Algorithmic Fairness and Vertical Equity:

Income Fairness with IRS Tax Audit Models

Abstract.

This study examines issues of algorithmic fairness in the context of systems that inform tax audit selection by the United States Internal Revenue Service (IRS). While the field of algorithmic fairness has developed primarily around notions of treating like individuals alike, we instead explore the concept of vertical equity—appropriately accounting for relevant differences across individuals—which is a central component of fairness in many public policy settings. Applied to the design of the U.S. individual income tax system, vertical equity relates to the fair allocation of tax and enforcement burdens across taxpayers of different income levels. Through a unique collaboration with the Treasury Department and IRS, we use access to detailed, anonymized individual taxpayer microdata, risk-selected audits, and random audits from 2010-14 to study vertical equity in tax administration. In particular, we assess how the adoption of modern machine learning methods for selecting taxpayer audits may affect vertical equity. Our paper makes four contributions. First, we show how the adoption of more flexible machine learning (classification) methods—as opposed to simpler models—shapes vertical equity by shifting audit burdens from high to middle-income taxpayers. Second, given concerns about high audit rates of low-income taxpayers, we investigate how existing algorithmic fairness techniques would change the audit distribution. We find that such methods can mitigate some disparities across income buckets, but that these come at a steep cost to performance. Third, we show that the choice of whether to treat risk of underreporting as a classification or regression problem is highly consequential. Moving from a classification approach to a regression approach to predict the expected magnitude of underreporting shifts the audit burden substantially toward high income individuals, while increasing revenue. Last, we investigate the role of differential audit cost in shaping the distribution of audits. Audits of lower income taxpayers, for instance, are typically conducted by mail and hence pose much lower cost to the IRS. We show that a narrow focus on return-on-investment can undermine vertical equity. Our results have implications for ongoing policy debates and the design of algorithmic tools across the public sector.

The annual tax gap, namely the difference between taxes owed and taxes paid, is estimated to be $440B in the United States ((IRS), [n. d.]b). Audits are the principal mechanism by which the Internal Revenue Service (IRS), the agency responsible for tax collection, verifies tax compliance and deters non-compliance. IRS resources are limited and the agency must use audits judiciously. During audits, the IRS typically solicits additional information from taxpayers to support information reported on filed returns. For the taxpayer, audits can be time-consuming, stressful, and costly (MacNabb, [n. d.]; Kiel and Eisinger, 2018). Low-income taxpayers, for whom refunds can comprise a substantial part of income, may wait “on their refunds to pay day-to-day living expenses such as rent, car repairs, or healthcare, and any delay can cause taxpayers significant hardship” (Advocate, 2019).

Since the 1970s, the IRS has used classification models as part of its audit selection process to detect which individuals are most likely to have misreported their tax liability. While the use of both classical and modern machine-learning models is foundational to many government agencies’ efforts to modernize predictive and allocative tasks (Engstrom et al., 2020), the adoption of such tools comes with considerable risks. The algorithmic fairness literature has amply documented how disparate impact and other negative outcomes can arise from the uncritical adoption and application of such models (Angwin et al., 2016; Lecher, 2018; Dastin, 2018). Given the scale and impact government decisions may have, mitigating these risks is a key priority for researchers and policy (Office, [n. d.]; President, [n. d.]). In this work we study the impact of, and safeguards for, fairness of machine learning models in the IRS tax audit context.

Specifically, our analysis focuses on fairness defined in terms of vertical equity, namely, appropriately accounting for relevant differences across individuals. This notion is central to public finance and public policy. By contrast, the algorithmic fairness literature has developed many formal definitions of fairness and techniques to satisfy notions of horizontal equity (treating like individuals alike) (Hardt et al., 2016; Dwork et al., 2012; Kusner et al., 2017). The applicability of these techniques to improve vertical equity has been little-explored. More generally, the literature on how to apply algorithmic fairness techniques to improve real-world systems remains in a nascent stage, especially in high-stakes policy settings where direct data and systems access can be challenging. Using anonymized IRS microdata, our work (i) examines the applicability of existing methods for promoting vertical equity in the tax audit context, (ii) introduces new algorithmic fairness problems motivated by vertical equity considerations, and (iii) provides a case study of addressing vertical equity concerns in a real-world algorithmic decision system. By introducing vertical equity to algorithmic fairness, we follow in the footsteps of others (Hutchinson and Mitchell, 2019; Heidari et al., 2019; Binns, 2018) that situate fairness in broader frameworks.

Our point of departure and the key motivation for our study is summed up in two key observations that, taken together, point to a discrepancy between the distribution of misreporting compared to the distribution of audits:

(1) the audit rate for lower-to-middle income earners is often as high or higher in recent recent years than that of high income earners; yet (2) an analysis of randomly conducted audits reveals that the amount of misreported tax liability (which we refer to, interchangeably, as the “misreport amount” or “adjustment”) is highest among the highest income earners and the rate of misreporting—defined as misreporting above $200—increases roughly monotonically with income.

With this context, our key research questions are as follows:

(1) To what extent does the choice of audit selection algorithm affect the noted discrepancy? Given the discrepancy between ground truth misreporting and audit allocations, we might expect that introducing a more accurate model may mitigate the issue.

However, we observe empirically that more flexible models, while indeed increasing accuracy, have the effect of even further concentrating of the audit burden on the lower-to-middle income taxpayers.

(2) Can existing algorithmic fairness methods, originally designed to promote horizontal equity, be applied to improve vertical equity?

In our context, one conception of vertical equity consists of monotonicity of the audit rate with respect to income. We show that, under some conditions, a selection process111By ‘selection process,’ we mean the prediction model and the process by which predictions are used to allocate audits together. that satisfies the well-known fairness metrics of equal true positive rates and equalized odds also requires monotonicity of the audit rate with respect to the misreport rate. Given our empirical findings, this also implies monotonicity with respect to income.

We thus divide taxpayers into income buckets

and explore to what extent conventional fairness methods applied to such buckets can resolve the apparent discrepancy between the audit rate and misreporting. We show that such methods come at a steep cost to revenue.

(3) What techniques can we use to more directly address vertical equity in the IRS audit allocation context?

We implement a direct approach to achieve monotonicity by imposing allocation constraints on model outputs, and find that this approach results in a modest cost to revenue. However, we find that

switching the prediction task from classification to regression not only also achieves a roughly monotonic shape, closely matching the audit distribution of an oracle with knowledge of the true misreport amount,

but also obtains significantly more revenue than even unconstrained classification. This is because regression shifts focus to taxpayers likely to have high amounts of underreporting rather than simply high probabilities of a misreport.

(4) Can differential audit costs explain the status quo mismatch?

We show that fully optimizing for return-on-investment with respect to the IRS’ audit costs concentrates audits nearly exclusively on lower income taxpayers, even when using predictions arrived at via regression. This suggests that IRS budgetary constraints may play an important role in shaping the agency’s ability to more equitably allocate audits without sacrificing the detection of under-reported taxes. A narrow focus on return-on-investment can seriously undermine vertical equity goals.

A major contribution of this paper is that we conduct all our experiments on real, detailed, audit data collected by the IRS. We view this collaboration as an important case study to assess and mitigate disparities in real-world, public sector settings that operate subject to binding operational constraints (see Holstein et al., 2019; Brown et al., 2019; Lamba et al., 2021; Obermeyer et al., 2019; Geyik et al., 2019). Our primary dataset consists of a stratified random sample of taxpayers collected as part of the IRS’ National Research Program (NRP), allowing us to avoid the selective labels problem (Lakkaraju et al., 2017), to draw inferences on a representative dataset, and to directly measure the risk of misreporting. Our work also connects to work that emphasizes the choice of prediction task (Obermeyer et al., 2019; Mullainathan and Obermeyer, 2021) and problem formulation (Passi and Barocas, 2019) for algorithmic fairness. In addition, our results speak to current policy debates about the fairness of tax administration (Kiel, [n. d.]) and appropriate funding levels for the IRS (Advocate, 2020).

The paper proceeds as follows. Section 1 provides background on the U.S. tax system and spells out the motivating stylized facts, setting up the question of what the IRS’s turn to machine learning may portend for vertical equity. Section 2 provides background on data and key definitions. Section 3 formally describes the audit problem, introduces notation, and discusses how extant fairness metrics might apply to the IRS context. Our main investigation is presented in four parts. First, Section 4 examines the impact of more powerful classifiers on audit distribution. Second, Section 5 presents the results of applying established algorithmic fairness techniques in our setting. Third, Section 7 studies the incorporation of monotonicity constraints as well as the simple but fundamental change of switching from classification to regression. Fourth, Section 8 examines the implications of accounting for audit costs. Section 9 concludes.

1. Background on the US Tax System

We examine individual federal income taxes in the US system. Taxes are assessed based on self-reported liability statements called tax returns, which can be time consuming and complicated to prepare; many taxpayers use commercial software or paid preparers. The tax rate on income is progressive, with marginal tax rates increasing in income.

As the tax code is very complicated, taxpayers (and their preparers (McTigue, [n. d.])) often make errors when calculating the amount they owe and are thus inadvertently non-compliant; others are willfully non-compliant, i.e., evade paying taxes. The annual gross tax gap, which measures total noncompliance, is approximately $440B ((IRS), [n. d.]b). In order to recover lost revenue, and to promote compliance with the income tax law, the IRS audits individuals that it believes may not be paying their full owed tax—due to, e.g., erroneously claiming credits or under-reporting income.

The IRS’ audit selection system is complex, with many parts. It principally relies on: (i) algorithmic methods to predict which taxpayers are most likely to underreport taxes, which serves as our main focus, (ii) a combination of simple rules that flag returns automatically; and, to a lesser extent, (iii) tips and other third party information, such as from whistleblowers. We focus on the algorithmic component of the IRS audit selection process, which has historically been a classification algorithm predicting individual taxpayer misreport (Hunter and Nelson, 1996). The details of existing modeling approaches are confidential, but historically, the basic approach involves a form of linear discriminant analysis.

Audits are conducted in different ways depending on the size and scope of issues identified. Some audits, including most involving the Earned Income Tax Credit (EITC), are conducted by mail at relatively low cost to the IRS. More complicated and extensive audits may be conducted by interview or by IRS examiner field visits. The timing of an audit relative to the processing of a return also varies. For instance, audits may be conducted on taxpayers claiming refunds before a check is sent out; this is known as revenue protection, and such audits are called “pre-refund”. Audits occurring after a check has been sent out to, or received from, the taxpayer are known as “post-refund.” These timing distinctions create differential impact on taxpayers, and may also affect the ease with which the IRS conducts audits.

Over the last eight years, budget cuts have decreased the audit rate, from an overall rate of 1% of individual filings receiving audits in 2010 to just 0.5% in 2016 ((IRS), [n. d.]a). The audit rate has decreased most significantly for individuals earning between $1-5M. Such individuals were audited at a rate of 8% in 2010 but just 2.2% in 2016 ((IRS), [n. d.]a). These changes in audit rates correspond to disproportionate reductions in examiners with more specialized expertise: while there was a 15% reduction in examiners conducting correspondence audits (i.e. audits by mail) from 2010 to 2019, there was a 25-40% reduction in examiners conducting in-person audits, which are utilized more for higher-income individuals ((IRS), [n. d.]c).

