Bernard, Pesenti and Vanduffel

Robust Distortion Risk Measures

Robust Distortion Risk Measures

Carole Bernard

\AFFDepartment of Accounting, Law and Finance, Grenoble Ecole de Management, France,

Department of Economics and Political

Science, Vrije Universiteit Brussel, Belgium \AUTHORSilvana M. Pesenti

\AFFDepartment of Statistical Sciences, University of Toronto, Canada, \EMAILsilvana.pesenti@utoronto.ca

\AUTHORSteven Vanduffel

\AFFDepartment of Economics and Political

Science, Vrije Universiteit Brussel, Belgium

03. February 2023

111First version 18. August 2020; revised version 18. May 2022

The robustness of risk measures to changes in underlying loss distributions (distributional uncertainty) is of crucial importance in making well-informed decisions. In this paper, we quantify, for the class of distortion risk measures with an absolutely continuous distortion function, its robustness to distributional uncertainty by deriving its largest (smallest) value when the underlying loss distribution has a known mean and variance and, furthermore, lies within a ball - specified through the Wasserstein distance - around a reference distribution. We employ the technique of isotonic projections to provide for these distortion risk measures a complete characterisation of sharp bounds on their value, and we obtain quasi-explicit bounds in the case of Value-at-Risk and Range-Value-at-Risk. We extend our results to account for uncertainty in the first two moments and provide applications to portfolio optimisation and to model risk assessment.

Risk Bounds, Distortion Risk Measures, Wasserstein Distance, Distributional Robustness, Range Value-at-Risk, Model Uncertainty \HISTORYEarlier versions have been presented at the Statistical Society of Canada Annual Meeting (virtual), the Conference on Quantitative Risk Management and Financial Technology (Waterloo, Canada), the INFORMS Annual Meeting (Seattle, USA), the Quantact lab (Montréal, Canada), the Workshop on Insurance Mathematics (London, Canada), the Bahnhofs Colloquium of the Swiss Actuarial Society (Zurich, Switzerland), the University of Waterloo (Canada), the Quantact (Montréal, Canada), and the University of Siegen (Germany).

1 Introduction

Many decisions in financial risk management are based on evaluations of so-called risk or performance measures, e.g., Value-at-Risk (VaR) and Tail Value-at-Risk (TVaR) (EIOPA 2009, BCBS 2013), which are limit cases of Range Value-at-Risk (RVaR) (Cont et al. 2010). Risk managers rely on such measures, as they provide a classification of risk severities by associating to every loss distribution a real number (Artzner et al. 1999). Many risk measures are, however, highly sensitive to changes in the underlying loss distribution, and this vulnerability can contribute to adverse decisions; see Cont et al. (2010), Kou et al. (2013), Embrechts et al. (2015), and Pesenti et al. (2016). Here, we quantify distributional uncertainty via bounds on the values of risk measures. Specifically, we study worst-case and best-case values of risk measures – that is, the largest (resp. smallest) value a risk measure can attain when the loss distribution belongs to a set of plausible alternative distributions.

The literature on risk bounds presents two main approaches. The first studies risk bounds for the aggregate portfolio loss given that the components have known marginal distributions but unknown interdependence; see, among others, Denuit et al. (1999), Embrechts and Puccetti (2006), Wang and Wang (2011), and Embrechts et al. (2013). Although explicit results can be derived in certain cases of interest, the bounds obtained are typically too wide to be practically useful. Specifically, the upper bound on a distortion risk measure is always at least as large as its value under the assumption of a comonotonic dependence, a situation that is arguably very extreme. Papers that study bounds with additional dependence constraints or by imposing modelling structures include Bernard et al. (2017), Lux and Rüschendorf (2019), and Wang et al. (2019). Another stream of the literature is concerned with deriving risk bounds of the aggregate loss under partial knowledge of its moments. Since only information on the moments of is required, these risk bounds apply to non-linear loss models, such as re-insurance portfolios, and to loss models for which the explicit aggregation is not known analytically, e.g., when is obtained via simulation models. As (higher) moments of the aggregate loss depend both on the marginal distributions and their interdependence, one thus retains some aspects of the marginal distributions and dependence information. Relevant papers include Hürlimann (2002) for the case of VaR and Cornilly et al. (2018) and Zhu and Shao (2018) for the case of (concave) distortion risk measures. Risk bounds that use additional refined information, such as uni-modality or symmetry, can be found in, e.g., Li et al. (2018).

This paper is situated in the second stream, in that we consider risk bounds of an aggregate loss under knowledge of its first two moments. However, we additionally impose a probability distance constraint on , specified via the Wasserstein distance. Specifically, all alternative aggregate loss distributions, over which the worst- and best- cases are sought – the uncertainty set – lie within a tolerance distance from a reference loss distribution. Thus, the size of the tolerance distance determines the uncertainty around the reference distribution, which may also entail uncertainties on its components. Indeed, if the tolerance is small enough, the uncertainty set contains only the reference distribution, whereas if the tolerance distance increases to infinity, we recover bounds with moments constraints only. Therefore, the tolerance distance allows for a refined notion of model risk, which results in a continuous spectrum of risk bounds interpolating from the risk of the reference distribution to the bounds on the aggregate loss under the knowledge of the first two moments only.

Worst- (best-) case values under probability distance constraints have been considered by Glasserman and Xu (2014) and Lam (2016), who use the Kullback-Leibler divergence, as well as by Blanchet and Murthy (2019), who utilise distances stemming from mass transportation. These papers, however, consider the expected value of a function of the loss random variable, whereas here we study the class of distortion risk measures. Moreover, we use a distance that allows for comparison of distributions on differing support, which is important in our context as it is not clear a priori whether the worst-case distribution shares the same support as the reference distribution. For example, a discrete reference distribution, together with a particular choice of distortion risk measure (e.g., inverse-S shaped), will result in a continuous worst-case distribution. In this work, we quantify the distance between the alternative distribution function and the reference distribution via the Wasserstein distance of order 2. The Wasserstein distance has been widely applied to model distributional uncertainty in financial contexts (see e.g., Pflug and Wozabal (2007), Bartl et al. (2020) and Chen and Xie (2021)), and as a distance from reference model (see e.g., Pesenti (2022) and Pesenti and Jaimungal (2021)).

A related stream of literature studies distributionally robust optimisation, leading to an optimum in the worst case. Relevant literature, in which the worst-case value of a distortion risk measure is considered includes Cai et al. (2020) and Pesenti et al. (2020). Cai et al. (2020) consider distortion risk measures under the assumption that the uncertainty set of the components is characterised by the knowledge of their moments, the components having compact support and additional convex constraints. Pesenti et al. (2020) consider signed Choquet Integrals (see Section 3.13 for a definition) and uncertainty sets characterised by so-called closedness-under-concentration. Neither of these works considers the Wasserstein distance, and the closedness-under-concentration condition is not compatible with uncertainty sets that are -Wasserstein balls around an (arbitrary) reference distribution.

In this paper, we derive for any given distortion risk measure (with absolutely continuous distortion function) its worst- and best-case values when the loss distribution has known first two moments and lies within a tolerance distance from a reference distribution, specified through the Wasserstein distance. To derive these bounds, we use the technique of isotonic projections (Németh (2003)). As a result, we obtain quasi analytical best- and worst-case bounds that significantly improve existing moment bounds. We find that for small Wasserstein tolerance distances, the worst-case distribution function (the distribution function attaining the worst-case value) is close (in a probabilistic sense) to the reference distribution, whereas for large tolerance distances the worst-case distribution function is no longer affected by the reference distribution. Thus, when the Wasserstein tolerance distance goes to infinity, the reference distribution becomes irrelevant, and we recover, as corollaries to our results, known moment bounds on distortion risk measures; see Li (2018) and Zhu and Shao (2018). Indeed, Li (2018) considers worst-case concave distortion risk measures with given mean and standard deviation, and Zhu and Shao (2018) consider the best-case and worst-case of the entire class of distortion risk measure under the knowledge of the first two moments. Neither considers a Wasserstein constraint.

We further apply our results to obtain quasi-explicit bounds on RVaR and (via a direct proof) VaR. We find that for small Wasserstein tolerance distances, the worst-case distribution functions for RVaR and VaR are no longer two-point distributions, thus making the bounds attractive for financial risk management applications.

This paper is structured as follows: Section 2 introduces the necessary notation and formulates the problem. The main results – the quasi-analytical best- and worst-case values of distortion risk measures under a Wasserstein distance constraint – are presented in Section 3. Section 4 contains two extensions. In Section 4.1, we calculate bounds of VaR and RVaR. In Section 4.3, we extend our results to complete moment uncertainty – that is, when the uncertainty set is a -Wasserstein ball around a reference distribution without any moment constraints. We provide applications of the risk bounds to portfolio optimisation and to model risk assessment of an insurance portfolio, including rationales for choosing the Wasserstein distance, in Section 5. All proofs are relegated to the appendix.

2 Problem Formulation

We consider an atomless probability space and let be the set of all square integrable random variables on that space. We denote by the corresponding space of distribution functions with finite second moment. The (left-continuous) inverse, also called the quantile function, of a distribution function is , and we denote its right-continuous inverse by . Throughout the exposition, we write for a standard uniform random variable on .

2.1 Distortion Risk Measures

In this section, we recall the class of distortion risk measures that contains risk measures commonly encountered in financial applications, such as VaR and TVaR. A distortion risk measure, evaluated at a distribution function , is defined via the Choquet integral

whenever at least one of the two integrals is finite. The function refers to a distortion function – that is, a non-decreasing function satisfying and . If is absolutely continuous, then the distortion risk measure has the following representation (Dhaene et al. 2012)

| (1) |

with weight function , which satisfies and where denotes the derivative from the left. In what follows, we may sometimes write instead of . {assumption} We assume that representation (1) holds and that .

Throughout the paper, we use the following three concave distortion risk measures to illustrate our results: the dual power distortion with parameter ,

| (2) |

the Wang transform (Wang 1996) with parameter ,

| (3) |

where and denote the standard normal distribution and its density, respectively; and the Tail Value-at-Risk (), also called Expected Shortfall, at level (Acerbi 2002) with

| (4) |

In Section 4.1, we also consider the case of Value-at-Risk (), , a distortion risk measure with that does not satisfy Assumption 2.1, i.e. it does not admit a representation as in (1) as a Lebesgue Integral.

2.2 Modelling Distributional Uncertainty

In financial risk management, distributional uncertainty is prevalent and bounds on the value of a risk measure, so-called worst- and best-case values or upper and lower bounds, are valuable tools for decision making. A worst- (best-) case value of a risk measure is defined as the largest (smallest) value a risk measure can attain when the underlying distribution belongs to a set of alternative distributions. Here, we consider subsets of that are characterised via a tolerance distance to a reference distribution, specified through the Wasserstein distance of order 2. Distribution functions belonging to such an uncertainty set may be viewed as alternatives to the reference distribution, representing model misspecification or alternative model assumptions. To formalise this, we recall the definition of the Wasserstein distance. The Wasserstein distance exhibits desirable properties, such as no restriction on the support of distribution functions, which is in contrast to the Kullback-Leibler divergence; see Villani (2008) for a discussion of the Wasserstein distance.

Definition 2.1 (Wasserstein distance of order 2)

The Wasserstein distance of order 2 between is (Villani 2008)

where the infimum is taken over all bivariate distributions with marginals and .

For distributions on the real line, the Wasserstein distance admits the following well-known representation (Dall’Aglio 1956)

Hence, the Wasserstein distance between and is uniquely determined by their corresponding quantile functions, and we may write instead of .

We denote by the reference distribution and its first two moments by and , respectively. Throughout, we fix the reference distribution and consider distributional uncertainty sets of the type

where , , and . The set thus contains all distribution functions whose first two moments are and , respectively, and that lie within a -Wasserstein ball around the reference distribution . The -constraint in the definition of is redundant when , and in this special case we denote the uncertainty set by . Note that in applications, one may often encounter that , but our set-up allows them to be different, which could for example be useful when their values are estimated using different data sources.

The best- and worst-case values of a distortion risk measure over the distributional uncertainty set are respectively defined by

In addition to the best- and worst-case values, we also study best-case and worst-case distribution functions if they exist – that is, the distribution functions attaining (5a) and (5b), respectively

Note that the square-integrability of in Assumption 2.1 is not restrictive. Indeed if , then problems (5a) and (5b) are both equal to . We provide a proof in Appendix 8, Lemma 8.1. We impose two additional conditions that are necessary in order to ensure that the considered optimisation problems are relevant and well-posed. {assumption} We assume that ; otherwise for all and problems (5) and (6) are obsolete. {assumption} We assume that contains at least two elements, and hence infinitely many; otherwise problems (5) and (6) are either ill-posed or trivial.

In this regard, Assumption 2.2 is equivalent to assuming that . To see this, note that for any

Hence, if , then , and if , then is a singleton, containing only one distribution with quantile function

Moreover, in this special case, coincides with the reference distribution if and only if and . Thus, from now on, we assume that .

3 Bounds on Distortion Risk Measures

For ease of exposition, we first study worst-case values (5b) and worst-case distribution functions (6b) for the class of concave distortion risk measures that are distortion risk measures with concave distortion function . The corresponding results for the case of general distortion risk measures are presented in Section 3.2 and those for best-case values (5a) and best-case distributions (6a) in Section 3.3.

3.1 Upper Bounds on Concave Distortion Risk Measures

Concave distortion risk measures are a subset of the class of distortion risk measures that are coherent and include the widely used TVaR. Furthermore, concave distortion risk measures span the class of law-invariant, coherent, and comonotone additive risk measures (Kusuoka 2001). For the special case of concave distortion risk measures, we obtain analytic solutions to problems (5b) and (6b), which are presented in the following theorem.

Theorem 3.1 (Worst-Case Values and Quantiles of Concave Distortions)

The worst-case value provided in Theorem 3.1 is sharp for all and attained by the worst-case quantile function . We observe that is a weighted average of the reference quantile function and the (non-decreasing) weight function from the distortion risk measure. As the worst-case value is non-decreasing in the tolerance distance , we obtain that is non-decreasing in , which in turn implies that is non-increasing in . Hence, we obtain that the influence of the reference distribution on the worst-case quantile function diminishes with increasing tolerance distance . Furthermore, for sufficiently large, i.e., under case 2. of Theorem 3.1, is zero and the worst-case quantile function is independent of the reference distribution. Note that when , the expression of in (7) is still valid and simplifies to .

As a direct corollary we obtain the worst-case values of TVaR. The proof is omitted as it follows by direct calculations from Theorem 3.1.

Corollary 3.2 (Worst-case Value of TVaR)

Theorem 3.1 generalises results that first appeared in Li (2018). This author derived sharp upper bounds on under the knowledge of the first two moments, i.e., without considering an -Wasserstein distance constraint or a reference distribution. Applying Theorem 3.1 with , we obtain his result, which is stated here for completeness; see also Cornilly et al. (2018) and Zhu and Shao (2018).

