Stability of shares in the Proof of Stake Protocol

– Concentration and Phase Transitions

Abstract.

This paper is concerned with the stability of shares in a cryptocurrency where the new coins are issued according to the Proof of Stake protocol. We identify large, medium and small investors under various rewarding schemes, and show that the limiting behaviors of these investors are different – for large investors their shares are stable, while for medium to small investors their shares may be volatile or even shrink to zero. For instance, with a geometric reward there is chaotic centralization, where all the shares will eventually concentrate on one investor in a random manner. This leads to the phase transition phenomenon, and the thresholds for stability are characterized. In response to the increasing activities in blockchain networks, we also propose and analyze a dynamical population model for the PoS protocol, which allows the number of investors to grow over the time. Numerical experiments are provided to corroborate our theory.

Key words: Blackwell-MacQueen urn, blockchain, concentration/anti-concentration, cryptocurrency, Pólya urn, Proof of Stake.

1. Introduction

In the past decade, blockchain technology has evolved tremendously, and is now regarded as an endeavor to facilitate the next generation digital exchange platform with a broad range of established or emerging applications including cryptocurrency (Nakamoto (2008); Wood (2014); Hileman and Rauchs (2017)), healthcare (McGhin et al. (2019); Donovan (2019); Tanwar et al. (2020)), supply chain (Saberi et al. (2019); Chod et al. (2020)), electoral voting (Wood (2018)) and new-born arts as non-fungible tokens (Wang et al. (2021); Dowling (2022)).

A blockchain is a growing chain of records or transactions, called blocks, which are jointly maintained by a set of miners or validators using cryptography. The idea of blockchain originated from distributed consensus, where multiple machines in a mission-critical system are required to make consistent decisions. The work of Lamport et al. (1982), which introduced the famous Byzantine Generals problem, laid the foundation for distributed consensus. From then on, distributed consensus has been deployed in many digital infrastructures such as Google Wallet and Facebook Credit. Since 2009, Bitcoin (Nakamoto (2008)) and various other cryptocurrencies have come around, and allowed the secure transfer of assets without an intermediary such as a bank or payment processing network. These cryptocurrencies achieved a new breakthrough in distributed consensus because they showed for the first time that consensus is viable in a decentralized and permissionless environment where anyone is allowed to work. This is in contrast with traditional trusted payment processing systems as well as distributed consensus-based computing infrastructures such as Google Wallet and Facebook Credit, where only a small number of permissioned personnels can participate. This way, Google Wallet and Facebook Credit are regarded as permissioned blockchains, while Bitcoin and other cryptocurrencies are permissionless blockchains.

At the core of a blockchain is the consensus protocol or smart contract, which specifies a set of voting rules allowing miners to agree on an ever-growing, linearly-ordered log of transactions forming the distributed ledger. There are several existing blockchain protocols, among which the most popular are Proof of Work (PoW, Nakamoto (2008)) and Proof of Stake (PoS, King and Nadal (2012); Wood (2014)).

-

•

In the PoW protocol, miners compete with each other by solving a puzzle, and the one who solves the puzzle first is allowed to append a new block to the blockchain. Thus, the probability of a miner being selected is proportional to the computational power that the miner has. The PoW coins include Bitcoin, Ethereum, Dogecoin…etc.

-

•

In the PoS protocol, the blockchain is updated by a randomly selected miner where the probability of a miner being drawn is proportional to the stake that the miner owns. The PoS coins include BNB, Cardano, Solana…etc.

As of May 28, 2022, Cryptoslate lists PoW coins with a total B () market capitalization, and PoS coins contributing a B () market capitalization. One disadvantage of the PoW protocol is that competition among miners has led to exploding levels of energy consumption. For instance, Mora et al. (2018) pointed out the unsustainability of PoW-based blockchains, and Platt et al. (2021) showed that energy consumption of Bitcoin is at least times higher than PoS-based blockchains. Chiu and Koeppl (2017); Saleh (2019); Cong et al. (2021) also discussed drawbacks of PoW blockchains from economic perspectives. Though PoS-based blockchains are still not as widely used as PoW-based ones, there is a strong incentive among blockchain practitioners to switch from a PoW to PoS ecosystem as is the case for Ethereum (Wickens (2021)).

A PoS blockchain mitigates the problem of energy efficiency and scalability; however, it receives several criticisms.

-

•

Security concern. PoS protocols may suffer from the Nothing-at-Stake problem, where it is effortless for (malicious) miners to copy every outdated history and participate in all of them. As shown in Bagaria et al. (2019), any miner with more than of the total stake can launch a double-spending attack, which seems to be less robust than the attack to a PoW-based blockchain. Brown-Cohen et al. (2019) also pointed out difficulties in detecting Nothing-at-Stake for incentive-compatible PoS protocols. One way to address this challenge is to come up with a clever block rewarding scheme, as discussed in Kiayias et al. (2017); Daian et al. (2019); Saleh (2021).

-

•

Centralization concern. Critics have argued that the PoS protocol induces wealth concentration, thus leading to centralization (Afram (2018); Irresberger (2018); Fanti et al. (2019)). As one key feature of a permissionless blockchain is decentralization, the problem of centralization may put questions to the necessity of using a permissionless blockchain since it yields concentration in voting mechanism as does a permissioned blockchain. Previous works (Alsabah and Capponi (2020); Arnosti and Weinberg (2022)) showed that the PoW protocol may generate concentration in mining power, and thus centralization in various settings. At a conceptual level, the effect of centralization or decentralization in both PoW and PoS blockchains arises from randomness. In a PoW blockchain, the randomness is external to the cryptocurrency, while in a PoS blockchain, the randomness comes from the cryptocurrency itself.

In this paper we consider the problem of wealth stability for different types of miners of a PoS blockchain. In the sequel, a PoS blockchain miner is also called an investor. The prominent work of Roşu and Saleh (2021) took the first step to study the long term evolution of large investor shares in a PoS cryptocurrency via a Pólya urn model. They proved under various reward assumptions that the shares in the long run do not deviate much from the initial ones as the initial coin offerings are large; that is,

That is to say, the rich-get-richer phenomenon does not occur when there is a small number of investors each having a large proportion of initial coins. Statistical analysis from (Foley et al. (2019); Tang et al. (2020)) suggested that there be increasing levels of activities from smaller investors in blockchain networks. Moreover, online platforms such as Robinhood Crypto allow for fractional trading. Thus, it is indispensable to understand the evolution of small investor shares as well. Typically for these investors, so the above relation holds trivially as ‘’. This prompts us to consider a more meaningful measure of evolution – the ratio , where ‘’ is indeterminate for small investors.

The first contribution of this work is to provide a systematic study of the aforementioned ratio under various rewarding schemes and for different types of investors in the setting of Roşu and Saleh (2021). The investors are categorized into large, medium and small ones in terms of their initial endowment of coins. The key observation is that for investors whose initial coins scale differently to the total initial coin offering, the ratio exhibits different asymptotic behaviors such as concentration and anti-concentration. This is a phase transition phenomenon, which has yet appeared in the literature on the economics of the PoS protocol. For instance, we prove that under a constant rewarding scheme, the ratio of evolution of shares concentrates at one for large investors, and converges to a Gamma random variable for medium investors, and decays towards zero for small investors (Theorem 2.1). Similar but slightly weaker results are established under a decreasing rewarding scheme (Theorem 2.2) and an increasing rewarding scheme (Theorem 2.3). In the case of a geometric reward, our result shows that with probability one, all the shares will eventually go to one investor in a completely random way. Such a behavior, which we call chaotic centralization, indicates that the geometric rewarding scheme induces long-run instability in a PoS blockchain. This, however, is not contradictory to Fanti et al. (2019) where it was shown that a geometric reward is optimal in a fixed time horizon.

As is clear from the growing popularity of blockchain technology, it may not be realistic to assume a fixed finite number of investors throughout. The second contribution of this paper is to propose a dynamical approach, which starts with a finite number of investors and evolves to an infinite number of investors. Our model can be viewed as an infinite population version of the Pólya urn model, and the idea comes from the Blackwell-MacQueen urn model in Bayesian nonparametrics, as well as species sampling in computational biology. In this dynamical population setting, we study the ratio of evolution of shares under various rewarding schemes (Theorem 3.4). Our result shows that under a decreasing rewarding scheme with a suitably large decay, the shares of the initial capitalists will be diluted in the long run. This observation is consistent with several existing practice (e.g. Bitcoin), and it may also provide guidance on the choice of rewarding schemes so that decentralization is incorporated in a PoS blockchain.

Let us also mention some relevant works. Tsoukalas and Falk (2020) studied the stake-based voting for crowd-sourcing on a blockchain, and showed that asymmetric information may lead to suboptimal outcomes. Benhaim et al. (2021) considered a committee-based protocol, and highlighted its advantage over other PoS protocols. To the best of our knowledge, it is the first time in this work that heterogeneity of investors is taken into account, leading to a phase transition in centralization vs decentralization. This paper also proposes and studies for the first time a dynamical model in which the number of investors is not fixed for the PoS protocol. Our paper thus contributes to both the literature on the decentralization of blockchains and that on the economics of the PoS protocol.

The remainder of the paper is organized as follows. In Section 2, we adopt the Pólya urn to model the PoS protocol, and study the ratio of evolution of shares under various rewarding schemes. In Section 3, we propose a dynamical population model which allows the number of investors to increase over the time. There we also provide analysis on the ratio of evolution of shares. We conclude with Section 4. All the proofs are given in Appendix.

2. Finite population model

In this section, we follow Roşu and Saleh (2021) to use a time-dependent Pólya urn model to describe the PoS protocol. Below we collect the notations that will be used throughout this paper.

