Risk-Aware Stability, Ultimate Boundedness, and Positive Invariance

Abstract

This paper introduces the notions of stability, ultimate boundedness, and positive invariance for stochastic systems in the view of risk. More specifically, those notions are defined in terms of the worst-case Conditional Value-at-Risk (CVaR), which quantifies the worst-case conditional expectation of losses exceeding a certain threshold over a set of possible uncertainties. Those notions allow us to focus our attention on the tail behavior of stochastic systems in the analysis of dynamical systems and the design of controllers. Furthermore, some event-triggered control strategies that guarantee ultimate boundedness and positive invariance with specified bounds are derived using the obtained results and illustrated using numerical examples.

I Introduction

Whether it is a financial portfolio or engineering system, we often need to accept a certain level of risk to balance the pros and cons of spending costs in the decision-making processes under uncertainties. This is particularly true when the uncertainty distributions have an unbounded support because a guarantee of 100% ideal satisfaction is impossible or requires an infinite amount of cost. Therefore, risk has been studied for a long time, not only in the financial industry [1, 2, 3, 4], but also in the wide areas of engineering [5, 6, 7] using many different approaches.

The notions of stability, ultimate boundedness, and positive invariance are fundamental in the analysis of dynamical systems and in the design of controllers [8]. To deal with stochastic uncertainties in dynamical systems, the concept of probabilistic stability was introduced in [9]. Later, the concepts of probabilistic set invariance and ultimate boundedness were introduced for discrete-time linear systems in [10] and extended to continuous-time linear systems in [11]. Those probabilistic notions are defined using chance constraints. Another popular approach to dealing with stochastic uncertainties is to consider mean square and -stability [12]. In this direction, ultimate boundedness [13] and positive invariance [14, 15] have been also investigated. However, those notions are not applicable to guarantee that the expected value of the constraint-violating cases is small.

To take into account this additional consideration of risk, this paper introduces the definitions of stability, ultimate boundedness, and positive invariance in terms of the worst-case Conditional Value-at-Risk (CVaR) for stochastic systems. CVaR is a relatively new risk measure that is defined as the conditional expectation of losses exceeding a certain threshold [16]. The worst-case CVaR is the supremum of CVaR over a set of possible disturbances [4, 17]. Using the (worst-case) CVaR, the tail behavior of the stochastic systems can be quantified; it quantifies the risk which has a low probability of occurring, but if it does occur, it will result in a large loss. Assessing the tail risk is especially beneficial when the uncertainty distribution has a fat tail. In such a case, the use of the chance constraints or standard expected value for analysis may result in a significant loss. Because the (worst-case) CVaR is a coherent risk measure [4], it enjoys nice mathematical properties. In particular, we see the worst-case CVaR on the squared norm of the states using the first two moments of the disturbance allows us to obtain elegant results for discrete-time linear stochastic systems. Such a problem setup can be easily applied to cases wherein the disturbance is non-Gaussian or the probability density function is not available.

The rest of the paper is organized as follows. After introducing notation, definitions, and properties of the worst-case CVaR as well as some basic results in Section II, Section III and Section IV present the definitions of stability, ultimate boundedness, and positive invariance using the worst-case CVaR, without inputs and with bounded inputs, respectively. Based on the results in Section IV, approaches to risk-aware event-triggered control are developed in Section V, which is followed by conclusion in Section VI.

II Preliminaries

II-A Notation

The sets of real numbers, real vectors of length , and real matrices of size are denoted by , , and , respectively. The sets of nonnegative numbers, nonnegative integers, and positive integers are denoted by , and , respectively. For , indicates is positive definite. denotes the transpose of a real matrix and denotes the trace of . denotes the identity matrix of size . The Kronecker product of two matrices and is denoted as . For , . For a vector , denotes the Euclidean norm. For a matrix , denotes the maximum singular value norm. Recall that a function is a function if it is continuous, strictly increasing and . A function is a function if for each fixed , with respect to and for each fixed , is decreasing with respect to and .

