Impacts of Public Information

on Flexible Information Acquisition††thanks: I thank seminar participants for valuable discussions and comments at Otaru University of Commerce. I acknowledge financial support by MEXT, Grant-in-Aid for Scientific Research (18H05217).

Abstract

Interacting agents receive public information at no cost and flexibly acquire private information at a cost proportional to entropy reduction. When a policymaker provides more public information, agents acquire less private information, thus lowering information costs. Does more public information raise or reduce uncertainty faced by agents? Is it beneficial or detrimental to welfare? To address these questions, we examine the impacts of public information on flexible information acquisition in a linear-quadratic-Gaussian game with arbitrary quadratic material welfare. More public information raises uncertainty if and only if the game exhibits strategic complementarity, which can be harmful to welfare. However, when agents acquire a large amount of information, more provision of public information increases welfare through a substantial reduction in the cost of information. We give a necessary and sufficient condition for welfare to increase with public information and identify optimal public information disclosure, which is either full or partial disclosure depending upon the welfare function and the slope of the best response.

JEL classification: C72, D82, E10.

Keywords: public information; private information; crowding-out effect; linear-quadratic-Gaussian game; optimal disclosure; information design; rational inattention.

1 Introduction

Consider a policymaker (such as a central bank) who discloses public information to agents (such as firms and consumers). Agents receive public information provided by the policymaker at no cost and flexibly acquire private information at a cost proportional to entropy reduction (Sims, 2003; Yang, 2015; Denti, 2020). When the policymaker provides more public information, agents acquire less private information, thus lowering information costs. Then, does the total amount of information about an unknown state increase or decrease? Should the policymaker provide more information to increase welfare? What is the optimal disclosure of public information maximizing welfare?

We address these questions in a two-stage game based on a symmetric linear-quadratic-Gaussian (LQG) game with a continuum of agents, where a payoff function is quadratic and an underlying state is normally distributed. In period 1, the policymaker chooses the precision of a normally distributed public signal. The policymaker’s objective function is social welfare, which is a material benefit minus the agents’ information cost, and the material benefit is an arbitrary quadratic function such as the aggregate payoff. In period 2, each agent flexibly acquires private information in the LQG game. The second-period subgame is essentially the same as those studied by Denti (2020) and Rigos (2020).

We measure the total amount of information in terms of the reduction in entropy caused by receiving public and private signals, i.e., the mutual information. By the chain rule of information, it can be represented as the sum of the mutual information of a public signal and a state and the conditional mutual information of a private signal and a state. When the policymaker provides more precise public information, the former increases, but the latter decreases. This effect of public information is referred to as the crowding-out effect (Colombo et al., 2014).111This effect is also found in Colombo and Femminis (2008), Wong (2008), Hellwig and Veldkamp (2009), Myatt and Wallace (2012), among others.

Our first main result shows that more provision of public information decreases the total amount of information if and only if the game exhibits strategic complementarity (i.e., the slope of the best response is strictly positive). This is because the crowding-out effect is more significant under strategic complementarity than under strategic substitutability (Colombo et al., 2014). Consider the benchmark case of no strategic interaction (i.e., the slope equals zero). In this case, public and private signals are perfect substitutes because an agent pays no attention to the opponents’ actions. Thus, when the policymaker increases one unit of public information, an agent reduces the same unit of private information, so the total amount of information remains constant. In a game with strategic complementarity, however, public and private signals are imperfect substitutes and each agent puts more value on public information than on private information from a coordination motive. Consequently, when the policymaker increases one unit of more valuable public information, an agent reduces more units of less valuable private information, so the total amount of information decreases.

To study the welfare implication of the above result, we represent the expected welfare (in the equilibrium of the second-period subgame) as a linear combination of the volatility (the variance of the average action) and the dispersion (the variance of individual actions around the average action) minus the cost of information. This follows Ui and Yoshizawa (2015) who study the social value of public information in the case of exogenous private information.

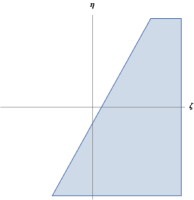

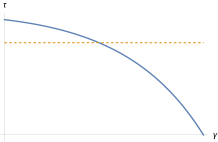

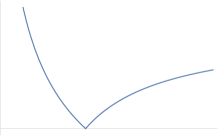

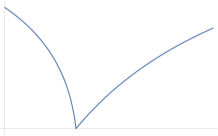

Our second main result is a necessary and sufficient condition for welfare to increase with public information, which depends upon the coefficients of volatility and dispersion and the slope of the best response. When the precision of public information is very low, more precise public information always increases welfare. This is because agents acquire a substantial amount of information facing considerable uncertainty, incurring an inefficiently large cost. When the precision of public information is not so low, more precise public information can reduce welfare if the coefficient of dispersion is greater than a threshold value determined by the coefficient of volatility (see Figure 1, where is the coefficient of dispersion, is that of volatility, and is the slope of the best response). In addition, the threshold value is increasing in the coefficient of volatility if the slope of the best response is not so large, but it is decreasing otherwise. This result is attributed to the following properties of dispersion and volatility. The dispersion decreases with public information because it equals the difference between the variance and the covariance of individual actions, and more precise public information brings them closer. In contrast, if the slope of the best response is not so large, the volatility increases with public information because it equals the covariance of individual actions, and more precise public information increases the covariance through an increase in the correlation coefficient. These properties are essentially the same as in the case of exogenous private information (Ui and Yoshizawa, 2015) or rigid information acquisition (Ui, 2022). However, if the slope of the best response is very large, there is a sharp difference. That is, the volatility decreases with public information due to the crowding-out effect enhanced by strong strategic complementarity.

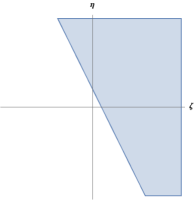

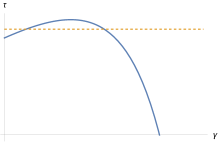

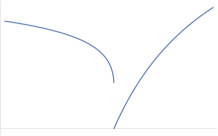

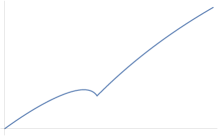

Our last main result identifies the optimal precision of public information. We show that full disclosure (i.e., the precision is infinite) is optimal if the coefficient of volatility is strictly positive and greater than a threshold value determined by that of dispersion; partial disclosure (i.e., the precision is finite) is optimal otherwise (see Figure 2a). It should be noted that no disclosure is always suboptimal, which is in sharp contrast to the case of exogenous private information. Ui and Yoshizawa (2015) study optimal disclosure of public information under exogenous private information and show that no disclosure is optimal if the coefficient of volatility is small enough (see Figure 2b). Even if the precision of private information is endogenously determined in the rigid information acquisition model (Colombo et al., 2014), no disclosure can be optimal (Ui, 2022).

