On Parametric Optimal Execution and Machine Learning Surrogates 111We would like to thank Kevin Webster and Nicholas Westray, as well as an anonymous referee, for their very valuable comments and suggestions. 222The accompanying Jupyter Notebook is available at https://github.com/moritz-voss/Parametric_Optimal_Execution_ML.

Abstract

We investigate optimal order execution problems in discrete time with instantaneous price impact and stochastic resilience. First, in the setting of linear transient price impact we derive a closed-form recursion for the optimal strategy, extending the deterministic results from [48]. Second, we develop a numerical algorithm based on dynamic programming and deep learning for the case of nonlinear transient price impact as proposed by [22]. Specifically, we utilize an actor-critic framework that constructs two neural-network (NN) surrogates for the value function and the feedback control. The flexible scalability of NN functional approximators enables parametric learning, i.e., incorporating several model or market parameters as part of the input space. Precise calibration of price impact, resilience, etc., is known to be extremely challenging and hence it is critical to understand sensitivity of the execution policy to these parameters. Our NN learner organically scales across multiple input dimensions and is shown to accurately approximate optimal strategies across a wide range of parameter configurations. We provide a fully reproducible Jupyter Notebook with our NN implementation, which is of independent pedagogical interest, demonstrating the ease of use of NN surrogates in (parametric) stochastic control problems.

- Keywords:

-

optimal execution, parametric control, neural network surrogates, stochastic resilience

1 Introduction

In the past decade an extensive literature has analyzed optimal execution of trades within a micro-structural framework that accounts for the interaction between trades, prices, and limit order book liquidity. For example, one notable strand follows the approach of Obizhaeva and Wang [48] which is able to generate closed-form formulas for optimal trading strategy with linear transient price impact. However, any practical use of these elegant mathematical derivations must immediately confront the strong dependence of the solution on the given model parameters. Concepts such as order book resilience or book depth are mathematical abstractions and are not directly available in the real world. Similarly, parameters such as inventory penalty, are model-specific and have to be entered by the user. Consequently, model calibration becomes highly nontrivial and in turn requires understanding the interaction between model parameters and the resulting strategy. In parallel, model risk, i.e., mis-specification of the dynamics, is also a major concern. Model risk can be partially mitigated by considering more realistic nonlinear models, but this comes at the cost of losing closed-form solutions.

Motivated by these issues, in this article we approach optimal execution using the lens of parametric stochastic control. To this end, we investigate numerical algorithms that determine the optimal execution strategy jointly in terms of the state variables (inventory and limit order book spread/mark-up), as well as model parameters (instantaneous price impact, resilience factor, inventory penalty, etc.). We consider augmenting 1-4 model parameters to the training space, yielding multi-dimensional control problems.

Our contribution is two-fold. In terms of the numerical methods, we propose a direct approach to parametric control that focuses on generating functional approximators to the value function. A concrete choice of such statistical surrogates that we present below are Neural Networks (NNs). Our approach employs NNs to approximate the Bellman equation and can be contrasted with other ways of using NNs, such as Deep Galerkin Methods [12, 13, 32] for PDEs; or parameterization of the feedback control [39, 14] in tandem with stochastic gradient descent. One advantage of our method is its conceptual simplicity; as such it as an excellent pedagogical testbed for machine learning methods. Indeed, given that optimal execution is now a core problem that is familiar to anyone working in mathematical finance, we believe that this example offers a great entryway to students or researchers who wish to understand and “play” with modern numerical tools for stochastic control. To this end, we provide a detailed Python Jupyter notebook that allows a fully reproducible checking of our results. Our notebook is made as simple as possible, in order to distill where the statistics tools come in, and aiming to remove much of the “ML mystique” that can be sometimes present. Our approach also emphasizes the questions of how to train the statistical surrogate, and how to approximate the optimal control, both important implementation aspects whose discussion is often skipped.

In terms of the financial application, we contribute to the optimal execution literature in several ways that would be of independent interest to experts in that domain. Specifically, our optimal execution modeling framework builds on the discrete-time, linear transient price impact model with exponential decay from [48] and additionally allows for (i) nonlinear, power-type price impact à la [22, 21], [30], [6], [26], [25]; (ii) a stochastic transient price impact driven by its own noise, akin to the continuous-time model in [18]; and (iii) a risk-aversion-type running quadratic penalty on the inventory as arising, e.g., in [53]. In other words, our model nests various existing proposals in the literature, offering a unified discrete-time framework that we investigate in detail. Other related work on optimal order execution with (exponentially) decaying (linear) transient price impact in discrete and continuous time include, e.g., [5], [8], [51], [9], [31], [46], [7], [3], [17], [4], [28, 29], [33], [44], [37], [24], [2, 1], [27], [47]; we also refer to the recent monograph by [54] for an excellent overview and discussion of price impact modeling. Moreover, in the linear case, we also establish a new explicit formula, see Proposition 1, for the optimal execution strategy with stochastic transient price impact and inventory penalty, which extends the explicit deterministic solution from [48] and allows us to also accurately benchmark our machine learning approach. Therefore, our numerical experiments provide new reliable insights on the interaction between different model parameters and the optimal strategy. Obtaining these insights, in other words building a better intuition on how the model behaves in different regimes, was the original motivation for our work, and is valuable for practitioners who must develop gut feelings on how the model reacts as the real world (i.e., calibrated parameters) changes. In particular, our numerical analysis complements the studies on deterministic optimal execution strategies with non-linear transient price impact carried out in [26] and [25].

In the broader context of machine learning methods for stochastic optimal control, our work is related to other applications of neural networks to financial problems, see [39, 14, 40]. Perhaps the closest is [43] who also study execution problems, but in a model with only temporary and permanent price impact à la [19], [10], [23]; see also [50] for a similar study. For other approaches in optimal execution in the presence of temporary price impact more in the flavor of reinforcement learning see, e.g., the recent survey articles by [35] and [41] and the references therein.

This article is organized as follows. Section 2 formulates our generalized optimal execution setting. Section 3 presents an explicit reference solution for unconstrained trading strategies. Section 4 describes our methodology for parametric stochastic control via statistical surrogates. Section 5 presents the numerical experiments and resulting insights. Following a brief conclusion in Section 6, Section 7 contains the proofs.

2 Problem formulation

Let be a discrete-time filtered probability space with trivial -field and a terminal time horizon . We consider a financial market with one risky asset whose -adapted real-valued unaffected fundamental price process is denoted by . We set .

Suppose a large trader dynamically trades in the risky security and incurs price impact in an adverse manner. Specifically, for , by choosing her number of shares in the risky asset at time , she trades shares in the -th trading period and confronts the -th fundamental random shock . Her action permanently affects the future evolution of the mid-price process which becomes

| (1) |

after the -th order is executed (we set ). The parameter represents linear permanent price impact.

In addition, the trader’s market orders are filled at a deviation from the mid-price in (1). The post-execution dynamics of these deviations from the mid-price after trading shares at time are modeled as

| (2) | ||||

with denoting the given initial deviation. Thus, in the absence of the large trader’s actions, the deviation tends to revert exponentially to zero at rate , with the latter parameter known as the book resilience. The resilience captures the transience of the instantaneous price impact, with representing the fraction by which the deviation from the mid-price incurred by past trades diminishes over a trading period. Empirically, the deviation process can be calibrated by considering the limit order book (LOB) spread and depth.

Due to finite market depth, which is measured by , the trader’s turnover of shares pushes the deviation in the trade’s direction by a constant factor times the instantaneous price impact, which is assumed to be , . Following, e.g., [21, 22], the latter power-type term generalizes the common linear situation from [48] where the instantaneous price impact is . However, empirically the instantaneous price impact is observed to be concave (at least for relatively small ), so that seems more realistic; see [45], [21], [15].

The -valued, -adapted sequence of zero-mean random variables represents additional small perturbations in the deviation stemming, e.g., from market and limit orders, which are placed at time by other small market participants, making the transient price impact captured by the deviation process stochastic; cf., e.g., [18].

