Distributionally Robust Policy Learning with Wasserstein Distance††thanks: The data used in this study are derived from data files made available to researchers by the MDRC. The author remains solely responsible for how the data have been used or interpreted. I am grateful to Xiaohong Chen, Riccardo D’Adamo, Takanori Ida, Toru Kitagawa, Shosei Sakaguchi, Jörg Stoye, and Takahide Yanagi for their helpful comments. I also thank the anonymous referees and the seminar participants at the 2021 Kansai Econometrics Meeting, 2022 IAAE, 2022 AMES, and 2022 SETA. Finally, this work was supported by a Grant-in-Aid for JSPS Fellows, Grant Number 19J20984.

The effects of treatments are often heterogeneous, depending on the observable characteristics, and it is necessary to exploit such heterogeneity to devise individualized treatment rules (ITRs). Existing estimation methods of such ITRs assume that the available experimental or observational data are derived from the target population in which the estimated policy is implemented. However, this assumption often fails in practice because of limited useful data. In this case, policymakers must rely on the data generated in the source population, which differs from the target population. Unfortunately, existing estimation methods do not necessarily work as expected in the new setting, and strategies that can achieve a reasonable goal in such a situation are required. This study examines the application of distributionally robust optimization (DRO), which formalizes an ambiguity about the target population and adapts to the worst-case scenario in the set. It is shown that DRO with Wasserstein distance-based characterization of ambiguity provides simple intuitions and a simple estimation method. I then develop an estimator for the distributionally robust ITR and evaluate its theoretical performance. An empirical application shows that the proposed approach outperforms the naive approach in the target population.

Keywords: Individualized treatment rule, External validity, Distributionally robust optimization

1 Introduction

The effects of treatments are often heterogeneous based on observable covariates. In the presence of multiple treatments, an important decision for a policymaker is to choose a rule that specifies a treatment for each value of covariates to maximize their objective function. Such a rule is often called an individualized treatment rule (ITR), and its significance has been acknowledged in many areas including healthcare (Bertsimas et al.,, 2017), homeless services (Kube et al.,, 2019), and energy conservation (Ida et al.,, 2021).

The typical decision-making process of a policymaker is as follows. They are interested in a specific population, called the target population. Population here refers to the joint distribution of potential outcomes and covariates. In determining an ITR, they can use experimental or observational data generated from another population, which is referred to as the source population. Note that they can identify they source covariate distribution and source distribution of potential outcome associated with each treatment conditional on a possible value of covariates from this data. Based on this data, they decide upon an ITR, and then, the resulting ITR is applied to the target population. Finally, the average outcome attained by the ITR is realized as the policymaker’s reward. The average outcome is often called welfare; therefore, a policymaker’s primal goal is to choose an optimal ITR that maximizes the target population’s welfare.

Most existing studies have developed efficient estimation methods of optimal ITRs under the implicit assumption that the target and source populations are essentially identical. Under this assumption, the target population’s welfare attained by arbitrary ITRs can be point-identified. Consequently, the optimal ITR for the target population also becomes identifiable. Based on this fact, previous studies have proposed an estimation method of optimal ITR utilizing the inverse-probability weighting (e.g., Kitagawa and Tetenov,, 2018; Swaminathan and Joachims,, 2015; Zhao et al.,, 2012) and augmented inverse-probability weighting (e.g., Athey and Wager,, 2021; Dudík et al.,, 2011; Zhou et al.,, 2022).

However, in practice, whether this assumption is valid is controversial. For example, imagine that a state government wants to decide whether or not to allow each individual to participate in an employment support program to improve average earnings in the state. The available data on the program come from a randomized controlled trial conducted in another state. In the framework above, two available treatments exist: one is to force an individual to participate in the program, and the other is to exclude the individual from the program. Associated with each treatment, the potential outcome is earnings that would be realized when the individual is assigned to the treatment. In addition, observable individual attributes, such as age and previous earnings, compose covariates. The joint distribution of potential outcomes and covariates in the former state corresponds to the target population, and that in the latter state corresponds to the source population. The critical question is whether the former and latter states can be considered the same. The demographics of the two states may be different. In addition, the response to the program may also be different because of differences in other economic circumstances. In such cases, it would be unrealistic to assume that the two populations are the same. The scenarios in which the assumption can be violated are not limited to the above example. For instance, when the state government wants to exploit a randomized controlled trial conducted earlier in its state to determine the current optimal ITR for the state, it must consider the validity of the assumption judiciously.

When the source and target populations are different, it is challenging to estimate the optimal ITR via the straightforward application of existing methods. However, in some cases, a slight modification in existing methods is sufficient to estimate the optimal ITR for the target population. Suppose that a difference exists between the source and target populations only in terms of covariate distribution and the density ratio of the target and source covariate distributions is known or identifiable with additional covariates data from the target population. In this case, the target population’s welfare attained by an ITR remains identifiable by reweighting the outcome with the density ratio of source and target covariate distributions. Kitagawa and Tetenov, (2018, Remark 2.2) and Uehara et al., (2020) discuss estimation methods that are tailored to this situation. Instead, if the distributions of covariates or distributions of potential outcomes associated with each treatment conditional on a value of covariates differ between the source and target populations in an unknown and unidentifiable way, it is impossible to estimate the optimal ITR for the target population. In the first place, the target population’s welfare attained by an ITR cannot be point-identified, which is a contrast to the case where the two populations are the same. This implies that the optimal ITR for the target population cannot be identified; the estimation goal itself is unclear.

Motivated by this identification problem in such a situation, one strand of recent literature has proposed replacing the unidentifiable goal with an identifiable one. In particular, Mo et al., (2021), Si et al., (2020, 2021), and Zhao et al., (2019) consider utilizing the concept of distributionally robust optimization (DRO) to obtain a reasonable learning goal. DRO begins with constructing an ambiguity set, which is a set of populations, based on the available knowledge and additional assumptions regarding the relationship between the source and target populations. Then, for each feasible ITR, it evaluates the distributionally robust welfare, which is the worst-case value of welfare over the ambiguity set. Finally, it chooses the ITR that maximizes the distributionally robust welfare. Following Mo et al., (2021), this study refers to such an ITR as a distributionally robust ITR (DR-ITR). By choosing the DR-ITR, it is guaranteed that the target population’s welfare is at least tantamount to its distributionally robust welfare, as long as the target population belongs to the ambiguity set. From this perspective, the DR-ITR would be a reasonable goal.

Although these attempts are the same, when they are applications of DRO, they vary based on underlying assumption. Zhao et al., (2019) and Mo et al., (2021) assume that the target population is absolutely continuous with respect to the source population and that a difference in the source and target populations exists only in the covariate distribution. Then, with the available data being the experimental or observational data generated from the source population, they construct the ambiguity set on the unknown target covariate distribution. Instead, Si et al., (2020, 2021) include the case where the conditional distributions can also differ in the two populations, while assuming that the target population is absolutely continuous with respect to the source population. Using the experimental or observational data, which are derived from the source population, they construct the ambiguity set on the target population. As is clear from the current discussion, these attempts may not be appropriate when the assumed absolute continuity does not hold.

