Abstract

In recent years it has become possible to collect GPS data from drivers and to incorporate this data into automobile insurance pricing for the driver. This data is continuously collected and processed nightly into metadata consisting of mileage and time summaries of each discrete trip taken, and a set of behavioral scores describing attributes of the trip (e.g, driver fatigue or driver distraction) so we examine whether it can be used to identify periods of increased risk by successfully classifying trips that occur immediately before a trip in which there was an incident leading to a claim for that driver. Identification of periods of increased risk for a driver is valuable because it creates an opportunity for intervention and, potentially, avoidance of a claim. We examine metadata for each trip a driver takes and train a classifier to predict whether the following trip is one in which a claim occurs for that driver. By achieving a area under the receiver-operator characteristic above 0.6, we show that it is possible to predict claims in advance. Additionally, we compare the predictive power, as measured by the area under the receiver-operator characteristic of XGBoost classifiers trained to predict whether a driver will have a claim using exposure features such as driven miles, and those trained using behavioral features such as a computed speed score.

keywords:

Telematics; Usage Based Insurance; Risk Mitigation1 \issuenum1 \articlenumber0 \datereceived \dateaccepted \datepublished \hreflinkhttps://doi.org/ \TitleNightly Automobile Claims Prediction from Telematics-Derived Features: A Multilevel Approach \TitleCitationTitle \AuthorAllen R. Williams 1, Yoolim Jin 2, Anthony Duer 2, Tuka Alhani 3 and Mohammad Ghassemi 4,* \AuthorNamesAllen R. Williams, Yoolim Jin, Anthony Duer, Tuka Alhanai, and Mohammad Ghassemi \AuthorCitationWilliams, A.R.; Jin, Y.; Duer, A.; Alhanai, T. Ghassemi, M. \corresCorrespondence: ghassem3@msu.edu;

1 INTRODUCTION

1.1 Motivation

Classical automobile insurance pricing is based on static features often indirectly and non-causally related to the risk propensity of the driver. There has been an increasing trend toward integrating driving habits and patterns into the insurance pricing equation. Policies which incorporate information about a policy holder’s driving habits are often referred to as usage based insurance and can include policy types such as pay-as-you-drive (PAYD) which offers a lower premium pricing for drivers who drive fewer annual miles, and pay-how-you-drive (PHYD) which uses features derived from a driver’s actual driving patterns (e.g, braking event counts or cornering event counts) to assess a driver’s claims propensity and determine a premium price Arumugam and Bhargavi (2019). There are several advantages to usage based insurance including a fairer distribution of cost among the population of insured drivers, an expectation of savings on insurance costs for the majority of drivers (especially drivers in the lower income category), increased traffic safety through a reduction in miles driven, and an opportunity to provide feedback to drivers thereby reducing the total risk in an insurer’s portfolio Tselentis et al. (2016); Litman (2004).

1.2 Objective

We were primarily interested in three research questions in this study. First, can we use telematic behavioral measures to determine which drivers were more likely to have a claim; that is, can we assess the risk propensity of a driver based on the telematics derived features? Second, can we determine which trips were more likely to result in claims using only features derived from previous trips? Finally, would the classification tasks be improved by combining the results of the driver risk assessment and journey risk assessment?

1.3 Literature Review

1.3.1 Telematics Data

There are multiple ways of collecting telematics data for usage based insurance, and even more ways of processing this data into usable features for determining the risk propensity of a driver. Driven distance and location (e.g, miles driven in urban areas) have been used as measures of a driver’s exposure to risk Guillen et al. (2019). The exact relationship between distance driven and claims frequency has been debated, with some authors describing a learning effect, which offsets some of the increased risk exposure from additional miles driven Boucher et al. (2017), however it has been argued that the effect is due to a residual heterogeneity which is inappropriately captured by the model used, meaning that low distance drivers have certain traits that are different from high mileage drivers other than just their distances driven Boucher and Turcotte (2020). The argument is that increased mileage should not be viewed as risk reducing, since a driver who decides to drive more miles has a fixed claims probability for their original driven distance and the additional distance can only increase that probability, although the marginal increase in probability of claims per mile may decrease with additional miles driven. Some studies have examined drowsiness detection using wearable headbands Rohit et al. (2017), or fatigue using computer vision techniques Abulkhair et al. (2015). There have been studies analyzing driver behavior using information acquired from a vehicle’s CAN bus, detailing sequences of actions including braking and turning events, steering wheel angle, and vehicle speed, most often in an attempt to identify drivers based on the information obtained from the CAN bus. Carfora et al. used a combination of mobile GPS data along with information from the CAN bus to derive two clusters which they identify as highway driving and urban road driving Carfora et al. (2019).

