Neural network model for imprecise regression

with interval dependent variables

111This work has been partially funded by the Engineering and Physical Science Research Council (EPSRC) through programme grant “Digital twins for improved dynamic design”, EP/R006768/1.

Abstract

This paper presents a computationally feasible method to compute rigorous bounds on the interval-generalisation of regression analysis to account for epistemic uncertainty in the output variables. The new iterative method uses machine learning algorithms to fit an imprecise regression model to data that consist of intervals rather than point values. The method is based on a single-layer interval neural network which can be trained to produce an interval prediction. It seeks parameters for the optimal model that minimizes the mean squared error between the actual and predicted interval values of the dependent variable using a first-order gradient-based optimization and interval analysis computations to model the measurement imprecision of the data. An additional extension to a multi-layer neural network is also presented. We consider the explanatory variables to be precise point values, but the measured dependent values are characterized by interval bounds without any probabilistic information. The proposed iterative method estimates the lower and upper bounds of the expectation region, which is an envelope of all possible precise regression lines obtained by ordinary regression analysis based on any configuration of real-valued points from the respective -intervals and their -values.

keywords:

imprecise regression, interval data, neural network, uncertainty1 Introduction

In real-life applications in science and engineering, data are often imperfect and contain uncertainty which arises, for example, from lack of knowledge, limited or inaccurate measurements, approximation or poor understanding of physical phenomena. This type of uncertainty is called epistemic uncertainty or incertitude [1, 2, 3] and can be modelled, for example, by interval bounds which is the simplest method for projecting such uncertainty through mathematical expressions. This type of interval uncertainty can arise in various cases including non-detects and data censoring [4], periodic observations, plus-or-minus measurement uncertainties, interval-valued expert opinions [5], privacy requirements, theoretical constraints, bounding studies, etc. [6, 7, 8].

Interval data can be considered as an alternative to \saysymbolic data modelled with uniform distributions over the interval ranges [9, 10, 11], which corresponds to Laplace’s principle of indifference with respect to the censored interval. All values within each interval are assumed to be equally likely. This assumption makes it relatively straightforward to calculate sample statistics for data sets containing such intervals. The alternative approach using only the ranges represents interval uncertainty purely in the form of bounds [12, 13, 6]. This approach is consistent with the theory of imprecise probabilities [14, 15, 16]. It models each interval as a set of all possible values, and calculations result in a class of distribution functions, corresponding to the different possible values within the respective intervals.

Regression analysis problems have been extensively studied for many years, and special focus has been given to regression models with interval-valued data. In the setting of symbolic data analysis, Billard and Diday [10] did pioneering work in which a linear regression model is fitted to the midpoint of the interval values. Over several decades various regression methods have been developed such as methods for linear regression models where the dependent variable has been either rounded or interval-censored [17, 18], methods for models that have interval-valued covariates and a precise dependent variable [19], interval-based algorithms for the data-fitting problem where measurement errors are supposed to be bounded and known [20, 21], some probabilistic [22] and likelihood-based [23] methods, non-parametric methods [24, 25], and others [26, 27]. In general, probabilistic models provide a more detailed uncertainty model, however interval-based techniques usually require fewer assumptions and provide theoretical guarantees on the reliability and robustness of the results. The method proposed in this paper combines these two approaches.

Regression analysis using artificial neural networks is widely used due to the ability to learn the complex relationship between the explanatory variables and their response. Neural networks are capable of modeling complex systems, analyzing data and making predictions in a variety of research fields. Uncertainty quantification is essential in neural network predictions because of imperfect models and limited or imprecise data. Depending on the form of the data and how it was collected, uncertainty can be modelled by non-probabilistic or probabilistic methods. Traditionally, it has been very common to make Gaussian assumptions about error structures. Such methods include Bayesian neural networks [28, 29], variational inference [30], the Monte Carlo dropout technique [31]. Gaussian assumptions can be used in classification problems [32, 33, 34] as well as regression problems. For instance, linear regression residuals are classically assumed to be normally distributed. However, this assumption of precise Gaussian distributions may not always be tenable for fully characterizing uncertainty when it includes both scatter and measurement imprecision.

We propose a new iterative method for fitting an imprecise linear regression model to data that include epistemic uncertainties. The method is based on a single-layer interval neural network (SLINN) which can be trained to produce an interval prediction. An additional extension to a multi-layer neural network is also presented. We consider the explanatory variables to be precise point values, and the dependent variables are presumed to have interval uncertainty. We assume that our imprecisely measured variables are surely enclosed within their respective censoring intervals, without necessarily knowing the distribution function characterizing the position of these values inside the intervals. Thus, the imprecision is modeled non-probabilistically even while the scatter of dependent values is modeled probabilistically by homoscedastic Gaussian distributions. The main contributions of this paper are that it introduces a computationally inexpensive way to compute rigorous bounds on the interval-generalisation of regression analysis to account for epistemic uncertainty in the output (dependent) variables. The method escapes computational difficulties associated with intervals and generalizes the notion of a regression line. We compare this approach and review several related ideas in regressions that take account of epistemic uncertainty in the -variable.

Section 2 familiarizes with interval arithmetic and the dependency problem. Section 3 provides comparison with alternative strategies. Section 4 describes the proposed approach for imprecise linear regression with interval-valued -data. Section 5 presents two first-order gradient-based optimization algorithms adapted to eliminate the dependency problem during interval computations. Sections 6 and 7 consider nonlinear regressions and multi-layer interval neural networks. Section 8 applies the proposed methods to synthetic and real data sets, and 9 offers conclusions.

2 Interval Analysis

2.1 Interval operations and functions

An interval can be denoted

where is the lower bound and is the upper bound, and is the set of all intervals. For intervals and , the basic interval operations are defined by

| (1) | ||||

Additional operations for computing midpoint, width, and absolute value are defined as

| (2) | ||||

An -interval vector is a vector with interval inputs

| (3) |

and an interval matrix is a matrix with interval entries .

For a general real function which maps an -vector to an -vector, the interval extension of is a function such that

| (4) |

For monotonically increasing (or decreasing) functions including elementary functions such as , , and others, the interval extension that produces sharp bounds can be computed using only endpoints

| (5) |

An interval function is called inclusion monotonic if for , where .

2.2 The dependency problem

The dependency problem is a huge stumbling block in the efficient application of interval arithmetic which can lead to much wider bounds for the computed output than the exact range of the expression implies. The dependency problem happens when a mathematical expression includes multiple instances of an interval variable. Naive replacement of floating point computations by intervals in an existing expression is not likely to lead to results that are best-possible. As an example, the interval-arithmetic computation of for yields

which is true but arguably not best-possible if we hold that is zero no matter what possible values might have, in which case a better answer would be .

To overcome the dependency problem in interval computations a number of special-purpose algorithms have been developed to obtain best-possible results for a variety of particular scenarios where algebraically removing repetitions is impossible or problematic. This includes centered, slope and mean value forms [35, 36], affine arithmetic [37, 38], Taylor models [39, 40], Bernstein polynomials [41], contractors, subpavings and other refinement strategies [42, 36, 43].

In this paper we will use the mean value form which is a second-order inclusion monotone approximation for an interval-valued extension of the real function

| (6) |

where is an interval inclusion of the Jacobian matrix of the function. In the case of an interval vector the second term in (6) reads , where is an interval extension of the partial derivatives .

3 Related Work

Classical regression methods. Billard Diday [10] proposed the center method (CM) which deals with interval-valued data in linear regression. This approach only takes into account the center points of the intervals, while leaving out other important information such as the widths of the intervals. Subsequent improvements to this method had been proposed in [44, 11, 45, 46] including separate regression models for the center and the range of the intervals, constrained linear regression models, and models based on the symbolic sample covariance. The center and range method (CRM) proposed by De Carvalho and Lima Neto [44] estimates the parameters for a linear model using both the center points and widths of the ranges of the interval-valued data as two independent models. The constrained center and range method (CCRM) [47] mathematically ensures that the lower bound is less or equal to the upper bound.

The sharp collection region. The methodology of imprecise probabilities offers powerful methods for reliable handling of coarse data [14, 48], which includes all situations where data are not observed in perfect resolution. The proposed iterative approach can be compared to an alternative strategy for handling interval data in the dependent variable of regression models. The sharp collection region (SCR) is one of three types of so-called \sayidentification regions that are discussed by Schollmeyer and Augustin in [18], which are sets of all parameters compatible with the interval data and model. This collection region has been studied, e.g., in [49, 50, 17] (cf., also [51]).

