Limit results for distributed estimation of invariant subspaces in multiple networks inference and PCA

Abstract

We study the problem of distributed estimation of the leading singular vectors for a collection of matrices with shared invariant subspaces. In particular we consider an algorithm that first estimates the projection matrices corresponding to the leading singular vectors for each individual matrix, then computes the average of the projection matrices, and finally returns the leading eigenvectors of the sample averages. We show that the algorithm, when applied to (1) parameters estimation for a collection of independent edge random graphs with shared singular vectors but possibly heterogeneous edge probabilities or (2) distributed PCA for independent sub-Gaussian random vectors with spiked covariance structure, yields estimates whose row-wise fluctuations are normally distributed around the rows of the true singular vectors. Leveraging these results we also consider a two-sample test for the null hypothesis that a pair of random graphs have the same edge probabilities and we present a test statistic whose limiting distribution converges to a central (resp. non-central) under the null (resp. local alternative) hypothesis.

keywords:

and

1 Introduction

Distributed estimation, also known as divide-and-conquer or aggregated inference, is used in numerous methodological applications including regression [aggregated_inference_huo, ridge_regression_dobriban], integrative data analysis [jive, feng2018angle, hector], multiple networks inference [arroyo2019inference], distributed PCA and image populations analysis [population_svd, sagonas2017robust, tang2021integrated, fan2019distributed, chen2021distributed], and is also a key component underlying federated learning [federated_survey]. These types of procedures are particularly important for analyzing large-scale datasets that are scattered across multiple organizations and/or computing nodes where both the computational complexities and communication costs (as well as possibly privacy constraints) prevent the transfer of all the raw data to a single location.

In this paper, we focus on distributed estimation of the leading singular vectors for a collection of matrices with shared invariant subspaces, and we analyze an algorithm that first estimates the projection matrices corresponding to the leading singular vectors for each individual matrix, then computes the average of the projection matrices, and finally returns the leading eigenvectors of the sample averages. One widely studied example of this problem is distributed PCA in which there are independent -dimensional sub-Gaussian random vectors with common covariance matrix scattered across computing nodes, and the goal is to find the leading eigenspace of . Letting be the matrix whose columns are the subsample of stored in node , the authors of [fan2019distributed] analyze a procedure where each node first computes the matrix whose columns are the leading left singular vectors of . These are then sent to a central computing node which outputs the leading eigenvectors of as the estimate for the principal components of . An almost identical procedure is also used for simultaneous dimension reduction of high-dimensional images , i.e., each is a matrix whose entries are measurements recorded for various frequencies and various times, and the goal is to find a “population value decomposition” of each as . Here and are and matrices (with ) representing population frames of references, and are the subject-level features; see [population_svd] for more details. The procedure in [fan2019distributed, population_svd] can also be used for estimating the invariant leading eigenspace of multiple adjacency matrices generated from the COSIE model [arroyo2019inference] where and (resp. ) represents the common structure (resp. possibly heterogeneity) across . As a final example, a typical setting for integrative data analysis assumes that there is a collection of data matrices from multiple disparate sources and the goal is to decompose each as , where share a common row space which captures the joint structure among all , represent the individual structure in each , and are noise matrices. Several algorithms, such as aJIVE and robust aJIVE [feng2018angle, ponzi2021rajive], compute an estimate of by aggregating the leading (right) singular vectors of and then estimate each individual by projecting onto the orthogonal complement of the .

1.1 Outline of results

Despite the wide applicability of the distributed estimators for invariant subspaces described above, their theoretical results are still somewhat limited. For example, the papers that proposed the aJIVE/rAJIVE procedures [feng2018angle, ponzi2021rajive] and the PVD [population_svd] do not consider any specific noise models and thus also do not present explicit error bounds for the estimates. Similarly, in the context of the COSIE model and distributed PCA, [arroyo2019inference] and [population_svd, tang2021integrated, fan2019distributed, chen2021distributed], only provide Frobenius norm upper bounds between and . In this paper we present a general framework for analyzing these types of estimators, with special emphasis on uniform error bounds and normal approximations for the row-wise fluctuations of around . A key contribution of our paper is summarized in the following result (see Section 1.2 for a description of the notations used here).

Theorem 1.

Let be a collection of matrices of size , with for all . Let denote the number of columns of and define . Now let be any arbitrary collection of matrices and denote as the matrix whose columns are the leading left singular vectors of each . Suppose that for each one has the expansion

where is a orthogonal matrix and satisfy

| (1.1) |

for some constant . Define the quantities

| (1.2) |

Now let be the matrix whose columns are the leading eigenvectors of and let be a minimizer of over all orthogonal matrix . Then

| (1.3) |

where is a matrix satisfying

| (1.4) | ||||

Given , let be the matrix whose columns are the leading left singular vectors of and let be a minimizer of over all orthogonal matrix . Then for all we have

| (1.5) |

where is a matrix satisfying the same upper bounds as those for .

Theorem 1 is a deterministic matrix perturbation bound which combines the individual expansions for into a single expansion for . The upper bounds for and in Theorem 1 depend only on and . While bounds for these quantities can be derived for many different settings, in this paper for conciseness and ease of presentation we analyze these quantities only for the COSIE model and distributed PCA as (1) both problems are widely studied and yet (2) our results are still novel. In particular, the COSIE model is a natural extension of the multi-layer SBM, and although there are a wealth of theoretical results for multi-layer SBMs (see e.g., [paul2020spectral, chen2020global, jing2021community, lei2020bias]), they are mainly based on procedures that first aggregate the individual networks (either through a joint likelihood or by taking a weighted sum of the adjacency matrices) before computing an estimate, and are thus conceptually quite different from the distributed estimators considered in Theorem 1 (where the aggregation is done on the individual estimates); see Section 2.2 for a detailed comparison. Similarly, existing results for distributed PCA [chen2021distributed, charisopoulos2021communication, fan2019distributed, liang2014improved] mainly focus on spectral/Frobenius error bounds for and are thus coarser than the row-wise limiting results presented here.

The structure of our paper is as follows. In Section 2 we study parameters estimations for the COSIE model for both undirected networks (where as considered in [arroyo2019inference]) and directed networks (where ). We show that the rows of the estimates and are normally distributed around the rows of and , respectively, and that for all , also converges to a multivariate normal distribution centered around with a specific bias. We then consider two-sample (and multi-sample) testing for the null hypothesis that a collection of graphs from the COSIE model have the same edge probabilities matrices, and leveraging the theoretical results for , we derive a test statistic whose limiting distribution converges to a central (resp. non-central ) under the null (resp. local alternative) hypothesis. In Section 3 we apply Theorem 1 to the distributed PCA setting, and derive normal approximations for the rows of the leading principal components when the data exhibit a spiked covariance structure. Numerical simulations and experiments on real data are presented in Section 4. Detailed proofs of all stated results are presented in the supplementary material.

1.2 Notations

We summarize some notations used in this paper. For a positive integer , we denote by the set . For two non-negative sequences and , we write (, resp.) if there exists some constant such that (, resp.) for all , and we write if and . The notation (, resp.) means that there exists some sufficiently small (large, resp.) constant such that (, resp.). If stays bounded away from , we write and , and we use the notation to indicate that and . If , we write and . We say a sequence of events holds with high probability if for any there exists a finite constant depending only on such that for all . We write (resp. ) to denote that (resp. ) holds with high probability. We denote by the set of orthogonal matrices. Given a matrix , we denote its spectral, Frobenius, and infinity norms by , , and , respectively. We also denote the maximum entry (in modulus) of by and the norm of by

where denote the th row of , i.e., is the maximum of the norms of the rows of . We note that the norm is not sub-multiplicative. However, for any matrices and of conformal dimensions, we have

see Proposition 6.5 in [cape2019two]. Perturbation bounds using the norm for the eigenvectors and/or singular vectors of a noisily observed matrix norm had recently attracted interests from the statistics community, see e.g., [chen2021spectral, cape2019two, lei2019unified, damle, fan2018eigenvector, abbe2020entrywise] and the references therein.

2 COSIE Model

Inference for multiple networks is an important and nascent research area with applications to diverse scientific fields including neuroscience [bullmore2009complex, battiston2017multilayer, de2017multilayer, kong2021multiplex], economics [schweitzer2009economic, lee2016strength], and social sciences [papalexakis2013more, greene2013producing]. One of the simplest and most widely-studied models for a single network is the stochastic blockmodel (SBM) [holland1983stochastic] where each node of is assigned to a block and the edges between pairs of vertices are independent Bernoulli random variables with success probabilities . Here denotes the number of blocks and is a symmetric matrix with real-valued entries in specifying the edge probabilities within and between blocks. A natural generalization of the SBM is the multi-layer SBM [tang2009clustering, kumar2011co, han2015consistent, paul2016consistent, lei2020bias, paul2020spectral] wherein there are a collection of SBM graphs on the same vertex set with a common community assignment but possibly different block probabilities matrices . The single and multi-layer SBMs can be viewed as edge-independent graphs where the edge probabilities matrices have both a low-rank and block constant structure. More specifically let be a multi-layer SBM and denote by the matrix with binary entries such that if and only if the th vertex is assigned to the th block. Then is the edge probabilities matrix for each , i.e., the edges of are independent Bernoulli random variables with success probabilities given by entries of .

Another class of model for multiple networks is based on the notion of generalized random dot product graphs (GRDPG) [young2007random, grdpg1]. A graph is an instance of a GRDPG if each vertex is associated with a latent position and the edges between pairs of vertices are independent Bernoulli random variables with success probablities where denotes a (generalized) inner product in . The edge probabilities matrix of a GRDPG can be written as where the rows of are the (normalized) latent positions associated with the vertices in and is a matrix representing a (generalized) inner product; is also low-rank but, in contrast to a SBM, needs not to have any constant block structure. The GRDPG thus includes, as special cases, the SBM and its variants including the degree-corrected, mixed-memberships, and popularity adjusted block models [sengupta_chen, karrer2011stochastic, Airoldi2008]. A natural formulation of the GRDPG for multiple networks is to assume that each is an edge independent random graph where the edge probabilities are . The resulting networks share a common latent structure induced by but with possibly heterogeneous connectivity patterns across networks as modeled by . Examples of the above formulation include the common subspace independent edge graphs (COSIE) model [arroyo2019inference] where are arbitrary invertible matrices and the multiple eigenscaling model [nielsen2018multiple, wang2019joint, draves2020bias] where are diagonal matrices. In this paper we consider a slight variant of the COSIE model that is suitable for directed networks.

Definition 1 (Common subspace independent edge graphs).

Let and be matrices with orthonormal columns and let be matrices such that for all and . Here and denote the th and th row of and , respectively. We say that the random adjacency matrices are jointly distributed according to the common subspace independent-edge graph model with parameters if, for each , is a random matrix whose entries are independent Bernoulli random variables with . In other words,

We write to denote a collection of random graphs generated from the above model, and we write to denote the (unobserved) edge probabilities matrix for each graph . We note that the COSIE model in [arroyo2019inference] is for undirected graphs wherein and are symmetric. Our subsequent theoretical results, while stated for directed graphs, continue to hold for the undirected COSIE model once we account for the symmetry of ; see Remark 9 for more details. Finally we emphasize that are not necessarily independent in the statement of Definition 1. Indeed, while the assumption that are mutually independent appears extensively in the literature (see e.g., the original COSIE model [arroyo2019inference], multi-layer GRDPGs [jones2020multilayer], multi-layer SBMs [han2015consistent, tang2009clustering, paul2016consistent, lei2020bias, paul2020spectral], and the multiNESS model [macdonald2022latent]), it is either not needed or can be relaxed for the theoretical results in this paper. See Remark 5 for more details.

Remark 1.

Recall that in the multi-layer SBM, where with entries in and for all represents the consensus community assignments (which does not change across graphs), and with entries in represent the varying community-wise edge probabilities. The multi-layer SBM is a special case of the COSIE model with and ; see Proposition 1 in [arroyo2019inference] for more details.

Given , we will estimate and using the same idea as that in [arroyo2019inference] (see Algorithm 1 for a detailed description). As we alluded to in the introduction, an almost identical procedure is also used for distributed PCA [fan2019distributed] and “population value decomposition” of images [population_svd].

-

1.

For each , obtain and as the matrices whose columns are the leading left and right singular vectors of , respectively.

-

2.

Let and be matrices whose columns are the leading left singular vectors of and , respectively.

-

3.

For each , compute .

2.1 Main results

We shall make the following assumptions on the edge probabilities matrices for . We emphasize that, because our theoretical results address either large-sample approximations or limiting distributions, these assumptions should be interpreted in the regime where is arbitrarily large and/or . For ease of exposition we also assume that the number of graphs is bounded as (1) there are many applications for which we only have a finite number of graphs and (2) if the graphs are not too sparse then having makes inference for and easier while not having detrimental effect on estimation of .

Assumption 1.

The following conditions hold when is arbitrarily large.

-

•

The matrices and are matrices with bounded coherence, i.e.,

-

•

There exists a factor depending on such that for each , is a matrix with where for some sufficiently large but finite constant . We interpret as the growth rate for the average degree of the graphs generated from .

-

•

have bounded condition numbers, i.e., there exists a finite constant such that

where (resp. ) denotes the largest (resp. smallest) singular value of .

Remark 2.

We now provide some brief discussions surrounding Assumption 1. The first condition of bounded coherence for (resp. ) is a prevalent and typically mild assumption in random graphs and many other high-dimensional statistics inference problems including matrix completion, covariance estimation, and subspace estimation, see e.g., [candes_recht, fan2018eigenvector, lei2019unified, abbe2020entrywise, cape2019two, cai2021subspace]. Bounded coherence together with the second condition also implies that the average degree of each graph grows poly-logarithmically in . This semisparse regime is generally necessary for spectral methods to work, e.g., if then the singular vectors of any individual are no longer consistent estimate of and . The last condition of bounded condition number implies that are full-rank and hence the column space (resp. row space) of each is identical to that of (resp. ). The main reason for this condition is to enforce model identifiabilitity as it prevents pathological examples such as when are rank matrices with no shared common structure but, by defining (resp. ) as the union of the column spaces (resp. row spaces) of , can still correspond to a valid (but vacuous) COSIE model.

We now present uniform error bounds and normal approximations for the row-wise fluctuations of and around and , respectively. These results provide much stronger theoretical guarantees than the Frobenius norm error bounds for and that is commonly encountered in the literature. See Section 2.2 for more detailed discussions. For ease of exposition we shall assume that the dimension of and is known and we set in Algorithm 1. If is unknown then it can be estimated using the following approach: for each let be the number of eigenvalues of exceeding in modulus where denotes the max degree of and take as the mode of the . We can then show that is, under the conditions in Assumption 1, a consistent estimate of by combining tail bounds for (such as those in [rinaldo_2013, oliveira2009concentration]) and Weyl’s inequality; we omit the details. Finally, for the COSIE model, the entries of noise are (centered) Bernoulli random variables. Our theoretical results, however, can be easily adapted to the more general setting where each can be decomposed as the sum of two mean-zero random matrices and where have independent bounded entries with and have independent sub-Gaussian entries with . In particular our proofs in Section A.2 and Section A.3 are written for this more general noise model. The reason for presenting only (centered) Bernoulli noise in this section is purely for simplicity of presentation as the COSIE model ties in nicely with many existing random graph models.

Theorem 2.

Let be a collection of full rank matrices of size , be matrices of size with orthonormal columns, and let be a sample of random adjacency matrices generated from the model in Definition 1. Let and suppose that and satisfy the conditions in Assumption 1. Let and be the estimates of and obtained by Algorithm 1. Let minimize over all orthogonal matrix and define similarly. We then have

| (2.1) |

where and is a random matrix satisfying

| (2.2) | ||||

with high probability. Eq. (2.1) implies

| (2.3) |

with high probability. The matrix has an expansion similar to Eq. (2.1) but with , , , and replaced by , , , and , respectively.

Remark 3.

If we fix an and let denote the leading left singular vectors of then there exists an orthogonal matrix such that

where satisfy the same bounds as those for . This type of expansion for the leading eigenvectors of a single random graph is well-known and appears frequently in the literature; see e.g., [cape2019signal, xie2021entrywise, abbe2020entrywise]. The main conceptual and technical contribution of Theorem 2 is in showing that, while is a non-linear function of , the expansion for is nevertheless still given by a linear combination of the expansions for . Finally, as we mentioned previously, Theorem 2 does not require to be mutually independent. As a simple example, let and suppose is an edge-independent random graph with edge probabilities while is a partially observed copy of where the entries are set to with probability completely at random for some . is dependent on but is also marginally, an edge independent random graph with edge probabilities . Hence, by Theorem 2, we have

where satisfies the bounds in Eq. (2.2) with high probability. The difference between (which depends only on ) and thus corresponds to .

Theorem 3.

Consider the setting in Theorem 2 and furthermore assume that are mutually independent. For any and , let be a diagonal matrix whose diagonal elements are of the form

Define as the symmetric matrix

Note that . Finally suppose that and . We then have

as , where and denote the th row of and , respectively. A similar result holds for the rows of and of with , , and replaced by , , and , respectively.

Remark 4.

Theorem 3 assumes instead of the weaker . This is done purely for ease of exposition, i.e., the normal approximations in Theorem 3 still hold in the regime . More specifically, let be the th row of . Then, for any fixed index , we derive the normal approximations in Theorem 3 by showing that (1) the th row of converges to a multivariate normal and (2) . Now the limiting normality for the th row of still holds in the regime. Meanwhile, we show by using the high-probability bound for given in Theorem 2; however the resulting bound only guarantees in the regime. Thus for we need to bound directly and this can be done with some careful book-keeping of and . Here is the th row of the matrices that appeared in the proof of Theorem 1; see Eq. (A.6). More specifically for any fixed we have with probability converging to , and this is sufficient to guarantee when . The details are tedious and mostly technical and thus, for conciseness and mathematical expediency, we only state normal approximations for the regime in this paper.

Theorem 3 also assumes that the minimum eigenvalue of grows at rate , and this condition holds whenever the entries of are homogeneous, e.g., suppose , then for any we have and hence

Weyl’s inequality then implies

The main reason for requiring a lower bound for the eigenvalues of is that we do not require to converge to any fixed matrix as and thus we cannot use directly in our limiting normal approximation. Rather, we need to scale by and, in order to guarantee that the scaling is well-behaved, we need to control the smallest eigenvalue of .

Remark 5.

For simplicity of presentation we had assumed in Theorem 3 that are mutually independent, but our result also holds under weaker conditions. More specifically the normal approximations in Theorem 3 is based on writing as

where is negligible in the limit. If are mutually independent then the above is (ignoring ) a sum of independent mean random vectors and we can apply the Lindeberg-Feller central limit theorem to show that is approximately multivariate normal. Now suppose we make the weaker assumption that, for a fixed index , are mutually independent random vectors where for each . Then under certain mild conditions on the covariance matrices for , we have

as where is a covariance matrix of the form

For example, suppose that the entries of are pairwise uncorrelated, i.e., for all and all . Then is a diagonal matrix for all in which case coincides with as given Theorem 3. As another example, suppose that and are pairwise -correlated random graphs [zheng2022vertex] for all . Then

Theorem 2 and Theorem 3, formulated for the COSIE model, assume that the subspaces and are shared across all . We now extend these results to the case where share some common invariant subspaces and but also have possibly distinct subspaces . More specifically, we assume that for each , is of the form

| (2.4) |

Here is a matrix, is a matrix (all with orthonormal columns), and is the matrix formed by concatenating the columns of and ; has a similar structure. Note that the number of columns in , which is denoted by , can be different from that for , and furthermore one of and can even be .

Now suppose we have a collection of edge independent graphs with edge probabilities of the form in Eq. (2.4). We can once again use Algorithm 1 to estimate (resp. ) where, in Step 2, we set (resp. ). We then have the following result.

Theorem 4.

