A Robustness Test for Estimating Total Effects with Covariate Adjustment

Abstract

Suppose we want to estimate a total effect with covariate adjustment in a linear structural equation model. We have a causal graph to decide what covariates to adjust for, but are uncertain about the graph. Here, we propose a testing procedure, that exploits the fact that there are multiple valid adjustment sets for the target total effect in the causal graph, to perform a robustness check on the graph. If the test rejects, it is a strong indication that we should not rely on the graph. We discuss what mistakes in the graph our testing procedure can detect and which ones it cannot and develop two strategies on how to select a list of valid adjustment sets for the procedure. We also connect our result to the related econometrics literature on coefficient stability tests.

1 Introduction

Suppose we are interested in estimating the total (causal) effect of a treatment on an outcome from observational data. One popular approach to estimate such an effect is covariate adjustment, also known as adjusting for confounding. Deciding which covariates to adjust for is a difficult problem, but it can be answered precisely if we have knowledge of the underlying causal structure in the form of a graph [Pearl, 2009]. In particular, the class of covariate sets we may adjust for has been fully graphically characterised [Shpitser et al., 2010, Perković et al., 2018]. We refer to sets in this class as valid adjustment sets.

In some cases there is more than one valid adjustment set, which raises the question how we can exploit this. One approach is to try and select from the available valid adjustment sets the one that provides the most statistically efficient estimator [Kuroki and Miyakawa, 2003, Rotnitzky and Smucler, 2020, Witte et al., 2020, Henckel et al., 2022].

Another natural approach is to use multiple valid adjustment sets and test whether they all in fact lead to estimators of the same quantity. Such a test would be a simple and targeted robustness check on the causal graph we are relying on. Here we say targeted in the sense that the test would only detect mistakes in the graph that are relevant to our goal of estimating the total effect of interest, which is easier than checking whether the entire graph is correct.

In the econometrics literature, it is already common practice to estimate the total effect with multiple estimators and then check whether the estimates differ by a large margin [e.g. Dikova et al., 2019, Yigezu and El-Shater, 2021, Schlegel et al., 2021]. This approach is often called testing for coefficient stability [Walter and Tiemeier, 2009] or simply called a robustness check [Lu and White, 2014].

Practitioners often verify coefficient stability in a heuristic manner, but there is also a theoretical literature on the topic, especially for instrumental variable estimators [Frank et al., 2013, Oster, 2019].

For covariate adjustment estimators, Lu and White [2014] have proposed a formal test for coefficient stability. Their framework is not based on graphical models and therefore it is harder to decide which adjustment sets to use for their test. They propose to fix what they call a core of covariates and then create additional adjustment sets by adding what they call non-core covariates to the core. Here, the status of being core or non-core depends on certain conditional independences. In the graphical framework it becomes clear that this approach is too restrictive as, for example, two valid adjustment sets may be disjoint. As a result their approach may consider too few sets which leads to a loss of power.

There exists a more general literature on validation tests for structural equation models. This literature, however, has focused on tests that either validate the entire model [Bollen, 1989, Bollen and Ting, 1993, Spirtes et al., 2000] or rely on instrumental variables [Kirby and Bollen, 2009]. Another related literature focuses on identifying valid adjustment sets by relying on an auxiliary variable, typically called an anchor, whose causal relationship to the treatment has to be known from domain knowledge [Entner et al., 2013, Gultchin et al., 2020, Shah et al., 2021, Cheng et al., 2022].

In this paper, we adopt the framework of a linear structural equation model compatible with an unknown directed acyclic graph (DAG). We propose a targeted robustness test that given a pair and a candidate DAG tests whether the valid adjustment sets with respect to in lead to estimates of the same quantity.

We first discuss, which mistakes in the candidate graph our robustness test has power for and how this depends on the valid adjustment sets we use for the test. We then propose a simple -test, similar to the one proposed by Lu and White [2014], although it differs in that we do not require a fixed core of covariates. We show that in general the joint asymptotic covariance matrix of the estimators we wish to compare is degenerate and that we need to know its rank for the test. This problem was acknowledged but not addressed by Lu and White [2014].

In response to the problem of the degenerate asymptotic covariance matrix, we propose two strategies. The first is to estimate the rank. This is a difficult statistical problem and may be unstable, especially in small samples. The upside of this approach, however, is that it allows us to use all valid adjustment sets for our test, which maximises its power.

The second strategy carefully selects a subset of the valid adjustment sets in a way that ensures the following two properties are likely to hold. First, the asymptotic covariance matrix is not degenerate. Second, we do not lose power completely against mistakes in the graph we had power for when using all valid adjustment sets. These two strategies represent different trade-offs between the stability of our testing procedure and its power to detect mistakes in the candidate graph.

Finally, we investigate with a simulation study how well our testing procedure controls the type-I error rate and how much power it has in finite samples. We do so for both of the strategies we propose, in order to compare and contrast their respective advantages and disadvantages. We also illustrate our testing procedure on a real data problem. All proofs are given in the supplementary materials. An implementation of our testing procedure and the code for our simulation study are made available at https://github.com/zehaosu/RoCA.

2 Preliminaries

We consider a linear structural equation model compatible with a DAG, where nodes represent random variables and edges represent direct effects. We now provide the most important definitions. The remaining definitions are provided in Section A of the supplementary materials.

Linear structural equation models. Let be a DAG. Then follows a linear structural equation model compatible with if for all

with edge coefficients and jointly independent errors with zero mean and finite variance. We do not assume that the errors are normally distributed.

Total effects. Consider a pair of random variables. The total effect of on is the partial derivative of the expectation with respect to . This is the instantaneous change of the average of in the world where is set to [Pearl, 2009]. In a linear structural equation model, the partial derivative is a constant slope that does not depend on . As a result, the total effect is simply a number .

Causal and forbidden nodes. Consider two nodes and in a DAG . The causal nodes relative to in , denoted , are all nodes on directed paths from to , excluding . The descendants of in , denoted , are all nodes such that there exists a directed path from to in . The forbidden nodes relative to in , denoted , are all nodes that are descendants of causal nodes, including . The non-forbidden nodes relative to in , denoted , are the nodes in .

Notation for regression coefficients. Consider random variables and , random vectors and the collection of adjustment sets . Let indicate the population level regression coefficient of in the ordinary least squares regression of on and . Let denote the corresponding estimator. Let denote the stacked population regression coefficients and the corresponding estimator. Finally, let be the population level residuals for the ordinary least squares regression of on and be the corresponding vector of sample residuals.

Valid adjustment sets. Consider nodes and in a DAG . A node set is a valid adjustment set relative to in if for all linear structural equation models compatible with , . We say a valid adjustment set is minimal if for all , is not a valid adjustment set. The class of valid adjustment sets has been fully characterised as follows.

Adjustment criterion. [Shpitser et al., 2010, Perković et al., 2018] A (possibly empty) set is a valid adjustment set relative to in if and only if

-

1.

contains no node in , and

-

2.

blocks all paths between and in that are not directed from to .

d-separation. Consider three disjoint node sets and in a DAG , such that follows a linear structural equation model compatible with . We can read off from whether is independent of given with a graphical criterion called d-separation [Pearl, 2009] which we define formally in the supplementary materials. We use the notation to denote that is d-separated from given in .

3 A Targeted Robustness Test for Covariate Adjustment

3.1 The Null Hypothesis and its Properties

Suppose we wish to estimate the total effect of a treatment on a response variable . Let denote the unknown true underlying casual graph and suppose we have a candidate causal graph that describes our understanding of the underlying causal structure but that we are not certain about. We would like to check whether the candidate graph is plausible, so we can rely on it to estimate with some confidence. In order to do so, we use to identify a collection of valid adjustment sets with respect to in . If is correct each of these sets corresponds to a consistent estimator of , i.e.,

| (1) |

If consists of more than one set, then equation (1) imposes an over-identifying constraint on the total effect . We use this constraint to test the plausibility of the candidate graph . The more valid adjustment sets we use, the more mistakes in the test can detect.

