The likelihood ratio test for structural changes in factor models222 We would like to thank editors Elie Tamer and Serena Ng, and two anonymous referees for their insightful suggestions. We extend our thanks to the participants of the 2022 NBER/NSF Time Series Conference at Boston University. Jiangtao Duan’s research is partially supported by National Nature Science Foundation of China (No.12101146, 12371263).

Jushan Bai1, Jiangtao Duan2, Xu Han3

1Columbia University, 2Xidian University and 3City University of Hong Kong

Abstract:

A factor model with a break in its factor loadings is observationally equivalent to a model without changes in the loadings but with a change in the variance of its factors. This approach effectively transforms a high-dimensional structural change problem into a low-dimensional problem. This paper considers the likelihood ratio (LR) test for a variance change in the estimated factors. The LR test implicitly explores a special feature of the estimated factors: the pre-break and post-break variances can be a singular matrix under the alternative hypothesis, making the LR test diverging faster and thus more powerful than Wald-type tests. The better power property of the LR test is also confirmed by simulations. We also consider mean changes and multiple breaks. We apply this procedure to the factor modeling of the US employment and study the structural change problem using monthly industry-level data.

Key words and phrases: High-dimensional factor models, Structural breaks, LR test

JEL classification: C12, C38, C55

1 Introduction

Factor models are effective tools for summarizing information in large datasets and are widely used in economics and finance. Examples include diffusion index forecasting (Stock and Watson, 2002, 2009), asset pricing (Ross, 1976; Fama and French, 1992; Feng et al., 2020), and macroeconomic policy evaluation (e.g., Bernanke et al., 2005; Han, 2018). Structural change is a common phenomenon in economic variables and is more likely to occur in high-dimensional data. To better understand the data structure and ensure the validity of subsequent analyses, it is useful to check the structural stability of factor models.

This paper focuses on testing structural breaks in the factor loading matrix. It is known that a factor model with structural breaks in its factor loading matrix is observationally equivalent to a model with time-invariant loadings but a potentially larger number of factors (hereinafter referred to as “pseduo-factors”) than the original model. This approach effectively translates the original and challenging high-dimensional testing problem into a low-dimensional problem. Based on this fact, the literature proposes numerous procedures to examine the moments of the pseudo-factors. For example, Chen, Dolado, and Gonzalo (2014) (CDG hereafter) propose Wald and Lagrange multiplier (LM) tests to examine the coefficients in the regression of the first estimated factor on the remaining factors. Han and Inoue (2015) (HI hereafter) develop Wald and LM tests that compare the pre- and post-break second moments of the estimated factors. Baltagi et al. (2021) generalize HI’s results and propose tests for multiple breaks in the factor loading matrix. Although these tests are consistent under certain alternative hypotheses, simulation evidence shows that they may not be powerful for moderate breaks in finite samples.

We consider a (quasi-)LR test. Our research is motivated by Duan, Bai, and Han (2022, DBH hereafter), who show that the quasi-maximum likelihood (QML) estimator of the break point is consistent when the subsample covariances of the pseudo-factors are singular. By consistency, we mean that the probability that the estimated break date is exactly equal to the true break date approaches one as the sample size grows. This implies a faster rate than the usual -consistency in terms of break fractions.

By construction, the LR test statistic is equal to the likelihood function evaluated at the estimated break point estimator. Thus, the faster convergence of the QML break estimator (under the alternative) is expected to correspond to a more powerful test of the LR statistic. In contrast, the sup-Wald and sup-LM statistics of CDG (2014) and HI do not generate consistent estimators for the break point under the alternative. Therefore, these tests are less powerful than the LR statistic.

LR tests are studied by Qu and Perron (2007) and Perron, Yamamoto, and Zhou (2020) for observable variables. In factor models, because the factor process is unobservable and is estimated subject to normalization restrictions, the limiting distributions of our LR tests are different from those in Qu and Perron (2007), except for the case of testing a single change. The limiting distribution depends on the increments of the Brownian bridge instead of Brownian motion. Interestingly, the normalization restrictions make the derivation of the limiting distribution even easier. The LR test is asymptotically equivalent to HI’s sup-Wald test under the null hypothesis. But its behavior under the alternative is more difficult to analyze for factor models. Inspired by the results in DBH (2022), we show that the LR test is diverging faster than the Wald test under the alternative. The higher power of our LR test is related to the insight that using multiple time series helps identify a break point (Bai et al., 1998). This insight culminates in the finding in Bai (2010) that it is possible to precisely identify the break point for common mean and variance breaks in large panels. Under the latent factor setup, the large cross-section still plays an important role, as it helps enforce the singularity for subsample pseudo-factor variance as grows, which is responsible for the superior power and accurate estimation of the break point under the alternative. Bai (2010) further show that even in the absence of a change in variance, QML allowing a variance change provides a more efficient estimator of the break point (in mean) than imposing the correction assumption of no change in variance. Taken together, these results support our use of the likelihood approach for testing structural changes.

Our paper is also related to, but substantially different from, other studies examining structural changes in factor models. The earlier literature focuses on the low-dimensional testing problem of whether the factor loadings of an individual variable have structural changes (e.g., Stock and Watson, 2009; Breitung and Eickmeier, 2011; and Yamamoto and Tanaka, 2015). In comparison, we are interested in testing changes in the entire loading matrix. Cheng et al. (2016) develop a Lasso estimator to determine whether there is a change in the factor loading matrix or the number of factors. While they concentrate on consistent model selection, our emphasis is on hypothesis testing. Su and Wang (2020) propose a test for identifying smooth changes in factor loadings using local principal components, while our test employs a quasi-maximum likelihood approach. Another related area of research focuses on the consistent estimation of factors under time-varying factor loadings. For example, Bates et al. (2013) established conditions under which the time variation of factor loadings can be ignored. However, our framework violates Bates et al.’s conditions because a significant proportion of factor loadings undergo a break at a common time under the alternative hypothesis. Mikkelsen et al. (2019) assumed factor loadings following stationary VAR processes, but our framework’s factor loadings experience a one-time shift, which means they are not stationary over time. Therefore, their method cannot be applied to our setting, unlike their setting where the time variation in factor loadings can be absorbed as idiosyncratic components.

Our work is further related to the literature on break point estimation for large factor models (e.g., Chen, 2015; Cheng et al., 2016; Baltagi et al., 2017; Barigozzi et al., 2018; Ma and Su, 2018; Bai et al., 2020). Most of the research is not likelihood-based, with the exception of DBH (2022), as explained above. Bai (2000) study the QML estimation of mean and variance breaks, but in a low-dimensional vector autoregressive setting. In addition, there is a large literature that tests breaks in a traditional time series setting, such as Andrews (1993), Bai and Perron (1998) and Bergamelli et al. (2019), among others.

The rest of this paper is organized as follows. Section 2 introduces the representation of the factor model with a single break in the factor loading matrix. Section 3 describes the LR test, establishing its asymptotic distribution under the null hypothesis and furthering deriving the divergence rate of the statistic under the alternative hypothesis. Section 4 generalizes the LR test to allow for factor mean changes and multiple breaks in the loading matrix. Section 5 investigates the finite-sample properties of the LR procedure via simulations. Section 6 implements the LR test for monthly US industry-level employment data.

The following notations are used. For an real matrix , we denote its Frobenius norm as . For a real number , represents the integer part of . denotes the cardinality of a set . vech is equal to the column-wise vectorization of a square matrix with the upper triangular excluded.

2 The factor model and hypotheses

Consider the following factor model that allows for a structural break in the factor loading matrix:

| (2.1) |

where is the -dimensional demeaned observation at time ; is an dimensional vector of unobserved common factors and ; is an unknown break date; and are the pre- and post-break factor loadings, respectively; and is the idiosyncratic error that may have serial and cross-sectional dependence along with heteroskedasticity. We define as the break fraction, which is assumed to be a fixed constant. This implies that is a sequence that depends on . For notational simplicity, we suppress the dependence of on .

We are interested in testing the null hypothesis of no structural break in the factor loadings, i.e.,

| (2.2) |

against the alternative hypothesis that a non-negligible portion of the cross sections have a break in their loadings at a common time, i.e.,

| (2.3) |

where as .

Under , (2.1) is a standard factor model with time-invariant factor loadings and denotes the number of original factors. Under , it is well known that the factor model is observationally equivalent to a model with time-invariant loadings and potentially more pseudo-factors (e.g., HI, 2015; Baltagi et al., 2017). To capture the factor dimension augmentation caused by the break, we follow the framework of DBH (2022) and set as the number of pseudo-factors in (2.1). We set

where is an matrix with full column rank , and are matrices, , and .

For a given split point , define

Thus, (2.1) can be rewritten in the following matrix format:

| (2.10) | |||||

| (2.13) | |||||

| (2.14) |

which is an observationally equivalent representation with a time-invariant loading matrix and pseudo-factors with .

The representation in (2.14) is flexible for both the null and alternative hypotheses. and are the numbers of factors before and after the break. Accordingly, under we can set , and pseudo-factors coincide with the original factors. Under , we can incorporate different types of changes by controlling the ranks of and . Following DBH (2022), loading changes can be divided into three types: Type (1), in which both and are singular (i.e., both and are less than , so (2.14) can capture the factor dimension enlargement caused by the break); Type (2), in which only or is singular (emerging or disappearing factors); and Type (3), in which both and are nonsingular (rotational change in loadings). In practice, Types (1) and (2) are more common than Type (3).

