Robust multiscale estimation of time-average variance for time series segmentation

Abstract

There exist several methods developed for the canonical change point problem of detecting multiple mean shifts, which search for changes over sections of the data at multiple scales. In such methods, estimation of the noise level is often required in order to distinguish genuine changes from random fluctuations due to the noise. When serial dependence is present, using a single estimator of the noise level may not be appropriate. Instead, it is proposed to adopt a scale-dependent time-average variance constant that depends on the length of the data section in consideration, to gauge the level of the noise therein. Accordingly, an estimator that is robust to the presence of multiple mean shifts is developed. The consistency of the proposed estimator is shown under general assumptions permitting heavy-tailedness, and its use with two widely adopted data segmentation algorithms, the moving sum and the wild binary segmentation procedures, is discussed. The performance of the proposed estimator is illustrated through extensive simulation studies and on applications to the house price index and air quality data sets.

Keywords: change point analysis, time-average variance constant, robust estimation, moving sum procedure, wild binary segmentation

1 Introduction

Dating back to the 1950s (Page,, 1954), change point analysis has a long tradition in statistics. The area continues to be an active field of research due to its importance in many applications where data is routinely collected in highly nonstationary environments. Data segmentation, a.k.a. multiple change point detection, enables partitioning of a time series into stationary regions and thus provides a simple framework for modelling nonstationary time series.

We consider the problem of detecting multiple change points in the piecewise constant mean of an otherwise stationary time series. We briefly review the existing literature on multiple change point detection in the presence of serial dependence, and refer to Aue and Horváth, (2013) and Truong et al., (2020) for a comprehensive overview. One line of research takes a parametric approach and simultaneously estimates the serial dependence and change points. For example, Chakar et al., (2017), Fang and Siegmund, (2020) and Romano et al., (2021) assume an autoregressive (AR) model of order one, while Lu et al., (2010), Cho and Fryzlewicz, (2021) and Gallagher et al., (2022) permit an AR model of arbitrary order.

Another line of research focuses on extending the use of the methodologies developed for independent data to time series settings. Lavielle and Moulines, (2000) and Cho and Kirch, (2021) adopt information criteria originally developed for a sequence of independent, Gaussian random variables (Yao,, 1988), to data exhibiting serial correlations and heavy tails, which requires the choice of an appropriate penalty that depends on the tail behaviour of noise. Tecuapetla-Gómez and Munk, (2017), Eichinger and Kirch, (2018), Dette et al., (2020) and Chan, (2022) propose estimators of the long-run variance (LRV) for quantifying the level of noise that are robust to the presence of multiple mean shifts. We also note that Wu and Zhou, (2020) and Zhao et al., (2021) extend self-normalisation-based change point tests to the data segmentation problem.

In this paper, we propose a robust estimator of the scale-dependent time-average variance constant (TAVC, Wu,, 2009). It is closely related to the literature on estimation of the LRV, namely for a stationary time series , but distinct in that our interest lies in estimating

| (1) |

for a given scale . We argue that such a scale-dependent TAVC estimator is well-suited to be combined with a class of multiscale change point detection methodologies, examples of which include the moving sum (MOSUM) procedure (Eichinger and Kirch,, 2018) and the wild binary segmentation (WBS, Fryzlewicz,, 2014) algorithm. Such approaches locally apply change point tests for single change point detection, to data sections of varying lengths and achieve good adaptivity in multiple change point detection (Cho and Kirch,, 2021). We motivate the use of scale-dependent TAVC in (1) in combination with such multiscale methods in the following examples.

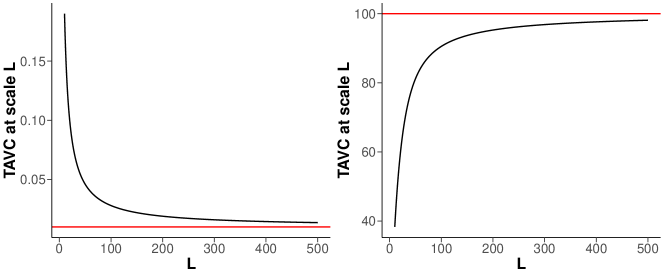

Example 1.

Consider an MA() process and an AR() process , where is a white noise process with . Figure 1 shows the TAVC of and for increasing , along with the true LRV, which highlights the large gap between and particularly at a small scale . This discrepancy has an impact on the performance of change point detection methods.

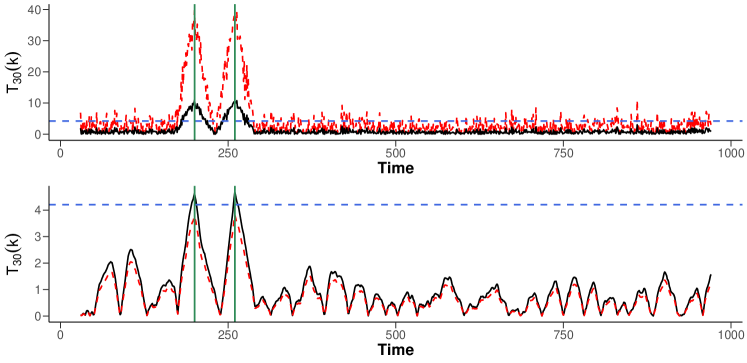

Figure 2 further illustrates this point by plotting the MOSUM detector statistics generated with a moving window of length (see Equation (11) for its definition), on the data generated by adding and to a piecewise signal with two change points at times and , respectively (). Then, the detector statistics are scaled by the proposed estimator of TAVC (solid) and the true LRV (dashed). For accurate detection of the change points, we expect that a sequence of appropriately scaled detector statistics forms two prominent peaks at the change points that exceed a theoretically motivated threshold, while away from the change points, detector statistics remain below the threshold, see Section 3.1 for further details. In combination with the TAVC estimator, the detector statistics exhibit the desired behaviour such that both change points are detectable from the scaled MOSUM statistics. However, due to the lack of adaptivity of the LRV to the scale-dependent variability of the detector statistics, its use leads to either a large number of false positives (spurious peaks above threshold, see the top panel of Figure 2), or false negatives (MOSUM detector statistics scaled by the LRV do not exceed the threshold near , see the bottom panel of Figure 2).

Example 1 demonstrates that adopting the global LRV may fail to reflect the degree of variability in the local data sections that are used in computing change point detector statistics adopted by multiscale data segmentation algorithms, which in turn may result in false negatives or positives. Moreover, when the LRV is close to zero as in the case of in Example 1, some estimators of the LRV have been observed to take negative values (Hušková and Kirch,, 2010), which further makes their use in change point problems undesirable.

To ensure that the scale-dependent TAVC estimator is robust to the mean shifts, we adopt the robust -estimation framework of Catoni, (2012), which was first proposed in the independent setting for mean and variance estimation and further extended to the serially dependent setting for LRV estimation in Chen et al., (2021). We establish the consistency of the proposed robust estimator of scale-dependent TAVC under general conditions permitting heavy tails and serial dependence decaying at a polynomial rate. Then, we discuss its application with multiscale change point detection methods such as the MOSUM procedure and the WBS algorithm, and provide a heuristic approach to accommodate local stationarity in the data.

The remainder of the article is organised as follows.

Section 2 introduces the scale-dependent TAVC and

its robust estimator and establishes its consistency.

Section 3 discusses its application with multiscale data segmentation algorithms and an extension to local stationarity.

In Section 4, we examine the performance of the proposed methodology

on simulated data sets and two real data examples on house price index and air quality.

Section 5 concludes the paper.

All proofs, algorithmic descriptions of multiscale change point methods

and additional numerical results are given in the appendix.

Accompanying R software implementing the methodology is available from https://github.com/EuanMcGonigle/TAVC.seg.

2 Scale-dependent TAVC and its robust estimation

2.1 Multiscale change point detection in the mean

We consider the problem of multiple change point detection under the following model:

| (2) |

Under the model (2), the piecewise constant signal contains change points at locations , , with the notational convention that and . The errors are assumed to be a (weakly) stationary time series satisfying with finite LRV , and are permitted to be serially correlated and heavy-tailed (see Assumption 1 below). Our aim is to consistently estimate the total number and the locations of the change points. While our primary focus is on detecting changes in the mean, it does not exclude the possibility of applying the proposed method to detecting changes in stochastic properties other than the mean via suitable data transformation as outlined in Cho and Kirch, (2021).

A common approach to this problem is closely related to the change point testing literature, which scans the data for the detection and estimation of multiple change points by locally applying a test well-suited for detecting a single change. Such a procedure typically involves comparing a test statistic of the form to a threshold, say . Here,

| (3) |

denotes a change point detector evaluated at some locations , which are determined in a method-specific way (see Section 3 below), denotes a measure of variability in the data section , and its estimator. Under the stationarity assumption on , a natural choice is , the scale-dependent TAVC defined in (1) with as the scale. Then, if does not contain any change point well within the interval, we expect , while it signals the presence of such a change point when . The key challenge lies in separating genuine mean shifts from the natural fluctuations due to serial correlations, which requires a careful selection of the estimator that correctly captures the variability in the section of the data under consideration.

It is well-documented that multiscale application of such a test on data sections of varying lengths, improves the adaptivity of the change point methodology to detect both large, frequent changes and small changes over long stretches of stationarity (Cho and Kirch,, 2021). For such a multiscale procedure, Example 1 demonstrates the potential pitfalls associated with using an estimator of the global LRV in place of , regardless of the length of the interval on which the detector statistic in (3) is computed. In the next section, we propose an estimator of the scale-dependent TAVC in (1) that is robust to the presence of multiple mean shifts, for the standardisation of multiscale change point detectors.

2.2 Robust estimation of multiscale TAVC

For notational convenience, suppose that is an even number, and let denote the block size. Then, for some starting point with number of blocks , we define

Analogously, we define

Then, the following sum

| (4) |

takes into account the temporal dependence in the local data sections of length . Further, we have for (see Theorem 1 below), such that is indicative of the level of variability albeit being inaccessible (as it is defined with in place of ). Its accessible counterpart, , on the other hand, is typically biased due to the mean shifts and thus is inappropriate as an estimator of the scale-dependent TAVC.

To obtain an estimator that is robust to multiple mean shifts, we adopt the robust -estimation framework of Catoni, (2012). Let denote a non-decreasing influence function as

| (5) |

The robust estimator of the TAVC at scale and starting point , denoted , is defined as the solution of the -estimation equation

| (6) |

where for some ; we specify the condition on later. If there are multiple solutions to Equation (6), any of them may be chosen.

2.3 Theoretical properties

We establish the consistency of the scale-dependent TAVC estimator under the following assumption on the error process .

Assumption 1.

-

(i)

We assume that , where is a sequence of i.i.d. random variables and for some constants and for all .

-

(ii)

There exists a fixed constant such that satisfies .

-

(iii)

We operate under either of the following two conditions on the distribution of .

-

(a)

There exists a fixed constant such that .

-

(b)

There exist fixed constants and such that for all .

-

(a)

The linearity of the process assumed in Assumption 1 (i) facilitates the controlling of the functional dependence in . The condition permits the temporal dependence to decay at an algebraic rate. Assumption 1 (ii) is made to ensure that the LRV is well-defined. Assumption 1 (iii) (iii)(a) allows heavy-tailed , while (iii)(b) assumes a stronger condition that requires sub-Weibull (Wong et al.,, 2020) tail behaviour on which includes sub-Gaussian () and sub-exponential () distributions as special cases.

For sequences of positive numbers and , write if there exists some positive constants and such that as . The following theorem establishes the consistency of the estimator of the scale-dependent TAVC, see Appendix C for the proof.

Theorem 1.

