Adversarial Counterfactual Environment Model Learning

Abstract

An accurate environment dynamics model is crucial for various downstream tasks, such as counterfactual prediction, off-policy evaluation, and offline reinforcement learning. Currently, these models were learned through empirical risk minimization (ERM) by step-wise fitting of historical transition data. However, we first show that, particularly in the sequential decision-making setting, this approach may catastrophically fail to predict counterfactual action effects due to the selection bias of behavior policies during data collection. To tackle this problem, we introduce a novel model-learning objective called adversarial weighted empirical risk minimization (AWRM). AWRM incorporates an adversarial policy that exploits the model to generate a data distribution that weakens the model’s prediction accuracy, and subsequently, the model is learned under this adversarial data distribution. We implement a practical algorithm, GALILEO, for AWRM and evaluate it on two synthetic tasks, three continuous-control tasks, and a real-world application. The experiments demonstrate that GALILEO can accurately predict counterfactual actions and improve various downstream tasks, including offline policy evaluation and improvement, as well as online decision-making.

1 Introduction

A good environment dynamics model for action-effect prediction is essential for many downstream tasks. For example, humans or agents can leverage this model to conduct simulations to understand future outcomes, evaluate other policies’ performance, and discover better policies. With environment models, costly real-world trial-and-error processes can be avoided. These tasks are vital research problems in counterfactual predictions Swaminathan and Joachims (2015); Alaa and van der Schaar (2018), off-policy evaluation (OPE) Liu et al. (2018); Nachum et al. (2019), and offline reinforcement learning (Offline RL) Levine et al. (2020); Yu et al. (2020). In these problems, the core role of the models is to answer queries on counterfactual data unbiasedly, that is, given states, correctly answer what might happen if we were to carry out actions unseen in the training data. However, addressing counterfactual queries differentiates environment model learning from standard supervised learning (SL), which directly fits the offline dataset for empirical risk minimization (ERM). In essence, the problem involves training the model on one dataset and testing it on another with a shifted distribution, specifically, the dataset generated by counterfactual queries. This challenge surpasses the SL’s capability as it violates the independent and identically distributed (i.i.d.) assumption Levine et al. (2020).

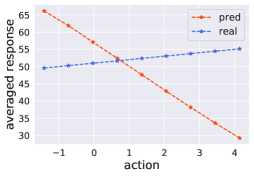

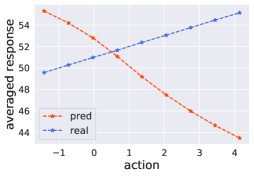

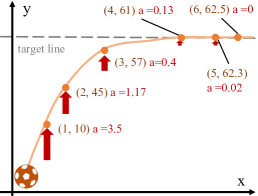

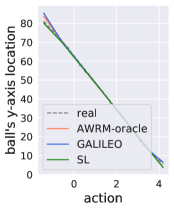

In this paper, we concentrate on faithful dynamics model learning in sequential decision-making settings like RL. Specifically, we first highlight a distinct situation of distribution shift that can easily lead to catastrophic failures in the model’s predictions: In many real-world applications, offline data is often gathered using a single policy with exhibiting selection bias, meaning that, for each state, actions are chosen unfairly. As illustrated in Fig. 1(a), to maintain the ball’s trajectory along a target line, a behavior policy applies a smaller force when the ball’s location is nearer to the target line. When a dataset is collected with such selection bias, the association between the states (location) and actions (force) will make SL hard to identify the correct causal relationship of the states and actions to the next states respectively (see Fig. 1(c)). Then when we query the model with counterfactual data, the predictions might be catastrophic failures. The selection bias can be regarded as an instance of the distributional-shift problem in offline model-based RL, which has also received great attention Levine et al. (2020); Yu et al. (2020); Chen et al. (2021); Lu et al. (2022). However, previous methods employing naive supervised learning for environment model learning tend to overlook this issue during the learning process, addressing it instead by limiting policy exploration and learning in high-risk regions. So far, how to learn a faithful environment model that can alleviate the problem directly has rarely been discussed.

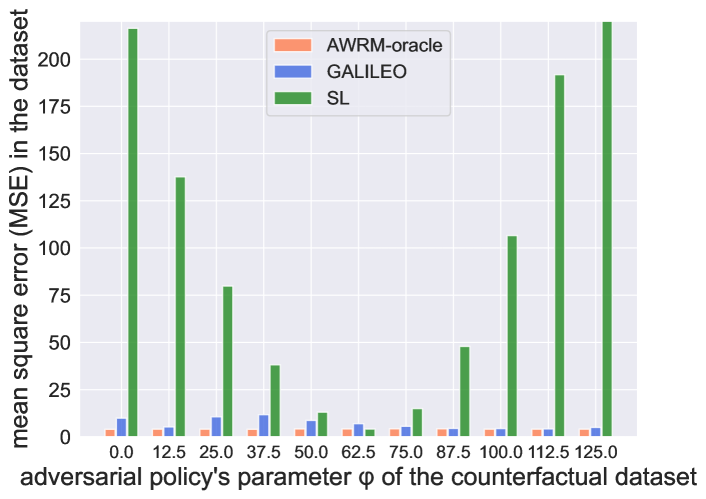

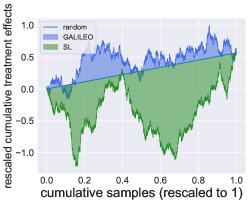

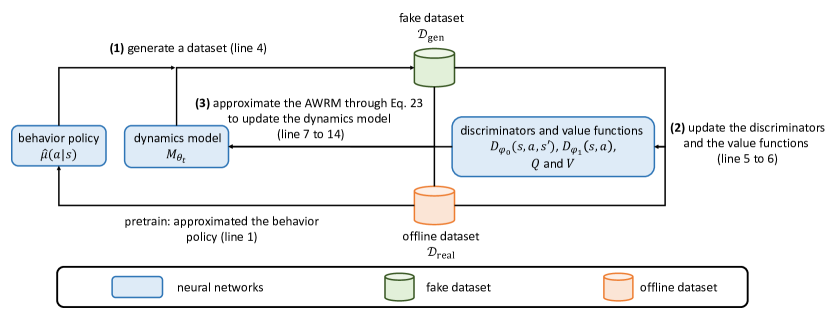

In this work, for faithful environment model learning, we first introduce weighted empirical risk minimization (WERM), which is a typical solution to solve the selection bias problem in causal inference for individual treatment effects (ITEs) estimation in many scenarios like patients’ treatment selection Imbens (1999); Alaa and van der Schaar (2018). ITEs measure the effects of treatments on individuals by administering treatments uniformly and evaluating the differences in outcomes. To estimate ITEs from offline datasets with selection bias, they estimate an inverse propensity score (IPS) to reweight the training data, approximating the data distribution under a uniform policy, and train the model under this reweighted distribution. Compared with ITEs estimation, the extra challenge of faithful model learning in sequential decision-making settings include: (1) the model needs to answer queries on numerous different policies, resulting in various and unknown target data distributions for reweighting, and (2) the IPS should account for the cumulative effects of behavior policies on state distribution rather than solely focusing on bias of actions. To address these issues, we propose an objective called adversarial weighted empirical risk minimization (AWRM). For each iteration, AWRM employs adversarial policies to construct an adversarial counterfactual dataset that maximizes the model’s prediction error, and drive the model to reduce the prediction risks under the adversarial counterfactual data distribution. However, obtaining the adversarial counterfactual data distribution is infeasible in the offline setting. Therefore, we derive an approximation of the counterfactual data distribution queried by the optimal adversarial policy and provide a tractable solution to learn a model from the approximated data distribution. As a result, we propose a practical approach named Generative Adversarial offLIne counterfactuaL Environment mOdel learning (GALILEO) for AWRM. Fig. 2 illustrates the difference in the prediction errors learned by these algorithms.

Experiments are conducted in two synthetic tasks, three continuous-control tasks, and a real-world application. We first verify that GALILEO can make accurate predictions on counterfactual data queried by other policies compared with baselines. We then demonstrate that the model learned by GALILEO is helpful to several downstream tasks including offline policy evaluation and improvement, and online decision-making in a large-scale production environment.

2 Preliminaries

We first introduce weighted empirical risk minimization (WERM) through inverse propensity scoring (IPS), which is commenly used in individualized treatment effects (ITEs) estimation Rosenbaum and Rubin (1983). It can be regarded as a scenario of single-step model learning . We define as the one-step environment, where denotes the state vector containing pre-treatment covariates (such as age and weight), denotes the treatment variable which is the action intervening with the state , and is the feedback of the environment. When the offline dataset is collected with a behavior policy which has selection bias, a classical solution to handle the above problem is WERM through IPS Shimodaira (2000); Assaad et al. (2021); Jung et al. (2020):

Definition 2.1.

The learning objective of WERM through IPS is formulated as

| (1) |

where , and denote the policies in testing and training domains, and the joint probability in which is the distribution of state. is the model space. is a loss function.

The is also known as importance sampling (IS) weight, which corrects the sampling bias by aligning the training data distribution with the testing data. By selecting different to approximate to learn the model , current environment model learning algorithms employing reweighting are fallen into the framework. For standard ITEs estimation, (i.e., is a uniform policy) for balancing treatments, where is an approximated behavior policy . Note that it is a reasonable weight in ITEs estimation: ITEs are defined to evaluate the differences of effect on each state under a uniform policy.

In sequential decision-making setting, decision-making processes in a sequential environment are often formulated into Markov Decision Process (MDP) Sutton and Barto (1998). MDP depicts an agent interacting with the environment through actions. In the first step, states are sampled from an initial state distribution . Then at each time-step , the agent takes an action through a policy based on the state , then the agent receives a reward from a reward function and transits to the next state given by a transition function built in the environment. , , and denote the policy, state, and action spaces.

3 Related Work

We give related adversarial algorithms for model learning in the following and leave other related work in Appx. F. In particular, in ITEs estimation, GANTIE Yoon et al. (2018) uses a generator to fill counterfactual outcomes for each data pair and a discriminator to judge the source (treatment group or control group) of the filled data pair. The generator is trained to minimize the output of the discriminator. Bica et al. (2020) propose SCIGAN to extend GANITE to continuous ITEs estimation via a hierarchical discriminator architecture. In real-world applications, environment model learning based on Generative Adversarial Imitation Learning (GAIL) has also been adopted for sequential decision-making problems Ho and Ermon (2016). GAIL is first proposed for policy imitation Ho and Ermon (2016), which uses the imitated policy to generate trajectories by interacting with the environment. The policy is learned with the trajectories through RL which maximizes the cumulative rewards given by the discriminator. Shi et al. (2019); Chen et al. (2019) use GAIL for environment model learning by regarding the environment model as the generator and the behavior policy as the “environment” in standard GAIL. Eysenbach et al. (2021) further inject the technique into a unified objective for model-based RL, which joints model and policy optimization. Our study reveals the connection between adversarial model learning and the WERM through IPS, where previous adversarial model learning methods can be regarded as partial implementations of GALILEO, explaining the effectiveness of the former.

4 Adversarial Counterfactual Environment Model Learning

In this section, we first propose a new offline model-learning objective for sequential decision-making setting in Sec. 4.1; In Sec. 4.2, we give a surrogate objective to the proposed objective; Finally, we give a practical solution in Sec. 4.3.

4.1 Problem Formulation

In scenarios like offline policy evaluation and improvement, it is crucial for the environment model to have generalization ability in counterfactual queries, as we need to query accurate feedback from for numerous different policies. Referring to the formulation of WERM through IPS in Def. 1, these requirements necessitate minimizing counterfactual-query risks for under multiple unknown policies, rather than focusing on a specific target policy . More specifically, the question is: If is unknown and can be varied, how can we generally reduce the risks in counterfactual queries? In this article, we call the model learning problem in this setting “counterfactual environment model learning” and propose a new objective to address the issue. To be compatible with multi-step environment model learning, we first define a generalized WERM through IPS based on Def. 1:

Definition 4.1.

In an MDP, given a transition function that satisfies and satisfies , the learning objective of generalized WERM through IPS is:

| (2) |

where , and the training and testing data distributions collected by policy and respectively. We define for brevity.

In an MDP, for any given policy , we have where denotes the occupancy measure of for policy . This measure can be defined as Sutton and Barto (1998); Ho and Ermon (2016) where is the discounted state visitation probability that the policy visits at time-step by executing in the environment and starting at the state . Here is the discount factor. We also define for simplicity.

With this definition, can be rewritten: . In single-step environments, for any policy , . Consequently, we obtain , and the objective degrade to Eq. (1). Therefore, Def. 1 is a special case of this generalized form.

Remark 4.2.

is referred to as density ratio and is commonly used to correct the weighting of rewards in off-policy datasets to estimate the value of a specific target policy in off-policy evaluation Nachum et al. (2019); Zhang et al. (2020). Recent studies in offline RL also provide similar evidence through upper bound analysis, suggesting that offline model learning should be corrected to specific target policies’ distribution using Yang et al. (2022). We derive the objective from the perspective of selection bias correlation, further demonstrate the necessity and effects of this term.

In contrast to previous studies, in this article, we would like to propose an objective for faithful model learning which can generally reduce the risks in counterfactual queries in scenarios where is unknown and can be varied. To address the problem, we introduce adversarial policies that can iteratively induce the worst prediction performance of the current model and propose to optimize WERM under the adversarial policies. In particular, we propose Adversarial Weighted empirical Risk Minimization (AWRM) based on Def. 4.1 to handle this problem.

Definition 4.3.

Given the MDP transition function , the learning objective of adversarial weighted empirical risk minimization through IPS is formulated as

| (3) |

where , and the re-weighting term is conditioned on the distribution of the adversarial policy . In the following, we will ignore and use for brevity.

In a nutshell, Eq. (3) minimizes the maximum model loss under all counterfactual data distributions to guarantee the generalization ability for counterfactual queried by policies in .

4.2 Surrogate AWRM through Optimal Adversarial Data Distribution Approximation

The main challenge of solving AWRM is constructing the data distribution of the best-response policy in since obtaining additional data from can be expensive in real-world applications. In this paper, instead of deriving the optimal , our solution is to offline estimate the optimal adversarial distribution with respect to , enabling the construction of a surrogate objective to optimize without directly querying the real environment .

In the following, we select as the negative log-likelihood loss for our full derivation, instantiating in Eq. (3) as: , where denotes . Ideally, for any given , it is obvious that the optimal is the one that makes assign all densities to the point with the largest negative log-likelihood. However, this maximization process is impractical, particularly in continuous spaces. To provide a tractable yet relaxed solution, we introduce an regularizer to the original objective in Eq. (3).

| (4) |

where denotes the regularization coefficient of and .

Now we present the final results and the intuitions behind them, while providing a full derivation in Appx.A. Suppossing we have representing the approximated data distribution of the approximated best-response policy under model parameterized by , we can find the optimal of (Eq. (4)) through iterative optimization of the objective . To this end, we approximate via the last-iteration model and derive an upper bound objective for :

| (5) |

where denotes , is a convex and lower semi-continuous (l.s.c.) function satisfying , which is also called function in -divergence Ali and Silvey (1966), , and denotes the entropy of .

Remark 4.4 (Intuition of ).

After derivation, we found that the optimal adversarial data distribution can be approximated by (see Appx. A), leading to the upper-bound objective Eq. (5), which is a WERM dynamically weighting by . Intuitively, assigns more learning propensities for data points with (1) larger discrepancy between (generated by model) and (real-data distribution), or (2) larger stochasticity of the real model . The latter is contributed by the entropy , while the former is contributed by the first two terms combined. In particular, through the definition of -divergence, we known that the discrepancy of two distribution and can be measured by , thus the terms can be interpreted as the discrepancy measure unit between and , while serves as a baseline on and measured by to balance the discrepancy contributed by and , making focus on errors on .

In summary, by adjusting the weights , the learning process will iteratively exploit subtle errors of the current model in any data point, regardless of how many proportions it contributes in the original data distribution, to eliminate potential unidentifiability on counterfactual data caused by selection bias.

4.3 Tractable Solution

In Eq. (5), the terms are still intractable. Thanks to previous successful practices in GAN Goodfellow et al. (2014) and GAIL Ho and Ermon (2016), we achieve the objective via a generator-discriminator-paradigm objective through similar derivation. We show the results as follows and leave the complete derivation in Appx. A.4. In particular, by introducing two discriminators and , we can optimize the surrogate objective Eq. (5) via:

| (6) |

where is a simplification of , , and and are the parameters of and respectively. We learn a policy via imitation learning based on the offline dataset Pomerleau (1991); Ho and Ermon (2016). Note that in the process, we ignore the term for simplifying the objective. The discussion on the impacts of removing is left in App. B.

In Eq. (6), the reweighting term from Eq. (5) is split into two terms in the RHS of the equation: the first term is a GAIL-style objective Ho and Ermon (2016), treating as the policy generator, as the environment, and as the advantage function, while the second term is WERM through . The first term resembles the previous adversarial model learning objectives Shang et al. (2019); Shi et al. (2019); Chen et al. (2019). These two terms have intuitive explanations: the first term assigns learning weights on data generated by the model . If the predictions of the model appear realistic, mainly assessed by , the propensity weights would be increased, encouraging the model to generate more such kind of data; Conversely, the second term assigns weights on real data generated by . If the model’s predictions seem unrealistic (mainly assessed by ) or stochastic (evaluated by ), the propensity weights will be increased, encouraging the model to pay more attention to these real data points when improving the likelihoods.

Based on the above implementations, we propose Generative Adversarial offLIne counterfactuaL Environment mOdel learning (GALILEO) for environment model learning. We list a brief of GALILEO in Alg. 1 and the details in Appx. E.

Input:

: offline dataset sampled from where is the behavior policy; : total iterations;

Process:

5 Experiments

In this section, we first conduct experiments in two synthetic environments to quantify the performance of GALILEO on counterfactual queries 111code https://github.com/xionghuichen/galileo.. Then we deploy GALILEO in two complex environments: MuJoCo in Gym Todorov et al. (2012) and a real-world food-delivery platform to test the performance of GALILEO in difficult tasks. The results are in Sec. 5.2. Finally, to further verify the abiliy GALILEO, in Sec. 5.3, we apply models learned by GALILEO to several downstream tasks including off-policy evaluation, offline policy improvement, and online decision-making in production environment. The algorithms compared are: (1) SL: using standard empirical risk minimization for model learning; (2) IPW Spirtes (2010): a standard implementation of WERM based IPS; (3) SCIGAN Bica et al. (2020): an adversarial algorithms for model learning used for causal effect estimation, which can be roughly regarded as a partial implementation of GALILEO (Refer to Appx. E.2). We give a detailed description in Appx. G.2.

