A Heteroskedasticity-Robust Overidentifying Restriction Test with High-Dimensional Covariates††thanks: The authors contributed equally to this work. An earlier working paper version of the paper circulated as “Q Test” (which integrates to our power enhancement procedure now) is available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4097813.

Abstract

We propose a new overidentifying restriction test for linear instrumental variable models. The novelty of the proposed test is that it allows the number of covariates and/or instruments to be larger than the sample size and is robust to heteroskedastic errors. We show that the test has the desired theoretical properties under sparse high-dimensional models and is more powerful than existing overidentification tests. First, we introduce a test based on the maximum norm of multiple parameters that could be high-dimensional. The theoretical power based on the maximum norm is shown to be higher than that in the modified Cragg-Donald test (Kolesár,, 2018), which is the only existing test allowing for large-dimensional covariates. Second, following the principle of power enhancement (Fan et al.,, 2015), we introduce the power-enhanced test, with an asymptotically zero component used to enhance the empirical power against some extreme alternatives with many locally invalid instruments. Focusing on hypothesis testing, we also provide a feasible estimator of endogenous effects for practitioners when instrument validity is not rejected. The simulation results show the superior performance of the proposed test, and the empirical power enhancement is clear. Finally, an empirical example of the trade and economic growth nexus demonstrates the usefulness of the proposed tests.

JEL classification: C12, C21, C26, C55

Keywords: overidentification test, maximum test, heteroskedasticity, power enhancement, data-rich environment.

1 Introduction

The instrumental variable (IV) approach is essential for the estimation and inference of endogenous treatment effects. Recently, the high-dimensional model has been the focal point of some IV-related studies, motivated by the increasing availability of large datasets, such as large survey data, clinical data, and administrative data. It is common to consider high-dimensional IV models where the number of covariates is vast, the number of potential IVs is enormous, or both. The consistency and asymptotic normality of IV estimation depend on the validity of the IVs. This paper concerns the overidentifying restriction test for IV validity in high dimensions, where the number of covariates and/or IVs could be even larger than the sample size.

The classic Sargan test (Sargan,, 1958) and J test (Hansen,, 1982) deal with a fixed number of IVs. Some recent overidentification tests consider a model with a large number of IVs. For example, Lee and Okui, (2012) proposed a modified Sargan test compatible with an increasing number of IVs under homoskedasticity. Chao et al., (2014) proposed an overidentification test robust to many IVs and heteroskedasticity following jackknife IV estimation (Angrist et al.,, 1999). Carrasco and Doukali, (2021) extended this method based on regularized jackknife IV estimation (Hansen and Kozbur,, 2014; Carrasco and Doukali,, 2017) to allow the number of IVs to be larger than the sample size.

All the tests mentioned above require the number of covariates in the structural equation to be fixed. A closely related earlier work is Kolesár, (2018), which extended Anatolyev and Gospodinov, (2011) and proposed a modified Cragg-Donald (MCD) test that allows a growing number of covariates. However, this test requires the total number of instruments () and covariates (), , to be less than the sample size , and the test has poor empirical power when . Within the context of overidentification tests, we refer to tests (including the MCD test and Chao et al., (2014)) that are based on a limiting distribution as “-type tests”. None of the existing -type tests allows with large .

Recent works (Belloni et al.,, 2014; Chernozhukov et al.,, 2015; Guo et al., 2018a, ) have proposed estimation and inference methodologies for endogenous treatment effects under high dimensions with . An overidentifying restriction test on IV validity is still unavailable for this scenario. This motivates our work. The proposed test allows the number of covariates and/or IVs to be greater than the sample size and is robust to heteroskedastic errors. It can check the validity of any overidentified subset of IVs and is scale invariant, making it a useful tool for empirical researchers. Although our paper focuses on the overidentification test, we suggest an endogenous treatment effect estimator when the null hypothesis is not rejected. Both the theoretical and numerical results support the suitability of this estimator.

1.1 Main Results and Contributions

First, we propose testing IV validity by designing a maximum test (M test) based on a maximum norm of multiple parameters that may be high dimensional. We call this test statistic the M statistic. Under some commonly imposed sparsity assumptions (Belloni et al.,, 2012, 2014), the M test has the correct asymptotic size; the M test has advantages for the setting of , where existing -type tests are not feasible. Moreover, the M test has better power than -type tests under sparsity when grows with the sample size but . Second, we propose an add-on asymptotically zero quadratic statistic (Q statistic) to improve the empirical power when the model includes many “locally invalid” IVs (meaning the alternatives have weak individual signals; for details, see Section 3.2) in finite samples. The resulting test, called the power-enhanced M test (PM test), rejects the null hypothesis when either the M or Q statistic is greater than the critical value of the significance level . Our paper extends the principle of power enhancement developed by Fan et al., (2015) and Kock and Preinerstorfer, (2019) to the popular IV model and overidentification test. The PM test always has noninferior theoretical power to the original M test by design. In simulations, we show that the empirical power of the PM test is indeed noninferior to that of the M test, and it is substantially improved when many IVs are locally invalid.

The PM test is an indispensable complement to the literature on postselection estimation and inference for endogenous treatment effects in high-dimensional settings (Belloni et al.,, 2012, 2014). These popular methodologies for sparse high-dimensional IV models are based on known IV validity. In practice, the IV validity is usually unknown. Our overidentification test is necessary for applications with many covariates and the IV set being either high- or low-dimensional.

We construct the tests using bias-corrected high-dimensional estimators. Specifically, the M test is implemented based on the maximum norm of the high-dimensional IV invalidity level estimator following the maximum test in a linear regression model (Chernozhukov et al.,, 2013; Zhang and Cheng,, 2017). The asymptotically zero Q statistic follows an inferential procedure for a quadratic form of high-dimensional parameters (Guo et al.,, 2019; Cai and Guo,, 2020; Guo et al.,, 2021). We extend the literature on quadratic form inference to the heteroskedasticity case.

In theory, we show that the M test has the correct asymptotic size with asymptotic power one when the maximum norm of the IV invalidity vector is of order . When is fixed, the M test can detect invalid IVs at a parametric rate, the same order of magnitude as the Sargan test in low dimensions. For sparse models with a growing , the M test is shown to achieve higher asymptotic power than the existing -type tests; the latter can only consistently detect the alternatives at the rate (for details, see Section 3, Remark 9). Furthermore, the asymptotically zero Q statistic guarantees a higher asymptotic power of the PM test than the -type tests when is proportional to (see Section 3, Remark 10). Computationally, the test can be easily implemented following the steps in Algorithm 1.

The simulation studies show that the M test has an apparent power improvement over the MCD test. For with large , for which our proposal is the only feasible method, the M test shows satisfactory performance in terms of size and power. Under many locally invalid IVs, the PM test substantially improves the power compared to the original M test, with empirical type I error controlled at the nominal level.

In the empirical study, we revisit the effect of trade on economic growth. We perform different tests on an IV model with a large number of covariates. We consider an overidentified set of instruments, including several possibly invalid instruments, such as energy usage and business environment. The PM test strongly rejects the null hypothesis of the correct specification well under the 1% level. In contrast, the M test rejects the null hypothesis under 5%, and the MCD test fails to reject at the 5% level, indicating the superiority of the PM test under high-dimensional IV models.

We summarize the main contributions as follows:

-

(i)

We propose an overidentification test for IV models with high-dimensional data. To our knowledge, this is the first overidentification test for with large . It is more powerful than existing -type tests under certain sparsity restrictions when .

-

(ii)

Our test is robust to heteroskedasticity, which is essential in IV models. Our paper extends the current high-dimensional statistical literature on the maximum norm or quadratic form inference to heteroskedastic data.

-

(iii)

We develop a power enhancement procedure in the context of an IV validity test. The asymptotically zero component improves empirical power against many local violations of the null hypothesis.

1.2 Other Related Literature

Often with the assumption of sparsity, regularized regression methods are commonly used to address high-dimensional problems with more covariates and IVs than the sample size (Belloni et al.,, 2012, 2014; Chernozhukov et al.,, 2015). A strand of literature has studied the estimation and inference of endogenous treatment effects without prior knowledge about IV validity (Kang et al.,, 2016; Guo et al., 2018a, ; Windmeijer et al.,, 2019, 2021; Sun et al.,, 2021; Ye et al.,, 2021; Fan and Wu,, 2022; Liang et al.,, 2022). Among these works, Guo et al., 2018a discussed inference for the treatment effect in the presence of possibly invalid IVs and high-dimensional covariates. However, these methods often require assumptions on the proportion of valid IVs, such as the majority rule Kang et al., (2016); Windmeijer et al., (2019). In addition, Guo, (2021) pointed out that the selection of valid IVs might suffer from selection error in finite samples. Our M test and its power-enhanced version work even if the majority rule is violated, and they show desirable finite sample performance based on our simulation and empirical results. Our test is also related to general signal detection works, including Donoho and Jin, (2004); Arias-Castro et al., (2011), and high-dimensional testing problems (Ingster and Suslina,, 2003). Our theoretical framework does not cover the examiner or judge designs (Arnold et al.,, 2022; Frandsen et al.,, 2023) with high-dimensional dummy IVs, which is a popular standalone application. This interesting case is left for future study. In addition, our methodology relates to the study of high-dimensional IV models from the perspective of estimation (Donald and Newey,, 2001; Okui,, 2011; Bai and Ng,, 2010; Carrasco,, 2012; Bekker and Crudu,, 2015; Fan and Zhong,, 2018; Zhu,, 2018). We also refer to Andrews et al., (2019) for a recent and comprehensive review of the weak IV literature.

Other literature (Liao,, 2013; Cheng and Liao,, 2015; Caner et al.,, 2018; Chang et al., 2021b, ) has studied moment condition selection under the GMM framework, requiring prior information about some moment conditions known to be valid. Chang et al., 2021a considered the overidentification test in high-dimensional settings using marginal empirical likelihood ratios and a selective subset of moment conditions. This paper also relates to a growing body of literature on quadratic form inference, such as Fan et al., (2021), with applications to the Markowitz mean-variance portfolio.

Finally, let us discuss the link between our paper and the inspiring power enhancement literature (Fan et al.,, 2015; Kock and Preinerstorfer,, 2019). For our overidentification test, the main task is primarily performed by the M test, although its empirical power can be further enhanced with a specific type of alternative (many local violations). There is a possibility of further improving the theoretical power of the overidentification test proposed by this paper. Nonetheless, additional efforts will be needed to fill the gap between the principle of power enhancement and the specific context of the overidentification test with high-dimensional covariates. Another point to consider is the choice of vector norm suggested by Kock and Preinerstorfer, (2021), who constructed an optimal high-dimensional test based on norm-based tests with in a general framework. In light of Kock and Preinerstorfer, (2021), asymptotically unbiased estimators of norms are required to build a bridge from the theoretical power enhancement results to practical implementations with . The theoretical properties of bias-corrected Lasso estimators for the maximum norm (Zhang and Cheng,, 2017) and squared norm (Cai and Guo,, 2020) are well known. However, this is not the case for the general norm. Due to these technical complications, and to focus on the central message of the current paper, we employ more easily implemented methodologies based on the maximum norm and norm for the case. More details are given in the last several paragraphs of Section 3.2.