This study also aims to define a reasonable ITR when the target population’s welfare is not identifiable by exploiting the concept of DRO. Specifically, this study mainly deals with the situation where the policymaker has access to the experimental data from the source population and the covariate data from the target population. In other words, the policymaker has no knowledge about the target conditional distribution of potential outcomes. In contrast to the aforementioned attempts (Mo et al.,, 2021; Zhao et al.,, 2019; Si et al.,, 2020, 2021), this study does not assume that the target conditional distribution of potential outcomes is absolutely continuous with respect to that of the source population, while the absolute continuity of the covariate distributions is maintained. To construct the ambiguity set without absolute continuity, I employ Wasserstein distance or order 1. This is a metric over probability distributions that does not require the Radon-Nykodim derivative, and thus, the proposed method can cover broader scenarios.

In addition to this advantage, the proposed Wasserstein-style ambiguity set is computationally attractive. In particular, with this ambiguity set, one can obtain the analytical solution of the distributionally robust welfare. Owing to this analytical simplicity, one can draw a lot of intuition. For example, it can be shown that obtaining an ITR by replacing the unknown target conditional distribution of potential outcomes with that of the source population is already distributionally robust under special cases in the Wasserstein sense. This provides a justification for the assumption that the source and target conditional distributions of potential outcomes are the same. In addition, by utilizing the technique developed in Mo et al., (2021) or Zhao et al., (2019), one can easily extend the proposed method to a situation where no covariate data are available from the target population.

For the estimation of the DR-ITR, the derived closed-from of the distributionally robust welfare implies a simple estimator. I assess its theoretical performance in terms of regret, which is in line with the literature on policy learning. Finally, I demonstrate the proposed DR-ITR using data from experimental evaluations of the changes in welfare-to-work programs in the early 1980s. The results show that the DR-ITR attains higher welfare in the target population than the ITR obtained by a naive approach.

Related Literature

This study contributes to the literature on ITRs (e.g., Kitagawa and Tetenov,, 2018; Zhao et al.,, 2012; Swaminathan and Joachims,, 2015; Athey and Wager,, 2021; Dudík et al.,, 2011; Zhou et al.,, 2022). The methods developed in existing studies are intended for use in situations where the source and target populations are the same. The policy learnings when the two populations are different are not well-explored. This study designs a DR-ITR that works appropriately in such situations.

The fundamental problem that motivates this study is the so-called external validity (Campbell,, 1957). The studies that explore external validity include (Hotz et al.,, 2005; Cole and Stuart,, 2010; Stuart et al.,, 2011, 2015, 2018; Allcott,, 2015; Andrews and Oster,, 2019; Dehejia et al.,, 2021; Pritchett and Sandefur,, 2013; Hartman et al.,, 2015; Gechter et al.,, 2019; Vivalt,, 2020; Tipton,, 2013, 2014). The primary interest of the literature is to obtain a point identification of the average treatment effect for the target population. To achieve this goal, the literature often assumes that the conditional distributions of potential outcomes are the same between the source and target populations. By contrast, this study allows a difference in the conditional distributions, and DRO attempts to obtain the lower bound of the target population’s welfare.

As mentioned earlier, the idea of this study stems from DRO with a Wasserstein-style ambiguity set. For a comprehensive review of DRO, see Rahimian and Mehrotra, (2019). A typical application of Wasserstein-DRO constructs an ambiguity set around the empirical distribution and lets its radius shrink to zero depending on the sample size to capture sampling uncertainty (e.g., Mohajerin Esfahani and Kuhn,, 2018; Blanchet et al.,, 2019; Shafieezadeh-Abadeh et al.,, 2015, 2019; Gao et al.,, 2017; Gao,, 2020). By contrast, the ambiguity set considered in this study is not centered around empirical distribution, but is centered around the source population, which differs from empirical distribution. In addition, its radius is set at a fixed positive value and does not converge to zero.

Adjaho and Christensen, (2022) conducted a similar study.111This study and Adjaho and Christensen, (2022) are independent contributions made public almost simultaneously in the arXiv repository. They also apply Wasserstein-DRO to a similar situation to develop a method that works when the source and target populations are different. One apparent difference is a concrete form of the Wasserstein-style ambiguity set. Specifically, Adjaho and Christensen, (2022, Section 3) deals with a similar situation as that in this study, but the derived results are different due to the difference in the ambiguity set. Their result implies that the modifications discussed in Kitagawa and Tetenov, (2018, Remark 2.2) and Uehara et al., (2020) are already distributionally robust, while the result of this study implies that the distributional robustness of the modifications does not necessarily hold and this study’s proposed approach outperforms the modifications in some aspects. In addition, Adjaho and Christensen, (2022, Section 4) extends Wasserstein-DRO to the case where both the target covariate distribution and target conditional distribution of potential outcomes are unknown and unidentifiable, without imposing the assumption of the absolute continuity of the covariate distributions. Their result implies that the resulting distributionally robust welfare remains unidentifiable without further assumptions. By contrast, this study extends the proposed method to such a case while maintaining the assumption of the absolute continuity of the covariate distributions, and adopts the DRO technique developed in Mo et al., (2021); Zhao et al., (2019).

Structure of the paper

In Section 2, I formally introduce the underlying model considered in this study. Then, in Section 3, I discuss the application of Wasserstein-DRO to the model of Section 2. Section 4 develops the estimation method of the proposed DR-ITR and provides the theoretical guarantee of the estimator. Finally, Section 5 demonstrates the proposed DR-ITR using experimental data. The additional information and proofs of the theoretical results are presented in the supplementary materials.

Notation

For any metric space , I use to denote Borel -algebra, which is the -algebra generated from the metric topology of . In addition, I write for the set of all probability measures on . For a probability measure , the support of the measure is denoted by . Given a measure space , another measurable space , and a measurable map , I denote the induced probability measure on by ; that is, for all . In addition, if , the expectation of with respect to the measure is denoted by .

2 Model

Here, I formally introduce the underlying model considered in this study (Section 2.1). After introducing the model, I explain the naive approach that assumes that the two populations differ only in the covariate distributions (Section 2.2). This approach often works as a bench mark. Before delving into details, a note of caution: Sections 2 and 3 exclude the consideration of identification and estimation and focus on the problem of interest in the population level. In particular, I often assume that a policymaker has the knowledge of a certain population, which is a joint distribution of potential outcomes and covariates, although the joint distribution of potential outcomes is never identified even with the experimental data. The identification and estimation will be discussed in Section 4.

