Tuning Parameter-Free Nonparametric Density Estimation from Tabulated Summary Data

Abstract

Administrative data are often easier to access as tabulated summaries than in the original format due to confidentiality concerns. Motivated by this practical feature, we propose a novel nonparametric density estimation method from tabulated summary data based on maximum entropy and prove its strong uniform consistency. Unlike existing kernel-based estimators, our estimator is free from tuning parameters and admits a closed-form density that is convenient for post-estimation analysis. We apply the proposed method to the tabulated summary data of the U.S. tax returns to estimate the income distribution.

Keywords: grouped data, income distribution, maximum entropy

JEL codes: C14, D31

1 Introduction

Researchers can often access a tabulated summary of data more easily than the original data containing confidential information at the individual level. Examples include administrative tax data containing detailed information about individual-level records of income. Tax authorities often release summary statistics of the income distributions in a tabulated format, such as the number of taxpayers and their average income, grouped by bins of income levels. Despite their lack of details, such tabulated summary data are still useful for researchers in analyzing income distributions, especially for historically old times for which micro data are no longer available.

A typical econometric method for estimating the cross-sectional distribution of a continuous random variable, such as the kernel density estimator and the empirical cumulative distribution function, requires individual-level information, and thus is not suitable when researchers only have access to tabulated summaries. In this paper, we propose a novel method for nonparametrically estimating the probability density function of an absolutely continuous distribution from tabulated summary data based on the maximum entropy (ME) principle. This ME density estimator enjoys a number of desirable properties. First, it is piecewise exponential, which allows for analytical post-estimation integration to calculate cumulative distribution estimates such as the mean, variance, top income shares, Lorenz curve, and the Gini coefficient. Second, and more importantly, unlike alternative kernel-based estimators (Blower and Kelsall, 2002; Sun, 2014), the ME density estimator is free from tuning parameters such as the bandwidth. This feature is attractive in practice and provides a complete theoretical justification of the method, unlike the existing kernel-based methods for which the theory fails to formally account for the tuning parameter choice in practice. We establish the strong uniform consistency for the ME density and cumulative distribution estimators under the asymptotic framework in which the resolution of bins in the table becomes finer at certain rates as the underlying sample size increases.

To illustrate our proposed method, we consider two applications. The first is a simulation study of the calculation of top income shares. Compared to the existing methods, our proposed method generates smaller bias and root mean squared error (RMSE). The second is the estimation of the income distribution and top income shares from the tabulated summaries of the U.S. tax returns data. Unlike the popular Pareto interpolation method of Piketty (2003), which relies on parametric assumptions in the upper tail, our method allows for the estimation in mid-sample as well as in the tails without parametric assumptions.

Related literature

Our paper is related to a large literature in economics on inequality measures as well as in statistics and econometrics of estimation with grouped data.

Applied researchers working with income inequality measures have long been studying the interpolation problem from grouped data; see for instance Cowell and Mehta (1982) for an early review. The parametric methods for estimating the Lorenz curve (and hence computing the Gini coefficient) of Kakwani and Podder (1976) and Villaseñor and Arnold (1989) have been used by the World Bank. Feenberg and Poterba (1993) and Piketty (2003) interpolate the upper tail of the income distribution by the Pareto distribution with local Pareto exponents estimated from a tabulated summary. See Piketty and Saez (2003) for an application to the U.S. income distribution. More recently, Blanchet et al. (2022) apply spline interpolation to what they call the inverted Pareto coefficients. Compared to this applied literature, our approach enjoys several advantages such as that 1. the method is supported by the rigorous econometric theory that guarantees the performance in large samples, 2. the method is nonparametric across the entire distribution of income, and 3. the output is a closed-form density that is analytically tractable and convenient for post-estimation analysis.

In terms of estimating the income distribution with tabulated data, our proposed method differs from the existing methods, which can be categorized into parametric and nonparametric ones. For the former, Hajargasht et al. (2012) assume a parametric income distribution and develop a generalized method of moment (GMM) estimator for the unknown parameters. See also Chen (2018) and Hajargasht and Griffiths (2020) for other GMM methods relying on parametric assumptions. Despite their good fit in some data sets (e.g., Jorda et al., 2021), parametric methods in general suffer from model misspecifications. Specifically, although the estimator of the coefficients in the parametric model might still converge to some pseudo true values, the implied density estimator is in general inconsistent. The theoretical effect of misspecification on further estimations of other features, say moments and top income shares, are unknown. They may exhibit large biases in finite samples, as we show by simulation studies in Section 4. In contrast, our estimator is nonparametric and relatively robust to parametric assumptions.

For nonparametric estimation with binned/grouped data, Scott and Sheather (1985) study the kernel density estimator when the observations are equally spaced. On the other hand, we do not require data to be equally spaced. Without the equal spacing restriction, Blower and Kelsall (2002) propose an alternative estimator with Gaussian kernel function, which Sun (2014) extends by allowing for other kernel functions. These kernel approaches require a bandwidth as a tuning parameter, whose choice is challenging in practice especially under the nonstandard sampling setup of binned/grouped/tabulated data. In contrast, our proposed ME estimator is free from tuning parameters and therefore more attractive in practice. Furthermore, this tuning-parameter-free feature of our proposed method provides a complete theoretical justification under weak regularity condition. Reyes et al. (2016) derive the orders of magnitude of the bias and the variance of Scott and Sheather’s estimator under very strong conditions: 1. the bin size is of a smaller order than , where denotes the bandwidth of the kernel estimator and 2. the underlying distribution function is seven-times differentiable with bounded derivatives. The first condition implies that the group structure is negligible and hence the bias and the variance are asymptotically the same as in the case with individual observations. The second condition is strong and rules out some candidate distributions, such as double Pareto, which is used in empirical studies of income distribution. Unlike the existing kernel-based methods, our ME estimator only requires the underlying density to be Lipschitz continuous and is based on minimizing the Kullback-Leibler divergence, which lead to both numerical and theoretical advantages. See Section 3 for details.

Finally, our paper is related to the large literature that applies the maximum entropy (ME) principle. Historically, the ME principle was developed in physics to infer the population distribution (e.g., energy distribution of gas molecules) from macroscopic variables (e.g., temperature); see Jaynes (1957). In economics, applications of the ME method include general equilibrium theory (Foley, 1994; Toda, 2010, 2015), diagnosis of asset pricing models (Stutzer, 1995), derivative pricing (Stutzer, 1996), discretization of probability distributions and stochastic processes (Tanaka and Toda, 2013, 2015; Farmer and Toda, 2017), among others. In this paper, we apply the ME principle as a tool to impose moment restrictions implied by the tabulated summary data. Applications in econometrics include Kitamura and Stutzer (1997) and Wu (2003), among others. To our knowledge, none of the existing ME methods work for tabulated summary data.

Organization of the paper

Section 2 introduces the general data framework and previews the U.S. tax return data set used in the application. Section 3 introduces the nonparametric density estimator and proves its strong uniform consistency. Section 4 presents simulation studies. Section 5 applies the proposed method to the U.S. tax return data set.

2 Tabulated summary data

2.1 General data framework

Consider the latent sample , which is not directly observed by the researcher. Denote the order statistics in descending order by such that

For each , define the partial sum of top order statistics

| (2.1) |

Consider a positive number of bins, where denotes the sequence of bin threshold values such that

Let be the number of order statistics included in the top bins, that is, . The tabulated data are summarized as , which is observed by the researcher.

2.2 Example: summary of income data by tax authorities

As a concrete example of the data framework just described, consider the latent sample of the values of income, where indexes potential taxpayers and is the sample size. Due to confidentiality concerns, in general there is no public access to administrative data of income. Publicly available data on the income distribution released from tax authorities often take the form of the tabulated summary .

