Repro Samples Method for Finite- and Large-Sample Inferences

Abstract

This article presents a novel, general, and effective simulation-inspired approach, called repro samples method, to conduct statistical inference. The approach studies the performance of artificial samples, referred to as repro samples, obtained by mimicking the true observed sample to achieve uncertainty quantification and construct confidence sets for parameters of interest with guaranteed coverage rates. Both exact and asymptotic inferences are developed. An attractive feature of the general framework developed is that it does not rely on the large sample central limit theorem and is likelihood-free. As such, it is thus effective for complicated inference problems which we can not solve using the large sample central limit theorem. The proposed method is applicable to a wide range of problems, including many open questions where solutions were previously unavailable, for example, those involving discrete or non-numerical parameters. To reduce the large computational cost of such inference problems, we develop a unique matching scheme to obtain a data-driven candidate set. Moreover, we show the advantages of the proposed framework over the classical Neyman-Pearson framework. We demonstrate the effectiveness of the proposed approach on various models throughout the paper and provide a case study that addresses an open inference question on how to quantify the uncertainty for the unknown number of components in a normal mixture model. To evaluate the empirical performance of our repro samples method, we conduct simulations and study real data examples with comparisons to existing approaches. Although the development pertains to the settings where the large sample central limit theorem does not apply, it also has direct extensions to the cases where the central limit theorem does hold.

Key words: Artificial samples; Conformal or matching samples; Discrete and continuous parameters; Parametric and nonparametric settings; Mixture model; Nuisance parameters

1 Introduction

Statistical inference includes quantifying uncertainty inherited from sampling based on an observed copy of data. The approach of repeatedly creating similar artificial (Monte-Carlo) data to help assess the uncertainty has proved in the literature to be an effective method. Examples include bootstrap, approximate Bayesian computing (ABC), generalized fiducial inference (GFI) algorithm, permutation, among others; see, e.g., Efron and Tibshirani (1993); Fishman (1996); Robert (2016); Hannig et al. (2016), and references therein. Most of these works, however, rely on the large sample central limit theorem (CLT) or approximations to justify their validity of statistical inference. Their applicability to some complicated inference problems, especially those to which the large sample CLT does not apply, is limited. In this article, we develop a novel and wide reaching artificial-sample-based inferential framework, which we support with both finite and large sample theories. The proposed framework has the advantage of providing valid inference without relying on likelihood functions or large sample theories. It is especially effective for difficult inference problems such as those involving discrete and/or non-numerical parameters (e.g., the unknown number of clusters, model A, B, C, etc.) among others. Although the repro samples method pertains to settings in which the large sample CLT does not apply, it also has direct extensions to the cases where the large sample theorem does hold.

Suppose that the sample data are generated from a model where is the true value of the model parameters that can be either numerical or nonnumerical or a mixture of both. We assume (and assume only) that we know how to simulate data from , given . Often, can be re-expressed in a structure equation form (also referred to as an “algorithmic model”):

| (1) |

where is a known mapping from and , , is a random vector whose distribution is known or from which it can be simulated. The reason that we adopt the formulation of (1) is that this model specification is very general. For example, it includes the traditional statistical model specification using a density function as its special case: Let be a sample from a density function with true parameter value . We then express in the form of (1) as where , and is the cumulative distribution function of . Additional examples, including more complicated ones, will be provided throughout the paper.

The repro samples method uses a simple yet fundamental idea: study the performance of artificial samples that are obtained by mimicking the sampling mechanism of the observed data; the artificial samples then help to quantify the uncertainty in estimation of the associated model and parameters. Specifically, let

be the realized observations, where is the corresponding unobserved (thus unknown) realization of . For any and a copy of , we can obtain a copy of artificial sample , which we refer to in this paper as repro samples. Note that, when and matches , the corresponding repro sample will match . However, both and are unknown. Since and are both realizations from the same distribution, we use this fact, together with a so-called nuclear mapping function on , , to quantify how likely a is a potential match for . For the collection of ’s that are deemed as “likely” matches, we look for the corresponding that produces a matching repro sample with . We use these to help recover . We formally formulate the procedure and show that a subset of constructed by this procedure has a desired frequency coverage rate and thus is a confidence set for .

In Section 2, we formally describe the repro samples framework. For a given potential value of , we construct a fixed level- Borel set of through a nuclear mapping function, and analyze whether any in the Borel set produces repro samples that match . By controlling through the fixed Borel set and seeking for the matching, we obtain a theoretically guaranteed level- confidence set for . The use of nuclear mapping functions is new and general, and it greatly increases the flexibility and utility of the repro samples method. If the distribution of the nuclear mapping has an explicit form, so does the confidence set. When the the confidence set cannot be explicitly expressed, we provide a generic algorithm. Moreover, the repro samples method can also be used to obtain p-values to conduct hypothesis testing for a wide range of problems. In addition, we further extended the framework beyond the parametric model (1), where the data generating model is not completely known. Although the repro samples method shares many insights with some Bayesian and fiducial procedures, its development is purely under the frequentist paradigm. It sidesteps the need to specify a likelihood or a loss function, and also the need to use large sample theories or the Dumpster-Shafer calculus. It has a wide range of applications, including problems involving any type of parameter spaces, exact and asymptotic inferences, parametric and nonparametric models, among others.

Section 3 provides additional developments we use to facilitate our understanding and broaden the application of the repro samples method. In Section 3.1, we explore the relationship of our repro samples method with the classical Neyman-Pearson hypothesis testing procedure by considering a special case in which we choose a test statistic as our nuclear mapping function. In general, a nuclear mapping function does not need to be a test statistics. Even in special cases in which the nuclear mapping is defined by a typical test statistics, we show that a confidence set obtained by the repro samples method is either the same or smaller than the one obtained by inverting the classical Neyman-Pearson hypothesis testing procedure.

We also obtain a set of optimality results. Furthermore, we develop in Section 3.2 a general technique to handle nuisance parameters through profiling. The method maintains the desired coverage rates for confidence sets constructed for target parameters, even in finite sample settings. Finally in Section 3.3, we improve the computational efficiency by investigating the use of data-dependent candidate sets to greatly reduce the search region in the parameter spaces. Using a candidate set is particularly effective when the target parameter of the inference is discrete, since we can take advantage of a many-to-one mapping that is uniquely inherent in a repro samples procedure. We provide a Monte-Carlo approach to obtain the candidate set and supporting theories to ensure the coverage rate of the final confidence set.

To demonstrate the utility and performance of the repro samples method, we use a normal mixture model as a case study example in Section 4. Accounting for uncertainty in an estimation of the unknown number of components in a mixture model, say , is a notoriously difficult and unsolved inference problem (e.g., Roeder, 1994; Chen et al., 2012), partly because the parameter space of is discrete and the large sample CLT does not apply on any point estimator of . Here, we construct a finite-sample confidence set for the number of components in the normal mixture model. We demonstrate that the repro samples method can effectively solve this open inference problem while handling a large and varying number of nuisance parameters. We perform simulation and real data analyses, and provide comparisons to existing frequentist and Bayesian approaches. The analyses is revealing. First, the regular criterion-based point estimators (even consistent estimators such as the BIC estimators) are often biased for smaller and they rarely recover the true . Second, existing (frequentist) likelihood-based procedures do not provide any upper bounds, and they have low power and work only asymptotically. Third, Bayesian credible sets obtained using the posteriors of perform poorly in terms of covering in repeated runs, even when a uniform flat prior of (over a range including the true value ) is used. In addition, credible sets for are very sensitive to the prior choices of both the target parameter and also (surprisingly) the nuisance parameters. By contrast, the proposed repro sample confidence sets always recover with the desired coverage rate. They also provide a full picture of the sampling uncertainty pertaining to the estimation of .

