#1##1 \xpatchcmd#1##1

Forecasting macroeconomic data with Bayesian VARs: Sparse or dense? It depends!

Abstract

Vectorautogressions (VARs) are widely applied when it comes to modeling and forecasting macroeconomic variables. In high dimensions, however, they are prone to overfitting. Bayesian methods, more concretely shrinking priors, have shown to be successful in improving prediction performance. In the present paper, we introduce the semi-global framework, in which we replace the traditional global shrinkage parameter with group-specific shrinkage parameters. We show how this framework can be applied to various shrinking priors, such as global-local priors and stochastic search variable selection priors. We demonstrate the virtues of the proposed framework in an extensive simulation study and in an empirical application forecasting data of the US economy. Further, we shed more light on the ongoing “Illusion of Sparsity” debate, finding that forecasting performances under sparse/dense priors vary across evaluated economic variables and across time frames. Dynamic model averaging, however, can combine the merits of both worlds.

Keywords: density forecasting, hierarchical priors, illusion of sparsity, (semi-)global-local shrinkage, stochastic volatility

1 Introduction

The recent literature suggests that predictions of macroeconomic variables benefit from exploiting large data sets. Especially vectorautoregressions (VARs), where the number of free parameters is relatively large compared to the limited length of macroeconomic time series, are prone to overfitting. Bayesian methods have shown to be an effective regularization technique in order to reduce estimation uncertainty by imposing additional structure on the model (e.g., Litterman,, 1986; Sims and Zha,, 1998; Koop,, 2013; Giannone et al.,, 2015; Chan, 2021b, ; Luo and Griffin,, 2022).

Prior elicitation for VARs is a long-standing issue which goes back at least to the Minnesota prior in Litterman, (1986). It stipulates that lagged coefficients of the respective dependent variables are shrunken less than lagged coefficients of other variables, and that coefficients are generally shrunken stronger with an increasing number of lags. The Minnesota prior, therefore, is a classic example of a prior based on domain knowledge. On the other side of the spectrum, hierarchical priors such as stochastic search variable selection (SSVS) priors or global-local (GL) priors – where the latter most recently attract more and more attention in combination with large VARs (e.g., Follett and Yu,, 2019; Huber and Feldkircher,, 2019; Kastner and Huber,, 2020) – offer off-the-shelf shrinkage, since they are neither problem-specific nor designed for VARs per se.

The first contribution of this paper is that we introduce the class of semi-global priors, which aims at combining the merits of domain knowledge with off-the-shelf shrinkage. In short, this framework is characterized by shrinkage parameters acting on pre-specified subgroups of the parameter space, i.e., on the semi-global level. It can easily be applied to already existing priors, e.g., it can be applied to any GL prior or to all kinds of SSVS priors. The framework is very flexible and nests other extension to GL priors, like the extensions to the normal-gamma prior in Huber and Feldkircher, (2019) and Chan, 2021b , as special cases. We propose a grouping of the coefficients which mimics some features of the Minnesota prior, namely the discrimination between lags in general, and within lags the discrimination between own-lag and cross-lag coefficients.

Second, we provide a concise comparison of shrinking priors that are commonly used in the VAR literature, but are scattered across different works and consequently lack a systematic comparison. Here, our attempt is to shed more light on the “prior zoo” by an in-depth comparison focusing on the two most important features of shrinking priors: a) the concentration at zero for shrinking noise, and b) the tail robustness for detecting the relevant signals. This in turn gives guidance for practitioners in meaningfully selecting hyperparameters. The priors under scrutiny are: The Minnesota prior, a semi-hierarchical version of the Minnesota prior (SHM), the stochastic search variable selection (SSVS) prior as in George et al., (2008), the Horseshoe (HS) prior (Carvalho et al.,, 2010), the normal-gamma (NG) prior (Brown and Griffin,, 2010), the Dirichlet-Laplace (DL) prior (Bhattacharya et al.,, 2015) and the -induced Dirichlet decomposition (R2D2) prior (Zhang et al.,, 2022). Concerning the latter and to the best of our knowledge, we are the first who investigate the R2D2 prior in the context of VARs.

Third, we contribute to the ongoing “Illusion of Sparsity” (IoS) debate (Cross et al.,, 2020; Fava and Lopes,, 2021; Giannone et al.,, 2021). Loosely speaking, within the Bayesian framework, there are two contrasting approaches in order to reduce parameter uncertainty in high dimensions. On the one hand, there are sparse modeling techniques that aim at selecting a small set of important predictors. On the other hand, dense modeling techniques support the assumption that all possible explanatory variables might be important; their individual impact for prediction, however, is expected to be small. Giannone et al., (2021) design one specific prior – which is basically a discrete mixture prior with point mass at zero – in order to detect whether specific datasets are best summarized by means of many equally important covariates or rather by a small subset of covariates. Analyzing the posterior results, they conclude that macroeconomic data is rather dense. Fava and Lopes, (2021) show that with little changes to the prior used in Giannone et al., (2021), i.e., using fatter tailed distributions, the posterior results appear to be sparser.

In light of these results, it becomes clear that the level of posterior sparsity can be very sensitive to prior assumptions. Thus, we augment the narrative by quantifying the sparseness of our considered priors before looking at the data. By applying the Hoyer sparseness measure (Hoyer,, 2004) to simulated data from the prior distributions, we demonstrate that they can be ordered from sparse to dense. Sparsity is best expressed by GL priors; denseness is best expressed by Minnesota(-type) priors. In addition, we find that prior sparseness translates to posterior sparseness. In other words, the prior and the posterior “sparsity ranking” is similar.

Other than Fava and Lopes, (2021) and Giannone et al., (2021), who investigate a linear model with a single response variable, the flexible framework of VARs allows us to analyze results for different response variables with only one data set. In an extensive simulation study based on various data generating processes (DGPs), we test the validity of our claims. In sparse DGPs, the variants of GL priors have the highest concentration around the true model parameters. In purely dense DGPs, the Minnesota priors seem to be superior to all competing models.

The gold standard of model evaluation in economic and financial applications is comparing forecasting performance: A model is considered good if it performs well in predicting the future. In our empirical application, we adopt a variant of the quarterly data set of the US economy proposed by Stock and Watson, (2012) and provided by McCracken and Ng, (2021). Overall, the semi-global versions of GL priors, with specific shrinkage for own-lag and cross-lag coefficients, achieve the highest support from the data in terms of one-step-ahead predictive likelihoods. Nevertheless, we find heterogeneity in model performance over time. The heterogeneous results demonstrate that there is no prior, and hence no sparse or dense modeling approach, that performs best during the whole evaluation period and for all variables. To combine the merits of different priors, we also discuss the possibility of dynamic model averaging (Raftery et al.,, 2010).

Overall, this paper provides a broad overview of specification choices with respect to Bayesian VARs in their reduced forms featuring stochastic volatility (SV). Although all of our considered priors have originally been proposed or put forward to the VAR framework using the reduced form, lately, many authors opt for using the structural form (e.g., Cross et al.,, 2020; Chan, 2021b, ). Placing priors on the structural form coefficients is alluring because then one can employ a faster Markov chain Monte Carlo (MCMC) algorithm. Nevertheless, placing the prior on the structural coefficients constitutes a different model where posteriors are (potentially substantially) different as well. Beyond that, there is early empirical evidence that modeling reduced-form coefficients leads to better out-of-sample forecasting performance (Bernardi et al.,, 2023). Modeling reduced-form coefficients, however, comes at the cost of a higher computational burden. To render MCMC computation feasible, we apply the corrected triangular algorithm as in Carriero et al., (2022).111Carriero et al., (2022) present a correction to the broadly applied algorithm based on equation per equation estimation put forward in Carriero et al., (2019).

The remainder of the paper is organized as follows: Section 2 describes the econometric framework and lays out the various prior specifications, while Section 3 compares the shrinking behavior and sparsity of the priors. Section 4 presents the results of an extensive simulation study considering different time series length within sparse and dense data-generating scenarios. In Section 5, we apply the different model setups to data of the US economy. After inspecting the posterior distributions, we perform a forecasting exercise to assess the predictive performance of the considered models. Finally, Section 6 concludes the article.

2 Econometric framework

For , let denote an -dimensional column vector containing observations on time series variables. In a model of order , , is determined by222For simplicity of exposition we omit the intercept in the following (which we nonetheless include in the empirical application).

| (1) |

where is an matrix of coefficients, the lag a positive integer, and an -dimensional vector of errors.

We assume the distribution of the errors to be multivariate Gaussian with time varying variance-covariance matrix, i.e., , and follow Cogley and Sargent, (2005) in applying the decomposition in the form of

| (2) |

where is an upper triangular matrix with ones on the diagonal, and is a diagonal matrix. We denote the free off-diagonal elements in as . The transformed errors then have a diagonal variance-covariance matrix . Borrowing from Jacquier et al., (1994) and Kim et al., (1998), the orthogonalized errors are assumed to follow univariate SV models: For ,

| (3) | ||||

| (4) |

where and are assumed to be i.i.d. . Hence, the th element of is . The log-variance process is initialized by . Here, is the level of log-variance, the persistence of log-variance, and the volatility of log-variance.

To facilitate prior implementation, it proves to be convenient to rewrite the model in matrix form. Define a vector of predictors and a matrix of coefficients , where is the number of vectorautoregressive coefficients per equation. Then the VAR can be written as

| (5) |

where , , and . and are matrices and is a matrix. Further, let , where denotes the number of autoregressive coefficients.

As our approach to inference is Bayesian, we have to specify prior distributions. The generic prior for the coefficient vector is multivariate normal:333Instead of modelling the reduced-form coefficients, one could also model the structural-form coefficients . Often, this is done to speed up computations, as it would allow for embarrassingly parallel “equation per equation” estimation (Carriero et al.,, 2019). Discussing whether it is better to shrink the reduced-form or the structural-form coefficients is out of scope of this paper. However, note that prior distributions are not translation invariant per se, and any comparison amongst the different settings must be treated with great care (cf. Appendix D for a demonstration). Performance of state-of-the art shrinkage priors in the structural setting are discussed in Cross et al., (2020) and Chan, 2021b . . For growth rates and/or approximately stationary transformed data it is common to center the prior at zero (e.g., George et al.,, 2008; Koop and Korobilis,, 2010; Cross et al.,, 2020; Kastner and Huber,, 2020), whereas for data in levels often the prior mean of own-lag coefficients in the first lag is set to one (Litterman,, 1986; Sims and Zha,, 1998). Moreover, is a diagonal matrix with diagonal elements . The shrinkage priors under scrutiny which are to be detailed in Sections 2.1 to 2.3 distinguish themselves in their treatment of . In view of the next sections, we want to highlight that the prior for the VAR coefficients does not depend on and hence neither on . This implies, that all considerations in Sections 2.1 to 2.3 and Sections 3.1 to 3.2 also apply to other specifications of the error covariance matrix, e.g. the order-invariant factor stochastic volatility specification without restrictions on the factor loadings proposed in Kastner and Huber, (2020) or the order invariant stochastic volatility specification in Chan et al., (2021).

2.1 Shrinkage based on domain knowledge: Minnesota priors

Traditional Minnesota prior

The prior proposed in Litterman, (1986) – we refer to as traditional Minnesota prior (MP_LIT) in the following – is mainly characterized by two assumptions based on domain knowledge: First, own-lags are assumed to account for most of the variation of a given variable. Second, recent lags are assumed to be more important in predicting current values than distant lags. Hence, is structured in a way, such that the sub-diagonal elements of are shrunken less than the off-diagonal elements. And, coefficients associated with more recent lags are shrunken less than the ones associated with more distant lags. We follow Koop and Korobilis, (2010) in setting the notation: Denote the block of that corresponds to the coefficients in the th equation, and let be its diagonal elements. The diagonal elements are set to

| (6) |

where is the OLS variance of a univariate AR(6) model of the th variable. We set to regularize cross-lag coefficients more heavily. The term in the denominator automatically imposes more shrinkage on the coefficients towards their prior mean as lag length increases. The term adjusts not only for different scales in the data, it is also intended to account for different scales of the responses of one economic variable to another (Litterman,, 1986).

Semi-hierarchical Minnesota prior

The semi-hierarchical Minnesota (SHM) prior is a generalization of the traditional Minnesota prior. Instead of fixing the shrinking parameters and , SHM treats them as unknown quantities and learns them in a data-based fashion. That is, the strong assumption that is now replaced with the weaker assumption that own-lags and cross-lags might account for different amounts in the variation of a given variable. We follow Huber and Feldkircher, (2019) in imposing gamma priors on and , i.e., where denotes the probability density function of the gamma distribution with shape and rate .

As default choice, we set for . The resulting gamma distribution has expectation 1 and variance 100. Moreover, the density diverges to infinity as . As most mass of this distribution is at zero, the prior can heavily shrink the parameters if necessary, though as soon as there are some moderate to large nonzero coefficients (in absolute values), the shrinkage will be only moderate to weak. Since the prior variances of cross-lag coefficients still have to be scaled with , it is not a fully hierarchical prior, and we refer to it as the semi-hierarchical Minnesota prior.

2.2 Off-the-shelf shrinkage: Global-local priors

Other than the Minnesota priors, global-local (GL) shrinkage priors are not built upon domain knowledge and are neither specifically designed for VARs nor for forecasting macroeconomic data. They are very popular in sparse and high-dimensional applications, and therefore also well suited for large VARs (Follett and Yu,, 2019; Huber and Feldkircher,, 2019; Kastner and Huber,, 2020). Following Polson and Scott, (2011), GL priors can be written as continuous scale mixture distributions. Let denote a symmetric unimodal density with variance , then a typical GL prior is of the following form:

| (7) |

where represents the global shrinkage and the local shrinkage. While the global parameter determines the overall shrinkage, the local parameters act to detect the relevant signals. Hence, is usually a density with substantial mass at zero. In case of being very small, must be a heavy-tailed density such that can override the effect of for a nonzero coefficient. GL priors distinguish themselves in their choices for and , which will be discussed in the next section.

2.3 Structured semi-global(-local) shrinkage

In this section, we aim at building a framework that allows to put more structure on off-the-shelf shrinkage priors, but with as little restrictions as possible.

Even though many applications have shown that a simple prior like the traditional Minnesota prior – where all hyperparameters are treated as known and therefore are not estimated from the data in a hierarchical fashion – can be very competitive, it lacks flexibility. First, due to the fact that own-lag shrinkage and cross-lag shrinkage are fixed a priori, the traditional Minnesota prior is not (automatically) adaptable. Especially in higher dimensions, well-established default values are difficult to determine, which in turn makes selecting them hard to justify. This issue is partly dealt with by considering semi-hierarchical versions of the prior (cf. Section 2.1). Second, it relies on tuning the prior variances with OLS estimates in order to adapt for the different scales of the endogenous variables. Third, shrinkage of higher order lags is deterministic, i.e., prior variances are additionally scaled by where denotes the lag and usually . Theoretically, GL priors could remedy those shortcomings with their local scales, which individually adjust the regularization for each coefficient. A problem arises, however, when the noise level and the absolute level of the coefficients are different in different parts of the parameter space. Then, the adjustment is probably not strong enough. In what follows, we introduce a simple framework that tackles this problem. It only needs little input from the researcher and does not require any pre-tuning of hyperparameters.

Let denote the generic index set that labels the coefficients of the th group in (e.g., the first group could be the own-lag coefficients associated with the first lag, the second group could be the cross-lag coefficients associated with the first lag, etc.), and let denote the number of elements in . Then, as a semi-global local prior with groups, we define the following hierarchical representation:

| (8) |

The only additional input required is the partitioning of into subgroups. We propose a partitioning that mimics two features of the Minnesota prior, namely the distinction between own-lag and cross-lag coefficients and the distinction between lags in general: In each lag, the diagonal elements (the own-lags) and the off-diagonal elements (the cross-lags) constitute separate groups, which makes groups in total.

The semi-global framework nests other modifications to global-local priors within the VAR framework as special cases. E.g., Huber and Feldkircher, (2019) consider both, equation-specific and covariate-specific shrinkage. The first means that the covariates of each equation form separate groups (individual degree of shrinkage for each equation) and the latter that the specific covariates across all equations form separate groups (individual degree of shrinkage for each covariate across all equations). The multiplicative lag-wise specification considered in the same paper, however, is not nested in the semi-global framework, since we assume independence across the groups. The adaptive Minnesota prior in Chan, 2021b could also be cast in the semi-global framework. It is the unification of the Minnesota prior with a global-local prior, namely the normal-gamma prior (Brown and Griffin,, 2010). That is, there are two semi-global shrinkage parameters: One for own-lags and one for cross-lags. Additionally, each coefficient is assigned a local scale. The prior variances are rounded off with the scaling term of the Minnesota prior in analogy to Eq. 6. Besides using quantities estimated from the data to tune the prior variances, the adaptive Minnesota prior differs from our approach as it is a prior for the structural coefficients.

