Spectral Analysis and Preconditioned Iterative Solvers for Large Structured Linear Systems

Nikos Barakitis

ATHENS UNIVERSITY OF ECONOMICS AND BUSINESS

SCHOOL OF INFORMATION SCIENCES AND TECHNOLOGY

DEPARTMENT OF INFORMATICS

Acknowledgment

I would firstly like to thank my supervisor, Associate Professor Paris Vassalos and my advisor, Professor Stefano Serra-Capizzano, for the unlimited help and support they offered to me during my studies. I would also like to thank Emeritus Professor Evaggelos Mageirou for his throughout invaluable help and guidance, and my advisor Professor Dimitrios Noutsos for being member of the advising commitee and generously sharing ideas with the team.

I would also like to thank my collaborator researchers, Sven-Erik Erkstrom and Paola Ferrari for the fruitful collaboration we had, and their patience.

Finally, I would like to thank Associate Professor Stavros Toumpis and Professor Panagiotis Katerinis for their attitude toward me at several moments which helped me to build my self confidence and made me to believe that the completion of this dissertation could be feasible.

Thank you,

Nikos Barakitis, Athens 2021.

Introduction

The use of iterative methods for solving large structured linear systems has been of interest for more than half a century, and the development of the field has gone together with the improvement of computer systems. In fact, the solution of a large linear system of the form

| (1) |

where the size of is and is a column vector of size , is often the central and most time- and storage-consuming part of the computation.

Iterative methods for solving linear systems first appeared in the works of Gauss, Seidel, and Jacobi in the 19-th century, with further progress in these methods being made in the first half of the 20-th century. These methods are typically referred to as stationary, as opposed to the other classes of iterative techniques that appeared later and relied on solution searches in Krylov subspaces. For the latter methods, the story began in 1952 with the development of the conjugate gradient (CG) method [30]. This method was proposed for solving symmetric and positive-definite linear systems. Initially, it was considered a direct method, because it was proved analytically to reach the exact solution in at most steps, or actually in as many steps as the number of distinct eigenvalues of the coefficient matrix. However, in practice, owing to the limited accuracy of floating-point arithmetic, especially in presence of ill-conditioning the method requires more iterations than expected for a satisfactory approximation of the solution. Besides this, when considered as a direct method, it required more arithmetic operations than the Gauss elimination. This method has remained out of interest for two decades. As applications required larger linear systems to be solved, the poor computational escalation of direct methods was overshadowed by the rapid improvement of computers and the evolution of computational methods.

This attitude regarding CG changed in the 70s following a publication from J. Reid [58]. Thereafter, it became clear that for well-conditioned systems, the number of steps that the CG requires to reach the solution with a given accuracy is independent of the size of the system. This work brought Krylov methods back into the focus of the research community. The list of Krylov methods, limited until then, was enriched with methods for non-definite symmetric systems [e.g., the minimum residual method (MINRES) [51]] and methods for non-symmetric systems [e.g., the generalised minimum residual method (GMRES) [61]].

Published by O. Axelson and G. Lindskog in 1986 [2]. Since then, the paper has been included in the references of almost every work relating to the solution of linear systems using iterative Krylov-subspace-theory based methods. In this study, it was proved that the efficiency of the preconditioned CG method depends on the clustering of the eigenvalues of the preconditioned matrix, which are clustered at and yet certainly far from zero. The notion of eigenvalue clustering will be defined later: Hereafter, preconditioning was officially upgraded to the first research target in the field numerical solution of linear systems.111It must be mentioned here that for methods such as the Generalized Minimum Residual method, applied to non-symmetric systems, the eigenvalue distribution may not exactly describe the convergence[19]. However, in every case, a clustered spectrum and a minimal eigenvalue far from zero ensure fast convergence of the method..

Preconditioning of a linear system refers to the replacement of the system (1) with

for left, split, and right preconditioning, respectively. In each case, the preconditioned matrix has a better condition number and superior spectral properties to the original one. For preconditioning to be feasible, the preconditioner must have two somewhat contradictory properties:

-

•

The preconditioned system must be easily solvable.

-

•

The determination and the application of the preconditioner must be easy.

The first property suggests that the preconditioner must be fairly close to the coefficient matrix of the system; however, this is generally difficult to solve and contradicts with the second property. To conclude, the next phrase, taken from [60], summarises a view widely adopted in the research community:

”Finding a good preconditioner to solve a given sparse linear system is often viewed as a combination of art and science.”

In general, two classes of preconditioning techniques are available. The first includes purely algebraic methods that use only the information contained in the coefficient matrix. Such methods are typically based on some type of incomplete factorisation or some type of sparse approximate inverse of the coefficient matrix [6, 60]. These methods achieve reasonable efficiency for a wide range of problems; however, they might not be the optimal choice for any one particular problem. The other class of methods, primarily applicable to problems arising from PDEs, involves the design of algorithms that are problem-specific. Such methods might be optimal for any specific problem; however, they require complete knowledge of the problem in advance, especially from a spectral point of view. In these methods, the preconditioners are selected by specific classes of matrices; furthermore, for their construction, a detailed spectral analysis of the coefficient matrix is required.

In the first part of this thesis, preconditioning strategies to solve (using Krylov subspace methods) linear systems arising from two specific problems are proposed. In the first problems, the coefficient matrix of the system emerges as an analytic function of a real Toeplitz matrix. This strategy utilises symmetrisation and preconditioning of the coefficient matrix. Preconditioners are selected from matrix algebras according to the spectral properties of the symmetrised coefficient matrix sequence. The properties of the matrix sequence are extensively analyzed. The second class of problems involves the numerical solution of partial differential equations with a fractional derivative order. These problems have been thoroughly investigated in recent years; however, a new category of preconditioners is here proposed. The new class of preconditioners exhibits optimal behaviour in relation to the proposals given so far in the literature, especially in dimensions of more than one. This behaviour is theoretically confirmed by the numerical results.

The first part of this thesis is structured as follows: The first chapter introduces all the necessary definitions and summarises the theory used to analyse the spectral properties of the coefficient matrix sequences. In the second chapter, the problem of symmetrising the large matrices that emerge as analytic functions of real Toeplitz matrices is considered. In the third chapter, is studied the numerical solution of fractional partial differential equations.

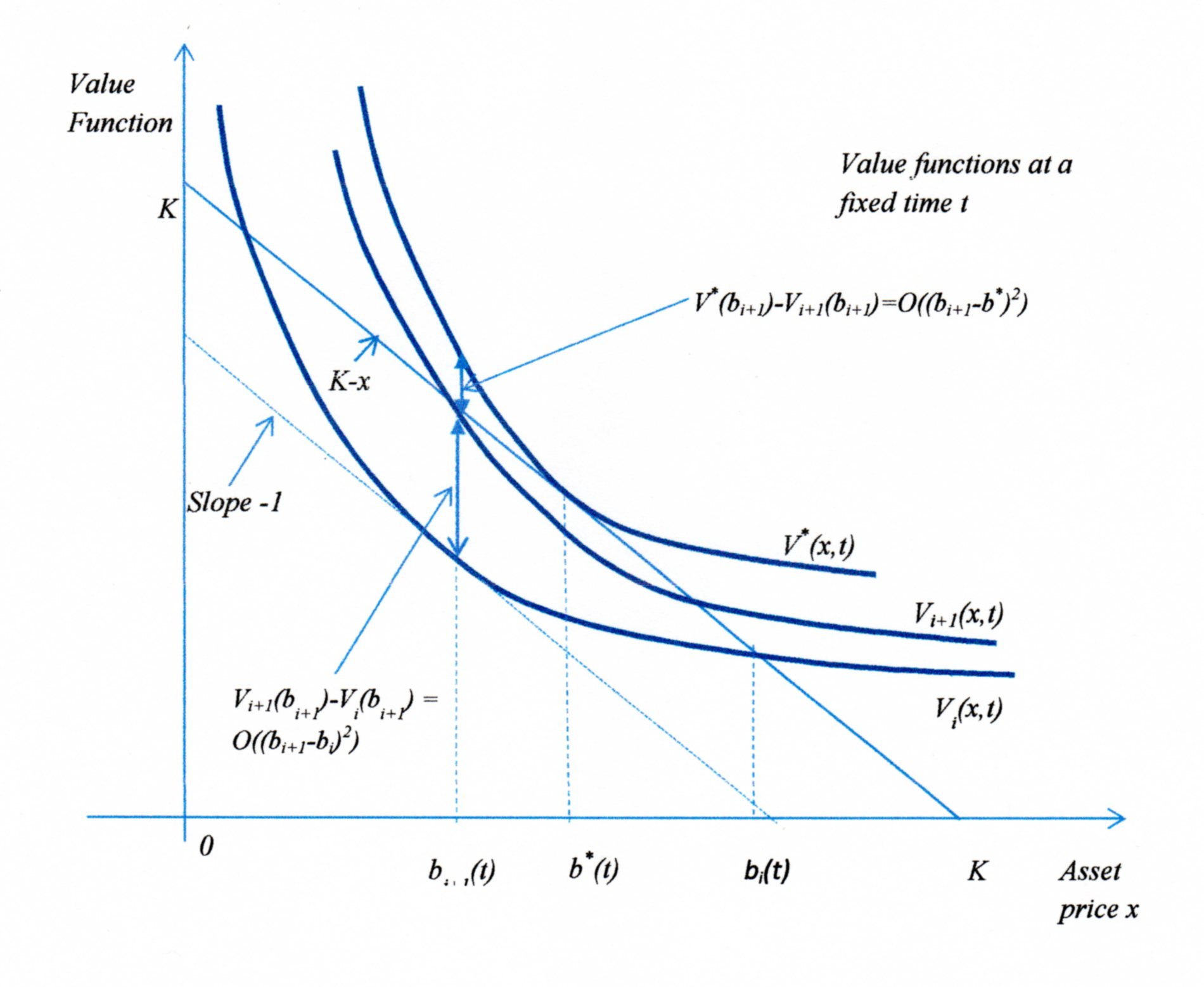

In the second part the numerical solution of a problem arising in finance is considered. In detail a numerical technique based again on an iterative algorithm is used for pricing an American put option. A put option is a financial derivative that gives the right (but not the obligation) to the holder to sell an asset for a pre-specified price , the exercise or strike price. The other party, the writer of the option, must accept the sale for the exercise price regardless of the current price of the asset at the time of exercise. The right can be exercised either only on the pre-determined expiry or maturity date in case of the European put option, or any day up to the pre-determined expiry date in the American put option. In any case, because the holder does not have an obligation to sell, the right will be exercised only if the current price is lower than . In this case, the profit of the seller will be .

