Optimal day-ahead offering strategy for large producers based on market price response learning

2Department of Statistics and UC3M-BS Institute for Financial Big Data (IFiBiD), University Carlos III of Madrid, Avenida de la Universidad, 30, 28911 Leganés, Spain. Email: caruizm@est-econ.uc3m.es

)

Abstract

In day-ahead electricity markets based on uniform marginal pricing, small variations in the offering and bidding curves may substantially modify the resulting market outcomes. In this work, we deal with the problem of finding the optimal offering curve for a risk-averse profit-maximizing generating company (GENCO) in a data-driven context. In particular, a large GENCO’s market share may imply that her offering strategy can alter the marginal price formation, which can be used to increase profit. We tackle this problem from a novel perspective. First, we propose an optimization-based methodology to summarize each GENCO’s step-wise supply curves into a subset of representative price-energy blocks. Then, the relationship between the resulting market price and the energy block offering prices is modeled through a probabilistic forecasting tool: a Distributional Neural Network, which also allows us to generate stochastic scenarios for the sensibility of the market towards the GENCO strategy via a set of linear constraints. Finally, this predictive model is embedded in the stochastic optimization model employing a constraint learning approach. Results show how allowing the GENCO to deviate from her true marginal costs renders significant changes in her profits and the marginal price of the market. Additionally, these results have also been tested in an out-of-sample validation setting, showing how this optimal offering strategy is effective in a real-world market contest.

Keywords: OR in energy, Constraint learning, Data-driven optimization, Electricity market, Optimal pricing strategy

1 Introduction

1.1 Background and Aim

Power systems worldwide are undergoing a major transformation aimed at their decarbonization while securing their reliability. One of the main players in this transition is the massive integration of renewable generating technologies from different sources. These are characterized by their low CO2 emissions and negligible marginal costs, but at the same time, by a non-dispatchable nature that introduces high levels of uncertainty in the operation of electrical systems. From the market perspective, especially for those based on marginal pricing, a high share of non-dispatchable producers implies high levels of price volatility, with important economic implications for all the market players. In this regard, producers with dispatchable technologies are exposed to fast-changing market conditions which may endanger the appropriate recovery of their (usually) high investment costs. On the one hand, these technologies are needed to complement renewables and guarantee system stability through the real-time balance of supply and demand. On the other hand, if they are finally dispatched, they usually set and raise the marginal price, which further contributes to price volatility.

In this uncertain environment, Generating Companies (GENCOs) need to develop effective strategies to participate in wholesale markets to guarantee a cost-effective dispatch and a reliable operation. Hence, we focus on the problem addressed by a GENCO that participates in a day ahead electricity market based on uniform marginal pricing, and seeks to derive the daily optimal offering strategy to be submitted. Furthermore, based on historical data from a real-world system, we verify that there is indeed a capacity of this GENCO to alter the price formation of the market with its offer curve. This relationship can be approximated by a machine learning forecasting tool, and embedded in the optimization problem employed in the decision-making process. The main novelty of this approach is that it is fully data-driven, making no exogenous assumptions on the market response once the offer curves are submitted. Moreover, uncertainty is explicitly modeled by a new probabilistic based methodology which allows anticipating potential unfavorable market realizations.

1.2 Approach

The proposed approach is based on learning the functional relationship between a large GENCO’s offer curve and the cleared marginal price, and use it to optimize her offering strategy. To this end, we consider a two-stage decision-making process. In the first-stage, the GENCO determines the offer curve to submit to the market. In the second-stage, the market price and dispatched quantities are revealed. Motivated by power systems where participants exhibit some degree of market power, we explicitly assume that the marginal price (and hence the dispatched quantities) is a second-stage decision variable dependent on first-stage decisions (offers), external factors, and uncertain data. This is a reasonable assumption in electricity markets based on uniform marginal pricing, in which suppliers and consumers submit their offers and bids (first-stage decisions) to the market operator. The intersection of the aggregated offering and bidding curves will generate an hourly marginal price for the market (which can be considered a second-stage decision for a player with sufficient market power). Therefore, the decisions made in the first stage by market agents have a direct impact on the formation of the marginal price and therefore on the profit they can obtain.

To learn this relationship (offer curve vs market price), we make use of an extension of the recently introduced Constraint Learning (CL) methodology, an empirical approach that has been receiving attention from the scientific community [7]. In this sense, we will employ historical data from the day-ahead market to relate historical GENCO’s offers with the final marginal price cleared in the market by means of fitting a machine learning model. The structure of this model will allow, despite its non-linear nature, to transform it to a set of piece-wise linear constraints, allowing its embedding in a stochastic mixed-integer optimization (MIO) problem.

Furthermore, as the classical point-predictive CL methodology employed generally in the literature does not capture uncertainty around the prediction, we make use of the Distributional Constraint Learning (DCL) developed by [2], which allows probabilistic-based scenario generation for learned variables. Note that the extension of CL methodology to account for uncertainty has already been employed to solve energy-related problems, like the one addressed by [20], where a retailer had to set an optimal price for consumers. However, it is solved under a stylized and simulation-based application and making use of a simple linear regression method, with limited forecast accuracy.

Therefore, the employment of the DCL methodology allows to address the GENCO’s stochastic optimization problem in a fully data-driven framework, i.e., not making any assumptions on the rest of the market’s participants behavior, that solely relies on historical market data. This is a novel approach that can be extrapolated to other applications where a complex system (market, network, organization, patient, etc.) responds to a decision maker actions, and sufficient amounts of data of these interactions are available.

1.3 Literature Review and Contributions

The problem of optimal offering from a large GENCO has been widely addressed in the literature from different perspectives. Some of the most common approaches are discussed in this section.

Multi-level optimization. These optimization models usually try to combine market clearing and optimal offering by using different optimization levels. For example, in a bi-level problem, the first level could be the offering strategy formulation, while the second level could be the market clearing. Since the market-clearing can admit a linear or convex formulation, KKT optimality conditions can be used to transform the bi-level approach into a mathematical program with equilibrium constraints. This bi-level formulation was used in works such as [22]. [13] deals with the problem of setting an offering strategy for a virtual problem plant with a stochastic three-stage bi-level approach. In contrast, in [19], a two-stage stochastic approach was used to establish the optimal strategy of a virtual power plant selling and purchasing energy from the day-ahead and the balancing markets seeking to maximize its profit. In [10], the optimal strategy for a photovoltaic power plant is established by a bi-level stochastic program, dealing with the uncertainty of the competitors and its photovoltaic output. On the other hand, [9] employs a robust approach for a wind-storage aggregator under a bi-level optimization framework. Works employing multi-level optimization usually share a common limitation: they are based on strong assumptions about the offering/bidding strategies of the rest of the market competitors.

Game theoretic approach. When multiple generating companies can act as price makers, Nash Equilibrium (NE) approaches can be employed to study the offering/bidding dynamics within the market. In the context of optimal offering, an NE is a set of offers such that, given all other competitors’ offers, no price-maker producer can improve her revenue by unilaterally changing her offer. Under this approach, [12] developed an iterative scheme that solves an NE in a market with two price-maker producers. [16] employed an equilibrium problem with equilibrium constraints together with a diagonalization method to identify a meaningful NE to study the operation of a distribution network composed of distributed energy resources and multi-microgrids with storage devices. More recently, in works such as the one from [5], reinforcement learning approaches have been combined with game-theoretical ones to improve the computational efficiency of the solution. However, as stated by [24], game theoretic models are of most interest to regulators, which seek to analyze market design or performance, on the basis of agents’ rationality.

Market / Competitors’ offering curves learning. As indicated, one of the challenges of the optimal offering problem is the lack of knowledge about the rivals’ offering strategies. In this sense, multiple works have been developed in order to identify these strategies. For example, [23] employs inverse optimization to estimate the rival producers’ offer prices that have been marginal assuming that the GENCO has knowledge of the daily market results. On the other side, [15] make use of a bayesian approach to unveil competitors offering curves. Despite the insightful information that can be obtained from estimating rivals’ offering curves, this information is already provided a posteriori in European day-ahead markets. However, learning (and predicting) competitors’ offers can be useful for a better characterization of scenarios in multi-level optimization approaches. Finally, in [4], an Extreme Learning Machine is employed to find the relationship between the prosumer strategy and the obtained profits and costs in distribution grids. This is, indeed, an example of applying CL in an energy market context with an out-of-sample validation scheme like the one proposed in this work, but on a smaller scale and without taking uncertainty into account.

Therefore, the main contributions of this work with respect to the state of the art in optimal offering problem are the following:

-

–

to develop a complete data-driven optimization model for a risk-averse GENCO offering strategy, making use of real world datasets without making assumptions regarding competitors’ behaviour.

-

–

to propose an optimization-based reduction technique to summarize past realizations of the market participants’ hourly offering curves.

-

–

to take uncertainty into account through the recently introduced Distributional Constraint Learning (DCL) methodology.

-

–

to show the validity of the optimal pricing strategy obtained in a real-world out-of-sample application based on the Spanish electricity market.

1.4 Article Organization

This article is organized as follows. Section 2 describes the stochastic optimization problem faced by GENCO when offering her energy blocks in the day-ahead market. Section 3 details the proposed methodology, from the constraint learning background, to the optimal discretization of supply curves and the final stochastic optimization problem under the DCL approach. Then, a case study is presented in Section 4, including out-of-sample testing of the optimal strategy. Finally, Section 5 draws the main conclusions of this work.

2 GENCO’s Stochastic Optimization Problem

In this section, we describe the optimization problem that the GENCO employs to derive her optimal offering strategy. The problem is formulated using a risk-averse two-stage stochastic approach in which the marginal price of the market is unknown but dependent on her block offers. This relationship can be explicitly modeled later employing piece-wise linearizable machine learning methods trained from historical data.

2.1 Notation

The notation employed to formulate the stochastic problem is described in this subsection for quick reference.

Indices and sets:

-

–

: Set of energy blocks, indexed by .

-

–

: Set of hourly periods within a day, indexed by .

-

–

: Set of stochastic scenarios, indexed by .

Variables:

-

–

: Price offered for block at time .

-

–

: Quantity of energy produced from block at time and scenario .

-

–

: Binary decision variable indicating whether price from block at time and scenario is below the marginal electricity price or not.

-

–

, : Auxiliary variables for CVaR formulation.

-

–

Marginal market price at time and scenario .

-

–

Offered quantity at price zero from renewable resources at time .

Parameters:

-

–

Contextual information that may have an influence on the marginal price formation.

-

–

Marginal generating cost for block at time .

-

–

: Allowed variability for the -th block price offer with respect to its generating cost at time .

-

–

Probability assigned to each scenario .

-

–

: Fraction of the profit distribution to be used in the CVaR calculation.

-

–

: Weight assigned to the CVaR against the expected profit.

2.2 Formulation

We assume the GENCO knows in advance of sending her offers the maximum energy quantity she can produce for each time and energy block, and its associated variable production cost . In an efficient market, the producer would directly send these offers (true marginal cost of production) which can be imposed in the current model by fixing . However, positive values of the parameter will let us adjust the degree to which producers with market power can modify their offers and deviate from perfect competition.

The stochastic model is formulated as follows:

| (1a) | ||||

| s.t. | ||||

| (1b) | ||||

| (1c) | ||||

| (1d) | ||||

| (1e) | ||||

| (1f) | ||||

| (1g) | ||||

| (1h) | ||||

| (1i) | ||||

| (1j) | ||||

| (1k) | ||||

where is the set of optimization variables.

The objective function (1a) represents the weighted sum of the GENCO expected value and the CVaR of her profit. CVaR will be employed to measure the risk taken by the producer, which equals the expected value of % scenarios with the lowest profit. In particular, we use the linear formulation of the CVaR proposed by [21]. The parameter is used to model the risk aversion level of the producer. Thus, when is equal to zero the producer acts as a risk-neutral decision-maker. On the other hand, when is equal to one, the producer can be considered risk-averse, and his decisions will focus on improving the left tail of the profit distribution. The expected profit is computed as the sum of the profits over the set of scenarios multiplied by their respective probabilities . The profit is composed of the revenues of the dispatched energy blocks, paid at a marginal price , minus their production costs.

Constraint (1b) establishes that the produced renewable energy at time equals the estimated one in order to send block offers to the pool . Constraints (1c)-(1e) model whether the price requested for one block is lower than the marginal price , or not. In particular, (1c) assigns variable a binary domain while (1d) and (1e) are employed through the big-M method in order to assign a value of one if the price of the block is under the marginal price, and zero otherwise.

With this assigned value of , equation (1f) will establish the dispatched energy. That is, will be equal to the estimated energy that can be produced for the block if the price requested for that block is under the marginal price. On the other hand, the value of will be zero if the price of that block is over the marginal price. That is, it is not a dispatched energy block.

Equation (1g) establishes that the stochastic marginal price can be estimated through a model , and therefore is dependent on the offering block prices , and external contextual information . This contextual data may include information that usually has an influence on the marginal price of the market, such as renewable energy production or demand. The specific methodology to generate each scenario realization of the price in (1g) is introduced in Section 3.3.

Constraint (1h) determines the producer flexibility of setting a block price above or below its true marginal cost , as a function of parameter . In particular, the impact of will be used to study how the GENCO can increase her profit by modifying the offering block prices. Equation (1i) ensures an increasing offering curve, a condition required in most electricity markets (see Figure 1). Finally, constraints (1j) and (1k) will be employed in order to characterize the CVaR. In particular, the value of would be equal to the Value at Risk at the optimal solution to the problem (1).

One of the advantages of this formulation is that it can be easily transformed into a mixed-integer linear problem, as the only non-linear term is the product between two variables: , which according to (1f) is equivalent to . The product involves a continuous variable and a binary one, which can be linearized without approximation (big-M approach).

3 Methodology

3.1 Distributional Constraint Learning Framework

As we have seen from the literature review exposed in Section 1.3, most approaches for setting optimal offerings are based on large assumptions or theoretical modeling, far from the real knowledge we can obtain from historical observation of the market. In this sense, our aim is to develop a fully data-driven methodology that allows us to estimate the marginal price (crucial in the optimal offering) based on the GENCO offers. This relationship can be embedded as sets of constraints under the so-called constraint learning (CL) framework [7].

An generalization of the CL framework can be seen in the optimization problem (2), which aims to minimize the expected value of the cost function (2a). This cost depends not only on the decision variables and (equivalent to and in our application (1), respectively), but also on external contextual information and uncertainty . Note that additional constraints could be applied through known functions on and , as stated in the constraint (2b).

| (2a) | ||||

| s.t. | ||||

| (2b) | ||||

| (2c) | ||||

The learned constraint is established in (2c). The relationship between and (and contextual information and uncertainty ) is modeled using a piece-wise linearizable prediction model , which is trained using a data set . Similarly, we can consider the offering strategy of the GENCO as and the response of the market .

Recently, the Distributional Constraint Learning (DCL) methodology was developed in order to take into account statistical uncertainty around the learned decision variable [2]. This approach makes the CL framework suitable for its implementation in stochastic optimization problems. An example of the DCL methodology can be seen in (3). In this case, the output from the piece-wise linearizable machine learning model will be composed of an estimate of the mean and the standard deviation for the distribution of the learned variable (3c).

| (3a) | ||||

| s.t. | ||||

| (3b) | ||||

| (3c) | ||||

A neural network can be employed as predictive model , which its structure and peculiarities for generating decision-dependent scenarios are exposed later on in this section.

3.2 Optimal discretization of supply curves and marginal price formation

As has been mentioned before, the GENCO’s optimization problem is based on deciding the prices offered to the market for her blocks of energy while predicting their possible impact on the marginal market price.

In general, in day-ahead electricity markets based on uniform marginal pricing, data from the hourly supply curve of each GENCO is composed of production units’ power blocks with their corresponding offering prices, i.e., prices that each unit is willing to accept to produce that amount of power for one hour. In a fair, transparent, and audited market, this price must reflect the marginal generating cost of that production unit.

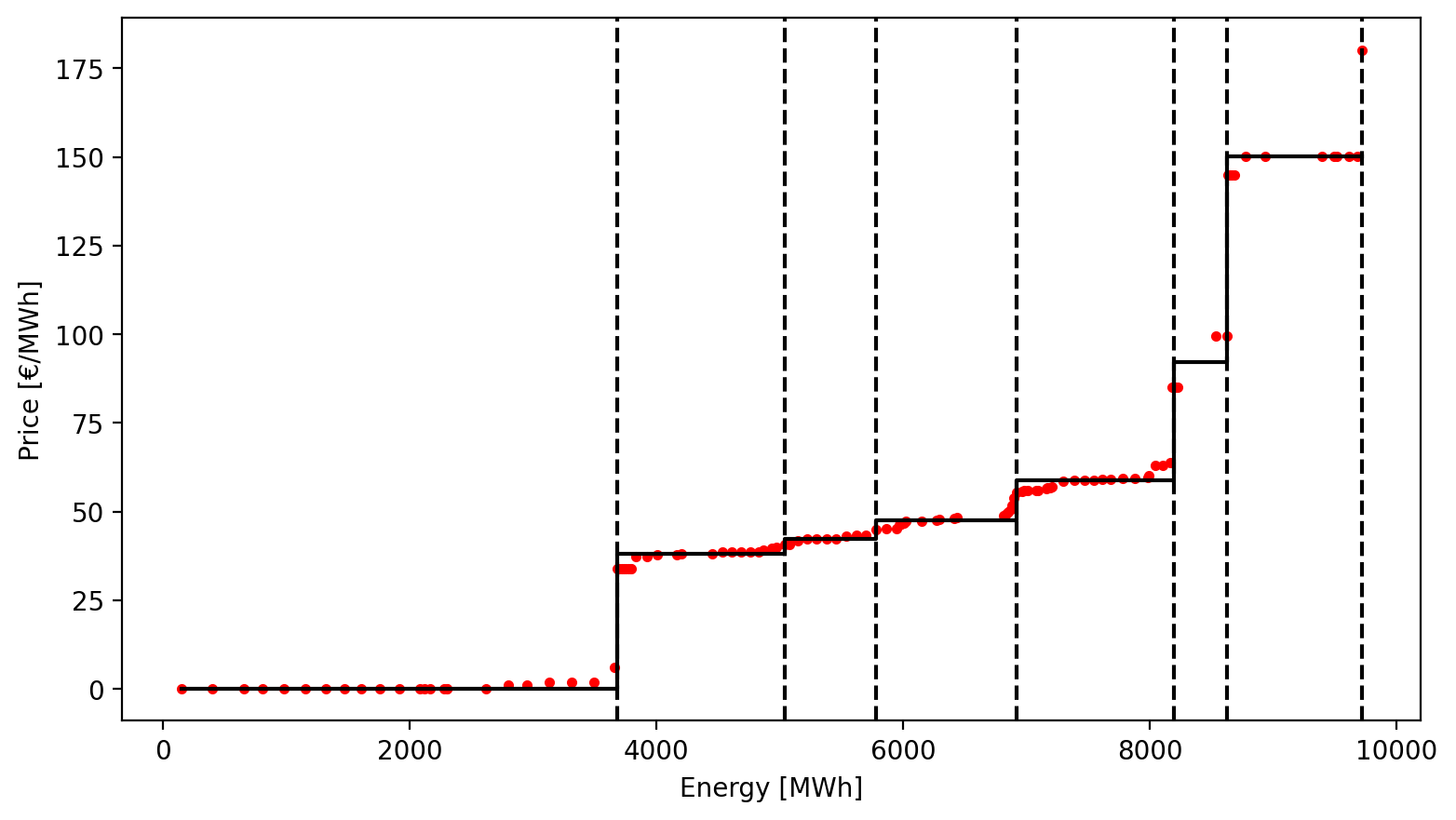

To build the GENCOS’ aggregated supply curve for each hour, production blocks are ordered by their price, from the lowest to the largest. Regarding the energy quantity, a cumulative sum is performed so that each price faces the cumulative quantity of energy of those blocks with prices below. This renders an increasing step-wise curve. An illustrative example can be seen in Figure 1, where for a given hour and particular GENCO, red points represent her production units with their price and cumulative quantity within the supply curve.