It is generally not possible to directly test the constraint from equation with observational data because we do not know the true total effect . It is, however, possible to test the relaxed null hypothesis

Let denote the null hypothesis associated with equation (1). As holds whenever does, it follows that any test with type-I error rate control for testing also has type-I error rate control for testing . In addition, any rejection of implies a rejection of and as a result of the candidate graph . It is therefore reasonable to test as a proxy for .

There is an even more restrictive null hypothesis . However, as we are interested in estimating one specific total effect, it is not necessary to validate the entire candidate graph , and the distinction between and is irrelevant for the purposes of this paper. There are, however, cases where holds but does not and in these cases any test for will have no power to reject . This occurs whenever holds but for all , . Whether this is the case depends on the choice of candidate sets and is more likely if contains few sets. In particular, this is impossible if contains even a single valid adjustment set from the true graph . In response, it is natural to use all available valid adjustment sets relative to in to maximise the number of sets in . However, even for a moderately sized the number of valid adjustment sets relative to the pair can be very large, e.g., there are in the graph and in the graph from Figure 1. This raises the question whether it is possible to select the collection in a way that minimises the risk of having no power for , while simultaneously limiting its size.

We now provide a necessary condition on under which the problematic case that holds but does not is rare, and as a result testing is a good proxy for testing .

Theorem 1.

Consider nodes and in a DAG such that . Let be a collection of node sets in . Suppose there exists a , such that and is not a valid adjustment set relative to in . Further, suppose that . If we sample the edge coefficients and error variances for a linear structural equation model compatible with from a distribution such that is absolutely continuous with respect to the Lebesgue measure, then -almost surely there exists a such that

Verifying that Theorem 1 holds requires knowledge of the true DAG , which we do not have. Nonetheless, it gives two important but also intuitive insights on how to select . First, the sets in should cover as many nodes as possible, i.e., ideally all non-forbidden nodes in the candidate graph . This maximises the chances that . Second, we should minimise the number of nodes that appear in all sets , and some of the candidate sets should be as small as possible. This maximises the chance that for at least one . Note that this is very different from the strategy proposed by Lu and White [2014].

Example 2.

Consider the graphs from Figure 1 and the linear structural equation model compatible with , where all edge coefficients and error variances equal 1. We are interested in estimating the total effect , which here is simply the edge coefficient of the edge and therefore by the path tracing rules for total effects from Wright [1934].

We now illustrate for three candidate graphs that differ from , whether we can use tests for the null hypothesis to detect the mistakes in the candidate graphs and how this depends on the choice of sets .

Consider the candidate graph and the collection

of three valid adjustment sets relative to in . A direct calculation shows that , none of which are equal to the total effect . In this case, the null hypothesis is true even though the null hypothesis is false, i.e., testing will not detect that there is a mistake in the candidate graph. However, if we add the set of non-forbidden nodes to , then no longer holds as is a valid adjustment set in and therefore . In this case testing will detect that there is a mistake in the candidate graph.

Consider now the candidate graph . It has exactly the same valid adjustment sets relative to as the true graph . Testing will therefore not detect that there is a mistake in the candidate graph, irrespective of the collection of valid adjustment sets. Since the two graphs are equivalent with respect to estimating the total effect with covariate adjustment this is not a concern.

Consider now the candidate graph . All valid adjustment sets relative to in result in estimates of . Therefore testing will not detect that there is a mistake in the candidate graph, irrespective of the collection of valid adjustment sets. Interestingly, in the graph equal to but with the edge removed, we can detect the mistakes by testing with, for example, the collection of all valid adjustment sets in . This is an example of using an instrument to detect omitted variables bias [cf. Chen and Pearl, 2015], which our test implicitly exploits.

3.2 The Test Statistic

As a preparatory result and for completeness, we first derive the asymptotic distribution of the estimator .

Lemma 3.

Consider a -dimensional random vector that follows a distribution where for all . Given two random variables , let , , be a collection of random subvectors of that do not contain or , and let for . Then the random vector converges in distribution to a multivariate normal random variable with mean zero and covariance matrix

| (2) |

where and .

In general the covariance matrix of the limiting normal distribution will not be of full rank, that is, the distribution will be degenerate. To illustrate this, we now give an example.

Example 4.

Consider again the DAG and the linear structural equation model from Example 2. Let

The asymptotic covariance matrix of is the rank-3 matrix

We now reformulate and slightly generalise the null hypothesis from Section 3.1 as follows. Consider a pair of random variables and a collection of random vectors . Define a contrast matrix such that and and consider the null hypothesis: . Based on the joint asymptotic normality of we now construct an asymptotically -distributed test statistic for this null hypothesis.

Definition 5 (Rank- Moore-Penrose inverse).

Consider the spectral decomposition of an positive semidefinite matrix , where is the orthonormal matrix of eigenvectors and with the ordered eigenvalues of . The rank- Moore-Penrose inverse of is the matrix , where and .

Theorem 6.

Assume the same conditions as in Lemma 3. Let be the covariance matrix of the limiting distribution of and given a contrast matrix , define . Suppose that is a consistent estimator of and that is a consistent estimator of . Let denote the rank- Moore-Penrose inverse of . Then under the null hypothesis , the test statistic

| (3) |

converges in distribution to a -distributed random variable.

We can estimate consistently by plugging in sample residuals for the population level residuals in equation (2). We refer to this estimator as the plug-in estimator and denote it . For a detailed argument, see Lemma 12 in the supplementary materials. Note also that for simplicity, we only consider the contrast matrix with at the entries and at the entries for , and with zeroes at the remaining entries in this paper.

3.3 The Degrees of Freedom

To compute the Moore-Penrose inverse and the degrees of freedom for the test statistic in equation (3), it is necessary to know the rank of . There are two possible approaches to this problem. The first is to estimate the rank with some estimate . The second approach is to select the candidate sets in a way that ensures the matrix is invertible. We now develop tools for both approaches.

3.3.1 Estimating the Degrees of Freedom

A standard approach to estimating the rank of a matrix from a noisy observation is information criterion based model selection. This is equivalent to conducting sequential hypothesis tests [Camba-Méndez and Kapetanios, 2009] for the possible ranks. In order to apply such model selection to the rank estimation of , we first derive that the half-vectorised plug-in estimator based on the plug-in estimator is asymptotically normal.

Proposition 7.

Under the same conditions as in Lemma 3, , where for some positive semidefinite matrix , with scaling matrix . Here, is the elimination matrix, and is the duplication matrix.

Based on Proposition 7 and a consistent estimator of the matrix , we may construct a rank estimation procedure from the minimum discrepancy function (MDF) test statistic [Cragg and Donald, 1997, Donald et al., 2007], which has the form

| (4) |

This procedure, however, has only been shown to be consistent if either is of full rank [Cragg and Donald, 1997] or, in slightly adapted form, if the true rank of is known [Ratsimalahelo, 2003].

As we cannot estimate the rank of to estimate the rank of , we instead propose using a simplified estimator based on the MDF statistic from equation (4) which we call the pseudo-MDF estimator:

| (5) | ||||

where is the best rank- reconstruction of based on spectral decomposition such that . Note that we effectively assume that the matrix is the identity matrix. In doing so, we ignore the covariance structure between the elements of . Although the elements of are likely correlated, the pseudo-MDF rank estimate nonetheless works well empirically (see Section 4).

3.3.2 Selecting to Ensure Full Rank

Depending on the choice of candidate sets , the asymptotic covariance matrix may be of full rank. This is, for example, trivially true if there is only one set in . Whenever is invertible, the matrix is also invertible. We now propose a strategy to select , such that is likely to be of full rank and that also follows the guidelines derived from Theorem 1 in Section 3.1.

Lemma 8.

