Timing is Everything: Learning to Act Selectively with Costly Actions and Constraints

Abstract

Many real-world settings involve costs for performing actions; transaction costs in financial systems and fuel costs being common examples. In these settings, performing actions at each time step quickly accumulates costs leading to vastly suboptimal outcomes. Additionally, repeatedly acting produces wear and tear and ultimately, damage. Determining when to act is crucial for achieving successful outcomes and yet, the challenge of efficiently learning to behave optimally when actions incur minimally bounded costs remains unresolved. In this paper, we introduce a reinforcement learning (RL) framework named Learnable Impulse Control Reinforcement Algorithm (LICRA), for learning to optimally select both when to act and which actions to take when actions incur costs. At the core of LICRA is a nested structure that combines RL and a form of policy known as impulse control which learns to maximise objectives when actions incur costs. We prove that LICRA, which seamlessly adopts any RL method, converges to policies that optimally select when to perform actions and their optimal magnitudes. We then augment LICRA to handle problems in which the agent can perform at most actions and more generally, faces a budget constraint. We show LICRA learns the optimal value function and ensures budget constraints are satisfied almost surely. We demonstrate empirically LICRA’s superior performance against benchmark RL methods in OpenAI gym’s Lunar Lander and in Highway environments and a variant of the Merton portfolio problem within finance.

1 Introduction

There are many settings in which agents incur costs each time they perform an action. Transaction costs in financial settings (Mguni, 2018a), fuel expenditure (Zhao et al., 2018), toxicity as a side effect of controlling bacteria (Sootla et al., 2016) and physical damage produced by repeated action that produces wear and tear are just a few among many examples (Grandt Jr, 2011). In these settings, performing actions at each time step is vastly suboptimal since acting in this way results in prohibitively high costs and undermines the service life of machinery. Minimising wear and tear is an essential attribute to safeguard against failures that can result in catastrophic losses (Grandt Jr, 2011).

Reinforcement learning (RL) is a framework that enables autonomous agents to learn complex behaviours from interactions with the environment (Sutton & Barto, 2018). Within the standard RL paradigm, determining optimal actions involves making a selection among many (possibly infinite) actions; a procedure that must be performed at each time-step as the agent decides on an action. In unknown settings, the agent cannot immediately exploit any topological structure of the action set. Consequently, learning not to take an action i.e performing a zero or null action, involves expensive optimisation procedures over the entire action set. Since this must be done at each state, this process is vastly inefficient for learning optimal policies when the agent incurs costs for acting.

In this paper, we tackle this problem by developing an RL framework for finding both an optimal criterion to determine whether or not to execute actions as well as learning optimal actions. A key component of our framework is a novel combination of RL with a form of policy known as impulse control (Mguni, 2018d; a). This enables the agent to determine the appropriate points to perform an action as well as the optimal action itself. Despite its fundamental importance as a tool for tackling decision problems with costly actions (Korn, 1999; Mitchell et al., 2014), presently, the use of impulse control within learning contexts (and unknown environments) is unaddressed.

We present an RL impulse control framework called LICRA, which, to our knowledge, is the first learning framework for impulse control. To enable learning optimal impulse control policies in unknown environments, we devise a framework that consists of separate RL components for learning when to act and, how to act, optimally. The resulting framework is a structured two-part learning process which differs from current RL protocols. In LICRA, at each time step, the agent firstly makes a decision whether to act or not leading to a binary decision space . The second decision part determines the best action to take. This generates a subdivision of the state space into two regions; one in which the agent performs actions and another in which it does not act at all. We show the set of states where the agent ought to act is characterised using an easy-to-evaluate criterion on the value function and, LICRA quickly learns this set within which it then learns which actions are optimal.

We then establish theory that ensures convergence of a Q-learning variant of LICRA to the optimal policy for such settings. To do this, we give a series of results namely:

i) We establish a dynamic programming principle (DPP) for impulse control and show that the optimal value function can be obtained as a limit of a value iterative procedure (Theorem 1) which lays the foundation for an RL approach to impulse control.

ii) We extend result i) to a new variant of Q-learning which enables the impulse control problem to be solved using our RL method (Theorem 2). Thereafter, we extend the result to (linear) function approximators enabling the value function to be parameterised (Theorem 3).

iii) We characterise the optimal conditions for performing an action which we reveal to be a simple ‘obstacle condition’ involving the agent’s value function (Proposition 1). Using this, the agent can quickly determine whether or not it should act and if so, then learn what the optimal action is.

iv) In Sec. 6, we extend LICRA to include budgetary constraints so that each action draws from a fixed budget which the agent must stay within. Analogous to the development of i), we establish another DPP from which we derive a Q-learning variant for tackling impulse control with budgetary constraints (Theorem 4). A particular case of a budget constraint is when the number of actions the agent can take over the horizon is capped.

Lastly, we perform a set of experiments to validate our theory within the Highway driving simulator and OpenAI’s LunarLander (Brockman et al., 2016).

As we demonstrate in our experiments, LICRA learns to compute the optimal problems in which the agent faces costs for acting in an efficient way which outperforms leading RL baselines. Second, as demonstrated in Sec. 6, LICRA handles settings in which the agent has a cap the total number of actions it is allowed to execute and more generally, generic budgetary constraints. LICRA is able to accommodate any RL algorithm unlike various RL methods designed to handle budgetary constraints.

2 Related Work

In continuous-time optimal control theory (Øksendal, 2003), problems in which the agent faces a cost for each action are tackled with a form of policy known as impulse control (Mguni, 2018d; a; Al-Fagih, 2015). In impulse control frameworks, the dynamics of the system are modified through a sequence of discrete actions or bursts chosen at times that the agent chooses to apply the control policy. This distinguishes impulse control models from classical decision methods in which an agent takes actions at each time step while being tasked with the decision of only which action to take. Impulse control models represent appropriate modelling frameworks for financial environments with transaction costs, liquidity risks and economic environments in which players face fixed adjustment costs (e.g. menu costs) (Korn, 1999; Mguni, 2018b; Mundaca & Øksendal, 1998).