For the rest of the paper, we assume that are independent and square integrable random variables with mean zero. The perturbations in (2) are i.i.d. normally distributed random variables with mean zero and variance , and independent of as well. We also refer to the case where for every . Finally, we let the filtration be given by for all .

2.1 Optimal Trade Execution

From now on, we suppose that the large trader wants to carry out a buying program to buy shares by executing market buy orders , . She starts with zero inventory and we use to denote the remaining number of shares she needs to buy after step to reach her target. That is, we set

| (3) |

where represents her remaining order to be filled after she executed her -th trade .

As common in the literature, in order to describe the evolution of the large trader’s cash balance, we assume that the -th transaction affects the mid-price and deviation gradually. More precisely, half of the -th order is filled at the pre-transaction’s mid-price , as well as the refreshed pre-transaction’s deviation , whereas the other half is executed at the less favorable post-transaction quantities (before the -th fundamental random shock hits the stock price) and (before the -th random perturbation of the deviation). Hence, assuming zero interest rates, the self-financing condition dictates that changes in the trader’s cash balance with initial value are only due to her buying activity of the risky asset which is executed at the previously described average execution prices:

| (4) | ||||

Lemma 1.

The terminal cash position at time of a buying schedule with for all and terminal state constraint is given by

| (5) |

Proof.

Next, in order to introduce the trader’s optimization problem let us denote for all time steps the collection of admissible buying strategies by

| (7) |

The trader aims to maximize her expected terminal cash position given in (5) while also controlling for inventory risk. The latter is modeled through a quadratic urgency penalty for an urgency parameter on her outstanding order. Combining the two terms, the objective is to minimize

| (8) |

Note that is the remaining order to be filled; our notation emphasizes the role of and as the state variables, and as the control. As it is well-known in the literature, we remark that the permanent impact disappears in (8) and from our further discussion since it only adds a fixed offset to the terminal cash position, irrespective of the trading strategy. Similarly, the martingale term in (5) disappears as well after taking expectations thanks to the independence of price increments.

We introduce for all the value function as

| (9) | ||||

To characterize , we use the corresponding dynamic programming (DP) equation. Since at the last period , the admissible set is a singleton , we have the terminal condition

| (10) |

and then for

| (11) |

with as postulated in (2) and the expectation being with respect to the Gaussian noise .

The DP equation (2.1) has two primary state variables . Below, we will also consider its dependence on the static parameters . Recall that is the book resilience (smaller increases the transient price impact); is the instantaneous price impact (larger makes trades affect more); is the urgency parameter (larger encourages larger buys to mitigate inventory risk); is the exponent of the instantaneous price impact function ( leads to convex (resp. concave) price impact) and is the standard deviation of the one-step-ahead deviation . Note that while and are dimensionless, the value of should be thought of relative to the initial inventory , and the values of should be picked relative to fluctuations in . For example, if (buying program of a hundred thousand shares) then should be on the order of , should be on the order of (so that is on the order of 10-100), and should be on the order of 1.

Remark 1 (Unconstrained Problem).

In the above formulated optimal trade execution problem it is tempting to a priori allow for trading in both directions (buy orders and sell orders ) as in the discrete-time linear transient price impact model in [2]; i.e., to compute

| (12) | ||||

over the set of unconstrained order schedules

| (13) |

However, as it will become apparent in Section 3, the exogenous noise in the deviation process in (2) would then trigger price manipulation in the sense of [38]. That is, there would exist profitable round-trip trades, i.e., nonzero strategies that generate strictly negative expected costs with by exploiting a nonzero deviation for some . This can be ruled out by either introducing a bid-ask spread or confining trading in one direction only; see also the discussion on price manipulation in [2, 29, 28] for the linear case , as well as [8, 30, 25] for the nonlinear case .

3 Explicit Solution for the Unconstrained Linear Case

The unconstrained optimal trade execution problem in (12) and (13) can be solved explicitly in the case of linear transient price impact () following a similar computation as done by [48]. They derived a solution in the deterministic case () without inventory penalty () and with initial deviation .

Proposition 1.

Let and let . Define

| (14) |

and, recursively, for all , set

| (15) |

Then the value function in (12) is quadratic in its arguments and given by

| (16) |

Moreover, the optimal order execution strategy is given by

| (17) | ||||

where and

| (18) |

for all .

Remark 2.

Observe that for every the optimal execution policy in (17) is given as a deterministic linear feedback function of the controlled random state variables and . Also, the coefficients of this linear function do not depend on . Therefore, in the deterministic version of the problem where , the optimal policy is given by the exact same feedback law in (17). Moreover, since the state variables and are themselves linear in and the i.i.d. zero-mean Gaussian noise , it follows that the optimal trades of the stochastic version of the problem with are in fact just a Gaussian-distributed perturbation from the corresponding deterministic solution with mean given by the latter.

Corollary 1.

On average, the optimal order executions in (17) coincide with for the deterministic problem with . Moreover, viewed as a random variable, has a Gaussian distribution with the above mean.

Remark 3 (Profitable Round-Trip Strategies).

Let . By virtue of Lemma 2 below, we obtain that the coefficients in (15) are all strictly negative for . As a consequence, if and taking zero initial buying volume outstanding (), we have in (16) for . In other words, the resulting optimal strategy in (17) is a profitable round-trip strategy in the sense of [38]. This happens because the feedback policy readily exploits a nonzero deviation and its resilience as it arises; see also the detailed discussion in [2, 28, 29]. Similarly, in line with the latter references, observe that there are no profitable round-trip strategies (nor transaction triggered price manipulation strategies in the sense of [9]) in the deterministic resilience case , as long as the initial deviation satisfies (because and for all ).

3.1 Deterministic Resilience Case

In the deterministic case , the solution presented in Proposition 1 can be rewritten in an explicit closed-form without backward recursion in (15) and forward feedback policy in (17). In view of Corollary 1, this is useful for revealing the dependence of the average optimal order executions on the model parameters , and .

Proposition 2.

Observe that in Proposition 2 the deterministic optimal strategy in (21) is fully characterized by the first trade in (20) and the size of the orders vary over time . A further simplification is obtained when there is no urgency/inventory penalty, i.e., . Specifically, all intermediate trades are flat and determined as a -fraction of the first order , shifted by a proportion of .

Corollary 2.

Set in Proposition 2. Then in (19) it holds that

| (23) |

and the optimal intermediate trades in (21) with initial trade in (20) are constant and simplify to

| (24) |

with defined in (48) below. The final trade is given by . The optimally controlled deviation process and remaining inventory in (22) simplify to

| (25) |

In particular, if it holds that

| (26) |

Corollary 2 shows that in the deterministic case without urgency penalty the optimal execution strategy in (24) is constant for the intermediate trades from to and keeps the deviation process in (25) flat until . If, in addition, (i.e., the setup in [48]) the optimal strategy simplifies to the symmetric U-shaped (26) and becomes independent of the instantaneous price impact parameter (as observed in [48]). Initial and last trades are the same and all remaining intermediate trades are simply prescribed as a constant -fraction of the initial trade. In particular, for full resilience all trades are just equal to .

3.2 Optimal Execution Profiles

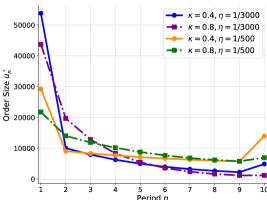

Figure 1 illustrates the behaviour of an optimal buying program from Proposition 2 with linear transient price impact () for different values of the model parameters . We consider buying shares in trades, with initial deviation . As discussed, when we obtain the well-known U-shape for the buying schedule, driven only by . With positive several novel qualitative effects appear: (i) the optimal strategy now depends on both resilience rate and temporary price impact ; (ii) intermediate trades are in general not flat anymore; and (iii) the overall pattern may shift from a U-shaped to a monotonically decreasing sequence of trades. The presence of an inventory penalty creates an incentive to buy faster in the beginning, which becomes more pronounced for small . Consequently, the case of and small might lead to a decreasing execution schedule, cf. the purple curve in Figure 1.

