∎

11institutetext:

Hu Zhang 22institutetext: School of Mathematical Sciences, Shanghai Jiao Tong University, China.

22email: jd_luckymath@sjtu.edu.cn

33institutetext: Yi-Shuai Niu 44institutetext: Department of Applied Mathematics, The Hong Kong Polytechnic University, Hong Kong;

School of Mathematical Sciences and SJTU-Paristech, Shanghai Jiao Tong University, China.

44email: yi-shuai.niu@polyu.edu.hk, niuyishuai@sjtu.edu.cn

A Boosted-DCA with Power-Sum-DC Decomposition for Linearly Constrained Polynomial Program††thanks: This work is supported by the National Natural Science Foundation of China (Grant 11601327).

Abstract

In this paper, we introduce a difference-of-convex (DC) decomposition for polynomials based on power-sum representation, which can be established by solving a sparse linear system. A boosted DCA with exact line search (BDCAe) is proposed to solve the DC formulation of the linearly constrained polynomial program. We show that the exact line search is equivalent to finding roots of a unary polynomial in an interval, which has a closed-form solution in many applications. The subsequential convergence of BDCAe to a critical point is proved, and the convergence rate under Kurdyka-Łojasiewicz property is established. Moreover, a fast dual proximal gradient (FDPG) method is applied to efficiently solve the resulting convex subproblems. Numerical experiments on the Mean-Variance-Skewness-Kurtosis (MVSK) portfolio optimization model via BDCAe, DCA, BDCA with Armijo line search, as well as FMINCON and FILTERSD solvers are reported, which demonstrates good performance of BDCAe.

Keywords:

Power-sum DC decomposition Polynomial optimization Boosted DCA Exact line search FDGP method Portfolio optimizationMSC:

90C26 90C3091G101 Introduction

We are interested in solving the polynomial optimization problem with linear constraints:

| (POPL) |

where is a multivariate polynomial and is a nonempty convex polyhedral set (not necessarily bounded), defined by

where and . Throughout the paper, we use a bold face letter as for a vector and for the i-th coordinate of the vector . The polynomial function is assumed to be bounded from below over , i.e.,

This problem arises in many applications such as the higher-order moment portfolio selection dinh2016dc ; Niu2011 ; niu2019higher , the eigenvalue complementarity problem le2012dc ; niu2013efficient ; niu2015solving ; niu2019improved , the tensor complementarity problem song2016properties , the Euclidean distance matrix completion problem bakonyi1995euclidian , the copositivity of matrix bras2016copositivity ; burer2009copositive ; dur2013testing ; you2022refined , the Boolean polynomial program niu2019discrete , the linear and bilinear matrix inequalities boyd1994linear ; niu2014dc , and so on.

The (POPL) is indeed a special class of the difference-of-convex (DC) program hartman1959functions ; hiriart1985generalized ; le2018dc , defined as below:

| (P) |

where and are convex polynomials. There are some related works on DC decompositions for polynomials. The DC decomposition for quadratic functions has been studied in hoai2000efficient ; bomze2004undominated ; le1997solving based on the eigenvalue decomposition of real symmetric matrices. However, in the case of general multivariate polynomials, this technique is no longer available and the DC decomposition is more difficult to obtain (especially in dense polynomials). Niu et al. Niu2011 proposed a DC decomposition for general polynomials in the form of where is obtained by estimating an upper bound of the spectral radius of the Hessian matrix of over a compact convex set. This technique has been successfully applied to several real-world applications such as the higher-order moment portfolio optimization Niu2011 and the eigenvalue complementarity problems niu2013efficient ; niu2015solving ; niu2019improved . Ahmadi et al. ahmadi2018dc explored DC decompositions for polynomials via algebraic relaxation techniques. They showed in ahmadi2012convex that convexity is different from sos-convexity, and characterized the discrepancy between convexity and sos-convexity in ahmadi2013complete for polynomials. Several DC decompositions are proposed in ahmadi2018dc by solving linear, second-order cone, or semidefinite programs. Meanwhile, Niu defined in niu2018difference the so-called Difference-of-Convex-Sums-of-Squares (DC-SOS) decomposition for general polynomials and developed several practical DC-SOS decomposition techniques. Some of these decomposition techniques can be also parallelized. The DC decomposition technique proposed in this paper is indeed a special DC-SOS decomposition in form of power-sums of linear forms, namely the power-sum DC (PSDC) decomposition. We will show that this decomposition can be established by solving a sparse linear system, which is discussed in Section 3.

Concerning the solution method for DC programming formulation (P), the most popular method is DCA, introduced by Pham 1988Duality in 1985 as an extension of the subgradient method, and extensively developed by Le Thi and Pham since 1994 (see, e.g., le1997solving ; tao2005dc ; le2018dc ; 1997Convex ; tao1998dc and the references therein). The main idea of DCA is to minimize a sequence of convex majorizations of the DC objective function by linearizing the second DC component at the current iterate. The general convergence theorem of DCA ensures that every limit point of the generated sequence by DCA is a critical point of (P) (see, e.g., 1997Convex ; tao2005dc ). Recent years, some accelerated DCAs are established. Artacho et al. artacho2018accelerating proposed a boosted DCA (BDCA) by incorporating DCA with an Armijo-type line search to potentially accelerate DCA under the smoothness assumption of both and . This method is extended to the non-smooth case of component in aragon2018boosted . Meanwhile, Niu et al. niu2019higher further extended BDCA to the convex constrained DC program for both smooth and nonsmooth cases. The global convergence theorem is established under the Łojasiewicz subgradient inequality. Besides, some other accelerations based on the heavy-ball method polyak1964some and Nesterov’s extrapolation nesterov1983method are also proposed. The inertial DCA (InDCA) de2019inertial is established by de Oliveira as a heavy-ball type polyak1964some accelerated DCA. Le Thi et al. proposed in nhat2018accelerated a Nesterov-type accelerated DCA (ADCA). Wen et al. wen2018proximal proposed a proximal DCA algorithm with Nesterov-type extrapolation gotoh2018dc . In this paper, based on BDCA for convex constrained DC program established in niu2019higher , we introduce an exact line search to accelerate DCA for solving (POPL), namely BDCA. The exact line search is equivalent to searching roots of a unary polynomial in an interval, which has a closed-form solution in many applications. We provide a verifiable necessary and sufficient condition for checking the feasibility of the line search direction (namely, the DC descent direction, generated by two consecutive iterates of DCA), and an upper bound for the initial stepsize along the DC descent direction is estimated. Moreover, a fast dual proximal gradient (FDPG) method beck2017first is proposed to effectively solve the convex subproblems in DCA and BDCA by exploiting the special structure of the power-sum DC decomposition. The convergence of BDCA is proved and its convergence rate under the Kurdyka-Łojasiewicz property is established.