When is true, the pre- and post-break second moments of the pseudo-factors are and , respectively. Thus, various tests (e.g., the sup-Wald and sup-LM type statistics developed by Chen et al. (2014) and Han and Inoue (2015)) propose to compare the subsample second moments of the factors under the assumption that is constant over time. Although these tests are consistent under the alternative hypothesis (e.g., Han and Inoue, 2015), simulation evidence shows that they have limited power in small samples when the break size is moderate.

To develop a more powerful test, we take a different route. Instead of comparing the variance of the factors before and after the break, we construct the maximum of LRs (sup-LR) based on the quasi-likelihood functions of the factors evaluated at different potential break points. The proposed LR test is expected to be more powerful than the sup-Wald type test because the QML estimator for the break point under the alternative is more precise than the estimators based on the least squares estimators (the maximum of Wald-type estimators). DBH (2022) show that the break point estimated by QML is equal to , with a probability approaching one as when or or both are singular. The Wald-type estimators do not have this property and are only stochastically bounded around .

3 Likelihood ratio test

Because is unobserved, we need an estimator of to construct our test statistic. Let denote the principal components (PC) estimator of under the usual identification condition:

| (3.1) |

Thus, is times the eigenvectors corresponding to the largest eigenvalues of the matrix . Because the data are demeaned, the PC estimator satisfies . For a given split point , we estimate the pre- and post- factor variances by

Here, we do not subtract the subsample mean, which is considered later. The quasi-Gaussian likelihood for a break point at is given by

| (3.2) |

Because the sample variance of is always equal to an identity by (3.1), the log-likelihood of no change for the entire sample is

Thus, the LR for testing the null hypothesis of no change against the alternative of a change occurring at is , which can be written as

The identification condition (3.1) is chosen for computational convenience, but the LR test can be employed under any valid identification condition. The explanation is provided in the Appendix.

3.1 Assumptions

To study the limiting null distribution of the LR test statistics, we make the following standard assumptions for the approximate factor model that allow for the functional central limit theorem.

Assumption 1.

, , where is positive definite, and uniformly for .

Assumption 2.

Let be the -th row of . for , for some positive definite matrix .

Assumption 3.

There exists a positive constant such that

-

(i)

and for all and ;

-

(ii)

and for every ;

-

(iii)

with for some and for all and for every ;

-

(iv)

, and

-

(v)

For every , .

Assumption 4.

There exists a positive constant such that

Assumption 5.

The eigenvalues of are distinct where .

Assumption 6.

There exists an

such that for all and and for each ,

(i) ;

(ii) .

Assumption 7.

For , .

Assumption 8.

Let . Under the null (i.e., ), , where is an Gaussian process.

Assumptions 1 and 2 are standard in the literature on approximate factor models (e.g., Bai, 2003). The time-invariant second moment of is commonly used for identification purposes because a change in the variance of is observationally equivalent to a rotation of the factor loadings. A variance change in can be absorbed by the matrix or in (2.14). The uniform convergence of in Assumption 1 is similar to Assumption A11 of Qu and Perron (2007). Assumptions 3 allows weakly correlated and heteroskedastic idiosyncratic errors. Assumptions 4 and 5 correspond to Assumptions D and G of Bai (2003). Assumption 6(i) corresponds to Bai’s (2003) Assumption F1. Assumption 6(ii) strengthens Bai’s (2003) Assumption F3 and ensures the consistency of the heteroskedasticity and autocorrelation consistent (HAC) covariance estimator of . Assumption 7 follows from Assumption 10 of DBH (2022) or Assumption 8 of HI (2015). Assumption 8 states that a basic functional central limit theorem holds for the sums of under the null hypothesis of no break.

3.2 Limiting distribution of sup-LR under the null hypothesis

It is well known that is an estimator of , where and denotes the eigenvalues of . Bai’s (2003) Proposition 1 shows that , where is the probability limit of and an diagonal matrix of the eigenvalues of , and is the eigenvector of . Thus,

which implies that

| (3.4) |

The following theorem establishes the asymptotic distribution of the sup-LR statistic under the null hypothesis.

Theorem 1.

(i)

| (3.5) |

where

and is an vector of independent Brownian motion.

(ii) Define the HAC estimator

| (3.6) |

where is a kernel function and is a bandwidth parameter. Then,

Note that the limiting null distribution of sup-LR depends on the long-run singular variance . Part (ii) of Theorem 1 states that the infeasible can be replaced with the HAC estimator in (3.6) computed using the estimated factors . Note that is only consistent for (Theorem 2 of HI (2015)), but inconsistent for . However, it can be shown that for some orthonormal matrix . Because a pre-multiplication by does not change the distribution of an independent standard normal vector, we can still replace with when simulating the limiting null distribution.

Note that the presence of in (3.5) is due to the potentially misspecified likelihood function (3.2), which assumes that are i.i.d. Gaussian under the null hypothesis. If (3.2) correctly specifies the likelihood, then the limiting distribution reduces to

| (3.7) |

where is an vector of independent Brownian motions. The distribution in (3.7) is the same as that used in conventional supreme type tests for a structural break, and the critical values can be found in Andrews (1993).

If are i.i.d. Gaussian and the null hypothesis is true, the sup-LR statistic is numerically close to HI’s (2015) sup-Wald and sup-LM statistics, which compare the subsample variances of . For example, HI’s (2015) sup-Wald statistic is defined as

where

and is an unconstrained estimator for the variance of . Under the null hypothesis, Theorem 2 provides an alternative formulation to approximate the proposed sup-LR statistic and establishes its connection to the sup-Wald statistic of HI (2015).

Theorem 2.

(i)

(ii) in addition, if ’s are i.i.d. Gaussian, then

Under the null hypothesis, Theorem 2(i) provides an approximation of the sup-LR statistic, which involves a comparison between and . Part (ii) of Theorem 2 shows that the sup-LR test is asymptotically equivalent to the sup-Wald test under Gaussianity and the null hypothesis of no break. Although the LR test is asymptotically equivalent to the Wald test under the null, as we show below, the LR test is more powerful under the alternative hypothesis. In addition, the LR test has better finite-sample size properties in simulation.

3.3 Power against the alternative hypothesis

To show that the new test is consistent under the alternative hypothesis, we need the additional assumption set forth below.

Assumption 9.

With probability approaching one (w.p.a.1), the following inequality holds:

as , where is a constant, and denotes the largest eigenvalue of a symmetric matrix.

This assumption is made in DBH (2022). It is a reasonable assumption, because . This ensures that the smallest eigenvalues of and are less than for a positive constant w.p.a.1, according to DBH’s (2022) Proposition 1. The theorem set forth below establishes the asymptotic property of the new test under the alternative hypothesis.

Theorem 3.

(i) if Assumption 9 holds and the factor loading matrix has a break such that either or in (2.14) is singular and , then there exists a constant such that

as ; and

(ii) if the factor loading matrix has a break such that both and in (2.14) are nonsingular with , then there exists a constant such that

as .

Theorem 3 proves that the sup-LR test is consistent under the alternative hypothesis. Part (i) states that the divergence rate of LR is , which is faster than the regular rate of conventional tests. This faster rate is caused by the singularity of or . If is singular, for instance, converges in probability to the singular matrix for . In finite samples, is nearly singular, and its smallest eigenvalue has an upper bound for some under the assumption at the same rate (see the technical details in the appendix). Thus, the term diverges at the faster rate for with . In contrast, conventional tests (such as HI’s sup-Wald test) that compare and do not take advantage of the near singularity of the sample covariance matrices and thus are less powerful than our sup-LR test.

Remark 1.

Define two break point estimators for based on our LR test and HI’s Wald test.

is the QML estimator proposed by DBH (2022), whereas can be viewed as an LS estimator analogous to the estimator developed by Baltagi et al. (2017). The LS estimator is inconsistent and has an estimation error , whereas the QML estimator is consistent in the sense that as if or is singular. The ability of the QML estimator to precisely identify the break point is translated into a more powerful sup-LR test.

Remark 2.

The alternative hypothesis requires a significant proportion of the cross sections to have a break in their loadings at a common time, and this setup is frequently utilized in the literature (e.g., Han and Inoue, 2015; Baltagi et al. 2021). If only a small number of series have breaks, there will be a power loss. The reason is the following. In a factor model with changes in the factor loading matrix, we can express it as a misspecified model with constant loadings, and the changes in the loadings can be absorbed using the idiosyncratic errors, resulting in correlations in the idiosyncratic errors. However, changes in a fixed number of loading coefficients only produce a limited level of correlation in the idiosyncratic errors of the misspecified model. Therefore, the factors can still be estimated consistently up to a rotation, and the sample factor variance will remain asymptotically the same before and after the break, leading to a loss of power in the test.

