Bayesian Additive Regression Trees for Probabilistic programming

Abstract

Bayesian additive regression trees (BART) is a non-parametric method to approximate functions. It is a black-box method based on the sum of many trees where priors are used to regularize inference, mainly by restricting trees’ learning capacity so that no individual tree is able to explain the data, but rather the sum of trees. We discuss BART in the context of probabilistic programming languages (PPL), i.e., we present BART as a primitive that can be used as a component of a probabilistic model rather than as a standalone model. Specifically, we introduce the Python library PyMC-BART, which works by extending PyMC, a library for probabilistic programming. We showcase a few examples of models that can be built using PyMC-BART, discuss recommendations for the selection of hyperparameters, and finally, we close with limitations of our implementation and future directions for improvement.

Keywords Bayesian inference non-parametrics PyMC Python binary trees ensemble method

1 Introduction

Bayesian Additive Regression Trees introduced by Chipman et al. [2010], have been demonstrated to be competitive compared with alternatives such as Gaussian processes, random forests, or neural networks. The main reason is that BART needs minimal user input and tuning while maintaining a good performance [Chipman et al., 2010, Rockova and Saha, 2018, Hill et al., 2020, Sparapani et al., 2021]. Additionally, and similar to other probabilistic methods like Gaussian processes, BART provides uncertainty quantification via probable intervals.

BART has been applied to solve numerous applications in recent years including estimation of causal effects [Leonti et al., 2010, Hill, 2011, Hu et al., 2022, Steele and Schwartz, 2022, Chen et al., 2022], species distribution modelling [Carlson, 2020], estimating indoor radon concentrations [Kropat et al., 2015], modeling of asteroid diameters [de Souza et al., 2021], genomics [Li et al., 2022], just to name a few.

Variable selection has also been an area of interest by BART researchers, achieving reasonable results [Bleich et al., 2014, Linero, 2018]. The main approach is based on counting how many times a given covariable is incorporated into the trees relative to the other covariables in the same model. In order to improve the performance of this very simple variable selection procedure, Linero [2018] introduced a sparsity-inducing Dirichlet hyperprior on the splitting proportions of the regression tree prior.

In the literature, it is common to find specific BART models associated with specific samplers and thus specific implementations [Chipman et al., 2010, Pratola et al., 2020, Lamprinakou et al., 2020, Orlandi et al., 2021]. In other words, general methods to sample from BART posteriors are not common and instead, conjugate priors are used to define such BART models. Likewise, packages like BART R [Sparapani et al., 2021], Xbart [He et al., 2019] or bartpy [Coltman, 2022] have been designed as standalone packages restricted to predefined models and not as tools to build arbitrary probabilistic models with BART components.

In this work, we present PyMC-BART an implementation of BART that removes the conflation of inference and modeling. As far as we know, this is the first package introducing BART as a primitive for a probabilistic programming language, and we are only aware of two previous proposals related to generalizing BART. Namely, Tan and Roy [2019] presented the general BART framework unifying BART extensions that were previously presented as separated models and Linero [2022] introduced a reversible jump Markov chain Monte Carlo algorithm to bypass the need for conjugacy. Abstracting away the implementation of inference from modeling, as we do with PyMC-BART, has been key to the success of applied Bayesian modeling in recent years, and the main reason for the popularity of PPLs like PyMC [Abril-Pla et al., 2023].

As previously mentioned, PyMC-BART works by extending PyMC’s functionality. From the user’s perspective, the main new object introduced is a BART random variable that can use together with the built-in PyMC random variables to build arbitrary probabilistic models in PyMC. We also provided a new inference method111or step methods, using the PyMC nomeclature called PGBART, which works exclusively for BART variables. For most users, there is no need to directly interact with PGBART. Instead, it is designed in such a way that PyMC will automatically use it whenever a BART variable occurs as part of a model. Thus, other than using a BART variable in a model, all other modeling aspects remain the same from a user perspective. Including model building, conditioning on observed data, fitting the model, computing posterior predictive samples, etc. Even more, due to the tight integration of PyMC with ArviZ, tasks such as assessing the fit, comparing to other models, assessing convergence, and other exploratory analysis of Bayesian models’ tasks [Kumar et al., 2019, Martin et al., 2021] are immediately accessible to users of PyMC-BART without the need to learn a new set of tools or syntax. Finally, we provide a set of tools specifically designed to work with the posterior distribution of trees, including tools to aid in the interpretation of the fitted function, to help users perform variable selection, and also to help diagnose the MCMC samples.

For the rest of this article, we will focus primarily on the practical aspects of BART. We start by giving a very brief overview of the BART model in Section 2, then we continue with Section 3 describing the PyMC-BART’s API, including which hyperparameters are available to users. In Section 4 we demonstrate basic usage through examples. And in Section 5 we discuss how to choose the number of trees for BART, arguably the most important hyperparameter PyMC-BART users can change. Finally, we conclude with Section 6 discussing some limitations of the current state of our implementation and the future of PyMC-BART. While the target audience of this manuscript is practitioners interested in adding BART to their Bayesian toolkit, we also provide details of the sampler we use to approximate the posterior over the trees in Appendix A, which we hope will help others interested in contributing to the base code.

PyMC-BART is available from the Python Package Index at https://pypi.org/project/pymc-bart and it can also be installed using conda. The package documentation, including installation instructions and examples of how to use BART to conduct different statistical analyses, can be found at https://www.pymc.io/projects/bart.

The version of PyMC-BART used for this article is 0.5.1 and the version of PyMC is 5.1.2 [Abril-Pla et al., 2023]. All analyses are supported by extensive documentation in the form of interactive Jupyter notebooks [Kluyver et al., 2016] available in the paper repository on GitHub https://github.com/Grupo-de-modelado-probabilista/BART/tree/master/experiments, enabling readers to re-run, modify, and otherwise experiment with the models described here on their own machines. This repository also includes instructions on how to set up an environment with all the dependencies used when writing this manuscript.

2 The BART model

A BART model can be represented as:

| (1) |

where are the covariates and the response variable. The sum is done over trees. Each is a binary tree with structure, i.e., specifies the set of interior nodes (also known as splitting nodes) and the associated splitting rules, and the set of terminal nodes (also known as leaf nodes). represents the values at the terminal nodes. For an example of a single tree used for regression, see Figure 1. represents an arbitrary probability distribution and parameters of that are not modeled as a sum of trees, like the standard deviation for a Normal likelihood.

The model is completed by specifying priors for and . For , independent priors are set for the depth of the trees, the splitting variables, and the splitting values. Details for such priors can be found in Appendix A. The overall effect of the BART priors is to prevent overfitting by making trees shallow, making leaf node values small on the scale of the data, and regularizing statistical interactions.

We can think of BART as priors over step functions, i.e., priors over piecewise constant functions. Furthermore, in the limit of the number of trees , BART converges to a nowhere-differentiable Gaussian Process [Linero and Yang, 2018]. One may object that BART cannot directly model smooth functions, which are arguably the most common cases for most datasets. Still, BART is useful in practice, as judged by all its applications. Figure 2 shows an example of BART fitted to data generated from 3 simple functions, a line, a sine, and a step function. In all the examples, the sample size is 200. We can see the effect of m on the result, the HDI (blue band) becomes narrower, and the mean predicted function better fit the curves, in Section 5 we provide some guidance on how to select m.

BART is part of the ensemble models family. Members of this family are based on modeling a function and making predictions, from a combination of simple models instead of from a single complex one. In the case of BART, the simple models are the binary trees. Generally, ensemble models have desirable properties, like being less prone to over-fit [Zhou, 2012, Kuhn and Johnson, 2013]. A drawback of ensemble methods, as well as other black-box methods, is that a meaningful and direct interpretation of the fitted model is difficult or even impossible; instead, models are assessed via evaluations at given values of the covariates. Later, we present examples of partial dependence plots [Friedman, 2001], which can be efficiently computed with PyMC-BART and can aid users in the interpretation of the results from BART models.

3 API

PyMC-BART seamlessly integrates with PyMC and ArviZ; for example, priors for in Equation 1, i.e., non-BART related parameters, can be arbitrarily set by the user using the standard PyMC syntax. The same goes for fitting the model: users need only to call the pm.sample() function, as they would normally do for regular models.

Additionally, PyMC uses ArviZ’s InferenceData object [Kumar et al., 2019, Martin et al., 2022] to store posterior samples, prior/posterior predictive samples, sampler statistics, etc. (see Figure 5). InferenceData is a rich data structure based on Xarray [Hoyer and Hamman, 2017]. For PyMC models with a BART variable from PyMC-BART, the InferenceData object will also store the variable inclusion record. This data can then be processed by helper functions provided by PyMC-BART, to obtain variable importance plots, as we show in Section 4. Users can also use ArviZ for convergence diagnostics including , effective sample size, trace plots, and rank plots [Vehtari et al., 2021a, Martin et al., 2021].

In the text, we assume the PyMC package has been imported with the pmb alias.

We now discuss the 3 main elements provided by PyMC-BART :

-

•

A BART random variable. This behaves similarly to default PyMC random variables and can be used together with them, allowing users to build arbitrary probabilistic models.

-

•

The PGBART step method. A method to sample from a BART random variable. The user does not need to interact with this sampler, as PyMC will automatically assign it to a BART variable if such a variable is part of the model.

-

•

A collection of helper functions to aid the user interpret the results.

3.1 BART random variables

For those familiar with PyMC syntax, defining BART models is straightforward. A pmb.BART random variable behaves like other PyMC variables, with a few caveats. It requires two mandatory arguments: X, a 2D NumPy array or a pandas DataFrame representing the covariate matrix, and Y, a 1D NumPy array or a pandas DataFrame representing the response vector. Y is needed because PyMC-BART uses it to define the starting point when sampling from the BART posterior and the variance of the leaf nodes.

Another difference is that a pmb.BART variable does not accept other PyMC random variables as arguments. The main reason is that, as in other implementations, the priors for the BART variables are not directly set by the users, but instead hyperparameters are used to adjust them indirectly222While this seems to work in practice, extensions could be considered in the future, like using a prior over , instead of a fixed number.. The hyperparameters that can be changed by the user are:

-

•

The number of trees m. This is a positive integer that defaults to 50. For some datasets, values as low as 20 could provide a good approximation; for others, values as high as 200 may be needed. The value of m can be defined using cross-validation. In our experiments, we found that Pareto smoothed importance sampling leave-one-out cross-validation (PSIS-LOO-CV) [Vehtari et al., 2017, 2021b], can be used to find reasonable values of m (see Section 5).

-

•

The value of alpha and beta, controlling the node depth. These parameters are the same as those originally proposed by Chipman et al. [2010].

-

•

The prior over the splitting variables. This is uniform over the covariates X. Users can pass an array, of the same length as the total number of covariates, if they have prior information about the relative importance of the variables.

-

•

The response. How the leaf node values are computed. Available options are constant (a single value at each leaf node), linear (a linear regression) or mix (both options selected at random). Defaults to constant. Options linear and mix are still experimental.