2.1 Problem Setup

Let be a finite set of possible treatments. Each individual in a population is characterized by a tuple , where denotes the potential outcome that would be realized if one received treatment . I assume that for any , takes a value in the outcome space , which is a closed subset of a Euclidean space. Then, a tuple takes values in , which is assumed to be equipped with the -distance; that is, for any pair , the distance is measured by . The last component denotes the individual’s observable characteristics, which take value in a Polish space . Let ; thus, a tuple takes values in . A particular population is characterized by a probability measure over . For an arbitrary population , let denote the conditional distribution of potential outcomes, given by , and let denote the marginal distribution of .222In this study, the conditional distributions of potential outcomes are understood as a regular conditional probability measure. The existence of a regular conditional probability measure is guaranteed by Bogachev, (2007, Theorem 10.4.14) because the covariate space is Polish. Hence, any conditional distribution of potential outcomes can be regarded as a proper probability measure in the outcome space, as compared to the case where one defines a conditional probability as a Radon-Nikodym derivative. Additionally, I define the conditional mean response (CMR) function as for and .

An ITR is a measurable mapping from to , and a set of candidate ITRs is denoted by . As emphasized in Kitagawa and Tetenov, (2018) and often assumed in subsequent studies, the set may not necessarily contain all measurable mappings. For any ITR , the welfare of ITR in population is given by

| (1) |

where the last equality comes from the law of iterated expectations. Hence, the welfare of ITR can be calculated using the knowledge of the covariate distribution and CMR function of population . Clearly, the welfare of ITR varies with the population under consideration.

A policymaker focuses on the target population , and aims to maximize the target population’s welfare. Namely, given the target population , their goal would be to obtain the optimal ITR for the target population as summarized in the following optimization problem:

| (2) |

It is obvious that the policymaker can achieve the goal if they have complete knowledge about . More precisely, knowledge about the target covariate distribution and target CMR function for all and is necessary and sufficient to solve problem 2. In other words, the policymaker cannot obtain the best ITR without such knowledge.

In this study, I consider the situation where the policymaker has no knowledge on the target conditional distribution of potential outcomes. Contrarily, I assume that they have knowledge on the target covariate distribution and source population , which differs from the target population. The two populations can differ in an arbitrary way as long as the following assumption is satisfied.

Assumption 2.1.

The target population and source population satisfy the following properties:

-

(i)

The target covariate distribution is absolutely continuous with respect to the source’s covariate distribution .

-

(ii)

The source CMR function is -almost surely bounded for all .

Similar assumptions to 2.1.(i) have been imposed in the literature on external validity (e.g., Hotz et al.,, 2005, Assumption 3). 2.1.(ii) is satisfied when potential outcomes are -almost surely bounded. In summary, the policymaker does not know anything about the target CMR function, but instead knows the source and target covariate distribution and source CMR function. This implies that they cannot calculate the target population’s welfare , whatever the ITR is. Consequently, they cannot obtain the optimal ITR for the target population.

2.2 Naive Approach

The reason the policymaker cannot obtain the optimal ITR for the target population is that the target CMR function is unknown, in contrast to the source CMR function . Thus, a naive approach is to replace the target CMR function with the source CMR function and solve the optimization problem; that is,

| (3) |

Note that the problem 3 is well-defined as an optimization problem due to 2.1.(i); otherwise, there exists a point such that is not uniquely determined. Hereafter, I refer to this approach as the naive approach and denote its optimal solution by , as indicated in 3.

When the target and source CMR functions are the same, the objective function in 3 corresponds to the target population’s welfare , and hence, equals . This is the case where one assumes that the source and target conditional distributions of potential outcomes are the same, as often assumed in the literature on external validity (e.g., Assumption 2 of Hotz et al.,, 2005). Unfortunately, however, one cannot verify this assumption from the available knowledge.

3 DR-ITR

This section formally discusses the application of DRO to the current setting. First, I define the DR-ITR with an arbitrary ambiguity set, which is a set of populations. Generally, an ambiguity set is constructed based on available knowledge. I denote the ambiguity set by . As a policymaker has knowledge of the source population and target covariate distribution, it is natural that the ambiguity set can depend on and . Given the ambiguity set, DRO solves the following optimization problem:

| (4) |

where

| (5) |

The object is the distributionally robust welfare, which is the worst-case value of welfare over the ambiguity set. Thus, DRO’s goal is to choose the DR-ITR that maximizes the distributionally robust welfare.333One of the potential drawbacks of DRO is that the max-min criterion may be too conservative to generate a valid policy. This drawback can be alleviated by adopting the Hurwicz criterion, which allows a policymaker to decide the extent to which they become conservative (Hurwicz,, 1951). Then, the objective function can be defined as a convex combination of the worst-case and best-case values for welfare. All the results presented in this study are easily extensible with minor modifications. Suppose that the target population is contained in the ambiguity set . In this case, the optimal ITR for the target population defined in 2 performs better than the distributionally robust policy in terms of the target population’s welfare; that is, . However, it is infeasible to obtain with the current knowledge. Instead, choosing the DR-ITR ensures that the ex-post target population’s welfare is at least equal to its distributionally robust welfare; that is, .

In the aforementioned DR-ITR formulation, several important issues remain unclear. First, I introduced the ambiguity set in an abstract manner. The choice of the ambiguity set is left to the policymaker’s discretion, and they can construct the set based on the available information and their belief in the difference between the source and target populations. Section 3.1 instantiate the DR-ITR with a Wasserstein-style ambiguity set. Second, given the specific choice of the ambiguity set, the DR-ITR must evaluate the distributionally robust welfare for each ITR . However, this is deemed difficult because the minimization problem in 5 generally involves an infinite number of distributions. Nevertheless, Section 3.2 shows that the distributionally robust welfare can be calculated very efficiently. In addition to these issues, I discuss what kind of population is determined as the worst case by Wasserstein DRO (Section 3.3) and some equivalence of the DR-ITR and naive-ITR under special cases (Section 3.4).

3.1 Ambiguity Set Based On Wasserstein Distance

In this study, the ambiguity set is constructed with the Wasserstein distance of order 1. Wasserstein distance is a kind of distance of probability measures that utilizes the structure of the underlying metric space. In the current setup, for a pair of probability measures in , the Wasserstein distance of order 1 is defined by

| (6) |

where denotes the set of all the joint distributions of , such that and . It is well-known that there exists that attains the infimum on the right-hand side of 6. In addition, in our current application, it is important that the distance does not require Radon-Nikodym derivative. For a more detailed explanation, see Villani, (2009, Chapter 6).

Based on Wasserstein distance, I introduce the ambiguity set considered in this study. Concretely, given the source population , the target covariate distribution , and a real number , the ambiguity set is defined as

| (7) |

Note that the ambiguity set 7 is well-defined under 2.1.(i) as the source conditional distribution of potential outcomes, , is unique for all . A population is contained in the ambiguity set 7 only if it satisfies the following properties: (i) for each in support of the target covariate distribution , its conditional distribution of potential outcomes at point differs from the counterpart of the source population by at most in terms of Wasserstein distance; (ii) its marginal distribution of covariates equals the target covariate distribution, . That is, the ambiguity set point wisely constructs Wasserstein balls with the source conditional distribution of potential outcomes as the center and as the radius. Importantly, this allows the conditional distribution of potential outcomes to differ from that of the source population.