4 Extensions

4.1 Allowing mean change in

First we note that testing a change in variance also has power for changes in the mean. Nevertheless, it might be interesting to explicitly allow for a shift in the mean of . It is common practice to first demean the data and then extract the principal components so that the full sample average is always exactly zero by construction. This property is used here. To incorporate a mean change in , we simply redefine the pre-break and post-break variance estimators:

where the dependence of and on is omitted for notational simplicity. The likelihood function takes the same form as in (3.2)

Define the LR test that allows for a structural break in both the mean and the variance of as

| (4.1) |

We make the following assumption about the weak convergence of the joint processes.

Assumption 10.

Let . Under the null (i.e., ),

where the right-hand side is a Gaussian process with independent increments.

Theorem 4.

(i)

where is an -dimensional independent Brownian motion process, and

(ii) If is uncorrelated with , then

where and are -dimensional and -dimensional independent Brownian motion processes, respectively, and

Part (ii) of Theorem 4 makes the additional assumption that and are uncorrelated. In this case, the limiting null distribution is similar to the result obtained by Qu and Perron (2007), which can be decomposed as the sum of two components, one corresponding to the mean change and the other corresponding to the variance change. Part (i) allows a more general setup with correlated and , and the critical values can be obtained by simulating dimensional Brownian motions and estimating the long-run variance . This long-run variance can be estimated by replacing with .

Remark 3.

Remark 4.

Note that and , so the terms and weakly converge to Brownian bridge type processes (see the proof of Theorem 4 for the technical details). Thus, a Wald test that allows a factor mean change can be defined without directly comparing and . Define

where is the corresponding long-run variance. Note that here we use instead of . The limit is similar to that of the usual Wald test,

where is an standard Brownian motion. This test is nuisance-parameter free.

Consider the simple weighting by , let . Take the maximum over the range say . The limiting distribution is simply

and the critical values do not depend on trimming parameter .

4.2 Testing multiple changes

In this section, we extend the sup-LR test to multiple changes. We consider testing the null hypothesis of no change versus the alternative hypothesis of a prespecified number of changes. To allow for changes under the alternative hypothesis, let and define

where

We define the set and .

Theorem 5.

The limiting distribution in Theorem 5 is different from the case with an observed , as in Bai and Perron (1998). Each term in the sum involves an increment of the Brownian bridge instead of Brownian motion because of the PC normalization in (3.1).

To allow for both mean and variance changes, we define the following statistic

where

Theorem 6.

These results depend on , but does not have to be correctly specified. We can also consider the double max type of test and the conditional test for multiple breaks as in Bai and Perron (1998), but we leave these as future research topics.

4.3 Determining the number of breaks

In practice, the number of breaks in a factor model is often unknown. We follow Bai’s (1997) sequential testing procedure to provide a consistent estimate for the true number of breaks. The procedure involves treating the model as if there is only one change point at each time.

To be specific, we first identify the initial break point, , using the QML method in DBH. To determine the presence of any additional breaks, we split the entire sample into two subsamples: and . For each subsample, we conduct the sup-LR test with as outlined in (4.3) or (4.4), and employ the QML method to estimate a break point for the subsample where the null hypothesis is rejected at a significance level of . We then split the corresponding subsample into further subsamples at the newly estimated break point and repeat the LR tests for each subsample. This process continues until the LR test is not rejected for all subsamples. The number of break points is equal to the number of subsamples minus one, and the location of the change points can be estimated in the procedure. The following corollary shows that the number of breaks can be consistently estimated when converges to zero slowly.

Corollary 1.

The proof of this corollary is similar to Proposition 11 in Bai (1997), and the details are omitted here. In practice, one can choose a small value. In our simulation, we set to be 0.05.

5 Monte Carlo simulations

In this section, we investigate the finite sample properties of the proposed LR and LRm tests for the factor models with a single break point. We compare the performance of our LR and LRm tests with HI’s Wald test and the LM test for various sample sizes and different setups for the factors and factor loadings in Tables 1-9. As shown below, we use Wald(HAC) and LM(HAC) to denote HI’s Wald and LM tests, respectively, using HAC variances with a Bartlett kernel. All of the HAC estimates are based on Newey and West’s (1994) method.

The asymptotic critical values for HI’s tests are provided by Andrews (1993), and the asymptotic critical values for the proposed tests are obtained by simulation. In all of the simulations, we set the time length of the Brownian motions equal to 2,000 and repeat them 1,000 times to obtain the critical values.

We investigate these tests’ size in Tables 1-4, and their power in Tables 5-9. The number of factors is selected by of Bai and Ng (2002). In all of the Monte Carlo experiments, we calculate size and power based on 2,000 replications for each data generating process (DGP).

Each factor is generated by the following AR(1) process:

where is i.i.d. for and is i.i.d. . The scalar captures the serial correlation of factors, and the idiosyncratic errors are i.i.d. . We set the break date in all of the setups. We consider the following DGPs for factor loadings and investigate the performance of the tests for the different types of breaks discussed in the previous section.

Tables 1 and 2 present the simulation results under the null hypothesis when the permissible break dates are between and for different nominal sizes of , , and . We set and for Tables 1 and 2, respectively, and set for and . Under the null hypothesis, . From Tables 1 and 2, we can see that all of these tests have effective sizes approaching the nominal levels as the sample size increases. Tables 3 and 4 show similar simulation results under the null hypothesis when the permissible break dates are from to for different nominal sizes.

Table 5 reports how the power of these tests changes as the sample size increases. We set , for , , and the permissible break dates are from to . This setup shows that the post-break factor loadings undergo a random shift. In each estimation, we use Bai and Ng’s (2002) to estimate the number of factors. Table 5 shows that all of these tests become powerful when the sample size increases. However, we can find that LR and LRm are more powerful than Wald(HAC) and LM(HAC) under small sample sizes. When , the power of Wald(HAC) and LM(HAC) is less than , but that of LR test is almost . These results consolidate Theorem 3.

Table 6 reports how power changes in these tests as the magnitude of the break in factor loadings increases. We set , for , , , and the permissible break dates are from to . When , the rejection frequency represents the size under the null hypothesis. As increases, all of these tests become powerful, although the power of Wald(HAC) and LM(HAC) is not monotonically increasing in . When and , LR and LRm are more powerful than Wald(HAC) and LM(HAC). The power of LR and LRm increases substantially and approaches one as approaches one. Although the power of Wald(HAC) and LM(HAC) increases as increases, the power when is smaller than the case of . As T increases from to , the power of Wald(HAC) and LM(HAC) increases, but they are still less powerful than LR and LRm. When and , LR and LRm also demonstrate superior power relative to the Wald and LM tests. The power of Wald(HAC) and LM(HAC) is poor when the sample size is small, even if the break magnitude is large. When and , the power of Wald(HAC) is less than , and the power of LM(HAC) is less than . When increases to , the power of Wald(HAC) and LM(HAC) improves but is still smaller than the power of LR and LRm.

Table 7 reports the power when the loading matrix undergoes a rotational change. We set , , . When , the rejection frequency represents the size under the null hypothesis. As the value of a increases, all of the tests become more powerful, except for Wald(HAC) and LM(HAC) when . The LR test has the highest power under this DGP. The power of the LRm test increases at a slower rate as increases. Our Theorem 3 demonstrates that the sup-LR diverges at the same rate as the conventional sup-Wald when both pre-break and post-break pseudo-factors have nonsingular variances. However, our simulation results indicate that sup-LR remains more powerful than sup-Wald under this scenario, as reported in Table 7. Specifically, when the loading matrix undergoes a rotational change, sup-LR is notably more powerful than sup-Wald with HAC variance. While we acknowledge that the theoretical power comparison under this setup may require analysis under local alternatives, we leave this as a future research topic.

Table 8 presents the power against changes in the number of factors. The post-break loadings are equal to pre-break loadings multiplied by an matrix, i.e., . We set , , . From Table 8, we find that the LR and LRm tests have higher than Wald(HAC) and LM(HAC).

Table 9 shows the power when the factors undergo a mean change. The factors are generated in the same way as above, except that we add a constant to the post-break factors, i.e., and , where and are the original factors and is a constant. We set , , . It is remarkable that all of the test statistics have power under this type of break. Unsurprisingly, LRm is the most powerful statistic under this DGP.

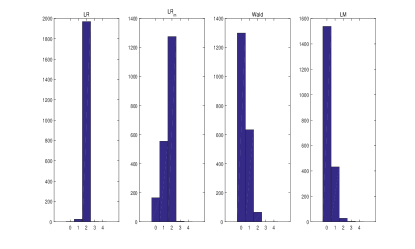

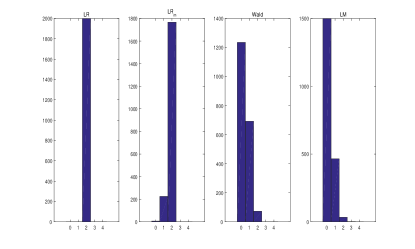

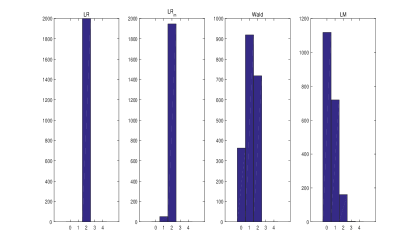

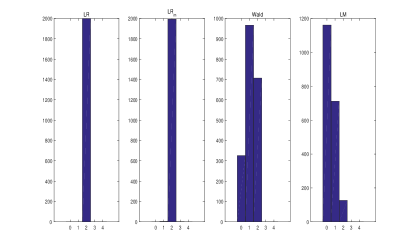

Figure 1 displays the number of breaks estimates using the sequential method based on sup-LR, sup-LRm, sup-Wald(HAC) and sup-LM(HAC) tests. The data generating process (DGP) is the same as that used in Table 5, except that the loadings experience two breaks at and . The loadings in the first regime are generated as for . The loadings in the second and third regimes are generated as and , respectively, where both and are iid draws from . We set . The sequential procedure uses tests, as in Bai (1997).

