RECAPP: Crafting a More Efficient Catalyst

for Convex Optimization

Abstract

The accelerated proximal point algorithm (APPA), also known as “Catalyst”, is a well-established reduction from convex optimization to approximate proximal point computation (i.e., regularized minimization). This reduction is conceptually elegant and yields strong convergence rate guarantees. However, these rates feature an extraneous logarithmic term arising from the need to compute each proximal point to high accuracy. In this work, we propose a novel Relaxed Error Criterion for Accelerated Proximal Point (RECAPP) that eliminates the need for high accuracy subproblem solutions. We apply RECAPP to two canonical problems: finite-sum and max-structured minimization. For finite-sum problems, we match the best known complexity, previously obtained by carefully-designed problem-specific algorithms. For minimizing where is convex in and strongly-concave in , we improve on the best known (Catalyst-based) bound by a logarithmic factor.

1 Introduction

A fundamental approach to optimization algorithm design is to break down the problem of minimizing into a sequence of easier optimization problems, whose solution converges to . A canonical “easier” problem is proximal point computation, i.e., computing

Here is a regularization parameter which balances between how close computing is to minimizing , and how easy it is to compute—as decreases tends to the true minimizer but becomes harder to compute.

The classical proximal point method [40, 39] simply iterates , and (for convex ) minimizes with rate for . This rate can be improved, at essentially no additional cost, by carefully combining proximal steps, i.e. , with gradient steps using [18]. This accelerated method converges with rate , a quadratic improvement over proximal point.

To turn this conceptual acceleration scheme into a practical algorithm, one must prescribe the accuracy to which each proximal point needs to be computed. Güler [18], Salzo & Villa [41] provided such conditions, which were later refined in independently-proposed accelerated approximate proximal point algorithm (APPA) [12] and Catalyst [27, 28]. Furthermore, APPA/Catalyst obtained global convergence guarantees for concrete problems by using linearly convergent algorithms to compute the proximal points to their required accuracy. The APPA/Catalyst framework has since been used to accelerate full-batch gradient descent, coordinate methods, finite-sum variance reduction [12, 28], eigenvalue problems [14], min-max problems [49], and more.

However, the simplicity and generality of APPA/Catalyst seems to come at a practical and theoretical cost: satisfying existing proximal point accuracy conditions requires solving subproblems to fairly high accuracy. In practice, this means expending computation in subproblem solutions that could otherwise be used for more outer iterations. In theory, APPA/Catalyst complexity bounds feature a logarithmic term that appears unnecessary. For example, in the finite sum problem of minimizing where each is convex and -smooth, APPA/Catalyst combined with SVRG [21] and finds an -optimal point of in computations of , a nearly optimal rate [47]. A line of work devoted to designing accelerated method tailored to finite sum problems [42, 2, 25] attains progressively better practical performance and theoretical guarantees, culminating in an complexity bound [44].

Given the power of APPA/Catalyst, it is natural to ask whether the additional logarithmic complexity term is fundamentally tied to the black-box structure that makes it generally-applicable? Indeed, Lin et al. [28] speculate that the logarithmic term “may be the price to pay for a generic acceleration scheme.”

Our work proves otherwise by providing a new Relaxed Error Condition for Accelerated Proximal Point (RECAPP) which standard subproblem solvers can satisfy without incurring an extraneous logarithmic complexity term. For finite-sum problems, our approach combined with SVRG recovers the best existing complexity bound of .111Our framework gives accelerated linear convergence for strongly-convex objectives via a standard restarting argument; see Proposition 2. Preliminary experiments on logistic regression problem indicate that our method is competitive with Catalyst-SVRG in practice.222Code available at: github.com/yaircarmon/recapp.

As an additional application of our framework, we consider the problem of minimizing for a function that is -smooth, convex in and -strongly-convex in . The best existing complexity bound for this problem is evaluations of , using an extension of APPA/Catalyst to min-max problems [49], and mirror-prox [22, 33, 4] as the subproblem solver.333Yang et al. [49] also establish the same rate for the dual problem of maximizing over . Since our acceleration framework is primal-only, we are currently unable to remove the logarithmic factor from that rate. Our framework (also combined with mirror-prox) removes this logarithmic factor, finding a point with expected suboptimality in gradient queries (up to lower order terms), which is asymptotically optimal [37]. We summarize our complexity bounds in Table 1.

| Objective | Reg. | ApproxProx complexity | WarmStart complexity | Overall complexity | Ref. |

|---|---|---|---|---|---|

| general | Thm. 1 | ||||

| Prop. 2 | |||||

| Thm. 2 | |||||

| Thm. 4 | |||||

Technical overview.

Our development consists of four key parts. First, we define a criterion on the function-value error of the proximal point computation (Definition 1) that significantly relaxes the relative error conditions of prior work; see Section 4.3 for a detailed comparison. Second, instead of directly bounding the distance error of the approximate proximal points (as most prior works implicitly do), we follow Asi et al. [3] and require an unbiased estimator of the proximal point whose variance is bounded similarly to the function-value error (Definition 2). We prove that any approximation satisfying these guarantees has the same convergence bounds on its (expected) error as the exact accelerated proximal points method. Third, we use the multilevel Monte Carlo technique [16, 7, 3] to obtain the required unbiased proximal point estimator using (in expectation) a constant number of queries to any method satisfying the function-value error criterion. Finally, we show how to use SVRG and mirror-prox to efficiently meet our error criterion, allowing us to solve finite-sum and minimax optimization problems without the typical extra logarithmic factors incurred by previous proximal point frameworks.

Even though we maintain the same iteration structure as APPA/Catalyst, our novel error criterion induces two nontrivial modifications to the algorithm. First and foremost, our relaxed error bound depends on the previous approximate proximal point as well as the current query point (see Algorithm 1). This dependence strongly suggests that the subproblem solver should depend on somehow. For finite-sum problems we use as the reference point for variance reduction, while for max-structured problems we initialize mirror-prox with and (approximately) . The second algorithmic consequence, which appeared previously in Asi et al. [3], stems from the fact that our function-value error and zero-bias/bounded-variance requirements are leveraged for distinct parts of the algorithm (the prox step and gradient step, respectively). This naturally leads to using distinct approximate prox points for each part: one directly obtained from the subproblem solver and one debiased via MLMC.

2 Additional Related Work

Beyond the closely related work already described, our paper touches on several lines of literature.

Finite-sum problems.

The ubiquity of finite-sum optimization problems in machine learning has led to a very large body of work on developing efficient algorithms for solving them. We refer the reader to Gower et al. [17] for a broad survey and focus on accelerated finite-sum methods, i.e., with a leading order complexity term scaling as (or as for strongly-convex problems with condition number ). Accelerated Proximal Stochastic Dual Coordinate Ascent [42] gave the first such accelerated rate for an important subclass of finite-sum problems. This method was subsequently interpreted as a special case of APPA/Catalyst [27, 12], which can also accelerate several other finite-sum optimization problems. Since then, research has focused on designing more practical and theoretically efficient accelerated algoirthms by opening the APPA/Catalyst black box. The algorithms Katyusha [2], Varag [25] and VRADA [44] offer improved complexity bound at the price of the generality and simplicity of APPA/Catalyst. Our approach matches the best existing guarantee (due to VRADA) without paying this price.