Corollary 3.3 (Worst-Case Values for ; Li (2018))

Example 3.4

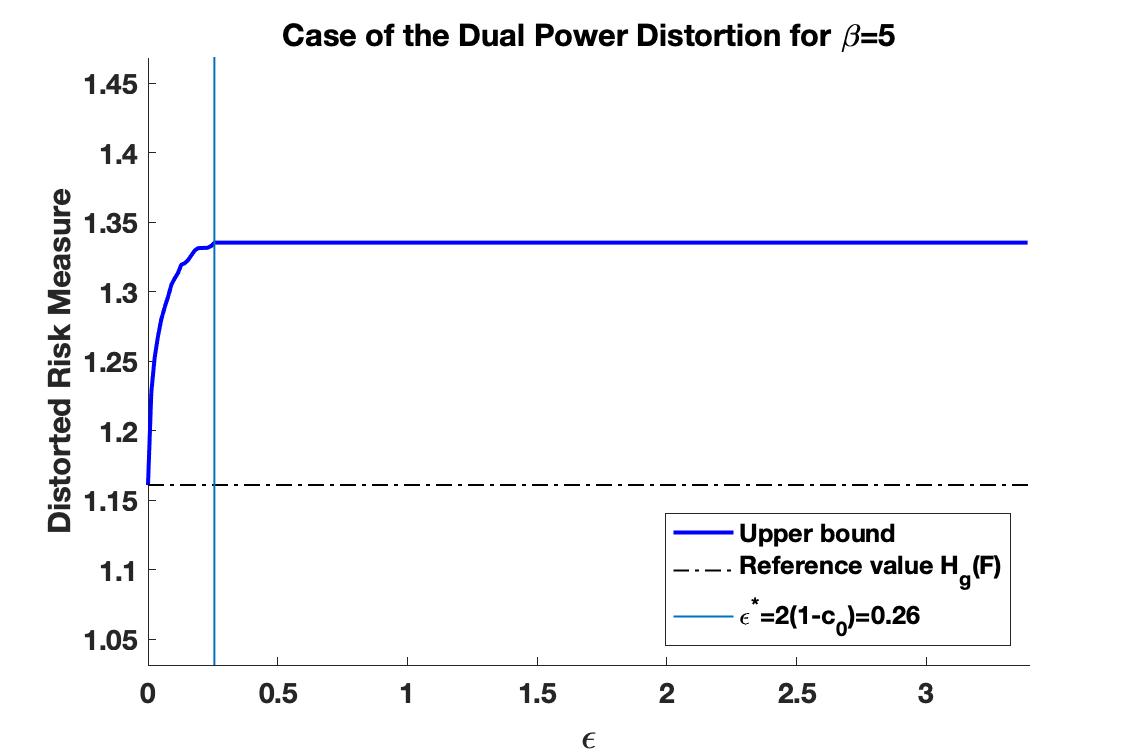

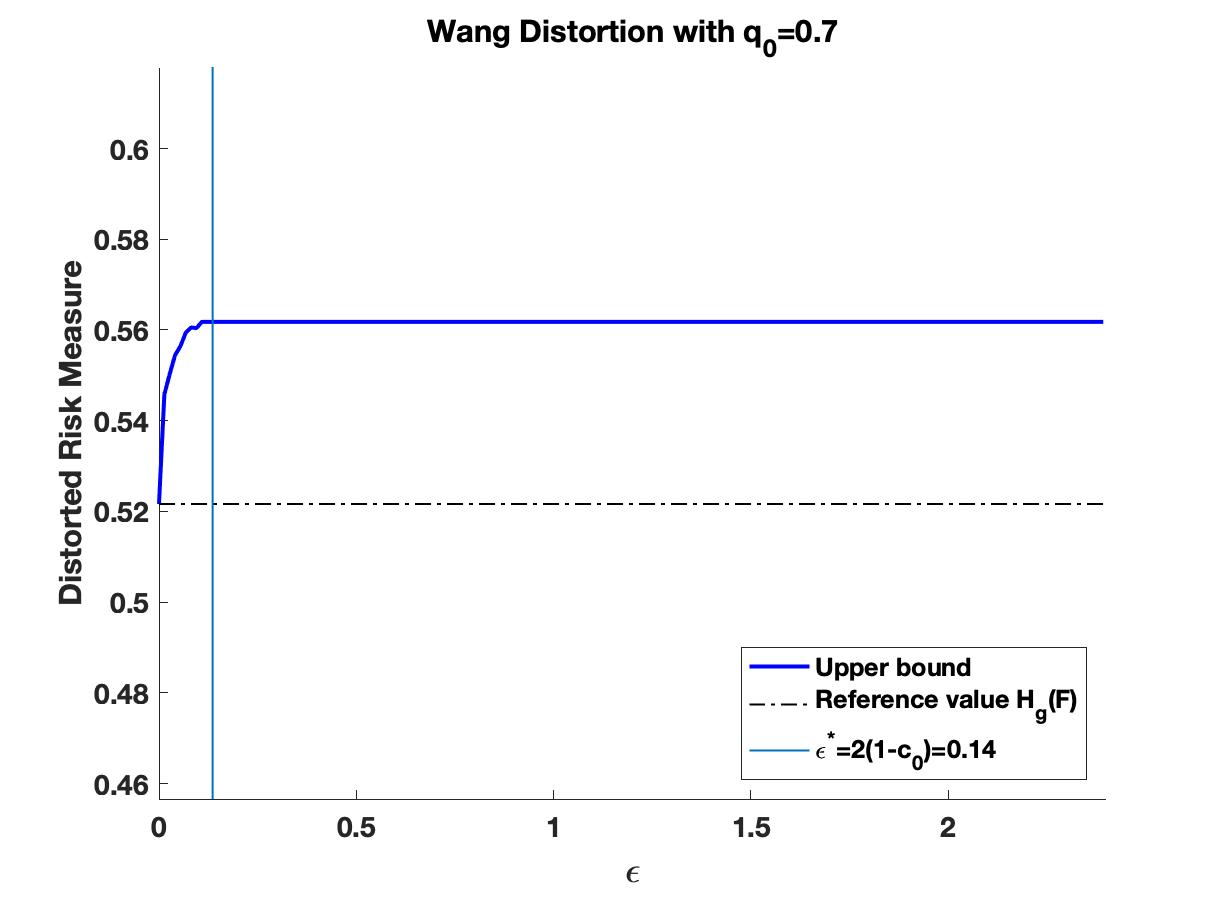

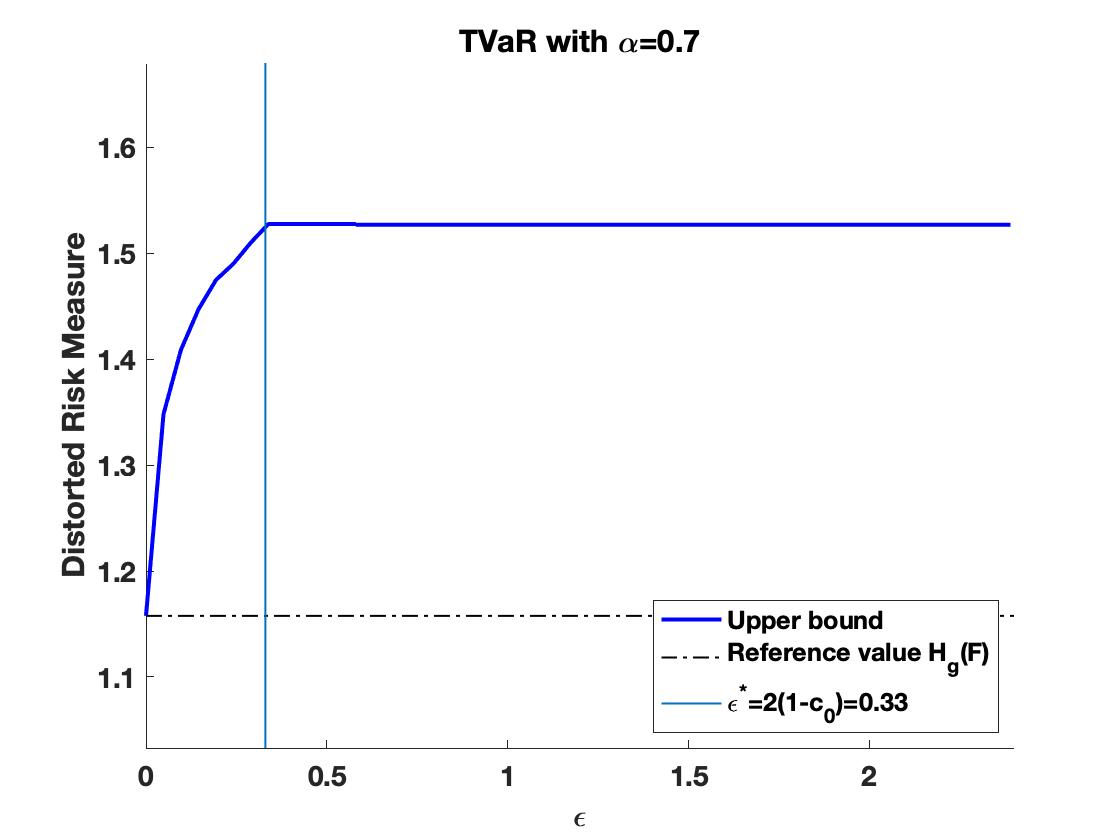

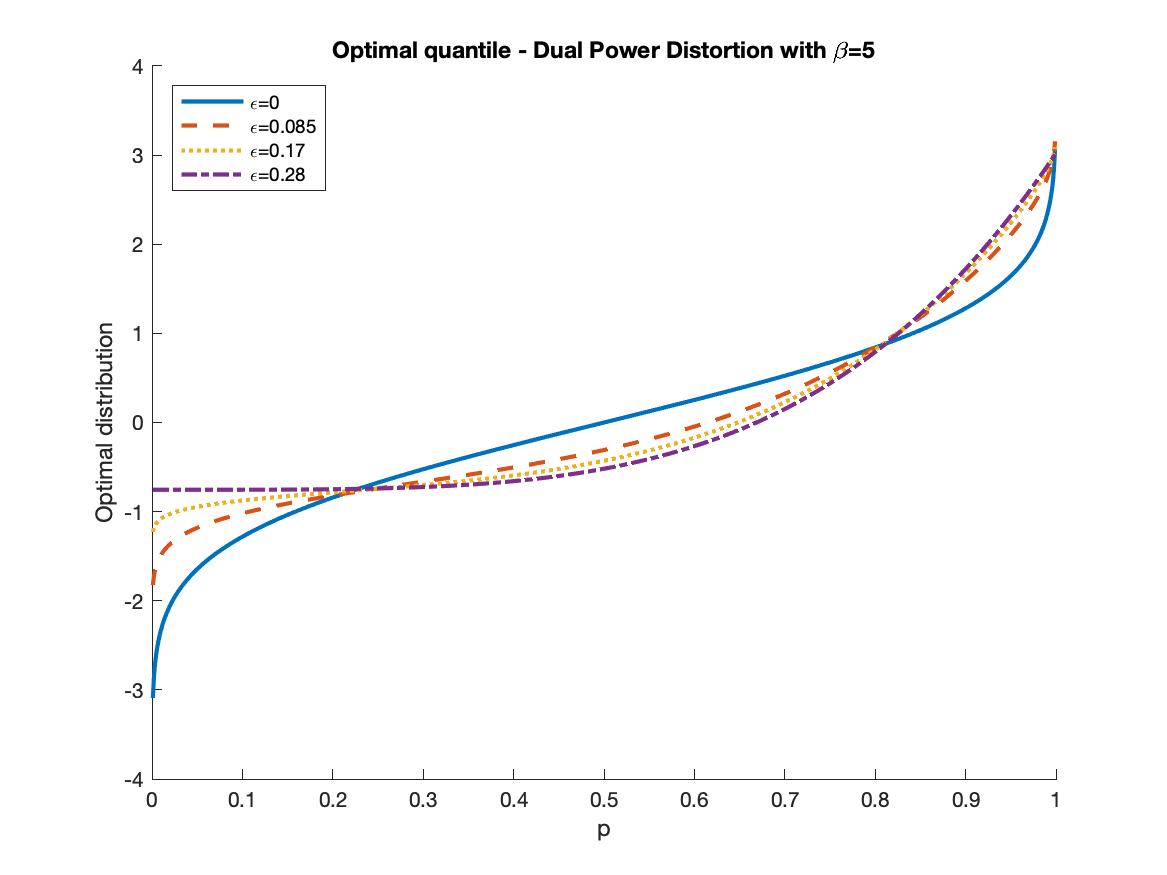

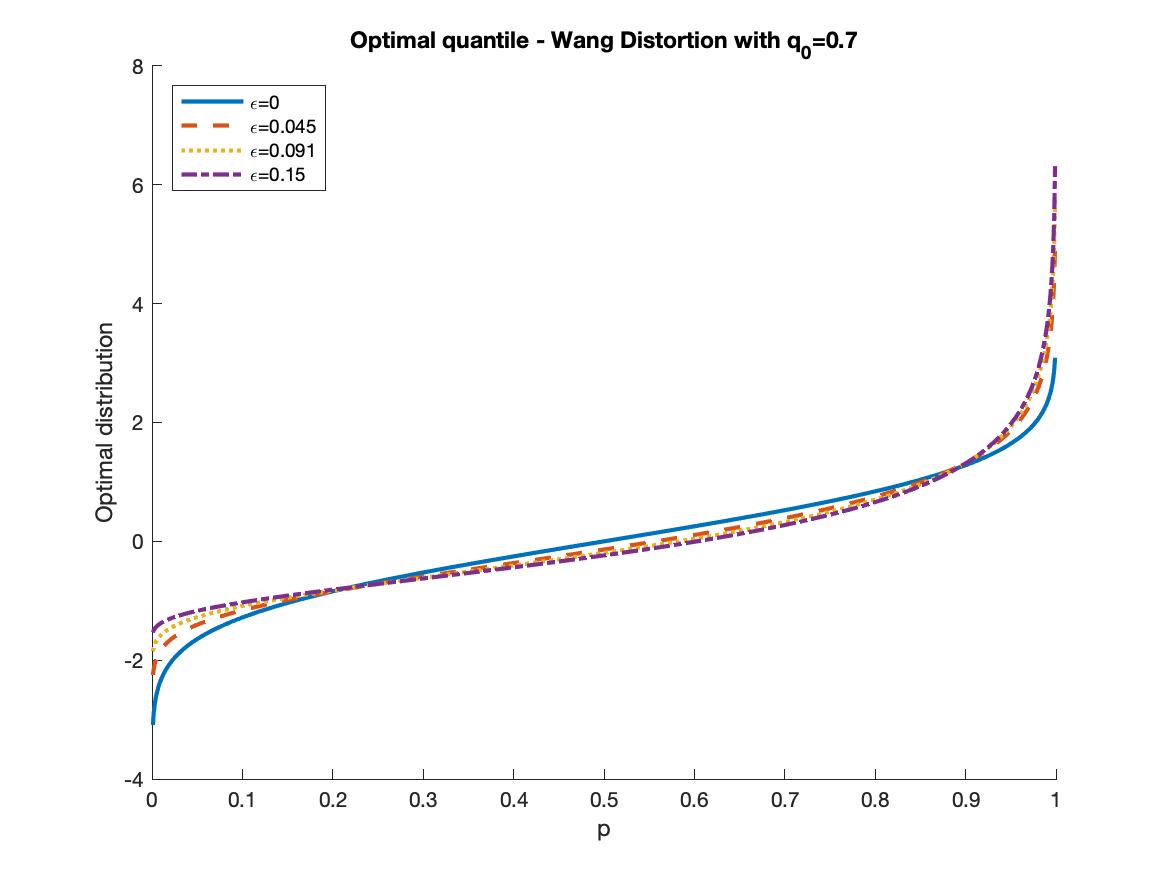

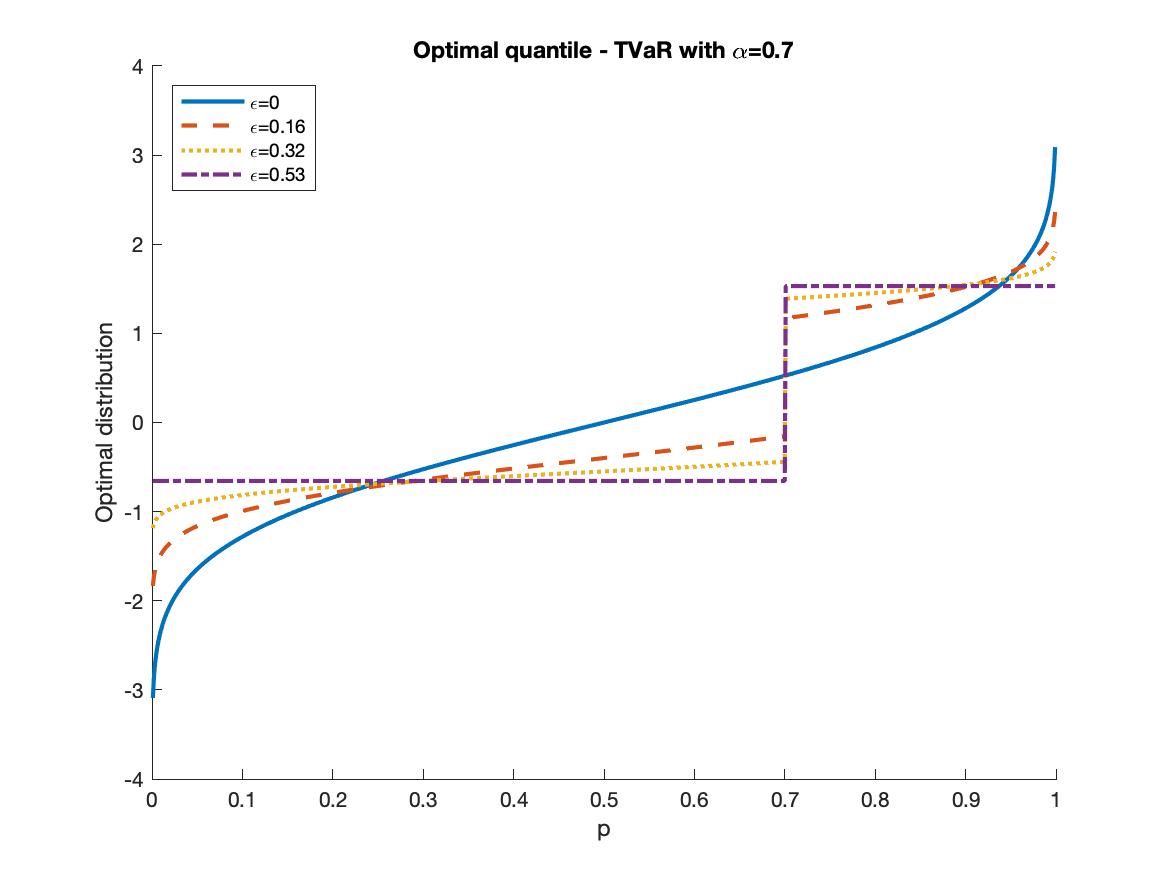

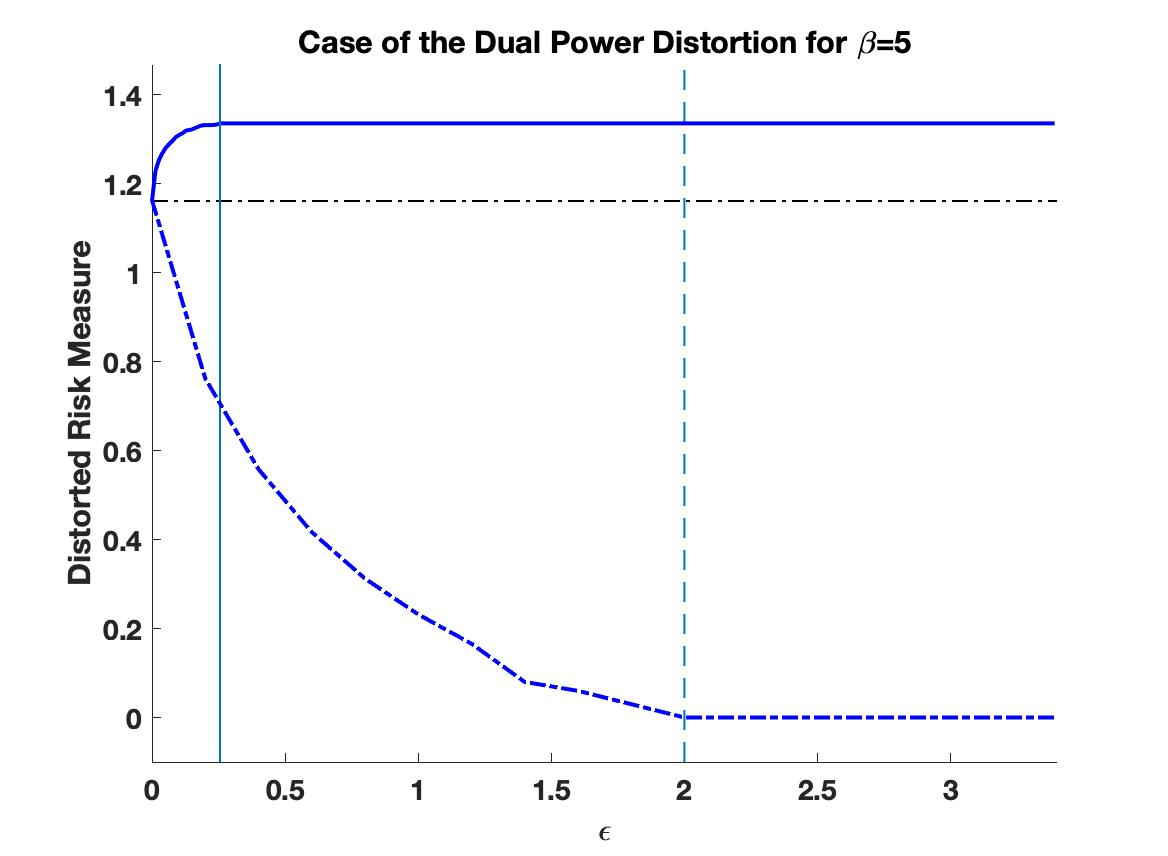

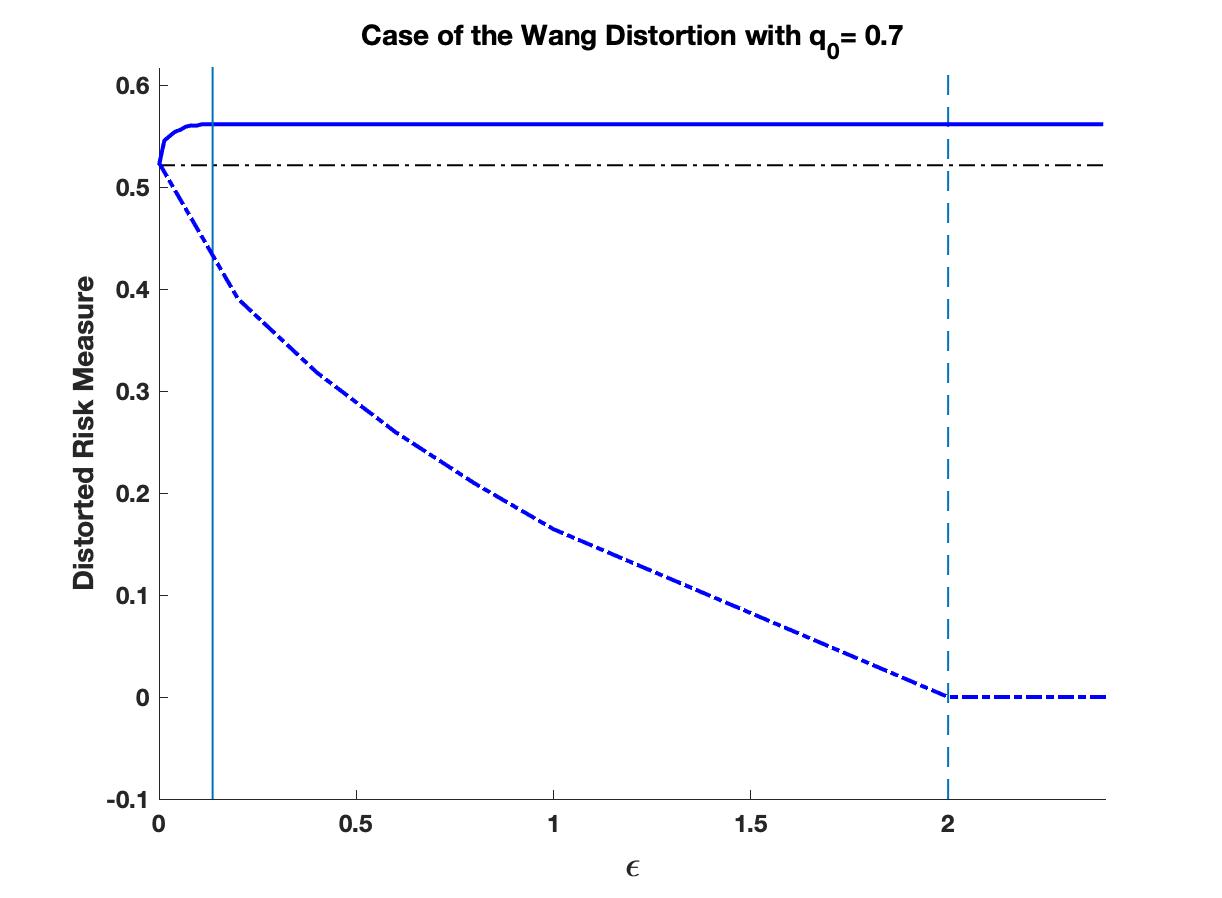

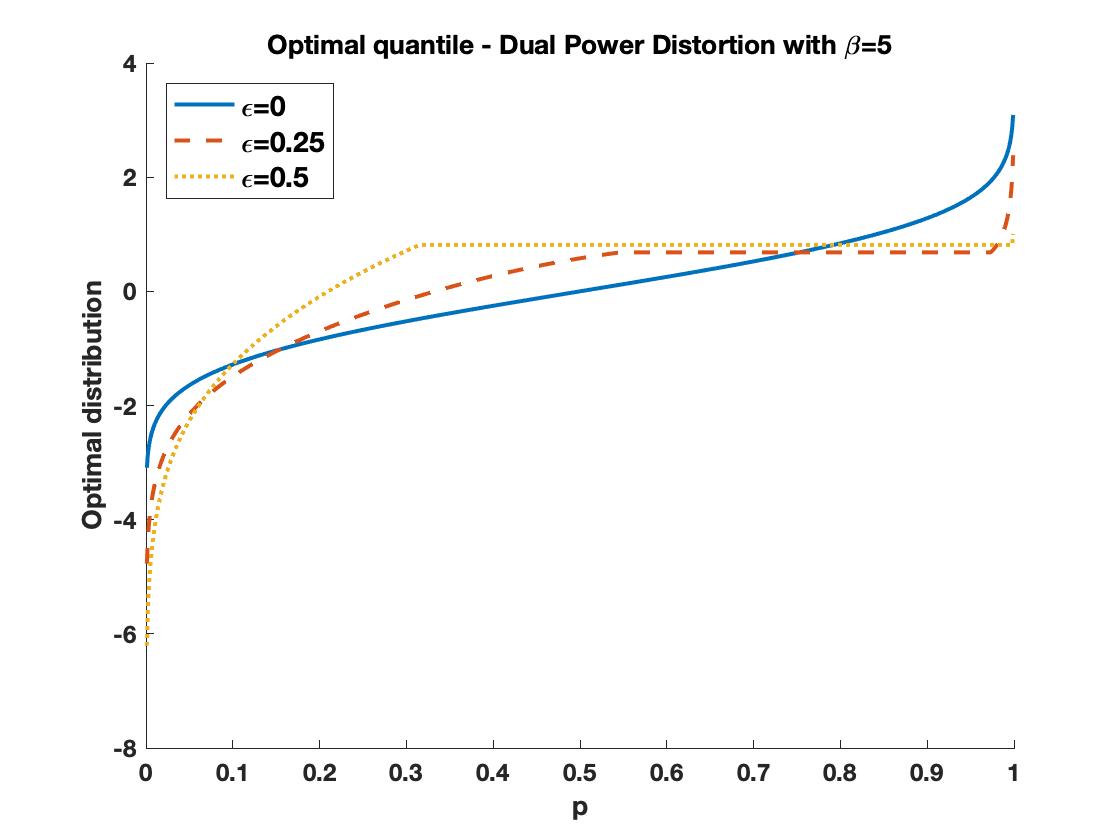

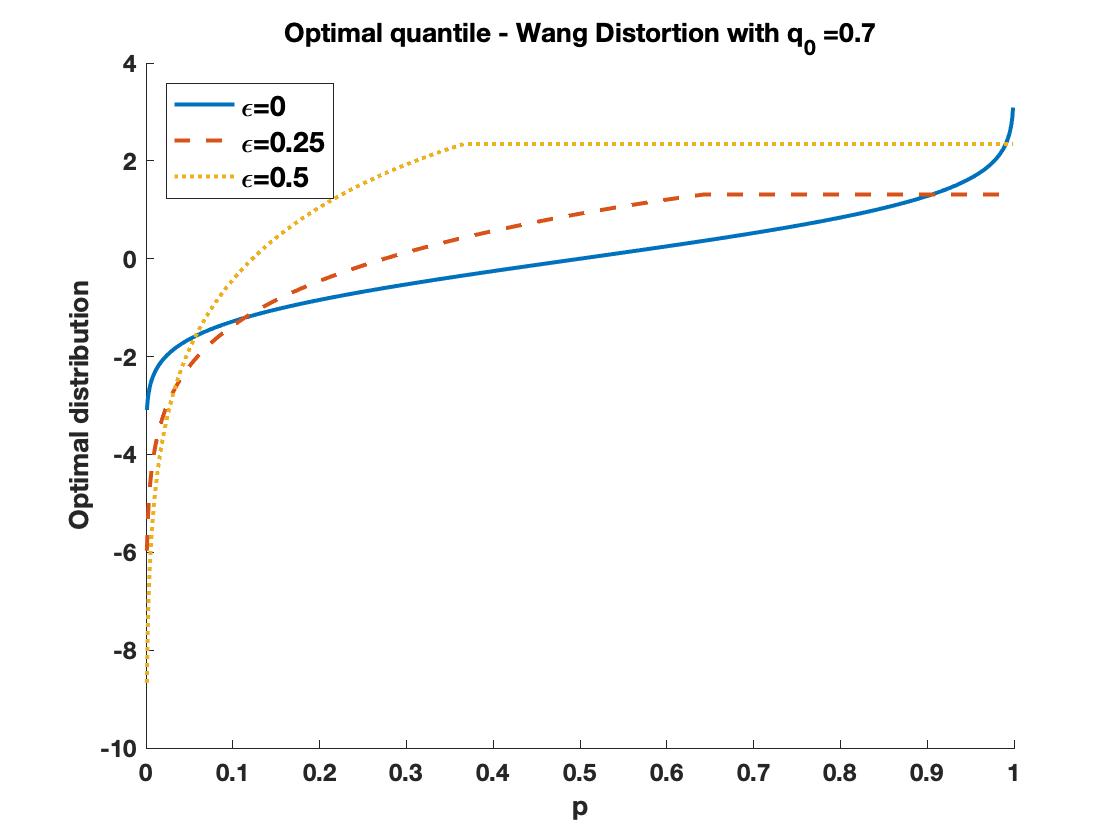

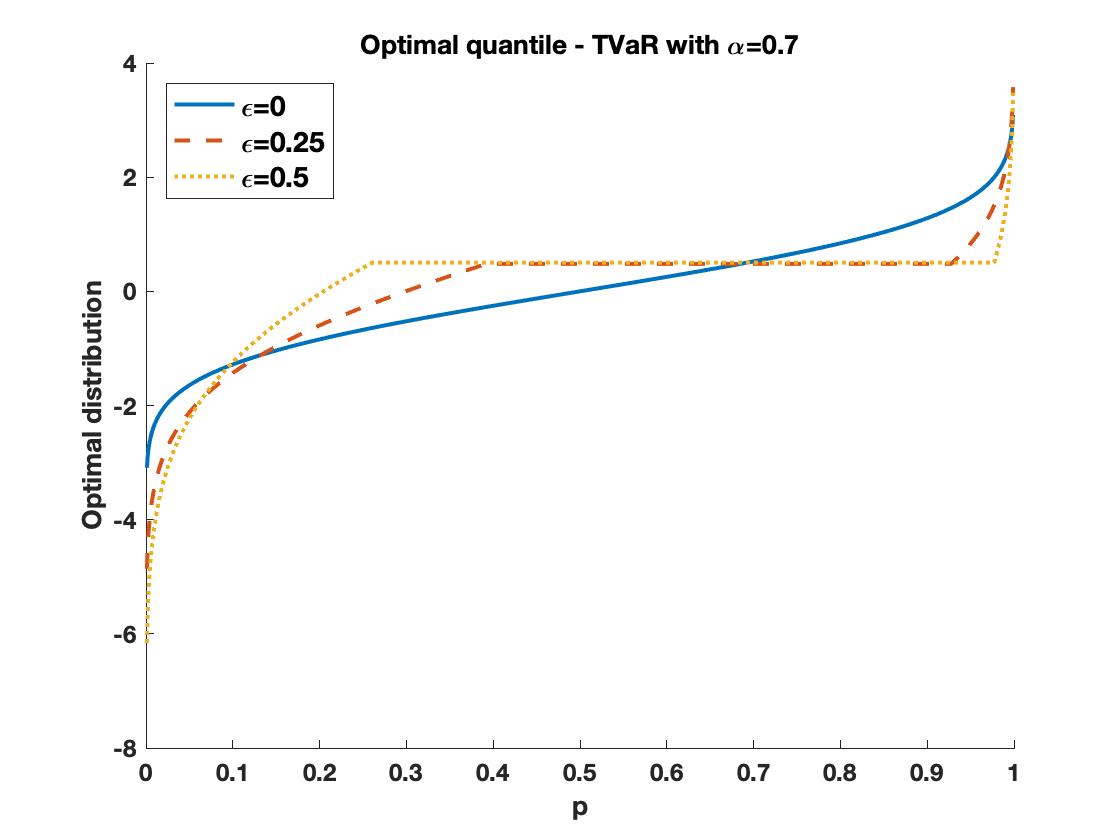

We illustrate the worst-case values of Theorem 3.1 for three concave distortion risk measures: the dual power distortion, the Wang transform, and TVaR defined in (2), (3), and (4), respectively. The reference distribution is chosen to be standard normal, and we further set and .

| Dual Power Distortion | Wang Distortion | TVaR distortion |

|---|---|---|

|

|

|

|

|

|

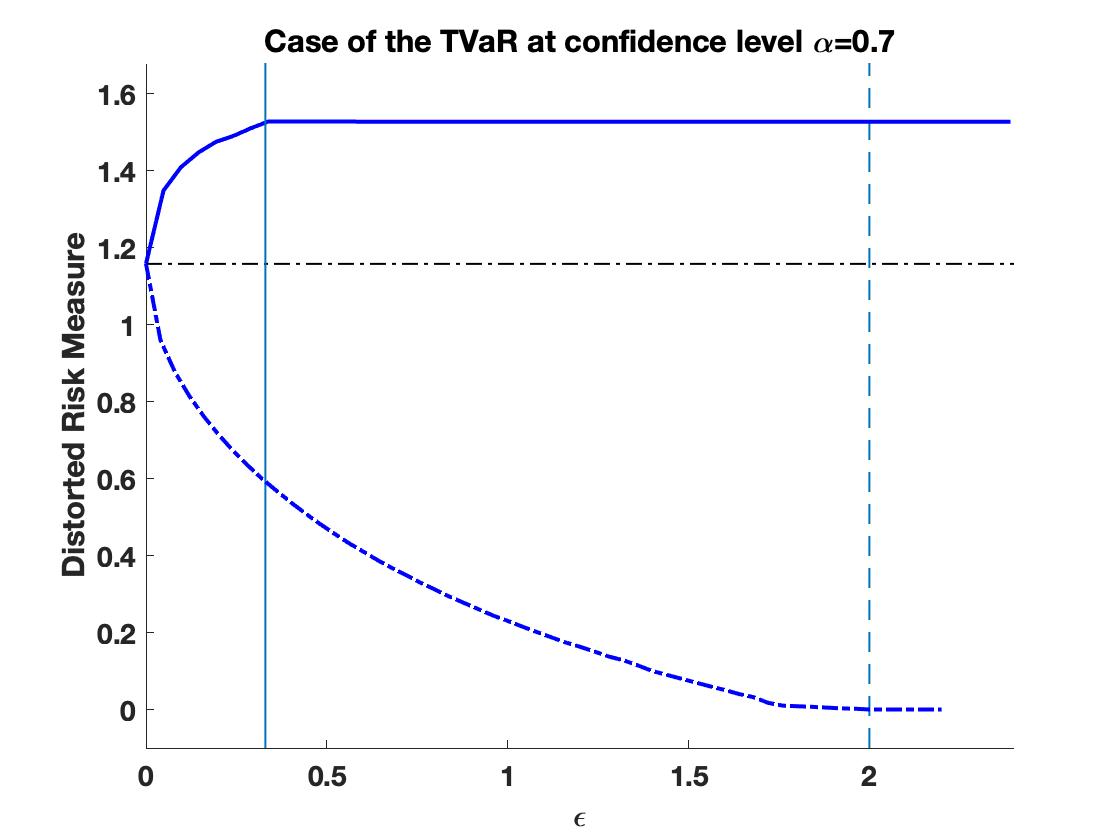

In the top panels of Figure 1, we observe that the upper bounds are indeed non-decreasing and continuous functions of . The turquoise coloured vertical lines display . The parameter value indicates the transition from case 1. to case 2. in Theorem 3.1; indeed, for case 2. of Theorem 3.1 applies and the worst-case value is independent of . For with (top right panel), the worst-case value is equal to , and we recover the well-known Cantelli upper bound.

The bottom panels of Figure 1 display the worst-case quantile functions for selected values of . We observe that for , the worst-case quantile functions are equal to the reference quantile functions (blue solid line). When the Wasserstein distance increases, the influence of the reference distribution diminishes and, if , the worst-case quantile function (violet dash-dotted line) is independent of the reference distribution. This can be seen clearly for TVaR, where the violet dash-dotted quantile function corresponds to a two-point distribution.

3.2 Upper Bounds on General Distortion Risk Measures

To characterise the worst-case values and quantile functions of general distortion risk measures we introduce the concept of isotonic projections; see e.g., Németh (2003). For this, we denote the space of square-integrable, non-decreasing, and left-continuous functions on by

| (8) |

Definition 3.5

For , denote by the isotonic projection of onto the space of square-integrable non-decreasing and left-continuous functions on – that is, the unique solution to

| (9) |

where denotes the norm. Whenever , we write instead of , as is indeed the isotonic projection of alone.

The isotonic projection differs from the isotonic regression (Barlow et al. 1972), which is a metric projection onto the set of finite dimensional and component-wise increasing vectors. We refer to Appendix 7 for further details and properties of isotonic projections.