Consider nodes and in a DAG such that . Consider a collection of

where , , are minimal valid adjustment sets relative to in . If for all , and we sample the edge coefficients and error variances for a linear structural equation model compatible with from a distribution , such that is absolutely continuous with respect to the Lebesgue measure, then the asymptotic covariance matrix for the random vector is -almost surely of full rank.

In general, the collection of all minimal valid adjustment sets will not fulfil the distinct node condition of Lemma 8. It is, however, easy to prune the set of all minimal valid adjustment sets to obtain a subset that fulfils the conditions of Lemma 8 and still covers the same set of nodes as the collection of all minimal valid adjustment sets.

3.4 The testing procedure

We propose a testing procedure that, given a pair of nodes in a candidate graph and a data set, tests whether adjusting for the valid adjustment sets relative to in leads to estimators that converge to the same quantity. The procedure uses the test statistic from equation (3) and we propose two strategies to select the collection of valid adjustment sets .

The first strategy, which we call , considers all available valid adjustment sets. This strategy is likely to lead to the best power for the test, but it requires estimating the degrees of freedom for the test statistic’s asymptotic distribution. This is a difficult problem (see Section 3.3.1) and as a result the solution we propose does not have a formal consistency guarantee, although it performs well in practice (see Section 4). In addition, computing all valid adjustment sets is very computationally expensive, especially for moderate to large graphs, and as a result this strategy may often not be computationally feasible.

The second strategy, which we call , is to prune the collection of all minimal valid adjustment sets as explained in Section 3.3.2 and then add the set of all non-forbidden nodes, which under the assumption is always a valid adjustment set (see Lemma 17 in the supplementary materials). This approach avoids estimating the degrees of freedom but may lead to a loss of power. Note that if we would need to replace the non-forbidden nodes with another large set such as [Perković et al., 2018]. However, if every set that d-separates and is a valid adjustment set and therefore our problem reduces to checking d-separation statements, for which there exists a wide literature on conditional independence tests [e.g. Spirtes et al., 2000]. Therefore, we disregard this case.

Another major advantage of the strategy is that it avoids the computationally heavy task of computing all valid adjustment sets. The number of minimal valid adjustment sets is typically much smaller than the number of valid adjustment sets and as a result the polynomial-delay algorithm by Van der Zander et al. [2014], which we use to estimate the set of all minimal valid adjustment sets, is generally quite fast. We verify this in a small simulation study, where the strategy ran on sparse graphs of size up to (see Section C.3 in the Supplementary Materials).

We summarise the testing procedure in Algorithm 1. As discussed in Section 3.1, the test cannot detect all types of mistakes in , but it nonetheless serves as a simple and targeted robustness check.

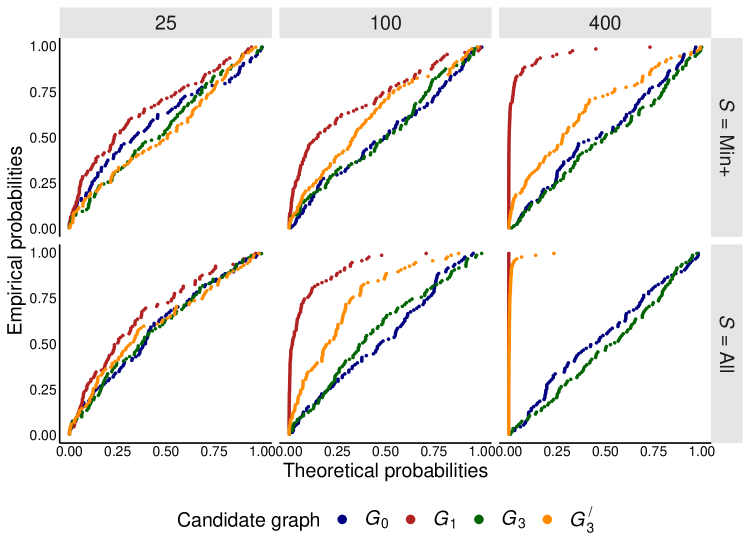

Example 9.

To illustrate our testing procedure, we revisit the linear structural equation model from Example 2 as well as the true graph and candidate graphs shown in Figure 1. In addition, we also consider the candidate graph which is the graph with the edge deleted. To each candidate graph we apply the testing procedure with both testing strategies (see Algorithm 1). Recall that for the candidate graphs and the null hypothesis is true, while it is false for the candidate graphs and . We sample data sets with observations, sets with observations, and another sets with observations from the underlying linear structural equation model and apply our testing procedure to each of these data sets. The resulting -values are shown as probability-probability plots against the standard uniform distribution in Figure 2. We explain the construction of these plots more thoroughly in Section C.1 of the Supplementary Materials. When the null hypothesis is true, we see that both strategies lead to close to uniform -values, especially when . We do not consider as it is equivalent to in terms of valid adjustment sets. We also observe reasonable power for and , especially with strategy . For on the other hand the power is mediocre except for and .

4 Simulations

We investigate the finite sample performance of the testing procedure from Algorithm 1 in a simulation study. The study is structured as follows. We randomly generate DAGs for each graph size from . The expected neighbourhood size is sampled uniformly from for each graph. Then, for each DAG we randomly generate a compatible linear structural equation model by (i) sampling the edge coefficients uniformly from the interval , (ii) sampling the error distribution uniformly to either be normal, , uniform or logistic for all errors and (iii) uniformly sampling scale parameters which depend on the error distribution such that the error variances are in the interval . We randomly choose a pair of nodes such that and that there exist at least two valid adjustment sets relative to in .

For each true DAG we then sample data sets from the corresponding linear structural equation model. The sample size is for half of these data sets, and for the other half. With each of these data sets we estimate a causal graph using either the Greedy Equivalence Search (GES) algorithm [Chickering, 2002], if the errors of the linear structural equation model are normal or the Linear Non-Gaussian Acyclic Models (LiNGAM) algorithm [Shimizu et al., 2006], otherwise. We do this to generate a large number of plausible candidate causal graphs for our testing procedure. We use the sample sizes and to ensure that some of the candidate graphs contain more errors and some fewer. We refer to the candidate graphs that were generated using the sample size as low accuracy candidate graphs and to those that were generated with the sample size as high accuracy ones.

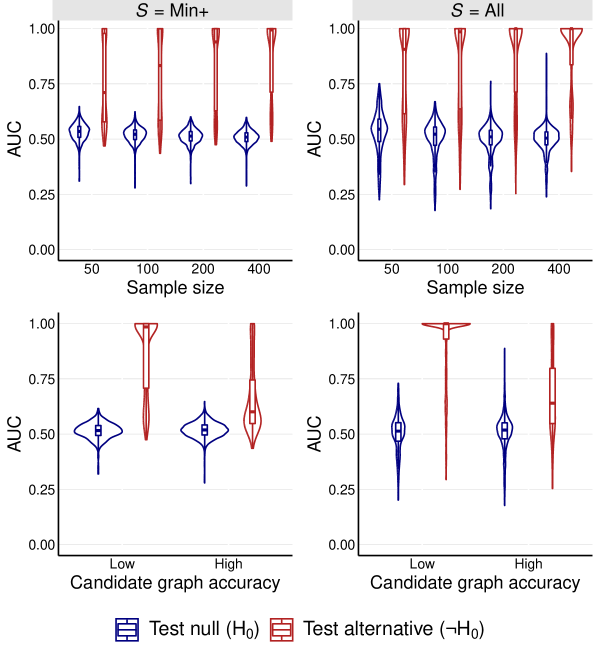

For each candidate graph and each sample size we do the following procedure. We sample an additional data sets with sample size from the corresponding true linear structural equation model. Given these data sets, the pair and the candidate graph , we apply Algorithm 1 using both strategies for graphs with or nodes. To measure the performance of our testing procedure we then compute the area under the curve (AUC) of the probability-probability plot of the -values against the uniform distribution. This means that in total we obtain AUCs for each candidate graph, i.e., for each testing strategy and for each sample size. Figure 3 gives an illustration of the layered simulation scheme. We give further details for the design of the simulation study in Section C.2 of the Supplementary Materials.

