A deep learning method for solving stochastic optimal control problems driven by fully-coupled FBSDEs

Abstract

In this paper, we mainly focus on the numerical solution of high-dimensional stochastic optimal control problem driven by fully-coupled forward-backward stochastic differential equations (FBSDEs in short) through deep learning. We first transform the problem into a stochastic Stackelberg differential game(leader-follower problem), then a cross-optimization method (CO method) is developed where the leader’s cost functional and the follower’s cost functional are optimized alternatively via deep neural networks. As for the numerical results, we compute two examples of the investment-consumption problem solved through stochastic recursive utility models, and the results of both examples demonstrate the effectiveness of our proposed algorithm.

Keywords stochastic optimal control, FBSDEs, deep learning, Stackelberg differential game, recursive utility

1 Introduction

Bismut [Bis73] first introduced linear backward stochastic differential equations (BSDEs in short) as the adjoint equation of the classical stochastic optimal control problem. In 1990, Pardoux and Peng firstly proved the existence and uniqueness of nonlinear BSDEs with Lipschitz condition [PP90]. Since then, the theory of BSDEs has been studied by many researchers and applied in a wide range of areas, such as in stochastic optimal control and mathematical finance [EKPQ97, Pen90]. When a BSDE is coupled with a (forward) stochastic differential equation (SDE in short), the system is usually called a forward-backward stochastic differential equation (FBSDE in short). We can refer to the literatures in [PW99, Ant93, CM96, HP95, PT99, MPY94] which studied the existence, uniqueness and the applications of coupled or fully-coupled FBSDEs.

In 1993, Peng [Pen93] first established a local stochastic maximum principle (SMP) for stochastic optimal control problems driven by FBSDEs. Then, the local SMP for other related problems were studied by Dokuchaev and Zhou [DZ99], Ji and Zhou [JZ06], Yong and Zhou [YZ99] ( see also the references therein). When the control domain is non-convex, Yong [Yon10] studied a fully coupled controlled FBSDE with mixed initial-terminal conditions. Wu [Wu13] studied a stochastic recursive optimal control problem. Hu [Min17], Hu et al. [HJX18] built the global stochastic maximum principle for stochastic optimal control problems driven by BSDEs and FBSDEs respectively. On the other hand, the dynamic programming principle (DPP) and related Hamilton-Jacobi-Bellman (HJB) equations have been intensively studied by Li and Wei [LW14], Hu et al. [HJX19] for this kind of stochastic optimal control problems. Furthermore, Hu et al. [HJX20] revealed the relationship between the SMP and the DPP for a stochastic optimal control problem where the system is governed by a fully coupled FBSDE. However, few literature has studied the numerical method for solving the stochastic optimal control problems driven by FBSDEs.

In this paper, we aim to solve the high-dimensional stochastic optimal control problem where the state equation is governed by

| (1.1) |

and the cost functional is defined by

| (1.2) |

Recall that for the high-dimensional classical stochastic optimal control problem where the state equation is a SDE, Han and E [HE16] solved it through deep learning method. In more details, they developed a feed-forward neural network to approximate the control and regard the cost functional as the optimization objective (see also [CL]). Comparing with the classical stochastic optimal control problem, the difficulty of our problem lies in that we need to deal with the high-dimensional FBSDE (1.1) firstly. And it is well-known that to obtain the numerical solution of (1.1) itself is a difficult problem.

The traditional methods for solving the FBSDEs include the partial differential equation (PDE in short) methods and the probabilistic methods, such as [Tad12, BT04, JJZ08, BZ08, FZZ16, MT04, FZT16, HRO16]. However, most of these methods can not deal with high-dimensional FBSDEs. In this paper, we reformulate the fully-coupled FBSDE (1.1) as a stochastic optimal control problem with the cost functional given by the error between the terminal condition and the solution of the FBSDE,

and build two feed-forward neural networks to approximate the control variables . This idea for solving (1.1) is currently a common method in solving high-dimensional BSDEs and FBSDEs (see e.g. [HJE18, EHJ17, HL18, JPPZ20, HPW20, PWG21, BEJ19]).

Based on the above analysis, we put forward the following ideas to solve our stochastic optimal control problem (1.1)-(1.2) by a novel deep learning method. Firstly, we transform (1.1)-(1.2) into a stochastic Stackelberg differential game(leader-follower problem). The goal of the follower is to find a pair of optimal control which minimizes the functional under a given control , while the goal of the leader is to find an optimal control which minimizes the cost functional . Secondly, a cross-optimization method is introduced to solve the high-dimensional stochastic Stackelberg differential game.

Specifically, we construct a feed-forward neural network to approximate the control and regard the cost functional as the optimization objective for the leader. We also build two feed-forward neural networks to approximate the control and regard as the optimization objective for the follower. As for the parameter updates of the neural networks, we update the parameters approximating through and the parameters approximating through alternatively. In more details, in each training step, we first fix an approximated to perform times updates for the parameters approximating , then based on the obtained , we perform one time update for the parameters approximating . The training will be repeated until a convergence result is obtained. Note that under a given , the follower should choose the optimal such that . Here in order to improve the computation efficiency, we use a relaxation method in the parameter update process. That is, instead of forcing , we control the number of updates by choosing an enough large coefficient so that can obtain a sufficiently small value which is close to , but not strictly equal to . We call this method the cross-optimization method (CO method).