Machine learning approaches have been applied to the task of predicting claims from features derived from telematics. Most papers have focused on the task of predicting which drivers are likely to have a claim. Pesantez-Narvarez, Guillen, and Alcanez explored both logistic regression and XGBoost on a small dataset to predict the existence of claims. They found that XGBoost performed favorably, but noted a difficulty in interpretation of XGBoost when tree models are used as the base learner due to the difficulty in extracting model coefficients. They argue that the modest performance gain of XGBoost over logistic regression on their dataset did not justify its use over logistic regression given the relatively lower interpretability of results. They also note the need for careful hyperparameter optimization with XGBoost due to its many hyperparameters and its ability to determine complex nonlinear decision boundaries Pesantez-Narvaez et al. (2019). Several other authors have also had success using an XGBoost classifier for claims prediction using telematics data on datasets of up to rows Hanafy and Ming (2021); Abdelhadi et al. (2020). Our use of telematics data is different from the above in that we predict claims at multiple levels of resolution and recombine the individual classifier outputs in order to predict which journeys occur immediately before a claim, so that we can identify periods of relatively higher risk for a driver, in the hopes that an intervention can be made and the increased risk can be mitigated.

1.3.2 Imbalanced Data

Insurance claims prediction is an example of a classification task in which data is almost always strongly class imbalanced. A dataset is considered to be class imbalanced if one class occurs much more often than the others. In a binary classification task the minority class is often referred to as the positive class, while the majority class is called the negative class. The focus of this section and the remainder of the paper will be on binary classification rather than multiclass classification. Learning from imbalanced datasets presents several challenges and there have been a variety of tools developed to address these challenges. Many classifiers will learn the majority class more effectively than the minority class, and will misclassify examples of the minority class more often than they do examples of the majority class. Moreover in domains where imbalanced data is common, it is often the case that correctly classifying minority class (positive) examples is more important than correctly classifying majority class (negative) examples López et al. (2013). Class imbalanced datasets often arise when the event that is to be detected is rare, so in addition to the relative scarcity of samples in the minority class in comparison to samples of the majority class, there may also be an inadequate number of samples of the minority class for the minority class which creates a difficulty in distinguishing signatures of the minority class from dataset noise Haixiang et al. (2017). See Figure 1 for an illustration of the class imbalance problem.

A related problem is class overlap. Overlap is said to occur when there are regions in the feature space with similar proportions of minority samples and majority samples. If a dataset is separable in the feature space then there is no class overlap; on the other hand, if examples of the two classes are distributed uniformly over the feature space then there is maximal class overlap. See Figure 2 for an illustration of the concept of class overlap.

Class overlap alone is a significant problem for classification however it presents even greater difficulties in the presence of class imbalance. Denil and Treppenberg explored the relationship between class imbalance and class overlap and found then when each was examined separately class overlap presented much more serious difficulties than class imbalance, and that the presence of both class imbalance and class overlap presented unique and catastrophic difficulties that did not occur with either class imbalance or class overlap alone Denil and Trappenberg (2010).

Class Imbalance and class overlap can be addressed at multiple different levels. At the data level sampling methods can be used to increase the proportion of minority class examples. Some of the simplest sampling techniques are random over/under sampling, in which either some samples from the minority class are chosen at random to be repeated in the training set, or samples from the majority class are chosen at random to be omitted from the training set. A problem with the random oversampling approach is that it does not often aid in recognition of the minority class, rather forces the decision boundary to be focused on more specific areas within the feature space Chawla et al. (2002). Alternatively oversampling techniques like SMOTE and its many variants produce new minority class samples thereby expanding the decision boundary and often aiding in the recognition of the minority class. SMOTE, in particular, works by selecting nearest neighbors for each minority sample (where is a hyperparameter) and for some proportion of these neighbors randomly choosing a point along the line connecting the minority sample with its neighbor and adding a new sample at that point, thereby augmenting the training data and expanding the decision boundary. Tomek link removal is a method for undersampling which can also help to address the class overlap problem Kotsiantis et al. (2006). A Tomek-link is a pair of samples who are each other’s nearest neighbor but have opposite class labels. Formally in the finite dataset where is a population of samples and the corresponding labels, write , let , and let , that is is the projection of onto . Then the pair are a Tomek link if and

Where is any metric, often Euclidean distance.

Another level at which the class imbalance problem can be addressed is at the classifier level. Often a weight is applied to samples in the minority class so that misclassification of minority samples is weighted more heavily in the loss function. Another commonly used method of dealing with class imbalance at the classifier level is ensemble classifiers. Most often these involve either bagging or boosting ensembles. Bagging (Bootstrap Aggregating) is an ensemble method in which a dataset is split into multiple datasets by sampling with replacement (Bootstrapping) and models are trained on each of the bootstrap samples, then at prediction time the predictions of each of the models is aggregated in some way (this could be a majority vote, an average, or more complex aggregation methods). Boosting is another ensemble method that iteratively trains a collection of weak learners and aggregates their predictions to form a more powerful ensemble. The weights of samples are chosen in each boosting round to incentivize the correct classification of samples which had been misclassified by the weak learners in earlier boosting rounds. The weight of each classifier toward the final prediction is inversely proportional to its error Shalev-Shwartz and Ben-David (2014).

2 METHODS

Herein we describe the data, methods, and validation approach used to develop models that assess the risk of driver- and journey-level claims using telematics data.

