Time-Varying Multivariate Causal Processes

∗Jiti Gao and ∗Bin Peng and †Wei Biao Wu and ∗Yayi Yan

∗Department of Econometrics and Business Statistics, Monash University,

and †Department of Statistics, University of Chicago

Abstract

In this paper, we consider a wide class of time-varying multivariate causal processes which nests many classic and new examples as special cases. We first prove the existence of a weakly dependent stationary approximation for our model which is the foundation to initiate the theoretical development. Afterwards, we consider the QMLE estimation approach, and provide both point-wise and simultaneous inferences on the coefficient functions. In addition, we demonstrate the theoretical findings through both simulated and real data examples. In particular, we show the empirical relevance of our study using an application to evaluate the conditional correlations between the stock markets of China and U.S. We find that the interdependence between the two stock markets is increasing over time.

Keywords: Local Linear Quasi-Maximum Likelihood Estimation; Multivariate Causal Process; Simultaneous Confidence Interval.

JEL Classification: C14, C32, G15.

1 Introduction

The family of vector autoregressive (VAR) models and the family of multivariate (G)ARCH models are among some of the most popular frameworks for modelling dynamic interactions of multiple variables. The VAR family usually captures the dynamic by imposing structures on the time series itself, while the (G)ARCH family imposes restrictions on the conditional second moments. We acknowledge the vast literature of both families, and have no intention to exhaust all relevant studies in this paper for the sake of space. We refer interested readers to Stock & Watson (2001) and Bauwens et al. (2006) for excellent review on both families.

Although both families have rich literature on their own, to the best of the authors’ knowledge not many works have been done to bridge them. Among limited attempts (e.g., Ling & McAleer 2003, Bardet & Wintenberger 2009), most (if not all) of these studies rely on the stationarity assumption. While the stationarity assumption comes in handy when deriving asymptotic properties, it may not be very realistic in practice (Preuss et al. 2015, Chen et al. 2021). For example, economic and financial data always include different macro shocks, as a consequence the behaviour can be quite volatile; the climate data may contain certain time trend which recently has attracted lots of attention due to greenhouse emission; etc. Anyway, certain nonstationarity may always occur.

To account for nonstationarity, locally stationary processes have received considerable attention since the seminal work of Dahlhaus (1996), Dette et al. (2011), Zhang & Wu (2012), Truquet (2017), Dahlhaus et al. (2019), among others. In contrast to the unit root process, the locally stationary process nicely balances stationarity and nonstationarity by allowing for the simultaneous presence of both types of behaviours in one time series process. In a very recent paper, Karmakar et al. (2022) consider simultaneous inference for a general class of univariate -Markov processes with time-varying coefficients, which covers several time-varying versions of the classical univariate models (e.g., AR, ARCH, AR-ARCH) as special cases. Despite its generality, their study still rules out the time-varying versions of some widely used models (e.g., ARMA, GARCH, ARMA-GARCH). Also, it is worth mentioning this line of research heavily focuses on univariate time series, which somewhat limits the popularity of locally stationary processes.

That said, it is reasonable to call for a framework which can marry the VAR family and the (G)ARCH family while allowing for nonstationarity. To provide a concrete example, consider a time-varying multivariate GARCH model, which can model the co-movements of financial returns. Detailed investigation on such a model can help answer research questions like (i). Is the volatility of a market leading the volatility of other markets? (ii) Whether the correlations between asset returns change over time? (iii). Are they increasing in the long run, perhaps because of the globalization of financial markets? These are of great practical importance for both investors and policymakers (Bauwens et al. 2006, Diebold & Yilmaz 2009).

To allow for flexibility as much as possible from the modelling perspective, we consider a class of multivariate causal processes as follows:

| (1.3) |

where , is an -dimensional random vector, is an -dimensional random matrix, is a time-varying parameter of interest with each element belonging to , and is a sequence of independent and identically distributed (i.i.d.) random vectors. Note that the value of usually depends on the value of , and the connection becomes clear once a specific model is considered. As far as we are concerned, both of and are fixed throughout the paper. Notably, both and are known, and share the same unknown parameter . The setting for regulates the time series for the periods that we do not observe, which is commonly adopted when certain nonstationarity gets involved (e.g., Vogt 2012). Essentially, it requires the initial time period does not have a diverging behaviour.

Before proceeding further, we provide two examples to briefly illustrate the rationality behind (1.3), and leave the detailed investigation on these examples to Section 2.4. We refer interested readers to Ling (2003), Ling & McAleer (2003) and Bardet & Wintenberger (2009) for extensive investigation on the parametric counterparts of these examples.

Example 1: Consider the time-varying VARMA() model

| (1.4) |

It is not hard to show that (1.4) admits a presentation in the form of (1.3), and

| (1.5) |

where .

Example 2: Consider the time-varying multivariate GARCH() model

| (1.6) |

where stands for the element of , and . The model (1) generalizes the models of Bollerslev (1990) and Jeantheau (1998). Similar to Example 1, we show that (1) admits a representation in the form of (1.3), and

| (1.7) |

In view of the development of Example 1 and Example 2 in Section 2.4, one may further show the time-varying counterparts of the parametric models mentioned in Bardet & Wintenberger (2009) are also covered by (1.3). To this end, we argue that (1.3) does not only allows for nonstationarity and conditional heteroskedasticity, but also provides sufficient flexibility to cover many well adopted models in the literature.

In this paper, our contributions are in the following four-fold: (1). we consider a wide class of time-varying multivariate causal processes which nests many classic and new examples as special cases; (2). we prove the existence of a weakly dependent stationary approximation for the model (1.3) at any given time of interest (i.e., ), which is the foundation in order to establish asymptotic properties associated with the model; (3). we establish the estimation theory, and provide both point-wise and simultaneous inferences on the coefficient functions of which both are important for practical works (Zhou & Wu 2010); (4). we demonstrate the theoretical findings through both simulated and real data examples.

