Semiparametric Single-Index Estimation for Average Treatment Effects††thanks: We are grateful to Qi Li, Bin Peng and Yundong Tu and the seminar participants in International Association for Applied Econometrics Annual Conferences, Econometric Society Australasia Meeting, Econometric Society Asian Meeting, and Monash University for valuable comments. Huang gratefully acknowledges financial support from the Australian Government through the Research Training Program (RTP). Gao gratefully acknowledges financial support from the Australian Government through Australian Research Council under Grant Number: DP170104421. Oka gratefully acknowledges financial support from the Australian Government through the Australian Research Council’s Discovery Projects (DP190101152). Any mistakes, errors, or misinterpretations are our alone.

Difang Huang† and Jiti Gao† and Tatsushi Oka†,‡ †Department of Econometrics and Business Statistics, Monash University

‡AI Lab, CyberAgent

Abstract

We propose a semiparametric method to estimate the average treatment effect under the assumption of unconfoundedness given observational data. Our estimation method alleviates misspecification issues of the propensity score function by estimating the single-index link function involved through Hermite polynomials. Our approach is computationally tractable and allows for moderately large dimension covariates. We provide the large sample properties of the estimator and show its validity. Also, the average treatment effect estimator achieves the parametric rate and asymptotic normality. Our extensive Monte Carlo study shows that the proposed estimator is valid in finite samples. We also provide an empirical analysis on the effect of maternal smoking on babies’ birth weight and the effect of job training program on future earnings.

Keywords: Average treatment effects; Causal inference; Hermite series expansion; Propensity score.

1 Introduction

The literature on program evaluation has received considerable attention and

provided primary tools for empirical studies in social science.

One of the measures frequently used for program evaluation is the average treatment effect (ATE).

The ATE is often estimated with

restrictive parametric conditions on either the propensity score function or the outcome equation.

However, when those parametric assumptions are violated,

the estimator may suffer from

non-negligible finite-sample bias.

In this paper, we develop a semiparametric estimation method for the ATE

to alleviate the issue of possible misspecifications.

Our semiparametric approach imposes a single-index structure on the propensity score function while allowing for a flexible link function that can be approximated by Hermite polynomials.

We estimate the index parameter and the link function simultaneously in the infinitely dimensional function space.

Our approach is practically tractable and can be applied to models with a large class of error distributions.

We establish the identification of the model under some regularity conditions,

which are incorporated

in our estimation procedure,

and

show that the proposed average treatment effect estimator

achieves the parametric convergence rate and asymptotic normality. Also, by extending the propensity score residual approach in Lee (2017), we propose an estimator that is valid even when the propensity score approaches zero or one.

There are a variety of approaches for estimating the average treatment effects under the assumption of unconfoundedness (see Abadie and

Cattaneo, 2018, for an overview). The doubly robust estimators,

including the inverse probability weighting estimator augmented with additional terms (e.g. Robins

et al., 1994; Robins and

Rotnitzky, 1995) and the regression imputation estimator with the propensity score as an additional regressor (e.g. Robins

et al., 1992; Scharfstein et al., 1999), have been widely used due to the robustness against model misspecifications. The estimators are valid as long as the specification of either propensity score function or the outcome equation is correct. For example, Bang and

Robins (2005), Robins (2000), and Rotnitzky et al. (2012) combine inverse propensity score weighting and matching method with imputation and projection to estimate the treatment effects, while the efficiency of these estimators depends on the choice of tuning parameters and computational implementation. Tan (2006, 2010) proposes a nonparametric doubly robust estimation approach and show that the estimators are efficient if the parametric propensity score model is correctly specified. However, Kang and

Schafer (2007) and Vansteelandt et al. (2012) show the doubly robust estimation approach suffers from non-trivial finite sample bias when one of the two models is misspecified, with the bias being large when both models are misspecified.

In order to address concerns about bias reduction, a fast-growing literature focuses on improving the robustness of doubly robust estimators. Hirano

et al. (2003) consider a nonparametric method to estimate the propensity score and treatment effects. However, this approach is not feasible for moderately large dimension covariates. Vermeulen and

Vansteelandt (2015, 2016) propose a novel data-driven method to reduce estimation bias under the potential misspecification of both models. Farrell (2015) provides an inference approach on average treatment effects that is robust to model selection errors. Sloczynski and

Wooldridge (2018) propose a general approach for the doubly robust estimators of average treatment effects under unconfoundedness. Chernozhukov et al. (2018) provide a general method to estimate unknown functions in the nonparametric influence function and apply it to debias the estimators of average treatment effects that are feasible in high-dimensional datasets.

We contribute to this strand of literature by proposing a new average treatment effect estimator that does not rely on either propensity score function or outcome equation specification. Our estimator is computationally simple and easy to implement in empirical studies. The asymptotic variance has a simple explicit form that does not need to be estimated through bootstrapping. The estimator can work well in datasets that are limited overlap in the covariate distributions and is not influenced by the extreme observations in empirical applications. By adopting a flexible assumption on the single index structure of propensity score function, our estimator performs well when there are many covariates compared with nonparametric approaches.

This paper is also related to the literature on the estimation of binary outcome models. Hirano

et al. (2003) and Wang

et al. (2010) use a nonparametric kernel method to approximate the propensity score function, while the estimation results tend to worsen for many covariates and may not be feasible for moderately large dimension covariates due to the curse of dimensionality. Semiparametric approach with single-index structure can retain flexible specification while avoiding the curse of dimensionality. Sun

et al. (2021) propose the semiparametric single-index model for propensity score and use the kernel method to estimate its function form semiparametrically. Liu et al. (2018) relate treatment indicator with the low-dimensional linear structure of the covariates and estimate the propensity score function with a nonparametric link function. Both papers assume the boundedness of the link function and the boundedness of function support, imposing additional constraints on asymptotic theory and numerical performance.

By relaxing the parametric assumption on the propensity score model, we estimate the conditional probability using an orthogonal series-based estimation method. Compared with the approach in Liu et al. (2018) and Sun

et al. (2021), our estimation approach requires neither the boundedness of the support of the regression function nor the boundedness of the regression function itself (see Chen, 2007; Dong

et al., 2016, 2021; Li and Racine, 2007). It is computationally tractable and allows for moderately large dimension covariates. Our propensity score estimator has a super convergence rate along the direction of the true parameter and has a standard convergence rate along with all other directions, where is the sample size. Our method can be further extended by assuming the conditional probability depends on the covariates vector through several linear combinations (see Koenker and

Yoon, 2009; Li

et al., 2016; Ma and Zhu, 2012, 2013; Racine and

Li, 2004, among others).

The rest of this paper is organized as follows. Section2 introduces

treatment effect parameters of interest and Section3 explains our semiparametric estimation method. We provide the large sample properties of the estimators in Section4

and simulation results in Section5.

We present the empirical results regarding the effect of maternal smoking on babies’ birth weight and the effect of job training program on future earnings

in Section6 and conclude in Section7. Appendix A finally gives the proof of the main theorem of this paper. Due to the space limitation, there are some additional details with results about sieve expansions in Appendix B, detailed proofs in Appendix C, extra simulation results in Appendix D, and extra empirical results in Appendix E.

2 Model and Identification

2.1 Setup

We consider the setup of the binary treatment and

adopt the potential outcome framework proposed by Rubin (1974).

We use and

to denote the potential outcome without and with the treatment, respectively.

Also, is the treatment indicator taking 1

if an individual receives the treatment and 0 otherwise.

For each unit, we observe either or , and the observed outcome is

given by:

Suppose that we observe a vector of covariates with the support of

and

define

the propensity score function

.

As a measure of treatment effects, we consider the ATE, defined as:

Alternatively, Angrist (1998) discusses the variance weighted ATE, defined as:

where

.

Because

,

the weight

assigns higher weights to a subpopulation if its propensity score is closer to .