To show the feasibility of our proposed method, we compute the investment-consumption problem for stochastic recursive utilities in a financial market. The concept of stochastic recursive utility was first introduced by Duffie and Epstein [DE92]. In fact, the stochastic recursive utility is associated with the solution of a particular backward stochastic differential equation (BSDE). From the BSDE point of view, El Karoui et al. [EKPQ97, EKPQ01] considered a more general class of recursive utilities defined as the solutions of BSDEs. In this paper, we compute two examples. In the first example, the stochastic recursive utility is described by a linear BSDE. For this case, the investment-consumption problem can be transformed to a classical stochastic optimal control problem. In this way, we can compare our computation results with those obtained by the numerical methods (such as the method in [HE16]) for solving classical stochastic optimal control problems. The numerical results show that the value of the recursive utility functions obtained by the two methods are very close. In the second example, we consider a more general recursive utility problem whose generator contains the term (refer to [EKPQ97, EKPQ01, CE02]). Chen and Epstein [CE02] studied the recursive utility problem with term, in which is regarded as the volatility of utility. The computation results show that our proposed method is also effective for this general case.

This paper is organized as follows. In section 2, we describe the stochastic optimal control problem driven by fully-coupled FBSDEs and reformulate it as a stochastic Stackelberg differential game problem. In section 3, we present our proposed CO method for solving the stochastic Stackelberg differential game via deep learning. As the numerical results, we compute the investment-consumption problem for stochastic recursive utilities in section 4. In section 5, we make a brief conclusion.

2 Statement of the problem

2.1 The stochastic control problem driven by FBSDE

On a given complete probability space , let be a standard -dimensional Brownian motion defined on a finite interval for some given constant . We denote

the natural filtration of and . contains all the -null set in and is right continuous. is denoted as the space of all mean square-integrable -adapted and -valued processes. It is a Hilbert space with the norm

We also denote as

is denoted as the Euclidean norm of an element and is denoted as the Euclidean inner product of elements .

In this paper, we consider the following controlled fully-coupled FBSDE,

| (2.1) |

where

are given functions with respect to . The process taking value in a given nonempty convex set in the system (2.1) is called an admissible control. For a given admissible control , the corresponding solution of the system (2.1) is denoted by

The set of all admissible control is denoted as , and the corresponding 4-tuple is called an admissible 4-tuple.

For a given control , are functions of . For these functions, we need to introduce some assumptions.

Given an full-rank matrix and set

where , and

Assumption 2.1.

-

(i)

is uniformly Lipschitz with respect to ;

-

(ii)

for each , ;

-

(iii)

is uniformly Lipschitz with respect to .

The following monotonic conditions firstly introduced in [PW99] are also needed.

Assumption 2.2.

| (2.2) | ||||

or

| (2.3) | ||||

where and are non-negative constants with , . Moreover we have (resp. ) when (resp. ).

We also introduce the following Lemma 1 without proof, and the proof of this lemma can be found in [PW99, Wu98].

Lemma 1.

For any given admissible control , let Assumption 2.1 and Assumption 2.2 hold. Then the FBSDE (2.1) has a unique adapted solution .

In the following, we define the cost functional of the stochastic optimal control problem by

| (2.4) |

where

are given functions with respect to . The 4-tuple process satisfies equation (2.1). Then the stochastic control problem driven by FBSDE can be described as following.

Problem 1.

The optimal control problem is to find an admissible control over such that

| (2.5) |

If there exists a control which minimizes over , then we call it an optimal control. (2.1) is called the optimal state equation and its solution is called an optimal trajectory.

Remark.

In Problem 1 and Lemma 1, we study the stochastic control problem driven by fully-coupled FBSDE (2.1), which needs some strong conditions (such as the monotonic conditions Assumption 2.1 and Assumption 2.2). If the forward SDE in (2.1) does not contain and terms, such strong conditions can be relaxed [Pen93].

2.2 The Equivalent problem

As discussed in [KZ00, LZ01, Yon10, Wu13], can be regarded as a control variable and in (2.1) can be seen as a terminal state constraint. Then Problem 1 can be reformulated as the following stochastic control problem to minimize

| (2.6) |

over , the state equation is given as

| (2.7) |

with the terminal state constraint

| (2.8) |

In this paper, our idea is to relax the terminal state constraint as an optimization objective which must be met firstly. Following this idea, the above stochastic control problem (2.6) becomes a stochastic Stackelberg differential game problem (leader-follower problem). In more details, we assume that there is one follower and one leader, and their cost functionals are given as follows

| (2.9) | ||||

For any choice of the leader and a fixed initial state , the goal of the follower is to minimize the functional over where is the set of all admissible . Denote the optimal of the follower as which clearly depends on of the leader. Then, the goal of the leader is to minimize the cost functional over .

In a more rigorous way, for in (2.7) and in (2.9), we introduce the following additional assumptions.

Assumption 2.3.

-

(i)

and are continuously differential;

-

(ii)

the derivatives of are bounded;

-

(iii)

the derivatives of are bounded by ;

-

(iv)

the derivatives of and are bounded by and , respectively.

Then the optimal control problem (2.5) (Problem 1) can be reformulated as the following Stackelberg differential game.

Problem 2.

Under Assumption 2.3, for any given and the initial state , there exists a strong solution to (2.7). If the above optimal pair in Problem 2 exists, we have and is an optimal control of Problem 1. The advantage of Problem 2 is that it does not need the regularity/integrability on , and the state equation is a forward SDE instead of a backward SDE as in Problem 1. The difficulty for solving Problem 2 is that it has to treat another optimization goal .

For simplicity, we denote the leader’s cost functional by , and the follower’s cost functional by in the following of the paper.

3 Deep neural network for solving the stochastic Stackelberg differential game

In this section, we consider to solve Problem 2 with deep neural network. As shown in section 2, Problem 2 is an optimal control problem with forward state equations, it contains two optimization goals, and the follower’s cost functional should be optimized in priority to the leader’s cost functional. In order to solve Problem 2, instead of using the penalty method which multiply the follower’s cost functional by a penalty parameter and adding it to the leader’s cost functional , we propose a cross-optimization method (CO method in brief). We optimize these two cost functionals alternatively and spend more computational cost on the follower’s cost functional . In this way, on the one hand, Problem 2 become unconstrained with respect to the control. On the other hand, we do not have to choose the approximate penalty parameter, which is usually hard to choose in the penalty method. The detailed process for optimizing these two functionals can be found in subsection 3.2.