2.1 Data

All data for this study was sourced from CSAA Insurance Group. Our dataset consisted of journeys taken by distinct drivers. For each journey, telematics features are derived from data collected from users’ smartphones by the telematics data collection and processing company The Floow. The telematics data are represented as a collection of scores and event counts. We do not use any traditional insurance features such as age or gender in this study Ma et al. (2018).

2.2 Outcome

For model development purposes, our outcome of interest were two binary variables that indicated the existence or absence of a claim at the driver and journey resolutions. A journey’s class label is set to if the following journey resulted in a claim for that driver while the driver’s class label is set to if the driver had a claim on any recorded journey. Our outcome was strongly class imbalanced; only of the journeys (and drivers) had in a claim.

2.3 Features

The telematics data are represented as a collection of scores and event counts. The telematic scores summarize the driving habits based on characteristics such as a drivers tendency toward distraction, fatigue, and time of day - metrics which have been shown previously to be associated with risk propensity. Scores are computed at two different levels: globally (at the driver level) and locally (at the trip level). The trip level scores are computed for each trip taken at the conclusion of the trip and thus can change significantly even for the same driver on different trips, and the driver level scores are global scores for a driver summarizing his or her driving more succinctly. There are six scores for each driver, and six scores for each journey. The data providers of this study informed us that higher scores are considered better in all categories, i.e, a driver with an Overall score of is considered to be less risky than a driver with an Overall score of if all else is equal.

The telematic event counts are computed for each trip for categories like braking, acceleration, and cornering; for each of these events, an intensity level ranging from mild to extreme is also captured. We also use aggregate measurements like the number of trips a driver has taken, or the number of miles the driver has driven as features for the assessment of driver risk propensity and the distance and duration of a trip for the assessment of relative riskiness of the trip.

2.3.1 Driver Risk Assessment

To assess the risk profile of drivers we take into account the global scores provided for each driver, the number of miles driven, the number of discrete trips taken, and the days since the last heartbeat (a periodic signal used to verify connectivity between the driver’s mobile device and the company’s receiver). We divide these features into two distinct subsets, those derived from a driver’s behavior and those measuring a driver’s risk exposure (See table 1 for a list of scores and summary statistics).

| Overall | Smooth Driving | Mobile Distraction | Time of Day | Fatigue | Speed | Driven Journeys | Miles Driven | |

| Mean | 80.61 | 71.30 | 86.33 | 75.53 | 83.59 | 79.90 | 418.01 | 3991.22 |

| Stdev | 5.28 | 8.54 | 9.14 | 3.41 | 9.17 | 5.18 | 435.79 | 5123.85 |

2.3.2 Journey Risk Assessment

Journey scores are provided as a sequence of scores and event counts for each driver (See Table 1 for a list of behavioral scores and summary statistics).

| Journey | Smooth Driving | Mobile Distraction | Time of Day | Fatigue | Speed | Duration (min) | Miles | |

