Sequential Learning and Economic Benefits from Dynamic Term Structure Models

Abstract

We explore the statistical and economic importance of restrictions on the dynamics of risk compensation from the perspective of a real-time Bayesian learner who predicts bond excess returns using dynamic term structure models (DTSMs). The question on whether potential statistical predictability offered by such models can generate economically significant portfolio benefits out-of-sample, is revisited while imposing restrictions on their risk premia parameters. To address this question, we propose a methodological framework that successfully handles sequential model search and parameter estimation over the restriction space in real time, allowing investors to revise their beliefs when new information arrives, thus informing their asset allocation and maximising their expected utility. Empirical results reinforce the argument of sparsity in the market price of risk specification since we find strong evidence of out-of-sample predictability only for those models that allow for level risk to be priced and, additionally, only one or two of these risk premia parameters to be different than zero. Most importantly, such statistical evidence is turned into economically significant utility gains, across prediction horizons, different time periods and portfolio specifications. In addition to identifying successful DTSMs, the sequential version of the stochastic search variable selection (SSVS) scheme developed can be applied on its own and also offer useful diagnostics monitoring key quantities over time. Connections with predictive regressions are also provided.

1 Introduction

1.1 Restrictions and out-of-sample Economic Benefits

Accurately estimating and forecasting bond risk premia, in real time, is of central economic importance for the transmission mechanism of monetary policy as well as for investors’ portfolio strategies. Even more important is understanding and identifying the contribution of risk premia to longer term interest rates, which largely depends on our ability to accurately infer expectations for the future path of the short end of the yield curve111See, Kim and Wright (2005) and Cochrane and Piazzesi (2009), among others, for studies that attempt to decompose forward rates into expectations of short rates and risk premia.. To successfully do so, it is essential to account for no-arbitrage, which implies restrictions on the cross-sectional and time series dynamics of the term structure (see, Joslin et al. (2011) and Bauer (2018)). The latter are largely exploited in related literature by dynamic term structure models (DTSMs), which impose tight restrictions on the dynamics of risk compensation, an essential component of the models. Failure to impose such restrictions, as in the unrestricted maximally flexible model widely used by almost all existing studies, leads to absence of no-arbitrage and, as such, to the generation of artificially stable short rate expectations and highly volatile risk premia (Kim and Orphanides 2012, Bauer 2018).

The importance of the market price of risk specification, and the associated restrictions related to it, has been extensively studied in earlier research (see, Dai and Singleton (2000), Duffee (2002), Ang and Piazzesi (2003), Kim and Wright (2005)), which has mainly focused on imposing ad hoc222Ad-hoc restrictions, are used in Dewachter and Lyrio (2006), and Rudebusch and Wu (2008), among others. Furthermore, the route of imposing prior restrictions is followed by Ang et al. (2007). zero restrictions on the parameters governing the dynamics of the risk premia333A common practice used is to, first, estimate an unrestricted maximally flexible model, and at a second step, to re-estimate it by setting to zero those parameters that have large standard errors. According to Bauer (2018), such an approach often leads to the wrong model.. This practice, however, has been criticised (see, Kim and Singleton (2012) and Bauer (2018)), since it raised concerns about, first, the joint significance of the constraints, second, the magnitude of the associated standard errors444According to Kim and Singleton (2012), it is unclear how small these have to be in order to set a parameter to zero. and, third, the failure to provide meaningful economic justification for the estimated parameters and the resulting state variables. Only recently, a few studies have investigated more systematic approaches to imposing restrictions on the dynamics of risk compensation555See, Cochrane and Piazzesi (2009) for a 4-factor affine model, Joslin et al. (2014) for an unspanned macro-finance DTSM, and Duffee (2011) and Bauer (2018) for yields-only versions of DTSMs. An alternative approach is followed by Chib and Ergashev (2009), who impose strong prior restrictions such that the yield curve is (on average) upward sloping, an assumption that is empirically and economically plausible.. In particular, Cochrane and Piazzesi (2009) and Duffee (2011) introduce tight restrictions, driven by prior empirical analysis, while Joslin et al. (2014) select zero restrictions. Bauer (2018) promotes the use of Bayesian variable selection samplers to identify such restrictions on risk prices.

Although the literature has noted the importance of restrictions, yet, no study has, so far, addressed and quantified their statistical and economic importance, out-of-sample666Empirical tests in Duffee (2011) suggest that the choice of no-arbitrage restrictions does not influence the out-of-sample performance of the models, given that they produce forecasts with indistinguishable differences.. Most importantly, there is no prior evidence as to how restrictions ’react’ to changes in the monetary environment, considering that existing studies on monetary policy effects (see, Piazzesi et al. (2006), Ang and Longstaff (2011), and Orphanides and Wei (2012)) suggest that restrictions selected based on the in-sample process may not be economically plausible around periods of monetary policy shifts, interventions, or under fragile economic conditions. With this in mind, in this paper we study the out-of-sample performance of yields-only DTSMs, in light of the alternative restrictions imposed on the dynamics of risk compensation and attempt to explore whether a real-time Bayesian investor can actually exploit statistical predictability, when making investment decisions. Are DTSMs, which utilise yield curve information only, capable of consistently predicting bond risk premia777Failure of the EH implies that bond returns are strongly predictable (see, Fama and Bliss (1987), Campbell and Shiller (1991) and Cochrane and Piazzesi (2005), for studies that utilise information coming solely from the yield curve.). In particular, Fama and Bliss (1987) and Campbell and Shiller (1991) propose forward and yield spreads as predictors and suggest that spreads have predictive power on excess returns, while Cochrane and Piazzesi (2005) use a linear combination of five forward rates as predictors. Such evidence, however, is purely statistical. and generating systematic economic gains to bond investors, out-of-sample?

Some recent literature (e.g. Duffee (2011), Barillas (2011), Adrian et al. (2013), Joslin et al. (2014)), suggests that yields-only DTSMs cannot capture the predictability of bond risk premia, since the required information to predict premia is not spanned888The spanning hypothesis suggests that the yield curve contains all relevant information required to forecast future yields and excess returns. Unspanned factors are not explained by the yield curve, while at the same time they are useful for predicting risk premia (see, Cochrane and Piazzesi (2005), Duffee (2011), Joslin et al. (2014) and Cieslak (2018)). by the cross section of yields, implying that more (mainly unspanned) factors are needed. In that respect, Duffee (2011) implements a five-factor yields-only DTSM aiming to capture hidden information in the bonds market, while Wright (2011), Barillas (2011), Joslin et al. (2014) and Cieslak and Povala (2015) use measures of macroeconomic activity to predict bond excess returns999In a recent study however, Bauer and Hamilton (2018) cast doubt on prior conclusions, suggesting that the evidence on variables other than the three yield factors predicting excess returns is not convincing.. In contrast, Sarno et al. (2016) and Feunou and Fontaine (2018), implement extended versions of yields-only DTSM and argue that their approaches help those models capture the required predictability, thus, overturning prior evidence. A similar conclusion is reached by Bauer (2018), who studies DTSMs under alternative risk price restrictions. In this study, we attempt to revisit evidently conflicting results on bond excess return predictability based on DTSMs.

Importantly, the above-mentioned studies, either do not consider the out-of-sample economic performance (as in Duffee (2011), Bauer (2018), Feunou and Fontaine (2018) and Giacoletti et al. (2021), etc.) or do not fully explore potential economic benefits for bond investors when compared to the non-predictability (constant risk premia) Expectations Hypothesis (EH) benchmark, which is the second empirical question we target in this paper. In fact, existing literature on economic value finds evidence of statistical predictability, which nevertheless does not translate into positive economic gains to bond investors (see, Della Corte et al. (2008), Sarno et al. (2016) and recently Andreasen et al. (2021)). In particular, using a dynamic mean-variance allocation strategy, framed within a DTSM, Della Corte et al. (2008) and Sarno et al. (2016) find that statistical predictability is not turned into superior portfolio performance when compared to the EH benchmark. Consistent results are also presented in Andreasen et al. (2021), in the context of a regime-switching macro-finance term structure model, who suggest that it is difficult to translate evidence of time-variation in expected excess returns into economic benefits to investors. Qualitatively similar results are found in the literature on economic value generated from predictive regression models101010Such models are not directly comparable to DTSMs, as the latter make different and stronger modelling assumptions, such as the absence of arbitrage, aiming to explicitly model several aspects of the market (e.g. accurately inferring short-rate expectations and term premia) and obtain further insights on the term structure of risk premia. on bond excess returns (see for example, Thornton and Valente (2012), Gargano et al. (2019), Bianchi et al. (2021) and Wan et al. (2022)). As in the DTSMs case, the evidence from such studies is conflicting, in some cases pointing towards a negative answer (as in Thornton and Valente (2012), Ghysels et al. (2018)111111According to Ghysels et al. (2018) (and Wan et al. (2022)), economic benefits vanish when fully revised macroeconomic information is replaced by real-time data. Our approach is not reliant on macroeconomic data and, as such, our analysis is independent on the debate between ’fully-revised’ vs. ’real-time’ macros. and Wan et al. (2022)), while in more recent studies (such as Gargano et al. (2019)121212In fact, Gargano et al. (2019) find some evidence of economic value for the Fama–Bliss (FB) predictive model. Concurrently, the model by Cochrane–Piazzesi (CP) fails to offer any positive economic gains to bond investors. and Bianchi et al. (2021)) some economic value is retained even for the yields-only case. Motivated in part by the case of predictive regression models, our aim in this paper is to explore, in the context of yields-only DTSMs, whether it is possible to achieve both statistical predictability and economic value by imposing restrictions in the price of risk specification.