Max-structured problems.

Objectives of the form are very common in machine learning and beyond. Such objectives arise from constraints (via Lagrange multipliers) [6], robustness requirements [5, 13, 30], and game-theoretic considerations [32, 43]. When is convex in and concave in , the mirror-prox algorithm minimizes to accuracy epsilon in gradient evaluations (with respect to both and ), where is the diameter of . This rate can be improved when is -strongly-concave in . For the special bilinear case , where a “simple” -strongly-convex function, an improved complexity bound of has long been known [35].

More recent work studies the case of general convex-strongly-concave . Thekumparampil et al. [46] and Zhao [50] establish complexity bounds of , which Lin et al. [29] improve to using an algorithm loosely based on APPA/Catalyst. Yang et al. [49] present a more direct application of APPA/Catalyst to min-max problems, further improving the complexity to , with logarithmic dependence on only in a lower order term. Similarly to standard APPA/Catalyst, the min-max variant requires highly accurate proximal point computation, e.g., to function-value error of . In contrast, RECAPP requires constant (relative) suboptimality and removes the final logarithmic factor from the leading-order complexity term. Yang et al. [49] also provide extensions to finite-sum min-max problems and problems where is non-convex in , which would likely benefit from out method as well (see Section 7).

Independent work. In recent independent work, Kovalev & Gasnikov [23] develop a method that minimizes assuming -strong-concavity in and -strong-convexity in . They attain an essentially optimal complexity proportional to times a logarithmic factor depending on problem parameters. Their method is tailored to saddle point problems, working in an expanded space by using point-wise conjugate function and applying recent advances in monotone operator theory. We note that RECAPP with restarts attains the same complexity bound (see Theorem 4). However, it is unclear whether the algorithm of [23] can recover the RECAPP’s complexity bound in the setting where is not strongly convex in .

Monteiro-Svaiter-type acceleration.

Monteiro-Svaiter [31] propose a variant of the accelerated proximal point method that uses an additional gradient evaluation to facilitate approximate proximal point computation. The Monteiro-Svaiter method and its extensions [15, 8, 9, 10, 45, 23, 11] also allow for the regularization parameter to be determined dynamically by the procedure approximating the proximal point. Ivanova et al. [20] leverage this technique to develop a variant of Catalyst that offers improved adaptivity and, in certain cases, improved complexity. We provide additional comparison between the approximation condition of [31, 20] and RECAPP in Section 4.3.

Multilevel Monte Carlo (MLMC).

MLMC is a method for debiasing function estimators by randomizing over the level of accuracy [16]. While originally conceived for PDEs and system simulation, a particular variant of MLMC due to Blanchet & Glynn [7] has found recent applications in the theory of stochastic optimization [26, 19]. Our method directly builds on the recent proposal of Asi et al. [3] to use MLMC in order to obtain unbiased estimates of proximal points (or, equivalently, the Moreau envelope gradient). Asi et al. [3] apply this estimator to de-bias proximal points estimated via SGD and improve several structured acceleration schemes. In contrast, we apply MLMC on linearly convergent algorithms, allowing us to configure it much more aggressively and avoid the extraneous logarithmic factors that appeared in the rates of Asi et al. [3].

Paper organization.

After providing some notation and preliminaries in Section 3, we present our improved inexact accelerated proximal point framework in Section 4. We then instantiate our framework: in Section 5 we consider finite-sum problems and SVRG (providing preliminary empirical results in Section 5.1) and in Section 6 we consider min-max problems and mirror-prox. We conclude in Section 7 by discussing limitations and possible extensions.

3 Preliminaries

General notation.

Throughout, and refer to closed, convex sets, with diameters denoted by and respectively (when needed). We use to denote a convex function defined on . For any parameter and point , we let

| (1) |

denote the proximal regularization of around , and let .

Distances and norms.

We consider Euclidean space throughout the paper and use to denote standard Euclidean norm. We denote a projection of onto a closed subspace by . For a convex function , we denote the Bregman divergence induced by as

for every . We denote the Euclidean Bregman divergence by

Smoothness, convexity and concavity.

Given a differentiable, convex function , we say is -smooth if its gradient is -Lipschitz. We say is -strongly-convex if for all ,

A function is -strongly concave if is -strongly convex. For that is convex in and concave in , the point is a saddle-point if for all .

4 Framework

In this section, we present our Relaxed Error Criterion Accelerated Proximal Point (RECAPP) framework. We start by defining our central algorithms and relaxed error criteria (Section 4.1). Next, we state our main complexity bounds (Section 4.2) and sketch its proof. Then, we illustrate our new relaxed error criterion by comparing it to the error requirements of prior work (Section 4.3). Finally, as an illustrative warm-up, we show our framework easily recovers the complexity bound of Nesterov’s classical accelerated gradient descent (AGD) method [34].

4.1 Methods and Key Definitions

Algorithm 1 describes our core accelerated proximal method. The algorithm follows the standard template of the (inexact) accelerated proximal point method, except that unlike most such methods (but similar to the methods of Asi et al. [3]), our algorithm relies on two distinct approximations of with different relaxed error criterion. We now define each approximation in turn.

Our first relaxed error criterion constrains the function value of the approximate proximal point and constitutes our key contribution.

Definition 1 (ApproxProx).

Given convex function , parameter , and points , the point is an approximate minimizer of such that for ,

| (2) |

Beyond the prox-center , our robust error criterion depends on two additional points: (which in Algorithm 1 is also set the prox-center ) and (which in Algorithm 1 is set to the previous iterate ). The criterion requires the suboptimality of the approximate solution to be bounded by weighted combination of two distances: the Euclidean distance between the true proximal point and , and the Bregman divergence (induced by ) between and . In Section 4.3 we provide a detailed comparison between our criterion and prior work, but note already that—unlike APPA/Catalyst—the relative error we require in (2) is constant, i.e., independent of the desired accuracy or number of iterations. This constant level of error is key to enabling our improved complexity bounds.

Our second relaxed error criterion constrains the bias and variance of the approximate proximal point.

Definition 2 (UnbiasedProx).

Given convex function , parameter , and points and , the point is an approximate minimizer of such that , and

| (3) |

Note that the any satisfies the distance bound (3) (due to -strong-convexity of ), but the zero-bias criterion is not guaranteed. Nevertheless, an MLMC technique (Algorithm 2) can extract an UnbiasedProx from any ApproxProx. Algorithm 2 repeatedly calls ApproxProx a geometrically-distributed number of times (every time with and equal to the last output), and outputs a point whose expectation equals to an infinite numbers of iterations of ApproxProx, i.e., the exact . Moreover, we show that the linear convergence of the procedure implies that the variance of the result remains appropriately bounded (see Proposition 1 below). Algorithm 2 is a variation of an estimator by Blanchet & Glynn [7] that was previously used in a context similar to ours [3]. However, prior estimators typically have complexity exponential in , whereas ours are linear in .

Finally, we define a warm start procedure required by our method.

Definition 3 (WarmStart).