-

•

split_rules. Allows using different split rules for different columns. The default is ContinuousSplitRule. The two other options are OneHotSplitRule and SubsetSplitRule [Deshpande, 2023], both meant for categorical variables.

-

•

shape. Specify the shape of the response vector. Defaults to the length of . It can be used to model more than one BART random variable per model. By default, the tree structure is shared for all BART random variables but the leaf values are independent. This can be changed by separate_trees hyperparameter.

-

•

separate_trees. Default to False. When training multiple trees (by setting a shape parameter), the default behavior is to learn a joint tree structure and only have different leaf values for each. This flag forces a fully separate tree structure to be trained instead. This is unnecessary in many cases and is considerably slower, multiplying run-time roughly by the number of dimensions.

3.2 PGBART

PyMC is capable of automatically assigning different sampling algorithms to different parameters in the same model. Thus, PyMC will use the pmb.PGBART sampler for BART variables, and use one of the built-in PyMC samplers for . If is a continuous parameter, then PyMC will automatically choose the pm.NUTS sampler [Hoffman and Gelman, 2014]. pmb.PGBART is a sampler we have specifically developed for BART variables, see Appendix A for details. These are the hyperparameters related to the sampler:

-

•

num_particles. The number of particles used to sample a new tree. Defaults to 10. In cases where the values [Vehtari et al., 2021a] are too high, increasing the number of particles can help.

-

•

batch. Number of trees out of the m trees fitted per step. Defaults to "auto", which is 10% of m during and after tuning. Users can provide a tuple, with the first element being the batch size during tuning and the second the batch size after tuning. Increasing batch can help to reduce but in our experience, it is better to increase the number of particles.

3.3 Helper functions

PyMC-BART currently offers 4 utility functions.

-

•

pmb.plot_pdp: A function to generate partial dependence plots [Friedman, 2001]. Its main inputs are a BART random variable (once a model has been fitted), and the covariate matrix.

-

•

pmb.plot_ice: A function to generate individual conditional expectation plots [Goldstein et al., 2013]. Its main inputs are a BART random variable (once a model has been fitted), and the covariate matrix.

-

•

pmb.plot_variable_importance: A function to estimate the variable importance. Its main inputs are an InferenceData object containing the "variable_inclusion" record in sample_stats group, a BART random variable (once a model has been fitted), and the covariate matrix.

-

•

pmb.plot_convergence: A function that plots the empirical cumulative distribution for the effective sample size and values for the BART random variables. Its main inputs are InferenceData and the name of the BART variable.

pmb.plot_variable_importance returns two subplots (see Figure 9). The top one shows the values of the relative variable importance, estimated as the count of each variable across all sampled trees and then normalized so the sum of all variables’ importance is 1. This is a standard plot in the BART literature. The bottom subpanel shows the square of the Pearson correlation coefficient333also known as the coefficient of determination between the full model with all covariates and models with fewer covariates. It can be used to find the minimal model capable of making predictions that are close to the full model. To generate this plot, we make two important approximations in order to reduce the computational cost:

-

•

We do not evaluate all possible combinations of variables, we simply add one variable at a time, following their relative importance.

-

•

We do not refit the model for 1 to n components; instead, we approximate the effect of removing variables by traversing trees from the posterior distribution computed for the full-model and pruning branches without the variable of interest, see Figure 3. This is similar to the procedure to compute the partial dependence plots, with the difference that for the plots we excluded all but one variable, and for the variable importance we start by excluding all but the most important one, then all but the two most important ones, until we include all variables.

4 Examples

In this section, we use a few examples to show how to build PyMC model with BART random variables. We are assuming the reader is already familiar with the PyMC syntax. If that’s not the case we recommend readers spend some time reading PyMC’s official documentation https://www.pymc.io.

4.1 Bikes

For our first example, we will use a dataset from the University of California Irvine’s Machine Learning Repository https://archive.ics.uci.edu/ml/datasets/bike+sharing+dataset. As the response variable, we use the number of bikes rented per hour. And for the covariates we use the hour of the day, the temperature, the humidity, and the speed of the wind.

The proposed model is:

Where we have followed the import conventions import pymc as pm and import pymc-bart as pmb. As was mentioned, the posterior samples are stored in ArviZ’s InferenceData object [Kumar et al., 2019, Martin et al., 2022]. Figure 5 shows an HTML representation of this object.

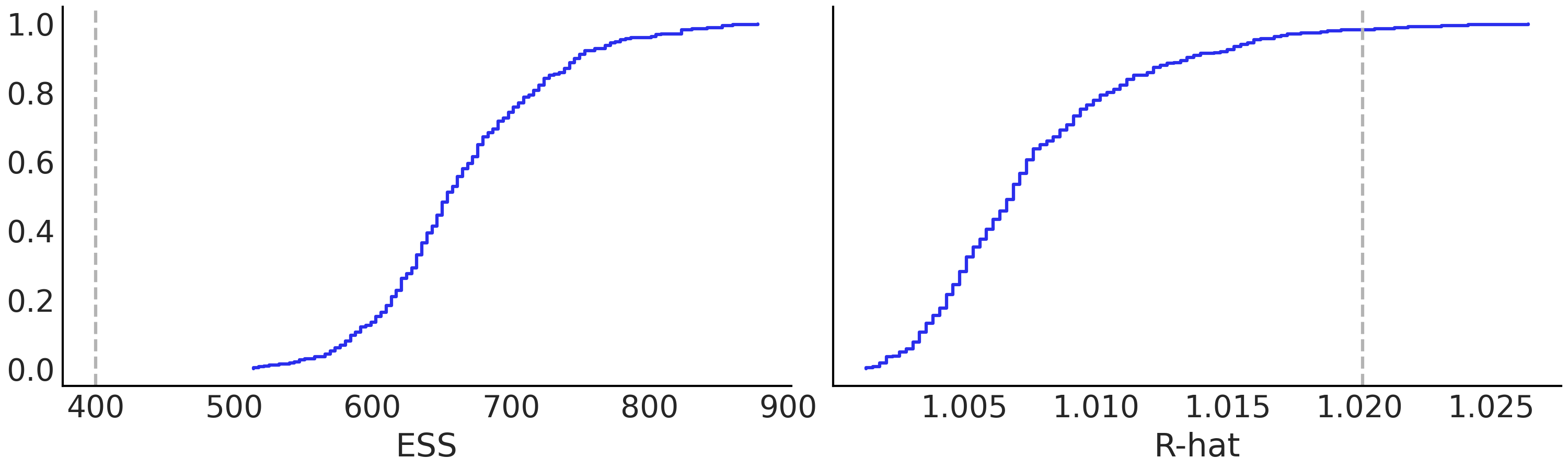

Figure 6 shows a visual diagnostics for the non-BART random variable in model_bikes such plots are a common, and useful, way to visualize sampling convergence. On the other hand, this kind of plot can be less useful to diagnose BART random variables. For that reason PyMC-BART offers the function pmb.plot_convergence (see Figure 7).

From Figure 7 we can see, on the left, that all values of the effective sample size are above the recommended threshold (dashed vertical line) value of 400 (100 per chain). And on the right, we see that most, but not all, of the values, have below the recommended threshold, taking a few more samples could potentially fix this issue. The value of the threshold for is computed automatically using a multiple comparison adjustment.

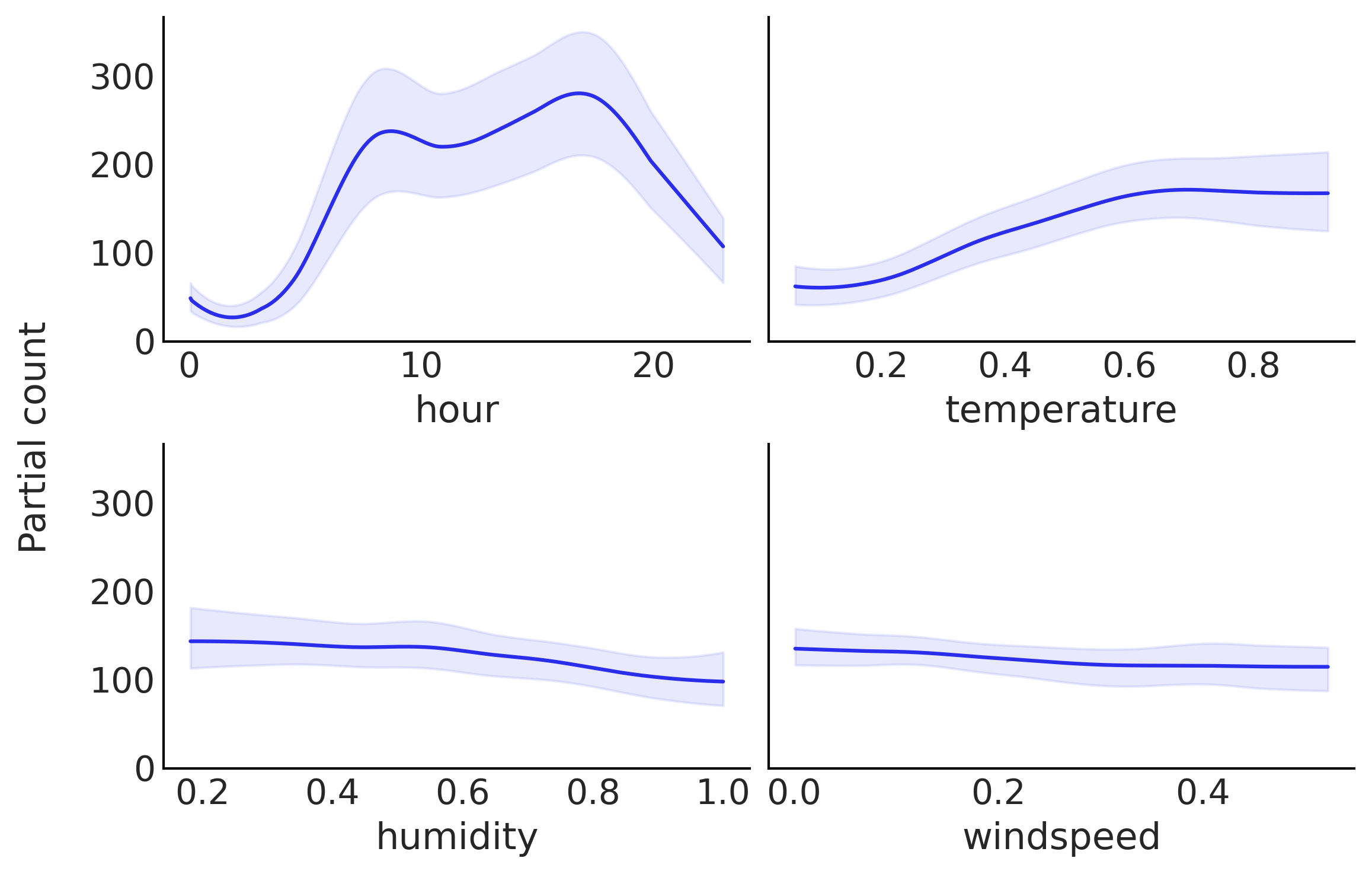

Besides extending PyMC with BART random variables and the PGBART sampler, we also offer a few helper functions, one of which can be used to compute partial dependence plots [Friedman, 2001]. For instance, the command pmb.plot_pdp(idata_bikes, X=X, Y=Y, grid=(2, 2)) generates Figure 8. This allows the user to analyze the partial contribution of each variable.

