Price Interpretability of Prediction Markets: A Convergence Analysis

Abstract.

Prediction markets are long known for prediction accuracy. This study systematically explores the fundamental properties of prediction markets, addressing questions about their information aggregation process and the factors contributing to their remarkable efficacy. We propose a novel multivariate utility (MU) based mechanism that unifies several existing automated market-making schemes. Using this mechanism, we establish the convergence results for markets comprised of risk-averse traders who have heterogeneous beliefs and repeatedly interact with the market maker. We demonstrate that the resulting limiting wealth distribution aligns with the Pareto efficient frontier defined by the utilities of all market participants. With the help of this result, we establish analytical and numerical results for the limiting price in different market models. Specifically, we show that the limiting price converges to the geometric mean of agent beliefs in exponential utility-based markets. In risk-measure-based markets, we construct a family of risk measures that satisfy the convergence criteria and prove that the price can converge to a unique level represented by the weighted power mean of agent beliefs. In broader markets with Constant Relative Risk Aversion (CRRA) utilities, we reveal that the limiting price can be characterized by systems of equations that encapsulate agent beliefs, risk parameters, and wealth. Despite the potential impact of traders’ trading sequences on the limiting price, we establish a price invariance result for markets with a large trader population. Using this result, we propose an efficient approximation scheme for the limiting price. Numerical experiments underscore the accuracy of this approximation across various scenarios, outperforming existing approximation methods. Our findings serve to aid market designers to better tailor and adjust the market-making mechanism for more effective opinions elicitation.

1. Introduction

Information, often scattered among the crowd, is valuable yet hard to aggregate. Throughout the centuries, researchers and practitioners have invented various tools in an attempt to piece them together. Classical mechanisms like polls, surveys, and brainstorming work fine.111According to (Berg et al., 2008), polls only accurately predict the outcome in of cases in presidential elections. (Pathak et al., 2015) find that expert forecasts performed worse than polls and prediction markets. In the corporate setting, (Cogwill and Zitzewitz, 2015) discover that expert forecasts had a higher mean square error compared to prediction markets. However, they lack the commitment to let people put their money where their mouth is. Over the past two decades, the prediction market, a mechanism designed specifically for information elicitation and aggregation, has gained much popularity. For example, the Iowa Electronic Markets (IEM), arguably the pioneer of all existing prediction markets designed primarily for various elections, almost consistently beats professional opinion polls (Berg et al., 2008). Other success stories include corporate consensus pooling, box office forecasting, and online recreational sports betting (e.g., (Chen et al., 2005; Cowgill et al., 2009; Cogwill and Zitzewitz, 2015)). There is theoretical evidence that prediction markets are robust against price manipulation (Hanson and Oprea, 2009). Overall, prediction markets have become a popular tool for information aggregation (e.g., (Wolfers and Zitzewitz, 2004; Arrow et al., 2008)).

Due to the liquidity issue, a prediction market is usually organized by an automated market maker (Hanson, 2003).222The “liquidity issue” refers to a phenomenon where buyers’ or sellers’ orders face delays or extended waiting times before being matched. In prediction markets, which usually have fewer traders than financial markets, one approach to address this issue is introducing a market maker to provide liquidity for buy and sell orders (Wolfers and Zitzewitz, 2004). In this market, traders exchange specialized securities with a market maker. These securities offer rewards based on uncertain outcomes, revealed once the true state is known. Traders, guided by their subjective beliefs, trade with the market maker to gain expected utility. Simultaneously, the market maker gathers valuable information through trading to enhance the overall accuracy of predictions. While the prediction market literature has primarily focused on designing effective market-making mechanisms (e.g., (Chen and Pennock, 2007; Abernethy et al., 2013; Othman et al., 2013; Slamka et al., 2013)), there have been relatively few attempts to explore the market’s evolutionary behavior. In this paper, we aim to narrowing this gap by addressing the following questions and providing additional insights into the analysis of prediction markets.

-

(1)

Under what conditions can we expect a prediction market to reach a consensus? That is, when does the trading process (market price) converge?

-

(2)

How to interpret the limiting price? What is the relation between such limiting price with each trader’s belief, wealth and their risk attitude?

In line with the spirit of (Sethi and Vaughan, 2016), we explore a dynamic prediction market model with multiple securities, involving a finite number of myopic, risk-averse traders with heterogeneous beliefs interacting with an automated market maker. We make several contributions that enhance the understanding and effectiveness of prediction markets.

Firstly, we introduce a unified multivariate utility (MU)-based mechanism that incorporates several market making mechanisms (e.g., (Hanson, 2003, 2007; Chen and Pennock, 2007; Agrawal et al., 2011)) into a consistent framework. Based on this framework, we propose a method for establishing market convergence that subsumes and extends the existing results in (Frongillo et al., 2015) and (Sethi and Vaughan, 2016). More importantly, we demonstrate that the limiting wealth distribution is Pareto optimal with respect to the utility of each trader. Additionally, this approach allows us to bypass the challenges of analyzing transient behavior in price dynamics and enables a direct examination of the limiting price.

By leveraging the general convergence result, we study the convergence properties of various utility types. Specifically, we derive the analytical form of price dynamics for the exponential utility-based market, revealing that the limiting price is the geometric mean of agents’ beliefs and is independent of the trading sequences. We extend this result to the convex risk-measure-based market. Specifically, we present an explicit method to construct risk measures that satisfy the convergence requirements. For a wide range of convex risk measures, we derive the analytical form of the limiting price, which emerges as a weighted power mean of agent beliefs.

Furthermore, we explore the more commonly used market model where all participants adopt the utility with constant relative risk aversion (i.e., CRRA utility) to make decisions. We analyze traders’ optimal trading decisions and examine the limiting wealth distribution resulting from the aggregate Pareto-optimization problem. It reveals that the limiting price can be characterized through a system of equations including all participants’ risk parameters, initial wealth allocation, and subjective beliefs. Crucially, we establish a fundamental result indicating that, even though trading sequences can influence the limiting price, their impact diminishes to insignificance as the trader population increases. Using these results, we introduce a heuristic weight called Pareto Optimal Induced (POI) weights and derive the associated approximate price formula that underscores the important role of risk aversion and initial wealth in price determination. To evaluate this approximation scheme, we conduct numerical experiments, which demonstrate that our POI price can closely track the actual price resulting from the trading with high accuracy across various settings. Through further comparison, our approximation scheme consistently outperforms previous attempts in the literature, such as the one presented in (Sethi and Vaughan, 2016). This performance improvement significantly advances the state-of-the-art in our comprehension of market prices.

Our findings hold significant potential for various applications. Firstly, the MU-based mechanism offers extensive flexibility in designing pricing formulations, empowering the market designer to tailor markets for diverse purposes. Secondly, our theoretical results establish a link between the parameters and the limiting price, enhancing the market designer’s ability to elicit traders’ beliefs effectively. Specifically, this suggests that market maker should exercise caution when selecting risk and wealth parameters to balance liquidity and accuracy. Our theoretical result on price stability in a random trading market suggests attracting more traders to achieve a reliable limiting price. Moreover, in scenarios like artificial prediction markets ((Chakravorti et al., 2023)), where traders are artificially generated supervised learners, our results provide guidance for configuring hyper-parameters for these artificial traders. Lastly, our convergence scheme and the subsequent price analysis can be effortlessly extended to prediction markets without a market maker. As an ancillary outcome, the theoretical proof of market convergence is closely related to the distributional algorithm of weakly-coupled multi-objective optimization. This proof can be extended to address more generalized problems sharing a similar structure.

This paper is organized as follows. In the remainder of this section, we review the related literature. In Section 2, we introduce the market model and the multivariate utility (MU)-based pricing mechanism. In Section 3, we present the general convergence result. In Section 4, we study the exponential utility-based market and the risk measure-based market. We then explore the CRRA utility-based market in Section 5. In Section 6, we discuss the price-volume relationship and the non-stationary market setting. We conclude the paper in Section 7. All the proofs and related results are provided in the Appendix.

1.1. Related Research

Our work is closely related to the research on automated market-making mechanisms in prediction markets. The logarithm market scoring rule (LMSR) introduced by (Hanson, 2003, 2007), stands out as one of the most popular mechanisms in internet prediction markets due to its desirable properties. In practice, LMSR can be implemented in the form of a cost function (Chen and Vaughan, 2010). This cost function-based mechanism has been refined in various directions (e.g., (Othman et al., 2013; Abernethy et al., 2013, 2014b)). Furthermore, (Chen and Pennock, 2007) propose a univariate utility function-based framework, which strongly motivates our adoption of the multivariate utility (MU)-based mechanism. Additionally, (Agrawal et al., 2011) introduce the sequential convex pari-mutuel mechanisms, allowing the market to accept limit orders. Partial equivalence among these mechanisms has been established (Chen and Pennock, 2007; Chen and Vaughan, 2010; Agrawal et al., 2011). To deal with the liquidity-adaption problem in practical implementation, (Othman et al., 2013) propose a liquidity-sensitive mechanism. Recent developments have extended these mechanisms in various directions (e.g., (Freeman et al., 2017; Ban, 2018; Freeman and Pennock, 2018)). As for the performance comparison of different mechanisms, (Slamka et al., 2013) provide simulation studies.

In prediction markets, trading-generated prices serve as predictors of future events, reflecting an aggregate estimate of the likelihood of a certain event occurring ((Manski, 2006; Wolfers and Zitzewitz, 2006)). As for the market convergence and price interpretation, there are generally two streams of studies. The first one involves a common prior and heterogeneous information. (Ostrovsky, 2012) and (Iyer et al., 2014) find that when all participants are risk-neutral or risk-averse, prices converge to a common posterior. These findings align with the well-known theorem established by (Aumann, 1976), stating that people with a common prior must have a common posterior if all posteriors are common knowledge, or in short, people cannot agree to disagree. The second stream of the model is characterized by heterogeneous priors but common information. In this model, several researchers adopt the static equilibrium model, where the price results from the market clearing condition. Following this idea, (Gjerstad and Hall, 2005) and (Manski, 2006) find a bias between traders’ mean beliefs and the equilibrium price. However, (Pennock, 1999) and (Wolfers and Zitzewitz, 2006) show that the market equilibrium coincides with the wealth-weighted average of trader’s beliefs when traders adopt the logarithm utility to make decisions.

