Stochastic Multi-armed Bandits with Non-stationary Rewards Generated by a Linear Dynamical System

Abstract

The stochastic multi-armed bandit has provided a framework for studying decision-making in unknown environments. We propose a variant of the stochastic multi-armed bandit where the rewards are sampled from a stochastic linear dynamical system. The proposed strategy for this stochastic multi-armed bandit variant is to learn a model of the dynamical system while choosing the optimal action based on the learned model. Motivated by mathematical finance areas such as Intertemporal Capital Asset Pricing Model proposed by Merton and Stochastic Portfolio Theory proposed by Fernholz that both model asset returns with stochastic differential equations, this strategy is applied to quantitative finance as a high-frequency trading strategy, where the goal is to maximize returns within a time period.

I Introduction

The stochastic multi-armed bandit (MAB) problem, proposed by Thompson in 1933 [1], has provided a powerful modeling framework to investigate a large class of decision making problems. In MAB, a learner interacts with the environment where in each interaction, called a round, the learner chooses an action and receives a reward. The performance of policies is usually evaluated as the expectation of the cumulative difference between chosen and optimal actions, and defined as regret. In its basic formulation rewards are sampled from a stationary distribution, a very popular algorithm, called the Upper Confidence Bound (UCB) algorithm [2], guarantees logarithmic growth of regret [3].

MAB has seen different applications in several areas such as machine learning, dynamic pricing, and portfolio management. In machine learning, the MAB formulation can be used to find a set of hyperparameters to increase the performance of the learning process [4]. This has been extended further by applying MAB to algorithm selection, where a learner searches for a high-performing algorithm to use for training [5]. For dynamic pricing, when selling a set of products, the price needs to be set according to the current demand in order to maximize profit. To find the optimal pricing, MAB is used where the model for demand is based on a low-dimensional demand model [6] or a differential equation [7]. In portfolio selection, MAB formulation is natural in the case where the manager creates a portfolio with multiple assets [8, 9].

In the examples mentioned above, the environments that the learner interacts with has time correlations and correlations between the rewards for each action. Hyperparameter optimization can be viewed as optimizing a cost function with correlated decision variables [10] and the training process is dynamic [4]. In dynamic pricing, the pricing for each product can be correlated with each other based on a low dimensional demand model [6] and the demand changes over time [7]. As for portfolio management, equations used in Intertemporal Capital Asset Pricing Model (ICAPM) proposed by Merton [11] and Stochastic Portfolio Theory proposed by Fernholz [12] model asset returns using stochastic differential equations. The examples above motivate the need to investigate non-stationary stochastic MAB where the rewards are sampled from a stochastic dynamical system. Here the reward can be expressed as the inner product between the action vector and a dynamic unknown parameter vector. Previous work in non-stationary MAB studies the case where the change in magnitude of the unknown parameter vector is bounded [13, 14] or when such vector is is sampled from a predefined set [15, 16]. In both cases the unknown parameter vector changes the distribution of the reward, making the original stochastic MAB formulation non-stationary. To the best of our knowledge, the bulk of papers in non-stationary MAB focus on the piece-wise stationary case, where the distributions are stationary within set intervals. Papers for the piece-wise stationary case focus on remembering-vs-forgetting trade-off using either discounting or sliding windows [17] to forget early recorded rewards or detecting the change in the distribution to decide when to restart the learning process [18, 19, 20, 21]. Other papers in non-stationary MAB bound the cumulative change of the reward mean in the form of variational budget [22, 23]. However, the rewards sampled from a stochastic dynamical system change in a very different manner, making previous work not well suited. In this paper we tackle the stochastic multi-armed bandit problem when the rewards are sampled from an unknown stochastic linear dynamical system driven by Gaussian noise. Since the rewards are now dynamic, the paper introduces a methodology that focuses on finding the optimal decision while learning a model of the system. We will leverage and adapt results in [24] to learn the linear model. We then use such model to design a policy based on reward predictions. To illustrate the concept, we apply the algorithm to a simple trading example.

The framework of the paper is as follows: Section II reviews the stochastic multi-armed bandit and introduces a variant where the rewards are sampled from a linear dynamical system. In section III, a methodology to model and predict rewards is presented. Section IV then uses the model to develop a strategy to maximize cumulative reward over a horizon. Section V performs regret analysis and provides a theoretical upper bound for the regret of the proposed algorithm. Section VI shows an application of the proposed algorithm to a simple high frequency trading example. Finally, section VII provides conclusions and future directions.