Notation. We consider as a function of and discuss the asymptotics where and jointly diverge to infinity. The phrase “with probability approaching one as ” is abbreviated as “w.p.a.1”. An absolute constant is a positive, finite constant that is invariant with the sample size. We use “” and “” to denote convergence in probability and distribution, respectively. For any positive sequences and , “” means there exists some absolute constant such that , “” means , and “” indicates and . Correspondingly, “”, “” and “” indicate that the aforementioned relations “”, “” and “” hold w.p.a.1. We use for some to denote the integer set . For a -dimensional vector , the number of nonzero entries is , the norm is , the norm is , and its maximum norm is . For a matrix , we define the norm and the maximum norm . “” implies the positive definiteness of . For any positive definite with spectral decomposition , we define with being the diagonal matrix composed of the square roots of the corresponding diagonal elements of . We use to denote the diagonal matrix composed of the diagonal elements of . We define and for any vectors . We use to denote the null vector, to denote the all-one vector, and to denote the -dimensional identity matrix. The indicator function is . Finally, for any , we use and to denote and , respectively.

The remainder of the paper is organized as follows. In Section 2, we introduce the model and a treatment effect estimator. Section 3 provides the M test and its power-enhanced version with their asymptotic properties. Section 4 demonstrates the finite sample performance of the PM test by Monte Carlo simulations. Section 5 provides an empirical example. Section 6 concludes the paper. Technical proofs and additional simulation results are given in the Appendix.

2 The Model and Endogenous Treatment Effect Estimation

We consider the following classic linear IV model: for ,

| (1) | |||||

where denotes the outcome variable, denotes the endogenous variable, and and denote the covariates and the instrumental variables, respectively. We focus on the setting of a scalar endogenous variable , which is common in the literature (Kolesár,, 2018; Windmeijer et al.,, 2019; Mikusheva and Sun,, 2020). The parameter of interest is interpreted as the treatment effect. , , , and are coefficients of conformable dimensions in the model. is endogenous due to the correlation between and , even conditional on all instruments and covariates. Our proposed overidentification test operates via a random sample . We denote , , and .

We allow heteroskedastic errors in model (1) so that and may vary with . As discussed in Section 1, the test allows for any combination of and . We also impose a sparsity assumption on model (1), following the literature on similar models with high-dimensional IVs and baseline covariates (e.g., Belloni et al.,, 2012, 2014; Kolesár et al.,, 2015; Guo et al., 2018b, ).

We consider the reduced form of model (1),

| (2) | |||

where , and with and . Following the literature on high-dimensional models, we impose the sparsity assumption on model (2). We define the sparsity index . For simplicity, we also use to regulate the sparsity of and , which can be induced by the sparsity of the coefficient vectors in model (1). We further specify the rate of the sparsity index in Assumption 4 below. As a general approach to handling high-dimensional sparse models, we apply the Lasso method (Tibshirani,, 1996) to estimate the high-dimensional parameters in (2) and customized (according to the functional form) debiasing methods for eventual estimators or test statistics.

We define as an design matrix with We define , , , and , for Let .

By , the treatment effect can be expressed as

| (3) |

where , and we choose

| (4) |

for data scale invariance with , for . We define . Note that , and we have under the null hypothesis of Thus, we aim to estimate and for an estimator of .

Remark 1.

When , the TSLS estimator actually estimates with the empirical Gram matrix . The Sargan test weights by the same matrix, and its power is determined by . However, the empirical Gram matrix of can be singular when . In our test, we employ the diagonal weighting matrix that applies to both low- and high-dimensional IVs. This choice of automatically satisfies the bounded norm required for our Lasso-based procedure (in Proposition B2).

2.1 A Debiased Lasso-Based Estimator of

Similar to the classic Sargen test, our test requires an initial estimator of . We introduce an estimator of that is fitting for our high-dimensional setting. This estimator helps construct our overidentification test based on the debiased Lasso estimator of . We derive its desired theoretical property at the end of this section.

Recall that when . With the estimators and specified later, can be estimated by

| (5) |

We call (5) the IQ estimator since it is given by the ratio of estimators of an inner product and a quadratic form. We have the following decomposition of the estimation error:

| (6) |

as . The asymptotic normality of follows from the asymptotic normality of and .

We use Lasso to estimate and in (2):

| (7) |

| (8) |

where are positive tuning parameters that are selected by cross-validation in practice. The estimation of obtained by plugging in the Lasso estimators in (7) and (8) causes bias and invalidates asymptotic normality. Therefore, we introduce a debiasing procedure for . Here, we generalize the debiasing method for the quadratic form of high-dimensional parameters presented in the recent literature (Guo et al.,, 2019, 2021). Since depends on quadratic transformations of the high-dimensional parameters, our debiasing procedure differs from well-known debiased Lasso methods such as Javanmard and Montanari, (2014), Zhang and Zhang, (2014), and van de Geer et al., (2014). We specify our bias correction procedure below. First, for , the denominator of , the estimation error of the plug-in estimator is

| (9) |

The second term on the RHS of (9) is negligible. We thus only need to estimate the first term, which is the key bias component induced by plugging in the Lasso estimators. The main idea is to estimate the leading bias term by , where is a projection vector to be constructed at (14). Intuitively, the term is proportional to the subgradient of the norm at the Lasso solution . Thus, by adding a linear projection of this term, the procedure compensates for the bias introduced by the penalty in the Lasso estimator (Javanmard and Montanari,, 2014).

For this purpose, we decompose the estimation error as follows:

| (10) |

where is a zero vector and is the projection direction vector constructed to minimize the estimation error. Then, if we estimate by

| (11) |

we will have

| (12) |

As mentioned earlier, is negligible. The first term on the RHS is also asymptotically negligible since we construct so that is sufficiently close to zero. Consequently, the approximation is expected, where . The asymptotic normality result stems from the second term.

Following the same line of argument, we can estimate by

| (13) |

where . We estimate by the constrained -minimization for inverse matrix estimation (CLIME) estimator (Cai et al.,, 2011), which is widely used to regularize the behavior of estimation in high-dimensional models. The CLIME procedure is defined by (A1) with the properties described in Lemma B4.

Here, we use instead of minimization as used in Javanmard and Montanari, (2014) since convergence of the CLIME estimator, specified by (B11), is required for the testing problem in this paper, which also appeared in the literature (Zhang and Cheng,, 2017; Gold et al.,, 2020). The projection vectors are formally defined as

| (14) |

To derive the asymptotic properties of , we make the following assumptions.

Assumption 1.

Suppose that are independent and identically distributed sub-Gaussian vectors such that for any and , where and are absolute constants. The population covariance matrix satisfies for absolute positive constants .

Assumption 2.

Suppose that and are centered sub-Gaussian variables such that and for some , where and are absolute constants. Assume , and for some absolute constants . In addition, there exist some absolute constants and such that for . Further assume that .

Remark 2.

Assumption 1 is a sub-Gaussian tail condition for both the covariates and IVs, with eigenvalue bounds for the population covariance matrix. Assumption 2 imposes sub-Gaussianity and bounded conditional moment conditions on the error terms. We also avoid perfect correlation between the two error terms by bounding the correlation coefficient away from one.

Assumption 3.

Define the class of population precision matrices

| (15) |

where . Suppose that with and .

Remark 3.

Assumption 3 includes mild sparsity conditions on the precision matrix (Cai et al.,, 2011) with and norms bounded by certain quantities to bound the estimation error of the CLIME estimator. This assumption is widely used for inferential procedures in high-dimensional models (Breunig et al.,, 2020; Gold et al.,, 2020; Cai and Guo,, 2020).

Assumption 4.

Suppose that , where is an absolute constant.

Assumption 5 (Tuning Parameters).

Suppose the following conditions hold:

-

(i)

The Lasso tuning parameters satisfy for , where with a sufficiently large absolute constant .

-

(ii)

The tuning parameters for the CLIME estimator in (A1) satisfy with a sufficiently large absolute constant .

Remark 4.

Assumption 4 constructs the asymptotic scheme, which also imposes restrictions on the number of nonzero coefficients . It bounds the estimation errors of the estimators. Assumption 4 further implies with , which is required for the Gaussian approximation property used for the M test in the next section. It also provides an asymptotic lower bound for the global IV strength . In classical low-dimensional IV models, strong IVs satisfy . Here, we only need global, not individual, strength for high-dimensional ; the latter is required in the literature on high-dimensional IV regression (Guo et al., 2018a, ; Guo et al., 2018b, ).

With the assumptions specified, we are ready to consider the asymptotic normality of our IQ estimator .

Theorem 1 shows that we can use for inference on the treatment effect when all IVs are valid. This makes the IQ estimator an alternative to the existing postselection procedures (Belloni et al.,, 2014; Chernozhukov et al.,, 2015) with known IV validity. The suitability of is further demonstrated by the simulation results in Appendix C.2. In the next section, we use this initial estimator to construct the overidentification test for convenience in deriving the asymptotic properties of the test statistic. Overidentifying restriction tests based on other existing postselection estimators of might be possible, but we will use our estimator because of its clear path to the asymptotic theories.

3 Overidentifying Restriction Test

In this section, we propose testing procedures for the following null hypothesis:

| (17) |

For data scale invariance, we use the weighted version with . Subtracting from the structural equation in (1) yields

| (18) |

where , and . Note that we identify , not , from (18). Obviously, when , implies and hence . Next, we derive the if and only if condition for equivalence between and . The weighted quadratic form of , , is useful in the following discussions. For simplicity of notation, we use for . By the definition of and some basic calculations, we have

| (19) |

where is the relatedness between and . By (19), if and only if or . Then, if it is equivalent to work with for the ultimate test of (17):

| (20) |

Remark 5.

The inequality means that the weighted vectors and are not perfectly parallel. A specific counterexample is , which entails that . This is why our test, like all other tests for IV validity, requires overidentifying conditions. In Appendix A.2, we provide more detailed discussions with several examples concerning and the relation between and . In the following theoretical results, we focus on the identifiable .

In the following subsections, we present the testing procedure for (20). Section 3.1 introduces the baseline testing procedure for (20) using the maximum norm . Intuitively, the maximum test has good power when the alternative set has strong signals of for some . In practice, when there are many locally invalid IVs, can be much smaller than under finite samples. Inspired by the principle of power enhancement (Fan et al.,, 2015; Kock and Preinerstorfer,, 2019), in Section 3.2, we construct an asymptotically zero quadratic statistic by an estimator of to enhance the empirical power of the original M test. The power enhancement procedure utilizes the high power of the M test under sparsity and the desired empirical power enhancement of the Q statistic. Next, we give the details of the M and Q statistics.

3.1 The M Test

In what follows, we propose a maximum test that addresses (20). We use the following procedure to construct an estimator of .

Substituting by in equation (18), we have

| (21) |

where , and 111Throughout the paper, the subscript stands for a transformed variable or parameters using the unknown . In addition, for generic notation , stands for the transformed variables or parameters using the estimator , denotes Lasso estimators or residuals, and represents debiased Lasso estimators.. The LHS, , is analogous to the “residuals” in the Sargan test. We apply Lasso to estimate from (21),

| (22) |

where is a positive tuning parameter selected by cross-validation. The bias-corrected estimator for is given as

| (23) |

where is defined by (A1). We use this in the maximum test.

