Efficient Algorithms for Minimizing Compositions of Convex Functions and Random Functions \RUNAUTHORChen et al. \TITLEEfficient Algorithms for Minimizing Compositions of Convex Functions and Random Functions and Its Applications in Network Revenue Management

Xin Chen1, Niao He2, Yifan Hu3, Zikun Ye4

\AFF

1 ISyE, Georgia Institute of Technology, Atlanta, US, \EMAILxin.chen@isye.gatech.edu

2 Department of Computer Science, ETH Zürich, Switzerland,

\EMAILniao.he@inf.ethz.ch

3 College of Management of Technology, EPFL, Switzerland, \EMAILyifan.hu@epfl.ch

4

Michael G. Foster School of Business, University of Washington, Seattle, US,

\EMAILzikunye@uw.edu

We study a class of stochastic nonconvex optimization in the form of , i.e., is a composition of a convex function and a random function . Leveraging an (implicit) convex reformulation via a variable transformation , we develop stochastic gradient-based algorithms and establish their sample and gradient complexities for achieving an -global optimal solution. Interestingly, our proposed Mirror Stochastic Gradient (MSG) method operates only in the original -space using gradient estimators of the original nonconvex objective and achieves complexities, which matches the lower bounds for solving stochastic convex optimization problems. Under booking limits control, we formulate the air-cargo network revenue management (NRM) problem with random two-dimensional capacity, random consumption, and routing flexibility as a special case of the stochastic nonconvex optimization, where the random function , i.e., the random demand truncates the booking limit decision . Extensive numerical experiments demonstrate the superior performance of our proposed MSG algorithm for booking limit control with higher revenue and lower computation cost than state-of-the-art bid-price-based control policies, especially when the variance of random capacity is large.

stochastic nonconvex optimization, hidden convexity, air-cargo network revenue management, gradient-based algorithms

1 Introduction

A wide range of operations management problems are special cases of the following stochastic optimization model,

| (1) |

where , is a random vector, is component-wise non-decreasing in , and is convex. Throughout the paper, we assume that the distribution remains unknown, and we can only generate independent and identically distributed (i.i.d.) samples from .

The optimization problem (1) arises pervasively in supply chain management and revenue management. A notable example is , where denotes component-wise minimum. In inventory control problems with supply capacity uncertainty, the amount delivered by suppliers is the minimum of the replenishment order quantity and the realized random capacity , i.e., (see, e.g., Ciarallo et al. 1994, Chen et al. 2015, 2018, Feng and Shanthikumar 2018, Chen and Gao 2019, Feng et al. 2019), in network revenue management problems using booking limit control policies, the accepted reservation is the minimum of the booking limit decision and the random demand (see, e.g., Brumelle and McGill 1993, Karaesmen and Van Ryzin 2004, Li and Pang 2017, Chen et al. 2018).

For these applications, an intrinsic challenge is that the random function is generally nonlinear in ; thus, the objective function is nonconvex in even if is (strongly) convex. For example, when and , it is easy to verify that is nonconvex. As a result, how to efficiently solve the nonconvex problem (1) to global optimality remains unclear. The aim of this paper is to design efficient algorithms that solve the optimization problem to global optimality. We focus on stochastic gradient-based methods as they can handle online data and are suitable for large-scale problems. We measure the efficiency of our proposed algorithms by sample complexity and gradient complexity, i.e., the number of samples and the number of evaluations of needed to achieve an -optimal solution, respectively. Despite the aforementioned advantages of gradient-based methods, they generally can only converge to approximate stationary points of nonconvex objectives.

Interestingly, under some technical conditions on the random function , an equivalent convex reformulation of the nonconvex problem (1) exists (Feng and Shanthikumar 2018):

| (2) |

where , is the image of on and is convex, and is the inverse of for simplicity. With the convex reformulation, it is promising to solve the original nonconvex objective to global optimality. However, to the best of our knowledge, no algorithm has been developed to solve either the original nonconvex problem or the convex reformulation, which we address in this paper.

Note that existing gradient-based methods, like projected stochastic gradient descent (SGD) (Nemirovski et al. 2009), are not directly applicable to solving the convex reformulation . Indeed, since involves the unknown distribution , is unknown. As a result, it is hard to build unbiased gradient estimators for . For the same reason, the closed-form of is unknown; hence, it is hard to perform projection onto .

To address these issues, a natural idea is to utilize sample average approximation (SAA) (Kleywegt et al. 2002) and apply projected SGD on the empirical convex reformulation constructed via the empirical distribution. We denote such a method as SAA+SG (Algorithm 3 with detailed discussion in Appendix 11). Although SAA+SG is intuitive and converges globally, it has several drawbacks. First, it requires access to offline data, limiting its applicability to the online setting. Second, the algorithm needs to estimate at each iteration, which requires solving an additional optimization subproblem and adds additional computational costs.

Instead, we consider algorithms that only operate in the original space, i.e., algorithms that do not require updating the transformed decision variable . Specifically, we propose the Regularized Stochastic Gradient descent (RSG) in Algorithm 1 and the Mirror Stochastic Gradient descent (MSG) in Algorithm 2. RSG performs regularized projected SGD updates on problem (1) and converges to a specific approximate stationary point. Under mild conditions, we show that the converging point corresponds to an approximate global optimal solution. MSG performs an update on the original space that mirrors a virtual SGD update on the convex reformation problem (3) and finds an approximate global optimal solution of the convex reformulation (2) but only updates implicitly via updating . To achieve such mirror behavior, MSG uses number of samples at each iteration to build a preconditioning matrix (see (8)).

| Algorithm | Properties | Sample Complexity | Gradient Complexity |

|---|---|---|---|

| SAA+SG | Requires a batch of offline data | ||

| (Algorithm 3) | requires less assumption on | ||

| RSG | simple to implement | ||

| (Algorithm 1) | one sample per-iteration | ||

| MSG | samples per-iteration | ||

| (Algorithm 2) | optimal sample & gradient complexity |

We establish the global convergence of SAA+SG, RSG, and MSG. Table 1 summarizes the sample and gradient complexities. For a more comprehensive summary of assumptions and complexity bounds, see Table 5 in Appendix 10. RSG achieves a complexity bound while MSG achieves better sample and gradient complexities, where hides the constant terms and additionally hides the logarithmic dependence. In terms of lower bounds for solving the original problem (1), utilizing the analysis of lower bounds on black-box stochastic gradient methods for stochastic convex optimization (Agarwal et al. 2009), we obtain a lower bounds for problem (1). It implies that the performance of MSG matches the optimal possible black-box stochastic gradient method in terms of the dependence on accuracy if ignoring the logarithmic factor.

We apply the proposed methods to solve an air-cargo network revenue management (NRM) problem with booking limit control, as well as a passenger NRM problem as a special case of the air-cargo NRM problem. We first formulate the NRM problem as two-stage stochastic programming and show that it is a special case of the nonconvex stochastic problem (1). Specifically, during the first stage, we first set up booking limits and then accept the amount of demand up to booking limits truncated by uncertain demand , i.e., . In the second stage, we make capacity allocation and routing decisions to serve the accepted demand after the reveal of the random capacity. A notable advantage of such modeling is that it only requires the aggregated level of demand over the whole reservation period rather than the arrival rate in each period, which is typically assumed to be accessible in dynamic models. Note that the focus of the paper is to find an optimal booking limit control. Thus we reduce the usual online NRM problem to a stochastic optimization problem, and we are interested in analyzing the sample efficiency for solving the problem. We leave the design of the online booking limit control policy as an interesting future direction.

We further conduct extensive numerical experiments to demonstrate the effectiveness and generalizability of the booking limit control in NRM problems, comparing to several different bid-price based control policies, including deterministic linear programming (DLP), dynamic programmings decomposition (DPD) (Erdelyi and Topaloglu 2010), and the state-of-the-art virtual capacity and bid price control (VCBP) (Previgliano and Vulcano 2021) in passenger NRM problem, and the state-of-art DPD (Barz and Gartner 2016) specifically designed for air-cargo NRM problem.

1.1 Contributions

Algorithm design and global convergence with non-asymptotic guarantees. We propose three algorithms, SAA+SG, RSG, and MSG, and establish the first non-asymptotic global convergence guarantees for the nonconvex stochastic optimization (1). In addition, RSG and MSG operate only in the original -space, and MSG achieves the optimal complexity bounds.

NRM modeling and algorithm. To the best of our knowledge, we are the first in the literature to propose booking limit control for the air-cargo network revenue problem that takes into account random show-ups, random capacity, random consumption, and routing flexibility at the same time. Our algorithms provide non-asymptotic global guarantees under some mild assumptions, while the VCBP algorithm only converges asymptotically to stationary points.

Numerical Results. Our numerical results demonstrate the superior performance of the proposed algorithms and provide strong justification for utilizing booking limit control in these NRM problems. In passenger NRM (a special case of air-cargo NRM), the booking limit control policy obtained by MSG significantly outperforms bid-price-based methods DLP, DPD, and VCBP with 43.6%, 8.3%, and 4.8% revenue improvement, respectively, and achieves the lowest computation time. In air-cargo NRM, our method outperforms the state-of-the-art DPD (Barz and Gartner 2016) by 12.86% under the fixed-route setting and 17.22% under the routing flexibility setting, which indicates the advantage of the booking limit control policy in dealing with routing flexibility. In addition, the numerical results indicate that booking limit control gains more revenue improvement against bid-price-based control policies, especially when the random capacity has a large variance.

1.2 Literature Review

We next review three streams of related literature.