II-B Conditional Value-at-Risk

Let be the mean and be the covariance matrix of the random vector under the true distribution , which is the probability law of . Thus, it is implicitly assumed that the random vector has finite second-order moments. Let denote the set of all probability distributions on that have the same first- and second-order moments as , i.e.,

Here denotes the Kronecker delta and denotes the expectation with respect to . The true underlying probability measure is not known exactly, but it is known that .

Definition II.1 (Conditional Value-at-Risk [16, 18])

For a given measurable loss function , a probability distribution on and a level , the CVaR at with respect to is defined as

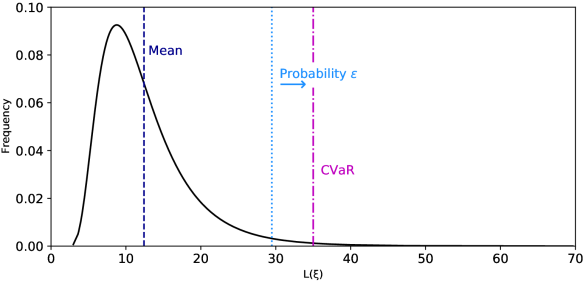

CVaR is the conditional expectation of loss above the ()-quantile of the loss function [18] and quantifies the tail risk (see Figure 1).

The worst-case CVaR is the supremum of CVaR over a given set of probability distributions as defined below:

Definition II.2 (Worst-case CVaR [18])

The worst-case CVaR over is given by

Here, the exchange between the supremum and infimum is justified by the stochastic saddle point theorem [19].

If is quadratic with respect to , the worst-case CVaR can be computed by a semidefinite program [18], [20]. Furthermore, if the mean of the random vector is zero, the following easy-to-compute bounds are obtained.

Lemma II.3 (Bounds for worst-case CVaR [21])

Suppose and with some , and , then

If and , then it follows that

To deal with dynamical systems, the following is a simple, but useful result.

Lemma II.4

Suppose are independent and identically distributed random vectors under the true distribution . Let . Then, is a random vector with the mean zero and covariance . Thus, the true underlying probability measure for satisfies , where

Moreover, for a matrix , it holds that

Proof:

Follows from the assumption that are independent and identically distributed. The second part follows from Lemma II.3. ∎

One reason that the (worst-case) CVaR is popular for risk assessment is its mathematically attractive properties of coherency.

Proposition II.5 (Coherence properties [4, 22])

The worst-case CVaR is a coherent risk measure, i.e., it satisfies the following properties: Let and be two measurable loss functions.

-

•

Sub-additivity: For all and ,

-

•

Positive homogeneity: For a positive constant ,

-

•

Monotonicity: If almost surely,

-

•

Translation invariance: For a constant ,

II-C Useful Result

This paper repeatedly utilizes the following inequality.

Lemma II.6 (Cauchy-Schwarz inequality)

For two vectors , it holds that

III Linear System without Inputs

This section considers linear systems subject to stochastic disturbances. After introducing a system model, stability, ultimate boundedness, and positive invariance are investigated.

III-A System Model

Consider the discrete-time linear stochastic system

| (1) |

where is the state and is the disturbance, respectively, at discrete time instant . and are constant matrices. It is assumsed that the initial condition is given, and that are independent and identically distributed random vectors with the mean zero and covariance for all . The true underlying probability measure is not known exactly, but it is known that , where

| (2) |

III-B Practical Stability and Ultimate Boundedness

Here, the stability notion in terms of the worst-case CVaR is introduced.

Definition III.1 (Practical stability)

The system (1) is practically asymptotically worst-case CVaR stable if there exist and a constant such that

| (6) |

The following lemma provides a sufficient condition for a system to be practically asymptotically worst-case CVaR stable.

Lemma III.2 (Sufficient condition for practical stability)

If and is reachable, then the linear system (1) is practically asymptotically worst-case CVaR stable.