5.1 Environment Settings

Synthetic Environments

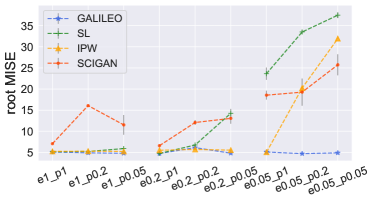

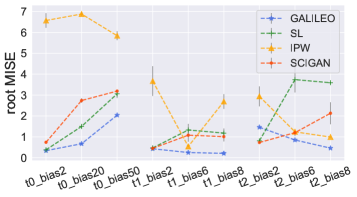

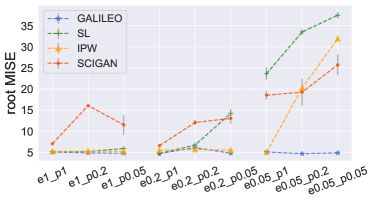

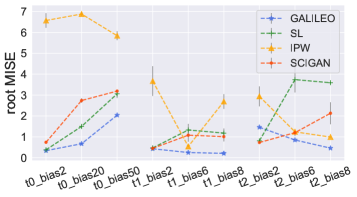

Previous experiments on counterfactual environment model learning are based on single-step semi-synthetic data simulation Bica et al. (2020). As GALILEO is compatible with single-step environment model learning, we first benchmark GALILEO in the same task named TCGA as previous studies do Bica et al. (2020). Based on the three synthetic response functions, we construct 9 tasks by choosing different parameters of selection bias on which is constructed with beta distribution, and design a coefficient to control the selection bias. We name the tasks with the format of “t?_bias?”. For example, t1_bias2 is the task with the first response functions and . The details of TCGA is in Appx. G.1.2. Besides, for sequential environment model learning under selection bias, we construct a new synthetic environment, general negative feedback control (GNFC), which can represent a classic type of task with policies having selection bias, where Fig. 1(a) is also an instance of GNFC. We construct 9 tasks on GNFC by adding behavior policies with different scales of uniform noise with probabilities . Similarly, we name them with the format “e?_p?”.

Continuous-control Environments

We select 3 MuJoCo environments from D4RL Fu et al. (2020) to construct our model learning tasks. We compare it with a standard transition model learning algorithm used in the previous offline model-based RL algorithms Yu et al. (2020); Kidambi et al. (2020), which is a standard supervised learning. We name the method OFF-SL. Besides, we also implement IPW and SCIGAN as the baselines. In D4RL benchmark, only the “medium” tasks is collected with a fixed policy, i.e., the behavior policy is with 1/3 performance to the expert policy), which is most matching to our proposed problem. So we train models in datasets HalfCheetah-medium, Walker2d-medium, and Hopper-medium.

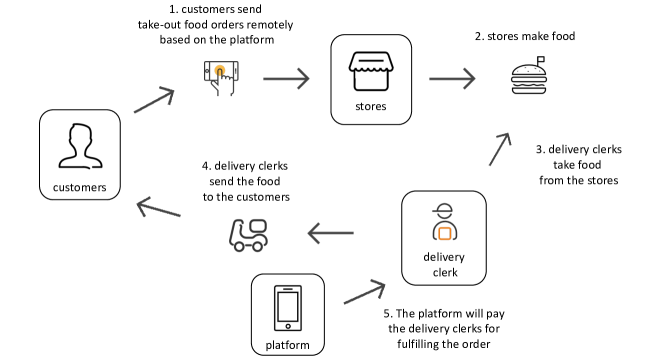

A Real-world Large-scale Food-delivery Platform

We finally deploy GALILEO in a real-world large-scale food-delivery platform. We focus on a Budget Allocation task to the Time period (BAT) in the platform (see Appx. G.1.3 for details). The goal of the BAT task is to handle the imbalance problem between the demanded orders from customers and the supply of delivery clerks in different time periods by allocating reasonable allowances to those time periods. The challenge of the environment model learning in BAT tasks is similar to the challenge in Fig. 1: the behavior policy is a human-expert policy, which tends to increase the budget of allowance in the time periods with a lower supply of delivery clerks, otherwise tends to decrease the budget (We gives a real-data instance in Appx. G.1.3).