We further define

and set . Finally, we define for the quantile function

| (10) |

with and . Note that is well-defined whenever , as the function is non-constant for all ; see also Proposition 7.1 in Appendix 7.

Before stating the worst-case value of general distortion risk measures, we need a further assumption. {assumption} We assume that . Note that Assumption 3.5 is a requirement on the weight function and the reference distribution. Assumption 3.5 is satisfied, for instance, when is bounded and the reference distribution has a quantile function that is unbounded to the right, i.e. for .

Theorem 3.6 (Worst-Case Values and Quantiles of General Distortions)

Let Assumptions 2.1, 2.2, 2.2, and 3.5 be fulfilled. Further, let be a distortion function and denote . Then, the following statements hold:

- 1.

-

2.

Let . If is not constant, then case applies with . If is constant, then the solution to (5b) is equal to but cannot be attained in general.

Remark 3.7

If is non-increasing, equivalently the distortion function is convex, then its isotonic projection is constant and thus equal to 1. Hence, for sufficiently large, case 2. of Theorem 3.6 implies that the upper bound is equal to . However, the well-known Hoeffding bounds for the expectation of a product of two random variables with given marginal distributions imply that for any admissible quantile function , it holds that (note that and is assumed to be non-constant). Hence, the upper bound is not attained. However, if for example there exists such that and , then the upper bound is attained. To see this, consider the quantile function in which takes value on , value on , and value zero otherwise. It verifies that the mean of is whereas its variance is equal to . Moreover, , thus attains the worst-case bound. An example of satisfying these conditions is if on and on .

If is non-decreasing, equivalently is concave, then is non-decreasing and thus equal to its isotonic projection. Hence, Theorem 3.6 reduces to Theorem 3.1 in the case of concave distortion risk measures. Theorem 3.6 generalises results by Zhu and Shao (2018), who analyse problem (5b) in the special case in which the Wasserstein constraint is redundant, which we state in the subsequent corollary.

Corollary 3.8 (Worst-Case Values for )

Let Assumptions 2.1, 2.2, and 3.5 be fulfilled. Further, let be a distortion function; then, the following statements hold:

-

1.

If is not constant, then

(11) The bound is sharp and attained by a distribution with quantile function defined in (10).

-

2.

If is constant, then

and the bound cannot be attained in general.