Let be a parameter space and be a statistical model associated with the unobserved random variable and the three observable random variables , assuming . With we denote the unknown true model and with the corresponding expectations. The sharp collection region is defined as

| (7) |

where is a joint distribution of the random variables under the model, is the joint distribution under a possible true model, and is a loss function which is zero if and only if the arguments are equal. The range of the expectation denotes the set of all values fulfilling the condition . The sharp collection region is the collection of all models that describe a possible random variable consistent with the boundaries in the best way in terms of the loss function . For a linear model and the classical quadratic loss function we have

| (8) |

It actually turns out that for the special case of linear regression under quadratic loss, the collection region is identical to the SLINN method. However, the SLINN approach is far more flexible and can be more widely adapted, e.g., to non-linear regression. A comparison of the proposed method, the sharp collection region and the center and range methods for a linear regression is presented in Section 8.

Monte Carlo simulations. We also compare the proposed single-layer interval neural network to a brute-force strategy based on Monte Carlo simulations which simply wiggles the points within the respective -intervals and searches for extreme cases. The most serious limitation of Monte Carlo simulations is that it represents all uncertainties as random variables. For example, in a large-scale problem which has many uncertain variables (like imprecise regression does), or which is computationally expensive to evaluate, the cost of Monte Carlo computations can become prohibitive. However, there are a number of special algorithms such as low-discrepancy sequences and Latin-hypercube sampling that can speed up the convergence of Monte Carlo.

Neural networks. The first ideas to incorporate interval-valued data in neural networks were described by Ishibuchi et al. [52] and Hernandez et al. [53] in training feed-forward neural networks and extending the backpropagation learning algorithm. Additional improvements to this strategy in the context of fuzzy regression analysis and nonlinear interval models were reported in [54, 55]. Traditional interval neural networks such as [54] and other versions mentioned above are based on interval arithmetic, but the authors apply only three interval operations (scalar multiplication and addition and multiplication of intervals) and avoid the subtraction operation. Thus their loss function which we denote [54] is not an interval and does not require general interval computations as it is defined as a sum of the differences between the upper and lower bounds separately. We believe that such a definition is valid under specific conditions, however only the use of pure interval arithmetic can guarantee that the obtained results are rigorous.

Other recent developments of the artificial neural networks for interval-valued data prediction such as [56, 57, 58, 59] are based on the CM and the CRM methods for linear regression. These neural networks exploit the loss function which is a weighted Euclidean distance between the predicted intervals and observed intervals such that

| (9) |

where is the weighting parameter which measures the relative importance of center points and radii. The use of this loss function is somewhat similar to Ishibuchi’s method in terms of avoiding an intervalized loss function and direct subtraction operations. In addition there is the bother of specifying the constant which may affect the results in an unclear way.

In [60] Sadeghi et al. presented an alternative way to efficiently train interval neural networks for imprecise data using the framework of interval predictor models (IPM). The IPM [61, 62] maps some observable variables (system inputs) into an interval that is used to predict an inaccessible variable. The regression model is tuned according to the minimax criterion of best fit, which amounts to selecting the parameters that minimize the maximum deviation from the observed by , i.e. . Unlike standard regression techniques, these models try to bound an envelope of the data using a conceptualization of fit different from the traditional least squares criterion, which produce interval estimates for the regression even from point-valued input data.

Summarizing the above, for the case of interval imprecision in the output variables with pairs we have

where is the loss function for the traditional approach [54], is the loss function for Sadeghi’s interval predictor model [60], and is our loss function. Several comparative examples are presented in Section 8. The loss functions proposed in this paper apply to regression problems. No attempt has been made to generalise them for other problems like classification or cross entropy.

4 Imprecise Regression

4.1 Statistical model and caveats

We consider a general linear model with one dependent variable where is a vector of observations on the dependent variable, is a augmented matrix with independent variables for observations including a constant term which is represented by column of ones, is an vector of random Gaussian errors, and is a vector of parameters to be estimated from the regression model

| (10) |

or, in matrix form,

| (11) |

In order to obtain a vector of regression coefficients we use ordinary least squares estimation which minimizes the sum of squared residuals

| (12) |

and yields a closed-form solution

| (13) |

When the dependent values in have uncertainty, they can each be replaced by interval bounds that guarantee the true value lies within them. In this case equation (13) becomes

| (14) |

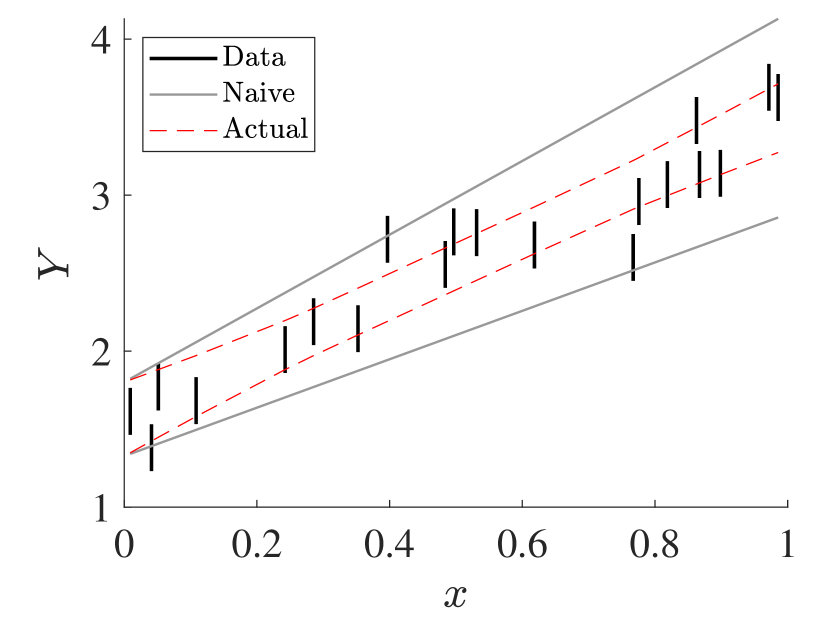

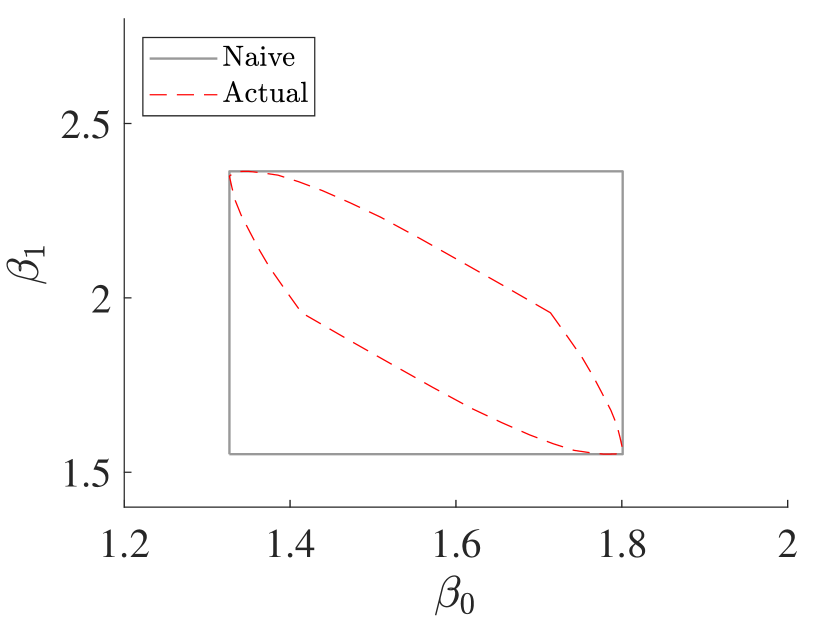

which gives the estimated interval coefficients . In the case of simple linear regression (), a naive solution would lead to these overly wide results

| (15) |

because the interval -values each appear two times in the expression for the -values. This naive approach uses a single step to solve closed-form equation (14) and forms the rectangle for all possibles values with bounds . An illustrative example is presented in Fig. 1 where solid grey lines correspond to the naive approach and red lines show the best-possible bounds considering all possible configurations of the -data within their respective interval as an expectation region which is a generalization of a regression line. We call these best-possible bounds the ‘actual’ bounds.

The identification region depicted within the red dashed lines in Fig. 1b was computed using an algorithm based on the insight that this region is the image of a multidimensional cuboid under a linear map (i.e., a zonotope, cf., [17]) for the sharp collection region [18].