The propensity score function can be used to obtain consistent estimators for the average treatment effect . Rosenbaum and

Rubin (1983) show that under the assumption of unconfoundedness given covariates, the confounding bias can be removed using the propensity score function. Hahn (1998) proposes the regression imputation estimator that achieves the semiparametric efficiency bound for estimating average treatment effect . Hirano

et al. (2003) show that the inverse probability weighting approach can achieve semiparametric efficiency by estimating propensity score in a nonparametric fashion, while this approach may suffer from the curse of dimensionality in empirical analysis.

2.2 Identification of the Treatment Effect

This subsection

introduces assumptions and

presents an identification result.

The following conditions are introduced.

Assumption 1.

have a joint distribution

satisfying:

(a)

,

(b)

.

1(a), referred as the “unconfoundedness assumption” by Rosenbaum and

Rubin (1983), has been widely used in the studies on the treatments effects and program evaluation (e.g., Dehejia and

Wahba, 1999; Heckman

et al., 1998). The validity of this assumption can be assessed by nonparametric approach (see Rosenbaum, 2002; Ichino

et al., 2008, for example).

1(b) ensures that

the conditional probability of treatment occurrence for both treated and non-treated units is positive, usually imposed in the inverse propensity weighting approach (Hirano

et al., 2003; Firpo, 2007). Rosenbaum and

Rubin (1983) refer to the combination of these two assumptions as “strongly ignorable treatment assignment”.

Since

we can identify the propensity score

given the data,

we can examine this assumption in practice.

For the estimation of ATE, we consider the following regression model:

(1)

We use the following weighted regression model for the weighted ATE:

(2)

where

is the variance of the treatment status

conditional on . The weight based on the variance

assigns a higher weight for a more precise subsample and lower weight to a less precise subsample as the weight function associated with the reaches a maximum at and declines towards 0 when approaches to 0 or 1. In the equations above,

and are scalar parameters,

and

is error term.

The lemma below shows that, under 1,

the ATE and weighted ATE can be identified from the data; its proof is given in Appendix C.

Parameter in Equation (1)

is equivalent to the weighted ATE,

or

.

(b)

Parameter

in Equation (2)

is equivalent to the ATE,

or .

The ATE is derived by taking out the average of individual treatment effects with equal weights, while the weighted ATE assigns higher weights to sub-population that is deemed to be more important and more precise estimators and lower weights to less precise estimators.111Lee (2017) and Li

et al. (2018) also show that variance-weighted ATE is the OLS estimand in the regression of the outcome on the treatment and the vector of covariates.

3 Estimation

This section proposes the estimator of the treatment effect parameters explained

in the previous section.

Suppose that we have a sample of size equals to and observe ,

which are independent copies of .

From

Lemma 1,

we can estimate

and ,

applying a least square estimation

for Equations (1) and (2),

once the propensity score is obtained.

Thus, we shall focus on the estimation of the

propensity score.

Section3.1

presents a semiparametric estimation method for the propensity

score function

and

Section3.2 explains a practical estimation procedure.

3.1 Estimation of the Propensity Score

For the estimation of the propensity score function,

we consider a semiparametric approach,

in which the propensity function is assumed to have a single-index structure.

More specifically, the propensity score is given by

(3)

where

is a known link function

and specified as the logistic function

in our analysis

i.e.,

for ,

is an unknown nonparametric function

and

is a vector of unknown parameters.

The link function

ensures that the propensity score function

is confined to be within the unit interval.

We assume that the parameters

is an element of the compact parameter space

and

set to satisfy that and

for the purpose of identification.

The model permits general forms of heteroskedasticity in the function form of the propensity score.

The semiparametric approach with a single-index constraint can retain flexible specifications while avoiding the curse of dimensionality.

Our method relies on the optimization with the constraint of the identification condition to derive the estimator of parameter .

Compared with the semiparametric approach using nonparametric kernel method (see Liu et al., 2018; Sun

et al., 2021), our estimator does not impose restrictions on the link function or its support and establishes the asymptotic theory for inference.

We consider the case where

the nonparametric function

resides in

the Hilbert space

with

a norm

for .

The Hilbert space contains all polynomials, all power functions and all bounded, real-valued functions, which are often encountered in both applications and econometric theory (see Chen, 2007, for a review).222We explain the properties of Hilbert space used for this paper in Appendix B.

Let

be the orthonormal basis

for the Hilbert space.

Then, we have the orthogonal series expansion for

any function :

(4)

where the inner product

.

In practice,

one has to choose a truncation parameter

to approximate the infinite series, such that:

where

and

.

For the estimation of the single-index model,

we consider the maximum likelihood framework

and define the log-likelihood function as follows:

The estimators

and

of and

are defined as the solution to the following maximization problem:

(5)

Letting

,

we have an estimator of the propensity score function:

(6)

Our estimation approach for the propensity score is based on Dong

et al. (2019) that investigate a semi-parametric single-index model where the link function is allowed to be unbounded and has unbounded support. The link function is regarded as a point in an infinitely many dimensional function space and the index parameter and the link function can be estimated simultaneously from an optimization with the constraint of identification condition for the index parameter.

Compared with the least squares approach in Dong

et al. (2019), our approach considers the maximum likelihood estimation for propensity score. While we may obtain the estimation results using the delta method based on the least squares approach in Dong

et al. (2019), our approach can lead to more efficient estimation for propensity score function.

Our estimator has nice finite sample properties. First, compared with a parametric approach, such as probit and logit, our propensity score estimator is more flexible and less prone to misspecification. Second, the estimator can be used for cases with multiple regressors and avoids the curse of dimensionality commonly encountered in nonparametric methods (e.g., Hahn, 1998; Hirano

et al., 2003). Finally, we do not impose any distributional assumptions on the covariates by including continuous, discrete, and categorical variables.

3.2 Estimation Procedure

This subsection provides an estimation procedure for the nonlinear constrained optimization problem in Equation (5) and a procedure for the selection of the truncation parameter among a set of suitable candidate values.333To the best of our knowledge, existing works examine the choice of optimal truncation parameter for non-parametric models (e.g. Gao

et al., 2002), while there are limited theoretical research on the optimal choice for the single-index model. We leave it for future work.

Given a truncation parameter , we obtain the estimators

and

as follows:

Algorithm 1. For a fixed truncation parameter ,

(i) Use a linear regression estimator

as the initial estimator

(ii) Obtain the estimator

as the solution to the problem:

.

(iii) Given the estimator

,

obtain the estimator as the solution to

the constrained optimization problem:

where is a scalar Lagrange multiplier.

The truncation error becomes negligible

asymptotically under the regularity conditions.

For the choice of the truncation parameter,

we propose the leave-one-out cross-validation as follows:

Algorithm 2.

Let be

a set of candidate values of the truncation parameter.

(i) For each , we apply Algorithm 1 for the observations without using -th observation and

obtain the leave-one-out estimate,

denoted by .

(ii) The optimal truncation parameter

minimizes the prediction mean of squares:

4 Asymptotic Properties

To establish asymptotic properties for the average treatment effect estimator, we assume the following conditions and provide justifications for the following assumptions.

Assumption 2.

(a)

The observations are

independent copies of .

(b)

Define the population objective function

, where .

Let

be a subset of such that .

(i)

All derivatives for and .

(ii)

has the unique maximum at .

(iii)

,

for some .

(c)

The truncation parameter

satisfies that

and as .

2(b) covers assumptions that are commonly used in the existing literature on sieve estimation (see Chen, 2007, for a review) and binary choice model (e.g., Coppejans, 2001; Cosslett, 1983; Ichimura, 1993; Klein and

Spady, 1993) as a special case and includes many commonly used distributions such as normal distribution and those possessing compact support. Recall we impose with for identification purpose. The estimator is derived from an optimization with the constraints for index parameter, and we do not need to impose additional parameter normalization conditions.444Ma et al. (2021) develops a semiparametric single index estimator for the propensity score with a one-step maximum likelihood-type estimator that imposes parameter normalizations. Our approach relax such restrictions on parameters including function form and parameter as long as the identification condition with holds.2(c) imposes the smoothness restrictions on the link function and the divergence restrictions on the truncation parameter to guarantee the truncation error is negligible.

