volume+number+eid

Forecast combinations: an over 50-year review

Abstract

Forecast combinations have flourished remarkably in the forecasting community and, in recent years, have become part of the mainstream of forecasting research and activities. Combining multiple forecasts produced from single (target) series is now widely used to improve accuracy through the integration of information gleaned from different sources, thereby mitigating the risk of identifying a single “best” forecast. Combination schemes have evolved from simple combination methods without estimation, to sophisticated methods involving time-varying weights, nonlinear combinations, correlations among components, and cross-learning. They include combining point forecasts and combining probabilistic forecasts. This paper provides an up-to-date review of the extensive literature on forecast combinations, together with reference to available open-source software implementations. We discuss the potential and limitations of various methods and highlight how these ideas have developed over time. Some important issues concerning the utility of forecast combinations are also surveyed. Finally, we conclude with current research gaps and potential insights for future research.

Keywords: Combination forecast; Cross learning; Forecast combination puzzle; Forecast ensembles; Model averaging; Open-source software; Pooling; Probabilistic forecasts; Quantile forecasts.

1 Introduction

The idea of combining multiple individual forecasts dates back at least to Francis Galton, who in 1906 visited an ox-weight-judging competition and observed that the average of 787 estimates of an ox’s weight was remarkably close to the ox’s actual weight; see [244] for more details of the story. About sixty years later, the famous work of [21] popularized the idea and spawned a rich literature on forecast combinations. More than fifty years have passed since [21]’s (\citeyearBates1969-yj) seminal work, and it is now well established that forecast combinations are beneficial, offering substantially improved forecasts on average relative to constituent models; see [52] and [253] for extensive earlier literature reviews.

In this paper, we aim to present an up-to-date modern review of the literature on forecast combinations over the past five decades. We cover a wide variety of forecast combination methods for both point forecasts and probabilistic forecasts, contrasting them and highlighting how various related ideas have developed in parallel.

Combining multiple forecasts derived from numerous forecasting methods is often a better approach than identifying a single “best forecast”. These are usually called “combination forecasts” or “ensemble forecasts” in different domains. Observed time series data are unlikely to be generated by a simple process specified with a specific functional form because of the possibility of time-varying trends, seasonality changes, structural breaks, and the complexity of real data generating processes [57]. Thus, selecting a single “best model” to approximate the unknown underlying data generating process may be misleading, and is subject to at least three sources of uncertainty: data uncertainty, parameter uncertainty, and model uncertainty [206, 151]. Given these challenges, it is often better to combine multiple forecasts to incorporate multiple drivers of the data generating process and mitigate uncertainties regarding model form and parameter specification.

Potential explanations for the strong performance of forecast combinations are manifold. First, the combination is likely to improve forecasting performance when multiple forecasts to be combined incorporate partial (but incompletely overlapping) information. Second, structural breaks are a common motivation for combining forecasts from different models [253]. In the presence of structural breaks and other instabilities, combining forecasts from models with different degrees of misspecification and adaptability can mitigate the problem, and helps explains the empirical success of forecast combinations. See, e.g., [224, 225] for an extensive discussion on forecast combinations in the presence of instabilities. Indeed, one can consider the competing forecasts as a form of intercept correction relative to a baseline forecast, providing potential gains in forecast accuracy if there are either structural breaks or deterministic misspecifications [122]. Finally, [122] noted that forecast combination can be viewed as an application of Stein-James shrinkage estimation [138]. Specifically, if the unknown future value is considered as a “meta-parameter” of which all the individual forecasts are estimates, then averaging has the potential to provide an improved estimate.

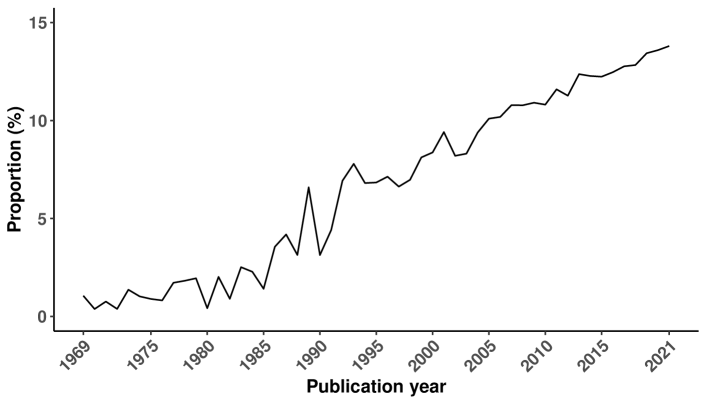

In light of their superiority, forecast combinations have appeared in a wide range of applications such as retail [170], energy [274], economics [1], and epidemiology [220]. Among all published forecasting papers included in the Web of Science, the proportion of papers concerning forecast combinations has been trending upward over the past years, reaching in , as shown in Figure 1. As a consequence, it is timely and necessary to review the extant literature on this topic.

The gains from forecast combinations rely on not only the quality of the individual forecasts to be combined, but the estimation of the combination weights assigned to each forecast [253, 42]. Numerous studies have been devoted to discussing critical issues concerning the constitution of the model pool and the selection of the optimal model subset, including but not limited to the accuracy, diversity, and robustness of individual models [20, 178, 250, 165, 140]. On the other hand, combination schemes vary across studies and have evolved from simple combination methods that avoid weight estimation [54, 199, 97, 114, 210, e.g.,] to sophisticated methods that tailor weights for different individual models [21, 191, 147, 163, 186, 140, 260, e.g.,]. Accordingly, forecast combinations can be linear or nonlinear, static or time-varying, series-specific or cross-learning, and ignore or cover correlations among individual forecasts. Despite the diverse set of forecast combination schemes, forecasters still have little guidance on how to solve the “forecast combination puzzle” [241, 235, 50, 45] — simple averaging often empirically dominates sophisticated weighting schemes that should (asymptotically) be superior.

Initial work on forecast combinations after the seminal work of [21] focused on dealing with point forecasts [52, 253, see, for example,]. In recent years considerable attention has moved towards the use of probabilistic forecasts [118, 105, 145, 180, e.g.,] as they enable a rich assessment of forecast uncertainties. When working with probabilistic forecasts, issues such as diversity among individual forecasts can be more complex and less understood than combining point forecasts [215], and additional issues such as calibration and sharpness need to be considered when assessing or selecting a combination scheme [100]. Additionally, probabilistic forecasts can be elicited in different forms (i.e., density forecasts, quantiles, prediction intervals, etc.), and the resulting combinations may have different properties such as calibration, sharpness, and shape; see [164] for further analytical details.

We should clarify that we take the individual forecasts to be combined as given, and we do not discuss how the forecasts themselves are generated. We focus our attention on combinations of multiple forecasts derived from separate and non-interfering models for a given time series. Nevertheless, the literature involves at least two other types of combinations that are not covered in the present review. The first is the case of generating multiple series from the single (target) series, forecasting each of the generated series independently, and then combining the outcomes. Such data manipulation extracts more information from the target time series, which, in turn, can be used to enhance the forecasting performance. [209] referred to this category of forecast combinations generally as “wisdom of the data” and provided an overview of approaches in this category. In this particular context, the combination methods reviewed in this paper can function as tools to aggregate (or combine) the forecasts computed from different perspectives of the same data. The second type of forecast combination we do not cover is forecast reconciliation for hierarchical time series, which has developed over the past ten years since the pioneering work of [129]. Forecast reconciliation involves reconciling forecasts across the hierarchy to ensure that the forecasts sum appropriately across the levels of the hierarchy, and hence is a type of forecast combination.