In the remainder, we briefly describe several state-of-the art off-the-shelf shrinkage priors and how they can (in one case even have to) be modified, such that the pooling strategy introduced by the semi-global framework materializes.

DL prior

The Dirichlet-Laplace (DL) prior, introduced in Bhattacharya et al., (2015) and put forward to the VAR framework in Kastner and Huber, (2020), takes the following hierarchical form:

| (9) |

where denotes the double exponential (sometimes called Laplace) distribution with variance , and denotes the Dirichlet distribution on the open simplex with concentration parameters . Letting for and , it can be shown that independently for , (cf. Lemma IV.3 in Zhou and Carin,, 2012). Using this result, it becomes clear that the proposed semi-global pooling strategy is not compatible with the vanilla DL prior, since there is no information sharing on the (semi-)global level. Therefore, to make things work, we replace the global shape parameter with the semi-global shape parameter , . Applying the Lemma, the semi-global-local DL prior has the following form:

| (10) |

where . Posterior results can be very sensitive to the choice of , as it is the parameter that controls the strength of regularization (cf. Section 3). Hence, we place i.i.d. discrete hyperpriors on for , where is the vector of strictly positive support points. Updates of are straightforward, as the full conditional posterior is again discrete on the same support points.

Last but not least, the DL prior can be expressed as a Gaussian scale mixture by introducing the auxiliary scaling parameter , s.t. . Consequently, for DL, .

NG prior

The normal-gamma prior proposed by Brown and Griffin, (2010) is nowadays well-established in different kinds of multivariate time-series modelling setups (e.g., Huber and Feldkircher,, 2019; Kastner,, 2019; Bitto and Frühwirth-Schnatter,, 2019). It takes the following form:

| (11) |

i.e., for NG, . As with DL, we place on , , i.i.d. discrete hyperpriors , where is the vector of strictly positive support points.

R2D2 prior

Only recently, Zhang et al., (2022) proposed the -induced Dirichlet decomposition (R2D2) prior. It is based on a beta prior on , where denotes the sum of all prior variances. The induced prior then takes the following form:

| (12) |

Apart from a higher level of hierarchy, it has a similar structure to the DL prior. A major difference is that, for R2D2, the prior variance follows a gamma distribution, whereas for DL, the prior scale follows a gamma distribution. Using the same result as before, conditional on , independently. Exploiting the scaling property of the gamma distribution, the R2D2 prior can be cast in the form of Eq. 8:

| (13) |

where and . By introducing auxiliary scaling parameters , the R2D2 prior can be written as a Gaussian scale mixture, s.t. , i.e. for R2D2, .

The R2D2 prior and the NG prior are closely related. For R2D2, the variance of a double exponential distribution follows a gamma distribution, whereas for NG, the variance of a normal distribution follows a gamma distribution. The special case of NG with , hence, could be seen as an -induced Dirichlet decomposition prior with a normal kernel.

As with DL and NG, we place on , , i.i.d. discrete hyperpriors , where is the vector of strictly positive support points.

Horseshoe

The horseshoe (HS) prior proposed in Carvalho et al., (2010) is given by

| (14) |

where denotes the half-Cauchy distribution. Other than NG and R2D2, HS places the hyperprior distributions on the standard deviation, rather than on the variance. Compared to all other priors discussed so far, it has the advantage that no tuning parameter has to be specified by the user.

Stochastic search variable selection

Another popular prior for BVARs is the stochastic search variable selection prior (SSVS, George et al.,, 2008), which is a discrete mixture of two normal distributions. Although this prior is neither a global-local shrinkage prior nor a continuous scale mixture prior, it can be modified in order to comply with the semi-global-local framework. In hierarchical form and adapted to the semi-global-local framework, the prior is given through

| (15) |

where is an auxiliary dummy variable, should be small (close to zero) and it must hold that . Intuitively speaking, if is assigned to the spike variance , it is virtually constrained to zero. If is assigned to the slab variance , it is shrunken depending on how is chosen. Further, we assume that the prior inclusion probability might differ between the groups. In order to learn the parameter in a data-based fashion, we impose i.i.d beta priors on each , : . Note, that for prediction purposes and for inference on the joint posterior , learning in a data-based fashion only has an effect if there is information sharing between coefficients. In the case where each constitutes a separate group, i.e., each is assigned an independent (as in, e.g., Cross et al.,, 2020), it is straightforward to show that the full conditional posterior only depends on the prior expectation of .

2.4 Priors for the variance-covariance matrix

To complete the models, we have to specify the priors on the decomposed variance-covariance matrix . Note that the precision matrix – the inverse of the variance-covariance matrix – can be written as . It is well-known that the precision matrix should be a sparse matrix, as zero entries on the off-diagonals imply conditional independence among the respective equations (West,, 2020). Hence, for , we choose the HS prior: , , , and .444In Section 5.5, we provide some robustness checks regarding different priors for . Following Kim et al., (1998), for , we choose a normal prior for the level of the log variance, , and for the persistence parameter, , a beta distribution on . Finally, we follow Kastner and Frühwirth-Schnatter, (2014) by imposing a gamma prior on the variance of the log variance, .

3 Shrinking behavior and sparsity of various priors

3.1 Univariate analysis

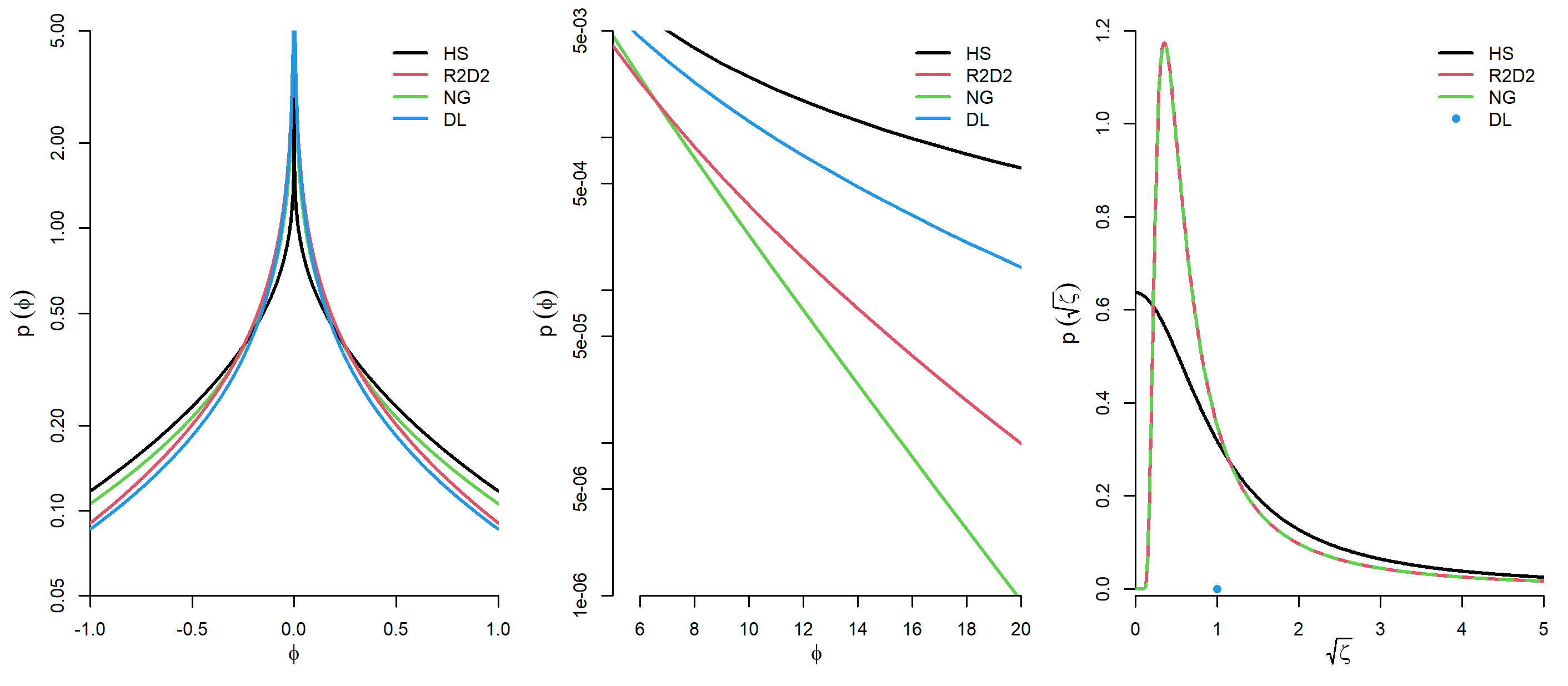

The limiting behavior of univariate global-local prior densities is typically analyzed conditionally on the global scale (e.g., Carvalho et al.,, 2010; Brown and Griffin,, 2010), i.e. marginalized over the local scales only. Since the global parameters often introduce dependence among all , , , we follow this line of thinking and conduct the analysis in Section 3.1 in terms of univariate conditionally independent prior densities , where stands for all global hyperparameters.

Theorem 3.1 (Limiting behavior of shrinkage priors).

-

a)

Tail behavior

For , the marginal densities satisfy

(16) (17) (18) (19) (20) (21) -

b)

Concentration at zero

For , the marginal densities satisfy

(22) (23) (24) (25) The marginal densities of SHM/MP_LIT and SSVS have no singularity at zero.

For the proofs of Theorem 3.1a)(16) and the first part of 3.1b)(22), we refer to Zhang et al., (2022), and for 3.1a)(19) and 3.1b)(25), we refer to Carvalho et al., (2010). The remaining proofs can be found in Appendix A.

Some noteworthy remarks follow. All global-local priors share a pole at , at least for certain hyperparameter settings, which is important for handling vectors with many zero elements. The Minnesota priors and SSVS do not diverge to infinity at zero, which could be seen as a disadvantage in sparse settings. For , , and , DL, NG and R2D2, respectively, diverge to infinity with polynomial speed; this is faster than HS. Concerning the tails: HS has the heaviest (Cauchy-like) tails. It is followed by DL and R2D2, respectively, which are still heavy-tailed in the sense that they have heavier tails than the exponential distribution. For , NG is not heavy-tailed, but still heavier-tailed than the Minnesota priors and SSVS, which have Gaussian-like tails.555A marginal note w.r.t. R2D2: Zhang et al., (2022) claim that R2D2 is polynomial in both regions at zero and in the tails, which seems contradictory to Theorem 3.1a)(18). For the avoidance of doubt, we want to clarify that the univariate density of R2D2 is polynomial in the tails only if the global scale is integrated out. This is somewhat misleading, since for all other priors under scrutiny in both papers, i.e. here and in Zhang et al., (2022), the global scale is fixed.

Figure 1 depicts the univariate densities conditional on the global scales and the prior densities for the global scales separately. For reasons of comparability, we show the densities for for all priors. It can easily be verified that for NG and R2D2, the gamma hyperpriors on imply generalized gamma hyperpriors on . Clearly, the division of tasks among global and local scales varies among different GL priors. Whereas the global scale of HS has considerable mass at zero, the global scale of NG and R2D2 is bounded away from zero. The global scale of DL is a Dirac-mass at one. That is, for DL, NG, and R2D2, the task of the local scales is twofold: In addition to detecting signals, they must be able to overwhelm the global scale in shrinking the zero coefficients to zero.

3.2 Multivariate analysis

In order to describe the implied level of sparsity of the different priors, we now analyze their multivariate distributions. We begin by characterizing the sparsity of the priors qualitatively and continue by quantifying it via a sparseness measure.