The paper is organized as follows. Section 2 presents the theoretical findings associated with the stationary approximation, estimation and inferences. In Section 3, we conduct extensive simulation studies to examine the theoretical findings, and further investigate the time-varying conditional correlations between the Chinese and U.S. Stock market. Section 4 concludes. Due to space limit, we give the proofs of the main results to the online appendices of the paper.

Before proceeding further, it is convenient to introduce some notation: the symbol denotes the Euclidean norm of a vector or the spectral norm for a matrix; and for short; denotes the Kronecker product; denotes the Hadamard product; stands for an identity matrix; stands for an matrix of zeros, and we write for short when ; for a function , let be the derivative of , where and ; , where and stand for a nonparametric kernel function and a bandwidth respectively; let and for integer ; is a diagonal matrix with the vector on its main diagonal, while creates a vector from the diagonal of matrix ; finally, let and denote convergence in probability and convergence in distribution, respectively.

2 Estimation and Asymptotics

In this section, we first prove the existence of a weakly dependent stationary approximation for the model (1.3) in Section 2.1; we then provide the estimation approach using the local linear quasi-maximum-likelihood estimation and establish the asymptotic properties of the proposed estimator in Section 2.2; Section 2.3 provides results on both point-wise and simultaneous inferences; Section 2.4 gives some detailed examples to justify the usefulness of our study.

2.1 Stationary Approximation

To study (1.3), the first challenge lies in the fact that the model may not be stationary. Therefore, for , we initial our analysis by finding a stationary approximation for each with . By doing so, we are able to measure the weak dependence of using the nonlinear system theory in Wu (2005), which then provides us a framework to derive the asymptotic properties accordingly.

To be clear on the dependence measure, consider an example in which is a stationary process, and admits a causal representation with being a measurable function. See Tong (1990) for discussion on nonlinear time series of this kind. For , we define the following dependence measure:

| (2.1) |

where is an independent copy of . Being able to measure the time series dependence such as (2.1) is the starting point for time series analyses.

We now introduce some basic assumptions.

Assumption 1.

-

1.

is a sequence of i.i.d. random vectors with , , and for some .

-

2.

For and , there exist nonnegative sequences and such that

where and are the columns of and respectively.

-

3.

For , lies in the interior of , where

and is a compact set of .

Assumption 1.1 is standard when studying dynamic time series model (Lütkepohl 2005). In Assumption 1.2, is a generic vector, and has the same length as . This assumption imposes Lipschitz-type conditions on and , which are rather minor, and can be easily fulfilled by a variety of models such as those mentioned in Section 1. See Propositions 2.3-2.4 below for details. Assumption 1.3 does not only guarantee a stationary approximation for each , but also ensures the approximated process has some proper moments. Similar conditions have also been adopted in Bardet & Wintenberger (2009).

With these conditions in hand, we present the following proposition which facilitates the development in what follows.

Proposition 2.1.

It is worth mentioning that for a univariate -Markov process

Karmakar et al. (2022) show that there exists such that based on the development of Wu & Shao (2004). From a methodological viewpoint, we give a set of new proofs which allow us to measure the dependence of multivariate causal processes with infinity memory. The term in the second result of Proposition 2.1 arises due to the infinity memory structure of . Thus, the dependence relies on the choice of and the decay rates of the coefficients and .

To ensure can approximate reasonably well, we impose more structure below.

Assumption 2.

-

1.

There exists a nonnegative sequence with such that for and

-

2.

Let and for some .

2.2 Estimation

We point out a few facts to facilitate the setup of the likelihood function. First, let include all the information of up to the time period . However, in practice, our observation on only starting from , so we have to work with the truncated version of for each :

| (2.2) |

Second, we note that when is sufficiently close to ,

| (2.3) |

Therefore, we are able to parametrize , and consider the maximum-likelihood estimation for each given . Finally, since may not be normally distributed, we consider the local linear quasi-maximum-likelihood estimation (QMLE) method.

Thus, our likelihood function is specified as follows:

| (2.4) |

where

Accordingly, for , is estimated by

| (2.5) |

where and is a compact set.

We impose more structures in order to derive the asymptotic distribution.

Assumption 3.

-

1.

for some .

-

2.

For any , and a.s. imply for some , where .

Assumption 4.

-

1.

and are twice continuously differentiable with respect to .

-

2.

There exists a nonnegative sequence with and some such that for any and any :

where , and .

Assumption 5.

Let be a symmetric and positive kernel function defined on with . Moreover, is Lipschitz continuous on . As , .

Assumption 3.1 ensures the positive definiteness of the covariance matrix of the likelihood function, and is widely adopted when studying the multivariate time series (e.g., page 2736 of Bardet & Wintenberger 2009). In fact, the validity of this assumption is easy to justify in view of (2.4) and (2.16) for Example 1 and Example 2 below. Assumption 3.2 imposes an standard identification condition in the literature of M-estimation (e.g., Proposition 3.4 of Jeantheau 1998). It is noteworthy that the current form of Assumption 3 accommodates the flexibility of the model (1.3), which is in fact unnecessary if we have a detailed model in practice. See Section 2.4 for example.

Assumption 4 imposes the Lipschitz-type conditions on the first and second order derivatives of and to ensure the smoothness of their functional components.

Assumption 5 is a set of regular conditions on the kernel function and the bandwidth.

With these conditions in hand, we summarize the first theorem of this paper below.

Theorem 2.1.

(1). If , then for any

where , and

(2). In addition, if is normally distributed, we have and thus .

After deriving the asymptotic distribution, we will establish both the point-wise inference and the simultaneous inference in the following.

2.3 Inference

In this section, we first discuss how to conduct point-wise inference, and then move on to derive the asymptotic results associated with the simultaneous inference. Specifically, for some preassigned significance level , we shall construct a asymptotic simultaneous confidence band (SCB) for in the sense that

Notably, the simultaneous inference nests the traditional constancy test as a special case. It does not only allow one to examine whether a time-varying model should be preferred to its parametric counterpart, but also allows one to test any particular functional form of interest. For example, if a horizontal line can be embedded in the SCB , then we accept the hypothesis that some elements of are constant.