Theorem 1 shows that the proposed robust estimator consistently estimates the TAVC at scale . The estimation error is decomposed into the error from approximating by in (9), and that in estimating by . In deriving the second error, we make explicit the influence of multiple mean shifts on the estimator by the term in (7)–(8), as well as the effect of the innovation distribution in the remaining terms. A careful examination of the proof of Theorem 1 shows that

| (10) |

therefore as increases, the scale- TAVC approximates the global LRV as expected.

Remark 1 (Maximum time-scale for TAVC estimation).

The error due to approximating with decreases with as in (9). On the other hand, the error of estimating with increases with as in (7)–(8); this is attributed to the effect of mean shifts that grows with , and the decrease in the number of available blocks. To balance between the two, we suggest setting a maximum time-scale, say , to be used in combination with a multiscale change point detection algorithm. That is, when the change point detector involves , we scale the detector with the estimator of , the TAVC at the corresponding scale . On the other hand, if , we propose to scale the detector with the estimator of , the TAVC at the maximum time-scale , which satisfies .

3 Applications and extensions

We now describe explicitly how the robust estimator of the scale-dependent TAVC proposed in Section 2, is applied within the algorithms that scan moving sum (MOSUM) and cumulative sum (CUSUM) statistics of the form (3), for multiple change point detection.

3.1 MOSUM procedure

The MOSUM procedure (Chu et al.,, 1995; Eichinger and Kirch,, 2018) evaluates the change point detector over a moving window. For a given bandwidth , the MOSUM detector for a change in mean at time point is given by

| (11) |

Eichinger and Kirch, (2018) propose to estimate the total number and the locations of multiple change points by identifying all significant local maximisers of , say , satisfying

| (12) |

for some . Here, denotes a critical value at a significance level , which is drawn from the asymptotic null distribution of the MOSUM test statistic obtained under mild conditions permitting heavy-tailedness and serial dependence, and takes the form

where and are known constants depending on and only. The single-bandwidth MOSUM procedure achieves consistency in estimating the total number and the locations of multiple change points, provided that as sufficiently fast while , see Theorem 3.2 of Eichinger and Kirch, (2018) and Corollary D.2 of Cho and Kirch, (2022) for explicit conditions. The requirement on indicates that the single-scale MOSUM procedure performs best with the bandwidth chosen as large as possible while avoiding situations where there are more than one change point within the moving window at any time. Consequently, it lacks adaptivity when the data sequence contains both large changes over short intervals and small changes over long intervals.

Multiscale extensions of the single-bandwidth MOSUM procedure, i.e. applying the MOSUM procedure with a range of bandwidths and then combining the results, alleviate the difficulties involved in bandwidth selection and provide adaptivity. In this paper, we consider the multiscale MOSUM procedure combined with the ‘bottom-up’ merging as proposed by Messer et al., (2014) (see also Meier et al., (2021)). Denoting the range of bandwidths by , let denote the set of estimators detected with some bandwidth . Then, we accept all estimators in returned with the finest bandwidth to the set of final estimators and, sequentially for , accept if and only if (with identical to that in (12)). That is, we only accept the estimators that do not detect the change points which have previously been detected at a finer scale.

We propose to apply the multiscale MOSUM procedure with bottom-up merging, in combination with the robust estimator of multiscale TAVC as follows. For each , the TAVC at scale is estimated by solving (6), provided that . Here, denotes the maximum scale which is set in relation to the sample size , see Remark 1. Then, we use in place of the global estimator in (12) to standardise the MOSUM detector . When , we use in place of for MOSUM detector standardisation. In doing so, we ensure that change point detectors at multiple scales are standardised by the scale-dependent TAVC that accurately reflects the degree of variability over the moving window (see Example 1) , while taking into account the presence of possibly multiple mean shifts therein. We refer to Algorithm 1 in Appendix A for the pseudocode of the multiscale MOSUM procedure with the robust estimator of scale-dependent TAVC.

3.2 Wild binary segmentation

The binary segmentation algorithm (Scott and Knott,, 1974; Vostrikova,, 1981) and its extensions, such as wild binary segmentation (WBS, Fryzlewicz,, 2014; 2020) and seeded binary segmentation (Kovács et al.,, 2020), recursively search for multiple change points using the CUSUM statistic of the form (3), with and that are identified iteratively. These methods have primarily been analysed for the data segmentation problem under (2) assuming i.i.d. Gaussianity on the . Consequently, some robust estimators of have been considered for standardising the CUSUM statistic. Here, we discuss the application of the WBS2 algorithm (Fryzlewicz,, 2020) in the time series setting with the proposed robust estimator of the scale-dependent TAVC.

Let denote the collection of all intervals within for some , and denote its subset selected either randomly or deterministically (see Cho and Fryzlewicz, (2021) for one approach to deterministic grid selection) with for some given . Starting with , we identify

| (13) |

for some threshold and denoting the proposed robust estimator of the TAVC at scale (when is odd, we use instead). As in Section 3.1, a maximum scale is set so that the CUSUM statistic over any interval of length greater than is standardised using . Following the recommendation made in Fryzlewicz, (2014), we adopt the threshold where is a universal constant.

If that fulfils (13) exists, it signals the presence of a change point so that the data is partitioned into and , and the same step of detecting and identifying a single change point is repeated on each partition separately. If no such exists, or when the user-specified minimum segment length is reached, then the search for change points is terminated on . We provide a pseudocode of the WBS2 algorithm with the robust estimator of scale-dependent TAVC in Algorithm 2 of Appendix A.

3.3 Extension to local stationarity

We propose a heuristic extension of the robust estimator of scale-dependent TAVC to the setting where the second-order structure of varies smoothly over time. Suppose that there exists an appropriately chosen window size such that may be regarded as being approximately second-order stationary over all . Then, we propose to perform the robust estimation described in Section 2.2 in a localised fashion.

To this end, define the time-varying TAVC at scale and time by

| (14) |

For notational convenience, we set for some integer , and let be the number of blocks for window size . For , we estimate by , the solution of the following -estimation equation

| (15) |

with . We apply a boundary extension so that and . The estimator of the local TAVC at time and scale is obtained analogously as that of the global TAVC at scale described in Section 2.2, except that we only use the windowed data region starting at time and ending at for the estimation of the former. Then, the MOSUM detector and the CUSUM statistic described in Sections 3.1–3.2 are standardised in a time-dependent way using and , respectively. In practice, we observe that taking the running median of as an estimator of further improves the performance, as it ‘smoothes’ out the local estimators and enhances the robustness to mean changes.

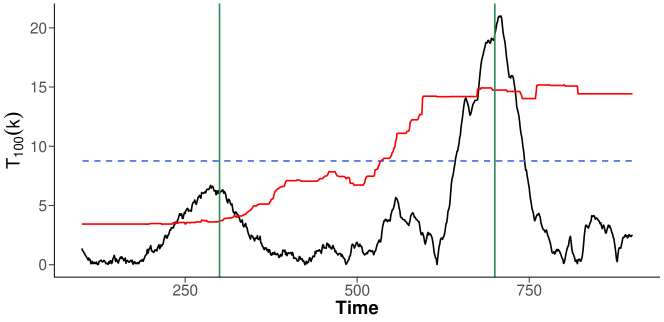

We illustrate the benefit of adopting the time-varying adaptation of the proposed robust estimator using the following example. Consider a time series of length , where the errors follow a time-varying AR(1) model: , with for , for , and . There are two changes in the mean at and , with change sizes and , respectively. In Figure 3, we show the MOSUM detector statistic in (11) calculated using bandwidth . We also plot the threshold at the significance level , multiplied by the square root of the global TAVC estimator at scale (i.e. ) in dashed blue line, and that multiplied by the square root of the local estimators of the scale- TAVC (i.e. ) in solid red line. We see that using the global approach misses the change at time due to the global scale- TAVC estimator being too large, whilst the localised approach successfully detects both changes.

Lastly, we mention that the robust estimation of time-varying and scale-dependent TAVC is of independent interest beyond the context of change point analysis, with possible extensions including the estimation of other second-order properties. For example, the procedure can be used to obtain a robust estimator of the spectrum of a locally stationary wavelet process (Nason et al.,, 2000) while the time series undergoes shifts in the mean.

4 Numerical results

4.1 Practical considerations

We provide guidance on the selection of tuning parameters required for the proposed robust TAVC estimator and its application with multiscale change point detection methods.

Parameter in (6).

We select where is a fixed constant for a given . For the problem of robust mean estimation, Catoni, (2012) recommends the standard deviation in the place of and in a similar vein, Chen et al., (2021) propose to use a trimmed mean

| (16) |

where are the ordered . Another approach is to use an appropriately scaled median of , in a similar fashion to McGonigle et al., (2021). In this case, the necessary scaling constant to ensure unbiasedness can be chosen by noting that is asymptotically Gaussian as , and thus is asymptotically scaled . This leads to the choice

| (17) |

where . In simulation studies, we report the results obtained with , , in setting the parameter where we observe that both choices return similarly good results.

Parameters and in (6).

As a further step to ensure greater robustness of the estimator, we obtain the estimator for a range of and take their median as the final estimator . Informally, we may get unlucky with some starting value that leads to many of the contaminated by the mean changes, and taking the median over a range of values of helps in alleviating this. We take in practice which yields good performance.

Maximum time-scale .

We recommend as the coarsest scale at which the scale-dependent TAVC is estimated. This choice is made to balance between mitigating the effect of change points, and ensuring that the TAVC at coarser scales is well-approximated by .

Tuning parameters for the multiscale MOSUM procedure.

We follow Cho and Kirch, (2022) and generate as a sequence of Fibonacci numbers. For the simulation studies reported in Section 4.2 and Appendix B, we consider where for with

.

For other tuning parameters, we adopt the recommended default values of the R package mosum (Meier et al.,, 2021), and set and .

Tuning parameters for the WBS2 algorithm.

For the threshold, we set the constant and draw deterministic intervals at each iteration, which are suggested choices in Fryzlewicz, (2014) and Cho and Fryzlewicz, (2021) respectively. As we permit the presence of serial correlations, it is reasonable to impose a minimum length requirement on the intervals considered in the WBS2 algorithm. We set this minimum length to be , with the finest scale considered by the MOSUM procedure.

Window size for time-varying TAVC estimation.

We utilise a scale-dependent window size . Setting gives data points used in the solving of the -estimation equations. We advise setting , which ensures that the influence of change points is negated and that the window size is large enough to include enough data points for reliable estimation of the TAVC.

4.2 Simulation study

In this section, we evaluate the performance of the proposed robust estimator of scale-dependent TAVC applied with the two multiscale change point detection procedures discussed in Sections 3.1–3.2. We compare with other methods that account for serial dependence under (2) and whose implementations are readily available in R,

with a variety of scenarios for generating serially correlated .

4.2.1 Settings

We assess the performance of different methods both in the case of no changes () and multiple changes (), under a variety of error structures. Unless stated otherwise, we generate with .

-

(M1)

.

-

(M2)

, where are i.i.d. -distributed random variables.

-

(M3)

AR(1) model: , with and .

-

(M4)

AR(2) model: , with and , with .

-

(M5)

MA(1) model: , with .

-

(M6)

ARCH(1) model: with , where , .

-

(M7)

Time-varying AR(1) model: , with .

-

(M8)

Time-varying AR(1) model: , with and .

-

(M9)

Time-varying MA(1) model: , with .