Since they were invented, such rights have been traded on the market as assets; therefore, a fair pricing process is needed. In a viable, where arbitrage opportunities are not allowed market model, the value of such a right at time before the maturity date should be equal to the price of a portfolio which has the same expected payoff value as the option at the exercise date at time . For the European put option, it has been shown that the fair price at time before the maturity date and for asset price must satisfy the Black–Scholes equation. At maturity time , the value of the option must be equal to the payoff function.

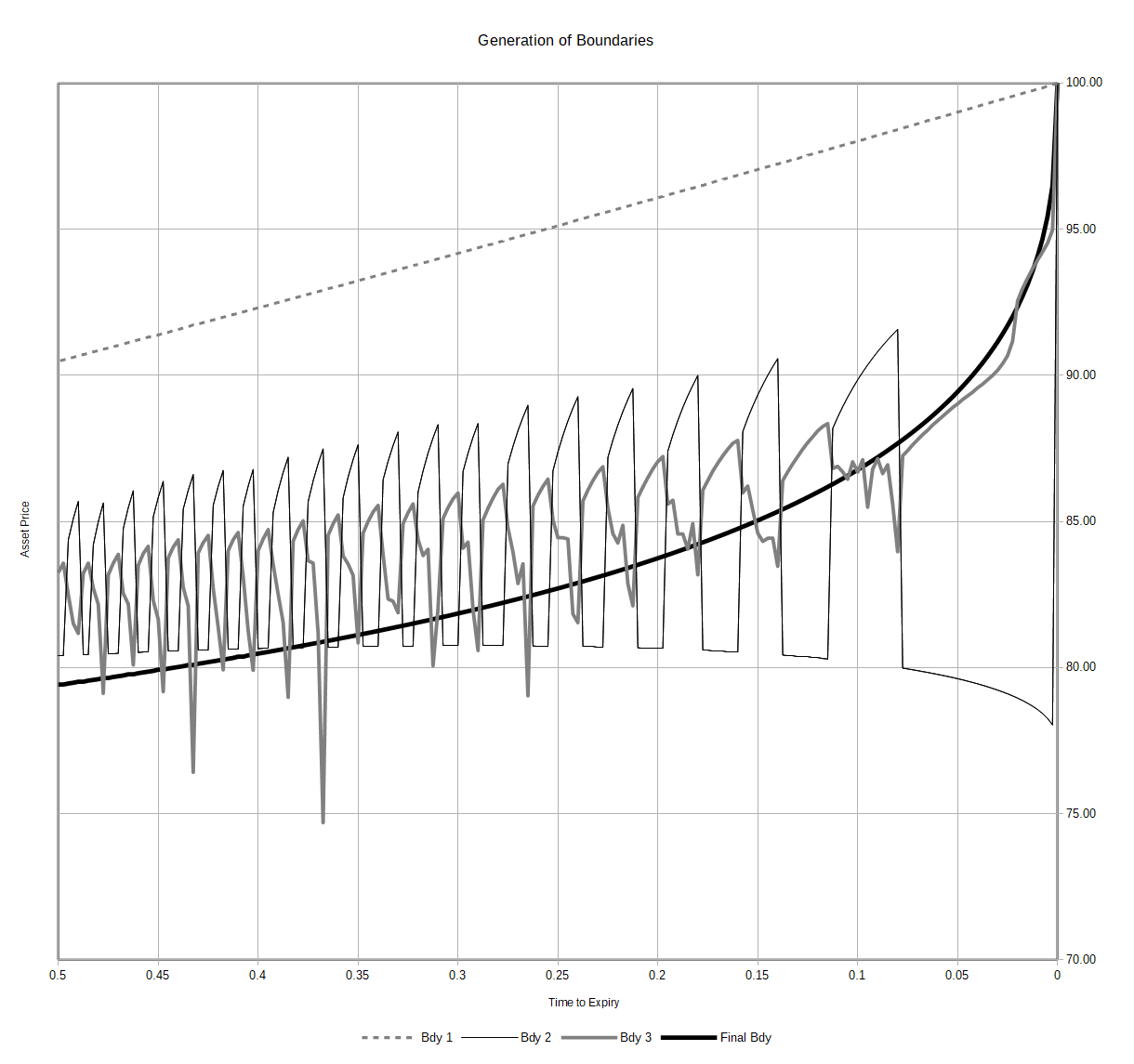

Despite the similarities between the two types of put options, the American put, compared with the European put, gives its holder the additional advantage in that it can be exercised any day before the maturity date, thereby offering them additional profit opportunities. It is fair, therefore, that this privilege should be taken into account in the pricing process of the option. Moreover, according to the process in which the price of the option at time is equal to the price of a portfolio (with the same expected payoff on the exercise day) at time , all the possible exercise times between should be taken into account. Although many of the characteristics of the value function of an American put option have been extensively analysed the pricing of such an options is a problem that has not yet been solved analytically.

Taking advantage of the known characteristics of the optimal value function, the iterative algorithm presented here, which utilises the principles of dynamic programming, iteratively improves exercise policies, obtains monotonically increasing value functions and converges quadratically under reasonable assumptions. The exact meaning of a policy will be defined in relevant chapter.

Part I Spectral Analysis and Preconditioned Iterative Solvers for Large Structured Linear Systems

Chapter 1 Generalized Locally Toeplitz Matrix Sequences

As mentioned in the introduction, the preconditioners for a large class of linear systems are constructed following analysis of the properties of the initial problem, which relate to the effective application of iterative methods. These properties include the condition number, asymptotic distribution of the eigenvalues, and singular values of the system coefficient matrix sequence. The theory used here to study matrix sequences is that of generalised locally Toeplitz (GLT) matrix sequences. This theory unifies, and essentially provides all the tools needed to study the asymptotic behaviour of the eigenvalues and singular values of matrix sequences obtained from the discretisation of differential or integral equations (as well as more besides).

The theory was introduced in Paollo Tilli’s paper on locally Toeplitz (LT) matrix sequences [71]. The idea was further developed by Stefano Serra-Capizzano in [67, 68] and also in a series of subsequent papers. A complete presentation of the theory can be found in [15, 16]. In the following, we define a matrix sequence as a sequence of the form , where and . The abbreviations LT and GLT matrix sequences denote locally Toeplitz and generalised locally Toeplitz matrix sequences, respectively.

1.1 Singular Value, Eigenvalue Distribution, and Clustering of Matrix Sequences

Definition 1.1.

Let be a function and be a matrix sequence. has an eigenvalue distribution described by , and we write if

| (1.1) |

where is the Lebesgue measure of , and is the set of all continuous functions defined on , whose support111The support of a function , denoted by , is the set is a closed and bounded subset of .

We say that has a singular value distribution described by , and we write if

| (1.2) |

where and is the set of all continuous functions defined on , whose support is a closed and bounded subset of .

Intuitively speaking, if the matrix sequence has an eigenvalue distribution described by , then under the condition that is continuous 222a.e.: almost anywhere. If is not continuous over a set of zero measures at most, then is continuous almost anywhere., the properly rearranged eigenvalues are close to a sampling of on an equispaced grid on . This definition allows eigenvalues to be out of the range of ; however, the total number of such eigenvalues is at most . The same is true in the singular value case.

Remark 1.1.

If is a normal matrix for all , then implies that , because every singular value of each matrix is the absolute value of the corresponding eigenvalue of that matrix.

In the following definition, the notion of the expansion of a set is used. The expansion of the set is defined as , where is the disc centred at with radius

Definition 1.2.

If is a matrix sequence and , we say that the eigenvalues of are strongly clustered at if, for every and every , the total number of eigenvalues of outside of is bounded by a constant which does not depend on . That is, for every , we have that

| (1.3) |

We say that the eigenvalues of are weakly clustered at if, for every and every , the total number of eigenvalues of outside of is bounded by a function . That is, for every , we have that

| (1.4) |

We similarly define the notion of the strong and weak clustering of singular values of a matrix sequence on a subset of .

Theorem 1.1.

If the distribution of eigenvalues of is described by , then the eigenvalues of the matrix sequence are weakly clustered in the essential range of 333The essential range of a function , denoted by , is the set , for which . Therefore, if takes a value outside , then ..

1.2 Approximation in Space of Matrix Sequences

The basic tool used in the theory of GLT matrix sequences to determine the eigenvalue and singular value distributions and clusters of a matrix sequence is the closeness of the sequence with others whose distributions and clusters are already known. The theorems presented in this section indicate the direction in which the concept of closeness between two matrix sequences should be defined to obtain identical eigenvalue and singular value distribution and clusters. (See [15] for more details.)

Definition 1.3.

A matrix sequence is said to be sparsely vanishing if for every there exists such that, for ,

where .

Theorem 1.2.

Let and be two matrix sequences for which, under a sufficiently large , . Then, the following apply:

-

•

If the singular values of are clustered at , then the singular values of are also clustered at the same set. If the matrices of the two sequences are Hermitian, the same is true for the eigenvalues.

-

•

If , then . If the matrices of the sequences are Hermitian, then implies . The above assertions apply even if .

-

•

If the matrices of are invertible, and if furthermore for every , the eigenvalues of are strongly clustered at .

-

•

If the condition is replaced by the relaxed one,

then all the above apply, with the difference being that the eigenvalues (singular values) of are weakly clustered at sets that are clustered, weakly or strongly, the eigenvalues (singular values) of . The eigenvalues (singular values) of are weakly clustered at , if is sparsely vanishing [66].

Proof.

To prove the first assertion, we consider the case in which the matrices of the sequences are Hermitian. Then, we assume that the eigenvalues of are clustered at a set , and that when is sufficiently large, . Thus, we have

where the first inequality comes from the well-known theorem of Hoffman and Wielandt. For any , we define . Then,

Let be the total number of elements of . Then, we have . That is, there are at most pairs of eigenvalues such that

If is the number of eigenvalues of lying outside and , respectively, for , then

The bound does not depend on , because we assume strong clustering at for the eigenvalues of .

