Frank-Wolfe Meets Metric Entropy

Abstract.

The Frank-Wolfe algorithm has seen a resurgence in popularity due to its ability to efficiently solve constrained optimization problems in machine learning and high-dimensional statistics. As such, there is much interest in establishing when the algorithm may possess a “linear” dimension-free iteration complexity comparable to projected gradient descent.

In this paper, we provide a general technique for establishing domain specific and easy-to-estimate lower bounds for Frank-Wolfe and its variants using the metric entropy of the domain. Most notably, we show that a dimension-free linear upper bound must fail not only in the worst case, but in the average case: for a Gaussian or spherical random polytope in with vertices, Frank-Wolfe requires up to iterations to achieve a error bound, with high probability. We also establish this phenomenon for the nuclear norm ball.

The link with metric entropy also has interesting positive implications for conditional gradient algorithms in statistics, such as gradient boosting and matching pursuit. In particular, we show that it is possible to extract fast-decaying upper bounds on the excess risk directly from an analysis of the underlying optimization procedure.

1. Introduction & Related Work

Constrained, high-dimensional convex optimization problems are ubiquitous in modern statistics and machine learning, and many promising approaches have emerged to solve them. In particular, for well-behaved objectives, the projected gradient descent algorithm of Beck and Teboulle (2009) has been shown to need only iterations to find an -aproximate solution (Bubeck, 2015). Unfortunately, it can require a costly “projection step” at each iteration, which is particularly expensive in high dimensional problems.

In contrast, conditional gradient algorithms such as Frank-Wolfe only require the solution of a linear program at each iteration, which is a major improvement when the ambient dimension is large (Frank and Wolfe, 1956; Jaggi, 2013). However, even for well-behaved objectives, the worst case dimension-free iteration complexity scales as . This has led to a search for algorithmic variants and high-level conditions that produce a “linear” iteration complexity, where the polyhedral geometry of the domain has played a major role.111See e.g. Garber and Hazan (2015, 2016); Lacoste-Julien and Jaggi (2015); Beck and Shtern (2017); Peña and Rodríguez (2019).

A noteworthy aspect of conditional gradient algorithms is that they produce solutions which are sparse: each iteration of the procedure yields a convex combination of at most atoms. This is true of all related algorithms known to the authors. Sparsity has made conditional gradient algorithms particularly useful in problems such as statistical estimation, signal recovery, and the construction of coresets (Li and Barron, 2000; Zhang, 2003; Zhang and Yu, 2005; Clarkson, 2010; Tropp, 2004).

It is therefore reasonable to expect that sparsity might place additional restrictions on the convergence rate, and this is the direction we pursue here.222It may be desirable to replace sparsity with the number of calls to a linear maximization oracle; we unfortunately do not know how to do this. However, since each call to a linear oracle will output a single atom, it would require some creativity to construct a solution using atoms from oracle queries. In fact, all existing lower bounds for Frank-Wolfe make essential use of sparsity (Jaggi, 2013; Garber and Hazan, 2016; Mirrokni et al., 2017; Lan, 2020). However, instead of constructing a single, hard instance, as in prior work,333All papers known to the authors construct a hard instance using the simplex. Mirrokni et al. (2017) also derive a sharper lower bound from a random polytope with vertices drawn from the hypercube. here we derive domain specific lower bounds that can be adapted to a wide variety of settings using geometric data.

At the core of the paper is a basic and well-known geometric idea: if every point in the domain can be approximated by a sparse set of atoms, then the metric entropy of cannot be too large. Running the argument in reverse, we see that if the metric entropy of is large then it takes many atoms—hence many conditional gradient iterations—to produce a good approximate solution.

This approach is simultaneously flexible enough to handle a wide variety of settings—and even to conduct an average case analysis—yet it is powerful enough to produce tight results: in particular, to show that in many real-world settings the best dimension-free guarantee possible is . We demonstrate this to be true for the -ball, for the nuclear norm ball, and for a spherical or Gaussian random polytope with a polynomial-in- number of vertices (with high probability). Moreover, these results each follow from a single, generic argument using basic information: the volume of a polytope and its number of vertices.

| Domain | Dimension | # Vertices | Lower Bound | Upper Bound |

| Random polytope | * | ? | ||

| Probability simplex | ||||

| Ball | ||||

| Nuclear-norm Ball | * | |||

| Ball | * | |||

| Strongly convex set |

1.1. Discussion of Results

Table 1 summarizes our results on lower bounds for Frank-Wolfe in various settings. In the first four examples, the best possible dimension-free rate is , and the upper and lower bounds match in the regime (or in the matrix case). In the fifth example (-ball), the same is true, but the bounds match in the regime , which is only relevant for extreme values of . The upper bounds are quoted from the works of Jaggi (2013), Garber and Hazan (2015), Garber and Hazan (2016), and Lacoste-Julien and Jaggi (2015).

Our results also highlight necessary conditions for accelerated dimension-free rates: the set of extreme points must be roughly “as complex” as the entire domain. This holds in particular for strictly convex sets, underscoring the open problem posed by Garber and Hazan (2015) of establishing or refuting linear convergence in strongly convex domains.