Given convex function , parameter and diameter bound , is a procedure that outputs such that .

Note that the exact proximal mapping satisfies all the requirements above; replacing , , and with recovers the exact accelerated proximal method.

4.2 Complexity Bounds

We begin with a complexity bound for implementing UnbiasedProx via Algorithm 2 (proved in Appendix A).

Proposition 1 (MLMC turns ApproxProx into UnbiasedProx).

For any convex and parameter , Algorithm 2 with and implements UnbiasedProx and makes calls to ApproxProx in expectation.

We now give our complexity bound for RECAPP and sketch its proof, deferring the full proof to Appendix A.

Theorem 1 (RECAPP complexity bound).

Given any convex function and parameters , RECAPP (Algorithm 1) finds with , within iterations using one call to WarmStart, and calls to ApproxProx and UnbiasedProx. If we implement UnbiasedProx using Algorithm 2 with and , the total number of calls to ApproxProx is in expectation.

Proof sketch. We split the proof into two steps.

Step 1: Tight idealized potential decrease. Consider iteration of the algorithm, and define the potential

where is a minimizer of in . Let and be the “ideal” values of and obtained via an exact prox-point computation, where for simplicity we ignore the projection onto . Using these points we define the idealized potential

Textbook analyses of acceleration schemes show that [36, 31]. Basic inexact accelerated prox-point analyses proceed by showing that the true potential is not much worse that the idealized potential, i.e., , which immediately allows one to conclude that for , and therefore that , implying the optimal rate of convergence as long . However, obtaining such a small to be that small naively requires approximating the proximal points to very high accuracy, which is precisely what we attempt to avoid.

Our first step toward a relaxed error criterion is proving stronger idealized potential decrease. We show that,

While the potential decrease term is well known and has been thoroughly exploited by prior work [12, 28, 31], making use of the term is, to the best of our knowledge, new to this work.

Step 2: Matching approximation errors. With the improved potential decrease at bound in hand, our strategy is clear: make the approximation error cancel with the potential decrease. That is, we wish to show

so that overall we have and consequently , with the last bound following form the warm-start condition and .

It remains to show that the ApproxProx and UnbiasedProx criteria provide the needed error bounds. For the function value, Definition 1 implies

where for the last inequality we use the property that due to the strong convexity of and the approximate optimality of guaranteed by ApproxProx (see (16) and the derivations before it in Appendix).

For , Definition 2 implies and

Substituting back into the expressions for and and using the fact that , we obtain the desired bound on and conclude the proof.444The need to have a lower bound like is the reason RECAPP does not take and requires a warm-start.

∎

Complexity bound for strongly-convex functions.

For completeness, we also include a guarantee for minimizing a strongly-convex function by restarting RECAPP. See Appendix A for pseudocode and proofs.

Proposition 2 (RECAPP for strongly-convex functions).

For any -strongly-convex function , and parameters , , restarted RECAPP (Algorithm 7) finds such that , using one call to WarmStart, and calls to ApproxProx and UnbiasedProx. If we implement UnbiasedProx using Algorithm 2 with and , the number of calls to ApproxProx is in expectation.

4.3 Comparisons of Error Criteria

We now compare ApproxProx (Definition 1) to other proximal-point error criteria from the literature. Throughout, we fix a center-point and let .

Comparison with Frostig et al. [12].

The APPA framework, which focuses on -strongly-convex functions, requires the function-value error bound

to hold for all . To compare this requirement with ApproxProx, note that in the unconstrained setting

where the last equality is due to the fact that minimizes and therefore . Consequently, the error of is

Therefore, in the unconstrained setting and the special case of we require a constant factor relative error decrease, while APPA requires decrease by a factor proportional to , or with the standard conversion . Thus, our requirement is significantly more permissive.

Comparison with Lin et al. [28].

The Catalyst framework offers a number of error criteria. Most closely resembling ApproxProx is their relative error criterion (C2):

with which is of the order of for most iterations. Setting in the Catalyst criterion would satisfy for any . Furthermore, ApproxProx allows for an additional error term proportional to , which does not exist in Catalyst. In our analysis in the next sections this additional term is essential to efficiently satisfy our criterion.

Comparison with the Monteiro-Svaiter (MS) condition.

Ivanova et al. [20] and Monteiro & Svaiter [31] consider the error criterion

This criterion implies the bound , making it stronger that the Catalyst C2 criterion when . However, Monteiro & Svaiter [31] show that by updating of using , any constant value of in suffices for obtaining rates similar to those of the exact accelerated proximal point method. The ApproxProx criterion is strictly weaker than the MS criterion with .

Ivanova et al. [20] leverage the MS framework and its improved error tolerance to develop a reduction-based method that, for some problems, is more efficient than Catalyst by a logarithmic factor. However, for the finite sum and max-structured problems we consider in the following sections, it is unclear how to satisfy the MS condition without incurring an extraneous logarithmic complexity term.

Stochastic error criteria.

It is important to note that in contrast to APPA and Catalyst, RECAPP is inherently randomized. The unbiased condition of UnbiasedProx is critical to our analysis of the update to . Although in many cases (such as in finite-sum optimization) efficient proximal point oracles require randomization anyhow, we extend the use of randomness to the acceleration framework’s update itself. It is an interesting question to determine if this randomization is necessary and comparable performance to RECAPP can be obtained based solely on deterministic applications of ApproxProx.

4.4 The AGD Rate as a Special Case

For a quick demonstration of our framework, we show how to recover the classical complexity bound for minimizing an -smooth function using exact gradient computations. To do so, we set and note that is -strongly convex and -smooth. Therefore, for each with we can implement ApproxProx by taking gradient steps starting from , since these steps produce an satisfying

and therefore

5 Finite-sum Minimization

In this section, we consider the following problem of finite-sum minimization:

| (4) |

where each is -smooth and convex.

We solve the problem by combining RECAPP with a single epoch of SVRG [21], shown in Algorithm 3. Our single point of departure from this classical algorithm is that the point we center our gradient estimator at () is allowed to differ from the initial iterate (). Setting to be the point of ApproxProx allows us to efficiently meet our relaxed error criterion.

Corollary 1 (ApproxProx for finite-sum minimization).

Given finite-sum problem (4), points , and , OneEpochSvrg (Algorithm 3) with , , and implements (Definition 1) using gradient queries.

Corollary 1 follows from a slightly more general bound on OneEpochSvrg (Proposition 4 in Appendix B). Below, we briefly sketch its proof.

Proof sketch. We begin by carefully bounding the variance of the gradient estimator . In Lemma 6 in the appendix we show that

| (5) |

Next, standard analysis on variance reduced stochastic gradient method [48] shows that

Plugging in the variance bound (5) at iteration , rearranging terms and telescoping for , we obtain

where we use smoothness of , and the choices of and . Noting that satisfies by convexity concludes the proof sketch. ∎

Warm-start implementation.

We now explain how to reuse OneEpochSvrg for obtaining a valid warm-start for RECAPP (Definition 3). Given any initial iterate with function error , we show that a careful choice of step size for OneEpochSvrg leads to a point with suboptimality in gradient computations (Lemma 8). Repeating this procedure times produces a point with suboptimality , which is a valid warm-start for . We remark that Song et al. [44] achieve the same complexity with a different procedure that entails changing the recursion for in Algorithm 1 of Algorithm 1. We believe that our approach is conceptually simpler and might be of independent interest.

