Treatment Choice with Nonlinear Regret††thanks: We would like to thank Tommaso Denti, Takashi Hayashi, Keisuke Hirano, Charles Manski, Francesca Molinari, José Luis Montiel Olea, Jörg Stoye, Aleksey Tetenov, Davide Viviano, Kohei Yata, and the participants at ASSA 2023, Bristol Econometric Study Group Conference, Boston College, Chicago, Cowles Foundation Conference, Cornell Brown Bag Seminar, Greater NY Metropolitan Area Econometrics Colloquium, IAAE 2022, Indiana Bloomington, Interactions Conference 2022, Michigan State, NASMES 2022, Northwestern and Penn State for helpful comments. The authors gratefully acknowledge financial support from ERC grants (numbers 715940 for Kitagawa and 646917 for Lee), the ESRC Centre for Microdata Methods and Practice (CeMMAP) (grant number RES-589-28-0001) and NSF grant (number SES-2315600).

Abstract

The literature focuses on the mean of welfare regret, which can lead to undesirable treatment choice due to sensitivity to sampling uncertainty. We propose to minimize the mean of a nonlinear transformation of regret and show that singleton rules are not essentially complete for nonlinear regret. Focusing on mean square regret, we derive closed-form fractions for finite-sample Bayes and minimax optimal rules. Our approach is grounded in decision theory and extends to limit experiments. The treatment fractions can be viewed as the strength of evidence favoring treatment. We apply our framework to a normal regression model and sample size calculations.

Keywords: Statistical decision theory, treatment assignment rules, mean square regret, limit experiments

1 Introduction

Evidence-based policy making using randomized control trial data is becoming increasingly common in various fields of economics. How should we use data to inform an optimal policy decision in terms of social welfare? Building on the framework of statistical decision theory as laid out in Wald (1950), the literature on statistical treatment choice initiated by Manski (2004) analyzes how to use data to inform a welfare optimal policy. Following Savage (1951) and Manski (2004), researchers often focus on the average of welfare regret across the sampled data (called expected regret) and obtain an optimal decision rule by minimizing a worst-case expected regret.

When it comes to the ranking of different statistical decision rules, once we eliminate those that are stochastically dominated, it becomes less obvious how we should compare decision rules that do not stochastically dominate each other. Focusing on the expected regret, as suggested by Manski (2004), provides a natural starting point. In general, regardless of whether we consider a Bayes or minimax criterion, optimal decision rules defined in terms of their expected regret are singleton rules, i.e., given a sample, optimal decision rules either treat everyone, or no-one in the population. There is, however, no compelling argument why we should limit our attention to the mean of regret, as has been acknowledged by Manski and Tetenov (2023) and Manski (2021a). In fact, focusing solely on the mean of regret and ignoring other features of the distribution of regret (e.g., second- or higher-order moments and tail probabilities) can lead to rules that incur a large welfare loss due to random sampling errors, especially when the sample size is small. As an artificial example, suppose that the outcome of interest is or (success or failure) and imagine that we observe 100 successes and 99 failures (the status quo is zero for everyone). The empirical success (ES) rule, which is asymptotically optimal in terms of the mean of regret, suggests that everyone in the entire population should be treated. If there is a swing of one outcome from to though, then the same ES rule now dictates that no-one should be treated. Such high sensitivity of treatment decisions with respect to sampling uncertainty implies that, given a sample, there is a non-negligible probability that ES rule incurs a large welfare loss.

To address these concerns, this paper proposes a novel approach to statistical treatment choice by optimizing a nonlinear transformation of welfare regret. In what follows, we let be a nonlinear transformation of the regret. We assess the performance of each treatment rule via the expected value of the transformed regret loss that it delivers. In the spirit of Wald (1950), this average nonlinear regret over realizations of the sampling process becomes the risk function. We refer to this risk as a nonlinear regret risk. Due to the nonlinearity of , information relating to other moments of the regret distribution is encoded in the risk function. For example, when , the associated risk function is the sum of the squared expected regret and the variance of regret, penalizing decision rules that lead to a high variance of regret. We refer to this nonlinear regret risk as mean square regret.111As shown in Remark 2.2, the variance regret is equivalent to the variance of welfare. Thus, compared to the expected regret criterion, our mean square regret can also be viewed as penalizing rules with a high variance of welfare.

This shift of criterion towards a nonlinear transformation of regret changes optimal rules drastically. We show that, under general conditions, singleton decision rules are not essentially complete. That means fractional rules cannot be eliminated from consideration once we take other moments or features of the regret distribution into account. Moreover, for many nonlinear transformations and for distributions in the one-parameter exponential family, many singleton threshold rules are in fact dominated by fractional decision rules. These results offer a novel decision-theoretic justification for implementing a fractional treatment assignment rule, which differs from justifications given in the existing literature so far, which all use the conventional expected regret as the criterion. See, for example, Manski (2009) for a detailed review of fractional rules with standard regret under ambiguity and other non-standard settings, including nonlinear welfare, interacting treatments, learning and other non-cooperative aspects. More specifically, when the linear welfare is partially identified, Manski (2000, 2005, 2007a, 2007b) shows that minimax regret optimal rules are fractional even with the true knowledge of the identified set.222There are two approaches to go without asuming the true knowlege of the identified set. One approach is to plug in an estimate of the identified set, treating it as if it is the true object (Manski, 2013; Cassidy and Manski, 2019; Manski, 2021b). The other approach is to directly consider finite sample minimax regret optimal rules, which can be also fractional (Stoye, 2012; Yata, 2021; Manski, 2022) if model ambiguity is sufficiently large compared to statistical uncertainty. Manski and Tetenov (2007) and Manski (2009) justify fractional rules via a nonlinear welfare in a point-identified setting. As shown by Munro (2023), fractional rules also arise when agents response with strategic behavior.

Our results justify fractional rules in a standard setting without model ambiguity, nonlinear welfare or other strategic aspects. We provide general results on Bayes and minimax optimal rules based on nonlinear regret risks. For mean square regret, we derive both Bayes and minimax optimal decision rules, not only in Gaussian finite samples with known variance but also asymptotically. These optimal rules are fractional, with the fraction of the population assigned to the treatment dependent on the -statistic for the average treatment effect estimated from experimental data. The form of the fractional assignment has a simple and insightful expression that is easy to compute in practice. For example, an asymptotically minimax optimal rule for the previous artificial example would only allocate 54% of the population to the treatment, dropping to 46% if one outcome switches. Due to their fractional nature, our optimal rules are useful even beyond the treatment decision paradigm: researchers may conveniently interpret our rule as a summary statistic that quantifies the strength of evidence in support of the treatment versus control. See Section 5.2 for further discussions on this matter.

We show that the form that our treatment rules take is closely related to the posterior distribution for the average treatment effect. In particular, the minimax mean square regret rule coincides with the posterior probability-matching assignment under the least favorable prior. The posterior probability-matching assignment, known as the Thompson sampling algorithm (Thompson, 1933), possesses a desirable exploration-exploitation property in bandit problems. Our results show that the posterior probability-matching assignment can be justified in terms of minimax mean square regret, even in the static treatment choice problem where the exploration motive does not exist.

Given a nonlinear regret risk and a prior for the underlying potential outcome distributions, we obtain the Bayes optimal rules. Consistent with our incompleteness and inadmissibility results, Bayes optimal rules are, in general, also fractional rules. For mean square regret, we show that the Bayes optimal rule is a tilted posterior-probability matching rule, where the probability of random assignment corresponds to the posterior probability tilted by a certain weighting term. In a special case where the prior for the average treatment effect is supported only on two symmetric points, the tilting term is nullified and the Bayes optimal rule boils down to the Thompson-sampling type posterior-probability matching rule. For the minimax optimal rule in a Gaussian experiment with known variance, we can show that a least favorable prior is supported on two symmetric points. Hence, the minimax optimal rule follows the posterior-probability matching assignment rule, and is a logistic transformation of the sample mean. This minimax mean square regret rule is easy to compute and tuning- or hyper-parameter free.