The current setting is intimately related to the optimal stopping problem which widely occurs in finance, economics and computer science (Mguni, 2019; Tsitsiklis & Van Roy, 1999). In the optimal stopping problem, the task is to determine a criterion that determines when to arrest the system and receive a terminal reward. In this case, standard RL methods are unsuitable since they require an expensive sweep (through the set of states) to determine the optimal point to arrest the system. The current problem can be viewed as an augmented problem of optimal stopping since the agent must now determine both a sequence of points to perform an action or intervene and their optimal magnitudes — only acting when the cost of action is justified (Øksendal & Sulem, 2019). Adapting RL to tackle optimal stopping problems has been widely studied (Tsitsiklis & Van Roy, 1999; Becker et al., 2018; Chen et al., 2020) and applied to a variety of real-world settings within finance (Fathan & Delage, 2021) and network operating systems (Alcaraz et al., 2020). Our work serves as a natural extension of RL approaches to optimal stopping to the case in which the agent must decide at which points to take a series of actions. As with optimal stopping, standard RL methods cannot efficiently tackle this problem since determining whether to perform a action requires a costly sweep through the action space at every state (Tsitsiklis & Van Roy, 1999). In (Pang et al., 2021) the authors introduce “sparse action” with a similar motivation as impulse control. However, the authors treat only the discrete action space case. Moreover, (Pang et al., 2021) do not provide a general theoretical framework of dealing with “sparse actions” but develop purely algorithmic solutions. Additionally, unlike the approach taken in (Pang et al., 2021), the problem setting we consider is one in which the agent faces a cost for each action - this produces a need for the agent to be selective about where it performs actions (but does not necessarily constrain the magnitude or choice of those actions).

Our framework bears resemblance to hierarchical RL (HRL) (Barto & Mahadevan, 2003). Policies in this hierarchy have usually different objectives. For example in sub-goal learning (Noelle, 2019), a top-level policy decides the goal of a low-level policy. In this case, the top-level policy gives control to the low-level policy for a number of time steps and/or until the sub-goal is achieved. In contrast, LICRA’s top-level policy must make a decision at every time step. One can note further similarities with a specific HRL framework — RL with options (Precup et al., 1998; Klissarov & Precup, 2021). There the agent chooses an option and then selects an action (or a sequence of actions) based on the current state and the chosen option. Therefore, there are two policies that the agent learns. Options and HRL offer abstraction frameworks with higher levels of internal structure than most of the standard RL algorithms. This can significantly speed up learning in many situations. For example, in a setting with sparse rewards, a subgoal discovery algorithm can guide the agent to an optimal policy more quickly. Our impulse control framework offers an even higher level of structure than options and HRL in order to determine when to act (Jinnai et al., 2019). This is achieved by exploiting the specificity of the impulse control setting which includes a cost of acting while employing a structure that enables isolating null actions from the action space.

3 Preliminaries

In RL, an agent sequentially selects actions to maximise its expected returns. The underlying problem is typically formalised as an MDP where is the set of states, is the (continuous) set of actions, is a transition probability function describing the system’s dynamics, is the reward function measuring the agent’s performance and the factor specifies the degree to which the agent’s rewards are discounted over time (Sutton & Barto, 2018). At time the system is in state and the agent must choose an action which transitions the system to a new state and produces a reward . A policy is a probability distribution over state-action pairs where represents the probability of selecting action in state . The goal of an RL agent is to find a policy that maximises its expected returns given by the value function: where is the agent’s policy set. The action value function is given by .

We consider a setting in which the agent faces at least some minimal cost for each action it performs. With this, the agent’s task is to maximise:

| (1) |

where for any state and any action , the functions and are given by where is the indicator function which is when and otherwise and where is a strictly positive (cost) function that introduces a cost each time the agent performs an action. Examples of the cost function is a quasi-linear function of the form where and is a positive real-valued constant. Since acting at each time step would incur prohibitively high costs, the agent must be selective when to perform an action. Therefore, in this setting, the agent’s problem is augmented to learning both an optimal policy for its actions and, learning at which states to apply its action policy. Examples of problem settings of this kind include financial portfolio problems with transaction costs (Davis & Norman, 1990) where each investment incurs a fixed minimal cost and robotics where actions produce mechanical stress leading to fatigue (Grandt Jr, 2011).

4 The LICRA Framework

In RL, the agent’s problem involves learning to act at every state including those in which actions do not significantly impact on its total return. While we can add a zero action to the action set and apply standard methods, we argue that this may not be the best solution in many situations. We argue the optimal policy has the following form:

| (2) |

which implies that we simplify policy learning by determining the set first — the set where we actually need to learn the policy.

We now introduce a learning method for producing impulse controls which enables the agent to learn to select states to perform actions. Therefore, now agent is tasked with learning to act at states that are most important for maximising its total return given the presence of the cost for each action. To do this effectively, at each state the agent first makes a binary decision to decide to perform an action. Therefore, LICRA consists of two core components: first, an RL process and a second RL process . The role of is to determine whether or not an action is to be performed by the policy at a given state . In LICRA, the policy first proposes an action which is observed by the policy . If activated, the policy determines the action to be selected. Therefore, prevents actions under for which the change in expected return does not exceed the costs incurred for taking such actions. While we consider now two policies , , the cardinality of the action space does not change. Crucially, the agent must compute optimal actions at only the subset of states chosen by . By isolating the decision of whether to act or not, the LICRA framework may also reduce the computational complexity in this setting.

LICRA consists of two independent procedures: a learning process for the policy and simultaneously, a learning process for the impulse policy which determines at which states to perform an action. In Sec. 5, we prove the convergence properties of LICRA. In our implementation, we used proximal policy optimisation (PPO) (Schulman et al., 2017) for the policy and for the impulse policy , whose action set consists of two actions (intervene or do not intervene) we used a soft actor critic (SAC) process (Haarnoja et al., 2018). LICRA is a plug & play framework which enables these RL components to be replaced with any RL algorithm of choice. Above is the pseudocode for LICRA, we provide full details of the code in Sec. 9 of the Appendix.

5 Convergence and Optimality of LICRA with Q-Learning

A key aspect of our framework is the presence of two RL processes that make decisions in a sequential order. In order to determine when to act the policy must learn the states to allow the policy to perform an action which the policy must learn to select optimal actions whenever it is allowed to execute an action. In this section, we prove that LICRA converges to an optimal solution of the system. Our proof is instantiated in a Q-learning variant of LICRA which serves as the natural basis for other extensions such as actor-critic methods. We then extend the result to allow for (linear) function approximators. We provide a result that shows the optimal intervention times are characterised by an ‘obstacle condition’ which can be evaluated online therefore allowing the policy to be computed online.

Given a function and , , we define the intervention operator by .111Note for the term , the action input of the function is a dummy variable decided by the operator . The interpretation of is the following: suppose that at time the system is at a state and the agent performs an immediate action . A cost of is then incurred by the agent and the system transitions to whereafter the agent executes the policy . Therefore is the expected future stream of rewards after an immediate action minus the cost of action. This object plays a crucial role in the LICRA framework which as we later discuss, exploits the cost structure of the problem to determine when the agent should take an action. Denote by the intervention operator acting on when the immediate action is chosen according to an epsilon-greedy policy. Given any , the Bellman operator is:

| (3) |

The Bellman operator captures the nested sequential structure of the LICRA method. In particular, the structure in (3) consists of an inner structure that consists of two terms: the first term is the estimated expected return given the current best estimate of the optimal action is executed and the policy is executed thereafter. The second term isolates the estimated expected return following no action and when the policy is executed thereafter. Lastly, the outer structure is an optimisation which compares the two quantities and selects the maximum. Note that when is a continuous (dense) set, this reduces the burden on an optimisation (possibly over a function approximator) to extract the point in the action space when it is optimal not to act.