In contrast to the above static model, another line of research explores the dynamic trading model. (Othman and Sandholm, 2010) investigate a market with risk-neutral traders with heterogeneous beliefs. In this setting, a finite number of traders interact with the market only once, resulting in a dependence between the trading order and the last posted price. In a related study, (Frongillo and Reid, 2015) adopt risk measures to model traders’ preferences in a market equipped with a cost function-based mechanism. When the traders trade with the market maker in random order, the dynamic trading process exhibits similarities with a machine learning algorithm that aims to minimize aggregate risk. While they develop some convergence conditions, their approach critically relies on the translation invariance property of risk measures ((Föllmer and Knispel, 2015)), which cannot be directly applied in our general MU-based market. Our work shares more similarities with (Sethi and Vaughan, 2016), who establish price convergence for a binary predication market with risk-averse traders and an LMSR-based market maker. However, our research focuses on a broader market setting, encompassing multiple securities, a general market-making mechanism, and a variety of trading decision paradigms. These complexities make it challenging to apply their approaches effectively to analyze our general model. We also note that (Bonnisseau and Nguenamadji, 2013) have considered a discrete Walrasian process, which is related to our model. However, the key difference is that their process involves pure exchange without a market maker. In contrast, our model is more intricate due to the externality introduced by the market maker and the pairwise trading restriction. The conditions required for market convergence in this scenario remain unclear, which partially motivates our current research.

Additionally, several studies have examined prediction markets with specific market structures. For example, (Abernethy et al., 2014a) analyze the equilibrium properties of a market with traders whose beliefs are drawn from exponential family distributions. (Carvalho, 2017) demonstrates that in a binary prediction market with an LMSR-based mechanism and risk-neutral budget-constrained traders, the price converges to the median belief of traders. (Tarnaud, 2019) investigates the asymptotic properties of a simple binary market with an LMSR-based mechanism and two traders. As valuable tools for forecasting and information aggregation, prediction markets also receive attention in the operations research and management science societies. For example, (Chen et al., 2008) develop a diffusion model for predicting the price of political events in prediction markets, while (Berg et al., 2009) use prediction markets to forecast market capitalization before an initial public offering. (Healy et al., 2010) investigate different trading mechanisms in small markets with complex environments. (Atanasov et al., 2017, 2022) systematically compare prediction markets with other popular information elicitation methods. Through several large-scale experimental tests, they find these two methods have advantages in different situations. (Jian and Sami, 2010) and (Choo et al., 2022) study the accuracy of prediction markets when there is price manipulation.

Besides the human-populated markets, artificial prediction markets with artificial agents (bot-traders) are developed as supervised learning tools for probability estimation and the aggregation of weak classifiers (e.g., (Storkey et al., 2012; Chakravorti et al., 2023)). Tuning the hyper-parameters (i.e., wealth, risk parameter, and beliefs of each bot-trader) in these artificial markets is a key challenge, as highlighted by (Chakravorti et al., 2023). Our convergence result and interpretation of the limiting price provide potential guidance for tuning these hyper-parameters.

Notations: A vector is denoted by a boldface letter, i.e., stands for a column vector . Let and be the all-one and all-zero vectors in the appropriate dimension, respectively. Given vectors and in , the notation means that for all , while indicates that and there exists an such that . Notations and represent the recession cone of the convex set and the convex function , respectively (as defined in Bertsekas et al. 2003). The domain of function is denoted as , and the probability simplex is represented as , where denotes the set of nonnegative real numbers.

2. Market Model and Trading Process

In this section, we introduce the market model. We consider a state space with , comprising mutually exclusive and exhaustive outcomes. Each state corresponds to an Arrow-Debreu security, which pays dollar if state occurs. These securities are traded in a prediction market organized by a central market maker. A total of traders engage in repeated transactions with the market maker at discrete time points . We represent the market maker’s wealth at time as and their outstanding securities position (i.e., the number of securities already sold) as . The market maker’s initial values are and . For each trader indexed by , we use and to denote their wealth and security positions at time . The initial values are and .

At each time , one trader interacts with the market maker (we will specify the order of arrivals of the traders in later discussions) by submitting an order . For instance, in the context of a football match outcome, such an order might be expressed as , representing shares for a buying order on “win”, share for a buying order on “loss”, and share for a selling order on “tie”. At any time , if the -th trader pays to the market marker (if , then it means the trader is paid by the market maker) and buys share of security, then the market state is updated as follows:333In this work, most of the results are irrelevant to the condition of the nonnegative wealth restriction (bankruptcy restriction). However, we specify the difference when it is necessary.

| (1) |

The other traders’ positions keep unchanged, i.e., and , for and .

To price an order , the market maker adopts a multivariate-utility (MU)-based mechanism described as follows. Suppose the market marker’ MU function is , which maps the net wealth position to some real value. We call the net wealth position because it represents all the possible wealth level if the final state is revealed at time .444For example, let and be the -th element of . Then, the -th element of is which represents the wealth after paying the obligation if -th event occurs. Similar to the utility-based pricing mechanism in (Chen and Pennock, 2007), the price of the order is determined by solving the following optimization problem:555Note that the domain of function , denoted by , may not necessarily be . As a result, in problem (), we explicitly add the constraint . This constraint can typically be expressed by some linear or nonlinear inequalities.

| (2) | Subject to: | |||

The minimizer of problem is the price of the order . Constraint (2) can also be written as , which means that the utility of the updated net wealth position is no less than that of the initial state. This is consistent with the utility-preserving property proposed in (Chen and Pennock, 2007), i.e., the market maker tries to find the lowest possible charge for the order such that the post-trade utility level is no less than the initial level.

To ensure the above pricing problem is well-posed, throughout this paper, we assume satisfies the following assumptions.

Assumption 1.

satisfies the following conditions: (i) it is continuous, concave and its domain is convex with ; (ii) it is monotonically increasing.666In this paper, we call a multivariate function monotonically increasing, if and only if for any , if , then and inequality holds strictly when .

Assumption 1 is mild and natural for the utility function except for the requirement which means that the utility is well-defined even if the wealth goes to infinity. Under Assumption 1, it can be verified that the MU-based pricing rule satisfies the axioms proposed in (Abernethy et al., 2013). These axioms serve as general requirements for a reasonable pricing mechanism. Furthermore, the MU-based pricing rule possesses several other desirable properties. For instance, it demonstrates responsiveness to any finite order with a unique price, effectively eliminates arbitrage opportunities for surebets, and exhibits a finite worst-case loss (under mild conditions). Moreover, there is abundant freedom to construct MU functions (see examples in Appendix B.1). The following result establishes the relation between the MU-based pricing rule with the MSR and the cost function-based mechanism.

Proposition 2.1.

An MU-based mechanism with a utility function satisfying Assumption 1 is equivalent with a cost function-based mechanism with a corresponding cost function. Furthermore, if an MU-based mechanism has a bounded loss under worst-case scenario, then the underlying utility can induce a proper scoring rule. Conversely, any proper scoring rule can induce an MU-based mechanism that has bounded worst-case loss.

The detailed proof of the above proposition is provided in Appendix B.2. In this work, we adopt the MU-based pricing rule in our analysis mainly due to the following reasons. First, as shown in Proposition 2.1, the MU-based pricing rule is general enough to cover existing classical pricing rules. More importantly, the MU-based mechanism provides a tractable way to study the convergence property of prices generated by a dynamic trading process. Once we have these convergence results, they can be directly applied to other pricing rules. Second, compared with the cost function-based pricing rule (Chen and Pennock, 2007; Abernethy et al., 2013) and the LMSR (Hanson, 2003), the MU-based mechanism could explicitly incorporate the risk preferences and the heterogeneous beliefs of all participants in a unified framework, which enables us to explore how these heterogeneous factors affect the final prices of these securities. Third, it is more convenient to construct the MU function in practice compared with the other mechanisms. For example, using risk-measure to define the cost function needs it to be convex and translation invariant, which means that the cost function should not be strictly convex. Indeed, it is usually not an easy task to customize a valid cost function in an analytical form.777Although (Föllmer and Schied, 2011) show that any convex risk measure (cost function) can be defined numerically via an acceptance set or by the dual representation, it requires solving a constrained optimization problem whenever a new order is submitted. In contrast, the MU-based utility only requires the function to be concave and monotone, and it can be constructed in various ways, including the classic expected utility theory (EUT) (Chen and Pennock, 2007) and convex risk measures (e.g., (Chen and Pennock, 2007; Föllmer and Schied, 2011; Hu and Storkey, 2014; Frongillo et al., 2015)). Moreover, the price of an order can be computed by a simple line search. We provide additional properties of the MU function and some examples in Appendix B.

On the trader’s side, we assume that each trader also adopts an MU function, , to evaluate his/her net wealth position.888The choice of trader’s MU function is similar to that of the market maker’s MU function . It can be based on conventional expected utility or constructed using a convex risk measure. Typically, in these formulas, the trader’s subjective belief is explicitly specified. Following the spirit of (Sethi and Vaughan, 2016), the -th trader solves the following problem to decide the amount of securities to trade,

| subject to | ||||

| (3) |

In this problem, the term in the objective function represents the -th trader’s net wealth position after the current trading. Problem can be viewed as a bi-level optimization problem. It fully characterizes all the information in one round of trading, i.e., the size of the order is determined by the upper-level problem, and the payment of the order , is determined by the subproblem in constraint (3). The lower level subproblem in constraint (3) is nothing but the problem . To guarantee the whole trading process is well defined, we impose the following conditions for , .

Assumption 2.

Each satisfies the following conditions: (i) it is continuous and strictly concave for non-equivalent wealth vectors999We call and are equivalent wealth, if and only if for some . Strictly concavity of non-equivalent wealth means that, for any who are not equivalent wealth vectors, it has for any .; (ii) is convex with and ; (iii) it is monotonically increasing.

