Distributional Uncertainty Propagation via Optimal Transport

Abstract

This paper addresses the limitations of standard uncertainty models, e.g., robust (norm-bounded) and stochastic (one fixed distribution, e.g., Gaussian), and proposes to model uncertainty via Optimal Transport (OT) ambiguity sets. These constitute a very rich uncertainty model, which enjoys many desirable geometrical, statistical, and computational properties, and which: (1) naturally generalizes both robust and stochastic models, and (2) captures many additional real-world uncertainty phenomena (e.g., black swan events). Our contributions show that OT ambiguity sets are also analytically tractable: they propagate easily and intuitively through linear and nonlinear (possibly corrupted by noise) transformations, and the result of the propagation is again an OT ambiguity set or can be tightly upper bounded by an OT ambiguity set. In the context of dynamical systems, our results allow us to consider multiple sources of uncertainty (e.g., initial condition, additive noise, multiplicative noise) and to capture in closed-form, via an OT ambiguity set, the resulting uncertainty in the state at any future time. Our results are actionable, interpretable, and readily employable in a great variety of computationally tractable control and estimation formulations. To highlight this, we study three applications in trajectory planning, consensus algorithms, and least squares estimation. We conclude the paper with a list of exciting open problems enabled by our results.

uncertainty propagation, optimal transport, distributionally robust control, stochastic optimization.

1 Introduction

Uncertainty modeling is a fundamental step in any decision-making problem across all areas of science and engineering. Designing a good uncertainty model is a very challenging problem on its own, due to the many aspects and trade-offs that need to be taken into consideration. From a practical standpoint, the uncertainty model should be expressive enough to capture relevant uncertainty behaviors present in real-world systems, while avoiding being too ‘coarse’ and leading to overly conservative decisions. From a theoretical standpoint, the expressivity should not compromise the analytical (e.g., propagate in closed-form through dynamical systems) and computational (i.e., lead to tractable decision-making) properties of the model. Additionally, it is highly desirable to have a unique uncertainty model, which enables a unified study of decision-making problems.

To further complicate the modeling process, the modeler often has access only to partial statistical information about the uncertainty. For example, the support of the uncertainty might be known (e.g., from first principles), but not the likelihood of its possible realizations. Alternatively, a limited number of samples from the uncertainty might be available (e.g., in data-driven scenarios), but no information on the support. Finally, the probability distribution of the uncertainty might be available at present, but no information about future distribution shifts. In all these cases, one is confronted with distributional uncertainty, whereby not only is the system affected by uncertainty, but also the underlying probability distribution of the uncertainty is unknown and only partially observable. All these aspects cannot be addressed in a unifying manner by either the robust (i.e., norm-bounded uncertainty) or stochastic (i.e., one fixed distribution, e.g., an empirical or Gaussian distribution) models, and call for a distributionally robust uncertainty description.

In this paper, we propose to model uncertainty via Optimal Transport (OT) ambiguity sets. OT ambiguity sets are balls of probability distributions constructed using an OT distance (e.g., the celebrated Wasserstein distance), and centered at a reference probability distribution. These constitute a very rich uncertainty model, which generalizes both the robust and stochastic models. Moreover, they capture many additional real-world uncertainty phenomena, such as (specific types of) black swan events, i.e., unpredictable rare events with dramatic consequences (see Section 2.1). Finally, their inherent distributionally robust formulation naturally captures many classes of distribution shifts. All these properties highlight the expressivity of OT ambiguity sets.

So far, OT ambiguity sets have been primarily employed in Distributionally Robust Optimization (DRO) problems, with many recent papers showing that this approach leads to computationally tractable formulations that successfully robustify state-of-the-art data-driven optimization and machine learning models; see [1, 2, 3, 4, 5] and references therein. Recently, such methodology has also spread in control, establishing an exciting new direction in (OT-based) Distributionally Robust Control (DRC). Existing work has been primarily focused on optimal control and MPC [6, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16], estimation and filtering [17, 18, 19, 20, 21], and uncertainty quantification [22, 23, 24, 25]. For non-OT-based works, see [26, 27, 28, 29, 30] and references therein.

Differently from DRO, which is a static optimization problem, DRC is a dynamic problem involving the interplay between a stochastic dynamical system and a real-time distributionally robust (optimal) control algorithm. Due to its dynamic nature, a key challenge in developing and analysing DRC methods is represented by the ability to predict the future behavior of the system. This, in turn, is accomplished by understanding how OT ambiguity sets propagate through the system dynamics.

In this paper, we address this problem in the context of both linear and nonlinear stochastic dynamical systems, with additive or multiplicative uncertainty. To do so, we take a step back and start by studying how OT ambiguity sets propagate through (i) arbitrary deterministic maps (which boil down to in the linear case), and (ii) stochastic maps of the form or (i.e., pointwise sum and product), for an uncertain random vector . This is done in Sections 3 and 4, respectively. We then specialize our results to stochastic dynamical systems and DRC problems in Section 5. The proposed framework is coined (OT-based) Distributional Uncertainty Propagation (DUP), which we believe to be the fundamental link between static DRO and dynamic DRC problems (see Fig. 1).

Our main contributions can be summarized as follows:

-

0)

Expressivity of OT ambiguity sets. We present a tutorial on the modeling power of OT ambiguity sets; see Section 2.

-

1)

DUP via deterministic nonlinear maps. In Theorem 4, we study the propagation of OT ambiguity sets through both arbitrary and structured (bijective, injective, and surjective) nonlinear maps . First, we show that OT ambiguity sets are exactly (in closed-form) propagated through bijective maps, and they are closed under propagation (i.e., the result of the propagation is again an OT ambiguity set). These properties are crucial features of OT ambiguity sets, which highlight their advantage over other stochastic uncertainty models, such as standard stochastic models consisting of a fixed distribution (e.g., Gaussian) or other types of distributionally robust descriptions (e.g., moment ambiguity sets). Secondly, we show that in the remaining cases, the result of the propagation can be upper bounded by an OT ambiguity set.

-

2)

DUP via deterministic linear maps. In Theorem 6, we restrict our attention to linear maps and prove a chain of inclusions that strenghtens Theorem 4 (when restricted to linear transformations). Moreover, we show that for linear maps the exactness and closedness of the propagation can be further extended from bijective to surjective maps.

-

3)

DUP via stochastic additive and multiplicative maps. In Theorems 11 and 16, we study the convolution and Hadamard product of two OT ambiguity sets. These two probabilistic operations correspond to the pointwise sum and product of two uncertain random vectors, respectively. In both cases, we show that the result of the convolution can be upper-bounded by another OT ambiguity set.

-

4)

Applications. In Section 5, we employ our DUP results in the context of control and estimation problems. Specifically, we start by employing the results in 1)-3) for discrete-time linear time-invariant (LTI) systems with (i) uncertain initial condition, (ii) additive uncertainty, and (iii) multiplicative uncertainty. In all three cases, we show that the distributional uncertainty in the state can be captured in closed-form by an OT ambiguity set. We then study three distinct applications: trajectory planning, consensus, and least squares estimation. We conclude the paper with preliminary results for nonlinear systems and a discussion on future research directions.