The rest of this paper is organized as follows. In Section 2, we recall some notations and preliminaries required in this paper. In Section 3, we establish two power-sum DC decompositions to get two DC programming formulations of (POPL). The corresponding BDCA to the two DC formulations are proposed in Section 4. The convergence analysis and the convergence rate of BDCA are proved in Section 5. The FDPG method for solving the convex subproblem are presented in Section 6. Some numerical experiments on the Mean-Variance-Skewness-Kurtosis portfolio optimization model by comparing BDCA with the classical DCA, BDCA with the Armijo line search, as well as the solvers FILTERSD and FMINCON are reported in Section 7. Some concluding remarks and potential research topics are discussed in the final section.

2 Notations and preliminaries

The inner product of two vectors is denoted by , while denotes the induced norm, defined by The gradient of a differentiable function at is denoted by .

A function is said to be -strongly convex () if

for all and which is equivalent to that is convex. A function is called Lipschitz continuous, if there is some constant such that

and is said to be locally Lipschitz continuous if, for each , there exists a neighborhood of such that restricted to is Lipschitz continuous.

The definition of the cone of feasible directions at is defined as

and the set of active constraints at is denoted by

Then, it is classical (see, e.g., (aragon2019nonlinear, , Proposition 4.14)) to get the next equality

Let be the set of all extended real-valued proper closed convex functions from to . A function is said to be difference-of-convex (DC) if with . We call that and are DC components of and is a DC decomposition of .

For a proper and closed (or lower semicontinuous) function , the Fréchet subdifferential of at is defined by

and if , then we take A point is called a (Fréchet) critical point for , if The effective domain of is defined by

Particularly, when is convex, then coincides with the classical subdifferential in convex analysis, defined by

Moreover, if is a DC function with , and is differentiable at , then one has the following equality:

Let be the indicator function of the polyhedral convex set defined by if and if . Then belongs to and where is the normal cone to at defined by

A point is a (Fréchet) critical point of (P) with differentiable at iff

The set of real polynomials with degree up to in variables is denoted by . The set of all -variate and -degree homogeneous polynomials (forms) is defined by , i.e.,

where and . Let us denote by the cardinality of and rewrite as .

A form is said to have a power-sum representation, if there exist linear forms and scalars () such that

A proper and closed function is said to have the Kurdyka–Łojasiewicz property at if there exist , a concave function and a neighborhood of , such that

-

(i)

-

(ii)

belongs to the class on

-

(iii)

on

-

(iv)

with , we have the KL inequality

The class of functions having the KL property is very ample. For example, all semialgebraic and subanalytic functions satisfy the KL inequality bolte2007lojasiewicz ; kurdyka1994wf ; lojasiewicz1993geometrie , so as to polynomial functions and indicator functions of polyhedral sets.

3 Power-Sum-DC decompositions of polynomials

3.1 Power-sum representation

It is known (see, e.g., trove ) that any form can be represented as weighted power-sum of linear forms (cf. the power-sum representation). For a given form, its power-sum representation (if exists) is not unique in general and nontrivial to be constructed. This kind of representations dates back to the Waring decomposition of homogeneous polynomials in complex space, defined as finding the smallest positive integer for a power-sum representation of a polynomial, which is notoriously difficult to determine in general. To date, only a few particular families are known (see, e.g., buczynska2013waring ; carlini2012solution ; mella2009base ). The situation in the real case is more complicated blekherman2015typical , and little is known. In the next lemma, we have a power-sum representation of a form by solving a linear system.

Lemma 1

For any form , i.e., one has the following power-sum representation for some :

| (1) |

Proof

Let , the multinomial equation reads as

| (2) |

where . It follows from

that

| (3) |

where the matrix

Let and . Then by the nonsingularity of niu2021power ; shelton1986multinomial , we can rewrite (3) as

Let . Then

with . ∎

Remark 1

Lemma 1 indicates that a power-sum representation of a form can be generated by solving the linear system:

| (4) |

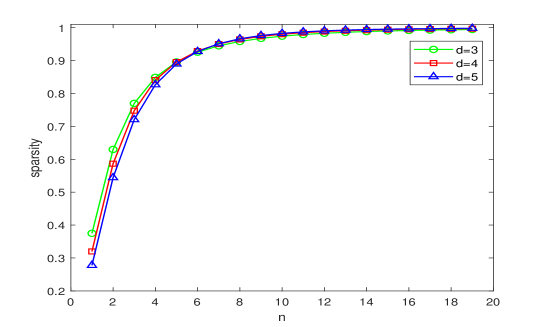

is asymmetric in general and the size of is , which could be very large even if and are not too large. For instance, when and , the size of goes up to millions. Fortunately, in many applications of polynomial optimization, the number of variables is much bigger than the degree , in this case, the matrix appears to be very sparse, whose analysis is demonstrated in niu2021power . As a consequence, the density of the matrix goes to as for any fixed . In Fig. 1, we observe that for , the sparsity of with respectively is more than . Thanks to the sparsity of the matrix , the power-sum representation of a form can be generated effectively by solving the sparse linear system (4).

3.2 Power-sum difference-of-convex decompositions

In this section, we establish the DC decomposition for any polynomial in two ways: the termwise power-sum-DC (TPSDC) decomposition and the homogenizing-dehomogenizing power-sum-DC (HDPSDC) decomposition.

TPSDC decomposition

: Applying Lemma 1 to a form, we can establish a power-sum-DC (PSDC) decomposition of any homogeneous polynomial in two cases: odd degree forms and even degree forms.

Corollary 1

Let .

-

(i)

If the degree is even, then we have a PSDC decomposition as

(5) where and

-

(ii)

If the degree is odd, then we have a PSDC decomposition as

(6) where and

Proof

The case (i) is followed by Lemma 1. To prove the case (ii), we can multiply with an additional variable to get an even degree form . Then, by applying the case (i) to and setting , we get immediately the case (ii). ∎

Any polynomial can be written as a finite sum of forms with Hence, applying Corollary 1 to each forms , we obtain a so-called termwise power-sum (TPSDC) decomposition of , which is described in Algorithm 1.

