Solving the Poisson equation using coupled Markov chains

Abstract

This article shows how coupled Markov chains that meet exactly after a random number of iterations can be used to generate unbiased estimators of the solutions of the Poisson equation. We establish connections to recently-proposed unbiased estimators of Markov chain equilibrium expectations. We further employ the proposed estimators of solutions of the Poisson equation to construct unbiased estimators of the asymptotic variance of Markov chain ergodic averages, involving a random but finite computing time. We formally study the proposed methods under realistic assumptions on the meeting times of the coupled chains and on the existence of moments of test functions under the target distribution. We describe experiments in toy examples such as the autoregressive model, and in more challenging settings.

1 Introduction

1.1 Central Limit Theorem and the Poisson equation

Markov chain Monte Carlo (MCMC) methods form a convenient family of simulation techniques with many applications in statistics. With a measurable space and a probability measure of statistical interest, MCMC involves simulation of a discrete-time, time-homogeneous Markov chain , with a -invariant Markov transition kernel and some initial distribution . Letting , where , the interest is to approximate for some function .

In particular, after simulating the chain until time , one may approximate an integral of interest via the average . Under weak assumptions, such averages converge almost surely to as , and under stronger but still realistic assumptions on , and that hold in many applications, they satisfy central limit theorems (CLTs),

| (1.1) |

where is the asymptotic variance associated with the Markov kernel and the function (see, e.g., Jones, 2004). One standard route to proving a CLT is via a solution of the Poisson equation for associated with , i.e. any function such that

| (1.2) |

where is viewed as a Markov operator and is the identity. In particular, if then (1.1) holds with initial distribution by Douc et al. (2018, Theorem 21.2.5), and

| (1.3) |

where indicates that . We focus on solutions with defined as follows.

Definition 1.

Let , define and the function

| (1.4) |

If is well-defined, then it is straightforward to deduce that so that is indeed fishy. In addition, is fishy for any constant . Moreover, if then , and by Douc et al. (Lemma 21.2.2, 2018) any other fishy function is equal to up to an additive constant. Inserting the function in place of in (1.3) leads to the expression

| (1.5) |

where the subscript indicates that . That familiar expression can be obtained with simple calculations from .

1.2 Monte Carlo methods using the Poisson equation

Despite its convenience for theoretical analysis, the Poisson equation is not analytically solvable for most Markov chains and functions of interest, and consistent approximations have been lacking. As a result, the asymptotic variance is commonly estimated using batch-means, spectral variance (see, e.g., Flegal & Jones, 2010; Vats et al., 2018, 2019; Chakraborty et al., 2022), or initial sequence estimators (Geyer, 1992; Berg & Song, 2022). On the other hand, inconsistent approximations of the solution of the Poisson equation have been proposed for the purpose of variance reduction via control variates. This involves replacing by in an ergodic average, where , so that and the limit of the MCMC estimator is unchanged, but the variance may be smaller with a judicious choice of . A convenient family of is since by construction and indeed an optimal choice of is . Approximations of have been considered for this purpose in, e.g., Andradóttir et al. (1993); Henderson (1997); Dellaportas & Kontoyiannis (2012); Mijatović & Vogrinc (2018); Alexopoulos et al. (2023).

We aim to contribute to methodological aspects of the Poisson equation, with a focus on asymptotic variance estimation via (1.3). We develop novel approximations of the solution , which are unbiased under fairly weak conditions, using coupled Markov chains. Couplings have often been used as formal techniques to analyze the marginal convergence of Markov chains (e.g. Jerrum, 1998), but many couplings are also implementable, with applications to exact sampling (Propp & Wilson, 1996), unbiased estimation (Glynn & Rhee, 2014), convergence diagnostics (Johnson, 1996), or variance reduction (Neal & Pinto, 2001). Here we find new uses for couplings of MCMC algorithms: in Section 2 we propose unbiased estimators of evaluations of the solution . Then we find strong connections between these estimators and the family of unbiased estimators of pioneered by Glynn & Rhee (2014), which we leverage to obtain new results on unbiased MCMC (Jacob et al., 2020). In Section 3 we use the proposed estimators of to approximate (1.3) in combination with unbiased MCMC, leading to novel estimators of that are unbiased and with finite variance under fairly mild conditions. The proposed asymptotic variance estimators are studied numerically in Section 4.

2 Coupled chains and fishy functions

2.1 Coupled Markov chains

For a given -invariant Markov kernel , we consider the time-homogeneous, discrete-time Markov chain with Markov kernel , which is a “faithful” coupling of with itself (Rosenthal, 1997), i.e. it satisfies

| (2.1) |

and for all . We observe that and are both time-homogeneous, discrete-time Markov chains with kernel . We use subscripts to denote the distribution of . For example is the law of when , and indicates . When only one chain is referenced, e.g. , we may similarly write and to indicate and , respectively. An important random variable when using coupled Markov chains is the meeting time,

| (2.2) |

which is the first time at which and take the same value. Since is faithful, with probability for all times . Johnson (1998); Jacob et al. (2020) and others have shown how to construct the coupled kernel for various MCMC algorithms, such that has finite expectation; see Appendix A for pointers.

The main assumption throughout this paper is that has a finite th moment, , when , the product measure of and itself.

Assumption 2.

The Markov kernel is -irreducible and for some ,

The assumption implies a polynomially decaying survival function of order and, conversely, one may verify the assumption by showing that decays polynomially with order with a dependence on that is not too strong. The proof of the next result is in Appendix D.1.

Proposition 3.

If Assumption 2 holds then for all ,

and for -almost all . Conversely, if for some , there exists with such that for -almost all , we have for all ,

then .

Our assumption on the moments of the meeting time allows us to employ the CLT of Theorem 4, that provides that the expression of at the basis of our proposed estimators in Section 3. The proof in Appendix D.2 relies heavily on the strategy of Douc et al. (2018, Section 21.4.1) but features from Definition 1 more prominently, and uses the CLT condition from Maxwell & Woodroofe (2000) rather than Douc et al. (2018, Theorem 21.4.1). Note that the CLT does not require .

2.2 Unbiased approximation of fishy functions

In the Markov chain setting, solutions of the Poisson equation for , or fishy functions for brevity, have been studied extensively (see, e.g., Duflo, 1970; Glynn & Meyn, 1996; Glynn & Infanger, 2022). It is known, for example, that fishy functions exist under fairly weak conditions. We focus on the particular, and more restrictive, core expression of from Definition 1.

Although is not necessarily well-defined -almost everywhere in general, Assumption 2 implies that for , for when and are sufficiently large in relation to ; see Theorem 24. We now define a family of fishy functions that will play a central role in what follows.

Definition 5.

For , the function

| (2.3) |

is fishy if is well-defined, since is a constant. When is fixed, in the sequel we may write instead of .

A priori, links between couplings of Markov chains and fishy functions may not appear as obvious. However, the definition of lends itself naturally to unbiased approximation via coupled Markov chains.

Definition 6.

For , the proposed estimator of is, with ,

| (2.4) |

where and are defined in Section 2.1. In particular, the dependence of on and is that the law of is in (2.4), and so we may omit the subscript when there is no ambiguity. We will also denote by below, in places where the explicit mention of is unnecessary.

The simple intuition behind Definition 6 is that we can equivalently write

and upon justifying the interchange of expectation and infinite sum as we do in Appendix D.3,

Theorem 7.

Under Assumption 2, let for some . For -almost all , and for such that , .

Theorem 34 in Appendix D.3, also provides bounds on moments of . For our subsequent analysis of asymptotic variance estimators, it is important that this is a pointwise result. The random variable may be simulated using Algorithm 2.1 with . The cost of sampling is the cost of running a pair of chains until they meet, which is typically comparable to twice the cost of running one chain for the same number of steps, i.e. on average.

As a generalization of Definition 6 we might sample , for an arbitrary distribution , and then generate given , which, under adequate assumptions, would be unbiased for the fishy function

| (2.5) |

Input: initial states , , Markov kernel , coupled kernel , lag .

-

1.

Set , .

-

2.

If , for , sample from .

-

3.

For , sample from until .

Output: coupled chains and the meeting time defined as the smallest at which .

Remark 8.

The above reasoning demonstrates how one can approximate the difference between two fishy function evaluations. In contrast, to unbiasedly approximate we would need to estimate and in an unbiased manner, for an arbitrary distribution , and take their difference.

An alternative estimator to Definition 6 could employ a random “truncation” variable as in Glynn & Rhee (2014) or Agapiou et al. (2018). This would allow the use of coupled chains that do not exactly meet, as long as the distance between them goes to zero fast enough. We do not pursue this generalization here, as exact meetings can be obtained in a variety of MCMC settings (Jacob et al., 2020).

2.3 Recovering Glynn–Rhee estimators

Through the Poisson equation we can recover the unbiased estimation techniques of Glynn & Rhee (2014) and Jacob et al. (2020). First observe that we may rearrange (1.2) as

| (2.6) |

where the left-hand side does not depend on and is any fishy function for . It then seems natural to estimate by estimating the terms on the right-hand side, for any . With we may write

| (2.7) |

where the right-hand side is a familiar quantity in the light of Glynn & Rhee (2014). In particular, one may run Algorithm 2.1 with : starting from , sample , and iteratively sample for , where is as defined in Section 2.1. The generated process is such that is Markov and almost surely for all large enough. Since is the expectation of both and , the estimator is unbiased for under suitable assumptions.

This same perspective on (2.6) suggests that for any we may define the equivalent and notationally convenient approximation , where , and it is clear that if for -almost all and , then

The initialization of the chains can be generalized from a point mass at to any probability distribution . Indeed, a re-arranged and integrated Poisson equation is

| (2.8) |

and this suggests the following estimator of , with essentially the same justification as above.

Definition 9.

For , denote the approximation of by

| (2.9) |

where marginally , and for some probability measure . We denote by the joint probability measure for , since this features in our analysis, noting that this is a coupling of and .

The estimator in Definition 9 is identical to the estimator denoted by in Jacob et al. (2020) if one chooses and is drawn from some coupling of with itself. We can also retrieve the more efficient variants proposed in Jacob et al. (2020). By changing the initial distribution , Definition 9 also admits the estimators denoted by for some in Jacob et al. (2020), and the estimators denoted by are obtained as averages of over a range of values of . Unbiased estimators based on chains coupled with a lag (Vanetti & Doucet, 2020) can be retrieved as well by considering the Poisson equation associated with the iterated Markov kernel . To make this precise, we make the following definition.

Definition 10.

The -lagged and -offset approximation of is

where , , is a time-homogeneous Markov chain with Markov kernel , and is a Markov chain with transition kernel and initial distribution and independent of . In particular, . We also define for any with , the average of such estimators as

The following result is established in Appendix D.4, as a particular case of Proposition 40, where upper bounds are given for . This result can be compared with Jacob et al. (Proposition 1, 2020) and Middleton et al. (Theorem 1, 2020), which provide only finite second moments. The latter obtains the same conditions on and for . The bounded assumption allows one to avoid the less explicit assumption that and can often be verified in practice.

Theorem 11.

Under Assumption 2, let with , and with . Then for any with , and for such that , .

Remark 12.

By Theorem 11 it is sufficient that and for to have a finite variance. On the other hand, Theorem 4 implies that a CLT holds for if and , which is weaker. The stronger condition in Theorem 11 is because finite second moment of the unbiased estimator is shown via finite second moment of the approximation of , and this requires .

Remark 13.

There are known links between bias of MCMC estimators and fishy functions. Kontoyiannis & Dellaportas (2009, Section 4) observe that the average has expectation given , thus represents the leading term in the asymptotic bias:

| (2.10) |

To numerically quantify that asymptotic bias, if and an approximation of is available, we may use the identity to approximate . On the other hand, even without accounting for , the behaviour of may be informative about the asymptotic bias, e.g. how changes as increases, as illustrated in Section 4.1.

2.4 Subsampled unbiased estimators

In practice, it can be convenient to view the estimator in Definition 10 as equivalent to the integral of with respect to an unbiased signed measure ; details are presented in Appendix B. This perspective allow us to define a subsampled version of the estimator with lower computational cost, for example if evaluations of are expensive in comparison to the simulation of , and this is particularly beneficial for the asymptotic variance estimator proposed in the sequel. The computational benefits of subsampling in this context are related to the thinning ideas in Owen (2017).

The following result is established in Appendix D.4 as a simplification of Proposition 42. It demonstrates that the sufficient conditions for lack-of-bias and finite th moments are identical for both and the subsampled estimator for any .