In Figure 1, the estimated number of breaks becomes more accurate as and increase for all tests. However, the estimates obtained using LR and LRm are more accurate than those obtained using Wald and LM. The advantage of LR and LRm is particularly pronounced when the sample size is small.

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | ||

| 100,100 | 0.012 | 0.004 | 0.000 | 0.011 | 0.005 | 0.003 | 0.049 | 0.021 | 0.002 | 0.128 | 0.084 | 0.050 | |

| 100,200 | 0.034 | 0.015 | 0.002 | 0.027 | 0.010 | 0.003 | 0.070 | 0.029 | 0.005 | 0.054 | 0.023 | 0.011 | |

| 100,500 | 0.064 | 0.025 | 0.003 | 0.064 | 0.026 | 0.002 | 0.086 | 0.039 | 0.004 | 0.055 | 0.017 | 0.003 | |

| 200,200 | 0.035 | 0.012 | 0.001 | 0.024 | 0.010 | 0.001 | 0.063 | 0.022 | 0.003 | 0.035 | 0.016 | 0.007 | |

| 200,500 | 0.072 | 0.028 | 0.005 | 0.072 | 0.026 | 0.004 | 0.083 | 0.044 | 0.008 | 0.054 | 0.018 | 0.001 | |

| 500,500 | 0.054 | 0.024 | 0.003 | 0.055 | 0.021 | 0.003 | 0.068 | 0.034 | 0.005 | 0.044 | 0.018 | 0.002 | |

| 100,100 | 0.031 | 0.010 | 0.002 | 0.033 | 0.011 | 0.002 | 0.069 | 0.029 | 0.004 | 0.121 | 0.083 | 0.047 | |

| 100,200 | 0.075 | 0.028 | 0.002 | 0.055 | 0.021 | 0.004 | 0.092 | 0.041 | 0.005 | 0.071 | 0.035 | 0.010 | |

| 100,500 | 0.130 | 0.068 | 0.014 | 0.109 | 0.053 | 0.012 | 0.112 | 0.059 | 0.011 | 0.078 | 0.031 | 0.008 | |

| 200,200 | 0.081 | 0.035 | 0.003 | 0.071 | 0.031 | 0.009 | 0.097 | 0.041 | 0.010 | 0.056 | 0.027 | 0.009 | |

| 200,500 | 0.129 | 0.061 | 0.014 | 0.103 | 0.051 | 0.009 | 0.108 | 0.050 | 0.014 | 0.077 | 0.032 | 0.005 | |

| 500,500 | 0.123 | 0.067 | 0.017 | 0.100 | 0.050 | 0.012 | 0.114 | 0.054 | 0.013 | 0.076 | 0.038 | 0.010 | |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 100,100 | 0.012 | 0.001 | 0.000 | 0.013 | 0.004 | 0.001 | 0.041 | 0.012 | 0.000 | 0.110 | 0.073 | 0.046 |

| 100,200 | 0.02 | 0.011 | 0.000 | 0.031 | 0.009 | 0.001 | 0.054 | 0.018 | 0.001 | 0.029 | 0.012 | 0.006 |

| 200,200 | 0.026 | 0.009 | 0.001 | 0.019 | 0.008 | 0.001 | 0.057 | 0.021 | 0.004 | 0.036 | 0.016 | 0.009 |

| 200,500 | 0.061 | 0.025 | 0.003 | 0.060 | 0.021 | 0.003 | 0.076 | 0.030 | 0.004 | 0.050 | 0.012 | 0.002 |

| 500,500 | 0.050 | 0.019 | 0.002 | 0.049 | 0.018 | 0.001 | 0.060 | 0.023 | 0.003 | 0.043 | 0.013 | 0.001 |

| 100,100 | 0.029 | 0.007 | 0.001 | 0.029 | 0.013 | 0.002 | 0.061 | 0.022 | 0.003 | 0.120 | 0.077 | 0.037 |

| 100,200 | 0.074 | 0.028 | 0.003 | 0.069 | 0.031 | 0.007 | 0.079 | 0.031 | 0.006 | 0.055 | 0.024 | 0.010 |

| 100,500 | 0.119 | 0.057 | 0.014 | 0.089 | 0.042 | 0.011 | 0.093 | 0.049 | 0.011 | 0.074 | 0.032 | 0.009 |

| 200,200 | 0.084 | 0.034 | 0.009 | 0.077 | 0.036 | 0.006 | 0.094 | 0.047 | 0.011 | 0.056 | 0.024 | 0.008 |

| 200,500 | 0.119 | 0.061 | 0.010 | 0.086 | 0.044 | 0.010 | 0.100 | 0.037 | 0.007 | 0.080 | 0.035 | 0.008 |

| 500,500 | 0.130 | 0.065 | 0.011 | 0.096 | 0.044 | 0.009 | 0.102 | 0.046 | 0.009 | 0.075 | 0.031 | 0.009 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 100,100 | 0.009 | 0.001 | 0.000 | 0.019 | 0.007 | 0.004 | 0.056 | 0.019 | 0.002 | 0.128 | 0.086 | 0.058 |

| 100,200 | 0.037 | 0.013 | 0.002 | 0.038 | 0.013 | 0.002 | 0.061 | 0.027 | 0.002 | 0.040 | 0.016 | 0.009 |

| 100,500 | 0.062 | 0.034 | 0.004 | 0.048 | 0.024 | 0.002 | 0.064 | 0.033 | 0.006 | 0.038 | 0.015 | 0.001 |

| 200,200 | 0.029 | 0.012 | 0.002 | 0.026 | 0.011 | 0.002 | 0.056 | 0.019 | 0.003 | 0.048 | 0.024 | 0.010 |

| 200,500 | 0.061 | 0.030 | 0.005 | 0.055 | 0.022 | 0.003 | 0.073 | 0.027 | 0.003 | 0.033 | 0.009 | 0.001 |

| 500,500 | 0.071 | 0.030 | 0.004 | 0.056 | 0.024 | 0.004 | 0.076 | 0.032 | 0.007 | 0.040 | 0.015 | 0.002 |

| 100,100 | 0.017 | 0.003 | 0.001 | 0.036 | 0.021 | 0.005 | 0.068 | 0.022 | 0.005 | 0.109 | 0.073 | 0.044 |

| 100,200 | 0.079 | 0.032 | 0.007 | 0.072 | 0.039 | 0.010 | 0.088 | 0.04 | 0.005 | 0.065 | 0.034 | 0.012 |

| 100,500 | 0.154 | 0.081 | 0.017 | 0.106 | 0.053 | 0.017 | 0.108 | 0.054 | 0.013 | 0.063 | 0.031 | 0.010 |

| 200,200 | 0.080 | 0.032 | 0.005 | 0.072 | 0.036 | 0.013 | 0.084 | 0.030 | 0.007 | 0.052 | 0.023 | 0.006 |

| 200,500 | 0.156 | 0.080 | 0.022 | 0.108 | 0.056 | 0.018 | 0.102 | 0.043 | 0.011 | 0.066 | 0.027 | 0.007 |

| 500,500 | 0.158 | 0.084 | 0.020 | 0.121 | 0.069 | 0.020 | 0.111 | 0.059 | 0.014 | 0.066 | 0.039 | 0.014 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 100,100 | 0.004 | 0.002 | 0.000 | 0.015 | 0.008 | 0.003 | 0.028 | 0.007 | 0.000 | 0.128 | 0.090 | 0.061 |

| 100,200 | 0.038 | 0.018 | 0.002 | 0.023 | 0.008 | 0.001 | 0.048 | 0.016 | 0.002 | 0.032 | 0.012 | 0.006 |

| 100,500 | 0.065 | 0.028 | 0.006 | 0.051 | 0.024 | 0.002 | 0.063 | 0.023 | 0.004 | 0.028 | 0.008 | 0.000 |

| 200,200 | 0.031 | 0.011 | 0.001 | 0.036 | 0.011 | 0.001 | 0.045 | 0.016 | 0.002 | 0.046 | 0.022 | 0.009 |

| 200,500 | 0.066 | 0.025 | 0.002 | 0.056 | 0.023 | 0.003 | 0.068 | 0.028 | 0.001 | 0.031 | 0.008 | 0.001 |

| 500,500 | 0.069 | 0.033 | 0.005 | 0.056 | 0.027 | 0.006 | 0.064 | 0.029 | 0.002 | 0.030 | 0.008 | 0.001 |