Notation. To denote the transpose of a matrix, the notation ⊤ is used. For norms, is the -norm norm for vectors. The trace of a matrix is denoted with . For a normal distribution, notation is used, where is the mean and is the covariance of the distribution. Inner product is where . The term is big-O notation. For the equality

this implies that for some constant and , for all [25].

II Problem Framework

Suppose that for given actions , the reward is sampled from the following stochastic linear dynamical system

| (1) |

where the unknown parameter vector is the state of the system. For each round , , the learner observes the reward based on the chosen action and the context . The context is a value that the learner always observes and its observation matrix is constant. The processes , , and are i.i.d. normally distributed, i.e. , , and . The matrices , , , , , vectors , , , and scalars , () are assumed to be unknown. The dimension is unknown, but dimension is known as it is the dimension of the context. For notation, given that there are vectors , we denote to be which vector is chosen. The system has the following assumptions

Assumption 1

The matrix pair is observable. The matrix is positive definite.

Assumption 2

The matrix is Schur, i.e. .

The goal of the learner is to maximize cumulative reward over a finite time horizon . To prove the performance of the learning strategy, regret analysis is used [26]. Regret is defined as the cumulative, over all rounds, expected difference between the highest reward (denoted as ) and the reward for the chosen action at time , i.e.

| (2) |

III Modeling the System from Data

If the learner knew (1), then the Kalman filter could be used to predict the state and consequently the reward for each action :

| (3) |

where and is the sigma algebra generated by previous contexts . Since the Kalman gain matrix converges thanks to assumption 1, then using the steady-state Kalman filter is reasonable where the prediction of the state and the estimate of the state can be combined into one equation

| (4) |

Since using the steady-state Kalman filter prediction provides a good prediction of , then learning the steady-state Kalman filter will intuitively provide a good prediction of the reward for each action . Therefore, to learn the steady-state Kalman filter, a variation of [24] is used. Let be the horizon length of how far we look into the past. We define a matrix for each and a vector below

| (5) |

Using and defined above, it can be shown that the reward has the following expression

| (6) |

where

Note that since is Schur by construction, then the magnitude of the term decreases as increases. If given a set of time instants then (6) can be rearranged in the following form

| (7) |

A regularized least squares estimate for (7) is

| (8) |

where is defined to be

| (9) |

and is the regularization parameter. Note that the is added so that that is positive definite and therefore invertible.

IV Bandit Strategy

The action the learner ought to choose is the action that the learner predicts will output the highest reward. This prediction is based on the matrix , which is an estimate of the matrix . Therefore, the learner should focus on learning for each action at the beginning and then choose an action based on after the initial phase.

The proposed strategy the learner will use is the following. The parameter to set is , where a larger value decreases the bias term in (6) which impacts the identification error . At the start of the algorithm, the learner will cycle through each action round to round . The learner will start computing once . After round , the learner will choose the action that has the largest value and update .

V Regret Analysis of SB-ETC

The following theorem below provides a bound for regret defined in (2).

Theorem 1

Given a failure rate of , regret as in (2) has the following bound with a probability of at least :

| (10) |

where , and are defined to be

| (11) | ||||

| (12) | ||||

| (13) |

and is a bound such that with a probability of at least :

| (14) |

Proof:

Using the law of iterated expectations [27], the instanteneous regret for one round is

| (15) |

where and are defined in (11) and (12). In the following, we will provide an upper bound for . Consider the following event

| (16) |

which implies that modeling error leads to selecting an action rather than the optimal one. Note that is the following probability

| (17) |

implying that . Adjusting the inequality in provides the following

| (18) |

Thus, the -2 norm is

| (20) |

Since , the estimate is bounded. For the product , based on theorem 1 in [28], since is conditionally -sub-Gaussian and is measurable, then given a failure rate , this term is bounded with a probability of at least . Therefore, (14) is satisfied with a probability of at least . Denote (14) as . Now assuming is given, the inequality (19) can be rewritten as

| (21) |

Let (21) be denoted as . Based on the Markov inequality [29], the following concentration bound is given

| (22) |

Note that is true if the following inequality is true.

| (24) |

Since (24) is satisfied with a probability of at least based on (14), then with a probability of at least . Therefore, (15) has the following upper bound

∎

Based on theorem 1, the regret performance is based on the bound for model error . Therefore, if the model is known, then sets the bound to be zero after which is reasonable. Note that is based on the number of times action is chosen, which can affect the upper bound. For now, the exploration period is set to so that the learner has samples for each action . Future work will focus on what is a more effective length for the exploration period.