We note that forecast combination and model averaging are sometimes used without distinction in the literature. The two terms overlap, but their focuses are different. “Model averaging” is a general term allowing for model uncertainty, particularly in parameter estimation, which can lead to better estimates and more reliable forecasts and prediction intervals than model selection (selecting a single best model). Several approaches to model averaging have been developed in statistics, econometrics, and machine learning. Two main strands can be identified: frequentist approaches [87, e.g.,] and Bayesian approaches [237, e.g.]. “Forecast combination” is a more focused terminology describing the combination of forecasts to generate a better forecast; the component forecasts could be outcomes from model averaging, individual models, or expert forecasts, for example. As with model averaging, weights can be used to combine the component forecasts. Unlike model averaging, however, forecast combination also has some underlying assumptions on the forecasts to ensure that the forecast combinations are unbiased or optimal.

This paper aims to contribute a broad perspective and historical overview of the main developments in forecast combinations. The paper is organized into two main sections on point forecast combinations (Section 2) and probabilistic forecast combinations (Section 3). Section 4 concludes the paper and identifies possible future developments in the future.

2 Point forecast combinations

2.1 Simple point forecast combinations

A considerable literature has accumulated over the years regarding how individual forecasts are combined, with the unanimous conclusion that simple combination schemes are hard to beat [139, 52, 86, 241, 165]. That is, equally weighted averages, which ignore past information regarding the precision of individual forecasts and correlations between forecast errors, work reasonably well compared to more sophisticated combination schemes.

The vast majority of studies on combining multiple forecasts have dealt with point forecasting, even though point forecasts (without associated measures of uncertainty) provide insufficient information for decision-making. The simple arithmetic average of forecasts based on equal weights stands out as the most popular and surprisingly robust combination rule [39, 54, 240, 97, see], and can be effortlessly implemented.

An early example of an equally weighted combination is from the M-competition, the first forecasting competition run by Spyros Makridakis and Michèle Hibon, involving 1001 time series; see [173] and [128] for more details of the competition. [173] reported that the simple average outperformed the individual forecasting models. [52] provided an extensive bibliographical review of the early work on the combination of forecasts, and then addressed the issue that the arithmetic means often dominate more refined forecast combinations. [177] concluded empirically that a larger number of individual methods included in the simple average scheme would help improve the accuracy of combined forecasts and reduce the variability associated with the selection of methods. [199] concisely summarized the advantages of adopting simple averaging into three aspects: (i) combination weights are equal and do not have to be estimated; (ii) simple averaging significantly reduces variance and bias by averaging out individual bias in many cases; and (iii) simple averaging should be considered when the uncertainty of weight estimation is taken into account. Additionally, [253] pointed out that the outstanding average performance of simple averaging depends strongly on model instability and the ratio of forecast error variances associated with different forecasting models.

More attention has been given to other strategies, including using the median and mode, as well as trimmed and winsorized means [46, 241, 97, 134, 114, e.g.,], due to their robustness in the sense of being less sensitive to extreme forecasts than a simple average [165]. For example, the early work of [92] observed that the “middlemost” of 787 estimates of an ox’s weight is within nine pounds of the ox’s actual weight, and thus advocated for the median forecast as the “vox populi” [91]. However, there is little consensus in the literature on whether the mean or the median of individual forecasts performs better in terms of point forecasting [147]. Specifically, [184] found no significant difference between the mean and the median, while the results of [241] supported the mean and [4, 92] recommended the median. [135] studied the forecasting performance of the mean and median, as well as the trimmed and winsorized means. Their results suggested that the trimmed and winsorized means are appealing, particularly when there is a high level of variability among the individual forecasts, because of their simplicity and robust performance. [152] compared empirically the mean, mode and median combination operators based on kernel density estimation, and found that the three operators deal with outlying extreme values differently, with the mean being the most sensitive and the mode operator the least. Based on these experimental results, they recommended further investigation of the use of the mode and median operators, which have been largely overlooked in the relevant literature.

Compared to various complicated combination approaches and machine learning algorithms, simple combinations seem outdated and uncompetitive in the big data era. However, the results from the recent M4 competition [175] showed that simple combinations continue to achieve relatively good forecasting performance and are still competitive. Specifically, a simple equal-weight combination ranked the third for yearly time series [232] and a median combination of four simple forecasting models achieved the sixth place for point forecasting [210]. [97] encompassed a variety of combination methods in the case of forecasting GDP growth and the unemployment rate. They found that the simple average sets a tough benchmark, with few combination schemes outperforming it. Moreover, simple combinations have a lower computational burden and can be implemented more efficiently than alternatives. Therefore, simple combination rules have been consistently the choice of many researchers and practitioners, and provide a challenging benchmark to measure the effectiveness of the newly proposed weighted forecast combination algorithms [174, 241, 175, 186, 141, 260, e.g.,].

Despite the ease of implementing simple combination schemes, their success still depends largely on the choice of the forecasts to be combined. Intuitively, we prefer that the component forecasts fall on opposite sides of the truth (the realization) [21, 159], so that the forecast errors tend to cancel each other out. However, this rarely occurs in practice, as the component forecasts are usually trained based on overlapping information sets and use similar forecasting methods. If all component forecasts are established similarly based on the same, or highly overlapping sets of information, forecast combinations are unlikely to be beneficial for the improvement of forecast accuracy. [178] and [165] emphasized two critical issues concerning the performance of simple combination rules: one for the level of accuracy (or expertise) of the forecasts in the pool and another for diversity among individual forecasts. Involving forecasts with low accuracy in the pool can decrease the combination performance. Additionally, a high degree of diversity among component models facilitates the achievement of the best possible forecast accuracy from simple combinations [250]. In conclusion, simple, easy-to-use combination rules can provide good and robust forecasting performance, especially when properly considering issues such as the accuracy and diversity of the individual forecasts to be combined.

2.2 Linear combinations

Despite the simplicity and performance of simple combination rules, it makes sense to assign greater weight to the most accurate forecast methods. But how to choose those weights? The problem of point forecast combinations can be defined as seeking a one-dimensional aggregator that integrates an -dimensional vector of -step-ahead forecasts involving the information up to time , , into a single combined -step-ahead forecast , where is the number of forecasts to be combined and is an -dimensional vector of combining weights. The class of combination methods represented by the mapping, , comprises linear and nonlinear combinations, as well as series-specific and cross-learning combinations. Additionally, the combination weights can be static or time-varying along the forecasting horizon. Below we discuss in detail the use of various approaches to determining combination weights associated with individual forecasts.

Typically, the combined forecast is constructed as a linear combination of the individual forecasts, which can be written as

where is an -dimensional vector of linear combination weights assigned to individual forecasts.

Optimal weights

The seminal work of [21] proposed a method to find the so-called “optimal” weights by minimizing the variance of the combined forecast error, and discussed only combinations of pairs of forecasts. [191] then extended the method to combinations of more than two forecasts. Specifically, if the individual forecasts are unbiased and their error variances are consistent over time, then the combined forecast obtained by a linear combination will also be unbiased. Differentiating with respect to and solving the first order condition, the variance of the combined forecast error is minimized by taking

| (1) |

where is the covariance matrix of the -step forecast errors and is an -dimensional unit vector. This is implemented, for example, in the R package ForecastComb [264]. In practice, the elements of the covariance matrix are usually unknown and need to be estimated.