| 100,100 | 0.021 | 0.008 | 0.000 | 0.037 | 0.020 | 0.007 | 0.053 | 0.021 | 0.003 | 0.107 | 0.073 | 0.048 |

| 100,200 | 0.068 | 0.029 | 0.006 | 0.084 | 0.046 | 0.014 | 0.085 | 0.038 | 0.008 | 0.052 | 0.030 | 0.013 |

| 100,500 | 0.151 | 0.087 | 0.023 | 0.101 | 0.047 | 0.015 | 0.093 | 0.043 | 0.009 | 0.054 | 0.021 | 0.006 |

| 200,200 | 0.071 | 0.030 | 0.006 | 0.082 | 0.043 | 0.010 | 0.066 | 0.028 | 0.003 | 0.050 | 0.024 | 0.008 |

| 200,500 | 0.150 | 0.085 | 0.019 | 0.115 | 0.063 | 0.023 | 0.090 | 0.041 | 0.007 | 0.051 | 0.022 | 0.005 |

| 500,500 | 0.156 | 0.085 | 0.024 | 0.108 | 0.066 | 0.021 | 0.090 | 0.045 | 0.008 | 0.059 | 0.027 | 0.006 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| , | ||||||||||||

| 100,100 | 0.651 | 0.498 | 0.259 | 0.325 | 0.254 | 0.135 | 1.000 | 1.000 | 0.998 | 1.000 | 0.999 | 0.937 |

| 100,200 | 0.995 | 0.989 | 0.878 | 0.880 | 0.729 | 0.503 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.994 |

| 100,500 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.998 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 200,200 | 0.998 | 0.992 | 0.880 | 0.876 | 0.720 | 0.505 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 200,500 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.999 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 500,500 | 1.000 | 1.000 | 1.000 | 1.000 | 0.999 | 0.998 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 100,100 | 0.614 | 0.467 | 0.229 | 0.322 | 0.256 | 0.139 | 1.000 | 1.000 | 0.999 | 1.000 | 0.998 | 0.869 |

| 100,200 | 0.998 | 0.984 | 0.792 | 0.861 | 0.704 | 0.424 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.997 |

| 100,500 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 200,200 | 1.000 | 0.980 | 0.784 | 0.860 | 0.702 | 0.419 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.999 |

| 200,500 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.998 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 500,500 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| , | ||||||||||||

| 0.015 | 0.005 | 0.000 | 0.026 | 0.007 | 0.002 | 0.055 | 0.018 | 0.003 | 0.158 | 0.111 | 0.074 | |

| 0.036 | 0.011 | 0.001 | 0.058 | 0.022 | 0.003 | 0.098 | 0.034 | 0.004 | 0.139 | 0.090 | 0.059 | |

| 0.221 | 0.128 | 0.043 | 0.184 | 0.108 | 0.039 | 0.413 | 0.320 | 0.232 | 0.330 | 0.270 | 0.140 | |

| 0.561 | 0.388 | 0.171 | 0.321 | 0.223 | 0.124 | 0.917 | 0.883 | 0.844 | 0.865 | 0.834 | 0.507 | |

| 0.568 | 0.424 | 0.203 | 0.290 | 0.232 | 0.145 | 0.996 | 0.994 | 0.983 | 0.990 | 0.981 | 0.715 | |

| 0.530 | 0.385 | 0.188 | 0.260 | 0.216 | 0.133 | 1.000 | 1.000 | 0.996 | 1.000 | 0.997 | 0.841 | |

| , | ||||||||||||

| 0.039 | 0.017 | 0.003 | 0.047 | 0.020 | 0.003 | 0.075 | 0.028 | 0.003 | 0.057 | 0.026 | 0.012 | |

| 0.130 | 0.061 | 0.004 | 0.162 | 0.088 | 0.016 | 0.192 | 0.099 | 0.021 | 0.089 | 0.041 | 0.010 | |

| 0.755 | 0.689 | 0.560 | 0.749 | 0.634 | 0.378 | 0.809 | 0.744 | 0.642 | 0.686 | 0.625 | 0.561 | |

| 0.993 | 0.971 | 0.803 | 0.77 | 0.660 | 0.432 | 0.999 | 0.998 | 0.994 | 0.997 | 0.992 | 0.972 | |

| 0.996 | 0.973 | 0.800 | 0.762 | 0.629 | 0.407 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.982 | |

| 0.993 | 0.967 | 0.797 | 0.749 | 0.619 | 0.411 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.990 | |

| , | ||||||||||||

| 0.029 | 0.011 | 0.000 | 0.070 | 0.027 | 0.006 | 0.074 | 0.031 | 0.007 | 0.150 | 0.101 | 0.056 | |

| 0.054 | 0.017 | 0.002 | 0.106 | 0.047 | 0.007 | 0.115 | 0.051 | 0.009 | 0.138 | 0.086 | 0.052 | |

| 0.204 | 0.117 | 0.035 | 0.184 | 0.096 | 0.035 | 0.393 | 0.318 | 0.255 | 0.338 | 0.271 | 0.133 | |

| 0.484 | 0.336 | 0.130 | 0.281 | 0.186 | 0.095 | 0.885 | 0.860 | 0.827 | 0.835 | 0.771 | 0.420 | |

| 0.529 | 0.374 | 0.170 | 0.284 | 0.211 | 0.132 | 0.990 | 0.986 | 0.978 | 0.982 | 0.948 | 0.622 | |

| 0.522 | 0.372 | 0.183 | 0.256 | 0.195 | 0.130 | 1.000 | 1.000 | 0.998 | 1.000 | 0.988 | 0.747 | |

| , | ||||||||||||

| 0.076 | 0.030 | 0.003 | 0.086 | 0.044 | 0.007 | 0.080 | 0.037 | 0.002 | 0.072 | 0.034 | 0.008 | |

| 0.159 | 0.071 | 0.015 | 0.192 | 0.095 | 0.025 | 0.185 | 0.094 | 0.020 | 0.085 | 0.040 | 0.015 | |

| 0.718 | 0.644 | 0.469 | 0.681 | 0.550 | 0.276 | 0.757 | 0.698 | 0.612 | 0.641 | 0.594 | 0.536 | |

| 0.986 | 0.922 | 0.685 | 0.756 | 0.624 | 0.382 | 0.997 | 0.996 | 0.991 | 0.990 | 0.983 | 0.953 | |

| 0.986 | 0.931 | 0.682 | 0.715 | 0.556 | 0.35 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.979 | |

| 0.994 | 0.932 | 0.721 | 0.723 | 0.568 | 0.366 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.980 | |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 1.0 | 0.012 | 0.002 | 0.000 | 0.012 | 0.006 | 0.003 | 0.050 | 0.018 | 0.002 | 0.145 | 0.107 | 0.067 |

| 1.1 | 0.009 | 0.001 | 0.000 | 0.023 | 0.007 | 0.002 | 0.054 | 0.018 | 0.003 | 0.127 | 0.086 | 0.055 |

| 1.2 | 0.011 | 0.004 | 0.000 | 0.043 | 0.021 | 0.003 | 0.114 | 0.038 | 0.004 | 0.096 | 0.059 | 0.030 |

| 1.3 | 0.029 | 0.006 | 0.000 | 0.053 | 0.022 | 0.002 | 0.252 | 0.112 | 0.009 | 0.101 | 0.051 | 0.024 |

| 1.4 | 0.035 | 0.010 | 0.000 | 0.079 | 0.029 | 0.004 | 0.457 | 0.241 | 0.040 | 0.121 | 0.057 | 0.020 |

| 1.5 | 0.060 | 0.013 | 0.002 | 0.070 | 0.028 | 0.003 | 0.653 | 0.405 | 0.100 | 0.162 | 0.073 | 0.016 |

| 1.6 | 0.055 | 0.013 | 0.001 | 0.072 | 0.029 | 0.006 | 0.771 | 0.538 | 0.161 | 0.192 | 0.084 | 0.021 |

| 1.7 | 0.076 | 0.016 | 0.001 | 0.064 | 0.025 | 0.006 | 0.904 | 0.708 | 0.253 | 0.262 | 0.119 | 0.033 |

| 1.8 | 0.084 | 0.013 | 0.000 | 0.048 | 0.012 | 0.004 | 0.946 | 0.800 | 0.328 | 0.301 | 0.130 | 0.034 |

| 1.9 | 0.097 | 0.021 | 0.001 | 0.045 | 0.012 | 0.004 | 0.976 | 0.884 | 0.378 | 0.350 | 0.145 | 0.043 |

| 2.0 | 0.108 | 0.016 | 0.000 | 0.047 | 0.012 | 0.001 | 0.989 | 0.919 | 0.460 | 0.404 | 0.161 | 0.049 |

| 1.0 | 0.026 | 0.008 | 0.002 | 0.044 | 0.021 | 0.006 | 0.065 | 0.030 | 0.007 | 0.120 | 0.086 | 0.043 |

| 1.1 | 0.024 | 0.009 | 0.001 | 0.044 | 0.018 | 0.004 | 0.071 | 0.028 | 0.004 | 0.100 | 0.068 | 0.040 |

