Constrained optimal stopping under a regime-switching model

Abstract

We investigate an optimal stopping problem for the expected value of a discounted payoff on a regime-switching geometric Brownian motion

under two constraints on the possible stopping times: only at exogenous random times and only during a specific regime.

The main objectives are to show that an optimal stopping time exists as a threshold type under some boundary conditions and

to derive expressions of the value functions and the optimal threshold.

To this end, we solve the corresponding variational inequality and show that its solution coincides with the value functions.

Some numerical results are also introduced. Furthermore, we investigate some asymptotic behaviors.

Keywords: Optimal stopping, Regime-switching, Variational inequality, Real option.

1 Introduction

In the real options literature, the following type of optimal stopping problems appears frequently:

| (1.1) |

where is the exogenous discount rate, is a stochastic process, which we call the cash flow process, is the set of all stopping times that investors can choose, and is an -valued function, which we call the payoff function. We can regard (1.1) as a function on , which we call the value function. Problem (1.1) concerns the optimal investment timing for an investment whose payoff is given by the random variable when executed at time . The most typical example of is

| (1.2) |

which expresses the value of an investment that starts at time with an initial cost and that brings to the investor perpetually an instantaneous return at each time . Remark that the right-hand side of (1.2) becomes a function on when the process has the strong Markov property such as a geometric Brownian motion. The main concern of (1.1) is to show that an optimal stopping time exists and can be expressed as

for some . This type of optimal stopping is called threshold type, and is called its optimal threshold. It is significant to examine whether an optimal stopping is of threshold type. If so, the optimal strategy becomes apparent, and the optimal stopping time can be explicitly described. McDonald and Siegel [17] has undertaken this framework of optimal stopping problems. See also Chapter 5 of Dixit and Pindyck [6]. Here we focus on discussing (1.1) when is a regime-switching geometric Brownian motion under two constraints on .

Regime-switching models, widely studied in mathematical finance ([2], [3], [4], [9], [10], [11] and so forth), are models in which the regime, representing, e.g., the economy’s general state, changes randomly. In this paper, we consider a regime-switching model with two regimes . Let be a stochastic process expressing the regime at time . In particular, is a -valued continuous-time Markov chain. Then the cash-flow process is given by the solution to the following stochastic differential equation (SDE):

| (1.3) |

where and for , and is a one-dimensional standard Brownian motion independent of . Considering a regime-switching model, we need to define a value function for each initial regime, that is, for each , we define the value function as

| (1.4) |

Furthermore, we impose two constraints on . Liquidity risk and other considerations mean that investment is not always possible. Therefore, it is significant to analyze models with constraints on investment opportunities and timing. Hence, we impose two constraints simultaneously in this paper. One is the random arrival of investment opportunities. More precisely, we restrict stopping only at exogenous random times given by the jump times of a Poisson process independent of and . Another is the regime constraint. We restrict that stopping is feasible only during regime .

Now, we introduce some related works. Bensoussan et al. [1] discussed the problem (1.1) for the same cash flow process as defined in (1.3) without restriction on stopping. They treated the case where is given as (1.2) and showed that an optimal stopping time exists as a threshold type by an argument based on PDE techniques. Nishihara [19] discussed the same problem for a two-state regime-switching model with under the regime constraint, but the cash flow process is still a geometric Brownian motion. Note that [19] assumed that an optimal stopping exists as a threshold type. In addition, Egami and Kevkhishvili [8] also studied the same problem for the case where is a regime-switching diffusion process but without restriction on stopping. On the other hand, the restriction of stopping to exogenous random times has been undertaken by Dupuis and Wang [7]. They considered the case where the cash flow process is a geometric Brownian motion and the payoff function is of American call option type, i.e., , and did not deal with regime-switching models. In [7], they first derived a variational inequality (VI) through a heuristic discussion. Solving it, they showed by a probabilistic argument that the solution to the VI coincides with the value function. There are other many works dealing with this issue such as [12], [13], [15], [16], [18] and so forth.

To our best knowledge, this paper is the first study that deals with the constrained optimal stopping problem on a regime-switching geometric Brownian motion. It is also new to simultaneously impose the random arrival of investment opportunities and the regime constraint. Remark that the discussion in this paper is based on the approach in [7].

