Robust -Divergence MDPs

Abstract

In recent years, robust Markov decision processes (MDPs) have emerged as a prominent modeling framework for dynamic decision problems affected by uncertainty. In contrast to classical MDPs, which only account for stochasticity by modeling the dynamics through a stochastic process with a known transition kernel, robust MDPs additionally account for ambiguity by optimizing in view of the most adverse transition kernel from a prescribed ambiguity set. In this paper, we develop a novel solution framework for robust MDPs with -rectangular ambiguity sets that decomposes the problem into a sequence of robust Bellman updates and simplex projections. Exploiting the rich structure present in the simplex projections corresponding to -divergence ambiguity sets, we show that the associated -rectangular robust MDPs can be solved substantially faster than with state-of-the-art commercial solvers as well as a recent first-order solution scheme, thus rendering them attractive alternatives to classical MDPs in practical applications.

1 Introduction

Markov decision processes (MDPs) are a flexible and popular framework for dynamic decision-making problems and reinforcement learning [39, 48]. A practical limitation of the standard MDP model is that it assumes the model parameters, such as transition probabilities and rewards, to be known exactly. In reinforcement learning and other applications, these parameters must be estimated from sampled data, which introduces estimation errors. Optimal MDP solutions, referred to as policies, are well known to be sensitive to errors and may fail catastrophically when deployed [25, 56].

Robust MDPs (RMDPs) mitigate the sensitivity of MDPs to estimation errors by computing a policy that is optimal for the worst plausible realization of the transition probabilities. This set of plausible transition probabilities is known as the ambiguity set. Most prior work considers ambiguity sets that are rectangular. In this work, we focus on s-rectangular ambiguity sets, which assume that the worst transition probabilities are chosen independently in each state [25, 56]. While several other models of rectangularity have been studied [9, 13, 21, 28], -rectangular ambiguity sets are popular due to their generality and their performance both in-sample and out-of-sample [56]. However, even though polynomial-time algorithms based on dynamic programming concepts have been developed for -rectangular sets, those algorithms may be too slow in practice. Solving RMDPs requires the solution of a convex optimization problem in every step of value or policy iteration, which can become prohibitively slow even in moderatly sized problems with 100s of states [5, 9, 14, 19].

Motivated by the difficulty of solving RMDPs, several fast algorithms have been proposed for -rectangular RMDPs [5, 9, 14, 19]. The preponderance of the earlier work has focused on ambiguity sets defined in terms of - and -norms. These ambiguity sets are polyhedral, and they can be analyzed using linear programming techniques which offer fruitful avenues to exploit the structure inherent to those sets. However, recent statistical studies point to the superior solution quality offered by nonlinear ambiguity sets defined in terms of the Kullback-Leibler (KL) divergence, the -norm and other metrics [17]. Linear optimization solvers are not applicable to RMDPs with -rectangular ambiguity sets defined in terms of non-polyhedral ambiguity sets, as the corresponding optimization problems are in general convex conic programs (e.g., exponential cone program in the case of KL divergence); thus, they are currently solved using first-order methods [14] or general convex conic solvers such as MOSEK [3], which tend to be complex, closed-source and slow.

As our main contribution, we propose a new suite of fast algorithms for solving RMDPs with -divergence constrained -rectangular ambiguity sets. -divergences, also known as f-divergences, constitute a generalization of the KL divergence that encompasses the Burg entropy as well as the - and weighted -norms as special cases [4, 6]. Moreover, -divergence ambiguity sets benefit from rigorous statistical performance guarantees, and they are optimal among all (known and unknown) data-driven optimization paradigms for certain types of worst-case out-of-sample performance guarantees [35]. The radii of -divergence ambiguity sets can be selected either via cross-validation or via statistical bounds [26, 32, 55]. Robust MDPs with -divergence sets are challenging and unexplored for both -rectangular and -rectangular ambiguity sets. Solving -divergence RMDPs using value iteration requires the solution of seemingly unstructured min-max problems. Our main insight is that these min-max problems can be reduced to a small number of highly structured projection problems onto a probability simplex. We use this insight to develop tailored solution schemes for the projection problems corresponding to several popular -divergence ambiguity sets, which in turn give rise to efficient solution methods for the respective RMDPs. Ignoring tolerances, our algorithms achieve an overall or time complexity to compute the robust Bellman operator, where and denote the numbers of states and actions, respectively. Since the evaluation of a non-robust Bellman operator requires a runtime of , our algorithms only incur an additional logarithmic overhead to account for robustness in the transition probabilities. This computational complexity compares favorably with the larger time complexity of a recent first-order solution scheme for KL divergence-constrained -rectangular RMDPs (which we will elaborate on later in the paper) as well as a minimum complexity of for the naïve solution with state-of-the-art interior-point algorithms. Our framework is general enough to readily accommodate for -divergences that have not been studied previously in the context of -rectangular ambiguity sets, such as the Burg entropy and the -distance. For other -divergences, such as the -norm, our framework results in the same complexity at substantially simplified proofs.

The algorithms developed in this paper speed up the computation of robust Bellman updates, and so they can be used in combination with a variety of RMDP solution schemes. In particular, they can be used to accelerate the standard robust value iteration, policy iteration, modified policy iteration [22] and partial policy iteration [19]. They can also be combined with a first order gradient method [14] that has been introduced recently. In addition, fast algorithms for computing the Bellman operator also play a crucial role when scaling robust algorithms to value function approximation [50], model-free reinforcement learning [33, 42], and robust policy gradients [49]. In this paper, we focus on the model-based setting, which is currently under active study [24, 29, 31] and has many important real-life applications [12, 20, 58]; moreover, it also serves as an important building block to constructing model-free algorithms. While this paper focuses on the -rectangular ambiguity sets, the proposed algorithms in this paper can also be applied to the special case of -rectangular ambiguity sets.

The remainder of the paper proceeds as follows. Section 2 reviews relevant prior work and Section 3 describes our basic RMDP setting. Then, Section 4 shows how the robust Bellman operator for a large class of ambiguity sets can be reduced to a sequence of structured projections onto a simplex. We describe novel algorithms for efficiently computing the simplex projections for several -divergences in Section 5. Finally, Section 6 presents experimental results that compare the runtime of our algorithms with general conic solvers as well as a recent first-order optimization algorithm [14].

Notation. We denote by the vector of all ones, whose context determines its dimension. We refer to the probability simplex in by . For , we let (similar for the maximum operator), and we define component-wise as , . We refer to the conjugate of a function by . Random variables are indicated by a tilde.

