Risk of Stochastic Systems for Temporal Logic Specifications

Abstract.

The wide availability of data coupled with the computational advances in artificial intelligence and machine learning promise to enable many future technologies such as autonomous driving. While there has been a variety of successful demonstrations of these technologies, critical system failures have repeatedly been reported. Even if rare, such system failures pose a serious barrier to adoption without a rigorous risk assessment. This paper presents a framework for the systematic and rigorous risk verification of systems. We consider a wide range of system specifications formulated in signal temporal logic (STL) and model the system as a stochastic process, permitting discrete-time and continuous-time stochastic processes. We then define the STL robustness risk as the risk of lacking robustness against failure. This definition is motivated as system failures are often caused by missing robustness to modeling errors, system disturbances, and distribution shifts in the underlying data generating process. Within the definition, we permit general classes of risk measures and focus on tail risk measures such as the value-at-risk and the conditional value-at-risk. While the STL robustness risk is in general hard to compute, we propose the approximate STL robustness risk as a more tractable notion that upper bounds the STL robustness risk. We show how the approximate STL robustness risk can accurately be estimated from system trajectory data. For discrete-time stochastic processes, we show under which conditions the approximate STL robustness risk can even be computed exactly. We illustrate our verification algorithm in the autonomous driving simulator CARLA and show how a least risky controller can be selected among four neural network lane keeping controllers for five meaningful system specifications.

1. Introduction

Over the next decade, large amounts of data will be generated and stored as devices that perceive and control the world become more affordable and available. Impressive demonstrations of data-driven and machine learning enabled technologies exist already today, e.g., robotic manipulation (Levine et al., 2016), solving games (Silver et al., 2018; Mnih et al., 2015), and autonomous driving (Dosovitskiy et al., 2017). However, occasionally occurring system failures impede the use of these technologies particularly when system safety is a concern. For instance, neural networks, frequently used for perception and control in autonomous systems, are known to be fragile and non-robust (Goodfellow et al., 2014; Su et al., 2019). Especially the problem of long tails in training data distributions poses challenges, e.g., natural variations in weather and lightning conditions (Robey et al., 2020).

Moving forward, we expect that system failures appear less frequently due to advancing technologies – nonetheless, algorithms for the systematic and rigorous risk verification of such systems is needed. For instance, the National Transportation Safety Board emphasized in a statement in connection with an Uber accident from 2018 “the need for safety risk management requirements for testing automated vehicles on public roads” (Board, 2019). In this paper, we show how to reason about the risk of systems that are modeled as stochastic processes. We consider a wide range of system specifications formulated in signal temporal logic (STL) (Maler and Nickovic, 2004; Bartocci et al., 2018) and present a systematic way to quantify and compute the risk of a system lacking robustness against failure.

1.1. Related Work

Depending on the research disciplines and applications, risk can have various interpretations. While risk is often defined as a failure probability, it can also be understood in more general terms as a metric defined over a cost distribution, e.g., the expected value or the variance of a distribution. We focus on tail risk measures to capture the rare yet costly events of a distribution. In particular, we consider the value-at-risk (VaR), i.e., quantiles of a distribution, and the conditional value-at-risk (CVaR) (Rockafellar and Uryasev, 2000, 2002), i.e., the expected value over a quantile. Tail risk measures are more frequently being used in robotics and control applications where system safety is important (Majumdar and Pavone, 2020).

Risk in control. Control design under risk objectives and constraints is increasingly been studied among control theorists as machine learning components integrated into closed-loop systems cause stochastic system uncertainty. Oftentimes, the CVaR risk measure is used to capture risk due its convexity and the property of being an upper bound to the VaR. For instance, the authors in (Samuelson and Yang, 2018) consider a stochastic optimal control problem with CVaR constraints over the distance to obstacles. Linear quadratic control under risk constraints was considered in (Tsiamis et al., 2021) to trade off risk and mean performance. A similar idea is followed for the risk constrained minimum mean squared error estimator in (Kalogerias et al., 2020). Risk-aware model predictive control was considered in (Singh et al., 2018; Hyeon et al., 2020), while (Schuurmans and Patrinos, 2020; Coulson et al., 2021) present data-driven and distributionally robust model predictive controllers. Risk-aware control barrier functions for safe control synthesis were proposed in (Ahmadi et al., 2022), while (Nyberg et al., 2021) demonstrates the use of risk in sampling-based planning. We remark that we view these works to be orthogonal to our paper as we provide a data-driven framework for the risk assessment under complex temporal logic specifications, and we hope to inform future control design strategies.

Stochastic system verification. System verification has a long history in complementing and informing the control design process of systems, e.g., using model checking (Baier and Katoen, 2008; Cassandras and Lafortune, 2009). When dealing with stochastic systems, system verification becomes computationally more challenging (Kwiatkowska et al., 2007). Statistical model checking has recently gained attention by relying on availability of data instead of computation (Legay et al., 2019; Agha and Palmskog, 2018; Zuliani et al., 2010; Fan et al., 2017). Another line of work considers stochastic barrier functions for safety verification of dynamical systems (Prajna et al., 2007; Jagtap et al., 2018). The authors in (Jasour et al., 2021b, a) deal with the verification of stochastic dynamial systems during runtime. Motivated by the fragility and sensitivity of neural networks (Goodfellow et al., 2014; Su et al., 2019), a special focus has recently been on verifying neural networks in open-loop (Katz et al., 2019; Singh et al., 2019) and closed-loop (Ivanov et al., 2019). We remark that our algorithms presented in this paper permit verification of general classes of systems, including systems with neural networks, as long as we can obtain data, e.g., from a simulator. The guarantees obtained in these previous works are either worst case guarantees or in terms of failure probabilities. Towards incorporating tail risk measures, the authors in (Chapman et al., 2019b, a) propose a risk-aware safety analysis framework using the CVaR. We are instead interested in system verification under more complex temporal logic specifications and risk.

Temporal logics. We use signal temporal logic to express a wide range of system specifications, e.g., surveillance (“visit regions A, B, and C every sec”), safety (“always between sec stay at least m away from region D”), and many others. For deterministic signals, STL allows to calculate the robustness by which a signal satisfies an STL specification. Particularly, the authors in (Fainekos and Pappas, 2009) proposed the robustness degree as the maximal tube around a signal in which all signals satisfy the specification. The size of the tube consequently measures the robustness of this signal with respect to the specification. As the robustness degree is in general hard to calculate, the authors in (Fainekos and Pappas, 2009) proposed approximate yet easier to calculate robust semantics. Many forms of robust semantics have appeared such as space and time robustness (Donzé and Maler, 2010), the arithmetic-geometric mean robustness (Mehdipour et al., 2019), the smooth cumulative robustness (Haghighi et al., 2019), averaged STL (Akazaki and Hasuo, 2015), and (Rodionova et al., 2016) in which a connection with linear time-invariant filtering is established allowing to define various types of robust semantics.

For stochastic signals, the authors in (Tiger and Heintz, 2020; Li et al., 2017; Kyriakis et al., 2019; Sadigh and Kapoor, 2016; Jha et al., 2018) propose notions of probabilistic signal temporal logic in which chance constraints over predicates are considered, while the Boolean and temporal operators of STL are not changed. Similarly, notions of risk signal temporal logic have recently appeared in (Lindemann et al., 2021b; Safaoui et al., 2020; Li et al., 2022) by defining risk constraints over predicates while not changing the definitions of Boolean and temporal operators. In this paper, we instead define risk over the whole STL specification. The work in (Farahani et al., 2018) considers the probability of an STL specification being satisfied instead of using chance or risk constraints over predicates. The authors in (Wang et al., 2019) consider hyperproperties in STL, i.e., properties between multiple system executions. More with a control synthesis focus and for the less expressive formalism of linear temporal logic, the authors in (Bharadwaj et al., 2018; Vasile et al., 2016; Lahijanian et al., 2015) consider control over belief spaces, while the authors in (Guo and Zavlanos, 2018) consider probabilistic satisfaction over Markov decision processes. Complementary to these works, (Baharisangari et al., 2021; Puranic et al., 2021) propose techniques to infer STL specifications from data towards explaining the underlying data.

Risk verification with temporal logics. In this paper, we quantify and compute the risk of lacking robustness against failure. We argue that the consideration of robustness in system verification is crucial and are particularly motivated by the fact that system failures are often caused by missing robustness to modeling errors, system disturbances, and distribution shifts in the underlying data generating process. The authors in (Anevlavis et al., 2022) further highlight the importance of robustness in system verification. Probably closest to our paper are the works in (Salamati et al., 2020, 2021; Jackson et al., 2021) and (Bartocci et al., 2013, 2015). In (Salamati et al., 2020, 2021; Jackson et al., 2021), the authors combine data-driven and model-based verification techniques to obtain information about the satisfaction probability of a partially known system. The authors in (Bartocci et al., 2013, 2015) present a purely data-driven verification technique to estimate probabilities over robustness distributions of the system. Conceptually our work differs in two directions. First, we consider general risk measures to be able to focus on the tails of the robustness distribution. We also show how to estimate the robustness risk from data with high confidence. Second, we use the robustness degree as defined in (Fainekos and Pappas, 2009) to obtain robustness distributions. This in fact allows us to obtain a precise geometric interpretation of risk. This paper is based on our previous work (Lindemann et al., 2021a). We here permit continuous-time stochastic processes and the CVaR as a risk measure. We also show under which conditions the STL robustness risk can exactly be calculated, while presenting exhaustive simulations within the autonomous driving simulator CARLA (Dosovitskiy et al., 2017).

1.2. Contributions and Paper Outline

Our general goal is to analyze the robustness of stochastic processes, and to quantify and compute the risk of a system lacking robustness against system failure. We make the following contributions:

-

•

We consider discrete-time and continuous-time stochastic processes and show under which conditions the robust semantics and the robustness degree of STL are random variables. This enables us to define risk over these quantities.

-

•

We define the STL robustness risk as the risk of a system lacking robustness against failure of an STL specification. The definition permits general classes of risk measures and has a precise geometric interpretation in terms of the size of permissible disturbances. We also define the approximate STL robustness risk as a computationally tractable upper bound of the STL robustness risk.

-

•

For the VaR and the CVaR, we show how the approximate STL robustness risk can be estimated from system trajectory data. Importantly, no particular restriction on the distribution of the stochastic process has to be made. For discrete-time stochastic processes with a discrete state space, we show how the approximate STL robustness risk can even be computed exactly.