5.2 Prediction Accuracy on Shifted Data Distributions

Test in Synthetic Environments

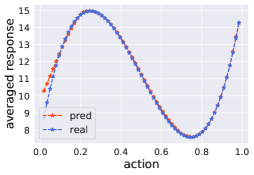

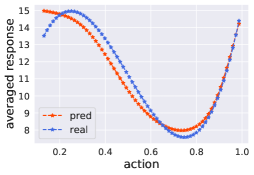

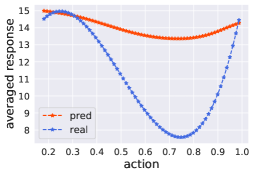

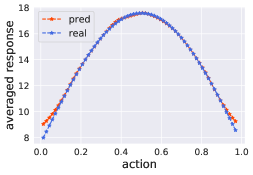

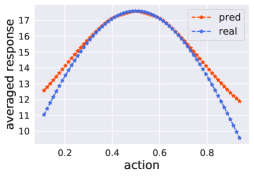

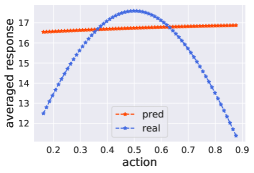

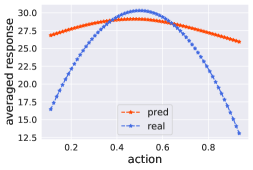

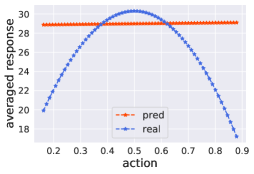

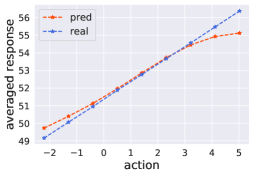

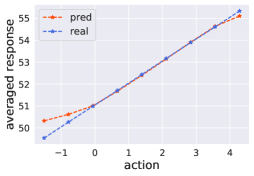

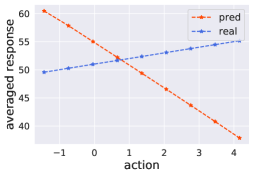

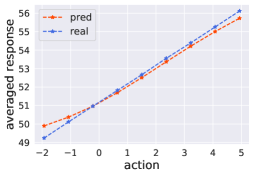

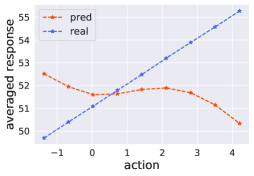

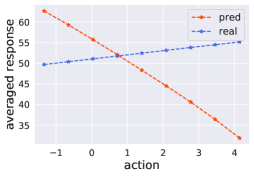

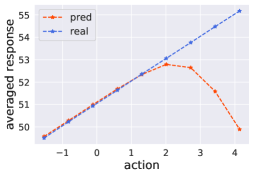

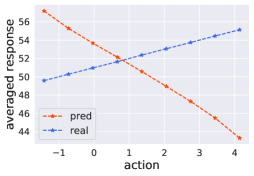

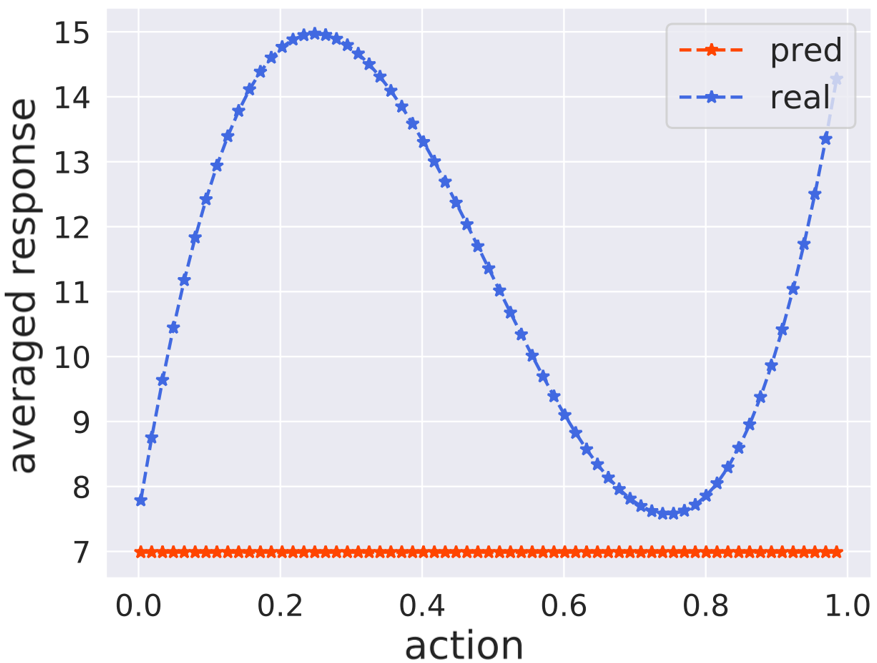

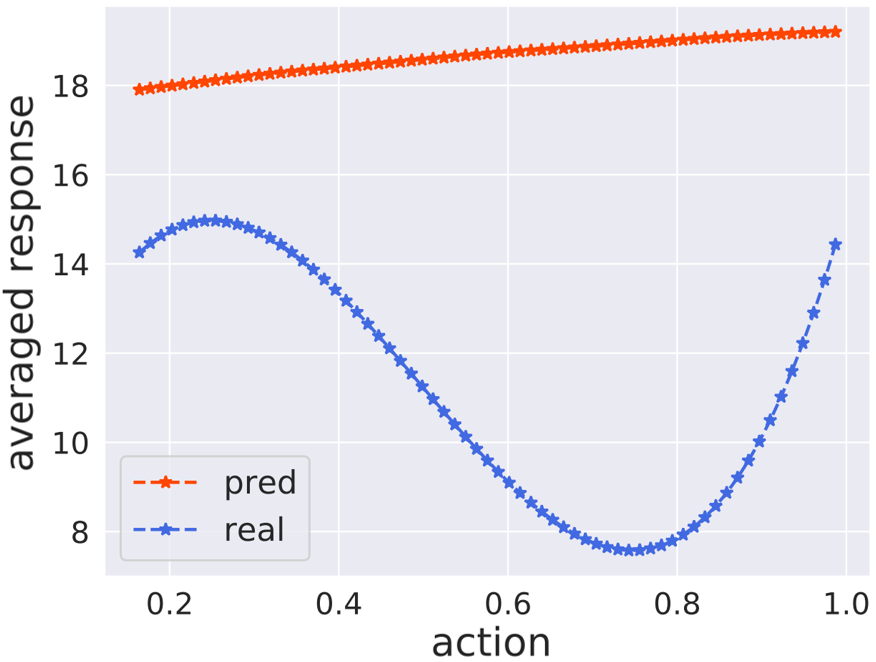

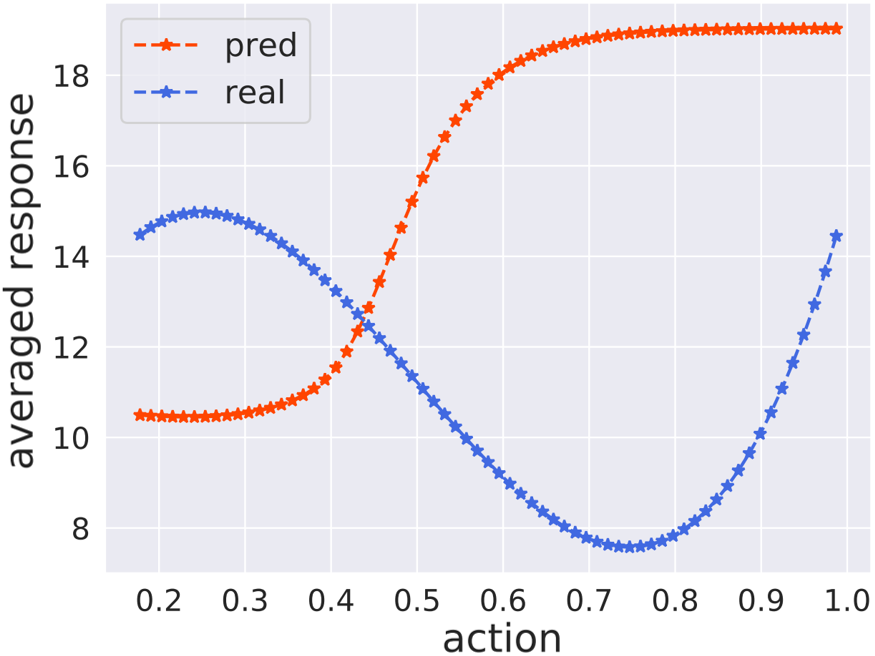

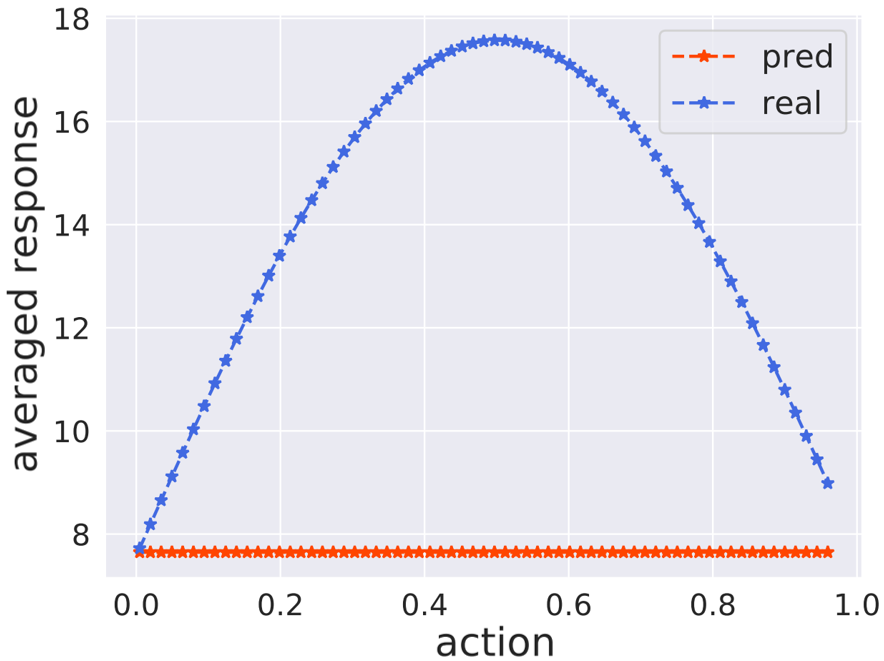

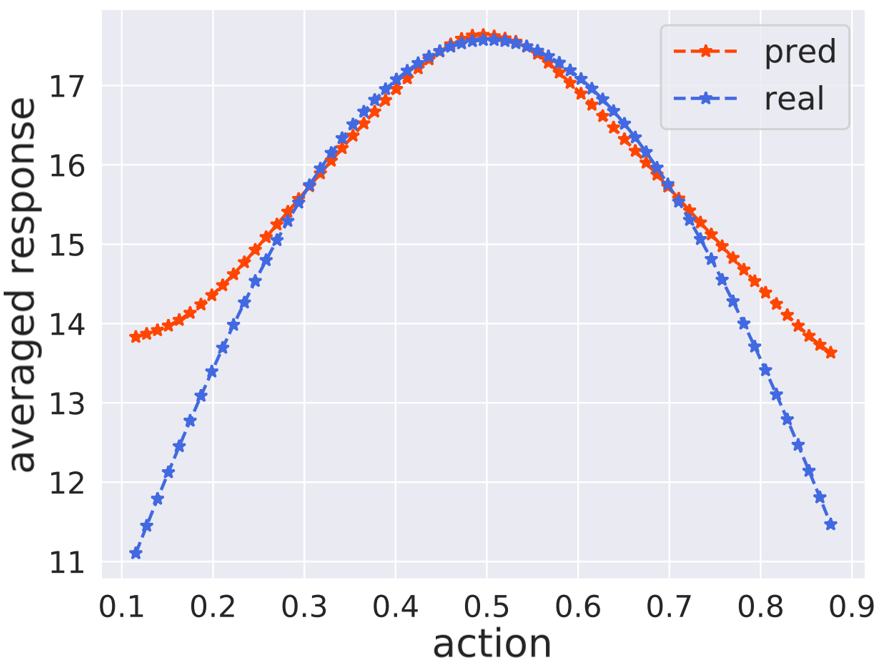

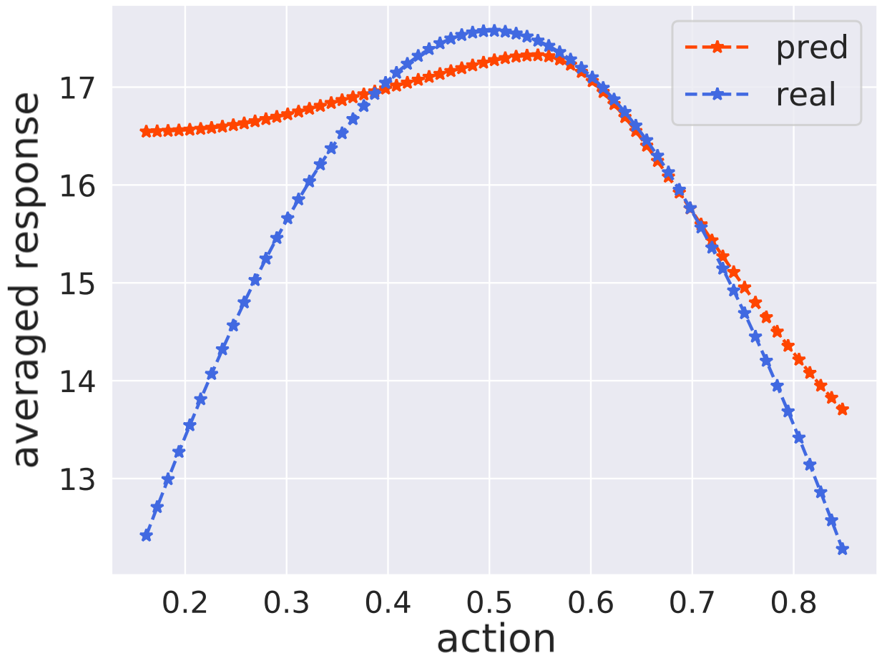

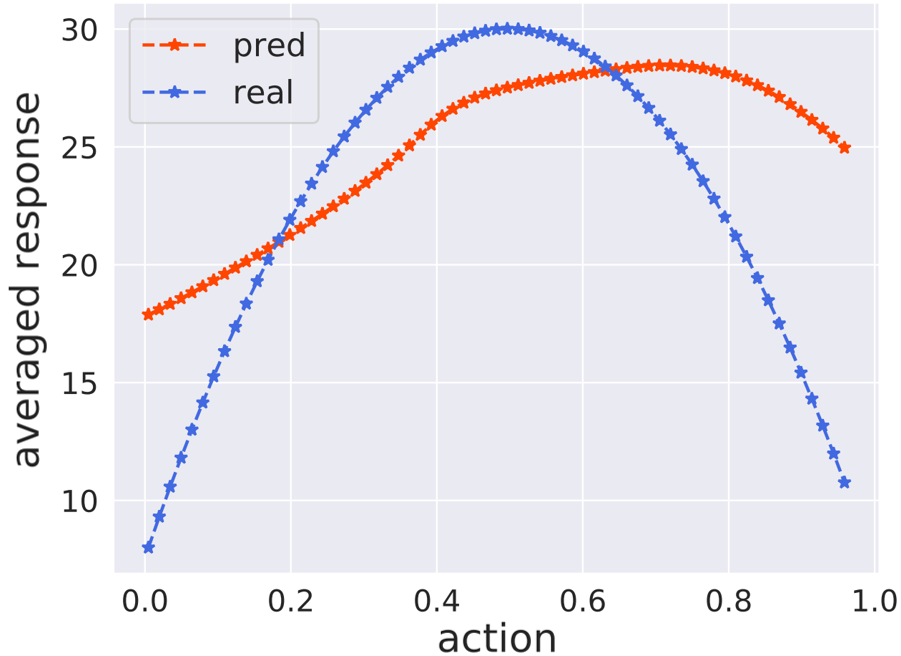

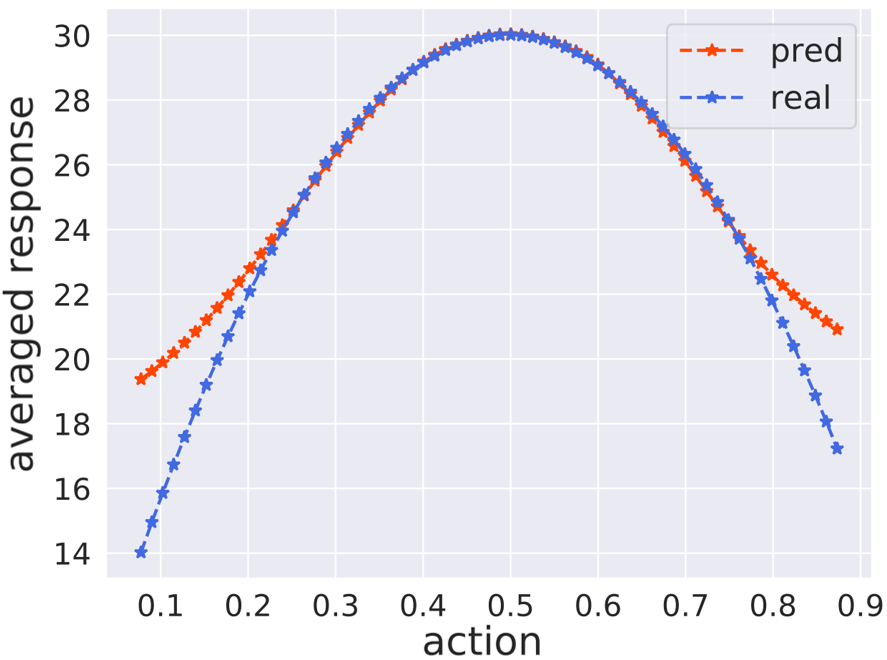

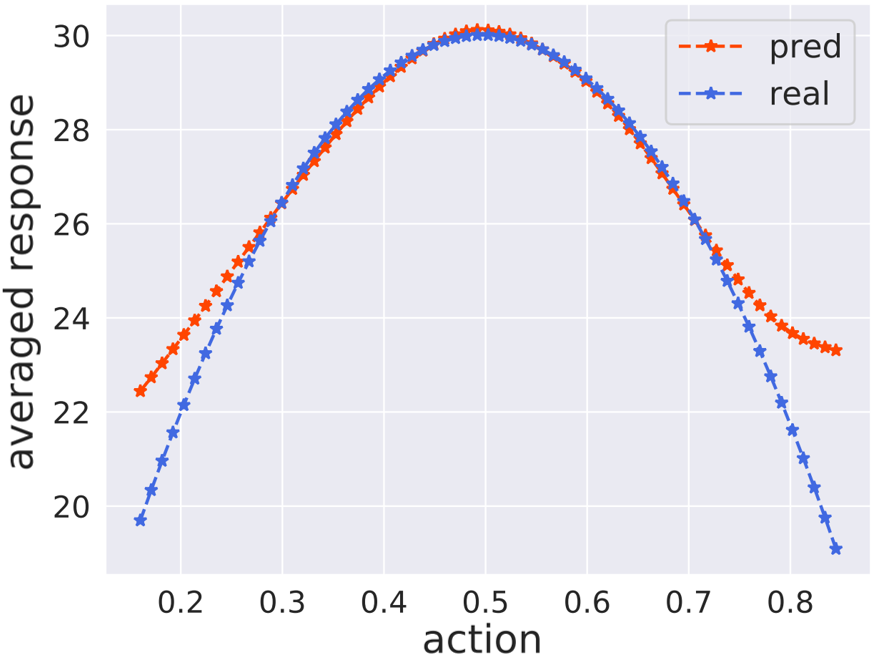

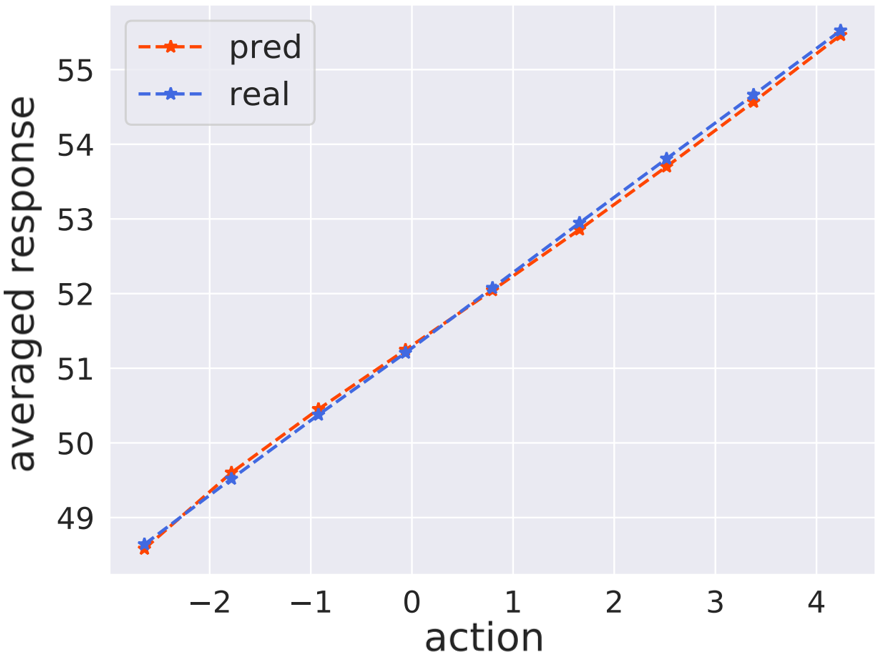

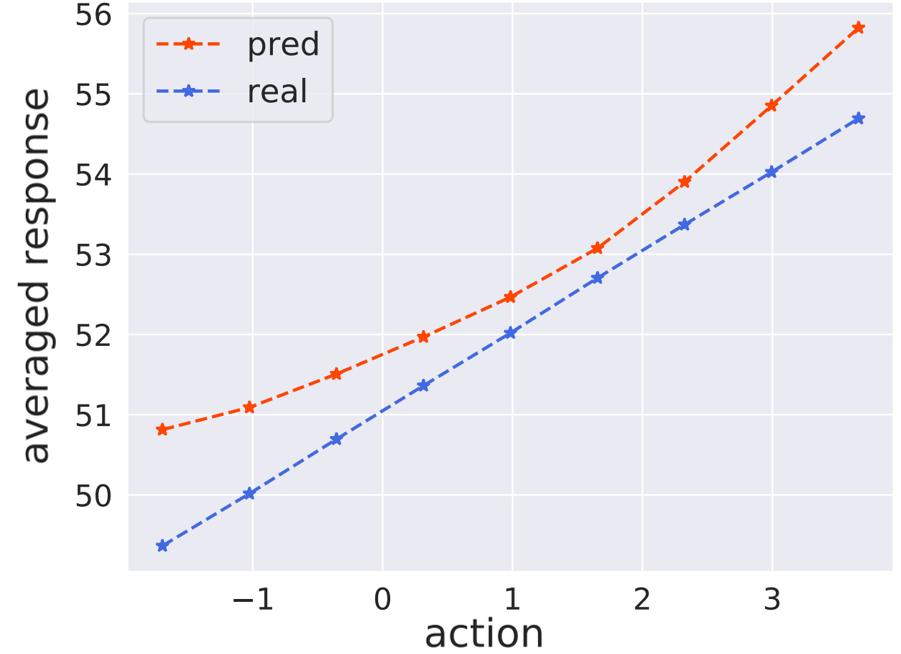

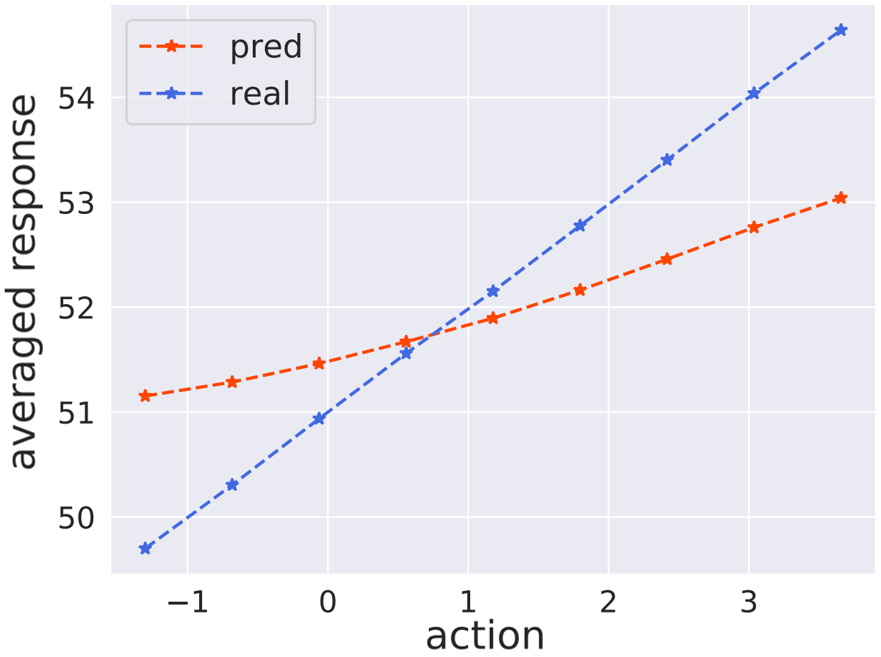

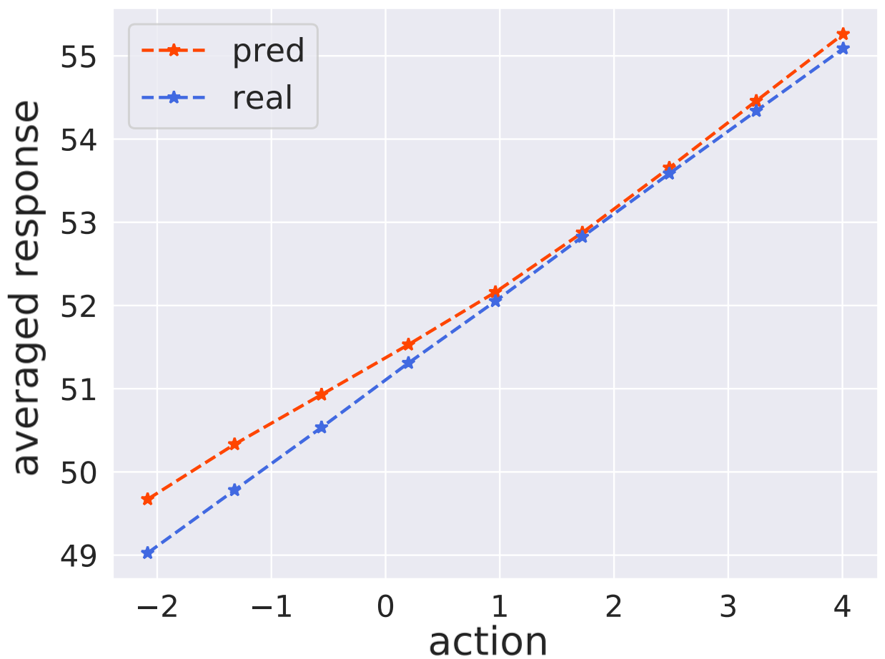

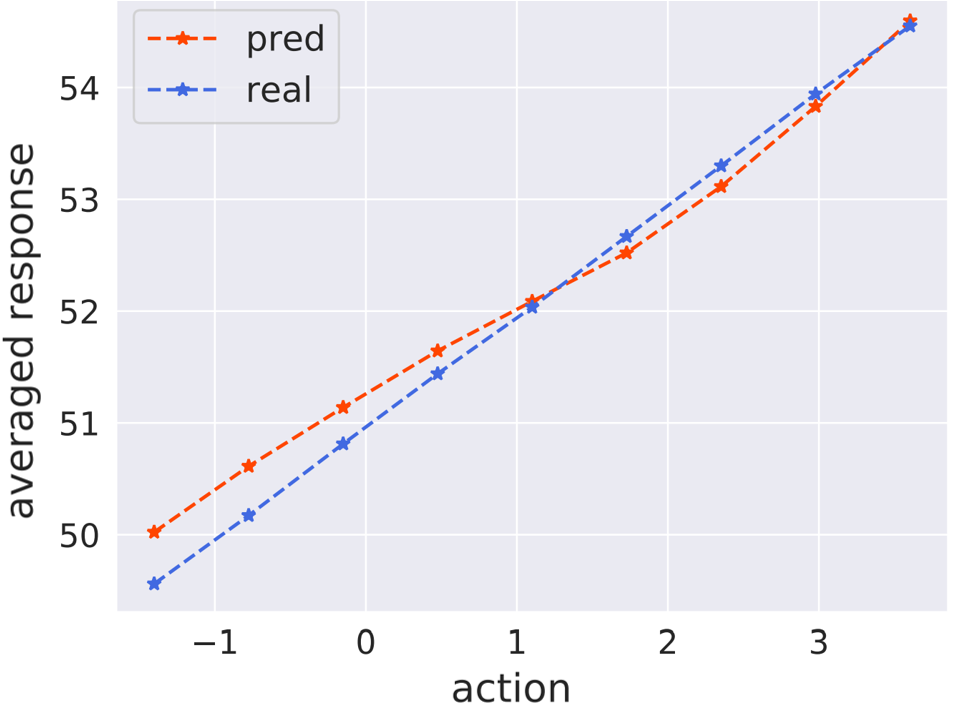

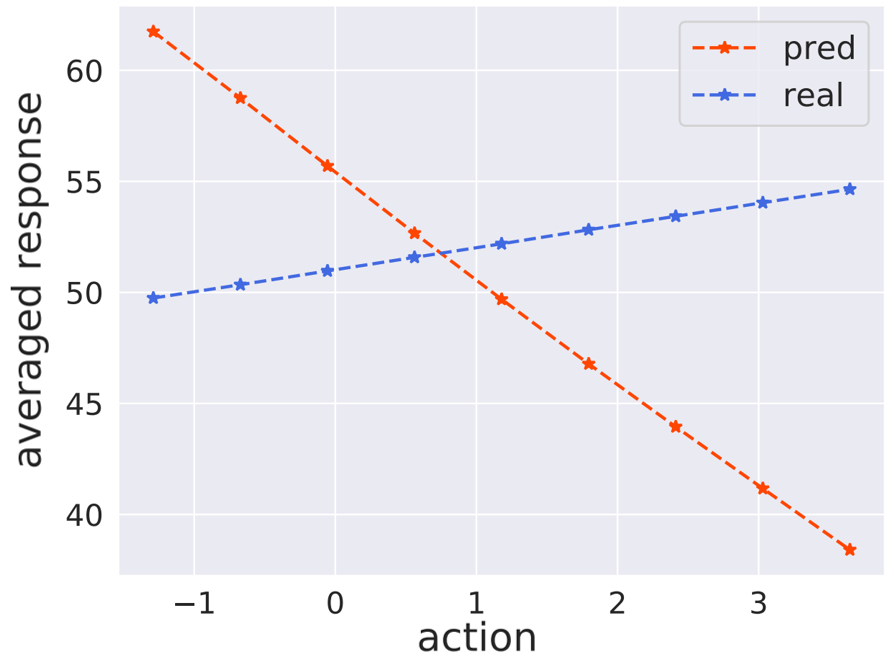

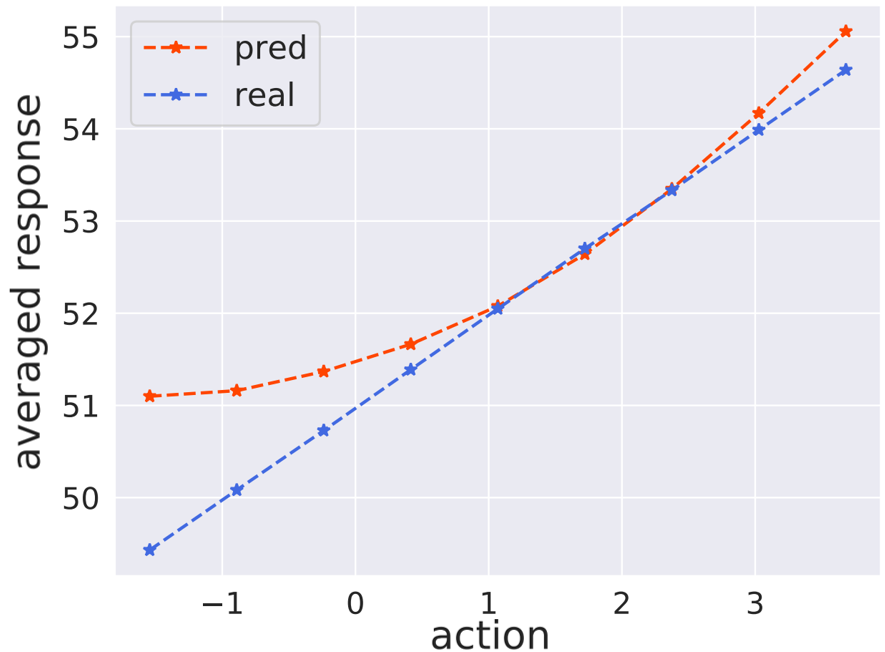

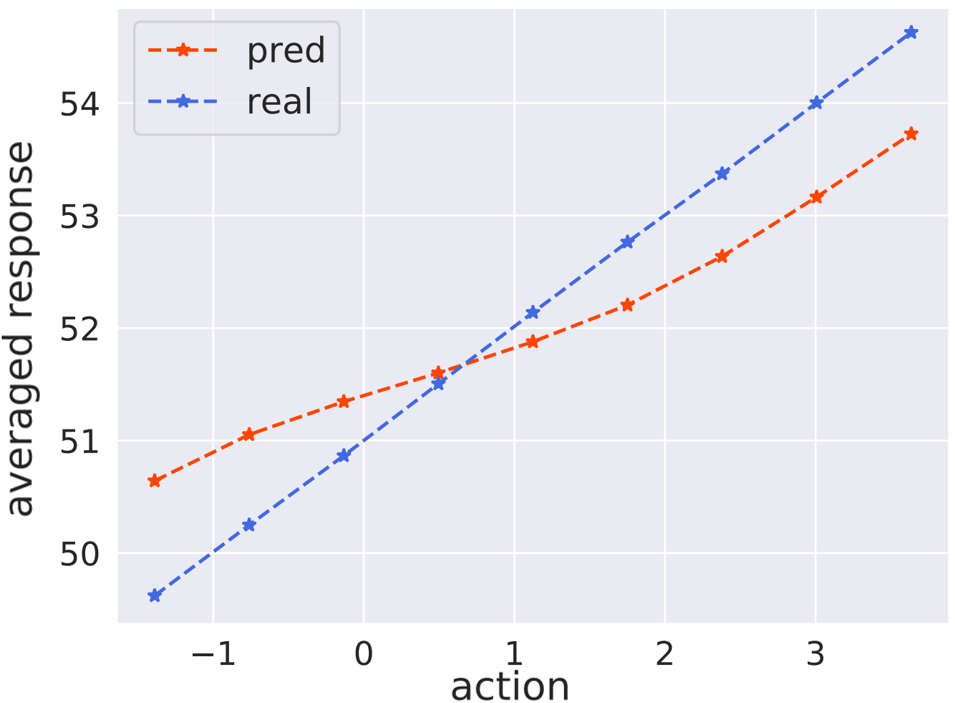

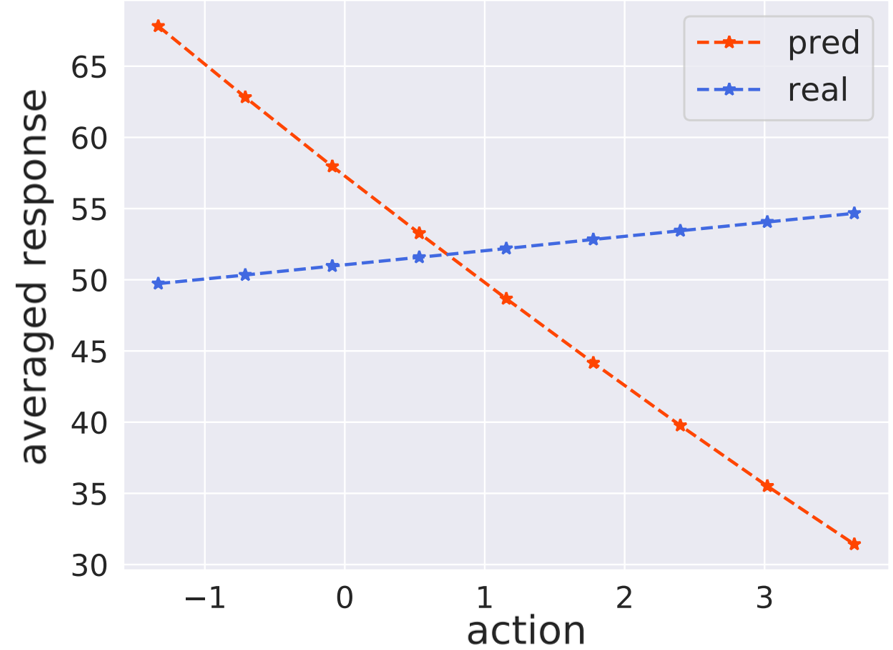

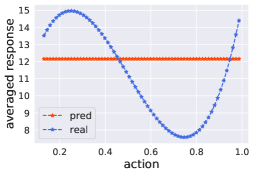

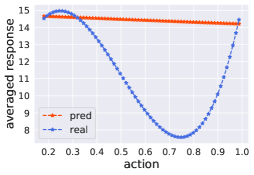

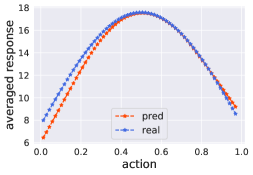

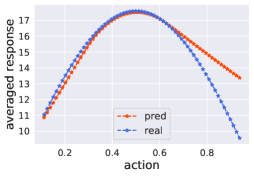

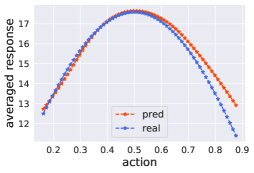

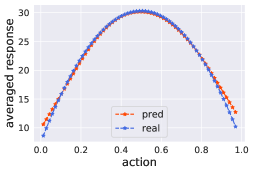

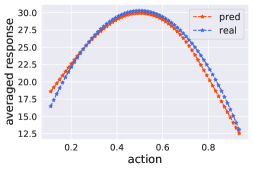

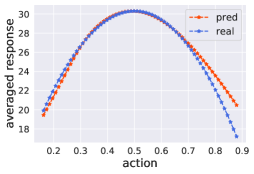

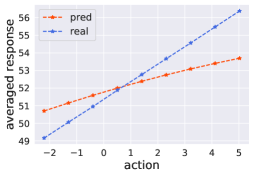

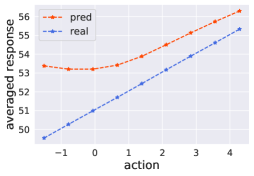

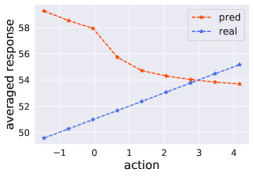

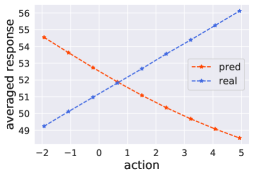

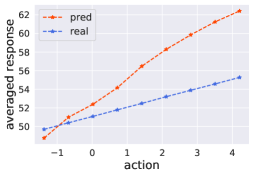

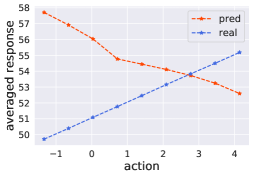

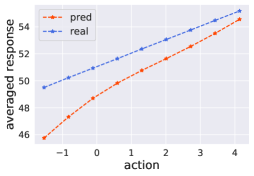

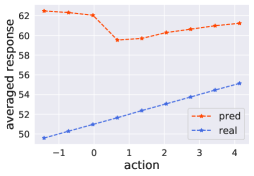

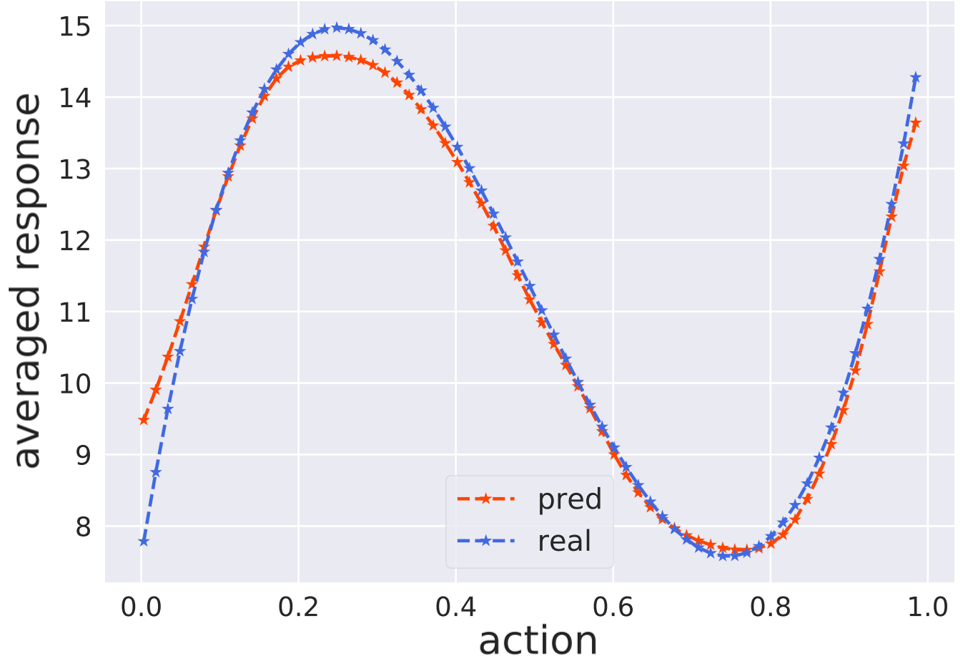

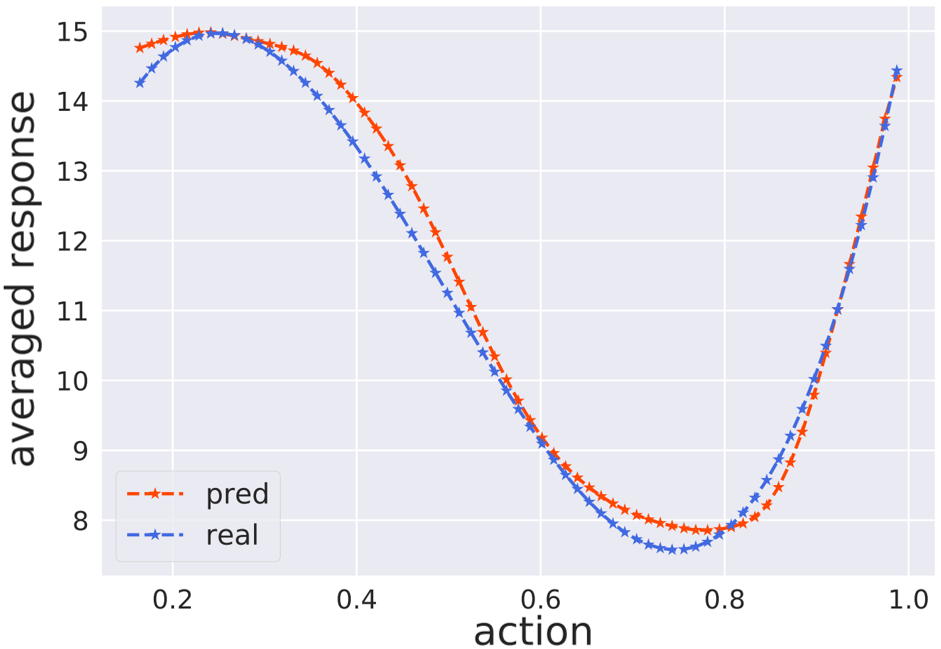

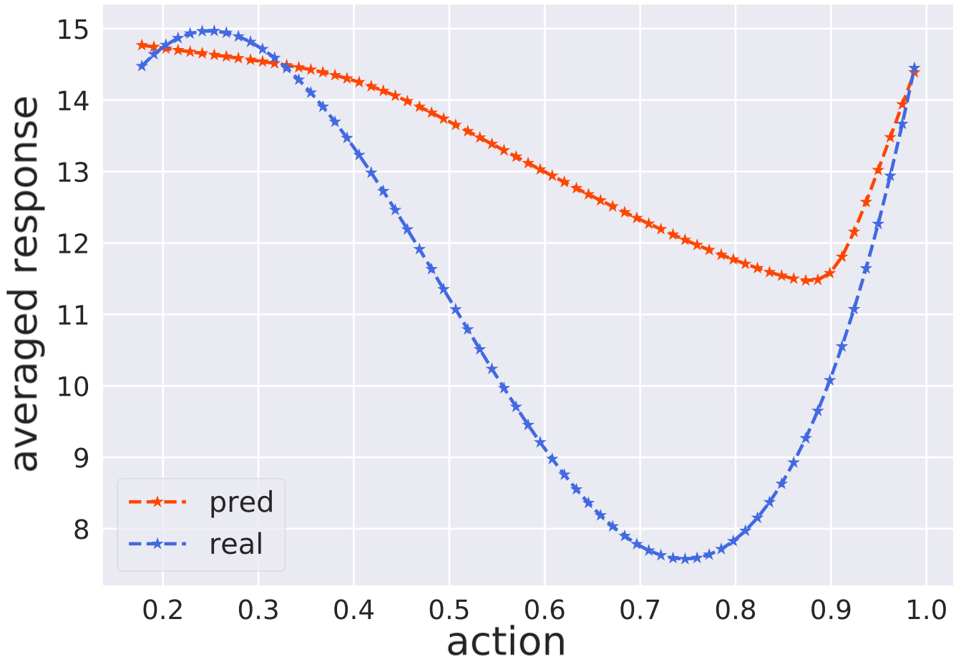

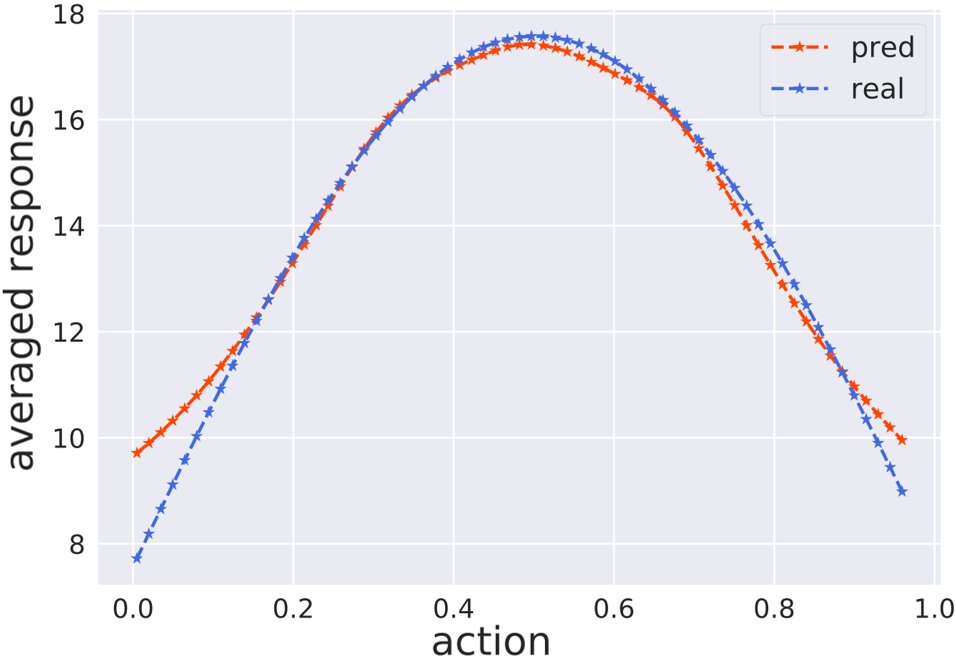

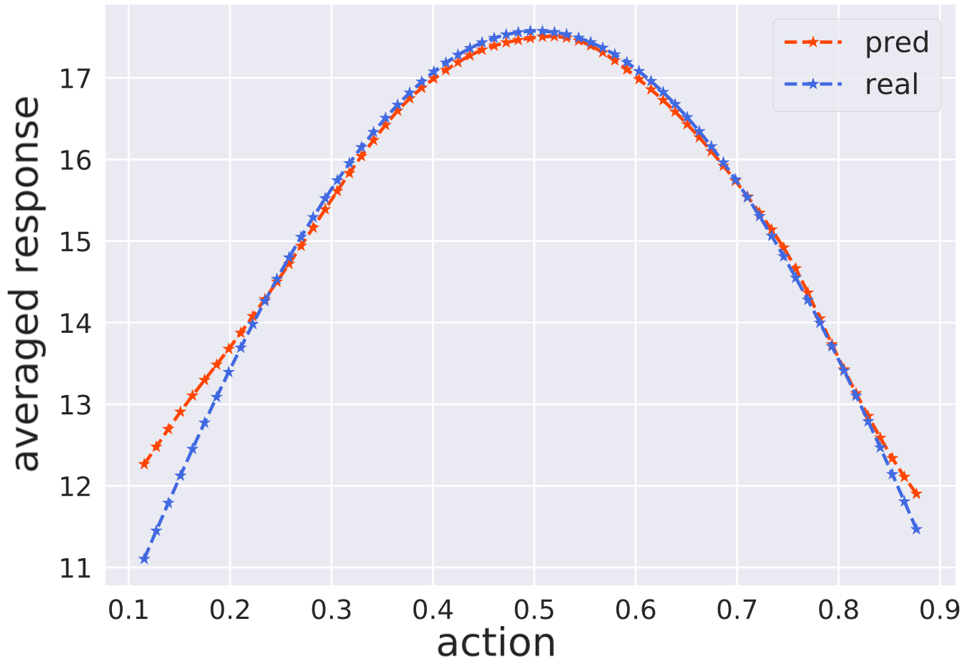

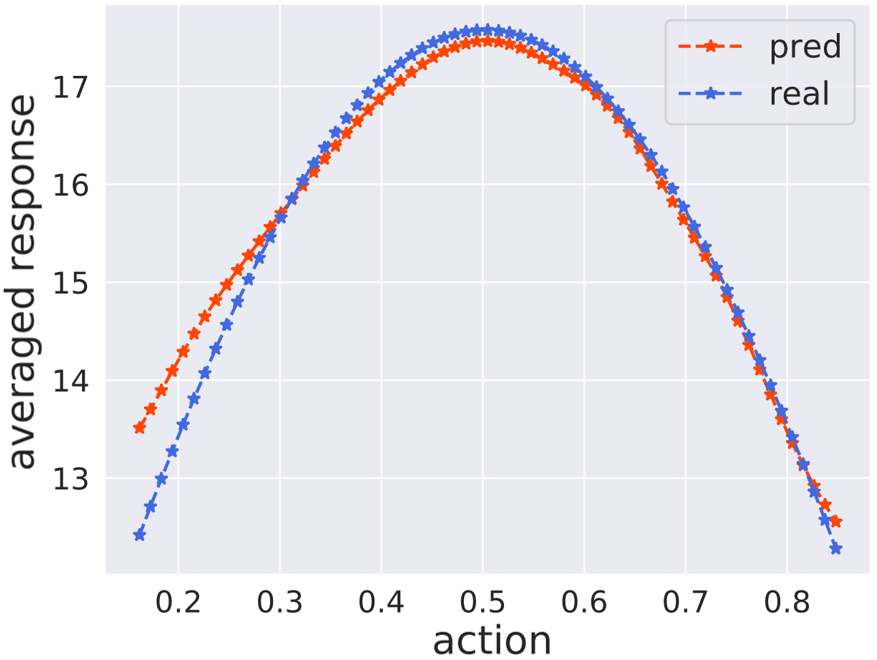

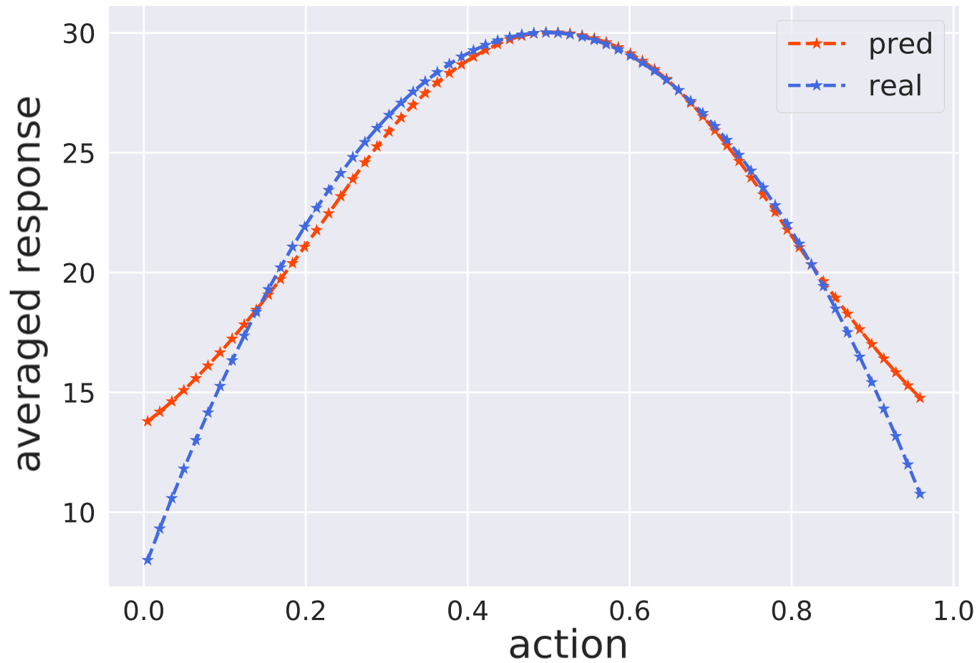

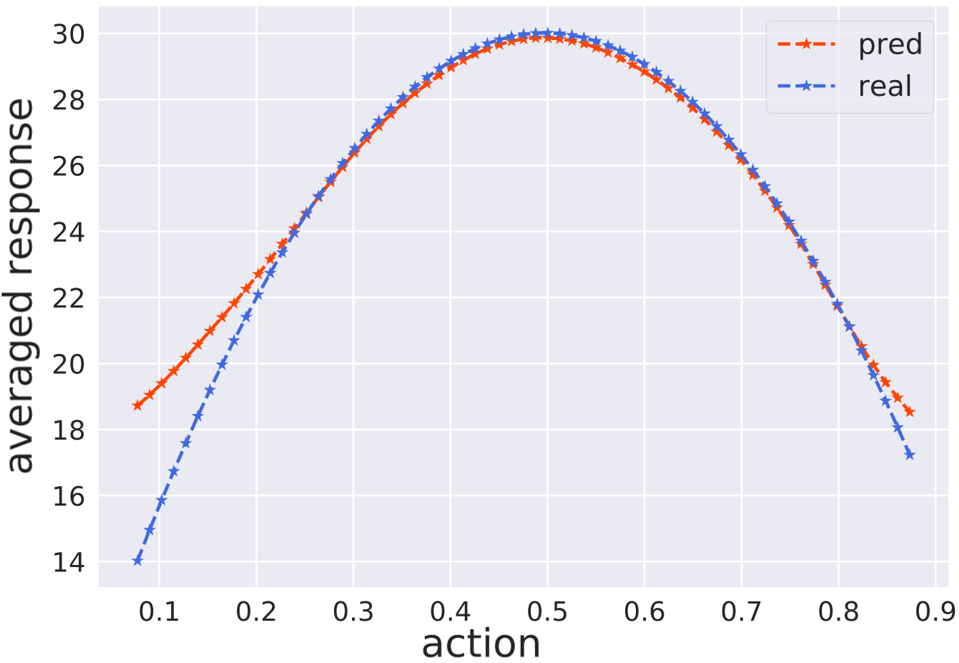

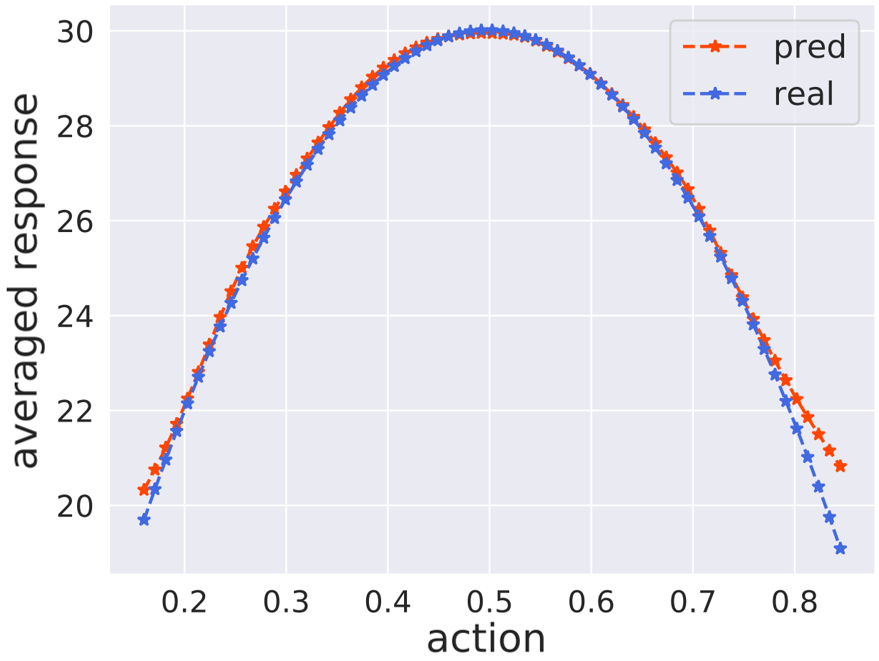

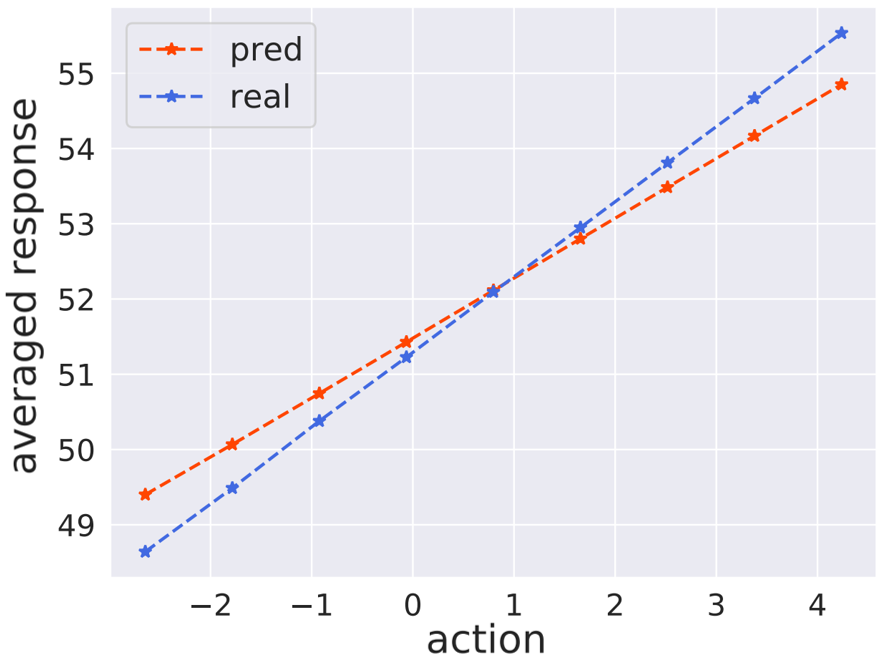

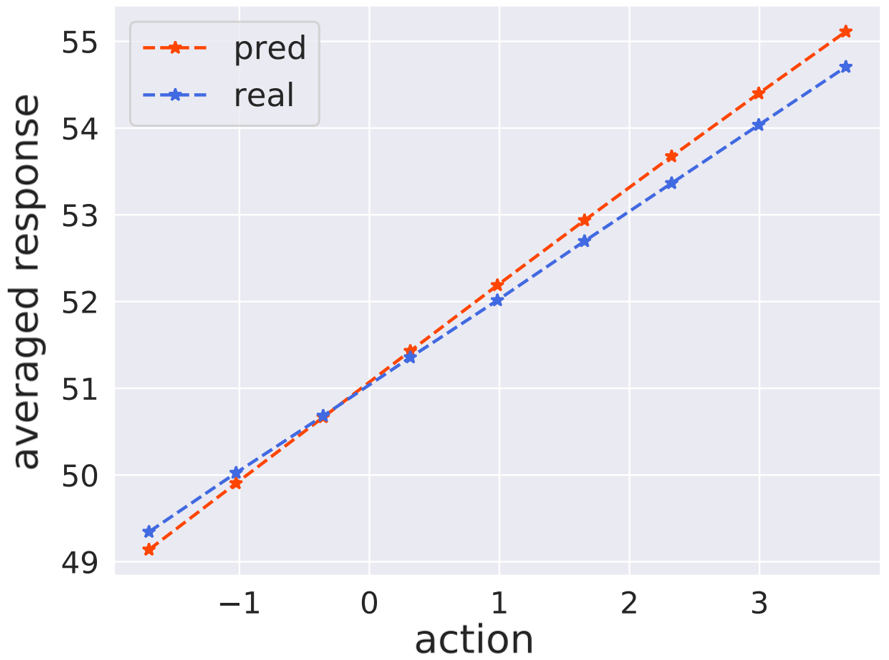

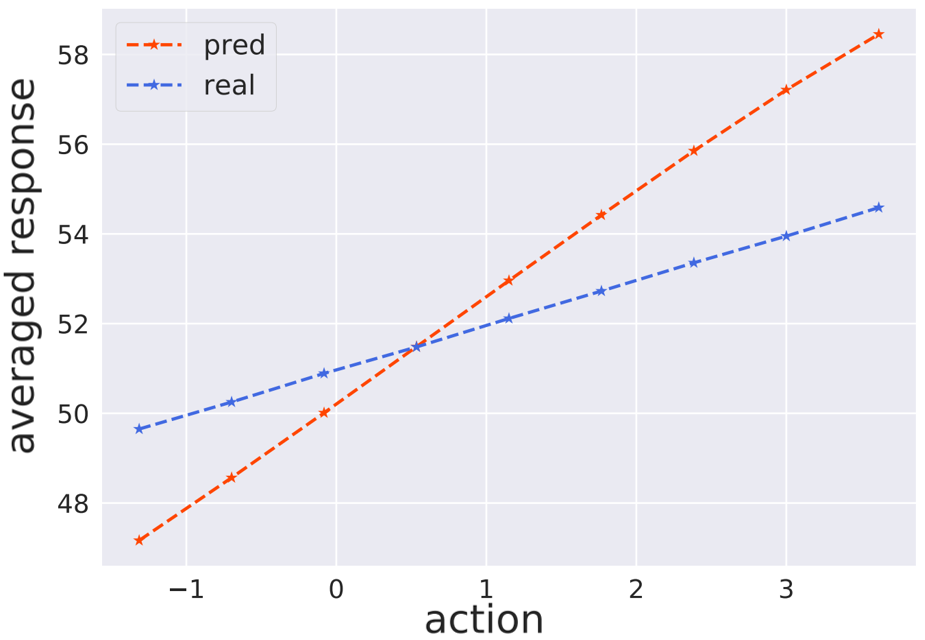

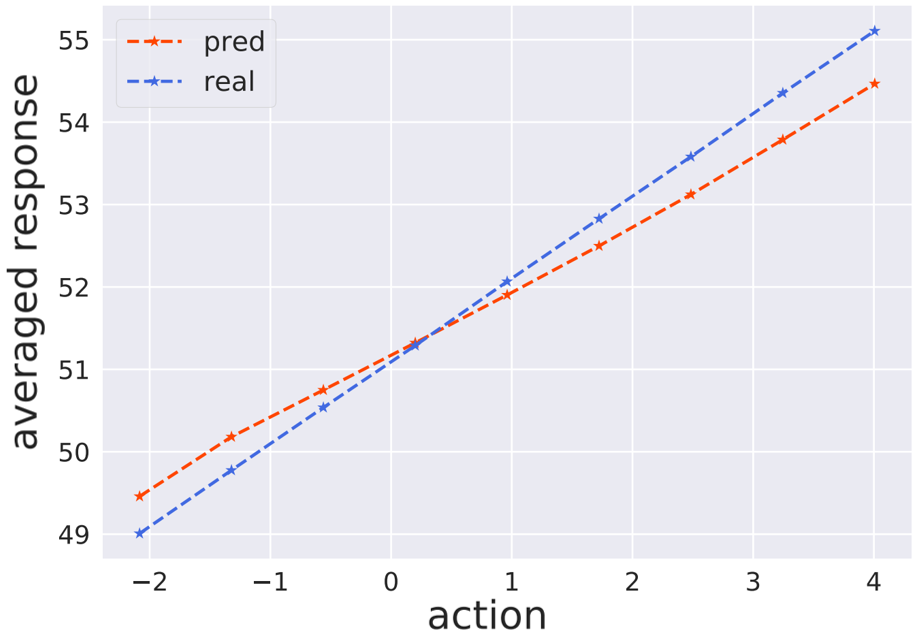

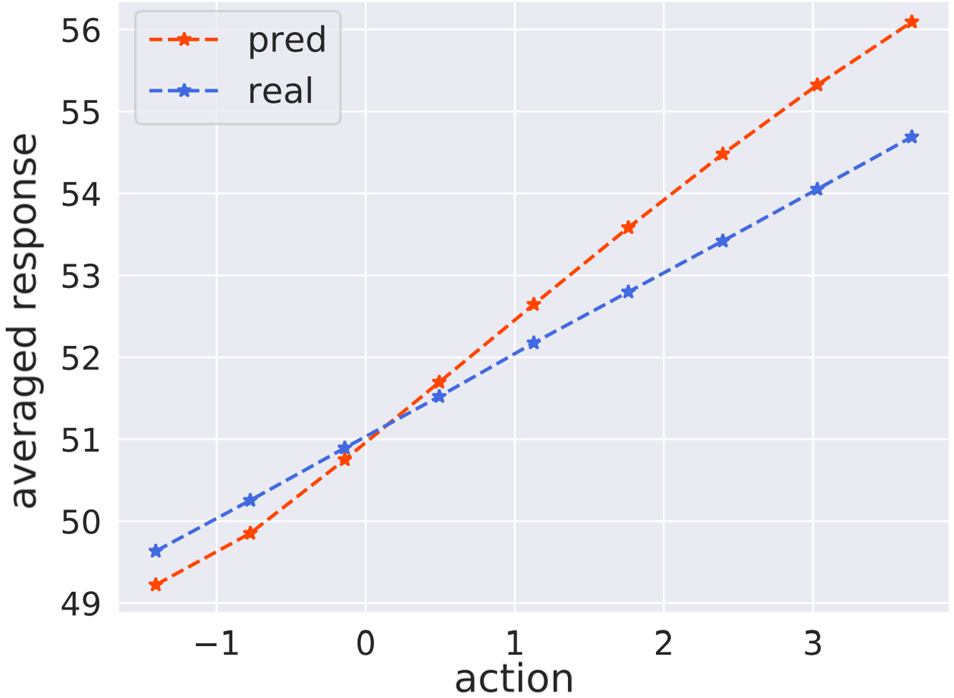

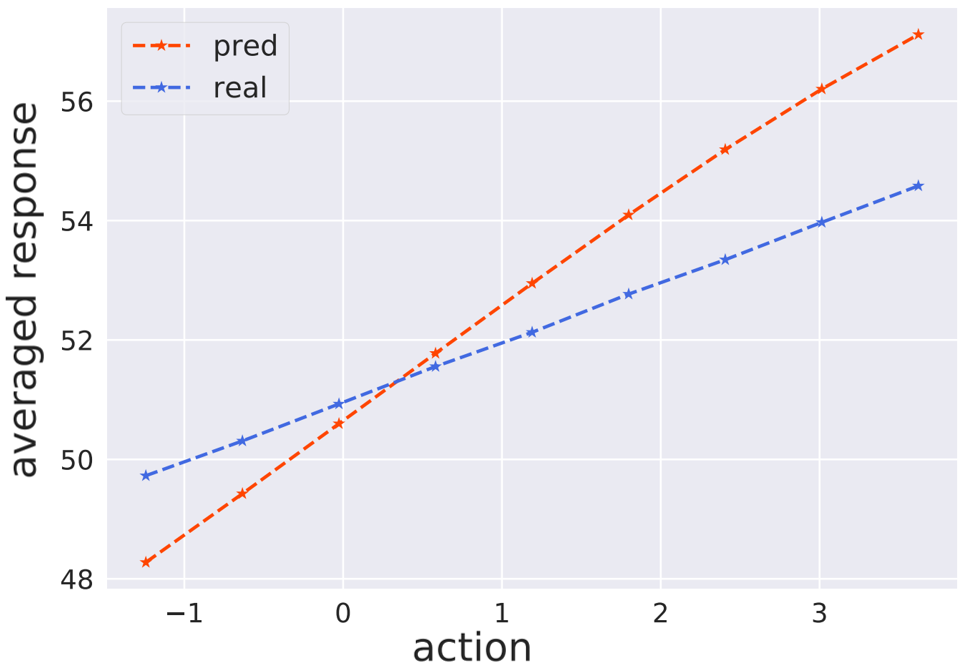

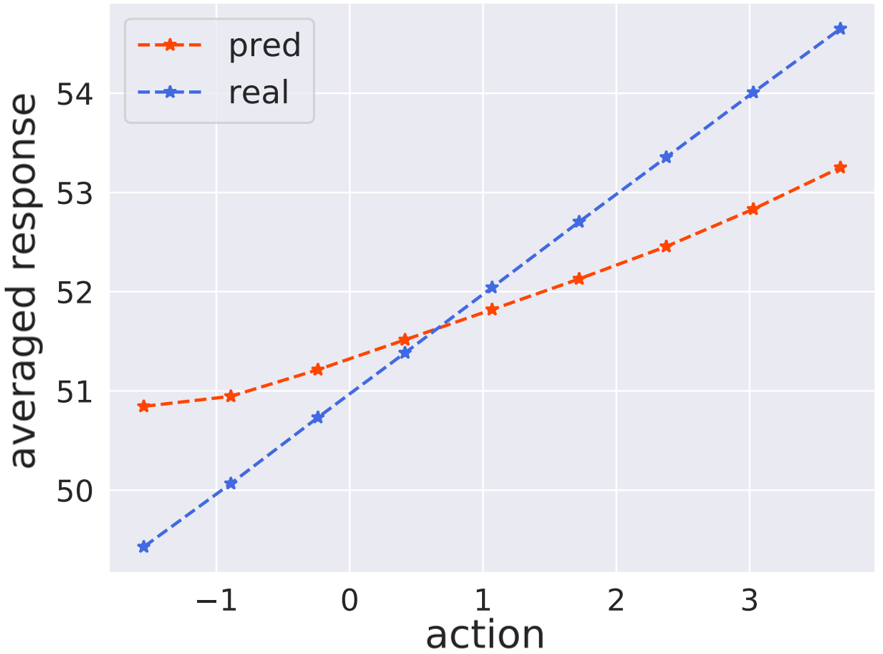

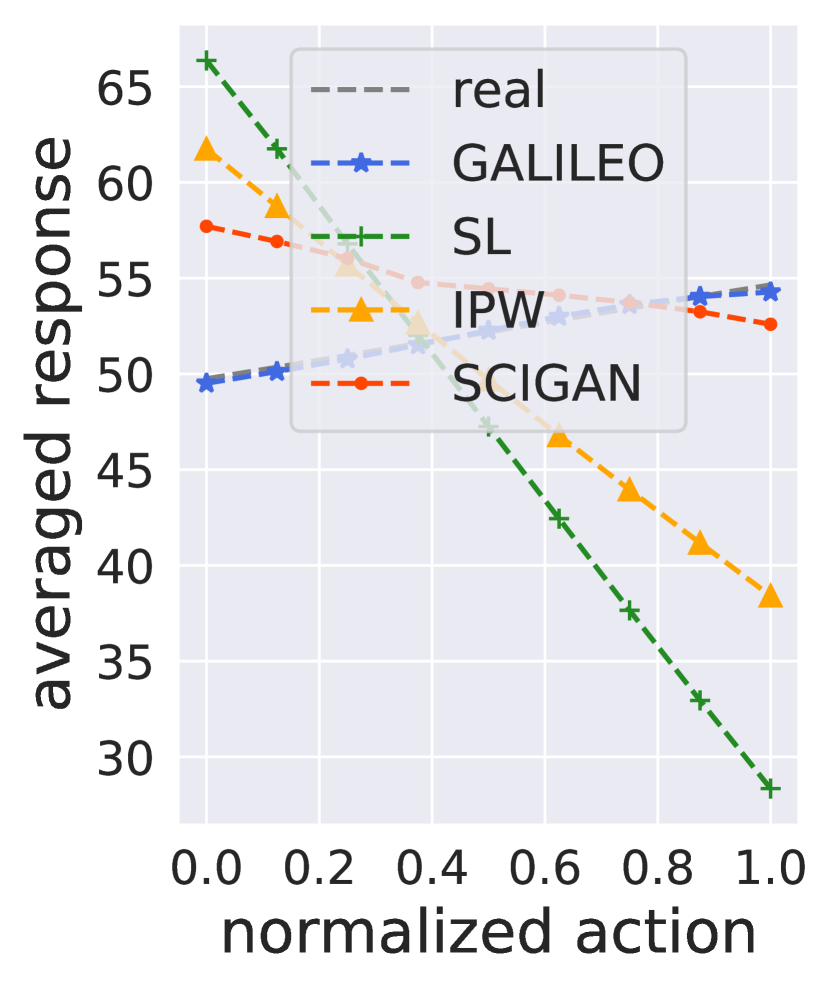

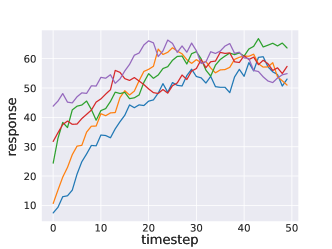

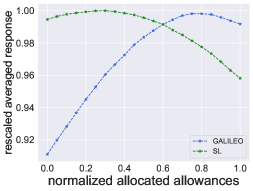

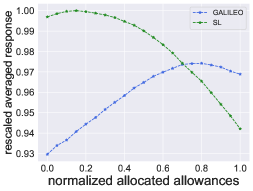

