Fool SHAP with Stealthily Biased Sampling.

Abstract

SHAP explanations aim at identifying which features contribute the most to the difference in model prediction at a specific input versus a background distribution. Recent studies have shown that they can be manipulated by malicious adversaries to produce arbitrary desired explanations. However, existing attacks focus solely on altering the black-box model itself. In this paper, we propose a complementary family of attacks that leave the model intact and manipulate SHAP explanations using stealthily biased sampling of the data points used to approximate expectations w.r.t the background distribution. In the context of fairness audit, we show that our attack can reduce the importance of a sensitive feature when explaining the difference in outcomes between groups while remaining undetected. More precisely, experiments performed on real-world datasets showed that our attack could yield up to a 90% relative decrease in amplitude of the sensitive feature attribution. These results highlight the manipulability of SHAP explanations and encourage auditors to treat them with skepticism.

1 Introduction

As Machine Learning (ML) gets more and more ubiquitous in high-stake decision contexts (e.g. , healthcare, finance, and justice), concerns about its potential to lead to discriminatory models are becoming prominent. The use of auditing toolkits (Adebayo et al., 2016; Saleiro et al., 2018; Bellamy et al., 2018) is getting popular to circumvent the use of unfair models. However, although auditing toolkits can help model designers in promoting fairness, they can also be manipulated to mislead both the end-users and external auditors. For instance, a recent study of Fukuchi et al. (2020) has shown that malicious model designers can produce a benchmark dataset as fake “evidence” of the fairness of the model even though the model itself is unfair.

Another approach to assess the fairness of ML systems is to explain their outcome in a post hoc manner (Guidotti et al., 2018). For instance, SHAP (Lundberg & Lee, 2017) has risen in popularity as a means to extract model-agnostic local feature attributions. Feature attributions are meant to convey how much the model relies on certain features to make a decision at some specific input. The use of feature attributions for fairness auditing is desirable for cases where the interest is on the direct impact of the sensitive attributes on the output of the model. One such situation is in the context of causal fairness (Chikahara et al., 2021). In some practical cases, the outputs cannot be independent from the sensitive attribute unless we sacrifice much of prediction accuracy. For example, any decisions based on physical strength are statistically correlated to gender due to biological nature. The problem in such a situation is not the statistical bias (such as demographic parity), but whether the decision is based on physical strength or gender, i.e. the attributions of each feature.

The focus of this study is on manipulating the feature attributions so that the dependence on sensitive features is hidden and the audits are misled as if the model is fair even if it is not the case. Recently, several studies reported that such a manipulation is possible, e.g. by modifying the black-box model to be explained (Slack et al., 2020; Begley et al., 2020; Dimanov et al., 2020), by manipulating the computation algorithms of feature attributions (Aïvodji et al., 2019), and by poisoning the data distribution (Baniecki et al., 2021; Baniecki & Biecek, 2022). With these findings in mind, the current possible advice to the auditors is not to rely solely on the reported feature attributions for fairness auditing. A question then arises about what “evidence” we can expect in addition to the feature attributions, and whether they can be valid “evidence” of fairness.

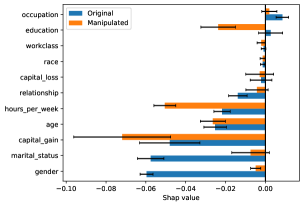

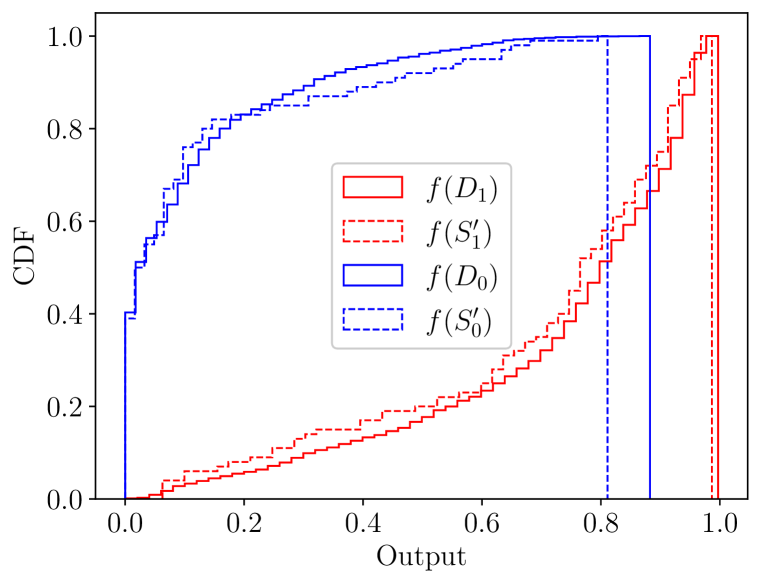

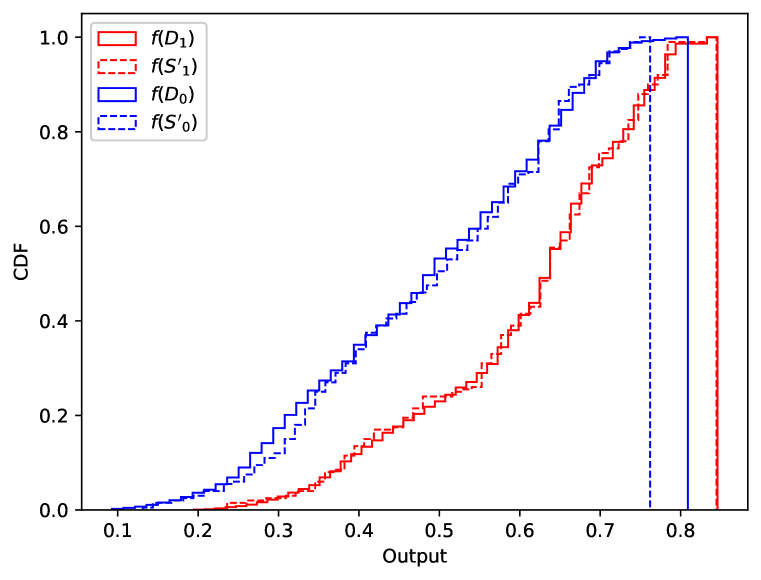

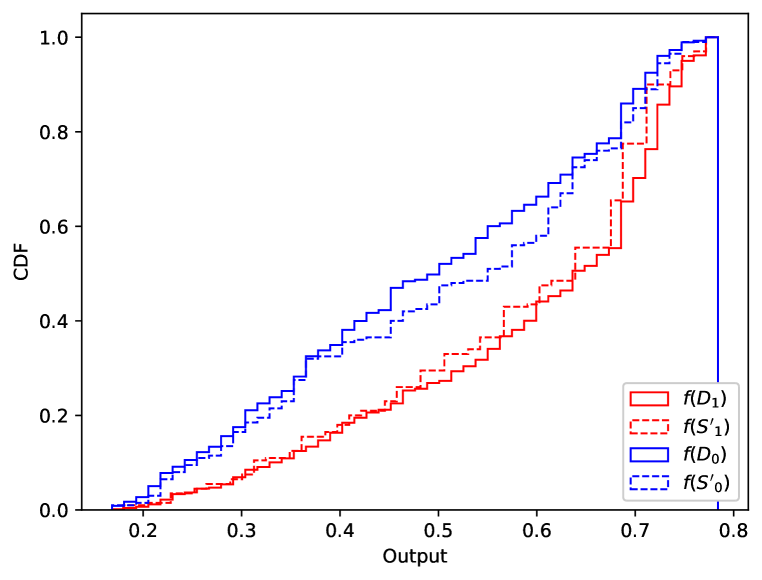

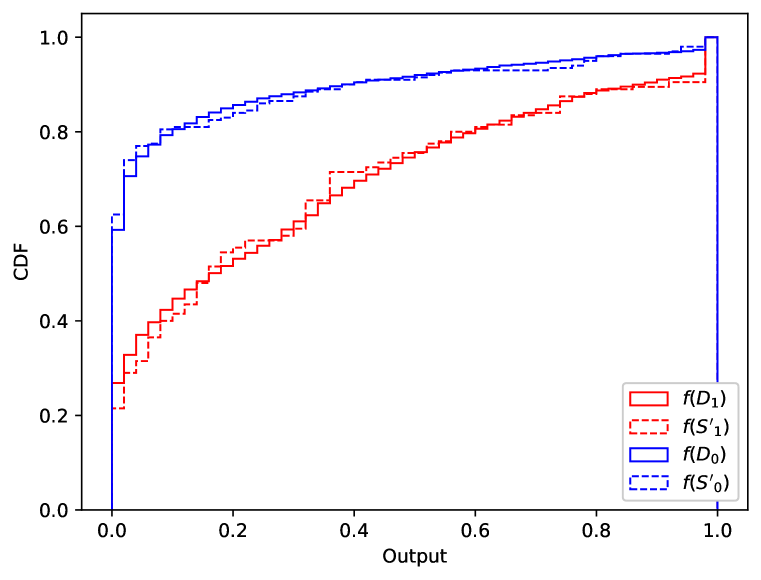

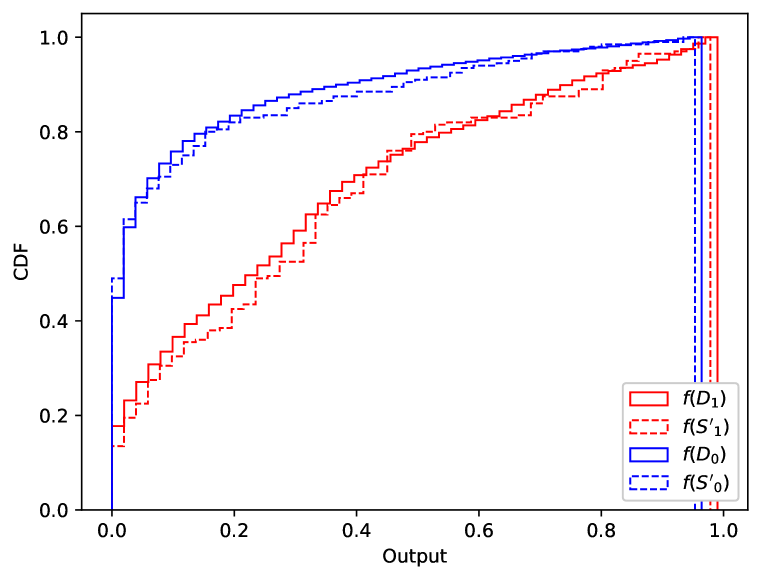

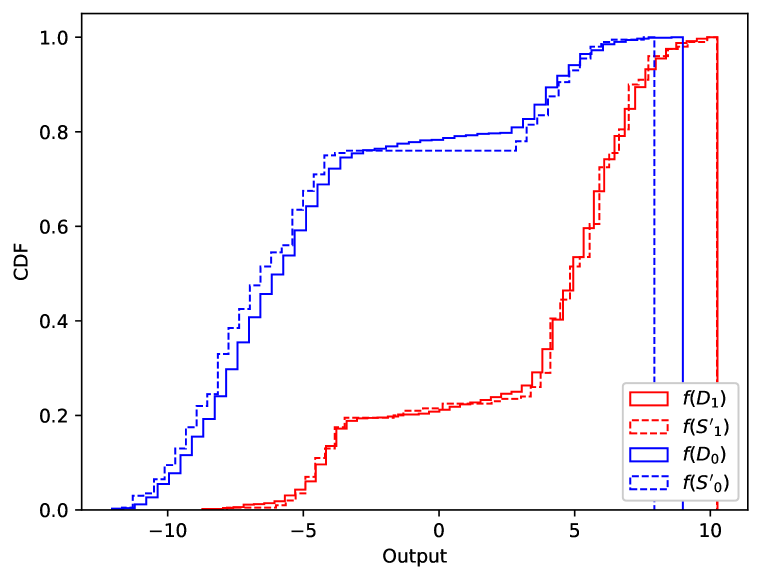

In this study, we show that we can craft fake “evidence” of fairness for SHAP explanations, which provides the first negative answer to the last question. In particular, we show that we can produce not only manipulated feature attributions but also a benchmark dataset as the fake “evidence” of fairness. The benchmark dataset ensures the external auditors reproduce the reported feature attributions using the existing SHAP library. In our study, we leverage the idea of stealthily biased sampling introduced by Fukuchi et al. (2020) to cherry-pick which data points to be included in the benchmark. Moreover, the use of stealthily biased sampling allows us to keep the manipulation undetected by making the distribution of the benchmark sufficiently close to the true data distribution. Figure 1 illustrates the impact of our attack in an explanation scenario with the Adult Income dataset.