-

•

We estimate the risk of four neural network lane keeping controllers within the autonomous driving simulator CARLA. We show how to find the least risky controller.

In Section 2, we present background on signal temporal logic, stochastic processes, and risk measures. In Section 3, we define the STL robustness risk and the STL approximate robustness risk. Section 4 shows how the approximate STL robustness risk can be estimated from data, while Section 5 shows under which conditions it can be computed exactly. The simulation results within CARLA are presented in Section 6 followed by conclusions in Section 7.

2. Background

We first provide background on signal temporal logic, stochastic processes, and risk measures.

2.1. Signal Temporal Logic

Signal temporal logic (STL) is based on deterministic signals where denotes the time domain (Maler and Nickovic, 2004). We particularly consider continuous time (the set of real numbers) and discrete time (the set of natural numbers). The atomic elements of STL are predicates that are functions where is the set of Booleans consisting of the true and false elements and , respectively. Let us associate an observation map with a predicate that indicates regions within the state space where the predicate is true, i.e.,

where denotes the inverse image of under the function . We assume throughout the paper that the sets and are non-empty and measurable, which is a mild technical assumption. In other words, the sets and are elements of the Borel -algebra of .

Remark 1.

For convenience, the predicate is often defined via a predicate function as

for . In this case, we have .

The syntax of STL, which recursively allows to formulate system specifications, is defined as

| (1) |

where and are STL formulas and where is the future until operator with time interval , while is the past until-operator. The Boolean operators and encode negations and conjunctions, respectively. We say that an STL formula as in (1) is bounded if the time interval is restricted to be compact. Based on these elementary operators, we can define the set of operators

| (past always operator). |

2.1.1. Semantics

To determine whether or not a signal satisfies an STL formula , we define the semantics of by means of the satisfaction function .111We use the notation to denote the set of all measurable functions mapping from the domain into the domain , i.e., an element is a measurable function . In particular, indicates that the signal satisfies the formula at time , while indicates that does not satisfy at time . While the intuitive meanings of the Boolean operators (‘not’), (‘and’), and (‘or’) are clear, we note that the future until operator encodes that holds until holds. Specifically, means that holds for all times after (not necessarily at time ) until holds within the time interval .222We use the notation and to denote the Minkowski sum and the Minkowski difference, respectively. Similarly, encodes that holds eventually within , while encodes that holds always within . For a formal definition of , we refer to Appendix A.

We are usually interested in the satisfaction function which determines the satisfaction of by at time zero, the time at which we assume to be enabled. An STL formula is hence said to be satisfiable if such that . The following example is taken from Lindemann et al. (2021a) and used as a running example throughout the paper.

Example 0.

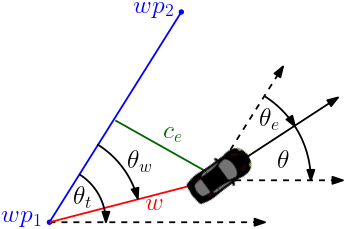

Consider a delivery robot that needs to perform two time-critical delivery tasks in regions and sequentially while avoiding areas and , see Fig. 2. We consider the STL formula

| (2) |

where the regions , , , and are encoded by the predicates , , , and , respectively, that are defined below. Let the state of the system at time be

where is the robot position at time and where , , , and denote the center points of the regions , , , and that are defined as

The predicates , , , and are now defined by their observation maps

| (3) | ||||

| (4) |

where is the Euclidean and is the infinity norm. In Fig. 2, six different robot trajectories - are shown. It can be seen that the signal that corresponds to violates , while - satisfy , i.e., we have and for all .

Remark 2.

The operators and are the strict non-matching versions of the until operators. In particular, is: 1) strict as it does not require to hold at the current time , and 2) non-matching as it does not require that and have to hold at the same time. When dealing with continuous-time stochastic systems later in this paper, we replace the strict non-matching versions and by the non-strict matching versions that we denote by and , see Appendix A for their formal definitions. We note that STL with until operators and is more expressive than STL with and . When excluding Zeno-signals, there is however no difference between these two notions (Furia and Rossi, 2007). As one rarely encounters Zeno-signals, we argue that the restriction to the non-strict matching version of the until operator for continuous-time stochastic processes is not restrictive in practice.

2.1.2. Robustness Degree

Importantly, one may also be interested in the quality of satisfaction and additionally ask how robustly the signal satisfies the STL formula at time . To answer this question, the authors in Fainekos and Pappas (2009, Definition 7) define the robustness degree that we recal next in a slightly modified manner. If , the robustness degree quantifies how much the signal can be perturbed by additive noise before changing the value of . Towards a formal definition, let us first define the set of signals that violate at time as

To measure distances between signals, let us define the metric as

where is the set of nonnegative extended real numbers and where is a metric assigning a distance in , e.g., the Euclidean norm. Throughout the paper, we use the extended definitions of the supremum and infimum operators, e.g., . Note that is the norm of the signal and measures the distance between the signals and .

To set some general notation, for a metric space with metric we denote by

the distance of a point to a nonempty set . Using this definition, the robustness degree is now defined via the metric as the distance of the signal to the set of violating signals .

Definition 0 (Robustness Degree333The robustness degree in Fainekos and Pappas (2009, Definition 7) is defined slightly differently by instead considering the signed distance of the signal to the set of violating signals .).

For a signal and an STL formula , the robustness degree is defined as

where denotes the closure of the set .

By definition of the robustness degree, the following properties hold. If , then , i.e., the signal satisfies at time . It further follows that all signals with are such that . The robustness degree defines in fact a robust neighborhood, which is a set strictly containing , so that for all in this robust neighborhood we have . Finally note that may imply either or , i.e., the signal either satisfies or violates at time .

2.1.3. Robust Semantics

Note that it is in general difficult to calculate the robustness degree as the set is hard to calculate. The authors in Fainekos and Pappas (2009) introduce the robust semantics as an alternative way of finding a robust neighborhood where is, in direct analogy to , the set of extended real numbers.

Definition 0 (Robust Semantics).

For a signal and an STL formula , the robust semantics are recursively defined as

Remark 3.

Importantly, by slight modification of Fainekos and Pappas (2009, Theorem 28), we know that

| (5) |

The robust semantics hence provides a tractable under-approximation of the robustness degree . The robust semantics are sound in the sense that if and if (Fainekos and Pappas, 2009, Proposition 30).

Example -1.

(continued) Consider again the trajectories shown in Fig. 2. We obtain , , and for all . The reason for having negative robustness lies in intersecting with the region . Marginal robustness of is explained as only marginally avoids the region while all other trajectories avoid the region robustly.

2.2. Random Variables and Stochastic Processes

Instead of interpreting an STL specifications over deterministic signals, we will interpret over stochastic processes. Consider therefore the probability space where is the sample space, is a -algebra of , and is a probability measure.

Let denote a real-valued random vector, i.e., a measurable function . When , we say is a random variable. We refer to as a realization of the random vector where . Since is a measurable function, a probability space can be defined for so that probabilities can be assigned to events related to values of .444Particularly, this probability space is where, for Borel sets , the probability measure is defined as where is the inverse image of under . Consequently, a cumulative distribution function (CDF) can be defined for . Given a random vector , we can derive other random variables. Assume for instance a measurable function , then becomes a derived random variable since function composition preserves measureability, see e.g., Durrett (2019) for more details.

A stochastic process is a function where is a random vector for each fixed . A stochastic process can be viewed as a collection of random vectors that are defined on a common probability space and that are indexed by . For a fixed , the function is a realization of the stochastic process. Another interpretation is that a stochastic process is a collection of deterministic functions of time that are indexed by .

2.3. Risk Measures

A risk measure is a function that maps from the set of real-valued random variables to the real numbers. In particular, we refer to the input of a risk measure as the cost random variable since typically a cost is associated with the input of . Risk measures hence allow for a risk assessment in terms of such cost random variables.

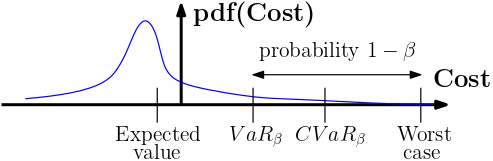

In this paper, we particularly use the expected value, the value-at-risk , and the conditional value-at-risk at risk level which are commonly used risk measures, see Figure 3. The of a random variable is defined as

i.e., the right quantile of . The of is defined as

where . When the CDF of is continuous, it holds that , i.e., is the expected value of conditioned on the events where is greater or equal than .

There are various desriable properties that a risk measure may satisfy, see Majumdar and Pavone (2020) for more information. We emphasize that our presented method is compatible with any monotone risk measure, where monotonicity of is defined as follows:

-

•

For two cost random variables , the risk measure is monotone if

The assumption of considering monotone risk measures is very mild, and both the value-at-risk and the conditional value-at-risk as well as the expected value are monotone.

3. The Risk of Lacking Robustness against Failure

We interpret STL formulas over stochastic processes instead of deterministic signals . It is, however, not immediately clear how to interpret the satisfaction of by . One way is to argue about the probability of satisfaction, see e.g., Farahani et al. (2018), but probabilities provide no information about the risk and the robustness of with respect to . In fact, some realizations of may satisfy robustly, while some other realizations of may satisfy only marginally or even violate . This observation leads us to the use of risk measures to be able to argue about the risk of the stochastic process lacking robustness against failure of the specification .

3.1. Measurability of Semantics, Robustness Degree, and Robust Semantics

To define the risk of a stochastic process , we first need to show under which conditions the semantics , the robustness degree , and the robust semantics are derived random variables. For discrete-time stochastic processes, no assumptions have to be made.

Theorem 1.

Let be a discrete-time stochastic process, i.e., . Let be an STL specification as in (1). Then , , and are measurable in for a fixed , i.e., , , and are random variables.

For continuous-time stochastic processes, however, we have to impose additional technical assumptions. Particularly, we have to restrict the class of STL formulas in (1) and make further assumptions on the stochastic process .

Theorem 2.

Let be a continuous-time stochastic process, i.e., . Let be a bounded STL specification as in (1), but where the strict non-matching until operators and are replaced with the non-strict matching until operators and . Then is measurable in for a fixed , i.e., is a random variable. If is measureable555Here, we mean measurable with respect to the Borel -algebras induced by the Skorokhod metric, see (Bartocci et al., 2015) for details., then is measurable in for a fixed , i.e., is a random variable, and if additionally is a cadlag function666Cadlag functions are right continuous functions with left limits. for each , then is measurable in for a fixed , i.e., is a random variable.777The result for measurability of is mainly taken from (Bartocci et al., 2015, Theorem 6).