It follows that if is determined by Equation (1), one can identify a combined forecast with no greater error variance than the minimum error variance of all individual forecasts. The fact was further explored by [253] to illustrate the diversification gains offered by forecast combinations, by simply considering combinations of pairs of forecasts. Under mean squared error (MSE) loss, [253] characterized the general solution of the optimal linear combination weights by assuming a joint Gaussian distribution of the outcome and available forecasts .

The loss assumed in [21] and [191] is quadratic and symmetric. [82] examined forecast combinations under more general loss functions accounting for asymmetries as well as skewed forecast error distributions. They demonstrated that the optimal combination weights strongly depend on the degree of asymmetry in the loss function and skewness in the underlying forecast error distributions. Subsequently, [201] demonstrated that the properties of optimal forecasts established under MSE loss are not generally robust under more general assumptions about the loss function. In addition, the properties of optimal forecasts were generalized to consider asymmetric loss and nonlinear data generating processes.

Regression-based weights

The seminal work by [110] provided an important impetus for approximating the “optimal” weights under a linear regression framework. They recommended the strategy that the combination weights can be estimated by ordinary least squares (OLS) in regression models having the vector of past observations as the response variable and the matrix of past individual forecasts as the predictor variables. Three alternative approaches imposing various possible restrictions were considered

| (2) | |||

| (3) | |||

| (4) |

The R package ForecastComb [264] provides the corresponding implementations. The constrained OLS estimation of the regression in Equation (2), in which the constant is omitted and the weights are constrained to sum to one, yields results identical to the “optimal” weights proposed by [21]. [110] further suggested that the unrestricted OLS regression in Equation (4), which allows for a constant term and does not require the weights to sum to one, is superior to the popular “optimal” method regardless of whether the constituent forecasts are biased. However, [64] argue that when using the unrestricted regression, one needs to consider the stationarity of the series being forecast, the possible presence of serial correlation in forecast errors [68, 61, see also], and the issue of multicollinearity.

Generalizations of the combination regressions have been considered in a large body of literature. [68] exploited serial correlated errors in the least squares framework by characterizing the combined forecast errors as autoregressive moving average (ARMA) processes, leading to improved combined forecasts. [117] and [7] provided an empirical analysis to compare the performance of various combination strategies, including the simple average, the unrestricted OLS regression, the restricted OLS regression where the weights are constrained to sum to unity, and the restricted OLS regression where the weights are constrained to be nonnegative. The results revealed that constraining weights to be nonnegative is at least as robust and accurate as the simple average and yields superior results compared to other combinations based on a regression framework. [59] addressed the problem of determining the combination weights by imposing both restrictions (that the weights should be nonnegative and sum to one), which turns out to be a special case of a LASSO regression. [61] found that allowing a lagged dependent variable in forecast combination regressions can achieve improved performance. Instead of using the quadratic loss function, [193] applied the absolute loss function in the unrestricted regression, also implemented in the ForecastComb package for R, to yield the least absolute deviation regression which is more robust to outliers than OLS combinations.

Forecast combinations using changing weights have also been developed to solve various types of structural changes in constituent forecasts. For instance, [71] explored rolling weighted least squares as well as time-varying parameter techniques in the basic regression framework, including both deterministic and stochastic time-varying parameters. Specifically, the combination weights are either described as deterministic nonlinear (polynomial) functions of time or allowed to involve random variation. They showed, via numerical examples based on various types of structural change in the constituent forecasts, that time-varying weights substantially help in improving forecasting ability in the presence of instabilities. [67] allowed the combination weights to evolve immediately or smoothly using switching regression models and smooth transition regression models. [248] generalized the regression method by incorporating time-varying coefficients that are assumed to follow a random walk process. The generalized model can be interpreted as a state space model and then estimated using Kalman filter updating. Following the spirit of [248], [213] achieved an accelerated inference process by using forgetting factors in the recursive Kalman filter updating.

Researchers have also worked on including many forecasts in a regression framework to take advantage of many models. However, [46] examined a wide range of combination methods and showed that OLS combinations have very poor performance when (the number of forecasts to be combined) is very large. Factor methods are a common way of condensing information when modeling and forecasting. They have also been used explicitly in forecast combination settings, and are especially attractive when the number of forecasts to be combined is very large (); see, e.g., [46] for a dynamic factor model framework for forecast combinations. The common factors in approximate dynamic factor models can be estimated by principal components [239]. Principal components regression (PCR) is typically motivated as an ad hoc tool for the solution of multicollinearity. [46] and [241] explicitly applied PCR to forecast combinations, resulting in a two-step procedure. The first step extracts the principal components, while the second step produces the final forecasts utilizing OLS regression. The superiority of PCR over OLS combinations was also supported by [216] and [211]. In turn, these methods relate to the question of whether one should forecast with variables (competing point forecasts in our paper’s context), factors (extracted from the competing forecasts), or both; see, e.g., [44] for a detailed discussion.

In large cases, given the estimation problems that arise when , researchers also frequently relate forecast combinations to shrinkage-type approaches (whether frequentist or Bayesian) that facilitate estimation of the forecast combination regression even when ; e.g. see [241]. [73] considered methods for selection and shrinkage in regression-based forecast combinations to address the estimation problem. They shed light on how machine learning can be used to optimally combine a large set of forecasts by introducing a LASSO-based procedure that consists of two steps. The first step involves setting some combination weights to zero using LASSO, and the second step shrinks the combination weights of the survivors toward equal weights. Additionally, [5] argued in favor of clustering the individual forecasts using the -means clustering algorithm based on their historical performance. For each cluster, a pooled (average) forecast is computed, which precedes the estimation of combination weights for the constructed clusters.

Performance-based weights

Estimation errors in the “optimal” weights and regression-based weights tend to be particularly large due to difficulties in properly estimating the covariance matrix , especially in situations with many forecasts to combine. Instead, [21] suggested weighing the constituent forecasts in inverse proportion to their historical performance, ignoring mutual dependence. In follow-up studies, [191] and [271] generalized this idea in the sense of considering more time series, more individual forecasts, and multiple forecast horizons. Their extensive results demonstrated that combinations ignoring correlations are more successful than those attempting to take account of correlations, and consequently reconfirmed [21]’s (\citeyearBates1969-yj) argument that correlations can be poorly estimated in practice and should be ignored when calculating combination weights.

Let be the -dimensional vector of -step forecast errors computed from the individual forecasts. Then the five procedures suggested in [21] for estimating the combination weights when is unknown, are extended to the general case as follows:

| (5) | |||

| (6) | |||

| (7) | |||

| (8) | |||

| (9) |

These weighting schemes differ in the factors, as well as the choice of the parameters, , , and . Correlations across forecast errors are either ignored by treating the covariance matrix as a diagonal matrix or estimated via the usual sample estimator (which may lead to quite unstable estimates of given highly correlated forecast errors). Some estimation schemes suggest computing or updating the relative performance of individual forecasts over rolling windows of the most recent observations, while others base the weights on exponential discounting with higher values of giving larger weights to more recent observations. Consequently, these weighting schemes are well adapted to allow a non-stationary relationship between the individual forecasting procedures over time [191]. However, they tend to increase the variance of the parameter estimates and work quite poorly if the data generating process is truly covariance stationary [253].