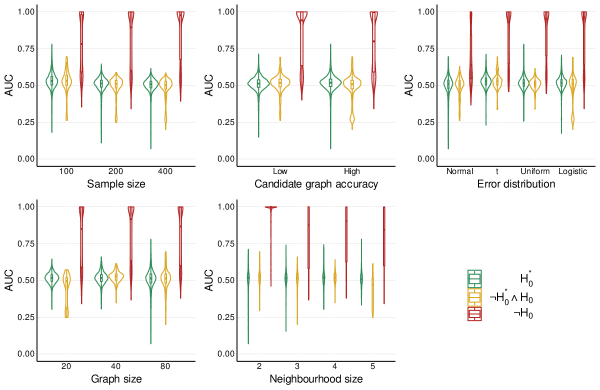

Figure 4 is an ensemble of violin plots of the AUCs from the simulation study. As we have access to the true graph, we can decide for each candidate graph and testing strategy, whether the null hypothesis for the test, i.e. , is true or false and plot these cases separately. Figure 4 shows that as the sample size of the data set used for our testing procedure increases, the AUCs in the cases where the null hypothesis is true become centred around . This indicates that both strategies control the type-I error rate asymptotically. There are, however, very large and small AUCs when we use the strategy with small sample sizes and for the more accurate candidate graphs. This is likely due to the rank estimation step required for this strategy and indicates that as expected the strategy is more stable than .

In the cases where the null hypothesis is false, i.e., the candidate graph contains a mistake that the test can detect, the AUCs have a cluster close to which is especially pronounced for the larger sample sizes. This indicates that our testing procedure has good power in many cases. Unsurprisingly, the AUCs are smaller for the candidate graphs with fewer errors, since it is more difficult to detect that there is a mistake in an almost correct graph than in a glaringly incorrect one. Nonetheless, the AUCs remain respectable and there continue to be AUCs close to . In general, the AUCs for strategy are larger than those for , although this gain is obtained at the price of a loss in stability.

| Cand. graph | Null () | Alternative () | |||

|---|---|---|---|---|---|

| accuracy | |||||

| Low | 50 | 0.0753 | 0.0903 | 0.5570 | 0.7396 |

| 100 | 0.0634 | 0.0626 | 0.6352 | 0.7880 | |

| 200 | 0.0540 | 0.0510 | 0.7132 | 0.8341 | |

| 400 | 0.0494 | 0.0468 | 0.7887 | 0.8812 | |

| High | 50 | 0.0781 | 0.0887 | 0.1543 | 0.1697 |

| 100 | 0.0631 | 0.0585 | 0.2026 | 0.2094 | |

| 200 | 0.0559 | 0.0499 | 0.2838 | 0.3010 | |

| 400 | 0.0540 | 0.0471 | 0.3838 | 0.4152 | |

The AUCs we consider do not capture the behaviour of our testing procedure fully, so we also calculate the proportion of tests rejected at level among all tests performed in the simulation study as an additional metric. The results are given in Table 1. They indicate that for both strategies our testing procedure controls the type-I error rate asymptotically and at the same time has good power for the alternative.

Note that for conciseness we have only analysed the performance of our procedure for testing the test null and not the stricter . However, since is in fact the null-hypothesis our procedure is formally testing, the performance does not differ meaningfully between the two cases that (i) holds and that (ii) does not hold but does. We verify this in Section 4 of the Supplementary Materials. We also investigate how often the problematic case that holds but does not occur in our simulation study, i.e., the testing procedure has no power to detect a meaningful mistake in the candidate graph: it never occurs in more than of the cases where holds although the actual percentage is much lower for some settings of our simulation study (see Table 2 in the Supplementary Materials).

We also investigate the performance of our testing procedure in an additional simulation study with graphs of size , and . Here, we only consider the strategy as the is too computationally expensive. Due to space constraints we provide the results in Section C.3 of the Supplementary Materials, but they do not differ meaningfully from the results for the smaller graphs.

5 Real data example

We apply our testing procedure to the single cell data collected for the investigation of human primary naïve CD T cell signalling networks by Sachs et al. [2005]. This data set consists of measurements from a total of experimental conditions. We will only use the data from the observational regime, which corresponds to the experimental setting with reagent anti-CD3/CD28. This subset of the data consists of measurements of phosphorylated proteins and phospholipids. The observational data is thought to be consistent with the conventionally accepted molecular interaction network (also called the consensus graph, , Figure 5 left). We use alternative graph proposed in Sachs et al. [2005] (, Figure 5 right) to evaluate the results of the analysis.

We consider as the candidate graph . We extract all pairs of nodes that satisfy . There are such node pairs in the graph. For every pair, we apply our testing procedure with strategy to the log-transformed and centred observational data. After a Bonferroni correction only the -values for the pairs (PKA, Erk) and (PKA, Akt) are significant at level ( and ).

We now take a closer look at these two node pairs. The collection of all valid adjustment sets relative to (PKA, Erk) in the consensus graph consists of sets. The test rejects the null hypothesis that these adjustment sets lead to estimates of the same quantity. To illustrate a potential error in , we consider the valid adjustment sets and {PLCg, PIP2, PIP3, Akt, PKC, p38, JNK}. If we consider the alternative graph as a more appropriate representation of the true data generating mechanism, the rejection is justifiable. The covariate Akt is a forbidden node in because it opens a collider path PKA Akt Erk. On the other hand, the empty set is a valid adjustment set also in . A similar argument applies to the the pair (PKA, Akt). The collection relative to this node pair also has a size of , among which we can look at adjustment sets and {Raf, Mek, PLCg, PIP2, PIP3, Erk, PKC, p38, JNK}. Using Erk is problematic as it is a forbidden node in because it blocks the causal path PKA Erk Akt. This indicates that in both cases our testing procedure is detecting a mistake in the consensus graph.

Our testing procedure produces rank estimates of mostly at ( out of cases), even though the size of goes up to . This illustrates how a large number of adjustment sets does not necessarily mean a large number of effective over-identifying constraints on the total effect for the test. It is unsurprising that our testing procedure with the strategy detects the same two pairs of nodes as problematic (p-values and .

6 Conclusion and discussion

In this paper, we propose a robustness test that checks whether it is reasonable to use a candidate causal graph to estimate a total effect of interest with covariate adjustment. This is a useful model validation tool for practitioners who wish to estimate a total effect with covariate adjustment and rely on causal graphs obtained from domain knowledge.

We develop our testing procedure assuming that the candidate graph is a DAG. In applications with unmeasured confounding between the covariates, it is more natural to assume that the candidate graph is an acyclic directed mixed graph (ADMG) with bi-directed edges that represent error correlations induced by the presence of unmeasured confounding. If the candidate ADMG contains at least two valid adjustment sets, it is also possible to apply our testing procedure in this setting with one limitation. The set may not be a valid adjustment set and as a result the strategy fails. We believe it is possible to adapt to an ADMG by replacing with a suitable alternative large valid adjustment set but we leave this for future research.

Another interesting idea for future research is that in general, given a valid adjustment set and a forbidden node, adding the node to the set should change the limit of the resulting estimator. It may be possible to exploit this in order to devise a testing procedure similar to the one proposed in this paper but that also exploits the information contained in the forbidden nodes of the candidate causal graph.

Acknowledgements.

We thank Milan Kuzmanovic for proposing the idea for Lemma 8. We also thank Vi Thanh Pham, Nicola Gnecco and Jonas Peters for feedback and insightful discussions. LH was supported by a research grant (18968) from VILLUM FONDEN.References

- Andrews [1987] Donald WK Andrews. Asymptotic results for generalized wald tests. Econometric Theory, 3(3):348–358, 1987.

- Bollen [1989] Kenneth A. Bollen. Structural Equations with Latent Variables. Wiley New York, 1989.

