Dynamics of a Binary Option Market with Exogenous Information and Price Sensitivity

Abstract

In this paper, we derive and analyze a continuous of a binary option market with exogenous information. The resulting non-linear system has a discontinuous right hand side, which can be analyzed using zero-dimensional Filippov surfaces. Under general assumptions on purchasing rules, we show that when exogenous information is constant in the binary asset market, the price always converges. We then investigate market prices in the case of changing information, showing empirically that price sensitivity has a strong effect on price lag vs. information. We conclude with open questions on general -ary option markets. As a by-product of the analysis, we show that these markets are equivalent to a simple recurrent neural network, helping to explain some of the predictive power associated with prediction markets, which are usually designed as -ary option markets.

I Introduction

Market models have been studied extensively both through simulation and in theory in the econophysics literature Castiglione and Stauffer (2001); Bonanno et al. (2006); Samanidou et al. (2007); Slanina (2001); Szczypińska and Piotrowski (2008); Rothenstein and Pawelzik (2003); Medo and Zhang (2008); Chang and Stauffer (2001); Hammel and Paul (2002); Trimborn et al. (2018). In contrast to traditional stock or bond markets, prediction markets have assets corresponding to future events (e.g., elections Berg et al. (1997), sports outcomes Thaler and Ziemba (1988) etc.) that can be bought and sold causing changes in the underlying asset prices. Asset prices may be interpreted as probabilities Manski (2006); Wolfers and Zitzewitz (2006). Prediction markets were first studied by Hanson Hanson (1990, 1991, 1995); Ray (1997). Since this initial work, they have been studied extensively Wolfers and Zitzewitz (2004); Servan-Schreiber et al. (2004); Manski (2006); Berg and Rietz (2003); Wolfers and Zitzewitz (2006); Dai et al. (2020); Chakraborty and Das (2016). For a survey of work in this area through 2007 see Tziralis and Tatsiopoulos (2007). These prediction markets are archetypical examples of binary option markets (in the two outcome case) Breeden and Litzenberger (1978). Their use on Wall Street dates to the 1800’s Rhode and Strumpf (2004). Artificial prediction markets were first explored by Chen et al. Chen et al. (2008); Chen and Vaughan (2010); Abernethy et al. (2011). This work shows a connection between learning and the prediction market showing that if a prediction market has a cost function with bounded loss, then it has an interpretation as a no-regret learning algorithm Chen and Vaughan (2010). This work is generalized in Abernethy et al. (2011). In the finance literature, binary options are usually used as a theoretical construct since they have a particularly simple Black-Scholes formulation Hull (2003).

In this paper, we study the potential dynamics of prediction markets under continuum limits. In particular, we generalize and then extend the market model described in Nakshatri et al. (2021) to a continuous time dynamic. The results of this paper are:

-

1.

We show that under a constant information assumption, all asset prices converge. This explains empirical results found in Nakshatri et al. (2021). The result follows from an argument on Filippov surfaces.

-

2.

We then study the impact of dynamic information on market dynamics and empirically quantify the effect of price sensitivity and on lag between the market price and the information signal.

The remainder of the paper is organized as follows: We show the model derivation in Section II. In Section III we show that with constant information, all binary prediction markets converge to a constant price. In Section IV, we study the numerical results of a non-constant information. We conclude and present future directions in Section VI.

II Model

Assume units of Asset 0 and Asset 1 at time have been sold. We assume the market is composed of a collection of agents with infinite cash and that the market price is fixed by a logarithmic market scoring rule (LMSR) so that the spot prices are given by:

| (1) | |||

| (2) |

Notice because a Boltzmann distribution is being used we have for all time. Here, term is a liquidity factor Lekwijit and Sutivong (2018) that adjusts the amount the price will increase or decrease given a change in the asset quantities. We denote the spot-price vector . Assume that .

In general, trade costs are not given by , since LMSR incorporates a market maker cost. The trade costs are given by:

where is the change in the quantify of Asset as a result of purchases by an agent. For mathematical simplicity we will assume agents purchase one share at a time so that . Let:

be the price of single share purchase of Asset .

II.1 Agent Purchase Logic and Information

Following Nakshatri et al. (2021), we assume agents specialize in the purchase of a specific asset class (either or ) and that there is some (possibly time-varying) external information that will inform this purchase decision.

Assume agents are indexed in and suppose that agent purchases only assets in class . We assume agents have an infinite cash reserve and do not sell assets back to the market maker. Following Nakshatri et al. (2021), we assume that each agent uses a characteristic function to reason about information so that its decision to buy an asset in class is governed by:

| (3) |

Here . In Nakshatri et al. (2021), this is assumed to be a logistic sigmoid function:

and is the unit step function defined as at . We note that any mapping can be used in the remainder of this paper. The expression defines the value Agent places on Asset as a function of the current asset price(s) and the information . Thus just in case:

Nakshatri et al. (2021) assumes that is a vector in an appropriate feature space and for some scalar proposes that should define a convex region in . Thus, a collection of (price sensitive) agents encode a set of time-varying sets in feature space and an agent purchases a share of a relevant asset if and only if the information encoded in the (constant) feature and price vector is an element of the region defined by . Nakshatri et al. (2021) shows that price insensitive agents can be used to define an arbitrary covering region to encode a binary classification problem but observes in discrete time that minor oscillations can occur in the price. We show that this cannot happen in continuous time assuming a constant feature vector and then explore the affects of a non-constant feature vector.

II.2 Continuous Model

Consider . We can rewrite this as:

We know that , so we have:

For , we can approximate the exponential and logarithmic functions with a Taylor series: and to see:

Since we assume , we may assume .

Following Nakshatri et al. (2021), let be the set of agents that buy only Asset and let be the set of agents that buy only Assert . Using our approximation from Eq. 3 we have:

If we assume that transaction times are proportional to a time slice so that:

| (4) |

then, taking the limit as , we obtain the non-linear differential equation:

| (5) | ||||

| (6) |

Using Eqs. 1 and 2 and the quotient rule we can compute:

These results are consistent with Tuyls et al. (2003); Bernasconi et al. (2022) for multi-agent systems using a Boltzmann (soft-max) learning rule assuming a two-class outcome.