For tractability of the subsequent piece-wise linearizable predictive model (which will be employed under the DCL methodology), we propose to summarize first each aggregated supply curve into a smaller number of blocks by using an optimization approach (4). The aim is to obtain a minimum-error-based discretization of GENCO’s hourly supply curve, apart from setting clear decision variables for the optimization problem (1).

| (4a) | ||||

| s.t.: | ||||

| (4b) | ||||

| (4c) | ||||

| (4d) | ||||

| (4e) | ||||

In this problem, we seek to obtain grouped power blocks from a total of original ones. is the energy price, is the real price observed, and is the amount of energy of each block . The objective function of the model (4a) aims to minimize the absolute distance between the real prices and the optimized ones , weighted by the energy quantity of the block. Constraints (4b) and (4c) allow one to assign the same price to all the values that belong to the same grouped block. The sum of in constraint (4d) ensures that cuts are obtained, and therefore grouped blocks, since is defined as a binary variable (4e).

The solution to this problem will let us know the different prices and positions where a step in the curve can be set to obtain an optimal cut and, therefore, an optimal grouped block. As an example, let us assume that we want to get grouped blocks from the curve (red dots) presented in Figure 1. The optimization problem will render the solid black step-wise curve as a solution. In this way, the dashed vertical lines represent the different cuts, and solid horizontal lines the energy price associated with each grouped block. Note that, for simplicity, an extra vertical line has been added in the last production unit to set the last block.

As can be seen, this solution will appropriately summarize the information within the original supply curve, as it results in a finer discretization for those parts of the curve with higher price variations. This will also lead to obtain a historical dataset of summarized offering block prices and energy quantities, which is needed for the later training of the machine learning model under the DCL methodology.

Once we obtain the optimal discretization of the GENCO supply curve, the same procedure can be applied to the rest of the offers on the market, that is, the supply curves of the competitors. Considering both the GENCO’s and competitors’ supply curves, and ordering all the blocks by their price, the cumulative energy quantity can be computed to build the aggregated discretized market supply curve.

Note that it is also possible to achieve a summarized curve by directly discretizing the original aggregated supply curve. However, splitting GENCO’s units and the ones from the competitors will allow us to know the weight of the producer within the market and to get insights on how its pricing strategy can modify the market outcomes.

Nevertheless, to set a marginal price, a demand curve is also needed. For the sake of simplicity, we will assume an inelastic demand curve, which will cut the supply curve and establish the price producers will be paid for each MWh of energy offered below this price.

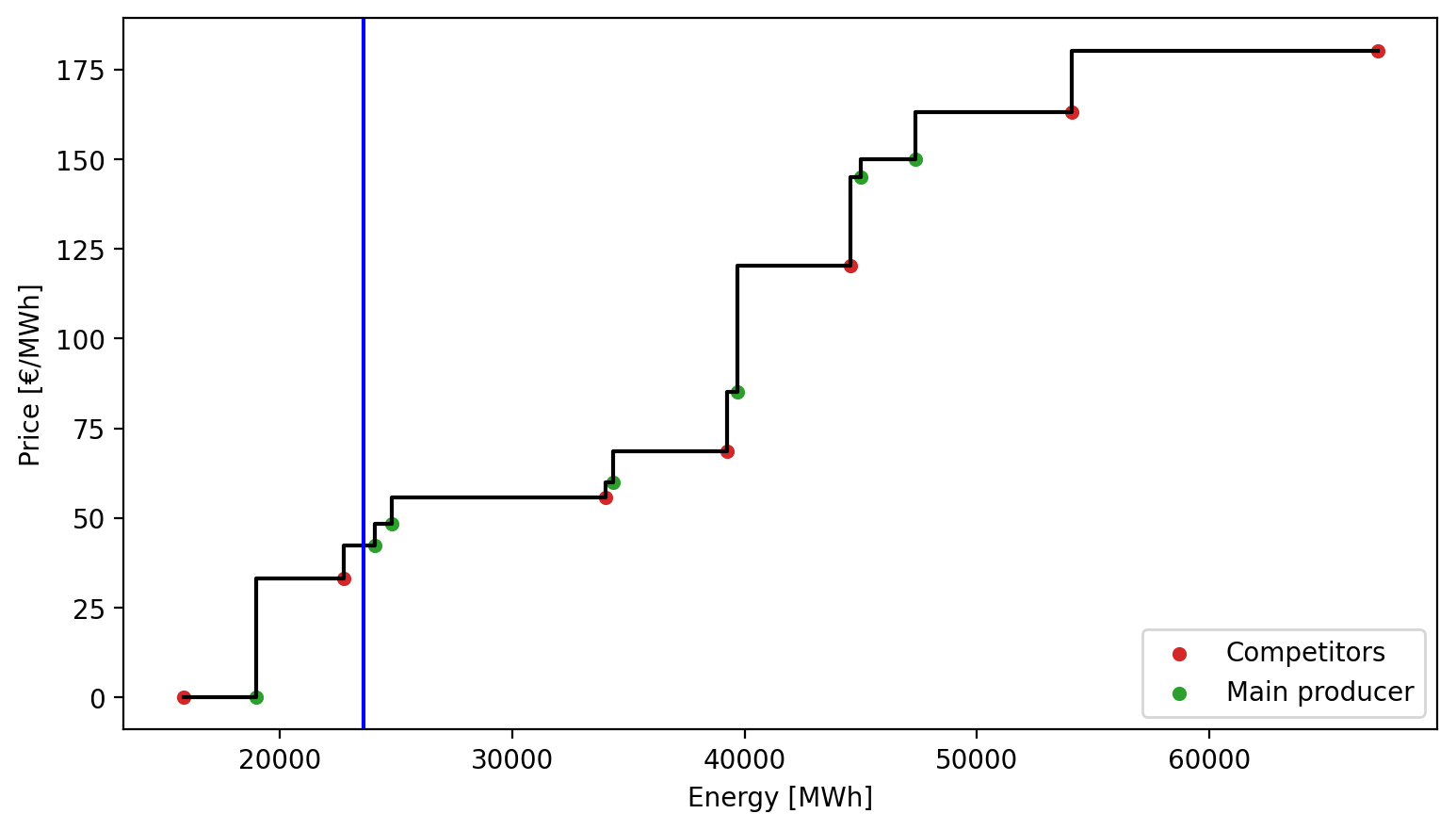

An example of this procedure is shown in Figure 2, where the increasing step-wise curve represents the aggregated market supply curve, the vertical line is the inelastic demand, and the green and red colors identify the blocks offered by the GENCO (main producer) and the rest of the competitors, respectively. We can see a total dispatched energy of 24000 MWh at a price of 42 €/MWh. Notice how the marginal price is set by a block from the main producer in this case. This motivates the study of how small variations in the offered price can directly change the marginal market price.

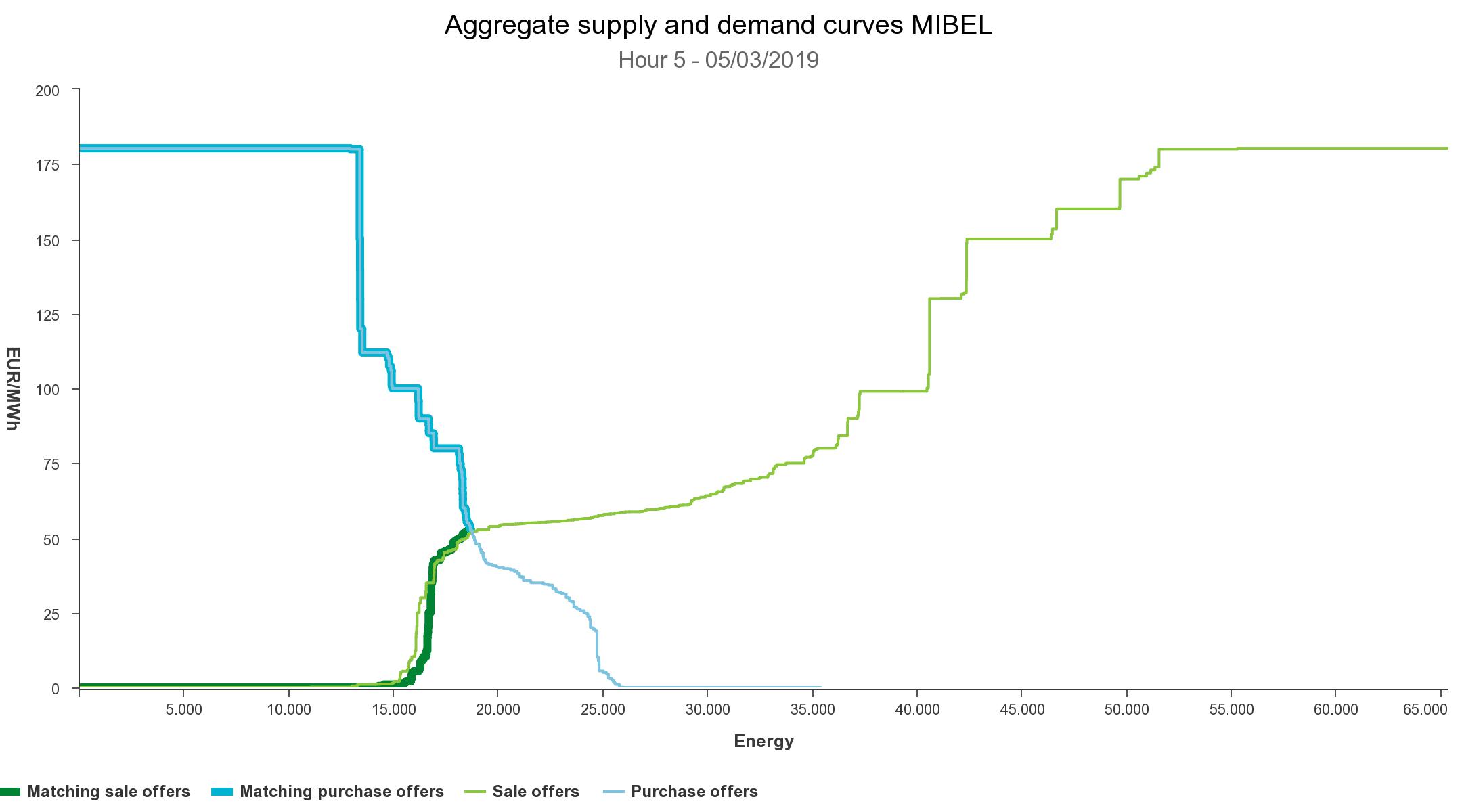

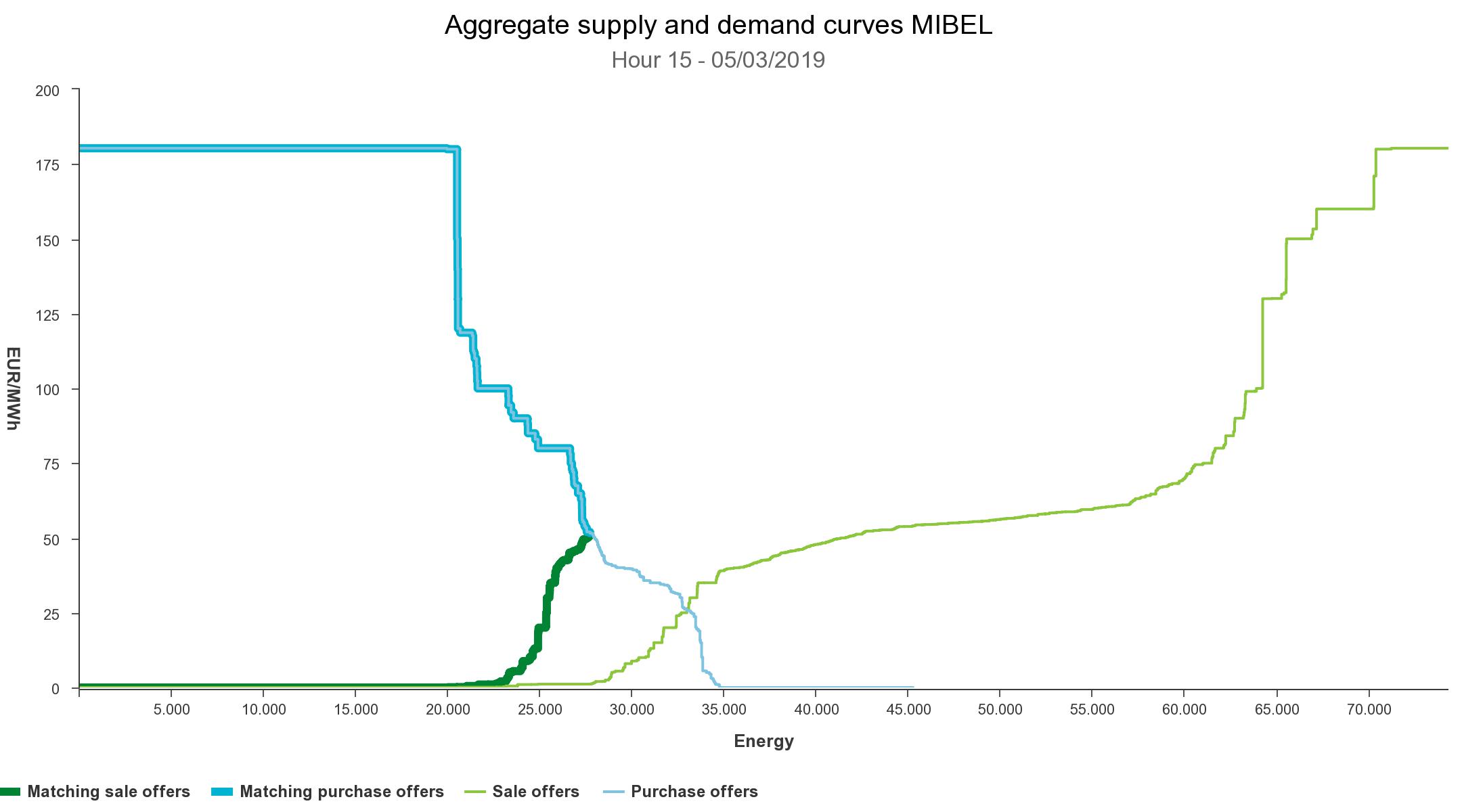

However, in real day-ahead electricity markets, the price resulting from the cut of the submitted demand and supply curves is not necessarily the resulting market marginal price (e.g., Spain and Portugal). In fact, it is common to observe that the final supply curve from the market suffers changes (withdraw of some operation units) due to the system operator’s ex-pot verification of technical constraints. We can take as an example the market curves presented in Figure 3. There, two different hourly marginal price formation procedures are shown within the same day in the Iberian Electricity Market [14]. The differences between the sale offers and the matching (dispatched) sale offers can be easily noticed at hour 15.

Therefore, when analyzing historical market data, it is important to consider this fact by statistically characterizing the differences between the matching supply curve and the offered one. This will allow us to validate the optimal strategy in real life (out-of-sample). That is, we can set the optimal blocks with real data and use competitors’ blocks, jointly with the demand and the approximated displacement of the supply curve to study the differences in profit according to the producer risk aversion and other relevant features.

3.3 Marginal price predictive model and scenario generation

To strategically derive the GENCO’s optimal offered prices within her supply curve (one for each block) is necessary to find a function accurate enough to predict the response of the marginal electricity price. That is, assuming that the strategic GENCO can alter the market marginal price, we will characterize it as a function of its price block offers and other external covariates, such as different marginal price lags, the expected demand, or levels of renewable energy production, for example.

Let us assume we have a dataset of observations of the type , where represents the marginal price, are the block price offers done by the GENCO, and are the values for the rest of auxiliary variables (covariates) the marginal price depends on, known at the time of the decision making.

In this way, it is possible to characterize the marginal price as a piece-wise linear function of and , allowing its inclusion in optimization problem (1) as a set of constraints. Following the DCL methodology, a Distributional Neural Network (DNN) can be employed for this task [17]. This DNN is fitted by minimizing the Gaussian negative log-likelihood, that is, we assume the estimation for the dependent variable is a random variable that follows a normal distribution.

The structure of this DNN is similar to a classical fully-connected neural network. It is made up of an input layer, a single or multiple hidden layers, and an output layer. Each of these layers is composed at the same time of neurons, where matrix operations and non-linear functions are applied. In general, for a given hidden layer of the DNN with nodes , the value of a node , denoted as , is calculated using the weighted sum of the node values of the previous layer, followed by a non-linear activation function . This value is given as:

| (5) |

where represents the bias term, and the weights for node in layer . This computation will continue in the following layers, taking as input the output of the previous layers, until the final one is reached.