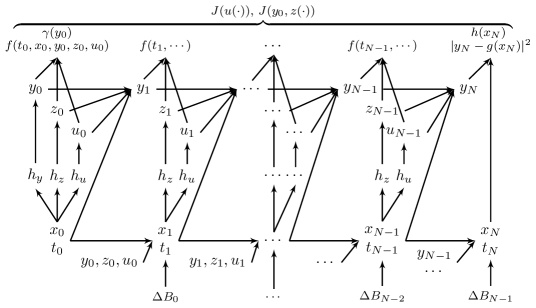

Before showing the approximation algorithm of Problem 2, we firstly need to discretize the forward state equation (2.7). Let and so that

is sufficiently small. Define and , where , for . We apply the Euler-Maruyama scheme to the forward state equation (2.7), then we have

| (3.1) |

For easier expression, we denote as here.

We use Monte Carlo sampling to approximate the expectations in the cost functionals. Then, the leader’s cost functional (2.4) can be evaluated by the following schemes:

| (3.2) |

where represents the number of Monte Carlo samples. Similarly, the follower’s cost functional can be approximated by

| (3.3) |

Here the numbers of Monte Carlo samples in (3.2) and (3.3) may be different. Without causing confusion, we use the same notation to represent the Monte Carlo sampling number, and the same notation and as in the continuous form to represent the corresponding discrete cost functionals.

3.1 Neural network architecture

In this subsection, we present the neural network architecture for solving Problem 2 approximately. Let be a sufficiently large natural number, and be a Borel measurable function.

Now we let the function with suitable be the approximation of the control :

| (3.4) |

for . is the trainable parameter in this neural network. We represent the function with a multilayer feed-forward neural network of the form

| (3.5) |

where

-

•

is a positive integer specifying the depth of the neural network,

-

•

are functions of the form

where the matrix weights and the bias vector are trainable parameters such that , is the number of nodes in layer , and represents the inputs of the neural network;

-

•

are the nonlinear activation functions, such as sigmoid, ReLU, ELU, etc.;

-

•

is a given function, in this paper, we set and .

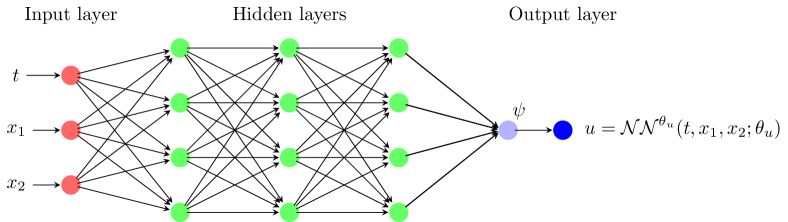

We treat the time as a part of input variables and the dimensions of the input and output in the neural network are and , respectively. Figure 1 shows an example of a single neural network for , .

In this paper, as the time is treated as an input variable, we use a common neural network, i.e. we share the parameters of the neural network among all the time points. The neural network is constructed with 5 layers, including 1 input layer with neurons, 3 hidden layers with neurons and 1 output layer with neurons. We adopt ReLU as the activation functions through the network, and add a batch normalization layer for each layer.

For approximating the controls and , we also construct two different feed-forward neural networks and , respectively.

| (3.6) |

The architectures of and are similar to that of , and the trainable parameters of them are and , respectively. They have the same depth, the same dimensions for the hidden layers, the same activation functions with the neural network , but different input and output dimensions. The dimensions of the input and output for are and , while that of the input and output for are and . We also add a batch normalization layer for each layer in the two neural networks. The whole neural network structure is shown in Figure 2.

3.2 Updating the parameters in the neural networks

From the formulation of Problem 2, two objective functionals and should be optimized, and the follower’s cost functional should be optimized in priority to the leader’s cost functional. Which means that we should make much more effort on optimizing the follower’s cost functional . A commonly used method for solving this problem is the penalty method, the idea of which is to treat as a penalty and add it to the leader’s cost functional :

| (3.7) |

where is a sufficiently large penalty parameter. And the aim is to find the optimal control of (3.7), in this way, Problem 2 is transformed to a classical stochastic optimal control problem without state constraint.

In this paper, different from the penalty method (3.7), we develop a novel deep learning method (the CO method) for solving this kind of stochastic Stackelberg differential game. In the neural network architecture, we update the network parameters through cross-optimization of the two cost functionals (3.2) and (3.3). For a given network parameter , we update the network parameters through the discrete follower’s cost functional (3.3). Then, under the approximation of with the updated , we update the network parameters through the discrete leader’s cost functional (3.2). In other words, in each training step, the network parameters for optimizing (3.2) and for optimizing (3.3) are updated alternatively. As mentioned above, the minimum of the follower’s cost functional should be satisfied in priority to the leader’s cost functional. Therefore in each training step, the update times of will be much higher than that of in practice.

Formally speaking, for a certain , a training step contains two different sub-steps

| (3.8) |

where and are given functions of parameters and their gradients. They represent the parameter update operations for the cost functionals (3.2) and (3.3), respectively. When the parameter is updated through , parameters remain unchanged, and when parameters are updated through , the parameter remains unchanged. Here we call the penalty updating coefficient, which represents the ratio of the number of optimizations of to that of .

In the actual calculation process, since the updates of and are carried out alternatively, it is feasible to perform the first update for or . And we only need to ensure that is large. The pseudo code of the proposed algorithm is given in Algorithm 1.