Our contributions can be summarized as follows:

-

•

Theoretically, we formalize a notion of foreground distribution that can be used to extend Local Shapley Values (LSV) to Global Shapley Values (GSV), which can be used to decompose fairness metrics among the features (Section 2.2). Moreover, we formalize the task of manipulating the GSV as a Minimum Cost Flow (MCF) problem (Section 4).

-

•

Experimentally (Section 5), we illustrate the impact of the proposed manipulation attack on a synthetic dataset and four popular datasets, namely Adult Income, COMPAS, Marketing, and Communities. We observed that the proposed attack can reduce the importance of a sensitive feature while keeping the data manipulation undetected by the audit.

Our results indicate that SHAP explanations are not robust and can be manipulated when it comes to explaining the difference in outcomes between groups. Even worse, our results confirm we can craft a benchmark dataset so that the manipulated feature attributions are reproducible by external audits. Henceforth, we alert auditors to treat post-hoc explanation methods with skepticism even if it is accompanied by some additional evidence.

2 Shapley Values

2.1 Local Shapley Values

Shapley values are omnipresent in post-hoc explainability because of their fundamental mathematical properties (Shapley, 1953) and their implementation in the popular SHAP Python library (Lundberg & Lee, 2017). SHAP provides local explanations in the form of feature attributions i.e. given an input of interest , SHAP returns a score for each feature . These scores are meant to convey how much the model relies on feature to make its decision . Shapley values have a long background in coalitional game theory, where multiple players collaborate toward a common outcome. In the context of explaining model decisions, the players are the input features and the common outcome is the model output . In coalitional games, players (features) are either present or absent. Since one cannot physically remove an input feature once the model has already been fitted, SHAP removes features by replacing them with a baseline value . This leads to the Local Shapley Value (LSV) which respect the so-called efficiency axiom (Lundberg & Lee, 2017)

| (1) |

Simply put, the difference between the model prediction at and the baseline is shared among the different features. Additional details on the computation of LSV are presented in Appendix B.1.

2.2 Global Shapley Values

LSV are local because they explain the prediction at a specific and rely on a single baseline input . Since model auditing requires a more global analysis of model behavior, we must understand the predictions at multiple inputs sampled from a distribution called the foreground. Moreover, because the choice of baseline is somewhat ambiguous, the baselines are sampled from a distribution colloquially referred to as the background. Taking inspiration from Begley et al. (2020), we can compute Global Shapley Values (GSV) by averaging LSV over both foreground and background distributions.

Definition 2.1.

| (2) |

Proposition 2.1.

The GSV have the following property

| (3) |

2.3 Monte-Carlo Estimates

In practice, computing expectations w.r.t the whole background and foreground distributions may be prohibitive and hence Monte-Carlo estimates are used. For instance, when a dataset is used to represent a background distribution, explainers in the SHAP library such as the ExactExplainer and TreeExplainer will subsample this dataset 111https://github.com/slundberg/shap/blob/0662f4e9e6be38e658120079904899cccda59ff8/shap/maskers/_tabular.py#L54-L55 by selecting 100 instances uniformly at random when the size of the dataset exceeds 100. More formally, let

| (4) |

represent a categorical distribution over a finite set of input examples , where is the Dirac probability measure, , and . Estimating expectations with Monte-Carlo amounts to sampling instances

| (5) |

and computing the plug-in estimate

| (6) | ||||

When a set of samples is a singleton (e.g. ), we shall use the convention to improve readability. In Appendix B.2, is shown to be a consistent and asymptotically normal estimate of meaning that one can compute approximate confidence intervals around to capture with high probability. In practice, the estimates are employed as the model explanation which we see as a vulnerability. As discussed in Section 4, the Monte-Carlo estimation is the key ingredient that allows us to manipulate the GSV in favor of a dishonest entity.

3 Audit Scenario

This section introduces an audit scenario to which the proposed attack of SHAP can apply. This scenario involves two parties: a company and an audit. The company has a dataset with and that contains input-target tuples and also has a model that is meant to be deployed in society. The binary feature with index (i.e. ) represents a sensitive feature with respect to which the model should not explicitly discriminate. Both the data and the model are highly private so the company is very careful when providing information about them to the audit. Hence, is a black box from the point of view of the audit. At first, the audit asks the company for the necessary data to compute fairness metrics e.g. the Demographic Parity (Dwork et al., 2012), the Predictive Equality (Corbett-Davies et al., 2017), or the Equal Opportunity (Hardt et al., 2016). Note that our attack would apply as long as the fairness metric is a difference in model expectations over subgroups. For simplicity, the audit decides to compute the Demographic Parity

| (7) |

and therefore demands access to the model outputs for all inputs with different values of the sensitive feature : and , where and are subsets of the input data of sizes and respectively. Doing so does not force the company to share values of features other than nor does it requires direct access to the inner workings of the proprietary model. Hence, this demand respects privacy requirements and the company will accept to share the model outputs across all instances, see Figure 2(a). At this point, the audit confirms that the model is indeed biased in favor of and puts in question the ability of the company to deploy such a model. Now, the company argues that, although the model exhibits a disparity in outcomes, it does not mean that the model explicitly uses the feature to make its decision. If such is the case, then the disparity could be explained by other features statistically associated with . Some of these other features may be acceptable grounds for decisions. To verify such a claim, the audit decides to employ post-hoc techniques to explain the disparity. Since the model is a black-box, the audits shall compute the GSV. The foreground and background are chosen to be the data distributions conditioned on and respectively

| (8) |

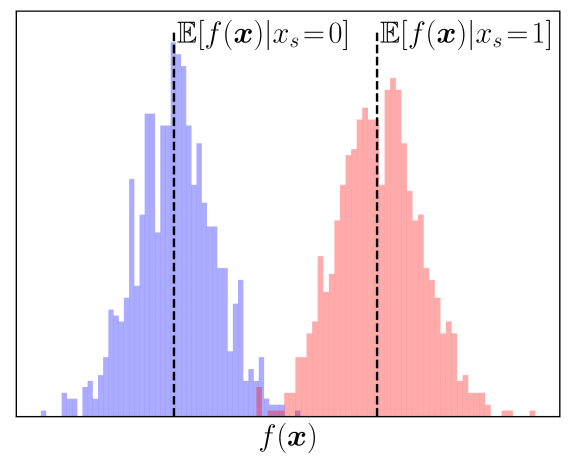

According to Equation 3, the resulting GSV will sum up to the demographic parity (cf. Equation 7). If the sensitive feature has a large negative GSV , then this would mean that the model is explicitly relying on to make its decisions and the company would be forbidden from deploying the model. If the GSV has a small amplitude, however, the company could still argue in favor of deploying the model in spite of having disparate outcomes. Indeed, the difference in outcomes by the model could be attributed to more acceptable features. See Figure 2(b) for a toy example illustrating this reasoning.

To compute the GSV, the audit demands the two datasets of inputs and , as well as the ability to query the black box at arbitrary points. Because of privacy concerns on sharing values of across the whole dataset, and because GSV must be estimated with Monte-Carlo, both parties agree that the company shall only provide subsets and of size to the audit so they can compute a Monte-Carlo estimate . The company first estimate GSV on their own by choosing uniformly at random from and (cf. Equation 5) and observe that indeed has a large negative value. They realize they must carefully select which data points will be sent, otherwise, the audit may observe the bias toward and the model will not be deployed. Moreover, the company understands that the audit currently has access to the data and representing the model predictions on the whole dataset (see Figure 2(a)). Therefore, if the company does not share subsets that were chosen uniformly at random from , it is possible for the audit to detect this fraud by doing a statistical test comparing to and to . The company needs a method to select misleading subsets whose GSV is manipulated in their favor while remaining undetected by the audit. Such a method is the subject of the next section.

4 Fool SHAP with Stealthily Biased Sampling

4.1 Manipulation

To fool the audit, the company can decide to indeed sub-sample uniformly at random . Then, given this choice of foreground data, they can repeatedly sub-sample , and choose the set leading to the smallest . We shall call this method “brute-force”. Its issue is that, by sub-sampling from , it will take an enormous number of repetitions to reduce the attribution since the GSV is concentrated on the population GSV .

A more clever method is to re-weight the background distribution before sampling from it i.e. define with and then sub-sample . To make the model look fairer, the company needs the computed with these cherry-picked points to have a small magnitude.

Proposition 4.1.

Let be fixed, and let represent convergence in probability as the size of the set increases, we have

| (9) |

We note that the coefficients in Equation 9 are tractable and can be computed and stored by the company. We discuss in more detail how to compute them in Appendix B.3. An additional requirement is that the non-uniform distribution remains similar to the original . Otherwise, the fraud could be detected by the audit. In this work, the notion of similarity between distributions will be captured by the Wasserstein distance in output space.

Definition 4.1 (Wassertein Distance).

Any probability measure over is called a coupling measure between and , denoted , if and . The Wassertein distance between and mapped to the output-space is defined as

| (10) |

a.k.a the cost of the optimal transport plan that distributes the mass from one distribution to the other.

We propose Algorithm 1 to compute the weights by minimizing the magnitude of the GSV while maintaining a small Wasserstein distance. The trade-off between attribution manipulation and proximity to the data is tuned via a hyper-parameter . We show in the Appendix A.2 that the optimization problem at line 5 of Algorithm 1 can be reformulated as a Minimum Cost Flow (MCF) and hence can be solved in polynomial time (more precisely as in Fukuchi et al. (2020)).

4.2 Detection

We now discuss ways the audit can detect manipulation of the sampling procedure. Recall that the audit has previously been given access to representing the model outputs across all instances in the private dataset. The audit will then be given sub-samples of on which they can compute the output of the model and compare with . To assess whether or not the sub-samples provided by the company were sampled uniformly at random, the audit has to conduct statistical tests. The null hypothesis of these tests will be that were sampled uniformly at random from . The detection Algorithm 2 with significance uses both the Kolmogorov-Smirnov and Wald tests with Bonferonni corrections (i.e. the terms in the Algorithm). The Kolmogorov-Smirnov and Wald tests are discussed in more detail in Appendix C.