Using the fact that for all time and substituting in our expressions for and , we obtain a single ODE in terms of , which we now write simply as :

| (7) |

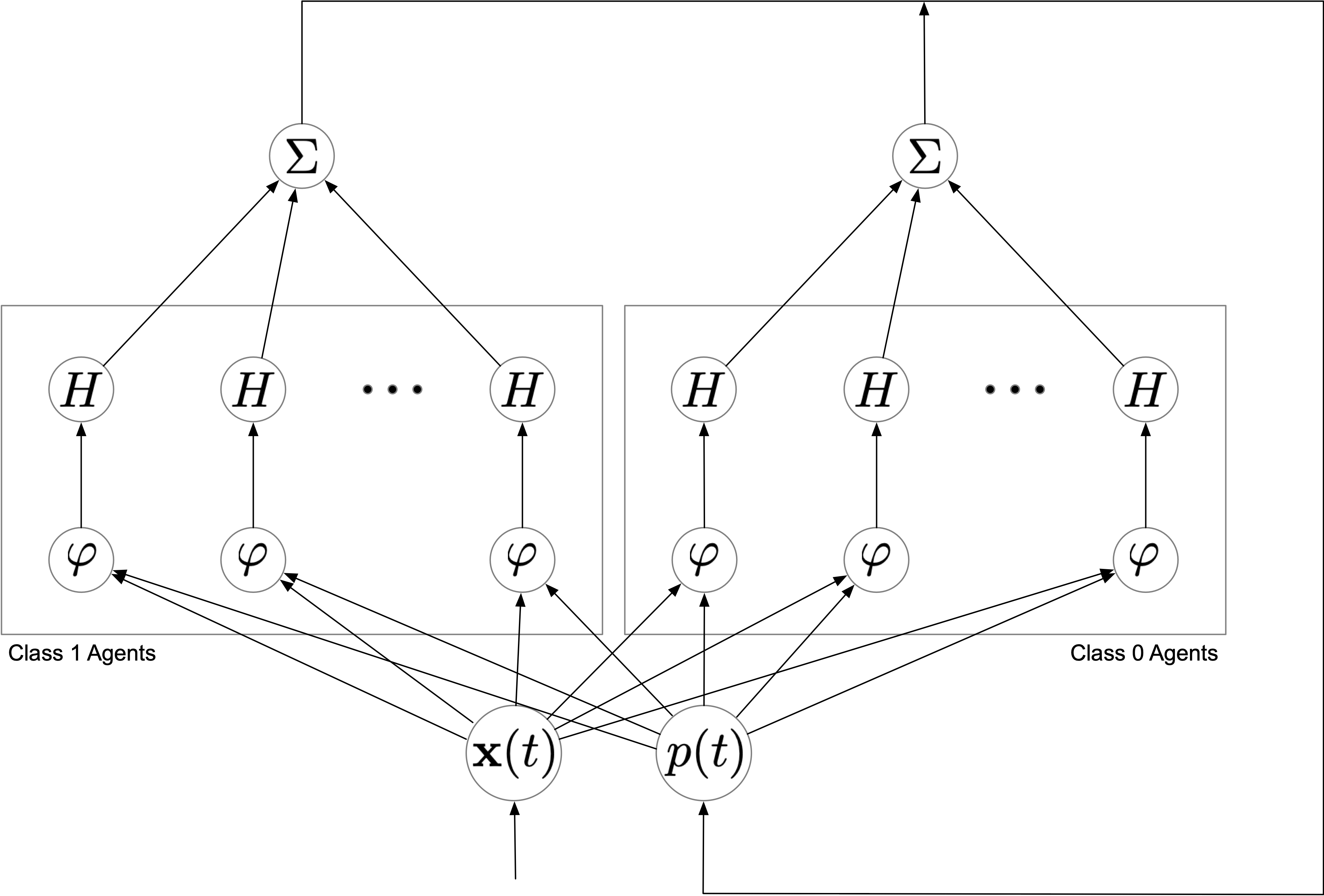

Notice unlike the work in Tuyls et al. (2003); Bernasconi et al. (2022), this ODE has a piecewise smooth and bounded right-hand-side with jump discontinuities. Therefore it is a Filippov system Filippov (1967, 2013). Moreover, this system can be described by a continuous time recurrent neural network, shown in Fig. 1.

The step function acts as an activation function for the non-linear neurons computing:

Thus, the dynamics of the neural network can be completely determined the exogenously specified dynamics of and Eq. 7.

III Asymptotic Market Behavior for Constant Information

Assume is constant so that where . The dynamics of are then:

| (8) |

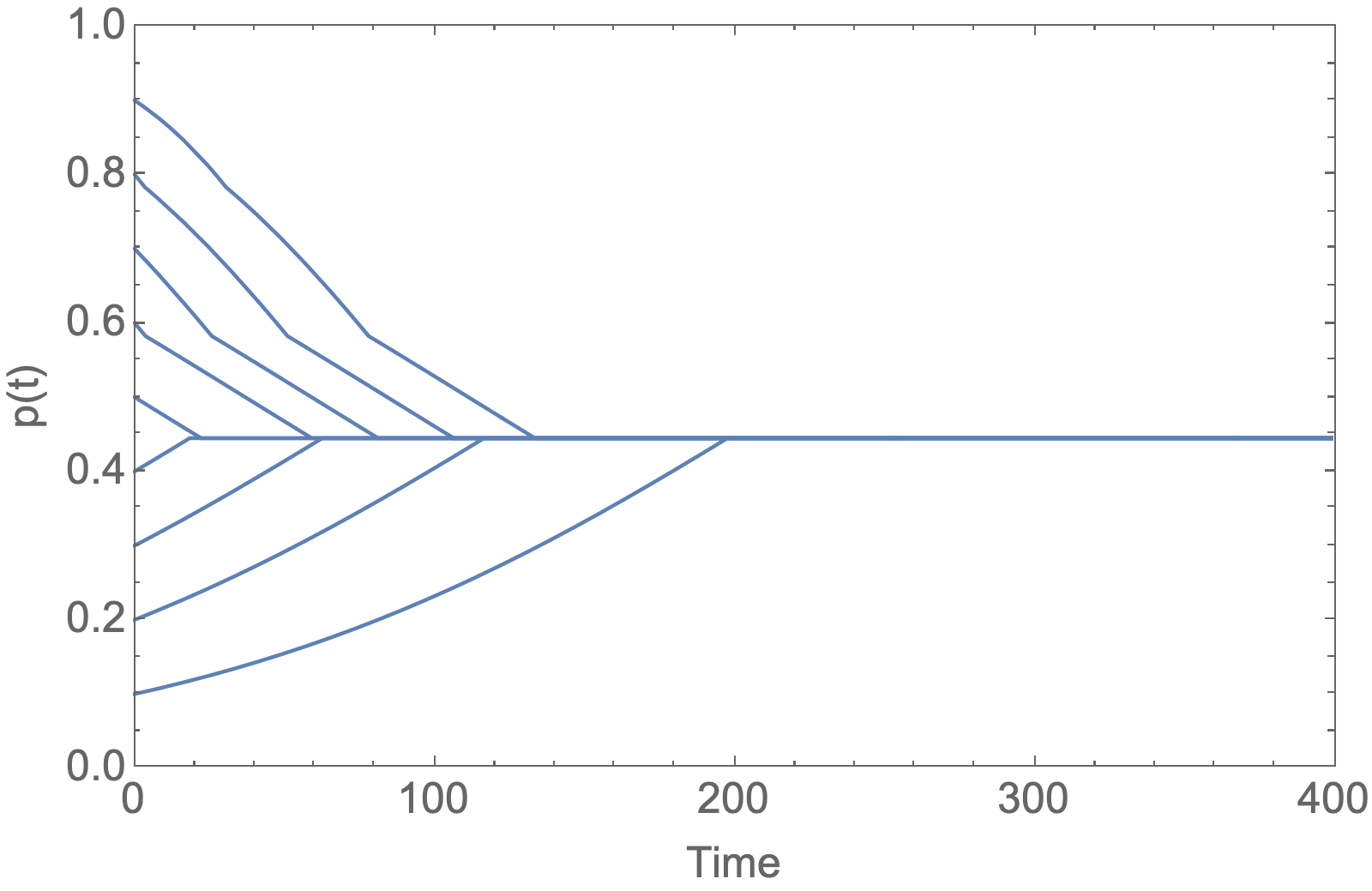

The right-hand-side is piecewise smooth and bounded and therefore a solution to this ODE exists Filippov (2013). It is clear that and are fixed points of Eq. 8. Therefore, for , if Eq. 7 if is a solution, then for all time.

We have just shown that the dynamics of are contained entirely in the smooth manifold . Thus the flow at any point is defined by a scalar (since the dimension of is 1). By convention positive flow moves toward . A sliding mode fixed point or fixed point on a Filippov surface is a point (a zero dimensional manifold) where the flow to the left of is positive and the flow to the right of is negative and the flow at may take either a positive or negative or zero value Filippov (2013). That is, the flow around this point is moving in opposite directions. Naturally, this definition can be extended to higher dimensional flows (see Filippov (2013)) but we do not require this level of complexity.

Let:

This is a discontinuous integer valued function with maximum value and minimum value . We can re-write Eq. 7 as:

From this, we see that for any fixed integer , Eq. 7 is just a logistic differential equation, which has a global solution. We deduce at once that Eq. 7 has a global continuous solution composed of piecewise smooth solutions to the individual logistic differential equations.

We now show that these solutions are monotonic and either asymptotically approach a value as time goes to infinity or reach a fixed point in finite time.

If , then is the solution for all time. On the other hand, suppose , then is initially decreasing and we have three possibilities.

- Case I:

-

If remains negative as decreases, then decreases for all time, asymptotically approaching the fixed point .

- Case II:

-

If increases as decreases and there is a finite such that , then for all , .

- Case III:

-

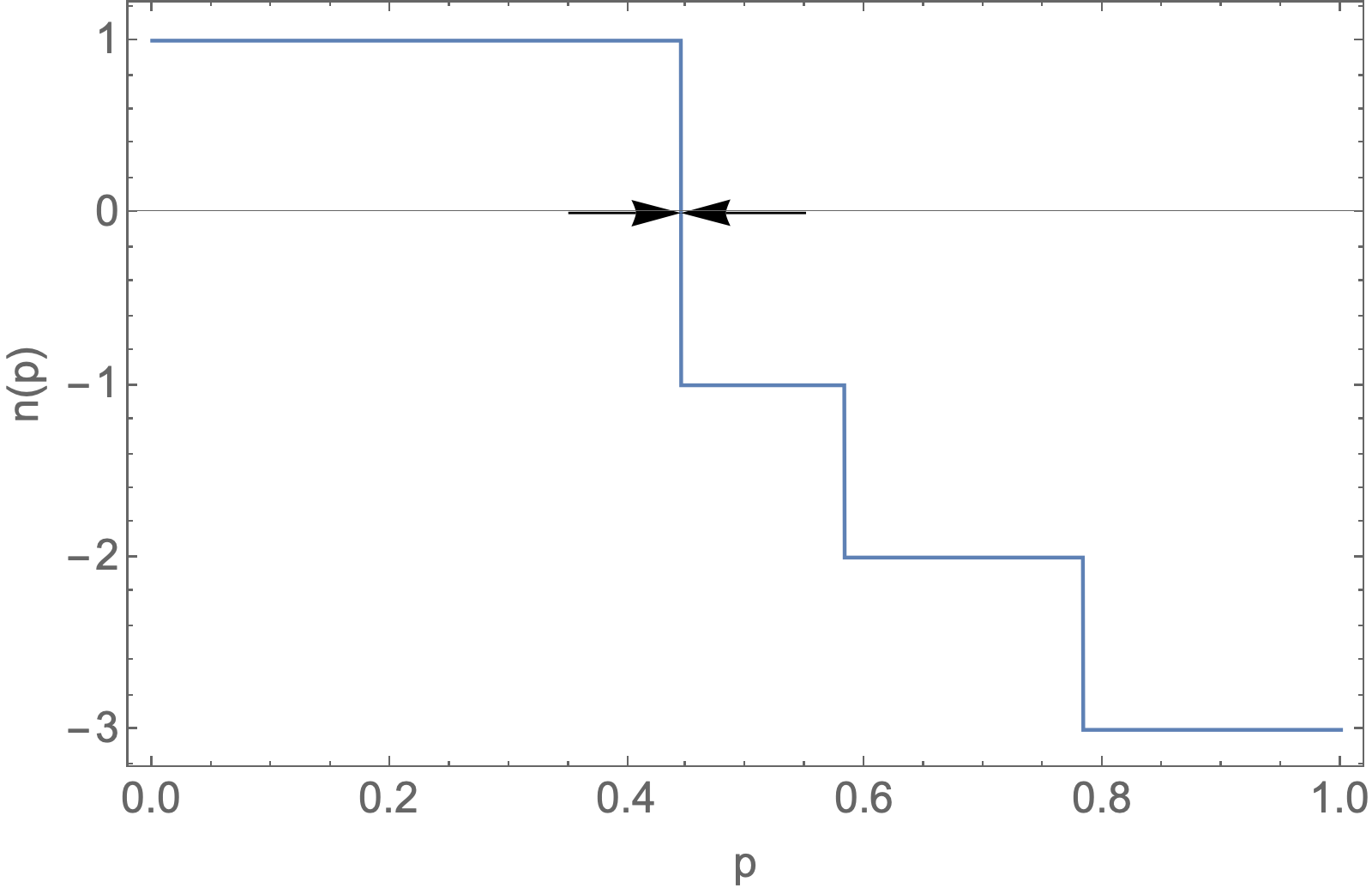

If increases as decreases and there is a smallest time so that for all , and , then is a sliding mode fixed point. Consequently, the value of becomes fixed at the location of the jump discontinuity in . This is illustrated in Fig. 2.

The argument for the case when is symmetric. Thus, we have shown that: (i) Every instance of Eq. 7 has a global continuous and piecewise smooth solution. (ii) Solutions are monotonic. (iii) Every solution either asymptotically approach or or reaches a constant value infinite time.

IV Numerical Results with Non-Constant Information

When is non-constant, the market will track the function through the function:

If there is some time so that for all we have (, respectively) then clearly must converge.

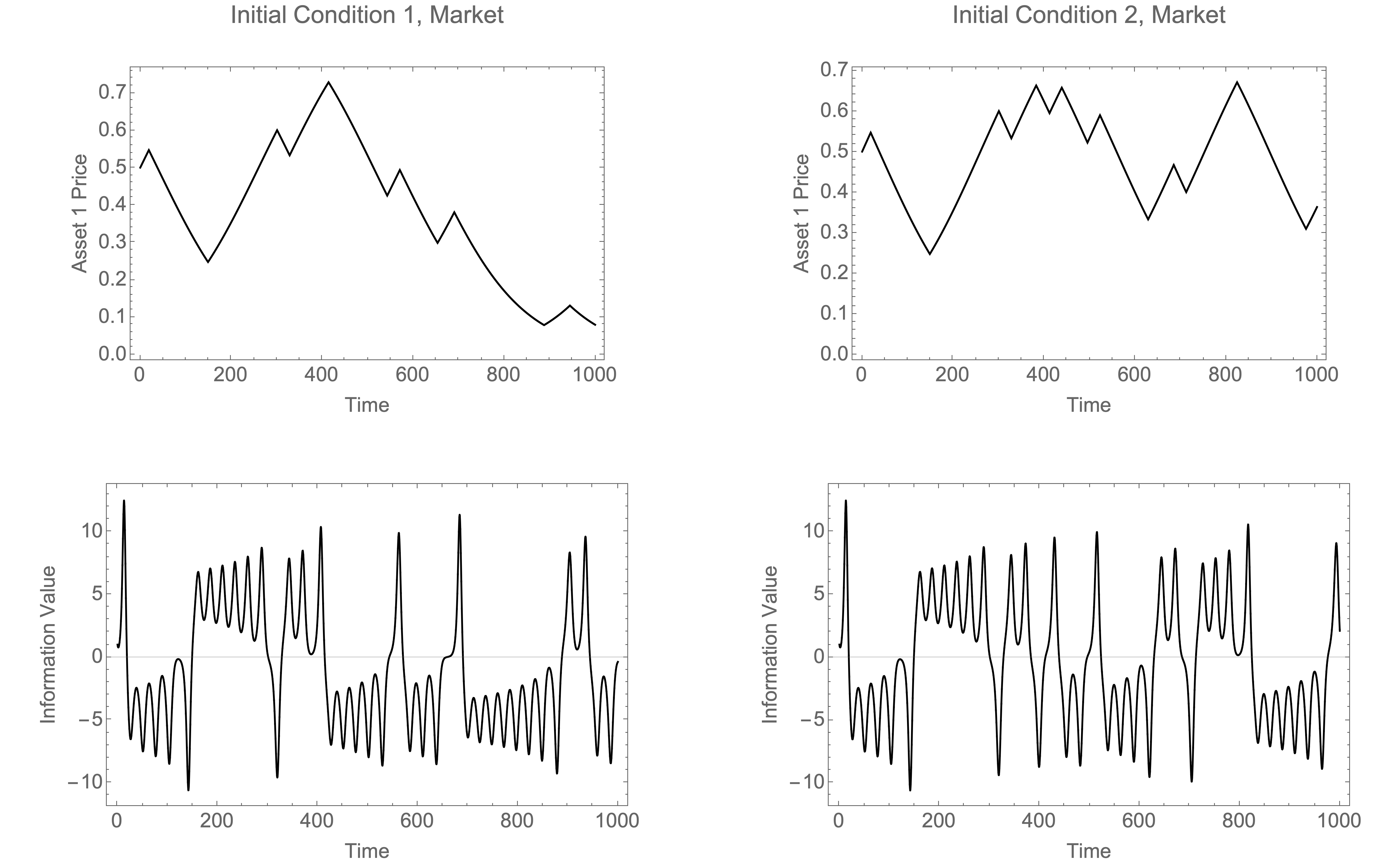

When remains above (or below) , the market will lag the information content in the and the market will smooth the information in the signal . By way of example, let be a solution to the Lorenz system and define:

where is the first dimension of the three dimensional curve . Then:

The dynamics are shown in Fig. 3 for two different initial conditions.

This shows that the market preserves the sensitive dependence on initial conditions (as expected) and smooths the dynamics of the Lorenz system. Numerical solution of the differential equation systems is described in B.