Let be the submatrix composed of the last rows of . Similar to Theorem 6 of Javanmard and Montanari, (2014), has the following decomposition:

| (24) |

where is a higher-order term. When , we have . Premultiplying on both sides of (24), we obtain

The first term implies that the asymptotic distribution of is intrinsically involved in our maximum test. The bounding of (B65) in the proof of Proposition B8 shows that . Thus, we can derive the following approximation under the null hypothesis :

| (25) |

The asymptotic covariance matrix of (25) can be approximated by

| (26) |

where and . Following Chernozhukov et al., (2013), it is shown that the distribution of can be well approximated by that of , where conditional on the observed data. Define the M statistic as

| (27) |

Then, under any significance level , the M test rejects the null hypothesis when

| (28) |

where the critical value is given as

| (29) |

following Chernozhukov et al., (2013), where is the probability measure induced by with the observable covariance matrix fixed. In practice, can be approximated by simulating independent draws (Chernozhukov et al.,, 2013; Zhang and Cheng,, 2017).

We then define the alternative set for theoretical justifications of the M test. We discuss the alternatives based on the probability limit of , given as

| (30) |

where , . Define the relatedness between and as

| (31) |

similar to the relatedness used in (19) with weighting matrix . Define the alternative set of (and treat all other parameters such as , as given), for any , as

| (32) |

for some absolute constant , where and are defined similarly to and with replaced by . We have the following technical assumptions, which are important for the theoretical properties of the M test.

Assumption 6.

The Lasso tuning parameter for (22) satisfies , where with some sufficiently large absolute constant .

Remark 6.

Recall that (26) estimates the asymptotic variance of , whose limiting form is defined as (B62) in the supplement. Based on its definition, , where and is positive definite. The maximum test requires the asymptotic individual variance of each component in the debiased estimator (i.e., each diagonal element of ) to be lower-bounded away from zero. This condition can be violated in general since is rank-deficient. The following assumption is sufficient for the required lower bounds of individual variances.

Assumption 7.

Remark 7.

Assumption 7 can be interpreted as the following overidentification condition: the weighted global IV strength cannot be dominated by only one of the IVs. In other words, the model needs to be overidentified by two dominating IVs with the same order of strength.

We are now ready to state the main theoretical result for the asymptotic size and power of the M test.

Theorem 2.

Remark 8.

Remark 9.

Here, we discuss the power comparison in the case of growing . For simplicity of illustration, we assume (only in this remark) that . In the literature (Donald et al.,, 2003; Okui,, 2011; Chao et al.,, 2014), overidentification tests take the form of a test. It is worth noting that the only existing test that also allows for growing is the MCD test of Kolesár, (2018), which takes the same form as the test and hence has the same asymptotic power rate. It is widely discussed in the aforementioned studies that -type tests have asymptotic power one against invalid IVs, as . This implies , where is the number of invalid IVs. Thus, under the sparsity condition , the M test has higher asymptotic power than the -type tests.

Now, we have established the theoretical property of the baseline M test. As discussed earlier, the finite sample performance of the M test might be harmed by many local violations of the null hypothesis in which the signal of the maximum norm is weak. We will next consider a procedure for empirical power enhancement by an asymptotically zero quadratic statistic.

3.2 Empirical Power Enhancement

The power enhancement procedure is inspired by Fan et al., (2015); Kock and Preinerstorfer, (2019). Theorem 2 shows that the M statistic defined by (28) satisfies as . Suppose that we have another statistic as . Define . Then, the PM test

| (35) |

also has asymptotic size with power at least the same as that of the M test . This subsection constructs the asymptotically zero Q statistic to obtain the PM test.

Following the same idea about the debiased estimators of and in (3), we construct a projection direction and propose the following bias-corrected estimator of :

| (36) |

We then define the Q statistic as

| (37) |

For ease of discussion of the asymptotic properties of the induced test (notice we do not perform this test individually) based on this Q statistic, we define a new alternative set with defined by (31). We have the following results in favor of the asymptotically zero Q statistic .

Theorem 3.

Remark 10.

Theorem 3 implies that when . Compared to the -type tests that consistently detect invalid IVs when , the asymptotically zero Q statistic guarantees higher asymptotic power than the -type tests when . Here, we again emphasize that when with high-dimensional covariates, our test is still feasible, while the -type tests break down.

The PM test (35) has asymptotic power one when either (C1): or (C2): , for some absolute constant , where (C1) and (C2) are the sufficient conditions for and , respectively.

Recall that denotes the number of invalid IVs. Note that even under the alternative, we require for any absolute constant with sufficiently large (implied by Assumption 4) to bound the bias term in (38) to derive the asymptotic size and power in theory. When is diagonal, condition (C1) implies

| (39) |

where the last inequality applies , which is necessary for a consistent estimator of . Condition (39) is exactly (C2). Thus, (C1) implies (C2). Under our model setting, the power enhancement is invisible from a theoretical point of view. Without estimation consistency, the power analysis becomes much more difficult.

Nevertheless, the power enhancement procedure is still favorable in practice. As mentioned below in Remark 5, in practice, there can be many locally invalid IVs with small . Consequently, the empirical norm of the target vector is much larger than the empirical maximum norm. The power enhancement by the Q statistic directly captures the norm and thus should have higher empirical power. The numerical studies in the next section show this is the case: the empirical power is enhanced in practice in this scenario, with the empirical type I error almost unaffected.

Practitioners can easily implement our test with a high-dimensional dataset222The computer code for the implementation of the above method is available at https://github.com/ZiweiMEI/PMtest.. The steps for the PM test are summarized in Algorithm 1.

4 Simulations

4.1 Setup

The simulation DGP follows Model (1). We focus on high-dimensional covariates where . For each pair , we set to consider both low- and high-dimensional instrumental variables. The exogenous variables are independently generated by a multivariate Gaussian distribution with mean zero and covariance matrix . We construct the error terms as follows:

where , and are i.i.d. variables. We set for homoskedasticity and for heteroskedasticity so that the R-square333According to Footnote 11 of Bekker and Crudu, (2015), . for the regression of on the IVs equals 0.2.

We fix . For each combination , we set and . We consider two sparse settings of

-

•

The relevant IVs are all strong: ;

-

•

There is a mixture of strong and weak IVs: .

Throughout the simulation study, we set and . For IV validity, we first consider , where only the first IV is invalid. To demonstrate the necessity of power enhancement, we also consider another setting of , given as

Compared to , contains more invalid instruments with a smaller maximum norm. The tests focused on the norm are likely to be more powerful than the M test. We will see the benefits of power enhancement in the simulation results.

The Lasso problems are solved by the glmnet R package. The tuning parameter is selected by cross-validation with the one-standard-error rule that is also favored in the current literature (Windmeijer et al.,, 2019). We use the efficient fastclime package (Pang et al.,, 2014) to solve Problem (A1) for the CLIME estimator of the precision matrix . In addition to the M test and PM test, we report the simulation results of the MCD test proposed by Kolesár, (2018) as a representative of -type tests, which allows many covariates with the restriction as .

4.2 Simulation Results

| Homoskedasticity | Heteroskedasticity | |||||||

| MCD | M | PM | MCD | M | PM | |||

| 150 | 50 | 10 | 0.022 | 0.073 | 0.073 | 0.023 | 0.042 | 0.042 |

| 100 | NA | 0.044 | 0.068 | NA | 0.035 | 0.044 | ||

| 100 | 10 | 0.023 | 0.057 | 0.057 | 0.021 | 0.056 | 0.056 | |

| 100 | NA | 0.038 | 0.061 | NA | 0.023 | 0.028 | ||

| 300 | 150 | 10 | 0.025 | 0.056 | 0.056 | 0.032 | 0.044 | 0.044 |

| 100 | 0.056 | 0.047 | 0.047 | 0.044 | 0.030 | 0.030 | ||

| 250 | 10 | 0.033 | 0.058 | 0.058 | 0.038 | 0.079 | 0.079 | |

| 100 | NA | 0.039 | 0.039 | NA | 0.038 | 0.038 | ||

| 500 | 350 | 10 | 0.035 | 0.052 | 0.052 | 0.028 | 0.052 | 0.052 |

| 100 | 0.057 | 0.041 | 0.041 | 0.050 | 0.051 | 0.051 | ||

| 450 | 10 | 0.041 | 0.048 | 0.048 | 0.042 | 0.054 | 0.054 | |

| 100 | NA | 0.038 | 0.038 | NA | 0.037 | 0.037 | ||

| 150 | 50 | 10 | 0.023 | 0.068 | 0.069 | 0.020 | 0.045 | 0.045 |

| 100 | NA | 0.044 | 0.067 | NA | 0.030 | 0.041 | ||

| 100 | 10 | 0.022 | 0.05 | 0.05 | 0.023 | 0.061 | 0.061 | |

| 100 | NA | 0.039 | 0.06 | NA | 0.023 | 0.028 | ||

| 300 | 150 | 10 | 0.029 | 0.057 | 0.057 | 0.028 | 0.039 | 0.039 |

| 100 | 0.057 | 0.044 | 0.044 | 0.041 | 0.030 | 0.030 | ||

| 250 | 10 | 0.031 | 0.056 | 0.056 | 0.035 | 0.056 | 0.056 | |

| 100 | NA | 0.040 | 0.040 | NA | 0.039 | 0.039 | ||

| 500 | 350 | 10 | 0.036 | 0.053 | 0.053 | 0.026 | 0.044 | 0.044 |

| 100 | 0.055 | 0.041 | 0.041 | 0.047 | 0.054 | 0.054 | ||

| 450 | 10 | 0.041 | 0.047 | 0.047 | 0.041 | 0.051 | 0.051 | |

| 100 | NA | 0.039 | 0.039 | NA | 0.039 | 0.039 | ||

Note: “MCD”, “M”, “PM” are the abbreviations of the modified Craig–Donald test, the maximum test and the power-enhanced maximum test, respectively. “NA” means “not available”.

Table 1 shows the empirical type I errors of different tests under . The MCD test controls the type I error below or close to the nominal size, and it is robust to heteroskedastic errors under finite samples. However, it is infeasible when . In comparison, our M test and PM test are robust to high-dimensional covariates and instruments. The most severe overrejection case occurs under , which is no more than 0.03 off from the target rejection rate of 5%. In most cases, the rejection rate is close to the nominal size. The slight bias in Type I error is offset by substantial power gains compared to the MCD test, as shown below. In addition, the empirical type I errors are similar between the M test and PM test, indicating that the power enhancement for the M test has almost no effect on the empirical size. In Appendix C.2, we also show the simulation results of our proposed IQ estimator (5) if the null hypothesis is not rejected. The IQ estimator has satisfactory performance in estimation and inference for .