The repro samples method stems from several existing artificial-sample-based inference procedures across Bayesian, frequentist and fiducial (BFF) paradigms, particularly, approximate Bayesian computing (ABC), generalized fiducial inference (GFI) and bootstrap methods, in which artificial samples are used to help quantify inference uncertainty. It also extends a key idea of the inferential model (IM) (Martin and Liu, 2015) that the inference uncertainty is quantified through the auxiliary . We view the repro samples approach as an improvement over the current existing inference methods and provide comparisons throughout the paper when the topic arises, At the outset, we emphasize that the repro samples method side-steps many restrictions encountered in the aforementioned BFF approaches. First, bootstrap, GFI and ABC methods rely on large sample CLT or some version of Bernstein von Mises-type theorem (thus CLT) to justify their (frequentist) frequency performance, therefore does not guarantee Small sample frequency performance. Second, both ABC and GFI methods are approximation methods that require a predetermined threshold to judge whether an artificial sample is sufficiently close to the observed sample. Their supporting theories need at a fast rate as the sample size . However, when at a fast rate, the sample rejection rate in their algorithms tends to . Thus, how to choose an appropriate to balance the procedures’ computational efficiency and inference validity is an unsolved problem (Li and Fearnhead, 2018). Finally, IM method is designed for epistemic probabilistic inference, and its complexity and reliance on Dempster-Shafer calculus make it hard to implement under complex settings. The IM method is not easily adaptable for asymptotic inference, and the restriction of using an ancillary to quantify uncertainty also limits its use in applications. The repro samples method, developed fully following the frequentist setting, addresses or sidesteps all these issues.

The remainder of this article is arranged as follows. Section 2 develops the general framework of the repro samples method with supporting theories and associated algorithms. Sections 3 considers several important aspects that further support the general development, including connection to the Neyman-Pearson procedure, handling of nuisance parameters, and a unique approach of getting a data-driven candidate set to improve computational efficiency. Section 4 is a case study on a normal mixture model that addresses a long standing open problem in statistical inference. Section 5 contains further remarks and discussions.

2 A general inference framework by repro samples

Let be a probability space and is a measurable random vector on with . Suppose is the sample data from (1) and the vector , , is a function (or a summary) of the sample data . A slightly more general model than (1) is to assume that is directly generated from

| (2) |

where is a given mapping from . In the special case that is the identity mapping function, then , and model (2) reduces to model (1); thus (1) is a special case of (2).

Let be the observed and be the (unknown) realization of associated with . By (2), we have

For any given and a simulated , we can thereafter construct an artificial (‘fake’) copy of :

We call a repro sample of and a repro copy of .

The goal of Section 2.1-2.3 is to present how to use repro samples to construct a confidence set, based on the observed , for the unknown parameter with a guaranteed coverage rate. In Section 2.1 we consider the case of giving the algorithmic model (2) where is completely known. Section 2.2 contains a generic algorithm when an explicit mathematical expression of the confidence set is not available. Section 2.3 extends the developments to a more general case in which the algorithmic model is not completely given.

2.1 A general formulation of a basic repro samples method

Under the algorithmic model (2) with a fixed , the sampling uncertainty of is solely determined by the uncertainty of , whose distribution is free of the unknown model parameters . Let us first focus on the easier task of quantifying the uncertainty in . Specifically, let be a level- Borel set such that Although is unknown, we have more than -level confidence that . If is confined within the same set (i.e., requiring ) and we collect any potential values that can create a repro sample that matches , then it leads to a subset on :

| (3) |

where s.t. is short for such that. In another words, for a potential value , if there exists a such that the repro sample matches with , then we keep this in the set. Since , if then . Similarly, under the model , we have . Thus, by construction,

The set constructed in (3) is a confidence set for . Here, is any single fixed set. As long as , the validity statement holds.

To expand the scope of this development, the requirement is replaced by

| (4) |

for any , where is a mapping function from , for some . Then, the constructed confidence set in (3) becomes

| (5) |

The function , which we refer to as a nuclear mapping, adds much flexibility to our repro-sampling method, as we will show throughout the paper. For the moment, we assume that the nuclear mapping is given; further discussions are provided in later sections.

From now on the set refers to the general expression of (5) instead of the special case in (3), unless specified otherwise. In the construction of in (5), for any potential value , we impose two constraints: (a) The repro error is confined by the restriction ; (b) The repro sample generated using matches the observed sample, i.e., . The quantification of inference uncertainty is achieved only through constraint (a) requiring for the given , and it does not involve the unknown true that generates . The input of the observed sample is discernible by matching the artificial repro sample with in constraint (b).

As an illustration of the method, we consider below a simple binomial example:

Example 1 (Binomial sample).

Assume , , and we observe . We can re-express the model as for . It follows that where is the realization of corresponding to .

For a given vector , we consider the nuclear mapping function , and we have , for each given . Let , where

| (6) |

is the pair of in that makes the shortest interval . By a direct calculation, it follows that , for any . The confidence set in (5) is then

The last equation holds, because for any given there always exists at least a such that , i.e., .

Table 1 provides a numerical study comparing the empirical performance of (Repro) against 95% confidence intervals obtained using the traditional Wald method and the fiducial approach (GFI) of Hannig (2009), both of which are asymptotic methods that can ensure coverage only when is large. The rerpo sampling method is an exact method that improves the performance of existing methods, especially when (a rule of thumb on asymptotic approximation of binomial data; cf., Casella and Berger (1990, p.106)).

| Coverage | Width | Coverage | Width | Coverage | Width | ||||

| Repro | 0.949(0.007) | 0.281(0.059) | 0.963(0.006) | 0.408(0.026) | 0.959(0.006) | 0.342(0.045) | |||

| Wald | 0.877(0.010) | 0.236(0.052) | 0.927(0.008) | 0.418(0.028) | 0.915(0.009) | 0.332(0.071) | |||

| GFI | 0.988(0.003) | 0.293(0.065) | 0.963(0.006) | 0.438(0.022) | 0.973(0.004) | 0.365(0.056) | |||

The next theorem states that in (5) is a level- confidence set.

Theorem 1.

We provide a proof of the theorem is in the Appendix. The in Theorem 1 may or may not depend on sample size . In examples involving large sample approximations, is often a function of with as . However, there are also examples in which does not involve . For example, suppose that . Then, , when is large. So, if we take , , for any Borel set , thus . Here, is the density function of .

Moreover, the repro samples method can be used to do hypothesis testing. From Theorem 1, we have the following corollary. A proof is given in Appendix.

Corollary 1.

Suppose we are interested in testing a hypothesis vs . In that case, we can define a p-value as

where is the level- repro samples confidence set defined in (5). Rejecting when leads to a size test, for any .

Although the repro samples method is developed following the frequentist principles, thus making it a completely frequentist approach, it is also closely related to several existing approaches across the Bayesian, fiducial, and frequentist (BFF) paradigms. In Remarks 2.1 - 2.3 below, we provide discussions to connect and compare these approaches. See also Appendix II for further and more elaborated discussions.

Remark 2.1 (comparison with Neyman-Pearson testing method). Corollary 1 suggests that we can conduct hypothesis testing using the repro samples method. Section 3.1 further investigates the relationship between the repro samples method and the classical Neyman-Pearson (N-P) hypothesis testing procedure under a special case where a nuclear mapping in (5) is chosen through a test statistic, i.e., we set where is a copy of data generated by the given and is a test statistic of a hypothesis testing problem. In general, the repro samples approach is broader than the classical N-P procedure. In particular, the nuclear mapping does not need to be a test statistic since it is not necessarily a function of data Allowing the nuclear mapping to be a function of provides more flexibility for developing inference procedures than the conventional testing approach. We illustrate this point using a simple example where a single observation is generated by , To get a confidence set for , we can let , and define Then, following (5), we construct the repro samples confidence set Apparently, is not a function of , since it is impossible to solve for in the structure equation when given . In this case, is not a test statistic. Section 3.1 provides further discussion and additional examples comparing the repro samples methods and the classical N-P method. We show that the repro samples method can always produce an either equal or smaller confidence set than the traditional N-P method when the nuclear mapping is chosen through a test statistic. There are also options in which the nuclear mapping function is not a test statistic.

Remark 2.2 (comparison with GFI and ABC methods) In modern statistical practice, R.A. Fisher’s fiducial method is understood as an inversion method that solves the structural equation for parameter with any (cf., Brenner et al., 1983; Hannig et al., 2016; Thornton and Xie, 2022). The matching equation in (5) plays a key role in the GFI development (Hannig et al., 2016). Hannig et al. (2016) and Thornton and Xie (2022) have also explored the connection of GFI to the Bayesian ABC method, noting that trying to match with is a key step in both GFI and ABC procedures. However, as stated in Hannig et al. (2016), an exact matching of for any given is difficult and sometime even impossible. Both GFI and ABC methods adopts a tuning threshold value to judge whether an artificial sample is close to the observed . Unfortunately, the use of approximating threshold has piratical issues. For instance, as shown in Li and Fearnhead (2018), the validity of the ABC method requires that at a fast rate, but this fast rate in turn leads to inefficient sampling with a high (often 100%) rejection rate. How to choose an appropriate to balance inferential validity and computational efficiency is still an unaddressed question in both ABC and GFI. Our repro sample approach avoids this issue of using a threshold by directly working with a set of and multiple copies of for each given . As further explained in Appendix II the repro samples method in effect compares with multiple copies of at each given and thus enabling us to use a confidence (significant) level to replace the arbitrary . In addition, the repro sample method can provide finite sample inference whereas GFI does not. Finally, ABC is a Bayesian procedure that not only requires additional prior assumption, but also requires a sufficient summary statistic in its algorithm. The repro samples approach compares favorably in that it does not have these constraints.