Finally, we show that improved dimension-free guarantees for Frank-Wolfe (or its variants) can be used to derive fast rates in dictionary aggregation problems. Most notably, we show that in the convex aggregation problem the distance of the risk minimizer to the boundary plays a role analogous to the “margin condition” in classification, allowing one to establish a fast rate of convergence in excess risk (Tsybakov, 2003; Lecué, 2007). Our argument is similar to Zhang and Yu (2005) in that it relies essentially on early stopping, but the outcome is quite novel.

2. Preliminaries

We now introduce the central objects studied in the paper.

Definition 1.

Given a subset of a Hilbert space , the -convex hull is given by

where denotes the probability simplex in . The regular (closed) convex hull is denoted .

This motivates our definition of a sparse programming algorithm, namely an optimization algorithm over whose outputs take values in .

Definition 2.

A -sparse programming algorithm is a function which, given access to a cost function and a set , outputs some . The set of all such functions is denoted

We do not restrict the computational complexity of the candidate function in any way, nor the manner in which it depends on and , as that is irrelevant for our results. By definition, the iterate of Frank-Wolfe and all of its usual variants comprises a -sparse programming algorithm—including the “away steps” and “fully corrective” variants, as well as the local oracle construction of Garber and Hazan (2016). Since we ignore all properties other than sparsity, the central quantity we study is the following.

Definition 3.

For a given error tolerance , the sparse programming complexity of a set , relative to a class of cost functions , is the smallest integer such that

We always consider the distance-squared cost functions

and suppress the subscript . Note that this class of cost functions is somewhat ideal in that all its elements are -smooth and -strongly convex. This serves to isolate the dependence of our lower bounds on the geometry of the domain alone.

The starting point of our work is the relation between the sparse programming complexity and the classical approximate Carathéodory problem in convex geometry, which aims to bound the following quantity.

Definition 4.

The compressibility of a set is given by

| (1) |

where denotes the unit ball in .

In other words, these numbers quantify how many points of are necessary to -approximate the convex hull. Since finding such that is equivalent to finding an -approximate minimizer of the cost function , which belongs to , we deduce the following.

Lemma 1.

For any , the compressibility satisfies

| (2) |

This relation was noted by Combettes and Pokutta (2021), who showed that modern convergence guarantees for Frank-Wolfe can be used to improve estimates on compressibility. In other words, a convergence guarantee for any sparse programming algorithm provides a deterministic proof of low compressibility.

In this work, we pursue a similar line of reasoning using a classical idea often attributed to Maurey that relates the compressibility to the metric entropy (Pisier, 1980). The metric entropy may be defined as follows.

Definition 5.

The covering number of a set with respect to a metric is defined as the smallest cardinality of a set such that

The metric entropy is the natural logarithm of the covering number, .

Unless otherwise indicated, we take to be the norm in and omit this argument. It is straightforward to show that the metric entropy of satisfies the following bound, which forms the basis for our results.

Lemma 2.

Let be a subset of the unit ball in . Then

| (3) |

We observe that if the compressibility satisfies , the metric entropy of cannot be much larger than that of . By (3), the metric entropy of is in turn only roughly times the metric entropy of .

Thus, a lower bound on the metric entropy of relative to that of can be translated into a domain-specific lower bound on the compressibility. By (2), we recover a lower bound on the sparse programming complexity. This is the essence of Proposition 1 and Theorem 3 below.

Remark 1.

Carathéodory’s theorem (Artstein-Avidan et al., 2015, Theorem A.1.3), a classical result in convex geometry, implies that for ,

Thus, the above argument cannot give a non-trivial lower bound on the iteration complexity that is larger than the ambient dimension, . It is therefore quite surprising that it recovers tight bounds on the iteration complexity of the form .

2.1. Notation

Throughout the paper, the notation will be used to denote an inequality that holds up to some universal positive constant, and will be used interchangeably with . Similarly, , , , etc. will denote a placeholder for a sufficiently large positive constant, which may not be the same across displays. A glossary of these and other notational conventions may be found in Appendix A.

3. Lower Bounds

In view of the above discussion, bounds on the metric entropy can be used to place restrictions on the convergence rate of any sparse programming algorithm. This section explores various applications of this observation, both for constructing general-purpose bounds and for studying specific examples. Omitted proofs are contained in Appendix B. We begin with the following result.

Proposition 1.

Let be a polytope in with vertices, of unit diameter, whose covering numbers are denoted Then, for any the sparse programming complexity for quadratic objectives over satisfies

Proof.

Without any loss of generality, we may assume that is a subset of the unit ball. Suppose that there exists a sparse programming algorithm which, for all , converges to within a tolerance of for the objective in fewer than iterations. Then, for each there exist vertices and with the property that

Now, let be a minimal covering of in at resolution , and let denote the projection of onto the nearest element of (breaking ties arbitrarily). It is straightforward to verify the following facts.

Lemma 3.

If with for all , and , then we have

| (4) |

Lemma 4.