2 Related Work

While RMDPs have been studied since the seventies [45], they have witnessed significant recent interest due to their widespread adoption in applications ranging from assortment optimization [43], medical decision-making [12, 62] and hospital operations management [16], production planning [58] and energy systems [20] to model predictive control [10], aircraft collision avoidance [23], wireless communications [57] and the robustification against approximation errors in aggregated MDPs [37].

Efficient implementations of the robust value iteration have been first proposed by [11, 21, 32] for RMDPs with -rectangular ambiguity sets, where the worst transition probabilities are considered separately for each state and action. The authors study ambiguity sets that bound the distance of the transition probabilities to some nominal distribution in terms of finite scenarios, interval matrix bounds, ellipsoids, the relative entropy, the KL divergence and maximum a posteriori models. Subsequently, similar methods have been developed by [57] for interval matrix bounds as well as likelihood uncertainty models, by [37] for -norm ambiguity sets as well as by [62] for interval matrix bounds intersected with a budget constraint. All of these contributions have in common that they focus on -rectangular ambiguity sets where the existence of optimal deterministic policies is guaranteed, and it is not clear how they could be extended to the more general class of -rectangular ambiguity sets where all optimal policies may be randomized.

In contrast to -rectangular ambiguity sets, -rectangular ambiguity sets restrict the conservatism among transition probabilities corresponding to different actions in the same state, which tends to lead to a superior performance in data-driven settings. [56] solve the subproblems arising in the robust value iteration of an -rectangular RMDP as linear or conic optimization problems using commercial off-the-shelf solvers. Despite their polynomial-time complexity, general-purpose solvers cannot exploit the structure present in these subproblems, which renders them suitable primarily for small problem instances. More efficient tailored solution methods for -rectangular RMDPs have subsequently been developed by [5, 18, 19]. [18] develop a homotopy continuation method for RMDPs with -rectangular and -rectangular weighted -norm ambiguity sets, while [5] adapt the algorithm of [18] to unweighted -norm ambiguity sets. [19] embed the algorithms of [18] in a partial policy iteration, which generalizes the robust modified policy iteration proposed by [22] for -rectangular RMDPs to -rectangular RMDPs.

While the present paper focuses on the robust value iteration for ease of exposition, we note that our algorithms can also be combined with the partial policy iteration of [19] to obtain further speedups. [9] establish a relationship between -rectangular RMDPs and twice regularized MDPs, which they subsequently use to propose efficient Bellman updates for a modified policy iteration. While their approach can solve RMDPs in almost the same time as a classical non-robust MDPs, the obtained policies can be conservative as the worst-case transition probabilities are not restricted to reside in a probability simplex and, therefore, may be negative and/or add up to more or less than . Finally, [14] propose a first-order framework for RMDPs with -rectangular KL and spherical ambiguity sets that interleaves primal-dual first-order updates with approximate value iteration steps. The authors show that their algorithms outperform a robust value iteration that solves the emerging subproblems using state-of-the-art commercial solvers. We compare our solution method for KL ambiguity sets with the approach proposed by [14] in terms of its theoretical complexity and numerical runtimes.

While this paper exclusively studies -rectangular uncertainty sets, alternative generalizations of -rectangular ambiguity sets have been proposed in the literature as well. For example, [28] consider -rectangular ambiguity sets where the transition probabilities of different states can be coupled, [13] study factor ambiguity model ambiguity sets where the transition probabilities depend on a small number of underlying factors, and [51] construct ambiguity sets that bound marginal moments of state-action features defined over entire MDP trajectories. Moving beyond the model-based setting, there is also an active line of research on robust reinforcement learning, such as least squares policy iteration [33], analysis on sample complexity [34], robust Q-learning and robust TDC algorithms [42, 53], and robust policy gradient [54]. We also note the papers [7, 15, 60] which study the related problem of distributionally robust MDPs whose transition probabilities are themselves regarded as random objects that are drawn from distributions which are only partially known. The connections between RMDPs and multi-stage stochastic programs as well as distributionally robust problems are explored further by [44, 46, 47].

3 Preliminaries

Robust MDPs

We study RMDPs with a finite state space and a finite action space . We assume an infinite planning horizon, but all of our results immediately extend to a finite time horizon. Without loss of generality, we assume that every action is admissible in every state . The RMDP starts in a random initial state that follows the known probability distribution from the probability simplex in . If action is taken in state , then the RMDP transitions randomly to the next state according to the conditional probability distribution . We condense the transition probabilities to the tensor . The transition probabilities are only known to reside in a non-empty, compact ambiguity set . For a transition from state to state under action , the decision maker receives an expected reward of . As with the transition probabilities, we condense these rewards to the tensor . Without loss of generality, we assume that all rewards are non-negative.

We denote by the set of all stationary (i.e., time-independent) randomized policies. A policy takes action in state with probability . The transition probabilities and the policy induce a stochastic process on the space of sample paths. We refer by to expectations with respect to this process. The decision maker is risk-neutral but ambiguity-averse and wishes to maximize the worst-case expected total reward under a discount factor ,

| (1) |

Note that the maximum and minimum in (1) are both attained by the Weierstrass theorem since and are non-empty and compact, while the objective function is finite since .

Rectangular Ambiguity Sets

For general ambiguity sets , evaluating the inner minimization in (1) is NP-hard even if the policy is fixed [56]. For these reasons, much of the research on RMDPs and their applications has focused on rectangular ambiguity sets. Among the most general rectangular ambiguity sets are the -rectangular ambiguity sets satisfying

see [25, 56, 59, 61]. In contrast to the simpler class of -rectangular ambiguity sets, -rectangular ambiguity sets restrict the choice of transition probabilities corresponding to different actions applied in the same state . This limits the conservatism of the resulting RMDP (1) and typically leads to a better performance of the optimal policy [56]. Although Bellman’s optimality principle extends to -rectangular RMDPs and there is always an optimal stationary policy, all optimal policies of an -rectangular RMDP may be randomized.

We study a new general class of -rectangular ambiguity sets that can be expressed as

| (2) |

where is the uncertainty budget and the distance functions , , are -divergences (also known as f-divergences) satisfying

Here, is a convex function satisfying . Intuitively, a -divergence measures the distance between two probability distributions. With an appropriate choice of , it generalizes other metrics including the KL divergence, the Burg entropy, - and -norms and others [4, 6]. Table 1 reports some popular -divergences that we study in this paper. The variation distance coincides with the -based -rectangular ambiguity sets studied in earlier work [18, 19]. Note that although we assume that is the same for different state-action pairs, the proposed approach also works for the more general case where .

| Divergence | Complexity of | Prior Art | ||

|---|---|---|---|---|

| Kullback-Leibler | ||||

| Burg Entropy | no poly-time | |||

| Variation Distance | ||||

| -Distance |

Robust Value Iteration

A standard approach for computing the optimal value and the optimal policy of an RMDP (1) is the robust value iteration [21, 32, 25, 56]: Starting with an initial estimate of the state-wise optimal value to-go, we conduct robust Bellman iterations of the form , , where the robust Bellman operator is defined component-wise as

| (3) |

This yields the optimal value , where the limit is approached component-wise at a geometric rate. The optimal policy , finally, is recovered state-wise via

4 Robust Bellman Updates via Simplex Projections

In this section, we show that the robust Bellman operator reduces to a generalized projection problem. This reduction is important because it underlies our fast algorithms for computing .