Our first result proves is a contraction operator in particular, the following bound holds:

Lemma 1

The Bellman operator is a contraction, that is the following bound holds:

where are elements of a finite normed vector space. We can now state our first main result:

Theorem 1

Given any , the optimal value function is given by where is the optimal policy pair.

The result of Theorem 1 enables the solution to the agent’s impulse control problem to be determined using a value iteration procedure. Moreover, Theorem 1 enables a Q-learning approach (Bertsekas, 2012) for finding the solution to the agent’s problem.

Theorem 2

Consider the following Q-learning variant:

| (4) |

then converges to with probability , where and .

We now extend the result to (linear) function approximators:

Theorem 3

Given a set of linearly independent basis functions with . LICRA converges to a limit point which is the unique solution to where and satisfies: .

The theorem establishes the convergence of the LICRA Q-learning variant to a stable point with the use of linear function approximators. The second statement bounds the proximity of the convergence point by the smallest approximation error that can be achieved given the choice of basis functions.

Having constructed a procedure to find the optimal agent’s optimal value function, we now seek to determine the conditions when an intervention should be performed. Let us denote by the points at which the agent decides to act or intervention times, so for example if the agent chooses to perform an action at state and again at state , then and . The following result characterises the optimal intervention policy and the optimal times .

Proposition 1

The policy is given by: , where is the solution in Theorem 1, is the intervention operator and is the Heaviside function, moreover the intervention times are .

Prop. 1 characterises the (categorical) distribution . Moreover, given the function , the times can be determined by evaluating if holds. A key aspect of Prop. 1 is that it exploits the cost structure of the problem to determine when the agent should perform an intervention. In particular, the equality implies that performing an action is optimal.

6 Budget Augmented LICRA via State Augmentation

We now tackle the problem of RL with a budget. To do this, we combine the above impulse control technology with state augmentation technique proposed in (Sootla et al., 2022) The mathematical formulation of the problem is now given by the following for any :

| (5) |

where is a fixed value that represents the maximum number of allowed interventions and is equal to one if an impulse was applied at time and zero if it was not. In order to avoid dealing with a constrained MDP, we propose to introduce a new variable tracking the remaining number of impulses: . We treat as another state and augment the state-space resulting in the transition :

| (6) |

To avoid violations, we reshape the reward as follows: where is a large enough hyper-parameter ensuring there are no safety violations. To summarise, we aim to solve the following budgeted impulse control (BIC) problem , where the policy now depends on the variable . Note in Equation 6 is a Markov process and, the rewards are bounded given the boundedness of . Therefore, we can apply directly the results for impulse control. We denote the augmented MDP by , where is the space of the augmented state. We have the following:

Theorem 4

Consider the MDP for the BIC problem, then:

a) The Bellman equation holds, i.e. such that , where the optimal policy for has the form ; b) Given a , the stable point solution for is given by , where is an optimal policy and is the Bellman operator of .

The result has several important implications. The first is that we can use a modified version of LICRA to obtain the solution of the problem while guaranteeing convergence (under standard assumptions). Secondly, our state augmentation procedure admits a Markovian representation of the optimal policy.

7 Experiments

We will now study empirically the performance of the LICRA framework. In experiments, we use different instances of LICRA, one where both policies are trained using PPO update (referred to as LICRA_PPO) and one where the policy deciding whether to act is trained using SAC and the other policy trained with PPO (referred to as LICRA_SAC). We have benchmarked both of these algorithms together with common baselines on environments, where it would be natural to introduce the concept of the cost associated with actions. We performed a series of ablation studies (see Appendix) which examine i) LICRA’s ability to handle different cost functions including the case when . ii) the benefits of LICRA in settings with a varying intervention regions. iii) the performance of the LICRA Q-learning variant in a discrete state space environment. In the following experiments, all algorithms apply actions that are drawn from an action set which contains a action. When this action is executed it produces costs and exerts no influence on the transition dynamics.

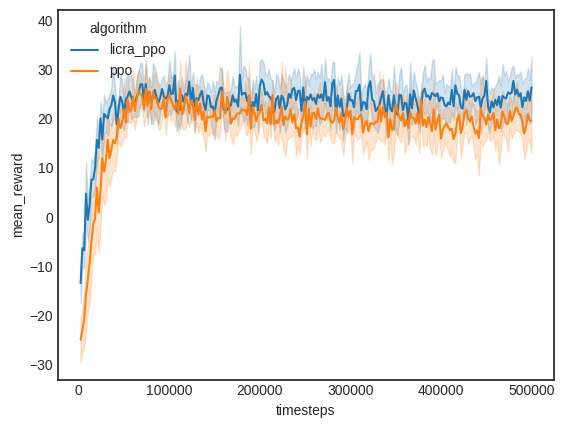

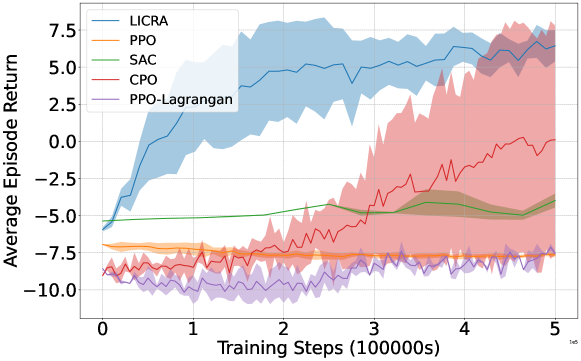

Merton’s Portfolio Problem with Transaction Costs. To exemplify the problem in an applied setting, we choose a well-known problem in finance known as the Merton Investment Problem with transaction costs (Davis & Norman, 1990). In this simple environment, the agent can decide to move its wealth between a risky asset and a risk-free asset. The agent receives a reward only at the final step, equal to the utility of the portfolio with a risk aversion factor equal to . If the final wealth of risky asset is and final wealth of risk-free asset is , then the agent will receive a reward of . The wealth evolves according to the following SDE:

| (7) |

where is the current wealth (the state variable), is an increment of Brownian motion and is the proportion of wealth invested in the risky asset. We set the risk-free return , risky asset return and volatility . We discretise the action space so that at each step the agent has three actions available: move % of risky asset wealth to the risk-free asset, move % of risk-free asset wealth to the risky asset or do nothing. Each time the agent moves the assets, it incurs a cost of i.e. a transaction fee. The agent can act after a time interval of seconds and the episode ends after steps. The results of training are shown in Fig. 1 which clearly demonstrates that LICRA_PPO learns faster than standard PPO.