1.1. Motivating Facts

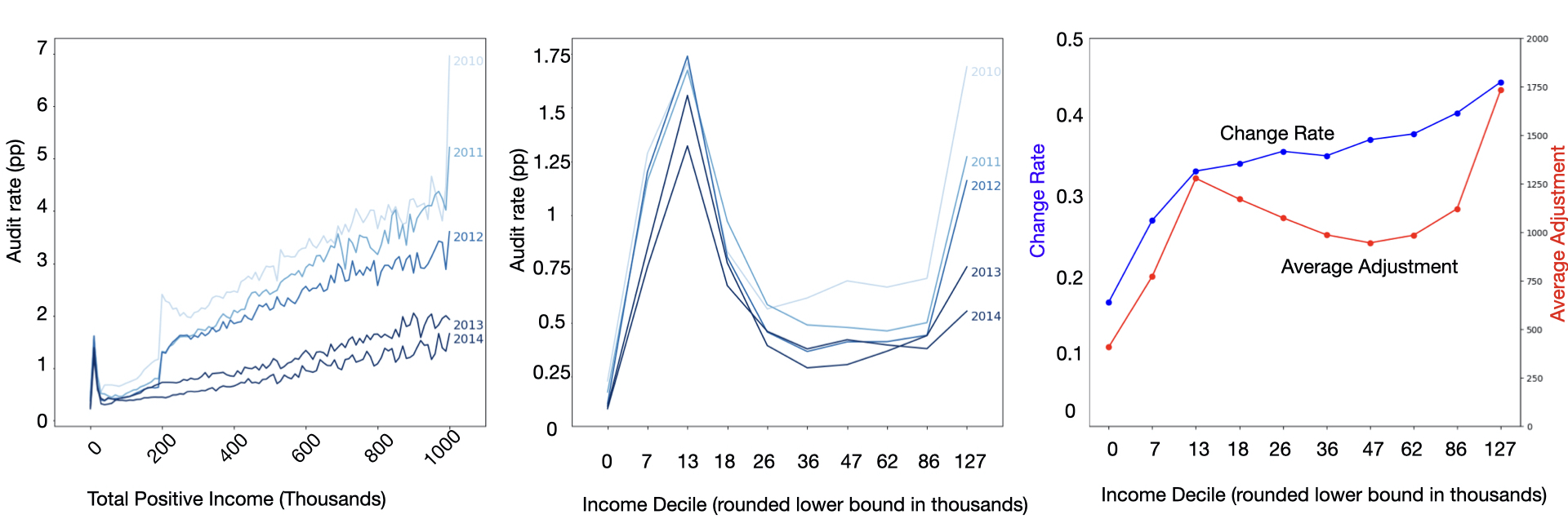

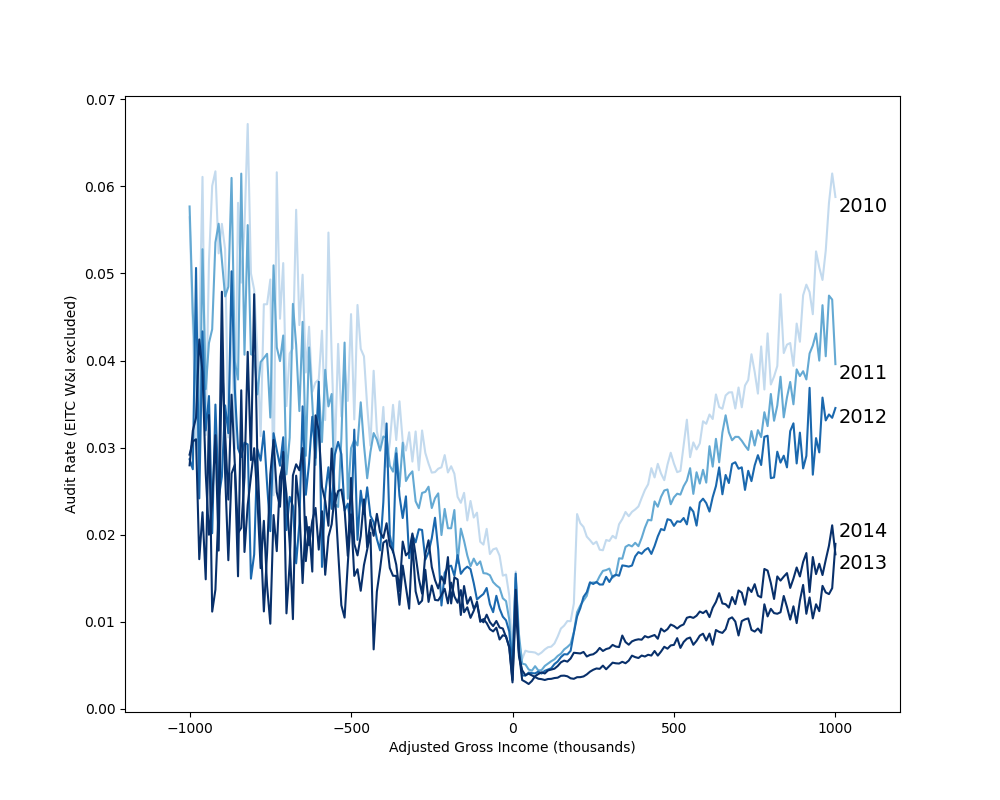

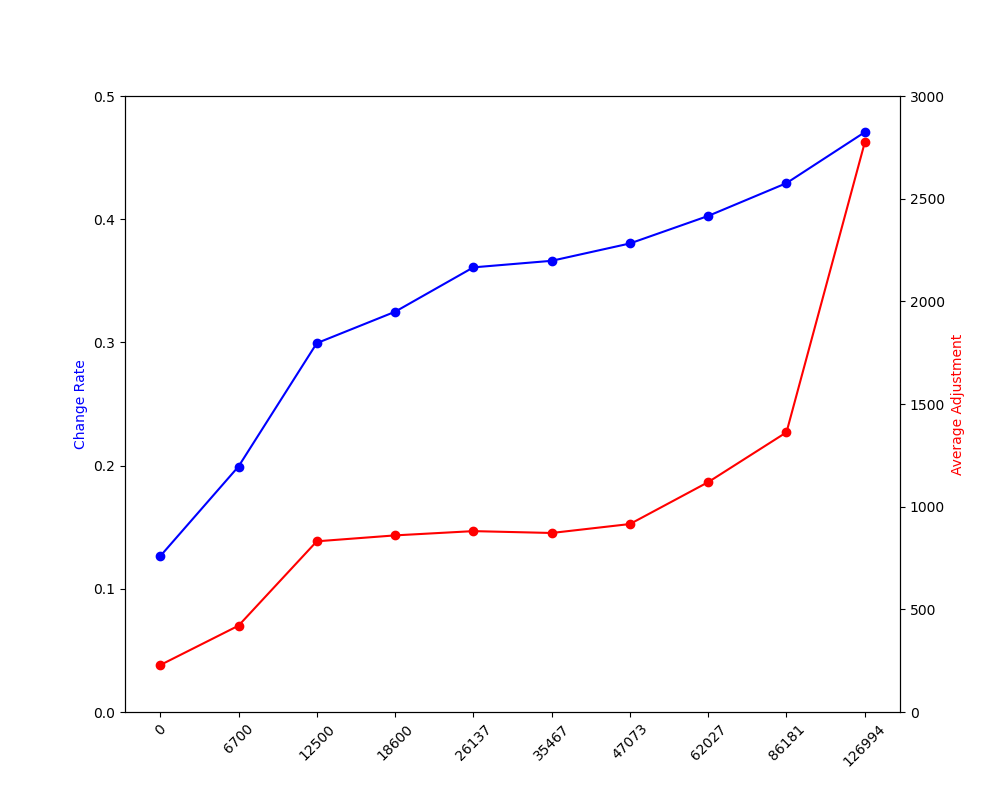

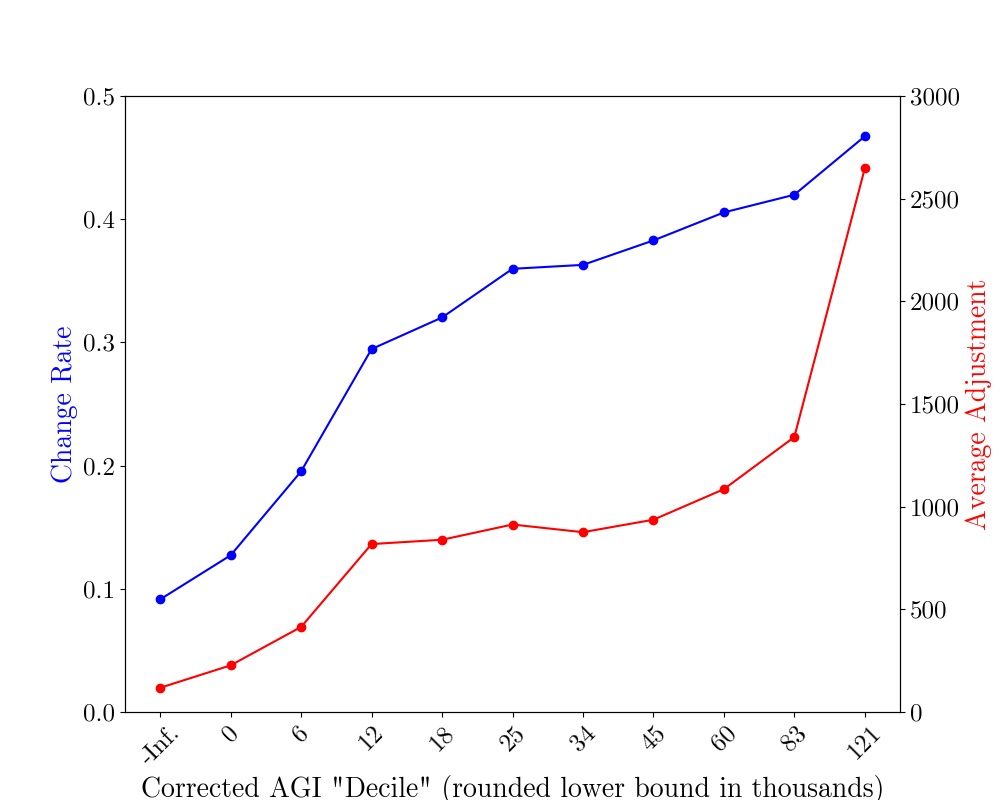

We highlight two motivating facts relevant to our investigation. First, in the most recent years, the lowest income earners have been audited at the same rate as the highest income earners. The left panel of Figure 1 plots income in $10K bins from $0 to $1M on the x-axis against the audit rate on the y-axis. Each line represents one year, from 2010 in lightest to 2014 in darkest blue. This panel shows the clear trend of the declining overall audit rate over time, which affects higher income groups most acutely. In addition, while audit rates generally increase in income, there is a large spike of audits in the lowest income groups. In 2014, the lowest earners are audited at a higher rate than all other income groups, except for those earning nearly $1M. The middle panel depicts the same data using income deciles. After 2010, low-to-middle income taxpayers (i.e. those in the 2nd-4th income deciles from $6.7K to $26K), were audited at a higher rate than all higher income deciles. This reflects the particular focus on pre-refund audits done principally by mail.

Second, the rate at which taxpayers understate their tax liability increases monotonically with income and average adjustments are highest in the highest income decile. The right panel presents audit outcomes estimated on the NRP data (described in Section 2 below). The blue line in this panel depicts the estimated fraction of audits in each decile with a true misreport of at least $200, while the red line depicts the average adjustment by decile. Because this is a stratified random sample with corresponding sampling weights, it is free of the selection bias inherent in measuring outcomes among risk-selected audits, and can thus be used to construct consistent estimates of population non-compliance.

These facts raise the motivating questions of this work: if adjustments are highest in the highest income decile, and the misreport rate increases monotonically with income, then why are audits so highly concentrated on lower-to-middle income taxpayers? To what extent can such patterns be exacerbated or mitigated by machine learning techniques? And are there opportunities for improving vertical equity given this mismatch?

2. Data and Key Terminology

We address these questions through a unique collaboration with the Treasury Department and IRS, which provides us access to two data sets previously unexplored in the computer science literature: (1) the NRP data, which consists of line-by-line audits of a stratified random sample of the US population (n=71.9K ) from 2010-14 ((IRS), [n. d.]d); and (2) all Operational Audits (OP) for 2014 (n=791.9K), which are risk-selected audits to identify tax evasion. Each observation contains information filed in a tax return. All dollar amounts are adjusted for inflation to 2014 dollars.

We train and evaluate our machine learning models on NRP data, as this data is a random, representative sample of the US population and does not suffer from selection bias (Lakkaraju et al., 2017).222That is, when a return is selected for OP audit, the IRS has reason to believe that the return represents a misreport. Hence, the return is likelier to have a large adjustment than a randomly selected return from the population, and may be more generally non-representative as well. That said, one limitation is that prior work has found that NRP data under-reports higher income tax evasion (Guyton et al., 2021). We note that the OP audit data includes observations that were selected for audit not solely through machine learning tools, but also through rule-based flags such as internal inconsistencies, and other methods of selecting audits. We use the OP data to display the status quo of audit selection in the IRS as of 2014, for example, in the left-most graphs in Figure 1.

In this data, three concepts are particularly important. First, by income, we mean the taxpayer’s reported total positive income (TPI). TPI captures all positive income an individual receives, gross of any losses.333Not all this income is taxable—for instance, tax deductions for losses or charitable contributions may reduce the total amount of taxable income. We focus on reported (rather than audit-adjusted) income because that is what the IRS observes at the time it selects taxpayers for audit, and we focus on TPI (rather than taxable income) because it represents a simple measure of earnings that is less likely to be affected by audit determinations. Many of the analyses in this paper will be over binned income, i.e. discretized income into equal-sized buckets, typically taken to be deciles of the income distribution.444While these bins and associated thresholds are relevant to our analysis and implemented algorithms, to our knowledge they are not currently used by IRS to categorize returns or to determine taxpayer eligibility for benefits.

Second, we refer to the amount by which a taxpayer’s return understates true tax liability as the misreport amount. If a taxpayer overstates their tax liability, then their misreport amount is negative. Throughout, we use the terms “adjustment” and misreport amount interchangeably. For classification, we define a significant misreport as whether the taxpayer’s understated tax liability exceeds a de minimis amount ($200). For brevity, we refer to these simply as misreports. Our findings are consistent across different choices of threshold (see Appendix C).

Third, we define the cost of an audit to the IRS as the total cost of the auditor’s time recorded on the particular audit, which we compute from auditor time555Notably, our available data for auditor time does not account for auditor time spent on audit appeals. and wage data. In principle, audit costs also include other components, such as overhead or attorney’s fees for litigated cases, but these are not possible for us to measure with our data. Note that we are focusing only on the budgetary costs of audits to the IRS, not the broader societal costs imposed on taxpayers.

3. The Audit Problem

To explore vertical fairness in audit allocations, we start with the tools most readily available to improve the fairness of algorithmic tools: the now-canonical fairness definitions applied in the literature (Hardt et al., 2016; Verma and Rubin, 2018). In this section, we first formalize the audit selection problem. Second, we discuss vertical equity in the context of the audit allocation problem, and consider how common fairness definitions may improve vertical as well as horizontal equity in this context. Third, we discuss implementation of these metrics and model evaluation.

3.1. Formal Definitions and Preliminaries

In this paper we define the basic audit problem as the following: given a budget and a set of taxpayers with associated features and audit costs, return a selection of taxpayers for audit that detects and recovers as much under-reported tax liability as possible within the given budget.666In practice, the audit problem undertaken by the IRS must balance a variety of objectives, including revenue maximization, deterrence, minimization of taxpayer burden, and reduction of improper payments.

For the majority of this paper, we model the budget as a fixed number of audited tax returns, which we represent as a percentage of the population. We use a budget of , which is the average percentage of audit coverage between 2010-2014. Taxpayers are indexed by and have features . One of the features in is , the taxpayer’s income. The income bucket of the taxpayer is the decile of . Taxpayers submit a report of tax liability , which may be different than their true liability . We let denote the taxpayer’s adjustment or misreport amount. We will also use for an indicator variable being above the misreport threshold . In our main experiments, we set , and write . We denote the cost incurred to the IRS by auditing an individual as . We use as an indicator for whether taxpayer is audited, and for a probabilistic relaxation. Occasionally, we use to indicate prediction, e.g. as predicted misreport amount.