4.3 Whole procedure

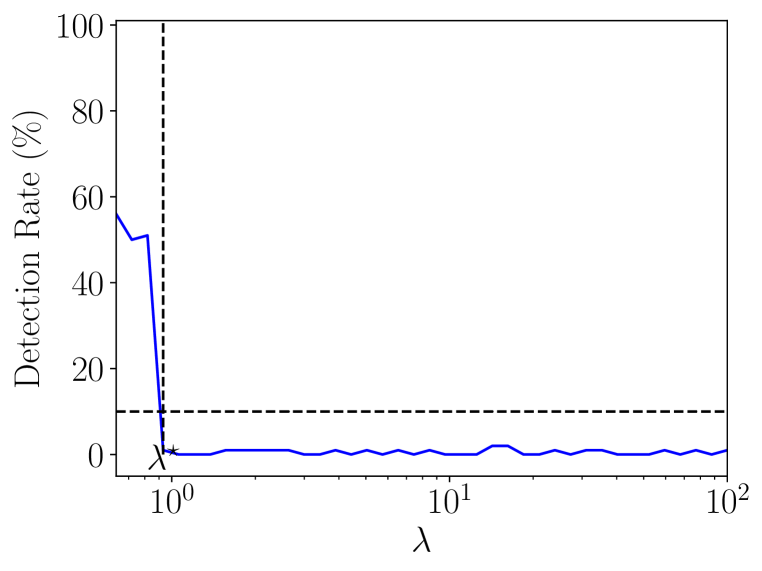

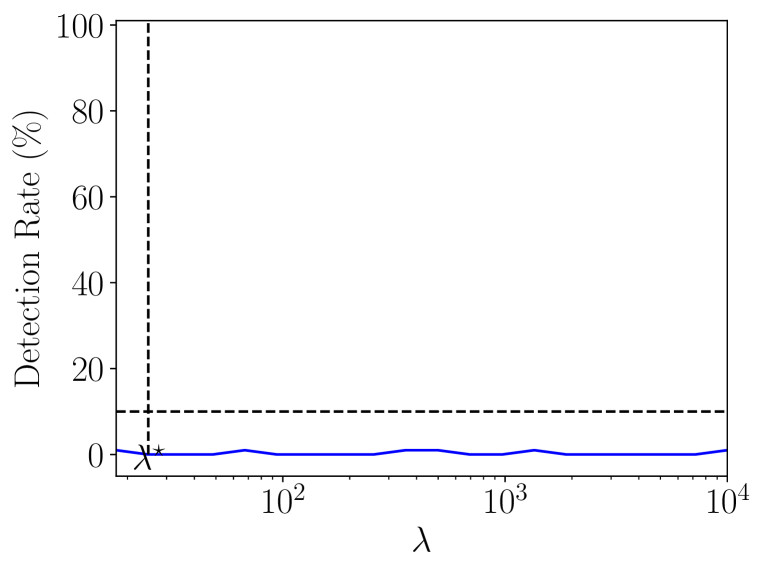

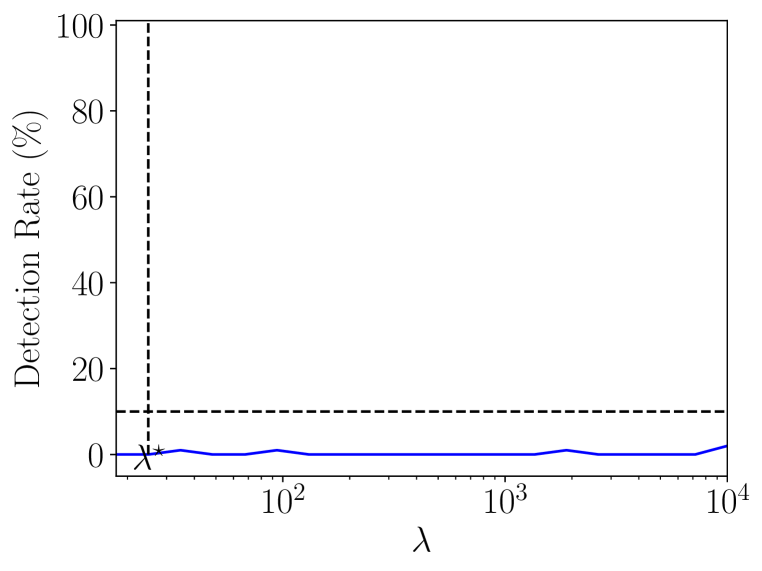

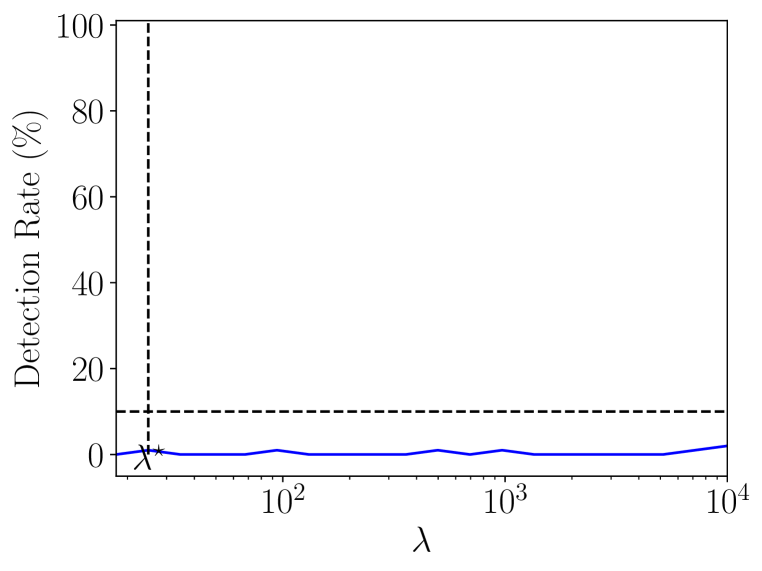

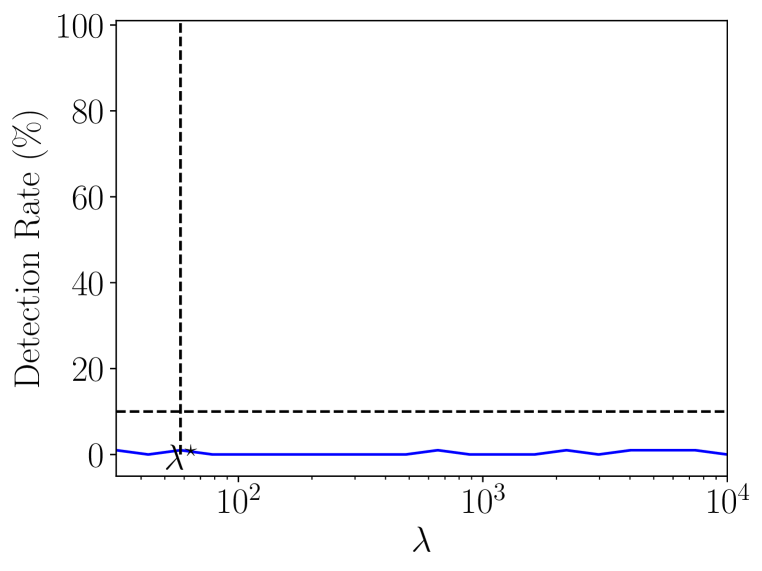

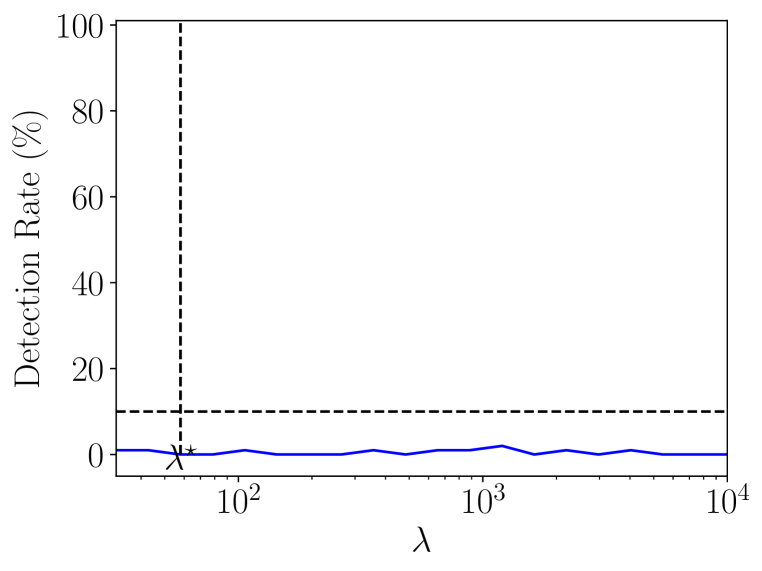

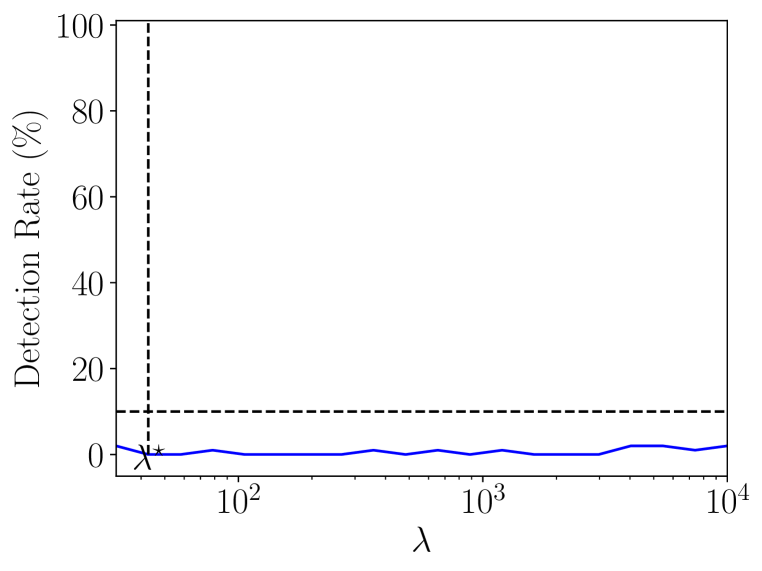

The procedure returning the subsets is presented in Algorithm 3. It conducts a log-space search between and for the hyper-parameter (line 6) in order to explore the possible attacks. For each value of , the attacker runs Algorithm 1 to obtain (line 7), then repeatedly samples (line 10) and attempts to detect the fraud (line 11). The attacker will choose that minimizes the magnitude of while having a detection rate below some threshold (line 12). An example of search over on a real-world dataset is presented in Figure 3.

One limitation of Fool SHAP is that it manipulates a single sensitive feature. In Appendix E.4, we present a possible extension of Algorithm 1 to handle multiple sensitive features and present preliminary results of its effectiveness. A second limitation is that it only applies to “interventional” Shapley values which break feature correlations. This choice was made because most methods in the SHAP library222except the TreeExplainer when no background data is provided are “interventional”. Future work should port Fool SHAP to “observational” Shapley values that use conditional expectations to remove features (Frye et al., 2020).

![[Uncaptioned image]](/html/2205.15419/assets/x4.png)

4.4 Contributions

The first technique to fool SHAP with perturbations of the background distribution was a genetic algorithm Baniecki & Biecek (2022). Although promising, the cross-over and mutation operations it employs to perturb data do not take into account feature correlations and can therefore generate unrealistic data. Moreover, the objective to minimize does not enforce similarity between the original and manipulated backgrounds. We show in Appendix E.3 that these limitations lead to systematic fraud detections. Hence, our contributions are two-fold. First, by perturbing the background via non-uniform weights over pre-existing instances (i.e. ) rather than a genetic algorithm, we avoid the issue of non-realistic data. Second, by considering the Wasserstein distance, we can control the similarity between the original and fake backgrounds.

Since the Stealthity Biased Sampling technique introduced in Fukuchi et al. (2020) also leverages a non-uniform distribution over data points and the Wasserstein distance, it makes sense to adapt it to fool SHAP. Still, the approach of Fukuchi et al. is different from ours. Indeed, in their work, they minimize the Wasserstein distance while enforcing a hard constraint on the number of instances that land on the different bins for the target and sensitive feature, That way, they can set the Demographic Parity to any given value while staying close to the original data. In our setting of manipulating the model explanation, we leave the Demographic Parity intact and instead manipulate its feature attribution. In terms of the optimization objective, we now minimize a Shapley value with a soft constraint on the Wasserstein distance.

