Hierarchical Constrained Stochastic Shortest Path Planning via Cost Budget Allocation

Abstract

Stochastic sequential decision making often requires hierarchical structure in the problem where each high-level action should be further planned with primitive states and actions. In addition, many real-world applications require a plan that satisfies constraints on the secondary costs such as risk measure or fuel consumption. In this paper, we propose a hierarchical constrained stochastic shortest path problem (HC-SSP) that meets those two crucial requirements in a single framework. Although HC-SSP provides a useful framework to model such planning requirements in many real-world applications, the resulting problem has high complexity and makes it difficult to find an optimal solution fast which prevents user from applying it to real-time and risk-sensitive applications. To address this problem, we present an algorithm that iteratively allocates cost budget to lower level planning problems based on branch-and-bound scheme to find a feasible solution fast and incrementally update the incumbent solution. We demonstrate the proposed algorithm in an evacuation scenario and prove the advantage over a state-of-the-art mathematical programming based approach.

I Introduction

As human beings, making decisions is one of the daily tasks to improve our lives, where many, if not most, decisions are sequential. Sequential decision making has been one of the core topics in Artificial Intelligence (AI) to support those pervasive tasks [ernst2004power, silver2017mastering, cassandra1998survey]. The major role of sequential decision making is generating a course of actions that achieves the goals of an agent. Actions are defined from the domain of the problem and describe the states where they can be executed and how the states are changed by executing them. In commercial aircraft operation, for example, nominal unit operations are based on air route segments and standard departure/arrival procedures, and hence those can be reasonable choices of actions sets.

In sequential decision making problems, a crucial assumption is that the actions are well defined and an agent is capable of executing those actions. For many real-world problems, however, such assumption is too strong to hold, especially for online applications. Again, in aircraft operations, even though each air route segment is well established and can be flown as a routine procedure, there might be a novel circumstance that prohibits an aircraft from flying the segment as published, such as convective weather conditions. In such situation, travelling the air route segment forms another planning problem, which makes the problem hierarchical.

In fact, hierarchical structure in the planning problem has been widely studied in stochastic sequential decision making problems [sutton1999between, theocharous2004approximate, lim2011monte, omidshafiei2017decentralized, amato2014planning]. In those works, options, also known as macro actions or skills, were introduced to abstract the underlying problem space into a higher-level space to scale both learning and planning processes. However, most of the works in hierarchical planning focus on minimizing the expected cost (or maximizing the expected reward). In many of the real-world applications, however, naively minimizing the expected cost might not be desirable. For example, when we want an aircraft to navigate to the destination as fast as possible, it is also important to ensure the aircraft can complete the mission with the onboard fuel or stays outside of the unsafe region for safety.

Despite being non-hierarchical, stochastic sequential decision making problems have been widely extended to include constraints. One of the most well-known frameworks is constrained stochastic shortest path problems (C-SSPs) [altman1999constrained], which optimize the primary cost function while constraining the secondary cost functions. In this paper, we propose a new framework, hierarchical constrained stochastic shortest path problem (HC-SSP), that extends C-SSP to hierarchical problem structure. To the authors’ knowledge, this extension has been little attempted, yet there is some work on this direction [feyzabadi2015hcmdp]. However, the previous work focuses on abstracting the existing state space to find an approximated solution to the original problem. In our approach, on the other hand, we focus on finding (near-)optimal solution given the hierarchical structure of the problem.

Although the extension from C-SSP to HC-SSP looks straightforward, this extension poses a unique challenge that has not been present in the previous works. A hierarchical approach has its advantage based on decoupled high-level actions that can be learned individually. However, with a constraint, they are no longer decoupled due to shared cost budget given by the constraint. To address this problem, we propose a cost budget allocation approach based on the well-known branch-and-bound scheme.

This paper makes two main contributions. First, we propose a hierarchical constrained stochastic shortest path problem (HC-SSP) that extends C-SSP with hierarchical structure. Second, we propose a budget-allocation-based algorithm that finds a deterministic hierarchical policy to a HC-SSP in an anytime fashion. The algorithm is shown to be theoretically optimal given a specific condition and can be approximated based on the user-defined approximation level. The experimental results show that the algorithm can find near-optimal solutions in most cases even with high approximation level.