The radius represents the ambiguity level of the target population, and its choice depends on the policymaker. On the one hand, the value should be large enough that the target population is contained in the ambiguity set; otherwise, it is not guaranteed that the distributionally robust welfare of the DR-ITR is a lower bound of its target population’s welfare. On the other hand, the value should also be small. When the value is excessively large, the decision based on DRO can be too conservative to be helpful. Hence, the optimal value of would be . Unfortunately, such a choice is infeasible in the current setup as knowledge on the target conditional distribution is lacking. Instead, Corollary 3.1 shows the relationship between certain welfare-relevant parameters and the value of , which guides the choice of .

Corollary 3.1.

Suppose that Assumption 2.1 is in force, and assume that a population is in the ambiguity set given in 7. Then, the population satisfies the following inequalities:

-

(i)

For all and ,

-

(ii)

For all and ,

-

(iii)

For all ,

-

(iv)

For all ,

The first two items characterize the difference in the conditional distributions of potential outcomes for each possible . In particular, the first one states that as long as a population is in the ambiguity set, its CMR function differs from the source CMR function by at most . Similarly, the second one states that the difference in the CMR functions between any pairs of treatments differs from the counterpart of the source population by at most . The latter two items characterize the difference in the marginal distributions of potential outcomes, while focusing on its mean. For the third item, the upper bound consists of the ambiguity level and an additional term that essentially measures the difference in the covariate distributions and . A similar interpretation holds for the fourth item. Note that this result does not address the tightness of the aforementioned inequalities. In particular, the result does not imply the existence of a distribution with for some and . The existence of such distributions are guaranteed in Corollary 3.2, which will be presented later.

Remark 3.1 (Ambigutiy set based on the Wasserstein distance of general order).

One can construct the ambiguity set using the Wasserstein distance of general order. Specifically, for , the Wasserstein distance of order is defined by

for any pair .

Remark 3.2 (Ambiguity set based on -divergence).

For a convex function , the -divergence between distributions and with is defined by

This definition includes the Kullback-Leibler (KL) divergence, Hellinger distance, or -divergence as a special case. One can construct -divergence based ambiguity set in 7 by replacing with . The crucial advantage of Wasserstein over -divergence is that a ball based on -divergence requires the support of each element in the ball to be included in the support of the central distribution, whereas the ball based on Wasserstein distance does not. Such requirements highly restrict the applicability of DRO.

3.2 Tractable Reformulation via Strong Duality

To solve problem 4, one must evaluate the distributionally robust welfare in 5. However, the infimum generally involves an infinite number of distributions and is not easy to calculate directly. In this section, I provide a tractable reformulation of the problem 4 by exploiting the strong duality results from Blanchet and Murthy, (2019), which simplifies our analysis.

First, the law of iterated expectations implies that the minimization problem 5 can be solved component-wise. Specifically, it can be written as , where

| (8) |

for each . The object can be interpreted as the worst-case conditional welfare of policy at covariate value . With these notations, the evaluation must be reduced to for all and .

One can obtain the strong dual problem of 8 by applying the results of Blanchet and Murthy, (2019). In LABEL:sec:review-of-BM, I briefly review their result. The significant advantage of this result in our application is that the dual problem involves only the source conditional distribution and that the dual problem involves a one-dimensional concave programming with respect to the dual argument. By explicitly solving this dual problem, the following theorem is obtained.

Theorem 3.1.

Suppose that Assumption 2.1 is in force. Then, for each and , it holds that

where is the infimum of outcome space , and it is set to when is unbounded from below. Therefore, the DR-ITR can be equivalently represented by

| (9) |

As is clear from the first equation of Theorem 3.1, the worst-case conditional welfare can be written in a simpler form, and its interpretation becomes simple as well. Consider an ITR that assigns treatment to individuals with the covariate . The worst-case conditional welfare of the ITR for these individuals is obtained by translating the source CMR function of treatment by (when such a translation is unrealistic owing to the lower bound of the outcome space, the worst-case value is set at the lower bound). Because of this simplification, the DR-ITR becomes tidy, as shown in 9. This result provides an interesting connection with the naive approach in Section 3.4, and also underlies the estimation method discussed in Section 4. Note that the above result does not address the existence of a worst-case population that attains the infimum in 5, which will be discussed in Section 3.3.

Remark 3.3.

Even when the ambiguity set is specified using the Kullback-Leibler divergence instead of the 1-Wasserstein distance, the worst-case conditional welfare can be simplified using its strong dual representation. Specifically, the strong duality result from (Hu and Hong,, 2012, Theorem 1 and Theorem 2) implies that the worst-case conditional welfare of the ITR at can be obtained as the optimal value for the following problem:

However, as opposed to the case of the 1-Wasserstein distance, the optimization problem cannot be analytically solved for the general source population. Therefore, such a concise representation of the DR-ITR as 9 is not available for the KL divergence-based ambiguity set. This will introduce computational complexity when considering the estimation procedure.

3.3 Existence of the Worst-Case Population

It is natural to question whether there exists a worst-case population that attains the infimum in 5, and if so, what kind of population it is. This section discusses the existence and characterization of such populations in the DR-ITR for specific outcome spaces. Again, the application of the results of Blanchet and Murthy, (2019) helps determine the existence and characterization of the worst-case population, as shown in Corollary 3.2.

Corollary 3.2.

Suppose that , .

-

(i)

If is convex and unbounded from below, the worst-case conditional distribution, which attains the infimum in 8, exists. Moreover, one of such distributions is characterized as an induced measure , with

-

(ii)

If is convex and bounded from below, the worst-case conditional distribution, which attains the infimum in 8, exists. Moreover, one of such distributions is characterized as an induced measure , with

Corollary 3.2 shows the existence of the worst-case conditional distribution of potential outcomes, which attains the infimum in (8) when the outcome space is a convex subset of . The result indicates that the worst-case conditional distribution of potential outcomes always exists when the outcome space is convex. Then, one can obtain the worst-case population by incorporating the worst-case conditional distribution with the target covariate distribution .

The corollary also gives examples of the worst-case conditional distribution. When the outcome space is convex and unbounded from below, one worst-case conditional distribution can be obtained by simply moving the source conditional distribution by along the -th dimension. Consequently, the worst-case conditional welfare is equal to . When the outcome space is convex but bounded from below, the characterization depends on whether it is logically possible to decrease the source CMR by . When , the worst-case distribution can be obtained by reducing the source CMR by and concentrating more mass around the mean. Conversely, if , the worst-case conditional distribution concentrates on for the -th dimension. Note that the distributions given in the corollary are merely examples of worst-case conditional distributions. For example, when , the worst-case distribution can also be characterized as an induced measure using a map

given . Finally, this result implies that the bound given in 3.1.(i) is tight.

3.4 Relation Between the DR-ITR and Naive-ITR

This subsection discusses an interesting relationship between the DR-ITR and naive-ITR in Section 2.2, which provides a justification for the naive approach from the perspective of Wasserstein DRO. Let be the first best ITR for the source population such that -a.s.. I additionally impose the following assumption.

Assumption 3.1.

Either of the following is true:

-

(i)

The first best ITR for the source population is an element of .

-

(ii)

For any policy , it holds -almost surely that .