|

|

| (a) | (b) |

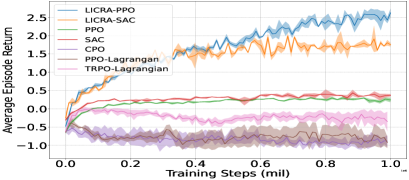

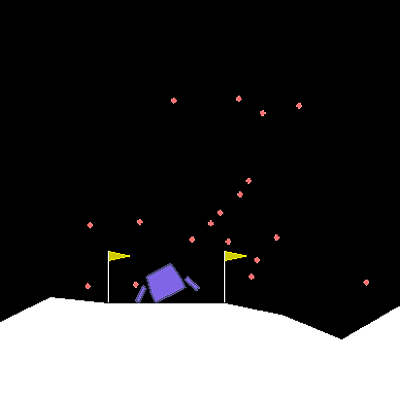

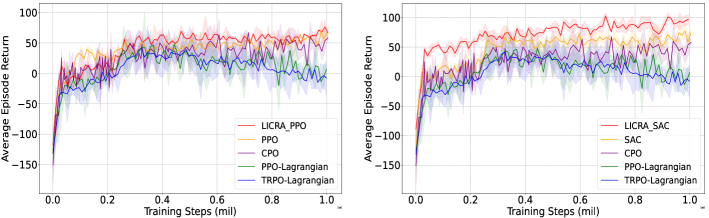

Driving Environment Fuel Rationing. We studied an autonomous driving scenario where fuel-efficient driving is a priority. One of the main components of fuel-efficient driving is controlled usage of acceleration and braking, in the sense that 1) the amount of acceleration and braking should be limited 2) if accelerations should be slowly and gently. We believe this is a problem where LICRA should thrive as the impulse control agent can learn to restrict the amount of acceleration and braking in the presence of other cars and choose when to allow the car to decelerate naturally. We used the highway-env (Leurent, 2018) environment on a highway task (see Fig (2. a)) where the green vehicle is our controlled vehicle and the goal is to avoid crashing into other vehicles whilst driving at a reasonable speed. We add a cost function into the reward term dependent on the continuous acceleration action, , where is a fixed constant cost of taking any action, and , with larger values of acceleration or braking being penalised more. The results are presented in Fig. (2.b). Notably, LICRA is able to massively outperform the baselines, especially our safety specific baselines which struggle to deal with the cost function associated with the environment. We believe one reason for the success of LICRA is that it is far easier for it to utilise the null action of zero acceleration/braking than the other algorithms, whilst all the algorithms have a guaranteed cost at every time step whilst not gaining a sizeable reward to counter the cost.

|

|

| (a) | (b) |

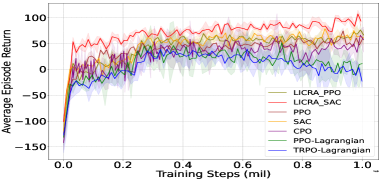

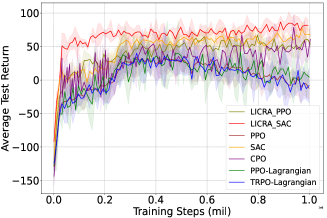

Lunar Lander Environment. We tested the ability of LICRA to perform in environment that simulate real-world physical dynamics. We tested LICRA’s performance the Lunar Lander environment in OpenAI gym (Brockman et al., 2016) which we adjusted to incorporate minimal bounded costs in the reward definition. In this environment, the agent is required to maintain both a good posture mid-air and reach the landing pad as quickly as possible. The reward function is given by:

where is the distance to the landing pad, is the velocity of the agent, and is the angular velocity of the agent at time . is the indicator function of taking actions, which is when the statement is true and when is false. Considering the limited fuel budget, we assume that we have a fixed cost for each action taken by the agent here, and doing nothing brings no cost. Then, to describe the goal of the game, we define the function of the final status by hasLanded(), which is when not landing; when the agent has landed softly on the landing pad; and when the lander runs out of fuel or loses contact with the pad on landing. The reward function rewards the agent for reducing its distance to the landing pad, decreasing its speed to land smoothly and keeping the angular speed at a minimum to prevent rolling. Additionally, it penalises the agent for running out of fuel and deters the agent from taking off again after landing.

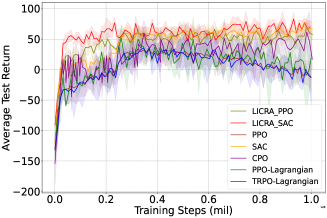

By introducing a reward function with minimally bounded costs, our goal was to test if LICRA can exploit the optimal policy. In Fig. 3, we observe that the LICRA agent outperforms all the baselines, both in terms of sample efficiency and average test return (total rewards at each timestep). We also observe that LICRA enables more stable training than PPO, PPO-Lagrangian and CPO.

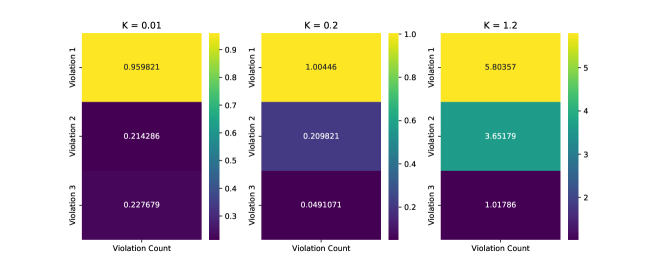

Ablation Study 1. Prioritisation of Most Important Actions. We next tested LICRA’s ability to prioritise where it performs actions when the necessity to act varies significantly between states. To test this, we modified the Drive Environment to now consist of a single lane, a start state and a goal state start (at the end) where there is a reward. With no acceleration, the vehicle decreases velocity. To reach the goal, the agent must apply an acceleration . Each acceleration incurs a cost as defined above. At zones of the lane, if the vehicle is travelling below a velocity , it is penalised by a strictly negative cost where . As shown in Fig. 4, when the intervention cost increases i.e. when , LICRA successfully prioritises the highest penalty zones to avoid incurring large costs.

