Constructing Trinomial Models Based

on Cubature Method on Wiener Space: Applications to Pricing Financial Derivatives

Abstract

This contribution deals with an extension to our developed novel cubature methods of degrees 5 on Wiener space. In our previous studies, we have shown that the cubature formula is exact for all multiple Stratonovich integrals up to dimension equal to the degree. In fact, cubature method reduces solving a stochastic differential equation to solving a finite set of ordinary differential equations. Now, we apply the above methods to construct trinomial models and to price different financial derivatives. We will compare our numerical solutions with the Black’s and Black–Scholes models’ analytical solutions. The constructed model has practical usage in pricing American-style derivatives and can be extended to more sophisticated stochastic market models.

keywords: Cubature method, Stratonovich integral, Wiener space, stochastic market model

1 Introduction and outline of the paper

In mathematical finance, it is common to describe the random changes in risky asset prices by stochastic differential equations (SDEs). SDEs can be re-written in their integral forms. However, it is not possible to calculate all stochastic integrals in closed form. Therefore, proper numerical methods should be used to estimate the value of such stochastic integrals.

One of the most popular numerical method to estimate stochastic integrals is Monte Carlo method (estimate). In particular, according to [17], cubature methods and consequently cubature formulae construct a probability measure with finite support on a finite-dimensional real linear space which approximates the standard Gaussian measure. A generalisation of this idea, when a finite-dimensional space is replaced with the Wiener space, can be used for constructing modern Monte Carlo estimates (see [1] for the exact sense of modern Monte Carlo estimate). The idea of cubature method on Wiener space, among others, was developed in [11]. The extension of this idea were developed and studied in [12, 13, 14, 17].

Our objective is to use cubature method and a cubature formula of degree 5 on Wiener space to estimate the expected values of functionals defined on the solutions of SDEs. This means that we use an extension to our developed novel cubature methods of degrees 5 to estimate the (discounted) expected values of European call and put payoff functions defined on the solutions of Black–Scholes and Black’s SDEs. This extension includes a construction of a recombining trinomial tree model. The underlying asset prices in Black–Scholes and Black’s models are log-normally distributed and the price dynamics follow geometric Brownian motion. Moreover, both models have closed form solutions to find the price of European call and put options. Availability of closed form solutions of these models provides us with an opportunity to investigate if the sequence of our trinomial models converges to a geometric Brownian motion or not. Also, we can compare our numerical results with analytical ones and consequently estimate the corresponding errors of our method. We would like to emphasize that the constructed trinomial tree has practical usage and applications in pricing path-dependent and American-style options.

The outline of this paper is as follows. In Section 2, we briefly look at the cubature method on Wiener space and at the applications of cubature formula in Black–Scholes and Black’s models. Then, in Section 3, we construct a trinomial model based on cubature formula on Black–Scholes model. After that, in Section 4, we study the convergence of the sequences of constructed trinomial model to a geometric Brownian motion. In Section 5, we will study the conditions which makes the probability measure in our trinomial model a martingale measure, i.e., risk-neutral probability measure. Later, in Section 6, we will extend our results for more cases and give some concrete examples where we study the behaviour of the constructed trinomial model in Black–Scholes and Black’s model. Finally, we close this paper by a discussion section.

2 Cubature formula in Black–Scholes and Black’s model

In this section, we briefly review how the cubature method on Wiener space can be used in the Black–Scholes and Black’s models.

2.1 Black–Scholes model via cubature formula

Given a filtered probability space , let be time- price of a (non-dividend-paying) risky asset, and be drift (risk-free interest rate) and diffusion (volatility of asset price) coefficients and be the standard one-dimensional Wiener process. The dynamics of risky asset prices in the Black–Scholes model [4, 15], under equivalent martingale probability measure , satisfies the following SDE (originally proposed by Samuelson [20])

| (1) |

The solution to the SDE (1) is an Itô process. After applying the Stratonovich correction, the above equation can be written in its Stratonovich form (see [18])

| (2) |

We note that, cubature formula is valid in time interval with length one. Applying the results of cubature method on Wiener space in Equation (2) yields to [13, 17]

where is the th possible trajectory, and stands for the number of trajectories in the cubature formula of degree .

Rearranging the last equation and calculating the integral of both hand sides gives

| (3) |

with and . In a cubature formula of degree , the number of trajectories is and one of the possible solutions becomes

| (4) |

where , i.e., the trajectories start from time and stop at time , , and with weight and coefficients summarized in Table 1.

| 1 | ||||

|---|---|---|---|---|

| 2 | ||||

| 3 |

Using Equation (4), we calculate and . For simplicity, denote by Now, let us ignore the intermediate partitions in . This reduces Equation (3) to

| (5) |

Equation (5) works for the time interval of length one, i.e. . Let be the time to maturity for an option. Right now, we can only consider . We would like considering yearly interest rate, yearly volatility and yearly time to maturity in a more flexible way. So, we modify the drift and diffusion terms in Equation (5). This modification yields to

| (6) |

Now, it is easy to calculate for . Then, the price of an option will be equal to its discounted expected payoff. For example, the price of an European call option () and the price of an European put option () with strike price will be given by

Equation (6) works better for very small time to maturity. Later in this paper, we will try to improve the performance of our model by extending it into a trinomial tree model.

