ESG-Valued Portfolio Optimization and Dynamic Asset Pricing

Abstract

ESG ratings provide a quantitative measure for socially responsible investment.

We present a unified framework for incorporating numeric ESG ratings into dynamic pricing theory.

Specifically, we introduce an ESG-valued return that is a linearly constrained transformation of financial return and ESG score.

This leads to a more complex portfolio optimization problem in a space governed by reward, risk and ESG score.

The framework preserves the traditional risk aversion parameter and introduces an ESG affinity parameter.

We apply this framework to develop ESG-valued: portfolio optimization; capital market line; risk measures;

option pricing; and the computation of shadow riskless rates.

Keywords

ESG scores, optimal portfolio, efficient frontier, option pricing, riskless rates

1 Introduction

Socially responsible investing (SRI) is a broad approach advocating investment in activities and companies that produce positive impact on the environment and society. The definition of SRI is quite general; its practices span a heterogeneous system of policies and scopes [27, 73]. The heterogeneity within the SRI movement and forces driving differing SRI outlooks have been studied on four levels: terminological, definitional, strategic and practical [43, 66]. Within the vast realm of SRI, a more focused approach in investment is emerging based upon ESG ratings, wherein each company is separately evaluated in three categories: environmental, social and governance. Evaluation is performed on the basis of factors within each category. The total ESG score of a company is then determined by a combination of three category scores, providing a “sustainability ordering” between firms.

ESG investing is experiencing fast growth as institutional investors, such as mutual and pension funds, now provide SRI-related financial products. (See for instance the recent report from the Organization for Economic Co-operation and Development on ESG investing [18], and references therein.) Different approaches have been taken by asset managers to integrate ESG factors into investment decisions [3, 71]. These approaches generally fall into three strategy groups. The first strategy, an exclusionary approach, “filters out certain companies based upon products or certain corporate behavior” [13]. The second strategy, the inclusionary approach, “involves adjusting the weights of an investment in a firm according to whether its behavior is more or less socially responsible” (ibid). There is a degree of subjectivity in both approaches. In the third, empirical-based strategy, asset managers seek for more exposure in companies with higher ESG scores, thus avoiding the subjectivity of the exclusionary and inclusionary approaches through the use of an empirical measure that does not exclude participation in less virtuous entities. According to the work of Berry at al. [13], most socially responsible financial products focus on the exclusionary approach. In contrast, they found that investors prefer to reward firms who display overall positive social policies, rather than exclude the less responsible through negative screening. A similar conclusion was reached by Amel-Zadeh and Serafeim [3]. These results could explain the slow reception of SRI, and drive new approaches to implement the third class of strategies.

Research has highlighted two main reasons behind the push for ESG products: ethical beliefs and improved financial performance [41]. Investigation of the connection between stakeholder preferences (ethical beliefs) and responsible investing includes the work of Bénabou and Tirole [11], Krüger [51], Lins et al. [53], Liang and Renneboog [52], and Starks at al. [68]. Krüger investigated how stock markets react to positive and negative events connected with corporate social responsibility, finding a strong reaction to negative events. Starks at al. found that long-term investors are more attracted toward higher rated ESG companies, “tilting their portfolios towards firms with high-ESG profiles”.

The literature has been more focused on the performance of ESG investing compared to conventional return-centric investing. An extensive literature review of over 2000 articles [33] concludes that 90% of the studies “find a nonnegative ESG [to] corporate financial performance relation” and that this relationship appears to be stable over time. Brooks and Oikonomou [19] obtain similar conclusions after reviewing a large set of studies focusing on the connection between ESG disclosure and performance and their effects on firm value. They found “a positive and statistically significant but economically modest link” between corporate social performance and firm financial perfomance. They also found a strong negative relationship between financial risk, whether systematic or idiosyncratic, and corporate social performance. Bello [10] performed a comparison between socially responsible and traditional mutual funds to attempt to quantify the impact of ethical screening on portfolio diversification and overall performance. He reported that the two classes of mutual funds do not differ statistically in the characteristics of assets they hold, in diversification, or in overall performance. In constrast, a similar study [1] on European mutual funds reports a superior “efficiency” of funds that focus on high ESG rated securities. Giese et al. [39] studied ESG causality on (as opposed to “correlation with”) financial performance by considering transmission channels of systematic and idiosyncratic risk within a standard discounted cash flow model, through which ESG ratings data (specifically MSCI ESG ratings data) impact valuation and performance. An interesting outcome of their study relates to the intensity and longevity of ESG signals (ESG rating changes) compared with factors such as momentum or volatility.

A component of the literature has focused on the effect of specific components of the three ESG categories. In the area of governance, Pan et al. [61] found a negative relationship between returns and high pay ratios. They claim that, in 2018, inequality-averse investors decreased the relative amount invested in stocks with a high pay ratio. Krueger at al. [50] surveyed institutional investors on whether, and how, they integrate climate risk into their financial decisions. The majority of those interviewed consider climate change to have relevant implication for financial performance and have consequently taken action in their practices to accommodate such risk. Görgen et al. [40] have investigated the impact of carbon risk on equity prices of “brown” and “green” firms. Their research uncovered two opposing effects: while brown firms display higher average returns, companies that become less green show a drop in returns.

Other relationships between ESG ratings and the financial system have been studied. Examples include the effect of ESG scores on credit ratings [7, 32] and on the fixed income market [44, 45, 46]. The analysis of ESG factors associated with a fixed income security, especially one issued by a government, involves dealing with complex methodological and technical implications [44]. The literature identifies two main approaches to translating ESG ratings into the fixed income market. The first is to issue products specifically designed to fund projects having positive environmental or social impact. Examples of securities issued with the specific purpose of financing projects related to environmental and climate change objectives are green and blue bonds111 The first green bond was issued by the European Investment Bank in 2007. https://www.eib.org/en/investor-relations/cab/index.htm [29, 31]. Ehlers et al. [31] have documented lower credit spreads222 The spread of yield at issuance over the yield curve of an appropriate treasury security of the same maturity at issuance date. on borrowing green bonds compared to that of a traditional counterpart issued by the same institutions. Polbennikov at al. [63] found that ESG corporate bond portfolios have experienced a modest positive incremental return. The second approach has a broader view. It consists of assigning the ESG rating of the company to their fixed income products, imposing a tighter connection between the global business activity of the issuer and the bond rating [2, 60]. A related issue is the ESG valuation of general fixed income securities backed by governments or municipalities [6].

A major concern of ESG ratings is the variability of scores among different rating agencies, which raises the issues of reliability and potential bias selection; see for instance [12, 15, 21, 25, 38], and references therein. Berg et al. [12] analyzed ESG scores from six large providers. They decomposed the spread among scores into three main sources:

-

i)

scope (56%), defined by the range of company attributes that the score intends to measure;

-

ii)

measurement (38%), the methodology used to compute a particular attribute; and

-

iii)

weights (6%), how the attribute values are combined to form a final score;

and were able to attribute the percentage weight (quoted above) to each source. The main source of variability found among ESG scoring systems was the selection of attributes (the scope). The authors warn of possible bias effects involved in the assignment of ESG scores as well as in research attempting to study the link between ESG scores and financial performance. For example, a “rater effect” was discovered under which “a rater’s overall view of a firm influences the measurement of specific categories”. Bilio et al. [15] found substantially low agreement in the assignment of ESG scores by four rating agencies. They investigated the impact of this variability on financial performance by comparing the Jensen-alpha for two equi-weighted portfolios: one formed by those companies that were rated by all four ESG rating agencies and the other composed of companies that were rated by none of the agencies. They found no evidence for a difference in financial performance between these two portfolios.

The construction of optimal portfolios is one corner-stone of modern finance theory. The traditional approach is based on two measures: financial reward and financial risk. The reward measure is usually represented by the expected value of future portfolio returns. Several measures have been proposed to quantify the risk related to the unpredictable component of the variability of portfolio returns; the most common of these are: the standard deviation [56], the absolute deviation [49], the value at risk (VaR) [54], and the conditional value at risk (CVaR) [65]. A common optimization approach consists of minimizing the reward-risk trade-off on the basis of a statistical model for future asset returns, see for instance [48] and [55]. The idea of incorporating ESG information or more general SRI aspects in this optimization problem was first pursued in the framework of negative screening. An example is the portfolio strategy approach proposed by Geczy and Guerard [36], which combined negative screening with a factor model and mean-variance optimization.

A more complex set of approaches have added ESG information directly to the portfolio selection and/or optimization problem. Bilbao at al. [14] introduced a two step optimization model. In the first step, an efficient frontier is computed using expected value of wealth as the reward measure and either mean-variance or CVaR as the risk measure. An investor social behavior satisfaction index is then computed on the efficient frontier. In the second step, the portfolio showing the best financial and social behavior is selected. The approach taken by Hirschberger et al. [42] and Utz et al. [70] involves portfolio selection in which sustainability is modeled, after risk and return, as a third selection criterion. Gasser at al. [35] have incorporated an ESG score as a linear term in the classical mean-variance optimization. Chen at al. [23] proposed a three step approach: the first step applies data envelopment analysis to the scores in each of the three ESG categories to obtain a more informative total score; the second step creates a restricted investment universe using financial attributes and the ESG scores obtained from the first step; the third step applies standard mean-variance optimization to the restricted portfolio. Pedersen et al. [62] integrated the relative ESG score of each asset into the objective function and studied the differential impact of environmental and governance scores on portfolio performance. Schmidt [67] added the portfolio ESG value to the objective function. Asset weights in a long-only portfolio were then optimized in terms of return, mean variance and ESG value. In Cesarone et al. [20], the ESG dimension is added as a hard constraint under mean-variance optimization with long-only positions solved numerically under data-driven scenarios. Their analysis is conducted on four investment universes: DJIA, Euro Stocxx 50, FTSE100, NASDAQ100 and S&P500. They find that optimal portfolios with highest ESG constraints gave better results only within the DJIA and S&P500 universes.

The discussion above underscores the fact that SRI investing and ESG ratings are “here to stay”, and that societal pressures will require that the optimization of financial returns be considered within a larger SRI framework. We note that ESG scores are an “SRI measure” that, to first-order approximation, is independent of the traditional return and risk-measures used in portfolio optimization.333 Literature reviews such as those done by Friede et al. [33] and Brooks and Oikonomou [19] have revealed less-than-conclusive results regarding the strength of correlation between ESG scores and financial performance. It is our goal, in this and further work, to produce a consistent, ESG-based, asset pricing framework upon which pricing, optimization, and risk management practices can be based. Our objective is to add the ESG score as a third dimension, while preserving the main machinery developed in dynamic asset pricing theory (see for instance [30]). As a result, we will be able to find optimal reward-risk-ESG asset allocations, but also be able to hedge the ESG-valued risk by pricing any contingent claims traded in financial markets. Our work has commonality with approaches discussed above in that we propose a linearly constrained combination of asset returns and ESG scores to produce ESG-valued returns. Our work then builds consistently upon this ESG-valued framework, extending its development into principle components of modern finance theory.

In Section 2 we present this linearly constrained transformation; in Section 3 we develop its application to portfolio optimization, and analyze empirically the ESG-valued efficient frontier using a portfolio of stocks from the Dow Jones Industrial Average. In Section 4 we consider ESG-valued measures appropriate for evaluating the performance of ESG-valued optimizations. In Section 5, we extend the results by developing an ESG-valued risk-free rate to enable the identification of tangent portfolios to the ESG-valued efficient frontier, thus formulating an ESG-valued capital asset pricing model (CAPM). The extension to an ESG-valued model for valuing European contingent claims is covered in Section 6. A numerical study is also presented. In Section 7 we investigate the effect of the ESG-adjustment on the computation of a riskless rate in markets having no riskless asset; the so-called shadow riskless rate as defined by Rachev et al. [64]. Final discussion is presented in Section 8.

