Rapid Regression Detection in Software Deployments through Sequential Testing

Abstract.

The practice of continuous deployment has enabled companies to reduce time-to-market by increasing the rate at which software can be deployed. However, deploying more frequently bears the risk that occasionally defective changes are released. For Internet companies, this has the potential to degrade the user experience and increase user abandonment. Therefore, quality control gates are an important component of the software delivery process. These are used to build confidence in the reliability of a release or change. Towards this end, a common approach is to perform a canary test to evaluate new software under production workloads. Detecting defects as early as possible is necessary to reduce exposure and to provide immediate feedback to the developer.

We present a statistical framework for rapidly detecting regressions in software deployments. Our approach is based on sequential tests of stochastic order and of equality in distribution. This enables canary tests to be continuously monitored, permitting regressions to be rapidly detected while strictly controlling the false detection probability throughout. The utility of this approach is demonstrated based on two case studies at Netflix.

1. Introduction

Many companies have invested in optimizing the software release process to make developers more agile and permit new features to reach users faster. Over the years, best practices have evolved to continuous and progressive delivery models, where software can be deployed at any time with a great deal of automation (Humble and Farley, 2010). This has resulted in rapid development cycles where changes are rolled out constantly, dramatically reducing the time taken for new features to reach end users. However, these changes pose an inherent risk as it is inevitable that something will go wrong. For Internet companies such as Netflix, this has the potential to degrade the user experience and increase user abandonment (Kohavi et al., 2013).

While test suites can be successful in catching functional problems within internal test environments, performance regressions may, at times, only appear under production workloads (Foo et al., 2015). Furthermore, it can be expensive to comprehensively test the quality and performance of software via internal testing (Xia et al., 2019). Maintaining an integration and testing environment that fully replicates the production environment is challenging and perhaps impossible. There are likely to be many differences between the state of the test environment and the state of the production environment. Therefore, it’s inevitable that software changes will make it past sophisticated test suites, enter into the production environment, and degrade the user experience. Quality gates (Schermann et al., 2016) within the software delivery process are therefore needed that are able to quickly and accurately detect defective software under production workloads.

1.1. Regression-Driven Experiments

To minimize the risk of deploying defective software, engineering practices have evolved towards regression-driven experimentation, namely canary testing (Schermann et al., 2018; Schermann, 2017). This practice involves exposing a change to a small group of users or traffic and studying its effects under production workloads (Humble and Farley, 2010). This approach reduces the negative impact of defective software by first validating the change on a subset of the population. If no significant effects are observed, the change is then rolled out to the entire population.

One common approach to canary testing is to treat it as a controlled experiment (Graff and Sanden, 2018; Štěpán Davidovič and Beyer, 2018; Tarvo et al., 2015). In this approach, a small portion of users or traffic are randomly assigned to one of two variants: control or treatment. The treatment represents the release candidate and contains the change to be tested while the control is a copy of the previous version. This approach is related to an A/B test design found in online controlled experiments. The benefit of this approach is that it establishes a causal relationship between the software and a change in performance.

A major shortcoming of existing approaches is the reliance on fixed- tests. These are statistical tests that provide statistical guarantees, such as type I (false detection) error control, when used strictly once. Historically these were developed to possess optimal statistical properties in applications where there was only one possible time to perform the analysis, such as when a statistician is simply handed a dataset or when all observations arrive simultaneously. However, in a canary test, observations can arrive sequentially which provide many opportunities for testing. Herein lies the difficulty of using fixed- tests in sequential applications; the choice of when to perform the test. Perform the test too early, and small regressions may go undetected (a high type II error probability). Perform the test too late and large regressions have been permitted to cause harm. Ideally one seeks to detect large regressions as soon as possible and end the test, preventing further experimental units from being exposed. In contrast to fixed- methodology, a natural form of scientific inquiry in sequential applications is to continue to collect data until a hypothesis has been proven or disproven.

Without sufficient statistical tooling, an erroneous practice of “peeking” has evolved where fixed- tests are repeatedly applied on an accumulating set of data (Johari et al., 2017). The problem with this practice is a lack of control over type I errors. One wants to apply the test frequently, to detect regressions as soon as possible, but the probability of making a type I error with a fixed- test increases with each usage (Armitage et al., 1969). We posit that canary tests should always have a strict type I error guarantee. Otherwise, the experiment would be unreliable, producing many false alerts which can increase manual intervention and reduce delivery cadence.

This issue can be resolved by the development of modern sequential statistical tests, which are optimized for applications where data arrives sequentially. The type I error is controlled no matter how many times they are used, even after every datapoint if desired, allowing experiments to be continuously monitored. This provides the ability to perform optional stopping, stopping the experiment in a data-dependent way as soon as a hypothesis is rejected i.e. when a regression is detected. Towards this end, sequential tests for difference-in-means of Gaussian random variables have already been widely used for online A/B experiments (Johari et al., 2015, 2017; Zhao et al., 2018). However, we argue that performing inference about means is too limited for canary tests, for not all bugs or performance regressions can be captured by differences in the mean alone, as the following example demonstrates. Consider PlayDelay, an important key indicator of the streaming quality at Netflix, which measures the time taken for a title to start once the user has hit the play button. It is possible for the mean of the control and treatment to be the same, but for the tails of the distribution to be heavier in the treatment, resulting in an increased occurrence of extreme values. Large values of PlayDelay, even if infrequent, are unacceptable and considered a severe performance regression by our engineering teams. Differences in the mean are therefore too narrow in scope for defining performance regressions.