2.2 Black’s model via cubature formula

In the Black’s model [3], the dynamics of risky forward rate prices satisfies

The Stratonovich form of the above SDE becomes

Following the same procedure as in Section 2.1, we get

| (7) |

3 Constructing a trinomial tree via cubature formula

In this section, we develop, modify and revise the idea of constructing a trinomial model via cubature formula on Wiener space presented in [13]. The idea of constructing an -step trinomial tree is to divide the time interval by steps. In each step, the price can go up by an amount of with probability , go in middle by an amount of with probability and go down by an amount with probability . Also, , and . In other words, we create more trajectories (paths) for the underlying process in discrete time in order to get more accurate possible prices. If a trinomial model is recombining, then the number of nodes in the constructed recombining trinomial tree is . Using trinomial expansion, we can find all trinomial coefficients which represent the number of possible paths to reach each node. Note that the sum of all trinomial coefficients is equal to the number of all possible paths in the constructed trinomial tree, that is, to . Moreover, we can simply calculate the corresponding probabilities and prices at each step of the tree and for each node. Figure 1 illustrates the idea, where the dashed-arrows represent a recombining binomial tree (e.g., see CRR binomial model in [5]). We observe that for example in node , and in node .

The constructed tree can (among other possible applications) be used for pricing European, American-style and path-dependent derivative options.

A trinomial tree approximation for the Black–Scholes model

Let , substituting and in Equation (6) (from now on we type instead of ), we introduce up, middle and down factors by

| (8) |

Observe that the factors , , and depend on through . To simplify notation, we omit this dependence.

Proposition 1.

The above trinomial construction produces a recombining trinomial tree.

Proof.

We simply calculate

Since and are positive, . Equivalently, . ∎

As an example, assume that the stock price , time to maturity of a year, strike price , yearly interest rate , yearly volatility and the number of steps in our trinomial tree .

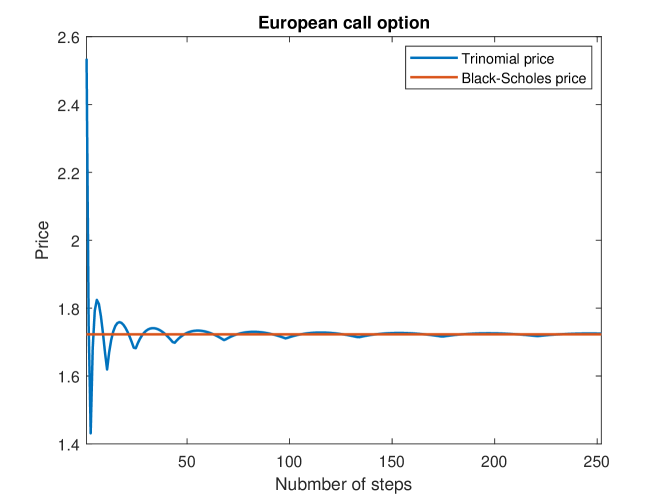

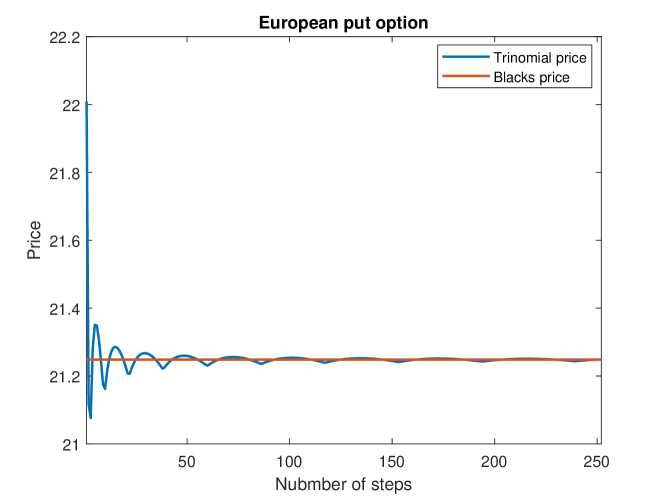

Now, given the above parameters, we write a script in MATLAB®, where we use the Black–Scholes formulae to calculate analytical prices, and apply the constructed trinomial tree model to estimate numerical prices of European call and put options. The option prices are summarized in Table 2. Moreover, the behavior of trinomial tree prices (for call option) is depicted in Figure 2. The absolute value of difference between Black–Scholes and trinomial prices for call option is 0.0020704969 and for put is 0.00207049733.

| ($) Black–Scholes | ($) Trinomial | ($) Black–Scholes | ($) Trinomial |

|---|---|---|---|

| 1.722901670 | 1.724972167 | 20.23223773 | 20.234308227 |

4 Convergence to geometric Brownian motion

As Figure 2 suggests, our (numerical) trinomial price may converge to the (analytical) Black–Scholes price. Now, we will consider a more general case and show that the sequence of our trinomial model (weakly) converges to a geometric Brownian motion. We first prove the convergence in distribution and then we prove the sequence of measures is tight. Let us start by reviewing the necessary definitions given in [2].

