What’s the Harm? Sharp Bounds on the Fraction Negatively Affected by Treatment

Abstract

The fundamental problem of causal inference – that we never observe counterfactuals – prevents us from identifying how many might be negatively affected by a proposed intervention. If, in an A/B test, half of users click (or buy, or watch, or renew, etc.), whether exposed to the standard experience A or a new one B, hypothetically it could be because the change affects no one, because the change positively affects half the user population to go from no-click to click while negatively affecting the other half, or something in between. While unknowable, this impact is clearly of material importance to the decision to implement a change or not, whether due to fairness, long-term, systemic, or operational considerations. We therefore derive the tightest-possible (i.e., sharp) bounds on the fraction negatively affected (and other related estimands) given data with only factual observations, whether experimental or observational. Naturally, the more we can stratify individuals by observable covariates, the tighter the sharp bounds. Since these bounds involve unknown functions that must be learned from data, we develop a robust inference algorithm that is efficient almost regardless of how and how fast these functions are learned, remains consistent when some are mislearned, and still gives valid conservative bounds when most are mislearned. Our methodology altogether therefore strongly supports credible conclusions: it avoids spuriously point-identifying this unknowable impact, focusing on the best bounds instead, and it permits exceedingly robust inference on these. We demonstrate our method in simulation studies and in a case study of career counseling for the unemployed.

1 Introduction

Before making changes to an online platform, product managers regularly conduct experiments (“A/B tests”) to make sure a change does not negatively impact users’ experience. Similarly, extensive program evaluations, whether experimental or observational, are a corner stone of evidence-based policymaking and help avoid harmful policy changes. These tests and evaluations focus on assessing the causal effect of a change on key metrics, whether user engagement or retention on online platforms or outcomes like employment for social programs. Average treatment effects, heterogeneous treatment effects, and distributional treatment effects on these outcomes quantify the quality of the intervention in terms of aggregate impacts on the population or on subpopulations. This is in its essence a statistical solution to the fundamental problem of causal inference: assess aggregate effects since the impact on any one individual can never be observed. We can never know whether a user that churned under arm “B” would have been retained under arm “A,” but we can characterize the distribution of retention under each arm, even segmenting the population by observable features.

While unknowable, the impact of changes on individuals is clearly of material importance to the decision to implement a change or not. This individual impact can have downstream effects, whether user-behavioral, reputational, or operational. Moreover, quantifying how negative this impact can be is crucial to understanding fairness with respect to the welfare of the individuals, rather than just focusing on social (i.e., average) welfare, the welfare of the decision-making entity, or the welfare of observable groups. Specifically, even if the average treatment effect is zero, there can still be a sizable subpopulation that is negatively affected by the change. That is, a change with zero average effect cannot in earnest be called “harmless." In this paper we consider measuring the fraction that are negatively affected. The aim is to be able to flag changes that may individually harm many. Unfortunately this fraction cannot be identified from data, even experimental data, but we may still be able to bound it. For example, if, in an A/B test, half of users click (or buy, or watch, or renew, etc.) whether exposed to the standard experience “A" or a new one “B," hypothetically it could be because the change affects no one, because the change positively affects half the user population to go from no-click to click while negatively affecting the other half, or anything in between. Such a large bound on the range of possibilities, however, is very crude and uninformative.

In this paper, we derive the sharp bounds on the fraction of individuals negatively affected by treatment using all baseline features available, and we develop tools to conduct robust inferences on these bounds. That is, we characterize the tightest-possible interval that contains all values of this unknowable quantity consistent with all observable information, in particular crucially leveraging unit feature information. We consider both the fraction negatively affected under a wholesale change from one treatment regime to another as well as under an optimal policy that assigns each observable subpopulation the treatment with best average outcomes for the subpopulation. Then, we tackle how to actually assess these theoretical bounds based on actual data, namely, how to estimate the interval endpoints and construct confidence intervals (CIs) that account for sampling error, on top of the inherent epistemic uncertainty characterized by the bounds. The bounds involve potentially complex functions such as the conditional average treatment effect (CATE) function, so we develop inference methodology that is exceedingly robust to learning these functions. Namely, our inferences are valid and calibrated even when these complex functions are learned nonparametrically at slow rates, and our estimated bounds remain valid, albeit conservative, even when these are learned inconsistently, so that conclusions as to the presence of harm based on our tools can be highly credible. We demonstrate our tools in a simulation study and in a case study of French reemployment assistance programs.

2 Problem Set Up and the Fraction Negatively Affected

The Population

Each individual in the population is associated with baseline covariates (observable characteristics), , and two binary potential outcomes, , corresponding to each of two treatment options, and . Examples include: two versions of product on an online platform and whether user is retained in the next quarter, or two versions of a job training program for the unemployed and whether the participant is reemployed within the following year. We will consider the generalization to non-binary outcomes in Remarks 1 and 3.

The individual treatment effect is the difference in potential outcomes: We assume that an outcome value of corresponds to a better outcome (e.g., retained, reemployed) and to a worse outcome (e.g., churned, unemployed). Thus, if treatment 0 represents status quo and treatment 1 represents a proposed change, then individuals with ( or ) are unaffected by the change, individuals with () benefit from the change, and individuals with () are harmed by the change. This list of potential-outcome combinations is exhaustive.

The Data

We consider data from either a randomized experiment or an observational study, wherein we never observe both and simultaneously. Each individual is associated with a treatment , and we observe the factual outcome corresponding to . We never observe the counterfactual . That is, the data consists of observations of .

In particular, the distribution of the data only reflects part of the full population distribution involving both potential outcomes. Let denote the distribution of . Define the coarsening function , which has the pre-image . Then the distribution induced on is given by (as measures). That is, the data distribution is given by taking a draw from and coarsening it by . The data then consists of independent draws, for . We use to denote expectations with respect to , respectively. Note that both have the same -distribution, so anything involving only will be the same. For any function of we let be the -norm with respect to .

We assume throughout that all endogeneity is explained by , known as unconfoundedness: . That is, controlling for , treatment assignment is independent of an individual’s idiosyncrasies as relevant to their potential outcomes. Randomized experiments ensure this by design, often with (complete randomization). Our results extend to observational settings assuming unconfoundedness, which is a common assumption in this setting [27]. For our purposes, the only technical difference between the experimental and observational settings is whether or not we exactly know the propensity score, defined as We assume throughout that almost surely, known as overlap. Note that assuming also encapsulates non-interference [50].

In the following it will also be useful to define the conditional mean of potential outcomes:

| (1) |

where the last equality follows from unconfoundedness and overlap, showing only depends on . We also define the conditional average treatment effect (CATE) and sum (CATS) functions as

| (2) |

2.1 Parameters of Interest

The primary parameter of interest we consider is the fraction negatively affected (FNA) by a wholesale change from treatment 0 to treatment 1:

In particular, this quantity stands in contrast to the average treatment effect, A zero or positive ATE is generally interpreted to indicate a neutral or favorable treatment. However, having need not mean having . A simple example is , which has but .