Point-wise Inference: First, we construct a bias-corrected estimator in order to remove the asymptotic bias of Theorem 2.1. Specifically, we let

| (2.6) |

where is defined in the same way as but using the bandwidth .

After tedious development (Lemma B.7 of Appendix B), we have uniformly over

where that is essentially a fourth-order kernel. It then infers that under the conditions of Theorem 2.1,

| (2.7) |

where .

It is noteworthy that the construction of (2.6) is different from directly using the fourth-order kernel in the regression. In terms of bandwidth selection, the traditional methods (e.g., cross-validation) still remain valid for (2.6) (Richter et al. 2019). However, if one directly employs the fourth-order kernel in the regression, it remains unclear how to select the optimal bandwidth in practice.

Now we discuss how to estimate which is constructed by and . Intuitively, we consider the following estimator

| (2.8) |

where

Note that we consider a local constant estimator in (2.8) rather than a local linear one, that is to avoid an implementation issue for finite sample studies (i.e., nonpositive definite covariance may occur when the local linear approach is employed). Such a numerical problem has been well explained and investigated in the literature. See Chen & Leng (2015) for example.

The following corollary summarizes the asymptotic property of (2.8).

Corollary 2.1.

Simultaneous Inference: We now consider the simultaneous inference. To allow for flexibility, we first introduce a selection matrix with full row rank, which selects the parameters of interest as follows:

| (2.9) |

Accordingly, the estimator and the corresponding asymptotic covariance matrix become

| (2.10) |

Theorem 2.2.

Under the conditions of Theorem 2.1.1, suppose further that

for some . In addition, let with and . Then

where

and is the Gamma function.

In Theorem 2.2, is slightly smaller than as we only require to be slightly larger than . Hence, the usual optimal bandwidth satisfies the conditions and .

As shown in Theorem 2.2, the convergence rate of the simultaneous confidence intervals for is of logarithmic rate and is therefore slow. In order to improve the rate, we consider a bootstrap method which shows a much better finite sample performance. We summarize the result in the following corollary.

Corollary 2.2.

Under the conditions of Theorem 2.2. Suppose that with . Then, on a richer probability space, there exists i.i.d. -dimensional standard normal variables such that

where , , ,

By Corollary 2.2, we propose the following numerical procedure to construct the SCB of :

- Step 1

-

Step 2

Generate i.i.d. -dimensional standard normal variables and calculate the quantity , in which .

-

Step 3

Repeat Step 2 times to obtain the empirical quantile of .

-

Step 4

Calculate using (2.8), and construct the SCB of by , where is the unit ball, and is the rank of .

2.4 Examples

Below, we demonstrate the usefulness of the aforementioned results by considering Example 1 and Example 2 of Section 1.

Example 1 (Cont.) — For , simple algebra shows that the approximated stationary process is defined by

| (2.11) |

where has been defined in (1.5), and

| (2.12) |

Additionally, in (2.4), is yielded as follows:

| (2.13) |

where and .

Then we are able to present the following proposition.

Proposition 2.3.

We note that the detailed identification conditions required for VARMA processes (e.g., the final equations form or echelon form) can be found in Lütkepohl (2005). We no longer discuss them here in order not to derivative from our main goal.

Example 2 (Cont.) — We further let

| (2.14) |

For , the corresponding approximated stationary process is defined as

| (2.15) |

where

| (2.16) | |||||

Note that is generated as follows:

| (2.17) |

where and .

Consequently, we can present the following proposition.

Proposition 2.4.

Suppose that there is a compact set

such that (1). for , lies in the interior of , (2). for some , (3). all the roots of are outside the unit circle with ’s and ’s being squared matrices of nonnegative elements, (4). is a vector of positive elements, (5). and are coprime and the formulation of the GARCH part is minimal, where and . Then the results Theorems 2.1 and 2.2 hold for model (1).

For the identification conditions of the GARCH process, we refer readers to Proposition 3.4 of Jeantheau (1998), who proves that assuming the minimal representation is enough for ensuring Assumption 3 holds.

In the following section, we conduct numerical studies using both simulated and real data to evaluate the finite-sample performance of the proposed estimation and inferential methods.

3 Numerical Studies

In this section, we first present the details of the numerical implementations in Section 3.1, and then conduct extensive simulations in Section 3.2. Section 3.3 presents a real data example on the conditional correlations between the Chinese and U.S. stock markets.

3.1 Numerical Implementation

Throughout the numerical studies, the Epanechnikov kernel is adopted. Following Zhou & Wu (2010), we use for the biased corrected estimator, where is the bandwidth selected by the cross-validation method of Richter et al. (2019).

Specifically, define the leave-one-out local linear QMLE

| (3.1) |

where

Then, the bandwidth is chosen by

| (3.2) |

As shown in Richter et al. (2019), this cross validation method works well as long as is uncorrelated, which implies that this desirable property should hold in our case.

Notably, when considering some specific models, the implementation may be further simplified. We provide more discussions along this line in Appendix B.4.

3.2 Simulation Results

In the simulation studies, we examine the empirical coverage probabilities of simultaneous confidence intervals for nominal levels . We consider the time-varying VARMA() and multivariate GARCH() model as follows:

-

1.

, where are i.i.d. draws from , , ,

Here we use final equations form to ensure the uniqueness of the VARMA representation.

-

2.

, where , , are i.i.d. draws from , ,

Let the sample size be () for the VARMA model (the GARCH model). We conduct replications for each choice of . Several different bandwidths close to are reported to check the sensitivity of bandwidth selection.