1.2. Contributions

The contributions of this paper are to provide developers with a new statistical framework for the rapid testing of rich hypotheses in canary tests. We first extend the statistical definition of bugs and performance regressions beyond simple differences in the mean, and provide a decision-theoretic approach to reasoning about the control and treatment. We propose a sequential canary testing framework using sequential tests of equality and stochastic ordering between distributions to automate testing. These allow any difference across the entire distribution, not just the mean, to be tested in real-time and identified as soon as possible. This captures a much broader class of bugs and performance regressions, while providing strict type I error guarantees specified by the developer.

Our statistical methodology is based on the confidence sequences and sequential tests of Howard and Ramdas (2022). We build upon their tests by providing sequential -values for testing equality and stochastic ordering among distributions, a complementary stopping rule for accepting approximately true null hypotheses, and an upper bound on the time taken for the test to stop. The contribution of sequential -values is necessary if one wishes to measure the strength of evidence against the null hypothesis and also if one wishes to use multiple testing corrections to control the false discovery rate (Johari et al., 2015). The complementary stopping rule is necessary if one wishes the test to stop in finite time. Without such a stopping rule the test is ”open-ended”, meaning it only stops when the null is rejected. If the null is true, then with probability at least the test would run indefinitely. In practise, developers need the canary test to finish in a finite time. Our contribution allows developer to stop the canary test and conclude with a high degree of confidence that any difference, if it exists, is not practically meaningful.

The complementary stopping rule also provides an upper bound on the maximum number of samples required by the test to reject the null or accept an approximate null at a user-specified tolerance and confidence level. This gives the developer a meaningful maximum number of samples required for the canary test and helps with planning. We also emphasize along the way that estimation is just as valuable as testing in this context. While the hypothesis testing component is useful for automating the logic that terminates the experiment, we stress the use of “anytime-valid” confidence sequences across all quantiles of each distribution. These can be visualized at any time, without any need to be concerned about peeking, and can be used by developers for anytime-valid insights into what would otherwise be a black box. This gives a precise description of the differences between control and treatment and aids in developer learnings.

This paper is organized as follows. In Section 2 we present related work. Section 3 introduces the statistical methodology, first by developing the mathematics for the fixed- case, and then generalizing it to work sequentially. Section 4 demonstrates the utility of this approach based on two case studies from Netflix. In Section 5 we reflect on our learnings and conclude the paper in Section 6.

2. Related Work

Canary testing systems (Tarvo et al., 2015; Štěpán Davidovič and Beyer, 2018) have been proposed for developers who wish to conduct regression-driven experiments. These systems are based on the design of a controlled experiment and rely upon statistical tests that provide a type I error guarantee when used exactly once. Due to this, these systems can suffer from the erroneous practice of “peeking” if developers repeatedly apply the statistical tests in an attempt to detect regressions early.

At Netflix, Kayenta (Graff and Sanden, 2018) has been used extensively for canary testing. Similar to (Tarvo et al., 2015; Štěpán Davidovič and Beyer, 2018), this approach is based on the design of a controlled experiment. To evaluate the outcome of the canary test, Kayenta uses fixed- statistical tests such as the Mann-Whitney U test. While these tests should be used strictly once we have found that developers will perform the tests multiple times during an experiment in an attempt to detect regressions early. This motivated our investment into sequential testing.

The statistics literature on sequential testing dates back at least to (Wald, 1945) with the introduction of the mixture sequential probability ratio test (mSPRT). Introductory texts to the subject can be found in (Wald, 1947; Siegmund, 1985). Johari et al. (Johari et al., 2015, 2017) proposed an “anytime-valid” sequential inference framework for differences in the means of Gaussian random variables using the mSPRT to provide confidence sequences and sequential -values. In addition to being used in commercial A/B testing software, (Zhao et al., 2018) use this framework for managing the automated rollout of new software features. However, they formulate performance regressions as differences in the mean which are too narrow in scope to capture the breadth of potential problems.

Our approach is based on the results of Howard et al. (Howard and Ramdas, 2022). The authors provide confidence sequences that hold uniformly over time across all quantiles of a distribution, which they use in the appendix to construct sequential tests of equality in distribution and stochastic dominance.

3. Statistical Methodology

In this section, we first define a performance regression in statistical terms. Then, we will describe the sequential test. For brevity, we’ll refer to the control and treatment simply as arms A and B of the experiment.

3.1. Beyond Inference on the Mean

A canary testing system aims to identify bugs and performance regressions by observing changes in the distribution of key metrics between arms. There is a strong concern that small performance regressions accumulate and substantially degrade the user experience over time. Usually, there is a directional notion of “desirable” and “undesirable” changes in the distribution of a metric. Consider, for example, PlayDelay. PlayDelay is the time taken, in milliseconds, for a title to begin streaming after being requested by the user. A shift in the distribution of PlayDelay toward larger values results in a poorer streaming experience, whereas a shift toward smaller values could be considered an improvement.

Many of the earlier works formulate performance regressions as differences in the mean between arms A and B (Zhao et al., 2018), with a performance regression occurring if the mean shifts in the undesirable direction of that metric. We argue from a decision-theoretic perspective that comparing means alone is insufficient to define a performance regression. Consider two users, one with a fast internet connection, the other with a slow internet connection, and consider the effect of PlayDelay on their satisfaction with the service. The former user is less affected by increases in PlayDelay, as the resulting values are likely still small and manageable, but the latter user is more affected, as their values were already high to begin with. As streaming performance is correlated with user dissatisfaction, increases in PlayDelay increase the risk of the latter user churning more than they do for the former. In other words, increases in PlayDelay are not nearly as important for the average user as they are for users already at risk, and increases in the mean are not as important as increases in the tail of the distribution.