Corollary 2 (WarmStart-Svrg for finite-sum minimization).

Consider problem (4) with minimizer , smoothness parameter , and some initial point with , for any , Algorithm 4 with , implements with gradient queries.

By implementing ApproxProx and WarmStart using OneEpochSvrg, RECAPP provides the following state-of-the-art complexity bound for finite-sum problems.

Theorem 2 (RECAPP for finite-sum minimization).

Given a finite-sum problem (4) on domain with diameter , RECAPP (Algorithm 1) with parameters and , using OneEpochSvrg for ApproxProx, and WarmStart-Svrg for WarmStart, outputs an such that . The total gradient query complexity is in expectation. Further, if is -strongly-convex with , restarted RECAPP (Algorithm 7) finds an -approximate solution using gradient queries in expectation.

5.1 Empirical Results

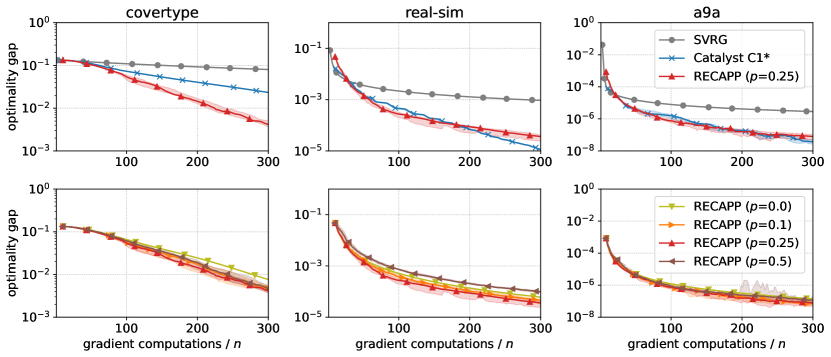

In this section, we provide an empirical performance comparisons between RECAPP and SVRG [21] and Catalyst [28]. Specifically, we compare to the C1* variant of Catalyst-SVRG, which Lin et al. [28] report to have the best performance in practice. We implemented all algorithms in Python, using the Numba [24] package for just-in-time compilation which significantly improved runtime. Our code is available at: github.com/yaircarmon/recapp.

Task and datasets.

We consider logistic regression on three datasets from libSVM [1]: covertype (, ), real-sim (, ), and a9a (, ). For each dataset we rescale the feature vectors to using unit Euclidean norm so that each is exactly -smooth. We do not add regularization to the logistic regression objective.

SVRG implementation.

We implement the SVRG iterates as in Algorithm 3, using and (i.e., the inverse of the smoothness of each function). However, instead of outputting the average of all iterates, we return the average of the final iterates.

Catalyst implementation.

Our implementation follows closely Catalyst C1* as described in [28], where for the subproblem solver we use repeatedly called Algorithm 3 with the parameters and averaging modification described above, checking the C1 termination criterion between each call.

RECAPP implementation.

Our RECAPP implementation follows Algorithms 1 and 2, with Algorithm 3 and Algorithm 4 implemented ApproxProxand WarmStart, respectively, and Algorithm 3 configured and modified and described above. In Algorithm 2 we set the parameters and we test . The setting which corresponds to setting in Algorithm 1) is a baseline meant to test whether MLMC is helpful at all. For we change the parameter in Algorithm 3 such that the expected amount of gradient computations is the same as for . Slightly departing from the pseudocode of Algorithm 1, we take to be computed in Algorithm 2, rather than , since it is always a more accurate proximal point approximation. We note that our algorithm still has provable guarantees (with perhaps different constant factors) under this configuration.

Parameter tuning.

For RECAPP and Catalyst, we tune the proximal regularization parameter (called in [28]). For each problem and each algorithm, we test values of the form , where is the objective smoothness, is the dataset size and in the set . We report results for the best value for each problem/algorithm pair.

Findings.

We summarize our experimental findings in Figure 1. The top row of Figure 1 shows that RECAPP is competitive with Catalyst C1*: on covertype RECAPP is significantly faster, on a9a it is about the same, and on real-sim it is a bit slower. Note that Catalyst C1* incorporates carefully designed heuristics and parameters for choosing the SVRG initialization and stopping time, while the RECAPP implementation directly follows our theoretical development. The bottom row of Figure 1 shows that provides a modest but fairly consistent improvement over the no-MLMC baseline. This provides evidence that MLMC might be beneficial in practice.

6 Max-structured Minimization

In this section, we consider the following problem of the max-structured function minimization:

| (6) |

where is smooth, convex in (for every ) and -strongly-concave in (for every ).

We solve (6) by combining RECAPP with variants of mirror-prox method [33], shown in Algorithm 5. Given a convex-concave -smooth objective , MirrorProx (Algorithm 5) starts from initial point , and finds in gradient queries an approximate solution satisfying for any ,

| (7) |

Our main observation is that applying such a mirror-prox method to the regularized objective , initialized at where we define the best response oracle , outputs solution satisfying the relaxed error criterion of after steps. We formalize this observation in Lemma 1.

Lemma 1 (ApproxProx for max-structured minimization).

Given max-structured minimization problem (6) and an oracle that outputs for any , MirrorProx in Algorithm 5 initialized at implements the procedure using a total of gradient queries and one call to .

Before providing a proof sketch for the lemma, let us remark on the cost of implementing the best response oracle. Since for any fixed the function is -strongly-concave and -smooth, we can use AGD to find an -accurate best response to in gradient queries. Therefore, even for extremely small values of we can expect the best-response computation cost to be negligible compared to the complexity of the mirror-prox iterations required to implement ApproxProx.

Proof sketch. We run MirrorProx for steps on . By (7) the output satisfies for , and arbitrary constant ,

The optimality of gives . Combining with the above implies

| (8) |

We now bound the two sides of (8) separately. The strong concavity of in allows us to show that

For the right-hand side, the definition of as a best response to yields

Plugging both inequalities into (8), and choosing sufficiently small , we see the output satisfies the condition of a oracle, concluding the proof sketch. ∎

Warm-start implementation.

We now explain how to apply accelerated gradient descent (AGD) and a recursive use of MirrorProx for obtaining a valid warm-start for RECAPP (Definition 3).

Lemma 2 (WarmStart for max-structured minimization).

Consider problem (6) where , are diameter bounds for , respectively. Given initial point , Algorithm 6, with parameters , and Algorithm 6 implemented using AGD, implements with

gradient queries.

By implementing ApproxProx and WarmStart using MirrorProx and WarmStart-Minimax, RECAPP provides the following state-of-the-art complexity bounds for minimizing the max-structured problems.

Theorem 3 (RECAPP for minimizing the max-structured problem).

Given with diameter bounds , on , , respectively, RECAPP (Algorithm 1) with parameters and and MirrorProx (Algorithm 5) to implement ApproxProx, and WarmStart-MirrorProx (Algorithm 6) to implement WarmStart, outputs a solution such that . The algorithm uses

gradient queries in expectation and calls to a best-response oracle . Further, if is -strongly-convex, restarted RECAPP (Algorithm 7) with parameters , , finds an -approximate solution using gradient queries in expectation and calls to .