If the matrices of the sequences are non-Hermitian, we define

which are Hermitian, and their eigenvalues are and , respectively. In addition, 444If is a singular value decomposition of the matrix and , then the unitary matrix that diagonalizes is .. Therefore, because the assumption of the theorem is satisfied, by applying the above arguments to the modified sequences and , we can conclude that the singular values of and are clustered in the same sets.

To prove the second inequality under the condition that , we first assume that the matrices of the sequences are Hermitian. Again, we define

For , , and the total number of its elements is at most ; for , we have

where is the modulus of continuity of , 555The modulus of continuity of a function is defined as ..

Remark 1.2.

The existence of in the representation of must be interpreted as follows. If we want , we can take a value of that is sufficiently small for and a value of large enough that .

If the matrices of the sequences are non-Hermitian, we apply the above conclusion to the modified sequences and , for which—as previously mentioned—it follows that and their eigenvalues are and , respectively. Therefore, for every , and for a sufficiently large , we have

If, in the above equation, we limit the test functions to , we obtain the desired result.

To prove the third inequality , we need the following propositions.

Proposition 1.2.1.

For every matrix , .

If is the Schur form of the matrix, is a complex, upper triangular matrix with eigenvalues of on its diagonal, and is the singular value decomposition, we have

Proposition 1.2.2.

If , then .

In this case, if is the -th column of , we have

Thus, we write

Using Proposition 1.2.2 and the assumptions of the theorem, we have

meanwhile, from Proposition 1.2.1, we have

Using the same arguments as in the proof of the first part, we deduce that, for every , a maximum of (independent of ) eigenvalues of are greater in absolute value than . Therefore, the eigenvalues of are clustered at , and the eigenvalues of are clustered at .

To prove the last part, it only needs to replace the constant in the three proofs above with a function which is of . Then, following the same steps as the proof of the first part, we deduce that the eigenvalues (singular values) of are weakly clustered at the same set where the eigenvalues (singular values) of are. Accordingly, we deduce that the eigenvalues of are weakly clustered at and those of are clustered at . The proof of the second part is entirely unaffected, because if is constant, and is a function, then

Theorem 1.3.

Let and be two matrix sequences, for which we have that, for every , where does not depend on . Then, the following apply:

-

•

If the singular values of are clustered at a set , the singular values of are also clustered at the same set. In addition, the singular values of one of the matrix sequences are strongly clustered at a set if and only if the same applies for the singular values of the other sequence. If the matrices of the sequences are Hermitian, the same holds for the eigenvalues of the sequences.

-

•

If , then . If the matrices of the sequences are Hermitian and , then .

-

•

If every matrix of is invertible, then the eigenvalues of are strongly clustered at .

-

•

If the condition is replaced by , the eigenvalues (singular values) of are weakly clustered at the sets where the eigenvalues (singular values) of are clustered. The eigenvalues of are also weakly clustered at . Furthermore,

meanwhile, if the matrices of the sequences are Hermitian,

Proof.

To prove the first part, we assume that the matrices of the sequences are Hermitian. Then,

where and are symmetric and positive definite, with

From Weyl’s theorem and conclusions deduced therefrom, we have

Therefore, the number of eigenvalues of lying outside for some set can differ from

the number of eigenvalues of lying outside , at a maximum of . If the matrices of the sequences are Hermitian, we use the sequences and , as in the previous theorem. Then, using the same arguments, we deduce that the singular values of the initial sequences are clustered in the same sets.

To prove the second assertion, we again assume that the matrices of the sequences are Hermitian. According to Lemma 3.3 in[73], it is enough to prove that the condition

is met for each indicator function , where if , else 666Every continuous function with bounded suport can be approximated by a simple staircase function of the form . From the first part of the theorem, we deduce that the total number of eigenvalues of the two sequences lying inside an interval can differ at a maximum of . This means that

and so the conclusion applies to all continuous with bounded support functions. This conclusion is also valid for the case in which . Analogous to the previous theorems, we can expand the conclusion to the case in which the matrices are non-Hermitian, and we conclude that the sequences have the same singular value distribution.

For the third assertion, we only have to observe that

where .

If , the total number of eigenvalues of lying outside of for a set can differ from the number of eigenvalues of lying outside of at a maximum of . Thus, we can conclude that has weakly clustered eigenvalues (singular values), even in sets where the eigenvalues (singular values) of are strongly clustered. Similarly, the eigenvalues of are weakly clustered at . The proof of the second part is unaffected, because

Theorem 1.4.

Let us suppose that and are two matrix sequences, for which and for a sufficiently large we have

Then,

-

•

If the singular values of are clustered at a set , then the singular values of are weakly clustered at the same set. If the matrices of the sequences are Hermitian, the same is valid for the eigenvalues.

-

•

Furthermore,

whereas for Hermitian sequence matrices,

Proof.

Applying Theorem 1.3 to sequences and , we conclude that the eigenvalues (singular values) of are clustered in the same sets and have the same distribution as the eigenvalues (singular values) of . Then, applying theorem 1.2 to sequences and , we conclude that the eigenvalues (singular values) of are clustered at the same sets and have the same distribution as the eigenvalues (singular values) of , and consequently with those of .

1.3 Approximating Classes of Sequences

Remark 1.3.

In the space of matrix sequences, we define the operations of summation, multiplication, and scalar multiplication as an extension of the corresponding matrix operations. Analogously, we define the conjugate transpose of a matrix sequence. In other words, if are matrix sequences, then and , then

According to Theorem 1.4, two different matrix sequences have the same singular value distribution and clusters (or eigenvalue distribution if their matrices are Hermitian) if their difference can be written as the sum of two matrix sequences, as follows: The rank of the matrices of the first sequence and the Frobenius norm of the matrices of the other sequence are small compared with their size. Thus, we define the concept of convergence of matrix sequences in the context of the theory of approximating classes of sequences. Therefore, the spectral properties of the limit sequence are drawn from the spectral properties of the sequences that constitute the tail of the sequence of matrix sequences. In what follows, the abbreviation a.c.s is used for approximating classes of sequences.

Definition 1.4.

Let be a matrix sequence and be a sequence of matrix sequences. We say that is an a.c.s. for , and we write if, for every , there exists an such that, for ,

| (1.5) |

where depends only on , and . denotes the spectral norm.

Proposition 1.3.1.

The sequence of matrix sequences is an a.c.s. for if and only if, for every , there exists an such that for every , there exists an such that for every , we have .

According to this definition, it is clear that, as , the difference between the sequences and can be analysed in two sequences, as follows: The rank of the matrices of the first sequence is asymptotically small compared to the matrix size, whereas the size of the matrices of the other sequence is small weighted in the norm. That is, as , the conditions of Theorem 1.4 are exactly met, with the difference that in the theorem, the Frobenius norm is used instead of the spectral norm used in the definition of the a.c.s.. However, this difference is of minor importance, as stated in the following proposition.

Proposition 1.3.2.

Let be a matrix sequence and be a sequence of matrix sequences. Then,

where , if and only if,

where and .

Proof.

To prove the direct, we set

Applying the equivalent definition of a.c.s. (Proposition 1.3.1) (i.e., for every , there exists an such that for , we have and ), we find that, for ,

which completes the proof. To prove the opposite, we observe that if , then

Because p is the total number of singular values of that exceed , we can write , where and . Then, we set

and the proof is complete.

The consequences and importance of the above definition are summarised in the two theorems that follow.

Theorem 1.5.

Let be a matrix sequence and be a sequence of matrix sequences such that . Let and

Thus, .

Theorem 1.6.

Let be a matrix sequence and be a sequence of matrix sequences such that Hermitians. Let and

Then, .

The proof of the two theorems is a direct consequence of the definition of the a.c.s sequences and Theorem 1.4. As , the requirements of the theorem are satisfied, and the singular value distribution (eigenvalue distribution) of is close to that of . Therefore, for the singular value case and for , we have

We have proven that the first term in the above sum has a limit at zero as , whereas the second term has a limit at zero for each as , by definition. The difference between the two integrals has a limit at zero as , because of the requirement that in the measure of the two theorems. A similar situation occurs in the eigenvalue case.

It must be mentioned that these two theorems can be proven without changing the norm to , though this proof is rather technical and straightforward. The approach used here has been chosen to clarify the two directions and the corresponding tolerance limits of deviation allowed between nearby elements in the space of matrix sequences. In the following proposition, are summarised the algebraic properties of the a.c.s. sequences.

Proposition 1.3.3.

Let , be matrix sequences, , and

-

•

,

-

•

.

Then,

-

•

,

-

•

.

-

•

Suppose that, for each , the total number of singular values of that are further from as is bounded by a function , where ; the same applies for . Then

.

1.3.1 Zero Distributed Sequences

A central role in the theory of approximation in the space of matrix sequences and in the theory of GLT matrix sequences is played by the class of matrices whose singular values are distributed to zero. The exact definition of the class and the theorem that uses the conclusions of a.c.s are as follows:

Definition 1.5.

We say that a matrix sequence is zero distributed if . That is,

It can be shown that a matrix sequence is zero-distributed if and only if

or, equivalently,

A matrix sequence is zero distributed if and only if

If is zero distributed, and the matrices of the sequence are Hermitian, then , because in that case, . Clearly, in that case,

and

Theorem 1.7.

Let , , and be matrix sequences, where is zero distributed and also applies that . Then,

If the matrices of the sequences are Hermitian,

Proof.

Let (where ) represent the singular value decomposition of . We define

where is the indicator function of . In other words, the singular values of are the singular values of which are greater than or equal to , while the remainder are zero. The singular values of are the values of which are less than , whilst the others are zero. We now define

Clearly, . Let and . By definition, if , then . In addition, because is zero distributed, such that if , . Thus, .

From the above, it is clear that . Then, applying Theorem 1.5 for , we deduce that . If the matrices are Hermitian, we follow the same steps using eigenvalues instead of singular values and apply Theorem 1.6; thus, we deduce that .

1.4 Circulant and Toeplitz Matrices

Circulant matrices are those of the form

Circulant matrices are diagonalised using the unitary discrete Fourier transform. Their spectrum is known; furthermore, because of their properties, they play a major role in the analysis and design of techniques for solving structured linear systems. Here, in addition to presenting their basic properties, they are used as an example of the use of a.c.s. theory to analyse the distribution of Toeplitz matrix sequences.