- Bollen and Ting [1993] Kenneth A Bollen and Kwok-fai Ting. Confirmatory tetrad analysis. Sociological methodology, pages 147–175, 1993.

- Buja et al. [2019] Andreas Buja, Lawrence Brown, Richard Berk, Edward George, Emil Pitkin, Mikhail Traskin, Kai Zhang, Linda Zhao, et al. Models as approximations I: Consequences illustrated with linear regression. Statistical Science, 34(4):523–544, 2019.

- Camba-Méndez and Kapetanios [2009] Gonzalo Camba-Méndez and George Kapetanios. Statistical tests and estimators of the rank of a matrix and their applications in econometric modelling. Econometric Reviews, 28(6):581–611, 2009.

- Chen and Pearl [2015] Bryant Chen and Judea Pearl. Exogeneity and robustness. Technical report, University of California, Los Angeles, 2015.

- Cheng et al. [2022] Debo Cheng, Jiuyong Li, Lin Liu, Kui Yu, Thuc Duy Le, and Jixue Liu. Toward unique and unbiased causal effect estimation from data with hidden variables. IEEE Transactions on Neural Networks and Learning Systems, 2022.

- Chickering [2002] David Maxwell Chickering. Learning equivalence classes of Bayesian-network structures. Journal of Machine Learning Research, 2:445–498, 2002.

- Cragg and Donald [1997] John G Cragg and Stephen G Donald. Inferring the rank of a matrix. Journal of econometrics, 76(1-2):223–250, 1997.

- Dikova et al. [2019] Desislava Dikova, Andrei Panibratov, and Anna Veselova. Investment motives, ownership advantages and institutional distance: An examination of russian cross-border acquisitions. International Business Review, 28(4):625–637, 2019.

- Donald et al. [2007] Stephen G Donald, Natércia Fortuna, and Vladas Pipiras. On rank estimation in symmetric matrices: the case of indefinite matrix estimators. Econometric Theory, pages 1217–1232, 2007.

- Ekstrøm [2020] Claus Thorn Ekstrøm. MESS: Miscellaneous Esoteric Statistical Scripts, 2020. URL https://CRAN.R-project.org/package=MESS.

- Entner et al. [2013] Doris Entner, Patrik Hoyer, and Peter Spirtes. Data-driven covariate selection for nonparametric estimation of causal effects. In Artificial Intelligence and Statistics, pages 256–264. PMLR, 2013.

- Frank et al. [2013] Kenneth A Frank, Spiro J Maroulis, Minh Q Duong, and Benjamin M Kelcey. What would it take to change an inference? using rubin’s causal model to interpret the robustness of causal inferences. Educational Evaluation and Policy Analysis, 35(4):437–460, 2013.

- Gultchin et al. [2020] Limor Gultchin, Matt Kusner, Varun Kanade, and Ricardo Silva. Differentiable causal backdoor discovery. In International Conference on Artificial Intelligence and Statistics, pages 3970–3979. PMLR, 2020.

- Henckel et al. [2022] Leonard Henckel, Emilija Perković, and Marloes H. Maathuis. Graphical criteria for efficient total effect estimation via adjustment in causal linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 84(2):579–599, 2022.

- Kalisch et al. [2012] Markus Kalisch, Martin Mächler, Diego Colombo, Marloes H. Maathuis, and Peter Bühlmann. Causal inference using graphical models with the R package pcalg. Journal of Statistical Software, 47(11):1–26, 2012.

- Kirby and Bollen [2009] James B Kirby and Kenneth A Bollen. 10. using instrumental variable tests to evaluate model specification in latent variable structural equation models. Sociological Methodology, 39(1):327–355, 2009.

- Kuroki and Miyakawa [2003] Manabu Kuroki and Masami Miyakawa. Covariate selection for estimating the causal effect of control plans by using causal diagrams. Journal of the Royal Statistical Society. Series B. Statistical Methodology, 65(1):209–222, 2003.

- Lu and White [2014] Xun Lu and Halbert White. Robustness checks and robustness tests in applied economics. Journal of econometrics, 178:194–206, 2014.

- Nandy et al. [2017] Preetam Nandy, Marloes H Maathuis, and Thomas S Richardson. Estimating the effect of joint interventions from observational data in sparse high-dimensional settings. Annals of Statistics, 45(2):647–674, 2017.

- Oster [2019] Emily Oster. Unobservable selection and coefficient stability: Theory and evidence. Journal of Business & Economic Statistics, 37(2):187–204, 2019.

- Pearl [2009] Judea Pearl. Causality. Cambridge University Press, second edition, 2009.

- Perković et al. [2018] Emilija Perković, Johannes Textor, Markus Kalisch, and Marloes H Maathuis. Complete graphical characterization and construction of adjustment sets in Markov equivalence classes of ancestral graphs. Journal of Machine Learning Research, 18(220):1–62, 2018.

- Ratsimalahelo [2003] Zaka Ratsimalahelo. Strongly consistent determination of the rank of matrix. Technical report, EERI Research Paper Series, 2003.

- Rotnitzky and Smucler [2020] Andrea Rotnitzky and Ezequiel Smucler. Efficient adjustment sets for population average causal treatment effect estimation in graphical models. Journal of Machine Learning Research, 21:188–1, 2020.

- Sachs et al. [2005] Karen Sachs, Omar Perez, Dana Pe’er, Douglas A Lauffenburger, and Garry P Nolan. Causal protein-signaling networks derived from multiparameter single-cell data. Science, 308(5721):523–529, 2005.

- Schlegel et al. [2021] Tobias Schlegel, Curdin Pfister, Dietmar Harhoff, and Uschi Backes-Gellner. Innovation effects of universities of applied sciences: an assessment of regional heterogeneity. The Journal of Technology Transfer, pages 1–56, 2021.

- Shah et al. [2021] Abhin Shah, Karthikeyan Shanmugam, and Kartik Ahuja. Finding valid adjustments under non-ignorability with minimal dag knowledge. arXiv preprint arXiv:2106.11560, 2021.

- Shimizu [2014] Shohei Shimizu. Lingam: Non-gaussian methods for estimating causal structures. Behaviormetrika, 41(1):65–98, 2014.

- Shimizu et al. [2006] Shohei Shimizu, Patrik O Hoyer, Aapo Hyvärinen, and Antti Kerminen. A linear non-gaussian acyclic model for causal discovery. Journal of Machine Learning Research, 7(Oct):2003–2030, 2006.

- Shpitser et al. [2010] Ilya Shpitser, Tyler VanderWeele, and James Robins. On the validity of covariate adjustment for estimating causal effects. In Proceedings of the Twenty-Sixth Annual Conference on Uncertainty in Artificial Intelligence (UAI-10), pages 527–536, Corvallis, Oregon, 2010. AUAI Press.

- Spirtes [1995] Peter Spirtes. Directed cyclic graphical representations of feedback models. In Proceedings of the Eleventh Conference on Uncertainty in Artificial Intelligence (UAI-95), pages 491–498, San Francisco, USA, 1995. Morgan Kaufmann Publishers Inc.

- Spirtes et al. [2000] Peter Spirtes, Clark Glymour, and Richard Scheines. Causation, Prediction, and Search. MIT Press, Cambridge, MA, second edition, 2000.

- Stewart [1998] Gilbert W Stewart. Perturbation theory for the singular value decomposition. Technical report, University of Maryland, 1998.

- Van der Zander et al. [2014] Benito Van der Zander, Maciej Liskiewicz, and Johannes Textor. Constructing separators and adjustment sets in ancestral graphs. In Proceedings of the UAI 2014 Conference on Causal Inference: Learning and Prediction, CI’14, pages 11–24, 2014.

- Walter and Tiemeier [2009] Stefan Walter and Henning Tiemeier. Variable selection: current practice in epidemiological studies. European journal of epidemiology, 24(12):733–736, 2009.