Let be a metric space. For the purposes of this paper it is enough to consider the case of with the distance

Let be the -field of Borel sets in . For a probability space , consider a measurable map . By this definition, for a point , the image is a continuous function on . That is, is a stochastic process with continuous sample paths.

Definition 1.

The distribution of is the probability measure on the -field given by

Remark 1.

In other words, we describe the one-to-one correspondence between the family of stochastic processes with continuous trajectories and the family of probability measures on .

Definition 2.

A sequence of stochastic processes converges in distribution to a stochastic process if the sequence of their distributions weakly converges to the distribution of the stochastic process , that is, for any continuous function we have

Let be a positive integer, and let , …, be arbitrary distinct points in .

Definition 3.

The natural projection is the map given by

Definition 4.

The finite-dimensional distributions of a stochastic process are the measures on the Borel -field of the space given by

Definition 5.

A family of probability measures on is called relatively compact if every sequence of elements of contains a weakly converging subsequence.

Theorem 1.

If the sequence of the distributions of stochastic processes is relatively compact and the finite-dimensional distributions of converge weakly to those of a stochastic process , then converges in distribution to .

Thus, proof of convergence in distribution of the sequence of trinomial trees to the geometric Brownian motion is naturally dividing into two parts, which will be given in the next two subsections.

4.1 Convergence of finite-dimensional distribution

Let us study the convergence of our model in the following 3 steps.

Step 1. (Preliminaries)

Consider Equation (8) and let , where . Then, the price at each step of the tree can be found using

| (9) |

Denote the number of times that the price goes up, up to time , i.e., step , by , down by and middle by , then the set of possible prices can be expressed by

If we substitute , the above set reduces to

Put , the space of paths, and as the -field of Borel sets. Let such that and be given. Now, we define the probability measure on supported by a finite subset of sample space with elements.

Step 2. (Description of the measure )

Consider the set of “words” consisting of letters, where each letter is either or or . Let

-

•

be the sequence of independent and identically distributed (IDD) random variables with ,

-

•

and , ,

-

•

be the function that takes the following values:

-

1.

-

2.

-

3.

the value in an arbitrary “intermediate” point, say , is given by linear interpolation, that is

-

1.

-

•

represents the number of letters ,

-

•

represents the number of letters ,

-

•

represents the number of letters .

Now, we define the probability measure on the Borel -field supported by the subset of sample space with atoms by

Finally, let be the measure that corresponds to the geometric Brownian motion

that is, , .

Step 3. (Proof of convergence)

Define the sequence of random variables on the probability space and on as . Following [19], we define

Note that, the sequence is a sequence of independent and identically distributed (IID) random variables.

Let be the stochastic process that corresponds to the measure . By the constructions in “Step 2.”, the values of the process (for simplicity denote it by ) in our trinomial tree can be expressed by re-writing Equation (9) as the following trinomial stock price

| (10) |

We observe that and . Using the equation above, we obtain following mean

| (11) |

and variance

where for the first term on the right hand side of the above equation, we have

and for the second term

Subtracting second term from first one gives

Thus,

| (12) |

Substituting the values , and , confirms the construction of our trinomial tree. That is,

where . Moreover,

In the next step, we would like to prove that the sequence of finite-dimensional distributions of our trinomial trees converges to those of the geometric Brownian motion. In one dimensional case, we prove in our trinomial model converges in distribution to in geometric Brownian motion as . First, we iterate Equation (10). This yields to

| (13) |

Note that for , the random variables are IID random variables. Now, we use Equation (10) and define as the standardized random variable of the sum, . That is,

Using the obtained mean and variance values in Equations (4.1) and (12)

multiplying numerator and denominator by ,

where for all and

Thus,

and using central limit theorem (see [10]), we have

where is the standard normal distribution function.

Doing a little algebra, we calculate the following terms in Equation (13)

| (14) |

where, , , and are given in Equation (8). Substituting the above values into Equation (13) (for an arbitrary ), we get

As the result, we showed that the one-dimensional distributions of our trinomial tree model converge (in distribution) to those of the geometric Brownian motion as . The generalization to -dimensional distributions is straightforward and uses the fact that the stochastic processes and have independent increments, see [2] for details. It remains to prove that the corresponding sequence of measures is relatively compact.

4.2 Relative compactness

To prove the relative compactness of the sequence of measures, we firstly denote the stock price, up, middle and down factors as functions of . That is, and . Secondly, we use the modulus of continuity’s definition given in [2, Equation 7.1] and Theorem [2, Theorem 7.5].

Definition 6 (Modulus of continuity).

The modulus of continuity for (an arbitrary) function on is defined by

Theorem 2 (Tightness and compactness in ).

Let be random functions. If for all

holds and if for each positive

holds, then .

On the one hand, we have already shown that the sequence of our trinomial models converges (in distribution) to the geometric Brownian motion. Therefore, condition holds. On the other hand, using Definition 6 and since are piece-wise linear, we have

Let , then . Thus, for condition in Theorem 2, we have

5 Martingale probability measure

In this section, we would like to investigate if there exists a martingale (risk-neutral) probability measure equivalent to the physical probability measure such that the discounted price process becomes a martingale.