Theorem 14.

Under Assumption 2, let for some , , with , and be the unbiased signed measure associated with . Define for some ,

where are conditionally independent random variables with

for some constants independent of . Then and for such that , .

Remark 15.

The more detailed Proposition 42 in Appendix D.4 provides a bound on but this bound does not depend on the value of . For , we can see that increasing decreases the variance of , through the law of total variance

Hence, there is a tradeoff between computational cost and variance, with increasing potentially improving efficiency up to point where the variance is dominated by .

3 Asymptotic variance estimation

3.1 Ergodic Poisson asymptotic variance estimator

We consider the task of estimating the asymptotic variance in the CLT, in (1.3). Various techniques have been proposed to estimate from one or multiple MCMC runs (see the references provided in Section 1.2), and these estimators are consistent when the length of each chain goes to infinity. Here we employ coupled Markov chains, as generated by Algorithm 2.1, to define new estimators of : we start with a consistent estimator before introducing unbiased estimators in the next section. We first re-express (1.3) as

| (3.1) |

where is the variance of under . Expectations with respect to can be consistently estimated from long MCMC runs. Using steps after burn-in we define the empirical measure . We can thus approximate and using the empirical mean and variance, denoted by and , and these are typically consistent as .

The difficulty is in the term in (3.1), since cannot be evaluated exactly. We employ unbiased estimators in Definition 6 in place of evaluations . This leads to the following estimator of , which we call the ergodic Poisson asymptotic variance estimator (EPAVE),

| (3.2) |

where each is conditionally independent of all others given . The proposed EPAVE might be practically relevant, but in this paper we view it as an intermediate step toward the estimators of Section 3.2, which have the advantage of being unbiased.

Remark 16.

In Appendix D.7, we show that this estimator is strongly consistent and satisfies a -CLT under Assumption 2 and moment assumptions on . The following summarizes Proposition 52 and Theorem 53. An expression for the asymptotic variance can be extracted from the proof, which depends implicitly on the coupling used to define . Note that standard asymptotic variance estimators do not in general converge at the Monte Carlo rate (see, e.g., Chakraborty et al., 2022, regarding batch means). On the other hand, EPAVE requires unbiased fishy function estimates in addition to Markov chain trajectories.

3.2 Subsampled unbiased asymptotic variance estimator

Starting again from (3.1), we propose an unbiased estimator of by combining unbiased estimators of with unbiased approximations of (Glynn & Rhee, 2014; Jacob et al., 2020), as reviewed in Appendix B. We thus assume that we can generate random signed measures , where is a random integer, are -valued random weights, and are -valued random variables. The random measure is such that for a class of test functions , where the expectation is with respect to coupled lagged Markov chains as generated by Algorithm 2.1, with initialized from an arbitrary coupling of with itself. Combining these measures with in (2.4), each term in (3.1) can be estimated without bias, as we next describe. First, unbiased estimators of can be obtained using two independent unbiased measures and , by computing

| (3.3) |

Unbiased estimation of the term in (3.1) is more involved. We first provide an informal reasoning that motivates the proposed estimator given below in (3.5) and described in pseudo-code in Algorithm 3.1. Consider the problem of estimating without bias, and assume that we can generate unbiased measures of and estimators with expectation equal to for all . Then we can generate , where all are conditionally independent of one another given . Conditioning on , we have

and then taking the expectation with respect to yields , under adequate assumptions on . However, the variable requires estimators of the fishy function for all locations, and could be large. Alternatively, after generating we can sample an index according to a Categorical distribution with strictly positive probabilities , and given we can generate . Then we observe that, conditioning on , integrating out the randomness in given , and then the randomness in ,

and therefore is an unbiased estimator of that requires only one estimation of at . The estimator proposed below employs estimators of the fishy function for each signed measure , where is a tuning parameter. Its choice and the selection probabilities are discussed in Section 3.3.

Input: generator of unbiased signed measures , generator of unbiased fishy function estimators , method to compute selection probabilities , integer .

We can finally introduce the proposed estimator, for which empirical performance is illustrated in Section 4. We write as for . Given , we sample integers with probabilities , independently for . Noting that each is the expectation of given , we obtain

| (3.4) |

Our proposed unbiased estimator of is thus

| (3.5) |

and its generation is described in Algorithm 3.1. The total cost of will typically be dominated by the cost of obtaining two signed measures for and estimators of evaluations of . We call the subsampled unbiased asymptotic variance estimator (SUAVE).

We show that under Assumption 2, is unbiased and has finite moments whenever has sufficiently many moments. For simplicity the statement here assumes that for all , but the results are more flexible. The following statement combines Theorem 50 and Remark 51 in Appendix D.6.

Theorem 18.

Under Assumption 2, let for some . Assume for . Then for any and -almost all , and for such that , .

Remark 19.

Parallel processors can be employed to generate independent copies of , and their average constitutes the proposed approximation of . If each has finite variance and finite expected cost, then is unbiased, consistent as and with a variance of order .

Remark 20.

If Assumption 2 holds for all (respectively for all , one requires only slightly more than moments of (respectively ) to estimate the asymptotic variance consistently and slightly more than moments of (respectively ) to approximate the asymptotic variance with a variance in , if is the number of independent unbiased estimators averaged. This seems close to tight, since moments of are required for the sample variance to have a finite variance in the simpler setting of independent and identically distributed random variables.

3.3 Implementation and improvements

Tuning of unbiased MCMC.

The proposed estimator relies on unbiased signed measures of . In the notation of Appendix B, for all experiments below we generate lagged chains, record the meeting times, and choose and as large quantiles of the meeting times. Then we choose as a multiple of such as , following the suggestions in Jacob et al. (2020): this ensures a low proportion of discarded iterations.

Choice of .

The proposed estimator requires setting to define as in Definition 5 and its estimator in Definition 6. Then is generated for various which are approximately distributed according to . As should preferably have a smaller cost and a smaller variance, we should set such that two chains starting at and are likely to meet quickly. Thus should preferably be in the center of the mass of , or generated according to an approximation of . We experiment with the choice of in Section 4.4, where we see that it can have a significant impact on computational efficiency.

Selection probabilities.

To implement SUAVE we need to choose selection probabilities given , the number of atoms in the signed measure . We set these probabilities to as a default choice. We can also try to minimize the variance of the resulting estimators with respect to . This requires information on the variance of . Indeed, if we condition on the realizations of , , then the variance of the term

| (3.6) |

is minimized over as follows. Since its expectation is independent of , we can equivalently minimize its second moment, thus we define

| (3.7) |

The use of leads to a second moment equal to , but for any such that , the Cauchy–Schwarz inequality implies . Therefore in (3.7) results in the smallest variance of the term in (3.6). It might sometimes be possible to approximate as a function of using pilot runs. We investigate this with numerical experiments in Section 4.1.

Choice of .

We also need to choose , where is the number of states in at which the fishy function is estimated. We can guide the choice of numerically by monitoring the inefficiency defined as the product of expected cost and variance, which can be approximated from independent copies of the proposed estimator. In all of our experiments we observed gains in efficiency when using greater than , as reported in multiple tables in Section 4. Recall that the total cost of is 1) the cost of generating two unbiased signed estimators of plus 2) the cost of fishy function estimators. Therefore, if we choose such that these two sub-costs are matched, at most half our computing efforts are allocated sub-optimally. We note that when we run SUAVE for a given choice of , we can also easily output estimators corresponding to smaller values of , at no extra cost, which helps in assessing the impact of .

Reservoir sampling.

A naive implementation of SUAVE with Algorithm 3.1 could incur a large memory cost when each state in is large, as in phylogenetic inference (Kelly et al., 2023). Indeed storing all the atoms of the generated signed measures might be cumbersome. However, for SUAVE we only need to select within each measure atoms at which to evaluate and to estimate ; see Line 3c in Algorithm 3.1. We can address the memory issue by setting for all and by using reservoir sampling (Vitter, 1985). This technique allows to sample uniformly in , times independently, without knowing in advance and keeping only objects in memory.

We mention other methodological variations that we do not investigate further in this manuscript. Instead of sampling atoms from each signed measure with replacement, we could sample without replacement. Also the estimators employed in (3.5) could be generated jointly instead of independently. In particular, we can couple chains starting from , with a common chain starting from : in other words, we could simulate a single coupling of chains instead of simulating couplings of two chains.

3.4 Multivariate extension

Using the Cramér–Wold theorem (Billingsley, 1995, Theorem 29.4), we can also consider the multivariate case where the test function takes values in . Write , and write . Consider the Poisson equation for each and introduce the associated solutions denoted by , and . The sum can be re-written as . Observe that is a martingale difference sequence for which a central limit theorem applies, with asymptotic variance as in (1.3), with instead of . Write . For any vector , we find that is a martingale difference sequence as well, and by the Cramér–Wold theorem the multivariate asymptotic variance is

| (3.8) |

Next, the multivariate extension of the alternate representation in (3.1) is obtained by developing the product of terms, then by using pointwise, and elementwise. Eventually we obtain

| (3.9) |

The -th entry of that matrix can be written

| (3.10) |

Therefore we can estimate multivariate asymptotic variances with the proposed technique, using pairs of independent unbiased signed measure approximations of , and unbiased estimators of evaluations of each coordinate of the fishy function .

3.5 Assessing the efficiency of unbiased MCMC without long runs

Although the asymptotic variance is of independent interest, we consider how its approximation may aid tuning of unbiased MCMC estimators. Consider the following CLT for in Definition 10.

Proof.

Under these conditions, for suitably large the concentration of is similar to the standard MCMC estimator of a similar computational cost, noting that one is simulating only a single chain after the meeting time. The approximation of the asymptotic variance typically requires long chains. Therefore, articles on unbiased estimation such as Glynn & Rhee (2014); Agapiou et al. (2018); Jacob et al. (2020) include efficiency comparisons relative to ergodic averages based on long chains. The proposed estimator of enables such efficiency comparisons without ever running long chains. The comparison can then be used to validate choices of , and , as well as the chosen coupling. We illustrate this in Sections 4.3 and 4.4.

4 Numerical experiments

We investigate the performance of the proposed estimators and some of their distinctive features. In Section 4.1 we start with visualizations of the fishy functions associated with two MCMC algorithms targeting the same distribution, and consider the effect of the number of selected atoms and of the selection probabilities . Section 4.2 focuses on a simple autoregressive process, for which can be computed analytically, and we compare SUAVE against standard asymptotic variance estimators. In Section 4.3 we consider Bayesian high-dimensional regression with shrinkage priors (Biswas et al., 2022), and we use SUAVE to assess the efficiency of unbiased MCMC. In Section 4.4 we consider a particle marginal Metropolis–Hastings algorithm (Andrieu et al., 2010; Middleton et al., 2020), which is known to be polynomially and not geometrically ergodic, and we investigate the effect of the number of particles, and of the choice of location in the definition of and .

4.1 Comparing two MCMC algorithms

The target is the posterior distribution in a Cauchy location model, with a Normal prior on the location parameter denoted by . We observe measurements , assumed to be realizations of . The prior on is . We consider the test function . The first algorithm considered here is the Gibbs sampler described in Robert (1995), alternating between Exponential and Normal draws:

where is the prior variance. The coupling of this Gibbs sampler is done using common random numbers for the -variables, and a maximal coupling for the update of ; see Appendix A.

We can show that Assumption 2 holds for all for this coupled Gibbs sampler. Consider any pair , , and the pair of next values, , . Write and for the auxiliary variables in each chain. First observe that the means of the Normal distributions, being of the form

takes values within with , since it is a weighted average of multiplied by a value in . Therefore the mean of the next is within a finite interval that does not depend on the previous . Regarding the variance , note that , where is Uniform, thus and finally . Also, . The distribution of does not depend on , thus we can define an interval and , independently of and , such that and simultaneously with probability .

Therefore, with probability , the pair is drawn from a maximal coupling of two Normals, which means and variances are in finite intervals defined independently of . Two such Normals have a total variation distance that is bounded away from one, therefore there exists some such that, overall, , for some , and all ,. Therefore the meeting time has Geometric tails.

The second algorithm is a Metropolis–Rosenbluth–Teller–Hastings (MRTH) algorithm with Normal proposal, with standard deviation . Its coupling employs a reflection-maximal coupling of the proposals. Verification of Assumption 2 can be done using Proposition 4 in Jacob et al. (2020). Indeed Jarner & Hansen (2000) describe a generic drift function for MRTH when the target is super-exponential: . This applies here because the prior is Normal and the likelihood is upper-bounded. We conclude that the meeting times have Geometric tails and thus Assumption 2 holds for any .