-

•

denotes the set of positive integers, and denotes the set of positive real numbers.

-

•

The symbol means that is bounded from above as ; the symbol means that is bounded from below and above as ; and the symbol or means that decays towards zero as .

Let be the number of investors, and be the number of initial coins/tokens in a PoS blockchain. The investors are indexed by , and investor ’s initial endowment of coins is with . We define the investor share as the fraction of coins each investor owns. So the initial investor shares are given by

| (2.1) |

Similarly, we denote by the number of coins owned by investor at time , and the corresponding share is

| (2.2) |

Here is the total number of coins at time , and thus . Clearly, for each forms a probability distribution on .

Now we provide a formal description of the PoS dynamics. At time , investor is selected at random among investors with probability . Once selected, the investor receives a deterministic reward of coins. Let be the random event that investor is selected at time . Thus, the number of coins owned by each investor evolves as

| (2.3) |

It was shown in (Roşu and Saleh, 2021, Proposition 5) that investors have no incentive to trade their coins under some risk neural conditions. Without loss of generality, we exclude the possibility of exchanges among investors. Note that the total number of coins satisfies . Combining (2.2) and (2.3) yields a recursion of the investor shares:

| (2.4) |

Let be the filtration as the -algebra generated by the random events . It is easily seen that for each , the process of investor ’s share is an -martingale. By the martingale convergence theorem (see e.g. Durrett (2019)),

| (2.5) |

where is some random probability distribution on .

We consider the evolution of the investor shares , as well as its long time limit . One major problem is to know whether the PoS protocol triggers the rich-get-richer, or concentration phenomenon by comparing the investor shares at the initial time and in the long time limit. As briefly discussed in the introduction, Roşu and Saleh (2021) were concerned with large investors, i.e. or equivalently . They proved under various reward assumptions that

| (2.6) |

That is, the rich-get-richer phenomenon does not occur typically when there is a small number of investors each having a significant proportion of initial coins. However, there may also be medium or even small investors whose initial shares is relatively small. For instance,

-

•

When the number of investors , there are less rich investors with initial endowment of coins such that but , and small investors with initial number of coins .

-

•

When the number of investors , there may also exist small investors who own fractional number of coins .

In these cases, we have , so for each fixed the probability always goes to as . Thus, it is more reasonable to consider the ratios or instead of the differences. In the following subsections, we study the ratio of evolution of shares under various rewarding schemes and for different types of investors, encompassing all the above instances. In particular, we observe phase transitions for different types of investors in terms of wealth stability.

2.1. Constant reward

We start with the constant reward (e.g. Blackcoin). Let be the Gamma function. Recall that the Dirichlet distribution with parameters , which we simply denote , has support on the standard simplex and has density

| (2.7) |

For , the Dirichlet distribution reduces to the beta distribution which is denoted by . It is easily seen that if then for each . The following result is concerned with the evolution of shares in a PoS protocol with a constant reward.

Theorem 2.1.

Assume that the coin reward is . Then the investor shares have a limiting distribution

| (2.8) |

Moreover,

-

(i)

For such that as (i.e. ), we have for each and each or :

(2.9) which converges to as .

-

(ii)

For (i.e. ), we have the convergence in distribution:

(2.10) where is a Gamma random variable with density .

-

(iii)

For (i.e. ), we have as . Moreover, for each :

(2.11)

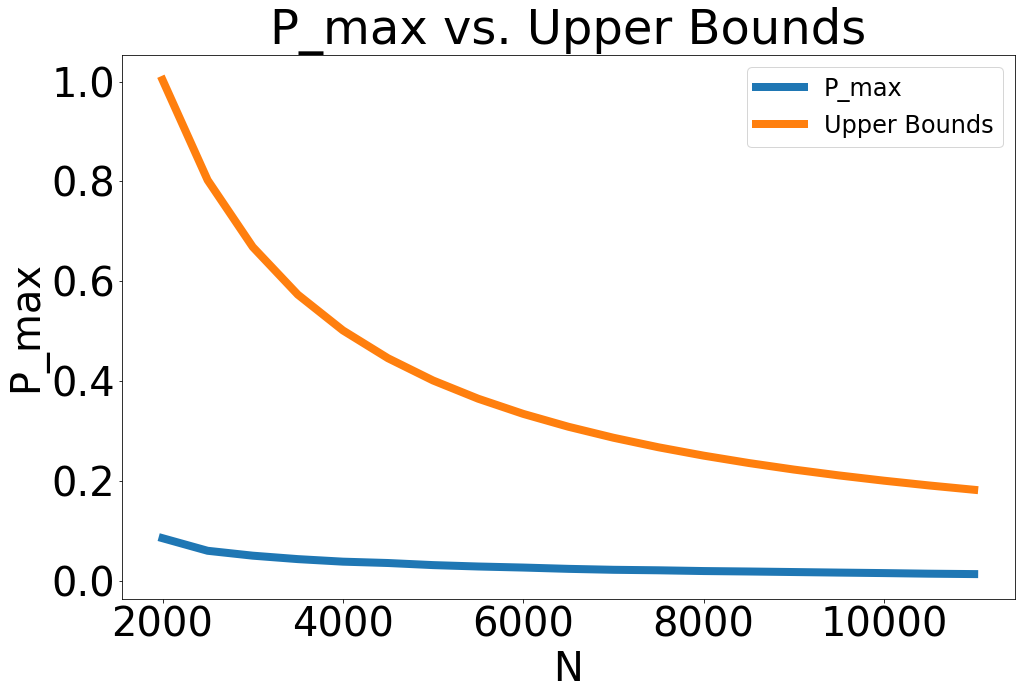

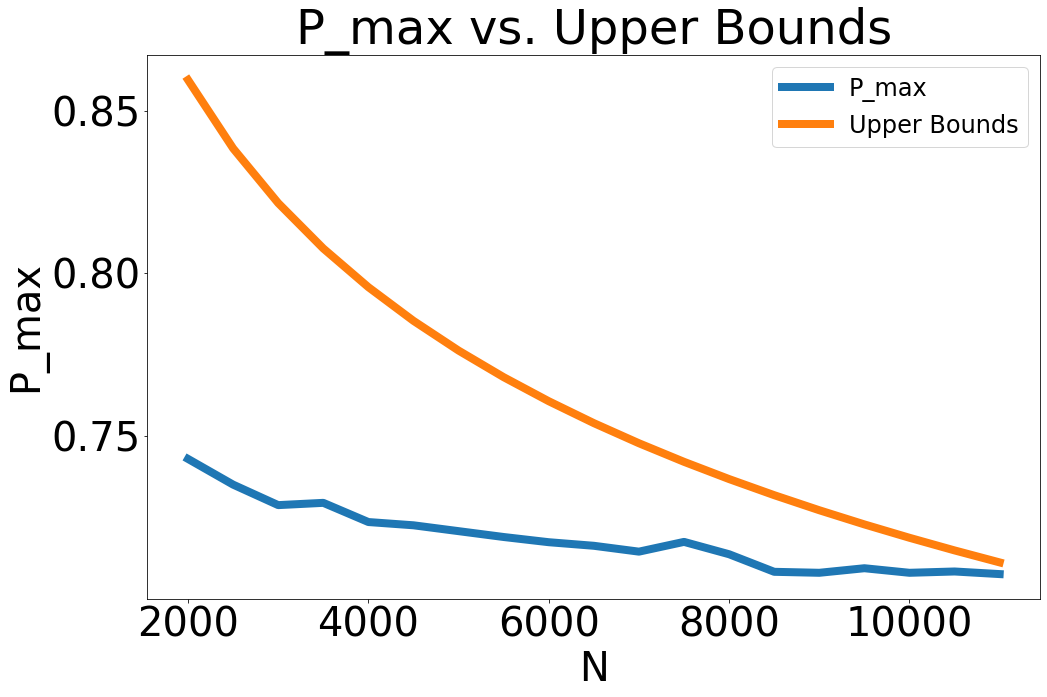

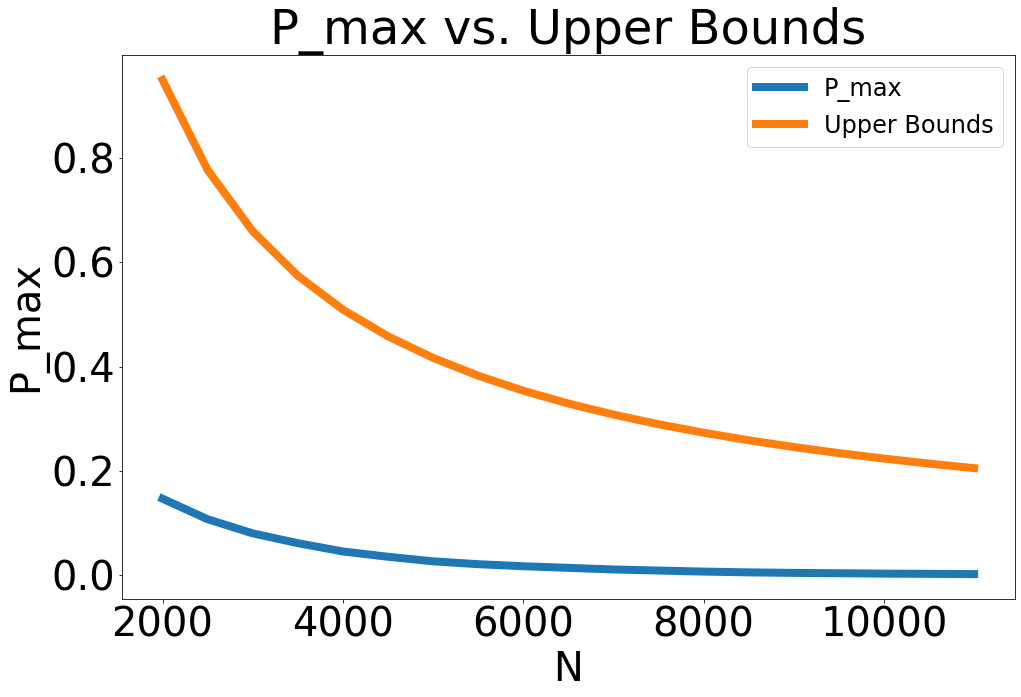

The proof of Theorem 2.1 is given in Appendix A. Let us make a few comments. The theorem reveals a phase transition of shares in the long run between large, medium and small investors. Part () shows that for large investors, their shares are stable in the sense that the ratio between the share at a later time and the initial share, i.e. , converges in probability to as the initial coin offerings . In particular, for extremely large investors with initial coins this is equivalent to the stability as defined by (2.6). The stability also holds for less rich large investors with but . Note that the concentration bound (2.9) is uniform in time , implying that the rich-get-richer phenomenon does not occur at any time. See Figure 1 for an illustration of the bound.