Let be a collection of full rank matrices of size , be a collection of matrices of size with orthonormal columns where the invariant subspaces and have and columns, respectively, and let be a sample of random adjacency matrices generated from the probability matrices as described in Eq. (2.4). Suppose that and satisfy the conditions in Assumption 1, and furthermore, there exists a constant not depending on and such that Let be the estimate of obtained by Algorithm 1. Let be a minimizer of over all orthogonal matrix . Then

| (2.5) |

where and is a random matrix satisfying

with high probability, where . Eq. (2.5) implies

with high probability. Given let denote the leading left singular vectors of . Let be a minimizer of over all orthogonal matrix . We then have

where is a random matrix satisfying the same upper bound as that for . The estimates and have similar expansions with and replaced by and , and then swapping the roles of and with , and , respectively.

Once again, for ease of exposition, we assume that (resp. ) is known in the statement of Theorem 4. If (resp. ) is unknown then it can be consistently estimated by choosing the number of eigenvalues of (resp. ) that are approximately , e.g., let denote the eigenvalues with descending order and choose Under Assumption 1 we have (resp. ) almost surely. Finally, while Theorem 4 is stated for having (centered) independent Bernoulli entries, the same result also holds when are of the form described in Assumption 2 (see Section A.2).

Given the expansions in Theorem 4, we can derive row-wise normal approximations for and following the same argument as that for Theorem 3, with the only difference being the form of the limiting covariance matrix. In particular let and denote the th row of and . Then as where

Remark 6.

We now describe two potential applications of Theorem 4, namely to the MultiNeSS model for multiplex networks of [macdonald2022latent] and the joint and individual variation explained (JIVE) model for integrative data analysis of [jive]. One formulation of the MultiNeSS model assumes that we have a collection of symmetric matrix ; here is a diagonal matrix with “1” and “-1” on the diagonal. Then, given a collection of noisily observed where the (upper triangular) entries of are independent mean random variables, the authors of [macdonald2022latent] propose estimating and by solving a convex optimization problem of the form

| (2.6) |

where the minimization is over the set of matrices ; here is some loss function (e.g., negative log-likelihood of the assuming some parametric distribution for the entries of ), is the nuclear norm, and are tuning parameters. Denoting the minimizers of Eq. (2.6) by , [macdonald2022latent] provides upper bounds for and . Letting (resp. ) be the minimizer of (resp. ) over all with the same dimensions as (resp. ), [macdonald2022latent] also provides upper bounds for and where the minimization is over all (indefinite) orthogonal matrices of appropriate dimensions. See Theorem 2 and Proposition 2 in [macdonald2022latent] for more details.

Instead of solving Eq. (2.6) one could also estimate and using Algorithm 1. Furthermore we surmise that, by applying Theorem 4, one could derive norm error bounds for these estimates, which will then yield uniform entrywise bounds and . These error bounds and uniform entrywise bounds can be viewed as refinements of the Frobenius norm upper bounds in [macdonald2022latent]. Due to space constraints, we leave these theoretical results and their derivations to the interested reader and only present, in Section 4.2, some numerical results comparing the estimates obtained from Algorithm 1 with those in [macdonald2022latent].

The JIVE model [jive] for integrative data analysis assumes that there are data matrices where each is of dimension ; the columns of correspond to experimental subjects while the rows correspond to features. Furthermore, are modeled as where share a common row space (denoted as ), represent individual structures, and denote additive noise perturbations. The authors of [feng2018angle] propose the aJIVE procedure for estimating and that is very similar to the procedure described in Theorem 4. More specifically they first estimates using the leading left singular vectors of where contains the leading right singular vectors of . Given a , the aJIVE procedure then estimates by truncating the SVD of where is the orthogonal projection onto the row space of . While the authors of [feng2018angle] present criteria for choosing the dimensions for and , they do not provide theoretical guarantees for the estimation of and ; this is partly because they did not consider any noise model on . We surmise that, if have independent mean sub-Gaussian entries then, by modifying Theorem 4 slightly (to allow for rectangular matrices) we can obtain norms error bounds for estimation of and . Once again, due to space constraints, we leave the precise bounds and their derivations to the interested reader.

We now resume our discussion of the COSIE model by presenting a normal approximation for the estimation of using .

Theorem 5.

Consider the setting in Theorem 2. For any , let be the estimate of given in Algorithm 1. Let and be diagonal matrices with entries

Also let be the diagonal matrix with diagonal entries

for any . Now let be given by

Note that . Next define as the symmetric matrix

Now suppose (note that always hold). Then for we have

| (2.7) |

as . Furthermore, are asymptotically mutually independent. Finally, if we have

as .

Remark 7.

The normal approximation in Theorem 5 requires as opposed to the much weaker condition of in Theorem 3. The main reason for this discrepancy is that Theorem 3 is a limit result for any given row of while Theorem 5 requires averaging over all rows of ; indeed, is a quadratic form in . The main technical challenge for Theorem 5 is in showing that this averaging leads to a substantial reduction in variability (compared to the variability in any given row of ) without incurring significant bias, and currently we can only guarantee this for . While this might seems, at first blush, disappointing it is however expected as the threshold also appeared in many related limit results that involve averaging over all rows of . For example [li2018two] considers testing whether the community memberships of the two graphs are the same and their test statistic, which is based on the - distance between the singular subspaces of the two graphs, converges to a standard normal under the condition for some ; see Assumption 3 in [li2018two]. As another example, [han_fan] studied the asymptotic distributions for the leading eigenvalues and eigenvectors of a symmetric matrix under the assumption that where is an unobserved low-rank symmetric matrix and is an unobserved generalized Wigner matrix, i.e., the upper triangular entries of are independent mean random variables. Among the numerous conditions assumed in their paper there is one sufficient condition for several of their main results to hold, i.e., that for all . Here is the random variable for the th entry of and is the th largest eigenvalue (in modulus) of ; see Eq. (13) in [han_fan] for more details. Suppose we fix an and let , , and (note that estimates for the eigenvalues of can be extracted from the entries of ). Then, assuming the conditions in Assumption 1, we have , and , and thus the condition in [han_fan] is simplified to , or equivalently that .

In addition, Theorem 5 assumes that the minimum eigenvalue of grows at rate . This condition is analogous to the condition for in Theorem 2 and is satisfied whenever the entries of are homogeneous. Furthermore, as we will see in the two-sample testing of Section 2.3, both and are generally unknown and need to be estimated, and consistent estimation of needs not imply consistent estimation of (and vice versa) unless we can control .

Remark 8.

We now compare our inference results for the COSIE model against existing results for spectral embedding of a single network. In particular the COSIE model with is equivalent to the GRDPG model [grdpg1] and thus our limit results for is the same as those for adjacency spectral embedding of a single GRPDG; e.g., Theorem 3.1 in [xie2021entrywise] and Theorem 3 in [tang2018eigenvalues] corresponds to special cases of Theorem 2 and Theorem 4 in the current paper. If and for all then, for any , we have where is the asymptotic covariance matrix (such as that given in Theorem 3.1 of [xie2021entrywise]) for the adjacency spectral embedding (ASE) of a single GRDPG with edge probabilities . If the are heterogeneous then the has a more complicated form (as it depends on the whole collection ) but nevertheless we still have . In summary, having graphs with a common subspace lead to better estimation accuracy for and compared to ASE for just a single GRDPG as we can leverage information across these multiple graphs. A formal statement of this claim is provided in Proposition 1 below. In contrast, the estimation accuracy of is not improved even when we have graphs (see Theorem 5) and this is because the are possibly heterogeneous and thus each is estimated using only a single .

Proposition 1.

Consider the setting in Theorem 2. We then have

with high probability. A similar result holds for with and replaced by and .

Remark 9.

Theorems 2, 3 and 5, with minimal changes, also hold under the undirected setting. In particular, the expansion for in Eq. (2.1) still holds for undirected graphs with and, given this expansion, the normal approximations in Theorem 3 and Theorem 5 can be derived using the same arguments as those presented in the supplementary material, with the main difference being that the covariance matrix in Theorem 5 now has to account for the symmetry in . More specifically let denote the half-vectorization of a matrix and let denote the diagonal matrix with diagonal entries . Denote by the duplication matrix which, for any symmetric matrix , transforms into . Define

and Theorem 5, when stated for undirected graphs, becomes

as . Here denotes the elimination matrix that, given any symmetric matrix , transforms into .

2.2 Related works

Although there have been multiple GRDPG-based models and estimating procedures proposed in the literature, their theoretical properties are still quite incomplete. For example, when are diagonal matrices both [nielsen2018multiple, wang2019joint] uses alternating gradient descent to estimate but do not provide error bound for the resulting estimates, except for the very special case where are scalars. We now summarize and compare a selection of more interesting results from [draves2020bias, arroyo2019inference, jones2020multilayer] with those in the current paper.

The authors of [draves2020bias] consider a special case of the multiple-GRPDG model wherein they assume, for each , that are diagonal matrices with positive diagonal entries, and study parameters estimation using a joint embedding procedure described in [levin2017central]. The joint embedding requires (truncated) eigendecomposition of a matrix and is thus more computationally demanding than Algorithm 1, especially when is large and/or is moderate. More importantly, it also leads to a representation of dimension corresponding to related (but still separate) node embeddings for each vertex, and this complicates the interpretations of the theoretical results. Indeed, it is unclear how (or whether if it is even possible) to extract from this joint embedding some estimates of the original parameters and . The results in [draves2020bias] are therefore not directly comparable to our results.

The model and estimation procedure in [arroyo2019inference] are identical to that considered in this paper, with the slight difference being that [arroyo2019inference] discusses the undirected graphs setting while we consider both the undirected and directed graphs settings; see Remark 9. The theoretical results in [arroyo2019inference] are, however, much weaker than those presented in the current paper. Indeed, for the estimation of , the authors of [arroyo2019inference] also derive a Frobenius norm upper bound for that is slightly less precise than our Proposition 1 but they do not provide more refined results such as Theorem 2 and Theorem 3 for the norm and row-wise fluctuations of . Meanwhile, for estimating , [arroyo2019inference] shows that converges to a multivariate normal distribution but their result does not yield a proper limiting distribution as it depends on a non-vanishing and random bias term which they can only bound by . In contrast Theorem 5 shows and thus can be replaced by the deterministic term in the limiting distribution. This replacement is essential for subsequent inference, e.g., it allows us to derive the limiting distribution for two-sample testing of the null hypothesis that two graphs have the same edge probabilities matrices (see Section 2.3), and is also technically challenging as it requires detailed analysis of using the expansions for and from Theorem 2 (see Sections A.5 and C.2 for more details).

The authors of [jones2020multilayer] consider multiple GRDPGs where the edge probabilities matrices are required to share a common left invariant subspace but can have possibly different right invariant subspaces, i.e., they assume where is a orthonormal matrix, are matrices and are possibly distinct matrices. The resulting model is then a special case of the model in Theorem 4 with . Given a realization of this multiple GRDPGs, [jones2020multilayer] define as the matrix whose columns are the leading left singular vectors of the matrix obtained by binding the columns of the and also define as the matrix whose columns are the leading (right) singular vectors of ; represents an estimate of the column space associated with . They then derive norm bounds and normal approximations for the rows of and . Their results, at least for estimation of , are qualitatively worse than ours. For example, Theorem 2 in [jones2020multilayer] implies the bound

which is worse than the bound in Theorem 4 by a factor of ; recall that can converge to at rate . As another example, Theorem 3 in [jones2020multilayer] yields a normal approximation for the rows of that is identical to Theorem 3 of the current paper, but under the much more restrictive assumption instead of . In addition [jones2020multilayer] does not discuss the estimation of .

We now discuss the relationship between our results and those for multi-layer SBMs; recall that multilayer SBMs are special cases of multilayer GRDPGs where so that . We first emphasize that our paper estimates using an “estimate then aggregate” approach, and thus we assume that as this guarantees that the individual are consistent estimates of . Furthermore we also assume that is bounded as (1) the problem is easier when increases with and (2) in many applications we only have a small number of graphs, even when the number of vertices of these graphs are rather large. Under this regime, by combining our result in Theorem 2 with the same argument as that for showing exact recovery in a single SBM (see e.g., Theorem 2.6 in [lyzinski2014perfect] or Theorem 5.2 in [lei2019unified]) one can also show that -means or -medians clustering on the rows of will, asymptotically almost surely, exactly recover the community assignments in a multi-layer SBM provided that as . The condition almost matches the lower bound for exact recovery in single-layer SBMs in [abbe2015exact, mossel2015consistency, abbe2020entrywise]; note, however, that [abbe2015exact, mossel2015consistency, abbe2020entrywise]; only consider the case of balanced SBMs where the block probabilities satisfy and for all .

Existing results for multi-layer SBMs, in contrast, are generally based on the “aggregate-then-estimate” approach. For example, the authors of [paul2020spectral] study community detection using two different procedures, namely a linked matrix factorization procedure (as suggested in [tang2009clustering]) and a co-regularized spectral clustering procedure (as suggested in [kumar2011co]) and they show that if then the estimation error bound of for these two procedures are

with high probability, where is an arbitrary but fixed constant. See the proofs of Theorem 2 and Theorem 3 in [paul2020spectral] for more details. As another example [jing2021community] proposes a tensor-based algorithm for estimating in a mixture multi-layer SBM model and shows that if then

with high probability; see the condition in Corollary 1 and the proof of Theorem 5.2 in [jing2021community] for more details. Our bound in Proposition 1 is thus either equivalent to or quantitatively better than those cited above, and our conditions is equivalent to the above conditions when is bounded by a constant not depending on . Finally, [lei2020bias] consider the sparse regime with for some constant not depending on and , and propose estimating using the leading eigenvectors of where, for each , denotes the diagonal matrix whose diagonal entries are the vertex degrees in ; the subtraction of corresponds to a bias-removal step and is essential as the diagonal entries of are heavily biased when the graphs are extremely sparse. Let denote the matrix containing these eigenvector. Theorem 1 in [lei2020bias] shows that if then

with high probability.

The above results for Frobenius norms estimation error of either or only guarantee weak recovery of the community assignment . We now discuss more refined error bounds in norms for estimating . The authors of [cai2021subspace] study subspace estimation for unbalanced matrices such as by using the leading eigenvectors of where zeroes out the diagonal entries of a matrix and thus serve the same purpose as as the subtraction of described above. Let denote the resulting leading eigenvectors. Now suppose and . Then by Theorem 1 in [cai2021subspace] we have

| (2.8) |

with high probability. See Section 4.3 in [cai2021subspace] for more details; note that the discussion in Section 4.3 of [cai2021subspace] assumes that is the adjacency matrix for a bipartite graph but the same argument also generalizes to the multi-layer SBM setting. Eq. (2.8) implies that clustering the rows of achieves exact recovery of .

The above norm bound can be further refined using results in [yan2021inference] wherein the diagonal entries of are iteratively imputed while computing its truncated eigendecompositions. In particular, let and let be a non-negative integer. Then, for , set where is the best rank- approximation to , and denotes the operation which zeros out the off-diagonal entries of a matrix. See Algorithm 7 in [yan2021inference] for more details. Let denote the leading eigenvectors of (the estimate in Eq. (2.8) corresponds to the case ). Also let denote the SVD of and denote . Once again suppose , , and choose . Then by Theorem 10 in [yan2021inference], there exists such that

| (2.9) |

where satisfies

with high probability. Eq. (2.9) also yields a normal approximation for the rows of but with more complicated covariance matrices than those given in Theorem 3; we leave the precise form of these covariance matrices to the interested reader. See Section C.6 for further discussion on Eq. (2.8) and Eq. (2.9).

2.3 Two-sample hypothesis testing

Detecting similarities or differences between multiple graphs is of both practical and theoretical importance, with applications in neuroscience and social networks. One typical example is testing for similarity across brain networks, see e.g., [zalesky2010network, rubinov2010complex, he2008structural]. A simple and natural formulation of two-sample hypothesis testing for graphs is to assume that they are edge-independent random graphs on the same vertices such that, given any two graphs, they are said to be from the same (resp. “similar”) distribution if their edge probabilities matrices are the same (resp. “close”); see e.g., [tang2017semiparametric, ginestet2017hypothesis, ghoshdastidar2020two, li2018two, levin2017central, durante2018bayesian] for several recent examples of this type of formulation.

Nevertheless, many existing test statistics do not have known non-degenerate limiting distribution, especially when comparing only two graphs, and calibration of their rejection regions have to be done either via bootstrapping (see e.g., [tang2017semiparametric]) or non-asymptotic concentration inequalities (see e.g., [ghoshdastidar2020two]). Both of these approaches can be sub-optimal. For example, bootstrapping is computationally expensive and has inflated type-I error when the bootstrapped distribution has larger variability compared to the true distribution, while non-asymptotic concentration inequalities are overtly conservative and thus incur a significant loss in power.

In this section we consider two-sample testing in the context of the COSIE model and propose a test statistic that converges to a distribution under both the null and local alternative hypothesis. More specifically suppose we are given a collection of graphs and are interested in testing the null hypothesis against the alternative hypothesis for some indices . As , this is equivalent to testing against . We emphasize that this reformulation transforms the problem from comparing matrices to comparing matrices.

Our test statistic is based on a Mahalanobis distance between and , i.e., by Theorem 5 we have

as . Now suppose the null hypothesis is true. Then and, with , we have

| (2.10) |

as . Our objective is to convert Eq. (2.10) into a test statistic that depends only on estimates. Toward this aim, we first define as a matrix of the form

| (2.11) |

where is a diagonal matrix whose diagonal elements are

for any and ; here we set . The following lemma shows that is a consistent estimate of .

Lemma 1.

Given Lemma 1, the following result provides a test statistic for that converges to a central (resp. non-central) under the null (resp. local alternative) hypothesis.

Theorem 6.

Consider the setting in Theorem 5 where . Fix and let and be the estimates of and given by Algorithm 1. Suppose and define the test statistic

where and are as given in Eq. (2.11). Then under , we have as . Next suppose that is a finite constant and that satisfies a local alternative hypothesis where

We then have as where is the noncentral chi-square distribution with degrees of freedom and noncentrality parameter .

Remark 10.

Theorem 6 indicates that for a chosen significance level , we reject if , where is the percentile of the distribution with degrees of freedom. The assumption is the same as that for the normal approximation of in Theorem 5; see Remark 7 for more discussion on this threshold. Now if the average degree grows at rate then we still have and thus under . We can therefore use as a test statistic and calibrate the rejection region for via bootstrapping. We note that the test statistic was also used in [arroyo2019inference], with the main difference being that [arroyo2019inference] only assumed (but did not show theoretically) that under the null hypothesis.

We end this section by noting that Theorem 6 can be extended to the multi-sample setting, i.e., testing against for some (generally) unknown pair . Our test statistic is then a sum of the (empirical) Mahalanobis distance between and . More specifically, define

| (2.12) |

where . Let and suppose . Then under we have as . Next let be a finite constant and suppose that satisfies a local alternative hypothesis of the form

where . Then we also have as . See Section A.7 for a proof sketch of these limit results.

Thus, for a chosen significance level , we reject if exceeds the percentile of the distribution with degrees of freedom. Furthermore, if we reject this then we can do post-hoc analysis to identify pairs where by first computing the -values of the test statistics in Theorem 6 for all and then applying Bonferroni correction to these -values. The test statistic in Eq. (2.12) also works for testing the hypothesis for all against for some possibly unknown , which is useful in the context of change-point detections for time series of networks. Once again if we reject this then we can identify the indices where by applying Bonferroni correction to the -values of the in Theorem 6 for all .