8 Conclusion

We presented a novel method to tackle the problem of learning how to select when to act in addition to learning which actions to execute. Our framework, which is a general tool for tackling problems of this kind seamlessly adopts RL algorithms enabling them to efficiently tackle problems in which the agent must be selective about when it executes actions. This is of fundamental importance in practical settings where performing many actions over the horizon can lead to costs and undermine the service life of machinery. We demonstrated that our solution, LICRA which at its core has a sequential decision structure that first decides whether or not an action ought to be taken under the action policy can solve tasks where the agent faces costs with extreme efficiency as compared to leading reinforcement learning methods. In some tasks, we showed that LICRA is able to solve problems that are unsolvable using current reinforcement learning machinery. We envisage that this framework can serve as the basis extensions to different settings including adversarial training for solving a variety of problems within RL.

References

- Al-Fagih (2015) Luluwah Al-Fagih. The british knock-out put option. International Journal of Theoretical and Applied Finance, 18(02):1550008, 2015.

- Alcaraz et al. (2020) Juan J Alcaraz, Jose A Ayala-Romero, Javier Vales-Alonso, and Fernando Losilla-López. Online reinforcement learning for adaptive interference coordination. Transactions on Emerging Telecommunications Technologies, 31(10):e4087, 2020.

- Barto & Mahadevan (2003) Andrew G Barto and Sridhar Mahadevan. Recent advances in hierarchical reinforcement learning. Discrete event dynamic systems, 13(1-2):41–77, 2003.

- Becker et al. (2018) Sebastian Becker, Patrick Cheridito, and Arnulf Jentzen. Deep optimal stopping. arXiv preprint arXiv:1804.05394, 2018.

- Benveniste et al. (2012) Albert Benveniste, Michel Métivier, and Pierre Priouret. Adaptive algorithms and stochastic approximations, volume 22. Springer Science & Business Media, 2012.

- Bertsekas (2012) Dimitri P Bertsekas. Approximate dynamic programming. Athena scientific Belmont, 2012.

- Brockman et al. (2016) Greg Brockman, Vicki Cheung, Ludwig Pettersson, Jonas Schneider, John Schulman, Jie Tang, and Wojciech Zaremba. Openai gym. arXiv preprint arXiv:1606.01540, 2016.

- Caplin & Spulber (1987) Andrew S Caplin and Daniel F Spulber. Menu costs and the neutrality of money. The Quarterly Journal of Economics, 102(4):703–725, 1987.

- Chen et al. (2020) Shuhang Chen, Adithya M Devraj, Ana Bušić, and Sean Meyn. Zap q-learning for´ optimal stopping. In 2020 American Control Conference (ACC), pp. 3920–3925. IEEE, 2020.

- Davis & Norman (1990) Mark HA Davis and Andrew R Norman. Portfolio selection with transaction costs. Mathematics of operations research, 15(4):676–713, 1990.

- Fathan & Delage (2021) Abderrahim Fathan and Erick Delage. Deep reinforcement learning for optimal stopping with application in financial engineering. arXiv preprint arXiv:2105.08877, 2021.

- Grandt Jr (2011) F Grandt Jr. Damage tolerant design and nondestructive inspection-keys to aircraft airworthiness. Procedia Engineering, 17:236–246, 2011.

- Haarnoja et al. (2018) Tuomas Haarnoja, Aurick Zhou, Kristian Hartikainen, George Tucker, Sehoon Ha, Jie Tan, Vikash Kumar, Henry Zhu, Abhishek Gupta, Pieter Abbeel, et al. Soft actor-critic algorithms and applications. arXiv preprint arXiv:1812.05905, 2018.

- Jaakkola et al. (1994) Tommi Jaakkola, Michael I Jordan, and Satinder P Singh. Convergence of stochastic iterative dynamic programming algorithms. In Advances in neural information processing systems, pp. 703–710, 1994.

- Jinnai et al. (2019) Yuu Jinnai, Jee Won Park, David Abel, and George Konidaris. Discovering options for exploration by minimizing cover time. In International Conference on Machine Learning, pp. 3130–3139. PMLR, 2019.

- Klissarov & Precup (2021) Martin Klissarov and Doina Precup. Flexible option learning. Advances in Neural Information Processing Systems, 34:4632–4646, 2021.

- Korn (1999) Ralf Korn. Some applications of impulse control in mathematical finance. Mathematical Methods of Operations Research, 50(3):493–518, 1999.

- Leurent (2018) Edouard Leurent. An environment for autonomous driving decision-making. https://github.com/eleurent/highway-env, 2018.

- Mguni (2018a) David Mguni. Duopoly investment problems with minimally bounded adjustment costs. arXiv preprint arXiv:1805.11974, 2018a.

- Mguni (2018b) David Mguni. Optimal capital injections with the risk of ruin: A stochastic differential game of impulse control and stopping approach. arXiv preprint arXiv:1805.01578, 2018b.

- Mguni (2018c) David Mguni. Optimal selection of transaction costs in a dynamic principal-agent problem. arXiv preprint arXiv:1805.01062, 2018c.

- Mguni (2018d) David Mguni. A viscosity approach to stochastic differential games of control and stopping involving impulsive control. arXiv preprint arXiv:1803.11432, 2018d.

- Mguni (2019) David Mguni. Cutting your losses: Learning fault-tolerant control and optimal stopping under adverse risk. arXiv preprint arXiv:1902.05045, 2019.

- Mitchell et al. (2014) Daniel Mitchell, Haolin Feng, and Kumar Muthuraman. Impulse control of interest rates. Operations research, 62(3):602–615, 2014.

- Mundaca & Øksendal (1998) Gabriela Mundaca and Bernt Øksendal. Optimal stochastic intervention control with application to the exchange rate. Journal of Mathematical Economics, 2(29):225–243, 1998.

- Noelle (2019) David C Noelle. Unsupervised methods for subgoal discovery during intrinsic motivation in model-free hierarchical reinforcement learning. In KEG@ AAAI, 2019.

- Øksendal (2003) Bernt Øksendal. Stochastic differential equations. In Stochastic differential equations, pp. 65–84. Springer, 2003.

- Øksendal & Sulem (2019) Bernt Øksendal and Agnès Sulem. Approximating impulse control by iterated optimal stopping. In Applied Stochastic Control of Jump Diffusions, pp. 255–272. Springer, 2019.

- Pang et al. (2021) Jing-Cheng Pang, Tian Xu, Sheng-Yi Jiang, Yu-Ren Liu, and Yang Yu. Sparsity prior regularized q-learning for sparse action tasks. arXiv preprint arXiv:2105.08666, 2021.

- Precup et al. (1998) Doina Precup, Richard S Sutton, and Satinder Singh. Theoretical results on reinforcement learning with temporally abstract options. In European conference on machine learning, pp. 382–393. Springer, 1998.

- Schulman et al. (2017) John Schulman, Filip Wolski, Prafulla Dhariwal, Alec Radford, and Oleg Klimov. Proximal policy optimization algorithms. CoRR, abs/1707.06347, 2017.