We present the empirical coverage probabilities associated with the SCB in Tables 1–2. For the vector- or matrix-valued unknown coefficients, we take an average across the elements. A few facts emerge from the tables. First, the finite sample coverage probabilities are smaller than their nominal level when () for the VARMA model (the GARCH model), but are fairly close to their nominal level as () for the VARMA model (the GARCH model). Second, the behaviour of the estimated simultaneous confidence intervals is not sensitive to the choices of bandwidths. Third, the GARCH model requires more data to reach a reasonable finite sample performance.

| 0.845 | 0.877 | 0.821 | 0.847 | 0.905 | 0.915 | 0.889 | 0.905 | ||||

| 0.865 | 0.875 | 0.847 | 0.876 | 0.912 | 0.930 | 0.897 | 0.909 | ||||

| 0.862 | 0.895 | 0.847 | 0.878 | 0.915 | 0.930 | 0.898 | 0.919 | ||||

| 0.875 | 0.895 | 0.847 | 0.876 | 0.905 | 0.945 | 0.901 | 0.920 | ||||

| 0.895 | 0.925 | 0.887 | 0.884 | 0.960 | 0.960 | 0.947 | 0.947 | ||||

| 0.910 | 0.927 | 0.886 | 0.890 | 0.940 | 0.967 | 0.940 | 0.930 | ||||

| 0.917 | 0.939 | 0.901 | 0.899 | 0.947 | 0.959 | 0.948 | 0.939 | ||||

| 0.937 | 0.932 | 0.908 | 0.895 | 0.957 | 0.957 | 0.947 | 0.937 | ||||

| 0.802 | 0.810 | 0.784 | 0.889 | 0.869 | 0.876 | 0.838 | 0.945 | ||||

| 0.824 | 0.820 | 0.791 | 0.879 | 0.882 | 0.866 | 0.843 | 0.945 | ||||

| 0.832 | 0.820 | 0.796 | 0.874 | 0.889 | 0.872 | 0.859 | 0.945 | ||||

| 0.820 | 0.823 | 0.792 | 0.879 | 0.892 | 0.881 | 0.871 | 0.950 | ||||

| 0.827 | 0.835 | 0.841 | 0.889 | 0.897 | 0.881 | 0.901 | 0.950 | ||||

| 0.829 | 0.825 | 0.843 | 0.884 | 0.892 | 0.881 | 0.903 | 0.940 | ||||

| 0.849 | 0.833 | 0.871 | 0.900 | 0.900 | 0.888 | 0.910 | 0.950 | ||||

| 0.852 | 0.835 | 0.873 | 0.910 | 0.907 | 0.889 | 0.910 | 0.950 | ||||

| 0.879 | 0.879 | 0.882 | 0.869 | 0.929 | 0.932 | 0.943 | 0.920 | ||||

| 0.899 | 0.879 | 0.882 | 0.859 | 0.950 | 0.944 | 0.943 | 0.919 | ||||

| 0.904 | 0.899 | 0.879 | 0.838 | 0.950 | 0.947 | 0.946 | 0.950 | ||||

| 0.867 | 0.857 | 0.884 | 0.898 | 0.929 | 0.944 | 0.946 | 0.960 | ||||

3.3 A Real Data Example

In this subsection, we investigate the time-varying conditional correlations between the Chinese and U.S. stock markets using the time-varying multivariate GARCH model. Recently, there is a growing literature to study the relationship of the two stock markets (e.g., Zhang & Li 2014, Pan et al. 2022), as the Chinese stock market has become the world’s second largest stock market after 2009. Understanding the interactions among different financial markets is important for investors and policymakers Diebold & Yilmaz (2009), BenSaïda (2019). For example, high equity market interdependence implies poor diversification benefits from portfolios, but highlights the possibility of better hedging benefits.

Previous research documents a strong positive link between the degree of globalization and equity market interdependence Baele (2005). Along this line of research, one important question is that whether the interdependence between the Chinese and U.S. stock markets has increased over time due to globalization so that estimates from historical data are unreliable for modern policy analysis, asset pricing and risk management. The existing results present many discrepancies, which may be due to the fact that the relationship evolves with time. Apparently, the results also indicate that one should use time-varying GARCH model to accommodate potential nonstationarity inherited in these financial variables. In addition, as pointed out by Caporin & McAleer (2013), dynamic conditional correlation (DCC) GARCH model represents the dynamic conditional covariances of the standardized residuals, and hence does not yield dynamic conditional correlations; DCC yields inconsistent two step estimators; DCC has no asymptotic properties. In what follows, we address these issues using the newly proposed approach. The estimation is conducted in exactly the same way as in Section 3.1, so we no longer repeat the details.

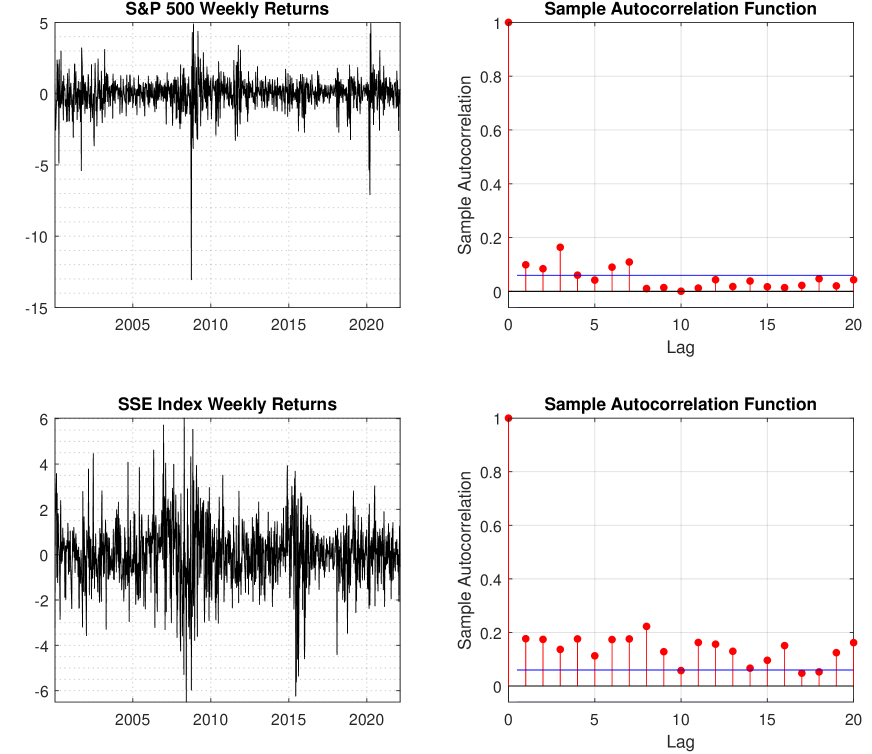

We calculate the Chinese and U.S. stock returns based on weekly Shanghai Stock Exchange (SSE) Composite Index and S&P 500 Index as they are the most comprehensive and diversified stock indices. The sample employed in this study spanning from January 2000 to February 2022 provides observations111The data are collected from Yahoo Finance at https://finance.yahoo.com/.. Figure 1 plots the two weekly returns as well as sample autocorrelation functions of squared data, which shows the typical “volatility clustering” phenomenon.