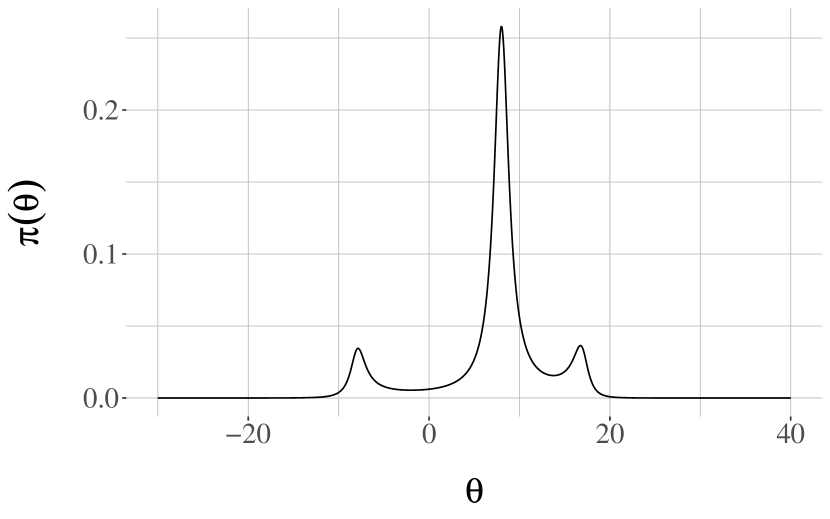

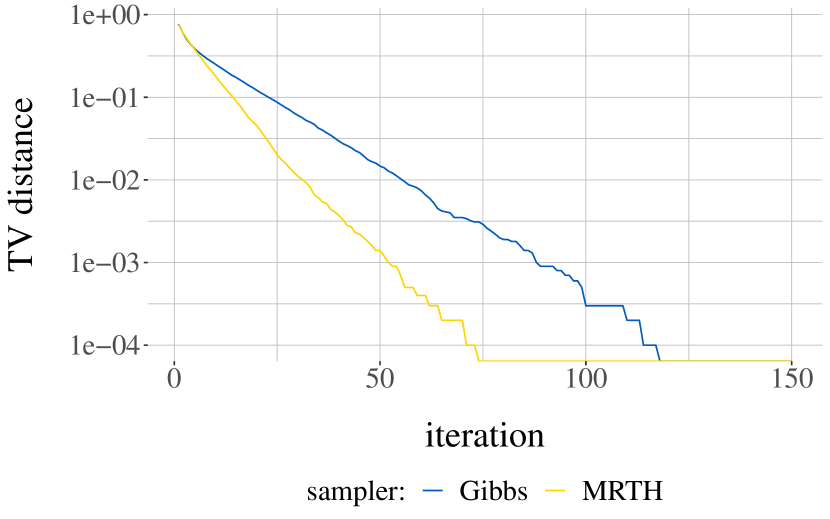

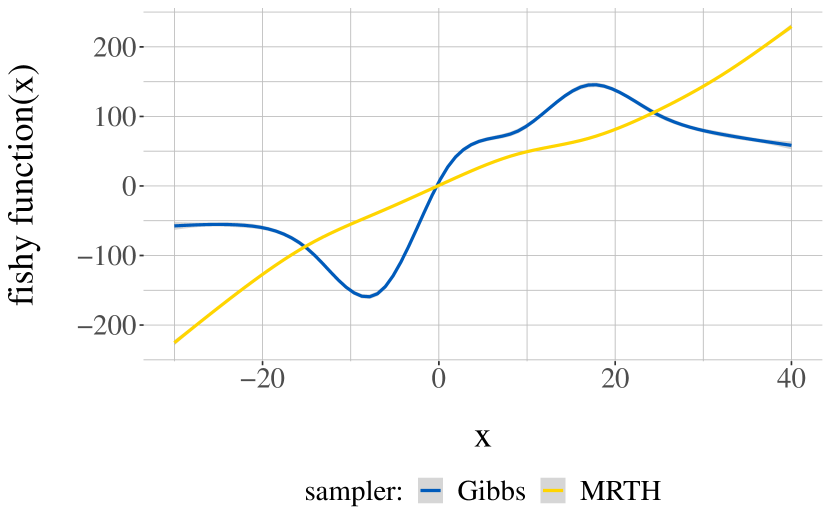

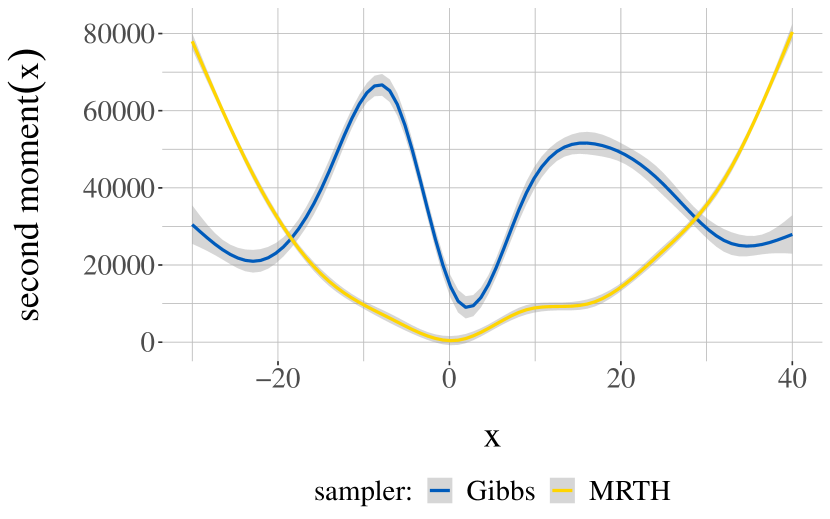

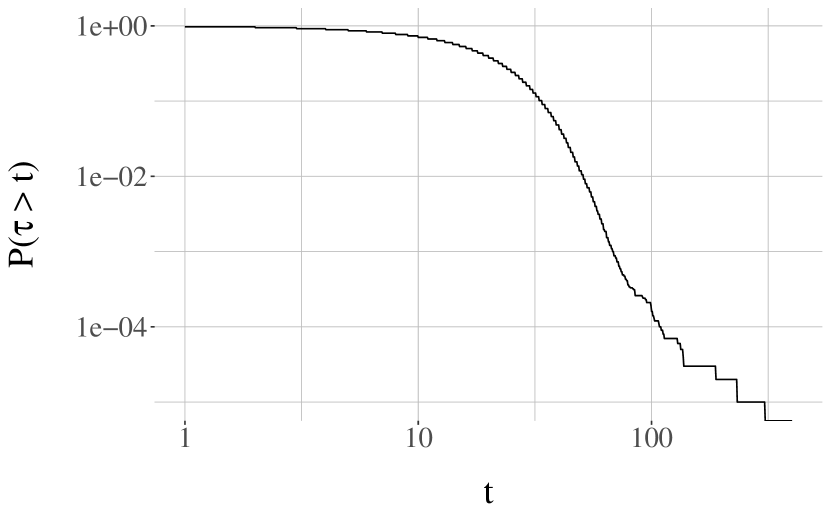

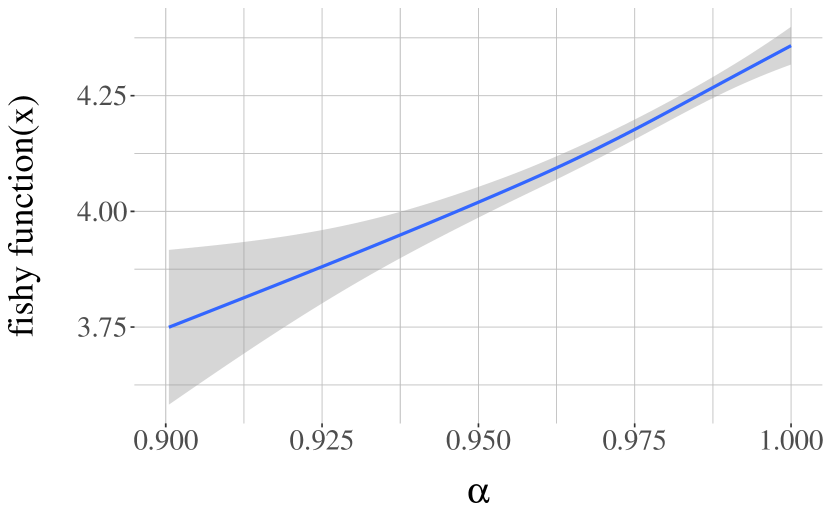

The initial distribution, for both chains, is set to , for which one can verify that is bounded. Figure 4.1(a) shows the target density and Figure 4.1(b) provides upper bounds on for the two algorithms, using the method of Biswas et al. (2019). The state used to define in (2.3) is set to zero. Figure 4.2(a) shows the estimated fishy functions for the two algorithms, and Figure 4.2(b) shows the estimated second moments , for a grid of values of and using independent repeats of for each . Here the fishy functions are markedly different for both algorithms. If we interpret the fishy function as an indication of the asymptotic bias of MCMC as in Remark 13, we see that this bias diverges for MRTH whereas it seems uniformly bounded for the Gibbs sampler. Indeed by inspecting the updates of the Gibbs sampler, we note that if goes to infinity, the -variables will be drawn from Exponential distributions with increasingly high rates, and in turn the next will be drawn from a Normal distribution with mean going to zero and variance going to . Thus the bias of estimators produced by the Gibbs sampler does not increase arbitrarily when the starting point diverges, as it does with the MRTH sampler.

From Figure 4.1(b) we select , for the Gibbs sampler, and , for MRTH. In both cases we use . We generate SUAVE estimators using different values of , for both MCMC algorithms. We first use uniform selection probabilities, . The results of independent runs are shown in Tables 4.1 and 4.2. Each entry shows a confidence interval obtained with the nonparametric bootstrap from the independent replications. The columns correspond to: 1) : the number of atoms in each signed measure at which fishy function estimators are generated, 2) estimate: overall estimate of , obtained by averaging independent estimates, 3) total cost of each proposed estimate, in units of “Markov transitions” 4) fishy cost: subcost associated with the fishy function estimates (increases with ), 5) empirical variance of the proposed estimators (decreases with ), and 6) inefficiency: product of variance and total cost (smaller is better). We observe that it is worth increasing up to the point where the fishy cost accounts for a significant portion of the total cost. From these tables we can confidently conclude that MRTH leads to a smaller asymptotic variance than the Gibbs sampler. Combined with an implementation-specific measure of the wall-clock time per iteration this can lead to a practical ranking of these two algorithms.

| R | estimate | total cost | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|---|

| 1 | [736 - 992] | [1049 - 1054] | [32 - 36] | [3e+06 - 6.4e+06] | [3.1e+09 - 6.7e+09] |

| 10 | [835 - 923] | [1349 - 1363] | [332 - 345] | [4.7e+05 - 5.9e+05] | [6.4e+08 - 8e+08] |

| 50 | [849 - 903] | [2686 - 2713] | [1667 - 1696] | [1.7e+05 - 2.1e+05] | [4.7e+08 - 5.6e+08] |

| 100 | [856 - 903] | [4379 - 4423] | [3361 - 3406] | [1.4e+05 - 1.7e+05] | [6.3e+08 - 7.4e+08] |

| R | estimate | total cost | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|---|

| 1 | [299 - 388] | [786 - 788] | [23 - 25] | [4e+05 - 7.3e+05] | [3.2e+08 - 5.8e+08] |

| 10 | [331 - 364] | [996 - 1003] | [233 - 240] | [6.2e+04 - 7.9e+04] | [6.3e+07 - 7.8e+07] |

| 50 | [333 - 351] | [1947 - 1966] | [1185 - 1203] | [1.9e+04 - 2.3e+04] | [3.8e+07 - 4.6e+07] |

| 100 | [335 - 349] | [3139 - 3168] | [2376 - 2405] | [1.3e+04 - 1.6e+04] | [4.2e+07 - 5e+07] |

Using the fishy function estimates shown in Figure 4.2, we fit generalized additive models (Wood, 2017) with a cubic spline basis for the function in order to approximate the optimal selection probabilities in (3.7). We then run the proposed estimators of , for both algorithms, with and independent replicates, using the approximated optimal . The results are shown in Table 4.3. We report the fishy cost, and we note that it is impacted by the optimal tuning of selection probabilities: for Gibbs it increases, while for MRTH it decreases. The variance of the estimator decreases, as expected. Overall the inefficiency decreases by a factor of or in this example.