The machine learning models we use throughout this paper which we integrate into the audit selection process either predict probability of misreporting (for classification models), or expected amount of misreporting (for regression models). In order to create an audit allocation from these predictions, however, we must select only of the population, which is in practice much less than the percentage of individuals predicted to not comply. Thus in order to create an audit allocation from machine learning model predictions, we rank model outputs by magnitude of prediction and take the top . The audit problem can be formalized as: .

If we consider to denote a dollar budget as opposed to an audit rate budget, as we do in Section 8, the constraint will be changed to . In practice, we use or to approximate .777As stated, this is an integer program, but we solve the linear relaxation due to computing constraints and because observations represent many people.

3.2. Algorithmic Fairness and Vertical Equity

We now discuss vertical equity in the IRS audit allocation context and its connection to several common algorithmic fairness metrics from the literature.

Vertical Equity. Vertical equity requires that different individuals be treated appropriately differently. In the taxation and audit context, we focus on vertical equity with respect to the appropriate treatment of taxpayers at different income levels. Appropriately different treatment depends on context-specific considerations and value judgments. To illustrate, given the fact that audits are costly for taxpayers (in terms of money as well as time, effort, and mental stress), policymakers may wish to avoid models that concentrate audits on low-income taxpayers out of concern for distributional social goals and in recognition of the declining marginal utility of taxpayers’ income. Other potential baselines for setting policy in this space are aligning audit rates with true rates of non-compliance, or with an Oracle-based selection, i.e. an allocation which selects individuals in order of true misreport amount. In our setting, because under-reporting rates increase with income (Figure 1) and an oracle places a higher probability of selection as income increases, these factors would suggest that audit rates should increase in income as well. Motivated by such considerations, we explore formalizing the notion of vertical equity as monotonicity and evaluate the discrepancy between audit allocation and true rates of misreport as an important component of vertical equity. Our focus on monotonicity is intended to illustrate how one might incorporate vertical equity concerns into algorithmic fairness, but we note that a fuller analysis from an optimal tax framework is beyond our scope here.888A full optimal policy analysis would have to consider such factors as heterogeneity in the audit burden or in the deterrence effect of audits by income. For example, audits of higher income taxpayers can be more involved, but audits of lower-income taxpayers may require obtaining harder to produce information and often involve freezing refunds for liquidity-constrained taxpayers while the audit proceeds. A fuller optimal policy analysis would also need to consider how audit policies interact with other tax variables (such as the income tax schedule and underpayment penalties) for achieving revenue and distributional goals. Each of these factors may impact vertical equity.

Montonicity Monotonicity (with respect to income) would require that the audit probability increase as income increases. Formally, given income buckets and , . We consider directly constraining the audit allocation to be monotonic in Section 6.

Oracle Allocation An oracle is a theoretical omniscient model with access to the true amounts of misreporting in the data (i.e. the ground truth labels). Formally, the oracle represents the model , where is the amount of true misreport of individual . The oracle creates an audit allocation by selecting individuals for audit in order of their true amount of misreport amount until exhausting the allocation budget. Thus, the audit allocation selected by the oracle is naturally aligned with true incidence of misreport. Although we do not explicitly enforce this behavior, we evaluate the vertical equity of model allocations by the extent to which they match the audit rate by income of the oracle model.

Demographic Parity. Demographic Parity (DP) requires, in our context, equal audit probability across income buckets. That is: Note that with a fixed budget and groups of equal size, asking for DP amounts to requiring the same audit rate for each group, which weakly satisfies monotonicity. Compared to the status quo described in Figure 1, this would result in lower audit rates for low-to-middle income taxpayers as well as very high income taxpayers, and higher audit rates for middle-to-upper income taxpayers. Important limitations to DP include that (1) as noted, equal audit rates do not imply equal audit burdens if taxpayers bear different costs, and (2) a perfectly accurate classifier would not satisfy DP unless the misreporting rates are exactly equal, which they are not.

Equal True Positive Rates (Hardt et al., 2016). Equal True Positive Rates (TPR) requires that the audit probability of non-compliant taxpayers not depend on income group, i.e., . Equal TPR ensures that no group of non-compliant taxpayers can expect a higher or lower chance of audit based solely on their income, but this does not mean that compliant taxpayers of each income group face the same chance of an audit.

Equalized Odds. Equalized Odds (EO) asks that the audit probability of both compliant and non-compliant taxpayers should not depend on their income group, i.e.: , and . EO extends equal TPR fairness by requiring audits of compliant taxpayers at the same rate across groups in addition to auditing non-compliant taxpayers at the same rate across groups.

In Appendix A, we consider conditions under which equal TPR or EO will result in monotonicity of the audit rate with respect to income. Specifically, we consider a hypothetical allocation that audits all taxpayers with , and show that under certain (differing) conditions, audit allocations that satisfy either either equal TPR or EO will result in monotonicity of the audit rate with respect to the misreport rate. Because the misreport rate increases with income (Figure 1), this suggests that enforcing one of the fairness constraints on a model generating audit allocations may also lead to monotonicity of audits with respect to income. We note that this result is suggestive, since models that satisfy a fairness constraint for the hypothetical allocation described above need not do so for the actual audit allocation induced after imposing a budget. Thus, we must ultimately test whether the targeted fairness constraints are satisfied on the audit allocation that results from a model once a budget is incorporated. Next, we describe algorithms to instantiate these conditions and evaluate the performance tradeoffs. We implement these algorithms and report results in Section 5.

3.3. Model Evaluation

In order to compare model allocations, we will consider several performance metrics. First, in order to approximate how well an audit allocation matches the ground truth rate of misreport, we consider how closely audit rates correspond to selection based on an oracle. Specifically, we calculate the overlap between a model’s allocation and the oracle’s, formally, the size of the intersection of the model and oracle’s audit allocation over the total number of audits in an allocation: , where and represent audit indicators for the oracle and a model respectively, is the audit budget as a percentage of the population, and is the total number of taxpayers.999The total number of taxpayers, taking into account the sampling weights. This metric is equivalent to the top-k intersection of model outputs, where is the audit allocation budget. This metric is often used to compare model-generated explanations (Ghorbani et al., 2019; Dombrowski et al., 2019; Black et al., 2021). Note that the overlap will be between 0 and 1, with 1 representing an exact match of the oracle’s allocation. We consider models that more closely match the oracle allocation with respect to income to have preferable vertical equity performance in our context.

Second, we consider revenue collected, which is simply the sum of adjustments over all audits. Recovering revenue is one of the key goals of the IRS and is itself relevant for distributive policy, since it funds services provided to citizens. We define revenue as follows: .101010We take sampling weights into account in this calculation, so in practice we calculate revenue as , where is the size of the NRP data set, and is the sample weight assigned to each row.

Third, we consider the no-change rate, which is the fraction of audits resulting in no (substantial) adjustment. No-change audits are undesirable from both IRS and taxpayer perspective, as both the auditor and taxpayer could have saved significant time, effort, and stress. We define the no-change rate as .

Fourth, we consider the cost of the audit to the IRS, which is important both in terms of the feasibility of an audit policy and its net revenue implications. We define cost as , where is our estimate of cost per return.111111Similarly to revenue, in practice, we calculate cost as . We describe how we obtain cost estimates in Section 8. In Sections 4-7, we hold audit rates fixed and measure incurred cost. In Section 8, however, we consider constraints on the total dollar cost of policies, and show how they may help explain the existing discrepancy between income and the audit rate.

3.4. Model Implementation

There exists a large body of research surrounding how to best implement and guarantee the common fairness metrics outlined above (Agarwal et al., 2018; Kearns et al., 2018; Donini et al., 2018; Celis et al., 2019; Zafar et al., 2019; Hardt et al., 2016). From this rich literature, we choose to rely on a technique developed by Agarwal et al. (Agarwal et al., 2018), which intervenes in a model’s training process to add a constraint during optimization which incentivizes the model to satisfy a given constraint in its predictions (Agarwal et al., 2018; Donini et al., 2018). Methods that enforce fairness constraints during training time are often described as “in-processing,” as opposed to those which intervene at prediction time, which are called “post-processing.” Agarwal et al.’s (in-processing) technique allows for demographic parity, true positive rate parity, equalized odds, and other constraints to be satisfied in expectation in a model’s predictions on the training distribution. We include results from other methods of enforcing fairness constraints, including post-processing techniques, as a discussion of the differences between various methods in Appendix F.

4. Flexible classifiers and audit classification

| Model Type | Label | Fairness | Revenue | No-Change | Cost | Net Revenue | Oracle |

|---|---|---|---|---|---|---|---|

| Type | Constraint | ($B) | Rate | ($B) | ($B) | Overlap | |

| Oracle | - | × | |||||

| LDA | Class | × | |||||

| Random Forest | Class | × | |||||

| Grad Boosted | Class | × | |||||

| Random Forest | Class | ✓(DP) | |||||

| Random Forest | Class | ✓(TPR) | |||||

| Random Forest | Class | ✓(EO) | |||||

| Random Forest | Class | ✓(Mono) | |||||

| Random Forest | Reg | × | |||||

| Grad Boost | Reg | × |

We begin by examining the hypothesis that the disproportionately high audit rate observed for low income earners may stem from using simpler classification models in guiding audit allocations. We demonstrate that (i) the disparity displayed in audit rates does not appear to arise from the less complex models similar to those the IRS has historically used; and, (ii) applying more complex models—in this case, Random Forests and Gradient Boosting— actually exacerbates the burden on lower income taxpayers.

4.1. Experimental Setup

In this section, we consider the audit allocation determined by Linear Discriminant Analysis (LDA) (an approximation of the historical choice by the IRS), a Random Forest Classifier, and a Gradient Boosting Classifier. In principle, classifiers may perform well at reducing the no-change rate, furthering IRS’s objective to avoid burdening compliant taxpayers. To be clear, the audit allocation is not simply the model’s predictions, but rather the individuals most highly predicted for misreport up to the audit budget, as described in Section 3.1. We use NRP data from 2010-2014 to train all models in this paper to predict the likelihood of misreporting. We randomly split this data into a train and validation (75%) and test (25%) sets. We search for optimal hyperparameters using sklearn’s GridSearchCV method with 5-fold cross validation.121212As described in detail in Appendix B, we train all but LDA models with sampling weights provided in the NRP data, meant to ensure the data is representative of the taxpayer population. For LDA models, we sub-sample a dataset from the NRP data that respects the sample weights by randomly selecting (with replacement) rows from the weighted training data according to the weights. For example, suppose that each row has a sample weight , and the sum of all weights in the training set is . Then each observation has a chance of getting selected as any given row in the sub-sampled data.

All results in this and following sections are calculated on the test set, which is reserved for reporting results. Results are reported by rescaling costs and revenues to reflect estimated average annual values for the full population (averaged between 2010-2014). For each classification model, we sort taxpayers in descending order of predicted misreport probability to produce a ranking. We then apply an audit rate budget of % of the population, reflecting the average audit rate from 2010-2014, and select audits by taking the top % of the population (i.e. 1125000 audits)in rank order. Further details are in Appendix B.