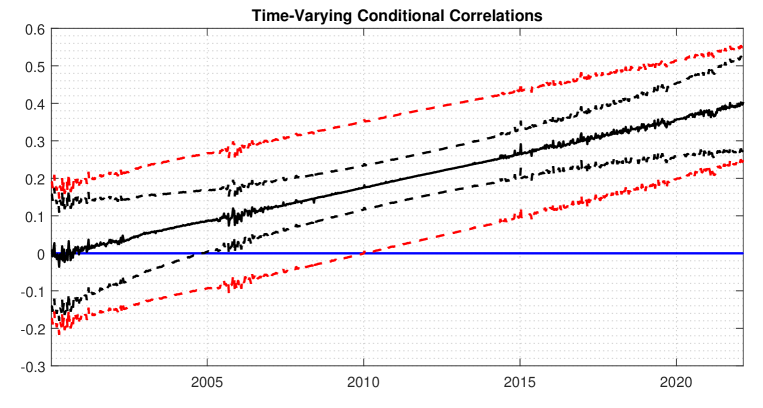

We next fit the data to a time-varying multivariate GARCH(1,1) model and are particularly interested in the estimates of time-varying conditional correlations, i.e.,

where is defined in (2.14). Figure 2 plots the estimates (black solid line) of time-varying conditional correlations between the two stock markets as well as 95% simultaneous confidence intervals (red dashed line) and 95% pointwise confidence intervals (black dashed line). Based on the simultaneous confidence intervals, apparently, the conditional correlations vary with respect to time. Moreover, as clearly presented in Figure 2, the interdependence between the two stock markets is increasing over time. By examining the pointwise confidence intervals, we can conclude that the two stock markets are not significantly correlated before 2005, but the relationship has been greatly enhanced in recent years. These results have important implications for investment and risk management. For example, it implies that the Chinese and U.S. investors who use cross-country portfolio strategies to eliminate country specific risks may be benefit from hedging. However, all types of investors should be cautious since the relations between the Chinese and U.S. stock markets are time-varying.

4 Conclusions

In this paper, we consider a wide class of time-varying multivariate causal processes which nests many classic and new examples as special cases. We first prove the existence of a weakly dependent stationary approximation for the model (1.3) which is the foundation to establish the corresponding asymptotic properties. Afterwards, we consider the QMLE estimation approach, and provide both point-wise and simultaneous inferences on the coefficient functions. In addition, we demonstrate the theoretical findings through both simulated and real data examples. In particular, we show the empirical relevance of our study using an application to evaluate the conditional correlations between the stock markets of China and U.S. We find that the interdependence between the two stock markets is increasing over time.

There are several directions for possible extensions. The first one is to consider quantile regression methods for such locally stationary multivariate causal processes. The second one is to propose a more powerful test based on the weighted integrated squared errors for testing whether some coefficients are time-invariant. We wish to leave such issues for future study.

5 Acknowledgements

The authors of this paper would like to thank George Athanasopoulos, David Frazier and Gael Martin for their constructive comments on earlier versions of this paper. Thanks also go to seminar participants for their insightful suggestions. Gao and Peng would also like to acknowledge the Australian Research Council Discovery Projects Program for its financial support under Grant Numbers: DP170104421 & DP210100476.

References

- (1)

- Baele (2005) Baele, L. (2005), ‘Volatility spillover effects in european equity markets’, Journal of Financial and Quantitative Analysis 40(2), 373–401.

- Bardet & Wintenberger (2009) Bardet, J.-M. & Wintenberger, O. (2009), ‘Asymptotic normality of the quasi-maximum likelihood estimator for multidimensional causal processes’, Annals of Statistics 37(5B), 2730–2759.

- Bauwens et al. (2006) Bauwens, L., Laurent, S. & Rombouts, J. V. (2006), ‘Multivariate garch models: a survey’, Journal of Applied Econometrics 21(1), 79–109.

- BenSaïda (2019) BenSaïda, A. (2019), ‘Good and bad volatility spillovers: An asymmetric connectedness’, Journal of Financial Markets 43, 78–95.

- Bollerslev (1990) Bollerslev, T. (1990), ‘Modelling the coherence in short-run nominal exchange rates: a multivariate generalized ARCH model’, Review of Economics and Statistics 72(3), 498–505.

- Caporin & McAleer (2013) Caporin, M. & McAleer, M. (2013), ‘Ten things you should know about the dynamic conditional correlation representation’, Econometrics 1(1), 115–126.

- Chen et al. (2021) Chen, L., Wang, W. & Wu, W. B. (2021), ‘Inference of breakpoints in high-dimensional time series’, Journal of the American Statistical Association 0(0), 1–13.

- Chen & Leng (2015) Chen, Z. & Leng, C. (2015), ‘Local linear estimation of covariance matrices via cholesky decomposition’, Statistica Sinica 25(3), 1249–1263.

- Dahlhaus (1996) Dahlhaus, R. (1996), ‘On the kullback-leibler information divergence of locally stationary processes’, Stochastic Processes and Their Applications 62(1), 139–168.

- Dahlhaus et al. (2019) Dahlhaus, R., Richter, S. & Wu, W. B. (2019), ‘Towards a general theory for nonlinear locally stationary processes’, Bernoulli 25(2), 1013–1044.

- Dette et al. (2011) Dette, H., Preuß, P. & Vetter, M. (2011), ‘A measure of stationarity in locally stationary processes with applications to testing’, Journal of the American Statistical Association 106(495), 1113–1124.