1.2.1 Stochastic Gradient-Based Algorithms.

(Projected) SGD and its numerous variants form one of the most important families of algorithms for solving classical stochastic optimization. For strongly convex and convex stochastic optimization (Nemirovski et al. 2009, Bottou et al. 2018), the complexity to achieve an -global optimality is and , respectively (For SGD, sample complexity equals gradient complexity). For nonconvex stochastic optimization, the gradient complexity to achieve an -stationary point is (Ghadimi and Lan 2013, Ghadimi et al. 2016). An extension of the stochastic gradient method is the stochastic primal-dual method (Agrawal and Devanur 2014, Li and Ye 2022). They are usually designed to handle functional constraints that do not admit easy projection.

1.2.2 Solving Nonconvex Optimization to Global Optimality.

For nonconvex optimization, there are several conditions that allow design efficient algorithms with global optimality guarantees, 1) hidden convexity, i.e., the problem admits a convex reformulation, 2) bisection methods for low-dimensional nonconvex problems, 3) Polyak-Łojasiewicz (PL) condition (Karimi et al. 2016), 4) structured nonconvex optimization (Sun 2021).

For hidden convex optimization problems, Chen and Shi (2023), Miao and Wang (2021) considered a pricing-based NRM problem with a nonconvex objective and nonconvex constraints that admits a convex reformulation. Due to the nonconvex constraint, their algorithm performs updates on the space of the convex reformulation. Chen and Shi (2023) achieved sample complexity in terms of the number of demands and Miao and Wang (2021) improved the complexity to via a sophisticated ellipsoid method with cutting planes. Differently, our problem has a convex box constraint, and thus, our algorithms operate in the original space. The proposed MSG method achieves sample complexity. Chen et al. (2022) considered a lost-sale inventory control problem with random supply in the limiting regime, which becomes a special case of problem (1) when the dimension . To achieve a global solution, they used a bisection method rather than leveraging the hidden convexity. Note that the complexity of the bisection method scales exponentially in , and thus, it is not suitable when is large.

Kunnumkal and Topaloglu (2008) studied finding an optimal base-stock policy in an inventory system with lost sales. They demonstrated the asymptotic stationary convergence of a stochastic approximation method and established the relationship between an approximate stationary point and an approximate global solution. The analysis of the RSG algorithm follows a similar idea, yet we characterize the non-asymptotic sample complexity.

Balseiro et al. (2023) designed a primal-dual method to solve a nonconvex online resource allocation problem to global optimality. They address the nonconvexity via the Shapley-Folkman Theorem (Starr 1969) that the primal-dual gap can be upper bounded by a constant that is independent of iterations. Han et al. (2020) designed an elimination method to achieve global solutions in nonconvex auctions. Yuan et al. (2021) combined SGD with bandit algorithm to search for optimal policy in the nonconvex inventory systems with fixed costs. The key to overcoming nonconvexity is that the objective is convex in while nonconvex in . Thus one could discretize the space and adapt a bandit algorithm to find approximate optimality for each .

Recently, various papers studied the Polyak-Łojasiewicz (PL) condition and other error bound conditions (Karimi et al. 2016). These conditions ensure that first-order stationary points are also globally optimal, and thus one could utilize first-order methods to find global optimality despite nonconvexity. The sample complexity of SGD to achieve an -global optimal solution is (Hu et al. 2021). Note that policy optimization with certain policy parameterization for reinforcement learning problems satisfies the PL condition (Bhandari and Russo 2019, Agarwal et al. 2020). However, one can easily verify that the PL condition does not hold for (1) when .

For more structured nonconvex optimization problems that admit efficient algorithms with global optimality guarantees, we refer interested readers to the website (Sun 2021). Although our problem belongs to the hidden convex problem class, the transformation function in our problem is unknown, and thus the methodology developed therein is generally not applicable.

1.2.3 Network Revenue Management.

One popular approach to network revenue management problems is booking limit control. It sets a threshold for each reservation class and accepts all requests until the threshold is met. Karaesmen and Van Ryzin (2004) solved a two-stage stochastic model via SGD to obtain an overbooking limit in the setting where the demand is assumed to be infinity (i.e., no truncation), and they demonstrate asymptotic convergence of the algorithm. Wang (2016) obtained integral booking limits from a one-period stochastic integer programming considering discrete random demands with the truncation and discrete random resource capacities. However, their focus is on the integral decision space and does not consider routing flexibility as we do in the paper. Wang et al. (2021) modeled the problem as two-stage stochastic programming under the special case when there is only one-dimensional deterministic capacity and one fixed route. In contrast, our models with the booking limit control for network revenue problems can incorporate the multi-dimensional random demand and capacity and allow flexibility in routing. Furthermore, the proposed algorithms are readily applicable and have non-asymptotic global convergence guarantees.

In addition to booking limit control, another pervasively applied approach uses bid price control, which can be derived from deterministic linear programming (DLP) (Talluri and Van Ryzin 1998). One can treat bid prices as prices for the resources, and the reservation is accepted if its revenue is higher than the sum of the bid prices of the required resources. More sophisticated time-dependent bid price control can be obtained from dynamic programming. Erdelyi and Topaloglu (2010) propose a DPD approach to jointly make overbooking and capacity allocation decisions in passenger revenue management, but they do not consider the random capacity. Compared with passenger revenue management, air-cargo network revenue management problems receive significantly less attention in the literature because of their complication, which prevents the direct application of existing techniques developed in the passenger NRM problems. Barz and Gartner (2016) consider an air-cargo network setting with both random capacities and routing flexibility. They develop a DPD approach to obtain the bid price policy, which depends on the time and the expected consumption of total accepted requests. However, they only deal with the routing flexibility in a heuristic way, while our approach considers optimal routing decisions after the realization of the random demand and capacity.

Organizations

The rest of the paper is organized as follows. In Section 2, we discuss the convex reformulation and the intuition behind RSG and MSG. In Section 3, we demonstrate the sample and gradient complexities for RSG and MSG. In Section 4, We discuss a number of operations management applications to illustrate the broad applicability of our algorithms.. We further formulate the NRM problem as a two-stage stochastic model, a special case of the studied stochastic nonconvex optimization. In Section 5, we present numerical experiments in various NRM settings.

Preliminaries

For an abuse of notation, let denote derivative, (sub)gradient, Clarke subdifferential, and Jacobian. For , and , let , , , where a subscript denotes the corresponding coordinate of a vector. We use to denote norm for vector and matrix. Note that the norm for a matrix is also known as the spectral norm, i.e., the largest singular value of a matrix. In addition, it holds that for any . Let denote projection from onto set . A function is -Lipschitz continuous on if it holds that for any . If the gradient of a function is Lipschitz continuous, we also call this function smooth. If a function satisfies for some constant , we say is -strongly convex if , is convex if , and is -weakly convex if . Note that any -smooth function is also -weakly convex by definition. We use to denote the set of subscript. We use to denote the transpose of the inverse of a matrix . We mainly focus on the complexity bounds in terms of the accuracy : we use to hide constants that do not depend on the desired accuracy and use to further hide the term.

2 Convex Reformulation and Algorithmic Design

In this section, we first formally state the convex reformulation of the optimization problem (1) and the corresponding conditions. Then, we discuss the intuition behind the algorithmic design of our proposed gradient-based methods. Recall the transformed problem:

| (3) |

where , , and with . Next, we list conditions for problem (3) to be an equivalent convex reformulation of problem (1). {assumption} We assume

-

(a).

Random vector is coordinate-wise independent.

-

(b).

Function is non-decreasing in for any given and any .

-

(c).

Function is stochastic linear in midpoint111Definition 1 in Feng and Shanthikumar (2018): A function for some convex is stochastically linear in midpoint if, for any , there exist and defined on a common probability space such that (i) and (ii) where denotes equal in distribution and denotes concave order. for any .

Feng and Shanthikumar (2018) showed that stochastic linearity in midpoint property holds for various functions used in supply chain management applications with dimension . Below we list four examples of function commonly used in operations management, including in our NRM applications.

-

(i)

, (ii) for , , ,

-

(iii)

, (iv) for some and .

Here is a non-negative random vector, and ; thus, is non-decreasing in . Example (i) appears in inventory problems with random yield. Example (ii) appears in a supply function in procurement from multiple suppliers (Dada et al. 2007). Example (iii) is the mostly studied random function. Example (iv) appears in the random supply from one producer with total production quantity to multiple firms (Tang and Kouvelis 2014). Firm orders quantity , and other firms order in total, which is unobserved to firm . So the proportional delivery quantity to firm is . We elaborate on more applications satisfying these functions in Section 4.1.

Proposition 2.1 (Feng and Shanthikumar 2018)

The proposition shows that for convex , the reformulated problem is a convex optimization problem under certain conditions. Feng and Shanthikumar (2018) demonstrated the proof of the proposition when dimension . Since the random vector is component-wise independent, the proof of the one-dimensional case can be extended to the high-dimensional setting, following Theorem 7.A.8 and Theorem 7.A.24 in Shaked and Shanthikumar (2007) for convex and component-wise convex , respectively. In addition, we make the following technical assumptions.

We assume

-

(a)

Domain has a finite radius , i.e., .

-

(b)

Function is convex, -Lipschitz continuous, and continuously differentiable.

-

(c)

Random function is -Lipschitz continuous in for any .

-

(d)

For any , random function is differentiable in almost surely.

Assumption 2(a), that domain is bounded, is widely seen in supply chain management and revenue management. Assumption 2(b) about convexity is necessary for the convex reformulation (3). For our NRM applications in Section 4, as we will show in Lemma 13.2, the function is convex if all accepted demands show up and is component-wise convex otherwise. The assumption that is -Lipschitz continuous and continuously differentiable is standard. One can easily verify that all four widely-used functions mentioned above satisfy Assumption 2(c)(d) under mild conditions, e.g., when and is a nonnegative random vector. Below we list a key assumption on the transformation function . Various combinations of and can guarantee it. {assumption} For the transformation function , we assume

-

(a)

Matrix is positive semi-definite for any and some constant .

-

(b)

Jacobian matrix is -Lipschitz continuous in , i.e., for any .