1.2 Sequential Learning and DTSMs with Sparsity

From a statistical or machine learning viewpoint, imposing restrictions may be thought of as guarding against overfit. If more parameters than needed are used to extract the signal of the market price of risk, it becomes more likely to capture noise rather than systematic patterns, thus leading to poor predictive performance. With this in mind, we propose a novel methodological framework which successfully handles sequential model searches over the space of all possible restrictions in real time, allowing investors to revise their beliefs when new information arrives, thus informing their asset allocation and maximising their expected utility. Setting up in the context of Bauer (2018), we construct a sequential learning scheme following the principles of Chopin (2002) and Del Moral et al. (2006). The modelling approach utilises Bayesian inference and forecasting simultaneously, while allowing for model and parameter uncertainty to be incorporated in a sequential manner. We use the developed setup to predict bond excess returns and explore the out-of-sample statistical and economic importance of restrictions.

Our approach differs from previous studies, allowing us to overcome a number of important challenges and offers several advantages. First, in a similar style to Wan et al. (2022) but tailored to the context of DTSMs, it allows us to update the estimates and predictive density as new data arrive, without the need to rerun everything from scratch. Second, it allows for potentially more powerful prediction techniques, such as Bayesian model averaging, to be implemented. In this paper, we develop a sequential version of the stochastic search variable selection (SSVS) scheme (can also be used for Gibbs Variable Selection) that allows incorporating model and parameter uncertainty in a sequential manner. This is of particular importance taking into account that investors often face model uncertainty, which highlights the need for a framework that is capable of monitoring, identifying and adjusting models in real time. Third, it provides a more robust alternative to the Markov Chain Monte Carlo (MCMC) sampler and model choice algorithms of Bauer (2018) and Gargano et al. (2019), as its sequential setup naturally provides inference in a parallel way that can potentially overcome issues such as poor mixing, slow convergence properties, and multi-modalities. While such issues do not seem to arise for a given set of restrictions and under the canonical setup of Joslin et al. (2011) as in Bauer (2018), the sequential scheme is useful in more challenging setups, such as the exploration of the restriction sets space.

Our evaluation framework consists of two stages. First, we evaluate the predictive performance using metrics such as the out-of-sample of Campbell and Thompson (2008) () or the log score (LS) as in Geweke and Amisano (2010). Second, to investigate the economic significance of the out-of-sample excess return forecasts generated by alternative models, we construct a dynamically rebalanced portfolio as in Della Corte et al. (2008) and Thornton and Valente (2012), for an investor with power utility preferences, and compute standard metrics (see, Johannes et al. (2014) and Gargano et al. (2019), among others) in both univariate and multivariate asset allocation setups.

Our results lead to a host of interesting conclusions regarding the US market. Initially, we confirm Sarno et al. (2016) in that yields-only DTSMs with some or no restrictions on the risk premia show evidence of statistical predictability which nevertheless is not translated into systematic economic gains for bond investors. However, we also complement Sarno et al. (2016) in that the situation is reversed when heavy restrictions are placed either by sequential model averaging schemes introduced in this paper or by two specific models identified by our framework. The latter are in line with Cochrane and Piazzesi (2009) and Duffee (2011) in that only level risk is priced, but place even heavier restrictions allowing only one or two free risk premia parameters. Those schemes and models offer improved out-of-sample portfolio performance and economically meaningful gains.

1.3 Outline

The remainder of this paper is organised as follows. Section 2 describes the modelling framework. Section 3 presents the sequential learning and forecasting procedure along with the framework for assessing the predictive and economic performance of models. Section 4 discusses the data and the sample period used and presents the best models inferred through the sequential SSVS scheme. Section 5 discusses the results both in terms of predictive performance and economic value. Section 6 provides connections with predictive regression models. Finally, Section 7 concludes the paper by providing some relevant discussion.

2 Dynamic Term Structure Model, Likelihood, and Restrictions

In this section we briefly describe the adopted model and the associated likelihood function in order to set up the notation and formulate our research question explicitly. More details can be found in Joslin et al. (2011) where this framework was introduced. The model belongs to the no-arbitrage class of Affine Term Structure Models (ATSMs) (see, Ang and Piazzesi (2003) and Cochrane and Piazzesi (2005)), under which the one period risk-free interest rate 131313Working with monthly data implies that is the 1-month yield. is assumed to be an affine function of an vector of state variables , namely

| (1) |

where is a scalar and is a vector. In Gaussian ATSMs, the physical probability measure is assumed to be a first-order Gaussian Vector Autoregressive (VAR) process

| (2) |

where , is an lower triangular matrix, is a vector and is a matrix. Lack of arbitrage implies the existence of a pricing kernel , defined as

| (3) |

with being the time-varying market price of risk which is assumed to be affine in the state 141414This is the ‘essentially-affine’ specification introduced in Duffee (2002). Existing studies have proposed alternative specifications for the market price of risk, such as the ‘completely-affine’ model of Dai and Singleton (2000), the ‘semi-affine’ model of Duarte (2004), and the ‘extended-affine’ model of Cheridito et al. (2007). See Feldhütter (2016) for a useful comparison of the models.

| (4) |

where is a vector and is a matrix. Assuming that the pricing kernel prices all bonds in the economy and we let denote the time-t price of an n-period zero-coupon bond, then the price of the bond is computed from and leads to the dynamics

| (5) |

where , and . Define the observed time-t, n-period yield as

| (6) |

The vector of the yields , denoted by , is also an affine function of the state vector

| (7) |

where the loading vector and the loading matrix are calculated using the above recursions, as and .

In theory, it is possible to specify the likelihood function based on (2) and (7) but, in practice, estimation and identification of these formulations has been proven to be challenging (see, Ang and Piazzesi (2003), Ang et al. (2007), Chib and Ergashev (2009), Duffee and Stanton (2012), Hamilton and Wu (2012), and Bauer (2018)), especially if ATSMs are expressed in terms of an unobserved latent . Additional restrictions need to be imposed to ensure identifiability, such as the canonical setup of Joslin et al. (2011) that is adopted in this paper. More specifically, is assumed to be linearly related to the observed yields, and as such, perfectly priced by the no-arbitrage restrictions. We rotate to match the first principal components (PCs) of the observed yields

| (8) |

with being the matrix that contains the PCs’ loadings. Following common practice, we consider the case of , noting that the first three extracted PCs are typically sufficient to capture most of the variation in the yield curve and often correspond to its level, slope, and curvature respectively (Litterman and Scheinkman 1991). Statistical inference can proceed using the observations . The likelihood factorises into two parts stemming from the and respectively. In order to specify the latter, henceforth denoted as likelihood, the affine transformation of (8) is applied to (5) to obtain the dynamics of under

| (9) |

and, similarly, the yield equation (7) can be rewritten as a function of 151515According to Duffee (2011), outside of knife-edge cases, the matrix is invertible, and as such, contains the same information as .

| (10) |

where , , , and are given in Online Appendix A. Note that in (7) and (10), yields are assumed to be observed without any measurement error. Nevertheless, an -dimensional observable state vector cannot perfectly price yields, and as such, we further assume that the bond yields used in the estimation are observed with independent measurement errors. An equivalent way to formulate this is to write

| (11) |

and to consider the dimension of as effectively being .