Remark 2.3 (comparison with IM method). Inferential model (IM) (Martin and Liu, 2015) also works directly on to quantify inference uncertainty, but contains notable differences from the proposed repro samples method. First and foremost, the IM method exists to provide an epistemic probabilistic inference for , a task not considered under the current frequentest framework; cf., Martin and Liu (2015). The repro samples on the other hand is a frquentist approach developed fully within the frequentist framework. Also importantly, the IM method uses random sets to quantify the uncertainty of the auxiliary term . But the repro samples method quantifies inference uncertainty through a nuclear mapping function that involves a potential parameter and an associated Borel set. Only one fixed level- Borel set is needed. Although IM can sometimes potentially provide some finer details in special cases (since Dempster-Shefer calculus automatically includes both upper and lower probabilities; i.e., plausible and belief functions), with additional constraints, the application of IM is more limited than repro samples method, especially under more complicated settings. Moreover, using a nuclear mapping function involving greatly extends the scope and flexibility of the repro samples method. As a special case, we are able to directly work on auxiliary by setting . To the best of our knowledge, the framework of IM method cannot be easily extended to incorporate varying . Furthermore, IM development requires Dempster-Shefer calculus and asymptotic inference is not available under the development. When both apply, the IM and repro samples methods provide either the same or comparable inference conclusions. Finally, the repro samples development affords us the opportunity to explore the unique aspect of matching to obtain a data-driven candidate set and greatly reduce computational burden; details are provided in Section 3.3. On the other hand, how to incorporate a data-driven candidate set with the IM method to reduce computational cost is not apparent.

2.2 A general Monte-Carlo algorithm

In Example 1, the distribution of has an explicit form, enabling us to express the level- confidence set in (5) explicitly. In cases when the distribution of is not explicit, we can use a Monte-Carlo method to obtain a level- Borel set in (4) and then construct the level- confidence set in (5) as stated in Algorithm 1 below:

(a) Compute , from which obtain an empirical distribution of . Based on the empirical distribution, we get a level- Borel set .

(b) Check whether there exists a such that and . If both of the above criteria are satisfied, keep the .

This general algorithm, grid search algorithm, searches the space of and is used only when an explicit expression of ’s distribution is not available. Our remarks on the implementation of the algorithm are as follows.

Remark 2.4 To obtain the level- Borel set for a given in Step 2(a), w often need to compute the (empirical) distribution of based on the set of Monte-Carlo points , . Then according to the empirical distribution, we can always numerically calculate . If is a scalar, we just directly compute its empirical distribution and use the (upper/lower) quantiles of to obtain a level- interval as the Borel set . When is a vector, say in , we can use data depth and follow Liu et al. (2021, §3.2.2) to construct the Borel set . Specifically, we let be the empirical depth function for any that is computed based on the Monte-Carlo points in , and be the empirical CDF of Then, following Lemma 1 (a) of Liu et al. (2021), the level- (empirical) central region is a level- Borel set on . See also Example 2 (B) of Section 2.3 for a numerical example, where the empirical depth function is computed by R package ddalpha (Pokotylo et al., 2019).

Remark 2.5 The algorithm needs to calculate the empirical distribution of for each . To improve the computing efficiency (at the cost of potentially losing the flexibility of the repro samples method), we can sometimes choose a nuclear mapping function whose distribution of is free (or approximately free) of . In this case, in (4) is free (or approximately free) of with . A benefit of using this type of nuclear mapping function is that we can modify Algorithm 1 to save computing time: in step 2(a), we only need to obtain for a single value of instead of for each grid value of

Remark 2.6 Later in Section 3.3, we will discuss the technique of using a data-driven candidate set to significantly reduce the search space. From the outset, we would like to comment that the search algorithm works in most cases that one commonly encounter. In many statistical analysis, for instance the commonly used likelihood-based inference, the regular conditions on the parameter space include that is a continuous space and the test statistic is also continuous (and often differentiable) in its inner space . Similarly, if the nuclear mapping function is continuous in and is a continuous space, one can in principle use a grid search method to carry out an analysis in this situation. What is new in the repro samples development is that can either be a discrete space or a set of non-numerical subjects. In this case, even if is (countable) infinite, we provide in Section 3.3 a way to take advantage of a many-to-one mapping structure inherited in the repro samples procedure to create a finite candidate set and carry out an efficient grid search method. See Section 3.3 for further details.

2.3 A further extension to more general cases

In this section, we further extend the framework developed above to settings where the matching equation (2) of the algorithmic model is not available. This includes some nonparametric inference problems that are not covered by the existing ABC or GFI methods. Consider the example of making inference for a population quantile of a completely unknown distribution , say, , the -th quantile parameter of . Since for , we have equation , where . Now suppose we observe data , for a fixed , then the equation becomes

| (8) |

where and . The corresponding realized version is . Equation (8) can not be expressed in the form of either (1) or (2). In fact, one cannot generate a repro sample based on (8) that is directly comparable to the observed sample . However, we can still use a repo sampling approach to provide an exact inference for such a nonparametrc inference problem.

In particular, we consider the following generalized data generating equation:

| (9) |

where is a given mapping function from and is a vector as defined at the start of Section 2. The corresponding realization version is . Equation (8) is a special case of (9) with .

The level- confidence set in (5) is modified to be

| (10) |

We have the following theorem for the set defined in (10). The proof is similar to that of Theorem 1 and is briefly described in Appendix I.

Theorem 2.

Assume the generalized model equation (9) holds. If the inequality (4) holds exactly, then for defined in (10) the following inequality holds exactly,

| (11) |

Furthermore, if (4) holds approximately with , then (11) holds approximately with , for , where is a small value that may depend on sample size .

As discussed in Sections 2.2, when the distribution of cannot be explicitly expressed, we may use a Monte-Carlo algorithm to carry out the construction of . Specifically, we may still use Algorithm 1 to get but replace the matching equation in the algorithm with .

The example below provides an illustration of this extended framework. Part (A) is on nonparametric quantile inference and part (B) is on censored quantile regression where making a finite-sample (semi-parametric) inference for model parameters is new and previously unavailable in the literature. Both parts demonstrate that the repro samples method performs well and is compared favorably to the corresponding large sample bootstrap methods.

Example 2 (Nonparametric and semi-parametric inference of quantiles).

(A) Assume are from an unknown distribution . We are interested in making inference about the population quantile , for a given . Write , where and . We define . It follows that and , where and are defined in (6). By (10), a finite sample level- confidence set is where is the th order statistic of the sample , and are the infimum and supremum of support of

Figure 1 provides a numerical study to compare the empirical performance of against 95% intervals obtained by the conventional bootstrap method under two types of . The repro samples method works well even for ’s close to or , whereas the bootstrap method has coverage issues under these settings.