3 Distributed PCA

Principal component analysis (PCA) [hotelling1933analysis] is the most classical and widely applied dimension reduction technique for high-dimensional data. Standard uses of PCA involve computing the leading singular vectors of a matrix and thus generally assume that the data can be stored in memory and/or allowed for random access. However, massive datasets are now quite prevalent and these data are often-times stored across multiple machines in possibly distant geographic locations. The communication cost for applying traditional PCA on these datasets can be rather prohibitive if all the data are sent to a central location, not to mention that (1) the central location may not have the capability to store and process such large datasets or (2) due to privacy constraints the raw data cannot be shared between machines. To meet these challenges, significant efforts have been spent on designing and analyzing algorithms for PCA in either distributed or streaming environments, see [garber2017communication, charisopoulos2021communication, chen2021distributed, fan2019distributed, pmlr-streaming-PCA] for several recent developments in this area.

A succinct description of distributed PCA is as follows. Let be iid random vectors in with and suppose the are scattered across computing nodes with each node storing samples where, for simplicity (and with minimal loss of generality), assume . Denote by the matrix formed by the samples stored on the th node. As we mentioned in the introduction, a natural distributed procedure (see e.g., [fan2019distributed]) for estimating the leading principal components of is: (1) each node computes the matrix whose columns are the leading eigenvectors of the sample covariance matrix (2) are sent to a central node (3) the central node computes the matrix whose columns are the leading left singular vectors of the matrix .

In this section we investigate the theoretical properties of distributed PCA assuming the following spiked covariance structure for , namely that

| (3.1) |

where is a such that and with . The columns of are the leading eigenvectors of . Covariance matrices of the form in Eq. (3.1) are studied extensively in the high-dimensional statistics literature, see e.g., [Spiked, sparse_AOS, sparse_AOS1, sparse, Tony_sparse, bai_sample_cov] and the references therein. A common assumption for is that it is sparse, e.g., the quasi-norms, for some , of the columns of are bounded. Note that sparsity of also implies sparsity of . In this paper we do not impose sparsity constraints on but instead assume that has bounded coherence, i.e., . The resulting will no longer be sparse. Bounded coherence is also a natural condition in the context of covariance matrix estimation, see e.g., [cape2019two, yan2021inference, chen2021distributed, xie2018bayesian] as it allows for the spiked eigenvalues to grow with while also guaranteeing that the entries of the covariance matrix remain bounded, i.e., there is a large gap between the spiked eigenvalues and the remaining eigenvalues. In contrast if is sparse then the spiked eigenvalues grows with if and only if the variance and covariances in also grow with , and this can be unrealistic in many settings as increasing the dimension of the (e.g., by adding more features) should not change the magnitude of the existing features.

We now state the analogues of Theorem 2, Theorem 3 and Proposition 1 in the setting of distributed PCA. We emphasize that these results should be interpreted in the regime where both and are arbitrarily large or .

Theorem 7.

Suppose we have iid mean zero -dimensional multivariate Gaussian random samples with covariance matrix of the form in Eq. (3.1) and they are scattered across computing nodes, each of which stores samples. Now suppose that , , and for some . Let be the effective rank of and let minimize over all orthogonal matrix where is the distributed PCA estimate of described above. Define

We then have, for that

| (3.2) |

where is a random matrix satisfying

with high probability. Furthermore, if , we have

| (3.3) |

with high probability, where .

Remark 11.

Theorem 7 assumes that the leading (spiked) eigenvalues of grows with at rate for some while the remaining (non-spiked) eigenvalues remain bounded. Under this condition the effective rank of satisfies and thus and correspond to the cases where is growing with and remains bounded, respectively. The effective rank serves as a measure of the complexity of ; see e.g., [vershynin_hdp, tropp2, luo_xiao_bunea]. The condition assumed for Eq. (3.2) is thus very mild as we are only requiring the sample size in each node to grow slightly faster than the effective rank . Similarly the slightly more restrictive condition for Eq. (3.3) is also quite mild as it leads to a much stronger (uniform) row-wise concentration for . If then the above two conditions both simplify to and thus allow for the dimension to grow exponentially with . Finally, Theorem 7 also holds for , with the only minor change being that the sample size requirement for Eq. (3.3) continue to be for .

Remark 12.

The proof of Theorem 7 (see Section A.8) is almost identical to that of Theorem 2 for the COSIE model (see Section A.2). More specifically, after deriving an expansion for for each (see Lemma 8 in Section A.8) we apply Theorem 1 to combine these individual expansions for into a single expansion for . We also note that the main difference between the leading terms in Theorem 2 and Theorem 7 is the appearance of the projection matrix . This difference arises because for the COSIE model, are low-rank matrices while for distributed PCA the are not necessarily low-rank.

Theorem 8.

Consider the setting in Theorem 7 and further suppose . Let and denote the th row of and , respectively. Define Then for any we have

as .

The condition stated in Theorem 8 is slightly more restrictive than the condition for Eq. (3.3). This is done purely for ease of exposition as the normal approximation for when requires more tedious book-keeping of . See Remark 4 for similar discussions.

Proposition 2.

Proposition 2 is almost identical to Theorem 4 in [fan2019distributed], except that [fan2019distributed] presented their results in term of the Orlicz norm for . We note that, for a fixed and , the error bound in Proposition 2 converges to at rate where is the total number of samples, and is thus reminiscent of the error rate for traditional PCA (where ) in the low-dimensional setting; see also the asymptotic covariance matrix in Theorem 8.

Remark 13.

For ease of exposition the previous results are stated in the case where is known and thus, without loss of generality, we can assume . If is unknown, we have to demean the data before doing PCA. More specifically let be the covariance matrix for the th server where . Then, with , we have

Bounds for are given in the proof of Theorem 7. Next, as , we have

with high probability. We thus have, from Eq. (B.12) and Eq. (B.13) in [chen2021classification], that

with high probability. Therefore and are all of smaller order than the corresponding terms for . We can thus ignore all terms depending on in the proofs of Theorem 7, Theorem 8 and Proposition 2, i.e., these results continue to hold even when is unknown.

Remark 14.

The theoretical results in this section can be easily extended to the case where all have the same eigenspace but possibly different spiked eigenvalues. More specifically, suppose that the data on the th server have covariance matrix

with for all and for some finite constant not depending on and . Then under this setting the expansion in Theorem 7 changes to

while the limit result in Theorem 8 holds with covariance matrix

where is the th diagonal element of and represents the variance of the th coordinate of not captured by the leading principal components in . The bound in Proposition 2 remains unchanged.

Finally, all results in this section can also be generalized to the case where are only sub-Gaussians. Indeed, the same bounds (up to some constant factor) for as those presented in the current paper are also available in the sub-Gaussian setting, see e.g., [Lounici2017, chen2021classification, chen2021spectral], and thus the arguments presented in the supplementary material still carry through. The only minor change is in the covariance in Theorem 8, i.e., if is mean and sub-Gaussian then

where is the th row of and contains the fourth order (mixed) moments of and thus needs not depend (only) on . In the special case when then where is the commutation matrix, and this implies (see Eq. (A.54)).

3.1 Related works

We first compare our results for distributed PCA with the minimax bound for traditional PCA given in [cai2013sparse]. For ease of exposition we state these comparisons in terms of the - distance between subspaces as these are equivalent to the corresponding Procrustes distances. Let be the family of spiked covariance matrices of the form

where , and are fixed constants. Then for any , we have from Proposition 2 that

| (3.4) |

with high probability, provided that has bounded coherence. Meanwhile, by Theorem 1 in [cai2013sparse], the minimax error rate for the class is

| (3.5) |

where the infimum is taken over all estimators of . If then the error rate in Eq. (3.4) for distributed PCA is the same as that in Eq. (3.5) for traditional PCA while if then there is a (multiplicative) gap of order at most between the two error rates. Note, however, that Eq. (3.4) provides a high-probability bound for which is a slightly stronger guarantee than the expected value in Eq. (3.5).

We now compare our results with existing results for distributed PCA in [garber2017communication, charisopoulos2021communication, chen2021distributed]. We remark at the outset that our norm bound for in Theorem 7 and the row-wise normal approximations for in Theorem 8 are, to the best of our knowledge, novel as previous theoretical analysis for distributed PCA focused exclusively on the coarser Frobenius norm error of and . The authors of [garber2017communication] propose a procedure for estimating the first leading eigenvector of by aligning all local estimates (using sign-flips) to a reference solution and then averaging the (aligned) local estimates. The authors of [charisopoulos2021communication] extend this procedure to handle more than one eigenvector by using orthogonal Procrustes transformations to align the local estimates. Let denote the resulting estimate of . If we now assume the setup in Theorem 7 then by Theorem 4 in [charisopoulos2021communication], we have

| (3.6) |

with high probability. The error rates for and are thus almost identical, cf., Eq. (3.4). The authors of [chen2021distributed] consider distributed estimation of by aggregating the eigenvectors associated with subspaces of whose dimensions are slightly larger than that of . While the aggregation scheme in [chen2021distributed] is considerably more complicated than that studied in [fan2019distributed] and the current paper, it also requires possibly weaker eigengap conditions and thus a detailed comparisons between the two sets of results is perhaps not meaningful. Nevertheless if we assume the setting in Theorem 7 then Theorem 3.3 in [chen2021distributed] yields an error bound for equivalent to Eq. (3.4).

In this paper we assume that grows with as the case where is fixed has been addressed in several classic works. For example Theorem 13.5.1 in [anderson1962introduction] states that converges to a multivariate normal distribution in provided that the eigenvalues of are distinct. This result is subsequently extended to the case where the are from an elliptical distribution with possibly non-distinct eigenvalues (see Sections 3.1.6 and 3.1.8 of [kollo2005advanced]) or when they only have finite fourth order moments [davis1977asymptotic]. These cited results are for the joint distribution of all rows of and are thus slightly stronger than row-wise results presented in this paper (which currently only imply that the joint distribution for any finite collection of rows of converges to multivariate normal).

Finally we present another variant of Theorem 7 and Theorem 8 but with different assumptions on and . More specifically, rather than basing our analysis on the sample covariances , we instead view each as where and represent the “signal” and “noise” components, respectively. Let , and note that

The column space of is, almost surely, the same as that spanned by . Furthermore the leading eigenvectors of are also the leading left singular vectors of and thus they can be considered as a noisy perturbation of the leading left singular vectors of (see Section 3 of [yan2021inference] for more details). Note that has mutually independent entries; in contrast, the entries of are dependent. We then have the following results.

Theorem 9.

Assume the same setting as that in Theorem 7 and suppose that

| (3.7) |

Let minimize over all orthogonal matrix . We then have

where denotes the Moore-Penrose pseudo-inverse and the residual matrix satisfies

with probability at least .

Theorem 10.

Consider the setting in Theorem 9 and further suppose that

Let and denote the th row of and , respectively. Define Then for any we have

as .

| Result | Conditions | |

|---|---|---|

| Theorem 7 and Theorem 8 |

|

|

| Theorem 9 and Theorem 10 |

|

Remark 15.

As we mentioned above, the conclusions of Theorems 7 and 8 are the same as those for those in Theorem 9 and Theorem 10. In particular the leading term in Theorem 7 is equivalent to the leading term in Theorem 9; see the derivations in Section C.7 for more details. Similarly, the covariance matrix in Theorem 8 is identical to that in Theorem 10. Thus, the only difference between these sets of results is in the conditions assumed for and (see Table 1). More specifically, Theorem 7 and Theorem 8 only require to be large compared to , i.e., while Theorem 9 and Theorem 10 require to be large but not too large compared to , i.e., . The main reason behind these discrepancies is in the noise structure in (independent entries) compared to (dependent entries). For example, if is fixed then in probability and . In contrast, for a fixed we have as but with high probability. The signal to noise ratio () in Theorem 7 thus behaves quite differently from the signal to noise ratio () in Theorem 9 as increases. Finally, if then and, by combining Theorems 8 and 10, under the very mild condition of .

4 Simulation Results and Real Data Experiments

4.1 COSIE model

We demonstrate the theoretical results for the COSIE model with numerical simulations. We consider the setting of directed multi-layer SBMs with graphs and blocks. More specifically we let be the number of vertices and generate and randomly where are iid with for and similarly are also iid with for ; and specify the outgoing and incoming community assignment for the th vertex. Next let be the matrix representing the such that if and otherwise, and define similarly. We then simulate adjacency matrices using the edge probabilities matrices where the entries of are independent random variables. Given we estimate , and with Algorithm 1.