HDPSDC decomposition

: It is well-known that: an -variate -degree form can be dehomogenized to a polynomial in variable of degree not more than by fixing a variable to 1 (cf. dehomogenization); conversely, a polynomial can be converted into a form by multiplying some powers of a new variable to each monomial as (cf. homogenization). Based on this fact, we propose a PSDC representation for any polynomial as follows:

Proposition 1

For any polynomial , one has the following PSDC decomposition:

| (7) |

where 111 is the ceiling function of a number. and

Proof

Let be an -variate and -degree polynomial in . If is even, applying Lemma 1 for the homogenized polynomial and setting , then we have the result immediately. If is odd, by homogenizing as a -variate -degree form, i.e.,

then incorporating Lemma 1 and dehomogenizing it by setting , we get the desired representation. ∎

As a consequence, the homogenizing-dehomogenizing power-sum-DC (HDPSDC) decomposition is summarized in Algorithm 2.

Comparison of TPSDC and HDPSDC:

We implemented and tested two decomposition algorithms on MATLAB R2021a with a laptop equipped with Intel Core i5-1035G1 CPU 1.19GHz and 8GB RAM. The CPU time (in seconds) of the two proposed decompositions are reported in Table 1. We observe that the average CPU time for Algorithm 2 (HDPSDC) is about 1.5 times faster than Algorithm 1 (TPSDC) when ; while they perform almost the same in the case of . This indicates that HDPSDC performes faster than TPSDC for large . Furthermore, the CPU time increases slowly with respect to , while sharply with respect to , and both methods are more sensitive to than .

| Algorithms | 11 | 18 | 25 | 32 | 39 | 46 | |

|---|---|---|---|---|---|---|---|

| Algorithm 1 | 3 | 0.03 | 0.02 | 0.06 | 0.17 | 0.40 | 1.26 |

| 4 | 0.01 | 0.03 | 0.11 | 0.32 | 0.72 | 2.29 | |

| Algorithm 2 | 3 | 0.01 | 0.02 | 0.06 | 0.17 | 0.39 | 1.09 |

| 4 | 0.02 | 0.02 | 0.06 | 0.18 | 0.40 | 1.19 |

3.3 DC reformulations of (POPL) based on PSDC

4 DCA and BDCA for solving (T–P) and (HD–P)

-

1

Initialization : Let be an initial point, be a small stopping tolerance, and ;

General step:

Niu et al. proved in (niu2019higher, , Proposition 1) that the direction in DCA is a descent direction (namely, DC descent direction) of at if (1) , (2) is a feasible direction of at , and (3) is strongly convex. In this case, proceeding a line search (exact or inexact) along will gain an extra decrease in the value of the objective function, which ensures an acceleration of DCA. Next, we present a Boosted DCA with exact line search (BDCA) to problem (T–P) and (HD–P) as described in Algorithm 4.

-

1

Initialization: Let be an initial point, be a small stopping tolerance, and ;

General step:

Note that when for all , then BDCA is reduced to DCA. The convention is applied for computing . Next, we will discuss several aspects in BDCA including: how to check the feasibility of the direction at over ; how to estimate an upper bound for the line search step-size; and the exact line search procedure.

Checking the feasibility of the direction at over

: We propose the next Lemma to check the feasibility of at over , which is different from the way in (niu2019higher, , Proposition 2) by comparing the active sets and .

Lemma 2

Proof

If , the conclusion is obvious by the definition of the cone of feasible directions .

If , then for and , we have

Invoking the fact that , we deduce

The last equivalent condition implies that the conclusion holds. ∎

Upper bound estimation for the line search step-size

: The next proposition provides us an upper bound for the line search step-size along the direction as (if ) by ensuring that .

Proposition 2

Let and be generated in Algorithm 4 and . Then

-

(i)

If , , then we have .

-

(ii)

If , , then we have for each ; moreover, , there exists such that

Proof

(i) If , we have for . and , we observe that the fact

holds for and . Therefore, we have .

(ii) If , we get from Lemma 2 that . and , we observe that the fact

| (8) |

holds for .

On the other hand, we verify the result from two aspects:

Case 1: If , it implies , we get that

Case 2: If , it implies . The similar augment to (a) can be used to deduce

Moreover, , we have some such that

By taking , we have

Therefore, we conclude ∎

Exact line search

: The exact line search in Step 4 is described in Algorithm 5, which is based on the minimization problem (ELS):

| (ELS) |

Without loss of generality, we suppose that has a representation in form of Proposition 1, i.e.,

| (9) |

Then plugging into Equation (9) with and , we have

where

| (10) |

Combined with Proposition 2, the problem (ELS) is shown as the following unary polynomial minimization problem:

| (11) |

Remark 2

The minimization problem (11) is well-defined. In fact, if , then . The assertation is verified. If , then we have . Since by the assumption that .

Remark 3

In contrast to the Armijo inexact line search in artacho2018accelerating ; niu2019higher , our approach requires to computing in Equation (10) and solving the problem (11) instead of computing the objective function values. The minimization of problem (11) can be done by finding the roots of the derivative of . In the case of , the roots of can be computed efficiently by root formula, which covers many cases in applications and provides optimal step-size for line search.

5 Convergence analysis for BDCA

Assumption 1

The component is -strongly convex with .

Note that this assumption is easy to be satisfied for problems (T–P) and . Since for a DC function with convex and , we can take and with a small to ensure the strong convexity of .

Lemma 3

niu2019higher Under Assumption 1. For the sequences , and generated by Algorithm 4, it holds that

| (12) |

Theorem 5.1

Proof

(i) To simplify the proof, we use (resp. ) instead of (resp. ) for . Invoking Step 4 and Step 5 of Algorithm 4, we have

Combining the previous inequality and Lemma 3, we obtain

| (13) |

as is decreasing and

we can conclude (i).

(ii) Since is bounded. Assume that is any limit point of sequence and is a subsequence of converging to , as , we get from (13) that

From the boundness of the sequence , we obtain . Since

Hence, for all ,

Taking , since and are continuously differentiable, we have

This implies that is a critical point for problem (T–P) (or (HD–P)).