(B) Consider a censored regression model (Powell, 1986), , where are independent error terms from an unknown distribution with medium . Following Bilias et al. (2000), the estimating equation for performing a quantile regression is , where is the quantile level and the parameter of interest is . Since , equation (9) can be expressed as where We consider a nuclear mapping function . Since the distribution of does not have an explicit expression, we use Algorithm 1 to obtain a level- confidence set for . Here, is a vector (of the same length of ) and is obtained using the data-depth approach described in Remark 2.4. Table 2 provides a numerical study to compare in (10) with the confidence sets obtained using the enhanced bootstrap method of Bilias et al. (2000). Again, the repro samples method provides level- confidence sets with finite sample coverage guarantee and it works well for this difficult inference problem even at a small , while the asymptotic bootstrap method has coverage issues under the same settings for . For both methods provide good coverage rates, but the bootstrap confidence sets are much larger.

| Quantile | Error Distribution | Repro Samples | Bootstrap | Relative Volume |

|---|---|---|---|---|

| (a) Normal | 0.945(0.007) | 0.885(0.010) | 0.779(0.028) | |

| (b) Mixture | 0.927(0.008) | 0.891(0.010) | 0.784(0.040) | |

| (c) Heteroscedastic | 0.943(0.007) | 0.893(0.010) | 0.762(0.008) | |

| (a) Normal | 0.945(0.007) | 0.970(0.005) | 17.518(2.723) | |

| (b) Mixture | 0.949(0.007) | 0.977(0.005) | 214.962(9.595) | |

| (c) Heteroscedastic | 0.951(0.007) | 0.980(0.004) | 346.202(11.403) |

3 Test statistic, nuisance parameters and candidate set

For any nuclear mapping function , as long as we have a set such that (4) holds, the set constructed accordingly is a level- confidence set for . In other words, it is possible that one might have multiple choices of that all lead to valid (and perhaps different) confidence sets. Therefore, the role of under the repro samples framework is similar to that of a test statistic under the classical (Neyman-Pearson) hypothesis testing framework. Accordingly, a good choice for is problem specific and we do not have a unique solution to all situations. In this section, we investigate the choice of the nuclear mapping function in two specific yet common settings. Specifically, in Section 3.1, we consider the special case of using a test statistic, including an (approximate) pivot quantity such as a likelihood ratio test statistic, as a nuclear mapping function. We provide comparisons to Neyman-Pearson testing methods. In Section 3.2, we consider the situation of existing nuisance parameters and provide a method to define a nuclear mapping function while minimizing the impact of the nuisance parameters.

To improve the efficiency of computing Algorithms 1, we also discuss the use of a pre-screening candidate set in Section 3.3. We pay special attention to discrete target parameters, a unique and also important development under the repro samples framework.

3.1 Define a nuclear mapping through a test statistic

In a classical testing problem versus , one often constructs a test statistic, say , and assume that we know the distribution of for generated under . Under the Neyman-Pearson framework, we can derive a level- acceptance region , where the set satisfies . By the property of test duality, a level- confidence set is

Suppose the nuclear mapping function is defined through this test statistic:

| (12) |

where . Since for the same , a level- confidence set of (5) by the repro samples method is

We have the following lemma suggesting . See Appendix I for a proof.

Lemma 1.

If the nuclear mapping function is defined through a test statistic as in (12), then we have . The two sets are equal , when .

It is possible that is strictly smaller than with . The following is an example in which is strictly smaller than .

Example 3.

Suppose is a set of sample from the model , , . Here, , . The point estimator is unbiased (and also -consistent). Let’s use the test statistic . Since follows a Irwin-Hall distribution when is the true value , by the classical testing method a level- confidence interval is . Here, is the quantile of the Irwin-Hall distribution. If we use the repro samples method, our confidence set is then . Since the constraint is non-trivial, the strictly smaller statement holds for non-trivially many realizations of .

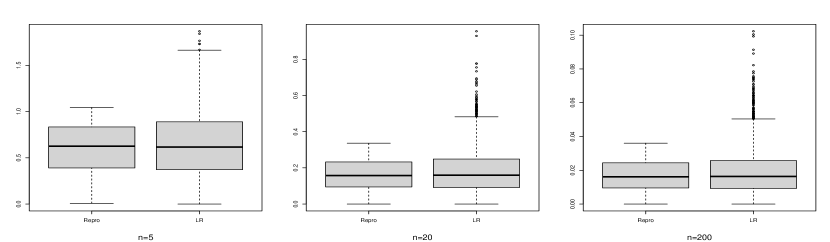

As an illustration, consider the case and , in which . Suppose we have a sample realization . By a direct calculation, and . Clearly, . We repeated the experiment times. The coverage rates of and are both . Among the repetitions, times and times . The average lengths of and are and , respectively.

As mentioned in Remark 2.2, a nuclear mapping function does not need to be a test statistic. However, if it is defined through a test statistics by (12), there are some immediate implications from Lemma 1. First, the confidence set by the repro samples method is either smaller or the same as the one obtained using the test statistic by the classical testing approach. So the set by the repro samples method is more desirable. Second, if the test statistic is optimal (in the sense that it leads to a powerful test), then the confidence set constructed by the corresponding nuclear mapping function is also optimal. In particular, we have the following corollary. Here, a level- uniformly most accurate (UMA) confidence set (also called Neyman shortest) refers to a level- confidence set that minimizes the probability of false coverage (i.e., probability of covering a wrong parameter value) over a class of level- confidence sets; cf., Casella and Berger (1990, §9.3.2). See Appendix I for a proof of the corollary.

Corollary 2.

(a) If the test statistic corresponds to the uniformly most powerful test and is a level- UMA confidence set, then the set by the corresponding repro sample method is also a level- UMA confidence set.

(b) If the test statistic corresponds to the uniformly most powerful unbiased test and is a level- UMA unbiased confidence set, then the confidence set by the corresponding repro sample method is also a level- UMA unbiased confidence set.

Finally, we can define the nuclear mapping through a pivot or an approximately pivot quantity, which is often used as a test statistic. The probability distribution of a pivot quantity does not depend on the unknown parameters. Hence it is convenient to define the nuclear mapping function through a pivot or an approximately pivot quantity, i.e., set , where is a pivot quantity whose distribution satisfies or an approximately pivot quantity whose distribution satisfies Here, is a density function that is free of the unknown parameter and is any Borel set, and is a small number as defined in Theorems 1 and 2. In this case, we have simplified in (4) that the set is free or approximately free of .

Let’s consider the example of a likelihood ratio test (LRT) statistic, which is often regarded as the most commonly used asymptotic pivot quantity; cf., Reid and Cox (2015). Example 4 below compares the repro sample method works with the LRT test.

We both consider an example where the LRT is asymptotically chi-square distributed, and revisit Example 3 where the regular asymptotic result does not hold. It demonstrates the flexibility of the repro samples method and its ability to achieve improved performance over the commonly used likelihood inference especially in finite sample settings.

Example 4 (Likelihood inference).

(a) Assume is the likelihood function corresponding to model (2). The LRT statistic for test vs is . Suppose the nuclear mapping function is defined as . A level- confidence set by the repro sample method is then where is a set that satisfies (4). This is an exact level- confidence set, if can be obtained for each given or directly using Algorithm 1. Frequently, as and under some regularity conditions, is asymptotically -distributed with degrees of freedom (Casella and Berger, 1990, p381), thus asymptotically free of . It follows that an asymptotic level- confidence set is where is the -th quantile of the distribution and is the confidence set obtained by the regular LRT method. By Corollary 2, preserves the optimality of when is optimal.

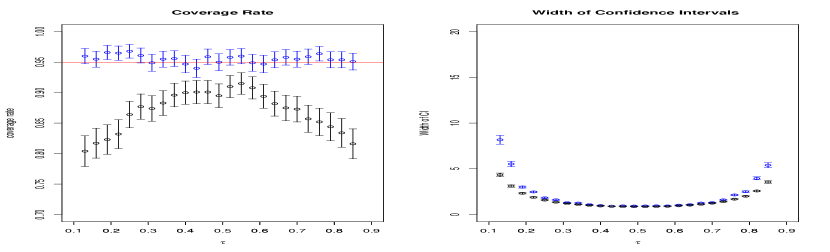

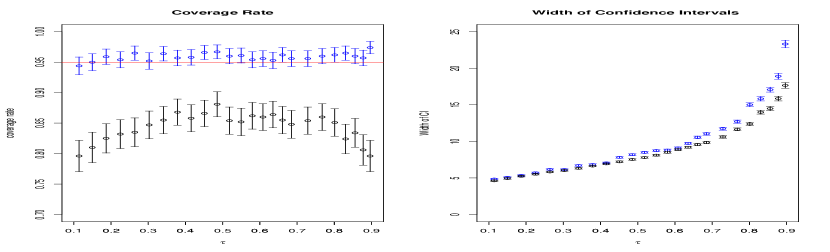

(b) We now revisit Example 3, where the likelihood function The LRT statistic is and does not converge to a distribution. However, is decreasing in . So, the LRT rejects with a large , which leads to a level- confidence set . Although we could directly define our nuclear mapping function through to obtain a repro sample confidence interval, we consider here an alternative choice of a vector nuclear mapping function , where is the th order statistic of a sample from . Let be a solution of . We can show for . Thus, a level- confidence set is . We have conducted a numerical study with true and , respectively. In all cases, the coverage rates of both confidence intervals are right on target around in 3000 repetitions. The intervals by the repro sample method are consistently shorter than those obtained using the LRT method across all sample sizes, as evidenced in Figure 2. Although a LRT is uniformly most powerful for a simple-versus-simple test by the Neyman-Pearson Lemma, it is not the case for the two-sided test in this example. we are able to explore and use the repro samples method to obtain a better confidence interval.

