Short-time asymptotics for non self-similar

stochastic volatility models

Abstract

We provide a short-time large deviation principle (LDP) for stochastic volatility models, where the volatility is expressed as a function of a Volterra process. This LDP does not require strict self-similarity assumptions on the Volterra process. For this reason, we are able to apply such an LDP to two notable examples of non self-similar rough volatility models: models where the volatility is given as a function of a log-modulated fractional Brownian motion [Bayer et al., Log-modulated rough stochastic volatility models. SIAM J. Financ. Math, 2021, 12(3), 1257-1284], and models where it is given as a function of a fractional Ornstein-Uhlenbeck (fOU) process [Gatheral et al., Volatility is rough. Quant. Finance, 2018, 18(6), 933-949]. In both cases we derive consequences for short-maturity European option prices, implied volatility surfaces and implied volatility skew. In the fOU case we also discuss moderate deviations pricing and simulation results.

Keywords: rough volatility, stochastic volatility, implied volatility, European option pricing, short-time asymptotics, fractional Brownian motion, fractional Ornstein-Uhlenbeck, modulated models, Volterra processes.

2020 Mathematics Subject Classification: 91G20, 60H30, 60F10, 60G22.

JEL Classifications: C32, C63, G12.

Acknowledgements: We are grateful to Christian Bayer, Lucia Caramellino for discussion and support. Barbara Pacchiarotti acknowledges the support of Indam-GNAMPA (research project “Stime asintotiche: principi di invarianza e grandi deviazioni”), of the MIUR Excellence Department Project awarded to the Department of Mathematics, University of Rome Tor Vergata (CUP E83C18000100006) and of University of Rome Tor Vergata (research program “Beyond Borders”, project “Asymptotic Methods in Probability”(CUP E89C20000680005)).

1 Introduction

Recent years have seen wide interest in volatility modelling with Volterra processes in the quantitative finance community. This has been spurred by the success of rough volatility models, where volatility is a non-Markovian, fractional process (Gatheral et al., 2018). In many instances, in order to produce this type of dynamics, volatility is expressed as a function of a Volterra process, i.e. a suitable deterministic kernel integrated against a Brownian motion. In this context a very useful feature of such kernel and of the corresponding fractional process is self-similarity.

When looking at approximation formulas and asymptotics, self-similarity is usually key as it enables the translation of a small-noise result into a short-time one through space-time rescaling. This can then be used to price short maturity options (see the discussion at the end of Section 3 in Gulisashvili (2020), and Gulisashvili (2018)). Based on this procedure, several short-time formulas are available for rough volatility models, if the volatility process is expressed as a function of a fractional Brownian motion (fBM) (Forde and Zhang, 2017), as a function of a Riemann-Liouville process (RLp), as in the rough Bergomi model (Bayer et al., 2019; Friz et al., 2022; Fukasawa, 2020), or as a solution to a fractional SDE, as in the fractional Heston model (Forde et al., 2021).

However, obtaining short-time approximation formulas is more difficult if volatility depends on a process which is not self-similar, such as the fractional Ornstein-Uhlenbeck (fOU) process (Horvath et al., 2019; Garnier and Sølna, 2017, 2018a, 2020b, 2019, 2020a), or the log-modulated fBM (log-fBM) (Bayer et al., 2021). In this paper, we address this issue, providing a short-time large deviation principle (LDP) for Volterra-driven stochastic volatilities, where the usual self similarity assumption is replaced by a weaker scaling property for the kernel, that needs to hold only in asymptotic sense (see conditions (K1) and (K2) below). We prove this general result starting from (Cellupica and Pacchiarotti, 2021), where a pathwise LDP for the log-price was proved when the volatility is function of a family of Volterra processes, and the price is solution to a scaled differential equation. Here, under suitable short-time asymptotic assumptions on the Volterra kernel, we prove a short-time LDP for the log-price process.

With our general result, we analyse more in depth models with volatility given as a function of fOU or log-fBM, neither of which is self-similar. However, we note that both these processes can be seen as a perturbation of self-similar processes, so that our general result can be applied, assuming that the price process is a martingale and a moment condition on the price.

The first class of processes to which we apply our LDP are log-modulated rough stochastic volatility models, introduced in Bayer et al. (2021) as a logarithmic perturbation of a more standard power-law Volterra stochastic volatility model, with volatility depending on a log-fBM. These models allow for the definition of a “true”, continuous volatility process with roughness (Hurst) parameter (including the “super-rough” case ), at the price of losing the self-similar structure of the power-law kernel. Differently from our LDP setting, however, in Bayer et al. (2021) Edgeworth-type asymptotics are considered, meaning that log-moneyness is of the form ( representing the time to maturity), while in order to observe a large deviations behavior we look here at a suitable log-moneyness regime (cf. equation (4.2)). This regime is consistent with Forde-Zhang LDP for rough volatility (Forde and Zhang, 2017) and the related large deviation results discussed below. When , we obtain a short-time LDP for the log-price process and consequent short-time option pricing, implied volatility and implied skew asymptotics. For this class of processes the rate function only depends on the self-similar power-law kernel, while the speed depends also on the modulating logarithmic function. It is shown in Bayer et al. (2021) that when the implied volatility skew explodes as (with a logarithmic correction), realising the model free bound in Lee (2005). Even though our proof only holds in the case, the expression we obtain for skew asymptotics, computed for , is consistent with this model free bound. We note that Baldi and Pacchiarotti (2022) have recently proved that in the case, even if the log-modulated model is well defined, an LDP cannot hold.

The second class of models to which we apply our LDP have a stochastic volatility given by a function of a fractional Ornstein-Uhlenbeck process. We find that, in short-time, such model behaves exactly as the analogous model, with volatility process given as the same function, computed on a fBM (i.e., the model studied in Forde and Zhang (2017)). More precisely, we mean that the two models satisfy an LDP with same speed and rate function. It follows that also the short-time implied skew (computed as a suitable finite difference) is the same for fOU and fBM-driven stochastic volatility models. For small time scales, fOU is, in a sense, close to fBM (see equation (3.6)), even though fOU is not self-similar. It is not uncommon when dealing with rough stochastic volatility, starting from the groundbreaking work Gatheral et al. (2018), to consider at times fBM, at times fOU, depending on which is most convenient for the problem at hand. Our result can be seen as a justification of this type of procedure, as it shows that pricing vanilla options with one or the other volatility does not matter (too much) for short maturities. Moreover, the fOU process is the most standard choice for a stationary process with a fractional correlation structure. This is one of the reasons why it has been used as volatility process for option pricing and related issues111note that both fBM and RLp (as in Rough Bergomi) are non-stationary and give rise to non-stationary volatility processes (Horvath et al., 2019; Garnier and Sølna, 2017, 2018a, 2020b, 2019, 2020a).