The covering numbers of the probability simplex satisfy

| (5) |

By (4) and the triangle inequality, we have

Moreover, the total number of possible values taken by the expression

can be upper bounded as

where we use the estimate of given by (5). Thus,

Rearranging and noting that the choice of sparse programming algorithm was arbitrary, we deduce that

Noting that , the proof is complete. ∎

As a first illustration of our result, let’s consider the unit ball in , which we’ll denote by . Plugging in the number of vertices and a volumetric estimate of the covering number gives the following lower bound.

Example 1 ( ball).

Thus, when the dimension is comparable to the inverse error tolerance , the number of iterations required for any sparse programming algorithm is .

Proof.

The above example illustrates a general approach for constructing lower bounds for arbitrary polytopes by means of the volume argument.

Theorem 1.

Let be a polytope of diameter at most . Then

| (6) |

where is the ratio between and the volume of the unit Euclidean ball, .

Note that can be isometrically transformed to lie inside the unit ball, hence is at most . By restricting to the affine hull of we must have or else the bound is vacuous. Meanwhile, for the naive implementation of Frank-Wolfe to be tractable in moderate to high dimension, we must have , so the first summand of the denominator would be at most .

We show subsequently that a random polytope with vertices has , so our lower bound for the ball applies in the average case, up to constants. Thus, it appears that the “curse of dimensionality,” namely the necessity for iterations to achieve an error tolerance of order , is a somewhat generic phenomenon.

Remark 2.

In a hypothetical scenario where and , our result (6) would imply that iterations are required to achieve a constant error tolerance , which would contradict the known dimension-free iteration complexity of Frank-Wolfe (Jaggi, 2013, Theorem 1). This implies that any sequence of polytopes containing an fraction of their circumscribed spheres cannot have a polynomial-in- number of vertices.

Indeed, Maurey’s lemma (see Pisier (1980, Lemma 2)), which may be derived as a consequence of Frank-Wolfe (Mirrokni et al., 2017; Combettes and Pokutta, 2021), tells us that a polytope of unit diameter on vertices has entropy at most , while implies the entropy is at least (by the volume argument). Choosing verifies that .

We complete our study of finite polytopes with an average-case lower bound showing that the inequality satisfied by the ball is generically satisfied by a polytope with polynomially many vertices.

Theorem 2.

Let be points independently distributed according to the uniform measure on the sphere , with . Let denote their convex hull. Then there exists a universal such that if for some , it holds with probability that

Moreover, for any particular choice of , the two statements hold with probability at least .

Proof.

We will provide a proof for the spherical case stated above; the promised extension to Gaussian random polytopes is postponed to the Appendix C.6. The basis of the proof is a bound due to Dyer et al. (1992) and adapted to our context by Pivovarov (2007), who also gives an analogous result for the Gaussian case. While the full proof can be found in the referenced paper, a sketch of the argument is provided in Appendix C.4 for the reader’s convenience.

Lemma 5 (Pivovarov (2007, Lemma 2.12)).

Let denote the unit ball in , and suppose that . Then

| (7) |

where is the measure of the spherical cap of height , namely for a unit vector .

In order to complete the argument, we need a good lower bound on the quantity so that the probability bound in (7) converges to . Fortunately, we are able to show the following.

Lemma 6.

For all ,

The bound follows from a more general lower bound on the size of spherical caps (Proposition 4 in the appendix), which uses a coupling of the high-dimensional spherical and Gaussian distributions. Armed with this bound, we have

as long as for some large enough universal constant . Finally, we note that on the complimentary event, we have

which is what we aimed to show. On this event, we may lower bound the sparse programming complexity by plugging the above volume estimate into Theorem 1 with . Noting that , we find that

Since we have assumed , the extra terms in the denominator may be absorbed into an appropriate universal constant factor adjoining , yielding the result. ∎

Remark 3.

It is evident from the proof of Lemma 5 that the result can be extended to any independent random points each satisfying

for some , i.e. the vertices cannot be too concentrated near any linear subspace.

Large or infinite vertex sets

If the domain admits a more sophisticated linear programming oracle—for example, in cases where a self-concordant barrier can be efficiently computed—then it is possible to dispense with the requirement that , which improves the situation considerably.

As an example in which our lower bounds begin to fail, we consider the suitably normalized unit cube , and rescale the error tolerance accordingly.

Example 2 (Unit cube).

In particular, taking , we find that iterations are required to achieve an error tolerance of .

Remark 4.

Here, the number of iterations required to achieve a constant error tolerance is . This would seem to contradict an bound, but reflects the fact that the diameter of the domain—in this case —is hidden in the constant of the usual bound (see e.g. Jaggi (2013)).

In this case the dimension must be exponential in the number of iterations for an upper bound to be tight. For more reasonable values of and , the lower bound behaves like . We therefore cannot rule out an iteration complexity upper bound for conditional gradient on the cube, nor even for reasonable values of and .

This differs significantly from the best known upper bounds for conditional gradient procedures on the unit cube, which take the form (Lacoste-Julien and Jaggi, 2015; Garber and Hazan, 2016; Peña and Rodríguez, 2019). In fact, as we remarked in the introduction, the sparse programming complexity in dimension can never be greater than for any , by Carathéodory’s theorem.