| 1.2 | 0.025 | 0.009 | 0.001 | 0.055 | 0.028 | 0.010 | 0.124 | 0.045 | 0.008 | 0.104 | 0.071 | 0.040 |

| 1.3 | 0.029 | 0.011 | 0.001 | 0.058 | 0.025 | 0.011 | 0.178 | 0.082 | 0.015 | 0.094 | 0.060 | 0.031 |

| 1.4 | 0.049 | 0.016 | 0.003 | 0.071 | 0.034 | 0.007 | 0.292 | 0.144 | 0.028 | 0.073 | 0.041 | 0.020 |

| 1.5 | 0.042 | 0.015 | 0.003 | 0.073 | 0.034 | 0.008 | 0.433 | 0.244 | 0.056 | 0.114 | 0.057 | 0.023 |

| 1.6 | 0.048 | 0.020 | 0.001 | 0.067 | 0.026 | 0.008 | 0.567 | 0.352 | 0.103 | 0.122 | 0.053 | 0.023 |

| 1.7 | 0.063 | 0.019 | 0.003 | 0.053 | 0.023 | 0.007 | 0.687 | 0.456 | 0.142 | 0.166 | 0.080 | 0.029 |

| 1.8 | 0.061 | 0.014 | 0.002 | 0.048 | 0.016 | 0.002 | 0.794 | 0.557 | 0.162 | 0.192 | 0.087 | 0.033 |

| 1.9 | 0.065 | 0.017 | 0.002 | 0.044 | 0.012 | 0.003 | 0.865 | 0.656 | 0.218 | 0.251 | 0.117 | 0.034 |

| 2.0 | 0.079 | 0.020 | 0.000 | 0.039 | 0.009 | 0.001 | 0.916 | 0.743 | 0.270 | 0.294 | 0.127 | 0.030 |

| 1.0 | 0.032 | 0.014 | 0.001 | 0.024 | 0.007 | 0.001 | 0.061 | 0.026 | 0.001 | 0.048 | 0.025 | 0.011 |

| 1.1 | 0.060 | 0.026 | 0.005 | 0.060 | 0.026 | 0.003 | 0.117 | 0.046 | 0.002 | 0.053 | 0.021 | 0.008 |

| 1.2 | 0.179 | 0.083 | 0.012 | 0.207 | 0.101 | 0.017 | 0.368 | 0.213 | 0.048 | 0.120 | 0.043 | 0.007 |

| 1.3 | 0.444 | 0.225 | 0.027 | 0.428 | 0.219 | 0.039 | 0.756 | 0.591 | 0.241 | 0.309 | 0.129 | 0.017 |

| 1.4 | 0.704 | 0.446 | 0.074 | 0.612 | 0.347 | 0.068 | 0.948 | 0.871 | 0.568 | 0.532 | 0.269 | 0.067 |

| 1.5 | 0.867 | 0.635 | 0.111 | 0.714 | 0.383 | 0.066 | 0.996 | 0.977 | 0.770 | 0.700 | 0.353 | 0.094 |

| 1.6 | 0.951 | 0.779 | 0.175 | 0.768 | 0.408 | 0.053 | 1.000 | 0.998 | 0.911 | 0.816 | 0.453 | 0.112 |

| 1.7 | 0.983 | 0.858 | 0.193 | 0.807 | 0.404 | 0.033 | 1.000 | 1.000 | 0.962 | 0.879 | 0.505 | 0.110 |

| 1.8 | 0.991 | 0.901 | 0.221 | 0.833 | 0.400 | 0.025 | 1.000 | 1.000 | 0.984 | 0.923 | 0.563 | 0.100 |

| 1.9 | 0.994 | 0.934 | 0.252 | 0.852 | 0.409 | 0.012 | 1.000 | 1.000 | 0.993 | 0.961 | 0.611 | 0.078 |

| 2.0 | 0.997 | 0.952 | 0.260 | 0.867 | 0.376 | 0.014 | 1.000 | 1.000 | 0.997 | 0.975 | 0.685 | 0.079 |

| 1.0 | 0.080 | 0.034 | 0.005 | 0.081 | 0.041 | 0.012 | 0.075 | 0.030 | 0.007 | 0.067 | 0.034 | 0.011 |

| 1.1 | 0.090 | 0.035 | 0.007 | 0.094 | 0.048 | 0.012 | 0.123 | 0.052 | 0.011 | 0.060 | 0.029 | 0.010 |

| 1.2 | 0.152 | 0.065 | 0.013 | 0.179 | 0.090 | 0.022 | 0.250 | 0.125 | 0.033 | 0.085 | 0.041 | 0.016 |

| 1.3 | 0.280 | 0.137 | 0.023 | 0.290 | 0.149 | 0.036 | 0.507 | 0.333 | 0.096 | 0.141 | 0.069 | 0.023 |

| 1.4 | 0.446 | 0.230 | 0.037 | 0.380 | 0.175 | 0.033 | 0.759 | 0.579 | 0.225 | 0.228 | 0.103 | 0.030 |

| 1.5 | 0.609 | 0.327 | 0.049 | 0.481 | 0.212 | 0.023 | 0.909 | 0.789 | 0.420 | 0.385 | 0.182 | 0.045 |

| 1.6 | 0.726 | 0.439 | 0.065 | 0.557 | 0.246 | 0.015 | 0.974 | 0.908 | 0.578 | 0.502 | 0.256 | 0.072 |

| 1.7 | 0.846 | 0.574 | 0.079 | 0.646 | 0.273 | 0.016 | 0.996 | 0.971 | 0.756 | 0.652 | 0.355 | 0.106 |

| 1.8 | 0.887 | 0.620 | 0.081 | 0.662 | 0.264 | 0.017 | 0.999 | 0.985 | 0.829 | 0.751 | 0.405 | 0.099 |

| 1.9 | 0.931 | 0.710 | 0.097 | 0.705 | 0.271 | 0.016 | 0.999 | 0.996 | 0.912 | 0.839 | 0.493 | 0.106 |

| 2.0 | 0.949 | 0.736 | 0.089 | 0.741 | 0.278 | 0.003 | 1.000 | 0.998 | 0.937 | 0.885 | 0.579 | 0.127 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 100,100 | 0.265 | 0.144 | 0.033 | 0.199 | 0.114 | 0.041 | 0.999 | 0.995 | 0.934 | 0.926 | 0.755 | 0.365 |

| 100,200 | 0.896 | 0.738 | 0.397 | 0.772 | 0.530 | 0.211 | 1.000 | 1.000 | 1.000 | 0.998 | 0.988 | 0.898 |

| 100,500 | 1.000 | 1.000 | 0.999 | 1.000 | 1.000 | 0.975 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.998 |

| 200,200 | 0.904 | 0.775 | 0.401 | 0.792 | 0.542 | 0.207 | 1.000 | 1.000 | 1.000 | 1.000 | 0.999 | 0.982 |

| 200,500 | 1.000 | 1.000 | 0.999 | 1.000 | 1.000 | 0.978 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 500,500 | 1.000 | 1.000 | 0.998 | 1.000 | 1.000 | 0.978 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 100,100 | 0.243 | 0.127 | 0.029 | 0.210 | 0.123 | 0.047 | 0.995 | 0.986 | 0.897 | 0.893 | 0.722 | 0.352 |

| 100,200 | 0.824 | 0.668 | 0.324 | 0.708 | 0.474 | 0.191 | 1.000 | 1.000 | 0.999 | 0.998 | 0.983 | 0.869 |

| 100,500 | 1.000 | 0.998 | 0.985 | 0.998 | 0.996 | 0.934 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 0.999 |

| 200,200 | 0.844 | 0.677 | 0.333 | 0.736 | 0.498 | 0.187 | 1.000 | 1.000 | 0.999 | 1.000 | 0.998 | 0.956 |

| 200,500 | 0.999 | 0.999 | 0.984 | 0.999 | 0.997 | 0.951 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 500,500 | 1.000 | 0.999 | 0.985 | 0.998 | 0.995 | 0.934 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| sup-Wald(HAC) | sup-LM(HAC) | sup-LR | sup-LRm | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | 10% | 5% | 1% | |

| 100,100 | 0.048 | 0.014 | 0.000 | 0.071 | 0.026 | 0.005 | 0.128 | 0.049 | 0.005 | 0.196 | 0.106 | 0.037 |

| 100,200 | 0.202 | 0.103 | 0.018 | 0.215 | 0.109 | 0.022 | 0.269 | 0.141 | 0.028 | 0.551 | 0.335 | 0.101 |

| 100,500 | 0.653 | 0.499 | 0.221 | 0.649 | 0.508 | 0.222 | 0.678 | 0.531 | 0.256 | 0.967 | 0.919 | 0.611 |

| 200,200 | 0.199 | 0.096 | 0.020 | 0.215 | 0.107 | 0.019 | 0.277 | 0.149 | 0.032 | 0.556 | 0.341 | 0.115 |

| 200,500 | 0.651 | 0.501 | 0.245 | 0.644 | 0.511 | 0.239 | 0.668 | 0.525 | 0.271 | 0.974 | 0.917 | 0.590 |

| 500,500 | 0.638 | 0.501 | 0.241 | 0.639 | 0.508 | 0.228 | 0.669 | 0.526 | 0.267 | 0.982 | 0.932 | 0.607 |