We have found the concept of stochastic ordering helpful in elevating directional comparisons beyond comparisons of the mean. Let and denote single observations from arms A and B, respectively. Let denote a loss function that defines the loss associated with the value of an observation. A developer will then prefer arm B over arm A if

| (1) |

i.e. if the expected loss (risk) is lower for arm B than it is for A. If the loss is linear, , the arm with the smaller risk is simply the arm with the smaller mean. As illustrated with PlayDelay, however, many practical loss functions are not linear. Increases of in PlayDelay are worse for users with already large values i.e. for . This implies that the loss function is not linear but convex, and clearly illustrates why defining regressions in terms of the mean alone is insufficient. Fortunately, can be guaranteed for all nondecreasing loss functions if is stochastically less than or equal to .

Let and be random variables with distributions and , respectively. is said to be stochastically less than or equal to , written , if . If, in addition, for some , then is said to be strictly stochastically less than . This condition is also known as first-order stochastic dominance. The practical significance behind stochastic ordering is that if and only if for all non-decreasing loss functions (Hadar and Russell, 1969).

The previous result is helpful because it removes the burden of fully specifying a developer’s subjective loss function . While different developers may disagree about the exact functional form of , all agree that this function is non-decreasing because increases in the distribution toward larger values are undesirable. If all developers agree that decreases in the distribution toward smaller values are undesirable, then all agree that the loss function is non-increasing. In the end, the exact values of and are not specifically of interest. It is only relevant to know if and vice versa.

To give a concrete example, let us return to studying the distribution of PlayDelay in a canary test. Developers would like to catch “increases” in PlayDelay in the release candidate, while no action is necessary for “decreases”. Therefore, our null hypothesis is that observations from arm B are stochastically less than or equal to observations from arm A, , while the alternative is the complement of this, which we can summarize as

| (2) |

Note that the complement of the null hypothesis is not as stochastic ordering is only a partial ordering. If the null is indeed rejected, it is the responsibility of the developer to use their judgement. Metrics for which “decreases” are bad can be tested similarly by replacing and with and respectively.

In many cases, the release candidate is not expected to have an effect on metrics at all. If the developer does not specify a direction, or one is not available from the application domain, then we test for any difference in the distribution

| (3) |

Although the decision for a canary test to succeed or fail is formulated in terms of a hypothesis test, we stress that an equally important objective of a canary test is estimation, that is, about learning the quantile functions of arms A and B.

3.2. Fixed- Inference

To build up to our full inferential procedure, we first consider the simpler fixed- case and then generalize it to the sequential case in Section 3.3. The procedure is quite intuitive: estimate the distribution and/or quantile functions and then use these estimates to test hypotheses. For example, one could test the null hypothesis by asking if the confidence bands on and fail to intersect.

3.2.1. One-Sample Distribution Function Confidence Band

Consider first the Dvoretzky–Kiefer–Wolfowitz (DKWM) inequality (Dvoretzky et al., 1956; Massart, 1990)

| (4) |

where is the empirical distribution function and is the sup-norm. It follows directly that a confidence band on the distribution function with coverage probability at least can be constructed with

| (5) |

where

| (6) |

(for details see example 2.2.4. from (Bickel and Doksum, 1977)).

3.2.2. One-Sample Quantile Function Confidence Band

Alternatively, one can construct a confidence band on the quantile function instead, via

| (7) |

where

is the upper empirical quantile function (the right continuous inverse of the empirical distribution function and equal to the order statistic of the data). is the lower quantile function (the left continuous inverse of the empirical distribution function and equal to the order statistic of the data), with the definition extended to be when .

3.2.3. Two-Sample Distribution/Quantile Function Confidence Bands

Suppose one has two sets of i.i.d. samples resulting from an A/B test. Let the distribution function, empirical distribution function, sample size and sample from arm A be denoted , , and respectively. Similarly let the distribution function, empirical distribution function, sample size and sample from arm B be denoted , and respectively. To obtain confidence bands on the distribution functions of arm A and arm B that hold simultaneously with probability at least , then one can apply a union bound, yielding

| (8) |

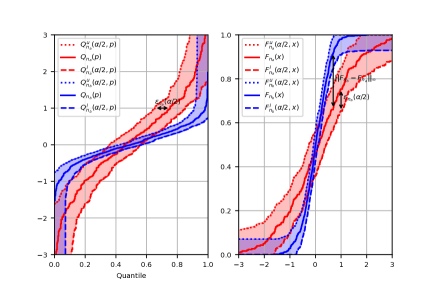

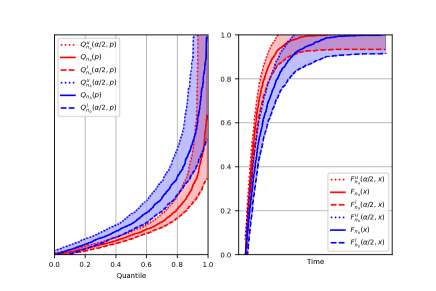

The confidence bands for the quantile functions are handled similarly, and both are illustrated in 1.