Imagine the outcome of interest now follows a normal distribution with unit mean and unit variance, whereas the status quo is zero for everyone. In this scenario, the infeasible optimal rule is to treat everyone and the regret of any decision rule is supported on . Suppose the planner observes one observation from the distribution and needs to make a treatment choice. The ES rule is optimal in terms of expected regret, but could be far from ideal in terms of other features of the regret and welfare distribution. In fact, if the planner adopted ES rule, then there would be a mass of 16% probability that she ended up with the largest possible regret of one (and the smallest possible welfare of zero). In contrast with the mean regret criterion commonly used in the literature, our mean square regret criterion penalizes rules with large variance of the regret distribution (and equivalently, large variance of welfare). If, instead, the planner implemented our proposed minimax rule, she could avert such high chance of welfare loss: the probability of incurring a regret larger than 0.95 (and a welfare smaller than 0.05) is only 1.4%. Also see Figure 1.1 for a comparison of the distributions of the regret and welfare for ES rule and our proposed mean square regret minimax optimal rule.

| ES rule | Our proposed minimax rule | ||

|---|---|---|---|

| Mean of regret | 0.1587 | 0.2087 | |

| Standard deviation of regret | 0.3654 | 0.2698 | |

| Mean of welfare | 0.8413 | 0.7913 | |

| Standard deviation of welfare | 0.3654 | 0.2698 | |

| Mean square regret | 0.1587 | 0.1133 |

Our approach can find their counterparts in decision theory from the work of Hayashi (2008), which builds a model that axiomatizes a class of regret-driven choices, including mean square regret and many other nonlinear regret criteria. In particular, our mean square regret criterion corresponds to what Hayashi (2008) calls regret aversion. We discuss the connection of our approach and the results of Hayashi (2008) more in detail in Section 5.1.

We demonstrate the usefulness of our approach in two applications. First, using our general theory, we derive a minimax optimal rule in a normal regression model with binary treatment, a specification frequently used by many practitioners. Second, in practice, the planner often has a preference for singleton rules, and calculates a sufficient sample size for their randomized experiment based on these singleton rules. We show that implementing these singleton rules can lead to a large efficiency loss in terms of mean square regret.

Following Hirano and Porter (2009, 2020), we extend our finite sample results to a large sample setting by engaging with the limit experiments framework introduced by Le Cam (1986). Even when potential outcome distributions are non-Gaussian but belong to a regular parametric class, we can obtain a Gaussian limit experiment with known variance. Therefore, we can apply our results from a finite sample Gaussian experiment to a limit experiment and find feasible and asymptotically optimal rules with some efficient estimator of the parameters. Interestingly, in the limit experiment, the Bayes optimal rule under the mean square regret remains different from the minimax optimal rule, although the resulting mean square regret is quantitatively similar between the two rules. This is in contrast with the linear regret risk, for which it is known that the Bayes optimal and minimax optimal rules in the limit experiment are the same empirical success rule.

In a series of papers, Manski and Tetenov have explored optimal treatment rules in frameworks that go beyond the classical paradigm of the statistical decision theory laid out by Wald (1950). Manski (1988, 2011) argues to maximize a functional of the welfare distribution that at least weakly respects stochastic dominance. Manski and Tetenov (2023) consider the performance of a statistical treatment rule measured in terms of quantiles of the welfare. Our approach is distinct from the approaches taken by the aforementioned papers. In particular, we select treatment rules based on the distributions of their regret. Motivated by the risk aversion of policy makers, Manski and Tetenov (2007) consider a concave and monotone transformation of welfare measured in terms of a binary outcome, and define regret in terms of the transformed welfare. That is, Manski and Tetenov (2007) take a concave transformation of the welfare and keep the associated regret linear, while our approach looks at a nonlinear transformation of regret, keeping the welfare linear. These two approaches share a similar motivation: they advocate that decision makers may wish to take other aspects of the regret distribution into consideration when ranking decision rules. However, how they implement such a motivation and how technically tractable they are (to pin down different optimal rules) are significantly different. See Online Appendix B for further discussions on these matters.

The literature on the treatment choice problem has become an area of active research since the pioneering works of Manski (2000, 2002, 2004) and Dehejia (2005) introduced a decision theoretic framework to the problem. When the welfare is point-identified, minimax regret treatment choice rules for finite samples are derived in Schlag (2006) and Stoye (2009). Tetenov (2012) considers asymmetric regret criteria. Hirano and Porter (2009, 2020) introduce an asymptotic framework to analyze treatment rules with limit experiments. When the welfare is partially identified, Manski (2000, 2005, 2007a, 2007b, 2009) analyzes the treatment choice given the knowledge of the identified set. Treatment allocation analyses without the knowledge of the identified set but with finite sample data include Stoye (2012), Christensen et al. (2020), Ishihara and Kitagawa (2021), Yata (2021), Manski (2022), Ishihara (2023) and Montiel Olea et al. (2023). Chamberlain (2011) investigates a Bayesian approach to treatment choice, and Christensen et al. (2020) and Giacomini et al. (2021) discuss a robust Bayesian approach.

There is a growing literature on learning in the context of individualized treatment rules that map an individual’s observable characteristics to a treatment. See Manski (2004), Bhattacharya and Dupas (2012), Kitagawa and Tetenov (2018, 2021), Mbakop and Tabord-Meehan (2021), and Athey and Wager (2021), among others. Our analysis does not incorporate individuals’ observable covariates. Since the nonlinear regret risk aggregates the conditional nonlinear regret risk additively, it is straightforward to incorporate observable discrete covariates into our analysis, i.e., an optimal individualized fractional assignment rule that applies an optimal fractional assignment rule to each subpopulation of individuals sharing the same covariate value.

The rest of the paper is organised as follows. Section 2 introduces our setup. Section 3 studies the admissibility and completeness of decision rules with nonlinear regret risk. Section 4 presents finite sample results on Bayes and minimax optimal decision rules. In Section 5, we discuss the axiomatic foundation of our criteria and the interpretation of our rules as a measure of strength of evidence. Section 6 extends our results to the limit experiment framework and derives asymptotically optimal decision rules. Section 7 applies our theory to an example of treatment choice in a normal regression model and an example of sufficient sample size calculation in randomized control trials. Section 8 concludes. Proofs and lemmas are reserved for the Appendix.

2 Setup

Consider the assignment of a binary treatment to an infinitely large population of individuals whose treatment effects can be heterogeneous. Let be the potential outcome when (with treatment) and be the potential outcome when (no treatment). Denote by the joint distribution of , where is a set of distributions under consideration. Define and as the means of the potential outcomes and under the distribution . We assume that the welfare of the planner is determined by the mean outcome in the population. Defining the population average treatment effect as , the infeasible optimal treatment policy is as follows: allocate to each individual in the population if and allocate everyone otherwise.

We also assume the decision problem is nontrivial in the sense that the image of the mapping contains both positive and negative values. Since the sign of is unknown, the planner collects an experimental sample of the observed outcomes of units randomly drawn from the population , and the experimental design is known to the planner. The experiment generates a random vector , where is the observed outcome of unit , is the treatment status of unit , and is the sampling space. Let be the sampling distribution of , which depends on as well as the known experimental design.333For example, for a randomized control trial with a known treatment probability , the joint likelihood of is written as , where and are the marginal densities of and , respectively. Our setup also accommodates other experimental designs. The derivation of is analogous but may be more involved if the experimental design is complicated. Also, we use the uppercase letter to denote a random vector and use lowercase letter to denote a realized value of . After observing data , the planner chooses a statistical treatment rule that maps to a real number between 0 and 1, i.e.,

where is the proportion of the population receiving the treatment. Denote by the set of all statistical decision rules under consideration.

Remark 2.1.

In our setting, the action space of the planner is , instead of . That is, the planner is allowed to make fractional treatment allocation and to differentiate the treatment statuses of individuals in the population. Following the terminology from Manski (2004, 2021a), we say is a singleton rule if for almost all . We say is fractional if is not a singleton rule. Intuitively, after observing data, a singleton rule either treats everyone, or no one in the population, whereas a fractional rule allocates an interior fraction of the population to the treatment, leaving the rest of the population untreated. A fractional rule may be implemented according to some randomization device after observing .

Applying the statistical treatment rule to the population yields a welfare of

to the planner. The infeasible optimal treatment policy that maximizes welfare is . Following Savage (1951) and Manski (2004), we define the regret of as its welfare compared to the welfare of , i.e.,

Since is a random object that depends on realizations of the random vector , Manski (2004) follows Wald (1950) in measuring the performance of using its risk, i.e., the expected regret across realizations of the sampling process:

where denotes the expectation with respect to .

