Understanding the Generalization Performance of Spectral Clustering Algorithms

Abstract

The theoretical analysis of spectral clustering mainly focuses on consistency, while there is relatively little research on its generalization performance. In this paper, we study the excess risk bounds of the popular spectral clustering algorithms: relaxed RatioCut and relaxed NCut. Firstly, we show the convergence rate of their excess risk bounds between the empirical continuous optimal solution and the population-level continuous optimal solution. Secondly, we show the fundamental quantity in influencing the excess risk between the empirical discrete optimal solution and the population-level discrete optimal solution. At the empirical level, algorithms can be designed to reduce this quantity. Based on our theoretical analysis, we propose two novel algorithms that can not only penalize this quantity, but also cluster the out-of-sample data without re-eigendecomposition on the overall samples. Experiments verify the effectiveness of the proposed algorithms.

1 Introduction

Spectral clustering is one of the most popular algorithms in unsupervised learning and has been widely used for many applications Von Luxburg (2007); Dhillon (2001); Kannan et al. (2004); Shaham et al. (2018); Liu et al. (2018). Given a set of data points independently sampled from an underlying unknown probability distribution, often referred to as the population distribution, spectral clustering algorithms aim to divide all data points into several disjoint sets based on some notion of similarity. Spectral clustering originates from the spectral graph partitioning Fiedler (1973), and one way to understand spectral clustering is to view it as a relaxation of searching for the best graph-cut since the latter is known as an NP-hard problem Von Luxburg (2007). The core method of spectral clustering is the eigendecomposition on the graph Laplacian, and the matrix composed of eigenvectors can be interpreted as a lower-dimensional representation that preserves the grouping relationships among data points as much as possible. Subsequently, various methods such as -means Ng et al. (2001); Shi and Malik (2000), dynamic programming Alpert and Kahng (1995), or orthonormal transform Stella and Shi (2003) can be used to get the discrete solution on the matrix and therefore the final group partitions.

However, compared with the prosperous development of the design and application, the generalization performance analysis of spectral clustering algorithms appears to be not sufficiently well-documented. Hitherto, the theoretical analysis of spectral clustering mainly focuses on consistency Von Luxburg et al. (2008, 2004); Cao and Chen (2011); Trillos and Slepčev (2018); Trillos et al. (2016); Schiebinger et al. (2015); Terada and Yamamoto (2019). Consistency means that if it is true that as the sample size collected goes to infinity, the partitioning of the data constructed by spectral clustering converges to a certain meaningful partitioning on the population level Von Luxburg et al. (2008), but consistency alone does not indicate the sample complexity Vapnik (1999). To our best knowledge, there is only one research that investigates the generalization performance of kernel NCut Terada and Yamamoto (2019). They use the relationship between NCut and the weighted kernel -means Dhillon et al. (2007), based on which they establish the excess risk bounds for kernel NCut. However, their analysis focuses on the graph-cut solution, not the solution of spectral clustering that we used in practice. We leave more discussions about the related work in the Appendix.

Motivated by the above problems, we investigate the excess risk bound of the popular spectral clustering algorithms: relaxed RatioCut and relaxed NCut. To compare with the RatioCut and NCut that are without relaxation, we refer to spectral clustering as relaxed RatioCut and relaxed NCut in this paper. It is known that spectral clustering often consists of two steps Von Luxburg (2007): (1) to obtain the optimal continuous solution by the eigendecomposition on the graph Laplacian; (2) to obtain the optimal discrete solution, also referred to as discretization, from the continuous solution by some heuristic algorithms, such as -means and orthonormal transform. Consistent with the two steps, we first investigate the excess risk bound between the empirical continuous optimal solution and the population-level continuous optimal solution. In deriving this bound, an immediate emerging difficulty is that the empirical continuous solution and the population-level continuous solution are in different dimensional spaces, making the empirical solution impossible to substitute into the expected error formula. To overcome this difficulty, we define integral operators, and use the spectral relationship between the integral operator and the graph Laplacian to extend the finite-dimensional eigenvector to the infinite-dimensional eigenfunction. Thus the deriving can proceed. We show that for both relaxed RatioCut and relaxed NCut, their excess risk bounds have a convergence rate of the order . Secondly, we investigate the excess risk bound between the empirical discrete optimal solution and the population-level discrete optimal solution. We observe the fundamental quantity in influencing this excess risk, whose presence is caused by the heuristic algorithms used in step (2) of spectral clustering. This fundamental quantity motivates us to design algorithms to penalize it from the empirical perspective, reducing it as small as possible. Meanwhile, we observe that the orthonormal transform Stella and Shi (2003) is an effective algorithm for penalizing this term, whose optimization objective corresponds to the empirical form of this fundamental quantity. Additionally, an obvious drawback of spectral clustering algorithms (relaxed NCut and relaxed RatioCut) is that they fail to generalize to the out-of-sample data points, requiring re-eigendecomposition on the overall data points. Based on our theoretical analysis, we propose two algorithms, corresponding to relaxed NCut and relaxed RatioCut, respectively, which can cluster the unseen samples without the eigendecomposition on the overall samples, largely reducing the time complexity. Moreover, when clustering the unseen samples, the proposed algorithms will penalize the fundamental quantity for searching for the optimal discrete solution, decreasing the excess risk. We have numerical experiments on the two algorithms, and the experimental results verify the effectiveness of our proposed algorithms. Our contributions are summarized as follows:

-

•

We provide the first excess risk bounds for the continuous solution of spectral clustering.

-

•

We show the fundamental quantity in influencing the excess risk for the discrete solution of spectral clustering. We then propose two algorithms that can not only penalize this term but also generalize to the new samples.

-

•

The numerical experiments demonstrate the effectiveness of the proposed algorithms.

2 Preliminaries

In this section, we introduce some notations and have a brief introduction to spectral clustering. For more details, please refer to Von Luxburg (2007).