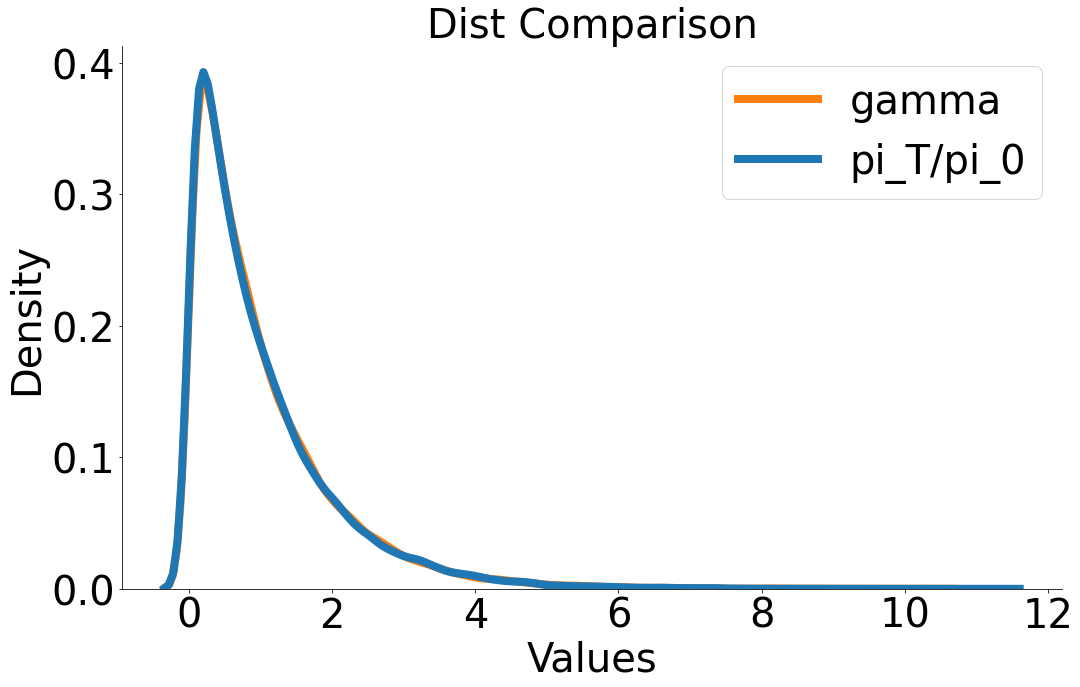

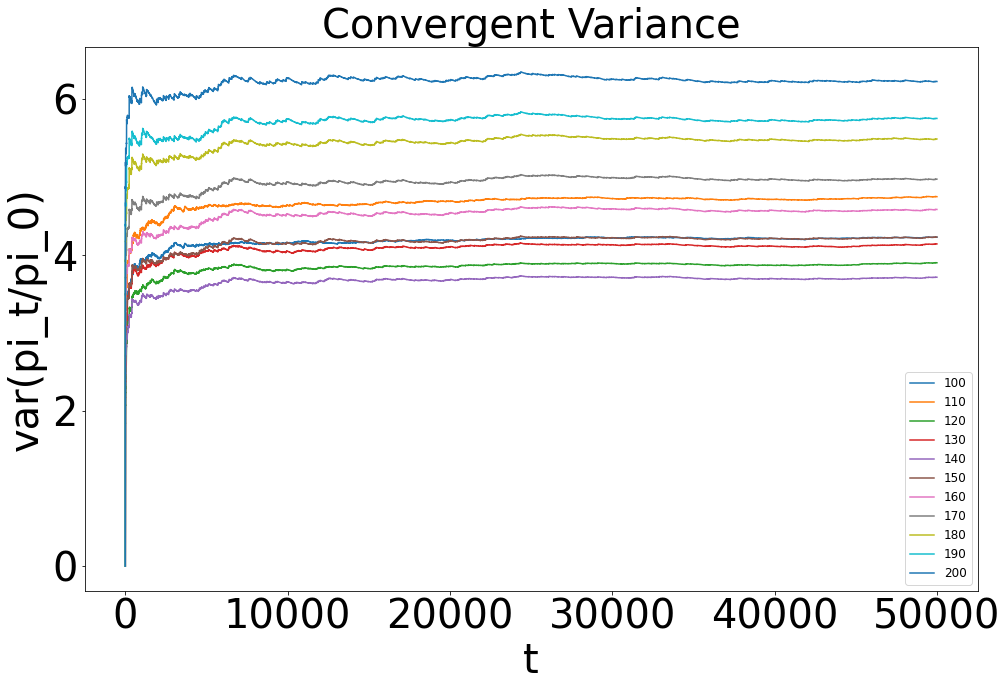

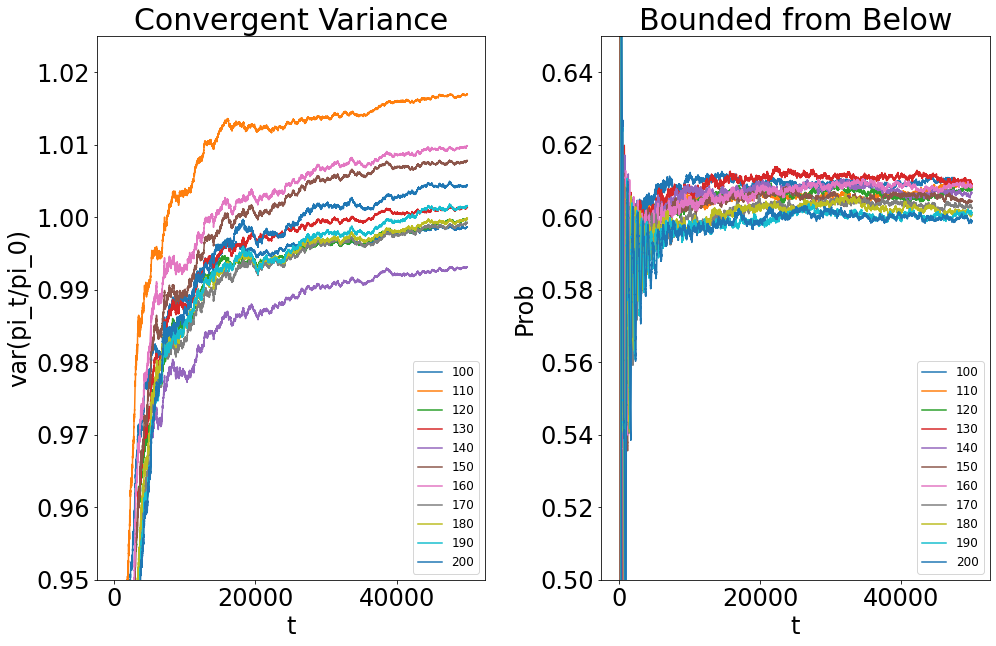

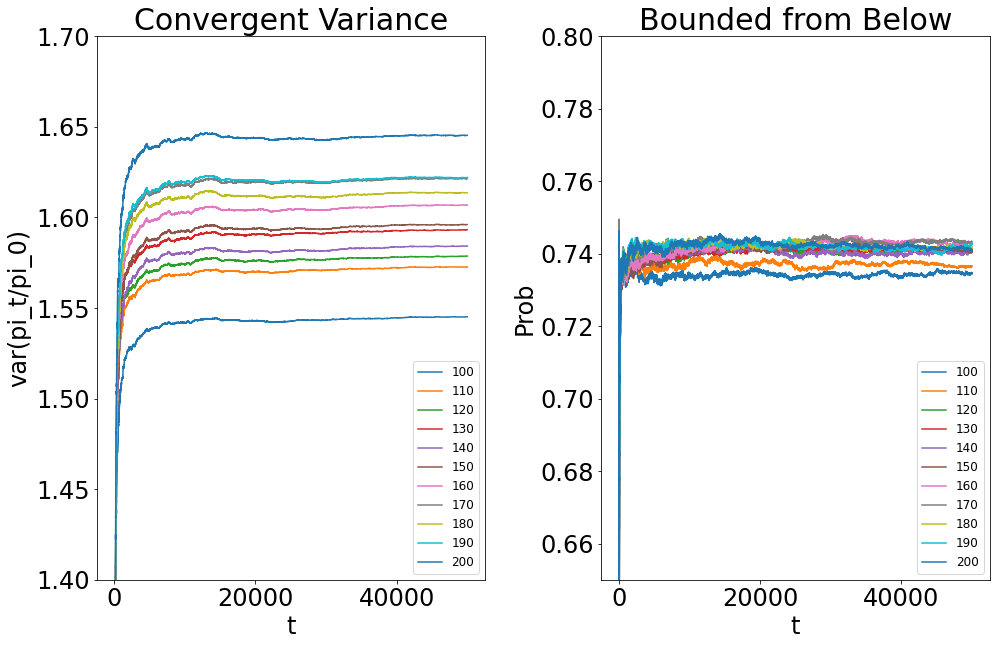

On the other hand, the evolution of shares for medium or small investors has very different limiting behaviors. Part () shows that medium investor’s shares are volatile in such a way that the ratio is approximated by a gamma distribution independent of the initial coin offerings, and hence . For instance, if the limiting distribution of the ratio reduces to the exponential distribution with parameter . See Figure 2(a) for an illustration of this approximation. In this case, we have