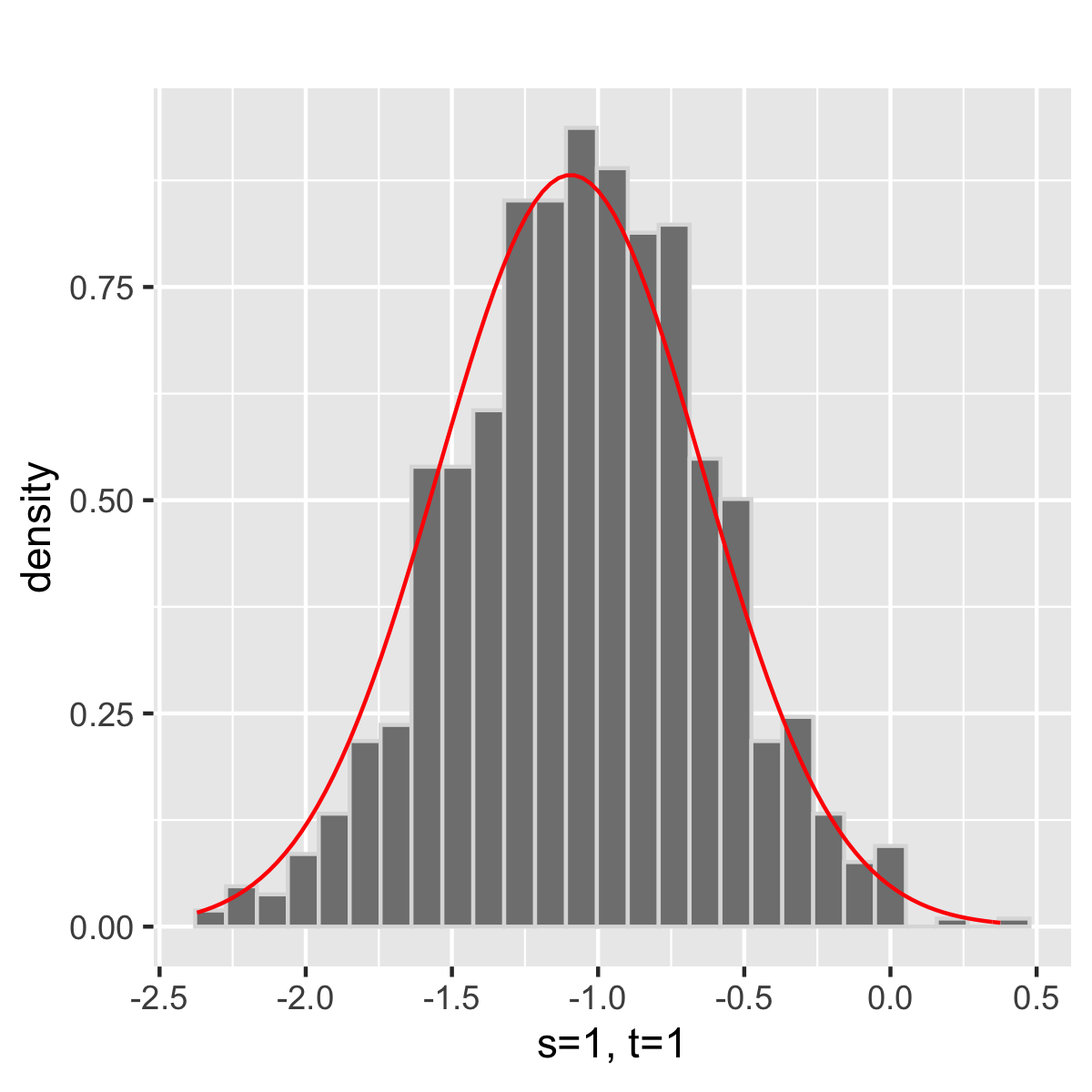

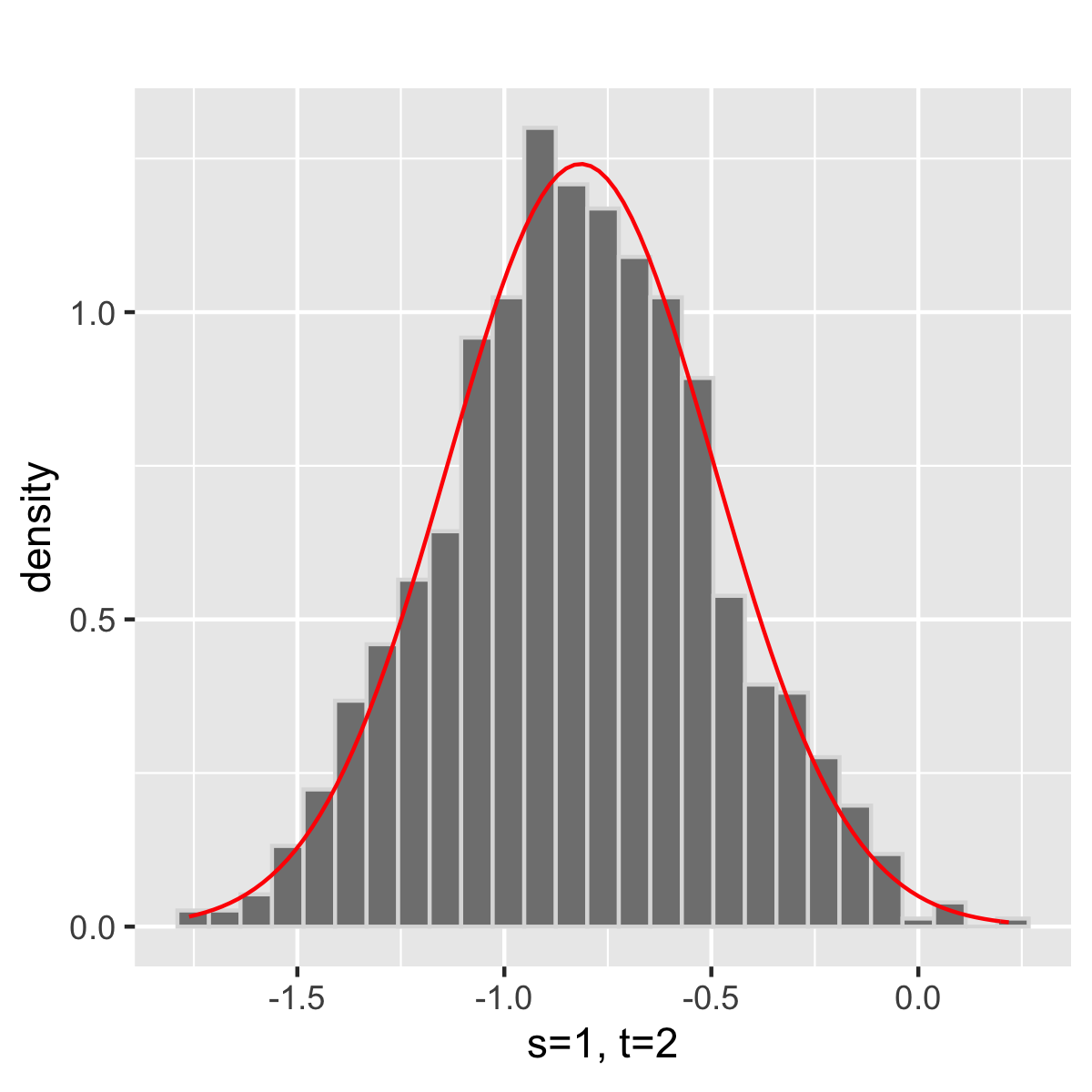

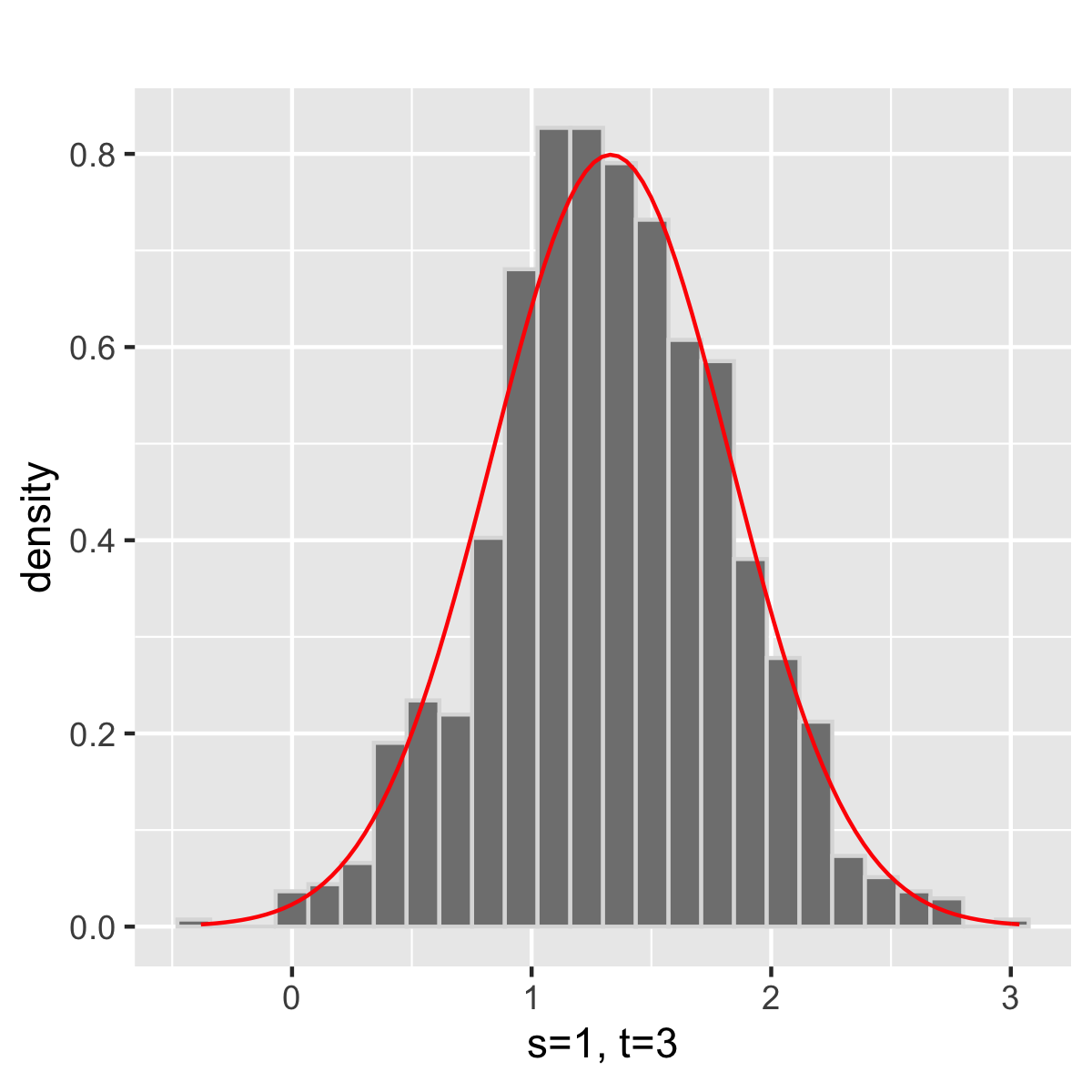

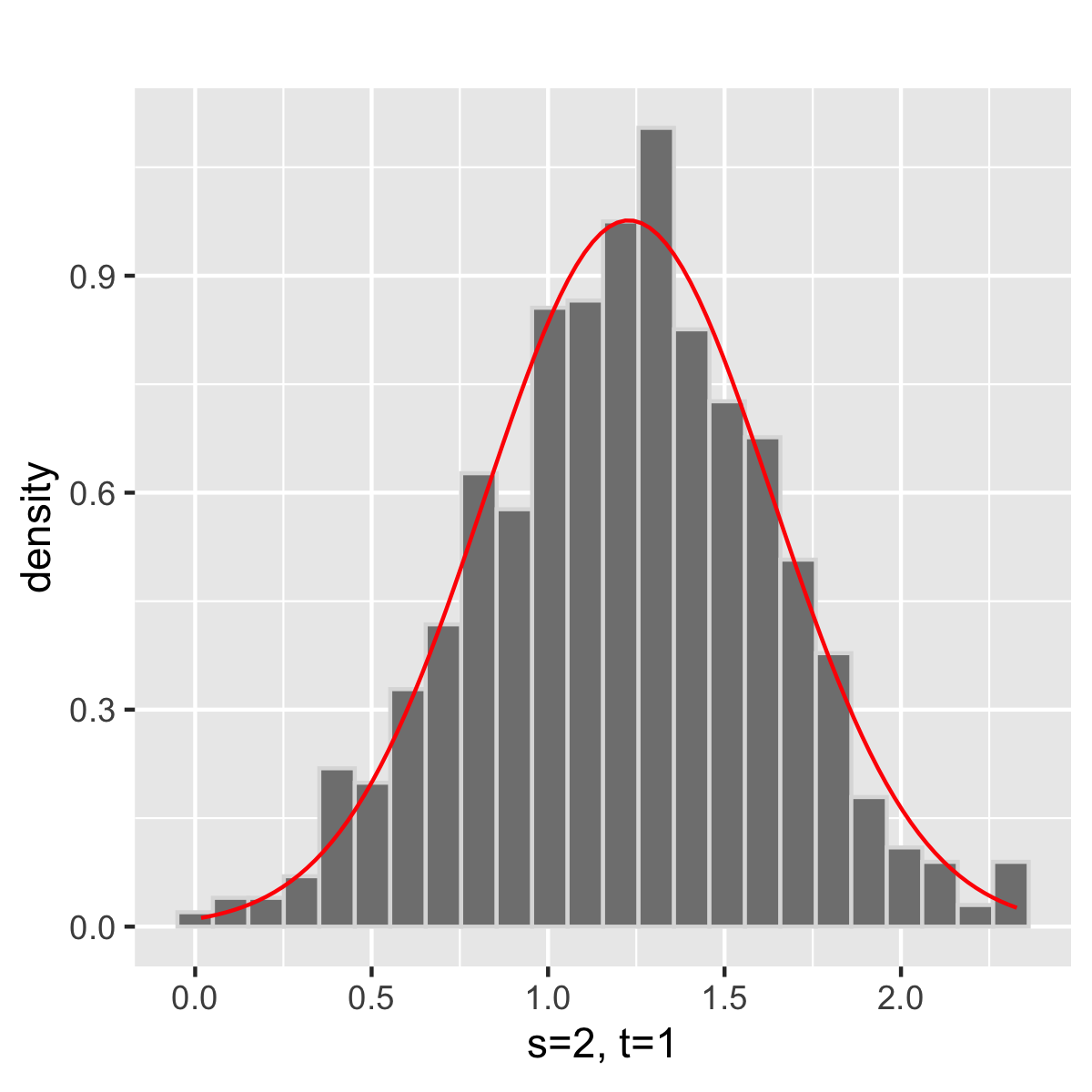

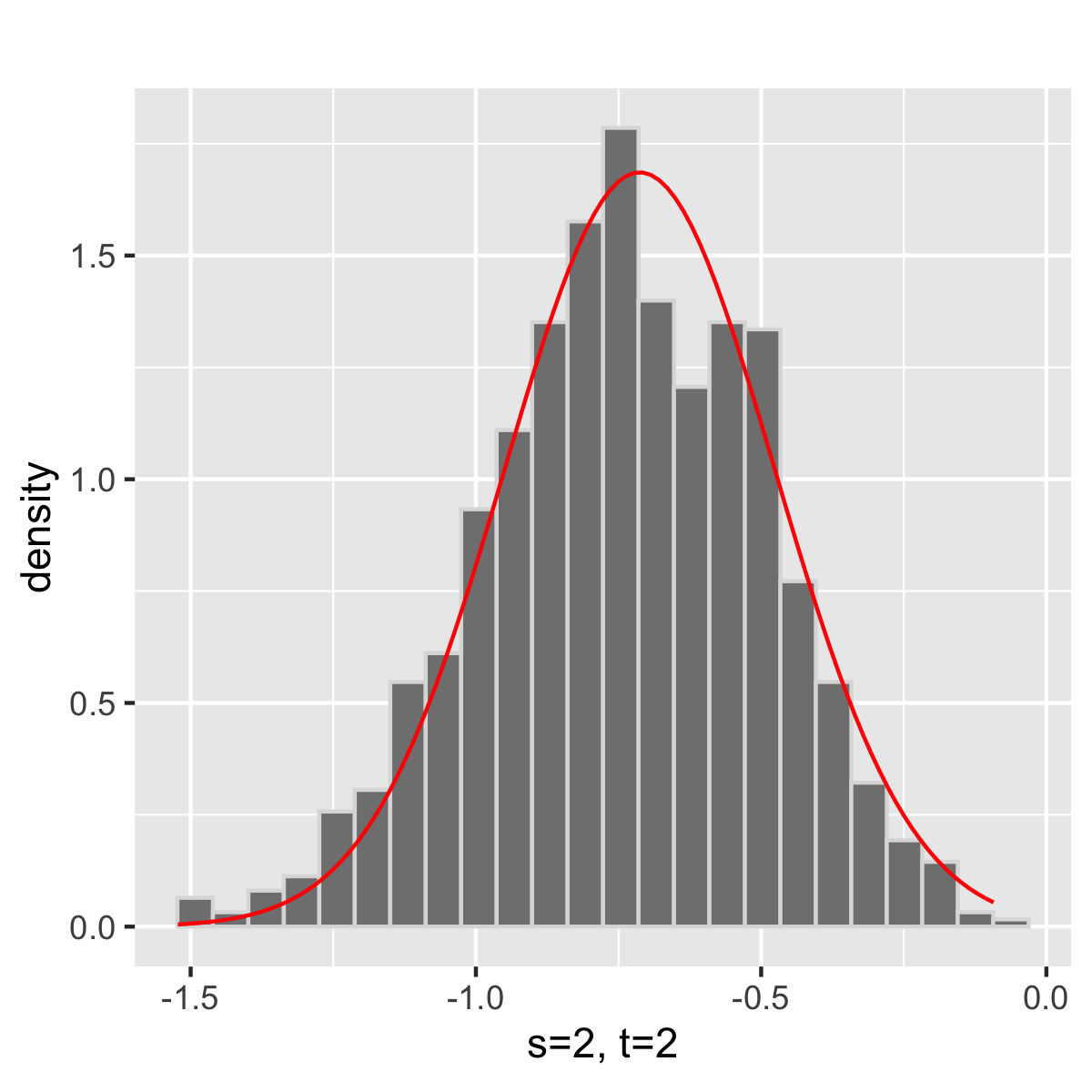

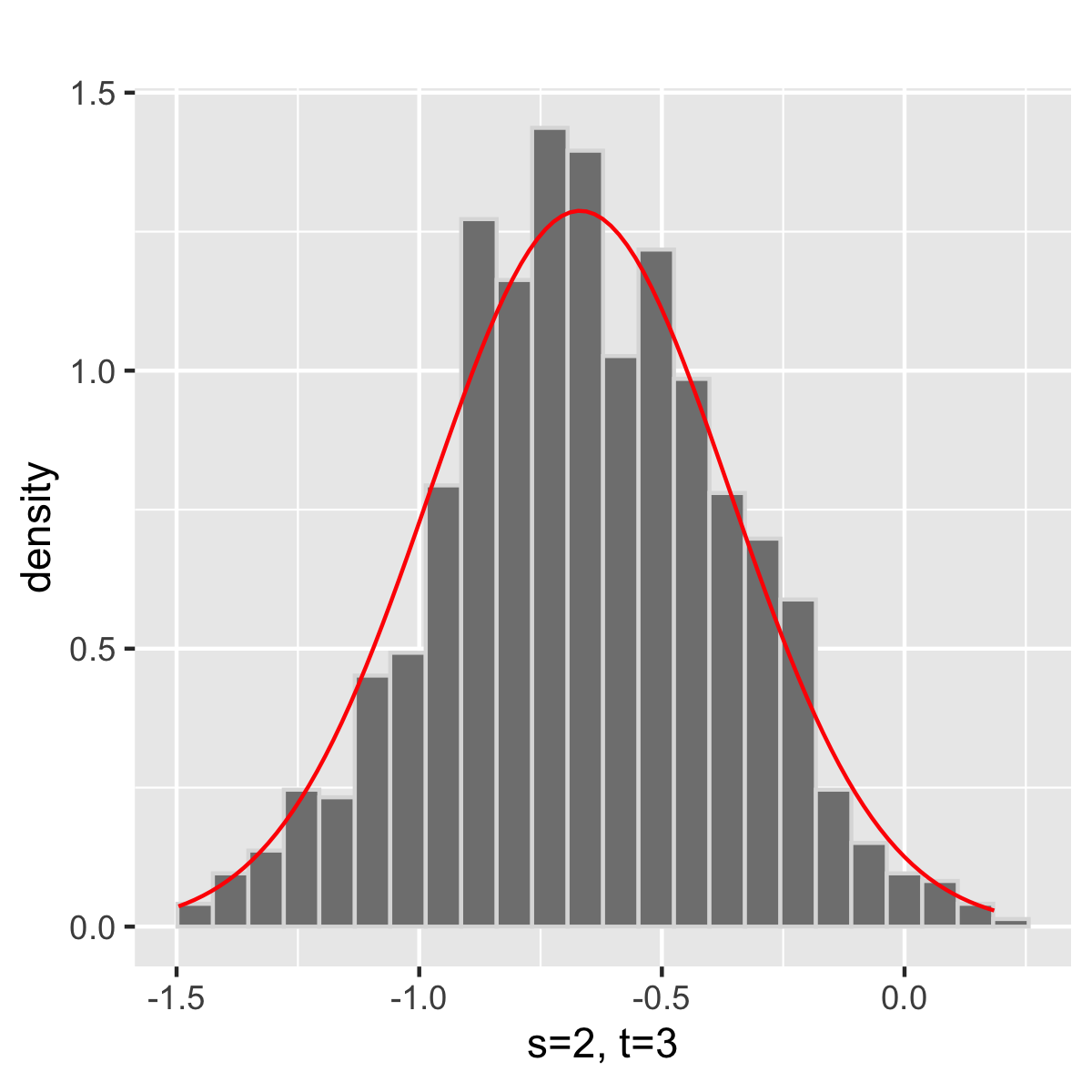

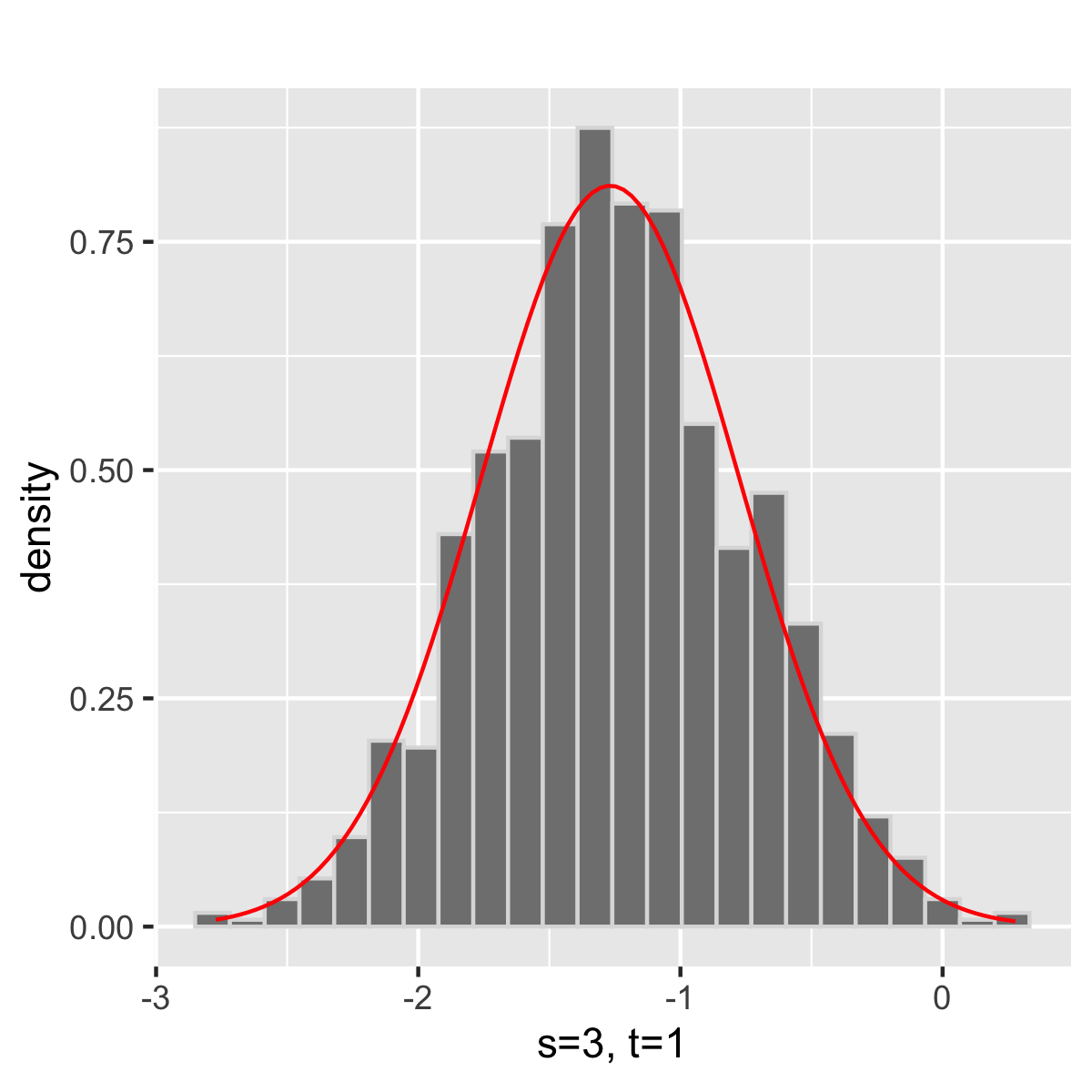

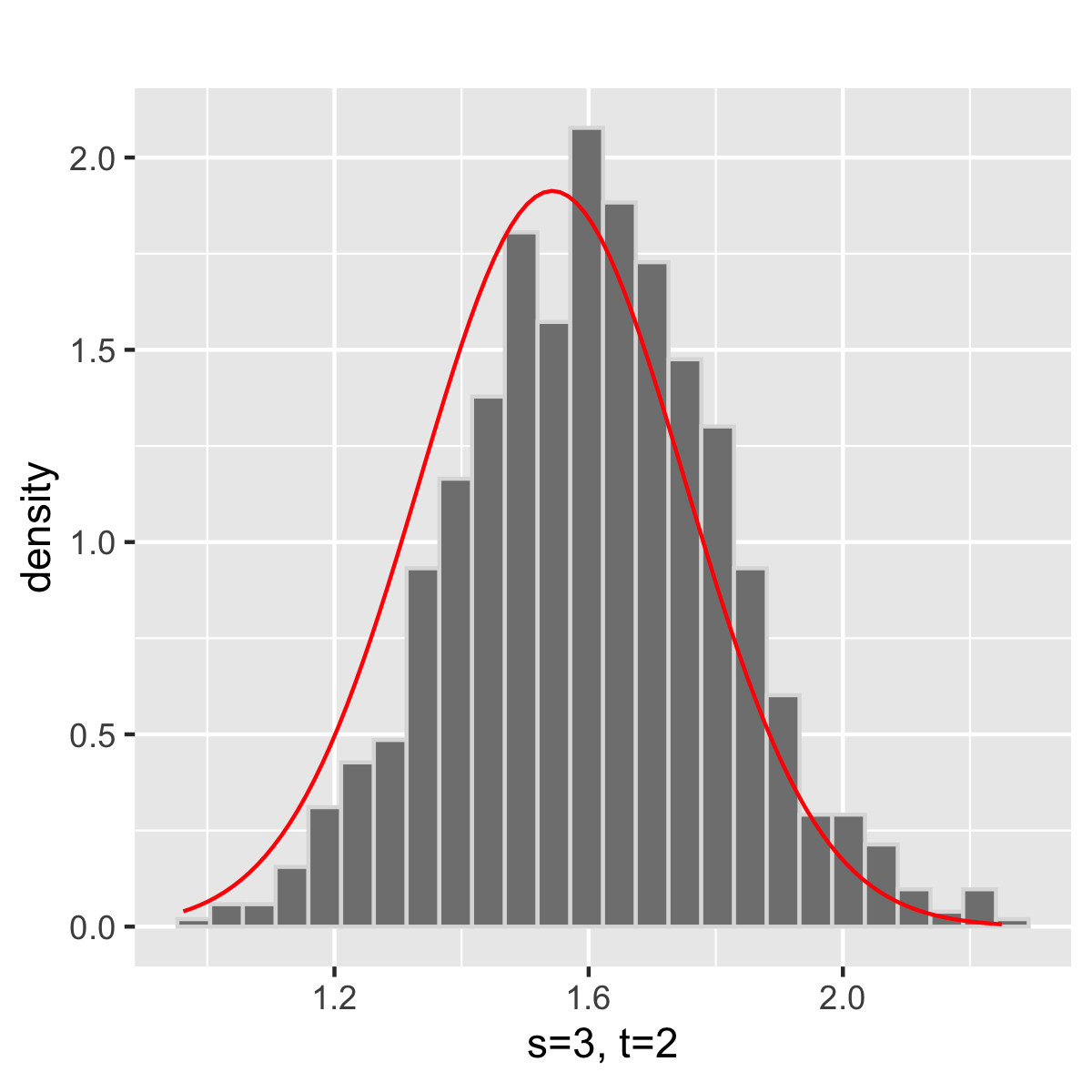

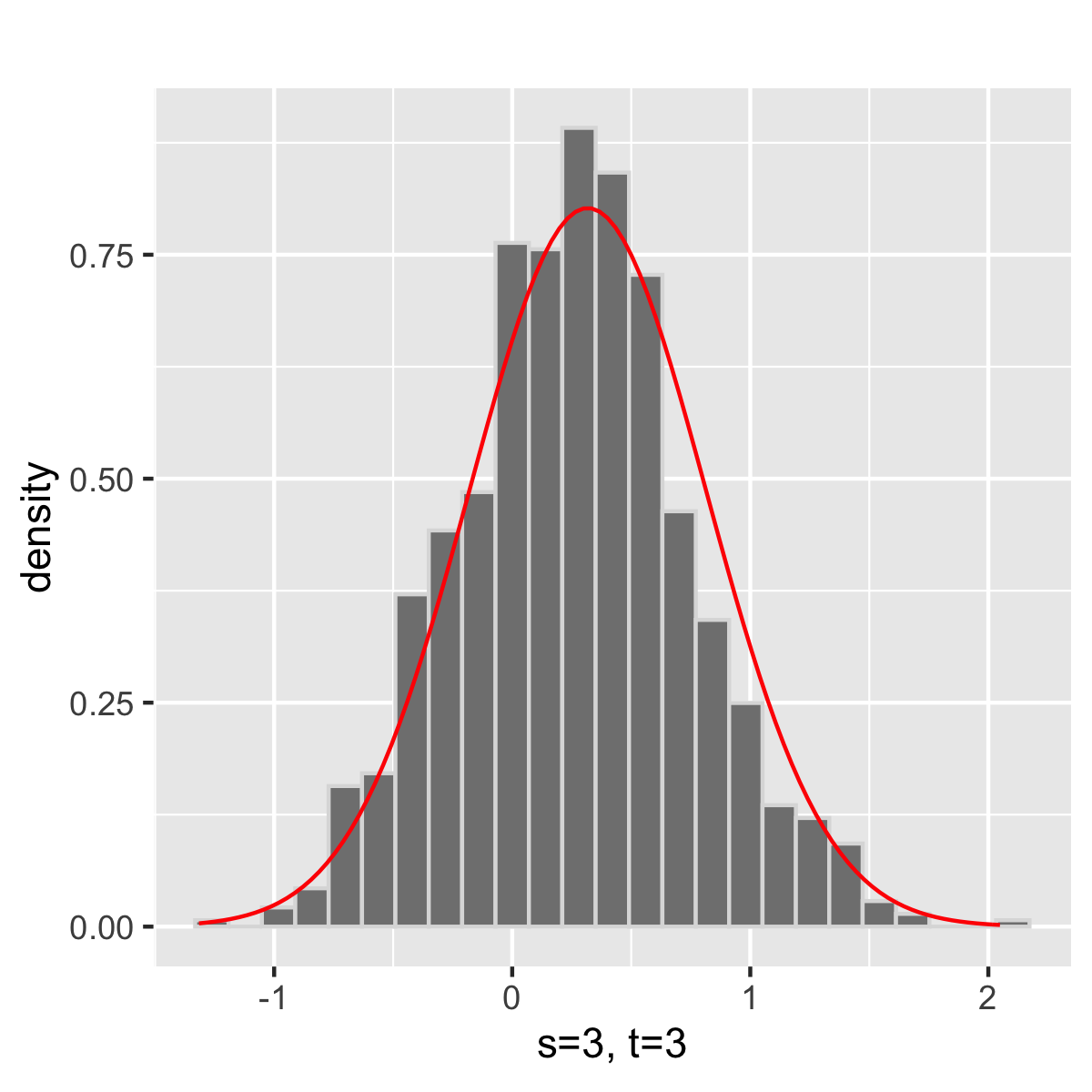

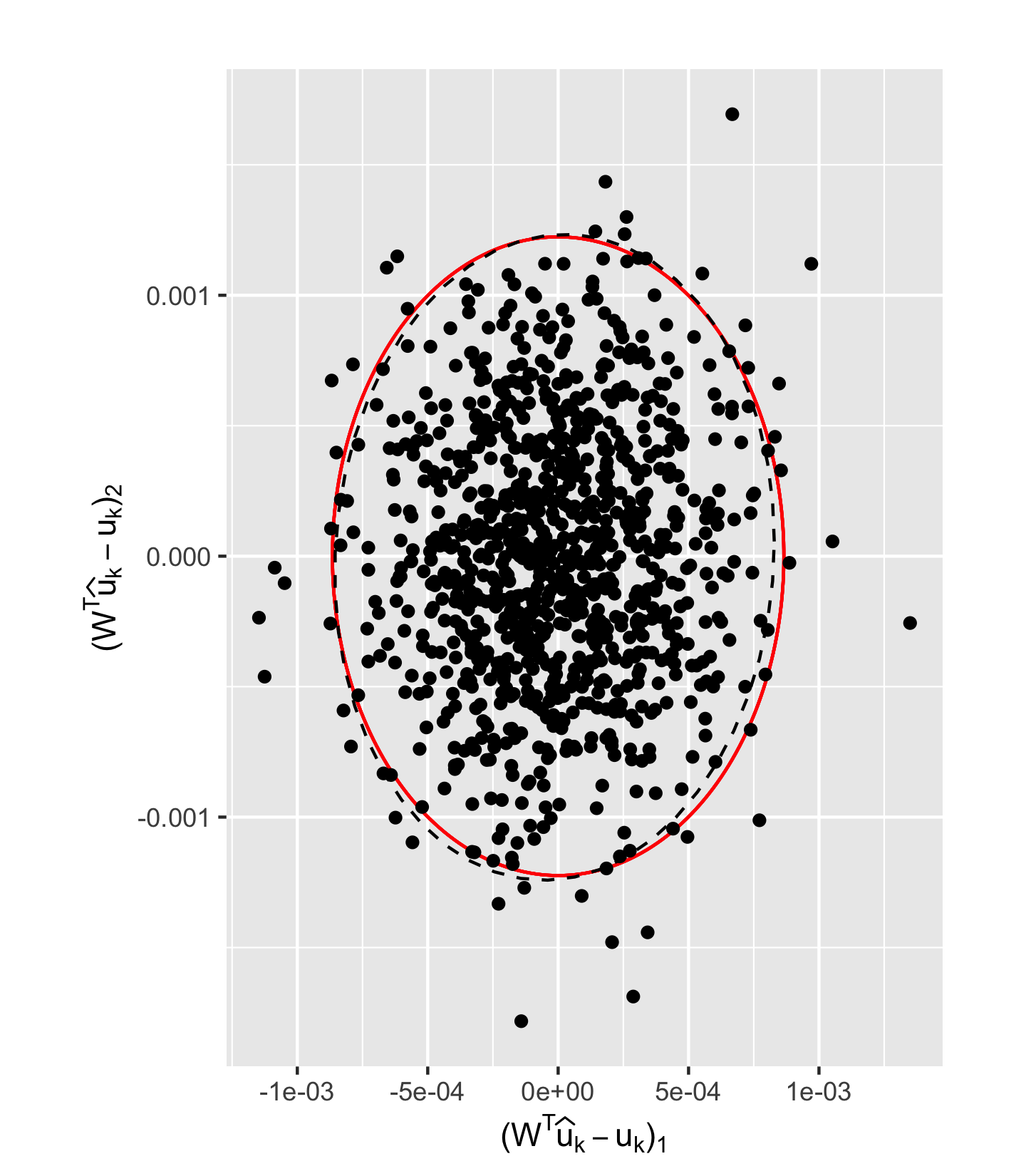

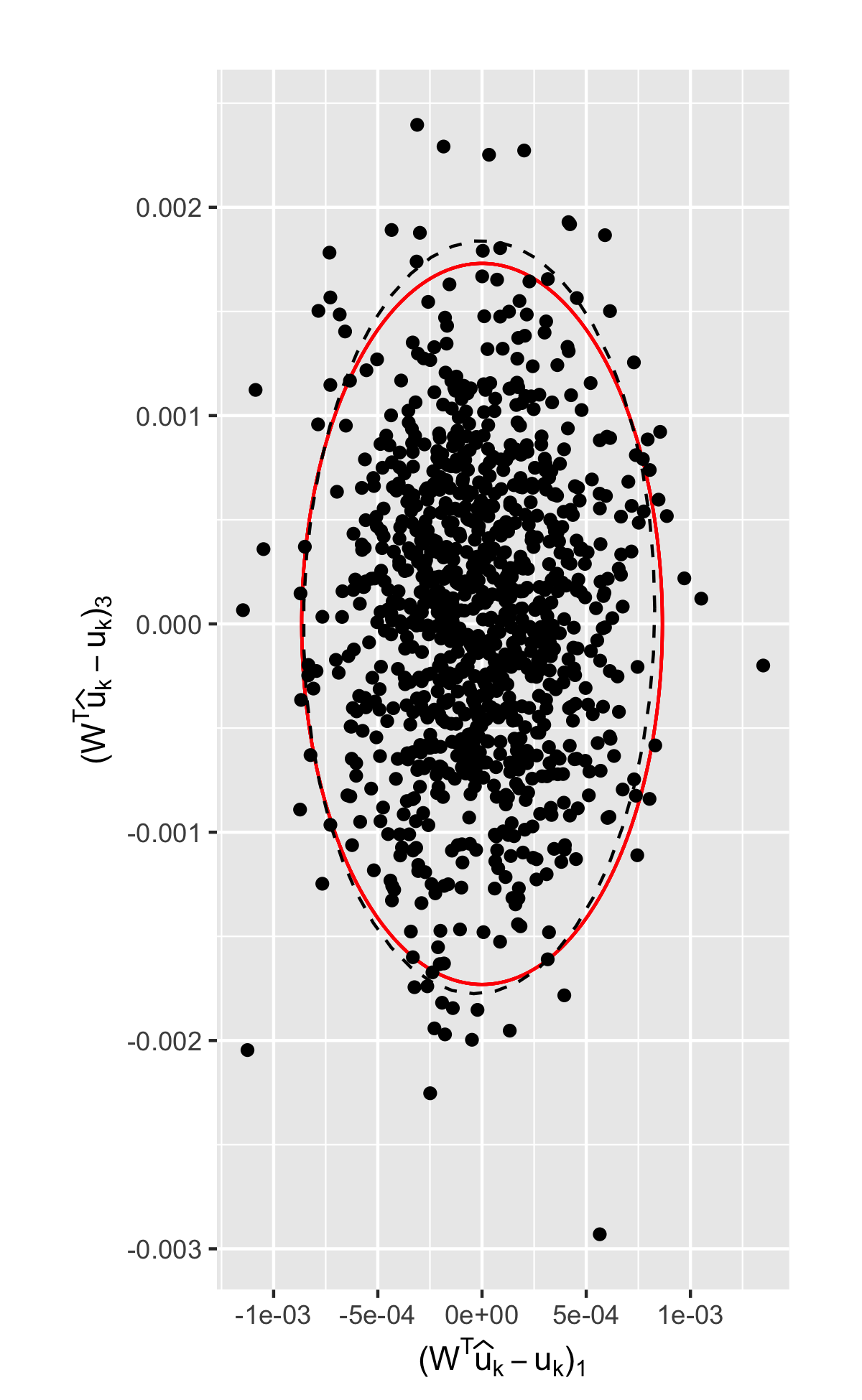