The DUP results show that OT ambiguity sets are analytically tractable, and constitute a promising well-posed uncertainty model for dynamical systems and control. Specifically, they allow to consider multiple sources of distributional uncertainty (e.g., from initial condition, additive noise, multiplicative noise) and capture via OT ambiguity sets the resulting distributional uncertainty in the state at any future time step. Moreover, our results are exact for a great variety of practical cases.

For linear systems (and certain classes of nonlinear systems), the resulting OT ambiguity sets are also computationally tractable, and can be directly employed in various DRC formulations which can be reformulated as tractable convex programs using, for example, the DRO results in [5] for many cases of practical interest. An initial effort in this direction has been made in [7], where the DUP framework has been exploited to formulate a Wasserstein Tube MPC which: (i) is a direct generalization of the deterministic Tube MPC to the stochastic setting, (ii) is recursively feasible, and (iii) can achieve an optimal trade-off between safety and performance.

Aside from the computational advantages, we envision that the DUP framework can be directly employed in the analysis of the closed-loop properties (e.g., invariance, stability) of systems affected by distributional uncertainty.

1.1 Mathematical Notation and Preliminaries

Throughout the paper, whenever we use and we implicitly assume that they are Polish spaces, i.e., separable and completely metrizable topological spaces (e.g., and spaces with ). We denote by the space of Borel probability distributions on . The support of a distribution is denoted by , and the delta distribution at is denoted by . Given , we denote by their product distribution. We denote by the fact that is distributed according to . We implicitly assume that all maps are Borel. Projection maps are denoted by , and the identity map on is (or simply whenever the context is clear). The indicator function of the set is denoted by . Finally, given , denotes their Hadamard (or pointwise) product, defined element-wise by for .

We focus on three classes of transformations of probability distributions: pushforward via a transformation, convolution with another distribution, and Hadamard product with another distribution. We start by defining the pushforward.

Definition 1.

Let and . Then, the pushforward of via is denoted by , and is defined as , for all Borel sets .

Definition 1 says that if , then is the probability distribution of the random variable . We now consider and define the convolution and the Hadamard product.

Definition 2.

Let . The convolution is defined by for all Borel sets .

Definition 3.

Let . The Hadamard product is defined by for all Borel sets .

The convolution captures the sum of independent random variables: if and are independent, then is distributed according to . Similarly, the Hadamard product captures element-wise multiplication of independent random variable: if and are independent, then is distributed according to . We exemplify these three definitions in the case of empirical probability measures:

Example 1.

Let and be empirical distributions with and samples. Then, , , and . In particular, all distributions are empirical and supported on the propagated samples.

2 Optimal Transport Ambiguity Sets

In this section, we formally define OT ambiguity sets and explore their modeling power for uncertainty quantification. Consider a non-negative lower semi-continuous function (henceforth, referred to as transportation cost) and two probability distributions . Then, the OT discrepancy between and is defined by

| (1) |

where is the set of all probability distributions over with marginals and , often called transport plans or couplings [31]. The semantics are as follows: we seek the minimum cost to transport the probability distribution onto the probability distribution when transporting a unit of mass from to costs . If , for some norm on , boils down to the celebrated (type-) Wasserstein distance. Intuitively, quantifies the discrepancy between and , and it naturally provides us with a definition of ambiguity in the space of probability distributions (see, e.g., Fig. 2). In particular, the OT ambiguity set of radius and centered at is defined as

| (2) |

In words, contains all probability distributions onto which can be transported with a budget of at most . This includes both continuous and discrete distributions, distributions not concentrated on the support of , and even distributions whose mass asymptotically escapes to infinity, as shown next.

Example 2.

Let , , , and let be the Gaussian distribution with mean and variance . Then, . Moreover, , and for all .

These properties cease to hold if the discrepancy between probability distributions is measured via the Kullback-Leibler (KL) divergence or Total Variation (TV) distance [32]. We conclude this subsection by highlighting that OT ambiguity sets are well-behaved under monotone changes in and .

Lemma 1.

Let , be transportation costs over , and .

-

1.

If then ;

-

2.

If , then .

In words, an increase in the transportation cost shrinks the OT ambiguity set, whereas an increase of the radius enlarges it. These simple observations arm practitioners with actionable knobs to control the level of distributional uncertainty.

2.1 Robustness in (space, likelihood)

OT ambiguity sets are attractive to model distributional uncertainty for various reasons, which we detail next. Differently from standard uncertainty models, namely robust (i.e., norm-bounded uncertainty) and stochastic (i.e., one fixed distribution), OT ambiguity sets capture uncertainty in both space (i.e., the support of the distribution) and likelihood (i.e., the probability of specific events). These are encoded in through and : given a reference distribution and a radius (intended as transportation ‘budget’), the transportation cost controls the displacement of probability mass from , and consequently the shape and size of . Specifically, given in the support of , then higher the value of , less probability mass is transported from to . This automatically bounds the likelihood of the value for any distribution in the OT ambiguity set . In particular, if is large enough for all in the support of and all , for some , then no distribution inside will be supported on .

This feature of OT ambiguity sets allows us to capture a great variety of uncertainty phenomena, as detailed next.

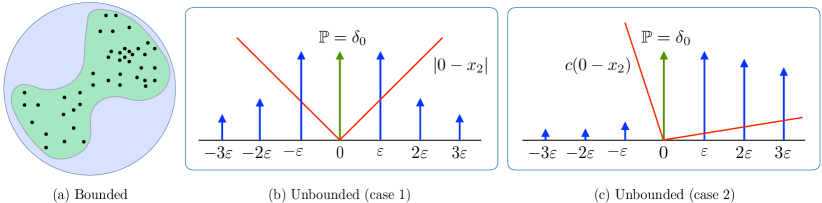

(i) bounded. In this case, naturally interpolates between the robust and the stochastic uncertainty models. Specifically, if , then recovers the probabilistic representation of the robust model (i.e., the set of all delta distributions for all ). If instead , then recovers the stochastic model. This interpolation between the two models allows to reduce the conservativeness of the robust model, while robustifying the stochastic model. Importantly, this property opens the door to studying decision-making formulations which optimally trade between safety and performance (see [7] for a control application). This is particularly important in data-driven scenarios, where is an empirical distribution supported on a finite number of samples from the uncertainty. This is illustrated in Fig. 3(a), where the black dots are the samples, the green shape is the support of the true unknown uncertainty distribution, and the blue circle is the robust model. In this case, can be properly designed to capture with high probability only the green area.