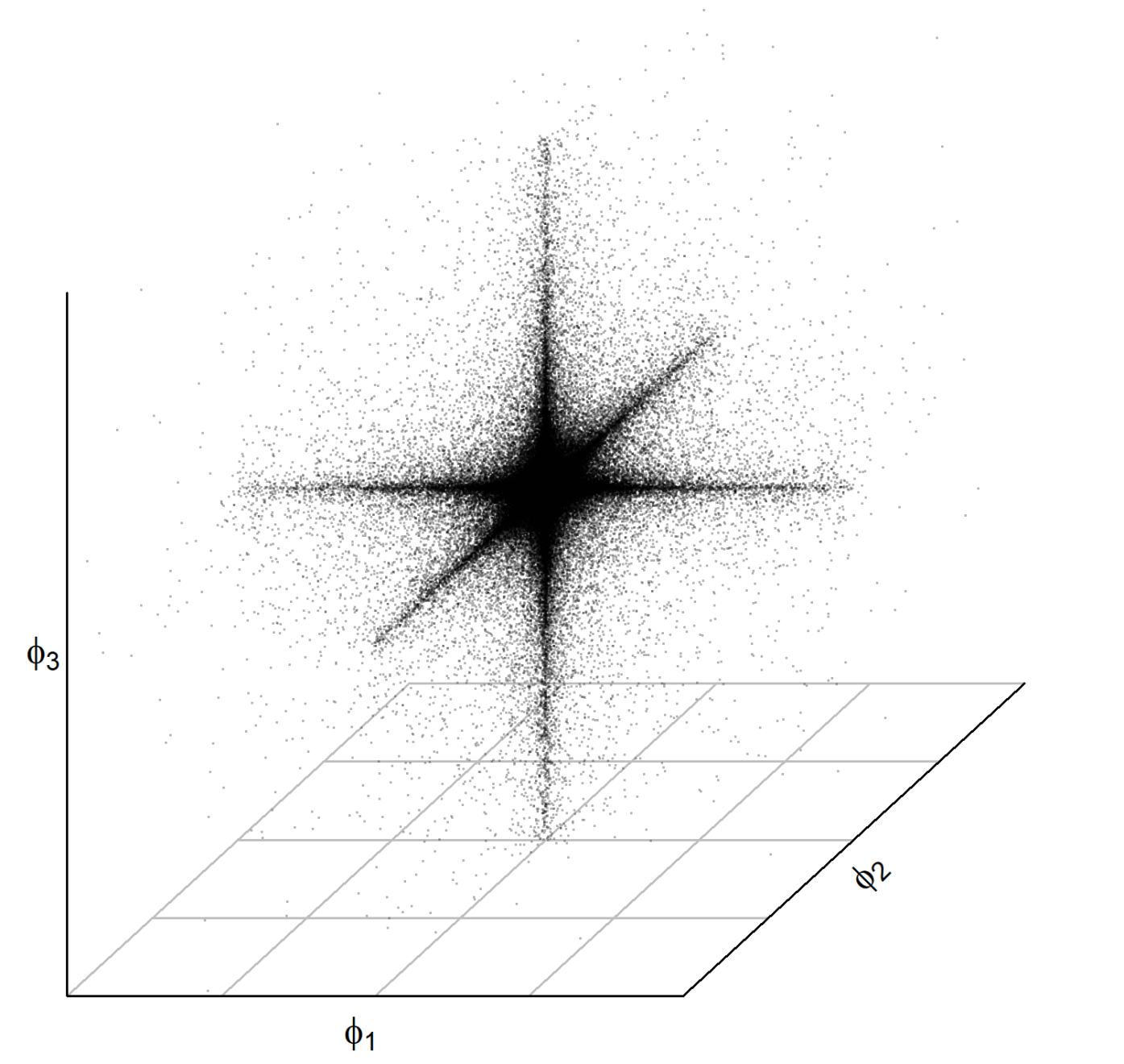

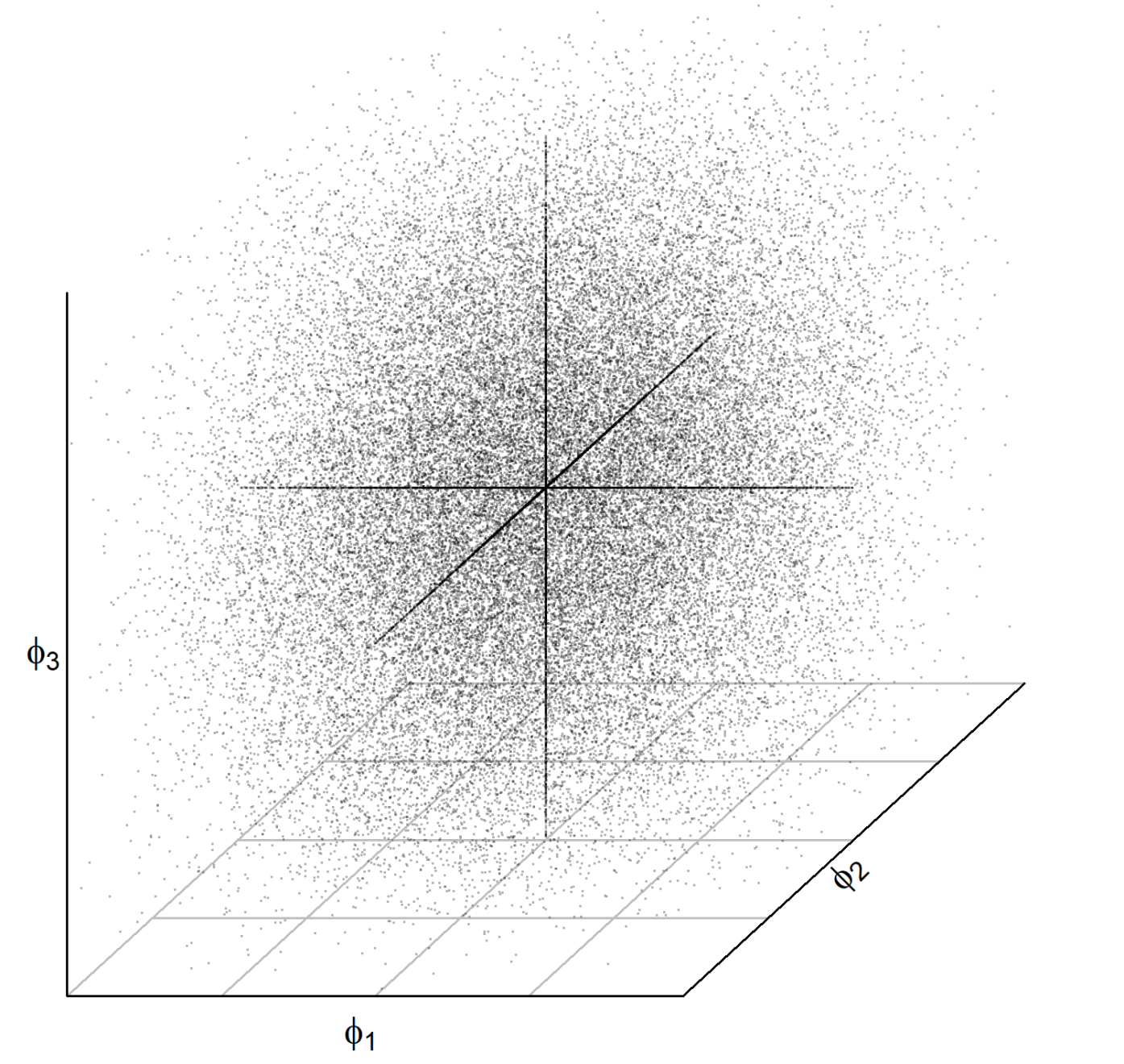

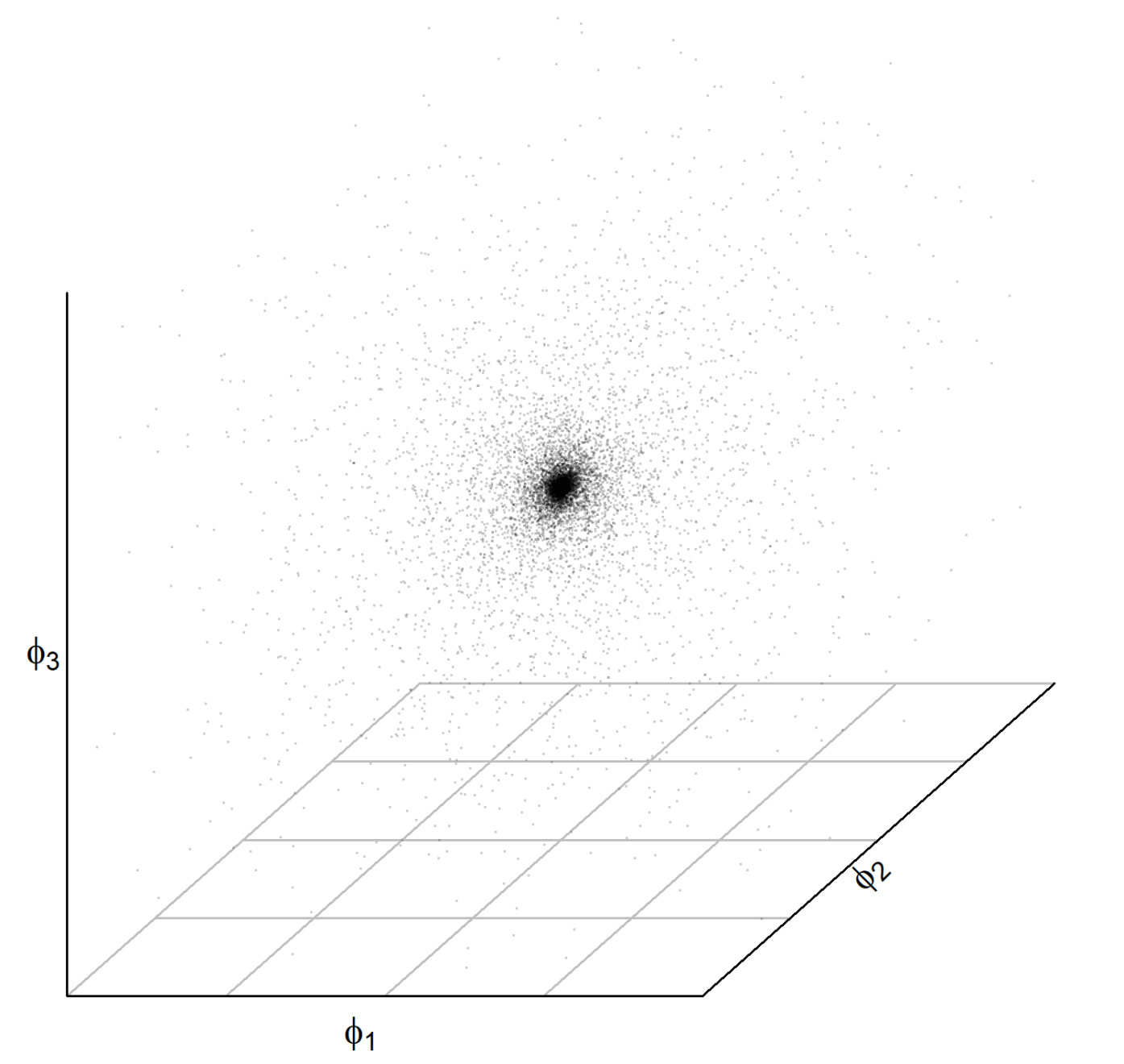

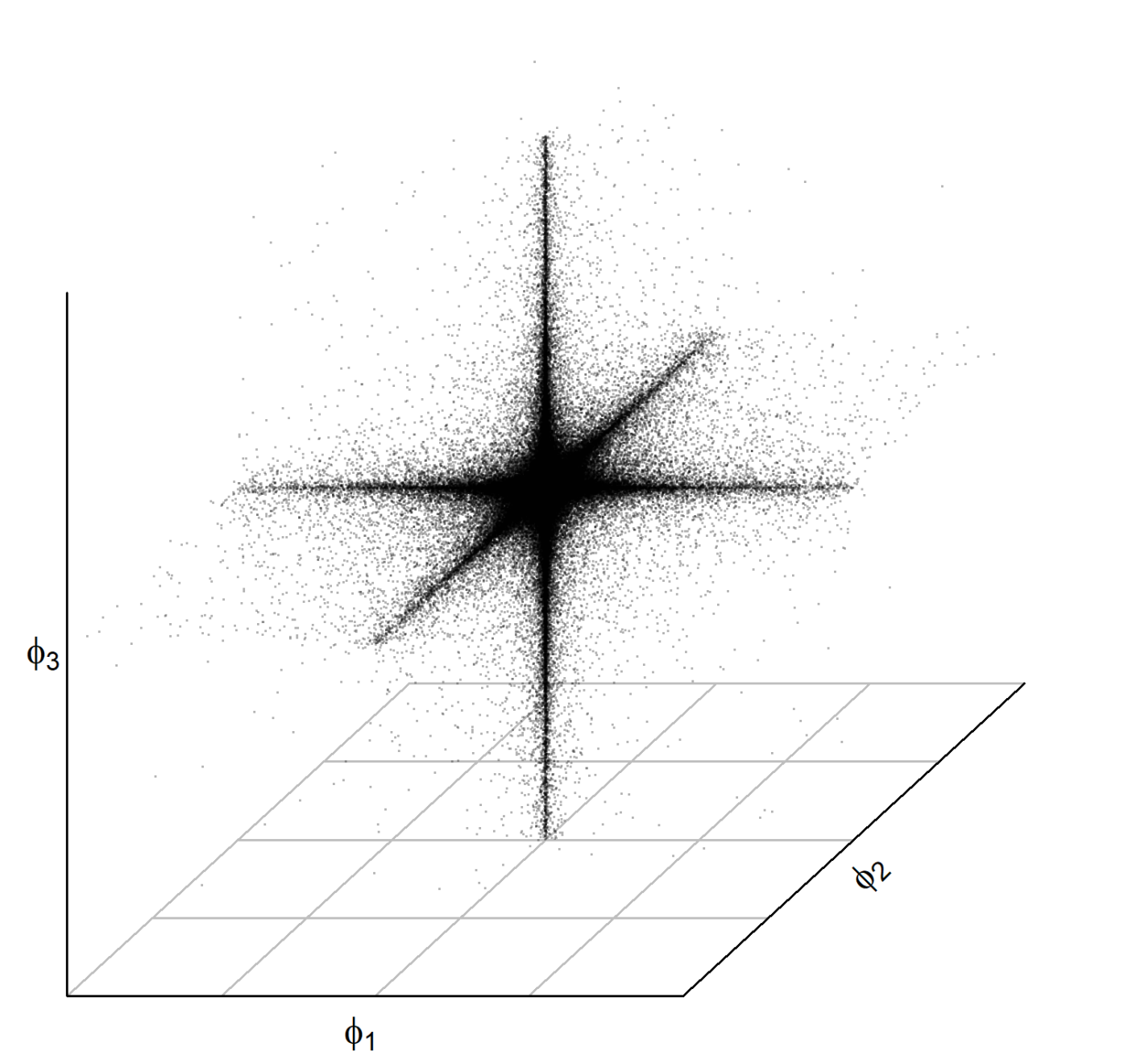

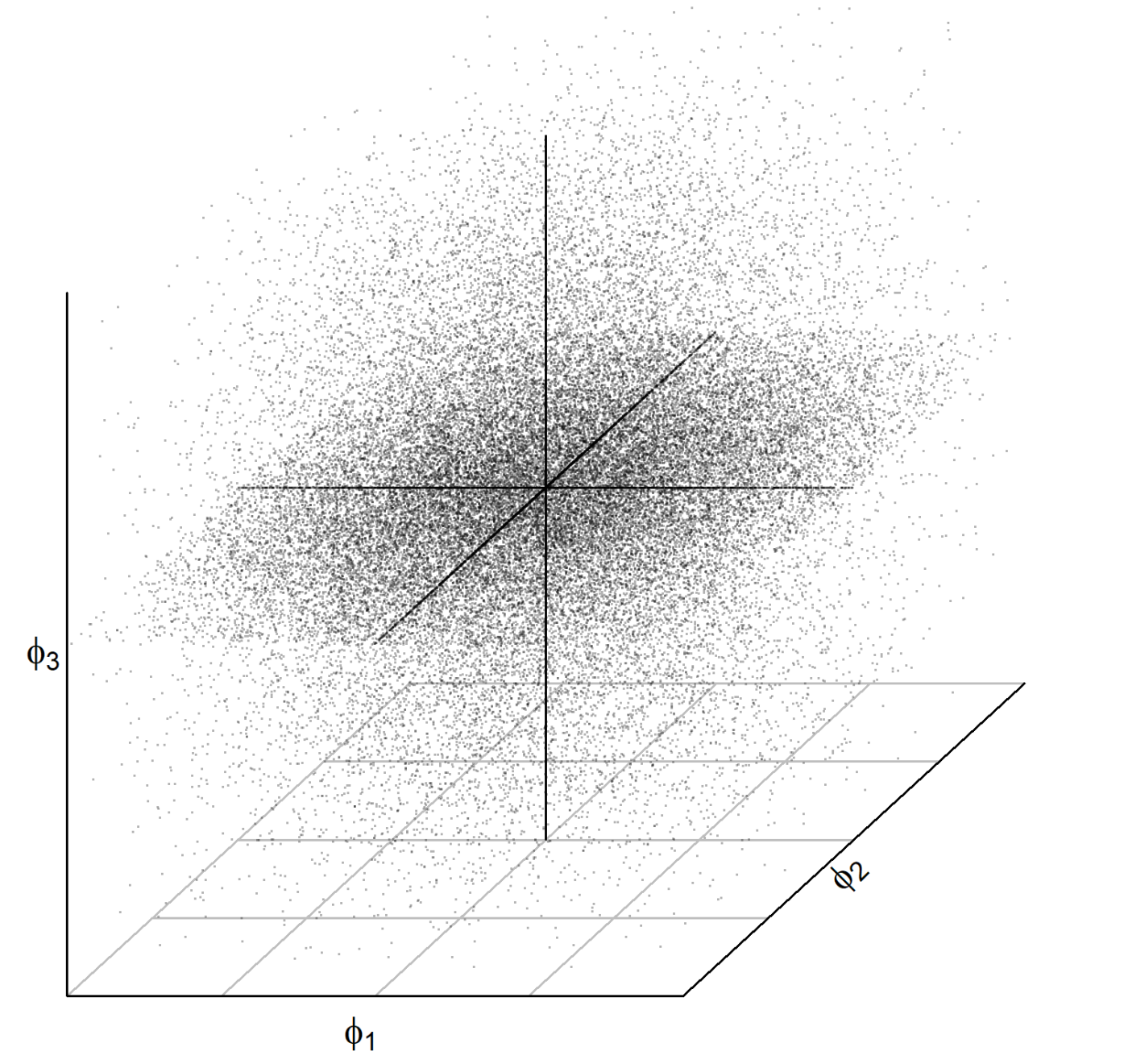

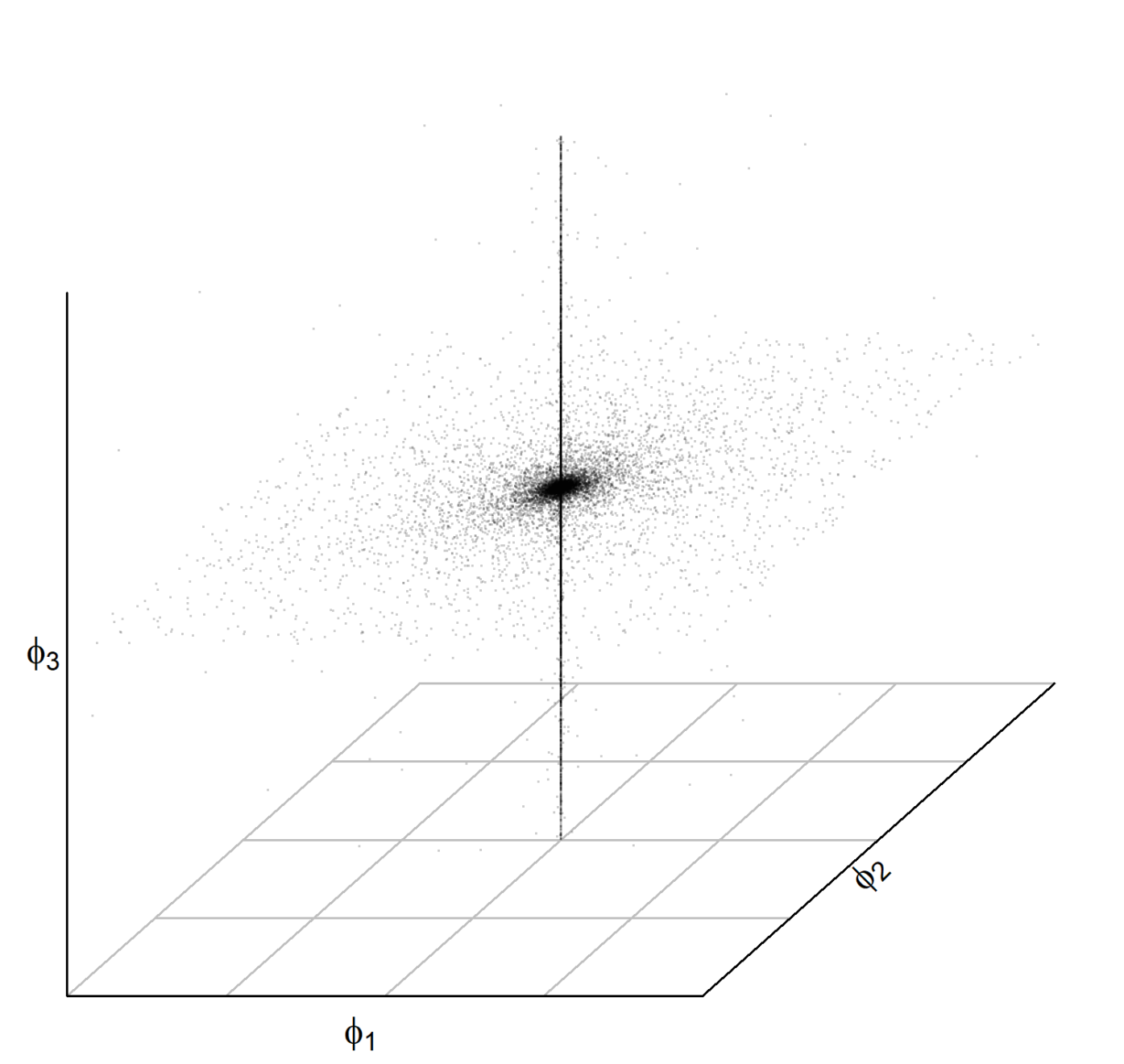

Figure 2 depicts three-dimensional scatter plots of prior simulations. The star-like shapes of GL priors (here the HS prior) have most of its mass where all coefficients are almost zero or where at most one is substantial different from zero, indicating sparseness. By contrast, the ball-like shape of SHM, which does not allow for outliers, indicates denseness. SSVS is somewhere in the middle of the contrasting approaches. The figure also demonstrates the effect of structured shrinkage. Assume and , then for all priors there is relatively more mass where or else , i.e., the structuring introduces discrimination between the groups. For GL priors, this implies discrimination between groups, while being sparse within groups. On the other hand, SHM only discriminates between own-lag and cross-lag coefficients. Within own-lag and within cross-lag coefficients it remains dense, which explains the spinning-top shape.

We quantify the sparseness of each prior by means of the Hoyer sparseness measure (Hoyer,, 2004). The Hoyer measure for the vector ,

| (26) |

is a normalized measure where indicates maximum sparseness, i.e., only one single nonzero value, and indicates maximum denseness, i.e., the absolute values of all components are equal. More importantly, it can express sparseness when all elements of are nonzero, but when almost all are very close to zero and only very few are large (in absolute values). This is important, as we analyze continuous prior distributions which never strictly exclude single coefficients.

| MP_LIT/SHM | HS | DL | R2D2 | NG | SSVS | |

|---|---|---|---|---|---|---|

| A | 0.21 | 0.89 | 0.51 | 0.45 | 0.37 | 0.45 |

| B | - | - | 0.99 | 0.98 | 0.98 | 0.95 |

We estimate the Hoyer measure through Monte Carlo simulation. Table 1 reports the arithmetic means stemming from a Monte Carlo simulation with iterations and simulated vectors of length . Interestingly, the simulation suggests that for MP_LIT/SHM, i.e., all priors of the form , , regardless the specific choice of , the expectation of the Hoyer measure converges to for . This behavior of the measure is convenient, since sparsity should not depend on the overall noise level. For the remaining priors, results can be sensitive to the choice of hyperparameters; thus, for each prior, we consider two different scenarios. In scenario A, the hyperparameters for DL, R2D2, and NG are selected to ensure that the concentration at zero is comparable to the one of HS. In scenario B, we select the hyperparameters such that the concentration at zero is higher compared to scenario A: For DL we set , for R2D2 we set and for NG we set , which results in the same behavior around the origin for those three priors. Our numerical experiments suggest, that the sparseness of DL, R2D2, and NG does not depend upon choices for the global hyperparameters. For SSVS, we set and in both scenarios. We set in scenario A and in scenario B.