Table 1 presents an example data set from the 2019 U.S. tax returns.111Table 1 shows partial information from Internal Revenue Service, Statistics of Income (SOI) Individual Income Tax Returns Publication 1304 (https://www.irs.gov/statistics/soi-tax-stats-individual-income-tax-returns-complete-report-publication-1304), Table 1.4 under “Basic Tables”. Adjusted gross income (AGI) is AGI less deficit. We omit the row corresponding to negative income. In this example, the number of income groups is . Column (1) shows the lower threshold of adjusted gross income (AGI) for each income group . Column (2) shows the number of taxpayers within each income group , which corresponds to in our notations, where we set by convention. Column (3) shows the total income (AGI) accruing to taxpayers in each income group in units of 1,000 U.S. dollars, which corresponds to in our notations, where we set by convention. We thus observe the tabulated summary data of AGI, where .

| Income group | Adjusted gross income (AGI) | ||

|---|---|---|---|

| (1) | (2) | (3) | |

| AGI threshold | # returns | Total income | |

| 18 | $1 | 9,866,880 | 24,439,988 |

| 17 | $5,000 | 9,925,940 | 74,584,857 |

| 16 | $10,000 | 11,087,737 | 138,230,399 |

| 15 | $15,000 | 10,039,446 | 175,255,963 |

| 14 | $20,000 | 9,493,968 | 213,660,160 |

| 13 | $25,000 | 9,289,939 | 254,877,708 |

| 12 | $30,000 | 16,090,602 | 560,073,192 |

| 11 | $40,000 | 12,503,041 | 560,258,808 |

| 10 | $50,000 | 22,238,948 | 1,366,892,948 |

| 9 | $75,000 | 14,118,568 | 1,222,947,425 |

| 8 | $100,000 | 21,997,582 | 3,004,363,636 |

| 7 | $200,000 | 7,297,883 | 2,090,808,696 |

| 6 | $500,000 | 1,162,371 | 781,920,814 |

| 5 | $1,000,000 | 254,197 | 305,561,848 |

| 4 | $1,500,000 | 103,075 | 176,961,208 |

| 3 | $2,000,000 | 143,514 | 425,088,995 |

| 2 | $5,000,000 | 34,738 | 237,781,553 |

| 1 | $10,000,000 | 20,876 | 590,230,011 |

3 Main results

This section investigates a method to characterize a well-behaved density function of the distribution of from the tabulated summary data introduced in Section 2. We first consider the case when the sample size is infinite and there are no sampling errors in bin probabilities and conditional means. We next propose a feasible estimator and study its asymptotic properties as the sample size tends to infinity.

3.1 Maximum entropy density

Let denote the true cumulative distribution function (CDF) of , which is assumed to be absolutely continuous with probability density function denoted by . Suppose that the thresholds satisfy

and let denote the interval for the top -th bin with top fractile denoted by . For each , the bin probability and conditional mean are defined by

| (3.1a) | ||||

| (3.1b) | ||||

where denotes the indicator function indicating that the argument belongs to the set .

Obviously, given only the finite tabulation , we do not have sufficient moment restrictions to pin down the true density function . The maximum entropy (ME) method is useful when only certain moment conditions are given. In our context of characterizing the distribution of from a tabulation, we can proceed as follows.

Letting denote a generic density, the given moment conditions consistent with (3.1) are

| (3.2a) | ||||

| (3.2b) | ||||

for each . The ME density is defined by the density on that minimizes the Kullback-Leibler divergence (with respect to the improper uniform density)

| (3.3) |

subject to the moment restrictions (3.2). Below, we let denote the equivalence class (identified by the norm) of nonnegative, measurable, and integrable functions . The following proposition characterizes the solution to the ME problem.

Proposition 1.

Let be the thresholds and be the average of in group . Then the function

| (3.4) |

is strictly concave in and achieves a unique maximum , which satisfies

| (3.5) |

The ME problem has a unique solution , which is piecewise exponential and satisfies

| (3.6) |

for . The minimum value of the Kullback-Leibler divergence (3.3) is given by

| (3.7) |

3.2 Estimation

This section proposes a feasible analog of the ME density characterized in Section 3.1 for estimation of the true density function of . We then establish its strong uniform consistency.

We construct a feasible ME density estimator by replacing and with their empirical analogs and , respectively. Letting denote the vector of thresholds, we thus define the sample-analog ME estimator of as the solution to the constrained optimization prblem of minimizing (3.3) subject to (3.2) with and in place of and , respectively.

We now establish the almost sure uniform consistency of for the true density function over any compact subset of the domain of as . To this end, consider the following conditions.

Assumption 1.

The following conditions hold.

-

(i)

is iid with density .

-

(ii)

The density is Lipschitz continuous with constant , that is, for all we have

-

(iii)

There exist some constants and such that

(3.8) Furthermore, letting be the domain of , we have and .

Condition (i) assumes a random sample. Condition (ii) implies that is almost everywhere differentiable with a bounded derivative, which is much weaker than typical assumptions on kernel estimators that require high-order smoothness conditions. Condition (iii) requires that the length of any bin is neither too large nor too small, as well as that the interval covers the domain of . With these conditions, the following theorem establishes the strong uniform consistency of the maximum entropy density estimator for the true density function over any compact subset of the domain and also bounds the convergence rate. The proof is non-trivial and deferred to Appendix B.

Theorem 2.

Suppose that Assumption 1 holds and let be compact. Then, as , we have

| (3.9a) | ||||

| (3.9b) | ||||

A few remarks are in order regarding this result on the convergence rate. First, while the rate is decomposed into the the deterministic part and the stochastic part, we do not have a control over the trade-off between these two components in the absence of a tuning parameter. This implies a drawback of the tuning parameter-free approach. Second, the rate depends on the parameters and of bin lengths. Slowly vanishing bin lengths (i.e., small and ) yield small variances at the expense of large biases. Quickly vanishing bin lengths (i.e., large and ) yield small biases at the expense of large variances. Third, suppose for simplicity. Then, implies that the stochastic part dominates, while implies that the deterministic part dominates. In the latter case, the limit distribution has a biased center, and it is difficult to conduct statistical inference in general. This is another limitation of the tuning parameter-free approach.

Reyes et al. (2016) derive the convergence rate of the kernel estimator proposed by Scott and Sheather (1985). Reyes et al. (2016) assume that the bin lengths are , where denotes the bandwidth satisfying and as . This condition implies that the group/bin structure is asymptotically negligible, and the resulting orders, and , of the deterministic and stochastic parts, respectively, are the same as those in the standard case with individual observations. On the one hand, choosing a certain bandwidth could lead to a smaller bias or variance than our ME estimator. On the other hand, the assumption that the bin lengths are is very restrictive and could be violated in empirical studies where the bins are not too small. Furthermore, Reyes et al. (2016) assume that the underlying distribution function is seven-times differentiable with bounded derivatives. In contrast, our ME estimator only requires Lipschitz continuity for , which is another advantage.

Having established the strong uniform consistency of the density, it is straightforward to establish the same for the cumulative distribution function (CDF) and quantiles. Define the estimator of by

The following corollary shows the strong uniform consistency of .

Corollary 3.

Suppose that Assumption 1 holds and let be compact. If , then, as , we have

Let denote the -th quantile of . Given , we can estimate by the analog . The following corollary shows that this quantile estimator is also consistent.

Corollary 4.

Suppose that Assumption 1 holds and let be compact. If and , then, as , we have .

3.3 Discussion

In an early review of interpolation methods from grouped data of income, Cowell and Mehta (1982) list the following ten desirable properties (with slight rewording) that the hypothetical interpolated distribution should possess.

-

(i)

The bin probability and conditional mean ( and in our notation in (3.2)) of the estimated density agree with the tabulated summary.

-

(ii)

.

-

(iii)

is continuous within any interval .

-

(iv)

is continuous.

-

(v)

is differentiable.

-

(vi)

.

-

(vii)

.

-

(viii)

has “few” turning points within each bin.

-

(ix)

The range of is “small” on any given interval.

-

(x)

admits a closed-form expression to compute inequality measures.

In addition to these properties, we would like to add:

-

(xi)

converges to the true density as the sample size tends to infinity.

The methods reviewed in Cowell and Mehta (1982) as well as those proposed thereafter satisfy only a few of these properties. For instance, the recent method of Blanchet et al. (2022) does not satisfy (viii) and (ix) (because it uses polynomial interpolation), (x) (because it interpolates the inverted Pareto coefficients, not the density), or (xi) (they do not provide formal theorems).

In contrast, our ME density estimator satisfies all properties except (iv) and (v). To see this, property (i) holds by construction and (xi) is established in Theorem 2. All other properties (except (iv) and (v)) hold because is piecewise exponential explicitly given by (3.6) and hence is nonnegative, continuously differentiable, and monotonic on each interval. Regarding properties (iv) and (v), they clearly hold except at bin thresholds.

To illustrate property (x) further, we present some integral formulas that are useful when computing the CDF and top income shares when the density is piecewise exponential. Consider the piecewise exponential density (3.6). To simplify the notation, let , , , and . Therefore, for , the density is

The counter CDF (tail probability) can be computed using

Applying integration by parts, the tail expectation can be computed using

Putting all the pieces together, we obtain the following closed-form expressions for the CDF and tail expectation. (We assume for simplicity, and we use the notation .)

4 Simulation studies

We conduct three simulation studies that examine the performance of our proposed ME method relative to existing methods.