At the core of the robust value iteration is the solution of the max-min problem (3). By applying the minimax theorem, the right-hand side of (3) equals to

| (4) |

The above optimization problem can be solved via bisection on its objective value; that is, we seek the lowest possible such that , for each where satisfies the constraints in (4). For any given in the bisection method, we check whether such exists by solving the following generalized -projection problem of the nominal transition probabilities :

| (5) |

Here, are the decision variables and , and are parameters. For any fixed , we compute and construct where is the optimal solution of the associated projection problem . We can then distinguish between the following two cases:

-

1.

If , then the constructed is a feasible solution to (5). Therefore, upper bounds the optimal objective value.

-

2.

If , then there is no feasible such that the objective value attains or less. Therefore, lower bounds the optimal objective value.

As a consequence of the cases above, one can compute the robust Bellman update (3) efficiently by bisection if the projection problem (5) can be solved efficiently. The proof of Theorem 1 describes further details needed to implement this algorithm, including the initial upper and lower bounds on and bounds on the precision needed when solving the projection problems.

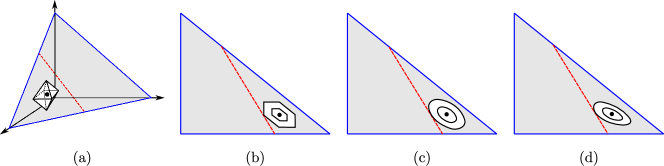

Note that problem (5) is infeasible if and only if . Moreover, problem (5) is trivially solved by with an optimal objective value of whenever . To avoid these trivial cases, we assume throughout the paper that and . We illustrate the feasible region and optimal solution to problem (5) for different -divergences in Figure 1.

Our generalized -projection (5) relates to the rich literature on projections onto simplices, which we review in the next section. In fact, our algorithms in the next section solve a variant of the simplex projection problem that is restricted by an additional inequality constraint. We therefore believe that our algorithms may find additional applications outside the RMDP literature.

In the following, we say that for a given estimate of the optimal value function, the robust Bellman iteration (3) is solved to -accuracy by any satisfying . We seek -optimal solutions because our ambiguity sets are nonlinear and hence the exact Bellman iterate may be irrational even if is rational. To simplify the exposition, we define as an upper bound on all , and .

For divergence-based ambiguity sets, the projection problem (5) is generically nonlinear and can hence not be expected to be solved to exact optimality. To account for this additional complication, we say that for a given , and , the generalized -projection is solved to -accuracy by any pair satisfying and .

Theorem 1.

Theorem 1 reduces the evaluation of the robust Bellman iterator , which involves the solution of a max-min optimization problem over an -rectangular ambiguity set that couples all actions , to a sequence of much simpler and highly structured projection problems that are no longer coupled across different actions . The next section describes efficient solution schemes for the projection problem (5) in the context of several -divergence ambiguity sets. The runtimes of these solution schemes are summarized in Table 1. Note that the evaluation of a non-robust Bellman operator requires a runtime of , which implies that our algorithms only incur an additional logarithmic overhead to account for robustness in the transition probabilities.

5 Fast Projections on -Divergence Simplices

We next describe fast algorithms for computing generalized projections onto the probability simplex. Combined with the results from Section 4, these algorithms can be used to efficiently compute the robust Bellman operator. Note that some -divergences, such as the KL divergence and the -distance, imply that if for some and , then for all with , and thus we can remove indices with . For other -divergences, such as the Burg entropy and the variation distance, one can readily verify that our results remain valid no matter whether or not, but the formulations and proofs require additional case distinctions and/or limit arguments. To simplify the exposition, we therefore assume that .

Proposition 1.

For the distance function , the optimal value of the projection problem (5) equals the optimal value of the bivariate convex problem

| (6) |

Proposition 1 reduces the -dimensional projection problem (5) to a two-dimensional optimization problem over the dual variables and . In the following, we show that for the -divergences from Table 1, problem (6) can be further simplified to univariate convex optimization problems that can be solved efficiently via bisection, binary search or sorting.

5.1 Kullback-Leibler Divergence

We first show that for the KL divergence , the reduced projection problem (6) can be further simplified to a univariate convex optimization problem.

Proposition 2.

For the KL divergence , the optimal value of the projection problem (5) equals the optimal value of the univariate convex problem

| (7) |

We next show that the univariate optimization problem (2) admits an efficient solution via bisection.

Theorem 2.

If for some , then the projection problem (5) can be solved to any -accuracy in time .

Note that the projection problem (5) is infeasible whenever . The condition in the statement of Theorem 2 can thus be interpreted as a strict feasibility requirement. It is worth contrasting the result of Theorem 2 with the solution of the projection problem (5) as an exponential cone program. The latter would result in a practical complexity of , assuming that—which is often observed in practice—the number of iterations of the employed interior-point solver does not grow with the problem dimensions. A theoretically guaranteed complexity, on the other hand, does not seem to be available at present as the commercial state-of-the-art solvers for exponential conic programs are not proven to terminate in polynomial time.

Corollary 1.

The robust Bellman iteration (3) over a KL divergence ambiguity set can be computed to any accuracy in time .

[14] propose a first-order framework for RMDPs over -rectangular KL divergence ambiguity sets whose robust Bellman update enjoys a complexity of , where is the iteration number. A careful analysis results in an overall convergence rate for the optimal MDP policy of . In contrast, the convergence rate of our robust value iteration amounts to . Treating the problem parameters , and as constants, our convergence rate simplifies to , which compares favourably against the convergence rate of the first-order scheme. Our numerical results in Section 6 show that this theoretical difference appears to carry over to a favourable empirical performance on test instances as well.

We finally note the related work [1], which optimizes a linear function over the intersection of a probability simplex with a constraint on the KL divergence to a nominal distribution. While one could in principle modify that algorithm to solve our projection problem (5), the resulting algorithm would require an additional bisection and would thus be significantly slower than ours.

5.2 Burg Entropy

Similar to the KL divergence, the reduced projection problem (6) can be further simplified to a univariate convex optimization problem for the Burg entropy .

Proposition 3.

For the Burg entropy , if , then the optimal value of the projection problem (5) equals the optimal value of the univariate convex problem

| (8) |

Similar to the KL divergence, the univariate optimization problem (8) can be solved efficiently.