From our short-time LDP we formally derive the corresponding moderate deviations result, consistent with the one holding for self-similar rough volatility (Bayer et al., 2019). We provide numerical evidence for both these large and moderate deviations results and for the skew asymptotics. We investigate on simulations how the choice between fOU and fBM dynamics in the volatility affects volatility smiles and skews, how accurate are our approximations, and how they depend on the mean reversion parameter.

Background. In recent years, rough volatility has been widely used in option pricing, due to the great fits it provides to observed volatility surfaces (Bayer et al., 2016) and its ability to capture fundamental stylized facts of the implied volatility, notably the power-law explosion of the implied skew in short-time, which explodes as under rough volatility (Alòs et al., 2007; Fukasawa, 2011, 2017). Many authors have argued that is actually positive but very close to (Bayer et al., 2016; Fukasawa, 2020), which would give an extreme skew explosion close to . This is a model-free bound (Lee, 2005), that can be reached pricing options using “singular” local (or local-stochastic) volatility models (Pigato, 2019; Friz et al., 2021), but it is hard to obtain with (rough) stochastic volatility, as in the limit the volatility process usually degenerates and can be defined only as a distribution, not as a genuine process (Forde et al., 2020, 2021; Neuman and Rosenbaum, 2018; Hager and Neuman, 2021). Moreover, one observes a skew-flattening phenomenon, as , in some of these models. This was the main motivation, in Bayer et al. (2021), to introduce the log-modulation of the power law kernel, allowing the corresponding stochastic volatility to be defined as a genuine process also in the limit. Technically, the logarithmic correction ensures that the variance remains finite even for , that in turn avoids the subsequent definition problems as , as well as the skew-flattening problem. We refer to Bayer et al. (2021) and references therein for a detailed discussion of the problem.

Volatility was already taken as an exponential function of a fOU process with when rough volatility was first proposed in Gatheral et al. (2018). On the one hand, mostly because of the desired self-similarity property of the volatility process, the exponential of a fBM or of a RLp222RLp is the stochastic process driving the volatility in the rough Bergomi model (Bayer et al., 2016), are often used for pricing options. On the other hand, it is argued, e.g. in Gatheral et al. (2018), that taking a fOU with small mean reversion is not very different from taking a fBM in the volatility, with the considerable advantage that fOU is a stationary process (Cheridito et al., 2003), while fBM and RLp are not. For a thorough discussion on fOU driven volatilities and related implied volatilities we refer in particular to Garnier and Sølna (2017, 2020a), for the relation of fOU to fast mean reverting Markov stochastic volatility we refer to Garnier and Sølna (2018a, 2019), for hedging under fOU volatility we refer to Garnier and Sølna (2020b), for portfolio optimization using fast mean reverting fOU process with we refer to Fouque and Hu (2018). A small-noise LDP under fOU volatility, with other related results, has been proved in Horvath et al. (2019), and LDP and moderate deviation principles for the rough Stein-Stein and other models, also in short-time, have been discussed in Jacquier and Pannier (2022) (see Remark 4.9 for details).

In this paper we consider short-time pricing asymptotics, i.e. pricing short maturity European options. This is a widely studied topic, as these short maturity pricing formulas provide methods for fast calibration, a quantitative understanding of the impact of model parameters on generated implied volatility surfaces, led to some widely used parametrizations of the volatility surface, and help in the choice of the most appropriate model to be fitted to data (Ait-Sahalia et al., 2020). Short maturity approximations are also used to obtain starting points for calibration procedures, which are then based on numerical evaluations. They have applications also to hedging, trading and risk management.

For notable results on short maturity valuation formulas under Markovian stochastic volatility we refer to Osajima (2015), and to Medvedev and Scaillet (2003, 2007) for Markovian stochastic volatility with jumps. Short-time skew and curvature under rough volatility have been discussed in Fukasawa (2017); Alòs and Leon (2017). Short maturity valuation formulas for European options and implied volatilities under rough stochastic volatility are given, e.g., in Forde and Zhang (2017); El Euch et al. (2019); Bayer et al. (2019); Friz et al. (2021, 2022); Fukasawa (2020). Short maturity local volatility under rough volatility is studied in Bourgey et al. (2023). Pathwise large and moderate deviation principles for rough stochastic volatility models are established in Horvath et al. (2019); Jacquier et al. (2018); Jacquier and Pannier (2022); Gulisashvili (2018, 2020, 2021, 2022); Gulisashvili et al. (2018a, b); Cellupica and Pacchiarotti (2021); Catalini and Pacchiarotti (2023).

Content of the paper. We consider in Section 2 an LDP for stochastic volatility models with volatility driven by general Volterra processes. In particular, in Section 2.2 we prove a short-time LDP for such models without relying on self-similarity. In Section 3 we see how these results provide short-time LDPs in relevant, non self-similar examples such as the log-fBM and the fOU process. In Section 4 we derive practical consequences for option pricing and implied volatility, for volatility models where the volatility depends on log-fBM or fOU, at the large deviations regime. In the case of fOU, we also consider moderate deviations. A numerical study of the accuracy and dependence on relevant parameters of our results in the fOU case concludes the paper in Section 5.

2 Large deviations for Volterra stochastic volatility models

2.1 Small-noise large deviations for the log-price

We are interested in stochastic volatility models with asset price dynamics described by

| (2.1) |

where we set, without loss of generality, the initial price. The time horizon is , and are two independent standard Brownian motions, is a correlation coefficient and , so that is a standard Brownian motion -correlated with . We assume that the process is a non-degenerate, continuous Volterra type Gaussian process of the form

| (2.2) |

Here, the kernel is a measurable and square integrable function on , such that , for all and

One can verify that the covariance function of the process defined as above is given by

We introduce now the modulus of continuity of the kernel , defined as

In order to ensure the continuity of the paths of , we assume that satisfies the following condition.

-

(A1)

There exist constants and such that for all .

Let us recall that the unique solution to equation (2.1) is , where the log-price process is defined by

| (2.3) |

Definition 2.1.

A modulus of continuity is an increasing function such that and . A function defined on is called locally -continuous, if for every there exists a constant such that for all , inequality holds.

Remark 2.2.

For instance, if , , the function is locally -Hölder continuous. If , the function is locally Lipschitz continuous.

We consider the following assumptions on the volatility function .

-

()

is a locally -continuous function for some modulus of continuity .

-

()

There exist constants such that

From now on, we denote by (respectively ) the set of continuous functions on (respectively the set of continuous functions on starting at ), endowed with the topology induced by the sup-norm.