A simple example in which 3.1.(i) is satisfied is the case where consists of all measurable mappings from to . 3.1.(ii) informally states that the source CMR function is sufficiently distant from the lower bound of the outcome space. One typical case is where the outcome space is unbounded from below; that is, . In this case, the assumption holds regardless of the value of and the class of the ITRs. Under Assumption 3.1, one has the following theorem:

Theorem 3.2.

Suppose that Assumptions 2.1 and 3.1 hold. Then, any naive-ITR is also a DR-ITR.

At first glance, this result seems unnatural. The naive approach imposes a somewhat strong assumption so that the target and source CMR functions become identical, and then searches for the best ITR. Contrarily, the DR-ITR considers populations with CMR functions that can deviate from the source CMR function more flexibly and optimizes against the worst-case over such populations. Hence, there appears to be a difference between the ITRs resulting from these two approaches. However, when the ambiguity set is specified using the 1-Wasserstein distance as in 7 and Assumption 3.1 holds, the naive-ITR is already distributionally robust.

I explain the relation between Assumptions 3.1 and 3.2 in more depth. For 3.1.(i), notice that Theorem 3.1 implies that the worst-case conditional welfare is always maximized by choosing the first best ITR . Thus, also maximizes the worst-case welfare . Therefore, as long as the first best ITR is in , it is one of the DR-ITRs. However, when 3.1.(ii) holds, Theorem 3.1 implies that

for all . That is, the worst-case welfare is obtained by translating the objective function of the naive approach by . Thus, maximizing the distributionally robust welfare is equivalent to maximizing the objective function of the naive approach.

Finally, I note that this consequence does not hold when Assumption 3.1 is not satisfied as exemplified in Example 3.1. In addition, such a relation does not necessarily hold when the ambiguity set is constructed using other metrics as demonstrated in Remark 3.3.

Example 3.1.

Suppose that , , , , and such that

In addition, assume that the source CMR function and target covariate distribution are given as follows:

where . Observe that Assumption 3.1 does not hold in this setting; in fact, one has , although . It is easily shown that the naive approach chooses , while DRO chooses .

Remark 3.4.

When the ambiguity set is specified using the Kullback-Leibler divergence, the naive-ITR and DR-ITR generally do not agree. Consider the case in which and for each and . In this case, is distributed according to a log-normal distribution with the parameters and . Hence, its expectation is represented by . Based on the strong duality result discussed in Remark 3.3, DRO with the Kullback-Leibler based ambiguity set maximizes the following function over the policy class:

It is evident that the objective function differs from that of the naive approach; hence, the solutions of these two approaches are not similar.

3.5 Consideration Regarding the Unknown Covariate Shift

Thus far, it has been assumed that the target covariate distribution is known. However, what if it is unknown? Even in such a case, one can construct another ambiguity set on the target covariate distribution, and seek a DR-ITR that is distributionally robust against the unknown covariate shifts as well. In particular, if 2.1.(i) is satisfied, the ambiguity set (e.g., Mo et al.,, 2021; Zhao et al.,, 2019) can be utilized.

Here, I incorporate the above idea with the ambiguity set based on -divergence. Suppose that a policymaker has no knowledge about the target population, but instead has knowledge on the source population. In addition, I assume that Assumption 2.1 holds. Then, one can incorporate unknown covariate shifts by using the following ambiguity set:

for . With this ambiguity set, the DR-ITR is an ITR that maximizes the worst-case welfare over the ambiguity set; that is, . As the constraints on the conditional distribution of potential outcomes and the covariate distribution are independent, one can calculate the distributionally robust welfare in a two-step procedure: (i) obtain the worst-case conditional welfare and (ii) calculate the worst-case value of the marginalized worst-case conditional welfare over the ambiguity set. Thus, Theorem 3.1 implies that the distributionally robust welfare is expressed as

As in Section 3.4, Assumption 3.1 provides an interesting result. Specifically, it can be shown that under the assumption it holds that

Thus, the DR-ITRs obtained by ignoring the possible difference in conditional distributions of potential outcomes are also distributionally robust. This result specifically reinforces the DR-ITR considered in Mo et al., (2021).

4 Estimation

In this section, I discuss the identification and estimation of the DR-ITR . Then, I evaluate the theoretical performance of its estimator. The estimation method is based on Theorem 3.1.

Suppose that the experimental or observational data generated from the source population and the covariate data generated from the target population are available. Specifically, the data from the source population are , where refers to the observable pre-treatment covariates of individual , denotes the individual’s treatment assignment, and is the post-treatment observed outcome. The sample is an i.i.d. draw from a joint distribution of . I assume that it satisfies unconfoundedness, the overlap condition, and consistency, and that its marginal distribution of is the same as the source population . However, the covariate data from the target population is , where each is an i.i.d. draw from .

The following are identifiable from this data; the marginal distributions of the source conditional distribution of potential outcomes for each and , the source covariate distribution , and the target covariate distribution . Thus, it is obvious from Theorem 3.1 that the distributionally robust welfare is identifiable, and thus, a natural estimator for can be constructed as follows:

-

(i)

Using data , estimate to obtain for all and .

-

(ii)

Solve

(10) where

(11)

The object is an estimator of the distributionally robust welfare. The estimator is constructed by replacing the unknown source CMR function with the estimated CMR function , and replacing the unknown target covariate distribution with the empirical distribution based on . Arbitrary method can be used as the estimator for the source CMR function.

Remark 4.1.

As demonstrated in Section 3.4, when one assumes Assumption 3.1, it suffices to seek a naive-ITR, to obtain a DR-ITR. Hence, the problem boils down to the question of how to estimate the objective function in 3. This problem has already been analyzed in existing studies, for example, Kitagawa and Tetenov, (2018, Remark 2.2) and Uehara et al., (2020).

4.1 Theoretical Guarantee

In line with the literature on policy learning, I evaluate the estimator’s performance using a kind of regret. Usually, the regret of the ITR is defined as the difference in the target population’s welfare between the optimal ITR for the target population and the ITR ; that is, the usual regret is defined as . However, the goal of DRO is different from that of standard policy learning; therefore, it is natural to modify the definition of regret. Specifically, I focus on the distributionally robust regret of the ITR defined by

In contrast to the usual regret, distributionally robust regret is defined as the difference in the distributionally robust welfare between the true DR-ITR and the ITR . The same concept is also considered by, for example, Lee and Raginsky, (2018); Si et al., (2021); Tu et al., (2019). In the following, I derive a high probability bound on .

I begin by listing some assumptions necessary for the analysis. Thereafter, I denote the expectation with respect to the distribution of data by .

Assumption 4.1.

The data generating process satisfies the following conditions:

-

(i)

.

-

(ii)

One has access to an estimator for such that are bounded almost surely and

for as .

Assumption 4.2.

There exist constants , , and such that for all .

Assumption 4.1 is the assumption on the data generating process. Assumption 4.2 is included to control the complexity of the ITR class. The object in the assumption is the covering number of , with as the radius and the Hamming distance as the distance. For its precise definition, see Definition 4 of Zhou et al., (2022). Then, under Assumption 4.2, I introduce the entropy integral by . Combining these assumptions, the next theorem follows.