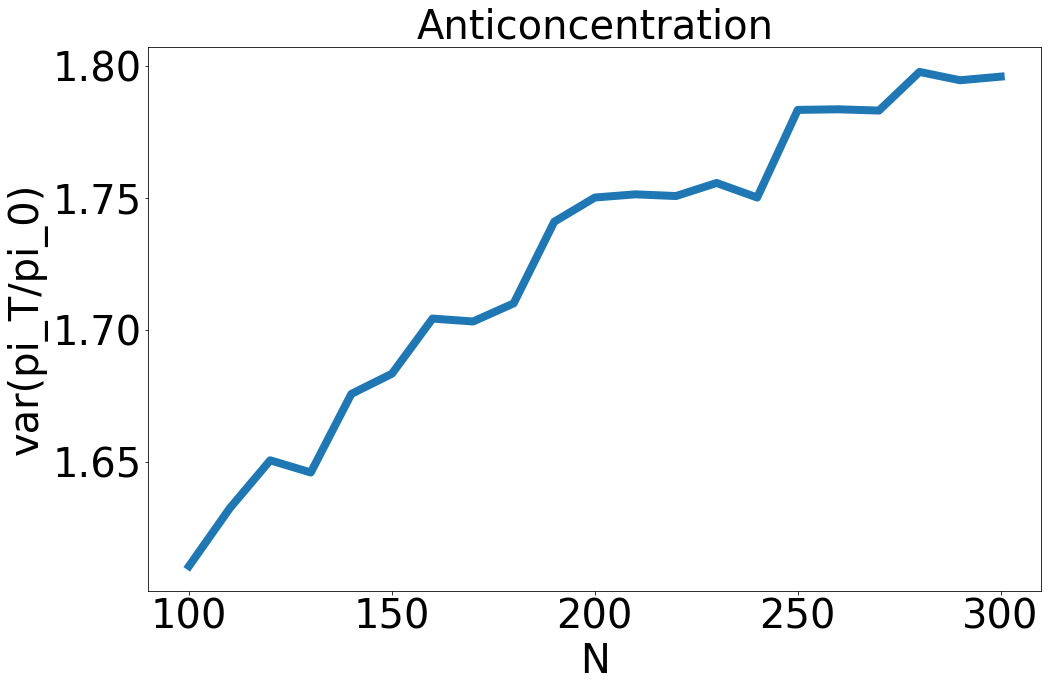

So with probability a medium investor’s share will double, and with probability this investor’s share will be halved. Part () shows that for small investors, their shares will be shrinking along the time, and the ratio converges to in probability as . This is indeed the poor-get-poorer phenomenon as illustrated in Figure 2(b).

Finally, we note that the results in Theorem 2.1 hold jointly for a finite number of investors belonging to the same category. That is,

-

•

For with satisfying the conditions in (),

-

•

For with satisfying the condition in (),

where are independent Gamma random variables.

-

•

For with satisfying the conditions in (),

2.2. Decreasing reward

We consider the decreasing reward such that for each (e.g. Bitcoin). The following theorem shows that the ratio of evolution of shares is more complicated in the PoS protocol with a decreasing reward scheme, and the phase transition may depend on how the reward function decreases over the time.

Theorem 2.2.

Assume that the coin reward is with for each .

-

(1)

If is bounded away from , i.e. , then

-

(i)

For such that as (i.e. ), we have for each and each or :

(2.12) which converges to as .

-

(ii)

For (i.e. ), we have . Moreover, there is independent of such that for sufficiently small:

(2.13) -

(iii)

For (i.e. ), we have as .

-

(i)

-

(2)

If for , then

-

(i)

For such that as (i.e. ), we have for each and each or :

(2.14) which converges to as .

-

(ii)

For (i.e. ), we have .

-

(iii)

For (i.e. ), we have as .

-

(i)

-

(3)

If for , then

-

(i)

For such that as (i.e. ), there is independent of and such that for each and each or :

(2.15) which converges to as .

-

(ii)

For (i.e. ), we have . Moreover, there is independent of such that for sufficiently small:

(2.16) -

(iii)

For (i.e. ), we have as .

-

(i)

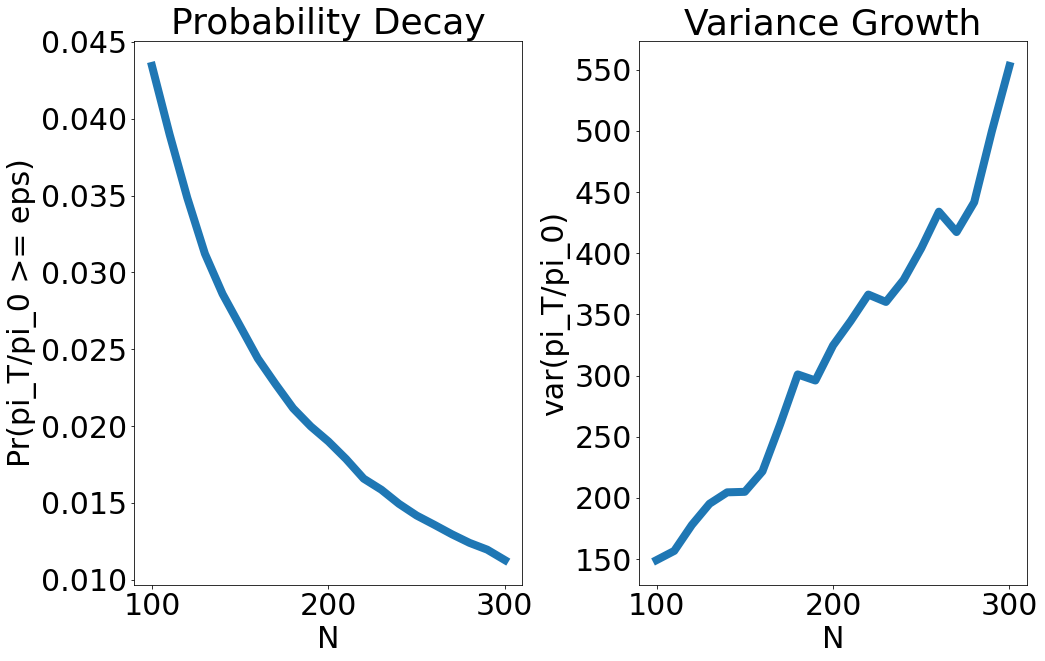

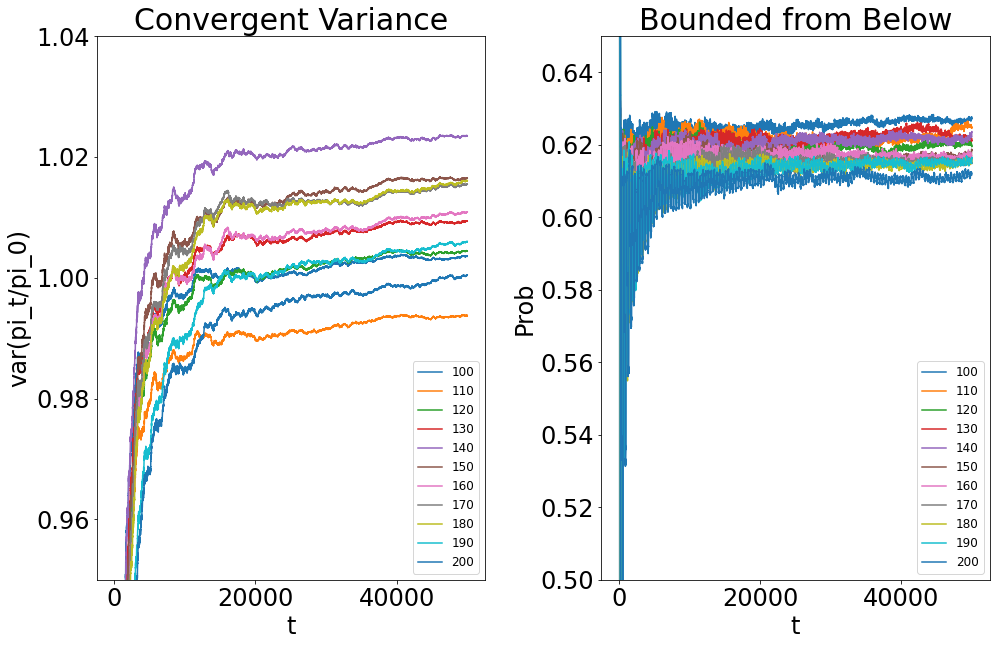

The proof of Theorem 2.2 is given in Appendix B. The theorem distinguishes three ways that the reward function decreases, leading to different thresholds in the phase transition to categorize large, medium and small investors. Part () assumes that the reward function decreases to a nonzero value. In this case, the threshold to identify large, medium and small investors is , which is the same as that of the PoS protocol with a constant reward. This may not be surprising, since the underlying dynamics is not much different from the one with a constant reward in the long run. For large investors, the ratio concentrates at ; while for medium investors there is the anti-concentration bound (2.13), indicating that the evolution of a medium investor’s share is no longer stable, and may be volatile. For small investors, we know that the variance of is large.