Let be an infinitesimal, decreasing function, i.e. , as . For every , we consider the following scaled version of equation (2.1)

The log-price process in the scaled model is

| (2.4) |

Here the Brownian motion is multiplied by a small-noise parameter and the Volterra process is of the form

where is a suitable kernel. It can be verified that the covariance function of the process , for every is given by

In the setting above, we are interested in an LDP for the family (we recall basic facts and notations on LDP in Appendix A). Such an LDP holds under the following conditions on the covariance functions, as seen in Theorem 7.4 in Cellupica and Pacchiarotti (2021).

-

(K1)

There exist an infinitesimal function and a kernel (regular enough to be the kernel of a continuous Volterra process) such that

(2.5) and

uniformly for

-

(K2)

There exist constants , such that, for every

Theorem 2.3.

Let be an infinitesimal function. Suppose Assumptions (K1) and (K2) are fulfilled. Then satisfies an LDP on with speed and good rate function

where

where is defined in equation (2.5) and is the Cameron-Martin space.

If Assumptions () and () hold for the volatility function , we also have a sample path LDP for the family of processes and for the family of random variables (see Section 7 in Cellupica and Pacchiarotti (2021) for details). Let us denote for .

Theorem 2.4.

Under Assumptions (), (), (K1) and (K2), we have: i) the family of processes satisfies an LDP with speed and good rate function

| (2.6) |

ii) the family of random variables satisfies an LDP with speed and good rate function

| (2.7) |

Remark 2.5.

From Theorem 4.8 in Forde and Zhang (2017), it follows that

2.2 Short-time large deviations for the log-price

It is well known that if the Volterra process is self-similar we can pass from small-noise to short-time regime (see the discussion at the end of Section 3 in Gulisashvili (2020)). However, in general this is not possible if the process is not self-similar. In this section, we obtain a short-time LDP that does not rely on the self-similarity assumption, by using the results of the previous section.

Let be a sequence decreasing to zero, i.e. as . For every and , if is a Volterra process as in (2.2) we have

| (2.8) |

with . Therefore for every and , if is as in (2.3), we have

Define and suppose the family of processes satisfies an LDP with speed (depending on ). Suppose furthermore that the family satisfies an LDP with speed (for details on this topic see Section 7 and in particular Theorem 7.4 in Cellupica and Pacchiarotti (2021)) and let be the process defined in (2.4). If we consider the processes, defined on the same space, we have

Let us recall that two families and of random variables are exponentially equivalent (at the speed , with as ) if for any ,

As far as the LDP is concerned, exponentially equivalent families are indistinguishable. See Theorem 4.2.13 in Dembo and Zeitouni (1998).

Theorem 2.6.

Under Assumptions (), (), (K1) and (K2), the two families and are exponentially equivalent and therefore satisfy the same LDP. In particular,

(i) the family satisfies an LDP with speed and good rate function given by (2.6);

(ii) the family of random variables satisfies an LDP with speed and good rate function given by (2.7).

Proof. We have

where and . The family satisfies an LDP with a good rate function. Then, it is exponentially tight (at the inverse speed ). Therefore for every , there exists a compact set (of equi-bounded functions) such that , with indicating the complementary set. Thus, for every ,

since the set is eventually empty.

3 Applications

In this section, we consider some (non self-similar) Volterra processes that satisfy assumption (A1) and such that the corresponding family defined by equation (2.8) satisfies conditions (K1) and (K2). We also suppose that assumptions () and () on the volatility function are satisfied and . From Theorem 2.6 we obtain a short-time LDP for the corresponding log-price processes.

3.1 Log-fractional Brownian motion and modulated models

Let us consider the kernel, for ,

| (3.1) |

where , and is a constant. The corresponding Volterra process essentially amounts to the log-fBM introduced in Bayer et al. (2021). There, an additional cutoff of the logarithm function was introduced in order to normalize the variance of the volatility at time one, but we can avoid here this complication as it does not affect our analysis in any way, since we only consider short-time asymptotics.

Condition (A1) for this kernel was proved in Bayer et al. (2021) with . Note that is the well known kernel of the RLp, which also satisfies Assumption (A1) with .

For large enough, we set

Let us verify that conditions (K1) and (K2) are satisfied for . No small time LDP can be verified in the case , as shown in Section 5.4 in Baldi and Pacchiarotti (2022).

(K1) For , , since we can suppose , we have

| (3.2) |

and therefore

Then, thanks to Lebesgue’s dominated convergence Theorem, for ,

so that .

This convergence is actually uniform, since

and therefore the sequence is a monotone sequence of continuous functions converging pointwise to a continuous function. Then (K1) is proved (with and ).

Let us prove that

The map defines a decreasing function in a neighbourhood of and an increasing function for . Then, for large enough, for , we have

Therefore,

Therefore conditions (K1) and (K2) are verified with infinitesimal function , limit kernel , and . A short-time LDP holds with inverse speed and limit kernel

The results proved for the log-fBM can be extended to a class of processes, that we refer to as modulated Volterra processes, defined, for , as

| (3.3) |

Here, is the kernel of a self-similar Volterra process of index , i.e.

| (3.4) |

that satisfies Assumption (A1), modulated by a slowly varying function , i.e. a function such that

for every . Thanks to (2.8) and (3.4), we have

First we note that here for , and

Note that the limit kernel is independent of . For these processes, if assumptions (K1) and (K2) are satisfied, we have a short-time LDP with the same rate function as the self-similar process and inverse speed . Therefore, the rate function does not depend on the modulating function , but the speed of the LDP does.

3.2 Fractional Ornstein-Uhlenbeck process

Let us recall that the Mandelbrot-Van Ness fBM is the centered continuous Gaussian process with covariance function

This process is self-similar with exponent and admits a Volterra representation with kernel (see e.g. Nualart (2006))

| (3.5) |

where

For and , we consider the fOU process, solution to

which is given explicitly, with initial condition , by333 Let us mention that, for other purposes, one could consider the stationary solution to the fractional SDE above (see for example Gatheral et al. (2018)), explicitly given by However, we are interested in this paper in option valuation, so we take as volatility driver the process above, with , so that is spot volatility in (4.6).

Here, the stochastic integral with respect to can be defined, by integration by parts and the stochastic Fubini theorem, as

| (3.6) |

We note from this equation that self-similarity for fOU is approximately inherited from the fBM, for small time scales. From (3.6) we obtain, for , the Volterra representation

with

and as above (see, e.g., Section 2 in Cellupica and Pacchiarotti (2021)). Condition (A1) for this process, with , was established in Lemma 10 in Gulisashvili (2018). Here we have

Let us verify that conditions (K1) and (K2) are satisfied.

(K1) It is enough to observe that

where is a constant independent of . Therefore

uniformly for . Therefore also

uniformly for and (K1) is proved (with and ).