It is important to note that there is a functional dependence between the slope and intercept which fills only a proper subset of the rectangle. Not all combinations are allowed. An optimal generalization of regression analysis to interval data would instead identify the envelope of all possible lines from regressions based on any possible configuration of points within the respective intervals . All such lines use only permissible combinations of and . As Fig. 1 suggests, the separate intervals for the slope and intercept are correct, but ignoring their dependence yields unnecessarily wide answers.

4.2 Iterative approach

The proposed iterative method is based on machine learning algorithms which fit an imprecise linear regression model to observations that include interval values. The regression model assumes that is linear in the unknown interval parameters to be estimated from the data. It generalises a single-layer neural network consisting of an input layer and output layer which replaces as the prediction. Generally, any layer of a neural network can be considered as an affine transformation with subsequent application of an activation function forming

where is a weight matrix and is a column-vector containing bias terms.

The proposed iterative method is a single-layer interval neural network, a supervised learning algorithm in a regression setting with interval-valued dependant variables. In the context of linear regression an activation function is not needed, and the SLINN iteratively optimises and by minimizing the interval mean squared error loss function

| (16) |

which is assumed to be defined and differentiable with respect to both and .

Training the interval extension of a real-valued neural network includes the following major steps:

-

1.

performing forward propagation to calculate an interval prediction ,

-

2.

computing the loss function at each training iteration which quantifies the distance between the actual and predicted values ,

-

3.

computing the gradient of the loss function with respect to interval parameters,

-

4.

minimizing the loss function with gradient descent or another optimization technique.

To perform interval arithmetic computations during the training process we use the specialized Matlab toolbox INTLAB [37] which provides powerful and rigorous tools for matrix operations. In this paper we consider two first-order gradient-based optimization algorithms and adapt them to interval computations eliminating the dependency problem.

5 Optimization Algorithms

5.1 Gradient descent

We shall first consider the most straightforward and popular first-order iterative optimization algorithm known as gradient descent [63, 64]. The algorithm updates the parameters adaptively at each iteration in the direction of the negative gradient of the loss function

| (17) | ||||

| (18) |

where is the learning rate which controls the size of the steps we take to reach minima.

Interval operations provide results that are rigorous in the sense that they bound all possible answers. The results are best-possible when they cannot be any tighter without excluding some possible answers. However, a direct naive substitution of the interval vector to the loss function (16) will cause the dependency problem as discussed in Section 2. The updating rules (17) and (18) add extra instances of intervals on each iteration to , which results in inflated bounds. Here and below we omit the use of square brackets for interval values and output for simplicity. Consider, for example, the sequence of iterations for updating the weights

| (19) |

At any iteration is the linear function

| (20) |

with respect to initial and . In order to overcome the dependency problem in the iterative approach, we use the mean value form to approximate the interval-valued function (20). The key idea is to apply form (6) to equation (17) so that for any interval variable we have

| (21) |

In more general cases when and the initial guesses are intervals equation (21) can be written in expanded form

| (22) |

The first term in (22) is nothing more than the standard updating rule for with precise midpoint values. Because the equation (20) is a linear function, the mean value form yields best-possible results even though it has multiple repeated interval variables, so the Jacobian matrix has only precise values without any uncertainty.

All three derivatives at iteration can be computed using the chain rule

| (23) | ||||

| (24) | ||||

| (25) |

The same argument applies to the biases and their derivatives from the Jacobian. Taking formula (23) as example, notice that the first multiplier in the first term is a constant coefficient for any . We call this structure a neighboring derivative which needs to be computed only once at the beginning of an iterated sequence. The second multiplier in the first term comes from the previous iteration. The same logic about the neighboring derivative applies to the second term in (23), where the second multiplier comes from the th result of the iteration. These interlinked iterations can be easily computed because the linearity of the first-order structure of the optimisation algorithm reveals each next derivative to be a combination of the derivative from the previous iteration multiplied by the neighboring derivative which is constant for any , across the linked iterations.

Although and can be optimally evaluated for any , naively computing the interval output layer also yields inflated uncertainty because of the unseen dependence between and caused by the repeated -values. To overcome this, the mean value form can be used for as well. The relevant derivatives are

| (26) |

and the resulting mean value form expression is

| (27) |

The first term in (27) is the precise central line fitted to midpoints taken from the interval inputs. We denote it as which will be useful in Section 7. Equation (27) can be thus written more compactly as

| (28) |

5.2 Gradient descent with momentum

Gradient descent is known to be slow compared to other optimization algorithms and can converge to a local minimum or saddle point when the loss function is highly non-convex. Choosing too small a learning rate leads to terribly slow convergence, while large can lead to divergence or to oscillating effects across the slope of the ravine. Also the learning process can be slow when an update is performed through all observations.

As an alternative, we adapt another optimization algorithm which is very similar to gradient descent but helps to accelerate it in the relevant direction. Gradient descent with momentum keeps in memory previous updates and has the following update rules:

| (29) | ||||

| (30) | ||||

| (31) | ||||

| (32) |

where is a hyperparameter called momentum that takes a value from 0 to 1. This momentum method uses an exponentially weighted average for and values and smooths down gradient measures. In order to adapt the momentum method to interval computations and reduce the interval dependency we rewrite equations (29-30) as

| (33) | ||||

and define the intermediate functions ,

| (34) | ||||

As in Section 5.1 we use the mean value form to approximate the interval functions and , which requires computing derivatives of and in (33) with respect to interval values. We can assume, for simplicity, that our initial guesses for are certain values, so formula (22) becomes a bit easier for this case:

| (35) |

Taking the full derivative of the multivariable function with respect to the interval vector for iterations yields

| (36) | ||||

| (37) | ||||

| (38) | ||||

so for iteration we have

| (39) |

The number of terms in (39) increases with each iteration because the updating rules for momentum include the functions and from previous iterations unlike the standard gradient descent. However, expression (39) depends on the previously computed and and has same neighboring derivatives as in formula (23) which should be computed once. In addition, we use the relationships between the derivatives

| (40) |

Thus, the two last terms in (38) are nothing more than the two last terms from (37) multiplied by . Assuming (40) and the sequential dependency on previous iterations, it is possible to rewrite (39) in a more compact form

| (41) |

where , and for

| (42) |

The particular derivatives needed for the linear and nonlinear regression settings are shown in A.

6 Other Forms of Nonlinear Regression Analysis

The model that we use here is linear with respect to unknown interval parameters, but not necessarily in the input variables . Therefore, it is possible to augment the model by replacing the input variables with nonlinear basis functions of the input variables for the one-dimensional case such as , where the are the regression coefficients. One of the possible options for a basis is to set , where . Such functional relationship is called polynomial regression, which is considered to be a special case of multiple linear regression. For this case the general design matrix in (10) can be rewritten as

| (43) |

Because the matrix is constant and doesn’t contain any uncertain variables, this makes it straightforward to compute the imprecise regression model with polynomial basis functions using the SLINN as , where . This expression does not have bias (intercept) term because we are using an augmented matrix which includes a column of ones. As an additional option we can replace with trigonometric terms, e.g.,

| (44) |

where is the order of the trigonometric model and .

These two extensions show how to use a linear model to characterise an nonlinear relationship between the independent variable and the corresponding conditional mean of . This generality can also be extended to the imprecise case where input data for the dependent variable has the form of intervals. The next section shows examples of such applications.

7 Nonlinear Regression as a Two-layer Neural Network

Exploiting the idea from Section 6, we can also use other basis functions which can be more flexible and provide broader tools for constructing imprecise regression models. For instance, let’s consider another tunable basis function which is commonly used in artificial neural networks as an activation function . We can construct a linear combination of sigmoid functions with some additional internal non-interval parameters

| (45) |

or in matrix form

| (46) |

This combination actually represents a feedforward two-layer neural network which consists of layers for hidden and output variables based on an input layer, as depicted in Fig. 2. The coefficients from (45) here are weights and biases of the hidden layer. Using now conventional denotations for the forward propagation we have

| Input: | ||

|---|---|---|

| Hidden layer: | ||

| Output: |

where the sigmoid function is used for . We use square brackets to emphasize that the hidden layer doesn’t contain interval weights and biases unlike the output layer.