3.2.4. Confidence Sets on the Difference

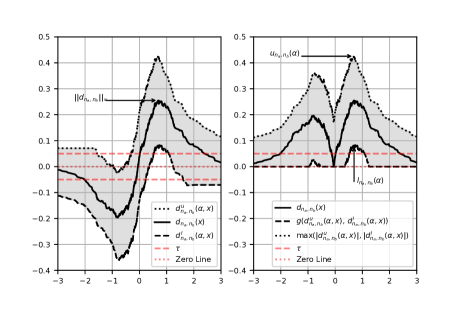

Ultimately we would like to test hypotheses about the difference between and , and so in this section we derive useful confidence statements about the difference. This section provides a confidence band on the function and a confidence interval for . Figures that complement figure 1 in visualizing the difference between distribution functions are provided in Appendix A.

Proposition 3.1.

Let the difference between distribution and empirical distribution functions be denoted and , respectively, with , , , defined as in equation (8), then

| (9) |

where

The confidence band on is an immediate consequence of the confidence bands on and .

Corollary 3.2.

Corollary 3.3.

| (10) |

where

3.2.5. A Test of

Theorem 3.4.

The null hypothesis can be rejected at the -level if

The -value for this test, , is the root of

| (11) |

where and .

The proof is provided in Appendix B. When , the root of equation 25 can be computed analytically as

| (12) |

When is large the -value is small. When the root of equation (11) must be found numerically. Some “bracketing” root-finding algorithms require the specification of an interval in which to seek the root, such as the bisection method (Conte and Boor, 1980). To construct lower and upper bounds on the -value, define

| (13) |

The -value is lower-bounded by , and upper-bounded by .

Corollary 3.5.

The null hypothesis can be rejected at the -level if

The -value for this test, , is the root of

| (14) |

where .

3.2.6. A Test of

The null hypothesis is the intersection of the hypotheses and i.e. and for all . This means that the results of the previous section can be re-purposed. The null hypothesis can be rejected at the -level if or . Similarly, the -value can be defined as . When , , otherwise it is sandwiched between and .

To gain some intuition for the mathematics, it is useful to recognize that the following are equivalent

-

•

The lower confidence bound for , , is greater than zero

-

•

Either or

-

•

The confidence band for the difference function in equation (9) excludes 0 for some

-

•

The confidence bands for the distribution functions in equation (8) fail to intersect for some

-

•

The confidence bands on the quantile functions fail to intersect for some

These statements are visualized with the help of figures 1 and 6.

3.2.7. Sample Size Calculations

A sample size calculation can be performed to obtain a confidence band for of a desired radius. When a radius of at most can be achieved with

| (15) |

A choice of can help reason if the difference is practically meaningful. Suppose one considers differences between distribution functions less than to be practically irrelevant. By choosing the diameter of the confidence band is less than . If the confidence band contains 0 for all , then and , which implies . One can conclude with confidence that .

3.3. Sequential Inference

The aforementioned coverage and type I error probabilities of the statistical procedure constructed from the DKWM inequality hold when the analysis is performed only once. This is an example of a fixed- test which is appropriate when the analysis is to be performed only once. This test is, however, not appropriate when data arrives sequentially and the analysis is intended to be performed continuously, as is the case with canary testing. To allow continuous monitoring we seek a confidence sequence

| (16) |

This extends the confidence band in (5) to hold for all . This, in turn, allows the previous results for two samples in section 3.2 to be extended for all . This can be achieved by using elegant “drop-in” replacements for in equation 6. Darling and Robbins (1968) propose using

| (17) |

This provides an -level confidence sequences that holds for all . Szorenyi et al. (2015) provide a result that holds by using

| (18) |

Their results follows directly from a union bound of the DKWM inequality in (4) over and using . Howard and Ramdas (2022) obtain a tighter confidence sequence with the same guarantee by using

| (19) |

The authors use these results to derive sequential tests of and (Darling and Robbins, 1968; Howard and Ramdas, 2022). We choose to work with equation (19) moving forward. We complement these results by contributing sequential -values, stopping logic for accepting an approximately true null hypothesis, and an upper bound on the number of observations required for the test to stop.

3.3.1. Sequential -values

A sequential -value satisfies the following

| (20) |

-values are often requested by developers as a measure of strength against the null hypothesis and are also necessary inputs for procedures controlling false discovery rate (Johari et al., 2015). The sequential -value for testing is equal to the root of (11), except that is replaced by its new definition in equation (19). When , the sequential -value is given by

otherwise it is sandwiched between and where

and can be computed numerically via bracketed root finding algorithms. Sequential -values for testing and are obtained by replacing with and , respectively. Practically, this permits the analysis to be performed as frequently as desired while maintaining coverage and type I error guarantees. In particular, it permits the use of a data-dependent stopping rule. The null hypothesis can be rejected at the level as soon as the corresponding sequential -value falls below .

Observations are received in the experiment in no specific order from arms A and B, they may even arrive at different rates. Let be an enumeration of in the order in which they occur. One can define a new sequential -value by computing the running minimum with , which satisfies

| (21) |

Confidence sequences on , and can be constructed similarly, and are provided in Appendix D.

3.3.2. Accepting an Approximate Null Hypothesis

One can continue to observe additional datapoints and tighten confidence bands on quantile and distribution functions forever. The more datapoints that are observed, the tighter these confidence bands become. For this reason, any difference in these functions is guaranteed to be revealed eventually i.e. the test is asymptotically power 1 (Howard and Ramdas, 2022).

In practice, developers want to stop the test in a finite time, such as when they are satisfied that the distributions are “similar enough”. Let denote a subjective tolerance specified by the developer, such that any departure from the null hypothesis by less than is practically irrelevant. We provide the developer a complementary stopping rule such that if the null is not already rejected, one can at least conclude with confidence that the difference is less than the desired tolerance.