| Mean | 80.04 | 68.92 | 86.53 | 76.22 | 93.81 | 81.78 | 18.02 | 9.71 |

| Stdev | 9.19 | 12.85 | 14.99 | 6.72 | 6.66 | 10.05 | 25.33 | 19.43 |

| Max. | 100 | 100 | 100 | 93.28 | 100 | 100 | 2,204.08 | 841.3 |

| Min. | 13.90 | 6.98 | 21.88 | 21.85 | 42.86 | 37.50 | 3.0 | 0.0 |

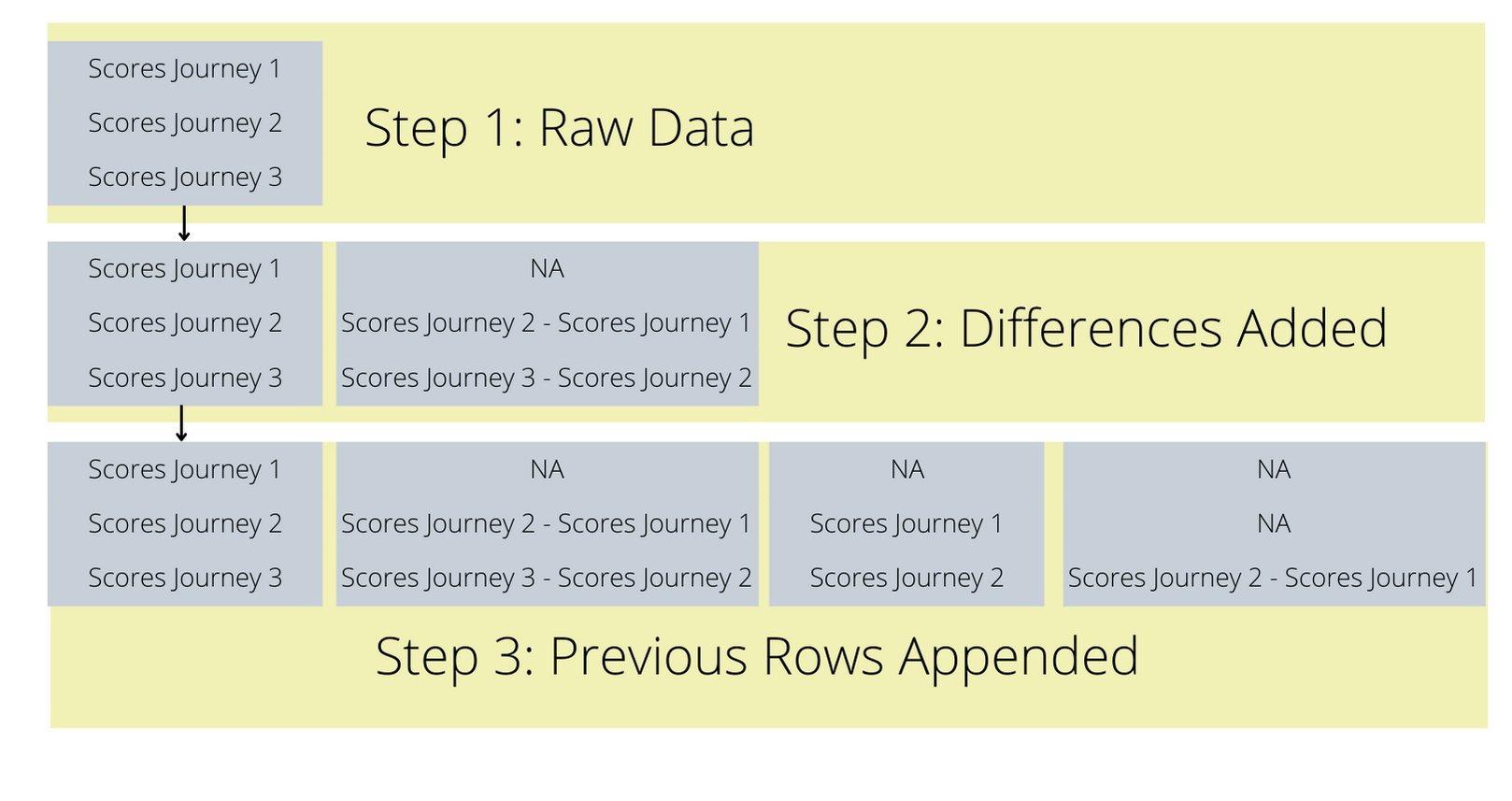

Because we want to determine patterns in scores which are indicative of future claims we expand samples to include features from the previous trips, including their labels, and we also provide and order differences in scores to the classifier (see Figure 3 for an abbreviated illustraion of the dataset widening process described.)