(ii) unbounded. In this case, OT ambiguity sets have the ability to capture arbitrarily large uncertainty values, together with the information about how rare those events are. We illustrate this reasoning in Fig. 3(b), where for simplicity of exposition we consider , (represented by the red lines), (i.e., the reference distribution is empirical and supported on the point ). Then, a simple calculation shows that for all . In words, captures the uncertainty value together with the information that the probability of this value is at most . This reasoning extends to more general scenarios (e.g., arbitrary and general ; see Fig. 3(c)) and makes OT ambiguity sets particularly suitable to model and robustify against black swan events, i.e., extreme outliers with catastrophic effects which are impossibly difficult to predict. This is experimentally validated in [33], in the context of day-ahead energy trading in energy markets.

3 Pushforward of OT Ambiguity Sets

In this section, we study how OT ambiguity sets propagate via linear and nonlinear transformations. We start by showing that naive approaches (in particular, propagation of the center only, or propagation based on Lipschitz bounds) fail to effectively capture the propagation of distributional uncertainty.

3.1 Naive Approaches and their Shortcomings

Given the OT ambiguity set , one might be tempted to approximate the result of the propagation by . This approach suffers from fundamental limitations already in very simple settings, easily resulting in crude overestimation or catastrophic underestimation of the distributional uncertainty, as shown in the next example.

Example 3.

Let on .

-

1.

Let . Then, only contains (regardless of ), whereas contains all distributions whose second moment is at most . Therefore, overestimates the true distributional uncertainty.

-

2.

Let , and . Then, . In Theorem 4 we show that . Thus, underestimates the true uncertainty.

Moreover, one might be tempted to bound the propagated distributional uncertainty with the Lipschitz constant of , i.e., to upper bound with . However, this approach suffers from three major limitations. First, many transformations are not Lipschitz continuous. Second, the transportation cost might not be , which makes the Lipschitz bound not directly applicable. Indeed, already in Example 3, an increase by a factor of 2 in the radius does not alleviate the underestimation of the true ambiguity set: one needs to use to account for the quadratic transportation cost . Finally, even if the transportation cost is , Lipschitz bounds might be overly conservative, as shown next.

Example 4.

Let on , , and be a diagonal matrix with diagonal entries (thus ). Then, eliminates all the distributional uncertainty in the last dimensions. However, contains, among others, all distributions of the form with , and satisfying .

These shortcomings prompt us to study the exact propagation of OT ambiguity sets.

3.2 Nonlinear Transformations

We seek to characterize the ambiguity set for a general Borel map . We proceed in three steps. In Lemma 2, we prove a result at the level of the set of couplings between two probability distributions and . Armed with this result, in Proposition 3 we study the pushforward at the level of the OT discrepancy. Our analysis culminates in Theorem 4, where we show how general OT ambiguity sets propagate under pushforward via arbitrary (nonlinear) maps.

At the level of couplings, the propagation is well behaved: the set of couplings between and , i.e., , corresponds to the pushforward via of .

Lemma 2.

Let , and consider an arbitrary transformation . Then,

We now study the OT discrepancy (1) between the pushforward of two probability distributions. Lemma 2 stipulates that, instead of optimizing over the set of all couplings , we can equivalently optimize over the pushforward of all couplings . This helps us shed light on the relation between the OT discrepancy between and and the OT discrepancy between and .

Proposition 3.

Let , consider a transformation , and let be a transportation cost on . Then,

| (3) |

Moreover, let be a transportation cost on . Then, we have the following cases:

1) If is bijective, with inverse , then

| (4) |

2) If is injective, with left inverse , then

| (5) |

3) If is surjective, with right inverse , then

| (6) |

Proposition 3 states that if the transportation cost on is of the form , for some transportation cost on , then the OT discrepancies and coincide. This a priori assumption of the transportation cost can be dropped if the function satisfies additional assumptions. For instance, if is bijective or injective (and thus, a left inverse exists), then for any transportation cost on , the OT discrepancies and coincide. We can now state the main result of this subsection.

Theorem 4 (Nonlinear transformations).

Let , consider an arbitrary transformation , and let be a transportation cost on . Then,

| (7) |

Moreover, let be a transportation cost on . Then, we have the following cases:

-

1.

If is bijective, with inverse , then

(8) -

2.

If is injective, with left inverse , then

(9) -

3.

If is surjective, with right inverse , then

(10)

Remark.

We highlight the striking similarity between the propagation of OT ambiguity sets in Theorem 4 and the propagation of deterministic bounded sets defined as . Simple calculations show that for a bijective transformations we have . Surprisingly, an analogous result, namely (8), holds in probability spaces for OT ambiguity sets. This shows that propagating OT ambiguity sets is as easy as propagating standard deterministic sets.

Remark.

In general, inclusion (9) cannot be improved to equality. For instance, consider the map defined by , with left inverse . Clearly, is injective. Moreover, consider the transportation cost , . Let . By construction, cannot be obtained from the pushforward via of a probability distribution over , and so . However, , and so .

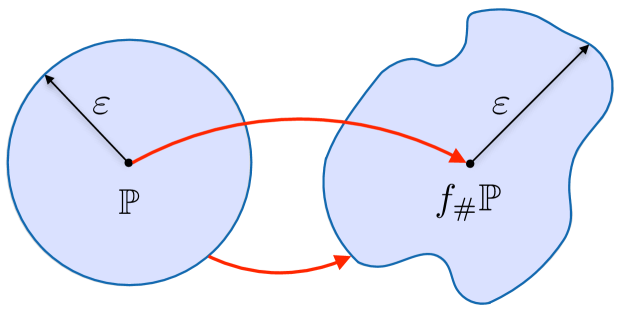

In a nutshell, Theorem 4 asserts that the pushforward of an OT ambiguity set of radius centered at via an invertible map coincides with an OT ambiguity set with the same radius centered at , constructed with the transportation cost ; see Fig. 4. When is only injective, the equality reduces to inclusion. In the surjective case, an upper bound for can be easily recovered from Lemma 1:

Corollary 5.

We exemplify Corollary 5 in the case of norms.

Example 5.

Let be defined by , where is a norm on . Clearly, is surjective, and a right inverse is given by for some with . Then, . Consider a transportation cost , for monotone . Elementary calculations show that . Therefore, Corollary 5 yields the inclusion .

3.3 Linear Transformations

We now investigate linear transformations between finite-dimensional Euclidean spaces, defined by a matrix . The linear structure, together with mild assumptions on the transportation cost, allow us to strengthen the results of Section 3.2 in three ways. First, we will derive an upper bound on even if the linear map defined by is not injective or surjective. In such case, right and left inverses do not exist, and Theorem 4 is not applicable. Second, we will prove a chain of inclusions that strenghtens the statements of Theorem 4 (when restricted to linear transformations). Finally, we will show that the equality (8) can be extended to arbitrary surjective linear maps.

To accomplish this, we restrict the analysis to finite-dimensional Hilbert spaces. Consider , with , for symmetric and positive definite, and , with symmetric and positive definite. Given , let denote its adjoint and denote its Moore-Penrose inverse.

Remark.

Following the definition of and , it can be easily shown that . In particular, if and , we recover the standard inner product and (i.e, the adjoint is the transpose). Moreover, if is full rank, then has a closed-form expression. Specifically, if is full row-rank then , and if is full column-rank then .