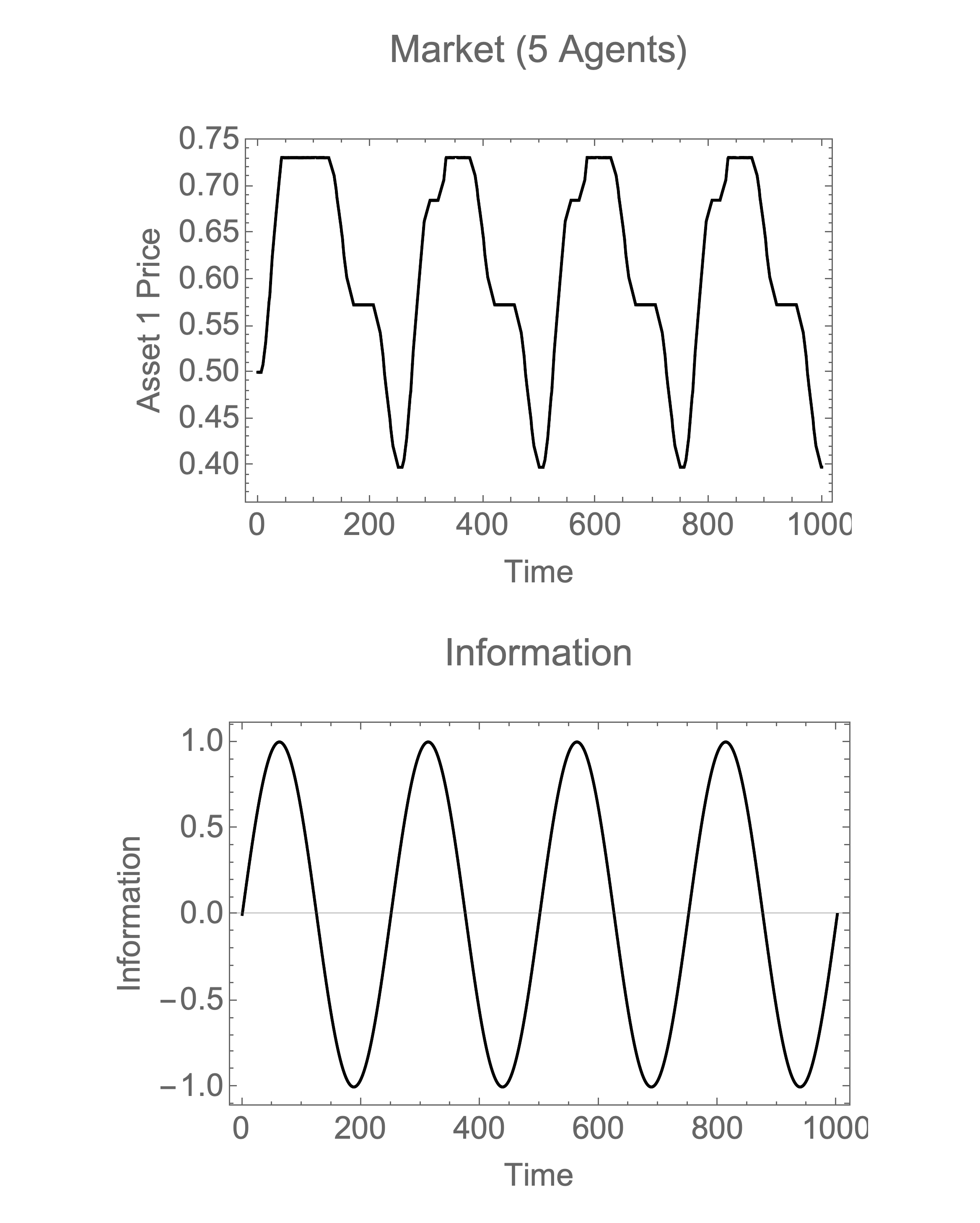

There is a lag in the market price as new information is assimilated into the asset price. To study this lag and the effect of various market conditions, we assume that . For our experiments, we set and . Define a set of agents by random intervals where if , then and and if , then and . When is large, with high probability these intervals cover the . Assume:

Then the market will classify as it moves from to over time. This is illustrated in Fig. 4 for two different agent sizes.

The market with smaller numbers of agents tracks the information but there are times when is not in any interval defining an agent and so buying stops. This leads to plateaus in the data.