These considerations extend naturally to other polytopes with exponentially many vertices that arise in combinatorial optimization such as matroid polytopes, flow polytopes, the Birkhoff polytope, and the -marginal polytope on an -clique.

Infinite vertex sets

It is also possible to consider optimization over convex sets for infinite sets , provided one replaces the cardinality with the covering number at scale . The proof follows along the same lines as Proposition 1, and is deferred to the Appendix C.7.

Theorem 3.

Let be a subset of the unit Euclidean ball. Then, for any the sparse programming complexity for quadratic objectives over satisfies

A nice application of Theorem 3 is given by the nuclear norm ball, which is another setting where Frank-Wolfe finds frequent use and where a sharp lower bound may be derived from the entropy calculation.

Example 3 (Nuclear norm ball).

Remark 5.

A corresponding linear rate for the nuclear norm ball cannot be derived from results known to the authors, since the set of extreme points is not discrete. Thus, sharpness of the lower bound remains unresolved.

Strictly convex sets

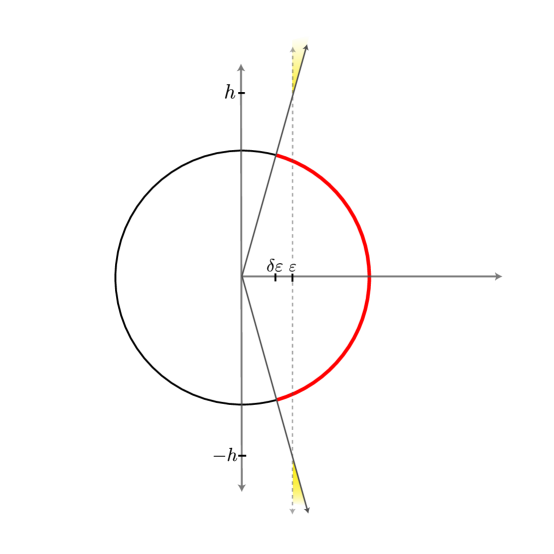

As the most extreme example in which our lower bound fails, let denote the boundary of a closed, strictly convex set . In this case, the entropy of and are equal up to constants and an additive factor , and our lower bound is at most constant, for any value of .

This underscores the open problem highlighted by Garber and Hazan (2015) of determining whether dimension-independent linear rates (or linear rates of any kind) are attainable for conditional gradient algorithms over strongly convex sets.

Lemma 7.

Let be a strictly convex subset of the unit ball, namely for some function which satisfies for , and let denote the boundary. Then

Proof.

Let be an arbitrary unit vector and put . Then, is a closed and bounded interval , and we can easily verify using strict convexity that . It follows that , since is a convex combination of and . The proof is then complete by applying Lemma 2. ∎

4. Stochastic Sparse Programming

In this section, we’ll show that it is possible to extract statistical guarantees simply by analyzing the convergence rate of a conditional gradient algorithm. This is done by appealing to the low complexity of the set of conditional gradient iterates.

For simplicity of exposition, we’ll illustrate this section’s results using the Gaussian sequence model. Let’s suppose we observe

where is a standard Gaussian in and is unknown. We will be interested in controlling the excess mean square error relative to some class , namely

We now state a bound that allows us to exploit the sparsity of Frank-Wolfe iterates as a form of regularization, although it applies to other forms of regularization as well.

Proposition 2.

Let be an -approximate minimizer of the empirical risk that takes values in , let be the minimizer of the true risk, and suppose that is convex. Then

| (8) |

Remark 6.

The utility of the above bound is that it is a sharp, localized bound, for example capable of recovering the oracle rates in sparse recovery, and yet it only depends on the local complexity of the approximating set and the approximation quality .

Suppose we would like to approximate using a finite, normalized dictionary,

To simplify computations, we assume . Let denote the error obtained by running a sparse programming algorithm for steps with the objective (the empirical risk), and note that the output of the procedure belongs to the linear span of at most elements of . Putting , we can compute that

| Note that the inner supremum is over a subset of a norm ball in a hyperplane of dimension , so it is -subgaussian (Lemma 11) with expectation at most . Thus we have | ||||

by the standard sub-Gaussian maximal inequality (Lemma 12). We obtain the following

Proposition 3.

Let denote the output of running a sparse programming algorithm for steps to minimize the empirical risk in some convex class , and let denote the optimization error. Then with probability at least ,

| (9) |

Convex Aggregation

If we take , it is straightforward to show that

which matches the minimax rate in the convex aggregation problem, attained by the exact empirical risk minimizer (Tsybakov, 2003). Now, if the empirical risk minimization problem is “well-conditioned” for Frank-Wolfe, so that with high probability

for some , then we may improve upon the minimax rate. For one concrete example, suppose belongs to the -relative interior of , for some . We can then appeal to the following result adapted from Garber and Hazan (2015).

Theorem 1.

Suppose belongs to the -relative interior of . Then the sub-optimality of the iterate of Frank-Wolfe for the objective satisfies

Applying the result to our context, we obtain the following rate. The crux of the proof is showing that under the same hypotheses, also belongs to the relative interior with high probability.