A broader set of combination weights based on the relative performance of individual forecasting techniques has been developed and examined in a series of studies. For example, [238] generalized the rolling window scheme in Equation (5) in the sense that the weights on the individual forecasts are inversely proportional to the th power of their MSE. The weights with correspond to assigning equal weights to all forecasts, while more weights are placed on the best performing forecasts by considering . Other forms of forecast error measures, such as the root mean squared error (RMSE) and the symmetric mean absolute percentage error (sMAPE), have also been considered to lead to performance-based combination weights [193, 204, e.g.,]. A weighting scheme with the weights depending inversely on the exponentially discounted errors was proposed by [241] as an upgraded version of the scheme in Equation (8), and was used in several subsequent studies [51, 97, e.g.,] to achieve gains from combining forecasts. The pseudo out-of-sample performance used in these weighting schemes is commonly computed based on rolling or recursive (expanding) windows [238, 51, 97, e.g.,]. It is natural to adopt rolling windows in estimating the weights to deal with structural changes, but the window length should not be too short without the estimates of the weights becoming too noisy [23].

Compared to constructing the weights directly using historical forecast errors, a new form of combinations that is more robust and less sensitive to outliers was introduced based on the “ranking” of individual forecasts. Again this kind of combination ignores correlations among forecast errors. The simplest and most commonly used method in the class is to use the median forecast as the output. [5] constructed the weights proportional to the inverse of performance ranks (sorted according to increasing order of forecast errors), which were later employed by [8] for tourism demand forecasting. The R package ForecastComb [264] provides tools for rank-based combinations. Another weighting scheme which attaches a weight proportional to to the th ordered constituent forecast was adopted in [275] and [77] to combine forecasts obtained from artificial neural networks (ANNs), where is a scaling factor. However, as mentioned by [8], this class of combination methods limits the weights to only a discrete set of possible values.

Criteria-based weights

Information criteria, such as Akaike’s information criterion [6, AIC,], the corrected Akaike information criterion [243, AICc,], and the Bayesian information criterion [230, BIC,], are often used for model selection in forecasting. However, choosing a single model out of the candidate model pool may be misleading because of the information loss from the alternative models. An alternative approach proposed by [40] is to combine multiple models based on information criteria to mitigate the risk of selecting a single model. It is also worth mentioning that the R packages MuMIn [17] and mmSAR [116] have been developed to perform model selection and multimodel averaging based on the use of information-theoretic approaches introduced by [40].

One such common approach is using Akaike weights. Specifically, in light of the fact that AIC estimates the Kullback-Leibler distance [157] between a model and the true data generating process, differences in the AIC can be used to weight different models, providing a measure of the evidence for supporting a given model relative to other constituent models. Given individual models, the Akaike weight of model can be derived as:

| where |

Akaike weights calculated in this manner can be interpreted as the probability that a given model performs best at approximating the unknown data generating process, given the model set and the available and historical data [147]. Similar weights from AICc, BIC, and other variants with different penalties, can be derived analogously.

The outstanding performance of weighted combinations based on information criteria has been supported in several studies. For instance, [147] used weights derived from AIC, AICc and BIC to combine exponential smoothing forecasts, and obtained superior accuracy over selecting a model using the same information criteria. A similar strategy was adopted by [206] to separately explore the benefits of bootstrap aggregation (bagging) for time series forecasting. Additionally, an empirical study by [207] showed that a weighted combination based on AIC improves the performance of the statistical benchmark they used.

Bayesian weights

Some effort has been directed towards Bayesian approaches to updating forecast combination weights in the face of new information gleaned from various sources. Recall that obtaining reliable estimates of the covariance matrix (the time and horizon subscripts are dropped for simplicity) of forecast errors is a major challenge in practice regardless of whether correlations among forecast errors are ignored or not. With this in mind, [38] suggested the idea of Bayesian combinations on the basis of the probability of each forecasting model performing the best on any given occasion. Considering the beta and the Dirichlet distributions as the conjugate priors for the binomial and multinomial processes respectively, the suggested non-parametric method performs well when there is relatively little past data by means of attaching prior subjective probabilities to individual forecasts [39, 64]. [196] presented another approach to using subjective probability in a Bayesian updating scheme based on the self-scoring weights proportional to the evaluation of the expert’s forecasting ability.

A different strand of research has also advocated the incorporation of prior information into the estimation of combination weights, but with the weights being shrunk toward some prior mean under a regression-based combination framework [192]. Assuming that the vector of forecast errors is normally distributed, [54] developed a Bayesian approach with the conjugate prior for represented by an inverted Wishart distribution with covariance matrix and scalar degrees of freedom . Again we drop time and horizon subscripts for simplicity. If the last observations are used to estimate , the combination weights derived from the posterior distribution for are

where is the precision matrix and is the sample covariance matrix. Compared to estimating using the standard sample covariance estimator or treating it as a diagonal matrix, the proposed approach provides a more stable estimation and allows for correlations between methods. The subsequent work by [72] allowed the incorporation of the standard normal-gamma conjugate prior by considering a normal regression-based combination

where and are -dimensional vectors of historical data and residuals, respectively, and is the matrix of constituent one-step forecasts. This approach results in estimated combination weights that can be viewed as a matrix-weighted average of those for the two polar cases (least squares and prior weights), and it can provide a rational transition between the subjective and data-based estimation of the combination weights. In light of the fact that Bayesian approaches have been mostly employed to construct combinations of probability forecasts, we will elaborate on other newly developed methods of determining combination weights from a foundational Bayesian perspective in Section 3.7.

2.3 Nonlinear combinations

Linear combination approaches implicitly assume a linear dependence between constituent forecasts and the variable of interest [76, 88], and may not result in the best forecast [233], especially if the individual forecasts come from nonlinear models or if the true relationship between combination members and the best forecast is characterized by nonlinear systems [13]. In such cases, it is natural to relax the linearity assumption and consider nonlinear combination schemes of higher complexity; these have received very limited research attention so far.

As [253] identified, two types of nonlinearities can be incorporated in forecast combinations. One involves nonlinear functions of the individual forecasts, but with the unknown parameters of the combination weights given in the linear form. The other allows a more general combination with nonlinearities directly considered in the combination parameters. Neural networks are often employed to estimate the nonlinear mapping because they offer the potential of learning the underlying nonlinear relationship between the future outcome and individual forecasts. The design of a neural network model is nevertheless time-consuming, and sometimes leads to overfitting and poor forecasting performance as more parameters need to be estimated.

[76] used ANNs to obtain the combined forecasts by the following form

| (10) | ||||

| (11) |

where , and denote the in-sample mean and in-sample standard deviation respectively, , and . This approach permits special cases of both purely linear combinations ( and ) and nonlinear combinations ( and ). Building on this, [119] proposed to evolve ANNs and demonstrated their utility, but only using a single time series. [156] and [13] employed neural network approaches with various activation functions to approximate the nonlinear dependence of individual forecasts and achieve nonlinear mapping, resulting in variants of Equation (10). The empirical results of nonlinear combinations from these studies generally dominate those from traditional linear combination strategies, such as simple average, OLS weights, and performance-based weights. However, the empirical evidence provided is based on fewer than ten time series, possibly hand-picked to lead to this result. Additionally, these nonlinear combination methods suffer from other drawbacks including the neglect of correlations among forecast errors, the instability of parameter estimation, and the multicollinearity caused by the overlap in the information sets used to produce individual forecasts. Thus, the performance of nonlinear combinations relative to linear combinations needs further investigation.