For testing , we propose to stop when the time-uniform version of the upper confidence bound on , , in corollary 3.2 is less than . This ensures with confidence at least that the null is approximately true i.e. for all . When testing , stopping when ensures with confidence at least that for all . Lastly, when testing , stopping when ensures with confidence at least that for all .

| Hypothesis | Reject | Approximate Accept |

|---|---|---|

3.3.3. Stopping Rules

We provide a summary of the stopping rules for each null hypothesis in table 1 (note that these definitions use the time-uniform version of in equation (19)). The probability that the incorrect conclusion is drawn is at most . Similar ”open-ended” versions of these can be found in Howard and Ramdas (2022, Appendix B.2.). The stopping logic for testing is quite simple when stated in plain English. With a slight abuse of mathematical verbiage, is rejected as soon as the confidence band on is strictly positive for some , and approximately accepted when it is less than for all . is rejected as soon as the confidence band on excludes zero for some , and approximately accepted when it is within and for all . Note that is simply the logical OR of the rejection criteria of tests and , while is the logical AND of the acceptance criteria.

Alternatively, one needn’t reject immediately. A developer can continue observing datapoints until the confidence bands on the quantile or distribution functions are precise enough to satisfy their curiosity. In this case, the sequential -value can be used as a final measure of evidence against the null hypothesis. One can also obtain a maximum number of observations required by the canary test by considering the number required to give a confidence band on of desired radius, which allows the developer to reason about meaningful differences, as discussed in section 3.2.7. When , The number of observations required for a confidence band of radius satisfies , which can be solved numerically for .

3.4. Count Metrics

In general a datapoint from arm in a canary test is a 2-tuple of a measurement and an arrival timestamp . The measurement is often continuous, like PlayDelay in milliseconds, and is a timestamp corresponding to when the measurement was taken or when it was received. In addition to testing hypotheses about the distribution of the measurement, it is also very relevant to test hypotheses about the timestamps. If the distributions of the measurements are equal among arms, but datapoints are received at a different rates, then this is also a cause for concern.

An extremely important example is when the metric corresponds to a particular error. In this example the measurement is simply an indicator that an error has occurred and the timestamp records when the error occurred. It would be highly alarming if the release candidate produced errors at a faster rate. Netflix carefully monitors playback errors which indicate a failure to play a title. If arm B experiences a higher volume of errors, then this is a strong signal of a regression. A fixed- approach is simply to test whether the number of errors produced in a window of time by arm B is greater or less than arm A. For this reason we refer to these as count metrics.

The raw data for a count metric is simply an ordered sequence of timestamps. Consequently, we model this as a one-dimensional point process. Kuo and Yang (1996) model the point process of software failure times as a time-inhomogeneous Poisson point process, or equivalently, the epoch’s of failure times as a time-inhomogeneous exponential process. We would prefer, however, not to make such strong assumptions. Instead, we model the sequence of timestamps as a general renewal process.

A renewal process is a stochastic process in time with waiting times between successive timestamps (epochs) drawn i.i.d. from a renewal distribution. In contrast to the Poisson point process assumption, no further assumptions are made about the renewal distribution. Suppose the canary test begins at time and the current time is . During this time, a sequence of datapoints has arrived in arm A at times . Let be the renewal distribution of arm A. The likelihood for given the observed times is then

| (22) |

where is the Radon–Nikodym derivative of with respect to Lebesgue measure. Associated with each event can be an additional measurement modelled as a random variable from the distribution . Our proposal is to sequentially test for differences in both the measurement distributions and as well as the renewal distributions and . Testing for differences in the renewal distribution is as simple as feeding the time differences for arms A and similarly for B into the procedure described in section 3.3.

4. Case Studies

In this section, we describe two case studies which demonstrate the approach described above in the context of canary testing client applications at Netflix. These tests are based on a controlled experiment where a randomized group of users are assigned to receive the release candidate while a control group receive the existing version of the client application. These tests are configured to run until the null is rejected or approximately accepted. Towards this end, our approach was deployed as a quality gate in the existing software delivery pipeline for the client applications under evaluation. These quality gates were configured to alert developers when a regression was detected with the release candidate.

4.1. Increase in PlayDelay

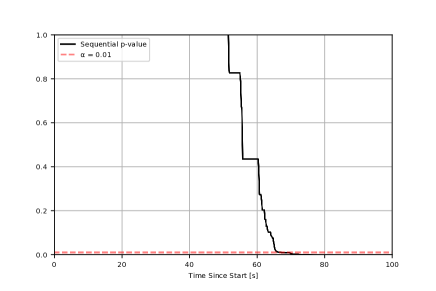

In the following case study, we show how the sequential methodology successfully detected a performance regression in PlayDelay and prevented the release candidate from reaching the production environment. The data is taken from a canary test in which the behavior of the client application was modified. The null hypothesis was that observations of PlayDelay in the release candidate should be stochastically less than or equal to observations in the existing version (). Figure 2 shows the sequential -value for this hypothesis as a function of time since the beginning of the canary test. The -value falls below after approximately 65 seconds.