- Witte et al. [2020] Janine Witte, Leonard Henckel, Marloes H. Maathuis, and Vanessa Didelez. On efficient adjustment in causal graphs. Journal of Machine Learning Research, 21(246):1–45, 2020.

- Wright [1934] Sewall Wright. The method of path coefficients. The Annals of Mathematical Statistics, 5(3):161–215, 1934.

- Yigezu and El-Shater [2021] Yigezu A Yigezu and Tamer El-Shater. Socio-economic impacts of zero and reduced tillage in wheat fields of the moroccan drylands. Agricultural Economics, 2021.

Supplementary Materials

Appendix A Graphical preliminaries

Graphs

A graph is a tuple of a node set and an edge set . We consider simple directed graphs where there is at most one edge between any pair of vertices and the edges are of the form .

Walks, paths and cycles

Two vertices are adjacent if there is an edge between them. A walk between and is a sequence of vertices such that successive vertices are adjacent. A path between and is a walk between and where all vertices are distinct. A directed path from to is a path between and where all the edges point towards . A cycle is a path plus an edge between and . A directed cycle is a directed path from to plus an edge . Given a path , let , denote the path segment from to and let . Given two paths and , let . We call any node on a path such that a collider on and any node that is not a collider on , a non-collider on .

DAG

A directed acyclic graph (DAG) is a directed graph without directed cycles.

Parents, children, ancestors and descendants

If , then is a parent of and is a child of . If there is a directed path from to , then is an ancestor of and is a descendant of . Any node is an ancestor and a descendant of itself. For any node , the sets of parents, children, ancestors and descendants of in are denoted by , , and , respectively. This definition applies disjunctively to sets of nodes. For example, the parents of the set of vertices are defined as . The non-descendants of are .

-separation

A path between and is blocked by a set if at least one of the following conditions holds:

-

(i)

There is a non-collider on that is in ;

-

(ii)

There is a collider on such that neither itself nor any other of its descendants are in .

A path that is not blocked is said to be open. If all paths between and are blocked by , then and are -separated by , denoted by . Otherwise, they are said to be -connected by .

Faithfulness

Consider a DAG such that follows a linear structural equation model compatible with . If for all disjoint subsets and of such that is independent of given , then we say that the distribution of is faithful to .

Appendix B Proofs

B.1 Proof of Theorem 1

Proof.

Consider the set . By assumption, and, nonetheless, is not a valid adjustment set. Thus, there must exist a non-causal path from to in that is open given . Suppose that is of the form . By assumption and therefore which in turn implies that . As a result, . But as it follows that , which contradicts our assumption that is open given . We can therefore assume that is not of the form which implies that must contain at least one non-collider. If every non-collider on is in , it follows that every node on is in . But this contradicts our assumption that is non-causal and open given . We can therefore conclude that contains at least one non-collider that is not in . But as by assumption, must be blocked by some set .

Consider the potential colliders on . As is open given for each collider , there must exist a causal path to some node in , where we choose to be the shortest possible such path. If any of the intersects, drop the longer of the two paths. If any contains , replace with and repeat our argument. Consider now the following linear structural equation: set all edge coefficients not on or our list of paths to . The resulting model is clearly compatible with but also to a pruned graph where we drop all edges with edge coefficient 0. Clearly, in the path is still open given and closed given . Furthermore, is the only path from to in , and as a result, we can conclude that and . We have therefore shown that there exists a linear structural equation model compatible with , such that .

Consider now the term as a function in the edge coefficients and error variances from the underlying linear structural equation model. By the same arguments as given in Section 13.3 of Spirtes et al. [2000] the function is equivalent to a polynomial in the edge coefficients and error variances of the linear structural equation model. As we have shown that there exists one linear structural equation model such that , this polynomial is non-trivial. Our claim then follows from the fact that the zero set of non-trivial polynomials has Lebesgue measure . ∎

B.2 Proof of Lemma 3

Lemma 10 (Orthogonality between covariates and regression residual, [Buja et al., 2019]).

In a least squares regression of on , the minimiser of the optimisation problem is the population regression coefficient . The residual is orthogonal to , i.e., .

Unless specified otherwise, serif letters denote random samples for scalar random variables. For example, is an -dimensional vector containing i.i.d. copies of . Bold serif letters denote random samples for vector random variables. For example, is an matrix where each row is i.i.d. as .

Lemma 11 (Regression error representation of OLS coefficients, [Buja et al., 2019]).

The difference between sample and population regression coefficient of from regressing on is

where is the vector of sample residuals from regressing on .

Proof of Lemma 3.

The proof is inspired by the results in Appendix E.5 of Buja et al. [2019]. We first observe from Lemma 11 that for every set , ,

| (6) |

where is the sample residuals from regressing on .

Numerator of (6).

For the second term on the last line it holds that

since by Lemma 10 and converges in distribution to a multivariate normal random variable by the central limit theorem, which is appropriate since by assumption, the fourth moments of are finite.

Denominator of (6).

Using the convention that the hat matrix , the average squared sample residuals

The second to last step follows because by Lemma 10.

We are now ready to present the asymptotic joint normality of . Since , together with the fact that the fourth moments of are finite, we can apply the multivariate central limit theorem to conclude that

where the entries have the form for all . Therefore, the random vector

due to the fact that the second vector converges in distribution to a vector of zeroes. Based on the discussion of the denominator term, we can conclude that

The target quantity can then be written as

where the convergence follows from Slutsky’s Theorem, and the asymptotic covariance matrix is as specified in the theorem statement. ∎

Remark.

If are all valid adjustment sets relative to in for a linear structural equation model compatible with a DAG , we can simplify the diagonal terms due to the independence between and (see proof of Proposition 3.1 in Supplement from Henckel et al. [2022]). Therefore, the corresponding terms are . It can also be shown that is root- consistent for the total effect for any valid adjustment set [Nandy et al., 2017]. In this case, in order to apply the central limit theorem separately on every entry of , we only need the finite variance assumption for the error terms of the linear structural equation model. In such a model, both and can be expressed as linear functions of the error terms, say and . Furthermore,

| (7) |

due to the independence between and . The order of each term cannot be larger than in (7) for all . Therefore, is finite for all whenever for all .

We also show that a consistent estimator of the covariance matrix can be obtained by plugging in the sample residuals.

Lemma 12 (Consistency of plug-in estimator of ).

Proof of Lemma 12.

Consider

The denominator converges in probability to by the proof of Lemma 3. The numerator can be written as

where the remainder term contains the rest of the products from the expansion: product with no -term, products with -term, products with -terms and products with -terms. Below we will show that the remainder term , and it follows that the numerator converges in probability to . By the continuous mapping theorem, follows.

We will discuss one case from each category, as the results can be shown similarly for other products in the same category. The use of parentheses in the subscript denotes a particular entry of a vector. For example, is the -th entry of the -th observation and is the -th entry of the vector . With the finite fourth moment assumption on , and for any and .

No -term.

where , the constant term exists due to the finite fourth moment assumption on .

One -term.

where , the constant term exists due to the finite fourth moment assumption on .

Two -terms.

where , the constant term exists due to the finite fourth moment assumption on .

Three -terms.

where , the constant term exists due to the finite fourth moment assumption on . ∎

Remark.

If the ’s are valid adjustment sets, the diagonal terms simplify to , and their convergence follows by the proof of Lemma 3 on the denominator.

B.3 Proof of Proposition 7

Proof.

The proof aims to show that the half-vectorised asymptotic covariance matrix estimator , after subtracting their true values in , will converge to a zero-mean normal distribution.

For the -th entry, we write

The numerator of the expression above is expanded as

where collects the remainder term resulting from replacing the sample residuals with population residuals.

We now subtract and add back the expected squared population residuals from the average squared population residuals. That is,

The first term converges to a zero-mean normal distribution by the central limit theorem and the finite fourth moment assumption on . The remainder term by analogous arguments to the ones used in the proof of Lemma 12. The second term on the second to last line disappears asymptotically, which entails that .