Theorem 3.

If for some , then the projection problem (5) can be solved to any -accuracy in time .

As with the KL divergence, the projection problem (5) corresponding to the Burg entropy can be solved in a practical complexity of as an exponential cone program, whereas we are not aware of any state-of-the-art solvers equipped with theoretical guarantees. To our best knowledge, RMDPs with -rectangular Burg entropy ambiguity sets have not been studied previously in the literature.

Corollary 2.

The robust Bellman iteration (3) over a Burg entropy ambiguity set can be computed to any accuracy in time .

Similar to the previous subsection, we note that the related paper [1] optimizes a linear function over the intersection of a probability simplex with a bound on the Burg entropy to a nominal distribution. While that algorithm could in principle be employed to solve our projection problem (5), the resulting solution scheme would not be competitive due to the inclusion of an additional bisection.

5.3 Variation Distance

We first provide an equivalent univariate optimization problem for the reduced projection problem (6) corresponding to the variation distance .

Proposition 4.

For the variation distance , the optimal value of the projection problem (5) equals the optimal value of the univariate convex problem

| (9) |

Once more, the univariate optimization problem (9) admits an efficient solution.

Theorem 4.

The projection problem (5) can be solved exactly in time .

Note that in contrast to the previous results, Theorem 4 employs a binary search and thus offers an exact solution to the projection problem (5). Our result of Theorem 4 matches the complexity of the homotopy continuation method proposed by [19]. The correctness and runtime of their algorithm, however, relies on lengthy ad hoc arguments, whereas Theorem 4 relies on the groundwork laid by Theorem 1 and Proposition 1. Problem (5) can also be solved as a linear program with a practical complexity of and a theoretical complexity of .

Corollary 3.

The robust Bellman iteration (3) over a variation distance ambiguity set can be computed to any accuracy in time .

[40] study the related problem of optimizing a linear function over the intersection of a probability simplex with an unweighted -norm constraint, and they identify structural properties of the optimal solutions. Since the linear function and the norm constraint are in different places of the optimization problem, however, their findings are not directly applicable to our setting.

5.4 -Distance

In contrast to the previous subsections, we directly solve the bivariate problem (6) for the -distance without first formulating an associated univariate optimization problem.

Theorem 5.

For the -distance , the optimal value of the projection problem (5) can be computed exactly in time .

Theorem 5 splits the bivariate piecewise quadratic optimization problem (6) corresponding to the -distance into bivariate quadratic problems by sorting the components of . Each of these problems can be reduced to the solution of univariate quadratic problems that themselves admit analytical solutions.

Corollary 4.

The robust Bellman iteration (3) over a -distance ambiguity set can be computed to any accuracy in time .

The projection problem (5) for the -distance ambiguity set can be solved as a quadratic program with a practical complexity of as well as a theoretical complexity of .

The first-order framework of [14] also applies to RMDPs over -rectangular spherical uncertainty sets. In that case, the robust Bellman update enjoys a complexity of , where is the iteration number. A careful analysis results in an overall convergence rate for the optimal MDP policy of . In contrast, the convergence rate of our robust value iteration amounts to . Treating the parameter as a constant, our convergence rate simplifies to , which compares favourably against the convergence rate of [14]. We remark, however, that the spherical ambiguity sets of [14] differ from the -distance ambiguity sets studied here, and as such the two methods are not directly comparable. We also note that our -distance ambiguity sets enjoy a strong statistical justification [4, 6].

Computing unweighted -norm projections of points onto -dimensional probability simplices has manifold applications in image processing, finance, optimization and machine learning [1, 8]. [30] proposes one of the earliest algorithms that computes this projection in time by iteratively reducing the dimension of the problem using Lagrange multipliers. The minimum complexity of is achieved, among others, by [27] through a linear-time median-finding algorithm and by [36] through a filtered bucket-clustering method. Note, however, that these algorithms do not account for the weights and the additional inequality constraint present in our generalized projection (5). The unweighted -norm projection of a point onto the intersection of the -dimensional probability simplex with an axis-parallel hypercube is computed by [52] through a sorting-based method and by [2] through Newton’s method, respectively. [38] optimize a linear function over the intersection of a probability simplex with an unweighted -norm constraint through an iterative dimension reduction scheme. [1], finally, study algorithms that optimize linear functions over the intersection of a probability simplex and a bound on the unweighted -norm distance to a nominal distribution.

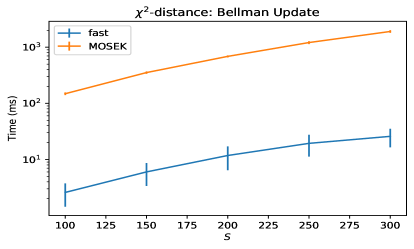

6 Numerical Results

We compare our fast suite of algorithms with the state-of-the-art solver MOSEK 9.3 [3] (commercial) and the first-order method of [14]. All experiments are implemented in C++, and they are run on a 3.6 GHz 8-Core Intel Core i9 CPU with 32 GB 2667 MHz DDR4 main memory. The source code is available at https://sites.google.com/view/clint-chin-pang-ho.

MOSEK fast MOSEK/fast 1,000 47.56 0.20 243.23 1,500 71.00 0.29 241.92 2,000 89.57 0.39 231.46 2,500 114.82 0.48 239.11 3,000 139.13 0.58 241.86 MOSEK fast MOSEK/fast 100 3,383.35 22.32 151.56 150 15,353.40 51.67 297.17 200 46,049.30 83.86 549.10 250 104,709.00 130.34 803.35 300 215,871.00 176.35 1,224.05

| f-o (3 its) | f-o (5 its) | fast | f-o/fast (3 its) | f-o/fast (5 its) | |

|---|---|---|---|---|---|

| 100 | 175.80 | 489.66 | 22.32 | 7.88 | 21.94 |

| 150 | 397.84 | 1,103.53 | 51.67 | 7.70 | 21.36 |

| 200 | 704.93 | 1,955.05 | 83.86 | 8.41 | 23.31 |

| 250 | 1,051.25 | 2,921.71 | 130.34 | 8.07 | 22.42 |

| 300 | 1,542.03 | 4,283.27 | 176.36 | 8.74 | 24.29 |

MOSEK fast MOSEK/fast 1,000 49.94 0.05 981.91 1,500 76.61 0.08 945.99 2,000 93.13 0.11 854.39 2,500 123.16 0.14 879.72 3,000 153.06 0.17 917.18 MOSEK fast MOSEK/fast 100 148.63 2.59 57.40 150 353.58 6.01 58.85 200 687.14 11.78 58.34 250 1,212.30 19.38 62.54 300 1,908.92 25.84 73.87

For our experiments, we synthetically generate random RMDP instances as follows. For the projection problem, we sample each component of uniformly at random between 0 and 1. Similarly, we sample each component of uniformly at random between 0 and 1 and subsequently scale so that its elements sum up to 1. The parameter , finally, is uniformly distributed between and to adhere to the assumptions of our paper. For the robust Bellman update, all vectors and all transition probabilities , and , are generated according to the above procedure. The parameter is also sampled from a uniform distribution supported on .