Consequently, the probabilities , , and 888We use the shorthand notations , , and instead of , , and , respectively. are well defined for measurable sets from the corresponding measurable spaces. This enables us to define the STL robustness risk in the next section.

Remark 4.

We first note that the assumption of a bounded STL formula with the non-strict matching until operator is made for a technical reason. While the restriction to bounded formulas limits our expressivity to finite time specifications, the consideration of the non-strict matching until operator is not restrictive as discussed in Remark 2. We remark that Bartocci et al. (2015) showed measurability of under the assumption of a bounded STL specification with non-strict matching until operators, while we additionally show measurability of the semantics and the robustness degree without any additional continuity assumptions on . Lastly, we recall that we do not need to assume that is bounded for a discrete-time stochastic process as per Theorem 1.

3.2. The STL Robustness Risk

One way of defining the risk associated with a stochastic process is to consider the satisfaction function . However, not much information about the robustness of can be inferred due to binary encoding of . Instead, we consider the risk of the stochastic process lacking robustness against failure of the specification by considering the robustness degree .

Example -1.

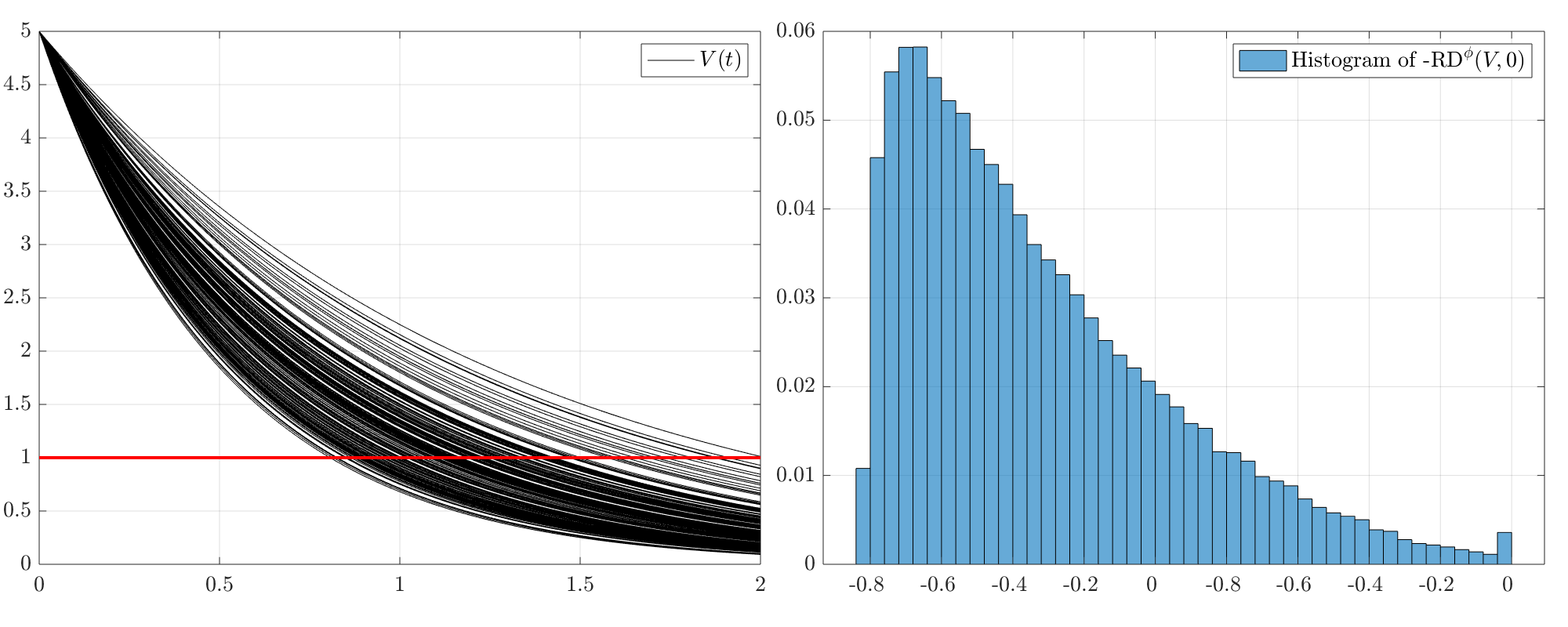

Consider an electric RC circuit consisting of a resistor with resistance and a capacitor with capacitance . If the capacitor is initially charged with , then the capacitor discharges its energy over time once the circuit is closed. In fact, the voltage over the capacitor is described by

where is the time constant. Assume that the resistance is unknown and modeled as where is a random variable following a beta distribution with probability density function where is the beta function with parameters and . Consequently, the voltage becomes a stochastic process of which we plot realizations in Fig. 4 (left). As a specification , we want that the voltage drops below after s, i.e.,

In Fig. 4 (right), we show the histogram of the negative robustness degree for realizations. To estimate the risk of the stochastic process lacking robustness against failure of , we can now compose with a risk measure . For instance, the value-at-risk at level is . Recall that is the quantile of . This means that with a probability of at least the robustness degree is not smaller (i.e., greater) than or, in other words, that in at most percent of the cases the robustness is smaller than . This information is useful as it allows us to quantify how much uncertainty our system can handle, e.g., when we do not know the value of exactly.

The previous example motivates the following definition for the risk of the stochastic process lacking robustness against failure of to which we refer as the STL robustness risk for brevity.

Definition 0 (STL Robustness Risk).

Given an STL formula and a stochastic process , the risk of lacking robustness against failure of at time is defined as

We remark that a large positive value of for a realization indicates robust satisfaction of . Therefore, the negative robustness degree is the cost random variable that is chosen as the input for the risk measure . This way, a large robustness degree results in a low cost. Finally, note that implies that the stochastic process is less risky than the stochastic process with respect to the specification .

3.3. The Approximate STL Robustness Risk

Unfortunately, the STL robustness risk can in general not be calculated as the robustness degree in Definition 2 is difficult to calculate. Instead, we will focus on using the robust semantics as an approximation of the STL robustness risk.

Definition 0 (Approximate STL Robustness Risk).

Given an STL formula and a stochastic process , the approximate risk of lacking robustness against failure of at time is defined as

Fortunately, the approximate STL robustness risk over-approximates the STL robustness risk when is a monotone risk measure as shown next.

Theorem 6.

Let be a stochastic process, be an STL specification as in (1), and be a monotone risk measure. Then it holds that

The previous result is important as using instead of will not result in an optimistic risk assessment. Especially in safety critical applications, it is desirable to be more risk-averse as opposed to being overly optimistic.

Sometimes one may be interested in scaling the robustness degree to associate a monetary cost with to reflect the severity of events with low robustness. Let us for this purpose consider an increasing cost function .

Corollary 0.

Let be a stochastic process, be an STL specification as in (1), be a monotone risk measure, and be an increasing cost function. Then it holds that

4. Data-Driven Estimation of the Approximate STL Robustness Risk

In this section, we show how the approximate STL robustness risk can be estimated from data. We assume that we have observed independent realizations of the stochastic process , i.e., we know realizations where are drawn independently and according to the probability measure . A practical example would be a simulator from which we can unroll trajectories . For brevity, we denote by . In this way, one can think of as independent copies of . We emphasize that we do not need knowledge of the distribution of . Our goal is to derive upper bounds of that hold with high probability. Let us, for convenience, first define the random variable

For further convenience, let and let us also define the tuple

We consider the value-at-risk , the conditional value-at-risk , and the mean . Particularly, we derive upper bounds , , and that hold with a probability of at least . By Theorem 6 and Propositions 1, 2, and 3 (presented in the remainder), we then have computational algorithms to find tight upper bounds for the approximate STL robustness risk and hence for the STL robustness risk, and it hold that with a probability of

4.1. Value-at-Risk (VaR)

For a risk level of , recall that the VaR of is given by

where denotes the CDF of . To estimate , we define the empirical CDF as

where denotes the indicator function defined as

Let now be a probability threshold. Inspired by Szorenyi et al. (2015), we calculate an upper bound of as

and a lower bound as

where we recall that for being the empty set due to the extended definition of the infimum operator. We next show that and are upper and lower bounds of , respectively, with a probability of at least .

Proposition 0.

Assume that is continuous and let be a probability threshold and be a risk level. Let and be based on the data . With a probability of at least , it holds that

4.2. Conditional Value-at-Risk (CVaR)

For a risk level of , recall that the CVaR of is given by

where . For estimating from data , we focus here on the case where the random variable (and hence ) has bounded support for fixed . In particular, we assume that . Note that has bounded support when the function is bounded, which can be achieved either by construction of or by clipping off outside the interval for some a priori chosen constants and , i.e., values outside this interval are clipped to the end points and of the interval. We remark that clipping off is not restrictive in most practical applications, i.e., realizations of that are larger than a sufficiently large value of indicate robust satisfaction of and will not affect the risk associated with while realizations of smaller than violate the specification already.999In practice, it hence makes sense to select a negative value for and to select based on physical intuition that we may have - either from trajectories that we may have already observed or from domain knowledge, e.g., for a lane keeping controller in autonomous driving the value of meter is a good robustness. We will provide illustrative examples in our simulations in Section 6. This boundedness assumption enables us now to directly leverage results from Wang and Gao (2010) to estimate upper and lower bounds of . Let us first define the empirical estimate of as

Based on Wang and Gao (2010, Theorem 3.1), we can now calculate an upper bound of as

and a lower bound as

We would like to highlight that the upper and lower bounds and , respectively, become less accurate with larger values of which we can account for by increasing the number of observed trajectories . The following proposition follows immediately from Wang and Gao (2010, Theorem 3.1).

Proposition 0.

Let be a probability threshold and be a risk level. Assume that . Let and be based on the data . With a probability of at least , it holds that

4.3. Mean

Define the empirical estimate of the mean as

By the law of large numbers, converges to with probability one as goes to infinity. For finite and when again has bounded support, i.e., , we can apply Hoeffding’s inequality and calculate an upper of the mean as

and a lower bound as

Similarly to the observation that we made for CVaR, note that the upper and lower bounds and , respectively, become less accurate with increasing values of , and more accurate with increasing . We next show that we indeed obtain valid upper and lower bounds.

Proposition 0.

Let be a probability threshold. Assume that . Let and be based on the data . With a probability of at least , it holds that

Example -3.