3.3 Lower Bounds on General Distortion Risk Measures

In a similar way as in Section 3.2, we first introduce the notation and assumptions needed to derive the best-case values and quantile functions of general distortion risk measures.

Definition 3.9

For , denote by the isotonic projection of onto the set of square-integrable non-increasing functions and left-continuous – that is, the unique solution to

| (12) |

Whenever , we write instead of , as is indeed the isotonic projection of onto the non-increasing functions.

Further, we define

and for all the quantile function

| (13) |

with and . Note that is well-defined whenever , as the function is non-constant for all ; see also Proposition 7.1 in Appendix 7.

We assume that . The next theorem states the best-case values and quantile functions of general distortion risk measures.

Theorem 3.10 (Best-Case Values and Quantiles of General Distortions)

Theorem 3.10 implies that for that is sufficiently large, i.e., in case 2., the lower bound of any concave distortion risk measure is equal to and not attained. The next corollary collects the results for .

Corollary 3.11 (Best-Case Values for )

Let Assumptions 2.1, 2.2, and 3.3 be fulfilled. Further, let be a distortion function; then, the following statements hold:

-

1.

If is not constant, then

The bound is sharp and is attained by a distribution with quantile function defined in (13).

-

2.

If is constant, then

and the bound cannot be attained.

Remark 3.12

Distortion risk measures have an alternative representation that makes it possible to write minimisation problems in terms of maximisation problems. Specifically,

| (14) |

where is the dual distortion of , given by , and , denote the distribution functions of the random variables and , respectively. Equation (14) follows from the fact that ; see e.g., Dhaene et al. (2012). This observation makes it possible to obtain Corollary 3.11, the statements on lower bounds, from Corollary 3.8, the corresponding statements on upper bounds, in a more direct manner. Such reasoning, however, cannot be extended when dealing with the Wasserstein distance constraints considered in this paper.

Remark 3.13

Theorems 3.6 and 3.10 can be generalised to signed Choquet integrals. A signed Choquet integral is, for a distribution function , defined by , where is of bounded variation with . Signed Choquet integrals generalise the class of distortion risk measures in that the distortion function can be decreasing. For absolutely continuous , the signed Choquet integral admits a representation as in (1), see Wang et al. (2020), thus, Theorems 3.6 and 3.10 can be extended to signed Choquet integrals with absolutely continuous distortion function.