For theoretical developments, we need to assume additional regularity conditions. Since these conditions are standard in the literature,

we state the conditions as 3.

Assumption 3.

Let be a relatively small positive number and , and be positive constants. Suppose that the following conditions hold:

(a)

For ,

(b)

Let and , where .

We assume that

and

,

where and denote the minimum and maximum eigenvalues of a square matrix , respectively.

(c)

Suppose that (i) ; (ii) .

3(a) covers commonly used conditions in the existing literature and imposes the uniform convergence of in a small neighborhood. For instance, Yu and

Ruppert (2002) require the uniform convergence in a small neighborhood and can be derived using the results of Lemma A2 in Newey and

Powell (2003). For simplicity, we impose condition (ii) and (iii) in 3(a) directly. 3(b) is similar with Assumption 2 of Newey (1997) and Assumption 3 of Su and Jin (2012) and the restrictions on the derivatives of orthogonal Hermite functions

can be derived using the results in Belloni et al. (2015). 3(c) is the under smoothing condition (see Belloni et al., 2015; Chang

et al., 2015) that guarantees the negligibility of the truncation error terms and asymptotic normality of estimator.

Assumption 4.

Let be a relatively small positive number. As let uniformly in , where

4 imposes restrictions on the probability distribution functions of the regressors and to make the functions reduce to as we use Hermite polynomials to decompose the link function in the function space and the link function is potentially unbounded and with unbounded support.

We are now ready to establish the large sample properties of the estimators for ATE and variance weighted ATE defined in Section3.2 where the propensity score is estimated based on the series estimation approach in Section3.1. The proof of Theorem1 below is given in Appendix A.

Theorem 1.

Suppose that Assumptions 2–4 hold. Then, as ,

(a)

,

(b)

,

where

and

.

Our proposed estimator has several advantages over other estimators including the inverse propensity score weighting (Hirano

et al., 2003; Imbens, 2010), matching (Abadie and

Imbens, 2006, 2011, 2016), regression adjustment (Lane and

Nelder, 1982), and doubly robust estimators (Tan, 2010; Tsiatis, 2006; Wooldridge, 2007; Liu et al., 2018).

First, our estimator is computationally simple and easy to implement. There is no need to specify the propensity score function form and truncation parameter. Second, our estimator has a simple explicit form of asymptotic variance that works well even in small samples, and we do not need to estimate the asymptotic variance through bootstrap procedures. Third, compared with the inverse propensity score approach, our estimation method works well in the datasets that are limited overlap in the covariate distributions and is not influenced by extreme observations in empirical applications.555Wooldridge (2007) proposes the inverse probability weighted M-estimation under a general missing data scheme and shows the misspecication of the error distribution is negligible under some regularity conditions, including the existence of pseudo-parameters. Our approach relaxes the requirement and our simulation and empirical results, reported in Sections 5 and 6, show some advantages of our approach in finite samples. Fourth, by adopting a flexible assumption on the single index structure of propensity score function, our estimator performs well when there are many covariates.

For statistical inferences,

we need to estimate the asymptotic variances

and .

Following the sample analog principles,

we can estimate the asymptotic variances

by using the sample moments based on

the observables:

,

,

and

.

We denote

by

and

the estimator of and , respectively.

The proposition below shows that those estimators are consistent. The proof of Proposition1 is given in Appendix C.

Proposition 1.

Let Assumptions 2–4 hold. Then, as ,

(a) ; and (b) .

5 Monte Carlo studies

We conduct an extensive simulation study for the finite sample properties of our semiparametric estimator proposed in Section3.2 for the average treatment effect. We repeat each experiment 10,000 times with sample size = 400, 800, or 1600 and set the truncation parameter equal to .666Our simulation results are valid and robust to a range of truncation parameters, as demonstrated in Appendix D.

Setting 5A: , where and the vector of covariates are generated from independent standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 5B: , where and the vector of covariates are generated from independent standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 5C: ,

where and the vector of covariates are generated from independent standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 5D: ,

where and the vector of covariates are generated from independent standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

We summarize the simulation results in Table1. In all four simulation settings, our estimators perform well according to bias and standard deviation criteria. For all the sample sizes under consideration, the estimators have relative small biases and standard deviations. The finite–sample simulation results support that the asymptotic normal approximation is accurate and the rate of convergence is consistent with the results in Theorem1.

Table 1: Simulation Results the Estimators of Average Treatment Effect of Settings 5A to 5D.

Setting

Setting

Bias

5A

400

0.0049

5C

400

-0.0054

800

-0.0003

800

0.0002

1600

-0.0001

1600

-0.0002

5B

400

0.0042

5D

400

0.0028

800

-0.0005

800

-0.0011

1600

-0.0001

1600

-0.0003

Std

5A

400

0.0418

5C

400

0.0403

800

0.0289

800

0.0277

1600

0.0225

1600

0.0180

5B

400

0.0380

5D

400

0.0366

800

0.0274

800

0.0243

1600

0.0201

1600

0.0167

In Appendix D, there are many more simulation results to show that both the proposed model and the estimation method work well numerically.777We also compare our estimator with recent approaches to propensity score estimation based on covariates balancing (e.g., Sant’Anna

et al., 2022; Imai and

Ratkovic, 2014; Zubizarreta, 2015) and high-dimensional selection (e.g., Belloni et al., 2017; Chernozhukov et al., 2018; Sun and Tan, 2021). These results are available upon request.

6 Empirical Study

In this section, we apply the proposed semiparametric method to analyze two real data examples. We study the effect of maternal smoking on babies’ birth weight in the main context and consider the effects of the job training program on future earnings in Appendix E.888As shown in Cattaneo

et al. (2015), the assumption that maternal smoking is exogenous to the babies’ birth outcome may not hold. We apply our approach for this empirical study as it is widely used in treatment effects studies as a benchmark. We also provide the effects of the job training program on future earnings in Appendix E as an additional empirical study.

In both cases, we demonstrate the validity of our estimation and inference method for the datasets with potential misspecification of propensity score and datasets with limited overlap.

We apply our semiparametric method to analyze the ATE of maternal smoking on babies’ birth weight. Low birth weight may increase infant mortality rates and economic costs, including late entry into kindergarten, repeated grades, and longer-term labor market outcomes (Arcidiacono and

Ellickson, 2011; Permutt and

Hebel, 1989; Rosenzweig and

Wolpin, 1991).

Although a large body of research confirms the negative effect of maternal smoking on babies’ birth weight, there is no consensus on its exact magnitude (Abrevaya, 2001, 2006; Chernozhukov and

Fernandez-Val, 2011; Evans and

Ringel, 1999). We use the dataset of low birth weight initially by Almond

et al. (2005). This is a rich database of singletons in Pennsylvania with 4,642 detailed observations of mothers and their infants’ birth information.

The outcome variable is infant birth weight measured in grams. The binary treatment variable is the mother’s smoking status ( indicates mother is a smoker, indicates mother is a non-smoker). The covariates include mother’s age, mother’s marital status, an indicator variable for alcohol consumption during pregnancy, an indicator for whether there was a previous birth where the newborn died, mother’s education, father’s education, number of prenatal care visits, mother’s race, an indicator of firstborn baby, and months since last birth (see Cattaneo, 2010).

The critical assumption in our application is that the mother’s smoking status is independent of the infant’s birth weight conditional on all observed demographic variables, implying that maternal smoking may impact the babies’ birth weights only through its effect on observed covariates. We show the summary statistics for all variables in Table2, which provides the summary statistics for baby birth weight data, where denotes sample size. For each variable, we report the sample average (Mean) and sample standard deviation (Std). *, **, and *** indicate the significance level at 10%, 5%, and 1%, respectively. As it reveals, the comparison between these two groups show that control group is quite different from the treated group.

Table 2: Summary Statistics for Baby Birth Weight data.