Given we observe baseline covariates, we can more generally consider personalized treatment policies that assign treatments based on the value of . Let denote any two such policies and let us define the fraction harmed by a change from to as

This more general construct gives rise to several parameters of interest:

-

1.

First, we recover our primary parameter of interest, where (or, ) stands for the constant policy taking value (or, ) everywhere.

-

2.

Second, given a proposed personalized treatment policy , the quantity is the fraction negatively affected by changing from a status quo of 0 to deploying the proposed policy , which intervenes to treat the subpopulation with covariates such that .

-

3.

Third, we can recover the misclassification rate of the policy :

This represents the fraction of individuals negatively affected by being misclassified by : they should be treated by one treatment but are being given the other.

-

4.

Of particular interest is the misclassification rate of the optimal personalized treatment policy, which assigns the treatment with larger conditional average outcome:

We are interested in . The policy can equivalently be characterized as the policy maximizing social welfare, , or as minimizing misclassification, , both over all policies . Given this, one hopes but cannot rule out that avoids negative impact.

3 Sharp Bounds

In this section, we derive sharp bounds on our parameters of interest. For the sake of generality we focus on the parameter as it captures all of our parameters of interest using different . The sharp bounds describe the set of values that can take if all we know is the distribution of the data, . This characterizes the most we can hope to learn at the limit of infinite data since this distribution is the most we can learn from draws from it, that is, our data.

To define this formally, recall that is given by via coarsening. However, this mapping from to need not be invertible. Given a parameter that depends on the full distribution , we define its identified set as the set of all values consistent with , that is, that could be explained by some that gives rise to the given data distribution and satisfies unconfoundedness:

We are interested in the identified set of and sharp bounds on the parameter .

When , we say that is identifiable because it is uniquely specified by the distribution of the data. Otherwise, we say it is unidentifiable: even given infinite data (equivalently, the distribution of the data), we cannot determine the value of based on the data alone since many values are consistent with the observations. For example, ATE is identifiable because and Eq. 1 shows that depends on alone.

Is identifiable? Our first result characterizes exactly when, showing that generally, no.

Theorem 1 (Identifiability).

is identifiable if and only if, for almost all , either or or .

Thm. 1 shows that only in degenerate cases is identifiable. Generally, there will exist a non-negligible (positive probability) set of ’s where the policies differ and neither conditional outcome distribution is constant. Then, by Thm. 1, would be unidentifiable.

We are now prepared to state our main theorem characterizing the sharp bounds on . Since is generally unidentifiable, the best we can do using the data is measure the set . The sharp lower and upper bounds are and , respectively, as these are precisely the largest (resp., smallest) lower (resp., upper) bounds on the set of possible values. The following result gives the sharp bounds and moreover shows the identified set is closed and convex so it is in fact an interval with the bounds as its endpoints.

Theorem 2 (Sharp Bounds on FNA).

Fix any . Set

| (3) | ||||

| (4) | ||||

Then, the identified set is the interval .

The proof of Thm. 2 proceeds by applying the Fréchet-Hoeffding bounds [21, 51] for each level of and showing this remains sharp. Eqs. 3 and 4 simplify a lot for the change from all-0 to all-1:

| (5) |

We can also simplify when considering the optimal policy. Plugging in the optimal policy we get:

| (6) |

Unlike most policies, it is always plausible that the optimal policy affects no one negatively: because , we always have . On the other hand, it is generally also plausible that it does, that is, is generally nonzero. In agreement with Thm. 1, it is in fact zero only when or for almost all .

Remark 1 (The Non-Binary Case).

We can generalize Thm. 2 to the non-binary-outcome case as well. Consider now general scalar outcomes , whether continuous, discrete, or mixed. Define the general parameter:

Then, , , and .

Theorem 3.

Fix . We then have

We recover Eqs. 3 and 4 by min/maximizing over . For inference, we focus on the binary case. The non-binary case can be handled similarly but is more complicated as it requires learning the functions that optimize the above and for each . (Nonetheless, even if we learn the wrong functions we will get valid, albeit not sharp, bounds; see Thms. 7 and 6.)

Remark 2 (Tail Expectations of Individual Treatment Effects).

Kallus [28] considers bounds on the conditional value at risk (CVaR) of individual treatment effects (ITEs): for ,

This is equal to the smallest subgroup-ATE among all -sized fractions of the population, that is, the average effect on the -worst affected. It is generally unidentifiable from data. While Kallus [28] considers general real-valued outcomes, in the special case of binary outcomes considered here, is a function of just FNA and ATE:

Lemma 1.

For , .

As a consequence of Thms. 2 and 1, we immediately have that the identified set for for is the interval , with as defined in Eq. 5. Consequently, the endpoints are the sharp lower and upper bounds on .

Kallus [28] gives the upper bound and shows it is tight given only in the sense that is always realizable by some with the same distribution of . However, this bound is generally not sharp, that is, it need not be realizable given , which characterizes more than just . In contrast, plugging into Lemma 1 gives the sharp upper bound in the special case of binary outcomes, that is, this bound fully uses all the information in . Moreover, we have a finite sharp lower bound, whereas Kallus [28] shows that no lower bound exists when given only . Nonetheless, Kallus [28] crucially handles general real-valued outcomes. In particular, the CVaR curve as varies is most interesting in settings with non-binary outcomes, since in binary settings, two numbers – the ATE and FNA – summarize all relevant information per Lemma 1.

4 Inference Methodology

In the previous section we characterized the sharp (meaning, tightest possible) bounds on FNA given the distribution of the data, that is, the best we could do if we had infinite data. We now address how to estimate these from actual data and characterize the uncertainty. That is, how to do inference on the parameters . Recall our data is independent draws for .

In order to systematically handle all of parameters of interest, we will develop a generic, robust method for a large class of parameters that include all of our parameters of interest as special cases.

4.1 Average Hinge Effects

We consider a class parameters we call Average Hinge Effects (AHEs), parametrized by a positive integer , a vector of signs , and a set of functions for :

| (7) | ||||

The AHE is so called because is called the hinge function. AHEs cover all of our parameters of interest: , , , , and . For now, we focus on any given .

4.2 Re-formulating the AHE

The AHE is defined as an average of a function of . The only unknown part of this function is . A naïve approach would be to estimate by , plug it into Eq. 7 and replace by a sample average over . This estimate, however, will not behave like a sample average approximation of Eq. 7. In particular, it has a nonzero derivative in , so that the errors in directly translate to errors in AHE estimation. For example, even if converges as fast as , this will introduce significant errors on the same order as the convergence of sample averages, which can imperil both efficiency and inference. And, if it converges more slowly, as would generally be the case when using flexible machine learning methods for estimating (as parametric ones will inevitably be misspecified), it can even affect the convergence rate of the final estimate. Worst yet, if is inconsistent for we have no hope of consistency for our estimate or an understanding of the direction of its bias. Generally, we would like to avoid depending on how exactly we fit , provide guarantees even when it is estimated slowly and regardless of what method is used to estimate it, and even provide guarantees when its estimation is inconsistent.