5 Experiments

5.1 Toy experiment

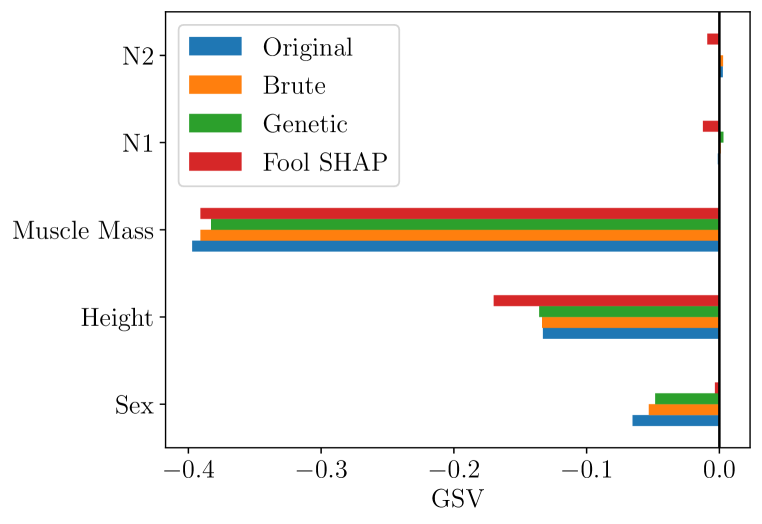

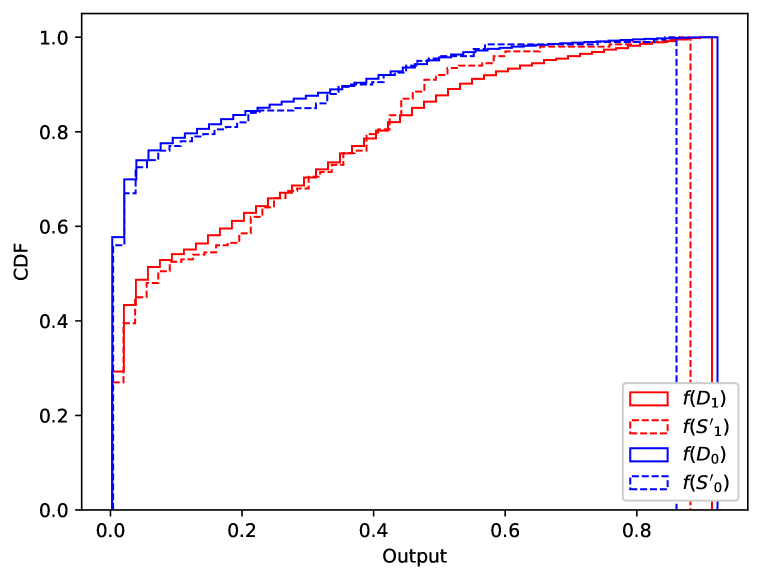

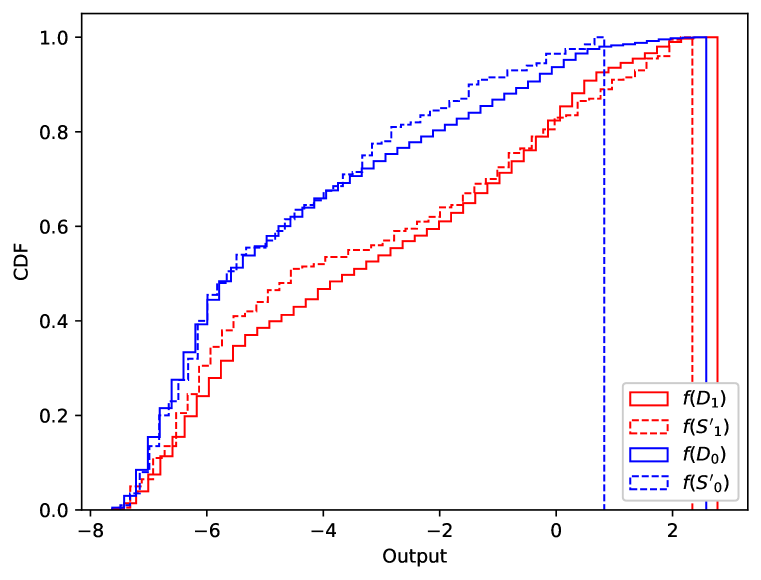

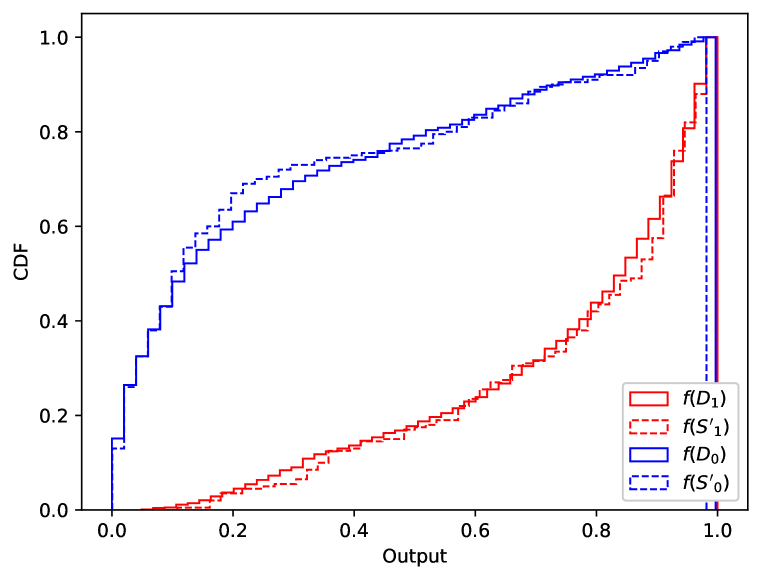

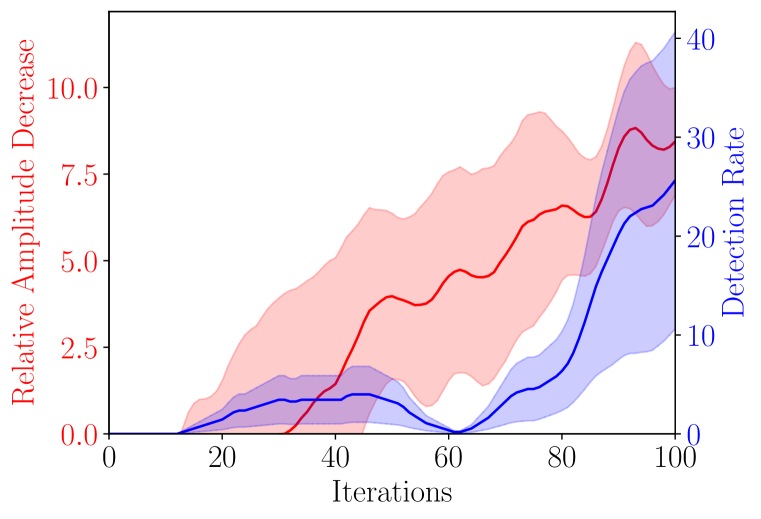

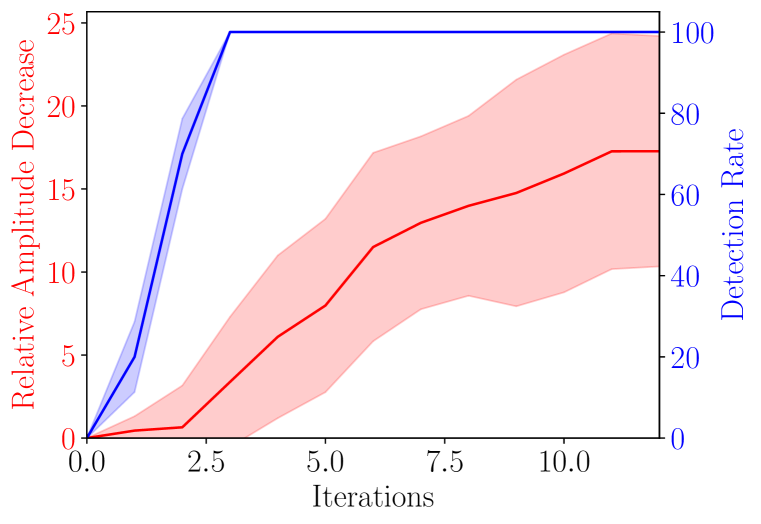

The task is predicting which individual will be hired for a job that requires carrying heavy objects. The causal graph for this toy data is presented in Figure 4 (left). We observe that sex () influences height (), and that both these features influence the Muscular Mass (). In the end, the hiring decisions () are only based on the two attributes relevant to the job: and . Also, two noise features were added. More details and justifications for this causal graph are discussed in Appendix D.1. Since strength and height (two important qualifications for applicants) are correlated with sex, any model that fits the data will exhibit some disparity in hiring rates between sexes. Although, if the model decisions do not rely strongly on feature , the company can argue in favor of deployment. GSV are used by the audit to measure the amount by which the model relies on the sex feature, see Figure 4 (Middle). By employing Fool SHAP with , the company can reduce the GSV of feature considerably compared to the brute-force and genetic algorithms. More importantly, the audit is not able to detect that the provided samples were cherry-picked, see Figure 4 (Right). More results are presented in Appendix E.1.

5.2 Datasets

We consider four standard datasets from the FAccT literature, namely COMPAS, Adult-Income, Marketing, and Communities.

-

•

COMPAS regroups 6,150 records from criminal offenders in Florida collected from 2013-2014. This binary classification task consists in predicting who will re-offend within two years. The sensitive feature is race with values for African-American and for Caucasian.

-

•

Adult Income contains demographic attributes of 48,842 individuals from the 1994 U.S. census. It is a binary classification problem with the goal of predicting whether or not a particular person makes more than 50K USD per year. The sensitive feature in this dataset is gender, which took values for female, and for male.

-

•

Marketing involves information on 41,175 customers of a Portuguese bank and the binary classification task is to predict who will subscribe to a term deposit. The sensitive attribute is age and took values for age 30-60, and for age not30-60

-

•

Communities & Crime contains per-capita violent crimes for 1994 different communities in the US. The binary classification task is to predict which communities have crimes below the median rate. The sensitive attribute is PercentWhite and took values for PercentWhite<90%, and for PercentWhite>=90%.

Three models were considered for the two datasets: Multi-Layered Perceptrons (MLP), Random Forests (RF), and eXtreme Gradient Boosted trees (XGB). One model of each type was fitted on each dataset for 5 different train/test splits seeds, resulting in 60 models total. Values of the test set accuracy and demographic parity for each model type and dataset are presented in Appendix D.2.

5.3 Detector Calibration

| mlp | rf | xgb | |

|---|---|---|---|

| COMPAS | 4.0 | 4.6 | 4.0 |

| Adult | 4.3 | 4.3 | 4.2 |

| Marketing | 4.9 | 5.0 | |

| Communities | 3.8 | 4.2 |

Detector calibration refers to the assessment that, assuming the null hypothesis to be true, the probability of rejecting it (i.e. false positive) should be bounded by the significance level . Remember that the null hypothesis of the audit detector is that the sets provided by the company are sampled uniformly from . Hence, to test the detector, the audit can sample their own subsets uniformly from at random from , run the detection algorithm, and count the number of detection over 1000 repeats. Table 1 shows the false positive rates over the five train-test splits using a significance level . We observe that the false positive rates are indeed bounded by for all model types and datasets implying that the detector employed by the audit is calibrated.

5.4 Attack Results and Discussion

The first step of the attack (line 3 of Algorithm 3) requires that the company run SHAP on their own and compute the necessary coefficients to run Algorithm 1. For the COMPAS and Adults datasets, the ExactExplainer of SHAP was used. Since Marketing and Communities contain more than 15 features, and since the ExactExplainer scales exponentially with the number of features, we were restricted to using the TreeExplainer (Lundberg et al., 2020) on these datasets. The TreeExplainer avoids the exponential cost of Shapley values but is only applicable to tree-based models such as RFs and XGBs. Therefore, we could not conduct the attack on MLPs fitted on Marketing and Communities.

The following step is to solve the MCF for various values of (line 7 of Algorithm 3). As stated previously, solving the MCF can be done in polynomial time in terms of , which was tractable for a small dataset like COMPAS and Communities, but not for larger datasets like Adult and Marketing. To solve this issue, as was done in Fukuchi et al. (2020), we compute the manipulated weights multiple times using 5 bootstrap sub-samples of of size 2000 to obtain a set of weights which we average to obtain the final weights .