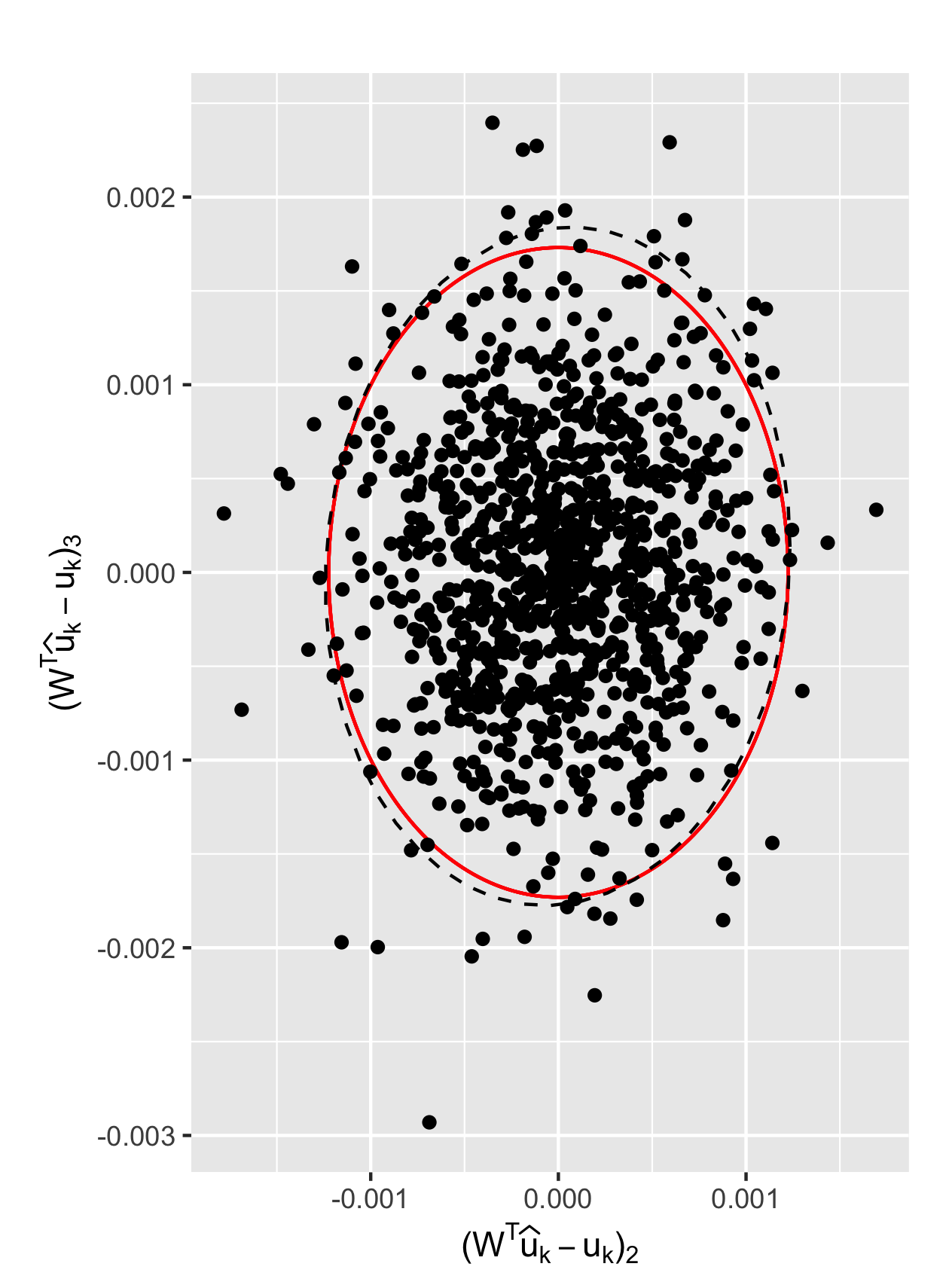

We repeat the above steps for Monte Carlo iterations to obtain an empirical distribution of which we then compare against the limiting distribution given in Theorem 5. The results are summarized in Figure 1. The Henze-Zirkler’s normality test indicates that the empirical distribution for is well-approximated by a multivariate normal distribution and furthermore the empirical covariances for are very close to the theoretical covariances.