Let be a unitary discrete Fourier transform. That is,

| (1.6) |

It is known that , where is the conjugate transpose operator.

If is the column , then

because . Taking the common factor for at the -line, the above becomes

where and .

Now, we assume a trigonometric polynomial of order , , and a circulant matrix of size (with ), , whose elements are defined as follows:

| (1.7) | ||||

| (1.8) | ||||

| (1.9) |

Then, the eigenvalues of according to the above are for . However, then we have

Finally, the eigenvalues of are the values of at the points ; in other words, the eigenvalues of the matrix constitute a uniform sampling of the function at the interval . It is clear that the eigenvalues of are distributed as . Because the matrix is normal, the same applies to its singular values. To summarise,

| (1.10) |

1.4.1 Toeplitz Matrices and Toeplitz Matrix Sequences

It is known from Fourier analysis that if is a Lebesgue integral function, defined at , and

| (1.11) |

then

The above series is called the Fourier series of the function , and it extends periodically across the real line. The coefficients are the Fourier coefficients of the function.

Definition 1.6.

The Toeplitz matrix of size , which is related to the function via , is defined as

The is referred to as the generating function of the matrix sequence .

In the following, several properties of the Toeplitz matrices are given [15]. Let , and let . Then,

-

•

.

-

•

.

-

•

If is real, then the is Hermitian and its eigenvalues are contained in the interval , where , .

-

•

if is not constant almost everywhere. Otherwise . If then almost everywhere and .

The eigenvalue and singular value distribution of the matrix sequence have been extensively studied. Initially, Szegő in [20] proved that if , then the eigenvalues of the Toeplitz matrix sequence are distributed as . Since then, this conclusion has been extended to sequences with the generating function complex [1, 54, 73, 72, 78, 17]. The results of this evolutionary research process are summarised in the following theorem, for which a proof borrowed from [15] is given here as an example of the use of a.c.s. to find the distribution of matrix sequences.

Theorem 1.8.

Let and be the Toeplitz matrix with generating function . Then,

If is real, then,

Proof.

Let be a trigonometric polynomial of order , and let be a circulant matrix of size , related to and defined as in (1.7)–(1.9). Then,

and . Then, defining

Clearly, the sequence is zero distributed, and according to Theorem 1.7, we have that

If the polynomial is real, then all the matrices are Hermitian, and using the same theorem again gives

Let now , , and . Then,

Owing to the uniform convergence of to at the interval , we have . In addition, the uniform convergence of to implies convergence in measure to in the same interval. So,

Clearly, is an a.c.s for . Provided that the other conditions of Theorem 1.5 also apply, we have that

If is real, all the matrices are Hermitian, and all the conditions of Theorem 1.6 apply. Consequently,

1.5 LT and GLT Matrix Sequences

The main source (although certainly not the only one) of problems in the case of large and typically sparse matrices is the discretisation of differential and integral equations. The structures of the matrices appearing in such problems depend on the numerical scheme selected for the discretisation of the specific differential or integral operator. Because this scheme is unchanged in terms of displacement, the matrices produced are Toeplitz. The elements of the coefficient matrix are constant over each diagonal, because the same scheme is chosen for the discretisation of the operator at each point of the unknown function’s domain. However, when the unknown function appears in the equation with a non-constant coefficient, all non-zero elements of the Toeplitz matrix are multiplied by the corresponding values of the function. In other words, a sampling of the coefficient function of the differential equation lies along the non-zero diagonals, the coefficient matrix is no longer Toeplitz, and its spectral distribution is not given by the known theorems. In the context of the GLT theory, almost every matrix sequence produced from the discretisation of a differential or integral equation can be approximated in an a.c.s sense by another matrix sequence for which the spectral distribution is known.

The basic definitions and conclusions of the theory are presented in the following subsections.

1.5.1 LT Matrix Sequences

Definition 1.7.

Let , , and . Then,

-

•

The locally Toeplitz operator is defined as an matrix,

where is the diagonal matrix of size , and the elements are a uniform sampling of in . That is,

(1.12) -

•

Provided that the function is Riemann integrable and , then we can define as a locally Toeplitz sequence, with symbol , if

For a locally Toeplitz sequence with symbol , we write .

Theorem 1.9.

Let and . Then, for each and , we apply

-

•

-

•

-

•

If are Riemann integrable777 The requirement for the function to be Riemann integrable is necessary to obtain For example, we define with if , and otherwise. In this case, is not Riemann integrable. Then, , whilst almost everywhere. and ; then,

-

•

If the matrices of the sequences are Hermitian, then are real almost everywhere, and .

The most important consequence of the classification of a matrix sequence as LT is the immediate characterisation of the distribution of its singular values, or its eigenvalues in the Hermitian case.

It can be proved that the Toeplitz matrix sequences, the sequences of diagonal matrices whose elements are a uniform sampling of a function , and the zero distributed sequences belong to LT class. More specifically,

-

•

,

-

•

for , then

-

•

.

1.5.2 GLT Matrix Sequences

A matrix sequence is GLT if it is the limit in the a.c.s. sense of a finite sum of LT sequences. That is,

Definition 1.8.

Let be a matrix sequence and be a measurable function. is a GLT sequence, with symbol ; then, we write ; if, for each , there exists a finite number of LT sequences such that

-

•

in measure,

-

•

.

On the one hand, owing to the definition of GLT sequences, it is expected that

On the other hand, sequences resulting from basic operations between GLT sequences also belong to the GLT class, with the symbol resulting from the same operations between the symbols of the initial sequences. The most important properties of the GLT sequences are summarised below.

- GLT1

-

Every GLT sequence is related with a function , , which is the symbol of the sequence. The singular values of the sequence are distributed as the function. If the matrices of the sequence are Hermitian, the eigenvalues of the sequence are distributed as the .

- GLT2

-

The set of all GLT sequences is an *-algebra. That is, it is closed under linear combinations, multiplications, conjugate transpositions, and inversions, provided that the symbol of the sequence is zero at a set of zero measure. Therefore, a sequence obtained by operations between GLT sequences is GLT with a symbol produced by identical operations between the symbols.

- GLT3

-

Every Toeplitz sequence, with generating function is GLT, with symbol .

- GLT4

-

Every diagonal matrix, whose elements are a uniform sampling of an almost everywhere continuous function is GLT with symbol .

- GLT5

-

Every zero-distributed sequence is GLT with symbol .

- GLT6

-

, if and only if there exist GLT sequences such that converge to in measure and is an a.c.s. for .

Chapter 2 Asymptotic spectra of large matrices coming from the symmetrisation of Toeplitz structure functions and applications to preconditioning

The symmetrisation of a real, non-symmetric Toeplitz system was first proposed by Jennifer Pestana and Andrew Wathen [55]. The symmetry is obtained by multiplying the system by , where

| (2.1) |

The use of Krylov subspace methods in symmetric linear systems offers significant advantages over the methods used in non-symmetric systems. For the conjugate gradient and minimum residual methods (and other similar methods), which are applied to symmetric positive definite and symmetric non-definite systems, respectively, it is known that the convergence depends on the eigenvalues of the coefficient matrix of the system. Thus, if the eigenvalue distribution of such a system is determined, it is theoretically guaranteed to converge within a number of iterations; however, there is no analogue result for methods applied to non-symmetric systems. In addition, for each iteration of the above methods, the cost is minimal, in the sense that only some table-vector multiplications are required.

The singular value and eigenvalue distribution of symmetrised matrix sequences have been studied in detail in [13, 38, 21]. The results are presented in the following sections.

2.1 Eigenvalue Distribution of Symmetrised Toeplitz Matrix Sequences

Definition 2.1.

Let be a given function defined in . We set in as follows:

| (2.2) |

Theorem 2.1.

Let with real Fourier coefficients, , as in (LABEL:anti_identity_matrix), and let be the Toeplitz matrix with generating . Then,

Proof.

The proof of the first result is trivial. Because is unitary, the singular values of match those of [Theorem 1.8]. To prove the second result, we first assume that . Then,

where is the Hankel matrix, which contains the Fourier coefficients of the function , starting from at position to at position . Analogously, is the Hankel matrix, which contains the Fourier coefficients of the function , starting from at position to at position . is exactly the Hankel matrix, with generating , as defined in [11]. For this matrix, it was proven that if is a Lebesgue integrable function, then . Because and is clearly Lebesgue integrable, . In addition , the singular values of match those of . The singular values of , because it is a block diagonal, are the singular values of the two blocks. Let be a singular value decomposition of . Then,

Now, let . Then,

where

The unitary matrix that diagonalizes is

while its eigenvalues are the same with those of with the addition of 0. Clearly, . Furthermore,

contains the Fourier coefficients of , starting from at position to at position ; thus, we observe that and is Lebesgue integrable. Therefore, and, analogously, . The rank of the second matrix is 2; hence, applying the singular values interlacing theorem for the two matrices, we deduce the sequences and ; therefore, are distributed at zero.

Then, based on Theorem 1.7 for symmetric matrices, .

2.2 Eigenvalue distribution of large matrices produced by the symmetrisation of Toeplitz structure functions

2.2.1 Matrix functions

Let the function be analytic at . Then, is analytic in an open sphere of radius centred at . Thus,

where . If with for a natural matrix norm111The natural matrix norm is any norm derived from the rule , where is a vector norm, the series converges, and the function is well defined. If is the spectral radius of , then the condition is necessary and sufficient for for some natural norm .

Crucially for symmetrisation, Toeplitz matrices are persymmetric. That is,

Otherwise, is symmetric. If is real, then is real symmetric and therefore normal. Furthermore,

that is, is also persymmetric. The above equation applies to all persymmetric matrices.

Proposition 2.2.1.

Let be analytic to . If is persymmetric and , then is persymmetric.

In the following, we refer only to series with real coefficients, so that is real symmetric.

2.2.2 Basic Results

Proposition 2.2.2.

Let with real Fourier coefficients , as defined in (LABEL:anti_identity_matrix), and let be the Toeplitz matrix with generating . Then, for every polynomial , we have

Proof.