Models (M1)–(M6) represent stationary error scenarios. Model (M1) is the setting commonly adopted in the literature while (M2), taken from Cho and Kirch, (2021), is adopted to examine whether a method works well in the presence of non-Gaussian errors. Models (M3) and (M4) allow strong autocorrelations in . Under Model (M5), the LRV is close to zero, which makes its accurate estimation difficult. Model (M6) is a non-linear process. Models (M7)–(M9) consider time-varying dependence structure; variants of (M7) and (M8) were studied in McGonigle et al., (2021) and Cho and Fryzlewicz, (2021), respectively. For Models (M1)–(M6), we use the global scale-dependent TAVC estimator described in Section 2.2 while for (M7)–(M9), we use the window-based estimator of the local scale-dependent TAVC described in Section 3.3.

We assess the performance of the methods both when and . In the latter case, the time series contains the change points at , with the (signed) change size . In (M1)–(M4) and (M6), we set and in the case of (M5), we set . In (M7)–(M9), we set where denotes the time-varying LRV.

We implement the robust TAVC estimation within both the multiscale MOSUM and WBS2 procedures as described in Sections 3.1 and 3.2, which are referred to as MOSUM.TAVC[ℓ] and WBS2.TAVC[ℓ], respectively. Here, the subscript with , refers to the choice of the tuning parameter involved in the parameter , see (16)–(17). For the choice of the tuning parameters, we refer to Section 4.1. For illustrative purposes, we also report the results of the ‘oracle’ versions of the MOSUM and WBS2 procedures referred to as MOSUM.oracle and WBS2.oracle, respectively. These methods are implemented with the true LRV ( in the case of Models (M7)–(M9)) for standardising the detector statistics, while all other tuning parameters are kept the same.

Additionally, we consider DepSMUCE (Dette et al.,, 2020), DeCAFS (Romano et al.,, 2021) and WCM.gSa (Cho and Fryzlewicz,, 2021) for comparison. DepSMUCE extends SMUCE (Frick et al.,, 2014) to dependent data using a difference-type estimator of the LRV. Although not its primary objective, DeCAFS detects multiple change points in the mean assuming that the noise is a stationary AR() process. The WCM.gSa method performs model selection on the sequence of models generated by the WBS2 algorithm, using an information criterion-based model selection strategy which assumes that follows an AR model of an arbitrary order. For DepSMUCE, we consider significance levels . Other tuning parameters not mentioned here are chosen as recommended by the authors.

4.2.2 Results

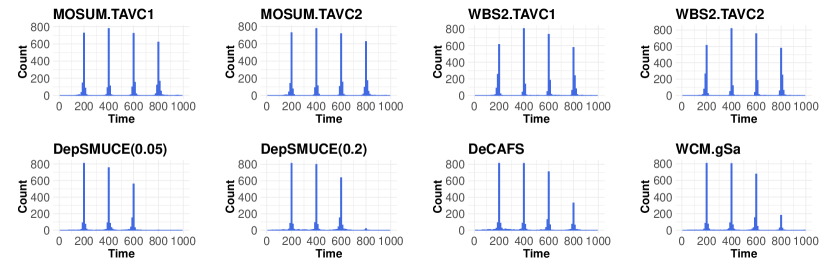

Table LABEL:table:sim:results summarises the results of the comparative simulation study from replications of time series of length generated as in (M1)–(M9) with . Results for other values of are given in Appendix B, where we make similar observations as below.

When , we report the proportion of falsely detecting any change point out of the realisations (see the column ‘Size’ in Table LABEL:table:sim:results). When , we report the relative mean squared error (RMSE)

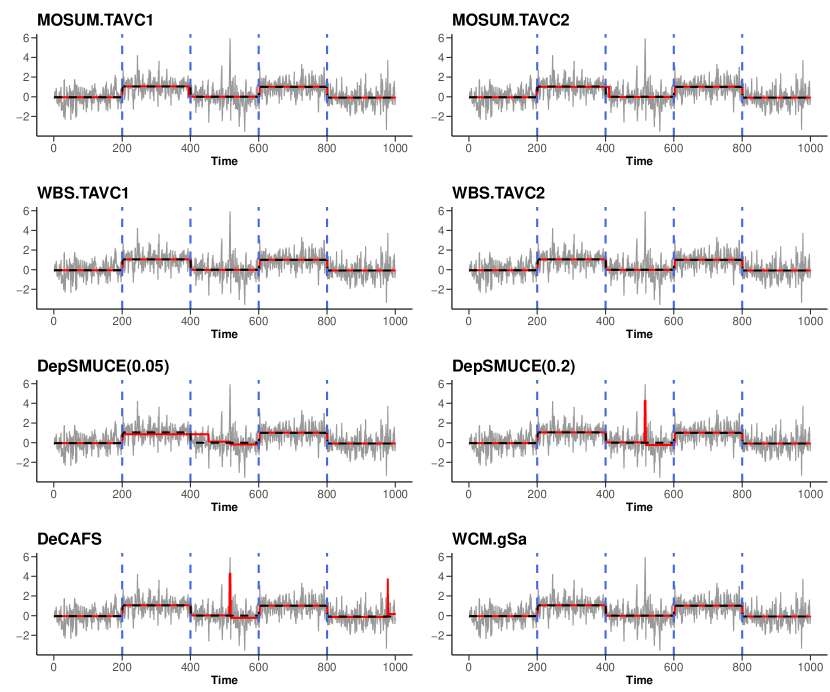

where is the piecewise constant signal constructed with the estimated change points, and is the oracle estimator constructed with the true change points. For illustration, Figure 4 plots obtained from different methods in consideration and the oracle estimator , on a realisation from Model (M6). We also report the distribution of the estimated number of change points, as well as the covering metric (CM). The covering metric (Arbelaez et al.,, 2010) measures the quality of the resulting segmentation as defined by the location of the detected changes, and is recommended in van den Burg and Williams, (2020) as an evaluation metric for comparing change point detection algorithms. The CM take values between and , with a value of corresponding to a perfect segmentation. Its explicit definition can be found in Appendix B. For each measure, we report its average over the realisations.

| Model | Method | Size | CM | RMSE | |||||

| (M1) | MOSUM.TAVC[1] | 0.135 | 0.000 | 0.006 | 0.980 | 0.014 | 0.000 | 0.967 | 6.098 |

| MOSUM.TAVC[2] | 0.091 | 0.000 | 0.015 | 0.978 | 0.007 | 0.000 | 0.965 | 6.234 | |

| WBS2.TAVC[1] | 0.049 | 0.000 | 0.004 | 0.996 | 0.000 | 0.000 | 0.976 | 4.605 | |

| WBS2.TAVC[2] | 0.028 | 0.001 | 0.017 | 0.982 | 0.000 | 0.000 | 0.973 | 4.787 | |

| DepSMUCE(0.05) | 0.010 | 0.000 | 0.014 | 0.986 | 0.000 | 0.000 | 0.972 | 4.859 | |

| DepSMUCE(0.2) | 0.066 | 0.000 | 0.001 | 0.998 | 0.001 | 0.000 | 0.976 | 4.566 | |

| DeCAFS | 0.015 | 0.000 | 0.000 | 0.970 | 0.029 | 0.001 | 0.976 | 4.798 | |

| WCM.gSa | 0.007 | 0.000 | 0.000 | 0.978 | 0.020 | 0.002 | 0.975 | 4.733 | |

| MOSUM.oracle | 0.040 | 0.000 | 0.000 | 0.861 | 0.132 | 0.007 | 0.965 | 5.782 | |

| WBS2.oracle | 0.004 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.977 | 4.567 | |

| (M2) | MOSUM.TAVC[1] | 0.149 | 0.001 | 0.004 | 0.979 | 0.015 | 0.001 | 0.967 | 6.512 |

| MOSUM.TAVC[2] | 0.086 | 0.003 | 0.008 | 0.981 | 0.008 | 0.000 | 0.965 | 6.595 | |

| WBS2.TAVC[1] | 0.040 | 0.001 | 0.006 | 0.993 | 0.000 | 0.000 | 0.976 | 4.702 | |

| WBS2.TAVC[2] | 0.014 | 0.004 | 0.011 | 0.985 | 0.000 | 0.000 | 0.974 | 4.899 | |

| DepSMUCE(0.05) | 0.586 | 0.000 | 0.004 | 0.611 | 0.161 | 0.224 | 0.946 | 13.784 | |

| DepSMUCE(0.2) | 0.747 | 0.000 | 0.000 | 0.420 | 0.180 | 0.400 | 0.934 | 15.828 | |

| DeCAFS | 0.898 | 0.000 | 0.000 | 0.105 | 0.040 | 0.855 | 0.886 | 29.258 | |

| WCM.gSa | 0.009 | 0.000 | 0.000 | 0.978 | 0.020 | 0.002 | 0.975 | 4.789 | |

| MOSUM.oracle | 0.037 | 0.000 | 0.000 | 0.843 | 0.143 | 0.014 | 0.964 | 6.300 | |

| WBS2.oracle | 0.012 | 0.000 | 0.000 | 0.996 | 0.004 | 0.000 | 0.978 | 4.650 | |

| (M3) | MOSUM.TAVC[1] | 0.147 | 0.000 | 0.000 | 0.998 | 0.002 | 0.000 | 0.995 | 1.810 |

| MOSUM.TAVC[2] | 0.082 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.994 | 1.789 | |

| WBS2.TAVC[1] | 0.062 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.998 | 1.258 | |

| WBS2.TAVC[2] | 0.034 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.998 | 1.264 | |

| DepSMUCE(0.05) | 0.968 | 0.000 | 0.000 | 0.920 | 0.078 | 0.002 | 0.992 | 1.494 | |

| DepSMUCE(0.2) | 0.996 | 0.000 | 0.000 | 0.739 | 0.232 | 0.029 | 0.978 | 1.888 | |

| DeCAFS | 0.597 | 0.000 | 0.000 | 0.590 | 0.342 | 0.068 | 0.982 | 1.236 | |

| WCM.gSa | 0.053 | 0.000 | 0.000 | 0.731 | 0.135 | 0.134 | 0.959 | 2.086 | |

| MOSUM.oracle | 0.001 | 0.000 | 0.000 | 0.891 | 0.097 | 0.012 | 0.988 | 2.012 | |

| WBS2.oracle | 0.000 | 0.000 | 0.000 | 0.979 | 0.021 | 0.000 | 0.997 | 1.321 | |

| (M4) | MOSUM.TAVC[1] | 0.123 | 0.000 | 0.003 | 0.992 | 0.005 | 0.000 | 0.987 | 3.133 |

| MOSUM.TAVC[2] | 0.073 | 0.001 | 0.004 | 0.992 | 0.003 | 0.000 | 0.986 | 3.232 | |

| WBS2.TAVC[1] | 0.053 | 0.001 | 0.000 | 0.999 | 0.000 | 0.000 | 0.994 | 1.715 | |

| WBS2.TAVC[2] | 0.035 | 0.003 | 0.002 | 0.995 | 0.000 | 0.000 | 0.993 | 1.755 | |

| DepSMUCE(0.05) | 0.678 | 0.000 | 0.000 | 0.979 | 0.021 | 0.000 | 0.993 | 1.827 | |

| DepSMUCE(0.2) | 0.907 | 0.000 | 0.000 | 0.891 | 0.105 | 0.004 | 0.986 | 2.089 | |

| DeCAFS | 0.734 | 0.000 | 0.000 | 0.241 | 0.224 | 0.535 | 0.935 | 2.258 | |

| WCM.gSa | 0.022 | 0.000 | 0.000 | 0.778 | 0.111 | 0.111 | 0.966 | 2.684 | |

| MOSUM.oracle | 0.008 | 0.000 | 0.000 | 0.972 | 0.028 | 0.000 | 0.986 | 3.087 | |

| WBS2.oracle | 0.001 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.995 | 1.705 | |