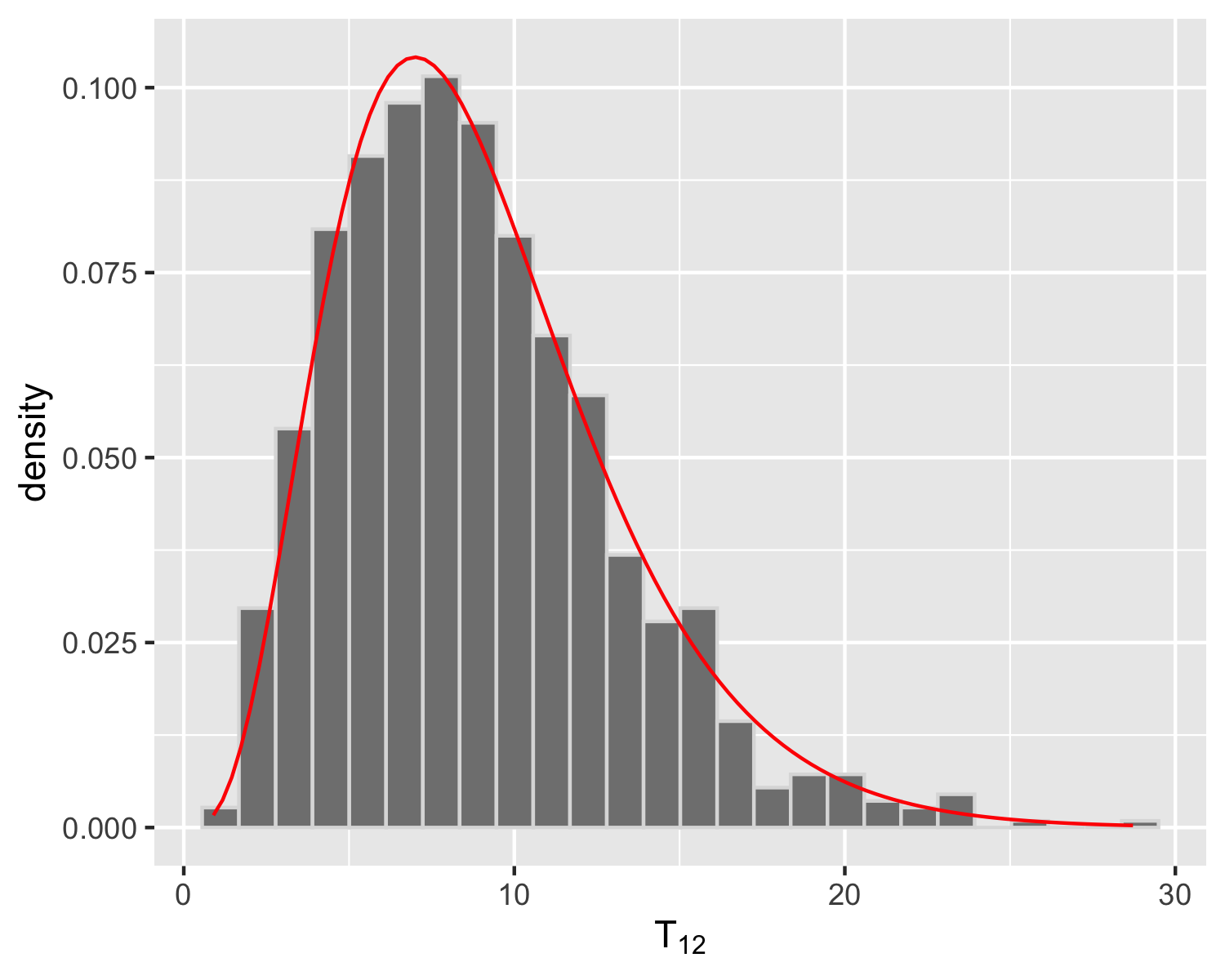

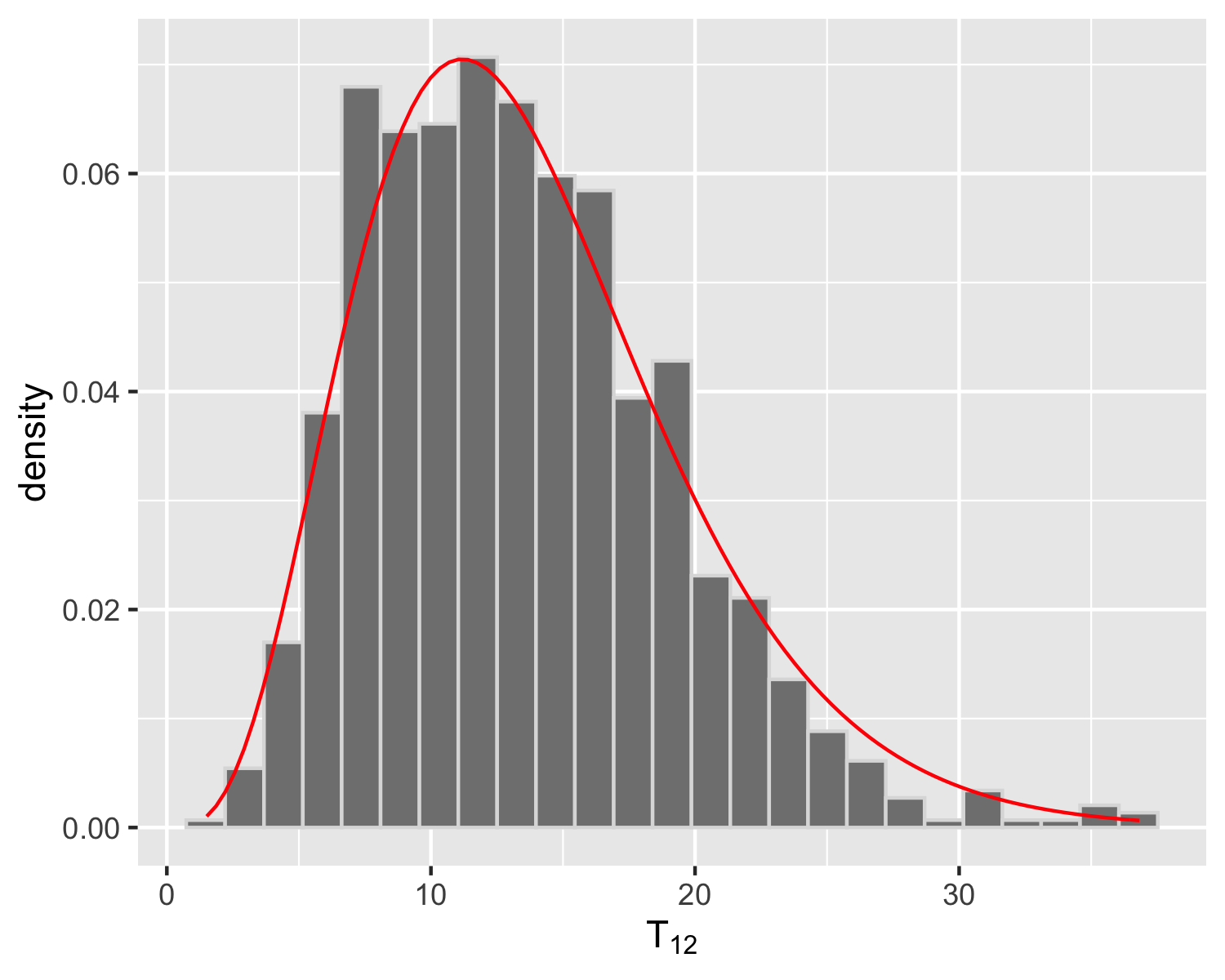

We next consider the problem of determining whether or not two graphs and have the same distribution, i.e., we wish to test against . We once again generate Monte Carlo replicates where, for each replicate, we generate a directed multi-layer SBM with graphs, blocks using a similar setting to that described at the beginning of this section, except now we set either or . These two choices for correspond to the null and local alternative, respectively. For each Monte Carlo replicate we compute the test statistic in Theorem 6 and compare its empirical distributions under the null and alternative hypothesis against the central and non-central distribution with degrees of freedom. The results are summarized in Figure 2 and we see that are indeed well approximated by the distributions.

4.2 MultiNeSS model

In Remark 6, we introduce the generalized model where all share some invariant subspaces but also have possibly distinct subspaces, and introduce how to estimate the subspaces with our algorithm. In this section we will show the performance of our algorithm for recovering the common and individual structures in a collection of matrices generated from the MultiNeSS model [macdonald2022latent] with Gaussian errors. More specifically, for any , let be a matrix of the form

where . Let be the common structure across all , and let be the individual structure for . We then generate where is a symmetric random matrix whose upper triangular entries are iid random variables.

Given we first compute as the matrix whose columns are the leading eigenvectors of for each . Next we let be the matrix whose columns are the leading left singular vectors of and be the matrix containing the leading left singular vectors of for all . Finally we compute the estimates of via

where and .

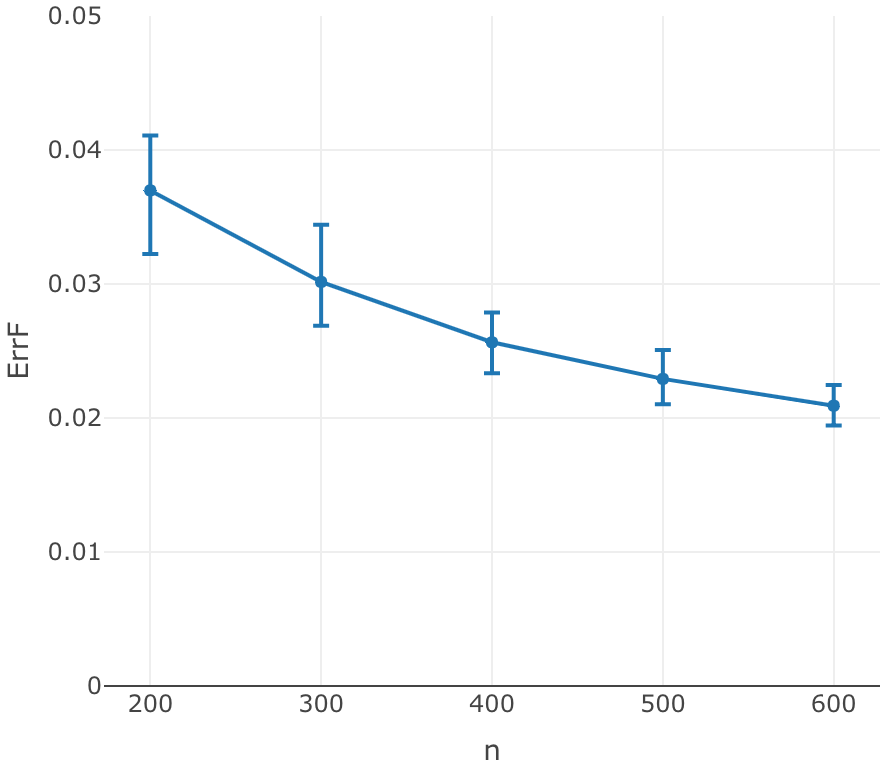

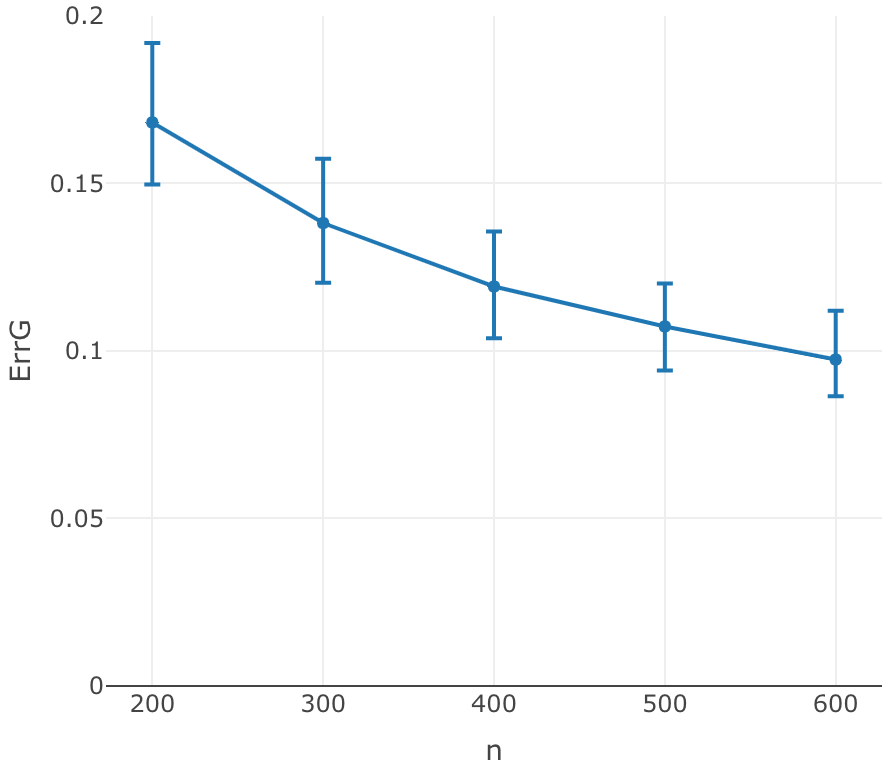

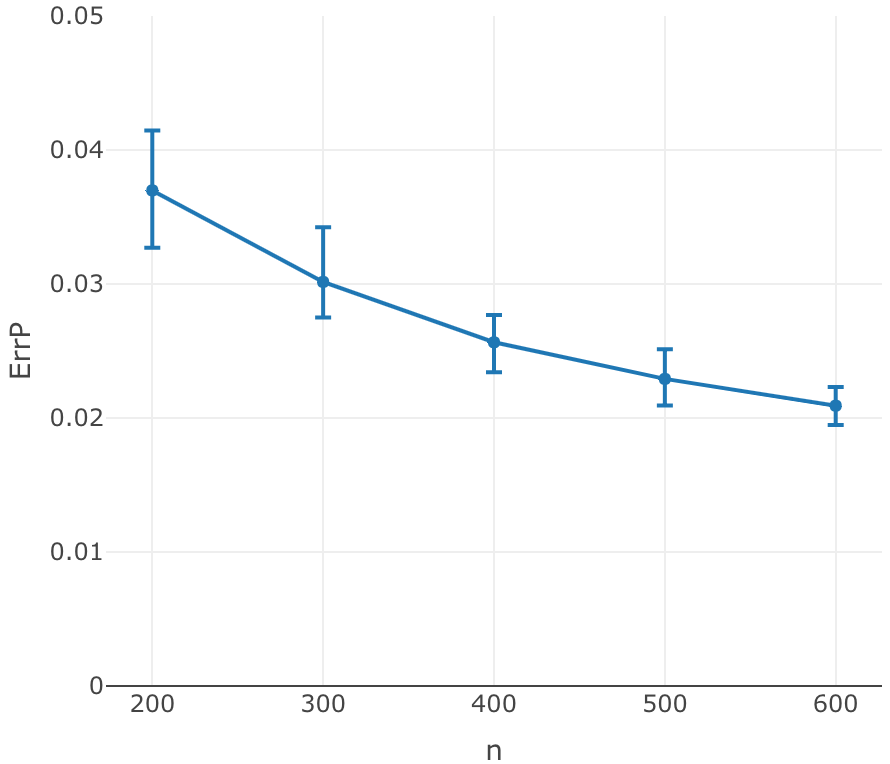

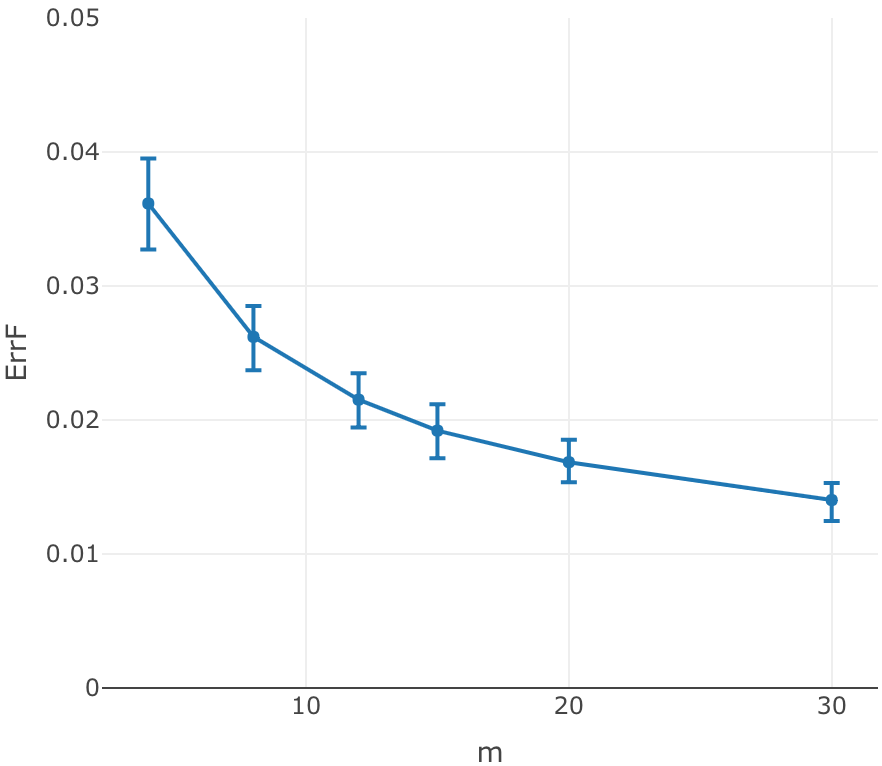

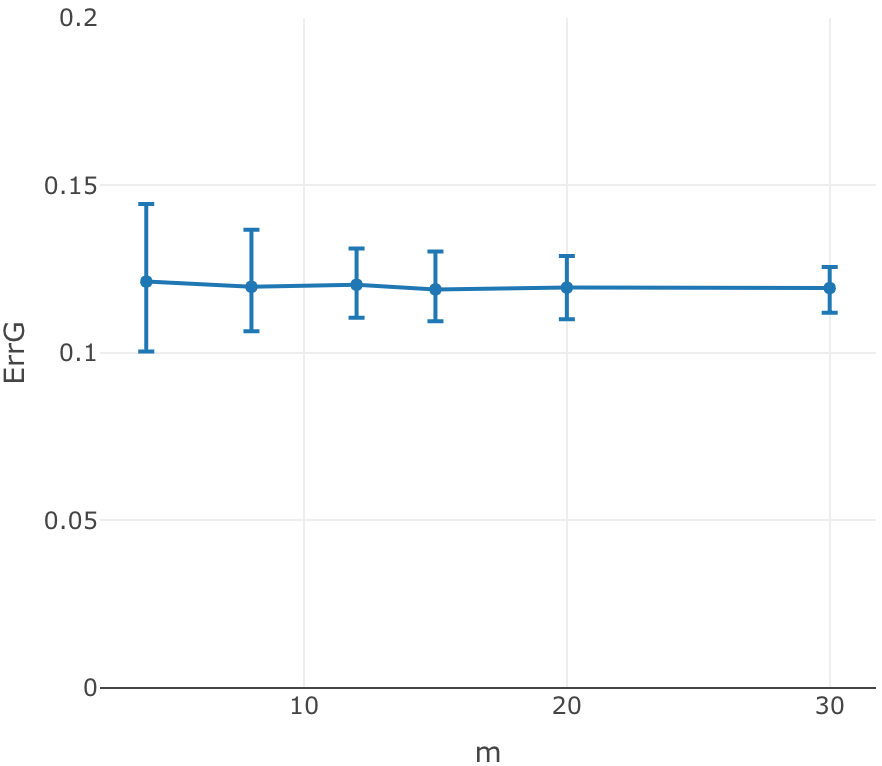

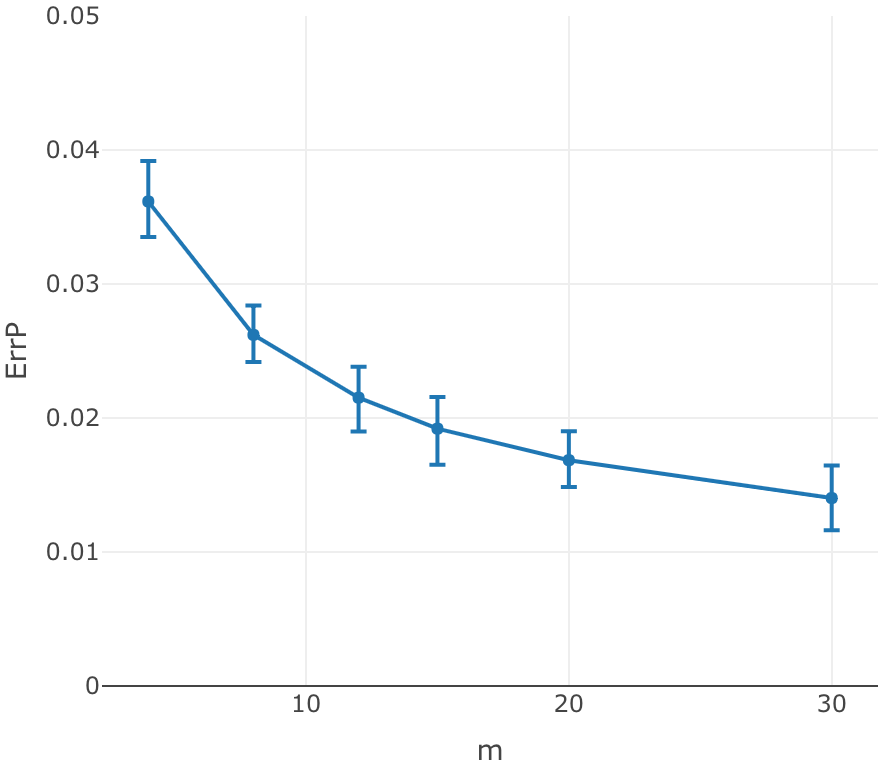

We use the same setting as that in Section 5.2 in [macdonald2022latent]. More specifically we fix , and either fix and vary or fix and vary . The estimation error for and are also evaluated using the same metric as that in [macdonald2022latent], i.e., we compute

where denote the Frobenius norm of a matrix after setting its diagonal entries to . The results are summarized in Figure 3 and Figure 4. Comparing the relative Frobenius norm errors in Figure 3 and Figure 4 with those in Figure 2 of [macdonald2022latent], we see that the two set of estimators have comparable performance. Nevertheless, our algorithm is slightly better for recovering the common structure (smaller ErrF) while the algorithm in [macdonald2022latent] is slightly better for recovering individual structure (smaller ErrG). Finally for recovering the overall edge probabilities , our ErrPs are always smaller than theirs. Indeed, as varies from to , the mean of our ErrP varies from about to while the mean in [macdonald2022latent] varies from about to . Simialrly, as varies from to , the mean of our ErrP varies from about to while the mean in [macdonald2022latent] varies from about to . In summary, while the two algorithms yield estimates with comparable performance, our algorithm has some computational advantage as (1) it is not an interative procedure and (2) it does not require any tuning parameters (note that the embedding dimensions and are generally not tuning parameters but rather chosen via some dimension selection procedure).