In order to specify the likelihood we note that dynamics of are of equivalent form to (9) with and , where is a vector and is a matrix reflecting the market price of risk in terms. We also follow the identification scheme of Joslin et al. (2011) (proposition 1), where the short rate is the sum of the state variables, namely with being a vector of ones, and the parameters and of the -dynamics are given as and , where denotes a vector containing the real and distinct eigenvalues of 161616Alternative specifications for the eigenvalues are considered in Joslin et al. (2011); however, real eigenvalues are found to be empirically adequate.. The joint likelihood (conditional on ) can now be written as

| (12) |

where the -likelihood components, , are given by (11) and capture the cross-sectional dynamics of the risk factors and the yields, whereas -likelihood components, , capture the time-series dynamics of the observed risk factors. The parameter vector is set to .

Note that in the case of all entries in , being non-zero, also known as the maximally flexible model, the mapping between and is 1-1. This allows for the following equivalent likelihood specification

| (13) |

Hence, loosely speaking, under the maximally flexible model the parameters are estimated mainly from the likelihood, in other words based solely on cross-sectional information and without reference to the real-world dynamics171717According to Joslin et al. (2011), the ordinary least squares estimates of parameters and are almost identical to those estimated using maximum likelihood.. But if one or more entries of the , are set to zero, in other words if restrictions are imposed, then the mapping from to is no longer 1-1, allowing only the likelihood specification of (12) that directly links parameters with time series information.

Nevertheless, this raises the issue of how to choose between the possible sets of restrictions in the , matrices; e.g. in the case of there are distinct sets of restrictions. Bauer (2018) suggests using Bayesian model choice, aiming to maximise the model evidence of each restriction specification. In this paper we propose choosing the restriction set with the optimal predictive performance among all possible restriction sets. Models that are optimal in the Bayesian sense, i.e. achieving the highest model evidence, are typically parsimonious and therefore are expected to exhibit good predictive performance. In a related argument, Fong and Holmes (2020) show that model evidence is formally equivalent with exhaustive leave--out cross-validation combined with the log posterior predictive scoring rule. Hence, it will not be surprising if the same set of restrictions was obtained from both approaches; in fact this is the case in data from the US market as we illustrate in Section 4. Nevertheless, this is not always guaranteed to be the case and, in situations where different answers are obtained, the predictive performance criterion may be more relevant in the context of DTSMs from an investor’s point of view.

3 Sequential Estimation, Model Choice, and Forecasting

In this section we develop a sequential Monte Carlo (SMC) framework for Gaussian ATSMs. We draw from the work of Chopin (2002, 2004) (see also Del Moral et al. (2006)), and make the necessary adaptations to tailor the methodology to the data and models considered in this paper. Furthermore, we extend the framework to allow for sequential Bayesian model choice by incorporating the SSVS algorithm that allows searching over models; see Schäfer and Chopin (2013) for some relevant work in the linear regression context. Overall, the developed framework allows the efficient performance of tasks such as sequential parameter estimation, model choice, and forecasting. We begin by providing the main skeleton of the scheme and then provide the details of its specific parts, such as the MCMC scheme for exploring the model space, and the framework for obtaining and evaluating the economic benefits of predictions.

3.1 Sequential Framework

Let denote all the data available up to time , such that . Similarly, the likelihood based on data up to time is and is defined in (12). Combined with a prior on the parameters , see Online Appendix B.1 for details, it yields the corresponding posterior

| (14) |

where is the model evidence based on data up to time t. Moreover, the posterior predictive distribution, which is the main tool for Bayesian forecasting, is defined as

| (15) |

where is the prediction horizon. Note that the predictive distribution in (15) incorporates parameter uncertainty by integrating out according to the posterior in (14). Usually, prediction is carried out by expectations with respect to (15), e.g. but, since (15) is typically not available in closed form, Monte Carlo can be used in the presence of samples from . This process may accommodate various forecasting tasks; for example forecasting several points, functions thereof, and potentially further ahead in the future. A typical forecasting evaluation exercise requires taking all the consecutive times from the nearest integer of, say, to . In each of these times, serves as the training sample, and points of after are used to evaluate the forecasts. Hence, carrying out such a task requires samples from (15), and therefore from , for several times . Note that this procedure can be quite laborious and in some cases infeasible.

An alternative approach that can handle both model choice and forecasting assessment tasks is to use sequential Monte Carlo (see, Chopin (2002) and Del Moral et al. (2006)) to sample from the sequence of distributions for . A general description of the Iterated Batch Importance Sampling (IBIS) of Chopin (2002)’s algorithm, see also Del Moral et al. (2006) for a more general framework, is provided in Table 1.

Initialise particles by drawing independently with importance weights , . For and each time for all :

-

(a)

Calculate the incremental weights

-

(b)

Update the importance weights to .

-

(c)

If some degeneracy criterion (e.g. ESS()) is triggered, perform the following two sub-steps:

-

(i)

Resampling: Sample with replacement times from the set of s according to their weights . The weights are then reset to one.

-

(ii)

Jittering: Replace s with s by running MCMC chains with each as input and as output.

-

(i)

The degeneracy criterion is usually defined through the Effective Sample Size (ESS) which is equal to

| (16) |

and is of the form for some , where is the vector containing the weights.

The IBIS algorithm provides a set of weighted samples, or else particles, that can be used to compute expectations with respect to the posterior, , for all using the estimator . Chopin (2004) shows consistency and asymptotic normality of this estimator as for all appropriately integrable . The same holds for expectations with respect to the posterior predictive distributions, ; the weighted samples can be transformed into weighted samples from by simply applying . A very useful by-product of the IBIS algorithm is the ability to compute , which is the criterion for conducting formal Bayesian model choice. Computing the following quantity in step (a) in Table 1 yields a consistent and asymptotically normal estimator of

| (17) |

An additional benefit provided by sequential Monte Carlo is that it provides an alternative choice when MCMC algorithms have poor mixing and convergence properties and, in general, is more robust when the target posterior is challenging, e.g. multimodal. Finally, as we demonstrate in Section 4, the sequential nature of the algorithm allows it to produce informative descriptive output to monitor the evolution of key parameters in time.

In order to apply the IBIS output to models and data in this paper, the following adaptations or extensions are needed. First, the choice of defining the incremental weights in step (a) in Table 1, also known as data tempering, is suitable for getting access to sequences of predictive distributions, needed to assess forecasting performance, but at the same time it is quite prone to numerical stability issues and very low effective sample sizes, in particular early on, that is at the initial time points. This is because the learning rate is typically higher at the beginning, especially when transitioning from a vague prior. An alternative approach that guarantees a pre-specified minimum effective sample size level, and therefore some control over the Monte Carlo error, is to use adaptive tempering; see, for example, Jasra et al. (2011). In order to combine the benefits of both approaches we use a hybrid adaptive tempering scheme which we present in Online Appendix B.2. The idea of this scheme is to use adaptive tempering within each transition between the posteriors based on and for each . Similar ideas have been applied in Schäfer and Chopin (2013) and Kantas et al. (2014). Second, and quite crucially in this paper, we extend the framework presented in Section 3.2 to handle sequential model searches over the space of all possible risk price restrictions. Third, we note that the MCMC sampler, used in sub-step (ii) of step (c) in Table 1, needs to be automated as it will have to be rerun for each time point and particle without the luxury of having initial trial runs, as it is often the case when running a simple MCMC on all the data. The problem is intensified by the fact that the MCMC algorithm used here, developed in Bauer (2018), consists of independence samplers that are known to be unstable. To address this, we utilise the IBIS output and estimate posterior moments to obtain independence sampler proposals; see Online Appendix B.2 for details. Finally, we connect the IBIS output with the construction of a model-driven dynamically rebalanced portfolio of bond excess returns and calculate its economic value.