This paper is organized as follows: Some mathematical preparations and the formulation of our optimal stopping problem will be given in Section 2. Section 3 introduces the corresponding VI and solves its modified version in which two boundary conditions are replaced. We shall derive explicit expressions of the solution to the modified VI, which involves solutions to quartic equations, but it can be numerically computable easily. In Section 4, assuming that the two boundary conditions replaced in Section 3 are satisfied, we prove that the solution to the VI coincides with the value functions and the optimal threshold for our optimal stopping problem. In addition, we introduce some numerical results. Section 5 is devoted to illustrating some results on asymptotic behaviors, and Section 6 concludes this paper.

2 Preliminaries and problem formulation

We consider a regime-switching model with state space and suppose that the regime process is a -valued continuous-time Markov chain with generator

where . Now, we make the convention . Note that the length of regime follows the exponential distribution with parameter . We take the process defined in (1.3) as the cash flow process, and assume throughout this paper that

| (2.1) |

Let be a Poisson process with intensity independent of and , and denote by its th jump time for with the conventions and , where . Note that the process generates exogenous random times when an investment opportunity arrives. In other words, for , represents the th investment opportunity time. Suppose that , , and are defined on a complete probability space . In addition, we denote by the filtration generated by , and . Assume that satisfies the usual condition. Furthermore, we restrict stopping to only when the regime is . Thus, the set of all possible stopping times is described by

where is the set of all -valued stopping times and . Next we formulate the payoff function as follows:

| (2.2) |

for some , and , but we exclude the case where since the optimal threshold is obviously in this case. This formulation includes treated in [7], and in [19]. Moreover, (2.2) covers the payoff function introduced in (1.2). In fact, [1] showed that

In the setting described above, we define the value functions as follows:

| (2.3) |

for , where and means the expectation with the initial condition and . In fact, we should define as in terms of (1.4), but the above definition (2.3) is justified by the following:

where and are independent copies of and , respectively, and is the set of all possible stopping times defined based on and . We discuss the optimal stopping problem (2.3) in the following sections.

3 Variational inequality

We discuss the variational inequality (VI) corresponding to the value functions . From the same sort of argument as Section 3 in [7], the VI is given as follows:

Problem 3.1.

Find two nonnegative -functions and a constant satisfying

| (3.1) | |||||

| (3.2) | |||||

| (3.3) | |||||

| (3.4) | |||||

| (3.5) | |||||

| (3.6) | |||||

| (3.7) |

where , , and are the infinitesimal generators of under regime defined as

for -function .

This section aims to solve the following modified version of Problem 3.1, in which we replace the boundary conditions (3.6) and (3.7) with (3.8) below:

To solve Problem 3.2, we need some preparations. For and , is the quadratic function on defined as

The equation has one positive and one negative solution, denoted by and , respectively. For each , we denote

and consider the quartic equation . Since , , and as tends to , the equation has four different solutions, two of which are positive, and two of which are negative. Now, for the equation , we denote the larger positive solution by and another positive solution by . Note that is positive, and holds since . Thus, holds for . A similar argument can be found in Remark 2.1 of Guo [10]. Furthermore, the same holds for the quartic equation . Let and be the larger and other negative solutions to , respectively, that is, holds for . In addition, we define the following constants:

| (3.9) |

and

| (3.10) |

With the above preparations, we solve Problem 3.2 as follows:

Proposition 3.3.

Proof.

For the time being, we use instead of , that is, we rewrite (3.4) and (3.5) as follows:

| (3.15) | |||||

| (3.16) |

Step 1: For , a general solution to (3.2) and (3.3) is expressed as (3.11) with some and some . Remark that the non-negativity of and is derived from the condition (3.1). Without loss of generality, we may assume that . Substituting (3.11) for (3.2) and (3.3), we obtain that

for any , which is equivalent to that and for . Thus, satisfies , that is, . In addition, the same is true for . Thus, as defined above, and are the larger and smaller positive solutions to the equation . Moreover, and satisfy the following:

| (3.17) |

Step 2: Next, we discuss the case where . Firstly, we need to find a special solution to (3.2) and (3.15), since (3.15) is inhomogeneous. Note that is of linear growth. For each , we can then write a special solution as . Substituting for (3.2) and (3.15), we have that

| (3.18) |

for any , in other words, all coefficients in (3.18) are 0, from which and satisfy (3.9).

Now, we derive for in the same way as the previous step. For each , we can write a general solution to (3.2) and (3.15) as

with some and . By (3.2), (3.15) and (3.18), it follows that

for . Thus, by the same way as Step 1, and are solutions to the quartic equation . On the other hand, if either at least or is positive, then (3.8) is violated since any positive solution is greater than 1. Thus, and are the negative solutions, and we may take them so that without loss of generality. Moreover, we have

| (3.19) |

Step 3: By the -property of and the boundary condition (3.16), it follows that

Solving the above, together with (3.17) and (3.19), we obtain (3.14).