As applications of the above results, we consider a Cournot game (Vives, 1988) and an investment game (Angeletos and Pavan, 2004) adopting the total net profit as a measure of firms’ welfare. Mathematically, both games belong to the same class of games with different slopes of the best response: a Cournot game has a negative slope exhibiting strategic substitutability, and an investment game has a positive slope exhibiting strategic complementarity. In the case of exogenous private information, more precise public information can reduce the total profit if and only if the game exhibits strong strategic substitutability, in which case no disclosure can be optimal (Bergemann and Morris, 2013; Angeletos and Pavan, 2004). This result remains valid in the case of rigid information acquisition (Ui, 2022). A contrasting result holds in the case of flexible information acquisition. That is, more precise public information can reduce the total profit if and only if the game exhibits strong strategic complementarity, while full disclosure is always optimal. The difference arises from the crowding-out effect enhanced by strategic complementarity.

We also apply our results to a beauty contest game (Morris and Shin, 2002). The welfare is the negative of the mean squared error of an individual action from the state minus the cost of information. In the case of exogenous private information, it is known that more precise public information can be harmful to welfare if the slope of the best response is greater than a threshold value (Morris and Shin, 2002). In the case of flexible information acquisition, a similar result holds, but the threshold value is less than in the case of exogenous private information; that is, welfare is more likely to decrease due to the crowding-out effect enhanced by strategic complementarity. This result is in clear contrast to the case of rigid information acquisition: the threshold value is greater than in the case of exogenous private information (Colombo and Femminis, 2008; Ui, 2014, 2022).

This paper is organized as follows. We introduce the model and discuss an equilibrium of the second-stage subgame in Sections 2 and 3, respectively. The relationship between the total amount of information and the provision of public information is studied in Section 4. Section 5 derives the representation of welfare in terms of the volatility and dispersion. We study the welfare effect of public information in Section 6 and identify the optimal disclosure in Section 7. Section 8 is devoted to applications. All proofs are relegated to the appendices.

1.1 Related literature

Flexible information acquisition is modeled in the rational inattention framework (Sims, 2003).222For a recent survey, see Mackowiak et al. (2021). There are two types of flexible information acquisition in games. Yang (2015) considers independent information acquisition focusing on global games, where agents pay attention to a state alone. Denti (2020) considers correlated information acquisition, where agents pay attention not only to the state but also to the opponents’ signals. Rigos (2020) studies LQG games under independent information acquisition,333The price-setting model of Mackowiak and Wiederholt (2009) is also an LQG game with independent information acquisition, but information acquisition technology is different. and Denti (2020) (in an earlier version) studies them under correlated information acquisition. The second-period subgame of our model corresponds to the models of Rigos (2020) and Denti (2020). We start with the assumption of correlated information acquisition and show that the set of equilibria in the second-period subgame is the same for both types of information acquisition.

Hébert and La’O (2021) consider agents who flexibly acquire information about a state, a public signal, and the opponents’ signals under a large class of information costs and study how properties of information costs relate to properties of equilibria. In particular, they examine whether agents correlate their actions with a public signal, which generates non-fundamental volatility, by assuming that a public signal is costly. In our paper, we assume that agents receive a public signal at no cost to study the direct impacts of public information provided by the policymaker.

This paper contributes to the literature on the role of public information in symmetric LQG games with a continuum of agents.444LQG games are introduced by Radner (1962). See Vives (2008) and Ui (2009, 2016). In the case of exogenous private information, Morris and Shin (2002) show that more provision of public information can be detrimental to welfare in a beauty contest game and attribute the harmful effect to agents’ overreaction to a public signal under strategic complementarity. Angeletos and Pavan (2007) study a symmetric LQG game and find a key factor for the social value of public information, which is referred to as the equilibrium degree of coordination relative to the socially optimal one. Bergemann and Morris (2013) characterize the set of all Bayes correlated equilibria in this game and advocate a problem of finding optimal ones.555Ui (2020) considers information design in general LQG games by formulating it as semidefinite programming. Ui and Yoshizawa (2015) solve the problem for an arbitrary quadratic welfare function by providing a necessary and sufficient condition for welfare to increase with private or public information. Colombo et al. (2014) integrate the symmetric LQG game and the model of rigid information acquisition with convex information costs and compare the equilibrium precision of private information with the socially optimal one.666Other models of information acquisition in symmetric LQG games are studied by Hellwig and Veldkamp (2009), Myatt and Wallace (2012, 2015), among others. Ui (2022) studies the welfare effect of public information in the model of Colombo et al. (2014) and identifies the optimal disclosure that maximizes welfare and the robust disclosure that maximizes the worst-case welfare, where the policymaker is uncertain about agents’ information costs. In our paper, we assume flexible information acquisition and demonstrate that the impacts of public information are essentially different from the cases of exogenous private information and rigid information acquisition. We also show that the harmful effect of public information can be attributed to the crowding-out effect enhanced by strategic complementarity.

This paper is also related to the literature on Bayesian persuasion and information design777See survey papers by Bergemann and Morris (2019) and Kamenica (2019) among others. with a receiver who costly acquires information. Lipnowski et al. (2020) and Bloedel and Segal (2020) consider a rationally inattentive receiver who can learn less information than what a sender provides. In Bloedel and Segal (2020), a receiver pays costly attention to the sender’s signals. In Lipnowski et al. (2020), a receiver pays costly attention to a state, but the information is less than that provided by the sender. Bizzotto et al. (2020) and Matysková and Montes (2021) consider a receiver who can acquire additional information after receiving a sender’s signal at no cost, which is closer in spirit to our model. The models in the above papers are based on the Bayesian persuasion framework (Kamenica and Gentzkow, 2011), and the sender’s payoff is independent of the receiver’s information cost. Our model is an extension of a symmetric LQG game, and the policymaker’s concern includes the agents’ information costs.