4.1 Density estimation

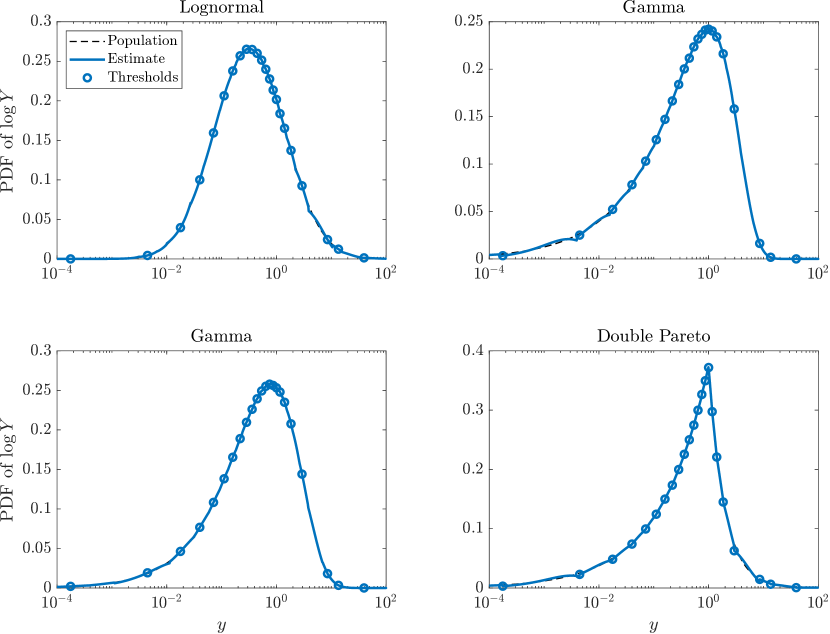

We first present density estimates from one large simulation draw with the sample size comparable to those in our empirical data. We consider four typical models for income distribution, namely lognormal, gamma, Weibull, and double Pareto. In each case, we choose the scale parameter so that the population mean normalizes to 1. Table 2 summarizes these distributions.

| Name | Density | Normalization | Parameter(s) |

|---|---|---|---|

| Lognormal | |||

| Gamma | |||

| Weibull | |||

| Double Pareto |

The simulation design is as follows. For each model, we generate a random sample with size . Such a large is coherent with the number of tax payers in our empirical data set; see Table 1. We set the top fractiles to

(so ) and define the -th threshold as the top -th quantile of . We then estimate the ME density as in Section 3.

Figure 1 shows the population and estimated densities for each model. Because the population densities are skewed, for visibility we plot the density of . In each case, the two densities and are nearly identical.

4.2 Top income shares

Next, we estimate the top income shares, which correspond to the Lorenz curve flipped along the 45 degree line. There are many existing methods for estimating the Lorenz curve as discussed in Section 1. We implement those proposed by Kakwani and Podder (1976) (henceforth KP) and Villaseñor and Arnold (1989) (henceforth VA), both of which have been used by the World Bank. In addition, we implement a more recently developed method by Hajargasht, Griffiths, Brice, Rao, and Chotikapanich (2012) (henceforth HGBRC), which has been further extended by Chen (2018) and Hajargasht and Griffiths (2020). The KP and VA methods impose some parametric assumptions on the Lorenz curve and essentially run linear regressions of the group mean ( in our notation) on some transformation of the proportion of each group ( in our notation). The HGBRC method imposes some parametric assumptions on the underlying density and constructs a generalized method of moments estimation. Regarding KP, we implement their Method III as described in their Section 4. Regarding VA, we implement their method with and as described in their Section 4. Regarding HGBRC, we adopt their assumption of the generalized beta distribution of the second kind (GB2, McDonald, 1984) and the diagonal weighting matrix as proposed by Chotikapanich et al. (2007).

Our data generating process is as follows. We suppose that the population distribution is double Pareto with parameters , , and (normalization). There are two reasons for using the double Pareto distribution with these parameters. First, this distribution has been shown to fit the income distribution very well; see for instance Toda (2012, Fig. 1(a)). Second, unlike other parametric distributions used in Figure 1, the double Pareto distribution admits a closed-form CDF and Lorenz curve as discussed in Appendix D, which is convenient for numerical evaluation. Appendix F considers other distributions.

We treat the population top percentiles as the observed thresholds () and compute the population top income shares. Next, we generate random samples with sizes from the population distribution222Since the logarithm of a double Pareto random variable is Laplace, which is double exponential, we can generate a double Pareto random variable using , where are independent exponential random variables with parameter 1. Therefore , where are independent uniform random variables on . and record the proportions of observations and their average incomes within each group, which we treat as our data.

Implementing our proposed ME, the KP, the VA, and the HGBRC methods, we report their relative bias and relative root mean squared error (RMSE) for the income shares of the top fractile with . More specifically, let denote the true top income share and the estimator in the -th simulation draw with . We define the relative bias and RMSE by

| Relative Bias | |||

| Relative RMSE |

respectively. Table 3 presents the results based on simulations.

Relative Bias 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME 0.007 0.003 0.001 0.001 0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 KP -0.353 -0.348 0.025 0.125 0.101 0.033 -0.020 -0.036 -0.031 -0.014 0.002 0.005 -0.349 -0.343 0.023 0.123 0.099 0.032 -0.020 -0.037 -0.031 -0.014 0.002 0.005 -0.347 -0.342 0.023 0.123 0.099 0.032 -0.021 -0.037 -0.031 -0.014 0.002 0.005 VA 0.257 0.052 0.020 0.029 0.021 -0.011 -0.039 -0.035 -0.019 -0.005 0.002 0.002 0.253 0.049 0.018 0.027 0.020 -0.012 -0.039 -0.035 -0.019 -0.005 0.002 0.002 0.253 0.049 0.017 0.027 0.020 -0.012 -0.039 -0.035 -0.019 -0.005 0.002 0.002 HGBRC -0.094 -0.054 -0.015 0.003 0.017 0.009 -0.007 -0.007 -0.004 -0.001 0.000 0.000 -0.049 -0.023 0.001 0.012 0.019 0.010 -0.005 -0.005 -0.002 -0.001 0.000 0.000 -0.039 -0.019 0.003 0.012 0.019 0.010 -0.005 -0.005 -0.002 -0.001 0.000 0.000 Relative RMSE 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME 0.440 0.133 0.053 0.033 0.019 0.012 0.009 0.006 0.004 0.002 0.001 0.000 0.136 0.042 0.017 0.010 0.006 0.004 0.003 0.002 0.001 0.001 0.000 0.000 0.046 0.014 0.005 0.003 0.002 0.001 0.001 0.001 0.000 0.000 0.000 0.000 KP 0.427 0.370 0.062 0.130 0.102 0.035 0.021 0.037 0.031 0.014 0.002 0.005 0.357 0.346 0.029 0.123 0.099 0.032 0.021 0.037 0.031 0.014 0.002 0.005 0.348 0.343 0.024 0.123 0.099 0.032 0.021 0.037 0.031 0.014 0.002 0.005 VA 0.268 0.079 0.051 0.048 0.034 0.022 0.041 0.036 0.020 0.005 0.002 0.002 0.254 0.052 0.023 0.030 0.022 0.013 0.039 0.035 0.019 0.005 0.002 0.002 0.253 0.049 0.018 0.027 0.020 0.012 0.039 0.035 0.019 0.005 0.002 0.002 HGBRC 0.223 0.137 0.071 0.044 0.027 0.015 0.011 0.009 0.005 0.002 0.001 0.000 0.093 0.049 0.024 0.019 0.021 0.011 0.006 0.005 0.003 0.001 0.000 0.000 0.054 0.026 0.011 0.015 0.020 0.011 0.005 0.005 0.002 0.001 0.000 0.000

The findings can be summarized as follows. First, our proposed ME method performs very well in terms of both bias and RMSE. They decrease as increases and are smaller than those of the other three methods for most of the combinations, especially the bias. Second, the KP and the VA methods both impose some parametric assumptions on the Lorenz curve and hence implicitly on the underlying density. In particular, the VA method imposes that the Lorenz curve is a part of an ellipse. This assumption implies that the underlying density (after a location- and scale-transformation) is proportional to , which is the Student distribution with two degrees of freedom (Villaseñor and Arnold, 1989, Theorem 4). The KP method introduces a new coordinate system and imposes another parametric form on the Lorenz curve. The implied density is still parametric but does not have a closed-form expression. The HGBRC method assumes the GB2 density, which has Pareo upper and lower tails. Therefore, its performance is substantially better than those of KP and VA. In summary, these and any other parametric assumptions could lead to large bias and RMSE caused by misspecification, which do not decrease with .