Assumption 2 is similar to Assumption 1 except that it requires to be strictly concave except along the direction . This condition is necessary to establish trading process convergence in the later part of this paper. Note that such an assumption is weaker than global strict concavity, and it can also accommodate risk measure-based MU function, which is linear along direction .

Although the state fully represents the trading process, it is complicated to study the convergence of the trading process by solving problem directly. It is more convenient to use the net wealth position to characterize the trading process. Specifically, at time , let and be the -th trader’s and the market maker’s net wealth position, respectively. At time , it has and . In each round of trading, when an order is placed at price , the variation of market maker’s wealth is denoted as . Then, the dynamics (1) transform into if the -th trader interacts with the market at time , and for , along with the market maker’s wealth update, . It is worth noting that the market total wealth adheres to the following condition:

| (4) |

for all , where is the total wealth of all participants in the market. Eq. (4) suggests that the total net wealth position in the market maintains at a constant level throughout the trading process.

Using the wealth vectors and , the utility preserving property (2) can be expressed as . This formulation motivates us to consider an equivalent formulation of the -th trader’s decision problem:

| (5) | Subject to: | |||

for given and satisfying (4). The following result establishes equivalence between problems and in the sense of the optimal solutions.

Proposition 2.2.

The above result suggests that captures all the essence of market evolution encoded in the original problem . It greatly simplifies the original market process characterized by , , and with the pricing problem . Therefore, in the consequent analysis, we focus on the formulation .

Remark 1 (No-bankruptcy Restriction).

In practical applications, traders often operate under the no-bankruptcy restriction, which means that the constraint holds for all and . When the problem includes such constraints, we denote the corresponding problem as .

To facilitate analysis, we make an additional assumption.101010 Assumption 3 is not necessary to define the MU-based pricing mechanism and not necessary for general convergence result. Imposing these assumptions helps simplify the analysis in dynamic trading process.

Assumption 3.

and , are continuously differentiable functions.

Before we analyze the convergence property, we discuss how to compute the instantaneous prices of the securities under the MU-based mechanism. The instantaneous prices of the securities can be viewed as an integrated forecast of the corresponding event (see, e.g., Wolfers and Zitzewitz 2004). Let be the market maker’s net wealth posisition. The instantaneous price of each security is defined as the marginal cost per share for purchasing an infinitesimal quantity of this security. The instantaneous price of the -th security, , can be computed by pricing the order where is a small number and is the -th unit vector. If is the solution of problem , then the instantaneous price of the -th security is . Under some assumptions of , the price can be explicitly computed.

Proposition 2.3.

If we aggregate all in a vector , then the price vector is exactly the normalized gradient of , i.e., . Note that, when the assumptions in Proposition 2.3 fail to hold, the domain boundary of will affect the solution of problem . In those cases, one can still compute the price by using the envelope theorem. However, it will be much more complicated as it will involve the form of the boundary of . We omit the detailed discussions for those cases.

3. Convergence of Market States in General Setting

In this section, we study the convergence properties of the market states (wealth and prices) generated by the sequential interactions between the traders and the market maker. We define the trading sequence as an infinite sequence of traders indexed by time, denoted by with . We say a sequence satisfies the infinite participation or simply the IP property, if for any , the set has infinite elements. We denote all trading sequences satisfying the IP property by . In other words, contains all trading sequences such that each trader interacts with the seller for an infinite number of times.111111Note that the IP property is a weaker condition than the assumption made in (Sethi and Vaughan, 2016). In Assumption 1 of (Sethi and Vaughan, 2016), it is assumed that there exists a constant such that each trader must trade once during any period of length . Obviously, this implies the IP property but not the reverse. Therefore, our assumption allows a more flexible trading pattern than that in (Sethi and Vaughan, 2016). Given a sequence , we can define the trading process as follows (which is referred to as Trading Process 1):

In Trading Process 1, we use , , to denote the instantaneous price of the securities at time . Given , can be computed by (6). As , if and converge to some limits and , respectively, then we call and the limiting wealth allocation for trader and the limiting price of the -th security. Some important questions arise naturally: Does the wealth allocation generated from the Trading Process 1 converge to some limiting allocation? If so, what property does the limiting wealth allocation have? Similarly, does the price generated from the Trading Process 1 converge and what property does the limiting price have?

To answer these questions, we first define the feasible set of all possible market states generated by the Trading Process 1 as follows,

| (7) |

It is not hard to prove that the feasible set is a compact set. We then introduce the definition of Pareto optimality of the wealth allocation with respect to the MU function for .

Definition 3.1.

A wealth allocation is called a Pareto optimal allocation if the following two conditions hold: (i) ; (ii) there does not exist any such that and for all with strict inequality holds for at least one .

The Pareto optimal allocation means that, for each trader, it is not possible to increase his/her own utility without decreasing the utility of any other traders. All the Pareto optimal wealth allocations form the Pareto efficient set. Note that, the concavity of guarantees that any Pareto efficient wealth allocation can be achieved by some weighting parameters (see, e.g., Mas-Colell et al. 1995) by solving the following optimization problem:

| (8) | ||||

We then present our main result which states that the Trading Process 1 converges to some Pareto optimal allocation.

Theorem 3.2.

Under Assumptions 1, 2 and 3, the wealth allocation and generated from Trading Process 1 for any given trading sequence converge to some limit and , i.e., for all and , if either one of the following conditions holds: (i) ; or (ii) can be expressed as with and satisfies and is finite if . Furthermore, the limiting allocation must be a Pareto optimal allocation.

In the above result, two alternative conditions (condition (i) and (ii)) are imposed to ensure that the limit of wealth allocation is an interior point in the domain of the utility function. Condition (i) is easy to understand, while condition (ii) is a generalization of the Inada condition, which is commonly used in conventional utility optimization. Theorem 3.2 states that, as the Trading Process 1 goes on, eventually, no trader would like to modify their wealth position anymore, i.e., the wealth process converges to some limiting wealth allocation. Moreover, the limiting wealth allocation must locate on the Pareto optimal set defined in Definition 3.1. The Pareto optimality of the limiting allocation formally confirms the theoretical foundations of prediction markets: a prediction market can indeed incentivize people to participate, and the limiting price is a “good price” in the sense that it is supported by a wealth allocation where the well-being (measured by utility level) of any trader cannot be improved anymore without decreasing some other traders’ utility.

Remark 2.

We emphasize that the requirement is necessary for achieving overall Pareto optimality. The trading process will still converge if one or more traders cease trading from time and the remaining traders will still reach their own Pareto optimality. However, if a trader only interacts with the market maker a finite number of times, then he/she may still be willing to trade after his/her last transaction, but is deprived of that opportunity. Consequently, this trader’s final wealth along with other traders’ wealth may not be located in the Pareto optimal set.

A direct result of Theorem 3.2 is that the price of the security also converges to some limiting price. Such a limiting price can be computed as follows.

Corollary 3.3.

When the assumptions in Theorem 3.2 are met and the trading process converges, the limiting price is given by,

| (9) |

where is the market maker’s the limiting wealth allocation.

The price formula (9) is a natural generalization of the one derived for the scalar-valued utility function in (Chen and Pennock, 2007). In the upcoming sections, we will study how the market forms prices by aggregating traders’ beliefs. To represent these beliefs, we use and to denote the market maker’s and the -th trader’s subjective beliefs (probabilities) on the outcomes, respectively. Unless otherwise stated, we assume that these beliefs remain constant throughout the trading process. We will use to denote the price vector generated by Trading Process 1, where .

4. Exponential Utility and Risk Measure-Based Market

The previous section demonstrated market states converging to Pareto optimal allocations but provided limited insight into how the market forms equilibrium prices. In this section, we explore two special cases: exponential utility-based and risk measure-based MU functions. We will derive the price convergence results for these market models.

4.1. Exponential Utility Based Market

We first consider the exponential utility functions-based market. The exponential utility has a constant risk aversion coefficient, which leads to trading decisions independent of the trader’s wealth level (Makarov and Schornick, 2010). This feature eliminates the wealth effect in the trading process and allows us to clearly illustrate the impacts of traders’ beliefs and risk preferences upon the limiting prices. It is important to note that adopting the exponential utility to price the security is equivalent to using the LMSR pricing rule, which is a widely adopted mechanism (see Appendix B.2 or (Chen and Pennock, 2007)). Specifically, given market state vectors and for , the market maker’s MU function and the -th trader’s utility function are

| (10) |

respectively, where and are the risk aversion coefficients for the market maker and the -th trader, respectively.

Since the exponential utility-based MU function satisfies the conditions outlined in Theorem 3.2, both wealth allocation and instantaneous prices converge to their respective limiting values. The following results characterize the evolution of market prices generated by Trading Process 1.

Proposition 4.1.

In a market equipped with the exponential utility functions defined in (10), given the market state with the price at time , it has the following results: (a) If the -th trader trades with the market maker, then the optimal trading amount is with

| (11) |

where . (b) The price is updated to

(c) As , for any , price converges to the limiting price , where

| (12) |

The above result demonstrates that the limiting price corresponds precisely to the geometric mean of the risk-adjusted beliefs held by all participants, including the traders and the market maker. It is worth noting that this limiting price, , remains unaffected by the chosen trading sequence, represented by , as long as . Price formulation (12) is closely connected to the concept of the Logarithm Opinion Pool mentioned in (Chakraborty and Das, 2015)121212The Logarithm Opinion Pool refers to the normalized weighted geometric mean of different opinions which is originated from the early works such as (Morris, 1974) and (Bordley, 1982) in area of the opinion pooling.. In (Chakraborty and Das, 2015), as it only focuses on the static trading model, it suggests one potential research direction as extending these findings to a market involving multiple agents engaging in repeated trading until market states converge. By providing an explicit outcome for this scenario, Proposition 4.1 effectively addresses such a question raised by (Chakraborty and Das, 2015).

Remark 3.

It is also important to note that, although the risk-neutral utility is a special case of the exponential utility,131313If we let or in (10), then the exponential utilities become risk-neutral utilities, i.e., and for all . the result in Proposition 4.1 does not hold for the risk-neutral case as it needs the assumption and for all . Even when the market maker adopts the exponential utility, but the trader’s utility is risk neutral, the whole trading process may not converge due to violating the strictly convex condition in Assumption 2. Indeed, under the risk-neutral setting, after the -th trader interacts with the market, the price of the -th security will be modified exactly to the -th trader’s belief, , which leads to price oscillation (see the detail in Appendix A.7).