For all of the tasks, we select mean-integrated-square error as the metric, which is a metric to measure the accuracy in counterfactual queries by considering the prediction errors in the whole action space. The results are summarized in Fig. 3 and the detailed results can be found in Appx. H. The results show that the property of the behavior policy (i.e., and ) dominates the generalization ability of the baseline algorithms. When , almost all of the baselines fail and give a completely opposite response curve, while GALILEO gives the correct response. (see Fig. 4). IPW still performs well when but fails when . We also found that SCIGAN can reach a better performance than other baselines when , but the results in other tasks are unstable. GALILEO is the only algorithm that is robust to the selection bias and outputs correct response curves in all of the tasks. Based on the experiment, we also indicate that the commonly used overlap assumption is unreasonable to a certain extent especially in real-world applications since it is impractical to inject noises into the whole action space.

The problem of overlap assumption being violated, e.g., in our setting, should be taken into consideration otherwise the algorithm will be hard to use in practice if it is sensitive to the noise range. On the other hand, we found the phenomenon in TCGA experiment is similar to the one in GNFC, which demonstrates the compatibility of GALILEO to single-step environments.

We also found that the results of IPW are unstable in TCGA experiment. It might be because the behavior policy is modeled with beta distribution while the propensity score is modeled with Gaussian distribution. Since IPW directly reweight loss with , the results are sensitive to the error of .

Finally, we plot the averaged response curves which are constructed by equidistantly sampling action from the action space and averaging the feedback of the states in the dataset as the averaged response. One result is in Fig. 4 (all curves can be seen in Appx. H). For those tasks where baselines fail in reconstructing response curves, GALILEO not only reaches a better MISE score but reconstructs almost exact responses, while the baselines might give completely opposite responses.

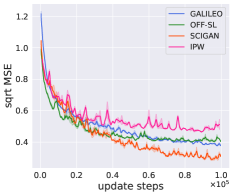

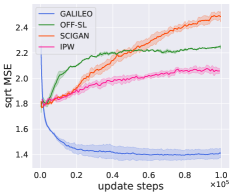

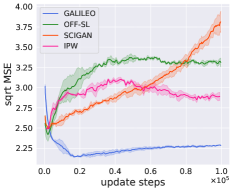

Test in MuJoCo Benchmarks

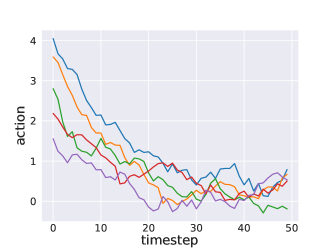

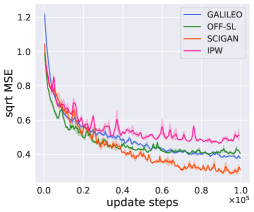

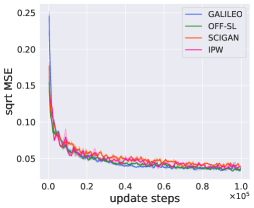

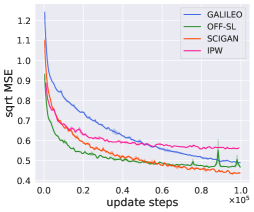

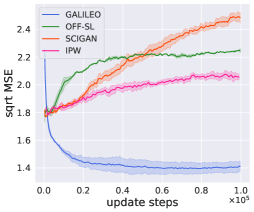

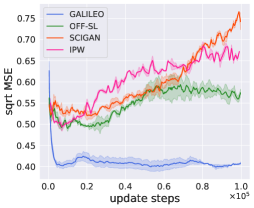

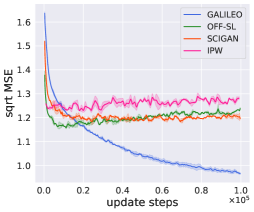

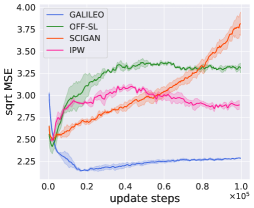

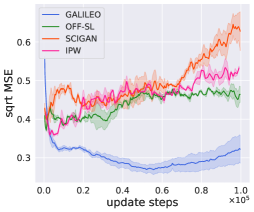

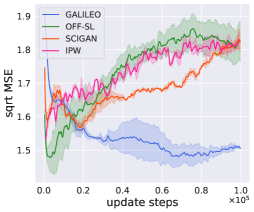

We test the prediction error of the learned model in corresponding unseen “expert” and “medium-replay” datasets. Fig. 5 illustrates the results in halfcheetah. We can see that all algorithms perform well in the training datasets. OFF-SL can even reach a bit lower error. However, when we verify the models through “expert” and “medium-replay” datasets, which are collected by other policies, the performance of GALILEO is more stable and better than all other algorithms. As the training continues, the baseline algorithms even gets worse and worse. The phenomenon are similar among three datasets, and we leave the full results in Appx. H.5.

Test in a Real-world Dataset

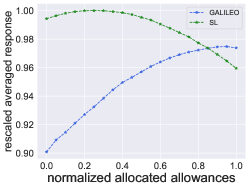

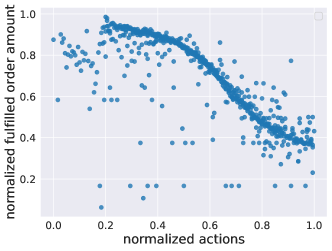

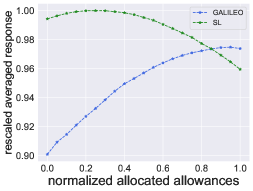

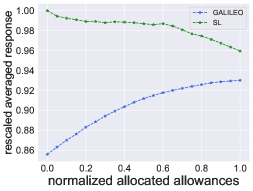

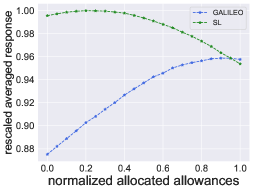

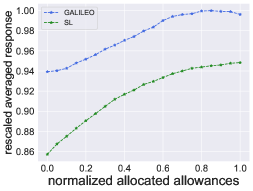

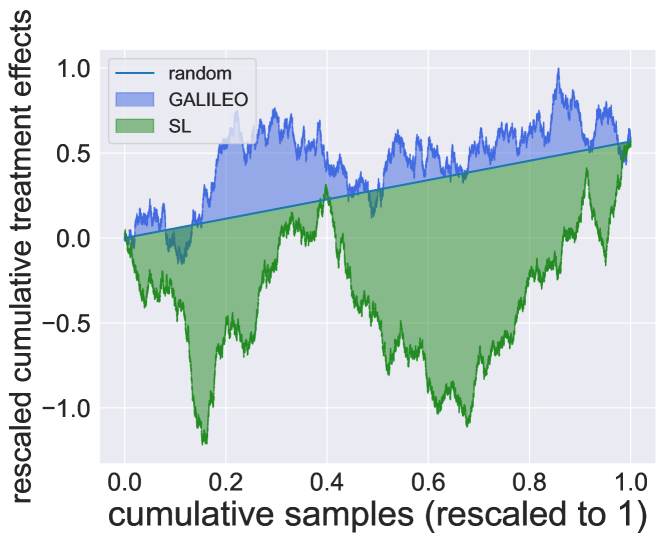

