Uplifting Bandits

Abstract

We introduce a multi-armed bandit model where the reward is a sum of multiple random variables, and each action only alters the distributions of some of them. After each action, the agent observes the realizations of all the variables. This model is motivated by marketing campaigns and recommender systems, where the variables represent outcomes on individual customers, such as clicks. We propose UCB-style algorithms that estimate the uplifts of the actions over a baseline. We study multiple variants of the problem, including when the baseline and affected variables are unknown, and prove sublinear regret bounds for all of these. We also provide lower bounds that justify the necessity of our modeling assumptions. Experiments on synthetic and real-world datasets show the benefit of methods that estimate the uplifts over policies that do not use this structure.

1 Introduction

MAB is an important framework for sequential decision making under uncertainty (Lai and Robbins, 1985; Bubeck and Cesa-Bianchi, 2012; Lattimore and Szepesvári, 2020). In this problem, a learner repeatedly takes action and receives their rewards, while the outcomes of the other actions are unobserved. The goal of the learner is to maximize their cumulative reward over time by balancing exploration (select actions with uncertain reward estimates) and exploitation (select actions with high reward estimates). MAB (MAB) has applications in online advertisement, recommender systems, portfolio management, and dynamic channel selection in wireless networks.

One prominent question in the MAB literature is how the dependencies between the actions can be exploited to improve statistical efficiency. Popular examples working toward this goal include linear bandits (Dani et al., 2008) and combinatorial bandits (Cesa-Bianchi and Lugosi, 2012). In this work, we study a different structured bandit problem with the following three features: \edefnn(\edefnit\selectfonti\edefnn) the reward is the sum of the payoffs of a fixed set of variables; \edefnn(\edefnit\selectfonti\edefnn) these payoffs are observed; and \edefnn(\edefnit\selectfonti\edefnn) each action only affects a small subset of the variables. This structure arises in many applications, as discussed below.

-

(a)

Online Marketing. An ecommerce platform can opt among several marketing strategies (actions) to encourage customers to make more purchases on their website. As different customers can be sensitive to a different marketing strategy, regarding each of them as a variable, it is natural to expect that each action would likely affect only a subset of the variables. The payoff associated to a customer can be for example the revenue generated by that customer; then the reward is just the total revenue received by the platform.

-

(b)

Product Discount. Consider a company that uses discount strategies to increase their sales. It is common to design discount strategies that only apply to a small subset of products. In this case, we can view the sales of each product as a variable and each discount strategy as an action, and assume that each action only has a significant impact on the sales of those products discounted by this action.

-

(c)

Movie Recommendation. Consider a bandit model for movie recommendation where actions correspond to different recommendation algorithms, and the variables are all the movies in the catalog. For each user, define a set of binary payoffs that indicate whether the user watches a movie in the catalog, and the reward is the number of movies from the catalog that this user watches. Since a recommendation (action) for this user contains (promotes) only a subset of movies, it is reasonable to assume that only their associated payoffs are affected by the action.

Our Contributions.

To begin with, we formalize an uplifting bandit model that captures the aforementioned structure. The term uplift is borrowed from the field of uplift modeling (Radcliffe, 2007; Gutierrez and Gérardy, 2017) and indicates that the actions’ effects are incremental over a certain baseline. We consider a stochastic model, that is, the payoffs of the variables follow an unknown distribution that depends on the chosen action, and study this problem under various assumptions on the learners’ prior knowledge about \edefnn(1\edefnn) the baseline payoff of each variable and \edefnn(2\edefnn) the set of affected variables of each action. Our first result (Section 3) shows that when both 1 and 2 are known, a simple modification of the UCB (UCB) algorithm (Auer, 2002) (Algorithm UpUCB (bl)) for estimating the uplifts has a much lower regret than its standard implementation. Roughly speaking, when is the number of variables and is the number of variables affected by each action, we get a regret bound instead of . This results in major regret reduction for , and is a distinguishing feature of all our results.

Going one step further, we design algorithms that have minimax optimal regret bounds without assuming that either 1 or 2 is known in Sections 5 and 6. When 1 the baseline payoffs are unknown and 2 the affected variables are known, we compute differences of UCBs to estimate the uplifts (Algorithm UpUCB). In contrast to standard UCB methods, these differences are not optimistic; this is because the feedback of the actions also reveals important information about the baseline. When 2 the affected variables are also unknown, we identify them on the fly to maintain suitable estimates of the uplifts. We study two approaches, which differ in what they know about the affected variables. Algorithm UpUCB-nAff knows an upper bound on number of affected variables, whereas Algorithm UpUCB-iLift knows a lower bound on individual uplift. Our regret bounds are summarized in Table 1. These results are further completed with lower bounds that justify the need for our modeling assumptions (Section 4).

| Algorithm | UCB | UpUCB (bl) | UpUCB | UpUCB-nAff | UpUCB-iLift |

| Affected variables known | No | Yes | Yes | No | No |

| Baseline payoffs known | No | Yes | No | No | No |

| Regret Bound | |||||

Organization.

We introduce our uplifting bandit model along with its various variations in Section 2. Over Sections 3, 5, 6, we provide regret bounds for these variations. Lower bounds and numerical experiments are presented in Section 4 and Section 7. To demonstrate the generality of our setup and how our algorithmic ideas extend beyond vanilla multi-armed bandits, we further discuss contextual extensions of our model in Section 8. Comparison to related work is deferred to Section 9.

2 Problem Description

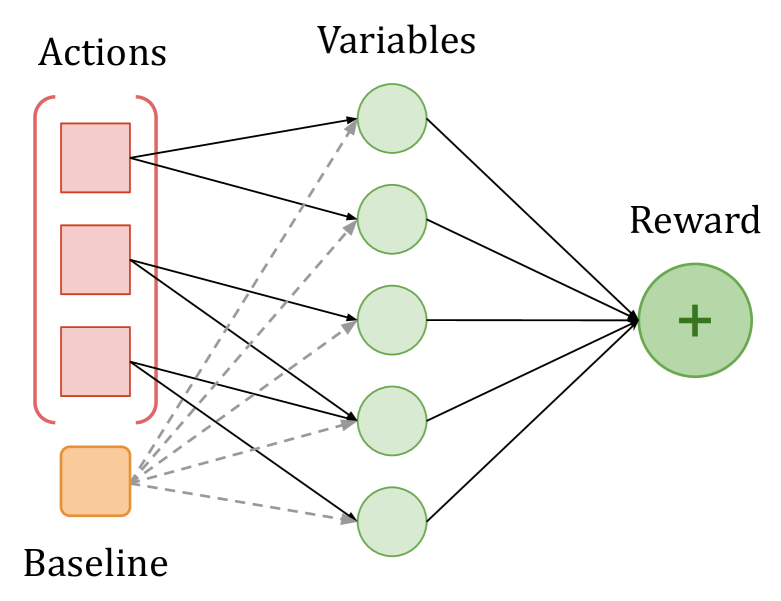

We start by formally introducing our uplifting bandit model. We illustrate it in Figure 1 and summarize our notations in Table 2. Contextual extensions of this model are discussed in Section 8.

A -uplifting bandit is a stochastic bandit with actions and underlying variables. Each action is associated with a distribution on . At each round , the learner chooses an action and receives reward where the set of all variables and is the payoff vector.111The terms reward and payoff distinguish and . Our model is distinguished by the two assumptions that we describe below.

-

(I)

Limited Number of Affected Variables. Let be the subset of variables affected by action and be the baseline distribution that the variables’ payoffs follow when no action is taken. By definition and have the same marginal distribution on , the variables unaffected by action .222If the actions in fact have small impact on the variables in , our model is misspecified and incurs additional linear regret whose size is proportional to the impact of the actions on . An interesting question is how we can design algorithms that self-adapt to the degree of misspecification. While the above condition is always satisfied with , we are interested in the case of , meaning only a few variables are affected by . We define as a uniform bound on , so that . For convenience of notation, we write and .

-

(II)

Observability of Individual Payoff. In addition to the reward , we assume that the learner observes all the payoffs after an action is taken in round .

Uplift and Noise.

Let be a random variable with distribution . We define and respectively as the expected value of and the noise in . We use (resp. ) to denote the vector of (resp. ), and refer to as the baseline payoffs. The individual uplift associated to a pair is defined as . An individual uplift can be positive or negative. We obtain the (total) uplift of an action by summing its individual uplifts over all the variables affected by that action

| (1) |

Let be the expected reward of an action or of pure observation. We also have since as long as .

A real-value random variable is said to be -sub-Gaussian if for all , it holds . Throughout the paper, we assume that is -sub-Gaussian for all and . Note that we do not assume that are independent, i.e., the elements in the noise vector may be correlated, for the following two reasons:

-

•

The independence assumption is not always realistic. In our first example, it excludes any potential correlation between two customers’ purchases.

-

•

While a learner can exploit their knowledge on the noise covariance matrix to reduce the regret, as for example shown in (Degenne and Perchet, 2016), incorporating such knowledge complicates the algorithm design and the accompanying analysis. We however believe this is an interesting future direction to pursue.

Regret.