4.2. Risk Measure-Based Market

We have demonstrated that the exponential utility-based market can converge to a unique limiting price, regardless of the trading sequence. This subsection delves deeper into the risk-measure-based MU function, which exhibits a similar property under specific conditions. Although some literature (e.g., (Hu and Storkey, 2014; Frongillo et al., 2015)) has investigated the risk-measure-based prediction market and developed convergence results, the existing studies provide limited information about the general convergence condition and the method to compute the limiting price. This section aims to complete these missing pieces.

We mainly focus on the convex risk measures, which possess some promising properties ((Föllmer and Schied, 2011)) that have emerged as a valuable tool in decision-making. However, directly utilizing the convex risk measure to construct the MU functions in trading problem may not satisfy the conditions outlined in Assumptions 1 and 2, which leads to a potential non-convergence in the trading process. To illustrate such a case, we provide a counter-example in Appendix A.3 (Example A.2). In order to address this issue, we need additional mild conditions on the risk-measure-based MU functions. Specifically, we assume the -th trader’s MU function and the market maker’s MU function are respectively constructed by some risk measures as follows,

| (13) |

where for are differentiable convex risk measures. Recall that a convex risk measure has the following dual representation (see e.g., (Föllmer and Schied, 2011)):

| (14) |

where is called the penalty function for . We assume is differentiable for all and define its partial derivative as follows. For some , the derivative of is denoted as:

| (15) |

If we impose some mild conditions on , the market constructed by the risk measures will also converge to a unique limiting state.

Proposition 4.2.

If the functions defined in (15) satisfy the following two conditions: (i) is continuously differentiable and strictly increasing; and (ii) is finite and for all and , then the MU function satisfies Assumption 1, the MU functions , , satisfy Assumption 2. In addition, both and satisfy Assumption 3. Thus, the market constructed by (13) meets the conditions in Theorem 3.2 and the market state converges to a Pareto optimal allocation.

Based on the above result, to check whether the market constructed by the risk measures (13) converges, we only need to check whether the penalty functions meet the conditions in Proposition 4.2.

We then focus on characterizing the limiting wealth allocation and the correspondent limiting price. We have the following result.

Theorem 4.3.

In risk measure-based market which satisfies the condition in Proposition 4.2, the following results are true: (i) The limiting wealth allocation is the unique solution of problem by setting . (ii) For any trading sequence , the unique limit price generated by Trading Process 1 is where and are the solution of problem . Furthermore, the price vector is given by where is defined in (14) for .

One surprising result of this theorem is that the limiting price can be independent of the initial wealth allocation. The root cause is the translation invariance property of risk measures. Indeed, considering the -th trader’s decision problem, the objective function is equivalent to . Therefore, the initial wealth can initially be eliminated from the individual problem. Hence, all subsequent trades become independent of the initial wealth. A similar observation holds for the market maker. As a result, the limiting , which determines the limiting price , is independent of the initial wealth allocation.

With the help of Theorem 4.3, it becomes feasible to explicitly compute the limiting price when the formulation of the risk measures is provided. We now consider a particular type of risk measure constructed using a dual formulation. We maintain the same notations as in Section 4.1, employing and to represent the beliefs of the market maker and the -th trader, respectively. The following result establishes that the limiting price can be expressed as the power-weighted mean of all participants’ beliefs.

Corollary 4.4.

Let , , be some parameters. If the penalty functions take the following form, and for with some , then the limiting price is

| (16) |

for .

The price formula (16) shows that the limit price is a weighted power mean of the traders’ beliefs where the weight is a trader dependent parameter . When , the penalty function becomes the cross entropy, i.e., with for , and the corresponding limiting price becomes the arithmetic weighted mean of trader beliefs. Regarding the selection of parameter , one particular choice is the initial wealth of each trader. In some application, such as the artificial prediction market (Chakravorti et al., 2023), these parameters can be viewed as the hyper-parameters which control the overall model performance.

5. Limiting Price for CRRA Utility

5.1. Price Variability

The preceding section demonstrates that, under certain conditions, the price sequence produced by the exponential utility-based and risk-measure-based markets can converge to a unique limit price for any trading sequence that satisfies the IP property. This motivates us to inquire if a similiar outcome can be extended to more commonly used utility functions. In this section, we mainly explore a market model constructed by the utility with constant relative risk aversion (i.e., CRRA utility). The CRRA utility enjoys widespread usage in economic modeling and analysis. In the CRRA utility-based market, we assume the market maker’s and the -th trader’s MU functions are

| (17) |

respectively, where and are the traders’ and market maker’s risk aversion parameters, respectively; and are the wealth vectors; and are the associated subjective beliefs as we defined in previous sections. Under the above setting, the trader’s decision problem generally lacks a closed-form solution. Nonetheless, when all participants have identical risk parameters, the trader’s decision can be solved as follows.

Proposition 5.1.

In the CRRA uitlity-based market definied by (17) with , given and at time , the solution of the -th trader’s decision problem is for , and the market states are updated to

| (18) |

where , for and , and is the solution to the following equation,

| (19) |

This proposition shows that in a CRRA-utility-based market, the initial wealth of each trader is recursively adapted into the wealth vector of the market maker, hence the limiting may be affected by the initial wealth allocation, as opposed to the risk measure-based markets. The following example demonstrates how the initial wealth, risk parameters, and trading sequence could affect limiting price.

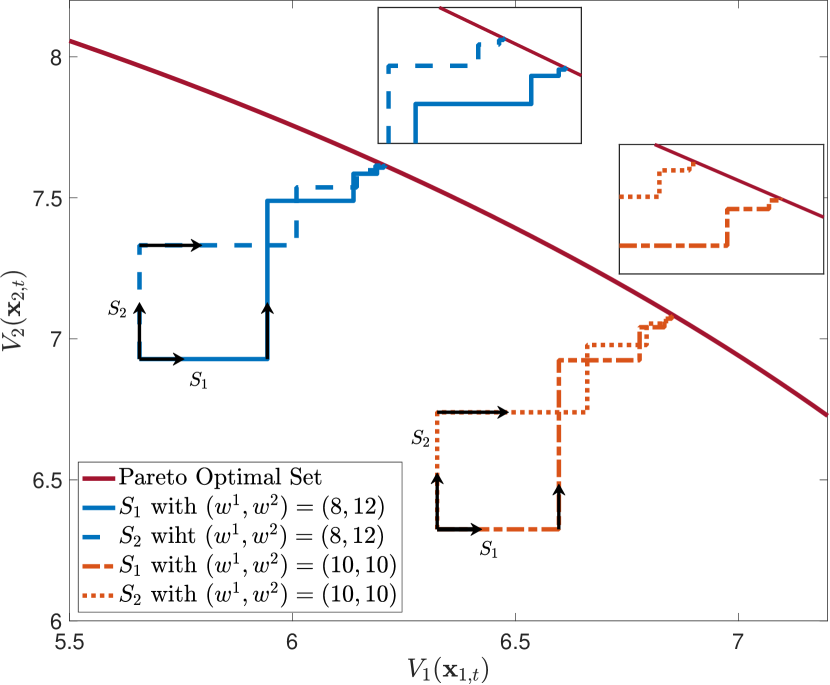

Example 5.2.

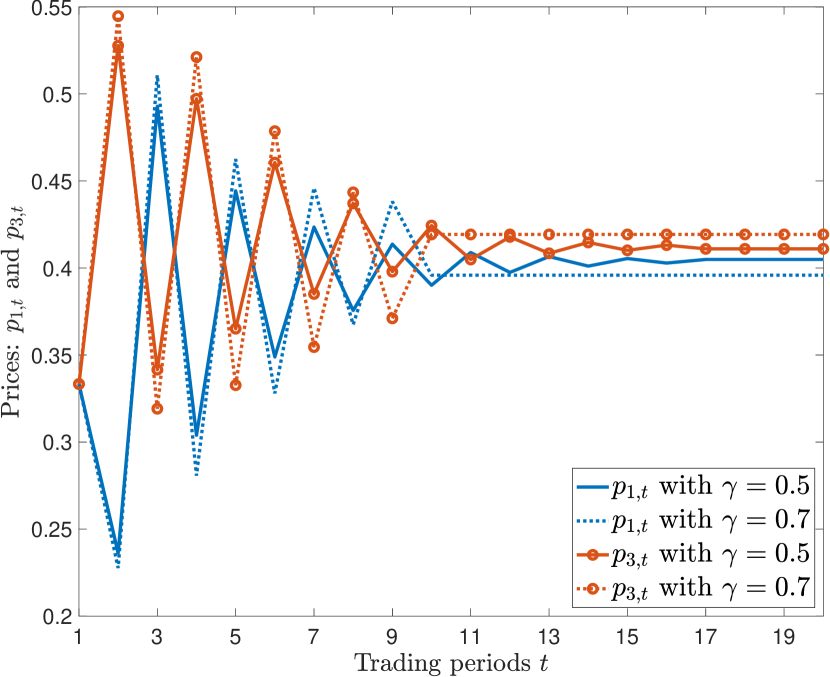

We consider a CRRA utility-based market with three assets () and two traders () whose belief are and , respectively. The market maker’s parameters are , and . The two traders’ initial wealth are and where we vary the parameters to examine their impact on the limiting prices. In Trading Process 1, we consider two trading sequences: and .141414Note that if the same trader arrives twice in a row, the second trade is vacuous because the first one is already utility maximizing. Figure 1(a) depicts the utility value trajectories generated by these trading processes for different when . The Pareto efficient frontier (represented by the solid line) is obtained by solving problem for different . This figure illustrates that, for a given wealth distribution and fixed trading sequence (either or ), the utility value trajectories indeed converge to points on the Pareto efficient frontier, confirming the result in Theorem 3.2. However, even for identical initial wealth, different trading sequences may generate different utility paths (and hence different limiting prices). Figure 1(b) demonstrates the impact of the risk parameter. It shows the price trajectories of and when for the trading sequence . This illustration makes it clear that a change in the risk aversion parameter, e.g., from to , has an effect on the limiting prices. Table 1 provides details of the limiting prices for different and . A closer examination reveals that even with fixed initial wealth, the limiting price may vary under different trading sequences, although both and satisfy the IP property.151515It is worth noting that when there are only two traders, and are effectively the only possible sequences that satisfy the IP property. The impact of the trading sequence is also discussed in (Sethi and Vaughan, 2016). However, among these factors, the trading sequence has less impact compared to the initial wealth and the risk parameter.