According to Item GLT3, every Toeplitz sequence is a GLT with symbol . In addition, according to Item GLT2, every sequence obtained with operations between GLT sequences is GLT with a symbol produced via the same operations as between the symbols of the sequences. Finally, according to GLT1, the singular values of a GLT sequence with symbol are distributed as . In the present case, .

Theorem 2.2.

Let with real Fourier coefficients , as defined in (LABEL:anti_identity_matrix), and let be a Toeplitz matrix with generating . Let be an analytic function, with real coefficients and a radius of convergence such that . Then, we have the following distributions:

| (2.3) |

and

| (2.4) |

Proof.

The condition implies that , where is the spectral norm; thus, . Therefore, matrix is well defined.

If , we use the Taylor series at for . That is, . For every , we define the polynomial,

Thus, the following properties apply:

-

1.

for every ,

-

2.

,

-

3.

in measure.

The first property is a consequence of Proposition 2.2.2. To prove the second property, we write

Then, we observe that , where . This property follows by setting and .

For the third property, because we assume that , is analytic at the set almost everywhere for . Therefore, converges almost everywhere at . In addition, because the domain is bounded, converges to .

Applying Theorem 1.5, it immediately follows that .

Item GLT6 implies that the matrix sequence is a GLT with symbol .

To prove (2.4), we set

Because , we have that

In addition, from the property GLT2, we find that the matrix sequence is a GLT, since is the difference between the two GLT sequences. Its symbol is the difference between the initial sequences symbols. So,

Because is unitary, we have

That is, is zero distributed, according to the Definition 1.5. Then,

where , as proved in Theorem 2.2, and is zero distributed. Thus, by applying Theorem 1.7, it immediately follows that

2.3 Numerical Results

In this section, the eigenvalue and singular value distributions of the sequence are numerically investigated. Considering this distribution, several circulant preconditioners are proposed, and the spectrum of the preconditioned sequence is also investigated.

2.3.1 Spectrum of the

The results presented in this section confirm the claims of Theorem 2.2. Specifically, for trigonometric polynomial and , either analytic function either polynomial is confirmed in the following four examples, that the distribution of the eigenvalues of the sequence is described by . It is also numerically confirmed that the singular value distribution of is described by .

Example 2.1.

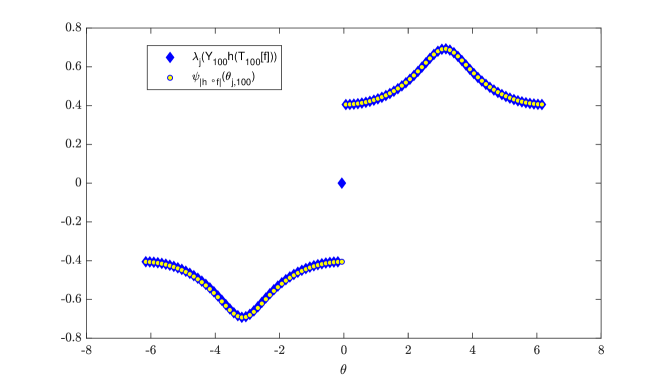

In this example the analytic function whose Taylor series converges throughout the complex plane, and the trigonometric polynomial are considered. Figure 2.1 shows that for , the eigenvalues of are well approximated by the uniform sampling of over , except for the presence of an outlier. This indicates that Definition 1.1 does not rule out the existence of such eigenvalues.

Example 2.2.

In the second example, for the analytic function , whose Taylor series at 0 converges with a radius of convergence equal to 1 is used the trigonometric polynomial with , as Theorem 2.2 demands. Figure 2.2, shows that except one outlier, the eigenvalues of for are well approximated by a uniform sampling of over .

Example 2.3.

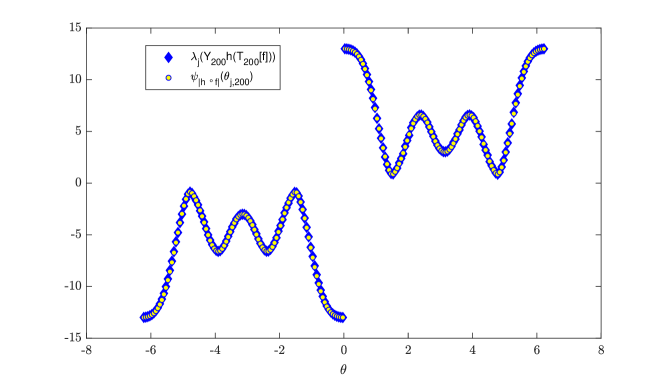

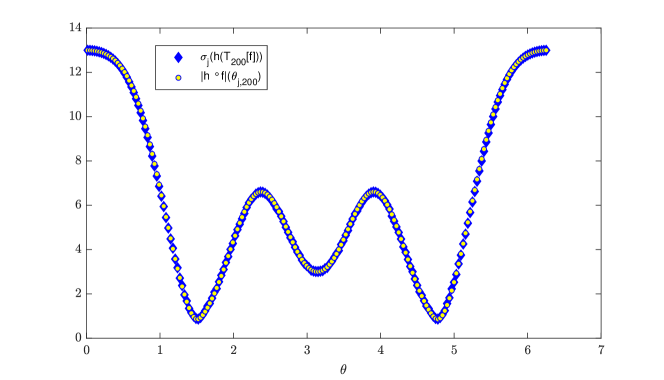

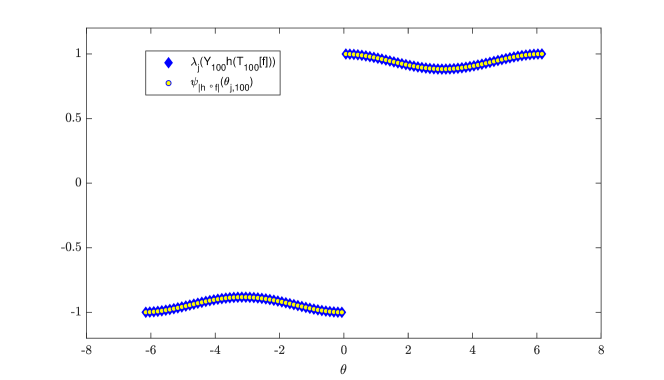

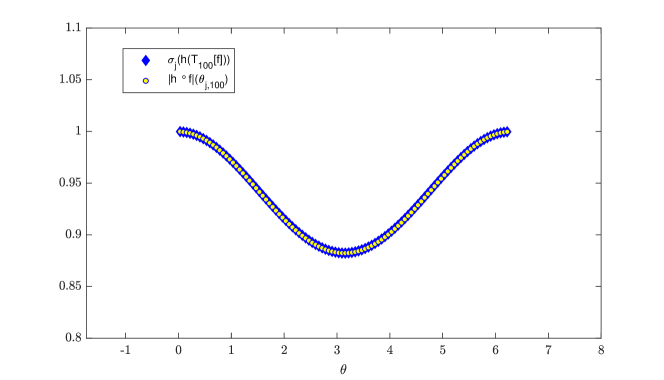

This example was taken from [22]. Following the same procedure as Examples 1–2 , Figure 2.3 shows the spectrum of for ; the function , whose Taylor series in 0 converges in the whole complex plane; and the trigonometric polynomial . In the present example, there are no outliers, and the eigenvalues of are approximated by the uniform sampling of over . Moreover, to numerically confirm the relation (2.3) of Theorem 2.2, it is verified that the singular values of the matrix can be approximated by a uniform sampling of over . Indeed, Figure 2.4 shows that the expected approximation holds true already for a moderate size such as .

Example 2.4.

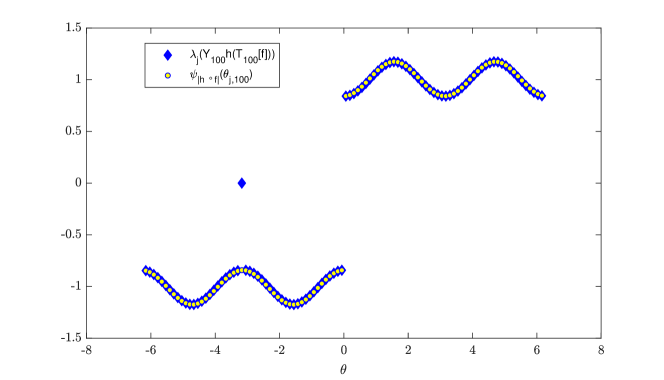

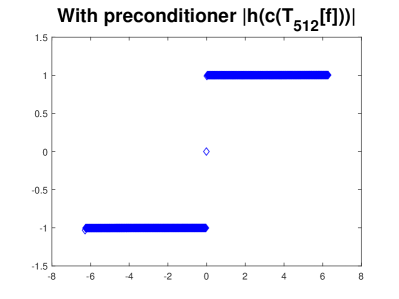

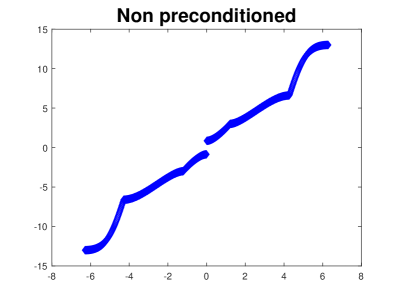

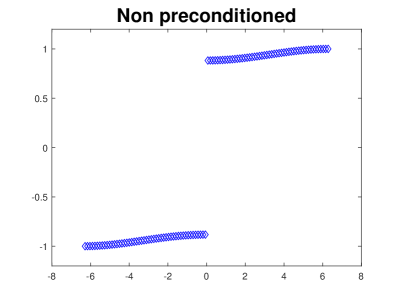

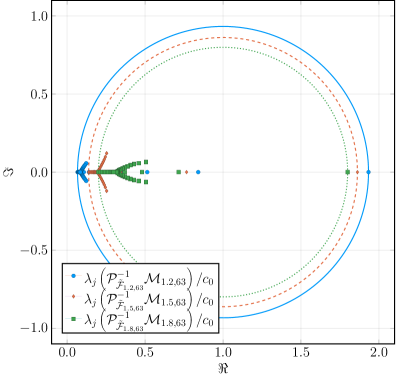

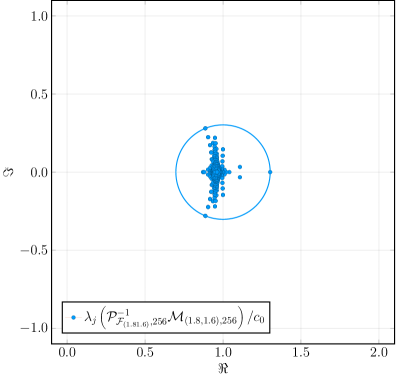

The last example is a practical case taken from [32, 31]. Here, we have the case of the exponential of a real non-symmetric Toeplitz matrix derived from computational finance (more specifically, from the option pricing framework in jump-diffusion models), where a partial integro-differential equation (PIDE) must be solved. The discretisation of a PIDE can be transformed into a matrix exponential problem which is equivalent to considering the analytic function , whose Taylor series centred at converges in the whole complex plane, as well as a trigonometric polynomial defined by the following Fourier coefficients:

| (2.5) | ||||

| (2.6) | ||||

| (2.7) | ||||

| (2.8) |

Here, is a normal distribution function with mean and standard deviation , the parameter is the expectation of the impulse function, is the spatial step size, is the stock return volatility, is the risk-free interest rate, and is the arrival intensity of the Poisson process.