The learner’s performance is characterized by their regret. To define it, we denote by an action with the largest expected reward and the largest expected reward. The regret of the learner after rounds is then given by

| (2) |

where is the suboptimality gap of action . In words, we compare the learner’s cumulative (expected) reward against the best we can achieved by taking an optimal action at each round. For posterity, we write for the minimum non-zero suboptimality gap and refer to it as the suboptimality gap of the problem.

UCB for Uplifting Bandits.

The UCB algorithm (Auer, 2002), at each round, constructs an UCB (UCB) on the expected reward of each action and chooses the action with the highest UCB. When applied to our model, we get a regret of , as the noise in the reward is -sub-Gaussian (recall that we do not assume independence of the payoffs). However, this approach completely ignores the structure of our problem. As we show in Section 3, we can achieve much smaller regret by focusing on the uplifts.

Problem Variations.

In the following sections, we study several variants of the above basic problem that differ in the prior knowledge about that the learner possesses.

-

(a)

Knowledge of Baseline Payoffs. We consider two scenarios based on whether the learner knows the baseline payoffs or not.

-

(b)

Knowledge of Affected Variables. We again consider two scenarios based on whether the learner knows the affected variables associated with each action or not.

3 Case of Known Baseline and Known Affected Variables

We start with the simplest setting where both the affected variables and the baseline payoffs are known. To address this problem, we make the crucial observation that for any two actions, the difference in their rewards equals to that of their uplifts. As an important consequence, uplift maximization has the same optimal action as total reward maximization, and we can replace rewards by uplifts in the definition of the regret (2). Formally, we write for the largest uplift; then

By making this transformation, we gain in statistical efficiency because can now be estimated much more efficiently under our notion of sparsity. Since both and are known, we can directly construct a UCB on . For this, we define for all rounds , actions , and variables the following quantities.

| (3) |

where is a tunable parameter. In words, , , and represent respectively the number of times that action is taken, the empirical estimate of , and the associated radius of CI calculated at the end of round . The UCB for action and variable at round is . We further define as the uplifting index, and refer to UpUCB (bl) as the algorithm that takes an action with the largest uplifting index at each round (Algorithm 1). Here, the suffix (bl) indicates that the method operates with the knowledge of the baseline payoffs.

Since UpUCB (bl) is nothing but a standard UCB with transformed rewards , and defines exactly the same regret as the original reward, a standard analysis for UCB yields the following result.

Proposition 1.

Let . Then the regret of UpUCB (bl) (Algorithm 1), with probability at least , satisfies:

| (4) |

As expected, the regret bound does not depend on and scales with . This is because the transformed reward of action is only -sub-Gaussian. The improvement is significant when . However, this also comes at a price, as both the baseline payoffs and affected variables need to be known. We address these shortcomings in Sections 5 and 6.

Estimating Baseline Payoffs from Observational Data.

In practice, the baseline payoffs can be estimated from observational data, which gives confidence intervals where lie with high probability. The uplifting indices can then be constructed by subtracting the lower confidence bounds of from . If the number of samples is , the widths of the confidence intervals are in . Identification of is possible only when the sum of these widths over variables is at most , which requires . Otherwise, these errors persist at each iteration and must be in the order of to ensure regret.

About Expected and Gap-Free Bounds.

In Proposition 1, we state a high-probability instance-dependent regret bound, and we will continue to do so for all the regret upper bounds that we present for the non-contextual variants. This type of result can be directly transformed to bound on by taking . Following the routine of separating into two groups depending on their scale, most of our proofs can also be easily modified to obtain a gap-free regret bound, which is typically in the order of . We will not state these results to avoid unnecessary repetitions.

4 Lower Bounds

In this section, we discuss the necessity of our modeling assumptions for obtaining the improved regret bounds of Proposition 1. We prove these results in Appendix B, where we also introduce a general information-theoretic lower bounds for bandit problems with similar design.

Intuitively, the regret can be improved both because the noise in the effect of an action is small, and because the observation of this effect does not heavily deteriorate with noise. These two points correspond respectively to assumptions (I) and (II). Moreover, the knowledge on allows the learner to distinguish between problems with different structures. Without such distinction, there is no chance that the learner can leverage the underlying structure. Therefore, the aforementioned three points are crucial for obtaining (4). Below, we establish this formally for algorithms that are consistent (Lai and Robbins, 1985) over the class of -sub-Gaussian uplifting bandits, which means the induced regret of the algorithm on any uplifting bandit with -sub-Gaussian noise satisfies for all .

For conciseness, in the following we say that an uplifting bandit has parameters if the number of actions, the number of variables, the suboptimality gaps, and the number of affected variables of this instance are respectively , , , and . We focus on instance-dependent lower-bounds and assume that the learner has full knowledge of the baseline distribution. (Of course, the problem only becomes more challenging if the learner does not know the baseline distribution.)

Proposition 2.

Let be a consistent algorithm over the class of -sub-Gaussian uplifting bandits that at most uses knowledge of , , and the fact that the noise is -sub-Gaussian. Let and sequence satisfy . Assume either of the following holds.

-

(a)

for all , so that in the bandits considered below all actions affect all variables.

-

(b)

Only the reward is observed.

-

(c)

The algorithm does not make use of any prior knowledge about the arms’ expected payoffs (in particular, the knowledge of is not used by ).

Then, there exists a -sub-Gaussian uplifting bandit with parameters such that the regret induced by on it satisfies:

As discussed above, Proposition 2 shows that there would be a higher regret in absence of any of the following: \edefnn(a\edefnn) Limited number of affected variables, \edefnn(b\edefnn) Side information about variables beyond reward, and \edefnn(c\edefnn) Some prior knowledge on how the variables are affected. We discuss below these three points in detail.

-

(a)

This point justifies the necessity of assumption (I). It can be further refined to account for non-uniform numbers of affected variables.

Proposition 3.

Let be a consistent algorithm over the class of -sub-Gaussian uplifting bandits that at most uses knowledge of , , and the fact that the noise is -sub-Gaussian. Then, for any and sequence with , there exists a -sub-Gaussian uplifting bandit such that the regret induced by on it satisfies

(5) Proposition 3 essentially posits that the regret must scale with the magnitudes of the noises. The stated lower bound (5) matches an expected version of (4) up to a constant factor, suggesting the minimax optimatlity of Proposition 4. One way to argue this lower bound holds is by reducing a carefully designed uplifting bandits with parameters to a -arm bandit with the corresponding noise scales. We will take a different approach in Appendix B that allows us prove all the lower bounds following the same schema.

-

(b)

This point partially justifies assumption (II). Note that it is however not always necessary to observe all the payoffs. For example, observing the aggregated payoff is sufficient for computing the uplifting indices of UpUCB (bl). Having observation of the entire payoff vector is particularly relevant for the case of unknown affected variables since it helps identify the affected variables relatively easily, as we will see in Section 6.

-

(c)

This point justifies the learner using knowledge about the affected variables. To get some more intuition on the meaning of this condition, let us consider two bandits with exactly the same baseline and noise distributions and very close expected payoffs of the arms. Then, with finite observations, they provide very similar feedback which prevents the learner from distinguishing between the two problems. However, the two bandits may have completely different structures, and in particular, one of them may have all variables affected by all actions since slight perturbation to the baseline would mean that a variable is affected. Therefore, the lower bound from a applies to this instance. Now, provided that the learner is doomed to treat the two instances equally, the lower bound applies to the other instance as well. Of course, one can argue that it is unnatural that the regrets of two similar problems differ significantly even when the learner is provided some prior knowledge. We believe this is the drawback of the asymptotic analysis that we look at here, since these differences may indeed be small within a reasonable number of runs. This is exactly related to the problem of misspecified model that we mentioned in Footnote 2.

With Proposition 2, what remains unclear at this point is whether similar improvement of the regret is still possible when the baseline is unknown or when the learner only has access to more restricted knowledge than . We give affirmative answers to these two questions in the next two sections.

Remark 1.

Our lower bounds are derived with respect to the worst correlation structure of the noise. It is also possible to obtain lower bounds that depend on the covariance of the noise. For example, if the variables are independent, the lower bound in (5) only scales linearly with .

5 Case of Unknown Baseline

In this section, we consider the situation where the sets of affected variables are known by the learner, but not the baseline payoffs. Missing proofs are in Appendix A.

Since the actual uplift at each round is never observed, the uplifts of the actions can hardly be estimated directly without knowing the baseline payoffs. Instead, we follow a two-model approach. Leveraging the fact that and have the same marginal distribution on , we can estimate the baseline payoffs by aggregating information from the feedback of different actions. This leads to

| (6) |

Compared to (3), we notice that both and are functions of . This is because for each taken action , we only increase the counters for those , which causes a non-uniform increase of . Then, by looking at all the rounds that variable is not influenced by the chosen action, we manage to compute , an estimate of . An alternative here is to consider a specific ‘action ’ and estimate the baseline payoffs only using feedback from this action. However, this necessarily requires action to be taken sufficiently often and would thus result in a very high regret. As we will see, our algorithm does not make use of this specific action and achieves regret comparable to the one presented in Proposition 1. To proceed, we define the following UCB indices for all the pairs

| (7) |

The second and the third lines of (7) contain the usual definition of UCBs using the empirical estimates and the radii of the confidence intervals defined in (3) and (6). In the special case that a variable is affected by all the actions (recall that we do not use ‘action ’), it is impossible to estimate but it is enough to compare directly against for any two actions , so we just set to in this case.