| Wealth | Risk | Limiting Price | ||||

|---|---|---|---|---|---|---|

| 10 | 10 | 0.5 (0.7) | 0.4044 (0.3959) | 0.1839 (0.1849) | 0.4117 (0.4192) | |

| 0.4045 (0.4004) | 0.1838 (0.1841) | 0.4117 (0.4155) | ||||

| 8 | 12 | 0.5 (0.7) | 0.4436 (0.4449) | 0.1745 (0.1726) | 0.3819 (0.3825) | |

| 0.4440 (0.4800) | 0.1743 (0.1741) | 0.3817 (0.3459) | ||||

| 12 | 8 | 0.5 (0.7) | 0.3624 (0.3463) | 0.1933 (0.1959) | 0.4443 (0.4578) | |

| 0.3621 (0.3776) | 0.1933 (0.2044) | 0.4446 (0.4180) | ||||

As demonstrated in Example 5.2, the trading sequence can impact the limiting price. A key observation for understanding this phenomenon is that can be equivalently viewed as preceded by an extra Trader 1 action. Such an action results in an initial market state different from that of the original . As Proposition 5.1 suggests, different initial wealth results in a different limiting price; thus the limiting prices for the two sequences and are different. To illustrate, we consider Example 5.2 with . The extra action of (the first trade) yields market states , , and . After the first trade, sequence becomes identical to . However, for , the initial condition is , , and , which is different from the states yield from after the first trading, thus the two sequences result in different limiting prices.

Practically, traders interact with the market maker randomly, leading to a random trading path. Consequently, the limiting price becomes a trading-sequence-dependent random variable. However, our next result characterizes the limiting price for a given trading sequence and demonstrates that price invariance can be achieved when the trader population is large.

Theorem 5.3.

For the CRRA-utility-based market, we have the following results:

(i) Given a trading sequence , the Trading Process 1 converges to the limiting wealth allocation characterized by problem with some weights ; and the limiting price is given by

| (20) |

where is the unique solution of the following equations:

| (21) |

where .

(ii) In Trading Process 1, if traders’ beliefs and initial wealth are independently and identically distributed random variables for ; with each trader having an equal probability of trading with the market maker at each trading instance, then the solution defined in Eq. (21) and the associated limiting price generated by each trading sample path converge almost surely to a pair of constant vectors as the trader population .

The first result in Theorem 5.3 provides an explicit method for computing the limiting price for a sepecified trading sequence with the associated weighting parameters . It is worth noting that the functional form of the limiting price (20) and (21) remain consistent, as the influence of the trading sequence is solely reflected through the weights . The second result in Theorem 5.3 is an interesting product of the price formula. One can consider it a prediction market analogue of the “Law of Large Numbers”. It implies that in a randomly trading market with a large trader population, the variation of limiting price induced by different trading sequences becomes negligible. This underscores the significance of trader participation in prediction markets, as it not only enhances liquidity but also increases the reliability of limiting prices. Imagine a prediction market that yields predictions (limiting price) that are heavily dependent on the trading sequence. In such a case, one cannot know whether its prediction truly represents the overall beliefs or only happens to be a biased result of a specific trading sequence. Such uncertainty will undermine the interpretability of prices and jeopardize the prediction accuracy.

Theorem 5.3 also provides several potentially useful insights for market maker designing. Combining Eqs. (20) and (21), the limiting price has the following decomposition:

| (22) |

This decomposition can be explained as follows. First, a smaller initial wealth can reduce the market maker’s impact on the limiting price. Second, a market maker with higher risk aversion (smaller ) also diminishes its influence on the limiting price because is a decreasing function of for . Third, the function exhibits an intriguing suppressive effect designed to mitigate the price distortion caused by the market maker’ externality. To explain further, reaches its maximum value of when . When the market consensus significantly deviates from the market maker’s belief , the term lessens its impact, effectively reducing the market maker’s influence on the limiting price. It is worth noting that such a suppressive effect stems from the utility preserving condition (8), underscoring the additional benefits of the MU-based mechanism.

With the above results, in the next section, we investigate how to approximate the limiting price under a finite trader scenario through choosing an appropriate weight .

5.2. Heuristic Weighting Parameters and Price Formula

The previous section has emphasized the vital role of determining the weighting parameters, , in solving problem to establish the limiting price. Given the practical difficulty of obtaining the “true” weighting parameters before trading converges, we propose an approximation using deterministic weights. Drawing inspiration from previous analysis, which highlights Pareto optimality of the limiting wealth allocation and underscores the significance of both the initial wealth distribution and the risk parameter in shaping the limiting price (e.g., see Table 1), we introduce the concept of Pareto Optimal Induced (POI) weights, denoted as defined as:

| (23) |

Applying Theorem 5.3, we replace with the POI weights in Eq. (21) to calculate the associated POI limiting price, denoted as , with its components given as follows:

| (24) |

where is the unique solution of the following equation,

| (25) |

Now we provide some interpretation for the POI limiting price. Eq (25) implies that the price is directly linked to a weighted average that considers all participants’ wealth and risk-adjusted beliefs regarding the -th asset. More specifically, the term represents the avarage risk-adjusted belief contributed from all the traders weighted by their own wealth. In contrast, the term which combines the risk difference and belief divergence, controls the contribution of market maker’s risk-adjusted belief in such a price.

The POI price formula (24) and (25) encompass specific market scenarios as special cases. When both market maker and traders adopt the logarithmic utilities, i.e., in (17), Eq. (25) will simplify to:

| (26) |

where representing the exponential Kullback-Leibler Divergence (KLD) between and . If we further set then the price formula (24) becomes the wealth-weighted average of market beilefs discussed in (Sethi and Vaughan, 2016).

We would like to highlight that the solution methodology for deriving the CRRA-utility based limiting price, e.g., Eq. (21) and the POI weights (23) remain applicable even when market participant’s MU functions extend beyond the CRRA family of utilities. One example is the hybrid market model where the market maker adopts exponential utility, as given by Eq. (10), while the traders adopt logarithmic utility. In this scenario, the POI limiting price remains the same as (24), but the equations for become:

| (27) |

We provide more details of Eq. (27) in Appendix A.5. Our numerical experiments (given in Appendix A.5) demonstrate that the price formula (27) outperforms the conventional wealth-weighted average price reported in (Sethi and Vaughan, 2016). The CRRA-utility-based pricing formula can also be extended to a more comprehensive market model where all participants adopt utilities with hyperbolic absolute risk aversion (HARA utility), which finds wide applications in economic modeling. A brief discussion of this model is presented in Appendix A.6.

5.3. Evaluation of Approximation Scheme

In this section, we first employ simulation to validate the accuracy of the POI weights (23) and the price formula (24) in estimating the true weighting coefficients and the true limiting price, respectively. Following this validation, we proceed to examine how the risk parameters and initial wealth impact the accuracy of our approximation.

We consider a CRRA-utility-based market with , , and . Traders are generated randomly as follows. The -th trader’s belief is sampled from , where is the baseline belief evenly sampled from and ; is uniformly distributed random noise on , and controls the market belief structure. We conduct simulations according to Trading Process 1, with each trader randomly selected with equal probability to interact with the market maker at each time period. For each set of parameters, we perform rounds of simulation, and we denote the -th sample of the limiting wealth allocation as .

-

•

Evaluation by limiting wealth: To verify the accuracy of the POI weights (23), we first solve the problem whose solution is denoted as . If the heuristic weight provides an accurate approximation for the “true” weighting parameter, then the wealth allocation should be close to the sample limiting wealth allocation generated by the simulation. We introduce the following quantity to measure the difference for each sample,

for . The sample mean and variance of is denoted by and , respectively.

-

•

Evaluation by limiting price: We denote the price associated with the -th sample of limting wealth as and we compute the POI price by using (24). To measure the difference between these prices, we employ the Kullback-Leibler Divergence (KLD), i.e., given two prices , the KLD of these prices is defined as . We then denote the KLD between the -th sample price and the POI price as for . We then compute the sample mean and sample variance of as and , respectively.

Table 2 reports the comparative results for different setups ( and ). For each set of risk parameters, denoted as (, ), we list the results for different values of . The results clearly show that, regardless of the different settings, the POI weights (23) and the POI price (24) perform exceptionally well, exhibiting minimal disparities in both wealth and price. A closer examination reveals several noteworthy patterns. Firstly, for a fixed set of risk parameters and , increasing the trader population enhances the accuracy of our approximation. This enhancement is evident as all error and variation indicators decrease with the increase in . Of particular significance is the observation that Table 2 also highlights a notable decrease in approximation variances, and , with a larger population. This reduction in variance can be attributed to the decrease in variation stemming from the trading sequence. Consequently, this pattern confirms the second result outlined in Theorem 5.3, which posits that a larger population leads to a more stable limit price. Secondly, for a given trader population, the approximation error is smaller in scenarios with compared to those with , suggesting that our approximation is more favorable for higher levels of risk aversion.