Corollary 1.

If belongs to the relative interior of for some , and for a sufficiently large universal constant , then we may choose and deduce that with probability

Remark 7.

Note that the radius of is , so values of are reasonable. Thus, the result reflects an unusual fast rate phenomenon that responds to the centrality of . One explanation for this (and Theorem 1) is that the volume of a high-dimensional polytope is generally concentrated at the boundary.

Remark 8.

It would be very interesting to design adaptive variants of the procedure considered in this section, using e.g. the duality gap. However, that is beyond the scope of our current work.

5. Conclusion

In this work, we have studied conditional gradient algorithms from the perspective that they output a convex (or linear) combination of at most atoms, where is the number of iterations. We establish that the set of outputs of any such procedure must has metric entropy bounded in terms of the number of iterations. If a convergence guarantee holds, this places restrictions on the entropy of the domain; we use this fact to derive domain-specific and sharp lower bounds in numerous settings of interest, as well as in canonical random domains with high probability. As a secondary application, we show that a dimension-free convergence rate which improves on the general bound can be used to establish fast rates in statistical estimation.

6. Acknowledgments

The author is generously supported by the MIT Jerry A. Hausman Graduate Dissertation Fellowship

References

- Adler et al. (2007) Robert J Adler, Jonathan E Taylor, et al. Random Fields and Geometry, volume 80. Springer, 2007.

- Artstein-Avidan et al. (2015) Shiri Artstein-Avidan, Apostolos Giannopoulos, and Vitali Milman. Asymptotic Geometric Analysis, Part I, volume 202 of Mathematical Surveys and Monographs. American Mathematical Society, June 2015. ISBN 978-1-4704-2193-9 978-1-4704-2345-2 978-1-4704-2346-9. doi: 10.1090/surv/202.

- Beck and Shtern (2017) Amir Beck and Shimrit Shtern. Linearly convergent away-step conditional gradient for non-strongly convex functions. Mathematical Programming, 164(1):1–27, July 2017. ISSN 1436-4646. doi: 10.1007/s10107-016-1069-4.

- Beck and Teboulle (2009) Amir Beck and Marc Teboulle. A Fast Iterative Shrinkage-Thresholding Algorithm for Linear Inverse Problems. SIAM Journal on Imaging Sciences, 2(1):183–202, January 2009. ISSN 1936-4954. doi: 10.1137/080716542.

- Bubeck (2015) Sébastien Bubeck. Convex optimization: Algorithms and complexity. Foundations and Trends® in Machine Learning, 8(3-4):231–357, 2015.

- Chatterjee (2014) Sourav Chatterjee. Superconcentration and Related Topics, volume 15. Springer, 2014.

- Clarkson (2010) Kenneth L. Clarkson. Coresets, sparse greedy approximation, and the Frank-Wolfe algorithm. ACM Transactions on Algorithms, 6(4):63:1–63:30, September 2010. ISSN 1549-6325. doi: 10.1145/1824777.1824783.

- Combettes and Pokutta (2021) Cyrille W. Combettes and Sebastian Pokutta. Revisiting the approximate Carathéodory problem via the Frank-Wolfe algorithm. Mathematical Programming, November 2021. ISSN 1436-4646. doi: 10.1007/s10107-021-01735-x.

- Dyer et al. (1992) Martin E. Dyer, Zoltan Füredi, and Colin McDiarmid. Volumes spanned by random points in the hypercube. Random Structures & Algorithms, 3(1):91–106, 1992.

- Fazel et al. (2004) M. Fazel, H. Hindi, and S. Boyd. Rank minimization and applications in system theory. In Proceedings of the 2004 American Control Conference, volume 4, pages 3273–3278 vol.4, 2004. doi: 10.23919/ACC.2004.1384521.

- Frank and Wolfe (1956) Marguerite Frank and Philip Wolfe. An algorithm for quadratic programming. Naval Research Logistics Quarterly, 3(1-2):95–110, 1956. ISSN 1931-9193. doi: 10.1002/nav.3800030109.

- Garber and Hazan (2015) Dan Garber and Elad Hazan. Faster Rates for the Frank-Wolfe Method over Strongly-Convex Sets. In Proceedings of the 32nd International Conference on Machine Learning, pages 541–549. PMLR, June 2015.

- Garber and Hazan (2016) Dan Garber and Elad Hazan. A Linearly Convergent Variant of the Conditional Gradient Algorithm under Strong Convexity, with Applications to Online and Stochastic Optimization. SIAM Journal on Optimization, 26(3):1493–1528, January 2016. ISSN 1052-6234. doi: 10.1137/140985366.

- Jaggi (2013) Martin Jaggi. Revisiting Frank-Wolfe: Projection-Free Sparse Convex Optimization. In Proceedings of the 30th International Conference on Machine Learning, pages 427–435. PMLR, February 2013.

- Lacoste-Julien and Jaggi (2015) Simon Lacoste-Julien and Martin Jaggi. On the global linear convergence of Frank-Wolfe optimization variants. In Proceedings of the 28th International Conference on Neural Information Processing Systems - Volume 1, NIPS’15, pages 496–504, Cambridge, MA, USA, December 2015. MIT Press.