(continued)

We now modify Example 1 by considering that the regions and are not exactly known. Let and in (3) and (4), respectively, be Gaussian random vectors as

| (6) | |||

| (7) |

Consequently, the signals - become stochastic processes denoted by -. Let now denote the th observed realization of where . Our first goal is to estimate to compare the risk between the six robot trajectories -. We set and .101010We can select smaller at the cost of slightly more conservative estimates. The histograms of for each trajectory are shown in Fig. 5. For different risk levels , the resulting upper and lower bounds for the value-at-risk are shown in the next table.

| 1 | 0.434 | 0.467 | 0.508 | 0.577 | 0.407 | 0.432 | 0.465 | 0.505 |

| 2 | 0.261 | 0.295 | 0.335 | 0.424 | 0.232 | 0.259 | 0.292 | 0.332 |

| 3 | -0.075 | -0.044 | 0.001 | 0.086 | -0.1 | -0.077 | -0.046 | -0.003 |

| 4 | -0.25 | -0.222 | -0.177 | -0.086 | -0.25 | -0.25 | -0.225 | -0.182 |

| 5 | -0.249 | -0.228 | -0.18 | -0.084 | -0.249 | -0.249 | -0.23 | -0.185 |

| 6 | -0.249 | -0.249 | -0.249 | -0.249 | -0.249 | -0.249 | -0.249 | -0.249 |

Across all , it can be observed that the estimate of is relatively tight as the difference between upper and lower bounds is small. The table indicates that trajectories and are not favorable and are not robust. Recall that smaller risk values are favorable as only negative values indicate actual robustness. Trajectory is better compared to trajectories and , but worse than - in terms of the approximate STL robustness risk of . For trajectories -, note that a provides the information that the trajectories have roughly the same approximate STL robustness risk. However, once the risk level is increased to , , and , it becomes clear that is preferable over and . This matches with what one would expect by closer inspection of Fig. 2 and Fig. 5.

We next estimate and therefore restrict to lie within simply by clipping values that exceed this bound. This choice is motivated by our previous discussion in Section 4.2 and as is upper bounded by , see histograms in Fig. 5. For different risk levels , the resulting upper and lower bounds for the conditional value-at-risk are shown next.

| 1 | 0.577 | 0.607 | 0.645 | 0.707 | 0.32 | 0.31 | 0.282 | 0.193 |

| 2 | 0.432 | 0.471 | 0.527 | 0.637 | 0.175 | 0.174 | 0.164 | 0.12 |

| 3 | 0.1 | 0.136 | 0.193 | 0.301 | -0.16 | -0.161 | -0.17 | -0.213 |

| 4 | -0.078 | -0.04 | 0.019 | 0.13 | -0.335 | -0.336 | -0.344 | -0.384 |

| 5 | -0.08 | -0.042 | 0.019 | 0.134 | -0.337 | -0.338 | -0.344 | -0.38 |

| 6 | -0.146 | -0.13 | -0.103 | -0.042 | -0.403 | -0.426 | -0.466 | -0.556 |

In general, the same observations regarding the ranking of can be made based on the conditional value-at-risk. However, the risk levels are in general much higher as is more risk sensitive than . An important observation is that the estimates of are not as tight as before for as the difference is larger, particularly for larger due to the division by in the estimates of and . For completeness, we also report the estimated mean of .

| 1 | 0.227 | 0.207 |

| 2 | 0.043 | 0.023 |

| 3 | -0.194 | -0.214 |

| 4 | -0.233 | -0.253 |

| 5 | -0.233 | -0.253 |

| 6 | -0.24 | -0.26 |

5. Exact Computation of the Approximate STL Robustness Risk

In the previous section, we estimated the approximate STL robustness risk using observed realizations of the stochastic process . In this section, we instead assume to know the distribution of . There are two main challenges in computing the approximate STL robustness risk from the distribution of . First, note that exact computation of requires knowledge of the CDF of . However, the CDF of is in general not known and often hard to obtain analytically. Second, calculating may often involve solving high dimensional integrals for which in most of the cases no closed-form expressions exists. For these reasons, we assume in this section that the STL formula is bounded and that is a discrete-time stochastic process, i.e., , with a finite state space (i.e., the set consists of a finite set of elements).

Recall that the time intervals contained in a bounded STL formula are compact. The satisfaction of such an STL formula can hence be decided by finite signals. A bounded STL formula has a future formula length and a past formula length . The future formula length can be calculated, similarly to Sadraddini and Belta (2015), as

The past formula length can be calculated similarly as

A finite signal of length is now sufficient to determine if is satisfied at time . In particular, information from the time interval is sufficient to determine if is satisfied at time . Now, let be the discrete-time stochastic process under consideration where the state space is a finite set. Note that we can always obtain such a finite set from a continuous state space by discretization. Let the probability mass function (PMF) of be given. The next result is stated without proof as it follows immediately from the fact that and , and consequently the set of signals , are finite sets.

Proposition 0.

Let be a bounded STL formula with future and past formula lengths and , respectively. Let be a discrete-time stochastic process with a finite state space . For , we can calculate the PMF and the CDF of as

Note that holds as required. Having obtained the PMF and the CDF of , it is now straightforward to calculate for various risk measures . Note in particular that is a discrete random variable so that is discrete and is piecewise continuous, hence simplifying the calculation of as no high-dimensional integrals need to be solved.

Example -4.

(continued) Recall that and were assumed to be Gaussian distributed according to (6) and (7), respectively. We first discretize the distributions of and , see Appendix G for details. From the PMFs and , we can now calculate the PMF for any where and are the discretized domains of and . We can hence calculate according to Proposition 1. From this, the value at risk can be calculated which is reported in the next table.

| 1 | 0.403 | 0.429 | 0.461 | 0.509 |

| 2 | 0.225 | 0.255 | 0.29 | 0.348 |

| 3 | -0.102 | -0.067 | -0.049 | 0.003 |

| 4 | -0.249 | -0.249 | -0.222 | -0.162 |

| 5 | -0.25 | -0.25 | -0.222 | -0.157 |

| 6 | -0.249 | -0.249 | -0.249 | -0.249 |

It can be seen that the STL robustness risks reported above closely resemble the sampling-based estimates of from Section 4.

6. Simulations: Autonomous Driving in Carla

We consider the verification of neural network-based lane keeping controllers for lateral control in the autonomous driving simulator CARLA (Dosovitskiy et al., 2017), see Fig. 1 (left). Lane keeping in CARLA is achieved by tracking a set of predefined waypoints. For longitudinal control, a built-in PID controller is used to stabilize the car at 20 km/h. We particularly trained four different neural network controllers as detailed below. Our overall goal is to estimate and compare the risks of these four controllers for five different specifications during a double left turn, see Fig. 1 (middle).

For the verification and comparison of these controllers, we are particularly interested in the cross-track error, which is a measure of the closest distance from the car to the path defined by the set of waypoints as illustrated in Fig. 1 (right). Formally, let be the waypoint that is closest to the car and let be the waypoint proceeding . Then the cross-track error is defined as where is the vector pointing from to the car and is the angle between and the vector pointing from to . We are also interested in the orientation error between the orientation of the reference path and the orientation of the car .

The state of the car consists of the cross-track error , the orientation error , the velocity of the car, the internal state of the longitudinal PID controller, and the rate at which the orientation of the reference path changes. The control input for which we aim to learn and verify a lane keeping controller is the steering angle .

6.1. Training Neural Network Lane Keeping Controllers

We have trained four different neural network controllers. Two of these four controllers were obtained by using supervised imitation learning (IL) (Ross and Bagnell, 2010), while the other two controllers were obtained by learning control barrier functions (CBFs) from expert demonstrations (Lindemann et al., 2021c).

To obtain two imitation learning controllers, we used a CARLA built-in PID controller as an expert controller to collect expert trajectories, which are sequences of state and control input pairs. The first IL controller, denoted as IL, is trained using the full state as an input to the neural network, while the control input is the output. The second IL controller, denoted as IL, is trained by only using partial state knowledge. In particular, only the cross-track error , the orientation error , and the rate at which the orientation of the path changes are used here as an input to the neural network. We used one-layer neural networks with 20 neurons per layer and ReLU activation functions, and trained with the mean squared error as the loss function.

Remark 6.

For simplicity, we did not attempt to address the distribution shift between the expert controller and the trained controller, e.g., by using DAGGER (Ross et al., 2011). We remark that our primary goal lies in the verification and comparison of risk between controllers.

To obtain the CBF-based controllers, we again used the expert controller to get expert trajectories from which we learned robust control barrier functions following Lindemann et al. (2021c). The first controller, denoted as CBF, uses again full state knowledge of . The second controller, denoted as CBF, estimates the cross-track error from RGB dashboard camera images while assuming knowledge of the remaining states, see Lindemann et al. (2021c) for details. Both neural network controllers consist of two layers with 32 and 16 neurons and tanh activation functions.

6.2. Risk Verification and Comparison

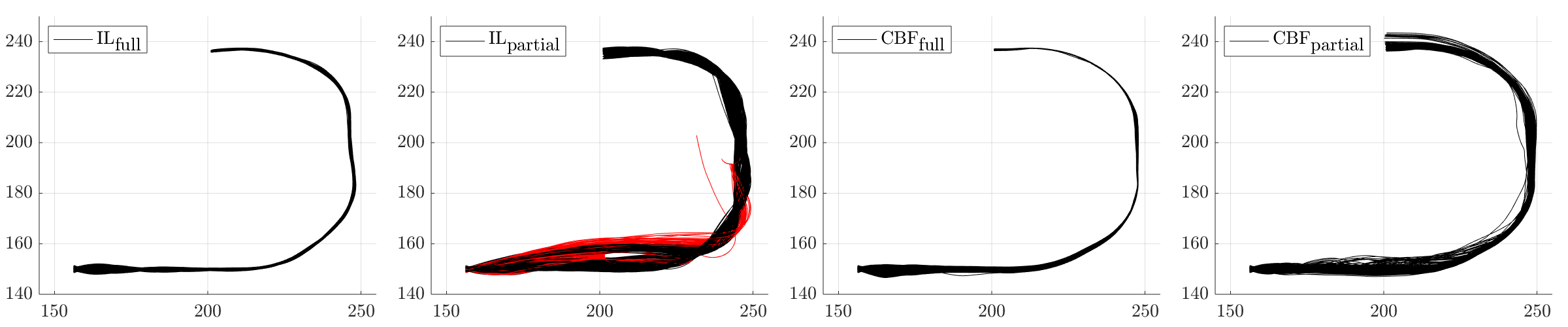

For the risk verification and comparison of these four controllers, we tested each of them on the training course, see Fig. 1 (middle). We uniformly sampled the initial position of the car in a range of m and rad and added normally distributed noise in a range of rad to the control input to simulate actuation noise so that the car becomes a stochastic process . We collected trajectories for each controller of which 600 are shown in Fig. 6. From a visual inspection, we can already see that the controllers that use full state knowledge (IL, CBF) outperform the controllers that only use partial state knowledge (IL, CBF). Videos of each controller from five different initial conditions are provided under https://tinyurl.com/48xjf545.