| algorithm | selection | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|

| Gibbs | uniform | [332 - 345] | [4.7e+05 - 5.9e+05] | [6.4e+08 - 8e+08] |

| Gibbs | optimal | [408 - 422] | [2.2e+05 - 2.8e+05] | [3.1e+08 - 4e+08] |

| MRTH | uniform | [233 - 240] | [6.2e+04 - 7.8e+04] | [6.2e+07 - 7.8e+07] |

| MRTH | optimal | [190 - 196] | [2.2e+04 - 2.7e+04] | [2.1e+07 - 2.6e+07] |

4.2 Comparison with standard asymptotic variance estimators

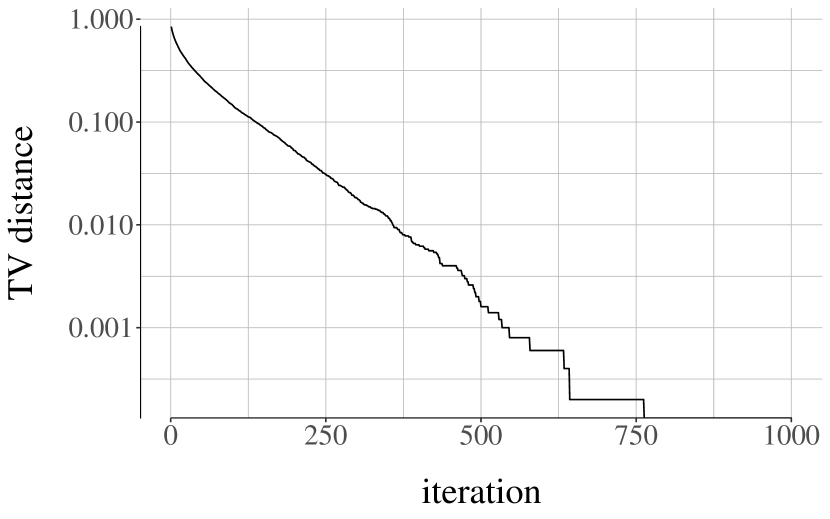

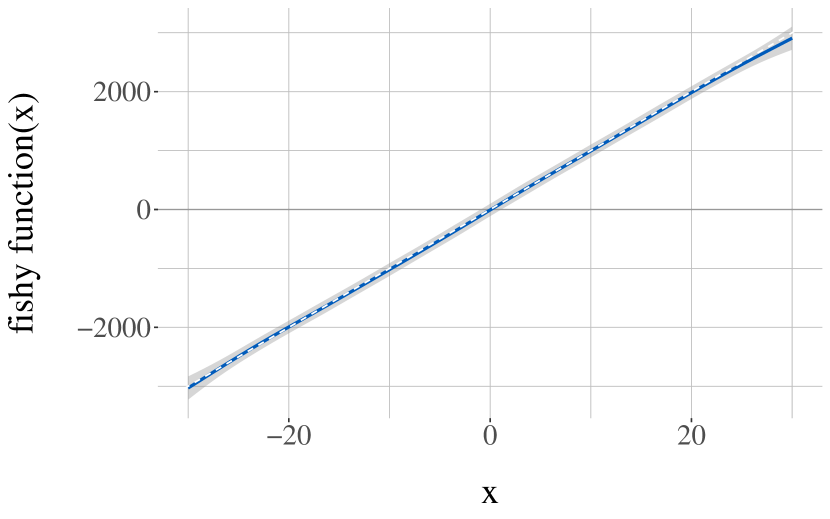

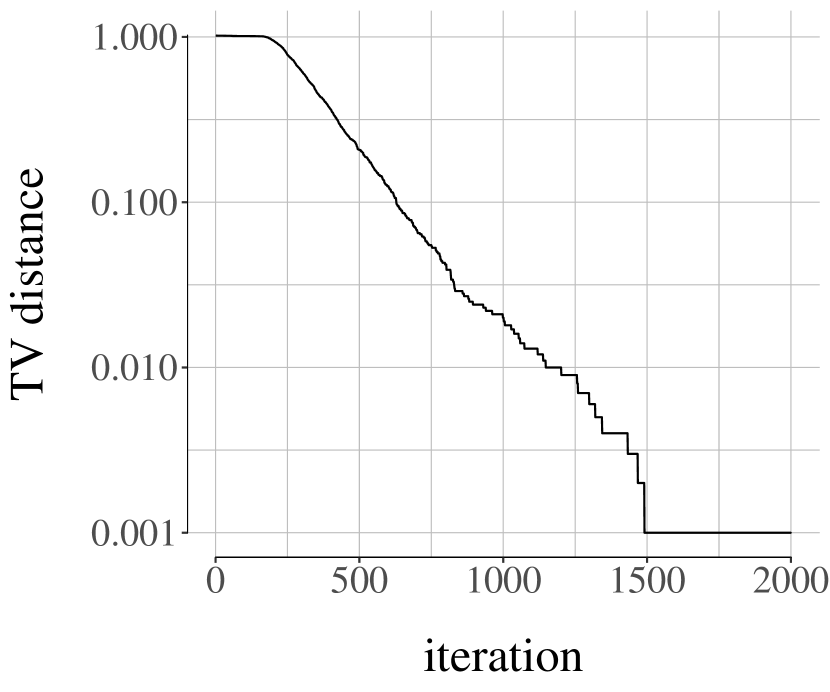

We consider the autoregressive process , where , and are independent. We set . The initial distribution is . The target distribution is , and for the asymptotic variance is . We use a reflection-maximal coupling to define the coupled kernel , see Appendix A. Appendix E verifies Assumption 2 for all . Figure 4.3(a) provides upper bounds on the TV distance to stationarity, and from this we will choose , , for unbiased MCMC approximations in the sequel. The state , used to define in (2.3), is set as . Figure 4.3(b) shows the estimated fishy function, from independent runs for a grid of values of . We can calculate that here is the function .

| R | estimate | total cost | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|---|

| 1 | [8178 - 10364] | [5234 - 5261] | [145 - 168] | [2.4e+08 - 4.8e+08] | [1.3e+12 - 2.5e+12] |

| 10 | [9414 - 10250] | [6676 - 6756] | [1585 - 1667] | [4e+07 - 5.5e+07] | [2.6e+11 - 3.7e+11] |

| 50 | [9748 - 10206] | [13148 - 13350] | [8069 - 8256] | [1.2e+07 - 1.5e+07] | [1.6e+11 - 2e+11] |

| 100 | [9840 - 10240] | [21259 - 21558] | [16163 - 16475] | [9.2e+06 - 1.1e+07] | [2e+11 - 2.4e+11] |

The performance of the proposed estimator of is shown in Table 4.4. The columns are as in Tables 4.1 and 4.2 in the previous section. The results are based on independent replicates. We see that increasing improves the efficiency with diminishing returns. Overall we obtain accurate estimates of with parallel runs that each costs of the order of iterations.

Next we compare the proposed estimator with the following “naive” strategy: generate a chain of length (post burn-in), compute the estimate , repeat times independently and compute the empirical variance of the estimates. We set to match the cost of our estimator with . We find that the naive strategy has a bias (as ) equal to , and an asymptotic variance of . This is about 10 times larger than the variance of the proposed estimator reported in Table 4.4.

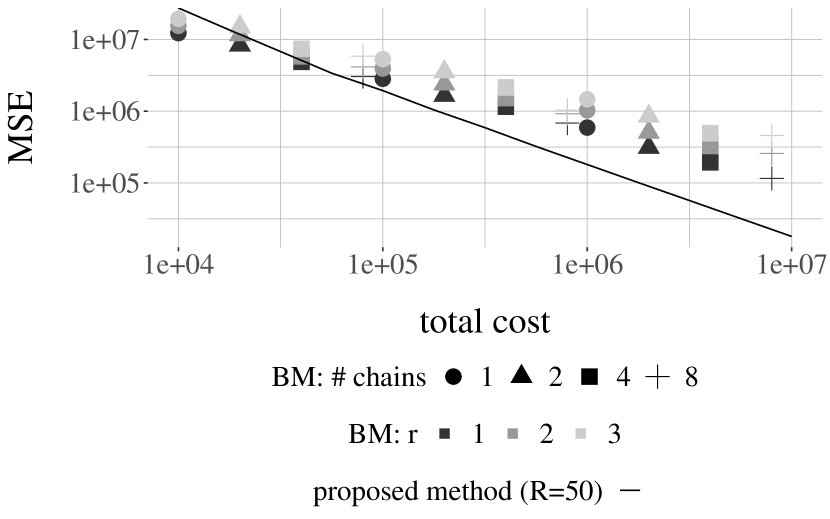

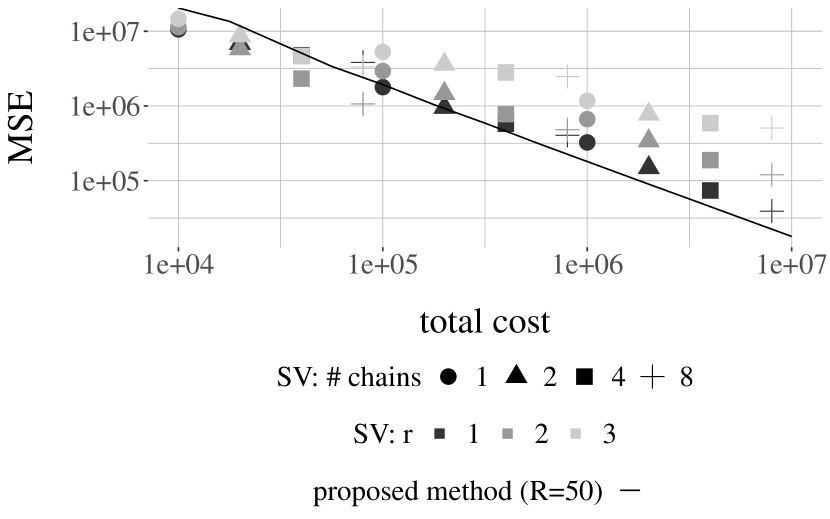

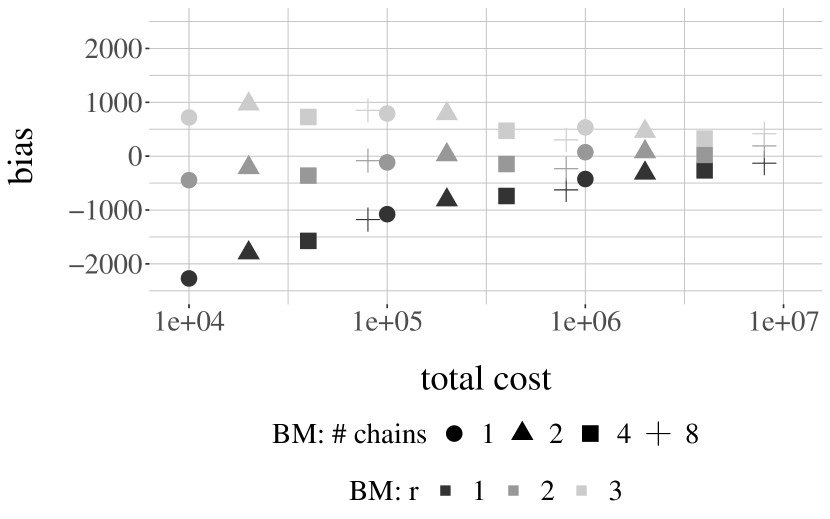

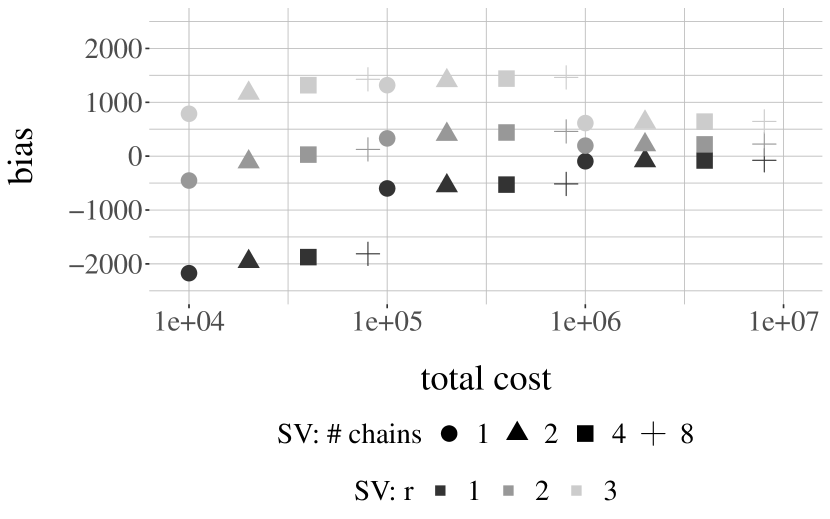

We continue the comparison with two standard families of asymptotic variance estimators: “batch means” (BM) and “spectral variance” (SV) as implemented in the mcmcse package (Flegal et al., 2020). These estimators are based on batch sizes determined with the method of Liu et al. (2022). For each class of methods, we use three values of the lugsail parameter, . We compute these estimators of using chains of lengths in , and numbers of parallel chains in . We base all the results on independent trajectories of length , so for example we obtain independent estimators based on one chain, based on two chains, etc. For each configuration we approximate the mean squared error (MSE), and the total cost is equal to number of chains multiplied by the time horizon. Finally, we report the MSE that would be achieved by our proposed method, using , if we generated sequentially a number of independent replicates of SUAVE corresponding to the given total cost. The comparison here does not account for any potential speed up on parallel architectures. The results are shown in Figure 4.4, where both axes are on logarithmic scale. Overall we note that our proposed method is competitive with standard asymptotic variance estimators. We also observe that the different estimators converge at different rates as a function of the total cost.