Following the same procedure as in Examples 1–3, we plot in Figure 2.5 the spectrum of for . In the present example, we observe that there are no outliers, and the eigenvalues of are well approximated by the uniform sampling of over .

2.3.2 Circulant Preconditioners for the Symmetrised Toeplitz Sequence

In the present section, preconditioners for the symmetrised system are proposed, and the distribution of the preconditioned sequence is numerically investigated.

For the construction of the preconditioners, the approach proposed in [22] is applied; however, taking into consideration the theoretical results proved here, another circulant preconditioner is also proposed. For the second preconditioner, a theoretical description of the preconditioned sequence distribution is provided. The results are presented in Examples 2.5, 2.6, and 2.7. As mentioned in the introduction, the preferred Krylov method for symmetric, non-definite systems is MINRES. This method has the advantage that the cost per iteration is minimal because only matrix–vector multiplications are required. In addition, if the eigenvalues of the preconditioned coefficient matrix are known, the number of iterations required for convergence with given accuracy is known. The preconditioner must be symmetric and positive-definite. All of the preconditioners proposed here are symmetric and positive definite.

Definition 2.2.

[55] For every circulant matrix , the absolute value circulant matrix of is defined as

where is defined as in (1.6) and is the diagonal matrix of size , whose elements are the absolute values of the eigenvalues of .

Definition 2.3.

The optimal Frobenius preconditioner for a Toeplitz matrix is the circulant , defined as

where is a diagonal matrix that contains the eigenvalues of . It is clear that .

Let and be the circulant matrix whose first column is . To explicitly derive the elements of , we define . We observe that for , the element of appears in two diagonals, in which the and elements of are located. The first of the two diagonals has elements, and the second has . Thus, we have

where must be determined. To satisfy the necessary conditions for the minimisation of , we require that

Therefore, the elements of the first column of are given by .

Remark 2.1.

The norm is produced by a positive inner product which makes , the space of complex matrices of size n (equipped with norm) a Hilbert space. The set of circulant matrices of size constitutes a non-empty, closed, and convex linear subspace of . Therefore, for every , there exists a unique circulant [[59] Theorem 3.32], such that

For more properties regarding see [64].

As mentioned in Definition 2.3, the diagonal matrix , whose elements are the eigenvalues of the optimal Frobenius preconditioner for , is the main diagonal of . The element in the diagonal is , where denotes the column of . Therefore, for , we have that

Finally, because , the above summation equates to

| (2.9) |

Let us suppose that is summable; that is, . Then, the partial sum uniformly converges to . We set . The partial sum uniformly converges to ; thus, for every , there exists an such that . We observe that for every , the sum (2.9) contains terms, for which the summation starts from a term of order and ends with a term of order . All these terms are at most far from the exact value of . We combined the remaining terms in pairs, to take two new terms. One of the orders was higher than , and the other was lower than . For example,

Hence, we have

Proposition 2.3.1.

Proposition 2.3.2.

Let summable, with real Fourier coefficients. Let be an analytic function with real coefficients and a radius of convergence such that . Then, the circulant matrices and are real, and we have that

| (2.10) |

In addition, the circulant , , , is real and symmetric, and

| (2.11) | ||||

| (2.12) |

Proof.

Under these assumptions, the function has real Fourier coefficients and belongs to . The matrix is real for every , because each of its elements represents the weighted average of certain elements of , which is real. The matrix is real for every because is real and has real coefficients. The first distribution at (2.10) is an immediate consequence of the implementation of Proposition 2.3.1 for . The second distribution is the consequence of the implementation of the same proposition for , in combination with property GLT2. In [21], it was proven that if is a real circulant, is real and symmetric. Finally, the distributions at (2.11) and (2.12) arise from the definition of the matrices and the application of the property GLT2.

The preconditioned matrices and are similar to real symmetric matrices, and therefore their eigenvalues are real. In fact, because is real, symmetric, and positive definite, it can be written in the form , where is real orthogonal and is diagonal with no negative elements. Hence,

which is symmetric because is symmetric. Analogously, we apply . The proposition that follows is a restatement (in matrix sequence terms) of Conclusion at [22].

Proposition 2.3.3.

[22] Let and be summable, with real Fourier coefficients. Let be an analytic function with real coefficients and a radius of convergence such that . If is the optimal Frobenius preconditioner for , then for the preconditioned sequence , we have that

where the matrices of are real orthogonal, and is zero-distributed.

A direct consequence of the proposition above and Theorem 1.7 is that the eigenvalues of the preconditioned sequence are distributed similarly to those of . The eigenvalues of a real orthogonal matrix can only be or . Finally, according to Theorem 1.1, the eigenvalues of the preconditioned sequence are clustered at . In the proposition that follows, we prove a similar conclusion for the preconditioned sequence .

Proposition 2.3.4.

Let and be summable, with real Fourier coefficients. Let be an analytic function with real coefficients and a radius of convergence such that . If is the optimal Frobenius preconditioner for , then for the preconditioned matrix sequence , we have that

where the matrices of are real orthogonal, and is zero-distributed.

Proof.

In Proposition 2.3.2, it was proved that

In addition, as Theorem 2.2 states, . By applying the property GLT2, we have

So, applying once more the property GLT2, we have

Therefore,

where is zero-distributed, as the sum of two zero-distributed sequences. The permutation of with the circulants can be achieved because they are real and Toeplitz.

Example 2.5.

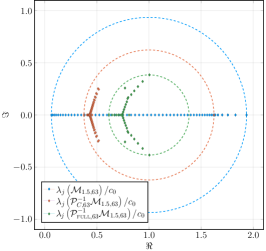

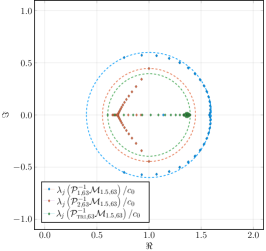

In this example, the efficiency of the absolute value circulant matrix as a preconditioner for the symmetrised matrix is tested and compared with ; for the functions and . In this case, , and thus, according to Theorem 2.1, it is reasonable to test as a preconditioner for and consequently for . The efficiency of the two preconditioners is shown in Figure 2.7. In the top panel of the figure, the eigenvalues of the non-preconditioned matrix for are sorted in increasing order. In the two panels that follow, the eigenvalues of the preconditioned matrix are . For the left graph, the preconditioner is , whereas for the right, the preconditioner is .

Remark 2.2.

According to Definition 2.3, for the construction of , it is necessary to know the Fourier coefficients of the function . However, these coefficients might not be known and must be calculated. In this case, their calculation should be included in the solution to the problem. These coefficients were not calculated analytically in the examples presented here. For the approximation of the integral (1.11) that defines each coefficient, the trapezoidal rule with a uniform partition over was used. This calculation can be performed using the Fast Fourier Transform. Specifically, the Fourier coefficient of the function is approximated by

The vector is exactly the Fourier transform of the vector

Given that , the chosen approximation of is . Setting and applying the above, we set necessary coefficients at a total cost of . This indicates that, if the function for which we seek the coefficients is a polynomial of a degree less that , this procedure returns the exact coefficients of the function [62].

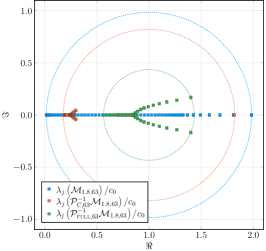

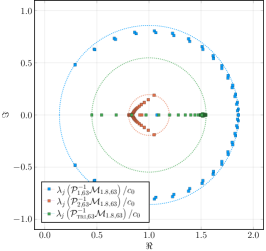

Example 2.6.

In the present example, the functions given in Example 2.3 are considered; that is, and . In Figure 2.8, is shown the behaviour of the eigenvalues of the matrix with and without the use of a preconditioning strategy. In particular, are shown the eigenvalues of the matrix , sorted in increasing order. In the bottom-left and bottom-right panels of Figure 2.8, the efficiency of both preconditioning strategies described in the previous example is tested. In both cases, is clear that the eigenvalues of the preconditioned matrix are clustered at -1 and 1, with up to outliers.

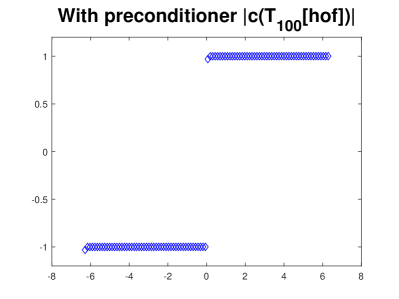

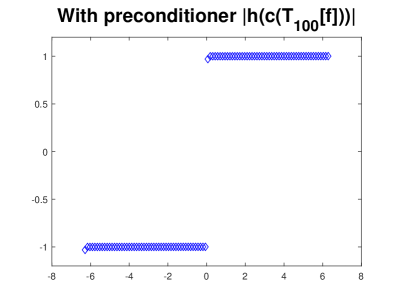

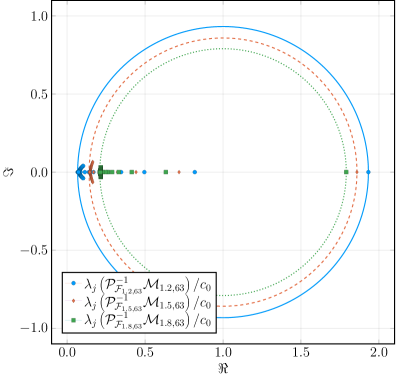

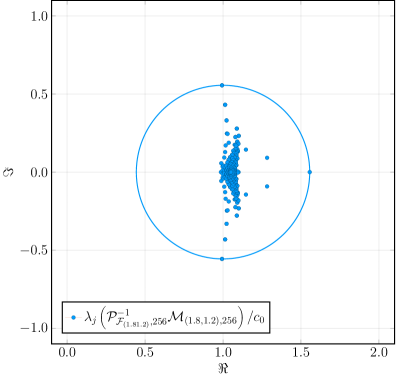

Example 2.7.