Our approach is based on focusing on an alternative formulation of AHE as a sample average where plugging in wrong values for some unknown functions does not affect the formulation too much.

Toward that end, let us first define by

| (8) |

Specifically, we have for , for , and for .

Given , understood as (possibly wrong) stand-ins for , define

If we plug in the correct values of the nuisance parameters , then we would have

| (9) |

Crucially, unlike the definition of AHE as an average in Eq. 7, we will show in Sec. 5 that this new representation as an average remains faithful even when we make small errors in the nuisances.

4.3 Inference Algorithm

Given our special construction of , our algorithm, presented in Alg. 1, follows a simple recipe: we estimate the nuisances in a cross-fold fashion and plug them into Eq. 9, approximating the expectation by a sample average. In Sec. 5 we will show that the special structure of affords this procedure a lot of robustness. The use of cross-fitting ensures nuisance estimates are independent of samples applied thereto [52, 12, 63]. This allows our analysis to only require lax rate assumptions on the nuisance fitting without requiring any additional regularity on restricting how the fitting is done. (If we assume nuisance estimates belong to a Donsker class with probability tending to 1, all of our results will hold even without cross-fitting; we omit this option for brevity.)

4.4 Nuisance Fitting

Our algorithm requires methods for fitting the nuisances . Fitting and amounts to binary regressions (probabilistic classification), which can be done with any of a variety of standard supervised learning methods, whether logistic regression, random forests, or neural nets.

There are different ways to fit . In particular, despite the fact that is determined by , we treat it as a separate nuisance to allow for specialized learners. Of course, the simplest way to fit it is to simply plugin an estimate for into the definition of in Eq. 8, and that is a legitimate option. For all of our parameters of interest, all nuisances are given by learning just two functions: and as in Eq. 2. Therefore, we may alternatively learn these directly and plug them into . For example, there exists a wide literature specialized to learning motivated by the observation that effect signals are often more nuanced and can therefore be washed out by the noise in baselines if we simply difference -estimates [26, 37, 34, 46, 3, 59]. We can similarly apply of all these approaches to learning by simply first mutating the outcome data as . Notably, [34, 46] give rates of convergence for -learning, which we can use to satisfy our assumptions in the next section.

5 Robustness Guarantees for Inference

We now show our inference method has some nice robustness guarantees. This will depend on showing that using our special renders Eq. 9 insensitive to errors in the nuisances. The specific level of errors allowed will depend on the sharpness of margin satisfied by , as defined below.

Definition 1.

We say that a given function satisfies a margin with sharpness (or, an -margin) if there exists such that for all . (We use the convention that if , , and if .)

Every trivially satisfies a 0-margin, but usually a sharper margin holds. If is almost surely either zero or bounded away from zero, then satisfies an infinitely sharp margin:

Lemma 2.

If for some then satisfies an -margin.

In particular, if has finite support, then we can always set . But, this also works more generally. Consider for . If , that is, the policies only differ either far from the boundary where is 0 or exactly on this boundary, then Lemma 2 ensures sharpness .

More generally, we should expect a margin with sharpness 1 in continuous settings.

Lemma 3.

If the cumulative distribution function (CDF) of is boundedly differentiable on for some , then satisfies a -margin.

Consider again the example of . If is a continuous random variable with a bounded density near , then Lemma 3 ensures a margin with sharpness 1. This holds for any two policies, including , which differ everywhere. The same conclusion would also hold if the CDF of was just continuously differentiable at .

Armed with the notion of margin, we can state in what sense the representation Eq. 9 is robust.

Theorem 4.

Fix any with , , for . Fix any . Suppose that either or (or both). Set if and otherwise set . Further assume that . Finally, suppose that satisfies a margin with sharpness . Then, for some constant , we have

In the above, we use the convention that .

5.1 Local Robustness, Confidence Intervals, and Efficiency

Thm. 4 has several important implications. Our first result shows that, if we estimate all nuisances correctly but potentially slowly at nonparametric rates, then we can ensure our estimator looks like a sample average approximation of Eq. 9 and our CIs are calibrated.

Theorem 5.

Suppose with , satisfies an -margin, and for , with , and . Then,

The conditions of Thm. 5 allow that we learn rather slowly. In particular, unlike naïvely plugging in a -estimate into Eq. 7 and taking sample averages, we do not depend at all on how is estimated and the uncertainty therein, provided some slow nonparametric rates hold. For example, learning in with -rates in -error suffices. Or, if is known, then consistently estimating without a rate suffices. For , if an -margin holds, it suffices to learn consistently (no rate) in -error or at -rates in -error. If a -margin holds, it suffices to learn at -rates in -error. While conditions like metric entropy imply -error rates [60], for many classes like smooth functions the error rates are even the same for all [54].

In fact, under one more condition, our estimator achieves the semiparametric efficiency lower bound.

Theorem 6.

Suppose for , . The semiparametric efficiency lower bound for is , whether or not is unknown (varies in the model) or known (fixed in the model).

Corollary 1.

5.2 Double Robustness and Double Validity

Next we show that Alg. 1 is very robust to incorrectly learning some nuisances.

Theorem 7.

Fix any with with . Set if and otherwise set . Suppose satisfies a margin with sharpness , and for that , , for some , and . If either or , then

| (double robustness) | |||

| (double validity, upper) | |||

| (double validity, lower) |

The first equation (double robustness) in Thm. 7 shows our estimator remain consistent for the AHE even if we incorrectly learn either or , bot not both, as long as we correctly learn .

The second two equations (double validity) in Thm. 7 show what happens when we also learn incorrectly. For upper double validity (second equation), we show that, as long as the that are misestimated correspond to convex terms in the AHE (), we remain consistent for an upper bound on the AHE, even if we also incorrectly learn either or , bot not both. In particular, for we only have convex terms, so we are guaranteed and upper bound on the upper bound, that is, we still estimate a valid upper bound on when we misestimate the CATE (which is for ) and one of or , it just may not be sharp. We also have a symmetric result for lower double validity (third equation), and applying it to we find that we will still estimate a valid upper bound, albeit possibly unsharp, on when we misestimate and one of or . The significance is that we can really trust the results of Alg. 1 are truly bounds on FNA, even if we make mistakes, and therefore conclusions about harm based on our estimates and inferences can be highly credible.

6 Empirical Investigation

We demonstrate our method in a simulation and a case study with data from a real experiment. Replication code is given in the supplement. Experiments were run on an AWS c5.24xlarge instance.