4.3 Comparison to kernel estimator

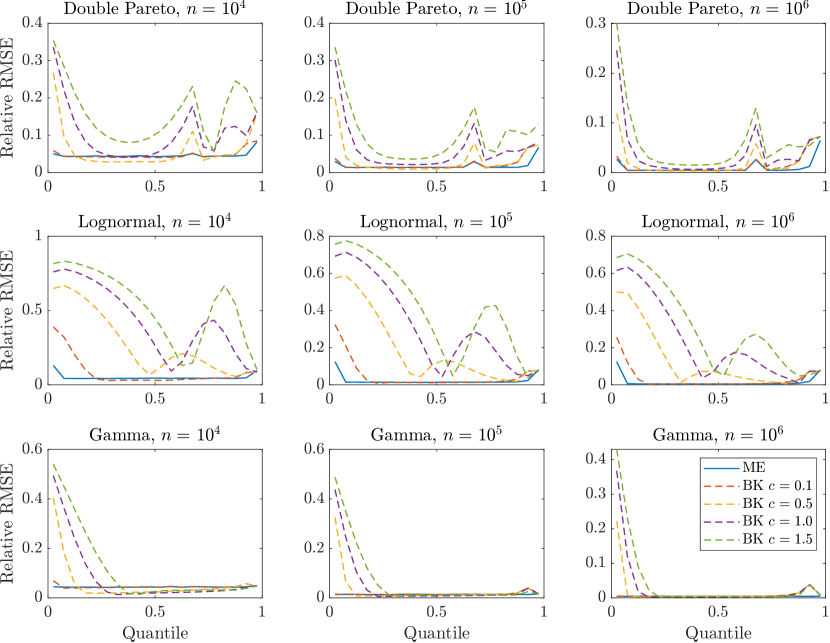

Finally, we compare our proposed ME estimator with the nonparametric kernel estimator proposed by Blower and Kelsall (2002). Given a bandwidth , define as the PDF of the normal distribution with mean zero and variance , that is,

We implement Blower and Kelsall (2002, eq.(1.4)) by constructing the density estimator

where is the histogram estimator

Using the fact that and is the normal density, we can simplify as follows:

where denotes the CDF of the standard normal distribution.

Blower and Kelsall (2002) do not derive any asymptotic properties of this estimator nor theoretical requirements on the choice of the bandwidth. We implement a variety of choices of to examine its finite sample performance. Specifically, we use the rule-of-thumb choice , where is the sample standard deviation based on individual observations (which is in principle infeasible given the tabulated data) and is some constant.

Figure 2 presents the relative RMSE for the density estimators when the data generating process is double Pareto, lognormal, and gamma as in Section 4.2 with sample size . Although these figures are not necessarily easy to read, the RMSEs for the ME (BK) estimator are indicated with solid (dashed) lines. As is clear from this figure, the RMSEs for the ME estimator is generally closest to the horizontal axis uniformly across quantiles, so the performance of our proposed ME method is outstanding. In addition, we also implement the kernel estimator studied by Reyes et al. (2016). Its performance is substantially worse than that proposed by Blower and Kelsall (2002) and hence not reported.

5 Income distribution in the United States

We consider two empirical applications of our method. First, we estimate the distribution of U.S. income distribution for particular years. Second, we estimate the top income shares (including mid-sample) over the past century.

5.1 Income distribution in 1946 and 2019

We estimate the distribution of U.S. adjusted gross income (AGI) in 1946 and 2019. We choose 2019 because it is the most recent year for which data is available. Before World War II, because only a small fraction of the population filed for taxes, the tax returns data is not representative for the population.333The fraction of tax filers among potential tax units has been stable at around 80–90% postwar but in the range of 1–20% before 1940; see the discussion in Piketty and Saez (2003). For this reason, we choose 1946 because it is one of the earliest years for which the tax returns data is representative for the population. Note that unlike in recent years, the tabulated summary data set is almost the only publicly available income data set in early years such as 1946.

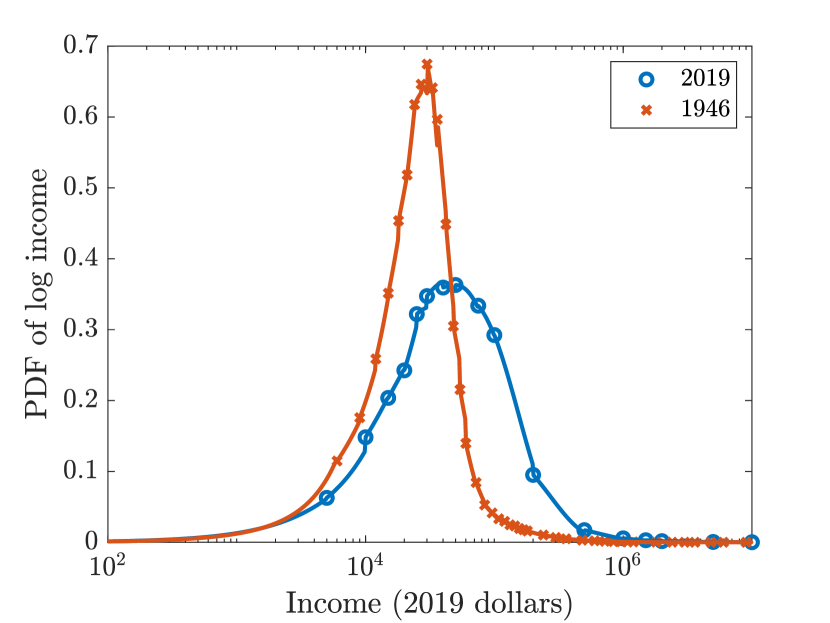

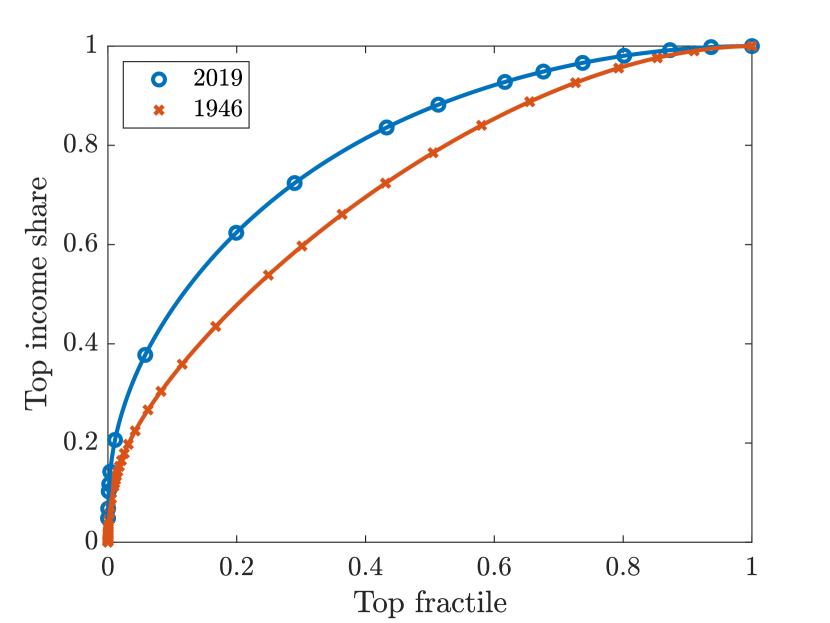

To make the results comparable across years, we measure income in 2019 dollars by adjusting with the Consumer Price Index (CPI). The number of income groups is for 1946 and for 2019. Figure 3(a) shows the ME density estimates of log income in a semi-log scale.