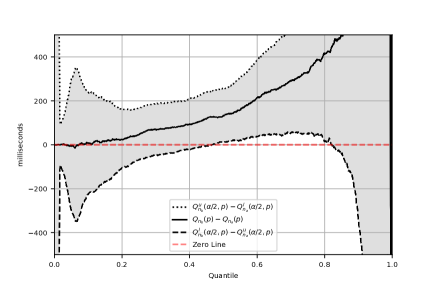

Figure 3 shows that the confidence bands for the quantile functions of arms A and B fail to intersect for many quantiles. While no quantiles are significantly lower in arm B, many are significantly greater, revealing a small but significant increase in PlayDelay. This is perhaps easier to see by considering the confidence band on the difference function in figure 8. The median value of PlayDelay increased by at least 11 and at most 255 milliseconds in arm B, while the 75-percentile increased by at least 51 and at most 635 milliseconds (based on a 0.99 confidence interval). If the developer wishes to get more precise estimates and tighter confidence intervals, they can continue the canary test without sacrificing coverage guarantees due to the time-uniform nature of these confidence sequences.

4.2. Drop in Successful Play Starts

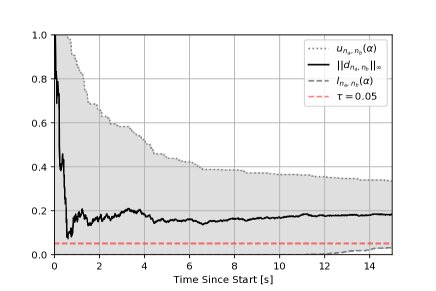

While PlayDelay captures the time taken by successful playbacks, it fails to capture unsuccessful playbacks (playback failures). To complement PlayDelay, Netflix also closely monitors the number of successful play starts. Simply, a Successful Play Start (SPS) event is sent to the central logging system by the client application whenever a title begins streaming after the viewer hits play, logging the successful start of the title. A significant drop in SPS events between arms therefore implies a significant increase in playback failures, and is an important metric for detecting software regressions. The following case study uses real data from a canary test where a software bug caused playback to fail for multiple devices.

The number of SPS events is an example of a count metric described in section 3.4. Consequently, we look at the time-differences between observed events (epochs) to study differences in the renewal distributions. In this example we test , where denotes the renewal distribution for arm .

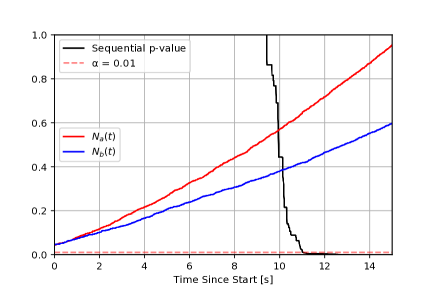

Let the counting process be defined as the number of events observed in the interval for arm . These are shown on the right axis of figure 4. Clearly there are fewer SPS events per unit time for arm B running the newer client application, suggesting a bug in the release candidate which prevents some users from streaming.

The left axis of figure 4 shows the sequential -value, which falls below in a mere seconds. From a different perspective, figure 7 shows the confidence sequence on . Note the sequential -value falls below at the same time the confidence sequence excludes zero, when .

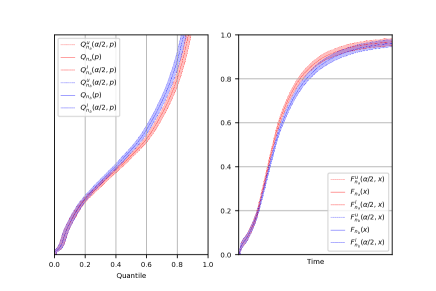

Figure 5 shows the empirical quantile and distribution functions with confidence bands at 15 seconds into the canary test. It is clear that many quantiles are shifted toward larger values, implying that the distribution of time-differences is shifted toward larger values and that SPS events are arriving less frequently.

We regard the confidence sequences on the quantile and distribution functions, as well as their differences, to be complementary to the automated stopping logic. They allow the developer to be kept in the loop as the canary test progresses and provide them insight into what would otherwise be a black-box system. Due to the time-uniform guarantees these can be visualized at any time without concern of peeking - the coverage guarantee holds for all time.

5. Discussion

The case studies presented above demonstrate the utility of our approach in rapidly detecting regressions. In both cases, our approach was successful in alerting developers to an issue within seconds. This is in contrast to the existing approach, based on fixed- tests, which would have taken upwards of 30 minutes or longer to detect the regression. This would have exposed the treatment population to a degraded experience for a prolonged period of time.

In practice, it can be tempting to apply fixed- tests for continuous monitoring. In our own experience, we have observed developers repeatedly applying these tests to quickly detect regressions. However, as demonstrated in Appendix E, the result of doing this is beyond just theoretical, i.e., it can result in an unacceptable number of false positives. This can erode trust in the canary test and impact deployment velocity as developers search for sources of regressions that do not exist.

For count metrics our methodology makes an assumption that the distribution of time-differences between successive observations is stationary. We have observed this to be a reasonable assumption for metrics with a high rate of events, as evinced in figure 4, because the run-time of the test is short. Count metrics for which data arrives very slowly, such as SPS for a rarely used device, take longer to reject or approximately accept the null. Therefore, over the course of a long-running canary test, it is likely that the assumption of a stationary renewal distribution is violated due to time-varying usage patterns of the Netflix application. Despite this, it is not clear to what extent the type I error guarantees of this system would degrade, given that it affects both arms equally. An alternative approach could be a sequential multinomial test to compare the proportion of counts across arms, which remains valid even in the presence of time-inhomogeneity (Lindon and Malek, 2020).