The interval \saylinear model of this two-layer neural network can be efficiently trained to find a set of interval parameters by the two optimization algorithms considered earlier. Some scholars [10, 17, 60] suggest that a precise result through the interval data can be approximated using central estimator. The values for the hidden layer will be those values that correspond to the central line fitted by a precise neural network with loss function

| (47) |

| (48) |

Having defined these we can use them to solve for and use the approach previously described for polynomial regression supposing is constant. Such an approach is not very efficient of course and may be time consuming.

More efficiently, the training process can be done in one step as in a regular neural network setting. Assuming that (47) is the midpoint of , then it is equivalent to the first term in (28) which represents the central line, hence the resulting interval approximation for the output layer at iteration () is

| (49) |

| (50) |

It should be noted, that equation (50) is analogous to (26) except that the latter has a constant matrix instead of layer . The Jacobian matrix has only one derivative with respect to because we assume that initial guesses for the weights and biases for both layers are certain values, but this could easily be generalised.

The concept of a network with interval weights and biases in the output layer can be generalized to a multi-layer network as

| (51) |

where is the layer number for and the square brackets denote interval values.

8 Numerical Examples

8.1 Linear regression model

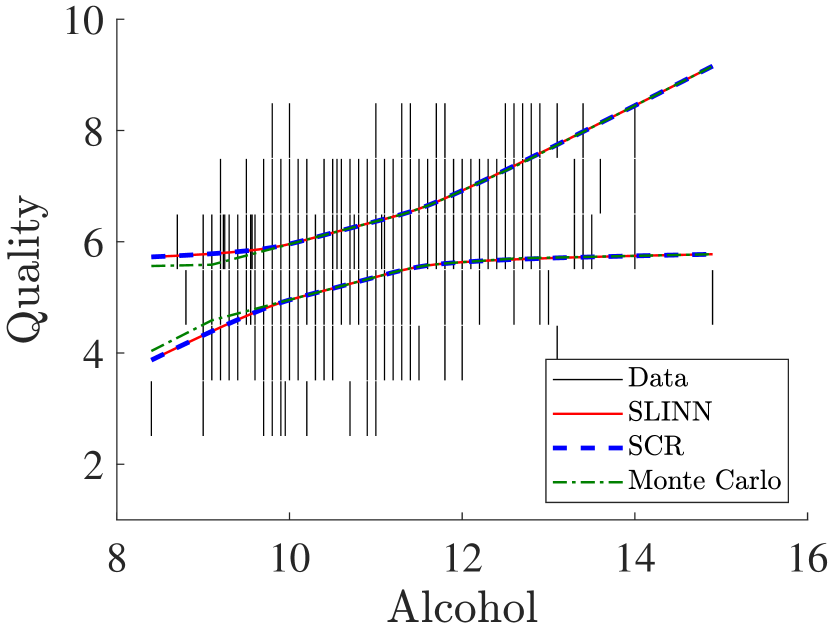

In order to illustrate the developed iterative method for computing the expectation band for a linear model with imprecise dependant variables, we use a publicly available red wine quality data set [65]. The data set contains a total of 12 variables, which were recorded for 1,599 observations. This section will illustrate a simple bivariate model and a more complex multivariable model with selected variables to predict wine quality based on chemical properties.

The dependent variable (assessed wine quality) has a discrete scale with six levels although we suppose that it is a proxy of a continuous variable. Because the wine quality is given as precise points, we assume that every expert provides an interval estimation of wine quality with width corresponding to the difference between levels so that the \saytrue wine quality is within the respective interval bounds. For example, a reported value of 7 is replaced with the interval [6.5, 7.5].

Simple model. For the simple bivariate model we used Alcohol amount as the independent variable and computed an imprecise regression model for Quality. The results of applying a single-layer interval neural network with the interval loss function defined in (16) is presented in Fig. 3 and compared to alternative strategies. The network was trained with constant learning rate , using batch gradient descent optimizer, momentum . The proposed method applied to these interval data yield an imprecise regression which is an expectation band (outlined with red curves).

Because this regression model is linear, the single-layer interval neural network and the sharp collection region [18] coincide and give the same interval bounds. The envelope of all regressions based on any possible configuration of points within the respective data intervals obtained from Monte Carlo simulation with replications is depicted by dash-dotted green lines. The lower and upper bounds obtained from the center and range method are depicted by black dashed lines. The CM [10] model has a slope but does not address the breadth of imprecision in the data. In contrast, the CRM [44] model yields two straight lines but seems to understate the uncertainty at extreme -values. The CCRM model gives exactly the same result as the CRM model. Table 1 shows computed interval coefficients for the simple model. All the center and range methods are able to predict the lower and upper bound of the interval value of the dependent variable, but do not give interval coefficients.

| SLINN | SCR | Monte Carlo | |

|---|---|---|---|

| (intercept) | [ -2.75, 5.46] | [-2.75, 5.46] | [-2.58, 5.29] |

| Alcohol | [ 0.02, 0.79] | [ 0.02, 0.79] | [ 0.03, 0.78] |

Selected model. Based on a correlation analysis we chose a subset of only highly correlated independent variables and performed multivariable linear regression to build an optimal prediction model for red wine quality. Thus, from the initial data set we obtained the selected model which includes 5 chemical properties (volatile acidity, citric acid, chlorides, sulphates, and alcohol). Table 2 shows the obtained interval coefficients for the selected model, and provides a comparison between the proposed method, the sharp collection region and Monte Carlo replications.

| SLINN | SCR | Monte Carlo | |

|---|---|---|---|

| (intercept) | [ -2.61, 7.48] | [-2.61 ,7.48 ] | [-1.68, 6.56 ] |

| Volatile acidity | [ -56.27, 20.55] | [-56.27, 20.56] | [-46.56, 10.85] |

| Citric acid | [ -37.93, 40.21] | [-37.93, 40.21 ] | [-29.85, 32.12 ] |

| Chlorides | [ -138.01, 73.44] | [-138.18, 73.53] | [-107.86, 43.21] |

| Sulphates | [ -18.78, 50.20] | [-18.78, 50.20 ] | [-14.63, 46.06 ] |

| Alcohol | [ -1.30, 10.73] | [ -1.30, 10.73] | [-0.96,10.39 ] |

The results show that the SLINN can produce similar estimates for interval coefficients as SCR. The Monte Carlo results suggest these intervals could not be much narrower.

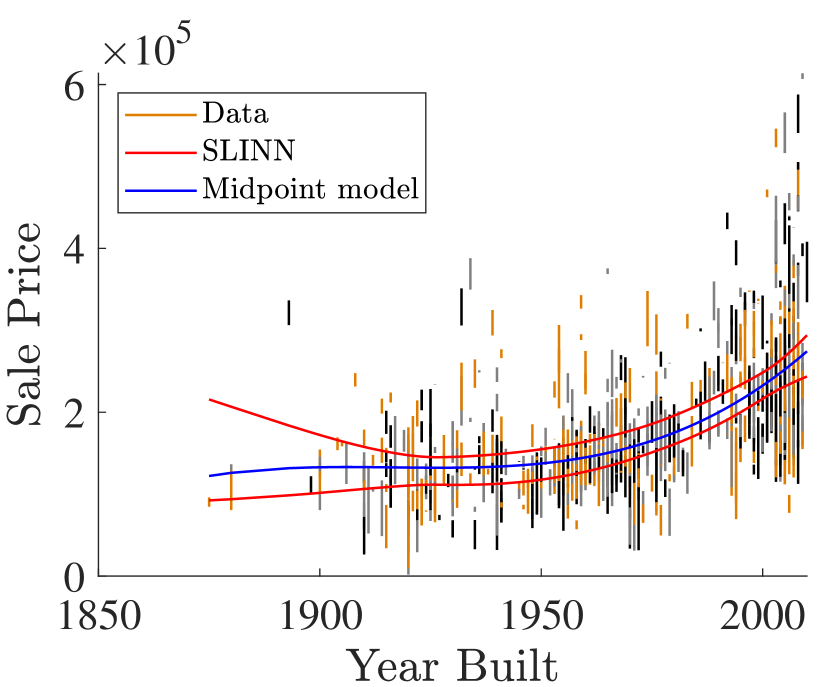

8.2 Polynomial regression

In this section we show the extension of linear imprecise models to capture non-linear relationships described in Section 6. To illustrate the use of imprecise polynomial regression on interval variables we will use the Ames housing data set [66]. This data set has 1460 collected samples with multiple features of houses sold during the 1880–2010 years. We fit a 3rd-order polynomial for Sale Price as a function of Year Built. The single-layer network was trained with constant learning rate , using batch gradient descent optimizer, momentum and 3000 epochs. The values of Sale Price are intervalized using the uniformly biased approach so that , where , and is the interval radius. A plot of the fitted imprecise regression model is presented in Fig. 4. The expectation band is marked by red solid lines, and the precise regression model based on midpoints is marked by a blue line. The interval data have variable color (black, gray and brown) for better display.