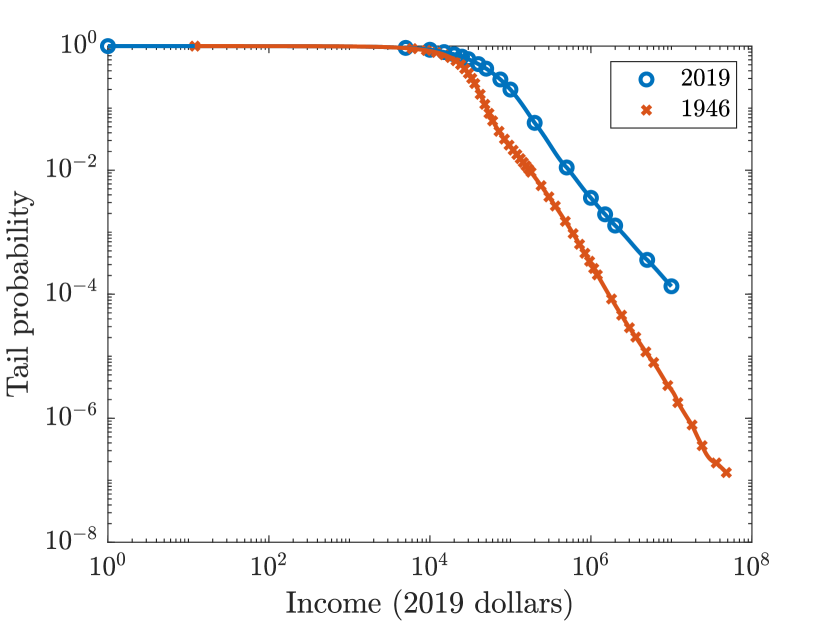

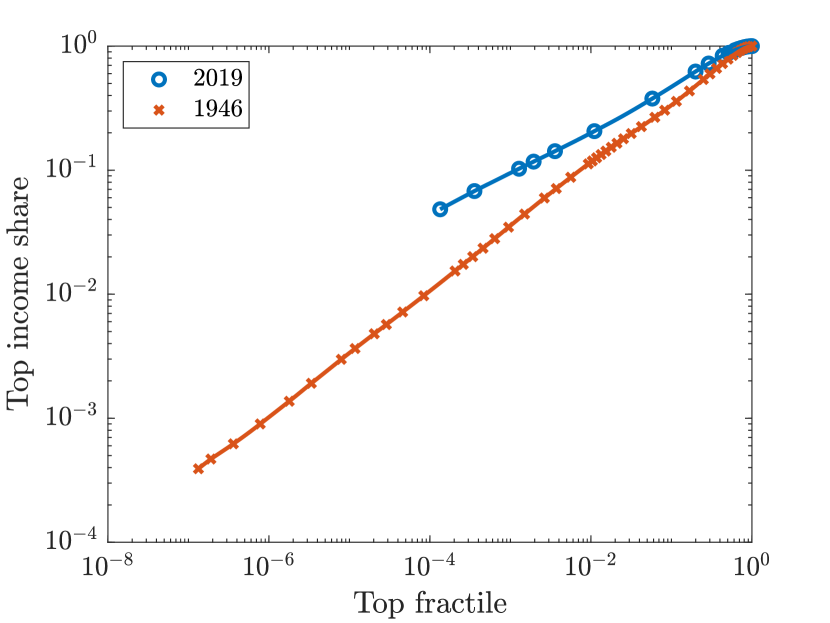

We can summarize the findings as follows. First, for each year the log income distribution is bell-shaped but slightly asymmetric. Second, observe that although is piecewise exponential, it is not necessarily continuous at the bin thresholds as can be seen from the spikes in the 1946 density. Third, the 2019 density is more spread-out than 1946, which suggests that income inequality has increased. Finally, Figure 3(b) shows the tail probability in a log-log scale, which is continuous. The fact that the 2019 tail probability is higher than 1946 implies that the 2019 (real) income distribution first-order stochastically dominates the 1946 one, possibly due to economic growth. The graphs also show a straight-line pattern for high incomes, which is consistent with a Pareto upper tail documented elsewhere; see for instance de Vries and Toda (2022) and the references therein. Because the slope is steeper for 1946 than in 2019, the income Pareto exponent is smaller (top income inequality is higher) in 2019.

Because the ME density is piecewise exponential, which is analytically tractable, it is straightforward to compute statistics such as top income shares; see Section 3.3. Figure 4 shows the top income shares, both in original and log-log scales. Figure 4(a) (original scale) is essentially the Lorenz curve flipped along the 45 degree line. The fact that the 2019 curve is above the 1946 one suggests that income inequality has increased. The straight-line pattern in log-log scale (Figure 4(b)) is consistent with a Pareto upper tail.

5.2 Top income shares over the century

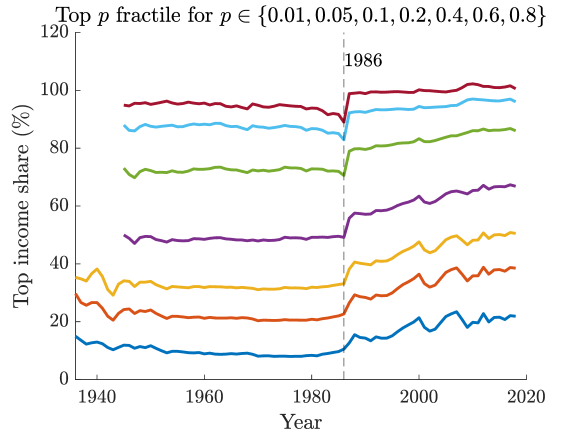

Finally, we apply the proposed method to estimate the top fractile income share for various values of . To construct the top income shares, we use the following approach. First, we collect the tabulated summaries of income similar to Table 1 for each year from the IRS Statistics of Income.444See the appendix in Lee et al. (2022) for specific details. These tables contain information on the number of tax units (an individual or a married couple with dependents if any) and their total income within each income group. As these tables contain only tax filers, we complement them with the total number of potential tax units and total income estimated by Piketty and Saez (2003).555We obtain the total number of tax units from the spreadsheet https://eml.berkeley.edu/~saez/TabFig2018.xls, Table A0, Column B, and total income from Column I. We suppose that non-filers are low income households and thus do not affect the calculation of the top fractile income share if is small enough. Because the fraction of tax filers among potential tax units exceeds 0.1 (0.8) since 1936 (1945), we construct the top fractile income share for since 1936 and also for for since 1945. Figure 5 shows the results.

The top 1%, 5%, 10% income shares exhibit an inverse U-shaped pattern, which is well known. To the best of our knowledge, the top income shares for mid-sample fractiles (e.g., ) have not been reported in the previous literature. We find that the mid-sample top income shares exhibit an abrupt upward jump between 1986 and 1987. This could be due to the Tax Reform Act of 1986, which significantly altered the treatment of capital gains income.666According to Piketty and Saez (2001, p. 40), the fraction of capital gains income included in AGI was 100% until 1933, 70% in 1934–1937, 60% in 1938–1941, 50% in 1942–1978, 40% in 1979–1986, and 100% since 1987. Because high income earners tend to hold more financial asset (and generate more capital gains), the large exclusion of capital gains in 1934–1986 likely causes the top income shares to be biased downwards.

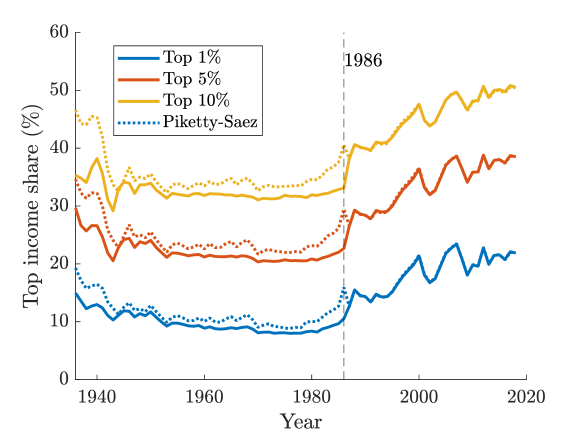

We next compare our top income shares to those constructed by Piketty and Saez (2003).777We obtain the top income shares from Table A3 in the spreadsheet https://eml.berkeley.edu/~saez/TabFig2018.xls. Piketty (2001, Appendix B, Section 1.1, pp. 592–599) provides the details of the method for constructing these top income shares. Since it is written in French, we describe the method in Appendix E for the convenience of the readers. Figure 6 shows the top 1%, 5%, 10% income shares constructed in two ways. We find that post-1986, our top income shares are nearly identical to those from Piketty and Saez (2003), even though our method is nonparametric while their method is parametric (assuming a Pareto upper tail). This is likely because the upper tail of the income distribution can be well approximated by the Pareto distribution. However, there are large discrepancies between the two series pre-1986 because we have used the raw AGI without adjusting for the excluded capital gains income discussed in Footnote 6.

6 Concluding remarks

Existing standard nonparametric estimators of density and cumulative distribution functions require individual-level data. Even when individual-level information is difficult to access due to confidentiality concerns, tabulated summaries of such data are often publicly available. Administrative data of income are the leading examples. In this paper, we propose a novel method of maximum entropy density estimation from tabulated summary data and establish the strong uniform consistency of the density and cumulative distribution estimators. This method enjoys many desirable properties. First, the estimator is piecewise exponential, which is analytically tractable. Using its functional form, it is straightforward to compute statistics such as top income shares. Second, and more importantly, our estimator is free from tuning parameters unlike existing kernel-based methods, which is attractive in practice. This feature provides a complete theoretical justification that our proposed estimator works in practice, unlike the existing kernel-based estimators for which the theory does not formally account for the effects of bandwidth choice in practice.

Appendix

Appenidx A provides a smoothed version of the proposed ME estimator. Appendix B contains mathematical proofs of the strong uniform consistency. Appendix C solves some numerical issues in constructing the proposed estimator. Appendix D computes the Lorenz curve for the double Pareto distribution. Appendix E describes the details of Piketty (2003)’s Pareto interpolation method, which was originally written in French. Appendix F contains additional simulation studies.

