A Unified Algorithm for Penalized Convolution Smoothed Quantile Regression

Abstract

Penalized quantile regression (QR) is widely used for studying the relationship between a response variable and a set of predictors under data heterogeneity in high-dimensional settings. Compared to penalized least squares, scalable algorithms for fitting penalized QR are lacking due to the non-differentiable piecewise linear loss function. To overcome the lack of smoothness, a recently proposed convolution-type smoothed method brings an interesting tradeoff between statistical accuracy and computational efficiency for both standard and penalized quantile regressions. In this paper, we propose a unified algorithm for fitting penalized convolution smoothed quantile regression with various commonly used convex penalties, accompanied by an R-language package conquer available from the Comprehensive R Archive Network. We perform extensive numerical studies to demonstrate the superior performance of the proposed algorithm over existing methods in both statistical and computational aspects. We further exemplify the proposed algorithm by fitting a fused lasso additive QR model on the world happiness data.

1 Introduction

Let be a scalar response variable of interest, and be a -dimensional vector of covariates. Since the seminal work of Koenker and Bassett (1978), quantile regression (QR) has become an indispensable tool for understanding pathways of dependence between and , which is irretrievable through conditional mean regression analysis via the least squares method. Motivated by a wide range of applications, various models have been proposed and studied for QR, from parametric to nonparametric and from low- to high-dimensional covariates. We refer the reader to Koenker (2005) and Koenker et al. (2017) for a comprehensive exposition of quantile regression.

Consider a high-dimensional linear QR model in which the number of covariates, , is larger than the number of observations, . In this setting, different low-dimensional structures have been imposed on the regression coefficients, thus motivating the use of various penalty functions. One of the most widely used assumption is the sparsity, which assumes that only a small number of predictors are associated with the response. Quantile regression models are capable of capturing heterogeneity in the set of important predictors at different quantile levels of the response distribution caused by, for instance, heteroscedastic variance. For fitting sparse models in general, various sparsity-inducing penalties have been introduced, such as the lasso (-penalty) (Tibshirani, 1996), elastic net (hybrid of /-penalty) (Zou and Hastie, 2005), smoothly clipped absolute deviation (SCAD) penalty (Fan and Li, 2001) and minimax concave (MC) penalty (Zhang, 2010). Other commonly used regularizers that induce different types of structures include the group lasso (Yuan and Lin, 2006), sparse group lasso (Simon et al., 2013) and fused lasso (Tibshirani et al., 2005), among others. We refer to the monographs Bühlmann and van de Geer (2011), Hastie et al. (2015) and Wainwright (2019) for systematic introductions of high-dimensional statistical learning.

The above penalties/regularizers have been extensively studied when applied with the least squares method, accompanied with the user-friendly and efficient software glmnet (Friedma et al., 2010). Quantile regression, on the other hand, involves minimizing a non-differentiable piecewise linear loss, known as the check function. Although a handful of algorithms have been developed based on either linear programming or the alternating direction method of multipliers (ADMM) (Koenker and Ng, 2005; Li and Zhu, 2008; Peng and Wang, 2015; Yu et al., 2017; Gu et al., 2018), there is not much software that is nearly as efficient as glmnet available for penalized quantile regressions. As the most recent progress, Yi and Huang (2017) proposed a semismooth Newton coordinate descent (SNCD) algorithm for solving a Huberized QR with the elastic net penalty; Yu et al. (2017) and Gu et al. (2018) respectively proposed ADMM-based algorithms for solving folded-concave penalized QR. See Gu et al. (2018) for a detailed computational comparison between the SNCD and ADMM-based algorithms, which favors the latter. The primary computation effort of each ADMM update is to evaluate the inverse of a or matrix. This can be computationally expensive when both and are large. Compared to sparsity-inducing regularization, the computational development of penalized QR with other important penalties, such as the group lasso, is still scarce. For instance, quantile regression with the group lasso penalty can be formulated as a second-order cone programming (SOCP) problem (Kato, 2011), solvable by general-purpose optimization toolboxes. These toolboxes are only adapted to small-scale problems and usually lead to solution with very high precision (low duality gap). For large-scale datasets, they tend to be too slow, or often run out of memory.

To resolve the non-differentiability issue of the check loss, Horowitz (1998) proposed to smooth the check loss directly using a kernel function. This approach, however, leads to a non-convex loss function which brings further computational issues especially in high dimensions. Recently, Fernandes et al. (2021) employed a convolution-type smoothing technique to introduce the smooth quantile regression (SQR) without sacrificing convexity. Convolution smoothing turns the non-differentiable check function into a twice-differentiable, convex and locally strongly convex surrogate, which admits fast and scalable gradient-based algorithms to perform optimization (He et al., 2021). Theoretically, the SQR estimator is asymptotically first-order equivalent to the standard QR estimator, and enjoys desirable statistical properties (Fernandes et al., 2021; He et al., 2021). For high-dimensional sparse models, Tan et al. (2022) proposed an iteratively reweighted -penalized SQR estimator that achieves oracle rate of convergence when the signals are sufficiently strong. They also proposed coordinate descent and ADMM-based algorithms for (weighted) -penalized SQR with the uniform and Gaussian kernels. These algorithms, however, do not adapt to more general kernel functions as well as penalties.