(iii) By summing inequality (13) from to , we obtain

therefore, we have ∎

Remark 4

Note that if the line search step-size is supposed to be bounded (e.g., let in (11) be some big enough value), then we will have a stronger convergence result based on (niu2019higher, , Theorem 11) that the sequence in BDCA is also convergent.

By employing the following useful lemma, we can obtain the rate of convergence of the sequence generated by Algorithm 4.

Lemma 4

Let be a nonincreasing and nonnegative real sequence converging to . Suppose that there exist and such that for all large enough ,

| (14) |

Then

-

(i)

if , then the sequence converges to in a finite number of steps;

-

(ii)

if , then the sequence converges linearly to with rate .

-

(iii)

if , then the sequence converges sublinearly to , i.e., there exists such that

(15) for large enough .

Proof

(i) If , then (14) implies that

It follows by and that converges to in a finite number of steps, and we can estimate the number of steps as:

Hence

(ii) If . Since , we have that for large enough . Thus, , and it follows by (14) that

for large enough . Hence

i.e., converges linearly to with rate for large enough .

(iii) If , then we have two cases:

Case 1: if converges in a finite number of steps, then the inequality (15) trivially holds.

Case 2: Otherwise, for all . Let and .

Suppose that . By the decreasing of and , we have

It follows from (14) that

Hence

| (16) |

for large enough .

Suppose that . Taking , then

Hence

It follows that :

In both cases, there exist a constant such that for large enough , we have

Summing for from to , we have

Then, by the decreasing of , we get

Hence, there exist some such that

for large enough , which completes the proof. ∎

We prove the convergence rate of the sequence generated by BDCA as the sequence has a limit point at which satisfies the Kurdyka–Łojasiewicz (KL) property frankel2015splitting ; lojaciewicz1964ensembles and is locally Lipschitz continuous.

Theorem 5.2

Consider the settings of Theorem 5.1, let are sequences generated by BDCA from a starting point . Denote by the set of limit points of . As is locally Lipschitz continuous and satisfies the KL property at each with for some and . The following estimations hold:

-

(i)

If , then the sequence converges to in a finite number of steps.

-

(ii)

If , then the sequence converges linearly to , that is, there exist positive constants and such that for all .

-

(iii)

If , then the sequence converges sublinearly to , that is, there exist positive constants and such that for all .

Proof

We conclude that shares the same value on . In fact, Since is continuously differentiable, the result is followed directly by

with any subsequence Since is locally Lipschitz continuous, for each , there exist some constant and such that

| (17) |

Moreover, since satisfies the Kurdyka–Łojasiewicz property at , there exists some constant , with such that the Kurdyka–Łojasiewicz inequality holds. Let we can construct an open cover of the set :

Since the sequence is bounded, then is a compact set. Therefore, there exist finite number of points such that

Let and Invoking the fact from Theorem 5.1 that and share the same set of limit points , there exists such that and for all . Thus, for all , there exists some such that Combined with (17), it implies that for all

| (18) |

On the other hand, since , there exist and such that for all . Setting and for each , we conclude that there exists some such that . Hence, for each and , we have

Since satisfies the Kurdyka–Łojasiewicz property and on , we have

| (19) |

Because we get that

using the previous equation, we obtain

Then it follows from (18) that

| (20) |

6 A FDPG method for solving the convex subproblem

We consider the PSDC representation in (HD–P) with a -strongly convex modulus () as bellow:

| (22) |

Hence, the related convex subproblem is as follow:

where denotes the gradient of at some point , i.e., By incorporating the indicator function of the constraint set into objective function, and we can rewrite the convex subproblem as:

| (23) |

Let us denote by and . By introducing new variables such that and taking

we can rewrite equivalently the problem (23) as:

| (24) |

where

The Lagrangian for problem (24) is

where Then minimizing the Lagrangian w.r.t. and , the dual problem is written as

By the strong duality theorem (see e.g., (beck2017first, , Theorem A.1)), then Consider the dual problem in its minimization form:

| (25) |

where Therefore, we have the following properties beck2017first :

-

is convex and -smooth with ;

-

is proper closed and convex.

Applying the classical FISTA (see, e.g., beck2017first ) for (25) and invoking that fact (beck2017first, , Lemma 12.5) that

holds if and only if

with , and combined with

-

Initialization: pick and

-

1

General step :

Step 1:

Remark 5

In Step 2 of Algorithm 6, the proximal operator of the convex functions can be computed by finding the unique real root of its derivative, and this can be done by the root formula as . In the case of , the efficient numerical method (e.g., Newton method) can be applied. Moreover, the computation of the proximal operator can be performed in parallelism.

The convergence result of the defined sequence is given bellow.

Lemma 5

(beck2017first, , Theorem 12.10) Suppose that is the sequence generated by Algorithm 6. Then for the unique optimal solution of problem (24) and any optimal solution of problem (25) and ,

Remark 6

By setting in Algorithm 6, we get from Lemma 5 that the convergence speed of the FDPG method for (24) is significantly affected by strong convexity modulus of function and initial point . This will be investigated further in the numerical experiment for solving the DC problem (HD–P). Finally, we point out that the FDGP method can also be applied to solve the convex subproblem of the problem (T–P).

7 Numerical experiment

In this section, we use our BDCA against the classical DCA and BDCA with Armijo line search proposed in niu2019higher applied to our new PSDC decompositions, as well as FILTERSD filtersdFletcher and FMINCON for solving the higher-order moment portfolio optimization model. All algorithms are implemented on MATLAB R2021a, and tested on a laptop equipped with Intel Core i5-1035G1 CPU 1.19GHz and 8GB RAM.

7.1 Higher-order moment portfolio optimization model

Let = be a random return vector of risky assets, be the -dimensional decision vector, where is the percentage invested in the -th risky asset, and be the expectation operator. The moments of the return are defined as followed:

-

The mean of the return denoted by and ,

-

The variance of the return denoted by and ,

-

The skewness of the return denoted by and ,

-

The kurtosis of the return denoted by and ,

Furthermore, the mean of a portfolio (first order moment) can be expressed as the variance of the portfolio (second order moment) as the skewness of the portfolio (third order moment) as

the kurtosis of the portfolio (fourth order moment) as

The mean-variance-skewness-kurtosis portfolio model can be studied as a weighted nonconvex polynomial minimization problem (see, e.g., niu2019higher ; Niu2011 ):

| (MVSK) |

where the parameter vector is the investor preference, the set with being the vector of ones is the -simplex, and . Note that this problem is known to be NP-hard in general. Moreover, due to the symmetry of (resp. and ), the computation complexity on (resp. and ) can be reduced from (resp. and ) to (resp. and ), see, e.g. Maringer2009GlobalOO ; Niu2011 . But for the larger (e.g., ), the total monomials of kurtosis can reach up to millions.