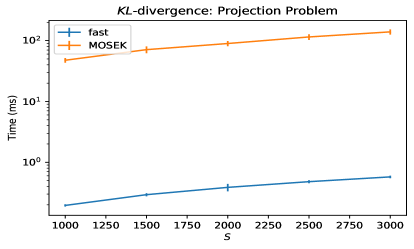

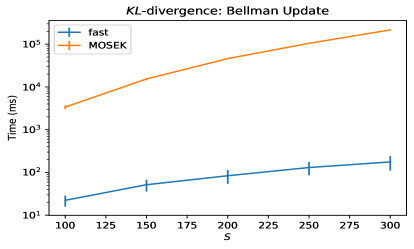

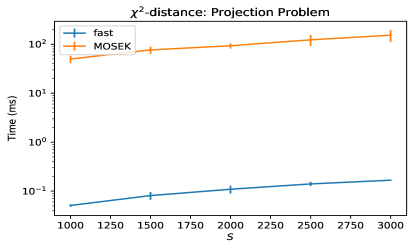

Tables 2–4 report average computation times over 50 randomly generated test instances for the KL-divergence and the -distance based ambiguity sets and show that the proposed algorithms outperform other methods. The tables reveal that our algorithms are about two orders of magnitude faster than MOSEK in solving the projection problem (5). For computing the robust Bellman update , our algorithms are also orders of magnitude faster than MOSEK, and this ratio increases with the problem size. The results also show that our algorithm outperforms the first-order method of [14]. The difference becomes more significant with an increasing number of robust Bellman updates. While our algorithms outperform the first-order scheme by a factor of 8 in the third Bellman iteration, they outperform it by a factor of about 20 in the fifth Bellman iteration. Since first-order methods are known to require many iterations for convergence, we conclude that our algorithm compares favorably in this experiment as well.

7 Conclusion

We study -rectangular robust MDPs with -divergence ambiguity sets. We develop efficient algorithms for computing robust Bellman updates for several important special cases of this ambiguity set. Our experimental results indicate that the proposed algorithms outperform MOSEK. Future work should address extensions to scalable model-free algorithms.

Acknowledgments

This work was supported, in part, by the Engineering and Physical Sciences Research Council (EPSRC) grant EP/W003317/1, by the CityU Start-Up Grant (Project No. 9610481), by the National Natural Science Foundation of China (Project No. 72032005), by the Chow Sang Sang Group Research Fund sponsored by Chow Sang Sang Holdings International Limited (Project No. 9229076), and by the NSF grant No. 1815275. Any opinion, finding, conclusion, or recommendation expressed in this material are those of the authors and do not necessarily reflect the views of the Engineering and Physical Sciences Research Council and the National Natural Science Foundation of China.

References

- Adam and Mácha [2020] L. Adam and V. Mácha. Projections onto the canonical simplex with additional linear inequalities. Optimization Methods & Software, Available online first, 2020.

- Ang et al. [2021] M. S. Ang, J. Ma, N. Liu, K. Huang, and Y. Wang. Fast projection onto the capped simplex with applications to sparse regression in bioinformatics. In Advances in Neural Information Processing Systems, volume 34, 2021.

- ApS [2019] MOSEK ApS. MOSEK Fusion API for C++ 9.3.20, 2019. URL https://docs.mosek.com/latest/cxxfusion/index.html.

- Bayraksan and Love [2015] G. Bayraksan and D. K. Love. Data-driven stochastic programming using phi-divergences. In D. M. Aleman and A. C. Thiele, editors, INFORMS TutORials in Operations Research, pages 1–19. 2015.

- Behzadian et al. [2021] B. Behzadian, M. Petrik, and C. P. Ho. Fast algorithms for -constrained s-rectangular robust MDPs. In Advances in Neural Information Processing Systems, volume 34, 2021.

- Ben-Tal et al. [2013] A. Ben-Tal, D. den Hertog, A. de Waegenaere, B. Melenberg, and G. Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- Chen et al. [2019] Z. Chen, P. Yu, and W. B. Haskell. Distributionally robust optimization for sequential decision-making. Optimization, 68(12):2397–2426, 2019.

- Condat [2016] L. Condat. Fast projection onto the simplex and the ball. Mathematical Programming, 158(1–2):575–585, 2016.

- Derman et al. [2021] E. Derman, M. Geist, and S. Mannor. Twice regularized MDPs and the equivalence between robustness and regularization. In Advances in Neural Information Processing Systems, volume 35, pages (Pre–Proceedings), 2021.

- Diehl and Bjornberg [2004] M. Diehl and J. Bjornberg. Robust dynamic programming for min-max model predictive control of constrained uncertain systems. IEEE Transactions on Automatic Control, 49(12):2253–2257, 2004.

- Givan et al. [2000] R. Givan, S. Leach, and T. Dean. Bounded-parameter Markov decision processes. Artificial Intelligence, 122(1):71–109, 2000.

- Goh et al. [2018] J. Goh, M. Bayati, S. A. Zenios, S. Singh, and D. Moore. Data uncertainty in Markov chains: Application to cost-effectiveness analyses of medical innovations. Operations Research, 66(3):697–715, 2018.

- Goyal and Grand-Clément [2018] V. Goyal and J. Grand-Clément. Robust Markov decision process: Beyond rectangularity. Available on arXiv, 2018.

- Grand-Clément and Kroer [2021a] J. Grand-Clément and C. Kroer. Scalable first-order methods for robust MDPs. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 12086–12094, 2021a.

- Grand-Clément and Kroer [2021b] J. Grand-Clément and C. Kroer. First-order methods for Wasserstein distributionally robust MDPs. In Proceedings of Machine Learning Research, volume 139, pages 2010–2019, 2021b.

- Grand-Clément et al. [2019] J. Grand-Clément, C. W. Chan, V. Goyal, and G. Escobar. Robust policies for proactive ICU transfers. Working Paper, 2019.

- Gupta [2019] Vishal Gupta. Near-optimal Bayesian ambiguity sets for distributionally robust optimization. Management Science, 65(9):4242–4260, 2019.

- Ho et al. [2018] C. P. Ho, M. Petrik, and W. Wiesemann. Fast Bellman updates for robust MDPs. In Proceedings of the 35th International Conference on Machine Learning, pages 979–1988, 2018.