In this paper, we introduce a major variant of the local adaptive majorize-minimization (LAMM) algorithm (Fan et al., 2018) for fitting convolution smoothed quantile regression that applies to any kernel function and a wide range of convex penalties. The main idea is to construct an isotropic quadratic objective function that locally majorizes the smoothed quantile loss such that closed-form updates are available at each iteration. The quadratic coefficient is adaptively chosen in order to guarantee the decrease of the objective function. In a sense, the LAMM algorithm can be viewed as a generalization of the iterative shrinkage-thresholding algorithm (ISTA) (Beck and Teboulle, 2009). Compared to the interior point methods (for solving linear programming and SOCP problems) as well as ADMM, LAMM is a simpler gradient-based algorithm that is particularly suited for large-scale problems, where the dominant computational effort is a relatively cheap matrix-vector multiplication at each step. The (local) strong convexity of the convolution smoothed quantile loss facilitates the convergence of such a first order method. A key advantage of the proposed algorithm over those in Tan et al. (2022) is that it can be applied to a broad class of convex penalties, typified by the lasso, elastic net, group lasso and sparse group lasso, and to any continuous kernel function. The proposed algorithm is implemented in the R package conquer (He et al., 2022) for fitting penalized (smoothed) quantile regression, including all the penalties considered in this paper.

The remainder of the paper is organized as follows. Section 2 briefly revisits quantile regression and its convolution smoothed counterpart. In Section 3, we describe a general local adaptive majorize-minimization principal for solving penalized smoothed quantile regression with four types of convex penalties, which are the lasso (-penalty), elastic net (hybrid of /-penalty), group lasso (weighted -penalty) and sparse group lasso (hybrid of - and weighted -penalty). The computational and statistical efficiency of the proposed algorithm is demonstrated via extensive simulation studies in Section 4. In Section 5, we further exemplify the the proposed algorithm by fitting a fused lasso additive QR model on the world happiness data.

2 Quantile Regression and Convolution Smoothing

Let be a -dimensional covariates and let be a scalar response variable. Given a quantile level of interest, assume that the -th conditional quantile of given follows a linear model , where . For notational convenience, we set such that is the intercept. Moreover, we suppress the dependency of on throughout the paper. Let be a random sample of size from . The standard quantile regression estimator is defined as the solution to the optimization problem (Koenker and Bassett, 1978)

| (2.1) |

where is the quantile loss, also known as the check function. Although the quantile loss is convex, its non-differentiability (even only at one point) prevents gradient-based algorithms to be efficient. In this case, subgradient methods typically exhibit very slow (sublinear) convergence and hence are not computationally stable. A more widely acknowledged approach is to formulate the optimization problem (2.1) as a linear program, solvable by the simplex algorithm or interior point methods. The latter has an average-case computational complexity that grows as a cubic function of (Portnoy and Koenker, 1997).

For fitting a sparse QR model in high dimensions, a natural parallel to the lasso (Tibshirani, 1996) is the -penalized QR (QR-lasso) estimator (Belloni and Chernozhukov, 2011), defined as a solution to the optimization problem

| (2.2) |

where is a regularization parameter that controls (indirectly) the sparsity level of the solution, and denotes the -norm. We refer to Wang et al. (2012) and Zheng et al. (2015) for further extensions to adaptive and folded concave penalties. Computationally, all of these sparsity-driven penalized methods boil down to solving a weighted -penalized QR loss minimization problem that is of the form

| (2.3) |

where for each . Thus far, the most notable methods for solving (2.2) or more generally (2.3) include linear programming (Koenker, 2022), coordinate descent algorithms (Peng and Wang, 2015; Yi and Huang, 2017) and ADMM-based algorithms (Yu et al., 2017; Gu et al., 2018). Among these, ADMM-based algorithms have the best overall performance as documented in Gu et al. (2018). The dominant computational effort of each ADMM update is the inversion of a or an matrix. For genomics data that typically has a small sample size, say in the order of hundreds, ADMM works well even when the dimension is in the order of thousands or tens of thousands. However, there is not much efficient algorithm, that is also scalable to , available for (weighted) -penalized QR, let alone for more general penalties.

To address the non-differentiability of the quantile loss, Fernandes et al. (2021) proposed a convolution smoothed approach to quantile regression, resulting in a twice-differentiable, convex and (locally) strongly convex loss function. On the statistical aspect, Fernandes et al. (2021) and He et al. (2021) established the asymptotic and finite-sample properties for the smoothed QR (SQR) estimator, respectively. Tan et al. (2022) further considered the penalized SQR with iteratively reweighted -regularization and proved oracle properties under a minimum signal strength condition. Let be a symmetric, non-negative kernel function, that is, for any , and . Given a bandwidth parameter , the -penalized SQR (SQR-lasso) estimator is defined as the solution to

| (2.4) |

Equivalently, the smoothed loss can be written as , where and “” denotes the convolution operator. Commonly used kernel functions include (i) uniform kernel, (ii) Gaussian kernel, (iii) logistic kernel, (iv) Epanechnikov kernel, and (v) triangular kernel. See Section 3 of He et al. (2021) for the explicit expressions of when the above kernels are used.

Statistical properties of convolution smoothed QR have been studied in the context of linear models under fixed-, growing- and high-dimensional settings (Fernandes et al., 2021; He et al., 2021; Tan et al., 2022). In the low-dimension setting “”, He et al. (2021) showed that the SQR estimator is (asymptotically) first-order equivalent to the QR estimator. Moreover, the asymptotic normality of SQR holds under a weaker requirement on dimensionality than needed for QR. In the high-dimensional regime “”, Tan et al. (2022) proved that the SQR-lasso estimator with a properly chosen bandwidth enjoys the same convergence rate as QR-lasso (Belloni and Chernozhukov, 2011). With iteratively reweighted -regularization, oracle properties can be achieved by SQR under a weaker signal strength condition than needed for QR.

Computationally, Tan et al. (2022) proposed coordinate descent and ADMM-based algorithms that are tailored to the uniform kernel and Gaussian kernel, respectively. These algorithms do not exhibit evident advantages over those for penalized QR, and also limit the choice of both kernel and penalty functions. This motivates us to develop a more efficient and flexible algorithm for penalized SQR, which accommodates general kernel functions and a broader range of convex penalties.