- Diebold & Yilmaz (2009) Diebold, F. X. & Yilmaz, K. (2009), ‘Measuring financial asset return and volatility spillovers, with application to global equity markets’, The Economic Journal 119(534), 158–171.

- Hall & Heyde (1980) Hall, P. & Heyde, C. C. (1980), Martingale Limit Theory and Its Application, Academic Press.

- Jeantheau (1998) Jeantheau, T. (1998), ‘Strong consistency of estimators for multivariate arch models’, Econometric theory 14(1), 70–86.

- Karmakar et al. (2022) Karmakar, S., Richter, S. & Wu, W. B. (2022), ‘Simultaneous inference for time-varying models’, Journal of Econometrics 227(2), 408–428.

- Ling (2003) Ling, S. (2003), ‘Adaptive estimators and tests of stationary and nonstationary short-and long-memory arfima–garch models’, Journal of the American Statistical Association 98(464), 955–967.

- Ling & McAleer (2003) Ling, S. & McAleer, M. (2003), ‘Asymptotic theory for a vector ARMA-GARCH model’, Econometric theory pp. 280–310.

- Lütkepohl (2005) Lütkepohl, H. (2005), New Introduction to Multiple Time Series Analysis, Springer Science & Business Media.

- Pan et al. (2022) Pan, Q., Mei, X. & Gao, T. (2022), ‘Modeling dynamic conditional correlations with leverage effects and volatility spillover effects: Evidence from the chinese and us stock markets affected by the recent trade friction’, The North American Journal of Economics and Finance 59, 101591.

- Preuss et al. (2015) Preuss, P., Puchstein, R. & Dette, H. (2015), ‘Detection of multiple structural breaks in multivariate time series’, Journal of the American Statistical Association 110(510), 654–668.

- Richter et al. (2019) Richter, S., Dahlhaus, R. et al. (2019), ‘Cross validation for locally stationary processes’, Annals of Statistics 47(4), 2145–2173.

- Stock & Watson (2001) Stock, J. H. & Watson, M. W. (2001), ‘Vector autoregressions’, Journal of Economic Perspectives 15(4), 101–115.

- Tong (1990) Tong, H. (1990), Non-linear Time Series: a Dynamical Systems Approach, Oxford University Press.

- Truquet (2017) Truquet, L. (2017), ‘Parameter stability and semiparametric inference in time varying auto-regressive conditional heteroscedasticity models’, Journal of the Royal Statistical Society: Series B 79(5), 1391–1414.

- Vogt (2012) Vogt, M. (2012), ‘Nonparametric regression for locally stationary time series’, Annals of Statistics 40(5), 2601–2633.

- Wu (2005) Wu, W. B. (2005), ‘Nonlinear system theory: Another look at dependence’, Proceedings of the National Academy of Sciences 102(40), 14150–14154.

- Wu & Shao (2004) Wu, W. B. & Shao, X. (2004), ‘Limit theorems for iterated random functions’, Journal of Applied Probability 41(2), 425–436.

- Wu & Zhou (2011) Wu, W. B. & Zhou, Z. (2011), ‘Gaussian approximations for non-stationary multiple time series’, Statistica Sinica pp. 1397–1413.

- Zhang & Li (2014) Zhang, B. & Li, X.-M. (2014), ‘Has there been any change in the comovement between the chinese and us stock markets?’, International Review of Economics & Finance 29, 525–536.

- Zhang & Wu (2017) Zhang, D. & Wu, W. B. (2017), ‘Gaussian approximation for high dimensional time series’, Annals of Statistics 45(5), 1895–1919.

- Zhang & Wu (2012) Zhang, T. & Wu, W. B. (2012), ‘Inference of time-varying regression models’, Annals of Statistics 40(3), 1376–1402.

- Zhou & Wu (2010) Zhou, Z. & Wu, W. B. (2010), ‘Simultaneous inference of linear models with time varying coefficients’, Journal of the Royal Statistical Society: Series B 72(4), 513–531.

Online Supplementary Appendices to

“Time-Varying Multivariate Causal Processes”

Jiti Gao∗ and Bin Peng∗ and Wei Biao Wu† and Yayi Yan∗

∗Monash University and †University of Chicago

The file includes Appendix A and Appendix B. We first present some technical tools in Appendix A.1, which will be repeatedly used in the development. We then provide the proofs of main results in Appendix A.2. We provide several preliminary lemmas in Appendix B.1 as well as some secondary lemmas in Appendix B.2, and then present the proofs of preliminary lemmas in Appendix B.3. Appendix B.4 discusses several computational issues of the local linear ML estimation.

In what follows, and always stand for some bounded constants, and may be different at each appearance.

Appendix A

A.1 Technical Tools

Projection Operator: Define the projection operator

where . By the Jensen’s inequality and the stationarity of , for , we have

where is a coupled version of with replaced by .

The Class :

Recall that we have defined in Assumption1. Let be a sequence of nonnegative real numbers with and be some finite constant. Let for any and , where is the column of . A function is in class if

If is vector- or matrix-valued, means that every component of is in .

Analytical Gradient:

Let

where . Then the first partial derivative is as follows:

| (A.1.1) | |||||

where is the element of .

By (A.1.1), the second partial derivative of is given by

| (A.1.2) | |||||

A.2 Proofs of the Main Results

Proof of Proposition 2.1.

(1). To prove the first result, we consider an approximated -Markov process defined by

| (A.2.1) | |||||

for , and

| (A.2.2) |

Let and .

By construction, we immediately obtain

where the second inequality follows from Assumption 1.

Recall that we have defined in the body of this proposition. As by Assumption 1, we have

Similarly, we have

Hence,

as .

According to the above development, we are readily to conclude that as in the space of . As a limit of strictly stationary process in , is a stationary process and .

(2). Let be an independent copy of . Similar to (A.2.1), we define the process , in which the difference is that we use when , and use when . In addition, define the process as , in which again the difference is that we use when , and use when . Further define .

By construction, for , and . For , Assumption 1 gives that

| (A.2.3) |

Since , by a recursion argument, we have for all .