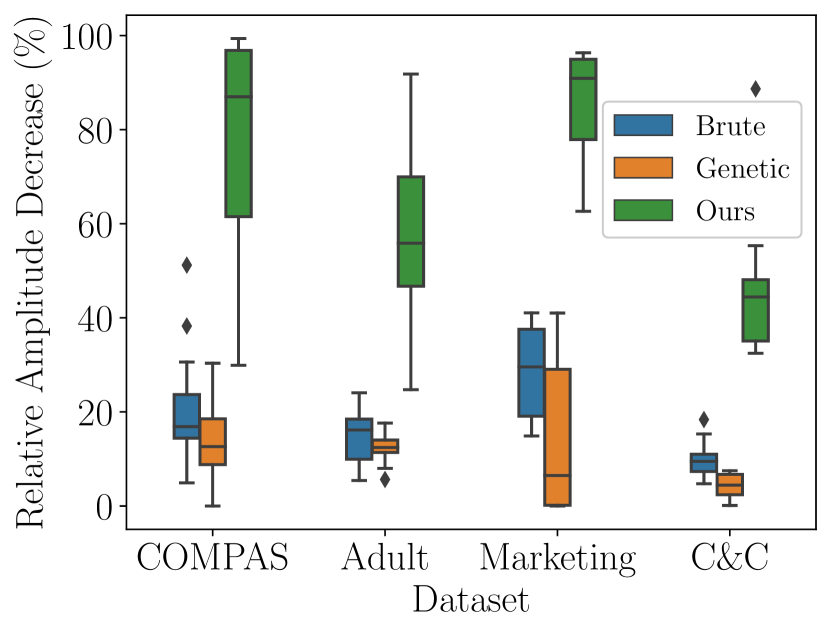

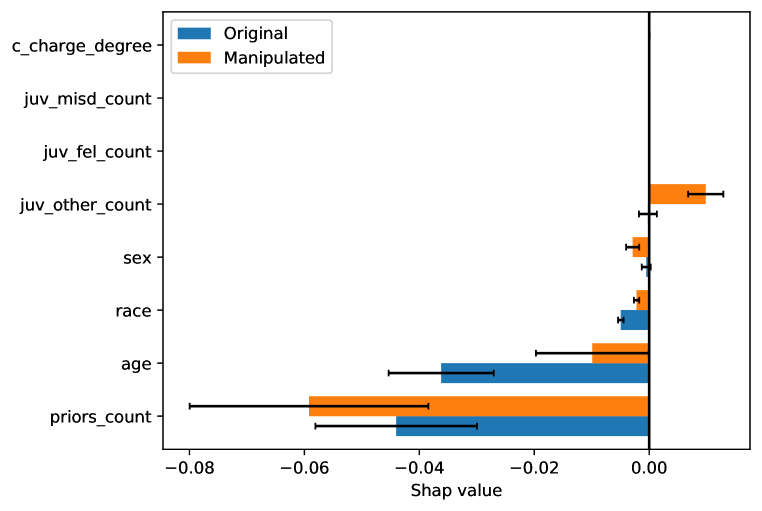

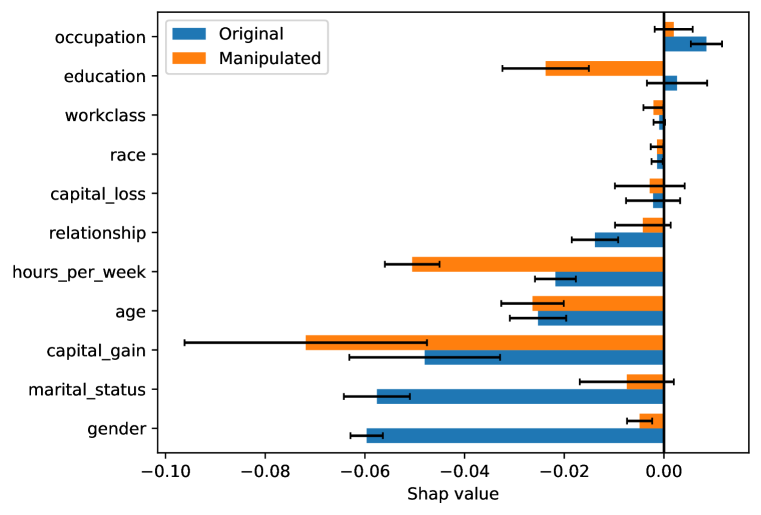

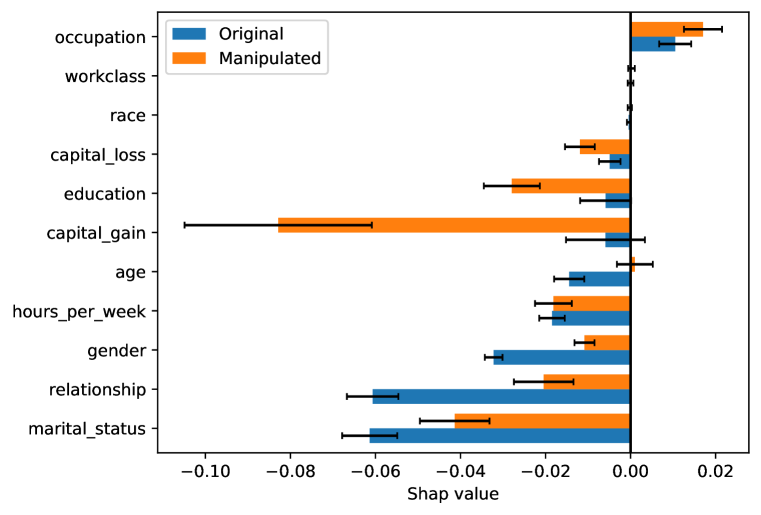

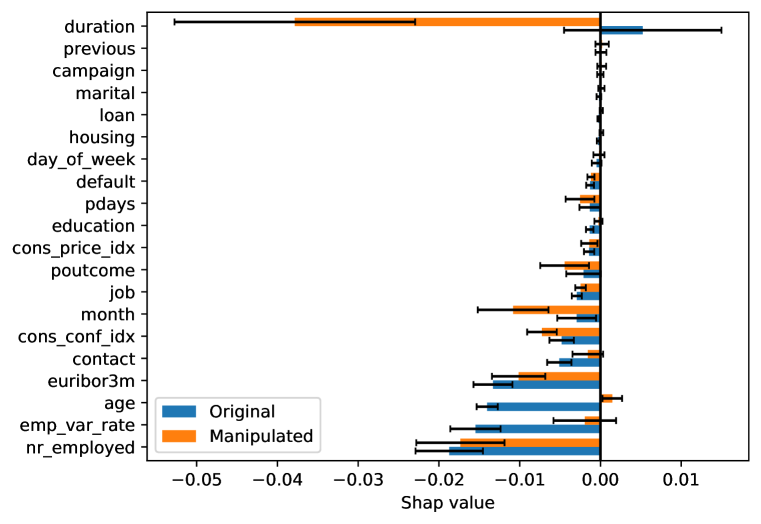

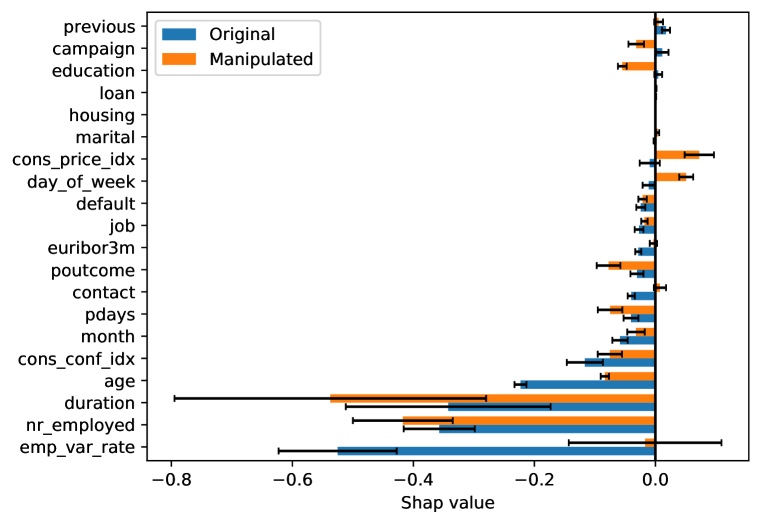

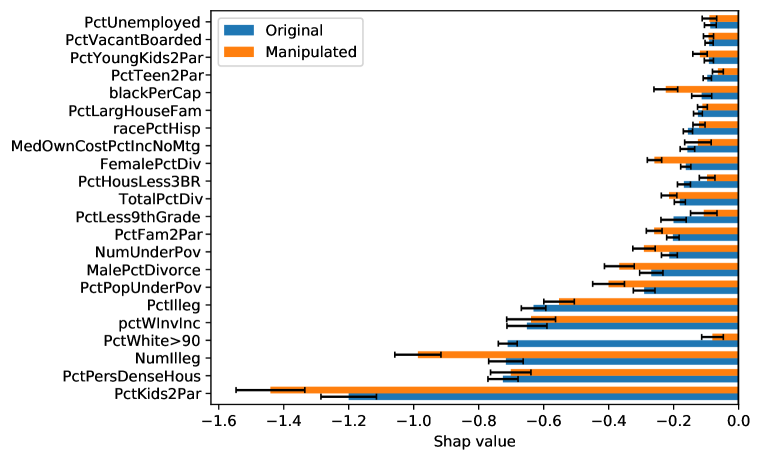

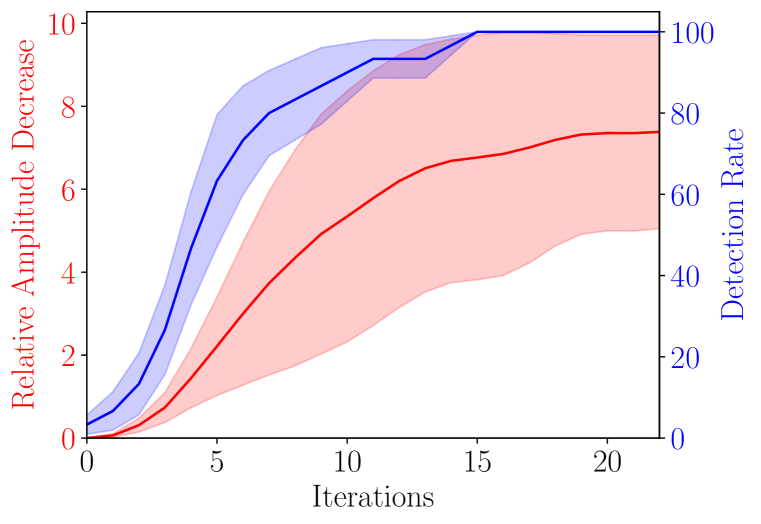

Results of 46 attacks with are shown in Figure 5. Specific examples of the conducted attacks are presented in Appendix E.2. As a point of reference, we also show results for the brute-force and genetic algorithms. To make comparisons to our attack more meaningful, the brute-force method was only allowed to run for the same amount of time it took to search for the non-uniform weights (about 30-180 seconds). Also, the genetic algorithm ran for 400 iterations and was stopped early if there were 10 consecutive detections. We note that, across all datasets, Fool SHAP leads to greater reductions of the sensitive feature attribution compared to brute-force search and the genetic perturbations of the background.

Now focusing on Fool SHAP, for the datasets COMPAS and Marketing, we observe median reductions in amplitudes of about . This means that our attack can considerably reduce the apparent importance of the sensitive attribute. For the Adult and Communities datasets, the median reduction in amplitude is about meaning that we typically reduce by half the importance of the sensitive feature. Still, looking at the maximum reduction in amplitude for Adult-Income and Communities, we note that one attack managed to reduce the amplitude by . Therefore, luck can play a part in the degree of success of Fool SHAP, which is to be expected from data-driven attacks.

Finally, the audit was consistently unable to detect the fraud using statistical tests. This observation raises concerns about the risk that SHAP explanations can be attacked to return not only manipulated attributions but also non-detectable fake evidence of fairness.

6 Conclusion

To conclude, we proposed a novel attack on Shapley values that does not require modifying the model but rather manipulates the sampling procedure that estimates expectations w.r.t the background distribution. We show on a toy example and four fairness datasets that our attack can reduce the importance of a sensitive feature when explaining the difference in outcomes between groups using SHAP. Crucially, the sampling manipulation is hard to detect by an audit that is given limited access to the data and model. These results raise concerns about the viability of using Shapley values to assess model fairness. We leave as future work the use of Shapley values to decompose other fairness metrics such as predictive equality and equal opportunity. Moreover, we wish to move to use cases beyond fairness, as we believe that the vulnerability of Shapley values that was demonstrated can apply to many other properties such as safety and security.

7 Ethics Statement

The main objective of this work is to raise awareness about the risk of manipulation of SHAP explanations and their undetectability. As such, it aims at exposing the potential negative societal impacts of relying on such explanations. It remains however possible that malicious model producers could use this attack to mislead end users or cheat during an audit. However, we believe this paper makes a significant step toward increasing the vigilance of the community and fostering the development of trustworthy explanations methods. Furthermore, by showing how fairness can be manipulated in explanation contexts, this work contributes to the research on the certification of the fairness of automated decision-making systems.

8 Reproducibility Statement

The source code of all our experiments is available online333https://github.com/gablabc/Fool_SHAP. Moreover, experimental details are provided in appendix D.2 for the interested reader.

References

- Adebayo et al. (2016) Julius A Adebayo et al. Fairml: Toolbox for diagnosing bias in predictive modeling. Master’s thesis, Massachusetts Institute of Technology, 2016.

- Aïvodji et al. (2019) Ulrich Aïvodji, Hiromi Arai, Olivier Fortineau, Sébastien Gambs, Satoshi Hara, and Alain Tapp. Fairwashing: the risk of rationalization. In International Conference on Machine Learning, pp. 161–170. PMLR, 2019.

- Baniecki & Biecek (2022) Hubert Baniecki and Przemyslaw Biecek. Manipulating shap via adversarial data perturbations (student abstract). 2022.

- Baniecki et al. (2021) Hubert Baniecki, Wojciech Kretowicz, and Przemyslaw Biecek. Fooling partial dependence via data poisoning. arXiv preprint arXiv:2105.12837, 2021.

- Begley et al. (2020) Tom Begley, Tobias Schwedes, Christopher Frye, and Ilya Feige. Explainability for fair machine learning. arXiv preprint arXiv:2010.07389, 2020.

- Bellamy et al. (2018) Rachel KE Bellamy, Kuntal Dey, Michael Hind, Samuel C Hoffman, Stephanie Houde, Kalapriya Kannan, Pranay Lohia, Jacquelyn Martino, Sameep Mehta, Aleksandra Mojsilovic, et al. Ai fairness 360: An extensible toolkit for detecting, understanding, and mitigating unwanted algorithmic bias. arXiv preprint arXiv:1810.01943, 2018.

- Chikahara et al. (2021) Yoichi Chikahara, Shinsaku Sakaue, Akinori Fujino, and Hisashi Kashima. Learning individually fair classifier with path-specific causal-effect constraint. In International Conference on Artificial Intelligence and Statistics, pp. 145–153. PMLR, 2021.

- Corbett-Davies et al. (2017) Sam Corbett-Davies, Emma Pierson, Avi Feller, Sharad Goel, and Aziz Huq. Algorithmic decision making and the cost of fairness. In Proceedings of the 23rd acm sigkdd international conference on knowledge discovery and data mining, pp. 797–806, 2017.

- Dimanov et al. (2020) Botty Dimanov, Umang Bhatt, Mateja Jamnik, and Adrian Weller. You shouldn’t trust me: Learning models which conceal unfairness from multiple explanation methods. In SafeAI@ AAAI, 2020.

- Dwork et al. (2012) Cynthia Dwork, Moritz Hardt, Toniann Pitassi, Omer Reingold, and Richard Zemel. Fairness through awareness. In Proceedings of the 3rd innovations in theoretical computer science conference, pp. 214–226, 2012.

- Frye et al. (2020) Christopher Frye, Damien de Mijolla, Tom Begley, Laurence Cowton, Megan Stanley, and Ilya Feige. Shapley explainability on the data manifold. arXiv preprint arXiv:2006.01272, 2020.