3 Local Adaptive Majorize-minimization Algorithm for Penalized SQR

In this section, we describe a unified algorithm to solve the optimization problem for penalized SQR, which has a general form

| (3.1) |

where is a generic convex penalty function and is the smoothed check loss given in (2.4). In this paper, we focus on the following four widely used convex penalty functions.

-

1)

Weighted lasso (Tibshirani, 1996): , where for ;

-

2)

Elastic net (Zou and Hastie, 2005): , where is a sparsity-inducing parameter and is a user-specified constant that controls the tradeoff between the penalty and the ridge penalty;

-

3)

Group lasso (Yuan and Lin, 2006): , where and is a sub-vector of corresponding to the th group of coefficients, and are predetermined weights;

-

4)

Sparse group lasso (Simon et al., 2013): .

We employ the local adaptive majorize-minimization (LAMM) principle to derive an iterative algorithm for solving (3.1). The LAMM principle is a generalization of the majorize-minimization (MM) algorithm (Lange et al., 2000; Hunter and Lange, 2004) to high dimensions, and has been applied to penalized least squares, generalized linear models (Fan et al., 2018) and robust regression (Pan et al., 2021). We first provide a brief overview of the LAMM algorithm.

Consider the minimization of a general smooth function . Given an estimate at the th iteration, the LAMM algorithm locally majorizes by a properly constructed function that satisfies the local property

| (3.2) |

where . The ensures the decrease of the objective function after each step, i.e., . Note that (3.2) is a relaxation of the global majorization requirement, , used in the MM algorithm (Lange et al., 2000; Hunter and Lange, 2004).

Motivated by the local property in (3.2), we now derive an iterative algorithm for solving (3.1). For notational convenience, let and let be the gradient of . We locally majorize given by constructing an isotropic quadratic function of the form

where is a quadratic parameter (to be determined) at the th iteration. Then, define the th iterate as the solution to

| (3.3) |

To ensure the descent of the objective function in (3.1) at each iteration, the parameter needs to be sufficiently large such that . Consequently,

where the second inequality is due to the fact that is a minimizer of (3.3). In practice, we choose by starting from a small value and successively inflate it by a factor until the majorization requirement is met at each iteration of the LAMM algorithm.

One of the main advantages of our approach is that the isotropic form of , as a function of , permits a simple analytic solution for different convex penalty functions . By the first-order optimization condition, satisfies

where denotes the subdifferential of . With certain convex penalties, a closed-form expression for can be derived from the above condition. Since a common practice is to leave the intercept term unpenalized, its update takes a simple form . Detailed update rules of for the above four convex penalties are summarized in Algorithm 1, in which denotes the shrinkage operator, where is the sign function and . For all the four penalty functions, the dominant computational effort of each LAMM update is a relatively cheap matrix-vector multiplication involving , thus with a complexity .

Input: kernel function , penalty function , regularization parameters, bandwidth , inflation factor , and convergence criterion .

Initialization: , .

Repeat the following steps until the stopping criterion is met, where is the th iterate.

-

1.

Set max{, }.

-

2.

repeat

-

3.

for (or for group lasso and sparse group lasso), update (or ) as follows:

weighted lasso . elastic net . group lasso . sparse group lasso . -

4.

If , set .

-

5.

until .

Output: the updated parameter .

4 Numerical Studies

In this section, we perform extensive numerical studies to evaluate the performance of the LAMM algorithm (Algorithm 1) for fitting penalized SQR with four convex penalties, the lasso ( penalty), elastic net, group lasso, and sparse group lasso. We implement Algorithm 1 using the Gaussian kernel. The numerical performance under other commonly used kernels, such the logistic kernel, Laplacian kernel and uniform kernel, are quite similar and thus we omit the correspondent results. As suggested in Tan et al. (2022), we set the default bandwidth value as throughout the numerical studies. The empirical evidence from He et al. (2021) and Tan et al. (2022) shows that the SQR estimator is not susceptible to the choice of in a reasonable range that is neither too small nor too large. In Section 4.1, we fit penalized SQR with the and elastic net penalties on simulated data with sparse regression coefficients. We also evaluate the computational efficiency of Algorithm 1, implemented by the conquer package, by comparing it to several state-of-the-art packages on penalized regression. In Section 4.2, we fit penalized SQR with the group lasso penalty on simulated data for which the groups of regression coefficients are sparse.

4.1 Simulated Data with Sparse Regression Coefficients

We start with generating from a multivariate normal distribution , where , and set . Given , we generate the response from the following linear heteroscedastic model:

| (4.1) |

where denotes the th quantile of the noise variable . We consider two noise distributions: (i) Normal distribution with mean zero and variance 2—, and (ii) -distribution with 1.5 degrees of freedom—. Moreover, the vector of regression coefficients takes the following two forms: (i) sparse with (intercept), , , , , , , , , , , and for all other ’s, and (ii) dense with (intercept), for , and otherwise.

We compare the proposed algorithm for penalized SQR with the and elastic net penalties to the -penalized QR implemented by the R package rqPen111The rqPen package does not have the elastic net penalty option. (Sherwood and Maidman, 2020). Note that the ADMM-based algorithm proposed by Gu et al. (2018), implemented in the R package FHDQR, is incompatible with the current version of R and hence is not included in this paper. The regularization parameter is selected via ten-fold cross-validation for which the validation error is defined through the quantile loss. We set the additional tuning parameter for the elastic net penalty as . To evaluate the statistical performance of different methods, we report the estimation error under the -norm, i.e., , as well as the true positive rate (TPR) and false positive rate (FPR), which are defined as the proportion of correctly estimated non-zeros and the proportion of falsely estimated non-zeros, respectively. The results for the sparse and dense , averaged over 100 replications, are reported in Tables 1 and 2, respectively.