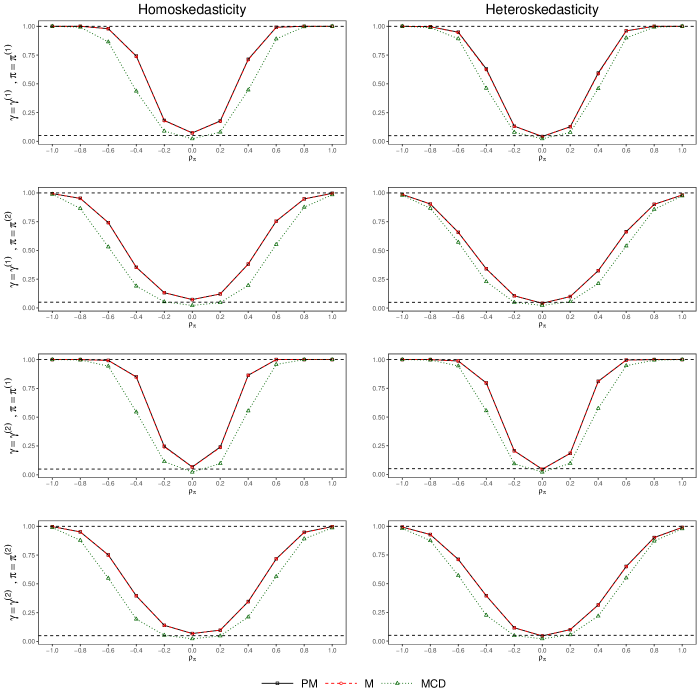

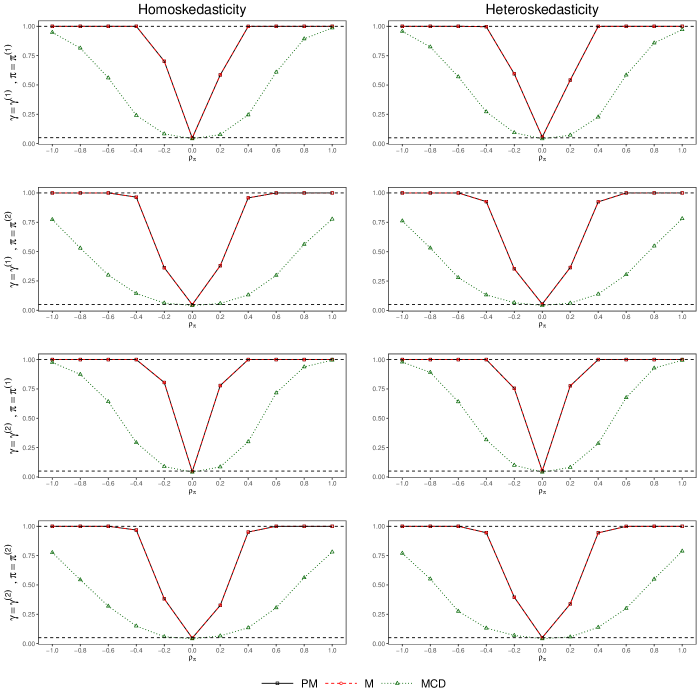

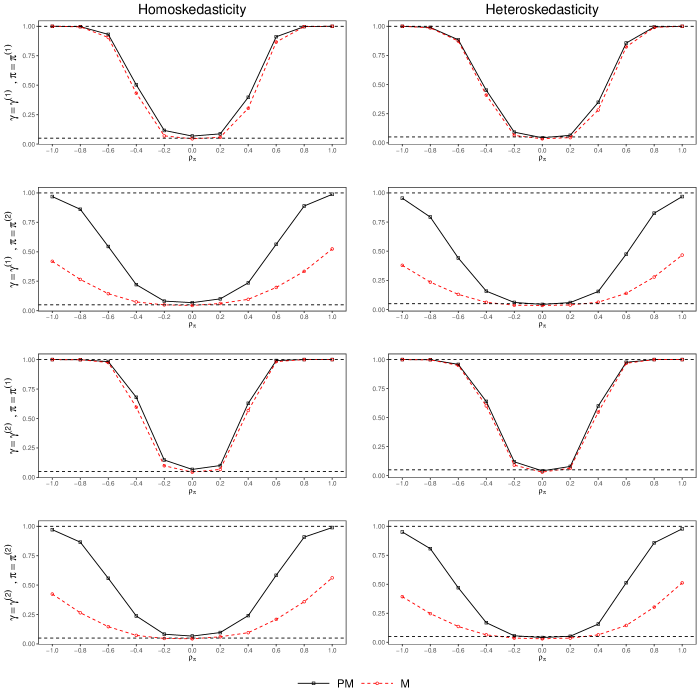

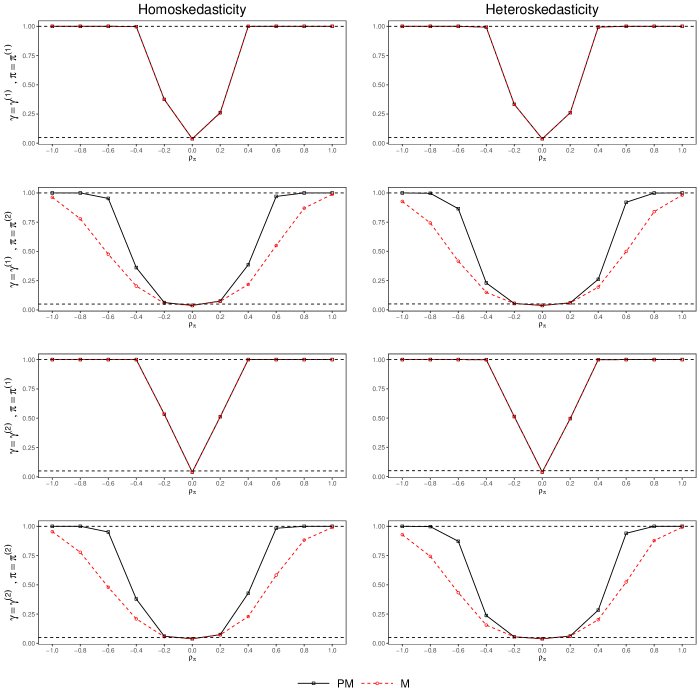

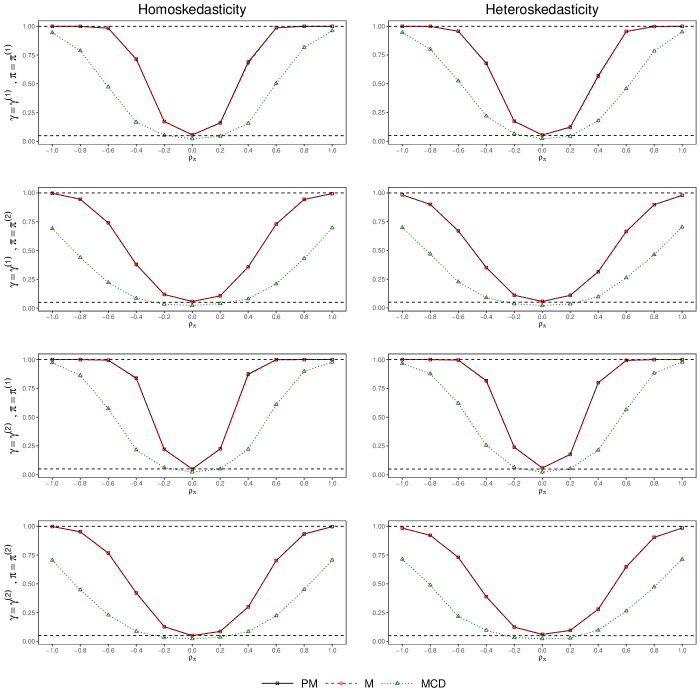

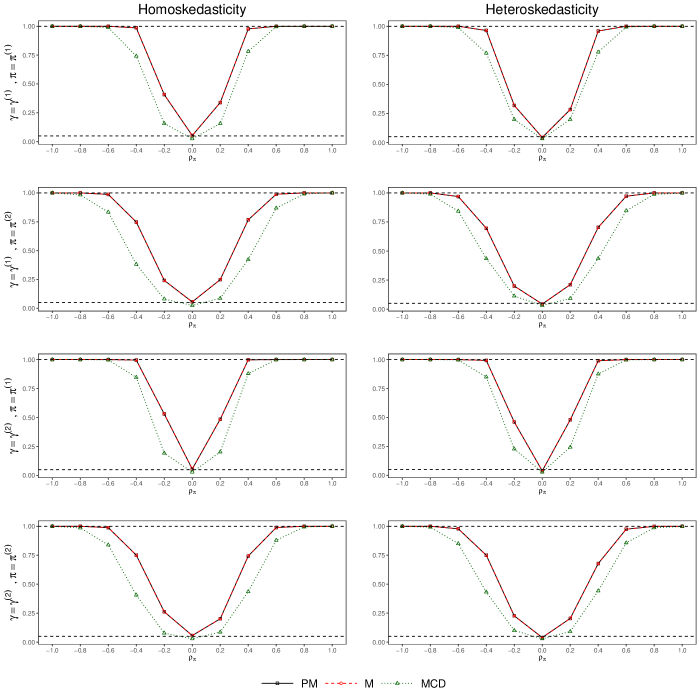

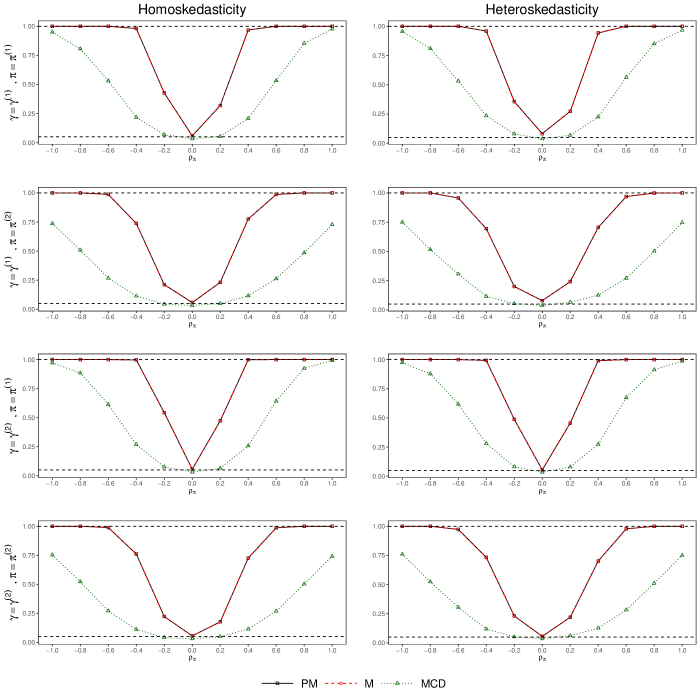

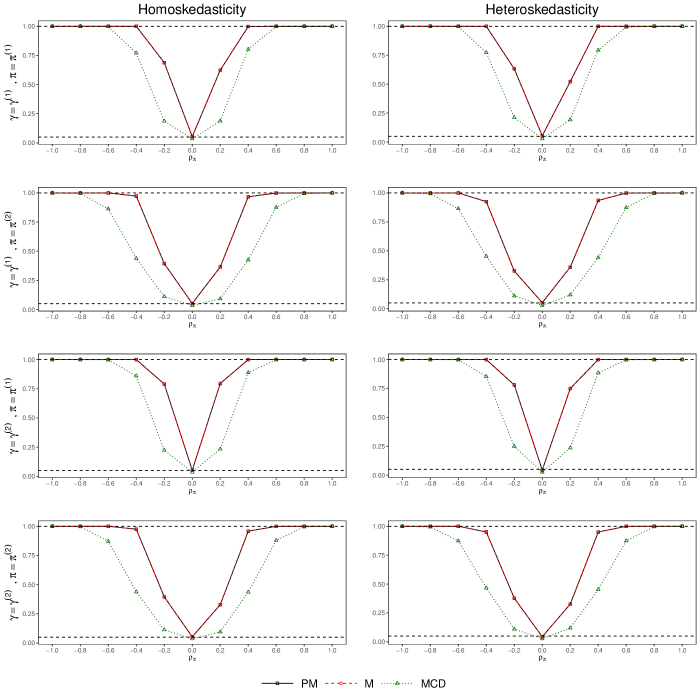

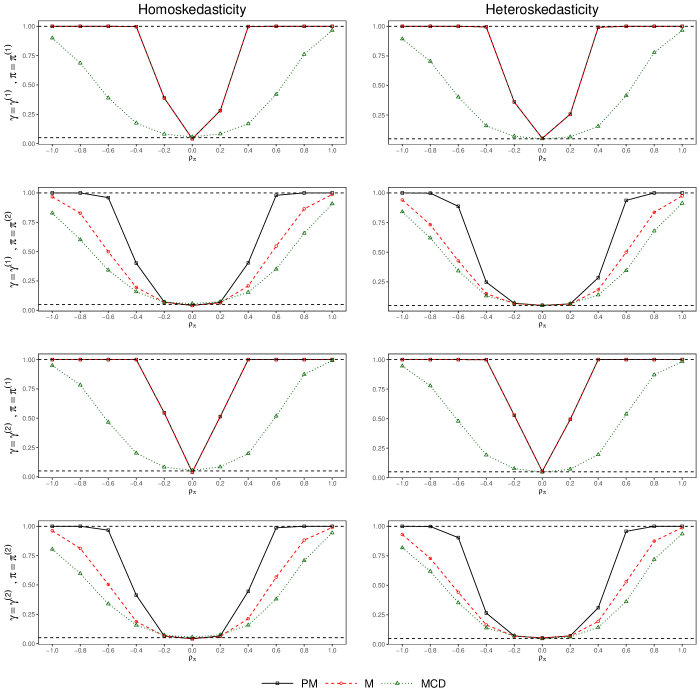

To save space, we only report the power curves in the main text under . The power curves for other settings are available in Appendix C.1. When so that , as shown in Figures 1 and 2, the M test and PM test have almost the same empirical power. When either one () or four IVs () are invalid, the M test on the maximum norm is at least as powerful as the test under a finite sample. In addition, both tests are more powerful than the MCD test. The power improvement is more evident when and , where is very close to the sample size .

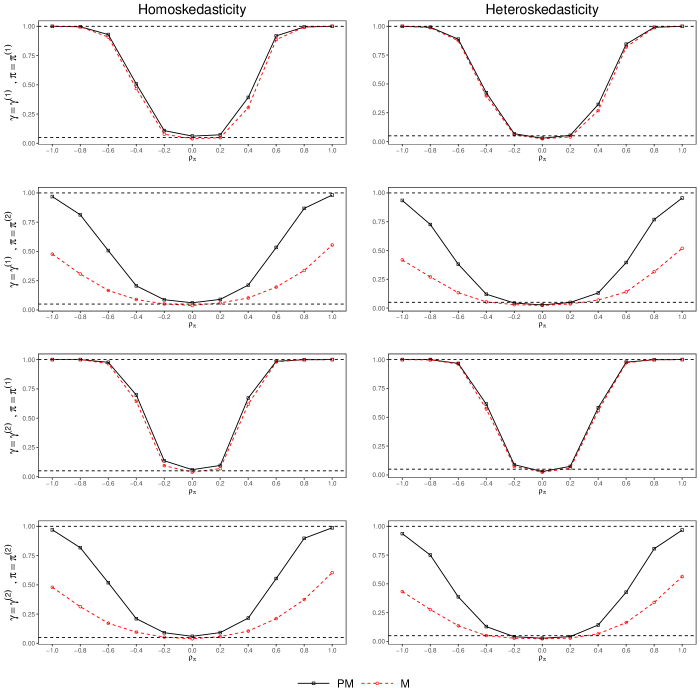

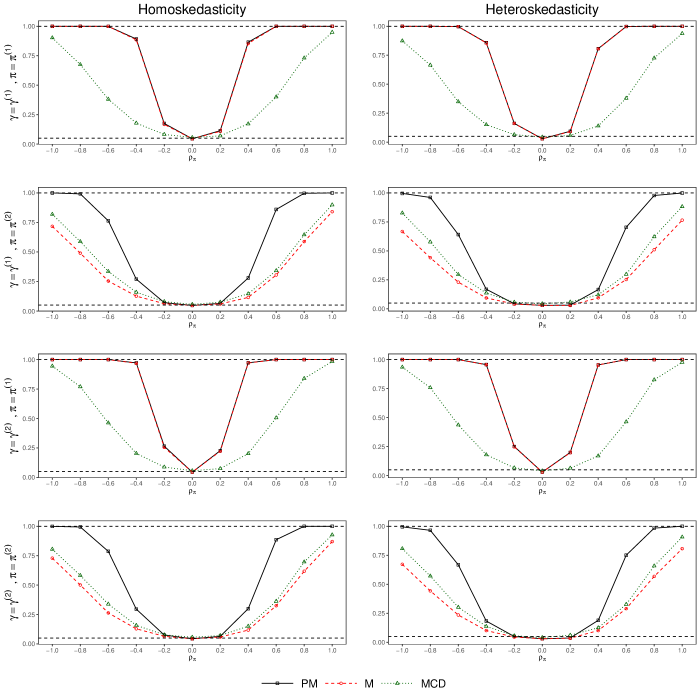

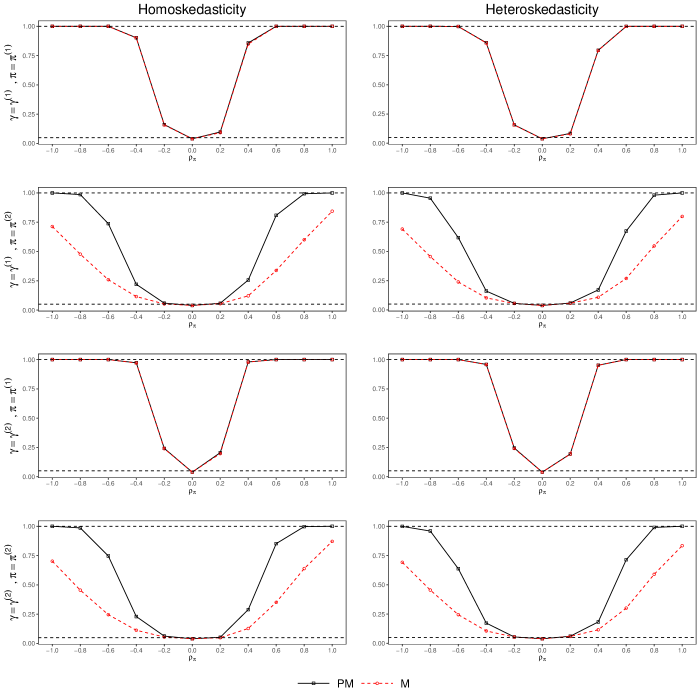

Figures 3 and 4 show the results when . Given , the -type MCD test becomes infeasible; hence, the results are unavailable in these two figures. With correct type I errors, the M test and PM test still have high power against invalid instruments under high dimensions, comparable to the performance under . Again, the power curves of the M test and PM test are close when there is only one invalid IV (), as shown in the first and third rows of the two figures. However, with 30 locally invalid instruments (, the second and fourth rows), the M test is outperformed by the PM test. This result shows that our power enhancement procedure makes the M test more robust to some extreme cases with many locally invalid instruments without significant impacts on type I errors.

5 Empirical Example

| Notation | Variable Name | Min | Median | Max | Mean | Std. Dev. |

| Log GDP | 7.463 | 10.422 | 12.026 | 10.184 | 1.102 | |

| Trade | 0.098 | 0.758 | 4.129 | 0.869 | 0.520 | |

| Log Population | -3.037 | 1.472 | 6.674 | 1.355 | 1.830 | |

| Log Area | 5.193 | 11.958 | 16.611 | 11.685 | 2.312 | |

| 0.015 | 0.079 | 0.297 | 0.092 | 0.052 | ||

| Languages | 1.000 | 1.000 | 16.000 | 1.887 | 2.129 | |

| Water Area | 0.000 | 2340.000 | 891163.000 | 25218.771 | 100518.984 | |

| Land Boundaries | 0.000 | 1881.000 | 22147.000 | 2819.987 | 3404.441 | |

| % Forest | 0.000 | 30.319 | 98.258 | 29.713 | 22.416 | |

| Arable Land | 0.558 | 42.035 | 82.560 | 40.760 | 21.611 | |

| Coast | 0.000 | 515.000 | 202080.000 | 4242.147 | 17399.583 | |

| 0.017 | 0.113 | 1.480 | 0.170 | 0.199 | ||

| 0.000 | 201.263 | 87556.265 | 1872.710 | 8160.430 | ||