On the one hand, using the fundamental asset pricing theorem, no arbitrage opportunity is possible if and only if there exists a risk-neutral probability measure (see [10]). This means that the average return on an asset should be equal to risk-free return, i.e.,

-

()

.

On the other hand, by definition the martingale conditions for an arbitrary discrete time stochastic process are:

-

()

-

()

.

In order to see under which conditions the discounted asset price process in a risk-neutral world is a martingale, we first define the stochastic process by on as , where

Now, we can write the stock price as

Firstly, for condition (), we have

Equating the above equation with the no arbitrage condition yields to

| (15) |

Secondly, for condition () and since , we have

Consequently, the expected value of discounted risky asset price becomes

6 Extension of the results and examples

The proof of convergence suggests us that there might be many solutions to a recombining trinomial tree.

We extend Equation (8) by introducing a finite positive parameter , that is

Also, we put and . Note that, with the above general formulations our proof of convergence remains to be valid. Indeed, Equation (4.1) holds for different values of . In our trinomial tree, , and . We would like to examine the convergence of Black–Scholes (BS) price and extension of our trinomial (Tri.) model price where .

Let the current stock price , time to maturity year, yearly interest rate and yearly volatility be given. We set (number of steps in the tree) (business days in 1 year). Now, we calculate the price of European call () and put () options with the described parameters for strike prices . We calculate the absolute error (Abs. error) by absolute value of the difference between analytical Black–Scholes (BS) price and trinomial price (Tri.). Using MATLAB®, the results are given in Table 3, 4 and 5.

| ($) BS | ($) Tri. | Abs. error | ($) BS | ($) Tri. | Abs. error | ||

|---|---|---|---|---|---|---|---|

| 1 | 1/2 | 25.578 | 25.583 | 0.0050237 | 2.8262 | 2.8315 | 0.0052915 |

| 3/2 | 1/3 | 25.578 | 25.579 | 0.0008575 | 2.8262 | 2.8272 | 0.0010584 |

| 2 | 1/4 | 25.578 | 25.574 | 0.0034202 | 2.8262 | 2.8229 | 0.0032862 |

| 3 | 1/6 | 25.578 | 25.581 | 0.0035653 | 2.8262 | 2.8297 | 0.0035653 |

| 4 | 1/8 | 25.578 | 25.581 | 0.0031566 | 2.8262 | 2.8292 | 0.0030227 |

| 5 | 1/10 | 25.578 | 25.568 | 0.0102440 | 2.8262 | 2.8157 | 0.0105120 |

| 10 | 1/20 | 25.578 | 25.585 | 0.0071857 | 2.8262 | 2.8324 | 0.0062482 |

| 20 | 1/40 | 25.578 | 25.591 | 0.0134450 | 2.8262 | 2.8374 | 0.0111680 |

| 30 | 1/60 | 25.578 | 25.511 | 0.0662680 | 2.8262 | 2.7563 | 0.0698850 |

| ($) BS | ($) Tri. | Abs. error | ($) BS | ($) Tri. | Abs. error | ||

|---|---|---|---|---|---|---|---|

| 1 | 1/2 | 13.517 | 13.523 | 0.0058724 | 10.078 | 10.084 | 0.00614020 |

| 3/2 | 1/3 | 13.517 | 13.522 | 0.0051641 | 10.078 | 10.083 | 0.00536490 |

| 2 | 1/4 | 13.517 | 13.522 | 0.0047397 | 10.078 | 10.083 | 0.00487370 |

| 3 | 1/6 | 13.517 | 13.520 | 0.0031506 | 10.078 | 10.081 | 0.00315060 |

| 4 | 1/8 | 13.517 | 13.518 | 0.0009543 | 10.078 | 10.079 | 0.00082035 |

| 5 | 1/10 | 13.517 | 13.516 | 0.0016326 | 10.078 | 10.076 | 0.00190050 |

| 10 | 1/20 | 13.517 | 13.500 | 0.0177320 | 10.078 | 10.059 | 0.01867000 |

| 20 | 1/40 | 13.517 | 13.460 | 0.0570400 | 10.078 | 10.018 | 0.05931700 |

| 30 | 1/60 | 13.517 | 13.416 | 0.1008700 | 10.078 | 9.9733 | 0.10449000 |

| ($) BS | ($) Tri. | Abs. error | ($) BS | ($) Tri. | Abs. error | ||

|---|---|---|---|---|---|---|---|

| 1 | 1/2 | 6.4401 | 6.4333 | 0.006796 | 22.313 | 22.306 | 0.00652820 |

| 3/2 | 1/3 | 6.4401 | 6.4424 | 0.002330 | 22.313 | 22.315 | 0.00253110 |

| 2 | 1/4 | 6.4401 | 6.4401 | 0.000055 | 22.313 | 22.313 | 0.00018848 |

| 3 | 1/6 | 6.4401 | 6.4363 | 0.003782 | 22.313 | 22.309 | 0.00378220 |

| 4 | 1/8 | 6.4401 | 6.4317 | 0.008373 | 22.313 | 22.304 | 0.00850690 |

| 5 | 1/10 | 6.4401 | 6.4481 | 0.008076 | 22.313 | 22.321 | 0.00780800 |

| 10 | 1/20 | 6.4401 | 6.4366 | 0.003491 | 22.313 | 22.308 | 0.00442890 |

| 20 | 1/40 | 6.4401 | 6.4442 | 0.004160 | 22.313 | 22.315 | 0.00188270 |

| 30 | 1/60 | 6.4401 | 6.3995 | 0.040562 | 22.313 | 22.269 | 0.04417800 |

Moreover, we investigate if the martingale condition holds for this example. This means, the following absolute value of difference (call it martingale condition) as or equivalently should tend to zero.