Part () considers a fast decreasing reward with . In this case, the threshold to identify different types of investors is , which is independent of the exact decreasing rate of . For large investors, the ratio concentrates at ; while for medium (resp. small) investors, the variance of is bounded (resp. tends to infinity).

Finally, part () deals with a slow decreasing reward with . In contrast with the previous cases, the threshold to identify different types of investors depends on the decreasing rate of . When , the threshold becomes which is consistent with that in part (), and when , the threshold becomes which agrees with that in part (). For large investors, the ratio concentrates at ; while for medium investors there is the anti-concentration bound (2.16). For small investors, the variance of is large.

2.3. Increasing reward

We consider the increasing reward of form for some and (e.g. EOS). The following theorem shows that the shares evolve very differently in the PoS protocol with a geometric reward vs a sub-geometric one.

Theorem 2.3.

Assume that the reward for some and .

-

(1)

If , then almost surely with

(2.17) -

(2)

If , then

-

(i)

For such that as (i.e. ), we have for each and each or :

(2.18) which converges to as .

-

(ii)

For (i.e. ), we have . Moreover, there exists independent of such that for sufficiently small:

(2.19) -

(iii)

For (i.e. ), we have as .

-

(i)

The proof of Theorem 2.3 is given in Appendix C. The theorem deals with two increasing reward schemes: a geometric reward and a sub-geometric one. Part () considers a geometric reward, and shows that with probability one, all the shares will eventually go to one investor in such a way that

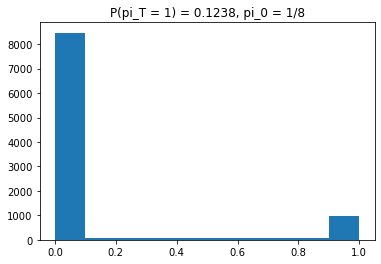

We call this chaotic centralization because the underlying dynamics will lead to the dictatorship, but the dictator is selected in a completely random manner. The investor with the largest initial coins will have the highest chance to control the PoS blockchain with a geometric reward.

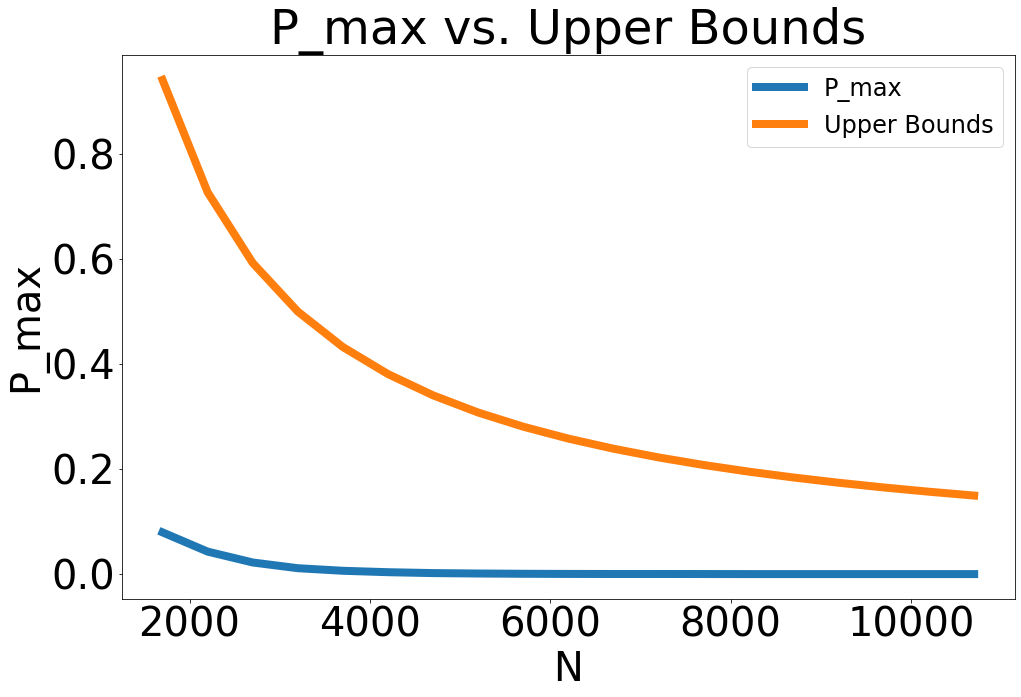

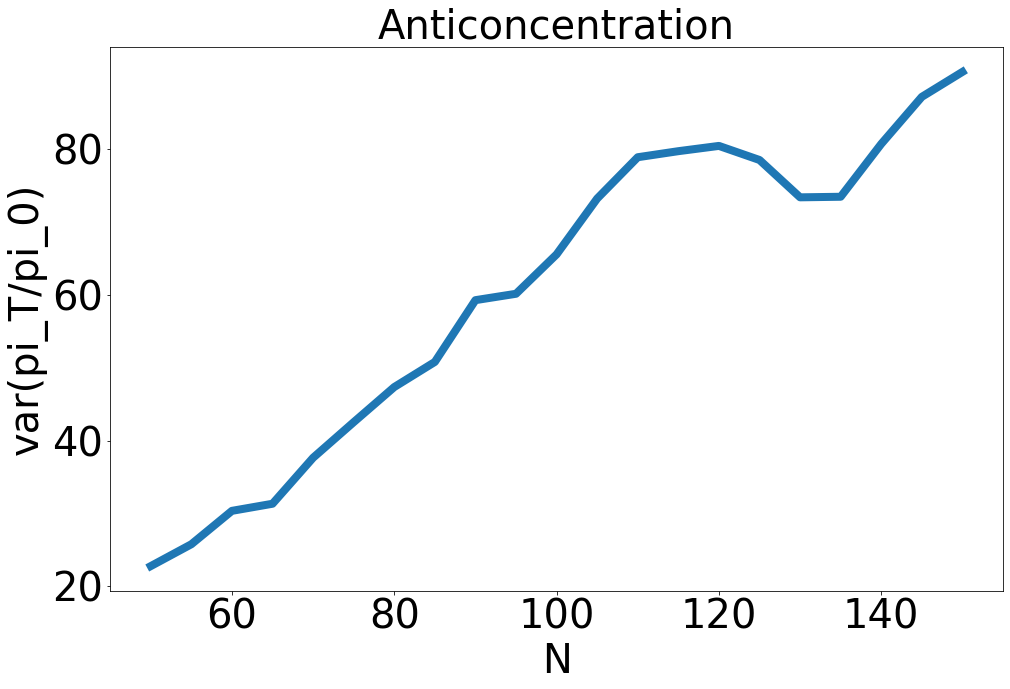

Part () considers a polynomial reward for . In this case, the threshold to distinguish large, medium and small investors is . For large investors, the ratio concentrates at ; while for medium investors there is the anti-concentration bound (2.19). For small investors, the variance of explodes. See Appendix E.2 for numerical illustrations related to Theorem 2.3.

3. Infinite population model

This section is concerned with modeling the PoS protocol which allows for an “infinite” number of investors in response to the growing popularity of blockchains. In Section 3.1, we start with a discrete infinite population model as a direct extension to the Pólya urn studied in Section 2. In Section 3.2, we consider an infinite population model sampled from a continuous space. Combining the ideas from these two subsections, we propose and analyze a dynamical population model for the PoS protocol in Section 3.3.

3.1. Discrete infinite population

In Section 2, we consider the Pólya urn model with a finite number of investors, i.e. , and study the limiting behavior of the ratio or as the initial coin offerings . Here we work directly with investors to model the PoS protocol.

We give a formal description of the model. The Pólya urn model with an infinite population is just as described in Section 2 but for . More precisely, there are a countably infinite number of investors indexed by . Let , be investor ’s endowment of coins at time with . At time , investor is selected at random among all investors with probability . Once selected, the investor receives a deterministic reward of . This way, the equations (2.1)–(2.4) hold for , and there are infinitely many small investors whose initial coins are (i.e. ). The investor shares are given by a vector of infinite length Again by the martingale convergence theorem,

| (3.1) |

where is random probability measure on .

We have seen in Theorem 2.1 that for a finite number of investors, if the reward is constant, the limiting investor shares have the Dirichlet distribution. For the Pólya urn model with an infinite population, one important problem is to understand limiting shares under constant or more general rewarding schemes. To this end, we recall the definition of the Dirichlet-Ferguson measure, or simply Dirichlet measure which was introduced by Ferguson (1973); Blackwell and MacQueen (1973) in the context of nonparametric Bayesian analysis.

Definition 3.1.

Let be a Polish space with Borel -field , and let be a positive measure on with . We say that has distribution if is a random distribution on such that for every measurable partition of , the random vector has distribution.

The following theorem studies the evolution of shares in a PoS protocol modeled by the Pólya urn with an infinite population.

Theorem 3.2.

Assume that the coin reward . Then the investor shares have a limiting distribution

| (3.2) |

where is a positive measure on with , . Moreover, for each investor or a finite number of investors in the same category, the results in Theorems 2.1, 2.2 and 2.3 hold under the corresponding rewarding schemes.

3.2. Infinite population from continuum

We consider an urn model with an infinite population which is sampled from a continuous space – we call it a PoS feature model. The motivation comes from understanding the influence induced by common features among investors in the PoS protocol. The influence of a particular feature is measured by the total shares that investors having this feature own. In many generic cases, features are represented or approximated by elements in a continuous sample space, e.g. geolocation of an investor, market experience of an investor measured in time, index assessing the level of risk aversion of an investor, and so on. Without loss of generality, we abstract the feature space as the unit interval .