Non-smoking Group

Smoking Group

Two-Sample

Difference

Mean

Std

Mean

Std

Infant birth weight

3412.91

570.69

3137.66

560.89

275.3***

Previous births with dead babys

0.25

0.43

0.32

0.47

-0.0724***

Mother’s age

26.81

5.65

25.17

5.30

1.644***

Mother’s education

12.93

2.53

11.64

2.17

1.291***

Father’s education

12.67

3.48

10.70

4.10

1.970***

Number of prenatal care visits

10.96

3.52

9.86

4.21

1.101***

Months since last birth

21.90

31.50

28.22

36.92

-6.322***

1 if mother married

0.75

0.43

0.47

0.50

0.278***

1 if alcohol consumed

0.02

0.14

0.09

0.29

-0.0726***

1 if mother is white

0.85

0.36

0.81

0.39

0.0388**

1 if first baby

0.45

0.50

0.37

0.48

0.0816***

Table 3: Average Treatment Effect Estimation for the Low Birth Weight Data.

ATE

Std

-statistics

-value

95% CI

AIPW

-231.20

27.35

-8.45

0.00

-284.82

-177.59

IPW

-232.73

26.63

-8.74

0.00

-284.93

-180.53

IPW-RA

-229.69

28.58

-8.04

0.00

-285.70

-173.67

MBC

-219.06

32.96

-6.65

0.00

-283.65

-154.47

PSM

-235.26

31.67

-7.43

0.00

-297.33

-173.20

RA

-234.97

25.25

-9.31

0.00

-284.46

-185.48

Efficient

-295.77

38.62

-7.66

0.00

-371.47

-220.07

Local

-306.32

54.50

-5.62

0.00

-413.14

-199.50

Logistic

-352.11

46.78

-7.53

0.00

-443.80

-260.42

Our Estimator ()

-217.90

22.82

-9.55

0.00

-262.63

-173.16

Table3 shows the estimation of average treatment effect based on our approach. The naive difference in the weight of babies belonging to non-smoking and smoking mothers is 275.3 grams. Given the potential confounding effects of covariates on the potential outcome, this result may not be a valid estimate of the average treatment effect. We next compare the results of average treatment effect estimation using the augmented inverse propensity weighting (AIPW) estimator (Tan, 2010; Tsiatis, 2006), inverse propensity weighting (IPW) estimator (Hirano

et al., 2003; Imbens, 2010), inverse propensity weighting with regression adjustment (IPW-RA) estimator (Wooldridge, 2007), bias-corrected matching (MBC) estimator (Abadie and

Imbens, 2006, 2011), propensity score matching (PSM) estimator (Rosenbaum and

Rubin, 1983; Abadie and

Imbens, 2016), regression adjustment (RA) estimator (Lane and

Nelder, 1982), doubly robust with either efficient propensity score estimation (Efficient) or parametric logistic estimation (Logistic) estimators (Liu et al., 2018; Ma and Zhu, 2013). We summarize the above estimation results for the average treatment effect of maternal smoking on babies’ birth weight in Table3 with the mean, standard deviation, -statistics, -value, and 95% confidence interval.

We note that the doubly robust estimator using the propensity score estimated by logistic regression is different from other estimators, suggesting that the parametric logistic form may not be suitable for the propensity score function in this data example. In comparison, our estimation approach is valid to potential misspecification of the propensity score function and provides a valid estimation and inference for the average treatment effect.

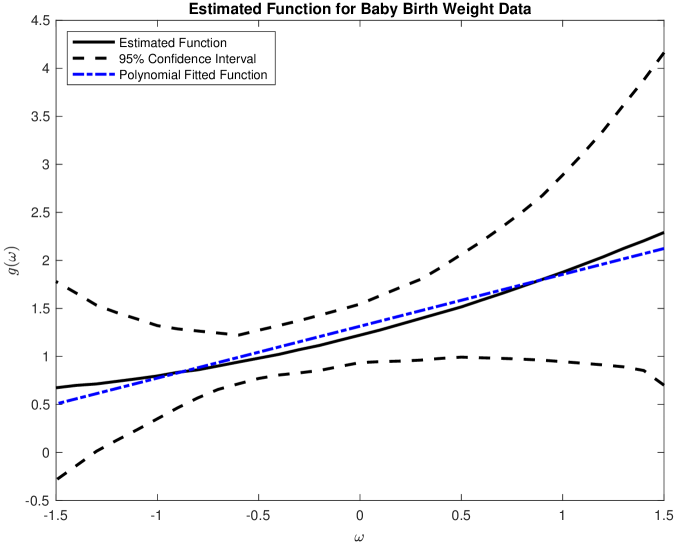

To further illustrate the potential misspecification of propensity score, we plot the estimated link function of propensity score using the wild bootstrap simulation with 500 bootstrap repetitions. As we use the logistic link function in Equation3, if the true DGP for propensity score in this data example is logistic, then the estimated link function should be identity function. We calculate the optimal truncation parameter based on the minimization of the prediction mean of squares. In this data example, the optimal truncation parameter . We estimate the approximated second-order polynomial fitted function using the ordinary least squares estimation approach as following (with standard errors in bracket):

where is the for .

Figure 1: Estimated nonparametric link function of the propensity score for the baby birth weight data.

We show the estimation in Figure1 with the estimated link function in solid line and the corresponding 95% confidence interval in dashed line. We also plot the approximated second-order polynomial fitted function using the ordinary least squares estimation approach as a reference. Our results show that the estimated link function does not seem to be an identity function. Such potential misspecification of propensity score may explain the differences for the treatment effect estimation between our estimator and the doubly robust estimator using the propensity score estimated by logistic regression. Both the estimated link function and the approximated second-order polynomial fitted function are close to each other, showing the estimation method work well in this empirical application.

7 Conclusion

To address the issue of possible misspecifications, we propose a semiparametric estimation method for the average treatment effect. Our approach assumes the propensity score function with a single-index structure, and a flexible link function is allowed. We estimate the index parameter and link function simultaneously in the infinitely dimensional function space and estimate the propensity score by implementing an optimization with the constraints of identification conditions and establish the large sample properties of our estimator. Our method is empirically applicable and can be used for models with a wide range of error distributions. Our approach also provides computational flexibility for moderately large dimension problems.

We conduct an extensive simulation study to evaluate the finite sample performance of our proposed estimator in finite samples. We provide the empirical results on the effect of maternal smoking on babies’ birth weight and the effect of the job training program on future earnings. We find that, compared to the widely used average treatment effect estimators, our approach is less prone to misspecification of the propensity score function and is valid when the propensity score approaches zero or one.

References

Abadie and

Cattaneo (2018)

Abadie, A. and M. D. Cattaneo (2018).

Econometric methods for program evaluation.

Annual Review of Economics10(1), 465–503.

Abadie and

Imbens (2006)

Abadie, A. and G. Imbens (2006).

Large sample properties of matching estimators for average treatment

effects.

Econometrica74(1), 235–267.

Abadie and

Imbens (2011)

Abadie, A. and G. Imbens (2011).

Bias-corrected matching estimators for average treatment effects.

Journal of Business & Economic Statistics29(1),

1–11.

Abadie and

Imbens (2016)

Abadie, A. and G. Imbens (2016).

Matching on the estimated propensity score.

Econometrica84(2), 781–807.

Abrevaya (2001)

Abrevaya, J. I. (2001).

The effects of demographics and maternal behavior on the distribution

of birth outcomes.

Empirical Economics26(1), 247–257.

Abrevaya (2006)

Abrevaya, J. I. (2006).

Estimating the effect of smoking on birth outcomes using a matched

panel data approach.

Journal of Applied Econometrics21(4), 489–519.

Almond

et al. (2005)

Almond, D., K. Y. Chay, and D. S. Lee (2005).

The costs of low birth weight.

The Quarterly Journal of Economics120(3),

1031–1083.

Angrist (1998)

Angrist, J. D. (1998, March).