The martingale conditions for different values of are illustrated in Table 6.

Remark 2.

| Martingale condition | ||

|---|---|---|

| 1 | 1/2 | |

| 3/2 | 1/3 | |

| 2 | 1/4 | |

| 3 | 1/6 | |

| 4 | 1/8 | |

| 5 | 1/10 | |

| 10 | 1/20 | |

| 20 | 1/40 | |

| 30 | 1/60 |

A trinomial tree approximation for Black’s model

So far, we have considered the Black–Scholes model. Constructing trinomial model and a recombining tree in the Black’s model is similar. Proofs of convergence to the geometric Brownian motion and martingale conditions can be achieved similar to what we have done in previous sections. We only have different up, middle and down factors. That is, using Equation (7)

Now, we try an example inspired by [7]. Assume that the current future price of a commodity , time to maturity of a year, strike price , yearly interest rate , yearly volatility and the number of steps in our trinomial tree . Programming in MATLAB®, we find the prices of European call futures and put futures options given in Table 7. Moreover, the behaviour of trinomial trees (for put futures option) as the number of steps increases is depicted in Figure 3.

| ($) Black | ($) Trinomial | ($) Black | ($) Trinomial |

|---|---|---|---|

| 1.496683230 | 1.497311844 | 21.248239239 | 21.248867854 |

The absolute value of difference between Black’s and trinomial prices for call futures option is 0.0006286140 and for put is 0.0006286144.