Step 4: In this step, we shall derive (3.13). Since and are continuous at , we have

Using (3.14) and cancelling , we obtain

and denote this as . Recall that and . Thus, , and hold. Moreover, we can see easily that , , , and . Thus, all the terms in are positive, and are negative. We have then , that is, (3.13) holds.

Step 5: We show that are -valued in this last step. Since as and for , there is an such that for any and . Now, we denote

and assume that . We have then , , and . When , it follows that

| (3.20) |

Thus, we have , which contradicts to the assumption that . Next, consider the case where . If , then (3.20) holds. This is a contradiction. When , we have

The second, third and fourth terms are non-negative. In addition, the fifth term is also non-negative since . Thus, , which is a contradiction. Lastly, when , for any , there is a such that , and hold for any . We have then for any from the view of (3.20), which means that holds. This is a contradiction. Consequently, are -valued. In particular, we have , from which follows. Thus, satisfy (3.4) and (3.5) since and for any . Consequently, gives the unique solution to Problem 3.2. This completes the proof of Proposition 3.3.

Remark 3.4.

It is very complicated to show that the function satisfies the boundary conditions (3.6) and (3.7). However, we can confirm that the conditions are met by implementing numerical computation for many parameter sets. In fact, with and fixed, and the values of and as , and , , , and as , satisfies (3.6) and (3.7) for all parameter sets. Thus, we can expect the boundary conditions (3.6) and (3.7) to be satisfied for any parameter set. We leave making sure of this fact to future research.

4 Verification

In this section, we show that the functions given in Proposition 3.3 coincide with the value functions defined by (2.3), and an optimal stopping time exists as a threshold type with the optimal threshold given in (3.13). To this end, we assume that satisfies the boundary conditions (3.6) and (3.7).

Let us start with some preparations. First of all, it is immediately apparent that the following lemma holds.

Lemma 4.1.

For , is bounded, and there is a such that for any .

In addition, we define

for with the conventions and . Note that represents the th time when stopping is feasible, and is described as

Now, we define

with the convention . Note that is an -valued stopping time, where . Hereafter, we write when a random variable follows the exponential distribution with parameter .

The following theorem is our main result.

Theorem 4.2.

Proof.

We show this theorem by dividing five steps.

Step 1: In this step, we fix and , and denote .

For , we denote by a geometric Brownian motion starting at under regime , that is, the solution to the following SDE:

In the following, when we write , its independent copy may be taken if necessary. Note that holds if , and . Now, we see the following:

| (4.1) |

To this end, we define firstly

| (4.2) |

Ito’s formula implies that

Taking expectation on both sides, we have

The first equality is due to (3.2); the second is due to the independence of and and . The last equality is obtained from the boundedness of by Lemma 4.1 and the integrability of . From the view of (4.2), we obtain

Since from Lemma 4.1 and from (2.1), we have

which tends to 0 as . As a result, since , the monotone convergence theorem implies (4.1).

Since , (4.1) can be rewritten as

| (4.3) |

From the view of (2.3), showing , we obtain immediately. In what follows, we focus on the proof of .

Step 2: Throughout the rest of this proof, we fix and . Now, we define

We can then unify (3.3) and (3.4) into

| (4.4) |

Here we aim to show the following by a similar argument to Step 1:

| (4.5) |

To this end, we define

where . In addition, recall that , that is, the first investment opportunity time. Noting that , we obtain

from Ito’s formula and (4.4). By the same sort of argument as Step 1, (4.5) follows.

Step 3: This step is devoted to preparing some notations. First of all, we define two sequences of stopping times inductively as follows: and, for ,

We call the time interval the th phase. Note that each phase begins when the regime changes into , moves to regime midway through, and ends when it returns to regime again. Moreover, we define the following two sequences of i.i.d. random variables:

Note that each expresses the length of regime in the th phase, and and are independent for any . For , we denote by the first investment opportunity time after the start of the th phase, that is,

Note that is not necessarily in the th phase, and may take the value of . In addition, we define , which represents the length of time from the start of the th phase until the arrival of the first investment opportunity.

Step 4: In this step, we shall show

| (4.6) |

Recall , that is, the time when stopping becomes feasible for the first time.