Throughout this subsection, we require the following assumption on the transportation cost.

Assumption 1.

The transportation cost is

-

(i)

translation-invariant: ;

-

(ii)

orthomonotone: for all satisfying .

Following Assumption 1, the transportation cost becomes a function . Accordingly, we use the simplified notation instead of ; i.e., .

Remark.

All transportation costs of the form , where is the norm induced by the inner product , and is monotone and lower semi-continuous, are translation-invariant and orthomonotone. Indeed, for all such that ,

We are now ready to state the main result of this subsection.

Theorem 6 (Linear transformations).

In words, Theorem 6 asserts that the result of the propagation is itself an OT ambiguity set (or can be upper bounded by one), with the same radius , propagated center , and an -induced transportation cost . The following example shows that the equality (14) does generally not hold for non-surjective linear maps.

Example 6.

Consider , and with pseudoinverse , the quadratic transportation cost , and the probability distribution . Let . Since , does not belong to regardless of . However, . Thus, , and .

Theorem 6 continues to hold if the OT ambiguity set is defined over a subset (i.e., contains only distributions supported on ). This is summarized in the next corollary, whose proof follows similar lines to the proof of Theorem 6 and is therefore omitted.

Corollary 7.

Let , and let be defined over . Moreover, let be full-row rank and let satisfy 1. Then, with restricted to all distributions supported on .

Theorems 4 and 6 provide a full description for the case of full-rank matrices. For invertible and full column-rank matrices (i.e., the injective case), the result follows directly from Theorem 4 with no assumption on the transportation cost (i.e., for a general ). The surjective case, instead, relies on Theorem 6, and therefore requires the transportation cost to be translation-invariant and orthomonotone.

We conclude this section with the application of Theorems 4 and 6 to some important special cases.

Corollary 8.

Let , be a translation-invariant transportation cost over , and .

-

1.

If is a translation, i.e., for , then

-

2.

If is a scaling, i.e., for , and satisfies , for some , then In particular, if , then .

-

3.

If is a rotation (resp., reflection) map, i.e., , where is an orthogonal matrix with determinant 1 (resp., ), and for , then

-

4.

Let the assumptions of Theorem 6 be satisfied. If is an orthogonal projection matrix, i.e., satisfies and , then

4 Convolution and Hadamard Product of OT Ambiguity Sets

In this section, we study the effect of additive and multiplicative uncertainty. In the probability space, these two operations correspond to the convolution and Hadamard product of probability distributions (see Definitions 2 and 3). As in the previous section, we do not restrict ourselves to fixed probability distributions but allow the uncertainty to be described by an OT ambiguity set. Accordingly we seek to characterize the two objects and . Throughout this section, we assume that (endowed with any distance).

4.1 Convolution

We start with the convolution of OT ambiguity sets. We proceed in three steps. In Lemma 9, we prove a result at the level of the set of couplings. Armed with this result, in Proposition 10 we study the convolution at the level of the OT discrepancy, which is used to define OT ambiguity sets. Our analysis culminates in Theorem 11, where we show that the convolution of OT ambiguity sets can be captured by another OT ambiguity set. Throughout this subsection, we require the following assumption on the transportation cost.

Assumption 2.

-

(i)

The transportation cost is translation-invariant: .

-

(ii)

There exists so that satisfies triangle inequality; i.e., for all .

2 is satisfied in particular by any power of a norm on . At the level of coupling, we can provide a “lower bound”: the set of couplings between and contains the set of couplings between and convolved with .

Lemma 9.

Let . Then,

| (15) |

Remark.

In general, the inclusion (15) cannot be improved to equality. For instance, let and . Then, . Moreover, let . Then, , i.e., it contains only one coupling. However, , and so , which is not a singleton since there are infinitely many couplings between and itself (e.g., , , etc.).

We now study the OT discrepancy between two probability distributions, both convolved with . Thanks to Lemma 9, we can produce an upper bound on the OT discrepancy by restricting ourselves to couplings of the form . This observation yields a contraction property.

Proposition 10.

Let and let satisfy 2(i). Then,

| (16) |

Proposition 10 shows that the OT discrepancy between and is upper bounded by the OT discrepancy between and . Adding noise to probability distributions before computing the Wasserstein distance has been used in machine learning to devise a smoothed version of the Wasserstein distance. With Proposition 10, we can give a general result on the convolution of OT ambiguity sets.

Theorem 11 (Convolution).

Let , and let satisfy 2. Then,

| (17) |

Remark.

In general, the upper bound 17 cannot be improved to equality. For instance, let , , , and . Let and , and consider the OT ambiguity set . The probability distribution belongs to . However, , since the convolution of any distribution in with is supported on at least two distinct points. Thus, . Nonetheless, in some special cases, we do have ; e.g., if , then convolution with is a translation by , and the equality follows from Corollary 8.

Theorem 11 continues to hold if the OT ambiguity sets and are defined over some subsets . This is summarized in the next corollary, whose proof follows similar lines to the proof of Theorem 11 and is thus omitted.

Corollary 12.

Let and , with . Moreover, let be defined over and be defined over . Finally, let satisfy 2. Then,

| (18) |

with restricted to all distributions supported on the Minkowski sum .

We conclude this subsection by specializing Theorem 11 to the case of a known probability distribution .

Corollary 13.

Let , and let satisfy 2. If and is positive definite, then and .

4.2 Hadamard Product

We now study the Hadamard product of OT ambiguity sets. As above, we proceed in three steps. In Lemma 14, we prove a result at the level of the set of couplings. Armed with this result, in Proposition 15 we study the Hadamard product at the level of the OT discrepancy. Our analysis culminates in Theorem 16, where we show that the Hadamard product of OT ambiguity sets can be captured by another OT ambiguity set. Throughout this subsection, we require the following assumption on the transportation cost.

Assumption 3.

-

(i)

The transportation costs is translation-invariant and satisfies for all .

-

(ii)

There exists such that satisfies triangle inequality; i.e., for all ;

3 is satisfied in particular by any power of a norm on . Similarly to Lemma 9 for the convolution operation, at the level of coupling we can provide a “lower bound”: the set of couplings between and contains Hadamard product of and .

Lemma 14.

Let . Then,

We now study the OT discrepancy between two and . Thanks to Lemma 14, we can produce an upper bound of the OT discrepancy by restricting ourselves to couplings of the form .

Proposition 15.

Let , and let satisfy 3(i). Then,

| (19) |

Proposition 15 states that the OT discrepancy satisfies the analogous of 3(i) in the probability space, namely the inequality (19). Armed with Proposition 15, we can now study the Hadamard product of OT ambiguity sets.

Theorem 16 (Hadamard product).

Let , and let satisfy 3. Then,

| (20) | ||||

Remark.

In general, the upper bound 20 cannot be improved to equality. As for the convolution, let , , , and . Let and , and consider the OT ambiguity set . The probability distribution belongs to . However, , since the Hadamard product of any distribution in with is supported on at least two distinct points (with the only possible exception for ). Thus, .