Observe that relatively small changes in model parameters generate significant impact on the optimal strategy . For example, the initial trade can be over 55% of total when is small and is small (which causes the emphasis to be on inventory risk), and less than 25% of for large and large (where strong resilience and strong temporary impact encourage to trade nearly equal amounts at each step). Also note the non-monotone behavior of the strategies, where the curves cross each other at different steps.

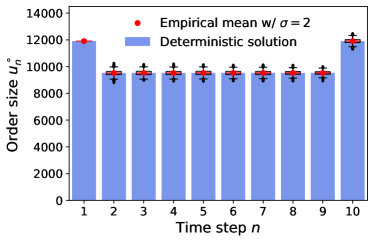

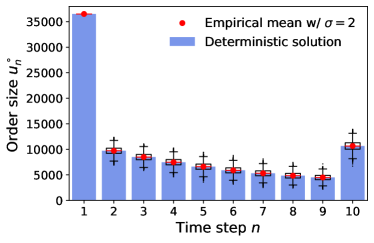

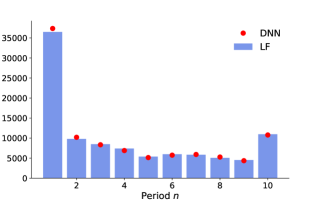

In the right panel of Figure 2 we illustrate how the pathwise strategies for from Proposition 1 are normally distributed and coincide on average with the deterministic solution, cf. Corollary 1. In the plot the blue bars correspond to the optimal deterministic solution from Proposition 2 and Corollary 2; and the boxplots show the distribution of from Proposition 1. We take and average over 10,000 paths, considering both the classical case with (left panel with U-shaped strategy) and our extension to positive inventory penalty (right panel). In line with Corollary 1, the empirical means match the deterministic solution. Since this feature is true for any configuration of the above qualitative effects can be deduced for the stochastic optimal feedback controls in (17).

4 Numerical Implementation

In the case of nonlinear transient price impact , no closed-form solution is possible and numerical methods are needed to compute an optimal solution for the minimization problem in (8). A numeric algorithm is also needed for to handle the constrained buy-only setting . Finally, the algorithm will be useful to study the dependence of on model parameters. Our algorithm to compute the value function and the optimal strategy relies on the Bellman equation (2.1) which provides a recursive characterization for and therefore for . Given the parametric setup, we consider a generic state that fuses stochastic states and some (or none) of the aforementioned model parameters; and for the rest of this section treat and as a function of .

In order to solve (2.1) we need to be able to evaluate its right-hand side. This entails (i) evaluating ; (ii) evaluating the conditional expectation; (iii) taking the over . None of those steps are possible to do analytically and numerical techniques are necessary.

Below, we propose and implement a direct approach based on constructing a functional approximator, also known as a surrogate, , to the value function that is trained via an empirical regression. This method is also known as Approximate Dynamic Programming (ADP) and Projected Value Iteration (PVI) in the literature; see, e.g., [42] and the references therein. Specifically, we consider the use of (feed-forward) Neural Networks (NN) for the latter. Note that our method is based on the DP equation; we do not make any reference to Hamilton-Jacobi-Bellman equations that are used in continuous-time setups, and which admit their own suites of NN approaches. Neither do we consider reinforcement learning (RL) that dispenses with the divide-and-conquer paradigm underlying the Bellman equation and the value function, and aims to maximize total trading revenue on the entire horizon. Namely, RL solves for all ’s in parallel over while we maintain the sequential backward learning of .

Instead, our approach is conceptually faithful to the classical DP philosophy and offers the following advantages:

-

•

It is straightforward to understand and implement, in some sense offering the most immediate approach to employing surrogate and other machine learning techniques for DP. As such, we bypass the more subtle ideas that have been advanced, offering a pedagogic-flavored setup;

-

•

It provides modularization, emphasizing that NN solvers are just one type of many potential surrogates. Thus, it de-mystifies deep learning, simply treating it as a choice among many. Indeed, our implementation requires just a few lines of code to substitute a different surrogate type.

4.1 Building a Surrogate

Denote by the state space of the surrogate, which includes the bona fide inputs , as well as all the relevant model parameters among which we wish to capture. In the examples below we consider , with the main illustrative example being where we take , i.e., we simultaneously learn the value function and the strategy as a function of , the resilience and the instantaneous price impact for some fixed and .

We denote by the one-step transition function of given external noise and action . For example,

Our resolution of the DP equation (2.1) operates as-is with each of the underlying sub-steps. This means that considering a generic intermediate step of the backward recursion and given a surrogate we first substitute it in place of . Next, the expectation in (2.1) is over the stochastic shocks which are one-dimensional Gaussian random variables. We employ Gaussian quadrature to replace the respective integral with a finite sum. Specifically, we rely on the optimal quantization of [49, 16] to select weights and respective knots to approximate

| (27) |

Remark 5.

One can straightforwardly consider non-Gaussian (e.g., heavy tailed) noise distributions for thereby providing a different nonlinear generalization. Non-Gaussian just reduces to taking a different set of ’s.

The optimization over the number of shares to buy is done via a numerical optimizer, namely the standard gradient-free optimization routine (such as L-BFGS) that is available in any software package. Note that is scalar, allowing the use of fast one-dimensional root finding algorithms. In our implementation, we do not evaluate any gradients of although that is feasible. In order to restrict to and rule out any selling, we optimize on the above bounded interval, straightforwardly supported by such solvers.

Finally, it remains to construct . As a machine learning task, the goal is to learn the true input-output map . Such functional approximation, aka surrogate construction [34], is carried out by selecting a collection of training inputs , evaluating (a noisy version of) and then fitting a statistical representation that can interpolate to new, out-of-sample ’s. The evaluation of is achieved by direct computation via the nonlinear optimizer and the quantized integral on the right-hand-side of (2.1):

| (28) | ||||

Observe that (28) uses and so leads to a recursive construction backward in time, fully mimicking the dynamic programming equation. This recursion is instantiated with the exact terminal condition and then run for . Our notation emphasizes the pointwise nature of the optimization for by taking the static parameters as part of the training design, hence varying in .

4.2 Policy Approximation

The primary output of the numerical solver is the execution strategy, given in feedback form as . Indeed, the strategy is what the controller is ultimately after, and yields a clear interpretation of how many shares the solver recommends to buy next. In contrast, the approximate value function is harder to interpret (since it is not in pure monetary dollars but potentially also involves the abstract inventory costs) and moreover due to the intermediate approximations does not have any concrete probabilistic representation. Indeed, while the true is the expected cost of the strategy, is not an expectation on , since it is obtained from one-step recursions.

Conventionally, is characterized as the of the Bellman recursion (2.1), so that to obtain one must re-do the optimization over . This is time-consuming, inefficient and non-transparent to the user. Instead we seek a direct representation for and in the spirit of the machine learning mindset (specifically actor-critic frameworks) propose to construct a second surrogate, auxiliary to the one describing . Accordingly, we construct a separate surrogate that is trained based on the recorded , the optimal execution amounts for each . Note that the fitting of is independent of the main loop above, so can be done in parallel with or after-the-fact.

Even when the training inputs are in the range , it is not generally guaranteed that this would be true for the fitted prediction . In order to enforce this constraint, we train based on the fractions and use a sigmoid transformation to intrinsically restrict all predictions (again interpreted as fractions of current inventory to be bought) into .

Remark 6.

In our setup, we first pointwise approximate and then fit a statistical surrogate to those samples; in [39, 14] the strategy is the opposite: first parametrize potential through a neural network with weights ; then use back-propagation to optimize the respective hyper-parameters . In that sense, their resulting is not a solution of any optimization problem, and there is no underlying dataset like for our approach.

4.3 Neural Network Solvers

A popular class of surrogates consists of feed-forward neural networks (NN). NN’s allow efficient fitting of high-dimensional parametric surrogates using back-propagation and a variety of stochastic optimization techniques, such as stochastic gradient descent.