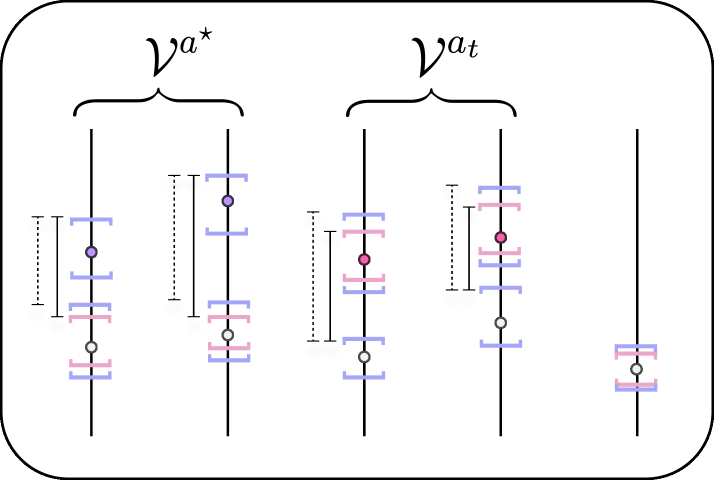

We outline the proposed method, UpUCB, in Algorithm 2. The uplifting indices are given by . It may be counter-intuitive to compare the differences between two UCBs. Indeed, is no longer an optimistic estimate of the uplifting effect , but it captures the essential trade-off between learning action ’s payoffs and learning the baseline . To provide some intuition, we give an informal justification of UpUCB in Figure 2(a): If a suboptimal action is taken in round , the estimates of all move closer to the actual mean from above. As a result, decreases, since all for do. Thus action is less likely to be taken next. Moreover, increases, since decrease for any affected by but not . Thus is more likely to be taken next. The effectiveness of UpUCB is confirmed by the following theorem.

Theorem 1.

Let . Then the regret of UpUCB (Algorithm 2) with probability at least , satisfies:

| (8) |

As in Proposition 1, the regret is . In fact, all decisions in UpUCB are made on uncertain estimates of at most variables; thus the statistical efficiency scales with and not . Moreover, for any action , the width of the confidence intervals for baseline estimates are lower than those of whenever . The factors thus play a secondary role in the analysis of the regret. A detailed comparison with Proposition 1 reveals that the difference is in the order of ; this is only significant when the optimal actions affect many more variables then the suboptimal ones. Hence, the price of not knowing the baseline payoffs is generally quite small.

6 Case of Unknown Affected Variables

Now we study the more challenging setting where the affected variables are unknown to the learner. Proposition 2 states that improvement is impossible if the learner does not possess any prior knowledge that allow them to exploit the structure. To circumvent this negative result, we study two weak assumptions motivated by practice: the learner has either access to \edefnn(\edefnit\selectfonti\edefnn) an upper bound on the number of affected variables or \edefnn(\edefnit\selectfonti\edefnn) a lower bound on individual uplift.

6.1 Known Upper Bound on Number of Affected Variables

Here we assume that we have a known upper bound on number of affected variables (i.e., ). We design algorithms with regret bounds that takes as input. We consider the cases of known and unknown baseline payoffs.

6.1.1 Known Baseline Payoffs

To illustrate our ideas, we start by assuming that the baseline payoffs are known. We propose an optimistic algorithm that maintains a UCB on the total uplift with an overestimate in the order of . Let , , and be defined as in (3). The UCB, uplifting indices, and the confidence intervals for each (action, variable) pair are

| (9) | ||||

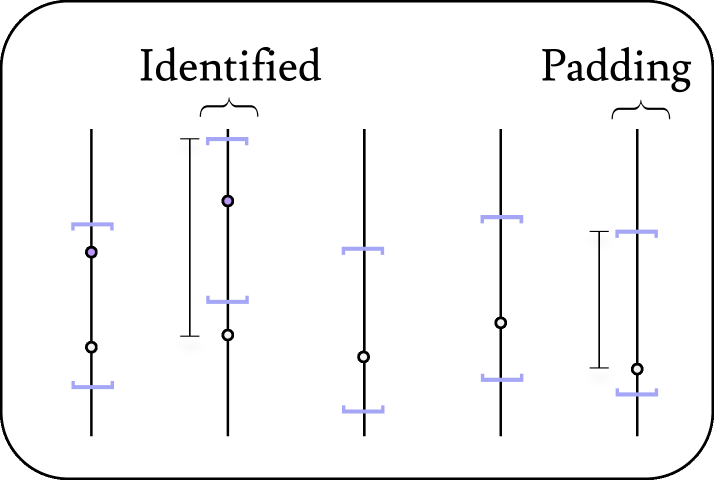

In the sequel, we refer to as the individual uplifting index of the pair . It serves as an estimate of the individual uplift . Our algorithm, UpUCB-nAff (bl), leverages two important procedures to compute an optimistic estimate of the uplift : identification of affected variables, and padding with variables with the highest individual uplifting indices.

To begin, in line 6, UpUCB-nAff (bl) constructs the set of identified variables

This set is contained in with high probability. In fact, by concentration of measure, with high probability , in which case indicates . However, is not guaranteed to capture all the affected variables, so we also need to provide an upper bound for , the uplift contributed by the unidentified affected variables. Since the individual uplifting index is in fact a UCB on the individual uplift here and , we can simply choose the variables in with the largest individual uplifting index , as done in line 8 of Algorithm 3. We refer to this set as . We then get a proper UCB on the uplift of action by computing in line 9. This process is summarized in Algorithm 3 and illustrated in Figure 2(b).

6.1.2 Unknown Baseline Payoffs

Now we focus on the most challenging setting, where also the baseline payoffs are unknown. In this case, neither the sets of identified variables nor the uplifting indices of UpUCB-nAff (bl) can be defined. We also cannot estimate the baseline payoffs using (6) since the sets of affected variables are unknown. To overcome these challenges, we note that for any two actions , and only differ on , and . Therefore, and differ in at most variables, and we recover a similar problem structure by taking the payoffs of any action as the baseline.

Combining this idea with the elements that we have introduced previously, we obtain UpUCB-nAff (Algorithm 4). In each round, UpUCB-nAff starts by picking a most frequently taken action (Line 4) whose payoffs are treated as the baseline during this round. Then, in Line 6, UpUCB-nAff chooses variables that are guaranteed to be either in or . This generalizes the identification step of UpUCB-nAff (bl). The individual uplifting indices are computed in Line 7. The definition as differences of UCBs is inspired by similar construction in UpUCB. Lines 8 and 9 constitute the padding step, during which variables with the highest uplifting indices are selected, and finally in Line 10 we combine the above to get the uplifting index of the action.

The similarity between UpUCB-nAff and UpUCB-nAff (bl) can be shown by supposing that one action has been taken frequently. Then the baseline payoffs are precisely estimated and do not change much between consecutive rounds.

6.1.3 Regret Bounds

Both UpUCB-nAff (bl) and UpUCB-nAff choose variables for estimating the uplift of an action, and the decisions are made based on these estimates. Therefore, the statistical efficiencies of these algorithms only scale with and not . This in turn translates into an improvement of the regret, as demonstrated by the theorem below.

Theorem 2.

Let . Then the regret of UpUCB-nAff (bl) (Algorithm 3) (resp. UpUCB-nAff, Algorithm 4), with probability at least , satisfies:

| (10) |

where (resp. ) in the above inequality.

The proof of Theorem 2 (Section A.3) is notable for two reasons. First, tracking of the identified variables guarantees that the uplifting index does not overestimate the uplift much. Take UpUCB-nAff (bl) as an example. An alternative to constructing a UCB on is to choose the variables with the highest individual uplifting indices . However, this would result in a severe overestimate when a negative individual uplift is present. Second, to prove (10) for UpUCB-nAff, we use that the widths of confidence intervals of the chosen are always smaller than those of the taken action. This is ensured by taking as the most frequent action (Line 4 in Algorithm 4).

6.2 Known Lower Bound on Individual Uplift

In this second part of this section, we assume a lower bound on individual uplift is known. This means the learner has access to satisfying that for all and , . This gives us an indicator on how many times we need to take each action in order to identify all the affected variables. Similar assumption was made by Lu et al. (2021) to identify which node in the causal graph affects the reward variable.

Again in this scenario, we derive regret bounds for both when the baseline payoffs are known or not to the learner. Our algorithms combine UCB, successive elimination (Even-Dar et al., 2006), and the idea that the affected variables can be identified after an action is taken sufficiently many times. Our regret bounds feature the ratio , suggesting that this knowledge is helpful when is relatively large.

Hereinafter, for any with , we use to denote the clipping function that restricts to the interval , i.e., . Missing proofs are collected in Section A.4.