First of all, we can rewrite (4.5) as

| (4.7) |

since is independent of and . Using (4.3) and (4.7), we have

Note that all random variables in the above are independent. Now, we denote

for , , and

for . Remark that, for , we can rewrite as follows:

| (4.8) |

when and . We have then, for any ,

From Lemma 4.1 and the independence of all random variables, it follows that

since

As a result, we obtain . Since each is non-negative, the monotone convergence theorem implies that

Thus, (4.8) provides that

On the other hand, holds. Since is a non-negative supermartingale, it converges to a.s. as by, e.g., Problem 1.3.16 of [14]. As a result, we have

from which (4.6) follows.

Step 5: We define a filtration as and a process as , where . We have then, for any ,

where is an independent copy of . Thus, is a non-negative -supermartingale, and converges to a.s. as . On the other hand, Lemma 1 of [7] implies

| (4.9) |

Since for any , the optional sampling theorem, e.g., Theorem 16 of Chapter V in [5], together with (4.6), yields that

for any -valued -stopping time . Taking supremum on the right-hand side over all such ’s, we obtain from the view of (2.3) and (4.9).

Next, we see the reverse inequality . To this end, we recall and define for . As shown in Lemma 4.3, is a uniformly integrable martingale, which implies that

since for any , and . Consequently, we obtain

and thus, the stopping time is optimal. This completes the proof of Theorem 4.2.

Lemma 4.3.

is a uniformly integrable martingale.

Proof.

We shall prove this lemma by the same sort of argument as Step 2 of Section 3.2 in [7]. First of all, for any , we have

where is an independent copy of . As a result, is a -martingale.

Next, we show the uniform integrability. To see this, we have only to show that

Since , it suffices to see that

| (4.10) |

Note that

Now, we take a satisfying for any . Denoting

we can see that is a nonnegative -supermartingale. Thus, the optional sampling theorem, e.g., Theorem 16 of Chapter V in [5], implies that

holds for any , from which (4.10) follows.

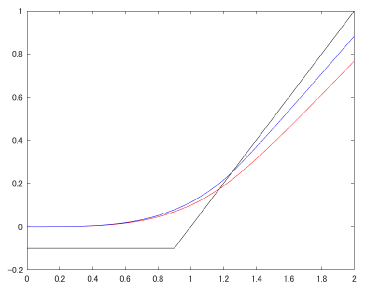

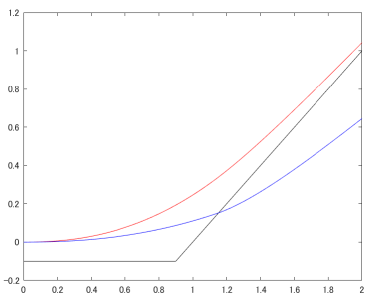

By Theorem 4.2, an optimal stopping time exists as a threshold type with the optimal threshold if in Proposition 3.3 satisfies the boundary conditions (3.6) and (3.7). Moreover, (3.11), (3.12) and (3.13) give expressions of the value functions and the optimal threshold , respectively. Although these expressions contain solutions to quartic equations, we can compute the value of numerically and illustrate the value functions , e.g., for the case where , , , , , , , and , we obtain approximately

and . Figure 2 illustrates the functions , and by red, blue, and black curves. Furthermore, it is immediately seen that the value functions are non-negative non-decreasing convex functions and as for . However, the magnitude relationship of and depends on how we take parameters. The function is larger in the above example but simply replacing the values of and with and , respectively, reverses the magnitude relationship between and as illustrated in Figure 2. Besides, for this case takes the value of .

5 Asymptotic behaviors

This section discusses asymptotic behaviors of the value functions and the optimal threshold when some parameter goes to . To compare with results in preceding literature, we consider the case where is a geometric Brownian motion given as , that is, and . Then, simple calculations show that

| (5.1) |

5.1 Asymptotic behaviors as

When , investment opportunities arrive continuously, which means only the regime constraint remains. First of all, we have

| (5.2) |

respectively, but the values of and are independent of . In addition, it follows that

| (5.3) |

as . By (3.10) and (5.2), we can see that

as , and converge to 0. By Proposition 3.3, Theorem 4.2 and (5.1), we obtain

where and are given in (5.1), and given in (5.5) below. Now, we assume that for any . Since and , we have

by (3.17). In addition, the continuity of at , togther with (5.3) and , implies that

where by (5.2), and

| (5.4) |

From the view of (5.4), we have

and

Substituting for (3.13) these limits and the limits obtained so far, we get the following:

| (5.5) |

We can see that holds. In addition, for the case where and , we can confirm that the above result coincides with Proposition 1 of [19].