Let be a subset of , be a probability measure on , and be the empirical measure. Given a set of samples independently drawn from the population distribution , the weighted graph constructed on can be specified by , where denotes the set of all nodes, denotes the set of all edges connecting the nodes, and is a weight matrix calculated by the weight function . Let denotes the number of all data points to be grouped. To cluster points into groups is to decompose into disjoint sets, i.e., and , . We define the degree matrix to be a diagonal matrix with entries . Then, the unnormalized graph Laplacian is defined as , and the asymmetric normalized graph Laplacian is defined as .

We now present some facts about spectral clustering. Let , where are vectors. We define the following empirical error:

| (1) |

where means the -th component of the -th vector . The optimization objective of RatioCut can be written as:

| (2) |

where denotes the number of vertices of a subset of a graph. The optimization objective of NCut can be written as:

| (3) |

where denotes the summing weights of edges of a subset of a graph. Since searching for the optimal solution of RatioCut and NCut is known as an NP-hard problem Von Luxburg (2007), spectral clustering often involves a relaxation operation, which allows the entries of to take arbitrary real values Von Luxburg (2007). Thus the optimization objective of relaxed RatioCut can be written as:

| (4) |

where is the identity matrix. The optimal solution of relaxed RatioCut is given by choosing as the matrix which contains the first eigenvectors of as columns Von Luxburg (2007). Similarly, the optimization objective of relaxed NCut can be written as:

| (5) |

The optimal solution of relaxed NCut is given by choosing the matrix which contains the first eigenvectors of as columns Von Luxburg (2007).

3 Excess Risk Bounds

We consider the real space in this paper. Let be a symmetric continuous weight function such that

| (6) |

measuring the similarities between pairs of data points . Since is not necessary to be positive definite and positive is more common in practice, we assume that to be positive in this paper. We now define the degree function as , and then define the function: if and otherwise, which is the population counterpart of the degree matrix. Let denotes the space of square integrable functions with norm .

3.1 Relaxed RatioCut

Based on the function , we define the function

which is symmetric. When is restricted to for any positive integer , the corresponding matrix is positive semi-definite (refer to proposition 1 in Von Luxburg (2007)), thus is a kernel function and associated with a reproducing kernel Hilbert space (RKHS) with scalar product (norm) (). In Section 3.1, we assume and to be continuous, which are common assumptions in spectral clustering. The elements in are thus bounded continuous functions, and the corresponding integral operator

is thus a bounded operator. The operator is the limit version of the Laplacian Rosasco et al. (2010). In other words, the matrix is an empirical version of the operator .

To investigate the excess risk bound, we need to define the population-level error, a limit version of Eq. (1):

where consists of functions . Further, the optimization objective of the population-level error of relaxed RatioCut, analogous to Eq. (4), can be defined as:

| (7) |

Let be the optimal solution of Eq. (7). Actually, are eigenfunctions of the operator Rosasco et al. (2010), that is , where is an eigenvalue of the operator , .

With the population-level error of relaxed RatioCut, we begin to analyze the excess risk bound. Excess risk measures on the population-level how the difference between the error of the empirical solution and the error of the population optima performs related to the sample size Biau et al. (2008); Liu (2021); Li and Liu (2021), formalized as , where is the optimal solution of the empirical error of relaxed RatioCut, i.e., Eq. (4), and, actually, are the eigenvectors of Laplacian Von Luxburg (2007). However, an immediate difficulty to derive the bound of is that and are in different spaces. Specifically, related to sample size is in finite-dimensional space, while is in infinite-dimensional function space. The fact that for different sample size , the elements in live in different spaces, making the term impossible to be calculated. To overcome this challenge, we define operator :

where . And we denote as the first eigenfunctions of the operator . Rosasco et al. (2010) shows that and have the same eigenvalues (up to zero eigenvalues) and their corresponding eigenfunctions and eigenvectors are closely related. If is a nonzero eigenvalue and , are the corresponding eigenvector and eigenfunction of and (normalized to norm l in and ) respectively, then

| (8) | ||||

where is the -th component of .

From Eq. (8), one can see that the eigenvectors of are the empirical version of the eigenfunctions of . In other words, if the eigenfunction is restricted to the dataset , it can be mapped into the eigenvector . Meanwhile, the eigenfunctions of are the extensions of the eigenvectors of , which are infinite-dimensional. Back to the term , we can replace the vectors in by its corresponding extended eigenfunctions in . Therefore, we now can investigate the excess risk bound between the empirical continuous optimal solution and the population-level continuous optimal solution by bounding the term . Additionally, the relations between the eigenvectors in and the eigenfunctions in can be applied to cluster out-of-sample data points. One can approximately calculate the eigenvectors of the out-of-sample data by the eigenfunctions in . Details will be shown in Section 4. We now present the first excess risk bound for relaxed RatioCut.

Theorem 1.

Suppose for any such that , then for any , with probability at least , the term is upper bounded by

where and are positive constants, is the clustering number.

Remark 1.

Theorem 1 shows that the excess risk bound of relaxed RatioCut between the empirical continuous optimal solution and the population-level continuous optimal solution has a convergence rate of the order if we assume that the eigenfunctions of operator are bounded, i.e., . This assumption is mild. Since we assume the kernel function and is continuous, the elements in associated with are bounded. The definition of operator is: , so it is reasonable to assume the eigenfunctions of are bounded, that is . in Theorem 1 comes from Eq. (6). We provide the proof of Theorem 1 in Appendix B.

Remark 2.

We highlight that we investigate the excess risk of spectral clustering. Compared with the generalization error bound that measures the difference between the empirical error of the empirical solution and the population-level error of the population-level solution, excess risk analysis is much more difficult because can not be calculated in expectation . The generalization error bound of relaxed RatioCut is easier to obtain since can be directly substituted into to calculate, and its proof indeed is included in the proof of Theorem 1. We show the generalization error bound as a corollary in the following.