Estimating the labor market impact of voluntary military service

using social security data on military applicants.

Econometrica66(2), 249.

Arcidiacono and

Ellickson (2011)

Arcidiacono, P. and P. Ellickson (2011).

Practical methods for estimation of dynamic discrete choice models.

Annual Review of Economics3(1), 363–394.

Bang and

Robins (2005)

Bang, H. and J. M. Robins (2005).

Doubly robust estimation in missing data and causal inference models.

Biometrics61(4), 962–973.

Belloni et al. (2015)

Belloni, A., V. Chernozhukov, D. Chetverikov, and K. Kato (2015).

Some new asymptotic theory for least squares series: Pointwise and

uniform results.

Journal of Econometrics186(2), 345–366.

Belloni et al. (2017)

Belloni, A., V. Chernozhukov, I. Fernandez-Val, and C. Hansen (2017).

Program evaluation with high-dimensional data.

Econometrica85(1), 233–298.

Cattaneo (2010)

Cattaneo, M. (2010).

Efficient semiparametric estimation of multi-valued treatment effects

under ignorability.

Journal of Econometrics155(2), 138–154.

Cattaneo

et al. (2015)

Cattaneo, M., B. Frandsen, and R. Titiunik (2015).

Randomization inference in the regression discontinuity design: An

application to party advantages in the u.

S. Senate. Journal of Causal Inference3(1), 1–24.

Chang

et al. (2015)

Chang, J., S. X. Chen, and X. Chen (2015).

High dimensional generalized empirical likelihood for moment

restrictions with dependent data.

Journal of Econometrics185(1), 283–304.

Chen (2007)

Chen, X. (2007).

Chapter 76 large sample sieve estimation of semi-nonparametric

models.

Volume 6 of Handbook of Econometrics, pp. 5549–5632.

Elsevier.

Chernozhukov et al. (2018)

Chernozhukov, V., D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, W. Newey,

and J. Robins (2018, 01).

Double/debiased machine learning for treatment and structural

parameters.

The Econometrics Journal21(1), C1–C68.

Chernozhukov and

Fernandez-Val (2011)

Chernozhukov, V. and I. Fernandez-Val (2011).

Inference for extremal conditional quantile models, with an

application to market and birthweight risks.

The Review of Economic Studies78(2), 559–589.

Coppejans (2001)

Coppejans, M. (2001).

Estimation of the binary response model using a mixture of

distributions estimator (mod).

Journal of Econometrics102(2), 231–269.

Cosslett (1983)

Cosslett, S. R. (1983).

Distribution-free maximum likelihood estimator of the binary choice

model.

Econometrica51(3), 765–782.

Dehejia and

Wahba (1999)

Dehejia, R. and S. Wahba (1999).

Causal effects in nonexperimental studies: Reevaluating the

evaluation of training programs.

Journal of the American Statistical Association94(448), 1053–1062.

Dong

et al. (2019)

Dong, C., J. Gao, and B. Peng (2019).

Series estimation for single-index models under constraints.

Australian & New Zealand Journal of Statistics61(3), 299–335.

Dong

et al. (2016)

Dong, C., J. Gao, and D. B. Tjostheim (2016).

Estimation for single-index and partially linear single-index

integrated models.

Annals of Statistics44(1), 425–453.

Dong

et al. (2021)

Dong, C., O. Linton, and B. Peng (2021).

A weighted sieve estimator for nonparametric time series models with

nonstationary variables.

Journal of Econometrics222(2), 909–932.

Evans and

Ringel (1999)

Evans, W. N. and J. S. Ringel (1999).

Can higher cigarette taxes improve birth outcomes.

Journal of Public Economics72(1), 135–154.

Farrell (2015)

Farrell, M. (2015).

Robust inference on average treatment effects with possibly more

covariates than observations.

Journal of Econometrics189(1), 1–23.

Firpo (2007)

Firpo, S. (2007).

Efficient semiparametric estimation of quantile treatment effects.

Econometrica75(1), 259–276.

Gao

et al. (2002)

Gao, J., H. Tong, and R. Wolff (2002, April).

Adaptive orthogonal series estimation in additive stochastic

regression models.

Statistica Sinica12(2), 409–428.

Hahn (1998)

Hahn, J. (1998).

On the role of the propensity score in efficient semiparametric

estimation of average treatment effects.

Econometrica66(2), 315–331.

Heckman

et al. (1998)

Heckman, J., H. Ichimura, and P. Todd (1998).

Matching as an econometric evaluation estimator.

Review of Economic Studies65(2), 261–294.

Hirano

et al. (2003)

Hirano, K., G. Imbens, and G. Ridder (2003).

Efficient estimation of average treatment effects using the estimated

propensity score.

Econometrica71(4), 1161–1189.

Ichimura (1993)

Ichimura, H. (1993).

Semiparametric least squares (SLS) and weighted SLS estimation of

single-index models.

Journal of Econometrics58(1-2), 71–120.

Ichino

et al. (2008)

Ichino, A., F. Mealli, and T. Nannicini (2008).

From temporary help jobs to permanent employment: What can we learn

from matching estimators and their sensitivity?

Journal of Applied Econometrics23(3), 305–327.

Imai and

Ratkovic (2014)

Imai, K. and M. Ratkovic (2014).

Covariate balancing propensity score.

Journal of The Royal Statistical Society Series B-statistical

Methodology76(1), 243–263.

Imbens and

Rubin (2015)

Imbens, G. and D. Rubin (2015).

Causal Inference in Statistics, Social, and Biomedical

Sciences.

Cambridge University Press.

Imbens (2010)

Imbens, G. W. (2010).

Better late than nothing: Some comments on Deaton (2009) and

Heckman and Urzua (2009).

Journal of Economic Literature48(2), 399–423.

Kang and

Schafer (2007)

Kang, J. and J. Schafer (2007).

Demystifying double robustness: A comparison of alternative

strategies for estimating a population mean from incomplete data.

Statistical Science22(4), 523–539.

Klein and

Spady (1993)

Klein, R. W. and R. H. Spady (1993).

An efficient semiparametric estimator for binary response models.

Econometrica61(2), 387.

Koenker and

Yoon (2009)

Koenker, R. and J. Yoon (2009).

Parametric links for binary choice models: A fisherian-bayesian

colloquy.

Journal of Econometrics152(2), 120–130.

LaLonde (1986)

LaLonde, R. J. (1986).

Evaluating the econometric evaluations of training programs with

experimental data.

The American Economic Review76(4), 604–620.

Lane and

Nelder (1982)

Lane, P. W. and J. A. Nelder (1982).

Analysis of covariance and standardization as instances of

prediction.

Biometrics38(3), 613–621.

Lee (2017)

Lee, M.-J. (2017).

Simple least squares estimator for treatment effects using propensity

score residuals.

Biometrika105(1), 149–164.

Levin and

Lubinsky (1992)

Levin, A. and D. S. Lubinsky (1992).

Christoffel functions, orthogonal polynomials, and nevai’s conjecture

for freud weights.

Constructive Approximation8(4), 463–535.

Li

et al. (2016)

Li, D., X. Wang, L. Lin, and D. K. Dey (2016).

Flexible link functions in nonparametric binary regression with

gaussian process priors.

Biometrics72(3), 707–719.

Li

et al. (2018)

Li, F., K. L. Morgan, and A. M. Zaslavsky (2018).

Balancing covariates via propensity score weighting.

Journal of the American Statistical Association113(521), 390–400.

Li and Racine (2007)

Li, Q. and J. S. Racine (2007).

Nonparametric Econometrics: Theory and Practice.

Princeton University Press.

Liu et al. (2018)

Liu, J., Y. Ma, and L. Wang (2018).

An alternative robust estimator of average treatment effect in causal

inference.

Biometrics74(3), 910–923.

Ma and Zhu (2012)

Ma, Y. and L. Zhu (2012).

A semiparametric approach to dimension reduction.

Journal of the American Statistical Association107(497), 168–179.