An NN represents as a composition, using linear hidden units at each layer, a user-chosen activation function across layers, and a user-selected number of layers. In our context, the precise architecture of the feed-forward NN is not conceptually important. The NN parameters are optimized via batch stochastic gradient descent. Relative to other statistical models, NN is overparametrized with thousands of parameters, known as the weights. Nevertheless NN is known to enjoy excellent empirical convergence (i.e., the algorithms find near-optimal weights), especially for large scale datasets, including in other stochastic control applications [14, 36, 40, 39].

Training an NN requires specifying the training inputs and initializing the NN weights. For the former, we propose a space-filling experimental design, matching the standard approach in statistics. As default, we select a hyper-rectangular training domain and sample each coordinate of uniformly and independently on the respective training interval, for example we sample the inventory . One may also implement joint sampling in , such as Latin Hypercube Sampling (LHS). A further option is to use low-discrepancy Quasi Monte Carlo (QMC) sequences to achieve a space filling training set of arbitrary size . Compared to i.i.d. Uniform sampling, LHS and QMC offer lower variance and better coverage, avoiding any clusters or gaps in the training locations, which is relevant when is relatively small compared to the dimension of . Note that training sets are indexed by ; we sample fresh ’s at each step, so that the training inputs vary across ’s, although they have the same size and shape.

To initialize the weights, we found it very beneficial to rescale the inputs to the unit hypercube, which permits the use of standard NN weight priors (namely Truncated Normal with mean zero). Similarly, for we re-scale the training outputs to be in the range too. For training the policy surrogate we apply a sigmoid activation function on the output layer of the NN that directly ensures that . The latter fraction is multiplied by the current inventory to get the number of shares to trade.

Our implementation (see the supplementary Jupyter Notebook) employs the TensorFlow library in Python, which provides one of the most popular engines for NNs. We employ “factory defaults” to construct our neural networks using the tensorflow.keras.Sequential architecture. This is a linear stack of layers; we use the same number of neurons per layer and the same activation function across layers. For the experiments below we utilize 4 layers and 20 neurons, with the ELU activation function, . Training uses the Adam algorithm with default learning rate, batch size of 64 and epochs. The latter represents a single pass through all training data, and many epochs are needed given the high noise in the underlying stochastic gradient descent optimizer of the NN weights. With the above choices, training a NN takes just a few lines in TensorFlow. Indeed, it takes more code to scale/re-scale the inputs and outputs than to actually build and fit the Neural Net. Other neural network libraries, such as scikit-learn or PyTorch could be straightforwardly substituted.

We end this section with a few final remarks:

-

•

It is completely straightforward to modify the NN architecture. For instance, to replace a 4-layer “deep” architecture with a single layer, it takes just commenting out 3 lines in our code. Similarly, one can add more layers with a single line change.

-

•

Because we maintain the underlying Dynamic Programming paradigm, the NNs are fitted one-by-one. Therefore, one has complete flexibility in modifying any aspect of the fitting procedure to make it step-dependent. This includes the size and shape of the training set ; the parameters for the NN optimization, including the initial NN weights; the NN architecture, such as the number of neurons; and even the surrogate type itself. For example, one could mimic RL techniques to select time-dependent training regions to reflect the natural time-dependency of the solution, such as the remaining order to fill decreasing over time.

-

•

The convergence of the stochastic gradient descent to find a good is quite slow. We find that epochs are necessary to achieve good results. The number of epochs is the primary determinant of fit quality, cf. Section 5.3.

-

•

Any surrogate can be re-trained/updated at any point of the overall backward loop. For example, we suggest training ’s for all ’s and then training more (i.e., run the backward loop again with same training samples or newly generated ones) as one way to improve empirical convergence. This process is completely transparent and just requires loading the existing NN objects corresponding to ’s rather than initializing new ones. Similarly, one can straightforwardly implement warm starting, using the fitted NN weights at step as an initial guess for the weights of .

-

•

A typical failure point for surrogates is unstable prediction when extrapolating beyond the range of the training region. Thus, care must be taken to select the training domain in order to minimize extrapolation. Usually the modeler knows a priori the test cases of interest and so can ensure that the training range is at least as large. For example, below we wish to test for and therefore we train on to mitigate any issues with prediction at or beyond the edge of the training domain.

Remark 7.

Other surrogate types could be employed in place of NNs. For example, Gaussian Processes (GP) [52] is a kernel regression method where the kernel hyperparameters are fitted using maximum likelihood. They are implemented in, e.g., scikit-learn in Python. GPs offer variable selection through automatic relevance determination, which allows to “turn off” covariates/parameters that make little impact on the response. GP surrogates are known for excellent performance on limited datasets and are very popular for emulating expensive computer and stochastic experiments. Another surrogate type are LASSO linear models that explicitly project onto the span of the basis functions , . The respective coefficients are determined from the (-penalized) least squares equations. Finally, we note that not all regression methods are appropriate; non-smooth frameworks like Random Forests would yield unstable or discontinuous estimates of and therefore should not be applied.

4.4 Workflow

To summarize, the algorithmic workflow to solve the parametric optimal execution problem is given in Algorithm 1. We provide a TensorFlow implementation of the above in the supplementary fully-reproducible Jupyter notebook.

| (29) |

5 Numerical Experiments

5.1 Comparison to Reference Model

With linear price impact , the unconstrained strategy is available by parsing recursively the formulas in Proposition 1. This yields a concrete benchmark to evaluate our numerical algorithms. In this section we compare an NN surrogate to the above ground truth. Even though is not feasible (since it can and does turn negative in some states), this comparison is still useful. For the chosen parameter configurations, (cf., Fig 2) so that the non-negativity constraint is not binding on the vast proportion of the paths and hence is very nearly optimal for the constrained problem as well; that is, with denoting the minimizer in (8). This “near”-optimality is confirmed by the closeness between the constrained NN-strategy and the unconstrained strategy (LF), offering an additional consistency check on the NN solver.

To enable an apples-to-apples assessment of , we fix the set of “noise” that feed into the realized ’s, and employ this fixed database of ’s to generate the test forward trajectories both for the NN approximator and for the exact solution. Since depends on the past execution amounts, the trajectories of the approximating strategy will differ at each and every step . Thus, we are not making a pairwise comparison between and from (17), but compare in terms of the final execution cost in (29). Indeed, due to stochastic fluctuations, on any given path the realized costs from the latter may be higher or lower than the costs of the benchmark strategy, however the Law of Large Numbers guarantees that for large, the average execution cost must be at least as much as the benchmark.

For illustration purposes, we train an NN that takes in the four inputs and compute the corresponding . The respective 4-dimensional training domain is taken to be a hyper-rectangle specified as . The remaining parameters are fixed as . We then select training points i.i.d. uniformly in the above domain, independently for each step . Note that while we kept the same training domain across steps, one can vary this as changes. The ranges of the training domain are ultimately driven by the desired test configurations. For example, below we show the results for the test set with and initial condition . The latter affect the range of . Since and , we train on the range . The range for depends on and . With , we expect to buy up to 50-60K shares in the first step, which with would lead to . Note that is highly sensitive to , hence the respective training range should reflect the bounds on values. The range for the resilience covers the test case of and is simultaneously quite wide to cover a range of market conditions (calibration of is known to be difficult). The range for the instantaneous impact is similarly chosen to cover a range of market conditions, with leading to impact that is 5 times stronger than that of . The quantization of the conditional expectation in (27) uses knots.

|

|

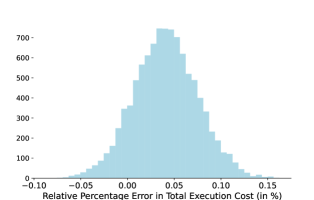

The left panel of Figure 3 shows the histogram of the difference between the realized execution costs coming from an NN approximator and the benchmark, across test trajectories. We observe that on average the former are 0.041% higher. Note that for about 11.6% of the paths, the realized costs from our approximate strategy were less than from the benchmark. Conversely, on more than 95.5% of the paths, the NN-based costs were less than 0.1% higher than those from the reference strategy, which is practically a very good level of accuracy.