2 The model

There are a policymaker and a continuum of agents indexed by . We consider the following two-period setting. In period 1, the policymaker chooses the precision of public information about an uncertain state and provides public information to agents at no cost. In period 2, each agent flexibly acquires private information at a cost proportional to the mutual information and chooses an action.

Let denote an uncertain state, which is normally distributed with mean and precision (the reciprocal of the variance). Public information is given as a random variable , which is normally distributed such that the posterior distribution of given is a normal distribution with mean and precision ; that is, and . Such a random variable exists and statisfies . In particular, if , then . We call the precision of public information, which is chosen by the policymaker in period 1.888In the literature, public information is often given as , where is a normally distributed noise term with precision . The conditional distribution of given is a normal distribution with mean and precision . Thus, we can translate into by letting and because .

Agent ’s action is a real number . We write , , and . Agent ’s payoff to an action profile is

| (1) |

which is symmetric and quadratic in and . This game exhibits strategic complementarity if and strategic substitutability if . We assume , which guerantees the existence and uniquenss of a symmetric equilibrium under a symmetric Gaussian information structure. We also assume without loss of generality. By completing the square, we obtain

| (2) |

where . Thus, agent ’s best response equals the conditional expectation of a target . We call the slope of the best response. Note that has no influence on the best response, so we can assume when we study equilibria.

Agent acquires private information about a target (Denti, 2020). The cost of information is proportional to the mutual information of a private signal and a target . The mutual information of two random variables and is denoted by

where is the joint density function of , and and are the marginal density functions of and , respectively. We write for the mutual information with respect to the conditional distribution of given a public signal :

Then, the cost of a private signal is

where is constant.

Without loss of generality, we restrict attention to a direct signal that suggests an optimal action, as justified by the revelation principle. Agent ’s direct signal is optimal if it is a solution of an optimization problem

| (3) |

where follows an arbitrary distribution, and denotes the conditional expectation operator when a public signal is given. An optimal direct signal must satisfy .

Anticipating the agents’ decision in period 2, the policymaker chooses in period 1 to maximize the expected value of a welfare function given by

| (4) |

where is symmetric and quadratic in and , i.e.,

| (5) |

A typical case is the aggregate payoff, i.e., .

3 The second-period subgame

This section focuses on the second-period subgame and calculates an equilibrium. Denti (2020) (in an earlier version) obtains an equilibrium assuming , which guarantees the existence and uniquness of equilibrium. We drop this assumption and obtain the set of equilibria for all using a parameter called the information fraction (Bowsher and Swain, 2012), which will play an essential role in our analysis.

In the second-stage subgame, a public signal with precision is given, and it is common knowledge that is normally distributed with mean and precision . Thus, throughout this section, every probability distribution is understood as the conditional one given . Let and denote the conditional variance of and the conditional covariance of and , respectively. For example, . Henceforth, conditional will be omitted until the end of this section.

We focus on a symmetric equilibrium in which is jointly normally distributed. A joint distribution of is said to be an equilibrium if it satisfies the following conditions.

-

1.

is jointly normaly distributed, where and .

-

2.

is an optimal direct signal.

-

3.

, , and .

The last condition must hold because and an equilibrium is symmetric, i.e., for all , , , and .

We characterize an equilibrium using the ratio of the variance of an action to that of a target , which is denoted by

and referred to as the information fraction (Bowsher and Swain, 2012). It is known that the information fraction equals the square root of the correlation coefficient between and . Thus, it measures the amount of information about contained in . In fact, the mutual information of and is represented as

when and are jointly normally distributed. Note that if and only if and that because the cost of information is infinite when .

The next proposition shows that satisfies either

| (6) |

or with in every equilibrium.

Proposition 1.

There exists an equilibrium with if and only if there exists satisfying (6). There exists an equilibrium with if and only if . The number of equilibria is determined by , , , and .

-

(i)

Suppose that . Then, an equilibrium is unique: if and if .

-

(ii)

Suppose that .

-

(a)

If or , an equilibrium is unique: in the former case and in the latter case.

-

(b)

If or , two equilibria exist: in one of them.

-

(c)

If , three equilibria exist: in one of them.

-

(a)

In every equilibrium, . In an equilibrium with ,

| (7) | |||

| (8) | |||

| (9) | |||

| (10) |

This proposition says that there are two types of equilibria depending upon and . In the first type with , agents acquire information. In the second type with and , agents do not acquire information. For later use, we calculate the set of possible information fractions in the first type (a straightforward proof is omitted), which is illustrated in Figure 3.

Lemma 1.

For each , the set of information fractions satisfying is

where

In addition, if and .

The number of equilibria also depends upon the slope of the best response . If the slope is not too large (i.e., ), an equilibrium is unique. However, if the slope is large enough (i.e., ), multiple equilibria arise, which results from strong strategic complementarity. In a game with strategic complementarity, not only an action but also information is a strategic complement (Hellwig and Veldkamp, 2009). Thus, it can be an equilibrium strategy to acquire a small amount of information as well as a large amount of information when . On the other hand, an equilibrium is unique in the following cases. When , each agent has a strong incentive to acquire a large amount of information under considerable uncertainty, irrespective of how much information the opponents possess; when , each agent has no incentive to acquire information under little uncertainty.

In an equilibrium with , and are completely determined by and affine in , as (7) implies. Thus, actions are conditionally independent given because, otherwise, must also depend on the correlated component of actions. In addition, the mutual information of and equals that of and . This means that Proposition 1 remains valid under the alternative assumption of independent information acqusition (Yang, 2015) that

-

•

agents acquire private information about a state (rather than a target ) at a cost proportional to the mutual information, i.e., ,

-

•

private signals are conditionally independent given .

Rigos (2020) calculates the set of equilibria in this case, which is shown to coincide with that in Proposition 1.

Because Denti (2020) and Rigos (2020) do not show the equivalence of the two equilibrium concepts and do not use the information fraction to represent an equilbrium, we provide a proof for Proposition 1. It is an immediate consequence of the following well-known result.999This result is a restatement of Theorem 10.3.2 of Cover and Thomas (2006) and its proof.