(K2) For we have

Therefore, denoting by a constant (not depending on ), we have

since (see for example Lemma 8 in Gulisashvili (2018))

Condition (K2) is verified with infinitesimal function , and limit kernel . Therefore, the short-time asymptotic behaviour of the model with volatility given as a function of the fOU process is exactly the same as the one of the model with volatility given as a function of the fBM, meaning that they both satisfy LDPs where the speed and rate function are the same. Indeed, the rate function in (2.7) is the same that was found in Forde and Zhang (2017). This can be computed numerically as we do in Section 5.

4 Short-time asymptotic pricing and implied volatility

In this section we discuss applications to option pricing and behaviour at short maturities of implied volatility for certain stochastic volatility models, using the LDP previously discussed. We denote

| (4.1) |

the European put and call prices with maturity and log-moneyness (i.e., strike , since ).

4.1 Large deviations pricing for log-modulated models

Let us consider the stochastic volatility model given by (2.1) and (3.3), i.e.

with kernel of a self-similar process, of exponent , that satisfies (A1), and slowly varying, such that satisfies (A1), (K1), (K2). In particular, this holds true for the kernel in (3.1), that essentially is the kernel of the log-fBM in Bayer et al. (2021), for . Let

where is the rate function in (2.7).

Let us write if (see also Appendix A).

Theorem 4.1.

Proof. We just prove the call asymptotics (the least straightforward). From Theorem 2.4 and Theorem 2.6, following the computations in Section 3.1, we have that the family satisfies an LDP with inverse speed and good rate function given by formula (2.7). Since (see Remark 2.5) we have for

for every sequence . Therefore, setting , so that , we have

i.e.,

| (4.3) |

Let us prove the upper bound. Let be small enough such that and fix . We have

where we have used Hölder’s inequality and the existence of such that . Moreover, is uniformly bounded as , using Doob’s maximal inequality for the martingale . Now from LDP (4.3) it follows

and we conclude by taking large enough (here we also use the goodness of the rate function, which implies that as .)

Now let us look at the lower bound. We have

Therefore

and the first summand goes to as . Therefore, for any ,

By continuity of (Forde and Zhang, 2017, Corollary 4.10) and the fact that the rate function is the same as for the self-similar process, this holds for as well and the lower bound is proved.

The following implied volatility asymptotics is a consequence of the previous result and an application of Gao and Lee (2014). Let us denote with asymptotic equivalence ( iff ).

Corollary 4.2.

For model (2.1), let us assume that (A1), (K1), (K2), (), () hold, that is a martingale and there exist such that . Then, with log-moneyness as in (4.2) and , the short-time asymptotics for implied volatility

| (4.4) |

holds. As a consequence, with , the finite difference implied volatility skew satisfies

| (4.5) |

Remark 4.3.

When taking the kernel in (3.1) with we have

in (4.5), and the finite difference skew at the LDP regime explodes as . We prove this for , because (K2) fails for . However, even for the process is defined and the skew asymptotics (4.5) can be computed and is consistent with the “Gaussian” result at the Edgeworth regime in Bayer et al. (2021). It is also clear that

is an approximation of for close to . Assuming smooth and, as one expects, and , we have

so that we can approximate the implied skew as

Note, however, that (4.5) and the asymptotics in Bayer et al. (2021) are different mathematical results. In addition, besides providing the at-the-money behaviour, result (4.4) can also be used to compute the whole short-dated smile, including the wings, so it can be used for calibration and, for example, for tail risk hedging. Since, as noted at the end of Section 3.1, the rate function is the same as for the self-similar process and does not depend on the modulating function , it can be computed as explained in Section 5 for fOU.

4.2 Large deviation pricing under fractional Ornstein-Uhlenbeck volatility

As consequence of Theorem 2.4 and Theorem 2.6 and the computations in Section 3.2, we can derive asymptotic pricing formulas for European put and call options under the price dynamics in (2.1), with volatility driven by the process given in (3.6). In this case, we are considering the stochastic volatility dynamics

| (4.6) |

with . Notice that this is written in differential form but could also be written explicitly as in (3.6). With the same arguments used in the proof of Theorem 4.1, we have

where . More explicitly, (2.7) reads

| (4.7) |

We have the following theorem.

Theorem 4.4.

Suppose (), () hold. If and , the put price in short-time satisfies

In addition, we now assume that the process is a martingale and there exist such that . If and , we have

Remark 4.5.

In both Theorems 4.1 and 4.4 the call price asymptotics holds under the assumption that the price process is a martingale, along with a moment condition. In the diffusive case () several related results are available. In particular, martingality holds if has exponential growth and (Sin, 1998; Jourdain, 2004; Lions and Musiela, 2007). Note that the assumption of negative correlation is justified from a financial perspective.

In the rough case, martingality is known to hold when has linear growth and the driving process is the fBM (Forde and Zhang, 2017). In Gassiat (2019), it is shown that for a class of rough volatility models with of exponential growth (that includes the rough Bergomi model) the stock price is a true martingale if and only if , while for , for any .

Models where the volatility is a function of a Gaussian process are considered in (Gulisashvili, 2020). If grows faster than linearly, conditions for the explosion of moments are given both in the correlated and uncorrelated case.

For models (3.3) and (4.6), these are open questions. We expect the conditions for the call asymptotics in Theorems 4.1 and 4.4 to hold in case and with exponential growth. In particular, martingality should definitely hold in the cases analogous to (Gassiat, 2019), but with fOU driver. Indeed, the distribution of the fOU process is more concentrated than the one of the fBM, because of the mean reversion property.

Proof. This follows from the classic argument that we spelled out in the proof of Theorem 4.1. The proof follows as in Appendix C, Proof of Corollary 4.13 in Forde and Zhang (2017). Again, from this call and put price asymptotics, an application of Corollary 7.1 in Gao and Lee (2014) gives the following result.

Corollary 4.6.

Under the assumptions of Theorem 4.4, writing , we have, for ,

| (4.8) |

As a consequence, the behavior of the implied skew at the large deviations regime under fOU-driven volatility is as follows.

Corollary 4.7.

Under the assumptions of Theorem 4.4, writing , we have, for ,

| (4.9) |

Remark 4.8 (On moderate deviations).

Model (4.6) should satisfy a moderate deviation result analogous to the ones in Bayer et al. (2019) and Theorem 3.13 in Friz et al. (2022). Let be as in (4.1), the price process given in (4.6). Assume that is times continuously differentiable. Let , and such that . Set . Then, we can formally compute the call asymptotics from Theorem 4.4, plugging as log price instead of , so that we substitute to in a Taylor expansion of at and get

Now, consider the speed in Theorem 4.4 and that if , recall from Forde and Zhang (2017) and Bayer et al. (2019) that and we find that the call price should satisfy the following moderate deviations asymptotics, as ,

We expect that a complete proof of this fact could be adapted from Proof of Theorem 3.13 in Friz et al. (2022) or Proof of Theorem 3.4 in Bayer et al. (2019). Assuming this call price asymptotics holds true, the following implied volatility asymptotics can be derived using Corollary 7.1, Equation (7.2) in Gao and Lee (2014) and that

| (4.10) |

Remark 4.9 (On related results).