| (M5) | MOSUM.TAVC[1] | 0.120 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.990 | 89.580 |

| MOSUM.TAVC[2] | 0.069 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.990 | 89.580 | |

| WBS2.TAVC[1] | 0.103 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.992 | 76.922 | |

| WBS2.TAVC[2] | 0.052 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.992 | 76.922 | |

| DepSMUCE(0.05) | 0.998 | 0.000 | 0.000 | 0.036 | 0.048 | 0.916 | 0.773 | 2535.266 | |

| DepSMUCE(0.2) | 1.000 | 0.000 | 0.000 | 0.003 | 0.004 | 0.993 | 0.634 | 1038.395 | |

| DeCAFS | 0.001 | 0.000 | 0.000 | 0.997 | 0.003 | 0.000 | 0.992 | 77.886 | |

| WCM.gSa | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.992 | 76.814 | |

| MOSUM.oracle | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.276 | 247.634 | |

| WBS2.oracle | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.278 | 207.555 | |

| (M6) | MOSUM.TAVC[1] | 0.168 | 0.000 | 0.000 | 0.978 | 0.021 | 0.001 | 0.973 | 6.246 |

| MOSUM.TAVC[2] | 0.112 | 0.000 | 0.001 | 0.993 | 0.006 | 0.000 | 0.973 | 6.246 | |

| WBS2.TAVC[1] | 0.064 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.981 | 4.833 | |

| WBS2.TAVC[2] | 0.030 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.981 | 4.844 | |

| DepSMUCE(0.05) | 0.507 | 0.000 | 0.000 | 0.740 | 0.176 | 0.084 | 0.963 | 8.026 | |

| DepSMUCE(0.2) | 0.716 | 0.000 | 0.000 | 0.564 | 0.252 | 0.184 | 0.949 | 9.934 | |

| DeCAFS | 0.755 | 0.000 | 0.000 | 0.191 | 0.066 | 0.743 | 0.911 | 25.250 | |

| WCM.gSa | 0.021 | 0.000 | 0.000 | 0.971 | 0.018 | 0.011 | 0.978 | 5.406 | |

| MOSUM.oracle | 0.021 | 0.000 | 0.000 | 0.881 | 0.109 | 0.010 | 0.969 | 6.300 | |

| WBS2.oracle | 0.005 | 0.000 | 0.000 | 0.995 | 0.005 | 0.000 | 0.981 | 4.863 | |

| (M7) | MOSUM.TAVC[1] | 0.247 | 0.000 | 0.002 | 0.970 | 0.025 | 0.003 | 0.973 | 5.232 |

| MOSUM.TAVC[2] | 0.171 | 0.000 | 0.004 | 0.972 | 0.023 | 0.001 | 0.972 | 5.310 | |

| WBS2.TAVC[1] | 0.184 | 0.000 | 0.004 | 0.988 | 0.008 | 0.000 | 0.971 | 5.004 | |

| WBS2.TAVC[2] | 0.125 | 0.000 | 0.010 | 0.987 | 0.003 | 0.000 | 0.970 | 5.114 | |

| DepSMUCE(0.05) | 0.747 | 0.000 | 0.175 | 0.718 | 0.107 | 0.000 | 0.928 | 7.807 | |

| DepSMUCE(0.2) | 0.921 | 0.000 | 0.019 | 0.716 | 0.258 | 0.007 | 0.960 | 5.416 | |

| DeCAFS | 0.830 | 0.000 | 0.000 | 0.652 | 0.171 | 0.177 | 0.958 | 6.217 | |

| WCM.gSa | 0.471 | 0.059 | 0.041 | 0.830 | 0.044 | 0.026 | 0.941 | 6.975 | |

| MOSUM.oracle | 0.015 | 0.000 | 0.000 | 0.903 | 0.094 | 0.003 | 0.969 | 5.312 | |

| WBS2.oracle | 0.005 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.975 | 4.884 | |

| (M8) | MOSUM.TAVC[1] | 0.244 | 0.000 | 0.001 | 0.947 | 0.052 | 0.000 | 0.969 | 6.884 |

| MOSUM.TAVC[2] | 0.154 | 0.000 | 0.001 | 0.961 | 0.038 | 0.000 | 0.969 | 6.918 | |

| WBS2.TAVC[1] | 0.160 | 0.000 | 0.002 | 0.995 | 0.003 | 0.000 | 0.967 | 6.565 | |

| WBS2.TAVC[2] | 0.107 | 0.000 | 0.003 | 0.994 | 0.003 | 0.000 | 0.967 | 6.658 | |

| DepSMUCE(0.05) | 0.219 | 0.032 | 0.641 | 0.306 | 0.019 | 0.002 | 0.817 | 17.602 | |

| DepSMUCE(0.2) | 0.483 | 0.000 | 0.252 | 0.633 | 0.105 | 0.010 | 0.904 | 10.411 | |

| DeCAFS | 0.341 | 0.001 | 0.002 | 0.652 | 0.153 | 0.192 | 0.953 | 9.188 | |

| WCM.gSa | 0.173 | 0.076 | 0.159 | 0.748 | 0.011 | 0.006 | 0.913 | 8.976 | |

| MOSUM.oracle | 0.045 | 0.000 | 0.000 | 0.841 | 0.142 | 0.017 | 0.962 | 7.206 | |

| WBS2.oracle | 0.013 | 0.000 | 0.000 | 0.996 | 0.004 | 0.000 | 0.971 | 5.960 | |

| (M9) | MOSUM.TAVC[1] | 0.311 | 0.000 | 0.008 | 0.915 | 0.076 | 0.001 | 0.963 | 7.027 |

| MOSUM.TAVC[2] | 0.204 | 0.000 | 0.020 | 0.931 | 0.049 | 0.000 | 0.962 | 7.026 | |

| WBS2.TAVC[1] | 0.234 | 0.000 | 0.020 | 0.972 | 0.008 | 0.000 | 0.958 | 8.451 | |

| WBS2.TAVC[2] | 0.167 | 0.000 | 0.029 | 0.968 | 0.003 | 0.000 | 0.958 | 8.143 | |

| DepSMUCE(0.05) | 0.130 | 0.181 | 0.806 | 0.013 | 0.000 | 0.000 | 0.743 | 13.448 | |

| DepSMUCE(0.2) | 0.380 | 0.022 | 0.874 | 0.094 | 0.010 | 0.000 | 0.774 | 11.770 | |

| DeCAFS | 0.075 | 0.034 | 0.414 | 0.431 | 0.078 | 0.043 | 0.858 | 10.028 | |

| WCM.gSa | 0.054 | 0.057 | 0.695 | 0.236 | 0.009 | 0.003 | 0.814 | 10.822 | |

| MOSUM.oracle | 0.101 | 0.000 | 0.000 | 0.760 | 0.211 | 0.029 | 0.957 | 7.436 | |

| WBS2.oracle | 0.080 | 0.000 | 0.000 | 0.827 | 0.171 | 0.002 | 0.950 | 7.927 | |

Overall, WBS2.TAVC displays better size control than MOSUM.TAVC. The multiscale MOSUM procedure with bottom-up merging has been noted to return false positives as it accepts all estimators from the finest bandwidth; see the simulation results reported in Cho and Kirch, (2022). Despite this known issue, MOSUM.TAVC shows better size control than some of the competitors such as DepSMUCE and DeCAFS. Between the two choices of the parameter used in (6), the one involving (17) (corresponding to the subscript ) yields the estimator of TAVC that returns better size control, e.g. closer to the nominal level for the multiscale MOSUM procedure. On the other hand, using the trimmed mean (corresponding to the subscript ) as in (16) sees improved power at the cost of larger size. This suggests that an approach combining the two choices of may yield a more balanced performance.

WBS2.TAVC performs the best across all metrics and scenarios among non-oracle methods when . Also, we observe that using the proposed robust estimator of scale-dependent TAVC, compares favourably to the multiscale methods applied with the true LRV (i.e. MOSUM.oracle and WBS2.oracle) and in some scenarios, the former outperforms the respective oracle counterpart. In particular, in Scenario (M5) where the LRV is close to , plugging in its true value leads to detecting many false positives. This shows that adopting the scale-dependent TAVC in place of the LRV for test statistic standardisation improves the finite sample performance when the change point detection procedure involves localised testing, as is the case for both the MOSUM and the WBS2 procedures. We make a similar observation about the performance of DepSMUCE which also sets out to estimate the LRV. DeCAFS exhibits good detection power but tends to over-estimate the number of change points as well as failing to control the size adequately even when it is applied to the correctly specified scenario (Model (M3)). WCM.gSa performs well in correctly estimating the number of change points regardless of whether or . However, its performance deteriorates in the presence of nonstationarities, see (M7)–(M9).

Further inspection of the results under (M9) demonstrates one advantage of the time-varying approach. Figure 5 plots the histogram of the estimated change point locations across the replications for each of the methods. We see that the competing approaches struggle to detect the final change point due to the decreased variability towards the end of the data sequence, whereas the proposed estimator of time-varying scale-dependent TAVC successfully extends to the locally stationary scenarios.

4.3 Data applications

We apply MOSUM.TAVC and WBS2.TAVC, the multiscale procedures combined with the robust estimator of scale-dependent TAVC, to two data examples. We select the parameter in (6) using (16) and select other tuning parameters as described in Section 4.1 unless specified otherwise.

4.3.1 House price index data

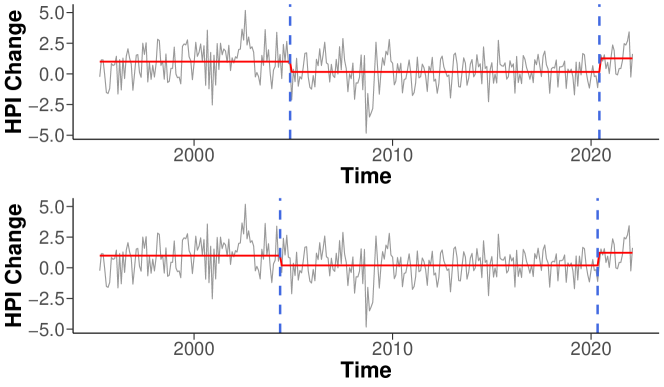

We analyse the monthly percentage changes in UK house price index (HPI), which provides insight into the estimated overall changes in house prices across the UK. The data are available from https://www.gov.uk/government/statistical-data-sets/, and a detailed description of the calculation of the HPI can be found from UK Land Registry, (2021). The HPI series for various regions of the UK have previously been analysed in Baranowski et al., (2019) and McGonigle et al., (2021). We analyse the HPI for detached properties in the area of Somerset West and Taunton between April 1995 and February 2022 ().

We set the tuning parameters as described in Section 4.1 except for the window size , (for WBS2.TAVC) and (for MOSUM.TAVC) due to the short length of the time series. We combine the multiscale change point detection procedures with the robust estimator of the time-varying, scale-dependent TAVC described in Section 3.3, with the bandwidths for the MOSUM procedure and the minimum interval length set at for WBS2. The data are shown in Figure 6, with the change points detected by WBS2.TAVC and MOSUM.TAVC as well as the resulting estimated mean signal given in the top and bottom panels, respectively. For comparison, we also apply DepSMUCE, DeCAFS and WCM.gSa to the data, see Table 2.

Both WBS2.TAVC and MOSUM.TAVC detect two changes. The first change, detected in May and November 2004 for the two methods, corresponds to a decrease in the mean of the HPI series. The second change, detected in May/June 2020, may be associated with the changing consumer demand for housing in the wake of the COVID-19 pandemic. The Taunton area saw the biggest increase in overall house prices in 2021, as the “race for space” saw buyers opt for “more space to work from home as well as more outdoor space” (The Guardian,, 2021).