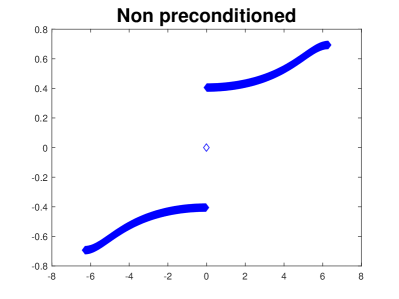

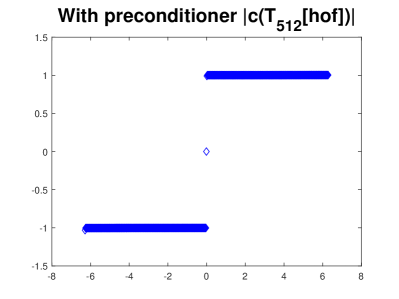

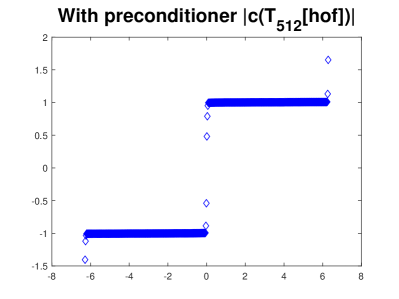

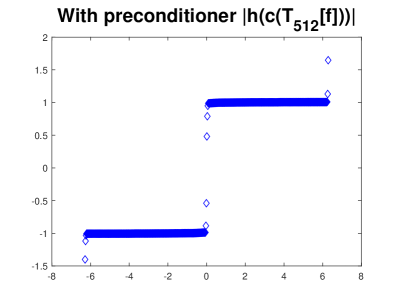

The last preconditioning test is performed on the computational finance case that was studied in Example 2.4. In other words, we have and , with defined as in (2.6)-(2.8). First, the preconditioning strategy approach introduced in [22] is applied; that is, . In the right-hand panel of Figure 2.9, the eigenvalues of the preconditioned matrix for are shown. The eigenvalues are clustered around -1 and 1, with up to two outliers. Analogously, we can study the eigenvalues of the preconditioned matrix , where . Indeed, we have and, by applying the results in [13], we have that is a valid preconditioner for the matrix . The left-hand panel of Figure 2.9 confirms that the eigenvalues of the preconditioned matrix are clustered around -1 and 1, with up to two outliers.

For each example, the validity of the two different preconditioning strategies was demonstrated. However, we have seen that, for sufficiently large matrices, the spectral results are remarkably similar. Other valid choices of preconditioning are possible; these produce a slightly different effect on the spectrum of the preconditioned matrix. Moreover, is highlighted that the strategy based on the results of [13, Theorem 5] provides an entire class of preconditioners suitable for symmetrised Toeplitz structure functions. Indeed, a preconditioner in this class is the absolute value of any circulant matrix such that the following singular value distribution is verified:

| (2.13) |

Concerning the choice of the preconditioning strategy based on this requirement, we used the Frobenius optimal circulant preconditioner because, from the properties of the considered and , relation (2.13) is satisfied.

Finally, we highlight that the choice of the optimal preconditioning strategy between the two approaches analysed in the examples depends on the computational aspects when constructing the matrix , which depends on the information available for the specific example. For instance, the computational cost of the construction of the preconditioner decreases if the Fourier coefficients of are known.

Chapter 3 Preconditioners for Fractional Diffusion Equations

Based on the Spectral Symbol

3.1 Introduction

Fractional calculus may be considered as an old and yet novel topic. Old because it dates back to a letter from L’Höpital to Leibniz in 1695; novel because it has been the object of specialised conferences and treatises for just a little over forty years. In recent years, considerable interest in fractional calculus has been stimulated by its applications in numerical analysis and modelling. Fractional differential equations (FDEs) are used to model anomalous diffusion or dispersion processes. Such phenomena are ubiquitous in natural and social sciences. Many complex dynamical systems exhibit anomalous diffusion. Fractional kinetic equations are usually an effective method to describe these complex systems, including diffusion, diffusive convection, and Fokker–Planck fractional differential equations. Because analytical solutions are rarely available, these types of equations are of numerical interest. When the fractional derivative , we obtain the standard diffusion process. With , we obtain a sub-diffusion process or a dispersive, slow diffusion process with an anomalous diffusion index; meanwhile, with , an ultra-diffusion process or an increased, fast diffusion process is realised.

Several definitions exist for the fractional derivative, and each definition approaches the ordinary derivative in the integer order limit. In [40, 41], the authors proposed two unconditionally stable finite difference schemes of first and second order accuracy based on the shifted Grünwald–Letnikov definition of fractional derivatives.

In [76], it was shown that once one of these methods is chosen, the coefficient matrix of the generated system can be seen as the sum of two structures, each of which is expressed as a diagonal matrix multiplied by a Toeplitz one. Because the efficient solution of such systems is of great interest, many iterative solvers have been proposed. Representative examples include the multigrid method (MGM) scheme proposed by [53], the circulant preconditioner [33] for the conjugate gradient normal residual (CGNR) method, and two structure-preserving preconditioners proposed in [9]. In the latter paper, the authors provide a detailed analysis, showing that the sequence of coefficient matrices belongs to the GLT class; furthermore, its spectral symbol, which describes the asymptotic singular and eigenvalue distributions, is explicitly derived. In [42], the analysis was extended to the two-dimensional case, and the authors compared the two-dimensional version of the structure-preserving preconditioner using a decomposition of the Laplacian [9] to a preconditioner based on an algebraic MGM.

By studying the simplest (but non-trivial), case of preconditioned Toeplitz systems generated by an even, non-negative function with zeros of any positive order, the authors prove [48] that the essential spectral equivalence between the matrix sequences and , (where is the sequence of symmetric positive definite (SPD) Toeplitz matrices generated by this function, and is the sequence of a specific matrix) is generated as

and

| (3.1) |

We recall here that is symmetric and orthogonal; therefore, it is the inverse of itself. Furthermore, ‘essential spectral equivalence’ means that all the eigenvalues of belong to an interval (except possible outliers) and do not converge to zero as the matrix size tends to infinity. For generating functions with the order of their zero lying in the interval , it is worth noting that there are no outliers.

According to the analysis given in the aforementioned works, the coefficient matrix of the system depends on the diffusion coefficients of the fractional DE. In the simplest case (i.e., where they are constant and equal), this is a diagonal times a real SPD Toeplitz matrix with a generating function that is even, positive, and real, having a zero at zero of real positive order between one and two, plus a positive diagonal with constant entries that asymptotically tend to zero. The analysis shows that this matrix is present in the more general case, where the diffusion coefficients are neither constant nor equal. In this case, a diagonal times a skew-symmetric real Toeplitz matrix is added to the coefficient matrix.

Taking advantage of this fact, we propose the preconditioner , where is a suitable diagonal matrix defined as follows: We show that this preconditioner can effectively retain the real part of the eigenvalues away from zero, whilst the sine transform maintains the cost per iteration , using a specific real algorithm or fast Fourier transform (FFT). It turns out that this preconditioner is very efficient, and although the structure-preserving preconditioners given in [9] are more efficient in the one-dimensional case, the proposed preconditioner is more efficient in two dimensions than the preconditioners described in [9] and [42].

3.2 Definition of Fractional Derivative

The fractional derivative has been defined in many ways. Each way has its own physical interpretations and applications. The classic form is given by the Riemann–Liouville integral.

Definition 3.1.

As the left Riemann–Liouville integral of order , we define the operator

to be applied on locally integrable functions over . Analogously, as the right Riemann–Liouville integral of order , we define the operator ,

to be applied in the same class of functions.

For the left Riemann–Liouville becomes

where the last equality is given by the Cauchy formula for times repeated integration. It is immediately apparent that, for , the operator is the order counter-derivative. That is,

For the right Riemann–Liouville integral of order , we have that

In general, for , we have that

and

The same applies for the right Riemann–Liouville integral.

If we now set 111The function is the ceiling function of and is equal to if ; otherwise, (the integer part of )+1.

In addition, we define the floor function of as if ; otherwise, (the integer part of )., the operator is well defined for the locally integrable functions over . So, if we set

we have a well-defined operator for which

Definition 3.2.

Let be integrable over , , and . The left-hand derivative of order , according to Riemann–Liouville, is defined as

The right derivative of order , according to Riemann–Liouville, is defined as

It can be proven that,

| (3.2) | |||

| (3.3) |

The definition of the fractional derivative of interest from a numerical point of view is given by Grünwald and is a generalisation of the definition of the derivative of integer order:

For , the left and right derivatives of order over are defined as

| (3.4) | |||

| (3.5) |

respectively. The Grünwald definition of the fractional derivative is equivalent (in the continuous limit) to the Riemann–Liouville definition and immediately provides a method for numerically approximating the fractional derivative of any function.