2.4 Model

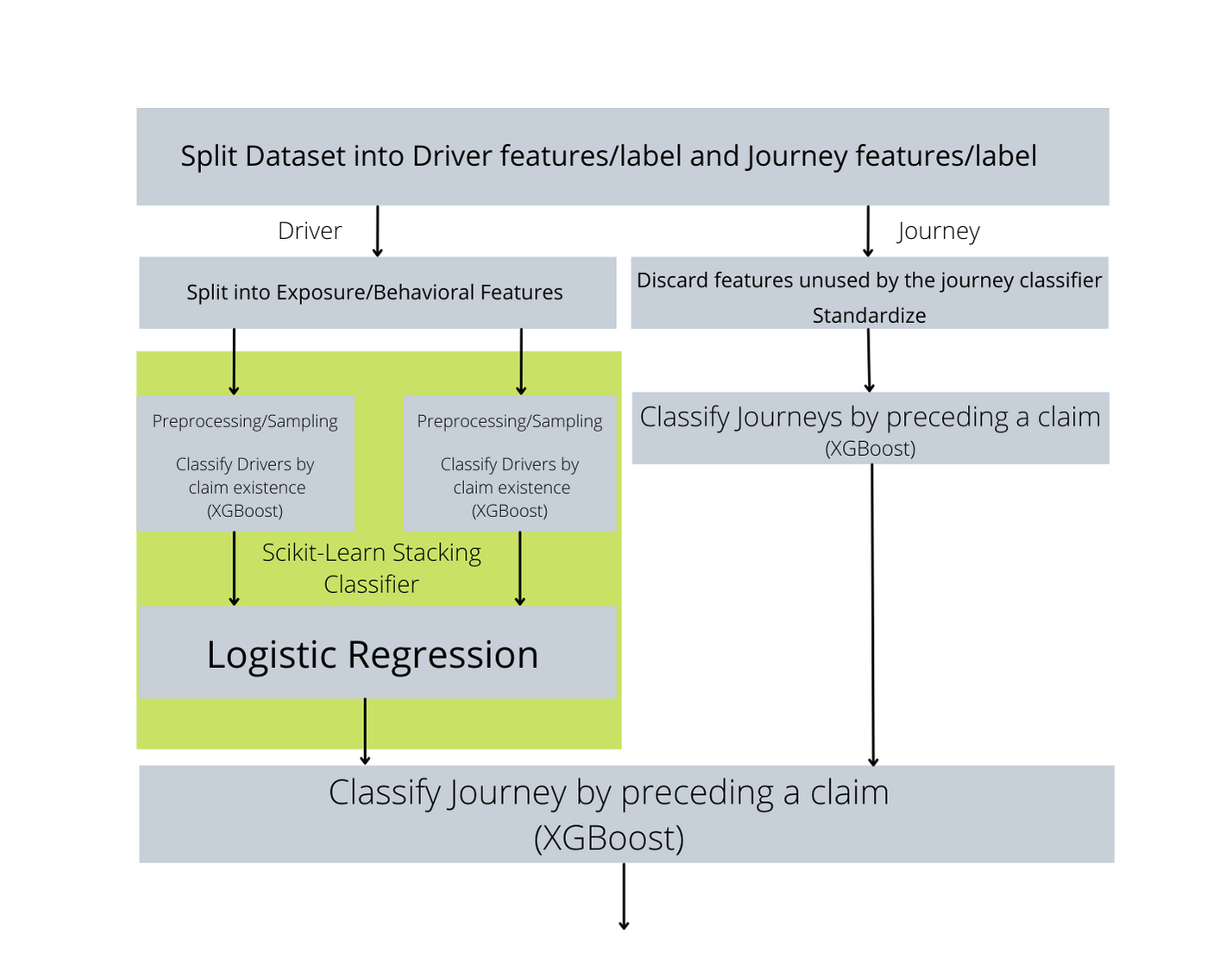

We use XGBoost as the classifier to predict driver- and journey-level claims using the telematics features. Chen and Guestrin (2016). XGBoost was chosen for its simplicity of use, interpretability, and ability to natively handle missing data. The process of stacking rows and taking differences necessarily creates a lot of missing cells (see Figure 3), and in this setting the missing cells carry information. For example the missing data created by taking differences and stacking rows conveys that there is no previous trip taken by the same driver. For the driver classification task we train two XGBoost models on different features and stack their outputs with a final logistic regression classifier. We also examine the performance of weighted and l2-regularized logistic regression. For the journey-level claims classification task we employ a model which combines the output of the driver and journey level classifiers. See Figure 4 for an illustration of our proposed final model for predicting journey risk.

Logistic regression comes with a natural means of extracting feature importances, namely its coefficients. Coefficients with a large magnitude are stronly associated with the target, and those with a low magnitude are not as important to the target prediction. Negative coefficients are inversely asoociated with target. XGboost provides a variety of feature importance scores, including cover, weight, and gain. Gain refers to the improvement in classification results obtained by splitting a decision tree on a particular feature. In the case of XGBoost there are many decision trees, and the gain feature importance score for each feature is averaged across all splits in which that feature is used. See Chen and Guestrin (2016) for an in-depth treatment of the objective function used by XGBoost and the types of feature importances it provides.

2.5 Performance Metric and Validation Approach

The model is evaluated by area under the receiver-operator characteristic, but cross-validation is done across drivers rather trips, using grouped stratified cross validation, where journeys are grouped by driver ID. Much like standard k-fold cross validation each journey is used exactly once in a test set, but in the grouped k-fold cross validation setting a driver’s trips are treated as a unit. Given an arbitrary driver ID, all trips taken by that driver ID will appear either in the test set or training set, and will never be split across the two sets. In this case it is also true that each driver appears in the test set for exactly one of the folds.

2.5.1 Feature Selection

We reduce the dimensionality of the feature space by fitting the XGBoost classifier to the training data with a small subset of features chosen for each tree and selecting the features preferred by the classifier based on average gain of a feature across all splits.

2.5.2 Addressing Class Imbalance

A significant challenge in this classification task is the class imbalance, as the vast majority of drivers have not had a claim. In order to address this challenge we use two sampling techniques: an oversampling technique call Synthetic Minority Oversampling TEchnique (SMOTE), followed by undersampling technique called Tomek link removal. In our case, we remove the majority class member of each Tomek-link pair. We also make use of modified scikit-learn pipelines provided by the imbalanced-learn package, and many preprocessing utilities from the scikit-learn package Kovács (2019); Lemaître et al. (2017); Pedregosa et al. (2011).

2.6 Combination of Journey-Driver Risk Assessment

After training the driver- and journey-level models separately, we trained a third model that combined the risk assessment from both models to provide an enhanced measure of risk at the journey-level.

That is, we use the driver risk scores estimated by the driver classifier, and the journey risk scores estimated by the journey classifier as input into a third classifier that predicts the same target as the journey classifier. We use an XGBoost classifier for this classification as well, and evaluate based on the same metrics with grouped stratified cross validation.