| 1000,1000 | 0.957 | 0.915 | 0.771 | 0.954 | 0.910 | 0.748 | 0.951 | 0.917 | 0.771 | 1.000 | 0.998 | 0.985 |

| 100,100 | 0.071 | 0.030 | 0.003 | 0.103 | 0.054 | 0.016 | 0.118 | 0.052 | 0.010 | 0.175 | 0.097 | 0.040 |

| 100,200 | 0.164 | 0.086 | 0.019 | 0.187 | 0.108 | 0.029 | 0.186 | 0.095 | 0.019 | 0.322 | 0.171 | 0.050 |

| 100,500 | 0.449 | 0.302 | 0.110 | 0.409 | 0.260 | 0.097 | 0.417 | 0.275 | 0.091 | 0.842 | 0.677 | 0.305 |

| 200,200 | 0.164 | 0.080 | 0.022 | 0.191 | 0.111 | 0.024 | 0.177 | 0.093 | 0.025 | 0.304 | 0.167 | 0.042 |

| 200,500 | 0.468 | 0.315 | 0.115 | 0.428 | 0.300 | 0.122 | 0.435 | 0.295 | 0.103 | 0.836 | 0.679 | 0.299 |

| 500,500 | 0.464 | 0.308 | 0.112 | 0.407 | 0.263 | 0.090 | 0.425 | 0.285 | 0.099 | 0.833 | 0.661 | 0.314 |

| 1000,1000 | 0.757 | 0.646 | 0.375 | 0.731 | 0.596 | 0.326 | 0.754 | 0.637 | 0.349 | 0.997 | 0.990 | 0.876 |

6 Empirical application

In this section, we estimate a factor model for the US industrial employment rates and apply the proposed tests to check whether the factor loadings have undergone a structural change in the past decade. Monthly data from January 2010 through April 2022 are available from the US Department of Labor for 84 industries. The data are a balanced panel with .

We use the information criteria and of Bai and Ng (2002), the (eigenvalue ratio) and (growth ratio) of Ahn and Horenstein (2013), the empirical distribution estimator of Onatski (2010), and the bridge estimator of Caner and Han (2014) to determine the number of common factors in the data. The maximum number of factors is set to 10. The estimated number of factors by and is three; the methods of Onatski (2010) and Caner and Han (2014) detect two factors; and and of Ahn and Horenstein (2013) choose one common factor. Therefore, we study the test results for the cases of one, two, and three common factors.

We apply our LR and LRm tests to examine whether there exists a structural break in factor loadings and estimate the break date if the null hypothesis is rejected. All of the settings for the two tests are the same as those used in the simulation studies.

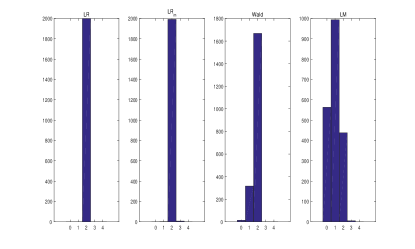

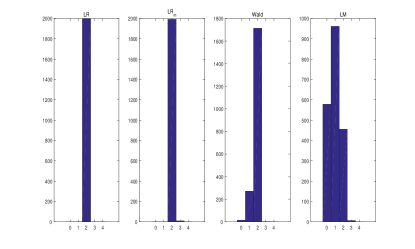

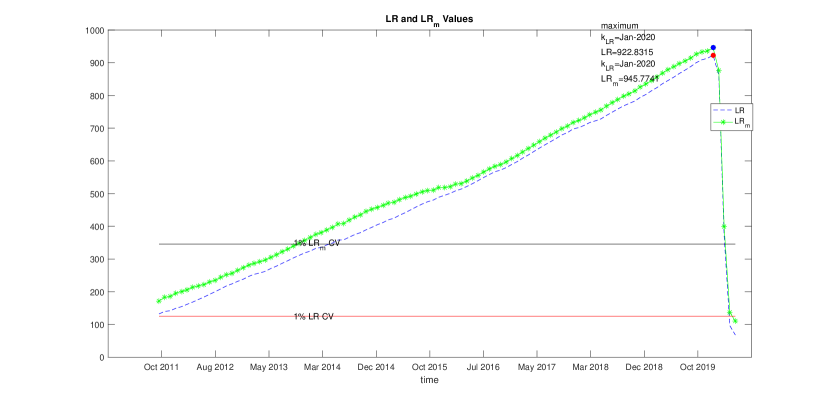

Table 10 reports the results of the LR and LRm tests at the , , and significance levels. Both the sup-LR and the sup-LRm reject the null hypothesis for . We also use the sup-LR and sup-LRm to estimate the break date. The sup-LR and sup-LRm show that the break date occurs in January 2020 (), regardless of the number of factors. We employed Wald and LM tests, both of which rejected the null hypothesis. Furthermore, we utilized a sequential procedure and determined that there was only one breakpoint present within the dataset.

Figure 2 shows the values of LR and LRm with different . The red and black horizontal lines are the sup-LR critical value and the sup-LRm critical value, respectively. The green and blue curves are the values of the LR and the LRm statistics, respectively. The red and blue points are the maximum points of the LR and the LRm, respectively. The break date in January 2020 means that employment has been changed to a new regime since February 2020, which is consistent with the observation that the stock market also fell sharply in late February.

We also separately performed LR and LRm tests on each single factor and found that all of them rejected the null hypothesis at the 1, 5, and 10 significance levels, except for the LRm test on the third factor at the 1 and 5 significance levels. The breakpoint positions for these single factors were identified at January 2020, February 2020, and March 2020, respectively. To explore the variations in factor contribution over time, we calculated the proportion of explained variation by summing the first three eigenvalues of and dividing it by the trace of , for data before and after the breakpoint. The results showed a significant increase in the proportion of explained variation value, from before the breakpoint to after the breakpoint, indicating a stronger degree of co-movement of employment across different industries during the pandemic.

| sup-LR | sup-LRm | |||||

| 10% | 5% | 1% | 10% | 5% | 1% | |

| 1 | 1 | 1 | 1 | 1 | 1 | |

| 1 | 1 | 1 | 1 | 1 | 1 | |

| 1 | 1 | 1 | 1 | 1 | 1 | |

1 means rejection.

7 Conclusions

This paper proposes an LR test for structural changes in the factor loading matrix. The new test is based on the LR principle under the assumption that the factors are normally distributed and serially uncorrelated. We show that the limiting null distribution of the test statistic is a function of a Brownian bridge that depends on a long-run variance term, which allows for non-normal and serially dependent factors. Under the alternative hypothesis, the test statistic diverges at a faster rate than regular Wald-type tests if the pseudo-factors have a singular variance before or after the break. The new LR tests are also generalized to allow for factor mean changes and multiple breaks. The simulation results confirm that our test is much more powerful than the Wald test of HI (2015). The test procedure is illustrated with a monthly US employment dataset and detects a structural break in early 2020.

Appendix

The LR test is invariant to the identification conditions

The identification problem in factor models occurs because one can set , where and for any nonsingular matrix . The identification condition essentially determines the rotation matrix .

To understand why the LR test is invariant to the choice of identification conditions, let denote the estimated factors under condition (3.1) and denote the factors estimated under an alternative identification condition. There must exist a nonsingular matrix such that

Thus, under the alternative identidication condition, the pre- and post- factor variances are given by

The quasi-Gaussian likelihood in (3.2) for a break point at is given by

The log-likelihood of no change for the entire sample becomes

because under (3.1). Thus, the likelihood ratio test under this alternative identification condition can be expressed as

Thus, the above is equivalent to the .

Proof. See the online appendix.

Proof of Theorem 1:

| (7.4) |

by Lemmas B2 and B3 of Bai (2003). Let (i.e., is an orthogonal matrix), so we have

| (7.5) | |||

| (7.6) |

under the condition that , where the first line uses (7.2), the second line uses (7.4), the fourth line follows from the definition of , and the last line follows from Assumption 8.

Because , it follows that

| (7.7) |

Moreover, (7.6) and (7.7) imply that

| (7.8) |

and the terms are uniform over for .

Consider the second order Taylor expansions of and at , so

where the terms are uniform over and follow from (7.8). Thus,

| (7.9) |

where the terms are uniform over . Because , we have

| (7.10) | |||||

by (7.6), (7.7), and the fact that is orthonormal. Because for a symmetric matrix , the result in (7.10) can be rewritten as

| (7.11) |

where means equality in distribution only,

and is an vector of independent Brownian motions.

(ii) Let , so using the definition of gives

Thus, the asymptotic distribution (The LR test is invariant to the identification conditions) can be expressed as

where in the second line means equality in distribution only and follows from the facts that is orthonormal and is a vector of independent Brownian motions. Thus, we can use an estimator for instead of to simulate the distribution. The HAC estimator in (3.6) is consistent for according to Theorem 2 of HI (2015).

Proof of Theorem 2: See the online appendix.