VI Application to trading

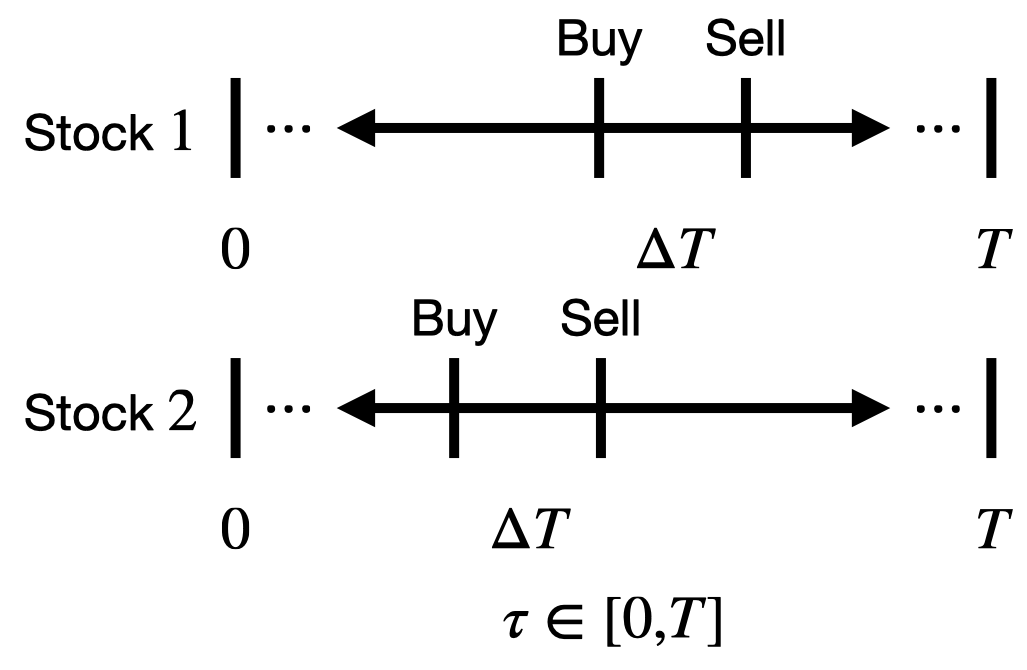

This section will exemplify the use of the proposed framework. Let there be two stocks, a trader is interested in. The trader can either buy then sell either stock 1 or 2, or refrain from trading for each round . Figure 1 provides an example timeline of the trader’s strategy.

The context represent the price change for the stock. The reward is the financial gain (loss) deriving from trading a stock. Both variables are sampled from the following stochastic linear dynamical system, where its derivation is in the Appendix.