- Fukuchi et al. (2020) Kazuto Fukuchi, Satoshi Hara, and Takanori Maehara. Faking fairness via stealthily biased sampling. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pp. 412–419, 2020.

- Guidotti et al. (2018) Riccardo Guidotti, Anna Monreale, Salvatore Ruggieri, Franco Turini, Fosca Giannotti, and Dino Pedreschi. A survey of methods for explaining black box models. ACM computing surveys (CSUR), 51(5):1–42, 2018.

- Hardt et al. (2016) Moritz Hardt, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. Advances in neural information processing systems, 29, 2016.

- Janssen et al. (2000) Ian Janssen, Steven B Heymsfield, ZiMian Wang, and Robert Ross. Skeletal muscle mass and distribution in 468 men and women aged 18–88 yr. Journal of applied physiology, 2000.

- Lee (2019) A J Lee. U-statistics: Theory and Practice. Routledge, 2019.

- Lundberg & Lee (2017) Scott M Lundberg and Su-In Lee. A unified approach to interpreting model predictions. Advances in neural information processing systems, 30, 2017.

- Lundberg et al. (2020) Scott M Lundberg, Gabriel Erion, Hugh Chen, Alex DeGrave, Jordan M Prutkin, Bala Nair, Ronit Katz, Jonathan Himmelfarb, Nisha Bansal, and Su-In Lee. From local explanations to global understanding with explainable ai for trees. Nature machine intelligence, 2(1):56–67, 2020.

- Massey Jr (1951) Frank J Massey Jr. The kolmogorov-smirnov test for goodness of fit. Journal of the American statistical Association, 46(253):68–78, 1951.

- Saleiro et al. (2018) Pedro Saleiro, Benedict Kuester, Loren Hinkson, Jesse London, Abby Stevens, Ari Anisfeld, Kit T Rodolfa, and Rayid Ghani. Aequitas: A bias and fairness audit toolkit. arXiv preprint arXiv:1811.05577, 2018.

- Shapley (1953) Lloyd S Shapley. A value for n-person games. Contributions to the Theory of Games, pp. 307–317, 1953.

- Slack et al. (2020) Dylan Slack, Sophie Hilgard, Emily Jia, Sameer Singh, and Himabindu Lakkaraju. Fooling lime and shap: Adversarial attacks on post hoc explanation methods. In Proceedings of the AAAI/ACM Conference on AI, Ethics, and Society, pp. 180–186, 2020.

- Wasserman (2004) Larry Wasserman. All of Statistics: A concise course in statistical inference. Springer, 2004.

Appendix A Proofs

A.1 Proofs for Global Shapley Values (GSV)

Proposition A.1 (Proposition 3).

The GSV have the following property

| (11) |

Proof.

As a reminder, we have defined the vector

| (12) |

whose components sum up to

| (13) | ||||

| (14) | ||||

| (15) | ||||

| (16) | ||||

| (17) |

where at the last step we have simply renamed a dummy variable. ∎

Proposition A.2 (Proposition 9).

Let be fixed, and let represent convergence in probability as the size of the set increases, then we have

| (18) |

Proof.

| (19) | ||||

Since is assumed to be fixed, then the only random variable in is which represents an instance sampled from the . Therefore, we can define and we get

| (20) | ||||

By the weak law of large number, the following holds as goes to infinity (Wasserman, 2004, Theorem 5.6)

| (21) |

Now, as a reminder, the manipulated background distribution is with . Therefore

| (22) | ||||

concluding the proof. ∎

A.2 Proofs for Optimization Problem

A.2.1 Technical Lemmas

We provide some technical lemmas that will be essential when proving Theorem A.1. These are presented for completeness and are not intended as contributions by the authors. Let us first write the formal definition of the minimum of a function.

Definition A.1 (Minimum).

Given some function , the minimum of over (denoted ) is defined as follows:

Basically, the notion of minimum coincides with the infimum (highest lower bound) when this lower bound is attained for some . By the Extreme Values Theorem, the minimum always exists when is compact and is continuous. For the rest of this appendix, we shall only study optimization problems where points on the domain set can be selected by the following procedure

-

1.

Choose some

-

2.

Given the selected , choose some , where the set is non-empty and depends on the value of .

When optimizing functions over these domains, one can optimize in two steps as highlighted in the following lemma.

Lemma A.1.

Given a compact domain of the form described above and a continuous objective function , the minimum is attained for some and the following holds

Proof.

Let , which is a well defined function on . We can then take its infimum . But is an infimum of ? By the definition of infimum

so that is a lower bound of . In fact, it is the highest lower bound possible so

| (23) |

By the Extreme Value Theorem, since is compact and is continuous, there exists s.t. . Since the infimum is attained on the left-hand-side of Equation 23, then it must also be attained on the right-hand-side and therefore we can replace all with in Equation 23, leading to the desired result. ∎

Lemma A.2.

Given a compact domain of the form described above and two continuous functions and , then

Proof.

Applying Lemma A.1 with the function proves the Lemma. ∎

A.2.2 Minimum Cost Flows

Let be a graph with vertices with directed edges , be a capacity and be a cost. Moreover, let be two special vertices called the source and the sink respectivelly, and be a total flow. The Minimum-Cost Flow (MCF) problem of consists of finding the flow function that minimizes the total cost

| (24) | ||||

| s.t. | ||||

where and are the outgoing and incoming edges from . The terminology of flow arises from the constraint that, for vertices that are not the source nor the sink, the outgoing flow must equal the incoming one, which is reminiscent of conservation laws in fluidic. We shall refer to as the flow from to .

Now that we have introduced minimum cost flows, let us specify the graph that will be employed to manipulate GSV, see Figure 6. We label the flow going from the sink to one of the left vertices as , and the flow going from to as . The required flow is fixed at .

Proof.

We begin by showing that the flow conservation constraints in the MCF imply that is a coupling measure (i.e. ), and is constrained to the probability simplex . Applying the conservation law on the left-side of the graph leads to the conclusion that the flows entering vertices must sum up to

This implies that is must be part of the probability simplex. By conservation, the amount of flow that leaves a specific vertex must also be , hence

For any edge outgoing from to the sink , the flow must be exactly . This is because we have edges with capacity going into the sink and the sink must receive an incoming flow of . As a consequence of the conservation law on a specific vertex , the amount of flow that goes into each is also 1

Putting everything together, from the conservation laws on , we have that , and . Now, to make the parallel between the MCF and Algorithm 1, we must use Lemma A.2. Note that is restricted to the probability simplex, while is restricted to be a coupling measure. Importantly, the set of all possible coupling measures is different for each because depends on . Hence, the domain has the same structure as the ones tackled in Lemma A.2 (where becomes and becomes ). Also, the set of possible and is a bounded simplex in so it is compact, and the objective function of the MCF is linear, thus continuous. Hence, we can apply the Lemma A.2 to the MCF.

Appendix B Shapley Values

B.1 Local Shapley Values (LSV)

We introduce Local Shapley Values (LSV) more formally. First, as explained earlier, Shapley values are based on coalitional game theory where the different features work together toward a common outcome . In a game, the features can either be present or absent, which is simulated by replacing some features with a baseline value .

Definition B.1 (The Replace Function).

Let be an input of interest , be a subset of input features that are considered active, and be a baseline input, then the replace-function is defined as

| (25) |

We note that this function is meant to “activate” the features in .

Now, if we let be a random permutation of features, and denote all features that appear before in , the LSV are computed via

| (26) |

where is the uniform distribution over permutations. Observe that the computation of LSV is scales poorly with the number of features hence model-agnostic computations are only possible with datasets with few features such as COMPAS and Adult-Income. For datasets with larger amounts of features the TreeExplainer algorithm (Lundberg et al., 2020) can be used to compute the LSV (cf. Equation 26) in polynomial time given that one is explaining a tree-based model.

B.2 Convergence

As a reminder, we are interested in estimating the GSV which requires estimating expectations w.r.t the foreground and background distributions. Said estimations can be conducted with Monte-Carlo where we sample instances

| (27) |

and compute the plug-in estimates

| (28) | ||||

We now show that, is a consistent and asymptotically normal estimate of

Proposition B.1.

Let be a black box, and be distributions on , and be the plug-in estimate of , the following holds for any and

where is the inverse Cumulative Distribution Function (CDF) of the standard normal distribution, and .

Proof.

The proof consists simply in noting that LSV are a function of two independent samples and . The model is assumed fixed and hence for any feature we can define . Now, the estimates of GSV can be rewritten

| (29) |

which we recognize as a well-known class of statistics called two-samples U-statistics. Such statistics are unbiased and asymptotically normal estimates of

| (30) |

The asymptotic normality of two-samples U-statistics is characterized by the following Theorem (Lee, 2019, Section 3.7.1).

Theorem B.1.

Let be a two-samples U-statistic with , moreover let have finite first and second moments, then the following holds for any

where and .

Proposition B.1 follows from this Theorem by choosing and noticing that having a model with bounded outputs () implies that which means that has bounded first and second moments. ∎

B.3 Compute the LSV

Running Algorithm 1 requires computing the coefficients for . To compute them, first note that they can be written in terms of LSV for all instances in

| (31) |

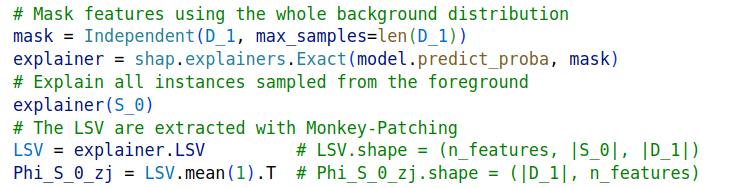

The LSV are computed deeply in the SHAP code and are not directly accessible using the current API. Hence, we had to access them using Monkey-Patching i.e. we modified the ExactExplainer class so that it stores the LSV as one of its attributes. The attribute can then be accessed as seen in Figure 7. The code is provided as a fork the SHAP repository. For the TreeExplainer, because its source code is in C++ and wrapped in Python, we found it simpler to simply rewrite our own version of the algorithm in C++ so that it directly returns the LSV, instead of Monkey-Patching the TreeExplainer.

Appendix C Statistical Tests

C.1 KS test

A first test that can be conducted is a two-samples Kolmogorov-Smirnov (KS) test (Massey Jr, 1951). If we let

| (32) |

be the empirical CDF of observations in the set . Given two sets and , the KS statistic is

| (33) |

Under the null-hypothesis for some univariate distribution , this statistic is expected to not be too large with high probability. Hence, when the company provides the subsets , the audit can sample their own two subsets uniformly at random from and compute the statistics and to detect a fraud.

C.2 Wald test

An alternative is the Wald test, which is based on the central limit theorem. If , then the empirical average of the model output over is asymptotically normally distributed as increases

| (34) |

where and are the expected value and variance of the model output across the whole background. The same reasoning holds for and the foreground . Applying the Wald test with significance would detect fraud when

| (35) |

where is the inverse of the CDF of a standard normal variable.