From Table 1 we see that when true signals are genuinely sparse, both -penalized SQR and QR outperform the elastic net SQR (with different values) in all three facets. Due to the large number of zeros in , the performance of the elastic net SQR deteriorates as decreases, where is a user-specified parameter that balances the penalty and the ridge () penalty. Table 2 summarizes the results under a dense that contains 100 non-zeros coordinates. In this case, the elastic net SQR estimators tend to have lower estimation error and high true positive rate, suggesting that the elastic net penalty may be beneficial when the signals are dense and the signal-to-noise ratio is relatively low.

| Linear Heteroscedastic Model with Sparse and | |||||||

| Noise | Methods | Error | TPR | FPR | Error | TPR | FPR |

| SQR (lasso) | 0.507 (0.009) | 1 (0) | 0.112 (0.006) | 0.861 (0.019) | 1 (0) | 0.070 (0.003) | |

| SQR (elastic net, ) | 0.943 (0.013) | 1 (0) | 0.280 (0.006) | 1.617 (0.020) | 1 (0) | 0.161 (0.004) | |

| SQR (elastic net, ) | 1.268 (0.014) | 1 (0) | 0.429 (0.008) | 2.119 (0.017) | 1 (0) | 0.270 (0.006) | |

| SQR (elastic net, ) | 1.602 (0.013) | 1 (0) | 0.635 (0.007) | 2.586 (0.013) | 1 (0) | 0.452 (0.013) | |

| rqPen (lasso) | 0.533 (0.010) | 1 (0) | 0.117 (0.006) | 0.915 (0.020) | 1 (0) | 0.076 (0.004) | |

| SQR (lasso) | 0.454 (0.010) | 1 (0) | 0.092 (0.004) | 0.825 (0.019) | 1 (0) | 0.065 (0.003) | |

| SQR (elastic net, ) | 0.899 (0.015) | 1 (0) | 0.265 (0.005) | 1.695 (0.020) | 1 (0) | 0.151 (0.004) | |

| SQR (elastic net, ) | 1.263 (0.016) | 1 (0) | 0.419 (0.008) | 2.265 (0.017) | 1 (0) | 0.231 (0.005) | |

| SQR (elastic net, ) | 1.642 (0.016) | 1 (0) | 0.620 (0.008) | 2.725 (0.013) | 1 (0) | 0.397 (0.006) | |

| rqPen (lasso) | 0.468 (0.011) | 1 (0) | 0.112 (0.005) | 0.851 (0.020) | 1 (0) | 0.070 (0.003) | |

| Linear Heteroscedastic Model with Sparse and | |||||||

| SQR (lasso) | 0.530 (0.011) | 1 (0) | 0.110 (0.005) | 0.895 (0.020) | 1 (0) | 0.066 (0.003) | |

| SQR (elastic net, ) | 0.988 (0.014) | 1 (0) | 0.269 (0.006) | 1.676 (0.020) | 1 (0) | 0.159 (0.004) | |

| SQR (elastic net, ) | 1.321 (0.016) | 1 (0) | 0.420 (0.008) | 2.189 (0.018) | 1 (0) | 0.250 (0.005) | |

| SQR (elastic net, ) | 1.672 (0.015) | 1 (0) | 0.615 (0.008) | 2.647 (0.013) | 1 (0) | 0.407 (0.010) | |

| rqPen (lasso) | 0.553 (0.012) | 1 (0) | 0.120 (0.005) | 0.947 (0.021) | 1 (0) | 0.070 (0.003) | |

| SQR (lasso) | 0.561 (0.014) | 1 (0) | 0.102 (0.004) | 1.023 (0.024) | 0.999 (0.001) | 0.063 (0.003) | |

| SQR (elastic net, ) | 1.073 (0.017) | 1 (0) | 0.258 (0.006) | 1.873 (0.021) | 0.999 (0.001) | 0.153 (0.004) | |

| SQR (elastic net, ) | 1.454 (0.018) | 1 (0) | 0.398 (0.008) | 2.421 (0.018) | 1 (0) | 0.225 (0.004) | |

| SQR (elastic net, ) | 1.842 (0.017) | 1 (0) | 0.595 (0.008) | 2.863 (0.014) | 1 (0) | 0.369 (0.005) | |

| rqPen (lasso) | 0.582 (0.015) | 1 (0) | 0.103 (0.005) | 1.060 (0.026) | 0.998 (0.001) | 0.068 (0.003) | |

| Linear Heteroscedastic Model with Dense and | |||||||

| Noise | Methods | Error | TPR | FPR | Error | TPR | FPR |

| SQR (lasso) | 1.441 (0.015) | 1 (0) | 0.246 (0.009) | 3.018 (0.034) | 0.996 (0.001) | 0.218 (0.011) | |

| SQR (elastic net, ) | 1.243 (0.013) | 1 (0) | 0.322 (0.009) | 2.184 (0.028) | 1 (0) | 0.259 (0.006) | |

| SQR (elastic net, ) | 1.210 (0.014) | 1 (0) | 0.440 (0.009) | 2.192 (0.034) | 1 (0) | 0.407 (0.008) | |

| SQR (elastic net, ) | 1.260 (0.014) | 1 (0) | 0.633 (0.007) | 2.787 (0.037) | 1 (0) | 0.718 (0.009) | |

| rqPen (lasso) | 1.512 (0.015) | 1 (0) | 0.246 (0.010) | 3.239 (0.039) | 0.993 (0.001) | 0.175 (0.006) | |