The risk criterion ranks treatment rules according to their mean regret. We, instead, consider a planner whose assessment of the performance of statistical treatment rules depends not only on the mean of regret but also on some other features of the regret distribution. To take other features of the regret distribution into consideration, we look at the nonlinear transformation of regret:

where is some nonlinear function. The planner’s preference over statistical decision rules is measured by the expected value of with respect to realizations of :

| (2.1) |

We refer to the criterion as the nonlinear regret risk.444The conventional mean regret risk function is a special case of our approach by taking to be linear. Due to the nonlinearity of , depends not only on the mean but also on other features of the regret distribution, including its higher-order moments. For instance, if we specify the quadratic function , the squared regret is

This squared regret constitutes the new loss function, and we can evaluate the performance of via mean square regret:

Remark 2.2.

Similar to the classical estimation theory, we can decompose

where is the mean regret risk, and is the variance of the regret defined as

Thus, ranking treatment rules by the mean square regret criterion has the benefit of penalizing rules with large regret variance. As

for each rule , the variance of its regret in fact equals the variance of the resulting welfare. The mean square regret criterion has the following equivalent representation

where denotes the variance under sampling distribution . Thus, compared to the mean regret criterion , the mean square regret penalizes rules that lead to a large variance of welfare. A decision maker who uses mean square regret criterion is averse to the volatility of their welfare (with respect to sampling uncertainty), while a decision maker who prefers the mean regret criterion ignores the volatility of their welfare.

3 Incompleteness and inadmissibility of singleton rules

Viewing the nonlinear regret risk defined in (2.1) as the risk criterion within Wald’s framework of statistical decision theory, we introduce the following standard definition of admissibility of a statistical treatment rule and the essential completeness of a class of rules.

Definition 3.1 (Admissibility, inadmissibility and essential completeness under nonlinear regret risk).

-

(i)

A statistical treatment choice rule is admissible under the nonlinear regret risk if no dominates , i.e., there is no such that holds for all with the inequality strict for some .

-

(ii)

A statistical treatment choice rule is inadmissible under the nonlinear regret if there exists a decision rule that dominates .

-

(iii)

A class of statistical treatment rules, , is essentially complete in , if, for an arbitrary rule not in , there exists a such that for all .

As in standard statistical decision theory, admissibility defined through nonlinear regret is a minimal requirement that a desirable statistical treatment rule should satisfy. The notion of an essentially complete class simplifies the task of finding a good decision rule, as there is no need to consider rules outside this class.

Assumption G (Nonlinear transformation).

The nonlinear transformation is continuously differentiable and is strictly increasing on with .

Assumption G puts mild restrictions on the shape of the nonlinear transformation. Together with Assumption G, our first theorem shows that, in terms of nonlinear regret risk, a wide class of singleton rules are not essentially complete, implying that fractional rules cannot be eliminated from consideration in general. Recall for each , denotes the distribution of data and depends on while keeping the experimental design intact.555For example, for a randomized control trial with treatment assignment probability , we have that for , . For an event , write as the probability of event under the sampling distribution .

Theorem 3.1.

Let be a class of singleton decision rules such that, for some that satisfy and , can be represented as , where

If Assumption G holds, then is not essentially complete in .

The incompleteness result in Theorem 3.1 is general, without relying on parametric specifications for or functional form restrictions on the decision rules. The class of singleton rules considered in Theorem 3.1 is also large, comprising both “non-degenerate singleton rules” () and “degenerate singleton rules” ( and ) under some pair of distributions, one with positive average treatment effect (), and the other negative ().666The assumption that the pair share the same absolute value of treatment effect is not essential. The proof still goes through as long as we have and for some . Intuitively, any singleton rule with a positive probability of making mistakes under such pair of distributions is contained in . For the same pair of distributions, would be the class of rules that treats everyone in the whole population with probability one, e.g., , which treats everyone and ignores data. In contrast, is the class of rules that treats no one in the population with probability one under and , and contains the trivial rule .

The results of Theorem 3.1 contrast sharply with the known result on the essentially completeness of singleton rules in more standard formulations of the treatment choice problem, where the (negative) expected welfare corresponds to the risk criterion in Wald’s framework of statistical decision theory. For hypothesis testing problems with monotone likelihood ratio distributions, Karlin and Rubin (1956) show that the class of singleton threshold rules is essentially complete. As exploited in Hirano and Porter (2009) and Tetenov (2012), the essential completeness of singleton threshold rules carries over to the treatment choice problem, implying that decision makers can discard fractional rules when in search of a good rule. Applying Theorem 3.1 to monotone likelihood ratio distributions, we can conclude that the same class of singleton threshold rules are no longer essentially complete when it comes to many nonlinear regret risk criteria. Therefore, fractional rules cannot be eliminated from the consideration. Theorem 3.1 is established with the following important observation:

Lemma 3.1.

Lemma 3.1 reveals that if we focus on a binary class of distributions with opposite treatment effects, then the class of nondegenerate singleton rules are dominated. Theorem 3.1 utilizes this dominance result in the restricted class of distributions to show that is not essentially complete in the unrestricted (possibly infinite) class of distributions .

In general, proving the inadmissibility of a rule (in ) is often more demanding, as one needs to find a dominating fractional rule not only for but all . The next theorem confirms that a large set of singleton threshold rules are indeed inadmissible, if we impose stronger shape restrictions on and more distributional assumptions for the data.

Theorem 3.2.

Suppose the nonlinear transformation is a nonzero, homogeneous function of degree . Moreover, there exists an estimator for , and the pdf or pmf of is a member of the following one-parameter exponential family:

| (3.3) |

where , are real valued functions, and for some . Then, any singleton threshold rule

| (3.4) |

where is in the interior of the support of , is inadmissible.

Theorem 3.2 is again in sharp contrast with the existing literature. For the same one-parameter exponential family distributions, results from Karlin and Rubin (1956) imply that singleton rules of the form (3.4) are in fact admissible for the decision criterion of mean regret. Our results offer an opposite conclusion, demonstrating that the ranking of statistical treatment rules crucially depends on which features of the regret distribution the decision maker wishes to exploit. The homogeneity assumption on the shape of is a particularly convenient one that enables us to explicitly pin down a dominating rule in the form of (3.1) over , but is not required and can be considerably weakened. This class of homogeneous functions also coincides with what Hayashi (2008) calls regret aversion.

4 Finite sample optimality

We measure the performance of a rule by its nonlinear regret risk , which depends on the true unknown . In this section we look at two optimality criteria and derive general results on optimal rules for these criteria. We illustrate the usefulness of our results using specific parametric models.

4.1 Bayes optimality

Definition 4.1 (Bayes nonlinear risk and the Bayes optimal rule).

Let be a prior distribution on . The Bayes nonlinear (regret) risk of with respect to the prior is

A Bayes optimal rule with respect to the prior is such that

Moreover, we say that a prior distribution is least favorable if for all prior distributions .777Our notion of Bayes optimality is specifically attached to the risk function , and is not an acronym for Bayes welfare criterion. See also Ferguson (1967); Berger (1985) for precedents of attaching Bayes optimality to a specific risk function in statistical decision theory.

We now characterize the Bayes optimal rule for the Bayes nonlinear risk. It turns out that under mild restrictions on the nonlinear transformation , the associated Bayes optimal rule is also fractional. To proceed, let be the posterior distribution of given a prior and .

Theorem 4.1.

Suppose Assumption G holds, and the following conditions are true:

-

(i)

There exists some treatment rule such that is finite.

-

(ii)

For almost all , the posterior distribution puts nonzero probability mass on both and .

Then for almost all , the Bayes optimal rule exists, is fractional, and satisfies

| (4.1) |

Remark 4.1.

In general, the Bayes optimal rule depends on the nonlinear transformation and the model specification for . The calculation of the posterior expectation in (4.1), which requires integration with respect to the posterior distribution of , can be complicated. To gain further insight, consider the simple case where and is parameterized by the one dimensional parameter , where (for example, the outcome is normal with known variance). It follows that the prior distribution is indexed by and written as , and the Bayes optimal rule with respect to the Bayes mean square regret

is characterized as

| (4.2) |

where is the posterior distribution of given the prior and data , with .

Further to this, if the prior is supported on two symmetric points for some , it follows that

which is the exact form of the posterior probability matching rule, as used by Thompson (1933). If the prior is not supported on two symmetric points, it holds that

| (4.3) |

where denotes the posterior distribution of conditional on . Thus, for the mean square regret, the Bayes optimal rule is a tilted version of the posterior probability matching rule.

Remark 4.2.

In contrast, for the linear regret risk , the Bayes optimal rule is

which is a singleton rule in general.