Corollary 1.

Under the above assumptions, for any , with probability at least ,

where is the clustering number.

In practice, after obtaining eigenvectors of the Laplacian , spectral clustering uses the heuristic algorithms on the eigenvectors to obtain the discrete solution. In analogy to this empirical process, we define the population-level discrete solution , which are functions in RKHS and are sought through by the population-level continuous solution . Let be the optimal solution of the minimal population-level error of RatioCut, i.e., optimal solution of the population-level version of Eq. (2). We then investigate the excess risk between the empirical discrete optimal solution and the population-level discrete optimal solution by bounding the term .

Theorem 2.

Suppose and for any such that , then for any , with probability at least , the term is upper bounded by

where and are positive constants, is the clustering number.

Remark 3.

In the proof of Theorem 2, we make an error decomposition: Term is proved by the empirical process theory, term is proved by spectral properties of the integral operator and the operator theory, while term can be derived easily. Bounds of the terms and give the result of Theorem 1. For term , we show that it can be bounded by (The proof is provided in Appendix C). We denote this quantity as , and the upper bound reveals that is a fundamental quantity in influencing the excess risk between the empirical discrete optimal solution and the population-level discrete optimal solution, which motivates us to penalize it as much as possible at the empirical level. We thus propose new algorithms in the next section. Additionally, since searching for the best graph-cut is known as an NP-hard problem Von Luxburg (2007), we investigate the generalization performance of the discrete solution obtained from the continuous solution in the practical spectral clustering process rather than the agnostic graph-cut solution. We hope that the theoretical study on such a kind of discrete solution can guide the design of novel spectral clustering algorithms.

3.2 Relaxed NCut

The basic idea of this subsection is roughly the same as Section 3.1. We consider relaxed NCut corresponding to the asymmetric normalized Laplacian . Bound (6) implies the corresponding integral operator

is well defined and continuous. To avoid notations abuse, we use symbols provided in Section 3.1. Corresponding minimal population-level error similar to Eq. (7) can be easily written from the empirical version in Eq. (5). For brevity, we omit it and just give some notations here. Let be the optimal solution of the minimal population-level error of relaxed NCut, which are eigenfunctions of the operator Rosasco et al. (2010). We denote as the optimal solution of minimal empirical error of relaxed NCut, i.e., Eq. (5), which actually are eigenvectors of the Laplacian Von Luxburg (2007).

Firstly, we aim to bound the term . However, another immediate difficulty is that the methods described in Section 3.1 are not directly applicable for relaxed NCut. The operator corresponding to in the previous subsection appears to be impossible to be defined for relaxed NCut since is not necessarily positive definite, so there is no RKHS associated with it. Moreover, even if is positive definite, the operator involves a division by a function, so there may not be a map from the RKHS to itself. To overcome this challenge, we use an assumption on introduced in Rosasco et al. (2010) to construct an auxiliary RKHS associated with a continuous real-valued bounded kernel . Here is the assumption:

Assumption 1.

Assume that is a positive, symmetric function such that

where is a family of continuous bounded functions such that all the (standard) deviations of orders exist and are continuous bounded functions.

According to Rosasco et al. (2010), Assumption 1 implies that there exists a RKHS with bounded continuous kernel such that: , where and . This allows us to define the following empirical operators

where . Let be the first eigenfunctions of the operator . Rosasco et al. (2010) shows that , and have closely related eigenvalues and eigenfunctions. The spectra of and are the same up to the eigenvalue . Moreover, if is an eigenvalue and , are the eigenvector and eigenfunction of and , respectively, then

| (9) | ||||

where is the -th component of the eigenvector . From Eq. (9), one can observe that the eigenvectors of are the empirical version of the eigenfunctions of . Moreover, the eigenfunctions of are the extensions of the eigenvectors of , which are infinite-dimensional. Therefore, given the eigenvectors of , we can extend it to the corresponding eigenfunctions. With this relationship, we can now investigate the excess risk between the empirical continuous optimal solution and the population-level continuous optimal solution by bounding the term . The following is the first theorem of relaxed NCut.

Theorem 3.

Under Assumption 1, suppose for any such that , then for any , with probability at least , the term is upper bounded by

where and are positive constants, is the clustering number.

Remark 4.

From Theorem 3, the excess risk of relaxed NCut has a convergence rate of the order . The proof techniques used in Theorem 3 conclude spectral properties of integral operators, operator theory, and empirical processes. in Theorem 3 comes from Eq. (6). We provide the proof of Theorem 3 in Appendix D. Moreover, the generalization error bound of relaxed NCut is shown below.

Corollary 2.

Under the above assumptions, for any , with probability at least ,

where is the clustering number.

As discussed before, the continuous solution of spectral clustering typically involves a discretization process, thus we then investigate the excess risk bound between the empirical discrete optimal solution and the population-level discrete optimal solution for relaxed NCut. In analogy to the previous subsection, we investigate , where ) are functions in RKHS and are sought through by the continuous eigenfunctions , and where is the optimal solution of the minimal population-level error of NCut, i.e., optimal solution of the population-level version of Eq. (3).

Theorem 4.

Under Assumption 1, suppose and for any such that , then for any , with probability at least , the term is upper bounded by

where and are positive constants, is the clustering number.

Remark 5.

From Theorem 4, one can see that the term is also a fundamental quantity in influencing the excess risk of relaxed NCut between the empirical discrete optimal solution and the population-level discrete optimal solution, which motivates us to propose algorithms in the next section to penalize this term to make the risk bound as small as possible. In addition to the difficulties mentioned above, proving excess risk bounds also has the following difficulties: (1) the objective function of spectral clustering (see Eq (1)) is a pairwise function, which can not be written as a summation of independent and identically distributed (i.i.d.) random variables so that the standard techniques in the i.i.d. case can not apply to it. In this paper, we use the -process technique introduced in Clémençon et al. (2008) to overcome this difficulty. (2) the operator involves a division by a function, thus the term can not be bounded directly by the proof technique of Theorem 2. We must introduce equivalent probability measures to construct equivalent vector space (please refer to Appendix D).