The right panel of Figure 3 compares the reference and the NN-based control on one sample forward trajectory. We observe that the two strategies are very close in a pathwise sense as well, confirming the high approximation quality.

5.2 Nonlinear Price Impact

We now proceed to consider strategies with nonlinear price impact . Two comparators are the linear feedback (LF) strategy defined by (17) and constrained to buys-only, which we denote by , and the volume-weighted average policy, known as VWAP. The first comparator utilizes the linear benchmark formula as a function of current , in other way it postulates the counter-factual even when is not unity. This means it will under-estimate price impact when , and will overestimate price impact when . The above over- or under-estimation of price impact can lead to severe instability in the execution strategy. The second VWAP comparator fixes . That strategy is completely model independent, and therefore its performance is little affected by . In that sense the VWAP is the opposite of the linear feedback policy which makes strong assumptions on the market environment; VWAP implements the same trades no matter the model parameters.

|

|

While for a fixed set of model parameters there are multiple ways to construct a nonlinear solver, this would be computationally intractable to do for a large collection of . Consequently, our parametric solver is indispensable to provide a comprehensive solution across many parameter configurations. Moreover, since we train jointly across a range of , the linear case is covered and can be used to indirectly assess the fit quality. In other words, we expect the performance of the NN surrogate for to be similar to its performance when .

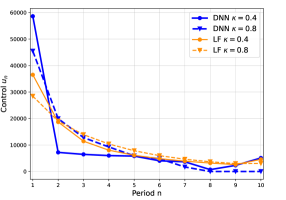

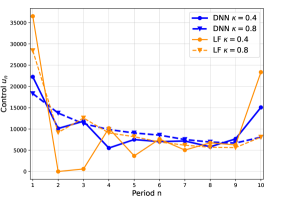

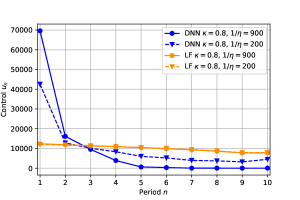

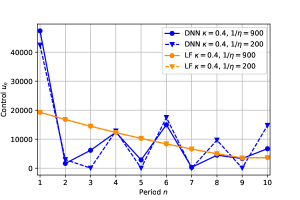

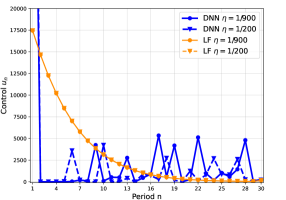

Figure 4 compares the resulting NN-based strategies to the linear feedback program restricted to buy-only. We observe that the linear feedback strategy is very sensitive to . For , LF generates oscillatory strategies, cf. the right panel of Figure 4. This occurs because the linear feedback underestimates the convex impact of trading on , so that it first over-shoots relative to the target , then under-shoots, etc. The unconstrained reference strategy actually tries to sell in the second step , as well as in the step. Forcing , we still obtain strong oscillations, no buying at and almost no buying at . In contrast, the (estimated) optimal strategy smoothly maintains throughout. Conversely for (left panel), the LF strategy underpurchases in the first trade since it does not correctly judge the reduced impact of large trades due to the concave price impact function.

For , price impact is much weaker and as a result the inventory urgency penalty dominates and leads to an L-shaped strategy, with a lot of buying in the first step or two, and a trickle for the rest of the steps. For , price impact is the dominant feature and yields U-shaped strategies, with largest trades at and . We also note that the dependence of the strategies on remains complex for . Since in all cases, total trades must add up to , as parameters change, the resulting effect on is non-monotone, i.e., more is traded at some steps and less in others. As a result, the various (average) strategy curves cross each other, often more than once.

Table 1 reports the performance of an NN solver versus the LF one. Specifically, we use a 5D NN solver that is parametric in . The NN strategy is found to lead to total execution costs that are 10-15% cheaper than LF, indicating that the differences observed in the respective strategies in Figure 4 are material. Gains are larger for larger and larger , i.e., for configurations where price impact is more short-lived and more severe. While we do not have a “gold standard” to compare against, we may use the performance (where LF is exact up to the non-negativity constraint that is almost never binding for this parameter configuration) as a yardstick for NN solution quality, since the NN solver is trained across different choices of .

| 10.33 | 7.33 | 15.05 | 10.58 | ||

| 10.34 | 8.70 | 13.01 | 5.85 | ||

5.3 NN Implementations

NN solvers necessarily contain multiple tuning parameters that must be chosen during implementation. It is a folk theorem that some finetuning is always necessary, one of the reasons that using NN is a bit of a “black art”.

In our setting, the feed-forward neural networks for and are very straightforward and do not require any bells and whistles. As mentioned, this simplicity of implementation is one of the reasons that we advocate this problem as a good pedagogical case study for building NN solvers for stochastic control problems. In particular, the NN architecture plays little significance: as long as one has sufficient flexibility, the choice of the number of neurons, the number of layers, etc., is very much secondary. Consequently, we default to the “canonical” setup with 16 neurons and 3 layers, that has been used in multiple prior works.

Nevertheless, there are certainly some tuning parameters that affect performance, first and foremost the effort spent on training. The latter is driven by the size of the training set, and the number of training epochs. The next set of experiments investigates in more detail how these parameters impact solution quality. In Table 2 we compare the average P&L of the NN strategy relative to LF for as we vary the number of epochs and the number of training points . As expected, accuracy increases as either or increase. We observe that the running time is roughly linear in (since the latter is a straightforward loop) and sub-linear in .

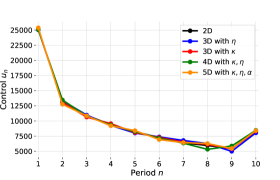

In addition, we also compare solvers that live in different dimensions, taking advantage of the fact that our implementation is fully dimension-agnostic and a single line change is needed to change . For NN training purposes, that dimension does not matter, so the running time is constant as changes. However, as expected, smaller implies more dense training sets (since the volume of the training domain shrinks) and hence better accuracy. This reflects the fundamental property that learning a functional approximator is more laborious on a larger domain, and the respective “volume” grows in . Thus, for the same , a 3D solver will be more accurate than a 4D one, and less accurate than a 2D one. This is the (computational) price to pay for learning simultaneously across multiple parameters.

| NN Configuration | Time (min) | |||

|---|---|---|---|---|

| 4D w/ | 0.10% | 1.43% | 2.73 | |

| 0.20% | 0.88% | 5.39 | ||

| 0.05% | 0.46% | 8.66 | ||

| 0.03% | 0.28% | 16.97 | ||

| 0.02% | 0.27% | 42.36 | ||

| 3D w/ | 0.04% | 0.24% | 8.38 | |

| 2D w/ | 0.03% | 0.15% | 8.14 |

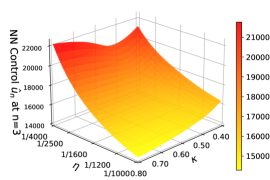

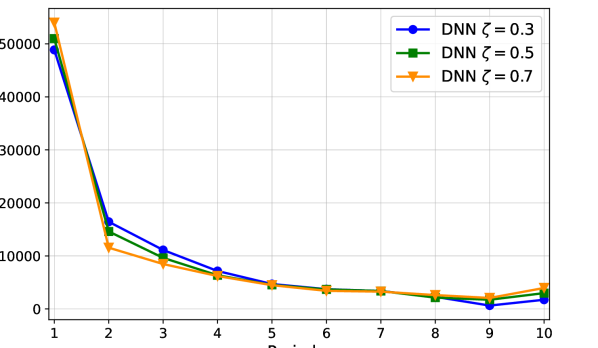

Figure 5 further compares solvers in different dimensions against each other in the nonlinear price impact case . We consider NN solvers in 2D that only take coordinates, as well as in 3D with coordinates, in 4D with and finally in 5D with . The fact that all solvers yield very similar strategies is an empirical indication of the convergence of the NNs.

|

|

Finally, the right panel of Figure 5 shows the fitted dependence of the control on at . Such dependence plots are the raison d’être of parametric solvers, providing the modeler with a direct view of the sensitivity of the strategy to model parameters. Without a parametric solver, it would be prohibitively expensive to generate such surfaces through re-solving each configuration one-by-one. We observe that at this intermediate step shrinks in and in .