8.3 Neural network numerical examples

Artificial data sets. In order to illustrate the developed iterative approach for training multiple-layer neural networks in an imprecise regression setting we first consider two artificial interval data sets derived from the following analytical functions:

-

1.

, ,

-

2.

, ,

where is the interval radius so that and .

For the test case #1 we trained 3 different interval neural networks on samples with 1 hidden layer containing 8 nodes. We use a mini-batch gradient descent optimizer with momentum, a sigmoid activation function and a constant learning rate. The weights were initialised using the uniform initialization . Summaries of the hyperparameters used in the numerical experiments are shown in Table 3.

| Parameter / Configuration | #1 | #2 |

| Hidden layers | 1 | 2 |

| Number of nodes | {8} | {16,16} |

| Activation function | Sigmoid | Tanh |

| Mini batch size, | 250 | 200 |

| Learning rate, | 0.005 | 0.005 |

| Momentum, | 0.9 | 0.9 |

| Number of training epochs | 6000 | 8000 |

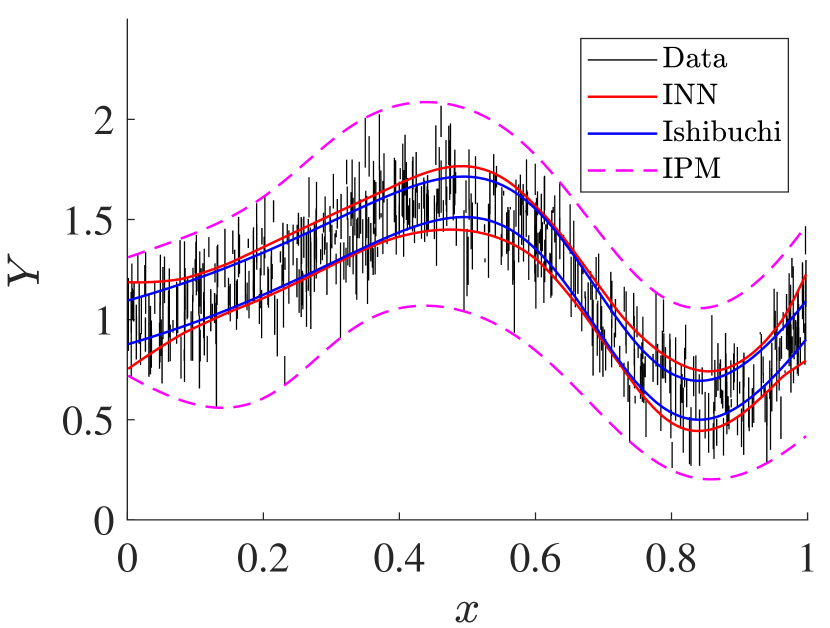

Fig. 5a shows fitted imprecise nonlinear models to interval data set by the proposed method (INN), IPM [60] and Ishibuchi’s method [54].

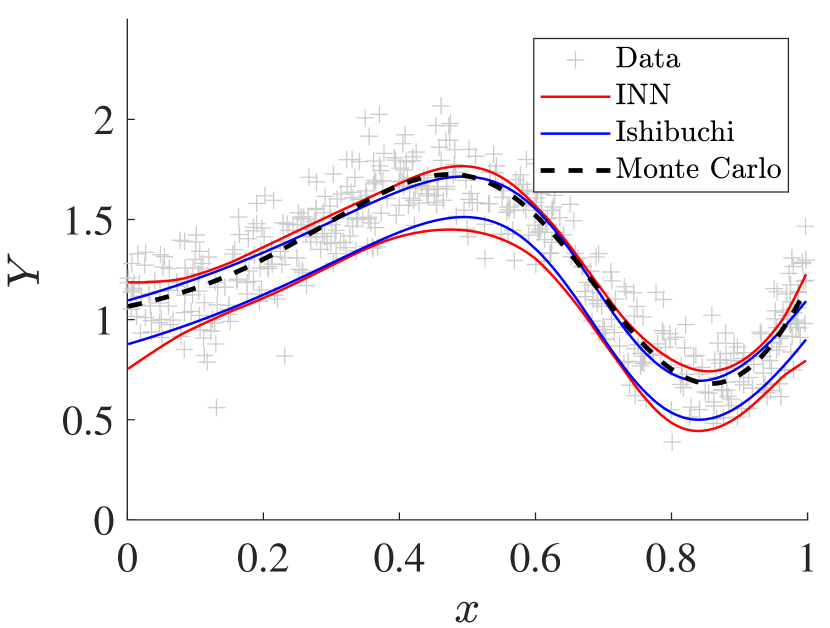

The expectation band (red lines) produced by the proposed method includes the interval output (blue lines) from the classical interval network which exploits the loss function defined as a sum of the differences between the upper and lower bounds separately. The IPM network produces robust bounds (dashed magenta lines) for all possible values in the data set. Fig. 5b shows a collection of points (gray crosses) taken randomly from the respective intervals in Fig. 5a with bias toward higher values. The result of using a precise neural network with the same architecture is depicted by the black dashed line. It is clearly visible that there are several regions where the dashed black line is outside of the blue intervals.

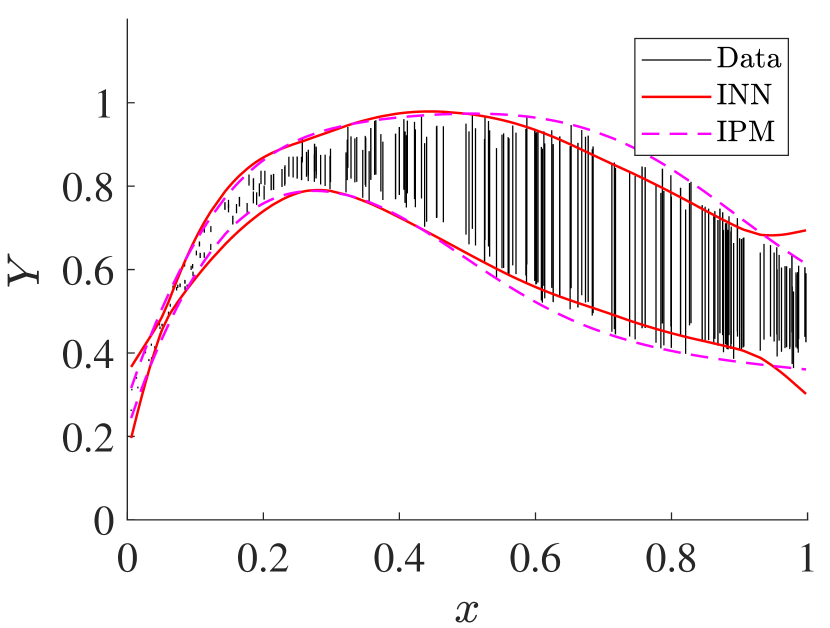

For the test case #2 we trained our INN and IPM on samples with 2 hidden layers, 16 nodes in each, and a hyperbolic tangent activation function. The hyperparameters are summarised in Table 3. Fig. 6 shows the computed expectation band (red lines) and interval bounds from the interval predictor model (dashed magenta lines).

Both the INN and the IPM methods seem to track not just the trend but also the change in imprecision.

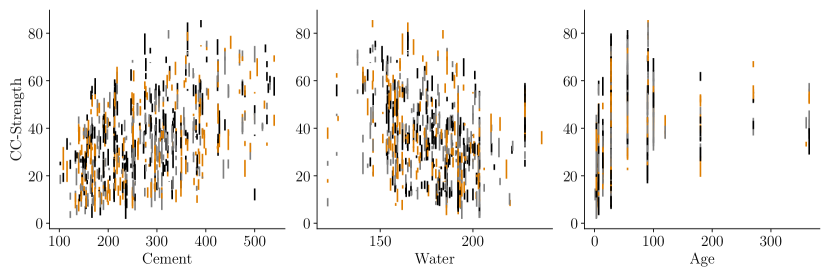

Engineering data set. As a next example we use the concrete compressive strength data set which determines the quality of concrete [67, 68]. The data set has 1030 collected samples with 9 attributes, where 8 of them are input variables (ingredients and age) and the target variable is concrete compressive strength (CC-Strength). We used all 8 variables to obtain the expectation band for the compressive strength of the concrete as a function of Cement, Age, Super Plasticizer, Blast Furnace Slag, Fly Ash, Coarse Aggregate, Fine Aggregate and Water. An expectation band, rather than a precise regression line, is needed because a rigorous interval approach is often important in civil engineering application and reliability analyses where extreme values are the primary focus of concern.