2 ESG-Valued Returns

We define the ESG-valued return as an affine combination of the ESG score for any asset and its return. Let be the ESG score for asset on day , and denote the value of appropriately normalized to the range .444 This normalization is discussed in Section 2.1. Since ESG scores are usually provided as positive values, the normalization to the range produces a positive (negative) shift in for those assets with ESG scores above (below) some determined “average” value of the original scale. For any , we then define the ESG-valued return

| (1) |

The constant is needed to insure that the ranges of and are comparable. The value of will depend on the return time period; for the daily returns considered here, we used the value to approximate the number of trading days in a year. Note that is chosen by the investor; for our purposes, we consider it to be independent of and . The ESG-valued return defined in (1) assigns more weight to the ESG score of each asset as . In the limit , the investor abandons any concern regarding the financial risk-reward trade-off and concentrates solely on the ESG risk-reward impact on the portfolio. Conversely, when , the investor abandons any interest in ESG.

To avoid confusion, the phrases “ESG-valued return” and “adjusted return” will always refer to . The word “return” used alone will refer to the financial return .

2.1 Scaling of ESG Values

To use the ESG-valued return (1), the investor has to determine a scoring system that reflects desired ESG criteria. As discussed in the Introduction, preference might, for example, be given to considering environmental implications over social aspects; the choice may be driven by ethical values or by consideration of profit maximization.555 Some literature has focused on the higher returns provided by portfolios based on certain ESG criteria. Pedersen at al. [62] found that governance factors are more linked to financial performance than those related to environmental impact. Choice of criteria will direct choice of scoring methodology and perhaps scoring agency.

Given a user-determined decision on the scoring system, we first consider the issue related to the time scale embedded in (1). Currently, ESG scores are provided on an annual basis,666 Although some providers distribute monthly scores, these data are usually expensive and are not provided on a regular basis. whereas the time scale (hence, the return data) required in (1) may vary from monthly to intra-day. Proceding with our choice of day, we discuss the issue of assigning values to on a daily basis. A straightforward approach is to utilize the last published ESG score for each date . While this takes advantage of the most recent ESG information, the ESG score for asset will remain constant over the period of a year. Under this approach, in (1) is the normalized value of for asset at the last yearly issue date, , of new ESG values. A clear drawback to this approach is the introduction of a (potentially large) jump discontinuity in the value of as the ESG year changes, with a consequent discontinuity in the value of the ESG-valued return. With ESG scores only available at yearly time points, a fill-in procedure to produce a smoothly varying daily ESG score would require both interpolation and extrapolation methods. An alternate approach would be to model the ESG score as a random variable. This approach, which should be more appropriate as the ESG score is affected by uncertainty, is challenging to implement given the current, relatively low frequency of ESG data, especially when compared to that of financial returns.

Taking the above considerations into account, we invoke the philosophy of using the most current data available and adopt the following procedure in this paper. In most financial computations (e.g. portfolio optimization, option pricing), a “look-back” window of days is required in order to compute statistics summarizing the random behavior of the assets under consideration. We utililze the most current ESG value available for each stock during the look-back period, regardless of the size of . For example, to obtain optimized portfolio weights for 06/06/2019 using a window of 510 days (5/25/2017 through 6/5/2019), the most recent ESG scores available from Refinitiv were from 12/31/2018. These ESG scores were used in (1) to compute adjusted returns for each day in the look-back period.

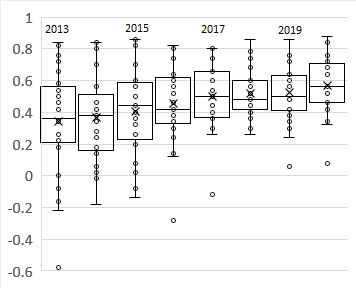

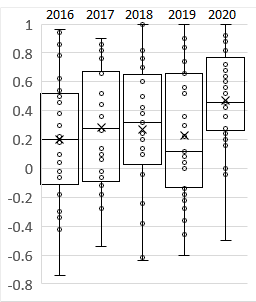

We consider next the issue of normalizing agency-provided ESG scores to the interval . While a linear normalization appears immediate and obvious, this is based upon inherent assumptions of linearity within the agency’s methodology. To illustrate this issue quantitatively we consider the ESG scores from Refinitiv for 29 of the stocks in the Dow Jones Industrial Average (DJIA). These are shown in Table A.1 for the years 2013 through 2020. Refinitiv ESG scores are based on a scale.777 Environmental, Social and Governance Scores from Refinitiv; Feb. 2021. https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/refinitiv-esg-scores-methodology.pdf We applied the obvious linear transformation to normalize these to . Box-whisker summaries of the resultant transformed scores are shown, by year, in Fig. 1. Very few of the stocks have scaled ESG values that are negative, implying very few (and none for 2018 through 2020) stocks have a Refinitiv score below 50. The ESG scores of the lower rated companies improved fairly rapidly over the period 2013 through 2017. Adjusting the ESG normalization to reflect a yearly change in the median ESG value (which might, for example, be interpreted as the appropriate percentile for separating “good” from “bad” ESG ratings) would introduce hidden variability into (1). Addressing this issue in further depth remains outside of the intended scope of this paper; therefore we proceed with the simple linear transformation to normalize the provided Refinitiv scores from to .

3 ESG-Valued Portfolio Optimization

We apply the ESG-valued return model to portfolio optimization. We consider a quite general framework; at the end of day888 We develop our formalism for daily returns. Reformulation for other time intervals is straightforward, assuming appropriate time-varying values for the ESG scores can be found. an investor has to decide how to reallocate the value of a portfolio among a universe of assets by selecting the fraction (the weight) to be invested in asset . The investor observes the series of previous asset returns and, based upon some discrete-state, parametric or non-parametric, statistical model, obtains a series of one-period-ahead returns . Under these assumptions, given the vector of portfolio weights , the simulated return of the portfolio between and is defined by the set of scenarios

| (2) |

The traditional approach is to assign weights by optimizing the trade-off between the financial risk and financial reward of the portfolio. The reward is usually measured by the expected value of the future return , whereas there are many choices for the risk measure .999 Artzner at al. [4] proposed an axiomatic approach to define the minimum set of propertie that should satisfy to be a coherent measure of risk. Frittelli at al. [34] have specified requirements to define a convex risk measure. Once the risk measure has been selected, the optimal portfolio can be obtained from the following minimization problem,

| (3) |

subject to the constraints

| (4) | |||

| (5) | |||

| (6) |

for some parameter that represents the risk-aversion attitude of the investor. Constraint (5) forces the portfolio turnover to be less than the pre-specified parameter ; here are the portfolio weights at time . Constraint (6) avoids short-selling and can be relaxed when the investor wishes to enter into such positions.

3.1 ESG Efficient Frontier

The ensemble of ESG-valued return scenarios is

| (7) |

where

| (8) |

We consider the portfolio optimization problem (3)-(6) when is replaced by . We illustrate ESG-valued optimization by application to a specific portfolio consisting of 29 of the 30 stocks101010 Due to its shorter span of existence, stock from DOW Inc is not included in the portfolio. comprising the DJIA. We use the ESG scores in Table A.1 provided by Refinitiv for each asset over the period 2013-2020. We employ the scaling methodology discussed in Section 2.1 for daily ESG scores.

To generate the ensemble of values in (8), we applied an ARMA()-GARCH(1,1) model to the set of historical returns . We employed the R package rugarch [37] to perform the ARMA-GARCH fits. The function autoarfima was used to fit the ARMA parameters and over the ranges , using the Bayesian information criterion. Separate fits were performed for each stock. For each asset, a GARCH(1,1) fit was then performed on the residuals of the best-fit ARMA model using the function ugarchfit and the assumption that the innovations are normal inverse Gaussian (NIG) [8, 9]. In the case in which ugarchfit failed to converge, the autocorrelation was computed to check for persistence. If no persistence was found, the GARCH(1,1) component was dropped in preference of a pure ARMA model.111111 Persistence was found to be both stock and time dependent; even for the same stock, the presence of persistence could change over time. The set of innovations resulting from the ensemble of ARMA()-GARCH(1,1) fits was then fit to a multidimensional NIG model using the R package ghyp [72]. From the parameterized, multidimensional NIG model, innovations were randomly generated. The generated innovations for asset were then fed into the ARMA()-GARCH(1,1) fit to generate sample returns for day for asset . The choice of the NIG distribution family for the innovations was motivated by its flexibility in modeling potentially different heavy-tailed behavior for each assset, while preserving asset return processes as semimartingales, a property that is necessary to perform option pricing. Since NIG distributions are closed under affine transformations, the ESG-valued returns (8) remain within the same distribution class as the unadjusted returns, again preserving the semimartingale property.

Two choices were used for the risk metric in (3), mean-variance (MV) and mean-CVaRβ (mCVaRβ) with and . Details on solving the minimization problem (3)-(6) using each of these measures are provided in Appendix B. Let denote the vector of optimal weights for any of these solutions.121212 For brevity we omit labeling the and dependence of . We can then define the optimal portfolio return and ESG-valued return,

| (9) | ||||

| (10) |

where are the realized asset returns on the close of trading day , from which the ESG-valued returns are computed. The portfolio price is computed in the usual manner,

| (11) |

The ESG-valued numeraire for the portfolio is similarly defined as

| (12) |

We assign the initial adjusted value of this numeraire to be . For simplicity we refer to as the ESG-valued price. For , the portfolio price (11) time series is just a scaled version of the ESG-valued price (12). Any significant differences only occur for . The normalized ESG score for the optimized portfolio is

| (13) |

As we have invoked a linear normalization , this is equivalent to

| (14) |

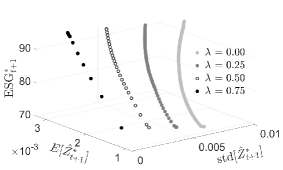

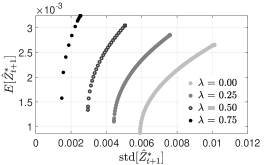

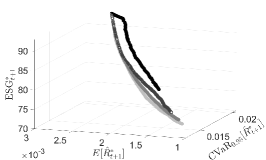

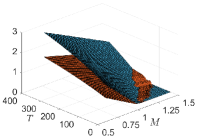

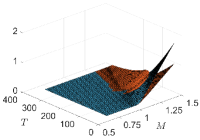

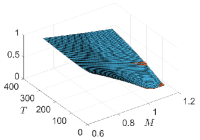

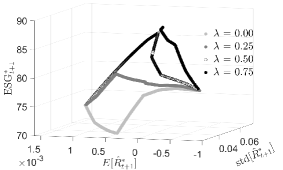

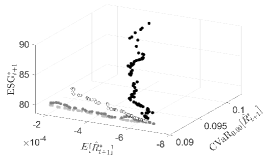

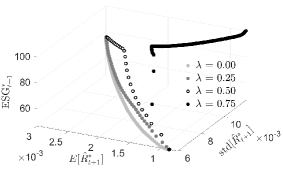

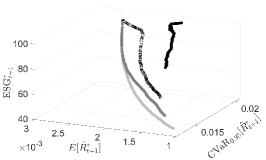

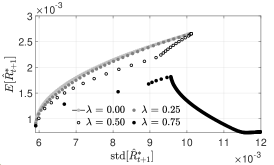

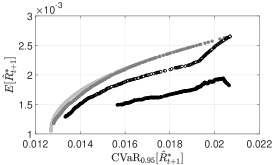

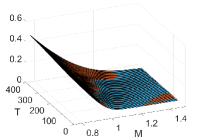

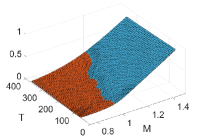

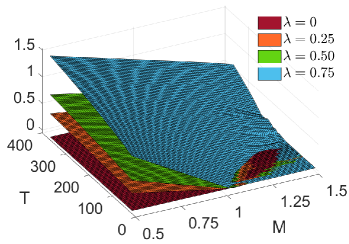

We illustrate the optimization procedure by solving for optimal weights for the date 12/30/2019 for our illustrative portfolio. We use a historical look-back period of days and generate simulated returns. Three optimizations were obtained, using MV, mCVaR0.95 and mCVaR0.99 risk measures. Optimizations were performed for four choices of . For each , the efficient frontier was computed using the sequence of values {0, 0.01, 0.02, …, 0.99}.131313 For this portfolio, there is essentially no change in the optimized solutions over the range . The efficient frontier can be examined either in the three-dimensional space or in . The efficient frontiers are plotted in space in Fig. 2.