In Algorithm 1, represents the total number of parameter update times. That is to say, we perform training steps. And in each training step, there are times updates for the parameters and one time update for the parameter . In this CO method, the choices of and are independent, and the training parameters, such as the learning rate, the optimizer, the neural network architecture, can be chosen separately. And we can choose an appropriate penalty updating coefficient in to make the follower’s cost functional small enough, instead of simply choosing the approximate penalty coefficient in the penalty method.

The above proposed algorithm can be regarded as a relaxation method for solving Problem 2. In Problem 2, the optimization of the leader’s cost functional should be based on that of the follower’s cost functional , thus we should firstly guarantee that . In our proposed CO method, we relax this constraint to improve the computation efficiency. We make the value of sufficiently close to 0, but not strictly equal to 0. Specifically, we make the coefficient to be large enough so that we can obtain an enough small value of the follower’s cost functional.

4 Numerical results

In this section, we show two optimal investment-consumption portfolio examples solved through recursive utility with our proposed algorithm. If not specially mentioned, we use a 5-layer fully connected neural network, 512 samples of Brownian motion in the test set, and the number of time points is . The implementations are performed through TensorFlow on a Lenovo computer with a 2.40 Gigahertz (GHz) Inter Core i7 processor and 8 gigabytes (GB) random-access memory (RAM).

Here we introduce a continuous and stochastic recursive utility problem which was first introduced by Duffie and Epstein [DE92]. Suppose there are assets trading continuously in the market, one of which is a risk-free asset whose price process is given as

| (4.1) |

where is the instantaneous rate of return. The other assets are risky assets satisfying

| (4.2) |

where is the appreciation rate, is the volatility of the stocks and is a standard Brownian motion valued in . All the processes are assumed to be -adapted.

An investor starts with a given initial wealth and his total wealth at time is denoted as . The wealth process is given by

| (4.3) |

where is called the portfolio of the investor and is called the consumption plan process. represents the proportion of total wealth invested in the -th risky asset and is taking value in , which means that the short-selling is prohibited. The remaining fraction valued in is thus the proportion of the left in the form of risk-free bond. In addition, we assume that the consumption process is non-negative (.

The utility of the investor at time is denoted as a function of the instantaneous consumption and the future utility. The utility process can be regarded as the solution of a BSDE given as

| (4.4) |

where is the terminal utility function. Under some regularity assumptions (such as Assumption 2.1, Assumption 2.2), equation (4.4) has a unique solution . More precisely, the recursive utility at time can be denoted by

| (4.5) |

where represents the natural filtration associated with the standard Brownian motion.

The goal of the investor is to choose the optimal investment and consumption to maximize the utility at time zero. Mathematically, he aims to find the optimal controls and , such that

| (4.6) |

where represents the set of all possible investment-consumption strategies and is the recursive utility given as (4.5). We rewrite as

| (4.7) |

and we suppose that is a generalized recursive utility function given as:

| (4.8) |

Here is the instantaneous utility function. The function is a differentiable function and can be regarded as a risk-aversion coefficient.

Actually, the recursive utility problem (4.6) is a special case of Problem 1, in which , and , therefore we can reformulate it to Problem 2, where the goal of the leader is to find the optimal controls which maximize (4.7), and the goal of the follower is to minimize

| (4.9) |

under the given controls . Then we solve the problem through our proposed CO algorithm presented in section 3.

In this example, in order to approximate the controls and , we need to construct two neural networks , , and both of the controls are supposed as the feedback controls of the time and the wealth process . The neural network approximating contains one -dimensional input layer, three -dimensional hidden layers and one -dimensional output layer. For the constraint of the portfolio, and for , we deal with it through a softmax function . The function is given as

which is often used in classification problems such as image classification. Intuitively, it makes sense to choose the softmax function because choosing the best investment asset based on the current state is essentially a classification problem. Moreover, we use a function to deal with the constraint . In addition, we construct the other two neural networks to approximate and , respectively. In all, four feed-forward neural networks are constructed in this example, the first for approximating the consumption rate , the second for approximating the wealth proportion , the third for approximating , and the last for approximating .

Note that in (4.9), is regarded as a control parameter which is approximated through deep neural network. While at the same time, it is the optimization objective in (4.7). In order to make difference, we call the in (4.7) the integral form and that in the neural network the parametric form. And we should emphasize that instead of optimizing the parametric form , we optimize the integral form with respect to . The reason is that the derivatives of the parametric form with respect to do not exist. What’s more, we compare the integral form with the parametric form of . We measure the distance of the values between the parametric form and the integral form and take it as a criterion for the effectiveness of our proposed algorithm.

4.1 Case 1: a linear driver

In the first example, we consider a linear driver and set , then the recursive utility functional we need to maximize is given as

| (4.10) |

In this case, (4.10) is equivalent to the stochastic functional

| (4.11) |

Thus the stochastic recursive utility problem (4.3) and (4.7) can degenerate to a classic stochastic optimal control problem as (4.3) and (4.11). There have been some deep learning methods for solving the stochastic control problem (4.3)-(4.11), such as the methods in [HE16, BHLP18, JPPZ21].

Here we suppose that is a quadratic utility function

and the terminal utility function is

We calculate the recursive utility problem with the previously mentioned investment-consumption model. Let the wealth process and trading assets processes satisfy (4.1)-(4.3). We set , , for , and the initial wealth is equal to . The parameters in is set to be . As a comparison, we also calculate the classic stochastic optimal control problem (4.3) and (4.11). Here we construct a similar neural network with that in [HE16] and regard the discrete time point as an input of the neural network.