Proof:

Using Lemma II.6 and norm sub-multiplicativity,

| (7) |

for any , where . Using Proposition II.5 along with Lemma II.4, it follows that

| (8) |

Here, we used

| (9) |

where is the solution to the Lyapunov equation

| (10) |

The last equality in (9) is due to is Schur and is reachable. Thus, choosing

| (11) |

satisfies Definition III.1. ∎

Remark III.3

For linear systems, assuming that is Schur is sufficient for practically asymptotically worst-case CVaR stability as for other kinds of stability. However, we impose the assumption in this paper, and Lemma III.2 is focused on such a case.

Here, we introduce a notion of worst-case CVaR ultimate bound, which is an extension of the probabilistic ultimate bound [10]. The notion of ultimate bound is closely related to practical asymptotic stability.

Definition III.4 (Ultimate bound)

Let . A domain is a worst-case CVaR ultimate bound for the system (1) if for every initial state , there exists such that for all .

A worst-case CVaR ultimate bound can be found as below:

Theorem III.5 (A ultimate bound)

III-C Positive Invariance

The notion of positive invariance is yet another important concept, which is intimately related to ultimate boundedness.

Definition III.6 (Positively invariant set)

Let be a continuous function. A domain is a worst-case CVaR positively invariant set for the system (1) if for any state for all .

A worst-case CVaR positively invariant set can be found as below:

Theorem III.7 (A positively invariant set)

IV Linear System with Bounded Inputs

In this section, linear systems with bounded inputs subject to stochastic disturbances are considered. To deal with such a case, the notion of input-to-state stability and robust positive invariance are developed using the worst-case CVaR.

IV-A System Model

Consider the discrete-time linear stochastic system

| (25) |

where is the state, is the bounded input and is the disturbance, respectively, at discrete time instant . , and are constant matrices. It is assumsed that the initial condition is given, and that are independent and identically distributed random vectors defined for (1).

We treat as a bounded disturbance and define

| (26) |

for a given .

IV-B Practical Stability and Ultimate Boundedness

As in the previous section, we define the input-to-state stability using the worst-case CVaR.

Definition IV.1 (Practical stability)

The system (25) is practically worst-case CVaR input-to-state stable if there exist , , and such that

| (29) |

Note that if a system is practically worst-case CVaR input-to-state stable, then it is practically asymptotically worst-case CVaR stable if there is no input.

The following lemma provides a sufficient condition for a system to be practically worst-case CVaR input-to-state stable.

Lemma IV.2 (Sufficient condition for practical stability)

If and is reachable, then the linear system (1) is practically worst-case CVaR input-to-state stable.

Proof:

Similar to the previous section, we introduce a notion of worst-case CVaR ultimate bound with bounded input.

Definition IV.3 (Ultimate bound)

Let . A domain is a worst-case CVaR ultimate bound with bounded input for the system (25) if for every initial state , there exists such that for all .

A worst-case CVaR ultimate bound can be found as below:

Theorem IV.4 (A ultimate bound)

IV-C Positive Invariance

The notion of robust positively invariant set can be defined for system with bounded input.

Definition IV.5 (Robust positively invariant set)

Let be a continuous function. A domain is a worst-case CVaR robust positively invariant set for the system (25) if for any state for all .

A robust positively invariant set can be found as follows.

Theorem IV.6 (A robust positively invariant set)

V Event-triggered Control

In this section, event-triggered control strategies are developed using the results in Section IV.

V-A System Model

Consider the discrete-time linear control system subject to stochastic disturbance

| (48) |

where is the state, is the control input and is the disturbance, respectively, at discrete time instant . , and are constant matrices. It is assumed that the initial condition is given and are independent and identically distributed random vectors defined for (1). It is also assumed that a linear state feedback control has been designed such that for (48) and is reachable.

In this section, we design event-triggered control strategies that guarantee ultimate boundedness and positive invariance for the system (48) with the set

| (49) |

To design trigger conditions, let us introduce the following notation: Let the triggering time sequence , and define the state used for the control input by

| (50) |

and the state error by

| (51) |

Then the control law can be written as

| (52) |

and the system (48) can be written as

| (53) |

The rest of this section considers the event-triggering mechanism in the form of

| (54) |

where the triggering function and the triggering threshold are to be designed. Note that such an event-trigger condition guarantees that for all .