The experiments reported in Figure 4.4 suggest that if the practitioner’s interest lies in very cheap but not necessarily accurate estimators of , SUAVE appears worse than BM and SV, and furthermore SUAVE involves the extra effort of designing and implementing couplings. However for accurate estimates SUAVE appears valuable, particularly for practitioners with access to parallel processors.

Finally we produce similar plots for the bias instead of the mean squared error, shown in Figure 4.5. The figure includes only batch means and spectral variance estimators since the proposed method is unbiased by design. We see that the lugsail parameter has a strong effect on the bias. In particular, the value that resulted in the smallest MSE in Figure 4.4 corresponds to a noticeable negative bias, that diminishes as the computing budget increases.

4.3 High-dimensional Bayesian linear regression

We examine a more challenging example, with a linear regression of responses on predictors of the riboflavin data set (Bühlmann et al., 2014). The model, MCMC algorithm and its coupling are taken from Biswas et al. (2022) and a self-contained description is provided in Appendix C; essentially we use a shrinkage prior on the coefficients (e.g. Bhadra et al., 2019) and the target distribution is the posterior distribution of the regression coefficients, denoted by , along with the global precision, the local precisions, and the variance of the observation noise. The state space is of dimension . This example motivates the implementation of reservoir sampling to select the states at which to estimate the fishy function, as described in Section 3.3. In this example, the meeting times have been shown to have Exponential tails in Biswas et al. (2022, Proposition 6) under mild assumptions, so that Assumption 2 holds for any .

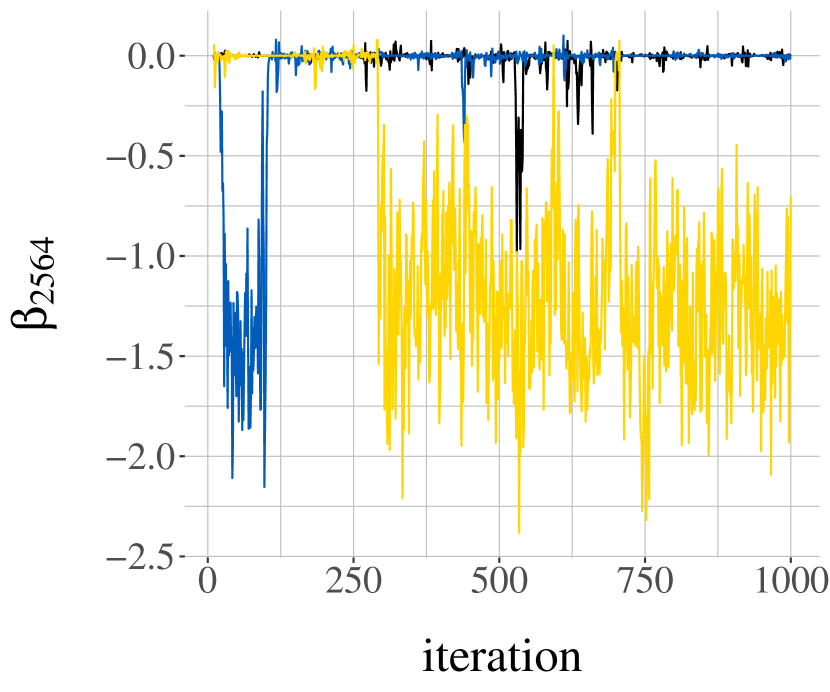

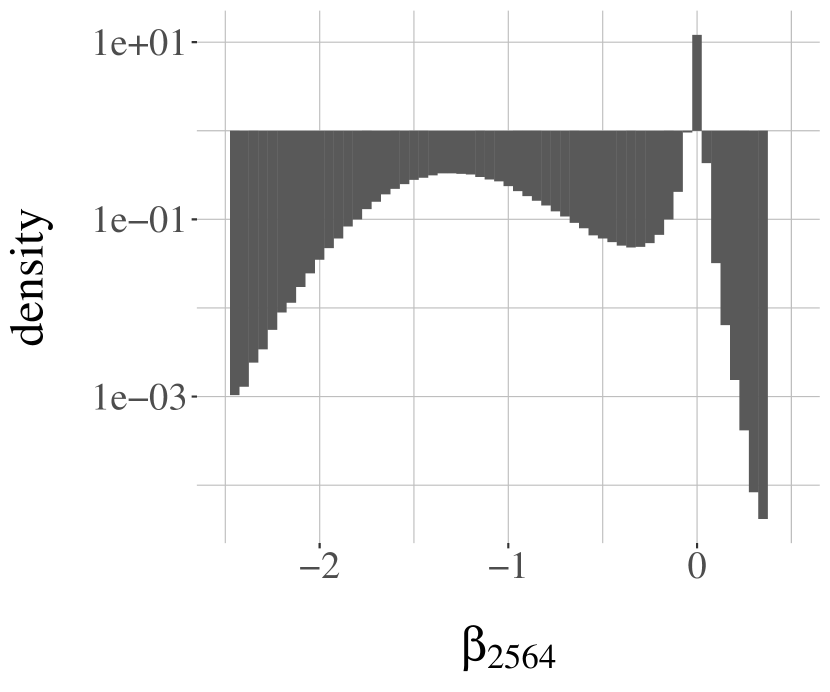

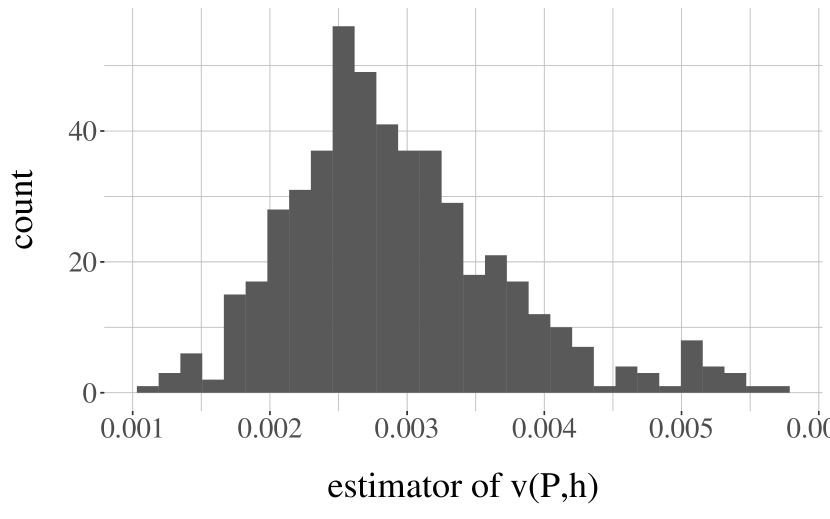

Based on preliminary runs, we choose the test function , which is a coordinate of the regression coefficients with a clearly bimodal marginal posterior distribution. Figure 4.6(a) shows three independent traces of over the first 1000 iterations. Figure 4.6(b) presents a histogram of , obtained from 10 independent chains run for 50,000 iterations each and discarding 2000 iterations as burn-in. Figure 4.6(c) shows upper bounds on obtained with the method of Biswas et al. (2019), using a lag and independent meeting times. From this we choose and .

To define , we draw once from the prior, and keep it fixed. We generate independent estimates of , for . The results are summarized in Table 4.5. We again observe tangible gains in efficiency when increasing , with diminishing returns. Overall we obtain relatively precise information about .

| R | estimate | total cost | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|---|

| 1 | [77 - 98] | [12310 - 12383] | [1522 - 1597] | [2.2e+04 - 3.3e+04] | [2.8e+08 - 4.1e+08] |

| 5 | [78 - 88] | [18466 - 18626] | [7687 - 7840] | [5.5e+03 - 6.9e+03] | [9.9e+07 - 1.3e+08] |

| 10 | [78 - 85] | [26225 - 26436] | [15437 - 15645] | [2.6e+03 - 3.1e+03] | [6.8e+07 - 8.2e+07] |

Next we illustrate the point made in Section 3.5 about the use of estimates of to tune unbiased MCMC estimators. Here, with , and , unbiased MCMC estimators of have an expected cost of and a variance of , leading to an inefficiency of . This is not much larger than the asymptotic variance , estimated to be around . Users can then decide whether increasing the values of , or is warranted.

4.4 Particle marginal Metropolis–Hastings

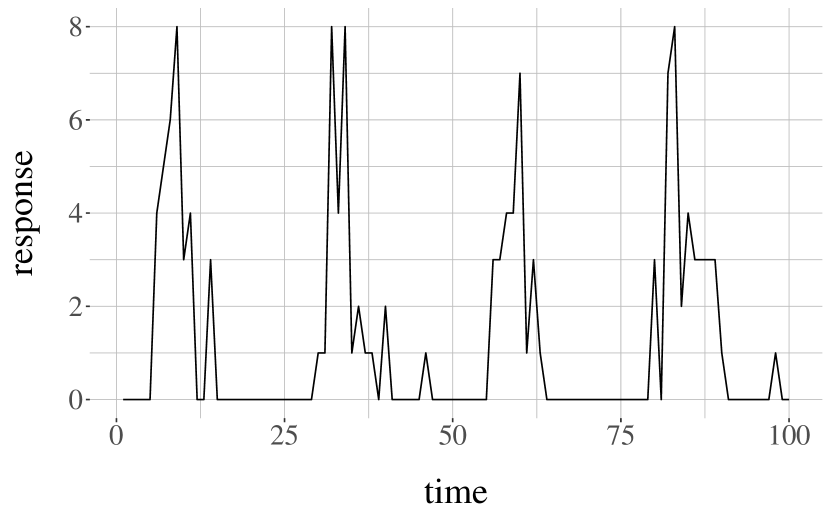

We consider the state space model (SSM) example in Middleton et al. (Section 4.2 2020), inspired by a model capturing the activation of neuron of rats when responding to a periodic stimulus. The observations are counts of neuron activations over experiments. We consider data points represented in Figure 4.7(a). They are modelled as

where and

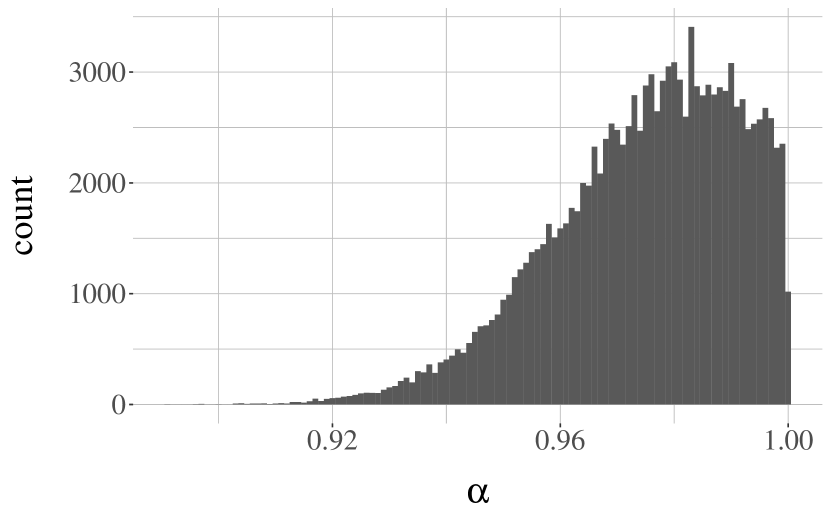

The prior is on , and is fixed to 1.5 here for simplicity. The likelihood is intractable but can be estimated using a particle filter. As in Middleton et al. (2020) we use controlled SMC (Heng et al., 2020), and we plug the likelihood estimator in the particle marginal Metropolis–Hastings algorithms (PMMH, Andrieu et al., 2010). We use 3 iterations of controlled SMC at each PMMH iteration. The proposal on is a Normal random walk, with a standard deviation drawn from at each iteration. The coupling operates with a reflection-maximal coupling of the proposals, and independent runs of SMC if the proposals differ. Formal verification of Assumption 2 is difficult, but relevant elements can be found in Middleton et al. (2020, Section 2.3). We initialize the chains from the prior . An approximation of the posterior distribution is shown in Figure 4.7(b), obtained from 14 chains of length and a burn-in of steps.