Remark 6.

This remark discusses why we use the asymmetric normalized Laplacian, not the symmetric normalized Laplacian. Using the asymmetric normalized graph Laplacian, we can analyze relaxed NCut in a unified form of the empirical error (i.e., Eq. (1)). While for the normalized symmetric Laplacian, we need to transform Eq. (1) to

Please refer to Proposition 3 and Eq. (11) in Von Luxburg (2007) for details.

Remark 7.

This remark discusses the relationship between this paper and Li and Liu (2021). Li and Liu (2021) study the clustering algorithm through a general framework and then gives excess risk bounds based on this framework. Specifically, the excess risk in Li and Liu (2021) is of the form . However, we have discussed that is impossible to be calculated for spectral clustering due to the dimensional issue. Thus, the bounds of established in Li and Liu (2021) do not hold for the specific spectral clustering problem, and that’s also the reason why we introduce the integral operator tool to revisit the spectral clustering problem. Hence, we highlight that the results of this paper, both the bounds and the algorithms, are novel compared to Li and Liu (2021).

4 Algorithms

From Theorems 2 and 4, the imperative is to penalize to make it as small as possible. Towards this aim, we should solve the following formula to find the optimal discrete solution :

where is any set of functions in RKHS . In the corresponding empirical clustering process, we should optimize this term . It can be roughly equivalent to optimize , to find the optimal discrete solution , where denotes the Frobenius norm. Stella and Shi (2003) propose an iterative fashion to optimize to get the discrete solution closest to the continuous optimal solution . At a high level, this paper provides a theoretical explanation on Stella and Shi (2003) from the population view.

The idea in Stella and Shi (2003) is based on that the continuous optimal solutions consist of not only the eigenvectors but of a whole family spanned by the eigenvectors through orthonormal transform. Thus the discrete optimal solution can be searched by orthonormal transform. With this idea, we can solve the following optimization objective to find the optimal discrete solution and orthonormal transform:

| s.t. |

where is a vector with all one elements, is any set of discrete vectors in the eigenspace, and is an orthonormal matrix. The orthonormal transform program finds the optimal discrete solution in an iterative fashion. This iterative fashion is shown below:

(1) given , solving the following formula:

(2) given , solving the following formula:

We denote this iterative fashion in Stella and Shi (2003) as (Program of Optimal Discretization).

4.1 GPOD

We now introduce our proposed algorithms, called algorithm, which can not only penalize the fundamental quantity in influencing the excess risk of the discrete solution but also allow clustering the unseen data points.

Firstly, for the samples , we can use the eigenvectors of (or ) to obtain its extensions based on Eq. (8) (or Eq. (9)), that is to obtain the eigenfunctions of (or ). Secondly, when the new data points come, we can calculate its eigenvectors with the help of the eigenfunctions . By mapping the eigenfunctions into finite dimensional space, we can approximately obtain the eigenvectors of the new samples . Specifically, we can use formula

to obtain the eigenvectors of for relaxed RatioCut and use

for relaxed NCut. Note that for relaxed RatioCut, since the underlying is unknown, the term can be empirically approximated by .

After obtaining the eigenvectors of the out-of-sample data points , we can use the iterative fashion to optimize the following optimization problem to seek the empirical optimal discrete solution:

| s.t. |

This optimization process can penalize the fundamental quantity for the out-of-sample data points.

The ability of our proposed algorithm in clustering unseen data points without the eigendecomposition on the overall data points makes the spectral clustering more applicable, largely reducing the time complexity. The concrete algorithm steps are presented in Appendix F, where we also analyze how the time complexity of our proposed algorithm is significantly improved in Remark 1. Overall, the proposed algorithms can not only penalize the fundamental quantity but also cluster the out-of-sample data points.

Remark 8.

Eqs. (8) and (9) hold when the denominator is not . This remark discusses the case when the denominator is , i.e., the or eigenvalue. According to the spectral projection view, for the unnormalized Laplacian, respectively the asymmetric graph Laplacian, the -eigenvalue, respectively the eigenvalue, doesn’t affect the performance of spectral clustering, see Proposition 9 and Proposition 14 in Rosasco et al. (2010), respectively. Thus, the or eigenvalue doesn’t influence the performance of in clustering the out-of-sample data.

4.2 Numerical Experiments

We have numerical experiments on the two proposed algorithms. Considering the length limit, we leave the experimental settings and results in Appendix G. The experimental results show that the proposed algorithms can cluster the out-of-sample data points, verifying their effectiveness.

5 Conclusions

In this paper, we investigate the generalization performance of popular spectral clustering algorithms: relaxed RatioCut and relaxed Ncut, and provide the excess risk bounds. According to the two steps of practical spectral clustering algorithms, we first provide a convergence rate of the order for the continuous solution for both relaxed RatioCut and relaxed Ncut. We then show the fundamental quantity in influencing the excess risk of the discrete solution. Theoretical analysis inspires us to propose two novel algorithms that can not only cluster the out-of-sample data, largely reducing the time complexity, but also penalize this fundamental quantity to be as small as possible. By numerical experiments, we verify the effectiveness of the proposed algorithms. One limitation of this paper is that we don’t provide a true convergence rate for the excess risk of the empirical discrete solution. We believe that this problem is pretty important and worthy of further study.

References

- Alpert and Kahng [1995] Charles J Alpert and Andrew B Kahng. Multiway partitioning via geometric embeddings, orderings, and dynamic programming. IEEE Transactions on Computer-aided Design of Integrated Circuits and Systems, 14(11):1342–1358, 1995.

- Arias-Castro et al. [2012] Ery Arias-Castro, Bruno Pelletier, and Pierre Pudlo. The normalized graph cut and cheeger constant: from discrete to continuous. Advances in Applied Probability, 44(4):907–937, 2012.