The exercise corroborates our preceding considerations. From sparse to dense, the priors can be ranked in the following order: DL, R2D2, NG, SSVS, HS, and at some distance SHM/MP_LIT. Moreover, the sparseness of DL, R2D2, NG, and SSVS is very sensitive to the choices of the parameters that control the concentration at zero, namely , , and , respectively.

4 Synthetic data exercises

This section aims at comparing the performances of the various priors on simulated data. Before that, the merits of the semi-global framework are illustrated on synthetic data.

4.1 Structured/informed shrinkage: An illustration

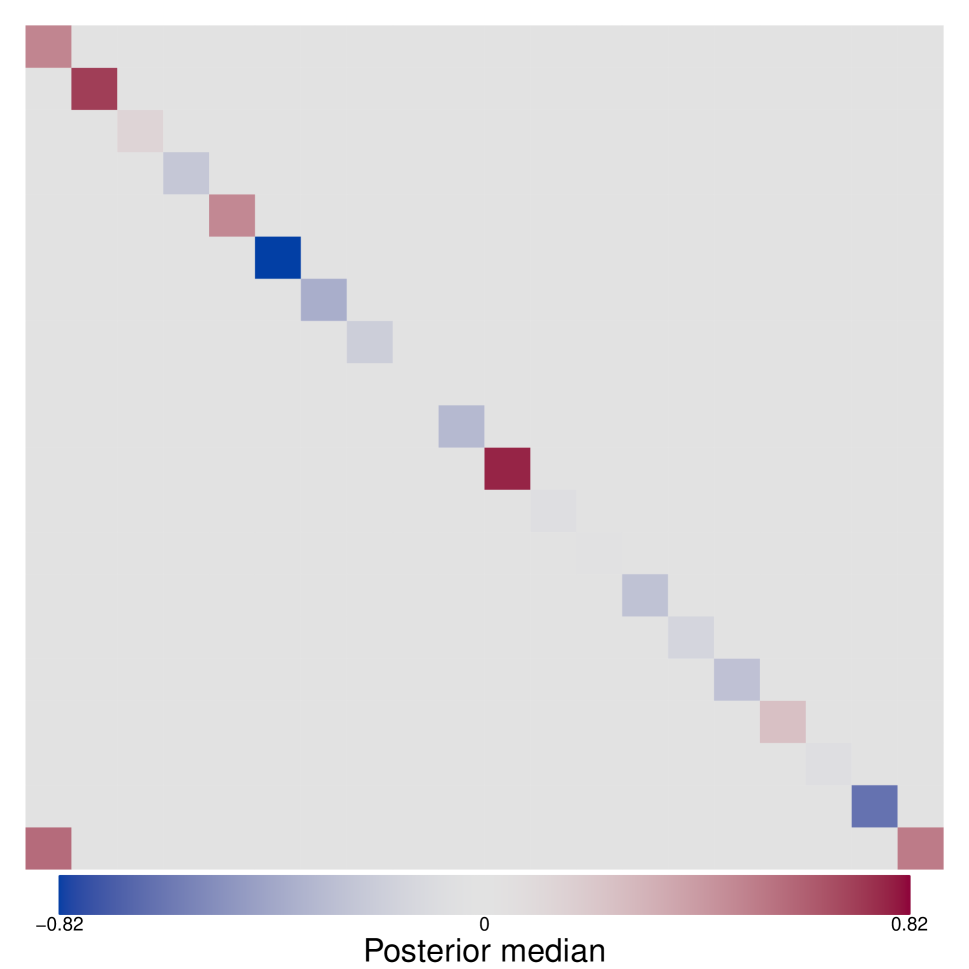

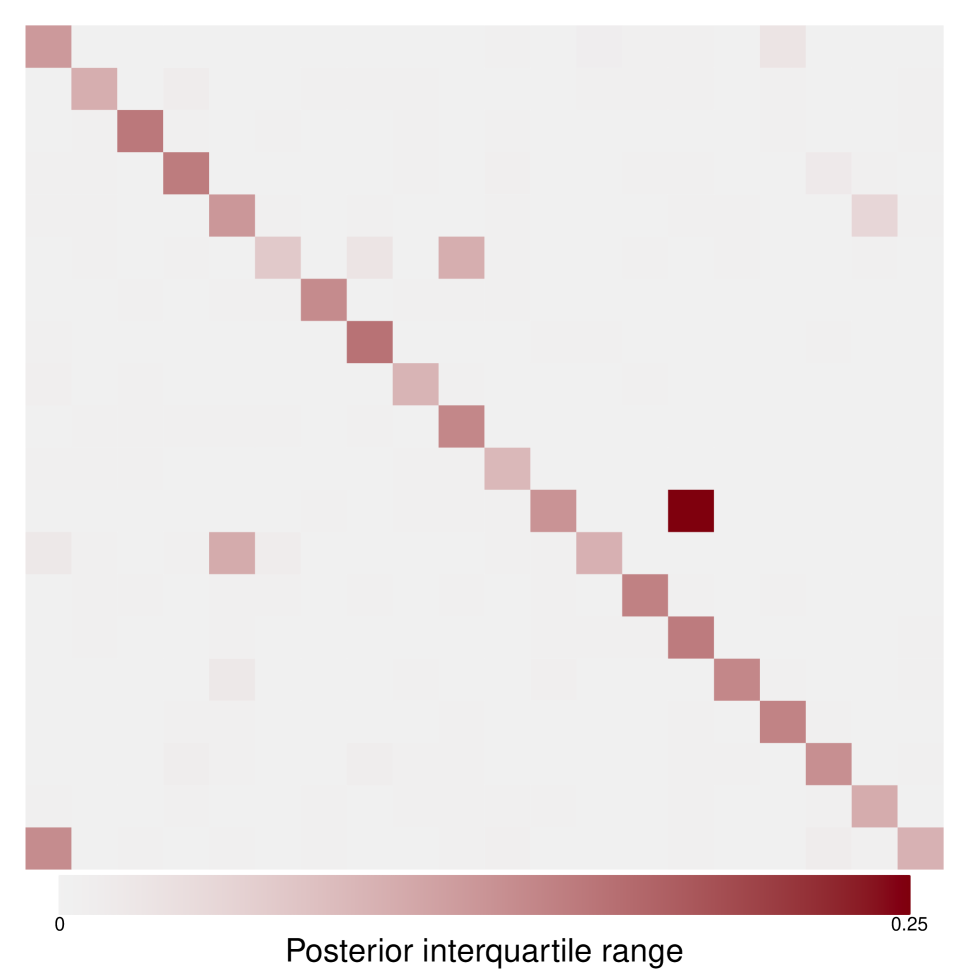

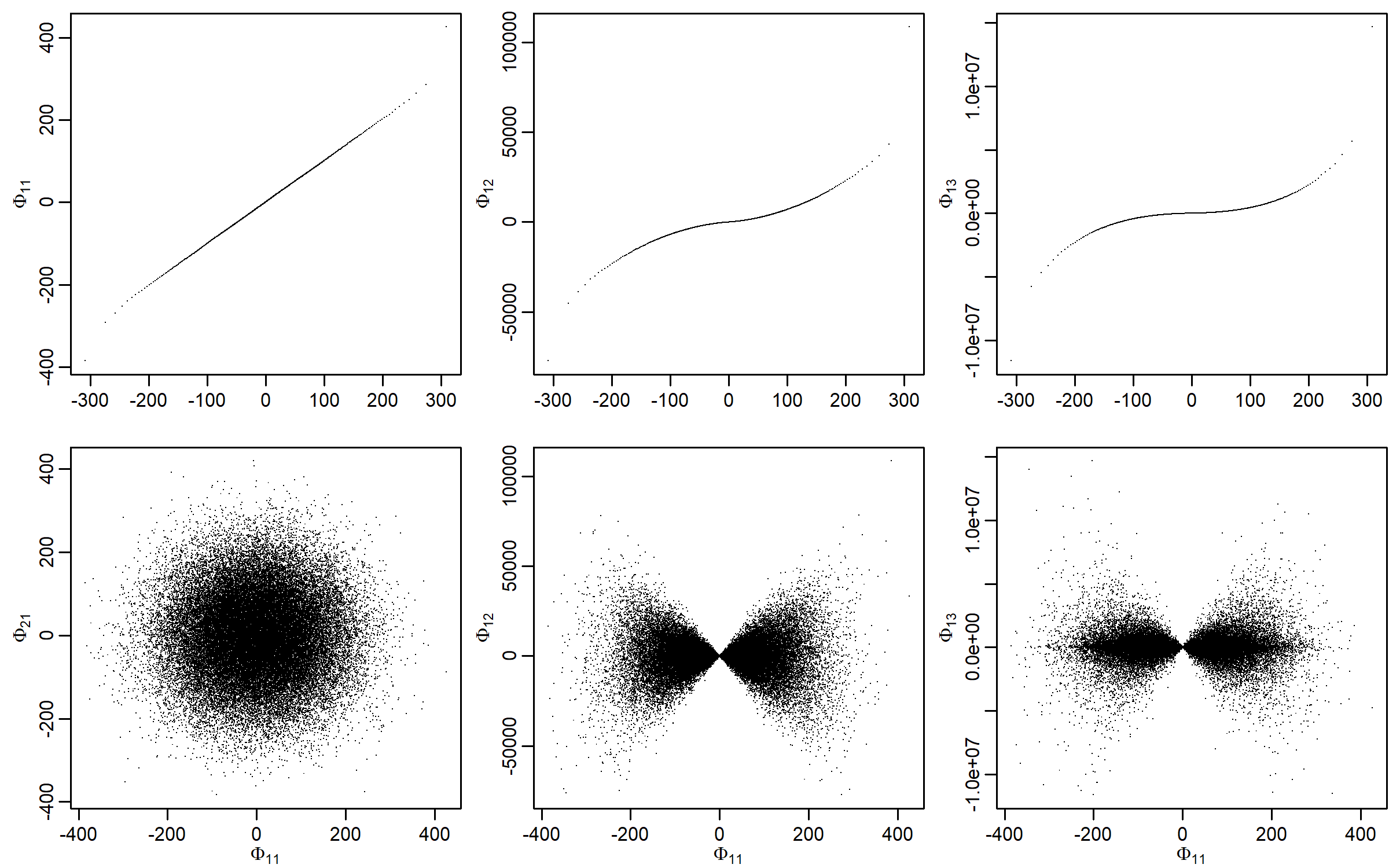

Consider the following example of a VAR(1): Assume that all diagonal elements of are nonzero, whereas there is only one nonzero off-diagonal element. That is, taken as a whole, is not sparse. Figure 3 demonstrates that a standard global-local prior – here the HS prior – overshrinks the diagonal elements and does not shrink the off-diagonal elements strong enough. The structured semi-global local version, however, adapts the degree of shrinkage in the two different subspaces of .

4.2 Simulation study

In this section, we compare the performances of the different priors on simulated data. The structure of the simulation study is borrowed from Kastner and Huber, (2020). We consider dense and sparse data generating processes (DGPs), as well as different dimensions in . Dimensionality is throughout. In each setting, we sample 20 replicates of the DGP. In all scenarios, we distinguish between own- and cross-lags. The nonzero coefficients of the DGPs are drawn from Gaussians with mean and standard deviation for , where and denote own-lag and cross-lag, respectively. In both scenarios, the probability of own-lag coefficients to be nonzero is 0.8, i.e., own-lags are always considered to be dense. The probability of cross-lag coefficients to be nonzero is 0.1 in the sparse and 0.8 in the dense scenario. Further, the scenarios differ regarding the signal-to-noise ratio. In the sparse scenario, we set . In the medium scenario, we set and . In the dense scenario, we set and . To simulate stable VAR processes, we control that none of the eigenvalues of the companion form have modulus greater than one (Lütkepohl,, 2005).

Elements in are nonzero with probability 0.01 in the sparse scenario, 0.1 in the medium scenario, and 0.8 in the dense scenario. In all scenarios, we set . The AR(1) processes driving the log-variances of the orthogonalized errors have mean , persistencies in the range and standard deviations in the range .