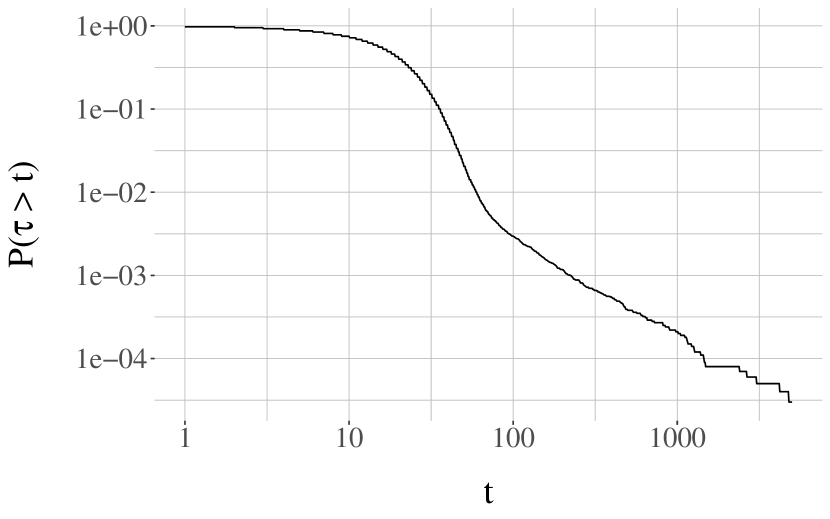

Expecting PMMH to be polynomially ergodic, we examine the tails of the distribution of the meeting times. We generate meeting times, either using 64 or 256 particles in each run of SMC within PMMH. The empirical survival functions of the meeting times , or more exactly of with a lag , are shown in Figure 4.8. Since both axes are on logarithmic scale, a straight line indicates a polynomial decay for . We indeed observe straight lines on the parts of figure where is large enough. Using linear regression we estimate the polynomial rate to be around 1 when using 64 particles (focusing on ), and above 2 when using 256 particles (focusing on ).

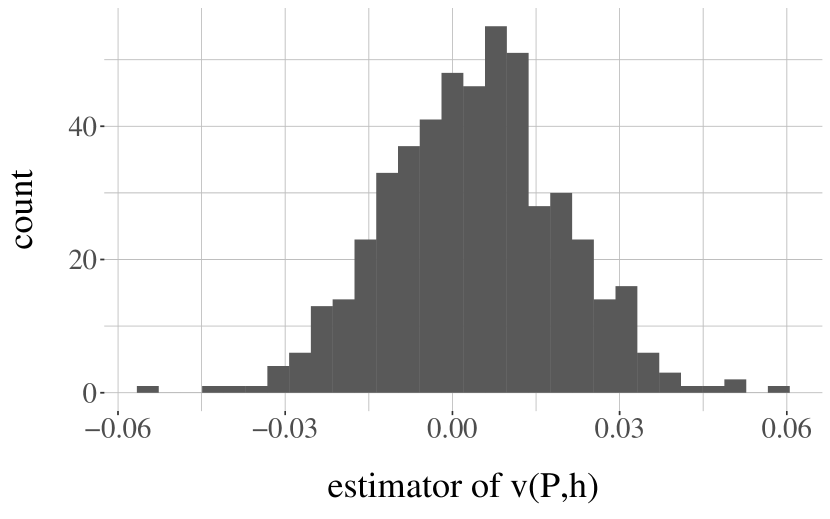

Given the heavy tails of when using 64 particles, we were not able to reliably estimate the associated . We thus focus on the use of 256 particles, and we generate SUAVE to estimate , times independently, for . We set in the definition of the fishy function estimator . We use and for unbiased MCMC approximations. We choose , the number of atoms at which is estimated per signed measure. From the SUAVE runs, we can extract all the locations at which is estimated by , along with the estimates. We then represent an approximation of in Figure 4.9(a), and a histogram of the estimates of in Figure 4.9(b). We see that the relative variance is fairly large, and notice that many estimates are negative.

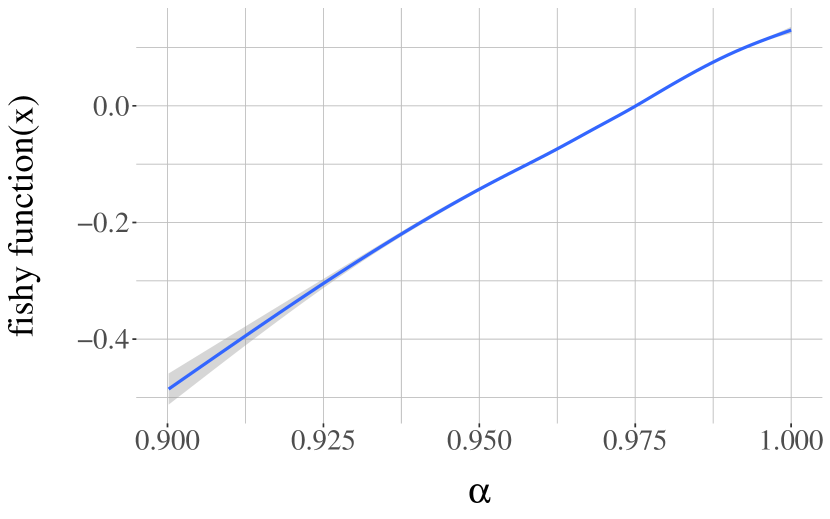

We then change from to , i.e. we place in the middle of the posterior distribution as shown in Figure 4.7(b), and reproduce the same plots in Figure 4.10. We see that the fishy function takes smaller values and its estimation is more precise. As a result, the distribution of is considerably more concentrated. The effect of the choice of is summarized in Table 4.6, where all entries are confidence intervals based on the nonparametric bootstrap. We observe that the choice of impacts the cost of fishy function estimation, as well as its variance and thus the variance of SUAVE. Here this results in orders of magnitude of difference in efficiency.

| y | estimate | fishy cost | variance of estimator | inefficiency |

|---|---|---|---|---|

| 0.5 | [2.64e-03 - 5.32e-03] | [3.62e+03 - 3.67e+03] | [2.2e-04 - 2.8e-04] | [1.9e+00 - 2.5e+00] |

| 0.975 | [2.85e-03 - 2.99e-03] | [1.01e+03 - 1.05e+03] | [5.4e-07 - 7.4e-07] | [3.3e-03 - 4.5e-03] |

Finally we can compare to the inefficiency associated with unbiased MCMC, here with and . We compute the variance and the expected cost of unbiased MCMC estimators of and find an inefficiency of , so the loss of efficiency of unbiased MCMC relative to standard MCMC is approximately .

5 Discussion

When a Markov chain admits an accessible atom , a solution of the Poisson equation (e.g. Glynn & Meyn, 1996) is , where . This allows approximation of pointwise by simulation if one can identify entries into and one can approximate pointwise. The approach we took in this article is different in that it does not rely on identifying atoms, and hence may be applicable in scenarios where this regenerative approximation is not implementable. For example, proper atoms may not exist for a given general state space Markov chain, and identification of hitting times of an atom for a suitable split chain as in Mykland et al. (1995) is not always feasible. While it is often possible to define a modified Markov chain that admits an easily identified, accessible atom (Brockwell & Kadane, 2005; Lee et al., 2014), the corresponding solution of the Poisson equation may not be similar to that of the original chain. Note also that, when atoms can be identified, one would often use regenerative simulation to approximate the asymptotic variance (Hobert et al., 2002), which can be expressed as (see, e.g., Bednorz et al., 2008).

Coupling techniques have been extensively used to study distances between a Markov chain at time and its limiting distribution. Couplings yield upper bounds on these distances and on the resulting mixing time, and these bounds are rarely sharp. Therefore, without matching lower bounds, coupling techniques cannot determine whether an algorithm converges faster than another. On the other hand, the proposed coupling-based asymptotic variance estimators are unbiased, even with sub-optimal couplings, under conditions presented in this article. Thus, with sufficient computing resources we can determine which algorithm leads to the smallest asymptotic variance.

Our experiments suggest that the proposed estimators of are practical and competitive. They only apply to settings where the requisite couplings are available, so that the proposed methods demand more from the user, compared to batch means and spectral methods. On the other hand, the proposed estimators are unbiased, with the important consequence that averages of independent copies achieves the Monte Carlo rate of convergence. This compares favourably to batch means estimators, for which, under general assumptions, convergence occurs at rate , where is the number of batches, and is often chosen as or where is the length of the chain (see Theorem 2.1, Chakraborty et al., 2022).

As with other works on unbiased MCMC, it is worth emphasizing that the performance depends on both the MCMC algorithm under consideration, its initialization and its coupling. We refer to the bimodal target in Section 5.1 of Jacob et al. (2020) for a situation where multimodality in the target distribution combined with a poor design of the MCMC sampler gives misleading estimates in finite samples, despite the lack of bias and the finite variance. In our theoretical results, we have prioritized assumptions on the moments of meeting times of the coupled Markov chains under strong but reasonable initialization assumptions, which can be cleanly separated from assumptions on the moments of functions. Given this emphasis, the results appear to be fairly strong and provide a sensible relationship between the moments of the meeting time and of moments of estimators. In applications, however, obtaining a precise estimate of the largest in Assumption 2 is not straightforward and in many ways is similar to obtaining non-asymptotic convergence bounds for Markov chains.

Appendix A contains reminders on practical couplings of MCMC algorithms, Appendix B contains reminders on unbiased MCMC, Appendix C provides details on the Gibbs sampler for high-dimensional Bayesian regression employed in Section 4.3, Appendix D contains proofs of our main results, and Appendix E verifies Assumption 2 for the AR(1) process considered in Section 4.2. Code to reproduce the figures of this article can be found at: https://github.com/pierrejacob/unbiasedpoisson/.

Acknowledgments.

Research of AL supported by EPSRC grant ‘CoSInES (COmputational Statistical INference for Engineering and Security)’ (EP/R034710/1). Research of DV supported by SERB (SPG/2021/001322).

References

- (1)

- Agapiou et al. (2018) Agapiou, S., Roberts, G. O. & Vollmer, S. J. (2018), ‘Unbiased Monte Carlo: Posterior estimation for intractable/infinite-dimensional models’, Bernoulli 24(3), 1726–1786.

- Alexopoulos et al. (2023) Alexopoulos, A., Dellaportas, P. & Titsias, M. K. (2023), ‘Variance reduction for Metropolis–Hastings samplers’, Statistics and Computing 33(1), 1–20.

- Andradóttir et al. (1993) Andradóttir, S., Heyman, D. P. & Ott, T. J. (1993), ‘Variance reduction through smoothing and control variates for Markov chain simulations’, ACM Transactions on Modeling and Computer Simulation (TOMACS) 3(3), 167–189.

- Andrieu et al. (2010) Andrieu, C., Doucet, A. & Holenstein, R. (2010), ‘Particle Markov chain Monte Carlo methods’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 72(3), 269–342.

- Bednorz et al. (2008) Bednorz, W., Latuszynski, K. & Latala, R. (2008), ‘A regeneration proof of the central limit theorem for uniformly ergodic Markov chains’, Electronic Communications in Probability 13, 85–98.

- Berg & Song (2022) Berg, S. & Song, H. (2022), ‘Efficient shape-constrained inference for the autocovariance sequence from a reversible Markov chain’.

- Bhadra et al. (2019) Bhadra, A., Datta, J., Polson, N. G. & Willard, B. (2019), ‘Lasso meets horseshoe: A survey’, Statistical Science 34(3), 405–427.