- Lan (2020) Guanghui Lan. Projection-free methods. In First-Order and Stochastic Optimization Methods for Machine Learning, pages 421–482. Springer International Publishing, Cham, 2020. ISBN 978-3-030-39568-1. doi: 10.1007/978-3-030-39568-1.

- Lecué (2007) Guillaume Lecué. Optimal rates of aggregation in classification under low noise assumption. Bernoulli. Official Journal of the Bernoulli Society for Mathematical Statistics and Probability, 13(4):1000–1022, 2007.

- Li and Barron (2000) Jonathan Li and Andrew Barron. Mixture Density Estimation. In Advances in Neural Information Processing Systems, volume 12. MIT Press, 2000.

- Mirrokni et al. (2017) Vahab Mirrokni, Renato Paes Leme, Adrian Vladu, and Sam Chiu-wai Wong. Tight Bounds for Approximate Carathéodory and Beyond. In Proceedings of the 34th International Conference on Machine Learning, pages 2440–2448. PMLR, July 2017.

- Peña and Rodríguez (2019) Javier Peña and Daniel Rodríguez. Polytope Conditioning and Linear Convergence of the Frank–Wolfe Algorithm. Mathematics of Operations Research, 44(1):1–18, February 2019. ISSN 0364-765X. doi: 10.1287/moor.2017.0910.

- Pisier (1980) Gilles Pisier. Remarques sur un résultat non publié de B. Maurey. Séminaire d’Analyse fonctionnelle (dit ”Maurey-Schwartz”), 1980.

- Pivovarov (2007) Peter Pivovarov. Volume thresholds for Gaussian and spherical random polytopes and their duals. Studia Math, 183(1):15–34, 2007.

- Talagrand (2014) Michel Talagrand. Gaussian processes and the generic chaining. In Upper and Lower Bounds for Stochastic Processes: Modern Methods and Classical Problems, pages 13–73. Springer Berlin Heidelberg, Berlin, Heidelberg, 2014. ISBN 978-3-642-54075-2. doi: 10.1007/978-3-642-54075-2.

- Tropp (2004) J.A. Tropp. Greed is good: Algorithmic results for sparse approximation. IEEE Transactions on Information Theory, 50(10):2231–2242, October 2004. ISSN 1557-9654. doi: 10.1109/TIT.2004.834793.

- Tsybakov (2003) Alexandre B Tsybakov. Optimal rates of aggregation. In Learning Theory and Kernel Machines, pages 303–313. Springer, 2003.

- Zhang (2003) Tong Zhang. Sequential greedy approximation for certain convex optimization problems. IEEE Transactions on Information Theory, 49(3):682–691, March 2003. ISSN 1557-9654. doi: 10.1109/TIT.2002.808136.

- Zhang and Yu (2005) Tong Zhang and Bin Yu. Boosting with early stopping: Convergence and consistency. The Annals of Statistics, 33(4):1538–1579, August 2005. ISSN 0090-5364, 2168-8966. doi: 10.1214/009053605000000255.

Appendix A Glossary of Notation

| inequality up to a universal constant | |

| (or | as |

| (or ) | asymptotic inequality up to a universal constant |

| (or ) | asymptotic inequality up to logarithmic factors |

| large universal constant (value may change across displays) | |

| sparse programming complexity | |

| compressibility | |

| -convex hull | |

| convex hull | |

| set of -sparse algorithms (functions) | |

| unit ball in | |

| Schatten ball in | |

| Frobenius norm | |

| Schatten norm | |

| Probability simplex in . |

Appendix B Section 2 Proofs

B.1. Proof of Lemma 2

We claimed that if is a subset of the unit ball then

Proof.

If then we may write

for and (the -ary probability simplex).

Now, let be a minimal covering of at resolution (in norm), and let be a minimal covering of at resolution (in norm). We may assume that is a subset of the unit ball in since the projection onto a closed, convex set cannot increase the distance to any point in that set (Bubeck, 2015, Lemma 3.1). For each index , let denote an element of such that , and let denote an element of such that . We have

Similarly, by Lemma 3 (proved independently in Appendix C.1 below), we have

By the triangle inequality, we obtain that

Note that right-hand sum can take on at most values. We have ; by Lemma 4 (proved independently in Appendix C.2 below), . We may therefore estimate

Taking logarithms gives the desired result. ∎

Appendix C Section 3 Proofs

C.1. Proof of Lemma 3

We claimed that for with for all , and , then

Proof.

We can verify that

as claimed. ∎

C.2. Proof of Lemma 4

We claimed that for all , the probability simplex satisfies

Proof.

To verify this, note that is contained within the unit ball . Thus, by Lemma 10, we have

where the final inequality holds for . ∎

Remark 9.

With a more careful application of the volume argument, one can show the upper bound . However, the two results are equivalent for our purposes.

C.3. Proof of Theorem 1

We claimed that

C.4. Sketch of Lemma 5

Here we sketch a proof of the inequality (7), proved by Pivovarov (2007), that if are independent points distributed according to the uniform measure on the Euclidean sphere in and denotes their convex hull, then

Proof.