Appendix A Smoothed ME estimation

Our estimator described in Section 3.1 in the main text is generally discontinuous at the bin thresholds . In practice, an ad hoc yet simple method to smooth the estimator is to replace it with some local polynomial function within small neighborhoods of . As a more systematic alternative, we can slightly shift the bin boundaries so that the implied ME estimator becomes continuous. To that end, we can treat as arguments and further minimize the Kullback-Leibler divergence (3.7) over as follows. Because the minimum threshold is unidentified, we set it to an arbitrary value , say, . Define the set of admissible thresholds by

| (A.1) |

which is a nonempty open interval in . The following theorem shows that in (3.7) always achieves a unique minimum on , which is continuous.

Theorem 5.

The proof is deferred to Appendix B.

Appendix B Proofs

Proof of Proposition 1.

To simplify notation, we suppress the dependence of , , etc. on . We use Fenchel duality (Borwein and Lewis, 1991) to solve the maximum entropy problem. The Lagrangian of the maximum entropy problem subject to the moment conditions (3.2) is

where and are the Lagrange multipliers corresponding to the moment conditions (3.2a) and (3.2b). The dual objective function is the minimum of over unconstrained . Taking the first order condition (Gâteaux derivative) pointwise, for we obtain

| (B.1) |

Hence the dual objective function becomes

The dual problem maximizes with respect to , which is a concave maximization problem. The first order condition with respect to is

| (B.2) |

Then (with a slight abuse of notation) the objective function becomes

| (B.3) |

where is given by (3.4). Since is additively separable, it suffices to maximize for each .

Let us now show that achieves a unique maximum over . It is straightforward to show the strict concavity of by applying Hölder’s inequality to the function . As , it follows from (3.4) that

because . Since is continuous and strictly concave on its domain, it achieves a unique maximum . When , we have for , and analytically maximizing for , we obtain the expression for in (3.5). Differentiating under the integral sign, we obtain

so can be signed as in (3.5).

Lemma 6.

Define the function by

| (B.4) |

where and . Then , , , , and .

Proof.

To simplify notation, let and . is trivial since as . Using the definition of and , we have , , and . Taking the derivative of , we have

Noting that as by Taylor’s theorem, a straightforward calculation yields .

To show , it suffices to show . To this end, define . Then and

for , so for . This shows . Taking the derivative once again, we have

Therefore to show , it suffices to show . To this end, define . Then

for , where the last inequality follows from for . Noting that , it follows that for , implying and hence . ∎

Below, extend the domain of in (B.4) to the entire real line by setting and for . Then , is strictly increasing, and is concave (convex) for (). Figure 7 shows its graph.

We need the following lemma to prove Theorem 2.

Lemma 7.

Let . Then the function

is strictly concave in and achieves a unique maximum . Furthermore, letting and , we have

| (B.5) |

Proof.

Proof of Theorem 2.

We divide our proof into four steps.

Step 1.

Reduction to the case when is an interval.

Since is Lipschitz, it is continuous, so the domain is open. Let be compact. For each we can take an open interval with and . Since is compact and , we can take a finite subcover . Therefore , so the uniform consistency on follows if we show the uniform consistency on each compact interval .

Below, to simplify the argument, fix and such that and . By relabeling the thresholds if necessary, without loss of generality we may assume by Condition (iii).

Step 2.

Let . As , we have

| (B.6a) | ||||

| (B.6b) | ||||

Let be the probability space over which the random variables are defined. For any , define the event

Let denote the indicator function of . Using , we obtain

where the last line follows from (3.8). Applying Hoeffding (1963)’s inequality to the last term, we obtain

| (B.7) |

Since by Assumption 1(iii), it follows that . By the Borel-Cantelli lemma, we have

Since is arbitrary, we obtain almost surely as .

To show that this term is for , for any , choose such that . Then the definition of and (B.7) imply

for all , so by the definition and that of the order in probability, we obtain (B.6a).

We next estimate the term . Using

and noting that (compact set) whenever , a similar calculation yields

| (B.8) |

Using the triangle inequality and , we obtain

| (B.9) |

Assumption 1(ii) implies that we can take such that . By the mean value theorem for integrals, for each , there exists some such that

| (B.10) |

Therefore dividing (B.9) by and using (B.10), we obtain

for each . Taking the maximum over , dividing by , and letting , we obtain (B.6b).

Step 3.

Let be the midpoint of , , and be the Lipschitz constant for . Then

| (B.11) |

Since by Assumption 1(ii) is Lipschitz continuous with constant , it is absolutely continuous. Theorem 3.35 of Folland (1999) implies that is almost everywhere differentiable with and we can apply the fundamental theorem of calculus (in particular, integration by parts). Therefore using and , we obtain

Therefore, for every , we have

Dividing both sides by and using (B.10), we obtain

uniformly over , which shows (B.11).

Step 4.

Strong consistency and the convergence rate of the estimator for uniformly over .

Letting , by assumption we have . Therefore for any , we can take such that . Using the moment conditions and the mean value theorem for the integrals, we can take such that

| (B.12a) | ||||

| (B.12b) | ||||

Therefore,

| (B.13) |

Using Assumption 1(ii), , and Assumption 1(iii), we can uniformly bound as

| (B.14) |

Noting that is exponential on and hence monotonic, it follows from the functional form in (3.6) and the mean value theorem that

| (B.16) |

By Step 2 and (B.10), we can bound the first term in the right-hand side of (B.16) as

| (B.17) |

To bound the second term, note from Steps 2 and 3 that

Therefore it follows from Lemma 7 that

| (B.18) |

Combining (B.16), (B.17) and (B.18), we obtain

| (B.19) |

The uniform bound (3.9b) follows from (B.13), (B.14), (B.15), (B.19), and Lemma 6. Noting that the term is also in this case, we also obtain the uniform strong consistency (3.9a). ∎

Proof of Corollary 4.

Since , there exists a -ball around such that . Also, since , by Assumption 1(ii). Furthermore, is continuous by Assumption 1(ii). Therefore, is bounded away from zero in a neighborhood of . That is, there exists a -ball and such that for all . Let .

We first show that

| (B.20) |

By way of contradiction, suppose that . Then, since and are continuous by construction,

and hence , which is a contradiction. Therefore, we must have . Sinimarly, must hold too. Therefore, (B.20) holds.

Since is non-decreasing by construction, and it is also strictly increasing on , (B.20) implies

| (B.21) |

Also, noting that , we obtain

| (B.22) |

Proof of Theorem 5.

Let be the closure of in (A.1), which is a nonempty compact interval. Let be the boundary of . Extend to by defining on .

We divide our proof into three steps.

Step 1.

is lower semicontinuous.

Motivated by (3.4) and (3.7), define by

where the case needs to be separately defined in the obvious way using (3.4). Then we can easily verify that is continuous. Therefore is lower semicontinuous.

Step 2.

is strictly convex.

Since and the supremum of convex functions is convex, it suffices to show that is strictly convex in . To this end it suffices to show that its Hessian is positive definite almost everywhere on . A tedious but straightforward calculation yields

| (B.23a) | ||||

| (B.23b) | ||||

| (B.23c) | ||||

| (B.23d) | ||||

which are valid for by setting . Collecting the partial derivatives (B.23) into a matrix, we obtain the Hessian

| (B.24) |

where

with strict inequality if . Since by (3.5) we have if and only if , we have for all almost everywhere on . Below, consider such .

As is well known, a real symmetric matrix is positive definite if and only if all leading principal minors are positive. In general, for a tridiagonal matrix

its determinant satisfies the three-term recurrence relation

| (B.25) |

where and (El-Mikkawy, 2004). Applying (B.25) to in (B.24) with , since and , we obtain

| (B.26) |

Clearly . Let us show by induction that

| (B.27) |

which implies for all . If , then because , so (B.27) holds. Suppose (B.27) holds for some . Then for , using (B.26) and the induction hypothesis, we obtain

so (B.27) holds for . This completes the proof of the strict convexity of in , and hence is strictly convex in .

Step 3.

There exists a unique that minimizes . For this , the maximum entropy density in (3.6) is continuous on .

Since is nonempty compact, is lower semicontinuous, and is finite-valued on , it achieves a minimum at some . Since on , it must be . Since is strictly convex on , the minimizer is unique.

Let us next show the continuity of . Since is piecewise exponential (hence continuous), it suffices to show the continuity at the thresholds . Since is differentiable, it follows from the first-order condition, the envelope theorem, and (B.23a) that

| (B.28) |

Appendix C Numerical issues

Although conceptually straightforward, numerically maximizing in (3.4) over can be unstable because the values of change by many orders of magnitude in typical data, for instance and in Table 1. For this reason it is useful to choose some scaling factor and consider . Define

Maximizing both sides over and using the definition of in Proposition 1, it follows that

Therefore to numerically compute and , we may maximize for some scaling factor (say so that ), multiply its maximizer by , and add to its maximum value.