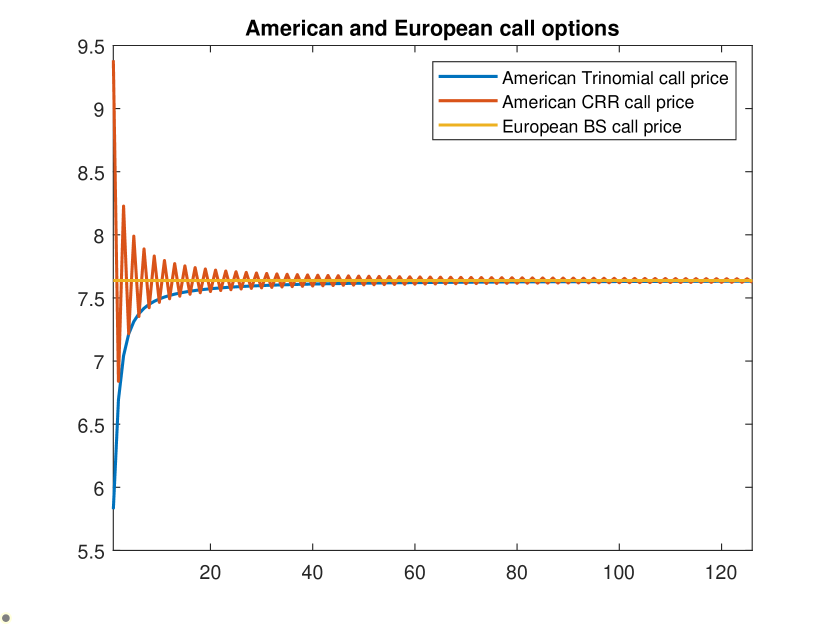

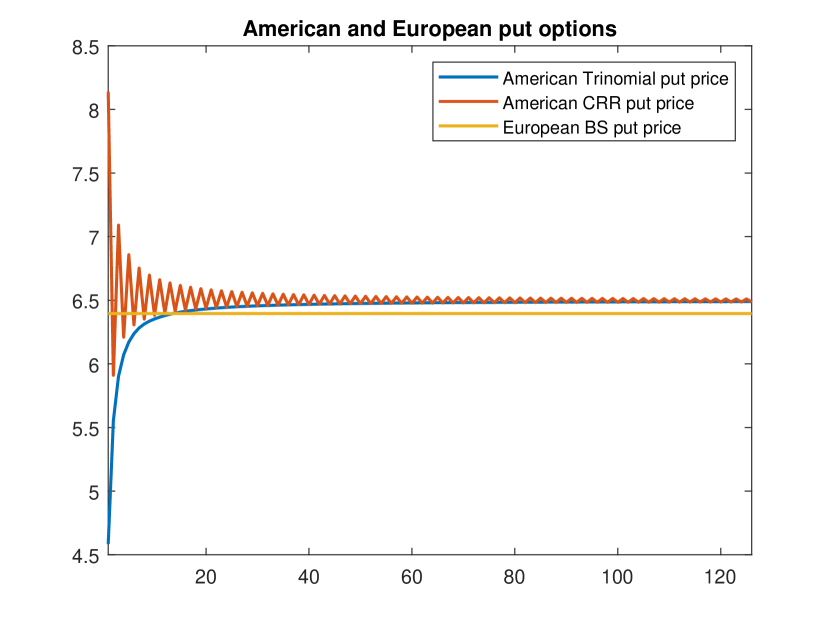

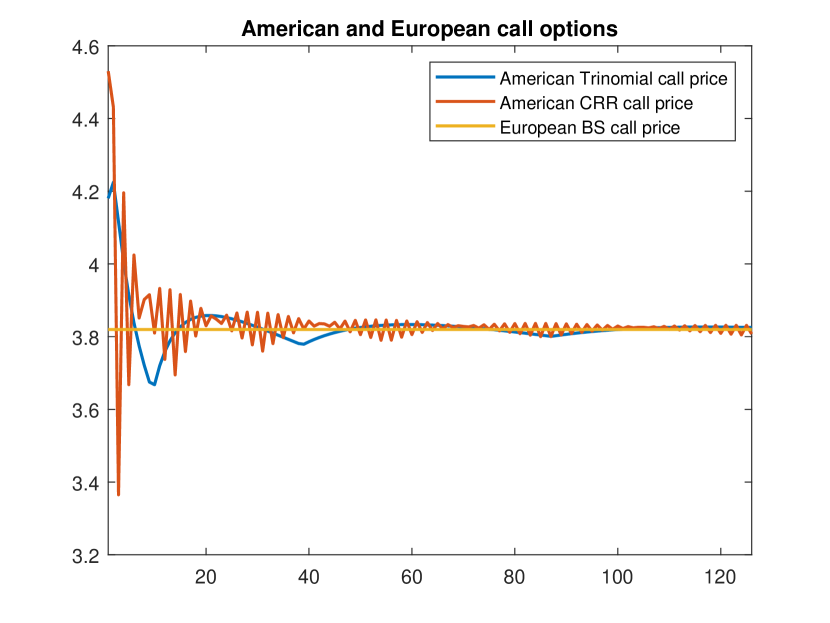

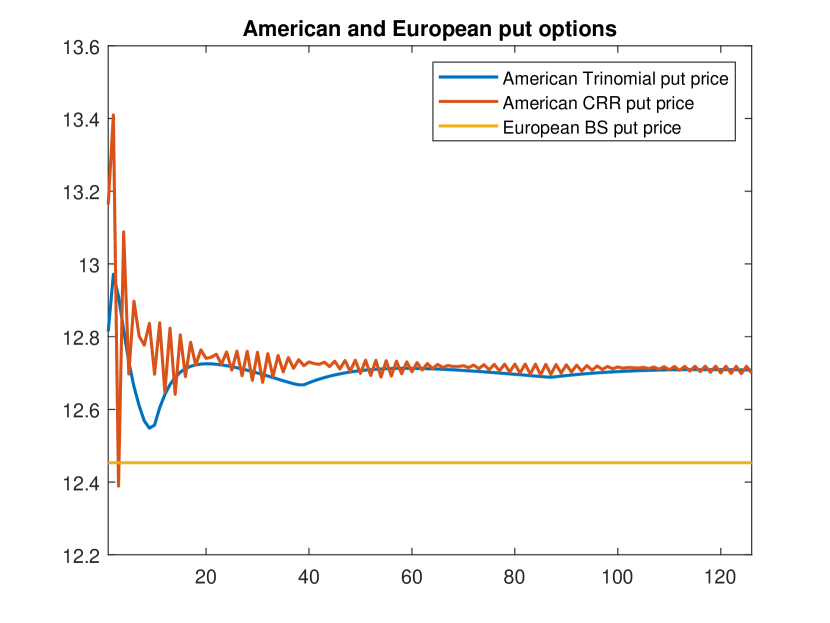

6.1 Pricing American options using the trinomial tree

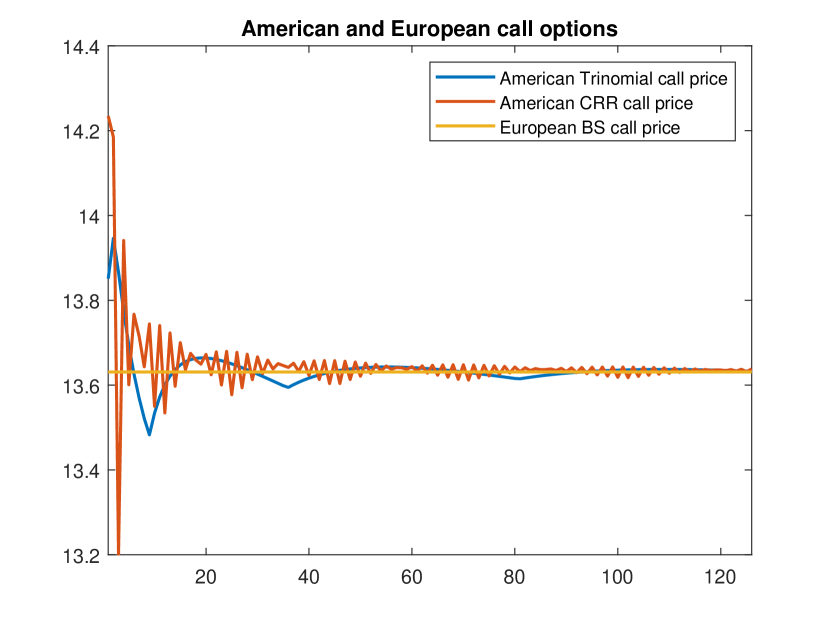

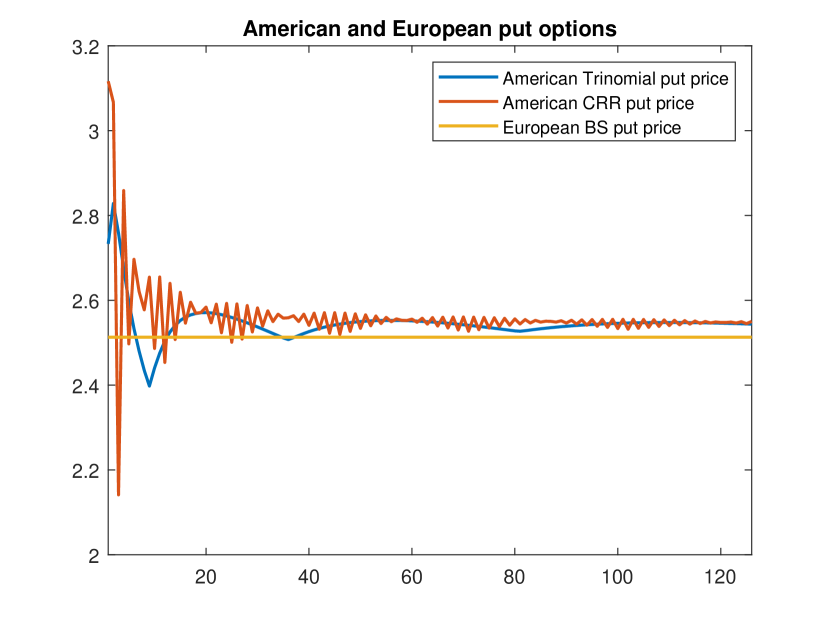

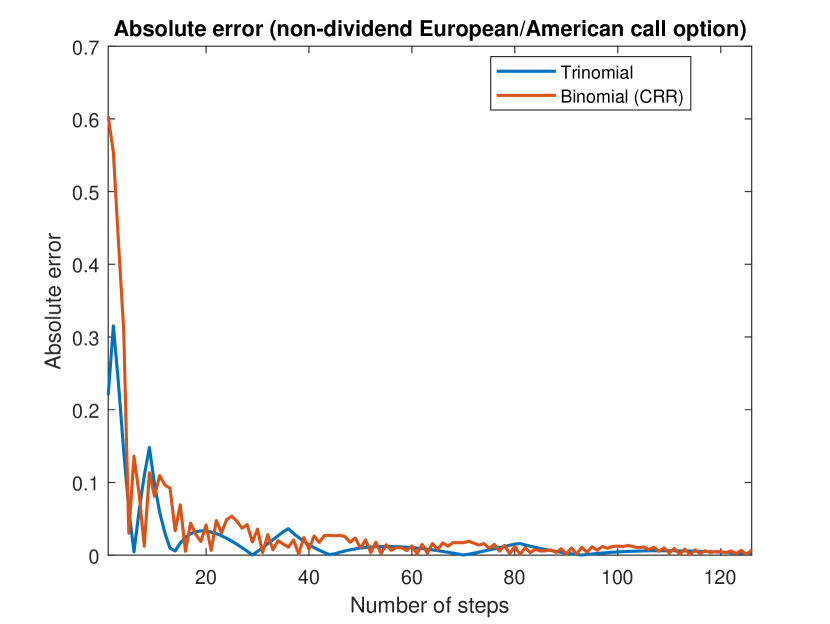

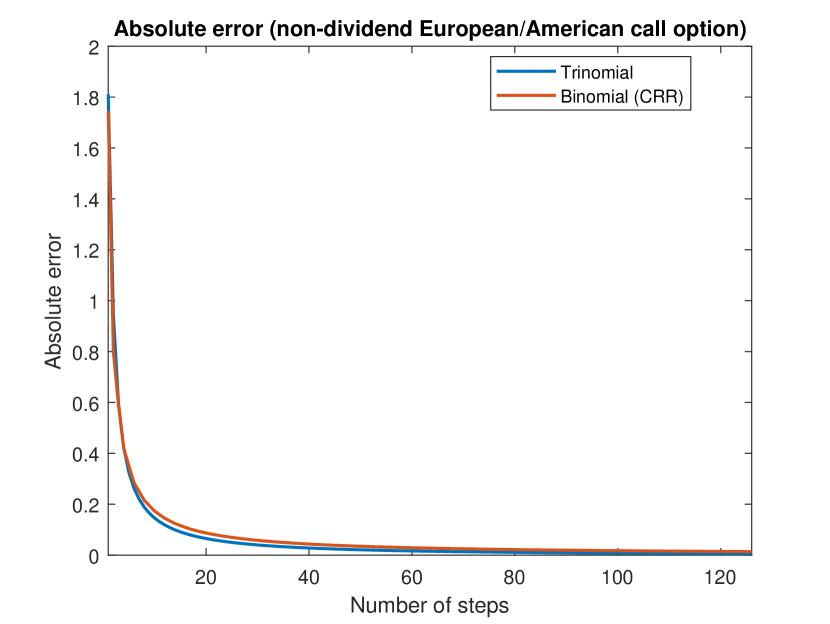

In this part, we will investigate the performance of our model in pricing American call and put options and compare it with classical CRR model. Let the current stock price , time to maturity year, yearly interest rate and yearly volatility be given. We increase the number of steps in the tree up to (business days in half a year). We would like to calculate the price of American call and put options with the described parameters for strike prices . The stock is non-dividend paying, thus the optimal time to exercise such an American call option is at maturity and therefore its price should coincide with a European call option. This fact help us to calculate the Black–Scholes (BS) price of European call option and calculate absolute errors of our trinomial model and CRR model for a call option.

Using MATLAB®, we implement backward recursion to preform these calculations. The results are given in Figure 4, 5, 6 and 7.

7 Discussion

In this paper, we briefly reviewed the cubature method on Wiener space where we specifically applied cubature method and cubature formula on Black–Scholes and Black’s models. We saw that using cubature formula of degree 5, solving Black–Scholes and Black’s SDEs reduces to solving 3 ordinary differential equations. This approach is not very accurate for long time intervals and therefore we constructed a trinomial tree model for very small time intervals using the