3 Results

Table 3 gives an snapshot of the results obtained by each classifier trained in this study. The following subsections provide individual results of the classifiers.

| Model | Target | Mean AUROC |

|---|---|---|

| Logistic Regression | Driver Claims | 0.69 |

| XGBoost (Exposure features) | Driver Claims | 0.70 |

| Stacking Classifier | Driver Claims | 0.70 |

| XGBoost | Journey Risk | 0.59 |

| Combined Classifier | Journey Risk | 0.62 |

3.1 Driver Classification Results

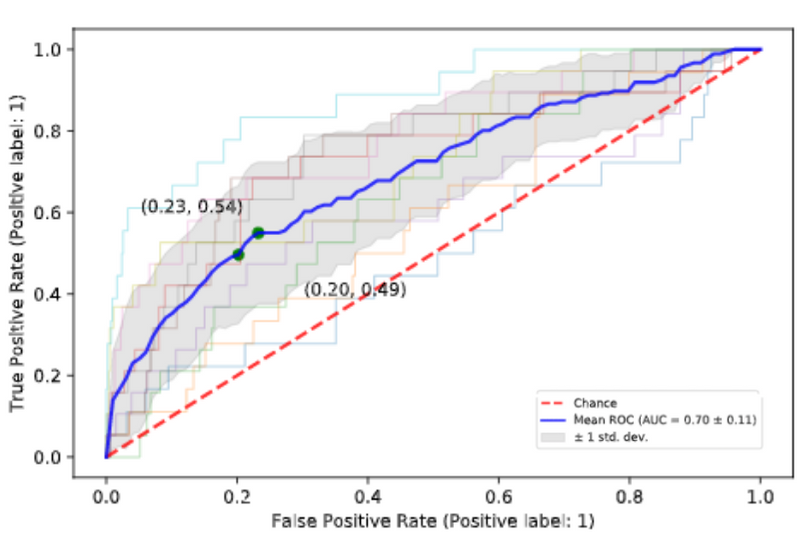

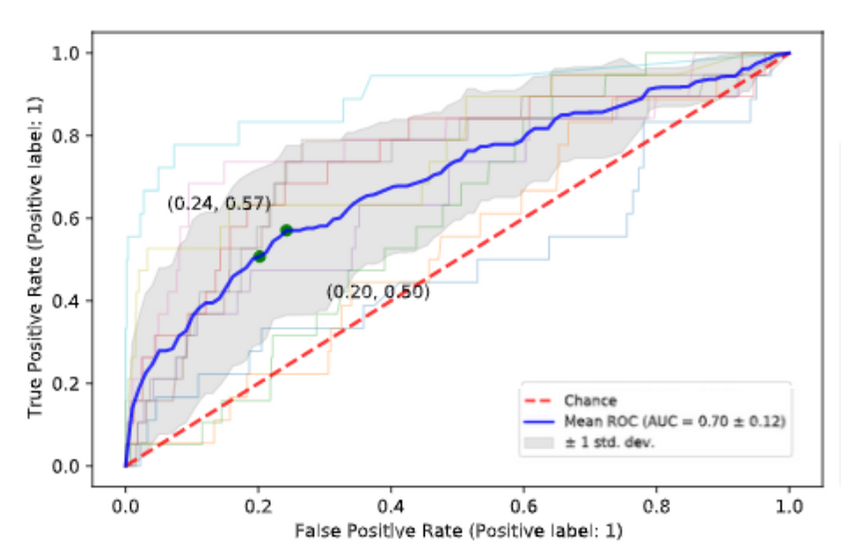

Our final driver-level model had an AUROC of across the ten test-set folds.

Additionally we obtained an area under the receiver-operator characteristic in the driver classification task of using only exposure features (i.e, Driven Journeys, Driven Distance, and Heartbeat Days Elapsed). We were unable to achieve an AUROC higher than using behavior features alone.

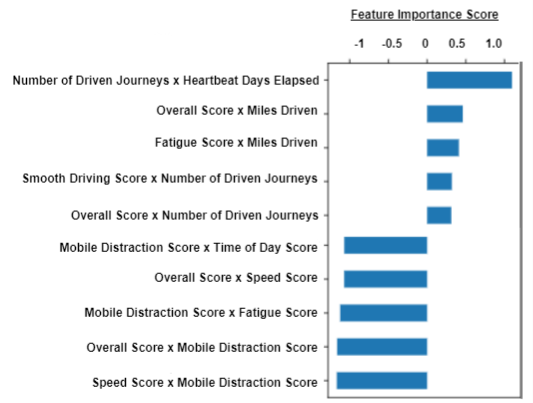

We find that scores are the most predictive in addition to either number of driven journeys, or total distance driven in miles. See Figure 5 for an illustration of the relative feature importance in the driver classification models.

3.2 Journey Classification Results

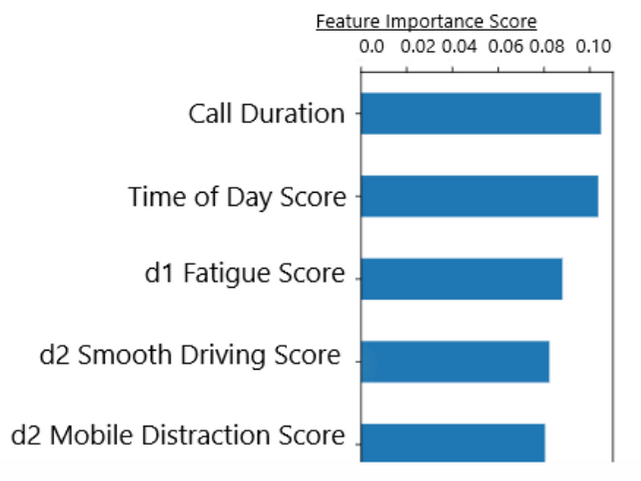

Our journey-level model had an AUROC of for the journey classification task in the absence of driver features. See figure 8 for a listing of feature importance scores from an XGBoost model trained on journey features.