3.2 Define a nuclear mapping and control nuisance parameters

Frequently researchers are interested in making inference only for a certain parameter, say , and the remaining parameters in are considered nuisance parameters. There is a large number of literature on this topic where profiling and conditional inference remain to be two major techniques that handle nuisance parameters (Cox and Reid, 1987; Davison, 2003, and references therein). These techniques typically lead to test statistics, say , that do not involve the nuisance parameter in expressions. Often times however the distributions of these test statistics still depend on the unknown nuisance parameter and thus not readily available. To obtain the distributions of , researchers often invoke large samples and assume that there exists a consistent plug-in estimator of the nuisance parameter; e.g., Reid and Cox (2015); Chuang and Lai (2000). In this subsection, however, we use a similar profiling idea to provide an alternative approach. The advantage of our approach is that it can give us a confidence set with a guaranteed finite-sample coverage rate.

Suppose is a mapping function from . For instance, we can often make , a test statistic mentioned above using either a profile or a conditional approach. Or, more generally can be any nuclear mapping function used to make a joint inference about . Suppose we have an artificial data point and let be a level- confidence set for , where has the expression of (5) or (10) but with replaced by the artificial data and the nuclear mapping function replaced by . Now, beside , let us consider another copy of parameter vector that has the same but perhaps a different . To explore the impact of a potentially wrong nuisance parameter , we define

| (13) |

From Corollary 1, we can interpret as a ‘-value’ when we test the null hypothesis that the data is from but in fact with . Our proposed profile nuclear mapping function for the target parameter is defined as

| (14) |

Although still depends on , including the unknown nuisance parameter , it is dominated by a random variable as stated in the lemma below. See Appendix I for a proof of the lemma.

Lemma 2.

Suppose is a profile nuclear mapping function from defined above. Then, we have

Based on the above lemma and following the construction outlined in Section 1, we define

| (15) |

The next theorem states that is a level- confidence set of the target parameter . A proof is provided in Appendix.

Theorem 3.

Suppose that is the true parameter with and is defined in (3.2), we have .

In cases when the distribution of is known, the function in (13) and the nuclear mapping function have explicit formulas. When the distribution of is not available, we can use a Monte-Carlo method to get for each given as described in the lemma below. See Appendix I for a proof.

Lemma 3.

Let be the empirical depth function that is computed based on the Monte-Carlo points in , where is the Monte-Carlo set defined in Algorithm 1 for a given . Let be the empirical CDF of then

where

Using Lemma 3, we can evaluate via (14), and then obtain the confidence set in (3.2). Note that, for any given , we can express as a function of only, so we can use a build-in optimization function in R (or another computing package) to obtain in (14). The following continuation of Example 2 illustrates constructing confidence interval (3.2) for a parameter of interests in presence of nuisance parameters. The case study example in Section 4 provides another illustration of a more difficult inference problem in a normal mixture model where the target parameter is the number of unknown components.

Example 2 (Continuation).

We continue Example 2(b) to obtain a confidence interval for a single regression coefficient in the censored quantile regression model (with the remaining coefficients as nuisance parameters), . We consider be the -th element of the vector that is previously used in Example 2(b) to make joint inference on the entire . Following Theorem 3 and Lemma 3, a confidence set for the single parameter is

where is defined in Lemma 3. Table 3 reports the performance of the above confidence interval for from simulation studies on the same setting as in Example 2(B). We observe that for , repro samples achieves the desirable coverage while the bootstrap method by Bilias et al. (2000) consistently under covers. The widths of the confidence intervals from the two approaches are similar. For =0.9, both approaches well cover the true parameter, but the bootstrap confidence intervals appear to be much wider.

| Quantile | Error Distribution | repro samples | Bootstrap | ||

|---|---|---|---|---|---|

| Coverage | Width | Coverage | Width | ||

| Normal | 0.944(0.007) | 0.747(0.006) | 0.920(0.009) | 0.727(0.007) | |

| Mixture | 0.950(0.007) | 0.832(0.007) | 0.935(0.008) | 0.839(0.008) | |

| Heteroscedastic | 0.940(0.008) | 0.826(0.007) | 0.921(0.009) | 0.844(0.009) | |

| Normal | 0.979(0.005) | 0.813(0.007) | 0.983(0.004) | 4.190 (0.424) | |

| Mixture | 0.973(0.005) | 1.407(0.013) | 0.973(0.005) | 3.260(0.312) | |

| Heteroscedastic | 0.945(0.007) | 1.149(0.009) | 0.967(0.006) | 4.124(0.439) | |

3.3 Finding candidate set for target parameter

Sometimes when an explicit expression of the confidence set is not available, one can use Algorithm 1 to search through the parameter space and construct . Finding a suitable candidate set to limit the search can greatly improve the computing efficiency of the algorithm. Here, a candidate set, say refers to a subset of the parameter space that is pre-screened using the observed data . In this section, we first provide a general result of the impact of using a data-dependent candidate set on the coverage. We then discuss the special case of a discrete target parameter in which we can take advantage of a many-to-one mapping that is unique in a repro samples setup to create an effective pre-screen candidate set to significantly reduce our computing cost.

The candidate set may be obtained using different pre-screening methods. The key is that we need to overcome the issue of a “double usage” of the data but still ensure an at least approximate coverage of the final output confidence set

| (16) |

we impose a condition that

| (17) |

where is a small number as described in Theorem 1. Here, the “double usage” refers to the fact that we use the observed data in constructing both the candidate set and confidence set . The corollary below contains a result showing that the output set is still an (approximate) level- confidence set. See Appendix I for a proof of the corollary.

Corollary 3.

Let and is a candidate set that satisfies (17). Then, we have

When the parameter space is continuous and the mapping function is continuous in , we may use a grid search method to cover the entire , as discussed in Remark 2.6. A data-dependent candidate set can help further narrow down to the grid search; cf., Example Example 2 (Continuation) and also Michael et al. (2019).

An intriguing yet unique situation in the repro samples development is when the parameter space is discrete. We can take advantage of a “many-to-one” mapping that often exists in the setup to get a data-dependent candidate set that is much smaller than . We describe the above key idea and a generic approach below. Section 4 includes a case study with with greater details to provide a specific illustration on how to obtain this kind of candidate set

For convenience of discussion, we rewrite (2) as , where is the true value of a discrete parameter with a parameter space and, if applicable, are the values of other (nuisance) parameters. Write . Our goal is to find a candidate set such that is significantly smaller than and satisfies (17).

Let us first examine a “many-to-one” mapping often inherited in a repro sample setup involving a discrete parameter . In particular, based on the equation we can rewrite as a solution of an optimization problem or, more generally,

| (18) |

where is a continuous loss function that measures the difference between two copies of data and . However, we do not know (observe) . By replacing with a repro copy in (18), we get

| (19) |

which maps a value to a . Typically, is uncountable and is countable, so the mapping in (19) is “many-to-one”; That is, many correspond to one . We are particularly interested in the subset , where for any the mapping in (19) produces . Since , . We assume is a nontrivial set containing many elements that can not be ignored.

Now suppose has a nontrivial probability. Then, we can use a Monte-Carlo method to obtain a candidate set such that . The idea is to simulate a sequence of , say, . When is large enough, with a high (Monte-Carlo) probability. That is with a high (Monte-Carlo) probability, where is our candidate set

| (20) |

We show next that , where as .

Let be an independent copy of . Formally, we assume the following condition:

-

(N1)

For any , there exists a neighborhood of , say , such that

(21) and , for a positive number .

Although the neighborhood and the number are problem specific, Condition (N1) is typically satisfied (or nearly satisfied) when is a continuous loss function and is uncountable. The following lemma suggests that, under Condition (N1) and as , in (20) satisfy condition (17). Here, the probability refers to the joint distribution of and Monte-Carlo ’s in . See Appendix I for a proof of the lemma.

Lemma 4.

Suppose Condition (N1) holds and is defined in (20). Then,

Based on the lemma, we propose the following theorem. Here, the probability refers to the condition distribution of given the set . See Appendix I for a proof.

Theorem 4.

Suppose Condition (N1) holds and is defined in (20). Then, there exists a positive number such that we have, in probability, (a) and (b) .