We first learn a model to predict the supply of delivery clerks (measured by fulfilled order amount) on given allowances. Although the SL model can efficiently fit the offline data, the tendency of the response curve is easily to be incorrect. As can be seen in Fig. 6(a), with a larger budget of allowance, the prediction of the supply is decreased in SL, which obviously goes against our prior knowledge. This is because, in the offline dataset, the corresponding supply will be smaller when the allowance is larger. It is conceivable that if we learn a policy through the model of SL, the optimal solution is canceling all of the allowances, which is obviously incorrect in practice. On the other hand, the tendency of GALILEO’s response is correct. In Appx. H.7, we plot all the results in 6 cities. We further collect some randomized controlled trials data, and the Area Under the Uplift Curve (AUUC) Betlei et al. (2020) curve in Fig. 6(b) verify that GALILEO gives a reasonable sort order on the supply prediction while the standard SL technique fails to achieve this task.

5.3 Apply GALILEO to Downstream Tasks

Off-policy Evaluation (OPE)

| Algorithm | Norm. value gap | Rank corr. | Regret@1 |

| GALILEO | 0.37 0.24 | 0.44 0.10 | 0.09 0.02 |

| Best DICE | 0.48 0.19 | 0.15 0.04 | 0.42 0.28 |

| VPM | 0.71 0.04 | 0.29 0.15 | 0.17 0.11 |

| FQE (L2) | 0.54 0.09 | -0.19 0.10 | 0.34 0.03 |

| IS | 0.67 0.01 | -0.40 0.15 | 0.36 0.27 |

| Doubly Rubost | 0.57 0.07 | -0.14 0.17 | 0.33 0.06 |

We first verify the ability of the models in MuJoCo environments by adopting them into off-policy evaluation tasks. We use 10 unseen policies constructed by DOPE benchmark Fu et al. (2021) to conduct our experiments. We select three common-used metrics: value gap, regret@1, and rank correlation and averaged the results among three tasks in Tab. 1. The baselines and the corresponding results we used are the same as the one proposed by Fu et al. (2021). As seen in Tab. 1, compared with all the baselines, OPE by GALILEO always reach the better performance with a large margin (at least 23%, 193% and 47% respectively), which verifies that GALILEO can eliminate the effect of selection bias and give correct evaluations on unseen policies.

Offline Policy Improvement

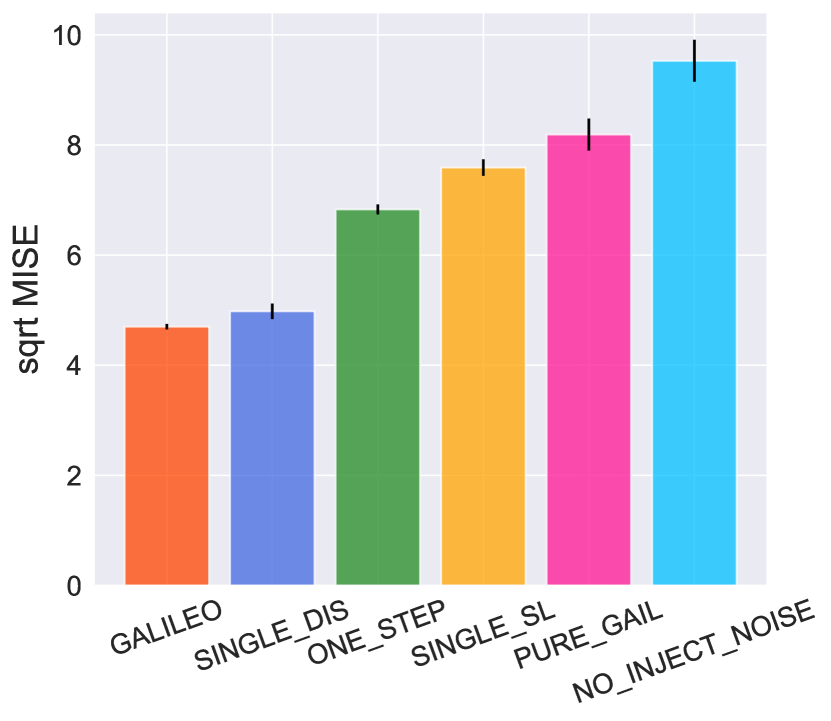

We then verify the generalization ability of the models in MuJoCo environments by adopting them into offline model-based RL. To strictly verify the ability of the models, we abandon all tricks to suppress policy exploration and learning in risky regions as current offline model-based RL algorithms Yu et al. (2020) do, and we just use the standard SAC algorithm Haarnoja et al. (2018) to fully exploit the models to search an optimal policy. Unfortunately, we found that the compounding error will still be inevitably large in the 1,000-step rollout, which is the standard horizon in MuJoCo tasks, leading all models to fail to derive a reasonable policy. To better verify the effects of models on policy improvement, we learn and evaluate the policies with three smaller horizons: . The results are listed in Tab. 2. We first averaged the normalized return (refer to “avg. norm.”) under each task, and we can see that the policy obtained by GALILEO is significantly higher than other models (the improvements are 24% to 161%). But in HalfCheetah, IPW works slightly