Lemma 2.

Let be a normally distributed random variable with mean and variance . Consider an optimization problem

| (11) |

where is a random variable with an arbitrary distribution. An optimal solution exists and satisfies the following.

-

•

If , then is a normally distributed random variable satisfying , , and .

-

•

If , then and .

Using this lemma, we can identify an optimal direct signal because (3) is (11) with and when and are jointly normally distributed. For example, consider a special case of no strategic interaction, i.e., , where a target is . By Lemma 2, if , then . By solving this, we obtain and . This is rewritten as , which is a special case of (6) with .

4 Total information

Each agent receives two types of information about , public information in period 1 and private information in period 2. When the policymaker provides more precise public information, agents acquire less precise private information in a unique equilibrium with information acquisition. This effect of public information on private information is referred to as the crowding-out effect. In the presence of the crowding-out effect, does the total amount of information about increase with public information? We address this question in terms of mutual information.

Assume that is sufficiently small, i.e., . Imagine that the policymaker chooses in period 1 and agents follow the unique equilibrium in period 2, where the information fraction is by Lemma 1. We measure the total amount of information about contained in by means of , i.e., the mutual information of and . By the chain rule of information, it holds that

where is the mutual information of and , and is the mutual information of and under the conditional probability distribution given . That is, the total amount of information is the sum of those of public information and private information, each of which is calculated as

| (12) |

Clearly, the public-information component is increasing in . In contrast, the private-information component is decreasing in because the information fraction is deceasing in .

Lemma 3.

If , then .

By (12), the total amount of information is

| (13) |

where the second equality follows from and (6). By differentiating (13) with respect to , we find that the total amount of information increases with the precision of public information if the game exhibits strategic substitutability and decreases if it exhibits strategic complementarity, as shown in the next proposition.

Proposition 2.

If and , then

| (14) |

Thus, is increasing in if , decreasing in if , and independent of if .

To provide another implication of (14), we divide both sides by and obtain

This implies that

| (15) |

We refer to as the marginal rate of substitution of public information for private information, which measures the crowding-out effect. The marginal rate of substitution is the change in the amount of private information resulting from a one-unit increase in the amount of public information . If is very large, a one-unit increase in public information substantially decreases private information, i.e., the crowding-out effect is significant. By (15), the crowding-out effect is larger in a game with strategic complementarity than strategic substitutability, which is another implication of Proposition 2.101010Colombo et al. (2014) obtain a similar result in the model of rigid information acquisition. See Remark 3.

In the benchmark case of , the marginal rate of substitution equals one; that is, public and private signals are perfect substitutes when there is no strategic interaction. Thus, when the policymaker increases the amount of public information, an agent reduces the amount of private information so that the total amount of information can remain constant.

If , however, the marginal rate of substitution is not constant; that is, public and private signals are imperfect substitutes. If the game exhibits strategic complementarity (i.e., ), the crowding-out effect is stronger, and the total amount of information decreases with public information. This is because agents put more value on public information to align their actions with the aggregate action,111111Indeed, the weight of in is by Proposition 1, which is increasing in . so that a one unit increase in more valuable public information compensates for a larger decrease in private information. In contrast, if the game exhibits strategic substitutability (i.e., ), the crowding-out effect is weaker, and the total amount of information increases with public information. This is because agents put less value on public information so that a one-unit increase in less valuable public information compensates for a smaller decrease in private information.

Before closing this section, we ask whether the marginal rate of substitution is monotone in , as suggested by (15). The answer depends upon which parameter to fix when changes. By (14), is represented as a function of :

We can verify that is not monotone in ; that is, the marginal rate of substitution is not necessarily increasing in for fixed . However, by plugging into , we can represent as a function of , which is monotone in :

| (16) |

That is, the marginal rate of substitution is increasing in for fixed . Consequently, when evaluated at the same information fraction, the crowing-out effect is larger in a game with a stronger degree of strategic complementarity. This observation will be used to provide intuition for results in the next section.

Remark 2.

Remark 3.

Colombo et al. (2014) study the model of rigid information acquisition and show that the substitutability between public and private information is increasing in the slope of the best response. In Appendix G, we discuss the case of rigid information acquisition with linear information costs and show that the total amount of information decreases with public information if and only if the game exhibits strategic complementarity, which is the same as Proposition 2. We also show that the crowding-out effect under flexible information acquisition is more significant than that under rigid information acquisition if and only if the game exhibits strategic complementarity. In other words, the crowding-out effect is more sensitive to the slope of the best response in the model of flexible information acquisition.

Remark 4.

We can conduct a similar analysis in the case of multiple equilibria, where and . Note that by Lemma 1. When , the above results remain valid; that is, the total amount of information decreases with public information because . When , however, we obtain the opposite result; that is, the total amount of information increases with public information. This is because agents acquire more precise private information when the policymaker provides more precise public information in the case of . See Appendix H.

5 The definition of optimality

In this section, we calculate the policymaker’s objective function and provide our definition of optimal disclosure. When the policymaker chooses and the agents follow equilibrium strategies, the expected welfare is calculated as

| (17) |

by (5), where is constant, because the expected values of and are constants independent of and by Proposition 1. We rewrite (17) using volatility and dispersion of actions, which follows Ui and Yoshizawa (2015) who characterize optimal disclosure in the case of exogenous private information. The volatility is the variance of the average action, , and the dispersion is the variance of the idiosyncratic difference, (Angeletos and Pavan, 2007; Bergemann and Morris, 2013).

Note that the first three terms in (17) are linearly dependent because

by (10) and the law of total variance. Thus, we can write (17) by means of volatility and dispersion,

| (18) |

where and . Consequently, the expected welfare is calculated as follows.

Lemma 4.

When the policymaker chooses and the agents follow an equilibrium with , the dispersion and volatility are given by

respectively, and the cost of information is given by . Thus, the expected welfare equals , where

Henceforth, we regard as the expected welfare, which equals either that under information acquisition, , or that under no information acquisition, . Note that is a function of and , and is uniquely determined by if or . If and , however, multiple equilibria arise and is not unique. In this case, we assume that the agents follow an equilibrium with the largest welfare (i.e., a sender-optimal equilibrium), following the standard Bayesian persuasion framework (Kamenica and Gentzkow, 2011).