4.2. Results

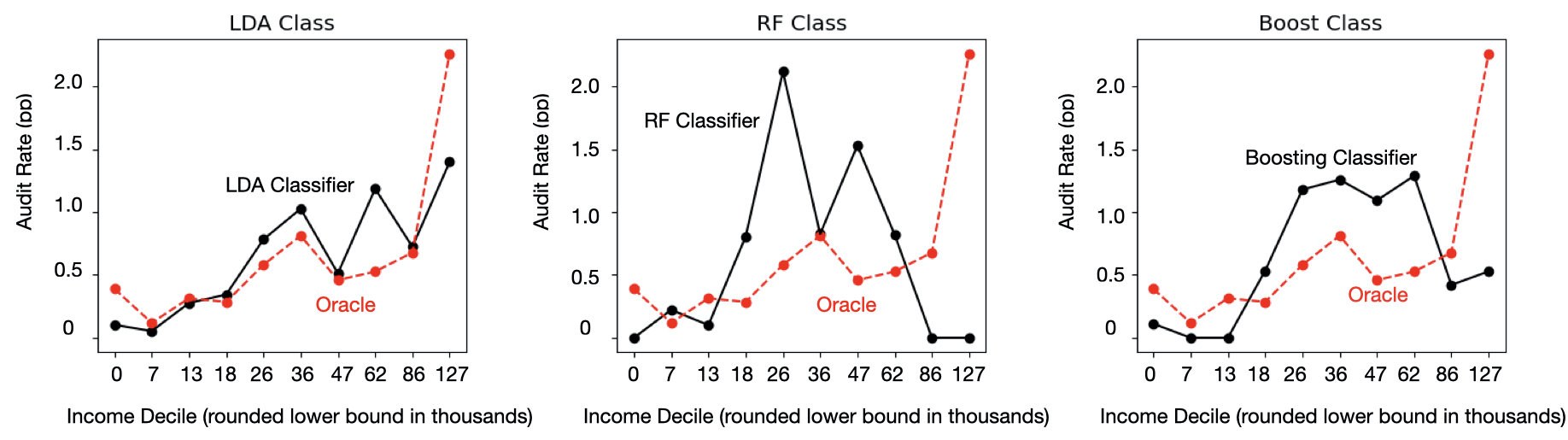

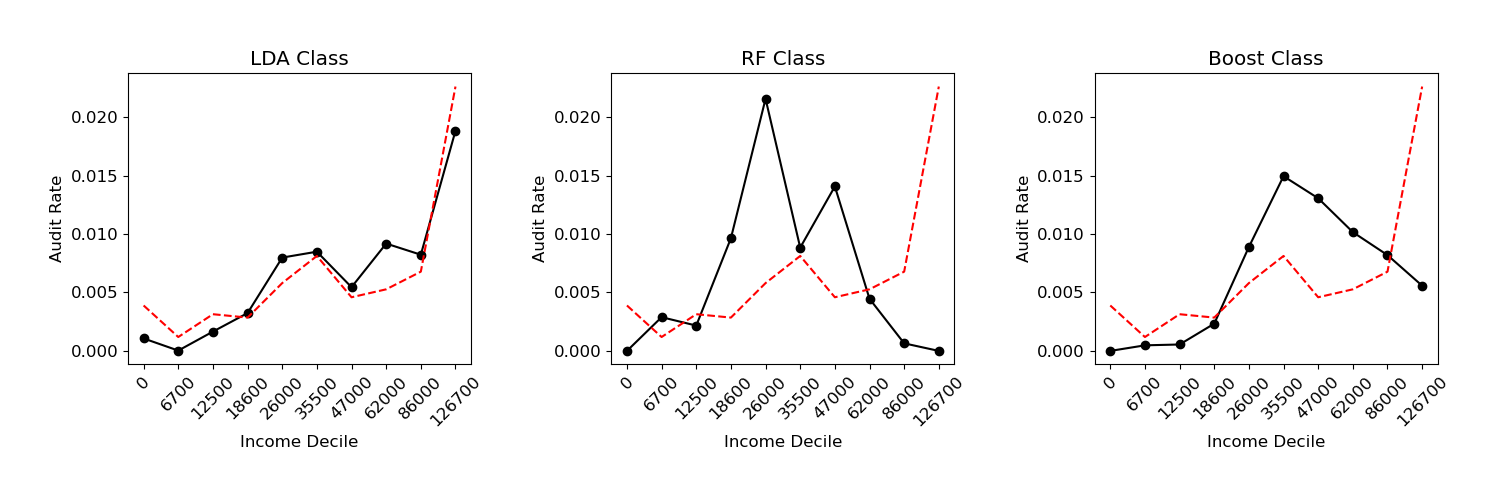

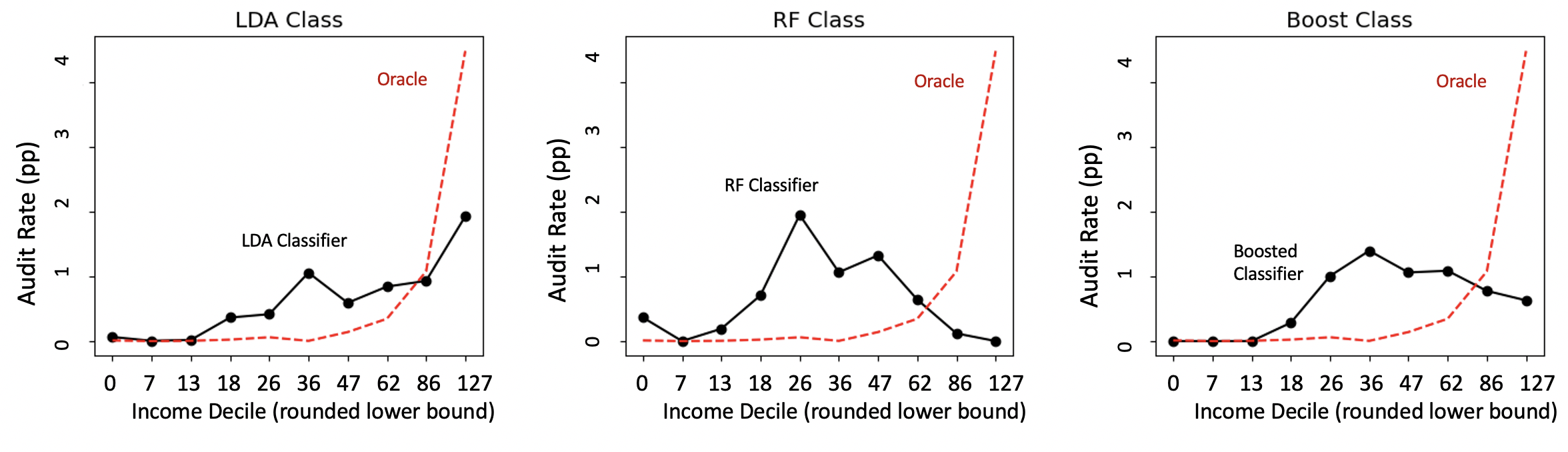

Figure 2 displays the audit rate by income of allocations obtained via ranking the predictions of LDA, Random Forest Classification, and Gradient Boosted models by predicted probability of misreport and selecting the top % of the population. Revenue and no-change rate of these models are included in Table 1. We highlight implications below.

First, higher model flexibility can lead to high audit focus on lower and middle income populations. As Table 1 shows, the Random Forest Classifier is well-optimized for the classification task: it has an extremely low no-change rate—just 3.5%—whereas simpler models have no-change rates higher than 12.8%. However, the Random Forest Classifier focuses almost exclusively on the lower-middle and middle of the income spectrum, not targeting the highest earning 20% at all. Similarly, the Gradient Boosted classification model concentrates most of the audit selection to the middle of the income spectrum (4-8th decile), with a strong drop-off for the top 20% of the population. (Appendix D shows that another simpler model (logistic regression) also results in rough monotonicity.)

Second, the simpler LDA model more closely matches the oracle. The LDA classifier has an audit selection curve that is roughly monotonic in income, with large increases in audit rate in the high income region. As LDA has been the IRS’ historical modeling approach (although it differs in practice with our implementation), this suggests that the large spike in operational audit selection rate on the lower end of the income spectrum apparent in 2014 may not stem directly from the predictions algorithmic components of the decision system, but rather other policy and modeling choices.

Third, increased classification accuracy does not imply increased revenue. Table 1 shows that the Random Forest and Gradient Boosted models have significantly lower no-change rates than the LDA model (3.5% and 4.2% vs. 12.8%), yet also substantially lower revenue ($3B and $4B vs. 6B). This highlights that improved performance on one objective (e.g., accuracy) may come at the expense of other seemingly intertwined objectives (e.g., revenue).

5. Fairness Constrained Classification

We now explore the use of bias mitigation methods to promote vertical equity.

5.1. Experimental Details

We enforce algorithmic fairness definitions on the Random Forest model at different points in the audit selection process: during training, or in-processing, following Agarwal et al. (Agarwal et al., 2018), and after training but before prediction, or post-processing (deferred to Appendix F, following Hardt et al. (Hardt et al., 2016)). Our setup for training the fairness-constrained models mirrors our setup for the fairness-unconstrained models, with the exception that we do not train the models with sampling weights, but rather subsample a dataset from the NRP weighted data as we do for LDA models as described in Section 4. This is because the in-processing methods are implemented using the FairLearn package (Bird et al., 2020), and the FairLearn package leverages sklearn’s sampling weight functionality in the course of their algorithm.