| SQR (lasso) | 1.575 (0.020) | 1 (0) | 0.216 (0.008) | 4.340 (0.188) | 0.976 (0.002) | 0.163 (0.006) | |

| SQR (elastic net, ) | 1.296 (0.015) | 1 (0) | 0.303 (0.008) | 2.479 (0.043) | 1 (0) | 0.239 (0.005) | |

| SQR (elastic net, ) | 1.247 (0.014) | 1 (0) | 0.434 (0.007) | 2.406 (0.029) | 1 (0) | 0.373 (0.005) | |

| SQR (elastic net, ) | 1.316 (0.014) | 1 (0) | 0.636 (0.006) | 2.709 (0.029) | 1 (0) | 0.594 (0.005) | |

| rqPen (lasso) | 1.628 (0.022) | 1 (0) | 0.234 (0.009) | 4.012 (0.055) | 0.970 (0.002) | 0.142 (0.004) | |

| Linear Heteroscedastic Model with Dense and | |||||||

| SQR (lasso) | 1.508 (0.015) | 1 (0) | 0.223 (0.008) | 3.054 (0.034) | 0.995 (0.001) | 0.194 (0.008) | |

| SQR (elastic net, ) | 1.289 (0.012) | 1 (0) | 0.309 (0.008) | 2.222 (0.024) | 1 (0) | 0.248 (0.005) | |

| SQR (elastic net, ) | 1.237 (0.012) | 1 (0) | 0.431 (0.007) | 2.174 (0.025) | 1 (0) | 0.383 (0.006) | |

| SQR (elastic net, ) | 1.291 (0.012) | 1 (0) | 0.634 (0.006) | 2.782 (0.036) | 1 (0) | 0.711 (0.010) | |

| rqPen (lasso) | 1.586 (0.016) | 1 (0) | 0.228 (0.009) | 3.356 (0.039) | 0.989 (0.001) | 0.166 (0.005) | |

| SQR (lasso) | 1.912 (0.029) | 1 (0) | 0.219 (0.007) | 4.896 (0.208) | 0.961 (0.003) | 0.172 (0.007) | |

| SQR (elastic net, ) | 1.487 (0.015) | 1 (0) | 0.302 (0.007) | 2.743 (0.043) | 0.999 (0) | 0.245 (0.005) | |

| SQR (elastic net, ) | 1.410 (0.014) | 1 (0) | 0.431 (0.007) | 2.600 (0.033) | 1 (0) | 0.372 (0.005) | |

| SQR (elastic net, ) | 1.491 (0.016) | 1 (0) | 0.643 (0.006) | 2.889 (0.036) | 1 (0) | 0.597 (0.006) | |

| rqPen (lasso) | 1.947 (0.025) | 1 (0) | 0.226 (0.008) | 4.543 (0.058) | 0.942 (0.004) | 0.129 (0.004) | |

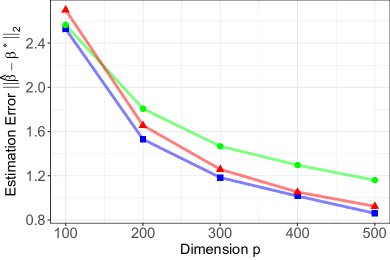

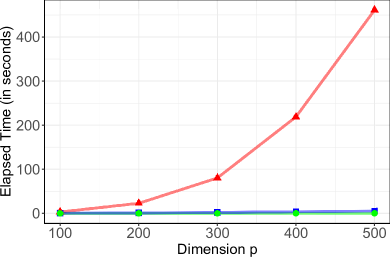

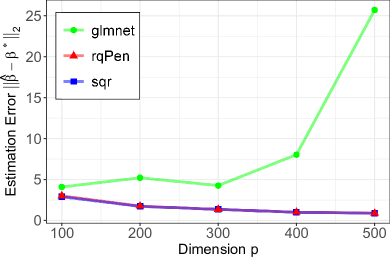

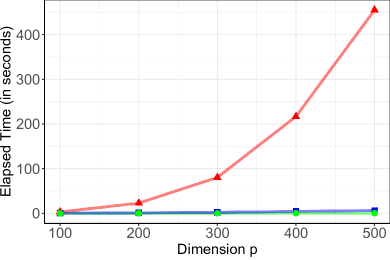

Furthermore, we provide speed comparisons of the three R packages, glmnet, rqPen and conquer, for fitting sparse linear models. As a benchmark, glmnet is used to compute the -penalized least squares (lasso) estimator, whereas rqPen and conquer are used to fit penalized quantile regression with . For each method, the regularization parameter is selected from a sequence of 50 -values via ten-fold cross-validation. The curves in panels (a) and (c) of Figure 1 represent the estimation error (under norm) as a function of dimension , and the curves in panels (b) and (d) of Figure 1 represent the computational time (in second) as a function of dimension . The sample size is taken to be . Under normal errors, the three estimators, lasso, QR-lasso and SQR-lasso, converge at similar rates as grows; while the lasso estimator is inconsistent when the error follows the -distribution. The SQR-lasso may even slightly outperforms the QR-lasso, indicating that smoothing can potentially improve finite-sample performance. In terms of computational efficiency, our conquer package exhibits a significant improvement over rqPen especially when is large, and is almost as efficient as glmnet.

4.2 Simulated Data with Sparse Groups of Regression Coefficients

We further assess the performance of penalized SQR with the group lasso penalty by comparing conquer with the R package sgl. The latter is used to compute the group lasso estimator. To this date, we are not aware of any existing R package that implements group lasso penalized quantile regression. The regularization parameter is once again selected by ten-fold cross-validation, and the weights are set as , where is the dimension of the sub-vector .