In the theorem, the small term tends to as the size of the Monte-Carlo set , and the result holds for any fixed (data) sample size . So the theorem is a small sample result. Also, the “in probability” statement regards the Monte-Carlo randomness of . Based on Theorem 4, we have a clean interpretation for the frequentist coverage statement: if we use the proposed Monte-Carlo method to obtain the candidate set , we have a near chance (i.e., in probability statement in ) that the coverage provability of the obtained set is no less than (i.e., frequency statement in ).

We will further discuss and provide an extension of Condition (N1) and Theorem 4 in Section 4.3.

4 Case study example: normal mixture with unknown number of components

Mixture distributions are a commonly used model in data science. However, a challenging task remains to be quantifying the uncertainty and making inference for the unknown number of components, say , in a finite mixture distribution. Although several existing procedures provide point estimates for , the question of how to assess the uncertainty of estimation of is still open. This difficulty is due in large part to the fact that the unknown is a discrete natural number and typical tools such as the large sample CLT are no long applicable to the point estimators of . In this section, we demonstrate how to use the repro samples method to solve this open question in a normal mixture model by constructing a finite sample level- confidence set for the unknown . This case study example also sheds light on how to address inference problems of discrete parameters and handle nuisance parameters in general cases.

4.1 Notations: normal mixture model

Suppose , one of the models in , for Write . Here, the model parameters are , where is the unknown (unobserved) membership assignment matrix, where and is the indicator of whether is from the th distribution , , . We denote by the corresponding true values , , , and , respectively. Because we are interested in inference of the unknown number of components and are therefore unknown nuisance parameters of the components’ means and variances.

We can re-express , where , in a vector form,

| (22) |

where . The realized version of (22) is where is the realized membership assignment matrix that generates . A typical setup further assumes that is a random draw from multinomial distribution with unknown proportion parameters , .

The literature confirms the identifiability issue in a mixture model that multiple sets of parameters could possibly generate the same data (Liu and Shao, 2003). To account for this identifiability issue, we re-define the true parameters as those that correspond to the ones with the smallest , i.e.,

| (23) |

when the identifiability issue arises. Here, and on the right hand side are the true parameter values that generates With a slight abuse of notation, we still use the same notations on the left hand side to denote the ones with the smallest . We further assume that defined in (23) is unique. We also assume that where and That is, among the components, none of the variance can completely dominate another , for any . The inference we develop is on the set of parameters defined in (23) with the smallest .

The inference problem for the target parameter is complicated. Here, we have both types of nuisance parameters of varying sizes: discrete nuisance parameters that are potentially high-dimensional and continuous nuisance parameters whose lengths change with . To have an effective repro samples approach that is computationally efficient, we handle the two types of nuisance parameters in two different ways. For the discrete nuisance parameter we take advantage of the many-to-one mapping described in Section 3.3 to obtain a manageable candidate set. For the continuous nuisance parameters , we utilize a specific feature of the normal mixture distribution, namely that, given , we can find sufficient statistics for and avoid searching through all possible values of . In Section 4.2, we define a nuclear mapping function that minimizes the impact of the nuisance parameters. In Section 4.3, we construct an effective candidate set of over the corresponding discrete parameter space to greatly improve our computing efficiency.

4.2 Nuclear mapping function for given

In most derivations of this subsection, is fixed. For notation simplicity, we suppress the subscripts in and simply write . Note that the vectors and have the length of that changes when varies. Also, let , be the submatrix of corresponding to the th component with being the index set corresponding component , and be the subvector of that is corresponding to the th component.

Corresponding to in (22), we can write as

where ,

|

|

For the given , is the sufficient statistics for and is the remaining normalized “noises” whose distribution is free of nuisance parameters . By its expression, depends only on , so we also write . To develop a nuclear mapping for while removing the impact of the nuisance parameters , we consider below a conditional probability given , the sufficient statistics for .

Let be any reasonable estimates of based on For instance, we can use a BIC-based estimator

where is the log-likelihood function of given We also denote the conditional probability and let

Conditional on , does not involve often unknown , as stated by the lemma below. See Appendix I for a proof of the lemma.

Lemma 5.

The function defined above is free of and so we can express

Next we follow Section 3.2 to remove the impact of the remaining latent discrete nuisance parameter . Specifically, let where , and it is a mapping from . We define a set in

This set only depends on the given and is free of nuisance parameters . Theorem 5 below states that is inside with a probability greater than , both conditionally and unconditionally. See Appendix I for a proof.

Theorem 5.

For any , the conditional probability

| (24) |

Therefore,

According to Lemma 2 and (3.2), we define

| (25) |

From Theorem 3 and a direct calculation, the corollary below states that can be further simplified and is a level confidence set for . See Appendix I for a proof.

Corollary 4.

The set defined in (25) can be further expressed as

| (26) |

where and are defined by replacing with in the definition of and Also, , so is a level confidence set for .

Corollary 4 suggests that, to construct we only need to calculate the function in (26) for each pair of and . This can be achieved with Monte-Carlo approach as follows. Given and we simulate a large number of and the collection of ’s forms a set . Let

The following theorem validates that we can approximate the conditional distribution of given and with the Monte-Carlo sampling distribution of See Appendix I for a proof.

Lemma 6.

Given a let and where then

4.3 Finding candidates for

We follow Section 3.3 to construct a data-driven candidate set for based on the observed data Corresponding to (19), we use a modified BIC as our lost function and define our many-to-one mapping for as

|

|

(27) |

By (20), a data-dependent candidate set for is

where is a collection of simulated , .

One complication under the mixture model setting is that the equation (21) in (N1) may not hold when hits certain directions (i.e., the two vectors and are on the same direction for some , ) or is extremely large. Fortunately, the probabilities of these events are arbitrarily small, resulting in the arbitrarily small difference between the probability bound in the following Theorem 6 and that in Theorem 4. In the theorem, See Appendix I for a proof.

Theorem 6.

Suppose Let the distance metric between and be then for any arbitrarily small there exist and also an interval of positive width such that when (a) , (b) where is defined in (28).

Remark 4.1 Compared to the standard BIC, the modified BIC many-to-one mapping (27) has an extreme term that involves the repro copy . We modified the term inside the log function so that the mapping (27) can give us when equals . We also allow the penalty on the model size to change by using instead of . This change adds some flexibility to help control the finite sample coverage probability as shown in Theorem 6. In practice, we usually still use since it is often in its required range for a small . For example, to achieve a coverage error we can take . Considering is usually it is likely that .

5 Numerical Studies: Real and simulated data

5.1 Real data analysis: red blood cell sodium-lithium countertransport (SLC) data

In this section we consider a data set that consists of Red blood cell sodium-lithium countertransport (SLC) activity measurements from 190 individuals (Dudley et al., 1991). SLC measurement is known to be correlated with blood pressure, and perceived as an essential cause of hypertension by some researchers. Moreover, SLC is usually easier to study than blood pressure that could be influenced by numerous environmental and genetic factors (Dudley et al., 1991). Roeder (1994) and Chen et al. (2012) both analyzed the SLC data set of 190 individuals using a normal mixture model, and perform a hypothesis testing on the number of components vs for a small integer Roeder (1994) concluded that is the smallest value of not rejected by the data assuming variance of each component is the same. Chen et al. (2012) argued instead that dropping the assumption of equal variances, the hypothesis of would not be rejected and thus a good fit for the data.

We use the repro samples approach developed in Section 4 to re-analyze the SLC data. Following Roeder (1994); Chen et al. (2012), we assume that the SLC measurements follow a normal mixture distribution with unknown number of components and obtain a 95% confidence set for that is After that, we fit the normal mixture model with on the SLC data with an EM algorithm, respectively. We provide the estimated mean, standard deviation and weight of each component in Table 4. The confidence set obtained by our repro samples approach suggests that both hypothesis and are plausible. Since, in genetics, a two-component mixture distribution corresponds to a simple dominance model and a three-component corresponds to an additive model (Roeder, 1994), evidently we can not rule out either of the two competing genetic models based on the SLC data alone.