We remark that for strongly-convex , the restarted Algorithm 9 not only yields a good approximate solution for , but also can be transferred to a good approximate primal-dual solution for by taking the best-response to the high-accuracy solution .

Generalization to the framework.

To obtain complexity bounds strictly in terms of gradient queries, we extend the framework of Section 4 to handle small additive errors at iteration when implementing the ApproxProx procedure as defined in (2). For we allow ApproxProx to return satisfying

| (9) |

This way, in Lemma 1 one can implement the best-response oracle (in Algorithm 5) to a sufficient high accuracy using gradient queries, using the standard accelerated gradient method [34]. This turns the method in Theorem 3 into a complete algorithm for solving (6), and only incurs an additional cost of gradient queries.

We state the main result here and refer readers to Appendix D for the generalization of RECAPP (Algorithm 8, Algorithm 9 and Proposition 5) and more detailed discussion.

Theorem 4 (RECAPP for minimizing the max-structured problem, without ).

Under the same setting of Theorem 3, Algorithm 8 with accelerated gradient descent to implement , outputs a primal -approximate solution and has expected gradient query complexity of

Further, if is -strongly-convex, restarted RECAPP (Algorithm 9) finds an -approximate solution and has expected gradient query complexity of

7 Discussion

This paper proposes an improvement of the APPA/Catalyst acceleration framework, providing an efficiently attainable Relaxed Error Criterion for the Accelerated Prox Point method (RECAPP) that eliminates logarithmic complexity terms from previous result while maintaining the elegant black-box structure of APPA/Catalyst.

The main conceptual drawback of our proposed framework (beyond its reliance on randomization) is that efficiently attaining our relaxed error criterion requires a certain degree of problem-specific analysis as well as careful subproblem solver initialization. In contrast, APPA/Catalyst rely on more standard and readily available linear convergence guarantees (which of course also suffice for RECAPP).

Nevertheless, we believe there are many more situations where efficiently meeting the relaxed criterion is possible. These include variance reduction for min-max problems, smooth min-max problems which are (strongly-)concave in but not convex in , and problems amenable to coordinate methods. All of these are settings where APPA/Catalyst is effective [49, 12, 28] and our approach can likely be provably better.

Moreover, even when proving improved rates is difficult, ApproxProx can still serve as an improved stopping criterion. This motivates further research into practical variants of ApproxProx that depend only on observable quantities (rather than, e.g. the distance to the true proximal point).

Acknowledgements

The authors thank anonymous reviewers for helpful suggestions. YC was supported in part by the Israeli Science Foundation (ISF) grant no. 2486/21 and the Len Blavatnik and the Blavatnik Family foundation. YJ was supported in part by a Stanford Graduate Fellowship and the Dantzig-Lieberman Fellowship. AS was supported in part by a Microsoft Research Faculty Fellowship, NSF CAREER Award CCF-1844855, NSF Grant CCF-1955039, a PayPal research award, and a Sloan Research Fellowship.

References

- [1] The LIBSVM data webpage. URL https://www.csie.ntu.edu.tw/~cjlin/libsvmtools/datasets/.

- Allen-Zhu [2016] Allen-Zhu, Z. Katyusha: The first direct acceleration of stochastic gradient methods. arXiv preprint arXiv:1603.05953, 2016.

- Asi et al. [2021] Asi, H., Carmon, Y., Jambulapati, A., Jin, Y., and Sidford, A. Stochastic bias-reduced gradient methods. arXiv preprint arXiv:2106.09481, 2021.

- Azizian et al. [2020] Azizian, W., Mitliagkas, I., Lacoste-Julien, S., and Gidel, G. A tight and unified analysis of gradient-based methods for a whole spectrum of games. In International Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- Ben-Tal et al. [2009] Ben-Tal, A., El Ghaoui, L., and Nemirovski, A. Robust optimization. Princeton University Press, 2009.

- Bertsekas [1999] Bertsekas, D. Nonlinear Programming. Athena Scientific, 1999.

- Blanchet & Glynn [2015] Blanchet, J. H. and Glynn, P. W. Unbiased Monte Carlo for optimization and functions of expectations via multi-level randomization. In 2015 Winter Simulation Conference (WSC), pp. 3656–3667, 2015.

- Bubeck et al. [2019] Bubeck, S., Jiang, Q., Lee, Y. T., Li, Y., and Sidford, A. Complexity of highly parallel non-smooth convex optimization. In Advances in Neural Information Processing Systems, 2019.

- Bullins [2020] Bullins, B. Highly smooth minimization of non-smooth problems. In Conference on Learning Theory, pp. 988–1030, 2020.

- Carmon et al. [2020] Carmon, Y., Jambulapati, A., Jiang, Q., Jin, Y., Lee, Y. T., Sidford, A., and Tian, K. Acceleration with a ball optimization oracle. In Advances in Neural Information Processing Systems, 2020.

- Carmon et al. [2022] Carmon, Y., Hausler, D., Jambulapati, A., Jin, Y., and Sidford, A. Optimal and adaptive monteiro-svaiter acceleration. arXiv:2205.15371, 2022.

- Frostig et al. [2015] Frostig, R., Ge, R., Kakade, S., and Sidford, A. Un-regularizing: approximate proximal point and faster stochastic algorithms for empirical risk minimization. In International Conference on Machine Learning, 2015.

- Ganin et al. [2016] Ganin, Y., Ustinova, E., Ajakan, H., Germain, P., Larochelle, H., Laviolette, F., Marchand, M., and Lempitsky, V. Domain-adversarial training of neural networks. The journal of machine learning research, 17(1):2096–2030, 2016.

- Garber et al. [2016] Garber, D., Hazan, E., Jin, C., Musco, C., Netrapalli, P., Sidford, A., et al. Faster eigenvector computation via shift-and-invert preconditioning. In International Conference on Machine Learning (ICML), 2016.

- Gasnikov et al. [2019] Gasnikov, A., Dvurechensky, P., Gorbunov, E., Vorontsova, E., Selikhanovych, D., Uribe, C. A., Jiang, B., Wang, H., Zhang, S., Bubeck, S., Jiang, Q., Lee, Y. T., Li, Y., and Sidford, A. Near optimal methods for minimizing convex functions with Lipschitz -th derivatives. In Conference on Learning Theory (COLT), 2019.

- Giles [2015] Giles, M. B. Multilevel Monte Carlo methods. Acta Numerica, 24:259–328, 2015.

- Gower et al. [2020] Gower, R. M., Schmidt, M., Bach, F., and Richtárik, P. Variance-reduced methods for machine learning. Proceedings of the IEEE, 108(11):1968–1983, 2020.

- Güler [1992] Güler, O. New proximal point algorithms for convex minimization. SIAM Journal on Optimization, 2(4):649–664, 1992.

- Hu et al. [2021] Hu, Y., Chen, X., and He, N. On the bias-variance-cost tradeoff of stochastic optimization. Advances in Neural Information Processing Systems (NeurIPS), 2021.