Theorem 4.1.

Suppose that Assumptions 2.1, 4.1 and 4.2 are satisfied. Then, for any , with a probability of at least , it holds that

where is an almost sure bound of .

Theorem 4.1 provides a high-probability bound on the distributionally robust regret. The first term of the upper bound is a high probability bound on the error generated using the empirical distribution of , instead of the true target covariate distribution . Contrastingly, the second term is a high probability bound on the error generated by using the estimator , instead of the true source CMR function . Overall, the distributionally robust regret with high probability converges to zero at a rate of .

5 Empirical Application

I demonstrate the proposed DR-ITR using data from the experimental evaluations of changes in welfare-to-work programs during the early 1980s. The program changes were aimed to increase employment and decrease welfare receipt. The new programs required single-parent families who were receiving benefits from Aid to Families with Dependent Children (AFDC), to participate in employment support programs as a condition for receiving the full amount of their monthly welfare payments. For a more detailed explanation of the program changes, see Friedlander and Robins, (1995), Hotz et al., (2005), and the references therein. Several states conducted randomized controlled trials (RCTs) to evaluate the effects of the program changes. Among these states, I focus on two experiments conducted in Arkansas and San Diego, because these two states seem to be very different in terms of the covariate distribution and conditional distribution of potential outcomes.

The new programs implemented and the corresponding experiments in Arkansas and San Diego differed slightly in terms of timing, central target family, and program components. The Arkansas WORK Program (WORK) targeted AFDC applicants and recipients with children aged at least three years and provided group job search and unpaid work experience. The corresponding experiment started in 1983 with 1,127 participants, of whom half were exposed to WORK and the rest were assigned to the control condition. Contrarily, the Saturation Work Initiative Model (SWIM) in San Diego targeted AFDC applicants and recipients with children aged at least six years and provided job search assistance, skills training, and unpaid work experience. The corresponding experiment started in 1985 with 3,211 participants, of whom half were exposed to the SWIM, and the remainder were assigned to the control condition. In both RCTs, the covariates related to personal characteristics and employment information were collected prior to the experiments. In addition, both experiments involved following up with participants at least two years after the start of the experiments, and collected earnings as outcome variables.

For the illustration of the DR-ITR, I consider the following hypothetical situation: Suppose that the government of Arkansas desires a good ITR that specifies whether an individual should participate in the WORK or not. Assume that the data available to the government are limited only to the data from RCT on the SWIM and the data of covariates from RCT on the WORK. In other words, I assume that the experimental assignment variable and the outcome variable of the WORK are not observed. Thus, according to the terminology of this study, the target population comprises single-parent families in Arkansas, whereas the source population comprises single-parent families in San Diego.

-

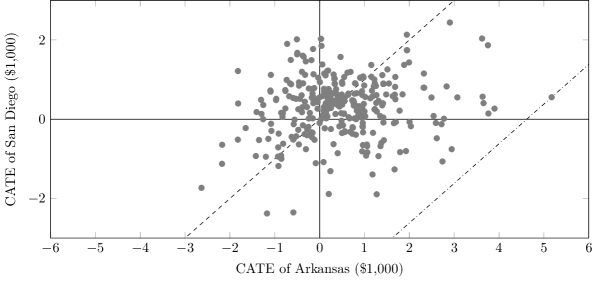

Notes: This figure illustrates the relation between Arkansas’s conditional average treatment effect (CATE) function and San Diego’s CATE function using a scatter plot. The CATE function of each location is estimated using the data from RCT conducted at the corresponding location. Each point represents an observed value of covariates in Arkansas’s RCT, and its -coordinate and -coordinate are an evaluation of the estimated CATE function for Arkansas and San Diego at that value of covariates. The dashed line shows that the two CATEs are the same. Thus, the more distant the point is from this line, the more different the two CATEs are. The dotted-dashed line passes through the point farthest from the reference line.

The source and target populations actually differ in terms of the covariate distribution and conditional distribution of potential outcomes. First, for the difference in the covariate distribution, LABEL:tab:covariate-summary lists the covariates used in the following estimation and provides the summary statistics of covariates by RCTs. In addition, it compares the means of each covariate in the two RCTs. The result implies that the two populations differ in terms of means of the covariates. To show that that conditional distributions of potential outcomes are also different, I focus on the difference in the conditional average treatment effect (CATE) functions of the two populations. Specifically, I estimate the CATE function of each location using S-learner with the random forest as the base learner (for a review of the CATE estimation, see Künzel et al.,, 2019; Jacob,, 2021). Then, I evaluate the two estimated CATE functions at the observed values of covariates in Arkansas’s RCT. Thus, the difference of the covariate distribution is essentially controlled, and any difference in the values of CATE derives from the difference in the conditional distribution of potential outcomes. Figure 1 visualizes the difference in the values of the CATE using a scatter plot. In the figure, each point represents an observation of covariates in Arkansas’s RCT, and its -coordinate and -coordinate are an evaluation of the estimated CATE function for Arkansas and San Diego at that value of covariates. If a point is on the dashed line, the CATEs of the two locations are the same. In other words, the more distant the point is from this line, the more different the two CATEs are. From this figure, one can observe that the CATE functions of the two locations are substantively different. The maximum distance between the two CATEs are about $4,618. In summary, the source and target populations are significantly different, and hence, the existing methods that assume two populations to be same are inappropriate.

I apply the proposed approach to the current setting and estimate the DR-ITR. The outcome is the total earnings in two years after the start of the WORK or SWIM, and thus the outcome space is non-negative real numbers. The source CMR function is estimated by the random forest with tuned hyper parameters using R package randomForest. The ambiguity level in 7 varies in . Note that the case of corresponds to the naive approach explained in Section 2.2, which is included for comparison. The ITR class consists of decision trees of depth 2 constructed by the covariates except sex and race information. These two variables are excluded because this information should not be used owing to ethical concerns. The optimization of the tree is conducted using R package policytree (Zhou et al.,, 2022). After obtaining the ITRs, I evaluate their performance by estimating the total earnings that would be attained in two years if each ITR was implemented in Arkansas. Note that this corresponds to the target population’s welfare. As the data from RCT conducted in Arkansas are actually available, it is possible to consistently estimate the welfare.

-

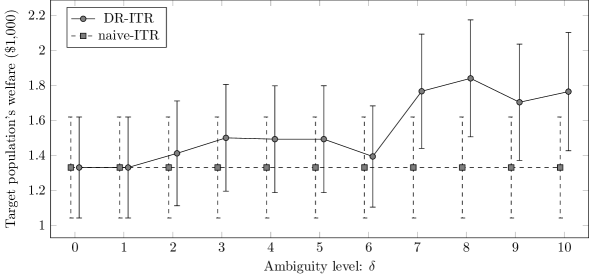

Notes: This figure summarizes the performance of the distributionally robust individualized treatment rule (DR-ITR) and naive-ITR in terms of the target population’s welfare, which is the average earnings in two years that would be attained if an ITR was implemented in Arkansas. The solid line with a circle represents the DR-ITR, while the dashed line with a square represents the naive-ITR. For each line, each error bar indicates the 95% confidence interval of the corresponding estimate.