6.2.1 Known Baseline Payoffs

As we have seen in Section 6.1.1, if the baseline payoffs are known, we can directly check whether is in the confidence interval. Moreover, with the knowledge for all , we deduce that can be identified correctly with probability after action is taken times. In fact, let be i.i.d. realizations of and be the empirical mean of variable . Applying the sub-Gaussian concentration inequality (17, Section A.1) gives

| (11) |

With a union bound we conclude that with probability at least it holds for all that . We distinguish between the following two situations

-

1.

, then .

-

2.

, then .

This implies that with the choice , we have effectively . One natural algorithm is to thus first pull each arm times and run UpUCB (bl) (Algorithm 1) in the remaining rounds by regarding as the variables that action affects. A direct computation shows that the regret of this algorithm is in with high probability.

However, can be arbitrarily large when gets closer to , and taking an action much fewer times is probably sufficient to deduce that action is not optimal (with high probability). We thus propose to implement the above idea in a more flexible manner: We run UpUCB (bl) with the uplifting indices , where

We refer to this algorithm as UpUCB-iLift (bl), with iLift standing for individual uplift, and summarize it in Algorithm 5. UpUCB-iLift (bl) has the following regret guarantee.

Theorem 3.

Let . Then the regret of UpUCB-iLift (bl) (Algorithm 5), with probability at least , satisfies:

| (12) |

Theorem 3 shows that Algorithm 5 provides a smooth transition between standard UCB and the naive strategy that tries to identify the affected variables of all the actions. When , the loss of taking action is so large that UCB prevents it from being taken further even if . Otherwise, the affected variables get identified after an action is taken sufficient number of times and the algorithm benefits from this knowledge to improve the estimate of the uplift. It is also quite straightforward to combine Algorithm 3 with Algorithm 5 when both and are known; this results in a regret bound that replaces by in (12).

6.2.2 Unknown Baseline Payoffs

Several additional challenges emerge when we want to adapt the aforementioned strategies to the case where the baseline payoffs are unknown. First, without additional assumption, it is impossible to tell whether two arbitrarily close estimates indicate the same effect of two actions on a variable. Then, without a proper baseline to compare with, we can never exclude the possibility that all the variables are affected by all the actions. To circumvent this issue, we make the following more stringent assumption.

Assumption 1.

The effect of any two actions on a variable differ by at least as long as one of them affects this variable, i.e., for all , , and , it holds .

In other words, is not only a lower bound on individual uplift, but also a lower bound on (individual) effect gap. Second, with a UCB-style algorithm, the optimal actions may not be taken sufficiently many times, in which case we can only conservatively assume that they affect all the variables. This would incur additional regret in the analysis when is unknown. Therefore, we would like to ensure that all the (potentially optimal) actions are taken the same number of times at the point that the affected variables get identified. This leads to a two-stage method as described in Algorithm 6.

In the first stage, we perform successive elimination until the uneliminated actions are taken sufficiently many times. Here is the empirical estimate of the reward associated to action and is the associated radius of confidence interval. Subsequently, for each variable we construct the set

| (13) |

where is the number of iterations in the elimination phase and the confidence intervals are defined as in (9). If Assumption 1 is verified, then with high probability only if . Therefore, the observed results from these arms can be used to estimate the baseline payoff of . On the other hand, the identified affected variables for action are then .

The second stage of the algorithm reuses the idea from UpUCB. We define the UCB indices following (9) for and for the baseline estimate we choose among the action that is taken the most frequently whenever this set is non-empty. Otherwise we arbitrarily set it to . That is,

| (14) |

The uplifting indices that guide the decision of the algorithm are defined by .

As shown below, the regret of Algorithm 6 takes roughly the same form as the one in Theorem 3, but as in Theorem 1, the number of variables that an optimal action affects also plays a crucial role in the regret bound.

Theorem 4.

Let Assumption 1 hold and . Then the regret of UpUCB-iLift (Algorithm 6), with probability at least , satisfies:

| (15) |

Remark 2.

A natural candidate for is the one that uses aggregated information as in (6). The problem of this choice is that how we aggregate the observations collected in the first phase are only determined at the end of the the phase, while this choice itself depends on these observations. Mathematically, this prevents us from defining a suitable martingale difference sequence for which we establish concentration bound. An easy fix is to only aggregate observations from the second phase, while the use of the observations from the first phase should be limited to those coming from just one arm.

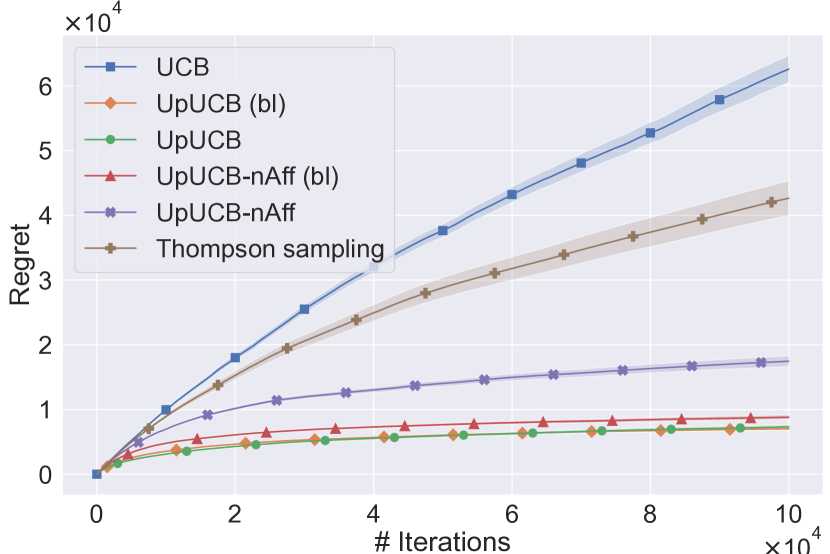

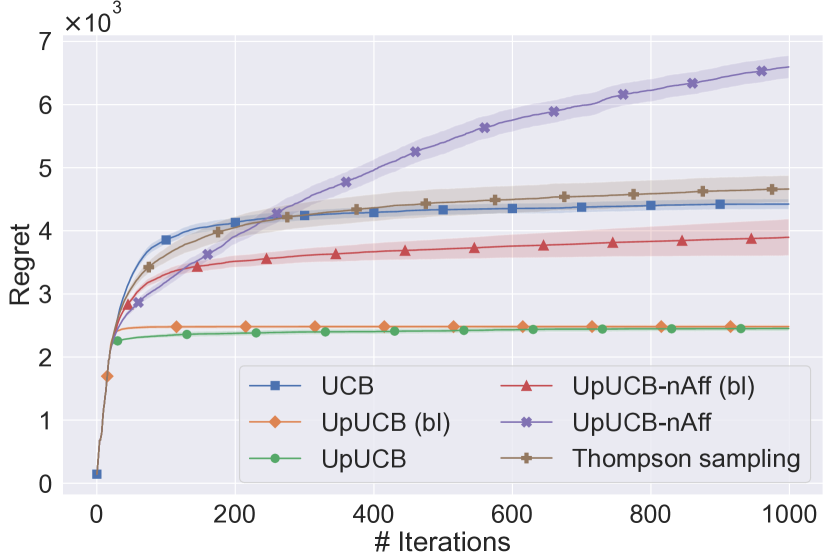

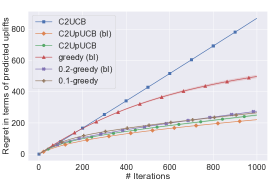

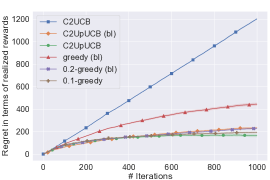

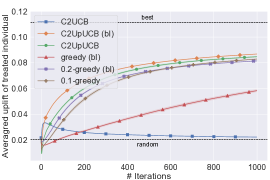

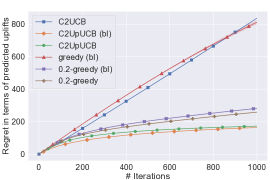

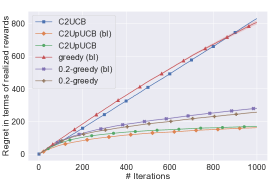

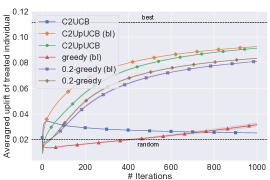

7 Numerical Experiments

In this section, we present numerical experiments to demonstrate the benefit of estimating uplifts in our model. We compare UpUCB (bl), UpUCB, UpUCB-nAff (bl), and UpUCB-nAff (Algorithms 1, 2, 3 and 4) against UCB and Thompson sampling with Gaussian prior and Gaussian noise that only use the observed rewards . To ensure a fair comparison, we tune all the considered algorithms and report the results for the parameters that yield the best averaged performance. The experimental setup details are provided in Appendix D. The experiments for the contextual combinatorial uplifting model introduced in Section 8 are presented in Section C.3.

Gaussian Uplifting Bandit.

We first study our algorithms in a Gaussian uplifting bandit, i.e., the noise vectors are Gaussian, with actions, variables, and meaning that each action affects variables. The expected payoffs are contained in , and the covariance matrix of the noise is taken the same for all the actions. The suboptimality gap of the created problem is around , and the variance of the total noise is around .