The root mean squared error (RMSE) between the posterior mean of the coefficients and the true parameter values is a common measure to evaluate the performances:

| (27) |

where denotes the -th posterior sample and is the posterior mean of the -th VAR coefficient.

The following prior specifications are considered: DL, NG, and R2D2 denote the standard global-local implementations with the concentration parameters being fixed. In DL, , the value proposed in Kastner and Huber, (2020). In NG and R2D2, , i.e. DL, NG, and R2D2 are specified to have the same concentration at zero. Further, in R2D2, , the value proposed in Zhang et al., (2022). In NG, and , such that NG and R2D2 differ only in their respective kernels: Whereas NG defines hyperpriors for the variance of a normal distribution, R2D2 defines hyperpriors for the variance of a double-exponential distribution. In DLa, NGa, and R2D2a, the support points of the discrete priors are equally spaced, and the probabilities are proportional to the density of an exponential distribution with rate . In MP_LIT, and . In SHM, for . For all SSVS priors, we closely follow the semiautomatic approach in George et al., (2008) by setting and . Here, denotes the variance of the posterior distribution resulting from a conjugate flat normal-Wishart prior, which is available in closed form. George et al., (2008) use the variance of the ordinary least squares (OLS) estimator. However, in situations where the number of covariates per equation exceeds the number of observations, the OLS estimator might not exist. For SSVS, , whereas SSVSp indicates that a is placed on . A superscript “∗” following a prior indicates a semi-global modification, e.g., the semi-global-local HS prior is denoted by HS∗.

| sparse | medium | dense | |||||||

|---|---|---|---|---|---|---|---|---|---|

| model | |||||||||

| MP_LIT | 5.64 | 4.68 | 4.03 | 5.09 | 4.49 | 4.08 | 3.18 | 2.89 | 2.59 |

| SHM | 5.46 | 4.71 | 4.13 | 5.56 | 4.56 | 4.07 | 3.27 | 2.54 | 2.00 |

| DL | 5.43 | 3.26 | 2.20 | 6.01 | 4.63 | 3.54 | 4.54 | 3.82 | 2.81 |

| DLa | 5.82 | 3.48 | 2.35 | 6.20 | 4.67 | 3.56 | 5.07 | 4.02 | 2.91 |

| DL | 5.28 | 3.23 | 2.21 | 6.07 | 4.59 | 3.41 | 4.75 | 3.84 | 2.77 |

| HS | 5.26 | 3.31 | 2.24 | 5.72 | 4.64 | 3.55 | 4.06 | 3.57 | 2.63 |

| HS∗ | 3.89 | 2.52 | 1.76 | 5.23 | 4.19 | 3.31 | 3.10 | 2.65 | 2.10 |

| NG | 5.26 | 3.20 | 2.24 | 5.69 | 4.66 | 3.54 | 4.09 | 3.69 | 2.72 |

| NGa | 5.55 | 3.47 | 2.37 | 5.78 | 4.60 | 3.53 | 4.42 | 3.82 | 2.84 |

| NG∗ | 4.95 | 3.08 | 2.11 | 5.69 | 4.63 | 3.48 | 4.04 | 3.53 | 2.67 |

| NG | 4.55 | 2.94 | 2.18 | 5.54 | 4.37 | 3.32 | 4.11 | 3.45 | 2.57 |

| R2D2 | 5.19 | 3.19 | 2.18 | 5.74 | 4.67 | 3.54 | 4.08 | 3.67 | 2.72 |

| R2D2a | 5.41 | 3.40 | 2.32 | 5.72 | 4.61 | 3.53 | 4.34 | 3.76 | 2.83 |

| R2D2∗ | 4.80 | 3.03 | 2.07 | 5.65 | 4.63 | 3.50 | 3.99 | 3.53 | 2.66 |

| R2D2 | 4.58 | 2.89 | 2.07 | 5.40 | 4.35 | 3.31 | 3.90 | 3.38 | 2.51 |

| SSVS | 5.54 | 3.80 | 2.67 | 5.95 | 5.23 | 4.31 | 4.09 | 3.73 | 2.96 |

| SSVSp | 6.07 | 4.17 | 2.42 | 6.09 | 5.51 | 4.72 | 4.23 | 3.98 | 3.28 |

| SSVS | 5.55 | 3.66 | 2.40 | 6.11 | 5.44 | 4.69 | 4.16 | 3.85 | 3.06 |

Table 2 reveals the results of the simulation study. HS∗ has the lowest RMSE in six out of nine scenarios: It is best in all sparse scenarios, in the medium scenarios with at least 100 observations and in the dense scenarios with only 50 observations. In the dense scenarios with at least 100 observations, SHM has the lowest scores. Concerning GL priors, the semi-global versions perform better than the standard versions in all scenarios. In the sparse and the medium scenarios, GL priors in general, i.e., the standard and the semi-global versions, tend to perform better than the Minnesota priors (with one notable exception). In the dense scenarios, SHM is overall best, closely followed by HS∗. SHM is considerably better than MP_LIT in the dense scenarios with at least 100 observations, whereas in the remaining scenarios their performances in terms of RMSEs is comparable. Turning to the various specifications of SSVS, we tend to observe competitive performance only in the sparse scenarios.

5 Empirical application to data of the US economy

In Section 5.1, we shortly summarize the data set, present the model specifications and the forecasting design. In Section 5.2, we inspect the posterior distributions of VAR coefficients arising from different prior distributions. In Section 5.3, we assess out-of-sample forecasting accuracy of the different models. In Section 5.4, we demonstrate the merits of combining forecasts of different models in a dynamic fashion via dynamic model averaging (DMA).

5.1 Data overview, model specification and forecasting design

The aim of the empirical application is to forecast economically relevant US time series. We use the quarterly data set provided by McCracken and Ng, (2021), which is based on the well-known Stock and Watson, (2012) data set. The sample period ranges from 1959:Q4 to 2020:Q1. All in all, we include quarterly time series with the intention to cover the most important segments of the US economy. The variables enter the models in log differences, except interest rates, which are already defined in rates and hence taken in levels. The complete list of all variables used in the following illustration is provided in Table 6 (Appendix C).

A very important and often underemphasized choice is the number of lags of endogenous variables included as predictors. In the Bayesian framework, fixing at a certain number implies prior information that higher lags do not carry any important information. Hence, Litterman, (1986) suggests estimating as many lags as is computationally feasible, in which the prior has to be designed such that irrelevant coefficients get shrunken to zero. However, the more lags we include, the severer the problem of overfitting becomes, and the harder it will be to regularize the parameter space. Not to mention the increase of computational burden. Typical choices for quarterly data in similar dimensions are either four or five lags (Chan, 2021b, ; Cross et al.,, 2020; Huber and Feldkircher,, 2019; Giannone et al.,, 2015). We estimate VAR()s for to investigate to what degree longer lags improve/worsen forecasting performance.

The forecasting performance is evaluated by means of a recursive pseudo out-of-sample forecasting exercise. Based on the initial estimation window ranging from 1959:Q4 to 1979:Q4, one-step ahead predictive densities are evaluated. After that, the estimation window is expanded by one quarter and the model is re-estimated. For each estimation step, we run ten independent MCMC chains. Per chain, we keep 15,000 draws after a burn-in of 5,000 iterations. This procedure is consequently repeated until the end of the sample 2020:Q1 is reached. The prior specifications we consider in the empirical application are the same as in Section 4.2.

5.2 Inspecting the posterior distributions

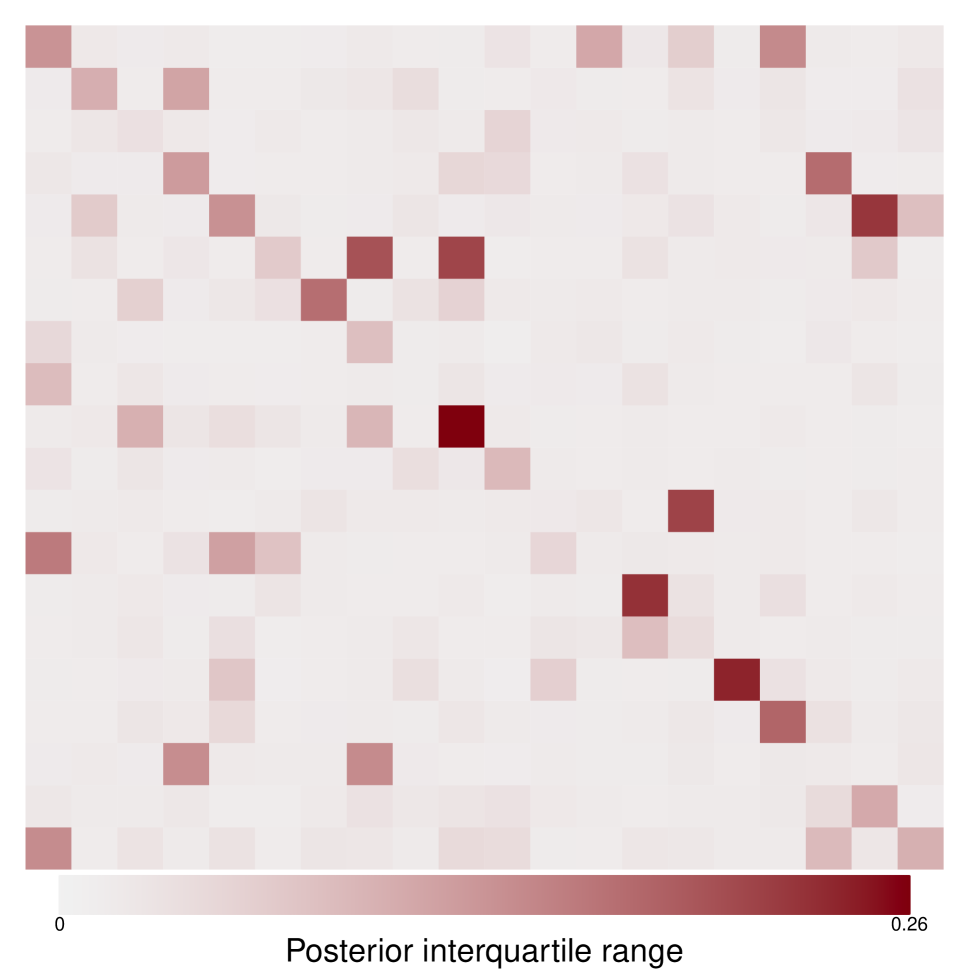

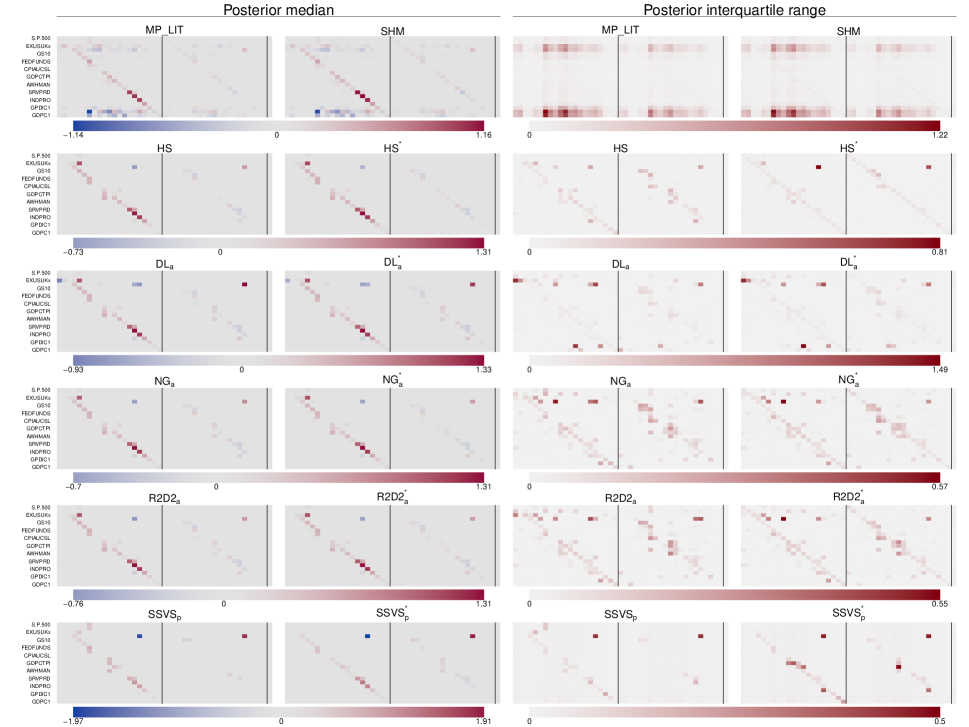

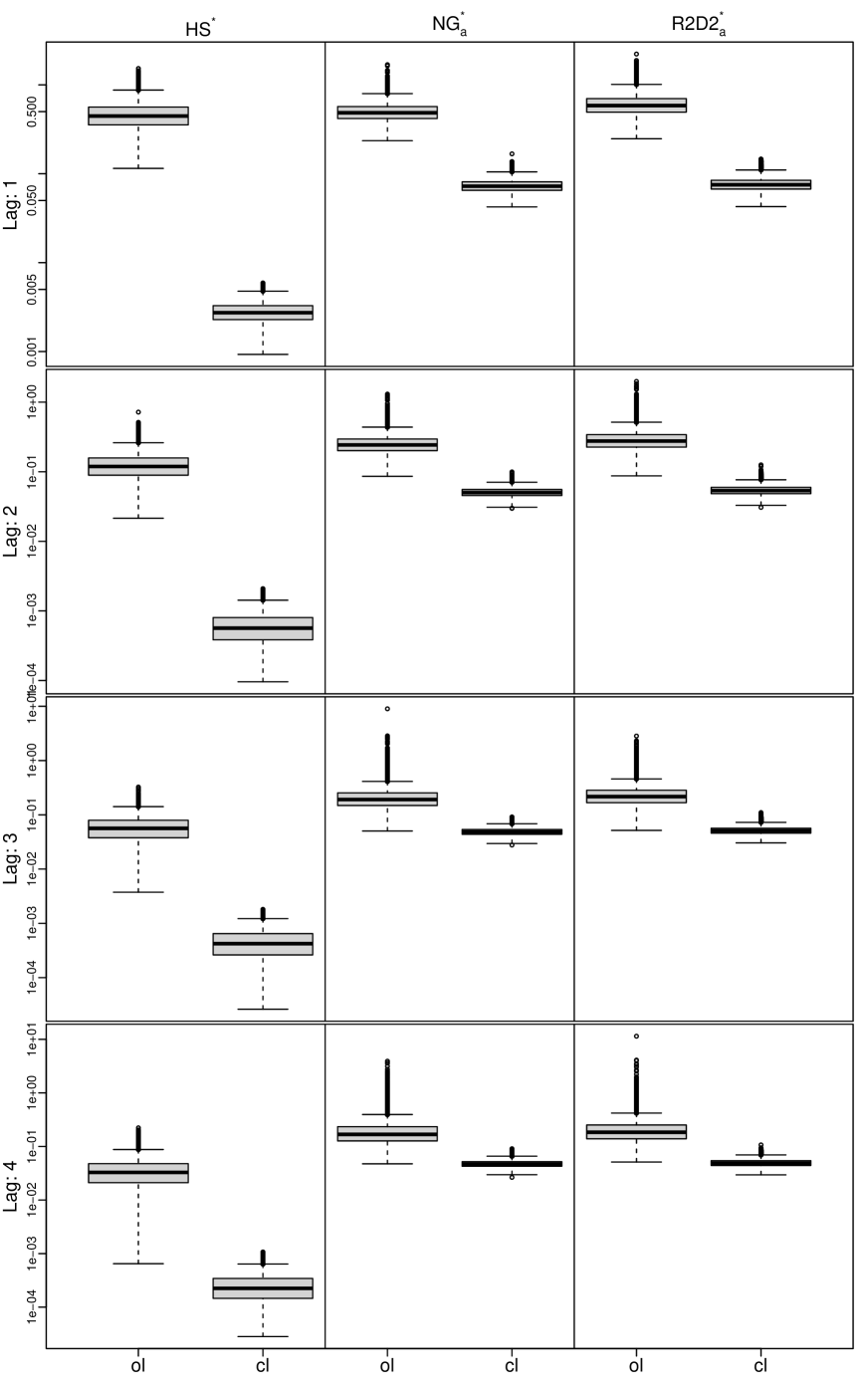

Before presenting the results of the forecasting exercise, it is worth analyzing the posterior distributions arising from the different priors. Figure 4 depicts posterior medians and posterior interquartile ranges of different VAR(2) models.666Although we find signals with higher lag orders, the out-of-sample results indicate that two lags usually are enough (cf. Section 5.3). All models, even the standard SSVS and GL priors, detect many signals associated with the first own-lag and little signals in the reaming part of the coefficient space. Concerning the cross-lag coefficients, the posteriors arising from the Minnesota priors show relatively high uncertainty, whereas the remaining priors only find sparse signals. The differences between the standard and the semi-global versions of SSVS and GL priors are hardly detectable by visual exploration only.