- Ivanova et al. [2021] Ivanova, A., Pasechnyuk, D., Grishchenko, D., Shulgin, E., Gasnikov, A., and Matyukhin, V. Adaptive catalyst for smooth convex optimization. In International Conference on Optimization and Applications, pp. 20–37. Springer, 2021.

- Johnson & Zhang [2013] Johnson, R. and Zhang, T. Accelerating stochastic gradient descent using predictive variance reduction. Advances in neural information processing systems (NeurIPS), 2013.

- Korpelevich [1976] Korpelevich, G. M. The extragradient method for finding saddle points and other problems. Ekonomika i Matematicheskie Metody, 12:747–756, 1976.

- Kovalev & Gasnikov [2022] Kovalev, D. and Gasnikov, A. The first optimal algorithm for smooth and strongly-convex-strongly-concave minimax optimization. arXiv:2205.05653, 2022.

- Lam et al. [2015] Lam, S. K., Pitrou, A., and Seibert, S. Numba: A llvm-based python JIT compiler. In Proceedings of the Second Workshop on the LLVM Compiler Infrastructure in HPC, pp. 1–6, 2015.

- Lan et al. [2019] Lan, G., Li, Z., and Zhou, Y. A unified variance-reduced accelerated gradient method for convex optimization. Advances in Neural Information Processing Systems (NeurIPS), 32, 2019.

- Levy et al. [2020] Levy, D., Carmon, Y., Duchi, J. C., and Sidford, A. Large-scale methods for distributionally robust optimization. Advances in Neural Information Processing Systems, 2020.

- Lin et al. [2015] Lin, H., Mairal, J., and Harchaoui, Z. A universal catalyst for first-order optimization. In Advances in Neural Information Processing Systems (NeurIPS), 2015.

- Lin et al. [2017] Lin, H., Mairal, J., and Harchaoui, Z. Catalyst acceleration for first-order convex optimization: from theory to practice. The Journal of Machine Learning Research, 18(1):7854–7907, 2017.

- Lin et al. [2020] Lin, T., Jin, C., and Jordan, M. I. Near-optimal algorithms for minimax optimization. In Conference on Learning Theory (COLT), 2020.

- Madry et al. [2018] Madry, A., Makelov, A., Schmidt, L., Tsipras, D., and Vladu, A. Towards deep learning models resistant to adversarial attacks. In International Conference on Learning Representations, 2018.

- Monteiro & Svaiter [2013] Monteiro, R. D. and Svaiter, B. F. An accelerated hybrid proximal extragradient method for convex optimization and its implications to second-order methods. SIAM Journal on Optimization, 23(2):1092–1125, 2013.

- Morgenstern & Von Neumann [1953] Morgenstern, O. and Von Neumann, J. Theory of games and economic behavior. Princeton university press, 1953.

- Nemirovski [2004] Nemirovski, A. Prox-method with rate of convergence for variational inequalities with Lipschitz continuous monotone operators and smooth convex-concave saddle point problems. SIAM Journal on Optimization, 15(1):229–251, 2004.

- Nesterov [1983] Nesterov, Y. A method of solving a convex programming problem with convergence rate . Soviet Mathematics Doklady, 27(2):372–376, 1983.

- Nesterov [2005] Nesterov, Y. Smooth minimization of non-smooth functions. Mathematical programming, 103(1):127–152, 2005.

- Nesterov [2018] Nesterov, Y. Lectures on convex optimization, volume 137. Springer, 2018.

- Ouyang & Xu [2021] Ouyang, Y. and Xu, Y. Lower complexity bounds of first-order methods for convex-concave bilinear saddle-point problems. Mathematical Programming, 185(1):1–35, 2021.

- Paquette et al. [2017] Paquette, C., Lin, H., Drusvyatskiy, D., Mairal, J., and Harchaoui, Z. Catalyst acceleration for gradient-based non-convex optimization. arXiv preprint arXiv:1703.10993, 2017.

- Parikh & Boyd [2014] Parikh, N. and Boyd, S. Proximal algorithms. Foundations and Trends in optimization, 2014.

- Rockafellar [1976] Rockafellar, R. T. Monotone operators and the proximal point algorithm. SIAM journal on control and optimization, 14(5):877–898, 1976.

- Salzo & Villa [2012] Salzo, S. and Villa, S. Inexact and accelerated proximal point algorithms. Journal of Convex analysis, 19(4):1167–1192, 2012.

- Shalev-Shwartz & Zhang [2014] Shalev-Shwartz, S. and Zhang, T. Accelerated proximal stochastic dual coordinate ascent for regularized loss minimization. In International conference on machine learning (ICML), 2014.

- Silver et al. [2017] Silver, D., Schrittwieser, J., Simonyan, K., Antonoglou, I., Huang, A., Guez, A., Hubert, T., Baker, L., Lai, M., Bolton, A., et al. Mastering the game of go without human knowledge. Nature, 550(7676):354–359, 2017.

- Song et al. [2020] Song, C., Jiang, Y., and Ma, Y. Variance reduction via accelerated dual averaging for finite-sum optimization. In Advances in Neural Information Processing Systems (NeurIPS), 2020.

- Song et al. [2021] Song, C., Jiang, Y., and Ma, Y. Unified acceleration of high-order algorithms under Hölder continuity and uniform convexity. SIAM journal of optimization, 2021.

- Thekumparampil et al. [2019] Thekumparampil, K. K., Jain, P., Netrapalli, P., and Oh, S. Efficient algorithms for smooth minimax optimization. Advances in Neural Information Processing Systems (NeurIPS), 2019.

- Woodworth & Srebro [2016] Woodworth, B. and Srebro, N. Tight complexity bounds for optimizing composite objectives. In Advances in Neural Information Processing Systems, pp. 3646–3654, 2016.

- Xiao & Zhang [2014] Xiao, L. and Zhang, T. A proximal stochastic gradient method with progressive variance reduction. SIAM Journal on Optimization, 24(4):2057–2075, 2014.

- Yang et al. [2020] Yang, J., Zhang, S., Kiyavash, N., and He, N. A catalyst framework for minimax optimization. Advances in Neural Information Processing Systems, 2020.

- Zhao [2020] Zhao, R. A primal dual smoothing framework for max-structured nonconvex optimization. arXiv:2003.04375, 2020.

Appendix A Proofs for Section 4

We first give a formal proof of Proposition 1.

See 1

Proof of Proposition 1.

Let and . By definition of ApproxProx and the strong strong-convexity of we have for ,

| (10) |

Further, for all ,

| (11) |

where we use the equality that , , the optimality of which implies for any , induction over and (10). Consequently, as . Further, since for all , the algorithm returns a point satisfying

which shows the output is an unbiased estimator of .

Next, to bound the variance, we use that for . Applying (10) and (11) yields that for all

Consequently,

and therefore,

Since this implies that the algorithm implements UnbiasedProx as claimed.

Finally, note that the expected number of calls made to ApproxProx is . Further, since is geometrically distributed with success probability . Consequently, the expected number of calls made to ApproxProx is as desired. ∎

See 1

Notation.