We now provide a simple example for which we derive the finite sample Bayes optimal rule with respect to a flat prior. This example also sheds some light on the form of the Bayes optimal rule in large samples, which is discussed in Section 6.

Example 4.1 (Testing an innovation with normal outcome and mean square regret).

Let . Suppose the distribution of is known to the planner and without loss of generality, . Therefore, the planner only needs to learn and in the experimental design she allocates all units to the treatment. Let be the sample average of observed outcomes. Assume is normally distributed with an unknown mean and a known variance normalized to one, with the likelihood function

| (4.4) |

Proposition 4.1.

In Example 4.1, consider the uniform (improper) prior on . Then the Bayes treatment rule with respect to the mean square regret is

where for any , and where and are the cdf and pdf of a standard normal random variable, respectively.

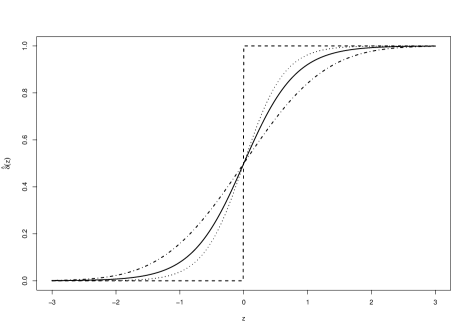

Proposition 4.1 is a direct application of Theorem 4.1. Since the prior is flat, the ‘posterior density’ is proportional to the likelihood (4.4). The form of the Bayes optimal rule then follows (4.3). The Bayes optimal rule is a product of two terms. The first term, , is the posterior probability that the treatment effect is positive given the uninformative prior, and corresponds to the posterior probability matching rule. The second term, , adjusts the first term upwards if , and adjusts it downwards if (note that ). Therefore, this Bayes optimal rule tilts the posterior probability matching rule and assigns treatment with a probability closer to zero or one. Also see Table 1 and Figure 6.2 for the magnitudes of the probability assignment of the Bayes optimal rule and posterior probability matching rule with respect to the uniform prior.

4.2 Minimax optimality

As an alternative to Bayes rule, this section studies minimax optimal rule for nonlinear regret risk.888As shown by Savage (1951); Manski (2004), maximin welfare criterion can be ultra-pessimistic and often leads to an optimal rule that always treats no-one in the population. Such ultra-pessimism carries over to maximin criterion applied to a nonlinear transformation of welfare. Echoing previous findings on minimax expected regret (e.g., Stoye, 2009; Tetenov, 2012), our results show that the ultra-pessimism also does not occur for the minimax criterion applied to many nonlinear regret risks.

Definition 4.2 (Minimax optimal rule).

A minimax optimal rule is such that

The following proposition characterizes the minimax optimal rule as a Bayes rule under a least favorable prior.

Proposition 4.2 (Lehmann and Casella (1998)).

Suppose is a distribution on such that

Then: (i) is minimax; (ii) is least favorable.

Proposition 4.2 is a direct result of Lehmann and Casella (1998, Theorem 5.1.4). Using Proposition 4.2, we can attempt to find the minimax optimal rule by adopting a ‘guess-and-verify’ approach: guess a least favorable prior and derive its associated Bayes optimal rule; verify that the resulting Bayes nonlinear regret risk equals the worst frequentist nonlinear regret risk of the Bayes optimal rule. In general, it can still be difficult to guess the least favorable distribution. However, in many parametric models, the support of the least favorable distribution is often discrete and finite, or the minimax optimal rule has a constant frequentist risk across its parameter space. See, for example, Kempthorne (1987). This greatly simplifies the problem. We now demonstrate the minimax optimal rule for Example 4.1.

Theorem 4.2.

| (4.5) |

or, equivalently, solves

| (4.6) |

where the expectation is with respect to . Moreover, a least favorable prior on is a two-point prior such that .

Remark 4.3.

The minimax optimal rule is a simple logistic transformation of the sample mean and is straightforward to calculate. Moreover, the minimax optimal rule agrees with the posterior probability matching rule, i.e., the treatment probability equals the posterior probability that the treatment effect is positive with respect to the least favorable prior, which is supported on two symmetric points around zero. In this way, we justify the posterior probability matching rule in a static environment without multiple exploration phases.

Remark 4.4.

On a more technical note, the proof of Theorem 4.2 relies on some different techniques from the existing treatment choice literature. For the mean regret criterion, singleton threshold rules form an essential complete class, so the minimax optimal rule with respect to mean regret can be found by directly minimizing the worst-case regret with respect to the threshold, without figuring out a least favorable prior (Tetenov, 2012). Stoye (2009) finds that a least favourable prior must be two-point symmetrically supported around zero. For this class of priors, the Bayes rule is always the ES rule. Therefore, the result of Stoye (2009) also does not need to pin down the exact location of the least favourable prior. However, for mean square regret, singleton rules are inadmissible, and it becomes essential to find the exact location of a least favorable prior. To find a least favorable prior and by observing the form of the mean square regret, we first conclude that a least favorable prior for mean square regret is also symmetric, such that

for some . Within this set of candidate least favorable priors indexed by , Theorem 4.1 implies the Bayes optimal rules admit the form . Furthermore, follows the form in (4.5), and is equivalent to the form in (4.6). Then, we guess that the least favorable prior is

where solves (4.5) or (4.6).999The exact location of the least favorable prior for the mean regret criterion is also different from and solves for Example 4.1. With this guess of the least favorable prior, we further establish that the following condition holds:

Condition 1.

.

The left-hand side of Condition 1 is the Bayes mean square regret of with respect to our hypothesized least favorable prior , and the right-hand side of Condition 1 is the worst mean square regret of . Thus, Proposition 4.2 implies that is a minimax optimal rule and is least favorable. See also Figure 4.1 for a graphical illustration. The full proof of Theorem 4.2 is left to Appendix A.

5 Further discussions

5.1 The microeconomic foundation of our approach

Our approach is naturally connected with the work of Hayashi (2008), which axiomatizes a class of regret-driven choices, including mean square regret and many other nonlinear transformations of regret. Below, we briefly discuss how the main results of Hayashi (2008) can be invoked to axiomatize and justify our nonlinear regret criteria.

Let be the product space of sample and the space of parameters indexing the distribution of the sample . Let be the set of statistical treatment choice rules and be the extended set of treatment choice rules which includes the infeasible oracle rule . For nonlinear transformation , we can express our nonlinear regret criterion with prior for as

The Bayes optimal nonlinear regret rule solves the following minimization

| (5.1) |

We can view the minimax optimal nonlinear regret rule as a solution to the following minimization:

| (5.2) |

where denotes the set of probability distributions on .

Let be the cardinality of , which is assumed to be finite in Hayashi (2008). Hayashi (Theorem 1, 2008) builds a general axiomatic model where the choice of a decision maker is represented by the following minimization:

| (5.3) |

where is a homothetic function and is viewed as the utility function. The function may be viewed as an aggregator that collects the decision maker’s regret in different states of the world. Note both (5.1) and (5.2) are special cases of (5.3) applied to finite . While Hayashi (2008) also discussed (5.1), the minimax nonlinear regret criterion (5.2) has not been considered elsewhere in the literature to the best of our knowledge. The case of is called regret aversion, which includes our mean square regret criterion as a special case.

Axiomatic results in decision theory, like (5.3), focus on decision making without sample data. Our criteria (5.1) and (5.2) are tailored for decision making with sample data, and deviate from (5.3) in the following two aspects. First, the menu used to calculate regret, , includes the infeasible oracle rule and is allowed to be different from the actual menu available to the decision maker. Second, the utility function is usually state dependent while in (5.3) the utility function is state independent. These two deviations, however, are standard practices in statistical decision theory, including criteria like minimax regret in the existing literature. Fully reconciling the differences between decision theory and statistical decision theory is beyond the scope of this paper. Manski (2021a, p. 2831) wrote: “As in decisions without sample data, there is no clearly best way to choose among admissible statistical decision functions (SDFs). Statistical decision theory has mainly studied the same criteria as has decision theory without sample data.” In view of Manski (2021a), our nonlinear regret criteria can find their counterparts in decision theory without sample data from Hayashi (2008).