Figure 2 compares the performance of the DR-ITR with that of the naive-ITR. In the figure, the solid line with a circle represents the welfare of the DR-ITR, while the dashed line with a square represents that of the naive-ITR. Note that the naive-ITR does not depend on the value of . It is clear that the DR-ITR outperforms the naive-ITR in terms of the point estimates of the target population’s welfare by appropriately choosing the value of . Specifically, the welfare due to the DR-ITR with positive ambiguity level is not less than that of the naive-ITR. Moreover, when , the t-test on the null hypothesis that the values of the target population’s welfare due to the DR-ITR and naive-ITR are the same is rejected at the 5% confidence level.

6 Conclusion

This study examined how one should determine a reasonable ITR when the population in which the estimated ITR is implemented differs from the population from which the available experimental or observational data are generated. Specifically, this study focuses on the unknown and unidentifiable difference in the conditional distribution of potential outcomes between the source and target populations, and proposes obtaining a DR-ITR that maximizes the worst-case value of welfare over a certain set of populations. In combination with the Wasserstein distance-based ambiguity set, the DR-ITR offers a simple intuition and estimation method. Additionally, it provides a justification for the naive approach, which assumes that the conditional distributions of potential outcomes are the same between the source and target populations. Thus, this study can be regarded as complementing the existing studies on this topic. In addition, an estimator for the distributionally robust policy is developed, and the theoretical analysis shows that the estimator has regret converging to zero.

Several interesting questions are left unanswered. First, a policy maker often has access to multiple sets of experimental data, each of which is generated from a different population. It is obscure how the proposed DR-ITR can be extended to such multiple-source population scenarios. Second, in the population level, the current problem discussed in Section 2 can be understood as a two-person zero-sum game between a policymaker who chooses an ITR to maximize the target population’s welfare and an adversary who chooses the target population to minimize the target population’s welfare. However, this study does not consider whether a Nash equilibrium exists or what types of strategies constitute the equilibrium. I leave these questions for future work.

Supplementary Materials of “Distributionally Robust Policy Learning with Wasserstein Distance” Daido KidoGraduate School of Economics, Kyoto University, Yoshida Honmachi, Sakyo, Kyoto, 606-8501, Japan. E-mail: kido.daidou.45m@st.kyoto-u.ac.jp

Structure of

LABEL:sec:suppementary-information-on-empirical-application provides the additional information on

References

- Adjaho and Christensen, (2022) Adjaho, C. and Christensen, T. (2022). Externally Valid Treatment Choice. arXiv preprint. arXiv:2205.05561.

- Allcott, (2015) Allcott, H. (2015). Site Selection Bias in Program Evaluation. The Quarterly Journal of Economics, 130(3):1117–1165.

- Andrews and Oster, (2019) Andrews, I. and Oster, E. (2019). A simple approximation for evaluating external validity bias. Economics Letters, 178:58–62.

- Athey and Wager, (2021) Athey, S. and Wager, S. (2021). Policy Learning With Observational Data. Econometrica, 89(1):133–161.

- Bertsimas et al., (2017) Bertsimas, D., Kallus, N., Weinstein, A. M., and Zhuo, Y. D. (2017). Personalized Diabetes Management Using Electronic Medical Records. Diabetes Care, 40(2):210–217.

- Blanchet et al., (2019) Blanchet, J., Kang, Y., and Murthy, K. (2019). Robust Wasserstein profile inference and applications to machine learning. Journal of Applied Probability, 56(3):830–857.

- Blanchet and Murthy, (2019) Blanchet, J. and Murthy, K. (2019). Quantifying Distributional Model Risk via Optimal Transport. Mathematics of Operations Research, 44(2):565–600.

- Bogachev, (2007) Bogachev, V. I. (2007). Measure Theory. Springer Berlin Heidelberg, Berlin Heidelberg, first edition.

- Bousquet, (2002) Bousquet, O. (2002). A Bennett concentration inequality and its application to suprema of empirical processes. Comptes Rendus Mathematique, 334(6):495–500.

- Bousquet, (2003) Bousquet, O. (2003). Concentration Inequalities for Sub-Additive Functions Using the Entropy Method. In Giné, E., Houdré, C., and Nualart, D., editors, Stochastic Inequalities and Applications, pages 213–247, Basel. Birkhäuser Basel.

- Campbell, (1957) Campbell, D. T. (1957). Factors relevant to the validity of experiments in social settings. Psychological Bulletin, 54(4):297–312.

- Cole and Stuart, (2010) Cole, S. R. and Stuart, E. A. (2010). Generalizing Evidence From Randomized Clinical Trials to Target Populations: The ACTG 320 Trial. American Journal of Epidemiology, 172(1):107–115.

- Dehejia et al., (2021) Dehejia, R., Pop-Eleches, C., and Samii, C. (2021). From Local to Global: External Validity in a Fertility Natural Experiment. Journal of Business & Economic Statistics, 39(1):217–243.

- Dudík et al., (2011) Dudík, M., Langford, J., and Li, L. (2011). Doubly Robust Policy Evaluation and Learning. In Getoor, L. and Scheffer, T., editors, Proceedings of the 28th International Conference on Machine Learning, ICML’11, pages 1097–1104, New York, NY, USA. ACM.

- Friedlander and Robins, (1995) Friedlander, D. and Robins, P. K. (1995). Evaluating Program Evaluations: New Evidence on Commonly Used Nonexperimental Methods. American Economic Review, 85(4):923–937.

- Gao, (2020) Gao, R. (2020). Finite-Sample Guarantees for Wasserstein Distributionally Robust Optimization: Breaking the Curse of Dimensionality. arXiv preprint. arXiv:2009.04382.

- Gao et al., (2017) Gao, R., Chen, X., and Kleywegt, A. J. (2017). Wasserstein Distributionally Robust Optimization and Variation Regularization. arXiv preprint. arXiv:1712.06050.

- Gechter et al., (2019) Gechter, M., Samii, C., Dehejia, R., and Pop-Eleches, C. (2019). Evaluating Ex Ante Counterfactual Predictions Using Ex Post Causal Inference. arXiv preprint. arXiv:1806.07016.

- Hartman et al., (2015) Hartman, E., Grieve, R., Ramsahai, R., and Sekhon, J. S. (2015). From sample average treatment effect to population average treatment effect on the treated: combining experimental with observational studies to estimate population treatment effects. Journal of the Royal Statistical Society: Series A (Statistics in Society), 178(3):757–778.

- Hotz et al., (2005) Hotz, V. J., Imbens, G. W., and Mortimer, J. H. (2005). Predicting the efficacy of future training programs using past experiences at other locations. Journal of Econometrics, 125(1):241–270.

- Hu and Hong, (2012) Hu, Z. and Hong, J. (2012). Kullback-Leibler Divergence Constrained Distributionally Robust Optimization. Optimization Online.