We first define the filtration and use the notation to denote the exact proximal mapping which iteration of the algorithm approximates. We note that , i.e., they are deterministic when conditioned on . We also recall in literature it is well-known that the coefficients we pick satisfy the condition that [38, 49].

For each iteration of Algorithm 1, we obtain the following bound on potential decrease (a special case and more careful analysis of its variant in Lemma 5 of Asi et al. [3]).

Proposition 3.

Under the assumptions of Theorem 1, let be a minimizer of . For every , the iterates of Algorithm 1 satisfy

This proposition can be proved directly by combining the following two lemmas.

Lemma 3 (Potential decrease guaranteed by exact proximal step).

At -th iteration of Algorithm 1, let and be the “ideal” values of and obtained via an exact prox-point computation, then we have

| (12) |

Proof.

We let and . Now we bound both sides of the quantity . First, note that

Since (see Fact 1.4 by Asi et al. [3]), is convex and , we have by update of and that

| (13) |

On the other hand to upper bound , note by definition of and ,

Combining the last two displays and rearranging, we obtain

∎

Lemma 4 (Potential difference between exact and approximate proximal step).

Following the same notation as in Lemma 3, for and defined as in Algorithm 1, we have

| (14) |

Proof.

To prove (4), we consider the effect of approximation errors of , in terms of , , respectively. First, by definition of and ApproxProx we have that

| (15) |

Now we further have

where we once again use the strong convexity of , the definition of ApproxProx and the triangle inequality that for any vectors . By rearranging terms and rescaling by a factor of this implies equivalently

| (16) |

Combining the above inequalities we have

| (17) |

where we use rearranging of terms and using the triangle inequality in (15), and plugging back the inequality (16).

Now that given definition of UnbiasedProx for so that and consequently

| (18) |

Proof of Theorem 1.

By requirement of WarmStart function, we have . Applying the potential decreasing argument in Proposition 3 recursively on thus gives

Multiplying both by and using the fact that for , , we show that output by Algorithm 1 satisfy that

The number of calls to each oracles follow immediately.

When implementing using MLMC, guarantees of Proposition 1 immediately implies the correctness and the total number of (expected) calls to . ∎

We now show an adaptation of our framework to the strongly-convex setting in Algorithm 7. We prove its guarantee as follows.

See 2

Proof of Proposition 2.

Let be the minimizer of , we show by induction that for the choice of , the iterates satisfy the condition that

| (19) |

For the base case , we have the inequality holds immediately by definition of procedure WarmStart. Now suppose the inequality (19) holds for . For , by Proposition 3 and proof of Theorem 1 we obtain

By our choice of , we have

and consequently by -strong convexity it holds that

Summing up the two inequalities together we obtain

which shows by math induction that the inequality (19) holds for .

Now by choice of , we have

which proves the correctness of the algorithm.

The algorithm uses one call to procedure WarmStart in Algorithm 7. The number of calls to procedures ApproxProx, UnbiasedProx is times the number of calls within each epoch , which is bounded by . The case when implementing UnbiasedProx by MLMC and ApproxProx follows immediately from Proposition 1.

∎

Appendix B Proofs for Section 5

Proposition 4 (Guarantee for OneEpochSvrg).

For any convex, -smooth , and parameter , consider the finite-sum problem where . Given a centering point , an initial point , and an anchor point , Algorithm 3 with instantiation of , outputs a point satisfying

The algorithm uses a total of gradient queries.

To prove Proposition 4, we first recall the following basic fact for smooth functions.

Lemma 5.

Let be an -smooth convex function. For any we have

| (20) |

and

| (21) |

We also observe the following few properties of Algorithm 3.

Lemma 6 (Gradient estimator properties).

For any , sample uniformly and let . It holds that , and for ,

| (22) |

Proof.

First, by definition of how we construct it holds that

This proves that is an unbiased estimator of .

Next, for such unbiased estimator we have

where we used that for any random . This proves the first inequality in (22).

For the second inequality, note

| (23) | ||||

where we use Cauchy-Schwarz inequality for Euclidean norms, and the property of smoothness of (see Eq. (21)).

The following proof on progress per step follows from the standard analysis by Xiao & Zhang [48] (as the constrained finite-sum minimization we consider is a special case of theirs), which we include the full statement here for completeness.

Lemma 7 (Progress per step of OneEpochSvrg, cf. Xiao & Zhang [48]).

Let where each is -smooth and convex. For , consider step in OneEpochSvrg, define and , it holds that

With these helper lemmas, we are ready to formally prove Proposition 4.

Proof of Proposition 4.

Consider the -th step of Algorithm 3, by Lemma 7 and , for we have

Our bounds on the variance of SVRG plus the -smoothness of yields

Thus we have by definition of and divergence,

| (24) |

Note is independent of . Telescoping bounds (24) and using optimality of so that for , we obtain

Rearranging terms, dividing over , and using convexity of , we have for and

where for inequality we use the fact that is -smooth, and the property of smoothness. ∎

To show how we implement the WarmStart procedure required in Algorithm 1, we first show the guarantee of the low-accuracy solver for finite-sum minimization of Algorithm 4.

Lemma 8 (Low-accuracy solver for finite-sum minimization).

For any problem (4) with minimizer , smoothness parameter , initial point so that , and any , Algorithm 4 with , finds a point after epochs such that .

Proof of Lemma 8.

We prove the argument by math induction and let . Note that for the base case , by Eq. (21). Now suppose the above inequality holds for , i.e. . Then for epoch by guarantee of Proposition 4 together given choice of and we have

where for the last inequality we note that series satisfies . ∎

Consequently, after epochs, we have

for any , which immediately proves the following corollary.

See 2

Now we give the formal proof of Theorem 2, the main theorem showing one can use our accelerated scheme RECAPP to solve the finite-sum minimization problem (4) efficiently.

See 2

Proof of Theorem 2.

We first consider the objective function without strong convexity. The correctness of the algorithm follows directly from Theorem 1, together with Corollary 1 and Corollary 2. For the query complexity, calling WarmStart-Svrg to implement the procedure of requires gradient queries following Corollary 2. The main Algorithm 1 calls of procedure , which by implementation of OneEpochSvrg each requires gradient queries following Corollary 1. Summing them together gives the claimed gradient complexity in total.

When the objective is -strongly-convex, the proof follows by the same argument as above and the guarantee of restarted RECAPP in Theorem 1. ∎

Appendix C Proofs for Section 6

We first consider a special case of standard mirror-prox-type methods [33] with Euclidean -divergence on and domains separately, i.e. . This ensures each step of the methods can be implemented efficiently. Below we state its guarantees, which is standard from literature and we include here for completeness.

Lemma 9 (-step guarantee of MirrorProx, cf. also Nemirovski [33]).

Let any be a convex-concave, -smooth function, in Algorithm 5 with initial points and step size outputs a point satisfying for any

| (25) |

Next we give complete proofs on the implementation of and , using MirrorProx (Algorithm 5) with proper choices of initialization , , and WarmStart-Minimax (Algorithm 6), respectively.

See 1

Proof of Lemma 1.