- Ho et al. [2021] C. P. Ho, M. Petrik, and W. Wiesemann. Partial policy iteration for -robust Markov decision processes. Journal of Machine Learning Research, 22:1–46, 2021.

- Huang et al. [2018] Q. Huang, Q.-S. Jia, and X. Guan. Robust scheduling of EV charging load with uncertain wind power integration. IEEE Transactions on Smart Grid, 9(2):1043–1054, 2018.

- Iyengar [2005] G. N. Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Kaufman and Schaefer [2013] D. L. Kaufman and A. J. Schaefer. Robust modified policy iteration. INFORMS Journal on Computing, 25(3):396–410, 2013.

- Kochenderfer and Chryssanthacopoulos [2011] M. J. Kochenderfer and J. P. Chryssanthacopoulos. Robust airborne collision avoidance through dynamic programming. Project Report ATC-371 for the Federal Aviation Administration, 2011.

- Kolarijani et al. [2021] M.A.S. Kolarijani, G.F. Max, and P. Mohajerin Esfahani. Fast approximate dynamic programming for infinite-horizon markov decision processes. In Advances in Neural Information Processing Systems, volume 34, pages 23652–23663, 2021.

- Le Tallec [2007] Y. Le Tallec. Robust, Risk-Sensitive, and Data-driven Control of Markov Decision Processes. PhD thesis, Massachusetts Institute of Technology, 2007.

- Love and Bayraksan [2015] D. Love and G. Bayraksan. Phi-divergence constrained ambiguous stochastic programs for data-driven optimization. Technical report, 2015.

- Maculan and de Paula Jr. [1989] N. Maculan and G. G. de Paula Jr. A linear-time median-finding algorithm for projecting a vector on the simplex of . Operations Research Letters, 8(4):219–222, 1989.

- Mannor et al. [2016] S. Mannor, O. Mebel, and H. Xu. Robust MDPs with -rectangular uncertainty. Mathematics of Operations Research, 41(4):1484–1509, 2016.

- Marjani et al. [2021] A. Al Marjani, A. Garivier, and A. Proutiere. Navigating to the best policy in markov decision processes. In Advances in Neural Information Processing Systems, volume 34, pages 25852–25864, 2021.

- Michelot [1986] C. Michelot. A finite algorithm for finding the projection of a point onto the canonical simplex of . Journal of Optimization Theory and Applications, 50(1):195–200, 1986.

- Nie et al. [2021] A. Nie, E. Brunskill, and C. Piech. Play to grade: Testing coding games as classifying markov decision process. In Advances in Neural Information Processing Systems, volume 34, pages 1506–1518, 2021.

- Nilim and Ghaoui [2005] A. Nilim and L. El Ghaoui. Robust control of Markov decision processes with uncertain transition matrices. Operations Research, 53(5):780–798, 2005.

- Panaganti and Kalathil [2021] K. Panaganti and D. Kalathil. Robust reinforcement learning using least squares policy iteration with provable performance guarantees. In Proceedings of the 38th International Conference on Machine Learning, pages 511–520, 2021.

- Panaganti and Kalathil [2022] K. Panaganti and D. Kalathil. Sample complexity of robust reinforcement learning with a generative model. In International Conference on Artificial Intelligence and Statistics, pages 9582–9602. PMLR, 2022.

- Parys et al. [2021] B. P.G. Van Parys, P. Mohajerin Esfahani, and D. Kuhn. From data to decisions: Distributionally robust optimization is optimal. Management Science, 67(6):3387–3402, 2021.

- Perez et al. [2020] G. Perez, M. Barlaud, L. Fillatre, and J.-C. Régin. A filtered bucket-clustering method for projection onto the simplex and the ball. Mathematical Programming, 182(1–2):445–464, 2020.

- Petrik and Subramanian [2014] M. Petrik and D. Subramanian. RAAM: The benefits of robustness in approximating aggregated MDPs in reinforcement learning. In Advances in Neural Information Processing Systems, volume 27, pages 1979–1987, 2014.

- Philpott et al. [2018] A. Philpott, V. de Matos, and L. Kapelevich. Distributionally robust SDDP. Computational Management Science, 15(3–4):431–454, 2018.

- Puterman [1994] M. L. Puterman. Markov Decision Processes: Discrete Stochastic Dynamic Programming. John Wiley & Sons, 1994.

- Rahimian et al. [2019] H. Rahimian, G. Bayraksan, and T. Homem-de-Mello. Identifying effective scenarios in distributionally robust stochastic programs with total variation distance. Mathematical Programming, 173(1–2):393–420, 2019.

- Rockafellar [1997] R. T. Rockafellar. Convex Analysis. Princeton University Press, 1997.

- Roy et al. [2017] A. Roy, H. Xu, and S. Pokutta. Reinforcement learning under model mismatch. In Advances in Neural Information Processing Systems, volume 30, 2017.

- Rusmevichientong and Topaloglu [2012] P. Rusmevichientong and H. Topaloglu. Robust assortment optimization under the multinomial logit choice model. Operations Research, 60(4):865–882, 2012.

- Ruszczyński [2010] A. Ruszczyński. Risk-averse dynamic programming for Markov decision processes. Mathematical Programming, 125(2):235–261, 2010.

- Satia and Jr. [1973] J. K. Satia and R. E. Lave Jr. Markovian decision processes with uncertain transition probabilities. Operations Research, 21(3):728–740, 1973.

- Shapiro [2016] A. Shapiro. Rectangular sets of probability measures. Operations Research, 64(2):528–541, 2016.

- Shapiro [2021] A. Shapiro. Distributionally robust optimal control and MDP modeling. Operations Research Letters, 49(3):809–814, 2021.

- Sutton and Barto [2018] R. S. Sutton and A. G. Barto. Reinforcement Learning: An Introduction. The MIT Press, second edition, 2018.

- Tamar et al. [2014a] A. Tamar, Y. Glassner, and S. Mannor. Policy gradients beyond expectations: Conditional value-at-risk. Available on arXiv, 2014a.

- Tamar et al. [2014b] A. Tamar, S. Mannor, and H. Xu. Scaling up robust MDPs using function approximation. In Proceedings of the 31st International Conference of Machine Learning, 2014b.

- Tirinzoni et al. [2018] A. Tirinzoni, X. Chen, M. Petrik, and B. D. Ziebart. Policy-conditioned uncertainty sets for robust Markov decision processes. In Advances in Neural Information Processing Systems, volume 31, pages 8953–8963, 2018.

- Wang and Lu [2015] W. Wang and C. Lu. Projection onto the capped simplex. Available on arXiv, 2015.