We consider static event-triggered control strategies that use a constant error threshold .

V-B Ultimate Boundedness

Event-triggered control strategies that guarantee ultimate boundedness are followed from Theorem IV.4.

Corollary V.1

Proof:

A similar result can be obtained using the error threshold on the control input error:

Corollary V.2

V-C Positive Invariance

Event-triggered control strategies that guarantee positive invariance are followed from Theorem IV.6.

Corollary V.3

Proof:

Follows from Theorem IV.6. ∎

A similar result can be obtained using the error threshold on the control input error:

Corollary V.4

Proof:

Follows from Theorem IV.6. ∎

V-D Numerical Examples

Here we observe the performances of the event-triggered controllers in the previous subsections using numerical examples.

Consider the system (48) with

| (66) |

subject to the zero-mean Gaussian disturbance with the covariance

| (67) |

and the state feedback gain

| (68) |

Choose to compute the worst-case CVaR.

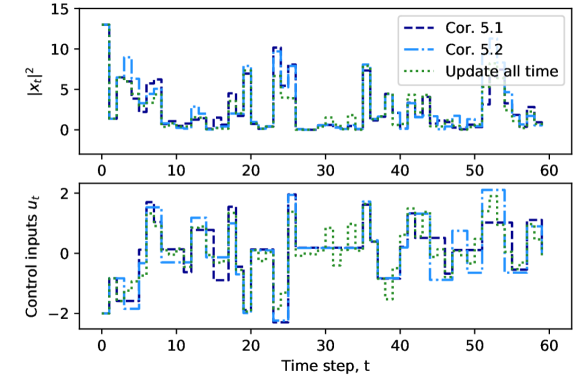

To see the performances of the controllers with Corollaries V.1 and V.2, choose and , which satisfy (58) and (60) with equalities, respectively. With those parameters, the event-triggered control performances and control inputs as well as those of a periodic controller (i.e., standard state feedback controller that updates the control input all the time) are shown in Figure 2. It is observed that the number of the control input updates were reduced to 27 and 25 during 60 time-steps, respectively, while is always smaller than , thus for sufficiently large is achieved.

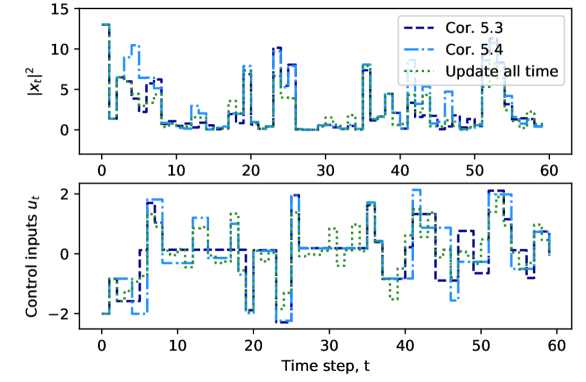

To see the performances of the controllers with Corollaries V.3 and V.4, choose and , which satisfy (63) and (65) with equalities, respectively. With those parameters, the event-triggered control performances and control inputs as well as those of a periodic controller are shown in Figure 3. The number of control input updates were 24 and 23 during 60 time-steps, respectively.

In all cases, it is observed that the number of control inputs achieved a 50% reduction while achieving the objectives. Those reductions are heavily dependent on the threshold . Large and , and a small help to reduce the number of updates.

VI Conclusion

This paper introduced the novel concepts of stability, ultimate boundedness, and positive invariance for stochastic systems using the worst-case Conditional Value-at-Risk (CVaR) to quantify the tail behavior of the stochastic systems. These notions extend the stochastic correspondences and allow us to consider risk in the decision-making processes. The introduced notions are used to design event-triggered controllers and their performances were illustrated using numerical examples.

References

- [1] H. M. Markowitz, Portfolio selection. Yale University Press, 1968.