The remainder of this paper is organized as follows. Section II summarizes the most relevant backgrounds to our work. Section III presents the proposed HC-SSP problem definition with an intuitive example. Section IV elaborates our proposed algorithm, followed by evaluation results in Section LABEL:sec_experiments. Finally, we conclude and present future work in Section LABEL:sec_conclusion.

II Preliminaries

II-A Constrained Stochastic Shortest Path Problem

A constrained stochastic shortest path problem (C-SSP) is a tuple in which is a set of discrete states; is the initial state; is a set of goal states; is a set of discrete actions; is the state transition function, where is the probability of being in state after executing action in state ; is the indexed set of cost functions , where each is the cost function and is the -th cost of executing action in the state and resulting in the state ; and is the indexed set of bounds , where is the bound for -th cost function for [altman1999constrained, trevizan2016heuristic].

A solution to a C-SSP is a policy which maps states to a probability distribution over actions. If a policy maps every state to a probability distribution with a single outcome, the policy is called “deterministic,” and is called “stochastic” otherwise. In the former case, we denote as the action selected by the policy for the state .

An optimal solution to a C-SSP is a policy which minimizes the total expected cost, but in addition, the expected cost of the secondary cost function should be upper bounded by for . In other words, an optimal policy for a C-SSP is defined as follows:

| s.t. |

where is the set of all policies and

Note that every optimal policy for a C-SSP might be stochastic [altman1999constrained]. In this paper, however, we limit the policy space to deterministic ones which are preferred due to explainability and reliability in the safety-critical applications such as aircraft operations. Note that it is known that limiting the policy space to deterministic ones significantly increases the complexity of the problem [feinberg2000constrained].

II-B Anytime Algorithm for C-SSPs

In this section, we introduce a recently developed anytime algorithm for C-SSPs in [hong2021anytime] which we use as a subroutine in our proposed method. The algorithm has two stages where the first stage finds a Lagrangian dual solution of a C-SSP and then the second stage incrementally closes a duality gap, if there is any. In the first stage, the Lagrangian function is defined as follows:

| (1) |

where and . Then the Lagrangian dual problem is defined as follows:

| (2) |

where

| (3) |

Note that the following statement holds, according to the weak duality [boyd2004convex]:

| (4) |

where is the primal optimal cost. If , where the strong duality holds, the dual solution coincides with a true optimal solution. However, strong duality usually does not hold in our problem and a duality gap exists. The purpose of the second stage is to reduce such gap and find a primal optimal solution.