5.2 Optimal rule as a summary statistic

The treatment probability of our suggested minimax optimal rule is always between zero and one. As such, our rule can be naturally viewed as a summary statistic that measures the strength of evidence in favor of treatment versus control. Therefore, the usefulness of our approach does not hinge on the decision theoretic framework. One does not have to literally make a treatment decision based on . Instead, empirical researchers may view as a degree of confidence gathered from data about the performance of the treatment in terms of welfare. Given finite sample from a single phase experiment, a larger value of means we are more in favor of the treatment, while a smaller value of signals less evidence supporting implementing the treatment. In contrast, in the standard mean regret paradigm, optimal rules are singleton and not fractional. Hence, it is not possible for applied researchers to solicit a measure of evidence strength from an optimal decision rule. Consider a scenario where is only slightly larger than zero. The empirical success rule would dictate everyone in the population to be treated, even though we may think that the evidence reflected from data in favor of the treatment is not entirely strong.

Viewing as a measure of the strength of evidence in a binary treatment setup, applied researchers may report as an alternative summary statistic to the widely used P value. Despite its popularity, P value is known to be unfit for a measure of support for its hypothesis (Schervish, 1996). Consider the setup in Example 4.1 again. The P value for one-sided hypotheses is . Since is in fact the posterior probability with respect to the flat prior, reporting the P value corresponds to reporting the posterior probability under a flat prior. However, reporting a posterior probability under a specific prior is not necessarily associated with any optimality criterion. Different from the P value, is an optimal treatment fraction under our mean square regret criterion. At the same time, is also a posterior probability under a least favorable prior. Note given , is quantitatively larger (smaller) than the P value. Therefore, reporting the P value would be more conservative than reporting in our mean square regret framework. In Section 7.1, we discuss how to calculate in a normal regression model with binary treatment.

6 Asymptotic optimality with mean square regret

In this section we derive asymptotically optimal rules via the limit experiment framework (Le Cam, 1986), following the approach taken by Hirano and Porter (2009). We first consider a local parametrization of the statistical model so that, in large samples, the treatment choice problem is equivalent to a simpler problem in a Gaussian limit experiment. Then, we examine and normalize our nonlinear regret in the limit, and find the corresponding optimal treatment rule. A feasible and asymptotically optimal treatment rule also follows if there exists an efficient estimator of the parameters in the original statistical model . For a review, see Hirano and Porter (2020).

6.1 Limit experiments

For simplicity, we focus on regular parametric models of with mean square regret . Semiparametric models and other nonlinear regret criteria can also be considered, albeit necessitating more technical analysis. Without loss of generality, consider a case where the distribution of is known and the mean of is zero. Suppose now the distribution of , denoted by , is parameterized by a finite dimensional parameter . Hence, the population average treatment effect is

Data is independently and identically drawn from . In particular, , where and is the support of . We now imagine a sequence of experiments in which the sample size grows. Let satisfy . We consider a sequence of local alternative parameters of the form , , the most challenging case in which to determine the optimal treatment rule, even in large samples.

Assumption DQM (Differentiability in Quadratic Mean).

There exists a function such that

and is nonsingular.

Assumption DQM is a standard assumption in the limit experiment framework (e.g., Van der Vaart, 1998). The function can usually be interpreted as the derivative of the loglikelihood function so that is the Fisher information under .

Assumption C (Convergence).

A sequence of treatment rules in the experiments is such that and for every as .

Compared to mean regret criterion, our mean square regret additionally depends on the second moment of decision rules. Thus, Assumption C assumes convergence of both first and second moments of decision rules, differing from Hirano and Porter (2009), who only look at convergence of the first moment of decision rules. Under Assumptions DQM and C, we first establish the following result that allows us to simplify the original treatment problem to a Gaussian experiment in large samples.

Proposition 6.1 (Van der Vaart (1998)).

Suppose satisfy Assumption DQM and a sequence of treatment rules in satisfy Assumption C. Then there exists a function such that for every ,

where is a multivariate normal distribution with mean and variance .

Proposition 6.1 is a special case of Van der Vaart (1998, Theorem 13.1 and Theorem 7.10) applied to the mean square regret setup, following Hirano and Porter (2009, Proposition 3.1). To use Proposition 6.1, note for any treatment rule in the experiments , the mean square regret is

which depends on only through and , to which we can apply Proposition 6.1. Thus, in terms of the mean square regret, any converging sequence of treatment rules is matched by some treatment rule in a simpler Gaussian experiment with unknown mean and known variance .

Let be the partial derivative of at . Since , it follows that as . Thus, for any rule ,

and as . Hence, normalizing by , for any converging rule in the sense of Proposition 6.1, we define the corresponding limit mean square regret as

| (6.1) | ||||

6.2 Feasible and asymptotically optimal rules

We first present results in terms of minimax optimality. Denote as convergence in distribution under the sequence of probability measures . Define to be the standard deviation of , where .

Theorem 6.1.

Suppose Proposition 6.1 holds, , and is differentiable at .

- (i)

-

(ii)

If, in addition, there exists a best regular estimator such that

(6.2) and there exists some estimator under , the feasible treatment rule

is locally asymptotically minimax optimal in terms of mean square regret:

where is a finite subset of and is the set of all decision rules that satisfy Assumption C (slightly abusing notation).

Theorem 6.1 extends our finite sample results to a large sample setting. Given a regular parametric model, the maximum likelihood estimator (MLE) usually satisfies (6.2). Thus, Theorem 6.1 suggests a simple way to construct an asymptotically minimax optimal rule in terms of mean square regret: estimate the parameters of via MLE, calculate a -statistic for the mean, and then carry out a simple logit transformation for the -statistic. This rule is always fractional and very easy to implement for practitioners. We expect that our result can also be extended to regular semiparametric models.

Next, we derive a feasible rule that is locally asymptotically Bayes optimal. Let be a positive and continuous prior density on (slightly abusing notation). For a treatment rule that satisfies Assumption C, the normalized Bayes mean square regret is

We define the Bayes mean square regret in the limit experiment when as

That is, as the Bayes mean square regret with respect to an uninformative prior. Then we can apply Theorem 4.1 to derive the Bayes optimal rule for the limit experiment. Given an MLE estimate of the parameters in , Theorem 6.2 further implies that a feasible and asymptotically optimal Bayes rule also follows with a simple transformation of the -statistic for the mean.

Theorem 6.2.

Suppose Proposition 6.1 holds, and is differentiable at . Let be the density of a prior distribution on that is continuous and positive at .

-

(i)

The Bayes optimal rule in terms of mean square regret in the limit experiment is

(6.3) where is defined in Proposition 4.1. That is, , where is the set of all treatment rules in the limit experiment.

-

(ii)

If, in addition, there exists a best regular estimator such that

and there exists some estimator under , the feasible treatment rule

is locally asymptotically Bayes optimal, i.e.,

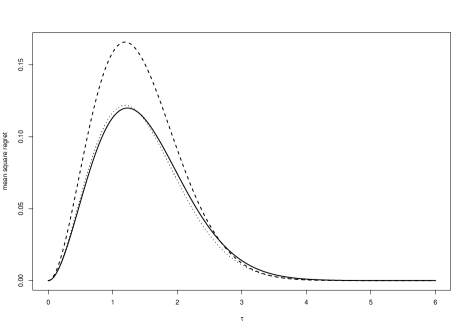

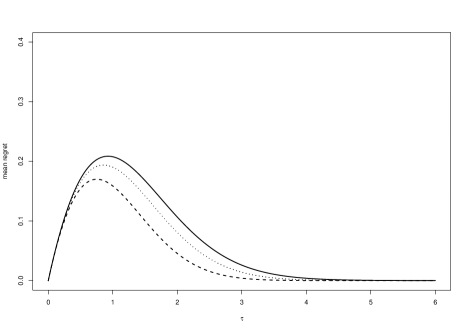

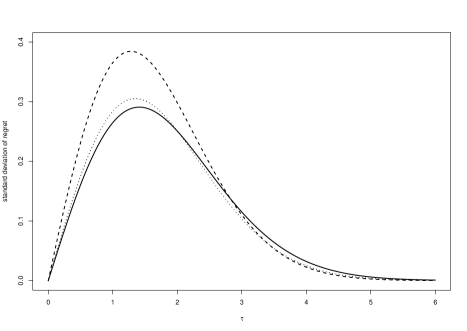

In the limit, the Bayes optimal rule is a tilted posterior probability matching rule with respect to the uninformative prior. Compared to the posterior probability matching rule, the Bayes optimal rule assigns treatment with a probability closer to zero or one. Compared to the limit minimax optimal rule, the Bayes optimal rule also assigns treatment with a probability close to zero or one. This contrasts with the case of linear regret risk, where it is known that the Bayes optimal and minimax optimal rules are the same empirical success rule. See Figure 6.2 and Table 1 for various rules in a Gaussian limit experiment with unit variance. It can be seen that all three fractional rules approach one as gets large. For sufficiently large positive values of (e.g., 2.33), the Bayes and minimax optimal rules are to effectively treat everyone. Even with a modest value of , the Bayes optimal rule recommends a probability of treatment of 0.94, which is quite high when compared with the corresponding probability of recommended by the posterior probability matching rule. Figures 6.2, 6.4 and 6.4 present the mean square regret, mean regret and standard deviation of regret of the optimal rules in the same Gaussian limit experiment with unit variance. We make several observations: firstly, although they admit different forms, our Bayes optimal and minimax optimal rules in the limit experiment exhibit a similar performance in terms of the mean square regret (Figure 6.2); secondly, the ES rule is minimax optimal in terms of mean regret (Figure 6.4), but its excessive variance (Figure 6.4) in those states where mean regret is high implies that it is not optimal in terms of mean square regret.