7.2 The numerical experiments of DCA, BDCA, BDCA, FILTERSD and FMINCON on (MVSK) model

We test on the dataset collected from monthly records from 1995 to 2015 of 48 industry-sector portfolios of the U.S stock market with the number of assets . For each , we test problems with three different investor’s preferences including risk-seeking (), risk-aversing () and risk-neutral (). In all tested methods, the initial points are generated by MATLAB function rand and the gradient is approximately computed by

where . We terminate DCA, BDCA and BDCA when

Settings of FDPG for solving convex subproblem

: (a) The initial point is set by and is the previous iterate in Algorithm 4. (b) We terminate FDPG when

Settings of Armijo rule in BDCA

: We reduce the initial stepsize by taking in BDCA niu2019higher where the reduction factor , until that

under the parameter and the initial stepsize

Numerical results

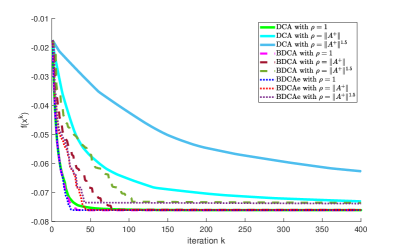

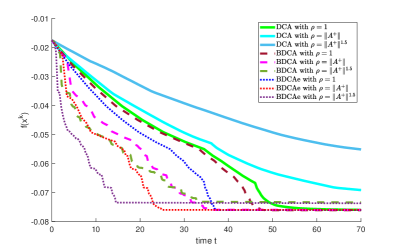

: In Fig. 2, we demonstrate the curve of the objective value with respect to the number of iterations and CPU time for DCA, BDCA, and BDCA with different modulus in (22) to solve the problem (HD–P). Fig. 2(a) shows that for all three methods, the smaller the modulus , the faster the objective values decrease with respect to the iterations, and better stationary point could be obtained. The reason is that the smaller modulus gives a better approximation of the objective function. Fig. 2(b) shows that the larger modulus will slow down DCA while speeding up BDCA and BDCA. There are two possible reasons to explain the speedup for BDCA and BDCA. The first is based on Lemma 5 that the larger will lead to faster convergence in solving convex subproblems. The second is perhaps due to the line search acceleration. In conclusion, Fig. 2 demonstrates that there is a trade-off in the choice of modulus for BDCA and BDCA. Increasing may lead to more acceleration but a bad critical point could be obtained.

In Table 2, we report the numerical results comparing BDCA with DCA, BDCA on objective function values, the CPU time (in seconds), and the iterations for (T–P) and (HD–P), as well as the solvers FILTERSD and FMINCON on objective values and the CPU time. We choose the modulus for DCA and for BDCA and BDCA based on Fig. 2. The average CPU time and the average iterations are also reported. On average CPU time, we observe that BDCA is the fastest method among the others for both (T–P) and (HD–P). Concerning the objective values, we observe that DCA and FILTERSD provide the best objective values in all tested examples. Our BDCA for both (T–P) and (HD–P) shares the same function values in most of cases except for instances of No. , and the differences in the objective values between BDCA and DCA as well as FILTERSD in these instances are within . Besides, we can see that BDCA for (HD–P) is about 1.5 times faster than BDCA and FMINCON, 2 times faster than FILTERSD, and more than 3 times faster than DCA on average CPU time. In conclusion, BDCA outperforms the other compared methods on (HD–P).

| No. | Algorithms for solving (T–P) | Algorithms for solving (HD–P) | FILTERSD | FMINCON | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| DCA | BDCA | BDCA | DCA | BDCA | BDCA | ||||||||||||||||||

| iter | time | obj | iter | time | obj | iter | time | obj | iter | time | obj | iter | time | obj | iter | time | obj | time | obj | time | obj | ||

| 1 | 11 | 1213 | 3.95 | -9.675e-02 | 27 | 0.17 | -9.675e-02 | 12 | 0.08 | -9.675e-02 | 1232 | 1.54 | -9.675e-02 | 26 | 0.08 | -9.675e-02 | 11 | 0.04 | -9.675e-02 | 0.03 | -9.675e-02 | 0.09 | -9.675e-02 |

| 2 | 11 | 505 | 2.34 | 5.625e-03 | 54 | 0.41 | 5.625e-03 | 13 | 0.08 | 5.625e-03 | 504 | 0.86 | 5.625e-03 | 48 | 0.13 | 5.625e-03 | 21 | 0.05 | 5.625e-03 | 0.03 | 5.625e-03 | 0.10 | 5.627e-03 |

| 3 | 11 | 305 | 1.43 | -9.993e-02 | 72 | 1.14 | -9.993e-02 | 17 | 0.11 | -9.993e-02 | 326 | 0.54 | -9.993e-02 | 50 | 0.17 | -9.993e-02 | 28 | 0.06 | -9.993e-02 | 0.08 | -9.993e-02 | 0.17 | -9.993e-02 |

| 4 | 16 | 225 | 4.10 | -1.522e-01 | 34 | 0.57 | -1.522e-01 | 15 | 0.27 | -1.522e-01 | 244 | 4.11 | -1.522e-01 | 33 | 0.40 | -1.522e-01 | 17 | 0.23 | -1.522e-01 | 0.14 | -1.522e-01 | 0.32 | -1.522e-01 |

| 5 | 16 | 486 | 6.19 | 8.175e-03 | 67 | 1.12 | 8.175e-03 | 29 | 0.42 | 8.175e-03 | 434 | 2.46 | 8.175e-03 | 51 | 0.49 | 8.175e-03 | 33 | 0.39 | 8.175e-03 | 0.19 | 8.175e-03 | 0.37 | 8.179e-03 |

| 6 | 16 | 396 | 4.39 | -8.260e-02 | 45 | 0.72 | -8.260e-02 | 21 | 0.35 | -8.260e-02 | 403 | 2.38 | -8.260e-02 | 43 | 0.35 | -8.260e-02 | 20 | 0.20 | -8.260e-02 | 0.15 | -8.260e-02 | 0.32 | -8.259e-02 |