6. Conclusion

This paper presents an approach to canary testing that has successfully detected performance regressions and bugs in software deployments at Netflix. The novel contributions of this approach are the formulation of regressions in terms of stochastic orderings and the sequential testing framework. Testing hypotheses of stochastic order enables developers to assign an undesirable direction to changes in a metric distribution beyond simply comparing the means. When no direction is available or appropriate, any difference in the distribution can be tested.

The sequential methodology permits canary tests to be continuously monitored, while retaining strict type I error guarantees. This allows automated stopping logic to be implemented for the canary test, removing the burden on the developer to monitor the release manually and freeing up time for them to return other tasks. The end effect is that bugs and performance regressions are detected rapidly, prevented from reaching the production environment and subsequent experimental units are saved from a degraded experience. Near-immediate feedback is given to the developer, allowing them to iterate quickly and remedy the issue.

Acknowledgements.

The authors would like to thank Minal Mishra, Toby Mao, Yanjun Liu, and Martin Tingley for their contributions. The authors would also like to thank the reviewers for their comments and suggestions.References

- (1)

- Armitage et al. (1969) P. Armitage, C. K. McPherson, and B. C. Rowe. 1969. Repeated Significance Tests on Accumulating Data. Journal of the Royal Statistical Society. Series A (General) 132, 2 (1969), 235–244.

- Bickel and Doksum (1977) Peter J. Bickel and Kjell A. Doksum. 1977. Mathematical statistics : basic ideas and selected topics. Vol. 2. Holden-Day San Francisco. 240–241 pages.

- Conte and Boor (1980) Samuel Daniel Conte and Carl W. De Boor. 1980. Elementary Numerical Analysis: An Algorithmic Approach (3rd ed.). McGraw-Hill Higher Education. 74–75 pages.

- Darling and Robbins (1968) D. A. Darling and Herbert Robbins. 1968. SOME NONPARAMETRIC SEQUENTIAL TESTS WITH POWER ONE. Proceedings of the National Academy of Sciences 61, 3 (1968), 804–809.

- Dvoretzky et al. (1956) A. Dvoretzky, J. Kiefer, and J. Wolfowitz. 1956. Asymptotic Minimax Character of the Sample Distribution Function and of the Classical Multinomial Estimator. The Annals of Mathematical Statistics 27, 3 (1956), 642 – 669.

- Foo et al. (2015) King Chun Foo, Zhen Ming (Jack) Jiang, Bram Adams, Ahmed E. Hassan, Ying Zou, and Parminder Flora. 2015. An Industrial Case Study on the Automated Detection of Performance Regressions in Heterogeneous Environments. In 2015 IEEE/ACM 37th IEEE International Conference on Software Engineering (Florence, Italy) (ICSE ’15). IEEE Press, 159–168.

- Graff and Sanden (2018) Michael Graff and Chris Sanden. 2018. Automated Canary Analysis at Netflix with Kayenta. https://medium.com/netflix-techblog/automated-canary-analysis-at-netflix-with-kayenta-3260bc7acc69. Netflix Tech Blog.

- Hadar and Russell (1969) Josef Hadar and William R. Russell. 1969. Rules for Ordering Uncertain Prospects. The American Economic Review 59, 1 (1969), 25–34.

- Howard and Ramdas (2022) Steven R. Howard and Aaditya Ramdas. 2022. Sequential estimation of quantiles with applications to A/B testing and best-arm identification. Bernoulli 28, 3 (2022), 1704 – 1728. https://doi.org/10.3150/21-BEJ1388

- Humble and Farley (2010) Jez Humble and David Farley. 2010. Continuous Delivery: Reliable Software Releases through Build, Test, and Deployment Automation (1st ed.). Addison-Wesley Professional.

- Johari et al. (2017) Ramesh Johari, Pete Koomen, Leonid Pekelis, and David Walsh. 2017. Peeking at A/B Tests: Why It Matters, and What to Do about It. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (Halifax, NS, Canada) (KDD ’17). ACM, New York, NY, USA, 1517–1525.

- Johari et al. (2015) Ramesh Johari, Leo Pekelis, and David J Walsh. 2015. Always Valid Inference: Bringing Sequential Analysis to A/B Testing. arXiv:1512.04922 [math.ST]

- Kohavi et al. (2013) Ron Kohavi, Alex Deng, Brian Frasca, Toby Walker, Ya Xu, and Nils Pohlmann. 2013. Online Controlled Experiments at Large Scale. In Proceedings of the 19th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (Chicago, Illinois, USA) (KDD ’13). ACM, New York, NY, USA, 1168–1176.

- Kuo and Yang (1996) Lynn Kuo and Tae Young Yang. 1996. Bayesian Computation for Nonhomogeneous Poisson Processes in Software Reliability. J. Amer. Statist. Assoc. 91, 434 (1996), 763–773. http://www.jstor.org/stable/2291671

- Lindon and Malek (2020) Michael Lindon and Alan Malek. 2020. Anytime-Valid Inference for Multinomial Count Data. arXiv:2011.03567 [stat.ME]

- Massart (1990) P. Massart. 1990. The Tight Constant in the Dvoretzky-Kiefer-Wolfowitz Inequality. The Annals of Probability 18, 3 (1990), 1269 – 1283.

- Schermann (2017) Gerald Schermann. 2017. Continuous Experimentation for Software Developers. In Proceedings of the 18th Doctoral Symposium of the 18th International Middleware Conference (Las Vegas, Nevada) (Middleware ’17). ACM, New York, NY, USA, 5–8.

- Schermann et al. (2016) Gerald Schermann, Jürgen Cito, Philipp Leitner, and Harald C Gall. 2016. Towards quality gates in continuous delivery and deployment. In 2016 IEEE 24th International Conference on Program Comprehension (ICPC). IEEE, 1–4.