- Sootla et al. (2016) Aivar Sootla, Diego Oyarzún, David Angeli, and Guy-Bart Stan. Shaping pulses to control bistable systems: Analysis, computation and counterexamples. Automatica, 63:254–264, 2016.

- Sootla et al. (2022) Aivar Sootla, Alexander I. Cowen-Rivers, Taher Jafferjee, Ziyan Wang, David Mguni, Jun Wang, and Haitham Bou-Ammar. Sauté RL: Almost surely safe reinforcement learning using state augmentation. arXiv preprint arXiv:2202.06558, 2022.

- Sutton & Barto (2018) Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- Tsitsiklis & Van Roy (1999) John N Tsitsiklis and Benjamin Van Roy. Optimal stopping of markov processes: Hilbert space theory, approximation algorithms, and an application to pricing high-dimensional financial derivatives. IEEE Transactions on Automatic Control, 44(10):1840–1851, 1999.

- Zhao et al. (2018) Pu Zhao, Yanzhi Wang, Naehyuck Chang, Qi Zhu, and Xue Lin. A deep reinforcement learning framework for optimizing fuel economy of hybrid electric vehicles. In 2018 23rd Asia and South Pacific design automation conference (ASP-DAC), pp. 196–202. IEEE, 2018.

Part I Appendix

9 Full Algorithms

In this supplementary section, we explicitly define two versions of the LICRA algorithm. Algorithm 2 describes the version where both agents use PPO. PPO_update() subroutine is a standard PPO gradient update done as in Algorithm 1 of (Schulman et al., 2017) with clipping surrogate objective with parameter . The gradient update utilises batch size , stepsize and performs update steps per episode. Algorithm 3 defines the LICRA_SAC version, utilising SAC for the switching agent. Here SAC_update() is analogously a standard soft actor-critic update done as in Algorithm 1 of (Haarnoja et al., 2018), where , and play the same role as in the PPO update.

10 Fuel Budget

We test the ability of LICRA (LICRA_SAC) in a budgeted Drive environment. We modified the Drive environment in Sec. 7 so that there is an additional scarce fuel level for the controlled vehicle. This fuel level decreases in proportion to the magnitude of the action taken by the agent. If the controlled vehicle runs out fuel then it receives a large negative reward, and therefore it is important that the agent learns to use minimal acceleration/braking to reach the final destination.

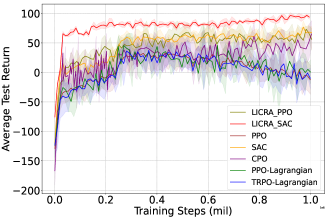

Fig. 5 shows the performance of LICRA and corresponding baselines. The majority of the baselines fail to learn anything in the environment, which we expect is due to the difficult of exploration due to low fuel levels (LICRA can counter this by exploring using the null action) and how easy it is to run out of fuel. In some seeds CPO is able to solve the environment to the same level as LICRA, but is not as stable over seeds and it is not as fast as LICRA in improving performance.

11 Ablation studies

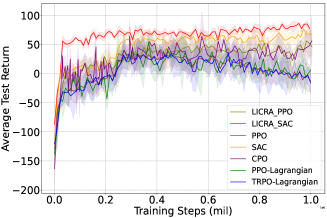

Fig. 3 shows the performance of LICRA variants and baselines when . In this section, we analyse LICRA’s ability to handle various functional forms of the intervention cost.

11.1 Ablation Study 2: Testing Different functional forms of the intervention costs

Intervention costs of the form .

In Sec. 4, we claimed that LICRA’s impulse control mechanism which first determines the set of states to perform actions then only learns the optimal actions at these states can induce a much quicker learning proceess. In particular, we claimed that LICRA enables the RL agent to rapidly learns which states to focus on to learn optimal actions.

In our last ablation analysis, we test LICRA’s ability to handle the case in which the agent faces no fixed costs so , therefore deviating from the form of the impulse control objective (1). In doing so, we test the ability of LICRA to prioritise the most important states for learning the correct actions in a general RL setting. As shown in Fig. 6 we present the average returns when . For this case, LICRA_SAC both learns the fastest indicating the benefits of the impulse control framework even in the setting in which the agent does not face fixed minimal costs for each action. Strikingly, LICRA also achieves the highest performance which demonstrates that LICRA also improves overall performance in complex tasks.

Intervention costs of the form .

We first analyse the behaviour of LICRA and leading baselines when the environment has intervention costs of the form where the fixed part is a strictly positive constant. Intervention costs of this kind are frequently found within economic settings where they are characterised as ‘menu costs’. This name derives from the fixed costs associated to a vendor adjusting their prices and serves as an explanation for price rigidities within the macroeconomy (Caplin & Spulber, 1987; Mguni, 2018c).

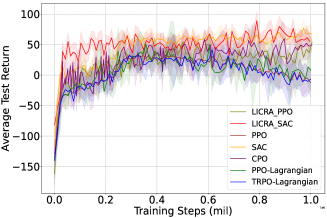

We next test the average returns when , , as shown in Fig. 7. Note that the action space is discrete and the intervention costs only occur when . In this case, LICRA_SAC both learns the fastest and achieves the highest performance. Moreover, unlike PPO which produces declining performance and does not converge, LICRA_PPO converges to a high reward stable point.

Intervention costs of the form .

We next analyse the behaviour of LICRA and leading baselines when the environment has intervention costs of the form where the fixed part and proportional part are strictly positive constants. Intervention costs of this kind are frequently found within financial settings in which an investor incurs a fixed cost for investment decisions e.g. broker costs (Davis & Norman, 1990; Mguni, 2018b). Note that the action space is discrete and the intervention costs only occur when .

We present the average returns when , in Fig. 7. As with previous case, LICRA_SAC both learns the fastest and achieves the highest performance. Moreover, unlike PPO which produces declining performance and does not converge, LICRA_PPO converges to a high reward stable point.

Intervention costs of the form .

In general, the intervention costs incurred by an agent for each intervention can be allowed to be a function of the state. For example, activating an actuator under adverse environment conditions may incur greater wear to machinery than in other conditions. The functional form of the cost function is the most general and produces the most complex decision problem out of the aforementioned cases. To capture this general case, we lastly analysed the behaviour of LICRA and leading baselines when the environment has intervention costs of the form where the fixed part and is a positive function.