Bernoulli Uplifting Bandit with Criteo Uplift.

We use the Criteo Uplift Prediction Dataset (Diemert et al., 2018) with ‘visit’ as the outcome variable to build a Bernoulli uplifting bandit, where the payoff of each variable has a Bernoulli distribution. This dataset is designed for uplift modeling, and has outcomes for both treated and untreated individuals. Thus it is suitable for our simulations. To build the model, we sample examples from the dataset, and use K-means to partition these samples into clusters of various sizes. The examples are taken as our variables. We consider actions that correspond to treating individuals of each cluster. Assuming that each cluster contains a single type of users that react in the same pattern, we sample the payoffs from independent Bernoulli distributions with means that equal the average visit rates of the treated or untreated individuals of the clusters, depending on which action is chosen. Here, and is around .

Results.

Figure 2 confirms that we can effectively achieve much smaller regret by restricting our attention to the uplift. Moreover, when the sets of affected are known, the loss of not knowing the baseline payoffs seems to be minimal. Not knowing the affected variables has a more severe effect, and in particular causes much larger regret in the second experiment. In fact, the design of UpUCB-nAff and UpUCB-nAff (bl) heavily rely on the additive structure of the uplifting index, and can thus hardly benefit from the payoff independence which allows the other four algorithms to achieve smaller regret in this case.

7.1 Ablation Study on Gaussian Uplifting Bandit

Below we further present ablation studies on the Gaussian uplifting bandit model.

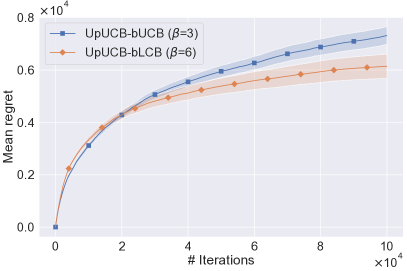

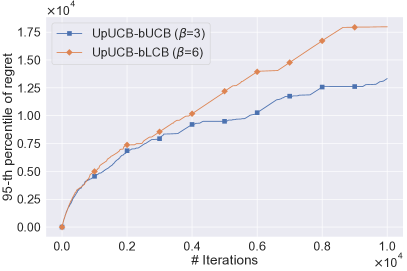

Baseline UCB versus Baseline LCB.

In Algorithm 2, we suggest subtracting the UCBs of the baseline payoffs from the UCBs of the actions. This could be counter-intuitive because to get an optimistic estimate of the uplift, we should instead subtract the LCBs of the baseline payoffs. However, the latter strategy prevents the learner from learning more about the baselines that are badly estimated, and can thus lead to failure more frequently. In the following, we refer to the two strategies respectively as UpUCB (bl)-bUCB and UpUCB (bl)-bLCB.

In Figure 3(a) (Left), we illustrate the mean regret of the two designs when their parameters are optimally tuned. It turns out there the two strategies perform similarly here. We would just like to highlight that to achieve the optimal performance, UpUCB (bl)-bLCB needs to use a larger exploration parameter. Therefore, in terms of average performance, it seems that the effect of using LCBs of the baseline is close to a shrinkage of the exploration parameter.

Next, we further inspect the robustness of the algorithms by plotting the th percentile of the regrets (which roughly corresponds to the th largest regret among those recorded in the runs). The same parameters give the optimal values for this metric. However, as shown in Figure 3(a) (Right), it turns out that UpUCB (bl)-bLCB achieves a much higher th percentile of regret, which indicates that it indeed fails more frequently.

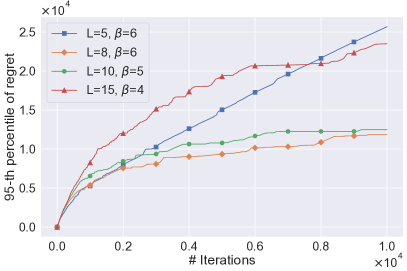

Misspecification of .

We also investigate the effect of misspecification of on Algorithm 3. For the bandit instance that we employ here, and thus according to Proposition 4, Algorithm 3 guarantees sublinear regret as long as it is provided with . On the flip side, the algorithm may incur linear regret if is underestimated.

To verify this, we run the algorithm with and plot the averaged regret and the -th percentile of regret for optimally tuned exploration parameters in Figure 3(b). We effectively observe sublinear regret when is overspecified, but the regret becomes much larger because the algorithm is more conservative and explores more. On the other hand, under severe underspecification of , the algorithm is doomed to fail whatever the exploration parameter used. Finally, it seems that slight underspecification of can be compensated by choosing a larger exploration parameter. In fact, in the figure we see that for choosing gives the smallest regret among the presented curves.

8 Contextual Extensions

In this section, we briefly discuss potential contextual extensions of our model. As in contextual bandits, context is a side information that helps the learner to make a more informed decision, which results in a higher reward. To incorporate context, one possibility is to associate each variable with a feature vector . The subscript indicates that the context can change from one round to another. We also associate each action with a function so that the expected payoff of action acting on a variable with feature is . The expected reward of choosing at round is then . The optimal action of round is and the regret of a learner that takes the actions is given by

As in Section 2, upon taking an action, the learner observes the noisy payoffs of all the variables. The key structure in our model is there exists a baseline payoff vector such that for any given action , the equality holds for most . Given context, this can be translated into the existence of a baseline function such that for any given and , the equality holds for most . The uplift of action is defined as

We provide two concrete examples of the contextual extension below.

Contextual Uplifting Bandit with Linear Payoffs.

In this model, each action is associated with an unknown parameter and the expected payoff is the scalar product of and the feature of the variable, i.e., . We also assume the aforementioned equality to hold for the baseline function and we use

for the variables affected by action at round . One sufficient condition for to be small is sparsity in both the parameter difference and the context vector . In fact, as long as the supports of and are disjoint. In the sequel, we assume is uniformly bounded by .

Clearly, our algorithms can be directly applied as long as we can construct a UCB on . This can for example be done using the construction of Linear UCB (Abbasi-Yadkori et al., 2011). In this way, the decision of the learner is again based on the uncertain estimates of at most variables, and we thus expect the improvements that we have shown in our theorems would persist. As an example, when both and are known, UpUCB (bl) adapted to this situation constructs UCB for , and it is straightforward to show that the regret of such algorithm can be as small as .333As in the previous sections, this bounds applies to the case where the noises are not necessarily independent. In contrast, if the learner works directly with the total reward, the regret is in .

Contextual Combinatorial Uplifting Bandit.

To demonstrate the flexibility of our framework, we also consider a different model that tackles the problem of targeted campaign. Here, we refer to the variables as individuals (customers) that we may want to treat (serve) with some treatment (campaign). To improve the overall return on investment, it is often beneficial to treat only a subset of the individuals. The bandit problem thus consists of finding the right set of individuals to treat at each round. Concretely, if the learner selects at most individuals to treat in a round, the action set can be written as , where is the number of non-zero coordinates of . In this form, the -th coordinate of is if and only if individual receives the treatment. Similar to before, we observe the payoffs of all the individuals after treatments are applied.

Here, we make a practical no interference assumption, that the payoff of each individual only depends on whether they are treated or not (i.e., independent of others). We can thus define functions for so that .444Strictly speaking, is a function of here. Considering the action of not treating any individual as the baseline, the uplift of action in round is given by

where is the set of individuals treated by action . For UCB-type methods, we should thus provide upper confidence bounds for . Depending on whether the baseline function is known or not, we may subtract or from to compute the uplifting indices for each individual. The algorithm then chooses the individuals with the highest uplifting indices. We refer to the resulting algorithm as C2UpUCB, where C2 is the abbreviation of “contextual combinatorial”. We provide its pseudo code in Algorithm 7 (where we suppose the baseline is unknown).

In Appendix C, we further present a generalization of the algorithm to the case of multiple treatments, a theoretical analysis thereof for linear payoffs, and accompanying numerical experiments.

9 Related Work

In this section, we link our work to other existing bandit models. To begin, as suggested by the name, the concept of uplift plays a crucial role in our approach. From a high-level perspective, the goals of both uplifting modeling and MAB is to help selecting the optimal action. The former achieves it by modelling the incremental effect of an action on an individual’s behavior. Despite this apparent connection between the two concepts, few papers explicitly link them together. We believe that this is because the resulting problem can often be solved by classic bandit algorithms with a redefined reward. This approach was taken in (Sawant et al., 2018; Berrevoets et al., 2019).

Instead, our paper focuses on bandit problems in which estimating the uplifts improves the statistical efficiency of the algorithms, and this is possible thanks to the ‘sparsity’ of the actions’ effects. Prior to our work, sparsity assumptions in bandits primarily concerned the sparsity of the parameter vectors in linear bandits, which could be of great interest in high-dimensional settings (Abbasi-Yadkori et al., 2012; Bastani and Bayati, 2020; Hao et al., 2021). A notable exception is Kwon et al. (2017) who studied a variant of the MAB where the sparsity is reflected by the fact that the number of arms with positive reward is small. Our work is orthogonal to all of these in that we look at a different form of sparsity. As we saw in Section 8, while sparsity in parameter can be a cause of sparsity in action effect, the improvement of regret is established with a different mechanism. In the upcoming paragraphs, we further exhibit how our model is related to causal and combinatorial bandits.