Some researchers have sought to construct nonlinear combinations via the inclusion of an additional nonlinear term to cope with the case where the individual forecast errors are correlated. The combination mechanism can be generalized to the following form

where is some nonlinear combination of forecasts and . In this way, the general framework for linear combinations is extended to deal with nonlinearities.

For example, [88] defined as the product of individual forecasts from different models, , while [3] took into account the linear correlations among the forecast pairs by including the term, , where and are the mean and standard deviation of the th model, respectively. Moreover, [2] defined the nonlinear term using , where denotes the standardized th individual forecast using the mean and standard deviation , and the term denotes the degree of mutual dependency between the th and th individual forecasts.

Clearly, combining forecasts nonlinearly requires further research. In particular, the forecasting performance of the various proposed nonlinear combination schemes should be properly investigated with a large, diverse collection of time series datasets along with appropriate statistical inference. There is also a need to develop nonlinear combination approaches that take account of correlations across forecast errors and the multicollinearity of forecasts.

2.4 Combining by learning

Stacked generalization [272, stacking,] provides a strategy to adaptively combine the available forecasting models. Stacking is frequently employed on a wide variety of classification tasks [280]; in the time series forecast context, it uses the concept of meta-learning to boost forecasting accuracy beyond that achieved by any of the individual models. Stacking is a general framework that comprises at least two levels. The first level involves training the individual forecasting models using the original data, while the second and any subsequent levels utilize an additional “meta-model”, using the prior level forecasts as inputs to form a set of forecasts. Thus, the stacking approach to forecast combinations weights individual forecasts adaptively using meta-learning processes.

There are many ways to implement the stacking strategy. Its primary implementation is to combine individual models in a series-by-series fashion. Individual forecasting models in the method pool are trained using only data of the single series they are going to forecast, while their forecast outputs are subsequently fed to a meta-model tailored for the target series to calculate the combined forecasts. This means that meta-models are required for separate time series data. Unsurprisingly, regression-based weight combinations discussed in Section 2.2 [110, 117, e.g.,] fall into this category and can be viewed as the most simple, common learning algorithm used in stacking. Instead of applying multiple linear regressions, [187] suggested a PCR model as the meta-model predominantly due to its desirable characteristics such as dimensionality reduction and avoidance of multicollinearity between the input forecasts of individual models. Similarly, LASSO regression, ANN, wavelet neural network (WNN), and support vector regression (SVR) can be conducted in a series-by-series fashion to achieve the same goal [76, 59, 222, 223, e.g.,]. One could use an expanding or rolling window method to ensure that enough individual forecasts are generated for the training of meta-models. Time series cross-validation, also known as “evaluation on a rolling forecasting origin” [130], is also recommended in the training procedures for both individual models and meta-models to help with the parameter estimation. Nevertheless, stacking approaches implemented in a series-by-series fashion still suffer from some limitations such as requiring a long computation time and long time series, and inefficiently using the training data.

An alternative way to perform the stacking strategy sheds some light on the potential of cross-learning. Specifically, the meta-model is trained using information derived from multiple time series rather than employing only a single series, thus various patterns can be captured along different series. The M4 competition organized by Spyros [175], comprising time series, recognized the benefits of cross-learning in the sense that the top three performing methods of the competition utilize the information across the whole dataset rather than a single series. Cross-learning can therefore be identified as a promising strategy to boost forecasting accuracy, at least when appropriate strategies for extracting information from large, diverse time series datasets are adopted [144, 231]. [279] trained a neural network model across the M4 competition dataset to learn how to combine individual models in the method pool. They adopted the temporal holdout strategy to generate the training dataset and utilized only the out-of-sample forecasts produced by standard individual models as the input for the neural network model.

An increasing stream of studies has shown that time series features characterizing each series in a dataset, provide valuable information for forecast combinations in a cross-learning fashion, leading to an extension of stacking. Numerous software packages have been developed for time series feature extraction, including the R packages feasts [195] and tsfeatures [132], the Python packages Kats [83], tsfresh [49] and TSFEL [16], the Matlab package hctsa [89], and the C-coded package catch22 [169]. These sets of time series features were empirically evaluated by [121].

The pioneering work by [58] developed a rule base consisting of rules to combine forecasts from four statistical models using time series features. [208] identified the main determinants of forecasting accuracy through an empirical study involving forecasting models and seven time series features. The findings can provide useful information for forecast combinations. More recently, [186] introduced a Feature-based FORecast Model Averaging (FFORMA) approach available in the R package M4metalearning [185], which employs statistical features (implemented using the R package tsfeatures) to estimate the optimal weights for combining nine different traditional models trained per series based on an XGBoost model. The FFORMA method reported the second-best forecasting accuracy in the M4 competition. Additionally, [170] highlighted the potential of convolutional neural networks as a meta-model to link the learnt features with a set of combination weights. [163] extracted time series features automatically with the idea of time series imaging, then these features were used for forecast combinations. [95] demonstrated the value of a collection of combination methods on a large and diverse amount of time series from the M3 [174], M4, M5 [171] datasets and FRED datasets555The FRED (Federal Reserve Economic Data) dataset is openly available at https://fred.stlouisfed.org.. In light of the fact that it is not clear which combination strategy should be selected, they introduced a meta-learning step to select a promising subset of combination methods for a newly given dataset based on extracted features.

In addition to the time series features extracted from the historical data, it is crucial to look at the diversity of the individual model pool in the context of forecast combinations [20, 250, 12, 165]. An increase in diversity among forecasting models has the potential to improve the accuracy of their combination. In this respect, features measuring the diversity of the method pool should be included in the feature pool to provide additional information possibly relevant to combining models. [161] calculated six diversity features and created an extensive feature pool describing both the time series and the individual method pool. Three meta-learning algorithms were implemented to link knowledge on the performance of individual models with the extracted features, and to improve forecasting performance. [140] utilized a group of features only measuring the diversity across the candidate forecasts to construct a forecast combination model mapping the diversity matrix to the forecast errors. The proposed approach yielded comparable forecasting performance with the top-performing methods in the M4 competition.

As expected, the implementations of stacking in a cross-learning manner also come with their limitations. The first limitation is the requirement for a large, diverse time series dataset to enable meaningful training outcomes. This issue can be addressed by simulating series on the basis of some assumed data generating processes [247] [131, implemented using the R package forecast,], or by generating time series with diverse and controllable characteristics [141] [143, implemented in the R package gratis,]. Moreover, given the considerable literature on feature identification and feature engineering [261, 142, 161, 186, 163, e.g.,], the feature-based forecast combination methods naturally raise some issues yet to receive much research attention including how to design an appropriate feature pool in order to achieve the best out of such methods, and what is the best loss function for the meta-model.

It is also worth mentioning that many neural network models rely on a model combination strategy, namely “ensembling” [43, see, e.g.,], that is applied internally to improve the overall forecasting performance. Due to the weak learning process in deep learning models, the overall forecasting results heavily depend on the combination of each forecasting result. They diversify the individual forecast via (1) varying the training data, (2) varying the model pool, and (3) varying the evaluation metric. For example, the N-BEATS model [198] utilized different strategies to diversify the forecasting results. For each forecasting horizon, individual models are trained with six window lengths. It also used three metrics sMAPE, MASE and MAPE to validate each model. In the end, a variety of models are used to make the median ensemble for results on the test set. One may refer to [93] for a general view of deep learning ensembles.