As shown in Fig. 7, for this case we present the average returns when , where represents the distance between the current position to the destination (determined by the state ). As before, the action space is discrete and the intervention costs only occur when . As with previous cases, LICRA_SAC both learns the fastest and achieves the highest performance, demonstrating LICRA’s ability to solve the more complex task. Moreover, as in the previous cases, unlike PPO which produces declining performance and does not converge, LICRA_PPO converges to a high reward stable point.

|

|

| (a) | (b) |

|

|

| (c) | (d) |

|

|

| (e) |

11.2 Ablation Study 3: Benefits of LICRA in Smaller Intervention Region

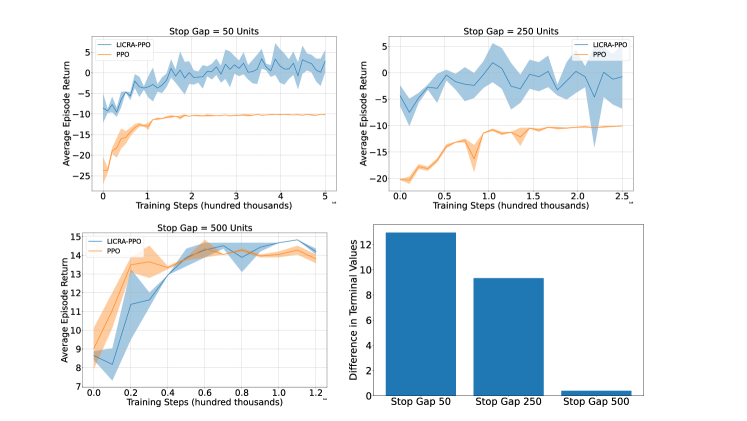

In Sec. 4, we claimed that LICRA enables efficient learning in setting in which the set of states in which the agent should act, which we call the intervention region is a subset of the state space. Moreover, we claimed that this advantage over existing methods is increased as the intervention region becomes small in relation to the entire state space.

To test these claims, we modified the Drive environment in Sec. 7 to a problem setting in which the agent is required to bring a moving vehicle to rest in a particular subregion of the lane or stop gap which we denote by . If the agent brings the vehicle to rest within the agent receives a reward and the episode terminates. If however the agent brings the vehicle to rest outside of the agent receives a lower reward the episode terminates. Lastly, if the agent fails to bring the vehicle to rest before the end of the lane the episode terminates and the agent receives reward. The length of the entire lane is units and we ablate the size of the region in which the agent is required to stop to receive the maximum reward. Now the agent gets to decide a magnitude which decelerates the vehicle i.e. how heavily to brake (at any given point, the agent can also choose not to brake at all). Each deceleration incurs a fixed minimal cost of where .

Fig. 8 shows the results of the ablation on the stop gap when is a length of units or of the entire state space through to i.e. when the intervention region is the entire state space.

As can be observed in Fig. 8, when the intervention region is comparatively small, LICRA_PPO produces a significant performance advantage over the base learner PPO. This performance gap is gradually decreased as the size of the stop gap increases and eventually becomes the entire state space (which is the case when the stop gap is ). Interestingly, LICRA_PPO still maintains a performance advantage over PPO even when .

12 Analysis of LICRA Q-learning Variant

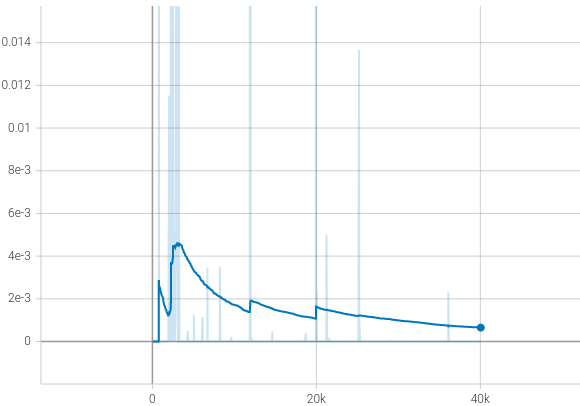

In order to validate the convergence of the Q-learning variant of LICRA (c.f. (4)), we ran an experiment where the LICRA Q-learning variant given in (4) can choose whether to act or not to act in a given discrete state (and continuous action space). In keeping with the problem setting we consider, there is a cost associated with any non-zero action. We consider a -by- grid world problem, where the start state is and the algorithm receives a positive reward only if it reaches the point . The action space is two-dimensional and continuous and the agent is moved in and dimensions by the number of grid tiles corresponding to the value of action projected to the nearest integer. Every non-zero action is associated with a cost of . Additionally, the region described by and is "windy" and the agent is pushed by one grid tile at each step in both dimensions. Hence the optimal policy is to wait for the first two time steps so that the agent is moved to without incurring any cost and then perform one final jump to . LICRA decides whether to act or not to act based on a tabular Q-learning rule given in (4) (using a normalised advantage function (NAF) to handle the continuous action space), where we store expected value for non acting in each cell. Fig. 9 shows that the TD-error of this tabular Q-learning setting converges to zero which validates the results of Theorem 2 and Theorem 3.

13 Hyperparameter Settings

In the table below we report all hyperparameters used in Merton Investment problem experiments.

| Hyperparameter | Value (PPO methods) | Value (SAC) |

|---|---|---|

| Clip Gradient Norm | 0.5 | None |

| Discount Factor | 0.99 | 0.99 |

| Learning rate | x | x |

| Batch size | 32 | 1024 |

| Steps per epoch | 2000 | 2000 |

| Optimisation algorithm | ADAM | ADAM |

In the next table, we report hyperparameters used in remaining experiments.

| Hyperparameter | Value |

|---|---|

| Clip Gradient Norm | 1 |

| 0.99 | |

| 0.95 | |

| Learning rate | x |

| Number of minibatches | 4 |

| Number of optimisation epochs | 4 |

| Number of parallel actors | 16 |

| Optimisation algorithm | ADAM |

| Rollout length | 128 |

| Sticky action probability | 0.25 |

| Use Generalized Advantage Estimation | True |

14 Notation & Assumptions

We assume that is defined on a probability space and any is measurable with respect to the Borel -algebra associated with . We denote the -algebra of events generated by by . In what follows, we denote by any finite normed vector space and by the set of all measurable functions.

The results of the paper are built under the following assumptions which are standard within RL and stochastic approximation methods:

Assumption 1. The stochastic process governing the system dynamics is ergodic, that is the process is stationary and every invariant random variable of is equal to a constant with probability .

Assumption 2. The function is in .

Assumption 3. For any positive scalar , there exists a scalar such that for all and for any we have: .

Assumption 4. There exists scalars and such that for any function satisfying for some scalars and we have that: .

Assumption 5. There exists scalars and such that for any we have that: .

15 Proof of Technical Results

We begin the analysis with some preliminary lemmata and definitions which are useful for proving the main results.