| Minimax | Bayes | Posterior probability | ES rule | |

|---|---|---|---|---|

| optimal rule | optimal rule | matching rule (flat prior) | ||

| 0 | 0.5 | 0.5 | 0.5 | |

| 0.2533 | 0.6507 | 0.6920 | 0.6 | 1 |

| 0.5244 | 0.7838 | 0.8430 | 0.7 | 1 |

| 0.8416 | 0.8877 | 0.9379 | 0.8 | 1 |

| 1.2816 | 0.9588 | 0.9851 | 0.9 | 1 |

| 1.6449 | 0.9827 | 0.9958 | 0.95 | 1 |

| 2.3263 | 0.9967 | 0.9997 | 0.99 | 1 |

7 Applications

7.1 Treatment choice in a normal regression model

Consider the following normal regression model frequently used by applied researchers:

| (7.1) |

where is the outcome variable, is the binary treatment and is a vector of covariates (including the intercept). Suppose the treatment effect is homogeneous. Then, the parameter is the population average treatment effect. Let and . (7.1) implies that the conditional density of given follows the parametric form

For now, assume the variance term is known to focus on the finite-sample analysis. Given a random sample , the MLE estimator for is

| (7.2) |

the usual OLS estimator. Let , the first entry of . It follows by standard algebra that

where denotes the th entry of matrix . By Theorem 4.2, the finite sample minimax optimal rule is

where is defined in Theorem 4.2. Even if is unknown, the MLE estimator for is , where is defined in (7.2), and

Applying Theorem 6.1, we may find a feasible asymptotically minimax optimal treatment rule as

Practitioners may report as an alternative to the P value associated with . Also see Section 5.2 for more discussions on this issue.

7.2 Sample size calculations

In practice, the planner often has a preference for singleton rules like the empirical success (ES) rule or the hypothesis testing (HT) rule, and calculates what is a sufficient sample size based on these singleton rules. In this section we discuss the implications for the efficiency loss in terms of mean square regret if singleton rules were implemented instead of our proposed minimax optimal rules. Compared to our minimax optimal rule, these singleton rules often require significantly more data and thus are much less efficient. A similar discussion can be had for the Bayes optimal rule, but we omit this for brevity.

Consider the Gaussian experiment in Example 4.1, but suppose now is the sample average calculated from experimental data with a sample size of and known variance . In this case the minimax optimal rule in terms of mean square regret is

where solves (4.5). Given each , we can select such that

i.e., the square root of the worst case mean square regret does not exceed . The worst case mean square regret can be calculated as

where is the worst case mean square regret of the minimax optimal rule in Example 4.1. Thus, the worst case mean square regret shrinks to zero at a rate of . In practice, we can choose to be proportional to , e.g., , so that the square root of the worst case mean square regret does not exceed 1% of the standard deviation.

Comparison with the ES rule

Manski and Tetenov (2016) choose a sufficient sample size for the ES rule via the optimal approach: a policy is optimal if, for all states of the world,

where is the infeasible optimal treatment rule or, equivalently,

| (7.3) |

for all states of the world. Given our Gaussian experiment , the worst case mean regret of the ES rule can be calculated exactly as

If the planner has a preference for the ES rule and decides to choose the sample size so that (7.3) holds with some , then the sample size should be at least

The worst case mean square regret of the ES rule, however, is

where . Hence, at , the worst case mean square regret of is . If, instead, the planner uses our minimax optimal rule, she only needs a sample size of for the worst case mean square regret not to exceed . Thus, to guarantee the same worst case mean square regret, the ES rule requires nearly 40% more observations than our minimax optimal rule.

Comparison with the HT rule

Practitioners who prefer the HT rule often select sample size by balancing Type I and II errors. In the Gaussian experiment , if the planner uses a size () HT rule

where is the quantile of a standard normal, then it is common for her to select sample size so that the power of the test is at least (), i.e., under the alternative , the probability of rejection is

Then the sample size should be at least

At this , we can also calculate the worst case mean square regret of the HT rule, which is approximately However, at this , the worst case mean square regret of our minimax rule is only . That is to say, with the same sample size , our minimax optimal rule guarantees that the worst case mean square regret is only around 8.3% of the corresponding value for the HT rule. Equivalently, to guarantee the same worst case mean square regret, the HT rule requires around 11 times more observations than our minimax optimal rule.

8 Conclusions

Our paper proposes a novel approach to measure the performance of statistical decision rules by considering a nonlinear transformation of regret. Such a shift of criterion can incorporate other features of the regret distribution (e.g., second- or higher-order moments and tail probabilities) into the decision-making process, and yields optimal rules that are drastically different from the existing literature. For a large class of nonlinear transformations, optimal rules are fractional, allocating only a proportion of the population to the treatment. For the mean square regret criterion, we also derive Bayes optimal and minimax optimal rules both for finite Gaussian samples and in asymptotic limit experiments. These rules have a simple and insightful form, and can be calculated easily by practitioners. As an extension, Kitagawa, Lee, and Qiu (2023) apply our mean square regret criterion to study optimal treatment choice problems when the welfare is only partially identified, and find that the fractional nature and the fundamental form of the minimax optimal rules found in our paper is preserved.

Our approach suggests that decision makers may display regret aversion, a notion related to but different from ambiguity aversion (Klibanoff et al., 2005; Denti and Pomatto, 2022). In particular, our nonlinear regret criteria can find their counterparts in decision theory from the work of Hayashi (2008) and thus are justified in terms of its microeconomic foundation.

Since our rules are always fractional, they naturally provide a degree of confidence in the performance of the treatment versus control. In that sense, our rule is useful for practitioners even outside the treatment choice paradigm. Implementing our rules also has the additional benefit of getting more data from randomized experiments that can be helpful for the inference of treatment effect, which would not be possible if singleton rules were implemented.

Appendix A Proofs of main results

Proof of Theorem 3.1

By Lemma C.1, there exists a rule that is not dominated in , and is such that

| (A.1) | |||

Suppose, on the contrary, that is essentially complete in . Then, there must exist some such that

and in particular,

| (A.2) |

as . Below, we show that no rule in can satisfy (A.2), forming a contradiction and completing the proof.

First of all, note both and are non-empty, as must contain the rule that treats everyone in the population irrespective of data, and must contain the rule that no one in the population irrespective of data.

Now, suppose is empty. Then, . However, no rule in or can satisfy (A.2). To this this, suppose did satisfy (A.2). Then, it must hold (as is not dominated in )

which violates (A.1). Similarly, if any did satisfy (A.2), it also must hold

which violates (A.1) too. Thus, a contradiction is formed and we conclude that is not essentially complete in .

Lastly, consider the case when is not empty. Then, . Clearly, the previous arguments still apply and no rule in satisfies (A.2). Furthermore, by Lemma 3.1, each is also dominated in . If any of the rule did satisfy (A.2), then must be dominated in as well due to (A.2), which violates the fact that is not dominated in . Thus, a contradiction is also formed and we conclude that is not essentially complete in .

Proof of Lemma 3.1

Given each , consider the fractional rule for some . When is implemented, the regret of is

The nonlinear regret risk of is

The derivative of with respect to at each is

As , it also holds . Thus, by Taylor’s theorem, we may write as

where is a number between and that depends on , and .