| p | ol/cl |

|---|---|

| 1 | ol |

| cl | |

| 2 | ol |

| cl | |

| 3 | ol |

| cl | |

| 4 | ol |

| cl | |

| 5 | ol |

| cl |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.29 | - | - | - | - |

| 0.78 | - | - | - | - |

| 0.37 | 0.48 | - | - | - |

| 0.82 | 0.84 | - | - | - |

| 0.37 | 0.54 | 0.68 | - | - |

| 0.82 | 0.84 | 0.85 | - | - |

| 0.37 | 0.55 | 0.71 | 0.76 | - |

| 0.83 | 0.85 | 0.85 | 0.88 | - |

| 0.38 | 0.55 | 0.74 | 0.76 | 0.78 |

| 0.83 | 0.85 | 0.85 | 0.87 | 0.84 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.26 | - | - | - | - |

| 0.78 | - | - | - | - |

| 0.33 | 0.39 | - | - | - |

| 0.82 | 0.84 | - | - | - |

| 0.33 | 0.45 | 0.64 | - | - |

| 0.82 | 0.84 | 0.86 | - | - |

| 0.32 | 0.46 | 0.62 | 0.73 | - |

| 0.83 | 0.85 | 0.85 | 0.88 | - |

| 0.33 | 0.45 | 0.68 | 0.72 | 0.76 |

| 0.82 | 0.85 | 0.86 | 0.87 | 0.85 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.23 | - | - | - | - |

| 0.60 | - | - | - | - |

| 0.30 | 0.19 | - | - | - |

| 0.60 | 0.61 | - | - | - |

| 0.31 | 0.22 | 0.22 | - | - |

| 0.61 | 0.61 | 0.61 | - | - |

| 0.31 | 0.21 | 0.22 | 0.25 | - |

| 0.61 | 0.61 | 0.61 | 0.61 | - |

| 0.31 | 0.22 | 0.22 | 0.25 | 0.26 |

| 0.61 | 0.61 | 0.61 | 0.61 | 0.61 |

| p | ol/cl |

|---|---|

| 1 | ol |

| cl | |

| 2 | ol |

| cl | |

| 3 | ol |

| cl | |

| 4 | ol |

| cl | |

| 5 | ol |

| cl |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.31 | - | - | - | - |

| 0.75 | - | - | - | - |

| 0.37 | 0.54 | - | - | - |

| 0.83 | 0.81 | - | - | - |

| 0.39 | 0.63 | 0.77 | - | - |

| 0.85 | 0.81 | 0.87 | - | - |

| 0.38 | 0.79 | 0.82 | 0.77 | - |

| 0.86 | 0.83 | 0.86 | 0.85 | - |

| 0.39 | 0.80 | 0.80 | 0.78 | 0.85 |

| 0.87 | 0.84 | 0.85 | 0.85 | 0.82 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.25 | - | - | - | - |

| 0.80 | - | - | - | - |

| 0.31 | 0.27 | - | - | - |

| 0.84 | 0.90 | - | - | - |

| 0.32 | 0.30 | 0.36 | - | - |

| 0.85 | 0.92 | 0.93 | - | - |

| 0.31 | 0.30 | 0.40 | 0.46 | - |

| 0.85 | 0.90 | 0.92 | 0.90 | - |

| 0.32 | 0.29 | 0.42 | 0.47 | 0.59 |

| 0.85 | 0.89 | 0.95 | 0.85 | 0.84 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.24 | - | - | - | - |

| 0.60 | - | - | - | - |

| 0.29 | 0.21 | - | - | - |

| 0.60 | 0.61 | - | - | - |

| 0.29 | 0.22 | 0.22 | - | - |

| 0.60 | 0.61 | 0.61 | - | - |

| 0.29 | 0.22 | 0.23 | 0.26 | - |

| 0.60 | 0.61 | 0.61 | 0.61 | - |

| 0.29 | 0.23 | 0.23 | 0.26 | 0.25 |

| 0.60 | 0.61 | 0.61 | 0.61 | 0.61 |

| p | ol/cl |

|---|---|

| 1 | ol |

| cl | |

| 2 | ol |

| cl | |

| 3 | ol |

| cl | |

| 4 | ol |

| cl | |

| 5 | ol |

| cl |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.30 | - | - | - | - |

| 0.75 | - | - | - | - |

| 0.37 | 0.47 | - | - | - |

| 0.79 | 0.79 | - | - | - |

| 0.37 | 0.56 | 0.66 | - | - |

| 0.81 | 0.77 | 0.81 | - | - |

| 0.36 | 0.62 | 0.67 | 0.71 | - |

| 0.80 | 0.76 | 0.78 | 0.79 | - |

| 0.38 | 0.62 | 0.72 | 0.74 | 0.75 |

| 0.80 | 0.76 | 0.78 | 0.78 | 0.79 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.25 | - | - | - | - |

| 0.77 | - | - | - | - |

| 0.32 | 0.31 | - | - | - |

| 0.80 | 0.78 | - | - | - |

| 0.32 | 0.36 | 0.57 | - | - |

| 0.80 | 0.78 | 0.82 | - | - |

| 0.31 | 0.36 | 0.58 | 0.69 | - |

| 0.80 | 0.77 | 0.81 | 0.80 | - |

| 0.32 | 0.38 | 0.64 | 0.69 | 0.7 |

| 0.80 | 0.77 | 0.81 | 0.79 | 0.8 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.29 | - | - | - | - |

| 0.76 | - | - | - | - |

| 0.37 | 0.48 | - | - | - |

| 0.80 | 0.79 | - | - | - |

| 0.38 | 0.54 | 0.68 | - | - |

| 0.81 | 0.77 | 0.81 | - | - |

| 0.37 | 0.62 | 0.70 | 0.72 | - |

| 0.82 | 0.78 | 0.79 | 0.81 | - |

| 0.39 | 0.63 | 0.73 | 0.75 | 0.77 |

| 0.82 | 0.77 | 0.79 | 0.79 | 0.79 |

| p | ol/cl |

|---|---|

| 1 | ol |

| cl | |

| 2 | ol |

| cl | |

| 3 | ol |

| cl | |

| 4 | ol |

| cl | |

| 5 | ol |

| cl |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.25 | - | - | - | - |

| 0.77 | - | - | - | - |

| 0.32 | 0.31 | - | - | - |

| 0.80 | 0.80 | - | - | - |

| 0.32 | 0.35 | 0.51 | - | - |

| 0.81 | 0.79 | 0.83 | - | - |

| 0.32 | 0.37 | 0.55 | 0.66 | - |

| 0.81 | 0.78 | 0.82 | 0.81 | - |

| 0.32 | 0.37 | 0.61 | 0.68 | 0.69 |

| 0.80 | 0.79 | 0.82 | 0.81 | 0.81 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.33 | - | - | - | - |

| 0.82 | - | - | - | - |

| 0.38 | 0.73 | - | - | - |

| 0.82 | 0.74 | - | - | - |

| 0.37 | 0.75 | 0.75 | - | - |

| 0.84 | 0.73 | 0.85 | - | - |

| 0.38 | 0.75 | 0.76 | 0.52 | - |

| 0.87 | 0.92 | 0.72 | 0.83 | - |

| 0.41 | 0.74 | 0.37 | 0.44 | 0.67 |

| 0.83 | 0.75 | 0.44 | 0.84 | 0.63 |

| l=1 | l=2 | l=3 | l=4 | l=5 |

|---|---|---|---|---|

| 0.30 | - | - | - | - |

| 0.81 | - | - | - | - |

| 0.37 | 0.54 | - | - | - |

| 0.89 | 0.88 | - | - | - |

| 0.33 | 0.72 | 0.37 | - | - |

| 0.86 | 0.88 | 0.32 | - | - |

| 0.34 | 0.81 | 0.85 | 0.59 | - |

| 0.84 | 0.43 | 0.61 | 0.93 | - |

| 0.36 | 0.82 | 0.36 | 0.37 | 0.41 |

| 0.81 | 0.60 | 0.78 | 0.31 | 0.31 |

Table 3 displays the posterior mean of the Hoyer measure.777We compute the Hoyer measure for every single coefficient posterior draw, which then provides us with the posterior distribution of the measure. In the first lag, the posteriors under all priors are dense, whereas for the Minnesota priors own-lags in general are dense. Moreover, the Minnesota priors are always denser than the remaining priors for all considered lag-lengths w.r.t. to both own-lag and cross-lag coefficients. Last but not least, especially on the off-diagonals, the posteriors under all priors except SHM can get extremely sparse. The heterogeneous results regarding sparsity show that posterior inference is strongly affected by the prior assumptions, which stresses the importance of careful prior elicitation. Hence, we think it is delusive to draw general conclusions about sparseness mainly by analyzing posterior quantities. Fava and Lopes, (2021) elaborate on how such posterior results often just spread illusions.

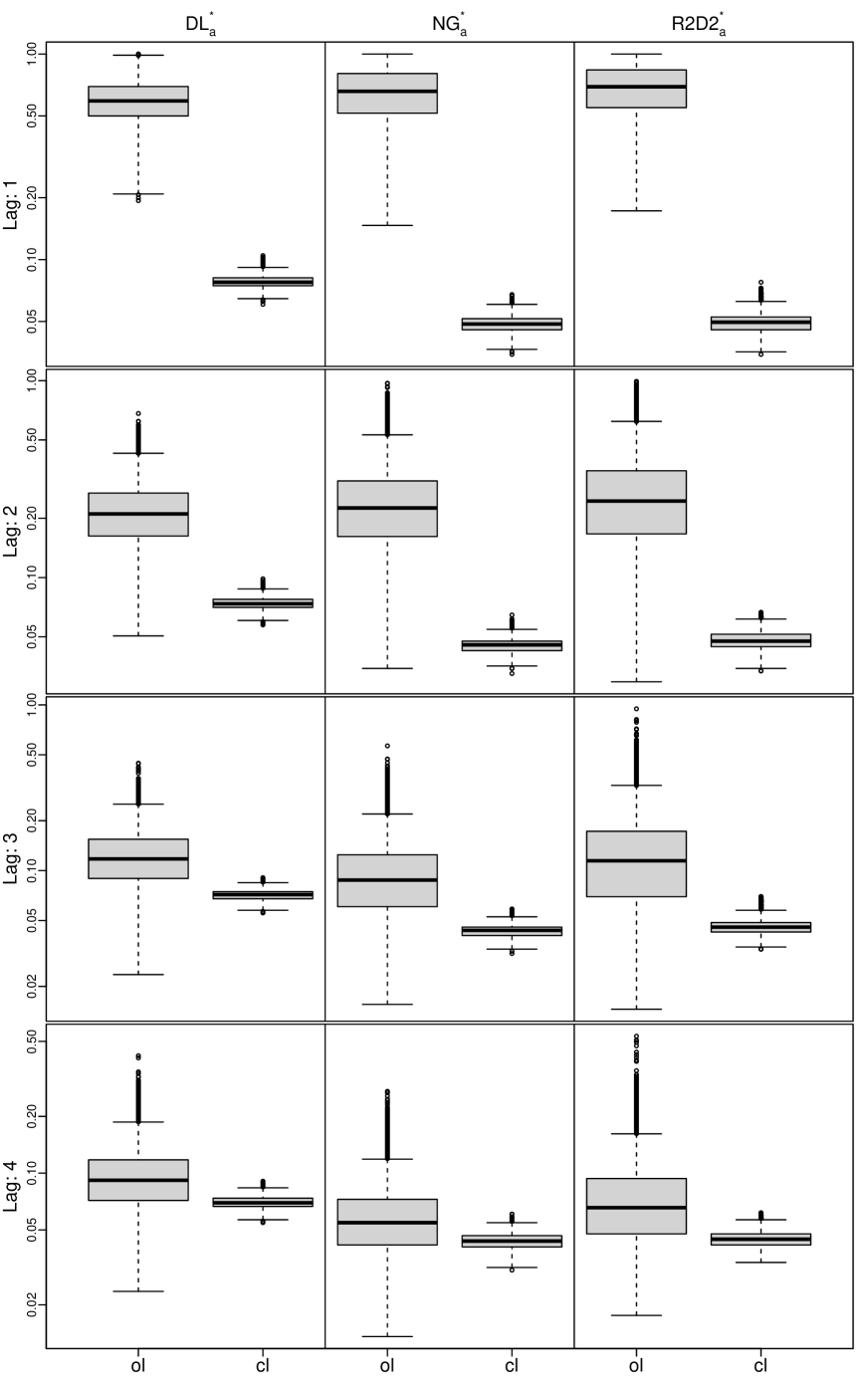

Comparing the sparseness between GL priors, we observe that the own-lag coefficients of the semi-global modifications are denser compared to their standard GL counterparts. HS∗ discriminates the strongest between own-lags and cross-lags in terms of sparsity, especially in more distant lags. In this context, it is worth analyzing the posterior distributions of the (semi-)global hyperparameters. Figure 5 depicts, exemplary for a VAR(4), box plots of the posterior distribution of for HS∗, NG, and R2D2, and the posterior distribution of for DL, for NG, for R2D2, . For all models there is a clear discrimination in all lags between own-lag and cross-lag, i.e., shrinkage is always stronger for cross-lag coefficients than for own-lag coefficients in all lags. The strength of discrimination between own-lag and cross-lag decreases with higher lags, and is the strongest for HS. Last but not least, the posterior distributions of the semi-global hyperparameters concentrate around smaller values for more distant lags than for closer lags, i.e., shrinkage increases with increasing lags.

5.3 Model evidence: Log predictive likelihoods

The marginal likelihood of the observed data, often referred to as model evidence, is of particular interest in Bayesian model comparison. It is the likelihood of the observed data, given the model assumptions. For non-conjugate priors, this real number is not analytically tractable. However, one-step-ahead predictive likelihoods (PLs) are intrinsically connected to the marginal likelihood: The marginal likelihood can be decomposed into one-step-ahead predictive likelihoods (cf., e.g., Geweke and Amisano,, 2010). Thus, the recursive forecasting design allows us to compute training-sample marginal likelihoods, i.e., marginal likelihoods conditioned on the initial estimation window ranging from 1970:Q1 to 1989:Q4. To compare two competing models A and B we consider log predictive Bayes factors, which are just the differences of log PLs.

| model | |||||

|---|---|---|---|---|---|

| MP_LIT | -63.35 | -18.84 | -7.99 | 0.00 | -10.48 |

| SHM | -46.53 | 7.74 | 9.88 | 18.45 | 7.42 |

| HS | -55.62 | -18.83 | -7.05 | -39.38 | -39.53 |

| DL | -39.61 | 10.89 | 24.49 | 2.70 | -7.65 |

| NG | -35.42 | 12.17 | 18.79 | -4.08 | -12.67 |

| R2D2 | -45.77 | 5.09 | 15.74 | 7.13 | -14.65 |

| DLa | -39.13 | 21.50 | 9.82 | -4.43 | -61.67 |

| NGa | -43.22 | 8.09 | 5.38 | -17.43 | -58.55 |

| R2D2a | -42.95 | 11.48 | 1.42 | -24.70 | -40.59 |

| NG∗ | -35.07 | 14.13 | 18.41 | 5.85 | -20.28 |

| R2D2∗ | -39.34 | 5.45 | 17.72 | 4.72 | -6.02 |

| HS∗ | -25.96 | 23.59 | 40.41 | 54.33 | 41.75 |

| DL | -29.59 | 36.92 | 26.75 | 11.56 | -29.39 |

| R2D2 | -17.67 | 44.37 | 32.56 | 13.31 | -7.36 |

| NG | -24.68 | 37.59 | 28.14 | 8.69 | -24.75 |

| SSVS | -65.09 | -29.15 | -38.91 | -55.41 | -80.25 |

| SSVSp | -89.23 | -53.66 | -68.89 | -94.91 | -115.56 |

| SSVS | -78.58 | -35.73 | -38.30 | -62.78 | -77.87 |

Table 4 depicts sums of one step ahead log-Bayes factors relative to the traditional Minnesota prior with four lags (MP_LIT(4)). The most important findings are the following: The overall best performance is achieved by the semi-global modification of HS with 4 lags (HS∗(4)). In almost all cases, the semi-global modifications clearly improve forecasting performance compared to their standard GL counterparts. Moreover, the semi-global modifications usually perform better than the Minnesota priors, whereas the “standard” GL priors do not. Comparing the scores of SHM and MP_LIT reveals that learning the shrinking parameters of the Minnesota prior from the data always improves forecasting performance, which corroborates findings in Giannone et al., (2015) and Cross et al., (2020). Among all considered priors, SSVS priors achieve the lowest scores.