At the higher values, both and increase rapidly for low-to-moderate values of the parameter . This is especially noticeable for the MV portfolios when and (Fig. 2(a)). Increasing the value of decreases the value of the ESG-valued risk measure and increases the value of the . The increase of with follows from (8); increasing puts more weight on optimizing the ESG score of the portfolio. The observed increase of with follows from the same reasoning. As we hold ESG scores constant throughout a year’s time, increasing puts more weight on resulting in the observed decrease of .

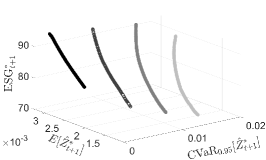

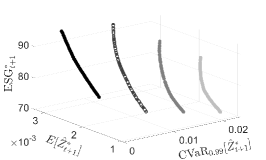

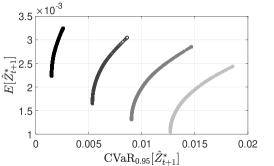

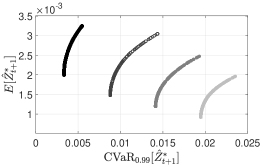

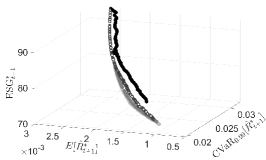

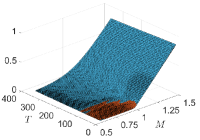

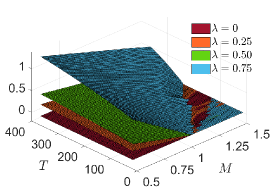

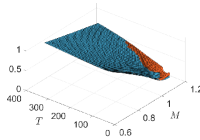

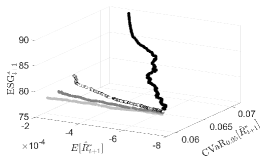

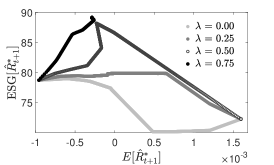

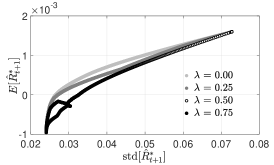

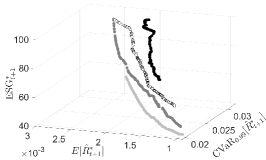

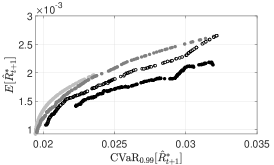

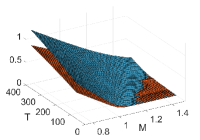

Fig. 3 investigates the results in space, using the traditional and axes.

The curve represents the traditional efficient frontier under which ESG scores are not considered. For this portfolio and date, on the frontier increases with increasing values of ; the choice of more risky portfolios giving rise to a higher ESG score. This is not a general result as it depends on the distribution of returns estimated at the particular date.141414 In the supplementary material to this paper we show the efficient frontier computed for a different date in which the portfolio ESG score initially increases with , but then decreases as and risk continue to increase. For the higher values, also increases rapidly for low-to-moderate values of the parameter ; again most noticeably for the MV portfolios when and (Fig. 3(a)). There is a nonlinear decrease in both and as increases (for any fixed value of ), which is seen most clearly in the projection on the plane. The most significant decrease in these values occurs when increases from 0.5 to 0.75. The behavior of this non-linear decrease changes with . When viewed in the full space, it is clear that this shift (at fixed ) in the efficient frontier shift is toward larger values. Noticeable on the efficient frontiers is a “kink” in its convex shape. For mCVaR0.99 optimization, the efficient frontier becomes less defined due to sparsity of data at the 99’th percentile.

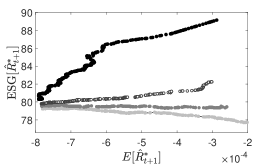

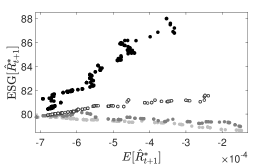

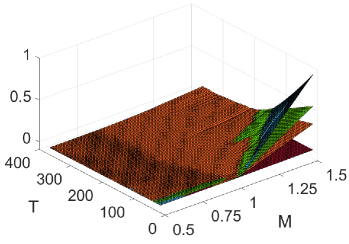

Since new ESG scores arrived on 12/31/2019, the choice of the optimization date of 12/30/2019 enabled a test of the stability of the optimization results by comparing the use of in-sample (released on 12/31/2018) versus out-of-sample (released on 12/31/2019) ESG scores. Fig. 4 plots the relative difference151515 The relative difference in the portfolio ESG score is defined in the usual manner as (ESG(out-of-sample) ESG(in-sample))/ESG(in-sample). between the ESG score of the optimal portfolio computed using individual asset ESG scores released on 12/31/2019 compared with the computations in Figs. 2 and 3 computed using the ESG data released on 12/31/2018.

In general, over all three risk measures, the relative difference does not exceed 5% percent, indicating a quite stable ESG portfolio value (at least for this date and these securities). The relative difference becomes zero as increases, approaching zero for smaller values of as increases. For the MV optimized portfolios, the relative ESG difference rapidly disappears over the range , The sensitivity of the MV optimal solution to ESG score dramatically decreases for values as the optimized portfolios become extremely concentrated in very few securities. The relative difference persists longest under mCVaR optimization, staying roughly constant until .

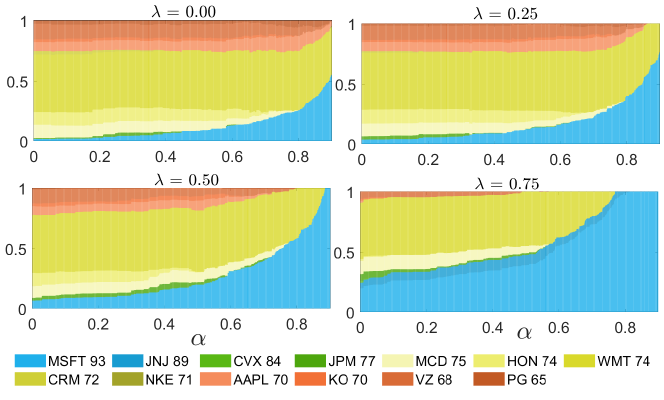

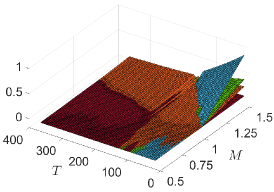

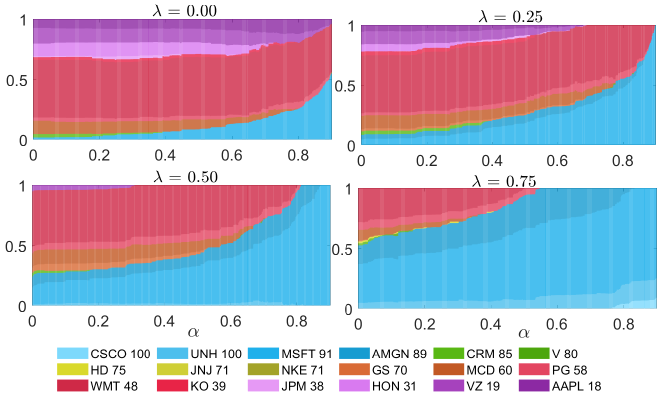

In Fig. 5 we depict the optimal portfolio weight composition along the efficient frontiers (i.e. as a function of ) of the mCVaR0.99 optimizations for each value of considered.

For a given choice of , the diversity of the portfolio decreases as increases; at high the optimizer focuses on those assets with highest expected return. For a fixed value of , an increase in leads to a portfolio composition that decreases the weight of lower ESG-scoring stocks. The effect is most noticeable for . Similar results (not shown) were obtained for the MV and mCVaR0.95 optimizations.

4 ESG-Valued Performance Measures

A common approach to evaluate the performance of an investment strategy is to use one or more reward-risk ratios (RRRs) to quantify the trade-off between expected reward and the risk associated with the strategy. There is an extensive list of such ratios, though not all of them posses the properties of a coherent risk measure; see Cheridito and Kromer [24] for a complete overview of RRRs and an analysis of their properties. For instance, the extensively used Sharpe ratio does not satisfy the monotonicity property. The development of ESG-valued RRRs involves deep questions concerning the desired properties that the measures should possess; for example, the coherent risk measure properties developed by Cherdito and Kromer may comprise a necessary, but not sufficient, set of properties for ESG-valued RRRs. The scope of this question is outside of this paper. We illustrate here a “straightforward” strategy for developing ESG-valued RRRs.

For any choice of an RRR, one strategy for developing an ESG-valued counterpart involves replacing the portfolio return in the definition of the RRR with the ESG-valued return . For illustration, we consider the stable tail adjusted return (STAR) ratio [58],

| (15) |

where is a risk-free rate appropriate for day . The ESG-valued STAR ratio is then

| (16) |

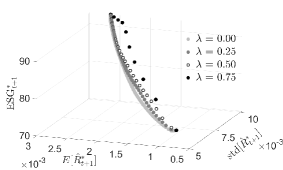

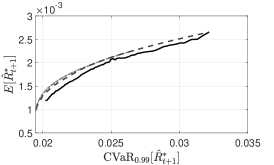

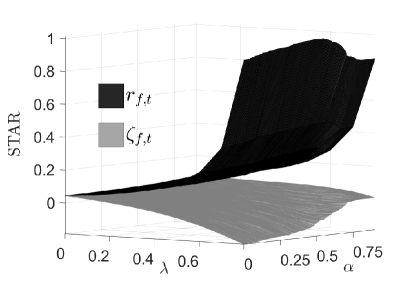

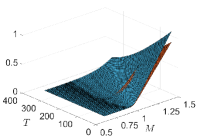

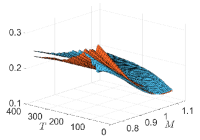

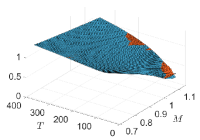

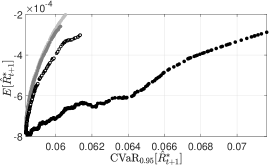

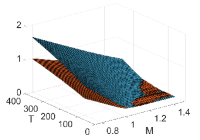

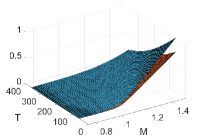

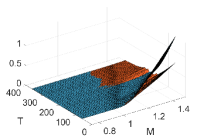

The ESG-valued STAR ratio satisfies all four properties of a coherent risk measure. As the STAR ratio will vary along the efficient frontier (i.e. with ) and from frontier to frontier (i.e. with ), in Fig. 6 we summarize the behavior of the STAR ratio as the surface STAR() for the mCVaR0.99 optimization.

(To compute the STAR ratio, we used the 10-year U.S. treasury yield rate to determine daily values for . Computation of the expectation and ETL in the STAR ratio is performed over the ensemble of ESG-valued returns generated for day based upon the information available at day .) As only four values for were computed while the grid is much finer, the smoothly interpolated surface appears coarser in the direction. The surface shows a generally convex relationship between the ESG-valued STAR ratio and and , although variation with is smaller. The “kink” that appears in the efficient frontier produces the non-convexity observed in the surface.