To obtain a more formal assessment, we next estimate the risk of each controller with respect to: 1) the cross-track error over the whole trajectory, during steady state, and during the transient phase, 2) the responsiveness of the controller, and 3) the orientation error.

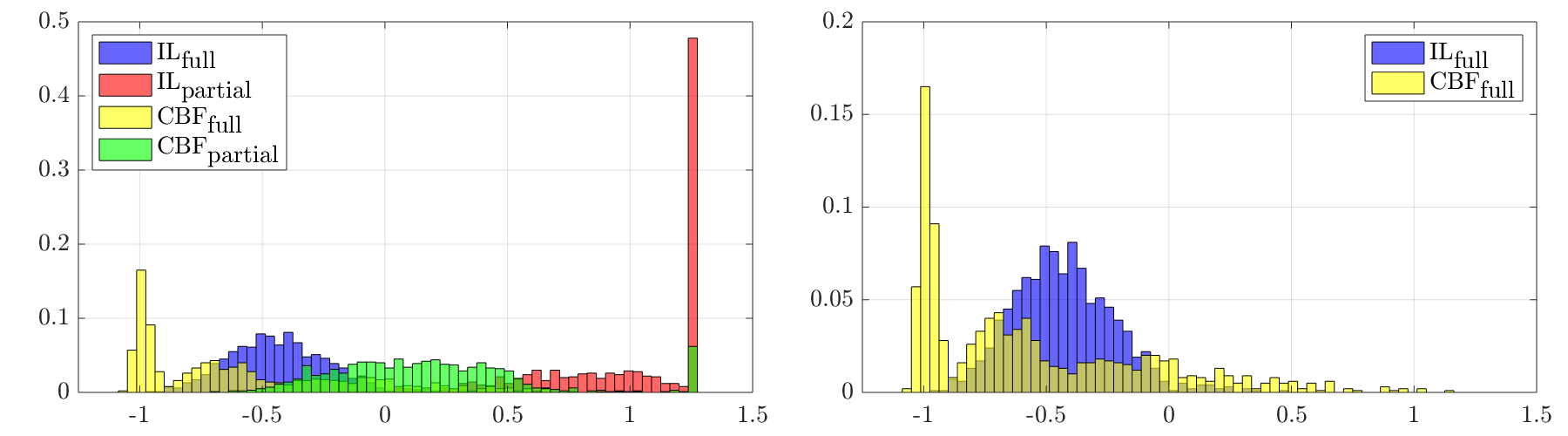

6.2.1. Cross-track error

The specification that we look at here is that the cross-track error should always be within the interval , where is a threshold that we selected based on the cross-track error induced by the expert controller . In STL language, we have

We show the histograms of for each controller in Fig. 7(a) (left).111111We restrict to lie within the interval , i.e., in this case we clip the values of to if . In the remainder, we clip - in the same way for the specifications -. We are particularly interested in the controllers IL and CBF and show their histograms isolated in Fig. 7(a) (right) for better readability. Selecting , the estimates of , , , and are reported in the table below. In the last column, we have additionally reported the empirical probability that the specification is satisfied which we calculate as

For each risk measure, we highlight the controller with the lowest risk in green.

| IL | -0.168 | 0.462 | 1.436 | -0.248 | -0.258 | -0.168 | -2.354 | -0.61 | 0.975 |

| IL | 1.25 | 1.25 | 2.776 | 1.166 | 1.25 | 1.25 | -1.014 | 0.806 | 0.005 |

| CBF | 0.135 | 1.125 | 1.818 | -0.375 | -0.125 | 0.105 | -1.972 | -0.736 | 0.863 |

| CBF | 0.58 | 1.25 | 2.42 | 0.357 | 0.44 | 0.58 | -1.37 | -0.003 | 0.364 |

Based on these risk estimates, we make the following observations:

-

•

As expected from the visual inspection of Fig. 6, the controllers IL and CBF perform poorly. Among these two, CBF performs slightly better in terms of risk than IL.

-

•

The controllers IL and CBF perform better. The risk of CBF in terms of the expected value is smaller than the risk of IL. Interestingly, the risk of IL in terms of the , , and is smaller than the risk of CBF. This is due to the long tail induced by CBF, see Fig. 7(a) (right). We hence argue that IL is the better choice with respect to .

-

•

The estimate of is not tight and very conservative. The difference between the upper and lower bounds is large. To make this bound tighter, more data is needed. We neglect the conditional value-at-risk in the remainder.

-

•

In this case, it can be observed that a low empirical satisfaction probability correlates with a high risk. We remark that this is not always the case as risk considers characteristics of the right tail of the distribution , while satisfaction probabilities focus on the left tail of this distribution. This can be observed when we present the results for specification .

We formulate the hypothesis that the long tail of CBF that makes CBF more risky than IL is induced by the transient behavior. We analyze this hypothesis in detail in the remainder looking at the specifications (steady-state) and (transient phase).

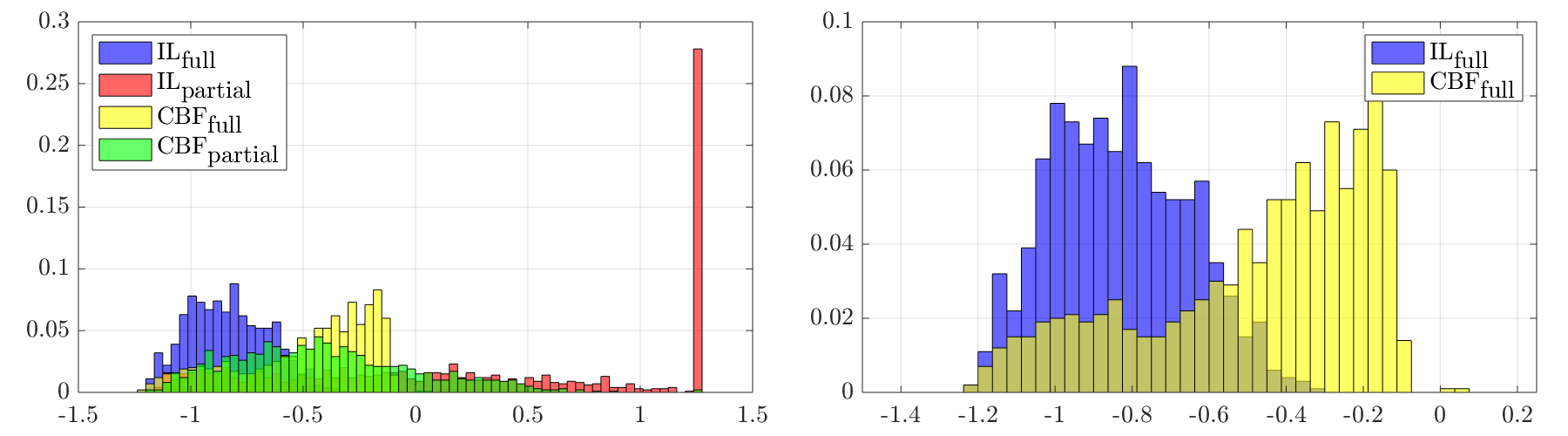

6.2.2. Steady-state

In the previous section, we concluded that IL is the best controller for the specification , i.e., when considering the cross-track error over the whole trajectory. We now study the steady-state behavior of each controller in terms of and reveal that CBF is the least risky controller when only looking at the steady-state. Therefore, we check if the cross-track error is always within the interval after s by the specification

We show the histograms of for each controller Fig. 7(b) and report the risk estimates below.

| IL | -0.168 | -0.078 | 0.462 | -0.254 | 0.975 |

| IL | 1.25 | 1.25 | 1.25 | 1.153 | 0.005 |

| CBF | -0.944 | -0.924 | -0.794 | -0.81 | 1 |

| CBF | 0.56 | 1.25 | 1.25 | 0.341 | 0.377 |

Based on these risk estimates, we make the following observations:

-

•

We see that our stated hypothesis is true and observe that CBF now has the least risky behavior for all risk measures with respect to , i.e., during steady state.

-

•

For CBF, we have . Consequently, for at most percent of the realizations the robustness is less than .

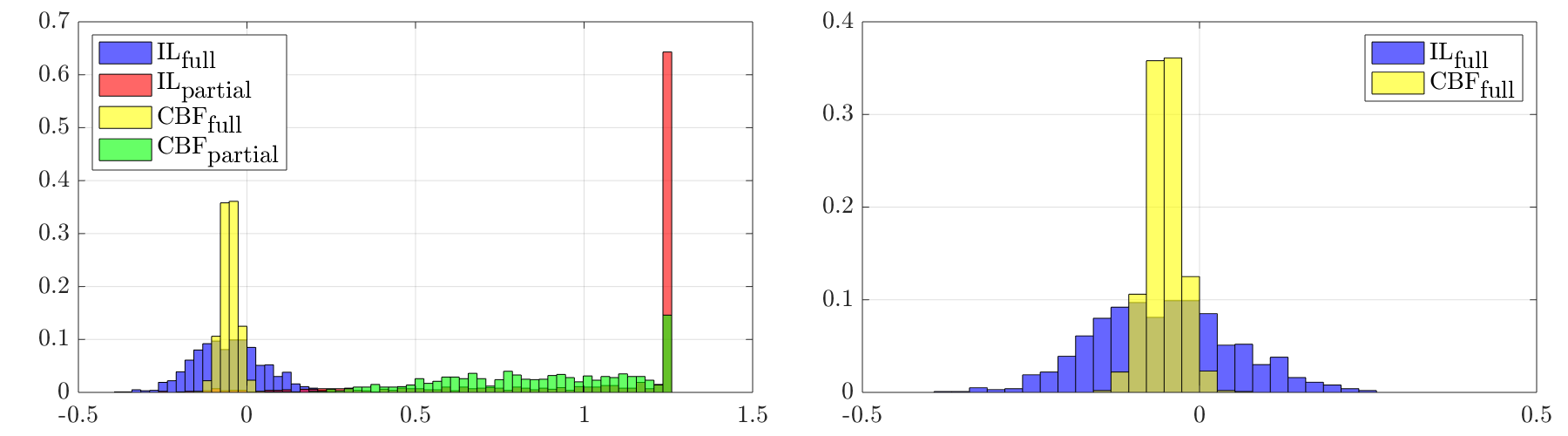

6.2.3. Transient phase

Complementary to the previous analysis, we now look at the transient behavior of the cross-track error of each controller by imposing the specification

In other words, the specification requires that eventually within the first s the absolute value of the cross-track error falls below the threshold for at least s. We show the histogram of each controller in Fig. 7(c) and report the corresponding risk estimates next.

| IL | -0.584 | -0.524 | -0.324 | -0.652 | 1 |

| IL | 1.25 | 1.25 | 1.25 | 0.493 | 0.42 |

| CBF | -0.157 | -0.137 | 0.063 | -0.297 | 0.998 |

| CBF | 0.2 | 0.38 | 1.25 | -0.221 | 0.83 |

For , we see a similar result as for in the sense that IL is the least risky controller, but now clearly indicating that IL is the less risky controller across all risk measures. It is also worth pointing out that CBF and CBF have almost the same expected value, while , , and indicate that CBF is less risky.