We generate the data according to (4.1) with 10 groups of regression coefficients . Specifically, we construct a block-diagonal covariance matrix , where , , and , and each block is an exchangeable covariance matrix with diagonal 1 and off-diagonal elements 0.6. We then generate the covariates from the multivariate normal distribution, and set . We construct that has a sparse group structure, i.e., with (intercept), , , , , , and .

To assess the performance of group lasso SQR, we calculate the group TPR and group FPR, defined as the proportion of groups that are correctly estimated to contain non-zeros, and the proportion of groups that are incorrectly estimated to contain non-zeros, respectively. Since -penalized methods do not induce group structures, the group TPR and FPR are not well defined. Results under Gaussian and -distributed random noise, averaged over 100 replications, are reported in Table 3. Under sparse group structures, the group lasso SQR achieves the best performance cross all settings as expected. This indicates that using the group lasso penalty may be beneficial when the covariates are highly correlated within predefined groups.

| Linear Heteroscedastic Model with Sparse Groups of and | |||||||

| Noise | Methods | Error | Group TPR | Group FPR | Error | Group TPR | Group FPR |

| SQR (lasso) | 0.707 (0.009) | NA | NA | 1.154 (0.016) | NA | NA | |

| rqPen (lasso) | 0.712 (0.009) | NA | NA | 1.223 (0.021) | NA | NA | |

| SQR (group) | 0.527 (0.006) | 1 (0) | 0.018 (0.004) | 0.745 (0.010) | 1 (0) | 0.046 (0.009) | |

| SGL (group) | 1.009 (0.044) | 1 (0) | 0.061 (0.011) | 1.395 (0.069) | 1 (0) | 0.070 (0.009) | |

| SQR (lasso) | 0.948 (0.032) | NA | NA | 1.510 (0.042) | NA | NA | |

| rqPen (lasso) | 0.663 (0.013) | NA | NA | 1.246 (0.023) | NA | NA | |

| SQR (group) | 0.662 (0.022) | 1 (0) | 0.001 (0.001) | 0.875 (0.020) | 1 (0) | 0.003 (0.002) | |

| SGL (group) | 2.502 (0.369) | 1 (0) | 0.139 (0.027) | 2.435 (0.151) | 1 (0) | 0.082 (0.019) | |

| Linear Heteroscedastic Model with Sparse Groups of and | |||||||

| SQR (lasso) | 0.753 (0.011) | NA | NA | 1.252 (0.019) | NA | NA | |

| rqPen (lasso) | 0.769 (0.011) | NA | NA | 1.299 (0.020) | NA | NA | |

| SQR (group) | 0.550 (0.007) | 1 (0) | 0.019 (0.005) | 0.780 (0.011) | 1 (0) | 0.050 (0.009) | |

| SGL (group) | 1.209 (0.053) | 1 (0) | 0.181 (0.012) | 1.585 (0.080) | 1 (0) | 0.181 (0.015) | |

| SQR (lasso) | 1.223 (0.044) | NA | NA | 1.896 (0.062) | NA | NA | |

| rqPen (lasso) | 0.822 (0.014) | NA | NA | 1.523 (0.028) | NA | NA | |

| SQR (group) | 0.862 (0.033) | 1 (0) | 0.001 (0.001) | 1.074 (0.030) | 1 (0) | 0.004 (0.002) | |

| SGL (group) | 2.591 (0.369) | 1 (0) | 0.145 (0.028) | 2.537 (0.152) | 1 (0) | 0.089 (0.019) | |

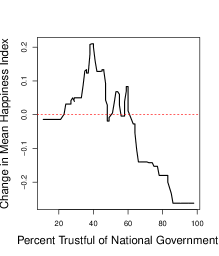

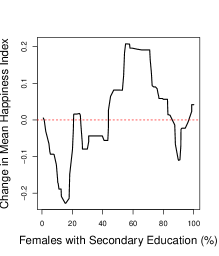

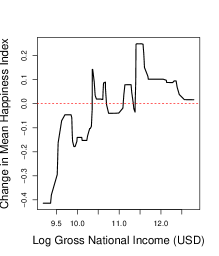

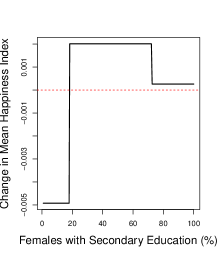

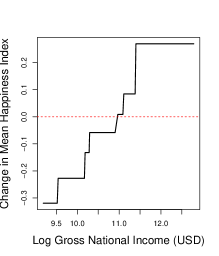

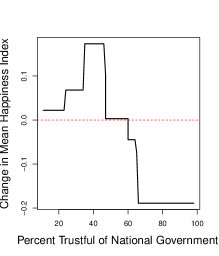

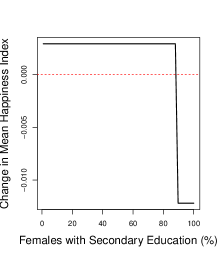

5 Fused Lasso Additive SQR and World Happiness Data

In this section, we employ the fused lasso additive smoothed quantile regression for flexible and interpretable modeling of the conditional relationship between country happiness level and a set of covariates, using the world happiness data (United Nations Development Programme, 2012; World Bank Group, 2012; Helliwell et al., 2013) previously studied in Petersen et al. (2016). Specifically, the goal is to study the conditional distribution of country-level happiness index, the average of Cantril Scale (Cantril, 1965) responses of approximately 3000 residents in each country, given twelve country-level predictors, including but are not limited to log gross national income (USD), satisfaction with freedom of choice, satisfaction with job, satisfaction with community, and trust in national government.