Simulation Study

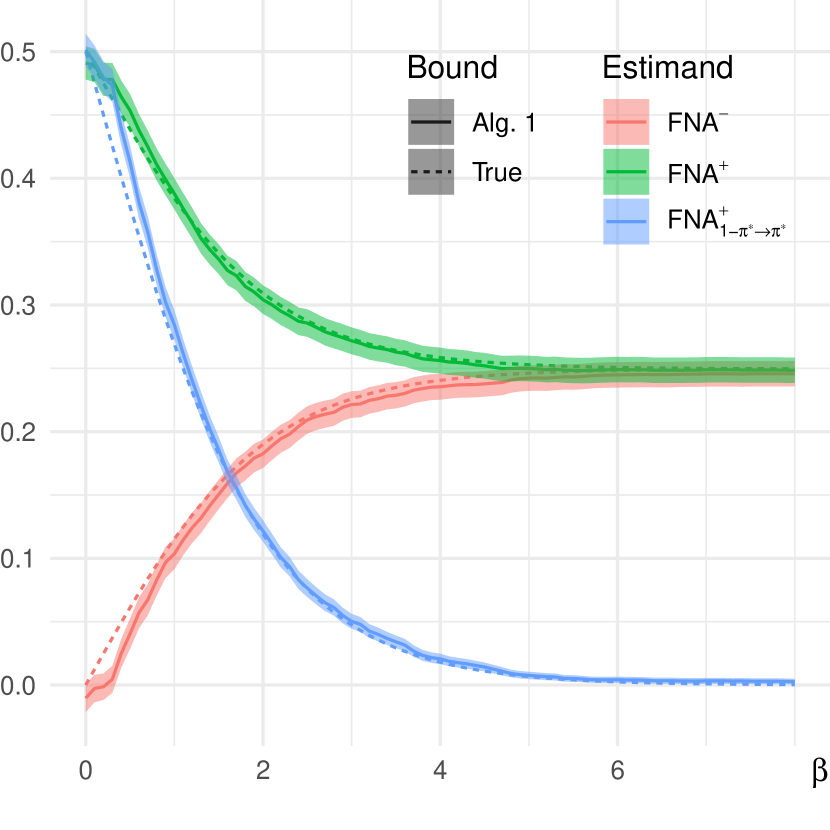

We consider -dimensional standard normal and set , where and . Here controls how much predicts . The dashed lines in Fig. 4 show the sharp bounds of Thm. 2 for and as we vary . We can see that, as becomes more predictive, the bounds go from to a point at . Note there is no true value for as we are not specifying the joint distribution of potential outcomes; instead, per Thm. 2, there are joint distributions with equal to any point between the bounds.

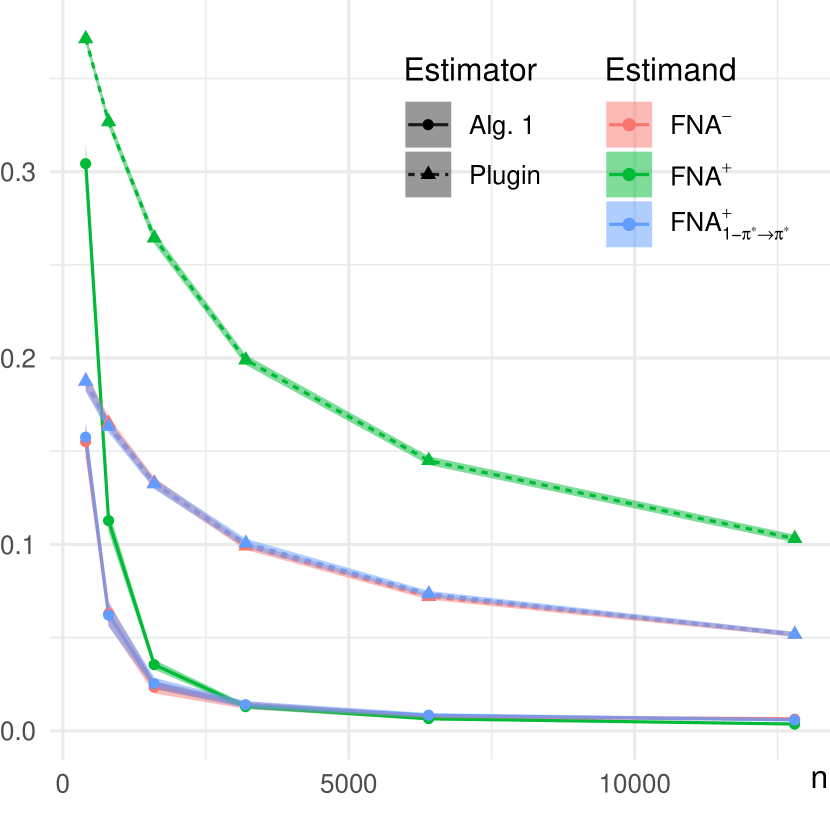

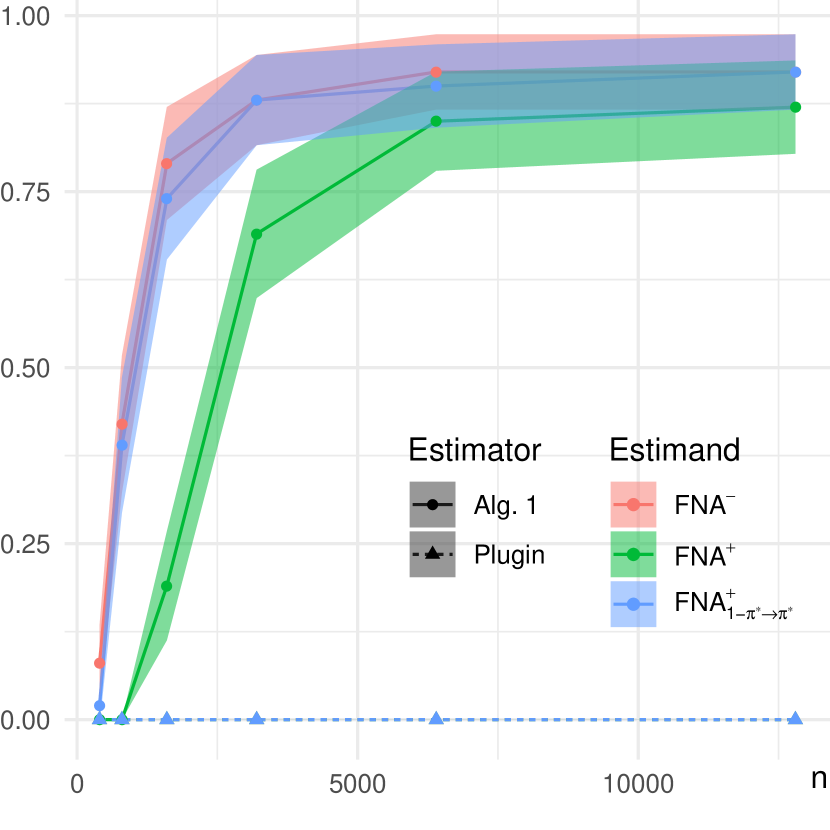

Next, we estimate these true bounds. We fix , and draw samples from , , . We apply Alg. 1 to this data with , estimating using random regression forests and using causal forests (all using R package grf with default parameters). The solid lines in Fig. 4 show the point estimate and 95%-CI output by Alg. 1 for a single draw of data for each . In Figs. 4 and 4 we plot the average root mean squared error of point estimates and coverage of CIs over replications with and varying . We compare the performance to the (cross-fitted) “plugin” estimator that just plugs in the (same) estimates for into Eq. 7 and approximate the expectation by a sample average. Shaded intervals denote 95%-CIs for performance (i.e., due to finite replications).