- Bhattacharya et al. (2016) Bhattacharya, A., Chakraborty, A. & Mallick, B. K. (2016), ‘Fast sampling with Gaussian scale mixture priors in high-dimensional regression’, Biometrika pp. 985–991.

- Billingsley (1995) Billingsley, P. (1995), Probability and Measure, third edn, John Wiley and Sons.

- Biswas et al. (2022) Biswas, N., Bhattacharya, A., Jacob, P. E. & Johndrow, J. E. (2022), ‘Coupling-based convergence assessment of some Gibbs samplers for high-dimensional Bayesian regression with shrinkage priors’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 84(3), 973–996.

- Biswas et al. (2019) Biswas, N., Jacob, P. E. & Vanetti, P. (2019), Estimating convergence of Markov chains with L-lag couplings, in ‘Advances in Neural Information Processing Systems’, pp. 7389–7399.

- Bou-Rabee et al. (2020) Bou-Rabee, N., Eberle, A. & Zimmer, R. (2020), ‘Coupling and convergence for Hamiltonian Monte Carlo’, The Annals of Applied Probability 30(3), 1209–1250.

- Brockwell & Kadane (2005) Brockwell, A. E. & Kadane, J. B. (2005), ‘Identification of regeneration times in MCMC simulation, with application to adaptive schemes’, Journal of Computational and Graphical Statistics 14(2), 436–458.

- Bühlmann et al. (2014) Bühlmann, P., Kalisch, M. & Meier, L. (2014), ‘High-dimensional statistics with a view toward applications in biology’, Annual Review of Statistics and Its Application 1, 255–278.

- Chakraborty et al. (2022) Chakraborty, S., Bhattacharya, S. K. & Khare, K. (2022), ‘Estimating accuracy of the MCMC variance estimator: Asymptotic normality for batch means estimators’, Statistics & Probability Letters 183, 109337.

- Chen (1999) Chen, X. (1999), Limit theorems for functionals of ergodic Markov chains with general state space, Vol. 139 of Memoirs of the American Mathematical Society, American Mathematical Society.

- Craiu & Meng (2022) Craiu, R. V. & Meng, X.-L. (2022), ‘Double happiness: enhancing the coupled gains of L-lag coupling via control variates’, Statistica Sinica 32, 1–22.

- Dellaportas & Kontoyiannis (2012) Dellaportas, P. & Kontoyiannis, I. (2012), ‘Control variates for estimation based on reversible Markov chain Monte Carlo samplers’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 74(1), 133–161.

- Devroye et al. (2018) Devroye, L., Mehrabian, A. & Reddad, T. (2018), ‘The total variation distance between high-dimensional Gaussians’, arXiv preprint arXiv:1810.08693 .

- Douc et al. (2018) Douc, R., Moulines, E., Priouret, P. & Soulier, P. (2018), Markov chains, Springer International Publishing.

- Duflo (1970) Duflo, M. (1970), ‘Opérateurs potentiels des chaînes et des processus de Markov irréductibles’, Bulletin de la Société Mathématique de France 98, 127–164.

- Flegal et al. (2020) Flegal, J. M., Hughes, J., Vats, D. & Dai, N. (2020), mcmcse: Monte Carlo Standard Errors for MCMC, Riverside, CA, Denver, CO, Coventry, UK, and Minneapolis, MN. R package version 1.4-1.

- Flegal & Jones (2010) Flegal, J. M. & Jones, G. L. (2010), ‘Batch means and spectral variance estimators in Markov chain Monte Carlo’, The Annals of Statistics 38(2), 1034–1070.

- Gerber & Lee (2020) Gerber, M. & Lee, A. (2020), ‘Discussion on the paper by Jacob, O’Leary, and Atchadé’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 82(3), 584–585.

- Geyer (1992) Geyer, C. J. (1992), ‘Practical Markov Chain Monte Carlo’, Statistical Science 7(4), 473 – 483.

- Glynn & Infanger (2022) Glynn, P. W. & Infanger, A. (2022), ‘Solving Poisson’s equation: Existence, uniqueness, martingale structure, and CLT’, arXiv preprint arXiv:2202.10404 .

- Glynn & Meyn (1996) Glynn, P. W. & Meyn, S. P. (1996), ‘A Liapounov bound for solutions of the Poisson equation’, The Annals of Probability pp. 916–931.

- Glynn & Rhee (2014) Glynn, P. W. & Rhee, C.-H. (2014), ‘Exact estimation for Markov chain equilibrium expectations’, Journal of Applied Probability 51(A), 377–389.

- Glynn & Whitt (1992) Glynn, P. W. & Whitt, W. (1992), ‘The asymptotic efficiency of simulation estimators’, Operations Research 40(3), 505–520.

- Griffeath (1975) Griffeath, D. (1975), ‘A maximal coupling for Markov chains’, Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete 31(2), 95–106.

- Hastings (1970) Hastings, W. K. (1970), ‘Monte Carlo sampling methods using Markov chains and their applications’, Biometrika 57(1), 97–109.

- Henderson (1997) Henderson, S. G. (1997), Variance reduction via an approximating Markov process, PhD thesis, Stanford University.

- Heng et al. (2020) Heng, J., Bishop, A. N., Deligiannidis, G. & Doucet, A. (2020), ‘Controlled sequential Monte Carlo’, The Annals of Statistics 48(5), 2904–2929.

- Heng & Jacob (2019) Heng, J. & Jacob, P. E. (2019), ‘Unbiased Hamiltonian Monte Carlo with couplings’, Biometrika 106(2), 287–302.

- Hobert et al. (2002) Hobert, J. P., Jones, G. L., Presnell, B. & Rosenthal, J. S. (2002), ‘On the applicability of regenerative simulation in Markov chain Monte Carlo’, Biometrika 89(4), 731–743.

- Jacob et al. (2020) Jacob, P. E., O’Leary, J. & Atchadé, Y. F. (2020), ‘Unbiased Markov chain Monte Carlo methods with couplings’, Journal of the Royal Statistical Society Series B (with discussion) 82(3), 543–600.

- Jarner & Hansen (2000) Jarner, S. F. & Hansen, E. (2000), ‘Geometric ergodicity of Metropolis algorithms’, Stochastic processes and their applications 85(2), 341–361.

- Jerrum (1998) Jerrum, M. (1998), Mathematical foundations of the Markov chain Monte Carlo method, in ‘Probabilistic methods for algorithmic discrete mathematics’, Springer, pp. 116–165.

- Johndrow et al. (2020) Johndrow, J., Orenstein, P. & Bhattacharya, A. (2020), ‘Scalable approximate MCMC algorithms for the horseshoe prior’, Journal of Machine Learning Research 21(73).

- Johnson (1996) Johnson, V. E. (1996), ‘Studying convergence of Markov chain Monte Carlo algorithms using coupled sample paths’, Journal of the American Statistical Association 91(433), 154–166.

- Johnson (1998) Johnson, V. E. (1998), ‘A coupling-regeneration scheme for diagnosing convergence in Markov chain Monte Carlo algorithms’, Journal of the American Statistical Association 93(441), 238–248.

- Jones (2004) Jones, G. L. (2004), ‘On the Markov chain central limit theorem’, Probability surveys 1, 299–320.

- Kelly et al. (2023) Kelly, L. J., Ryder, R. J. & Clarté, G. (2023), ‘Lagged couplings diagnose Markov chain Monte Carlo phylogenetic inference’, Annals of Applied Statistics (to appear) .

- Kontoyiannis & Dellaportas (2009) Kontoyiannis, I. & Dellaportas, P. (2009), ‘Notes on using control variates for estimation with reversible MCMC samplers’, arXiv preprint arXiv:0907.4160 .

- Lee et al. (2014) Lee, A., Doucet, A. & Łatuszyński, K. (2014), ‘Perfect simulation using atomic regeneration with application to sequential Monte Carlo’, arXiv preprint arXiv:1407.5770 .

- Liu et al. (2022) Liu, Y., Vats, D. & Flegal, J. M. (2022), ‘Batch size selection for variance estimators in MCMC’, Method. Comput. Appl. Prob. 24(1), 65–93.

- Maxwell & Woodroofe (2000) Maxwell, M. & Woodroofe, M. (2000), ‘Central limit theorems for additive functionals of Markov chains’, The Annals of Probability 28(2), 713–724.

- Metropolis et al. (1953) Metropolis, N., Rosenbluth, A., Rosenbluth, M., Teller, A. & Teller, E. (1953), ‘Equations of state calculations by fast computing machines’, J. Chem. Phys. 21(6), 1087–1092.

- Meyn & Tweedie (2009) Meyn, S. & Tweedie, R. (2009), Markov chains and stochastic stability, 2 edn, Cambridge University Press.

- Middleton et al. (2020) Middleton, L., Deligiannidis, G., Doucet, A. & Jacob, P. E. (2020), ‘Unbiased Markov chain Monte Carlo for intractable target distributions’, Electronic Journal of Statistics 14(2), 2842–2891.

- Mijatović & Vogrinc (2018) Mijatović, A. & Vogrinc, J. (2018), ‘On the Poisson equation for Metropolis–Hastings chains’, Bernoulli 24(3), 2401–2428.

- Mykland et al. (1995) Mykland, P., Tierney, L. & Yu, B. (1995), ‘Regeneration in Markov chain samplers’, Journal of the American Statistical Association 90(429), 233–241.

- Neal & Pinto (2001) Neal, R. M. & Pinto, R. L. (2001), Improving Markov chain Monte Carlo estimators by coupling to an approximating chain, Technical report, Department of Statistics, University of Toronto.

- Nguyen et al. (2022) Nguyen, T. D., Trippe, B. L. & Broderick, T. (2022), Many processors, little time: MCMC for partitions via optimal transport couplings, in ‘International Conference on Artificial Intelligence and Statistics’, PMLR, pp. 3483–3514.

- Nummelin (1984) Nummelin, E. (1984), General irreducible Markov chains and non-negative operators, number 83, Cambridge University Press.

- Owen (2017) Owen, A. B. (2017), ‘Statistically efficient thinning of a Markov chain sampler’, Journal of Computational and Graphical Statistics 26(3), 738–744.

- Propp & Wilson (1996) Propp, J. G. & Wilson, D. B. (1996), ‘Exact sampling with coupled Markov chains and applications to statistical mechanics’, Random structures and Algorithms 9(1-2), 223–252.

- Rio (1993) Rio, E. (1993), Covariance inequalities for strongly mixing processes, in ‘Annales de l’IHP Probabilités et statistiques’, Vol. 29, pp. 587–597.

- Robert (1995) Robert, C. P. (1995), ‘Convergence control methods for Markov chain Monte Carlo algorithms’, Statistical Science 10(3), 231–253.

- Rosenthal (1997) Rosenthal, J. S. (1997), ‘Faithful couplings of Markov chains: now equals forever’, Advances in Applied Mathematics 18(3), 372 – 381.

- Shaked & Shanthikumar (2007) Shaked, M. & Shanthikumar, J. G. (2007), Stochastic orders, Springer.

- Thorisson (2000) Thorisson, H. (2000), Coupling, stationarity, and regeneration, Vol. 14, Springer New York.

- Vanetti & Doucet (2020) Vanetti, P. & Doucet, A. (2020), ‘Discussion on the paper by Jacob, O’Leary, and Atchadé’, Journal of the Royal Statistical Society: Series B (Statistical Methodology) 82(3), 584–585.

- Vats et al. (2018) Vats, D., Flegal, J. M. & Jones, G. L. (2018), ‘Strong consistency of multivariate spectral variance estimators in Markov chain Monte Carlo’, Bernoulli 24(3), 1860–1909.

- Vats et al. (2019) Vats, D., Flegal, J. M. & Jones, G. L. (2019), ‘Multivariate output analysis for markov chain monte carlo’, Biometrika 106(2), 321–337.

- Vitter (1985) Vitter, J. S. (1985), ‘Random sampling with a reservoir’, ACM Transactions on Mathematical Software (TOMS) 11(1), 37–57.

- Wang et al. (2021) Wang, G., O’Leary, J. & Jacob, P. E. (2021), Maximal couplings of the metropolis–hastings algorithm, in ‘International Conference on Artificial Intelligence and Statistics’, PMLR, pp. 1225–1233.

- Wood (2017) Wood, S. (2017), Generalized Additive Models: An Introduction with R, 2 edn, Chapman and Hall/CRC.