2.5 Which forecasts should be combined?

Including forecast methods with poor accuracy degrades the performance of the forecast combination. One prefers to exclude component forecasts that perform poorly and to combine only the top performers. In judgmental forecasting, [178] highlighted the importance of the crowd’s mean level of accuracy (expertise). They argued that the mean level of expertise sets a floor on the performance of combining. The gains in accuracy from selecting top-performing forecasts for combination have been investigated and confirmed by a stream of articles such as [35] and [151]. [165] emphasized that the variance of accuracy across time series, which provides an indication of the accuracy risk, exerts a great influence on the performance of the combined forecasts. They suggested balancing the trade-offs between the average accuracy and the variance of accuracy when choosing component models from a set of available models.

Another key issue is diversity. Diversity among the individual forecasts is often recognized as one of the elements required for accurate forecast combination [20, 34, 250]. [12] utilized the bias-variance decomposition of MSE to study the effects of forecast combinations and confirmed that an increase in diversity among the individual forecasts is responsible for the error reduction achieved in combined forecasts. Diversity among individual forecasts is frequently measured in terms of correlations among their forecast errors, with lower correlations indicating a higher degree of diversity. The distance of top-performing clusters introduced by [161], where a -means clustering algorithm is applied to construct clusters, and a measure of coherence proposed by [250] are also considered as other measures to reflect the degree of diversity among forecasts.

In an analysis of a winner-take-all forecasting competition, [167] found that the optimal strategy for reporting forecasts is to exaggerate the forecasters’ own private information and down-weight any common information. This exaggeration results in gains in the accuracy of the simple average by amplifying the diversity of the individual forecasts. The gains were confirmed by [114], who looked more closely at the impact of private-signal exaggeration on forecast combinations, which translates into averaging forecasts that are overfitted and overconfident.

Ideally, we would choose independent forecasts to amplify the diversity of the component forecasts when forming a combination. However, the available individual forecasts are often produced based on similar training, similar models and overlapping information sets, leading to highly positively correlated forecast errors. Including forecasts that have highly correlated forecast errors in a combination creates redundancy and may result in unstable weights, especially in the class of regression-based combinations (see Section 2.2). In this respect, using different types of forecasting models (e.g., statistical, machine learning, and judgmental), or different sources of information (e.g., exogenous variables), can help improve diversity [12]. The results of the M4 competition reconfirmed the benefits of combinations of statistical and machine learning models [175].

It is often suggested that a subset of individual forecasts be combined, rather than the full set of forecasts, as there are decreasing returns to adding additional forecasts [9, 281, 123, 99, 73, 165]. Simply put, many could be better than all. In this regard, given a method pool with many forecasting models available, one can consider an additional step ahead of combining: subset selection. Instead of using all available forecasts in a combination, the step aims to eliminate some forecasts from the combination and select only a subset of the available forecasts.

The most common technique of subset selection is to include only the most accurate methods in the combination, discarding the worst-performing individual forecasts [109, e.g.,]. [178] investigated the gains in accuracy from this select-crowd strategy. [151] proposed a heuristic, where we exclude component forecasts that show a sharp drop in performance by using the outlier detection methods in boxplots. Their empirical results over four diverse datasets showed that this subset selection approach outperforms selecting a single forecast or combining all available forecasts. Nonetheless, the approach may suffer from a lack of diversity when formulating appropriate pools.

Early studies considering diversity used forecast encompassing tests for combining forecasts [146, 60, e.g.,]. The forecast encompassing literature ties in very closely with forecast combinations. Several forecast encompassing tests have been developed to test whether one forecast (or a set of forecasts) encompasses all information contained in another forecast (or another set of forecasts); see, e.g., [48] and [120]. A classical argument suggests that when fixed weights are used (as in an average), only non-encompassed individual models are worth combining [69]. However, [122] provided a counter example in processes subject to location shifts where previously encompassed models may later dominate, while the earlier dominant model may later fail badly.

The diversity of an available forecast pool has occasionally been explicitly considered for subset selection. [42] proposed an optimal subset selection algorithm for forecast combinations based on mutual information, which takes account of diversity among different forecasts. More recently, [165] developed a subset selection approach comprising two screens: one screen for removing individual models that perform worse than the Naïve2 benchmark, and another for excluding pairs of models with highly correlated forecast errors. In this way, both accuracy and diversity issues are addressed when forming a combination.

Subset selection techniques take advantage of allowing many forecasts to be considered when combining, reducing weight estimation errors and improving computational efficiency. However, subset selection has received scant attention in the context of forecast combinations, and it is mainly focused on trimming based on the principles of expertise. Therefore, automatic selection techniques considering both expertise and diversity merit further attention and development.

One approach is to note that subset selection is equivalent to assigning zero weights to some individual forecasts, which could be determined either statistically or judgmentally. [73] focused on weights that solve a penalized estimation problem. Specifically, they proposed a two-step LASSO-based procedure that selects a subset of forecasts to combine in the first step, and shrinks the weights of the selected candidates toward equality. An alternative idea can be using a pre-set threshold to select individual models with weights greater than the threshold to join the subsequent combination; see, e.g., [281, 260]. Of course, there is no guarantee that the zero weight over the training period will also be zero over the forecast horizon. Hence, time-varying subset selection is certainly one solution to this problem and can be achieved by applying a pre-set threshold to forecast combinations with time-varying weights [162].

2.6 Forecast combination puzzle

Despite the explosion of a variety of popular and sophisticated combination methods, empirical evidence and extensive simulations repeatedly show that the simple average with equal weights often outperforms more complicated weighting schemes. This somewhat surprising result has occupied a very large literature, including the early studies by [238, 240, 241], the series of Makridakis competitions [173, 174, 175], and also the more recent articles by [29, 30], etc. [52] surveyed the early combination studies and raised a variety of issues that remain to be addressed, one of which is “What is the explanation for the robustness of the simple average of forecasts?” In a recent study, [95] investigated the forecasting performance of a collection of combination methods on many time series from diverse sources and found that the winning combination methods differ for the different data sources, while the simple average strategies show, on average, more gains in improving accuracy than other more complex methods. [241] coined the term “forecast combination puzzle” for the phenomenon — theoretically sophisticated weighting schemes should provide more benefits than the simple average from forecast combination, while empirically the simple average has been continuously found to dominate more complicated approaches to combining forecasts.

Most explanations of why simple averaging might dominate complex combinations in practice have centered on the errors that arise when estimating the combination weights. For example, [253] noted that the success of simple combinations is due to the increased parameter estimation error with weighted combinations — simple combination schemes do not require estimating combination parameters, such as weights based on forecast errors. [235] demonstrated that the simple average is expected to overshadow the weighted average in a situation where the weights are theoretically equivalent. The results from simulations and an empirical study showed the estimation cost of weighted averages when the optimal weights are close to equality, thus providing an empirical explanation of the puzzle. Later, [50] provided a theoretical explanation for these empirical results. Taking the estimation of “optimal” weights (see Section 2.2) into account, [50] considered random weights rather than fixed weights during the optimality derivation and showed that, in this case, the forecast combination may introduce biases in combinations of unbiased component forecasts and the variance of the forecast combination may be larger than in the fixed-weight case, such as the simple average. More recently, [45] proposed a framework to study the theoretical properties of forecast combinations. The proposed framework verified the estimation error explanation of the “forecast combination puzzle” and, more crucially, provided additional insights into the puzzle. Specifically, the mean squared forecast error (MSFE) can be considered as a variance estimator of the forecast errors which may not be consistent, leading to biased results with different weighting schemes based on a simple comparison of MSFE values. [30] explained why, in practice, equal weights are often a good choice using the tradeoff between bias (reflecting the error resulting from underfitting training data when choosing equal weights) and variance (quantifying the error resulting from the uncertainty when estimating other weights).