The optimal precision maximizes the expected welfare under either information acquisition or no information acquisition. In the case of information acquisition (i.e., ), the optimal precision is given by

where is the maximum achievable welfare given under information acquisition. The domain of is , where

We refer to as the maximum precision under information acquisition. In the case of no information acquisition (i.e., and ), the optimal precision is given by

The globally optimal precision is defined as follows.

Definition 1.

We say that is optimal if one of the following holds.

-

•

and for .

-

•

and for .

We will identify the optimal precision in the above sense by means of four parameters: the coefficient of dispersion , the coefficient of volatility , the slope of the best response , and the coefficient of information costs .

6 The welfare effect of public information

In this section, we study the welfare effect of public information and obtain the optimal precision under information acquisition and that under no information acquisition . We assume that is sufficiently small, i.e., .

First, we consider the case of no information acquisition, i.e., and . The welfare is by Lemma 4, which is strictly increasing (decreasing) if the volatility’s coefficient is strictly positive (negative) because . Therefore, we have the following proposition.

Proposition 3.

It holds that

| (19) |

Next, we consider the case of information acquisition, i.e., . The welfare is by Lemma 4. Recall that the domain of is , and the corresponding range of the information fraction is

because is assumed. Note that, for each ,

Thus, to obtain , it is enough to solve the last optimization problem, and its solution is given by the following lemma, which is an immediate consequence of Lemma 4.

Lemma 5.

For each , it holds that

where

| (20) |

Thus, uniquely maximizes over .

Let . Then, Lemma 5 implies that uniquely maximixes over if .121212If , then for all , but we focus on the case with sufficiently small to make the discussion simple.

Proposition 4.

Assume that . Then, .

By Proposition 4, no disclosure () is suboptimal for sufficiently small . When the policymaker discloses no information, the agents acquire a substantial amount of information to reduce uncertainty, incurring inefficiently large costs. In fact, as approaches zero, the cost goes to infinity, so the expected welfare goes to minus infinity:

Using Lemma 5, we study the welfare effect of public information and gain intuition about the optimal precision . We focus on the case of and , i.e., the second-period equilibrium is unique. Because , we obtain

| (21) |

This leads us to the following proposition, which provides a necessary and sufficient condition for welfare to increase with public information.

Proposition 5.

If , it holds that

| (22) | ||||

| (23) |

The change in welfare, , consists of those in the dispersion term, the volatility term, and the cost term, which correspond to the three terms in (21) and (22), respectively. The last term in (22), , measures the cost reduction induced by the crowding-out effect, which is decreasing in and approaches infinity as goes to zero (becuase goes to one). This is why welfare increases with public information when public information is sufficiently imprecise. Note that the cost reduction is small when is large and the agents acquire a small amount of information.

On the other hand, welfare can decrease with public information only if by (23) (see Figure 1), which is equivalent to by (20). That is, when the coefficient of dispersion is large enough, more precise public information can be harmful. We can understand this by the fact that the dispersion is decreasing in :

This is because the dispersion equals the difference between the variance of an action and that of the average action, and more precise public information brings them closer. In contrast, when the coefficient of volatility is large enough, more precise public information is always beneficial if , yet it can be harmful if . This can be understood by the fact that the volatility is increasing in if and only if :

The volatility equals the covariance of actions since , which equals the corelation coefficient multiplied by the variance of an individual action. More precise public information increases the correlation coefficient but decreases the variance through the crowding-out effect. When , the crowding-out effect is so strong and a decrease in the variance is so large that the covariance decreases with public information.

7 The optimal disclosure rule

Using the result in Section 6, we obtain the optimal precision of public information. When , there are three candidates for the optimal precision, , , and , by Propositions 3 and 4. However, we can focus on and for the following reason: if , then ; if , then , and . Therefore, the optimal precision is if and if . This observation leads us to the following proposition.

Proposition 6.

Assume that . The optimal precision is uniquely given by

where . Both and are optimal in the other nongeneric case ( or ).

Figure 2a illustrates the optimal precision on the -plane. Full disclosure is optimal if is in the upper region, where the coefficient of volatility is positive and large enough; partial disclosure is optimal if is in the lower region. If , the volatility necessarily increases with public information, but if , it can decrease due to the crowding-out effect. Even in the latter case, when public information is sufficiently precise, the volatility necessarily increases with public information because the agents do not acquire private information and the crowding-out effect disappears. This is why a sufficiently large coefficient of volatility guarantees the optimality of full disclosure.

No disclosure is never optimal because public information reduces the cost of information, which is in sharp contrast to the case of exogenous private information. To see this, assume that an agent receives a private signal that follows a fixed normal distribution in the second period at no cost (Angeletos and Pavan, 2007). A private signal is conditionally independent across agents given and the precision of private information (defined as ) is exogenously fixed. Ui and Yoshizawa (2015) study optimal disclosure of public information in this case and show that no disclosure is optimal if is small enough, as illustrated in Figure 2b and formally stated in the next proposition.131313See Corollary 5 of Ui and Yoshizawa (2015).

Proposition 7 (Ui and Yoshizawa, 2015).

Assume that the precision of private information is exogenously fixed. For any precision of private information, the optimal precision is uniquely given by

In the other case, depends upon the precision of private information.

Even if the precision of private information is endogenously determined, no disclosure can be optimal as long as the cost is convex in the precision. To be more specific, assume that an agent chooses the precision of private information before receiving a private signal and that its cost is a convex function (Colombo et al., 2014). Information acquisition is rigid in the sense that the distribution is restricted to be normal. Ui (2022) studies optimal disclosure in this case and finds that no disclosure is optimal if is small enough.

In the model of rigid information acquisition, more precise public information also reduces the cost of information, but the reduction cannot be substantial enough to make no disclosure suboptimal. To see why, recall that the cost of information is assumed to be convex in the precision of private information. This implies that the precision is bounded above because the marginal cost is increasing and the marginal benefit approaches zero as the precision goes to infinity. Consequently, the cost of private information cannot be so substantial. In contrast, the precision and the cost of private information are unbounded in the model of flexible information acquisition, thus making no disclosure suboptimal.

8 Applications

8.1 Cournot and investment games

Suppose that in (1), and let be the aggregate payoff. Then, it can be readily shown that ; that is, in (18). Thus, the expected welfare equals the variance of an individual action minus the cost of information.