The PoS feature model is inspired from the Blackwell-MacQueen construction of a Pólya urn on general state spaces as described in Lemma D.1. At each time , an investor with some feature is selected to receive a deterministic reward . Now we specify the selection rule over the time. At time , the initial coin offering is , and these coins are distributed among the investors with features in according to a diffuse probability measure on . That is, the number of coins owned by investors with features in is . At time , an investor with feature is selected by the rule

| (3.3) |

and then receives a reward . So the total number of coins becomes . At time , an investor with feature is selected with probability . More generally, at time an investor with feature is selected by the rule:

| (3.4) |

The main difference between the PoS feature model (3.3)–(3.4) and the urn models discussed in the previous sections is that there are uncountably many features of the investors for selection, but there are only a countable number of investors selected at time Two questions arise naturally: (). How to label the features of the investors selected by the feature model (3.3)–(3.4)? (). What are the limiting shares corresponding to these features?

These problems are closely related to the problem of species sampling and exchangeable partitions studied in Pitman (1995, 1996). Let us spell out in the PoS setting as follows. For (1) the simplest way to label the features among the selected investors is by their order of appearance. For , denote as the feature to appear in the sequence of Let and for , with the convention . So is the index at which the feature appears for the first time, and on the event . For instance, if , then , , , and , , , For general rewards , it seems challenging to specify the limiting distribution of shares . One exception is for the constant reward as stated in the following theorem.

Theorem 3.3.

Assume that the coin reward . Let be the features appearing in the order of appearance of the PoS feature model specified by (3.3)–(3.4). Then there is the stick-breaking representation for the limiting shares:

| (3.5) |

where are independent and identically distributed as . Moreover, let be the number of features appeared among the first selected investors. Then almost surely.

The proof of Theorem 3.3 is given in Appendix D.2. Theorem 3.3 shows that whatever the initial distribution of features is, the PoS feature model (3.3)–(3.4) with a constant reward yields a limiting share distribution on a countable number of features. This distribution, which only depends on the initial coin offerings and the reward , is known as the Griths-Engen-McCloskey (GEM) distribution (Ewens (1990)).

We may also consider more general PoS feature models. One such instance is when the selection rule relies on the history of the features of previously selected investors. For , let be the number of times that the investors with feature (in the order of appearance) are selected up to time , and be the vector of counts of various features of the investors up to time . We can regroup the investors according to their features, and rewrite the selection rule (3.4) as

| (3.6) |

Here we look for general selection rules of form and for ,

| (3.7) |

for some functions , defined on . The meaning of the selection rule (3.7) is as follows: given the histogram of features of investors selected from time to time , an investor with feature is selected with probability for , and an investor with a new feature is selected with probability . It is easily seen the selection rule (3.6) is a special case of the general rule (3.7) with , with . A closely related selection rule is defined by the functions , for some . In this case, the limiting share distribution also has the stick-breaking representation (3.5) with independent, and distributed as . This is known as the Pitman-Yor distribution (Pitman (1996); Pitman and Yor (1997)).

In general, we need the following condition on to define the selection rule (3.7): and for , where is the number of nonzero entries in . Pitman (1996) provides an additional condition on in terms of the exchangeable partition probability functions (EPPFs) so that the sequence specified by the selection rule (3.3)–(3.7) is exchangeable, and thus the limiting share distribution is well-defined. Such a sequence is called the species sampling sequence, see also Hansen and Pitman (2000) for related discussions.

3.3. From finite to infinite population

In this final subsection, we propose a dynamical approach to model the PoS protocol. We start with a finite number of investors, and then at each time a new investor may come into the market, which evolves to an infinite number of investors. This combines the ideas from previous sections, especially the Blackwell-MacQueen urn model.

We proceed to the description of the model. At time there are investors indexed by . These investors are initial capitalists in the blockchain network, so they play a very important role in the PoS protocol. For , let be the initial endowment of coins of investor , and with be the corresponding shares. At time , there are two possibilities: either one of these initial investors are selected, or a new investor is selected from the population. This is realistic since many cryptocurrencies are initially owned by a handful of coin miners or venture capitalists, and then their shares will be diluted by new investors over the time. Since the population is large, we approximate the population space by the unit interval , and a new investor is selected from by a diffuse probability measure as in Section 3.2. We also introduce a dilution parameter , which is the weight that a new investor is introduced to the blockchain network. More precisely,

-

•

For each , investor is selected with probability .

-

•

A new investor with “index’ in is selected with probability .

By letting be the index of the investor selected at time , we have

| (3.8) |

and the selected investor receives a deterministic reward . More generally, at time the selection rule is given by

| (3.9) |

where is the number of coins that investor owns at time , is the number of coins that a new investor with index owns at time , and is the total number of coins up to time . There are three terms on the right side of the selection rule (3.9): the first one comes from the initial investors, the second term is from the new investors previously entering the market, and the third term is the probability that a new investor is introduced. The following theorem studies how the shares of the initial capitalists are diluted over the time.

Theorem 3.4.

For , let be the shares of investor at time under the PoS protocol (3.8)–(3.9). Then is a supermartingale. Consequently, the shares of initial investors almost surely for some random sub-probability distribution .

-

(1)

Assume that the coin reward is decreasing with for each .

-

(i)

If or for , we have , and .

-

(ii)

If for , we have almost surely.

-

(i)

-

(2)

Assume that the coin reward for . We have , and .

-

(3)

Assume that the coin reward . We have . Consequently, the results in Theorem 2.1 hold.

The proof of Theorem 3.4 is given in Appendix D.3. The theorem shows that for the dynamical PoS model (3.8)–(3.9), the shares of initial investors will decrease over the time. If the coin reward does not decay too fast, i.e. , the expectation of the ratio tends to as the initial coin offering is large. On the contrary, if the coin reward decays very fast, i.e. , the initial investors’ shares will be eventually diluted to zero. More is known if the coin reward is constant. As is clear in the proof, the selection rule (3.9) as a probability measure converges with probability one to a random discrete probability distribution , and given the indices of selected investors, i.e. are independent and identically distributed as . Recall that has the representation where has distribution, and are independent and identically distributed as and also independent of . Thus, the indices of new investors (in order of their appearance) are just independent and identically distributed as , and the limiting expectation of their total shares is . So the larger the initial coin offerings are, the less influence of new investors have.

4. Conclusion

In this paper, we study the evolution of investor shares in a PoS blockchain under various rewarding schemes and for different types of investors. In contrast with the previous works where only large investors are considered, we take the heterogeneity of investors into account, and show that medium to small investors may suffer from share instability – their shares may be volatile, or even shrink to zero in the long run. This leads to the phase transition phenomenon, where thresholds for stability vs instability are characterized under different rewarding schemes. In particular, for the PoS protocol with a geometric reward we observe chaotic centralization; that is, all the shares will go to one investor in a random manner. In response to the increasing activities in blockchain networks, we also propose and analyze a dynamical population model for the PoS protocol which allows the number of investors to grow over the time. Our quantitative analysis also provides guidance on the choice of rewarding schemes so that decentralization is indeed implemented in a PoS blockchain.

There are a few directions to extend this work. For instance, one can study the trading incentive in the dynamical population setting. This requires incorporating a game-theoretic component to the analysis, and formulating a suitable reward optimization problem. Another problem is to consider other types of urn dynamics to model the voting rule in the PoS protocol, e.g. square voting rule (Penrose (1946)), and study the problems of long time stability and reward incentives.

Acknowledgement: We thank Alex Y. Wu for the help with the numerical experiments and the careful reading of the manuscript. We thank David Yao for helpful discussions, and Agostino Capponi and Jing Huang for various pointers to the literature. We gratefully acknowledges financial support through an NSF grant DMS-2113779 and through a start- up grant at Columbia University.

Appendix A Proof of Theorem 2.1

Proof.

The fact that the investor shares converges almost surely as to with the Dirichlet distribution (2.8) is a classical result of Pólya urn, see e.g.(Johnson and Kotz, 1977, Section 6.3).

() Since is a martingale, we have . It follows from (Mahmoud, 2009, Corollary 3.1) or Lemma 2.2 of (Goldstein and Reinert, 2013, Lemma 2.2) that

| (A.1) |

Specializing (A.1) to , we obtain which recovers Corollary 1 of Roşu and Saleh (2021). By applying Chebyshev’s inequality, we get

| (A.2) |

which leads to (2.9) by noting that and .

() Since , we have . Now , by standard limit theorem we get . This implies the convergence in distribution (2.10).

() By () we have . Let so as by hypothesis. Then

Note that , and as . As a result, there exists a constant (independent of ) such that

which converges to as . This yields the convergence (2.11). ∎

Appendix B Proof of Theorem 2.2

To prove Theorem 2.2, we need a series of lemmas.

Lemma B.1.

The variance of investor ’s share is

| (B.1) |

where

| (B.2) |

The third central moment of investor ’s share satisfy the relation

| (B.3) |

and the fourth central moment of investor ’s share satisfy the relation

| (B.4) |

Proof.

Lemma B.2.

Proof.

(1) The upper bound follows from (Roşu and Saleh, 2021, Lemma A.4). By (B.2), we get . This implies that for ,

| (B.8) |

where the second inequality is due to the fact that is decreasing. By abuse of language, let be the linear interpolation of . Since is decreasing, we deduce from (B.8) that

which yields the lower bound in (B.6).