- Bartlett and Mendelson [2002] Peter L Bartlett and Shahar Mendelson. Rademacher and gaussian complexities: Risk bounds and structural results. Journal of Machine Learning Research, 3(Nov):463–482, 2002.

- Biau et al. [2008] Gérard Biau, Luc Devroye, and Gábor Lugosi. On the performance of clustering in hilbert spaces. IEEE Transactions on Information Theory, 54(2):781–790, 2008.

- Cao and Chen [2011] Ying Cao and Di-Rong Chen. Consistency of regularized spectral clustering. Applied and Computational Harmonic Analysis, 30(3):319–336, 2011.

- Clémençon et al. [2008] Stéphan Clémençon, Gábor Lugosi, Nicolas Vayatis, et al. Ranking and empirical minimization of u-statistics. The Annals of Statistics, 36(2):844–874, 2008.

- Dhillon et al. [2007] Inderjit S Dhillon, Yuqiang Guan, and Brian Kulis. Weighted graph cuts without eigenvectors a multilevel approach. IEEE transactions on pattern analysis and machine intelligence, 29(11):1944–1957, 2007.

- Dhillon [2001] Inderjit S Dhillon. Co-clustering documents and words using bipartite spectral graph partitioning. In Proceedings of the seventh ACM SIGKDD international conference on Knowledge discovery and data mining, pages 269–274, 2001.

- Fiedler [1973] Miroslav Fiedler. Algebraic connectivity of graphs. Czechoslovak mathematical journal, 23(2):298–305, 1973.

- Kannan et al. [2004] Ravi Kannan, Santosh Vempala, and Adrian Vetta. On clusterings: Good, bad and spectral. Journal of the ACM (JACM), 51(3):497–515, 2004.

- Kato [1987] Tosio Kato. Variation of discrete spectra. Communications in Mathematical Physics, 111(3):501–504, 1987.

- Lang [2012] Serge Lang. Real and functional analysis, volume 142. Springer Science & Business Media, 2012.

- Latała and Oleszkiewicz [1994] Rafał Latała and Krzysztof Oleszkiewicz. On the best constant in the khinchin-kahane inequality. Studia Mathematica, 109(1):101–104, 1994.

- Li and Liu [2021] Shaojie Li and Yong Liu. Sharper generalization bounds for clustering. In International Conference on Machine Learning, pages 6392–6402, 2021.

- Liu et al. [2018] Fuchen Liu, David Choi, Lu Xie, and Kathryn Roeder. Global spectral clustering in dynamic networks. Proceedings of the National Academy of Sciences, 115(5):927–932, 2018.

- Liu [2021] Yong Liu. Refined learning bounds for kernel and approximate -means. In Advances in Neural Information Processing Systems, 2021.

- Mohri et al. [2018] Mehryar Mohri, Afshin Rostamizadeh, and Ameet Talwalkar. Foundations of machine learning. MIT press, 2018.

- Ng et al. [2001] Andrew Ng, Michael Jordan, and Yair Weiss. On spectral clustering: Analysis and an algorithm. In Advances in neural information processing systems, pages 849–856, 2001.

- Pelletier and Pudlo [2011] Bruno Pelletier and Pierre Pudlo. Operator norm convergence of spectral clustering on level sets. The Journal of Machine Learning Research, 12:385–416, 2011.

- Rohe et al. [2011] Karl Rohe, Sourav Chatterjee, Bin Yu, et al. Spectral clustering and the high-dimensional stochastic blockmodel. The Annals of Statistics, 39(4):1878–1915, 2011.

- Rosasco et al. [2010] Lorenzo Rosasco, Mikhail Belkin, and Ernesto De Vito. On learning with integral operators. Journal of Machine Learning Research, 11(2), 2010.

- Schiebinger et al. [2015] Geoffrey Schiebinger, Martin J Wainwright, Bin Yu, et al. The geometry of kernelized spectral clustering. The Annals of Statistics, 43(2):819–846, 2015.

- Shaham et al. [2018] Uri Shaham, Kelly Stanton, Henry Li, Boaz Nadler, Ronen Basri, and Yuval Kluger. Spectralnet: Spectral clustering using deep neural networks. arXiv preprint arXiv:1801.01587, 2018.

- Shi and Malik [2000] Jianbo Shi and Jitendra Malik. Normalized cuts and image segmentation. IEEE Transactions on pattern analysis and machine intelligence, 22(8):888–905, 2000.

- Singer and Wu [2017] Amit Singer and Hau-Tieng Wu. Spectral convergence of the connection laplacian from random samples. Information and Inference: A Journal of the IMA, 6(1):58–123, 2017.

- Stella and Shi [2003] X Yu Stella and Jianbo Shi. Multiclass spectral clustering. In Computer Vision, IEEE International Conference on, page 313, 2003.

- Terada and Yamamoto [2019] Yoshikazu Terada and Michio Yamamoto. Kernel normalized cut: a theoretical revisit. In International Conference on Machine Learning, pages 6206–6214, 2019.

- Ting et al. [2011] Daniel Ting, Ling Huang, and Michael Jordan. An analysis of the convergence of graph laplacians. arXiv preprint arXiv:1101.5435, 2011.

- Trillos and Slepčev [2018] Nicolas Garcia Trillos and Dejan Slepčev. A variational approach to the consistency of spectral clustering. Applied and Computational Harmonic Analysis, 45(2):239–281, 2018.

- Trillos et al. [2016] Nicolás García Trillos, Dejan Slepčev, James Von Brecht, Thomas Laurent, and Xavier Bresson. Consistency of cheeger and ratio graph cuts. The Journal of Machine Learning Research, 17(1):6268–6313, 2016.

- Vapnik [1999] Vladimir Vapnik. The nature of statistical learning theory. Springer science & business media, 1999.