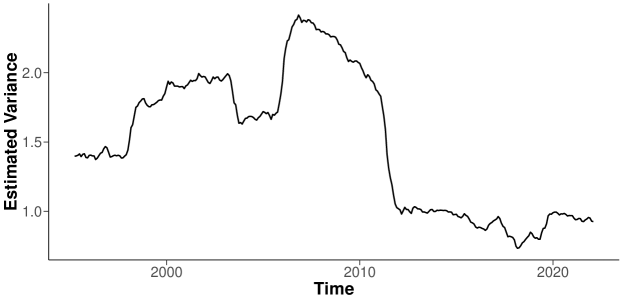

We observe that no changes are detected by either WBS2.TAVC or MOSUM.TAVC during the 2008–2009 period associated with the financial crisis. In contrast, DepSMUCE (with ), DeCAFS and WCM.gSa detect changes during this time period, possibly influenced by the increased variability during the financial crisis. Changes detected in the crisis period can be attributed to changes in variance (and autocorrelation), rather than those in mean, as noted in McGonigle et al., (2021). We further support this interpretation by estimating the time-varying variance after adjusting for the shifts in mean using the change point estimators returned by WBS2.TAVC, using the wavelet-based framework of Nason et al., (2000) implemented for non-dyadic data as described in McGonigle et al., (2022), see Figure 7. There is a clear period of increased variance between 2007–2010, likely due to the financial crisis. By utilising a time-varying TAVC estimator, our proposed methodology is able to capture the increased variability during this period, which ensures that potential false positives are not detected. Furthermore, by accounting for the decrease in variability towards the end of the series, our time-varying estimator of the scale-dependent TAVC allows for the detection of a change in 2020 that is missed by other methods.

| Method | Detected change points |

|---|---|

| WBS2.TAVC | 2004-11, 2020-06 |

| MOSUM.TAVC | 2004-05, 2020-05 |

| DepSMUCE(0.05) | 2004-11 |

| DepSMUCE(0.2) | 2008-09 |

| DeCAFS | 1999-05, 2003-01, 2008-08, 2009-01 |

| WCM.gSa | 1999-05, 2003-01, 2007-09, 2009-01, 2021-08 |

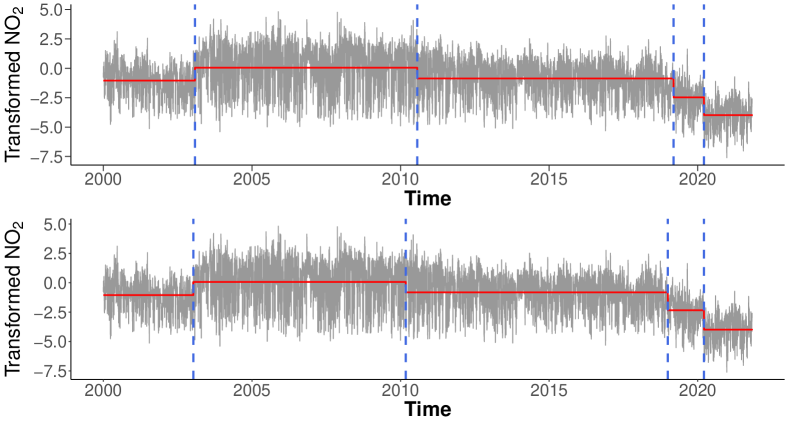

4.3.2 Nitrogen dioxide concentration in London

We analyse the daily average concentrations of nitrogen dioxide (NO2), measured in , recorded at Marylebone Road in London, UK. The measurements were taken from January 1st, 2000 until October 31st, 2021 (). The data set is available from https://www.londonair.org.uk and a similar dataset was analysed for shifts in the mean in Cho and Fryzlewicz, (2021) using the WCM.gSa method. The data take positive values and display both seasonality and effects due to bank holidays, as the main source of NO2 emissions at the site is likely to be road traffic. To mitigate these effects, we take the square root transform of the data and remove seasonality as described in Cho and Fryzlewicz, (2021).

We apply WBS2.TAVC and MOSUM.TAVC using the global TAVC estimator in (6), with the minimum interval length set at for WBS2.TAVC and the bandwidths set as for the MOSUM.TAVC. All other tuning parameters are selected as in Section 4.1. The transformed data are shown in Figure 8, with change points detected by WBS2.TAVC and MOSUM.TAVC and the resulting estimated mean signals given in the top and bottom panels, respectively. For comparison, we also apply DepSMUCE, DeCAFS and WCM.gSa to the data. Except for DeCAFS, which detects 17 change points, all methods return similar estimators. For brevity, the DeCAFS method is omitted from the results reported in Table 3.

Both WBS2.TAVC and MOSUM.TAVC detect four change points, some of which can be linked to policy changes likely affecting the levels of air pollutants. In February 2003, traffic management measures were introduced in central London which included modification of the pollutant filters of London buses and other heavy duty diesel vehicles, leading to an increase in their NO2 emissions (Air Quality Expert Group,, 2004). This corresponds to the change on January 31st, 2003 detected by all methods. Also, Marylebone Road lies within the ultra low emission zone (ULEZ) that was introduced in April 2019. The ULEZ places restrictions on the levels of pollutants of vehicles travelling in the zone, and can be linked to the change on March 10th, 2019 detected by WBS2.TAVC or earlier in 2018 by other methods considering the bias in the change point estimators. This corresponds to a decrease in the concentration of NO2. The final change point, detected by all methods on March 18th, 2020, aligns with the nationwide lockdown due to the COVID-19 pandemic on March 23rd, 2020, which resulted in drastically reduced levels of NO2 throughout the UK (Higham et al.,, 2021).

| Method | Detected change points |

|---|---|

| WBS2.TAVC | 2003-01-31, 2010-07-25, 2019-03-10, 2020-03-18 |

| MOSUM.TAVC | 2003-01-11, 2010-03-06, 2018-12-30, 2020-03-18 |

| DepSMUCE(0.05) | 2003-01-31, 2010-07-25, 2018-10-14, 2020-03-18 |

| DepSMUCE(0.2) | 2003-01-31, 2008-08-31, 2012-10-04, 2018-10-14, 2020-03-18 |

| WCM.gSa | 2003-01-31, 2009-12-09, 2018-10-14, 2020-03-18 |

5 Conclusions

We propose an estimator of scale-dependent TAVC that is robust to the presence of (possibly) multiple mean shifts. It is readily combined with multiscale change point detection methodologies which, by scanning for change points over data sections of varying lengths, provide good adaptivity to the problem of multiple change point detection. We show the consistency of the proposed estimator under general assumptions permitting heavy tails and serial dependence decaying at a polynomial rate, and investigate its use with the multiscale MOSUM procedure and the WBS2 algorithm.

Through extensive numerical studies, we demonstrate the benefit of adopting the proposed estimator of scale-dependent TAVC for improved finite sample performance, as it better reflects the level of variability in the local data sections involved in the multiscale methods.

In particular, the heuristic extension to local stationarity shows promising performance which provides a natural avenue for future research. An implementation of the methodology in the R programming language can be found at https://github.com/EuanMcGonigle/TAVC.seg.

References

- Air Quality Expert Group, (2004) Air Quality Expert Group (2004). Nitrogen dioxide in the United Kingdom. https://uk-air.defra.gov.uk/library/assets/documents/reports/aqeg/nd-chapter2.pdf. Accessed 01/03/2022.

- Arbelaez et al., (2010) Arbelaez, P., Maire, M., Fowlkes, C., and Malik, J. (2010). Contour detection and hierarchical image segmentation. IEEE Transactions on Pattern Analysis and Machine Intelligence, 33(5):898–916.

- Aue and Horváth, (2013) Aue, A. and Horváth, L. (2013). Structural breaks in time series. Journal of Time Series Analysis, 34:1–16.

- Baranowski et al., (2019) Baranowski, R., Chen, Y., and Fryzlewicz, P. (2019). Narrowest-over-threshold detection of multiple change points and change-point-like features. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 81(3):649–672.

- Catoni, (2012) Catoni, O. (2012). Challenging the empirical mean and empirical variance: A deviation study. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques, 48(4):1148–1185.

- Chakar et al., (2017) Chakar, S., Lebarbier, E., Lévy-Leduc, C., and Robin, S. (2017). A robust approach for estimating change-points in the mean of an AR(1) process. Bernoulli, 23(2):1408–1447.

- Chan, (2022) Chan, K. W. (2022). Optimal difference-based variance estimators in time series: A general framework. The Annals of Statistics, 50(3):1376–1400.

- Chen et al., (2021) Chen, L., Wang, W., and Wu, W. B. (2021). Inference of breakpoints in high-dimensional time series. Journal of the American Statistical Association, pages 1–13.

- Cho and Fryzlewicz, (2021) Cho, H. and Fryzlewicz, P. (2021). Multiple change point detection under serial dependence: Wild contrast maximisation and gappy Schwarz algorithm. arXiv preprint arXiv:2011.13884.

- Cho and Kirch, (2021) Cho, H. and Kirch, C. (2021). Data segmentation algorithms: Univariate mean change and beyond. Econometrics and Statistics (to appear).

- Cho and Kirch, (2022) Cho, H. and Kirch, C. (2022). Two-stage data segmentation permitting multiscale change points, heavy tails and dependence. Annals of the Institute of Statistical Mathematics, 74(4):653–684.

- Chu et al., (1995) Chu, C.-S. J., Hornik, K., and Kaun, C.-M. (1995). MOSUM tests for parameter constancy. Biometrika, 82(3):603–617.

- Dette et al., (2020) Dette, H., Eckle, T., and Vetter, M. (2020). Multiscale change point detection for dependent data. Scandinavian Journal of Statistics, 47(4):1243–1274.

- Eichinger and Kirch, (2018) Eichinger, B. and Kirch, C. (2018). A MOSUM procedure for the estimation of multiple random change points. Bernoulli, 24(1):526–564.

- Fang and Siegmund, (2020) Fang, X. and Siegmund, D. (2020). Detection and estimation of local signals. arXiv preprint arXiv:2004.08159.

- Frick et al., (2014) Frick, K., Munk, A., and Sieling, H. (2014). Multiscale change point inference. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(3):495–580.

- Fryzlewicz, (2014) Fryzlewicz, P. (2014). Wild binary segmentation for multiple change-point detection. The Annals of Statistics, 42(6):2243–2281.

- Fryzlewicz, (2020) Fryzlewicz, P. (2020). Detecting possibly frequent change-points: Wild binary segmentation 2 and steepest-drop model selection. Journal of the Korean Statistical Society, 49(4):1027–1070.

- Gallagher et al., (2022) Gallagher, C., Killick, R., Lund, R., and Shi, X. (2022). Autocovariance estimation in the presence of changepoints. Journal of the Korean Statistical Society, pages 1–20.

- Higham et al., (2021) Higham, J., Ramírez, C. A., Green, M., and Morse, A. (2021). UK COVID-19 lockdown: 100 days of air pollution reduction? Air Quality, Atmosphere & Health, 14(3):325–332.

- Hušková and Kirch, (2010) Hušková, M. and Kirch, C. (2010). A note on studentized confidence intervals for the change-point. Computational Statistics, 25(2):269–289.

- Kovács et al., (2020) Kovács, S., Li, H., Bühlmann, P., and Munk, A. (2020). Seeded binary segmentation: A general methodology for fast and optimal change point detection. arXiv preprint arXiv:2002.06633.

- Lavielle and Moulines, (2000) Lavielle, M. and Moulines, E. (2000). Least-squares estimation of an unknown number of shifts in a time series. Journal of Time Series Analysis, 21(1):33–59.