A Cournot game (Vives, 1988) is a special case when . Firm produces units of a homogeneous product at a quadratic cost . An inverse demand function is , where is constant and is normally distributed. Then, firm ’s gross profit excluding the cost of information is

which is reduced to (1) with and by normalization.

An investment game (Angeletos and Pavan, 2004) is also a special case when . Firm chooses an investment level at a quadratic cost and receives a return , where is constant. Then, firm ’s gross profit excluding the cost of information is

which is reduced to (2) with and by normalization.

To provide a benchmark for our result, assume that private information is exogenous. In a Cournot game, the total profit can decrease with public information, and no disclosure can be firm optimal (Bergemann and Morris, 2013). In an investment game, the total profit necessarily increases with public information (Angeletos and Pavan, 2004). These results are formally stated as follows (Ui and Yoshizawa, 2015).

Proposition 8.

Assume that the precision of private information is exogenously fixed and that . If , welfare necessarily increases with public information. If , welfare can decrease with public information. If , no disclosure is optimal when private information is sufficiently precise.

In brief, more precise public information can reduce the total profit if and only if the game exhibits strong strategic substitutability, in which case no disclosure can be optimal (see Figure 4). This result is essentially the same as in the case of rigid information acquisition (Ui, 2022).141414Under rigid information acquisition with strictly convex information costs (strictly convex in the precision of private information), more precise public information can reduce the total profit if and only if the game exhibits strong strategic substitutability, where the slope of the best response is smaller than in the case of exogenous private information.

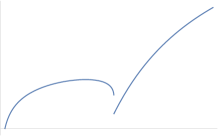

We provide a contrasting result in the case of flexible information acquisition as a corollary of Propositions 5 and 6. That is, more precise public information can reduce the total profit if and only if the game exhibits strong strategic complementarity, while full disclosure is always optimal. In other words, the total profit necessarily increases with public information in a Cournot game, whereas it can decrease with public information in an investment game.

Corollary 9.

Assume that . If , then is increasing. If , then is increasing for and decreasing for . In both cases, full disclosure is optimal.

The difference in the above results arises from the crowding-out effect enhanced by strategic complementarity. Recall that the total profit equals the gross profit minus the cost of information. When the policymaker provides more precise public information, the gross profit decreases if and increases if (see Figures 5a and 5b), while the cost of information decreases if and vanishes if . This is because the crowding-out effect reduces private information if and disappears if . Since the cost reduction is substantial when is very small, the total profit increases when is small enough as well as large enough, thus making full disclosure optimal (see Figures 5c and 5d). However, when the degree of strategic complementarity is sufficiently strong (i.e., ) and the cost reduction is modest (i.e., is close to ), a decrease in the gross profit is so substantial that the total profit decreases (see Figure 5d).

8.2 Beauty contest games

We consider a beauty contest game (Morris and Shin, 2002), where , , and . An agent’s target is the weighted mean of the state and the aggregate action, . The welfare is the negative of the mean squared error of an individual action from the state minus the cost of information, . Because the welfare has a negative value, full disclosure attains the maximum welfare and is optimal. It can be readily shown that and in (18).

In the case of exogenous private information, the following result is well known: if the degree of strategic complementarity is strong enough, more precise public information can be harmful to welfare.

Proposition 10 (Morris and Shin, 2002).

Assume that the precision of private information is exogenously fixed and that . If , welfare can decrease with public information.

The harmful effect arises from the fact that agents place too much weight on public information, which is entailed by a coordination motive under strong strategic complementarity, and overreact to public information.

In the case of flexible information acquisition, welfare can decrease with public information even if ; that is, welfare is more likely to decrease.

Corollary 11.

Assume that and . If , then is deceasing for , where .

This result is attributed to the crowding-out effect enhanced by strategic complementarity, which is essentially the same as the case of an investment game. When the policymaker provides more precise public information, the gross welfare excluding the cost of information decreases if due to the crowding-out effect (see Figures 6a). Nonetheless, the net welfare increases when is small enough because of a substantial decrease in the cost of information. However, when the degree of strategic complementarity is sufficiently strong (i.e., ) and the cost reduction is modest (i.e., is close to ), a decrease in the gross welfare is so substantial that the net welfare decreases.

Appendix A Proofs for Section 3

Proof of Proposition 1.

Assume that the distribution of is an equilibrium. Because , we have . By solving this for , we obtain .

Let and . Then, is an optimal solution of (11) and satisifes the condition in Lemma 2. Suppose . By Lemma 2,

which implies , i.e., (8).

We obtain a condition for the existence of . An agent acquires information about but does not pay attention to and separately (because it is more costly). Thus, we must have

| (A.1 ) |

Using the formula for conditional distributions, we obtain

| (A.2 ) |

because . Similarly,

| (A.3 ) |

because . Hence, we have

| (A.4 ) |

by (A.1), (A.2), and (A.3), and the variances of both sides are equal, i.e.,

| (A.5 ) |

which implies (9). Solving (A.4) for , we have , which implies (7) and

| (A.6 ) |

By multiplying both sides of by and taking the expectation, we have , which implies (10).

In summary, if an equilibrium with exists, then (7), (8), (9), and (10) hold. It is easy to prove the converse: if the joint normal distribution of satisfies these equations, then it is an equilibrium. We can also verify the following.

- •

- •

Next, we show that an equilibrium with no information acquisition exists if and only if . Suppose that an equilibrium with no information acquisition exists. Beacuse and are constant, we must have by Lemma 2. Conversely, suppose that . In an equilibrium, if is constant, then , so is also constant by Lemma 2. Because and , we have . ∎

Appendix B Proofs for Section 4

Appendix C Proofs for Section 5

Appendix D Proofs for Section 7

Proof of Proposition 6.

By direct calculation, we have

| (A.7 ) |

Thus, when ,

Similarly, when ,

This implies the following.

-

(a)

If and or if and , then .

-

(b)

If and or if and , then .

We show that the above conditions are equivalent to those in the proposition.

Consider (a). It is clear that the condition in (a) holds if and . To show the converse, assume first that and . Recall that implies . Since

| (A.8 ) |

we have

Next, assume that and . Note that , i.e., . This implies because if , then , and , contradicting .