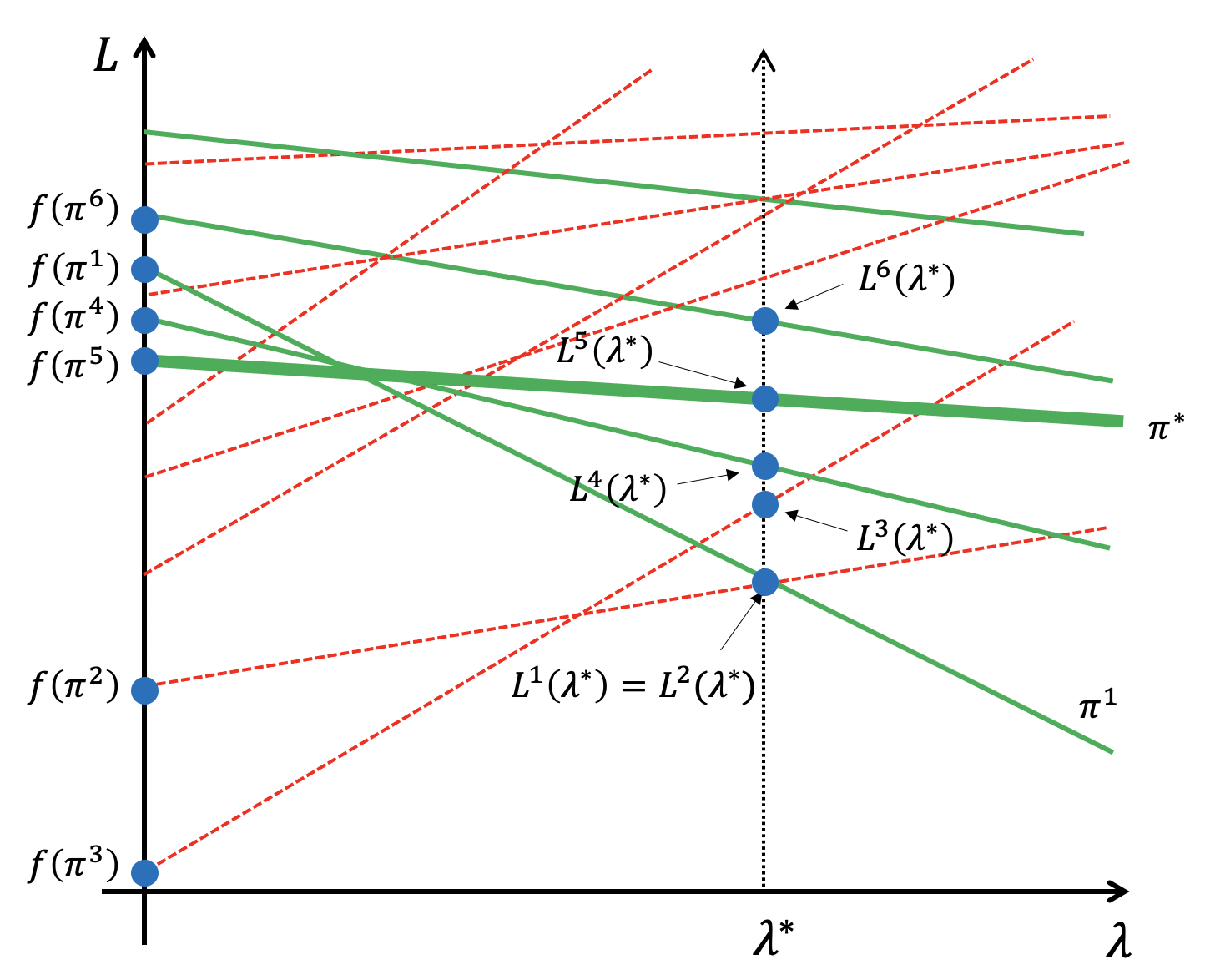

Conceptually, the way the algorithm obtains a primal optimal policy is quite simple. From the dual optimal policy, we can find a primal optimal solution by iteratively finding the next best solutions, with respect to the Lagrangian function value . This procedure is illustrated in Fig. 1 with an intuitive example which only includes a single secondary cost function. The figure shows all the deterministic policies in space, including feasible ones () and infeasible ones (), in green solid lines and red dotted lines, respectively. Note that the true primal optimal policy is indicated with a bold line. Fig. 1 also shows the Lagrangian function value for each policy as an intersection of the policy with the dotted vertical line at . Similarly, a -intercept of a policy is the primal cost . In addition, is the solution associated with which can be obtained from the first stage, where denotes -th best policy with respect to the Lagrangian function value . Starting from , we find the next best policies in terms of , in a non-decreasing manner, until we obtain a primal optimal policy , and update the incumbent policy whenever we obtain a better feasible policy. Note that the Lagrangian function value and incumbent cost at any time set lower and upper bounds on the optimal cost of the C-SSP, respectively. We refer to [hong2021anytime] for the details of the anytime algorithm.

III Hierarchical Constrained Stochastic Shortest Path Problem

In this section, we define a hierarchical constrained stochastic shortest path problem (HC-SSP). We begin this section with an intuitive example of a HC-SSP followed by a formal definition.