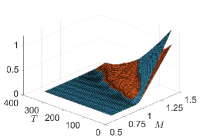

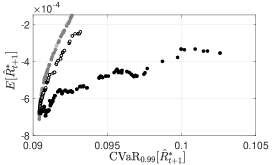

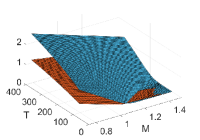

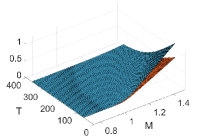

Another strategy would be to replace with an ESG-valued risk-free rate, such as that developed in equation (18) for defining tangent portfolios. Fig. 6 also shows the surface STAR() for the mCVaR0.99 optimization using the formulation

| (17) |

with defined in (18). Because the risk-free rate has no dependence, as increases the behavior of the STAR ratio is effectively that of which increases with . In contrast, the risk-free rate has strong dependence, especially so since this risk-free rate is assigned an ESG score of 100, larger that that of any assset in the optimized portfolio and, consequently, larger than that of the portfolio. As a result, for large the term becomes the dominating factor in the numerator and denominator of (17). Apparently this effect exists even for small, positive values of , resulting in a monotonic decrease in the STAR ratio as increases. In contrast to the surface, which shows no strong dependence, as increases, the dependence of the surface becomes more pronouced and the STAR ratio decreases with a decrease in (more risk-averse optimization producing smaller STAR ratios). The STAR ratio becomes negative under these conditions.

4.1 Performance Over Time

We now investigate the ESG-optimized investment results over time using the same DJIA-derived portfolio of stocks as in Section 3.1. We consider a daily investment horizon spanning the period 01/03/2017 through 12/30/2020. Using the procedure outlined in Section 3.1 involving 1-day ahead forecasting based upon two years of previous returns, for each day we computed an efficient frontier using the sequence of values for each value of , obtaining a set of optimal asset weights for each combination. We employed only the MV and mCVaR0.99 optimizations to examine central and tail behavior. Transaction costs were included in the evaluation by assuming a cost of 2 basis points for each buy and each sell order executed in rebalancing the portfolio. We imposed a daily turnover constraint of 0.4% ( in (5)) to approximate reasonable business practice. The results are compared to a benchmark consisting of the equally weighted, buy-and-hold portfolio (EWBH) of the same 29 DJIA stocks.161616 With reference to equations (9) and (10), the EWBH portfolio is defined as follows. ; the stock for Dow Inc. remains excluded. No scenario sets are generated; no optimization is performed. At , . For , the number of shares of each stock remains fixed at ; thus , where is the price of the asset at the close of trading day .

The efficient frontier portfolios were evaluated using standard performance measures: total return (Tot Rtn), annualized return (Ann Rtn), average turnover (AvgTO), expected tail loss (ETL95)171717 Also known as conditional value-at-risk or expected shortfall. and expected tail return (ETR95), both at 95% significance levels, and maximum drawdown (MDD). ETR95 is the reward counterpart of ETL95, measuring the average value of those returns above the 0.95 quantile. MDD is generally defined as the maximum drop of portfolio returns over all time intervals that can be formed as a partition of the investment period [22]. As performance measures, we also considered the average ESG score of a portfolio over the time period, as well as its standard deviation. Table A.2 presents time-averaged values for these summary performance measures for select () efficient frontier portfolios for both mCVaR0.99 and MV optimizations.

The total and annualized returns of the optimized portfolios are generally superior to that of the benchmark for values of for mCVaR0.99 and for MV optimizations. For fixed , as increases, AvgTO tends to fall below the daily constraint value of 0.4%. For fixed , AvgTO decreases with . This effect is of particular importance under MV optimization, which suffers from instability of solutions and high turnover rates which can downgrade financial performance [26, 47, 59]. For mCVaR0.99, except for the largest values of and , the magnitudes of ETL95 and ETR95 are less than that of the EWBH benchmark. For MV, these magnitudes generally exceed that of the benchmark. In the opimized portfolios, ETL95 always exceeds ETR95 in magnitude, with the suggestion that, for MV optimization, at large values of the magnitude difference decreases as increases. All optimal portfolios have lower MDD than the benchmark. For optimization under mCVaR0.99, the MDD decreases with for each fixed value of . Average ESG scores for the optimized portfolios virtually always exceed that of the benchmark. Under mCVaR0.99 optimization the standard deviation of the ESG score is generally smaller than that of the benchmark; for MV optimization the reverse is true.

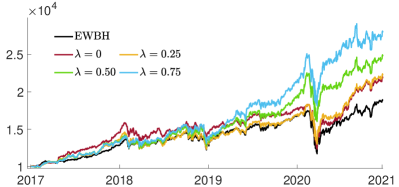

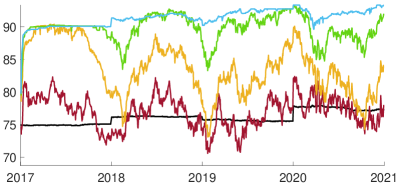

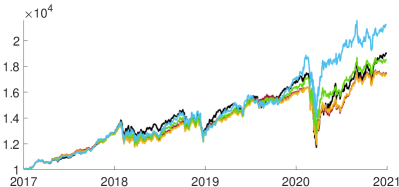

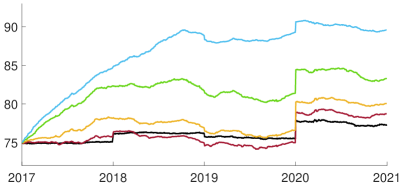

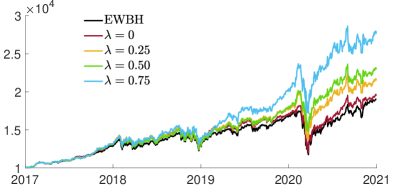

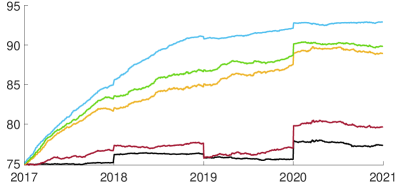

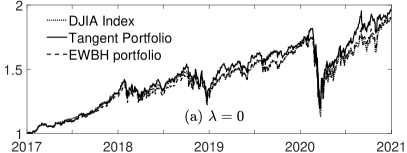

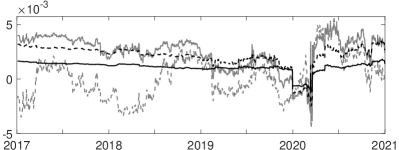

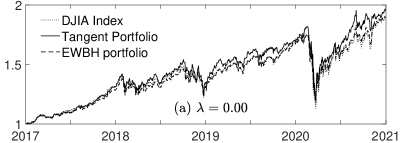

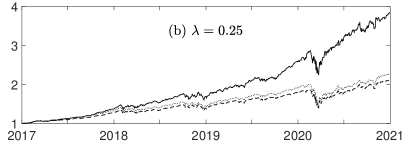

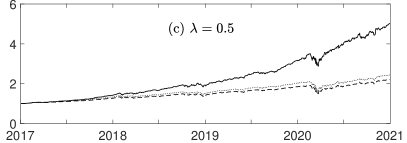

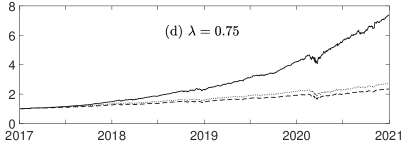

The time series for both the price (assuming an initial investment of $10,000) and ESG score for the point of the efficient frontiers of the mCVaR0.99 optimized portfolios are shown in Fig. 7. The values for the benchmark portfolio, EWBH, are also shown. As previously noted, the price and ESG time series were computed with a daily turnover constraint of 0.4%. For discussion purposes, these time series were also computed under optimization with no turnover constraint. The unconstrained time series are also plotted in Fig. 7. With no turnover constraints, the ESG optimized () portfolios outperform the benchmark, both in cumulative price and portfolio ESG value. With a realistic daily turnover constraint of 0.4% to control transaction costs, the EWBH benchmark outperforms the optimized portfolios until the Covid-19 pandemic. Post pandemic, the portfolio exhibits strong recovery while the portfolio displays recovery competitive with that of the benchmark. Each turnover-unconstrained portfolio rapidly establishes a separate ESG level (around which it displays variance). Under the turnover constraint, the portfolio ESG scores climb to their separate levels more slowly, but with much less variance. The noticeable discontinuity in portfolio ESG values on 01/01/2020 arises from rather large changes in the ESG ratings of a number of these companies in the 12/31/2019 data release compared to that of 12/31/2018. (See Table A.1.)

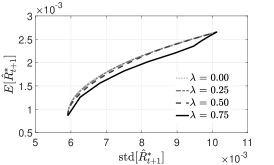

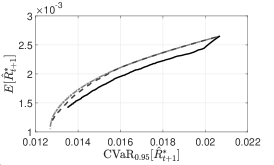

We computed moment values for the distribution of the returns for the same () selection of efficient frontier portfolios as in Table A.2. Specifically we consider the mean, median, standard deviation (Std), skewness (Skew), and excess kurtosis (ExKurt). Table A.3 summarizes these values for both optimizations. For each fixed value of , mean, median returns and the Std increase with , much more so under MV optimization. Skewness and ExKurt decrease as increases.

We also computed the portfolios’ performance relative to five popular RRRs: the Sharpe (SR), Sortino, STAR, Rachev and Gini ratios [24].181818 Here we define the Sharpe, Sortino and STAR ratios using only the portfolio returns and not the excess returns relative to a benchmark. These values are summarized in Table A.4. The optimized portfolios generally produce superior RRR values compared to the benchmark over all ranges of and . For and , the RRRs for MV generally outperform those for mCVaR0.99.

When , the choice of does not significantly alter the performance of the optimal portfolios as the investor is only concerned with the risk of the investment, which is unaffected by the ESG score.

5 ESG-Valued Tangent Portfolios

The efficient frontiers in the plane (see Fig. 2) can be used to identify the ESG-valued tangent portfolio. This approach will naturally lead to an ESG reformulation of the capital asset pricing model (CAPM), the security market line (SML), and the two-fund separation theorem [69]. Determining the tangent portfolio for each ESG-valued efficient frontier in this space requires identification of an appropriate risk-free rate process .

The appropriate risk-free rate to be used should also be ESG-valued as in (1). This raises the issue of assigning an ESG score to a fixed-income security, in particular to any government bond. As a first attempt to address this, we proceeded as follows. We used the yield on the 10-year U.S. treasury bond (appropriate scaled to daily rates) and assigned the government bond a maximum ESG score of 100.191919 Another possibility is to use an ESG score for the appropriate country for a government bond. Some agencies are beginning to provide such scores, though not necessarily in the same scale used for companies. The motivation behind this choice is that the risk-free rate is not among the set of choices available to the investor; any other ESG value for the risk-free rate will be more arbitrary than simply assigning the maximum value. From (1), the appropriate ESG-valued riskless rate is then

| (18) |

The ESG-valued tangent portfolio for date will be uniquely determine by the straight line from the point which is tangent to the -specified ESG-valued efficient frontier.