Now, let . Using (A.2.3) and the fact that is a nonincreasing sequence, we have for all . Then recursively . Since and , we have , i.e., .

The proof of the first result gives

The same bound holds for the quantity . Thus,

which completes the proof. ∎

Proof of Proposition 2.2.

(1). Write

where the second inequality follows from Assumption 1 and Assumption 2. In view of the stationarity of , rearranging the terms in the above inequality yields that

(2). Write

As for , by the first result of this proposition, we have

In addition, as and , we have

The proof is now complete. ∎

Proof of Theorem 2.1.

(1). First, we introduce a few notations to facilitate the development. Let , , and for . Recall that we have defined , and let be defined similarly with respect to the elements of .

Then we consider . Since each element of is in , we have , where with between and . Let . By the Mean Value Theorem, we have

with some . Since is in class by Lemma B.2, using Lemma B.8 and yields

The above analyses plus Lemma B.5 reveal that

In addition, by Lemma B.1, we have . To prove this theorem, by the Cramer-Wold device, it suffices to show that for any unit vector ,

Note that is a sequence of martingale differences, we prove the asymptotic normality by using the martingale central limit theorem Hall & Heyde (1980). We first consider the convergence of conditional variance. Let . By Lemma B.8, we have

In addition, by Proposition 2.1, is a sequence of stationary variables and thus we have

We next verify the Lindeberg condition. The sum is bounded by

which converges to zero since by Lemma B.8.3. The asymptotic normality is then obtained.

The proof of the first result is now complete.

(2). For notation simplicity, we abbreviate to in what follows. Note that

Hence, we have

| (A.2.4) | |||||

In addition, if is normal distributed, we have and , where is independent of , and is a commutation matrix. By (A.2.4), if is normal distributed, we have

Then we have if is normal distributed. The proof is now complete. ∎

Proof of Corollary 2.1.

By Lemma B.5 (2) and the proof of Theorem 2.1, we have

In addition, applying Lemma B.3 (4), Lemma B.5 (2) and Lemma B.3 (2) to , we have

as and .

For , as , here we use a different argument to prove the result, which leads to weaker moment conditions.

Define . By Lemma B.4.1, we have .

Define and

By partial summation, we have

Hence, we have . Note that forms a sequence of martingale differences. By the Doob’s maximal inequality, Burkholder’s inequality and the elementary inequality for , we obtain that

which shows that . The result then follows directly by Lemma B.3.2. ∎

Proof of Theorem 2.2.

Proof of Corollary 2.2.

By Lemma B.10, there exists i.i.d. -dimensional standard normal variables such that

with . Since is Lipschitz continuous and is a sequence of i.i.d. normal variables, we have

Combining the above analyses, we then complete the proof.

∎

Proof of Proposition 2.3.

Note that in this case is in class as by Lemma B.2. Hence, we only need that the innovation process has moments for some compared to moments needed in Theorem 2.2.

Consider Assumptions 1–2 first. For notation simplicity, we ignore the time-varying intercept, and rewrite model (2.11) as

where , and

Let and , we have

and thus . Then Assumption 1 is automatically met if . By using the property of block matrix determinants and for all (this implies the maximum eigenvalue of left upper matrix in is less than ), it can be shown that the maximum eigenvalue of , denoted by , is less than 1 uniformly over . Hence, we have and . In addition, . Then Assumption 2 is met.

However, by using techniques which are more specific to the VARMA models, the condition can be weakened to for all . Similar to the above analysis, we have with as for all , which implies that and .

For the identification conditions stated in Assumption 3, it is well known that the final form or echelon form is enough to ensure the uniqueness of the VARMA representation.

For verifying Assumption 4, one need the derivatives of . Define . Note that and , it is easy to show that

Hence, we have and . Similarly, we can verify the conditions imposed on second order derivatives.

The proof is now complete.

∎

Proof of Proposition 2.4.

Since is a positive and diagonal matrix, we have

Then Assumption 1 is automatically met if . In addition, as converges to zero with exponential rate and , similar to the proof of Proposition 2.3 we can easily verify Assumptions 2 and 4. For the identification conditions of the GARCH process, we refer readers to Proposition 3.4 of Jeantheau (1998), who proves that assuming the minimal representation is enough for ensuring Assumption 3 holds.

However, by using techniques which are more specific to the GARCH models, the condition can be weaken to . Define and . We first prove the existence of (which implies the existence of ) as well as its weak dependence property by means of a chaotic expansion. Since , by substitute recursively, we have

To prove the boundedness of , since are independent random variables, it suffices to show that

By using and , we have

Hence, we have . Next, we show that for some . Write

By using the same arguments as in the proof of Proposition 2.1, we have since and . Since for and is a positive diagonal matrix, for , we have

for some .

The proof is now completed.

∎

Appendix B

B.1 Preliminary Lemmas

First, we define a few notations for better presentation. First, let , where and are the same generic vectors as in (2.4). Let be a a kernel function being Lipschitz continuous and bounded on .

For and , define

| (B.1) |

where and . Let , denote the same quantity but with replaced by or .

In addition, let

| (B.2) |

where and some .

Lemma B.1.

Suppose Assumptions 1 and 3 hold. Then, is uniquely maximized at .

Lemma B.2.

Suppose Assumptions 3–4 hold. Then, for some and with and . In addition, if , .

Lemma B.3.

Suppose Assumptions 1–2 hold with . Then

-

1.

and ;

-

2.

;

-

3.

with .

In addition, suppose for some , then

-

4.

.

Lemma B.4.

Let , where for some and . Suppose Assumptions 1–2 hold with , and

Then we obtain

-

1.

;

-

2.

and , where ;

-

3.

and .

Lemma B.5.

Under the conditions of Lemma B.4 with , then

-

1.

with ,

-

2.

;

Suppose further and . Then

-

3.

.

Lemma B.6.

Suppose Assumptions 1–5 hold with , and

for and some . Then

where

Lemma B.7.

Under the conditions of Theorem 2.2,

where and .