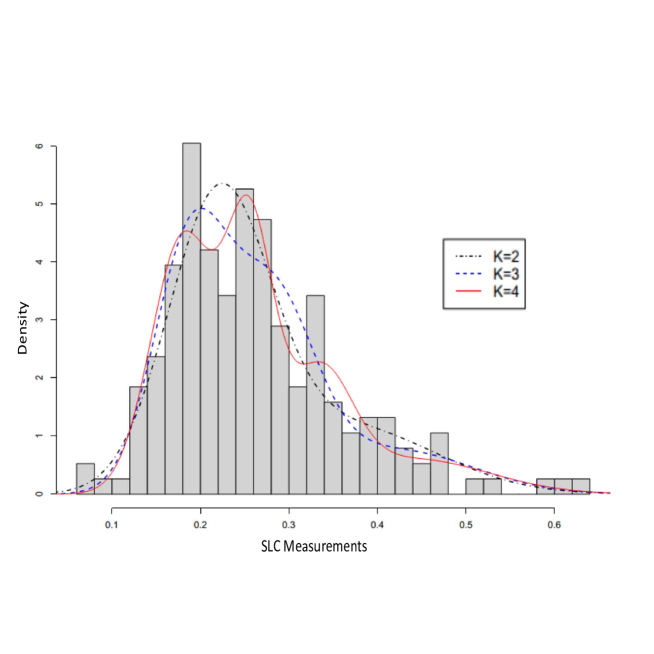

An advantage of the proposed repor samples method is that its confidence set provides both a lower bound and an upper bound for plausible values of supported by the data set, whereas inverting one-sided tests proposed by Roeder (1994) and Chen et al. (2012) can only lead to one sided confidence set. One formidable challenge of finding an upper bound is the fact that any distribution can be arbitrarily well approximated by a normal mixture distribution, therefore for a large can never be rejected. Here we manage to tackle this challenge by using repro samples to find a proper candidate set as described in Section 4.3. The upper bound of the confidence set for we find for the SLC data is In Figure 3, we plot the histogram of the SLC measurements together with estimated normal mixture densities with number of components using EM algorithm. It appears that only with , the normal mixture model could capture the three spikes in the histogram, while still smoothly fitting the rest of the histogram. Indeed, a normal mixture model with four components should demand further investigation, since it effectively represents the data without over fitting it.

| Component Mean | Component SD | Weight | |

|---|---|---|---|

| 2 | (0.2206,0.3654) | (0.0571,0.1012) | (0.7057,0.2943) |

| 3 | (0.1887,0.4199,0.2809) | (0.0414,0.0886,0.0474) | (0.4453,0.168,0.3866) |

| 4 | (0.1804,0.3351,0.2556,0.4403) | (0.0362,0.0359,0.0268,0.086) | (0.4018,0.1742,0.2941,0.1299) |

We also conducted a Bayesian analysis on the SLD data using R package mixAK (Komárek and Komárková, 2014), where the Bayesian inference procedure on Gaussian mixture model with unknown number of components is discussed in Richardson and Green (1997). We implement four different priors on in our analysis: uniform, truncated Poisson(0.4), truncated Poisson(1) and truncated Poisson(5) over The priors used on and are the default priors (i.e., Gaussian and inverse Gamma priors) in mixAK. The posterior distributions for the four priors are plotted in Figure 4, with corresponding 95% credible sets , , , , respectively. It turns out the posterior distributions and their corresponding 95% credible intervals (sets) of are quite different for different priors. Even in the cases with the same credible set using uniform and truncated Poisson(1) priors, their posterior distributions are quite different. It is clear that the Bayesian inference of is very sensitive to the choice of prior distribution. A simulation study in the next section affirms this observation. In addition, the simulation study further suggests that the Bayesian procedure is not suited for the task of recovering the true value (under repeated experiments) and Bayesian outcomes are also affected greatly by the default priors on and .

5.2 Simulation Study: Inference and Recovery of True

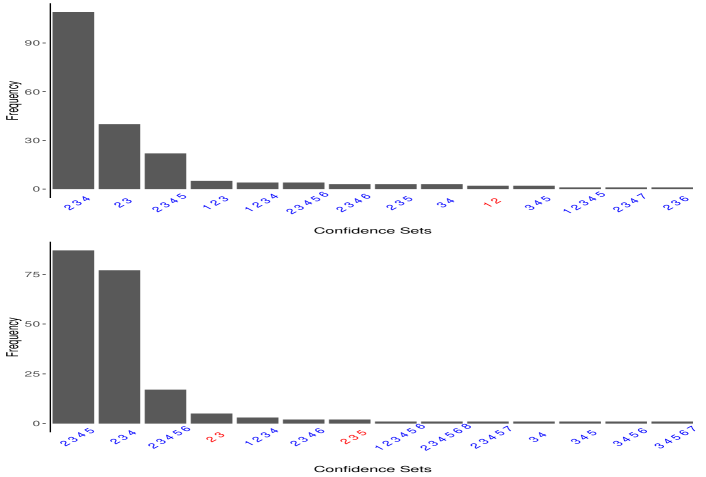

To further demonstrate the performance of the proposed confidence set, we carry out simulation studies in which the simulated data are generated using the estimated normal mixture model with and in Table 4, respectively. We keep the sample size at . For each simulated data, we apply the proposed repro samples method. We repeat the simulation and analysis 200 times, and subsequently summarize the 200 level-95% confidence sets using a bar plot in Figure 5, for and , respectively.

It appears that for both settings of and , the proposed confidence set for achieves coverage rates of 99% and 96.5% respectively, both greater than 95%. Note that the parameter space for is discrete, therefore, unlike confidence intervals for continuous parameters, it is not always possible to achieve an exact confidence level of 95%. For simulated data with the average size of the proposed confidence set is about 3, with a standard error of 0.05. In fact, we observe from Figure 5 that for the majority of the 200 simulations, our approach produces a confidence set of As for more than 80% of the times, we obtain a confidence set of either or , making the average size of the confidence set around 3.65, with a standard error of 0.05.

We compare the performance of the existing methods under the same simulation settings. First, the classical BIC method recovers the true value of only 13 times (6.5%) out of the 200 repetitions. The number of times drops to (out of 200 repetitions) when the true The results are not surprising, since with penalty terms point estimators of are often biased towards smaller values in practice, even though BIC estimator is a consistent estimator. These two extremely low rates of correctly recovering the true cluster sizes highlights the challenge of the traditional point estimation method in this simulation example, and more generally the risk of using just a point estimation in a normal mixture model. This result also suggests the necessity of quantifying the uncertainty of the estimation using a confidence set with desired coverage rate.

Additionally, when it comes to make an inference for , we also illustrate the advantage of our proposed confidence set over the existing one-sided hypothesis testing approach in the literature. In practice, researchers would usually favor the smallest model that can not be rejected, as discussed in Roeder (1994) and Chen et al. (2012). However, we observe from our simulation study that such practices could very well erroneously lead us to an overly small model, resulting in incorrect scientific interpretation. In particular, we find in our simulation study that, when the true and we perform the PLR test of Chen et al. (2012) on versus , only 74% times do we fail to reject . When the true and we perform the PLR test on versus , we fail 93% times to reject . These results suggest that most of time the PLR test would favor a wrong model over the true one. Furthermore, inverting either of the one-sided tests does not produce a useful confidence set, since the upper bound of the confidence set is . In conclusion, we believe that the proposed confidence set by the repro samples method is a more intact approach of conducting inference on compared to the one that uses only hypothesis testing.

(a) (b) (c)

Finally, we compare the performance of the Bayesian procedure described in Richardson and Green (1997) on analysis of the Gaussian mixtures with unknown number of components. Figure 6 summarizes the results from the Bayesian inference procedure produced by R package mixAK (Komárek and Komárková, 2014). The data is generated with the same setting as the lower panel of Figure 5 with The left panel of Figure 6 illustrates the results by imposing uniform prior on The middle panel displays results from Poisson(1) prior, which prefers smaller , and the right panel from Poisson(5) prior, which favors the truth since the mode of Poisson(5) is 4. We can see that the Bayesian level- credible sets consistently underestimate and fail to cover . With the uniform prior, the credible sets only covers 43 times out of the 200 simulations (21.5%). While with a truncated Poisson(1) prior that favors smaller the Bayesian approach completely fails to cover with none of the credible intervals including Even with an “oracle” truncated Poisson(5) prior that sides with the truth, the Bayesian approach manages to cover the truth only of the times. An additional issue with the Bayesian method is that the outcomes are sensitive to the specification of the prior on as evidenced by the differences among the three panels of Figure 6.

The underestimation of by the Bayesian method with a uniform prior for is a little surprising at the first appearance. However, further investigation reveals that the priors on and also have a large impact on the estimation of and the underestimation is attributable to the shrinkage effect of implementing a multilevel hierarchical model (see Richardson and Green (1997) for details). Indeed, it is well known that shrinkage is ubiquitous when parameters are modeled hierarchically in Bayesian analysis. Here both the means and the variances of each component would share a common prior, thus over promoting smaller as observed across all four plots in Figure 6.