Ma and Zhu (2013)

Ma, Y. and L. Zhu (2013).

Efficient estimation in sufficient dimension reduction.

The Annals of Statistics41(1), 250–268.

Newey (1997)

Newey, W. K. (1997).

Convergence rates and asymptotic normality for series estimators.

Journal of Econometrics79(1), 147–168.

Newey and

Powell (2003)

Newey, W. K. and J. L. Powell (2003).

Instrumental variable estimation of nonparametric models.

Econometrica71(5), 1565–1578.

Permutt and

Hebel (1989)

Permutt, T. and J. R. Hebel (1989).

Simultaneous-equation estimation in a clinical trial of the effect of

smoking on birth weight.

Biometrics45(2), 619–622.

Racine and

Li (2004)

Racine, J. and Q. Li (2004).

Nonparametric estimation of regression functions with both

categorical and continuous data.

Journal of Econometrics119(1), 99–130.

Robins (2000)

Robins, J. (2000).

Marginal Structural Models versus Structural nested Models as

Tools for Causal inference.

New York: Springer.

Robins and

Rotnitzky (1995)

Robins, J. and A. Rotnitzky (1995).

Semiparametric efficiency in multivariate regression models with

missing data.

Journal of the American Statistical Association90(429), 122–129.

Robins

et al. (1994)

Robins, J., A. Rotnitzky, and L. Zhao (1994).

Estimation of regression coefficients when some regressors are not

always observed.

Journal of the American Statistical Association89(427), 846–866.

Robins

et al. (1992)

Robins, J. M., S. D. Mark, and W. K. Newey (1992).

Estimating exposure effects by modelling the expectation of exposure

conditional on confounders.

Biometrics48(2), 479–495.

Rosenbaum (2002)

Rosenbaum, P. (2002).

Observational Studies.

New York: Springer.

Rosenbaum and

Rubin (1983)

Rosenbaum, P. and D. Rubin (1983).

The central role of the propensity score in observational studies for

causal effects.

Biometrika70(1), 41–55.

Rosenzweig and

Wolpin (1991)

Rosenzweig, M. R. and K. I. Wolpin (1991).

Inequality at birth: The scope for policy intervention.

Journal of Econometrics50(1), 205–228.

Rotnitzky et al. (2012)

Rotnitzky, A., Q. Lei, M. Sued, and J. M. Robins (2012).

Improved double-robust estimation in missing data and causal

inference models.

Biometrika99(2), 439–456.

Rubin (1974)

Rubin, D. (1974).

Estimating causal effects of treatments in randomized and

nonrandomized studies.

Journal of Educational Psychology66(5), 688–701.

Sant’Anna

et al. (2022)

Sant’Anna, P. H. C., X. Song, and Q. Xu (2022).

Covariate distribution balance via propensity scores.

Journal of Applied Econometricsn/a(n/a).

Scharfstein et al. (1999)

Scharfstein, D. O., A. Rotnitzky, and J. M. Robins (1999).

Adjusting for nonignorable drop-out using semiparametric nonresponse

models.

Journal of the American Statistical Association94(448), 1096–1120.

Sloczynski and

Wooldridge (2018)

Sloczynski, T. and J. Wooldridge (2018).

A general double robustness result for estimating average treatment

effects.

Econometric Theory34(1), 112–133.

Su and Jin (2012)

Su, L. and S. Jin (2012).

Sieve estimation of panel data models with cross section dependence.

Journal of Econometrics169(1), 34–47.

Sun and Tan (2021)

Sun, B. and Z. Tan (2021).

High-dimensional model-assisted inference for local average treatment

effects with instrumental variables.

Journal of Business & Economic Statistics0(0),

1–13.

Sun

et al. (2021)

Sun, Y., K. X. Yan, and Q. Li (2021).

Estimation of average treatment effect based on a semiparametric

propensity score.

Econometric Reviews40(9), 852–866.

Tan (2006)

Tan, Z. (2006).

A distributional approach for causal inference using propensity

scores.

Journal of the American Statistical Association101(476), 1619–1637.

Tan (2010)

Tan, Z. (2010).

Bounded, efficient and doubly robust estimation with inverse

weighting.

Biometrika97(3), 661–682.

Tsiatis (2006)

Tsiatis, A. A. (2006).

Semiparametric Theory and Missing Data.

New York: Springer.

Vansteelandt et al. (2012)

Vansteelandt, S., M. Bekaert, and G. Claeskens (2012).

On model selection and model misspecification in causal inference.

Statistical Methods in Medical Research21(1), 7–30.

Vermeulen and

Vansteelandt (2015)

Vermeulen, K. and S. Vansteelandt (2015).

Bias-reduced doubly robust estimation.

Journal of the American Statistical Association110(511), 1024–1036.

Vermeulen and

Vansteelandt (2016)

Vermeulen, K. and S. Vansteelandt (2016).

Data-adaptive bias-reduced doubly robust estimation.

The International Journal of Biostatistics12(1),

253–282.

Wang

et al. (2010)

Wang, L., A. Rotnitzky, and X. Lin (2010).

Nonparametric regression with missing outcomes using weighted kernel

estimating equations.

Journal of the American Statistical Association105(491), 1135–1146.

Wooldridge (2007)

Wooldridge, J. M. (2007).

Inverse probability weighted estimation for general missing data

problems.

Journal of Econometrics141(2), 1281–1301.

Yu and

Ruppert (2002)

Yu, Y. and D. Ruppert (2002).

Penalized spline estimation for partially linear single-index models.

Journal of the American Statistical Association97(460), 1042–1054.

Zubizarreta (2015)

Zubizarreta, J. R. (2015).

Stable weights that balance covariates for estimation with incomplete

outcome data.

Journal of the American Statistical Association110(511), 910–922.

Appendix

Appendix A provides proof for Theorem1. Appendix B gives some preliminary results about Hilbert space, Appendix C gives the proofs of the main results, Appendix D provides some additional numerical results, and Appendix E presents additional empirical application results.

We prove the asymptotic normality of and in two steps. In the first step, we take the first-stage errors into account when estimating the propensity score function . In the second step, we prove the asymptotic properties of sample analog of treatment effects estimators.

(a) We write

We first consider the asymptotic properties of , by the orthogonality, we write

where the first inequality follows from the Lipschitz continuity of , the third equality follows from the orthogonality of Hermite polynomials.

For , denote the term as . By 2(a), we have and . Applying the Lindeberg–Levy CLT, we have:

For , we write:

where the second equality follows from 2(a), the fourth inequality follows from the triangular inequality.

For , we write:

where the first inequality follows from 3(a), the second equality follows from mean value theorem, the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 2(b) and the fact that and is bounded by 1.

For , we write:

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 3(c) and Lemma A1 from Dong

et al.(2019).

For , we write

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, the fourth inequality follows from Lemma A4 in Dong

et al.(2019), and the last inequality follows from the definition of .

For , we write:

where the second equality follows from 2(a), the fourth inequality follows from the triangular inequality and similar proofs as .

For , we write:

where the second equality comes from the boundness of , the third inequality comes from triangular inequality, and the fourth equality comes from the similar proofs as .

In sum, we have shown the following asymptotic normality:

(b) We write:

Following similar derivations to those used for , we have

For , denote the term as . By 2(a), we have and . Applying the Lindeberg–Levy CLT, we have:

For , we write

where the second inequality follows from 2(a) and boundness of , and the third equality follows from the similar proofs as .

For , we write:

where the second inequality follows from 2(a) and boundness of , and the third equality follows from the similar proofs as .

For , we write:

where the second inequality follows from 2(a) and boundedness of , and the third equality follows from the similar proofs as .

Appendix B: Preliminary properties for Hilbert Space

In this section, we present the properties of the Hilbert Space that includes all polynomials, all power functions, all bounded functions, and even some exponential functions. More importantly, all functions in the space are defined on the entire real line.

An inner product for is given by:

Hermite polynomials form a complete orthogonal sequence in with each elements defined by:

for .