- Schermann et al. (2018) Gerald Schermann, Jürgen Cito, Philipp Leitner, Uwe Zdun, and Harald C. Gall. 2018. We’re doing it live: A multi-method empirical study on continuous experimentation. Information and Software Technology 99 (2018), 41–57.

- Siegmund (1985) David Siegmund. 1985. Sequential Analysis: Tests and Confidence Intervals. Springer.

- Szorenyi et al. (2015) Balazs Szorenyi, Robert Busa-Fekete, Paul Weng, and Eyke Hüllermeier. 2015. Qualitative Multi-Armed Bandits: A Quantile-Based Approach. In Proceedings of the 32nd International Conference on Machine Learning (Proceedings of Machine Learning Research, Vol. 37). PMLR, Lille, France, 1660–1668.

- Tarvo et al. (2015) Alexander Tarvo, Peter F. Sweeney, Nick Mitchell, V.T. Rajan, Matthew Arnold, and Ioana Baldini. 2015. CanaryAdvisor: A Statistical-Based Tool for Canary Testing (Demo). In Proceedings of the 2015 International Symposium on Software Testing and Analysis (Baltimore, MD, USA) (ISSTA 2015). ACM, New York, NY, USA, 418–422.

- Wald (1945) Abraham Wald. 1945. Sequential tests of statistical hypotheses. The annals of mathematical statistics 16, 2 (1945), 117–186.

- Wald (1947) Abraham Wald. 1947. Sequential Analysis. John Wiley & Sons, New York.

- Xia et al. (2019) Tong Xia, Sumit Bhardwaj, Pavel Dmitriev, and Aleksander Fabijan. 2019. Safe Velocity: A Practical Guide to Software Deployment at Scale using Controlled Rollout. In 2019 IEEE/ACM 41st International Conference on Software Engineering: Software Engineering in Practice (Montreal, Quebec, Canada) (ICSE-SEIP ’19). IEEE Press, 11–20.

- Zhao et al. (2018) Zhenyu Zhao, Mandie Liu, and Anirban Deb. 2018. Safely and Quickly Deploying New Features with a Staged Rollout Framework Using Sequential Test and Adaptive Experimental Design. In 2018 3rd International Conference on Computational Intelligence and Applications (ICCIA). IEEE Computer Society, Los Alamitos, CA, USA, 59–70.

- Štěpán Davidovič and Beyer (2018) Štěpán Davidovič and Betsy Beyer. 2018. Canary Analysis Service. Commun. ACM 61, 5 (2018), 54–62.

Appendix

Appendix A Confidence Band on

The confidence band on can be used to derive a confidence band on , this is illustrated in figure 6. Note that the image of under is if or otherwise. Define

then

| (23) |

Appendix B Proof of Theorem 3.4

The null hypothesis is equivalent to . It can be rejected at the -level if there exists an such that i.e. when the lower bound on the confidence interval of is greater than the upper bound on the confidence interval of . This is true if and only if .

To obtain a -value we seek the smallest such -level test that rejects the null i.e.

| (24) |

Let denote the positive part of the empirical difference function. If there exists an such that , this set is not empty, and is the root of the following equation

| (25) |

where . The intuition here comes from finding the largest confidence band radius such that the test still rejects. This critical value occurs when the confidence band radius is equal to the largest positive value of over the domain . For any , , which implies that and the null hypothesis is not be rejected.

Appendix C Additional Figures

Appendix D Confidence Sequences on

One can define confidence sequences for , and by taking running intersections, e.g.

| (26) |

| (27) |

| (28) |

Appendix E Simulation Study

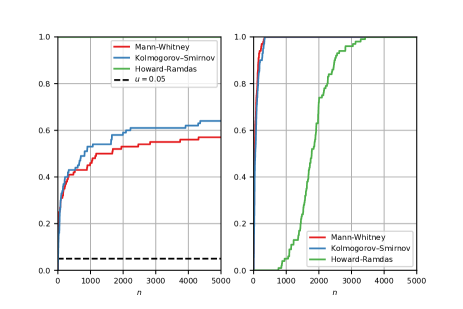

In this section, we present a simulation which demonstrates the advantages of the sequential test compared to fixed- methods. To illustrate the advantage of sequential over fixed- methods, we examine the empirical type I error probabilities under continuous monitoring, that is, performing a significance test after every datapoint. We generate 100 simulations where each simulation generates independent streams of i.i.d. random variables for each arm. After every new pair of observations a significance test configured at the level is performed. If the -value is less than 0.05, the null hypothesis is rejected and the stopping time is recorded, otherwise a new pair of observations is sampled from arms A and B. The tests compared the fixed- Kolmogorov-Smirnoff and Mann-Whitney tests to the sequential test in section 3.3. The random number generator is seeded consistently, so that each stream of random variables is identical for each test. To ease the computation, the simulations are terminated when 5000 observations are sampled from each arm.

The left of figure 9 clearly visualizes the problem with continuous monitoring for the Kolmogorov-Smirnoff and Mann-Whitney tests, which resulted in 64 and 57 false positives respectively. It also shows that no type I errors resulted from the sequential procedure. This can be explained by the fact that the sequential procedure must control the type I error probability for all , and so one expects the type I error probability in a smaller, finite window of time to be less than if it were to run indefinitely. The right of figure 9 shows the empirical probability of correctly rejecting the null by in simulations where the null is incorrect.