The values of CC-Strength are intervalized using the uniformly biased approach so that , where , and is the interval radius. In this way we model the interval uncertainty in measurements, which, for example, may arise due to the fact that these measurements are often performed under varying conditions or protocols, or by independent agents, or with different measuring devices. As an illustrative example, three scatter plots between CC-Strength and several features are shown in Fig. 7.

We train the proposed algorithm using a train-test split ratio of 0.3, with hyperbolic tangent activation functions on the scaled data set (in the range of 0 to 1) and with decaying learning rate , where step is the current epoch. Summaries of the hyperparameters used in the numerical experiment are shown in Table 4. Summaries of the results from the numerical experiments using training configuratrions #1-4 are presented in Table 5. For measuring performance and accuracy of the predictions we used several different interval metrics defined below. The mean minimum and maximum distances between interval predictions and targets are defined as

the mean endpoint distance is

and the midpoint mean absolute error .

| Parameter / Configuration | #1 | #2 | #3 | #4 |

| Hidden layers | 1 | 2 | 1 | 2 |

| Number of nodes | {8} | {8,8} | {24} | {24,24} |

| Activation function | Tanh | Tanh | Tanh | Tanh |

| Mini batch size, | 200 | 200 | 200 | 200 |

| Initial learning rate, | 0.01 | 0.01 | 0.01 | 0.01 |

| Decay rate | 0.96 | 0.96 | 0.96 | 0.96 |

| Decay steps | 1000 | 1000 | 1000 | 1000 |

| Momentum, | 0.9 | 0.9 | 0.9 | 0.9 |

| Number of training epochs | 12000 | 12000 | 12000 | 12000 |

| Metric / Config. | #1 | #2 | #3 | #4 | ||||

|---|---|---|---|---|---|---|---|---|

| Train | Test | Train | Test | Train | Test | Train | Test | |

| 1.13 | 1.52 | 1.66 | 2.06 | 0.79 | 1.09 | 0.34 | 0.58 | |

| 11.28 | 11.59 | 9.81 | 10.05 | 12.26 | 12.84 | 12.92 | 13.89 | |

| 7.21 | 7.61 | 6.05 | 6.34 | 8.14 | 8.82 | 8.79 | 9.86 | |

| 4.94 | 5.34 | 4.93 | 5.27 | 4.80 | 5.34 | 4.04 | 4.77 | |

The metric measures how the centers of the predictions and observed values compare with each other. According to the , training configuration #4 has better predictive capability compared to the other configurations in terms of matching the centers of the observed values and their predictions. The likewise says this configuration has the smallest distances between predictions and observations. Configuration #2 has the highest value of which means the fit is poorest among the four configurations, in the sense that the mean distance between observed and predicted intervals is smallest. Notice, however, this configuration has the lowest value of which indicates that the network is producing underestimated interval predictions that do not capture all the uncertainty (that is, both the imprecision and scatter) in the dependant variables. Although the match between the endpoints of the observed and predicted value is relatively good compared to the other configurations, the metric is sensitive only to the interval endpoints, and not to their centers. Care must be exercised in interpreting .

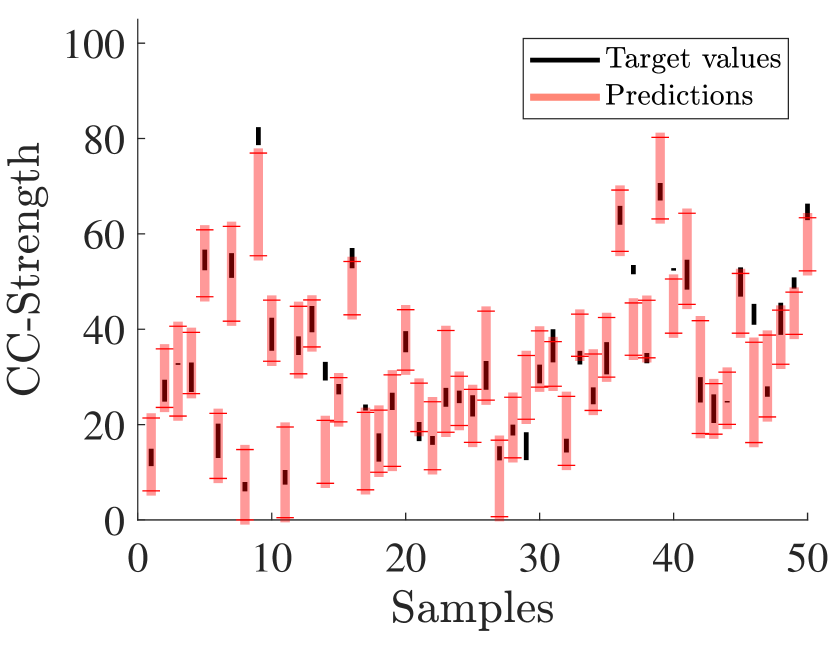

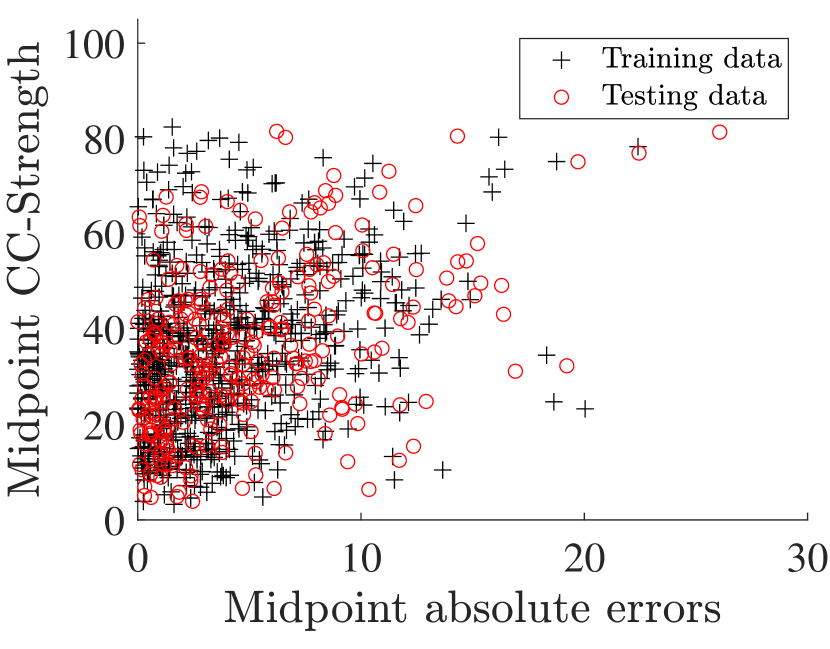

Fig. 8a shows 50 randomly selected target variables and their interval predictions from the test data for configuration #4. Fig. 8b presents the scatter plot of midpoint absolute errors for the train and test data sets.

Both figures show that the network’s predictions are in good agreement with target values, and absolute errors for the test and train data have similar trends in scattering.

9 Conclusions

We have presented a new iterative method for fitting an imprecise regression model to data with interval-valued dependant variables. The proposed method is a single-layer interval neural network, a supervised learning algorithm in a regression setting. An extended version for nonlinear regressions using a multi-layer interval neural network is also presented which gives stronger tools for modeling uncertainty. The main contributions of this paper are that it

-

•

introduces a computationally inexpensive way to compute rigorous bounds on the interval-generalisation of regression analysis to account for epistemic uncertainty in the output (dependent) variables;

-

•

introduces the notion of the expectation band as a generalisation of a regression line;

-

•

introduces the use of ‘neighboring derivatives’ to solve certain interval problems involving derivatives in iterated calculations in a efficient way;

-

•

escapes the problem of repeated variables (aka the dependency problem or wrapping effect) even though the loss function is an interval calculation in an iterative process; and

-

•

reviews several related ideas in regressions that take account of (epistemic) uncertainty in the -variable.