Consider the potential facets of , each determined by a subset of points (since no points are coplanar, almost surely). If , then at least one of these subsets must form a facet that intersects . We may thus bound the probability that a particular subset forms a facet that intersects , and then apply a union bound over all subsets.

To this end, suppose that for a given subset of indices of size , the corresponding points form a facet that intersects . Then both of the half-spaces determined by the affine hull of have probability at most with respect to the uniform distribution on the sphere. Moreover, since forms a facet, each of the remaining points must independently lie in the same one of these two half-spaces. This event can therefore have probability at most , conditional upon any realization of . By a union bound over all possible subsets , we get

where the latter inequality follows from standard estimates such as Stirling’s approximation. This completes our sketch of Lemma 5. ∎

Remark 10.

It is quite clear that this proof can be relaxed to arbitrary independent distributions of the points , where is replaced by any uniform upper bound on the probability that each point lies on either side of any hyperplane that intersects . For example, in the Gaussian case, this quantity is precisely , where denotes the Gaussian CDF.

C.5. Proof of Lemma 6

The claimed result was that for all

This follows from the following lower bound on the volume of a spherical cap of height , which is particularly useful in the regime where , and is a small constant, e.g. . Its proof uses the well-known coupling between the high dimensional spherical and Gaussian distributions.

Proposition 4.

Let for uniformly distributed on and a canonical basis vector in . Let denote the Gaussian CDF. For all and , it holds that

Starting from this proposition, we may take , , and use the lower bound to obtain

For , this quantity is at least .

Proof.

Let be a standard Gaussian random vector in . Since is uniformly distributed on the sphere , our problem is equivalent to stating a lower bound for the probability of the event

where is a canonical basis vector. We start by considering the alternative event

Since the is a unit normal random variable, we have that . Now, we have

so it suffices to bound the probability of . Indeed, rearranging the two corresponding inequalities yields

Note that by Jensen’s inequality. Since is the supremum of a Gaussian process with pointwise variance and , we deduce from Borell’s inequality (Theorem 1) that

| (10) |

Thus,

∎

C.6. Extension to Gaussian Polytopes

In this section we’ll prove an analogous result to Theorem 2 where the vertices are independently distributed according to the standard Gaussian measure in .

Proposition 5.

Let be independent standard Gaussian vectors in , with . Let denote their convex hull. Then there exists some , depending only on , such that if for some , it holds with probability that

Proof.

Let be given. We use the following result, whose proof mimics Lemma 5.

Lemma 8 (Pivovarov (2007, Lemma 2.7 & Eqn. 11)).

Let denote the Gaussian CDF. Then

| (11) |

In order to apply Theorem (1), we also need an appropriate estimate on the radius of . Note that is the supremum of a unit variance Gaussian process, so by Borell’s inequality (Theorem 1) we have

To estimate the expectation, note by (10), we have . Thus, by the sub-Gaussian maximal inequality (Lemma 12), we have that

Since , we obtain that

Absorbing negligible terms and simplifying, we obtain

for some sufficiently large which depends only on . By a union bound, it holds with probability that

Plugging this into Theorem 1 gives

which yields the result when we choose , simplify, and note that .

∎

C.7. Proof of Theorem 3

We claimed that if is a subset of the unit Euclidean ball, then for any the sparse programming complexity for quadratic objectives over satisfies

Proof.

We work forwards from Lemma 2, which says that

Combining this with the definition of compressibility (1) gives

since . Rearranging and applying (2) to relate compressibility to sparse programming complexity, we obtain a lower bound on the sparse programming complexity in terms of the gap between and :

| (12) |

The proof is complete after noting that , and . ∎

C.8. Proof of Example 2

We claimed that

Proof.

To verify the claim, note that the normalized unit cube has volume precisely and has vertices. On the other hand, the unit ball has volume

where we have used the standard inequality . It follows that . Combining this with Theorem 1 gives

which is precisely the claimed bound. ∎

C.9. Proof of Example 3

We claimed that whenever ,

Proof.

Firstly, note that the standard Euclidean inner product structure in coincides with the Frobeinus inner product . Recall that we have

We begin by estimating . For unit vectors and ,

and, each of these summands may be bounded as, e.g.,

using the fact that . Using the triangle inequality, we may conclude in this manner that

Now, suppose we are given a minimal covering (resp. ) of (resp. ) at resolution . We may assume without loss of generality that these coverings are subsets of the unit ball, since the nearest point map onto the unit ball does not increase the distance to any point in the unit ball (Bubeck, 2015, Lemma 3.1) . By the above computation, the set

is a covering of of size at resolution . By a volume argument (Lemma 10) we have that for all , since is a subset of the unit ball. We may therefore conclude that

To estimate , note that vector of singular values of has at most nonzero entries. Thus, if then . Appealing to the equivalence between the Frobenius and canonical Euclidean norms, we deduce that

By another volume argument (Lemma 9) this implies

Plugging these estimates into Theorem 3 gives

since . Finally, taking gives us

This completes the proof. ∎

Appendix D Proofs from Section 4

D.1. Proof of Proposition 2

The result follows from the following, slightly more general statement.