The particularity of the DNN lies in its output: it throws an estimate of the mean and standard deviation of the dependent variable distribution, assuming its normality as mentioned above. From these conditional distribution parameters, we will be able to generate scenarios for the marginal price stated in constraint (1g), as we will show later in this section.

For the embedding of the DNN within the optimization problem as a set of constraints, we have to take into account mainly the non-linear activation function . Some works like [3] have studied how to implement trained neural networks as mixed-integer formulations. One of the most employed options is to train the neural network using the Rectified Linear Unit (ReLU) as the non-linear activation function. This function is composed of a max operator, that can be easily transformed to a set of piece-wise linear constraints [3]

Once the predictive model has been fitted and embedded within the stochastic optimization problem, adding one simple constraint will allow us to generate scenarios for from the mean and standard deviation estimate of its distribution. In this way, we can turn the optimization problem (1) into the following one:

| (6a) | ||||

| s.t. | ||||

| (6b) | ||||

| (6c) | ||||

| (6d) | ||||

| (6e) | ||||

Now, in our optimization problem, constraint (6c) represents the DCL framework. As can be seen, the DNN will establish the relationship between our offering prices (and contextual information that has an influence on the marginal price of the market, such as renewable energy production or demand) with the parameters of the conditional distribution of the hourly marginal price , i.e., and . On the other hand, constraint (6d) allows us to generate random scenarios for the marginal price by reconstructing a normal distribution using random values from a standard normal sampled outside the optimization problem. The joint fulfillment of constraints (6c) and (6d) allows the generation of scenarios for the marginal price directly dependent on the GENCO’s decisions. Therefore, the producer will try to alter the marginal price distribution to maximize her own profit distribution.

4 Case study

The main objective of this case study is to analyze the optimal bidding strategy of a large GENCO in a data-driven context. For this purpose, real-world data will be employed during the study, jointly with an out-of-sample validation, to show how price variations in GENCO’s offered energy blocks can modify the marginal market price and make her profit increase.

4.1 The dataset

In this case study, we will focus on a large GENCO within the Spanish electricity market. This GENCO produces around 25% of the total energy in the system. As exposed in Sections 3, we will employ different types of data to characterize the problem.

Firstly, in order to obtain discretized energy blocks and compute a marginal price with the inelastic demand, the hourly supply curves for each GENCO in the day-ahead market are necessary. This information is open-access and provided by the designated electricity market operator for the Iberian Peninsula, OMIE [18]. Two years of data have been collected on an hourly frequency, from June 2017 to June 2019. This data includes day-ahead hourly supply curves (similar to Figure 1) for the production units from the large GENCO as well as from the competitors. That is, more than 30 million observations were processed. Hourly data from June 1st, 2017 to May 31st, 2019 will be mainly employed to train our linear model to predict the day-ahead marginal price. June 2019 will be used as a test, applying an out-of-sample validation approach.

The selection of this time range is due to two main reasons: there were no atypical external factors that made electricity price increase or decrease from the average price of the decade, and there were no significant changes in the renewable power installed capacity that could bias the analysis.

Regarding the covariates employed in the predictive model (price lags, demand, solar, and wind energy forecasts with their respective lags), they are obtained through the information system of Red Eléctrica Española (the Spanish system operator), ESIOS [6]. All this information is assumed to be known in advance at the decision-making time.

4.2 Applied methodology

The methodology for solving the GENCO’s optimization problem under the DCL approach is based on three steps. First, we discretize the market offering curves. Then, we train the DNN model to learn the relationship between the marginal price, GENCO’ offers, and the rest of the contextual variables. Lastly, we embed the fitted model into the optimization problem, and generate decision-dependent scenarios at decision-making time.

4.2.1 Market dicretization

The first step in the methodology process is to optimally discretize the offering supply curves. As exposed in Section 3, we will consider a specific supply curve discretization for the GENCO and another one for the rest of the competitors. This allows better characterizing the GENCO’s curve and gaining technological insights, which will be useful in designing the marginal price prediction model.

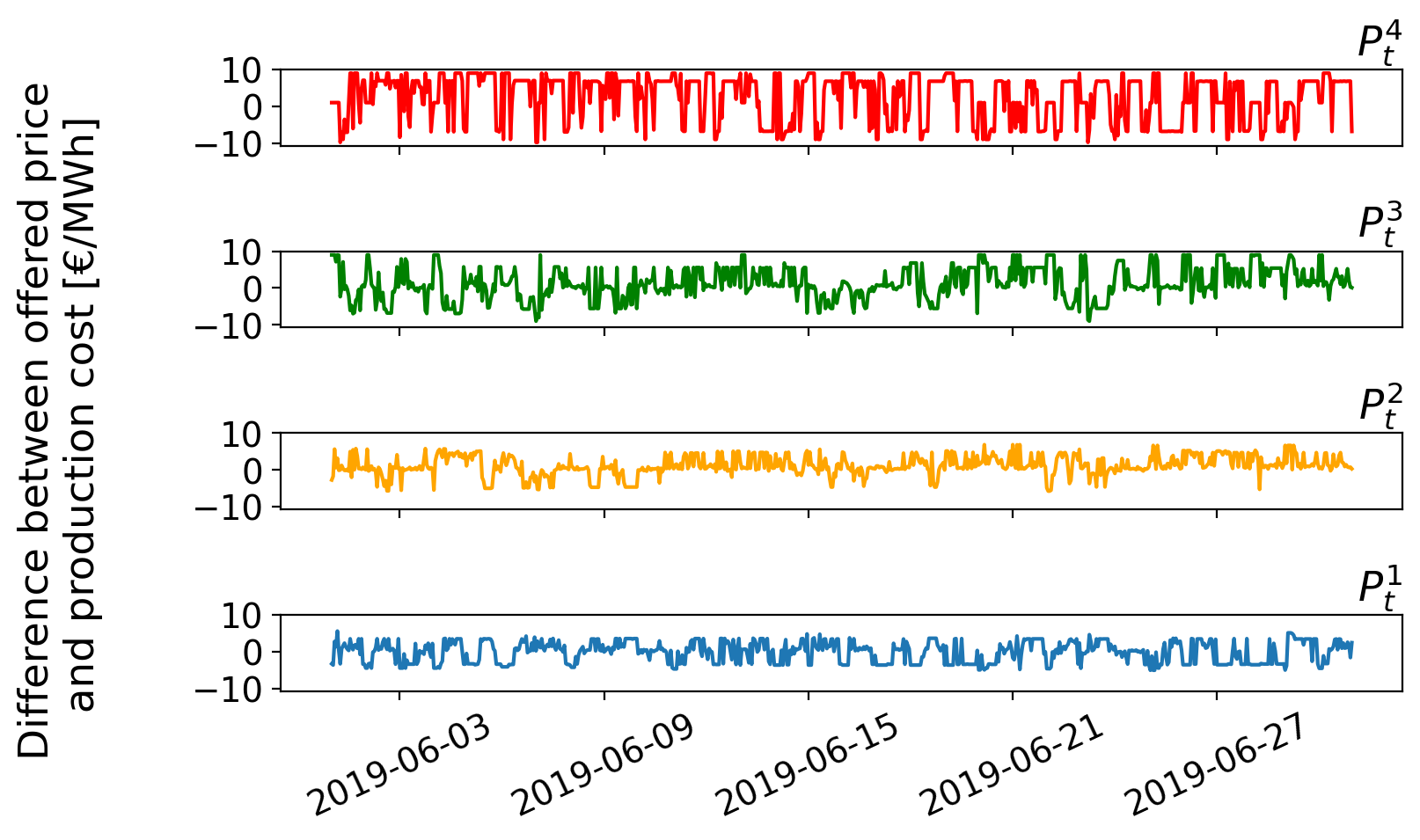

All the hourly supply curves will be discretized into 7 different blocks, both for the main producer and for the competitors. For each block, we assume its energy quantity and price represent how much quantity can be produced and at what cost. We consider 7 blocks as a reasonable number of blocks to capture the main functional properties of the supply curves, while not increasing in excess the dimensionality of the mixed-integer linear problem (1). The first block will always represent the amount of estimated renewable production (at zero cost), and the last two blocks, high-cost generating technologies that, as the historical data reflects, are never marginal. An example of this characterization was shown in Figure 1.

Once the discretized market supply curve is obtained, we approximate the hourly aggregated demand curve by an inelastic one. We get this value from the estimated hourly demand provided by ESIOS. This inelastic demand, jointly with the aggregated supply curve will render an intersection point, that sets a first marginal price with its corresponding total dispatched energy (Figure 2).

However, we know that this first intersection can be far from the resulting market price value, as technical restrictions come into play. These change the shape of the supply curve, creating a gap between the intersection of the curves and the resulting hourly marginal price (Figure 3).

This is a phenomenon that we can not precisely quantify without a detailed physical description of the electricity system, but that must be considered somehow by the GENCO, as it may modify the resulting market outcomes. Nevertheless, by using historical data, we have statistically characterized this difference, and used it to replicate the resulting supply curve including these technical corrections. The difference in energy quantities will allow us to displace our discretized supply curve and give a more accurate estimation of the market marginal price. After this displacement is applied, we compute our new intersection, obtaining the final market marginal price and the dispatched energy.

For fair out-of-sample model validation, the real hourly displacement due to the technical restrictions cannot be known in advance by the GENCO. Thus, as a proxy, we will employ the mean displacement of the last two months, grouped by hourly periods. We will see that this is an effective strategy to characterize this phenomenon.

4.2.2 Marginal price predictive model

Now that hourly marginal prices from the discretized supply curves have been computed, we seek the adequate predictive model (6c), i.e., to estimate the marginal price as a function of the offering prices and several covariates, to be embedded within the stochastic optimization problem (6).

As stated in Section 3, a DNN will be used under the DCL methodology in order to generate scenarios from the hourly day-ahead price distribution, conditioned on the GENCO’s offers. For every NN-based model, we must choose the size and shape of its structure. In our case, we will employ 1 hidden layer with 50 neurons in the DNN. This self-contained structure size has been chosen to deal with the trade-off between network complexity and performance [2].

For this DNN model, the following predictors have been used:

-

–

Quantity of renewable energy offered by the large GENCO power producer.

-

–

Block prices (6 decision variables) offered by the GENCO. These decision variables include all the block prices except the one related to the renewable energy, that is offered at zero price.

-

–

Demand estimation for the respective hour, and 7 lags (24, 48, …, 168 hours), 24 hour rolling mean, maximum and minimum.

-

–

Wind power estimation for the respective hour, and 7 lags (24, 48, …, 168 hours), 24 hour rolling mean, maximum and minimum.

-

–

Solar power estimation for the respective hour, and 7 lags (24, 48, …, 168 hours), 24 hour rolling mean, maximum and minimum.

-

–

7 marginal price lags (24, 48, …, 168 hours).

-

–

Calendar covariates: dummies for day of the week and month, and binary variable for holidays.

Therefore, the dataset will be formed by a total of 70 different predictors for the hourly market marginal price model, being trained in the two-year hourly period stated previously.

The trained DNN with the mentioned covariates can output a probabilistic forecast of the day-ahead price in the form of an estimate for its mean and standard deviation parameters assuming a normal distribution. The predictive performance of the DNN is not as simple to evaluate as in point estimation methods where we can check classical metrics like the mean absolute error or the mean squared error. To this end, we will focus on whether the values generated from the estimated distribution can cover the real value of the day-ahead price. In relation to this coverage of the distributions on the test days, we can say that by generating 300 samples from the estimated distributions, around 96% of the hourly prices are covered.

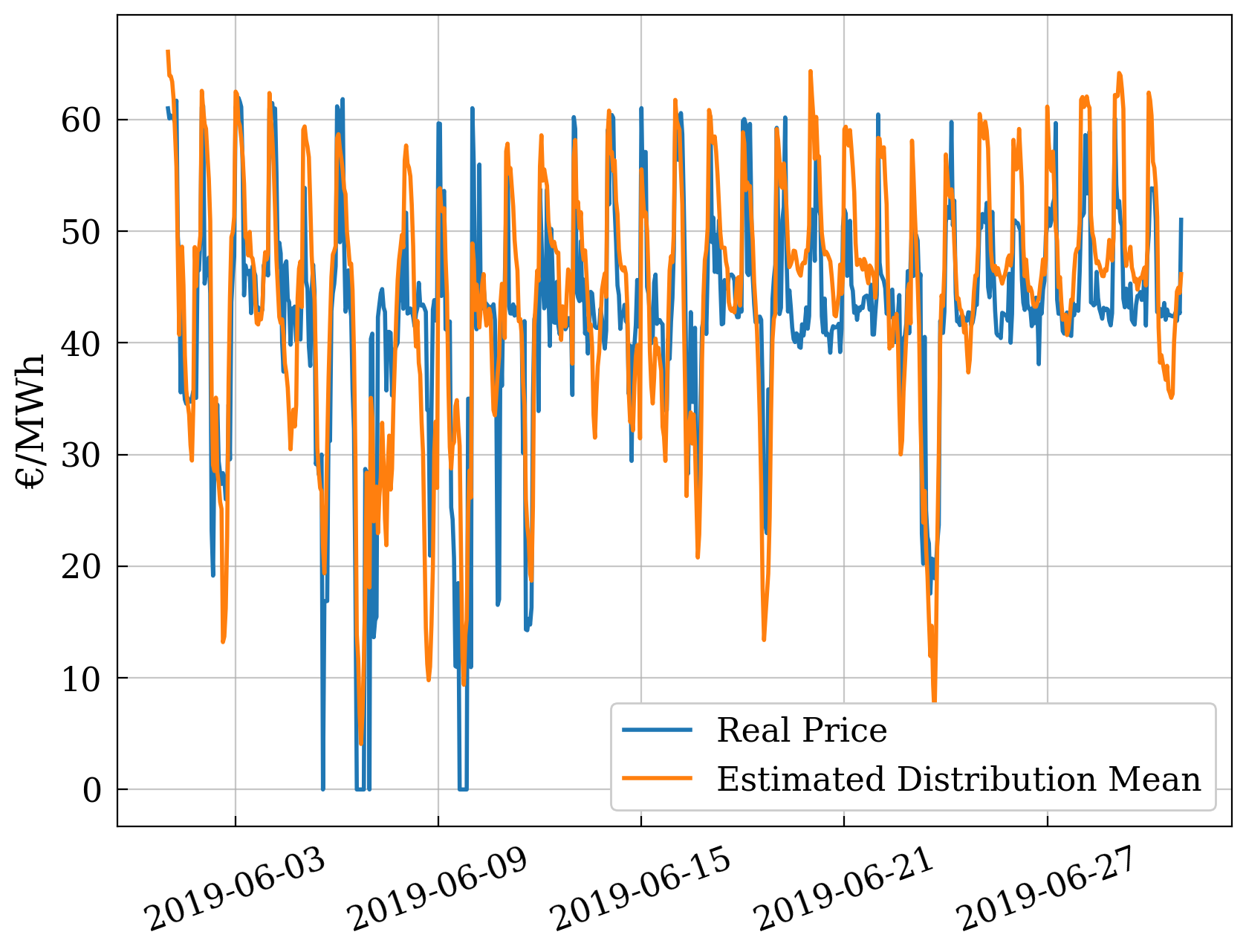

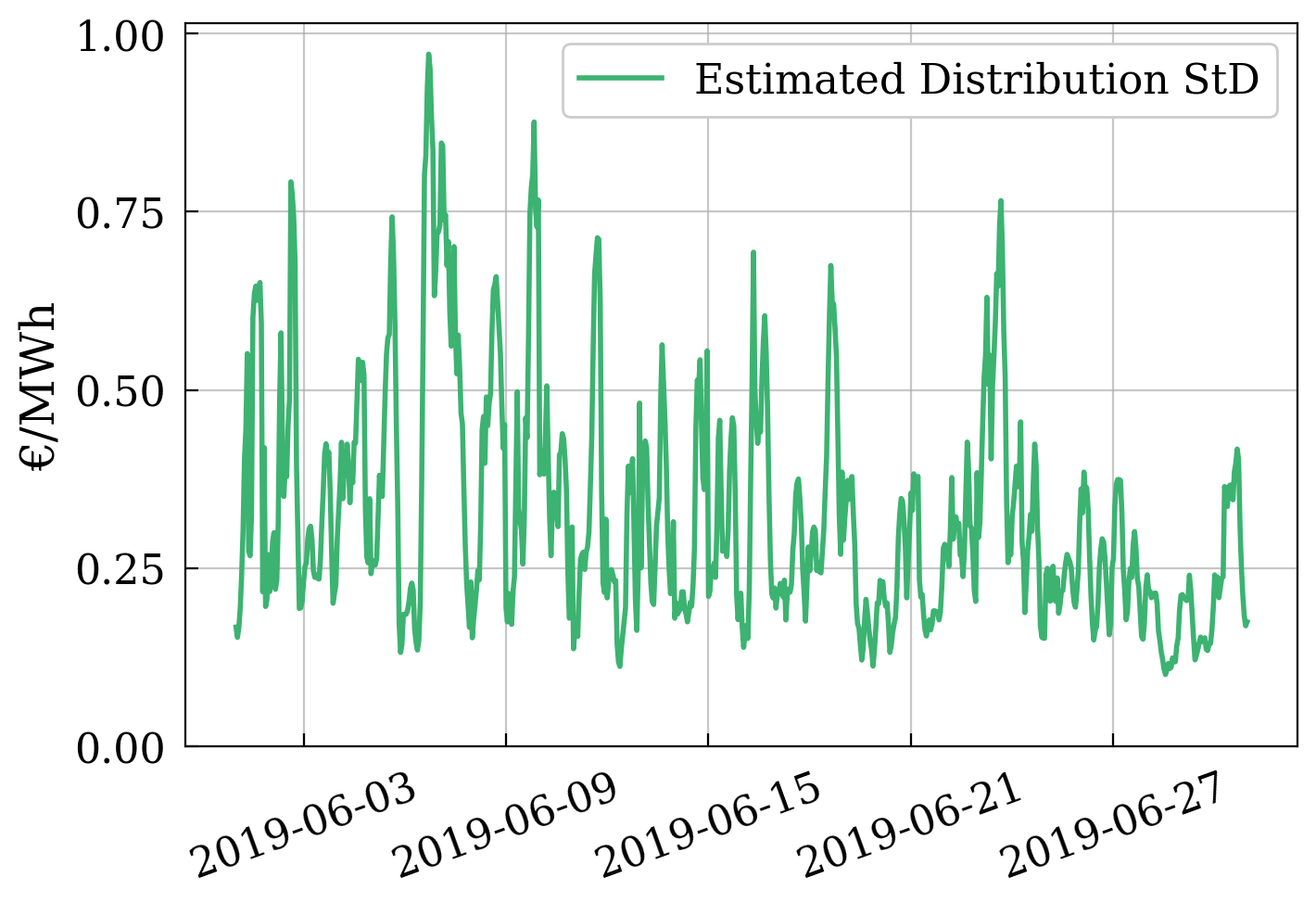

Now, we check whether the estimated mean from the distribution is far from the real price, and examine the value of the estimated standard deviation, which is directly related to the uncertainty around the prediction. We can check these estimated distribution parameters in Figure 4.