| (26) |

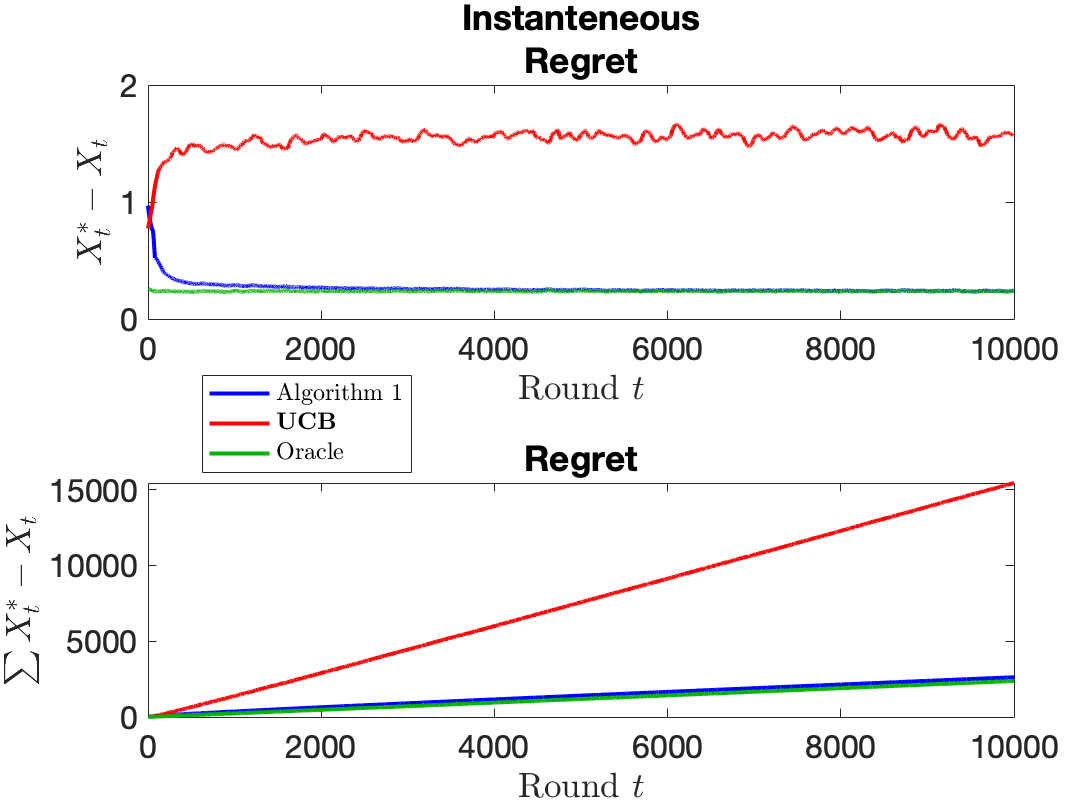

For the model, the number of previous contexts that are used is and the regularization parameter . Since is Schur, one could argue that the reward is just Gaussian distributed as . Therefore, using UCB is a reasonable method to use as a comparison. The parameter used in UCB is . To provide an upper bound on the algorithm’s performance we use an oracle that leverages optimal predicted awards generated by the Kalman filter (3) to choose the action .

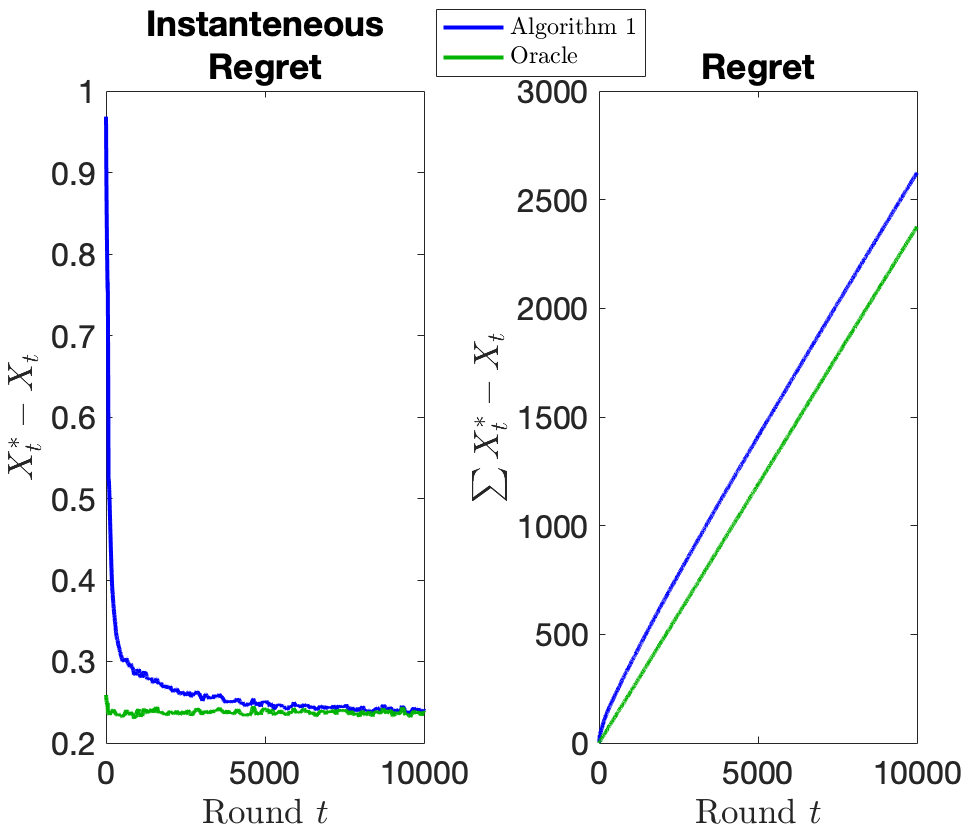

Figure 2 contains the instanteneous regret (the top plot) and regret (the bottom plot) of the learner using UCB (the red line), algorithm 1 (the blue line), and the oracle (the green line) averaged across 1,000 different simulations. Even though the system converges to the steady-state, UCB still performs sub-par compared to algorithm 1. Figure 3 is a comparison of just algorithm 1 and the oracle. It can be observed that algorithm 1 instantenous regret is converging to the oracle’s instanteneous regret.