3.2.1 Combination of Journey-Driver Risk Assessment Results

We report an area under the receiver-operator characteristic of with the majority of the importance placed on the journey risk rather than the driver risk. See table 3 for a summary of classifiers used, their targets, and area under the receiver-operator characteristic achieved.

4 Discussion

In this paper we have presented a model which is able to predict the likelihood on the next trip a driver takes with an AUROC of . We have also explored a stacked model composed of XGBoost classifiers which was able to slightly improve the AUROC and tighten the ROC variance compared to a classifier trained on exposure features alone. We have shown that telematics derived features are predictive of claims propensity for drivers, and that the risk of a claim can be predicted in advance with some level of accuracy, even with data computed only nightly rather than real-time data. Ultimately the prediction of claims risk in the near-future would allow an intervention and ideally a prevention of the claim. We note the significance of the work, some limitations and exciting possibilities for future work below.

4.1 Significance

Much of the work in telematics has been around the derivation of features from raw data or the use of features to classify risky drivers for insurance premium pricing. We have shown that these features can be used to predict claims in advance, which opens the possibility of preventing that claim. Claims range in severity but can cost tens of thousands of dollars and can result in injury or death of the driver or others. Since telematics data is already being collected and stored such a claims prevention model would be inexpensive to implement but could have a great benefit to both the insurer and the insured.

4.2 Limitations

The most important limitation of the present work is that it used black-box scores as features for classification, and data provided only at the trip level, rather than real-time. Although our model was able to predict risky trips with a surprisingly high AUROC using trip level data, examination of real-time driving behavior would allow exploration of patterns in driving behavior immediately before incidents resulting in claims occurred and could further improve the classificaton results. Secondly, our risk analysis is based on population level statistics, which could be improved by using a more individual and personalized assessment of risk. There is an analogy with personalized nutrition, where it is likely that personalized advice may outperform advice based solely on population level statistics Jinnette et al. (2021). In our case this introduces the questions

-

•

does influencing a driver away from patterns associated with claims at the population level decrease the claims propensity of that driver?

-

•

how can we best combine insights from population level studies and and personalized advice derived from a drivers own data only?

4.3 Future Directions

An interesting direction for future research would be to experimentally test whether influencing drivers toward scores associated with lower risk could truly reduce their claims propensity. Experimentally testing intervention strategies could address questions like

-

1.

After identifying that a driver is at increased risk, what is the best method of intervention?

-

2.

Does the timing of the intervention influence its effectiveness in reducing a driver’s risk?

-

3.

Can we identify the reason why the driver was considered to be at risk, and personalize the intervention to that individual? (e.g, are there signatures in the data indicative of anger, alcohol consumption or extreme stress?)

Another exciting direction for future work is the expansion of the statistics used in the classification of the journey risk. In our case, we used differences and stacked frames to allow the classifier which expects IID tabular data to use the sequences of data.

Finally we found that oversampling was helpful in classifying driver risk, especially when using behavioral variables, where the minority class was oversampled to produce approximately a 1:3 ratio of positive to negative samples, but due to the grouped and sequential nature of the journey classification task, we did not use any oversampling for the journey classification task. A suitable combination of oversampling and undersampling techniques may be of great use on such an imbalanced dataset. It would be worthwhile to explore dataset augmentation with generative sequence models that fit this use case and examine their efficacy as a preprocessing tool in the journey prediction task.

‘Conceptualization, A.R.W. and M.G.; methodology, A.R.W., M.G., and T.A.; software, A.R.W and Y.J; validation, A.R.W, M.G.;investigation, M.G. and A.R.W.; resources, Y.J.; data curation, A.D, Y.J.; writing—original draft preparation, A.R.W; writing—review and editing, M.G, A.D.; visualization, A.R.W; supervision, M.G.; funding acquisition, M.G. All authors have read and agreed to the published version of the manuscript.”

This work was funded by a grant from the CSAA Insurance Group

Not Applicable

Not Applicable

Due to the nature of this research, participants of this study did not agree for their data to be shared publicly, so supporting data is not available.

Y.J. and A.D. Were employed by the funding company at the time research was conducted.

no \appendixstart

References

References

- Arumugam and Bhargavi (2019) Arumugam, S.; Bhargavi, R. A survey on driving behavior analysis in usage based insurance using big data. Journal of Big Data 2019, 6, 1–21.

- Tselentis et al. (2016) Tselentis, D.I.; Yannis, G.; Vlahogianni, E.I. Innovative insurance schemes: pay as/how you drive. Transportation Research Procedia 2016, 14, 362–371.

- Litman (2004) Litman, T. Pay-as-you-drive pricing for insurance affordability. Victoria Transport Policy Institute (www. vtpi. org) 2004.

- Guillen et al. (2019) Guillen, M.; Nielsen, J.P.; Ayuso, M.; Pérez-Marín, A.M. The use of telematics devices to improve automobile insurance rates. Risk analysis 2019, 39, 662–672.