- Lu et al., (2010) Lu, Q., Lund, R., and Lee, T. C. (2010). An MDL approach to the climate segmentation problem. The Annals of Applied Statistics, 4(1):299–319.

- McGonigle et al., (2021) McGonigle, E. T., Killick, R., and Nunes, M. A. (2021). Detecting changes in mean in the presence of time-varying autocovariance. Stat, 10(1):e351.

- McGonigle et al., (2022) McGonigle, E. T., Killick, R., and Nunes, M. A. (2022). Trend locally stationary wavelet processes. Journal of Time Series Analysis, 43(6):895–917.

- Meier et al., (2021) Meier, A., Kirch, C., and Cho, H. (2021). mosum: A package for moving sums in change-point analysis. Journal of Statistical Software, 97(1):1–42.

- Messer et al., (2014) Messer, M., Kirchner, M., Schiemann, J., Roeper, J., Neininger, R., and Schneider, G. (2014). A multiple filter test for the detection of rate changes in renewal processes with varying variance. The Annals of Applied Statistics, 8(4):2027–2067.

- Nason et al., (2000) Nason, G. P., von Sachs, R., and Kroisandt, G. (2000). Wavelet processes and adaptive estimation of the evolutionary wavelet spectrum. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 62(2):271–292.

- Page, (1954) Page, E. S. (1954). Continuous inspection schemes. Biometrika, 41(1/2):100–115.

- Romano et al., (2021) Romano, G., Rigaill, G., Runge, V., and Fearnhead, P. (2021). Detecting abrupt changes in the presence of local fluctuations and autocorrelated noise. Journal of the American Statistical Association, pages 1–16.

- Scott and Knott, (1974) Scott, A. J. and Knott, M. (1974). A cluster analysis method for grouping means in the analysis of variance. Biometrics, 30(3):507–512.

- Tecuapetla-Gómez and Munk, (2017) Tecuapetla-Gómez, I. and Munk, A. (2017). Autocovariance estimation in regression with a discontinuous signal and m-dependent errors: A difference-based approach. Scandinavian Journal of Statistics, 44(2):346–368.

- The Guardian, (2021) The Guardian (2021). House prices shoot up in UK towns as ‘race for space’ continues apace. https://www.theguardian.com/money/2021/dec/30/house-prices-shoot-up-in-uk-towns-as-race-for-space-continues-apace. Accessed 01/05/2022.

- Truong et al., (2020) Truong, C., Oudre, L., and Vayatis, N. (2020). Selective review of offline change point detection methods. Signal Processing, 167:107299.

- UK Land Registry, (2021) UK Land Registry (2021). UK house price index. http://landregistry.data.gov.uk/app/ukhpi. Accessed 01/05/2022.

- van den Burg and Williams, (2020) van den Burg, G. J. and Williams, C. K. (2020). An evaluation of change point detection algorithms. arXiv preprint arXiv:2003.06222.

- Vostrikova, (1981) Vostrikova, L. J. (1981). Detecting ‘disorder’ in multidimensional random processes. Soviet Doklady Mathematics, 24:55–59.

- Wong et al., (2020) Wong, K. C., Li, Z., and Tewari, A. (2020). Lasso guarantees for -mixing heavy-tailed time series. The Annals of Statistics, 48(2):1124–1142.

- Wu and Zhou, (2020) Wu, W. and Zhou, Z. (2020). Multiscale jump testing and estimation under complex temporal dynamics. arXiv preprint arXiv:1909.06307.

- Wu, (2009) Wu, W. B. (2009). Recursive estimation of time-average variance constants. The Annals of Applied Probability, 19(4):1529–1552.

- Yao, (1988) Yao, Y.-C. (1988). Estimating the number of change-points via Schwarz’ criterion. Statistics & Probability Letters, 6(3):181–189.

- Zhang and Wu, (2017) Zhang, D. and Wu, W. B. (2017). Gaussian approximation for high dimensional time series. The Annals of Statistics, 45(5):1895–1919.

- Zhao et al., (2021) Zhao, Z., Jiang, F., and Shao, X. (2021). Segmenting time series via self-normalization. arXiv preprint arXiv:2112.05331.

Appendix A Algorithms and further description

A.1 Multiscale MOSUM procedure with bottom-up merging

Algorithm 1 provides a pseudocode for the multiscale MOSUM procedure with bottom-up merging combined with the robust estimation of TAVC.

A.2 Wild binary segmentation 2 algorithm

Algorithm 2 provides a pseudocode for the WBS2 algorithm combined with the robust TAVC estimation.

Appendix B Additional numerical results

In this section, we provide further information on the simulation study carried out in Section 4.2 and report additional numerical results to demonstrate the performance of the proposed robust estimator of the scale-dependent TAVC.

The covering metric (CM) used to assess the quality of the segmentation produced by the detected change point is defined as follows. The true change locations define a partition of the interval into disjoint sets such that is the segment . Similarly, the estimated change locations yield a partition of segments . Then, CM is defined by

The CM takes values between and , with a value of corresponding to a perfect segmentation, i.e. .

We repeat the simulations carried out in Section 4.2 with different values of . When , we introduce change points to the time series at times . For , we have change points at times . Lastly, is set analogously as in the main text. See Tables LABEL:table:sim:two–LABEL:table:sim:three for the results.

| Model | Method | Size | CM | RMSE | |||||

| (M1) | MOSUM.TAVC[1] | 0.116 | 0.006 | 0.033 | 0.944 | 0.017 | 0.000 | 0.944 | 7.188 |

| MOSUM.TAVC[2] | 0.061 | 0.010 | 0.086 | 0.897 | 0.007 | 0.000 | 0.930 | 8.261 | |

| WBS2.TAVC[1] | 0.068 | 0.008 | 0.041 | 0.951 | 0.000 | 0.000 | 0.949 | 6.411 | |

| WBS2.TAVC[2] | 0.037 | 0.036 | 0.092 | 0.872 | 0.000 | 0.000 | 0.922 | 9.082 | |

| DepSMUCE(0.05) | 0.015 | 0.006 | 0.220 | 0.774 | 0.000 | 0.000 | 0.890 | 12.896 | |

| DepSMUCE(0.2) | 0.067 | 0.000 | 0.033 | 0.965 | 0.002 | 0.000 | 0.953 | 6.334 | |

| DeCAFS | 0.023 | 0.000 | 0.000 | 0.964 | 0.035 | 0.001 | 0.961 | 6.062 | |

| WCM.gSa | 0.011 | 0.000 | 0.000 | 0.963 | 0.026 | 0.011 | 0.958 | 6.227 | |

| MOSUM.oracle | 0.025 | 0.000 | 0.000 | 0.879 | 0.115 | 0.006 | 0.948 | 6.863 | |

| WBS2.oracle | 0.008 | 0.000 | 0.000 | 0.997 | 0.003 | 0.000 | 0.963 | 5.749 | |

| (M2) | MOSUM.TAVC[1] | 0.131 | 0.003 | 0.033 | 0.944 | 0.020 | 0.000 | 0.946 | 7.020 |

| MOSUM.TAVC[2] | 0.079 | 0.016 | 0.067 | 0.906 | 0.011 | 0.000 | 0.931 | 8.195 | |

| WBS2.TAVC[1] | 0.077 | 0.017 | 0.033 | 0.950 | 0.000 | 0.000 | 0.948 | 6.183 | |

| WBS2.TAVC[2] | 0.040 | 0.042 | 0.081 | 0.877 | 0.000 | 0.000 | 0.924 | 7.635 | |

| DepSMUCE(0.05) | 0.371 | 0.003 | 0.153 | 0.643 | 0.125 | 0.076 | 0.883 | 20.031 | |

| DepSMUCE(0.2) | 0.572 | 0.000 | 0.022 | 0.609 | 0.200 | 0.169 | 0.917 | 15.960 | |

| DeCAFS | 0.746 | 0.000 | 0.000 | 0.232 | 0.096 | 0.672 | 0.894 | 26.581 | |

| WCM.gSa | 0.013 | 0.000 | 0.000 | 0.977 | 0.022 | 0.001 | 0.959 | 6.521 | |

| MOSUM.oracle | 0.040 | 0.000 | 0.000 | 0.862 | 0.129 | 0.009 | 0.948 | 6.813 | |

| WBS2.oracle | 0.015 | 0.000 | 0.000 | 0.995 | 0.004 | 0.001 | 0.964 | 5.335 | |

| (M3) | MOSUM.TAVC[1] | 0.168 | 0.000 | 0.003 | 0.992 | 0.005 | 0.000 | 0.991 | 2.038 |

| MOSUM.TAVC[2] | 0.113 | 0.000 | 0.016 | 0.981 | 0.003 | 0.000 | 0.989 | 2.153 | |

| WBS2.TAVC[1] | 0.144 | 0.000 | 0.002 | 0.998 | 0.000 | 0.000 | 0.997 | 1.484 | |

| WBS2.TAVC[2] | 0.096 | 0.001 | 0.017 | 0.982 | 0.000 | 0.000 | 0.992 | 1.698 | |

| DepSMUCE(0.05) | 0.963 | 0.000 | 0.000 | 0.893 | 0.106 | 0.001 | 0.987 | 1.841 | |

| DepSMUCE(0.2) | 0.993 | 0.000 | 0.000 | 0.750 | 0.218 | 0.032 | 0.972 | 2.196 | |

| DeCAFS | 0.574 | 0.000 | 0.002 | 0.646 | 0.276 | 0.078 | 0.976 | 1.302 | |

| WCM.gSa | 0.160 | 0.000 | 0.000 | 0.498 | 0.185 | 0.317 | 0.887 | 3.262 | |

| MOSUM.oracle | 0.001 | 0.000 | 0.001 | 0.991 | 0.008 | 0.000 | 0.991 | 2.037 | |

| WBS2.oracle | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.997 | 1.454 | |

| (M4) | MOSUM.TAVC[1] | 0.130 | 0.001 | 0.016 | 0.977 | 0.006 | 0.000 | 0.979 | 3.419 |

| MOSUM.TAVC[2] | 0.071 | 0.005 | 0.051 | 0.943 | 0.001 | 0.000 | 0.968 | 4.715 | |

| WBS2.TAVC[1] | 0.102 | 0.004 | 0.017 | 0.979 | 0.000 | 0.000 | 0.986 | 2.091 | |

| WBS2.TAVC[2] | 0.066 | 0.012 | 0.060 | 0.928 | 0.000 | 0.000 | 0.971 | 2.905 | |

| DepSMUCE(0.05) | 0.762 | 0.000 | 0.000 | 0.959 | 0.039 | 0.002 | 0.988 | 2.116 | |

| DepSMUCE(0.2) | 0.919 | 0.000 | 0.000 | 0.859 | 0.125 | 0.016 | 0.978 | 2.502 | |

| DeCAFS | 0.722 | 0.000 | 0.000 | 0.248 | 0.189 | 0.563 | 0.903 | 2.642 | |

| WCM.gSa | 0.113 | 0.000 | 0.000 | 0.623 | 0.156 | 0.221 | 0.921 | 3.682 | |

| MOSUM.oracle | 0.003 | 0.000 | 0.001 | 0.984 | 0.014 | 0.001 | 0.983 | 2.861 | |

| WBS2.oracle | 0.001 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.992 | 1.776 | |

| (M5) | MOSUM.TAVC[1] | 0.095 | 0.000 | 0.000 | 0.965 | 0.035 | 0.000 | 0.985 | 78.044 |

| MOSUM.TAVC[2] | 0.045 | 0.000 | 0.000 | 0.970 | 0.030 | 0.000 | 0.985 | 78.070 | |

| WBS2.TAVC[1] | 0.191 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.988 | 66.844 | |