From Figure 8, we can conclude that:

-

1.

The marginal contribution of the variable hour varies in a more complex way than for the other variables. Starting from a minimum between 0 and 3 hours approximately, it increases to a first peak at around 8; then it decreases slightly to a new, higher peak, at around 17, and finally, it decreases. This pattern can be interpreted as a relationship between working hours and the need to rent bikes.

-

2.

While the value of temperature increases, the number of rented bikes also increases, but at some point it stabilizes. This can be explained by saying that at higher temperatures people are more motivated to go out, but there comes a point where this is no longer the case.

-

3.

humidity seems to contribute in a very slightly negative way, which could be interpreted as meaning that high humidity does not contribute to people wanting to ride a bike. Nevertheless, the relationship (if any) seems to be tenuous.

-

4.

windspeed shows practically no contribution to the motivation to ride a bike.

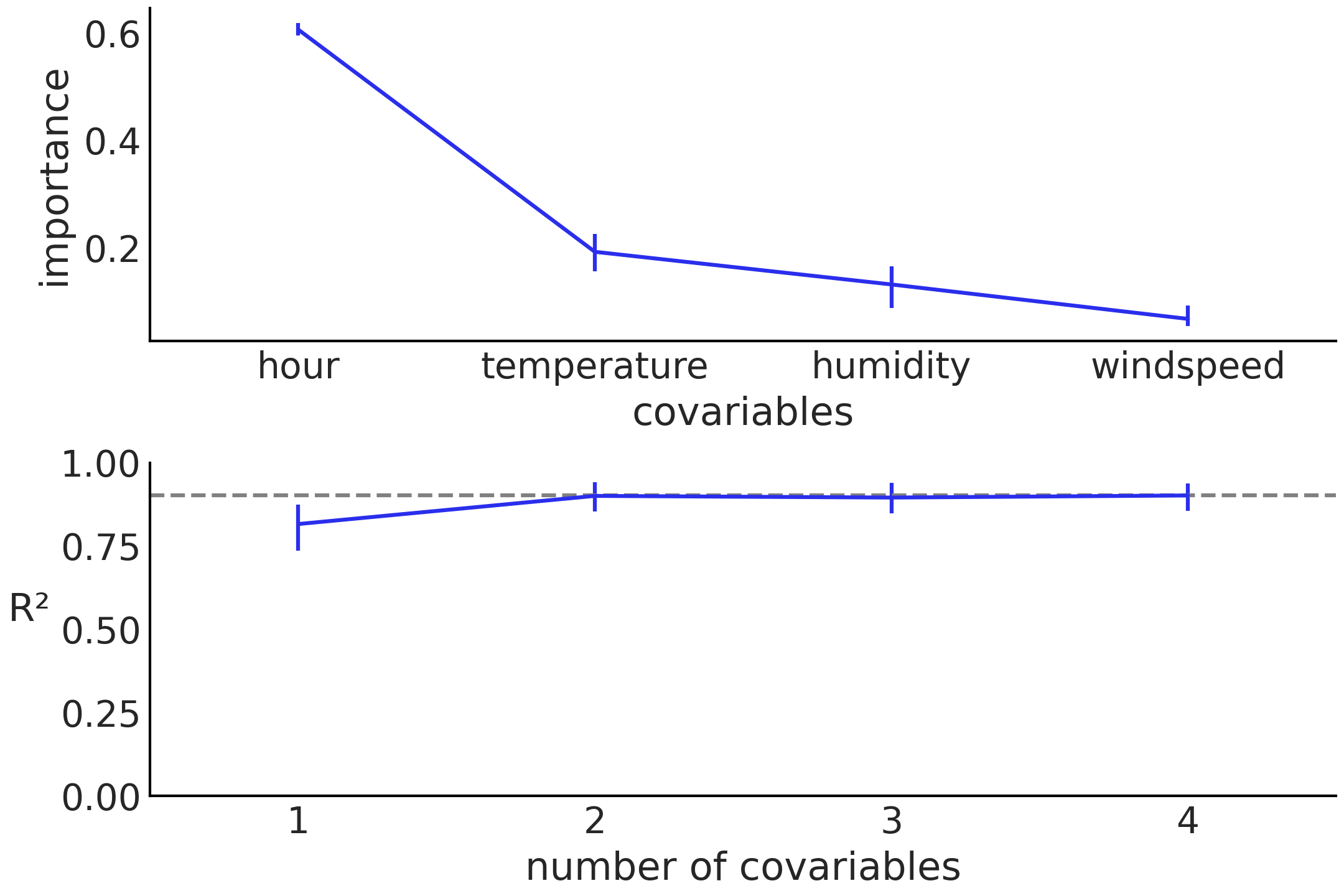

Now we move our focus to the analysis of variable importance. From the top panel of Figure 9 generated using the code pmb.plot_variable_importance(idata_bikes, , X, samples=100)

From the top panel, we can see that the variables hour and temperature are the most important covariates and that the other two are less important. Notice this is in line with the partial dependence plots from Figure 8. This kind of plot is useful to see the relative importance of a variable but is not very useful if we want to select a subset of the variables, as we do not have a clear criterion to separate the variables with “high” importance from those with “low” importance.

In order to provide a variable selection procedure from the computation of variable importance, we introduce a new plot. We can see an instance in the bottom panel of Figure 9. On the x-axis we have the number of variables and on the y-axis the square of the Pearson correlation coefficient between the predictions made by the full-model (all variables included) and the restricted models, i.e., those with only a subset of the variables in the full-model. The variables are included following the relative variable importance order, as shown in the top panel. Thus, in the bikes example, the first variable included is hour, then hour and temperature, followed by hour, temperature and humidity and finally the four variables hour, temperature, humidity, and windspeed, i.e., the full model. Hence, from Figure 9 we can see that even a model with a single component, hour can generate predictions that are very close to the full model. Moreover, the predictions from the model with the two components hour and temperature is, on average, indistinguishable from the full model. The error bars represent the 94 % highest density interval (HDI) of the posterior predictive distribution, that is, of the predictions of the model.

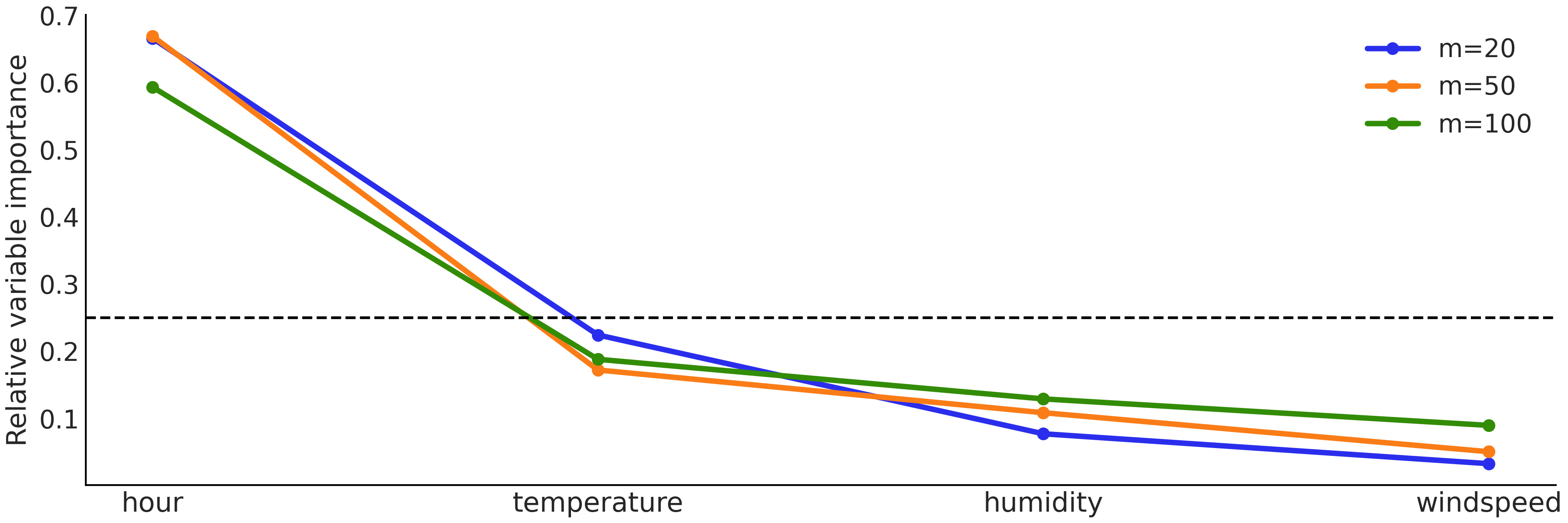

Finally, we close this example by showing that the computation of variable importance is robust with respect to the number of trees m, as can be seen from Figure 10. We notice this is contrary to the original proposal by Chipman et al. [2010] where they use a low number of trees (m=20 or 25) for variable importance and a higher one for inference. With PyMC-BART is possible to use the same value of m for both tasks. Hence, our suggestion is to calculate the importance of variables using the same number of trees as employed for inference, typically ranging from 50 to 200 trees. It’s important to ensure the adequacy of inference for our specific goals and to verify the absence of convergence issues before proceeding.

4.2 Friedman function

The second example uses the Friedman function [Chipman et al., 2010], which consists of generating data for the random variables where iid and , where .

We can see that only depends on the first five covariates . Thus, the rest of the covariates are completely irrelevant. This fact, plus the nonlinearities and interactions, make finding challenging for standard parametric methods, and thus a good test for BART models.

To fit the data generated from the Friedman function, we use the model:

We fit this model four times, changing at each instance the number of features (columns) in variable X, . That is, we evaluate BART for an increasing number of irrelevant features.