We show in Appendix 10.1 the general conditions to ensure Assumption 2. Further, Table 6 in Appendix 10.1 summarizes the conditions needed for all four functions and to ensure Assumption 2. For , , and , they satisfy Assumption 2 for a compact domain and any distribution that admits a nonnegative bounded support, which is common in operation management literature. For , we characterize the conditions on to ensure Assumption 2 in Lemma 4.1. In Section 4.3, we further characterize the performance of the proposed algorithm for when needed conditions on do not hold, with the analysis given in Appendix 10.4.

Next, we provide closed forms of the gradients of and . The proof is in Appendix 7.1.

2.1 Algorithmic Design of Global Converging Algorithms

In this subsection, we discuss the motivation for the global converging algorithm design.

2.1.1 Intuition of SAA+SG (Algorithm 3)

Since Proposition 2.1 provides an equivalent finite-dimensional convex reformulation (3) of the original nonconvex problem (1), intuitively, one may design gradient-based methods on to solve (3). A straightforward way is to perform projected stochastic gradient descent (PSGD) (Nemirovski et al. 2009) on the convex reformulation, i.e., where is an unbiased gradient estimator of and is drawn independently from .

However, since is unknown, the closed-forms of , , and remain unknown. It leads to two challenges: 1) it is hard to construct unbiased stochastic gradients of since we do not know ; 2) it is hard to perform projections onto . Thus the classical PSGD is not implementable on .

We can utilize SAA to estimate the unknown with the empirical distribution. Based on this idea, we design a SAA+SG algorithm. To the best of our knowledge, it is the first of its kind in the literature. Due to the page limit, we defer the detailed algorithmic construction, global convergence complexities, and related discussion in Appendix 11. Note that SAA+SG only requires Assumptions 2 and 2 to achieve a global convergence. Thus it requires fewer assumptions. However, SAA+SG requires access to a batch of samples in the beginning and requires computing the inverse of the estimated transformation function at each iteration, which can be costly.

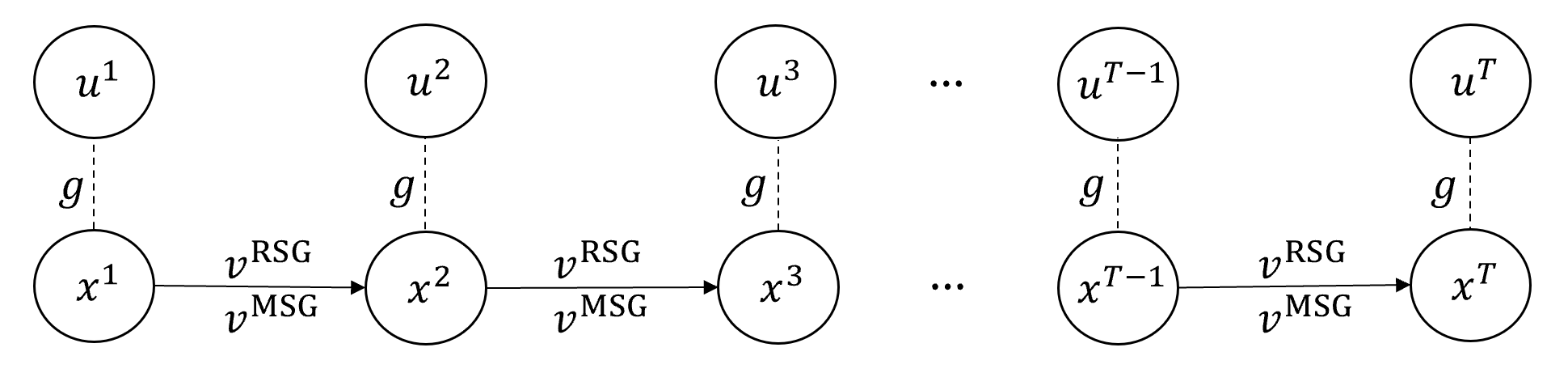

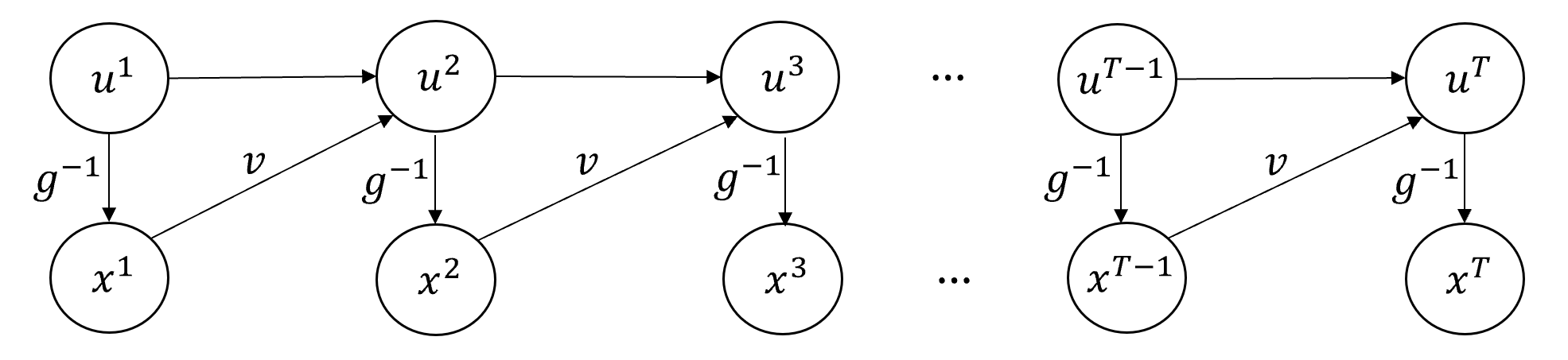

In the following subsections, we propose two algorithms, regularized stochastic gradient method (RSG) and mirror stochastic gradient method (MSG), to solve problem (1). A key property of RSG and MSG is that both algorithms operate only in the original space on , thus avoiding the indirect estimation of from . Figure 2 and Figure 3 in Appendix 11.1 illustrate the difference in the updating procedure in RSG and MSG compared to SAA+SG.

2.1.2 Intuition of RSG (Algorithm 1)

By Lemma 2.2, it holds for that Let and . By Proposition 2.1, we have . Utilizing the convexity of , we have

| (6) | ||||

where the first inequality uses convexity of , the second inequality uses the Cauchy-Schwarz inequality, the second equality holds by the relationship between and , and the third inequality uses the property of spectral norm. It implies that if is a stationary point of such that and is finite-valued, is also a global optimal solution.

To find an approximate stationary point of the original problem, we propose to solve problem (1) via regularized stochastic gradient method (RSG),

which is an unbiased gradient estimator of a regularized objective with a regularization parameter . Intuitively, any approximate stationary points of are approximate stationary points of for small . Next, we use an example with to illustrate why we add this regularization.

Example 2.3 (Example of RSG on )

When , an unbiased gradient estimator of is , where denotes a diagonal matrix with the -th diagonal entry being the indicator function . If for some , the -th coordinate of the gradient estimator is for any realization of . As a result, projected SGD may not perform any update on the -th coordinate and get stuck. RSG addresses this issue by adding a regularization. For such that for some , RSG would perform the update on the -th coordinate such that

| (7) |

Denote . (7) implies that RSG first shrinks the decision variable component-wisely to find a such that for any , and hence avoid convergence to any points in . According to (6), is exactly the set of local solutions that we intend to avoid. Hence, regularization ensures convergence to an approximate stationary point of such that is finite. For a small , such a is also an approximate stationary point of , and thus an approximate global optimal solution of by (6). In summary, RSG uses regularization to avoid vanishing gradient and ensure global convergence, while regularization in statistical learning literature is usually for avoiding overfit (Vapnik 1999).

2.1.3 Intuition of MSG (Algorithm 2)

As for MSG, the key step is to design a gradient estimator of such that each update on the original space mirrors the gradient update of the convex objective on the reformulated space . Denote the stepsize as .

Next, we illustrate how to build the gradient estimator . For ease of demonstration, consider the simplified setting when . The gradient descent update on for a point is Denote . If MSG mirrors the exact gradient descent update on using a gradient estimator , one should have Therefore, it holds that

| (8) | ||||

where we assume exists and use the first-order approximation in the second line. Notice that . As long as the stepsize is small, the approximation error is controlled by . It motivates us to design a stochastic estimator for . One can also interpret as a pre-conditioning matrix.

It remains to build efficient estimators of with small bias and small variance at a low sampling cost. To achieve that, we utilize the well-known equality for infinite series of matrices. Let be a symmetric random matrix, be its expectation and denote the identity matrix. Suppose that is invertible and . It holds that

where if and are i.i.d. samples. Utilizing a randomization scheme over , one can construct an estimator of . Particularly, for an integer , to estimate , we construct the following estimator: generate uniformly from , generate i.i.d. sample from , and form the following estimator

| (9) |

where is to ensure that . Although is a diagonal matrix in our problem, such estimators are used for more general matrix inverse estimation, e.g., estimating inverse Hessian matrix in bilevel optimization (Hong et al. 2020).

Lemma 2.4

Note that one could also use other distributions rather than the uniform distribution over . We defer related discussions and the proof to Appendix 7.2.

Based on the above discussion, we formally describe MSG in Algorithm 2. Line 2 and Line 3 in MSG are to build a stochastic gradient estimator of , where acts as a preconditioning matrix that rescale the gradient of the nonconvex objective . For , the -th diagonal entry of is , where is the cumulative distribution function of . Thus the preconditioning parameter enlarges all coordinates of . To analyze the convergence of MSG, we need to characterize the second moment of . To avoid potential dependence issues, we use two independent sets of samples of to estimate the first and the second terms in Line 2 of MSG. Also note that in MSG, we use the matrix inverse estimator (9) with for simplicity. In addition, we use an independent sample to build a gradient estimator of . The regularization term in line 3 of MSG is also used to avoid vanishing gradient issues in practice, as we did for RSG.