Example 3.14 (Continued)

Figure 2 illustrates the best- and worst-case values (Theorems 3.6 and 3.10) of three concave distortion risk measures: the dual power distortion, the Wang transform, and TVaR, with a standard normal reference distribution, , and . In the upper panels of Figure 2, the solid blue line corresponds to the upper bound and the dashed blue line corresponds to the lower bound. The black line depicts the reference risk measure and the vertical turquoise lines display the critical value for the transition between case 1. and case 2. in Theorem 3.6 (upper bound, solid line) and Theorem 3.10 (lower bound, dashed line).

As all three risk measures are concave, their lower bounds – for sufficiently large (case 2. in Theorem 3.10) – are all equal to but not attained. That the lower bounds are not attained can be seen in the lower panels, where the corresponding best-case quantile functions are displayed. The best-case quantile functions become flatter for larger , and for sufficiently large the quantile functions are no longer defined.

| Dual Power Distortion | Wang Distortion | TVaR distortion |

|---|---|---|

|

|

|

|

|

|

4 Extensions

In this section we consider two extensions. First, we derive explicit bounds on RVaR and (via a direct proof) the bounds on VaR. Second, we extend the results to the uncertainty sets solely described by the Wasserstein distance.

4.1 Bounds on Range Value-at-Risk, Value-at-Risk, and Tail Value-at-Risk

In this section we provide bounds on the risk measures RVaR, TVaR, and VaR. Specifically, we first calculate the best- and worst-case values of RVaR and then derive the TVaR bounds as limiting cases. The bounds on VaR are derived via a direct proof as VaR does not satisfy Assumption 2.1. The at levels is defined by (Cont et al. 2010)

By letting , we obtain TVaR; that is, for any it holds that

Next, recall that and denote . Both VaR and VaR+ are distortion risk measures ( with and with , see Dhaene et al. (2012)); however, they do not belong to the class of distortion risk measures considered in this paper as they do not satisfy Assumption 2.1. Furthermore, it holds that for any

The worst-case values of these risk measures under constraints on the first two moments but without a Wasserstein constraint have been extensively studied; indicatively see Kaas and Goovaerts (1986), Lo (1987), Grundy (1991), Hürlimann (2005), and De Schepper and Heijnen (2010) for the VaR, Li et al. (2018) for the RVaR, and Natarajan et al. (2010) for the TVaR. We collect the worst- and best-case values of these risk measures without a Wasserstein constraint in the subsequent corollaries. The bounds on TVaR and RVaR also follow from Corollary 3.8 and 3.11.

Corollary 4.1 (Worst-Case Values for )

For , the worst-case values of , and coincide; that is,

While the worst-case value of cannot be attained, the worst-case distribution of , and is a two-point distribution with quantile function

| (15) |

Corollary 4.2 (Best-Case Values for )

For , the best-case values of , , , and are

While the best-case values of and cannot be attained, the best-case distribution corresponding to the best-case has a quantile function given by (15) whereas for the best-case it is a two-point distribution with quantile function

Next, we study the lower and upper bound on RVaR when, in addition to the moment constraints, the distributions in the uncertainty set lie within an -Wasserstein ball of the reference distribution .

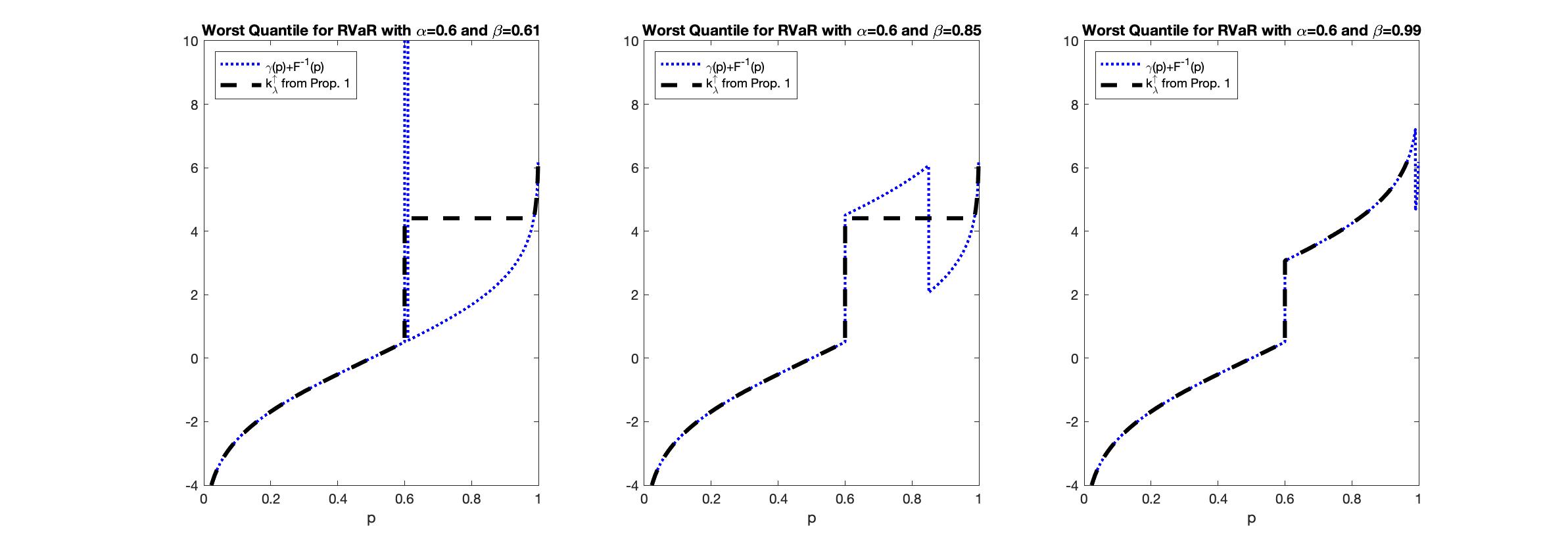

Proposition 4.3 (Worst-Case Quantiles of RVaR)

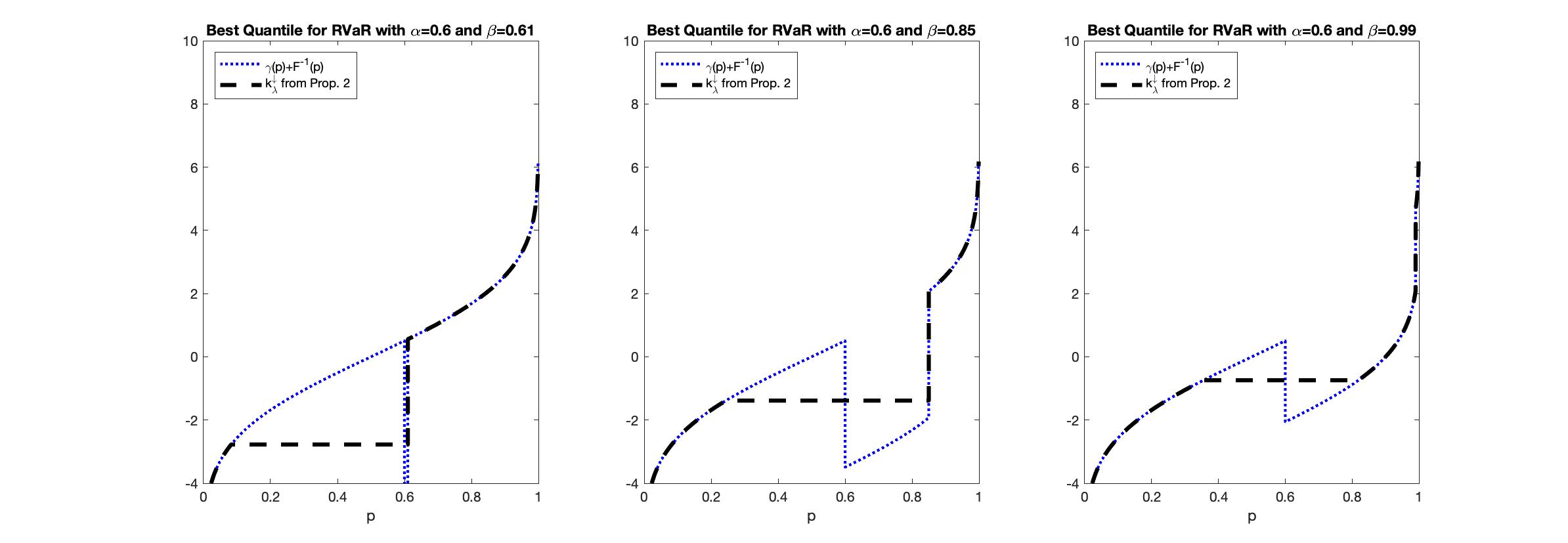

Proposition 4.4 (Best-Case Quantiles of RVaR)

We verified with numerical experiments that the closed-form expressions in (16) and (17) match well with numerically obtained isotonic and antitonic projections.333All numerically obtained isotonic projections are constructed using LSQISOTONIC, a built-in function in Matlab.

The subsequent corollary and proposition provide the best- and worst-case quantile functions of TVaR and VaR, respectively. The results are also summarised in Table 1.

Corollary 4.5 (Best- and Worst-Case Quantiles of TVaR)

As VaR and do not satisfy Assumption 1, we provide a direct proof of the next proposition.

Proposition 4.6 (Best- and Worst-Case Quantile of VaR)

| Risk measure | Best-case quantile | Worst-case quantile |

|---|---|---|

| Proposition 4.4; | Proposition 4.3; | |

| Proposition 4.4 with ; | not attained; | |

| not attained; | Proposition 4.3 with ; | |

| Proposition 4.4 with ; | Proposition 4.3 with and . |

for case 1. of Theorems 3.6 and 3.10, respectively; that is, for sufficiently small.

Example 4.7

Figures 3 and 4 illustrate the isotonic projections for the worst- and best-case quantile function of with and different values of . Specifically, Figure 3 displays and its isotonic projection onto the set of non-decreasing functions (derived in Proposition 4.3). Note that we chose sufficiently small such that the worst-case quantile functions of are not two-point distributions, and thus case 1. of Theorem 3.6 applies. Figure 4 displays the corresponding graphs for the best-case quantile functions.