- Von Luxburg et al. [2004] Ulrike Von Luxburg, Olivier Bousquet, and Mikhail Belkin. On the convergence of spectral clustering on random samples: the normalized case. In International Conference on Computational Learning Theory, pages 457–471, 2004.

- Von Luxburg et al. [2008] Ulrike Von Luxburg, Mikhail Belkin, and Olivier Bousquet. Consistency of spectral clustering. The Annals of Statistics, pages 555–586, 2008.

- Von Luxburg [2007] Ulrike Von Luxburg. A tutorial on spectral clustering. Statistics and computing, 17(4):395–416, 2007.

Appendix A Related Work

This section introduces related work on the theoretical analysis of spectral clustering algorithms. Existing theoretical research of spectral clustering mainly focuses on consistency, i.e., if it is true that as the sample size collected goes to infinity, the partitioning of the data constructed by the clustering algorithm converges to a certain meaningful partitioning on the population level. Von Luxburg et al. [2008] establishes consistency for the embedding by proving that as much as the eigenvectors of the Laplacian matrix converge uniformly to the eigenfunctions of the Laplacian operator. Rosasco et al. [2010] provides the simpler proof of this convergence. Cao and Chen [2011] constructs the consistency of regularized spectral clustering. Rohe et al. [2011] analyzes the consistency for stochastic block models, Ting et al. [2011] analyzes the spectral convergence, Pelletier and Pudlo [2011] analyzes the convergence of graph Laplacian, and Singer and Wu [2017] analyzes the convergence of the connection graph Laplacian. Trillos et al. [2016] proposes a framework and improves the results in Arias-Castro et al. [2012] by minimizing the discrete functionals over all possible partitions of the data points, while the latter just minimizes a specific family of subsets of the data points. Based on the framework in Trillos et al. [2016], Trillos and Slepčev [2018] provides a variational approach known as -convergence, proving the convergence of the spectrum of the graph Laplacian towards the spectrum of a corresponding continuous operator. Terada and Yamamoto [2019] investigates the kernel normalized cut, establishing the consistency by the weighted -means on the reproducing kernel Hilbert space (RKHS), and deriving the excess risk bound for kernel NCut. However, as we discussed in the main paper, they study the graph-cut solution, not the solution of spectral clustering that we used in practice. Different from the above research, we investigate the excess risk bound of the popular spectral clustering algorithms (relaxed RatioCut and relaxed NCut), not consistency. Our analysis is based on the practical steps of spectral clustering and spans two perspectives: the continuous solution and the discrete solution.

Appendix B Proof of Theorem 1

Proof.

The term can be decomposed as:

(1). For term , we have

Based on Eq. (8) in the main paper and by the transformation of elements between the RKHS and , we have

The term can be equivalently written as

where denotes the expectation and denotes the corresponding empirical average. Furthermore, denoted by . For any in RKHS , the term can be upper bounded by

We first apply the McDiarmid’s inequality Mohri et al. [2018] to control the deviation of the term from its expectation. For independent and identically distributed (i.i.d.) sampled data points and , we have

Since we assume , thus . Together with gives

Applying McDiarmid’s inequality with increment bounded by implies that with probability at least , we have

We use the Rademacher average Bartlett and Mendelson [2002] to bound the term . As mentioned in the main paper, the objective function of spectral clustering, i.e., Eq. (1), is a pairwise function, which can not be written as a summation of i.i.d. random variables, so that the standard techniques in the i.i.d. case can not apply to it. We use the -process technique introduced in Clémençon et al. [2008] to overcome this difficulty. Specifically, we define the following Rademacher complexity for spectral clustering:

Definition 1.

Assume is a space of functions , then the empirical Rademacher complexity of for spectral clustering is:

where is an i.i.d. family of Rademacher variables taking values and with equal probability independent of the sample , and is the largest integer no greater than . The Rademacher complexity of is .

With the Rademacher complexity, we begin to bound the term . Lemma A.1 in Clémençon et al. [2008] with and the index set allow us to derive

Let be i.i.d. samples independent of and let be a sequence of Rademacher variables. According to the Jensen’s inequality and a standard symmetrization technique, the term can be bounded by

where the last inequality uses the Khinchin-Kahane inequality Latała and Oleszkiewicz [1994]. Since and , thus we can bound the last formula by . Based on the above results, we derive that the term can be bounded by with probability at least .

(2). To bound the term , we need to define another operator: for relaxed RatioCut:

where . Rosasco et al. [2010] shows that and have the same eigenvalues (possibly up to some zero eigenvalues) and their corresponding eigenfunctions are closely related. A similar relation holds for and that we have mentioned in the main paper. The spectral properties between the operators and the Laplacian can help us to bound the term .

According to the spectral properties of the graph Laplacian, we know that is equivalent to the first smallest eigenvalues of Von Luxburg [2007]. Similarly, with operator spectral properties, is equivalent to the first smallest eigenvalues of operator . Specifically, can be written as:

where is the -th eigenvalue of the operator . Thus, for term , we have:

According to Proposition 8 and Proposition 9 in Rosasco et al. [2010] that demonstrates the relationship of eigenvalues between operator and operator , operator and matrix , respectively, we thus obtain that . Furthermore, it can be bounded by . Since and are self-joint operators Rosasco et al. [2010], from Theorem 5 in Kato [1987], we can bound by . Using the operator Theory Lang [2012], . From Theorem 7 in Rosasco et al. [2010], we know that with probability at least . From the above results, the term can be bounded by with probability at least . Based on the bounds of term and term , we derive that with probability at least . ∎

Appendix C Proof of Theorem 2

Proof.

The term can be decomposed as:

(1). Suppose ,

Since the eigenfunction is normalized to norm , and the discrete solution is also constrained to norm , so the term can be bounded by . And since , we finally bound by .

(2). Term and Term have been bounded in the proof of Theorem 1.