From Figure 4 (left), we can notice how the estimated mean parameter is close to the real price for most of the real hourly prices. There are only a few days where the estimated distribution mean lies further from the real price, like the 6th, 11th, or 20th. On the right side of Figure 4 we can check the estimated standard deviation of the distribution. It is interesting to notice how the 6th is also the day with the highest uncertainty, an insightful result, as we know the GENCO will face high levels of uncertainty at the time the standard deviation of the distribution is higher. With these results, we assert that the DNN is capable to model the behavior of the market given some contextual information and the block information of the GENCO. In this sense, we assume that GENCO decisions can affect the marginal price, and hence, their profits (which will be tested next).

4.2.3 Scenario generation

After embedding the trained DNN within our optimization problem, the last step is to generate scenarios . As it has been stated in Section 3, the scenario uncertainty will come from the fulfillment of constraint (6d), employing randomly generated values from a standard normal distribution. A total of 150 of these sampled values will be used, which implies a total of 150 scenarios per hour in the test month.

4.3 Results

We solve the stochastic optimization problem (6) through the scenario generation described in the previous section. This optimization problem will be solved for each day within the month of June 2019. In the Spanish market, producers send their offers at 12:00 for every hour of the following day. For that reason, the quantity offered per block ( ) and its true estimated cost () will be determined by solving the model (4) to obtain the respective blocks for the GENCO.

The proposed optimal offering problem has been solved through a Python 3.9.12 implementation, using Pyomo 6.3 [11]. The selected mathematical solver for all the computations was Gurobi [8] in its version 10.0. Besides, the computer employed included a CPU Intel Core i7 10700, RAM of 64 GB, and NVIDIA GeForce GTX 3060 graphic card. The computation time is dependent on the particular scenario set and the assigned parameters, especially , where a bigger value increases the decision space, and therefore, the computation time. In general, most computationally demanding experiments took around 1 hour per day of the testing set to reach a 1% optimality gap.

As indicated, we use to quantify possible deviations with respect to . For example, if the production cost of the first block at time is 25€, and we set a variability of 10%, will have a value of 2.5€. From now on, we will directly refer to as this percentage. This variability has been applied to the first four non-zero cost blocks. For the remaining two blocks, was set to zero, as their cost is so high that their price never intervenes in the marginal price formation. Moreover, the value affecting the CVaR formulation is set to 10%, that is, in the risk-averse case, we focus on improving the expected value of the scenarios below the 10th percentile of the profit distribution.

Regarding the rest of the covariates needed by the DNN to estimate the marginal price, they are also known at the time of the decision making, as the platform ESIOS offers open-access estimations of hourly demand, renewable production, etc. Thus, we consider this problem as a realistic data-driven approach.

Concerning the risk aversion level, we solve the optimization problem for the cases where the producer is risk-neutral () and risk-averse (). In the computation process, we used values 0.001 and 0.999 instead of 0 and 1 for stability in the results. A code example for a level of 10% and is openly available in a Github repository [1].

4.3.1 Aggregated results

First, we present a summary of the stochastic results for values (risk aversion level) of zero and one, and values of , and , in Table 4.3.1. Notice that the employment of as the value of leads to a heuristic approach where the GENCO does not modify her offering prices in comparison to her costs.

The idea of limiting to a specific set of small values comes from the employment of the DCL methodology. Allowing the GENCO to deviate too much from her cost can cause optimal solutions far from the data that was previously employed to train the predictive model, which may cause a risk of increasing the modeling error. Furthermore, we believe that in a complex, large, and marginal energy market, regulators will try to supervise large producers’ offering behavior, not allowing large deviations from their true costs (large value of ). In the same sense, we believe that the aforementioned deviation values are enough to study GENCO’s optimal offering, which is later validated out-of-sample.

Furthermore, we introduce two additional approaches for comparative purposes. First, what we denote as Deterministic Constraint Learning (Det. CL) transforms the stochastic problem into a deterministic one. In this sense, the NN will only output the mean estimate of the conditional distribution for the marginal price. This point prediction will be used to solve the problem (1) in a deterministic way, as no scenarios are generated. Once the optimal deterministic offering curve solution is obtained, it will be fixed and evaluated as a stochastic problem.

On the other hand, we will also compare our DCL methodology with its “wait and see” (perfect information) counterpart. In this case, the GENCO can anticipate the exact realization of the marginal price, which directly depends on the random values in the constraint (6d). A different optimal offering strategy will be obtained for each of the scenarios, and therefore reach the maximum possible profit assuming a perfect foresight of the future. This approach cannot be implemented in practice, but can be used as a benchmark to evaluate the performance of the stochastic model.

The three first columns of Table 4.3.1 represent the considered approach, the price flexibility over the cost of production, and the risk aversion level of the GENCO, respectively. The expected profit is calculated as the mean daily profit over the 30 days of testing; the same testing period is used to derive the expected CVaR. The sixth column represents the expected learned marginal price during June 2019, while the seventh column reports the expected dispatched energy, that is, the energy to be produced as its offered price is under the market marginal price. Finally, the last four columns present the mean price offered for each of the first four blocks (decision variables). Notice that, for the perfect information approach, we obtain a different offering curve per scenario.

| Solving | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Approach | Price | |||||||||

| Risk | ||||||||||

| (€/MWh) | ||||||||||

| Cost-based | 3639662.23 | 2601507.53 | 44.17 | 4180.31 | 37.23 | 49.70 | 60.84 | 77.51 | ||

| Det. CL | 3598446.52 | 2598663.84 | 43.82 | 4286.70 | 36.24 | 47.45 | 57.93 | 73.79 | ||

| 3544976.72 | 2566327.61 | 43.43 | 4406.60 | 34.22 | 45.72 | 55.63 | 70.36 | |||

| 3521603.35 | 2523788.04 | 43.40 | 4415.09 | 32.85 | 46.92 | 55.60 | 67.49 | |||

| DCL | 3679684.78 | 2640315.23 | 44.61 | 4162.07 | 37.28 | 50.17 | 61.28 | 78.22 | ||

| 3675169.19 | 2699748.15 | 44.52 | 4160.89 | 37.86 | 49.82 | 60.19 | 78.31 | |||

| 3726022.07 | 2691895.72 | 45.07 | 4155.91 | 37.08 | 50.83 | 62.12 | 80.04 | |||

| 3715318.89 | 2788887.77 | 45.03 | 4146.26 | 38.40 | 49.94 | 59.80 | 79.59 | |||

| 3775005.07 | 2741711.66 | 45.54 | 4133.73 | 37.16 | 51.47 | 62.61 | 80.75 | |||

| 3737565.67 | 2851544.87 | 45.30 | 4128.31 | 38.52 | 50.00 | 59.28 | 80.38 | |||

| W&S DCL | 3726485.52 | 2708032.38 | 45.86 | 4168.16 | 37.44 | 50.84 | 61.27 | 78.69 | ||

| 3797757.05 | 2799340.26 | 46.36 | 4167.51 | 37.46 | 51.97 | 62.04 | 79.89 | |||

| 3845251.09 | 2861349.73 | 46.82 | 4165.99 | 37.77 | 52.72 | 62.24 | 80.49 |

Regarding the deterministic approach, we can see how the expected profit decreases as the price flexibility level increases. This could be due to not taking uncertainty into account, as a point estimation maximization could lead to higher uncertainty () in the stochastic solution. However, more dispatched energy is obtained compared to the DCL approach. With the perfect information scenario, a higher profit is expected, but not far from the uncertain DCL approach. It is interesting to note that the CVaR of the risk-averse GENCO with the DCL approach is extremely close to the one obtained in the perfect information case.

By differentiating between levels of price flexibility within the DCL approach, we can see how the expected profit increases as this flexibility does. This is due to the offering price adjustments that the GENCO employs to modify the marginal price of the market. Starting from a marginal price of 44.17€/MWh when the GENCO makes offers at production cost, we can see an increment of the marginal price up to 45.54€/MWh where the flexibility is 15% of the production costs.

There are also differences regarding the risk aversion level. When the producer is risk-averse (), expected profits are slightly lower, but the CVaR improves significantly, as the marginal price does not increase as much as in the case where the producer is risk-neutral (). The dispatched energy differences across flexibility and risk aversion levels are small, making us guess that the GENCO is more interested in modifying the marginal price than increasing its dispatched quantities.

In relation to the block prices offered, significant differences appear when varying the price flexibility and risk aversion levels. For example, as flexibility increases, the mean price offered for the first block increases in the risk-averse GENGO, while maintaining its value close to its cost for the risk-neutral case. The price of the second block increases independently of the risk-aversion level with a larger flexibility, but this increment is on a lower scale on the risk-averse GENCO. This fact can be caused by the need for the producer to get some blocks dispatched. However, increasing the second block price will leave the blocks offered by competitors below and increase the marginal price. In the third block, risk-neutral producer offers over the marginal cost, while the risk-averse one does it below this cost. Finally, the same behavior of the second block can be appreciated in the fourth one.

4.3.2 Results by risk-aversion and flexibility level

What follows will graphically show the stochastic results for the complete testing period, studying the profit distribution and optimal block prices for different levels of risk aversion and price flexibility.