5.4 Square-Root Price Impact

We next investigate the special case where . This “square-root law” of price impact is advocated by some practitioners (c.f., [45, 11, 15]) and has also been addressed numerically in [25] via a brute force optimization of the cost function. In contrast, our case study highlights once more the usefulness of our parametric solver in that it readily computes an optimal execution schedule jointly across a range of different price impact parameters and , as well as urgency rates ; and thus unveils with ease after a single round of training the solution’s dependence on the latter under this square-root price impact regime. Specifically, for fixed, we train a 5D NN solver that is parametric in over the hyper-rectangle , , , , with i.i.d. uniformly selected training points, and set .

|

|

Figure 6 compares the resulting NN-based strategies to the linear feedback benchmark case and Table 3 reports their performances. We first note that the obtained strategy is very sensitive to whether the urgency parameter is zero or not. This is sensible because with , the magnitude of the incurred price impact is on the small scale and even further reduced by large values for . As a consequence, as soon as becomes nonzero, the focus on rapidly reducing outstanding inventory dominates the overall order schedule; see the left panel in Figure 6. In contrast, when inventory control is turned off (i.e., ) the NN strategy exhibits an oscillatory behavior: peaks of large buy orders are interrupted by near to zero-volume orders; see the right panel in Figure 6. This observation is somewhat consistent with the numerical results presented in [25, Section 4.4] where the computed strategy consists of a few bursts of buying interspersed with long periods of no trading. In terms of total execution costs, the NN solver always significantly outperforms the LF benchmark strategy in all considered parameter configurations for ; see Table 3. Apparently, the LF feedback policy overestimates the price impact which leads to an overall sub-optimal behavior.

| 54.85 | 17.56 | ||

| 30.40 | 28.11 |

5.5 Number of Periods

Our NN algorithm trivially scales in the number of periods as it involves a simple loop over . Financially speaking, the most common interpretation is to fix the business time horizon , and then pick the scheduling interval , so that . To illustrate this, we consider taking a larger number of intervals . To reflect the idea that is fixed, we need to re-scale some of the model parameters in terms of the frequency . Specifically, since the dynamics of are motivated by a discretization of a continuous-time kernel decay specification, we need to keep constant, in other words , where we explicitly indicate the dependence of the resilience parameter on . Indeed, as gets bigger, should shrink so that the persistence of increases. Similarly, the continuous-time volatility should be invariant, so that . Finally, the inventory penalty is also proportional to business time, hence . In contrast, the impact parameter has no time-units, hence does not change as a function of .

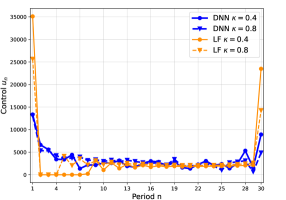

Returning to the closed-form formulas for , we observe that more fine scheduling frequency does not alter the fundamental U-shape (in the case ). In fact the initial and final trade amounts are only slightly affected by higher , while the intermediate trades are roughly inversely proportional to , maintaining the same trading rate in business time. Similar intuition carries over to the solution when . The left panel of Figure 7 shows the execution strategy for and , keeping all other parameters as in Figure 4 right, modulo re-scaling as described above. The right panel of Figure 7 shows the execution strategy for and . The latter plot is comparable to the right panel of Figure 6, taking zero inventory penalty . However, to prevent negative deviations , we must significantly decrease the noise amplitude to (compared to in Figure 6).

For and , the linear feedback strategy overshoots greatly, leading (for ) to no trades for periods , while the NN solution maintains a steady pace (with a decreasing trend due to the inventory penalty ) throughout. It gains about 10% in average cost savings compared to LF (11.2% for and 8.3% for ).

For and , we observe in Figure 7 bursty trading taking advantage of the concave price impact which discourages making small trades. Instead, the strategy executes every 2-4 periods, letting mean-revert back to zero in between. As in Figure 6, due to the first trade is very large, in our case about 65,000 for and about 78,000 for .

While the proposed dynamic programming approach implies error back-propagation as the iterations over are stepped through, we see very reasonable performance as is increased with exactly the same code. We do recommend to employ a different strategy (e.g., RL-like with a single neural network that incorporates time-dependence) for or so.

|

|

5.6 Multi-Exponential Decay Kernel

We conclude our numerical experiments by investigating the performance of our NN algorithm on an extended version of our model formulated in Section 2. Recall that the transient price impact process introduced in (2) for the studied buying program , , is given by

This deviation process belongs to a general class of decaying price impact processes, also called propagator models originally developed by [21, 22], and can be written as

| (30) |

with an exponential decay kernel

| (31) |

Therefore, it is very sensible to consider extensions of our model by allowing for different decay kernels in (31). Specifically, there is empirical evidence reported in the literature that price impact exhibits some memory effect and rather decays according to a power law function; cf., e.g., [22].

In order to retain a Markovian framework, we study in this section the generalization where the kernel is a convex combination of exponentially decaying kernels, namely it is of the form

| (32) |

for some with , and . Plugging this back into (30) yields

| (33) |

where

In other words, the total price distortion in (33) is now driven by processes which decay at different timescales . The ’s are fully correlated with the dynamics and

Moreover, the dynamics in (2) generalize to ,

In the special case , for all we retrieve the original setup from (2).

Augmenting the ’s to the state space and following the same reasoning as in Section 2.1, the objective function in (8) becomes

the corresponding value functions in (9) are given by

for all .

We next illustrate the above extension in the case so that the decay kernel is a mixture of two exponentials. Taking for the mixing weight , the associated dynamic programming (DP) equation in (10) and (2.1) modifies to

| (34) | ||||

| (35) |

for all .

Our NN agorithm can be easily extended to the DP equations in (34) and (5.6). In particular, we can also treat the mixing weight as a model hyperparameter that can be trained upon. In Figure 8 we illustrate the execution profiles of the NN solver for a model with a multi-exponential decay kernel as specified in (32) where , , and several values of . We train the solver across the 4 inputs with the latter in the range . The plot extends the configuration of the left panel in Figure 4 to a multi-exponential propagator and shows the corresponding NN policy (mean values across simulations) in the concave price impact regime with , and . As before, we take and periods and three different ’s.

As the accompanying table shows, misspecifying the decay kernel is costly: the DNN solver beats an LF strategy that assumes linear price impact and a single decay parameter by 9-12%. Of note, taking an exponential kernel with the larger does better than using an averaged . Even when the impact is linear, , the DNN beats the LF strategy (by 0.32%-1.51%) due to its mis-specification via an exponential kernel.

|

|

||||||||||||||||||||||||||||||||||||

6 Conclusion

In this article we have investigated neural network surrogates for solving optimal execution problems across a range of model parameters. Our approach jointly learns an optimal strategy as a function of the stochastic system state and of the market configuration.

The developed algorithm and the accompanying Jupyter Notebook can be used as a starting point for many other related analyses. For example, it would be straightforward to modify the code to handle parametric stochastic control problems of similar flavor (e.g., discrete-time hedging).

A further use case is to use the trained neural network as a building block in a more sophisticated setup. In particular, one may consider frameworks that explicitly account for model risk, in the sense of imprecisely known parameters. In the adaptive approach (including the Predictive Model Control popular in engineering), the modeler first develops learning dynamics, which convert static parameters, such as , into a stochastic process , where is the best estimate of the book resilience at step . Updating equations for in terms of the previous and new information from step (such as using the Bayesian paradigm) yield dynamics that can be merged with those of . One then plugs-in the resulting (and other similarly learned/updated parameters) into the NN-learned to obtain the adaptive strategy—which takes into account the latest parameter estimates, but does not solve the full Bellman equation. Conversely, one could also consider robust approaches that minimize over feasible parameter settings in order to protect against a worst-case situation. The latter again requires access to the computed as a building block. Finally, we may mention the adaptive robust approach [20] that combines dynamic learning with a worst-case min-max optimization to protect against incorrect estimates or mis-specified dynamics. The resulting numerical algorithms will be investigated in a separate, forthcoming sequel.