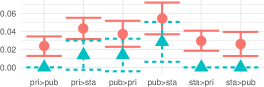

Case Study

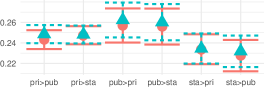

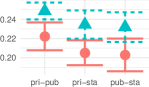

Using data from [6] (BSD license), we compare three different assistance programs offered to French unemployed individuals: the standard benefits (sta), access to public-run counseling (pub), and to private-run counseling (pri). Our binary outcome is reemployment within six months. For example, we can consider a hypothetical scenario where we change from a private to a public counseling provider. As reported by [6], the ATE for this hypothetically change is slightly positive, so a policymaker might therefore enact it, especially if, for example, it offered cost savings or other operational benefits. We consider who may be harmed by this: how many who remain unemployed under the new public program that would have been reemployed under the old private program.

For any pair of arms, we consider the sharp bounds on the FNA from one to other or the other way and on the misclassification rate of the optimal policy choosing between the two. Following Kallus [28], we set to all pre-treatment covariates in table 2 of Behaghel et al. [6]., and we consider the sharp bounds either with these or given no at all. We fit using linear regression and using doubly-robust pseudo-outcome linear regression. Since the propensity is known, in light of the guarantees of Thm. 7, we do not worry about misspecifying , only using it for variance reduction by accounting for main effects, and we do not worry about misspecifying , only hoping to tighten the bounds some from using no . The results are shown in Fig. 4. We see that, while covariates are somewhat uninformative, we are still able to tighten bounds compared to no . In particular, for the change from sta to pri or pub or the change from pri to pub, without the lower bounds on FNA are 0, while with the lower bounds as well as the lower confidence bounds on these bounds are strictly positive. This means that, with and the methods developed we can prove that there must be some harm by this change, something we could not do otherwise and such a finding can bolster further work to investigate and address this harm.

7 Connections, Limitations, Extensions, and Conclusions

Connections to partial identification

Partial identification of unknowable parameters has a long tradition in econometrics [55, 41, 43, 40, 45, 53, 11, 35]. Some approaches focus on average treatment effects in the presence of confounding [15, 17, 31, 49, 56, 62, 8, 13], among which [17, 62, 8, 13] are notable for conducting semiparametric inference on bounds, but for confounding rather than for individual effects, as we do. Some others, like us, focus on understanding the joint distribution of potential outcomes [25, 16, 1, 42, 18]. Like us, these heavily leverage the Fréchet-Hoeffding bounds [51, 21, 9, 61, 48]. Unlike these, we use efficient and robust inference that can aggregate across covariates to tighten bounds by leveraging machine learning of conditional-mean outcome functions.

Connections to fairness

Understanding the distribution of impact is a central problem in algorithmic fairness [44, 5]. Here, we specifically focused on the differential impact of interventions, which brought up issues of identification. In contrast, in algorithmic fairness one usually measures disparities in observed outcomes, such as in the form of the loss function of a model on a labeled example [33, 7, 22, 2]. A line of work specifically focuses on identification issues in algorithmic fairness [32, 10, 30, 29, 19, 38, 14, 36]. Notably, [32] also conduct semiparametric inference on sharp bounds derived from the Fréchet-Hoeffding bounds, but in the context of algorithm evaluation with unobserved protected labels rather than interventions with unobserved counterfactuals. And, [30] do consider unobserved counterfactuals in assessing equality of opportunity [24] for intervention-prioritization policies, but (appropriately in their own context) they assume away our primary focus here by assuming an a priori known bound on FNA (possibly zero, i.e., monotone treatment response).

Limitations and Extensions

Restricting outcomes to be binary is one limitation of our work, and extensions to continuous settings is an interesting avenue of future research. Another limitation is that, while we can bound the FNA, it can still be hard to asses who is negatively affected. This is, unfortunately, impossible for the same reason FNA is unidentifiable, but a place to start such analyses may be to consider who are individuals with and even characterize that group via summary statistics compared to the population. Indeed, per Eq. 5, the lower bound on FNA is exactly the (negative of the) ATE on this group. Another important consideration is whether the data is representative: FNA refers to the fraction of the studied population, which might differ from the population of interest. E.g., if an experiment did not enroll a representative sample, we may be systematically excluding some groups from consideration. If such unrepresentativeness is explained by covariates (i.e., missing at random), the solution is simple: we reweight. If not explained by (i.e., missing not at random), then we need to also account for this additional source of unidentifiability. An avenue for future research is to combine such ambiguity with counterfactual ambiguity. Another concern is whether the outcome represents the impact we want to measure [47].

Conclusions

Our tools support drawing credible conclusions about the potential negative impact of interventions: they both account for ambiguity due to unobserved counterfactuals (while mitigating it using covariates) as well as strongly guard against slow or inconsistent learning of necessary nuisances functions. Robust inference on the lower bounds, in particular, crucially provides watertight demonstrations of negative impact, which can bolster efforts to mitigate harm and improve equity.

Acknowledgments

I am grateful for the helpful comments of the anonymous reviewers and for many insightful and thought-inspiring conversations with my colleagues at Netflix.

References

- Abbring and Heckman [2007] Jaap H Abbring and James J Heckman. Econometric evaluation of social programs, part iii: Distributional treatment effects, dynamic treatment effects, dynamic discrete choice, and general equilibrium policy evaluation. Handbook of econometrics, 6:5145–5303, 2007.

- Agarwal et al. [2018] Alekh Agarwal, Alina Beygelzimer, Miroslav Dudík, John Langford, and Hanna Wallach. A reductions approach to fair classification. In International Conference on Machine Learning, pages 60–69. PMLR, 2018.

- Athey and Imbens [2016] Susan Athey and Guido Imbens. Recursive partitioning for heterogeneous causal effects. Proceedings of the National Academy of Sciences, 113(27):7353–7360, 2016.