Summarizing the observations from , , and , IL is the least risky controller during the transient phase and CBF is the least risky controller during steady-state.

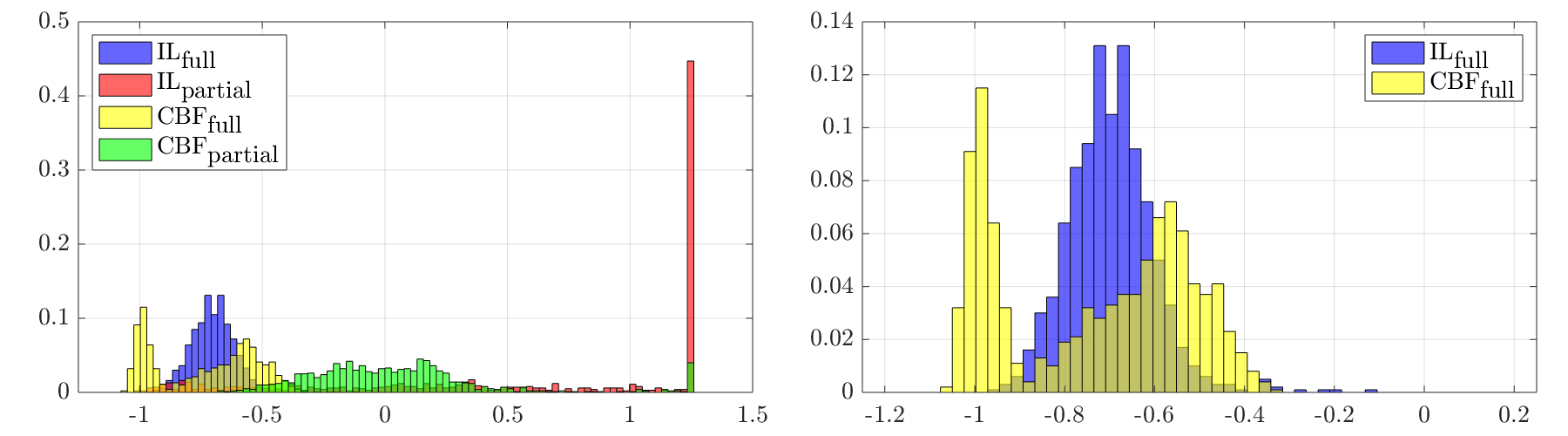

6.2.4. Responsiveness

So far, we focused on the cross-track error during steady-state and transient phase. We now analyze the responsiveness of the controllers when the cross-track error gets too large. We particularly analyze how responsive the controllers are in such situations and how quickly they can decrease the error again to an acceptable level. Let us therefore look at the specification

In other words, whenever the cross-track error leaves the interval after the transient phase has died out (approximately after s), it should hold that within the next s the cross-track error is again within the interval for at least s. We show the histogram of each controller in Fig. 7(d) and report the corresponding risk estimates below.

| IL | 0.088 | 0.128 | 0.248 | 0.127 | 0.703 |

| IL | 1.25 | 1.25 | 1.25 | 1.226 | 0.026 |

| CBF | -0.0152 | -0.005 | 0.055 | 0.129 | 0.974 |

| CBF | 1.25 | 1.25 | 1.25 | 1.054 | 0 |

The results are interesting in the sense that the risk of IL and CBF in terms of the expected value are almost identical, even slightly favoring IL, while the risk of CBF in terms of , , and is much smaller.

6.2.5. Orientation Error

Let us now focus on the orientation error . In general, an orientation error is expected when either the orientation of the reference path changes or the car tries to reduce the cross-track error by adjusting , e.g., when we need to reduce (see Fig. 1). To analyze how well the orientation error is adjusted when the cross-track error leaves the interval , we consider the specification

The specification encodes that, whenever the cross-track error leaves the interval , the orientation error should, within s, be such that the cross-track error decreases for at least s. We show the histogram of each controller in Fig. 7(e) and report the risk estimates below.

| IL | -0.58 | -0.54 | -0.13 | -0.517 | 1 |

| IL | 1.25 | 1.25 | 1.25 | 0.762 | 0.247 |

| CBF | -0.47 | -0.44 | -0.32 | -0.553 | 1 |

| CBF | 0.43 | 1.14 | 1.25 | 0.225 | 0.503 |

We can observe that the risk of IL is the lowest for and , while the risks of IL and CBF are roughly equal for the expected value . However, the distribution induced by IL has a long tail which is why the risk of CBF is the lowest for .

7. Conclusion

We defined the STL robustness risk to quantify the risk of a stochastic system lacking robustness against failure of an STL specification. The approximate STL robustness risk was defined as a computationally tractable upper bound of the STL robustness risk. It was shown how the approximate STL robustness risk is estimated from data for the value-at-risk and the conditional value-at-risk. We also provided conditions under which the approximate STL robustness risk can be computed exactly. Within the autonomous driving simulator CARLA, we trained four different neural network lane keeping controllers and estimated their risk for five different STL system specifications.

Acknowledgements.

This research was supported by NSF award CPS-2038873 and NSF CAREER award ECCS-2045834, and a Google Research Scholar award.References

- (1)

- Agha and Palmskog (2018) Gul Agha and Karl Palmskog. 2018. A survey of statistical model checking. ACM Transactions on Modeling and Computer Simulation 28, 1 (2018), 1–39.

- Ahmadi et al. (2022) Mohamadreza Ahmadi, Xiaobin Xiong, and Aaron D. Ames. 2022. Risk-Averse Control via CVaR Barrier Functions: Application to Bipedal Robot Locomotion. IEEE Control Systems Letters 6 (2022), 878–883.

- Akazaki and Hasuo (2015) Takumi Akazaki and Ichiro Hasuo. 2015. Time robustness in MTL and expressivity in hybrid system falsification. In Proceedings of the International Conference on Computer-Aided Verification. San Francisco, CA, 356–374.

- Anevlavis et al. (2022) Tzanis Anevlavis, Matthew Philippe, Daniel Neider, and Paulo Tabuada. 2022. Being correct is not enough: efficient verification using robust linear temporal logic. ACM Transactions on Computational Logic 23, 2 (2022), 1–39.

- Baharisangari et al. (2021) Nasim Baharisangari, Jean-Raphaël Gaglione, Daniel Neider, Ufuk Topcu, and Zhe Xu. 2021. Uncertainty-Aware Signal Temporal logic. arXiv preprint arXiv:2105.11545 (2021).

- Baier and Katoen (2008) Christel Baier and Joost-Pieter Katoen. 2008. Principles of Model Checking (1 ed.). The MIT Press, Cambridge, MA.

- Bartocci et al. (2013) Ezio Bartocci, Luca Bortolussi, Laura Nenzi, and Guido Sanguinetti. 2013. On the Robustness of Temporal Properties for Stochastic Models. In Proceedings of the Workshop on Hybrid Systems and Biology. Taormina, Italy, 3–19.

- Bartocci et al. (2015) Ezio Bartocci, Luca Bortolussi, Laura Nenzi, and Guido Sanguinetti. 2015. System design of stochastic models using robustness of temporal properties. Theoretical Computer Science 587 (2015), 3–25.

- Bartocci et al. (2018) Ezio Bartocci, Jyotirmoy Deshmukh, Alexandre Donzé, Georgios Fainekos, Oded Maler, Dejan Ničković, and Sriram Sankaranarayanan. 2018. Specification-based monitoring of cyber-physical systems: a survey on theory, tools and applications. In Lectures on Runtime Verification. Springer, 135–175.

- Bharadwaj et al. (2018) Suda Bharadwaj, Rayna Dimitrova, and Ufuk Topcu. 2018. Synthesis of surveillance strategies via belief abstraction. In Proceedings of the Conference on Decision and Control. Miami, FL, 4159–4166.

- Bhat and L. A. (2019) Sanjay P. Bhat and Prashanth L. A. 2019. Concentration of risk measures: A Wasserstein distance approach. Proceedings of the Conference on Neural Information Processing Systems 32 (2019), 11762–11771.

- Board (2019) National Transportation Safety Board. 2019. Collision Between Vehicle Controlled by Developmental Automated Driving System and Pedestrian. Highway Accident Report NTSB/HAR-19/03 (2019).

- Brown (2007) David B. Brown. 2007. Large deviations bounds for estimating conditional value-at-risk. Operations Research Letters 35, 6 (2007), 722–730.

- Cassandras and Lafortune (2009) Christos G. Cassandras and Stephane Lafortune. 2009. Introduction to discrete event systems. Springer Science & Business Media.

- Chapman et al. (2019b) Margaret P. Chapman, Jonathan Lacotte, Aviv Tamar, Donggun Lee, Kevin M. Smith, Victoria Cheng, Jaime F. Fisac, Susmit Jha, Marco Pavone, and Claire J. Tomlin. 2019b. A risk-sensitive finite-time reachability approach for safety of stochastic dynamic systems. In Proceedings of the 2019 American Control Conference. Philadelphia, PA, 2958–2963.

- Chapman et al. (2019a) Margaret P. Chapman, Jonathan P. Lacotte, Kevin M. Smith, Insoon Yang, Yuxi Han, Marco Pavone, and Claire J. Tomlin. 2019a. Risk-sensitive safety specifications for stochastic systems using Conditional Value-at-Risk. arXiv preprint arXiv:1909.09703 (2019).