Proposition 6.

Let be an -approximate minimizer of the empirical risk that takes values in , let be the minimizer of the true risk, and suppose that is convex. Then

| (13) |

Moreover, under the same conditions, it holds with probability that

| (14) |

where is given by the localized set

Proof.

Let denote the nearest point to in , so

By convexity of and Lemma 13, we have

Combining these two yields

Finally, since is an -approximate minimizer of in , we have

Writing the norm as an inner product and rearranging gives

Thus, we have

where . Note that since is star-shaped, the supremum must be attained at some satisfying

| (15) |

where the last step follows from linearity of the objective. Plugging this in, we get the first announced bound

For the second bound, we put

| (16) |

where we have used symmetry of the Gaussian distribution in the final step. By Borell’s inequality (Theorem 1) we have that with probability ,

| (17) |

Let be the subset of points satisfying (17). On the event where (17) holds, we have

This completes the proof. ∎

D.2. Proof of Proposition 3

We claimed that

Proposition 2 tells us that

| (18) |

Thus, it will be sufficient to state a high probability bound for the quantity

Note that by Borell’s inequality (Theorem 1), we must have

| (19) |

Moreover, we verified in the main text that

Note that the second summand is the expectation a maximum of variables , each of which satisfies (by another application of Borell’s inequality). Therefore, by Lemma 12, we have

| (20) |

using the standard bounds and . Combining this with (19) and inverting the probability bound gives us that with probability at least we have

Finally, plugging this into (18), expanding the square, and absorbing absolute constants gives us the claimed result so long as .

D.3. Proof of Proposition 1

We claimed that if belongs to the relative interior of for some , and for a sufficiently large universal constant , then for and with probability

Proof.

We begin by verifying that the empirical risk minimizer belongs to the -relative interior with high probability. Indeed, let denote the empirical risk minimizer, i.e. the minimizer of over . We have that by Proposition 2 with that

Moreover, we have that

by symmetry of the Gaussian distribution and the fact that a linear function over will be maximized at some point in . By the sub-Gaussian maximal inequality, this is at most , and combining this with Borell’s inequality (Theorem 1) we obtain

Now, on this event, since minimizes over the convex set , we have by Lemma 13 that

Thus, on this event we have , since . For the range of we consider, this is upper bounded by and hence the distance to the boundary is must be at least . Plugging this value into Theorem 1 gives us

when we choose . Combining this with Proposition 3 and a union bound gives us that with probability

which reduces to the claimed bound. ∎

Appendix E Technical Lemmas

E.1. Covering Lemmas

We make heavy use of the standard volume argument, which is stated for convenience below.

Lemma 9 (Artstein-Avidan et al. (2015, Theorem 4.1.13)).

Let be a convex subset of and let denote a norm in with unit ball . Then

| (21) |

We also use the following result, which is an easy corollary of Lemma 9.

Lemma 10 (Artstein-Avidan et al. (2015, Corollary 4.1.15)).

Let be centrally symmetric convex set, and let denote the norm in with unit ball . Then

| (22) |

E.2. Probability Lemmas

The following concentration result for Gaussian suprema, which is a consequence of the Gaussian isoperimetric inequality, is heavily used throughout the paper.

Theorem 1 (Borell’s Inequality, Adler et al. (2007, Theorem 2.1.1)).

Let be a separable and almost surely bounded Gaussian process, and put . Then,

In particular, noting that if is a standard Gaussian in and a subset of the unit ball, then is a separable and a.s. bounded Gaussian process indexed by and , we have the following immediate corollary.

Lemma 11.

Let be a standard Gaussian in and let be a subset of the unit ball in . Then

The final tools that we frequently use throughout the paper are the following maximal inequalities for Gaussian and sub-Gaussian random variables.

Lemma 12.

Suppose that we are given random variables , with , each of which satisfies

for all . Then we have

| (23) |

In the special case where the are independent Gaussian random variables, we have

| (24) |

Proof.

For (24), we refer the reader to Chatterjee (2014, Equation A.3) and its accompanying proof. For (23) we closely mimic the proof of Talagrand (2014, Lemma 2.2.3). By a union bound and the fact that a probability can be at most , for any we have

Then we can integrate the tail to obtain

| Making the substitution , we obtain | ||||

| Choosing gives | ||||

Since for , we deduce the result for all . Meanwhile, for the case we have that

since the Gaussian density is symmetric and integrates to . ∎

E.3. Other Useful Results

Lemma 13.

Given , a closed, convex subset of a Euclidean space , and a point , let denote the nearest point to in . Then, for any ,

Proof.

Note that by strict convexity of the squared norm, must be unique. By translation, we may assume . There are two cases. If then and the statement is trivial. On the other hand, suppose . Let be a minimal ball centered at which contains . Then, the tangent plane to at , which is perpendicular to must separate from (or else, using convexity of and strict convexity of the squared norm, we can find a better point than by interpolation). It follows that . Finally, we may compute

This completes the proof. ∎