Concerning the performance of GL priors compared to Minnesota priors: The standard GL priors do not produce more accurate forecasts than SHM. This contradicts results in Huber and Feldkircher, (2019) at first sight. The weaker performance of SHM in Huber and Feldkircher, (2019) can be explained (at least to some extent) by the vague prior imposed on , a normal prior with zero mean and variance 10. The fact that the prior choice for indeed plays a crucial role in terms of forecasting performance is demonstrated in Section 5.5. Interestingly, among the standard GL priors, HS has the lowest scores: For all orders, it has even lower scores than MP_LIT(4). The story changes radically, though, when looking at the semi-global modifications. For , HS∗ performs best. DL, R2D2 and NG with also perform considerably better than the best Minnesota prior, SHM(4).

Turning the focus to lag-length, we find that for the data set at hand, competitive forecasts require at least two lags of the endogenous variables as predictors. DL, R2D2, and NG perform best with , whereas MP_LIT, SHM, and HS∗ perform best with . Interestingly, the performances of HS, DL, DLa, DL, NG, NGa, NG, R2D2, R2D2a, and R2D2 deteriorate with . In this respect, HS∗ is the most robust prior.

The forecasting exercise also reveals both potentials and boundaries of the hierarchical treatment of hyperparameters. The Minnesota prior clearly benefits from treating both shrinking parameters as random variables. For GL priors, the story is more complex. On the one hand, DL, NG, and R2D2 in their standard implementations do not improve by placing priors on the concentration parameters , , and , respectively. On the other hand, the semi-global modifications of both NG and R2D2 unfold their full potential only if both and , , are equipped with hyperpriors. This finding confirms our conjecture that GL priors have limitations when the noise level and the sparsity differs in different regions of the parameter space.

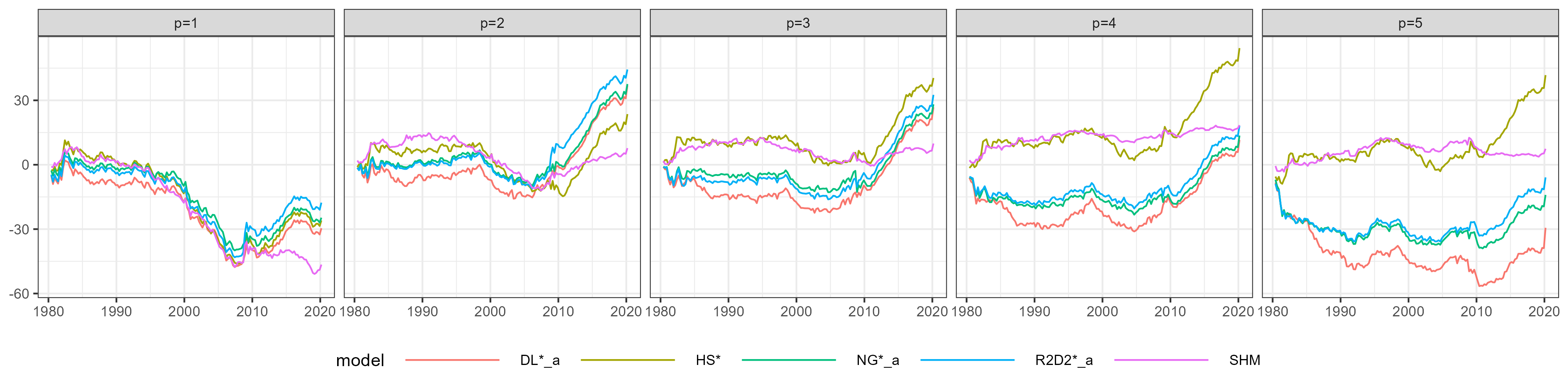

Figure 6 depicts how the forecasting scores evolve over time for an illustrative selection of different priors. It reveals that the financial crisis 2007/2008 marks a break in the evolution of the scores. After the crisis, the sparse models – the semi-global modifications of the GL priors – accumulate much higher scores than the “dense” SHM. Before the crisis, however, SHM is very competitive. The only sparse prior en par with SHM before the crisis is HS*. Overall, there is no single model that performs best over the whole evaluation period. Hence, there is no general answer to the question, whether sparse or dense modeling techniques perform better in forecasting economic data.

5.4 Dynamic model averaging

The previous sections highlighted the heterogeneity of model performance over time. The question arises, whether combining weighted forecasts can improve forecasting performance.

Dynamic model averaging (DMA, Raftery et al.,, 2010; Koop and Korobilis,, 2012; Onorante and Raftery,, 2016) is a straightforwardly implementable averaging scheme, where the weights are sequentially updated as new observations become available, depending on the forecasting performance up to this point in time. A model with strong support from the data for a given period will receive a higher weight for the following period. By contrast, a model performing relatively worse will receive a lower weight.

In a nutshell, DMA works as follows. Denote the one-step-ahead PL in for model within model space . The predicted weight associated with model is computed as follows,

| (28) |

where denotes a discount factor. The model updating equation then is

| (29) |

To shed more light on the discount factor: Standard (static) Bayesian model averaging is achieved by setting , as would be proportional to the (training-sample) marginal likelihood of model using data through the time . We follow Raftery et al., (2010) in specifying , indicating that receives as much weight as .

The sparse models that we consider for DMA are DL, HS∗, NG, and R2D2. MP_LIT and SHM, by contrast, are representing the dense models. Concerning lag-length, we average over VARs of order . Last but not least, we initialize the weights to be equally distributed over all considered models for the first prediction.

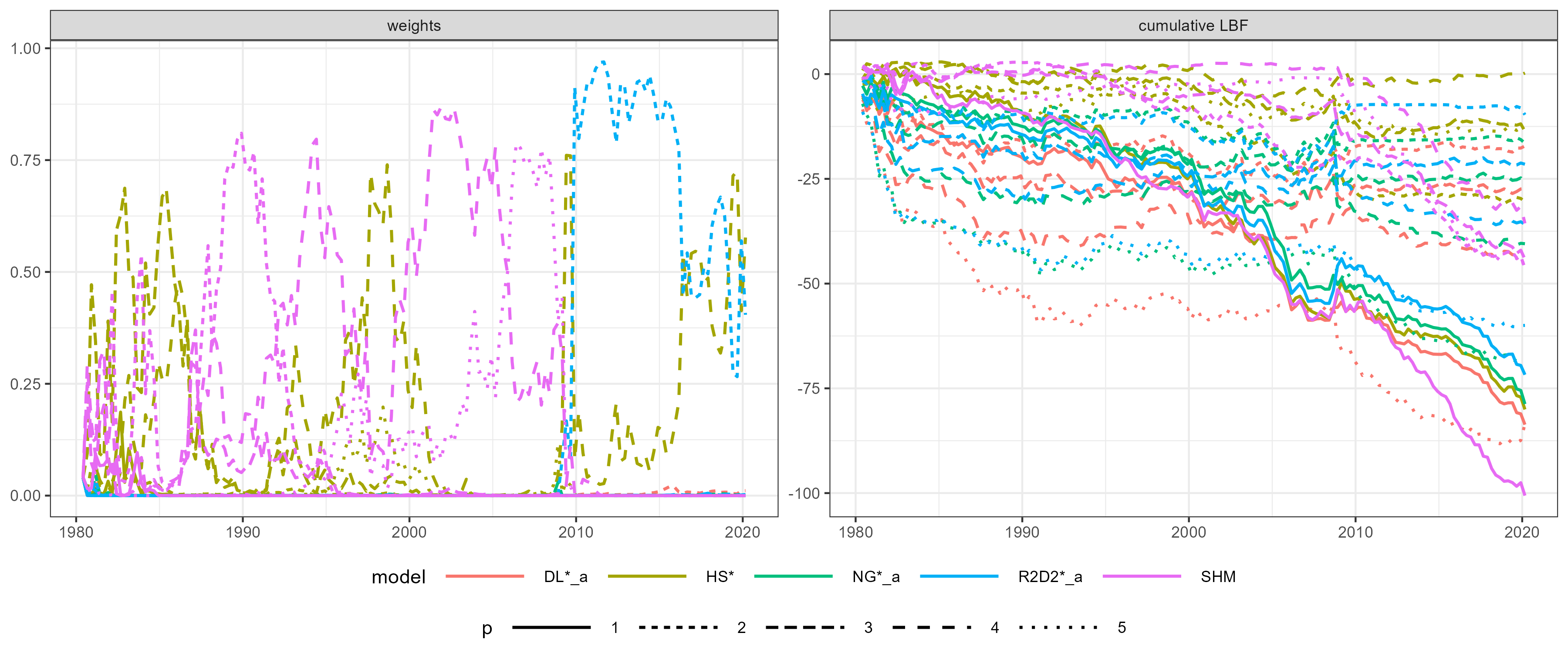

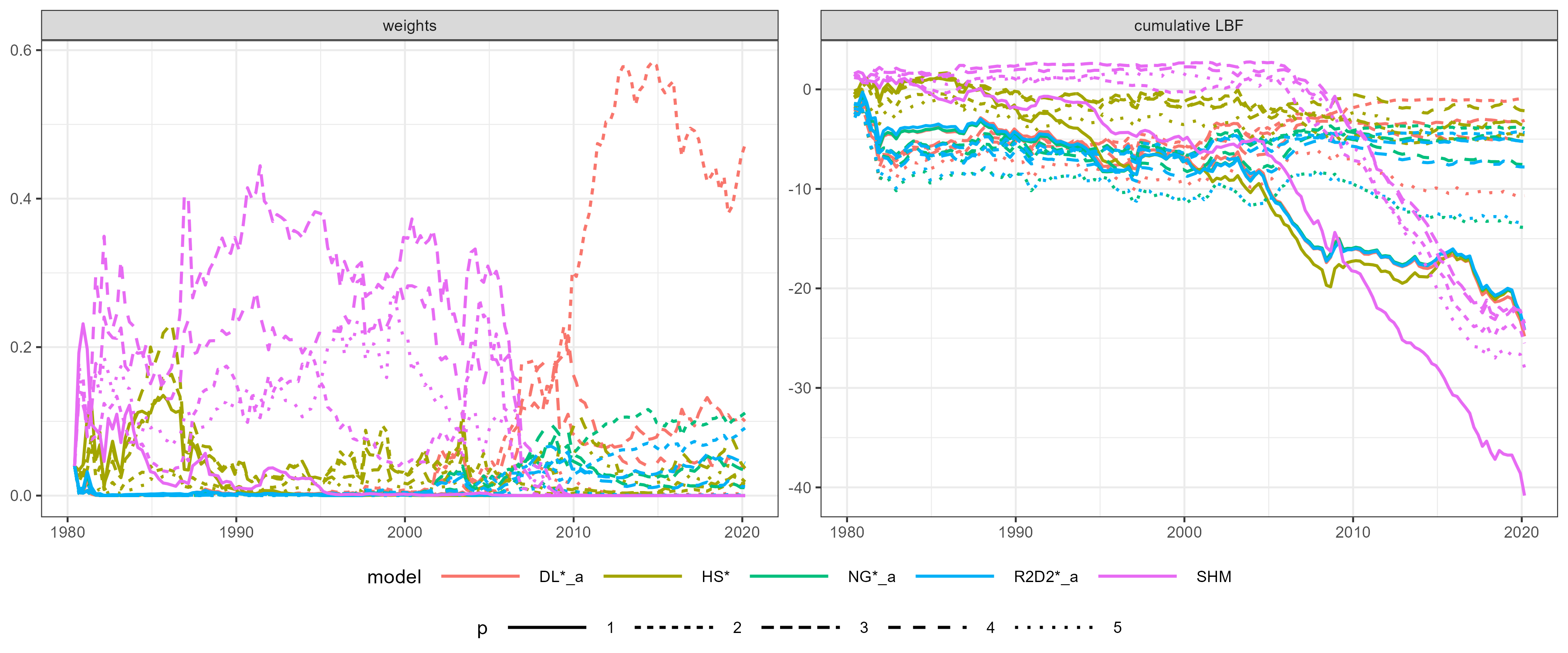

Turning towards the results, we first consider the one-step ahead predictive density of all 21 variables. Figure 7(a) shows the evolution of model weights and cumulative log Bayes factors (LBFs) of the considered models relative to DMA over the whole evaluation period. Until the end of the 2000s, SHM with and HS∗ with are dominating alternately. From 2010 up to 2015, R2D2 with two lags receives almost 100% of the weights and in the very end of the evaluation period R2D2∗ with two lags and HS∗ with four lags are sharing the weights fifty-fifty. Analyzing the cumulative LBFs, it turns out that DMA is practically never worse than any single model specification.

DMA can also improve forecasts if only a subset of variables is considered. Figure 7(b) depicts DMA model weights and cumulative LBFs relative to DMA when the predictive density of GDP, CPI and FFR is taken into account, only. By and large, the evolution of the predictive scores is similar to when all variables are considered. However, the analysis of model weights reveals that the distribution of weights over the models is now more dispersed. DL, which is practically not apparent when evaluating the full 21-dimensional predictive density, now receives the largest weights after 2010.

To sum up, model performance is not only heterogeneous over time, but also across evaluated variables. Model averaging is a very effective tool in combining the merits of various modeling techniques, in contrast to the unrewarding search for the single model that can do them all.

5.5 Sensitivity of results with respect to the prior for

In this section, we investigate the sensitivity of results w.r.t. different prior choices for . The elements in are often interpreted as contemporaneous coefficients. Hence, an obvious choice for would be to use a prior of the same family as the prior on , e.g., DL/DL on is combined with DL on . For DL on , we specify , where is the number of elements in . For NG and R2D2 on we set , such that for DL, NG, and R2D2, the concentration at zero is matched. As a second alternative, we investigate a relatively uninformative normal prior with zero mean and variance 10 for each element in , independently, which we refer to as FLAT prior. As a third option, we investigate a global(-but-not-local) shrinkage (GS) prior. More specifically, the prior is conditionally normal with zero mean and a global gamma hyperprior on the variance parameter: , . GS is similar in spirit to SHM. In combination with SHM on , then the contemporaneous coefficients represents the third distinct group besides own-lag and cross-lag coefficients.

| Prior on | Prior on | Prior on | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Prior on | HS | GS | FLAT | */* | HS | GS | FLAT | */* | HS | GS | FLAT | */* |

| MP_LIT | -18.84 | -90.87 | -57.89 | - | -7.99 | -78.46 | -68.52 | - | 0.00 | -88.61 | -61.50 | - |

| SHM | 7.74 | -70.25 | -38.87 | - | 9.88 | -70.41 | -53.82 | - | 18.45 | -77.53 | -50.24 | - |

| HS | -18.83 | -94.06 | -67.92 | -18.83 | -7.05 | -93.36 | -93.24 | -7.05 | -39.38 | -110.26 | -97.96 | -39.38 |

| DL | 10.89 | -55.09 | -39.91 | 5.71 | 24.49 | -69.40 | -62.52 | 13.78 | 2.70 | -84.44 | -65.32 | -0.16 |

| NG | 12.17 | -59.68 | -44.35 | 10.44 | 18.79 | -64.01 | -64.73 | 17.30 | -4.08 | -80.42 | -72.80 | 4.11 |

| R2D2 | 5.09 | -70.67 | -36.04 | 16.53 | 15.74 | -75.23 | -62.09 | 14.46 | 7.13 | -75.65 | -78.67 | 10.13 |

| SSVS | -29.15 | -94.68 | -75.24 | -18.81 | -38.91 | -94.92 | -101.08 | -17.65 | -55.41 | -120.77 | -116.59 | -39.28 |

| HS∗ | 23.59 | -54.07 | -21.24 | 23.59 | 40.41 | -44.08 | -30.45 | 40.41 | 54.33 | -38.14 | -17.25 | 54.33 |

| DL | 36.92 | -43.07 | -11.48 | 33.20 | 26.75 | -67.08 | -58.75 | 31.49 | 11.56 | -81.69 | -93.82 | 12.26 |

| NG | 37.59 | -48.52 | -12.96 | 41.91 | 28.14 | -55.97 | -51.76 | 37.93 | 8.69 | -72.27 | -63.34 | 21.32 |

| R2D2 | 44.37 | -42.85 | -12.77 | 42.50 | 32.56 | -59.10 | -47.42 | 37.64 | 13.31 | -58.10 | -57.82 | 21.63 |

Table 5 shows sums of one-step ahead Bayes factors for an illustrative selection of VARs. GS and FLAT on clearly deteriorates forecasting performance of all models compared to HS used in the main analysis. Interestingly, GS is even worse than FLAT, which indicates that there are few strong signals that GS simply overshrinks. GL priors and SSVS on are serious contenders to HS. NG, R2D2, and SSVS on even slightly improve the performances of NG, R2D2, and SSVS on , respectively. Overall, the results highlight the importance of a sparsity-inducing prior for . The sensitivity of forecasting performance w.r.t the prior choice for strengthen our view to use the same prior on for all models in the main analysis and also could explain to some extent the relatively weak performance of SHM in Huber and Feldkircher, (2019), where it is combined with the FLAT prior on .