Causal Bandits.

The term causal bandits captures the general idea that in a bandit model the generation of reward may be governed by some causal mechanism while the actions correspond to interventions on the underlying causal graph. This idea was first formalized in (Lattimore et al., 2016) and subsequently explored in a series of work (Lee and Bareinboim, 2018; Lu et al., 2020; Nair et al., 2021) that cover multiples variants of the problem, including both the minimization of simple and cumulative regrets. Our problem fits into the causal bandit framework by regarding Figure 1 as a simple causal graph where the variables consist of all the directed causes of the reward and the actions correspond to atomic interventions on the action nodes. The observability of these direct causes are also key assumptions in many of the aforementioned works. Moreover, in the unknown affected case our causal graph is in fact partially unknown. This is an intriguing problem in causal bandits as argued by (Lu et al., 2021). While we have shown improvement of the algorithms for this specific model, a interesting question is whether similar improvement can still be shown in more general causal bandit models under the assumption that each actions only affects a limited number of variables of the causal graph.

Combinatorial Bandits.

In combinatorial bandits (Cesa-Bianchi and Lugosi, 2012), the learner selects at each round a subset of ground items depending on which the reward is computed. In its simplest form, the reward is just the sum of the payoffs of the selected items. Of particular relevance to us is the semi-bandit setting (Chen et al., 2013; Kveton et al., 2015), which assumes that the payoffs of the selected items are also observed. This structure of the reward and observability of individual payoffs both suggest a strong similarity between our model and semi-bandits. However, this comes with an important conceptual difference: the set of items, or variables, for which we observe the outcomes are selected in semi-bandits, while for us they are fixed and inherent to the reward generation mechanism. As an example, in example (c), combinatorial bandit models optimize the number of movies that are watched among the recommended ones, while we also consider non-recommended movies. In fact, as argued in (Wang et al., 2020), a recommendation is only effective if the user actually watches the movie and would not watch it without the recommendation

On the other hand, mathematically, it is possible to fit our model into the stochastic combinatorial semi-bandit framework when the sets of affected variables are known. For this, consider a semi-bandit problem with items that correspond to the random variables . At each round, the learner selects items that depends on the taken action and observes the payoffs of the selected items. More precisely, when action is taken, the selected items are .

In terms of algorithm, let us consider the UpUCB algorithm described in Algorithm 2, which is based on selecting the action with the largest uplift index . We notice that the quantity is indeed an upper confidence bound on the reward of action and UpUCB is equivalent to choosing the action with the largest in each round. This observation indeed reduces UpUCB to CombUCB (Chen et al., 2013; Kveton et al., 2015) on the transformed model. Nonetheless, the UpUCB formulation has several advantages:

-

1.

It captures the fact that we really care about is the uplifting effect and the variables affected by each action.

-

2.

The uplifting interpretation facilitates algorithm design in more involved situations as we have shown in Section 6.

-

3.

While the general analysis of CombUCB yields a regret in , we have shown in Theorem 1 that the regret of UpUCB is in . Our analysis presented in Section A.2 also greatly benefits from the UpUCB formulation of the algorihhm.

10 Concluding Remarks

This paper addresses MAB problems whose rewards can be written as a sum of some observable variables. We showed that when each of the action only affects a limited number of these variables, much smaller regret can be achieved, and we developed algorithms with such guarantee under different variations of knowledge the learner possesses. While the focus of this paper is on UCBs for stochastic bandits, we believe understanding how similar problem structure can be exploited for other algorithms such as Thompson sampling, information directed sampling, or even methods for adversarial bandits is also important.

| Notation | Explanation | |

| Bandits | Number of actions | |

| An action | ||

| An optimal action, | ||

| The set of actions, | ||

| Round index | ||

| Number of rounds / Time horizon | ||

| The set of all the rounds, | ||

| Reward received at round | ||

| Expected reward of action | ||

| Largest expected reward, | ||

| Suboptimality gap of action , | ||

| Minimum non-zero suboptimality gap, i.e., | ||

| Uplifting Bandits | Number of underlying variables | |

| A variable | ||

| The set of variables, | ||

| Number of variables affected by action | ||

| Upper bound on number of affected variables, i.e., | ||

| The set of variables affected by action | ||

| 0 | A convenient notation to represent all quantities related to the baseline | |

| A notation to include both the actions and the baseline | ||

| Baseline reward | ||

| Expected uplift of action , | ||

| Largest expected uplift, | ||

| Payoffs observed at round , | ||

| Expected payoffs of action , | ||

| Baseline payoffs, | ||

| Expected individual uplifts of action , | ||

| The distribution of the payoffs associated to action | ||

| Baseline distribution of the payoffs | ||

| Lower bound on individual uplift, i.e., , | ||

| UCB | Number of times action is taken in the first rounds | |

| Empirical estimates of expected payoffs | ||

| Widths of confidence intervals | ||

| Confidence intervals | ||

| Upper confidence bounds | ||

| Uplifting index of action | ||

| Individual uplifting indices | ||

| Error probability provided as input for UCB-type algorithms |

References

- Abbasi-Yadkori et al. (2011) Yasin Abbasi-Yadkori, Dávid Pál, and Csaba Szepesvári. Improved algorithms for linear stochastic bandits. Advances in Neural Information Processing Systems, 24:2312–2320, 2011.

- Abbasi-Yadkori et al. (2012) Yasin Abbasi-Yadkori, David Pal, and Csaba Szepesvari. Online-to-confidence-set conversions and application to sparse stochastic bandits. In Artificial Intelligence and Statistics, pages 1–9. PMLR, 2012.

- Auer (2002) Peter Auer. Using confidence bounds for exploitation-exploration trade-offs. Journal of Machine Learning Research, 3(Nov):397–422, 2002.

- Bastani and Bayati (2020) Hamsa Bastani and Mohsen Bayati. Online decision making with high-dimensional covariates. Operations Research, 68(1):276–294, 2020.

- Berrevoets et al. (2019) Jeroen Berrevoets, Sam Verboven, and Wouter Verbeke. Optimising individual-treatment-effect using bandits. arXiv preprint arXiv:1910.07265, 2019.

- Bubeck and Cesa-Bianchi (2012) Sébastien Bubeck and Nicolo Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Machine Learning, 5(1):1–122, 2012.

- Burnetas and Katehakis (1996) Apostolos N Burnetas and Michael N Katehakis. Optimal adaptive policies for sequential allocation problems. Advances in Applied Mathematics, 17(2):122–142, 1996.

- Cesa-Bianchi and Lugosi (2012) Nicolo Cesa-Bianchi and Gábor Lugosi. Combinatorial bandits. Journal of Computer and System Sciences, 78(5):1404–1422, 2012.

- Chen et al. (2013) Wei Chen, Yajun Wang, and Yang Yuan. Combinatorial multi-armed bandit: General framework and applications. In International Conference on Machine Learning, pages 151–159. PMLR, 2013.

- Chung and Zhong (2001) Kai Lai Chung and Kailai Zhong. A course in probability theory. Academic press, 2001.

- Dani et al. (2008) Varsha Dani, Thomas P Hayes, and Sham M Kakade. Stochastic linear optimization under bandit feedback. In Conference on Learning Theory, pages 355–366, 2008.

- Degenne and Perchet (2016) Rémy Degenne and Vianney Perchet. Combinatorial semi-bandit with known covariance. In Advances in Neural Information Processing Systems, pages 2972–2980, 2016.

- Diemert et al. (2018) Eustache Diemert, Artem Betlei, Christophe Renaudin, and Massih-Reza Amini. A large scale benchmark for uplift modeling. In International Conference on Knowledge Discovery and Data Mining. ACM, 2018.

- Doob (1953) Joseph L. Doob. Stochastic processes. John Wiley & Sons, 1953.

- Even-Dar et al. (2006) Eyal Even-Dar, Shie Mannor, Yishay Mansour, and Sridhar Mahadevan. Action elimination and stopping conditions for the multi-armed bandit and reinforcement learning problems. Journal of machine learning research, 7(6), 2006.

- Filippi et al. (2010) Sarah Filippi, Olivier Cappe, Aurélien Garivier, and Csaba Szepesvári. Parametric bandits: The generalized linear case. In Advances in Neural Information Processing Systems, volume 23, pages 586–594, 2010.

- Gutierrez and Gérardy (2017) Pierre Gutierrez and Jean-Yves Gérardy. Causal inference and uplift modelling: A review of the literature. In International Conference on Predictive Applications and APIs, pages 1–13. PMLR, 2017.

- Hao et al. (2021) Botao Hao, Tor Lattimore, and Wei Deng. Information directed sampling for sparse linear bandits. In Advances in Neural Information Processing Systems, 2021.

- Kveton et al. (2015) Branislav Kveton, Zheng Wen, Azin Ashkan, and Csaba Szepesvari. Tight regret bounds for stochastic combinatorial semi-bandits. In Artificial Intelligence and Statistics, pages 535–543. PMLR, 2015.