The asymptotic covariance between two entries in

where

Analogous to the proof of Lemma 3, the joint normality follows by the multivariate Central Limit Theorem, which we can apply due to Slutsky’s Theorem and the assumption that the fourth moments of the errors are finite.

Define a deterministic mapping for subscript , such that it maps the -th element of to the -th entry of . The asymptotic covariance matrix of is a matrix whose entries are related to the expression of and by the mapping such that

for . The asymptotic covariance matrix of follows from the linear relationship . ∎

Remark.

Again we discuss the special situation where the ’s are valid adjustments sets. In this case, the diagonal terms

The numerator

where we can apply the central limit theorem because to the first term because and . The remainder term by analogous arguments used in the proof of Lemma 12. Similarly, the denominator converges in probability to . Then by Slutsky’s Theorem,

B.4 Proof of Theorem 6

Proof of Theorem 6.

Lemma 3 states that is asymptotically normal. We first show that to quantify the degrees of freedom of a Wald-type statistic, one only needs to look at the rank of covariance matrix .

Suppose where . Consider the eigendecomposition of , where is the orthonormal matrix containing the eigenvectors of , and with eigenvalues . It can be verified that the (unique) Moore-Penrose inverse of is defined as

because of the semi-positive definiteness. Under , denote . For all , . By joint normality of , and are independent. Moreover, since ,

| (8) |

The consistency of , i.e., , , implies that when taking , since both and are integer-valued.

Since is positive semidefinite, its spectral decomposition is , where with . The rank- spectral approximation of is then , where . Following Weyl’s inequality [Stewart, 1998] and Proposition 7, we have since the asymptotic covariance matrix of is finite. We now show that . For any ,

If , and . Otherwise if , because . Hence, for all . Since all entries of are bounded by , . Then by consistency of .

B.5 Proof of Lemma 8

Lemma 13 (Modified Lemma D.1 in Henckel et al. [2022]).

Consider a causal DAG such that and that is a valid adjustment set relative to in . Given a partition , if , then is a valid adjustment set relative to in .

Theorem 14 (Spirtes, 1995).

Consider DAG containing , and , where and does not contain or , is -separated from given if and only if the partial correlation coefficient for all linear structural equation models compatible with .

Corollary 15.

Consider nodes and , and a set in a DAG . Then is -separated from given if and only if for some linear structural equation model compatible with and faithful to .

Lemma 16.

Consider a causal DAG and let follow a linear structural equation model compatible with . Let be the set of independent errors from the linear structural equation model, where is the number of nodes in . Given two nodes such that and any valid adjustment set relative to in , the population regression residual is a linear combination of the error terms , in which the coefficient of is .

Proof.

We refer to the proof of Lemma B.4 in Henckel et al. [2022]. The residual can be written as a linear combination of errors. In particular, the coefficient of is

Since is a valid adjustment set relative to in , it cannot contain descendants of , which are forbidden nodes. Then the set is empty, because . The result is immediate using the convention that . ∎

We are now ready to present the proof of Lemma 8.

Proof of Lemma 8.

Consider a linear structural equation model that is faithful to . We will first only consider the minimal valid adjustment sets in the collection . The first step of the proof is to show that the regression residuals cannot be linearly dependent. Suppose on the contrary that there is a linear combination such that for some not all equal to . Without loss of generality, suppose that . Consider the first minimal valid adjustment set . It contains at least one unique node . We can thus write , where is the population OLS regression coefficient of on . Since is a minimal adjustment set, node is -connected with in given by Lemma 13. It follows from Corollary 15 that the regression coefficient of in cannot be zero. In this case, expanding into and rearranging the terms, the equation can be expressed equivalently as

| (9) |

where for and . Equation (9) cannot hold due to the fact that the covariance matrix of is non-singular. Therefore, we conclude that when . On the contrary, when , the argument above can be repeated for minimal adjustment sets with , so on and so forth until . Since the linear combination cannot evaluate to zero whenever for any , the inequality holds generally for all ’s not all equal to zero.

The second step is to show that the regression residual products cannot be linearly dependent either. Lemma 16 states that each contains the error term . For any valid adjustment set , (see proof of Proposition 3.1 in Supplement from Henckel et al. [2022]). Therefore, , when written in the form of error terms only, cannot contain . Consider now another linear combination . Suppose that for some ’s not all equal to . We can expand into plus some linear combination of the other errors. Singling out the terms involving in , we have that

| (10) |

since and is independent from the other errors. Due to the non-degeneracy of , the linear combination must evaluate to for some ’s not all equal to . However, this is impossible by independence between ’s shown in the first step, and we have reached a contradiction.

Following the proof of Lemma 3, the asymptotic covariance matrix is precisely the covariance matrix of , which is non-singular due to linear independence among ’s. Hence, the corresponding asymptotic covariance matrix also has full rank.

Now we consider the set of non-forbidden nodes. Let . The -connection condition of a unique node and faithfulness ensures a non-zero coefficient in front of in . Since is a valid adjustment set relative to in , we can repeat the argument above and conclude that the enlarged asymptotic covariance matrix is also non-singular.

When the edge coefficients and the error variances in the linear structural equation model are sampled from an absolutely continuous distribution with respect to the Lebesgue measure, the model is faithful with probability [Spirtes et al., 2000]. Therefore, since we showed that for all faithful models is invertible our claim follows. ∎

B.6 Lemma 17 and its proof

Lemma 17.

Consider nodes and in a DAG such that . Then is a valid adjustment set relative to in .

Proof.

Obviously, does not contain any forbidden nodes so it only remains to show that it blocks all paths from to that are not directed. Note first the only possible path from to that does not contain a non-collider is . By assumption and therefore this path is blocked by . Let be any other path from to that is not directed. It must therefore contain at least one non-collider. If any non-collider on is in , is blocked so suppose this is not the case, i.e., all non-collider on are in . Any collider on must be a descendant of a non-collider on and is therefore also in . In this case is again blocked given and therefore we can assume that does not contain any colliders and is therefore of the form . But any node in that is not is a descendant of and therefore or we would have a violation of the acyclicity assumption. But then is a directed path which contradicts out starting assumption for . ∎

Appendix C Simulation setup

C.1 Simulation in Example 9

The definition of the probability-probability plot that we employ in Example 6 is described as follows. Given a sample of p-values , we sort them in the increasing order: . Then we apply the empirical distribution function to get the empirical probabilities for , i.e., . These are simply assuming no ties. Since we wish to compare the sample to the standard uniform distribution, whose cumulative distribution function is for , we compute the theoretical probabilities . The plot is finally obtained by plotting against .

C.2 Simulation in Section 4

True graph

We generate causal DAGs as Erdős–Rényi random graphs. There are in total DAGs with nodes and DAGs with nodes. The expected neighbourhood size for each DAG is drawn uniformly from , with the function randDAG in R package pcalg [Kalisch et al., 2012].

Linear structural equation model

For our compatible linear structural equation we sample edge coefficients uniformly from . We then draw an error distribution uniformly from one of four distributions: normal, uniform, , or logistic. Note that we use the same error distribution for all errors in the model. We than sample variances for each error in our model as follows. The variance parameter of the normal errors is sampled uniformly from to . The location parameter of the uniform errors symmatric around zero is sampled uniformly from to . The -errors are sampled from a -distribution with degrees of freedom and then scaled by times the square root of a uniformly sampled number from to . The scale parameter of the logistic errors centred around zero is sampled uniformly from to . By sampling our parameters this way we ensure that the variances are approximately in the interval from to .

The pair

The node is randomly drawn from the true DAG , where we weight each node in by the number of its descendants minus 1. Once is fixed, we sample uniformly from the set . The sampling procedure is repeated until there are at least two valid adjustment sets relative to the selected pair in the completed partially directed acyclic graph (CPDAG) of .