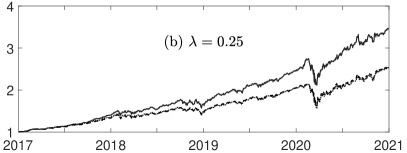

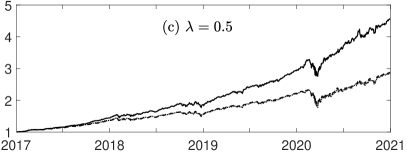

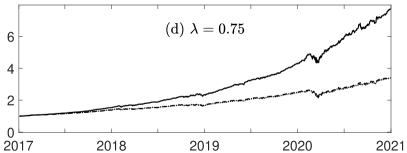

Using (18), the ESG-valued tangent portfolio can be identified on any efficient frontier parameterized by ().202020 It is critical to emphasize that the tangent portfolios are identified using the efficient frontiers computed in space and not in space. The optimization is performed in the former space, not the latter. As can be seen by comparing Figs. 2 and 3, convexity of the efficient frontiers can only be guaranteed in the former space. These ESG-valued tangent portfolios were identified for the (0.4% daily turnover constrained) portfolios computed in Section 4.1. Fig. 7 shows the price performance (obtained from the returns (9)) as well as the ESG scores for the tangent portfolios computed with mCVaR0.99 optimization. For , the price performance of these turnover constrained tangent portfolios is competitive with that obtained by the turnover unconstrained, efficient frontier portfolios (compare Figs. 7 (a) and (e)). Allowing for the initial transient behavior due to the turnover constraint, for the ESG scores for the turnover constrained tangent portolios are superior to those for the turnover unconstrained, efficient frontier portfolios (compare Figs. 7 (b) and (f)).

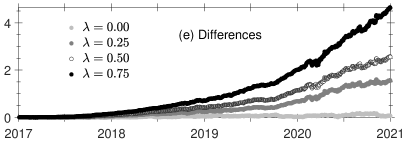

The time series are displayed in Fig. 8 for these mCVaR0.99 optimized tangent portfolios. time-series are also shown for the EWBH benchmark as well as for an ESG-valued DJIA index.212121 With reference to equations (9) and (10), the DJIA index is defined as follows. . No scenario sets are generated; where is the DJIA published weight for component and is the published weight for Dow Inc., which is excluded from our benchmark index. We utilized the published DJIA weights applicable to 30/12/2020 in composing our index. Note the close agreement between the EWBH and ESG-valued index values; both portfolios are comprised of the same stocks, with different weights applied. The differences between ESG-valued tangent portfolio and the ESG-valued index values are also plotted in Fig. 8. As noted earlier, the , ESG-valued plots are just scaled versions of the corresponding price plots. As increases, the differences between the optimized portfolio ESG-valued time series and those of the benchmarks (Fig. 8 (e)) grow more rapidly than the corresponding differences between optimized portfolio and benchmark price series (not shown, but can be inferred from Fig. 7).

Table A.5 provides the performance, moment, and RRR measures for these four tangent portfolios. At the higher values of , the tangent portfolios outperform the benchmark. Compared to the benchmark, total (and hence annualized) return almost doubles for the tangent portfolio as increases. With the exception of one Gini value, the value for every RRR considered is better than the benchmark as increases. Trivially the tangent portfolio average ESG score improves with . (The standard deviation of ESG decreases because more weight is given to the ESG score which remains constant over each year.) The average turnover considerably decreases as increases.

6 ESG-Valued Option Valuation

We consider the effect of ESG-valued returns on option pricing. Paralleling equations (11) and (12), we shall refer to the valuations given to options using ESG-valued returns as “ESG-valued option values” or simply “option values” and reserve the phrase “option price” to refer to the valuation of options based on traditional financial returns. When , ESG-valued option values become equal to option prices. For a given date , using the discrete methodology outlined in Appendix C, we computed European contingency claim option values for a sequence of expiration dates , and strike values using an ESG-valued tangent portfolio as the underlying. We chose the date corresponding to the efficient frontiers discussed in Sections 3.1 and 5. Option values were computed for each tangent portfolio. The same methodology was employed to obtain option values for the same date using the ESG-valued DJIA index as the underlying. We are interested in the difference between option values based upon the adjusted DJIA index and the tangent portfolios.

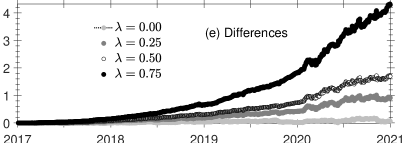

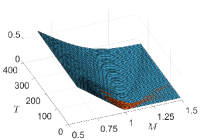

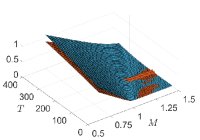

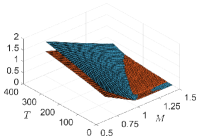

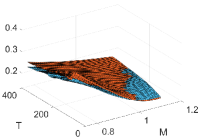

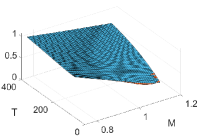

Call and put option values were expressed as functions of and “ESG-moneyness” , where is the ESG-valued price of the relevant portfolio on day . We considered ESG-moneyness values in the range and maturity times days. Comparisons of the call and put value surfaces based on the ESG-valued DJIA index and on the mCVaR0.99 optimized tangent portfolio for selected values of are given in Fig. 9.

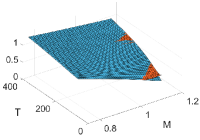

The respective call and put option value differences, and , between the tangent portfolios and the DJIA index are also given in Fig. 9.

When , call and put values (and hence, call and put option prices) written on the index and the mCVaR0.99 tangent portfolio are practically equal. The difference increases with , especially as strike values move further into-the-money. By construction, ESG-valued tangent portfolios have a higher ESG score, which in turn implies a positive shift in their aggregate value, creating higher call and put values. The effect of a positive on call and put values is different as a function of time to maturity; at constant in-the-money values of , call values increase with while put values decrease.

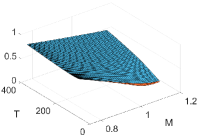

Fig. 10 compares implied volatility (IV) surfaces, computed by fitting to the Black-Scholes model, for call options based on the DJIA index and the mCVaR0.99-optimized tangent portfolios. For and in-the-money values, the IV surface of the DJIA index is above that of the tangent portfolio for short maturity times. For longer maturity dates it drops below. As increases, the two IV surfaces move upwards (overall volatility increases); the difference between the surfaces decreases; and the volatility “smirk” becomes steeper.

7 ESG-Valued Shadow Riskless Rate

The existence of a risk-free rate in the economy is a common and implicit assumption of modern financial theory. However, the situation in which the risk-free rate is not available for a market has been also considered. The seminal work is that of Black [16], who proposed a CAPM model without assuming the existence of a riskless rate. Black later introduced a “shadow real rate” as an option on fixed-income derivatives [17]. More recently, a different approach has been introduced by Rachev at al. [64], in which a shadow riskless rate is defined as a perpetual option on the set of risky securities selected as the investment universe. Rachev at al. computed analytic formulas for the shadow riskless rate under different models of the stochastic process driving the market uncertainty. The simplest case, where diffusion is driven by Brownian motions, is summarized in Appendix D.

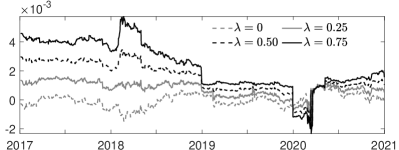

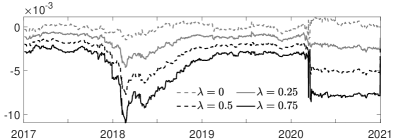

We analyze the effect of ESG-valued returns on the shadow riskless rate (SRR) derived in (D.3) of Appendix D for an investment universe defined by the 29 stocks comprising our ESG-valued DJIA index. For each trading date in the period from 01/03/2017 through 12/31/2020, using two-year moving windows we estimated the vector of mean values of, and the variance-covariance matrix for, the 29 stock returns. The asset (row) entries in were sorted in order of decreasing variance value. The elements required in (D.3) were obtained from the upper triangular matrix obtained from the Cholesky decomposition . To eliminate one dimension and obtain 28 Brownian motions, the last column of was replaced with a linear combination of its last two columns.

The SRR computations were performed on the DJIA index for the values .222222 We perform the SRR computations on the DJIA index rather than the optimized portfolios because the Dow Index is conventially recognized as an indicator of the general health of the US stock market (though there are valid arguments against this). The time series for the four SRRs are presented in Fig. 11. The SRR levels show separation in rough proportion to the value of ; however this proportion is affected by each year-end readjustment of ESG values. The separation between SRR curves appears to be roughly constant for the calendar years 2017 and 2019. Over 2018 the separations between the curves narrow. The Covid 19 crash in 2020 initially removes differences between SRR curves; after which they again begin to separate.

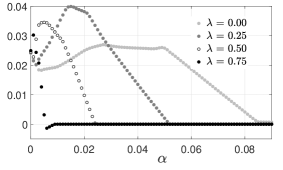

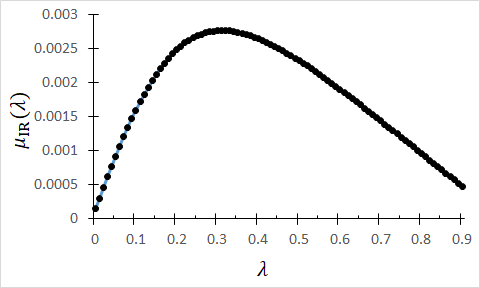

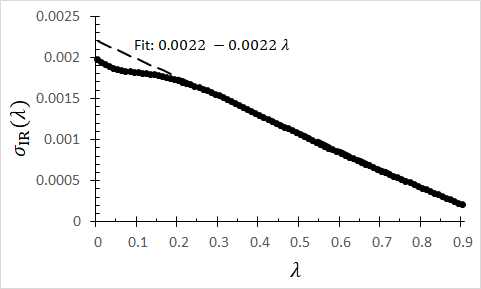

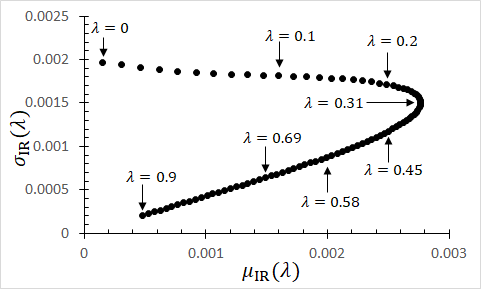

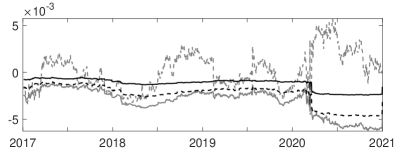

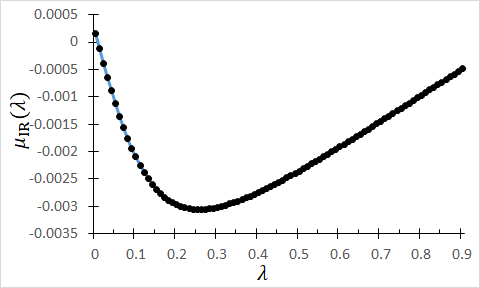

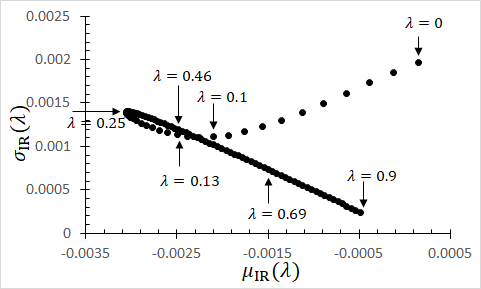

We define the standard deviation of the price deflator process by . This enables the definition of the SRR information ratio, IR. The four time series for IR are also plotted in Fig. 11. For each time series, the average and standard deviation values of IR can be computed. The behaviors of and for { 0,0.01,0.02,…,0.89,0.9} are presented in Fig. 12. The value of intially grows with , reaching a maximum time-averaged IR value at , after which the averaged SRR information ratio decreases. The standard deviation decreases with ; for , the decrease is linear. These results quantify the nonlinear impact of on the shadow riskless rate.

8 Discussion

In response to environmental changes and investor, societal, and governmental pressure, ESG ratings are assuming an important role in financial markets. Thus motivated, we have introduced a consistent ESG-valued framework for the inclusion of ESG ratings into dynamic pricing theory. There are two fundamental parameters in the framework; in addition to the traditional financial risk aversion parameter (), we introduce the ESG affinity parameter . When , our pricing framework reduces to traditional financial-risk versus financial-reward valuation. As increases, the framework places increased emphasis on the impact of ESG ratings on valuation. Thus our results are presented in terms of comparisons of valuations for compared with . In this work we have applied the ESG-valued framework to portfolio optimization, risk measures, option pricing, and the concept of shadow riskless rates. Although the ESG-valued return (1) is linearly dependent on ESG scores through , other non-linearities in portfolio and option valuation ultimately result in non-linear dependence on .