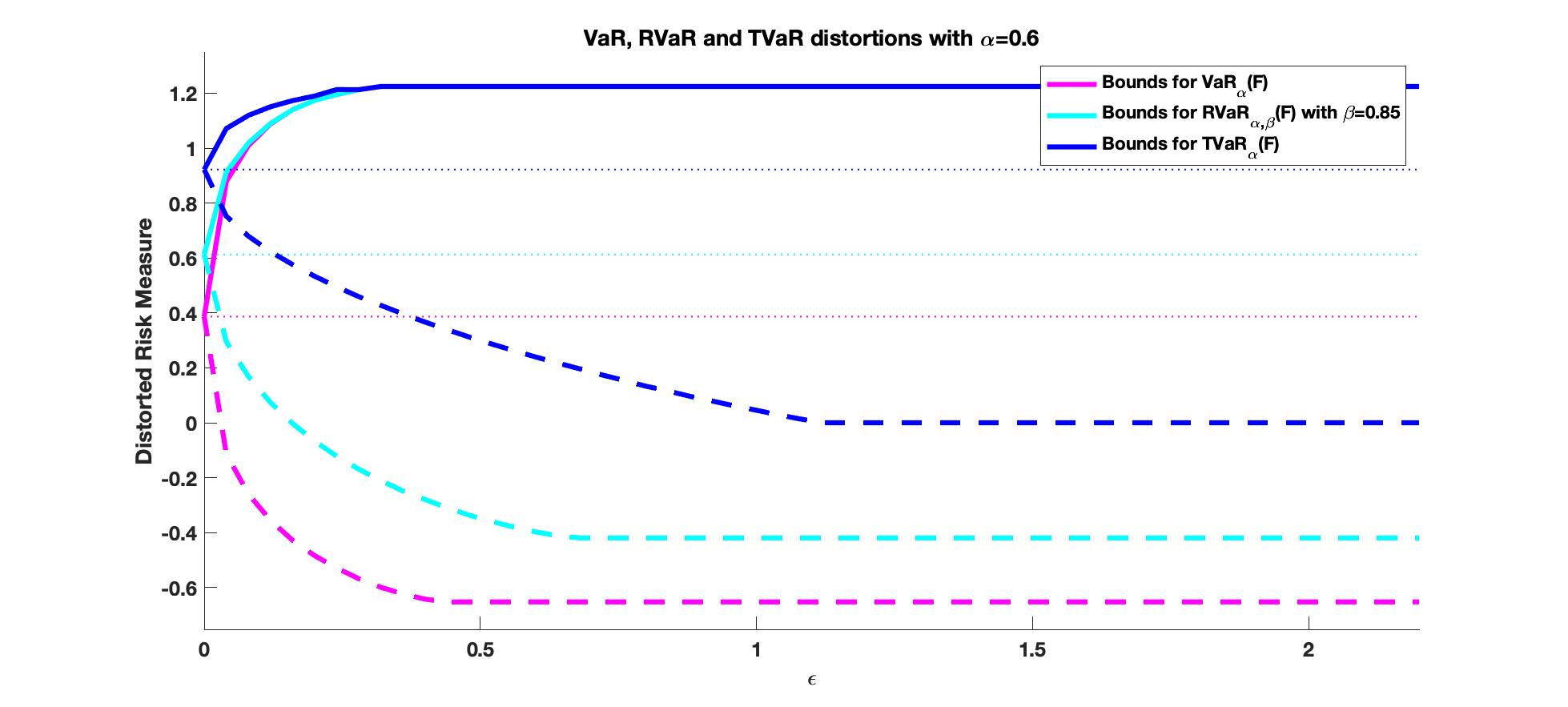

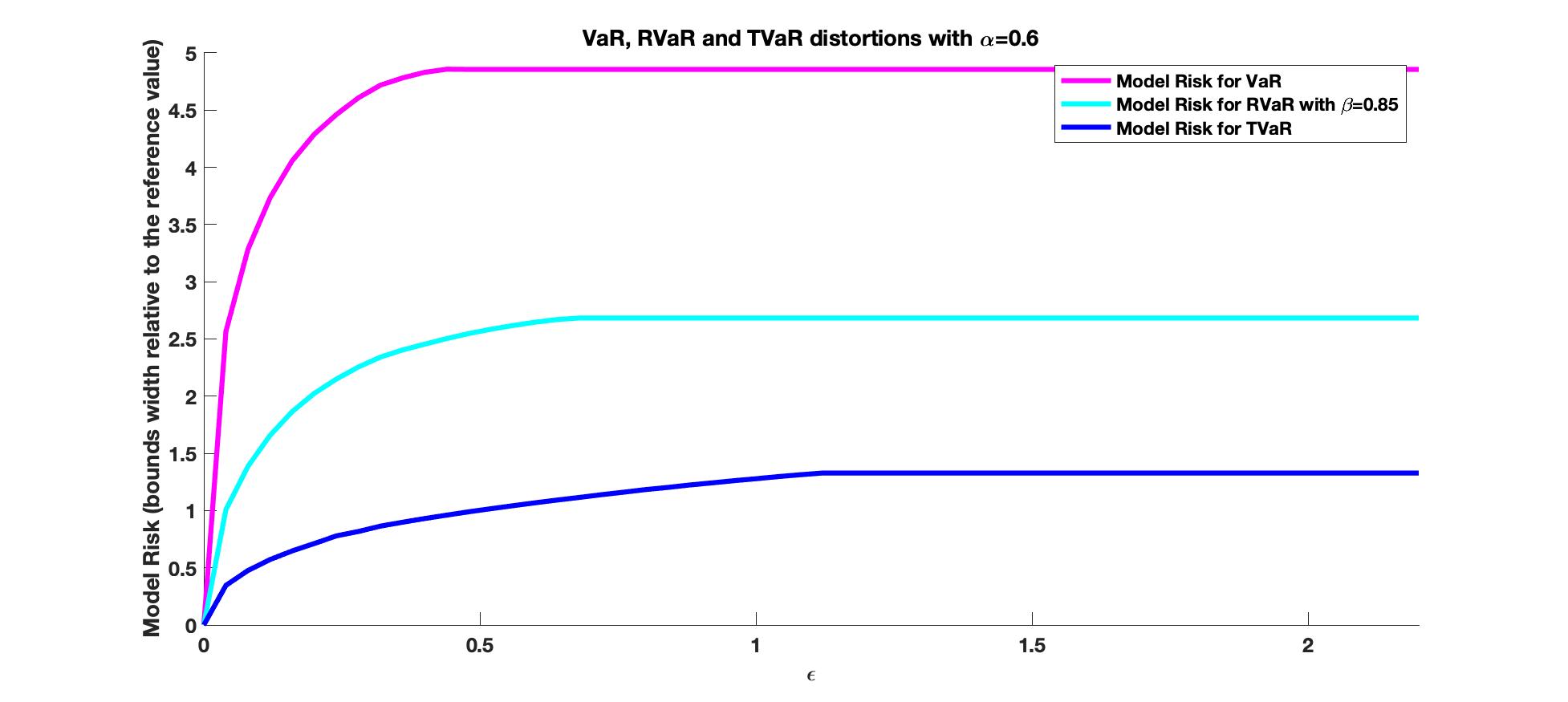

The left plot of Figure 5 displays the lower and upper bounds on , , and as a function of the Wasserstein distance . When is sufficiently large (case 2. in Theorems 3.6 and 3.10), the Wasserstein distance no longer affects the bounds; these bounds coincide with the well-known Cantelli bounds. The normalised lengths of the bounds on , , and as a function of are displayed in the right plot of Figure 5. The normalised length of the bounds are the differences between (5b) and (5a) divided by the risk measure evaluated at the reference distribution and have been introduced to assess model risk by Barrieu and Scandolo (2015). The length of the bounds on , for example, is .

|

|

We observe that the normalised length of the bounds on all three risk measures increases with respect to . Moreover, the normalised length of the VaR bounds is significantly larger than in the case of TVaR, a fact that is well-known for the case when (Embrechts et al. 2015).

4.2 Robustness to Moment Uncertainty

In practical applications, the mean and variance of loss distributions may themselves be prone to uncertainty, e.g., when estimated jointly, see Delage and Ye (2010). When uncertainty in the mean is prevalent, (5a) and (5b) should be considered with uncertainty set , where specifies the range of ambiguity on and . Proposition 4.8 provides the worst-case values when and are prone to marginal and elliptical uncertainty. Extensions to best-case values follow in a similar fashion and are omitted.

Consider the following cases

-

1.

(marginal) .

-

2.

(circlic) .

-

3.

(elliptical) , with .

Proposition 4.8 (Upper Bounds with Moment Uncertainty)

Let be a distortion function and given by case 1. 2. or 3 defined above. If for all , it holds that , then

and its solution is given in Theorem 3.6, case 1., with and given by

-

1.

(marginal) If , then

-

2.

(circlic) We have

(18) where with , and takes on the smaller value whenever .

-

3.

(elliptical) We have

(19) where takes on the smaller value whenever .

If for all , it holds that , then the solution to is given in Theorem 3.6, case 2.

4.3 Wasserstein Uncertainty Set

In this section we consider worst-case concave distortion risk measures under complete moment uncertainty. Specifically, we consider an uncertainty set that contains all distribution functions that lie within an -Wasserstein ball around the reference distribution, i.e., without a first and second moment constraint. Thus, the optimisation problem becomes

| (20) |

where is the set of all distribution functions that lie within a -Wasserstein ball around the reference distribution .

Theorem 4.9 (Wasserstein Uncertainty)

Let Assumptions 2.1 and 2.2 be fulfilled. Further, let be a concave distortion function; then, the solution to problem (20) exists, is unique, and has quantile function given by

with

where , , and are given in Theorem 3.1 and denotes the unique positive solution to , which is explicitly given in Theorem 3.1. The corresponding worst-case value is

Note that if , then the mean and standard deviation of the worst-case distribution fulfil and (recall that ). Thus, the worst-case distribution when the uncertainty set is only characterised by a Wasserstein ball has a larger mean and standard deviation than the benchmark. Thus, the uncertainty set with fixed and results in a different worst-case distribution compared to the uncertainty set characterised solely by the Wasserstein distance.

5 Applications

The tolerance distance i.e., the degree of the uncertainty, should be adequately chosen. Pesenti and Jaimungal (2021) study optimal portfolio choice and assume that the investor is prepared to accept terminal wealth distributions that stay within an -Wasserstein ball around some benchmark distribution. In this case, the Wasserstein tolerance distance reflects the investor’s tolerance of deviating from the benchmark portfolio strategy and its value is thus driven by the investor’s risk preferences. In most applications, however, the uncertainty set is constructed to contain all “plausible” distributions, i.e., the uncertainty set should be large enough to contain with high probability the true data-generating distribution and at the same time small enough to exclude pathological distributions, which would incentivise overly conservative decisions (Esfahani and Kuhn (2018)). In these settings, the tolerance distance should be driven by data considerations rather than being exogenously specified. In this regard, in various (data) contexts and under various assumptions Wozabal (2014) chooses via cross-validation whereas Blanchet et al. (2022) choose such that the true distribution function lies with a given probability within a Wasserstein ball around the empirical reference distribution. Additionally, including expert opinion in constructing the uncertainty set may provide valuable information, particularly in the case of limited available data (Clemen and Winkler (1999)). In the applications hereafter we do not pursue the estimation of in great length, but rather provide some guidelines for choosing it.

5.1 Portfolio Optimisation

We consider a portfolio optimisation problem in which an investor aims to construct a robust portfolio among returns , , in which is a suitable polyhedral set. We denote the multivariate distribution function of by and assume that it is subject to uncertainty in that only its mean vector and covariance matrix are known. For each portfolio , we denote by the (unknown) distribution function of the aggregate portfolio loss having mean and variance . There is a benchmark model under which the investor assumes444This assumption is fulfilled, for instance, when an elliptical multivariate distribution function is taken as reference model for . that the aggregate portfolio loss has distribution function belonging to a location-scale family, i.e., there is a distribution function such that

Then, for fixed , the Wasserstein distance between and is given by

| (21) |

The investor now aims to find the portfolio that has the smallest risk – measured via a concave distortion risk measure – among all possible portfolios whose aggregate loss lie within a Wasserstein distance of the benchmark portfolio. Specifically, we consider the optimisation problem

| (22) |

where is the set of all -dimensional distribution functions with mean vector and covariance matrix , and where we allow the tolerance distance to depend on , i.e., , .

Proposition 5.1

Note that problem formulation (22) is general in that the tolerances may depend on the portfolio at hand. As a consequence, it is not always possible to obtain the minimum in (23) in explicit form, and numerical procedures may be required.

From (21), however, we observe that the Wasserstein distance scales linearly with the standard deviation of the portfolio loss. Hence, it appears natural to take the tolerance of the form555If historical asset returns are available the value of can be determined as follows: using the historical returns we estimate for a given portfolio , the empirical distribution of the portfolio loss, its standard deviation , and the Wasserstein distance between and the (discretised version of the) reference distribution . By doing so for a set of portfolios , one can estimate by }. This procedure in particular guarantees that for each portfolio its corresponding empirical distribution lies in the uncertainty set. for . The next result considers this case. Its proof follows from Proposition 5.1 via direct calculation and is omitted.

Corollary 5.2

In all cases of Corollary 5.2, the robust portfolio optimisation problem reduces to solving a second order cone program. Specifically, for , there is no ambiguity and the investor aims to obtain the optimal portfolio under the assumption that for each portfolio the portfolio (loss) has known quantile function The optimal choice is the portfolio666If an elliptical multivariate distribution function is taken as the reference model for , then is also an elliptical distribution. for which attains

where we recall that . When , the Wasserstein distance becomes irrelevant and the optimal portfolio problem reduces to the one considered in Li (2018), i.e., to

In this regard, implies that in the case of no ambiguity (), more emphasis is placed on the expected return component than in the case in which the Wasserstein distance constraint is irrelevant (.) Moreover, in this instance, the optimal terminal wealth has a quantile function that is linear in the (non-negative) weight function (see Corollary 3.3), and thus is bounded from below, a feature that might be considered as not very realistic. The cases deal with situations that are between these extreme scenarios. Observe that is increasing in on the interval taking value when , and value when As and thus the degree of ambiguity increases, less emphasis is placed on the expected return leading to optimal portfolios that become more conservative. Note that in all intermediate cases the optimal quantile function inherits structure of the reference quantile function (see Theorem 3.1).

5.2 Insurance Portfolio of Risks

This section illustrates the best- and worst-case values of VaR on a simulated portfolio of dependent risks, that could e.g., arise from insurance activities. We consider the Pareto-Clayton model that offers a flexible way of modelling portfolios with dependent risks, see Oakes (1989) and Albrecher et al. (2011) for applications in insurance and Dacorogna et al. (2016) and Bernard et al. (2018) for applications in finance. In the Pareto-Clayton model, the portfolio components are, given , independent and Exponentially distributed with parameter , that is drawn from a Gamma distribution, i.e., . The aggregate portfolio risk thus follows, conditionally on , a Gamma distribution. By Dubey (1970) Equations 1.1 and 1.3, the scaled aggregate portfolio risk is a Beta distribution of the second kind. Thus, the quantile function of the aggregate portfolio risk and the first five moments are explicitly given by

where denotes the Beta function and the quantile function of the Beta distribution with parameters and .

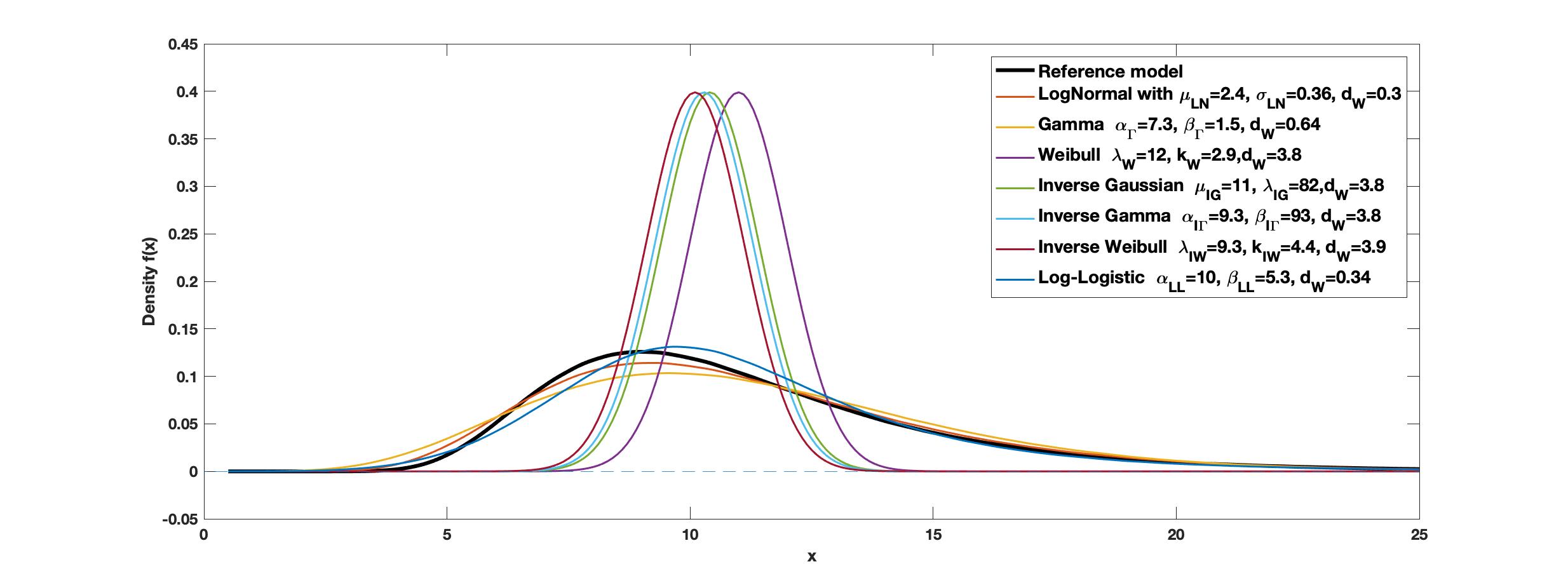

We consider the situation where modellers or experts may not fully agree on the reference Pareto-Clayton model, as available data or estimation may induce uncertainties or the distribution of might not seem appropriate. As alternative models for the distribution of the aggregate portfolio risk , we consider two-parameter distributions with support in that are commonly utilised for modelling insurance portfolios. Specifically, we consider a Lognormal model (LN), a Gamma model (), a Weibull model (W), an Inverse Gaussian model (IG), an Inverse Gamma model (I), an Inverse-Weibull model (IW), and a Log-Logistic model (LL). The different models are described in Table 2 and additional information is provided in Appendix 9. For the numerical simulations of the Pareto-Clayton model we use , , and , as in Bernard et al. (2018). The parameters of the alternative models, reported in Table 2, are obtained by matching the first two moments to those of the reference Pareto-Clayton model, i.e., and .

| Model | Abb. | Parameters | ||

|---|---|---|---|---|

| Lognormal model | LN | 0.298 | ||

| Gamma | 0.637 | |||

| Weibull | W | 3.787 | ||

| Inverse Gaussian | IG | 3.802 | ||

| Inverse Gamma | I | 3.792 | ||

| Inverse-Weibull | IW | 3.868 | ||

| Log-Logistic | LL | 0.345 | ||

We illustrate the reference Pareto-Clayton model (solid black) and the alternative models in Figure 6 via their densities. It is apparent that the considered alternative models can be grouped into light-tailed models (W, IG, I, IW) and heavy-tailed models (LN, , LL).