The implementation results with different dimensions and different terminal time are shown in Table 1. All the results are take from 5 independent runs. The number of iterations for parameter update is 18,000 and is set to be 19. That is to say, after 19 iterations of optimization for the follower’s cost functional (4.9), we perform one iteration of optimization for the leader’s cost functional (4.7). And the total number of training steps is . We show the integral form and the parametric form of (Inte. and Para. in the table, respectively), and calculate their mean values and variances among 5 independent runs. We also show the values calculated through the classic stochastic control problem (4.3) and (4.11) (Clas. in the table).

| Mean | Var. | Mean | Var. | Mean | Var. | Mean | Var. | ||

| Clas. | 0.06192 | 8.0998e-08 | 0.12323 | 7.2303e-08 | 0.18416 | 1.7761e-10 | 0.24314 | 3.9102e-07 | |

| Inte. | 0.06161 | 2.6347e-08 | 0.12269 | 9.8344e-08 | 0.18299 | 2.9634e-07 | 0.24216 | 7.3878e-07 | |

| Para. | 0.06146 | 3.1114e-07 | 0.12194 | 3.0065e-07 | 0.18217 | 3.3235e-06 | 0.24137 | 1.4374e-06 | |

| Clas. | 0.06183 | 1.2111e-07 | 0.12301 | 3.9042e-07 | 0.18389 | 1.1229e-07 | 0.24359 | 3.3391e-07 | |

| Inte. | 0.06169 | 2.3650e-08 | 0.12268 | 2.9813e-07 | 0.18248 | 3.5300e-07 | 0.24202 | 4.7493e-07 | |

| Para. | 0.06169 | 2.9493e-07 | 0.12238 | 8.1997e-07 | 0.18149 | 1.0537e-06 | 0.24084 | 5.2556e-06 | |

| Clas. | 0.06160 | 3.7891e-07 | 0.12282 | 6.4121e-07 | 0.18376 | 7.0530e-08 | 0.24315 | 8.0416e-07 | |

| Inte. | 0.06137 | 4.5255e-08 | 0.12203 | 1.9316e-07 | 0.18204 | 1.0402e-07 | 0.24268 | 6.7658e-07 | |

| Para. | 0.06036 | 3.8921e-07 | 0.12169 | 5.4307e-06 | 0.17921 | 4.2815e-07 | 0.24098 | 5.2413e-06 | |

| Clas. | 0.06171 | 1.1584e-07 | 0.11055 | 1.3581e-03 | 0.18333 | 4.5646e-07 | 0.24321 | 8.7775e-07 | |

| Inte. | 0.06142 | 2.0930e-08 | 0.12226 | 2.3594e-07 | 0.18235 | 1.6639e-07 | 0.24228 | 5.0222e-07 | |

| Para. | 0.06129 | 4.6174e-07 | 0.12092 | 2.7358e-06 | 0.18113 | 3.5940e-06 | 0.23994 | 4.3413e-06 | |

| Clas. | 0.06170 | 9.4358e-08 | 0.12303 | 2.7746e-07 | 0.18324 | 1.2237e-07 | 0.24126 | 1.9552e-06 | |

| Inte. | 0.06143 | 2.0046e-08 | 0.12222 | 6.9066e-08 | 0.18273 | 5.7814e-08 | 0.24134 | 3.6883e-07 | |

| Para. | 0.06077 | 2.7034e-06 | 0.12160 | 3.2163e-06 | 0.18115 | 1.3218e-06 | 0.23722 | 1.3412e-06 | |

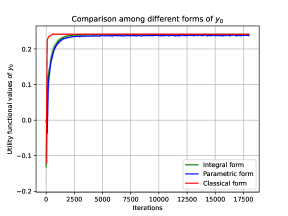

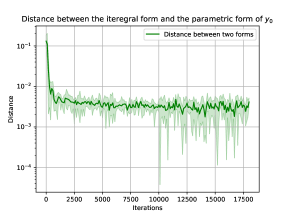

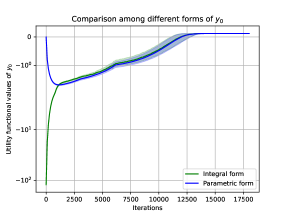

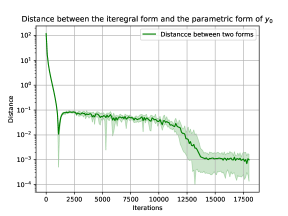

The results in Table 1 show that our proposed method is effective for the recursive utility problem. The values of the utility between the integral form and the parametric form are close, and both of the two forms are close to the value of the classic form. We also exhibit the curves of the utility values of different forms in Figure 3. The left figure shows the mean and scope for the different forms of among 5 independent runs. We can see that the values of the three different forms of are getting closer with the increase of the number of iterations. At the same time, the value of the integral form is getting larger which meets our objective to maximize the recursive utility functional (4.7) (see the green curve and scope). The right figure shows the mean and scope of the distance between the integral form and the parametric form.