3 Global Convergence and Complexities Bounds

In this section, we demonstrate the global convergence and the sample and gradient complexities of RSG and MSG to achieve an -optimal solution. For ease of reference, we summarize the assumptions needed for SAA+SG, RSG, and MSG and their sample complexities bounds in Table 5 in Appendix 10. The table also includes the global convergence of MSG for NRM applications when satisfies a discrete distribution. Note that the intuition of RSG and MSG discussed in Section 2 builds upon the unconstrained setting. When extended to a constrained setting, the following lemma is the key property that we use to address the hardness brought in by projection. We defer the proof to Appendix 7.3.

Lemma 3.1

Suppose that is a box constraint and Assumption 2(a)(b) holds. For any , we have

Lemma 3.1 says that one could exchange the projection operator and the transformation operator when both and are box constraints and is a component-wise non-decreasing function. In the proof of RSG, Lemma 3.1 plays a key role in establishing an upper bound of the gradient mapping of using the gradient mapping of (see (21)). In the proof of MSG, Lemma 3.1 enables us to conduct the analysis in a way similar to the unconstrained case. The following theorem establishes the global convergence of RSG. The proof is in Appendix 8.

Theorem 3.2

In the above theorem, the term comes from a stationary convergence of RSG, where the constant is explicitly given in the analysis, the term comes from adding the regularization, and the remaining terms come from building a relationship between stationary convergence and global convergence utilizing convexity of the reformulated problem. Theorem 3.2 implies that setting , and for any , we have . Since RSG uses one sample and computes one gradient of at each iteration, for to be an -optimal solution of , the sample and gradient complexities of RSG are both in terms of the dependence on the accuracy . We point out that the complexity of RSG has a dependence on the radius, which, in the worst case, is equivalent to a quadratic dependence on the dimension since is a box constraint. We will show later that such dependence does not have a significant impact on numerical experiments.

In terms of analysis, we first build up the stationary convergence of projected SGD on constrained smooth optimization measured by the norm of the gradient mapping (Davis and Drusvyatskiy 2018, Drusvyatskiy and Paquette 2019) and then establish a relationship between the stationary convergence and the global convergence.

The following theorem demonstrates the global convergence of MSG. We defer the proof to Appendix 9. Unlike RSG, the analysis of MSG does not require to be Lipschitz continuous as it directly demonstrates global convergence.

Theorem 3.3

In the right-hand-side of (10), the first term coming from a telescoping sum appears in SGD analysis (Nemirovski et al. 2009), the second terms comes from the variance of the estimator and the approximation error of MSG to the virtual SGD update on , the third term comes tje from regularization, and the fourth term comes from the bias of estimating matrix inverse .

Setting , , , and , we have . Since MSG uses at most number of samples per-iteration, the sample and gradient complexities of MSG are both . In terms of the dependence on the accuracy , the theorem implies that the nonconvex problem (1) under Assumption 2 and Assumption 2 is fundamentally no harder than the classical stochastic convex optimization. Note that the iteration complexity also depends on the radius of the domain , i.e., . Since is a box constraint, in the worst case, scales linearly in dimension , which is still better than that of RSG. We are unaware of any method that could get rid of the dimension dependence, and we leave it for future investigation.

Next, we discuss the efficiency of MSG via showing a lower bound for problem (1). For this purpose, note that Agarwal et al. (2009) developed an lower bounds on the gradient complexity of any black-box stochastic first-order algorithms for obtaining an -optimal solution of , where is convex and Lipschitz continuous. Interestingly, the hard instance that they used to construct the lower bound happens to be a special case of problem (1) when , and . It is easy to verify that Assumptions 2 and 2(c-f) hold for . Though the hard instance in Agarwal et al. (2009) is constructed by , Agarwal et al. (2009) considered lower bounds for black-box stochastic first-order algorithms, i.e., algorithms that uses a gradient estimator of that can be of any form as long as it is unbiased and has bounded variance but does not have to be . This is different from MSG, which additionally uses to build up a preconditioning matrix and thus is not a black-box algorithm. Though the results of Agarwal et al. (2009) is not directly applicable to MSG, we could use their analysis to establish a lower bound on the gradient complexity of any black-box stochastic first-order algorithms for solving problem (1). In addition, such lower bounds imply that the sample and gradient complexities of MSG match the best possible black-box stochastic gradient methods for solving (1) in terms of accuracy if ignoring the logarithmic term.

4 Applications

In this section, we first discuss the board applicability of the studied stochastic nonconvex optimization in operations management. Then, we model the air-cargo NRM problem with random demand, two-dimensional capacity, consumption, and routing flexibility under booking limit control as a special case of Problem (1). We further show the global convergence of MSG on the NRM problem. Interested readers please refer to Appendix 13 for the modeling of passenger NRM and to refer (Feng et al. 2015, Klein et al. 2020) for a comprehensive review of air-cargo NRM. Our booking limit control also adapts to two interesting extensions of managing uncertain capacity introduced in Previgliano and Vulcano (2021), see Appendix 14.1.

4.1 Operations Management Applications

Several operations management applications are special cases of the studied problem (1). Dynamic multisourcing problems with random capacities (Chen et al. 2018, Feng et al. 2019), assemble-to-rrder system with a random capacity (Chen et al. 2018, Feng et al. 2019) and lost-sale inventory problems with random supply (Chen et al. 2022) are special cases of problem (1) with . Newsvendor with procurement from multiple suppliers (Dada et al. 2007) is a special cases of problem (1) with and random supply from one producer to multiple firms (Tang and Kouvelis 2014) is a special case of problem (1) with . Interested readers may refer to other applications in Feng and Shanthikumar (2018, 2022). We also give an example of assemble-to-order systems in Appendix 12.

4.2 Modeling for Air-cargo Network Revenue Management

From a temporal perspective, the air-cargo NRM problem consists of reservation stage and service stage. During the reservation stage, we have to decide whether to accept reservation requests. Then at the service stage, we aim to minimize the penalty of rejecting show-ups by accommodating show-ups within the limited random capacity and potential routing options. Thus, there are four significant factors in air-cargo NRM problems, two-dimensional capacity (weight and volume), random capacity, random consumption, and routing flexibility (i.e., demand class with specified origin-destination pair can be shipped via any feasible route in the airline network). In this paper, we consider these four factors all at once. Barz and Gartner (2016) considered the same setting and proposed a DPD method. However, their DPD method only heuristically addressed the routing decision while we explicitly model the routing decisions as decision variables. In what follows, we formulate the problem using booking limit control as a two-stage stochastic optimization problem.

At the start of the reservation stage, we decide the booking limits, denoted by decision vector , for demand classes. Under booking limit control, we accept new requests for a demand class unless the booking limit is reached. We assume that the aggregated demand during the whole reservation stage, denoted by vector , is random and component-wise independent. Note that each request comes with a random weight and a random volume that are independent of and , and will reveal at the service stage. In total, we accept up to reservations during the reservation stage. At the end of the reservation stage, cancellations and no-shows are realized.

We use the random vector to represent the number of show-ups for the service. Thus, the number of show-ups can be written as a function of the booking limit and random demand, i.e., . We assume that follows a Poisson distribution with a coefficient and that is component-wise independent. Without loss of generality, we assume that the no-shows or cancellations are not refundable. Note that all-show-up setting is a special case with and . We focus on Poisson show-ups rather than the more practical binomial show-ups because Poisson is well suited to the continuous optimization framework, and the same justification can be found in Karaesmen and Van Ryzin (2004). Moreover, we consider the continuous booking limit , which allows fractional acceptance throughout the paper for the same reason. We also want to highlight that our algorithms can be heuristically adapted to the discrete booking limit and binomial show-up setting with more detailed discussions in Appendix 13.

At the service stage, there are inventory classes associated with a two-dimensional random capacity, where the first dimension is weight capacity and the second dimension is volume capacity . Each accepted demand from class has random weight and volume . We assume that both random weight and volume are realized at the beginning of the service stage and are independent of the booking limit and the aggregated demand . The revenue gained by accepting one unit reservation is a function of random weight and volume, denoted by . In the air-cargo industry, a common practice is to charge for demand class , with some constants (Barz and Gartner 2016). With the similar structure, we define as the penalty of rejecting one unit reservation. We assume each demand class can be satisfied by different routes and define the binary parameter to represent whether the inventory class is required to satisfy the demand from the route of demand class . During the service stage, the first decision is the amount of served show-ups under limited capacities, and the second decision is the routing decision, where we use variable to denote the amount of demand allocated to route of demand class . Let denote the penalty of rejecting accepted demand during the service stage. Then the air-cargo NRM problem under booking limit control has the following mathematical formulation:

| (11) |

where and

| s.t. | |||

In the above model, the first and the second constraints represent the weight and volume capacities constraints for all inventory classes . The third constraint indicates that the total accepted demand of class is allocated over different routes. From a modeling perspective, to the best of our knowledge, we are the first to explicitly model the optimal routing decisions under the booking limit control. In comparison, the DPD method proposed in Barz and Gartner (2016) only heuristically splits the reservations of class with the same origin-destination equally into fixed sub-classes.

4.3 Theoretical Results for NRM Applications

In this subsection, we discuss the global convergence of the proposed algorithms in NRM applications and discuss what happens if there lacks Assumption 2. The next lemma specifies the conditions needed for to ensure the assumptions needed for global convergence. We defer the proof to Appendix 10.2. We also specify conditions needed for the other three functions to ensure Assumption 2 in Appendix 10.1. A summary of the conditions is in Table 6.

Lemma 4.1

For with component-wise independent random vector , if the CDF of , , is -Lipschitz continuous and for any , then all needed assumptions on and to ensure global convergence of RSG and MSG hold.