- Audibert and Tsybakov [2007] Jean-Yves Audibert and Alexandre B Tsybakov. Fast learning rates for plug-in classifiers. The Annals of statistics, 35(2):608–633, 2007.

- Barocas et al. [2019] Solon Barocas, Moritz Hardt, and Arvind Narayanan. Fairness and Machine Learning. fairmlbook.org, 2019. http://www.fairmlbook.org.

- Behaghel et al. [2014] Luc Behaghel, Bruno Crépon, and Marc Gurgand. Private and public provision of counseling to job seekers: Evidence from a large controlled experiment. American economic journal: applied economics, 6(4):142–74, 2014.

- Bird et al. [2020] Sarah Bird, Miro Dudík, Richard Edgar, Brandon Horn, Roman Lutz, Vanessa Milan, Mehrnoosh Sameki, Hanna Wallach, and Kathleen Walker. Fairlearn: A toolkit for assessing and improving fairness in ai. Microsoft, Tech. Rep. MSR-TR-2020-32, 2020.

- Bonvini and Kennedy [2021] Matteo Bonvini and Edward H Kennedy. Sensitivity analysis via the proportion of unmeasured confounding. Journal of the American Statistical Association, pages 1–11, 2021.

- Cambanis et al. [1976] Stamatis Cambanis, Gordon Simons, and William Stout. Inequalities for e k (x, y) when the marginals are fixed. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 36(4):285–294, 1976.

- Chen et al. [2019] Jiahao Chen, Nathan Kallus, Xiaojie Mao, Geoffry Svacha, and Madeleine Udell. Fairness under unawareness: Assessing disparity when protected class is unobserved. In Proceedings of the conference on fairness, accountability, and transparency, pages 339–348, 2019.

- Chernozhukov et al. [2007] Victor Chernozhukov, Han Hong, and Elie Tamer. Estimation and confidence regions for parameter sets in econometric models 1. Econometrica, 75(5):1243–1284, 2007.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. Econometrics Journal, 21(1):C1–C68, 2018.

- Chernozhukov et al. [2021] Victor Chernozhukov, Carlos Cinelli, Whitney Newey, Amit Sharma, and Vasilis Syrgkanis. Omitted variable bias in machine learned causal models. arXiv preprint arXiv:2112.13398, 2021.

- Coston et al. [2021] Amanda Coston, Ashesh Rambachan, and Alexandra Chouldechova. Characterizing fairness over the set of good models under selective labels. In International Conference on Machine Learning, pages 2144–2155. PMLR, 2021.

- Cross and Manski [2002] Philip J Cross and Charles F Manski. Regressions, short and long. Econometrica, 70(1):357–368, 2002.

- Ding et al. [2019] Peng Ding, Avi Feller, and Luke Miratrix. Decomposing treatment effect variation. Journal of the American Statistical Association, 114(525):304–317, 2019.

- Dorn et al. [2021] Jacob Dorn, Kevin Guo, and Nathan Kallus. Doubly-valid/doubly-sharp sensitivity analysis for causal inference with unmeasured confounding. arXiv preprint arXiv:2112.11449, 2021.

- Firpo and Ridder [2008] Sergio Firpo and Geert Ridder. Bounds on functionals of the distribution of treatment effects. 2008.

- Fogliato et al. [2020] Riccardo Fogliato, Alexandra Chouldechova, and Max G’Sell. Fairness evaluation in presence of biased noisy labels. In International Conference on Artificial Intelligence and Statistics, pages 2325–2336. PMLR, 2020.

- Frank et al. [1987] Maurice J Frank, Roger B Nelsen, and Berthold Schweizer. Best-possible bounds for the distribution of a sum—a problem of kolmogorov. Probability theory and related fields, 74(2):199–211, 1987.

- Fréchet [1935] Maurice Fréchet. Généralisation du théoreme des probabilités totales. Fundamenta mathematicae, 1(25):379–387, 1935.

- Ghosh et al. [2021] Avijit Ghosh, Lea Genuit, and Mary Reagan. Characterizing intersectional group fairness with worst-case comparisons. In Artificial Intelligence Diversity, Belonging, Equity, and Inclusion, pages 22–34. PMLR, 2021.

- Hahn [1998] Jinyong Hahn. On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, pages 315–331, 1998.

- Hardt et al. [2016] Moritz Hardt, Eric Price, and Nati Srebro. Equality of opportunity in supervised learning. Advances in neural information processing systems, 29, 2016.

- Heckman et al. [1997] James J Heckman, Jeffrey Smith, and Nancy Clements. Making the most out of programme evaluations and social experiments: Accounting for heterogeneity in programme impacts. The Review of Economic Studies, 64(4):487–535, 1997.

- Imai and Ratkovic [2013] Kosuke Imai and Marc Ratkovic. Estimating treatment effect heterogeneity in randomized program evaluation. The Annals of Applied Statistics, 7(1):443–470, 2013.

- Imbens and Rubin [2015] Guido W Imbens and Donald B Rubin. Causal inference in statistics, social, and biomedical sciences. Cambridge University Press, 2015.

- Kallus [2022] Nathan Kallus. Treatment effect risk: Bounds and inference. arXiv preprint arXiv:2201.05893, 2022.

- Kallus and Zhou [2018] Nathan Kallus and Angela Zhou. Residual unfairness in fair machine learning from prejudiced data. In International Conference on Machine Learning, pages 2439–2448. PMLR, 2018.

- Kallus and Zhou [2019] Nathan Kallus and Angela Zhou. Assessing disparate impacts of personalized interventions: Identifiability and bounds. arXiv preprint arXiv:1906.01552, 2019.

- Kallus et al. [2019] Nathan Kallus, Xiaojie Mao, and Angela Zhou. Interval estimation of individual-level causal effects under unobserved confounding. In The 22nd international conference on artificial intelligence and statistics, pages 2281–2290. PMLR, 2019.

- Kallus et al. [2021] Nathan Kallus, Xiaojie Mao, and Angela Zhou. Assessing algorithmic fairness with unobserved protected class using data combination. Management Science, 2021.

- Kearns et al. [2018] Michael Kearns, Seth Neel, Aaron Roth, and Zhiwei Steven Wu. Preventing fairness gerrymandering: Auditing and learning for subgroup fairness. In International Conference on Machine Learning, pages 2564–2572. PMLR, 2018.

- Kennedy [2020] Edward H Kennedy. Optimal doubly robust estimation of heterogeneous causal effects. arXiv preprint arXiv:2004.14497, 2020.

- King [2013] Gary King. A solution to the ecological inference problem. In A Solution to the Ecological Inference Problem. Princeton University Press, 2013.

- Kleinberg et al. [2018] Jon Kleinberg, Himabindu Lakkaraju, Jure Leskovec, Jens Ludwig, and Sendhil Mullainathan. Human decisions and machine predictions. The quarterly journal of economics, 133(1):237–293, 2018.