VII Conclusion

This paper introduces a new variant of the stochastic multi-armed bandit where the rewards are sampled from an unknown stochastic linear dynamical system. To approach this problem, the learner first explores all the actions to learn the underlying linear model. Using the learned model, the learner uses the model to predict the action with the highest reward. Simulation results show how the proposed strategy yields near optimal actions after the learning phase. An application to high frequency trading is used to illustrate the methods and the results.

References

- [1] W. R. Thompson, “On the likelihood that one unknown probability exceeds another in view of the evidence of two samples,” Biometrika, vol. 25, no. 3/4, pp. 285–294, 1933.

- [2] R. Agrawal, “Sample mean based index policies by o (log n) regret for the multi-armed bandit problem,” Advances in Applied Probability, vol. 27, no. 4, pp. 1054–1078, 1995.

- [3] P. Auer, N. Cesa-Bianchi, and P. Fischer, “Finite-time analysis of the multiarmed bandit problem,” Machine learning, vol. 47, no. 2, pp. 235–256, 2002.

- [4] L. Li, K. Jamieson, G. DeSalvo, A. Rostamizadeh, and A. Talwalkar, “Hyperband: A novel bandit-based approach to hyperparameter optimization,” The Journal of Machine Learning Research, vol. 18, no. 1, pp. 6765–6816, 2017.

- [5] M. Gagliolo and J. Schmidhuber, “Algorithm selection as a bandit problem with unbounded losses,” in International conference on learning and intelligent optimization. Springer, 2010, pp. 82–96.

- [6] J. W. Mueller, V. Syrgkanis, and M. Taddy, “Low-rank bandit methods for high-dimensional dynamic pricing,” Advances in Neural Information Processing Systems, vol. 32, 2019.

- [7] S. Agrawal, S. Yin, and A. Zeevi, “Dynamic pricing and learning under the bass model,” in Proceedings of the 22nd ACM Conference on Economics and Computation, 2021, pp. 2–3.

- [8] W. Shen, J. Wang, Y.-G. Jiang, and H. Zha, “Portfolio choices with orthogonal bandit learning,” in Twenty-fourth international joint conference on artificial intelligence, 2015.

- [9] X. Huo and F. Fu, “Risk-aware multi-armed bandit problem with application to portfolio selection,” Royal Society open science, vol. 4, no. 11, p. 171377, 2017.

- [10] B. Shahriari, K. Swersky, Z. Wang, R. P. Adams, and N. De Freitas, “Taking the human out of the loop: A review of bayesian optimization,” Proceedings of the IEEE, vol. 104, no. 1, pp. 148–175, 2015.

- [11] R. C. Merton, “An intertemporal capital asset pricing model,” Econometrica: Journal of the Econometric Society, pp. 867–887, 1973.

- [12] R. Fernholz and B. Shay, “Stochastic portfolio theory and stock market equilibrium,” The Journal of Finance, vol. 37, no. 2, pp. 615–624, 1982.

- [13] W. C. Cheung, D. Simchi-Levi, and R. Zhu, “Learning to optimize under non-stationarity,” in The 22nd International Conference on Artificial Intelligence and Statistics. PMLR, 2019, pp. 1079–1087.

- [14] A. Javanmard, “Perishability of data: dynamic pricing under varying-coefficient models,” The Journal of Machine Learning Research, vol. 18, no. 1, pp. 1714–1744, 2017.

- [15] Y. Qin, T. Menara, S. Oymak, S. Ching, and F. Pasqualetti, “Non-stationary representation learning in sequential linear bandits,” arXiv preprint arXiv:2201.04805, 2022.

- [16] Y. Qin, T. Menara, S. Oymak, and F. Pasqueletti, “Representation learning for stochastic sequential linear bandits,” IEEE Conference on Decision and Control, 2021.