5.2. Results

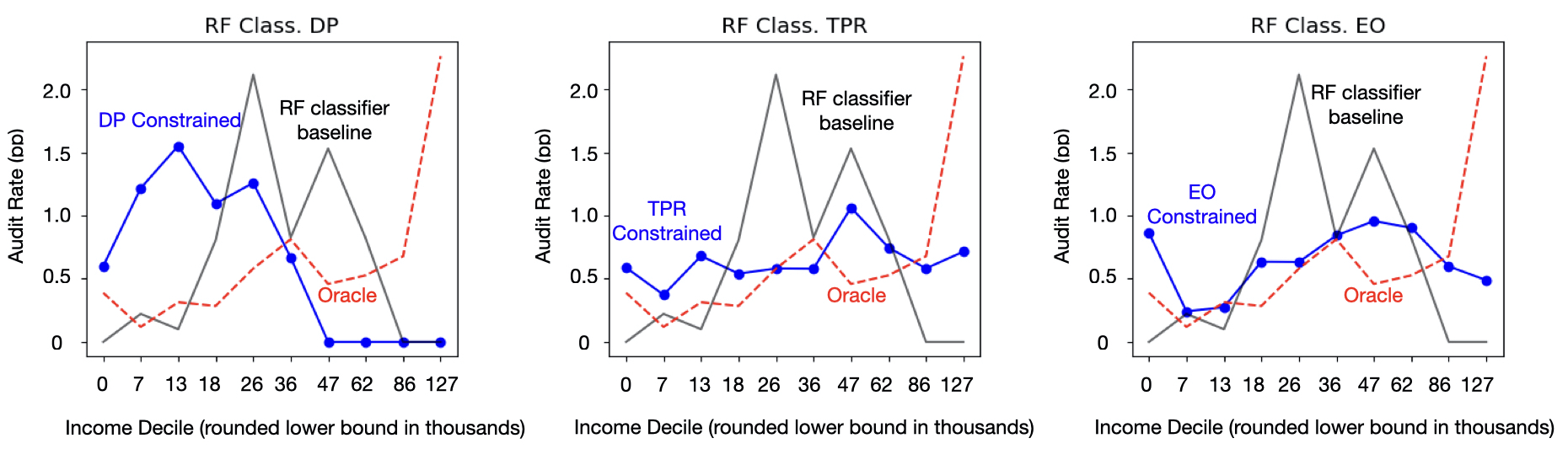

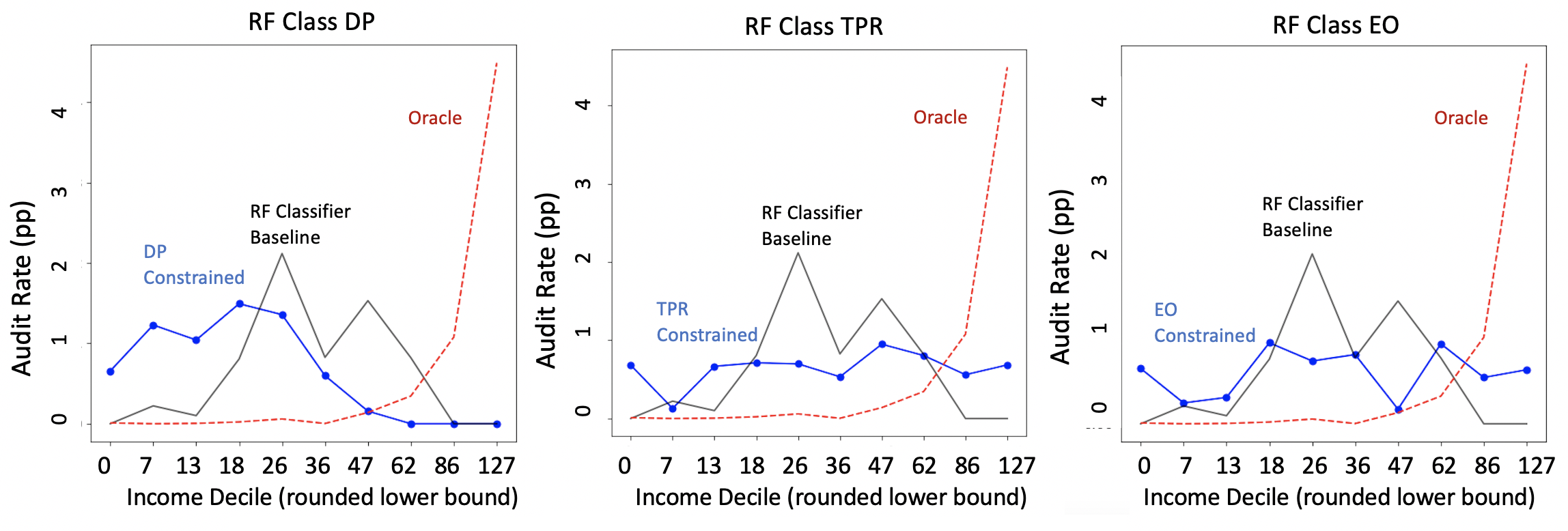

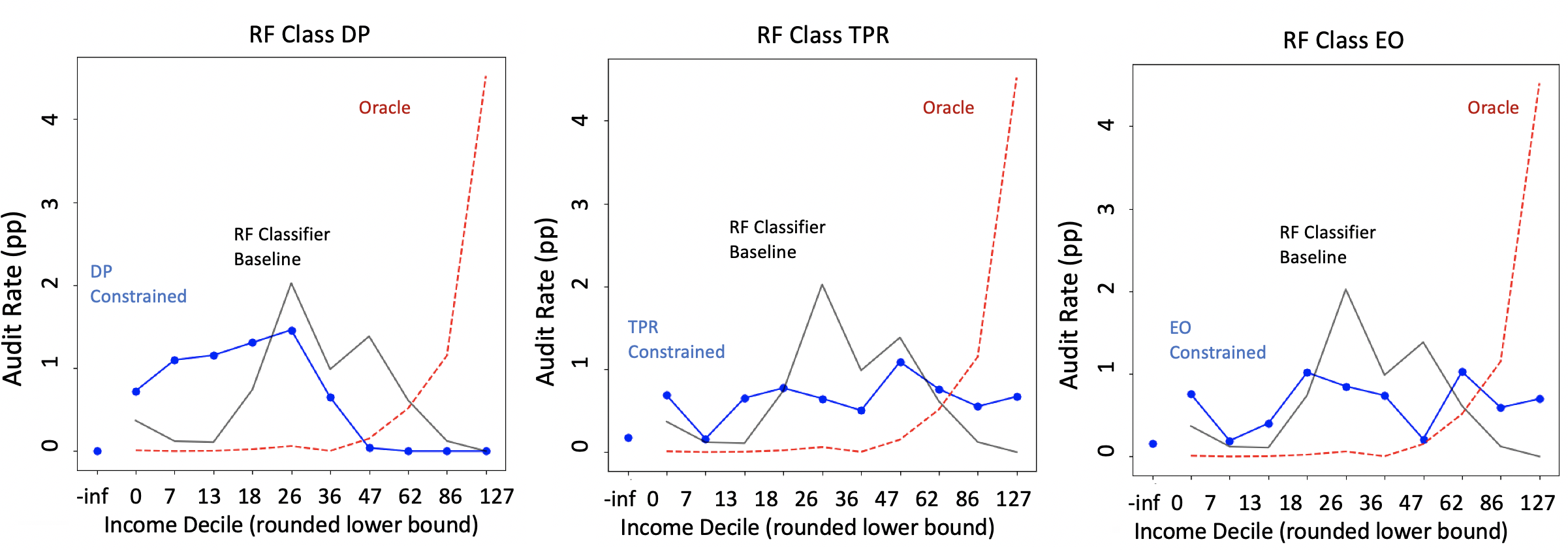

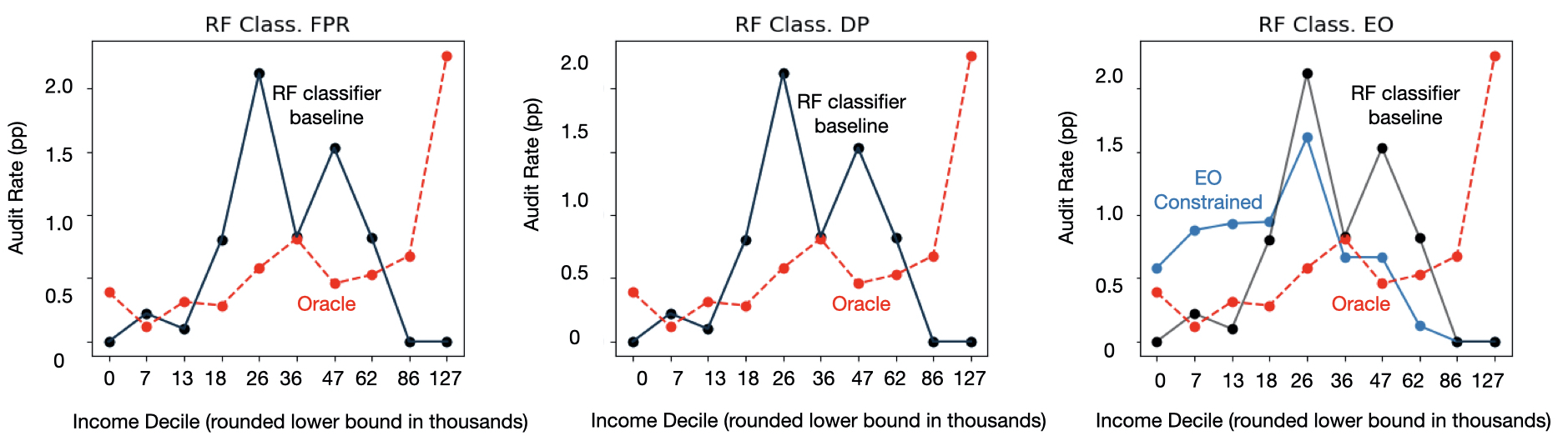

Our high-level result is that enforcing fairness constraints during training results in steep trade-offs with limited fairness payoffs for the budgeted allocation problem. Figure 3 displays audit rate by income decile for Random Forest Classifier trained to respect each of the fairness definitions considered. We present revenue and no-change rate in Table 1.

Equal TPR and EO models do lead to overall lower focus on low and middle income groups. However, they continue to under-target the highest end of the income spectrum when compared with the oracle predictor. And perhaps surprisingly, despite this shift to focus slightly more on higher ends of the income spectrum, enforcing these constraints actually leads to a large decrease in revenue: from over $3B to as low as $600M in revenue. We additionally notice a decrease in the no-change rate towards levels closer to the baseline LDA predictor. Finally, they imperfectly enforce the targeted fairness constraints once the audit budget is imposed: this is immediately evident in the allocation from a model constrained to respect demographic parity, as the audit rate is not equal across groups.

Given these results, we argue that enforcing fairness constraints during training is not an effective technique to improve vertical equity in an audit allocation setting. We highlight some broader implications of vertical equity for algorithmic fairness in Section 9.

6. Enforcing Monotonicity

In this section, we instead enforce monotonicity directly. We do this by solving the following linear program:

where all notation follows Section 3.1, represents sampling weights, and the Random Forest Classifier generates .

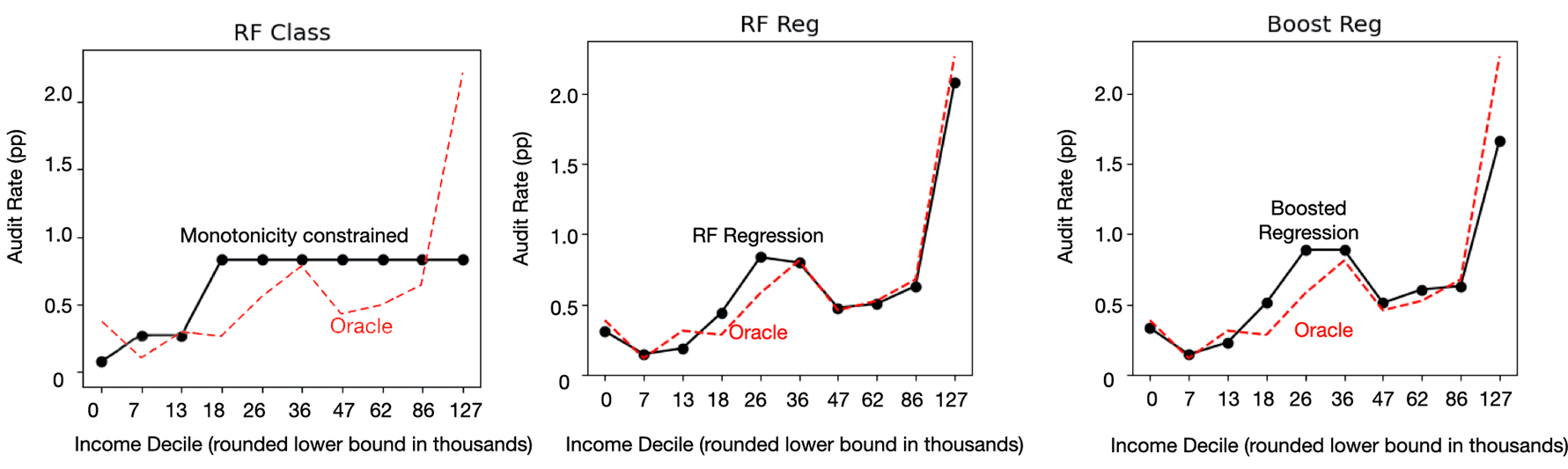

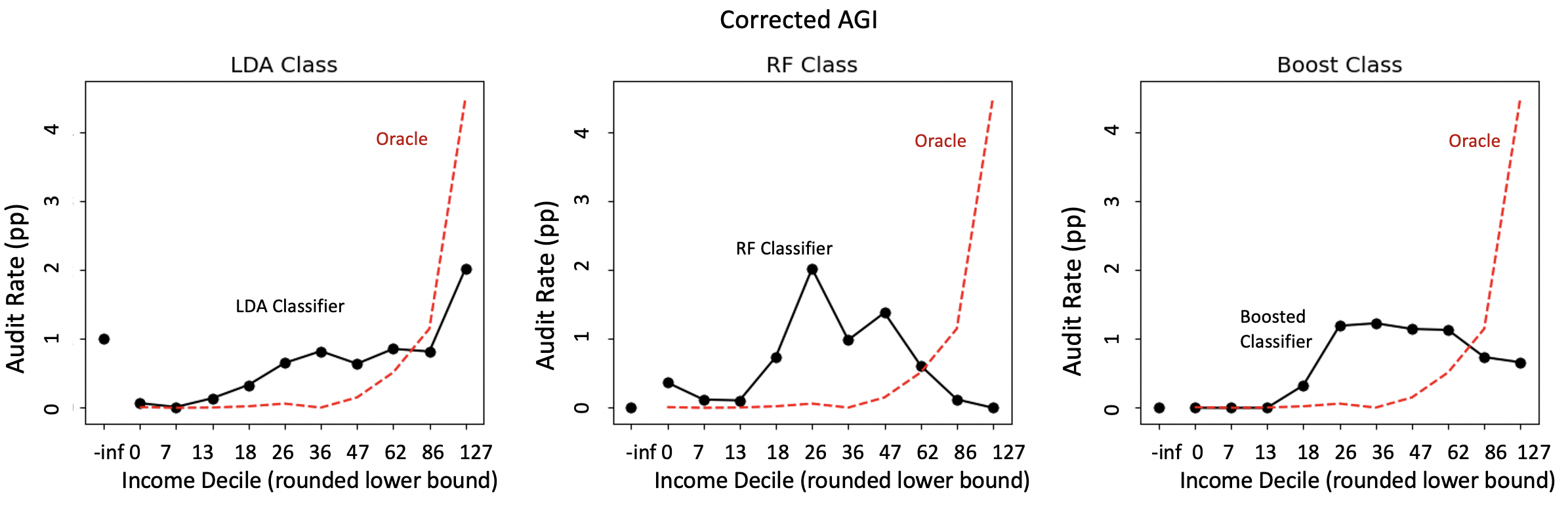

The leftmost panel of Figure 4 shows the audit distribution of the solution to the linear program. Notably, all income buckets from the fourth decile and above are audited at the same rate. In other words, the constrained solution audits higher income deciles at the minimum in order to focus most energy on the fourth decile. The trade-off with performance is relatively modest relative to the unconstrained classifier, as seen in Table 1: revenue does decrease, but by only $50 million; the no-change rate increases by half a percentage point. These results indicate that, especially compared to enforcing traditional fairness constraints, enforcing monotonicity may be a relatively economical approach to encourage (one notion of) vertical equity. The next section shows, however, that this approach may be far from optimal.

7. From Classification to Regression

We now demonstrate that changing the model’s prediction target from the probability of misreport to expected misreport amount—i.e. changing from a classification to regression algorithm— can reduce burden on lower-income taxpayers and make audit rates more closely mirror the oracle while also increasing revenue. This demonstrates that, in some circumstances, changing the model’s prediction task to reflect behavioral desiderata–rather than enforcing a constraint on top of a model optimizing for an imperfectly aligned task—is a more effective technique to reach equity goals.