Explaining the puzzle using estimation error requires a hypothesis that potential gains from the “optimal” combination are not too large so that estimation error overwhelms the gains. Special cases, such as where the covariance matrix of the forecast errors has equal variances on the diagonal, and all off-diagonal covariances are equal to a constant, are illustrated by [253] and [127] to arrive at equivalence between the simple average and the “optimal” combination. [81] characterized the potential bounds on the size of gains from the “optimal” weights over the equal weights and illustrated that these gains are often too small to balance estimation error, providing a supplementary explanation of the puzzle for the explanation of large estimation error.

Rather than focusing on the impact of combination weight estimation, [282] instead explored the impact of sampling variability in forecast combinations. They demonstrated that, asymptotically, the sampling variability in the performance of the combination forecast is driven entirely by the variability arising from the estimation of the constituent models, and combination weight estimation imparts no bias or variability to the performance of forecast combinations, which lies in opposition to the finding of [50]. These findings imply that, when the combination weights are theoretically equivalent, there will be little performance difference between a sophisticated forecast combination and an equally weighted combination, providing new insights into the “forecast combination puzzle”.

The examination and explanation of the “forecast combination puzzle” can provide decision makers with the following guidelines to identify which combination method to choose in specific forecasting problems.

-

•

Estimation errors are identified as “finite-sample estimation effects” in [235], which suggests that an insufficiently small sample size may be unable to provide robust weight estimates. Thus, if one has access to limited historical data, the simple average or estimated weights with covariances between forecast errors being neglected are recommended. In addition, alternative simple combination operators such as trimmed and winsorized means can be adopted to eliminate extreme forecasts, and thus, offer more robust estimates than the simple average.

-

•

Structural changes, which may cause different weight estimates in the training and evaluation samples, tend to impact sophisticated combination approaches more than the simple average. This case makes the simple average the better choice. The forecast combinations using changing weights can also be considered as a means to cope with structural changes, as suggested in [71] and [67].

-

•

If one has access to many component forecasts, the PCR and the clustering strategy (for details, see Section 2.2) might be useful to diminish estimation errors and solve the multicollinearity problem by reducing the number of parameters need to be estimated.

- •

In summary, forecasters are encouraged to analyze the data prior to identifying the combination strategy and to choose combination rules tailored to specific forecasting problems.

3 Probabilistic forecast combinations

3.1 Probabilistic forecasts

In recent years, probabilistic forecasts have received increasing attention. For example, the recent Makridakis competitions, the M4 and the M5 Uncertainty [176] competitions, encouraged participants to provide probabilistic forecasts of different types as well as point forecasts. Probabilistic forecasts are appealing for enabling optimal decision-making with better understanding of uncertainties and the resulting risks. A brief survey of extensive applications of probabilistic forecasting was offered by [101].

Probabilistic forecasts can be reported in various forms including density forecasts, distribution forecasts, quantiles, and prediction intervals, and how to combine them can vary. For example, although a quantile forecast is the inverse of the corresponding forecast represented by the cumulative distribution function, the combined quantile forecast and the combined probability forecast may not be equivalent. Simple examples of averaging quantiles and probabilities with equal weights are provided by [164].

Interval forecasts form a crucial special case and are often constructed using quantile forecasts where the endpoints are specific quantiles of a forecast distribution. For example, the lower and upper endpoints of a central prediction interval can be defined via the quantiles at levels and .

As with point forecasts, combining multiple probabilistic forecasts allows for diverse information sets and different types of forecasting models, as well as the mitigation of potential misspecifications derived from a single model. Empirical studies suggest that the relative performance of different models often varies over time due to structural instabilities in the unknown data generating process [28, e.g.,]. Thus, there has been a growing interest in bringing together multiple probabilistic forecasts to produce combined forecasts that integrate information from separate sources.

3.2 Scoring rules

Decision makers mainly focus on accuracy when combining point forecasts, while other measures such as calibration and sharpness need to be considered when working with combinations of probabilistic forecasts [100, 103, 158]. Calibration concerns the statistical consistency between the probabilistic forecasts and the corresponding realizations, thus serving as a joint property of forecasts and observations. In practice, a probability integral transform (PIT) histogram is commonly employed informally as a diagnostic tool to assess the calibration of probability forecasts regardless of whether they are continuous [63, 70] or discrete [105]: A uniform histogram indicates a probabilistically calibrated forecast. Sharpness refers to the concentration of probabilistic forecasts, and thus serves as a property of the forecasts only; the sharper a forecast is, the better it is. Sharpness is easily comprehended when considering prediction intervals: the sharper the forecasts, the narrower the intervals. In the case of probability forecasts, sharpness can be assessed in terms of the width of central prediction intervals. For more thorough definitions and diagnostic tools of calibration and sharpness, we refer to [101].

According to [100], the intent of probabilistic forecasting is to maximize the sharpness of the forecast distributions subject to calibration based on the available information set. In this light, scoring rules that reward both calibration and sharpness are appealing in the sense of providing summary measures for the quality of probabilistic forecasts, with a higher score indicating a better forecast. For a probabilistic forecast , a scoring rule is proper if it satisfies the condition that the expected score for an observation drawn from distribution is maximized when . It is strictly proper if the maximum is unique. [103] provides an excellent review and discussion on a diverse collection of proper scoring rules for probabilistic forecasts.

The schemes for combining multiple probabilistic forecasts have evolved from a simple distribution mixture to more sophisticated combinations accounting for correlations between distributions. Which type of strategy one might choose to use depends largely on the computational burden, and the overall performance of the combined forecasts with regard to accuracy, calibration, and sharpness.

3.3 Linear pooling

Probability forecasts strive to predict the probability distribution of quantities or events of interest. In line with the notations in previous sections, here we consider individual forecasts specified as cumulative probability distributions of a random variable at time , denoted , , using the information available up to time , . One popular approach is to directly take a mixture distribution of these individual probability forecasts with estimated weights, neglecting correlations between these individual components. This approach is commonly referred to as the “linear opinion pool” in the literature on combining experts’ subjective probability distributions, dating back at least to [242]. The linear pool of probability forecasts is defined as the finite mixture

| (12) |

where is the weight assigned to the th probability forecast. These weights are often set to be non-negative and sum to one to guarantee that the pooled forecast preserves properties of both non-negativity and integrating to one. The pooled probability forecast satisfies numerous properties such as the unanimity property (if all individual forecasters agree on a probability then the pooled forecast agrees also); see [56] for more details.

Linear pooling of probability forecasts allows us to accommodate skewness and kurtosis (fat tails), and also multi-modality, even under normal distributions of individual forecasts; see [258] and [118] for further discussion on this point.

Define and as the mean and variance of the th component forecast distribution and drop the time and horizon subscripts for simplicity. Then the linear combined probability forecast has the mean and variance,

| (13) | ||||

| and | (14) |

Note that the mean of the combination distribution is equivalent to the linear combination of the individual means. Thus, the associated combination point forecast is consistent with the linear combination point forecast.