- Coulson et al. (2021) Jeremy Coulson, John Lygeros, and Florian Dörfler. 2021. Distributionally robust chance constrained data-enabled predictive control. IEEE Trans. Automat. Control (2021).

- Donzé and Maler (2010) Alexandre Donzé and Oded Maler. 2010. Robust Satisfaction of Temporal Logic over Real-valued Signals. In Proceedings of the Conference on Formal Modeling and Analysis of Timed Systems. Klosterneuburg, Austria, 92–106.

- Dosovitskiy et al. (2017) Alexey Dosovitskiy, German Ros, Felipe Codevilla, Antonio Lopez, and Vladlen Koltun. 2017. CARLA: An open urban driving simulator. In Proceedings of the Conference on Robot Learning. Mountain View, California, 1–16.

- Durrett (2019) Rick Durrett. 2019. Probability: theory and examples. Vol. 49. Cambridge university press.

- Fainekos and Pappas (2009) Georgios E. Fainekos and George J. Pappas. 2009. Robustness of temporal logic specifications for continuous-time signals. Theoretical Computer Science 410, 42 (2009), 4262–4291.

- Fan et al. (2017) Chuchu Fan, Bolun Qi, Sayan Mitra, and Mahesh Viswanathan. 2017. DryVR: data-driven verification and compositional reasoning for automotive systems. In Proceedings of the International Conference on Computer Aided Verification. Heidelberg, Germany, 441–461.

- Farahani et al. (2018) Samira S. Farahani, Rupak Majumdar, Vinayak S. Prabhu, and Sadegh Soudjani. 2018. Shrinking horizon model predictive control with signal temporal logic constraints under stochastic disturbances. IEEE Trans. Automat. Control 64, 8 (2018), 3324–3331.

- Furia and Rossi (2007) Carlo Alberto Furia and Matteo Rossi. 2007. On the expressiveness of MTL variants over dense time. In Proceedings of the International Conference on Formal Modeling and Analysis of Timed Systems. Salzburg, Austria, 163–178.

- Goodfellow et al. (2014) Ian J. Goodfellow, Jonathon Shlens, and Christian Szegedy. 2014. Explaining and harnessing adversarial examples. arXiv preprint arXiv:1412.6572 (2014).

- Guide (2006) A Hitchhiker’s Guide. 2006. Infinite dimensional analysis. Springer.

- Guo and Zavlanos (2018) Meng Guo and Michael M Zavlanos. 2018. Probabilistic motion planning under temporal tasks and soft constraints. IEEE Trans. Automat. Control 63, 12 (2018), 4051–4066.

- Haghighi et al. (2019) Iman Haghighi, Noushin Mehdipour, Ezio Bartocci, and Calin Belta. 2019. Control from signal temporal logic specifications with smooth cumulative quantitative semantics. In Proceedings of the Conference on Decision and Control. Nice, France, 4361–4366.

- Hyeon et al. (2020) Eunjeong Hyeon, Youngki Kim, and Anna G Stefanopoulou. 2020. Fast Risk-Sensitive Model Predictive Control for Systems with Time-Series Forecasting Uncertainties. In Proceedings of the Conference on Decision and Control. Jeju Island, Republic of Korea, 2515–2520.

- Ivanov et al. (2019) Radoslav Ivanov, James Weimer, Rajeev Alur, George J. Pappas, and Insup Lee. 2019. Verisig: verifying safety properties of hybrid systems with neural network controllers. In Proceedings of the International Conference on Hybrid Systems: Computation and Control. Montreal, Canada, 169–178.

- Jackson et al. (2021) John Jackson, Luca Laurenti, Eric Frew, and Morteza Lahijanian. 2021. Formal Verification of Unknown Dynamical Systems via Gaussian Process Regression. arXiv preprint arXiv:2201.00655 (2021).

- Jagtap et al. (2018) Pushpak Jagtap, Sadegh Soudjani, and Majid Zamani. 2018. Temporal logic verification of stochastic systems using barrier certificates. In Proceedings of the International Symposium on Automated Technology for Verification and Analysis. Los Angeles, CA, 177–193.

- Jasour et al. (2021a) Ashkan Jasour, Weiqiao Han, and Brian Williams. 2021a. Real-Time Risk-Bounded Tube-Based Trajectory Safety Verification. arXiv preprint arXiv:2110.00233 (2021).

- Jasour et al. (2021b) Ashkan Jasour, Xin Huang, Allen Wang, and Brian C Williams. 2021b. Fast nonlinear risk assessment for autonomous vehicles using learned conditional probabilistic models of agent futures. Autonomous Robots (2021), 1–14.

- Jha et al. (2018) Susmit Jha, Vasumathi Raman, Dorsa Sadigh, and Sanjit A. Seshia. 2018. Safe autonomy under perception uncertainty using chance-constrained temporal logic. Journal of Automated Reasoning 60, 1 (2018), 43–62.

- Kallenberg (1997) Olav Kallenberg. 1997. Foundations of modern probability. Vol. 2. Springer.

- Kalogerias et al. (2020) Dionysios S. Kalogerias, Luiz F. O. Chamon, George J. Pappas, and Alejandro Ribeiro. 2020. Better Safe Than Sorry: Risk-Aware Nonlinear Bayesian Estimation. In Proceedings of the Conference on Acoustics, Speech and Signal Processing. Barcelona, Spain, 5480–5484.

- Katz et al. (2019) Guy Katz, Derek A Huang, Duligur Ibeling, Kyle Julian, Christopher Lazarus, Rachel Lim, Parth Shah, Shantanu Thakoor, Haoze Wu, Aleksandar Zeljić, et al. 2019. The marabou framework for verification and analysis of deep neural networks. In Proceedings of the International Conference on Computer Aided Verification. New York City, NY, 443–452.

- Kolla et al. (2019) Ravi Kumar Kolla, L. A. Prashanth, Sanjay P. Bhat, and Krishna Jagannathan. 2019. Concentration bounds for empirical conditional value-at-risk: The unbounded case. Operations Research Letters 47, 1 (2019), 16–20.

- Kwiatkowska et al. (2007) Marta Kwiatkowska, Gethin Norman, and David Parker. 2007. Stochastic model checking. In Proceedings of the International School on Formal Methods for the Design of Computer, Communication and Software Systems. Bertinoro, Italy, 220–270.

- Kyriakis et al. (2019) Panagiotis Kyriakis, Jyotirmoy V. Deshmukh, and Paul Bogdan. 2019. Specification mining and robust design under uncertainty: A stochastic temporal logic approach. ACM Transactions on Embedded Computing Systems 18, 5s (2019), 1–21.

- Lahijanian et al. (2015) Morteza Lahijanian, Sean B. Andersson, and Calin Belta. 2015. Formal verification and synthesis for discrete-time stochastic systems. IEEE Trans. Automat. Control 60, 8 (2015), 2031–2045.

- Legay et al. (2019) Axel Legay, Anna Lukina, Louis Marie Traonouez, Junxing Yang, Scott A. Smolka, and Radu Grosu. 2019. Statistical model checking. In Computing and Software Science. Springer, 478–504.

- Levine et al. (2016) Sergey Levine, Chelsea Finn, Trevor Darrell, and Pieter Abbeel. 2016. End-to-end training of deep visuomotor policies. The Journal of Machine Learning Research 17, 1 (2016), 1334–1373.

- Li et al. (2017) Jiwei Li, Pierluigi Nuzzo, Alberto Sangiovanni-Vincentelli, Yugeng Xi, and Dewei Li. 2017. Stochastic contracts for cyber-physical system design under probabilistic requirements. In Proceedings of the International Conference on Formal Methods and Models for System Design. Vienna, Austria, 5–14.

- Li et al. (2022) Xiao Li, Jonathan DeCastro, Cristian Ioan Vasile, Sertac Karaman, and Daniela Rus. 2022. Learning A Risk-Aware Trajectory Planner From Demonstrations Using Logic Monitor. In Proceedings of the Conference on Robot Learning. PMLR, 1326–1335.

- Lindemann et al. (2021a) Lars Lindemann, Nikolai Matni, and George J. Pappas. 2021a. STL Robustness Risk over Discrete-Time Stochastic Processes. In Proceedings of the Conference on Decision and Control. Austin, Texas, 1329–1335.

- Lindemann et al. (2021b) Lars Lindemann, George J. Pappas, and Dimos V. Dimarogonas. 2021b. Reactive and Risk-Aware Control for Signal Temporal Logic. IEEE Trans. Automat. Control (2021).

- Lindemann et al. (2021c) Lars Lindemann, Alexander Robey, Lejun Jiang, Stephen Tu, and Nikolai Matni. 2021c. Learning Robust Output Control Barrier Functions from Safe Expert Demonstrations. arXiv preprint arXiv:2111.09971 (2021).

- Majumdar and Pavone (2020) Anirudha Majumdar and Marco Pavone. 2020. How should a robot assess risk? Towards an axiomatic theory of risk in robotics. In Robotics Research. Springer, 75–84.

- Maler and Nickovic (2004) Oded Maler and Dejan Nickovic. 2004. Monitoring temporal properties of continuous signals. In Proceedings of the Formal Techniques, Modelling and Analysis of Timed and Fault-Tolerant Systems. Grenoble, France, 152–166.

- Massart (1990) Pascal Massart. 1990. The tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality. The annals of Probability (1990), 1269–1283.

- Mehdipour et al. (2019) Noushin Mehdipour, Cristian-Ioan Vasile, and Calin Belta. 2019. Arithmetic-geometric mean robustness for control from signal temporal logic specifications. In Proceedings of the American Control Conference. Philadelphia, PA, 1690–1695.

- Mhammedi et al. (2020) Zakaria Mhammedi, Benjamin Guedj, and Robert C. Williamson. 2020. Pac-bayesian bound for the conditional value at risk. Proceedings of the Conference on Advances in Neural Information Processing Systems 33 (2020), 17919–17930.

- Mnih et al. (2015) Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A. Rusu, Joel Veness, Marc G. Bellemare, Alex Graves, Martin Riedmiller, Andreas K. Fidjeland, Georg Ostrovski, et al. 2015. Human-level control through deep reinforcement learning. nature 518, 7540 (2015), 529–533.

- Munkres (2000) James R. Munkres. 2000. Topology (2nd ed.). Prentice Hall.

- Nikolakakis et al. (2021) Konstantinos E Nikolakakis, Dionysios S Kalogerias, Or Sheffet, and Anand D Sarwate. 2021. Quantile Multi-Armed Bandits: Optimal Best-Arm Identification and a Differentially Private Scheme. IEEE Journal on Selected Areas in Information Theory 2, 2 (2021), 534–548.