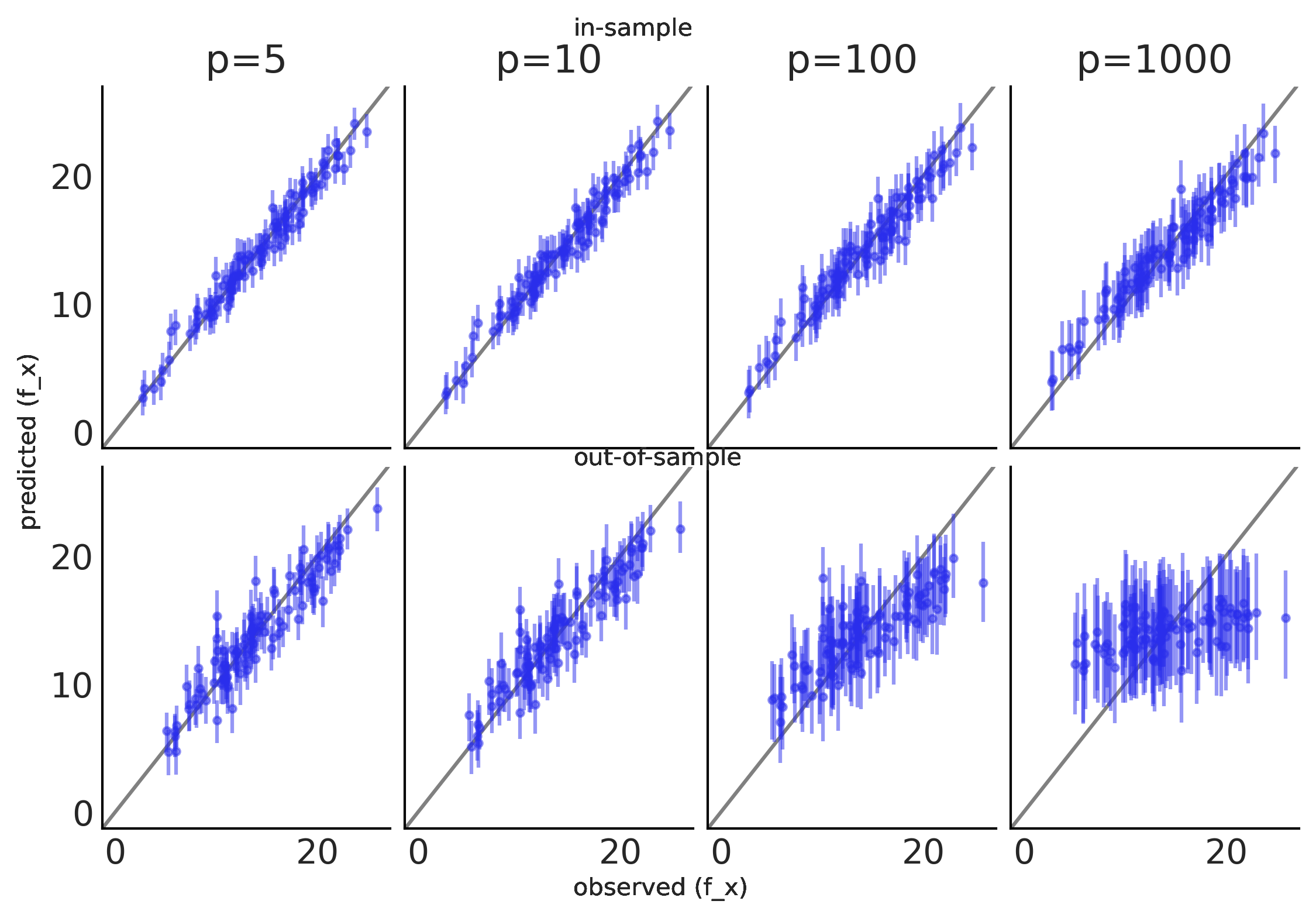

Figure 12 shows the correlation between predicted and observed data with different numbers of covariables , the true values are in the x-axis while the y-axis contains the in-sample predictions (top panel) and out-of-sample (bottom panel). The error bars represent the 90% HDI. The more closely the predictions are to the true function, the closer they will be to the black line at 45∘. For the in-sample predictions, we can see a very good agreement between predicted and observed data even when the number of irrelevant features is much larger than the relevant ones. As expected, out-of-sample predictions are worse than in-sample ones. When the number of irrelevant features is relatively high PyMC-BART predictions are not-robust enough to the number of irrelevant features as previously observed Linero [2018] with a sparsifying prior. Thus, our recommendation for when the number of irrelevant covariates is very large compared to the relevant ones, like when p=100 or p=1000 in this example, is to first check variable importance and if the non-relevant variables represent a very large fraction of the total number of covariates, then do a second run keeping only the most relevant covariates. If for some reason the user doesn’t want to remove variables from the model then increasing the number of tuning steps and the number of particles can help to improve the out-of-sample fit, at a higher computational cost.

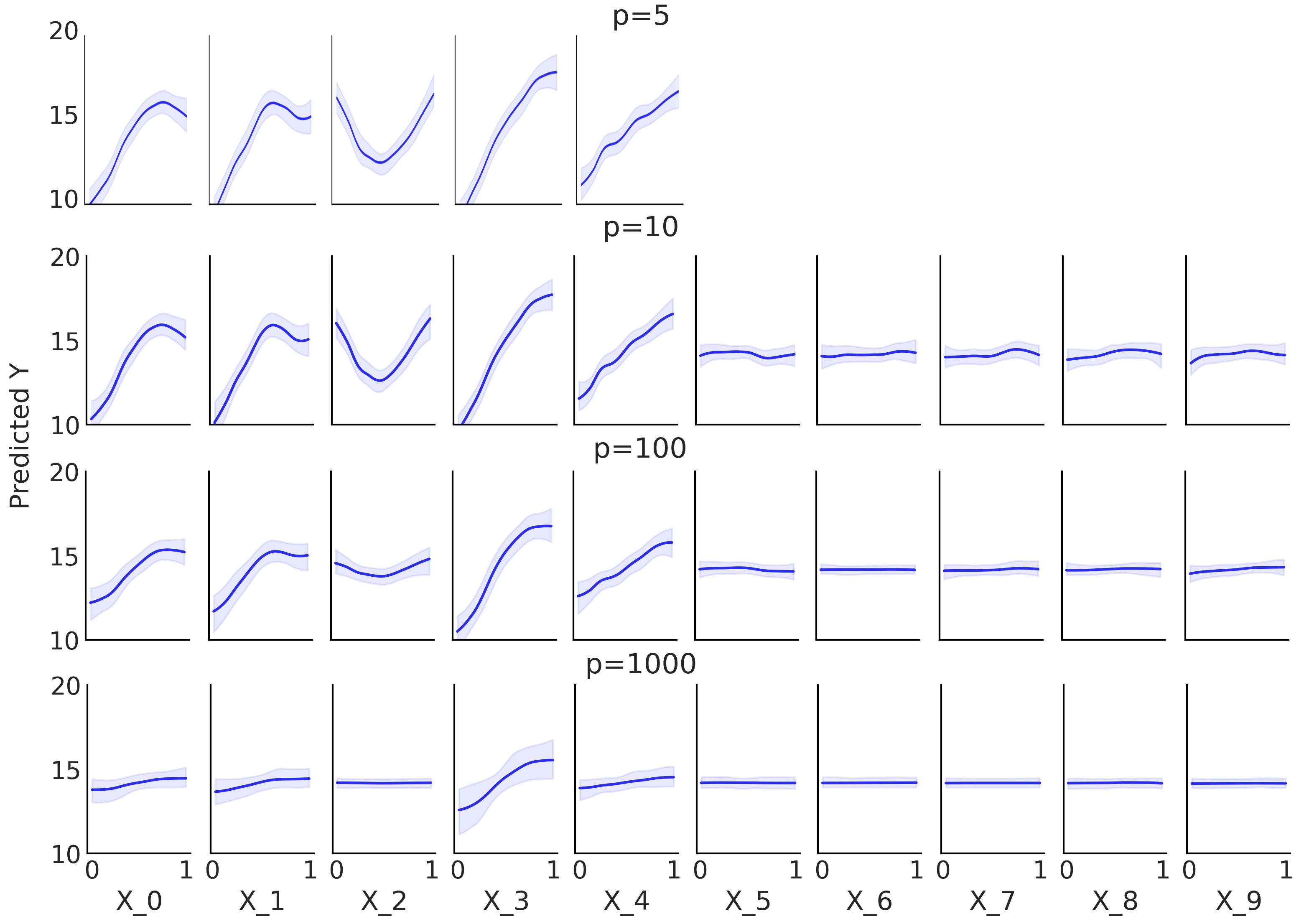

Figure 13 shows a partial dependence plot for the BART model model_friedman, with different number of covariables . We can see that the variables have almost zero contribution to the response variable 444With the rest of the variables , not shown here but following the same flat pattern., while the first 5 variables have a larger effect on . We can also see that, as we increase , the trends are quite robust, although the response becomes flatter. This effect is more clear for , and especially for .