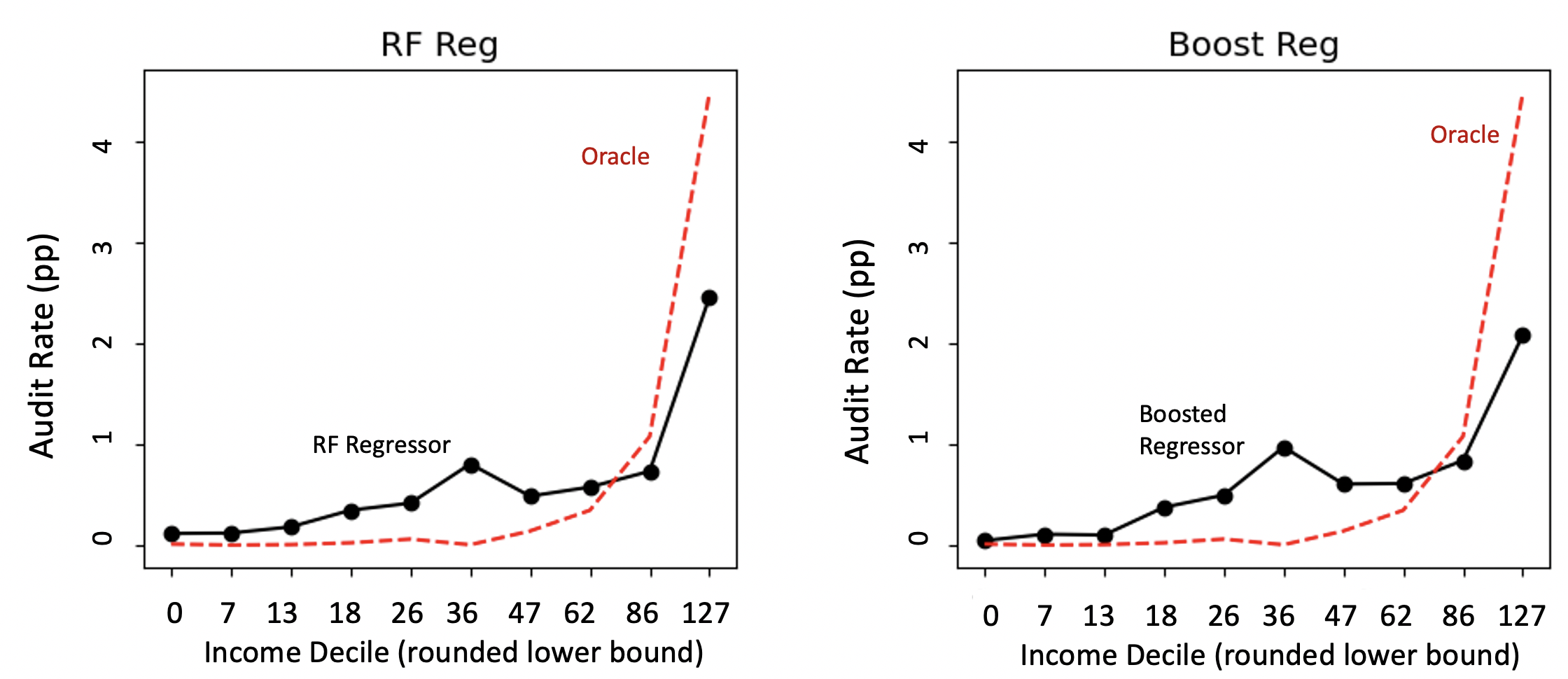

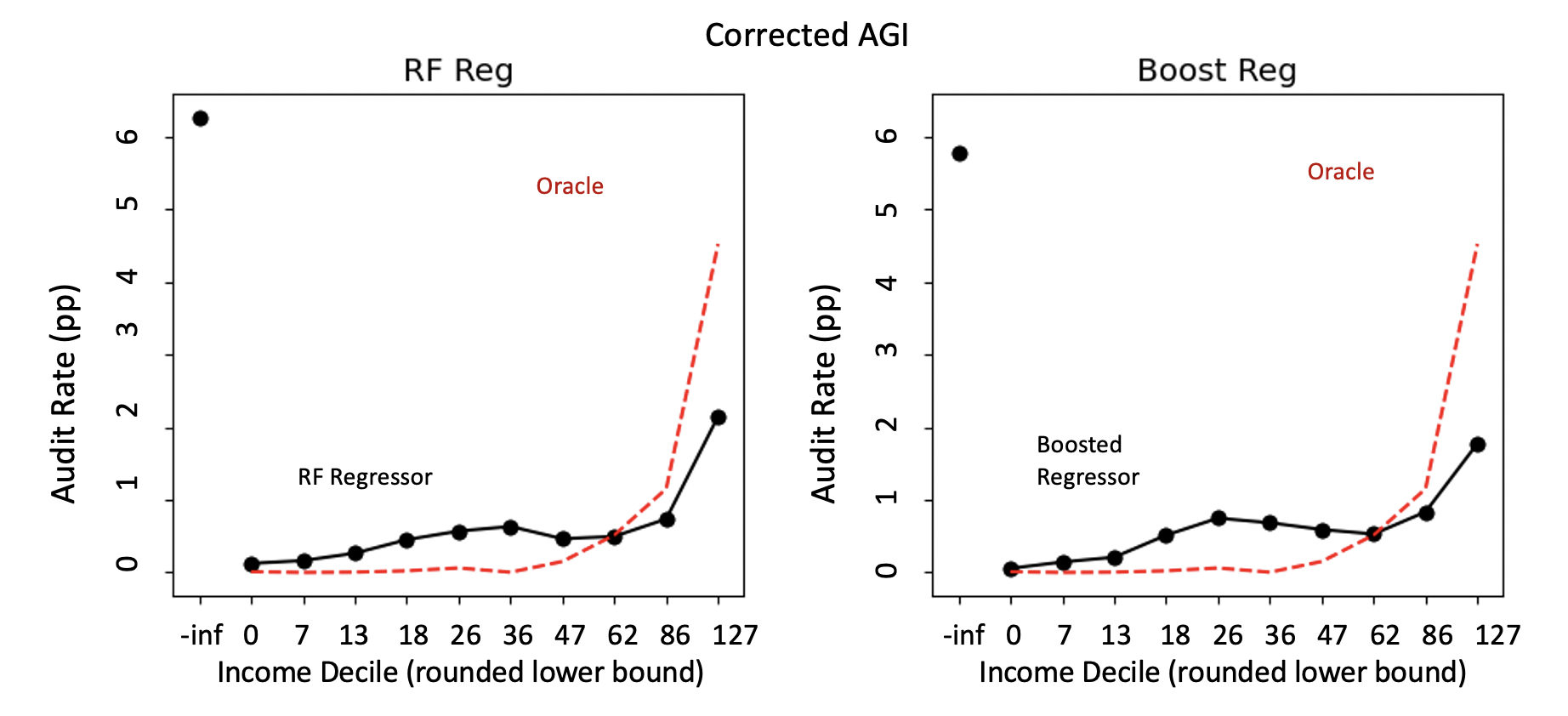

We train regression models with the same process described in Section 4 for classification models, but use the misreport amount as the label rather than to a binary indicator of misreport. The audit rate by income decile of Random Forest and Gradient Boosting regression models are displayed in black in Figure 4, along with the oracle in dashed red.

We highlight two chief results. First, shifting the prediction target from the probability of misreport (classification) to the expected amount of misreport (regression) shifts audit focus from lower income to higher income taxpayers, resulting an audit allocation that is not only nearly monotonic, but also closely matches the oracle allocation. As can be seen in Figure 4 and the right column of Table 1, the resulting allocation is in fact closer to the oracle than any other prior allocation. Thus, changing from a classification to a regression task can be seen as one method to directly optimize for (multiple notions of) vertical equity in the IRS context.

Second, while changing the prediction target from presence of significant misreport to amount of misreport does increase the no-change rate (up to 20-23%), it also results in a dramatic increase in revenue. Table 1 shows that assessed revenue under regression rises to $10B, compared to the $3.6B baseline of high-powered classification models.

Thus, within the set of higher complexity models, switching from classification to regression may provide an effective way to decrease the mismatch between audit allocations and ground truth levels of misreport, as well as decrease audit focus on lower and middle income individuals, while increasing under-reported tax liability detected by the IRS. We leave the discussion of how regression-based allocations interact with the IRS goal of broad-spectrum noncompliance deterrence—which may necessitate additional focus on lower-magnitude noncompliance—to future work.

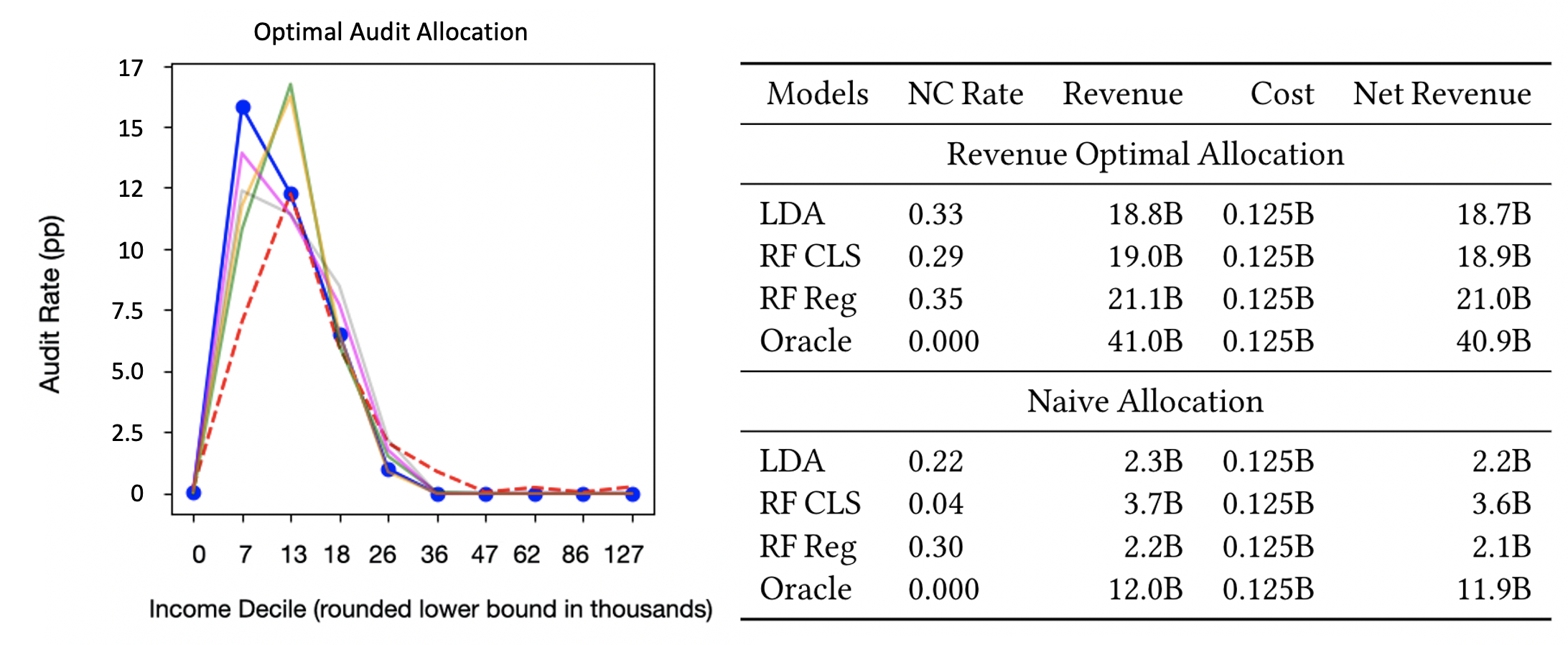

8. Agency Resources and The Impact of a Narrow Return-on-Investment Approach

We now turn to examining the relationship between vertical equity and agency resources. As noted, how an audit proceeds depends upon the type of noncompliance suspected: for example, many audits on lower-to-middle income individuals concern a potentially incorrectly claimed tax credit, whereas audits on higher income individuals more often involve insufficient taxes being paid on income or other assets ((IRS), [n. d.]c). Audits concerning tax credits are largely done via correspondence, where the IRS sends a letter to the taxpayer requesting verification of qualification for the claimed credit ((IRS), [n. d.]c). Other types of misreporting often incur in-person IRS audits ((IRS), [n. d.]c). Correspondence audits are extremely resource-efficient for the IRS. On the other hand, in-person audits require more time and expertise, and tend to incur much higher costs. Further, a non-response from a correspondence audit is taken as an admission of non-compliance, resulting in revenue returned to the IRS (Guyton et al., 2018), and keeping investigation costs low. One study on EITC correspondence audits found that up to 75% were determined to be noncompliant due to nonresponse, undeliverable mail, or insufficient response (Guyton et al., 2018). Thus, the ease of correspondence audits, coupled with the high nonresponse rate leading to frequent revenue returned to the IRS, may result in more reliably recovered income than in-person audits, in addition to their lower direct costs. Here, we use a simple model to explore whether a constrained monetary budget, coupled with differential cost of audits across the income spectrum, might affect audit allocation. We model the audit budget in terms of a dollar cost131313We note that a fixed monetary budget may not perfectly capture the resource constraints faced in practice; for instance, the limited number of auditors of a given expertise level may bind more tightly than any short-term dollar budgets. Still, this simplification captures important heterogeneity in the degree to which audits push against agency resource constraints. In addition to shedding light on the status quo audit distribution, such analysis may be interesting to the field of applied ML, as relatively few papers consider budget-constrained allocation models. as opposed to a constraint on the fraction of the population audited.

8.1. Experimental Details

In our consideration of the effects of agency resource limitations on audit allocation, we focus on the dollar cost of audits to the IRS and its budgetary constraints. We calculate a simplified version of cost that only takes into account the cost of the actual tax examination, based on data from previous real operational audits. We calculate cost as the product of the examiner’s time spent on a given audit with their hourly pay. We average this product over income deciles and activity code, which roughly corresponds to groupings of individuals based upon what tax forms they have filled out, to estimate audit cost. We incorporate cost into our analysis by directly including the dollar budget as an audit selection constraint, thus creating a linear program to maximize total predictive value (i.e. probability or amount of misreport) with respect to the dollar budget. As we show in Appendix G, this formulation is equivalent to a fractional knapsack problem; thus, the optimal solution is to select individuals in order of their ratio of cost to return to the IRS, in other words, return-on-investment. We use a dollar budget of $125M, the average estimated total cost of audits from years 2010-2014. Further details are in Appendix H.

8.2. Results

We present three main results. First, due to the differing audit costs to the IRS by income, return-on-investment focused audit selection results in an allocation which overwhelmingly targets lower income taxpayers. In the left panel of Figure 5, we show the optimal audit selection policy under a dollar budget with rankings from each of the models considered in our paper thus far. As described in Appendix G, the revenue-optimal audit allocation is to choose returns with the return on investment, i.e. the best ratio of predicted reward (adjustment in regression or change probability in classification) to audit cost. Based on our calculations of audit cost, audits in the highest income decile may cost up to 41 times the least costly audits. Given the disparities in audit costs over the income spectrum, the revenue-optimal audit selection method results in an allocation that almost exclusively targets lower income individuals.

Second, the return on investment of auditing lower income individuals may shed light on the status quo allocation’s focus on low and middle income individuals. We note that the optimal allocation with a dollar budget looks similar to the 2014 operational audit selection policy (Figure 1). Given the decreasing IRS budget over time, prioritization of net revenue maximization may influence the vertical equity of status-quo allocations. However, we note that the extremely low cost of audits on the lower end of the income spectrum result at least partially from a policy choice made to proceed with different types of audits in asymmetric ways: i.e., via correspondence audits on the lower end of the spectrum, and in-person audits on the higher end. This decision, coupled with the choice to view a lack of response as noncompliance, results in less time, and fewer resources, spent on audits for individuals in the lower end of the income spectrum, thus resulting in the constrained revenue-optimal allocation focusing so highly on low-income individuals.

Third, we find that to improve vertical equity and increase revenue collected, regression models require a higher dollar budget. As demonstrated in Section 7 and Table 1, regression models produce the highest net revenue allocations amongst models constrained to only audit a given percentage of the population (). However, the cost to the IRS of these allocations are considerably higher than classification methods—and indeed, higher than our approximation of average IRS budget between 2010-2014, $125M. At this low dollar budget, regression models under-perform on revenue compared to classification models, demonstrated in the right panel of Figure 5: this is because regression models target individuals in the higher income realm, where the audit cost is greater, thus preventing such allocations from targeting enough individuals to generate high revenue returns. This suggests that increasing the dollar budget available for audits may present an opportunity for not only more net revenue, but also in a more equitable allocation of audits.

9. Discussion

Through this unique collaboration with the Treasury Department and IRS, we have studied the impact of machine learning on vertical equity. Our work suggests that: (1) more accurate classifiers may exacerbate rather than improve income fairness concerns; (2) off-the-shelf fairness solutions are not well-suited for attaining income fairness; (3) fundamental modeling changes, like switching from a binary target to a regression target, can improve income fairness; and (4) external constraints, like institutional budgets, may influence fairness regardless of what underlying predictive model is used. Specifically, a return-on-investment focused audit allocation may undermine vertical equity under current conditions. More broadly, this work underscores the importance of vertical equity, in addition to horizontal equity, in real-world application areas of machine learning. To our knowledge, the term does not appear in the algorithmic fairness literature,141414Outside the fairness community, but inside the general umbrella of technology and engineering, the term has been used; in particular, (Yan and Howe, 2020) use both terms in a study of equity in access to transportation, and point towards a possible link to algorithmic fairness. However, their interpretation of vertical and horizontal equity are substantially different from ours; for instance, they suggest that group fairness should be linked to vertical equity. and traditional fairness metrics can be seen as focusing on horizontal, rather than vertical, equity. Given the importance of achieving vertical equity for policy, this work points towards further development of algorithmic fairness techniques as a promising path for future research.