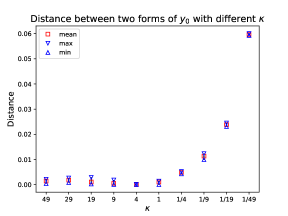

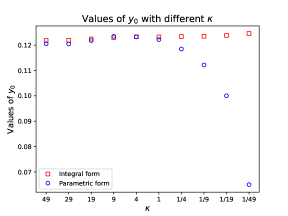

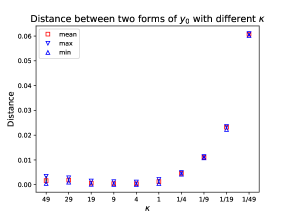

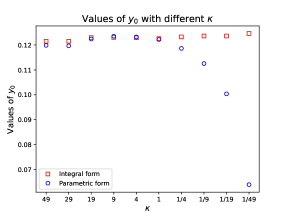

In order to show the impact of the penalty updating coefficient to the convergence of the algorithm, we vary the value of for and . The results with different are shown in Table 2 and Figure 4. In Figure 4, the left figure shows that the distances between the integral form and the parametric form are small when , which means that the value of (4.9) can be small enough when we perform more iterations on (4.9). The right figure shows the values of the utility functional are more stable for the case than the case . Here means that we perform more iterations of optimization on (4.7) than that on (4.9).

| Inte. | Para. | Distance | ||||

| Mean | Var. | Mean | Var. | Mean | Var. | |

| 0.12184 | 1.9438e-07 | 0.12056 | 1.9288e-06 | 0.00145 | 5.2404e-07 | |

| 0.12194 | 1.4726e-07 | 0.12045 | 2.4452e-06 | 0.00182 | 4.1077e-07 | |

| 0.12243 | 7.4394e-08 | 0.12182 | 6.7248e-07 | 0.00107 | 2.2293e-07 | |

| 0.12295 | 4.0809e-07 | 0.12347 | 1.2084e-08 | 0.00055 | 4.4437e-07 | |

| 0.12332 | 6.8988e-09 | 0.12326 | 2.2820e-09 | 0.00010 | 5.4356e-09 | |

| 0.12323 | 9.5936e-08 | 0.12218 | 5.6867e-08 | 0.00106 | 2.7134e-07 | |

| 0.12340 | 1.9741e-08 | 0.11848 | 1.3041e-07 | 0.00492 | 1.3164e-07 | |

| 0.12354 | 3.0263e-08 | 0.11218 | 6.6298e-07 | 0.01136 | 7.8541e-07 | |

| 0.12386 | 2.7079e-08 | 0.10002 | 3.1441e-07 | 0.02384 | 2.6049e-07 | |

| 0.12461 | 2.8228e-08 | 0.06496 | 9.7174e-08 | 0.05965 | 1.1475e-07 | |

4.2 Case 2: a nonlinear driver

In this case, the function is given as , , for , where is a given constant . The functions , and the other settings are the same as the linear driver.

The implementation results with different dimensions and different terminal times for this example are shown in Table 3. We set and the total number of iterations to be 18,000. The computation results are similar to that with the linear driver. The distances between the integral form and the parametric form of are small at the end of the training. In Figure 5, we show the curves for the values and the distances of between the integral form and the parametric form with and . We can see that the distances between the integral form and the parametric form of are getting closer to 0 when the number of iterations increases. Besides, the value of the integral form is getting larger, which shows that we can find the optimal investment-consumption strategy to maximize the recursive utility functional (4.7).

| Mean | Var. | Mean | Var. | Mean | Var. | Mean | Var. | ||

| Inte. | 0.06166 | 2.2275e-08 | 0.12293 | 7.4394e-08 | 0.18284 | 4.2424e-07 | 0.24182 | 1.0601e-06 | |

| Para. | 0.06110 | 4.1587e-07 | 0.12240 | 6.7248e-07 | 0.18236 | 6.0408e-07 | 0.23978 | 8.4018e-06 | |

| Distance | 0.00074 | 4.6313e-08 | 0.00064 | 2.2293e-07 | 0.00063 | 1.3188e-07 | 0.00236 | 2.5190e-06 | |

| Inte. | 0.06156 | 1.3603e-07 | 0.12266 | 1.6195e-07 | 0.18284 | 9.5716e-08 | 0.24167 | 2.7468e-06 | |

| Para. | 0.06123 | 1.2727e-06 | 0.12302 | 3.9956e-07 | 0.18352 | 8.2581e-07 | 0.24052 | 1.1217e-05 | |

| Distance | 0.00066 | 3.2714e-07 | 0.00054 | 7.1423e-08 | 0.00117 | 9.8714e-08 | 0.00164 | 1.7542e-06 | |

| Inte. | 0.06157 | 4.3009e-08 | 0.12270 | 8.5964e-08 | 0.18256 | 8.1253e-07 | 0.24257 | 7.8675e-07 | |

| Para. | 0.06126 | 4.5989e-07 | 0.12206 | 1.2343e-06 | 0.18123 | 4.9427e-06 | 0.24145 | 2.5426e-06 | |

| Distance | 0.00052 | 5.2667e-08 | 0.00109 | 3.3751e-07 | 0.00155 | 1.1978e-06 | 0.00112 | 5.7840e-07 | |

| Inte. | 0.06145 | 2.8057e-08 | 0.12221 | 3.3040e-07 | 0.18304 | 6.4776e-07 | 0.24183 | 3.4355e-07 | |

| Para. | 0.06089 | 5.5206e-07 | 0.12065 | 4.3699e-06 | 0.18207 | 3.0924e-06 | 0.23964 | 1.2486e-06 | |

| Distance | 0.00071 | 1.4810e-07 | 0.00183 | 1.5946e-06 | 0.00097 | 9.1203e-07 | 0.00218 | 4.1711e-07 | |

| Inte. | 0.06149 | 4.8995e-08 | 0.12251 | 1.1746e-07 | 0.18300 | 4.2698e-07 | 0.24273 | 9.6758e-08 | |

| Para. | 0.06109 | 7.2222e-07 | 0.12152 | 6.1477e-07 | 0.18203 | 1.6656e-06 | 0.24172 | 3.8806e-07 | |

| Distance | 0.00069 | 1.3734e-07 | 0.00099 | 2.3589e-07 | 0.00097 | 4.8985e-07 | 0.00101 | 1.3610e-07 | |

We also vary the value of for and . The computation results are shown in Table 4 and Figure 6, which also exhibit that the distances between the two different forms of are smaller and more stable when .