We incur MirrorProx with , smoothness initial point , and number of iterations . By guarantee (25) in Lemma 9, the algorithm outputs such that for any ,

Suppose has as its unique saddle-point, in particular we pick and in the above inequality to obtain

| (26) | ||||

where for the first inequality we use the definition that . Now for the LHS of (26), we have

| (27) |

Plugging (27) back to (26) and rearranging terms, we obtain

| (28) | ||||

where we use Cauchy-Schwarz inequality for Euclidean norm.

Further, to bound RHS of (28), we note that by definition of and ,

where we use strong convexity in of and convexity of .

Plugging this back in (28), we obtain

Thus we prove that can be implemented via MirrorProx properly. The total complexity includes one call to and gradient queries as each iteration in MirrorProx requires two gradients. ∎

See 2

Proof of Lemma 2.

Given domain diameter and the initialization , , we first use accelerated gradient descent (cf. Nesterov [34]) to find a -approximate solution of (which we set to be ) using gradient queries. We recall the definition of and thus

| (29) |

Now we incur MirrorProx with objective , smoothness , initial points . We let to denote its unique saddle point. Thus, we have by iterating guarantee of (25) in Lemma 9 with iterations, after calls to MirrorProx we have

where we use Cauchy-Schwarz inequality for Euclidean norms, and condition (29) and the fact that is -Lipschitz in .

Thus given being -smooth, we have

| (30) |

Note we also have

where we use that minimizes . Plugging this back to (30), we obtain .

The gradient complexity of mirror-prox part is . Summing this together with the gradient complexity for accelerated gradient descent used in obtaining gives the claimed query complexity.

∎

Appendix D Generalization of Framework and Proof of Theorem 4

In this section, we present a generalization of the framework, where we allow additive errors when implementing ApproxProx and UnbiasedProx (Definition 4 and 5). When the additive error is small enough, it would contributes to at most additive error in the function error and thus generalize our framework (Algorithm 8 and Proposition 5). In comparison to prior works APPA/Catalyst [12, 27, 28], in the application to solving max-structured problems our additive error comes from some efficient method with cheap total gradient costs, thus only contributing to the low-order terms in the oracle complexity (Theorem 4).

We first re-define the following procedures of ApproxProx and UnbiasedProx, which also tolerates additive (-)error.

Definition 4 ().

Given convex function : , regularization parameter , a centering point and two points , is a procedure that outputs an approximate solution such that for ,

| (31) |

Definition 5 ().

Given convex function : , regularization parameter , a centering point , two points , is a procedure that outputs an approximate solution such that , and

| (32) |

With the new definitions of -additive proximal oracles and -additive unbiased proximal point estimators, we can formally give the guarantee of Algorithm 8 in Proposition 5.

Proposition 5 (RECAPP with additive error).

For any convex function : , parameters , RECAPP with additive error (Algorithm 8) finds such that within iterations. The algorithm uses one call to WarmStart, and an expectation of oracle complexity

where we let , and use to denote some oracle complexity for calling each .

For any -strongly-convex : , parameters , restarted RECAPP (Algorithm 9) finds such that , using one call to WarmStart and an expectation of oracle complexity

where , , and for .

To prove the correctness of Proposition 5, we first show in Lemma 10 that implements an for given , , with the corresponding inputs. In comparison with the case presented in Section 4, the key difference is we need to ensure when we sample a large index (with tiny probability), the algorithm calls to smaller additive error , so as to ensure it contributes in total a finite additive term in the variance.

Lemma 10 (MLMC turns into ).

Given convex : , , , function in Algorithm 8 implements . Denote as some oracle complexity for calling each , then the oracle complexity for is .

Proof of Lemma 10.

Let , by definition of , we have

where we use the optimality of which implies for any , the equality that , the induction over .

In conclusion, this shows that as , and thus by choice of for , the algorithm returns a point satisfying

which shows the output is an unbiased estimator of .

For the variance, we have by a same calculation as in the proof of Proposition 1,

which proves the bound as claimed.

The query complexity is in expectation

∎

This shows that we can implement using , similar to the case without additive error , as in Proposition 1. Now we are ready to provide a complete proof of Proposition 5, which shows the correctness and complexity of Algorithm 8.

Proof of Proposition 5.

First of all we recall the notation of filtration , , , and as the minimizer of (see Appendix A for more detailed discussion).

The majority of the proof still lies in showing the potential decreasing lemma as in Proposition 3, while also taking into account the extra additive error when implementing oracles and .

Following (3), we recall the inequality that

| (33) |

Thus, by definition of , and we have that

Similarly to (18) and its analysis, we also have by definition of that

Plugging these back into (33), we conclude that

Recursively applying this bound for and together with the WarmStart guarantee we have

where we use the choice of and that . This shows the correctness of the algorithm.

The algorithm uses call to WarmStart. At each iteration , by guarantee of implementing using MLMC in Lemma 10, we have the query complexity with respect to is in expectation

which implies the total oracle complexity through calling by summing over .

The strongly-convex case follows by a similar analysis as in the proof of Proposition 2. We show by in duction

| (34) |

taking into account that by choice of , the contribution of the additive errors is always bounded by . This choice also implies the expected oracle complexity due to calling differently at each epoch and iteration. ∎

The additive errors allowed by this framework are helpful to the task of minimizing the max-structured convex objective . This is because we can then use accelerated gradient descent to solve for the best-response oracle needed in Algorithm 5 to high accuracy before calling calling Algorithm 5 , and show that MirrorProx formally implements a . The resulting gradient complexity has an extra logarithmic term on , but only shows up on a low-order terms.

Corollary 3 (Implementation of for minimizing max-structured function).

Proof of Corollary 3.

Given the initialization , we first use accelerated gradient descent Nesterov [34] to find a -approximate solution of (which we set to be ). We recall the definition of and thus

| (35) |

using gradient queries.

Then, we invoke MirrorProx with , initial point , and number of iterations . The rest of the proof is essentially the same as in Lemma 1, with the only exception that when bounding RHS of (28), we note that by choice of and the error bound in (35), it becomes

Plugging this new bound with additive error back in (28), we obtain

Thus the procedure implements . The total gradient complexity is the complexity in MirrorProx same as Lemma 2 plus the extra complexity in implementing using accelerated gradient descent, which sums up to as claimed. ∎

See 4

Proof of Theorem 4.

For the non-strongly-convex case, , the correctness of the algorithm follows directly from the non-strongly-convex case of Proposition 5, together with Corollary 3 and Lemma 2. For the query complexity, calling WarmStart-Minimax to implement the procedure of WarmStart to error requires gradient queries by Lemma 2. Following Proposition 5, denote to be the gradient complexity of implementing : we have by Corollary 3. Consequently, the total gradient complexity for implementing all is in expectation

where we use and choice of .

Summing the gradient query complexity from both WarmStart and procedures give the final complexity.

For the -strongly-convex case, the correctness of the algorithm follows directly from the strongly-convex case of Proposition 5, together with Corollary 3 and Lemma 2. The query complexity for calling one WarmStart-Minimax remains unchanged. Following Proposition 5, denote to be the gradient complexity of implementing : we have by Corollary 3. Consequently, the total gradient complexity for implementing all is in expectation

where we use and choice of and .

∎