- Künzel et al. [2019] Sören R Künzel, Jasjeet S Sekhon, Peter J Bickel, and Bin Yu. Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the national academy of sciences, 116(10):4156–4165, 2019.

- Lakkaraju et al. [2017] Himabindu Lakkaraju, Jon Kleinberg, Jure Leskovec, Jens Ludwig, and Sendhil Mullainathan. The selective labels problem: Evaluating algorithmic predictions in the presence of unobservables. In Proceedings of the 23rd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 275–284, 2017.

- Makarov [1982] GD Makarov. Estimates for the distribution function of a sum of two random variables when the marginal distributions are fixed. Theory of Probability & its Applications, 26(4):803–806, 1982.

- Manski [1995] Charles F Manski. Identification problems in the social sciences. Harvard University Press, 1995.

- Manski [1997a] Charles F Manski. The mixing problem in programme evaluation. The Review of Economic Studies, 64(4):537–553, 1997a.

- Manski [1997b] Charles F Manski. Monotone treatment response. Econometrica, pages 1311–1334, 1997b.

- Manski [2003] Charles F Manski. Partial identification of probability distributions, volume 5. Springer, 2003.

- Mitchell et al. [2021] Shira Mitchell, Eric Potash, Solon Barocas, Alexander D’Amour, and Kristian Lum. Algorithmic fairness: Choices, assumptions, and definitions. Annual Review of Statistics and Its Application, 8:141–163, 2021.

- Molinari [2020] Francesca Molinari. Microeconometrics with partial identification. Handbook of econometrics, 7:355–486, 2020.

- Nie and Wager [2021] Xinkun Nie and Stefan Wager. Quasi-oracle estimation of heterogeneous treatment effects. Biometrika, 108(2):299–319, 2021.

- Passi and Barocas [2019] Samir Passi and Solon Barocas. Problem formulation and fairness. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pages 39–48, 2019.

- Ridder and Moffitt [2007] Geert Ridder and Robert Moffitt. The econometrics of data combination. Handbook of econometrics, 6:5469–5547, 2007.

- Rosenbaum [2002] Paul R. Rosenbaum. Observtional Studies. Springer, 2002.

- Rubin [1986] Donald B Rubin. Comment: Which ifs have causal answers. Journal of the American statistical association, 81(396):961–962, 1986.

- Rüschendorf [1981] Ludger Rüschendorf. Sharpness of fréchet-bounds. Zeitschrift für Wahrscheinlichkeitstheorie und verwandte Gebiete, 57(2):293–302, 1981.

- Schick [1986] Anton Schick. On asymptotically efficient estimation in semiparametric models. Annals of Statistics, 14(3):1139–1151, 09 1986.

- Semenova [2017] Vira Semenova. Debiased machine learning of set-identified linear models. arXiv preprint arXiv:1712.10024, 2017.

- Stone [1982] Charles J Stone. Optimal global rates of convergence for nonparametric regression. The annals of statistics, pages 1040–1053, 1982.

- Tamer [2010] Elie Tamer. Partial identification in econometrics. Annu. Rev. Econ., 2(1):167–195, 2010.

- Tan [2006] Zhiqiang Tan. A distributional approach for causal inference using propensity scores. Journal of the American Statistical Association, 101(476):1619–1637, 2006.

- Tsiatis [2006] Anastasios A Tsiatis. Semiparametric theory and missing data. 2006.

- Van der Vaart [2000] Aad W Van der Vaart. Asymptotic statistics. Cambridge University Press, 2000.

- Wager and Athey [2018] Stefan Wager and Susan Athey. Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523):1228–1242, 2018.

- Wainwright [2019] Martin J Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press, 2019.

- Williamson and Downs [1990] Robert C Williamson and Tom Downs. Probabilistic arithmetic. i. numerical methods for calculating convolutions and dependency bounds. International journal of approximate reasoning, 4(2):89–158, 1990.

- Yadlowsky et al. [2018] Steve Yadlowsky, Hongseok Namkoong, Sanjay Basu, John Duchi, and Lu Tian. Bounds on the conditional and average treatment effect with unobserved confounding factors. arXiv preprint arXiv:1808.09521, 2018.

- Zheng and van der Laan [2011] Wenjing Zheng and Mark J van der Laan. Cross-validated targeted minimum-loss-based estimation. In Targeted Learning, pages 459–474. Springer, 2011.

Checklist

-

1.

For all authors…

-

(a)

Do the main claims made in the abstract and introduction accurately reflect the paper’s contributions and scope? [Yes] Provided sharp bounds and ways to do inference thereon

-

(b)

Did you describe the limitations of your work? [Yes] See Sec. 7

-

(c)

Did you discuss any potential negative societal impacts of your work? [Yes] See Sec. 7

-

(d)

Have you read the ethics review guidelines and ensured that your paper conforms to them? [Yes]

-

(a)

-

2.

If you are including theoretical results…

-

(a)

Did you state the full set of assumptions of all theoretical results? [Yes]

-

(b)

Did you include complete proofs of all theoretical results? [Yes]

-

(a)

-

3.

If you ran experiments…

-

(a)

Did you include the code, data, and instructions needed to reproduce the main experimental results (either in the supplemental material or as a URL)? [Yes]

-

(b)

Did you specify all the training details (e.g., data splits, hyperparameters, how they were chosen)? [Yes]

-

(c)

Did you report error bars (e.g., with respect to the random seed after running experiments multiple times)? [Yes]

-

(d)

Did you include the total amount of compute and the type of resources used (e.g., type of GPUs, internal cluster, or cloud provider)? [Yes]

-

(a)

-

4.

If you are using existing assets (e.g., code, data, models) or curating/releasing new assets…

-

(a)

If your work uses existing assets, did you cite the creators? [Yes]

-

(b)

Did you mention the license of the assets? [Yes]

-

(c)

Did you include any new assets either in the supplemental material or as a URL? [Yes]

-

(d)

Did you discuss whether and how consent was obtained from people whose data you’re using/curating? [N/A]

-

(e)

Did you discuss whether the data you are using/curating contains personally identifiable information or offensive content? [N/A]

-

(a)

-

5.

If you used crowdsourcing or conducted research with human subjects…

-

(a)

Did you include the full text of instructions given to participants and screenshots, if applicable? [N/A]

-

(b)

Did you describe any potential participant risks, with links to Institutional Review Board (IRB) approvals, if applicable? [N/A]

-

(c)

Did you include the estimated hourly wage paid to participants and the total amount spent on participant compensation? [N/A]

-

(a)

Supplementary Materials

Appendix A Proofs for Sec. 3

A.1 Proof of Thm. 1

Proof of Thm. 1.