Proof of Theorem 3:

(i) Without loss of generality, we consider the case in which is singular with and is nonsingular under the alternative. Given Assumption 9, it follows that

| (7.12) |

for by Proposition 1 of DBH (2022) for some . In addition, for and we have, as ,

by (7.2) and Assumption 1. Thus, for

| (7.13) |

where and the second line follows from (7.12). In addition, we have

| (7.14) |

The RHS of (7.14) is positive definite because is nonsingular, so

is also dominated by the leading term in (7.13). This completes the proof for part (i).

(ii) For , we have

Consider the function

where and . Note that

so for and for . Thus, takes its maximum equal to zero when for . Because , there must exist at least a for some so that . Thus,

which gives the desired result.

Proof of Theorem 4:

(i) Note that

| (7.15) |

where the term follows from (7.8) under the null hypothesis, the term follows from Assumption 10 and (7.1), and both terms are uniform over .

Thus, the second order Taylor expansion gives

where the term follows from (7.15) and is uniform over . Similarly,

Thus, we have

| (7.16) |

where the last equality follows from (7.8) and Assumption 10, and the term is uniform over . Similarly,

For the term , we have

| (7.17) |

with , where the first equality uses the fact that because PCs are estimated from demeaned data, and the term follows from (7.1) and is uniform over . This also implies that

| (7.18) |

By (7.18) we have

| (7.19) |

In addition,

| (7.20) |

where the second equality follows from the first equation in (7.7). By (7.19) and (7.20), we can obtain

| (7.25) | |||||

| (7.31) |

where the second equality follows from , (7.5) and (7.17), and the weak convergence follows from Assumption 10.

(ii) Under the additional assumption that is uncorrelated with , (7.19) reduces to

where is an -dimensional independent Brownian motion process and Therefore, together with the result in (The LR test is invariant to the identification conditions), the LR statistic has the following limiting distribution

Taking the supreme over yields the desired distribution.

Proof of Theorem 5:

(7.32) implies that is uniformly , so following arguments similar to those used in (7.8) and (7.9), we have

| (7.33) |

where the and terms are uniform over for . Because , we have

| (7.34) |

where the third line follows from (7.32) and the fact that , and the weak convergence follows from Assumption 8. The result in (7.34) can be written as

where means equality in distribution only,

and is an vector of independent Brownian motions. Thus, we have

where is a Brownian bridge process.

Proof of Theorem 6:

Following the steps in (7.17), we can obtain

References

- Ahn and Horenstein (2013) Ahn, S. and Horenstein, A. 2013. Eigenvalue ratio test for the number of factors. Econometrica 81, pp. 1203–1227.

- Andrews (1993) Andrews, D.W.K., 1993. Tests for parameter instability and structural change with unknown change point. Econometrica 61, pp. 821–856.

- Bai (1997) Bai, J., 1997. Estimaing multiple breaks one at a time. Econometric Theory 13, pp. 315–352.

- Bai (2000) Bai, J., 2000. Vector autoregressive models with structural changes in regression coefficients and in variance-covariance matrices. Annals of Economics and Finance 1, pp. 303–339.

- Bai (2010) Bai, J., 2010. Common breaks in means and variances for panel data. Journal of Econometrics 157, pp. 78–92.

- Bai and Ng (2002) Bai, J. and Ng, S. 2002. Determining the number of factors in approximate factor models. Econometrica 70, pp. 191–221.

- Bai (2003) Bai, J., 2003. Inferential theory for factor models of large dimensions. Econometrica 71, pp. 135–171.

- Bai et al. (2020) Bai, J., Han, X., Shi, Y., 2020. Estimation and inference of change points in high-dimensional factor models. Journal of Econometrics 219, pp. 66–100.

- Bai et al. (1998) Bai, J., R. L. Lumsdain, and J. H. Stock (1998): Testing for and Dating Common Breaks in Multivariate Time Series, Review of Economic Studies, 65, 395-432.

- Bai and Perron (1998) Bai, J., Perron, P., 1998. Estimating and testing linear models with multiple structural changes. Econometrica 66, pp. 47–78.

- Baltagi et al. (2017) Baltagi, B., Kao, C., Wang, F., 2017. Identification and estimation of a large factor model with structural instability. Journal of Econometrics 197, pp. 87–100.

- Baltagi et al. (2021) Baltagi, B., Kao, C., Wang, F., 2021. Estimating and testing high dimensional factor models with multiple structural changes. Journal of Econometrics 220, pp. 349–365.

- Barigozzi et al. (2018) Barigozzi, M., Cho, H., Fryzlewicz, P., 2018. Simultaneous multiple change-point andfactor analysis for high-dimensional time series. Journal of Econometrics 206, pp. 187–225.

- Bates et. al (2013) Bates, B. J., Plagborg-Mller, M., Stock, J. H., and Watson, M. W., 2013. Consistent factor estimation in dynamic factor models with structural instability. Journal of Econometrics 177, pp. 289–304.

- Bergamelli et. al (2019) Bergamelli, M., Bianchi, A., Khalaf, L. and Urga, G, 2019. Combining P-Values to Test for Multiple Breaks in Cointegrated Regressions. Journal of Econometrics 211, pp. 461–482.

- Bernanke et al. (2005) Bernanke, B., Boivin, J., Eliasz, P., 2005. Measuring the effects of monetary policy: a factor-augmented vector autoregressive (FAVAR) approach. The Quarterly journal of economics 120, pp. 387–422.

- Breitung and Eickmeier (2011) Breitung, J. and Eickmeier, S., 2011. Testing for structural breaks in dynamic factor models. Journal of Econometrics 163, pp. 71–84.

- Caner and Han (2014) Caner, M. and Han, X., 2014. Selecting the Correct Number of Factors in Approximate Factor Models: The Large Panel Case With Group Bridge Estimators. Journal of Business and Economic Statistics 32, pp. 359–374.

- Chen (2015) Chen, L., 2015. Estimating the common break date in large factor models. Economics Letters 131, pp. 70–74.

- Chen et al. (2014) Chen, L., Dolado, J.J. and Gonzalo, J., 2014. Detecting big structural breaks in large factor models. Journal of Econometrics 180, pp. 30–48.

- Cheng et al. (2016) Cheng, X., Liao, Z., Schorfheide, F., 2016. Shrinkage estimation of high-dimensional factor models with structural instabilities. Review of Economic Studies 83, pp. 1511–1543.

- Duan et al. (2022) Duan, J., Bai, J., and Han, X., 2022. Quasi-maximum likelihood estimation of break point in high-dimensional factor models. Journal of Econometrics 233, pp. 409–236.

- Fama (1992) Fama, E. and French, K., 1992. The cross-section of expected stock returns. Journal of Finance 47, pp. 427–465.

- Feng (2020) Feng, G., Giglio, S. and Xiu, D., 2020. Taming the factor zoo: A test of new factors. Journal of Finance 75, pp. 1327–1370.

- Han (2018) Han, X., 2018. Estimation and inference of dynamic structural factor models with over-identifying restrictions. Journal of Econometrics 202, pp. 125–147.

- Han and Inoue (2015) Han, X., Inoue, A., 2015. Tests for parameter instability in dynamic factor models. Econometric Theory 31, pp. 1117–1152.

- Ma and Su (2018) Ma, S., Su, L., 2018. Estimation of large dimensional factor models with an unknown number of breaks. Journal of Econometrics 207, pp. 1–29.

- Mikkelsen et. al (2019) Mikkelsen, J. G., Hillebrand, E., and Urga, G., 2019. Consistent estimation of time-varying loadings in high-dimensional factor models. Journal of Econometrics 208, pp. 535–562.

- Newey and West (1994) Newey, W., West, K., 1994. Automatic Lag Selection in Covariance Matrix Estimation. The Review of Economic Studies 61, pp. 631–653.

- Onatski (2010) Onatski, A., 2010. Determining the Number of Factors from Empirical Distribution of Eigenvalues. The Review of Economics and Statistics 92, pp. 1001–1016.

- Perron_Yamamoto (2020) Perron, P., Yamamoto, Y. Zhou, J. 2020. Testing jointly for structural changes in the error variance and coefficients of a linear regression model. Quantitative Economics 11, pp. 1019–1057.

- Qu and Perron (2007) Qu, Z. and Perron, P., 2007. Estimating and Testing Structural Changes in Multivariate Regressions. Econometrica 75, pp. 459–502.

- Ross (1976) Ross, S., 1976. The Arbitrage Theory of Capital Asset Pricing. Journal of Finance 13, pp. 341–360.

- Stock and Watson (2002) Stock, J.H. and Watson, M.W., 2002. Forecasting using principal components from a large number of predictors. Journal of the American Statistical Association 97, pp. 1167–1179.

- Stock and Watson (2009) Stock, J.H. and Watson, M.W., 2009. Forecasting in dynamic factor models subject to structural instability. In: Castle, J., Shephard, N. (Eds.), The Methodology and Practice of Econometrics, A Festschrift in Honour of Professor David F. Hendry. Oxford University Press, Oxford.

- Su and Wang (2020) Su, L., Wang, X., 2020. Testing for structural changes in factor models via anonparametric regression. Econometric Theory 36, pp. 1127–1158.

- Yamamoto and Tanaka (2015) Yamamoto, Y. and Tanaka, S., 2015. Testing for factor loading structural change under common breaks. Journal of Econometrics 189, pp. 187–206.