3.2 Sequential Model Choice Across Risk Price Restrictions

As mentioned in Section 2, the specification of the market price of risk is conducted via and . For brevity of further exposition, let and . If all the entries in are free parameters we get the maximally flexible model. Alternative models have also been proposed in the existing studies, e.g. Cochrane and Piazzesi (2009) and Bauer (2018), where some of these entries are set to zero. More specifically, in most models the set of unrestricted parameters is usually a subset of . A standard approach to facilitating Bayesian model choice is via assigning spike-and-slab priors (Mitchell and Beauchamp 1988, George and McCulloch 1993, Madigan and Raftery 1994) on each of the s, via the following mixture

| (18) |

where s are Bernoulli random variables taking zero value if the corresponding is small (almost equal to zero) or non-zero value if it is large (significantly different from zero). Hence is typically given a very small value, thus forcing the underlying parameter towards zero, while is set to a larger value so that the data determine the value of the parameter in question. More specifically for , we use the Zellner’s g-prior as in Bauer (2018), a rather standard choice to prevent over-penalisation of complex models, an issue often referred to as the Lindley’s paradox; see Online Appendix B.1 for more details. The s are also estimated using MCMC; see Online Appendix B.2 for details. The proportion of the MCMC draws in which each is equal to one provides the posterior probability of the corresponding being non-zero, also known as posterior inclusion probability.

We consider two approaches to Bayesian model choice in order to explore its links with predictive performance. The first approach is to implement the spike-and-slab approach on some data used for training purposes in order to select the top models. The sequential algorithm in Table 1 is then applied to each of them, without using spike-and-slab priors and with some being exactly equal to zero, extracting their predictive distributions and contrasting them with the observed data. Under the second approach, sequential inference on both the models and the parameters is drawn. This is implemented by running a single instance of the sequential algorithm in Table 1, modified to incorporate the SSVS algorithm based on the spike-and-slab priors. In this case, the parameter vector includes the s allowing us to calculate the inclusion probabilities, using the particle weights, at each time based on all the data up to and including .

This approach offers several advantages in exploring the landscape of the risk price restriction space as we can monitor potential changes in the importance of different s over time. Moreover, the global search nature of sequential Monte Carlo may be helpful in exploring this landscape across different models. Each particle contains a set of s and corresponds to a particular model. The set of particles therefore contains instances of the leading models among the possible ones. Every time resampling and jittering take place, the list of models can be potentially updated giving more focus to the cases with higher weights, or else posterior probability, and potentially depleting the ones with lower weights. Hence it is now less likely to get trapped in local modes when exploring the model space. Finally, this scheme allows combining different models and incorporating model uncertainty into forecasting via model averaging in a sequential manner.

3.3 Assessing Predictive Performance and Economic Value

Failure of the EH implies that bond returns are strongly predictable (see, Fama and Bliss (1987), Campbell and Shiller (1991), Cochrane and Piazzesi (2005), and Ludvigson and Ng (2009), among others). In this section, we attempt to revisit conflicting results reported in the existing studies (e.g. Duffee (2011), Barillas (2011), Adrian et al. (2013), Joslin et al. (2014), Sarno et al. (2016) and Feunou and Fontaine (2018)) on the ability of yields-only DTSMs to capture the predictability of risk premia in the US Treasury market. This is done while exploring sequentially the space of restrictions imposed on the dynamics of risk compensation. Furthermore, we attempt to explore whether statistical predictability, if any, can be turned into economic benefits for bond investors.

3.3.1 Bond Excess Returns:

The observed continuously compounded excess return of an -year bond is defined as the difference between the holding period return of the -year bond, expressed above in terms of log prices, and the -period yield as

| (19) |

where is defined in (6). If, instead of taking the observed one, we take the model-implied yield , from equation (10), we arrive at the predicted excess returns

| (20) |

where is observed and is a prediction from the model. Our developed framework, see Table 1, allows drawing from the predictive distribution of based on all information available up to time . More specifically, for each particle equation (9) can be used to obtain a particle of , which can then be transformed into a particle of via equation (20).

The predictive accuracy of bond excess return forecasts is measured in relation to an empirical benchmark. We follow related literature and adopt the EH as this benchmark, which essentially uses historical averages as the optimal forecasts of bond excess returns. This empirical average is

| (21) |

We consider two metrics to assess the predictive ability of models considered. First, following Campbell and Thompson (2008), we compute the out-of-sample () as

| (22) |

for being the mean of the predictive distribution. Positive values of this statistic mean that model-implied forecasts outperform the empirical averages and suggest evidence of time-varying return predictability. Second, in order to assess the entire predictive distribution offered by our scheme, rather than just point predictions, we use the log score181818The computational details, results and discussion of the log predictive score are presented in Online Appendix D.; a standard choice among scoring rules with several desirable properties, such as being strictly proper, see for example Dawid and Musio (2014). These metrics are aggregated over all prediction times ( to ) and maturities. In order to get a feeling for how large the differences from the EH benchmark are, we report the p-values from the Diebold-Mariano test (see, Gargano et al. (2019)) noting that these are viewed as indices rather than formal hypothesis tests. They are based on t-statistics computed taking into account potential serial correlations in the standard errors (see, Newey and West (1987)).

3.3.2 Economic Performance of Excess Return Forecasts:

From a bond investor’s point of view it is of paramount importance to establish whether the predictive ability of a model can generate economically significant portfolio benefits, out-of-sample. The portfolio performance may also serve as a metric to compare models that impose different sets of restrictions on the price of risk specification. In that respect, our approach is different from Thornton and Valente (2012) and Sarno et al. (2016), who test the economic significance for an investor with mean-variance preferences191919In fact, Sarno et al. (2016), also use an approximation of the power utility solution. Furthermore, they allow for the variance to be constant (or rolling window) and in-sample, in line with Thornton and Valente (2012). and conclude that statistical significance is not turned into better economic performance, when compared to the EH benchmark. It is more in line with Gargano et al. (2019) and Bianchi et al. (2021), who arrive at similar conclusions for models which utilise information coming solely from the yield curve (e.g. yields, forwards, etc.). Computationally, it is quite similar to the approach of Wan et al. (2022), tailored to the context of our paper.

We consider a Bayesian investor with power utility preferences,

| (23) |

where is an -period portfolio value and is the coefficient of relative risk aversion. If we let be a portfolio weight on the risky -period bond and be a portfolio weight of the riskless -period bond, then the portfolio value periods ahead is given as

| (24) |

where is the risk-free rate, here synonymous with the -period yield. Such an investor maximises her expected utility over h-periods in the future, based on

| (25) |

where is the predictive density described earlier. At every time , our Bayesian learner solves an asset allocation problem getting optimal portfolio weights by numerically solving

| (26) |

with being the number of particles from the predictive density of excess returns, weighted using importance weights , , which come from the IBIS algorithm.

To obtain the economic value generated by each model, we use the resulting optimum weights to compute the CER as in Johannes et al. (2014) and Gargano et al. (2019). In particular, for each model, we define the CER as the value that equates the average utility of each model against the average utility of the EH benchmark specification. Denoting realised utility from the predictive model as and realised utility from the EH benchmark as , we get

| (27) |

The above can be extended to multi-asset portfolio allocation by taking to be a vector.

4 Data and Models

The yield data set contains monthly observations of zero-coupon US Treasury yields with maturities of -years, spanning the period from January to the end of . In particular, yields used are the unsmoothed Fama-Bliss yields constructed by Le and Singleton (2013)202020We are grateful to Anh Le for generously providing the data set.. We consider two samples, one ending at the end of and that, as such, precludes the ensuing financial crisis, and a second one which includes the period after the end of , a period determined by, first, different monetary actions and establishment of unconventional policies and, second, interest rates hitting the zero-lower bound. The first sample has been used by most of the existing studies (see, Joslin et al. (2011), Joslin et al. (2014), Bauer (2018), and Bauer and Hamilton (2018)). Following related literature, we choose the starting date avoiding the early s, a period with evidence of the Fed changing its monetary policy. The post- global financial crisis period is excluded from our first sample due to concerns about the capability of Gaussian ATSMs to deal with the zero-lower bound (see, Kim and Singleton (2012) and Bauer and Rudebusch (2016)). These concerns are explored in the second sample, spanning the period from January to end of , as in Bauer and Hamilton (2018). The post period of the second sample coincides with the vast majority of the recent bond predictability literature (see, Bianchi et al. (2021), Wan et al. (2022), Borup et al. (2021) and Li et al. (2022)), thus allowing direct comparisons. Overall, the data contain different market conditions and monetary policy actions. In the analyses of the two samples the data are split into a warm-up period, where the data are used only for estimation purposes, and a testing period, starting immediately afterwards, where we start evaluating the model predictions while incorporating additional information as the data become available. Specifically, the training periods are and respectively. The data processing involves extracting the first three principal components from the yield curve, depicted in Figure 1 of Online Appendix C.