5.2 Asymptotic behaviors as

As tends to , the regime vanishes, and only the constraint on the random arrival of investment opportunities remains. In other words, the model converges to the one treated in Dupuis and Wang [7]. In this case, it follows that

| (5.6) |

Note that the value of is independent of . We have then , and

Moreover, as . By the same way as the previous subsection, we obtain that

and for any , where is the limit given in (5.6). As seen in [7], we can prove that holds and the boundary conditions (3.6) and (3.7) are satisfied. When and , the result in this subsection is consistent with [7].

6 Conclusions

We considered a two-state regime-switching model and discussed the optimal stopping problem defined by (2.3) under two constraints on stopping: the random arrival of investment opportunities and the regime constraint. Under the assumption that the boundary conditions (3.6) and (3.7) are satisfied, we showed that an optimal stopping time exists as a threshold type. In addition, we derived expressions of the value functions , and the optimal threshold , which include solutions to quartic equations, but can be easily computed numerically. Asymptotic behaviors of , and are also discussed. On the other hand, the assumption of the boundary conditions might be redundant, as mentioned in Remark 3.4. Thus, it is significant as future work to show that the boundary conditions (3.6) and (3.7) are always satisfied using, e.g., a PDE approach discussed in Bensoussan et al. [1].

Acknowledgments

Takuji Arai gratefully acknowledges the financial support of the MEXT Grant in Aid for Scientific Research (C) No.18K03422.

References

- [1] Bensoussan, A., Yan, Z., & Yin, G. (2012). Threshold-type policies for real options using regime-switching models. SIAM Journal on Financial Mathematics, 3(1), 667-689.

- [2] Bollen, N. P. (1998). Valuing options in regime-switching models. Journal of Derivatives, 6, 38-50.

- [3] Buffington, J., & Elliott, R. J. (2002). American options with regime switching. International Journal of Theoretical and Applied Finance, 5(05), 497-514.

- [4] Buffington, J., & Elliott, R. J. (2002). Regime switching and European options. In Stochastic Theory and Control (pp. 73-82). Springer, Berlin, Heidelberg.

- [5] Dellacherie, C., & Meyer, P. A. (1982). Probabilities and potential. B, volume 72 of. North-Holland Mathematics Studies, 30.

- [6] Dixit, R. K., & Pindyck, R. S. (2012). Investment under uncertainty. Princeton university press.

- [7] Dupuis, P., & Wang, H. (2002). Optimal stopping with random intervention times. Advances in Applied probability, 34(1), 141-157.

- [8] Egami, M., & Kevkhishvili, R. (2020). A direct solution method for pricing options in regime-switching models. Mathematical Finance, 30(2), 547-576.

- [9] Elliott, R. J., Chan, L., & Siu, T. K. (2005). Option pricing and Esscher transform under regime switching. Annals of Finance, 1(4), 423-432.

- [10] Guo, X. (2001). An explicit solution to an optimal stopping problem with regime switching. Journal of Applied Probability, 38(2), 464-481.

- [11] Guo, X., & Zhang, Q. (2004). Closed-form solutions for perpetual American put options with regime switching. SIAM Journal on Applied Mathematics, 64(6), 2034-2049.

- [12] Hobson, D. (2021). The shape of the value function under Poisson optimal stopping. Stochastic Processes and their Applications, 133, 229-246.

- [13] Hobson, D., & Zeng, M. (2019). Constrained optimal stopping, liquidity and effort. Stochastic Processes and their Applications.

- [14] Karatzas, I., & Shreve, S. (2012). Brownian motion and stochastic calculus (Vol. 113). Springer Science & Business Media.

- [15] Lange, R. J., Ralph, D., & Støre, K. (2020). Real-option valuation in multiple dimensions using Poisson optional stopping times. Journal of Financial and Quantitative Analysis, 55(2), 653-677.

- [16] Lempa, J. (2012). Optimal stopping with information constraint. Applied Mathematics & Optimization, 66(2), 147-173.

- [17] McDonald, R., & Siegel, D. (1986). The value of waiting to invest. The Quarterly Journal of Economics, 101(4), 707-727.

- [18] Menaldi, J. L., & Robin, M. (2016). On some optimal stopping problems with constraint. SIAM Journal on Control and Optimization, 54(5), 2650-2671.

- [19] Nishihara, M. (2020). Closed-form solution to a real option problem with regime switching. Operations Research Letters, 48(6), 703-707.