| WBS2.TAVC[2] | 0.098 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.988 | 66.844 | |

| DepSMUCE(0.05) | 0.968 | 0.000 | 0.000 | 0.237 | 0.125 | 0.638 | 0.856 | 751.323 | |

| DepSMUCE(0.2) | 0.993 | 0.000 | 0.000 | 0.057 | 0.054 | 0.889 | 0.754 | 1319.156 | |

| DeCAFS | 0.004 | 0.000 | 0.000 | 0.983 | 0.014 | 0.003 | 0.988 | 84.649 | |

| WCM.gSa | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.988 | 67.557 | |

| MOSUM.oracle | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.284 | 250.212 | |

| WBS2.oracle | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.289 | 201.271 | |

| (M6) | MOSUM.TAVC[1] | 0.174 | 0.001 | 0.013 | 0.969 | 0.016 | 0.001 | 0.958 | 7.016 |

| MOSUM.TAVC[2] | 0.079 | 0.005 | 0.030 | 0.955 | 0.010 | 0.000 | 0.953 | 7.527 | |

| WBS2.TAVC[1] | 0.105 | 0.007 | 0.017 | 0.975 | 0.001 | 0.000 | 0.963 | 6.226 | |

| WBS2.TAVC[2] | 0.058 | 0.015 | 0.048 | 0.937 | 0.000 | 0.000 | 0.951 | 7.041 | |

| DepSMUCE(0.05) | 0.389 | 0.000 | 0.075 | 0.802 | 0.097 | 0.026 | 0.930 | 12.034 | |

| DepSMUCE(0.2) | 0.579 | 0.000 | 0.014 | 0.727 | 0.178 | 0.081 | 0.939 | 11.923 | |

| DeCAFS | 0.647 | 0.000 | 0.000 | 0.304 | 0.120 | 0.576 | 0.906 | 24.573 | |

| WCM.gSa | 0.020 | 0.000 | 0.000 | 0.972 | 0.023 | 0.005 | 0.964 | 6.510 | |

| MOSUM.oracle | 0.025 | 0.000 | 0.000 | 0.922 | 0.073 | 0.005 | 0.958 | 7.303 | |

| WBS2.oracle | 0.006 | 0.000 | 0.000 | 0.993 | 0.006 | 0.001 | 0.969 | 5.939 | |

| (M7) | MOSUM.TAVC[1] | 0.230 | 0.009 | 0.058 | 0.912 | 0.021 | 0.000 | 0.940 | 6.810 |

| MOSUM.TAVC[2] | 0.160 | 0.015 | 0.102 | 0.866 | 0.017 | 0.000 | 0.928 | 7.928 | |

| WBS2.TAVC[1] | 0.205 | 0.017 | 0.087 | 0.871 | 0.024 | 0.001 | 0.918 | 8.715 | |

| WBS2.TAVC[2] | 0.141 | 0.038 | 0.124 | 0.823 | 0.015 | 0.000 | 0.904 | 10.482 | |

| DepSMUCE(0.05) | 0.335 | 0.002 | 0.325 | 0.620 | 0.050 | 0.003 | 0.868 | 11.388 | |

| DepSMUCE(0.2) | 0.577 | 0.000 | 0.095 | 0.717 | 0.183 | 0.005 | 0.924 | 7.381 | |

| DeCAFS | 0.399 | 0.002 | 0.002 | 0.713 | 0.184 | 0.099 | 0.940 | 6.843 | |

| WCM.gSa | 0.284 | 0.054 | 0.095 | 0.741 | 0.074 | 0.036 | 0.908 | 8.554 | |

| MOSUM.oracle | 0.016 | 0.000 | 0.000 | 0.924 | 0.073 | 0.003 | 0.954 | 5.573 | |

| WBS2.oracle | 0.006 | 0.000 | 0.000 | 0.997 | 0.003 | 0.000 | 0.957 | 5.822 | |

| (M8) | MOSUM.TAVC[1] | 0.247 | 0.007 | 0.058 | 0.897 | 0.037 | 0.001 | 0.938 | 8.065 |

| MOSUM.TAVC[2] | 0.164 | 0.013 | 0.087 | 0.877 | 0.021 | 0.002 | 0.929 | 8.329 | |

| WBS2.TAVC[1] | 0.195 | 0.016 | 0.058 | 0.898 | 0.028 | 0.000 | 0.922 | 9.555 | |

| WBS2.TAVC[2] | 0.142 | 0.027 | 0.114 | 0.848 | 0.011 | 0.000 | 0.906 | 10.293 | |

| DepSMUCE(0.05) | 0.180 | 0.063 | 0.712 | 0.213 | 0.012 | 0.000 | 0.748 | 16.963 | |

| DepSMUCE(0.2) | 0.397 | 0.009 | 0.434 | 0.482 | 0.072 | 0.003 | 0.832 | 12.487 | |

| DeCAFS | 0.301 | 0.006 | 0.023 | 0.662 | 0.199 | 0.110 | 0.930 | 9.065 | |

| WCM.gSa | 0.236 | 0.040 | 0.232 | 0.692 | 0.022 | 0.014 | 0.885 | 9.182 | |

| MOSUM.oracle | 0.034 | 0.000 | 0.001 | 0.863 | 0.131 | 0.005 | 0.947 | 6.526 | |

| WBS2.oracle | 0.014 | 0.000 | 0.000 | 0.989 | 0.011 | 0.000 | 0.949 | 6.549 | |

| (M9) | MOSUM.TAVC[1] | 0.261 | 0.005 | 0.251 | 0.703 | 0.040 | 0.001 | 0.886 | 8.747 |

| MOSUM.TAVC[2] | 0.163 | 0.014 | 0.348 | 0.615 | 0.023 | 0.000 | 0.861 | 9.839 | |

| WBS2.TAVC[1] | 0.178 | 0.010 | 0.329 | 0.633 | 0.028 | 0.000 | 0.855 | 10.803 | |

| WBS2.TAVC[2] | 0.117 | 0.025 | 0.440 | 0.520 | 0.015 | 0.000 | 0.825 | 11.536 | |

| DepSMUCE(0.05) | 0.121 | 0.058 | 0.924 | 0.017 | 0.001 | 0.000 | 0.709 | 11.780 | |

| DepSMUCE(0.2) | 0.309 | 0.008 | 0.897 | 0.084 | 0.011 | 0.000 | 0.725 | 11.289 | |

| DeCAFS | 0.084 | 0.004 | 0.660 | 0.224 | 0.081 | 0.031 | 0.774 | 11.858 | |

| WCM.gSa | 0.071 | 0.002 | 0.749 | 0.219 | 0.019 | 0.011 | 0.775 | 9.747 | |

| MOSUM.oracle | 0.137 | 0.000 | 0.000 | 0.754 | 0.216 | 0.030 | 0.941 | 7.328 | |

| WBS2.oracle | 0.150 | 0.000 | 0.000 | 0.768 | 0.228 | 0.004 | 0.917 | 8.366 | |

| Model | Method | Size | CM | RMSE | |||||

| (M1) | MOSUM.TAVC[1] | 0.126 | 0.000 | 0.000 | 0.983 | 0.017 | 0.000 | 0.975 | 5.979 |

| MOSUM.TAVC[2] | 0.068 | 0.000 | 0.005 | 0.991 | 0.004 | 0.000 | 0.974 | 6.185 | |

| WBS2.TAVC[1] | 0.018 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.981 | 4.781 | |

| WBS2.TAVC[2] | 0.006 | 0.000 | 0.007 | 0.993 | 0.000 | 0.000 | 0.981 | 4.851 | |

| DepSMUCE(0.05) | 0.007 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.982 | 4.764 | |

| DepSMUCE(0.2) | 0.067 | 0.000 | 0.000 | 0.998 | 0.001 | 0.001 | 0.981 | 4.769 | |

| DeCAFS | 0.006 | 0.000 | 0.000 | 0.985 | 0.014 | 0.001 | 0.981 | 4.844 | |

| WCM.gSa | 0.005 | 0.000 | 0.000 | 0.964 | 0.014 | 0.022 | 0.979 | 6.087 | |

| MOSUM.oracle | 0.040 | 0.000 | 0.000 | 0.821 | 0.171 | 0.008 | 0.972 | 6.023 | |

| WBS2.oracle | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.982 | 4.776 | |

| (M2) | MOSUM.TAVC[1] | 0.143 | 0.000 | 0.000 | 0.996 | 0.004 | 0.000 | 0.975 | 5.940 |

| MOSUM.TAVC[2] | 0.079 | 0.000 | 0.003 | 0.997 | 0.000 | 0.000 | 0.974 | 6.051 | |

| WBS2.TAVC[1] | 0.025 | 0.000 | 0.002 | 0.998 | 0.000 | 0.000 | 0.983 | 4.432 | |

| WBS2.TAVC[2] | 0.016 | 0.002 | 0.003 | 0.995 | 0.000 | 0.000 | 0.982 | 4.459 | |

| DepSMUCE(0.05) | 0.828 | 0.000 | 0.000 | 0.389 | 0.171 | 0.440 | 0.941 | 16.822 | |

| DepSMUCE(0.2) | 0.924 | 0.000 | 0.000 | 0.209 | 0.142 | 0.649 | 0.923 | 20.094 | |

| DeCAFS | 0.957 | 0.000 | 0.000 | 0.040 | 0.016 | 0.944 | 0.879 | 31.810 | |

| WCM.gSa | 0.005 | 0.000 | 0.000 | 0.961 | 0.014 | 0.025 | 0.980 | 4.686 | |

| MOSUM.oracle | 0.051 | 0.000 | 0.000 | 0.846 | 0.138 | 0.016 | 0.973 | 5.934 | |

| WBS2.oracle | 0.002 | 0.000 | 0.000 | 0.999 | 0.001 | 0.000 | 0.983 | 4.413 | |

| (M3) | MOSUM.TAVC[1] | 0.122 | 0.000 | 0.000 | 0.996 | 0.004 | 0.000 | 0.995 | 2.050 |

| MOSUM.TAVC[2] | 0.081 | 0.000 | 0.000 | 0.999 | 0.001 | 0.000 | 0.995 | 2.063 | |

| WBS2.TAVC[1] | 0.034 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.998 | 1.356 | |

| WBS2.TAVC[2] | 0.017 | 0.000 | 0.003 | 0.997 | 0.000 | 0.000 | 0.998 | 1.394 | |

| DepSMUCE(0.05) | 0.925 | 0.000 | 0.000 | 0.975 | 0.025 | 0.000 | 0.997 | 1.410 | |

| DepSMUCE(0.2) | 0.991 | 0.000 | 0.000 | 0.887 | 0.109 | 0.004 | 0.992 | 1.575 | |

| DeCAFS | 0.591 | 0.000 | 0.000 | 0.605 | 0.345 | 0.050 | 0.988 | 1.176 | |

| WCM.gSa | 0.007 | 0.000 | 0.000 | 0.643 | 0.150 | 0.207 | 0.959 | 2.336 | |

| MOSUM.oracle | 0.005 | 0.000 | 0.000 | 0.974 | 0.026 | 0.000 | 0.994 | 1.980 | |

| WBS2.oracle | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.998 | 1.356 | |

| (M4) | MOSUM.TAVC[1] | 0.092 | 0.000 | 0.000 | 0.992 | 0.008 | 0.000 | 0.990 | 3.017 |

| MOSUM.TAVC[2] | 0.060 | 0.000 | 0.003 | 0.995 | 0.002 | 0.000 | 0.990 | 3.024 | |

| WBS2.TAVC[1] | 0.020 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.996 | 1.808 | |