- Boucher et al. (2017) Boucher, J.P.; Côté, S.; Guillen, M. Exposure as duration and distance in telematics motor insurance using generalized additive models. Risks 2017, 5, 54.

- Boucher and Turcotte (2020) Boucher, J.P.; Turcotte, R. A longitudinal analysis of the impact of distance driven on the probability of car accidents. Risks 2020, 8, 91.

- Rohit et al. (2017) Rohit, F.; Kulathumani, V.; Kavi, R.; Elwarfalli, I.; Kecojevic, V.; Nimbarte, A. Real-time drowsiness detection using wearable, lightweight brain sensing headbands. IET Intelligent Transport Systems 2017, 11, 255–263.

- Abulkhair et al. (2015) Abulkhair, M.F.; Salman, H.A.; Ibrahim, L.F. Using mobile platform to detect and alerts driver fatigue. International Journal of Computer Applications 2015, 123.

- Carfora et al. (2019) Carfora, M.F.; Martinelli, F.; Mercaldo, F.; Nardone, V.; Orlando, A.; Santone, A.; Vaglini, G. A “pay-how-you-drive” car insurance approach through cluster analysis. Soft Computing 2019, 23, 2863–2875.

- Pesantez-Narvaez et al. (2019) Pesantez-Narvaez, J.; Guillen, M.; Alcañiz, M. Predicting motor insurance claims using telematics data—XGBoost versus logistic regression. Risks 2019, 7, 70.

- Hanafy and Ming (2021) Hanafy, M.; Ming, R. Machine learning approaches for auto insurance big data. Risks 2021, 9, 42.

- Abdelhadi et al. (2020) Abdelhadi, S.; Elbahnasy, K.; Abdelsalam, M. A proposed model to predict auto insurance claims using machine learning techniques. Journal of Theoretical and Applied Information Technology 2020, 98.

- López et al. (2013) López, V.; Fernández, A.; García, S.; Palade, V.; Herrera, F. An insight into classification with imbalanced data: Empirical results and current trends on using data intrinsic characteristics. Information sciences 2013, 250, 113–141.

- Haixiang et al. (2017) Haixiang, G.; Yijing, L.; Shang, J.; Mingyun, G.; Yuanyue, H.; Bing, G. Learning from class-imbalanced data: Review of methods and applications. Expert systems with applications 2017, 73, 220–239.

- Denil and Trappenberg (2010) Denil, M.; Trappenberg, T. Overlap versus imbalance. Canadian conference on artificial intelligence. Springer, 2010, pp. 220–231.

- Chawla et al. (2002) Chawla, N.V.; Bowyer, K.W.; Hall, L.O.; Kegelmeyer, W.P. SMOTE: synthetic minority over-sampling technique. Journal of artificial intelligence research 2002, 16, 321–357.

- Kotsiantis et al. (2006) Kotsiantis, S.; Kanellopoulos, D.; Pintelas, P.; et al. Handling imbalanced datasets: A review. GESTS international transactions on computer science and engineering 2006, 30, 25–36.

- Shalev-Shwartz and Ben-David (2014) Shalev-Shwartz, S.; Ben-David, S. Understanding machine learning: From theory to algorithms; Cambridge university press, 2014.

- Ma et al. (2018) Ma, Y.L.; Zhu, X.; Hu, X.; Chiu, Y.C. The use of context-sensitive insurance telematics data in auto insurance rate making. Transportation Research Part A: Policy and Practice 2018, 113, 243–258.

- Chen and Guestrin (2016) Chen, T.; Guestrin, C. XGBoost: A Scalable Tree Boosting System. Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining; ACM: New York, NY, USA, 2016; KDD ’16, pp. 785–794. doi:\changeurlcolorblack10.1145/2939672.2939785.

- Kovács (2019) Kovács, G. smote-variants: a Python Implementation of 85 Minority Oversampling Techniques. Neurocomputing 2019, 366, 352–354. (IF-2019=4.07), doi:\changeurlcolorblack10.1016/j.neucom.2019.06.100.

- Lemaître et al. (2017) Lemaître, G.; Nogueira, F.; Aridas, C.K. Imbalanced-learn: A Python Toolbox to Tackle the Curse of Imbalanced Datasets in Machine Learning. Journal of Machine Learning Research 2017, 18, 1–5.

- Pedregosa et al. (2011) Pedregosa, F.; Varoquaux, G.; Gramfort, A.; Michel, V.; Thirion, B.; Grisel, O.; Blondel, M.; Prettenhofer, P.; Weiss, R.; Dubourg, V.; et al. Scikit-learn: Machine Learning in Python. Journal of Machine Learning Research 2011, 12, 2825–2830.

- Jinnette et al. (2021) Jinnette, R.; Narita, A.; Manning, B.; McNaughton, S.A.; Mathers, J.C.; Livingstone, K.M. Does personalized nutrition advice improve dietary intake in healthy adults? A systematic review of randomized controlled trials. Advances in Nutrition 2021, 12, 657–669.