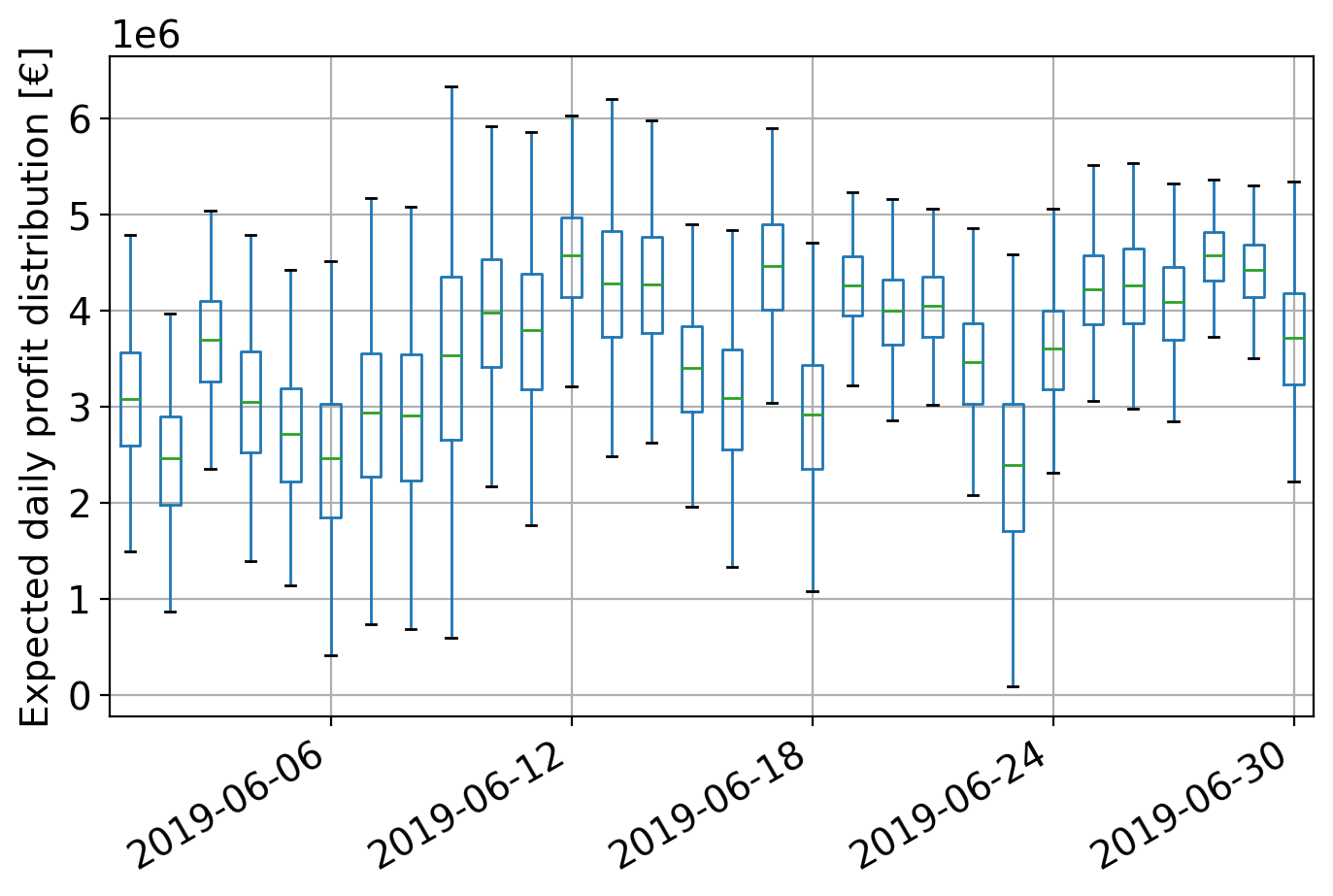

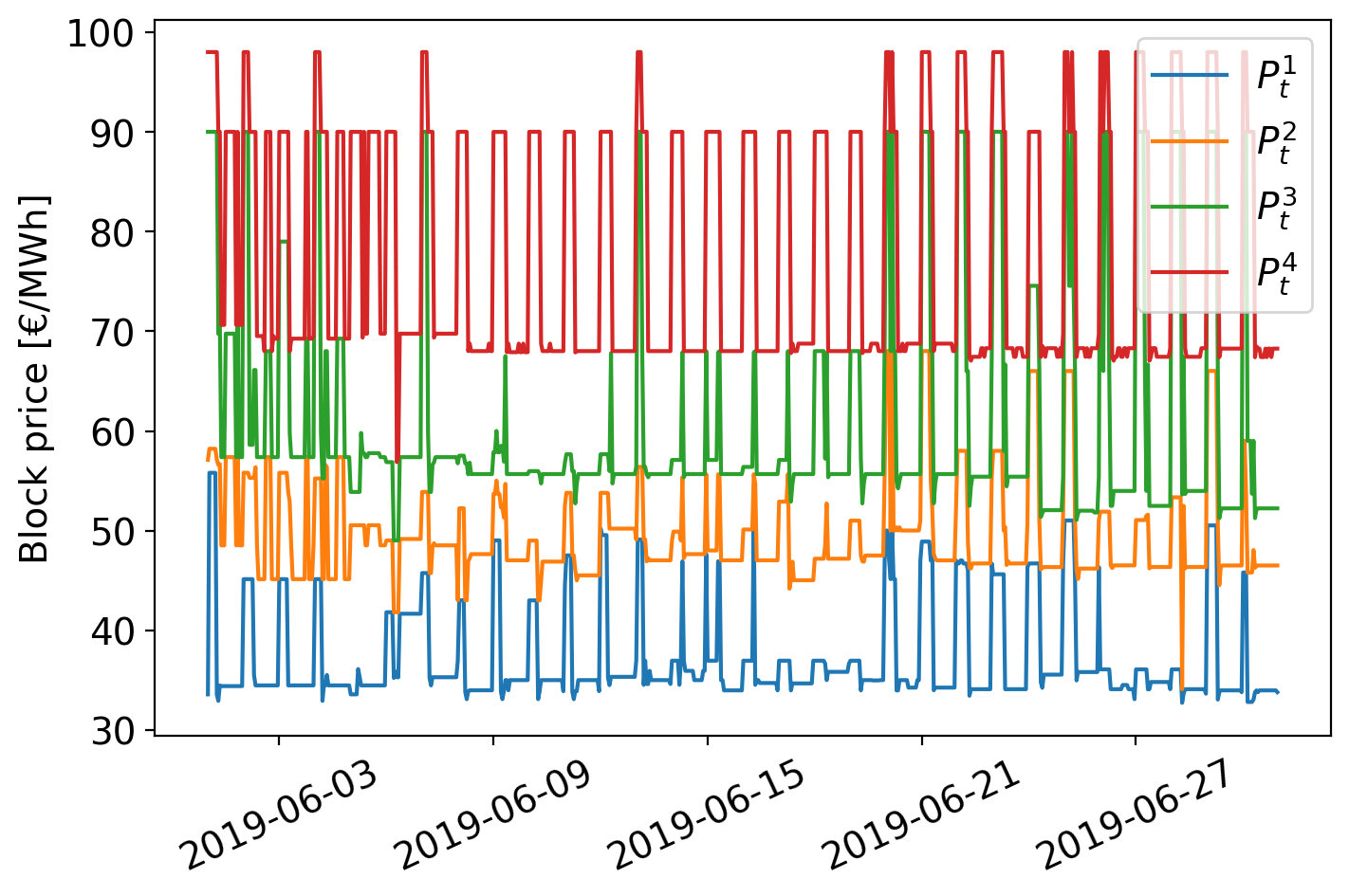

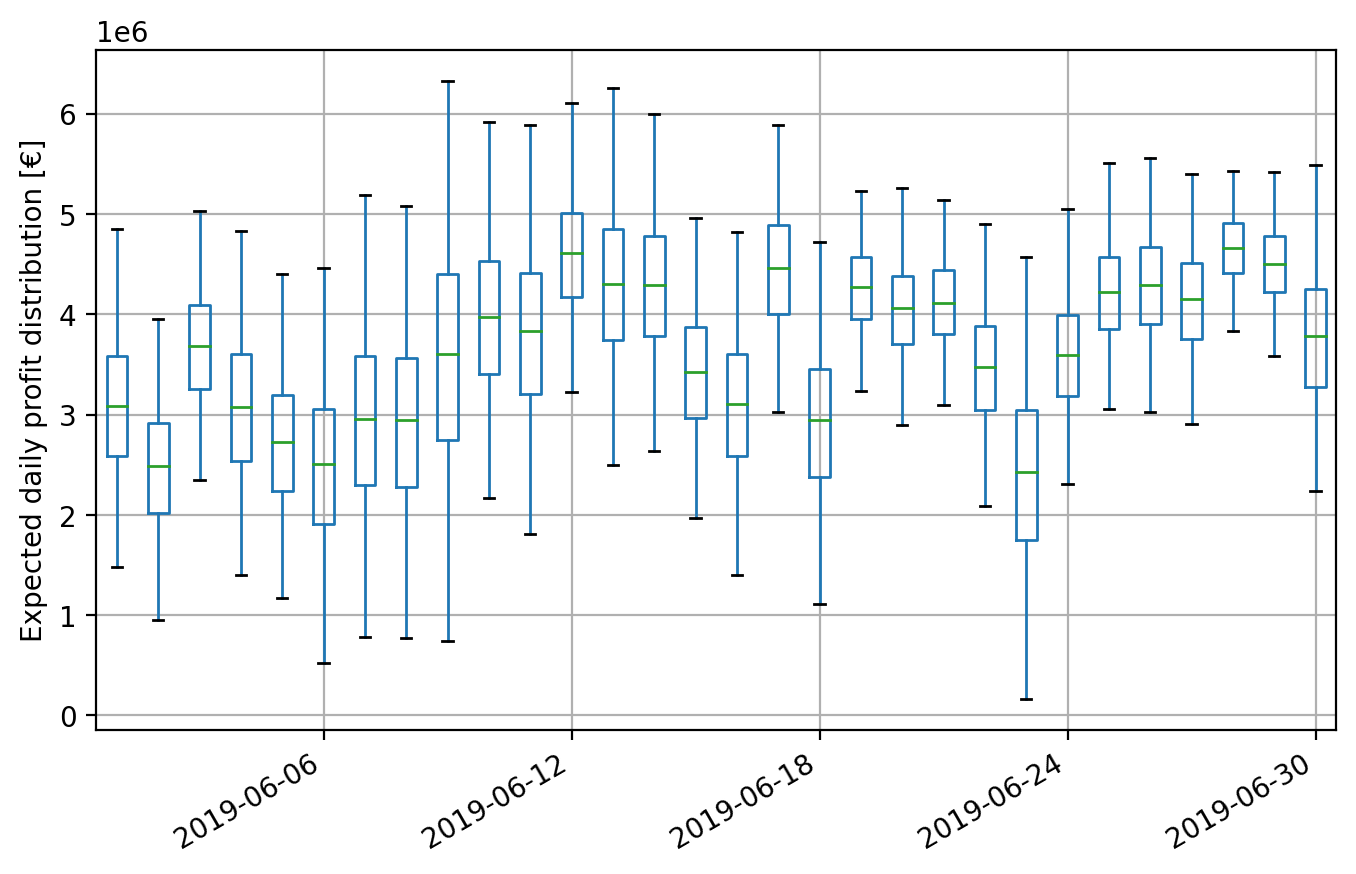

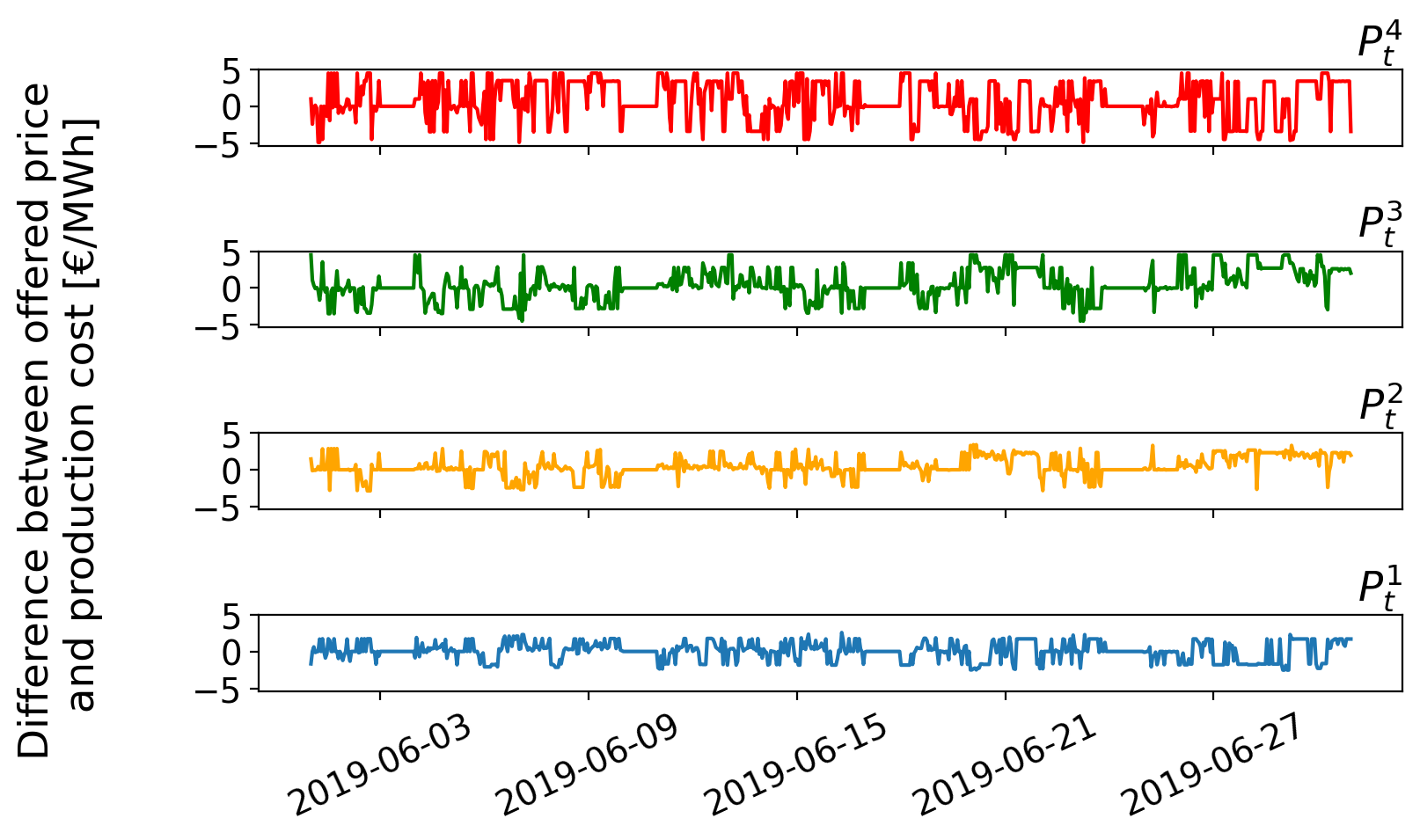

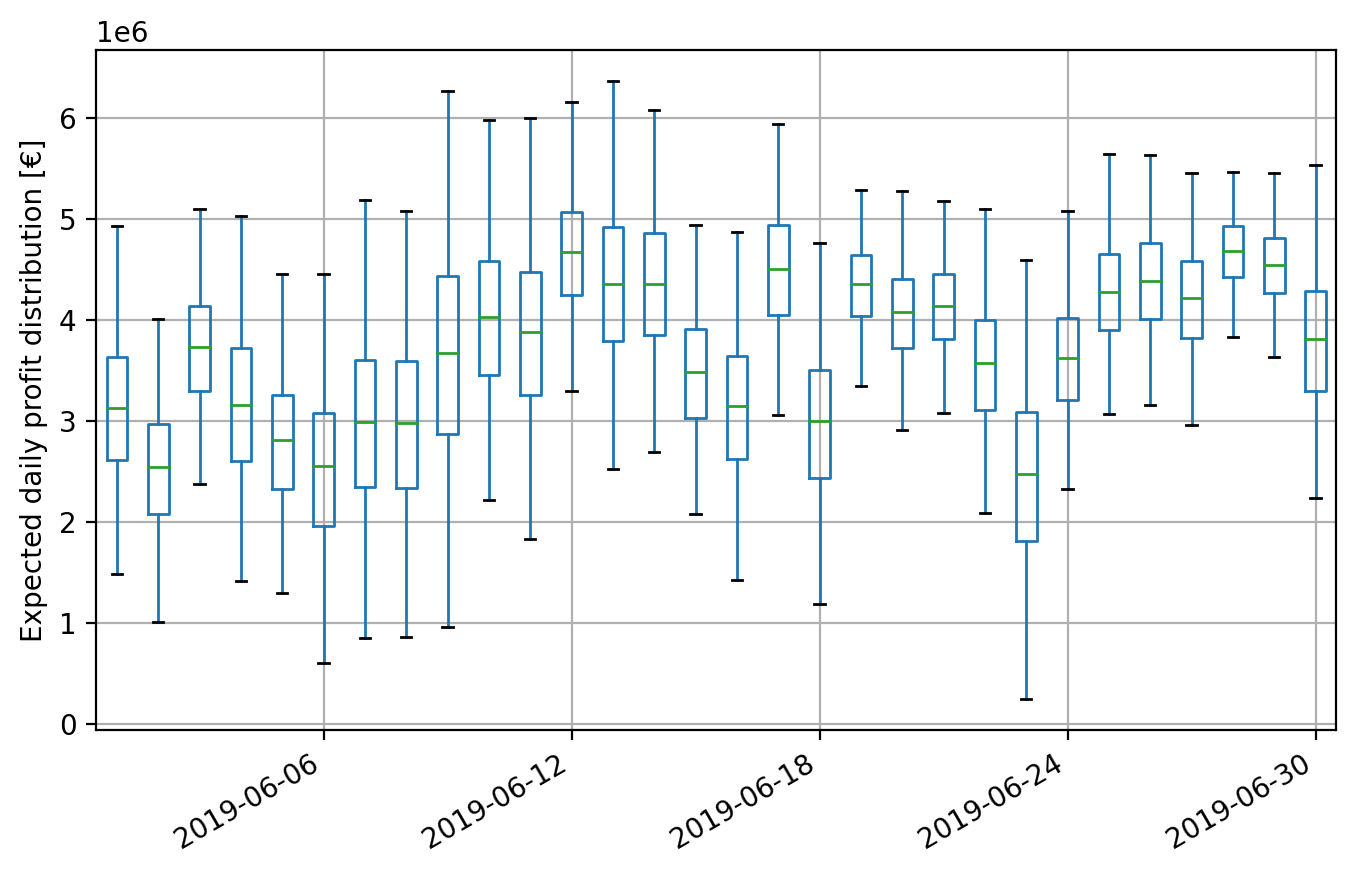

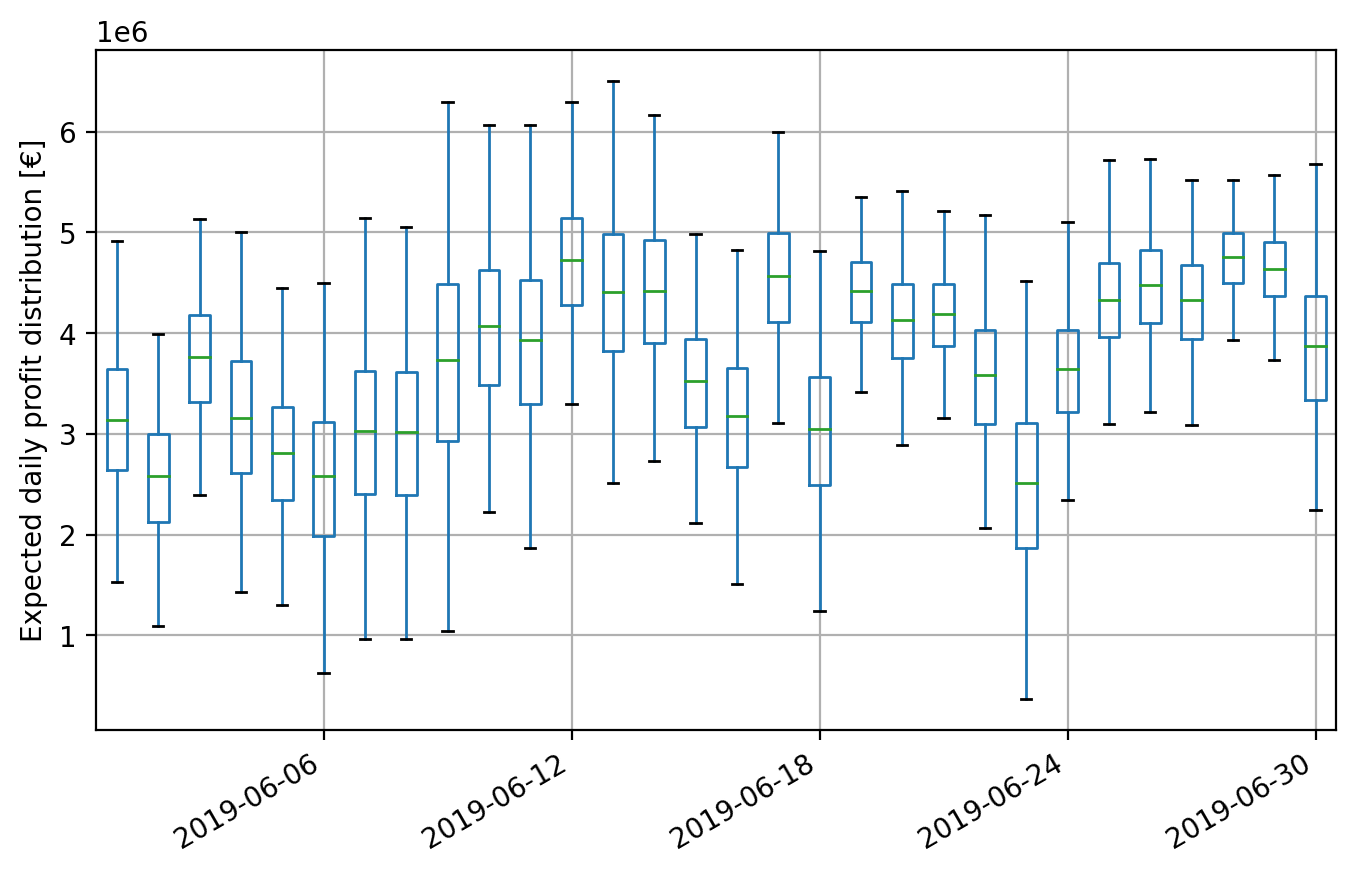

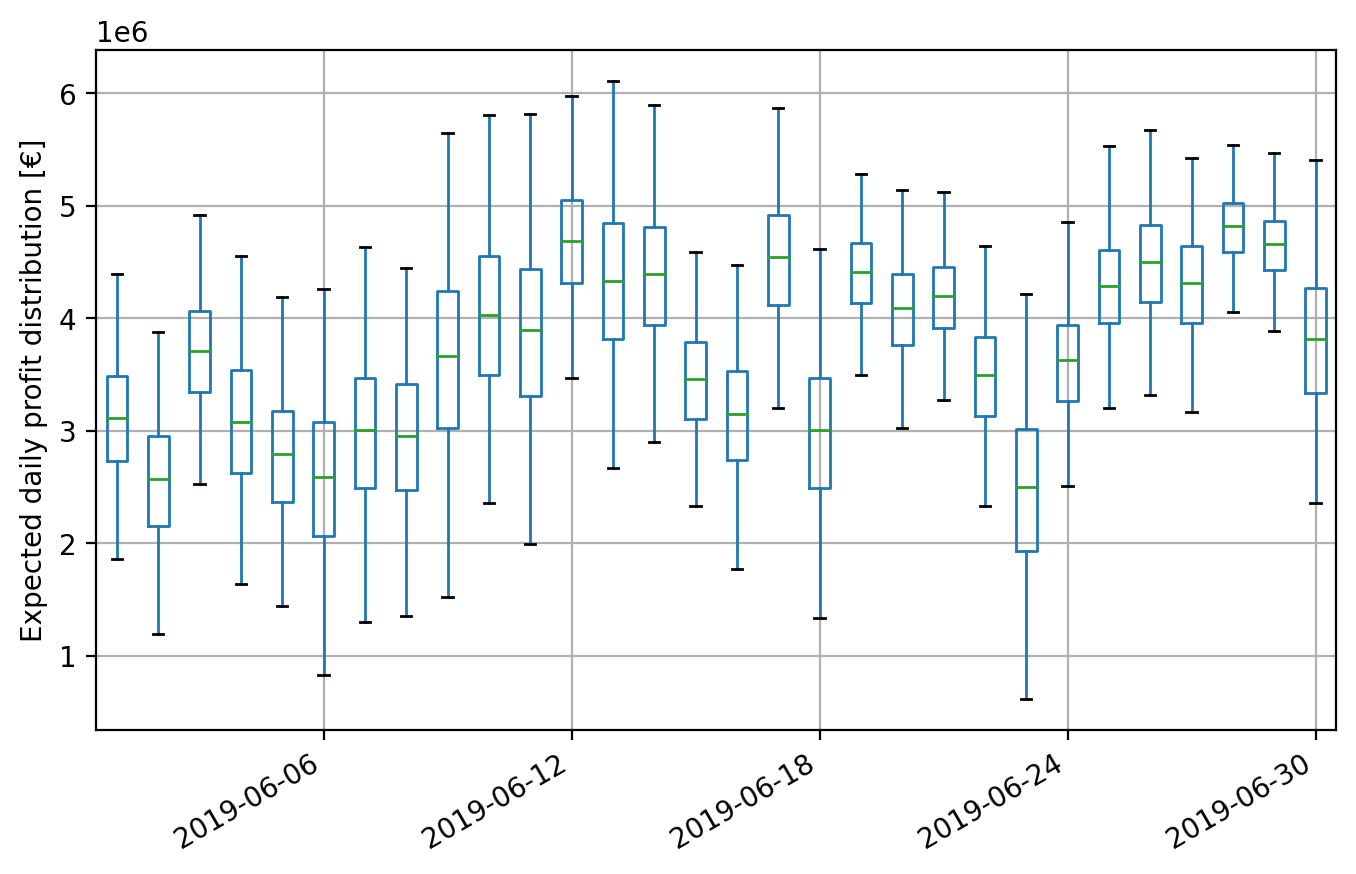

Firstly, in Figure 5, we show the expected daily profit distribution (left) and hourly block prices (right) when no strategic offering is allowed. That is, the price flexibility is 0% and the block prices are the production costs. With this level of price flexibility, the block prices show the real production cost during June 2019. These costs are obtained following the methodology presented in Section 3.2. That is, we discretized the original supply curve of the large GENCO and assumed the obtained values for each block to be the true costs. Regarding the expected profit distribution, we can see how it fluctuates between 2 and 6 million euros per day. Furthermore, we can see the different profit uncertainty levels the GENCO faces across the month. For example, the profit distribution on June 22 is much narrower than on June 24, giving us the idea of different levels of risk exposure.