In terms of models, as mentioned in Section 2, there are possible distinct sets of risk price restrictions in the case of three factors driving the state variables. The first model considered is the previously mentioned maximally flexible model, (), in line with previous empirical studies (e.g. Duffee (2011), Sarno et al. (2016), and Bauer (2018), among others), which places no restrictions on the risk premia parameters. The next three models were the ones suggested by our developed sequential SSVS scheme, as the models with the highest posterior probability, when it was run in the first warm-up period 1985-1996. The outcome of this run, confirmed the argument of sparsity in the market price of risk specification, since the best models only freed one or two risk price parameters. Specifically, the model with the highest posterior probability is the one that allows a single free parameter, , which we denote as . This is the parameter which drives variation in the price of level risk due to changes in the slope of the yield curve. The next model, denoted by , has two free risk price parameters, as and also , whereas under only is free. This suggests that the variation in the price of level risk is driven by changes in the level factor. Finally, we consider Bayesian model averaging with model weights obtained from our developed sequential SSVS scheme. We explore three formulations: the first one () assumes uniform prior distribution over models, where each element of is independently Bernoulli distributed with success probability , as in Bauer (2018). The second one () uses a hierarchical prior, namely Beta-Binomial; see for example Wilson et al. (2010) and Consonni et al. (2018). The list of models is completed with , a constrained version of with only and allowed to be non-zero.

5 Empirical Results

This section presents the main results on the statistical and economic performance of excess return forecasts. In particular, we assess models based on different sets of restrictions and explore the evident puzzling behaviour between statistical predictability and meaningful out-of-sample economic benefits for bond investors. Furthermore, we monitor how the optimum set of restrictions behaves around periods of monetary policy shifts, interventions, and fragile economic conditions.

5.1 Yield Curve and Risk Price Dynamics

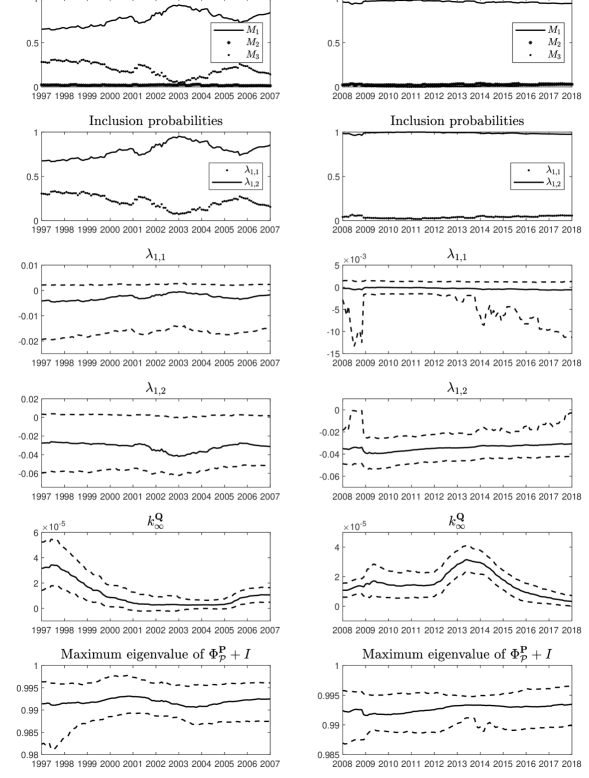

The yield curve behaviour through time (see Online Appendix C for more details) is captured from the sequential setup developed in this paper, which allows monitoring variations across time in the estimates of parameters, restrictions, and the importance thereof. Figure 1 contains the results obtained from fitting the model on the two previously mentioned samples, focusing on the testing periods. The plots depict information for the parameters , , their posterior inclusion probabilities, the associated posterior model probabilities, as well as the highest eigenvalue of and which is linked to the long-run mean of the short rate under . From the restrictions parameters, we chose to report only and as these were the only parameters with posterior inclusion probabilities not close to zero. In fact, based on the median probability principle that recommends keeping only variables with inclusion probabilities above , perhaps only the parameter should be allowed to be free, thus pointing to model . Nevertheless, as we discuss in the remainder of the paper, it may be helpful to consider freeing .

The posterior inclusion probabilities of the risk premia parameters are rather stable in the second sample, whereas they vary slightly in the first one in line with the changes in policy actions. During the conundrum period, the inclusion probability for increases while at the same time that for deteriorates. This suggests that the parameter, which links compensation for level risk to the slope factor, becomes more important during periods of yield curve steepening than periods when the curve flattens. Similarly, the parameter is more likely to be important during periods where the level of the term structure increases. In terms of model probabilities, performs better than , as follows from the posterior inclusions probabilities of and respectively. In the second sample the picture is clearer, as the model selection procedure suggest that only the parameter should be left free, and consequently is the clear winner.

It is also interesting to look at the long-run mean of the short rate under , over time, the posterior trajectory of which follows interest rate expectations and yield curve fluctuations. In the first sample, it starts at a high level and progressively moves down to zero until . This is followed by an increase during and after the conundrum period of -, due to the substantial increase of the federal funds rate. Qualitatively similar conclusions are made when looking at the second sample, where the long-run mean level starts slightly increasing after , reflecting the steepening of the curve due to the Fed’s policies. The increase is more pronounced during and peaks around the ’taper tantrum’ events, reflecting and capturing the sharp increase in medium-to-long maturity yields, and drops afterwards. Finally, we monitor the largest eigenvalue of the feedback matrix , where denotes the identity matrix. Its posterior mean remains nearly constant and very close to unity over the entire sample period, indicating a generally high -persistence, implied by the restrictions imposed on the risk-price parameters. This also reflects an enhanced time variation of short rate expectations and more stable risk premiums, implying a larger role of the expectation component over the risk premium component, in line with policy making and interventions.

5.2 Bond Return Predictability

This subsection presents results on the predictive performance exercise described in Section 3.3.1. Table 2 reports values for all models across bond maturities, prediction horizons and sub-periods. Results for the first sample (1985-2007), suggest that the maximally flexible model , widely used in the vast majority of prior studies, performs rather poorly out-of-sample compared to the EH benchmark, as showcased by predictive that are mostly negative, especially at the longer maturities (beyond -year). This is not the case for the second sample (1990-2018) where offers evidence of predictability for investment horizons bigger than month, generating scores which are mostly positive and highly significant, especially at the short end of the maturity spectrum and at longer prediction horizons.

Results are generally better when heavy restrictions are imposed on the risk price dynamics (models ), generating more accurate forecasts, as showcased by positive values, suggesting strong evidence of out-of-sample bond return predictability. Models and perform quite well in the second sample, which could be partly explained by the parameter being helpful when the curve steepens. On the other hand model , which does not contain , does better in the first sample. This reveals that shocks to the level of the yield curve, captured through , are important components of time-varying risk premia, mainly, during high yield and low uncertainty periods. In terms of the sequential model averaging schemes, they all perform consistently well doing slightly better in the second sample and at long prediction horizons.

Furthermore, we confirm that predictability is substantially higher following the post-crisis recession period, when the US market experienced high uncertainty and low interest rates, compared to the pre-crisis low volatility and high yield period, where are substantially lower. This finding is robust across models tested and methodologies applied.

These observations are in contrast to prior literature (see, Duffee (2011), Barillas (2011), Adrian et al. (2013), and Joslin et al. (2014)), which suggests that yields-only DTSMs are not capable of capturing the predictability of bond risk premia, and are more in line with the results of Sarno et al. (2016) and Feunou and Fontaine (2018) who argue that their modelling approaches help models to capture the required predictability of excess returns, in the context of DTSMs. Another message coming out of the analysis, despite the very good performance of models -, is that sequential model averaging can provide a reliable solution in both time periods. The results based on LS are also qualitatively similar and can be found in Online Appendix D.

5.3 Economic Performance

In this subsection, we concentrate on performance in terms of economic value, as described in Section 3.3. We therefore ask whether the predictive ability of models can be exploited by a real-time Bayesian investor when making investment decisions. We initially consider a univariate asset allocation setup which, then is extended to a multivariate allocation framework, where investor jointly models bond excess returns across maturities. To assess the robustness of our results and establish a better link with existing literature, we investigate the economic evidence considering three different scenarios for investors. The first two prevent them from taking extreme positions, while the third relaxes restrictions and allows for maximum leveraging and short-selling. In particular, in the first scenario we follow Thornton and Valente (2012), Sarno et al. (2016) and Gargano et al. (2019) and restrict portfolio weights to range in the interval , thus imposing maximum short-selling and leveraging of 100% respectively. Second, we follow Huang et al. (2020) and restrict portfolio weights to the interval which keeps maximum short-selling at 100% while increasing the upper bound, which now amounts to a maximum leveraging of 400%212121The results and discussion of this allocation scenario are presented in Online Appendix E.1.. Third, we follow Bianchi et al. (2021) and Wan et al. (2022) and impose no allocation restrictions to investors, allowing for portfolio weights to be unbounded. Finally, to make our results directly comparable to previous studies, we set the coefficient of risk aversion to , across scenarios.