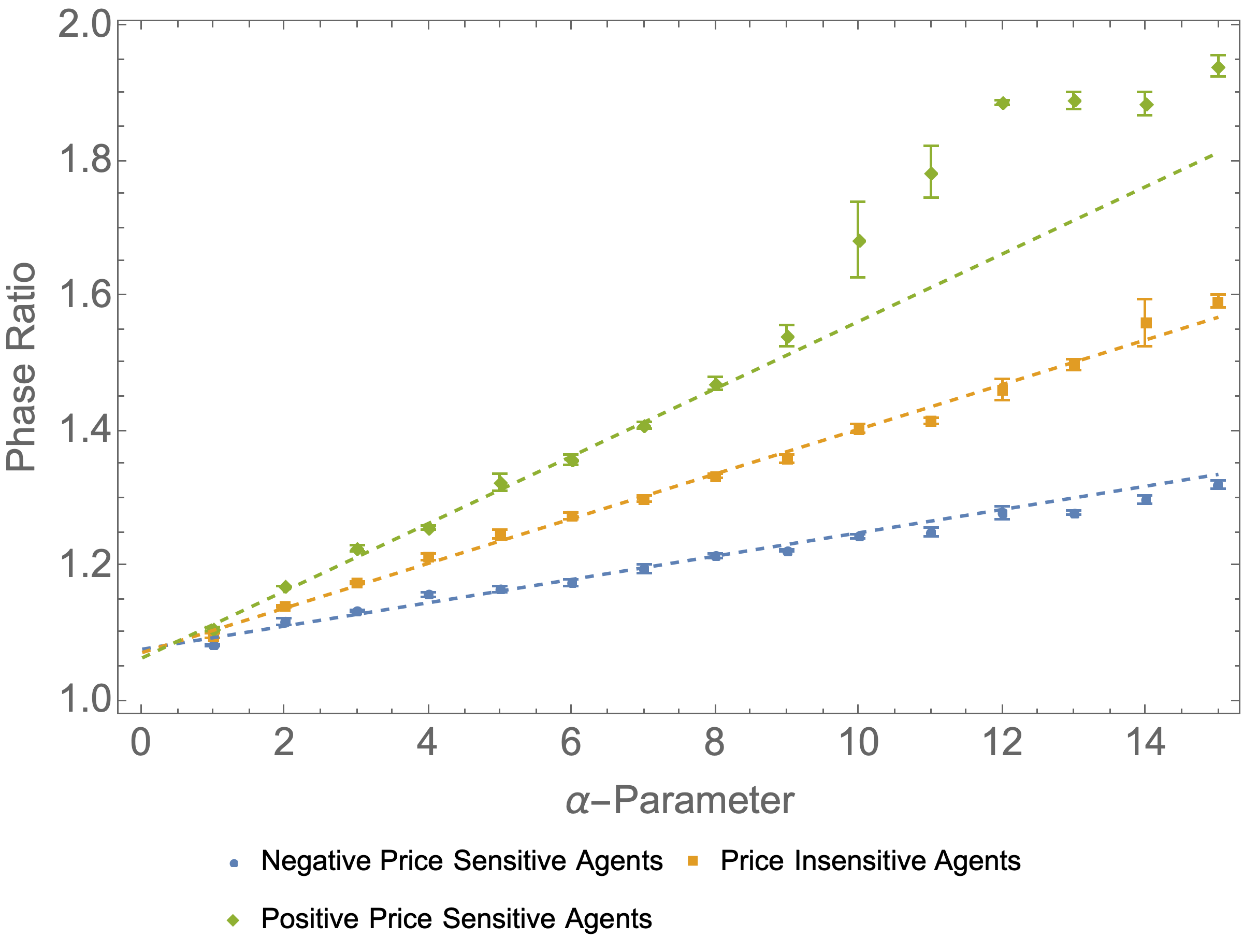

Introduce two parameters and so that:

we can examine the effect asset price sensitivity () and input gain () have on the lag in information uptake in the market. To do this, we use the measured phase difference between and using the argument of the Fourier transform of the solutions at the fundamental frequency . The ratio of the two phases provides a measure of the speed with which information is taken up by the market. We used markets with 250 agents (125 agents per class) and allows to vary from to and to vary in the set . For all experiments . When , there is no price sensitivity. When , agents are more sensitive to price and higher prices make them value the asset lower. Effectively, this creates additional friction in purchasing. When , agents are price sensitive and higher prices causes them to value an asset more. This creates additional force in the the market to purchase even at higher prices. We used 5 replications of each condition to construct confidence intervals on the mean of the phase ratios. Agent intervals were randomized in each replication. Throughout all experiments, was held constant with and . Results are shown in Fig. 5.

We conclude that agents with positive price sensitivity resulted in a higher phase ratio while agents with a negative price sensitivity had a lesser phase ratio for varying input gain (). Price insensitive agents’ phase ratio fell between the positive and negative price sensitive agents. Hence, when , information is taken up by the market faster than when and when . We also note that the phase ratio appears to exhibit saturation in the positive price sensitive agents, which should be expected.

V Generalization and Conjecture

Generalizing the dynamics of Eq. 7 to assets is straightforward. We obtain:

| (9) |

where:

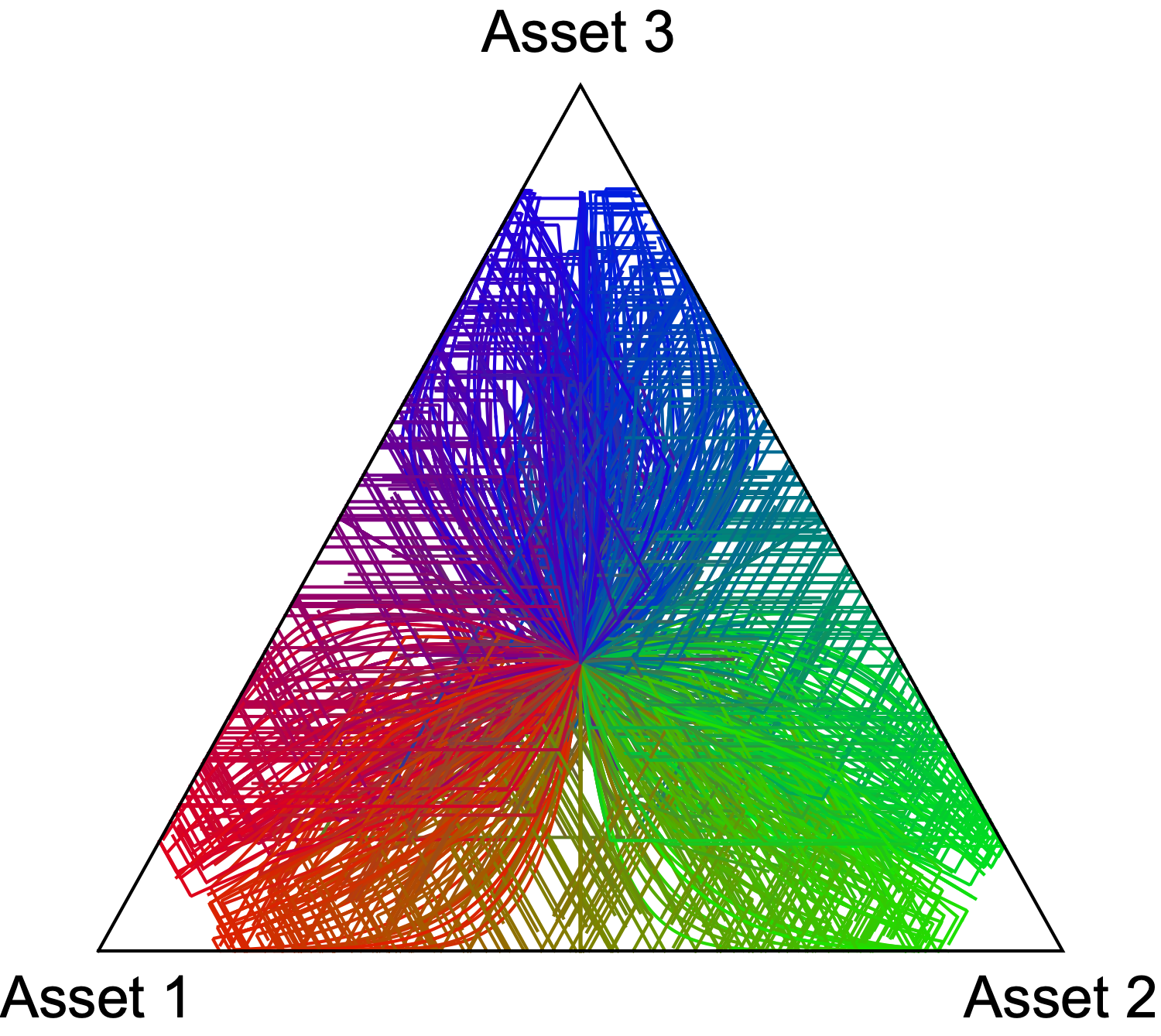

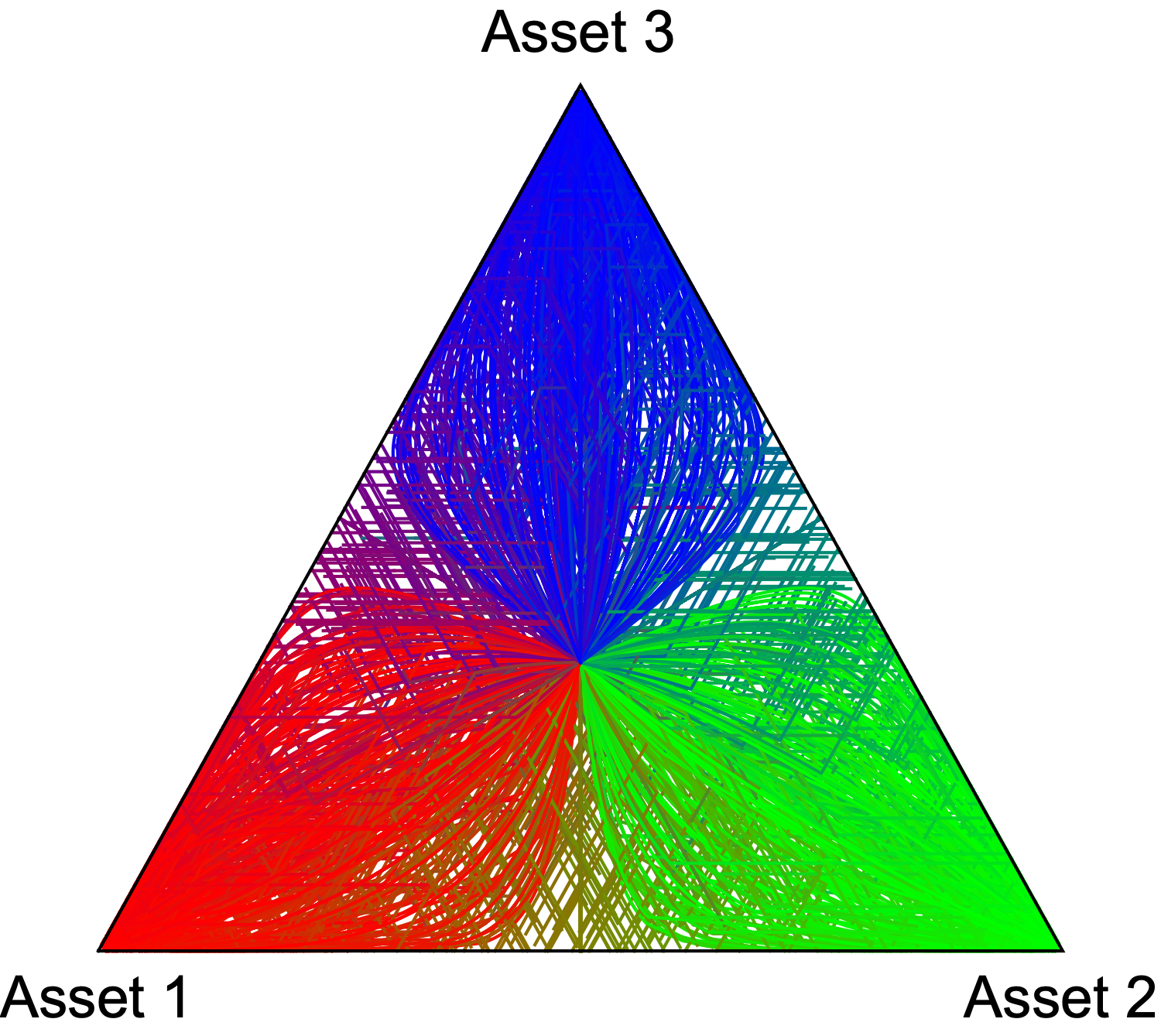

Here is the group of agents who specialize in purchasing assets in class and is the price of asset class . This equation is consistent with Tuyls et al. (2003); Bernasconi et al. (2022). The dynamics effectively describe a recurrent neural network with an embedded softmax layer (generalizing Fig. 1). We conjecture that with constant information, the resulting dynamics always converge, fully generalizing the result in Section III. We illustrate this conjecture in Fig. 6 for a three asset market simulated with over 3000 variations on the dynamics assuming:

where is randomly drawn from either or - see Fig. 6(left) or Fig. 6(right), respectively. The cardinality is randomly drawn from to , simulating a small market.

The figures show that oscillation is not present when information is held constant. In particular, our conjecture implies that the dynamics quickly reach an dimensional Filippov surface and then slide along it until they reach a fixed point (a zero dimensional subset of the Filippov surface) thus ensuring convergence of the system. Assuming this conjecture is correct, then synthetic prediction markets (of the type discussed in Nakshatri et al. (2021)) can be extended to arbitrary prediction classes and the use of continuous time markets will eliminate oscillations observed in the discrete time algorithm. In addition to the open question of the convergence of -array option markets with , we leave as an area of future research how best to design functions and () to recover desired market output values given input data .

VI Conclusion and Future Directions

In this paper, we have prove the convergence of price in a continuous binary option market with constant external information. This is proved by showing that the right-hand-side of the dynamics are piecewise smooth and bounded allowing us to reason about the Filippov surface on which the dynamics come to rest. Consequently, the price dynamics are always monotonic, continuous, and piecewise smooth and always converge. In the presence of non-constant external information, we show empirically that a positive price sensitivity (i.e., purchases increase in response to higher prices) causes larger market lags to external information change while negative price sensitivity (i.e., purchases decrease in response to higher prices) decrease market lag to external information.