III-A HC-SSP in a Nutshell

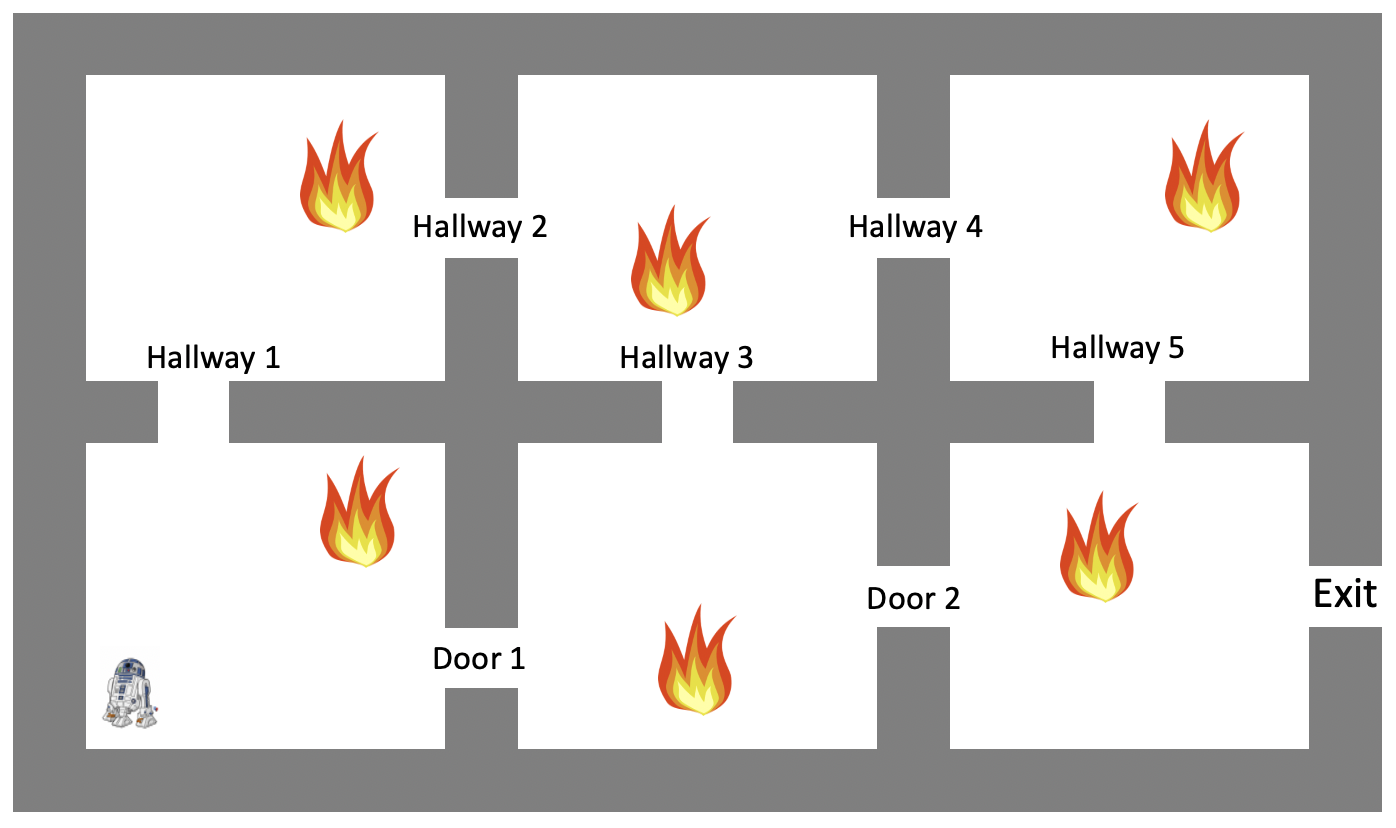

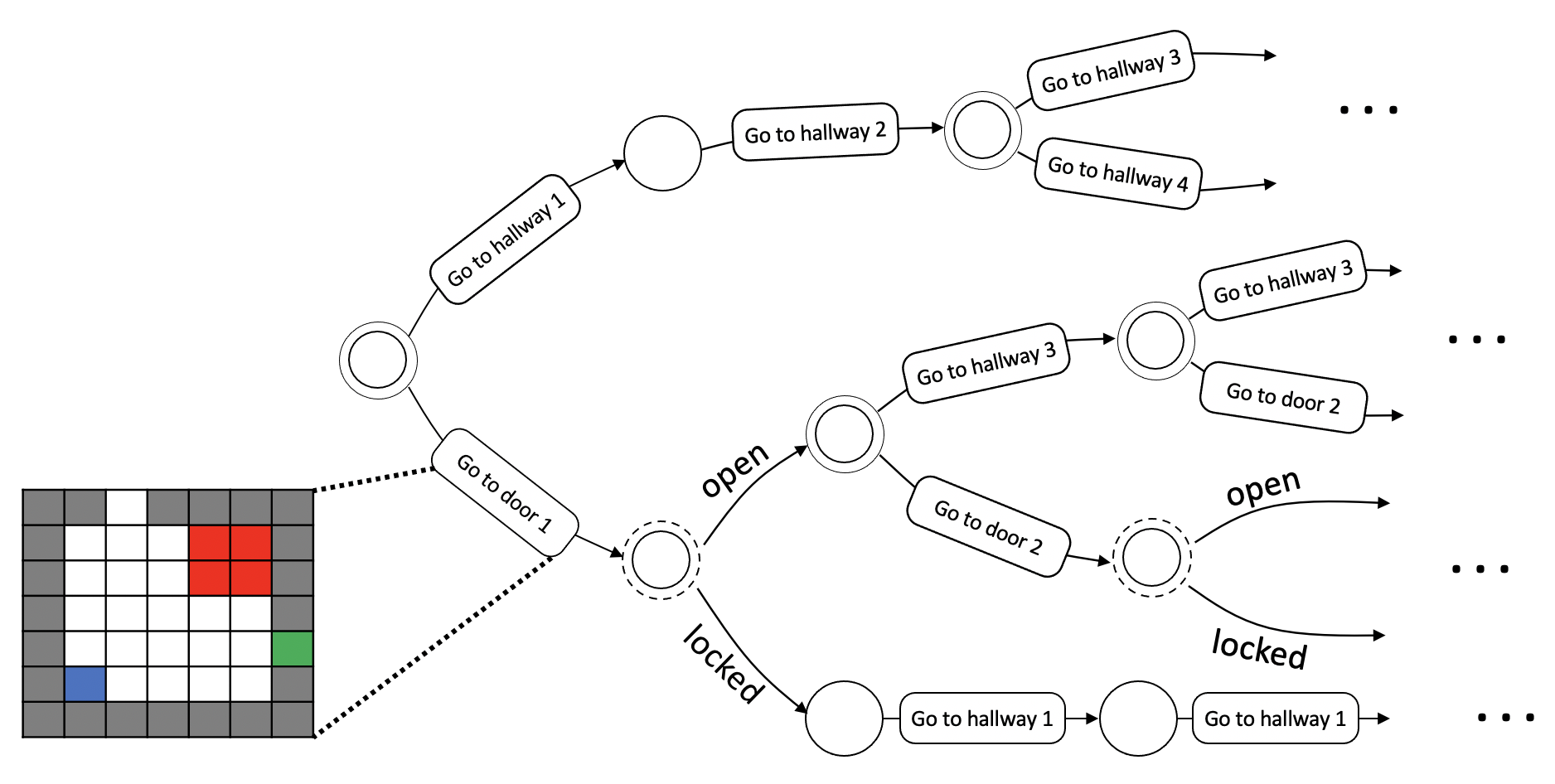

Consider a grounded example shown in Fig. 2, in which a robot is evacuating from a building with six rooms in a hazardous environment. In this example, a robot should make a series of decisions about which hallway or door to approach to get to the exit point. At a quick glance, using door 1 and door 2 seems to let the robot evacuate faster than the other options. However, the decision should be made carefully since the robot has only partial information on the building: the robot knows that the hallways are always clear, but also knows that the doors are locked with a 0.1 probability, in which case the robot should take a roundabout way. By assuming that a set of activities that move a robot from a specific landmark to another is well defined, the problem can be formulated as a conditional procedural planning problem, which is shown in Fig. 3 graphically. Note that, each circle and oval represents a notable event and activities, respectively. Also note that, double circle and dotted double circle represent controllable and uncontrollable choices, respectively.

One of the keys to our approach is noting that each activity (e.g., go-to-door1) is not necessarily predefined. Rather, each of the activities can be defined as an another planning problem with its own state and action space. For example, each activity can be considered as a stochastic shortest path problem in a grid world as shown in Fig. 3.