We first provide a brief overview of the fused lasso additive model in Petersen et al. (2016). The fused lasso additive model seeks to balance interpretability and flexibility by approximating the additive function for each covariate via a piecewise constant function. Let for and let be an matrix with entries and for , and for . Moreover, let be a permutation matrix that orders the elements of from least to greatest. The fused lasso additive model estimator in Petersen et al. (2016) can be obtained by solving the convex optimization problem

| (5.1) |

where is a fused lasso type penalty that encourages the consecutive entries of the ordered parameters to be the same. We refer the reader to Petersen and Witten (2019), Wu and Witten (2019), and Sadhanala and Tibshirani (2019) for a summary of recent work on flexible and interpretable additive models.

We now propose the fused lasso additive smoothed quantile regression for interpretable and flexible modeling of the conditional distribution of given at specific quantile levels. Specifically, we propose to solve the following optimization problem by substituting the squared error loss in (5.1) via the smoothed quantile loss in (2.4):

| (5.2) |

Optimization problem (5.2) is convex and can be solved using a block coordinate descent algorithm similar to that of Petersen et al. (2016), which we outline in Algorithm 2. Each iteration in Algorithm 2 involves solving a penalized smoothed quantile regression problem with a fused lasso type penalty (5.3). Tibshirani and Taylor (2011) showed that the fused lasso type penalty in (5.3) can be rewritten as a weighted lasso penalty through some transformation on the regression coefficients, and thus Algorithm 1 can naturally be employed to solve (5.3). We omit the derivations and refer the reader to Tibshirani and Taylor (2011) for the details.

Input: kernel function , regularization parameter , smoothing bandwidth parameter , and convergence criterion .

Initialization: , for .

Iterate: for each , until the stopping criterion is met, where is the value of obtained at the th iteration.

-

1.

Update the residual .

-

2.

Update as

(5.3) -

3.

Update the intercept .

-

4.

Center the parameters .

Output: the updated parameters .

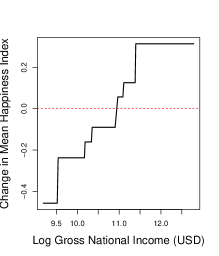

We apply the proposed method to investigate the conditional distribution of country-level happiness index at different quantile levels . We implement our proposed method under the Gaussian kernel with , and selected using cross-validation. The estimated fits for three selected covariates are shown in Figure 2: the first, second, and third rows in Figure 2 correspond to the results for , , and , respectively. For the estimated fits are similar to that of the fused lasso additive model presented in Petersen et al. (2016). In particular, we find that an increased in gross national income, up to a certain level, is associated with increased happiness, conditional on the other predictors. Moreover, the differences in conditional associations between country’s happiness level and both gross national income and percent trustful of national government are negligible for the three quantile levels. It is interesting to see that the conditional association between mean happiness index and females with secondary education are different for the three different quantile levels, suggesting that there are potential heterogenous effects.

References

- Beck and Teboulle (2009) Beck, A. and Teboulle, M. (2009). A fast iterative shrinkage-thresholding algorithm for linear inverse problems. SIAM Journal of Imaging Science 2 183–202.

- Belloni and Chernozhukov (2011) Belloni, A. and Chernozhukov, V. (2011). -penalized quantile regression in high-dimensional sparse models. Annals of Statistics 39 82–130.

- Bühlmann and van de Geer (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer, Heidelberg.

- Cantril (1965) Cantril, H. (1965) The Pattern of Human Concerns. Rutgers University Press.

- Fan and Li (2001) Fan, J. and Li, R. (2001). Variable selection via nonconcave regularized likelihood and its oracle properties. Journal of American Statistical Association 96 1348–1360.

- Fan et al. (2018) Fan, J., Liu, H., Sun, Q. and Zhang, T. (2018). I-LAMM for sparse learning: Simultaneous control of algorithmic complexity and statistical error. Annals of Statistics 46 814–841.

- Fernandes et al. (2021) Fernandes, M., Guerre, E. and Horta, E. (2021). Smoothing quantile regressions. Journal of Business & Economic Statistics 39 338–357.

- Friedma et al. (2010) Friedman, J., Hastie, T. and Tibshirani, R. (2010). Regularization paths for generalized linear models via coordinate descent. Journal of Statistical Software 33(1): 1–22.

- Helliwell et al. (2013) Helliwell, J., Layard, R. and Sachs, J. (2013). World Happiness Report 2013. Sustainable Development Solutions Network.

- Hunter and Lange (2004) Hunter, D. R. and Lange, K. (2004). A tutorial on MM algorithms. The American Statistician 58 30–37.

- Hunter and Lange (2000) Hunter, D. R. and Lange, K. (2000). Quantile regression via an MM algorithm. Journal of Computational and Graphical Statistics 9 60–77.

- Gu et al. (2018) Gu, Y., Fan, J., Kong, L., Ma, S. and Zou, H. (2018). ADMM for high-dimensional sparse regularized quantile regression. Technometrics 60 319–331.

- Hastie et al. (2015) Hastie, T., Tibshirani, R. and Wainwright, M. (2015). Statistical Learning with Sparsity: The Lasso and Generalizations. CRC Press, Boca Raton.

- He et al. (2021) He, X., Pan, X., Tan, K. M. and Zhou, W.-X. (2021). Smoothed quantile regression with large-scale inference. Journal of Econometrics, in press.

- He et al. (2022) He, X., Pan, X., Tan, K. M. and Zhou, W.-X. (2022). Package “conquer”, version . Reference manual: https://cran.r-project.org/web/packages/conquer/conquer.pdf.

- Horowitz (1998) Horowitz, J. L. (1998). Bootstrap methods for median regression models. Econometrica 66 1327–1351.