7 Proofs

We start with Lemma 2 which provides an intermediate computation relevant for showing in (16) (existence of round-trips) and characterizing the optimal in in (17).

Proof.

Proof of Proposition 1: In the linear case the unconstrained version of the optimal execution problem formulated in (12) is a linear quadratic stochastic control problem. Therefore, it is well known that for all the value functions are linear quadratic in and . This motivates the ansatz , where the coefficients are determined via backward induction by using the corresponding dynamic programming equations in (10) and (2.1).

First, the terminal condition in (10) yields as claimed in (14), as well as . Next, for the inductive step, let . The dynamic programming equation in (2.1) (for the considered unconstrained version of the problem) yields

| (37) |

Plugging in in (37) and solving the squares we obtain

| (38) | |||

where we used the fact that as well as . Minimizing (38) with respect to gives

| (39) |

and hence the feedback policy as claimed in (17). In particular, note that it follows from Lemma 2 that and that in (39) is indeed the unique minimum in (38). Moreover, inserting (39) back into (38) yields

which implies the desired recursive formulas provided in (15) and the representation of the value function in (16). Also note in (17) that is just a deterministic constant in and that is normally distributed for all . Indeed, since is linear in and , and the state variables and are linear in and the i.i.d. zero-mean Gaussian noise , one checks that is ultimately just a linear transformation of . As a direct consequence, we can conclude that is an admissible strategy in the set as defined in (13). Finally, the representation of in (18) follows directly from its state dynamics in (2). ∎

Proof of Proposition 2: In the case the optimal control problem in (12) (with ) is deterministic. We can introduce the corresponding cost functional given by

| (40) |

For all , considering the state variables and in (3) and (2) as functions in , we note that

In particular, we have the relation

| (41) |

Therefore, for all we can compute

| (42) |

where we used (41) in the last step. Similarly,

| (43) |

Hence, using (43) in (42) we obtain the recursive equation

| (44) |

Next, minimizing (40) under the constraint and denoting the Lagrangian multiplier, we obtain the first order conditions

| (45) |

which, together with (44), can be rewritten as

| (46) |

Computing the differences of the equations in (46) for successive and (for ) and rearranging the terms yields the recursive formula

| (47) |

where

| (48) |

Due to its linear structure, the recursion in (47) can be solved explicitly. We obtain the representation

| (49) |

where are given by ,

| (50) | ||||

for , as well as , which comes from the terminal condition . Moreover, (49) implies the representation

| (51) |

where are given by and

| (52) |

as well as

| (53) |

where are defined as and

| (54) |

In other words, the first order conditions in (46), together with the terminal state constraint , allow to express explicitly in terms of via (49) and it remains to minimize the costs in (40) as a linear quadratic function in only, namely

Proof of Corollary 2: In the case the constants introduced in (48) reduce to , and . Moreover, direct computations reveal that the coefficients in (50) simplify to

as well as , , . This yields the claim in (24). For the coefficients in (52) we obtain

and for the coefficients in (54) we have

This yields the claim in (25). Finally, directly computing and as defined in (19) gives the expressions in (23). ∎

References

- [1] Julia Ackermann, Thomas Kruse and Mikhail Urusov “Càdlàg semimartingale strategies for optimal trade execution in stochastic order book models” In Finance and Stochastics 25.4, 2021, pp. 757–810 DOI: 10.1007/s00780-021-00464-5

- [2] Julia Ackermann, Thomas Kruse and Mikhail Urusov “Optimal Trade Execution in an Order Book Model with Stochastic Liquidity Parameters” In SIAM Journal on Financial Mathematics 12.2, 2021, pp. 788–822 DOI: 10.1137/20M135409X

- [3] Aurélien Alfonsi and José Infante Acevedo “Optimal Execution and Price Manipulations in Time-varying Limit Order Books” In Applied Mathematical Finance 21.3 Routledge, 2014, pp. 201–237 DOI: 10.1080/1350486X.2013.845471

- [4] Aurélien Alfonsi and Pierre Blanc “Dynamic optimal execution in a mixed-market-impact Hawkes price model” In Finance and Stochastics 20.1, 2016, pp. 183–218 DOI: 10.1007/s00780-015-0282-y

- [5] Aurélien Alfonsi, Antje Fruth and Alexander Schied “Constrained portfolio liquidation in a limit order book model” In Advances in Mathematics of Finance Warsaw, Poland: Banach Center Publi. 83, Polish Acad. Sci. Inst. Math, 2008, pp. 9–25

- [6] Aurélien Alfonsi, Antje Fruth and Alexander Schied “Optimal execution strategies in limit order books with general shape functions” In Quantitative Finance 10.2 Routledge, 2010, pp. 143–157 DOI: 10.1080/14697680802595700

- [7] Aurélien Alfonsi and Alexander Schied “Capacitary Measures for Completely Monotone Kernels via Singular Control” In SIAM Journal on Control and Optimization 51.2, 2013, pp. 1758–1780 DOI: 10.1137/120862223

- [8] Aurélien Alfonsi and Alexander Schied “Optimal Trade Execution and Absence of Price Manipulations in Limit Order Book Models” In SIAM Journal on Financial Mathematics 1.1, 2010, pp. 490–522 DOI: 10.1137/090762786

- [9] Aurélien Alfonsi, Alexander Schied and Alla Slynko “Order Book Resilience, Price Manipulation, and the Positive Portfolio Problem” In SIAM Journal on Financial Mathematics 3.1, 2012, pp. 511–533 DOI: 10.1137/110822098

- [10] Robert Almgren and Neil Chriss “Optimal Execution of Portfolio Transactions” In Journal of Risk 03, 2001, pp. 5–40

- [11] Robert Almgren, Chee Thum, Emmanuel Hauptmann and Hong Li “Direct Estimation of Equity Market Impact” In RISK, 2005

- [12] Ali Al-Aradi, Adolfo Correia, Danilo Naiff, Gabriel Jardim and Yuri Saporito “Solving nonlinear and high-dimensional partial differential equations via deep learning” In arXiv preprint arXiv:1811.08782, 2018

- [13] Ali Al-Aradi, Adolfo Correia, Danilo de Frietas Naiff, Gabriel Jardim and Yuri Saporito “Applications of the deep Galerkin method to solving partial integro-differential and Hamilton-Jacobi-Bellman equations” In arXiv preprint arXiv:1912.01455, 2019

- [14] Achref Bachouch, Côme Huré, Nicolas Langrené and Huyen Pham “Deep neural networks algorithms for stochastic control problems on finite horizon, Part 2: numerical applications” In arXiv preprint arXiv:1812.05916, 2018

- [15] Emmanuel Bacry, Adrian Iuga, Matthieu Lasnier and Charles-Albert Lehalle “Market Impacts and the Life Cycle of Investors Orders” In Market Microstructure and Liquidity 01.02, 2015, pp. 1550009 DOI: 10.1142/S2382626615500094

- [16] Vlad Bally, Gilles Pagès and Jacques Printems “A quantization tree method for pricing and hedging multidimensional American options” In Mathematical Finance 15.1, 2005, pp. 119–168

- [17] Peter Bank and Antje Fruth “Optimal Order Scheduling for Deterministic Liquidity Patterns” In SIAM Journal on Financial Mathematics 5.1, 2014, pp. 137–152 DOI: 10.1137/120897511

- [18] Dirk Becherer, Todor Bilarev and Peter Frentrup “Optimal liquidation under stochastic liquidity” In Finance and Stochastics 22.1, 2018, pp. 39–68 DOI: 10.1007/s00780-017-0346-2

- [19] Dimitris Bertsimas and Andrew W. Lo “Optimal control of execution costs” In Journal of Financial Markets 1.1, 1998, pp. 1–50 DOI: https://doi.org/10.1016/S1386-4181(97)00012-8

- [20] Tomasz R Bielecki, Tao Chen, Igor Cialenco, Areski Cousin and Monique Jeanblanc “Adaptive robust control under model uncertainty” In SIAM Journal on Control and Optimization 57.2 SIAM, 2019, pp. 925–946