We conclude this subsection by specializing Theorem 16 to the case of a known probability distribution .

Corollary 17.

Let , and let satisfy 3. If and is positive definite, then .

5 Applications

In this section, we specialize the results presented in Theorems 6, 4, 11 and 16 to several applications in the context of (stochastic) dynamical systems and least squares estimation.

5.1 Stochastic Linear Control Systems

Our first application concerns the propagation of distributional uncertainty through a stochastic LTI control system. We focus on three sources of uncertainty: stochastic initial condition, additive process noise, and multiplicative noise. In all cases, we capture distributional uncertainty via OT ambiguity sets (using the translation-invariant and orthomonotone transportation cost ) and aim at quantifying the distributional uncertainty in the state at time .

Specifically, our three settings of interest are as follows:

-

1.

Deterministic LTI system with uncertain initial condition, whose distribution belongs to an OT ambiguity set:

(21) -

2.

Stochastic LTI system with deterministic initial condition, and with additive noise, where the distribution of the noise trajectory belongs to an OT ambiguity set:

(22) -

3.

Stochastic LTI system with deterministic initial condition, and with two sources of independent (element-wise) multiplicative noise whose distributions belong to two OT ambiguity sets:

(23)

These formulations encompass the scenario when one only has access to i.i.d. samples of the uncertainty and constructs an OT ambiguity set around these. For instance, in the case of unknown initial condition (case 1) above), suppose one has access to samples from . In this case, statistical concentration inequalities can be used to construct an OT ambiguity set around the empirical distribution which contains the true distribution with high probability; see [22, Section 4] for details.

We now use the theory of Sections 3 and 4 to capture the distributional uncertainty in . To ease notation, let

| (24) | ||||

Proposition 18 (Distributional uncertainty in LTI systems).

Remark.

The propagation in 1) is exact if is full row-rank and the propagation in 2) is exact if is full row-rank. In all other cases, Proposition 18 provides us with a (non-trivial) upper bound for the distributional uncertainty in .

Remark.

The results in Theorems 6, 11 and 16 can also be employed in scenarios where multiple (simultaneous) sources of uncertainty are present. For example, for stochastic LTI systems with both uncertain initial condition and additive noise, i.e.,

it can be easily shown that the OT ambiguity set

with , captures the distributional uncertainty in the state . Notice that this ambiguity set is not the result of a simple superposition of the two ambiguity sets in 1)-2) from Proposition 18.

5.2 Distributionally Robust Trajectory Planning

We now instantiate our results for distributionally robust trajectory planning. Consider the stochastic LTI system

| (25) |

where , , and all system matrices are of appropriate dimensions. We suppose that the noise trajectory is distributed according to an unknown probability distribution . In particular, we do not assume that and are uncorrelated.

For a horizon , we aim at steering (25) from a given initial condition to a target set defined as

| (26) |

where and . In what follows, we assume that defined in (24) is full row-rank. To deal with distributions with unbounded support and reduce conservatism, we say an input trajectory is feasible if the probability distribution of the terminal state , given by

| (27) |

satisfies the Conditional Value at Risk (CVaR) constraint:

| (28) |

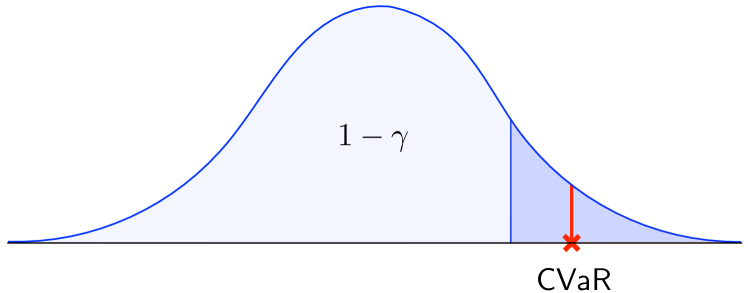

Due to space constraints, we refer to [22, Equation (1)] for the specific mathematical formulation of CVaR constraints, and simply recall here that: (i) represents the expectation of the right -tail of the distribution (see Fig. 5), and (ii) (28) is a convex constraint which implies that the terminal state belongs to the target set with probability of at least .

If the true distribution of the noise trajectory were known, we could directly leverage (27) and compute the cheapest control input via

| (29) |

We consider instead the case where the distribution is unknown and we only have access to i.i.d. noise sample trajectories

for . We capture the distributional uncertainty in the noise trajectories via an OT ambiguity set centered at the empirical distribution . By Proposition 18, the distributional uncertainty in the terminal state is therefore captured by the OT ambiguity set

In particular, the center of the OT ambiguity set is supported on the controlled state samples

Accordingly, the optimal input must satisfy the CVaR constraint (28) for all probability distribution belonging to the OT ambiguity set :

| (30) |

The semi-infinite problem (30) can be reformulated as a finite-dimensional convex program using [5, Proposition 2.12 and Theorem 2.16]. Due to space reasons, its proof is omitted.

Proposition 19 (Distributionally robust trajectory planning).

The distributionally robust trajectory planning (30) admits the finite-dimensional convex reformulation

with , and .

We evaluate our methodology on the two-dimensional linear system , , and , prestabilized with the LQR control gain (designed with ) and . We suppose that the decision-maker has access to 5 noise sample trajectories. We choose the set as the target (grey in Fig. 6) and select . We repeat our experiments for three values of and compare with propagation of the OT ambiguity set via the Lipschitz constant and propagation of the center only. As shown in Fig. 6, the feedforward input resulting from (red in Fig. 6) performs well on the 5 training sample trajectories, steering them to the boundary of the target set, but yields poor performance on unseen test samples. For larger (blue and green in Fig. 6), instead, the system trajectories are successfully steered to the target set, even for unseen noise realizations, at the price of a moderate increase in cost (8.5% larger cost for and 14.9% larger cost for , compared with ). Finally, the propagation via the Lipschitz constant yields instead 29.3% larger cost, whereas only propagating the center leads to infeasibility and is therefore not included in the plot.

5.3 Consensus in Averaging Algorithms

Our third application concerns uncertainty quantification in the context of discrete-time averaging algorithms. More specifically, we study how distributional uncertainty in the initial condition of averaging algorithms propagates to the consensus state that (under suitable assumption) the algorithm reaches. Formally, consider the discrete-time averaging algorithm

| (31) |

where is the row-stochastic adjacency matrix associated with a directed graph (which captures the interactions among the nodes/agents of the averaging). Under suitable assumptions on , the iterate resulting from (31) is known to reach consensus (i.e., all entries of the vector are equal). Such algorithms are ubiquitous in many applications, including network systems, multi-agent systems, and opinion dynamics; see [34] and references therein.

In many real-world settings, the initial probability distribution is unknown. For instance, in opinion dynamics, the distribution of users’ initial opinions is unknown but can be estimated via surveys (from which is constructed); in sensor networks, can be calibrated based on the sensors’ specifications. Accordingly, we can use an OT ambiguity set to capture its distributional uncertainty.