Table 3 reports results for the annualised CER values, generated using out-of-sample forecasts of bond excess returns across maturities and prediction horizons in the first sample. Panel A presents evidence under the first investment scenario. Results show evidence of positive out-of-sample economic benefits, mainly at longer maturities. In particular, we find that, in most models, corresponding CERs are positive and non-negligible, indicating that yields-only models with heavy restrictions on the dynamics of risk compensation, not only provide statistical evidence of out-of-sample predictability, but also generate valuable economic gains for bond investors relative to the EH benchmark. Concurrently, the maximally flexible model , fails to offer any positive out-of-sample economic benefits compared to the EH benchmark, generating CER values which are consistently negative across the maturity spectrum and investment horizons. Furthermore, consistent with the conclusions coming from the predictability analysis in Section 5.2, such models are identified to be the exact same ones, suggesting that only models which allocate one or two non-zero risk price parameters solely to the level factor are able to generate meaningful economic gains for investors who dynamically rebalance their portfolio when new information arrives. Finally, the developed sequential SSVS scheme, which only searches among the best models available, attains very good performance, generating CER values which are quantitatively similar, compared to model . Those findings are in contrast to the conclusions of Thornton and Valente (2012) and Sarno et al. (2016), who argue that bond investors who utilise information from the yield curve only are not able to systematically earn any economic premium out-of-sample.

Importantly, our results suggest larger gains from predictability at longer maturities (beyond 5-years) and investment horizons (beyond 6-months), reflecting substantially higher and statistically significant CER values and consequently more profitable investments. This is in line with prior empirical evidence (see, Bianchi et al. (2021)) which states that long-dated yields contain substantial predictive power beyond the first five years. For example, for model at the -month investment horizon, CER is () for a -year (-year) maturity bond, while at the -month horizon, corresponding CER is () and highly significant for a -year (-year) maturity bond. Qualitatively similar gains are generated for most of the models. In turn, for the sequential SSVS model , which searches only among the best models available, at the -month investment horizon, CER is () for a -year (-year) maturity bond, while at the -month prediction horizon, corresponding CER is () and highly significant for a -year (-year) maturity bond. In fact, during the first sub period, those two models appear to outperform all other models tested.

Comparing the performance of alternative model specifications over time sheds light on the importance of particular restrictions across monetary policy actions and market conditions. Table 4 displays CER values for the period ending in , which covers the aftermath of the recession of - as well as the most interesting phases of the unfolding of the Fed’s policy responses to it. Results reveal that economic benefits are even more pronounced compared to the pre-crisis period. Such an upturn in CER values occurs across the maturity spectrum with a tendency for substantially larger gains at the long end of the curve, where investments on the -year maturity bond remain the most profitable. In particular, looking at all models, other than and , CER values for a -year maturity bond almost double when compared to the pre-crisis period. For example, for model at the -month investment horizon, CER is up to for a -year maturity bond, while at the -month horizon, corresponding CER is and highly significant. Qualitatively similar results are observed for other models tested, as displayed in Table 4. Importantly, positive and significant gains are now generated at shorter maturities and investment horizons. For example, for model at the -month investment horizon, CER is and significant for a -year maturity bond, while for model at the -month horizon, CER is and significant for a -year maturity bond. Finally, models that have been inferred via the sequential SSVS scheme developed (e.g. model ) do very well offering qualitatively similar CER values to model .

Next, we move to investigate asset allocation using the scenario where no allocation restrictions are imposed on investors. Panels B in Tables 3 and 4 present results for the annualised CER values. Our results in this case, are even more pronounced compared to the constrained allocation scenario of Panel A, since CER values increase substantially, across the maturity spectrum. More specifically, we find that for model , at the -month investment horizon, CERs increase up to and significant for a -year maturity bond, while for model , at the -month horizon, CER value jumps to . Importantly, models with some or no restrictions on the risk price dynamics, such as the maximally flexible model , still fail to offer any positive out-of-sample economic benefits compared to the EH benchmark. No matter the bond maturity, the investment horizon and the period considered, generated CERs are consistently negative, revealing no benefits to investors, in line with Thornton and Valente (2012) and Sarno et al. (2016).

Turning to the multi-asset allocation exercise, results are presented in Table 5. Panel A reports annualised CER values for the first sample, while Panel B for the second sample. Our results remain qualitatively similar to the univariate allocation setup. In particular, results reveal that the maximally flexible model continues to fail offering any out-of-sample benefits to investors, generating CERs which are consistently negative across investment horizons and sub-periods. The situation is reversed for models with heavy restrictions on the dynamics of risk compensation (e.g. models and ) as well as for models inferred via the developed SSVS scheme (e.g. model ). In particular, results reveal larger gains from predictability at longer investment horizons (beyond -months), where CERs are positive and significant compared to the EH benchmark. In fact, corresponding CERs are higher (in some cases on the order of per annum) compared to the univariate case, suggesting that gains are not limited to specific maturities, as evidenced also in Bianchi et al. (2021). Similar conclusions, yet more pronounced are revealed during the second sample where economic benefits are substantially higher. Interestingly, model , which offers positive gains during the first sample, fails to produce any benefits to investors during the second sample, in line with the univariate allocation case.

6 Connections with Predictive Regression Models

Given the improved performance offered by the use of the sequential SSVS approach in DTSMs, it is natural to ask the question whether it can also be of help in similar contexts such as predictive regression models (see, Fama and Bliss (1987), Cochrane and Piazzesi (2005), Gargano et al. (2019), Bianchi et al. (2021), Wan et al. (2022), among many others). We consider inputs from yields-only data, in fact the s (PCs) are viewed as the only inputs, thus leading to the following model

| (28) |

where , are scalars, and is vector of the regression coefficients. Connecting with relevant literature, e.g. Gargano et al. (2019), these inputs are closer to the factor as they are linear combinations of the yield across maturities; in that paper the factors are maturity-specific whereas the factor contains macroeconomic information. To maximise relevance with our approach to DTSMs, we consider a variant of the model in (28) paired with a VAR model

| (29) | ||||

| (30) |

where , and are defined as before. The above model can provide forecasts for any ; in the case of a forecast is obtained directly from (30) whereas, for , a prediction of is drawn first from (29). In other words, for we get a standard predictive regression model and, for , we incorporate the VAR dynamics present in DTSMs. This allows us to take advantage of potential benefits from sparse VAR formulations while sparsity can also be imposed on the predictive regression coefficients. The exercise is quite challenging from a predictive regression perspective given the yields-only inputs and the time-constant parameters and volatility; e.g. in Gargano et al. (2019) such models based on the factor fail to generate economic value.

For a given and information up to time , the model defined by (29) and (30) can be estimated from the data , . Since the are assumed to be directly observed, the overall likelihood is given by the product of VAR and predictive regression likelihoods obtained from (29) and (30) respectively. We proceed by assigning spike and slab priors to all the elements , , and , as well as some standard conjugate priors on the remaining parameters, so that a Gibbs sampler is obtained; see Online Appendix F for details. In the presence of that Gibbs sampler, the IBIS algorithm can then be applied as before. It is worth noting that this algorithm is searching over models for each exploring both predictive regression coefficients and VAR parameters.

Table 6 contains figures concerning the economic values generated by the model in (29) and (30), using the sequential SSVS approach. In Panel B, corresponding to the second sample, the model succeeds in generating substantial economic value, mostly for large prediction horizons and small maturities, with results being more pronounced for the case of no portfolio weight restrictions. Nevertheless, in Panel A covering the first sample, the results models fail to generate economic value, except for a couple of cases corresponding to unconstrained portfolio weights. Overall, these preliminary results are encouraging and suggest that it would be worthwhile to explore this methodology further, with alternative inputs, time-varying parameters and volatility.