A pathwise small-noise LDP under fOU volatility has been proved in Horvath et al. (2019), with different hypothesis in particular on the function . From this LDP, a short-time result for a suitably renormalized process is also derived, with a time-scaling different from ours.

In Jacquier and Pannier (2022) asymptotic results are given for Volterra driven volatility models, including large and moderate deviations, also in small-time. Hypothesis on the models are different from ours, for example is of linear growth, or alternatively a moment condition of type for any holds. The rate function is given as an expression involving fractional derivatives of the minimiser. In particular, in (Jacquier and Pannier, 2022, Section 4.2.1) these results are applied to the rough Stein-Stein model, which is similar to (4.6), with the RLp instead of the fBM, and with the specific choice of volatility function . Analogous results should also hold with the fBM instead of the RLp as driver of the volatility.

Remark 4.10 (On applications).

As mentioned in the introduction, short-time asymptotic approximations to the implied volatility surface are used for model calibration, pricing and other applications. They give information on option prices with short maturity, with low computational burden. This helps for example in the creation of delta-hedging strategies that are sensitive to short-term moves in the underlying and in general in trading and risk management. Efficient and accurate methods for calibrating fOU-driven volatility models are relevant, for example, because these volatility models are used for computing option prices and implied volatilities (Garnier and Sølna, 2017, 2020a) and for hedging (Garnier and Sølna, 2020b). Furthermore, Garnier and Sølna (2018a) compare the price impact of fast mean-reverting Markov stochastic volatility models with the price impact of mean reverting rough volatility models (see also Garnier and Sølna (2019)). In Fouque and Hu (2018), a model with both return and volatility driven by a fast mean reverting fOU process are used for portfolio optimization, in the regime.

5 Numerical experiments

In this section we test the accuracy of short-time pricing formulas (4.8), and (4.10) and of the implied skew asymptotics (4.9). We do so for a stochastic volatility model with asset price dynamics given by (2.1), with both fBM-driven volatility (i.e., is the fBM) and fOU-driven volatility (i.e., is the fOU process, as in (4.6)). Recall that both fBM and fOU models lead to the same rate function.

For numerical experiments with log-fBM volatility, we refer to Bayer et al. (2021). In particular, the discussion in Remark 4.3 on the at-the-money implied skew for log-modulated models is consistent with the numerical evaluations of at-the-money skews in (Bayer et al., 2021, Section 7).

From Section 3.2, we have the Volterra representation of the fBM

where is the kernel in (3.5), and the Volterra representation of the fOU process

| (5.1) |

To evaluate the quality of approximations (4.8), (4.9) and (4.10), we first simulate Monte Carlo call prices under both these models, from which we then recover Black-Scholes implied volatilities. In both cases we consider a volatility function , depending on positive parameters given by

| (5.2) |

To compute these prices under our stochastic volatility dynamics, we need to simulate the asset price at the fixed time horizon . Hence we consider a time-grid , , and on this grid the random vector , first with and then . In both cases, it is a multivariate Gaussian vector with zero mean and known covariance matrix, that can be computed from the Volterra representation of the processes. The whole vector can be simulated using a Cholesky factorization of this covariance matrix. We then use this vector to construct an approximate sample of the log-asset price

by using a forward Euler scheme on the same time-grid

We produce i.i.d. approximate Monte Carlo samples , that we use to evaluate call option prices by standard sample average. Then, we compute the corresponding implied volatilities by Brent’s method (see Atkinson (2008), Press et al. (2012)), where is the maturity and the log-moneyness.

Note that Theorem 4.4, Corollary 4.6 and Corollary 4.7 do not apply to the model above, because does not satisfy the polynomial growth condition (). However, also in in the self-similar case, large deviations pricing results were first obtained under linear growth conditions in Forde and Zhang (2017) and then the conditions were weakened in Bayer et al. (2020); Gulisashvili (2018) to include exponential growth. Therefore, we chose here to test our result on the exponential volatility in (5.2), for which our result should hold as well. This choice is more realistic, being analogous to the rough Bergomi model, and being the volatility function considered e.g. in Garnier and Sølna (2020b).

To evaluate the accuracy of large deviations approximation (4.8), we follow the choice in Friz et al. (2022) and use as model parameters , and as mean reversion parameter in fOU we take or . These parameters are similar to the ones estimated on empirical volatility surfaces, as for example in Bayer et al. (2016). We take a rough, but not “extremely rough” ( instead of ) Hurst parameter , motivated by the recent study El Amrani and Guyon (2023).

We simulate Monte Carlo samples using discretization points. We estimate call option prices , where , and the corresponding implied volatility .

Then, we need to compute . The rate function in (4.7) can be approximated numerically using the Ritz method, as described in detail in (Gelfand and Fomin, 1963, Section 40), Forde and Zhang (2017), and (Friz et al., 2022, Remark 4.3 and Section 5.1). The rate function is obtained trough numerical optimization on a fixed, finite number of coefficients associated to a basis of the Cameron-Martin space . We take as basis the Fourier basis, i.e. with

that we truncate to (larger values of did not seem to improve the computation) and use the more explicit representation of the rate function in (4.7) given in Forde and Zhang (2017), (Bayer et al., 2019, Proposition 5.1), (Friz et al., 2022, Section 5.1).