better. However, compared with MAX-RETURN, it can be found that all methods fail to derive reasonable policies because their policies’ performances are far away from the optimal policy. By further checking the trajectories, we found that all the learned policies just keep the cheetah standing in the same place or even going backward. This phenomenon is also similar to the results in MOPO Yu et al. (2020). In MOPO’s experiment in the medium datasets, the truncated-rollout horizon used in Walker and Hopper for policy training is set to 5, while HalfCheetah has to be set to the minimal value: 1. These phenomena indicate that HalfCheetah may still have unknown problems, resulting in the generalization bottleneck of the models.

| Task | Hopper | Walker2d | HalfCheetah | avg. norm. | ||||||

| Horizon | H=10 | H=20 | H=40 | H=10 | H=20 | H=40 | H=10 | H=20 | H=40 | / |

| GALILEO | 13.0 0.1 | 33.2 0.1 | 53.5 1.2 | 11.7 0.2 | 29.9 0.3 | 61.2 3.4 | 0.7 0.2 | -1.1 0.2 | -14.2 1.4 | 51.1 |

| OFF-SL | 4.8 0.5 | 3.0 0.2 | 4.6 0.2 | 10.7 0.2 | 20.1 0.8 | 37.5 6.7 | 0.4 0.5 | -1.1 0.6 | -13.2 0.3 | 21.1 |

| IPW | 5.9 0.7 | 4.1 0.6 | 5.9 0.2 | 4.7 1.1 | 2.8 3.9 | 14.5 1.4 | 1.6 0.2 | 0.5 0.8 | -11.3 0.9 | 19.7 |

| SCIGAN | 12.7 0.1 | 29.2 0.6 | 46.2 5.2 | 8.4 0.5 | 9.1 1.7 | 1.0 5.8 | 1.2 0.3 | -0.3 1.0 | -11.4 0.3 | 41.8 |

| MAX-RETURN | 13.2 0.0 | 33.3 0.2 | 71.0 0.5 | 14.9 1.3 | 60.7 11.1 | 221.1 8.9 | 2.6 0.1 | 13.3 1.1 | 49.1 2.3 | 100.0 |

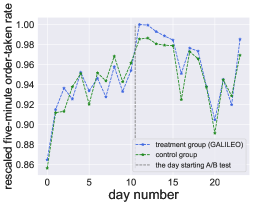

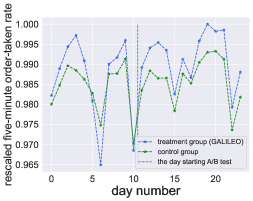

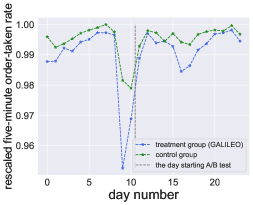

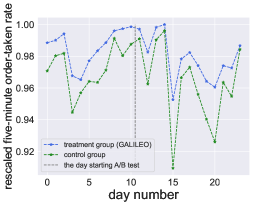

Online Decision-making in a Production Environment

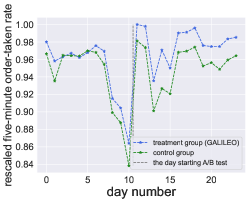

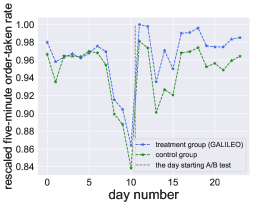

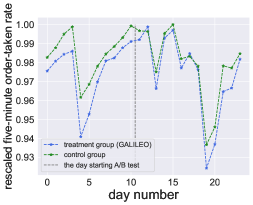

Finally, we search for the optimal policy via model-predict control (MPC) using cross-entropy planner Hafner et al. (2019) based on the learned model and deploy the policy in a real-world platform. The results of A/B test in City A is shown in Fig. 6(c). It can be seen that after the day of the A/B test, the treatment group (deploying our policy) significant improve the five-minute order-taken rate than the baseline policy (the same as the behavior policy). In summary, the policy improves the supply from 0.14 to 1.63 percentage points to the behavior policies in the 6 cities. The details of these results are in Appx. H.7.

6 Discussion and Future Work

In this work, we propose AWRM which handles the generalization challenges of the counterfactual environment model learning. By theoretical modeling, we give a tractable solution to handle AWRM and propose GALILEO. GALILEO is verified in synthetic environments, complex robot control tasks, and a real-world platform, and shows great generalization ability on counterfactual queries.

Giving correct answers to counterfactual queries is important for policy learning. We hope the work can inspire researchers to develop more powerful tools for counterfactual environment model learning. The current limitation lies in: There are several simplifications in the theoretical modeling process (further discussion is in Appx. B), which can be modeled more elaborately . Besides, experiments on MuJoCo indicate that these tasks are still challenging to give correct predictions on counterfactual data. These should also be further investigated in future work.