4.3 Distributed PCA

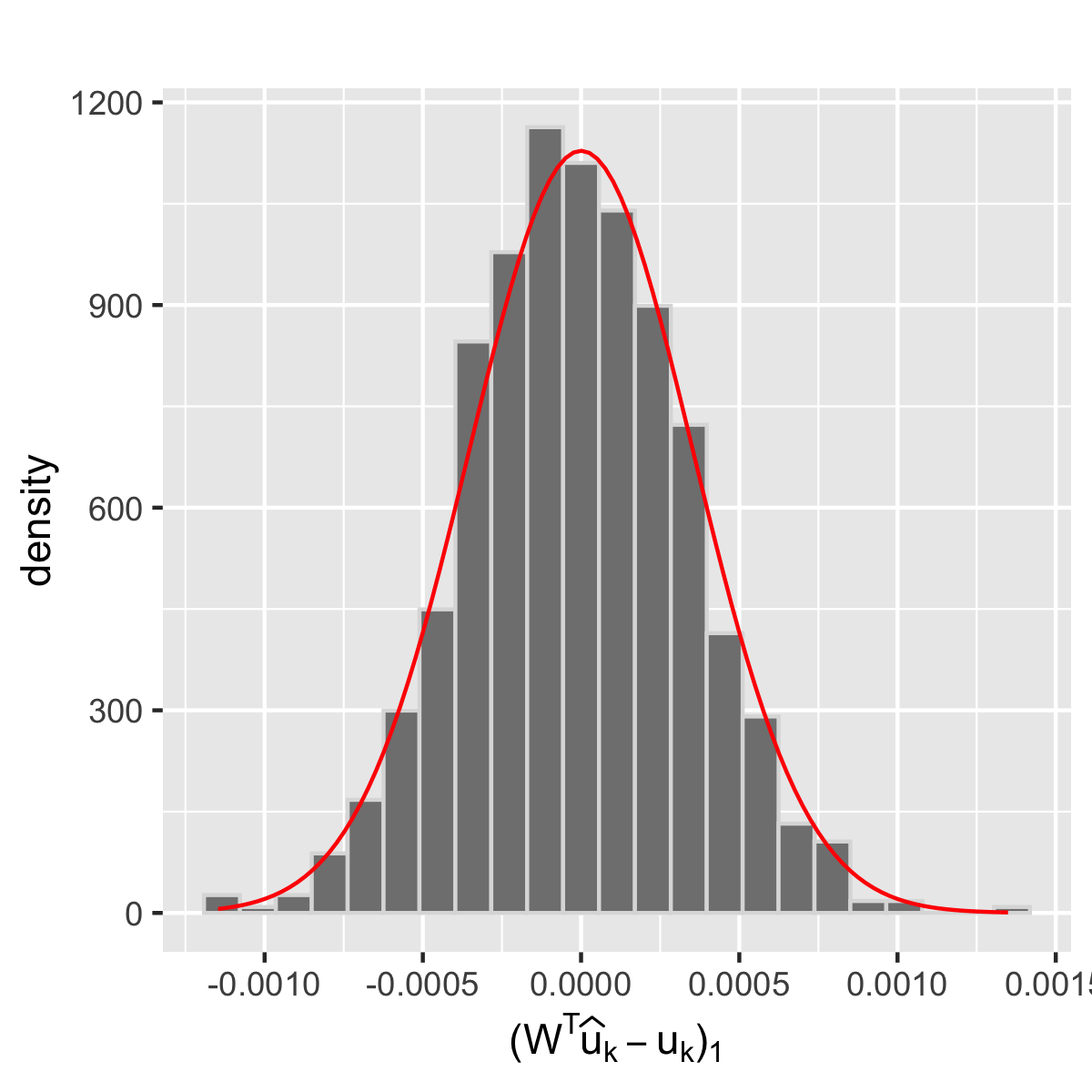

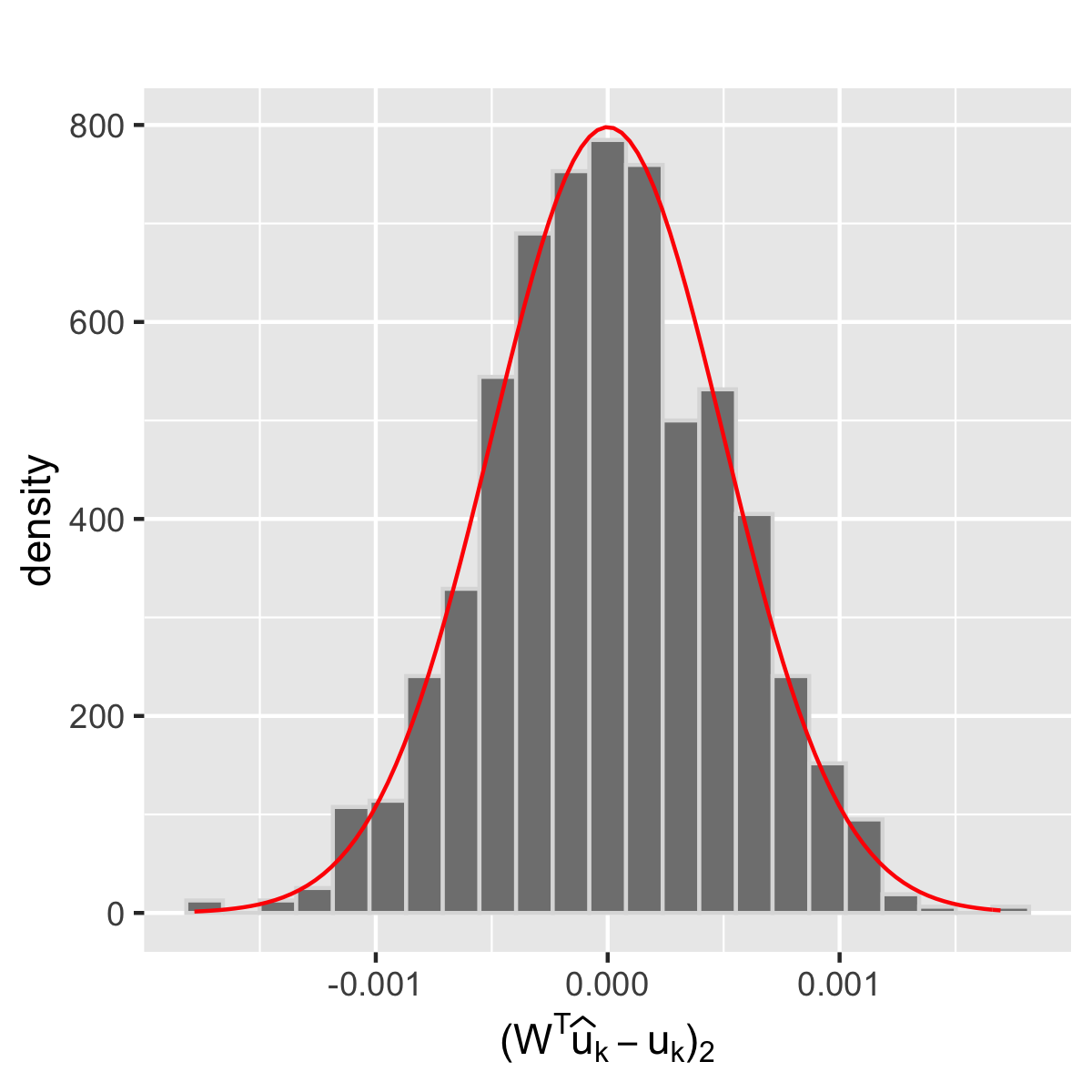

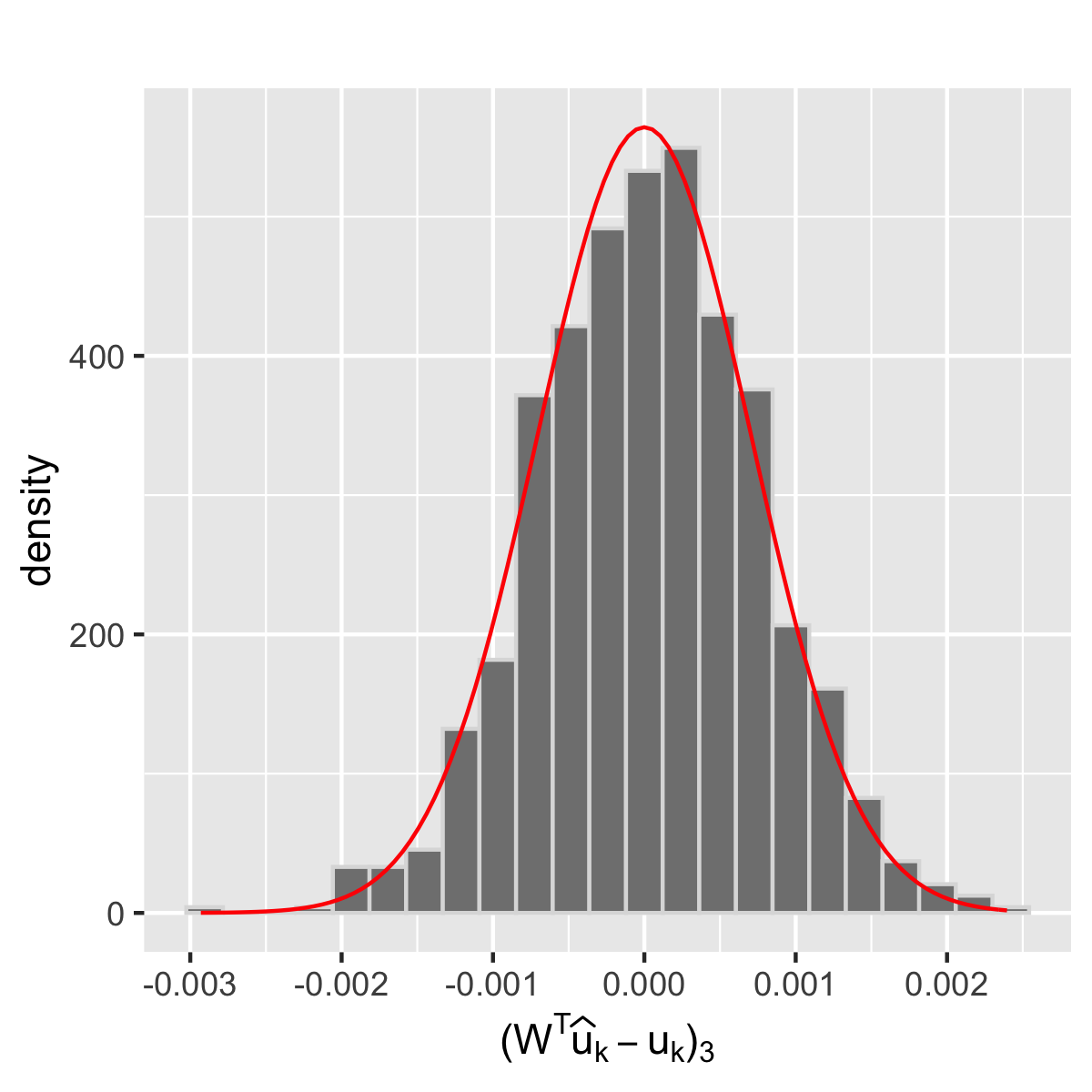

We now demonstrate our theoretical results for distributed PCA by simulations. Let , and be positive integers and be a collection of iid random vectors in with . Here with . The matrix is sampled uniformly from the set of matrices with and thus has spiked eigenvalues. Given we partition the data into subsamples, each having vectors, and then estimate using Algorithm 1 with .

We obtain an empirical distribution for based on Monte Carlo replications with and and compare it against the limiting Gaussian distribution specified in Theorem 8. Here and denote the first row of and , respectively. The Henze-Zirkler’s normality test fails to reject (at significance level ) the null hypothesis that the empirical distribution follows a multivariate normal distribution. For more details see Figure 5 for histograms plots of the marginal distributions of and Figure 6 for scatter plots of vs .

4.4 Connectivity of brain networks

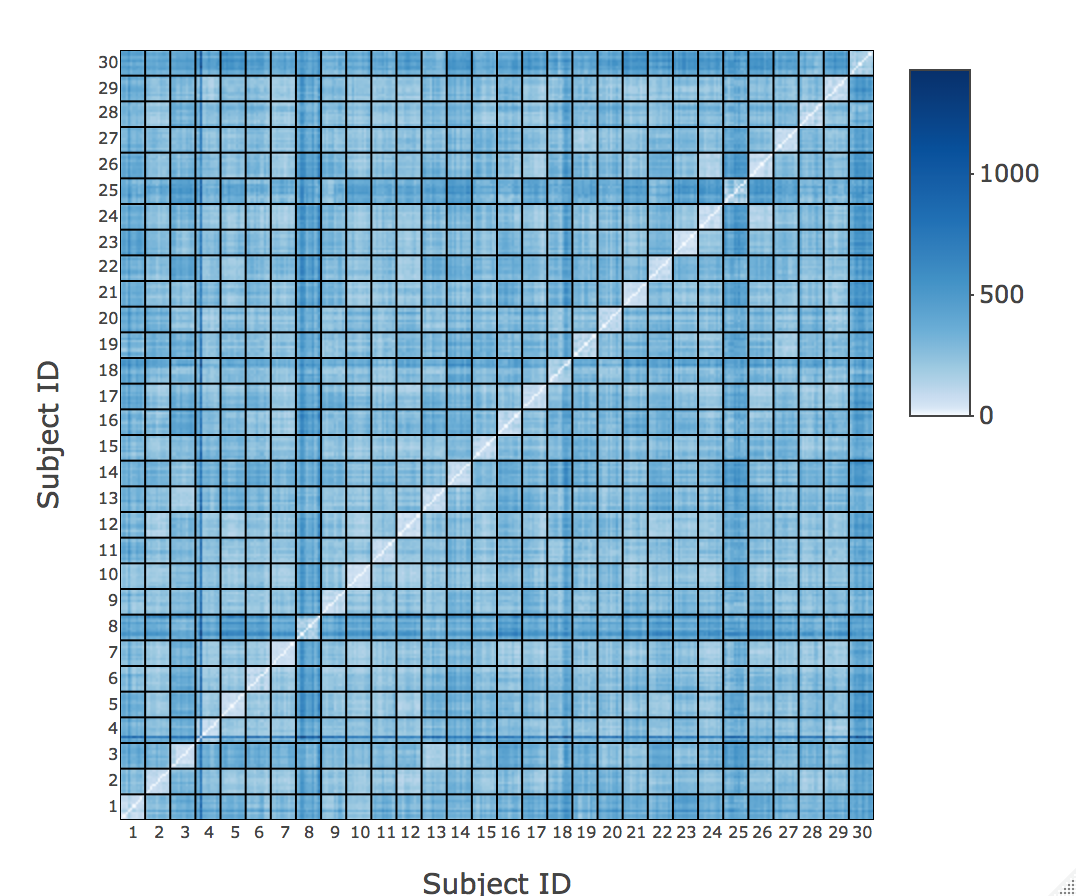

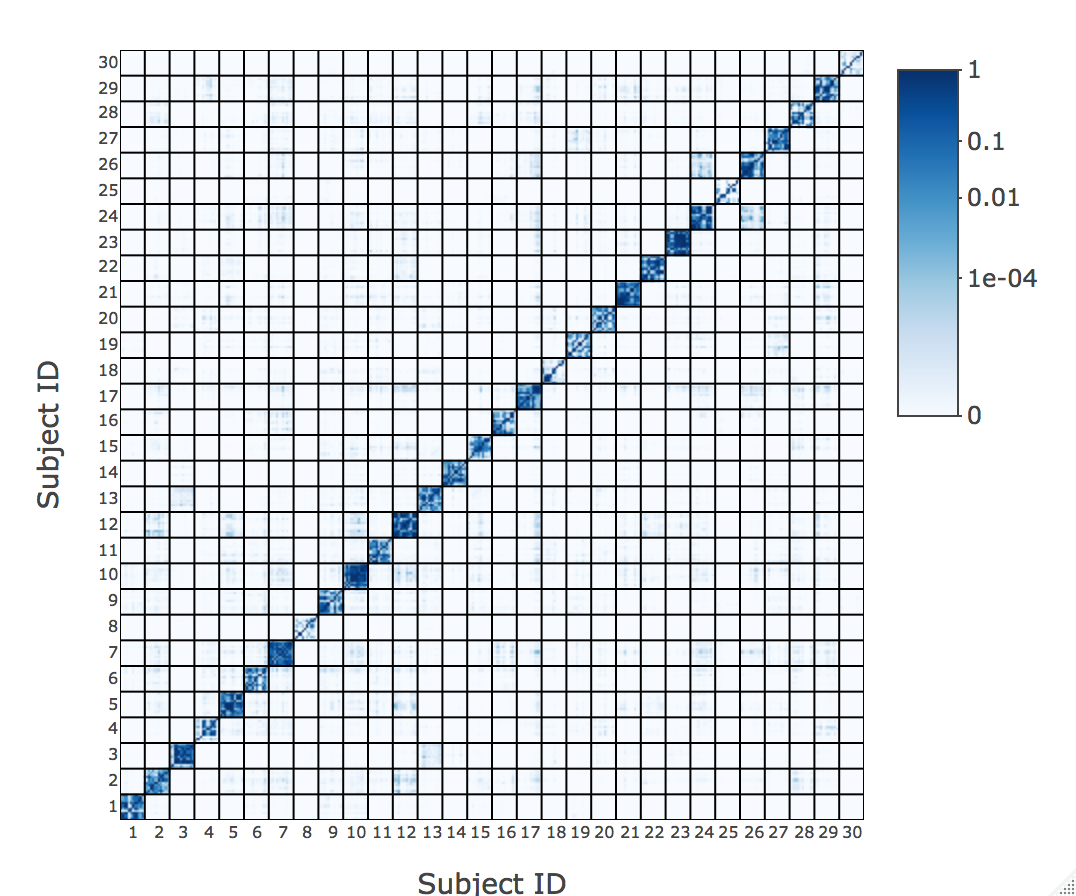

In this section we use the test statistic in Section 2.3 to measure similarities between different connectomes constructed from the HNU1 study [zuo2014open]. The data consists of diffusion magnetic resonance imaging (dMRI) records for healthy adults subjects where each subject received dMRI scans over the span of one month. The resulting dMRIs are then converted into undirected and unweighted graphs on vertices by registering the brain regions for these images to the CC200 atlas of [craddock2012whole].

Taking the graphs as one realization from an undirected COSIE model, we first apply Algorithm 1 to extract the “parameters estimates” associated with these graph. The initial embedding dimensions , which range from to , and the final embedding dimension are all selected using the (automatic) dimensionality selection procedure described in [zhu2006automatic]. Given the quantities and we compute for each graph (and truncate the entries of the resulting to lie in ) before computing using the formula in Remark 9. Finally we compute the test statistic for all pairs , as defined in Theorem 6.