| 0.000 | 184.863 | 2231.550 | 242.217 | 287.270 | ||

| 0.000 | 1.946 | 20.573 | 2.686 | 3.025 | ||

| 0.033 | 3.099 | 19.408 | 3.802 | 3.112 | ||

| 0.000 | 39.891 | 19854.247 | 352.687 | 1675.864 | ||

| PM2.5 | 5.861 | 22.252 | 99.734 | 27.868 | 19.436 | |

| Access to Electricity | 9.300 | 99.800 | 100.000 | 84.434 | 26.245 | |

| Ease of Doing Business Index | 1.000 | 85.000 | 188.000 | 88.356 | 54.022 |

To illustrate the usefulness of the proposed test with high-dimensional data, we revisit the empirical analysis of the effect of trade on economic growth (Frankel and Romer,, 1999, FR99 hereafter). Fan and Zhong, (2018) searched for instruments (all geographical variables) following the celebrated gravity theory of trade. In this paper, we update all data to 2018 and expand the set of IVs from Fan and Zhong, (2018) to include potentially invalid IVs from World Bank economic data. Following the literature, the outcome is the logarithm of GDP. There are countries, and , which includes (1) the constructed trade proposed by FR99 under the guidance of the gravity theory of trade, (2) the logarithms of population and land area describing the sizes of the countries and (3) other covariates and candidate IVs concerning geographical characteristics, energy, the environment and natural resources, and business activity variables444, and are instruments and covariates that have been widely recognized in the literature since FR99. To make better comparisons to the literature, we do not penalize them in the Lasso problems, following the suggestions in Belloni et al., (2014).. The outcome variable, the endogenous variable, the original FR99 covariates, and a subset of the baseline instruments used in Fan and Zhong, (2018), together with three additional and possibly invalid IVs, are summarized in Table 2. We perform overidentification tests using this (sub)set of IVs.

| Instrument Sets | MCD | M | PM |

| 0.062 | 0.029 | 0.000 | |

| 0.317 | 0.275 | 0.275 |

We standardize the data so that all variables have zero sample mean and unit standard deviation and then compare the results of different testing methods. Table 3 shows the p values of different tests performed on the real data. We first test the correct specifications of all 16 instruments in Table 2 and expect the null hypothesis to be rejected since at least some of the instruments (about climate), (about resources) and (about business activity) are likely to have a direct effect on economic growth. We can see that the M test and PM test reject the null hypothesis at the 5% and 1% levels, respectively, while MCD fails to reject the validity of IVs at the 5% level.