- Nyberg et al. (2021) Truls Nyberg, Christian Pek, Laura Dal Col, Christoffer Norén, and Jana Tumova. 2021. Risk-aware motion planning for autonomous vehicles with safety specifications. In 2021 IEEE Intelligent Vehicles Symposium (IV). IEEE, 1016–1023.

- Prajna et al. (2007) Stephen Prajna, Ali Jadbabaie, and George J. Pappas. 2007. A framework for worst-case and stochastic safety verification using barrier certificates. IEEE Trans. Automat. Control 52, 8 (2007), 1415–1428.

- Puranic et al. (2021) Aniruddh G. Puranic, Jyotirmoy V. Deshmukh, and Stefanos Nikolaidis. 2021. Learning from Demonstrations using Signal Temporal Logic. In Proceedings of the Conference on Robot Learning.

- Robey et al. (2020) Alexander Robey, Hamed Hassani, and George J. Pappas. 2020. Model-Based Robust Deep Learning: Generalizing to Natural, Out-of-Distribution Data. arXiv preprint arXiv:2005.10247 (2020).

- Rockafellar and Uryasev (2000) R. Tyrrell Rockafellar and Stanislav Uryasev. 2000. Optimization of conditional value-at-risk. Journal of risk 2 (2000), 21–42.

- Rockafellar and Uryasev (2002) R. Tyrrell Rockafellar and Stanislav Uryasev. 2002. Conditional value-at-risk for general loss distributions. Journal of banking & finance 26, 7 (2002), 1443–1471.

- Rodionova et al. (2016) Alena Rodionova, Ezio Bartocci, Dejan Nickovic, and Radu Grosu. 2016. Temporal logic as filtering. In Proceedings of the International Conference on Hybrid Systems: Computation and Control. Vienna, Austria, 11–20.

- Ross and Bagnell (2010) Stéphane Ross and Drew Bagnell. 2010. Efficient reductions for imitation learning. In Proceedings of the International Conference on Artificial Intelligence and Statistics. Sardinia, Italy, 661–668.

- Ross et al. (2011) Stéphane Ross, Geoffrey Gordon, and Drew Bagnell. 2011. A reduction of imitation learning and structured prediction to no-regret online learning. In Proceedings of the International Conference on Artificial Intelligence and Statistics. Ft. Lauderdale, FL, 627–635.

- Sadigh and Kapoor (2016) Dorsa Sadigh and Ashish Kapoor. 2016. Safe control under uncertainty with probabilistic signal temporal logic. In Proceedings of Robotics: Science and Systems XII. AnnArbor, Michigan.

- Sadraddini and Belta (2015) Sadra Sadraddini and Calin Belta. 2015. Robust temporal logic model predictive control. In Proceedings of the Conference on Communication, Control, and Computing. Monticello, IL, 772–779.

- Safaoui et al. (2020) Sleiman Safaoui, Lars Lindemann, Dimos V. Dimarogonas, Iman Shames, and Tyler H Summers. 2020. Control Design for Risk-Based Signal Temporal Logic Specifications. IEEE Control Systems Letters 4, 4 (2020), 1000–1005.

- Salamati et al. (2020) Ali Salamati, Sadegh Soudjani, and Majid Zamani. 2020. Data-Driven Verification under Signal Temporal Logic Constraints. IFAC-PapersOnLine 53, 2 (2020), 69–74.

- Salamati et al. (2021) Ali Salamati, Sadegh Soudjani, and Majid Zamani. 2021. Data-driven verification of stochastic linear systems with signal temporal logic constraints. Automatica 131 (2021), 109781.

- Samuelson and Yang (2018) Samantha Samuelson and Insoon Yang. 2018. Safety-aware optimal control of stochastic systems using conditional value-at-risk. In Proceedings of the American Control Conference. Milwaukee, WI, 6285–6290.

- Schuurmans and Patrinos (2020) Mathijs Schuurmans and Panagiotis Patrinos. 2020. Learning-Based Distributionally Robust Model Predictive Control of Markovian Switching Systems with Guaranteed Stability and Recursive Feasibility. In Proceedings of the Conference on Decision and Control. Jeju Island, Republic of Korea, 4287–4292.

- Silver et al. (2018) David Silver, Thomas Hubert, Julian Schrittwieser, Ioannis Antonoglou, Matthew Lai, Arthur Guez, Marc Lanctot, Laurent Sifre, Dharshan Kumaran, Thore Graepel, et al. 2018. A general reinforcement learning algorithm that masters chess, shogi, and Go through self-play. Science 362, 6419 (2018), 1140–1144.

- Singh et al. (2019) Gagandeep Singh, Timon Gehr, Markus Püschel, and Martin Vechev. 2019. An abstract domain for certifying neural networks. Proceedings of the ACM on Programming Languages 3 (2019), 1–30.

- Singh et al. (2018) Sumeet Singh, Yinlam Chow, Anirudha Majumdar, and Marco Pavone. 2018. A framework for time-consistent, risk-sensitive model predictive control: Theory and algorithms. IEEE Trans. Automat. Control 64, 7 (2018), 2905–2912.

- Su et al. (2019) Jiawei Su, Danilo Vasconcellos Vargas, and Kouichi Sakurai. 2019. One pixel attack for fooling deep neural networks. IEEE Transactions on Evolutionary Computation 23, 5 (2019), 828–841.

- Szorenyi et al. (2015) Balazs Szorenyi, Róbert Busa-Fekete, Paul Weng, and Eyke Hüllermeier. 2015. Qualitative multi-armed bandits: A quantile-based approach. In Proceedings of the International Conference on Machine Learning. Lille, France, 1660–1668.

- Thomas and Learned-Miller (2019) Philip Thomas and Erik Learned-Miller. 2019. Concentration inequalities for conditional value at risk. In Proceedings of the International Conference on Machine Learning. Long Beach, CA, 6225–6233.

- Tiger and Heintz (2020) Mattias Tiger and Fredrik Heintz. 2020. Incremental reasoning in probabilistic signal temporal logic. International Journal of Approximate Reasoning 119 (2020), 325–352.

- Tsiamis et al. (2021) Anastasios Tsiamis, Dionysios S. Kalogerias, Alejandro Ribeiro, and George J. Pappas. 2021. Linear Quadratic Control with Risk Constraints. arXiv preprint arXiv:2112.07564 (2021).

- Vasile et al. (2016) Cristian-Ioan Vasile, Kevin Leahy, Eric Cristofalo, Austin Jones, Mac Schwager, and Calin Belta. 2016. Control in belief space with temporal logic specifications. In Proceedings of the Conference on Decision and Control. Las Vegas, NV, 7419–7424.

- Wang and Gao (2010) Ying Wang and Fuqing Gao. 2010. Deviation inequalities for an estimator of the conditional value-at-risk. Operations Research Letters 38, 3 (2010), 236–239.

- Wang et al. (2019) Yu Wang, Mojtaba Zarei, Borzoo Bonakdarpour, and Miroslav Pajic. 2019. Statistical verification of hyperproperties for cyber-physical systems. ACM Transactions on Embedded Computing Systems (TECS) 18, 5s (2019), 1–23.

- Zuliani et al. (2010) Paolo Zuliani, André Platzer, and Edmund M Clarke. 2010. Bayesian statistical model checking with application to simulink/stateflow verification. In Proceedings of the International Conference on Hybrid Systems: Computation and Control. Stockholm, Sweden, 243–252.

Appendix A Semantics of Signal Temporal Logic

The satisfaction function determines whether or not the signal satisfies the specification at time . The definition of follows recursively from the structure of as follows.

Definition 0 (STL Semantics).

For a signal and an STL formula , the satisfaction function is recursively defined as

Appendix B Proof of Theorem 1

We prove the statement of Theorem 1 first for the the semantics , then for the robust semantics , and finally for the robustness degree .

B.1. Semantics

Let us define the power set of as . Note that is a -algebra of . To prove measurability of in for a fixed , we need to show that, for each , it holds that the inverse image of under for a fixed is contained within , i.e., that it holds that

We show measurability of in for a fixed inductively on the structure of .

: For , it trivially holds that since for all . This follows according to Definition 1 so that if and otherwise.

: Let be the indicator function of with if and otherwise. According to Definition 1, we can now write . Recall that is measurable and note that the indicator function of a measurable set is measurable again (see e.g., Durrett (2019, Chapter 1.2)). Since is measurable in for a fixed by definition, it follows that and hence is measurable in for a fixed . In other words, for , it follows that

: By the induction assumption, is measurable in for a fixed . Recall that is a -algebra that is, by definition, closed under its complement so that, for , it holds that

: By the induction assumption, and are measurable in for a fixed . Hence is measurable in for a fixed since the min operator of measurable functions is again a measurable function.

and : Recall the definition of the future until operator

By the induction assumption, and are measurable in for a fixed . First note that and are countable sets since . According to Guide (2006, Theorem 4.27), the supremum and infimum operators over a countable number of measurable functions is again measurable. Consequently, the function is measurable in for a fixed . The same reasoning applies to .

B.2. Robust semantics

The proof for follows again inductively on the structure of and the goal is to show that for each Borel set . The difference here, compared to the proof for the semantics presented above, lies only in the way predicates are handled. Note first that we can write as

| (8) | ||||

where we recall that we interpret and . Since the composition of the indicator function with , i.e., , is measurable in for a fixed as argued before, we only need to show that and are measurable in for a fixed . This immediately follows since is measurable in for a fixed by definition and since the function is continuous in its first argument, and hence measurable (see Guide (2006, Corollary 4.26)), due to being a metric defined on the set (see e.g., Munkres (2000, Chapter 3)) so that is measurable in for a fixed .

B.3. Robustness Degree

For , note that, for a fixed , the function maps from the domain into the domain , while maps from the domain into the domain . Recall now that and that is a metric defined on the set as argued in Fainekos and Pappas (2009). Therefore, it follows that the function is continuous in its first argument (see e.g., Munkres (2000, Chapter 3)), and hence measurable with respect to the Borel -algebra of (see e.g., Guide (2006, Corollary 4.26)). Consequently, the function is measurable in its first argument for a fixed . As is countable and is a discrete-time stochastic process, it follows that is measurable with respect to the product -algebra of Borel -algebras which is equivalent to the Borel -algebra of (see e.g., Kallenberg (1997, Lemma 1.2)). Since function composition preserves measurability, it holds that is measurable in for a fixed .