In this setting, we are interested in capturing the distributional uncertainty in the consensus state .

Proposition 20 (Consensus OT ambiguity set).

Let , and let be row stochastic with a unique eigenvalue in and all the other eigenvalues strictly inside the unit circle. Moreover, let be the distribution of the state , and be the distribution of . Finally, let denote the left eigenvector of associated to the eigenvalue (normalized so that ). Then,

| (32) |

where denotes the standard weak convergence. If additionally is doubly-stochastic, then and

| (33) |

In words, the distributional uncertainty is the same in all entries of , and it belongs to the OT ambiguity set , which therefore captures the distributional uncertainty in the consensus state. This way, for instance, we can quantify the worst-case probability that the consensus state resides outside of an interval of interest via

As above, this optimization problem admits a finite-dimensional convex reformulation [5].

5.4 Least Squares Estimation

Our fourth application concerns statistical estimation. Consider the linear inverse problem

| (34) |

where the aim is to estimate the parameter from noisy measurements (with ) of the form , with random measurement noise (possibly correlated). If has full column-rank, a standard solution is the ordinary least squares (OLS) estimator

| (35) |

The OLS estimator corresponds to the maximum likelihood estimation when the measurement noise are i.i.d. and standard normal with equal variances. Moreover, by the Gauss–Markov theorem [35], if are i.i.d. and have zero mean and equal finite variance, then the OLS estimator is the best linear unbiased estimator, i.e., it has the lowest sampling variance within the class of linear unbiased estimators.

Here, we depart from these assumptions and study a more general case, where we only have access to the i.i.d. samples , with , from an otherwise unknown measurement noise (joint) distribution (see remark below for the specialization to the i.i.d. case). In this scenario, we seek to understand how the distributional uncertainty in measurement noise, captured by an OT ambiguity set, propagates to the OLS estimator in (35). Especially when the OLS estimator is subsequently used for decision-making (e.g., in estimation or identification problems), it is crucial to accurately quantify uncertainty [36].

More formally, we construct an OT ambiguity set centered at the empirical distribution , which is guaranteed to contain the true probability distribution with high probability and study the resulting OT ambiguity set around the estimation error .

Remark (i.i.d. case).

If the noise measurements are i.i.d. according to an unknown noise distribution , and we have access to samples from , then [37, Theorem 2] can be used to construct an OT ambiguity set which contains with high probability. Subsequently, [22, Lemma 3] can be used to construct an OT ambiguity set for the probability distribution of (i.e., the product distribution ).

Our results readily allow us to quantify the distributional uncertainty in the OLS estimator.

Proposition 21 (Distributional uncertainty in OLS estimator).

Remark (i.i.d. case, continued).

In the i.i.d. setting of the previous remark, we therefore conclude that .

When the measurement noise has zero mean and variance , the covariance matrix of the OLS estimator is equal to [35]. However, except for basic cases (e.g., Gaussian measurement noise), the covariance does not entirely capture the distributional uncertainty in the OLS estimator. On the contrary, Proposition 21 enables us to fully capture the distributional uncertainty in the estimation error .

5.5 Nonlinear Dynamical Systems

Our last application concerns the propagation of the distributional uncertainty through a nonlinear dynamical system. Consider the deterministic dynamical system

| (37) |

with . We suppose that the initial condition is distributed according to some unknown probability distribution , which belongs to an ambiguity set , where, as above, could be an empirical distribution over finitely many samples. Theorem 4 allows us to propagate the distributional uncertainty encapsulated in the OT ambiguity set and, thus, to characterize the distributional uncertainty in .

Corollary 22.

Unfortunately, the nonlinearity of (37) prevents us from replicating our results in Proposition 18 for the LTI case (in particular, additive and multiplicative noise) without resorting to Lipschitz bounds. For instance, in the case of additive process noise, there is no explicit expression for the state as a function of and the noise trajectory , which was crucial to prove 2) in Proposition 18. We leave the analysis of additive and multiplicative noise in the context of nonlinear dynamical systems to future research, and conclude this section with an outlook on some exciting open problems.

1) Distributionally robust control. Our results can be directly employed in a variety of Distributionally Robust Optimal Control and MPC formulations, offering many advantages:

-

(i)

Computation. Propagating OT ambiguity sets from the noise to the state leads to much smaller optimization problems (as in Proposition 19), whose dimension is independent of the control horizon. Moreover, we envision that a disturbance affine feedback policy leads to convex reformulations of DRC problems, where it is possible to optimize over both the feedforward and feedback terms.

-

(ii)

Analysis. The propagated OT ambiguity set capturing the distributional uncertainty in the state (recall Proposition 18) unveils the role of the feedforward and feedback terms in the control input : controls the position, while controls the shape and size of this OT ambiguity set (see also [22, Section IV-B]).

2) Distributionally robust filtering. We envision that our results can play a major role in developing and studying novel distributionally robust filtering formulations, e.g., ensemble Kalman filter or particle filter. Specifically, we believe that the propagation of finitely many samples coupled with a robustification via OT ambiguity sets (which captures the underlying true distribution) allows us to rigorously quantify uncertainty in such filtering algorithms.

3) Robustify control in probability spaces. We envision that the distributionally robust results proposed in this paper can serve as the right baseline to robustify existing control approaches in the probability space (e.g., steering of distributions); see [38, 39, 40, 41, 42, 43, 44, 45, 46, 47], and the references therein.

4) Convergence, invariance, and stability analysis. Finally, we strongly believe that our results pave the way to studying the properties of dynamical systems affected by distributional uncertainty. Specifically, our exact propagation results allow to exactly embed such systems in the probability space as a sequence of controlled OT ambiguity sets. Then, convergence and invariance properties can be naturally formulated as convergence and invariance of OT ambiguity sets. Moreover, we envision that these results can be employed in studying the stability of systems affected by distributional uncertainty.

References

- [1] Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the Wasserstein metric: performance guarantees and tractable reformulations. Mathematical Programming, 171(1):115–166, 2018.

- [2] Aman Sinha, Hongseok Namkoong, Riccardo Volpi, and John Duchi. Certifying some distributional robustness with principled adversarial training. arXiv preprint arXiv:1710.10571, 2017.

- [3] Jose Blanchet and Karthyek Murthy. Quantifying distributional model risk via optimal transport. Mathematics of Operations Research, 44(2):565–600, 4 2019.

- [4] Rui Gao. Finite-sample guarantees for Wasserstein distributionally robust optimization: Breaking the curse of dimensionality. Operations Research, 2022.

- [5] Soroosh Shafieezadeh-Abadeh, Liviu Aolaritei, Florian Dörfler, and Daniel Kuhn. New perspectives on regularization and computation in optimal transport-based distributionally robust optimization. arXiv preprint arXiv:2303.03900, 2023.

- [6] Insoon Yang. Wasserstein distributionally robust stochastic control: A data-driven approach. IEEE Transactions on Automatic Control, 66(8):3863–3870, 2020.