Next, we increase the price flexibility level up to 5% and recast the results by risk aversion level in Figure 6. We represent the risk-neutral GENCO in Figures 6(a) and (b), and the risk-averse in Figures 6(c) and (d). Figures 6(a) and (c) show the distribution of daily profit increments compared to the base case when the GENCO offers her energy at production costs. This means that, for the same scenario, we compute the difference between the expected profit at a price flexibility level of 5%, and a level of 0%. On the other hand, Figures 6(b) and (d) represent the difference between the optimal prices offered for each block for a price flexibility level of 5% and the base case (the production cost in Figure 5). The same descriptive setting is applied for the rest of the analyzed cases with different flexibility levels in Figures 7 and 8.

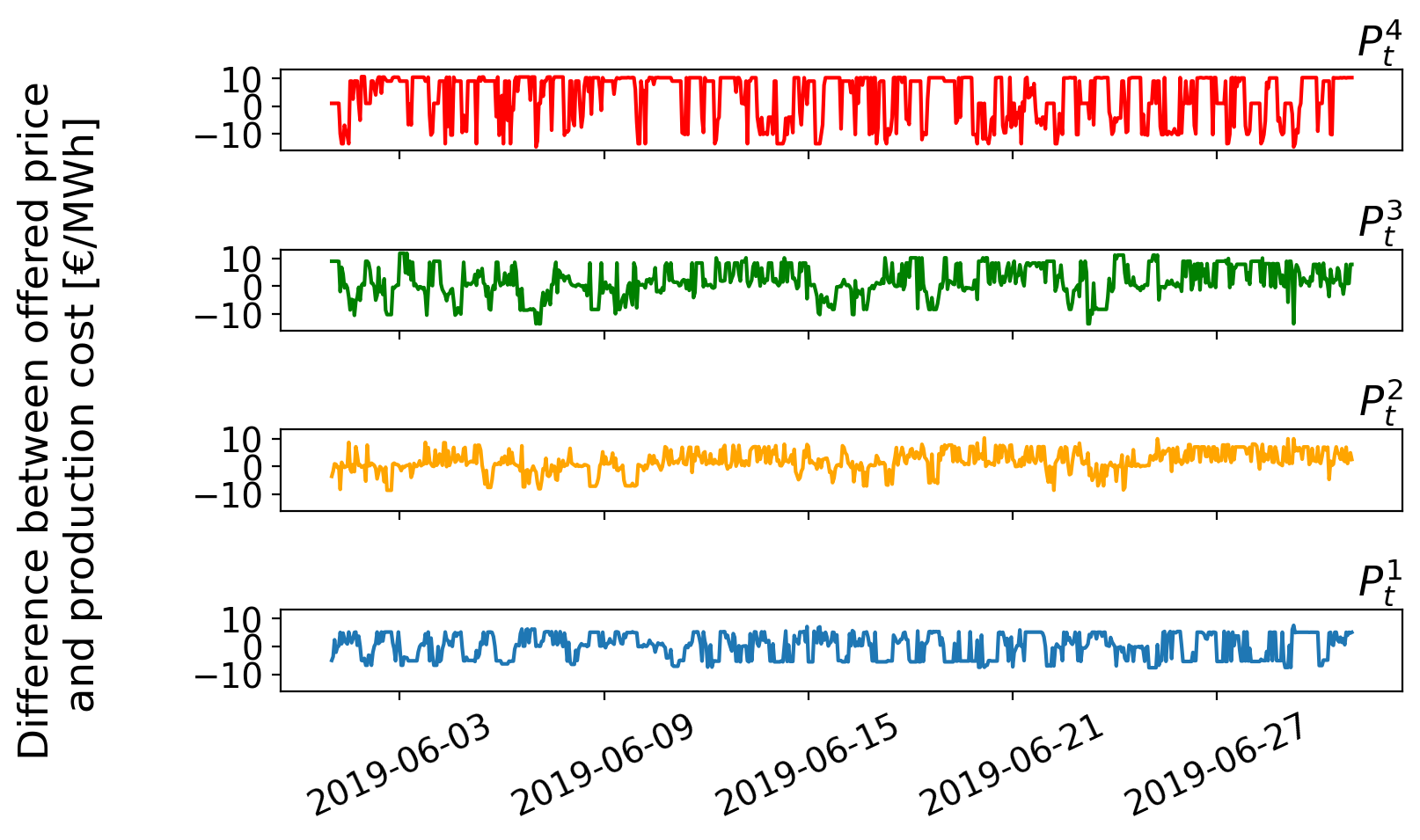

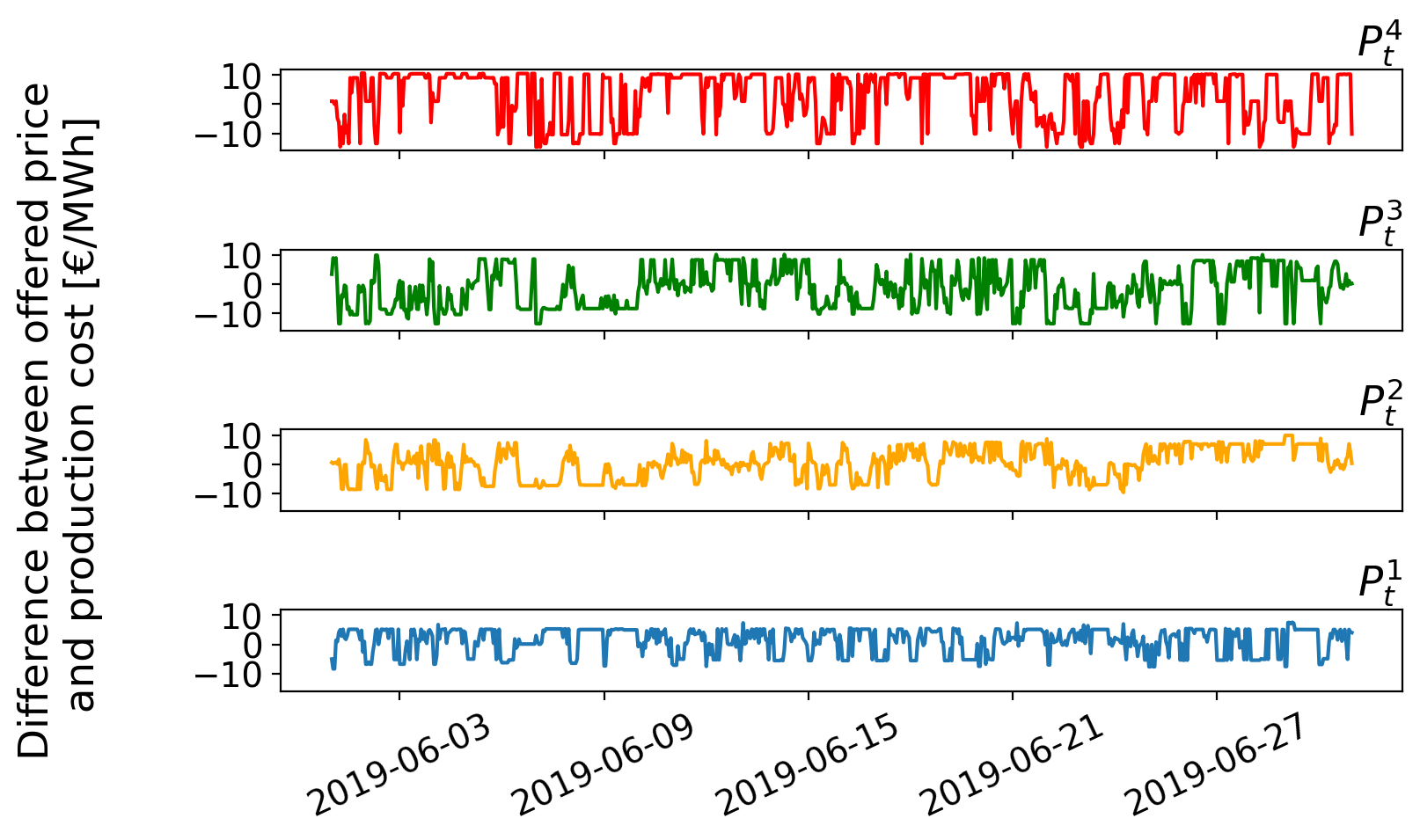

In Figure 6 we can see differences regarding the profit distribution by risk aversion level. Although there are not so many differences in the mean of the distribution (this mean is slightly bigger for the risk-neutral GENCO), we can appreciate the change in the distribution shape. For instance, the distribution for the risk-neutral GENCO has a higher variance than the risk-averse case, which can be noticed in the boxplot range on days like June 9th. Besides, we can notice how the risk-averse GENCO tries to improve the lower tail of the distribution, increasing the value of worst-case profit scenarios. This can be easily checked on the lower tail distribution from June 7th to June 9th. Concerning the offering strategy, we can see the main differences in the variance of the offered prices. Risk-averse GENCO modify to a larger extent her offers for trying to improve worst-case scenarios. Furthermore, we see that the price offered for the first block is close to the marginal cost (zero value in the figure) for the risk-neutral case, and how the risk-averse producer kept the prices high for the second block at the end of the month.