Another key to our approach is constraints on secondary costs defined over a set of activities. Consider a global constraint for the evacuation scenario is defined verbally as follows: “The damage caused by fire must be less than or equal to until evacuation.” With such constraint, the planning problem for go-to-door1 in Fig. 3 is now a constrained stochastic shortest path problem.

There is another yet more important implication of having such global constraint. Due to the global constraint, activities are no longer independent. Suppose we are planning for an activity go-to-door1 as a sub-problem for our evacuation planning problem. Then, how much of the cost out of the global damage budget should be allocated for this activity? For example, using budget parsimoniously in planning go-to-door1 might result in a conservative and sub-optimal plan if optimal solutions for other activities cause negligible damage. On the other hand, using too much of the budget in planning go-to-door1 might result in sub-optimality as well, since other activities could reduce global cost by using more budget. This motivates us to allocate the budget systematically for different activities to obtain global optimality which will be discussed in more detail in Section IV.

Finally, a solution to HC-SSP is a hierarchical policy that consists of both procedural policy and policies for every associated activity. There are two desirable properties for a solution. First, the solution should be feasible, which means that the solution should not violate any constraint. In the evacuation scenario, we only have one global constraint that requires the damage caused by fire to be less than or equal to . Therefore, the weighted sum of the damage cost for every activity that is selected by a procedural policy should be less than or equal to , where a weight for an activity is the likelihood of executing that activity. Second, the solution should minimize the expected cost. It is not always possible, however, to obtain an optimal solution, especially when the planning time is limited. Therefore, we want to develop a solution method with an anytime property which can output an incumbent feasible solution at timeout while the solution eventually converges to a true optimal solution with sufficient planning time.

III-B Problem Definition

A HC-SSP is a tuple , where

-

•

is a set of discrete states.

-

•

is the initial distribution.

-

•

is a set of notable events. Note that and are two special events, where is the start event and is the end event.

-

•

is a set of choice variables, each being a discrete, finite domain variable. Note that each is associated with an event , where we denote .

-

•

is a set of activities. An activity is activated if both start and end events of the activity are activated.

-

•

is a probabilistic transition function between events based on the assignments of choice variables, where is the probability of being in event after executing choice in event .

-

•

is an indexed set of constraints, where and is the number of constraints. Each is a tuple , where is a set of activities associated with the constraint , is an upper bound and is an index function for each that indicates which secondary cost function is used for . Note that in this paper we assume that a secondary cost function of an activity is included in at most one constraint for simplicity. This assumption, however, can be easily generalized with little modification.

A HC-SSP abstracts the underlying state-action space and dynamics based on events and activities, where the activities are selected by choice variables and the transitions between events are governed by transition function . Then each activity is defined over a subset of underlying state space and has its own action space and dynamics with its sub-goal. Formally, an activity is a tuple , where

-

•

are the start and end events of the activity, respectively.

-

•

is a set of discrete states.

-

•

is a set of discrete actions.

-

•

is the state transition function, where is the probability of being in state after executing action in state .

-

•

is an indexed set of cost functions, where each is the -th cost function that defines the -th cost of executing action in state and resulting in state and is the number of secondary cost functions for the activity .

-

•

is the set of goal state.

In this paper, we refer to the planning problem over the events and activities as procedural planning and the planning problem for each activity as activity planning, which will be discussed in more detail in Section IV-B.

III-C Solution to HC-SSP

A solution to a HC-SSP problem is a tuple , where

-

•

is a procedural policy which fully assigns every choice variable .

-

•

is a set of policies for every activated activity by , where a policy is a mapping from states to actions for an activity .

Note that, abusing the notation, if an activity is activated by , and otherwise. Then, an optimal solution to a HC-SSP is defined as follows:

| (5) | ||||

| s.t. | (6) | |||

| (7) | ||||

| (8) |

where and are initial and termination distributions of the policy for an activity , respectively, is a likelihood of executing an activity given procedural policy , and is the expected primary cost for an activity which is defined as follows:

and is the expected -th secondary cost for an activity which is defined as follows:

IV Approach

In this section, we present our proposed approach for a HC-SSP. We begin with an intuitive introduction of the approach and then present algorithms and formal analysis.