- [7] Liviu Aolaritei, Marta Fochesato, John Lygeros, and Florian Dörfler. Wasserstein tube mpc with exact uncertainty propagation. arXiv preprint arXiv:2304.12093, 2023.

- [8] Zhengang Zhong, Ehecatl Antonio Del Rio-Chanona, and Panagiotis Petsagkourakis. An efficient data-driven distributionally robust MPC leveraging linear programming. In 2023 American Control Conference (ACC), pages 2022–2027. IEEE, 2023.

- [9] Francesco Micheli, Tyler Summers, and John Lygeros. Data-driven distributionally robust mpc for systems with uncertain dynamics. In 2022 IEEE 61st Conference on Decision and Control (CDC), pages 4788–4793. IEEE, 2022.

- [10] Marta Fochesato and John Lygeros. Data-driven distributionally robust bounds for stochastic model predictive control. In 2022 IEEE 61st Conference on Decision and Control (CDC), pages 3611–3616. IEEE, 2022.

- [11] Christoph Mark and Steven Liu. Data-driven distributionally robust MPC: An indirect feedback approach. arXiv preprint arXiv:2109.09558, 2021.

- [12] Jeremy Coulson, John Lygeros, and Florian Dörfler. Distributionally robust chance constrained data-enabled predictive control. IEEE Transactions on Automatic Control, 67(7):3289–3304, 2021.

- [13] Atharva Navsalkar and Ashish R Hota. Data-driven risk-sensitive model predictive control for safe navigation in multi-robot systems. In 2023 IEEE International Conference on Robotics and Automation (ICRA), pages 1442–1448. IEEE, 2023.

- [14] Kihyun Kim and Insoon Yang. Distributional robustness in minimax linear quadratic control with wasserstein distance. SIAM Journal on Control and Optimization, 61(2):458–483, 2023.

- [15] Robert D McAllister and James B Rawlings. On the inherent distributional robustness of stochastic and nominal model predictive control. IEEE Transactions on Automatic Control, 2023.

- [16] Alireza Zolanvari and Ashish Cherukuri. Iterative risk-constrained model predictive control: A data-driven distributionally robust approach. arXiv preprint arXiv:2308.11510, 2023.

- [17] Soroosh Shafieezadeh Abadeh, Viet Anh Nguyen, Daniel Kuhn, and Peyman M Mohajerin Esfahani. Wasserstein distributionally robust kalman filtering. Advances in Neural Information Processing Systems, 31, 2018.

- [18] Shixiong Wang. Distributionally robust state estimation for nonlinear systems. IEEE Transactions on Signal Processing, 70:4408–4423, 2022.

- [19] Bingyan Han. Distributionally robust kalman filtering with volatility uncertainty. arXiv preprint arXiv:2302.05993, 2023.

- [20] Kyriakos Lotidis, Nicholas Bambos, Jose Blanchet, and Jiajin Li. Wasserstein distributionally robust linear-quadratic estimation under martingale constraints. In International Conference on Artificial Intelligence and Statistics, pages 8629–8644. PMLR, 2023.

- [21] Jean-Sébastien Brouillon, Florian Dörfler, and Giancarlo Ferrari-Trecate. Regularization for distributionally robust state estimation and prediction. IEEE Control Systems Letters, 2023.

- [22] Liviu Aolaritei, Nicolas Lanzetti, and Florian Dörfler. Capture, propagate, and control distributional uncertainty. arXiv preprint arXiv:2304.02235, 2023.

- [23] Liviu Aolaritei, Nicolas Lanzetti, Hongruyu Chen, and Florian Dörfler. Uncertainty propagation via optimal transport ambiguity sets. arXiv preprint arXiv:2205.00343, 2022.

- [24] Dimitris Boskos, Jorge Cortés, and Sonia Martínez. High-confidence data-driven ambiguity sets for time-varying linear systems. IEEE Transactions on Automatic Control, 2023.

- [25] Dimitris Boskos, Jorge Cortés, and Sonia Martínez. Data-driven ambiguity sets with probabilistic guarantees for dynamic processes. IEEE Transactions on Automatic Control, 66(7):2991–3006, 2020.

- [26] Bart PG Van Parys, Daniel Kuhn, Paul J Goulart, and Manfred Morari. Distributionally robust control of constrained stochastic systems. IEEE Transactions on Automatic Control, 61(2):430–442, 2015.

- [27] Peter Coppens and Panagiotis Patrinos. Data-driven distributionally robust MPC for constrained stochastic systems. IEEE Control Systems Letters, 6:1274–1279, 2021.

- [28] Mathijs Schuurmans and Panagiotis Patrinos. A general framework for learning-based distributionally robust MPC of markov jump systems. IEEE Transactions on Automatic Control, 2023.

- [29] Anushri Dixit, Mohamadreza Ahmadi, and Joel W Burdick. Distributionally robust model predictive control with total variation distance. IEEE Control Systems Letters, 6:3325–3330, 2022.

- [30] Licio Romao, Ashish R Hota, and Alessandro Abate. Distributionally robust optimal and safe control of stochastic systems via kernel conditional mean embedding. arXiv preprint arXiv:2304.00644, 2023.

- [31] Cédric Villani. Optimal Transport: Old and New. Springer-Verlag Berlin Heidelberg, 2009.

- [32] Alison L Gibbs and Francis Edward Su. On choosing and bounding probability metrics. International statistical review, 70(3):419–435, 2002.

- [33] Liviu Aolaritei, Boubacar Bangoura, Nicolas Lanzetti, Saverio Bolognani, and Florian Dörfler. Hedging against black swans in renewable energy markets via distributionally robust optimization. Work in Progress, 2023.

- [34] Francesco Bullo. Lectures on network systems, volume 1. Kindle Direct Publishing Seattle, DC, USA, 2020.

- [35] Timothy John Sullivan. Introduction to uncertainty quantification, volume 63. Springer, 2015.

- [36] Tyler Summers and Maryam Kamgarpour. Distributionally robust bootstrap optimization. arXiv preprint arXiv:2112.13932, 2021.

- [37] Nicolas Fournier and Arnaud Guillin. On the rate of convergence in Wasserstein distance of the empirical measure. Probability Theory and Related Fields, 162(3-4):707–738, 8 2015.

- [38] Yongxin Chen, Tryphon T Georgiou, and Michele Pavon. Optimal transport in systems and control. Annual Review of Control, Robotics, and Autonomous Systems, 4:89–113, 2021.

- [39] Daniel Owusu Adu, Tamer Başar, and Bahman Gharesifard. Optimal transport for a class of linear quadratic differential games. IEEE Transactions on Automatic Control, 67(11):6287–6294, 2022.

- [40] Rahul Singh, Isabel Haasler, Qinsheng Zhang, Johan Karlsson, and Yongxin Chen. Inference with aggregate data: An optimal transport approach. arXiv preprint arXiv:2003.13933, 2020.