- Kwon et al. (2017) Joon Kwon, Vianney Perchet, and Claire Vernade. Sparse stochastic bandits. In Conference on Learning Theory, volume 65, 2017.

- Lai and Robbins (1985) Tze Leung Lai and Herbert Robbins. Asymptotically efficient adaptive allocation rules. Advances in applied mathematics, 6(1):4–22, 1985.

- Lattimore et al. (2016) Finnian Lattimore, Tor Lattimore, and Mark D Reid. Causal bandits: Learning good interventions via causal inference. In Advances in neural information processing systems, 2016.

- Lattimore and Szepesvári (2020) Tor Lattimore and Csaba Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- Lee and Bareinboim (2018) Sanghack Lee and Elias Bareinboim. Structural causal bandits: where to intervene? Advances in Neural Information Processing Systems 31, 31, 2018.

- Lu et al. (2020) Yangyi Lu, Amirhossein Meisami, Ambuj Tewari, and William Yan. Regret analysis of bandit problems with causal background knowledge. In Conference on Uncertainty in Artificial Intelligence, pages 141–150. PMLR, 2020.

- Lu et al. (2021) Yangyi Lu, Amirhossein Meisami, and Ambuj Tewari. Causal bandits with unknown graph structure. In Advances in Neural Information Processing Systems, 2021.

- Nair et al. (2021) Vineet Nair, Vishakha Patil, and Gaurav Sinha. Budgeted and non-budgeted causal bandits. In International Conference on Artificial Intelligence and Statistics, pages 2017–2025. PMLR, 2021.

- Qin et al. (2014) Lijing Qin, Shouyuan Chen, and Xiaoyan Zhu. Contextual combinatorial bandit and its application on diversified online recommendation. In Proceedings of the 2014 SIAM International Conference on Data Mining, pages 461–469. SIAM, 2014.

- Radcliffe (2007) Nicholas Radcliffe. Using control groups to target on predicted lift: Building and assessing uplift model. Direct Marketing Analytics Journal, pages 14–21, 2007.

- Sawant et al. (2018) Neela Sawant, Chitti Babu Namballa, Narayanan Sadagopan, and Houssam Nassif. Contextual multi-armed bandits for causal marketing. In International Conference on Machine Learning, 2018.

- Szita and Szepesvári (2011) István Szita and Csaba Szepesvári. Agnostic KWIK learning and efficient approximate reinforcement learning. In Conference on Learning Theory, pages 739–772. JMLR Workshop and Conference Proceedings, 2011.

- Vershynin (2018) Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wang et al. (2020) Yixin Wang, Dawen Liang, Laurent Charlin, and David M Blei. Causal inference for recommender systems. In Fourteenth ACM Conference on Recommender Systems, pages 426–431, 2020.

Appendix A Proofs for Upper Bound Results

In this appendix, we provide proofs of the regret bounds from Sections 5 and 6. Our proofs have the following structure.

-

1.

Leveraging Lemmas 2 and 3 presented in Section A.1, we define a high-probability event on which all the expected payoffs belong to their confidence intervals.

-

2.

For UCB-like methods, we use the fact that the uplifting index of the taken action is larger than that of any optimal action by design to show that on event a suboptimal action can only be taken when its associated width of confidence interval is sufficiently large.

-

3.

The previous point allows us to bound the number of times that a suboptimal action is taken on .

-

4.

We conclude with the following regret decomposition (which was already stated in (2)).

(16)

A.1 Concentration Bounds

To prove the regret upper bounds, we will make use of concentration bounds that apply to quantities defined in (3) and (6). Underlying all these results is the following fundamental concentration inequality for -sub-Gaussian random variables [Vershynin, 2018]

| (17) |

However, the estimates in (3) and (6) aggregate observed values in a way that depend on the decisions that have been made. Therefore, concentration bounds for the sum of independent variables, which can be directly derived from (17), are not sufficient for our purposes. The standard trick to circumvent this issue in bandit literature is to combine Doob’s optional skipping ([Doob, 1953, Chap. 3], [Chung and Zhong, 2001, Chap. 9]) with concentration inequality for martingale difference sequence. The following lemma adapted from [Szita and Szepesvári, 2011, Lem. A.1] is proved exactly using this technique.

Lemma 1.

Let be a filtration and let be a sequence of - valued random variables such that is -measurable, and is -measurable and conditionally -sub-Gaussian, i.e., for all . Let and let , where we take when . Then, for any ,

| (18) |

Proof.

The proof of [Szita and Szepesvári, 2011, Lem. A.1] essentially applies. We just need to replace the use of Hoeffding-Azuma inequality by the use of concentration inequality for conditionally sub-Gaussian martingale difference sequences, which is itself derived from (17) and the fact that the sum of conditionally sub-Gaussian martingale differences is sub-Gaussian. ∎

In the following, will represent the natural filtration associated to such that is -measurable, and is -measurable. Applying Lemma 1 to properly defined along with the use of a union bound gives the following concentration results that are key to our analyses.

Lemma 2.

Let , , and let be defined as in (3). Then for any , it holds

Proof.

For , we define the random variables

We then define the failure events

It holds . In fact, if happens then for some and this is only possible when . With the definition , we further see that and . The latter means that we indeed have . Thus multiplying by gives exactly

which shows that happens as well. It is thus sufficient to prove that .

For , we apply Lemma 1 to and . Since , we recover the exact inequality that appears in the definition of . We conclude with a union bound taking ranging from to . ∎

Lemma 3.

Let , and let be defined as in (6). Then for any , it holds

A.2 Unknown Baseline: Proof of Theorem 1

See 1

Proof.

We first notice that while there are variables, not all of them are involved in estimating the uplifts. Therefore, we only need to focus on the set of relevant variables . Clearly, . With this in mind, we define the events

Lemma 2 and Lemma 3 in Section A.1 along with union bounds over and guarantee

It is thus sufficient to show that (8) holds on .

In the remainder of the proof, we consider an arbitrary realization of and prove that (8) indeed holds for this realization. From (16) it is clear that we just need to bound from above for all suboptimal action with . This is done by providing a lower bound on for any such that . To proceed, suppose that a suboptimal action is taken for the last time at round .555If the action is not taken anymore after the first runs. We have so the upper bound that we show later trivially holds. This implies and . By the definition of the uplifting indices, we get

Rearranging and dropping from both sides, we get

| (19) |

This is similar to the type of inequality that defines standard UCB. In fact, the left and the right hand sides of (19) are respectively upper confidence bounds on and upper confidence bounds on . We next bound these two quantities respectively from above and from below. Since both and hold, we have the following inequalities for the UCB indices

Combining the above, we obtain

Adding to both sides and rearranging leads to

From this we can derive an inequality between the suboptimal gap and the the widths of the confidence intervals as follows

| (20) | ||||

We next argue that for all we have and hence . In fact, if , then whenever action is taken, the count of also increases by . Formally,

Therefore, we further deduce . Equivalently,

A.3 Unknown Affected Variables: Proof of Theorem 2

Below we prove Theorem 2 separately for UpUCB-nAff (bl) and UpUCB-nAff.

Proposition 4 (Regret of UpUCB-nAff (bl)).

Let . If the learner knows and an upper bound on maximum number of variables an action affects and the baseline payoffs, then UpUCB-nAff (bl) (Algorithm 3), with probability at least , has regret bounded by:

| (21) |

Proof.

Let us consider the event

| (22) |

By Lemma 3 and a union bound we get immediately . In the following, we assume that occurs and prove (21).

First, by the definition of we have clearly . In fact, if then . The inclusion along with the condition imply ; in particular, and thus .

Next, for any , it holds . This implies , and accordingly . We can then write

Since on , we have ; subsequently

This shows that is effectively an upper bound of . With this in mind, we are ready to bound the number of times that a suboptimal action is taken.

Let with and assume that it is taken at round , which means that . We have shown that . It remains to provide an upper bound for that involves . For this, we again use and the fact that for all to decompose

| (23) |

The summation of the individual uplifting indices over is naturally related to . Since , for all it holds

In consequence,

| (24) |

What we need to show next is that the definition of guarantees to be small whenever . In fact, if , we have , and in particular , implying that

By definition, , and hence

| (25) |

Putting (23), (24), and (25) together, we get

With we deduce

Therefore, , and equivalently

Following the argument in the proof of Theorem 1, this translates into an upper bound on and we conclude by invoking the decomposition of (16). ∎

We notice that it is quite straightforward to adapt UpUCB-nAff (bl) and its analysis to the setting where the learner knows an action-dependent upper bound . The only change in (21) is that is replaced by . Thus we recover (4) up to a multiplicative constant when . To derive the regret bound for UpUCB-nAff, we combine idea from the proofs of Theorems 1 and 4.

Proposition 5 (Regret of UpUCB-nAff).

Let . Then the regret of UpUCB-nAff (Algorithm 4), with probability at least , satisfies:

| (26) |

Proof.

We again place ourselves in the event defined in (22), and prove (26) under this condition. Recall that is an action that is taken most frequently during the first rounds and the associated estimates serve as baselines at round . We define as the set of variables that are affected by either action or . Clearly, .

We first show that whenever occurs. Let . Under we have both and . Therefore, ; subsequently . The contrapositive of the above gives exactly .