In summary, we can conclude from the simulation study that the proposed repro samples method is effective and can always recover the true values of using confidence sets with guaranteed coverage rates. All existing methods, including the point estimation, existing hypothesis testing method and the Bayesian procedure, however regularly miss the true , with outcomes almost always biased toward smaller values. Furthermore, credible sets by the Bayesian method do not have the repeated coverage rates and its outcomes are also very sensitive to the choices of priors on and .

6 Further comments and discussion

This article develops a general and effective framework, named repro samples method, to making inference for a wide range of problems, including many difficult open questions for which solutions were previously unavailable or could not be easily obtained. It utilizes artificial sample sets generated by mimicking the observed data to quantify inference uncertainty. Our development has explicit mathematical solutions in many settings, while others it uses a Monte-Carlo algorithm to achieve numerical solutions. The repro samples method has several theoretical guarantees. Theoretical discussions in the article include guaranteed frequentist coverage in various situations in both finite and large sample settings, relationship and advantages to the classical hypothesis testing procedure and associated optimality results, effective handling of nuisance parameters, and use of a data-driven candidate set to improve computing efficiency, etc. We also discuss relationships to other artificial sample based approaches across Bayesian, fiducial and frequentist inferences and to that of the probabilistic IM method, with additional details provided in Appendix II. A distinct advantage of the proposed framework is that it does not need to rely on likelihood or large sample CLT to develop inference. It is particularly effective for a broad collection of challenging inference problems, especially those involving discrete target parameters.

The repro samples method is broadly applicable. This article includes a number of examples to illustrate several different aspects of the development. It further includes a case study example to construct a finite-sample confidence set for the unknown number of components in a mixed normal model, which is a well-known unsolved problem in statistical inference. Although it appears simple, the case study example requires a number of procedures to deal with the discrete target parameter and also a large number of nuisance parameters of varying lengths. Beside the examples in this article, we have also applied the repro samples method to solve another difficult problem on post-selection inference in high dimensional models where the model selection uncertainty are quantified and also incorporated in the inference of regression coefficients. Due to space limitation, we summarize the results of the post-selection inference problem in a separate paper, in Wang et al. (2022). Additional research involving discrete parameters (e.g., identification of root node(s) of a network, network membership, unknown number of clusters/mixtures, etc.) and also rare events data are currently underway. The research results will be reported in separate articles.

Indeed, the repro samples method can greatly extend the scope and reach of statistical inference by considering broad types of parameters and models. Besides the regular type of parameter space that is continuous, the parameter space in a repro samples method can be discrete or even mixed types. It sidesteps some regularity conditions commonly imposed in a traditional approach (e.g., the true is an inner point of parameter space ; Casella and Berger, 1990, Chapters 7 and 8). Furthermore, the algorithmic model (1) and its extension (9) are very general. In addition to covering the traditional Fisherian model specifications of using density functions (as illustrated throughout the paper), they cover complex models such as those specified in a sequence of differential equations in population genetics, astronomy, geology, etc., in which one can simulate a data set from the model given the model parameter . With the fast growth of data science, there is a pressing need to develop and expand the theoretical foundation for statistical inference and prediction. The development of the repro samples method is trans-formative and we anticipate that it will serve as a stepping stone to establish theoretical foundations for statistical inference and prediction in data science.

References

- (1)

- Barber et al. (2015) Barber, S., Voss, J. and Webster, M. (2015), ‘The rate of convergence for approximate bayesian computation’, Electronic Journal of Statistics 9(1), 80–105.

- Bickel and Freedman (1981) Bickel, P. J. and Freedman, D. (1981), ‘Some asymptotic theory for the bootstrap’, Annals of Statistics 9, 1196–1217.

- Bilias et al. (2000) Bilias, Y., Chen, S. and Ying, Z. (2000), ‘Simple resampling methods for censored regression quantiles’, Journal of Econometrics 99(2), 373–386.

- Brenner et al. (1983) Brenner, D., Fraser, D. and Monette, G. (1983), ‘On models and theories of inference; structural or pivotal analysis’, Statistische Hefte 24, 7–19.

- Casella and Berger (1990) Casella, G. and Berger, R. L. (1990), Statistical Inference, Wadsworth and Brooks/Cole, Pacific Grove, CA.

- Chen et al. (2012) Chen, J., Li, P. and Fu, Y. (2012), ‘Inference on the Order of a Normal Mixture’, Journal of the American Statistical Association 107(499), 1096–1105.

- Chuang and Lai (2000) Chuang, C.-S. and Lai, T. L. (2000), ‘Hybrid resampling methods for confidence intervals’, Statistica Sinica 10, 1–50.

- Cox and Reid (1987) Cox, D. R. and Reid, N. (1987), ‘Parameter orthogonality and approximate conditional inference’, Journal of the Royal Statistical Society. Series B (Methodological) 49(1), 1–39.

- Davison (2003) Davison, A. (2003), Statistical Models, Cambridge University Press.

- Dudley et al. (1991) Dudley, C. R., Giuffra, L. A., Raine, A. E. and Reeders, S. T. (1991), ‘Assessing the role of APNH, a gene encoding for a human amiloride-sensitive Na+/H+ antiporter, on the interindividual variation in red cell Na+/Li+ countertransport.’, Journal of the American Society of Nephrology 2(4), 937–943.

- Efron and Tibshirani (1993) Efron, B. and Tibshirani, R. J. (1993), An Introduction to the Bootstrap, Monographs on Statistics and Applied Probability, Chapman & Hall/CRC, Florida, USA.

- Fishman (1996) Fishman, G. (1996), Monte Carlo: concepts, algorithms, and applications, Springer Science & Business Media, New York, USA.

- Hannig (2009) Hannig, J. (2009), ‘On generalized fiducial inference.’, Statistica Sinica 19, 491–544.

- Hannig et al. (2016) Hannig, J., Iyer, H., Lai, R. C. S. and Lee, T. C. M. (2016), ‘Generalized fiducial inference: A review and new results’, Journal of American Statistical Association . To appear. Accepted in March 2016. doidoi:10.1080/01621459.2016.1165102.

- Komárek and Komárková (2014) Komárek, A. and Komárková, L. (2014), ‘Capabilities of R package mixAK for clustering based on multivariate continuous and discrete longitudinal data’, Journal of Statistical Software 59, 1–38.

- Li and Fearnhead (2018) Li, W. and Fearnhead, P. (2018), ‘On the asymptotic efficiency of approximate bayesian computation estimators’, Biometrika 105(2), 286–299.

- Liu et al. (2021) Liu, D., Liu, R. Y. and Xie, M. (2021), ‘Nonparametric fusion learning for multiparameters: Synthesize inferences from diverse sources using data depth and confidence distribution’, Journal of the American Statistical Association 0(0), 1–19.

- Liu and Shao (2003) Liu, X. and Shao, Y. (2003), ‘Asymptotics for likelihood ratio tests under loss of identifiability’, The Annals of Statistics 31(3), 807 – 832.

- Martin and Liu (2015) Martin, R. and Liu, C. (2015), Inferential Models: Reasoning with Uncertainty, Chapman & Hall/CRC.

- Michael et al. (2019) Michael, H., Thornton, S., Xie, M. and Tian, L. (2019), ‘Exact inference on the random-effects model for meta-analyses with few studies’, Biometrics 75(2), 485–493.

- Peters et al. (2012) Peters, G., Fan, Y. and Sisson, S. (2012), ‘On sequential monte carlo partial rejection control approximate bayesian computation’, Statistical Computing 22, 1209–1222.

- Pokotylo et al. (2019) Pokotylo, O., Mozharovskyi, P. and Dyckerhoff, R. (2019), ‘Depth and Depth-Based Classification with R Package ddalpha’, Journal of Statistical Software 91, 1–46.

- Powell (1986) Powell, J. L. (1986), ‘Censored regression quantiles’, Journal of Econometrics 32(1), 143–155.

- Reid (2022) Reid, N. (2022), Distributions for parameters, in J. Berger, X.-L. Meng, N. Reid and M. Xie, eds, ‘Handbook on Bayesian, Fiducial and Frequentist (BFF) Inferences’, Chapman & Hall. To appear.

- Reid and Cox (2015) Reid, N. and Cox, D. R. (2015), ‘On some principles of statistical inference’, International Statistical Review 83(2), 293–308.

- Richardson and Green (1997) Richardson, S. and Green, P. J. (1997), ‘On Bayesian Analysis of Mixtures with an Unknown Number of Components (with discussion)’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 59(4), 731–792.