| Market Par. | Price Diff. | Wealth Diff. | ||||

|---|---|---|---|---|---|---|

| -2 | -2 | 50 | ||||

| -2 | -2 | 100 | ||||

| -2 | -2 | 200 | ||||

| -2 | -2 | 400 | ||||

| -2 | 0.5 | 50 | ||||

| -2 | 0.5 | 100 | ||||

| -2 | 0.5 | 200 | ||||

| -2 | 0.5 | 400 | ||||

| 0.5 | -2 | 50 | ||||

| 0.5 | -2 | 100 | ||||

| 0.5 | -2 | 200 | ||||

| 0.5 | -2 | 400 | ||||

| 0.5 | 0.5 | 50 | ||||

| 0.5 | 0.5 | 100 | ||||

| 0.5 | 0.5 | 200 | ||||

| 0.5 | 0.5 | 400 | ||||

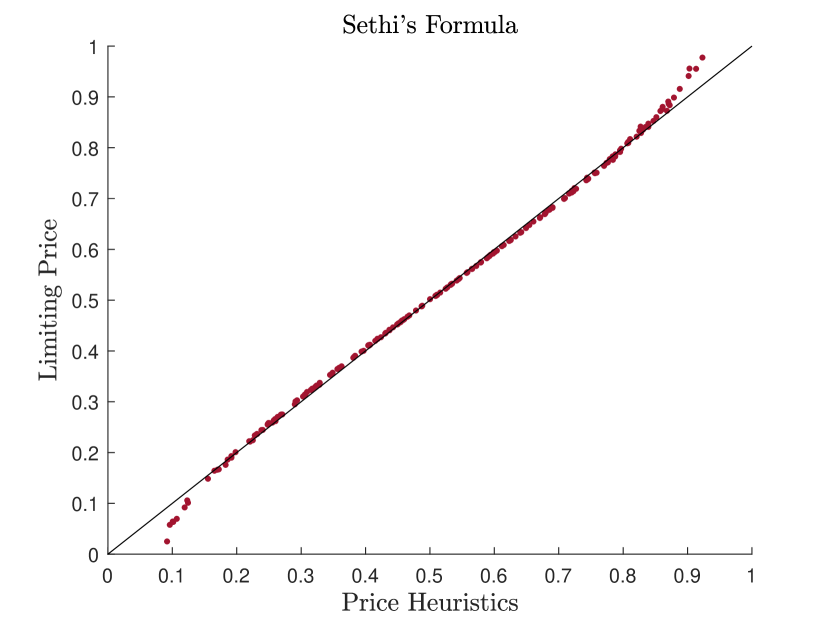

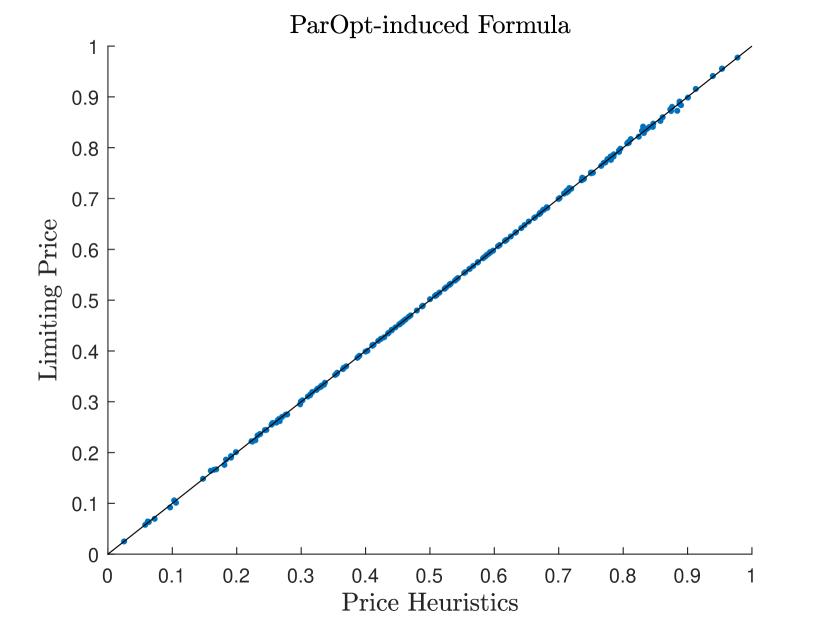

We proceed to examine how the risk parameters and initial wealth affect the quality of our approximation. To better illustrate the impact of these parameters, we introduce the conventional wealth-weighted price formula from (Sethi and Vaughan, 2016) as a benchmark, denoted as , where

| (28) |

We follow a simulation procedure similar to that in Table 2, using a fixed and . To highlight the impact of traders’ risk parameter , we vary its values and compare the resulting limiting prices obtained from the simulation with two heuristic price formulas: (24) and (28).

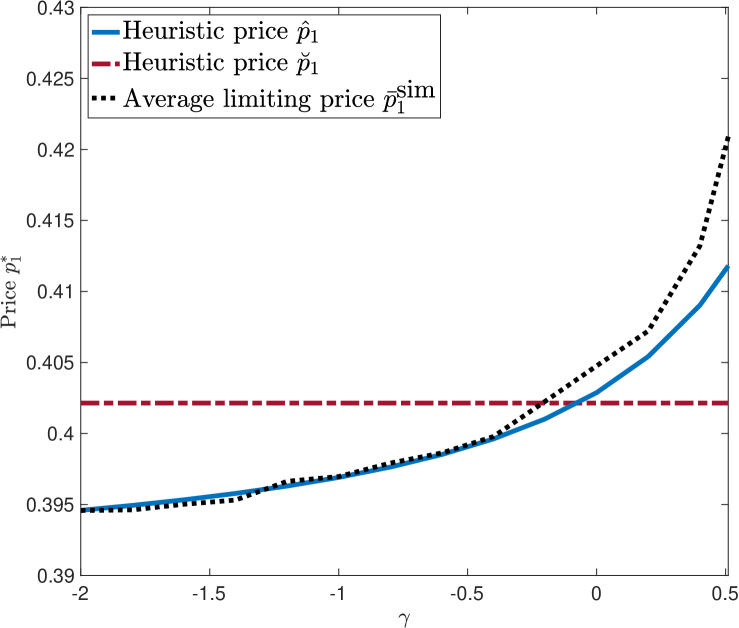

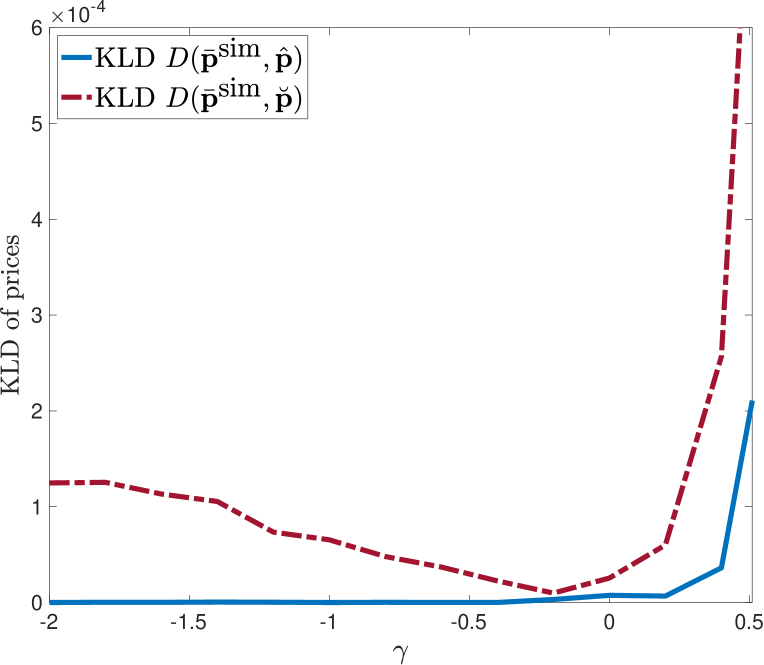

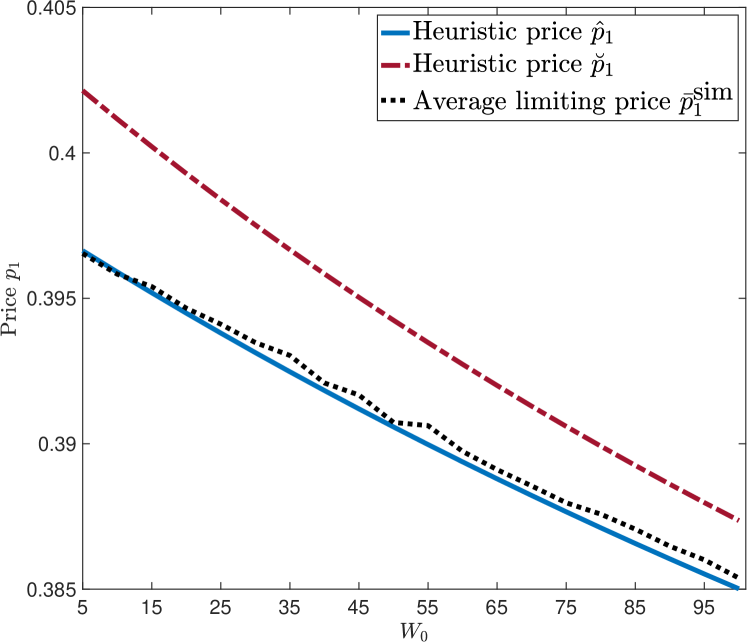

In Figure 2(a), the red curve represents the average price of the first security resulting from rounds of simulations, which exhibits an increasing trend as increases. Importantly, our POI price formula (24) effectively captures this trend, as indicated by the solid blue curve. In contrast, the conventional wealth-weighted formula (28) fails to exhibit such a distinct pattern as it does not account for the risk parameter. Figure 2(b) illustrates the approximation errors of the two heuristic prices where and measure the KLD between the simulated average price and the two heuristic prices, respectively. Notably, when deviates from , especially when it is below zero, our price formula (24) significantly outperforms the conventional wealth-weighted formula (28).