| 7 | 21 | 179 | 8.61 | -1.647e-01 | 44 | 3.26 | -1.647e-01 | 22 | 1.35 | -1.647e-01 | 189 | 11.42 | -1.647e-01 | 43 | 1.82 | -1.647e-01 | 22 | 1.03 | -1.647e-01 | 0.79 | -1.647e-01 | 0.68 | -1.647e-01 |

| 8 | 21 | 477 | 18.77 | 1.574e-03 | 88 | 8.51 | 1.574e-03 | 21 | 1.18 | 1.574e-03 | 444 | 7.29 | 1.574e-03 | 54 | 1.39 | 1.574e-03 | 22 | 0.65 | 1.574e-03 | 0.81 | 1.574e-03 | 1.58 | 1.579e-03 |

| 9 | 21 | 308 | 12.16 | -9.945e-02 | 240 | 16.56 | -9.945e-02 | 37 | 2.12 | -9.945e-02 | 313 | 8.08 | -9.945e-02 | 82 | 3.51 | -9.945e-02 | 25 | 1.03 | -9.945e-02 | 0.98 | -9.945e-02 | 1.18 | -9.945e-02 |

| 10 | 26 | 138 | 15.34 | -1.302e-01 | 56 | 5.26 | -1.302e-01 | 27 | 2.98 | -1.302e-01 | 224 | 13.94 | -1.302e-01 | 56 | 3.56 | -1.302e-01 | 28 | 2.16 | -1.302e-01 | 2.33 | -1.302e-01 | 2.20 | -1.302e-01 |

| 11 | 26 | 472 | 31.45 | 4.184e-03 | 68 | 10.16 | 4.185e-03 | 30 | 3.61 | 4.185e-03 | 457 | 16.84 | 4.184e-03 | 68 | 3.25 | 4.185e-03 | 28 | 1.42 | 4.185e-03 | 3.28 | 4.184e-03 | 4.52 | 4.191e-03 |

| 12 | 26 | 349 | 19.52 | -1.077e-01 | 102 | 11.10 | -1.077e-01 | 30 | 3.11 | -1.077e-01 | 373 | 13.97 | -1.077e-01 | 92 | 5.74 | -1.077e-01 | 32 | 2.30 | -1.077e-01 | 2.46 | -1.077e-01 | 3.08 | -1.077e-01 |

| 13 | 31 | 107 | 15.73 | -1.649e-01 | 58 | 9.59 | -1.649e-01 | 32 | 11.18 | -1.649e-01 | 166 | 19.45 | -1.649e-01 | 58 | 7.74 | -1.649e-01 | 31 | 5.04 | -1.649e-01 | 6.16 | -1.649e-01 | 4.31 | -1.649e-01 |

| 14 | 31 | 565 | 65.38 | 9.530e-04 | 77 | 12.52 | 9.543e-04 | 54 | 9.50 | 9.543e-04 | 545 | 29.18 | 9.530e-04 | 109 | 8.15 | 9.555e-04 | 46 | 3.86 | 9.566e-04 | 6.51 | 9.530e-04 | 9.18 | 9.613e-04 |

| 15 | 31 | 513 | 55.87 | -1.082e-01 | 129 | 37.56 | -1.082e-01 | 37 | 6.86 | -1.082e-01 | 535 | 30.66 | -1.082e-01 | 86 | 9.68 | -1.082e-01 | 42 | 4.87 | -1.082e-01 | 7.46 | -1.082e-01 | 7.75 | -1.082e-01 |

| 16 | 36 | 67 | 21.60 | -1.649e-01 | 64 | 18.56 | -1.649e-01 | 35 | 12.26 | -1.649e-01 | 106 | 24.12 | -1.649e-01 | 66 | 15.51 | -1.649e-01 | 33 | 9.76 | -1.649e-01 | 14.61 | -1.649e-01 | 9.00 | -1.649e-01 |

| 17 | 36 | 597 | 128.97 | 7.728e-04 | 85 | 26.76 | 7.769e-04 | 67 | 22.47 | 7.764e-04 | 591 | 53.18 | 7.728e-04 | 82 | 8.71 | 7.769e-04 | 34 | 4.29 | 7.740e-04 | 14.75 | 7.732e-04 | 20.67 | 7.824e-04 |

| 18 | 36 | 320 | 55.33 | -1.144e-01 | 85 | 22.47 | -1.144e-01 | 39 | 12.35 | -1.144e-01 | 336 | 37.12 | -1.144e-01 | 90 | 16.96 | -1.144e-01 | 47 | 13.85 | -1.144e-01 | 15.84 | -1.144e-01 | 15.95 | -1.144e-01 |

| 19 | 41 | 71 | 28.43 | -1.650e-01 | 75 | 33.74 | -1.650e-01 | 41 | 23.08 | -1.650e-01 | 87 | 28.83 | -1.650e-01 | 73 | 21.74 | -1.650e-01 | 40 | 14.84 | -1.650e-01 | 28.47 | -1.650e-01 | 15.81 | -1.650e-01 |

| 20 | 41 | 599 | 217.92 | 8.431e-04 | 117 | 51.56 | 8.436e-04 | 59 | 28.40 | 8.456e-04 | 592 | 81.15 | 8.431e-04 | 112 | 23.45 | 8.452e-04 | 75 | 18.25 | 8.484e-04 | 28.58 | 8.431e-04 | 34.87 | 8.540e-04 |

| 21 | 41 | 223 | 61.09 | -1.083e-01 | 88 | 35.27 | -1.083e-01 | 40 | 20.14 | -1.083e-01 | 238 | 41.35 | -1.083e-01 | 93 | 25.09 | -1.083e-01 | 44 | 16.36 | -1.083e-01 | 28.22 | -1.083e-01 | 21.93 | -1.083e-01 |

| 22 | 46 | 65 | 34.28 | -1.650e-01 | 77 | 51.42 | -1.650e-01 | 43 | 33.65 | -1.650e-01 | 71 | 25.71 | -1.650e-01 | 77 | 31.35 | -1.650e-01 | 44 | 22.85 | -1.650e-01 | 60.59 | -1.650e-01 | 29.71 | -1.650e-01 |

| 23 | 46 | 483 | 276.73 | 1.165e-03 | 111 | 78.71 | 1.168e-03 | 67 | 53.35 | 1.166e-03 | 474 | 104.54 | 1.165e-03 | 111 | 34.76 | 1.168e-03 | 72 | 26.76 | 1.165e-03 | 67.20 | 1.165e-03 | 74.03 | 1.177e-03 |

| 24 | 46 | 324 | 139.86 | -1.146e-01 | 102 | 61.48 | -1.146e-01 | 49 | 53.01 | -1.146e-01 | 336 | 87.68 | -1.146e-01 | 106 | 53.20 | -1.146e-01 | 49 | 36.87 | -1.146e-01 | 64.49 | -1.146e-01 | 48.95 | -1.146e-01 |

| average | 374 | 51.23 | 82 | 20.78 | 35 | 12.58 | 384 | 26.93 | 71 | 11.55 | 35 | 7.80 | 14.76 | 12.78 | |||||||||