We have shown several numerical examples in which the interval neural network was trained to quantify uncertainty with interval predictions. The imprecision was modeled non-probabilistically by interval bounds. Although interval computations can sometimes be computationally prohibitive, the proposed approach is free of this disadvantage. Because the interval approach is rigorous, the obtained results will be more reliable than approaches that neglect the imprecision.

This paper has presented a computationally feasible alternative to both traditional generalised linear regression and regressions based on Bayesian neural networks [29], which can be computationally costly. The huge literature from both camps is very diverse, but these applications can be contrasted with proposed method. The interval neural network does not require probabilistic assumptions, either about imprecision or about the scatter of dependent value, because it models uncertainty with interval bounds.

The interval bands produced by traditional and Bayesian methods that are created from point estimates of -values arise as confidence or prediction bands (as they are for ordinary least squares regression), not as interval characterisations of measurement imprecision. We defer discussion of the analogous confidence and prediction bands from the proposed approach to a future paper. The traditional and Bayes net methods handle regression when the -values are scattered according to probability distributions, almost always Gaussian distributions. The proposed approach solves a different problem, which is regression when the uncertainty about the measurements are characterised by intervals not associated with any particular probability distribution. The future paper will discuss the problem of regression for -values that are scattered according to some distribution but are known only through interval measurements.

10 Acknowledgements

We thank Jonathan Sadeghi, Marco de Angelis, Olena Posmitna for their very helpful comments. This work was supported by the UK Engineering and Physical Science Research Council through grant number EP/R006768/1. The authors would like to thank the anonymous reviewers for their helpful comments and suggestions.

Appendix A Derivatives

Neighbouring derivatives for the gradient descent optimizer in the linear regression setting when are scalars and is an matrix

| (52) | ||||

| (53) |

Operation sum() performs the summation along each column and is a column vector of all ones with size .

Neighbouring derivatives for the momentum optimizer and a two-layer neural network model

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) |

where is an identity matrix of size , is a hidden precise layer. The rest of derivatives with respect to are

| (58) |

| (59) | ||||

| (60) |

| (61) |

References

- [1] W. Oberkampf, J. Helton, and K. Sentz, “Mathematical representation of uncertainty,” in 19th AIAA Applied Aerodynamics Conference, American Institute of Aeronautics and Astronautics, June 2001.

- [2] H. G. Matthies, “Quantifying uncertainty: Modern computational representation of probability and applications,” in Extreme Man-Made and Natural Hazards in Dynamics of Structures (A. Ibrahimbegovic and I. Kozar, eds.), (Dordrecht), pp. 105–135, Springer Netherlands, 2007.

- [3] A. Der Kiureghian and O. Ditlevsen, “Aleatory or epistemic? Does it matter?,” Structural Safety, vol. 31, no. 2, pp. 105–112, 2009.

- [4] D. R. Helsel, Nondetects and Data Analysis: Statistics for Censored Environmental Data. John Wiley & Sons, 2005.

- [5] A. Speirs-Bridge, F. Fidler, M. McBride, L. Flander, G. Cumming, and M. Burgman, “Reducing overconfidence in the interval judgments of experts,” Risk Analysis, vol. 30, pp. 512–523, Mar. 2010.

- [6] S. Ferson, V. Kreinovich, W. Oberkampf, L. Ginzburg, and J. Hajagos, Experimental Uncertainty Estimation and Statistics for Data Having Interval Uncertainty. Sandia National Laboratories: SAND2007-0939, 2007.

- [7] K. Zaman, S. Rangavajhala, M. P. McDonald, and S. Mahadevan, “A probabilistic approach for representation of interval uncertainty,” Reliability Engineering & System Safety, vol. 96, no. 1, pp. 117–130, 2011.

- [8] H. T. Nguyen, V. Kreinovich, B. Wu, and G. Xiang, Computing Statistics under Interval and Fuzzy Uncertainty. Springer Berlin Heidelberg, 2012.

- [9] P. Bertrand and F. Goupil, “Descriptive statistics for symbolic data,” in Analysis of Symbolic Data (H.-H. Bock and E. Diday, eds.), (Berlin, Heidelberg), Springer Berlin Heidelberg, 2000.

- [10] L. Billard and E. Diday, “Regression analysis for interval-valued data,” in Data Analysis, Classification, and Related Methods (H. A. L. Kiers, J.-P. Rasson, P. J. F. Groenen, and M. Schader, eds.), (Berlin, Heidelberg), pp. 369–374, Springer Berlin Heidelberg, 2000.

- [11] L. Billard and E. Diday, Symbolic Data Analysis: Conceptual Statistics and Data Mining. John Wiley & Sons, Ltd, Dec. 2006.

- [12] C. Manski, Partial Identification of Probability Distributions. New York: Springer-Verlag, 2003.

- [13] G. Xiang, S. A. Starks, V. Kreinovich, and L. Longpré, “New algorithms for statistical analysis of interval data,” in Applied Parallel Computing. State of the Art in Scientific Computing (J. Dongarra, K. Madsen, and J. Waśniewski, eds.), (Berlin, Heidelberg), pp. 189–196, Springer Berlin Heidelberg, 2006.

- [14] P. Walley, Statistical Reasoning with Imprecise Probabilities. Chapman & Hall, 1991.

- [15] V. Kuznetsov, Interval Statistical Models (In Russian). Moscow: Radio and Sviaz, 1991.

- [16] T. Augustin, F. P. A. Coolen, G. de Cooman, and M. C. M. Troffaes, eds., Introduction to Imprecise Probabilities. John Wiley & Sons, Ltd, May 2014.

- [17] M. Černý and M. Rada, “On the possibilistic approach to linear regression with rounded or interval-censored data,” Measurement Science Review, vol. 11, no. 2, 2011.

- [18] G. Schollmeyer and T. Augustin, “Statistical modeling under partial identification: Distinguishing three types of identification regions in regression analysis with interval data,” International Journal of Approximate Reasoning, vol. 56, pp. 224–248, 2015.

- [19] G. Schollmeyer, “Computing simple bounds for regression estimates for linear regression with interval-valued covariates,” in Proceedings of the Twelveth International Symposium on Imprecise Probability: Theories and Applications (A. Cano, J. De Bock, E. Miranda, and S. Moral, eds.), vol. 147 of Proceedings of Machine Learning Research, pp. 273–279, PMLR, 06–09 Jul 2021.

- [20] S. P. Shary, “Maximum consistency method for data fitting under interval uncertainty,” Journal of Global Optimization, vol. 66, pp. 111–126, July 2015.

- [21] S. I. Kumkov, V. Kreinovich, and A. Pownuk, “In system identification, interval (and fuzzy) estimates can lead to much better accuracy than the traditional statistical ones: General algorithm and case study,” in 2017 IEEE International Conference on Systems, Man, and Cybernetics (SMC), IEEE, Oct. 2017.

- [22] V. Kreinovich and S. Shary, “Interval methods for data fitting under uncertainty: A probabilistic treatment,” Reliable Computing, vol. Vol. 23, pp. pp. 105–140, 07 2016.

- [23] M. E. Cattaneo and A. Wiencierz, “Likelihood-based imprecise regression,” International Journal of Approximate Reasoning, vol. 53, no. 8, pp. 1137–1154, 2012. Imprecise Probability: Theories and Applications (ISIPTA’11).

- [24] R. A. de A. Fagundes, R. J. A. Q. Filho, R. M. C. R. de Souza, and F. J. A. Cysneiros, “An interval nonparametric regression method,” in The 2013 International Joint Conference on Neural Networks (IJCNN), pp. 1–7, 2013.

- [25] R. Nasirzadeh, F. Nasirzadeh, and Z. Mohammadi, “Some nonparametric regression models for interval-valued functional data,” Stat, Dec. 2021.

- [26] H. Wang, R. Guan, and J. Wu, “Linear regression of interval-valued data based on complete information in hypercubes,” Journal of Systems Science and Systems Engineering, vol. 21, pp. 422–442, Dec. 2012.

- [27] A. Blanco-Fernández, A. Colubi, and G. González-Rodríguez, “Linear regression analysis for interval-valued data based on set arithmetic: A review,” in Towards Advanced Data Analysis by Combining Soft Computing and Statistics, pp. 19–31, Springer Berlin Heidelberg, 2013.

- [28] D. J. C. MacKay, “A Practical Bayesian Framework for Backpropagation Networks,” Neural Computation, vol. 4, pp. 448–472, 05 1992.