7 Discussion

In this paper we focused on the DTSMs, explored their predictability and whether it can translate into economic benefits for investors. Our findings complement Sarno et al. (2016) suggesting that economic value can only be obtained, in addition to predictability, if extreme and specific restrictions are placed on their market price of risk specification. In order to implement this approach, we adapted Bayesian variable selection, as in Bauer (2018), to a sequential setting that allows identifying the optimal set of restrictions in real time. The sequential version of the SSVS scheme developed successfully identifies such restrictions either directly, as it can be applied on its own, or indirectly by suggesting specific restrictions that set all risk premia parameters to zero, except for one or two of them ( and potentially ). The results are robust to several portfolio allocation scenarios and different time periods, with the performance in the post- recession period with no portfolio allocation restrictions being more pronounced, and are driven mostly by long prediction horizons and larger maturities.

From a statistical viewpoint the problem may be viewed as imposing sparsity. Standard approaches to sparsity include ridge and Lasso regression. However the former is equivalent to assigning normal priors on the risk premia parameters of the maximally flexible model and was implemented without success, whereas the Bayesian versions of the latter, which are essential to conduct portfolio allocation, are generally not associated with sparsity. Instead the use of spike and slab priors is one of the default approaches to impose sparsity in the Bayesian context. It may be useful to explore alternative options; see for example Polson and Scott (2011) and the references therein. In terms of identified optimal restrictions, our findings are in line with Cochrane and Piazzesi (2009) and Duffee (2011) in that only the level risk is priced, but our adopted models impose further restrictions. The findings of the empirical analysis suggest that these additional restrictions are necessary to produce economic value. An alternative market price of risk specification would be the reduced rank approach of Joslin et al. (2011), perhaps not directly, being less strict than the restrictions implied Duffee (2011), but paired with spike and slab priors. The sequential SSVS approach may also be useful in the context of predictive regressions, aiming to offer improved economic value to existing approaches.

Furthermore, our results reveal some evidence of time variation in the parameters and restrictions; for the latter this is only viewed in the first sample. The sequential SSVS approach can capture such variations to some extent but this is also closely linked to the choice of the data window. Using an expanding window, as in this paper, could work well for small and perhaps moderate changes, but is unlikely to capture extreme shocks such as the Covid-19 period where a shorter window would be more appropriate. Going forward, it would be interesting to consider DTSM models with time varying parameters, for example the mean under the pricing measure appears to be time varying as suggested from the output offered by the IBIS algorithm, or regime switching approaches tailoring for example Andreasen et al. (2021) to the context of DTSMs. Another promising future direction is to incorporate spanned or unspanned macroeconomic variables in the models; see, for example, Joslin et al. (2014).

References

- Adrian et al. (2013) Adrian T, Crump RK, Moench E (2013) Pricing the term structure with linear regressions. Journal of Financial Economics 110(1):110–138.

- Andreasen et al. (2021) Andreasen MM, Engsted T, Møller SV, Sander M (2021) The yield spread and bond return predictability in expansions and recessions. The Review of Financial Studies 34(6):2773–2812.

- Ang et al. (2007) Ang A, Dong S, Piazzesi M (2007) No-arbitrage taylor rules. Working Paper 13448, National Bureau of Economic Research.

- Ang and Longstaff (2011) Ang A, Longstaff FA (2011) Systemic sovereign credit risk: Lessons from the us and europe. Journal of Monetary Economics 60(5):493–510.

- Ang and Piazzesi (2003) Ang A, Piazzesi M (2003) A no-arbitrage vector autoregression of term structure dynamics with macroeconomic and latent variables. Journal of Monetary Economics 50(4):745–787.

- Barillas (2011) Barillas F (2011) Can we exploit predictability in bond markets? Working paper, Emory University.

- Bauer (2018) Bauer MD (2018) Restrictions on risk prices in dynamic term structure models. Journal of Business & Economic Statistics 36(2):196–211.

- Bauer and Hamilton (2018) Bauer MD, Hamilton JD (2018) Robust bond risk premia. The Review of Financial Studies 31(2):399–448.

- Bauer and Rudebusch (2016) Bauer MD, Rudebusch GD (2016) Resolving the spanning puzzle in macro-finance term structure models. Review of Finance 21(2):511–553.

- Bianchi et al. (2021) Bianchi D, Büchner M, Tamoni A (2021) Bond risk premiums with machine learning. The Review of Financial Studies 34(2):1046–1089.

- Borup et al. (2021) Borup D, Eriksen JN, Kjær MM, Thyrsgaard M (2021) Predicting bond return predictability. SSRN 3513340 .

- Campbell and Shiller (1991) Campbell JY, Shiller RJ (1991) Yield spreads and interest rate movements: A bird’s eye view. The Review of Economic Studies 58(3):495–514.

- Campbell and Thompson (2008) Campbell JY, Thompson SB (2008) Predicting excess stock returns out of sample: Can anything beat the historical average? The Review of Financial Studies 21(4):1509–1531.

- Cheridito et al. (2007) Cheridito P, Filipović D, Kimmel RL (2007) Market price of risk specifications for affine models: Theory and evidence. Journal of Financial Economics 83(1):123–170.

- Chib and Ergashev (2009) Chib S, Ergashev B (2009) Analysis of multifactor affine yield curve models. Journal of the American Statistical Association 104(488):1324–1337.

- Chopin (2002) Chopin N (2002) A sequential particle filter method for static models. Biometrika 89(3):539–552.

- Chopin (2004) Chopin N (2004) Central limit theorem for sequential monte carlo methods and its application to bayesian inference. The Annals of Statistics 32(6):2385–2411.

- Cieslak (2018) Cieslak A (2018) Short-rate expectations and unexpected returns in treasury bonds. The Review of Financial Studies 31(9):3265–3306.

- Cieslak and Povala (2015) Cieslak A, Povala P (2015) Expected returns in treasury bonds. The Review of Financial Studies 28(10):2859–2901.

- Cochrane and Piazzesi (2005) Cochrane JH, Piazzesi M (2005) Bond risk premia. The American Economic Review 95(1):138–160.

- Cochrane and Piazzesi (2009) Cochrane JH, Piazzesi M (2009) Decomposing the yield curve. Working paper, AFA 2010 Atlanta Meetings.

- Consonni et al. (2018) Consonni G, Fouskakis D, Liseo B, Ntzoufras I (2018) Prior Distributions for Objective Bayesian Analysis. Bayesian Analysis 13(2):627 – 679.

- Dai and Singleton (2000) Dai Q, Singleton KJ (2000) Specification analysis of affine term structure models. The Journal of Finance 55(5):1943–1978.

- Dawid and Musio (2014) Dawid AP, Musio M (2014) Theory and applications of proper scoring rules. METRON 72(2):169–183.

- Del Moral et al. (2006) Del Moral P, Doucet A, Jasra A (2006) Sequential monte carlo samplers. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 68(3):411–436.

- Della Corte et al. (2008) Della Corte P, Sarno L, Thornton DL (2008) The expectation hypothesis of the term structure of very short-term rates: Statistical tests and economic value. Journal of Financial Economics 89(1):158–174.

- Dewachter and Lyrio (2006) Dewachter H, Lyrio M (2006) Macro factors and the term structure of interest rates. Journal of Money, Credit and Banking 38(1):119–140.

- Duarte (2004) Duarte J (2004) Evaluating an alternative risk preference in affine term structure models. The Review of Financial Studies 17(2):379–404.

- Duffee (2002) Duffee GR (2002) Term premia and interest rate forecasts in affine models. The Journal of Finance 57(1):405–443.

- Duffee (2011) Duffee GR (2011) Information in (and not in) the term structure. The Review of Financial Studies 24(9):2895–2934.

- Duffee and Stanton (2012) Duffee GR, Stanton RH (2012) Estimation of dynamic term structure models. The Quarterly Journal of Finance 2(02):1250008.

- Duffie and Kan (1996) Duffie D, Kan R (1996) A yield-factor model of interest rates. Mathematical Finance 6(4):379–406.

- Fama and Bliss (1987) Fama EF, Bliss RR (1987) The information in long-maturity forward rates. The American Economic Review 680–692.

- Feldhütter (2016) Feldhütter P (2016) Can affine models match the moments in bond yields? Quarterly Journal of Finance 6(2):1650009.

- Feunou and Fontaine (2018) Feunou B, Fontaine JS (2018) Bond risk premia and Gaussian term structure models. Management Science 64(3):1413–1439.