If , then , , . As , note and . Then,

if Since , as . Also, is continuously differentiable on and , implying . Thus, there exists some small enough such that , so that it holds

| (A.3) |

If , , , . Write . Then,

Analogous arguments show that by choosing small enough, we have and

| (A.4) |

We then pick small enough so that both (A.3) and (A.4) hold, implying

Proof of Theorem 3.2

First note, for any rule that is a function of (including ), we can rewrite their nonlinear regret risk as , since the nonlinear regret risk of depends on only via . Given a singleton rule , Lemma C.2 establishes the existence of a fractional rule that dominates . The conclusion of the theorem directly follows.

Proof of Theorem 4.1

As and condition (i) of Theorem 4.1 holds, it is straightforward to show (see, for example, Theorem 4.1.1 in Lehmann and Casella (1998)) that the Bayes optimal rule is such that

| (A.5) |

provided the solution of (A.5) exists for almost all .

Then the existence of follows from continuity of the objective function (A.5) in , which itself follows from the fact that is continuously differentiable. To see for almost all , note for all because is strictly increasing on by Assumption G. Thus,

where the last inequality follows from Assumption G and condition (ii). Similarly,

The above calculations imply that we can always reduce by moving away from both 0 and 1 and toward an interior point. Therefore, must be such that , for almost all . Then, (4.1) follows from the first order condition for (A.5).

Proof of Proposition 4.1

The proof is similar to the proof of statement (i) of Theorem 6.2 and thus omitted.

Proof of Theorem 4.2

We split the proof into three steps by adopting the ‘guess-and-verify’ approach.

Step 1: Guess a least favorable prior. Note the worst case mean square regret of a minimax optimal rule is

| (A.6) |

where

By Lemma D.1, the support of the solution of (A.6) never contains zero. In Lemma D.2, we show that the support of the solution of (A.6) must be symmetric, i.e., if the support of the solution of (A.6) contains for some , it must also contain . Therefore, we conjecture that the least favorable prior is two-point supported. Moreover, Lemma D.3 shows that for a symmetric two-point prior to be least favorable, each point is equally likely to be realised. Thus, our guess for the least favorable prior is such that

Step 2: Derive the Bayes optimal rule associated with the hypothesized least favorable prior. For each , let be the Bayes optimal rule with respect to the two-point symmetric prior

Within the above set of candidate least favorable priors, we show: (1) the Bayes optimal rules admit the form ; (2) follows the form in (4.5), and is equivalent to the form in (4.6). Thus, our guess for the least favorable prior is

Indeed, the functional form of is derived by applying Theorem 4.1,

where is the posterior distribution of conditional on and admits:

where is the likelihood of , is the likelihood of , and is the marginal density of . Note

It follows that

Therefore, the Bayes mean square regret of admits the form in (4.5):

Since and , we see that (4.5) is equivalent to (4.6):

and by a change of variables,

Proof of Theorem 6.1

Proof of statement (i)

Let be a minimax optimal rule in the limit experiment. That is, solves

Following Hirano and Porter (2009), consider slicing the parameter space of in the following way: define

where is such that (without loss of generality) and Hence,

Note for each , the limit regret only depends on through . Thus, we can consider treatment rules of the form

where . Let solve the simpler minimax exercise

among rules of form . It follows by Lemma E.1 that is a minimax optimal rule. Define

Lemma E.2 shows that can be found by solving , and Lemma E.3 establishes the the form of , which is a minimax optimal rule in the limit experiment.

Proof of statement (ii)

Proof of Theorem 6.2

Proof of statement (i)

Applying Theorem 4.1 to the limit Bayes mean square criterion yields

Notice in the limit experiment, has a flat prior. It follows that the posterior distribution is proportional to a normal distribution with mean and variance . Then

where denotes the conditional expectation of a normal random variable with mean and variance given . By the properties of the normal distribution and truncated normal distribution,

Statement (i) follows.

Proof of statement (ii)

References

- Athey and Wager (2021) Athey, S. and S. Wager (2021): “Policy learning with observational data,” Econometrica, 89, 133–161.

- Berger (1985) Berger, J. (1985): Statistical decision theory and Bayesian analysis, Springer.

- Bhattacharya and Dupas (2012) Bhattacharya, D. and P. Dupas (2012): “Inferring welfare maximizing treatment assignment under budget constraints,” Journal of Econometrics, 167, 168–196.

- Cassidy and Manski (2019) Cassidy, R. and C. F. Manski (2019): “Tuberculosis diagnosis and treatment under uncertainty,” Proceedings of the National Academy of Sciences, 116, 22990–22997.

- Chamberlain (2011) Chamberlain, G. (2011): “Bayesian aspects of treatment choice,” in The Oxford Handbook of Bayesian Econometrics, ed. by J. Geweke, G. Koop, and H. van Dijk, Oxford University Press, 11–39.

- Christensen et al. (2020) Christensen, T., H. Moon, and F. Schorfheide (2020): “Robust Forecasting,” ArXiv:2011.03153 [econ.EM], https://doi.org/10.48550/arXiv.2011.03153.

- Dehejia (2005) Dehejia (2005): “Program evaluation as a decision problem,” Journal of Econometrics, 125, 141–173.

- Denti and Pomatto (2022) Denti, T. and L. Pomatto (2022): “Model and predictive uncertainty: A foundation for smooth ambiguity preferences,” Econometrica, 90, 551–584.

- Ferguson (1967) Ferguson, T. S. (1967): Mathematical statistics: A decision theoretic approach, Academic press.

- Giacomini et al. (2021) Giacomini, R., T. Kitagawa, and M. Read (2021): “Robust Bayesian Analysis for Econometrics,” Federal Board of Chicago Working Paper, No. 2021-11, https://doi.org/10.21033/wp-2021-11.

- Hayashi (2008) Hayashi, T. (2008): “Regret aversion and opportunity dependence,” Journal of economic theory, 139, 242–268.

- Hirano and Porter (2009) Hirano, K. and J. R. Porter (2009): “Asymptotics for statistical treatment rules,” Econometrica, 77, 1683–1701.

- Hirano and Porter (2020) ——— (2020): “Asymptotic analysis of statistical decision rules in econometrics,” in Handbook of Econometrics, Volume 7A, ed. by S. N. Durlauf, L. P. Hansen, J. J. Heckman, and R. L. Matzkin, Elsevier, vol. 7 of Handbook of Econometrics, 283–354.

- Ishihara (2023) Ishihara, T. (2023): “Bandwidth selection for treatment choice with binary outcomes,” The Japanese Economic Review, 1–11.

- Ishihara and Kitagawa (2021) Ishihara, T. and T. Kitagawa (2021): “Evidence Aggregation for Treatment Choice,” ArXiv:2108.06473 [econ.EM], https://doi.org/10.48550/arXiv.2108.06473.

- Karlin (1957) Karlin, S. (1957): “Pólya type distributions, II,” The Annals of Mathematical Statistics, 28, 281–308.

- Karlin and Rubin (1956) Karlin, S. and H. Rubin (1956): “The theory of decision procedures for distributions with monotone likelihood ratio,” The Annals of Mathematical Statistics, 272–299.

- Kempthorne (1987) Kempthorne, P. J. (1987): “Numerical specification of discrete least favorable prior distributions,” SIAM Journal on Scientific and Statistical Computing, 8, 171–184.

- Kitagawa et al. (2023) Kitagawa, T., S. Lee, and C. Qiu (2023): “Treatment choice, mean square regret and partial identification,” The Japanese Economic Review, 1–30.

- Kitagawa and Tetenov (2018) Kitagawa, T. and A. Tetenov (2018): “Who should be treated? Empirical welfare maximization methods for treatment choice,” Econometrica, 86, 591–616.

- Kitagawa and Tetenov (2021) ——— (2021): “Equality-minded treatment choice,” Journal of Business & Economic Statistics, 39, 561–574.

- Klibanoff et al. (2005) Klibanoff, P., M. Marinacci, and S. Mukerji (2005): “A smooth model of decision making under ambiguity,” Econometrica, 73, 1849–1892.

- Le Cam (1986) Le Cam, L. (1986): Asymptotic methods in statistical decision theory, Springer Science & Business Media.

- Lehmann and Casella (1998) Lehmann, E. L. and G. Casella (1998): Theory of point estimation, Springer Science & Business Media, second ed.

- Manski (1988) Manski, C. F. (1988): “Ordinal utility models of decision making under uncertainty,” Theory and Decision, 25, 79–104.

- Manski (2000) ——— (2000): “Identification problems and decisions under ambiguity: empirical analysis of treatment response and normative analysis of treatment choice,” Journal of Econometrics, 95, 415–442.

- Manski (2002) ——— (2002): “Treatment choice under ambiguity induced by inferential problems,” Journal of Statistical Planning and Inference, 105, 67–82.