Appendix D Lorenz curve for double Pareto distribution

Integrating the double Pareto density (with ), it is easy to show that the CDF of double Pareto is

Let us compute the Lorenz curve, which is implicitly defined by

where is the mean. If , then

If , then

Letting , the mean of double Pareto (assuming ) is

Thus if (or equivalently ), then

If (or equivalently ), then

Putting all the pieces together, the Lorenz curve for a double Pareto distribution with and is

Appendix E Piketty (2003)’s Pareto interpolation method

Piketty (2003)’s Pareto interpolation method for constructing top income shares is widely used, for example in Piketty and Saez (2003) and the World Inequality Database.888https://wid.world/ Because the detailed description of the method is relegated to Piketty (2001, Appendix B, Section 1.1, pp. 592–599), which is written in French, for completeness we describe the method here.

We use the same notation as in Section 3.1. For simplicity assume that we are interested in the income distribution and the top income shares of the taxpayers, so the sample size is . Suppose we observe the lower income threshold for income group , which we denote by . Let be the top fractile corresponding to the -th income threshold and

be the average income of taxpayers with income above .

Let be the ratio between the average income of individuals exceeding and the income threshold . If income is Pareto distributed (in the upper tail), then for large enough income level , the CDF takes the form for some and Pareto exponent . Therefore for any large enough income threshold , we have

| (E.1) |

Piketty (2001) refers to as the (local) Pareto coefficient. When the income distribution has a Pareto upper tail, the (local) Pareto exponent can be recovered from (E.1) as

| (E.2) |

Let and suppose we would like to construct the top fractile income share. For example, corresponds to the top 1% income share. Piketty (2001) proceeds as follows to construct the top fractile income share. First, let be the closest proportion to directly observed in the data, and and be the corresponding income threshold and local Pareto exponent. Then one supposes that the income distribution is locally exactly Pareto, and therefore the CDF is

The income threshold corresponding to the top fractile can be computed as

Noting that the sample size is , the total income of taxpayers in the top fractile can be computed as

| (E.3) |

The top fractile income share can then be computed as . If the researcher is interested in the top income share of all income earners (including those who do not file for taxes), one would adjust the sample size and the total income from other sources (e.g., population statistics and national accounts); see for example Piketty and Saez (2001, Appendix A).

Appendix F Additional simulations

In the main text, we used the double Pareto distribution to evaluate the bias and RMSE in the top income shares. Here, we repeat the analysis in Table 3 with data generated from lognormal, gamma, and Weibull distributions, which are described in Table 2. For the lognormal distribution, we set . For the gamma and the Weibull distributions, we set and , respectively, so that they are both identical to the exponential distribution with unit mean (for which it is possible to compute top income shares in closed-form). Other setups and the four estimation methods are the same as those described in Section 4. Tables 4 and 5 present the results.

Relative Bias 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME -0.016 -0.003 -0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 -0.003 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 -0.002 0.00 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 KP 0.897 0.112 -0.036 -0.034 -0.012 0.001 0.006 0.006 0.004 0.002 0.000 -0.001 0.907 0.113 -0.035 -0.034 -0.011 0.001 0.006 0.006 0.004 0.002 0.000 -0.001 0.908 0.113 -0.035 -0.034 -0.011 0.001 0.006 0.006 0.004 0.002 0.000 -0.001 VA 0.412 0.044 -0.016 -0.013 -0.004 0.001 0.003 0.004 0.003 0.002 0.001 0.000 0.411 0.044 -0.015 -0.012 -0.003 0.002 0.003 0.004 0.003 0.002 0.001 0.000 0.410 0.044 -0.015 -0.012 -0.003 0.002 0.003 0.004 0.003 0.002 0.001 0.000 HGBRC 0.296 0.078 0.018 0.007 0.002 0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.256 0.084 0.026 0.013 0.005 0.003 0.002 0.001 0.001 0.000 0.000 0.000 0.235 0.080 0.026 0.013 0.005 0.003 0.002 0.001 0.001 0.000 0.000 0.000 Relative RMSE 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME 0.342 0.106 0.037 0.022 0.011 0.006 0.004 0.002 0.001 0.001 0.000 0.000 0.109 0.033 0.012 0.007 0.004 0.002 0.001 0.001 0.000 0.000 0.000 0.000 0.036 0.010 0.004 0.002 0.001 0.001 0.000 0.000 0.000 0.000 0.000 0.000 KP 0.932 0.129 0.046 0.040 0.017 0.008 0.008 0.007 0.005 0.002 0.000 0.001 0.911 0.115 0.037 0.034 0.012 0.003 0.006 0.006 0.004 0.002 0.000 0.001 0.909 0.113 0.036 0.034 0.011 0.002 0.006 0.006 0.004 0.002 0.000 0.001 VA 0.423 0.071 0.038 0.027 0.013 0.008 0.005 0.004 0.003 0.002 0.001 0.000 0.412 0.047 0.019 0.014 0.005 0.003 0.004 0.004 0.003 0.002 0.001 0.000 0.411 0.044 0.016 0.013 0.003 0.002 0.003 0.004 0.003 0.002 0.001 0.000 HGBRC 0.587 0.190 0.067 0.037 0.018 0.010 0.006 0.004 0.002 0.001 0.001 0.000 0.313 0.101 0.032 0.016 0.007 0.004 0.002 0.001 0.001 0.001 0.000 0.000 0.254 0.084 0.026 0.013 0.006 0.003 0.002 0.001 0.001 0.000 0.000 0.000

Relative Bias 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME -0.020 0.001 0.001 0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 -0.002 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 KP -0.886 0.313 0.206 0.085 -0.003 -0.027 -0.029 -0.021 -0.011 -0.001 0.004 0.004 -0.905 0.313 0.205 0.084 -0.003 -0.027 -0.029 -0.022 -0.011 -0.001 0.004 0.004 -0.906 0.313 0.205 0.084 -0.003 -0.027 -0.029 -0.022 -0.011 -0.001 0.004 0.004 VA 11.773 1.777 0.236 -0.012 -0.107 -0.096 -0.062 -0.029 -0.008 0.002 0.003 0.001 11.763 1.775 0.235 -0.013 -0.108 -0.096 -0.062 -0.029 -0.008 0.002 0.003 0.001 11.761 1.774 0.235 -0.013 -0.108 -0.096 -0.062 -0.029 -0.008 0.002 0.003 0.001 HGBRC -0.002 -0.036 -0.022 -0.012 -0.004 -0.001 0.001 0.001 0.001 0.001 0.000 0.000 0.013 -0.010 -0.008 -0.005 -0.002 -0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.009 -0.007 -0.006 -0.004 -0.001 0.000 0.000 0.000 0.000 0.000 0.000 0.000 Relative RMSE 0.001 0.01 0.05 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 ME 0.316 0.097 0.038 0.024 0.013 0.009 0.006 0.004 0.002 0.001 0.001 0.000 0.103 0.031 0.012 0.008 0.004 0.003 0.003 0.001 0.001 0.000 0.000 0.000 0.032 0.009 0.004 0.002 0.001 0.001 0.001 0.000 0.000 0.000 0.000 0.000 KP 0.891 0.330 0.209 0.087 0.011 0.028 0.029 0.022 0.011 0.002 0.004 0.004 0.906 0.315 0.206 0.084 0.005 0.027 0.029 0.022 0.011 0.001 0.004 0.004 0.907 0.313 0.205 0.084 0.003 0.027 0.029 0.022 0.011 0.001 0.004 0.004 VA 11.776 1.777 0.237 0.019 0.108 0.096 0.062 0.030 0.008 0.002 0.003 0.001 11.763 1.775 0.235 0.014 0.108 0.096 0.062 0.030 0.008 0.002 0.003 0.001 11.761 1.774 0.235 0.013 0.108 0.096 0.062 0.030 0.008 0.002 0.003 0.001 HGBRC 0.285 0.113 0.046 0.027 0.014 0.008 0.006 0.004 0.002 0.001 0.001 0.000 0.090 0.035 0.015 0.009 0.004 0.003 0.002 0.001 0.001 0.000 0.000 0.000 0.027 0.013 0.007 0.004 0.002 0.001 0.001 0.000 0.000 0.000 0.000 0.000

Our findings here are similar to those presented in Section 4. First, our proposed ME method performs very well in terms of both the bias and RMSE. They are smaller than those of the other methods for most of the combinations, especially the bias. Second, the KP and the VA methods both impose some parametric assumptions on the Lorenz curve and hence implicitly on the underlying density. The misspecification biases could be quite large depending on the true data generating process, especially for the VA method.