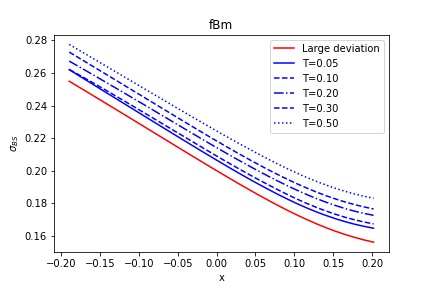

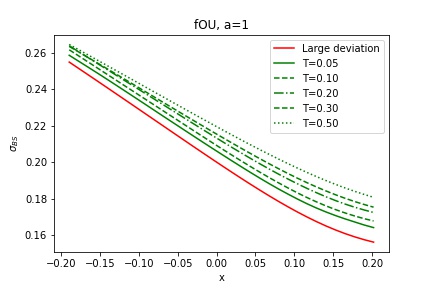

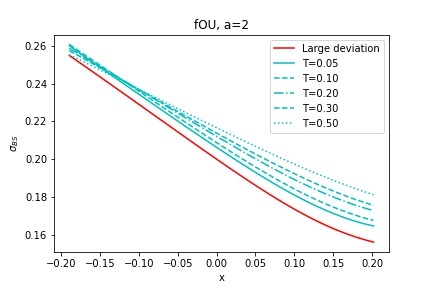

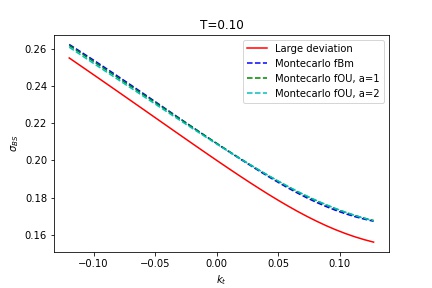

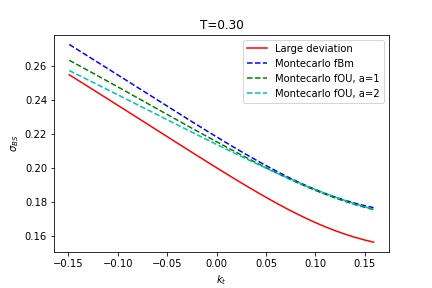

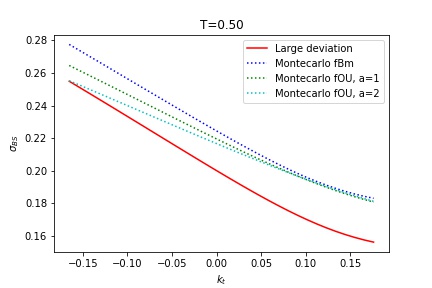

In Figure 1 we show for each model how, as the maturity becomes smaller, gets closer to the asymptotic limit in (4.8), where . We recall that is the option maturity and we numerically evaluate for and for equidistant points. The fact that, even for very small maturities, the short-time limit is not reached, can be explained by the fact that the error is of order (as shown in the self-similar case in Friz et al. (2022)), which vanishes as , albeit slowly, since .

In Figure 2, for each fixed maturity, we compare the implied volatility smiles produced by each model (fOU vs fBM-driven volatilities), in order to observe the influence of the magnitude of the mean reversion parameter on the volatility smiles. In particular, we note that implied volatilities generated by fOU-driven models seem to fall between the implied volatilities generated by fBM-driven models and the asymptotic smile, indicating convergence also if polynomial growth of is not satisfied in this example.

We test now the moderate deviation asymptotics in Remark 4.8. In order to do so, let us recall an expansion to the fourth order of the rate function that allows us to use the second order moderate deviation.444This expansion is given in (Friz et al., 2022, Lemma 6.1), where the kernel is used. However, in the proof of this result the specific shape of the kernel is not used, but only self-similarity, and therefore it holds for in (3.5) as well. We denote now and with the adjoint of in , so that , where again is the fBM kernel in (3.5).

Lemma 5.1 (Fourth order energy expansion).

Let us assume that is countinuously differentiable two times. Let be the energy function in (4.7). Then

| (5.3) |

where

and

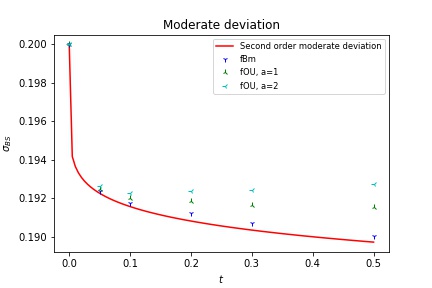

We plot in Figure 3 implied volatilities computed via Monte Carlo simulations and the corresponding approximation given in (5.4). We take again as in(5.2), with parameters , and . We first note that we fix in (4.10), and so we choose , that is the interval . With respect to our previous experiments, we also take the smaller vol of vol parameter , which is in line with the choices in Bayer et al. (2019); Friz et al. (2022). Indeed, the quality of the approximation deteriorates as grows, and for larger the asymptotic formula (5.4) is accurate on a smaller time interval.

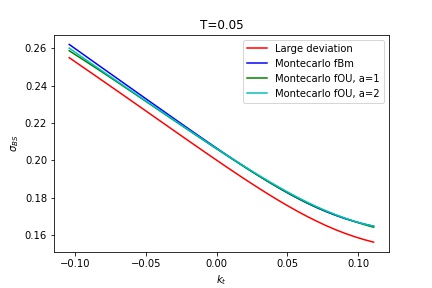

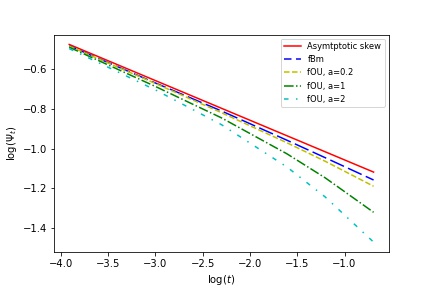

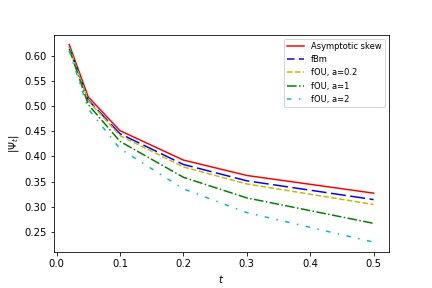

In Figure 4 we compare, with , , the absolute value of the large deviations finite difference implied skew

| (5.5) |

computed on fBm-driven and fOU-driven stochastic volatility models, with the asymptotic skew expected from Corollary 4.7, where we also use the approximation, as ,

We observe that, consistently with the smile slopes observed in Figure 2, larger mean-reversion parameters correspond to flatter smiles and smaller skews (in absolute value), smaller mean-reversion parameters correspond to steeper smiles and larger skews (in absolute value), fBm has a larger skew than fOU, and the asymptotic skew is even larger than the one generated from fBm, although very close to it. As maturity , the difference between all these skews vanishes.

This could reflect the fact that larger mean-reversion parameters give more concentrated volatility trajectories, with in (5.1) staying closer to and therefore the stochastic volatility path staying closer to the spot-vol . This may produce flatter implied volatility surfaces and explain smiles and skews observed in Figures 2, 3 and 4 corresponding to larger ’s. On the short end of the surface, however, all of these have to coincide due to our asymptotic results. Let us also mention that the discrepancy observed in Figure 2 on the level of the smile (regardless of the skew), between the asymptotic red line and all the simulated “positive maturity” lines is likely due to a term-structure term of order , for which we refer the reader to Friz et al. (2022) (large deviations setting) and El Euch et al. (2019) (central limit setting).

6 Conclusion

In this paper, we prove a short-time large deviation principle for stochastic volatility models, with volatility given as a function of a Volterra process. This result holds without strict self-similarity assumptions on the processes driving the model, and can therefore be applied to some notable examples of (non self-similar) rough volatility models.