- Manski (2004) ——— (2004): “Statistical treatment rules for heterogeneous populations,” Econometrica, 72, 1221–1246.

- Manski (2005) ——— (2005): Social choice with partial knowledge of treatment response, Princeton University Press.

- Manski (2007a) ——— (2007a): Identification for prediction and decision, Harvard University Press.

- Manski (2007b) ——— (2007b): “Minimax-regret treatment choice with missing outcome data,” Journal of Econometrics, 139, 105–115.

- Manski (2009) ——— (2009): “The 2009 Lawrence R. Klein Lecture: Diversified treatment under ambiguity,” International Economic Review, 50, 1013–1041.

- Manski (2011) ——— (2011): “Actualist rationality,” Theory and Decision, 71, 195–210.

- Manski (2013) ——— (2013): Public policy in an uncertain world: analysis and decisions, Harvard University Press.

- Manski (2021a) ——— (2021a): “Econometrics for decision making: Building foundations sketched by Haavelmo and Wald,” Econometrica, 89, 2827–2853.

- Manski (2021b) ——— (2021b): “Probabilistic Prediction for Binary Treatment Choice: with focus on personalized medicine,” Tech. rep., National Bureau of Economic Research.

- Manski (2022) ——— (2022): “Identification and Statistical Decision Theory,” arXiv preprint arXiv:2204.11318.

- Manski and Tetenov (2007) Manski, C. F. and A. Tetenov (2007): “Admissible treatment rules for a risk-averse planner with experimental data on an innovation,” Journal of Statistical Planning and Inference, 137, 1998–2010.

- Manski and Tetenov (2016) ——— (2016): “Sufficient trial size to inform clinical practice,” Proceedings of the National Academy of Sciences, 113, 10518–10523.

- Manski and Tetenov (2023) ——— (2023): “Statistical decision theory respecting stochastic dominance,” The Japanese Economic Review, 1–23.

- Mbakop and Tabord-Meehan (2021) Mbakop, E. and M. Tabord-Meehan (2021): “Model selection for treatment choice: Penalized welfare maximization,” Econometrica, 89, 825–848.

- Montiel Olea et al. (2023) Montiel Olea, J. L., C. Qiu, and J. Stoye (2023): “Decision Theory for Treatment Choice Problems with Partial Identification,” ArXiv:2312.17623 [econ.EM], https://doi.org/10.48550/arXiv.2312.17623.

- Munro (2023) Munro, E. (2023): “Treatment Allocation with Strategic Agents,” ArXiv:2011.06528 [econ.EM], https://doi.org/10.48550/arXiv.2011.06528.

- Savage (1951) Savage, L. (1951): “The theory of statistical decision,” Journal of the American Statistical Association, 46, 55–67.

- Schervish (1996) Schervish, M. J. (1996): “P values: what they are and what they are not,” The American Statistician, 50, 203–206.

- Schlag (2006) Schlag, K. H. (2006): “ELEVEN - Tests needed for a Recommendation,” Tech. rep., European University Institute Working Paper, ECO No. 2006/2, https://cadmus.eui.eu/bitstream/handle/1814/3937/ECO2006-2.pdf.

- Stoye (2009) Stoye, J. (2009): “Minimax regret treatment choice with finite samples,” Journal of Econometrics, 151, 70–81.

- Stoye (2012) ——— (2012): “Minimax regret treatment choice with covariates or with limited validity of experiments,” Journal of Econometrics, 166, 138–156.

- Tetenov (2012) Tetenov, A. (2012): “Statistical treatment choice based on asymmetric minimax regret criteria,” Journal of Econometrics, 166, 157–165.

- Thompson (1933) Thompson, W. R. (1933): “On the likelihood that one unknown probability exceeds another in view of the evidence of two samples,” Biometrika, 25, 285–294.

- Van der Vaart (1998) Van der Vaart, A. W. (1998): Asymptotic statistics, Cambridge university press.

- Wald (1950) Wald, A. (1950): Statistical Decision Functions, New York: Wiley.

- Yata (2021) Yata, K. (2021): “Optimal Decision Rules Under Partial Identification,” ArXiv:2111.04926 [econ.EM], https://doi.org/10.48550/arXiv.2111.04926.

Appendix for Online Publication

Appendix B Comparison with Manski and Tetenov (2007)

In this section, we clarify the differences between our approach of treatment choice with nonlinear regret criteria and the approach of risk averse welfare criteria taken by Manski and Tetenov (2007). To elaborate, let be a concave function. A concave transformation of is . For the concave transformation , the regret of treatment rule defined in terms of nonlinear welfare is

In contrast, our paper considers a nonlinear (possibly convex) transformation of regret measured in terms of the original welfare:

where is a nonlinear function that does not depend on , or . In other words, the loss function in Manski and Tetenov (2007) is while in our paper the loss function is . Note we may write (assuming is sufficiently differentiable)

Since , the expected regret based on nonlinear welfare is

Thus, a risk-averse decision maker in the sense of Manski and Tetenov (2007) also cares about the regret distribution beyond the mean. However, the nonlinear welfare approach effectively considers all moments of the regret (up to some limit determined by the specific ) additively. Moreover, how the decision maker weighs different moments of the regret is state-dependent. That is, different values of results in different relative importance of each moment. While our nonlinear regret approach also aims to bring other features of the regret distribution into consideration, a typical nonlinear regret criterion often only focuses on one particular moment of regret and is less convoluted. The following example further illustrates the differences.

Example B.1 (expected regret with a quadratic and concave transformation of welfare).

Suppose , , and is a quadratic and concave function. As , , and for all , it follows that

Thus, compared to our mean square regret, the criterion of expected regret based on a quadratic, concave transformation of welfare always gives more weight to the mean of regret when it comes to the ranking of different decision rules. In addition, with a positive treatment effect, would put more weight on when is smaller. If the treatment effect is negative, the relative importance of and stays the same.

Therefore, both our approach and that of Manski and Tetenov (2007) share a similar motivation: when it comes to the selection of a good rule, decision makers may wish to take other aspects of the regret distribution into account. As a result, fractional rules arise. However, how these two approaches operate is dramatically different, and it seems our approach offers a more tractable framework to work out different optimal rules. Below, we take a step further to show that these two approaches are inherently two different ways of ranking decision rules.

Proposition B.1.

Consider the following statement

| (B.1) |

Then (B.1) holds for some concave function and some function if and only if and for some constants and .

Proof.

The if part is straightforward to show. We focus on the only if part. Let and . Since convexity and concavity are preserved under the expectation operator, it holds that is concave too. Then, by assumption,

| (B.2) |

for all and , implying

| (B.3) |

Fixing , (B.3) implies

| (B.4) |

Since is concave, (B.4) implies is concave as well for all . Conversely, fixing , (B.3) implies

| (B.5) |

or, equivalently,

| (B.6) |

Since is concave, (B.6) implies is convex for all . Thus, must be both concave and convex for , implying is an affine function for all . This implies is affine and admits for some constants and . Since is affine, (B.4) implies that is affine for and for . Furthermore, for all , (B.5) implies , i.e., is affine for as well, and for . At , must hold, implying . Thus, and must hold or, equivalently, for some constants and . ∎

Given a concave transformation of the welfare considered in Manski and Tetenov (2007), Proposition B.1 shows that we cannot find a nonlinear transformation of the original regret such that the regret of nonlinear welfare defined in Manski and Tetenov (2007) equals our nonlinear regret risk for all rules and all states of the world. The results of Proposition B.1 can be extended in several ways. Firstly, Proposition B.2 shows that even if we consider either or to be convex, or we restrict the domain of to be positive, the results of Proposition B.1 continue to hold. For instance, suppose and a nonlinear welfare transformation were to exist so that

| (B.7) |

Proposition B.2 shows that such an does not exist. Secondly, one might argue that even though (B.1) does not hold, the risks of the two approaches could be affine transformations of each other, so that the optimal rules are the same. In Proposition B.3, we show that even in such a scenario, both and also have to be affine. Our approach in introducing nonlinear is inherently different from that of Manski and Tetenov (2007).

Proposition B.2.

-

(i)

(B.1) holds for some convex function and some function if and only if and for some constants and .

-

(ii)

(B.1) holds for some function and some convex function if and only if and for some constants and .

-

(iii)

(B.1) holds for some concave function , where is a compact interval, and some function if and only if and for some constants and .

Proof.

Statement (i): the proof is the same as that of Proposition B.1.