result of cubature formula. Then, we find the numerical prices of European call and put options using our developed cubature formula and compare our results with analytical prices of Black–Scholes model. Moreover, we proved that the sequences of constructed trinomial tree converges to the geometric Brownian motion. After that, we studied the martingale conditions and we extended the results. The extension of results (among other possible applications) included pricing American options.

References

- [1] C. Bayer and J. Teichmann. Cubature on Wiener space in infinite dimension. Proceedings of The Royal Society of London. Series A: Mathematical, Physical and Engineering Sciences, 464, 2097, 2493–2516, 2008.

- [2] P. Billingsley. Convergence of probability measures, 2nd ed., John Wiley & Sons, Inc., New York, 1999.

- [3] F. Black. The pricing of commodity contracts. J. Financial Economics, 1, 1, 167–169, 1976.

- [4] F. Black and M. Scholes. The pricing of options and corporate liabilities. J. Political Economy, 81, 3, 637–654, 1973.

- [5] J. Cox, S. Ross and M. Rubinstein. Option pricing: A simplified approach. J. Financial Economics, 7, 3, 229–263, 1979.

- [6] P. Glasserman. Monte Carlo methods in financial engineering, vol. 53 of Applications of Mathematics (New York), Springer, New York, 2004.

- [7] J. Hull. Options, futures, and other derivatives, 10th ed., Pearson, London, 2017.

- [8] R. Jarrow. Derivative securities, South-Western College Pub, Cincinnati, Ohio, 2000.

- [9] R. Jarrow and A. Rudd. Option pricing, Dow Jones-Irwin Homewood, IL, 1983.

- [10] M. Kijima. Stochastic processes with applications to finance, 2nd ed., CRC Press, Boca Raton, FL, 2013.

- [11] T. Lyons and N. Victoir. Cubature on Wiener space. Proceedings of The Royal Society of London. Series A. Mathematical, Physical and Engineering Sciences, 460, 2041, 169–198, 2002.