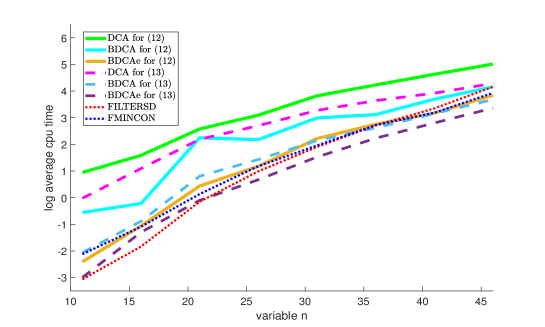

Fig. 3 demonstrates the average CPU time for the instances in Table 2 along the number of assets . We observe that DCA for (T–P) has the worst performance, while FILTERSD has the best performance when is less than about . As increases beyond , the best result is given by BDCA for (HD–P), and the methods BDCA for (HD–P), BDCA for (T–P), FMINCON, and FILTERSD have almost the same performance, which demonstrates that BDCA should be a promising approach to outperform the others on large-scale settings.

8 Conclusions

In this paper, we presented a novel DC-SOS decomposition technique based on the power-sum representation for polynomials. We proposed an accelerated DCA (BDCA) combining DCA with an exact line search along the DC descent direction for solving linearly constrained polynomial optimization problems. We proved that any limit point of the sequence generated by BDCA is a critical point of (POPL) and established the convergence rate of the sequence under the Kurdyka-Łojasiewicz assumption. We applied the FDPG method by exploiting the power-sum-DC structure for solving effectively the convex subproblems. The numerical experiments on the (MVSK) model indicated that BDCA outperformed BDCA with Armijo line search and DCA, as well as the solvers FILTERSD and FMINCON on average CPU time and almost always got the best objective values. In the future, one important question is to investigate a better way to generate power-sum-DC decompositions with a shorter basis or to generate a sparse power-sum-DC decomposition. Another important question is how to find an adaptive way to update strongly convex parameter for ensuring both acceleration and good computed solution. Moreover, taking advantage of the power-sum structure to more effectively solve convex subproblems is always an important research topic.

Acknowledgements.

This work is supported by the National Natural Science Foundation of China (Grant 11601327).References

- (1) Ahmadi, A.A., Hall, G.: DC decomposition of nonconvex polynomials with algebraic techniques. Mathematical Programming 169(1), 69–94 (2018)

- (2) Ahmadi, A.A., Parrilo, P.A.: A convex polynomial that is not sos-convex. Mathematical Programming 135(1), 275–292 (2012)

- (3) Ahmadi, A.A., Parrilo, P.A.: A complete characterization of the gap between convexity and sos-convexity. SIAM Journal on Optimization 23(2), 811–833 (2013)

- (4) Artacho, F.J.A., Fleming, R.M., Vuong, P.T.: Accelerating the dc algorithm for smooth functions. Mathematical Programming 169(1), 95–118 (2018)

- (5) Artacho, F.J.A., Goberna, M.A., López, M.A., Rodríguez, M.M.: Nonlinear optimization. Springer (2019)

- (6) Artacho, F.J.A., Vuong, P.T.: The boosted dc algorithm for nonsmooth functions. SIAM J. Optim. 30(1), 980–1006 (2020)

- (7) Bakonyi, M., Johnson, C.R.: The euclidian distance matrix completion problem. SIAM Journal on Matrix Analysis and Applications 16(2), 646–654 (1995)

- (8) Beck, A.: First-order methods in optimization. SIAM (2017)

- (9) Blekherman, G.: Typical real ranks of binary forms. Foundations of Computational Mathematics 15(3), 793–798 (2015)

- (10) Bolte, J., Daniilidis, A., Lewis, A.: The łojasiewicz inequality for nonsmooth subanalytic functions with applications to subgradient dynamical systems. SIAM Journal on Optimization 17(4), 1205–1223 (2007)

- (11) Bomze, I.M., Locatelli, M.: Undominated dc decompositions of quadratic functions and applications to branch-and-bound approaches. Computational Optimization and Applications 28(2), 227–245 (2004)

- (12) Boyd, S., El Ghaoui, L., Feron, E., Balakrishnan, V.: Linear matrix inequalities in system and control theory. SIAM (1994)

- (13) Brás, C., Eichfelder, G., Júdice, J.: Copositivity tests based on the linear complementarity problem. Computational Optimization and Applications 63(2), 461–493 (2016)

- (14) Buczyńska, W., Buczyński, J., Teitler, Z.: Waring decompositions of monomials. Journal of Algebra 378, 45–57 (2013)

- (15) Burer, S.: On the copositive representation of binary and continuous nonconvex quadratic programs. Mathematical Programming 120(2), 479–495 (2009)

- (16) Carlini, E., Catalisano, M.V., Geramita, A.V.: The solution to the waring problem for monomials and the sum of coprime monomials. Journal of algebra 370, 5–14 (2012)

- (17) Chambadal, L.: Algèbre linéaire et algèbre tensorielle (2017)

- (18) Dür, M., Hiriart-Urruty, J.B.: Testing copositivity with the help of difference-of-convex optimization. Mathematical Programming 140(1), 31–43 (2013)

- (19) Fletcher, R.: Filtersd–a library for nonlinear optimization written in fortran (2015). URL https://projects.coin-or.org/filterSD

- (20) Frankel, P., Garrigos, G., Peypouquet, J.: Splitting methods with variable metric for Kurdyka–Łojasiewicz functions and general convergence rates. Journal of Optimization Theory and Applications 165(3), 874–900 (2015)