As mentioned earlier, empirical researchers can also use our method to test whether a subset of IVs is valid. Here, we select the subset of IVs used in Fan and Zhong, (2018), including , as displayed in Table 2, and treat the other instruments as covariates. Therefore, the variable dimensions are now and . All the considered tests do not reject the null hypothesis, meaning there is no evidence that this subset of instruments is invalid.

The takeaway from this empirical exercise is that practitioners should be cautious in the interpretation of a failure to reject the null hypothesis by existing overidentification tests such as MCD when many covariates and/or instruments are present. Using tests with low power would result in further difficulty in the estimation and inference of the endogenous treatment effect. Our proposed test improves the power in different model settings; hence, it is recommended in a data-rich environment to detect invalid instruments.

6 Conclusion

In this paper, we develop a new test on overidentifying restrictions for linear IV models with high-dimensional covariates and/or IVs. This test is robust to heteroskedasticity. We show that under sparsity, our PM test has better theoretical power than the existing -type tests while having the size under control, even when . The higher power stems from the utilization of a sparse model structure. This substantially improves the empirical power against many locally invalid instruments. The procedure can be used to test any overidentifying restrictions of a subset. As high-dimensional data become more common in observational studies, the PM test should have many applications in detecting instrument misspecifications. From a technical perspective, this paper extends the inference of maximum and norms, allowing for heteroskedasticity, and shows applicability to triangular systems such as the linear IV regression model. We would like to pursue the theoretical discussion of many locally invalid IVs in the future.

References

- Anatolyev and Gospodinov, (2011) Anatolyev, S. and Gospodinov, N. (2011). Specification testing in models with many instruments. Econometric Theory, 27(2):427–441.

- Andrews et al., (2019) Andrews, I., Stock, J., and Sun, L. (2019). Weak instruments in IV regression: Theory and practice. Annual Review of Economics, 11:727–753.

- Angrist et al., (1999) Angrist, J. D., Imbens, G. W., and Krueger, A. B. (1999). Jackknife instrumental variables estimation. Journal of Applied Econometrics, 14(1):57–67.

- Arias-Castro et al., (2011) Arias-Castro, E., Candès, E. J., and Plan, Y. (2011). Global testing under sparse alternatives: Anova, multiple comparisons and the higher criticism. The Annals of Statistics, 39(5):2533–2556.

- Arnold et al., (2022) Arnold, D., Dobbie, W., and Hull, P. (2022). Measuring racial discrimination in bail decisions. American Economic Review, 112(9):2992–3038.

- Bai and Ng, (2010) Bai, J. and Ng, S. (2010). Instrumental variable estimation in a data rich environment. Econometric Theory, 26:1577–1606.

- Bekker and Crudu, (2015) Bekker, P. A. and Crudu, F. (2015). Jackknife instrumental variable estimation with heteroskedasticity. Journal of Econometrics, 185(2):332–342.

- Belloni et al., (2012) Belloni, A., Chen, D., Chernozhukov, V., and Hansen, C. (2012). Sparse models and methods for optimal instruments with an application to eminent domain. Econometrica, 80:2369–2429.

- Belloni et al., (2014) Belloni, A., Chernozhukov, V., and Hansen, C. (2014). Inference on treatment effects after selection among high-dimensional controls. The Review of Economic Studies, 81(2):608–650.

- Bickel et al., (2009) Bickel, P. J., Ritov, Y., and Tsybakov, A. B. (2009). Simultaneous analysis of lasso and dantzig selector. The Annals of Statistics, 37(4):1705–1732.

- Breunig et al., (2020) Breunig, C., Mammen, E., and Simoni, A. (2020). Ill-posed estimation in high-dimensional models with instrumental variables. Journal of Econometrics, 219(1):171–200.

- Bühlmann and van de Geer, (2011) Bühlmann, P. and van de Geer, S. (2011). Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media.

- Cai and Guo, (2020) Cai, T. T. and Guo, Z. (2020). Semisupervised inference for explained variance in high dimensional linear regression and its applications. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(2):391–419.

- Cai et al., (2011) Cai, T. T., Liu, W., and Luo, X. (2011). A constrained minimization approach to sparse precision matrix estimation. Journal of the American Statistical Association, 106(494):594–607.

- Cai et al., (2014) Cai, T. T., Liu, W., and Xia, Y. (2014). Two-sample test of high dimensional means under dependence. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(2):349–372.

- Caner et al., (2018) Caner, M., Han, X., and Lee, Y. (2018). Adaptive elastic net GMM estimation with many invalid moment conditions: Simultaneous model and moment selection. Journal of Business & Economic Statistics, 36(1):24–46.

- Carrasco, (2012) Carrasco, M. (2012). A regularization approach to the many instruments problem. Journal of Econometrics, 170:383–398.

- Carrasco and Doukali, (2017) Carrasco, M. and Doukali, M. (2017). Efficient estimation using regularized jackknife IV estimator. Annals of Economics and Statistics, (128):109–149.

- Carrasco and Doukali, (2021) Carrasco, M. and Doukali, M. (2021). Testing overidentifying restrictions with many instruments and heteroskedasticity using regularized jackknife IV. The Econometrics Journal, pages 1–27.

- (20) Chang, J., Chen, S., Tang, C. Y., and Wu, T. T. (2021a). High-dimensional empirical likelihood inference. Biometrika, 108:127–147.

- (21) Chang, J., Shi, Z., and Zhang, J. (2021b). Culling the herd of moments with penalized empirical likelihood. arXiv preprint arXiv:2108.03382.

- Chao et al., (2014) Chao, J. C., Hausman, J. A., Newey, W. K., Swanson, N. R., and Woutersen, T. (2014). Testing overidentifying restrictions with many instruments and heteroskedasticity. Journal of Econometrics, 178:15–21.

- Cheng and Liao, (2015) Cheng, X. and Liao, Z. (2015). Select the valid and relevant moments: An information-based lasso for GMM with many moments. Journal of Econometrics, 186(2):443–464.

- Chernozhukov et al., (2013) Chernozhukov, V., Chetverikov, D., and Kato, K. (2013). Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. The Annals of Statistics, 41(6):2786–2819.

- Chernozhukov et al., (2015) Chernozhukov, V., Hansen, C., and Spindler, M. (2015). Post-selection and post-regularization inference in linear models with many controls and instruments. American Economic Review, 105(5):486–90.

- Donald and Newey, (2001) Donald, S. and Newey, W. (2001). Choosing the number of instruments. Econometrica, 69:1161–1191.

- Donald et al., (2003) Donald, S. G., Imbens, G. W., and Newey, W. K. (2003). Empirical likelihood estimation and consistent tests with conditional moment restrictions. Journal of Econometrics, 117(1):55–93.

- Donoho and Jin, (2004) Donoho, D. and Jin, J. (2004). Higher criticism for detecting sparse heterogeneous mixtures. The Annals of Statistics, 32(3):962–994.

- Fan et al., (2015) Fan, J., Liao, Y., and Yao, J. (2015). Power enhancement in high-dimensional cross-sectional tests. Econometrica, 83(4):1497–1541.

- Fan et al., (2021) Fan, J., Weng, H., and Zhou, Y. (2021). Optimal estimation of functionals of high-dimensional mean and covariance matrix. arXiv preprint arXiv:1908.07460.

- Fan and Wu, (2022) Fan, Q. and Wu, Y. (2022). Endogenous treatment effect estimation with a large and mixed set of instruments and control variables. The Review of Economics and Statistics, pages 1–45.

- Fan and Zhong, (2018) Fan, Q. and Zhong, W. (2018). Nonparametric additive instrumental variable estimator: A group shrinkage estimation perspective. Journal of Business & Economic Statistics, 36(3):388–399.

- Frandsen et al., (2023) Frandsen, B., Lefgren, L., and Leslie, E. (2023). Judging judge fixed effects. American Economic Review, 113(1):253–277.

- Frankel and Romer, (1999) Frankel, J. A. and Romer, D. H. (1999). Does trade cause growth? American Economic Review, 89(3):379–399.

- Gold et al., (2020) Gold, D., Lederer, J., and Tao, J. (2020). Inference for high-dimensional instrumental variables regression. Journal of Econometrics, 217(1):79–111.

- Guo, (2021) Guo, Z. (2021). Post-selection problems for causal inference with invalid instruments: A solution using searching and sampling. arXiv e-prints, pages arXiv–2104.

- (37) Guo, Z., Kang, H., Cai, T. T., and Small, D. S. (2018a). Confidence intervals for causal effects with invalid instruments by using two-stage hard thresholding with voting. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 80(4):793–815.

- (38) Guo, Z., Kang, H., Cai, T. T., and Small, D. S. (2018b). Testing endogeneity with high dimensional covariates. Journal of Econometrics, 207(1):175–187.

- Guo et al., (2021) Guo, Z., Renaux, C., Bühlmann, P., and Cai, T. T. (2021). Group inference in high dimensions with applications to hierarchical testing. Electronic Journal of Statistics, 15(2):6633–6676.

- Guo et al., (2019) Guo, Z., Wang, W., Cai, T. T., and Li, H. (2019). Optimal estimation of genetic relatedness in high-dimensional linear models. Journal of the American Statistical Association, 114(525):358–369.

- Hall and Heyde, (1980) Hall, P. and Heyde, C. C. (1980). Martingale limit theory and its application. Academic Press.

- Hansen and Kozbur, (2014) Hansen, C. and Kozbur, D. (2014). Instrumental variables estimation with many weak instruments using regularized jive. Journal of Econometrics, 182(2):290–308.

- Hansen, (1982) Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica, pages 1029–1054.

- Ingster and Suslina, (2003) Ingster, Y. and Suslina, I. (2003). Nonparametric Goodness-of-fit Testing under Gaussian Models. Springer.

- Javanmard and Montanari, (2014) Javanmard, A. and Montanari, A. (2014). Confidence intervals and hypothesis testing for high-dimensional regression. The Journal of Machine Learning Research, 15(1):2869–2909.

- Kang et al., (2016) Kang, H., Zhang, A., Cai, T. T., and Small, D. S. (2016). Instrumental variables estimation with some invalid instruments and its application to mendelian randomization. Journal of the American Statistical Association, 111(513):132–144.