We shall now bound for any suboptimal action , from which the proof concludes by applying (16). Let satisfying . If it is taken at round , we have . This can be written as

| (27) |

Decomposition of Suboptimality Gap using the New Baseline.

Similar to before, we will use (27) to relate the widths of the confidence intervals to the suboptimality gap . For this, we notice that the suboptimality gap of can be rewritten as

| (28) | ||||

The last equality is true because outside , and the same holds when we replace by . Therefore, our goal is to lower bound the RHS of (27) by an expression that contains and upper bound the LHS of (27) by an expression that contains .

Lower Bound on RHS of (27).

Since is the maximum padding, we can lower bound the RHS of the inequality by . Formally, with we have and . Thus, by definition of ,

To further provide a lower bound on , we recall that , so with , , and , we get

| (29) | ||||

Upper Bound on LHS of (27).

To make the term appear, we first relate it to the sum of the uplifting indices using .

| (30) |

The last inequality uses . Next, to relate to the LHS of (27), we want to show \edefnn(\edefnit\selectfonti\edefnn) is small, and \edefnn(\edefnit\selectfonti\edefnn) We can add additional terms from to the LHS of (27). These two points correspond respectively to inequalities (25) and (23) in the proof of Proposition 4. Again, this can be done by looking at the definition of . In fact, if , then by definition , implying that

The above two inequalities respectively translate into

In other words, for any we have . Subsequently,

| (31) | ||||

| (32) |

Therefore

| (33) | ||||

The first inequality makes use of (31) and (32), and in particular the last term on the RHS is non-negative thanks to (32). The equality in the second line is true because . Finally, for the last inequality we use the fact that and . Along with (33) we get an upper bound on that involves .

Conclusion.

Combining (27), (29), (30), and (33), we obtain

By the choice of we have . With (28), it follows that and thus

Repeating the argument in the proof of Theorem 1 (i.e., choose to be the last time that action is taken if it is taken more than once and apply decomposition (16)) gives the desired result. ∎

See 2

Proof.

The proof follows by combining Propositions 4 and 5. ∎

A.4 Unknown Affected Variables: Proofs of Theorems 3 and 4

See 3

Proof.

As before, we prove (12) under the condition that defined in (22) occurs. Recall that we have shown in the proof of Proposition 4 that with our choice of , so this effectively leads to a high-probability regret bound.

In the following we assume that occurs and show that for any suboptimal action , it holds

| (34) |

The inequality (12) then follows directly from (16) and a rearrangement of the terms.

We first claim that for any if then . In fact, by the definition of , implies that . Therefore, as argued in the text, if and only if . Since for any and , this also proves that always holds (we have either or ).

Let be the last time that a suboptimal action is taken so that . This indicates , and hence . We distinguish between the following two cases:

-

1.

: Then so , which in turn leads to , or equivalently .

-

2.

: Then so , which in turn leads to , or equivalently .

Since we also have in the first case, the above gives

Plugging in the definition of we get immediately (34). ∎

See 4

Proof.

We shall again consider the event defined in (22), which holds with probability as argued in the proof of Proposition 4. Leveraging the decomposition in (16) it is sufficient to prove that on we have

| (35) |

We assume happens in the rest of the proof.

Let us first focus on the elimination phase, notice that event implies for every . In this case, the optimal actions never get eliminated. In fact, if , then for all it holds that

As a consequence, we also have and we conclude by the principle of induction. With this we further deduce that all action with gets eliminated after it is taken at most times. To see this, notice that for such action we have

Therefore, for all in phase \@slowromancapi@ of the algorithm, it is true that

| (36) |

This suggests that inequality (35) holds if the algorithm terminates in the elimination phase.

Otherwise, the algorithm constructs ’s, ’s, and switches to the UpUCB phase. Let us denote by the set of actions that do not affect variable and let be the actions that remain after phase \@slowromancapi@. We argue that the sets are constructed such that when occurs,

-

\edefnn(\edefnit\selectfonti\edefnn)

.

-

\edefnn(\edefnit\selectfonti\edefnn)

If there exist such that then we also have .

The second point is proved by observing that under we must have if . To show the first point, notice that after the elimination phase, each of the action in is taken exactly times and thus . By Assumption 1, if , then for all we have , which along with the definition of implies , and therefore .

The rest of the proof follows closely that of Theorem 1. Suppose that a suboptimal action is taken at round during phase \@slowromancapii@ of the algorithm. This means (recall that since happens), i.e.,

Rearranging the terms we get

If then . In particular, so is well-defined and . With we know that and accordingly by the fact that happens. This shows . Moreover, by the choice of ; hence, . The same argument applies to , and the UCB indices of and can be bounded from above and below as in previous proofs. In summary, we obtain

Equivalently,

| (37) |

To conclude, we claim that

| (38) |

Let us first show . The first inclusion is a consequence of :

As for the second inclusion we prove it’s contrapositive:

Notice that the second implication holds because is suboptimal and in particular . The inclusion can be proved in a similar way, and combining these results gives (38). Therefore, the RHS of (37) is exactly while the LHS of (37) is bounded from above by . In consequence,

Therefore, any suboptimal action that gets taken in the UpUCB phase satisfies

On the other hand, if an suboptimal action is not taken in the UpUCB phase then (36) applies, so in either case (35) is verified, which concludes the proof. ∎

Appendix B Lower Bounds

To prove our lower bounds, we fist establish in Section B.1 a general lemma for deriving instance-dependent lower-bounds for bandit problems with underlying variables, side observations, and prior knowledge on the distribution of the variables. Subsequently, in Section B.2 we regard uplifting bandit as a special case of this model and apply the lemma to prove Propositions 2 and 3.

B.1 A General Information-theoretic Lower Bound

Let be a random vector of variables that entirely determines the reward so that we can write for some deterministic reward function . Let be the distribution of action on the underlying variables and be the baseline distribution on these variables. At each round after taking an action, the learner observes a vector in that is itself a function of the variables, written as where is the observation function. The decision of which action to take can then only be based on the interaction history and some prior knowledge of the learner about the distributions of the variables .666For our purpose, we can regard this as a partition of the set of all bandit instances that the learner may encounter.

A class of action distributions is defined as where each is a set of distributions on . We say that is indistinguishable under if for all we have . A bandit problem with underlying variables, side observations, and prior knowledge on the variable distribution is thus defined by the quadruple . A policy is said to be consistent over if for all and all instance of , the regret of on the instance satisfies . A policy is compatible with observation and prior knowledge if it can be implemented by a learner that observes and has prior knowledge .

By abuse of notation, for any distributions on we will write as the expected reward when the variables follow distribution whenever this quantity is defined. We also write as the pushforward of along . Let be a set of distributions such that is well-defined for any . Let and such that . The following quantity is crucial to the analysis

where denotes the KL divergence of from . Intuitively, it quantities how difficult it is to learn that the expected reward is smaller than (smaller the value of the more difficult it is). The next lemma is a straightforward adaptation of [Burnetas and Katehakis, 1996, Th. 1],[Lattimore and Szepesvári, 2020, Th. 16.2] to our model. It provides a lower bound on the asymptotic regret

Lemma 4.

Let be a class of action distributions and be the reward function. Let be a consistent algorithm over that is compatible with prior knowledge function and observation function . Then, if is indistinguishable under , for all , it holds that

| (39) |

Proof.

The proof follow closely the one presented in [Lattimore and Szepesvári, 2020]. The key observation is that the same proof still carries out if we have a random vector and our reward and observation depends on this random vector. In particular, let and be the probability measure on the actions and the observations induced by the interaction of the policy with the bandit instances and for . The assumption that is compatible with and and that is indistinguishable under allows us to write , where are the observations of the learner, and are respectively the probability density functions of and , and is a probability kernel that can be chosen using prior knowledge.777Many technical details are omitted here. We refer the interested readers to [Lattimore and Szepesvári, 2020] for a rigorous treatment of such proof. We have a similar decomposition for . Then, following the proof of [Lattimore and Szepesvári, 2020, Lem. 15.1] we get immediately

In the above, means that the expectation is taken with respect to . The proof can be completed in the same way as done for [Lattimore and Szepesvári, 2020, Th. 16.2]. ∎

B.2 Lower Bounds for Uplifting Bandits– Proof

The following proposition includes both Proposition 2 and Proposition 3.

Proposition 6.

Let be a consistent algorithm over the class of -sub-Gaussian uplifting bandits that at most uses knowledge of , , and the fact that the noise is -sub-Gaussian. Then, for any and sequence with , there exists a -sub-Gaussian uplifting bandit with parameters such that the regret induced by on it satisfies

| (40) |

Moreover, if can be implemented under either of the following conditions

-

(a)

Only the reward is observed.

-

(b)

The learner does not have any prior knowledge about the arms’ expected payoffs.

Then, there exists a -sub-Gaussian uplifting bandit with parameters where the regret of is

| (41) |

Proof.

Let . Throughout the proofs, the lower bound will be shown for problem instances with and the following mean values for

| (42) |

By construction, we have if and only if and thus the number of mean-affected variables of is exactly . Clearly, is an optimal action and the suboptimality gap of action is .