| WBS2.TAVC[2] | 0.009 | 0.000 | 0.002 | 0.998 | 0.000 | 0.000 | 0.996 | 1.821 | |

| DepSMUCE(0.05) | 0.559 | 0.000 | 0.000 | 0.999 | 0.001 | 0.000 | 0.996 | 1.789 | |

| DepSMUCE(0.2) | 0.850 | 0.000 | 0.000 | 0.964 | 0.035 | 0.001 | 0.994 | 1.878 | |

| DeCAFS | 0.696 | 0.000 | 0.000 | 0.267 | 0.220 | 0.513 | 0.961 | 1.944 | |

| WCM.gSa | 0.013 | 0.000 | 0.000 | 0.723 | 0.113 | 0.164 | 0.967 | 2.803 | |

| MOSUM.oracle | 0.004 | 0.000 | 0.000 | 0.951 | 0.046 | 0.003 | 0.989 | 2.908 | |

| WBS2.oracle | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.996 | 1.800 | |

| (M5) | MOSUM.TAVC[1] | 0.133 | 0.00 | 0.000 | 1.000 | 0.000 | 0.000 | 0.993 | 87.796 |

| MOSUM.TAVC[2] | 0.071 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.993 | 87.796 | |

| WBS2.TAVC[1] | 0.066 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.994 | 74.530 | |

| WBS2.TAVC[2] | 0.029 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.994 | 74.530 | |

| DepSMUCE(0.05) | 1.000 | 0.000 | 0.0000 | 0.000 | 0.000 | 1.000 | 0.613 | 2496.320 | |

| DepSMUCE(0.2) | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.464 | 4116.486 | |

| DeCAFS | 0.000 | 0.000 | 0.000 | 0.993 | 0.007 | 0.000 | 0.994 | 77.484 | |

| WCM.gSa | 0.000 | 0.000 | 0.000 | 1.000 | 0.000 | 0.000 | 0.994 | 74.648 | |

| MOSUM.oracle | 1.000 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.265 | 222.751 | |

| WBS2.oracle | 0.978 | 0.000 | 0.000 | 0.000 | 0.000 | 1.000 | 0.265 | 188.806 | |

| (M6) | MOSUM.TAVC[1] | 0.192 | 0.000 | 0.002 | 0.988 | 0.010 | 0.000 | 0.979 | 6.112 |

| MOSUM.TAVC[2] | 0.117 | 0.000 | 0.002 | 0.995 | 0.003 | 0.000 | 0.979 | 6.259 | |

| WBS2.TAVC[1] | 0.054 | 0.000 | 0.001 | 0.999 | 0.000 | 0.000 | 0.985 | 4.641 | |

| WBS2.TAVC[2] | 0.029 | 0.001 | 0.001 | 0.998 | 0.000 | 0.000 | 0.985 | 4.662 | |

| DepSMUCE(0.05) | 0.767 | 0.000 | 0.000 | 0.549 | 0.232 | 0.219 | 0.960 | 9.668 | |

| DepSMUCE(0.2) | 0.931 | 0.000 | 0.000 | 0.336 | 0.257 | 0.407 | 0.944 | 11.982 | |

| DeCAFS | 0.903 | 0.000 | 0.000 | 0.090 | 0.040 | 0.870 | 0.911 | 28.388 | |

| WCM.gSa | 0.024 | 0.000 | 0.000 | 0.958 | 0.017 | 0.025 | 0.983 | 4.860 | |

| MOSUM.oracle | 0.029 | 0.000 | 0.000 | 0.892 | 0.101 | 0.007 | 0.978 | 6.151 | |

| WBS2.oracle | 0.006 | 0.000 | 0.000 | 0.997 | 0.002 | 0.001 | 0.985 | 4.631 | |

| (M7) | MOSUM.TAVC[1] | 0.297 | 0.000 | 0.000 | 0.957 | 0.043 | 0.000 | 0.979 | 4.854 |

| MOSUM.TAVC[2] | 0.214 | 0.000 | 0.001 | 0.971 | 0.027 | 0.001 | 0.979 | 4.840 | |

| WBS2.TAVC[1] | 0.178 | 0.000 | 0.000 | 0.992 | 0.008 | 0.000 | 0.979 | 4.959 | |

| WBS2.TAVC[2] | 0.120 | 0.000 | 0.001 | 0.997 | 0.002 | 0.000 | 0.979 | 4.984 | |

| DepSMUCE(0.05) | 0.445 | 0.004 | 0.292 | 0.616 | 0.088 | 0.000 | 0.917 | 9.351 | |

| DepSMUCE(0.2) | 0.726 | 0.000 | 0.035 | 0.670 | 0.284 | 0.011 | 0.963 | 5.326 | |

| DeCAFS | 0.557 | 0.000 | 0.000 | 0.492 | 0.216 | 0.292 | 0.961 | 6.242 | |

| WCM.gSa | 0.316 | 0.031 | 0.027 | 0.895 | 0.026 | 0.021 | 0.968 | 4.840 | |

| MOSUM.oracle | 0.036 | 0.000 | 0.000 | 0.878 | 0.111 | 0.011 | 0.975 | 4.933 | |

| WBS2.oracle | 0.005 | 0.000 | 0.000 | 0.997 | 0.003 | 0.000 | 0.983 | 4.154 | |

| (M8) | MOSUM.TAVC[1] | 0.304 | 0.000 | 0.000 | 0.939 | 0.058 | 0.003 | 0.976 | 5.985 |

| MOSUM.TAVC[2] | 0.195 | 0.000 | 0.000 | 0.960 | 0.039 | 0.001 | 0.976 | 5.934 | |

| WBS2.TAVC[1] | 0.142 | 0.000 | 0.000 | 0.994 | 0.006 | 0.000 | 0.976 | 5.958 | |

| WBS2.TAVC[2] | 0.081 | 0.000 | 0.001 | 0.998 | 0.001 | 0.000 | 0.977 | 5.796 | |

| DepSMUCE(0.05) | 0.277 | 0.077 | 0.704 | 0.210 | 0.009 | 0.000 | 0.833 | 15.628 | |

| DepSMUCE(0.2) | 0.595 | 0.004 | 0.361 | 0.514 | 0.113 | 0.008 | 0.901 | 10.853 | |

| DeCAFS | 0.368 | 0.000 | 0.000 | 0.594 | 0.199 | 0.207 | 0.965 | 7.261 | |

| WCM.gSa | 0.136 | 0.040 | 0.051 | 0.894 | 0.010 | 0.005 | 0.962 | 5.811 | |

| MOSUM.oracle | 0.060 | 0.000 | 0.000 | 0.805 | 0.174 | 0.021 | 0.971 | 6.190 | |

| WBS2.oracle | 0.004 | 0.000 | 0.000 | 0.997 | 0.003 | 0.000 | 0.980 | 5.162 | |

| (M9) | MOSUM.TAVC[1] | 0.382 | 0.000 | 0.003 | 0.922 | 0.072 | 0.003 | 0.974 | 6.551 |

| MOSUM.TAVC[2] | 0.259 | 0.000 | 0.004 | 0.953 | 0.042 | 0.001 | 0.974 | 6.549 | |

| WBS2.TAVC[1] | 0.231 | 0.000 | 0.005 | 0.985 | 0.010 | 0.000 | 0.973 | 7.309 | |

| WBS2.TAVC[2] | 0.181 | 0.000 | 0.003 | 0.993 | 0.004 | 0.000 | 0.974 | 7.153 | |

| DepSMUCE(0.05) | 0.231 | 0.741 | 0.251 | 0.008 | 0.000 | 0.000 | 0.731 | 13.329 | |

| DepSMUCE(0.2) | 0.540 | 0.269 | 0.616 | 0.106 | 0.008 | 0.001 | 0.784 | 13.165 | |

| DeCAFS | 0.081 | 0.262 | 0.022 | 0.574 | 0.092 | 0.050 | 0.890 | 8.834 | |

| WCM.gSa | 0.061 | 0.281 | 0.076 | 0.624 | 0.014 | 0.005 | 0.890 | 8.122 | |

| MOSUM.oracle | 0.097 | 0.000 | 0.000 | 0.754 | 0.215 | 0.031 | 0.968 | 6.883 | |

| WBS2.oracle | 0.067 | 0.000 | 0.000 | 0.957 | 0.042 | 0.001 | 0.967 | 6.774 | |

Appendix C Proof of Theorem 1

For sequences of positive numbers and , we write , or , if there exists some constant such that as . We write if there exists some positive constants and such that as . Without loss of generality, we set and drop the dependence on for notational simplicity; analogous arguments are applicable when other fixed values of are used.

We denote by the set of indices of the -th block of data for some . We adapt the proof of Theorem 5 in Chen et al., (2021) with modifications to our case with the TAVC estimator. We denote by

Then, . First, we consider the influence function constructed using the blocks which do not contain any change points:

Letting

define the functions

Then, it can be shown that satisfies the envelope property

| (C.1) |

To see this, note that since by Equation (5), we have

Similarly, from the fact that , the lower bound follows.

Next, we show that is concentrated about its mean. We deal with the different cases, Assumptions 1 (iii) (iii)(a) and (iii)(b), separately, in order to prove Equations (7) and (8) respectively. Applying Step 2 of the proof of Theorem 5 in Chen et al., (2021), we have that, for and ,

| (C.2) |

where is the -net for with and . For any random variable , denote by the centering operator, and let . Let , and , , be with therein replaced with its independent and identically distributed copy for all . Then for any random variable with measurable , let .

Proof of (7).

Under Assumption 1 (iii) (iii)(a), we show that satisfies appropriate functional dependence properties. Denote

Since , we have for any and ,

| (C.3) |

Further, let and . Then,

and we define

Noting that

it follows that

Next, by Assumption 1 (i), we have

| (C.4) |

for any arbitrarily small . Then, using (C.4),

| (C.5) | ||||

| (C.6) |

where the constants involved in depend on , and . Since we only consider , we bound in (C.3) for as

where the first inequality follows from Hölder’s inequality, the second from Burkholder’s inequality (see e.g. Lemma 2 of Chen et al., (2021)) with , the last from (C.5)–(C.6) and . Similarly, when , we have that . We can bound the term in (C.3) in a similar fashion, to obtain

| (C.7) |

Therefore, the dependence-adjusted norm

for with . Under Assumption 1 (iii) (iii)(a), having shown the bound on , we apply Lemma C.2 of Zhang and Wu, (2017) and yield, for any ,

where and the constant appearing in the depend on , , , and . Applying a Bonferroni bound with then yields

| (C.8) |

Taking , using Equations (C.2) and (C.8) we obtain

| (C.9) |

Recalling that and , we have that

| (C.10) |

Combining Equations (C.1), (C.9) and (C.10), we have that with probability tending to one,

| (C.11) |

uniformly for all , where

with . If

| (C.12) |

then possesses real roots. Denote the smallest root by , which satisfies

| (C.13) |

Under Assumption 1, we have for some ,

by (C.6) and Burkholder’s inequality. Therefore, from (C.13) and that ,

A similar bound can be obtained for , the largest root of and under Equation (C.11), we have that . Then, setting , we have (C.12) holds, and

∎

Proof of (8).

We proceed analogously as in the proof of (7), except that we control for the dependence-adjusted sub-exponential norm of , as

where the first inequality follows from (C.7) and the second from Assumption 1 (i). Therefore, we have with . Then applying Lemma C.4 of Zhang and Wu, (2017) with (C.2), we obtain

where depends on and through . Taking , we have that

| (C.14) |

Then, by the analogous arguments as those adopted in the proof of (7) with (C.14) replacing (C.9), we derive (8). ∎