Our results also reveal a subtle dimension of fairness when resources are allocated under a budget constraint. When there is greater uncertainty for high-income individuals, classification risk scores can shift audit allocations to lower-income individuals simply because misreports are easier to predict. Exploring the role of heterogeneity in uncertainty and its fairness implications might explain a wide range of other policies that have disparate impact (e.g., enforcement against blue collar vs. white collar crime). In the tax context, this insight also underscores the need for information collection mechanisms (e.g., third party reporting by offshore financial institutions) to reduce such uncertainty in the high income space, which has been the subject of significant policy debate (of the Treasury, 2021; Edelhertz, 1970).

We conclude by noting several limitations and opportunities for further work. First, we do not have access to the exact models employed by the IRS or the complete procedures, so we cannot make definitive inferences about past or current practice. Second, we only observe (an imperfect proxy of) the IRS cost of an audit, not taxpayer costs; the true societal cost of an audit may thus be materially different than what is used in Section 8. Third, our approach has not distinguished between underreporting from misreported income versus over-claimed refundable credits; some policymakers may view these forms of noncompliance differently. Finally, while the notion of monotonicity is motivated in part by the near-monotonicity of adjustments and the oracle results, it is not grounded in a full welfare analysis. Such an approach might take into account audit costs to taxpayers, deterrence effects, and other policy levers, such as tax rates or penalty amounts. Accounting for these dimensions may not necessarily yield strict monotonicity as a form of vertical equity, and we view this theoretical development as an important path to refining vertical fairness.

Despite these limitations, this work represents an important step given the policy significance and complexity of this setting. The scale of the problem is substantial — amongst U.S. taxpayers alone, improvements in this area can affect more than 100M individuals annually. Moreover, “government by algorithm” continues to grow (Engstrom et al., 2020), and understanding how to incorporate fundamental fairness and redistribution concerns in taxation may serve as a model for other governance-related settings. Finally, insights derived in this setting — such as the differing effects of costs when considered as a constraint rather than in the objective — may carry over to other unrelated settings. Our finding that a narrow return-on-investment approach may degrade rather than improve vertical equity may be critical in a range of policy contexts (Parrillo, 2013). Thus, both the technical concepts and policy problem are important and vital avenues for future research.

References

- (1)

- Advocate (2019) National Taxpayer Advocate. 2019. Annual Report to Congress. https://www.taxpayeradvocate.irs.gov/reports/2019-annual-report-to-congress/full-report/

- Advocate (2020) National Taxpayer Advocate. 2020. The IRS is Significantly Underfunded to Serve Taxpayers and Collect Tax. https://www.taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/Most-Serious-Problems-IRS-Significantly-Underfunded.pdf

- Agarwal et al. (2018) Alekh Agarwal, Alina Beygelzimer, Miroslav Dudík, John Langford, and Hanna Wallach. 2018. A reductions approach to fair classification. In International Conference on Machine Learning. PMLR, 60–69.

- Angwin et al. (2016) Julia Angwin, Jeff Larson, Surya Mattu, and Lauren Kirchner. 2016. Machine bias: There’s software used across the country to predict future criminals. And it’s biased against blacks. ProPublica (2016).

- Binns (2018) Reuben Binns. 2018. Fairness in machine learning: Lessons from political philosophy. In Conference on Fairness, Accountability and Transparency. PMLR, 149–159.

- Bird et al. (2020) Sarah Bird, Miro Dudík, Richard Edgar, Brandon Horn, Roman Lutz, Vanessa Milan, Mehrnoosh Sameki, Hanna Wallach, and Kathleen Walker. 2020. Fairlearn: A toolkit for assessing and improving fairness in AI. Technical Report MSR-TR-2020-32. Microsoft. https://www.microsoft.com/en-us/research/publication/fairlearn-a-toolkit-for-assessing-and-improving-fairness-in-ai/

- Black et al. (2021) Emily Black, Klas Leino, and Matt Fredrikson. 2021. Selective Ensembles for Consistent Predictions. arXiv preprint arXiv:2111.08230 (2021).

- Brown et al. (2019) Anna Brown, Alexandra Chouldechova, Emily Putnam-Hornstein, Andrew Tobin, and Rhema Vaithianathan. 2019. Toward algorithmic accountability in public services: A qualitative study of affected community perspectives on algorithmic decision-making in child welfare services. In Proceedings of the 2019 CHI Conference on Human Factors in Computing Systems. 1–12.

- Celis et al. (2019) L Elisa Celis, Lingxiao Huang, Vijay Keswani, and Nisheeth K Vishnoi. 2019. Classification with fairness constraints: A meta-algorithm with provable guarantees. In Proceedings of the conference on fairness, accountability, and transparency. 319–328.

- Celis et al. (2017) L Elisa Celis, Damian Straszak, and Nisheeth K Vishnoi. 2017. Ranking with fairness constraints. arXiv preprint arXiv:1704.06840 (2017).

- Dastin (2018) Jeffrey Dastin. 2018. Amazon scraps secret AI recruiting tool that showed bias against women. Reuters (2018).

- Dombrowski et al. (2019) Ann-Kathrin Dombrowski, Maximilian Alber, Christopher J Anders, Marcel Ackermann, Klaus-Robert Müller, and Pan Kessel. 2019. Explanations can be manipulated and geometry is to blame. arXiv preprint arXiv:1906.07983 (2019).

- Donini et al. (2018) Michele Donini, Luca Oneto, Shai Ben-David, John Shawe-Taylor, and Massimiliano Pontil. 2018. Empirical risk minimization under fairness constraints. arXiv preprint arXiv:1802.08626 (2018).

- Dwork et al. (2012) Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. 2012. Fairness through awareness. In Innovations in Theoretical Computer Science.

- Edelhertz (1970) Herbert Edelhertz. 1970. The nature, impact, and prosecution of white-collar crime. Vol. 2. National Institute of Law Enforcement and Criminal Justice.

- Engstrom et al. (2020) David Freeman Engstrom, Daniel E Ho, Catherine M Sharkey, and Mariano-Florentino Cuéllar. 2020. Government by algorithm: Artificial intelligence in federal administrative agencies. Administrative Conference of the United States (2020).

- Geyik et al. (2019) Sahin Cem Geyik, Stuart Ambler, and Krishnaram Kenthapadi. 2019. Fairness-aware ranking in search & recommendation systems with application to linkedin talent search. In Proceedings of the 25th acm sigkdd international conference on knowledge discovery & data mining. 2221–2231.

- Ghorbani et al. (2019) Amirata Ghorbani, Abubakar Abid, and James Zou. 2019. Interpretation of neural networks is fragile. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 33. 3681–3688.

- Guyton et al. (2021) John Guyton, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman. 2021. Tax evasion at the top of the income distribution: theory and evidence. Technical Report. National Bureau of Economic Research.

- Guyton et al. (2018) John Guyton, Kara Leibel, Dayanand S Manoli, Ankur Patel, Mark Payne, and Brenda Schafer. 2018. The effects of EITC correspondence audits on low-income earners. Technical Report. National Bureau of Economic Research.

- Hardt et al. (2016) Moritz Hardt, Eric Price, and Nati Srebro. 2016. Equality of opportunity in supervised learning. In Advances in Neural Information Processing Systems.

- Hardt (2016) Moritz et al. Hardt. 2016. Equality of Opportunity in Supervised Learning (NIPS’16).

- Heidari et al. (2019) Hoda Heidari, Michele Loi, Krishna P Gummadi, and Andreas Krause. 2019. A moral framework for understanding fair ml through economic models of equality of opportunity. In Proceedings of the conference on fairness, accountability, and transparency. 181–190.

- Holstein et al. (2019) Kenneth Holstein, Jennifer Wortman Vaughan, Hal Daumé III, Miro Dudik, and Hanna Wallach. 2019. Improving fairness in machine learning systems: What do industry practitioners need?. In Proceedings of the 2019 CHI conference on human factors in computing systems. 1–16.

- Hunter and Nelson (1996) William J Hunter and Michael A Nelson. 1996. An IRS production function. National Tax Journal 49, 1 (1996), 105–115.

- Hutchinson and Mitchell (2019) Ben Hutchinson and Margaret Mitchell. 2019. 50 years of test (un) fairness: Lessons for machine learning. In Proceedings of the Conference on Fairness, Accountability, and Transparency. 49–58.

- (IRS) ([n. d.]a) Internal Revenue Service (IRS). [n. d.]a. Compliance Presence. https://www.irs.gov/statistics/compliance-presence

- (IRS) ([n. d.]b) Internal Revenue Service (IRS). [n. d.]b. IRS Newsroom. https://www.irs.gov/newsroom/the-tax-gap

- (IRS) ([n. d.]c) Internal Revenue Service (IRS). [n. d.]c. IRS Update on Audits. https://www.irs.gov/newsroom/irs-update-on-audits

- (IRS) ([n. d.]d) Internal Revenue Service (IRS). [n. d.]d. National Research Program Overview. https://www.irs.gov/irm/part4/irm_04-022-001

- (IRS) ([n. d.]e) Internal Revenue Service (IRS). [n. d.]e. NRP Examining Process. https://www.irs.gov/irm/part4/irm_04-022-004r

- Kearns et al. (2018) Michael Kearns, Seth Neel, Aaron Roth, and Zhiwei Steven Wu. 2018. Preventing fairness gerrymandering: Auditing and learning for subgroup fairness. In International Conference on Machine Learning. PMLR, 2564–2572.

- Kiel ([n. d.]) Paul Kiel. [n. d.]. It’s Getting Worse: The IRS Now Audits Poor Americans at About the Same Rate as the Top 1%.

- Kiel and Eisinger (2018) Paul Kiel and Jesse Eisinger. 2018. Who’s more likely to be audited: A person making $20,000 or $400, 000.

- Kusner et al. (2017) Matt J Kusner, Joshua Loftus, Chris Russell, and Ricardo Silva. 2017. Counterfactual Fairness. In Advances in Neural Information Processing Systems.

- Lakkaraju et al. (2017) Himabindu Lakkaraju, Jon Kleinberg, Jure Leskovec, Jens Ludwig, and Sendhil Mullainathan. 2017. The selective labels problem: Evaluating algorithmic predictions in the presence of unobservables. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining. 275–284.

- Lamba et al. (2021) Hemank Lamba, Kit T Rodolfa, and Rayid Ghani. 2021. An Empirical Comparison of Bias Reduction Methods on Real-World Problems in High-Stakes Policy Settings. ACM SIGKDD Explorations Newsletter 23, 1 (2021), 69–85.

- Lecher (2018) Colin Lecher. 2018. What Happens When an Algorithm Cuts Your Health Care. The Verge (2018).

- MacNabb ([n. d.]) Jill MacNabb. [n. d.]. Study of Tax Court Cases In Which the IRS Conceded the Taxpayer was Entitled to Earned Income Tax Credit (EITC). https://www.taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/Research-Studies-Study-of-Tax-Court-Cases-in-Which-the-IRS-Conceded-the-Taxpayer-was-Entitled-to-Earned-Income-Tax-Credit-EITC.pdf

- McTigue ([n. d.]) Jamse R. Jr. McTigue. [n. d.]. In a Limited Study, Preparers Made Significant Errors.

- Mullainathan and Obermeyer (2021) Sendhil Mullainathan and Ziad Obermeyer. 2021. On the Inequity of Predicting A While Hoping for B. In AEA Papers and Proceedings, Vol. 111. 37–42.

- Obermeyer et al. (2019) Ziad Obermeyer, Brian Powers, Christine Vogeli, and Sendhil Mullainathan. 2019. Dissecting racial bias in an algorithm used to manage the health of populations. Science (2019).

- of the Treasury (2021) U.S. Department of the Treasury. 2021. How Financial Reporting Helps American Workers and Ensures that Top Earners Pay Their Fair Share. https://home.treasury.gov/news/featured-stories/how-financial-reporting-helps-american-workers-and-ensures-that-top-earners-pay-their-fair-share

- Office ([n. d.]) U.S. Government Accountability Office. [n. d.]. Artificial Intelligence: An Accountability Framework for Federal Agencies and Other Entities. ([n. d.]).

- Parrillo (2013) Nicholas R Parrillo. 2013. Against the Profit Motive: The Salary Revolution in American Government, 1780-1940. Yale University Press.

- Passi and Barocas (2019) Samir Passi and Solon Barocas. 2019. Problem formulation and fairness. In Proceedings of the Conference on Fairness, Accountability, and Transparency. 39–48.

- Pedregosa et al. (2011) F. Pedregosa, G. Varoquaux, A. Gramfort, V. Michel, B. Thirion, O. Grisel, M. Blondel, P. Prettenhofer, R. Weiss, V. Dubourg, J. Vanderplas, A. Passos, D. Cournapeau, M. Brucher, M. Perrot, and E. Duchesnay. 2011. Scikit-learn: Machine Learning in Python. Journal of Machine Learning Research 12 (2011), 2825–2830.

- President ([n. d.]) U.S. President. [n. d.]. Exec. Order No. 13985 86 Fed. Reg. 7009, Advancing Racial Equity and Support for Underserved Communities Through the Federal Government.

- Singh and Joachims (2018) Ashudeep Singh and Thorsten Joachims. 2018. Fairness of exposure in rankings. In Proceedings of the 24th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining. 2219–2228.

- Verma and Rubin (2018) Sahil Verma and Julia Rubin. 2018. Fairness definitions explained. In 2018 ieee/acm international workshop on software fairness (fairware). IEEE, 1–7.