References

- Blanchet et al. (2022) Thomas Blanchet, Juliette Fournier, and Thomas Piketty. Generalized Pareto curves: Theory and applications. Review of Income and Wealth, 68(1):263–288, March 2022. doi:10.1111/roiw.12510.

- Blower and Kelsall (2002) Gordon Blower and Julia E. Kelsall. Nonlinear kernel density estimation for binned data: Convergence in entropy. Bernoulli, 8(4):423–449, August 2002.

- Borwein and Lewis (1991) Jonathan M. Borwein and Adrian S. Lewis. Duality relationships for entropy-like minimization problems. SIAM Journal on Control and Optimization, 29(2):325–338, March 1991. doi:10.1137/0329017.

- Chen (2018) Yi-Ting Chen. A unified approach to estimating and testing income distributions with grouped data. Journal of Business & Economic Statistics, 36(3):438–455, 2018. doi:10.1080/07350015.2016.1194762.

- Chotikapanich et al. (2007) Duangkamon Chotikapanich, William E. Griffiths, and D. S. Prasada Rao. Estimating and combining national income distributions using limited data. Journal of Business & Economic Statistics, 25(1):97–109, January 2007. doi:10.1198/073500106000000224.

- Cowell and Mehta (1982) Frank A. Cowell and Fatemeh Mehta. The estimation and interpolation of inequality measures. Review of Economic Studies, 49(2):273–290, April 1982. doi:10.2307/2297275.

- de Vries and Toda (2022) Tjeerd de Vries and Alexis Akira Toda. Capital and labor income Pareto exponents across time and space. Review of Income and Wealth, 68(4):1058–1078, December 2022. doi:10.1111/roiw.12556.

- El-Mikkawy (2004) Moawwad E. A. El-Mikkawy. On the inverse of a general tridiagonal matrix. Applied Mathematics and Computation, 150(3):669–679, March 2004. doi:10.1016/S0096-3003(03)00298-4.

- Farmer and Toda (2017) Leland E. Farmer and Alexis Akira Toda. Discretizing nonlinear, non-Gaussian Markov processes with exact conditional moments. Quantitative Economics, 8(2):651–683, July 2017. doi:10.3982/QE737.

- Feenberg and Poterba (1993) Daniel R. Feenberg and James M. Poterba. Income inequality and the incomes of very high-income taxpayers: Evidence from tax returns. Tax Policy and the Economy, 7:145–177, 1993. doi:10.1086/tpe.7.20060632.

- Foley (1994) Duncan K. Foley. A statistical equilibrium theory of markets. Journal of Economic Theory, 62(2):321–345, April 1994. doi:10.1006/jeth.1994.1018.

- Folland (1999) Gerald B. Folland. Real Analysis: Modern Techniques and Their Applications. John Wiley & Sons, Hoboken, NJ, 2 edition, 1999.

- Hajargasht and Griffiths (2020) Gholamreza Hajargasht and William E. Griffiths. Minimum distance estimation of parametric Lorenz curves based on grouped data. Econometric Reviews, 39(4):344–361, April 2020. doi:10.1080/07474938.2019.1630077.

- Hajargasht et al. (2012) Gholamreza Hajargasht, William E. Griffiths, Joseph Brice, D. S. Prasada Rao, and Duangkamon Chotikapanich. Inference for income distributions using grouped data. Journal of Business & Economic Statistics, 30(4):563–575, October 2012. doi:10.1080/07350015.2012.707590.

- Hoeffding (1963) Wassily Hoeffding. Probability inequalities for sums of bounded random variables. Journal of the American Statistical Association, 58(301):13–30, March 1963. doi:10.1080/01621459.1963.10500830.

- Jaynes (1957) Edwin T. Jaynes. Information theory and statistical mechanics. Physical Review, 106(4):620–630, May 1957. doi:10.1103/PhysRev.106.620.

- Jorda et al. (2021) Vanesa Jorda, José María Sarabia, and Markus Jäntti. Inequality measurement with grouped data: Parametric and non-parametric methods. Journal of the Royal Statistical Society: Series A (Statistics in Society), 184(3):964–984, July 2021. doi:10.1111/rssa.12702.

- Kakwani and Podder (1976) Nanak C. Kakwani and Nripesh Podder. Efficient estimation of the Lorenz curve and associated inequality measures from grouped observations. Econometrica, 44(1):137–148, January 1976. doi:10.2307/1911387.

- Kitamura and Stutzer (1997) Yuichi Kitamura and Michael Stutzer. An information-theoretic alternative to generalized method of moments estimation. Econometrica, 65(4):861–874, July 1997. doi:10.2307/2171942.

- Lee et al. (2022) Ji Hyung Lee, Yuya Sasaki, Alexis Akira Toda, and Yulong Wang. Capital and labor income Pareto exponents in the United States, 1916–2019. June 2022. URL https://arxiv.org/abs/2206.04257.

- McDonald (1984) James B. McDonald. Some generalized functions for the size distribution of income. Econometrica, 52(3):647–663, May 1984. doi:10.2307/1913469.

- Piketty (2001) Thomas Piketty. Les Hauts Revenues en France au XX Siècle: Inégalités et Redistributions, 1901–1998. Bernard Grasset, Paris, 2001.

- Piketty (2003) Thomas Piketty. Income inequality in France, 1901–1998. Journal of Political Economy, 111(5):1004–1042, October 2003. doi:10.1086/376955.

- Piketty and Saez (2001) Thomas Piketty and Emmanuel Saez. Income inequality in the United States, 1913–1998. NBER Working Paper 8467, 2001. URL https://www.nber.org/papers/w8467.

- Piketty and Saez (2003) Thomas Piketty and Emmanuel Saez. Income inequality in the United States, 1913–1998. Quarterly Journal of Economics, 118(1):1–41, February 2003. doi:10.1162/00335530360535135.

- Reyes et al. (2016) Miguel Reyes, Mario Francisco-Fernández, and Ricardo Cao. Nonparametric kernel density estimation for general grouped data. Journal of Nonparametric Statistics, 28(2):235–249, March 2016. doi:10.1080/10485252.2016.1163348.

- Scott and Sheather (1985) David W. Scott and Simon J. Sheather. Kernel density estimation with binned data. Communication in Statistics - Theory and Methods, 14(6):1353–1359, January 1985. doi:10.1080/03610928508828980.

- Stutzer (1995) Michael Stutzer. A Bayesian approach to diagnosis of asset pricing models. Journal of Econometrics, 68(2):367–397, August 1995. doi:10.1016/0304-4076(94)01656-K.

- Stutzer (1996) Michael Stutzer. A simple nonparametric approach to derivative security valuation. Journal of Finance, 51(5):1633–1652, December 1996. doi:10.1111/j.1540-6261.1996.tb05220.x.

- Sun (2014) Xu Sun. Asymmetric kernel density estimation based on grouped data with applications to loss model. Communications in Statistics - Simulation and Computation, 43(3):657–672, March 2014. doi:10.1080/03610918.2012.712184.

- Tanaka and Toda (2013) Ken’ichiro Tanaka and Alexis Akira Toda. Discrete approximations of continuous distributions by maximum entropy. Economics Letters, 118(3):445–450, March 2013. doi:10.1016/j.econlet.2012.12.020.

- Tanaka and Toda (2015) Ken’ichiro Tanaka and Alexis Akira Toda. Discretizing distributions with exact moments: Error estimate and convergence analysis. SIAM Journal on Numerical Analysis, 53(5):2158–2177, 2015. doi:10.1137/140971269.

- Toda (2010) Alexis Akira Toda. Existence of a statistical equilibrium for an economy with endogenous offer sets. Economic Theory, 45(3):379–415, December 2010. doi:10.1007/s00199-009-0493-6.

- Toda (2012) Alexis Akira Toda. The double power law in income distribution: Explanations and evidence. Journal of Economic Behavior and Organization, 84(1):364–381, September 2012. doi:10.1016/j.jebo.2012.04.012.

- Toda (2015) Alexis Akira Toda. Bayesian general equilibrium. Economic Theory, 58(2):375–411, February 2015. doi:10.1007/s00199-014-0849-4.

- Villaseñor and Arnold (1989) José A. Villaseñor and Barry C. Arnold. Elliptical Lorenz curves. Journal of Econometrics, 40(2):327–338, February 1989. doi:10.1016/0304-4076(89)90089-4.

- Wu (2003) Ximing Wu. Calculation of maximum entropy densities with application to income distribution. Journal of Econometrics, 115(2):347–354, August 2003. doi:10.1016/S0304-4076(03)00114-3.