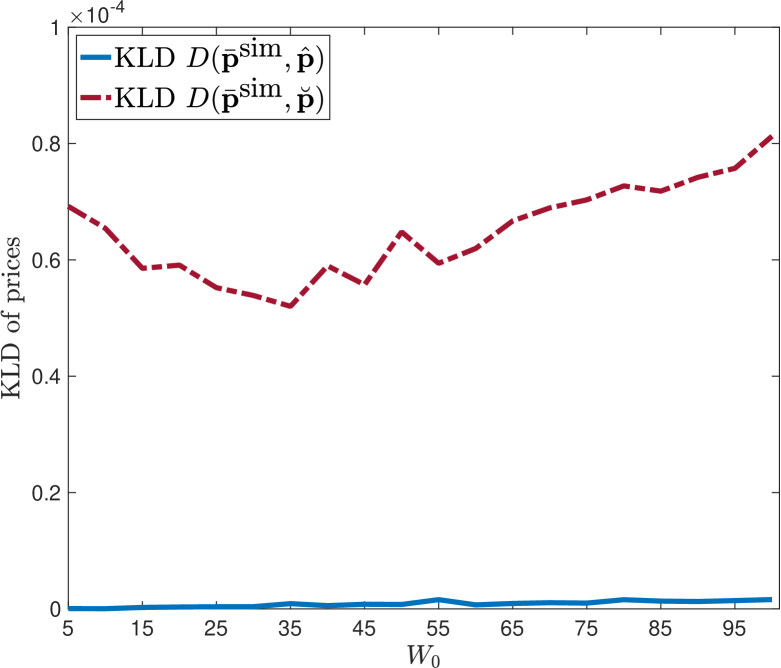

We then investigate the impact of the market maker’s initial wealth , which is a key design variable for providing liquidity. Holding , we incrementally raise from to . In Figure 3(a), the limiting price decreases as increases. This is because the price becomes increasingly biased towards the market maker’s own belief (i.e., ) as its wealth grows. Both formulas (24) and (28) display a similar trend. However, our price formula (24) closely tracks the limiting price, while the conventional one (28) tends to overestimate it significantly. Figure 3(b) provides a more detailed comparison of these approximation errors by evaluating the KLD. It becomes evident that our POI price formula (24) not only demonstrates greater accuracy but also exhibits much higher stability than formula (28) when varying the market maker’s wealth . This characteristic highlights that the quality of our heuristic price formula (24) is not sensitive to fluctuations in the market maker’s wealth level. Such a property may benefit the market maker in customizing the market-making mechanism.

In summary, the combination of the POI weights (23) with Eq. (21) offers an accurate estimation of the limiting price across various market scenarios. Although such a pricing formula is not entirely analytical, the parameters , given in Eqs. (21) provide comprehensive information on how the price is aggregated based on participants’ beliefs, risk attitudes, and wealth levels.

6. Price-Volume Relationship and Nonstationary Market

In this section, we provide analysis of the price-volume relationship resulted from our model and discuss the market behavior in a non-stationary market.

The price-volume relationship: Like microstructure analysis in the financial market, studying the relationship between the price and trading volume reveals how prices evolve during trading. To examine this, we consider the -th round of trading where the -th trader interacts with the market maker in Trading Process 1. Although it might seem like only one trader is trading at a time, we can think of this as a group of traders. For instance, the -th trader represents a group of traders holding the similar beliefs with the wealth being the aggregate wealth. Therefore, the order size in each round of trading represents an aggregate order for a group of traders. For simplicity, we consider a market with binary securities (). The -th trader solves problem to determine the optimal decision . Since the two securities are mutually exclusive, the trading volume is only related to the net demand where is the amount of the order.161616The last equality is from the definition of . The mutual exclusiveness also implies the prices satisfies . We then examine the relationship between the net demand and the security’s price for different market settings.

As the exponential MU-function-based market admits a closed-form solution for trading problem , it is an ideal vehicle to study the price-volume relationship. Using the expression (11) in Proposition 4.1, we can compute the net demand as,

| (29) |

where is defined in Proposition 4.1. We observe that the volume is proportional to the difference between the log odds of the -th trader’s belief and the security price. The demand decreases as the price increases, indicating a higher demand for the security at a lower price. Conversely, for a fixed price , the demand depends on the trader’s utility-adjusted belief . A trader trades more security if deviates further from the price. It is also evident that the net trade volume is discounted by a factor . That is to say, even if two traders have identical subjective beliefs, the trader who is more risk-averse trades less security than the one with less risk aversion. This finding further demonstrates the importance of including the risk parameter in our approximated pricing formula (25).

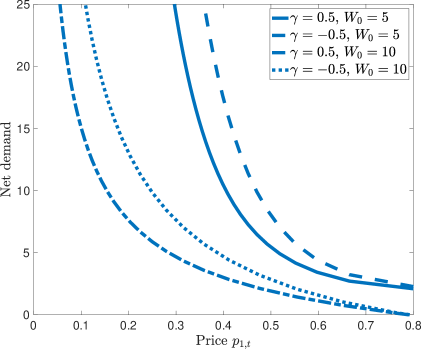

The above price-volume relationship also holds for the CRRA utility-based market. We slightly modify the market in Example 5.2 by aggregating the first two securities as a single security, which gives a binary market. That is, the two traders’ beliefs become and . Figure 4 plots trader 2’s net demand as a function of for diffferent paramters, i.e., and . Clearly, we can observe the pattern that the net demand is negatively correlated with the price and the risk aversion parameter. In addition, this figure also indicates that when the market maker has larger wealth, it may provide higher trading volume (higher liquidity).

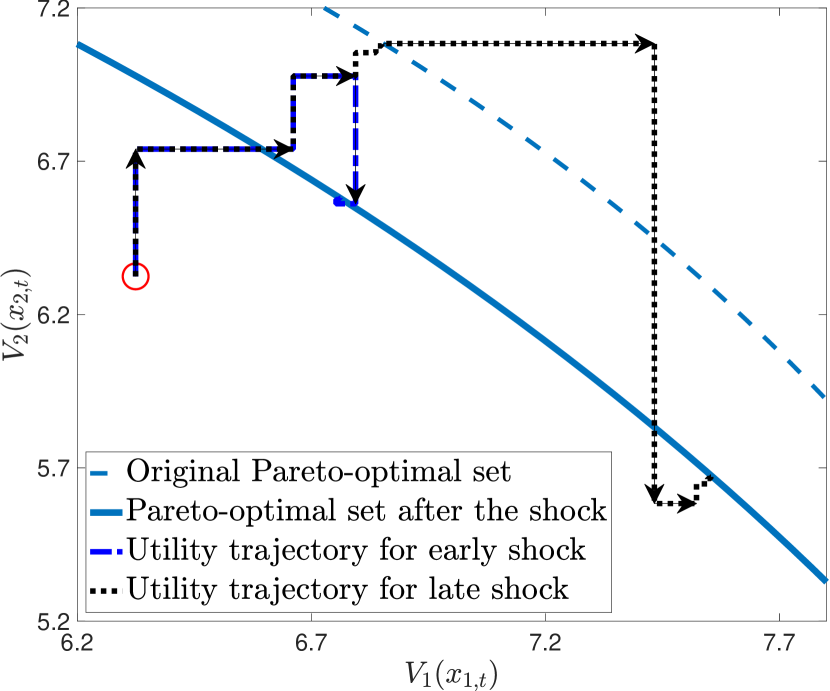

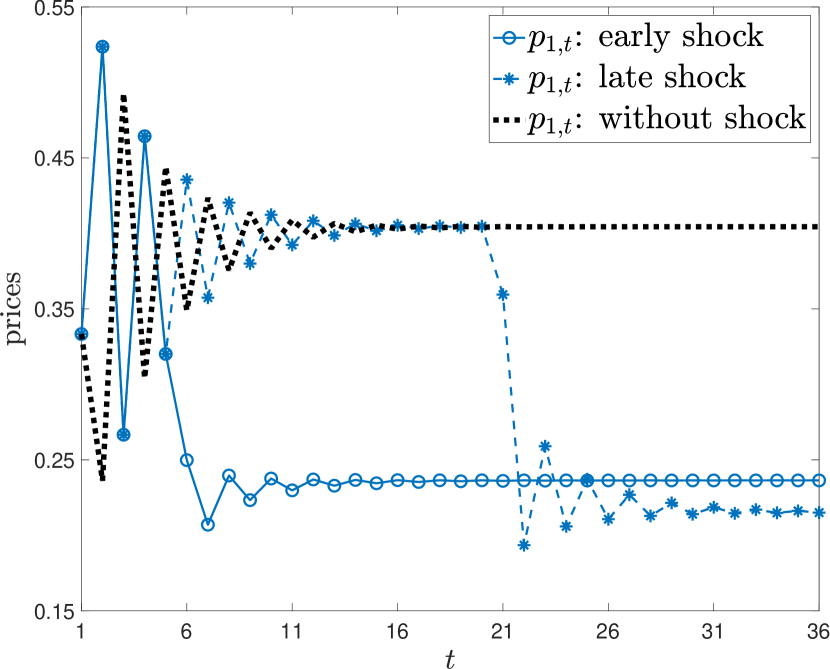

Nonstationary market: All the previous analysis is based on the stationary assumption, i.e., we assume that no new information comes to the market during trading. However, in reality, most prediction markets run for several months, and when an event shocks the market, traders’ beliefs are significantly changed. To show how new information affects security prices, we consider two situations: the shock happens at an early stage (before price convergence), and the shock happens at a late stage. We adopt Example 5.2 for illustration. The shock changes the traders’ beliefs on the second security, i.e., the original beliefs, and are modified to and , respectively. Figure 5(a) displays the trajectories of two traders’ utilities. The solid line and dash-dot line indicate the Pareto optimal frontiers of utility values generated by the original and modified beliefs, respectively. We can observe that, regardless of when the shock occurs, the utilities ultimately converge to the new Pareto-optimal set (i.e., the solid curve and the dashed curve indicate the Pareto-optimal sets for the market with and without the shock, respectively). However, the position of the limiting points varies. Figure 5(b) illustrates the trajectory of the first security’s price, . Similar to the utility values, when new information enters the market, the price responds rapidly to this new information. It is important to note that the limiting prices resulting from early and late shocks are different. This is a straightforward consequence of Theorem 5.3, which indicates that all traders’ initial conditions and beliefs determine the limiting price. If we consider the time at which the shock occurs as the new starting point, early and late shocks produce different initial conditions, thus potentially leading to different limiting prices.