The orthogonality of this basis system satisfies , where is the Kronecker delta. For , we have orthogonal series expansion:

For any truncation parameter , we split the orthogonal series expansion into two parts as following:

(B.1)

where , , , and the approximation residual is given by .

The quantity of is crucial for the asymptotic properties of our estimators, using the results in the Theorem 1.1 of Levin and

Lubinsky (1992) and Dong

et al. (2021), we have:

uniformly for and where is given.999In our context, . In addition, we can show that the order of is when the condition for satisfies as long as the truncation parameter diverge.

Appendix C: Proofs for the main results and other results

Proof of Lemma 2.1.

(a)

We have

under 1(b),

and thus the regression parameter can be written as:

It follows from the law of iterated expectation that:

This leads to the desired result.

(b)

Under 1(b) and the law of iterated expectation,

and thus the regression parameter can be written as:

Given the unconfoundedness under 1(a) and that , we have:

Thus, the desired result follows.

∎

In addition to the main results established in Section 4 of the submission, we have the following important results. The following lemma establishes the consistency of the estimators .

Lemma C.1: Define the norm

over the space .

Suppose that 2 holds. Then, we have, as ,

In Lemma C.2 below,

we establish the convergence rate and the limit distribution

of the estimator .

To present the result,

let

be a matrix.

Under the constraint of ,

can be considered as the projection matrix

that maps any vector

into the orthogonal complement space of true parameter .

Let

be a

matrix consisting of eigenvectors

associated with eigenvalue of 1.

Lemma C.2: Let Assumptions 2 and 3 hold. Then,

as ,

(a)

(b)

,

where

and

.

Lemma C.2(a) establishes the asymptotic normality of that utilizes the transformation of into as both and belongs to the unit ball of . Lemma C.2(b) is due to the constraint of . It measures the distance of to the surface of unit ball and indicates that along the direction of true value , the estimated value converges with a faster rate than in all other directions that are orthogonal to true value .

Proof of Lemma C.1.

Note that the objective function in Equation (5) is interchangeable with the sample version of population objective function .

Our proof is composited of two parts. In the first part, we prove the convergence of sample objective function to the population objective using Lemma A2 in Newey and

Powell(2003). In the second part, we prove the consistency of by contradiction.

(a) We begin to prove the convergence of sample objective function to the population objective :

We proceed by checking whether Conditions (i) to (iii) in Lemma A2 of Newey and

Powell(2003) hold.

For Condition (i), as we assume that is a compact subset of the parameter space and is defined with norm. Therefore, Condition (i) holds.

For Condition (ii), as we assume that the data generating process is independent and identically distributed in 2(a), therefore, we apply the Law of Large Numbers (LLN) and show that:

Therefore, Condition (ii) holds.

For Condition (iii), we prove by showing the continuity of holds, which indicates that the continuity of holds with probability approaching 1.

For any given and belonging to , we have:

For , we have:

where the second inequality follows from the fact that is a binary variable and the Cauchy-Schwarz inequality.

which indicates the continuity of . Therefore, Condition (iii) of Lemma A2 of Newey and

Powell(2003) holds. We then have shown .

(b) We next show the consistency of by contradiction. By definition of , regardless of the value of , we have:

By the uniform convergence and the continuity of , if , we have:

with probability approaching 1, which contradicts the definition of as the maximizer for the sample version of objective function.

Therefore, we have .

∎

Proof of Lemma C.2.

To simplify the notation, we denote the constrained maximization objective function in Equation (5) with:

where is the Lagrange multiplier.

We prove the asymptotic normality of in two parts. In the first part, we use the routine procedure in Yu and

Ruppert(2002) to study the objective function . In the second part, we analyze the asymptotic property of each function used in this procedure.

(1)

In the first part, by the definition of , we have:

By multiplying in both sides of ,

we have:

Multiplying to both sides of , we have:

where the second equality follows from Taylor expansion with lies between and , the third equality follows from , and the fourth equality follows from .

(2)

In the second part, we analyze the asymptotic property of and used in the above procedure. Similar to the proofs in Lemma C.1, it is easy to show . We therefore focus on a sufficiently small neighborhood of in the following proof.

In the following proofs, we will show ,

where lies between and .

We are also going to show .

(2.1)

We first focus on the function and note that:

For , we write:

Following Lemma A2 in Dong

et al.(2019) and 2(a), we write:

Therefore, we have the term uniformly.

For , we write:

For , we have:

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, the fourth inequality follows from Lemma A4 in Dong

et al.(2019), and the last inequality follows from the definition of .

For , we write:

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 3(c) and Lemma A1 from Dong

et al.(2019)

For , we write:

where lies between and the first inequality follows from 3(a), the second equality follows from mean value theorem, the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 2(b) and the fact that and is bounded by 1.

where the first inequality follows from 3(a) and the boundedness of function , the second inequality follows from Cauchy-Schwarz inequality, the

fourth inequality follows from 2(b) and 3(b), and the last equality follows from the definition of and Lemma C.1.

For , we write:

where the first inequality follows from the boundedness of function and 3(a), the third inequality

follows from Cauchy-Schwarz inequality, and the last equality follows from 2(b) and Lemma A1 in Dong

et al.(2019).

For , we write:

where lies between and , the first inequality follows from the boundedness of function and 3(a), the second equality follows from mean value theorem, the third inequality follows from triangular inequality and Cauchy-Schwarz inequality, and the last equality follows from 2(b) and .

For , we write :

Similar to the proofs for the term , uniformly.

For , we write:

For , we write:

where lies between and the first inequality follows from 3(a), the second equality follows from mean value theorem, the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 2(b) and the fact that and is bounded by 1.

For , we write:

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, and the last equality follows from 3(c) and Lemma A1 from Dong

et al.(2019).

For , we have:

where the first inequality follows from 3(a), the second inequality follows from Lipschitz continuity of , the third inequality follows from Cauchy-Schwarz inequality, the fourth inequality follows from Lemma A4 in Dong

et al.(2019), and the last inequality follows from the definition of .

Combing the above results, we conclude that: .

(2.2)

We next focus on the function and note that:

For , denote the term as . By 2(a), we have and . Applying the Lindeberg–Levy CLT, we have

For , we write:

where the first inequality follows from 3(c). In connection with similar proofs in Lemma C.1, we obtain . Similarly, we have .

For , we write:

where the first inequality follows from Cauchy-Schwarz inequality, and the second equality follows from 3(c).

For , we have:

where the first inequality comes from Cauchy-Schwarz inequality and the third equality follows from the boundness of function and 2(b).

For , we write:

where and both lie between and , and the second and fifth equalities follow from mean value theorem.

Note that , where has eigenvalues and for eigenvalue 0 with eigenvector . Therefore, we rotate the function using the matrix in order to have non-singular asymptotic variance covariance matrix.

Moreover, note that , we have

.

In sum, we have .

Given the asymptotic properties of and , we have:

(b)

Using

we have , where measures the distance from the coordinate to the surface of the unit ball and shows that the convergence speed of is faster in the direction of compared with all other directions orthogonal to .

where the first inequality comes from 3(a), the second equality comes from Cauchy-Schwarz inequality, the third equality comes from the consistency of such that and the similar proofs as .

For , we have:

where the first inequality comes from 3(a), and the second equality comes from the triangular inequality.

For , we have:

where the first inequality comes from 3(a), the second inequality comes from Cauchy-Schwarz inequality, and the third equality comes from the similar proofs as . Similarly, we have .

For , we have:

where the second inequality comes from 3(a), and the third equality comes from the consistency of such that and the similar proofs as .

For , by the Law of Large Numbers, we have

In sum, we have shown .

(b)

We write

For , we have:

where the first inequality comes from the boundness of , and the second equality comes from the similar proofs as .

For , we have:

where the third inequality comes from 3(a), the fourth inequality comes from Cauchy-Schwarz inequality, and the last inequality comes from the consistency of such that and the similar proofs as .