B.2 Secondary Lemmas

Before proceeding further, we introduce some extra notations. Assume that there exists some measurable function such that for , is well defined, where . Let

Assume that is Lipschitz continuous and its smallest eigenvalue is bounded away from uniformly over . In what follows, we let stand for the component of .

Lemma B.8.

Let . Let . Let and be two sequences of random variables. Assume that and . Then, we have

-

1.

;

-

2.

;

-

3.

.

Lemma B.9.

Assume that for

-

1.

with some ,

-

2.

,

-

3.

for some .

In addition, assume that and . Then

where

and is the Gamma function.

Lemma B.10.

Assume that for

-

1.

with some ,

-

2.

,

-

3.

for some .

Let . Then on a richer probability space, there exists i.i.d. k-dimensional standard normal variables and a process such that

where

B.3 Proofs of Preliminary Lemmas

Proof of Lemma B.1.

Let

By Assumption 1.1 and the construction of , we write

For any positive definite matrix with eigenvalues , we have

where the equality holds if in which case . Thus, is uniquely minimized at , which implies that is uniquely minimized at by Assumption 3.2. In addition, since is a positive definite matrix, then

is uniquely minimized at by Assumption 3.2. Hence, is uniquely maximized at . ∎

Proof of Lemma B.2.

We first consider . Write

where the definitions of and should be obvious, and .

For , we have

where the second inequality follows from the facts that

by using Assumption 1.2 twice.

By Assumption 3, it is easy to know that , which in connection with the fact is Lipschitz continuous on yields that

In addition, for an invertible matrix , , and for a positive definite matrix and symmetric matrix , . Hence, we have

Note that if , .

For , since is bounded by Assumption 3, we can obtain that

where . Similarly, if , .

For , write

Similar to the development for and , we can obtain that

where we again let . Also if ,

Combing the above analysis, we have shown . In addition, if , .

Similar to the development for , we can show , and if .

The proof is now complete. ∎

Proof of Lemma B.3.

(1). By Proposition 2.1.1, we have . Since , we have

Using , we have

In addition, by using the Lipschitz property of , we have

Combing the above analyses, the first result follows.

(2). By Lemma B.8.1 and Proposition 2.2, for , we have

Hence, we have

and

by the definition of Riemann integral and the stationarity of .

(3). Write

By the Lipschitz continuity of and (by Lemma B.8.3), we have

Similarly, by Lemma B.8.2 and , we have

By the Lipschitz continuity of , we have . Hence,

The proof is now complete.

(4). By Propositions 2.1.1 and 2.2.2, we have and . Hence, we have .

By Lemma B.8 and the definitions of and , we have

In addition, by Proposition 2.2.1 and for some , we have

Hence, we have

The proof of the fourth result is now complete. ∎

Proof of Lemma B.4.

(1). Let be a coupled version of with replaced by . By Lemma B.8, we have

By Proposition 2.1.2 and the conditions on and in the body of this lemma, we have for some . Hence, we have

The proof of the first result of this lemma is now complete.

(2)–(3). Since

the second result follows directly from the first result.

Since when , for each element of , we have

where is yielded by the coupled version.

The proof is now complete. ∎

Proof of Lemma B.5.

(1). Note that

in which is a sequence of martingale differences.

If , by the Burkholder’s inequality, for and Lemma B.4.1, we have

Similarly, for , by the Burkholder’s inequality and the Minkowski inequality, we have

The proof of the first result is now complete.

(2). For any fixed , let and be a discretization of such that for each one can find satisfying . Let denote the numbers of sets in . Write

By the Markov inequality, we have

Note that forms a sequence of martingale differences. By the Burkholder’s inequality and Lemma B.4.1, we have

which in connection with the fact is independent of yields that

(3). Let for short. Let further be a discretization of such that for each one can find satisfying . Define as a discretization of . For some constant , we have

Let , we have and for some by Lemma B.4.2. Let , we have

and

Note that and for some large enough. By using Theorem 6.2 of Zhang & Wu (2017) (the proof therein also works for the uniform functional dependence measure) with and to , we have

In addition, by the Markov inequality and Lemma B.3.1, we have

The proof is now complete. ∎

Proof of Lemma B.6.

By the Mean Value Theorem, we have

where

Proof of Lemma B.7.

(1). Let and . By Lemma B.5 and the proof of Theorem 2.1, we have

By the Taylor expansion, we have

where and with between and . By Lemma B.3 and Lemma B.5, we have

where and

By Lemma B.4.3 and the condition

for some , we have for some . By Lemma B.10, we have

Since , we further obtain that

using Lemma B.6.

Hence, by Lemma B.3.4, we have

Since

we have

for . Hence, we have and , where and are corresponding to the part in their definitions given in the beginning of this proof.

Write

The proof of the first result is now complete.

B.4 Computation of the Local Linear ML Estimates

In our numerical studies, we use the function fminunc in programming language MATLAB to minimize the negative of log-likelihood function. The initial guess is important when using optimization functions because these optimizers are trying to find a local minimum, i.e. the one closest to the initial guess that can be achieved using derivatives. In this section, we give a possible choice of initial estimates.

We could estimate the coefficients of time-varying VARMA() model

by kernel-weighted least squares method if the lagged were given. To obtain a preliminary estimator, we first fit a long VAR model and then use estimated residuals in place of true residuals. Consider the VAR model

where is set to be in our numerical studies. Then, we compute , where are the local linear least squares estimators. Given , we are able to estimate , and as well as their derivatives by local linear least squares method.

In order to achieve identifications, certain restrictions should be imposed on the coefficients of the VARMA model. Suppose there exists a known matrix and a vector satisfying

which follows that

where . Then the local linear estimator of is given by

where . Similarly, the local linear estimator of is given by

where .

We next consider the preliminary Estimation of Multivariate GARCH Models. Define and . We can rewrite model (1.4) as

with . Similar to the VARMA model, we are able to estimate , and as well as their derivatives by local linear least squares method. Consider the VAR model

where is set to be in our numerical studies. Then, we compute , and . Hence, the local linear estimator of is given by

where and stacks the lower triangular part of a square matrix excluding the diagonal.