7. Conclusion

This paper studies the prediction market convergence properties through the utilization of the multivariate utility (MU)-based market-making mechanism. This mechanism not only consolidates various existing market-making methods under specific conditions but also establishes a framework for examining the dynamic trading process within a market featuring a single market maker and a finite number of traders. Within this framework, we address one fundamental question arising in the prediction market: the formation of the limiting price (final price) by all market participants. We establish, under mild conditions, that traders’ wealth processes converge to a limiting wealth distribution, resulting in Pareto optimal utility levels for all participants. This outcome enables us to explore the limiting price across different market types. In exponential utility markets, we present an explicit formula for the limiting price. For convex risk-measure-based markets, we introduce a method to design MU functions via penalty functions and demonstrate that the limiting price is uniquely determined as a weighted power mean of trader beliefs. Regarding CRRA utility-based markets, we characterize the limiting price through a system of equations. Additionally, we present a theoretical result indicating that the impact of trading sequence variation becomes negligible as the trader population increases. This novel finding enables us to formulate an approximate price formula, suggesting that the limiting price can be construed as a wealth-weighted risk-adjusted average of all participants’ beliefs. Numerical experiments validate the high accuracy and robustness of this approximation.

There are several promising directions for future research. Firstly, although this work has derived price formulas under various theoretical settings, a critical next step is the empirical validation of these results using real market data.

Secondly, our model is built on the stationary assumption that participants’ beliefs remain constant. In real-world trading, traders and market maker typically adaptively revise their beliefs based on new information. While our preliminary analysis in Section 6 indicates that changes in traders’ beliefs can result in significant shifts in the limiting price, it remains unknown how traders and market maker should incorporate this new information into their decision-making process as part of a learning process. A recent study by (Birge et al., 2021) analyzes the profit maximization problem for market maker in the spread betting market, where market maker may learn the distribution of event outcomes during trading. To address the potential profit loss that Bayesian policies may suffer in the presence of strategic bettors, they propose a new policy that balances learning with bluff-proofing. Building on this line of research, our model has the potential to incorporate learning features for both traders and market maker.

Thirdly, in our model, we assume that traders’ decision problems are myopic, meaning that they focus on single-period decision problems. However, in the actual market, some traders exhibit forward-looking behavior. For example, some professional traders may possess significant insights into future market movements. Therefore, it is worthwhile to explore a model that incorporates traders who tackle forward-looking decision problems involving multi-period considerations. In such a scenario, the decision horizon spans multiple periods, which introduces more price uncertainty resulting from the trading activities of other market participants. Establishing a tractable multi-period decision problem for traders is a crucial step in exploring this forward-looking aspect in the market.

Lastly, it is well-known that classical risk-averse preferences cannot fully explain certain decision-making behaviors observed in empirical studies and psychological experiments (Tversky and Kahneman, 1992). Prospect theory (PT) is an influential alternative theory that accounts for psychological factors such as loss aversion, reference points, and probability distortion in individual decision-making ((Kahneman and Tversky, 2013; Barberis, 2013)). Recently, (Yu et al., 2022) adopt a PT-based utility and construct an equilibrium model to explain pricing anomalies in betting markets. In the context of pricing models, (den Boer and Keskin, 2022) incorporate the PT-based demand function into a dynamic pricing model with demand learning and propose an asymptotically optimal dynamic pricing policy. Incorporating PT-based traders into the current analysis could provide a more realistic representation of real-world trading. Furthermore, it would be intriguing to explore how such traders influence the limiting price. However, establishing market convergence could be challenging due to the non-convex nature of the PT-based model. To address this challenge, several key assumptions made in this work may require refinement.

References

- Abbott [2001] Stephen Abbott. Understanding Analysis, volume 2. Springer, 2001.

- Abernethy et al. [2013] Jacob Abernethy, Yiling Chen, and Jennifer Wortman Vaughan. Efficient market making via convex optimization, and a connection to online learning. ACM Transactions on Economics and Computation, 1(2):1–39, 2013.

- Abernethy et al. [2014a] Jacob Abernethy, Sindhu Kutty, Sébastien Lahaie, and Rahul Sami. Information aggregation in exponential family markets. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, pages 395–412, 2014a.

- Abernethy et al. [2014b] Jacob D. Abernethy, Rafael M. Frongillo, Xiaolong Li, and Jennifer Wortman Vaughan. A general volume-parameterized market making framework. In Proceedings of the Fifteenth ACM Conference on Economics and Computation, pages 413–430, 2014b.

- Agrawal et al. [2011] Shipra Agrawal, Erick Delage, Mark Peters, Zizhuo Wang, and Yinyu Ye. A unified framework for dynamic prediction market design. Operations Research, 59(3):550–568, 2011.

- Arrow et al. [2008] Kenneth J. Arrow, Robert Forsythe, Michael Gorham, Robert Hahn, Robin Hanson, John O. Ledyard, Saul Levmore, Robert Litan, Paul Milgrom, Forrest D. Nelson, George R. Neumann, Marco Ottaviani, Thomas C. Schelling, Robert J. Shiller, Vernon L. Smith, Erik Snowberg, Cass R. Sunstein, Paul C. Tetlock, Philip E. Tetlock, Hal R. Varian, Justin Wolfers, and Eric Zitzewitz. The promise of prediction markets. Science, 320(5878):877–878, 2008.

- Atanasov et al. [2022] P. Atanasov, J. Witkowski, B. Mellers, and P. Tetlock. Crowd prediction systems: Markets, polls, and elite forecasters. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 1013–1014, 2022.

- Atanasov et al. [2017] Pavel Atanasov, Phillip Rescober, Eric Stone, Samuel A Swift, Emile Servan-Schreiber, Philip Tetlock, Lyle Ungar, and Barbara Mellers. Distilling the wisdom of crowds: Prediction markets vs. prediction polls. Management Science, 63(3):691–706, 2017.

- Aumann [1976] Robert J Aumann. Agreeing to disagree. The Annals of Statistics, 4(6):1236–1239, 1976.

- Ban [2018] A. Ban. Strategy-proof incentives for predictions. In International Conference on Web and Internet Economics, pages 51–65. Springer, 2018.

- Barberis [2013] Nicholas C Barberis. Thirty years of prospect theory in economics: A review and assessment. Journal of Economic Perspectives, 27(1):173–196, 2013.

- Berg et al. [2008] Joyce E Berg, Forrest D Nelson, and Thomas A Rietz. Prediction market accuracy in the long run. International Journal of Forecasting, 24(2):285–300, 2008.

- Berg et al. [2009] Joyce E Berg, George R Neumann, and Thomas A Rietz. Searching for Google’s value: Using prediction markets to forecast market capitalization prior to an initial public offering. Management Science, 55(3):348–361, 2009.

- Bertsekas [2016] Dimitri Bertsekas. Nonlinear Programming. Athena, Scientific, 2016.

- Bertsekas et al. [2003] Dimitri P Bertsekas, Angelia Nedi, Asuman E Ozdaglar, et al. Convex Analysis and Optimization. Athena Scientific, 2003.

- Birge et al. [2021] J. R. Birge, Y. F. Feng, N. B. Keskin, and A. Schultz. Dynamic learning and market making in spread betting markets with informed bettors. Operations Research, 69(6):1446–1476, 2021.

- Bonnisseau and Nguenamadji [2013] Jean-Marc Bonnisseau and Orntangar Nguenamadji. Discrete Walrasian exchange process. Economic Theory, 52(3):1091–1100, 2013.

- Bordley [1982] R. F. Bordley. A multiplicative formula for aggregating probability assessments. Management Science, 28(10):1091–1213, 1982.

- Carvalho [2017] Arthur Carvalho. On a participation structure that ensures representative prices in prediction markets. Decision Support Systems, 104:13–25, 2017.

- Chakraborty and Das [2015] Mithun Chakraborty and Sanmay Das. Market scoring rules act as opinion pools for risk-averse agents. In Advances in Neural Information Processing Systems, pages 2359–2367, 2015.

- Chakravorti et al. [2023] T. Chakravorti, V. Singh, S. Rajtmajer, M. McLaughlin, R. Fraleigh, C. Griffin, A. Kwasnica, D. Pennock, and C. L. Giles. Artificial prediction markets present a novel opportunity for human-ai collaboration. In A. Ricci, W. Yeoh, N. Agmon, and B. An, editors, Proc. of the 22nd International Conference on Autonomous Agents and Multiagent Systems (AAMAS 2023), 2023.

- Chen et al. [2008] M Keith Chen, Jonathan E Ingersoll Jr, and Edward H Kaplan. Modeling a presidential prediction market. Management Science, 54(8):1381–1394, 2008.

- Chen and Pennock [2007] Yiling Chen and David M. Pennock. A utility framework for bounded-loss market makers. In Proceedings of the Twenty-Third Conference on Uncertainty in Artificial Intelligence, pages 49–56, 2007.

- Chen and Vaughan [2010] Yiling Chen and Jennifer Wortman Vaughan. A new understanding of prediction markets via no-regret learning. In Proceedings of the 11th ACM Conference on Electronic Commerce, pages 189–198. ACM, 2010.

- Chen et al. [2005] Yiling Chen, Chao-Hsien Chu, Tracy Mullen, and David M. Pennock. Information markets vs. opinion pools: An empirical comparison. In Proceedings of the 6th ACM Conference on Electronic Commerce, pages 58–67, 2005.

- Choo et al. [2022] Lawrence Choo, Todd R Kaplan, and Ro’i Zultan. Manipulation and (mis) trust in prediction markets. Management Science, 68(9):6716–6732, 2022.

- Cogwill and Zitzewitz [2015] Bo Cogwill and Eric Zitzewitz. Corporate prediction markets: Evidence from Google, Ford and Firm x. The Review of Economic Studies, 82(4):1309–1341, 2015.

- Cowgill et al. [2009] B. Cowgill, J. Wolfers, and Eric Zitzewitz. Auctions, Market mechanisms and Their Applications, chapter Using prediction markets to track information flows: Evidence from Google. Springer, 2009.

- den Boer and Keskin [2022] A. V. den Boer and N. B. Keskin. Dynamic pricing with demand learning and reference effects. Management Science, 68(10):7065–7791, 2022.

- Föllmer and Knispel [2015] Hans Föllmer and Thomas Knispel. Convex risk measures: Basic facts, law-invariance and beyond, asymptotics for large portfolios, chapter Chapter 30, pages 507–554. World Scientific Handbook in Financial Economics Series. World Scientific, 2015.