Appendix D Methodological Details

D.1 Toy Example

The toy dataset was constructed to closely match the results of the following empirical study comparing skeletal mass distributions between men and women (Janssen et al., 2000). Firstly, the sex feature was sampled from a Bernoulli

| (36) |

According to Table 1 of Janssen et al. (2000), the average height of women participants was 163 cm while it was 177cm for men. Both height distributions had the same standard deviation of 7cm. Hence we sampled height via

| (37) | ||||

It was noted in Janssen et al. (2000) that there was approximately a linear relationship between height and skeletal muscle mass for both sexes. Therefore, we computed the muscle mass as

| (38) | ||||

The values of coefficients 0.186, 0.128 and noise levels 5 and 4 were chosen so the distributions of would approximately match that of Table 1 in Janssen et al. (2000). Finally the target was chosen following

| (39) | ||||

Simply put, the chances of being hired in the past () were impossible for individuals with a smaller height than 160cm. Moreover, individuals with a higher mass skeletal mass were given more chances to be admitted. Yet, individuals with less muscle mass could still be given the job if they displayed sufficient determination. In the end, we generated 6000 samples leading to the following disparity in .

| (40) |

D.2 Real Data

The datasets were first divided into train/test subsets with ratio . The models were trained on the training set and evaluated on the test set. All categorical features for COMPAS, Adult, and Marketing were one-hot-encoded which resulted in a total of 11, 40, and 61 columns for each dataset respectively. A simple 50 steps random search was conducted to fine-tune the hyper-parameters with cross-validation on the training set. The resulting test set performance and demographic parities for all models and datasets, aggregated over 5 random data splits, are reported in Tables 2 and 3 respectively.

| mlp | rf | xgb | |

|---|---|---|---|

| COMPAS | |||

| Adult | |||

| Marketing | |||

| Communities |

| mlp | rf | xgb | |

|---|---|---|---|

| COMPAS | |||

| Adult | |||

| Marketing | |||

| Communities |

Appendix E Additional Results

E.1 Toy Example

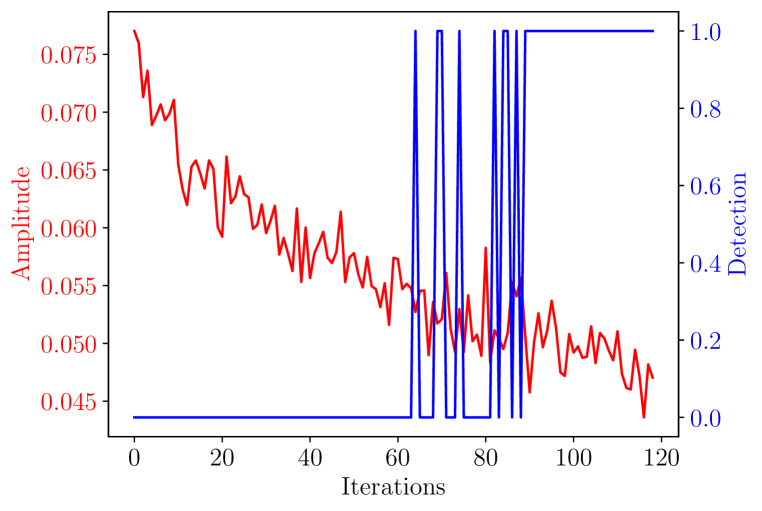

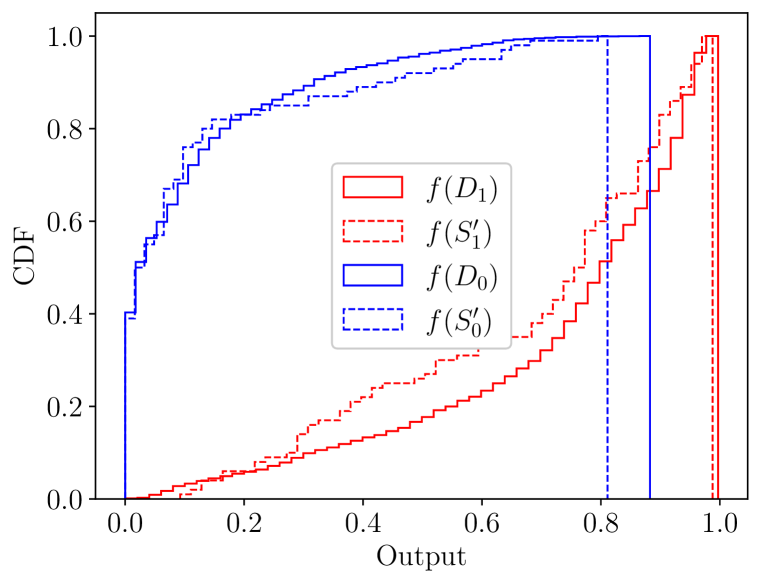

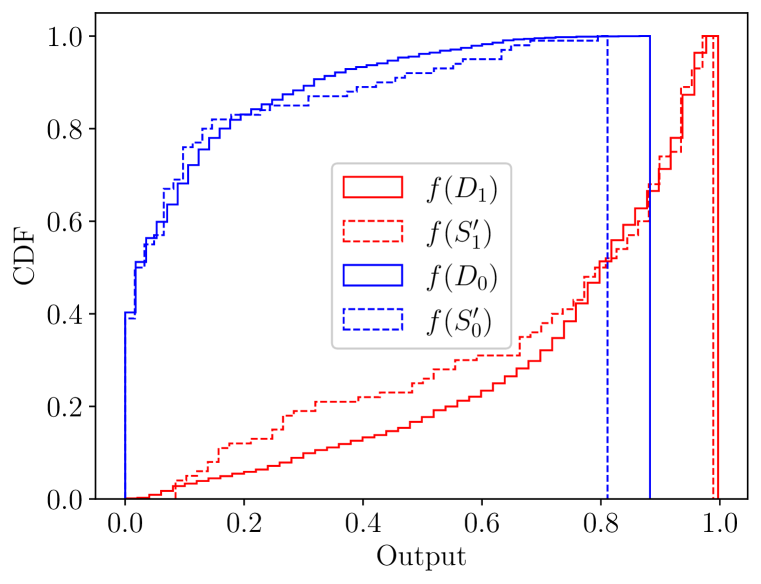

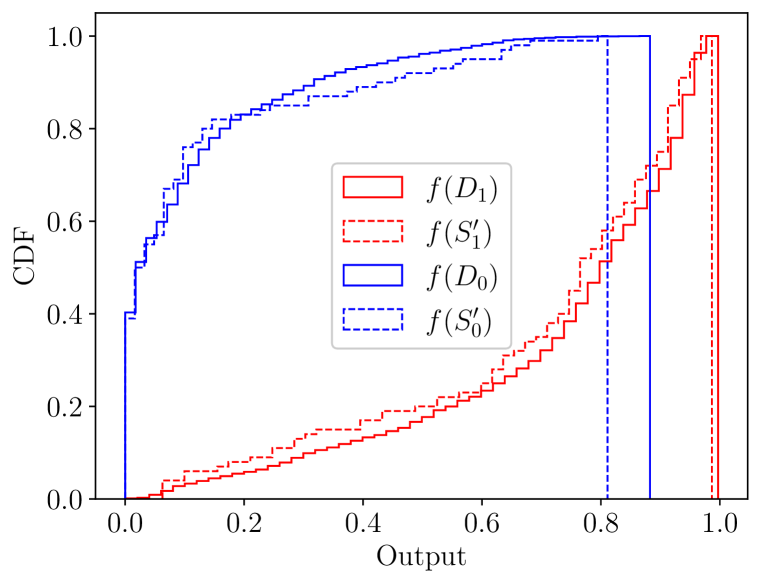

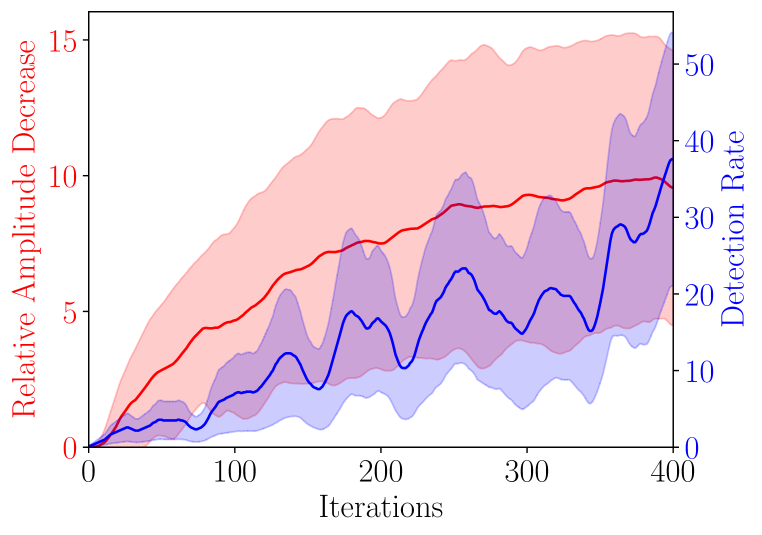

Figure 8 presents additional results for the toy example. More specifically, Figure 8 (a) illustrates the evolution of the detection and amplitude of the sensitive feature during the genetic algorithm. We note that beyond 90 iterations, the detector is systematically able to assert that the dataset is manipulated. The smallest value of amplitude that can be reached via the genetic algorithm without being detected is around . Figures 8 (b) (c) and (d) show the CDFs of where is chosen via the genetic algorithm, brute-force, and Fool SHAP respectively. We observe that Fool SHAP is the method where the resulting CDF for is closest to the CDF for . This is why the audit is not able to detect fraud using statistical tests. The fact that Fool SHAP generates fake CDFs that are close to the data CDFs is a consequence of minimizing the Wasserstein distance. These results highlight the superiority of Fool SHAP compared to the brute-force approach and the genetic algorithm.

E.2 Examples of Attacks

In this section, we present 8 specific examples of the attacks that were conducted on COMPAS, Adult, Marketing, and Communities.

E.3 Genetic Algorithm

This section motivates the use of stealthily biased sampling to perturb Shapley Values in place of the method of Baniecki et al. (2021), which fools SHAP by perturbing the background dataset via a genetic algorithm. In said genetic algorithm, a population of fake background datasets evolves iteratively following three biological mechanisms

-

•

Cross-Over: Two parents produce two children by switching some of their feature values.

-

•

Mutation: Some individuals are perturbed with small Gaussian noise.

-

•

Selection: The individuals with the smallest amplitudes are selected for the next generation.