The philosophy incorporated in our framework is that socially responsible investing places a value on an investment portfolio that is competitive with (or “additional to”) financial return. Individual investor emphasis on that value is adjusted through the ESG affinity parameter. As a consequence, our framework produces valuations (e.g. for portfolios, options, riskless rates) in terms of an ESG-valued numeraire which reduces to a standard financial price when . Standardization of such a numeraire will become necessary if ESG-valued valuation is to be adopted. This would require the development of market indices expressed in terms of a standard ESG (or SRI) numeraire.

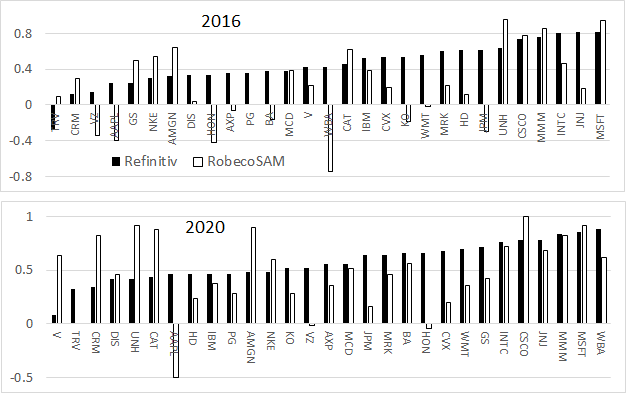

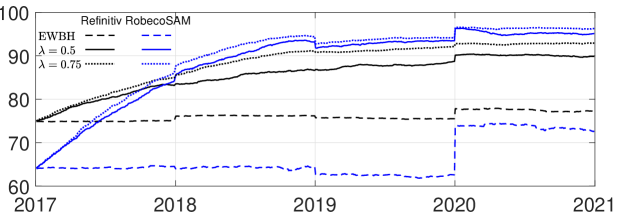

If adopted, a framework such as that developed here will require consideration of a myriad of issues, some of which are being pursued as described in the Introduction; others arise from considerations encountered while implementing the framework. In our view, one of the most important limitations is the deterministic nature of the ESG rankings employed here; we have ignored the variability of agency-provided ESG scores. As noted in the introduction, the definition of methodologies, and the consequent creation of databases related to ESG scores has experienced huge growth in the last ten years, resulting in a wide set of options in the choice of rating agency. Although it is not our intention to further address that issue in this paper, as it has been extensively explored in literature cited, we provide some insight on its impact on our ESG-valued valuation framework by considering scores from two different providers. In the supplement to this paper, we have repeated the computational results presented in this manuscript using ESG scores provided by RobecoSAM.

Despite the general disagreement of ESG scores between these two providers, we have observed that optimal portfolios performances, and hence efficient frontiers, on the DJIA index present relative stable results between the two scoring systems. This in turn implies stable results for the option pricing example in Section 6. However, optimized portfolio compositions can considerably change when computed with RobecoSAM scores. This in turn is reflected on the shadow riskless rate implicit in the market, even if computed under Gaussian hypotheses, exhibiting wide variation in the SRR depending on the score system used. This result confirms the need for a stronger effort toward a convergence of methodologies to asses ESG scores.

Given the current and foreseable variation in ESG rating systems and methodologies, our framework accommodates (and in fact argues in favor of) ESG ratings as random variables whose stochastic properties reflect these variations. Evaluation of these properties will become more definitive once ESG ratings are updated on time scales shorter than the calendar year. Ideally, company-specific ESG ratings would change on a time scale intrinsic with the company’s activity.

Our work reveals that adoption of an ESG-valued valuation framework will require resolution of critical research issues. (i) Our model requires that ESG-ratings be rescaled to be comparable to financial returns, which requires scaling to a bounded interval with , . This requires the identification of a threshold ESG value satisfying which effectively separates “good” ESG ratings from “bad” ESG ratings. (ii) Traditional financial-reward : financial-risk metrics must be modified to incorporate ESG ratings, thus becoming ESG-valued-reward : ESG-valued-risk metrics. This raises the research question of “coherence”, the necessary set of properties that such adjusted metrics should satisfy. (iii) As excess return is often measured relative to a government set risk-free rate, the concept of applying ESG ratings to governments and government-issued bonds becomes a required research focus. (iv) The option pricing model explored here is based upon a discretization of a continuum model which captures limited information (specifically, only the standard deviation of the financial returns of the underlying). Thus another research avenue is the application of this ESG-valued framework to option valuation models that are capable of capturing more of the microstructure of the underlying asset price (and, when it becomes available, that of its ESG ratings). (v) The methodology used here for the computation of the shadow riskless rate requires identification of the standard deviation parameters (equation (D.1) of Appendix D) from the elements of the variance-covariance matrix of asset returns. There is currently no theory governing this identification; the Cholesky decomposition approach used here is ad hoc.