- Fong and Holmes (2020) Fong E, Holmes CC (2020) On the marginal likelihood and cross-validation. Biometrika 107(2):489–496.

- Gargano et al. (2019) Gargano A, Pettenuzzo D, Timmermann A (2019) Bond return predictability: Economic value and links to the macroeconomy. Management Science 65(2):508–540.

- George and McCulloch (1993) George EI, McCulloch RE (1993) Variable selection via gibbs sampling. Journal of the American Statistical Association 88(423):881–889.

- Geweke and Amisano (2010) Geweke J, Amisano G (2010) Comparing and evaluating bayesian predictive distributions of asset returns. International Journal of Forecasting 26(2):216–230.

- Ghysels et al. (2018) Ghysels E, Horan C, Moench E (2018) Forecasting through the rearview mirror: Data revisions and bond return predictability. The Review of Financial Studies 31(2):678–714.

- Giacoletti et al. (2021) Giacoletti M, Laursen KT, Singleton KJ (2021) Learning from disagreement in the us treasury bond market. The Journal of Finance 76(1):395–441.

- Hamilton and Wu (2012) Hamilton JD, Wu JC (2012) Identification and estimation of Gaussian affine term structure models. Journal of Econometrics 168(2):315–331.

- Huang et al. (2020) Huang D, Jiang F, Li K, Tong G, Zhou G (2020) Are bond returns predictable with real-time macro data? Asian Finance Association (AsianFA) 2018 Conference.

- Jasra et al. (2011) Jasra A, Stephens DA, Doucet A, Tsagaris T (2011) Inference for lévy-driven stochastic volatility models via adaptive sequential monte carlo. Scandinavian Journal of Statistics 38(1):1–22.

- Johannes et al. (2014) Johannes M, Korteweg A, Polson N (2014) Sequential learning, predictability, and optimal portfolio returns. The Journal of Finance 69(2):611–644.

- Joslin et al. (2014) Joslin S, Priebsch M, Singleton KJ (2014) Risk premiums in dynamic term structure models with unspanned macro risks. The Journal of Finance 69(3):1197–1233.

- Joslin et al. (2011) Joslin S, Singleton KJ, Zhu H (2011) A new perspective on Gaussian dynamic term structure models. The Review of Financial Studies 24(3):926–970.

- Kantas et al. (2014) Kantas N, Beskos A, Jasra A (2014) Sequential monte carlo methods for high-dimensional inverse problems: a case study for the navier-stokes equations. SIAM/ASA Journal on Uncertainty Quantification 2:464–489.

- Kim and Orphanides (2012) Kim DH, Orphanides A (2012) Term structure estimation with survey data on interest rate forecasts. Journal of Financial and Quantitative Analysis 241–272.

- Kim and Singleton (2012) Kim DH, Singleton KJ (2012) Term structure models and the zero bound: an empirical investigation of japanese yields. Journal of Econometrics 170(1):32–49.

- Kim and Wright (2005) Kim DH, Wright JH (2005) An arbitrage-free three-factor term structure model and the recent behavior of long-term yields and distant-horizon forward rates. Working paper, Finance and Economics Discussion Series 2005-33, Federal Reserve Board of Governors.

- Le and Singleton (2013) Le A, Singleton KJ (2013) The structure of risks in equilibrium affine models of bond yields. Unpublished working paper, University of North Carolina at Chapel Hill .

- Li et al. (2022) Li J, Sarno L, Zinna G (2022) Risks and risk premia in the us treasury market. SSRN 3640341 .

- Litterman and Scheinkman (1991) Litterman RB, Scheinkman J (1991) Common factors affecting bond returns. The Journal of Fixed Income 1(1):54–61.

- Ludvigson and Ng (2009) Ludvigson SC, Ng S (2009) Macro factors in bond risk premia. The Review of Financial Studies 22(12):5027–5067.

- Madigan and Raftery (1994) Madigan D, Raftery AE (1994) Model selection and accounting for model uncertainty in graphical models using occam’s window. Journal of the American Statistical Association 89(428):1535–1546.

- Mitchell and Beauchamp (1988) Mitchell TJ, Beauchamp JJ (1988) Bayesian variable selection in linear regression. Journal of the American Statistical Association 83(404):1023–1032.

- Newey and West (1987) Newey WK, West KD (1987) A simple, positive semi-definite, heteroskedasticity and autocorrelation consistent covariance matrix. Econometrica 55(3):703–708.

- Orphanides and Wei (2012) Orphanides A, Wei M (2012) Evolving macroeconomic perceptions and the term structure of interest rates. Journal of Economic Dynamics and Control 36(2):239–254.

- Piazzesi et al. (2006) Piazzesi M, Schneider M, Benigno P, Campbell JY (2006) Equilibrium yield curves [with comments and discussion]. NBER Macroeconomics Annual 21:389–472.

- Polson and Scott (2011) Polson NG, Scott JG (2011) Shrink globally, act locally: sparse bayesian regularization and prediction. Bayesian statistics, Oxford University Press 9:501–538.

- Rudebusch and Wu (2008) Rudebusch GD, Wu T (2008) A macro-finance model of the term structure, monetary policy and the economy. The Economic Journal 118(530):906–926.

- Sarno et al. (2016) Sarno L, Schneider P, Wagner C (2016) The economic value of predicting bond risk premia. Journal of Empirical Finance 37:247–267.

- Schäfer and Chopin (2013) Schäfer C, Chopin N (2013) Sequential Monte Carlo on large binary sampling spaces. Statistics and Computing 23(2):163–184.

- Thornton and Valente (2012) Thornton DL, Valente G (2012) Out-of-sample predictions of bond excess returns and forward rates: An asset allocation perspective. The Review of Financial Studies 25(10):3141–3168.

- Wan et al. (2022) Wan R, Fulop A, Li J (2022) Real-time bayesian learning and bond return predictability. Journal of Econometrics 230(1):114–130.

- Wilson et al. (2010) Wilson MA, Iversen ES, Clyde MA, Schmidler SC, Schildkraut JM (2010) Bayesian model search and multilevel inference for SNP association studies. The Annals of Applied Statistics 4(3):1342 – 1364.

- Wright (2011) Wright JH (2011) Term premia and inflation uncertainty: Empirical evidence from an international panel dataset. The American Economic Review 101(4):1514–34.

| Panel A: Period - 1985 - 2007 | Panel B: Period - 1990 - 2018 | ||||||||||||

| h | 2Y | 3Y | 4Y | 5Y | 7Y | 10Y | h | 2Y | 3Y | 4Y | 5Y | 7Y | 10Y |

| 1m | 0.03*** | 0.01** | 0.00** | -0.02* | -0.03 | -0.08 | 1m | -0.02* | -0.02 | -0.03 | -0.02 | -0.01 | -0.02* |

| 3m | 0.06** | 0.02** | 0.01** | -0.04** | -0.06** | -0.22 | 3m | 0.08*** | 0.05** | 0.02** | 0.02** | -0.01* | -0.02** |

| 6m | 0.09** | 0.04** | 0.01** | -0.04** | -0.14* | -0.35 | 6m | 0.26*** | 0.20*** | 0.13*** | 0.10** | 0.06** | 0.03** |

| 9m | 0.07* | 0.02* | -0.02* | -0.07* | -0.20 | -0.43 | 9m | 0.39*** | 0.28*** | 0.19** | 0.16** | 0.14** | 0.09** |

| 12m | 0.08* | 0.02 | -0.03 | -0.06 | -0.22 | -0.43 | 12m | 0.48*** | 0.40*** | 0.28** | 0.25** | 0.21** | 0.16** |

| 1m | 0.05*** | 0.04*** | 0.03*** | 0.03** | 0.02** | 0.03** | 1m | 0.03*** | 0.05*** | 0.04*** | 0.04** | 0.03** | 0.04*** |

| 3m | 0.07** | 0.06** | 0.06** | 0.04* | 0.06** | 0.05** | 3m | 0.10*** | 0.12*** | 0.10*** | 0.10*** | 0.09*** | 0.12*** |

| 6m | 0.10** | 0.09* | 0.10** | 0.09* | 0.09* | 0.08** | 6m | 0.19*** | 0.23*** | 0.20*** | 0.18*** | 0.17*** | 0.20*** |

| 9m | 0.08 | 0.08 | 0.10* | 0.10* | 0.11* | 0.09* | 9m | 0.28*** | 0.35*** | 0.34*** | 0.32*** | 0.28*** | 0.32*** |