- Wang and Zou [2021] Y. Wang and S. Zou. Online robust reinforcement learning with model uncertainty. In Advances in Neural Information Processing Systems, volume 34, pages 7193–7206, 2021.

- Wang and Zou [2022] Yue Wang and Shaofeng Zou. Policy gradient method for robust reinforcement learning. In Proceedings of the 39th International Conference on Machine Learning, pages 23484–23526, 2022.

- Weissman et al. [2003] T. Weissman, E. Ordentlich, G. Seroussi, S. Verdu, and M. J. Weinberger. Inequalities for the deviation of the empirical distribution. Technical Report, https://www.hpl.hp.com/research/infotheory/papers/HPL-2003-97R1Web.pdf, 2003.

- Wiesemann et al. [2013] W. Wiesemann, D. Kuhn, and B. Rustem. Robust Markov decision processes. Mathematics of Operations Research, 38(1):153–183, 2013.

- Xiao et al. [2013] H. Xiao, K. Yang, and X. Wang. Robust power control under channel uncertainty for cognitive radios with sensing delays. IEEE Transactions on Wireless Communications, 12(2):646–655, 2013.

- Xin and Goldberg [2018] L. Xin and D. A. Goldberg. Distributionally robust inventory control when demand is a martingale. Available on arXiv, 2018.

- Xu and Mannor [2010] H. Xu and S. Mannor. Distributionally robust Markov decision processes. In Advances in Neural Information Processing Systems, volume 23, pages 2505–2513, 2010.

- Xu and Mannor [2012] H. Xu and S. Mannor. Distributionally robust Markov decision processes. Mathematics of Operations Research, 37(2):288–300, 2012.

- Yu and Xu [2016] P. Yu and H. Xu. Distributionally robust counterpart in Markov decision processes. IEEE Transactions on Automatic Control, 61(9):2538–2543, 2016.

- Zhang et al. [2017] Y. Zhang, L. N. Steimle, and B. T. Denton. Robust Markov decision processes for medical treatment decisions. Available on Optimization Online, 2017.

Appendix A Additional Results of the Experiments

Figures 2–4 provide error bars (with mean values as horizontal curves and standard deviations as vertical bars) for the numerical results reported in Tables 2–4.

Appendix B Proofs

The proof of Theorem 1 requires us to analyze the quantitative stability of the robust Bellman operator . To this end, we study the dual of problem (3’) on page 3’, which the proof of Theorem 1 will show to be equivalent to the robust value iteration (3):

| (10) |

Here, denotes the conjugate of the deviation function in the definition (2) of the ambiguity set , and the perspective function in (10) extends to in the usual way [41, Corollary 8.5.2]. Note also that strong duality holds between (3’) and (10) since problem (3’) affords a Slater point by assumption (K).

The proof of Theorem 1 relies on two auxiliary results, which we state and prove first.

Lemma 1.

Proof of Lemma 1. Using the notational shorthand , the KKT conditions for (3’) and (10) are:

Here, denotes the epigraphical variable used to linearize the objective function in (3’). The proof is split into two parts. We first show that for every there is such that

| (11) |

We next prove that for all and , we have

| (12) |

Since by the dual feasibility condition, (11) and (12) imply that for every there is such that . From this we obtain that

where the last inequality holds since by the second stationarity condition. This proves the statement of the lemma.

To show (11), we note that

since is convex by assumption (C) and by assumption (D). We thus have

and the fact that implies that

which is equivalent to (11).

We now prove (12). Aggregating the equations in the first stationarity condition according to the weights shows that for all , we have

| (13) |

since the primal feasibility condition guarantees that and the last complementary slackness condition ensures that . However, the first stationarity condition also implies

| (14) |

since due to the dual feasibility condition. Combining (13) and (14), finally, yields

which implies (12) since as by the dual feasibility condition, by the primal feasibility condition and by assumption. ∎

Lemma 2.

Proof of Lemma 2. Since , we have for fixed that

where belongs to any primal-dual pair and satisfying the KKT conditions of problems (3’) and (10). Indeed, since only the first term in the objective function in (10) depends on , the solution for the dual problem with budget remains feasible (but is typically not optimal) for the dual problem with budget , and its objective value decreases by precisely . The result now follows from Lemma 1. ∎

Proof of Theorem 1. We compute an -optimal solution to the robust Bellman iteration component-wise. To this end, consider any component , . We apply the classical min-max theorem to equivalently reformulate the right-hand side of (3) as the optimal value of the optimization problem

| (3’) |

In this reformulation, we have replaced the inner maximization over with the maximization over the extreme points of , which is allowed since the objective function is linear in .

We compute through a bisection on the optimal value of problem (3’). To this end, we set . We start the bisection with the lower and upper bounds and , respectively. Here, the lower bound satisfies , and it indeed constitutes a lower bound since the projection subproblem (5) is infeasible if which is set to be for each . Likewise, the upper bound is valid as long as our robust Bellman iteration operates on (approximate) lower bounds of the value function, which can be guaranteed, for example, by starting the robust Bellman iteration with the initial estimate . In each iteration , we consider the midpoint and compute the generalized -projections , , to -accuracy, resulting in the action-wise lower and upper bounds , respectively. When then update the interval bounds as follows:

We terminate the bisection once (i) or (ii) , whichever condition holds first. Note that both interval updates ensure that and remain valid bounds since

as well as

where the respective second implications hold since

and the latter is the case if and only if the optimal value of problem (3’) does not exceed , that is, if and only if for some .

At termination, in case (i) we have , which implies that is an -optimal solution to . If case (ii) is satisfied at termination, on the other hand, then

in which case is an exact optimal solution to the variant of the robust value iteration (3) where the budget in the ambiguity set is replaced with some . In this case, we have that

where the first inequality follows from the monotonicity of in its second argument, and the second inequality holds because of the following argument. If the constraint in problem (3’) is not binding at optimality, then . On the other hand, if the constraint in problem (3’) is binding at optimality, then by applying Lemma 2 in the appendix and using our definition of and the fact that , we have

One readily verifies that at most iterations of complexity are executed in each of the bisections, which concludes the proof. ∎

Proof of Proposition 1. For the deviation measure from the statement of this proposition, problem (5) becomes

| (15) |

The Lagrange dual function associated with this problem is

where and . Rearranging terms, we observe that

and the suprema inside this expression coincide with the convex conjugates , . The resulting optimization problem (6) is convex since the conjugates are convex. Moreover, since by assumption, problem (15) affords a feasible solution, and the linearity of the constraints implies that this solution constitutes a Slater point. We thus conclude that strong duality holds between (6) and (15), that is, their optimal objective values indeed coincide. ∎

Proof of Proposition 2. Plugging the convex conjugate of the KL divergence into the bivariate optimization problem (6), we obtain

By rearranging terms, the objective function can be expressed as

| (16) |

and the first-order optimality condition shows that for fixed , the function is maximized by

Substituting in (16), we obtain problem (7) as postulated. ∎

Proof of Theorem 2. We prove the statement in three steps. Step 1 shows that the optimal solution to (7) is lower and upper bounded by and , respectively. Note that is finite due to the assumed strict positivity of and . Step 2 derives a global upper bound on the derivative of , which we henceforth use to denote of the objective function of problem (7). In conjunction with the concavity of , this will allow us to bound the maximum objective function value over any interval . Step 3, finally, employs a bisection search to solve (7) to -accuracy in the stated complexity.