(2) Note that . Then for each ,

| (B.9) |

where the second inequality follows from (B.1) and the upper bound in (B.6), and the last inequality is due to the fact that . Also for each ,

| (B.10) |

Combining (B.1), (B) and (B.10), we get

| (B.11) |

Using the sum-integral trick as in (Roşu and Saleh, 2021, Lemma A.4) we deduce that for So the bound (B.11) leads to

Similarly, we get from (B.1) that

∎

Lemma B.3.

Proof.

Lemma B.4.

Assume that the reward is decreasing, i.e. for each , and that for .

-

(1)

Let be defined by (B.2). There exist independent of and such that

(B.15) - (2)

Proof.

(1) It follows from (B.8) and (B.14) that

Thus, we need to study the asymptotic behavior of as . Since for , we have:

| (B.17) |

for some independent of and . Again by the sum-integral trick, we get

| (B.18) |

Now for , we have

| (B.19) |

and

| (B.20) |

Combining (B.17), (B.18), (B) and (B) yields

This leads to the bounds (B.15).

Proof of Theorem 2.2.

(1) () By Chebyshev’ inequality and the upper bound in (B.6), we get

This proves (2.12): the ratio converges in probability to as .

Appendix C Proof of Theorem 2.3

To prove Theorem 2.3, we need the following lemma.

Lemma C.1.

Proof.

(1) The upper bound follows from (Roşu and Saleh, 2021, Lemma A.5). Recall that , and thus behaves asymptotically as . As a result, there is independent of and such that for sufficiently large. This also implies that for sufficiently large. By (B.8), we have

| (C.3) |

where the last equality is due to the fact that . Using the sum-integral trick, we get

| (C.4) |

for sufficiently large. Combining (C) and (C.4) yields the lower bound in (C.1).

Appendix D Proof of Theorems 3.2 – 3.4

D.1. Proof of Theorem 3.2

To prove Theorem 3.2, we need the following result of the Blackwell-MacQueen urn scheme which generalizes the Pólya urn scheme.

Lemma D.1 (Blackwell and MacQueen (1973)).

Let be a positive and finite measure on a Polish space . Define a sequence as follows: is distributed as , and for ,

| (D.1) |

where is the Dirac mass at point . Then

-

•

converges in total variation (and thus in distribution) almost surely to a random discrete distribution , which has distribution.

-

•

Conditional given , are independent and identically distributed as .

Proof of Theorem 3.2.

First assume that , and let be a positive measure on such that , so . Let be the index of the investor who is selected by the PoS protocol at time . By definition of the PoS scheme, we have

Lemma D.1 then implies the identity in distribution (3.2). By Definition 3.1, we get for each fixed , and thus the results in Theorem 2.1 hold. The results in Theorems 2.2 and 2.3 are stated for each investor , and do not depend on the number of investors. So these results also hold in the infinite population setting. ∎

D.2. Proof of Theorem 3.3

Proof.

The stick-breaking representation (3.5) follows from the Blackwell-MacQueen urn construction (Lemma D.1), along with various constructions of the Dirichlet measure by Ferguson (1973); McCloskey (1965). See e.g. (Pitman, 1996, Section 2.2) for a review of the circle of ideas. The fact that behaves asymptotically as is read from (Korwar and Hollander, 1973, Theorem 2.3 ). ∎

D.3. Proof of Theorem 3.4

Proof.

Note that with probability and with probability . As a result,

So is a supermartingale. By the martingale convergence theorem, converges almost surely to a random vector . Observe that which implies that

| (D.2) |

(1) Assume that is decreasing. If , we have , and if for , we have . In both cases, we get and thus the infinite product in (D.2) converges to some number in . If for , we have for sufficiently large. In this case, . Consequently, we get which implies that almost surely.

(2) Assume that for . If , it follows from the proof of Lemma C.1 that . We have . If , then and grows exponentially in . In both cases, we have which implies that the infinite product in (D.2) converges to some number in .

(3) It is easily checked that the PoS scheme (3.8)–(3.9) with a constant reward is just the Blackwell-MacQueen urn with . It follows from Lemma D.1 that selection probability (3.9) converges almost surely to a random discrete distribution , and given the indices of investors selected are independent and identically distributed as . This implies that the limiting share of investor is , and the results in Theorem 2.1 follow. ∎

Appendix E Numerical illustrations for Theorems 2.2 and 2.3

E.1. Numerical illustrations for Theorem 2.2: decreasing reward

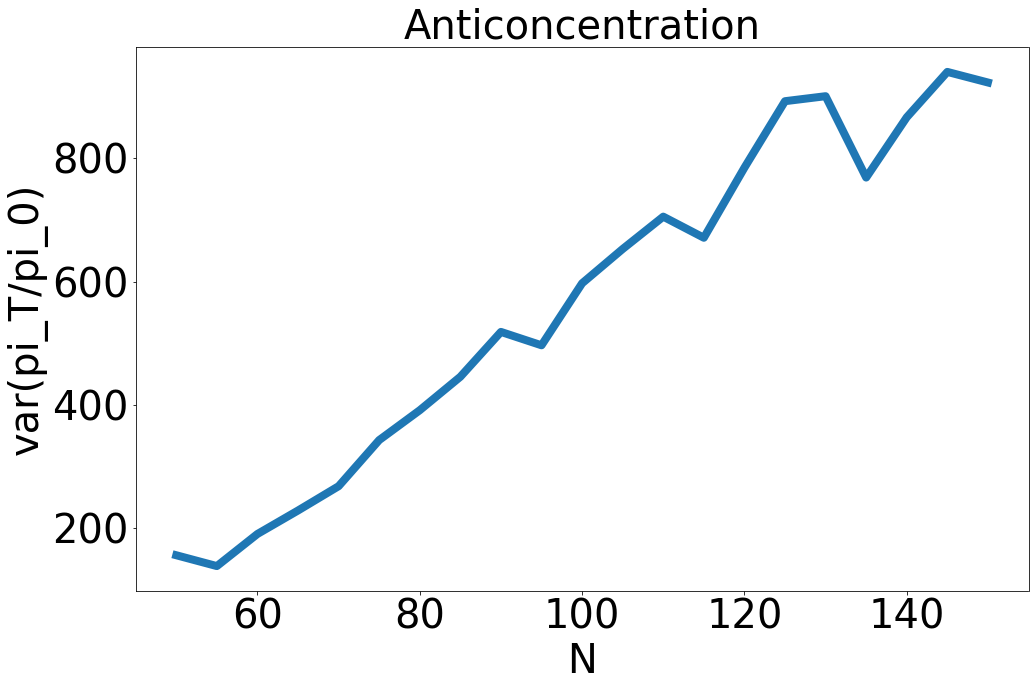

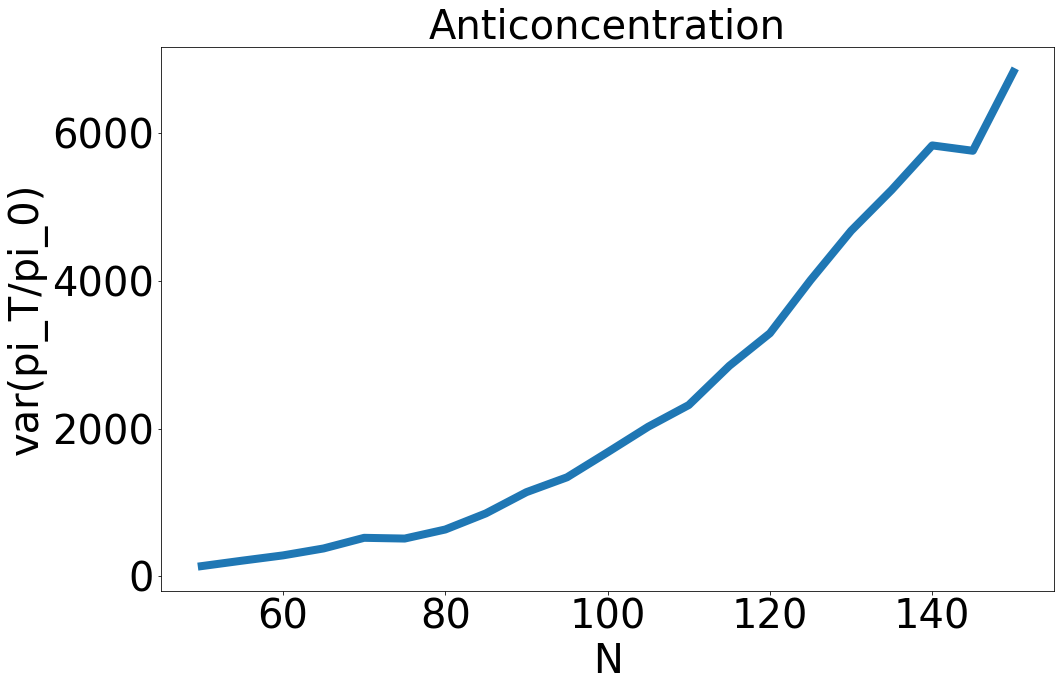

(1) is bounded from : Figure 3 shows the concentration bound (2.12) for large investors; Figure 4(a) shows the bounded variance and the anti-concentration bound (2.13) for medium investors; Figure 4(b) shows the exploding variance for small investors.

(2) for : Figure 5 shows the concentration bound (2.14) for large investors; Figure 6(a) shows the bounded variance for medium investors; Figure 6(b) shows the exploding variance for small investors.

(3) for : Figure 7 shows the concentration bound (2.15) for large investors; Figure 8(a) shows the bounded variance and the anti-concentration bound (2.16) for medium investors; Figure 8(b) shows the exploding variance for small investors.

E.2. Numerical illustrations for Theorem 2.3: increasing reward

(1) for : Figure 9 shows the chaotic centralization under a geometric reward.