Note that the convexity of the objective function and the gradient calculation follow a similar derivation in Karaesmen and Van Ryzin (2004) and are reproduced in Appendix 13 for completeness. Specifically, in the all-show-up case (there does not exist cancellations and no-shows) in NRM problems, the function in (11) is concave as NRM is a maximization problem. On the other hand, obtaining the gradient of requires solving a linear program (LP). Under the condition specified in in Lemma 4.1, Theorems 3.2 and 3.3 imply that for solving air-cargo NRM (11) under the all-show-up case, MSG requires solving number of LPs while RSG needs to solve number of LPs to achieve an -optimal solution.

In what follows, we discuss the convergence of MSG when Assumption 2(b), the smoothness of the transformation function , is missing. To ensure Assumption 2 (b) holds, it requires Lipschitz continuous CDF assumption on , meaning that is a continuous random vector. However, in NRM applications, the distribution of can be discrete, like Possion or multinomial. The next theorem shows the approximate global convergence rate of MSG without assuming is continuous. We defer the analysis to Appendix 10.4

Theorem 4.2

Suppose that Assumptions 2, 2 and 2(a) hold. For MSG with stepsizes , and regularization parameter , for a discrete distribution with a support over , the expected error of MSG is upper bounded by

| (12) |

When is a Poisson random vector with an arrival rate vector or a multinomial distributed random vector with number of trails, the expected error bound becomes

| (13) |

When is large, the approximation in (13) comes from Stirling’s formula and the property of Poisson and multinomial distributions. The theorem implies that the global convergence of MSG still holds even without the smoothness of . The reason is that both Poisson and multinomial distributions can be well approximated by continuous normal distribution when is large.

In Appendix 10.4, we further show that the performance of both RSG and MSG are also not influenced even if Assumption 2(a) is lacking. The reason follows a similar discussion in Example 2.3 that adding regularization can address the issue. Our numerical experiments also support such an observation that regularization is crucial to escape local solutions.

5 Computational Experiments and Results

For network revenue management problems, we conduct extensive numerical experiments implemented in Python using the Gurobi linear programming solver. The implementation details and revenue evaluation of the proposed RSG (Algorithm 1), MSG (Algorithm 2), and SAA+SG (Algorithm 3 in Appendix 11) and other benchmark strategies including DLP, DPDs (Erdelyi and Topaloglu 2010, Barz and Gartner 2016), and VCBP (Previgliano and Vulcano 2021), can be found in Appendix 14.1. Discussions on assumptions in numerical studies are in Appendix 14.2. Numerical convergence comparison of RSG, MSG, and SAA+SG on a specific instance is in Appendix 14.3.

5.1 Passenger Network Revenue Management with the Random Capacity

Experimental Setup. We use test examples from Erdelyi and Topaloglu (2010). Among these examples, the reservation stage is divided into discrete periods with specified arrival probability for each demand class at each period. We label these test instances by tuple with definitions given as follows. (1) : the network contains one hub and spokes (see Figure 1(a)); (2) : airline offers a high and a low fare itinerary in each origin-destination pair, where the high fare is times the price associated with low fare class. Thus, the number of inventory classes (flight legs) is , and the number of demand classes (itineraries) is ; (3) : penalty of rejecting one unit show-up from demand class is with ; (4) : show-up probability is given by , which follows binomial distribution and is the same for all demand classes; (5) : load factor is defined as total expected demand divided by total capacity; (6) : the random capacity follows the truncated Gaussian distribution with range and two different levels of coefficient of variation . In total, there are 96 different test instances.

Comparison to Other Control Policies. In the following, we compare proposed methods to other control policies in the existing literature in two aspects: expected revenue and computation time. We consider an alternative setting under binomial random show-ups as mentioned in the experimental setup. Thus the function is only component-wise convex rather than convex as required in our theory. We still apply our algorithms and report the results.

| Benchmark Strategies | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 4 | 8 | 4 | 8 | (4,0) | (8,0) | (1,1) | 0.9 | 0.95 | 1.2 | 1.6 | 0.1 | 0.5 | |

| MSG v.s. DLP | 23.9% | 63.2% | 43.8% | 43.3% | 9.1% | 57.3% | 64.2% | 42.3% | 44.7% | 65.0% | 22.1% | 10.4% | 76.7% |

| MSG v.s. DPD | 3.0% | 13.7% | 11.0% | 5.6% | 3.0% | 14.9% | 7.1% | 8.1% | 8.6% | 10.5% | 6.1% | 0.7% | 16.0% |

| MSG v.s. VCBP | 4.4% | 5.3% | 5.7% | 3.9% | 4.4% | 6.9% | 3.2% | 6.0% | 3.6% | 4.0% | 5.6% | 4.0% | 5.7% |