- (21) Gotoh, J., Takeda, A., Tono, K.: DC formulations and algorithms for sparse optimization problems. Mathematical Programming 169(1), 141–176 (2018)

- (22) Hartman, P.: On functions representable as a difference of convex functions. Pacific Journal of Mathematics 9(3), 707–713 (1959)

- (23) Hiriart-Urruty, J.B.: Generalized differentiability/duality and optimization for problems dealing with differences of convex functions. In: Convexity and duality in optimization, pp. 37–70. Springer (1985)

- (24) Kurdyka, K., Parusinski, A.: wf-stratification of subanalytic functions and the lojasiewicz inequality. Comptes rendus de l’Académie des sciences. Série 1, Mathématique 318(2), 129–133 (1994)

- (25) Le Thi, H.A.: An efficient algorithm for globally minimizing a quadratic function under convex quadratic constraints. Mathematical programming 87, 401–426 (2000)

- (26) Le Thi, H.A., Moeini, M., Pham, D.T., Judice, J.: A dc programming approach for solving the symmetric eigenvalue complementarity problem. Computational Optimization and Applications 51(3), 1097–1117 (2012)

- (27) Le Thi, H.A., Pham, D.T.: Solving a class of linearly constrained indefinite quadratic problems by DC algorithms. Journal of global optimization 11(3), 253–285 (1997)

- (28) Le Thi, H.A., Pham, D.T.: The DC (difference of convex functions) programming and DCA revisited with DC models of real world nonconvex optimization problems. Annals of operations research 133(1), 23–46 (2005)

- (29) Le Thi, H.A., Pham, D.T.: DC programming and DCA: thirty years of developments. Mathematical Programming 169(1), 5–68 (2018)

- (30) Łojasiewicz, S.: Ensembles semi-analytiques, institut des hautes etudes sci. Bures-sur-Yvette, France (1964)

- (31) Łojasiewicz, S.: Sur la géométrie semi et sous-analytique. In: Annales de l’institut Fourier, vol. 43, pp. 1575–1595 (1993)

- (32) Maringer, D., Parpas, P.: Global optimization of higher order moments in portfolio selection. Journal of Global optimization 43(2), 219–230 (2009)

- (33) Mella, M.: Base loci of linear systems and the waring problem. Proceedings of the American Mathematical Society 137(1), 91–98 (2009)

- (34) Nesterov, Y.E.: A method for solving the convex programming problem with convergence rate . In: Dokl. akad. nauk Sssr, vol. 269, pp. 543–547 (1983)

- (35) Niu, Y.S.: On difference-of-sos and difference-of-convex-sos decompositions for polynomials. arXiv :1803.09900 (2018)

- (36) Niu, Y.S., Glowinski, R.: Discrete dynamical system approaches for boolean polynomial optimization. to appear in Journal of Scientific Computing, arXiv preprint arXiv:1912.10221 (2019)

- (37) Niu, Y.S., Júdice, J., Le Thi, H.A., Pham, D.T.: Solving the quadratic eigenvalue complementarity problem by dc programming. In: Modelling, Computation and Optimization in Information Systems and Management Sciences, pp. 203–214. Springer (2015)

- (38) Niu, Y.S., Júdice, J., Le Thi, H.A., Pham, D.T.: Improved dc programming approaches for solving the quadratic eigenvalue complementarity problem. Applied Mathematics and Computation 353, 95–113 (2019)

- (39) Niu, Y.S., Pham, D.T.: DC programming approaches for bmi and qmi feasibility problems. In: Advanced Computational Methods for Knowledge Engineering, pp. 37–63. Springer (2014)

- (40) Niu, Y.S., Pham, D.T., Le Thi, H.A., Júdice, J.: Efficient dc programming approaches for the asymmetric eigenvalue complementarity problem. Optimization Methods and Software 28(4), 812–829 (2013)

- (41) Niu, Y.S., Wang, Y.J., Le Thi, H.A., Pham, D.T.: Higher-order moment portfolio optimization via an accelerated difference-of-convex programming approach and sums-of-squares. arXiv :1906.01509 (2019)

- (42) Niu, Y.S., Zhang, H.: Power-product matrix: nonsingularity, sparsity and determinant. arXiv:2104.05209 (2021)

- (43) de Oliveira, W., Tcheou, M.P.: An inertial algorithm for dc programming. Set-Valued and Variational Analysis 27(4), 895–919 (2019)

- (44) Pham, D.T., Le Thi, H.A.: Convex analysis approach to DC programming: theory, algorithms and applications. Acta mathematica vietnamica 22(1), 289–355 (1997)

- (45) Pham, D.T., Le Thi, H.A.: A DC optimization algorithm for solving the trust-region subproblem. SIAM Journal on Optimization 8(2), 476–505 (1998)

- (46) Pham, D.T., Le Thi, H.A., Pham, V.N., Niu, Y.S.: DC programming approaches for discrete portfolio optimization under concave transaction costs. Optimization letters 10(2), 261–282 (2016)

- (47) Pham, D.T., Niu, Y.S.: An efficient dc programming approach for portfolio decision with higher moments. Computational Optimization and Applications 50(3), 525–554 (2011)

- (48) Pham, D.T., Souad, E.B.: Duality in dc (difference of convex functions) optimization. subgradient methods. Trends in mathematical optimization pp. 277–293 (1988)

- (49) Phan, D.N., Le, H.M., Le Thi, H.A.: Accelerated difference of convex functions algorithm and its application to sparse binary logistic regression. In: IJCAI, pp. 1369–1375 (2018)

- (50) Polyak, B.T.: Some methods of speeding up the convergence of iteration methods. Ussr computational mathematics and mathematical physics 4(5), 1–17 (1964)

- (51) Shelton, R., Heuvers, K.J., Moak, D., Rao, K.B.: Multinomial matrices. Discrete mathematics 61(1), 107–114 (1986)

- (52) Song, Y., Yu, G.: Properties of solution set of tensor complementarity problem. Journal of Optimization Theory and Applications 170(1), 85–96 (2016)

- (53) Wen, B., Chen, X., Pong, T.K.: A proximal difference-of-convex algorithm with extrapolation. Computational optimization and applications 69(2), 297–324 (2018)

- (54) You, Y., Niu, Y.S.: A refined inertial dc algorithm for dc programming. Optimization and Engineering pp. 1–27 (2022)