- [21] Jean-Philippe Bouchaud, J. Farmer and Fabrizio Lillo “How Markets Slowly Digest Changes in Supply and Demand” In Handbook of Financial Markets: Dynamics and Evolution, Handbooks in Finance San Diego: North-Holland, 2009, pp. 57–160 DOI: https://doi.org/10.1016/B978-012374258-2.50006-3

- [22] Jean-Philippe Bouchaud, Yuval Gefen, Marc Potters and Matthieu Wyart “Fluctuations and response in financial markets: the subtle nature of ‘random’ price changes” In Quantitative Finance 4.2 Routledge, 2004, pp. 176–190 DOI: 10.1080/14697680400000022

- [23] Álvaro Cartea and Sebastian Jaimungal “Incorporating order-flow into optimal execution” In Mathematics and Financial Economics 10.3, 2016, pp. 339–364 DOI: 10.1007/s11579-016-0162-z

- [24] Ying Chen, Ulrich Horst and Hoang Hai Tran “Portfolio liquidation under transient price impact - theoretical solution and implementation with 100 NASDAQ stocks” Preprint on arXiv:1912.06426, 2019

- [25] Gianbiagio Curato, Jim Gatheral and Fabrizio Lillo “Optimal execution with non-linear transient market impact” In Quantitative Finance 17.1 Routledge, 2017, pp. 41–54 DOI: 10.1080/14697688.2016.1181274

- [26] Ngoc-Minh Dang “Optimal Execution with Transient Impact” In Market Microstructure and Liquidity 03.01, 2017, pp. 1750008 DOI: 10.1142/S2382626617500083

- [27] Martin Forde, Leandro Sánchez-Betancourt and Benjamin Smith “Optimal trade execution for Gaussian signals with power-law resilience” In Quantitative Finance 0.0 Routledge, 2021, pp. 1–12 DOI: 10.1080/14697688.2021.1950919

- [28] Antje Fruth, Torsten Schöneborn and Mikhail Urusov “Optimal trade execution and price manipulation in order books with time-varying liquidity” In Mathematical Finance 24.4, 2014, pp. 651–695 DOI: https://doi.org/10.1111/mafi.12022

- [29] Antje Fruth, Torsten Schöneborn and Mikhail Urusov “Optimal trade execution in order books with stochastic liquidity” In Mathematical Finance 29.2, 2019, pp. 507–541 DOI: https://doi.org/10.1111/mafi.12180

- [30] Jim Gatheral “No-dynamic-arbitrage and market impact” In Quantitative Finance 10.7 Routledge, 2010, pp. 749–759 DOI: 10.1080/14697680903373692

- [31] Jim Gatheral, Alexander Schied and Alla Slynko “Transient linear price impact and Fredholm integral equations” In Mathematical Finance 22.3, 2012, pp. 445–474 DOI: https://doi.org/10.1111/j.1467-9965.2011.00478.x

- [32] Maximilien Germain, Huyên Pham and Xavier Warin “Neural networks-based algorithms for stochastic control and PDEs in finance” In arXiv preprint arXiv:2101.08068, 2021

- [33] Paulwin Graewe and Ulrich Horst “Optimal Trade Execution with Instantaneous Price Impact and Stochastic Resilience” In SIAM Journal on Control and Optimization 55.6, 2017, pp. 3707–3725 DOI: 10.1137/16M1105463

- [34] Robert B Gramacy “Surrogates: Gaussian Process Modeling, Design, and Optimization for the Applied Sciences” ChapmanHall/CRC, 2020

- [35] Ben Hambly, Renyuan Xu and Huining Yang “Recent Advances in Reinforcement Learning in Finance” Preprint on arXiv:2112.04553, 2021

- [36] Jiequn Han and Weinan E “Deep learning approximation for stochastic control problems” NIPS 2016, Deep Reinforcement Learning Workshop In arXiv preprint arXiv:1611.07422, 2016

- [37] Ulrich Horst and Xiaonyu Xia “Multi-dimensional optimal trade execution under stochastic resilience” In Finance and Stochastics 23.4, 2019, pp. 889–923 DOI: 10.1007/s00780-019-00394-3

- [38] Gur Huberman and Werner Stanzl “Price Manipulation and Quasi-Arbitrage” In Econometrica 72.4, 2004, pp. 1247–1275 DOI: https://doi.org/10.1111/j.1468-0262.2004.00531.x

- [39] Côme Huré, Huyên Pham, Achref Bachouch and Nicolas Langrené “Deep neural networks algorithms for stochastic control problems on finite horizon, part I: convergence analysis” In arXiv preprint arXiv:1812.04300, 2018

- [40] Amine Ismail and Huyên Pham “Robust Markowitz mean-variance portfolio selection under ambiguous covariance matrix” In Mathematical Finance 29.1 Wiley Online Library, 2019, pp. 174–207

- [41] Sebastian Jaimungal “Reinforcement learning and stochastic optimisation” In Finance and Stochastics 26.1, 2022, pp. 103–129 DOI: 10.1007/s00780-021-00467-2

- [42] Arezou Keshavarz and Stephen Boyd “Quadratic approximate dynamic programming for input-affine systems” In International Journal of Robust and Nonlinear Control 24.3, 2014, pp. 432–449 DOI: https://doi.org/10.1002/rnc.2894

- [43] Laura Leal, Mathieu Laurière and Charles-Albert Lehalle “Learning a functional control for high-frequency finance” Preprint on arXiv:2006.09611, 2021

- [44] Charles-Albert Lehalle and Eyal Neuman “Incorporating signals into optimal trading” In Finance and Stochastics 23.2, 2019, pp. 275–311 DOI: 10.1007/s00780-019-00382-7

- [45] Fabrizio Lillo, J. Farmer and Rosario N. Mantegna “Master curve for price-impact function” In Nature 421.6919, 2003, pp. 129–130 DOI: 10.1038/421129a

- [46] Christopher Lorenz and Alexander Schied “Drift dependence of optimal trade execution strategies under transient price impact” In Finance and Stochastics 17.4, 2013, pp. 743–770 DOI: 10.1007/s00780-013-0211-x

- [47] Eyal Neuman and Moritz Voß “Optimal Signal-Adaptive Trading with Temporary and Transient Price Impact” In SIAM Journal on Financial Mathematics 13.2, 2022, pp. 551–575 DOI: 10.1137/20M1375486

- [48] Anna A. Obizhaeva and Jiang Wang “Optimal trading strategy and supply/demand dynamics” In Journal of Financial Markets 16.1, 2013, pp. 1–32 DOI: http://dx.doi.org/10.1016/j.finmar.2012.09.001

- [49] Gilles Pagès, Huyên Pham and Jacques Printems “An optimal Markovian quantization algorithm for multi-dimensional stochastic control problems” In Stochastics and Dynamics 4.4, 2004, pp. 501–545

- [50] Andrew Papanicolaou, Hao Fu, Prasanth Krishnamurthy, Brian Healy and Farshad Khorrami “An optimal control strategy for execution of large stock orders using long short-term memory networks” In Journal of Computational Finance 26.4, 2023, pp. 37–65 DOI: https://doi.org/10.21314/JCF.2023.003

- [51] Silviu Predoiu, Gennady Shaikhet and Steven Shreve “Optimal Execution in a General One-Sided Limit-Order Book” In SIAM Journal on Financial Mathematics 2.1, 2011, pp. 183–212 DOI: 10.1137/10078534X

- [52] Carl Edward Rasmussen and Christopher K.. Williams “Gaussian Processes for Machine Learning” The MIT Press, 2006

- [53] Alexander Schied, Torsten Schöneborn and Michael Tehranchi “Optimal Basket Liquidation for CARA Investors is Deterministic” In Applied Mathematical Finance 17.6 Routledge, 2010, pp. 471–489 DOI: 10.1080/13504860903565050

- [54] Kevin T Webster “Handbook of Price Impact Modeling” ChapmanHall/CRC, 2023