(3). is the continuous solution and is the discrete solution. The continuous solution space is a larger solution space, so we obtain .

Based on the above results of , , , and , we derive that with probability at least . ∎

Appendix D Proof of Theorem 3

Proof.

The term can be decomposed as:

(1). For term , we have

Based on Eq. (9) in the main paper, we have

The term can be equivalently written as

where is the expectation and is the corresponding empirical average. Denoted by . For any in the RKHS , the term can be bounded by

Till here, the following proof is the same as the proof of Theorem 1. For brevity, we omit it here. Since we assume , we have . Together with gives that with probability at least

(2). To bound the term , we also need to define the following bounded operators for relaxed NCut:

Rosasco et al. [2010] shows that , and have closely related eigenvalues and eigenfunctions, and the similar relations hold for , and . The spectral properties of these integral operators can help us to derive the term .

Similar to the proof of Theorem 1, the next key step is to prove the value of and . We first introduce a measure , having density w.r.t , is equivalent to since they have the same null sets. This implies that the spaces and are the same vector space and the corresponding norm are equivalent. In this proof, we regard as an operator from to , observing that its eigenvalues and eigenfunctions are the same as eigenvalues and eigenfunctions of , viewed as an operator from into Rosasco et al. [2010]. Let ,

where the last equality is obtained because eigenvalues and eigenfunctions of are the same in and Rosasco et al. [2010]. So for the relaxed NCut, , which is equal to the sum of the first smallest eigenvalues of . Similarly, by replacing with the empirical measure , is equal to the the sum of the first smallest eigenvalues of (This result can also be obtained by the spectral properties of Von Luxburg [2007]). Then we have

with probability at least .

Based on the above results, we derive that with probability at least .

∎

Appendix E Proof of Theorem 4

Proof.

Similarly, the term can be decomposed as:

(1). The proof of the term is the same as the proof of Theorem 1. Suppose , then we have

(2). The term and term have been bounded in the proof of Theorem 3.

(3). It is easily to have .

Based on the above results, we derive that with probability at least . ∎

Appendix F Algorithms

Algorithm 1 corresponds to relaxed RatioCut, while Algorithm 2 corresponds to relaxed NCut. We just show the pseudocode of clustering the out-of-sample data points in Algorithms 1 and 2. For clustering the original data , one can use the algorithm . We provide the pseudocode of in Algorithm 3 Stella and Shi [2003], please refer to Stella and Shi [2003] for more details. Additionally, line in Algorithms 1 and 2 aims to normalize the length of each row of the matrix so that they lie on a unit hypersphere centered at the origin and then can be searched for the discrete solution through orthonormal transform when performing in line 9. Moreover, in line , denotes vector diagonalization operation and returns the diagonal of its matrix argument in a column vector. The following iterative fashion in line 9 aims to find the empirical optimal discrete solution and the right orthonormal transform , see the details in Algorithm 3.

Input: weight function , cluster number , samples , new samples .

Phase 1: Based on , compute =-, then

compute the smallest eigenvalues and the corresponding eigenvectors .

Phase 2: Compute the eigenvectors of , then find the optimal discrete solution by the following steps:

Input: weight function , cluster number , samples , new samples .

Phase 1: Based on , compute , then

compute the smallest eigenvalues and the corresponding eigenvectors .

Phase 2: Compute the eigenvectors of , then find the optimal discrete solution by the following steps:

Remark 9.

[Comparison of time complexity.] For the original , the time complexity is mainly spent on the eigendecomposition and the SVD, whose complexity is all of the order Stella and Shi [2003]. If the iterative fashion in is performed times for samples, the time complexity of is of the order , because needs to compute time eigendecomposition and times SVD. Therefore, when the out-of-sample data points come, assuming the iteration fashion in is times on the overall data points of size , the time complexity of is , because they need to compute time eigendecomposition and times SVD on the overall data points. While for our proposed algorithm, assuming the iteration fashion in is times for samples , the time complexity is , because we can calculate the eigenvectors of with the help of the extended eigenfunctions , as discussed in the main paper. We just need to compute time eigendecomposition and times SVD on the out-of-sample data points . Besides, the size of may be not large in practice, thus the term will be much smaller than . Furthermore, a smaller may lead to faster convergence, thus may be much smaller than in practice. Based on the above analysis, one can see that our proposed algorithms significantly improve the time complexity when clustering unseen samples.

Input: matrix .

Appendix G Numerical Experiments

We have numerical experiments on the two proposed algorithms.

G.1 Toy Dataset

We first verify the effectiveness of the proposed algorithms on two popular toy datasets, circle datasets and moon datasets, implemented by scikit-learn which is a well-known tool for predictive data analysis in machine learning. The number of original samples is set as , and the number of unseen samples is set as . The weight function is used by Gaussian kernel function , where is set as for relaxed NCut and for relaxed RatioCut. The first row is four illustrations of the data points. Among them, the first two illustrations are the original samples and denote the circle datasets and moon datasets, respectively, while the last two illustrations are out-of-sample data points. We use the eigenvectors of the original data to cluster the unseen samples without requiring the eigendecomposition on the overall samples. Specifically, we use the information in the first illustration to predict the classification label of the samples in the third illustration, and the second illustration corresponds to the fourth illustration. The second row and the third row are clustering results for relaxed RatioCut and relaxed NCut, respectively. Among them, the first two illustrations are spectral clustering on the original samples, while the last two illustrations are spectral clustering on the out-of-sample samples. In each illustration, the samples are assigned one color: black or gray. From row 2, one can see that the unseen data points are correctly colored and correctly classified, suggesting that our proposed algorithms can use the eigenvectors of the original samples to correctly cluster the unseen samples. Similar results hold for row 3 which corresponds to relaxed NCut. In conclusion, from Figure 1, one can see that our two proposed algorithms are effective in clustering the unseen data points.