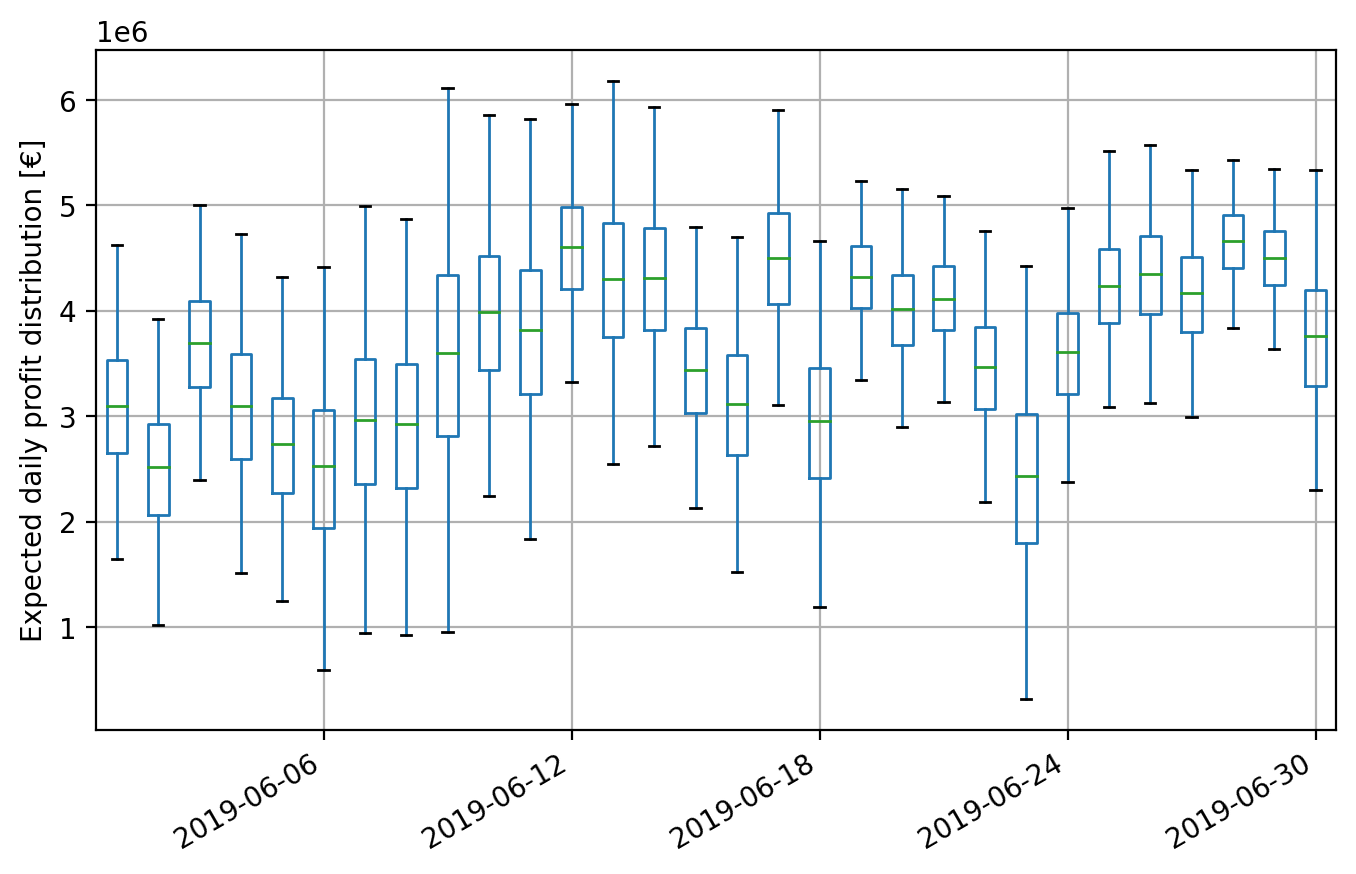

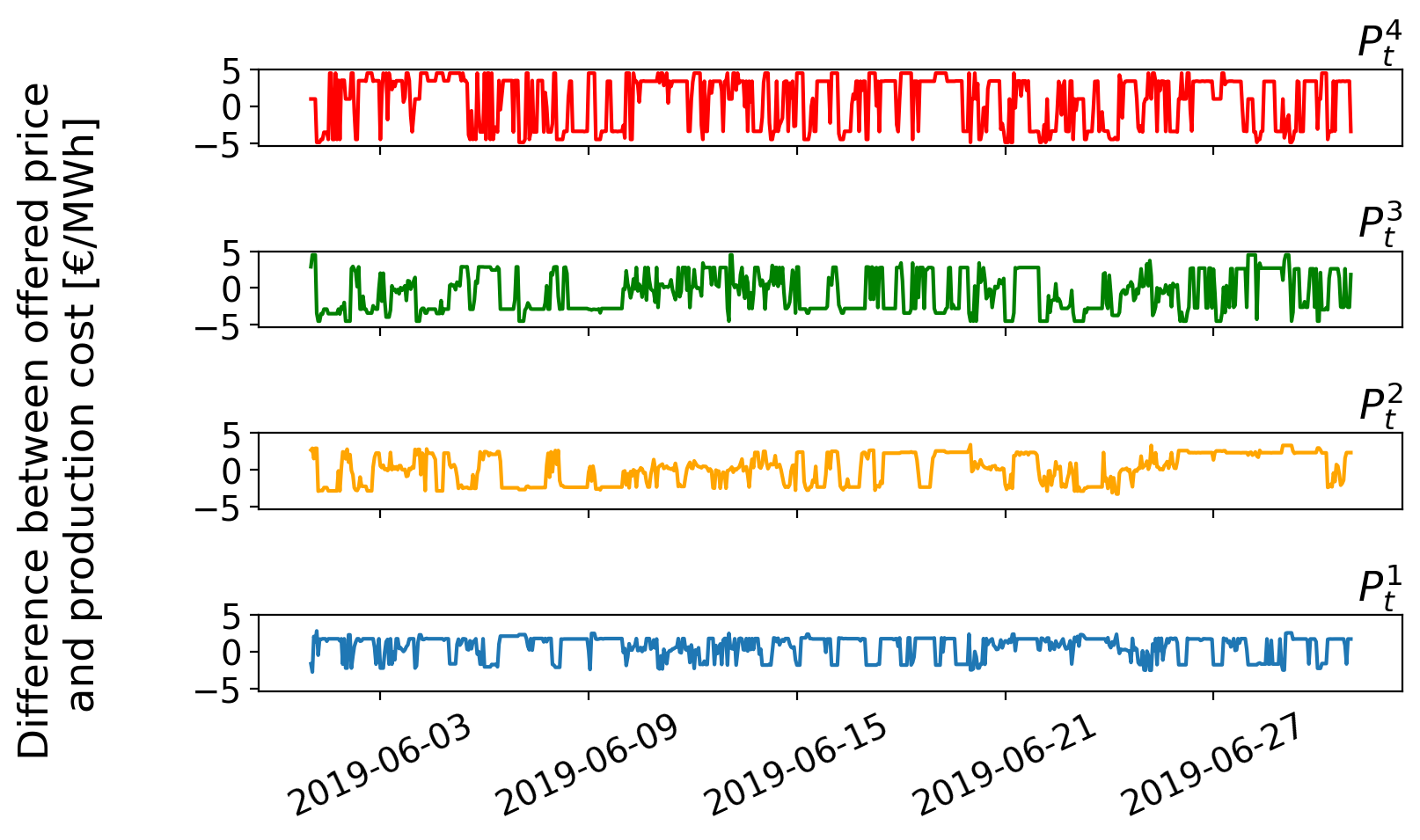

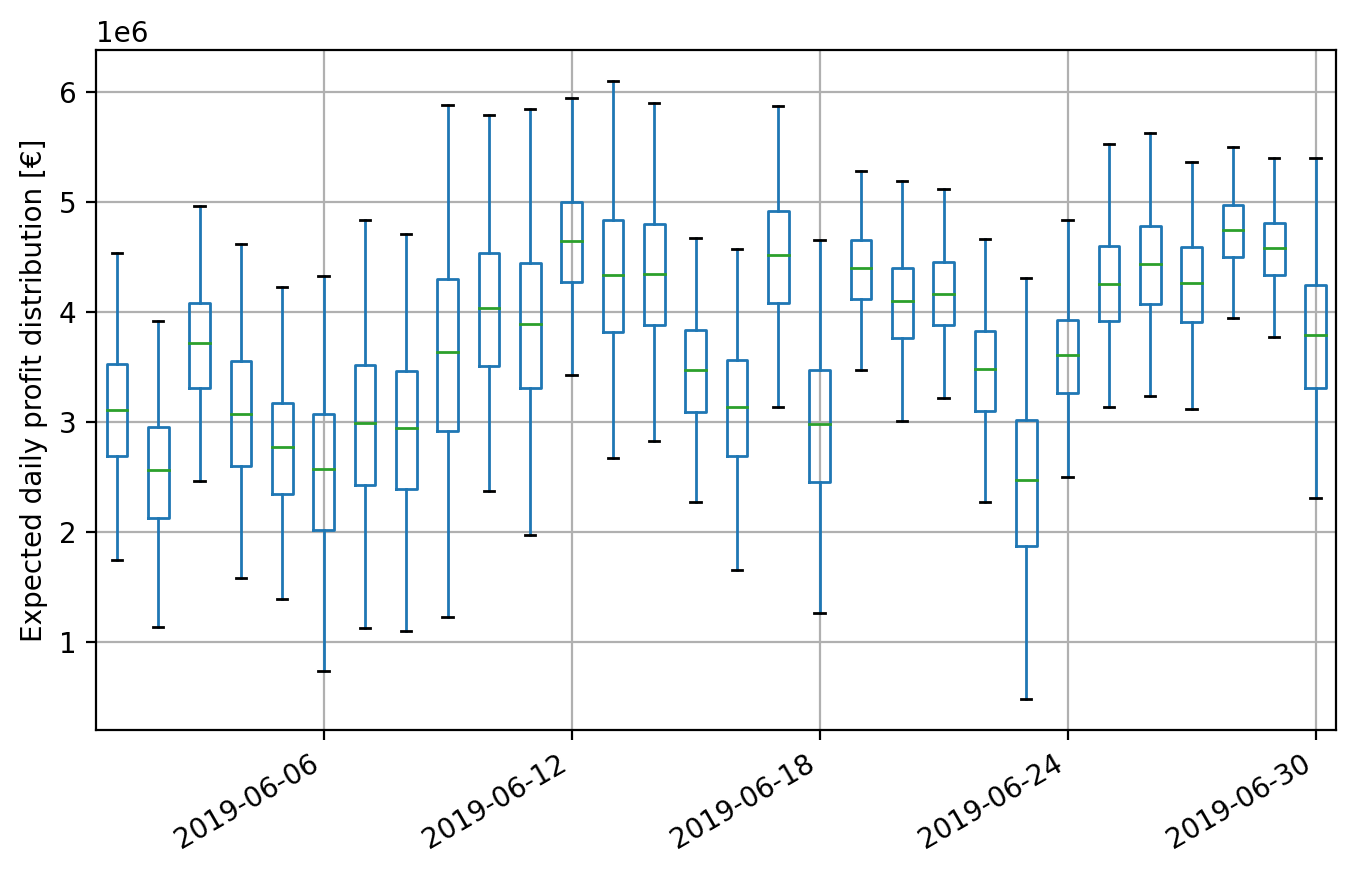

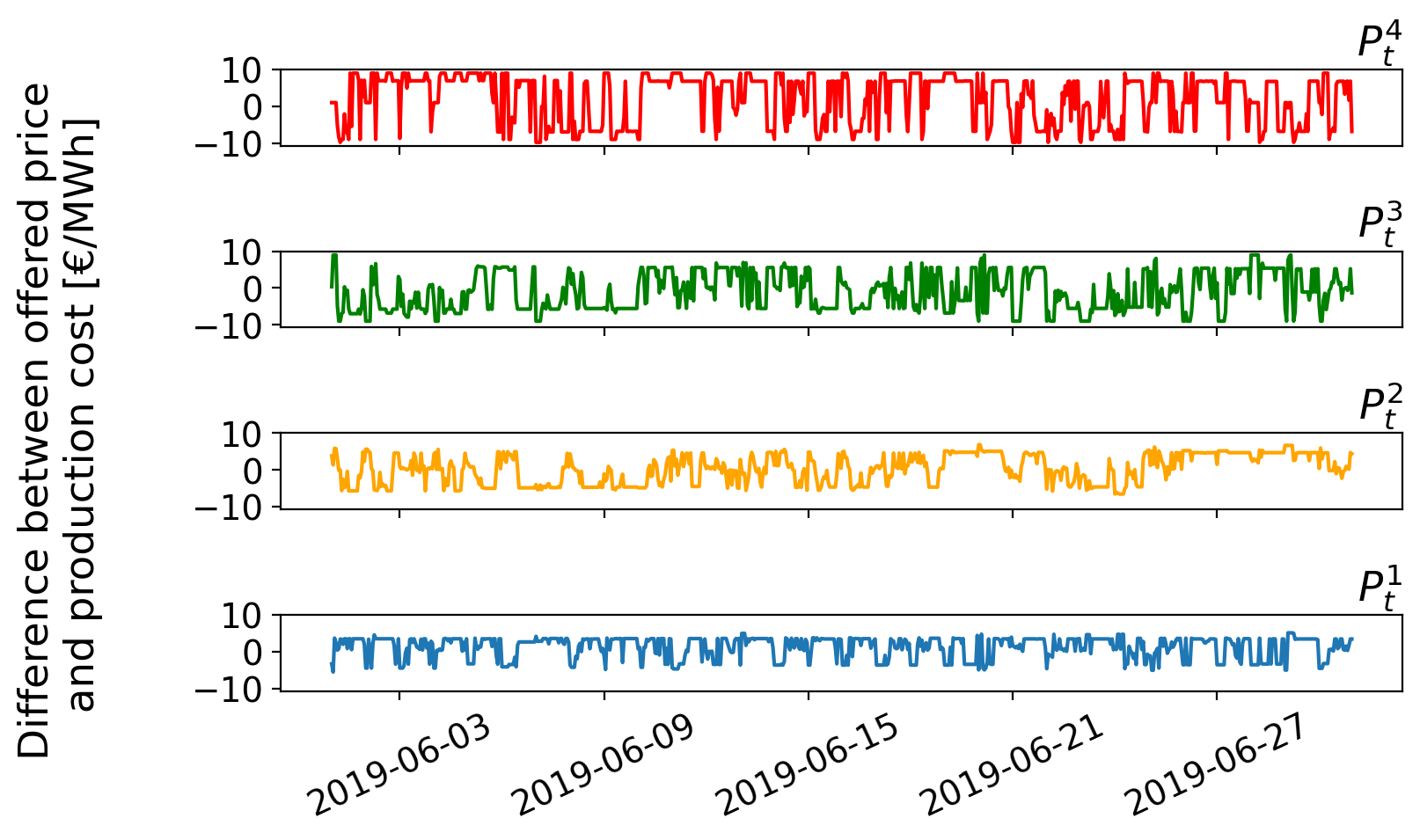

Following the increase of flexibility, we repeat our analysis for the case of in Figure 7. In this case, we can observe the same behavior regarding the distributions of daily profit increment. For the risk-neutral GENCO, we can see how more profit distributions reach 6 million € as the upper tail. In the opposite case, the risk-averse GENCO achieves to improve all lower tail distributions, with only a few below 1 million € compared to the 5% price flexibility case. In relation to the offered prices, both GENCOs take advantage of the price flexibility level by modifying their offers in a larger range regarding the production costs. The pricing behavior for the first and second blocks is still similar to that of the previous case, while in the third block, it is more noticeable how the risk-averse producer tries to minimize its value during more hours of the day.

We will finish this analysis with a 15% level of price flexibility case. Results are shown in Figure 8. We can appreciate the largest differences in profit variance in this case. The main goal of the risk-averse GENCO is to reduce the range of possible values in the profit distribution while improving the lower tail. This variability reduction can be easily seen on the first day of the test. Furthermore, there are almost no days with profits exceeding 6 million € or below 1 million € for the risk-averse case, while the risk-neutral GENCO tries to maximize the mean profit at the cost of having a large variability in the distribution. In relation to the block prices, the risk-averse GENCO tries to minimize the price of the third block on more occasions than the risk-neutral while also increasing the price of the second block, which suggests the target of joining the prices of both blocks. On the other hand, the risk-neutral GENCO keeps the difference between the price offered and the production cost around zero, while making this difference positive for most of the hours in the rest of the blocks.

4.3.3 Out-of-sample model validation

As we have seen, the stochastic optimization model illustrates how allowing strategic price offering for a GENCO can increase the day-ahead market marginal price. Furthermore, we see differences in offering prices, marginal prices, and expected profits in relation to the risk aversion level of the GENCO.

This analysis was based on the assumption that the distributional neural network model (6c) was an accurate representation of the market price response to the GENCO’ strategic offers. However, we aim to test if this stochastic optimal strategy would actually work in a real market. That is, we want to know what may occur when the GENCO sends her optimized supply curves to the Spanish day-ahead market. For this reason, we will follow an out-of-sample validation of the derived offering strategy, using data from June 2019.

For this purpose, the methodology will stand as follows:

-

1.

Once the optimal strategy by the GENCO is derived from (6), send the resulting supply curve to the market. Block quantities will be with prices , jointly with at zero cost.

-

2.

Aggregate the GENCO supply curve with the one collected by the market operator from the rest of the market competitors (also discretizated in 7 blocks, see Section 3), and use the inelastic demand forecast from ESIOS to obtain the initial marginal price.

-

3.

Displace the market supply curve employing the mean displacement of the last two months at its corresponding hour, to reproduce technical adjustments performed by the market operator.

After all these steps are done, we will finally get an estimated marginal price. Profits for the GENCO can be computed as the product of the dispatched quantities (those blocks below the resulting marginal price) times the marginal price minus the production costs of this energy.

These out-of-sample results have been computed for different levels of risk aversion () and price flexibility (). Table 4.3.3 summarizes the main obtained insights. The third column of the table shows the total daily profit increments for the GENCO in June 2019 when deviating her optimal offering from the production costs. The fourth and fifth columns indicate the first and third quantiles over this daily profit increment distribution. These two values will give us an interval guess for what value we should expect the profit increment to be. We find its standard deviation rightwards, to finally compute the mean hourly marginal price of the market.

| Price | ||||||

|---|---|---|---|---|---|---|

| flexibility | Risk | |||||

| (€/MWh) | ||||||

| 191095.45 | 0 | 6560.67 | 17623.90 | 43.51 | ||

| 214241.76 | 105.77 | 10541.40 | 19717.90 | 43.54 | ||

| 442832.52 | -374.17 | 25615.05 | 21189.03 | 43.59 | ||

| 262260.90 | -4647.12 | 18823.01 | 42586.82 | 43.59 | ||

| 504035.65 | -1084.16 | 30006.26 | 23461.30 | 43.63 | ||

| 501912.42 | -2812.18 | 31912.63 | 41281.07 | 43.67 |

The first and one of the most important results that we can confirm out-of-sample is that allowing the large GENCO offers to deviate from marginal costs makes the market marginal price increase. Notice that the mean day-ahead price offering at production cost would be 43.46 €/MWh

Furthermore, for both the risk-neutral and risk-averse GENCOs, their profit increments are directly related to the price flexibility that we allow them to take. This fact makes our stochastic results previously exposed true also in a real market test. We can see how the total profit increment for the risk-neutral GENCO is higher than the one for the risk-averse producer for the cases of price flexibility levels of 10% and 15%. When the GENCO employs a price flexibility level of 5% the total profit increase in the risk-averse case is greater than in the risk-neutral one.

Regarding the profit increment quantiles, i.e., on which values we expect the increment in profit to move on a daily basis; we can see that the range of values increases when also increasing the price flexibility level. For example, we can notice that for the 5% flexibility level, a daily profit increase with the optimal strategy should be expected to be below 10 thousand €.

In relation to the deviation of the profit increment when the optimal strategy is chosen, the risk-averse producer is not able to hold this variability as well as the risk-neutral GENCO. This fact can also be seen in the first quantile, which is generally lower in the risk-averse GENCO case. This is due to some specific days where the risk-averse optimal strategy is worse than offering at marginal cost, which can now be checked in the graphical analysis.

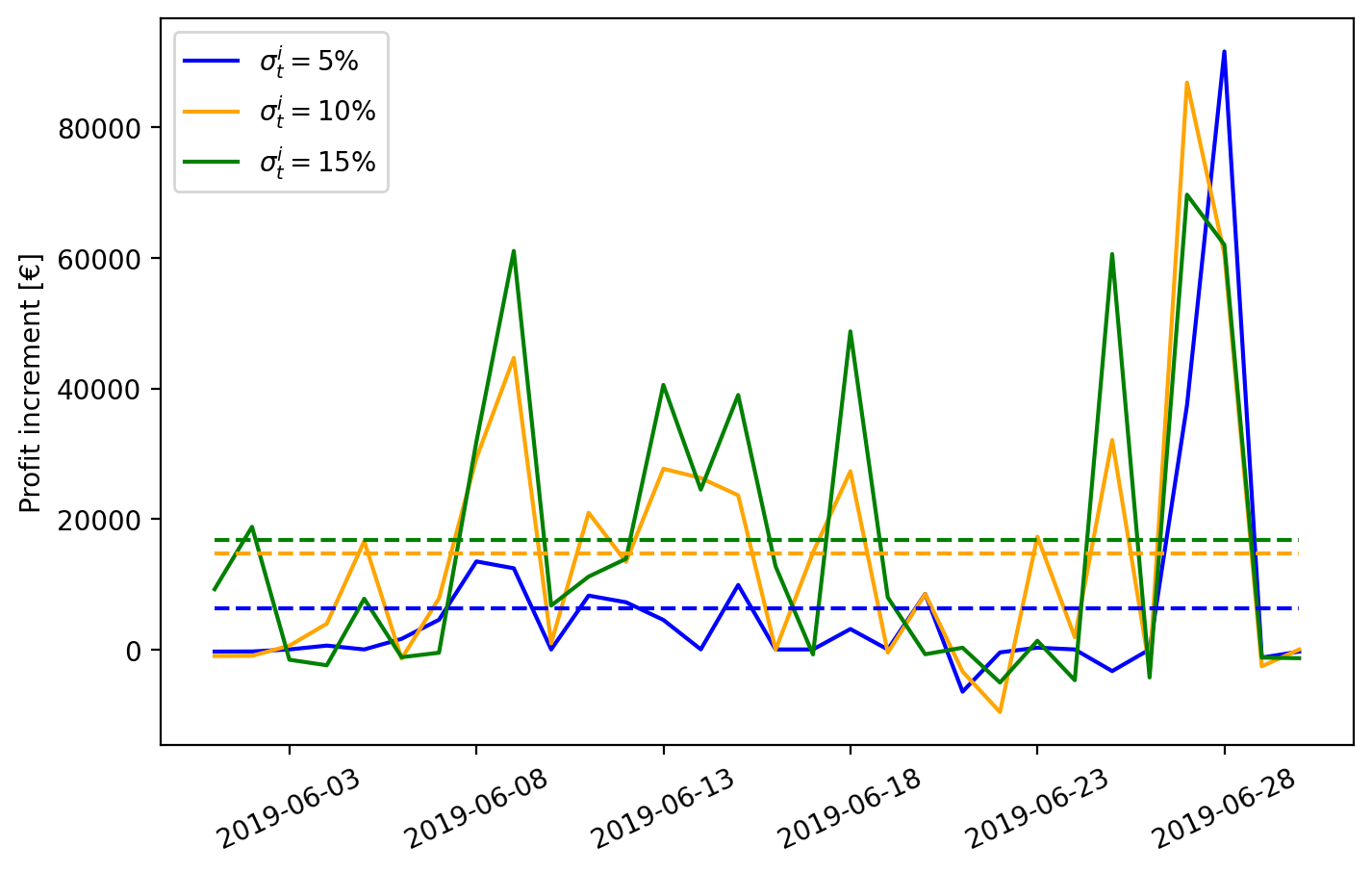

Therefore, to finish this section, we will show graphically the daily GENCO profit increase in the test period for different levels of price flexibility and risk aversion concerning the true generating cost offering strategy. Figure 9 shows the daily out-of-sample profit increment for risk-neutral (up) and risk-averse (down) GENCO for different levels of price flexibility. Dashed lines represent the mean for each pricing strategy.

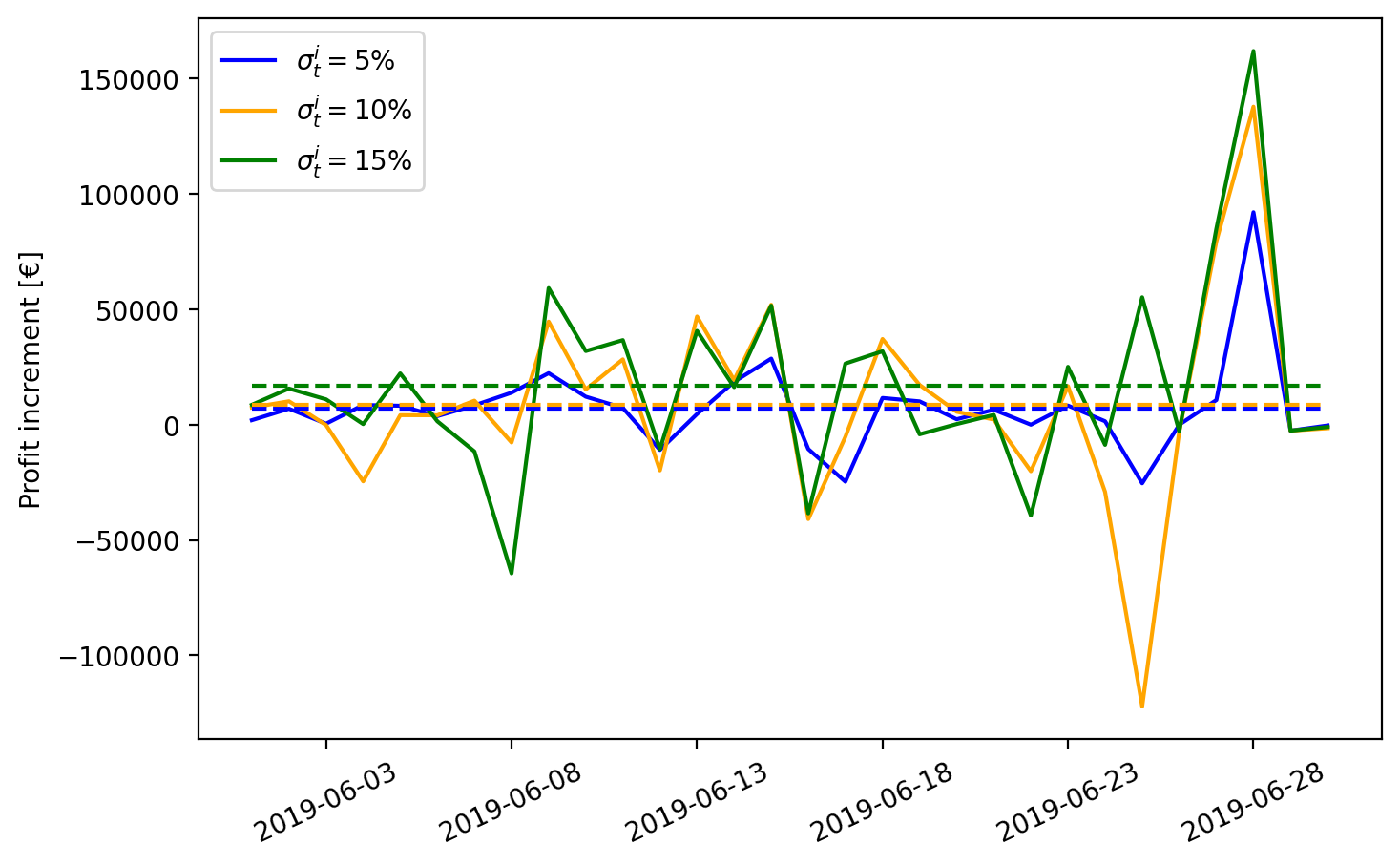

As can be seen, most days, the profit increment is slightly higher for cases where the price flexibility is different from zero, for both levels of risk aversion. Also, on some specific days, this profit difference is increased on a higher scale, for instance, June 9th, 13th, 17th, 27th, or 28th. It is interesting to notice that, for the risk-neutral case, the mean profit increment is quite similar for price flexibility levels of 10% and 15%. However, in the risk-averse case, the highest profit increase is clearly obtained for price flexibility of 15%, but at the cost of a larger variance in the results, with days obtaining big negative values of profit increment compared to the cost-offering strategy.