For , by the Law of Large Numbers, we have:

In sum, we have shown .

∎

Appendix D: Additional Simulation Results

Appendix D.1: Simulation Study: Estimating the Propensity Score Function

We first conduct a Monte Carlo study to investigate the finite sample properties of our semiparametric estimator proposed in Section3.1 for the propensity score.

We consider the following four functional forms (DGPs) with a vector of regressors :

1A. ,

where .

1B. ,

where is the same as in Setting 1A.

2A. , where

.

2B.

,

where is the same as in Setting 1B.

The propensity score function is defined as . The DGPs in Settings 1A and 1B satisfy the for identification purpose,

while the DGPs in Settings 2A and 2B violate .

Let

be the estimator of . We evaluate the estimators in terms of bias, standard deviation (std) and root mean-squared error (RMSE).

We summarize the simulation results in Table4. For the DGPs in Settings 1A and 1B that satisfy , the simulation results show that our estimator performs well. Moreover, by focusing on the bias and RMSE separately, it is clear that both terms vanish quickly as the sample size increases. The asymptotic normal approximation is accurate as the standard deviations become smaller as the sample size grows. Our estimation approach is valid for the polynomial single index structure or more complicated periodic single index form. More importantly, the convergence speed is along the direction of true parameter , consistent with the results in Lemma C.2.

Table 4: Simulation Results for the Estimators of Propensity Score Function of Settings 1A to 2B.

Setting

Setting

Bias

1A

400

-0.0030

0.0019

2A

400

-0.0114

-0.0094

800

0.0011

-0.0010

800

-0.0051

0.0050

1600

0.0003

0.0003

1600

0.0019

0.0015

1B

400

-0.0010

-0.0015

2B

400

0.0108

-0.0081

800

-0.0003

0.0005

800

-0.0052

0.0043

1600

0.0001

0.0003

1600

-0.0009

0.0009

Std

1A

400

0.0356

0.0482

2A

400

0.0439

0.0449

800

0.0232

0.0309

800

0.0305

0.0314

1600

0.0195

0.0249

1600

0.0215

0.0217

1B

400

0.0222

0.0349

2B

400

0.0471

0.0482

800

0.0138

0.0184

800

0.0317

0.0334

1600

0.0136

0.0167

1600

0.0268

0.0282

For the DGPs in Settings 2A and 2B that violate , the estimated value and converge to and -, respectively. For all sample sizes we studied, the estimators have relative small biases. The standard deviations of and become smaller as the sample size increases. The asymptotic normal approximation is accurate and the convergence speed is along all other direction orthogonal to the true value , in accordance with the results in Lemma C.2.

We further conduct the simulation study to investigate the performance of our estimators for six dimensions of covariates. We consider the following four DGPs for the propensity score with the vector of regressors :

•

3A. , where .

•

3B. , where is the same as in Setting 3A.

•

4A. ,

where .

•

4B.

, where

is the same as in Setting 4A.

The propensity score function is defined as . The DGPs in Settings 3A and 3B satisfy ,

while the DGPs in Settings 4A and 4B violate .

We show the simulation results for Settings 3A and 3B in Table5 and the results for Settings 4A and 4B in Table6, respectively. Our estimation approach is valid for the six dimensions of covariates we considered. All estimators have small biases for the three sample sizes we considered. The biases vanish quickly when the sample size increases and RMSEs generally decrease as the sample size increases. The asymptotic normal approximation is accurate as the standard deviations become smaller as the sample size grows. The convergence speed is consistent with the results in Lemma C.2.

Table 5: Simulation Results for the Estimators of Propensity Score Function of Settings 3A to 3B.

Setting

Bias

3A

400

-0.0059

-0.0047

-0.0076

0.0040

-0.0047

0.0042

800

0.0025

0.0024

-0.0028

-0.0017

0.0016

-0.0017

1600

0.0011

-0.0013

0.0011

-0.0009

-0.0005

0.0011

3B

400

0.0018

0.0036

0.0024

0.0031

-0.0014

0.0043

800

-0.0008

0.0010

-0.0009

0.0006

-0.0004

0.0009

1600

0.0001

-0.0001

-0.0001

0.0001

0.0002

0.0001

Std

3A

400

0.0524

0.0542

0.0629

0.0476

0.0384

0.0641

800

0.0340

0.0351

0.0392

0.0293

0.0230

0.0381

1600

0.0236

0.0244

0.0266

0.0199

0.0152

0.0253

3B

400

0.0326

0.0387

0.0387

0.0339

0.0244

0.0511

800

0.0203

0.0210

0.0232

0.0173

0.0137

0.0267

1600

0.0142

0.0147

0.0161

0.0120

0.0100

0.0165

Table 6: Simulation Results for the Estimators of Propensity Score Function of Settings 4A to 4B.

Setting

Bias

4A

400

0.0134

0.0219

-0.0234

-0.0165

-0.0092

0.0199

800

0.0123

0.0137

-0.0214

-0.0146

0.0086

-0.0142

1600

0.0029

0.0114

-0.0116

-0.0103

-0.0030

-0.0114

4B

400

0.0125

-0.0265

-0.0134

0.0195

0.0071

0.0189

800

0.0114

-0.0055

0.0125

0.0056

-0.0068

0.0070

1600

0.0033

0.0070

-0.0064

-0.0032

-0.0046

-0.0014

Std

4A

400

0.0601

0.0467

0.0557

0.0526

0.0537

0.0677

800

0.0420

0.0323

0.0395

0.0371

0.0378

0.0472

1600

0.0293

0.0226

0.0273

0.0260

0.0268

0.0332

4B

400

0.0432

0.0470

0.0487

0.0496

0.0426

0.0624

800

0.0337

0.0380

0.0374

0.0405

0.0319

0.0525

1600

0.0298

0.0271

0.0324

0.0287

0.0236

0.0375

We further conduct a Monte Carlo study to investigate the finite sample properties of our semiparametric estimator proposed in Section3.2, and examine the average treatment effect under potential misspecification of propensity score function and the relaxation of in Equation3. We consider the following eight DGPs for both the propensity score and potential outcome.

Setting 7A: , where , the vector of covariates are generated from standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 7B: , where , the vector of covariates are generated from standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 8A: , where is independent of , , the vector of covariates are generated from standard normal distributions . The outcome model is generated as , where and .

Setting 8B: , where is independent of , , the vector of covariates are generated from standard normal distributions . The outcome model is generated as , where and .

Setting 9A: , where and the vector of covariates are generated from standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where is the chi-square with 1 degree of freedom minus its median and .

Setting 9B: , where and the vector of covariates are generated from the standard normal distribution . The propensity score function is defined as and the outcome model is generated as , where is Cauchy distribution and .

Setting 10A: , where the vector of covariates are generated from standard normal distributions . The propensity score function is defined as and the outcome model is generated as , where and .

Setting 10B: , where is independent of and the vector of covariates are generated from standard normal distributions . The outcome model is generated as , where and .

The DGPs in Settings 7A and 7B violate in Equation3, the DGPs in Settings 8A and 8B have probit propensity score function and are supposed to be handled by our semiparametric single-index models, DGPs in Settings 9A and 9B have heavy-tail error distribution of the outcome equations, and DGPs in Settings 10A and 10B impose additional misspecification of propensity score function with respect to the semiparametric single-index model.

Table 7: Simulation Results the Estimators of Average Treatment Effect of Settings 7A to 10B.

Setting

Setting

Setting

Setting

Bias

7A

400

0.0044

8A

400

0.0046

9A

400

0.0039

10A

400

-0.0059

800

-0.0021

800

-0.0017

800

-0.0022

800

0.0027

1600

0.0002

1600

-0.0007

1600

-0.0002

1600

0.0002

7B

400

0.0028

8B

400

-0.0052

9B

400

-0.0026

10B

400

0.0046

800

-0.0011

800

0.0035

800

0.0011

800

-0.0019

1600

-0.0003

1600

-0.0007

1600

-0.0003

1600