Next, we discuss the choice of Wasserstein distance by means of model uncertainty. Specifically, we let be the maximum of all Wasserstein distances between the reference and a selection of alternative models. The constructed Wasserstein ball then includes all distribution functions whose Wasserstein distance is smaller or equal to the maximum of all Wasserstein distances between the reference and the considered alternative models and, in particular, all considered alternative models. We report the Wasserstein distances between the Pareto-Clayton model and all alternative models in Table 2 and observe that the Wasserstein distances between the reference distribution and the alternatives from the heavy-tailed models are significantly smaller compared to the alternatives from the light-tailed models. This illustrates that model uncertainty is considered with respect to the reference distribution, which in our case is heavy-tailed. Thus, in a model uncertainty context, changing from the heavy-tailed reference model, i.e., Pareto-Clayton, to a light-tailed model, e.g., Weibull, entails a higher level of uncertainty compared to other models from the heavy-tailed family, e.g., Lognormal.

| Uncertainty Set | |||

|---|---|---|---|

| with | ( 12.8 ; 18.8 ) | ( 14.6 ; 22.8 ) | ( 19.0 ; 35.1 ) |

| with | ( 10.7 ; 21.6 ) | ( 12.1 ; 26.1 ) | ( 15.0 ; 41.5 ) |

| # of moments | ( 0.0 ; 111.1 ) | ( 0.0 ; 222.2 ) | ( 1.1 ; 1000 ) |

| # of moments | ( 9.7 ; 23.4 ) | ( 10.2 ; 29.0 ) | ( 10.7 ; 51.9 ) |

| # of moments | ( 10.1 ; 22.5 ) | ( 10.8 ; 26.2 ) | ( 11.7 ; 38.7 ) |

| # of moments | ( 10.1 ; 22.5 ) | ( 11.5 ; 25.6 ) | ( 15.1 ; 32.9 ) |

| # of moments | ( 10.1 ; 22.4 ) | ( 11.5 ; 25.5 ) | ( 15.1 ; 32.9 ) |

| , , unimodal | ( 9.9 ; 18.7 ) | ( 10.3 ; 22.6 ) | ( 10.7 ; 38.1 ) |

The best- and worst-case values of , for , for various uncertainty sets are report in Table 3. The values of of the Pareto-Clayton model are respectively , , and . The uncertainty sets we consider are with , , and . The tolerance corresponds to model uncertainty with respect to heavy-tailed alternative models (LN, , LL), whereas allows for alternative models that are light-tailed (W, IG, I, IW). To compare these bounds with results in the literature, we calculate the lower and upper bounds on VaR when only the first , , moments are known (Bernard et al. 2018). Note that the forth row in Table 3 () corresponds to , i.e., with Wasserstein tolerance . It is apparent that the bounds with a tolerance distance that contain the heavy-tailed alternative models () are significantly smaller than the ones corresponding to both heavy-tailed and light-tailed alternative models (. Furthermore, we report in the last row of Table 3 the bounds on VaR for an uncertainty set with fixed mean, bounded standard deviation, and where the uncertainty set further contains only unimodal distributions (Bernard et al. 2020). We observe in Table 3, that the Wasserstein constraint significantly reduces the bounds and that information on higher moments only affects the bounds in a minor way. Moreover, when only heavy-tailed models are considered as alternatives (, the length of the bounds is of the length when both light- and heavy-tailed are valid alternative models (.

6 Conclusion

We derive quasi explicit best- and worst-case values of a large class of distortion risk measures when the underlying loss distribution has a given mean and variance and lies within a -Wasserstein ball around a given reference distribution. We find that for small Wasserstein tolerance distances the worst-case distribution function (the distribution function attaining the worst-case value) is probabilistically close to the reference distribution, whereas for large tolerance distances, the worst-case distribution function is no longer affected by the reference distribution. We also derive the worst-case distribution function for VaR and RVaR and show that for small Wasserstein tolerance distances, the worst-case distribution functions of VaR and TVaR are no longer two-point distributions, thus making the bounds attractive for risk management applications.

Our results generalise findings in Li (2018) and Zhu and Shao (2018), which correspond to a Wasserstein tolerance of . Furthermore, we illustrate the risk bounds on two applications, to portfolio optimisation and to model risk assessment of an insurance portfolio.

7 Isotonic Projection.

Here, we collect properties of the metric projection defined in (9). For this, we denote by the space of square-integrable functions on and consider the following metric projection from to (set defined by (8)):

A metric projection is called isotone if the projection preserves the order induced by (Németh 2003). The partial order on induced by is given, for any , by

Proposition 7.1 (Theorem 3. Németh (2003))

The metric projection is isotone and subadditive; that is, fulfils for all :

-

1.

Isotone: If , then .

-

2.

Subadditive: .

In this paper, we compare only projections of functions of the type , for fixed and . Thus, we view the projection of as a function of and define , .

Proposition 7.2

For fixed and , the metric projection is an isotonic projection with the following properties:

-

1.

Isotone: For , it holds that .

-

2.

Continuous: If , then

Proof 7.3

The next proposition collects a few properties of the isotonic projection and thus of . These properties follow from (Brunk 1965, Theorem 2.2. and Corollary 2.3) and we provide short proofs adapted to our setting. For this we denote by the inner product on – that is, , for .

Proposition 7.4

The isotonic projection satisfies the following properties for all and :

-

1.

;

-

2.

;

-

3.

.

Proof 7.5

Proof of Proposition 7.4. We follow the arguments of the proof of Theorem 1.3.2 by Barlow et al. (1972).

Property 1. For , , and define the function . By definition of the isotonic projection it holds that . Next, we consider the function

which obtains its minimum in , by definition of the isotonic projection of . The first order condition at , implies that

Property 2. By the definition of an isotonic projection, it holds that for all . Choosing with , we obtain

Thus, for and the above inequality becomes

Taking limits with and concludes the statement of the property.

Property 3. For and , we obtain, by first applying property 2. and then property 1.

8 Proofs.

We denote by the corresponding set of quantile functions in . Further, we denote .

Lemma 8.1

If , then

Proof 8.2

8.1 Proof of Theorem 3.1 and Corollary 3.3.

For the proof of Theorem 3.1 we need the following lemmas.

Lemma 8.3

Let , and be non-decreasing; then

has a unique solution given by

| (24) |

where and . Moreover, is continuous in , for .

Proof 8.4

Lemma 8.5

Proof 8.6

Proof of Lemma 8.5. Let defined in (24). Solving for such that amounts to solving

| (27) |

Using the expression of in (26), Equation (27) is simply

| (28) |

which ensures that . Using the expression of ,

Rearranging, we obtain

| (29) |

Next, denote by and , then the expression of becomes and the square of Equation (29) becomes

This is a second degree equation in , which can also be written as

| (30) |

| (31) |

Observe that if , then as the covariance between two comonotonic variables. by definition of as a covariance between two variables with respective variances and and that are not perfectly correlated, and , by definition of as a covariance between two variables with respective variances and . Thus, from the expression (31) we have that . As a consequence, (30) then has two roots, of which only one, , is positive. \Halmos

Proof 8.7

Proof of Theorem 3.1. For concave distortion risk measures, (5b) is equivalent to

| (32) |

where is non-decreasing. For , let denote the quantile function defined in (24). The Wasserstein distance between and is given by

where . Note that by Lemma 8.3 is continuous with and .

Case 1. Let . We split this part into three steps. First, we show that the optimal quantile function has to be of the form for some . Second, we show that the solution lies at the boundary of the Wasserstein ball. Third, we show uniqueness.

For the first step, let be a solution to problem (32) with and . Then, by continuity of , there exists and a corresponding such that . Moreover, it holds that

Applying Lemma 8.3, we obtain ; thus, improves upon and we conclude the first step.

For the second step, let be such that satisfies . By construction, it holds that

| (33) |

Furthermore, by Lemma 8.3 we have that , which, together with (33), implies

Therefore, we obtain that and hence that the solution lies at the boundary of the Wasserstein ball. Uniqueness follows from the uniqueness of as the solution of Lemma 8.3. The worst-case value is

The explicit expression for then follows from Lemma 8.5 and is given in (25).

Case 2. Let ; then and thus is admissible. Moreover, it is straightforward that for all , . Hence, solves problem (32). \Halmos

8.2 Proof of Theorem 3.6 and Corollary 3.8.

The following lemma is needed to prove Theorem 3.6.

Lemma 8.9

Let and be a distortion function with weight function . Then

has a unique solution given by

| (34) |

where and , and is given in (9). Moreover, is continuous in , for .

Proof 8.10

Proof of Lemma 8.9. For , note that the isotonic projection is non-constant, which implies that , as defined in (34), fulfils . Let ; then is a non-decreasing function. Moreover, it holds that . Thus, the following inequalities are equivalent:

Note that unless the inequalities are strict, which implies uniqueness of the solution. Finally, continuity of follows from continuity of the isotonic projection , property 2. in Proposition 7.2. \Halmos

Proof 8.11

Proof of Theorem 3.6. For , define as in (34) and note that . The Wasserstein distance between and is given by (see also Theorem 3.1) , where . By Lemma 8.9, is continuous in , with .

Case 1. Let . Similar to the proof of Theorem 3.1, we split the proof into three steps: first, the worst-case quantile function is of the form , second, the solution lies at the boundary of the Wasserstein ball, and third we show that it is unique. The first two steps follow along the lines of the proof of Theorem 3.1 case 1., replacing with and using in the second step the properties of the isotonic projection . Uniqueness follows from the uniqueness of as the solution to (8.9) in Lemma 8.9.

Case 2. If and is not constant, then Lemma 8.9 applies for all . Let be as defined in (34) with . Then . Moreover, for all it holds, applying Lemma 8.9 with , that . Hence, cannot be improved and thus yields the unique optimal solution.

If is constant, then we find that for all , , where the first inequality follows from the properties of the isotonic projection (Proposition 7.4, property 3.) and the equality follows from the fact that as (applying Proposition 7.4, property 3. with and ). Finally, we show that is indeed the supremum. Consider the case in which and define , for , and where is a non-negative non-decreasing function such that and . Hence, , for . Moreover, for every that are sufficiently small, there exists such that

For the proof is similar and is omitted. \Halmos

Proof 8.12

Proof of Corollary 3.8. Corollary 3.8 follows from Theorem 3.6. We prove only that equation (11) (when is not constant) is equivalent to the worst-case value in Theorem 3.6 (case 2.). From the characterisation of the isotonic projection - that is, applying Property 3. of Proposition 7.4 with - we obtain that ; thus, . Further, by Property 2. of Proposition 7.4, it holds that . Hence,

8.3 Proof of Theorem 3.10.

The following lemma is needed for the proof of Theorem 3.10.

Lemma 8.13

Let and be a distortion function. Then

has a unique solution given by

| (35) |

where and , and is given in (12). Moreover, is continuous in , for .

Proof 8.14

Proof of Lemma 8.13. For , note that is not constant and that , as defined in (35), fulfils . Let ; then is a non-increasing function. Moreover, it holds that . Thus, the following inequalities are equivalent:

Note that unless the inequalities are strict, which implies that the solution is unique. Finally, continuity of follows from continuity of the isotonic projection ; that is, Proposition 7.2, property 2. \Halmos

8.4 Proofs of Corollaries 4.1 & 4.2 and Propositions 4.3 & 4.4.

Proof 8.16

Proof of Corollary 4.1. These results are well-known and we provide here a proof using the statements derived in this paper. First, we prove the worst-case value of the TVaR. Recall that its weight function is non-decreasing and, hence, for all . Applying Corollary 3.8 we obtain and therefore

Next, we calculate the worst-case value of with weight function . To apply Corollary 3.8, we first derive the isotonic projection of . Using similar arguments as in the proof of Proposition 4.3 below, we find that the isotonic projection of is equal to on and constant on , on which it takes the value , which must be such that . Hence, , and the worst-case equals that of . Consider the right-continuous quantile function taking the value on , and the value on , and observe that it has mean and standard deviation . As it follows that

Finally, assume that , for some . One can easily construct a left-continuous quantile function having mean and standard deviation , such that . Hence,

Proof 8.17

Proof of Corollary 4.2. The results for the case of , and follow from Remark 3.12 and Corollary 3.8 in a straightforward manner.

For the lower bound on , observe that the isotonic projection of is constant, and thus that , as (applying Proposition 7.4, property 3. with and ). Hence,

Proof 8.18

Proof of Proposition 4.3. By Theorem 3.6 case 1., we have to calculate the isotonic projection of onto the space of non-decreasing functions. According to Lemma 5.1 in Brighi and Chipot (1994), the isotonic projection has the form

| (36) |

where is a countable index set, and , , are disjoint intervals, and for any , denotes the complement of the set .

We first show that contains only one element. For this, let be an optimal solution with representation given by (36). By definition minimises over all non-decreasing functions . Moreover,

| (37) |

Case 1: If , then the summand in (37) can be improved by choosing , for all , and where denotes the right endpoint of .

Case 2: If , then the summand in (37) can be improved by setting on , and where denotes the right endpoint of . Therefore, and the isotonic projection is constant on one interval , with . Define , . Then, crosses at and, moreover, crosses when , provided the jump is not too large. More precisely, for a given , and satisfy

Proof 8.19

Proof 8.20

Proof of Corollary 4.5. For the worst-case value, let denote the quantile function given in Proposition 4.3 with , , and . Direct calculations show that indeed attains the supremum given in Corollary 3.2. For the best-case value, recall that and that is an increasing function in . Thus, by Theorem 3.10

| (38) |

where , , and is given in Proposition 4.4. Tedious calculations show that the limit in (38) exists and is equal to , where has a quantile function given in Proposition 4.4 with . \Halmos

Proof 8.21

Proof of Proposition 4.6.

We first consider the worst-case of and second that of .

To show the worst-case value of we split the proof into three steps.

Step 1: We show that for any and the unique quantile function attaining

| (39) |

is given by

| (40) |

where and are the unique solutions to

First, we show that the solution to (39), denoted here by , lies at the boundary of the Wasserstein ball, i.e., . Assume by contradiction that lies in the interior of the Wasserstein ball; then there exists a such that and , which is a contradiction to the optimality of the solution. Next, we show that the optimal solution to (39) has to be of the form (40). For this, assume that is a solution with . By non-decreasingness of it holds that , for all . Thus, the Wasserstein distance has a lower bound given by

which is a contradiction to the fact that the optimal solution lies at the boundary of the Wasserstein ball. Uniqueness of the solution follows from the uniqueness of and .

Step 2: Denote by , , and the unique parameters such that has mean , variance , and Wasserstein distance . These indeed exist as the three equations for the optimal , , and are not linearly dependent. Next, we claim that is the solution to our problem:

| (41) |

To show this, note that problem (41) is equivalent to

| (42) |

Indeed, a quantile function is admissible to (41) if and only if it is admissible to (42). This is because and have the same mean and variance, which implies that if and only if if and only if if and only if . However, is the unique solution to (42) (because it solves (39) with , , and ). Hence, cannot be a solution to (41) unless it coincides with .