However, the variance of the combination distribution is larger than the linear combination of the individual variances when the individual means differ. Consequently, the common strategy of seeking diverse forecasts may harm the probabilistic forecast, while helping the point forecast; see [215] for a theoretical illustration and simulation study. Simply put, as the diversity among individual probability forecasts increases, the mixed forecast will lose sharpness and may become under-confident because of the spread driven by the disagreement between the individual probability forecasts [126, 258, 215].

Even in the ideal case in which individual forecasts are well calibrated, the resulting linear pooling combination may be poorly calibrated. Theoretical aspects of this finding and properties of linear pools of probability forecasts have been further studied in [126], [215], and [164].

On the other hand, [126] demonstrated, both from theoretical and empirical aspects, that linear pooling may work to provide better calibrated forecasts than the individual distributions when individual forecasts tend to be overconfident. This finding helps to account for the success of linear pooling in varied applications. [134] highlighted that if the experts are overconfident but have low diversity, the linear pool may remain overconfident. [164] identified three factors that manipulate the calibration of the probability forecast derived from linear pooling: (i) the number of constituent forecasts, (ii) the degree to which the constituent forecasts are overconfident, and (iii) the degree of the constituents’ disagreement on the location (e.g., mean) of the distribution.

In principle, probability forecasts can be recalibrated before or after the pooling to correct for miscalibration [255]. However, it is challenging to appraise the degree of miscalibration, which may vary considerably among different forecasts and over time, and therefore to recalibrate accordingly. Some effort has been directed toward the development of alternative combination methods to address the calibration issue. For example, [134] suggested the “trimmed opinion pool”, which trims away some individual forecasts from the “linear opinion pool” before mixing the component forecasts. Specifically, exterior trimming that trims away forecasts with low or high means values serves as a way to address under-confidence by decreasing the variance. Conversely, interior trimming that trims away forecasts with moderate means is suggested to mitigate overconfidence via increasing the variance. The improvement in forecasting performance offered by trimming was confirmed by [114] at a more foundational level.

Some researchers prefer nonlinear alternatives, including a generalized linear pool, the spread-adjusted linear pool, and the beta-transformed linear pool, in terms of delivering better calibrated combined probability forecasts; these are discussed in Section 3.5. Instead of mixing probability forecasts mentioned above, [164] recommended averaging quantile forecasts (see Section 3.9) based on the supportive results both theoretically and empirically.

The key practical issue determining the success (or failure) of linear pooling is how the weights for the individual probability forecasts in the finite mixture should be estimated. As with point forecast combinations, equal weights are worthy of consideration, while determining optimal weights is particularly challenging in the case of having access to probability forecasts with limited historical data.

Linear pooling with equal weights is easy to understand and implement, commonly yielding robust and stable outcomes. For reviews, see, e.g., [258] and [194]. A leading example is the survey of professional forecasters (SPF) in the US, which publishes mixed probability forecasts (in the form of histograms) for inflation and GDP growth using equal weights. As the experience of combining point forecasts has taught us, the equally weighted approach often turns out to be hard to beat. An important reason is that it avoids parameter estimation error that often exists in weighted approaches; see Section 2.6 for more details and illustrations.

Motivated by the “optimal” weights obtained in point forecast combinations by minimizing the MSE loss (see Section 2.2), [118] proposed obtaining the set of weights by minimizing the Kullback-Leibler information criterion (KLIC) distance between the combined probability forecast density and the true (but unknown) probability density , . The KLIC distance is defined as

Under the asymptotic assumption that the number of observations grows to infinity, the problem of minimizing the KLIC distance reduces to the maximization of the average logarithmic score of the combined probability forecast. Therefore, the optimal weight vector is given by

| (15) |

where . The use of the logarithmic scoring rule eliminates the need to estimate the unknown true probability distribution, and therefore simplifies the weight estimation for the component forecasts. This was followed by [203] documenting the properties of the optimal weights in Equation (15), centering on the asymptotic assumption used by [118]. Their simulations and empirical results indicated that the combination with optimal weights is inferior for small , while it is valid in minimizing the KLIC distance when is sufficiently large. Therefore, a sufficient training sample is recommended when solving the optimization problem.

Following in the footsteps of [118], many extensions and refinements of the combination strategy have been suggested. [59] devised a simple iterative algorithm to compute the optimal weights in Equation (15). The algorithm scales well with the dimension , and hence enables the combination of many individual probability forecasts. [99] provided a Bayesian perspective on an optimal linear pool, and provided a theoretical justification for the use of optimal weights. [162] conducted time-varying weights based on time-varying features from historical information, where the weights in the forecast combination were estimated via Bayesian logarithmic predictive scores. [133] put forward an exponential weighting scheme based on the recursive weights constructed using the relative past performance of each individual probability forecast in terms of the logarithmic score. In contrast to the optimal opinion pool based on the weights in Equation (15), in this case, the logarithmic score of the combined probability forecast is not necessarily maximized. The logarithmic scoring rule is appealing as it intuitively assigns a higher weight to a component forecast that better fits the realized value. On the other hand, forecast combinations with weights optimized by minimizing the continuously ranked probability score [103, CRPS,], which is a strictly proper scoring rule for distribution forecasts, have been considered in some research, see, e.g, [212], [252], and [251].

Furthermore, some special treatments were given to accommodate probability forecast combinations in applications such as energy forecasting, retail forecasting, and economic forecasting. For instance, [197] extended the idea of optimal combinations but estimated optimal weights by either maximizing the censored likelihood scoring rule [75] or minimizing a weighted version of the CRPS, allowing forecasters to limit themselves to a specific region of the target distribution. For example, we are more likely to be interested in avoiding out-of-stocks when working with retail forecasting. The tail of the distribution is also the main feature of interest when measuring downside risk in equity markets. Additionally, [282] showed that when forecasting during times of high volatility, forecast combinations produced by optimizing according to the censored likelihood scoring rule always lead to a better out-of-sample performance than “optimal” forecast combinations with weights optimized using the logarithmic score, which lends support to the use of a scoring rule that prioritizes accurate forecasts in a specific region. [74] instead constructed regularized mixtures of density forecasts using a variety of objectives and regularization penalties. The optimal regularization tends to spread probability mass from the center into both tails of the distribution, correcting for overconfidence and adjusting kurtosis. Besides, [202] proposed an approach to computing the optimal weights by maximizing the average logarithmic score subject to additional higher moments restrictions. Through constrained optimization, the combined probability forecast can preserve specific characteristics of the distribution, such as fat tails or asymmetry. [180] looked at mode misspecification, and showed via simulation and empirical results that score-specific optimization of linear pooling weights does not always achieve improvements in forecasting accuracy.

3.4 Bayesian model averaging

Bayesian model averaging (BMA) provides an alternative means of mixing individual probability forecasts with respect to their posterior model probabilities. BMA offers a conceptually elegant and logically coherent solution to the issue of accounting for model uncertainty [160, 78, 214, 94, see, e.g.,]. Under this approach, the posterior probability forecast is computed by mixing a set of individual probability forecasts distributions, , from model , and can be given as

| (16) |

where is the posterior probability of model . The decision makers update the prior probability of model being the true model, , via Bayes’ Theorem to compute the posterior probability

| (17) |

where

| (18) |