G.2 Real Dataset

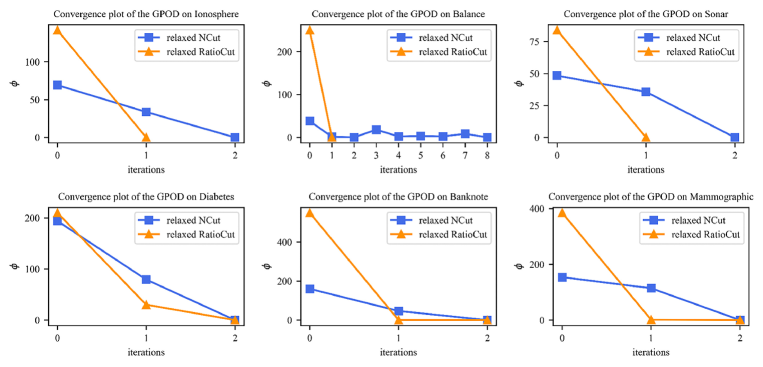

Additionally, six real datasets collected from the UCI machine learning repository are used for the experiments, which are commonly used in clustering. We compare with the relevant algorithm -means, where -means clusters the unseen data by choosing the closest cluster center. The details of the datasets are presented in Table 1. To measure the performance, we adopt Accuracy (ACC) and Normalized Mutual Information (NMI) as evaluation metrics. The closer the scores of these metrics are to , the better performance. For each dataset, we randomly choose of the samples as the training set (i.e., the original data) and the remaining as the testing set (i.e., the unseen samples). The Gaussian kernel function is chosen as the weight function as above. There are two hyperparameters in the experiments: the number of clusters denoted as and the Gaussian kernel function parameter denoted as . We set equal to the number of classes in the dataset, and the settings of parameter are given in Table 2. Here the parameter settings of relaxed NCut and relaxed RatioCut are denoted as setting[1] and setting[2] respectively. All algorithms are performed four times on each dataset to reduce the impact of randomness, and then the average performance is computed. From the experimental results in Table 3, one can see that outperforms -means. Meanwhile, the convergence of the is shown in Figure 2, where the six illustrations show the convergence speed of the algorithm on the six datasets, respectively. For each illustration, the horizontal axis represents the iteration steps and the vertical axis represents the optimization objective of the algorithm, the gap between the discrete and continuous solutions. As can be seen from Figure 2, the algorithm can converge quickly after a few iterations.

| Datasets | Instances | Attributes | Classes |

|---|---|---|---|

| Ionosphere | 351 | 34 | 2 |

| Balance | 625 | 4 | 3 |

| Sonar | 208 | 60 | 2 |

| Diabetes | 768 | 20 | 2 |

| Banknote | 1372 | 5 | 2 |

| Mammographic | 961 | 6 | 2 |

| Ionosphere | Balance | Sonar | Diabetes | Banknote | Mammographic | |

|---|---|---|---|---|---|---|

| relaxed NCut | 0.3970 | 0.0940 | 0.0245 | 0.1730 | 0.0520 | 0.0820 |

| relaxed RatioCut | 0.3970 | 0.0940 | 0.0245 | 5.5000 | 0.0480 | 0.0820 |

| Method | Metric | Datasets | |||||

|---|---|---|---|---|---|---|---|

| Ionosphere | Balance | Sonar | Diabetes | Banknote | Mammographic | ||

| -means | ACC | 76.1 | 52.5 | 55.7 | 67.5 | 56.0 | 64.8 |

| NMI | 0.1965 | 0.1399 | 0.0474 | 0.0581 | 0.0123 | 0.0710 | |

| GPOD[1] | ACC | 78.2 | 64.4 | 64.8 | 71.5 | 73.0 | 76.0 |

| NMI | 0.3058 | 0.2370 | 0.0697 | 0.0978 | 0.2750 | 0.2161 | |

| GPOD[2] | ACC | 79.1 | 66.9 | 58.2 | 74.0 | 88.3 | 74.8 |

| NMI | 0.3229 | 0.2937 | 0.0427 | 0.1417 | 0.4986 | 0.2012 | |

Appendix H Table of Notation

Please refer to Table 4.

| Notation | Description | Section |

| a subset of | 2 | |

| a probability measure on | 2 | |

| the empirical measure on | 2 | |

| a set of samples | 2 | |

| weighted graph constructed on | 2 | |

| , | set of all nodes and edges respectively | 2 |

| weight function | 2 | |

| weight matrix calculated by the weight function | 2 | |

| number of elements in set | 2 | |

| the clustering number | 2 | |

| degree matrix | 2 | |

| unnormalized graph Laplacian | 2 | |

| asymmetric normalized graph Laplacian | 2 | |

| a set of vectors | 2 | |

| the empirical error | 2 | |

| the summing weights of edges of a subset of a graph | 2 | |

| the space of square integrable functions | 3 | |

| a kernel function | 3.1 | |

| a reproducing kernel Hilbert space | 3.1 | |

| the supremum | 3.1 | |

| an integral operator | 3.1 | |

| a set of functions | 2 | |

| the population-level error | 3.1 | |

| optimal solution of the minimal population-level error of relaxed RatioCut (or NCut) | 3.1 (or 3.2) | |

| optimal solution of the minimal empirical error of relaxed RatioCut (or NCut) | 3.1 (or 3.2) | |

| a empirical operator of relaxed RatioCut | 3.1 | |

| the population-level discrete solution | 3.1 | |

| consisting of the first eigenfunctions of the operator (or ) | 3.1 (or 3.2) | |

| the optimal solution of the minimal population-level error of RatioCut (or NCut) | 3.1 (or 3.2) | |

| an integral operator | 3.2 | |

| a continuous real-valued bounded kernel | 3.2 | |

| , | empirical operators of relaxed NCut | 3.2 |

| an orthonormal matrix | 4 | |

| a set of new samples | 4.1 | |

| the eigenvectors of the new samples | 4.1 |