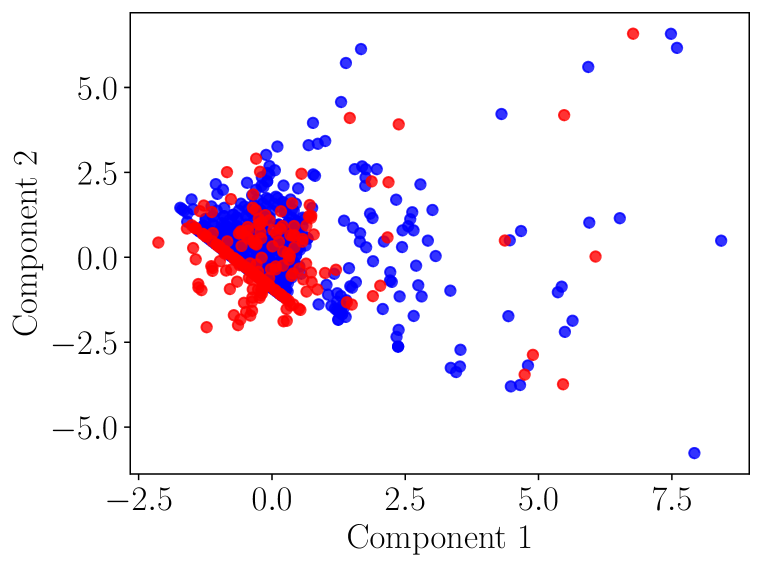

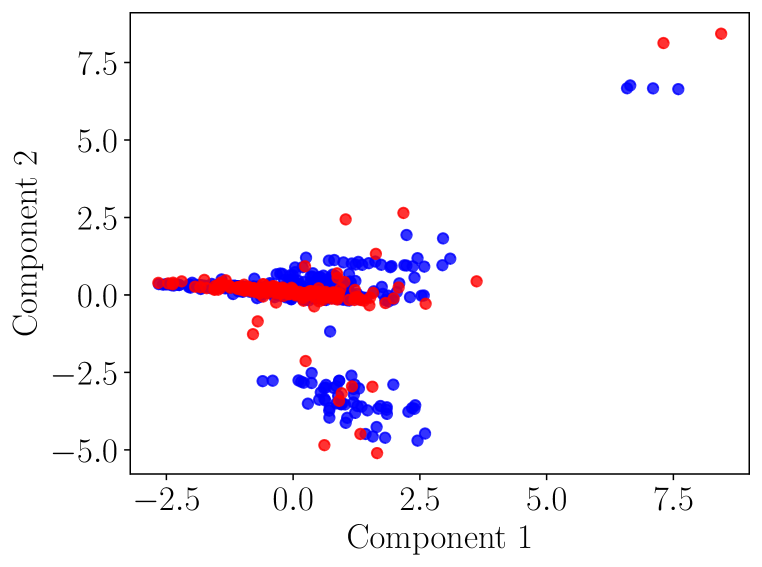

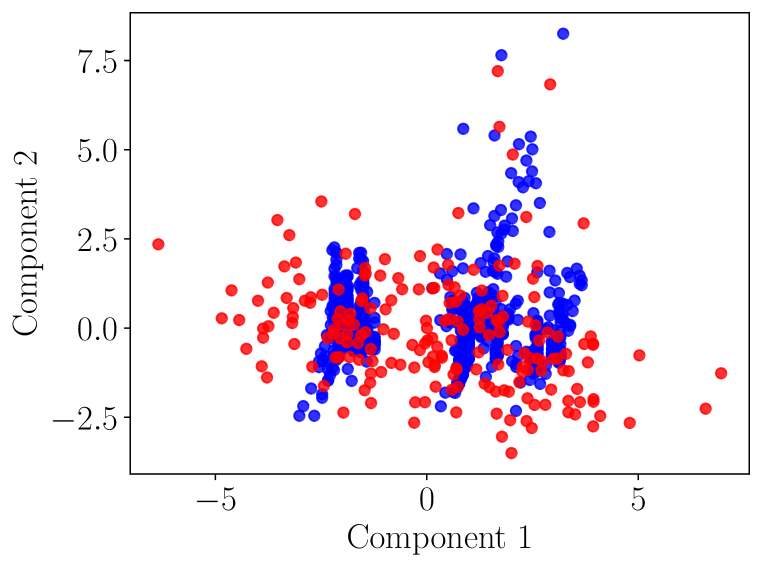

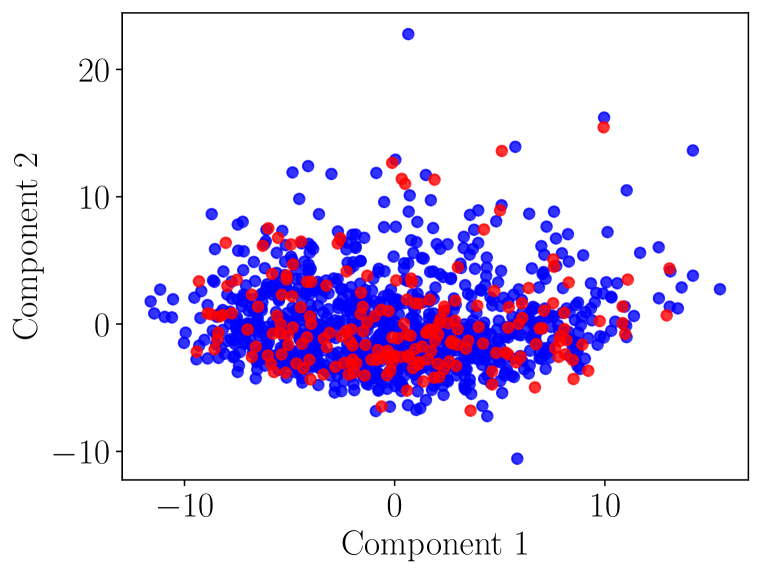

Although the use of a genetic algorithm makes the method of Baniecki et al. (2021) very versatile, its main drawback is that there is no constraint on the similarity between the perturbed background and the original one. Moreover, the mutation and cross-over operations ignore the correlations between features and hence the perturbed dataset can contain unrealistic instances. To highlight these issues, Figure 17 presents the first two principal components of and for the XGB models used in Section 5.4. On COMPAS and Marketing especially, we see that the fake samples lie in regions outside of the data manifold. For Adult-Income and Marketing, the fake data overlaps more with the original one, but this could be an artifact of only visualizing 2 dimensions.

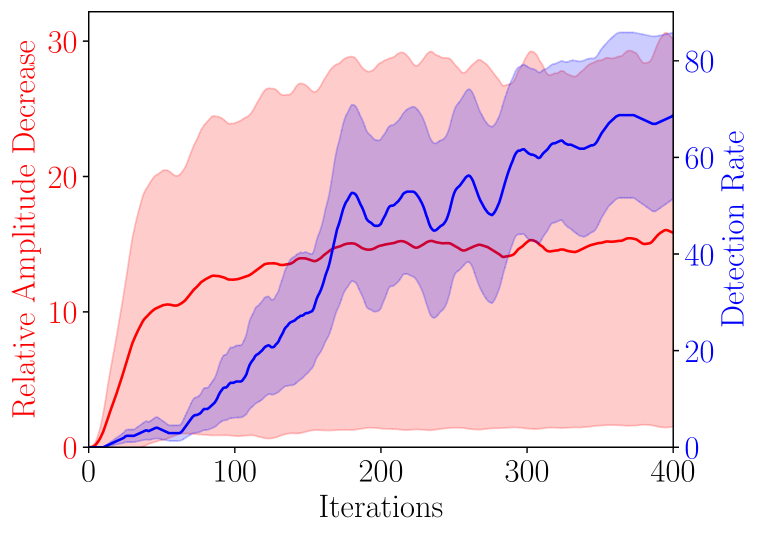

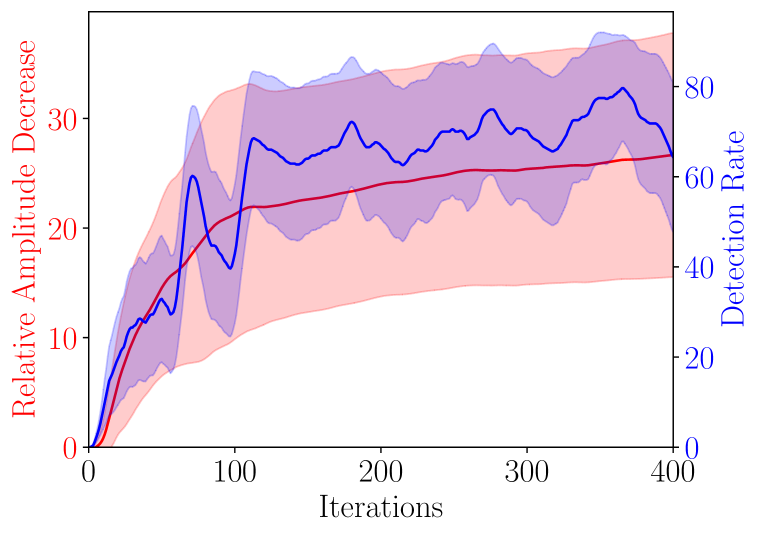

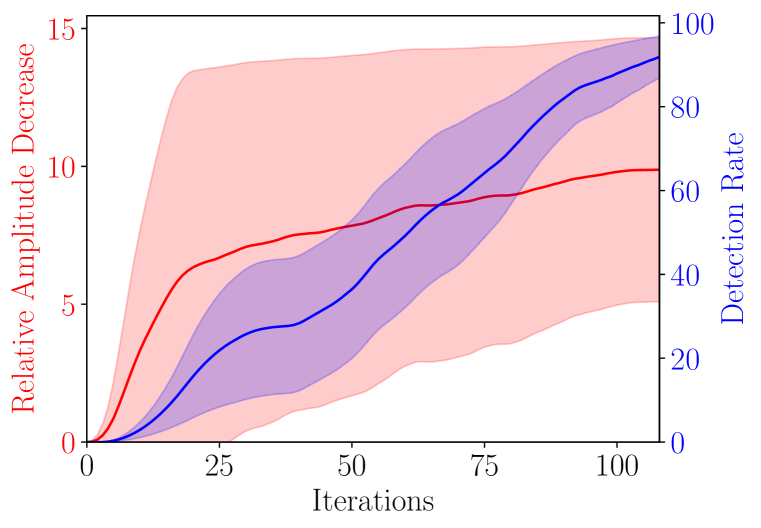

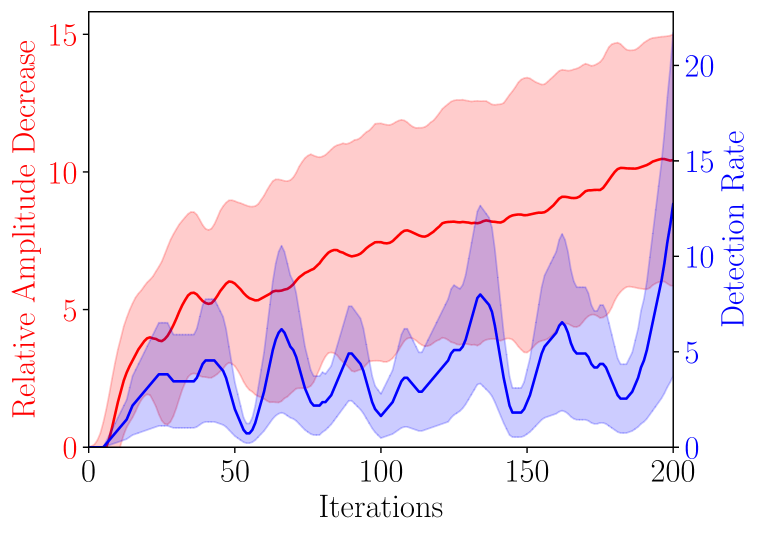

For a more rigorous analysis of “similarity” between and , we must study the detection rate of the audit detector. To this end, Figures 18 and 19, present the amplitude reduction and the detection rate after a given number of iterations of the genetic algorithm. These curves show the average and standard deviation across the 5 train/test splits employed in our main experiments. Moreover, window 20 convolutions were used to smooth the curves and make them more readable. On the Marketing and Communities datasets, we see that for both XGB and Random Forests models, the detector is quickly able to assert that the data was manipulated. We suspect the genetic algorithm cannot fool the detector on these two datasets because they contain a large number of features (Marketing has 20, Communities has 98). Such a large number of features could make it harder to perturbate samples while staying close to the original data manifold. Since the model behavior is unpredictable outside of the data manifold, it is impossible for the genetic algorithm to guarantee that the CDF of will be close to the CDF of . For adult-income, the detection rate appears to be lower but still, the largest reductions in amplitude of the sensitive feature were about , even after 2.5 hours of run-time.

Contrary to the genetic algorithm, our method Fool SHAP addresses both constraints of making the fake data realistic and keeping it close to the original dataset. Indeed, our objective is tuned to make sure that the Wasserstein distance between the original and perturbed data is small. Moreover, since we do not generate new samples but rather apply non-uniform weights to pre-existing ones, we do not run into the risk of generating unrealistic data.

.

E.4 Multiple Sensitive Attributes

We present preliminary results for settings where one wishes to manipulate the Shapley values of multiple sensitive features each part of a set . For example, in our experiments, we considered gender as a sensitive attribute for the Adult-Income dataset and we showed that one can diminish the attribution of this feature. Nonetheless, there are two other features in Adult-Income that share information with gender: relationship and marital-status. Indeed, relationship can take the value widowed and marital-status can take the value wife, which are both proxies of gender=female. For this reason, these two other features may be considered sensitive and decision-making that relies strongly on them may not be acceptable. Hence, we must derive a method that reduces the total attributions of the features in .

We first let for any . In our experiments, all these signs will typically be negative. The proposed approach is to minimize the norm

| (41) |

which we interpret as the total amount of disparity we can attribute to the sensitive attributes. Remember that converges in probability to (cf. Proposition 9). Therefore minimizing the norm will require minimizing

| (42) |

which is again a linear function of the weights. We present Algorithm 4 as an overload of Algorithm 1 that now supports taking multiple sensitive attributes as inputs.

The only difference in the resulting MCF is that we must use the cost for edges in the graph of Figure 6. This new algorithm is guaranteed to diminish the norm of the attributions of all sensitive features. However, that this does not imply that all sensitive attributes will diminish in amplitude. Indeed, minimizing the sum of multiple quantities does not guarantee that each quantity will diminish. For example, is smaller than although is smaller than and is higher than . Still, we see reducing the norm as a natural way to hide the total amount of disparity that is attributable to the sensitive features. Another important methodological change is the way we select the optimal hyper-parameter in Algorithm 3. Now at line 12, we use the norm as a selection criterion.

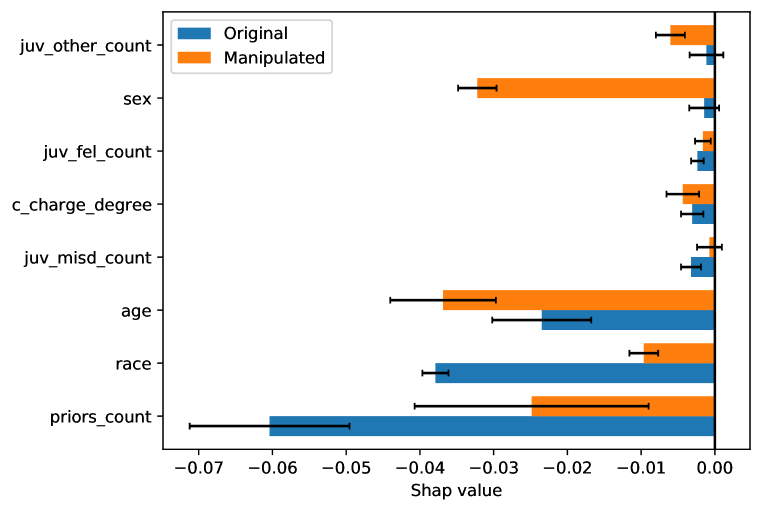

Figures 20 and 21 present preliminary results of attacks on three RFs/XGBs fitted on Adults with different train/test splits. We note that in all cases, before the attack, the three sensitive features had large negative attributions. By applying our method, we can considerably reduce the amplitude of the two sensitive attributes. The attribution of the remaining sensitive feature remains approximately constant or slightly becomes more negative. We leave it as future work to run large-scale experiments with multiple sensitive features for various datasets.

![[Uncaptioned image]](/html/2205.15419/assets/x43.png)

![[Uncaptioned image]](/html/2205.15419/assets/x44.png)

![[Uncaptioned image]](/html/2205.15419/assets/x45.png)

![[Uncaptioned image]](/html/2205.15419/assets/x49.png)

![[Uncaptioned image]](/html/2205.15419/assets/x50.png)

![[Uncaptioned image]](/html/2205.15419/assets/x51.png)