- Xu et al. (2021) Xu, K., Fjelde, T. E., Sutton, C. & Ge, H. (2021), Couplings for Multinomial Hamiltonian Monte Carlo, in ‘International Conference on Artificial Intelligence and Statistics’, PMLR, pp. 3646–3654.

Appendix A Coupling of MCMC algorithms

For completeness we recall some implementable coupling techniques for MCMC. We focus on Metropolis–Rosenbluth–Teller–Hastings (MRTH) algorithms (Metropolis et al. 1953, Hastings 1970). The goal is to couple generated trajectories such that exact meetings can occur. Various relevant considerations are presented in Jacob et al. (2020), Wang et al. (2021).

Algorithm A.1 describes a simple way of coupling and where is the transition associated with MRTH, with proposal transition and acceptance rate . In the algorithmic description, a maximal coupling of two distributions and for random variables and , respectively, refers to a joint distribution for with marginals and , and such that is maximized over all such joint distributions; examples are provided below.

-

1.

Sample from a maximal coupling of and .

-

2.

Sample .

-

3.

If , set , otherwise .

-

4.

If , set , otherwise .

-

5.

Return .

Next we provide details on how to sample from maximal couplings of and . A possibility, mentioned in Section 4.5 of Thorisson (2000), and called -coupling in Johnson (1998), is described in Algorithm A.2. The algorithm requires the ability to sample from and . The cost of executing Algorithm A.2 is random, its expectation is independent of and , and its variance goes to infinity as . A variant of the algorithm for which the variance is bounded for all is described in Gerber & Lee (2020).

-

1.

Sample .

-

2.

Sample .

-

3.

If , set .

-

4.

Otherwise, sample and

until , and set . -

5.

Return .

When and are Normal distributions with the same variance, an alternative maximal coupling procedure is described in Algorithm A.3; it was proposed in Bou-Rabee et al. (2020). Its cost is deterministic and independent of and . In the algorithmic description, refers to the probability density function of the standard Normal distribution.

-

1.

Let and .

-

2.

Sample , and .

-

3.

If , set ; else set .

-

4.

Set , and return .

In the case of univariate Normal distributions and , the procedure simplifies to Algorithm A.4. We used Algorithm A.4 to couple AR(1) processes in Section 4.2.

-

1.

Let .

-

2.

Sample , and .

-

3.

Set .

-

4.

If , set ; else set .

-

5.

Return .

Beyond MRTH, various MCMC algorithms can be coupled so as to trigger exact meetings, for example Hamiltonian Monte Carlo (Heng & Jacob 2019, Xu et al. 2021), Gibbs samplers to sample partitions (Nguyen et al. 2022), or samplers for phylogenetic inference (Kelly et al. 2023). However there is no automatic recipe to construct efficient couplings, and it remains a task to solve on a “per-algorithm” basis.

Appendix B Unbiased MCMC estimators

B.1 Unbiased estimators of expectations and signed measures

Glynn & Rhee (2014) show how coupled Markov chains can be employed to construct unbiased estimators of stationary expectations. These estimators were considered in the Monte Carlo setting by Agapiou et al. (2018). We recall here the variations presented in Jacob et al. (2020) and follow-up works, that rely on a coupled Markov kernel that induces meetings of the two chains. This removes the need to specify a truncation variable as in Glynn & Rhee (2014) and Agapiou et al. (2018).

Specifically, we construct the chains with a time lag , which is a tuning parameter. The construction is as in Algorithm 2.1. We also introduce a “starting time” , a “prospective end time” , with , which are tuning parameters. Under assumptions provided in Section D.4 (see also Jacob et al. 2020, Middleton et al. 2020), the following random variable is an unbiased estimator of :

| (B.1) |

Consider a range of integers for and associated estimators obtained from the same trajectories . All of these estimators are unbiased, so their average is unbiased and reads

We can find a simpler representation for the double sum in the above equation. Denote by the number of times that the term appears in the double sum. Then is the number of terms of the form equal to as moves in and . We can focus on in since for outside of that range. Note that, for a given , there can be at most one value of such that . So

We can re-write this as

where is the set of positive integers. In other words we are counting the positive multiples of within the range , for any . We can restrict that range to , since we cannot find a positive multiple of smaller than . Now the range is between two positive integers. This yields:

| (B.2) |

Indeed for two positive integers , the number of multiples of within is .

Thus we obtain

| (B.3) |

where refers to a “bias cancellation” term,

| (B.4) |

Instead of the above expressions that involve a test function , we can consider the signed measure

| (B.5) |

as an unbiased approximation of . This is of the form

| (B.6) |

where , are states from either or and are either , or of the form ; in particular the weights can be negative.

If we count the cost of sampling from the kernel as one unit, and the cost of sampling from as one unit if the chains have met already, and two units otherwise, then the random cost of obtaining (B.3), or (B.5), equals units.

The above unbiased estimators are to be generated independently in parallel, and averaged to obtain a final approximation of . Since they are unbiased, the mean squared error is equal to the variance. To compare unbiased estimators with different cost, e.g. to compare different configurations of the tuning parameters , we can compute the asymptotic inefficiency defined as the expected cost multiplied by the variance, as described in Glynn & Whitt (1992); the lower value, the better.

B.2 Upper bounds on the distance to stationarity

A by-product of the above estimator is an upper bound on (Jacob et al. 2020, Biswas et al. 2019, Craiu & Meng 2022), given by

| (B.7) |

The upper bound can be estimated using independent replications of the meeting time . To justify (B.7), first use the triangle inequality to write

where the second inequality comes from the employed coupling being sub-optimal, and in the last line is defined as . By writing , and interchanging the infinite sum and the expectation, we obtain

Recall that . If then the set in the above display is empty. If , then the set has cardinality equal to the number of multiples of within the range . Using the same formula as before this is . Finally we observe that and are identical when , which can be seen by considering the cases: and separately. Thus we retrieve (B.7).

Appendix C MCMC for Bayesian linear regression with shrinkage prior

We provide details for the numerical experiments of Section 4.3. The example is taken from Biswas et al. (2022), where the authors consider couplings of the Gibbs sampler of Johndrow et al. (2020). We provide here a short and self-contained description of one particular version of the Gibbs sampler and its coupling; many more algorithmic considerations can be found in Biswas et al. (2022).

C.1 Model

The context is that of linear regression, with individuals and covariates, with . The generative model is described below, where is the outcome, the vector of explanatory variables, the regression coefficients, the observation noise, is called the global precision and is the local precision associated with for ,

The distribution refers to the Student t-distribution with degrees of freedom, truncated on , with density up to a multiplicative constant. The hyper-parameters are set as . In our experiments we initialize Markov chains from the prior distribution.

C.2 Gibbs sampler

The main steps of the Gibbs sampler under consideration are as follows.

-

•

For , sample each given using slice sampling.

-

•

Given , sample :

-

–

given using an MRTH step,

-

–

given from an Inverse Gamma distribution,

-

–

given from a p-dimensional Normal distribution.

-

–

Overall the computational complexity is of the order of operations per iteration, therefore it can be used with large and moderate values of . Details on each step can be found below.

-update.

The conditional distribution of given the rest has density

which we can target with the slice sampler described in Algorithm C.1, applied independently component-wise.

-

1.

Sample .

-

2.

Sample by setting .

-

3.

Sample from the distribution with unnormalized density on , with and . This can be done by sampling and setting

where is the cdf of the distribution.

-update.

The conditional distribution of given has density

where is the marginal likelihood of the observations given and , and is the prior density for . We sample using a Metropolis–Rosenbluth–Teller–Hastings scheme. Given the current value of , propose , where we set . Then calculate the ratio

using

where . Set with probability , otherwise keep unchanged.

-update.

Using the same notation , the conditional distribution of given is Inverse Gamma:

-update.

With the notation , the distribution of given the rest is Normal with mean and covariance matrix . We can sample from such Normals in a cost of order using Algorithm C.2, as described in Bhattacharya et al. (2016).

-

1.

Sample ,

-

2.

Compute , .

-

3.

Compute where .

-

4.

Define as with the -th row divided by .

-

5.

Return

C.3 Coupled Gibbs sampler

We consider only one of the variants in Biswas et al. (2022), which is not necessarily the most efficient but achieves good performance in the experiments of Section 4.3 and is simpler than the “two-scale” coupling described in Biswas et al. (2022). We describe how to couple each update, with the first chain in state and the second in state .

-update.

We consider two strategies to couple the slice sampling updates of , as described in Algorithm C.1.

- 1.

-

2.

We can use a common uniform in the first step of Algorithm C.1, and then a common uniform in the third step. This is a pure “common random numbers” (CRN) strategy.

We adopt a “switch-to-CRN” strategy: we scan the components , and sample using the maximal coupling strategy above. If any component fails to meet, we switch to the CRN strategy for the remaining components.

-update.

To update , we draw the proposals in the MRTH step using a maximal coupling as in Algorithm A.2. We then employ a common uniform variable for the two acceptance steps.

-update.

To sample , we employ a maximal coupling of Inverse Gamma distributions implemented using Algorithm A.2.

-update.

We use a CRN strategy, which amounts to using the same draws in the first step of Algorithm C.2 to sample both and .

Appendix D Theoretical results

D.1 Assumption on the meeting time

Proof of Proposition 3.

The first part follows by Markov’s inequality:

For the second part, we have . Using Tonelli’s theorem,

which is finite since , and we conclude. ∎

The following sufficient condition for is used to ensure that is well-defined under Assumption 2 when has sufficiently many moments.

Proposition 22 (Douc et al. 2018, Prop. 21.2.3).

Let be a Markov kernel with unique invariant distribution . Let for some . If

then is fishy for and .

We consider here what Assumption 2 implies about the corresponding and its fishy functions. First, we observe that this assumption implies that is aperiodic, and also ergodic of degree (as defined e.g. in Nummelin 1984, Section 6.4), which implies e.g. that a CLT holds for ergodic averages of bounded functions.

Proposition 23.

Proof.

We now turn to the implication of Assumption 2 on properties of . In particular, we see that with sufficiently many moments of implies that .

Theorem 24.

Under Assumption 2, let for some . For such that , .

Proof.

Remark 25.

The results above and Theorem 4 rely only on the existence of meeting times with polynomial survival functions, so one can deduce that they hold for any Markov kernel such that with and , since then

Conversely, for such a Markov kernel there exists a possibly non-Markovian coupling that would satisfy Assumption 2 (see, e.g., Griffeath 1975), but we do not pursue this here.

D.2 Proof of Theorem 4

Lemma 26.

(Rio 1993, Theorem 1.1) Let and be integrable random variables such that

where the supremum is over all measurable sets. Then

where for a random variable , is the tail quantile function of , i.e. .

Lemma 27.

Assume that, for all ,

Then for , measurable functions, and , measurable sets,

Proof.

Denote the preimage of under as . We have

∎

Lemma 28.

Assume that

Then with such that , and ,

where is the tail quantile function of .

Proof.

We follow the same strategy as in Douc et al. (2018, Lemma 21.4.3). By Lemma 27 with , we obtain

for use in Lemma 26. It follows that

where is the tail quantile function of . Since has the same distribution as , . On the other hand by Douc et al. (2018, Lemma 21.A.3) we have . Hence, by Cauchy–Schwarz, we have

By interchanging the use of and , we obtain the final bound. ∎

The following lemma is similar to Douc et al. (2018, Theorem 21.4.4).

Lemma 29.

Assume that

and let . Then

-

1.

.

-

2.

If and , then .

Proof.

We have by Markov’s inequality

from which we may deduce that and so

By Lemma 28, it follows that

Moreover, if ,

from which we may conclude. ∎

Proof of Theorem 4.

Without loss of generality, assume . By Theorem 24, we have since and . Then, by Proposition 23 and Lemma 29 we obtain . For the CLT, we appeal to Maxwell & Woodroofe (2000), for which it is sufficient to show that

| (D.3) |

where , and is then equal to . We find using Lemma 29,

where we define by Proposition 23. Since is non-increasing, we may deduce that

It follows that

and this is for some since . Hence, and (D.3) is satisfied. Since , this implies that by Douc et al. (2018, Lemma 21.2.7), and we conclude. ∎

D.3 Unbiased approximation of fishy functions

The following technical lemma will be useful to obtain bounds on the moments of the fishy function estimator in Definition 6. For a random variable , we denote .

Lemma 30.

Let , be sequences of random variables, a non-negative, integer-valued and almost surely finite random variable, and . Then for any with ,

where is finite for .

Proof.

By Minkowski’s inequality, Hölder’s inequality and Markov’s inequality,

∎