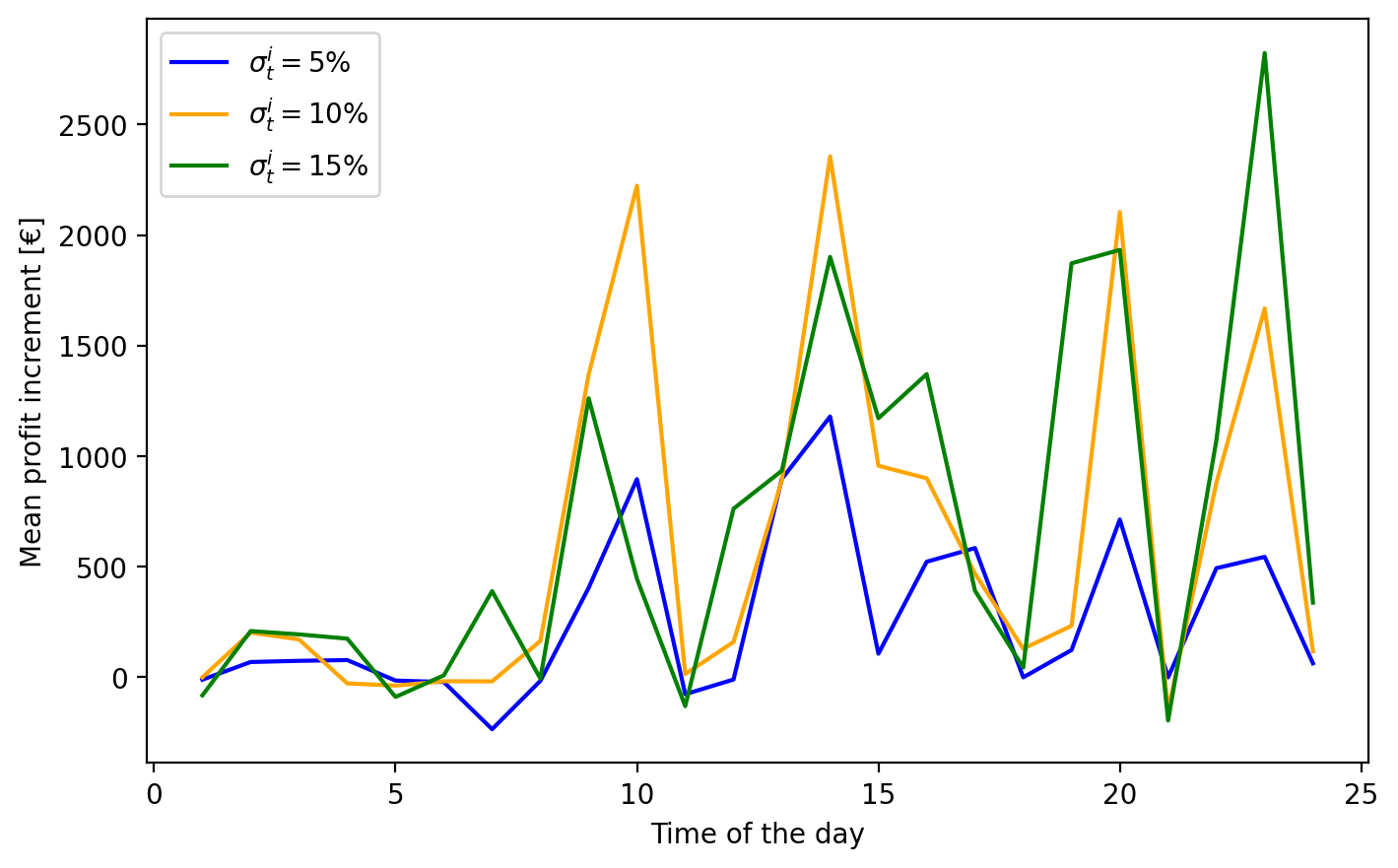

Furthermore, we can appreciate more differences when we show the average increase in profits on an hourly basis (Figure 10). As in the case above, we represent the profit increment for several levels of price flexibility and risk aversion: risk-neutral (up) and risk-averse (down). We can see how the biggest amount of profit increment can be made around 8:00, and in some specific hours like 13:00 to 17:00, 19:00 to 20:00, and 22:00 to 23:00 in a non-homogeneous way.

For the risk-neutral GENCO, we can notice how, on average, and in most of the hours of the day, a profit increment can be obtained by allowing price flexibility in her offering strategy. Besides, when the profit increases, it does it on a bigger scale when the maximum price flexibility is set. Furthermore, only in hours like 7:00 and 21:00 the profit increment is negative, i.e., a cost-offering strategy is better.

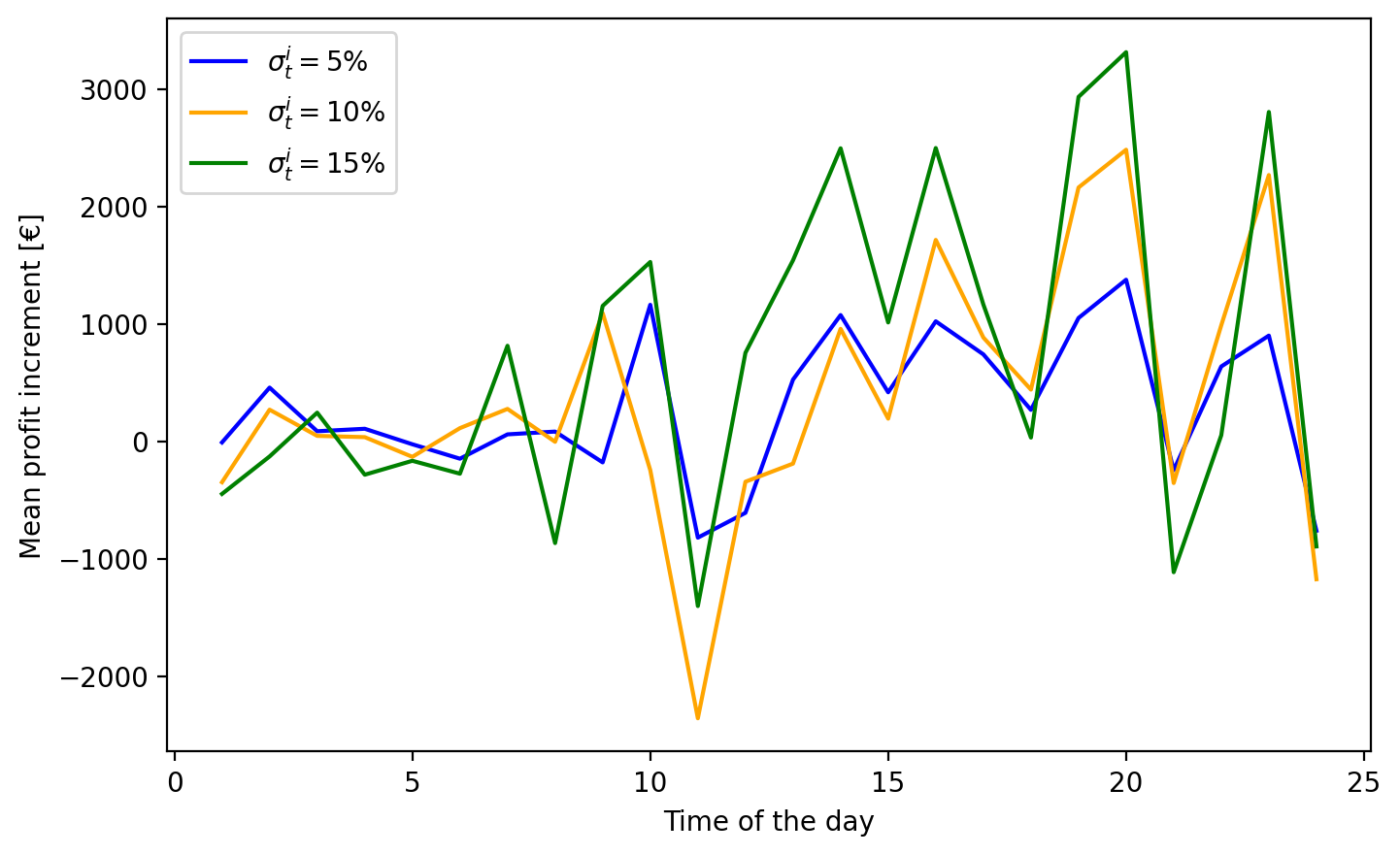

On the other hand, the behavior of the hourly profit increments is similar in the case of a risk-averse GENCO. However, there are more hours when the mean profit does not increase. In the case where the profit suffers an increment, it does it proportionally to the different levels of price flexibility. Nevertheless, the case of a 5% price flexibility allows the risk-averse GENCO to soften the decrease in profit.

These results show how the stochastic optimization model is optimistic about the profit increment. Nevertheless, the profit increments do occur, but at a lower scale than the reported stochastic model. This could be due to local limitations of the predictive model, as large variations in competitor block offers, which could change market outcomes, cannot be taken into account. However, the hourly behavior of the profit increment provides valuable insights and suggests that an hourly price flexibility strategy could be taken into account to further increase GENCO’s profits.

To sum up, this out-of-sample validation approach has allowed us to confirm in a real-life context how allowing a GENCO to deviate from its true generating costs makes her expected profits increase. Nevertheless, we have seen how an excessive value of the price flexibility may create too much volatility in the results, in particular, in the risk-averse GENCO. Finally, we have learned that the highest increase in profit can be achieved at some specific hours of the day.

5 Conclusions

In this work, we have dealt with the problem of finding an optimal offering strategy for a large GENCO. That is, knowing the amount of energy that the GENCO can produce and at what cost, setting the prices of the offered energy blocks for a profit-maximizing strategy.

We present a data-driven methodology where GENCO’s supply curves and the ones from the rest of the competitors are optimally discretized. This discretization allows to get important insights from their offering strategy, reproduce the market clearing to compute the resulting market price, and ease an out-of-sample validation of the proposed stochastic optimization model.

The relationship between the hourly market marginal price and the block prices offered by the GENCO is modeled through a Distributional Neural Network approach. The advantage of this approach is to obtain an accurate but piece-wise linearizable model in its structure, from which different scenarios for the market outcomes can be sampled from their predicted distribution with a simple linear constraint. This predictive model is embedded into a two-stage stochastic optimization model which accounts for risk aversion to derive the optimal supply curve to submit to the day-ahead market.

After an in-depth analysis, stochastic results have shown how allowing the GENCO to deviate from her marginal costs offer, results in a marginal market price increase, which also increases her profits. Besides, there are differences in the pricing behavior of the GENCO depending on her risk aversion level. In general, a risk-neutral GENCO achieves to increase the marginal price to a higher extent than the risk averse GENCO, but worsens the worst case profit scenarios.

One of the main novelties of this work is that the optimal offering strategy is tested out-of-sample. That is, we simulate the actual functioning of the market combining the demand and the offers from the GENCO and her competitors. We show how the proposed optimization model achieves a marginal price increment and a profit increase for risk averse and risk neutral GENCOs when they deviate from marginal cost offering. Besides, an hourly price flexibility strategy could further increase GENCO’s profit. Furthermore, these results warn us about the importance of executing effective audits in markets with uniform pricing based on marginal technologies. Minor increments in the block prices may significantly increase the marginal price which will be transferred to the consumers.

Future work is focused not only on studying the price strategy for the GENCO but also on allowing flexibility on the offered energy quantity. This would add more complexity to the optimization problem and the prediction model. Furthermore, hourly-trained models could be fitted to better capture different market dynamics.

Acknowledgements

The authors gratefully acknowledge the financial support from MCIN/AEI/10.13039/ 501100011033, project PID2020-116694GB-I00 and from the FPU grant (FPU20/00916).

References

- [1] Antonio Alcántara “opti-genco-offers”, 2022 URL: https://github.com/antonioalcantaramata/opti-genco-offers

- [2] Antonio Alcántara and Carlos Ruiz “A Neural Network-Based Distributional Constraint Learning Methodology for Mixed-Integer Stochastic Optimization” In arXiv preprint arXiv:2211.11392, 2022

- [3] Ross Anderson et al. “Strong mixed-integer programming formulations for trained neural networks” In Mathematical Programming 183.1 Springer, 2020, pp. 3–39

- [4] Kaixuan Chen, Jin Lin and Yonghua Song “Trading strategy optimization for a prosumer in continuous double auction-based peer-to-peer market: A prediction-integration model” In Applied energy 242 Elsevier, 2019, pp. 1121–1133

- [5] Yan Du, Fangxing Li, Helia Zandi and Yaosuo Xue “Approximating nash equilibrium in Day-ahead electricity market bidding with multi-agent deep reinforcement learning” In Journal of modern power systems and clean energy 9.3 SGEPRI, 2021, pp. 534–544

- [6] ESIOS “Red Eléctrica España”, 2022 URL: https://www.esios.ree.es

- [7] Adejuyigbe Fajemisin, Donato Maragno and Dick den Hertog “Optimization with constraint learning: A framework and survey” In arXiv preprint arXiv:2110.02121, 2021

- [8] Gurobi Optimization, LLC “Gurobi Optimizer Reference Manual”, 2022 URL: https://www.gurobi.com

- [9] Xuejiao Han and Gabriela Hug “A distributionally robust bidding strategy for a wind-storage aggregator” In Electric power systems research 189 Elsevier, 2020, pp. 106745

- [10] Xuejiao Han, Evaggelos G Kardakos and Gabriela Hug “Offering strategy of a price-maker pv power plant: multi-stage stochastic programming with probabilistic constraints” In 2018 Power Systems Computation Conference (PSCC), 2018, pp. 1–7 IEEE

- [11] William E Hart et al. “Pyomo-optimization modeling in python” Springer, 2017

- [12] Aswin Kannan, Uday V Shanbhag and Harrison M Kim “Strategic behavior in power markets under uncertainty” In Energy Systems 2.2 Springer, 2011, pp. 115–141

- [13] Evaggelos G Kardakos, Christos K Simoglou and Anastasios G Bakirtzis “Optimal offering strategy of a virtual power plant: A stochastic bi-level approach” In IEEE Transactions on Smart Grid 7.2 IEEE, 2015, pp. 794–806

- [14] MIBEL “Mercado Ibérico de la Electricidad”, 2022 URL: https://www.mibel.com/es/home_es/

- [15] Lesia Mitridati and Pierre Pinson “A Bayesian inference approach to unveil supply curves in electricity markets” In IEEE Transactions on Power Systems 33.3 IEEE, 2017, pp. 2610–2620

- [16] Amir Naebi et al. “EPEC approach for finding optimal day-ahead bidding strategy equilibria of multi-microgrids in active distribution networks” In International Journal of Electrical Power & Energy Systems 117 Elsevier, 2020, pp. 105702

- [17] David A Nix and Andreas S Weigend “Estimating the mean and variance of the target probability distribution” In Proceedings of 1994 ieee international conference on neural networks (ICNN’94) 1, 1994, pp. 55–60 IEEE

- [18] OMIE “OMIE”, 2022 URL: https://www.omie.es

- [19] Hrvoje Pandžić, Juan M Morales, Antonio J Conejo and Igor Kuzle “Offering model for a virtual power plant based on stochastic programming” In Applied Energy 105 Elsevier, 2013, pp. 282–292

- [20] Román Pérez-Santalla, Miguel Carrión and Carlos Ruiz “Optimal pricing for electricity retailers based on data-driven consumers’ price-response” In TOP Springer, 2022, pp. 1–35

- [21] R Tyrrell Rockafellar and Stanislav Uryasev “Optimization of conditional value-at-risk” In Journal of risk 2 Citeseer, 2000, pp. 21–42

- [22] Carlos Ruiz and Antonio J Conejo “Pool strategy of a producer with endogenous formation of locational marginal prices” In IEEE Transactions on Power Systems 24.4 IEEE, 2009, pp. 1855–1866

- [23] Carlos Ruiz, Antonio J Conejo and Dimitris J Bertsimas “Revealing rival marginal offer prices via inverse optimization” In IEEE Transactions on Power Systems 28.3 IEEE, 2013, pp. 3056–3064

- [24] Gregory Steeger, Luiz Augusto Barroso and Steffen Rebennack “Optimal bidding strategies for hydro-electric producers: A literature survey” In IEEE Transactions on Power Systems 29.4 IEEE, 2014, pp. 1758–1766