| Inte. | Para. | Distance | ||||

| Mean | Var. | Mean | Var. | Mean | Var. | |

| 0.12150 | 3.8599e-07 | 0.11983 | 2.0846e-06 | 0.00167 | 9.6376e-07 | |

| 0.12150 | 8.3208e-08 | 0.11965 | 7.7199e-07 | 0.00185 | 3.5862e-07 | |

| 0.12293 | 7.4394e-08 | 0.12240 | 6.7248e-07 | 0.00064 | 2.2293e-07 | |

| 0.12307 | 1.8615e-07 | 0.12350 | 6.5421e-10 | 0.00043 | 2.0767e-07 | |

| 0.12289 | 1.8920e-07 | 0.12322 | 1.3545e-09 | 0.00040 | 1.5793e-07 | |

| 0.12255 | 1.7449e-06 | 0.12219 | 1.3545e-09 | 0.00124 | 1.5793e-07 | |

| 0.12324 | 5.4207e-08 | 0.11862 | 2.6561e-08 | 0.00462 | 6.7300e-08 | |

| 0.12362 | 1.2905e-09 | 0.11254 | 2.7437e-08 | 0.01108 | 3.5992e-08 | |

| 0.12357 | 2.6459e-07 | 0.10039 | 9.0642e-09 | 0.02318 | 2.2544e-07 | |

| 0.12461 | 1.0065e-07 | 0.06392 | 7.9881e-10 | 0.06069 | 1.1117e-07 | |

The above results demonstrate that our proposed method is effective for solving the stochastic recursive utility problem. Besides, we should do more optimizations on the follower’s cost functionals, as verified by the implementation results.

5 Conclusion

In this paper, we propose a deep learning method for solving the stochastic control problem driven by fully-coupled FBSDEs. We transform it into a stochastic Stackelberg differential game and propose a CO method to solve this new problem. The CO method has high flexibility and we can set the training parameters of the neural networks seperately to optimize the leader’s cost functional and the follower’s cost functional independently. In order to show the performance of our algorithm, we give two optimal investment-consumption portfolio examples solved through the stochastic recursive utility models. The numerical results demonstrate remarkable performance.

References

- [Ant93] Fabio Antonelli. Backward-forward stochastic differential equations. Annals of Applied Probability, 3(3):777–793, 1993.

- [BEJ19] Christian Beck, Weinan E, and Arnulf Jentzen. Machine Learning Approximation Algorithms for High-Dimensional Fully Nonlinear Partial Differential Equations and Second-order Backward Stochastic Differential Equations. Journal of Nonlinear Science, 29(4):1563–1619, 2019.

- [BHLP18] Achref Bachouch, Come Hure, Nicolas Langrene, and Huyen Pham. Deep neural networks algorithms for stochastic control problems on finite horizon, part 2: numerical applications. arXiv: 1812.05916v1, 2018.

- [Bis73] Jeanmichel Bismut. Conjugate convex functions in optimal stochastic control. Journal of Mathematical Analysis and Applications, 44(2):384–404, 1973.

- [BT04] Bruno Bouchard and Nizar Touzi. Discrete-time approximation and monte-carlo simulation of backward stochastic differential equations. Stochastic Processes & Their Applications, 111(2):175–206, 2004.

- [BZ08] Christian Bender and Jianfeng Zhang. Time discretization and markovian iteration for coupled fbsdes. Annals of Applied Probability, 18(1):143–177, 2008.

- [CE02] Zengjing Chen and Larry Epstein. Ambiguity, risk, and asset returns in continuous time. Econometrica, 70(4):1403–1443, 2002.

- [CL] René Carmona and Mathieu Laurière. Convergence analysis of machine learning algorithms for the numerical solution of mean field control and games: ii – the finite horizon case. arXiv preprint arXiv:1908.01613.

- [CM96] Jakša Cvitanić and Jin Ma. Hedging options for a large investor and forward-backward sde’s. The annals of applied probability, 6(2):370–398, 1996.

- [DE92] Darrell Duffie and Larry G Epstein. Stochastic differential utility. Econometrica: Journal of the Econometric Society, pages 353–394, 1992.

- [DZ99] Nikolai Dokuchaev and Xun Yu Zhou. Stochastic controls with terminal contingent conditions. Journal of Mathematical Analysis and Applications, 238(1):143–165, 1999.

- [EHJ17] Weinan E, Jiequn Han, and Arnulf Jentzen. Deep learning-based numerical methods for high-dimensional parabolic partial differential equations and backward stochastic differential equations. Communications in Mathematics & Statistics, 5(4):349–380, 2017.

- [EKPQ97] Nicole El Karoui, Shige Peng, and Marie Claire Quenez. Backward stochastic differential equations in finance. Mathematical finance, 7(1):1–71, 1997.

- [EKPQ01] Nicole El Karoui, Shige Peng, and Marie Claire Quenez. A dynamic maximum principle for the optimization of recursive utilities under constraints. Annals of applied probability, pages 664–693, 2001.

- [FZT16] Yu Fu, Weidong Zhao, and Zhou Tao. Efficient spectral sparse grid approximations for solving multi-dimensional forward backward sdes. Discrete and Continuous Dynamical Systems - Series B, 22(9), 2016.

- [FZZ16] Yu Fu, Weidong Zhao, and Tao Zhou. Multistep schemes for forward backward stochastic differential equations with jumps. Journal of Scientific Computing, 69(2):1–22, 2016.

- [HE16] Jiequn Han and Weinan E. Deep learning approximation for stochastic control problems. NIPS Workshop on Deep Reinforcement Learning, 2016.