It is easiest to prove this as a consequence of Thm. 2, since we already prove the latter below. By Thm. 2, the statement that is identifiable is equivalent to the statement that , as defined in Eqs. 3 and 4. Note, moreover, that , where

and that is a nonnegative variable. Therefore, the statement that is identifiable is equivalent to the statement that . From the above simplification of and since , it is immediate that the event is equivalent to the -measurable event . Noting that is equivalent to completes the proof. ∎

A.2 Proof of Thm. 2

Proof.

By iterated expectations we can write

Let use first show that . Consider any feasible . By union bound, and since probabilities are in , we have

Similarly,

Therefore,

whence , as desired.

We next show that by exhibiting a that recovers it and is compatible with . First, we let have the same -distribution as . Next, for each , if , we set

and if , we set

Note that in each case, the 4 numbers are nonnegative and always sum to 1, and are therefore form a valid distribution on . Moreover, in each case, we have that and . Finally, we set , which ensures that we satisfy unconfoundedness and that . Therefore, since the -distribution as well as all -distributions match, we must have that is compatible with . Finally, we note that, under this distribution, we exactly have

Therefore, .

Next, we show that . Consider any feasible . Note that

Similarly,

Therefore,

the expectation of which is defined to be . Therefore, , as desired.

We next show that by exhibiting a that recovers it and is compatible with . First, we let have the same -distribution as . Next, for each , if , we set

and if , we set

Note that in each case, the 4 numbers are nonnegative and always sum to 1, and are therefore form a valid distribution on . Moreover, in each case, we have that and . Finally, we set , which ensures that we satisfy unconfoundedness and that . Therefore, since the -distribution as well as all -distributions match, we must have that is compatible with . Finally, we note that, under this distribution, we exactly have

Therefore, .

To complete the proof, note that is linear in and that is a convex set, so that is a convex set. ∎

A.3 Proof of Thm. 3

We first present the following restatement of theorems 1 and 2 of [39].

Lemma 4.

Let denote two given distributions on scalar variables. Then,

Proof.

We now turn to proving Thm. 3.

Proof.

Set

Note that

First, write

and similarly for . We now consider the inside of the expectation for every as the sum of two variables , where and , conditioned on . Then the result follows by Lemma 4. ∎

A.4 Proof of Lemma 1

Proof.

Because , we have

Since , the objective approaches as or . Thus, there are only three possible solutions that realize the supremum: . Plugging these in above, we obtain

First, we note that . Second, we note that

Substituting yields the result. ∎

Appendix B Proofs for Sec. 5

B.1 Preliminaries

Lemma 5.

Let be given. Suppose satisfies a margin with sharpness . Fix . Then, for some ,

| (10) | ||||

| (11) | ||||

| (12) | ||||

| (13) |

Proof.

Lemma 6.

Fix any with either or . Set if and otherwise set . Then,

Proof.

Because either or , we have that

If , then the first equation in the statement is immediate.

If , note that

Therefore, if, among all with , the sign is the same, then the biases in all go the same way, establishing the latter two inequalities in the statement. ∎

B.2 Proof of Lemmas 2 and 3

Proof of Lemma 2.

If then clearly . If then . Finally note that, . ∎

Proof of Lemma 3.

Let be the bound on the derivative of the CDF on . If then clearly . If then . Thus, . ∎

B.3 Proof of Thm. 4

Proof.

We first tackle the first inequality to be proven. We will proceed by bounding each of

| (14) | |||

| (15) |

We begin by bounding Eq. 14 considering separately the case that and that . For brevity let us set

In the case that , we bound Eq. 14 by bounding each of

| (16) | |||

| (17) |

Using iterated expectations to first take expectations with respect to and then with respect to , we find that Eq. 16 is equal to

| (18) | ||||

Iterating expectations the same way, we find that Eq. 17 is equal to 0.

In the case that , we bound Eq. 14 by bounding each of

| (19) | |||

| (20) |

Using iterated expectations to first take expectations with respect to and then with respect to , we find that Eq. 19 is again exactly equal to Eq. 18 and the same bound applies. Again, iterating expectations the same way, we find that Eq. 20 is equal to 0.

We now turn to Eq. 15. Using iterated expectations to first take expectations with respect to and then with respect to , we find that Eq. 15 is equal to

We proceed to bound each summand by applying one of Eqs. 10, 11, 12 and 13 of Lemma 5. Consider the term. Suppose (i.e., ). Then applying Eq. 10 if and Eq. 11 if yields the desired bound. Suppose . Since , we can bound the term by , where in the last equality we used . Applying Eq. 12 if and Eq. 13 if yields the desired bound.

We now turn to proving Eq. 15. We proceed by bounding each of the following:

| (21) | |||

| (22) | |||

| (23) |

Firstly, Eq. 21 is equal to

Secondly, Eq. 22 is equal to

B.4 Proof of Thm. 5

Proof.

For brevity, let . Define , , , and . We then have

| (24) | |||

| (25) |

By Chebyshev’s inequality conditioned on , we obtain that Eq. 25 is

By our nuisance-estimation assumptions and Thm. 4, we have that . Thus, Eq. 25 is .

The first equation is concluded by noting .

For the second equation, first note that the first equation together with the central limit theorem imply

Therefore, the result is concluded if we can show that . Note that and that . We have already shown that and continuous mapping implies the same holds for their squares. Next we study the convergence of . Using , we bound

Then, following the very same arguments used to prove the first equation we can show that . ∎

B.5 Proof of Thm. 6

Proof.

Define

Since , if the efficient influence functions of each of exist and are given by , respectively, then the efficient influence function of is given by .

Fix and let us derive the efficient influence function of . Let be a measure on dominating . Let be the counting measure on . Let be the counting measure on . Let be the product measure. Consider the nonparametric model consisting of all distributions on that are absolutely continuous with respect to . By theorem 4.5 of Tsiatis [57], the tangent space with respect to this model is given by

| where | |||

Consider any submodel passing through with density and score belonging to the tangent space . The efficient influence function is the unique function , should it exist, such that

for any such submodel.

Define . Then, by product rule, we have

| (26) |

where we used the fact that implies for almost every .

Note that

Note further that since densities integrate to 1 at all ’s, we have that,

| (27) | ||||

| (28) | ||||

| (29) |

Subtracting 0 from the right hand-side of Eq. 26 in the form of the left-hand side of Eq. 27 times plus the left-hand side of Eq. 29 times , we find that

Since

we conclude that their sum

is the efficient influence function for .

Since is just a weighted average of potential outcomes like the ATE, following the same arguments as in theorem 1 of Hahn [23] shows that

is the influence function for .

The sum of is exactly , which completes the proof for the case where is unknown.

For the model with fixed and known, the tangent space is given by just , that is, the tangent space component corresponding to the -model is the subspace . Since each only had components in and , it still remains within this more restricted tangent space and therefore is still the efficient influence function of . ∎