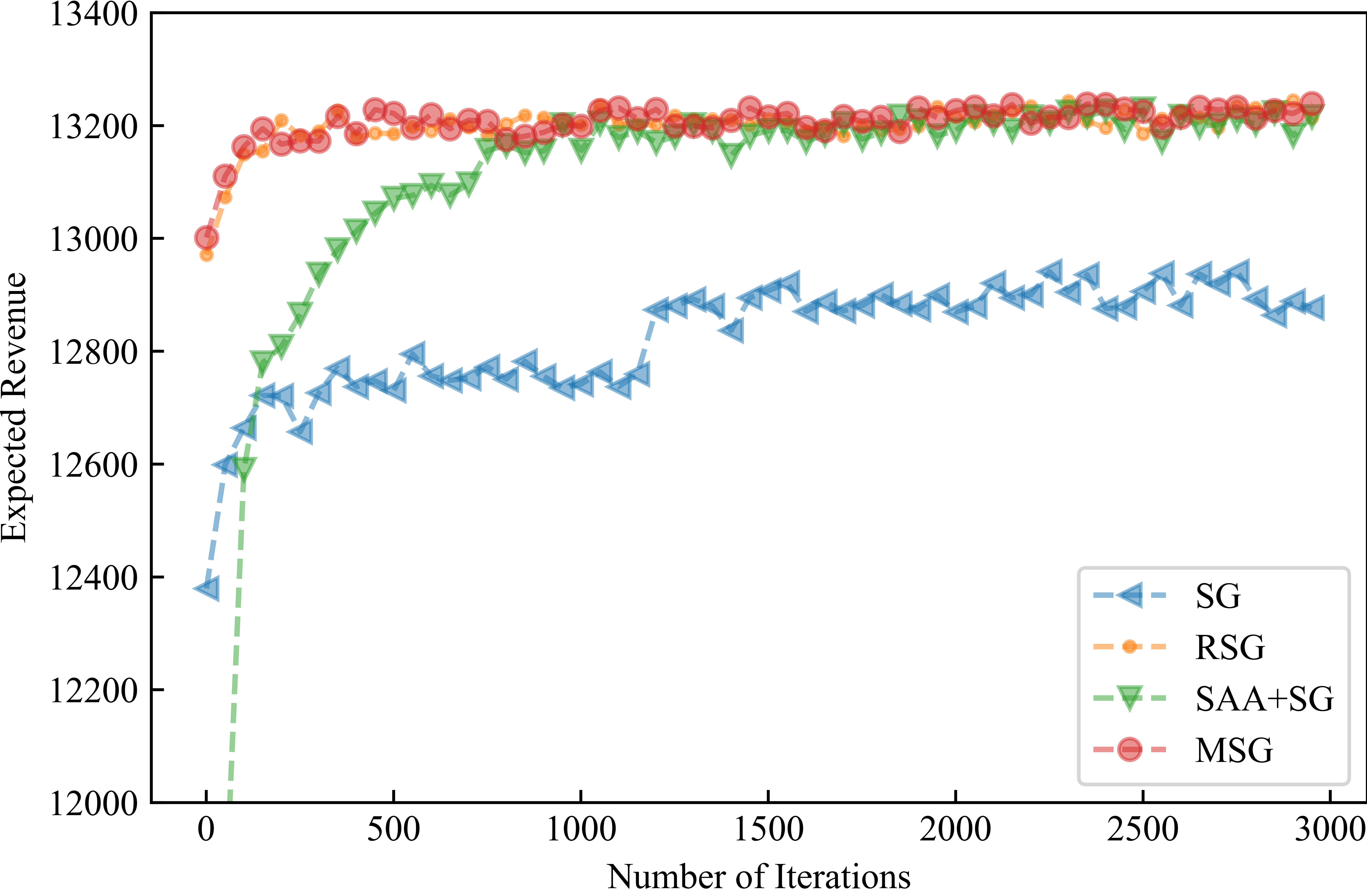

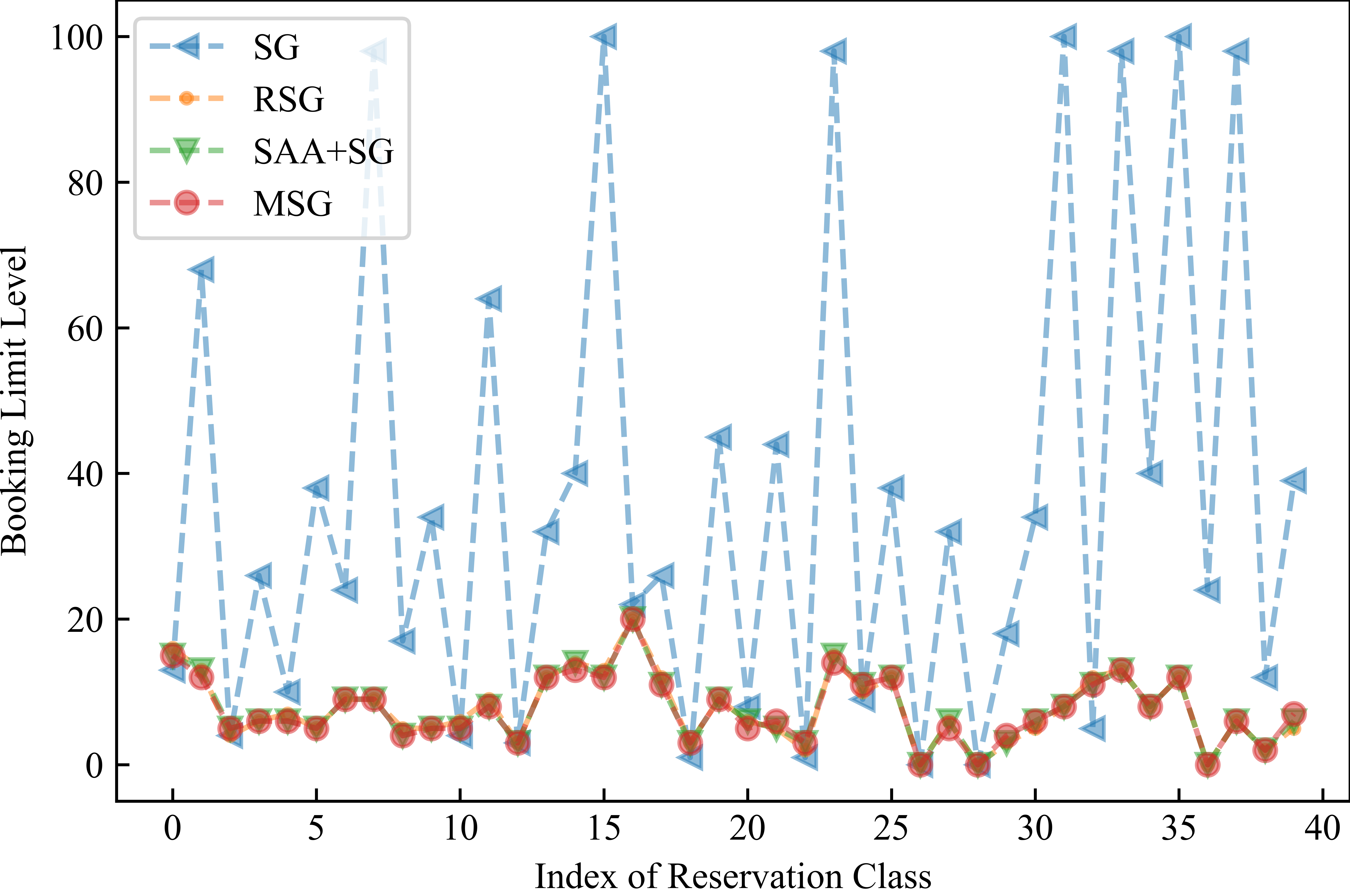

For the comparison in expected revenue, Table 7 in Appendix 14.4 documents the complete numerical results for all passenger NRM instances. In summary, there is no significant difference in the expected revenue between RSG, MSG, and SAA+SG. Thus, we only compare MSG to other control policies in the following. Averaging over all instances, MSG gains higher revenue than DLP, DPD, and VCBP by 43.6%, 8.3%, and 4.8%, respectively. It is not surprising that DLP performs worst among all control policies since it does not account for the variance in demands, show-ups, and capacities. There are some interesting observations when we fix one factor and average over all instances with the fixed factor. For instance, we evaluate the influence of the capacity variance factor by averaging over 48 instances with and the other 48 instances with . Table 2 summarizes such results. We find that DLP and DPD perform significantly worse in high capacity variance case than the low variance case , while our booking limit control and VCBP can deal with the random capacity setting much better. Previgliano and Vulcano (2021) report a similar result that VCBP performs better than DPD in high capacity variance cases. We point out that the implemented DPD (Erdelyi and Topaloglu 2010) method is designed for random show-ups with deterministic capacity. Although we extend their DPD method to incorporate the random capacity using the sample average to approximate the boundary value function, we admit there might exist other DPD methods specifically designed for the random capacity. For completeness, we compare our booking limit control to DPD under exactly the same 48 deterministic capacity instances (Table 1 and Table 2 in Erdelyi and Topaloglu (2010)) and report that DPD performs better than booking limit control by 1.22%. However, there is no significant revenue gap after we resolve our booking limit model 10 times. The test examples in two columns and in Table 2 have the increasing penalty of rejecting customers. The performance gap increases from the low penalty to the high penalty setting, indicating our booking limit control makes a better trade-off between the high-fare and low-fare classes.

| Benchmark Strategies | RSG | MSG | SAA+SG | VCBP | DPD | |

|---|---|---|---|---|---|---|

| Number of Spokes | 4 | 12 | 8 | 16 | 45 | 57 |

| 8 | 44 | 32 | 57 | 94 | 85 | |

The comparison in computation time is summarized in Table 3. Since the number of spokes is the key parameter that affects the computation time, we report average CPU seconds averaged over all or instances. The stopping criteria of VCBP, RSG, MSG, and SAA+SG are specified in Appendix 14.1. With different spokes , we get different test instances with demand classes and inventory classes. Next, we discuss the per-iteration computational costs. VCBP solves one LP with decision variables and constraints at each iteration and uses the backward path to get gradients with the computation cost of , where is the number of total arrivals. Our proposed algorithms solve the same size LP with decision variables and constraints at each iteration, and the computation cost of remaining arithmetic operations is mild compared to the LP solving. DPD solves single-leg dynamic programming, and the computation cost is bounded by . Our results in Table 3 show that MSG has the lowest computation cost at both and . However, the computation cost of the DPD method scales better with respect to . It is worth mentioning that the scalability with respect to of VCBP is the same as our algorithms as they all solve one LP of the same size at each iteration. In addition, although we only focus on fixed in our computation experiments and do not compare the scalability in , the computation cost of our proposed algorithms for booking limits is independent of since we aggregate the reservation periods into a single stage.

5.2 Air-cargo Network Revenue Management

Without Routing Flexibility Experimental Setup. Since we do not have access to all the test instances for air-cargo NRM in Barz and Gartner (2016), we construct similar instances based on parameters listed in Appendix 14.5, including the demand class label, average weight, average volume, the origin, the destination, and the per-unit-revenue. Note that the per-unit-revenue is the parameter in revenue introduced in Section 4.2.

We adopt a similar setup as Barz and Gartner (2016) and set parameters as follows: ; the penalty is 2.4 times of revenue, e.g., ; the coefficient of correlation between weight and volume consumption and the coefficient of correlation between the weight and volume capacity are both ; the planning horizon is , which is consistent with the previous passenger network revenue case; we neither consider the no-show nor cancellation, which can be easily incorporated, to be consistent with the air-cargo DPD (Barz and Gartner 2016) (ACDPD); all demand classes arrive with equal probability over the reservation stage; we consider two different levels of the coefficient of variation in the random consumption , two levels of the coefficient of variation in the random capacity , and two scenarios of the average load factor levels (i.e., [demand]/[capacity] with the fixed expected demand and varying expected capacity). The network structure is spoke-hub given in Figure 1 (a). Since this network only contains one feasible route for any given origin-destination pair, there is no routing flexibility.

As shown in Table 4 under “Without Routing Flexibility” columns, the booking limit control policy computed by MSG outperforms ACDPD by an average 12.86% among all test instances. We observe a similar trend as in passenger network instances (see the column in Table 2) that MSG outperforms ACDPD at a more significant level when the capacity and demand have higher variances, indicating that our MSG method accounts for randomness more effectively.

| Settings | Without Routing Flexibility | With Routing Flexibility | ||||||

|---|---|---|---|---|---|---|---|---|

| [D]/[C] | ACDPD | MSG | MSG v.s. ACDPD | ACDPD | MSG | MSG v.s. ACDPD | ||

| 0.1 | 0.1 | 1.0 | 10,028 | 10,115 | 9,284 | 9,328 | ||

| 2.0 | 5,828 | 6,193 | 6.3% | 5,126 | 5,684 | 10.9% | ||

| 0.4 | 1.0 | 5,975 | 6,989 | 17.0% | 5,197 | 6,262 | 20.5% | |

| 2.0 | 3,758 | 4,213 | 12.1% | 3,282 | 4,193 | 27.8% | ||

| 0.4 | 0.1 | 1.0 | 8,988 | 10,013 | 11.4% | 8,275 | 8,868 | 7.2% |

| 2.0 | 5,172 | 6,034 | 16.7% | 4,487 | 5,496 | 22.5% | ||

| 0.4 | 1.0 | 5,944 | 7,089 | 19.3% | 5,179 | 6,239 | 20.5% | |

| 2.0 | 3,506 | 4,216 | 20.2% | 3,172 | 4,076 | 28.5% | ||

-

•

Notes: Columns “ACDPD” and “MSG” are expected revenue. “MSG v.s. ACDPD” is a relative revenue increase at 95% confidence level. denotes there is no statistically significant difference between MSG and ACDPD at 95% confidence level.

With Routing Flexibility Experimental Setup. Figure 1 (b) demonstrates a network structure with routing flexibility. Compared to Figure 1 (a), there is an additional leg (link 9) from node 1 to node 3 on top of the spoke-hub network. With the additional link 9, the request from origin 1 to destination 3 can be served with two route options: 1) Route 1: leg 9; 2) Route 2: leg 1 from node 1 to node 5, then leg 7 from node 5 to node 3. We set the average capacity level (hence the total capacity level) the same way in the without-routing case by scaling the capacity levels of leg 1 to leg 8 by 8/9, and adding extra capacity to leg 9.

As shown in Table 4 under “With Routing Flexibility” columns, booking limit control outperforms ACDPD by an average 17.22% among all test instances. An important observation is that booking limit control outperforms ACDPD even more with routing flexibility compared to fixed routes setting. It is not surprising because ACDPD only heuristically deals with the routing decisions by splitting reservations of class with the same origin and destination equally into fixed classes with different routes. For example, the requests from origin 1 to destination 3 are equally divided into two routes during the reservation stage. In addition, we still observe a similar trend that higher variance leads to a larger performance gap between MSG and ACDPD.