References

- Alaa and van der Schaar (2018) A. M. Alaa and M. van der Schaar. Limits of estimating heterogeneous treatment effects: Guidelines for practical algorithm design. In Proceedings of the 35th International Conference on Machine Learning, volume 80, pages 129–138, Stockholm, Sweden, 2018.

- Ali and Silvey (1966) S. M. Ali and S. D. Silvey. A general class of coefficients of divergence of one distribution from another. Journal of the Royal Statistical Society: Series B (Methodological), 28(1):131–142, 1966.

- Assaad et al. (2021) S. Assaad, S. Zeng, C. Tao, S. Datta, N. Mehta, R. Henao, F. Li, and L. Carin. Counterfactual representation learning with balancing weights. In The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pages 1972–1980, Virtual Event, 2021.

- Ben-David et al. (2006) S. Ben-David, J. Blitzer, K. Crammer, and F. Pereira. Analysis of representations for domain adaptation. In Advances in Neural Information Processing Systems 19, pages 137–144, British Columbia, Canada, 2006. MIT Press.

- Ben-David et al. (2010) S. Ben-David, J. Blitzer, K. Crammer, A. Kulesza, F. Pereira, and J. W. Vaughan. A theory of learning from different domains. Mach. Learn., 79(1-2):151–175, 2010.

- Betlei et al. (2020) A. Betlei, E. Diemert, and M. Amini. Treatment targeting by AUUC maximization with generalization guarantees. CoRR, abs/2012.09897, 2020.

- Bica et al. (2020) I. Bica, J. Jordon, and M. van der Schaar. Estimating the effects of continuous-valued interventions using generative adversarial networks. In Advances in Neural Information Processing Systems 33, virtual event, 2020.

- Buesing et al. (2019) L. Buesing, T. Weber, Y. Zwols, N. Heess, S. Racanière, A. Guez, and J. Lespiau. Woulda, coulda, shoulda: Counterfactually-guided policy search. In 7th International Conference on Learning Representations, New Orleans, LA, 2019.

- Byrd and Lipton (2019) J. Byrd and Z. C. Lipton. What is the effect of importance weighting in deep learning? In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 872–881, Long Beach, CA, 2019.

- Chen et al. (2019) X. Chen, S. Li, H. Li, S. Jiang, Y. Qi, and L. Song. Generative adversarial user model for reinforcement learning based recommendation system. In Proceedings of the 36th International Conference on Machine Learning, pages 1052–1061, Long Beach, CA, 2019.

- Chen et al. (2021) X.-H. Chen, Y. Yu, Q. Li, F.-M. Luo, Z. T. Qin, S. Wenjie, and J. Ye. Offline model-based adaptable policy learning. In Advances in Neural Information Processing Systems 34, Virtual Conference, 2021.

- Cortes et al. (2010) C. Cortes, Y. Mansour, and M. Mohri. Learning bounds for importance weighting. In Advances in Neural Information Processing Systems 23, pages 442–450, British Columbia, Canada, 2010. Curran Associates, Inc.

- Eysenbach et al. (2021) B. Eysenbach, A. Khazatsky, S. Levine, and R. Salakhutdinov. Mismatched no more: Joint model-policy optimization for model-based RL. CoRR, abs/2110.02758, 2021. URL https://arxiv.org/abs/2110.02758.

- Fu et al. (2020) J. Fu, A. Kumar, O. Nachum, G. Tucker, and S. Levine. D4RL: datasets for deep data-driven reinforcement learning. CoRR, abs/2004.07219, 2020.

- Fu et al. (2021) J. Fu, M. Norouzi, O. Nachum, G. Tucker, Z. Wang, A. Novikov, M. Yang, M. R. Zhang, Y. Chen, A. Kumar, C. Paduraru, S. Levine, and T. Paine. Benchmarks for deep off-policy evaluation. In 9th International Conference on Learning Representations, Virtual Event, Austria, 2021.

- Goodfellow et al. (2014) I. J. Goodfellow, J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S. Ozair, A. C. Courville, and Y. Bengio. Generative adversarial nets. In Advances in Neural Information Processing Systems 27, pages 2672–2680, Montréal, Canada, 2014.

- Haarnoja et al. (2018) T. Haarnoja, A. Zhou, P. Abbeel, and S. Levine. Soft Actor-Critic: Off-policy maximum entropy deep reinforcement learning with a stochastic actor. In Proceedings of the 35th International Conference on Machine Learning, pages 1856–1865, Stockholmsmässan, Sweden, 2018.

- Hafner et al. (2019) D. Hafner, T. P. Lillicrap, I. Fischer, R. Villegas, D. Ha, H. Lee, and J. Davidson. Learning latent dynamics for planning from pixels. In Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 2555–2565, Long Beach, CA, 2019.

- Hassanpour and Greiner (2019) N. Hassanpour and R. Greiner. Counterfactual regression with importance sampling weights. In Proceedings of the 28th International Joint Conference on Artificial Intelligence, pages 5880–5887, Macao, China, 2019.

- Hiriart-Urruty and Lemaréchal (2001) J. Hiriart-Urruty and C. Lemaréchal. Fundamentals of Convex Analysis. 2001. ISBN 9783642564680.

- Hishinuma and Senda (2021) T. Hishinuma and K. Senda. Weighted model estimation for offline model-based reinforcement learning. In Advances in Neural Information Processing Systems 34, pages 17789–17800, virtual, 2021.

- Ho and Ermon (2016) J. Ho and S. Ermon. Generative adversarial imitation learning. In Advances in Neural Information Processing Systems 29, pages 4565–4573, Barcelona, Spain, 2016.

- Imbens (1999) G. Imbens. The role of the propensity score in estimating dose-response functions. Econometrics eJournal, 1999.

- Ionides (2008) E. L. Ionides. Truncated importance sampling. Journal of Computational and Graphical Statistics, 17(2):295–311, 2008.

- Johansson et al. (2018) F. D. Johansson, N. Kallus, U. Shalit, and D. Sontag. Learning weighted representations for generalization across designs. arXiv preprint arXiv:1802.08598, 2018.

- Jung et al. (2020) Y. Jung, J. Tian, and E. Bareinboim. Learning causal effects via weighted empirical risk minimization. In Advances in Neural Information Processing Systems 33, Virtual Event, 2020.

- Kidambi et al. (2020) R. Kidambi, A. Rajeswaran, P. Netrapalli, and T. Joachims. MOReL : Model-based offline reinforcement learning. CoRR, abs/2005.05951, 2020.

- Levine et al. (2020) S. Levine, A. Kumar, G. Tucker, and J. Fu. Offline reinforcement learning: Tutorial, review, and perspectives on open problems. CoRR, abs/2005.01643, 2020.

- Liu et al. (2018) Q. Liu, L. Li, Z. Tang, and D. Zhou. Breaking the curse of horizon: Infinite-horizon off-policy estimation. In Advances in Neural Information Processing Systems 31, pages 5361–5371, Montréal, Canada, 2018.

- Liu et al. (2020) Y. Liu, A. Swaminathan, A. Agarwal, and E. Brunskill. Provably good batch off-policy reinforcement learning without great exploration. In Advances in Neural Information Processing Systems 33, virtual event, 2020.

- Lu et al. (2022) C. Lu, P. J. Ball, J. Parker-Holder, M. A. Osborne, and S. J. Roberts. Revisiting design choices in offline model based reinforcement learning. In The 10th International Conference on Learning Representations, Virtual Event, 2022.

- Nachum et al. (2019) O. Nachum, Y. Chow, B. Dai, and L. Li. Dualdice: Behavior-agnostic estimation of discounted stationary distribution corrections. In Advances in Neural Information Processing Systems 32, pages 2315–2325, BC, Canada, 2019.

- Nguyen et al. (2010) X. Nguyen, M. J. Wainwright, and M. I. Jordan. Estimating divergence functionals and the likelihood ratio by convex risk minimization. IEEE Trans. Inf. Theory, 56(11):5847–5861, 2010.

- Nowozin et al. (2016) S. Nowozin, B. Cseke, and R. Tomioka. f-GAN: Training generative neural samplers using variational divergence minimization. In Advances in Neural Information Processing Systems 29, pages 271–279, Barcelona, Spain, 2016.

- Pitis et al. (2020) S. Pitis, E. Creager, and A. Garg. Counterfactual data augmentation using locally factored dynamics. In Advances in Neural Information Processing Systems 33, virtual, 2020.

- Pomerleau (1991) D. Pomerleau. Efficient training of artificial neural networks for autonomous navigation. Neural Computation, 3(1):88–97, 1991.

- Quinonero-Candela et al. (2008) J. Quinonero-Candela, M. Sugiyama, A. Schwaighofer, and N. D. Lawrence. Dataset shift in machine learning. Mit Press, 2008.

- Rosenbaum and Rubin (1983) P. R. Rosenbaum and D. B. Rubin. The central role of the propensity score in observational studies for causal effects. Biometrika, 70:41–55, 1983.

- Schulman et al. (2015) J. Schulman, S. Levine, P. Abbeel, M. I. Jordan, and P. Moritz. Trust region policy optimization. In Proceedings of the 32nd International Conference on Machine Learning, volume 37, pages 1889–1897, Lille, France, 2015.

- Schulman et al. (2017) J. Schulman, F. Wolski, P. Dhariwal, A. Radford, and O. Klimov. Proximal policy optimization algorithms. CoRR, abs/1707.06347, 2017.

- Shang et al. (2019) W. Shang, Y. Yu, Q. Li, Z. T. Qin, Y. Meng, and J. Ye. Environment reconstruction with hidden confounders for reinforcement learning based recommendation. In Proceedings of the 25th ACM SIGKDD International Conference on Knowledge Discovery & Data Mining, pages 566–576, Anchorage, AK, 2019.

- Shi et al. (2019) J. Shi, Y. Yu, Q. Da, S. Chen, and A. Zeng. Virtual-taobao: Virtualizing real-world online retail environment for reinforcement learning. In The 33th AAAI Conference on Artificial Intelligence, pages 4902–4909, Honolulu, Hawaii, 2019.

- Shimodaira (2000) H. Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2):227–244, 2000.

- Sontakke et al. (2021) S. A. Sontakke, A. Mehrjou, L. Itti, and B. Schölkopf. Causal curiosity: RL agents discovering self-supervised experiments for causal representation learning. In Proceedings of the 38th International Conference on Machine Learning, volume 139 of Proceedings of Machine Learning Research, pages 9848–9858, Virtual Event, 2021.

- Spirtes (2010) P. Spirtes. Introduction to causal inference. J. Mach. Learn. Res., 11:1643–1662, aug 2010. ISSN 1532-4435.

- Sutton and Barto (1998) R. S. Sutton and A. G. Barto. Reinforcement learning - an introduction. Adaptive computation and machine learning. MIT Press, 1998.

- Swaminathan and Joachims (2015) A. Swaminathan and T. Joachims. Batch learning from logged bandit feedback through counterfactual risk minimization. J. Mach. Learn. Res., 16:1731–1755, 2015.

- Todorov et al. (2012) E. Todorov, T. Erez, and Y. Tassa. MuJoCo: A physics engine for model-based control. In Proceedings of the 24th IEEE/RSJ International Conference on Intelligent Robots and Systems, pages 5026–5033, Vilamoura, Portugal, 2012.

- Voloshin et al. (2021) C. Voloshin, N. Jiang, and Y. Yue. Minimax model learning. In A. Banerjee and K. Fukumizu, editors, The 24th International Conference on Artificial Intelligence and Statistics, volume 130 of Proceedings of Machine Learning Research, pages 1612–1620, Virtual Event, 2021.

- Yang et al. (2022) S. Yang, S. Zhang, Y. Feng, and M. Zhou. A unified framework for alternating offline model training and policy learning. CoRR, abs/2210.05922, 2022.

- Yoon et al. (2018) J. Yoon, J. Jordon, and M. van der Schaar. GANITE: estimation of individualized treatment effects using generative adversarial nets. In 6th International Conference on Learning Representations, 2018.

- Yu et al. (2020) T. Yu, G. Thomas, L. Yu, S. Ermon, J. Y. Zou, S. Levine, C. Finn, and T. Ma. MOPO: model-based offline policy optimization. In Advances in Neural Information Processing Systems 33, virtual event, 2020.

- Zhang et al. (2020) R. Zhang, B. Dai, L. Li, and D. Schuurmans. Gendice: Generalized offline estimation of stationary values. In 8th International Conference on Learning Representations, Addis Ababa, Ethiopia, 2020.

- Zou et al. (2020) W. Y. Zou, S. Du, J. Lee, and J. O. Pedersen. Heterogeneous causal learning for effectiveness optimization in user marketing. CoRR, abs/2004.09702, 2020.

Appendix

Appendix A Proof of Theoretical Results

In the proof section, we replace the notation of with an integral for brevity. Now we rewrite the original objective as:

| (7) |

where and , which is the squared -norm. In an MDP, given any policy , where denotes the occupancy measure of for policy , which can be defined [46, 22] as where is the state visitation probability that starts at state in model and receive at timestep and is the discount factor.

The overall pipeline to model the tractable solution to AWRM is given in Fig. 7. In the following, we will summarize the modelling process based on Fig. 7. We first approximate the optimal distribution via Lemma. A.1.

Lemma A.1.

Note that the ideal best-response policy is not the real best-response policy . The distribution is an approximation of the real optimal adversarial distribution. We give a discussion of the rationality of the ideal best-response policy as a replacement of the real best-response policy in Remark A.4. Intuitively, has larger densities on the data where the divergence between the approximation model and the real model (i.e., ) is larger or the stochasticity of the real model (i.e., ) is larger.

However, the integral process of in Eq. (8) is intractable in the offline setting as it explicitly requires the conditional probability function of . Our solution to solve the problem is utilizing the offline dataset as the empirical joint distribution and adopting practical techniques for distance estimation on two joint distributions, like GAN [16, 34], to approximate Eq. (8). To adopt that solution, we should first transform Eq. (8) into a form under joint distributions. Without loss of generality, we introduce an intermediary policy , of which can be regarded as a specific instance. Then we have for any if . Assuming if , which will hold when overlaps with , then Eq. (8) can transform to:

where . We notice that the form is the integrated function in reverse KL divergence, which is an instance of function in -divergence [2]. Replacing that form with function, we obtain a generalized representation of :

| (9) |

where is a convex and lower semi-continuous (l.s.c.) function. gives a generalized representation of the optimal adversarial distribution to maximize the error of the model. Based on Eq. (9), we have a surrogate objective of AWRM which can avoid querying to construct :

Theorem A.2.

Let as the data distribution of the best-response policy in Eq. (4) under model parameterized by , then we can find the optimal of (Eq. (4)) via iteratively optimizing the objective , where is approximated via the last-iteration model . Based on Corollary A.9, we derive an upper bound objective for :

where denotes , is a l.s.c function satisfying , and .

Thm. A.2 approximately achieve AWRM by using and a pseudo-reweighting module . assigns learning propensities for data points with larger differences between distributions and . By adjusting the weights, the learning process will exploit subtle errors in any data point, whatever how many proportions it contributes, to correct potential generalization errors on counterfactual data.

Remark A.3.

In practice, we need to use real-world data to construct the distribution . In the offline model-learning setting, we only have a real-world dataset collected by the behavior policy , which is the empirical distribution of . Let , we have

which is Eq. (5) in the main body.

In Thm. A.2, the terms are still intractable. Thanks to previous successful practices in GAN [16] and GAIL [22], we achieve the objective via a generator-discriminator-paradigm objective through similar derivation. We show the results as follows and leave the complete derivation in Appx. A.4. In particular, by introducing two discriminators and , letting , we can optimize the surrogate objective Eq. (5) via:

where is a simplification of , , and and are the parameters of and respectively. We learn a policy via imitation learning based on the offline dataset [36, 22]. Note that in the process, we ignore the term for simplifying the objective. The discussion on the impacts of removing is left in App. B.

A.1 Proof of Lemma A.1

Proof.

Given a transition function of an MDP, the distribution of the best-response policy satisfies:

We know that the occupancy measure is a density function with a constraint . Assuming the occupancy measure has an upper bound , that is , constructing a regularization coefficient as a constant value given any , then we have

which is the optimal density function of Eq. (7) with .

Note that in some particular , we still cannot construct a that can generate an occupancy specified by for any . We can only claim the distribution of the ideal best-response policy satisfies:

| (10) |

where is a normalizer that . We give a discussion of the rationality of the ideal best-response policy as a replacement of the real best-response policy in Remark A.4.

∎

Remark A.4.

The optimal solution Eq. (10) relies on . In some particular , it is intractable to derive a that can generate an occupancy specified by . Consider the following case: a state in might be harder to reach than another state , e.g., , then it is impossible to find a that the occupancy satisfies . In this case, Eq. (10) can be a sub-optimal solution. Since this work focuses on task-agnostic solution derivation while the solution to the above problem should rely on the specific description of , we leave it as future work. However, we point out that Eq. (10) is a reasonable re-weighting term even as a sub-optimum: gives larger densities on the data where the distribution distance between the approximation model and the real model (i.e., ) is larger or the stochasticity of the real model (i.e., ) is larger.

A.2 Proof of Eq. (9)

The integral process of in Eq. (8) is intractable in the offline setting as it explicitly requires the conditional probability function of . Our motivation for the tractable solution is utilizing the offline dataset as the empirical joint distribution and adopting practical techniques for distance estimation on two joint distributions, like GAN [16, 34], to approximate Eq. (8). To adopt that solution, we should first transform Eq. (8) into a form under joint distributions. Without loss of generality, we introduce an intermediary policy , of which can be regarded as a specific instance. Then we have for any if . Assuming if , which will hold when overlaps with , then Eq. (8) can transform to:

| (11) | ||||

| (12) |

where .

Definition A.5 (-divergence).

Given two distributions and , two absolutely continuous density functions and with respect to a base measure defined on the domain , we define the -divergence [34],

| (13) |

where the generator function is a convex, lower-semicontinuous function.

We notice that the terms and are the integrated functions in reverse KL divergence, which is an instance of function in -divergence (See Reverse-KL divergence of Tab.1 in [34] for more details). Replacing that form with , we obtain a generalized representation of :

| (14) |

A.3 Proof of Thm. A.2

We first introduce several useful lemmas for the proof.

Lemma A.6.

Rearrangement inequality The rearrangement inequality states that, for two sequences and , the inequalities

hold, where is any permutation of .

Lemma A.7.

For two sequences and , the inequalities

hold.

Proof.

By rearrangement inequality, we have

Then we have

∎

Now we extend Lemma A.7 into the continuous integral scenario:

Lemma A.8.

Given , for two functions and that if and only if , the inequality

holds, where and and .

Proof.

Since , we have

∎

Corollary A.9.

Let where and , for , the inequality

holds if . It is not always satisfied for functions of -divergence. We list a comparison of on that condition in Tab. 3.

Proof.