IV-A Overview

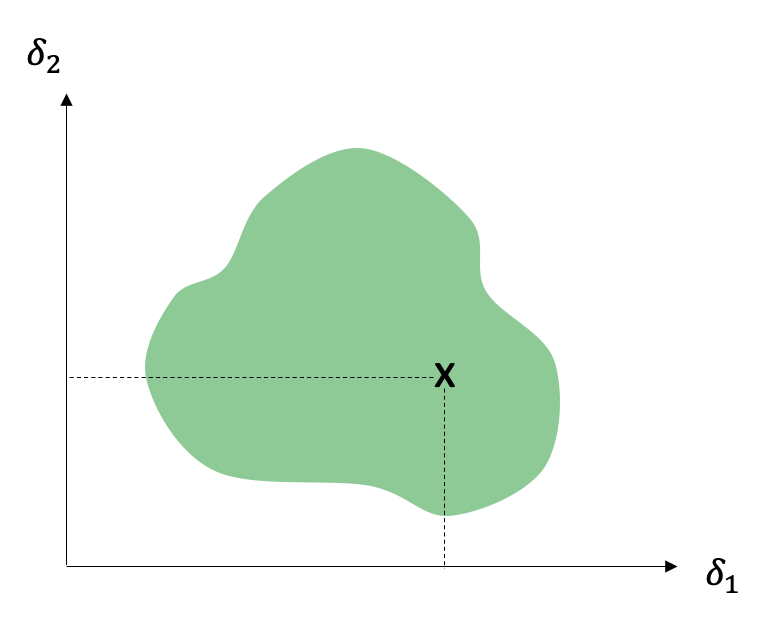

For the purpose of illustration, let us consider a simple problem shown in Fig. 4a which has two activities and a single constraint including both activities. Our approach is based on the fact that we can decouple the procedural and each activity planning problems if the constraint budget is allocated properly to each of the activities.

Fig. 4b shows the constraint budget allocation space for the example problem, where and axes are the allocated budget for activities and , respectively, and the green shaded region conceptually shows the region where a feasible solution to HC-SSP exists. Then if we allocate a specific budget to and , respectively, then we can find policies for each activity based on the allocation, which in turn allows us to find procedural policy based on and values of each activity. However, since the allocation space is continuous, it is computationally intractable to check every possible budget allocation to find an optimal solution. Instead, we frame the allocation problem based on the branch-and-bound scheme [balakrishnan1991branch, horst2013global].

Let and be lower and upper limits of budget allocation for a constraint and an activity . Then the allocation space that we are interested in, which we denote as , is defined as follows:

Note that a simple choice of such lower and upper limits for is and , where is the minimum likelihood of activity , although a more sophisticated bound can be found based on pre-processing. Then the branch-and-bound algorithm keeps splitting into smaller partitions and computes upper () and lower bounds () for the newly generated partitions, which can be used not only to guide the search toward an optimal solution but also to determine the quality of the current incumbent solution.

Algorithm 1 shows the branch-and-bound algorithm for a HC-SSP, where and denote upper and lower bounds for a partition , respectively, and and denotes global upper and lower bounds at the -th iteration, respectively. After initialization (lines 1–9), the algorithm splits a partition with the lowest lower bound into two partitions along its longest edge to form a new partition (lines 11–13). Then it computes lower and upper bounds for newly generated partitions (lines 14–19) and updates the global lower and upper bounds (lines 20–21). In addition, whenever a better feasible solution is found, it updates the incumbent solution (lines 4–6 and 16–18).

The core parts of Algorithm 1 are Compute-LB and Compute-UB subroutines which highly affect the performance of the algorithm. Before presenting the proposed Compute-LB and Compute-UB subroutines, let us begin with introducing procedural and activity planning in more detail, which has been briefly introduced in Section III-B.

IV-B Procedural and Activity Planning

In this section, we define procedural planning and activity planning, and then show that both of the planning problems can be reduced to an instance of C-SSP. Let us begin with the definition of procedural planning.

Definition 1.

(Procedural Planning) Suppose estimates for the primary and -th secondary cost functions for every activity and are given, where the former and the latter are denoted as and , respectively. Then we define planning for a procedural plan based on the given estimates as procedural planning.

Similarly, we define activity planning as follows.