Step 3: Finally, we can verify that coincides with the solution as stated in the statements of the corollary. For this, note first that both and are affine functions of , and we only need to show that for every there exist such that Let us first consider the case in which is close to one. First, assume that is constant on , where , then we take . By increasing we can bring arbitrarily close to on and will coincide with on as well as on Second, assume that is not constant on the right of , then for any close to we can find such that will coincide with on as well as on Hence, for any value of close to 1, it is possible to specify such that When , we can take , i.e., and By continuity of it thus follows that for all there exist such that

Next,we consider the worst-case . Clearly, the worst-case values of and are equal. The worst-case value of , however, is not attained. To see this, assume by contradiction that the worst-case is attained by . Then, there exists such that , for all . This, however, implies that , where attains the worst-case .

The proof of the best-case values of and follows similar steps to the worst-case values. Note that the best-case is attained while the best-case is not. \Halmos

8.5 Proof of Proposition 4.8.

Lemma 8.22

Proof 8.23

Proof of Lemma 8.22. We only prove the case . By Theorem 3.6 it holds that

| (43) |

As the isotonic projection does not depend on nor , the supremum in (43) can be taken over . For the three different cases of as defined in Proposition 4.8, and since , we have:

-

1.

If , then the maximum is attained at otherwise at .

-

2.

This case follows from case 3 with .

-

3.

If , is the negative root of the ellipse. Thus, optimisation (43) is equivalent to, replacing from the formula of the ellipse,

Taking the derivative with respect to , the maximum fulfils

Thus, and .

If , is the positive root of the ellipse and the proof follows similar steps.

Proof 8.24

Proof of Proposition 4.8. Let be one of the cases in Proposition 4.8. For , define the quantile function , , where and are unique and such that , and , are given in Proposition 4.8. The Wasserstein distance between and is , where . The remainder of the poof follows along the arguments of the proof of Theorem 3.6. \Halmos

8.6 Proof of Theorem 4.9.

Proof 8.26

Proof 8.27

Proof of Theorem 4.9. By Lemma 8.25 we only have to solve

We can rewrite as follows, using the expression of in (25):

where can be simplified as using (25) and (29). Thus,

Furthermore, recall that and that since is the covariance between two comonotonic variables in (28). We therefore obtain that

Observe that from the expression of in (26), , we have

Thus, when differentiating with respect to interpreted as a function of , we obtain

| (44) |

and when differentiating with respect to , we obtain

| (45) |

To solve , we first use that and then square the equation we aim to solve. There are two roots for characterised by But only one solves the original equation (45), which is given by

| (46) |

which then corresponds to . From the fact that in (45), we have that

Replacing this expression in (44), we find that is equivalent to . Using the expression of in (46), this gives which can be solved explicitly and has a unique root:

Recall the equation which can be simplified to the unique point

in which . Next, we verify that the Hessian matrix is negative-definite at this point (negative diagonal coefficients and positive determinant), which ensures that it is a global maximum.

In fact, the Hessian matrix at any point can be written as

where . Evaluating this Hessian matrix at , it can be simplified to

The diagonal coefficients are clearly negative and the determinant

is positive, which ensures that is locally concave at , which completes the proof. \Halmos

Proof 8.28

Proof of Proposition 5.1.

The general projection property (Theorem 1) in Popescu (2007) shows that for every portfolio and every distribution function having mean and variance there exists a multivariate distribution function such that the portfolio loss is distributed with As a consequence, optimisation (22) is equivalent to

| (47) |

where denotes the set of univariate distributions with mean and standard deviation . Applying Theorem 3.1 yields that (47) is equivalent to the minimisation problem

| (48) |

in which777Note that when , i.e., when , it follows that and thus that . with , , and , where we used equation (29) to obtain the expression for . Note that , where . Then, minimisation (48) becomes

which reduces to

Substituting and noting that concludes the proof. \Halmos

9 Application to a Portfolio of Risks

Here we collect the models used in Section 5.2. We provide the first two moments, which are used to calculate the models’ parameters by matching the first two moments to those of the reference Pareto-Clayton model.

-

1.

Lognormal Model (LN): We write as , where is a normally distributed random variable with mean and variance . The first two moments of are and .

-

2.

Gamma model (): The portfolio loss is Gamma distributed with parameters , , , and density , , where denotes the Gamma function.

-

3.

Weibull model (W): The portfolio loss follows a Weibull distribution with parameters , distribution function , , , and .

-

4.

Inverse Gaussian model (IG): The distribution of is Inverse Gaussian with parameters , distribution function , , , and .

-

5.

Inverse Gamma model (I): The portfolio loss follows a Inverse Gamma distribution with parameters , density function , , , and .

-

6.

Inverse Weibull model (IW): The distribution function of is Inverse Weibull with parameters and density , , , and .

-

7.

Log-Logistic Model (LL): The portfolio loss follows a Log-Logistic distribution with parameters , quantile function , , , and .

S. Pesenti acknowledges the support of the Natural Sciences and Engineering Research Council of Canada (NSERC) with funding reference numbers DGECR-2020-00333 and RGPIN-2020-04289. C. Bernard and S. Vanduffel acknowledge funding from FWO (FWOODYSS11).

References

- Acerbi (2002) Acerbi C (2002) Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking & Finance 26(7):1505–1518.

- Albrecher et al. (2011) Albrecher H, Constantinescu C, Loisel S (2011) Explicit ruin formulas for models with dependence among risks. Insurance: Mathematics and Economics 48(2):265–270.

- Artzner et al. (1999) Artzner P, Delbaen F, Eber JM, Heath D (1999) Coherent measures of risk. Mathematical Finance 9(3):203–228.

- Barlow et al. (1972) Barlow RE, Bartholomew D, Bremner JM, Brunk HD (1972) Statistical inference under order restrictions: the theory and application of isotonic regression (Wiley).

- Barrieu and Scandolo (2015) Barrieu P, Scandolo G (2015) Assessing financial model risk. European Journal of Operational Research 242(2):546–556.

- Bartl et al. (2020) Bartl D, Drapeau S, Tangpi L (2020) Computational aspects of robust optimized certainty equivalents and option pricing. Mathematical Finance 30(1):287–309.

- BCBS (2013) BCBS (2013) Consultative Document October 2013. Fundamental review of the trading book: A revised market risk framework. Technical report, Basel Committee on Banking Supervision, Bank for International Settlements.

- Bernard et al. (2018) Bernard C, Denuit M, Vanduffel S (2018) Measuring portfolio risk under partial dependence information. Journal of Risk and Insurance 85(3):843–863.

- Bernard et al. (2020) Bernard C, Kazzi R, Vanduffel S (2020) Range Value-at-Risk bounds for unimodal distributions under partial information. Insurance: Mathematics and Economics 94(1):9–24.

- Bernard et al. (2017) Bernard C, Rüschendorf L, Vanduffel S, Wang R (2017) Risk bounds for factor models. Finance and Stochastics 21(3):631–659.

- Blanchet et al. (2022) Blanchet J, Chen L, Zhou XY (2022) Distributionally robust mean-variance portfolio selection with Wasserstein distances. Management Science 68(9):6382–6410.

- Blanchet and Murthy (2019) Blanchet J, Murthy K (2019) Quantifying distributional model risk via optimal transport. Mathematics of Operations Research 44(2):565–600.

- Brighi and Chipot (1994) Brighi B, Chipot M (1994) Approximated convex envelope of a function. SIAM Journal on Numerical Analysis 31(1):128–148.

- Brunk (1965) Brunk H (1965) Conditional expectation given a -lattice and applications. The Annals of Mathematical Statistics 36(5):1339–1350.

- Cai et al. (2020) Cai J, Li J, Mao T (2020) Distributionally robust optimization under distorted expectations. Available at SSRN 3566708.

- Chen and Xie (2021) Chen Z, Xie W (2021) Sharing the Value-at-Risk under distributional ambiguity. Mathematical Finance 31(1):531–559.

- Clemen and Winkler (1999) Clemen RT, Winkler RL (1999) Combining probability distributions from experts in risk analysis. Risk Analysis 19(2):187–203.

- Cont et al. (2010) Cont R, Deguest R, Scandolo G (2010) Robustness and sensitivity analysis of risk measurement procedures. Quantitative Finance 10(6):593–606.

- Cornilly et al. (2018) Cornilly D, Rüschendorf L, Vanduffel S (2018) Upper bounds for strictly concave distortion risk measures on moment spaces. Insurance: Mathematics and Economics 82:141–151.

- Dacorogna et al. (2016) Dacorogna MM, Elbahtouri L, Kratz M (2016) Explicit diversification benefit for dependent risks. SCOR papers 38(1).

- Dall’Aglio (1956) Dall’Aglio G (1956) Sugli estremi dei momenti delle funzioni di ripartizione doppia. Annali della Scuola Normale Superiore di Pisa-Classe di Scienze 10(1-2):35–74.

- De Schepper and Heijnen (2010) De Schepper A, Heijnen B (2010) How to estimate the Value at Risk under incomplete information. Journal of Computational and Applied Mathematics 233(9):2213–2226.

- Delage and Ye (2010) Delage E, Ye Y (2010) Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations Research 58(3):595–612.

- Denuit et al. (1999) Denuit M, Genest C, Marceau É (1999) Stochastic bounds on sums of dependent risks. Insurance: Mathematics and Economics 25(1):85–104.

- Dhaene et al. (2012) Dhaene J, Kukush A, Linders D, Tang Q (2012) Remarks on quantiles and distortion risk measures. European Actuarial Journal 2(2):319–328.

- Dubey (1970) Dubey SD (1970) Compound gamma, beta and F distributions. Metrika 16(1):27–31.

- EIOPA (2009) EIOPA (2009) Directive 2009/138/ec of the European parliament and of the council. Technical report, European Insurance and Occupational Pensions Authority.

- Embrechts and Puccetti (2006) Embrechts P, Puccetti G (2006) Bounds for functions of dependent risks. Finance and Stochastics 10(3):341–352.

- Embrechts et al. (2013) Embrechts P, Puccetti G, Rüschendorf L (2013) Model uncertainty and VaR aggregation. Journal of Banking & Finance 37(8):2750–2764.

- Embrechts et al. (2015) Embrechts P, Wang B, Wang R (2015) Aggregation-robustness and model uncertainty of regulatory risk measures. Finance and Stochastics 19(4):763–790.

- Esfahani and Kuhn (2018) Esfahani PM, Kuhn D (2018) Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming 171(1-2):115–166.

- Glasserman and Xu (2014) Glasserman P, Xu X (2014) Robust risk measurement and model risk. Quantitative Finance 14(1):29–58.

- Grundy (1991) Grundy BD (1991) Option prices and the underlying asset’s return distribution. The Journal of Finance 46(3):1045–1069.

- Hürlimann (2002) Hürlimann W (2002) Analytical bounds for two Value-at-Risk functionals. ASTIN Bulletin 32(2):235–265.

- Hürlimann (2005) Hürlimann W (2005) Improved analytical bounds for gambler’s ruin probabilities. Methodology and Computing in Applied Probability 7(1):79–95.

- Kaas and Goovaerts (1986) Kaas R, Goovaerts MJ (1986) Best bounds for positive distributions with fixed moments. Insurance: Mathematics and Economics 5(1):87–92.

- Kou et al. (2013) Kou S, Peng X, Heyde CC (2013) External risk measures and Basel accords. Mathematics of Operations Research 38(3):393–417.

- Kusuoka (2001) Kusuoka S (2001) On law invariant coherent risk measures, volume 3 (Springer).

- Lam (2016) Lam H (2016) Robust sensitivity analysis for stochastic systems. Mathematics of Operations Research 41(4):1248–1275.

- Li (2018) Li JYM (2018) Closed-form solutions for worst-case law invariant risk measures with application to robust portfolio optimization. Operations Research 66(6):1533–1541.

- Li et al. (2018) Li L, Shao H, Wang R, Yang J (2018) Worst-case range Value-at-Risk with partial information. SIAM Journal on Financial Mathematics 9(1):190–218.

- Lo (1987) Lo AW (1987) Semi-parametric upper bounds for option prices and expected payoffs. Journal of Financial Economics 19(2):373–387.

- Lux and Rüschendorf (2019) Lux T, Rüschendorf L (2019) Value-at-Risk bounds with two-sided dependence information. Mathematical Finance 29(3):967–1000.

- Natarajan et al. (2010) Natarajan K, Sim M, Uichanco J (2010) Tractable robust expected utility and risk models for portfolio optimization. Mathematical Finance 20(4):695–731.

- Németh (2003) Németh A (2003) Characterization of a Hilbert vector lattice by the metric projection onto its positive cone. Journal of Approximation Theory 123(2):295–299.

- Oakes (1989) Oakes D (1989) Bivariate survival models induced by frailties. Journal of the American Statistical Association 84(406):487–493.

- Pesenti (2022) Pesenti SM (2022) Reverse sensitivity analysis for risk modelling. Risks 10(141).

- Pesenti and Jaimungal (2021) Pesenti SM, Jaimungal S (2021) Portfolio optimisation within a Wasserstein ball. Available at SSRN 3744994.

- Pesenti et al. (2016) Pesenti SM, Millossovich P, Tsanakas A (2016) Robustness regions for measures of risk aggregation. Dependence Modeling 4(1):348–367.

- Pesenti et al. (2020) Pesenti SM, Wang Q, Wang R (2020) Optimizing distortion riskmetrics with distributional uncertainty. Available at SSRN 3728638.

- Pflug and Wozabal (2007) Pflug G, Wozabal D (2007) Ambiguity in portfolio selection. Quantitative Finance 7(4):435–442.

- Popescu (2007) Popescu I (2007) Robust mean-covariance solutions for stochastic optimization. Operations Research 55(1):98–112.

- Villani (2008) Villani C (2008) Optimal transport: Old and new, volume 338 (Springer Science & Business Media).

- Wang and Wang (2011) Wang B, Wang R (2011) The complete mixability and convex minimization problems with monotone marginal densities. Journal of Multivariate Analysis 102(10):1344–1360.

- Wang et al. (2020) Wang Q, Wang R, Wei Y (2020) Distortion riskmetrics on general spaces. ASTIN Bulletin 50(3):827–851.

- Wang et al. (2019) Wang R, Xu ZQ, Zhou XY (2019) Dual utilities on risk aggregation under dependence uncertainty. Finance and Stochastics 23(4):1025–1048.

- Wang (1996) Wang S (1996) Premium calculation by transforming the layer premium density. ASTIN Bulletin 26(1):71–92.

- Wozabal (2014) Wozabal D (2014) Robustifying convex risk measures for linear portfolios: A nonparametric approach. Operations Research 62(6):1302–1315.

- Zhu and Shao (2018) Zhu W, Shao H (2018) Closed-form solutions for extreme-case distortion risk measures and applications to robust portfolio management. Available at SSRN .