6 Conclusion

Careful prior elicitation in Bayesian vectorautoregressions goes back at least to Litterman, (1986) and has been refined ever since. Our main contribution is a discussion of modern variants of prior choices, both established and novel, and a side-by-side comparison in terms of their structural (sparsity) behavior. In doing so, we borrow both from well-established (Minnesota-type) structural knowledge as well as from more automatic (shrinkage-type) approaches, thereby aiming at combining the best of both worlds. As a result of this aim, we propose what we term semi-global-local priors. We compare the various specifications in terms of their in- and out-of-sample performance on simulated data, as well as on a practically interesting (and notoriously hard) macroeconomic prediction problem. Whether sparse or dense priors fare better depends on a range of factors: the data at hand and the data transformations employed, the dimensionality of the predictive set, and the loss function used for evaluating the predictions. Finally, we investigate how dynamic model averaging can help to shed light on the temporal patterns representing historical regime shifts. It becomes clear that no single model dominates the others; much rather, we find that some models are sometimes better than others, and dynamically combining them is fruitful.

While trying to comprehensively and integratively shed light on the Illusion of Sparsity debate, we also want to point out that many questions remain unanswered. Issues left for future research include an in-depth analysis where forecasting performance between modeling reduced-form and modeling structural-form coefficients is compared side by side. Moreover, a systematic analysis of the various different approaches to modeling reduced-form VARs with time-varying variance-covariance matrices (e.g. Cholesky-SV vs. Factor-SV) is still missing. Lastly, we believe that the findings of this work could be used as a starting point for a systematic analysis of VARs with time-varying regression parameters (e.g. Bitto and Frühwirth-Schnatter,, 2019; Huber et al.,, 2019; Frühwirth-Schnatter-Schnatter and Knaus,, 2021) where the issue of choosing good shrinkage priors is exacerbated in the sense that in addition to shrinkage towards zero, shrinkage towards constancy needs to be dealt with.

References

- Bateman, (1953) Bateman, H. (1953). Higher transcendental functions, volume 1. McGraw-Hill Book Company, New York.

- Bernardi et al., (2023) Bernardi, M., Bianchi, D., and Bianco, N. (2023). Variational inference for large Bayesian vector autoregressions. arXiv:2202.12644 [econ.EM].

- Bhattacharya et al., (2015) Bhattacharya, A., Pati, D., Pillai, N. S., and Dunson, D. B. (2015). Dirichlet–Laplace priors for optimal shrinkage. Journal of the American Statistical Association, 110(512):1479–1490.

- Bitto and Frühwirth-Schnatter, (2019) Bitto, A. and Frühwirth-Schnatter, S. (2019). Achieving shrinkage in a time-varying parameter model framework. Journal of Econometrics, 210(1):75–97.

- Brown and Griffin, (2010) Brown, P. J. and Griffin, J. E. (2010). Inference with normal-gamma prior distributions in regression problems. Bayesian Analysis, 5(1):171–188.

- Carriero et al., (2022) Carriero, A., Chan, J., Clark, T. E., and Marcellino, M. (2022). Corrigendum to “Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors” [j. econometrics 212 (1) (2019) 137–154]. Journal of Econometrics, 227(2):506–512.

- Carriero et al., (2019) Carriero, A., Clark, T. E., and Marcellino, M. (2019). Large Bayesian vector autoregressions with stochastic volatility and non-conjugate priors. Journal of Econometrics, 212(1):137–154.

- Carvalho et al., (2010) Carvalho, C. M., Polson, N. G., and Scott, J. G. (2010). The horseshoe estimator for sparse signals. Biometrika, 97(2):465–480.

- (9) Chan, J. C. C. (2021a). Comparing stochastic volatility specifications for large Bayesian VARs. https://joshuachan.org/papers/ML-LargeVARSV.pdf ; accessed: 2021-05-19.

- (10) Chan, J. C. C. (2021b). Minnesota-type adaptive hierarchical priors for large Bayesian VARs. International Journal of Forecasting, 37(3):1212–1226.

- Chan et al., (2021) Chan, J. C. C., Koop, G., and Yu, X. (2021). Large order-invariant Bayesian VARs with stochastic volatility. arXiv:2111.07225 [econ.EM].

- Cogley and Sargent, (2005) Cogley, T. and Sargent, T. J. (2005). Drifts and volatilities: monetary policies and outcomes in the post WWII US. Review of Economic Dynamics, 8(2):262–302.

- Cross et al., (2020) Cross, J. L., Hou, C., and Poon, A. (2020). Macroeconomic forecasting with large Bayesian VARs: Global-local priors and the illusion of sparsity. International Journal of Forecasting, 36(3):899–915.

- Eddelbuettel and François, (2011) Eddelbuettel, D. and François, R. (2011). Rcpp: Seamless R and C++ integration. Journal of Statistical Software, 40(8):1–18.

- Eddelbuettel and Sanderson, (2014) Eddelbuettel, D. and Sanderson, C. (2014). Rcpparmadillo: Accelerating R with high-performance C++ linear algebra. Computational Statistics and Data Analysis, 71:1054–1063.

- Fava and Lopes, (2021) Fava, B. and Lopes, H. F. (2021). The illusion of the illusion of sparsity: An exercise in prior sensitivity. Brazilian Journal of Probability and Statistics, 35(4):699–720.

- Follett and Yu, (2019) Follett, L. and Yu, C. (2019). Achieving parsimony in Bayesian vector autoregressions with the horseshoe prior. Econometrics and Statistics, 11:130–144.

- Frühwirth-Schnatter-Schnatter and Knaus, (2021) Frühwirth-Schnatter-Schnatter, S. and Knaus, P. (2021). Sparse Bayesian state-space and time-varying parameter models. In Tadesse, M. G. and Vannucci, M., editors, Handbook of Bayesian Variable Selection, pages 297–326. Chapman & Hall.

- George et al., (2008) George, E. I., Sun, D., and Ni, S. (2008). Bayesian stochastic search for VAR model restrictions. Journal of Econometrics, 142(1):553–580.

- Geweke and Amisano, (2010) Geweke, J. and Amisano, G. (2010). Comparing and evaluating Bayesian predictive distributions of asset returns. International Journal of Forecasting, 26(2):216–230.

- Giannone et al., (2015) Giannone, D., Lenza, M., and Primiceri, G. E. (2015). Prior selection for vector autoregressions. The Review of Economics and Statistics, 97(2):436–451.

- Giannone et al., (2021) Giannone, D., Lenza, M., and Primiceri, G. E. (2021). Economic predictions with big data: The illusion of sparsity. Econometrica, 89(5):2409–2437.

- Hosszejni and Kastner, (2021) Hosszejni, D. and Kastner, G. (2021). Modeling univariate and multivariate stochastic volatility in R with stochvol and factorstochvol. Journal of Statistical Software, 100:1–34.

- Hoyer, (2004) Hoyer, P. O. (2004). Non-negative matrix factorization with sparseness constraints. The Journal of Machine Learning Research, 5:1457–1469.

- Huber and Feldkircher, (2019) Huber, F. and Feldkircher, M. (2019). Adaptive shrinkage in Bayesian vector autoregressive models. Journal of Business & Economic Statistics, 37(1):27–39.

- Huber et al., (2019) Huber, F., Kastner, G., and Feldkircher, M. (2019). Should I stay or should I go? A latent threshold approach to large-scale mixture innovation models. Journal of Applied Econometrics, 34(5):621–640.

- Jacquier et al., (1994) Jacquier, E., Polson, N. G., and Rossi, P. E. (1994). Bayesian analysis of stochastic volatility models. Journal of Business & Economic Statistics, 12(4):371–389.

- Kastner, (2019) Kastner, G. (2019). Sparse Bayesian time-varying covariance estimation in many dimensions. Journal of Econometrics, 210(1):98–115.

- Kastner and Frühwirth-Schnatter, (2014) Kastner, G. and Frühwirth-Schnatter, S. (2014). Ancillarity-sufficiency interweaving strategy (ASIS) for boosting MCMC estimation of stochastic volatility models. Computational Statistics & Data Analysis, 76:408–423.

- Kastner and Huber, (2020) Kastner, G. and Huber, F. (2020). Sparse Bayesian vector autoregressions in huge dimensions. Journal of Forecasting, 39(7):1142––1165.

- Kim et al., (1998) Kim, S., Shephard, N., and Chib, S. (1998). Stochastic volatility: Likelihood inference and comparison with ARCH models. The Review of Economic Studies, 65(3):361–393.

- Koop and Korobilis, (2010) Koop, G. and Korobilis, D. (2010). Bayesian multivariate time series methods for empirical macroeconomics. Foundations and Trends® in Econometrics, 3(4):267–358.

- Koop and Korobilis, (2012) Koop, G. and Korobilis, D. (2012). Forecasting inflation using dynamic model averaging. International Economic Review, 53(3):867–886.

- Koop, (2013) Koop, G. M. (2013). Forecasting with medium and large Bayesian VARs. Journal of Applied Econometrics, 28(2):177–203.

- Leydold and Hörmann, (2022) Leydold, J. and Hörmann, W. (2022). GIGrvg: Random Variate Generator for the GIG Distribution. R package version 0.7.

- Litterman, (1986) Litterman, R. B. (1986). Forecasting with Bayesian vector autoregressions: Five years of experience. Journal of Business & Economic Statistics, 4(1):25–38.

- Luo and Griffin, (2022) Luo, Y. and Griffin, J. E. (2022). Bayesian methods of vector autoregressions with tensor decompositions. arXiv:2211.01727 [stat.ME].

- Lütkepohl, (2005) Lütkepohl, H. (2005). New Introduction to Multiple Time Series Analysis. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Makalic and Schmidt, (2016) Makalic, E. and Schmidt, D. F. (2016). A simple sampler for the horseshoe estimator. IEEE Signal Processing Letters, 23(1):179–182.

- Mathai et al., (2009) Mathai, A. M., Saxena, R. K., and Haubold, H. J. (2009). The H-function: theory and applications. Springer Science & Business Media.

- McCracken and Ng, (2021) McCracken, M. W. and Ng, S. (2021). FRED-QD: A quarterly database for macroeconomic research. Federal Reserve Bank of St. Louis Review, 103(1):1–44.

- Onorante and Raftery, (2016) Onorante, L. and Raftery, A. E. (2016). Dynamic model averaging in large model spaces using dynamic Occam’s window. European Economic Review, 81:2–14.

- Polson and Scott, (2011) Polson, N. G. and Scott, J. G. (2011). Shrink globally, act locally: Sparse Bayesian regularization and prediction. In Bernardo, J. M., Bayarri, M. J., Berger, J. O., Dawid, A. P., Heckerman, D., Smith, A. F. M., and West, M., editors, Bayesian Statistics 9: Proceedings of the Ninth Valencia International Meeting, pages 501–538, Oxford, UK. Oxford University Press.

- R Core Team, (2022) R Core Team (2022). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- Raftery et al., (2010) Raftery, A. E., Kárný, M., and Ettler, P. (2010). Online prediction under model uncertainty via dynamic model averaging: Application to a cold rolling mill. Technometrics, 52(1):52–66. PMID: 20607102.

- Sims and Zha, (1998) Sims, C. A. and Zha, T. (1998). Bayesian methods for dynamic multivariate models. International Economic Review, 39(4):949–968.

- Stock and Watson, (2012) Stock, J. H. and Watson, M. W. (2012). Disentangling the Channels of the 2007–09 Recession. Brookings Papers on Economic Activity, pages 81–156.

- West, (2020) West, M. (2020). Bayesian forecasting of multivariate time series: scalability, structure uncertainty and decisions. Annals of the Institute of Statistical Mathematics, 72(1).

- Yu and Meng, (2011) Yu, Y. and Meng, X.-L. (2011). To center or not to center: That is not the question—an ancillarity–sufficiency interweaving strategy (ASIS) for boosting MCMC efficiency. Journal of Computational and Graphical Statistics, 20(3):531–570.

- Zhang et al., (2022) Zhang, Y. D., Naughton, B. P., Bondell, H. D., and Reich, B. J. (2022). Bayesian regression using a prior on the model fit: The R2-D2 shrinkage prior. Journal of the American Statistical Association, 117(538):862–874.

- Zhou and Carin, (2012) Zhou, M. and Carin, L. (2012). Negative binomial process count and mixture modeling. arXiv:1209.3442v1 [stat.ME].

- Zwillinger and Jeffrey, (2007) Zwillinger, D. and Jeffrey, A. (2007). Table of integrals, series, and products. Elsevier.

Appendix A Proof of Theorem 3.1.

In order to prove Theorem 3.1, we first have to establish the densities of the priors marginalized over the local scale .

Proposition A.1.

Given the DL prior (10), the density of for any , , marginalized over the local scale , is given by

| (A.1) |

where is the modified Bessel function of the second kind.888Modified Bessel function of the second kind: .

Proof.

Cf. Bhattacharya et al., (2015). ∎

Proposition A.2.

Given the NG prior (11), the density of for any , , marginalized over the local scale , is given by

| (A.2) |

Proof.

∎

Proposition A.3.

Proof.

The Meijer-G function nests many functions as special cases, e.g. . Hence,

The last equality follows from 9.31.(5) in Zwillinger and Jeffrey, (2007). Now, let . Then,

The last equality follows from 7.813.(2) in Zwillinger and Jeffrey, (2007).

The last equality follows from 9.31.(2) in Zwillinger and Jeffrey, (2007). ∎

Proposition A.4.

Given the HS prior (14), the density of for any , , marginalized over the local scales , is given by

| (A.6) |

where is the exponential integral function.

Proof.

Cf. Carvalho et al., (2010). ∎

Proof of Theorem 3.1a).

For (16) cf. Zhang et al., (2022), for (19) cf. Carvalho et al., (2010). (20) and (21) are standard and hence not derived.

(17): According to 10.25.3 in https://dlmf.nist.gov/10.25, when both and are real, if , then . Then as , using Proposition A.2,

Proof of Theorem 3.1b).

Case : According to 10.30.3 in https://dlmf.nist.gov/10.30, when , , . Given , , using Proposition A.1,

(23): Case : According to 10.27.3 in https://dlmf.nist.gov/10.27 . Moreover, according to 10.30.2 in https://dlmf.nist.gov/10.30, when , and is real, . Given , , using Proposition A.2,

Case : According 10.30.3 in https://dlmf.nist.gov/10.30, when , , . Given , , using Proposition A.2,

Appendix B A note on posterior estimation

Efficient computer implementations of all posterior samplers discussed in this paper are conveniently bundled into the R (R Core Team,, 2022) package bayesianVARs, interfacing to C/C++ via Rcpp (Eddelbuettel and François,, 2011) and RcppArmadillo (Eddelbuettel and Sanderson,, 2014) for increased computational efficiency. The package can be freely downloaded at https://github.com/luisgruber/bayesianVARs. In what is to follow, we thus refrain from describing the various posterior samplers in detail. Instead, we provide their main building blocks only: the necessary conditionals used for Gibbs sampling.