Results discussed in this paper can be extended in several ways. We have left an open conjecture on the generalization of the market convergence result to markets with asset classes. We assert that under constant external information these markets also converge. If this is true, then the use of continuous time -array asset markets as an approach to machine learning would be sensible. In this case, since we have shown -array option markets describe a recurrent neural network, investigating how to fit exogenous parameters defining the functions to build a classifier is an interesting and open question, especially considering the recurrent aspect of the neural structure. Finally further analysis in the case when the exogenous signal is non-constant may provide further insight into the behavior of these simple options markets.

Acknowledgement

Portions of this work were sponsored by the DARPA SCORE Program under Cooperative Agreement W911NF-19-2-0272.

Appendix A The Lorenz Attractor

For the example in Section IV, we use the standard Lorenz attractor:

To better illustrate the market effect, we slow the dynamics down by a factor of and set , , .

Appendix B Numerical Solution of Large Differential Equations

When is complex or there are more than a few agents, numerical solution of the differential equations can become unstable. To compensate for this, we can solve Eqs. 5 and 6 using a simple Euler forward step method using a small in Eq. 4 (see below):

We then compute using information for and up to time via Eq. 2. For small , the results match the output of an off-the-shelf ODE solver and are more numerically stable.

References

- Castiglione and Stauffer (2001) F. Castiglione and D. Stauffer, Physica A: Statistical Mechanics and its Applications 300, 531 (2001).

- Bonanno et al. (2006) G. Bonanno, D. Valenti, and B. Spagnolo, The European Physical Journal B-Condensed Matter and Complex Systems 53, 405 (2006).

- Samanidou et al. (2007) E. Samanidou, E. Zschischang, D. Stauffer, and T. Lux, Reports on Progress in Physics 70, 409 (2007).

- Slanina (2001) F. Slanina, Physical review e 64, 056136 (2001).

- Szczypińska and Piotrowski (2008) A. Szczypińska and E. W. Piotrowski, Physica A: Statistical Mechanics and its Applications 387, 3982 (2008).

- Rothenstein and Pawelzik (2003) R. Rothenstein and K. Pawelzik, Physica A: Statistical Mechanics and its Applications 326, 534 (2003).

- Medo and Zhang (2008) M. Medo and Y.-C. Zhang, Physica A: Statistical Mechanics and its Applications 387, 2889 (2008).

- Chang and Stauffer (2001) I. Chang and D. Stauffer, Physica A: Statistical Mechanics and its Applications 299, 547 (2001).

- Hammel and Paul (2002) C. Hammel and W. Paul, Physica A: Statistical Mechanics and its Applications 313, 640 (2002).

- Trimborn et al. (2018) T. Trimborn, M. Frank, and S. Martin, Physica A: Statistical Mechanics and its Applications 505, 613 (2018).

- Berg et al. (1997) J. Berg, R. Forsythe, and T. Rietz, in Understanding Strategic Interaction (Springer, 1997) pp. 444–463.

- Thaler and Ziemba (1988) R. H. Thaler and W. T. Ziemba, Journal of Economic perspectives 2, 161 (1988).

- Manski (2006) C. F. Manski, economics letters 91, 425 (2006).

- Wolfers and Zitzewitz (2006) J. Wolfers and E. Zitzewitz, Interpreting prediction market prices as probabilities, Tech. Rep. (National Bureau of Economic Research, 2006).

- Hanson (1990) R. Hanson, Foresight Update 10, 3 (1990).

- Hanson (1991) R. Hanson, Foresight Update 11 (1991).

- Hanson (1995) R. Hanson, (1995).

- Ray (1997) R. Ray, The Futurist 31, 25 (1997).

- Wolfers and Zitzewitz (2004) J. Wolfers and E. Zitzewitz, Journal of economic perspectives 18, 107 (2004).

- Servan-Schreiber et al. (2004) E. Servan-Schreiber, J. Wolfers, D. M. Pennock, and B. Galebach, Electronic markets 14, 243 (2004).

- Berg and Rietz (2003) J. E. Berg and T. A. Rietz, Information systems frontiers 5, 79 (2003).

- Dai et al. (2020) M. Dai, Y. Jia, and S. Kou, Journal of Econometrics (2020).

- Chakraborty and Das (2016) M. Chakraborty and S. Das, in IJCAI (2016) pp. 158–164.

- Tziralis and Tatsiopoulos (2007) G. Tziralis and I. Tatsiopoulos, The journal of prediction markets 1, 75 (2007).

- Breeden and Litzenberger (1978) D. T. Breeden and R. H. Litzenberger, Journal of business , 621 (1978).

- Rhode and Strumpf (2004) P. W. Rhode and K. S. Strumpf, Journal of Economic Perspectives 18, 127 (2004).

- Chen et al. (2008) Y. Chen, L. Fortnow, N. Lambert, D. M. Pennock, and J. Wortman, in Proceedings of the 9th ACM conference on Electronic commerce (2008) pp. 190–199.

- Chen and Vaughan (2010) Y. Chen and J. W. Vaughan, in Proceedings of the 11th ACM conference on Electronic commerce (2010) pp. 189–198.

- Abernethy et al. (2011) J. Abernethy, Y. Chen, and J. Wortman Vaughan, in Proceedings of the 12th ACM conference on Electronic commerce (2011) pp. 297–306.

- Hull (2003) J. C. Hull, Options futures and other derivatives (Prentice-Hall, 2003).

- Nakshatri et al. (2021) N. Nakshatri, A. Menon, C. L. Giles, S. Rajtmajer, and C. Griffin, Results in Control and Optimization 5, 100052 (2021).

- Lekwijit and Sutivong (2018) S. Lekwijit and D. Sutivong, Journal of Modelling in Management (2018).

- Tuyls et al. (2003) K. Tuyls, K. Verbeeck, and T. Lenaerts, in Proceedings of the second international joint conference on Autonomous agents and multiagent systems (2003) pp. 693–700.

- Bernasconi et al. (2022) M. Bernasconi, F. Cacciamani, S. Fioravanti, N. Gatti, F. Trovo, and E. Contribuition, (2022).

- Filippov (1967) A. Filippov, SIAM Journal on Control 5, 609 (1967).

- Filippov (2013) A. F. Filippov, Differential equations with discontinuous righthand sides: control systems, Vol. 18 (Springer Science & Business Media, 2013).