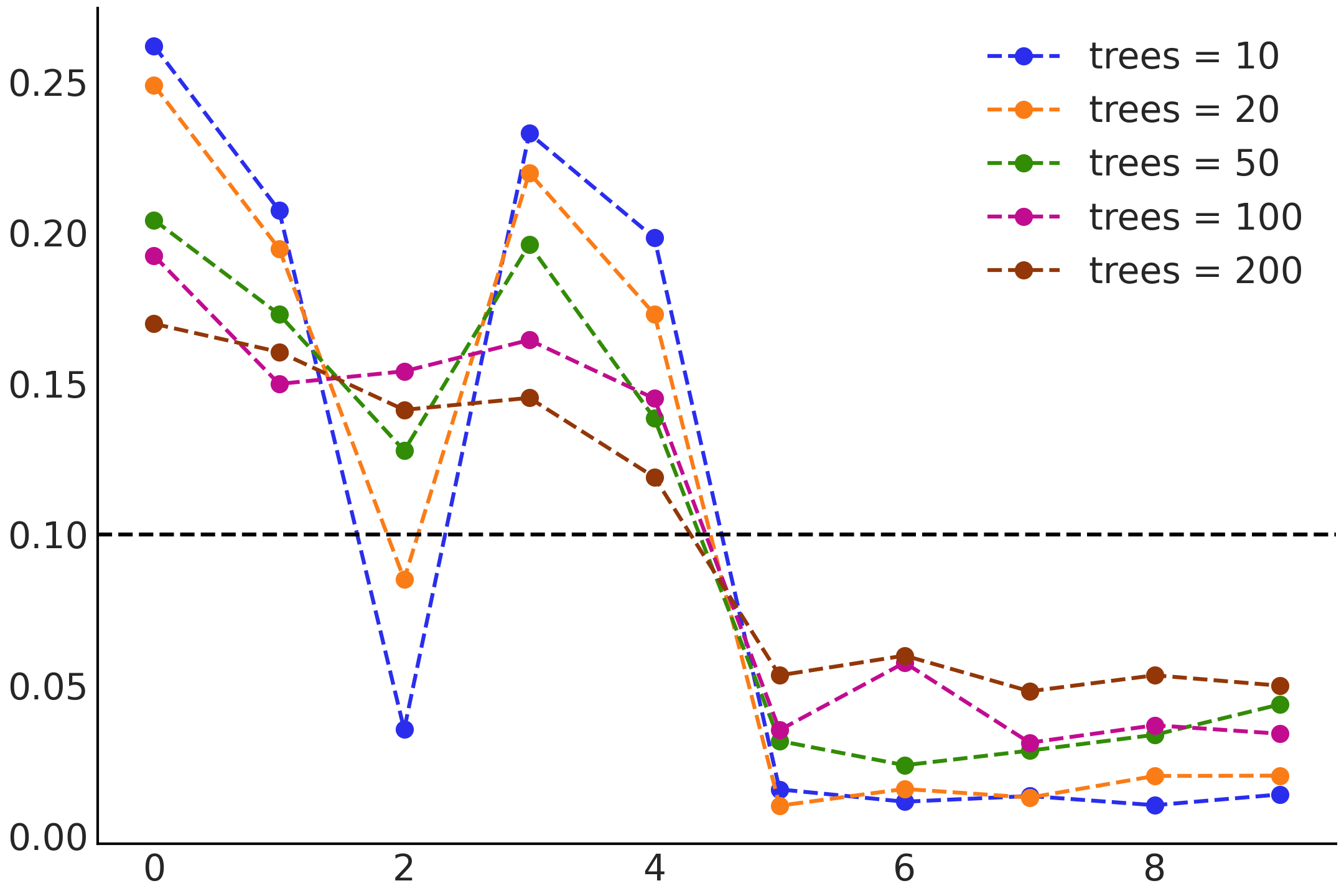

Next, we compute variable importance, using and model_friedman. We observe in Figure 14 that the first five variables are the more important ones. This is expected from the construction of , as we already mentioned that the variables are unrelated to the response variable . This is in agreement with Figure 13. Additionally, from Figure 14 we can see that variable importance is virtually insensitive to the values of m when m >= 50. With fewer trees, 10 or 20, the values of the importance variables have more dispersion, but even in that situation, the first 5 variables are the most important ones. Again, we can see a qualitative agreement with Figure 13.

Our results are similar to that of Chipman et al. [2010], with the important difference that, in our case, the variables have even less importance (almost nil), which is a better result.

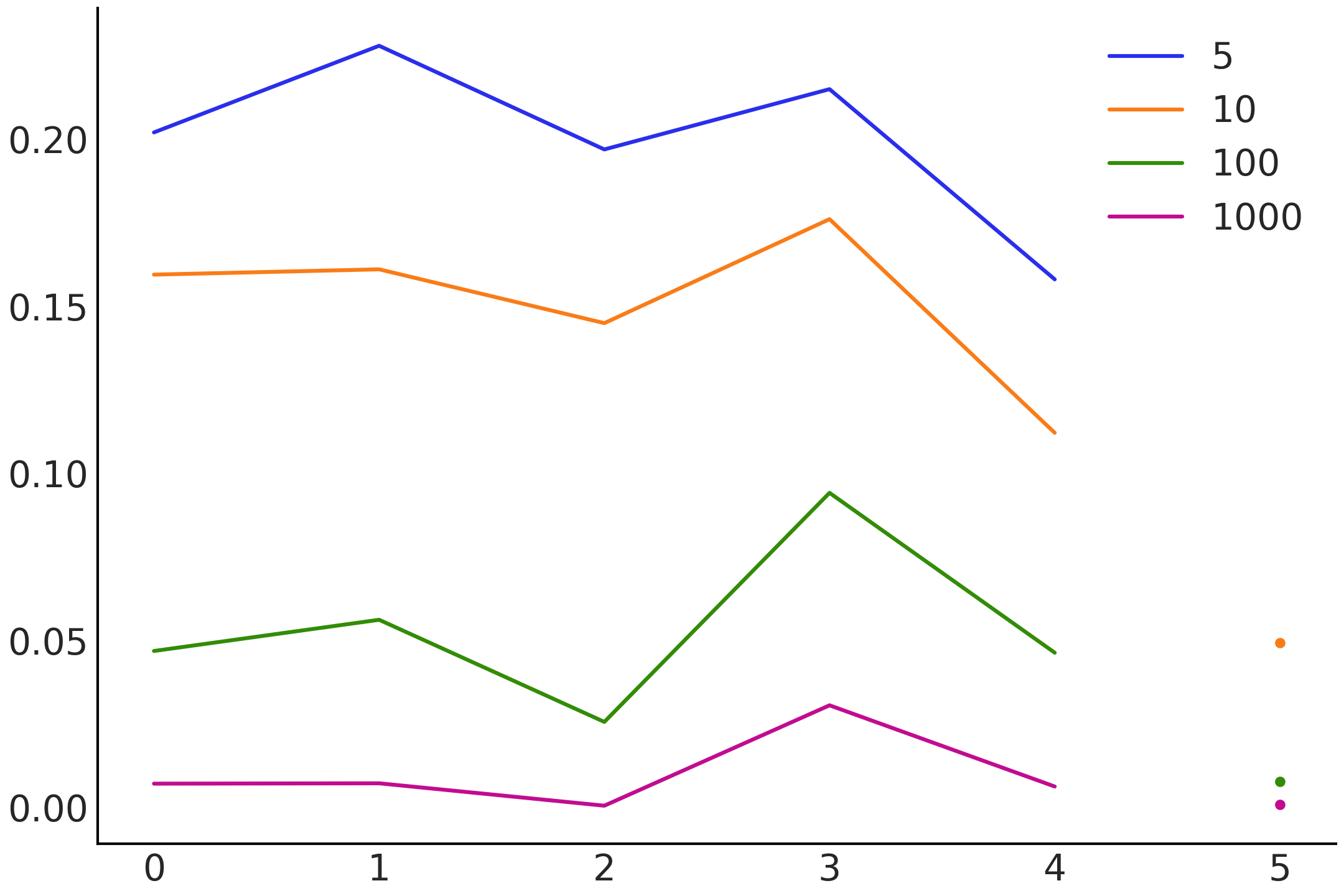

In Figure 15 we can observe that, as the number of irrelevant features increases, the relative importance of the first five covariates decreases, as expected, because the total importance of 1 has to be distributed among more covariates. But we can also see that the relative importance is robust with respect to an increase in the number of non-relevant covariates, because on average the variable importance for the non-relevant covariates is smaller than for the relevant ones.

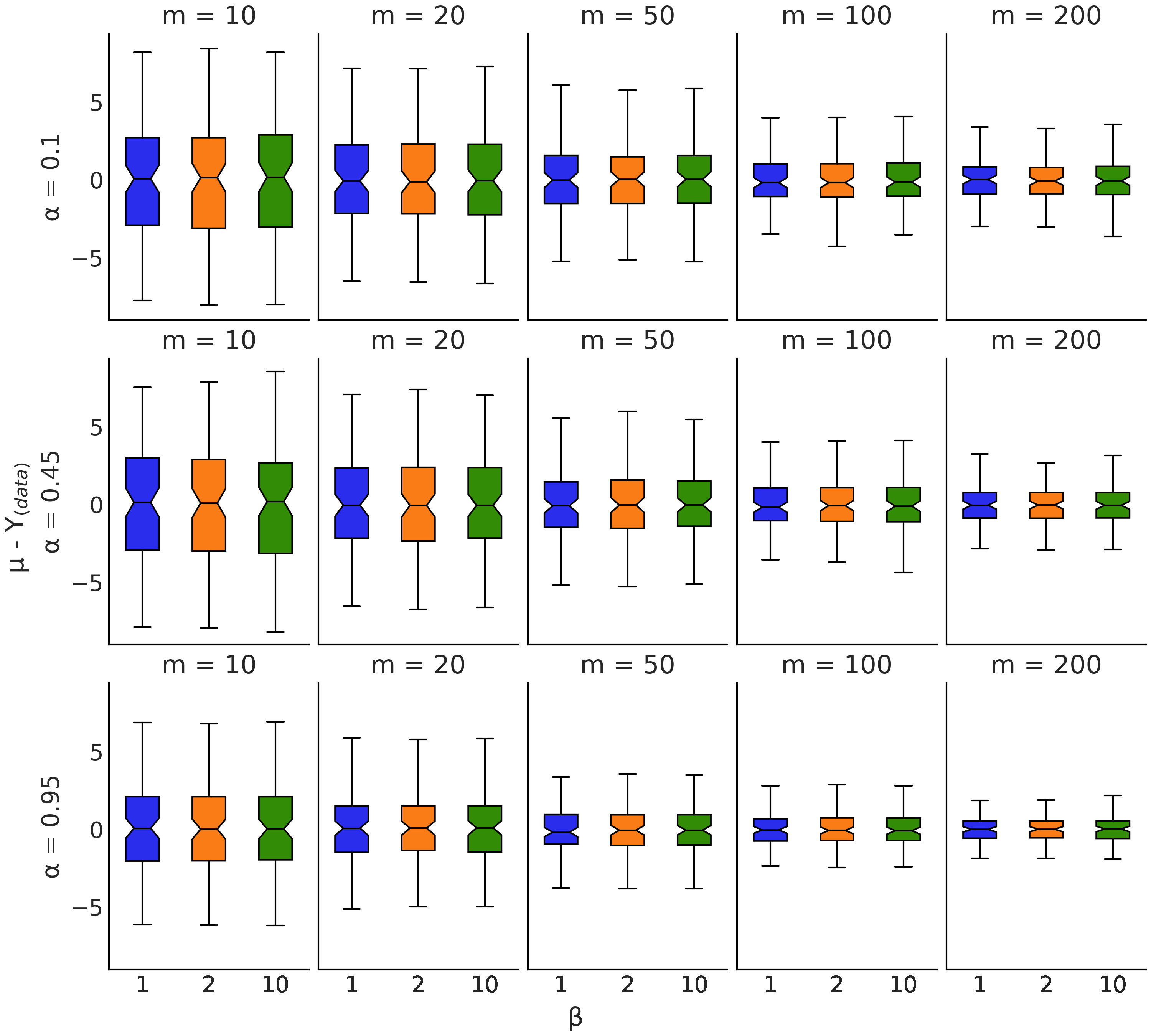

To evaluate the impact of the hyperparameters alpha and beta, which controls the prior for the depth of the trees, we use model_friedman for , iterating through m, alpha and beta, for , alpha and beta . In Figure 16 we can see that the effect of alpha parameter and beta parameter is overall small in comparison with the effect of . We repeat these calculations for models_bikes, models_coal, and the space influenza toy model with similar outcomes. Because deeper trees are needed to represent higher-order interactions, we created two modified versions of Friedman functions by adding, to the first term, one and two more interactions. Again, the effect of changing alpha is small. All results are available at https://github.com/Grupo-de-modelado-probabilista/BART/tree/master/experiments.

After this experiment and following Chipman et al. [2010], we decided to set alpha=0.95 and beta=2 as the default values.