(2) for : Figure 10 shows the concentration bound (2.18) for large investors; Figure 11(a) shows the bounded variance and the anti-concentration bound (2.19) for medium investors; Figure 11(b) shows the exploding variance for small investors.

References

- Afram (2018) E. Afram. Proof of Work vs Proof of Stake. 2018. Available at https://coingeek.com/proof-work-vs-proof-stake.

- Alsabah and Capponi (2020) H. Alsabah and A. Capponi. Pitfalls of bitcoin’s proof-of-work: R&d arms race and mining centralization. 2020. SSRN:3273982.

- Arnosti and Weinberg (2022) N. Arnosti and S. M. Weinberg. Bitcoin: A natural oligopoly. Management Science, 2022.

- Bagaria et al. (2019) V. Bagaria, A. Dembo, S. Kannan, S. Oh, D. Tse, P. Viswanath, X. Wang, and O. Zeitouni. Proof-of-stake longest chain protocols: Security vs predictability. 2019. arXiv:1910.02218.

- Benhaim et al. (2021) A. Benhaim, B. H. Falk, and G. Tsoukalas. Scaling Blockchains: Can elected committees help? 2021. arXiv:2110.08673.

- Blackwell and MacQueen (1973) D. Blackwell and J. B. MacQueen. Ferguson distributions via Pólya urn schemes. The Annals of Statistics, 1:353–355, 1973.

- Brown-Cohen et al. (2019) J. Brown-Cohen, A. Narayanan, A. Psomas, and S. M. Weinberg. Formal barriers to longest-chain proof-of-stake protocols. In Proceedings of the 2019 ACM Conference on Economics and Computation, pages 459–473, 2019.

- Chiu and Koeppl (2017) J. Chiu and T. V. Koeppl. The economics of cryptocurrencies–Bitcoin and beyond. 2017. SSRN:3048124.

- Chod et al. (2020) J. Chod, N. Trichakis, G. Tsoukalas, H. Aspegren, and M. Weber. On the financing benefits of supply chain transparency and blockchain adoption. Management Science, 66(10):4378–4396, 2020.

- Cong et al. (2021) L. W. Cong, Z. He, and J. Li. Decentralized mining in centralized pools. The Review of Financial Studies, 34(3):1191–1235, 2021.

- Daian et al. (2019) P. Daian, R. Pass, and E. Shi. Snow white: Robustly reconfigurable consensus and applications to provably secure proof of stake. In International Conference on Financial Cryptography and Data Security, pages 23–41, 2019.

- Donovan (2019) F. Donovan. Healthcare blockchain could save industry $100b annually by 2025. HIT Infrastructure, 2019. Available at https://hitinfrastructure.com/news/healthcare-blockchain-could-save-industry-100b-annually-by-2025.

- Dowling (2022) M. Dowling. Is non-fungible token pricing driven by cryptocurrencies? Finance Research Letters, 44:102097, 2022.

- Durrett (2019) R. Durrett. Probability—theory and examples. Cambridge University Press, 2019.

- Ewens (1990) W. J. Ewens. Population genetics theory—the past and the future. In Mathematical and statistical developments of evolutionary theory (Montreal, PQ, 1987), volume 299, pages 177–227. Kluwer Academic Publishers, 1990.

- Fanti et al. (2019) G. Fanti, L. Kogan, S. Oh, K. Ruan, P. Viswanath, and G. Wang. Compounding of wealth in proof-of-stake cryptocurrencies. In International Conference on Financial Cryptography and Data Security, pages 42–61, 2019.

- Ferguson (1973) T. S. Ferguson. A Bayesian analysis of some nonparametric problems. The Annals of Statistics, 1:209–230, 1973.

- Foley et al. (2019) S. Foley, J. R. Karlsen, and T. J. Putniņš. Sex, drugs, and bitcoin: How much illegal activity is financed through cryptocurrencies? The Review of Financial Studies, 32(5):1798–1853, 2019.

- Goldstein and Reinert (2013) L. Goldstein and G. Reinert. Stein’s method for the beta distribution and the Pólya-Eggenberger urn. Journal of Applied Probability, 50(4):1187–1205, 2013.

- Hansen and Pitman (2000) B. Hansen and J. Pitman. Prediction rules for exchangeable sequences related to species sampling. Statistics & Probability Letters, 46(3):251–256, 2000.

- Hileman and Rauchs (2017) G. Hileman and M. Rauchs. Global cryptocurrency benchmarking study. Cambridge Centre for Alternative Finance, 33:33–113, 2017.

- Irresberger (2018) F. Irresberger. Coin concentration of proof-of-stake blockchains. Leeds University Business School Working Paper, (19-04), 2018.

- Johnson and Kotz (1977) N. L. Johnson and S. Kotz. Urn models and their application: an approach to modern discrete probability theory. John Wiley & Sons, 1977.

- Kiayias et al. (2017) A. Kiayias, A. Russell, B. David, and R. Oliynykov. Ouroboros: A provably secure proof-of-stake blockchain protocol. In Annual International Cryptology Conference, pages 357–388, 2017.

- King and Nadal (2012) S. King and S. Nadal. Ppcoin: Peer-to-peer crypto-currency with proof-of-stake. 2012. Available at https://decred.org/research/king2012.pdf.

- Korwar and Hollander (1973) R. M. Korwar and M. Hollander. Contributions to the theory of Dirichlet processes. The Annals of Probability, 1:705–711, 1973.

- Lamport et al. (1982) L. Lamport, R. Shostak, and M. Pease. The Byzantine Generals Problem. ACM Transactions on Programming Languages and Systems, 4(3):382–401, 1982.

- Mahmoud (2009) H. M. Mahmoud. Pólya urn models. Texts in Statistical Science Series. CRC Press, 2009.

- McCloskey (1965) J. W. McCloskey. A model for the distribution of individuals by species in an environment. 1965. Thesis (Ph.D.)–Michigan State University.

- McGhin et al. (2019) T. McGhin, K.-K. R. Choo, C. Z. Liu, and D. He. Blockchain in healthcare applications: Research challenges and opportunities. Journal of Network and Computer Applications, 135:62–75, 2019.

- Mora et al. (2018) C. Mora, R. L. Rollins, K. Taladay, M. B. Kantar, M. K. Chock, M. Shimada, and E. C. Franklin. Bitcoin emissions alone could push global warming above 2 c. Nature Climate Change, 8(11):931–933, 2018.

- Nakamoto (2008) S. Nakamoto. Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review, page 21260, 2008.

- Penrose (1946) L. S. Penrose. The elementary statistics of majority voting. Journal of the Royal Statistical Society, 109(1):53–57, 1946.

- Pitman (1995) J. Pitman. Exchangeable and partially exchangeable random partitions. Probability Theory Related Fields, 102(2):145–158, 1995.

- Pitman (1996) J. Pitman. Some developments of the Blackwell-MacQueen urn scheme. In Statistics, Probability and Game theory, volume 30, pages 245–267. 1996.

- Pitman and Yor (1997) J. Pitman and M. Yor. The two-parameter Poisson-Dirichlet distribution derived from a stable subordinator. The Annals of Probability, 25(2):855–900, 1997.

- Platt et al. (2021) M. Platt, J. Sedlmeir, D. Platt, P. Tasca, J. Xu, N. Vadgama, and J. I. Ibañez. Energy footprint of blockchain consensus mechanisms beyond proof-of-work. 2021. arXiv:2109.03667.

- Roşu and Saleh (2021) I. Roşu and F. Saleh. Evolution of shares in a proof-of-stake cryptocurrency. Management Science, 67(2):661–672, 2021.

- Saberi et al. (2019) S. Saberi, M. Kouhizadeh, J. Sarkis, and L. Shen. Blockchain technology and its relationships to sustainable supply chain management. International Journal of Production Research, 57(7):2117–2135, 2019.

- Saleh (2019) F. Saleh. Volatility and welfare in a crypto economy. 2019. SSRN:3235467.

- Saleh (2021) F. Saleh. Blockchain without waste: Proof-of-stake. The Review of Financial Studies, 34(3):1156–1190, 2021.

- Tang et al. (2020) W. Tang, X. Guo, and F. Tang. The buckley-osthus model and the block preferential attachment model: statistical analysis and application. In International Conference on Machine Learning, pages 9377–9386. PMLR, 2020.

- Tanwar et al. (2020) S. Tanwar, K. Parekh, and R. Evans. Blockchain-based electronic healthcare record system for healthcare 4.0 applications. Journal of Information Security and Applications, 50:102407, 2020.

- Tsoukalas and Falk (2020) G. Tsoukalas and B. H. Falk. Token-weighted crowdsourcing. Management Science, 66(9):3843–3859, 2020.

- Wang et al. (2021) Q. Wang, R. Li, Q. Wang, and S. Chen. Non-fungible token (NFT): Overview, evaluation, opportunities and challenges. 2021. arXiv:2105.07447.

- Wickens (2021) K. Wickens. ’the Merge’ to end cryptocurrency mining on gaming GPUs won’t come until 2022. 2021. Available at https://www.pcgamer.com/the-merge-to-end-cryptocurrency-mining-on-gaming-gpus-wont-come-until-2022.

- Wood (2018) A. Wood. West Virginia secretary of state reports successful blockchain voting in 2018 midterm elections. 2018. Avalialbe at https://cointelegraph.com/news/west-virginia-secretary-of-state-reports-successful-blockchain-voting-in-2018-midterm-elections.

- Wood (2014) G. Wood. Ethereum: A secure decentralised generalised transaction ledger. Ethereum Project Yellow Paper, 151:1–32, 2014.