- Kock and Preinerstorfer, (2019) Kock, A. B. and Preinerstorfer, D. (2019). Power in high-dimensional testing problems. Econometrica, 87(3):1055–1069.

- Kock and Preinerstorfer, (2021) Kock, A. B. and Preinerstorfer, D. (2021). Consistency of -norm based tests in high dimensions: characterization, monotonicity, domination. arXiv preprint arXiv:2103.11201.

- Kolesár, (2018) Kolesár, M. (2018). Minimum distance approach to inference with many instruments. Journal of Econometrics, 204(1):86–100.

- Kolesár et al., (2015) Kolesár, M., Chetty, R., Friedman, J., Glaeser, E., and Imbens, G. W. (2015). Identification and inference with many invalid instruments. Journal of Business & Economic Statistics, 33(4):474–484.

- Lee and Okui, (2012) Lee, Y. and Okui, R. (2012). Hahn–Hausman test as a specification test. Journal of Econometrics, 167(1):133–139.

- Liang et al., (2022) Liang, X., Sanderson, E., and Windmeijer, F. (2022). Selecting valid instrumental variables in linear models with multiple exposure variables: Adaptive lasso and the median-of-medians estimator. arXiv preprint arXiv:2208.05278.

- Liao, (2013) Liao, Z. (2013). Adaptive GMM shrinkage estimation with consistent moment selection. Econometric Theory, 29(5):857–904.

- Mei and Shi, (2022) Mei, Z. and Shi, Z. (2022). On lasso for high dimensional predictive regression. arXiv preprint arXiv:2212.07052.

- Merlevède et al., (2011) Merlevède, F., Peligrad, M., and Rio, E. (2011). A Bernstein type inequality and moderate deviations for weakly dependent sequences. Probability Theory and Related Fields, 151(3):435–474.

- Mikusheva and Sun, (2020) Mikusheva, A. and Sun, L. (2020). Inference with many weak instruments. arXiv preprint arXiv:2004.12445.

- Okui, (2011) Okui, R. (2011). Instrumental variable estimation in the presence of many moment conditions. Journal of Econometrics, 165:70–86.

- Pang et al., (2014) Pang, H., Liu, H., and Vanderbei, R. J. (2014). The fastclime package for linear programming and large-scale precision matrix estimation in R. Journal of Machine Learning Research.

- Sargan, (1958) Sargan, J. D. (1958). The estimation of economic relationships using instrumental variables. Econometrica, pages 393–415.

- Sun et al., (2021) Sun, B., Liu, Z., and Tchetgen Tchetgen, E. (2021). On multiply robust mendelian randomization (mr2) with many invalid genetic instruments. medRxiv.

- Tibshirani, (1996) Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1):267–288.

- van de Geer et al., (2014) van de Geer, S., Bühlmann, P., Ritov, Y., and Dezeure, R. (2014). On asymptotically optimal confidence regions and tests for high-dimensional models. The Annals of Statistics, 42(3):1166–1202.

- Vershynin, (2010) Vershynin, R. (2010). Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027.

- Windmeijer et al., (2019) Windmeijer, F., Farbmacher, H., Davies, N., and Davey Smith, G. (2019). On the use of the lasso for instrumental variables estimation with some invalid instruments. Journal of the American Statistical Association, 114(527):1339–1350.

- Windmeijer et al., (2021) Windmeijer, F., Liang, X., Hartwig, F. P., and Bowden, J. (2021). The confidence interval method for selecting valid instrumental variables. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 83(4):752–776.

- Ye et al., (2021) Ye, T., Liu, Z., Sun, B., and Tchetgen Tchetgen, E. (2021). GENIUS-MAWII: For robust mendelian randomization with many weak invalid instruments. arXiv preprint arXiv:2107.06238.

- Zhang and Zhang, (2014) Zhang, C.-H. and Zhang, S. (2014). Confidence intervals for low dimensional parameters in high dimensional linear models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 76(1):217–242.

- Zhang and Cheng, (2017) Zhang, X. and Cheng, G. (2017). Simultaneous inference for high-dimensional linear models. Journal of the American Statistical Association, 112(518):757–768.

- Zhu, (2018) Zhu, Y. (2018). Sparse linear models and -regularized 2SLS with high-dimensional endogenous regressors and instruments. Journal of Econometrics, 202(2):196–213.

Appendices to “A Heteroskedastic-Robust Overidentifying Restriction Test with High-Dimensional Covariates”

Qingliang Fan†, Zijian Guo‡, Ziwei Mei†

†Department of Economics, The Chinese University of Hong Kong

‡Department of Statistics, Rutgers University

The Appendices include the following parts: Section A provides additional details and examples. Section B contains all technical proofs. Section C collects the omitted simulation results from the main text.

A Additional Details and Discussions

A.1 The CLIME Procedure

Define the CLIME estimator (Cai et al.,, 2011) as

| (A1) | ||||

where denotes the -th standard basis of whose components are all zero except the -th equaling one, and is a positive tuning parameter satisfying Assumption 5(ii). The restriction to solve controls the estimation error, and the transformation from to is for symmetry111The symmetrization is unnecessary for convergence, while we use the fastclime R package (Pang et al.,, 2014) for efficient computation, which follows Cai et al., (2011) to produce a symmetric estimator. such that . Lemma B4 provides the convergence rates of the CLIME estimator specified by (A1).

A.2 Relation between and

As discussed in Section 3 of the paper, the true is of our interest while we work with the data scale-invariant version of (or ). It is thus helpful to look into the relation between and the identified for a clearer picture of the alternative set defined as (32). Below are several illustrative examples. Example 1 shows that perfectly parallel and cause zero even if , and hence the M test, as well as all other overidentification tests, has no power against invalid IVs. Example 2 shows that when and are far away from perfectly parallel, the alternative set defined by is similar to that defined by under sparsity.

Example 1.

Recall that the discussions from (19) to (20) illustrate the absence of power when and are perfectly parallel. A trivial example is which obviously is not overidentified. Another example with is given as follows. For simplicity, let , and . Here measures the strength of IV invalidity. Then it is easy to compute the for any .

Example 2.

Recall that is defined as (31). Following the same arguments from (19) to (20), as is strictly bounded away from one, we have . Hence, when is diagonal,

where is the number of invalid IVs and is the number of relevant IVs222The last inequality applies and hence .. Consequently, for some sufficiently large absolute constant whenever for some absolute constant large enough. Following symmetric arguments, we deduce that

and hence any implies for some . Hence, when and are not perfectly correlated and is small, the alternative set induced by as (32) is almost equivalent to that induced by .

In summary, the alternative set induced by the data scale-invariant version of can fulfill the task of testing the validity of IVs measured by .

B Proofs

Throughout the proof, we use and to denote generic absolute constants that may vary from place to place. We first present some useful preliminary lemmas in Section B.1. Section B.2 includes the proofs of the theoretical results in Section 2 of the main text. Firstly, some essential propositions about the initial Lasso estimators and test statistics are summarized in Section B.2.1. Secondly, we give the proof of Theorem 1 in Section B.2.2. Section B.3 includes the proofs of the main theoretical results of the proposed tests in Section 3 of the main text. Firstly, some essential propositions are given in Section B.3.1. Secondly, we give the proofs of Theorems 2 and 3 in Sections B.3.2 and B.3.3, respectively.

B.1 Preliminary Lemmas

This subsection provides useful lemmas implied by (or directly from) other literature.

Define the restricted eigenvalue of the empirical Gram matrix , given as

| (B2) |

where the restricted set . Lemma B1 provides the Lasso convergence rate. This is a direct result of Lemma 1 in Mei and Shi, (2022) and Theorem 6.1 of Bühlmann and van de Geer, (2011).

Lemma B1.

Suppose that for . Then

| (B3) | ||||

with . In addition, if ,

| (B4) | ||||

Lemma B2 shows the probability bounds for the maximum norm of some sub-Gaussian and sub-exponential variables, and a lower bound of the restricted eigenvalue useful in the proofs.

Proof of Lemma B2.

By Assumption 1, (B5) is the result of

In terms of (B6) and (B7), the LHS of the inequalities is the maximum norm of sub-exponential vectors with mean zero. By Corollary 5.17 in Vershynin, (2010), when there exists some such that

and similar probability bound holds for . As for (B8), for any

for some absolute constant , where the last inequality applies . ∎

Lemma B3 shows that under certain conditions, linear transformations of sub-Gaussian vectors are still sub-Gaussian.

Lemma B3.

Suppose that all entries in the vector are centered sub-Gaussian variables such that and for any , for some absolute constants and . If there exists some matrix such that , then the entries in the vector are sub-Gaussian such that with some absolute constants and .

Proof of Lemma B3.

By the equivalence between Conditions 1 and 2 in Lemma 5.5 of Vershynin, (2010), we know that is equivalent to the fact that the sub-Gaussian norm

| (B9) |

is bounded by some absolute constant . Let denote the -th element of . By Proposition 5.10 of the same reference,

for some absolute constant , and Lemma B3 follows with and . ∎

Proof of Lemma B4.

By Lemma B3, each element of is sub-Gaussian with uniformly bounded sub-Gaussian norm defined as (B9). By Lemma 23 in Javanmard and Montanari, (2014), is a feasible solution w.p.a.1. in (A1) when with some sufficiently large absolute constant , i.e. w.p.a.1. By the definition of in (A1)

w.p.a.1, which verifies (B10). Besides,

Following the proof of (14) in Theorem 6 of Cai et al., (2011) we can deduce

The proof of Lemma B4 completes. ∎

Lemma B5 shows a more convenient asymptotic regime used in the proofs.

Lemma B5.

Under Assumption 4

| (B13) |

Lemma B6 shows the probability bounds for the maximum norms that are useful to bound the estimation errors of asymptotic variance.

Proof of Lemma B6.

We only show (B14). The other two inequalities can be verified following the same procedures. By Assumption 1, for any , we know that

for some absolute constants and . By Theorem 1 of Merlevède et al., (2011), we know that for any

where as defined in (2.8) of the same paper. Here measures an upper bound of the mixing coefficient for a time series, which can be arbitrarily small for independent data. Taking with . Then

where the second inequality applies that

Obviously, . Take and hence and . We thus also have as by Lemma B5. Hence,

and (B14) follows. ∎

B.2 Proofs of the Initial Estimator in Section 2

B.2.1 Essential Propositions

Proposition B1 provides probability upper bounds of the Lasso estimators of the reduced form estimators.

Proposition B2 provides probability upper bounds of the weighting matrix .

Proposition B2.

Proof of Proposition B2.

Proposition B3 provides some error bounds that are useful in deriving estimation error of the asymptotic variance. Recall that . Similarly, define where is defined below (32).

Proof of Proposition B3.