Definition 1

A.1 An operator is said to be a contraction w.r.t a norm if there exists a constant such that for any we have that:

| (8) |

Definition 2

A.2 An operator is non-expansive if we have:

| (9) |

Lemma 2

For any , we have that:

| (10) |

Proof 1

Lemma 3

A.4 The probability transition kernel is non-expansive, that is:

| (14) |

Proof 2

The result is well-known e.g. (Tsitsiklis & Van Roy, 1999). We give a proof using the Tonelli-Fubini theorem and the iterated law of expectations, we have that:

where we have used Jensen’s inequality to generate the inequality. This completes the proof.

Proof of Theorem 1

Proof 3 (Proof of Lemma 1)

In what follows, we employ the following shorthands:

For notational simplicity, where it will not cause confusion we also drop the dependence of the functions on the policy pair . With a slight abuse of notation we will write in which case the Bellman operator acting on a function by

| (15) |

To prove that is a contraction, we consider the three cases produced by (15), that is to say we prove the following statements:

i)

ii) (and hence is a contraction).

iii) .

We begin by proving i).

We now prove ii).

For any , define by . Now using the definition of we have that for any

using the fact that is non-expansive. The result can then be deduced easily by applying max on both sides.

We now prove iii). We split the proof of the statement into two cases:

Case 1:

| (16) |

We now observe the following:

where we have used the fact that for any scalars we have that and the non-expansiveness of .

Case 2:

For this case, first recall that for any , for some .

again using the fact that is non-expansive. Hence we have succeeded in showing that for any we have that

| (17) |

Gathering the results of the three cases gives the desired result.

To prove part ii), we make use of the following result:

Theorem 5 (Theorem 1, pg 4 in (Jaakkola et al., 1994))

Let be a random process that takes values in and given by the following:

| (18) |

then converges to with probability under the following conditions:

-

i)

and

-

ii)

, with ;

-

iii)

for some .

To prove the result, we show (i) - (iii) hold. Condition (i) holds by choice of learning rate. It therefore remains to prove (ii) - (iii). We first prove (ii). For this, we consider our variant of the Q-learning update rule:

After subtracting from both sides and some manipulation we obtain that:

where .

Let us now define by

Then

| (19) |

We now observe that

| (20) |

Now, using the fixed point property that implies , we find that

| (21) |

using the contraction property of established in Lemma 1. This proves (ii).

We now prove iii), that is

| (22) |

Now by (20) we have that

for some where the last line follows due to the boundedness of (which follows from Assumptions 2 and 4). This concludes the proof of the Theorem.

Proof of Convergence with Linear Function Approximation

First let us recall the statement of the theorem:

Theorem 3

LICRA converges to a limit point which is the unique solution to the equation:

| (23) |

where we recall that for any test function , the operator is defined by .

Moreover, satisfies the following:

| (24) |

The theorem is proven using a set of results that we now establish. To this end, we first wish to prove the following bound:

Lemma 4

For any we have that

| (25) |

so that the operator is a contraction.

Proof 4

Recall, for any test function , a projection operator acting is defined by the following

Now, we first note that in the proof of Lemma 1, we deduced that for any we have that

(c.f. Lemma 1).

Setting and it can be straightforwardly deduced that for any : . Hence, using the contraction property of , we readily deduce the following bound:

| (26) |

We now observe that is a contraction. Indeed, since for any we have that:

using (26) and again using the non-expansiveness of .

We next show that the following two bounds hold:

Lemma 5

For any we have that

-

i)

,

-

ii)

.

Proof 5

The first result is straightforward since as is a projection it is non-expansive and hence:

using the contraction property of . This proves i). For ii), we note that by the orthogonality property of projections we have that , hence we observe that:

after which we readily deduce the desired result.

Lemma 6

Define the operator by the following:

where we define by: .

For any we have that

| (27) |

and hence is a contraction mapping.

Proof 6

Lemma 7

Define by where

| (28) |

then is a fixed point of , that is .

Proof 7

We begin by observing that

Hence,

| (29) |

which proves the result.

Lemma 8

The following bound holds:

| (30) |

Proof 8

By definitions of and (c.f (28)) and using Jensen’s inequality and the stationarity property we have that,

| (31) |

Now recall that and , using these expressions in (31) we find that

Moreover, by the triangle inequality and using the fact that and that and (c.f. (30)) we have that

which gives the following bound:

from which, using Lemma 5, we deduce that , after which by (8), we finally obtain

as required.

Let us rewrite the update in the following way:

where the function is given by:

for any and for any . Let us also define the function by the following:

Lemma 9

The following statements hold for all :

-

i)

-

ii)

.

Proof 9

To prove the statement, we first note that each component of admits a representation as an inner product, indeed:

using the iterated law of expectations and the definitions of and .

We now are in position to prove i). Indeed, we now observe the following:

where in the last step we used the orthogonality of . We now recall that since is a fixed point of . Additionally, using Lemma 5 we observe that . With this we now find that

which is negative since which completes the proof of part i).

The proof of part ii) is straightforward since we readily observe that

as required and from which we deduce the result.

To prove the theorem, we make use of a special case of the following result:

Theorem 6 (Th. 17, p. 239 in (Benveniste et al., 2012))

Consider a stochastic process which takes an initial value and evolves according to the following:

| (32) |

for some function and where the following statements hold:

-

1.

is a stationary, ergodic Markov process taking values in

-

2.

For any positive scalar , there exists a scalar such that

-

3.

The step size sequence satisfies the Robbins-Monro conditions, that is and

-

4.

There exists scalars and such that

-

5.

There exists scalars and such that

-

6.

There exists a scalar such that

-

7.

There exists scalars and such that

-

8.

There exists some such that for all and .

Then converges to almost surely.

In order to apply the Theorem 6, we show that conditions 1 - 7 are satisfied.

Proof 10

Conditions 1-2 are true by assumption while condition 3 can be made true by choice of the learning rates. Therefore it remains to verify conditions 4-7 are met.

To prove 4, we observe that

Now using the definition of , we readily observe that using the non-expansiveness of .

Hence, we lastly deduce that

we then easily deduce the result using the boundedness of and .

Now we observe the following Lipschitz condition on :

using Cauchy-Schwarz inequality and that for any scalars we have that .

Using Assumptions 3 and 4, we therefore deduce that

| (33) |

Proof of Proposition 1

Proof 11

First let us recall that the intervention time is defined recursively where . The proof is given by establishing a contradiction. Therefore suppose that and suppose that the intervention time is an optimal intervention time. Construct the and policy switching times by and respectively. Define by and . By construction we have that

We now use the following observation

| (34) | |||

| (35) |

Using this we deduce that

where the first inequality is true by assumption on . This is a contradiction since is an optimal policy for Player 2. Using analogous reasoning, we deduce the same result for after which deduce the result. Moreover, by invoking the same reasoning, we can conclude that it must be the case that are the optimal switching times.