3.3 Fractional Diffusion Equations in One Dimension

We consider the following initial value problem:

| (3.6) |

Here, is the fractional derivative order, is the source term, and the positive functions are the diffusion coefficients. The left () and right () Riemann–Liouville partial fractional derivatives are defined as

| (3.7) | ||||

respectively. In the present work, to approximate the partial left and right fractional derivatives, two different numerical schemes will be used, and the effectiveness of the method proposed here can be immediately compared with already known methods. These schemes are based on Grünwald’s definition. The scheme is adapted in more than one dimension and shifted so that it is consistent and unconditionally stable. More specifically, the left and right partial derivatives (with respect to the spatial variable) of order are defined as

The following method for the discretisation of equation (3.6) was given by Meerschaert and Tadjeran in [40]. It combines discretisation in time via the implicit Euler method with discretisation of the left and right fractional derivatives (in space) using formulas (3.9) and (3.10), respectively. We define

We also set

Using the implicit Euler method, equation (3.6) becomes

Using formulas (3.9) and (3.10) for the approximation of the left and right fractional derivatives, respectively, we have the following finite difference scheme:

In matrix form, this becomes

| (3.11) |

where is the identity matrix of size ,

| (3.12) | ||||

and

| (3.20) |

If we define,

| (3.21) | ||||

then the system (3.11) becomes

| (3.22) |

For investigating the behaviour of the above system and to design an effective strategy for its solution, it is necessary to investigate the properties of fractional binomial coefficients.

Proposition 3.3.1.

Let and be as in (3.8). The following apply:

That and immediately follows from this definition. In addition, because , . If , then

From the above, it is clear that for , the term retains a positive sign and is less than . Additionally, using the known identity

| (3.23) |

we have,

Because the only negative term in the above zero sum is , the sum of the remaining terms must be equal to . Thus, it turns out that, on one hand, any partial sum is less than zero; on the other hand, the sum of the absolute values is equal to .

Using Proposition (3.3.1), we find that the matrix defined in (3.20) is strictly diagonally dominant, and therefore positive and invertible. In [76], it was proven that the coefficient matrix of the system (3.22) is also strictly diagonally dominant and invertible. More essential properties of the involved matrices are revealed using the theory of GLT matrix sequences below.

An interesting property of the matrix (3.20), arising from the operator that this matrix discretises, is given in the following proposition.

Proposition 3.3.2.

A linear system with a coefficient matrix of can be solved by a direct method, with a total cost of operations. In fact, only one Toeplitz matrix-vector multiplication [of cost ] and then a forward substitution [of cost ] are needed.

Proof.

According to the relationship (3.2), the left Riemann–Liouville fractional derivative of order is the left inverse operator of the Riemann–Liouville fractional integral of order in the space of integrable functions over an interval . For this integral, in the continuous limit, we apply

Inspired by this fact, we can pre-multiply any system of the form with the matrix that implements the inverse operator according to the above scheme; that is,

| (3.29) |

It is worth noting that is the inverse of the lower triangular Toeplitz matrix with the vector as the first column and it implements the fractional derivative of order without displacement. Then, is the following lower Hessenberg matrix:

| (3.35) |

Because the elements of the first column are all known, it is not necessary to make the multiplication explicitly, and we only need multiply the right-hand vector with . Of course, this multiplication can be performed with a cost of operations, whilst the system with the coefficient matrix is clear and can be solved with a forward substitution.

3.3.1 Second-order Finite Difference Discretisation

It can be shown [70] that,

| (3.36) | ||||

| (3.37) |

where

| (3.38) | ||||

| (3.39) |

and as defined in (3.8).

In this case, the matrix in the system (3.11) must be replaced by the following matrix:

| (3.47) |

Proposition 3.3.3.

Let and be as defined in (3.38)–(3.39). Thus, it is apparent from the definition that

Examining the sign of over , we find that

In addition, if , we have that , because is a weighted average of two positive terms. From the definition and properties of fractional binomial coefficients (3.3.1), we have

According to the above,

If , then the two negative terms in the above zero sum are and . Therefore, the sum of the remaining terms must be equal to , and thus,

Analogously, if , then the only negative term in the zero sum is , and we conclude that

In any case,

and if ,

3.4 Spectral Analysis of the Coefficient Matrices

In the present section, we present in detail the distribution of eigenvalues and singular values of the matrix sequences , , and appearing on the left-hand side of the system (3.22). For the first two, which are clearly Toeplitz, their spectral symbol 222In the definition of Toeplitz matrices (Definition 1.6), the term ’generating function’ is used instead of ’spectral symbol’ for the function whose Fourier coefficients compose the diagonals of the matrices of the sequence. Nevertheless, from the property GLT3, every Toeplitz sequence is GLT with a spectral symbol that is the same as the generating function. Hence, the term ’spectral symbol’ is used instead of ’generating function’ for reasons of homogeneity, because the spectral behaviour of all matrix sequences shown here can only be analysed using the GLT theory. is analyzed. The sequence belongs to the GLT class, and its spectral symbol is also considered. In addition, the distribution of the sequence appears in the second-order finite difference discretisation is considered.

Definition 3.3.

Let the sequence be such that . Then, the series converges uniformly to a continuous periodic function . The set of all these functions is the Wiener class.

Proposition 3.4.1.

[9] Let . The matrix sequences , , and are Toeplitz with spectral symbols

| (3.48) | |||

| (3.49) |

respectively.

We observe that

Based on the properties of the sequence (3.3.1) and the definition of the Wiener class (Definition 3.3), is well defined and belongs to that class.

Then,

Therefore, . It is clear that the spectral symbol of the sequence is the function , which, because the Fourier coefficients are real, entails that . Also,

The spectral distribution of the sequence was studied by [9]. The following propositions summarise the results required to design an effective strategy for solving 3.3.1.

Proposition 3.4.2.

Proposition 3.4.3.

If , the function has a zero of order at .333If is a continuous, non-negative, and real function over , we say that it has a zero of order at , if there exist such that and . For , and the proposition is true. For , and the proposition is untrue, because this trigonometric polynomial has a zero of order two.

Proposition 3.4.4.

For the functions and , as defined above, we apply

It is evident from the propositions above that the coefficient matrix of the system (3.22), , is in a bad condition, because its minimum singular value or eigenvalue if converges to zero with order . An effective strategy for preconditioning the system is to keep the singular values or eigenvalues of the system away from zero. It should be noted that, if the preconditioner is selected from the GLT class (e.g., as a band Toeplitz or circulant with a spectral symbol ), then from the property GLT2, and . In this case, if , the preconditioner is not optimal. This is because the singular values or eigenvalues of the sequence cannot be clustered at , because the spectral symbol is a nontrivial function of .

Proposition 3.4.5.

Proposition 3.4.6.

If , the function has a zero of order at 0.

3.5 Fractional Diffusion Equations in Two Dimensions

We consider the following initial value problem in two dimensions:

| (3.52) |

Here, is the fractional order of the derivative, is the source term, and the non-negative functions and are the diffusion coefficients.

In this case, the left () and right () Riemann–Liouville fractional derivatives are defined as

For the discretisation of Equation (3.52), we use a method that combines the Crank–Nicolson method in time with the second-order finite difference in spatial domain scheme (3.36)–(3.37), adapted for two dimensions. The method was proposed and proven to be consistent and unconditionally stable in [70].

We define,

and . For the unknown function , we set and

For the diffusion coefficients , , , and , we set

and . The corresponding discretisation is as follows:.

For the discretisation of the source term , we set and

We define and . In the equation, fractional derivatives of different orders and appear, and it is also possible to obtain different numbers of discretisation points in each spatial domain. Thus, we define the matrices , , and the matrices,

where is the identity matrix of size , and denotes the Kronecker product. Then, by using the Crank–Nicolson method, we obtain the system

where , . In compact form, the system is written

where

| (3.53) | ||||

Proposition 3.5.1.

[42] We suppose that and . We suppose also that for a given time , the functions , , , and are Riemman integrable over . Then,

where

Therefore

In addition, if we have,

3.6 The Preconditioners

3.6.1 The Preconditioner in one Dimension

In order that the results are directly combarable with that in [9], in one dimension will be used the first order finite difference scheme. Also, to simplify the notation the time mark will be ommited. Let now, as in (3.20) and as in (3.22).

As mentioned in the introduction of the chapter, the proposed preconditioner is a diagonal matrix , times a matrix, . Such a combination of two matrices as preconditioner is not a new proposal ([50],[49],[45]).

The form of the coefficient matrix of the system suggests for the diagonal the following matrix,

| (3.54) |

that has been used in other preconditioning strategies also [9]. Assuming that the functions do not have a common zero we conclude that the is uniformly bounded and

If we now define , , , and taking into consideration that the are no-negative, we have that and also,

Hence, can be written as

Since, from (3.4.1), and we have

| (3.55) |

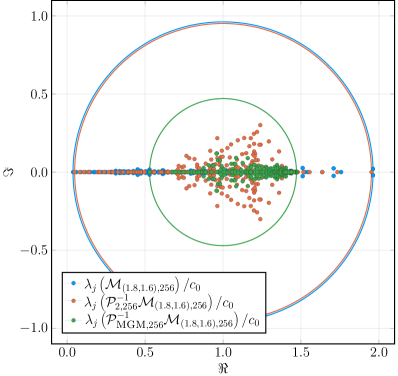

where , defined in (3.49), is real, positive and even. The above derivation of the matrix is of interest since it makes clear why it is reasonable to use the preconditioner. The first term of the above matrix, , is diagonal with positive and entries, since we have supposed that the functions do not have zero at the same point in the domain and . We mention here that although the entries are , its effect on the eigenvalues of the preconditioned matrix can be significant. The reason is explained in the end of this section. The third term in (3.55) is a diagonal matrix with entries in times a skew-symmetric Toeplitz matrix with generating function and consequently purely imaginary eigenvalues. If this term is vanishing while if the are constant but not equal it is a pure skew-symmetric Toeplitz (in that case for some constant ).

The term in (3.55), which is mainly responsible for the dispersion of the real part of the spectrum, is the second term, that is . The preconditioner will effectively cluster the eigenvalues of this matrix, and consequently the eigenvalues of the whole matrix . Hence, taking advantage of the ‘essential spectral equivalence’ between the matrix sequences and proven in [48], we propose a preconditioner expressed as

| (3.56) |

where

with defined in (3.54) and being the sine transform matrix reported in (3.1). Obviously, the proposed preconditioner is symmetric and positive definite.

Case I: are constants

In the case where the diffusion coefficient functions are constants, the (3.55) becomes:

i.e, is exactly the sum of a symmetric and a skew-symmetric Toeplitz matrix. It is worth noticing that according to the GLT machinery, the term which is added to the symbol of the first Toeplitz matrix sequence does not change the symbol of the sequence since is of order . However it affects the speed in which the minimum eigenvalue of the sequence approaches zero as the dimension of the matrix tends to infinity. Thus, in this special case, the part of preconditioner is defined as