Proof of (B22). We first need a bound for . Note that when ,

| (B26) |

and hence

| (B27) |

Thus, by Lemma B5 . This implies

| (B28) |

and by Proposition B2

We then deduce that

| (B29) |

which together with (B28) also implies

| (B30) |

In addition, we have

| (B31) |

Finally, by the boundness of defined in Assumption 2, each entry of is also sub-Gaussian. Thus the second moment is uniformly bounded. Following the proof of (B14) we deduce that

| (B32) |

and hence

| (B33) | ||||

Similarly,

| (B34) |

Proof of (B23). We only show the upper bound of the first term on the LHS since the second term goes through similarly. By the boundness of , each entry of is also sub-Gaussian. Thus the second moment is uniformly bounded. Following the proof of (B14) we deduce that

| (B35) |

and hence

Proof of (B25). We only prove the case with . Other cases can be verified in the same manner. Here . Note that

| (B36) | ||||

and hence

Note that the first term on the RHS of (B36) can be written as

where the last inequality applies Proposition B1. By sub-Gaussianity in Assumption 1, the fourth-moment is uniformly bounded by some absolute constant. Then by (B14)

As for the last two terms of (B36), by (B15), (B16) and Lemma B5,

and

Then (B25) follows. ∎

B.2.2 Proof of Theorem 1

Define and thus . We will show a stronger result: when for any absolute constant , the following asymptotic normality holds

| (B37) |

under the conditions in Theorem 1. The estimation error of can be decomposed as

By Proposition B1, Proposition B2.

Additionally, by Lemma B4,

where the last inequality applies and implied by Assumption 4 and Lemma B5.

Recall that and ,

| (B38) | ||||

where the last inequality applies Proposition B1 and Lemma B4. Then by (B38) and (B7)

Thus,

| (B39) |

The probability bound of the first term implied by (B7) is given as

which, together with (B39), implies that

| (B40) |

Besides, define and where .

and following the same procedures to derive (B39), we deduce that

| (B41) | ||||

where the last step applies . Then by (6), (B39) and (B41) we deduce that

| (B42) | ||||

and by (B7),

| (B43) |

Note that when , , which implies together with (B43). Thus,

| (B44) | ||||

Define the asymptotic variance of the first term on the RHS of (B44)

| (B45) |

The remaining of this proof will show that

Step 1. Show that . Recall that where . By the upper and lower bounds of conditional variances and covariances in Assumption 2, we deduce that

By (B28),

| (B49) |

and hence by the bound of the second term on the LHS of (B22), uniformly for all . In addition,

under Assumption 4, implying that

| (B50) |

Consequently,

Step 2. Define where is the -th element in the -dimensional vector . Thus we have and . By Corollary 3.1 of Hall and Heyde, (1980), it suffices to show the following conditional Lindeberg condition

| (B51) |

for any fixed . Following the same arguments in the proof of Lemma 24 in Javanmard and Montanari, (2014), each element of the matrix is sub-Gaussian. Consequently, when as implied by Assumption 4. Thus by Proposition B2 and (B46),

w.p.a.1 for some absolute constant . Besides, by (B30),

where the absolute constants and are defined in Assumption 2. Therefore, for any , w.p.a.1,

| (B52) | ||||

The upper bound as , as implied by Assumption 4. Then the Lindeberg condition (B51) holds. Therefore, we have shown Step 2.

Step 3. Show that . We decompose the estimation error of the asymptotic variance as

where

and

We first bound Note that by (B46) and (B37),

| (B53) |

Then by Lemma B5 and hence by (B30) and

| (B54) |

Then by Proposition B3, (B33), (B34), (B53), (B54) and the fact that , we deduce that

where the last inequality applies (B53) and (B54). In addition, by Lemma B3 we know the entries of are sub-Gaussian with uniformly bounded sub-Gaussian norms. Then similar upper bounds as Proposition B3 still hold with replaced by , which implies

and

Then, by Assumption 4, Lemma B5 and (B38),

where the last equality applies (B46).

B.3 Proofs of Theorems in Section 3

B.3.1 Essential Propositions

Proposition B4 provides Lasso estimation errors of the identified parameters that measure IV validity.

Proof of Proposition B4.

Remark B1.

Proposition B6 provides an intermediate result for lower bounded individual variances of the test statistic for the M test.

Proposition B6.

Proof of Proposition B6.

Note that is idempotent and hence

For any , is the -th diagonal element of given as

which is strictly bounded from below by . ∎

Proposition B7 shows the Gaussian Approximation property for the key component in the test statistic, which is the key for the asymptotic size and power of the M test. Define

| (B60) |

and .

Proposition B7.

Proof of Proposition B7.

By Corollary 2.1 of Chernozhukov et al., (2013), it suffices to show

-

1.

for all .

-

2.

for some large enough absolute constant . Here the constant is a counterpart of “” in Chernozhukov et al., (2013).

Then (B61) follows by Corollary 2.1 of Chernozhukov et al., (2013), given that implied by Assumption 4.

Step 1. Show . By the law of iterated expectations

Let be the -th standard basis vector of . Then by (B49) . Hence,

where the last inequality is deduced by Proposition B6. Similarly,

Step 2. It suffices to show that is sub-exponential satisfying for any , . Since is a sub-Gaussian vector with bounded sub-Gaussian norm and has norm bounded from above, by Lemma B3, the entries of are sub-Gaussian variables. By Sub-Gaussianity of , it turns out that , as an entry in the sub-exponential vector in , is sub-exponential. ∎

Proposition B8 provides a decomposition of the debiased Lasso estimator of the target vector .

Proposition B8.

Proof of Proposition B8.

By definition of ,

| (B64) | ||||

where is the submatrix composed of the last rows of , and

| (B65) |

Then by (B7), (B40) and (B30),

| (B69) | ||||

Then by (B68), (B69), Assumption 4, Lemma B5 and Proposition B2,

Bound . We first bound . Since

we deduce that

| (B70) |

Note that

where the first term on the RHS is bounded by

where the second inequality applies (B7), (B29) and (B70), and the last step applies Lemma B5. It thus suffices to show that

Note that by Proposition B2,

and hence and

Then by Proposition B2,

| (B71) | ||||

This implies

where the last inequality applies Lemma B5. This completes the proof of Proposition B8. ∎

Proposition B9 provides a probability upper bound for the estimation error of . Define

| (B72) |

with defined as (30). Recall that is the submatrix composed of the last rows of .

Proof of Proposition B9.

We bound the estimation error of as

| (B75) | ||||

where the last inequality applies (B10), (B70), Proposition B5 and that fact that follows the arguments above (B35). It remains to bound , and .

Bound .We first bound . Define

Note that

where the second inequality follows by (B71). We further bound the first term on the RHS that

Since by Proposition B1,

and by (B40),

We can deduce that

and thus,

| (B76) |

| (B77) |

B.3.2 Proof of Theorem 2

This proof follows the procedure in the proof of Theorem 2.2 in Zhang and Cheng, (2017). Conditional on the observed data, the normal vector is equal in distribution to

where are i.i.d. standard normal variables. Define

where denotes the -th row of the matrix , and

Here and are analogs of “” and “” in (14) of Chernozhukov et al., (2013), and is “” and “” in (15) of the same paper. Proposition B8 shows that and hence,

| (B78) |

where and . Furthermore, define with large enough and

Finally, define the critical value of

Following the same path to verify Theorem 3.2 of Chernozhukov et al., (2013), we can deduce that

where the comes from Proposition B7. By (B78)

Take . By (B9) and the definition of below (B78),

Thus

| (B79) |

as .

Prove (34). Let be the normal variable with covariance matrix as defined in Proposition B7. By Step 1 in the proof of the same lemma, we have for some absolute constant . By Lemma 6 of Cai et al., (2014), for any ,

as , which implies

By the bounds of , we deduce for some absolute constant ,

The Gaussian approximation result from Proposition B7 implies that

Then (B78) implies

| (B80) | ||||

B.3.3 Proof of Theorem 3

We have the following decomposition of

| (B83) | ||||

where

| (B84) |

and

| (B85) |

Recall that and Define . Note that by Proposition B2 we can deduce . Suppose that .

-

(a)

When , we have , and thus , . Then

- (b)

where the last step applies Lemma B5. Thus, w.p.a.1,

for any . Consequently, it suffices to show that

Show . By (B56), the definition and (B26),

| (B87) |

In addition, by (B87), Proposition B4, Lemma B4, Proposition B4 and Proposition B2,

and hence,

| (B88) | ||||

With (B87), (B88) and from Proposition B4, we can deduce that

Below we show the last step to derive the term by term. By Lemma B5 and (B86),

and

where the last equality applies , and

This completes the proof of .

Show . Note that by Propositions B4 and B2, Equation (B86) and Lemma B4,

where the last equality applies that . In addition,

Then applying the upper bounds of and derived above, together with Proposition B2, (B7), (B87) and (B86), the first term of is bounded by

where the last two steps apply Lemma B5. Besides, using the same set of probability upper bounds, the second term of is bounded by

This completes the proof of Theorem 3.

C Additional Simulation Results

C.1 Power Curves

C.2 Simulation Results for Estimation

| MAE | Coverage | Length | |||||||||

| IQ | LIML | mbtsls | IQ | LIML | mbtsls | IQ | LIML | mbtsls | |||

| 150 | 50 | 10 | 0.022 | 0.021 | 0.021 | 0.942 | 0.937 | 0.940 | 0.101 | 0.099 | 0.099 |

| 100 | 0.026 | NA | NA | 0.915 | NA | NA | 0.107 | NA | NA | ||

| 100 | 10 | 0.023 | 0.029 | 0.029 | 0.935 | 0.945 | 0.947 | 0.106 | 0.139 | 0.142 | |

| 100 | 0.027 | NA | NA | 0.895 | NA | NA | 0.108 | NA | NA | ||

| 300 | 150 | 10 | 0.015 | 0.016 | 0.016 | 0.935 | 0.949 | 0.952 | 0.070 | 0.080 | 0.080 |

| 100 | 0.016 | 0.016 | 0.017 | 0.931 | 0.953 | 0.962 | 0.072 | 0.084 | 0.087 | ||

| 250 | 10 | 0.015 | 0.030 | 0.030 | 0.945 | 0.941 | 0.941 | 0.072 | 0.141 | 0.143 | |

| 100 | 0.016 | NA | NA | 0.929 | NA | NA | 0.073 | NA | NA | ||

| 500 | 350 | 10 | 0.011 | 0.017 | 0.017 | 0.937 | 0.950 | 0.952 | 0.053 | 0.080 | 0.081 |

| 100 | 0.012 | 0.018 | 0.018 | 0.935 | 0.941 | 0.944 | 0.053 | 0.084 | 0.087 | ||

| 450 | 10 | 0.012 | 0.029 | 0.029 | 0.948 | 0.943 | 0.947 | 0.054 | 0.140 | 0.142 | |

| 100 | 0.011 | NA | NA | 0.953 | NA | NA | 0.054 | NA | NA | ||

| 150 | 50 | 10 | 0.036 | 0.036 | 0.036 | 0.924 | 0.943 | 0.943 | 0.163 | 0.174 | 0.175 |

| 100 | 0.040 | NA | NA | 0.892 | NA | NA | 0.167 | NA | NA | ||

| 100 | 10 | 0.036 | 0.052 | 0.053 | 0.931 | 0.943 | 0.947 | 0.168 | 0.248 | 0.255 | |

| 100 | 0.040 | NA | NA | 0.900 | NA | NA | 0.166 | NA | NA | ||