- [41] Antonio Terpin, Nicolas Lanzetti, and Florian Dörfler. Dynamic programming in probability spaces via optimal transport. arXiv preprint arXiv:2302.13550, 2023.

- [42] Amirhossein Taghvaei and Prashant G Mehta. Optimal transportation methods in nonlinear filtering. IEEE Control Systems Magazine, 41(4):34–49, 2021.

- [43] Vishaal Krishnan and Sonia Martínez. A probabilistic framework for moving-horizon estimation: Stability and privacy guarantees. IEEE Transactions on Automatic Control, 66(4):1817–1824, 2020.

- [44] Max Emerick and Bassam Bamieh. Continuum swarm tracking control: A geometric perspective in Wasserstein space. arXiv preprint arXiv:2303.15638, 2023.

- [45] Karthik Elamvazhuthi, Piyush Grover, and Spring Berman. Optimal transport over deterministic discrete-time nonlinear systems using stochastic feedback laws. IEEE control systems letters, 3(1):168–173, 2018.

- [46] Isin M Balci and Efstathios Bakolas. Exact SDP formulation for discrete-time covariance steering with Wasserstein terminal cost. arXiv preprint arXiv:2205.10740, 2022.

- [47] Vignesh Sivaramakrishnan, Joshua Pilipovsky, Meeko Oishi, and Panagiotis Tsiotras. Distribution steering for discrete-time linear systems with general disturbances using characteristic functions. In 2022 American Control Conference (ACC), pages 4183–4190. IEEE, 2022.

- [48] Filippo Santambrogio. Optimal Transport for Applied Mathematicians. Birkhäuser, Cham, 2015.

Appendix A Proofs

A.1 Proofs for Section 3

Proof of Lemma 2.

We start with the proof of the inclusion . We consider , and we want to prove that , i.e., the marginals of are and . For any Borel and bounded test function , we have that

and therefore , i.e., the first marginal of is . Analogously, .

We now prove . We consider and seek such that . For this, let , and . Since and , the Gluing Lemma [48, Lemma 5.5] ensures the existence of a measure satisfying and In particular, -a.e., since

Analogously, -a.e.. Consider now . We show that this is the probability distribution that we are looking for. In particular, since, for any Borel and bounded test function , we have that

which shows that . Analogously, . Finally, we show that . This follows from

for any Borel and bounded test function . Here, we used that -a.e.. This concludes the proof. ∎

Proof of Proposition 3.

Proof of Theorem 4.

We start by proving (7). Let . To establish that , we use (3):

| (38) |

Before proceeding with the proof, we highlight that the chain of equivalences (38) cannot be used to get equality of sets in (7). The reason for this is that not all the probability distributions in the ambiguity set can be written as the pushforward of a probability distribution over . This will become more clear for injective maps, in the proof of (9).

We will now prove the bijective case (8). The inclusion follows directly from (7), by considering , since . We will now prove the converse inclusion, i.e., :

where the inclusion follows from (7) reversing and .

We now proceed to the injective case (9). Similarly to the bijective case, notice that the inclusion follows directly from (7), with . Thus, we only have to prove that . Towards this end, we start by proving the inclusion . This follows immediately from since

We now focus on the converse direction:

We will now prove the surjective case (10). We start with the inclusion :

Proof of Theorem 6.

The linear structure, together with the translation invariance and orthomonotonicity of the transportation cost, allows us to prove the following relationship:

| (39) |

for an arbitrary matrix . In the nonlinear case, we did not have such a relationship, since there is no pseudoinverse for an arbitrary nonlinear transformation . Indeed, the equivalent of (39) for a nonlinear transformation is (7).

We will now prove the inclusion (39). Let . Then, can be shown as follows:

where the inequality follows from orthomonotonicity of and being the orthogonal projector onto :

With (39), we can now prove the chain of relationships (13). We start with the inclusion :

where the first equality follows from the definition of pseudoinverse (). We now prove the equality . The inclusion follows from

The converse inclusion follows from

Finally, follows from (39):

This concludes the proof for a general matrix .

We now focus on the full row-rank case and show with being the right inverse of . In virtue of (13), it suffices to prove that Let and be an optimal plan satisfying Define the coupling . For clarity, we define by , points in , by , points in , and by , points in . By the Finite Rank Lemma, and , i.e., each can be uniquely decomposed in with and is the orthogonal projection on . Thus, we see and as maps and , respectively. By the Disintegration Theorem [48, §2.3], there exists a -a.e. uniquely determined family of probability distributions on , such that Similarly, there exists a -a.e. uniquely determined family of probability distributions on , such that Consider now the probability distribution on defined by

We show that and . Notice that this is enough to conclude the proof. For any Borel and bounded test function , we have

showing that . In the rest of the proof, we will show that . For this, we first define the coupling

With the test function , we see -a.e.. We now claim . Indeed, for any Borel and bounded test function , we have

showing that the first marginal of is , and

showing that the second marginal of is . Finally, follows from

This concludes the proof of the inclusion and, with it, the proof of Theorem 6. ∎

A.2 Proofs for Section 4

Proof of Lemma 9.

Let . We want to show that is a coupling between and . For any Borel and bounded test function , we have

showing that the first marginal of is . Analogously, the second marginal of is . ∎

Proof of Proposition 10.

Proof of Theorem 11.

To start, 2(ii) implies that satifies triangle inequality. The proof follows analogously to the one of triangle inequality of the type- Wasserstein distance [48, Lemma 5.4]. Then, let and . This implies that and . Then,

where the first inequality follows from the triangle inequality. Thus, and (17) follows. ∎

Proof of Lemma 14.

Let . We want to show that is a coupling between and . For any Borel and bounded test function , we have

showing that the first marginal of is . Analogously, the second marginal is . ∎

Proof Proposition 15.

Proof of Theorem 16.

As in the proof of Theorem 11, 3(ii) ensures triangle inequality for . Then, let and ; i.e., and . Then,

where the first and the fourth inequality follow from the triangle inequality of the OT discrepancy. This establishes (20). ∎

A.3 Proofs for Section 5

Proof of Proposition 18.

We prove the three cases separately.

3) We prove the statement by induction. The base case is trivial. Suppose then the statement holds for . Then, since the element-wise product induces the Hadamard product of distributions and the sum induces the convolution of distributions, we have Since , we have that belongs to

where the first inclusion follows Theorem 6, the second from (since ), the third from Theorem 16 and Corollary 17 (since satisfies 3 with ), and the last one from Theorem 11 (since satisfies 2 with ). ∎

Proof of Proposition 20.

We first claim that , with as in the statement. If this is true, , and the result follows from Theorem 6. Since the transformation is surjective and is translation-invariant and orthomonotone, (14) implies that

with being the right inverse of . Notice that is an OT ambiguity set of probability distributions over . Then, . We now prove . A standard modal decomposition of gives for all . For any continuous and bounded test function , dominated convergence gives Then, (32) follows from and the definition of OT ambiguity set. If additionally , , which establishes (33). ∎