- [HJE18] Jiequn Han, Arnulf Jentzen, and Weinan E. Solving high-dimensional partial differential equations using deep learning. Proceedings of the National Academy of Sciences of the United States of America, 115(34):8505–8510, 2018.

- [HJX18] Mingshang Hu, Shaolin Ji, and Xiaole Xue. A global stochastic maximum principle for fully coupled forward-backward stochastic systems. SIAM Journal on Control and Optimization, 56(6):4309–4335, 2018.

- [HJX19] Mingshang Hu, Shaolin Ji, and Xiaole Xue. The existence and uniqueness of viscosity solution to a kind of hamilton–jacobi–bellman equation. SIAM Journal on Control and Optimization, 57(6):3911–3938, 2019.

- [HJX20] Hu, Mingshang, Ji, Shaolin, and Xue, Xiaole. Stochastic maximum principle, dynamic programming principle, and their relationship for fully coupled forward-backward stochastic controlled systems. ESAIM: COCV, 26:81, 2020.

- [HL18] Jiequn Han and Jihao Long. Convergence of the deep bsde method for coupled fbsdes. arXiv:1811.01165, 2018.

- [HP95] Ying Hu and Shige Peng. Solution of forward-backward stochastic differential equations. Probability Theory and Related Fields, 103(2):273–283, 1995.

- [HPW20] Côme Huré, Huyên Pham, and Xavier Warin. Deep backward schemes for high-dimensional nonlinear PDEs. arXiv:1902.01599 [cs, math, stat], June 2020.

- [HRO16] Thomas P Huijskens, Marjon Ruijter, and Cornelis W Oosterlee. Efficient numerical fourier methods for coupled forward-backward sdes. Journal of Computational and Applied Mathematics, 296:593–612, 2016.

- [JJZ08] M. A. Jin, Shen Jie, and Yanhong Zhao. On numerical approximations of forward-backward stochastic differential equations. Siam Journal on Numerical Analysis, 46(5):2636–2661, 2008.

- [JPPZ20] Shaolin Ji, Shige Peng, Ying Peng, and Xichuan Zhang. Three algorithms for solving high-dimensional fully coupled fbsdes through deep learning. IEEE Intelligent Systems, 35(3):71–84, 2020.

- [JPPZ21] Shaolin Ji, Shige Peng, Ying Peng, and Xichuan Zhang. Solving stochastic optimal control problem via stochastic maximum principle with deep learning method. 2021.

- [JZ06] Shaolin Ji and Xun Yu Zhou. A maximum principle for stochastic optimal control with terminal state constraints, and its applications. Communications in Information and Systems, 6(4):321 – 338, 2006.

- [KZ00] Michael Kohlmann and Xunyu Zhou. Relationship between backward stochastic differential equations and stochastic controls: a linear-quadratic approach. SIAM Journal on Control and Optimization, 38(5):1392–1392, 2000.

- [LW14] Juan Li and Qingmeng Wei. Optimal control problems of fully coupled fbsdes and viscosity solutions of hamilton–jacobi–bellman equations. SIAM Journal on Control and Optimization, 52(3):1622–1662, 2014.

- [LZ01] Andrew E. B. Lim and Xunyu Zhou. Linear-quadratic control of backward stochastic differential equations. SIAM Journal on Control and Optimization, 2001.

- [Min17] Hu Mingshang. Stochastic global maximum principle for optimization with recursive utilities. Probability, Uncertainty and Quantitative Risk, 2(1), 2017.

- [MPY94] Jin Ma, Philip Protter, and Jiongmin Yong. Solving forward-backward stochastic differential equations explicitly—a four step scheme. Probability theory and related fields, 98(3):339–359, 1994.

- [MT04] G. N. Milstein and M. V. Tretyakov. Numerical algorithms for forward-backward stochastic differential equations connected with semilinear parabolic equations. volume 28, pages 561–582, 2004.

- [Pen90] Shige Peng. A general stochastic maximum principle for optimal control problems. Siam Journal on Control and Optimization, 28(4):966–979, 1990.

- [Pen93] Shige Peng. Backward stochastic differential equations and applications to optimal control. Applied Mathematics and Optimization, 27(2):125–144, 1993.

- [PP90] Etienne Pardoux and Shige Peng. Adapted solution of a backward stochastic differential equation. Systems & Control Letters, 14(1):55–61, 1990.

- [PT99] Etienne Pardoux and Shanjian Tang. Forward-backward stochastic differential equations and quasilinear parabolic pdes. Probability Theory and Related Fields, 114(2):123–150, 1999.

- [PW99] Shige Peng and Zhen Wu. Fully coupled forward-backward stochastic differential equations and applications to optimal control. Siam Journal on Control and Optimization, 37(3):825–843, 1999.

- [PWG21] Huyên Pham, Xavier Warin, and Maximilien Germain. Neural networks-based backward scheme for fully nonlinear PDEs. SN Partial Differential Equations and Applications, 2:16, 2021.

- [Tad12] Eitan Tadmor. A review of numerical methods for nonlinear partial differential equations. Bulletin of the American Mathematical Society, 49(4):507–554, 2012.

- [Wu98] Zhen Wu. Maximum principle for optimal control problem of fully coupled forward-backward stochastic systems. Systems Science and Mathematical Sciences, 11(3):249–259, 1998.

- [Wu13] Zhen Wu. A general maximum principle for optimal control of forward backward stochastic systems. Automatica, 49(5):1473–1480, 2013.

- [Yon10] Jiongmin Yong. Optimality variational principle for controlled forward-backward stochastic differential equations with mixed initial-terminal conditions. SIAM Journal on Control and Optimization, 48(6):4119–4156, 2010.

- [YZ99] Jiongmin Yong and Xunyu Zhou. Stochastic Controls-Hamiltonian System and HJB Equations. Springer, 1999.