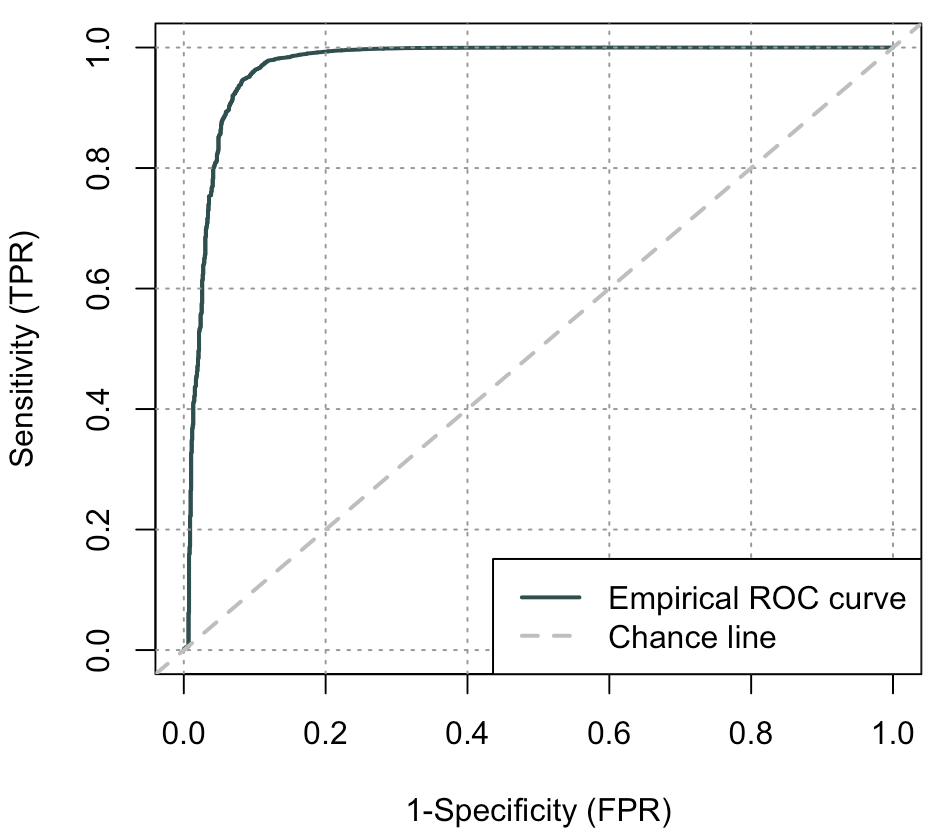

The left panel of Figure 7 shows the matrix of values for all pairs with while the right panel presents the -values associated with these (as compared against the distribution with degrees of freedom). Note that, for ease of presentation we have rearranged the graphs so that graphs for the same subject are grouped together and furthermore we only include, on the and axes marks, the labels for the subjects but not the individual scans within each subject. We see that our test statistic can discern between scans from the same subject (where are generally small) and scans from different subjects (where are quite large). Indeed, given any two scans and from different subjects, the -values for (under the null hypothesis that ) is always smaller than . Figure 8 shows the ROC curve when we use to classify whether a pair of graphs represents scans from the same subject (specificity) or from different subjects (sensitivity). The corresponding AUC is and is thus close to optimal.

The HNU1 data have also been analyzed in [arroyo2019inference]. In particular, [arroyo2019inference] proposes as test statistic, and instead of computing -values from some limiting distribution directly, [arroyo2019inference] calculates empirical -values by using 1) a parametric bootstrap approach; 2) the asymptotic null distribution of . By neglecting the effect of the bias term , [arroyo2019inference] approximates the null distribution of as a generalized distribution, and estimates it by Monte Carlo simulations of a mixture of normal distributions with the estimate and . Comparing the -values of our testing in Figure 7 with the results obtained by their two methods in Figure 15, we see that for different methods the ratios of the -values for the pairs from the same subject and that for the pairs from different subject are very similar. Thus both test statistics can detect whether the pairs of graphs are from the same subject well. Our test statistic however has the benefit that its -value is computed using large-sample approximation and is thus much less computationally intensive compared to test procedures which use bootstrapping and other Monte Carlo simulations.

4.5 Worldwide food trading networks

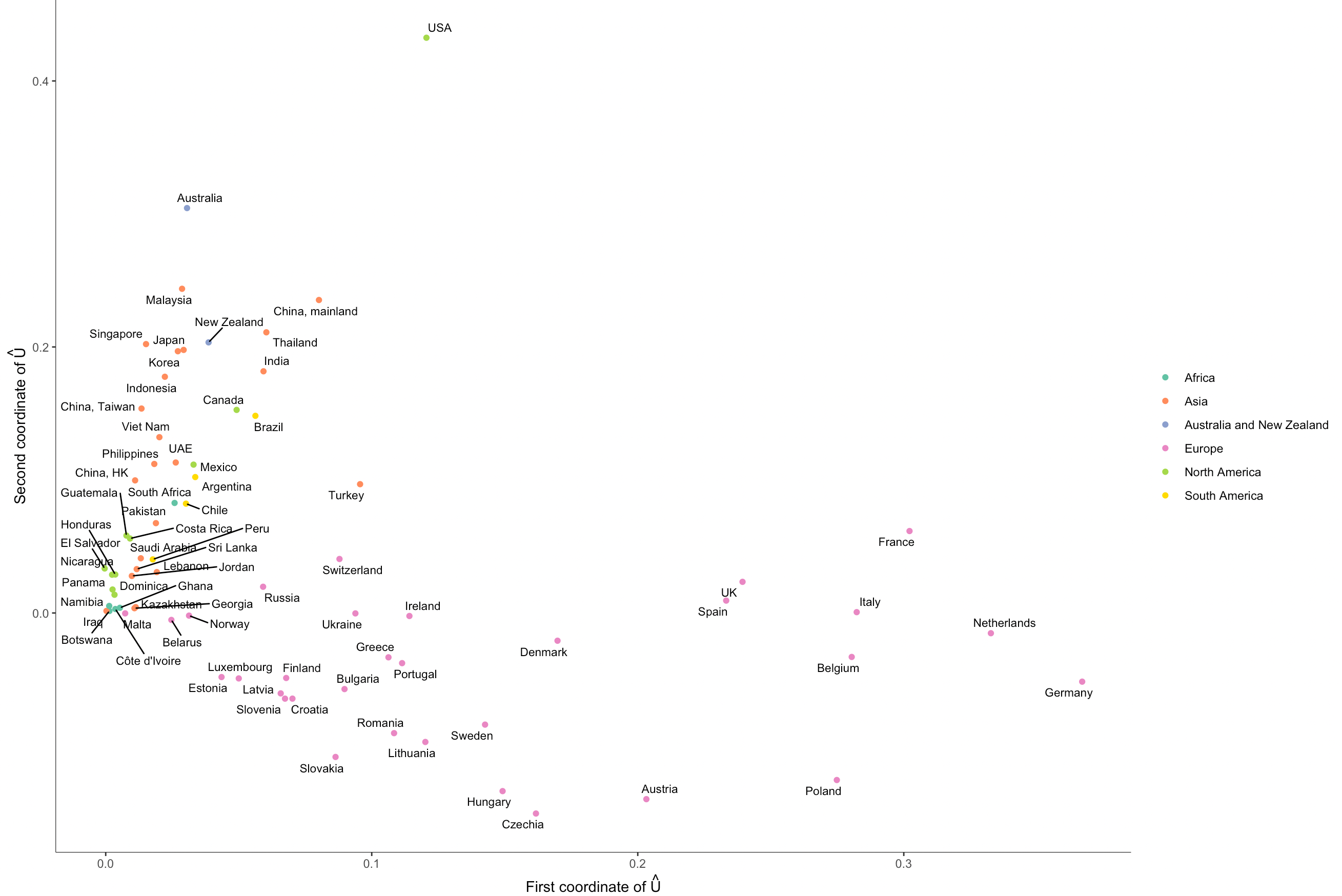

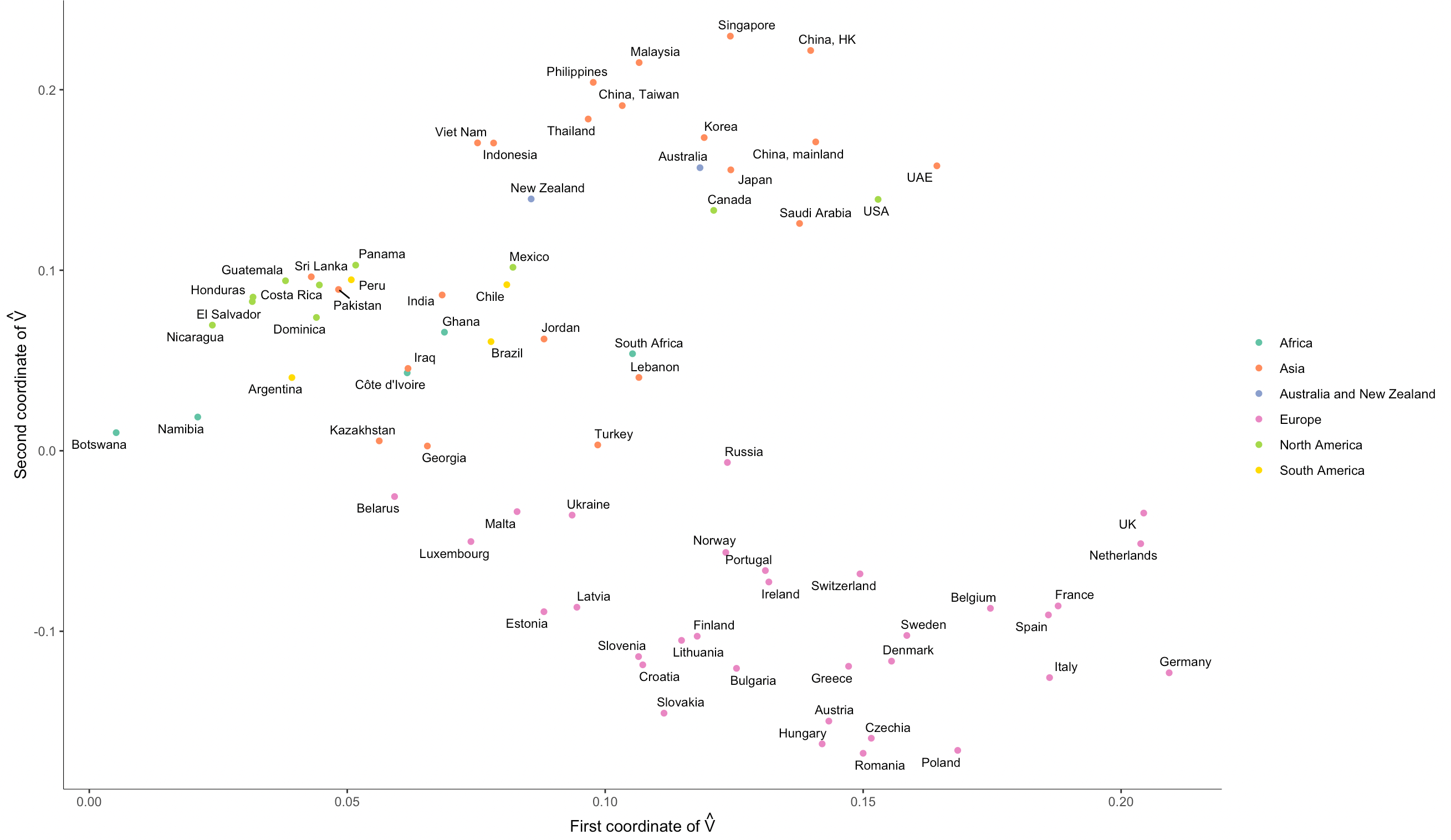

For the second example we use the trade networks between countries for different food and agriculture products during the year . The data is collected by the Food and Agriculture Organization of the United Nations and is available at https://www.fao.org/faostat/en/#data/TM. We construct a collection of networks, one for each product, where vertices represent countries and the edges in each network represent trading relationships between the countries; the resulting adjacency matrices are directed but unweighted as we (1) set if country exports product to country and (2) ignore any links between countries and in if their total trade amount for the th product is less than two hundred thousands US dollars. Finally, we extract the intersection of the largest connected components of and obtain networks on a set of shared vertices.

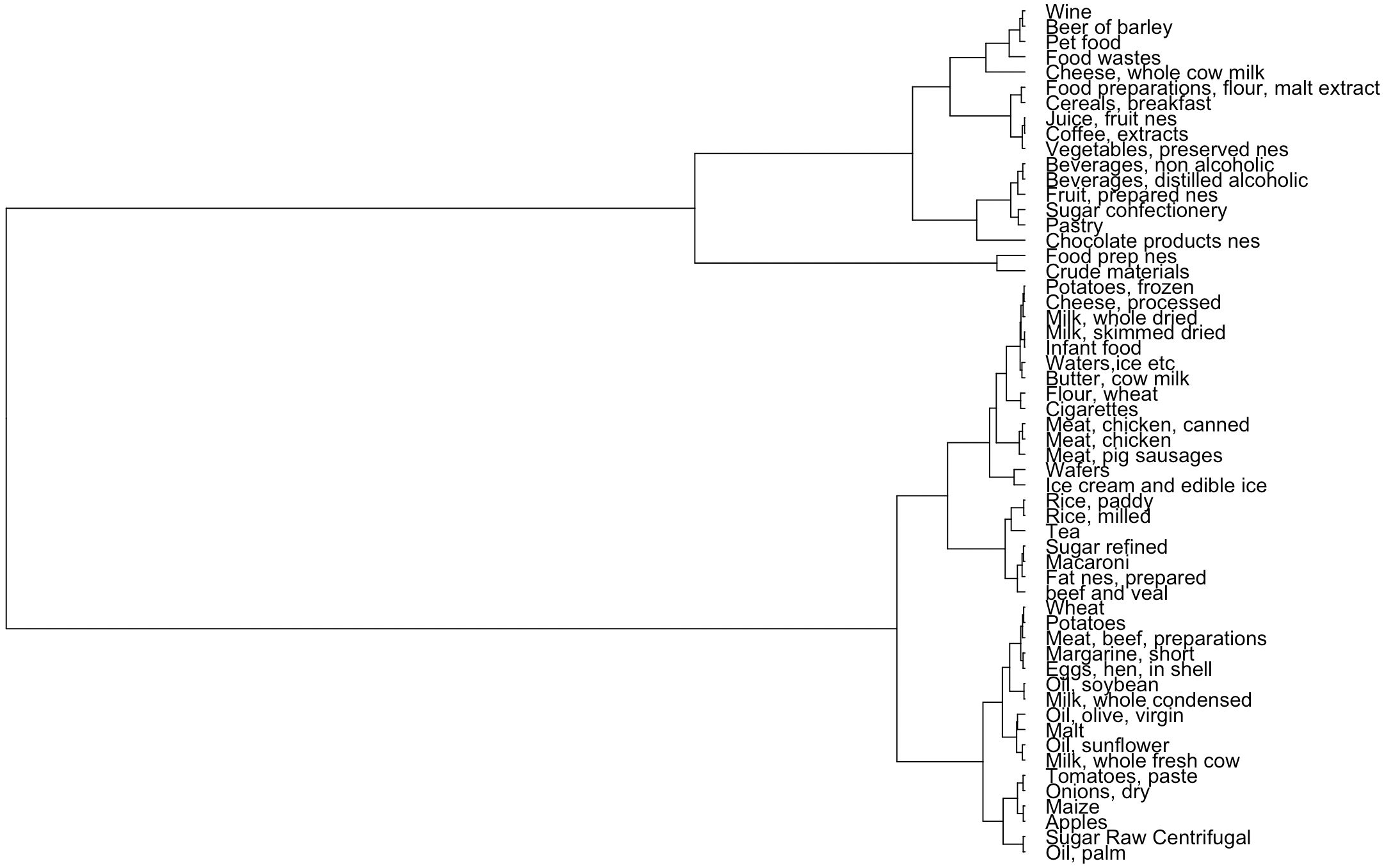

Taking the networks as one realization from a directed COSIE model, we apply Algorithm 1 to compute the “parameters estimates” associated with these graphs with initial embedding dimensions as well as the final embedding dimension all chosen to be . Figure 9 and Figure 10 present scatter plots for the rows of and , respectively; we interpret the th row of (resp. ) as representing the estimated latent position for this country as an exporter (resp. importer). We see that there is a high degree of correlation between these “estimated” latent positions and the true underlying geographic proximities, e.g., countries in the same continent are generally placed close together in Figure 9 and Figure 10.

Next we compute the statistic in Theorem 6 to measure the differences between and between all pairs of products . Viewing as a distance matrix, we organize the food products using hierarchical clustering [johnson1967hierarchical]; see the dendogram in Figure 11. There appears to be two main clusters formed by raw/unprocessed products (bottom cluster) and processed products (top cluster), and suggest discernable differences in the trading patterns for these types of products.

The trading dataset (but for 2010) have also been analyzed in [jing2021community]. In particular, [jing2021community] studies the mixture multi-layer SBM and proposes a tensor-based algorithm to reveal memberships of vertices and memberships of layers. For the food trading networks, [jing2021community] first groups the layers, i.e., the food products, into two clusters, and then obtains the embeddings and the clustering result of the countries for each food clusters. Our results are similar to theirs. In particular their clustering of the food products also shows a difference in the trading patterns for unprocessed and processed foods while their clustering of the countries is also related to the geographical location. However, as we also compute the test statistic for each pairs of products, we obtaine a more detailed analysis of the product relationships. In addition, as we keep the orientation for the edges (and thus our graphs are directed) we can also analyze the countries in term of both their export and import behavior, and Figures 9 and 10 show that there is indeed some difference between these behaviors, e.g., the USA and Australia are outliers as exporters but are clustered with other countries as importers.

4.6 Distributed PCA and MNIST

We now perform dimension reduction on the MNIST dataset using distributed PCA with and compare the result against traditional PCA on the full dataset. The MNIST data consists of grayscale images of handwritten digits of the numbers through . Each image is of size pixels and can be viewed as a vector in with entries in . Letting be the matrix whose rows represent the images, we first extract the matrix whose columns are the leading principal components of . The choice is arbitrary and is chosen purely for illustrative purpose. Next we approximate using distributed PCA by randomly splitting into subsamples. Letting be the resulting approximation we compute . We repeat these steps for independent Monte Carlo replicates and summarize the result in Figure 12 which shows that the errors between and are always substantially smaller than . We emphasize that while the errors in Figure 12 do increase with , this is mainly an artifact of the experiment setup as there is no underlying ground truth and we are only using as a surrogate for some unknown (or possibly non-existent) . In other words, is noise-free in this setting while is inherently noisy and thus it is reasonable for the noise level in to increases with . Finally we note that, for this experiment, we have assumed that the rows of are iid samples from a mixture of multivariate Gaussians with each component corresponding to a number in . As a mixture of multivariate Gaussians is sub-Gaussian, the results in Section 3 remain relevant in this setting; see Remark 14.

5 Conclusion

In this paper we present a general framework for deriving limit results for distributed estimation of the leading singular vectors for a collection of matrices with shared invariant subspaces, and we apply this framework to multiple networks inference and distributed PCA. In particular, for heterogeneous random graphs from the COSIE model, we show that each row of the estimate (resp. ) of the left (resp. right) singular vectors converges to a multivariate normal distribution centered around the row of the true singular vectors (resp. ) and furthermore that converges to a multivariate normal distribution for each . Meanwhile for the setting of distributed PCA we derive normal approximations for the rows of the leading principal components when the data exhibit a spiked covariance structure.