Causal structure learning

We use causal structure learning algorithms to generate large numbers of reasonable candidate graphs for our test procedure. If the error distribution is normal, we apply Greedy Equivalence Search (GES, Chickering [2002]) to estimate a completed partially directed acyclic graph (CPDAG). Note that the adjustment criterion also applies to CPDAGs. Otherwise, we apply LiNGAM [Shimizu, 2014] and estimate a DAG. We use the functions ges and lingam from R package pcalg with default options [Kalisch et al., 2012].

Untestable cases

If there is only one or no adjustment set in the candidate graph , the proposed test cannot be performed so we discard these cases. If the valid adjustment sets are simply those sets that d-separate from . As there is a large literature on conditional independence tests which are more suitable here than our test procedure, we discard this case. If the rank of is estimated to be , there is no effective over identifying constraint for our test procedure, so we discard these cases as well.

AUC calculation

Recall that for each candidate graph and sample size for testing , we perform our test times. We plot the probability-probability plot between the corresponding -values and the standard uniform distribution. We compute the area under the curve (AUC) of this curve with the function auc from R package MESS [Ekstrøm, 2020].

Determining whether null hypothesis is true

For every estimated graph and test strategy, we check using the true linear structural equation model whether the null hypothesis is true or false by computing the population level regression coefficients and checking whether they are all equal.

Version control

The simulation studies were conducted using R version 4.1.1.

C.3 Extra simulation results

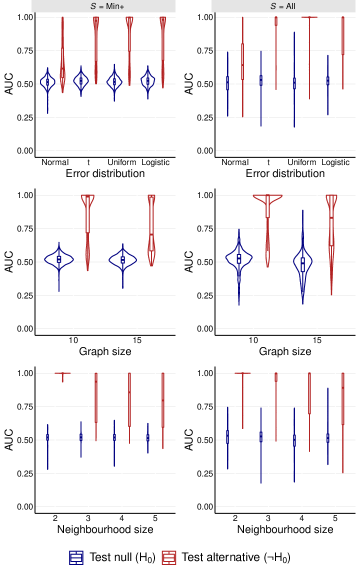

Figure 6 and Figure 7 show additional plots of the AUCs from the simulation study. In Figure 6 the AUCs are grouped by error distribution of the linear structural equation model, graph size of the true graph and expected neighbourhood size of the true graph, respectively. In Figure 6 they are additionally grouped by the sample size used for testing and the candidate graph accuracy. The plots show that of the three parameters only the error distribution seems to have an impact on the performance of our testing procedure. This is likely due to the fact that in cases with normally distributed errors we can only learn a CPDAG, which contain fewer valid adjustment sets than DAGs.

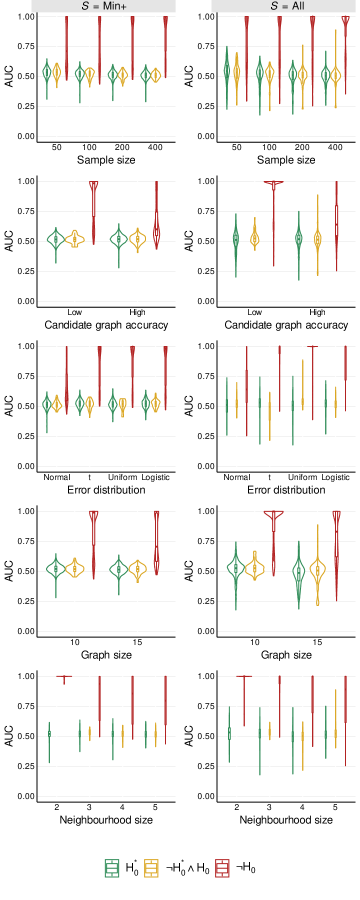

Table 2 summarises the proportions of candidate graphs (and strategies) where the null-hypothesis is true, the null hypothesis is false but the actual test null hypothesis is true and both are false, respectively. Unsurprisingly is true more often for the high accuracy candidate graphs. We can also see that the strategy always result in a higher proportions of cases where is false when compared to , which is due to the fact that consider a subset of the adjustment sets considers. The problematic cases where generally occur in around of the cases, and interestingly are more common for the larger graphs than for the smaller graphs.

| Factor | Strategy | ||||||

|---|---|---|---|---|---|---|---|

| Hypothesis | |||||||

|

Expected graph

accuracy |

Low | 42.82 | 1.98 | 55.20 | 36.14 | 1.98 | 61.88 |

| High | 85.64 | 5.48 | 8.88 | 84.71 | 5.27 | 10.02 | |

|

Graph

size |

10 | 81.12 | 3.08 | 15.8 | 77.73 | 3.08 | 19.19 |

| 15 | 55.24 | 7.46 | 37.3 | 54.31 | 6.99 | 38.69 | |

|

Neighbourhood

size |

2 | 92.18 | 0.00 | 7.82 | 88.83 | 0.00 | 11.17 |

| 3 | 93.31 | 1.49 | 5.20 | 88.61 | 1.24 | 10.15 | |

| 4 | 63.14 | 6.34 | 30.53 | 62.56 | 6.34 | 31.10 | |

| 5 | 54.52 | 7.47 | 38.01 | 52.49 | 7.24 | 40.27 | |

| Cand. graph | |||||||

|---|---|---|---|---|---|---|---|

| accuracy | |||||||

| Low | 50 | 0.0751 | 0.0909 | 0.0788 | 0.0759 | 0.5570 | 0.7396 |

| 100 | 0.0636 | 0.0636 | 0.0587 | 0.0385 | 0.6352 | 0.7880 | |

| 200 | 0.0543 | 0.0510 | 0.0488 | 0.0516 | 0.7132 | 0.8341 | |

| 400 | 0.0493 | 0.0466 | 0.0525 | 0.0503 | 0.7887 | 0.8812 | |

| High | 50 | 0.0786 | 0.0897 | 0.0711 | 0.0712 | 0.1543 | 0.1697 |

| 100 | 0.0634 | 0.0587 | 0.0585 | 0.0557 | 0.2026 | 0.2094 | |

| 200 | 0.0559 | 0.0500 | 0.0558 | 0.0476 | 0.2838 | 0.3010 | |

| 400 | 0.0543 | 0.0471 | 0.0492 | 0.0475 | 0.3838 | 0.4152 | |

Minimal adjustment sets in large sparse graphs

We ran a small simulation to demonstrate the scalability of the algorithm for minimal adjustment sets proposed by Van der Zander et al. [2014]. We simulated Erdős–Rényi graphs with graph size and expected neighbourhood size . For each combination above, we generated DAGs. For each DAG, we selected the pair of nodes in the same way as in the main simulation described in Section 4. We then ran the algorithm to extract minimal adjustment sets relative to and performed the rest of the testing procedure according to Algorithm 1. We allowed up to one hour on each DAG to finish the computation of minimal adjustment sets, and for the graph sizes , the percentages of completed algorithm runs were , respectively. The results suggest that the extraction of minimal adjustment sets is possible even for graphs with sizes in the order of s. We also noted, however, that the space required to store the adjustment sets can also exceed the GB RAM allocated.

strategy-only simulation on larger graphs

We conducted another simulation on graphs of size and with precisely the same setup as the simulation in Section 4 using only the strategy. As the strategy is computationally much fast than the strategy we, we were able to increase the graph sizes while keeping the other configurations unchanged. It is worth pointing out that attempting to run the simulation on graphs of nodes with the strategy in the same setup almost always exceeded the one-hour timeout. Figure 8 contains violin plots of AUCs framed by different parameters used in the simulation and coloured by their respective true hypotheses. The results are very similar to what we saw in the simulation in Section 4. The small bulks around AUC to for in Figure 8 are due to a specific DAG and structural equation model where our procedure was very conservative. One particular simulated graph of size was not included in the plots due to memory overflow during the computation of the minimal adjustment sets, which indicated that for graphs larger than , memory might have to be taken into account.