- Hurwicz, (1951) Hurwicz, L. (1951). The generalized Bayes minimax principle: a criterion for decision making under uncertainty. Cowles Commission Discussion Paper, No.335.

- Ida et al., (2021) Ida, T., Ishihara, T., Ito, K., Kido, D., Kitagawa, T., Sakaguchi, S., and Sasaki, S. (2021). Paternalism, Autonomy, or Both? Experimental Evidence from Energy Saving Programs. arXiv preprint. arXiv:2112.09850.

- Jacob, (2021) Jacob, D. (2021). CATE meets ML. Digital Finance, 3(2):99–148.

- Kitagawa and Tetenov, (2018) Kitagawa, T. and Tetenov, A. (2018). Who Should Be Treated? Empirical Welfare Maximization Methods for Treatment Choice. Econometrica, 86(2):591–616.

- Kube et al., (2019) Kube, A., Das, S., and Fowler, P. J. (2019). Allocating Interventions Based on Predicted Outcomes: A Case Study on Homelessness Services. Proceedings of the AAAI Conference on Artificial Intelligence, 33(01):622–629.

- Künzel et al., (2019) Künzel, S. R., Sekhon, J. S., Bickel, P. J., and Yu, B. (2019). Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the National Academy of Sciences, 116(10):4156–4165.

- Lee and Raginsky, (2018) Lee, J. and Raginsky, M. (2018). Minimax Statistical Learning with Wasserstein distances. In Bengio, S., Wallach, H., Larochelle, H., Grauman, K., Cesa-Bianchi, N., and Garnett, R., editors, Advances in Neural Information Processing Systems, volume 31. Curran Associates, Inc.

- Mo et al., (2021) Mo, W., Qi, Z., and Liu, Y. (2021). Learning Optimal Distributionally Robust Individualized Treatment Rules. Journal of the American Statistical Association, 116(534):659–674.

- Mohajerin Esfahani and Kuhn, (2018) Mohajerin Esfahani, P. and Kuhn, D. (2018). Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming, 171(1):115–166.

- Pritchett and Sandefur, (2013) Pritchett, L. and Sandefur, J. (2013). Context Matters for Size: Why External Validity Claims and Development Practice Don’t Mix. resreport 336, Center for Global Development.

- Rahimian and Mehrotra, (2019) Rahimian, H. and Mehrotra, S. (2019). Distributionally Robust Optimization: A Review. arXiv preprint. arXiv:1908.05659.

- Shafieezadeh-Abadeh et al., (2019) Shafieezadeh-Abadeh, S., Kuhn, D., and Mohajerin Esfahani, P. (2019). Regularization via Mass Transportation. Journal of Machine Learning Research, 20(103):1–68.

- Shafieezadeh-Abadeh et al., (2015) Shafieezadeh-Abadeh, S., Mohajerin Esfahani, P., and Kuhn, D. (2015). Distributionally Robust Logistic Regression. In Cortes, C., Lawrence, N., Lee, D., Sugiyama, M., and Garnett, R., editors, Advances in Neural Information Processing Systems, volume 28. Curran Associates, Inc.

- Si et al., (2020) Si, N., Zhang, F., Zhou, Z., and Blanchet, J. (2020). Distributionally Robust Policy Evaluation and Learning in Offline Contextual Bandits. In Daumé III, H. and Singh, A., editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 8884–8894. PMLR.

- Si et al., (2021) Si, N., Zhang, F., Zhou, Z., and Blanchet, J. (2021). Distributional Robust Batch Contextual Bandits. arXiv preprint. arXiv:2006.05630.

- Stuart et al., (2018) Stuart, E. A., Ackerman, B., and Westreich, D. (2018). Generalizability of Randomized Trial Results to Target Populations: Design and Analysis Possibilities. Research on Social Work Practice, 28(5):532–537.

- Stuart et al., (2015) Stuart, E. A., Bradshaw, C. P., and Leaf, P. J. (2015). Assessing the Generalizability of Randomized Trial Results to Target Populations. Prevention Science, 16(3):475–485.

- Stuart et al., (2011) Stuart, E. A., Cole, S. R., Bradshaw, C. P., and Leaf, P. J. (2011). The use of propensity scores to assess the generalizability of results from randomized trials. Journal of the Royal Statistical Society: Series A (Statistics in Society), 174(2):369–386.

- Swaminathan and Joachims, (2015) Swaminathan, A. and Joachims, T. (2015). Batch Learning from Logged Bandit Feedback through Counterfactual Risk Minimization. Journal of Machine Learning Research, 16(52):1731–1755.

- Talagrand, (1996) Talagrand, M. (1996). New concentration inequalities in product spaces. Inventiones mathematicae, 126(3):505–563.

- Tipton, (2013) Tipton, E. (2013). Improving Generalizations From Experiments Using Propensity Score Subclassification: Assumptions, Properties, and Contexts. Journal of Educational and Behavioral Statistics, 38(3):239–266.

- Tipton, (2014) Tipton, E. (2014). How Generalizable Is Your Experiment? An Index for Comparing Experimental Samples and Populations. Journal of Educational and Behavioral Statistics, 39(6):478–501.

- Tu et al., (2019) Tu, Z., Zhang, J., and Tao, D. (2019). Theoretical Analysis of Adversarial Learning: A Minimax Approach. In Wallach, H., Larochelle, H., Beygelzimer, A., d'Alché-Buc, F., Fox, E., and Garnett, R., editors, Advances in Neural Information Processing Systems, volume 32. Curran Associates, Inc.

- Uehara et al., (2020) Uehara, M., Kato, M., and Yasui, S. (2020). Off-Policy Evaluation and Learning for External Validity under a Covariate Shift. In Larochelle, H., Ranzato, M., Hadsell, R., Balcan, M. F., and Lin, H., editors, Advances in Neural Information Processing Systems, volume 33, pages 49–61. Curran Associates, Inc.

- Villani, (2009) Villani, C. (2009). Optimal Transport: Old and New, volume 338 of Grundlehren der mathematischen Wissenschaften. Springer, Berlin, Heidelberg, first edition.

- Vivalt, (2020) Vivalt, E. (2020). How Much Can We Generalize From Impact Evaluations? Journal of the European Economic Association, 18(6):3045–3089.

- Wainwright, (2019) Wainwright, M. J. (2019). High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press.

- Zhao et al., (2012) Zhao, Y., Zeng, D., Rush, A. J., and Kosorok, M. R. (2012). Estimating Individualized Treatment Rules Using Outcome Weighted Learning. Journal of the American Statistical Association, 107(499):1106–1118.

- Zhao et al., (2019) Zhao, Y., Zeng, D., Tangen, C. M., and Leblanc, M. L. (2019). Robustifying trial-derived optimal treatment rules for a target population. Electronic Journal of Statistics, 13(1):1717–1743.

- Zhou et al., (2022) Zhou, Z., Athey, S., and Wager, S. (2022). Offline Multi-Action Policy Learning: Generalization and Optimization. Operations Research. Advance online publication. https://doi.org/10.1287/opre.2022.2271.