- Yan and Howe (2020) An Yan and Bill Howe. 2020. Fairness in practice: a survey on equity in urban mobility. A Quarterly bulletin of the Computer Society of the IEEE Technical Committee on Data Engineering 42, 3 (2020).

- Zafar et al. (2019) Muhammad Bilal Zafar, Isabel Valera, Manuel Gomez-Rodriguez, and Krishna P Gummadi. 2019. Fairness constraints: A flexible approach for fair classification. The Journal of Machine Learning Research 20, 1 (2019), 2737–2778.

Appendix

Appendix A Fairness constraints and Monotonicity

In this section, we show that a selection process which achieves either equal true positive rates or equalized odds will, under certain (differing) conditions, satisfy monotonicity with respect to the ranking of bins by true misreport rate. That is, such models must choose a higher audit rate in a group with a higher rate of misreport than it chooses in a group with a lower rate of misreport. Given that, in our setting, misreport rate appears to be monotonic with respect to income, such results would imply audit rate monotonicity with respect to income as well.

For this section, we assume the following setup. There are two groups of observations and of equal size , and they have and positive labels respectively and and negative labels. An auditor selects observations for audit from and from such that the total audits is their audit budget . The auditor has access to a model which gives binary predictions . The auditor would like to select and in such a way that she maximizes true positives selected; we assume that - that is, the audit budget is much smaller than the total amount of positive predictions by the model.

After the auditor makes selections and , we define the as the false positive rate of the audits for ; that is,

In other words, is the false positive rate of the composition of whatever the auditor’s selection process is with the predictions of the model (not the false positive rate of the model itself). We define similarly. Additionally, we define as the true positive rate of the audits for , i.e.:

and similarly. Finally, let , often known as precision.

A.1. Equal TPR and Monotonicity

Our first lemma relates monotonicity to precision in the case of a selection process satisfying equal true positive rates:

Lemma A.1.

Suppose that the selection process satisfies equal true positive rates. Then with and defined as above: .

Proof.

Note that:

Then the true positive rate can be written as

But by assumption, , so

But this implies that

Hence, if and only if , or in other words:

∎

To interpret this lemma, suppose that Group 2 has a higher misreport rate than Group 1 by some factor. Then the lemma states that for any selection process satisfying equal true positive rates, monotonicity with respect to misreport rate requires precision in Group 2 greater than in Group 1 by at least the same factor, and vice versa.

A.2. Equalized Odds and Monotonicity

The following lemma shows that, in this setting, any allocation that satisfies equalized odds (i.e. and ) must audit the group with a higher misreport rate at a higher rate if the true positive rate is larger than the false positive rate; conversely, it must audit the group with a higher misreport rate at a lower rate if the true positive rate is lower than the false positive rate.

Lemma A.2.

Suppose that the allocation satisfies equalized odds. That is, and . If , then ; otherwise, .

Proof.

Note that is the sum of true and false positives in and is the sum of true and false positives in . Since

we can observe that:

and similarly for . But then:

But then we have that:

yielding the claimed result. ∎

Lemma A.2 shows that if the selection process as a whole satisfies equalized odds, then groups with higher misreport rates will be audited at a higher rate if and only if the process catches a larger fraction of misreporters than the fraction of non-misreporters it ensnares. In balanced settings and with good models, we might expect that generally the true positive rate will be higher than the false positive rate, and this is what provides intuition that imposing equalized odds might push the process towards monotonicity in misreport rate. But these rates interact with the overall audit budget: in the regime where the budget is very small and models are good, then it may be possible to obtain a low false positive rate but an even lower true positive rate. In that case, equalized odds will require that the group with higher non-compliance is audited less.

Appendix B Further Experimental Details

| Model Type | Label | Subsampled | Revenue | No-Change | Cost | Net Revenue | Oracle |

|---|---|---|---|---|---|---|---|

| Type | (Data Size) | ($B) | Rate | ($B) | ($B) | Overlap | |

| Oracle | - | × | |||||

| LDA | Class | ✓11M | |||||

| LDA | Class | ✓1100k | |||||

| Random Forest | Class | × | |||||

| Random Forest | Class | ✓1100k | |||||

| Grad Boost | Class | × | |||||

| Grad Boost | Class | ✓1100k |

In this paper, we compare LDA, Random Forest Classifier, Random Forest Regressor, Gradient Boost Classifier, and Gradient Boost Regressor models. We use the sklearn python package (Pedregosa et al., 2011) to implement all models except for gradient boosted models, and search for optimal hyperparameters using sklearn’s GridSearchCV method with 5-fold cross validation. Gradient boosted models are created through the XGBoost python package, and optimal hyperparameters are also found using GridSearchCV. We use NRP data from 2010-2014 to train all models in this paper, with dollar values scaled to 2014 values. Our threshold for determining what qualifies as a tax misreport is a $200 difference between paid tax and amount owed. We winsorize amount of misreport to the 1st and 99th percentiles. We split the data into train, test, and validation sets randomly. Our train and validation sets comprise 75% of the data, with a test set of 25% of the data.

We note that the IRS NRP data contains sampling weights, which are used to ensure that the NRP data is representative of the true underlying distribution of taxpayers ((IRS), [n. d.]e). We train all unconstrained models with sampling weights included in the NRP data using sklearn’s built in data-weighting feature, except LDA, whose sklearn implementation does not does not support training weights. For LDA, we create a representative dataset from the NRP data by randomly subsampling rows from the weighted training data according to the weights. For example, consider that each row has a weight , and the sum of all weights in the training set is . Then each observation has probability of getting selected as any given row in the subsampled data. This produces an unweighted training set reflecting the same proportions as the weighted training data, with one million samples. As mentioned in Section 5, the FairLearn package (Bird et al., 2020) requires the use of the sklearn training weights feature to implement its in-process fairness enforcement algorithms. As a result, we also use the subsampling technique to create training sets for in-process fairness models, but with samples of points, as the algorithm is extremely time-intensive on large datasets (over 48 hours for one model). In order to show that the use of sampling weights during training, or the difference in training set size from 100k to 1M, does not strongly affect the results presented in the paper, we show the audit allocations and revenue, cost, and no-change rates of the LDA, Random Forest, and XGBoost classifiers in Figure 6 and Table 2 respectively.

All analyses sections are produced on the test set. Cost and revenue calculations are reported by rescaling costs and revenues to reflect estimated annual values for the full population, for each year 2010-2014, and then dividing by five.

We sort taxpayers by descending order of predicted misreport probability from all classification models (using sklearn’s predict_proba()) method, in order to produce a ranking. We use sklearn’s predict method to return expected misreport for regression models. We use an audit rate budget of % of the taxpayer population, reflecting the average audit rate from 2010-2014, and select audits by taking the top % of the taxpayer population in rank order. This % corresponds to weighted percentage of the population, computed with sampling weights, i.e. where is an observation in the weighted dataset, is an indicator of whether to audit that observation, and is the number of people the observation represents to create a representative population from the sampling data. The audit budget of of the taxpayer population, is equivalent to 1125000 audits.

Appendix C Robustness Checks on Classification Thresholds

| Model Type | Label | Revenue | No-Change | Cost | Net Revenue | |

|---|---|---|---|---|---|---|

| Type | Threshold | ($B) | Rate | ($B) | ($B) | |

| Oracle | - | × | ||||

| LDA | Class | 200 | ||||

| Random Forest | Class | 200 | ||||

| Random Forest | Class | 1,000 | ||||

| Random Forest | Class | 5,000 | ||||

| Random Forest | Class | 10,000 | ||||

| LDA | Class | 1,000 | ||||

| LDA | Class | 5,000 | ||||

| LDA | Class | 10,000 |

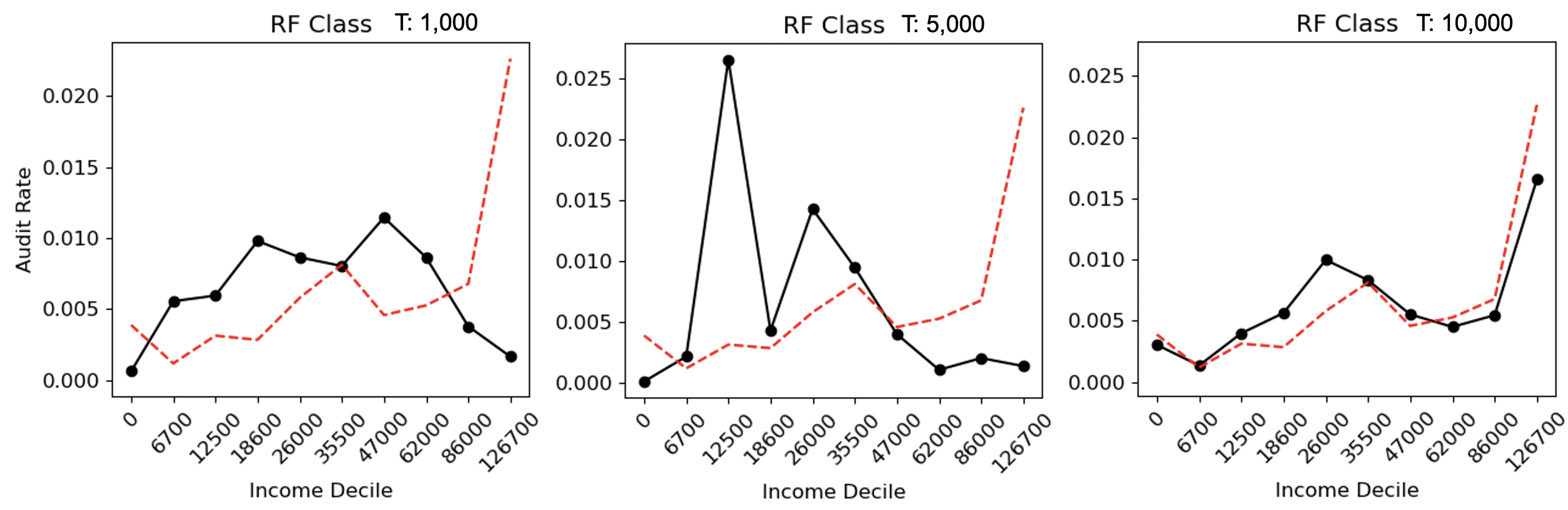

In this section, we compare the audit allocations of high-flexibility classification models (namely, random forest classifiers) with different thresholds for what constitutes a significant adjustment. In the main text, we use a threshold of $200 to signify a significant misreport. In these experiments, we consider thresholds of $1,000, $5,000, and $10,000. Experimental setup is identical to that described in Section B, with the exception of the change in threshold. We display our results in Figure 7, and Table 3.

The results show us that changing the threshold of a significant adjustment to $1,000 does not significantly impact audit allocation compared to the results presented in the main text. A threshold of $5,000 exacerbates the classification model’s excess focus on the lower end of the income spectrum, even beyond results shown in the main paper. Only a threshold of $10,000 makes a significant difference in terms of the audit allocation—shifting the focus to high income individuals almost exclusively— however, it results in an extremely high no-change rate.

Appendix D Increased Audit Focus on Lower-and-Middle Income only in High Complexity Models

| Model Type | Label | Subsampled | Revenue | No-Change | Cost | Net Revenue | Oracle |

|---|---|---|---|---|---|---|---|

| Type | (Data Size) | ($B) | Rate | ($B) | ($B) | Overlap | |

| Oracle | - | × | |||||

| LDA | Class | ✓11M | |||||

| Random Forest | Class | × | |||||

| Grad Boost | Class | × | |||||

| Log. Reg. | Class | × |

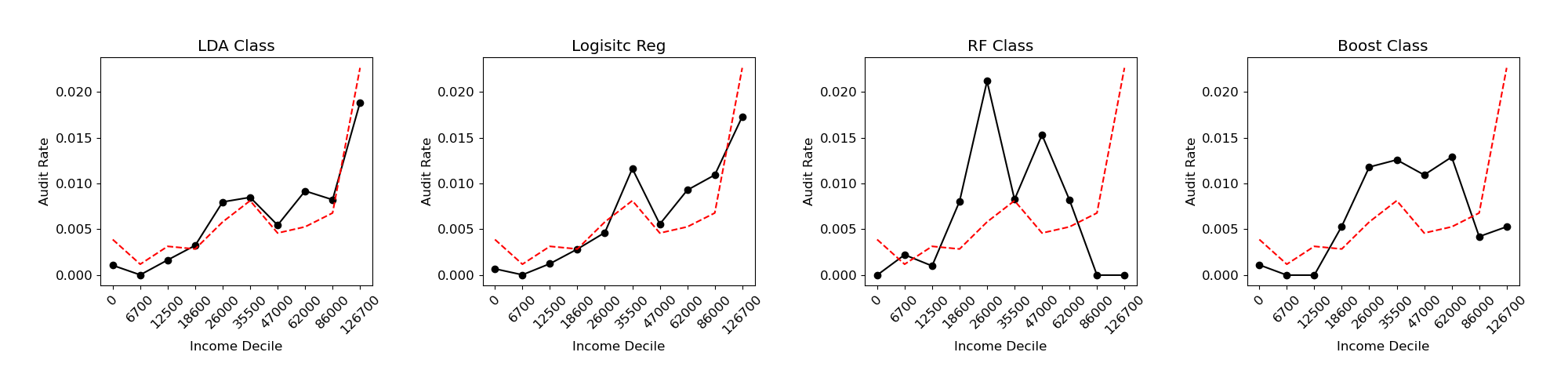

In this section, we provide results from a logistic regression model to further buttress the claim that only higher-complexity classification models result in audit allocations which exacerbate focus on lower and middle-income taxpayers. We train the Logistic Regression classification model with the same procedure outlined in Appendix B, with sampling weights directly included during training. The audit allocation is depicted in Figure 8: the allocation is more monotonic than the higher complexity classification models; and is apparent in Table 4, the no-change rate is higher, but the revenue is higher as well.

Appendix E Additional Robustness Checks