- [17] A. Garivier and E. Moulines, “On upper-confidence bound policies for non-stationary bandit problems,” arXiv preprint arXiv:0805.3415, 2008.

- [18] C. Hartland, N. Baskiotis, S. Gelly, M. Sebag, and O. Teytaud, “Change point detection and meta-bandits for online learning in dynamic environments,” in CAp 2007: 9è Conférence francophone sur l’apprentissage automatique, 2007, pp. 237–250.

- [19] F. Liu, J. Lee, and N. Shroff, “A change-detection based framework for piecewise-stationary multi-armed bandit problem,” in Proceedings of the AAAI Conference on Artificial Intelligence, vol. 32, no. 1, 2018.

- [20] Y. Cao, Z. Wen, B. Kveton, and Y. Xie, “Nearly optimal adaptive procedure with change detection for piecewise-stationary bandit,” in The 22nd International Conference on Artificial Intelligence and Statistics. PMLR, 2019, pp. 418–427.

- [21] J. Mellor and J. Shapiro, “Thompson sampling in switching environments with bayesian online change detection,” in Artificial intelligence and statistics. PMLR, 2013, pp. 442–450.

- [22] L. Wei and V. Srivastava, “Nonstationary stochastic multiarmed bandits: Ucb policies and minimax regret,” arXiv preprint arXiv:2101.08980, 2021.

- [23] O. Besbes, Y. Gur, and A. Zeevi, “Stochastic multi-armed-bandit problem with non-stationary rewards,” Advances in neural information processing systems, vol. 27, pp. 199–207, 2014.

- [24] A. Tsiamis and G. J. Pappas, “Finite sample analysis of stochastic system identification,” in 2019 IEEE 58th Conference on Decision and Control (CDC). IEEE, 2019, pp. 3648–3654.

- [25] D. E. Knuth, “Big omicron and big omega and big theta,” SIGACT News, vol. 8, no. 2, p. 18–24, Apr. 1976.

- [26] T. Lattimore and C. Szepesvári, Bandit algorithms. Cambridge University Press, 2020.

- [27] J. M. Wooldridge, Econometric analysis of cross section and panel data. MIT press, 2010.

- [28] Y. Abbasi-yadkori, D. Pál, and C. Szepesvári, “Improved algorithms for linear stochastic bandits,” in Advances in Neural Information Processing Systems, J. Shawe-Taylor, R. Zemel, P. Bartlett, F. Pereira, and K. Q. Weinberger, Eds., vol. 24. Curran Associates, Inc., 2011.

- [29] S. Boucheron, G. Lugosi, and P. Massart, Concentration inequalities: A nonasymptotic theory of independence. Oxford university press, 2013.

- [30] A. Gelb et al., Applied optimal estimation. MIT press, 1974.

- [31] C. Van Loan, “Computing integrals involving the matrix exponential,” IEEE transactions on automatic control, vol. 23, no. 3, pp. 395–404, 1978.

Appendix A Derivation for (26)

The trader models the price evolution of stock (denoted as ) using the following stochastic differential equation for based on [11].

| (27) |

where and , , are defined to be

| (28) |

The variable is the drift rate of stock , is the speed of reversion (the rate returns to its mean), and sets the magnitude of . Both and are independent Gaussian distributed random variables with a variance of with no time correlation, i.e. and where is the delta dirac function. Let . Using Itô’s lemma, the stochastic differential equation for is

| (29) | ||||

| (30) | ||||

| (31) |

This leads to the following stochastic differential equations:

| (32) |

Let the following matrices and vectors be defined as below:

| (35) |

| (36) |

This provides the stochastic linear dynamical system

| (37) |

System (37) is discretized with intervals of size () which gives the following discrete-time stochastic linear dynamical system

| (38) |

where and are defined below.

| (39) | ||||

| (40) |

Equations (39) and (40) are from [30]. Evaluating (40) is analytically intractable; therefore, [31] is used to approximate .

| (45) | ||||

| (46) |

Say that the trader uses the following strategy: the trader buys stock at the start of time and then sells that stock at time . Define reward for this time period to be

| (47) |

Therefore, the difference is the logarithm of the percentage increase/decrease of buying at and then selling at . We extend (38) by using the following matrices and vectors:

| (50) | ||||

| (53) | ||||

| (54) |

Finally, the eigenvectors of are computed, where is observable and is Schur. This transformation provides (26).