- Kato (2011) Kato, K. (2011). Group lasso for high dimensional sparse quantile regression models. arXiv preprint arXiv:1103.1458.

- Koenker (2005) Koenker, R. (2005). Quantile Regression. Cambridge University Press, Cambridge.

- Koenker (2022) Koenker, R. (2022). Package “quantreg”, version . Reference manual: https://cran.r-project.org/web/packages/quantreg/quantreg.pdf.

- Koenker and Bassett (1978) Koenker, R. and Bassett, G (1978). Regression quantiles. Econometrica 46 33-50.

- Koenker et al. (2017) Koenker, R., Chernozhukov, V., He, X. and Peng, L. (2017). Handbook of Quantile Regression. CRC Press, Boca Raton, FL.

- Koenker and Ng (2005) Koenker, R. and Ng, P. (2005). A Frisch-Newton algorithm for sparse quantile regression. Acta Mathematicae Applicatae Sinica 21 225–236.

- Lange et al. (2000) Lange, K., Hunter, D. R. and Yang, I. (2000). Optimization transfer using surrogate objective functions. Journal of Computational and Graphical Statistics 9 1–59.

- Li and Zhu (2008) Li, Y. and Zhu, J. (2008). -norm quantile regression. Journal of Computational and Graphical Statistics 17 163–185.

- Pan et al. (2021) Pan, X., Sun, Q. and Zhou, W.-X. (2021). Iteratively reweighted -penalized robust regression. Electronic Journal of Statistics 25 3287–3348.

- Peng and Wang (2015) Peng, B. and Wang, L. (2015). An iterative coordinate descent algorithm for high-dimensional nonconvex penalized quantile regression. Journal of Computational and Graphical Statistics 24 676–694.

- Petersen and Witten (2019) Petersen, A. and Witten, D. (2019). Data-adaptive additive modeling. Statistics in Medicine 38 583–600.

- Petersen et al. (2016) Petersen, A., Witten, D. and Simon, N. (2016). Fused lasso additive model. Journal of Computational and Graphical Statistics 25 1005–1025.

- Portnoy and Koenker (1997) Portnoy, S. and Koenker, R. (1997). The Gaussian hare and the Laplacian tortoise: Computability of squared-error versus absolute-error estimators. Statistical Science 12 279–300.

- Sadhanala and Tibshirani (2019) Sadhanala, V. and Tibshirani, R. (2019). Additive models with trend filtering. Annals of Statistics 47 3032–3068.

- Sherwood and Maidman (2020) Sherwood, B. and Maidman, A. (2020). Package “rqPen”, version . Reference manual: https://cran.r-project.org/web/packages/rqPen/rqPen.pdf.

- Simon et al. (2013) Simon, N., Friedman, J., Hastie, T. and Tibshirani, R. (2013). A sparse-group lasso. Journal of Computational and Graphical Statistics 22(2): 231–245.

- Tan et al. (2022) Tan, K. M., Wang, L. and Zhou, W.-X. (2022). High-dimensional quantile regression: Convolution smoothing and concave regularization. Journal of the Royal Statistical Society: Series B 84(1): 205–233.

- Tibshirani (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B 58 267–288.

- Tibshirani (2014) Tibshirani, R. (2014). Adaptive piecewise polynomial estimation via trend filtering. Annals of Statistics 42 285–323.

- Tibshirani et al. (2005) Tibshirani, R. and Saunders, M., Rosset, S., Zhu, J. and Knight, K. (2005). Sparsity and smoothness via the fused lasso. Journal of the Royal Statistical Society: Series B 67 91–108.

- Tibshirani and Taylor (2011) Tibshirani, R. and Taylor, J. (2011). The solution path of the generalized lasso. Annals of Statistics 39 1335–1371.

- United Nations Development Programme (2012) United Nations Development Programme. (2012). Human Development Indicators. United Nations Publications.

- Wainwright (2019) Wainwright, M. J. (2019). High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge University Press, Cambridge.

- Wang et al. (2012) Wang, L., Wu, Y. and Li, R. (2012). Quantile regression for analyzing heterogeneity in ultra-high dimension. Journal of American Statistical Association 107 214–222.

- World Bank Group (2012) World Bank Group. (2012). World Development Indicators 2012. World Bank Publications.

- Wu and Witten (2019) Wu, J. and Witten, D. (2019). Flexible and interpretable models for survival data. Journal of Computational and Graphical Statistics 28 954–966.

- Yang and Zou (2015) Yang, Y. and Zou, H. (2015). A fast unified algorithm for solving group-lasso penalized learning problems. Statistics and Computing 25 1129–1141.

- Yi and Huang (2017) Yi, C. and Huang, J. (2017). Semismooth Newton coordinate descent algorithm for elastic-net penalized Huber regression and quantile regression. Journal of Computational and Graphical Statistics 26 547–557.

- Yu et al. (2017) Yu, L., Lin, N. and Wang, L. (2017). A parallel algorithm for large-scale nonconvex penalized quantile regression. Journal of Computational and Graphical Statistics 26 935–939.

- Yuan and Lin (2006) Yuan, M. and Lin, Y. (2006). Model selection and estimation in regression with grouped variables. Journal of the Royal Statistical Society: Series B 68 49–67.

- Zhang (2010) Zhang, C.-H. (2010). Nearly unbiased variable selection under minimax concave penalty. Annals of Statistics 38 894–942.

- Zheng et al. (2015) Zheng, Q., Peng, L. and He, X. (2015). Globally adaptive quantile regression with ultra-high dimensional data. Annals of Statistics 43 2225–2258.

- Zou and Hastie (2005) Zou, H. and Hastie, T. (2005). Regularization and variable selection via the elastic net. Journal of the Royal Statistical Society: Series B 67 301–320.