- [2] R. W. Klein and V. S. Bawa, “The effect of estimation risk on optimal portfolio choice,” Journal of Financial Economics, vol. 3, no. 3, pp. 215–231, 1976.

- [3] H. M. Markowitz and G. P. Todd, Mean-variance analysis in portfolio choice and capital markets. John Wiley & Sons, 2000, vol. 66.

- [4] S. Zhu and M. Fukushima, “Worst-case conditional value-at-risk with application to robust portfolio management,” Operations research, vol. 57, no. 5, pp. 1155–1168, 2009.

- [5] C. A. Cornell, “Engineering seismic risk analysis,” Bulletin of the seismological society of America, vol. 58, no. 5, pp. 1583–1606, 1968.

- [6] P. Whittle, “Risk-sensitive linear/quadratic/Gaussian control,” Advances in Applied Probability, vol. 13, no. 4, pp. 764–777, 1981.

- [7] R. V. Whitman, “Evaluating calculated risk in geotechnical engineering,” Journal of Geotechnical Engineering, vol. 110, no. 2, pp. 143–188, 1984.

- [8] F. Blanchini, “Set invariance in control,” Automatica, vol. 35, no. 11, pp. 1747–1767, 1999.

- [9] H. J. Kushner, “On the stability of stochastic dynamical systems,” Proceedings of the National Academy of Sciences of the United States of America, vol. 53, no. 1, pp. 8–12, 1965.

- [10] E. Kofman, J. A. De Doná, and M. M. Seron, “Probabilistic set invariance and ultimate boundedness,” Automatica, vol. 48, no. 10, pp. 2670–2676, 2012.

- [11] E. Kofman, J. A. De Doná, M. M. Seron, and N. Pizzi, “Continuous-time probabilistic ultimate bounds and invariant sets: Computation and assignment,” Automatica, vol. 71, pp. 98–105, 2016.

- [12] D. Kannan and V. Lakshmikantham, Handbook of stochastic analysis and applications. CRC Press, 2001.

- [13] M. Zakai, “On the ultimate boundedness of moments associated with solutions of stochastic differential equations,” SIAM Journal on Control, vol. 5, no. 4, pp. 588–593, 1967.

- [14] A. Benzaouia, E. K. Boukas, and N. Daraoui, “Stability of continuous-time linear systems with Markovian jumping parameters and constrained control,” IFAC Proceedings Volumes, vol. 35, no. 1, pp. 43–48, 2002.

- [15] E. Boukas and A. Benzaouia, “Stability of discrete-time linear systems with Markovian jumping parameters and constrained control,” IEEE Transactions on Automatic Control, vol. 47, no. 3, pp. 516–521, 2002.

- [16] R. T. Rockafellar and S. Uryasev, “Optimization of conditional value-at-risk,” Journal of Risk, vol. 2, pp. 21–41, 2000.

- [17] D. Huang, S.-S. Zhu, F. J. Fabozzi, and M. Fukushima, “Portfolio selection with uncertain exit time: A robust cvar approach,” Journal of Economic Dynamics and Control, vol. 32, no. 2, pp. 594–623, 2008.

- [18] S. Zymler, D. Kuhn, and B. Rustem, “Distributionally robust joint chance constraints with second-order moment information,” Mathematical Programming, vol. 137, pp. 167–198, 2013.

- [19] A. Shapiro and A. Kleywegt, “Minimax analysis of stochastic problems,” Optimization Methods and Software, vol. 17, no. 3, pp. 523–542, 2002.

- [20] S. Zymler, D. Kuhn, and B. Rustem, “Worst-case value at risk of nonlinear portfolios,” Management Science, vol. 59, no. 1, pp. 172–188, 2013.

- [21] M. Kishida and A. Cetinkaya, “Risk-aware linear quadratic control using conditional value-at-risk,” IEEE Transactions on Automatic Control, 2022. [Online]. Available: https://doi.org/10.1109/TAC.2022.3142131

- [22] P. Artzner, F. Delbaen, J.-M. Eber, and D. Heath, “Coherent measures of risk,” Mathematical Finance, vol. 9, pp. 203–228., 1999.