. Suppose , we have if and only if holds. Thus if and only if holds for all . By defining and and using Lemma A.8, we have:

Then we know

holds. ∎

| Name | Generator function | If |

| Kullback-Leibler | False | |

| Reverse KL | True | |

| Pearson | False | |

| Squared Hellinger | False | |

| Jensen-Shannon | False | |

| GAN | True |

Theorem A.10.

Let as the data distribution of the best-response policy in Eq. (4) under model parameterized by , then we can find the optimal of (Eq. (4)) via iteratively optimizing the objective , where is approximated via the last-iteration model . Based on Corollary A.9, we have an upper bound objective for and derive the following objective

where , denotes , is the generator function in -divergence which satisfies , and is the parameters of . denotes a probability function with the same parameters as the learned model (i.e., ) but the parameter is fixed and only used for sampling.

Proof.

Let as the data distribution of the best-response policy in Eq. (4) under model parameterized by , then we can find the optimal of (Eq. (4)) via iteratively optimizing the objective , where is approximated via the last-iteration model :

| (15) | ||||

| (16) |

where is introduced to approximate the term and fixed when optimizing . In Eq. (15), for Eq. (7) is eliminated as it does not contribute to the gradient of . Assume , let , , and , the first inequality can be derived by adopting Corollary A.9 and eliminating the first since it does not contribute to the gradient of .

∎

A.4 Proof of the Tractable Solution

Now we are ready to prove the tractable solution:

Proof.

The core challenge is that the term is still intractable. In the following, we give a tractable solution to Thm. A.2. First, we resort to the first-order approximation. Given some , we have

| (17) |

where is the first-order derivative of . By Taylor’s formula and the fact that of the generator function is bounded in , the approximation error is no more than . Substituting with in Eq. (17), the pattern in Eq. (16) can be converted to , then we have:

Note that the part in can be canceled because of , but we choose to keep it and ignore . The benefit is that we can estimate from an empirical data distribution through data collected by in directly, rather than from a uniform distribution which is harder to be generated. Although keeping incurs extra bias in theory, the results in our experiments show that it has not made significant negative effects in practice. We leave this part of modeling in future work. In particular, by ignoring , we have:

| (18) | ||||

| (19) |

We can estimate and through Lemma A.11.

Lemma A.11 ( estimation [33]).

Given a function parameterized by , if is convex and lower semi-continuous, by finding the maximum point of in the following objective:

we have . is Fenchel conjugate of [20].

In particular,

then we have and . Given and , let , then we can optimize via:

Based on the specific -divergence, we can represent and with a discriminator . It can be verified that , , and proposed in [34] satisfies the condition (see Tab. 3). We select the former in the implementation and convert the tractable solution to:

| (20) |

where , is a simplification of .

∎

Remark A.12.

In practice, we need to use the real-world data to construct the distribution and the generative data to construct . In the offline model-learning setting, we only have a real-world dataset collected by the behavior policy . We can learn a policy via imitation learning based on [36, 22] and let be the policy . Then we can regard as the empirical data distribution of and the trajectories collected by in the model as the empirical data distribution of . Based on the above specializations, we have:

which is Eq. (6) in the main body.

Appendix B Discussion and Limitations of the Theoretical Results

We summarize the limitations of current theoretical results and future work as follows:

-

1.

As discussed in Remark A.4, the solution Eq. (10) relies on . In some particular , it is intractable to derive a that can generate an occupancy specified by . If more knowledge of or is provided or some mild assumptions can be made on the properties of or , we may model in a more sophisticated approach to alleviating the above problem.

-

2.

In the tractable solution derivation, we ignore the term (See Eq. (19)). The benefit is that in the tractable solution can be estimated through offline datasets directly. Although the results in our experiments show that it does not produce significant negative effects in these tasks, ignoring indeed incurs extra bias in theory. In future work, techniques for estimating [30] can be incorporated to correct the bias. On the other hand, is also ignored in the process. can be regarded as a global rescaling term of the final objective Eq. (19). Intuitively, it constructs an adaptive learning rate for Eq. (19), which increases the step size when the model is better fitted and decreases the step size otherwise. It can be considered to further improve the learning process in future work, e.g., cooperating with empirical risk minimization by balancing the weights of the two objectives through .

Appendix C Societal Impact

This work studies a method toward counterfactual environment model learning. Reconstructing an accurate environment of the real world will promote the wide adoption of decision-making policy optimization methods in real life, enhancing our daily experience. We are aware that decision-making policy in some domains like recommendation systems that interact with customers may have risks of causing price discrimination and misleading customers if inappropriately used. A promising way to reduce the risk is to introduce fairness into policy optimization and rules to constrain the actions (Also see our policy design in Sec. G.1.3). We are involved in and advocating research in such directions. We believe that business organizations would like to embrace fair systems that can ultimately bring long-term financial benefits by providing a better user experience.

Appendix D AWRM-oracle Pseudocode

We list the pseudocode of AWRM-oracle in Alg. 2.

Input:

: policy space; : total iterations

Process:

Appendix E Implementation

E.1 Details of the GALILEO Implementation

The approximation of Eq. (17) holds only when is close to , which might not be satisfied. To handle the problem, we inject a standard supervised learning loss

| (21) |

to replace the second term of the above objective when the output probability of is far away from ().

In the offline model-learning setting, we only have a real-world dataset collected by the behavior policy . We learn a policy via behavior cloning with [36, 22] and let be the policy . We regard as the empirical data distribution of and the trajectories collected by in the model as the empirical data distribution of . But the assumption might not be satisfied. In behavior cloning, we model with a Gaussian distribution and constrain the lower bound of the variance with a small value to keep the assumption holding. Besides, we add small Gaussian noises to the inputs of to handle the mismatch between and due to . In particular, for and learning, we have:

where is a simplification of and .

On the other hand, we notice that the first term in Eq. (20) is similar to the objective of GAIL [22] by regarding as the policy to learn and as the environment to generate data. For better capability in sequential environment model learning, here we introduce some practical tricks inspired by GAIL for model learning [42, 41]: we introduce an MDP for and , where the reward is defined by the discriminator , i.e., . is learned to maximize the cumulative rewards. With advanced policy gradient methods [39, 40], the objective is converted to , where , , and . in Eq. (20) can also be constructed similarly. Although it looks unnecessary in theory since the one-step optimal model is the global optimal model in this setting, the technique is helpful in practice as it makes more sensitive to the compounding effect of one-step prediction errors: we would consider the cumulative effects of prediction errors induced by multi-step transitions in environments. In particular, to consider the cumulative effects of prediction errors induced by multi-step of transitions in environments, we overwrite function as , where and . To give an algorithm for single-step environment model learning, we can just set in and to .

Input:

: offline dataset sampled from where is the behavior policy;

: total iterations;

Process:

By adopting the above implementation techniques, we convert the objective into the following formulation

| (22) | ||||

| (23) | ||||

| (24) | ||||

| (25) | ||||

| (26) |

where . In practice, GALILEO optimizes the first term of Eq. (22) with conservative policy gradient algorithms (e.g., PPO [40] or TRPO [39]) to avoid unreliable gradients for model improvements. Eq. (25) and Eq. (26) are optimized with supervised learning. The second term of Eq. (22) is optimized with supervised learning with a re-weighting term . Since is unknown, we use to estimate it. When the mean output probability of a batch of data is larger than or small than , we replace the second term of Eq. (22) with a standard supervised learning in Eq. (21). Besides, unreliable gradients also exist in the process of optimizing the second term of Eq. (22). In our implementation, we use the scale of policy gradients to constrain the gradients of the second term of Eq. (22). In particular, we first compute the -norm of the gradient of the first term of Eq. (22) via conservative policy gradient algorithms, named . Then we compute the -norm of the gradient of the second term of Eq. (22), name . Finally, we rescale the gradients of the second term by

| (27) |

For each iteration, Eq. (22), Eq. (25), and Eq. (26) are trained with certain steps (See Tab. 6) following the same framework as GAIL. Based on the above techniques, we summarize the pseudocode of GALILEO in Alg. 3, where and are set to and in all of our experiments. The overall architecture is shown in Fig. 8.

E.2 Connection with Previous Adversarial Algorithms

Standard GAN [16] can be regarded as a partial implementation including the first term of Eq. (22) and Eq. (25) by degrading them into the single-step scenario. In the context of GALILEO, the objective of GAN is

where . In the single-step scenario, . The term can convert to by replacing the gradient of with [46]. Previous algorithms like GANITE [51] and SCIGAN [7] can be regarded as variants of the above training framework.

Appendix F Additional Related Work

Our primitive objective is inspired by weighted empirical risk minimization (WERM) based on inverse propensity score (IPS). WERM is originally proposed to solve the generalization problem of domain adaptation in machine learning literature. For instance, we would like to train a predictor in a domain with distribution to minimize the prediction risks in the domain with distribution , where . To solve the problem, we can train a weighted objective with , which is called weighted empirical risk minimization methods [4, 5, 12, 9, 37]. These results have been extended and applied to causal inference, where the predictor is required to be generalized from the data distribution in observational studies (source domain) to the data distribution in randomized controlled trials (target domain) [43, 3, 19, 26, 25]. In this case, the input features include a state (a.k.a. covariates) and an action (a.k.a. treatment variable) which is sampled from a policy. We often assume the distribution of , is consistent between the source domain and the test domain, then we have , where and are the policies in source and target domains respectively. In [43, 3, 19], the policy in randomized controlled trials is modeled as a uniform policy, then . is also known as inverse propensity score (IPS). In [25], it assumes that the policy in the target domain is predefined as before environment model learning, then it uses as the IPS. The differences between AWRM and previous works are fallen in two aspects: (1) We consider the distribution-shift problem in the sequential decision-making scenario. In this scenario, we not only consider the action distribution mismatching between the behavior policy and the policy to evaluation , but also the follow-up effects of policies to the state distribution; (2) For faithful offline policy optimization, we require the environment model to have generalization ability in numerous different policies. The objective of AWRM is proposed to guarantee the generalization ability of in numerous different policies instead of a specific policy.

On a different thread, there are also studies that bring counterfactual inference techniques of causal inference into model-based RL [8, 35, 44]. These works consider that the transition function is relevant to some hidden noise variables and use Pearl-style structural causal models (SCMs), which is a directed acyclic graphs to define the causality of nodes in an environment, to handle the problem. SCMs can help RL in different ways: [8] approximate the posterior of the noise variables based on the observation of data, and environment models are learned based on the inferred noises. The generalization ability is improved if we can infer the correct value of the noise variables. [35] discover several local causal structural models of a global environment model, then data augmentation strategies by leveraging these local structures to generate counterfactual experiences. [44] proposes a representation learning technique for causal factors, which is an instance of the hidden noise variables, in partially observable Markov decision processes (POMDPs). With the learned representation of causal factors, the performance of policy learning and transfer in downstream tasks will be improved.

Instead of considering the hidden noise variables in the environments, our study considers the environment model learning problem in the fully observed setting and focuses on unbiased causal effect estimation in the offline dataset under behavior policies collected with selection bias.

In offline model-based RL, the problem is called distribution shift [52, 28, 11] which has received great attentions. However, previous algorithms do not handle the model learning challenge directly but propose techniques to suppress policy sampling and learning in risky regions [52, 27]. Although these algorithms have made great progress in offline policy optimization in many tasks, so far, how to learn a better environment model in this scenario has rarely been discussed.

We are not the first article to use the concept of density ratio for weighting. In off-policy estimation, [29, 32, 53] use density ratio to evaluate the value of a given target policy . These methods attempt to solve an accurate approximation of . The objective of our work, AWRM, is for the model to provide faithful feedback for different policies, formalized as minimizing the model error of the density function for any in the policy space . The core of this problem is how to obtain an approximation of the density function of the best-response corresponding to the current model, and then approximate the corresponding ). It should be emphasized that since is unknown in advance and will change as the induction bias of is changed, the solutions proposed in [29, 32, 53] cannot be applied to AWRM; Recently, [21, 50] use density ratio weighting to learn a model. The purpose of weighting is to make the model adapt to the current policy learning and adjust the model learning according to the current policy, which is the same as the WERM objective proposed in Def. 4.1. [49] also utilizes density ratio weighting to learn a model. Instead of estimating them based on the offline dataset and target policy as previous works do, they propose to design an adversarial model learning objective by constructing two function classes and , satisfying the target policy’s value and density ratio are covered, i.e., and . Different from previous articles, our approach uses adversarial weighting to learn a universal model that provides good feedback for any target policy , i.e., AWRM, instead of learning a model suitable to a specific target policy.

Appendix G Experiment Details

G.1 Settings

G.1.1 General Negative Feedback Control (GNFC)

The design of GNFC is inspired by a classic type of scenario that behavior policies have selection bias and easily lead to counterfactual risks: For some internet platforms, we would like to allocate budgets to a set of targets (e.g., customers or cities) to increase the engagement of the targets in the platforms. Our task is to train a model to predict targets’ feedback on engagement given targets’ features and allocated budgets.

In these tasks, for better benefits, the online working policy (i.e., the behavior policy) will tend to cut down the budgets if targets have better engagement, otherwise, the budgets might be increased. The risk of counterfactual environment model learning in the task is that: the object with better historical engagement will be sent to smaller budgets because of the selection bias of the behavior policies, then the model might exploit this correlation for learning and get a conclusion that: increasing budgets will reduce the targets’ engagement, which violates the real causality. We construct an environment and a behavior policy to mimic the above process. In particular, the behavior policy is

where is a sample noise, which will be discussed later. The environment includes two parts:

(1) response function :

(2) mapping function :

The transition function is a composite of . The behavior policies have selection bias: the actions taken are negatively correlated with the states, as illustrated in Fig. 9(a) and Fig. 9(b). We control the difficulty of distinguishing the correct causality of , , and by designing different strategies of noise sampling on . In principle, with a larger number or more pronounced disturbances, there are more samples violating the correlation between and , then more samples can be used to find the correct causality. Therefore, we can control the difficulty of counterfactual environment model learning by controlling the strength of disturbance. In particular, we sample from a uniform distribution with probability . That is, with probability and with probability . Then with larger , there are more samples in the dataset violating the negative correlation (i.e., ), and with larger , the difference of the feedback will be more obvious. By selecting different and , we can construct different tasks to verify the effectiveness and ability of the counterfactual environment model learning algorithm.

G.1.2 The Cancer Genomic Atlas (TCGA)

The Cancer Genomic Atlas (TCGA) is a project that has profiled and analyzed large numbers of human tumors to discover molecular aberrations at the DNA, RNA, protein, and epigenetic levels. The resulting rich data provide a significant opportunity to accelerate our understanding of the molecular basis of cancer. We obtain features, , from the TCGA dataset and consider three continuous treatments as done in SCIGAN [7]. Each treatment, , is associated with a set of parameters, , , , that are sampled randomly by sampling a vector from a standard normal distribution and scaling it with its norm. We assign interventions by sampling a treatment, , from a beta distribution, . controls the sampling bias and , where is the optimal treatment. This setting of ensures that the mode of is .

The calculation of treatment response and optimal treatment are shown in Table 4.

| Treatment | Treatment Response | Optimal treatment |

| 1 | ||

| 2 | ||

| 3 | , where | if , 1 if |

We conduct experiments on three different treatments separately and change the value of bias to assess the robustness of different methods to treatment bias. When the bias of treatment is large, which means is large, the training set contains data with a strong bias on treatment so it would be difficult for models to appropriately predict the treatment responses out of the distribution of training data.

G.1.3 Budget Allocation task to the Time period (BAT)

We deploy GALILEO in a real-world large-scale food-delivery platform. The platform contains various food stores, and food delivery clerks. The overall workflow is as follows: the platform presents the nearby food stores to the customers and the customers make orders, i.e., purchase take-out foods from some stores on the platform. The food delivery clerks can select orders from the platform to fulfill. After an order is selected to fulfill, the delivery clerks will take the ordered take-out foods from the stores and then send the food to the customers. The platform will pay the delivery clerks (mainly in proportion to the distance between the store and the customers’ location) once the orders are fulfilled. An illustration of the workflow can be found in Fig. 10.

However, there is an imbalance problem between the demanded orders from customers and the supply of delivery clerks to fulfill these orders. For example, at peak times like lunchtime, there will be many more demanded orders than at other times, and the existed delivery clerks might not be able to fulfill all of these orders timely. The goal of the Budget Allocation task to the Time period (BAT) is to handle the imbalance problem in time periods by sending reasonable allowances to different time periods. More precisely, the goal of BAT is to make all orders (i.e., the demand) sent in different time periods can be fulfilled (i.e., the supply) timely.

The core challenge of the environment model learning in BAT tasks is similar to the challenge in Fig. 1. Specifically, the behavior policy in BAT tasks is a human-expert policy, which will tend to increase the budget of allowance in the time periods with a lower supply of delivery clerks, otherwise will decrease the budget (Fig. 11 gives an instance of this phenomenon in the real data).

To handle the imbalance problem in different time periods, in the platform, the orders in different time periods will be allocated with different allowances . For example, at 10 A.M. (i.e., ), we add (i.e., ) allowances to all of the demanded orders. From 10 A.M. to 11 A.M., the delivery clerks who take orders and send food to customers will receive extra allowances. Specifically, if the platform pays the delivery clerks for fulfilling the order, now he/she will receive . For each day, the budget of allowance is fixed. We should find the best budget allocation policy of the limited budget to make as many orders as possible can be taken timely.

To find the policy, we first learn a model to reconstruct the response of allowance for each delivery clerk , where is the taken orders of the delivery clerks in state , is the allowances, denotes static features of the time period . In particular, the state includes historical order-taken information of the delivery clerks, current orders information, the feature of weather, city information, and so on. Then we use a rule-based mapping function to fill the complete next time-period states, i.e., . Here we define the composition of the above functions and as . Finally, we learn a budget allocation policy based on the learned model. For each day, the policy we would like to find is:

In our experiment, we evaluate the degree of balancing between demand and supply by computing the averaged five-minute order-taken rate, that is the percentage of orders picked up within five minutes. Note that the behavior policy is fixed for the long term in this application. So we directly use the data replay with a small scale of noise (See Tab. 6) to reconstruct the behavior policy for model learning in GALILEO.

Also note that although we model the response for each delivery clerk, for fairness, the budget allocation policy is just determining the allowance of each time period and keeps the allowance to each delivery clerk the same.

G.2 Baseline Algorithms

The algorithm we compared are: (1) Supervised Learning (SL): training a environment model to minimize the expectation of prediction error, without considering the counterfactual risks; (2) inverse propensity weighting (IPW) [45]: a practical way to balance the selection bias by re-weighting. It can be regarded as , where is another model learned to approximate the behavior policy; (3) SCIGAN: a recent proposed adversarial algorithm for model learning for continuous-valued interventions [7]. All of the baselines algorithms are implemented with the same capacity of neural networks (See Tab. 6).

G.2.1 Supervised Learning (SL)

As a baseline, we train a multilayer perceptron model to directly predict the response of different treatments, without considering the counterfactual risks. We use mean square error to estimate the performance of our model so that the loss function can be expressed as , where is the number of samples, is the true value of response and is the predicted response. In practice, we train our SL models using Adam optimizer and the initial learning rate on both datasets TCGA and GNFC. The architecture of the neural networks is listed in Tab. 6.

G.2.2 Inverse Propensity Weighting (IPW)