6 Conclusion and Future Directions

In this paper, we propose three gradient-based methods for solving a family of stochastic nonconvex optimization (1) to global optimality with non-asymptotic guarantees, in which the complexity of MSG matches the lower bounds. We model air-cargo NRM under booking limit control policy as two-stage stochastic optimization models and as special cases of the proposed model (1) and illustrate the superior performance of proposed algorithms theoretically and numerically.

Much remains open and requires further investigation. 1. When is a positively dependent random vector (Chen and Gao 2019), the convex reformulation (3) does not hold and there exists an infinitely-dimensional stochastic convex reformulation. There is a lack of efficient algorithms for solving such an infinite-dimensional problem despite some statistical results about the asymptotic performance of SAA (Deng et al. 2022) and (Singham and Lam 2020). 2. In this paper, our algorithms adjust the booking limit by leveraging the aggregated demand collected after each reservation period. It remains interesting to design an online booking limit control policy that adjusts the booking limit right after accepting or rejecting a demand request.

This research is partly supported by National Science Foundation Grants CMMI-1761699, CRII-1755829, and ZJU-UIUC Institute Research Program.

References

- Agarwal et al. (2020) Agarwal A, Kakade SM, Lee JD, Mahajan G (2020) Optimality and approximation with policy gradient methods in markov decision processes. Conference on Learning Theory, 64–66 (PMLR).

- Agarwal et al. (2009) Agarwal A, Wainwright MJ, Bartlett PL, Ravikumar PK (2009) Information-theoretic lower bounds on the oracle complexity of convex optimization. Advances in Neural Information Processing Systems, 1–9.

- Agrawal and Devanur (2014) Agrawal S, Devanur NR (2014) Fast algorithms for online stochastic convex programming. Proceedings of the twenty-sixth annual ACM-SIAM symposium on Discrete algorithms, 1405–1424 (SIAM).

- Balseiro et al. (2023) Balseiro SR, Lu H, Mirrokni V (2023) The best of many worlds: Dual mirror descent for online allocation problems. Operations Research 71(1):101–119.

- Barz and Gartner (2016) Barz C, Gartner D (2016) Air cargo network revenue management. Transportation Science 50(4):1206–1222.

- Bertsekas (2009) Bertsekas D (2009) Convex optimization theory, volume 1 (Athena Scientific).

- Bhandari and Russo (2019) Bhandari J, Russo D (2019) Global optimality guarantees for policy gradient methods. arXiv preprint arXiv:1906.01786 .

- Bottou et al. (2018) Bottou L, Curtis FE, Nocedal J (2018) Optimization methods for large-scale machine learning. Siam Review 60(2):223–311.

- Brumelle and McGill (1993) Brumelle SL, McGill JI (1993) Airline seat allocation with multiple nested fare classes. Operations Research 41(1):127–137.

- Chen et al. (2022) Chen B, Jiang J, Zhang J, Zhou Z (2022) Learning to order for inventory systems with lost sales and uncertain supplies. arXiv preprint arXiv:2207.04550 .

- Chen and Gao (2019) Chen X, Gao X (2019) Stochastic optimization with decisions truncated by positively dependent random variables. Operations Research 67(5):1321–1327.

- Chen et al. (2015) Chen X, Gao X, Hu Z (2015) A new approach to two-location joint inventory and transshipment control via l♮-convexity. Operations Research Letters 43(1):65–68.

- Chen et al. (2018) Chen X, Gao X, Pang Z (2018) Preservation of structural properties in optimization with decisions truncated by random variables and its applications. Operations Research 66(2):340–357.

- Chen and Shi (2023) Chen Y, Shi C (2023) Network revenue management with online inverse batch gradient descent method. Production and Operations Management .

- Ciarallo et al. (1994) Ciarallo FW, Akella R, Morton TE (1994) A periodic review, production planning model with uncertain capacity and uncertain demand—optimality of extended myopic policies. Management Science 40(3):320–332.

- Dada et al. (2007) Dada M, Petruzzi NC, Schwarz LB (2007) A newsvendor’s procurement problem when suppliers are unreliable. Manufacturing & Service Operations Management 9(1):9–32.

- Davis and Drusvyatskiy (2018) Davis D, Drusvyatskiy D (2018) Stochastic subgradient method converges at the rate on weakly convex functions. arXiv preprint arXiv:1802.02988 .

- Deng et al. (2022) Deng C, Xiong Y, Yang L, Yang Y (2022) A smoothing saa method for solving a nonconvex multisource supply chain stochastic optimization model. Mathematical Problems in Engineering 2022.

- Drusvyatskiy and Paquette (2019) Drusvyatskiy D, Paquette C (2019) Efficiency of minimizing compositions of convex functions and smooth maps. Mathematical Programming 178(1):503–558.

- Erdelyi and Topaloglu (2009) Erdelyi A, Topaloglu H (2009) Separable approximations for joint capacity control and overbooking decisions in network revenue management. Journal of Revenue and Pricing Management 8(1):3–20.

- Erdelyi and Topaloglu (2010) Erdelyi A, Topaloglu H (2010) A dynamic programming decomposition method for making overbooking decisions over an airline network. INFORMS Journal on Computing 22(3):443–456.

- Feng et al. (2015) Feng B, Li Y, Shen ZJM (2015) Air cargo operations: Literature review and comparison with practices. Transportation Research Part C: Emerging Technologies 56:263–280.

- Feng et al. (2019) Feng Q, Jia J, Shanthikumar JG (2019) Dynamic multisourcing with dependent supplies. Management Science 65(6):2770–2786.

- Feng and Shanthikumar (2018) Feng Q, Shanthikumar JG (2018) Supply and demand functions in inventory models. Operations Research 66(1):77–91.

- Feng and Shanthikumar (2022) Feng Q, Shanthikumar JG (2022) Applications of stochastic orders and stochastic functions in inventory and pricing problems. Production and Operations Management 31(4):1433–1453.

- Ghadimi and Lan (2013) Ghadimi S, Lan G (2013) Stochastic first-and zeroth-order methods for nonconvex stochastic programming. SIAM Journal on Optimization 23(4):2341–2368.

- Ghadimi et al. (2016) Ghadimi S, Lan G, Zhang H (2016) Mini-batch stochastic approximation methods for nonconvex stochastic composite optimization. Mathematical Programming 155(1):267–305.

- Han et al. (2020) Han Y, Zhou Z, Weissman T (2020) Optimal no-regret learning in repeated first-price auctions. arXiv preprint arXiv:2003.09795 .

- Hong et al. (2020) Hong M, Wai HT, Wang Z, Yang Z (2020) A two-timescale framework for bilevel optimization: Complexity analysis and application to actor-critic. arXiv preprint arXiv:2007.05170 .

- Hu et al. (2020a) Hu Y, Chen X, He N (2020a) Sample complexity of sample average approximation for conditional stochastic optimization. SIAM Journal on Optimization 30(3):2103–2133.

- Hu et al. (2021) Hu Y, Chen X, He N (2021) On the bias-variance-cost tradeoff of stochastic optimization. Advances in Neural Information Processing Systems 34.

- Hu et al. (2020b) Hu Y, Zhang S, Chen X, He N (2020b) Biased stochastic first-order methods for conditional stochastic optimization and applications in meta learning. Advances in Neural Information Processing Systems 33:2759–2770.

- Karaesmen and Van Ryzin (2004) Karaesmen I, Van Ryzin G (2004) Overbooking with substitutable inventory classes. Operations Research 52(1):83–104.

- Karimi et al. (2016) Karimi H, Nutini J, Schmidt M (2016) Linear convergence of gradient and proximal-gradient methods under the polyak-łojasiewicz condition. Joint European Conference on Machine Learning and Knowledge Discovery in Databases, 795–811 (Springer).

- Klein et al. (2020) Klein R, Koch S, Steinhardt C, Strauss AK (2020) A review of revenue management: Recent generalizations and advances in industry applications. European Journal of Operational Research 284(2):397–412.

- Kleywegt et al. (2002) Kleywegt AJ, Shapiro A, Homem-de Mello T (2002) The sample average approximation method for stochastic discrete optimization. SIAM Journal on Optimization 12(2):479–502.

- Kunnumkal and Topaloglu (2008) Kunnumkal S, Topaloglu H (2008) Using stochastic approximation methods to compute optimal base-stock levels in inventory control problems. Operations Research 56(3):646–664.

- Li and Pang (2017) Li D, Pang Z (2017) Dynamic booking control for car rental revenue management: A decomposition approach. European Journal of Operational Research 256(3):850–867.

- Li and Ye (2022) Li X, Ye Y (2022) Online linear programming: Dual convergence, new algorithms, and regret bounds. Operations Research 70(5):2948–2966.

- Miao and Wang (2021) Miao S, Wang Y (2021) Network revenue management with nonparametric demand learning: -regret and polynomial dimension dependency. Available at SSRN 3948140 .

- Nemirovski et al. (2009) Nemirovski A, Juditsky A, Lan G, Shapiro A (2009) Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization 19(4):1574–1609.

- Previgliano and Vulcano (2021) Previgliano F, Vulcano G (2021) Managing uncertain capacities for network revenue optimization. Manufacturing & Service Operations Management .

- Shaked and Shanthikumar (2007) Shaked M, Shanthikumar JG (2007) Stochastic orders (Springer Science & Business Media).

- Singham and Lam (2020) Singham DI, Lam H (2020) Sample average approximation for functional decisions under shape constraints. 2020 Winter Simulation Conference (WSC), 2791–2799 (IEEE).

- Starr (1969) Starr RM (1969) Quasi-equilibria in markets with non-convex preferences. Econometrica: journal of the Econometric Society 25–38.