We first consider an application to the log-modulated rough stochastic volatility models introduced in Bayer et al. (2021). We derive short-maturity asymptotics for European option prices and implied volatility surfaces. Our results on the implied skew at the large deviations regime are consistent with the results at the Edgeworth central-limit regime derived in Bayer et al. (2021), but allow for valuation of options further from the money.

Then we consider models where volatility is given as a function of a fractional Ornstein-Uhlenbeck process, as e.g. in the seminal work Gatheral et al. (2018). In this case we find that the limit short maturity behavior of option prices and implied volatilities, as well as the short time implied skew, is the same as the one of a model driven by a fractional Brownian motion. We investigate this fact numerically on simulation results, discussing also moderate deviations pricing and implied skew asymptotics.

Appendix A The large deviations principle

Large deviations give an asymptotic computation of small probabilities on an exponential scale (see e.g. Dembo and Zeitouni (1998) as a reference on this topic). We recall some basic definitions (see e.g. Section 1.2 in Dembo and Zeitouni (1998)). Throughout this paper a speed function is a sequence such that . A sequence of random variables , taking values on a topological space , satisfies the large deviation principle (LDP) with rate function and speed function if is a lower semicontinuous function,

for all open sets , and

for all closed sets . A rate function is said to be good if all its level sets are compact. Therefore, if an LDP holds, and is a Borel set such that ( and are the interior and the closure of respectively), then

where In this case we write

Moreover is exponentially tight with respect to the speed function if, for all , there exists a compact such that

The concept of exponential tightness plays a crucial role in large deviations; in fact this condition is often required to establish that the LDP holds for a sequence of random variables taking values on an infinite dimensional topological space. In this paper we refer to condition (8) and (9) in Section 2 in Macci and Pacchiarotti (2017)) which yield the exponential tightness when the topological space of the continuous function is equipped with the topology of the uniform convergence.

References

- Ait-Sahalia et al. (2020) Y. Ait-Sahalia, C. Li, and C.X. Li (2020) Implied stochastic volatility models. The Review of Financial Studies, 34:394–450.

- Alòs and Leon (2017) E. Alòs and J. A. León (2017) On the curvature of the smile in stochastic volatility models. SIAM Journal on Financial Mathematics, 8(1):373-399.

- Alòs et al. (2007) E. Alòs, J. A. León and J. Vives (2007) On the short-time behavior of the implied volatility for jump-diffusion models with stochastic volatility. Finance and Stochastics, 11(4):571–589.

- Atkinson (2008) K.E. Atkinson (2008) An introduction to numerical analysis, 2nd ed, Wiley India Pvt. Limited

- Baldi and Pacchiarotti (2022) P. Baldi and B. Pacchiarotti (2022) Large Deviations of continuous Gaussian processes: from small noise to small time. Preprint arXiv:2207.12037.

- Bayer et al. (2020) C. Bayer, P. K. Friz, P. Gassiat, J. Martin and B. Stemper (2020) A regularity structure for rough volatility. Mathematical Finance, 30(3):782–832.

- Bayer et al. (2016) C. Bayer, P. K. Friz and J. Gatheral (2016) Pricing under rough volatility. Quantitative Finance, 16(6):887–904.

- Bayer et al. (2019) C. Bayer, P. K. Friz, A. Gulisashvili, B. Horvath and B. Stemper (2019) Short-time near-the-money skew in rough fractional volatility models. Quantitative Finance, 19(5):779–798.

- Bayer et al. (2021) C. Bayer, F. Harang and P. Pigato (2021) Log-modulated rough stochastic volatility models. SIAM Journal on Financial Mathematics, 12(3):1257–1284.

- Bourgey et al. (2023) F. Bourgey, S. De Marco, P. K. Friz and P. Pigato (2023) Local volatility under rough volatility. Mathematical Finance, 33(4):1119-1145

- Catalini and Pacchiarotti (2023) G. Catalini and B. Pacchiarotti (2023) Asymptotics for multifactor Volterra type stochastic volatility models. Stochastic Analysis and Applications, 41(6):1025-1055.

- Cellupica and Pacchiarotti (2021) M. Cellupica and B. Pacchiarotti (2021) Pathwise Asymptotics for Volterra Type Stochastic Volatility Models. Journal of Theoretical Probability, 34(2):682–727.

- Cheridito et al. (2003) P. Cheridito, H. Kawaguchi and M. Maejima (2003) Fractional Ornstein-Uhlenbeck processes. Electronic Journal of Probability, 8:1–14.

- Dembo and Zeitouni (1998) A. Dembo and O. Zeitouni (1998) Large Deviations Techniques and Applications, Jones and Bartlett, Boston MA.

- El Euch et al. (2019) O. El Euch, M. Fukasawa, J. Gatheral and M. Rosenbaum (2019) Short-term at-the-money asymptotics under stochastic volatility models. SIAM Journal on Financial Mathematics, 10(2):491–511.

- Forde et al. (2020) M. Forde, M. Fukasawa, S. Gerhold and B. Smith (2022) The Riemann-Liouville field and its GMC as , and skew flattening for the rough Bergomi model. Statistics and Probability Letters, 181:10926.

- Forde et al. (2021) M. Forde, S. Gerhold and B. Smith (2021) Small-time, large-time and asymptotics for the rough Heston model. Mathematical Finance, 31:203–241.

- Forde and Zhang (2017) M. Forde and H. Zhang (2017) Asymptotics for rough stochastic volatility models. SIAM Journal on Financial Mathematics, 8(1):114–145.

- Friz et al. (2021) P.K. Friz, P. Gassiat and P. Pigato (2021) Precise asymptotics: Robust stochastic volatility models. Annals of Applied Probability, 31(2):896–940.

- Friz et al. (2022) P.K. Friz, P. Gassiat and P. Pigato (2022) Short dated smile under Rough Volatility: asymptotics and numerics. Quantitative Finance, 22(3):463–480.

- Friz et al. (2021) P.K. Friz, P. Pigato and J. Seibel (2021) The Step Stochastic Volatility Model. Risk magazine, June 2021, (Longer version available at at SSRN: https://ssrn.com/abstract=3595408).

- Fukasawa (2011) M. Fukasawa (2011) Asymptotic analysis for stochastic volatility: Martingale expansion. Finance and Stochastics, 15:635–654.

- Fukasawa (2017) M. Fukasawa (2017) Short-time at-the-money skew and rough fractional volatility. Quantitative Finance, 17(2):189–198.

- Fukasawa (2020) M. Fukasawa (2020) Volatility has to be rough. Quantitative Finance, 21(1):1–8.