Appendix A Tables

| Ticker | 12/31 | 12/31 | 12/31 | 12/30 | 12/29 | 12/31 | 12/31 | 12/31 |

|---|---|---|---|---|---|---|---|---|

| 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

| MMM | 88 | 90 | 86 | 88 | 88 | 87 | 89 | 92 |

| AXP | 50 | 51 | 51 | 68 | 73 | 73 | 78 | 78 |

| AMGN | 67 | 65 | 68 | 66 | 75 | 72 | 74 | 74 |

| AAPL | 61 | 57 | 54 | 62 | 69 | 70 | 67 | 73 |

| BA | 59 | 73 | 66 | 69 | 80 | 78 | 80 | 83 |

| CAT | 75 | 69 | 75 | 73 | 65 | 69 | 69 | 72 |

| CVX | 73 | 73 | 80 | 77 | 88 | 84 | 79 | 84 |

| CSCO | 83 | 85 | 85 | 87 | 87 | 88 | 88 | 89 |

| KO | 77 | 72 | 73 | 77 | 75 | 70 | 65 | 76 |

| GS | 63 | 67 | 72 | 62 | 70 | 73 | 86 | 86 |

| HD | 63 | 78 | 70 | 81 | 83 | 74 | 72 | 73 |

| HON | 68 | 53 | 63 | 67 | 68 | 74 | 75 | 83 |

| IBM | 79 | 73 | 81 | 76 | 77 | 80 | 71 | 73 |

| INTC | 86 | 91 | 91 | 90 | 87 | 88 | 88 | 88 |

| JNJ | 91 | 92 | 93 | 91 | 90 | 89 | 88 | 89 |

| JPM | 71 | 71 | 78 | 81 | 83 | 77 | 82 | 82 |

| MCD | 77 | 70 | 64 | 69 | 71 | 75 | 70 | 78 |

| MRK | 78 | 71 | 72 | 80 | 81 | 77 | 80 | 82 |

| MSFT | 92 | 92 | 93 | 91 | 90 | 93 | 93 | 93 |

| NKE | 68 | 65 | 75 | 65 | 70 | 71 | 72 | 74 |

| PG | 60 | 59 | 72 | 68 | 66 | 65 | 71 | 73 |

| CRM | 46 | 41 | 46 | 56 | 63 | 72 | 62 | 67 |

| TRV | 42 | 49 | 43 | 36 | 44 | 63 | 70 | 66 |

| UNH | 62 | 64 | 67 | 82 | 78 | 80 | 72 | 71 |

| VZ | 72 | 69 | 60 | 57 | 66 | 68 | 75 | 76 |

| V | 21 | 51 | 52 | 71 | 72 | 71 | 53 | 54 |

| WBA | 39 | 53 | 60 | 71 | 72 | 74 | 81 | 94 |

| WMT | 78 | 78 | 79 | 78 | 77 | 74 | 81 | 85 |

| DIS | 61 | 62 | 64 | 67 | 65 | 76 | 78 | 71 |

| Model | Tot. Ret | Ann. Ret | AvgTO | ETL95 | ETR95 | MDD | ESG* | ||

|---|---|---|---|---|---|---|---|---|---|

| (%) | (%) | (%) | (%) | (%) | (%) | avg | std | ||

| EWBH | 90.14 | 17.68 | 0.00 | -3.41 | 2.86 | 33.00 | 72.72 | 2.97 | |

| mCVaR0.99 | |||||||||

| 0.00 | 0.0 | 70.75 | 14.53 | 0.40 | -2.74 | 2.41 | 28.47 | 71.97 | 2.05 |

| 0.3 | 71.53 | 14.66 | 0.40 | -2.74 | 2.40 | 28.36 | 71.99 | 2.06 | |

| 0.5 | 71.85 | 14.71 | 0.40 | -2.75 | 2.41 | 28.36 | 72.02 | 2.01 | |

| 0.7 | 73.88 | 15.05 | 0.40 | -2.76 | 2.44 | 27.62 | 72.33 | 2.17 | |

| 0.9 | 82.60 | 16.49 | 0.40 | -2.90 | 2.55 | 28.23 | 72.61 | 2.93 | |

| 0.25 | 0.0 | 71.17 | 14.60 | 0.40 | -2.73 | 2.40 | 28.20 | 72.55 | 1.78 |

| 0.3 | 70.80 | 14.53 | 0.40 | -2.73 | 2.41 | 28.05 | 72.86 | 1.71 | |

| 0.5 | 71.60 | 14.67 | 0.40 | -2.73 | 2.41 | 27.66 | 73.17 | 1.68 | |

| 0.7 | 73.35 | 14.96 | 0.40 | -2.75 | 2.44 | 26.94 | 74.83 | 1.77 | |

| 0.9 | 92.13 | 18.00 | 0.39 | -2.96 | 2.65 | 25.71 | 78.59 | 2.53 | |

| 0.50 | 0.0 | 69.77 | 14.36 | 0.40 | -2.73 | 2.40 | 28.01 | 73.78 | 1.56 |

| 0.3 | 69.62 | 14.33 | 0.40 | -2.73 | 2.41 | 27.89 | 74.30 | 1.57 | |

| 0.5 | 84.62 | 16.81 | 0.39 | -2.86 | 2.57 | 25.23 | 80.36 | 2.72 | |

| 0.7 | 93.51 | 18.22 | 0.38 | -2.97 | 2.68 | 24.78 | 82.13 | 3.18 | |

| 0.9 | 112.02 | 20.98 | 0.36 | -3.20 | 2.94 | 24.37 | 84.51 | 4.14 | |

| 0.75 | 0.0 | 68.57 | 14.15 | 0.40 | -2.74 | 2.41 | 27.43 | 76.50 | 1.95 |

| 0.3 | 72.50 | 14.82 | 0.40 | -2.79 | 2.46 | 26.67 | 78.85 | 2.38 | |

| 0.5 | 80.31 | 16.12 | 0.39 | -2.84 | 2.53 | 25.69 | 80.89 | 2.87 | |

| 0.7 | 112.57 | 21.06 | 0.34 | -3.26 | 2.98 | 25.39 | 86.65 | 4.97 | |

| 0.9 | 143.49 | 25.30 | 0.33 | -3.61 | 3.35 | 27.40 | 88.19 | 5.66 | |

| MV | |||||||||

| 0.00 | 0.0 | 76.82 | 15.54 | 0.40 | -2.84 | 2.46 | 29.17 | 71.93 | 2.59 |

| 0.05 | 84.53 | 16.80 | 0.40 | -3.06 | 2.61 | 30.62 | 72.38 | 2.80 | |

| 0.10 | 90.68 | 17.77 | 0.38 | -3.33 | 2.80 | 32.39 | 73.49 | 3.22 | |

| 0.15 | 90.64 | 17.77 | 0.39 | -3.55 | 2.96 | 35.00 | 74.17 | 3.46 | |

| 0.20 | 88.69 | 17.46 | 0.40 | -3.73 | 3.08 | 37.27 | 74.30 | 3.63 | |

| 0.25 | 0.0 | 85.13 | 16.90 | 0.40 | -2.95 | 2.52 | 30.21 | 72.01 | 2.81 |

| 0.05 | 84.74 | 16.83 | 0.40 | -3.21 | 2.74 | 30.96 | 77.46 | 3.49 | |

| 0.10 | 102.24 | 19.54 | 0.40 | -3.51 | 3.08 | 30.64 | 81.10 | 4.29 | |

| 0.15 | 109.34 | 20.60 | 0.40 | -3.74 | 3.31 | 31.39 | 82.49 | 4.72 | |

| 0.20 | 114.60 | 21.36 | 0.40 | -3.87 | 3.43 | 32.07 | 83.14 | 5.01 | |

| 0.50 | 0.0 | 92.87 | 18.12 | 0.40 | -3.14 | 2.63 | 31.68 | 72.00 | 2.78 |

| 0.05 | 93.35 | 18.19 | 0.40 | -3.42 | 3.01 | 29.52 | 81.58 | 4.96 | |

| 0.10 | 144.99 | 25.50 | 0.35 | -3.76 | 3.54 | 27.01 | 86.22 | 5.80 | |

| 0.15 | 170.92 | 28.74 | 0.32 | -3.95 | 3.75 | 27.47 | 87.59 | 5.94 | |

| 0.20 | 180.31 | 29.86 | 0.30 | -4.05 | 3.84 | 27.72 | 88.01 | 5.99 | |

| 0.75 | 0.0 | 100.63 | 19.30 | 0.40 | -3.42 | 2.87 | 33.14 | 72.14 | 2.97 |

| 0.05 | 101.12 | 19.38 | 0.39 | -3.57 | 3.20 | 28.20 | 83.86 | 5.66 | |

| 0.10 | 166.27 | 28.18 | 0.31 | -3.88 | 3.67 | 27.43 | 87.69 | 6.04 | |

| 0.15 | 191.69 | 31.17 | 0.27 | -4.05 | 3.87 | 27.53 | 88.51 | 6.04 | |

| 0.20 | 202.70 | 32.41 | 0.26 | -4.15 | 3.96 | 28.03 | 88.76 | 6.11 | |

| Model | Mean | Median | Std | Skew | ExKurt | Model | Mean | Median | Std | Skew | ExKurt | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EWBH | 6.4 | 11.1 | 1.3 | -1.02 | 21.9 | |||||||

| mCVaR0.99 | MV | |||||||||||

| 0.00 | 0.0 | 5.3 | 8.3 | 1.1 | -0.92 | 22.1 | 0.00 | 5.7 | 9.3 | 1.1 | -0.93 | 20.4 |

| 0.3 | 5.4 | 8.0 | 1.1 | -0.92 | 22.2 | 0.05 | 6.1 | 10.7 | 1.2 | -1.08 | 22.9 | |

| 0.5 | 5.4 | 8.5 | 1.1 | -0.92 | 22.3 | 0.10 | 6.4 | 11.1 | 1.3 | -1.17 | 23.1 | |

| 0.7 | 5.5 | 9.6 | 1.1 | -0.90 | 22.4 | 0.15 | 6.4 | 11.2 | 1.4 | -1.32 | 23.9 | |

| 0.9 | 6.0 | 9.9 | 1.2 | -0.97 | 22.7 | 0.20 | 6.3 | 11.5 | 1.5 | -1.40 | 24.1 | |

| 0.25 | 0.0 | 5.3 | 8.7 | 1.1 | -0.88 | 21.8 | 0.00 | 6.1 | 10.1 | 1.1 | -1.02 | 21.0 |

| 0.3 | 5.3 | 8.6 | 1.1 | -0.89 | 21.8 | 0.05 | 6.1 | 10.6 | 1.3 | -1.05 | 23.2 | |

| 0.5 | 5.4 | 8.5 | 1.1 | -0.88 | 21.8 | 0.10 | 7.0 | 12.3 | 1.4 | -0.91 | 20.8 | |

| 0.7 | 5.5 | 10.2 | 1.1 | -0.82 | 22.1 | 0.15 | 7.4 | 12.5 | 1.5 | -0.90 | 20.2 | |

| 0.9 | 6.5 | 10.6 | 1.2 | -0.68 | 20.4 | 0.20 | 7.6 | 12.0 | 1.5 | -0.88 | 19.4 | |

| 0.50 | 0.0 | 5.3 | 9.6 | 1.1 | -0.83 | 21.2 | 0.0 | 6.5 | 11.7 | 1.2 | -1.08 | 22.3 |

| 0.3 | 5.3 | 9.5 | 1.1 | -0.83 | 21.4 | 0.05 | 6.6 | 10.6 | 1.4 | -0.74 | 22.0 | |

| 0.5 | 6.1 | 11.1 | 1.1 | -0.51 | 19.0 | 0.10 | 8.9 | 13.4 | 1.5 | -0.43 | 17.5 | |

| 0.7 | 6.6 | 11.2 | 1.2 | -0.43 | 18.7 | 0.15 | 9.9 | 12.6 | 1.6 | -0.46 | 16.2 | |

| 0.9 | 7.5 | 11.0 | 1.3 | -0.34 | 17.3 | 0.20 | 10.3 | 11.7 | 1.6 | -0.49 | 16.0 | |

| 0.75 | 0.0 | 5.2 | 9.4 | 1.1 | -0.70 | 19.8 | 0.0 | 6.9 | 12.3 | 1.3 | -1.11 | 23.3 |

| 0.3 | 5.4 | 10.4 | 1.1 | -0.60 | 19.0 | 0.05 | 7.0 | 12.2 | 1.4 | -0.52 | 20.1 | |

| 0.5 | 5.9 | 10.8 | 1.1 | -0.47 | 18.3 | 0.10 | 9.7 | 13.3 | 1.6 | -0.43 | 16.4 | |

| 0.7 | 7.5 | 11.5 | 1.3 | -0.23 | 15.8 | 0.15 | 10.7 | 11.8 | 1.6 | -0.48 | 15.8 | |

| 0.9 | 8.9 | 12.8 | 1.4 | -0.36 | 16.0 | 0.20 | 11.0 | 11.8 | 1.7 | -0.52 | 16.0 | |

| Model | SR | Sortino | STAR | Rachev | Gini | Model | SR | Sortino | STAR | Rachev | Gini | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | |||

| EWBH | 4.86 | 6.59 | 1.88 | 83.86 | 12.26 | |||||||

| mCVaR0.99 | MV | |||||||||||

| 0.00 | 0.0 | 4.87 | 6.69 | 1.94 | 87.79 | 12.42 | 0.0 | 5.09 | 6.96 | 2.00 | 86.56 | 12.97 |

| 0.3 | 4.91 | 6.75 | 1.96 | 87.84 | 12.55 | 0.05 | 5.09 | 6.92 | 1.99 | 85.10 | 13.03 | |

| 0.5 | 4.92 | 6.76 | 1.96 | 87.76 | 12.55 | 0.10 | 4.92 | 6.66 | 1.93 | 83.94 | 12.35 | |

| 0.7 | 4.98 | 6.85 | 2.00 | 88.42 | 12.66 | 0.15 | 4.62 | 6.21 | 1.81 | 83.29 | 11.47 | |

| 0.9 | 5.16 | 7.08 | 2.07 | 88.03 | 13.11 | 0.20 | 4.34 | 5.81 | 1.69 | 82.50 | 10.68 | |

| 0.25 | 0.0 | 4.91 | 6.76 | 1.96 | 87.99 | 12.53 | 0.0 | 5.34 | 7.28 | 2.08 | 85.36 | 13.70 |

| 0.3 | 4.89 | 6.73 | 1.95 | 88.13 | 12.46 | 0.05 | 4.85 | 6.60 | 1.90 | 85.36 | 12.30 | |

| 0.5 | 4.93 | 6.79 | 1.97 | 88.32 | 12.56 | 0.10 | 5.02 | 6.89 | 2.00 | 87.79 | 12.40 | |

| 0.7 | 4.95 | 6.84 | 1.99 | 88.64 | 12.61 | 0.15 | 4.93 | 6.78 | 1.97 | 88.48 | 12.05 | |

| 0.9 | 5.45 | 7.59 | 2.20 | 89.56 | 13.77 | 0.20 | 4.93 | 6.78 | 1.96 | 88.78 | 11.96 | |

| 0.50 | 0.0 | 4.85 | 6.67 | 1.93 | 87.92 | 12.33 | 0.0 | 5.38 | 7.31 | 2.08 | 83.94 | 13.87 |

| 0.3 | 4.83 | 6.65 | 1.92 | 88.02 | 12.27 | 0.05 | 4.82 | 6.66 | 1.92 | 88.23 | 12.03 | |

| 0.5 | 5.31 | 7.43 | 2.13 | 89.90 | 13.41 | 0.10 | 5.84 | 8.26 | 2.37 | 94.17 | 14.38 | |

| 0.7 | 5.49 | 7.72 | 2.21 | 90.18 | 13.81 | 0.15 | 6.18 | 8.76 | 2.51 | 94.89 | 15.14 | |

| 0.9 | 5.80 | 8.21 | 2.34 | 91.87 | 14.46 | 0.20 | 6.24 | 8.84 | 2.53 | 94.94 | 15.26 | |

| 0.75 | 0.0 | 4.78 | 6.60 | 1.90 | 88.23 | 12.05 | 0.0 | 5.22 | 7.08 | 2.03 | 83.98 | 13.32 |

| 0.3 | 4.90 | 6.80 | 1.95 | 88.27 | 12.36 | 0.05 | 4.87 | 6.80 | 1.95 | 89.64 | 11.97 | |

| 0.5 | 5.19 | 7.24 | 2.07 | 89.17 | 13.07 | 0.10 | 6.20 | 8.80 | 2.51 | 94.65 | 15.28 | |

| 0.7 | 5.77 | 8.17 | 2.30 | 91.53 | 14.39 | 0.15 | 6.48 | 9.20 | 2.63 | 95.40 | 15.94 | |

| 0.9 | 6.13 | 8.69 | 2.45 | 92.86 | 15.27 | 0.20 | 6.54 | 9.28 | 2.66 | 95.63 | 16.10 | |

| Model | Tot. Ret | Ann. Ret | AvgTO | ETL95 | ETR95 | MDD | ESG* | |||

|---|---|---|---|---|---|---|---|---|---|---|

| (%) | (%) | (%) | (%) | (%) | (%) | avg | std | |||

| EWBH | 90.14 | 17.69 | 0.00 | -3.41 | 2.86 | 32.87 | 72.72 | 2.97 | ||

| mCVaR0.99 | ||||||||||

| 0.00 | 95.01 | 18.45 | 0.40 | -3.48 | 2.92 | 34.06 | 74.04 | 3.49 | ||

| 0.25 | 114.91 | 21.40 | 0.35 | -3.80 | 3.38 | 31.09 | 82.98 | 4.67 | ||

| 0.50 | 129.63 | 23.46 | 0.33 | -3.60 | 3.36 | 26.86 | 84.58 | 4.69 | ||

| 0.75 | 176.66 | 29.43 | 0.23 | -3.97 | 3.78 | 27.49 | 88.08 | 5.83 | ||

| MV | ||||||||||

| 0.00 | 93.80 | 18.26 | 0.42 | -3.76 | 3.13 | 37.23 | 74.64 | 3.76 | ||

| 0.25 | 118.44 | 21.90 | 0.33 | -4.10 | 3.60 | 34.23 | 83.64 | 5.22 | ||

| 0.50 | 154.95 | 26.77 | 0.25 | -4.12 | 3.83 | 30.23 | 86.09 | 5.62 | ||

| 0.75 | 207.56 | 32.95 | 0.16 | -4.21 | 4.03 | 28.14 | 88.51 | 6.06 | ||

| Model | Mean | Median | Std | Skew | ExKurt | Mean | Median | Std | Skew | ExKurt |