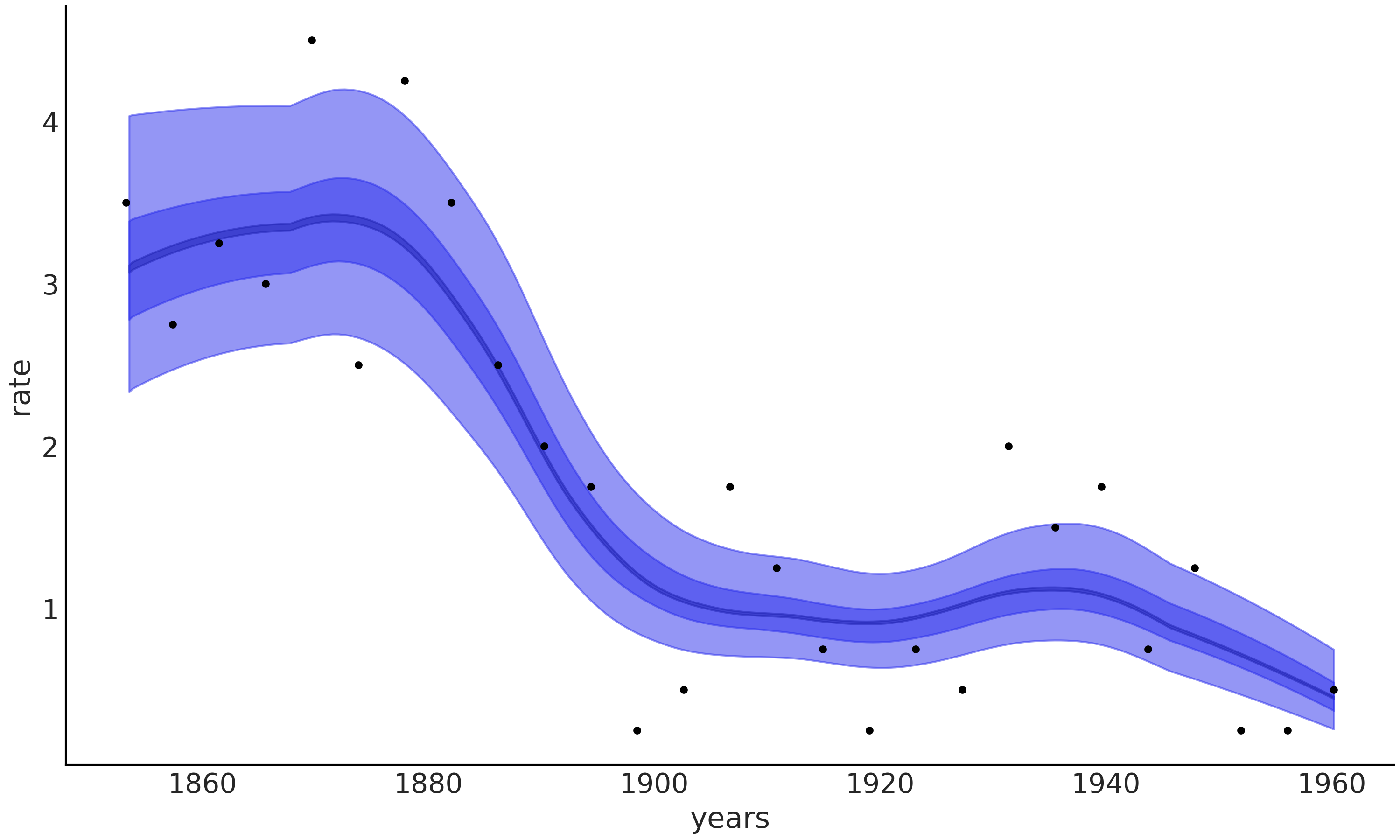

4.3 Cox processes

We now show how to use BART for a 1D discretized non-homogeneous Poisson process. We use the classical coal mining disaster dataset. The same example, but using Gaussian Processes, can be found in Martin [2018] and the documentation of GPstuff package [Vanhatalo et al., 2013].

The data consist of timestamps for when the disaster occurred. To be able to fit this data using a regression model, we bin the data as shown next

where the values of X correspond to the date of the disasters and Y are the number of accidents for that date. Because this is a simple function, we use m=20.

The BART model for this example is:

The main differences between this model to the ones seen so far are the use of a Poisson likelihood, the exponential inverse link function np.exp(), and a smaller number of trees m=20.

In Figure 19, the blue line represents the mean accident rate, and the dark and light blue bands represent the HDI 50% and 94% respectively. A notable decrease in accidents can be observed between the years 1880 and 1900.

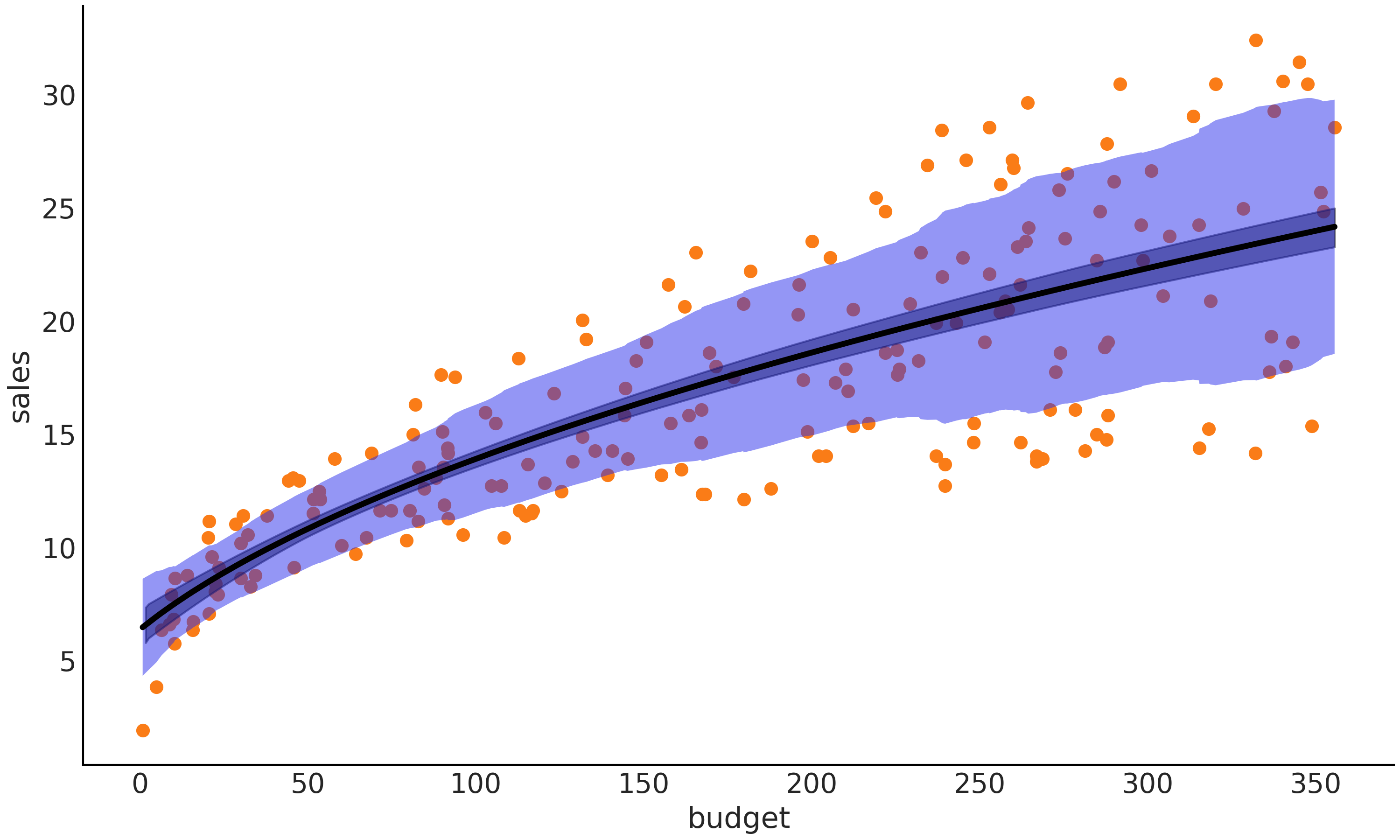

4.4 Heteroscedasticity

So far we have seen examples of PyMC-BART used to model the mean function, but we can also use it to model a non-constant variance. To exemplify such a scenario, we are going to make use of the marketing dataset [Kassambara, 2019]. We have the budget spent on YouTube advertisement vs the effect on sales. We decided to model the mean as a linear model, with a square root transformation, and let BART be in charge of the standard deviation. The model is:

In Figure 21 we see the mean function as a black line, the 94% HDI of the mean as a darker blue band, and the 94% HDI of the standard deviation as a lighter blue band.

Alternatively, we could go fully non-parametric with this example and use BART to model, both the mean and variance.

Notice, how BART is defined with a size = 2 argument and used to model both the mean and standard deviation of the Normal response. Alternative to size we can pass the shape argument, in this case it should be shape(2, 200), with the second dimension being the sample size.

5 Defining the number of trees

Finding a good value for the number of trees remains important when using BART in practice. Intuitively, as this number controls the flexibility of the BART function, it should be large enough so that the sum of trees is adequate to explain the data, but not so large that the function becomes too flexible. Another practical reason to avoid overshooting m is the computational cost of BART, both in terms of time and memory, which increases with m.

First, Chipman et al. [2010] and others later, have reported that usually the number of trees should be between 20 and 200. For implementations of BART without sparsifying prior over the splitting variables, authors recommend a lower value of m when computing variable importance than when doing inference. For PyMC-BART we observed that the computation of variable importance is robust with respect to the value of m (see for example Figures 10 and 14) and in general we recommend using the same value of m for both inference and variable importance assessment.

One way to tune m is to perform K-fold cross-validation, as recommended by Chipman et al. [2010]. Another option is to approximate cross-validation by using Pareto-smoothed importance sampling leave-one-out cross-validation (PSIS-LOO-CV) Vehtari et al. [2017, 2021b]. The main advantage of PSIS-LOO-CV is that we only need to fit the model once for each value of m, instead of K-times as in K-fold cross-validation. It has been reported that PSIS-LOO-CV can lead to overfitting Linero and Yang [2018] when used to select m and, hence, we decided to evaluate both PSIS-LOO-CV and 5-fold cross-validation with PyMC-BART. We used these two methods because PSIS-LOO-CV is a fast method to compare models, with strong empirical and theoretical support, and 5-fold cross-validation has been recommended by Chipman et al. [2010]. Notice that it is not our intention to perform a one-to-one comparison, instead, we are interested in providing practical recommendations for users to pick a value of m.

For five models and datasets, the 3 simple functions from Figure 2, the models model_bikes, the model_friedman, model_coal, and the space influenza model (a toy-model binary classification task taken from Martin [2018], Martin et al. [2021]) we computed PSIS-LOO-CV as implemented in ArviZ and 5-fold cross-validation. A common pattern we observed when using PSIS-LOO-CV is that, as we increase the value of m from 10 to 200, in successive steps, the values of the estimated expected log pointwise predictive density (ELPD) keep increasing or, at best, stop increasing. We observed the same pattern for 5-fold CV, i.e., the root-mean-square deviation (RMSD) decreases with m or, at best, stabilizes. All the results are available at https://github.com/Grupo-de-modelado-probabilista/BART/tree/master/experiments.