Appendix E Proofs for Section 8

Proof of Corollary 9.

When , if and if , which implies that . Because , full disclosure is optimal for all .

Consider . First, suppose that , where for all . Because , is decreasing, and thus is increasing because is decreasing. Next, suppose that . Because , is increasing if . Moreover, . Thus, for each , and because . This implies that is decreasing if because is decreasing. ∎

Proof of Corollary 11.

When and , if and if . Let as before.

Suppose that . Then, for all , so is decreasing for because is increasing for .

Suppose that . Recall that, for all , is decreasing and for . Note that . Thus, is increasing if . Consequently, for , is decreasing because . ∎

Appendix F Flexible acquisition with the Fisher information costs

In this appendix, we consider the model of flexible information acquisition with the Fisher information cost (Hébert and Woodford, 2021) instead of the mutual information cost and show that Propositions 1 and 2 remain valid. We also demonstrate that the crowding-out effect enhanced by strategic complementarity has the essentially same effect on welfare as in the case of the mutual information cost discussed in Section 8.

Let be a normally distributed random variable with mean and variance . Let be a signal about , which has a conditional probability density function given . By regarding as a parameter determining the distribution of when is given, we can define the log likelihood function . The following value is referred to as the Fisher information:

A cost of a private signal is called the Fisher information cost if it is proportional to the expected value of :

where is constant. The following result is a special case of Proposition 4 in Hébert and Woodford (2021).151515This result is closely related to the well-known result that the standard normal distribution has the smallest Fisher information for location among all distributions with variance less than or equal to one. See Huber and Ronchetti (2009), for example.

Lemma A.

Consider an optimization problem

where is a random variable with an arbitrary distribution. An optimal solution exists and satisfies the following.

-

•

If , then is a normally distributed random variable satisfying , , and .

-

•

If , then and .

Compare this lemma with Lemma 2. The distribution of the optimal signal in each lemma is the same when . Because the proofs of Propositions 1 and 2 rely only on the distribution of the optimal signal in Lemma 2, the same proofs go through under the assumption of the Fisher information cost. That is, Propositions 1 and 2 remain valid, where is replaced with .

From now on, let . In the second-period equilibrium with , the Fisher information cost is

By replacing the mutual information cost in Lemma 4 with the above Fisher information cost, we obtain the expected welfare:

For each , it holds that

which implies that maximizes over , where

Let be the maximum achievable welfare given . The domain of is the same as that of , i.e., . For , , and thus

As a consequence, Corollary 9 on Cournot and investment games has the following counterpart in the case of the Fisher information cost.

Corollary A.

Assume that . For , is increasing if and decreasing if .

That is, more precise public information can reduce the total profit if and only if the game exhibits strong strategic complementarity, which is essentially the same as in the case of the mutual information cost.

Similarly, Corollary 9 on a beauty contest game has the following counterpart in the case of the Fisher information cost.

Corollary B.

Assume that and . If , then is deceasing for .

That is, welfare can decrease with public information even if , which is also essentially the same as in the case of the mutual information cost.

We can also identify the optimal precision. No disclosure can be optimal, which is different from the case of the mutual information cost. The difference arises from the following fact: the mutual information cost is proportional to and unbounded, whereas the Fisher information cost is proportional to and bounded. That is, the cost reduction cannot be substantial enough to make no disclosure suboptimal in the case of the Fisher information cost.

Proposition C.

Assume that the agents have the Fisher information cost. Let . The optimal precision is uniquely given by

Proof.

Suppose that . The optimal precision is either or because is strictly increasing. By direct calculation,

which is strictly positive if and only if .

Suppose that . The optimal precision is either or because is strictly decreasing, and

which is strictly positive if and only if . ∎

Appendix G Rigid acquisition with linear information costs

In this appendix, we compare the model of rigid information acquisition with linear information costs (Colombo and Femminis, 2008; Colombo et al., 2014; Ui, 2022) with the model in this paper. We focus on linear information costs (linear in the precision of private information) because the crowding-out effect is largest among all convex information costs (Ui, 2014). We show that the crowding-out effect is larger in the case of flexible information acquisition than in the case of rigid information acquisition if and only if the game exhibits strategic complementarity.

An agent receives a private signal that follows a normal distribution in the second period at a cost , where is constant and is the the precision of private information defined as . A private signal is conditionally independent across agents given and . The second period subgame has a unique equilibrium (Colombo et al., 2014), and the precision of private information is given by161616See Colombo et al. (2014) and Ui (2022).

For , is linear and decreasing in , and is decreasing in ; that is, the crowding-out effect is more siginificant when is larger, which is essentially the same as in the case of flexible information acquisition.

The total amount of information also has the same property as in the case of flexible information acquisition. The mutual information of an agent’s signals and a state is calculated as

| (A.9 ) |

where denotes the determinant of the covariance matrix of a random vector . Then, we obtain the following counterpart for Proposition 2.

Proposition D.

If , then

| (A.10 ) |

Thus, is increasing in if , decreasing in if , and independent of if .

We compare and when , i.e., the total amount of information is the same for both types of information acquisition. If , the change in the total amount of information caused by a one-unit increase in public information is smaller under flexible information acquisition, which means that the crowding-out effect is larger. This is true if and only if the game exhibits strategic complementarity, as shown by the next proposition.

Proposition E.

Suppose that and . Then,

| (A.11 ) |

Proof.

In a game with strategic complementarity, a one-unit increase in public information causes a greater decrease in the total amount of information (i.e., the crowding-out effect is larger) under flexible information acquisition. In a game with strategic complementarity, it causes a greater increase in the total amount of information (i.e., the crowding-out effect is smaller) under flexible information acquisition. This implies that the crowding-out effect is more sensitive to the slope of the best response in the flexible information acquisition model than in the rigid information acquisition model.

Appendix H The crowding-in effect of public information

In this appendix, we study the problem of Section 4 in the case of multiple equilibria. Assume that and . By Lemma 1, . We focus on the equilibrium with and show that when more precise public information is provided, the agents acquire more precise private information, so the total amount of information increases. In contrast, in the equilibrium with , it is straightforward to show that every result in Section 4 remains valid.

As discussed in Section 4, more precise public information decreases private information in the equilibrium with . However, in the equilbrium with , more precise public information increases private information. This effect of public information is referred to as the crowding-in effect.