- Gao and Lee (2014) K. Gao and R. Lee. (2014) Asymptotics of implied volatility to arbitrary order. Finance and Stochastics, 18:349–392.

- Garnier and Sølna (2017) J. Garnier and K. Sølna (2017) Correction to Black-Scholes Formula Due to Fractional Stochastic Volatility. SIAM Journal on Financial Mathematics, 8:560–588.

- Garnier and Sølna (2018a) J. Garnier and K. Sølna (2018a) Option pricing under fast-varying and rough stochastic volatility. Annals of Finance, 14:489–516.

- Garnier and Sølna (2019) J. Garnier and K. Sølna (2019) Option pricing under fast-varying long-memory stochastic volatility. Mathematical Finance, 29:39–83.

- Garnier and Sølna (2020a) J. Garnier and K. Sølna (2020a) Implied Volatility Structure in Turbulent and Long-Memory Markets. Frontiers in Applied Mathematics and Statistics , 29 April 2020.

- Garnier and Sølna (2020b) J. Garnier and K. Sølna (2020b) Optimal hedging under fast-varying stochastic volatility. SIAM Journal on Financial Mathematics, 11(1):274–325

- Gassiat (2019) P. Gassiat (2019) On the martingale property in the Rough Bergomi model. Electronic Communications in Probability, 24:1–9

- Gatheral et al. (2018) J. Gatheral, T.Jaisson and M. Rosenbaum (2018) Volatility is rough. Quantitative Finance, 18(6):933–949.

- Gelfand and Fomin (1963) I.M. Gelfand and S.V. Fomin (1963) Calculus of variations. Revised English edition translated and edited by Richard A. Silverman Prentice-Hall.

- Gulisashvili (2018) A. Gulisashvili (2018) Large Deviation Principle for Volterra type Fractional Stochastic Volatility Models. SIAM Journal on Financial Mathematics, 9(3):1102–1136.

- Gulisashvili (2020) A. Gulisashvili (2020) Gaussian stochastic volatility models: scaling regimes, large deviations, and moment explosions. Stochastic Processes and their Applications, 130(6):3648–3686.

- Gulisashvili (2021) A. Gulisashvili (2021) Time-inhomogeneous Gaussian stochastic volatility models: Large deviations and super roughness. Stochastic Processes and their Applications, 139:37–79.

- Gulisashvili (2022) A. Gulisashvili (2022) Multivariate Stochastic Volatility Models and Large Deviation Principles. Preprint arXiv:2203.09015.

- Gulisashvili et al. (2018a) A. Gulisashvili, F. Viens and X. Zhang (2018a) Small-Time Asymptotics for Gaussian Self-Similar Stochastic Volatility Models, Applied Mathematics & Optimization, 1–41.

- Gulisashvili et al. (2018b) A. Gulisashvili, F. Viens and X. Zhang (2018b) Extreme-strike asymptotics for general Gaussian stochastic volatility models. Annals of Finance, 15(1):59–101.

- Guyon (2021) J. Guyon (2021) Dispersion-Constrained Martingale Schrödinger Problems and the Exact Joint S&P 500/VIX Smile Calibration Puzzle. Available at SSRN: https://ssrn.com/abstract=3853237 or http://dx.doi.org/10.2139/ssrn.3853237

- El Amrani and Guyon (2023) M. El Amrani and J. Guyon (2023) Does the term-structure of equity at-the-money skew really follow a power law? Risk magazine, July 2023, (Longer version available at at SSRN: https://ssrn.com/abstract=4174538).

- Fouque and Hu (2018) J.P. Fouque and R. Hu (2018) Optimal Portfolio under Fast Mean-Reverting Fractional Stochastic Environment SIAM Journal of Financial Mathematics, 9(2):564-601.

- Hager and Neuman (2021) P. Hager and E. Neuman (2021) The Multiplicative Chaos of Fractional Brownian Fields. Annals of applied probability, 32(3) 2139–2179.

- Horvath et al. (2019) B. Horvath, A. Jacquier and C. Lacombe (2019) Asymptotic behaviour of randomised fractional volatility models. Journal of Applied Probability, 56(2):496–523.

- Jacquier et al. (2018) A. Jacquier, M.S. Pakkanen and H. Stone (2018) Pathwise large deviations for the rough Bergomi model. Journal of Applied Probability, 55(4):1078–1092.

- Jacquier and Pannier (2022) A. Jacquier and A. Pannier (2022) Large and moderate deviations for stochastic Volterra systems, Stochastic Processes and their Applications, 149:142–187.

- Jourdain (2004) B. Jourdain (2004) Loss of martingality in asset price models with lognormal stochastic volatility, preprint Cermics, 267:2004.

- Lee (2005) R. W. Lee (2005) Implied volatility: Statics, dynamics, and probabilistic interpretation, in Recent Advances in Applied Probability, Springer, New York, 241-268.

- Lions and Musiela (2007) P. L. Lions and M. Musiela (2007) Correlations and bounds for stochastic volatility models, In Annales de l’Institut Henri Poincare (C) Non Linear Analysis, 24:1–16.

- Macci and Pacchiarotti (2017) C. Macci and B. Pacchiarotti (2017) Exponential tightness for Gaussian processes with applications to some sequences of weighted means. Stochastics 89(2):469–484.

- Medvedev and Scaillet (2003) A. Medvedev and O. Scaillet (2003) A simple calibration procedure of stochastic volatility models with jumps by short term asymptotics. Research Paper No. 93, September 2003, FAME International Center for Financial Asset Management and Engineering. Available at SSRN 477441, 2003.

- Medvedev and Scaillet (2007) A., Medvedev and O. Scaillet (2007) Approximation and calibration of short-term implied volatilities under jump-diffusion stochastic volatility. The Review of Financial Studies, 20(2):427–459.

- Neuman and Rosenbaum (2018) E. Neuman and M. Rosenbaum (2018) Fractional Brownian motion with zero Hurst parameter: a rough volatility viewpoint. Electronic Communications in Probability, 23(61):1–12.

- Nualart (2006) D. Nualart (2006) Malliavin Calculus and Related Topics, Springer, Berlin.

- Osajima (2015) Y. Osajima (2015) General asymptotics of Wiener functionals and application to implied volatilities. In Large Deviations and Asymptotic Methods in Finance, 137–173, Springer.

- Pigato (2019) P. Pigato (2019) Extreme at-the-money skew in a local volatility model. Finance and Stochastics, 23:827–859.

- Press et al. (2012) W. H. Press, S. A. Teukolsky, W. T. Vetterling and B. P. Flannery (2007) Numerical Recipes: The Art of Scientific Computing (3rd ed.). New York: Cambridge University Press.

- Sin (1998) C. A. Sin (1998) Complications with stochastic volatility models. Advances in Applied Probability, 30(1):256–268.