Regarding these results we want to highlight two facts, the first one is that we observed that even for low values of m PyMC-BART is able to capture the mean function approximately well and the effect of increasing m is to refine the fit with a decrease of the residuals. Second, we want to remind the reader that as m increases, the values of the leaf nodes are shrunk towards zero and, thus, this should help mitigate overfitting.

Thus, based on our experiments, and as a rule of thumb, we recommend using values of m around 50 or less during model building and exploration and switching to values of m around 200 to obtain the final result. For very simple models and/or small datasets, like the coal mining example in this paper, low values of m around 50, could be enough. Nevertheless, probably this is not the case for most common scenarios involving smooth functions and datasets around 100 data points or larger.

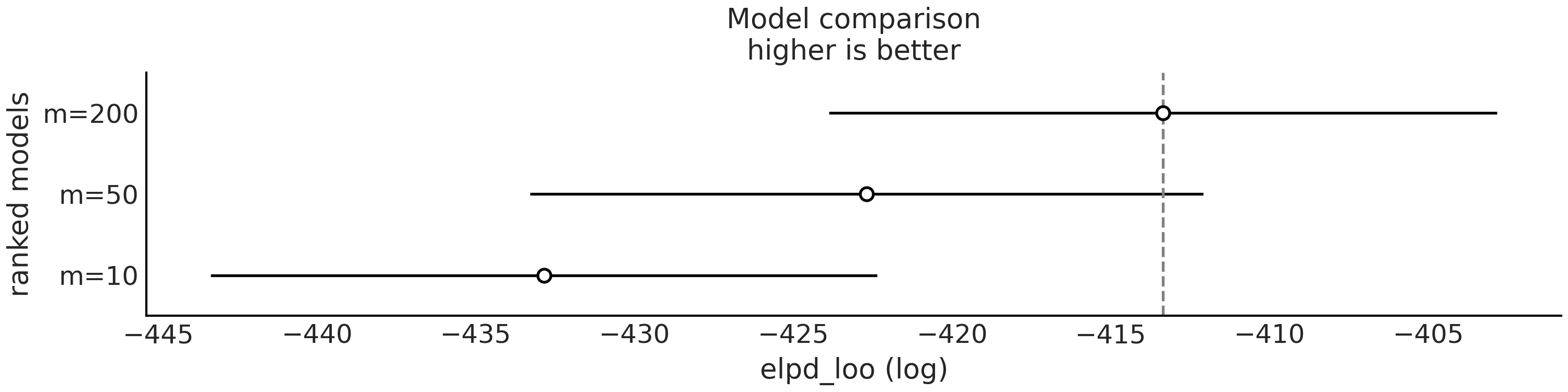

If values of m around 200 become too costly in terms of time and/or memory, so it becomes important to find smaller values for m, we recommend using PSIS-LOO-CV. Let’s say we want to find a suitable value of m for the model in the first row of Figure 2. We decide to fit the model 3 times with values of m 10, 50, and 100 and hence we will get 3 InferenceData objects, let’s call them idata_sfl_10, idata_sfl_50, idata_sfl_200. To compute LOO and obtain a plot like the one in Figure 24 we can do as follows:

From Figure 24, we can see that the value of the ELPD follows the order , indicating that we should pick m=200. But it is important to remark that differences equal to or smaller than 4 are considered irrelevant and that, additionally, the uncertainty of the estimated ELPD should also be considered. We can see that there is considerable overlap for m=50 and m=200. Thus, picking a value of m=50, should save time and memory without a practical impact on the fitting.

6 Discussion and Conclusion

PyMC-BART extends PyMC, effectively combining the flexibility of BART models with the power of a modern state-of-the-art probabilistic programming framework. Through a series of empirical evaluations, we have given an overview of how PyMC-BART can be used for inference of non-linear regression models and to assess variable importance or perform variable selection.

We hope that our contribution will help more users to adopt BART models as part of their toolbox, and we invite researchers and developers to further improve PyMC-BART, as well as to work on similar implementations in other probabilistic programming languages. Some aspects we believe could be improved in the future are: Reducing memory footprint by modifying our tree implementation (or using a Cython or Rust implementation), increasing the efficiency of the sampler (for example we might try to use a better proposal as described in Pratola [2016], or rotating splitting rules to explore a wider sample space and improve mixing Maia et al. [2022]), or add new visualizations like those in Inglis et al. [2022]. Additionally, we could increase efficiency by modifying the initialization and tuning routine of NUTS conditional to a BART variable in the model. Or explore other distributions for the leaf nodes such as Gaussian Processes Maia et al. [2022], Wang et al. [2022], which can reduce the necessary number of trees and improve extrapolation.

7 Acknowledgments

This research was supported by the National Agency of Scientific and Technological Promotion ANPCyT, Grant PICT-2018-02212 (O.A.M.) and National Scientific and Technical Research Council CONICET, Grant PIP-0087 to O.A.M. We thank NumFOCUS, a nonprofit 501(c)(3) public charity, for the operational and financial support of PyMC and PyMC-BART. We also want to thank Marcin Elantkowski for reporting a bug in an early version of our code, and also for creating a Rust implementation of PyMC-BART https://github.com/elanmart/rust-pgbart.

Appendix A Sampling from BART

We use a sampler inspired by the Particle Gibbs method introduced by Lakshminarayanan et al. [2015], but with some modifications in order to be able to define a generalized version of BART, see Algorithm 1. We implemented this sampler to work with PyMC, but it is important to note that it can be implemented in other probabilistic programming languages as well. One important consideration is that PGBART is designed to sample trees, and we relied on PyMC’s compound step feature to sample non-BART variables. That is, PyMC will automatically assign the PGBART sampler to a pmb.BART random variable, and if other random variables are present in the model it will assign other samplers to those variables. This makes our implementation of BART flexible enough to easily accommodate a large family of BART models, and even a combination of BART and other models, like, for example, linear regression.

In Algorithm 1 uppercase letters represent arrays, that is is an array of trees, represents the -th tree in the array, and is the output of the -th tree in the array. represents the log-likelihood of the -th particle tree. The first three lines are run once to initialize the algorithm, after that the main loop body (lines 5 to 20) constitutes one step of the sampling algorithm for a BART variable, which can be interleaved with one step of another sampling algorithm, like NUTS, for other variables. To reduce the computational cost at each step, we update a subset of the trees , by default is 10% of . To simplify the description of the algorithm, we have defined a few functions, that we now describe.

- initialize_trees

-

: We set all trees to the mean of divided by m. That is, we set the sum of trees, , at the mean of .

- initialize_particles

-

: In order to propose a new tree, we generate particle-trees. One of these particles is just the tree we want to replace, . This ensures that there is a non-zero probability of keeping the current tree, instead of accepting a new one. The rest of the particles are grown starting from scratch (see grow_tree function below) instead of being perturbations of an existing tree. This helps to explore larger regions.

- normalize_weights

-

: We normalize the weights, so they are between 0 and 1, and they sum up to 1; this is . We also compute , which is the sum of unnormalized weights, divided by the number of particles. After resampling, all particles will have the same weight.

- resample

-

: Based on, we use a systematic resampling, of all but the first two particles. This will remove particles with low probability and retain those with higher probability. The number of particles is kept constant, meaning some particles may be repeated.

- sample

-

: Based on, we select a single particle and its associated tree.

- variable_inclusion

-

: During tuning, this function updates alpha_vec, which is the vector with the proportions used to sample the splitting variables. After tuning, alpha_vec is fixed, and we instead update the variable_inclusion vector, which is then normalized and returned as the estimation of the variable importance. In both cases, the update is done by counting the splitting variables in the returned tree.

- grow_tree

-

function attempts to grow a tree based on the following criteria:

- node depth

-

: The probability that a node at depth is non-terminal is given by with and . This prior was proposed and studied by Chipman et al. [2010]. The default value is and .

- splitting variable

-

: We compute the distribution over the splitting variables from the data. We begin with a flat categorical distribution, , i.e., all covariates have the same chance of being used as splitting variables. During the tuning phase, we continuously update based on counting the splitting variables in the accepted trees. After the tuning phase, we fix this distribution and use it to sample from the splitting variables.

- splitting values

-

: Uniform over the observed values.

- leaf values

-

: We use , where is computed as the mean of the current sum of trees divided by the number of trees m. is initially computed from , being for binomial data and for data other than binomial. Because the prior variance on the leaf node parameters can be model dependent during the tuning phase the running variance of the predictions from each fitted tree is computed and used as a proposal. After tuning the variance remains fixed.

References

- Abril-Pla et al. [2023] O. Abril-Pla, V. Andreani, C. Carroll, L. Dong, C. J. Fonnesbeck, M. Kochurov, R. Kumar, J. Lao, C. C. Luhmann, O. A. Martin, M. Osthege, R. Vieira, T. Wiecki, and R. Zinkov. Pymc: A modern and comprehensive probabilistic programming framework in python. PeerJ Computer Science, 9:e1516, 2023. doi: 10.7717/peerj-cs.1516.

- Bleich et al. [2014] J. Bleich, A. Kapelner, E. I. George, and S. T. Jensen. Variable selection for bart: An application to gene regulation. The Annals of Applied Statistics, 8(3), Sep 2014. ISSN 1932-6157. doi: 10.1214/14-aoas755. URL http://dx.doi.org/10.1214/14-AOAS755.

- Carlson [2020] C. J. Carlson. embarcadero: Species distribution modelling with bayesian additive regression trees in r. Methods in Ecology and Evolution, 11(7):850–858, 2020. doi: https://doi.org/10.1111/2041-210X.13389. URL https://besjournals.onlinelibrary.wiley.com/doi/abs/10.1111/2041-210X.13389.

- Chen et al. [2022] X. Chen, M. O. Harhay, G. Tong, and F. Li. A bayesian machine learning approach for estimating heterogeneous survivor causal effects: Applications to a critical care trial, 2022. URL https://arxiv.org/abs/2204.06657.

- Chipman et al. [2010] H. A. Chipman, E. I. George, and R. E. McCulloch. BART: Bayesian additive regression trees. The Annals of Applied Statistics, 4(1):266–298, Mar. 2010. ISSN 1932-6157. doi: 10.1214/09-AOAS285. URL http://projecteuclid.org/euclid.aoas/1273584455.

- Coltman [2022] J. Coltman. Bartpy documentation, 2022. URL https://jakecoltman.github.io/bartpy/.

- de Souza et al. [2021] R. S. de Souza, A. Krone-Martins, V. Carruba, R. de Cassia Domingos, E. E. O. Ishida, S. Alijbaae, M. H. Espinoza, and W. Barletta. Probabilistic modeling of asteroid diameters from gaia DR2 errors. Research Notes of the AAS, 5(8):199, aug 2021. doi: 10.3847/2515-5172/ac205e. URL https://doi.org/10.3847/2515-5172/ac205e.