Lemma B.

If and , then and .

Proof.

To see why the crowding-in effect arises when , imagine that the policymaker provides more precise public information and, at the same time, the opponents acquire more precise private information. Then, private information is more valuable to an agent because both private information and public information are strategic complements in a game with strategic complementarity (Hellwig and Veldkamp, 2009). Because an agent acquires a small amount of information when , the marginal cost with respect to the information fraction, , is also small. Thus, an agent has a strong incentive to acquire more precise private information, making the crowding-in effect consistent with equilibrium.

Due to the crowding-in effect, more public information increases the total amount of information. More formally, the total amount of information when is given by

and we have .

References

- Angeletos and Pavan (2004) Angeletos, G.-M., Pavan, A., 2004. Transparency of information and coordination in economies with investment complementarities. Amer. Econ. Rev. 94, 91–98.

- Angeletos and Pavan (2007) Angeletos, G.-M., Pavan, A., 2007. Efficient use of information and social value of information. Econometrica 75, 1103–1142.

- Bergemann and Morris (2013) Bergemann, D., Morris, S., 2013. Robust predictions in games with incomplete information. Econometrica 81, 1251–1308.

- Bergemann and Morris (2019) Bergemann, D., Morris, S., 2019. Information design: A unified perspective. J. Econ. Lit. 57, 44–95.

- Bizzotto et al. (2020) Bizzotto, J., Rüdiger, J., Vigier, A., 2020. Testing, disclosure and approval. J. Econ. Theory 187, 105002.

- Bloedel and Segal (2020) Bloedel, A., Segal, I., 2020. Persuading a rationally inattentive agent. Working Paper.

- Bowsher and Swain (2012) Bowsher, C. G., Swain, P. S., 2012. Identifying sources of variation and the flow of information in biochemical networks. Proc. Natl. Acad. Sci. U.S.A. 109, E1320–E1328.

- Colombo and Femminis (2008) Colombo, L., Femminis, G., 2008. The social value of public information with costly information acquisition. Econ. Letters 100, 196–199.

- Colombo et al. (2014) Colombo, L., Femminis, G., Pavan, A., 2014. Information acquisition and welfare. Rev. Econ. Stud. 81, 1438–1483.

- Cover and Thomas (2006) Cover, T. M., Thomas, J. A., 2006. Elements of Information Theory. Wiley.

- Denti (2020) Denti, T., 2020. Unrestricted Information Acquisition. Working paper.

- Hébert and La’O (2021) Hébert, B., La’O, J., 2021. Information acquisition, efficiency, and non-fundamental volatility. NBER Working Paper 26771.

- Hébert and Woodford (2021) Hébert, B., Woodford, M., 2021. Neighborhood-based information costs. Amer. Econ. Rev. 111, 3225–3255.

- Hellwig and Veldkamp (2009) Hellwig, C., Veldkamp, L., 2009. Knowing what others know: coordination motives in information acquisition. Rev. Econ. Stud. 76, 223–251.

- Huber and Ronchetti (2009) Huber, P. J., Ronchetti, E. M., 2009. Robust Statistics. Wiley.

- Kamenica (2019) Kamenica, E., 2019. Bayesian persuasion and information design. Annu. Rev. Econ. 11, 249–72

- Kamenica and Gentzkow (2011) Kamenica, E., Gentzkow, M., 2011. Bayesian persuasion. Amer. Econ. Rev. 101, 2590–2615.

- Lipnowski et al. (2020) Lipnowski, E., Mathevet, L., Wei, D., 2020. Attention management. Amer. Econ. Rev.: Insights 2, 17–32.

- Mackowiak et al. (2021) Mackowiak, B., Matějka, F., Wiederholt, M., 2021. Rational inattention: A review. J. Econ. Lit. (forthcoming).

- Mackowiak and Wiederholt (2009) Mackowiak, B., Wiederholt, M., 2009. Optimal sticky prices under rational inattention. Amer. Econ. Rev. 99, 769–803.

- Matysková and Montes (2021) Matysková, L., Montes, A., 2021. Bayesian persuasion with costly information acquisition. Working paper.

- Morris and Shin (2002) Morris, S., Shin, H. S., 2002. Social value of public information. Amer. Econ. Rev. 92, 1521–1534.

- Myatt and Wallace (2012) Myatt, D. P., Wallace, C., 2012. Endogenous information acquisition in coordination games. Rev. Econ. Stud. 79, 340–374.

- Myatt and Wallace (2015) Myatt, D. P., Wallace, C., 2015. Cournot competition and the social value of information. J. Econ. Theory 158, 466–506.

- Radner (1962) Radner, R., 1962. Team decision problems. Ann. Math. Stat. 33, 857–881.

- Rigos (2020) Rigos, A., 2020. Flexible Information acquisition in large coordination games. Working paper.

- Sims (2003) Sims, C. A., 2003. Implications of rational inattention. J. Monet. Econ. 50, 665–690

- Ui (2009) Ui, T., 2009. Bayesian potentials and information structures: Team decision problems revisited. Int. J. Econ. Theory 5, 271–291.

- Ui (2014) Ui, T., 2014. The social value of public information with convex costs of information acquisition. Econ. Letters 125, 249–252.

- Ui (2016) Ui, T., 2016. Bayesian Nash equilibrium and variational inequalities. J. Math. Econ. 63, 139–146.

- Ui (2020) Ui, T., 2020. LQG information design. Working paper.

- Ui (2022) Ui, T., 2022. Optimal and robust disclosure of public information. Working paper.

- Ui and Yoshizawa (2015) Ui, T., Yoshizawa, Y., 2015. Characterizing social value of information. J. Econ. Theory 158, 507–535.

- Vives (1988) Vives, X., 1988. Aggregation of information in large Cournot markets. Econometrica 56, 851–876.

- Vives (2008) Vives, X., 2008. Information and Learning in Markets: the Impact of Market Microstructure. Princeton Univ. Press.

- Wong (2008) Wong, J., 2008. Information acquisition, dissemination, and transparency of monetary policy. Can. J. Econ. 41, 46–79.

- Yang (2015) Yang, M., 2015. Coordination with flexible information acquisition. J. Econ. Theory 158, 721–738.