- [29] M. Abdar, F. Pourpanah, S. Hussain, D. Rezazadegan, L. Liu, M. Ghavamzadeh, P. Fieguth, X. Cao, A. Khosravi, U. R. Acharya, V. Makarenkov, and S. Nahavandi, “A review of uncertainty quantification in deep learning: Techniques, applications and challenges,” Information Fusion, vol. 76, pp. 243–297, 2021.

- [30] D. M. Blei, A. Kucukelbir, and J. D. McAuliffe, “Variational inference: A review for statisticians,” Journal of the American Statistical Association, vol. 112, pp. 859–877, Apr. 2017.

- [31] N. Srivastava, G. Hinton, A. Krizhevsky, I. Sutskever, and R. Salakhutdinov, “Dropout: A simple way to prevent neural networks from overfitting,” Journal of Machine Learning Research, vol. 15, no. 56, pp. 1929–1958, 2014.

- [32] Y. Zhou, Y. Zhu, Q. Ye, Q. Qiu, and J. Jiao, “Weakly supervised instance segmentation using class peak response,” 2018 IEEE/CVF Conference on Computer Vision and Pattern Recognition, pp. 3791–3800, 2018.

- [33] Q. Bi, K. Qin, H. Zhang, and G.-S. Xia, “Local semantic enhanced convnet for aerial scene recognition,” IEEE Transactions on Image Processing, vol. 30, pp. 6498–6511, 2021.

- [34] A. Saseendran, K. Skubch, S. Falkner, and M. Keuper, “Shape your space: A gaussian mixture regularization approach to deterministic autoencoders,” in Advances in Neural Information Processing Systems (M. Ranzato, A. Beygelzimer, Y. Dauphin, P. Liang, and J. W. Vaughan, eds.), vol. 34, pp. 7319–7332, Curran Associates, Inc., 2021.

- [35] O. Caprani and K. Madsen, “Mean value forms in interval analysis,” Computing, vol. 25, no. 2, pp. 147–154, 1980.

- [36] R. E. Moore, R. B. Kearfott, and M. J. Cloud, Introduction to Interval Analysis. Society for Industrial and Applied Mathematics, Jan. 2009.

- [37] S. Rump, “INTLAB - INTerval LABoratory,” in Developments in Reliable Computing (T. Csendes, ed.), pp. 77–104, Dordrecht: Kluwer Academic Publishers, 1999. http://www.tuhh.de/ti3/rump/.

- [38] J. Stolfi and L. H. de Figueiredo, “An introduction to affine arithmetic,” Trends in Computational and Applied Mathematics, vol. 4, no. 3, pp. 297–312, 2003.

- [39] L. B. Rall, “Mean value and taylor forms in interval analysis,” SIAM Journal on Mathematical Analysis, vol. 14, no. 2, pp. 223–238, 1983.

- [40] M. Berz and K. Makino, “Verified integration of odes and flows using differential algebraic methods on high-order taylor models,” Reliable Computing, vol. 4, pp. 361–369, 1998.

- [41] G. G. Lorentz, Bernstein polynomials. American Mathematical Soc., 2013.

- [42] O. Caprani and K. Madsen, “Contraction mappings in interval analysis,” BIT Numerical Mathematics, vol. 15, pp. 362–366, 1975.

- [43] L. Jaulin, M. Kieffer, O. Didrit, and E. Walter, Applied interval analysis. Guildford, England: Springer, 2001 ed., Dec. 2012.

- [44] F. d. A. T. de Carvalho, E. d. A. Lima Neto, and C. P. Tenorio, “A new method to fit a linear regression model for interval-valued data,” in KI 2004: Advances in Artificial Intelligence (S. Biundo, T. Frühwirth, and G. Palm, eds.), (Berlin, Heidelberg), pp. 295–306, Springer Berlin Heidelberg, 2004.

- [45] E. de A. Lima Neto and F. de A.T. de Carvalho, “Constrained linear regression models for symbolic interval-valued variables,” Computational Statistics & Data Analysis, vol. 54, no. 2, pp. 333–347, 2010.

- [46] W. Xu, Symbolic data analysis: interval-valued data regression. PhD thesis, University of Georgia Athens, GA, 2010.

- [47] E. de A. Lima Neto and F. de A.T. de Carvalho, “Constrained linear regression models for symbolic interval-valued variables,” Computational Statistics & Data Analysis, vol. 54, no. 2, pp. 333–347, 2010.

- [48] J. L. Horowitz and C. F. Manski, “Imprecise identification from incomplete data.,” in ISIPTA, vol. 1, pp. 213–218, 2001.

- [49] A. Beresteanu, I. Molchanov, and F. Molinari, “Sharp identification regions in models with convex moment predictions,” Econometrica, vol. 79, no. 6, pp. 1785–1821, 2011.

- [50] A. Beresteanu and F. Molinari, “Asymptotic properties for a class of partially identified models,” Econometrica, vol. 76, no. 4, pp. 763–814, 2008.

- [51] M. Ponomareva and E. Tamer, “Misspecification in moment inequality models: back to moment equalities?,” The Econometrics Journal, vol. 14, no. 2, pp. 186–203, 2011.

- [52] H. Ishibuchi and H. Tanaka, “An extension of the BP-algorithm to interval input vectors-learning from numerical data and expert's knowledge,” in [Proceedings] 1991 IEEE International Joint Conference on Neural Networks, IEEE, 1991.

- [53] C. Hernandez, J. Espf, K. Nakayama, and M. Fernandez, “Interval arithmetic backpropagation,” in Proceedings of 1993 International Conference on Neural Networks (IJCNN-93-Nagoya, Japan), IEEE, 1993.

- [54] H. Ishibuchi, H. Tanaka, and H. Okada, “An architecture of neural networks with interval weights and its application to fuzzy regression analysis,” Fuzzy Sets and Systems, vol. 57, no. 1, pp. 27–39, 1993.

- [55] L. Huang, B.-L. Zhang, and Q. Huang, “Robust interval regression analysis using neural networks,” Fuzzy Sets and Systems, vol. 97, pp. 337–347, Aug. 1998.

- [56] D. Chetwynd, K. Worden, and G. Manson, “An application of interval-valued neural networks to a regression problem,” Proceedings: Mathematical, Physical and Engineering Sciences, vol. 462, no. 2074, pp. 3097–3114, 2006.

- [57] A. M. S. Roque, C. Maté, J. Arroyo, and Á. Sarabia, “iMLP: Applying multi-layer perceptrons to interval-valued data,” Neural Processing Letters, vol. 25, pp. 157–169, Feb. 2007.

- [58] D. Yang and Y. Liu, “L1/2 regularization learning for smoothing interval neural networks: Algorithms and convergence analysis,” Neurocomputing, vol. 272, pp. 122–129, 2018.

- [59] Z. Yang, D. K. Lin, and A. Zhang, “Interval-valued data prediction via regularized artificial neural network,” Neurocomputing, vol. 331, pp. 336–345, 2019.

- [60] J. Sadeghi, M. de Angelis, and E. Patelli, “Efficient training of interval neural networks for imprecise training data,” Neural Networks, vol. 118, pp. 338–351, Oct. 2019.

- [61] M. Campi, G. Calafiore, and S. Garatti, “Interval predictor models: Identification and reliability,” Automatica, vol. 45, no. 2, pp. 382–392, 2009.

- [62] S. Garatti and M. C. Campi, “L-inf layers and the probability of false prediction,” IFAC Proceedings Volumes, vol. 42, no. 10, pp. 1187–1192, 2009. 15th IFAC Symposium on System Identification.

- [63] R. Courant, “Variational methods for the solution of problems of equilibrium and vibrations,” Bulletin of the American Mathematical Society, vol. 49, no. 1, pp. 1–23, 1943.

- [64] C. Lemaréchal, “Cauchy and the gradient method,” 2012.

- [65] P. Cortez, A. Cerdeira, F. Almeida, T. Matos, and J. Reis, “Modeling wine preferences by data mining from physicochemical properties,” Decision Support Systems, vol. 47, no. 4, pp. 547–553, 1998.

- [66] D. D. Cock, “Ames, Iowa: Alternative to the boston housing data as an end of semester regression project,” Journal of Statistics Education, vol. 19, no. 3, p. null, 2011.

- [67] I.-C. Yeh, “Modeling of strength of high-performance concrete using artificial neural networks,” Cement and Concrete Research, vol. 28, no. 12, pp. 1797–1808, 1998.

- [68] “Concrete Compressive Strength Data Set.” https://archive.ics.uci.edu/ml/datasets/concrete+compressive+strength.