- Sun (2021) Sun J (2021) Provable nonconvex methods/algorithms URL https://sunju.org/research/nonconvex/.

- Talluri and Van Ryzin (1998) Talluri K, Van Ryzin G (1998) An analysis of bid-price controls for network revenue management. Management Science 44(11-part-1):1577–1593.

- Tang and Kouvelis (2014) Tang SY, Kouvelis P (2014) Pay-back-revenue-sharing contract in coordinating supply chains with random yield. Production and Operations Management 23(12):2089–2102.

- Vapnik (1999) Vapnik V (1999) The nature of statistical learning theory (Springer science & business media).

- Wang et al. (2021) Wang T, Meng Q, Wang S, Qu X (2021) A two-stage stochastic nonlinear integer-programming model for slot allocation of a liner container shipping service. Transportation Research Part B: Methodological 150:143–160.

- Wang (2016) Wang X (2016) Optimal allocation of limited and random network resources to discrete stochastic demands for standardized cargo transportation networks. Transportation Research Part B: Methodological 91:310–331.

- Yuan et al. (2021) Yuan H, Luo Q, Shi C (2021) Marrying stochastic gradient descent with bandits: Learning algorithms for inventory systems with fixed costs. Management Science 67(10):6089–6115.

Online Appendices

Organization of Appendices

The appendices are organized as follows. In Appendix 7, we show the technical details on the proof of Lemmas 2.2, 2.4, 3.1, 4.1, the second moment of the gradient estimators in MSG, and the auxiliary results related to stationary convergence of RSG. In Appendix 8, we demonstrate the analysis of the global convergence of RSG. In Appendix 9, we demonstrate the analysis of the global convergence of MSG. In Appendix 10, we discuss the conditions required for operations management applications to ensure that the assumptions needed by the global convergence results of RSG and MSG. We also discuss situations when certain assumptions do not hold and what happens to the practical performance of the proposed algorithm. In Appendix 11, we discuss the detailed construction of SAA+SG method, which builds an empirical convex reformulation via SAA and solves the empirical convex reformulation via SGD, and the sample and gradient complexities of SAA+SG. In Appendix 12, we give a model formulation of assemble-to-order systems as a special case of our nonconvex optimization problem. In Appendix 13, we further discuss the details of the NRM problem given in Section 4, including the modeling of the passenger NRM, concavity of the NRM models, computing the stochastic gradient of in NRM problems, and discussions about integer booking limits and Poisson show-ups in NRM problems. In Appendix 14, we discussed details of the numerical implementation and demonstrate the full numerical results.

7 Technical Details

7.1 Proof of Lemma 2.2

By Assumption 2(d), for any , the probability that is non-differentiable in is zero. In addition, is Lipschitz continuous in for any given . Without loss of generality, for a given , we define

| (14) |

For simplicity, we shall use and indifferently.

Proof.

Since is -Lipschitz continuous, it holds for any , , , and that

Since is component-wise independent and , without loss of generality, let us consider the first coordinate . The other coordinates follow directly.

where denotes the support of , the event and denotes the complement of , the second equality holds by definition of the derivative, the third equality holds naturally, the forth equality holds by dominated convergence theorem and mean-value theorem that one could switch the order of limit and integration as is Lipschitz continuous, the fifth equality holds by the definitions of derivative and conditional expectation, and the sixth equality holds as for any given , is uniformly upper and lower bounded by the Lipschitz continuous parameter and by Assumption 2(d). By (14), the last equality holds.

7.2 Proof of Lemma 2.4: Estimating Matrix Inverse

Remark: Note that the distribution of in Lemma 2.4 is a uniform distribution over the support . One could use other distributions to build up estimators for matrix inverse. For instance, when using a geometric distribution with parameter over support , the estimator is

One can show that is unbiased, has a bounded second moment, and needs number of samples in expectation to construct. However, with a small probability, the estimator could have very large entries.

Proof.

We first bound the bias. To simplify notation, we let for .

where the last equality holds as and dominated convergence theorem guarantees interchange of expectation and gradient. On the other hand, since for any , we have

As a result, the bias of the estimator is upper bounded.

where the first inequality holds by triangle inequality, the second and third inequality holds by spectral norm, the second equality holds as , and the last inequality holds by Assumptions 2(b). As for the second moment, since , we have

where the first inequality holds by spectral norm, and the second inequality holds as .

The average number of samples used to construct the estimator is

7.3 Proof of Lemma 3.1: Switching Projection and Transformation

Proof.

By definition, , .

It suffices to show the one-dimensional case because , is component-wise independent, and both and are box constraints. Without loss of generality, we denote and .

Case I: if , then . It holds that

Case II: if It holds that

Since , it holds that

On the other hand, since projection from to an interval is a non-decreasing function and is also non-decreasing for any , we have the following,

As a result, it holds that,

Case III: if . It holds that

Since , we have the following inequality,

On the other hand, due to the non-decreasing property of box projection and for any , we have the following,

Thus, . Summarizing all the cases, we obtain the desired result.

7.4 Second Moments of Gradient Estimators and in MSG

The following lemma characterizes the second moments of gradient estimators and used in the analysis of MSG.

Lemma 7.1

Proof.

By Lemma 2.4, we have for and . It holds that

where the first inequality uses the Cauchy-Schwarz inequality and the fact that is independent of , and the second inequality holds by Lemma 2.4 and Lipschitz continuity of and .

As for , we have

where the first inequality uses the Cauchy-Schwarz inequality, and the second inequality uses the Cauchy-Schwarz inequality and the fact that , , and are independent.

7.5 Auxiliary Results Related to Gradient Mapping

We first restate the definition of gradient mapping for constrained optimization problems. For a smooth objective over a convex domain , define for some . The definition of gradient mapping of is given as

| (16) |

The following lemmas are used in the proof of Theorem 3.2. In particularly, Lemma 7.2 establishes the optimality gap and the gradient mapping. Lemma 7.3 characterizes the convergence rate, measured in terms of the norm of gradient mapping, of projected SGD on weakly convex objectives.

Lemma 7.2

For a convex function over a convex domain with and for any , it holds for any that

Proof.

Define

Equivalently, we may rewrite

By the first-order optimality condition, it holds that

where denotes the subdifferential set of the convex function at . By definition of , , it holds that

where the first inequality uses convexity of and

Consider the general stochastic optimization problem:

where is a convex set. Recall the projected SGD updates with a independent random sample and stepsize :

Let be uniformly selected from . Denote

Function is the Moreau envelop of and is widely used in stationary convergence of nonconvex functions (Davis and Drusvyatskiy 2018, Hu et al. 2020b, Drusvyatskiy and Paquette 2019). By Davis and Drusvyatskiy (2018), the gradient of the Moreau envelop is given by

Lemma 7.3

If is -Lipschitz continuous in for any given and is -Lipschitz continuous in , the output of projected SGD with stepsize satisfies the following inequality:

Proof.

8 Proof of Theorem 3.2: Global Convergence of RSG

Proof.

Recall that is the output of RSG. By definition of gradient mapping given in (16), we have

RSG is equivalent to projected SGD on the regularized objective . Since is -Lipschitz continuous and -weakly convex, Lemma 7.3 implies that , the output of RSG with stepsize , satisfies

Denote

| (18) |

The gradient mapping of satisfies the following inequality.

| (19) | ||||

where the first inequality uses the Cauchy-Schwarz inequality, the second inequality uses the non-expansiveness property of the projection operator (Bertsekas 2009), i.e., for a convex closed set and any , and the third inequality utilizes the fact that is compact with radius . In what follows, we establish the relationship between optimality gap and gradient mapping convergence.

For and , recall that . The following inequality holds

| (20) | ||||

where (a) holds as , , and ; (b) holds according to Lemma 7.2; (c) holds by the Cauchy-Schwarz inequality; (d) uses the definition of gradient mapping and the fact that , ; (e) uses Lipschitz continuity of , and (since ) and the fact that is compact; (f) holds as is a box constraint with the -th coordinate interval being .

For coordinate , we divide the following analysis into two cases: 1) ; 2) . For the first case, we have

where the first inequality utilizes the fact that , , and the non-expansiveness of projection operator, the first equality holds as and is a diagonal matrix, the second equality holds as , and the second inequality holds by Assumption 2(b). For the second case, we have

| (21) | ||||

where the first equality holds as is a bijective mapping under Assumption 2, the inequality holds as is -Lipschitz continuous, and the second equality holds by Lemma 3.1.

If , it means . Since is a diagonal positive definite matrix and , it holds that . As a result, we have and thus . Hence, it holds that

A similar argument holds when . As a result, for the second case, we have

Summarizing the two cases, we have

Setting in (20) and taking full expectation, we have

where the last inequality holds by (19).

9 Proof of Theorem 3.3: Global Convergence of MSG

Proof.

Denote , . We have

| (22) |

We first establish an upper bound on the objective value to the optimal objective value . For this purpose, first note that

where (a) uses the fact that and the definition of specified by MSG, (b) follows from Lemma 3.1, which is the key step for handling the constraints, (c) utilizes the fact that projection operator is non-expansive and , (d) holds by expanding , (e) follows from the definition , and (f) follows from Theorem 2.1 that is convex. After rearranging terms and taking full expectation, we have

| (23) | ||||

Summing up (23) from to and dividing on both sides, we have

| (24) |

where the first equality holds as is selected uniformly from , and the second equality holds as and . It remains to upper bound the right-hand-side of (24). Note that sum of forms a telescoping sum that is widely used in derivation of gradient-based methods (Nemirovski et al. 2009).

| (25) |

Next we establish an upper bound on . By Assumption 2 that is -Lipschitz continuous in for any , is -Lipschitz continuous. As a result, we have

| (26) |

where the second inequality holds by Lemma 7.1 about the second moment of .

Upper bounding is another key step of the analysis. By definition, we have

| (27) | ||||