As for the first step, the validity of the lower bound follows directly from the non-negativity constraint in (7). In view of the upper bound , we note that

Since and while at the same time , we conclude from the concavity of that is indeed a valid upper bound on the maximizer of problem (7).

In view of the second step, we observe that

where the first inequality follows from the concavity of and the other two inequalities hold since . The concavity of then implies that for any , we have

Thus, if we find , sufficiently close such that , then we can closely bound the optimal objective value of problem (7) from below and above by and , respectively.

As for the third step, finally, we bisect on by starting with the initial bounds , halving the length of the interval in each iteration by verifying whether is positive and terminating once . Since , we have

and thus the length of the interval no longer exceeds once the iteration number satisfies

that is, after iterations. The interval then provides the -accurate solution to the projection problem (5). The statement now follows from the fact that evaluating the derivative in each bisection step takes time . ∎

Remark 1.

The proposed lower and upper bounds in Theorem 2 are tight up to constant factor. Indeed, consider the example where and with , and for . Then the objective function in problem (7) is

The above problem satisfies the setting in Theorem 2 since . We search for that satisfies the first order condition:

We thus have , that is, the upper bound on should be at least , when .

Proof of Corollary 1. The proof of Theorem 1 employs an outer bisection over that requires for each the repeated solution of the projection problem (7) with and (since the outer bisection is stopped when the interval length no longer exceeds ) to an accuracy of . In that case, for each we have

and . Plugging those estimates into the statement of Theorem 2, we see that the projection problem (7) is solved in time

Combining this estimate with the complexity from Theorem 1, we obtain

and a reordering of terms proves the statement of the corollary. ∎

Proof of Proposition 3. Plugging the convex conjugate of the Burg entropy into the bivariate optimization problem (6), we obtain

| (17) |

Here, the first constraint ensures that the logarithms in the objective function are well-defined (as usual, we assume that ). Unlike the proof of Proposition 2, the first-order optimality condition of this problem’s objective function does not lend itself to extracting the optimal value of . Instead, we consider the Karush-Kuhn-Tucker conditions for problem (17), which are:

The optimal value of problem (17) is non-negative since satisfies the constraints of (17). Hence, complementary slackness implies that , as otherwise would imply that the optimal objective value of problem (17) was . Multiplying the first stationarity condition with and the second one with and summing up then yields

where the right-hand side of the first line exploits the fact that and the last equivalence uses complementary slackness to replace with . The result now follows from substituting with in problem (17) and rescaling via . ∎

Proof of Theorem 3. Similar to the proof of Theorem 2, we show the statement in three steps. Step 1 argues that , which we henceforth use to denote of the objective function of problem (8), is well-defined and continuously differentiable on the half-open interval with a positive derivative at and a negative derivative close to , respectively. This ensures that the optimum is attained on the open interval . Step 2 derives a global upper bound on , which will allow us to bound the maximum objective function value over any interval due to the concavity of . Step 3, finally, employs a bisection search to solve (8) to -accuracy in the stated complexity.

In view of the first step, we note that for we have

and thus the expression inside the logarithm of is strictly positive for all . Here, the first inequality holds by assumption, and the last equivalence follows from a division by , which is strictly positive by assumption. We then observe that for , we have

In particular, we have , which is positive since by assumption. (Recall that the projection problem is trivial if .) For , on the other hand, the fractions in corresponding to the indices with evaluate to , whereas the other fractions evaluate to

and thus remain finite. In conclusion, we have for near .

As for the second step, we observe that

where the inequalities follow from the concavity of , the fact that as well as , and because , respectively. Similar arguments as in the proof of Theorem 2 then allow us to closely bound the optimal value of problem (8) from below and above by and , respectively, whenever .

In view of the third step, finally, we bisect on by starting with the initial bounds , halving the length of the interval in each iteration by verifying whether is positive and terminating once . Similar arguments as in the proof of Theorem 2 show that this is the case after iterations. The statement now follows since evaluating the derivative in each bisection step takes time . ∎

Proof of Corollary 2. The proof of Theorem 1 employs an outer bisection over that requires for each the repeated solution of the projection problem (7) with and (since the outer bisection is stopped when the interval length no longer exceeds ) to an accuracy of . In that case, for each we have . Plugging this estimate into the statement of Theorem 3, we see that the projection problem (8) is solved in time

Combining this estimate with the complexity from Theorem 1, we obtain

and a reordering of terms proves the statement of the corollary. ∎

Proof of Proposition 4. Plugging in the definition of , see Table 1, results in the following variant of problem (6):

Note that the constraints are equivalent to . The above objective function is piecewise linear in with coefficients that are all non-negative. Thus, . In this case, the problem simplifies to the problem in the statement of the proposition. ∎

Proof of Theorem 4. There must be an optimal solution to this problem that is attained at

Since the objective function is concave in , we can identify an optimal solution in iterations via a trisection search. Each evaluation requires time , thus resulting in an overall complexity of as claimed. ∎

Proof of Corollary 3. Combining the estimate from Theorem 4 with the complexity from Theorem 1, we obtain

and a reordering of terms proves the statement of the corollary. ∎

Proof of Theorem 5. To solve this problem, we sort the components of so that the associated expressions are monotonically non-decreasing (that is, are monotonically non-increasing). For each , we can then consider the subproblem

which due to the monotonically non-decreasing ordering of is equivalent to

| (18) |

The objective function of (18) can be re-expressed as

Recall that for a fixed value of , the constraints of (18) impose that . Therefore, for any fixed , problem (18) reduces to a convex quadratic optimization problem with one-dimensional box constraints. One can readily verify that this problem is solved by

We can consider each case separately. In the first case, we restrict the domain of so that , and problem (18) reduces to

Note that the constraint in this problem is equivalent to

Here, the last equivalence holds since the components of are sorted and . We have thus reduced the problem to a one-dimensional convex quadratic program with a box constraint, whose closed-form solution can be computed in . Similar formulations can be derived for the other two cases of .

In summary, the overall complexity is due to the sorting of the components of , while each of the subproblems can be solved in constant time . ∎