| EWBH | 6.4 | 11.1 | 1.3 | -1.02 | 21.9 | |||||

| mCVaR0.99 | MV | |||||||||

| 0.00 | 6.7 | 11.4 | 1.4 | -1.28 | 23.9 | 6.6 | 11.6 | 1.5 | -1.36 | 23.7 |

| 0.25 | 7.6 | 11.9 | 1.5 | -0.86 | 19.1 | 7.8 | 11.7 | 1.6 | -0.92 | 18.7 |

| 0.50 | 8.3 | 12.6 | 1.4 | -0.50 | 16.8 | 9.3 | 12.9 | 1.7 | -0.64 | 16.7 |

| 0.75 | 10.1 | 11.7 | 1.6 | -0.45 | 15.8 | 11.2 | 13.0 | 1.7 | -0.51 | 15.1 |

| Model | SR | Sortino | STAR | Rachev | Gini | SR | Sortino | STAR | Rachev | Gini |

| (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | (%) | |

| EWBH | 4.86 | 6.59 | 1.88 | 83.86 | 12.26 | |||||

| mCVaR0.99 | MV | |||||||||

| 0.00 | 4.87 | 6.57 | 1.91 | 83.82 | 12.19 | 4.48 | 6.00 | 1.75 | 83.05 | 11.02 |

| 0.25 | 5.02 | 6.92 | 2.00 | 88.87 | 12.18 | 4.79 | 6.57 | 1.90 | 87.84 | 11.51 |

| 0.50 | 5.69 | 8.01 | 2.30 | 93.20 | 13.92 | 5.61 | 7.85 | 2.26 | 92.94 | 13.57 |

| 0.75 | 6.29 | 8.93 | 2.55 | 95.31 | 15.44 | 6.52 | 9.25 | 2.66 | 95.70 | 15.88 |

Appendix B MV and mCVaRβ ESG-Valued Optimization

Extension of MV and mCVaRβ optimization to ESG-valued returns is straightforward. Consider a universe of assets and the corresponding series of simulated ESG-valued returns ; ; . For MV optimization, let (with transpose denoted by ) denote the vector of the sample means and the corresponding variance-covariance matrix computed from the adjusted returns. Let denote the portfolio weight232323 Without loss of generality, we consider long-only portfolio optimization. for asset . The ESG-valued MV optimization is obtained as the solution of the quadratic programming problem [56, 57]

| (B.1) |

subject to the constraints

| (B.2) | |||

| (B.3) |

for a particular choice of and , where is the risk-aversion parameter.

Appendix C ESG-Valued Option Valuation: Discrete Model

Consider the problem of pricing a European contingent claim on the underlying securuity on day having strike value and maturity date . We utilize the following discrete option pricing approach. Following the procedure in Section 3.1, we fit an ARMA()-GARCH(1,1) model to a two-year window of historical returns of , assuming that the innovations are distributed according to an NIG distribution. From the NIG fit, we randomly generate a set of of innovations which, using the fitted ARMA-GARCH parameters, is conveted into a return trajectory . We generate an ensemble of such return trajectories, . Using the ESG score for day , from (1) each trajectory can then be converted to a trajectory of ESG-valued returns and consequently a set of ESG-valued price trajectories .242424 As noted in Section 6, we used , .

We compute an ESG-valued price for call and put options in the standard way; the contract value is given by the discounted expected value of the contract pay-off, conditioned to a filtration , where the conditional expectation is with respect to a risk-neutral measure [28], which discounts expected values at the ESG-valued risk-free rate defined in (18),

| (C.1) |

Given the risk neutral probability measure , European call (c) and put (p) ESG-valued option values on the underlying can be computed as

| (C.2) | ||||

In the discrete setting of this paper,

and the option valuation problem is reduced to identifying through the coefficients . We solve for these coefficients by minimizing the Kullback-Leibler divergence between and the natural world probability [5]. This involves solving the convex problem

| (C.3) |

subject to the constraints

| (C.4) | |||

| (C.5) | |||

| (C.6) |

In (C.3), is the probability of trajectory under . As each trajectory is equally likely, . Option values are then computed from the discrete version of (C.2)

| (C.7) | ||||

Appendix D Shadow Riskless Rate

Consider a set of risky securities whose prices ; are driven by Brownian motions252525 More complex pricing models have been considered [64]; here we employ the basic Brownian motion model. . Thus

| (D.1) |

To eliminate arbitrage opportunities in the market defined by (D.1), we search for the unique state-price deflator

| (D.2) |

such that the discounted prices , are martingales. It is easy to show262626 This follows directly from Itô’s formula. that this requirement is equivalent to solving the linear system

| (D.3) |

for . Following the treatment in Duffie [30, Chapter 6D], the risk premium for each security is

| (D.4) |

where is the short-term, shadow riskless rate (SRR) observed in the market.

References

- [1] Abate, G., Basile, I., and Ferrari, P. The level of sustainability and mutual fund performance in europe: An empirical analysis using ESG ratings. Corporate Social Responsibility and Environmental Management 28, 5 (2021), 1446–1455.

- [2] Alessandrini, F., Baptista Balula, D., and Jondeau, E. ESG screening in the fixed-income universe. Swiss Finance Institute Research Paper, 21-77 (2021).

- [3] Amel-Zadeh, A., and Serafeim, G. Why and how investors use ESG information: Evidence from a global survey. Financial Analysts Journal 74, 3 (2018), 87–103.

- [4] Artzner, P., Delbaen, F., Eber, J.-M., and Heath, D. Coherent measures of risk. Mathematical Finance 9, 3 (1999), 203–228.

- [5] Avellaneda, M., Buff, R., Friedman, C., Grandechamp, N., Kruck, L., and Newman, J. Weighted Monte Carlo: A new technique for calibrating asset-pricing models. International Journal of Theoretical and Applied Finance 04, 01 (2001), 91–119.

- [6] BadÃa, G., Pina, V., and Torres, L. Financial performance of government bond portfolios based on environmental, social and governance criteria. Sustainability 11, 9 (2019).

- [7] Bannier, C. E., Bofinger, Y., and Rock, B. Corporate social responsibility and credit risk. Finance Research Letters 44 (2022), 102052.

- [8] Barndorff-Nielsen, O. E. Exponentially decreasing distributions for the logarithm of particle size. Proceedings of The Royal Society A: Mathematical, Physical and Engineering Sciences 353, 1674 (1977), 401–419.

- [9] Barndorff-Nielsen, O. E. Normal inverse Gaussian distributions and stochastic volatility modelling. Scandinavian Journal of Statistics 24, 1 (1997), 1–13.

- [10] Bello, Z. Y. Socially responsible investing and portfolio diversification. Journal of Financial Research 28, 1 (2005), 41–57.

- [11] Bénabou, R., and Tirole, J. Individual and corporate social responsibility. Economica 77, 305 (2010), 1–19.

- [12] Berg, F., Koelbel, J. F., and Rigobon, R. Aggregate confusion: The divergence of ESG ratings. MIT Sloan School of Management Cambridge, MA, USA, 2019.

- [13] Berry, T. C., and Junkus, J. C. Socially responsible investing: An investor perspective. Journal of Business Ethics 112, 4 (2013), 707–720.

- [14] Bilbao-Terol, A., Arenas-Parra, M., Cañal-Fernández, V., and Bilbao-Terol, C. Selection of socially responsible portfolios using hedonic prices. Journal of business ethics 115, 3 (2013), 515–529.

- [15] Billio, M., Costola, M., Hristova, I., Latino, C., and Pelizzon, L. Inside the ESG ratings: (dis)agreement and performance. Corporate Social Responsibility and Environmental Management 28, 5 (2021), 1426–1445.

- [16] Black, F. Capital market equilibrium with restricted borrowing. The Journal of Business 45, 3 (1972), 444–55.

- [17] Black, F. Interest rates as options. The Journal of Finance 50, 5 (1995), 1371–1376.

- [18] Boffo, R., and Patalano, R. ESG investing: Practices, progress and challenges. Tech. rep., OECD Paris, 2020.

- [19] Brooks, C., and Oikonomou, I. The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. The British Accounting Review 50, 1 (2018), 1–15. The Effects of Environmental, Social and Governance Disclosures and Performance on Firm Value.

- [20] Cesarone, F., Martino, M. L., and Carleo, A. Does ESG impact really enhance portfolio profitability?, January 2022.

- [21] Chatterji, A. K., Durand, R., Levine, D. I., and Touboul, S. Do ratings of firms converge? Implications for managers, investors and strategy researchers. Strategic Management Journal 37, 8 (2016), 1597–1614.

- [22] Cheklov, A., Uryasev, S., and Zabarankin, M. Drawdown measure in portfolio optimization. International Journal of Theoretical and Applied Finance 08, 01 (2005), 13–58.

- [23] Chen, L., Zhang, L., Huang, J., Xiao, H., and Zhou, Z. Social responsibility portfolio optimization incorporating ESG criteria. Journal of Management Science and Engineering 6, 1 (2021), 75–85.

- [24] Cheridito, P., and Kromer, E. Reward-risk ratios. Journal of Investment Strategies, Forthcoming (2013).

- [25] Christensen, D. M., Serafeim, G., and Sikochi, A. Why is corporate virtue in the eye of the beholder? The case of ESG ratings. The Accounting Review 97, 1 (04 2021), 147–175.

- [26] Clarke, R., de Silva, H., and Thorley, S. Portfolio constraints and the fundamental law of active management. Financial Analysts Journal 58, 5 (2002), 48–66.

- [27] Daugaard, D. Emerging new themes in environmental, social and governance investing: a systematic literature review. Accounting & Finance 60, 2 (2020), 1501–1530.

- [28] Delbaen, F., and Schachermayer, W. A general version of the fundamental theorem of asset pricing. Mathematische Annalen 300, 1 (1994), 463–520.

- [29] Dorfleitner, G., Utz, S., and Zhang, R. The pricing of green bonds: external reviews and the shades of green. Review of Managerial Science (2021), 1–38.

- [30] Duffie, D. Dynamic asset pricing theory, 3. ed ed. Princeton Univ. Press, Princeton, NJ, 2001.

- [31] Ehlers, T., and Packer, F. Green bond finance and certification. BIS Quarterly Review September (2017).

- [32] Fernandez, R., and Elfner, N. ESG integration in corporate fixed income. Journal of Applied Corporate Finance 27, 2 (2015), 64–72.

- [33] Friede, G., Busch, T., and Bassen, A. ESG and financial performance: aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance & Investment 5, 4 (2015), 210–233.

- [34] Frittelli, M., and Rosazza Gianin, E. Putting order in risk measures. Journal of Banking & Finance 26, 7 (2002), 1473–1486.

- [35] Gasser, S. M., Rammerstorfer, M., and Weinmayer, K. Markowitz revisited: Social portfolio engineering. European Journal of Operational Research 258, 3 (2017), 1181–1190.

- [36] Geczy, C. C., and Guerard, J. ESG and expected returns on equities: The case of environmental ratings. Wharton Pension Research Council Working Paper No. 2021-15 (August 2021).

- [37] Ghalanos, A. rugarch: Univariate GARCH models, 2012. R package version 1.0-16.

- [38] Gibson Brandon, R., Krueger, P., and Schmidt, P. S. ESG rating disagreement and stock returns. Financial Analysts Journal 77, 4 (2021), 104–127.

- [39] Giese, G., Lee, L.-E., Melas, D., Nagy, Z., and Nishikawa, L. Foundations of ESG investing: How ESG affects equity valuation, risk, and performance. The Journal of Portfolio Management 45, 5 (2019), 69–83.