- [12] A. Malyarenko, H. Nohrouzian and S. Silvestrov. An algebraic method for pricing financial instruments on post-crisis market. In Algebraic Structures and Applications. SPAS 2017, vol. 317 of Springer Proceeding in Mathematical Statistics, chapter 37, 839–856.

- [13] H. Nohrouzian and A. Malyarenko. Testing cubature formulae on Wiener space vs explicit pricing formulae. In Stochastic processes, statistical methods and engineering mathematics. SPAS 2019, vol. yyy of Springer Proceeding in Mathematical Statistics, chapter zz, xxx–xxx.

- [14] A. Malyarenko and H. Nohrouzian. Evolution of forward curves in the Heath–Jarrow–Morton framework by cubature method on Wiener space. Communications in Statistics: Case Studies, Data Analysis and Applications, 7, 4, 717–735, 2021.

- [15] R. Merton. Theory of rational option pricing. The Bell Journal of Economics and Management Science, 4, 1, 141–183, 1973.

- [16] H. Nohrouzian, Y. Ni and A. Malyarenko. An arbitrage-free large market model for forward spread curves. Applied Modeling Techniques and Data Analysis 2, vol. 8, chapter 6, 75–90, Wiley, 2021.

- [17] H. Nohrouzian, A. Malyarenko and Y. Ni. Pricing Financial Derivatives in the Hull–White Model Using Cubature Methods on Wiener Space. ACommunications in Statistics: Case Studies, Data Analysis and Applications, vol. 7, no.4, 717–735, E-ISSN 2373-7484, Taylor and Francis Online, 2021.

- [18] B. Øksendal. Stochastic Differential Equations: An Introduction with Applications, Springer, Berlin, 2013.

- [19] A. Pascucci. PDE and martingale methods in option pricing, Springer, Milan, 2011.

- [20] P. Samuelson. Rational theory of warrant pricing. Industrial Management Review, 6, 2, 13–31, 1965.