- Deshpande [2023] S. K. Deshpande. flexbart: Flexible bayesian regression trees with categorical predictors, 2023.

- Friedman [2001] J. H. Friedman. Greedy function approximation: A gradient boosting machine. The Annals of Statistics, 29(5):1189 – 1232, 2001. doi: 10.1214/aos/1013203451. URL https://doi.org/10.1214/aos/1013203451.

- Goldstein et al. [2013] A. Goldstein, A. Kapelner, J. Bleich, and E. Pitkin. Peeking inside the black box: Visualizing statistical learning with plots of individual conditional expectation. Journal of Computational and Graphical Statistics, 24:44 – 65, 2013.

- He et al. [2019] J. He, S. Yalov, and P. R. Hahn. Xbart: Accelerated bayesian additive regression trees. In K. Chaudhuri and M. Sugiyama, editors, Proceedings of the Twenty-Second International Conference on Artificial Intelligence and Statistics, volume 89 of Proceedings of Machine Learning Research, pages 1130–1138. PMLR, 16–18 Apr 2019. URL https://proceedings.mlr.press/v89/he19a.html.

- Hill et al. [2020] J. Hill, A. Linero, and J. Murray. Bayesian additive regression trees: A review and look forward. Annual Review of Statistics and Its Application, 7(1):251–278, 2020. doi: 10.1146/annurev-statistics-031219-041110. URL https://doi.org/10.1146/annurev-statistics-031219-041110.

- Hill [2011] J. L. Hill. Bayesian nonparametric modeling for causal inference. Journal of Computational and Graphical Statistics, 20(1):217–240, 2011.

- Hoffman and Gelman [2014] M. D. Hoffman and A. Gelman. The No-U-Turn Sampler: Adaptively Setting Path Lengths in Hamiltonian Monte Carlo. Journal of Machine Learning Research, 15(1):1593–1623, 2014.

- Hoyer and Hamman [2017] S. Hoyer and J. Hamman. Xarray: N-D Labeled Arrays and Datasets in Python. Journal of Open Research Software, 5(1), Apr. 2017. ISSN 2049-9647. doi: 10.5334/jors.148.

- Hu et al. [2022] L. Hu, J. Ji, R. D. Ennis, and J. W. Hogan. A flexible approach for causal inference with multiple treatments and clustered survival outcomes, 2022. URL https://arxiv.org/abs/2202.08318.

- Inglis et al. [2022] A. Inglis, A. Parnell, and C. Hurley. Visualizations for bayesian additive regression trees, 2022. URL https://arxiv.org/abs/2208.08966.

- Kassambara [2019] A. Kassambara. datarium: Data Bank for Statistical Analysis and Visualization, May 2019. URL https://CRAN.R-project.org/package=datarium.

- Kluyver et al. [2016] T. Kluyver, B. Ragan-Kelley, F. Pérez, B. Granger, M. Bussonnier, J. Frederic, K. Kelley, J. Hamrick, J. Grout, S. Corlay, P. Ivanov, D. Avila, S. Abdalla, and C. Willing. Jupyter notebooks – a publishing format for reproducible computational workflows. In F. Loizides and B. Schmidt, editors, Positioning and Power in Academic Publishing: Players, Agents and Agendas, pages 87 – 90. IOS Press, 2016.

- Kropat et al. [2015] G. Kropat, F. Bochud, M. Jaboyedoff, J.-P. Laedermann, C. Murith, M. Palacios, and S. Baechler. Improved predictive mapping of indoor radon concentrations using ensemble regression trees based on automatic clustering of geological units. Journal of Environmental Radioactivity, 147:51–62, 2015.

- Kuhn and Johnson [2013] M. Kuhn and K. Johnson. Applied Predictive Modeling. Springer-Verlang, New York, 1st ed. 2013, corr. 2nd printing 2018 edition edition, May 2013. ISBN 978-1-4614-6848-6.

- Kumar et al. [2019] R. Kumar, C. Carroll, A. Hartikainen, and O. A. Martin. Arviz a unified library for exploratory analysis of Bayesian models in python. Journal of Open Source Software, 4(33):1143, 2019. ISSN 2475-9066. doi: 10.21105/joss.01143.

- Lakshminarayanan et al. [2015] B. Lakshminarayanan, D. M. Roy, and Y. W. Teh. Particle gibbs for bayesian additive regression trees, 2015. URL https://arxiv.org/abs/1502.04622.

- Lamprinakou et al. [2020] S. Lamprinakou, E. McCoy, M. Barahona, A. Gandy, S. Flaxman, and S. Filippi. Bart-based inference for poisson processes, 2020. URL https://arxiv.org/abs/2005.07927.

- Leonti et al. [2010] M. Leonti, S. Cabras, C. S. Weckerle, M. N. Solinas, and L. Casu. The causal dependence of present plant knowledge on herbals—contemporary medicinal plant use in campania (italy) compared to matthioli (1568). Journal of Ethnopharmacology, 130(2):379–391, 2010.

- Li et al. [2022] Z. Li, S. Liu, W. Conaty, Q.-H. Zhu, P. Moncuquet, W. Stiller, and I. Wilson. Genomic prediction of cotton fibre quality and yield traits using Bayesian regression methods. Heredity, pages 1–10, May 2022. ISSN 1365-2540. doi: 10.1038/s41437-022-00537-x. URL https://www.nature.com/articles/s41437-022-00537-x. Publisher: Nature Publishing Group.

- Linero [2018] A. R. Linero. Bayesian regression trees for high-dimensional prediction and variable selection. Journal of the American Statistical Association, 113(522):626–636, 2018.

- Linero [2022] A. R. Linero. Generalized bayesian additive regression trees models: Beyond conditional conjugacy, 2022. URL https://arxiv.org/abs/2202.09924.

- Linero and Yang [2018] A. R. Linero and Y. Yang. Bayesian regression tree ensembles that adapt to smoothness and sparsity. Journal of the Royal Statistical Society B, 80(5):1087–1110, 2018. doi: https://doi.org/10.1111/rssb.12293. URL https://rss.onlinelibrary.wiley.com/doi/abs/10.1111/rssb.12293.

- Maia et al. [2022] M. Maia, K. Murphy, and A. C. Parnell. Gp-bart: a novel bayesian additive regression trees approach using gaussian processes, 2022. URL https://arxiv.org/abs/2204.02112.

- Martin [2018] O. Martin. Bayesian Analysis with Python: Introduction to Statistical Modeling and Probabilistic Programming Using PyMC3 and ArviZ, 2nd Edition. Packt Publishing, 2 edition edition, Dec. 2018.

- Martin et al. [2022] O. Martin, A. Hartikainen, C. Carroll, and O. Abril-Pla. Arviz, May 2022. URL https://doi.org/10.5281/zenodo.6547007.

- Martin et al. [2021] O. A. Martin, R. Kumar, and J. Lao. Bayesian Modeling and Computation in Python. Chapman and Hall/CRC, Boca Raton, 1st edition, 2021. ISBN 978-0-3678-9436-8.

- Orlandi et al. [2021] V. Orlandi, J. Murray, A. Linero, and A. Volfovsky. Density regression with bayesian additive regression trees, 2021. URL https://arxiv.org/abs/2112.12259.

- Pratola [2016] M. T. Pratola. Efficient Metropolis–Hastings Proposal Mechanisms for Bayesian Regression Tree Models. Bayesian Analysis, 11(3):885 – 911, 2016. doi: 10.1214/16-BA999. URL https://doi.org/10.1214/16-BA999.

- Pratola et al. [2020] M. T. Pratola, H. A. Chipman, E. I. George, and R. E. McCulloch. Heteroscedastic BART via Multiplicative Regression Trees. Journal of Computational and Graphical Statistics, 29(2):405–417, Apr. 2020. ISSN 1061-8600. doi: 10.1080/10618600.2019.1677243. URL https://doi.org/10.1080/10618600.2019.1677243. Publisher: Taylor & Francis _eprint: https://doi.org/10.1080/10618600.2019.1677243.

- Rockova and Saha [2018] V. Rockova and E. Saha. On theory for bart, 2018. URL https://arxiv.org/abs/1810.00787.

- Sparapani et al. [2021] R. Sparapani, C. Spanbauer, and R. McCulloch. Nonparametric machine learning and efficient computation with bayesian additive regression trees: The bart r package. Journal of Statistical Software, 97(1):1–66, 2021. doi: 10.18637/jss.v097.i01. URL https://www.jstatsoft.org/index.php/jss/article/view/v097i01.

- Steele and Schwartz [2022] K. M. Steele and M. H. Schwartz. Causal effects of motor control on gait kinematics after orthopedic surgery in cerebral palsy: a machine-learning approach. medRxiv, 2022. doi: 10.1101/2022.01.04.21268561. URL https://www.medrxiv.org/content/early/2022/01/05/2022.01.04.21268561.

- Tan and Roy [2019] Y. V. Tan and J. Roy. Bayesian additive regression trees and the general bart model. Statistics in Medicine, 38(25):5048–5069, 2019. doi: https://doi.org/10.1002/sim.8347. URL https://onlinelibrary.wiley.com/doi/abs/10.1002/sim.8347.

- Vanhatalo et al. [2013] J. Vanhatalo, J. Riihimäki, J. Hartikainen, P. Jylänki, V. Tolvanen, and A. Vehtari. GPstuff: Bayesian modeling with Gaussian processes. J. Mach. Learn. Res., 2013.

- Vehtari et al. [2017] A. Vehtari, A. Gelman, and J. Gabry. Practical Bayesian model evaluation using leave-one-out cross-validation and WAIC. Statistics and Computing, 27(5):1413–1432, Sept. 2017. ISSN 1573-1375. doi: 10.1007/s11222-016-9696-4. URL https://doi.org/10.1007/s11222-016-9696-4.

- Vehtari et al. [2021a] A. Vehtari, A. Gelman, D. Simpson, B. Carpenter, and P.-C. Bürkner. Rank-Normalization, Folding, and Localization: An Improved for Assessing Convergence of MCMC (with Discussion). Bayesian Analysis, 16(2):667 – 718, 2021a. doi: 10.1214/20-BA1221. URL https://doi.org/10.1214/20-BA1221.

- Vehtari et al. [2021b] A. Vehtari, D. Simpson, A. Gelman, Y. Yao, and J. Gabry. Pareto Smoothed Importance Sampling. arXiv:1507.02646 [stat], Feb. 2021b. URL http://arxiv.org/abs/1507.02646. arXiv: 1507.02646 version: 7.

- Wang et al. [2022] M. Wang, J. He, and P. R. Hahn. Local gaussian process extrapolation for bart models with applications to causal inference, 2022. URL https://arxiv.org/abs/2204.10963.

- Zhou [2012] Z.-H. Zhou. Ensemble Methods: Foundations and Algorithms. CRC press, Boca Raton, FL, 1 edition edition, June 2012. ISBN 978-1-4398-3003-1.